Aspiring to Excellence Annual Report 2005 - Kerry Properties ...

191

Aspiring to Excellence Annual Report 2005 (Incorporated in Bermuda with limited liability) Stock Code : 683

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Aspiring to Excellence Annual Report 2005 - Kerry Properties ...

13/F - 14/F, Cityplaza 314 Taikoo Wan RoadTaikoo Shing, Hong Kong

Telephone: (852) 2967 2200Facsimile: (852) 2967 9480

www.kerryprops.com

An

nu

al R

eport 2005

Aspiring to Excellence

Annual Report 2005(Incorporated in Bermuda with limited liability)

Stock Code : 683

Cover_eng.indd 1Cover_eng.indd 1 2006/4/7 2:59:19 PM2006/4/7 2:59:19 PM

3

The Group’s dedication towards quality and

service to customers across a fast expanding

network and the constant desire of our people

to progress and to innovate is the key to

creating value for our shareholders

1

PROPERTYThe property division of Kerry Properties Limited is engaged in the creation and management of distinguished residential neighbourhoods as well as prime-quality, strategically-located mixed-use developments. These are being presented as part of a real estate network offering innovative value-added features and services throughout the Asia-Pacifi c region.

LOGISTICS NETWORKKerry Logistics Network Limited (Kerry Logistics) has established a leading position as Asia’s premier supply chain management expert and third-party logistics service provider, both in terms of customer satisfaction and shareholder value. With a China focus and being an Asia specialist, Kerry Logistics has progressively built up world-class capabilities to access and empower the supply chains of niche customer sectors across the globe.

INFRASTRUCTUREThe infrastructure division’s strategy is to work side-by-side with strategic public or private-sector partners in infrastructure developments, committing itself to those projects that improve the quality of life and that contribute towards the conservation of our environment for future generations.

BOARD OF DIRECTORS

Executive DirectorsMr ANG Keng Lam

Chairman

Mr WONG Siu KongDeputy Chairman andManaging Director

Mr HO Shut Kan

Mr MA Wing Kai, William

Independent Non-executive DirectorsMr William Winship FLANZ

Mr LAU Ling Fai, Herald

Mr Christopher Roger MOSS, O.B.E.

Non-executive DirectorMr TSE Kai Chi

AUDIT COMMITTEEMr Christopher Roger MOSS, O.B.E.

Chairman

Mr LAU Ling Fai, Herald

Mr TSE Kai Chi

FINANCE COMMITTEEMr ANG Keng Lam

Mr WONG Siu Kong

Mr HO Shut Kan

REMUNERATION COMMITTEEMr ANG Keng Lam Chairman

Mr WONG Siu Kong

Mr William Winship FLANZ

Mr LAU Ling Fai, Herald

Mr Christopher Roger MOSS, O.B.E.

QUALIFIED ACCOUNTANTMs CHANG Yin Wa

COMPANY SECRETARYMs LI Siu Ching, Liz

PRINCIPAL BANKERSBank of China (Hong Kong) Limited

Bank of Communications Co., Ltd.

The Bank of East Asia, Limited

BNP Paribas

Calyon

China Construction Bank Corporation

Citigroup

DBS Bank Ltd

Hang Seng Bank Limited

The Hongkong and Shanghai Banking Corporation Limited

Industrial and Commercial Bank of China (Asia) Limited

Standard Chartered Bank (Hong Kong) Limited

AUDITORSPricewaterhouseCoopers

Certifi ed Public Accountants

PROPERTY VALUERSSavills (Hong Kong) Limited

DTZ Debenham Tie Leung Limited

LEGAL ADVISERS

Hong Kong LawDeacons

Stephenson Harwood & Lo

Bermudian LawAppleby Spurling Hunter

PRC LawFangda Partners

STOCK CODESStock Exchange of Hong Kong: 683

Bloomberg: 683 HK

Reuters: 683.HK

REGISTERED OFFICECanon’s Court22 Victoria StreetHamilton HM12Bermuda

HEAD OFFICE AND PRINCIPAL PLACE OF BUSINESS13/F & 14/F, Cityplaza 314 Taikoo Wan RoadTaikoo Shing, Hong Kong

