Assignment of Bank Management

19

Page 1 of 19 Assignment of Bank Management A Study Report on “Causes of Non-Performing Assets & its current status in “Central Bank of India” Submitted to: Submitted By: Ankana Thankur Ravindra Kumar MBA/15004/13 Faculty Madhusudan Kr MBA/15005/13 Birla Institute of Technology Pratik Bhushan MBA/15036/13 MESRA, Patna Campus Asiful Haque MBA/15056/13 Department of Management Birla Institute of Technology, MESRA Patna Campus

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of Assignment of Bank Management

Page 1 of 19

Assignment of Bank Management

A Study Report on

“Causes of Non-Performing Assets & its current status in

“Central Bank of India” Submitted to: Submitted By: Ankana Thankur Ravindra Kumar MBA/15004/13 Faculty Madhusudan Kr MBA/15005/13 Birla Institute of Technology Pratik Bhushan MBA/15036/13 MESRA, Patna Campus Asiful Haque MBA/15056/13

Department of Management

Birla Institute of Technology, MESRA Patna Campus

Page 2 of 19

PERFORMING ASSETS:-

An assets can be considered as a performing asset if,

Prompt realization of interest debited to the advance account at periodical intervals.

Prompt realization of instalments pertaining to the principal amount of the advance.

MEANING:-

An asset that causes to generate income for the bank is called Non-Performing Asset.

NON-PERFORMING ASSETS:-

NPA are advances that have ceased to perform. An advance asset will cease to be a

“Performing” asset and will be deemed to have become a “Non-Performing” asset when there

is,

A default in the payment of interest amounts, which are debited to the advance

account.

A default in the repayment of the instalments pertaining to the principal amount of

the advance.

In initial stages of Income recognition, Assets Classification Guidelines,

An amount due under any credit facility was treated as “Past Due” when it has not been paid

within 30 days from the due date. Due to the improvement in the payment and settlement

systems, recovery climate, up gradation of technology in the banking system,

etc., it was decided to dispense with “Past Due” concept, with effect from March 31, 2001.

Accordingly, a from that date, a Non-Performing Asset shell be an advance where,

(i) Interest and / or instalment of principal remain overdue for a period of more than

180 days in respect of a Term Loan,

(ii) The account remains ‘out of order for a period of more than 180 Days, in respect

of an Overdraft / Cash Credit,

(iii) The bill remains overdue for a period of more than 180 days in the case of Bills

Purchased and Discounted,

(iv) Interest and / or instalment of principal remains overdue for two harvest seasons

but for a period not exceeding two half in the case of an advance granted for

agriculture purpose, and

Page 3 of 19

(v) Any amount to be received remains overdue for a period of more than 180 days in

respect of other accounts.

With a view to moving towards international best practices and to ensure greater

transparency, it has been decided to adopt the ’90 days Overdue’ norm for identification of

NPAs, form the year ending March 31, 2004. Accordingly with effect from March 31, 2004, a

Non-Performing Asset shell be a loan or an advance where;

(i) Interest and / or instalment of principal remain overdue for a period of more than

90 days in respect of a Term Loan,

(ii) The account remains ‘out of order for a period of more than 90 Days, in respect

of an Overdraft / Cash Credit,

(iii) The bill remains overdue for a period of more than 90 days in the case of Bills

Purchased and Discounted,

(iv) In case of direct agricultural advances, the overdue norms specified below are

applicable;

(a) Loan granted for short duration crops will be treated as NPA, if instalment of

principal or interest thereon remains outstanding for two crop seasons.

(b) Loan granted for long duration crops will be treated as NPA, if instalment of

principal or interest thereon remains outstanding for one crop seasons.

(c) For Agriculture term loans, the norms would depend on type & crop cultivated

by Agriculturist.

Any amount to be received remains overdue for a period of more than 90 days in respect

of other accounts

ASSETS CLASSIFICATION:-

Classification of Assets should be done on the basis of objective criteria with uniform and

consistent application of norms duly ensured. There are generally three ways of classification

of assets, which are given as under:

Assets classification under Health Code System:-

Under the Health Code system, bank are required to classify the advances under any one of

the heads depending upon the status of the account, dealings, availability of security cover,

etc.

Asset Classification for Final Accounts:-

Banks are required to prepare their final accounts as per Third Schedule to the Banking

Regulation act, 1949 which bankers / auditors are well conversant with.

Page 4 of 19

Assets Classification under Prudential Norms:-

Under the prudential norms of asset classification, banks are now required to classify their

advances in the following four broad groups:-

(a) Standard Assets:-

These are assets which are ‘Performing’ and do not disclose any weakness and do not carry

more than normal business risk.

(b) Sub-Standard Assets:-

These are assets which have ceased to ‘Perform’ but which have not completed a period of

18 months (now 12 Months) after getting classified as Non-performing and there is no threat

to recovery on account of erosion in the realizable value of security or due to non-availability

of security or due to other factors, to the extent that the account is to be classified either as

Doubtful Assets or as Loss Assets. With effect from 31st March, 2005, a sub-standard asset

would be one, which has remained NPA for a period less than or equal to 12 months.

(c) Doubtful Asset:-

These are accounts which have completed a period of 18months (now 12 Months) after

getting classified as Sub-standard Assets. A loan classified as doubtful has all the weakness

inherent in assets that were classified as sub-standard, with the added characteristic that the

weakness make collection or liquidation in full on the basis of currently known facts,

conditions and values-highly questionable and improbable. With effect from March 31st,

2005, an asset would be classified as doubtful if remained in the sub-standard category 12

months.

