Assignment 2

17

Introduction The main objective of AASB 139 Financial Instruments: Recognition and Measurement is to provide the principles for recognizing and measuring financial assets and financial liabilities. It is applicable for annual reporting periods beginning on or after 1 January 2005. Nevertheless, criticisms against the AASB 139 arose with the awareness of the shortcomings under adoption of AASB 139. As a result, AASB 9 Financial Instruments with the purpose to setting out requirements for the classification, and aspects of measurement, recognition and de-recognition of both financial assets and financial liabilities will supersede AASB 139 from 1 January 2015 and early adoption is permitted. The new standard has retained most of the rules preset in AASB 139. Meanwhile, some changes were made to the fair value option for financial liabilities to address the issue of own credit risk. The main objective of this assignment is to discuss about the shortcomings and issues of AASB 139 which has given rise to AASB 9. Two Australian listed companies have been chosen to portrait a better picture of the impacts on the accounting for financial instruments in financial statement with the future application of AASB 9. First of all, Qantas is Australia’s largest domestic and international airline and their main business is the 1

-

Upload

umonash-my -

Category

Documents

-

view

0 -

download

0

Transcript of Assignment 2

Introduction

The main objective of AASB 139 Financial Instruments:

Recognition and Measurement is to provide the principles for

recognizing and measuring financial assets and financial

liabilities. It is applicable for annual reporting periods

beginning on or after 1 January 2005. Nevertheless,

criticisms against the AASB 139 arose with the awareness of

the shortcomings under adoption of AASB 139. As a result,

AASB 9 Financial Instruments with the purpose to setting out

requirements for the classification, and aspects of

measurement, recognition and de-recognition of both

financial assets and financial liabilities will supersede

AASB 139 from 1 January 2015 and early adoption is

permitted. The new standard has retained most of the rules

preset in AASB 139. Meanwhile, some changes were made to the

fair value option for financial liabilities to address the

issue of own credit risk.

The main objective of this assignment is to discuss about

the shortcomings and issues of AASB 139 which has given rise

to AASB 9. Two Australian listed companies have been chosen

to portrait a better picture of the impacts on the

accounting for financial instruments in financial statement

with the future application of AASB 9.

First of all, Qantas is Australia’s largest domestic and

international airline and their main business is the

1

transportation of passengers using two complementary airline

brands – Qantas and Jetstar. Quantas group is currently

recognizing their financial assets and financial liabilities

at fair value in accordance with AASB 139. On the other

hand, Australian United Investment Company Limited has early

adopted AASB 9 in recognition of their financial

instruments.

Shortcomings and criticisms of AASB 139

1. Fair value measurement considerations

AASB 139 (par 43-44) stated that the measurement of a

financial asset or financial liability upon initial

recognition must be at fair value. The debate on the use of

the fair value (FV) for the measurement and classification

of long-term financial instruments has the following two

opposing views.

Firstly, the pro-view is that disclosing risk reflects the

true value of the balance sheet and thereby allows

regulators, investors, and other users of accounting

2

information to better assess a risk profile. (Bentley &

Franklin, 2003)

In contrast, the contra-view has been presented by companies

in the banking and financial industry. It is claimed that

accounting for expected risks leads to excessive and

artificial volatility of financial statements. As a

consequence, the value of the balance sheets of financial

institutions may be driven by short-term fluctuations in the

market that do not reflect the value of the fundamentals and

the long-term values of assets and liabilities. (Allen &

Carletti, 2008).

In addition, AASB 139 (par 48-49) stated that quoted prices

in an active market provide the best evidence of fair value

of a financial asset or liability. If the market for a

financial instrument is not active, a valuation technique is

used to determine fair value.

The fair value of equity or bond holdings in another listed

firm was easy to determine. Nevertheless, trying to fair

value the shares, or debt, of unlisted entities is the main

problem. It would be difficult to measure the value of a

subsidiary or associated company if there is no market

price. It is pointless as the values of these were largely

eliminated on consolidation where the company was a

subsidiary, as most were. (Orizk.net, 2006)

2. Hedge accounting

3

The criteria for hedge accounting under AASB 139 (par 89-

102) are:

i) The hedge is expected to be highly effective (ie changes

in fair value or cash flows of hedged risk are offset by

changes in fair value or cash flows of hedging instrument).

ii) The effectiveness of the hedge can be reliably measured.

iii) The hedge is continually assessed and is highly

effective (i.e. 80-125%) throughout the period the hedge is

designated for.

In addition, the ineffective portion of the hedging

instrument is recognized directly in profit or loss under a

cash flow hedge.

The issue is whether firms are able to comply with the

exacting requirements contained in AASB 139 for hedge

accounting while reflecting the underlying economic

substance of the transactions. Alternatively, the question

of whether it is appropriate that firms required reporting

their hedging activities on a fair value basis which does

not reflect the economic substance of these transactions. If

so, the concern is that this will adversely impact the

relevance of the financial statements. (Willoe & Peter,

2008).

