ASSIGNMENT ON ACCOUNTING FOR DECISION MAKING MBA – MAY 2013 Course: BMAC5203: Accounting Decision...

23

ASSIGNMENT ON ACCOUNTING FOR DECISION MAKING MBA – MAY 2013 Course: BMAC5203: Accounting Decision Making

-

Upload

openmalaysiaoum -

Category

Documents

-

view

2 -

download

0

Transcript of ASSIGNMENT ON ACCOUNTING FOR DECISION MAKING MBA – MAY 2013 Course: BMAC5203: Accounting Decision...

ASSIGNMENT ON ACCOUNTING FOR DECISION MAKING

MBA – MAY 2013

Course: BMAC5203: Accounting Decision Making

TABLE OF CONTENTS

i. TASK - 1 ………………………………………………P 10 - 15

ii. TASK - 2 ……………………………………………….P 3 - 5

iii. TASK - 3 ……………………………………………….P 5 - 6

iv. TASK - 4 ……………………………………………….P 7 - 10

v. REFERENCES .………………………………………………P 16

2 | P a g e

Task 2A – Planning and Control

a.

1. Attendance

The expected participation was 45 members. However, it

was reported that the actual participation was 60

members. The above actual information has not been

compared with the relevant standard information. That is

not an acceptable practice.

2. Revenue

The actual revenue is RM 2,205/-. Therefore, the actual

number of participants should be 63.

As per the statement of the treasure, there were 60

members attended to the function. Hence, there would have

been another 3 nonmembers also attended the party.

3 | P a g e

3. Cost of food

Should be corrected as RM 945/- (63 x RM 15/-)

4. Cost of beverages

Should be corrected as RM 441/- (63 x RM 7/-)

5. The DJ was originally planned for 3 hours with a written

contract. However, RM 175/- was paid to DJ.

b. Revised budget

Actual (A) Revisedbudget (B)

(A) –(B)

Members 60

Revenue 2,205 2,100 105FFood 870 900 30FBeverages 480 420 60UFDJ 175 150 25UFFacility rental

200 200 NIL

50F

4 | P a g e

According to the above revised budget; the overall net

effect of the function is favourable (50F). However, the

function was not as successful as originally reported.

TASK 2B – Planning and Ethics

c. In this case the following problems can be observed.

1. Setting standards too high or low lead to a budgeting

slack (padding the budget). When managers are

deliberately overestimating costs and underestimating

revenue; that misleads the true picture of the future.

2. Sales Manager of the company has violated the

professional standards in executing her duties as a

professional.

3. The non-communication of true information fairly and

objectively is a violation of credibility.

5 | P a g e

It is not consistent with the professional responsibility

and integrity. The sales manager needs to contribute her

full potential to the organization.