(d) Loss Assets:-

A Borrower account in which a loss has been identified by the internal or external auditors or

by the RBI inspectors. The releasable value of security in the accounts is very little.

Guidelines for Classification of Assets:-

Classification of Assets in to above categories should be done taking into account the degree

of well-defined credit weakness and the extent of dependence on collateral security for

realization of dues.

Banks should establish appropriate internal systems to eliminate the tendency to delay or

postpone the identification of NPAs, especially in respect of high value accounts. The banks

may fix a minimum cut off point to decide what would constitute a high value account

depending upon their respective business level. The cut of point should be valid for the entire

accounting year. Responsibility and validation levels for ensuring proper asset classification

Page 5 of 19

may be fixed by the banks. The system should ensure that doubts in asset classification due

to any reason are settled through specified internal channels within one month from the date

on which the account would have been classified as NPA as per extant guidelines.

Up gradation of Loan Accounts classified as NPAs:-.

If arrears of interest and principal are paid by the borrower in the case of loan accounts

classified as NPAs, the account should no longer be treated as non-performing and may be

classified as ‘standard’ accounts.

Accounts regularized near about the balance date:-

The asset classification of borrower account where a solitary or a few credits are recorded

before the balance sheet date should be handled with care and without scope for subjectivity.

Where the account indicates inherent weakness on the basis of the data available, the

account should be deemed as a NPA. In other genuine cases, the banks must furnish

satisfactory evidence to the Statutory Auditors / Inspecting Officers about the manner of

regularization of the account to eliminate doubts on their performing status.

Asset Classification to be borrower-wise and not facility-wise:-

It is difficult to envisage a situation when only one facility to a borrower becomes a problem

credit and not others. Therefore, all the facilities granted by a bank to a borrower will have to

be treated as NPA and not the particular facility or part thereof which has become irregular.

If the debits arising out of devolvement of letters of credit or invoked guarantees are parked

in a separate account, the balance outstanding in that account also should be treated as a

part of the borrower’s principal operating account for the purpose of application of prudential

norms on income recognition, asset classification and provisioning.

Government guaranteed Advances:-

The credit facilities backed by guarantee of the Central Government though overdue may be

treated as NPA only when the Government repudiates its guarantee when invoked. This

exemption from classification of Government guaranteed advances as NPA is not for the

purpose of recognition of income. With effect from 1st, April, 2000, advances sanctioned

against State Government Guarantees should be classified as NPA in the normal course, if the

guarantee is invoked and remains in default for more than two quarters. With effect from

March 31st, 2001 the period of default is revised as more than 180 days and with effect from

March 31st, 2004 the period of default would be revised as more than 90 days.

Advances under rehabilitation approved by BIFR / TLI:-

Banks are not permitted to upgrade the classification of any advance in respect of which the

terms have been renegotiated unless the package of re-negotiated terms has worked

satisfactorily for a period of one year. While the existing credit facilities sanctioned to a unit

Page 6 of 19

under rehabilitation packages approved by BIFR / Term Lending Institutions will continue to

be classified as sub-standard or doubtful as the case may be, in respect of additional facilities

sanctioned under the rehabilitation packages, the Income Recognition, Asset Classification

norms will become applicable after a period of one year from the date of disbursement.

PROVISIONING NORMS:-

In order to narrow down the divergences and adequate provisioning by banks, it was

suggested that bank’s statutory auditors, if they so desire, could have a dialogue with RBIs

Regional Office / Inspectors who arrived out for bank’s inspection during the previous year

with regard to the accounts contributing to the difference.

Pursuant to this, regional offices were advised to forward a list of individual advances, where

the variance in the provisioning requirements between the RBI and the bank is above certain

cut off levels so that the bank and the statutory auditors take into account the assessment of

the RBI while making provisions for loan loss, etc.

The primary responsibility for making adequate provision for any diminution in the value of

loan assets, investment of other assets is that of the bank managements and the statutory

auditors The assessment made by the inspecting officer of the RBI is furnished to the bank to

assist the bank management and the statutory auditors in taking a decision in regard to

making adequate and necessary provisions in terms of prudential guidelines.

In conformity with the prudential norms, provisions should be made on the non-performing

assets on the basis of classification of assets into prescribed categories as detailed above.

Taking into account the time lag between an account becoming doubtful of recovery, its

recognition as such, the realization of the security and the erosion over time in the value of

security charged to the bank, the banks should make provision against loss assets, doubtful

assets and sub-standard assets as below:

(a) Loss Assets:-

The entire assets should be written off after obtaining necessary approval from the

competent authority. If the assets are permitted to remain in the books for any reason, 100

per cent of the outstanding should be provided.

In respect of an asset identified as a loss asset, full provision at 100 per cent should be made

if the expected salvage value of the security is negligible.

