Proceedings of the 20th Land Audit Committee Meeting held ...

Upload

khangminh22Category

view

0download

0

N o t i c e o f M e e t i n g

Audit and Transparency Committee

6.30pm on Thursday 14 April 2016

Committee Room 2, Kensington Town Hall, Hornton Street, London W8 7NX

Contact: Gavin Wilson

Tel: 020 7361 2264

E-mail: [email protected]

Website: www.rbkc.gov.uk

Issue Date: 6 April 2016

Town Clerk – Nicholas Holgate

Committee Membership:

Councillors Paul Warrick (Chairman), Robert Atkinson, William Pascall (Vice-Chairman) and Charles Williams.

Co-opted members:

Mr Andrew Ling BSc (Econ), FCA, Mr Ian Luder CBE, BSc (Econ), FCA., FTII.,

Dip PFS., FRSA and Ms Lorraine Mohammed MBA, ASI-IAQ.

Public Agenda

A1. Apologies for Absence

A2. Declarations of Interest

Any Member of the Committee, or any other Member present in the meeting room, who

has a disclosable pecuniary interest in a matter to be considered at the meeting is

reminded to disclose the interest to the meeting and to leave the room while any

discussion or vote on the matter takes place.

Members are also reminded that if they have any other significant interest in a matter to

be considered at the meeting, which they feel should be declared in the public interest,

such interests should be declared to the meeting. In such circumstances Members should

consider whether their continued participation, in the matter relating to the interest, would

be reasonable in the circumstances, particularly if the interest may give rise to a

perception of a conflict of interests, or whether they should leave the room while any

discussion or vote on the matter takes place.

A3. Minutes of the Meeting held on 1 February 2016 (attached)

A4. KPMG External Audit Plan 2015/16 (attached)

A5. Risk management in Adult Social Care and Public Health (attached)

A6. Risk Management (attached)

A7. End of year Anti-Fraud Report (attached)

A8. Progress on Internal Audit Work – 2015/16 (attached)

A9. Draft Audit Plan for 2016-17 (attached)

A10. Treasury Management Activity Report 1 October – 31 December 2015 (attached)

A11. KPMG Annual Report on Grants and Returns Work 2014/15 (attached)

[Each written report on the public part of the Agenda as detailed above:

(i) was made available for public inspection from the date of the Agenda;

(ii) incorporates a list of the background papers which (i) disclose any facts or matters on which

that report, or any important part of it, is based; and (ii) have been relied upon to a material

extent in preparing it. (Relevant documents which contain confidential or exempt

information are not listed.); and

(iii) may, with the consent of the Chairman and subject to specified reasons, be supported at

the meeting by way of oral statement or further written report in the event of special

circumstances arising after the despatch of the Agenda.]

Exclusion of the Press and Public

To exclude the press and public from the remainder of the proceedings by virtue of the exempt

nature of the following business to be transacted relating to any individual and the financial or

business affairs of any particular person (including the authority holding that information).

B1. Part B Minutes of the Meeting held on 1 February 2016 (attached)

There are no other matters scheduled to be discussed at this meeting that would appear to

disclose confidential or exempt information under the provisions Schedule 12A of the Local

Government (Access to Information) Act 1985.

Should any such matters arise during the course of discussion of the above items or should the

Chairman agree to discuss any other such matters on the grounds of urgency, the Committee will

wish to resolve to exclude the press and public by virtue of the private nature of the business to

be transacted.

The next ordinary meeting of this Committee will be held

on 28 June 2016

Minutes of a meeting of the Audit and Transparency Committee held in the Petrie

Room, Freeman Suite, Committee Room 2,

Kensington Town Hall, London W8 7NX at

6.30pm on 1 February 2016

1

PRESENT

Members of the Committee

Councillor Robert Atkinson Councillor Paul Warrick (Chairman)

Councillor William Pascall (Vice-Chairman) Councillor Charles Williams

Co-opted Members

Mr. Andrew Ling Mr. Ian Luder

Others in Attendance

Mr. John Barnett (Senior Audit Manager)

Mr. Kevin Bartle (Interim Director of Finance) Mr. Nick Dawe (Interim Bi-Borough Director of Corporate Services, MSP)

Mr. Nicholas Holgate (Town Clerk) Ms. Moyra McGarvey (Shared Services Director for Audit, Fraud, Risk and

Insurance)

Mr. Mike Sloniowski (Bi-Borough Risk Management Officer) Mr. Gavin Wilson (Governance Administrator)

A G E N D A - P A R T A

A1 APOLOGIES FOR ABSENCE

An apology for absence was received from Ms Mohammed.

A2 MEMBERS' DECLARATIONS OF INTEREST

Cllr Pascall declared that he was a Chairman of Governors at Marlborough

Primary School.

A3 MINUTES OF THE MEETINGS HELD ON 21 SEPTEMBER 2015 AND 3

DECEMBER 2015

The minutes of the meetings of the Committee held on 21 September 2015 and

3 December 2015 were agreed and were signed as a correct record by the Chairman.

EXCLUSION OF PRESS AND PUBLIC FROM THE MEETING

RESOLVED: to exclude the press and public from the meeting for Items B1 and B2 on the grounds that it is likely to involve the disclosure of exempt information as defined

in Part I of Schedule 12A to the Act, as amended, relating to any individual and the financial or business affairs of any particular person (including the authority holding

that information):

2

B1 PART B MINUTES OF THE MEETING HELD ON 3 DECEMBER 2015

The Part B minutes of the meeting of the Committee held on 3 December 2015 were agreed and signed as a correct record by the Chairman.

B2. MANAGED SERVICES PROGRAMME (MSP) – BT ASSURANCE REPORT Detailed consideration was given to a report incorporating a BT Planning

Assurance Report which had been produced following discussions with senior BT representatives in December 2015 regarding outstanding targets.

The report was received and noted.

A4. KPMG ANNUAL AUDIT LETTER 2014/15 The report was received and noted.

A5. SPECIAL EDUCATION NEEDS

Mr Barnett drew attention to the fact that Internal Audit had agreed to postpone until August their intended review, being after the completion of the Ernst Young

review of current arrangements supporting SEN assessments and the changes to the structures and procedures being implemented to meet new demands.

The Committee agreed that, once the Ernst Young report had been considered

within Children’s Services, the Committee should be provided with comments from the Department on the findings of the report and the value which it had

provided. Action: Mr Barnett; Mr Christie to note

A6. PROGRESS ON INTERNAL AUDIT WORK

Mr Barnett drew attention to the fact that recent recruitment to the Internal Audit team had corrected the underperformance in relation to the delivery of the

Audit Plan referred to in paragraph 2.1 of the report.

In response to an enquiry by Cllr Warrick regarding the threat of cyber security,

Mr Holgate said that there had been a number of serious attempts to breach the Council’s cyber security but to date, none had been successful. Ms McGarvey

added that officers were well aware that cyber attackers were continually inventing new ways of gaining illegitimate access to systems, and there was the

need for continuing vigilance in this area. Cllr Pascall referred to the increasing use of multi-agency working and mobile working as areas meriting future

consideration by Internal Audit. Ms McGarvey said that consideration was already being given by Internal Audit to the use of mobile devices.

Responding to Mr Luder’s point that it was to be regretted that not all social

workers within the Fostering and Adoption Service had been found to have up-to-date Disclosure and Barring Service (DBS) clearance, Mr Barnett said that

there had been only three instances; he explained the reason in each case, commenting that actions taken had satisfactorily addressed the issue.

The report was received and noted.