BRANCH OFFICE21/F, CITIC TowerNo 1 Tim Mei AvenueCentral, Hong Kong

WEBSITEwww.kerryprops.com

PRINCIPAL SHARE REGISTRAR AND TRANSFER OFFICEButterfi eld Fund Services (Bermuda) LimitedRosebank Centre11 Bermudiana RoadPembroke, Bermuda

HONG KONG BRANCH REGISTRAR AND TRANSFER OFFICEAbacus Share Registrars Limited26/F, Tesbury Centre28 Queen’s Road EastWanchai, Hong Kong

CONTACTCorporate Communications DepartmentKerry Properties Limited13/F & 14/F, Cityplaza 314 Taikoo Wan RoadTaikoo Shing, Hong KongTelephone: (852) 2967 2200Facsimile: (852) 2967 9480

KEY DATES

Closure of Registers of Members28 April 2006 to 3 May 2006

Annual General Meeting3 May 2006

Proposed Payment of Final Dividend/ Despatch of Share Certifi cates in respect of Scrip Dividend9 June 2006

Corporate Information & Key Dates

4 Financial Highlights

8 2005 Business Highlights

10 Chairman’s Statement

Management Discussion & Analysis

13 Overall Results

14 Review of Property Business

26 Review of Logistics Business

32 Review of Infrastructure Business

34 Financial Review

36 Particulars of Properties Held

49 Corporate Social Responsibility Report

51 2005 Awards

52 Corporate Governance Report

67 Audit Committee Report

68 Remuneration Committee Report

69 Internal Controls

70 Directors and Senior Management

73 Report of the Directors

91 Auditors’ Report

92 Consolidated Income Statement

93 Consolidated Balance Sheet

94 Balance Sheet

95 Consolidated Cash Flow Statement

97 Consolidated Statement of Changes in Equity

99 Notes to the Consolidated Financial Statements

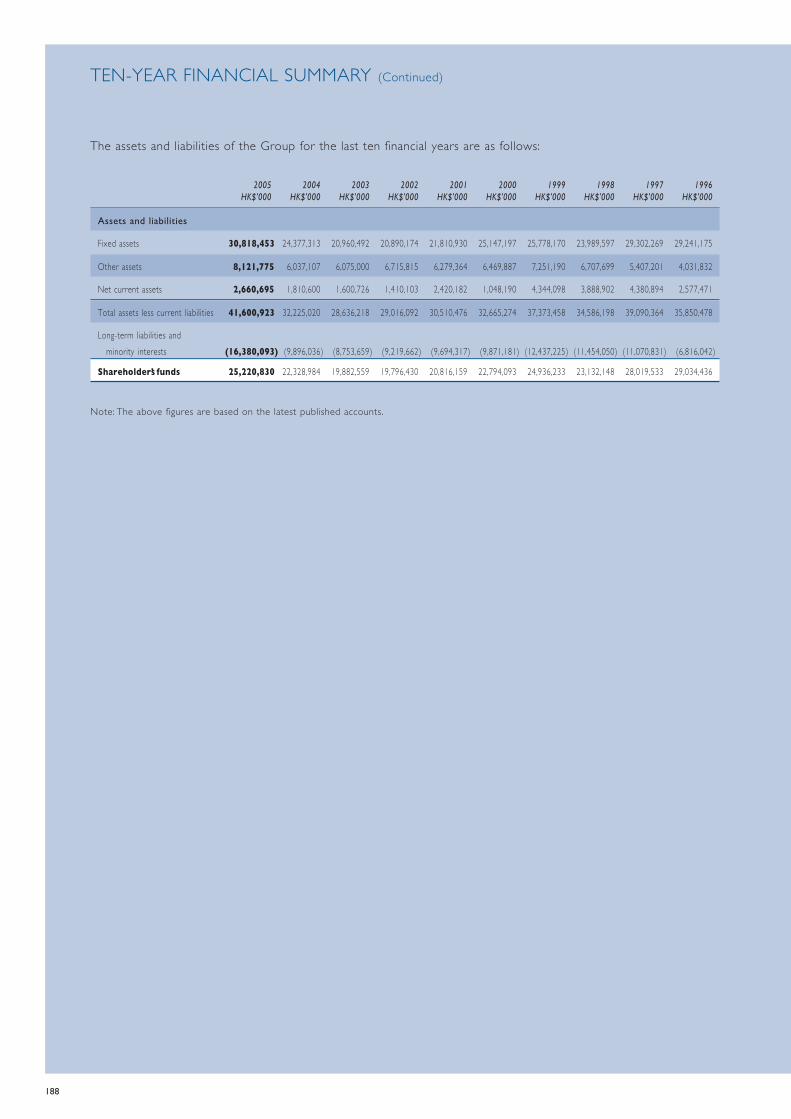

187 Ten-Year Financial Summary

Contents

4