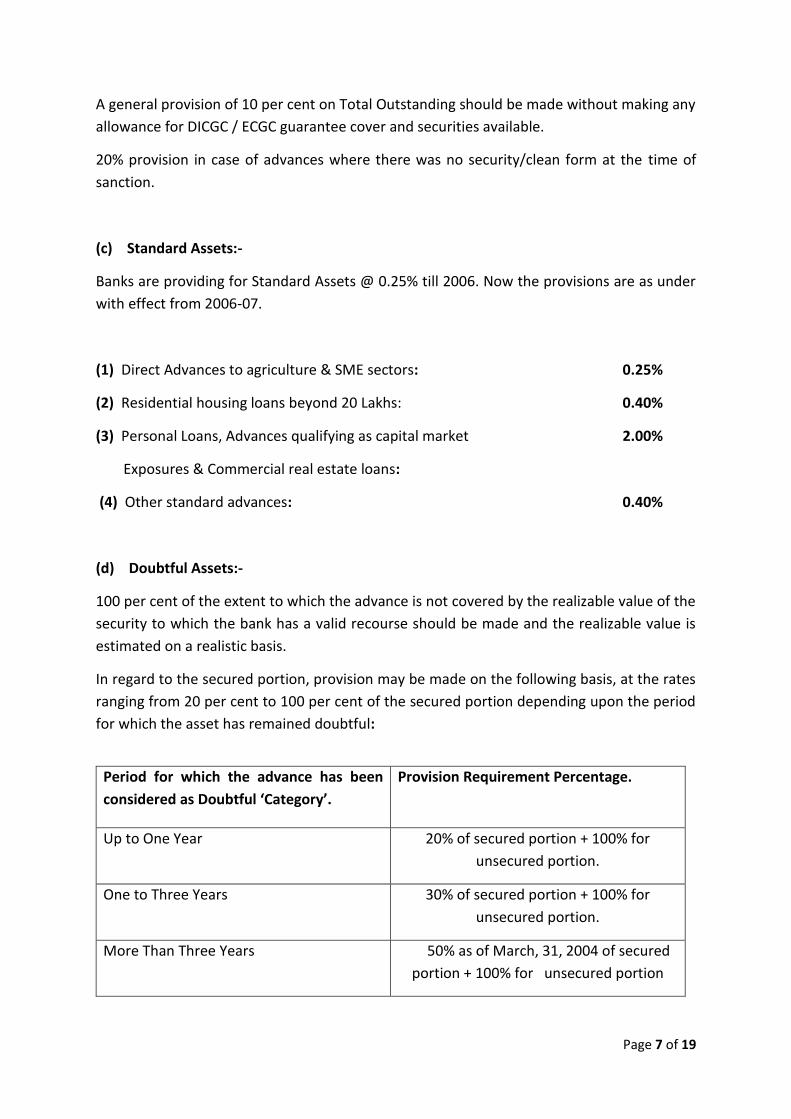

(b) Sub-standard Assets:-

Page 7 of 19

A general provision of 10 per cent on Total Outstanding should be made without making any

allowance for DICGC / ECGC guarantee cover and securities available.

20% provision in case of advances where there was no security/clean form at the time of

sanction.

(c) Standard Assets:-

Banks are providing for Standard Assets @ 0.25% till 2006. Now the provisions are as under

with effect from 2006-07.

(1) Direct Advances to agriculture & SME sectors: 0.25%

(2) Residential housing loans beyond 20 Lakhs: 0.40%

(3) Personal Loans, Advances qualifying as capital market 2.00%

Exposures & Commercial real estate loans:

(4) Other standard advances: 0.40%

(d) Doubtful Assets:-

100 per cent of the extent to which the advance is not covered by the realizable value of the

security to which the bank has a valid recourse should be made and the realizable value is

estimated on a realistic basis.

In regard to the secured portion, provision may be made on the following basis, at the rates

ranging from 20 per cent to 100 per cent of the secured portion depending upon the period

for which the asset has remained doubtful:

Period for which the advance has been

considered as Doubtful ‘Category’.

Provision Requirement Percentage.

Up to One Year 20% of secured portion + 100% for

unsecured portion.

One to Three Years 30% of secured portion + 100% for

unsecured portion.