3

A7. RISK MANAGEMENT

Mr Sloniowski referred to the implications of the recent ‘Lincolnshire incident’ (a zero-day security breach of I.T. systems at Lincolnshire County Council) and said that Mr

Garcez, Tri-Borough Chief Information Officer, would be reviewing the

implications for the Royal Borough.

It was agreed that future risk registers should be printed in colour in order to facilitate ease of consideration.

Action: Mr Wilson

Cllr Pascall suggested that, additionally, a method of presentation might be

employed which rendered the relevant information intelligible in a black and white format.

Mr Sloniowski to note

Cllr Williams observed that there seemed to be a degree of variability in the approaches adopted by departments in recording risks. In particular, it appeared

that not all the major operational risks in the case of the Planning and Borough Development Department were identified in Appendix 2. Mr Sloniowski said that

he would advise the PBD senior management team of the need to present

inclusive information in future reports. Action: Mr Sloniowski In response to an enquiry by Cllr Pascall regarding liaison with departments to

ensure consistency of approach, Mr Sloniowski advised that online guidance was provided, and departments were reminded of the need to refer to this.

The report and appendices were received and noted.

A8 TREASURY MANAGEMENT ACTIVITY REPORT: 1 JULY – 30 SEPTEMBER 2015

The report was received and noted.

The meeting ended at 8.04 p.m.

Chairman

External Audit Plan 2015/2016

Royal Borough of Kensington and Chelsea and Kensington and Chelsea Pension Fund

March 2016

1© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Headlines

Financial Statement Audit Value for Money Arrangements work£

There are no significant changes to the Code of Practice on Local Authority Accounting in 2015/16, which provides stability in terms of the accounting standards the Authority need to comply with.

MaterialityMateriality for planning purposes has set at £10 million for the Authority and £16.5 million for the Pension Fund.

We are obliged to report uncorrected omissions or misstatements other than those which are ‘clearly trivial’ to those charged with governance and this has been set at £500k for the Authority and £825k for the Pension Fund.

Significant risks Those risks requiring specific audit attention and procedures to address the likelihood of a material financial statement error have been identified as:■ Management override of controls■ Fraudulent Revenue Recognition■ Valuation of Property, Plant and Equipment ■ Managed Services implementation

Other areas of audit focusThose risks with less likelihood of giving rise to a material error but which are nevertheless worthy of audit understanding have been identified as:■ Cash■ Payroll and Non-Payroll Expenditure■ Accounting for Pension Costs and Liabilities■ Business rates and Council tax income■ HRA rental income and repairs & maintenance expenditure■ Housing benefits expenditure ■ Pension Fund Investments (PF)

Logistics

£

The National Audit Office has issued new guidance for the VFM audit which applies from the 2015/16 audit year. The approach is broadly similar in concept to the previous VFM audit regime, but there are some notable changes:

■ There is a new overall criterion on which the auditor’s VFM conclusion is based; and

■ This overall criterion is supported by three new sub-criteria.

Our risk assessment is ongoing and we will report VFM significant risks during our audit.

See pages 8 to 10 for more details.

Our team is:

■ Andy Sayers – Partner

■ Jodie Lusby – Manager

■ Antony Smith – Pension Fund Manager

■ Laura Hetherington – Assistant Manager

More details are on page 13.

Our work will be completed in four phases from January to September and our key deliverables are this Audit Plan and a Report to those charged with Governance as outlined on page 12.

Our fee for the audit is £121,425 (£159,300 2014/2015) for the Authority and £21,000 (£21,000 2014/15) for the Pension Fund see page 11.

2© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Financial Statements Audit

Our financial statements audit work follows a four stage audit process which is identified below. Appendix 1 provides more detail on the activities that this includes. This report concentrates on the Financial Statements Audit Planning stage of the Financial Statements Audit.

Value for Money Arrangements Work

Our Value for Money (VFM) Arrangements Work follows a five stage process which is identified below. Page 8 provides more detail on the activities that this includes. This report concentrates on explaining the VFM approach for the 2015/16.

Introduction

Background and Statutory responsibilities

This document supplements our Audit Fee Letter 2015/16 presented to you in April 2015, which also sets out details of our appointment by Public Sector Audit Appointments Ltd (PSAA).

Our statutory responsibilities and powers are set out in the Local Audit and Accountability Act 2014 and the National Audit Office’s Code of Audit Practice.

Our audit has two key objectives, requiring us to audit/review and report on your:

■ Financial statements (including the Annual Governance Statement): Providing an opinion on your accounts; and

■ Use of resources: Concluding on the arrangements in place for securing economy, efficiency and effectiveness in your use of resources (the value for money conclusion).

The audit planning process and risk assessment is an on-going process and the assessment and fees in this plan will be kept under review and updated if necessary.

Acknowledgements

We would like to take this opportunity to thank officers and Members for their continuing help and co-operation throughout our audit work.

Substantive Procedures CompletionControl

Evaluation

Financial Statements Audit

Planning

Risk Assessment

VFM audit work

Identification of significant

VFM risksConclude Reporting

3© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Financial statements audit planning

Financial Statements Audit Planning

Our planning work takes place during January to March 2016. This involves the following key aspects:

■ Risk assessment;

■ Determining our materiality level; and

■ Issuing this audit plan to communicate our audit strategy.

Risk assessment

Professional standards require us to consider two standard risks for all organisations. We are not elaborating on these standard risks in this plan but consider them as a matter of course in our audit and will include any findings arising from our work in our ISA 260 Report.

■ Management override of controls – Management is typically in a powerful position to perpetrate fraud owing to its ability to manipulate accounting records and prepare fraudulent financial statements by overriding controls that otherwise appear to be operating effectively. Our audit methodology incorporates the risk of management override as a default significant risk. In line with our methodology, we carry out appropriate controls testing and substantive procedures, including over journal entries, accounting estimates and significant transactions that are outside the normal course of business, or are otherwise unusual.

■ Fraudulent revenue recognition – We do not consider this to be a significant risk for local authorities as there are limited incentives and opportunities to manipulate the way income is recognised. We therefore rebut this risk and do not incorporate specific work into our audit plan in this area over and above our standard fraud procedures.

The diagram opposite identifies, significant risks and other areas of audit focus, which we expand on overleaf. The diagram also identifies a range of other areas considered by our audit approach.

£

Management override of

controls

Revenue recognition

Remuneration disclosures

Accounting for leases

Managed Services implementation

Key financial systems

Valuation of PPE

Pension Fund investments

Bad debt provision

Financial Instruments disclosures

Pension liability

assumptions

Provisions

Pension assets & liabilities

Compliance to the Code’s disclosure

requirements

Keys: Significant risk Other area of audit focus Example other areas considered by our approach

Cash

Payroll and Non-Payroll Expenditure

HRA Income and Expenditure

Housing Benefits

Expenditure

Business rates and Council tax income

4© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Significant Audit Risks

Those risks requiring specific audit attention and procedures to address the likelihood of a material financial statement error.

Financial statements audit planning (cont.)£

Managed Services

■ Risk: The Tri-borough councils implemented a new financial system on 1 April 2015 through a managed service partnership with BT. There have been a number of difficulties with the implementation which gives rise to a significant risk over the completeness of the balances in the financial statements. The difficulties we are aware of during 2015/16 include:

• reconciliations not being carried out in a timely manner and a large number of unreconciled items in the income and cash balances;

• expenditure payments not being made correctly;

• some income received by the Council is unallocated and being held in a suspense account; and

• not all employees were routinely paid each month.