TWO-YEAR OVERVIEWFY 2005 FY 2004 % Change

Turnover (HK$M) 8,009 5,102 +57%Gross profi t (HK$M) 2,273 1,840 +24%Gross profi t margin (%) 28.4 36.1Operating profi t (HK$M) 3,246 1,733 +87%Operating profi t margin (%) 40.5 34.0Profi t attributable to shareholders (HK$M) - before fair value change of properties 1,759 1,580 +11% - after fair value change of properties 3,067 2,271 +35%Net profi t margin (%) - before fair value change of properties 22.0 31.0

- after fair value change of properties 38.3 44.5Earnings per share (HK$) - before fair value change of properties 1.45 1.32 +10% - after fair value change of properties 2.53 1.90 +33%Shareholders’ equity (HK$M) 25,221 22,329 +13%Net borrowings (HK$M) 9,184 3,923 +134%Net asset value per share (HK$) 20.73 18.44 +12%Share price as at 31 December (HK$) 20.55 16.60 +24%Price earnings ratio# (times) - before fair value change of properties 14.2 12.6 - after fair value change of properties 8.1 8.7Market capitalization as at 31 December# (HK$M) 25,001 20,105 +24%Dividend per share (HK$) 0.7 0.6 +17%Dividend payout ratio (%) - before fair value change of properties 48.3 45.5 - after fair value change of properties 27.7 31.7Dividend cover (times) - before fair value change of properties 2.1 2.2 - after fair value change of properties 3.6 3.2Dividend yield# (%) 3.4 3.6Return on shareholders’ equity (%) - before fair value change of properties 7.0 7.1 - after fair value change of properties 12.2 10.2Gearing (%) 36 18Interest cover (times) - before fair value change of properties 9.9 12.2 - after fair value change of properties 16.1 14.0Current ratio (times) 1.7 1.6Liquidity ratio (times) 1.5 1.3Discount to net asset value# (%) 0.9 10.0