More Than Three Years 50% as of March, 31, 2004 of secured

portion + 100% for unsecured portion

Page 8 of 19

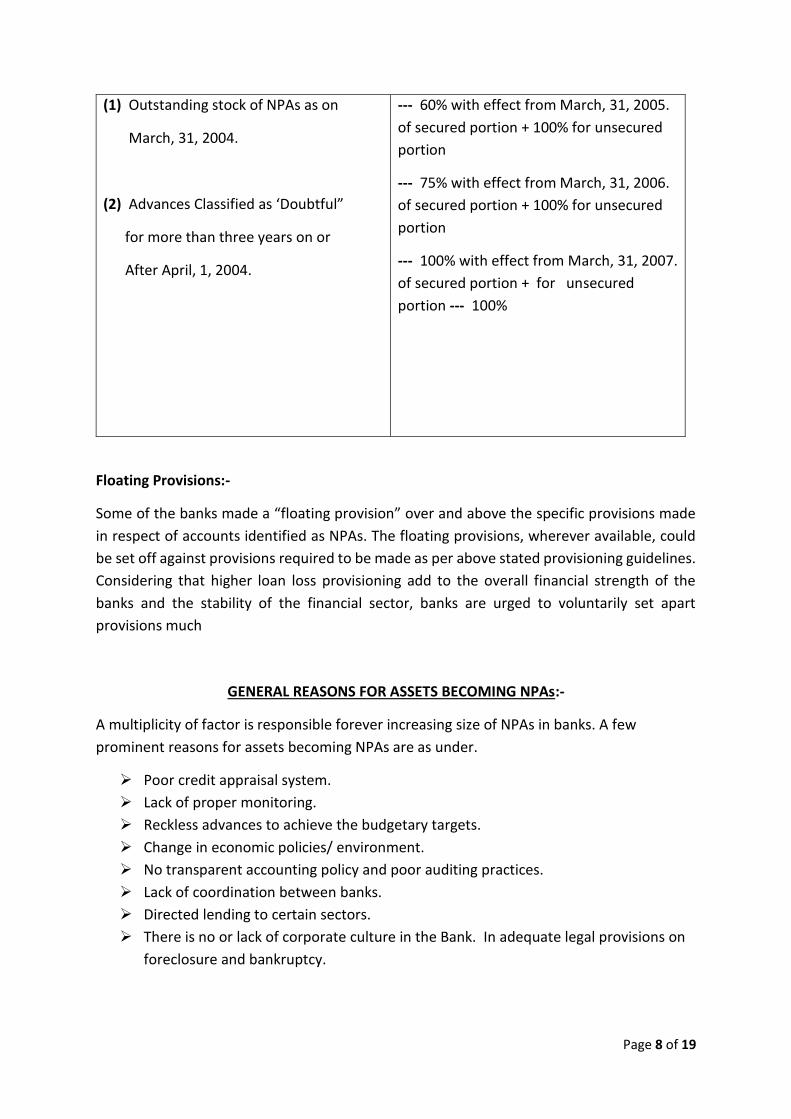

Floating Provisions:-

Some of the banks made a “floating provision” over and above the specific provisions made

in respect of accounts identified as NPAs. The floating provisions, wherever available, could

be set off against provisions required to be made as per above stated provisioning guidelines.

Considering that higher loan loss provisioning add to the overall financial strength of the

banks and the stability of the financial sector, banks are urged to voluntarily set apart

provisions much

GENERAL REASONS FOR ASSETS BECOMING NPAs:-

A multiplicity of factor is responsible forever increasing size of NPAs in banks. A few

prominent reasons for assets becoming NPAs are as under.

Poor credit appraisal system.

Lack of proper monitoring.

Reckless advances to achieve the budgetary targets.

Change in economic policies/ environment.

No transparent accounting policy and poor auditing practices.

Lack of coordination between banks.

Directed lending to certain sectors.

There is no or lack of corporate culture in the Bank. In adequate legal provisions on

foreclosure and bankruptcy.

(1) Outstanding stock of NPAs as on

March, 31, 2004.

(2) Advances Classified as ‘Doubtful”

for more than three years on or

After April, 1, 2004.

--- 60% with effect from March, 31, 2005.

of secured portion + 100% for unsecured

portion

--- 75% with effect from March, 31, 2006.

of secured portion + 100% for unsecured

portion

--- 100% with effect from March, 31, 2007.

of secured portion + for unsecured

portion --- 100%

Page 9 of 19

CAUSES OF NPA:-

There are many causes for performing assets becoming Non-performing. The following are

some of the general causes which Contribute to creation of NPAs and the same can be

categorized under three Classes:-

(1) Causes attributable to the Promoter / Borrower:-

Bad intention of securing wrongful gains from banks by availing advances by

misrepresentation of facts.

Financial indiscipline—diversion of funds for unapproved purposes.

Mismanagement of Units / Projects---wilful or otherwise.

Lack of professional management.

Death / disability of the chief promoter / person behind the show.

Inability to tie up the funds required as margin (promoters’ contribution) as per the

projection furnished.

Problems due to adverse exchange fluctuations faced by exporters/ importers.

Inadequate control / supervision resulting in time and cost overrun.

Low priority to technology up gradation and inadequate attention to research and

development, quality control etc.

Differences / disputes amongst promoters---family splits, lack of co-ordination among

partners, groupings among the directors of the company etc.

Huge deviation in the demand

(2) Causes attributable to the Bank:-

Delay in decision making and sanction of credit facilities.

Defective / deficient monitoring and supervision of advance accounts.

Improper /poor credit appraisal due to lack of expertise and scales required for critical

pre-sanction scrutiny of loan proposals.

Non-availability of reliable market and industry relevant data on demand / supply

scenario.

Compromise on project viability with overemphasis on security while assessing the

loan proposals.

Disbursement of advance facilities before compliance of terms ad condition of

sanction and incomplete / defective documentation.

Delayed and / or non-detection / diagnosis of warning signals and inaction in the

initiation of the remedial measures.

Long pending judicial proceedings and protracted legal battles in courts act more as a

cover to the defaulting borrowers.

Page 10 of 19

Lack of government support and apathy of public to bank’s recovery efforts.

Non observance of bank’s well laid down norms and systems and of preventive /

precautionary measures facilitating perpetration of frauds by insiders / outsiders.

(3) Causes beyond the control of banks and borrowers:-

Political uncertainties.

Frauds committed by outsiders, with or without the collusion of outsiders.

Inadequate infrastructure facilities such as supply of power and other essential inputs.

Debt Relief Schemes introduced by some states for political mileage have vitiated the

repayment culture and has resulted in a large number of wilful defaulters.

Inconsistency in judicial verdicts as a result of improper presentation of facts.

Outdated laws, labour unrest / lockouts / strikes, riots etc.