In the 2010 annual report of Qantas Group, all derivative

transactions undertaken represent economic hedges of

4

underlying risk and exposures and group did not enter into

speculative derivative transactions. Notwithstanding this,

AASB 139 requires certain mark-to-market movements in

derivatives which are classified as ‘ineffective’ to be

recognized immediately in the Consolidated Income Statement.

Qantas Group claimed that the recognition of derivative

valuation movements in reporting periods which differ from

the designated transaction causes volatility in statutory

profit that does not reflect the hedging nature of these

derivatives.

Besides that, the group has excluded certain impacts of AASB

139: Financial Instruments: Recognition and Measurement

(AASB 139) and items that management considered to be non-

recurring in nature in order to provide more useful

information that more accurately reflects the underlying

performance of the Group. (Qantas Group, 2010).

3. Complexity

There are numerous categories of financial assets in AASB

139 while each of which had its own classification criteria.

Different issues were found within each category of

financial assets. For example,

Held-to-Maturity Investments

The categorization of financial assets as held-to-

maturity investments reflects a combination of purpose-

led classification and, to an extent, management

5

discretion. It is purpose-led because management must

have the intention to hold the asset until maturity. But

categorizing financial assets that management intends to

hold to maturity as held-to-maturity investments is not

mandatory because management has the discretion to

designate them as at fair value through profit or loss,

subject to restrictions, such as being able to reliably

measure the fair value of investments in equity

instruments. (Loftus, J., 2006).

Overcoming of issues in AASB 139

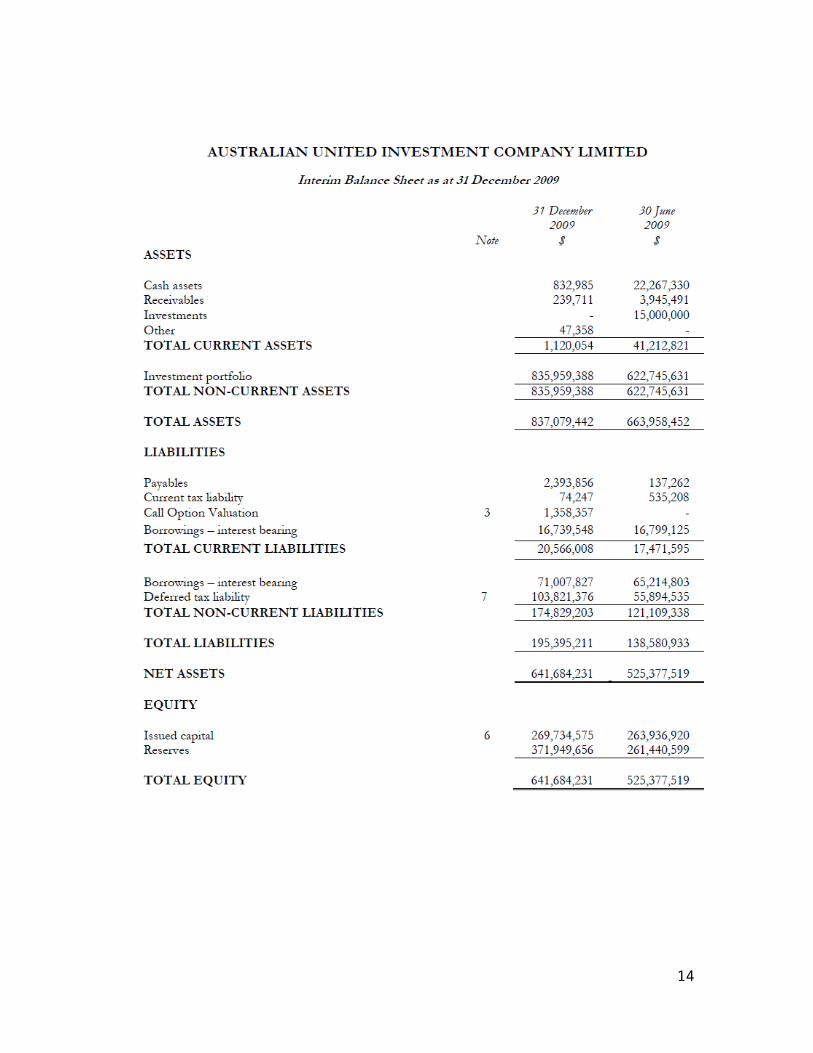

To overcome the issues faced in AASB 139 on the financial

reporting, Australian United Investment Company Limited has

early adopted AASB 9 Financial Instruments (AASB 9) with

initial application from 7 December 2009. In accordance with

AASB 9 the Company has designated its investments in equity

securities that were formerly designated as “available-for-

sale”, as “fair value through other comprehensive income” as

disclosed in their annual report of 2009. This results in

all realized and unrealized gains and losses from the

investment portfolio being recognized directly in equity

through “other comprehensive income” in the Statement of

Comprehensive Income.