# Based on share price as at 31 December 2005 and 31 December 2004, respectively.

Financial Highlights

5

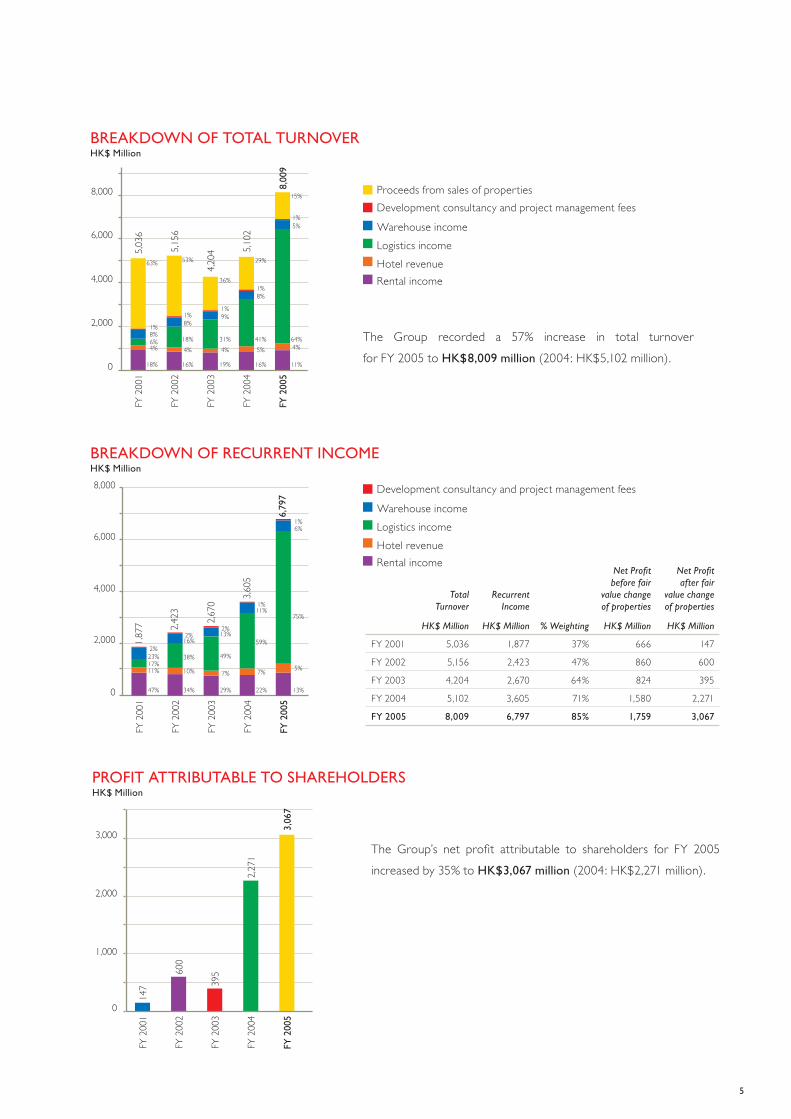

The Group’s net profi t attributable to shareholders for FY 2005 increased by 35% to HK$3,067 million (2004: HK$2,271 million).

The Group recorded a 57% increase in total turnoverfor FY 2005 to HK$8,009 million (2004: HK$5,102 million).

BREAKDOWN OF TOTAL TURNOVERHK$ Million

Hotel revenue

Warehouse income

Development consultancy and project management fees

Logistics income

Rental income

BREAKDOWN OF RECURRENT INCOMEHK$ Million

Total Turnover

HK$ Million

Recurrent Income

HK$ Million % Weighting

Net Profi t before fair

value change of properties

HK$ Million

Net Profi t after fair

value change of properties

HK$ Million

FY 2001 5,036 1,877 37% 666 147

FY 2002 5,156 2,423 47% 860 600

FY 2003 4,204 2,670 64% 824 395

FY 2004 5,102 3,605 71% 1,580 2,271

FY 2005 8,009 6,797 85% 1,759 3,067

PROFIT ATTRIBUTABLE TO SHAREHOLDERSHK$ Million

Hotel revenue

Warehouse income

Development consultancy and project management fees

Logistics income

Rental income

Proceeds from sales of properties

6

PROFIT ATTRIBUTABLE TO SHAREHOLDERS BY DIVISION (before fair value change of properties) HK$ Million

FY 2005

FY 2004

PROFIT ATTRIBUTABLE TO SHAREHOLDERS BY DIVISION (after fair value change of properties)HK$ Million

EARNINGS PER SHARE (before exceptional items)HK$

Profi t attributable to shareholders

(by division)

2005

HK$ Million

2004

HK$ Million % Change

PRC Property 295 441 -33%

Hong Kong Property 780 603 29%

Overseas Property 65 27 141%

Logistics Network 507 438 16%

Infrastructure 38 31 23%

Project, Property Management and Others 74 40 85%

1,759 1,580 11%

Profi t attributable to shareholders

(by division)