The Council is managing the service problems and is in regular contact with BT, including finance officers visiting the BT office regularly. In addition the Council has brought in additional resources to support the year end processes. Improvements were made to the transactional processing during the course of the year but there remains a risk to the audit opinion. Throughout the year we have been liaising with management to gain an understanding of the difficulties being encountered, the actions being taken to mitigate the impact and the progress in resolving the issues.

Approach: We will:

• review the testing carried out by the finance team to gain assurance over the accuracy of transactions being made by BT;

• review the Internal Audit work completed; and

• carry out substantive testing over material balances in the financial statements. As a result of the implementation of managed services we have reduced our performance materiality to 50% which will result in increased sample sizes.

Valuation of Property, Plant, and Equipment (PPE)

■ Risk: As at 31 March 2015 the value of the Council’s PPE was £1,338 million. Local authorities exercise judgement in determining the fair value of different classes of assets held and the methods used to ensure the carrying values recorded each year reflect those fair values. The Council is responsible for ensuring that the valuation of PPE is appropriate at each financial year end and for conducting impairment reviews that confirm the condition of these assets. We have assessed that the inherent uncertainty in valuation and high value of assets held by the Council creates a significant risk to the financial statements for 2015/16.

■ Approach: We will:

• review management’s assessment of property valuations and impairment calculations;

• confirm the information provided to the valuer from the Authority;

• compare the assumptions made by your valuer to benchmarks and to the assumptions used for 2014/15 for consistency;

• complete testing over new capital additions in year to confirm appropriately capitalised and that Council ownership is evidenced; and

• review disposals made in year and confirm appropriate removal from the PPE balance in 2015/16.

5© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Other areas of audit focus (continued)

Those risks with less likelihood of giving rise to a material error but which are nevertheless worthy of audit understanding.

Financial statements audit planning (cont.)

Housing Benefits Expenditure

■ Issue: Housing benefits in area of audit focus due to the size of the figures (£147m in 2014/15) and the degree of complexity inherent in the calculation of benefit payable.

■ Approach: We will gain an understanding over controls related to housing benefits expenditure; test the operating effectiveness of relevant controls; complete substantive analytical review of rent rebates and rent allowances; and reconcile expenditure to the subsidy claim form.

Business rates income

■ Issue: NDR is material (£286m in 2014/15), has complexity in the translation from Collection Fund into Council prime statements and a degree of judgment underlying the NDR appeals provision.

■ Approach: We will gain an understanding over controls related to business rates income; test the operating effectiveness of relevant controls; complete substantive analytical review of income; and agree precepts to underlying documentation. We will also consider the basis of the appeals provision.

£

Council tax income

■ Issue: Council tax is a material income stream for the Authority (£103m in 2014/15) and there is complexity surrounding the translation from Collection Fund into Council primary statements.

■ Approach: We will gain an understanding over controls related to Council tax income; test the operating effectiveness of relevant controls; complete substantive analytical review of income; and agree precepts to underlying documentation.

Pension Fund Investments (PF only)

■ Issue: The value of pension fund investment assets totalling £818m at 31 March 2015 is a material item in your financial statements, which can involve an element of judgment and uncertainty.

■ Approach: We will review the valuation of the Pension Fund investments, including the unlisted investments, and consider the independent assurance that is available in respect of the valuation processes and valuations of funds. We shall also review the disclosure notes in the light of relevant requirements

HRA Repairs and Maintenance and Management Expenditure

■ Issue: HRA expenditure over repairs & maintenance and supervision & management is an area of audit focus due to the material size (£13m and £14m in 2014/15, respectively).

■ Approach: We will gain an understanding over controls related to HRA expenditures; test the operating effectiveness of relevant controls; and complete substantive analytical review of expenditures. We will also link to our work over payroll and non-payroll expenditure.

HRA Rental Income

■ Issue: HRA dwelling rental income is an area of audit focus due to the material size (£42m in 2014/15).

■ Approach: We will gain an understanding over controls related to HRA rental income; test the operating effectiveness of relevant controls; and complete substantive analytical review of dwelling rent income and reconcile HRA amounts to the Authority’s CIES.

6© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Financial statements audit planning (cont.)£

Other areas of audit focus (continued)

Those risks with less likelihood of giving rise to a material error but which are nevertheless worthy of audit understanding.

Accounting for pension assets and liabilities

■ Issue: Pension valuations require a significant level of expertise, judgement and estimation and are therefore more susceptible to error. This is also a very complex accounting area increasing the risk of misstatement.

■ Approach: We will confirm the information provided to the actuary from the Authority; review the actuarial valuation and consider the disclosure implications; and consider the assumptions made by your actuaries to benchmarks, which are collated by our KPMG actuaries, and to the assumptions used for 2014/15 for consistency.

Payroll

■ Issue: Payroll represents a significant proportion of the Authority’s annual expenditure. Whilst not considered overly complex from a material error perspective, we consider that it is important from an audit perspective to understand the nature of the Authority’s expenditure in this area. This is also an area impacted by Managed Services.

■ Approach: We will review and test reconciliations for gross pay and deductions (e.g. pensions, tax and national insurance); and complete substantive analytical review of payroll costs and test supporting system information used to compile the review.

Cash

■ Issue: Cash has a pervasive impact on the financial statements and provides comfort for other areas of the financial statements. This is also an area impacted by Managed Services.

■ Approach: We will review controls over bank reconciliations; and confirm balances with external third parties.

Non-Payroll Expenditure

■ Issue: Non-payroll expenditure, specifically the accounts payable component, is an area of audit focus due to its pervasive impact on the financial statements and size. This is also an area impacted by Managed Services.

■ Approach: We will perform substantive tests of details to agree expenditures to third party documentation and cut-off testing of non-payroll expenditure to ensure costs are recorded in the correct period.

7© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Financial statements audit planning (cont.)

Materiality

We are required to plan our audit to determine with reasonable confidence whether or not the financial statements are free from material misstatement. An omission or misstatement is regarded as material if it would reasonably influence the user of financial statements. This therefore involves an assessment of the qualitative and quantitative nature of omissions and misstatements.

Generally, we would not consider differences in opinion in respect of areas of judgementto represent ‘misstatements’ unless the application of that judgement results in a financial amount falling outside of a range which we consider to be acceptable.

For the Authority, materiality for planning purposes has been set at £10 million for the Authority’s accounts. In 2015/16 we have capped our materiality in line with the level of general fund reserves.

For the Pension Fund, materiality for planning purposes has been set at £16.5 million.

We design our procedures to detect errors in specific accounts at a lower level of precision.

£

Reporting to the Audit and Transparency Committee

Whilst our audit procedures are designed to identify misstatements which are material to our opinion on the financial statements as a whole, we nevertheless report to the Audit Committee any unadjusted misstatements of lesser amounts to the extent that these are identified by our audit work.

Under ISA 260(UK&I) ‘Communication with those charged with governance’, we are obliged to report uncorrected omissions or misstatements other than those which are ‘clearly trivial’ to those charged with governance. ISA 260 (UK&I) defines ‘clearly trivial’ as matters that are clearly inconsequential, whether taken individually or in aggregate and whether judged by any quantitative or qualitative criteria.

In the context of the Authority, we propose that an individual difference could normally be considered to be clearly trivial if it is less than £0.5 million.

In the context of the Pension Fund, we propose that an individual difference could normally be considered to be clearly trivial if it is less than £825k.

If management have corrected material misstatements identified during the course of the audit, we will consider whether those corrections should be communicated to the Audit Committee to assist it in fulfilling its governance responsibilities.