Law and order problems affecting commercial and industrial activity in certain parts

of the country.

Natural calamities like earthquakes, draughts and floods, etc., resulting in large-scale

destruction of properties and life.

SOME OF THE INDICATORS SUGGESTING SLIPPAGES TO NPA:-

A borrower account will not become NPA overnight. Like a major disease to human body, it

does give symptoms beforehand. It is only up to the banker to take sight of these symptoms

and initiate timely remedial measures to prevent the account from actually slipping in to NPA.

On the basis of auditors’ experience of banks, the following notable indications would be

available in different types of borrower’s accounts:-

(1) Cash Credit / Overdraft:-

Increasing number of goods returned by the clients.

Increasing number of unreconciled book debts.

Increasing number of incidences of debit / credit notes in the books of accounts.

Self-Cheques presented through some other bank.

Huge cash withdrawals without proper explanation.

Frequent requests for temporary overdrawing.

Frequent requests for release / exchange of securities.

Increase in transactions in personal accounts of proprietor / partner / directors.

Unexplained delay in submission of financial statements and tax returns.

Page 11 of 19

(2) Bills Discounted / Purchased:-

Incidences of accommodation bills.

Gradual increase in realization period.

Frequent incidences of partial realization of bills.

Gradual increase in dishonour of bills discounted and return of bills purchased. As

guidance, dishonour / return of bills in excess of 5% of bills may be taken as the danger

signal.

Frequent requests for discount / purchase of bills draw on parties outside the list of

drawers approved by the bank.

Requests for meeting the amount of dishonoured / returned bills from out of discount

/ purchase of fresh bills.

(3) Letter of Credits / Bank Guarantees:-

Invocation of Bank Guarantees / development of Letter of Credit.

Non receipt of original LC / BGs bonds after expiry and several reminders.

(4) Term Loans:-

Misconception of the project.

Undue and unreported delay in project implementation.

Non-introduction of margin from time to time and wrong utilisation of loan proceeds.

Default in payment of instalments / interest.

Frequent breakdowns in plant and machinery.

Drastic fluctuations in operational efficiency and capacity utilization.

Labour unrest in the plant.

Disposal / replacement of vital plant and machineries without the consent of the bank

and without putting an effective alternative arrangement in place.

(5) Foreign Exchange Finance:-

Incidences of accommodation and kite flying.

Frequent overdue in PCL without genuine reasons.

Frequent cancellation of orders by the overseas buyers.

Increasing delay in realization of export bills.

Huge uncovered Foreign Exchange position.

Frequent return of goods.

Drastic changes in the economic / political atmosphere in the importer’s country.

Serious violation of FEMA / RBI Guidelines by the exporter’s attracting penal action.

Page 12 of 19

(6) Other General Warning Signals:-

Opening of bank accounts with other banks without the consent of the lending banker.

Unreconciled branch accounts where borrowers have branches elsewhere.

Unexplained swing in the behavioural pattern of the borrower.

Noticeable reduction in ancillary business like DDs, TTs, etc.

Notice by partner / director of the borrowing firm / company of irregularities.

Death of key person in the conduct of business of the borrower’s.

Suits filed against the borrowers other than in normal course of business.

Issuance of notices to the borrowers from the respective body for not meeting

statutory dues like Income Tax, Sales tax, Excise, ESIC etc.

Receipt of attachment orders as a result of non-payment of any of the above duties.

Material changes in the demand / supply scenario and supply of raw material potent

enough to pose serious threat to the economic viability of the project / business.

The above list is not exhaustive and each case of advance may require special attention

depending on each case. As the saying goes, a stitch in time saves nine. It is the alertness and

constant vigil exercised at the operational levels along with quality monitoring and timely

follow-up of borrower accounts that will prevent fresh slippages from performing to non-

performing. The practical banker should develop necessary skill to take note of the warning

signals and initiate necessary corrective action.

In order to build-up and maintain a portfolio of quality advances, it is essential to meticulously

follow the good and time-tested systems and procedures. The best way to tackle NPA

menace is to prevent fresh additions to this undesirable club and, at the same time, putting

vigorous efforts to reduce the size of existing NPA segment.