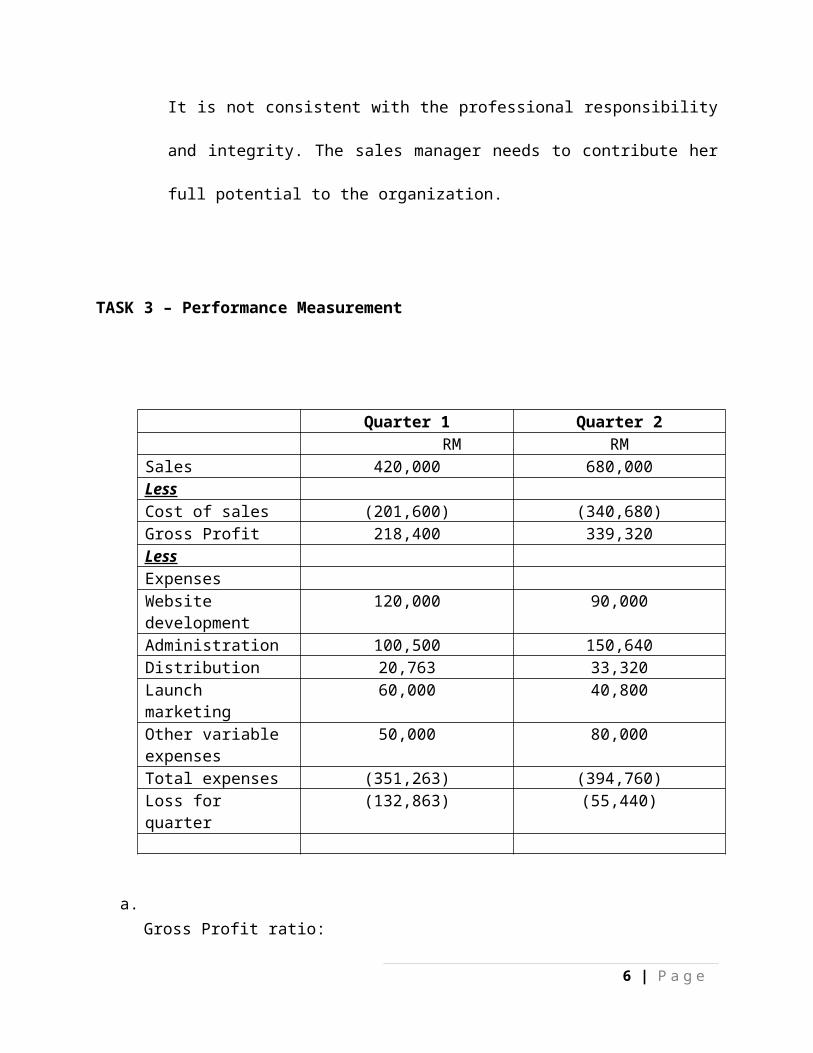

TASK 3 – Performance Measurement

Quarter 1 Quarter 2 RM RM

Sales 420,000 680,000LessCost of sales (201,600) (340,680)Gross Profit 218,400 339,320LessExpensesWebsite development

120,000 90,000

Administration 100,500 150,640Distribution 20,763 33,320Launch marketing

60,000 40,800

Other variable expenses

50,000 80,000

Total expenses (351,263) (394,760)Loss for quarter

(132,863) (55,440)

a.Gross Profit ratio:

6 | P a g e

Gross profit / Sales x 100

Quarter 1 Quarter 2218,400 / 420,000 x 100 =

52%339,320 / 680,000 x 100 =

49.9%

Web development expenses

Expenses / Sales

Quarter 1 Quarter 2120,000 / 420,000 = 2.86 90,000 / 680,000 = 0.13

b. The losses incurred for the two quarters cannot be accepted

as a true reflection of the financial position of the

company due to following reasons.

1. The owners of the business are drawing modest salaries

which are included in the administration expenses which

are a higher amount. This has resulted in increase in

total expenses.

7 | P a g e

2. Website development expenses were charged to the income

statement directly where it has future benefits that

should matched with its revenue. Website development cost

should be considered as a fixed asset. This cost has to

be charged to the income statement over a period of its

useful life.

3. They are in the opinion that marketing expenses incurred

in 1st and 2nd quarter as a future benefit. Hence, it

should be charged to the income statement for each

quarter on a fair basis.

TASK 4 – Decision Making

Rex Ltd.Installed capacity 2,000 chips / weekSelling price RM 100

8 | P a g e

Current production 1,600 chips / weekFixed cost RM 75,000Variable cost RM 80,000

a. Breakeven point:

Fixed cost / Contribution per unit

Variable cost per unit = Current total variable

cost / Current level of activity

= RM 80,000 / 1,600

= RM 50

Contribution per unit = Sales price – Variable

cost

= RM 100 – RM 50

= RM 50

Breakeven point = RM 75,000 / RM 50

= 1,500 units

At the breakeven point: profits will be “zero”

9 | P a g e

RMSales 1,500 x RM 100 150,000LessVariable cost 1,500 x RM 50 (75,000)Contribution margin

75,000

LessFixed cost (75,000)

Net income 0

b. Plant’s profit when it is running at full capacity :

Full capacity = 2,000 chip per week

RMSales 2,000 x RM 100 200,000LessVariable cost 2,000 x RM 50 (100,000)Contribution margin 100,000LessFixed cost (75,000)

Net income 25,000

c. Cost per unit at plant’s full capacity of 2,000 units per

week

10 | P a g e

Variable cost per unit

RM 80,000 / 1,600 units

RM 50

Variable cost RM 50 x 2,000 units

RM 100,000

Fixed cost RM 75,000Total cost RM 175,000

No. of units 2,000

Cost per unit RM 175,000 / 2,000units

RM 87.50

d. New customer’s order

200 chips per week @ RM 80 per chip

The decision of accepting or refusing the new order is based

on its contribution margin. Because, the fixed cost has been

already incurred. Hence, the decision has to be made based

on contribution.

New offer price RM 80 per unitLessVariable cost refer section (b) (RM 50)Contribution margin

RM 30 per unit

Total contribution for the order

RM 30 x 200 units RM 6,000

11 | P a g e

As per the above if the order is accepted; the profits willincrease by RM 6000.

Without the order With the orderSales RM 100 x 1,600

units =

RM 160,000

RM 100 x 1,600 units=RM 160,000+RM 80 x 200 units = RM 16,000

RM 176,000

LessVariable cost RM 50 x 1,600

units =(RM 80,000)

RM 50 x 1,800 units =(RM 90,000)

Contribution RM 80,000 RM 86,000LessFixed cost (RM 75,000) (RM 75,000)

Profit 5,000 11,000

e. In addition to the above mathematical calculations, there

some qualitative factors also to be considered in making a

make or buy decision.

i. Continuous supply - whether supplier has the capacity

to supply without delays in order to cater the demand

12 | P a g e

ii. Supplier’s reliability – his past track records and the

referrals

iii. Quality of goods – to make sure the required quality is

maintained

iv. Compliance issues – whether the supplier can meet the

legislative requirements.