2014/15

£667m

0

200

400

600

800Materiality based on prior year gross expenditure

Individual errors, where identified, reported to Audit Committee

Procedures designed to detect individual errors

£0.5m

£5m

£,000’s

8© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Value for money arrangements work

VFM audit risk assessment

Financial statements and other audit work

Identification of significant VFM risks (if

any) Conclude on arrangements to

secure VFM

No further work required

Assessment of work by other review agencies

Specific local risk based work

VFM

conclusion

Continually re-assess potential VFM risks

£

Informed decision making

Working with

partners and third parties

Sustainable resource

deployment

Overall criterion

In all significant respects, the audited body had proper arrangements to ensure it took properly informed decisions and deployed resources to achieve planned and

sustainable outcomes for taxpayers and local people.

Background to approach to VFM work

The Local Audit and Accountability Act 2014 requires auditors of local government bodies to be satisfied that the authority ‘has made proper arrangements for securing economy, efficiency and effectiveness in its use of resources’.

This is supported by the Code of Audit Practice, published by the NAO in April 2015, which requires auditors to ‘take into account their knowledge of the relevant local sector as a whole, and the audited body specifically, to identify any risks that, in the auditor’s judgement, have the potential to cause the auditor to reach an inappropriate conclusion on the audited body’s arrangements.’

The VFM approach is fundamentally unchanged from that adopted in 2014/2015 and the process is shown in the diagram below. However, the previous two specified reporting criteria (financial resilience and economy, efficiency and effectiveness) have been replaced with a single criteria supported by three sub-criteria. These sub-criteria provide a focus to our VFM work at the Authority. The diagram to the right shows the details ofthis criteria.

9© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Value for money arrangements work (cont.)£

VFM audit stage Audit approach

VFM audit risk assessment We consider the relevance and significance of the potential business risks faced by all local authorities, and other risks that apply specifically to the Authority. These are the significant operational and financial risks in achieving statutory functions and objectives, which are relevant to auditors’ responsibilities under the Code of Audit Practice.

In doing so we consider:

■ The Authority’s own assessment of the risks it faces, and its arrangements to manage and address its risks;

■ Information from the Public Sector Auditor Appointments Limited VFM profile tool;

■ Evidence gained from previous audit work, including the response to that work; and

■ The work of other inspectorates and review agencies.

Linkages with financial statements and otheraudit work

There is a degree of overlap between the work we do as part of the VFM audit and our financial statements audit. For example, our financial statements audit includes an assessment and testing of the Authority’s organisational control environment, including the Authority’s financial management and governance arrangements, many aspects of which are relevant to our VFM audit responsibilities.

We have always sought to avoid duplication of audit effort by integrating our financial statements and VFM work, and this will continue. We will therefore draw upon relevant aspects of our financial statements audit work to inform the VFM audit.

Identification ofsignificant risks

The Code identifies a matter as significant ‘if, in the auditor’s professional view, it is reasonable to conclude that the matter would be of interest to the audited body or the wider public. Significance has both qualitative and quantitative aspects.’

If we identify significant VFM risks, then we will highlight the risk to the Authority and consider the most appropriate audit response in each case, including:

■ Considering the results of work by the Authority, inspectorates and other review agencies; and

■ Carrying out local risk-based work to form a view on the adequacy of the Authority’s arrangements for securing economy, efficiency and effectiveness in its use of resources.

10© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Value for money arrangements work (cont.)£

VFM audit stage Audit approach

Assessment of work by other review agencies

and

Delivery of local risk based work

Depending on the nature of the significant VFM risk identified, we may be able to draw on the work of other inspectorates, review agencies and other relevant bodies to provide us with the necessary evidence to reach our conclusion on the risk.

If such evidence is not available, we will instead need to consider what additional work we will be required to undertake to satisfy ourselves that we have reasonable evidence to support the conclusion that we will draw. Such work may include:

■ Meeting with senior managers across the Authority;

■ Review of minutes and internal reports;

■ Examination of financial models for reasonableness, using our own experience and benchmarking data from within and without the sector.

Concluding on VFM arrangements

At the conclusion of the VFM audit we will consider the results of the work undertaken and assess the assurance obtained against each of the VFM themes regarding the adequacy of the Authority’s arrangements for securing economy, efficiency and effectiveness in the use of resources.

If any issues are identified that may be significant to this assessment, and in particular if there are issues that indicate we may need to consider qualifying our VFM conclusion, we will discuss these with management as soon as possible. Such issues will also be considered more widely as part of KPMG’s quality control processes, to help ensure the consistency of auditors’ decisions.

Reporting We will update our assessment throughout the year should any issues present themselves and report against these in our ISA260.

We will report on the results of the VFM audit through our ISA 260 Report. This will summarise any specific matters arising, and the basis for our overall conclusion.

The key output from the work will be the VFM conclusion (i.e. our opinion on the Authority’s arrangements for securing VFM), which forms part of our audit report.

11© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Other matters

Whole of government accounts (WGA)

We are required to review your WGA consolidation and undertake the work specified under the approach that is agreed with HM Treasury and the National Audit Office. Deadlines for production of the pack and the specified approach for 2015/16 have not yet been confirmed.

Elector challenge

The Local Audit and Accountability Act 2014 gives electors certain rights. These are:

■ The right to inspect the accounts;

■ The right to ask the auditor questions about the accounts; and

■ The right to object to the accounts.

As a result of these rights, in particular the right to object to the accounts, we may need to undertake additional work to form our decision on the elector's objection. The additional work could range from a small piece of work where we interview an officer and review evidence to form our decision, to a more detailed piece of work, where we have to interview a range of officers, review significant amounts of evidence and seek legal representations on the issues raised.

The costs incurred in responding to specific questions or objections raised by electors is not part of the fee. This work will be charged in accordance with the PSAA's fee scales.

Our audit team

Our audit team will be led by Andrew Sayers. We have this year added Jodie Lusby as your Manager, Jodie is well known to the finance team as she was your Assistant Manager last year and your Assistant Manager will be Laura Hetherington. Appendix 2 provides more details on specific roles and contact details of the team.

Reporting and communication

Reporting is a key part of the audit process, not only in communicating the audit findings for the year, but also in ensuring the audit team are accountable to you in addressing the issues identified as part of the audit strategy. Throughout the year we will communicate with you through meetings with the finance team and the Audit and Transparency Committee. Our communication outputs are included in Appendix 1.

Independence and Objectivity

Auditors are also required to be independent and objective. Appendix 3 provides more details of our confirmation of independence and objectivity.

Audit fee

Our Audit Fee Letter 2015/2016 presented to you in April 2015 first set out our fees for the 2015/2016 audit. This letter also sets out our assumptions. We have not considered it necessary to make any changes to the agreed fees at this stage.

The planned audit fee for 2015/16 is £121,425. This is a 25% reduction in audit fee, compared to the 2014/2015 of £159,300. The planned audit fee for 2015/16 is £21,000 for the Pension Fund. (2014/15 £21,000).

12© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Appendix 1: Key elements of our financial statements audit approach

Driving more value from the audit through data and analyticsTechnology is embedded throughout our audit approach to deliver a high quality audit opinion. Use of Data and Analytics (D&A) to analyse large populations of transactions in order to identify key areas for our audit focus is just one element. We strive to deliver new quality insight into your operations that enhances our and your preparedness and improves your collective ‘business intelligence.’ Data and Analytics allows us to:■ Obtain greater understanding of your processes, to

automatically extract control configurations and to obtain higher levels assurance.