The revised AASB 9 incorporates the IASB’s completed work on

Phase 1 of its project to replace AASB 139 Financial

Instruments: Recognition and Measurement on the

6

classification and measurement of financial assets and

financial liabilities. This Standard includes requirements

for the classification and measurement of financial

instruments, as well as recognition and de-recognition

requirements for financial instruments. Some changes in this

Standard compared with AASB 139 are described below.

(a) Financial assets are classified based on: the objective

of the entity’s business model for managing the financial

assets; and the characteristics of the contractual cash

flows. This replaces the categories of financial assets in

AASB 139, each of which had its own classification criteria.

In short, AASB 9 retains but simplifies the mixed

measurement model and establishes two primary measurement

categories for financial assets; amortized cost and fair

value, which will improve the reliability.

(b) Financial assets can be designated and measured at fair

value through profit or loss at initial recognition if doing

so eliminates or significantly reduces a measurement or

recognition inconsistency that would arise from measuring

assets or liabilities, or recognizing the gains and losses

on them, on different bases.

(c ) AASB 9 allows an irrevocable election on initial

recognition to present gains and losses on investments in

equity instruments that are not held for trading in other

comprehensive income. Dividends in respect of these7

investments that are a return on investment are recognized

in profit or loss and there is no impairment or recycling on

disposal of the instrument.

Conclusion

In conclusion, the objective of the standard change is to

establish principles for the financial reporting of

financial assets and financial liabilities that will present

relevant and useful information to users of financial

statements for their assessment of the amounts, timing and

uncertainty of an entity’s future cash flows. It is

appreciable as long as the standards accord with economic

development status and meet the needs of users since the

statements under new standards can provide more reliable and

useful information.

(1426

words)

References

Allen, F., &Carletti, E. (2008). Should financial

institutions mark-to-market?

Financial Stability Review, 12, 1-6. Retrieved from

http://www.banque-

france.fr/fileadmin/user_upload/banque_de_france/publications/Revue_d

8

_la_stabilite_financiere/etud1_1008.pdf

Australian United Investment Company Limited. (2009). Annualreport. Retrieved

from http://www.aui.com.au/resources/30%20June%202009%20-

%20Final%20Docs%20-%20AUI/AUI%20-

%20Annual%20Report%202009%20-%20Final.pdf

Australian Accounting Standards Board. (2004). AASB 139

‘Financial

Instruments: Recognition and measurement’. Vic.,

Australia: AASB

Australian Accounting Standards Board. (2009). AASB 9

‘Financial

Instruments. Vic., Australia: AASB

Bentley, P. A., Franklin, M. A. (2013). Which international

cultures favor

disclosure of risk. International Journal of Business, Accounting,

&

Finance. 7(2), 62-76.

Institute of Chartered Accountants Australia. (2012). AASB 9

Financial

instruments. Retrieved from

9

http://www.charteredaccountants.com.au/Industry-

Topics/Reporting/Australian-accounting-standards/

Analysis-of-AASB-

standards/AASB-9--Financial-instruments

Institute of Chartered Accountants Australia. (2012). AASB

139 Financial

instruments: recognition and measurement. Retrieved from

http://www.charteredaccountants.com.au/Industry-

Topics/Reporting/Australian-accounting-standards/

Analysis-of-AASB-

standards/AASB-139--Financial-instruments

AASB 139 (IAS 39) in Australia – The main challenges for

everyone else. (2006).

Retrieved from http://ozrisk.net/2006/09/28/aasb-139-ias-

39-in-australia-

the-main-challenges-for-everyone-else/

Loftus, J. (2006). What do you get when you mix measurement

methods and

priciples? Accounting for financial instruments.

Retrieved from

http://business.curtin.edu.au/files/Loftus.pdf

10

Qantas Group. (2010). Annual Report. Retrieved from

https://www.qantas.com.au/infodetail/about/investors/

2010AnnualReport.p

df

Willoe, F., Peter, W. (2008). Issues arising with the

implementation of AASB 139

Financial Instruments: Recognition and Measurement by

Australian firms

in the gold industry. 1-23. Retrieved from

http://epress.lib.uts.edu.au/research/bitstream/

handle/10453/11451/20080

01779.pdf?sequence=1

Appendixes

Australian United Investment Company Limited: Annual report

2009

11

12

13

14

Qantas Group: Annual report (2010)

15

16

17

![ASSIGNMENT 5 2 final edition[rev2]](https://static.fdokumen.com/doc/165x107/631535445cba183dbf07e436/assignment-5-2-final-editionrev2.jpg)