Page 13 of 19

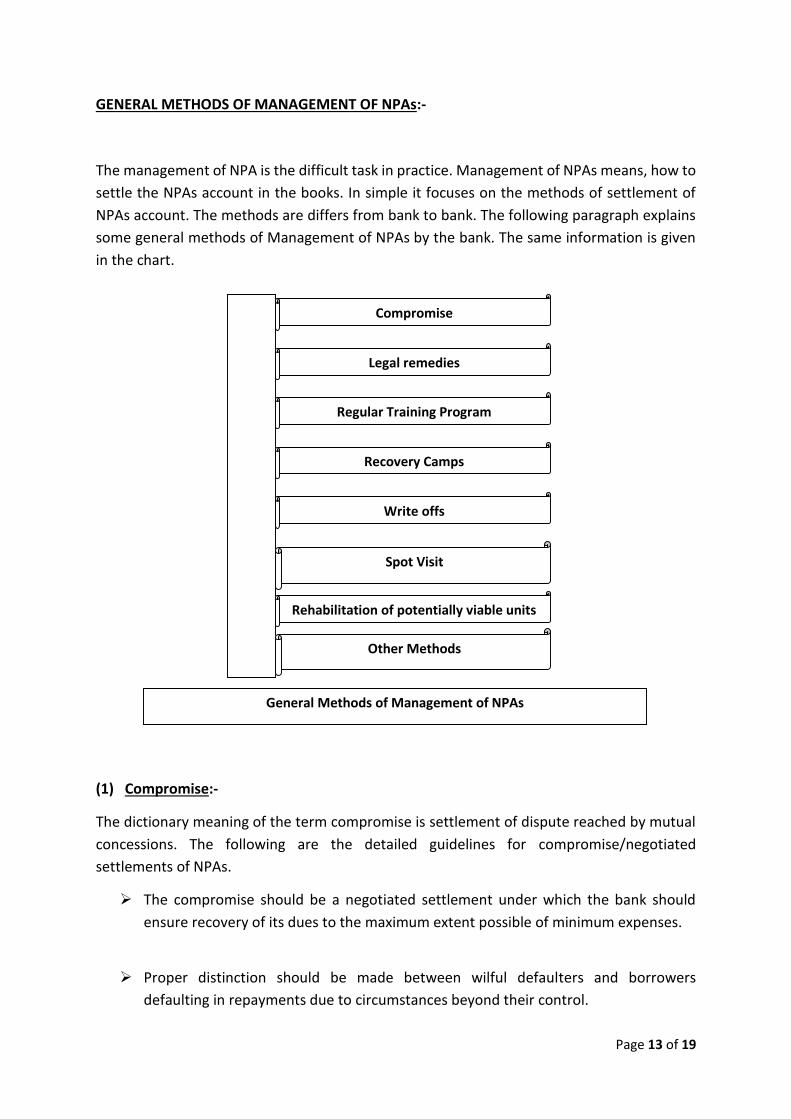

GENERAL METHODS OF MANAGEMENT OF NPAs:-

The management of NPA is the difficult task in practice. Management of NPAs means, how to

settle the NPAs account in the books. In simple it focuses on the methods of settlement of

NPAs account. The methods are differs from bank to bank. The following paragraph explains

some general methods of Management of NPAs by the bank. The same information is given

in the chart.

(1) Compromise:-

The dictionary meaning of the term compromise is settlement of dispute reached by mutual

concessions. The following are the detailed guidelines for compromise/negotiated

settlements of NPAs.

The compromise should be a negotiated settlement under which the bank should

ensure recovery of its dues to the maximum extent possible of minimum expenses.

Proper distinction should be made between wilful defaulters and borrowers

defaulting in repayments due to circumstances beyond their control.

General Methods of Management of NPAs

Compromise

Legal remedies

Regular Training Program

Recovery Camps

Write offs

Spot Visit

Rehabilitation of potentially viable units

Other Methods

Page 14 of 19

Where security is available for assessing the realizable value, proper weight age should

be given to the location, condition and marketable title and possession of such

security.

An advantage in settlement cases is that banks can promptly recycle the funds instead

of resorting to expensive recovery proceedings spread over a long period.

All compromise proposals approved by any functionary should be promptly reported

to the next higher authority for post facto scrutiny.

Proposal for write off/ compromise should be first by a committee of senior executives

of the bank.

(2) Legal remedies:-

The legal remedies are one of the methods of management of NPAs. The banks observed that

the borrower is making wilful default; no more time should be lost instituting appropriate

recovery proceedings. The legal remedies are:

Filing civil suits.

Filing criminal suits under sec.138.

Filing suits in DRT.

Use of SARFAESI Act for quick recovery.

Putting cases to Lokadalat.

(3) Regular Training Program:-

The all levels of Staff, Officers should undergo the regular training program on credit and NPA

management. It is very useful and helpful to the Staff, officers & Executives for dealing with

proper appraisal of advances & using correct techniques for NPA recovery & reduction.

(4) Recovery Camps:-

The banks should conduct the regular or periodical recovery camps in the bank premises or

some other common places; such type of recovery camps reduces the level of NPAs in the

Banks.

(5) Write offs:-

Page 15 of 19

Write offs is also one of the common management techniques of NPAs. The assets are treated

as loss assets, when the bank writes off the balances. The ultimate aim of the write off is to

clean the Balance sheet.

(6) Spot Visit:-

The bank officials should visit to the borrower’s business place or borrower’s field regularly

or periodically & should have continuous meaningful dialogue, it will help in proper diagnosis

of reasons and deciding correct course of action for recovery. It is also help full to the bank to

control or reduce the NPAs limit.

(7) Rehabilitation of potentially viable units:-

Technically feasible & economically viable NPA units can be rehabilitee through rescheduling,

rephrasing, additional financial support, interest rebate, etc. This will help the units to come

back on the track & start generating income to banks overdue & come out of NPA status.

(8) Other Methods:-

Persistent phone calls.

Media announcement.

Help of recovery agents.

Help of advocates for speedy disposals.

Up gradation of account through recovery of overdue amount.