■ Focus manual procedures on key areas of risk and on transactional exceptions.

■ Identify data patterns and the root cause of issues to increase forward-looking insight.

We anticipate using data and analytics in our work around key areas such as journals.

CompletionPlanning Control evaluation Substantive testing

Com

mun

icat

ion

Aud

it w

orkf

low

Continuous communication involving regular meetings between Audit Committee, Senior Management and audit team

Initial planning meetings and risk

assessment

Audit strategy and plan

Annual Audit Letter

ISA 260 (UK&I) Report

Interim audit

Year end audit of financial

statements and annual report

Sign audit

opinion

■ Perform risk assessment procedures and identify risks

■ Determine audit strategy

■ Determine planned audit approach

■ Understand accounting and reporting activities

■ Evaluate design and implementation of selected controls

■ Test operating effectiveness of selected controls

■ Assess control risk and risk of the accounts being misstated

■ Plan substantive procedures

■ Perform substantive procedures

■ Consider if audit evidence is sufficient and appropriate

■ Perform completion procedures

■ Perform overall evaluation

■ Form an audit opinion

■ Audit and Transparency Committee

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

D&AENABLED

AUDIT METHODOLOGY

13© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Appendix 2: Audit team

Your audit team has been drawn from our specialist public sector assurance department. Our audit team is detailed below. We have introduced a new Manager, Jodie Lusby. Jodie is well known to the finance team as she was the Assistant Manager last year.

Name Andrew Sayers

Position Partner/Director

‘My role is to lead our team and ensure the delivery of a high quality, valued added external audit opinion.

I will be the main point of contact for the Audit and Transparency Committee and the Town Clerk.’

Name Jodie Lusby

Position Manager

‘I provide quality assurance for the audit work and specifically any technical accounting and risk areas. I will work closely with Andrew to ensure we add value.

I will liaise with the Interim Finance Director and other Directors.’

Name Laura Hetherington

Position Assistant Manager

‘I will be responsible for the on-site delivery of our work and will supervise the work of our audit assistants.’

Name Antony Smith

Position Manager

‘My role is to lead our Pension Fund team and ensure the delivery of a high quality, pension fund audit’.

Andy SayersPartner

+ 44 [0]207 694 [email protected]

Antony SmithManager

+ 44 [0]207 311 [email protected]

Laura HetheringtonAssistant Manager

+ 44 [0]207 896 [email protected]

Jodie LusbyManager

+ 44 [0]207 311 [email protected]

14© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Appendix 3: Independence and objectivity requirements

Independence and objectivity

Professional standards require auditors to communicate to those charged with governance, at least annually, all relationships that may bear on the firm’s independence and the objectivity of the audit engagement partner and audit staff. The standards also place requirements on auditors in relation to integrity, objectivity and independence.

The standards define ‘those charged with governance’ as ‘those persons entrusted with the supervision, control and direction of an entity’. In your case this is the Audit and Transparency Committee.

KPMG LLP is committed to being and being seen to be independent. APB Ethical Standard 1 Integrity, Objectivity and Independence requires us to communicate to you in writing all significant facts and matters, including those related to the provision of non-audit services and the safeguards put in place, in our professional judgement, may reasonably be thought to bear on KPMG LLP’s independence and the objectivity of the Engagement Lead and the audit team.

Further to this auditors are required by the National Audit Office’s Code of Audit Practice to:

■ Carry out their work with integrity, independence and objectivity;

■ Be transparent and report publicly as required;

■ Be professional and proportional in conducting work;

■ Be mindful of the activities of inspectorates to prevent duplication;

■ Take a constructive and positive approach to their work;

■ Comply with data statutory and other relevant requirements relating to the security, transfer, holding, disclosure and disposal of information.

PSAA’s Terms of Appointment includes several references to arrangements designed to support and reinforce the requirements relating to independence, which auditors must comply with. These are as follows:

■ Auditors and senior members of their staff who are directly involved in the management, supervision or delivery of PSAA audit work should not take part in political activity.

■ No member or employee of the firm should accept or hold an appointment as a member of an audited body whose auditor is, or is proposed to be, from the same firm. In addition, no member or employee of the firm should accept or hold such appointments at related bodies, such as those linked to the audited body through a strategic partnership.

■ Audit staff are expected not to accept appointments as Governors at certain types of schools within the local authority.

■ Auditors and their staff should not be employed in any capacity (whether paid or unpaid) by an audited body or other organisation providing services to an audited body whilst being employed by the firm.

■ Auditors appointed by the PSAA should not accept engagements which involve commenting on the performance of other PSAA auditors on PSAA work without first consulting PSAA.

■ Auditors are expected to comply with the Terms of Appointment policy for the Engagement Lead to be changed on a periodic basis.

■ Audit suppliers are required to obtain the PSAA’s written approval prior to changing any Engagement Lead in respect of each audited body.

■ Certain other staff changes or appointments require positive action to be taken by Firms as set out in the Terms of Appointment.

Confirmation statement

We confirm that as of 15 March 2016 in our professional judgement, KPMG LLP is independent within the meaning of regulatory and professional requirements and the objectivity of the Engagement Lead and audit team is not impaired.

© 2016 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

Produced by Create Graphics/Document number: CRT053550A

This report is addressed to the Authority and has been prepared for the sole use of the Authority. We take no responsibility to any member of staff acting in their individual capacities, or to third parties. We draw your attention to the Statement of Responsibilities of auditors and audited bodies, which is available on Public Sector Audit Appointment’s website (www.psaa.co.uk).

External auditors do not act as a substitute for the audited body’s own responsibility for putting in place proper arrangements to ensure that public business is conducted in accordance with the law and proper standards, and that public money is safeguarded and properly accounted for, and used economically, efficiently and effectively.

We are committed to providing you with a high quality service. If you have any concerns or are dissatisfied with any part of KPMG’s work, in the first instance you should contact […], the engagement lead to the Authority, who will try to resolve your complaint. If you are dissatisfied with your response please contact the national lead partner for all of KPMG’s work under our contract with Public Sector Audit Appointments Limited, Andrew Sayers, by email to [email protected] After this, if you are still dissatisfied with how your complaint has been handled you can access PSAA’s complaints procedure by emailing [email protected] by telephoning 020 7072 7445 or by writing to Public Sector Audit Appointments Limited, 3rd Floor, Local Government House, Smith Square, London, SW1P 3HZ.

1

A5

THE ROYAL BOROUGH OF KENSINGTON AND CHELSEA

AUDIT AND TRANSPARENCY COMMITTEE 14 APRIL 2016

REPORT BY THE EXECUTIVE DIRECTOR FOR ADULT SOCIAL CARE

AND HEALTH

RISK MANAGEMENT IN ADULT SOCIAL CARE AND HEALTH

This report is intended to update the Audit and Transparency Committee on Adult Social Care Department’s key strategic and operational risks.

FOR INFORMATION

1. INTRODUCTION

1.1 The Audit and Transparency Committee is responsible for reviewing

the arrangements in place for identifying and managing key risks across the Council.

1.2 In accordance with that committee’s forward plan, this risk

management report is a joint report covering both Adult Social Care

and the Public Health services within the Shared Services Adults Social Care and Health department. It is presented to the Committee

for their information and review.