TASK 1 - Target Costing

a.

To : Managing Director - Target Company

From : Kanchana Wariyapola - Graduate School of

Management

Subject : Process of Target Costing

Date : 25.01.2012

With the emergence of global competition in business, the

companies faced immense challenge for survival in their

businesses. To ensure the survival they must make sure that they

13 | P a g e

are providing superior products that deliver the quality and the

functionality that customers demand while generating desired

profits. One of the ways to ensure that is to subject them to

Target Costing.

Target costing is a primarily a technique that strategically

manages company’s future profits. The objective of this technique

is to determine the life cycle cost at which a company must

produce a product with specified functionality and quality, if

the product is to be profitable at its anticipated selling price.

Target costing defines the cost as an input to the product

development process not as an outcome of the process.

Once the anticipated selling price is decided, the desired profit

margin will be subtracted and company arrives at the target cost.

Thereafter the key element is to design the product that

satisfies customers demand at its target cost. Many of the firms

that have adopted target costing successfully have learned to

view it as an integral part of product development process and

not as a standalone process.

14 | P a g e

For target costing to be effective, it has to be a highly

integrated process. There are 3 main steps can be identified.

This integration demands a high level of specificity about want

customers demand and what price they are prepared to pay. Market

analysis becomes crucial in the market driven costing part of

target costing by determining allowable costs. These allowable

costs are used to transmit the competitive cost pressures that

the company faces to product designers. This focuses on product

designer’s ability to meet these cost aspects.

Once the company established the product level target cost; it

transmits them into component level. Thus it passes its cost

pressures to the suppliers. They must in turn find ways to design

and produce company’s externally sourced components in order to

15 | P a g e

Source:

make adequate returns for them by supplying those to the company.

Thus component level costing focuses supplier’s creativity in

ways which benefit the customer. In light of the above facts I

would like to propose the following target costing process for

16 | P a g e

your company to adopt in order to achieve superior results.

17 | P a g e

b. Benefits of adopting Target Costing for Target Co.

i. This will give an early external focus to the

company in its product development. The market

driven costing part of target coasting begins at

product conceptualization level. This will give a

better insight about the customer demand and the

company’s position to compete with others will be

18 | P a g e

stronger. Internally driven traditional approaches

will not have the above benefit.

ii. Cost control will begin at the early stages of the

process. If it is noted that a cost gap exists, it

is much easier to take corrective actions by

design team; unlike in traditional approaches

where the cost control takes place at cost

incurring stage and it is far too late to make a

significant change in an expensive manufacturing

process.

iii. Target costing at early stage considers the

product which is demanded. Only the features that

are of value to the customers will be included.

Additional features that are unlikely to be valued

by the customers will be excluded. This doesn’t

normally happen in traditional cost plus methods.

iv. Cost per unit under target costing is lower than

in the other methodologies by about 20% - 40%

19 | P a g e

depending on the product and the market

conditions. Under other traditional approaches,

the company may not be aware of the constraints in

the external environment until the production

process starts and at this stage it is much

difficult to make significant changes as most of

the costs are already built in.

v. The company can reduce the lead time in

introducing the product to the market. Because,

this process has a greater external focus in the

inception itself and the company is sensitive to

the real demand in the market. This will help

company to get things right at the first time.

c. Possible steps to reduce the cost gap

i. Review the features of the product

The features which are of no value to the

customers should be removed from the product. This

20 | P a g e

will reduce the cost and the selling price should

not

be reduced. This is referred as value analysis.

ii. Review the whole supplier chain

The entire supplier chain has to be reviewed to

see whether there are possible cost reduction

points. The component level target costing can be

used to transit the pressure created at product

level target costing to its suppliers. This will

focus supplier’s creativity beneficial to the

buyer.

iii. Team approach

The best cost efficiencies can be achieved when

the team approach is adopted. Company must bring

the design, marketing, manufacturing and

distribution teams together to brainstorm to find

out the cost effective methodologies.

iv. Components

21 | P a g e

The company should look into the cost involvement

of the each component. New suppliers could be

sought and new materials can be tested while

making sure that the perceived quality of the

product is not damaged.

v. Work practices

The change of some working practices may result in

higher efficiencies and that will reduce the idle

time of the workers. The process automation can be

also considered under this. Creating a good

learning culture will reduce the labour cost per

unit.

vi. Overheads

Increase in productivity will help spreading the

fixed overheads over a large number of units. The

company can consider the ABC costing in its

22 | P a g e

overhead allocation. This may result in more

favourable cost allocation in the digital radio.

REFERENCES

1. Kaygusuz, S. Y. (2011). Target costing for new product development process. Business and Economic Research Journal, 2(4), 19-26.

2. Kokemuller, N. (2014). Target Costing. Small Business. 2014,Received from: http://smallbusiness.chron.com/benefits-target-costing-66494.html

23 | P a g e