Page 16 of 19

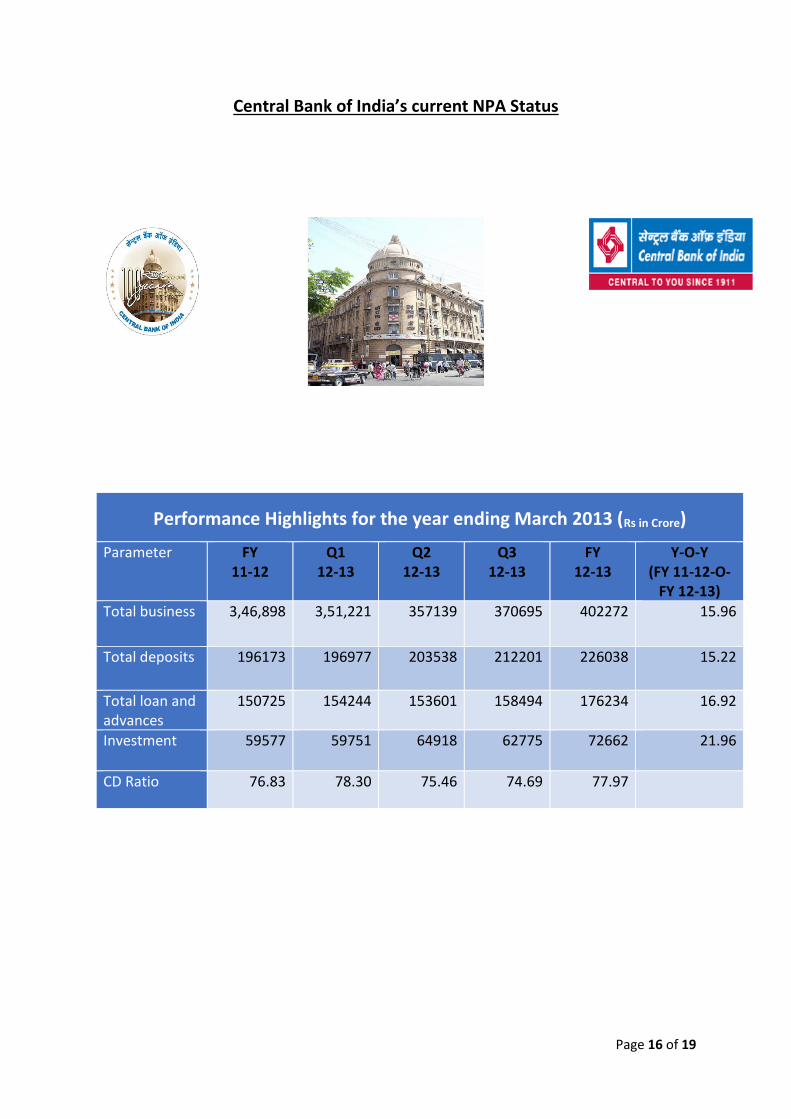

Central Bank of India’s current NPA Status

Performance Highlights for the year ending March 2013 (Rs in Crore)

Parameter FY 11-12

Q1 12-13

Q2 12-13

Q3 12-13

FY 12-13

Y-O-Y (FY 11-12-O-

FY 12-13)

Total business 3,46,898 3,51,221 357139 370695 402272 15.96

Total deposits 196173 196977 203538 212201 226038 15.22

Total loan and advances

150725 154244 153601 158494 176234 16.92

Investment 59577 59751 64918 62775 72662 21.96

CD Ratio 76.83 78.30 75.46 74.69 77.97

Page 17 of 19

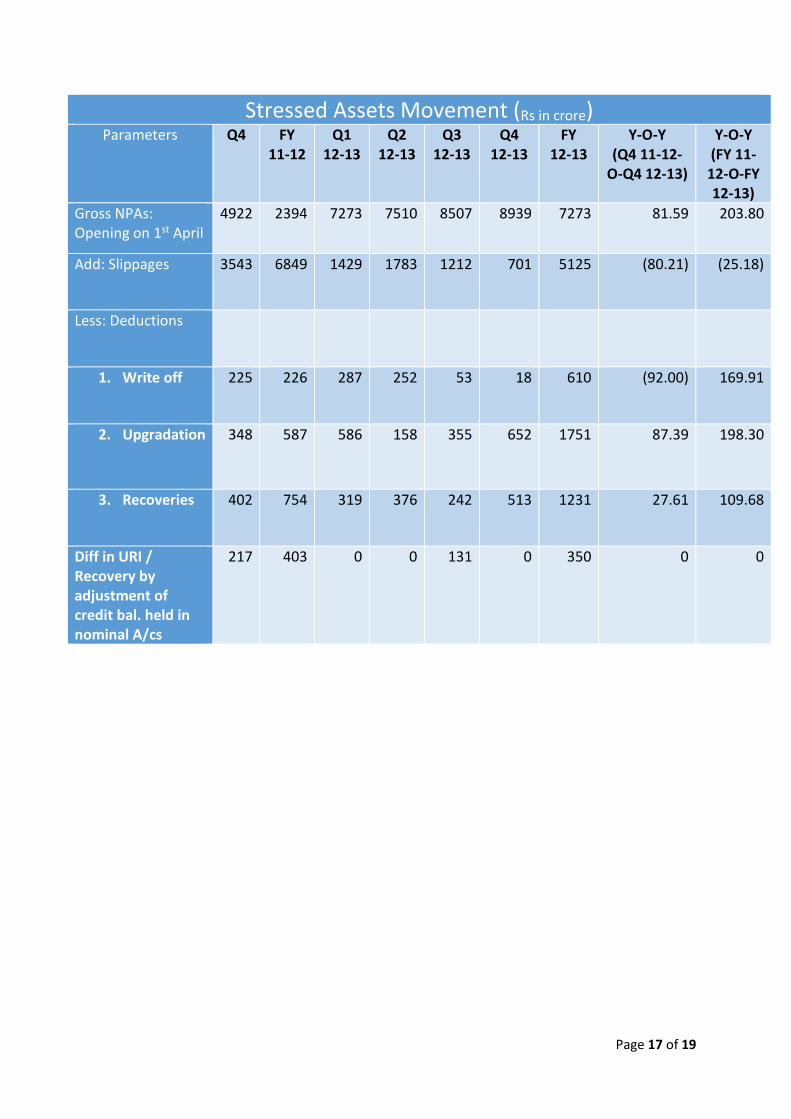

Stressed Assets Movement (Rs in crore)