2. RISK MANAGEMENT ARRANGEMENTS

2.1 Background

2.1.1 The Public Health service transferred into local government from the

NHS on 1 April 2013 and is a shared service across the three authorities (RBKC, LBHF and WCC). Initially a standalone service area,

hosted by WCC, it has formed part of the overall Adult Social Care and Public Health department in the portfolio of the Executive Director,

Adult Social Care, since mid-2014. The Director of Public Health reports to the Executive Director, Adult Social Care.

As a WCC-hosted service, the Public Health service initially adopted the WCC corporate Risk Management Strategy as the basis of its risk

management arrangements, and over the intervening period has adapted this as necessary to fit its particular situation as a shared

service across three boroughs.

2.1.2 Adult Social Care (ASC) services came together across Hammersmith

2

& Fulham, Kensington and Chelsea and Westminster in April 2012, as one of the first three-borough, shared services. At the time there

were three different corporate, borough based business planning and risk management policies and processes in place. An internal audit

of ASC risk management arrangements was carried in 2013. This identified the need for a more robust and consistent approach to risk

identification, ownership, management and mitigation across all service areas and embedding this within the business and

programme planning processes of the service. With the assistance of Corporate risk colleagues in February 2013 a new risk management

policy and process was implemented across ASC. This was followed

by an extensive programme of awareness raising and support to management boards and teams to embed the new approach.

2.1.3 In essence both the Public Health and Adult Social Care directorate’s

approach to risk management is a pragmatic one, based on and complying with the principles of the internationally-recognised Risk

Management standard AS/NZS 4360:2004. This Standard is principally concerned with ensuring that health and social care

organisations have the basic building blocks in place for managing risk through development and implementation of a robust risk

management system. Both services approach to risk management fully conforms to Shared Services corporate risk management

standards, including in respect of managing hazards, incidents, complaints and claims.

2.2 Outline of Adult Social Care & Health Risk Management processes

Within Adult Social Care and Health, there is a clearly-defined

structure and process in place for capturing and managing risks. This is structured as follows:

2.2.1 Senior Accountable Officers

The Executive Director of ASC and Director of Public Health, are the

relevant senior accountable officers, who have the responsibility for ensuring the risks identified by the ASC and Public Health

directorates respectively, are managed effectively. The accountable officers champion and have overall ownership of the risk

management process. They ensure that appropriate commitment and

compliance to the process occurs throughout the services.

2.2.2 Senior Management Teams (Senior Management Team (SMT) in Public Health, Adults Leadership Team (ALT) in Adult

Social Care)

A key responsibility of the senior management teams is to:

3

o monitor, manage and report on risks to the business

The senior management teams have primary responsibility for

ensuring that appropriate systems and processes are in place to

deliver effective risk management, across all the services for which they are responsible. The senior teams review the strategic risk

registers on at least a quarterly basis; this is more frequent with significant strategic risks which are subject to change.

In addition to their key role in reviewing and mitigating current risks,

the Adult Social Care Adult Leadership Team and Public Health

Senior Management Team also ensure that:

o there is full consideration of risk in the directorates’ annual business planning processes and that actions from identified risks

are fully factored into developing targets and objectives as part of business planning activities;

o there is regular horizon-scanning by all boards and teams for

emerging risks, both strategic and operational. All intelligence on such potential new risks are fed into the risk management and

business planning processes.

2.2.3 Directors, Deputy Directors and Heads of Service

Each Adult Social Care Director, Public Health Deputy Director and

Heads of Service are responsible for ensuring that risk management processes are adopted within their service area and that risks are

appropriately and timely managed, i.e. included directorate, programme, project or team Risk Registers and escalated/de-escalated

as appropriate.

2.2.4 Line managers and staff

All line managers and staff are expected to:

o Be aware of and comply with each directorate’s risk management

policy and processes.

o Participate fully in regular risk review processes.

o Assume responsibility for risks and mitigating controls within their

own areas of work.

2.2.5 Public Health Strategic Risk Register

The PH strategic risk register holds a record of all identified high-level and strategic risks likely to impact on the service area as a whole. This

4

Risk Register is maintained by the directorate’s nominated Risk Officer, with each risk being subject to review on at least a monthly basis.

For ease of reference, all risks in the PH directorate Risk Register are

categorised under one of the following four headings:

o Public Health Risks

o Contracts/Finance/Performance Risks

o Governance Risks

o Public Health Team Risks

The Public Health Strategic Risk Register is presented quarterly to the

Public Health Senior Management Team (SMT) for their review and recommendation on mitigating actions. SMT takes the view that

management of these risks will be most effective and efficient when undertaken in common, collective and portfolio terms, rather than on an

individual risk by risk basis or appetite by appetite basis varying across

different public health teams.

A number of the current strategically significant risks in the Public Health Strategic Risk Register are outlined in section 4 below and a summary is

attached as Appendix 1. The full Public Health Risk Register can be made available to members on request.

2.2.6 Adult Social Care Strategic Risk Register

The whole business of adult social care is associated with the

management of risk at an individual customer and carer case level and

at a strategic level, as relates to the meeting of the care needs of all adult residents with a limited budget and in partnership with health,

housing and care and support providers.

The Adult Social Care Strategic Risk Register holds a record of all identified high-level and strategic risks likely to impact on the service

area as a whole. This Risk Register is maintained by the directorate’s nominated Risk Officer, with each risk being subject to ongoing review.

On occasion risks can arise form an individual case which could have

strategic significance to the service and Council. All risks are assessed by using the corporate rating for impact and likelihood. Strategic risks

are those rated with significant potential impact. These are included in the strategic risk register and reported to Adult Social Care Leadership

Team on a quarterly basis as part of routine performance management

arrangements.

A number of the current strategically significant risks in the Adult Social

5

Care risk register are outlined in section 4 below and a summary is attached as Appendix 2. The full register can be made available to

members on request.

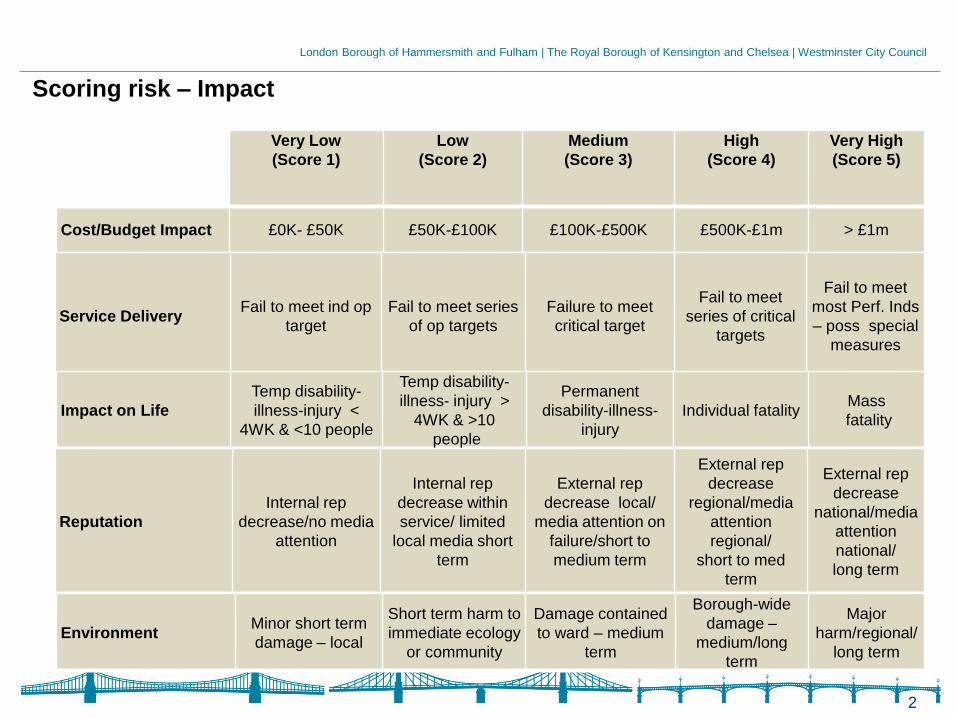

2.2.7 Assessing and Rating risks

All identified risks are assessed by using the corporate scales for rating both impact and likelihood. Impact is assessed across a number of

domains:

o Financial

o Reputational

o Service Delivery

o Impact on Life

o Environmental

Likelihood is evaluated by use of a scale ranging from Likely to Extremely

Unlikely. A risk score is then derived by multiplying the two resultant values together.