Parameters Q4 FY 11-12

Q1 12-13

Q2 12-13

Q3 12-13

Q4 12-13

FY 12-13

Y-O-Y (Q4 11-12-

O-Q4 12-13)

Y-O-Y (FY 11-

12-O-FY 12-13)

Gross NPAs: Opening on 1st April

4922 2394 7273 7510 8507 8939 7273 81.59 203.80

Add: Slippages 3543 6849 1429 1783 1212 701 5125 (80.21) (25.18)

Less: Deductions

1. Write off 225 226 287 252 53 18 610 (92.00) 169.91

2. Upgradation 348 587 586 158 355 652 1751 87.39 198.30

3. Recoveries 402 754 319 376 242 513 1231 27.61 109.68

Diff in URI / Recovery by adjustment of credit bal. held in nominal A/cs

217 403 0 0 131 0 350 0 0

Page 18 of 19

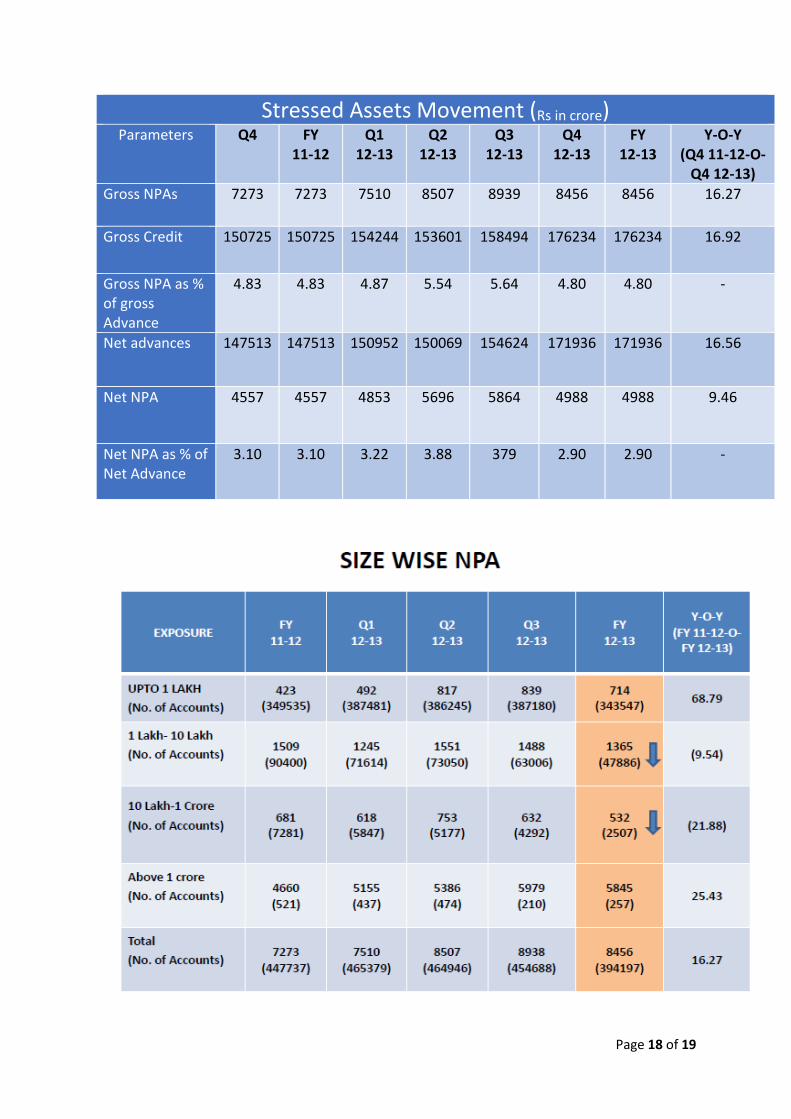

Stressed Assets Movement (Rs in crore)

Parameters Q4 FY 11-12

Q1 12-13

Q2 12-13

Q3 12-13

Q4 12-13

FY 12-13

Y-O-Y (Q4 11-12-O-

Q4 12-13)

Gross NPAs 7273 7273 7510 8507 8939 8456 8456 16.27

Gross Credit 150725 150725 154244 153601 158494 176234 176234 16.92

Gross NPA as % of gross Advance

4.83 4.83 4.87 5.54 5.64 4.80 4.80 -

Net advances 147513 147513 150952 150069 154624 171936 171936 16.56

Net NPA 4557 4557 4853 5696 5864 4988 4988 9.46

Net NPA as % of Net Advance

3.10 3.10 3.22 3.88 379 2.90 2.90 -

Page 19 of 19

***************************************************************************