At any time, a risk which is assessed as having a high impact rating, (irrespective of likelihood) is considered a strategic risk. These are

included on the strategic risk register and reported to Public Health Senior Management Team and/or Adult Leadership Team at least on a

quarterly basis as a key part of performance management arrangements.

2.2.8 Public Health Team Risk Registers

In addition to the Public Health Strategic Risk Register, each of the Public

Health Teams manages and maintains its own team risk register. These are intended to identify and hold risks which are more operational in

nature, and specific to that team’s work. These team risk registers are reviewed at least monthly as a standing item by each team at their

scheduled monthly team meeting.

However, both strategic and team risk registers are considered holistically within the Public Health service area. If considered

appropriate, risks can be escalated from a team risk register to the corporate risk register or alternatively de-escalated from the corporate

risk register to a team risk register in line with monthly reviews of actions taken to address risks and mitigating measures put in place.

6

2.2.9 Adult Social Care - Board Risk Registers

To ensure effective risk management across the whole of ASC business there are a number of key governance boards which have responsibility

for maintaining risk registers. These cover risks related to, transformation, key projects, operations, commissioning, financial,

safeguarding and other strategic, operational and service related areas:

o Portfolio Delivery Steering Group – covers the whole of the ASC

transformation programme, including ‘whole systems’ with health, the Better Care Fund and delivery of the medium term financial strategy.

Also reviews implementation, delivery and monitoring of impact of new duties as a result of the Care Act.

o Contracts and Commissioning Board – covers all procurement and commissioning activities, including the development of new

commissioning strategies.

o Workforce Development Board – covers the internal workforce

issues including, learning and organizational development, staff

recruitment and retention.

o Operations Board – covers the operational activities of the social

work services for older people and adults with a physical or learning disability.

o Mental Health Management Board – covers the operational social work services and partnership arrangements with West London Mental

Health Trust.

o Safeguarding Adults Board – oversees safeguarding strategy and processes across agencies.

o Home Care Board – this is a project board, but has strategic significance as it oversees the implementation of the new home care

framework contracts and monitors demand for and take up of home care services.

o Customer Journey Board – this is a project board, but has strategic significance as it oversees the redesign of social work and community

independence services.

o IT Programme Board – oversees the implementation of the ASC IT strategy and related systems.

o Information Governance Board – shared with Children’s Services, oversees information governance and information sharing issues.

o Provided Services Board – covers the management and operation of in house provided services for all care groups.

o Performance Board – recently established to manage and improve

performance across the department.

7

2.2.10 Governance structures with Health

There are specific partnership arrangements in place which manage the shared risk with the NHS. These are the:

o Health and Well-being Board – a statutory requirement in all boroughs, the Health & Well-being Board brings together health with

adults, children’s and public health to facilitate the systematic integration of public services.

o Better Care Fund Board – oversees the development of the Better Care Fund across the three boroughs.

o Joint Executive Team – brings together the senior executive teams

for Adult Social Care and the three CCGs across the three boroughs.

2.2.11 Internal Audit support Although risk management and internal controls are management’s responsibility, Internal Audit has a significant role to play in supporting the maintenance of effective internal control through its annual programme of audit work and reports.

Internal Audit adopts a risk-based approach to planning its work, and is likely to reference the various PH and ASC risk registers when identifying areas for undertaking audit work.

The Public Health and Adult Social Care corporate risk review process also includes an annual self-assessment of the Risk Management Controls Assurance Standard. Substantive compliance (i.e. 75% or above) is required. This standard is one of three core standards identified by the National Audit Office and is also therefore subject to independent verification by Internal Audit each year.

3. MANAGING CURRENT STRATEGIC RISKS

3.1 A summarised version of the Risk Registers for both Public Health and Adult Social Care, are provided at Appendix 1 and 2. These

include a record of all current key strategic risks which impact on the business and activities of both service areas. These are

subject to quarterly management review by the senior management teams of both services with associated mitigating

actions escalated or de-escalated as necessary. Key strategic risks for the information of the committee are described in more

detail below:

3.2 Public Health strategic risks

3.2.1 Public Health grant reductions and removal of the ring-fence (Appx. 1 Risk ref 1)

In October 2015 the Department of Health (DH) announced that Public

8

Health budgets would be reduced nationally by 6.2% after a national consultation exercise. The Government had initially proposed substantial

cuts to each of the three councils’ agreed public heath budgets. The most generous of the consultation options would see the Public Health

directorate’s budgets cut by 6.2%.

The Autumn Statement for Public Health Finance saw the government announce that the Public Health ring-fence will be maintained for

2016/17 and 2017/18. No announcement has been received about whether the ring-fence will be removed after this date, however, we

anticipate that this may happen and is therefore a risk.

The statement also announced that Councils had to deliver annual

average real terms savings of 3.9% over the next 5 years. The exact amount is yet to be announced, as consultation regarding the allocation

formula that will be used to determine future grant allocations is ongoing.

To mitigate the risks outcomes being impaired through the reduction to the grant and the potential removal of the ring-fence after 2017-18,

Public Health:

Finance managers continue to model various savings scenarios to mitigate the potential impact of any further cuts to the Public

Health grant. Commissioners are reviewing service specifications, contracts

and new ways of working to establish whether contracts can be

commissioned differently, more collaboratively to release efficiencies.

A task and finish group has been set up to review current and future years’ potential grant allocation and budget commitments

in a reducing grant context, with a view to aligning spend to the Public Health vision for the Councils.

The directorate continues to explore how the councils can continue to meet their public health duties, deliver their agreed

outcomes and the councils’ medium-term plans.

3.2.2 Clinical governance (APPX 1, Risk ref 3)

Clinical governance is a system through which NHS organisations are accountable for continuously improving the quality of their services and

safeguarding high standards of care by creating an environment in which

excellence in clinical care will flourish. Adequate assurances are required of our providers and their clinical governance processes.

Without these, we are not fully assured that services fully meet clinical governance requirements.

To mitigate these risks, contracts have clinical governance clauses

placed within them; placing a duty on providers to comply.

9

A review of current monitoring mechanisms will be undertaken, to ensure that these are up to date and provide sufficient assurances.

Clinical governance policies are to be developed, Staff to be provided with clinical governance guidelines

3.2.3 Public Health Restructure. (Appx 1 Risk Ref 4)

The uncertainty about the direction of Public Health and the instability in

PH team affects delivery of key outputs. Instability in PH team affects delivery of key outputs. This has wider implications and could affect

wider council and unrelated services.

To mitigate this risk, the following is taking place:

Team away days have been planned to engage staff and take them

through the next steps for the division. Preliminary consultation with staff is underway;

Managers are attending Leadership workshops, which focus on leading differently

One to one discussions are being undertaken with staff, as part of

annual appraisal

3.3 Adult Social Care strategic risks

3.3.1 Reducing resources to support people with care needs and

increasing demand due to demographic pressures (Appx 2, Risk ref 1)

In the financial year there is a funding hole nationally in ASC of £3bn. Through the MTFS, LBHF has already made efficiencies and savings in

recent years as the resources available for social care have significantly reduced. As a result of demographic changes the Council is already

supporting greater numbers of people with care needs and increasing numbers with complex needs who would have previously been supported

through health services. Therefore, the likelihood of this risk occurring remains very high.

3.3.2 Responding to changing legislation (Appx 2 Risk ref 2)

The Care Act began to be implemented from April 2015. There was a comprehensive programme in place in LBHF to ensure that ASC was

compliant with the new requirements. Although implementation of some

parts of the Act (e.g. the ‘care cap’) has been delayed until 2020 by the Government; ASC are left with delivering new responsibilities such as for

self-funders, carers and the wider health and wellbeing, without additional resources. There continues to be a lack of clarity from

Government about available funding to support additional demands for services,

10

To mitigate these risks we are continuing to: Further change our service model to put a greater focus on short term,

re-abling, interventions to help people regain skills and look after themselves for longer, so delaying the need for social and health care;

this is being delivered through the Customer Journey programme. Pursue opportunities to develop more integrated and closer working

with health colleagues, through initiatives such as the Better Care Fund and ‘whole systems’ programme.

Develop a new Commissioning Strategy which is exploring different mechanisms to resource and commission services in the future using

‘care pathways’, and different procurement models.

Develop an approach to prevention which focuses on reducing demand for social care and utilise some Public Health and wider

Council resources to help achieve this. Manage resource planning through the Department of Health, ADASS

network and LGA in relation to the Care Act.

3.3.3 Reducing customer satisfaction (Appx 2, Risk ref 3) There is increasing risk that customer and carer satisfaction and

outcomes will reduce. The scale of change around frontline social work and provider services and the greater emphasis on individuals finding

their own care solutions, time limited interventions and reablement, may lead to reduced satisfaction of some customers especially those who

have been supported for some time.

To mitigate this risk we are:

Developing a communications strategy and plan which informs residents of changes in the approach to health and social care services

locally. Closely analysing all customer and carer feedback, including that

through complaints and the statutory user and carer surveys and using this to help inform our planning.

Redesigning frontline social work services in the Customer Journey project, based on the ‘customer voice’ research which identified what

was important to people who use our services. Exploring new opportunities for co-production and design of new

services with customers and carers to ensure their needs and ideas are central to our approach.

- Specific responsibility for managing performance has been assigned to the Director of Whole Systems and a departmental

Performance Board has been established to improve

performance.

3.3.4 Workforce risks (Appx2 Risk ref 4) The recent Adult Social Care Peer Review highlighted a recruitment and

retention risk across London for social care staff. There is a risk that this is exacerbated locally as terms and conditions are not as competitive as

some authorities elsewhere. Additionally, there is significant change

11

fatigue across the ASC shared service and added complexity of working across three boroughs, which together create a significant recruitment

and retention risk. The whole commissioning service is currently in the middle of a restructure with 39 of the 63 posts in the new service

requiring external recruitment.

To mitigate this risk we have/are: Established a Workforce Board which is overseeing an ASC Workforce

Plan Exploring alternative ways to reward staff, for example through

tailored development programmes.

Improved internal staff communications from the senior management team by the use of blogs, team meetings and through the TriAngles

staff newsletter. Used the results of the Your Voice survey to address service, team

and staff concerns. Key change programmes have dedicated learning and development

plans attached to them, i.e. Customer Journey, Commissioning Review and home care implementation.

The Commissioning Review includes detailed transition planning including, knowledge and skills transfer; prioritisation of business over

transitional period. Specific recruitment issues have arisen as part of the implementation

of the Commissioning Review and specific short and medium term measures have been put in place to manage them.

3.3.5 Market unable to provide services required (Appx 2 Risk Ref 5) The ASC market is fragile and there is a risk that it is not able to develop

in the ways we will require in the future to meet local need; there is significant risk of market failure.

To mitigate this risk commissioners have:

Developed an updated Market Position Statement setting out our future commissioning intentions and direction of travel.

Ernst and Young are supporting the development of our new Commissioning Strategy and procurement forward plan. Further

analyses is being undertaken by the West London Alliance will link to our work and support the achievement of improvements in quality and

cost. Engaged with providers and are undertaking more excersies to

stimulate the development of the market. Helped providers to plan

better by publishing forward plans for tenders etc. Developed a Provider Failure and Service Interruption Policy.

12

3.4 Common strategic risk

3.4.1 Managed Services Programme (including Agresso System implementation). (Appx 1 Risk ref 10, Appx 2 Risk ref 5)

Both services are continuing to experience risks arising from a difficult

implementation of the Managed Services Programme. In addition to some problems around payment to suppliers, there are also significant

issues around the accuracy of staff information which have resulted in some staff getting incorrectly paid and lack of clarity about leave

arrangements. This situation if not resolved could have a significant

impact on the end of year accounts and financial controls.

To mitigate these risks, the Adult Social Care, Public Health finance and commissioning

managers have been where necessary arranging for ad-hoc emergency payments to be made to the smaller and more vulnerable

providers and suppliers. Some legacy systems have been retained (e.g. Abacus) to minimise

the impact on customers and charging. Working with HR to improve staffing information on Agresso.

Continue to lobby Corporate for more training and technical solutions. 4. RECOMMENDATION.

4.1 The Committee is requested to review the risk management arrangements that have been put in place by both the Adult Social

Care and Public Health services and to consider the mitigating actions

for each key high-level strategic risk identified in Section 3 below and note the respective Strategic Risk Registers attached as Appendices.

(Public Health - Appendix 1; Adults Social Care - Appendix 2.)

Liz Bruce, Executive Director Adult Social Care and Health

Background papers:

Contact officer: Martin Calleja Tel: 07534 224294 E-mail: [email protected]

Contact officer: Michael Sloniowski

Tel: 020 8753 2587 E-mail: [email protected]

Inherent Risk Mitigating actions

Ris

k R

ef

Re

pu

tati

on

al

Fin

anci

al

Serv

ice

Del

iver

y

Imp

act

on

life

Envi

ron

men

t

Initial risk

scoreCurrent likelihood

score Current impact score

Current risk

score

Movement of

risk exposure

since last

review What actions are planned to mitigate the risk ?

1PUBLIC HEALTH GRANT REDUCTIONS AND

REMOVAL OF THE RING-FENCEMike Robinson Mike Robinson

Quarterly

Review

Health outcomes will be impaired by the reduction of the Public Health

grant reductions and Public Healths ability to deliver against the Councils'

medium term plans

Yes Yes Yes Yes No 20 3 - Occasional 4- High 12

1. PH Finance Business partners continue to undertake scenario planning and prepare various

budget proposals about future reductions that the Public Health grant will be subject to an

annual average 3.0% reduction (in real terms) over the next 5 years. Consultation regarding the

allocation formula is still ongoing and we are awaiting the annoucement of how the public health

grant will be allocated in future years.

2. The announced in-year reduction to the grant of 6.2% has been met.

3. Review of commissoning, contracts and procurement programes to identify where efficiencies

can be achieved for future years.

4. A task and finish group has been set up to review current and future years potential grant

allocation and budget commitments in a reducing grant context, with a view to aligning spend to

the Public Health vision for the Councils.

2