2005

HK$ Million

2004

HK$ Million % Change

PRC Property 372 548 -32%

Hong Kong Property 1,429 1,187 20%

Overseas Property 69 27 156%

Logistics Network 1,085 438 148%

Infrastructure 38 31 23%

Project, Property Management and Others

74 40 85%

3,067 2,271 35%

EARNINGS PER SHARE (after exceptional items)HK$

FY 2005

FY 2004

Financial Highlights (Continued)

7

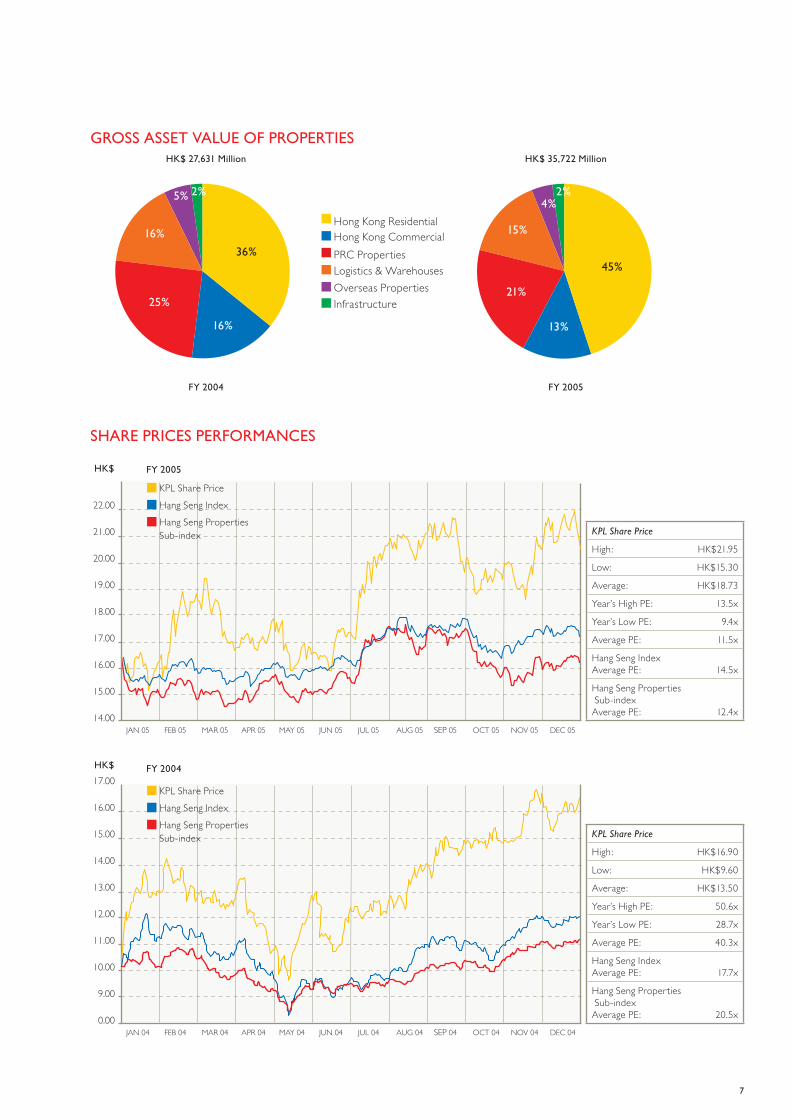

GROSS ASSET VALUE OF PROPERTIESHK$ 27,631 Million

36%

16%

25%

2%

16%

5%

45%

13%

21%

2%

15%

4%

FY 2005FY 2004

HK$ 35,722 Million

Hong Kong Residential

PRC Properties

Infrastructure

Logistics & WarehousesOverseas Properties

Hong Kong Commercial

HK$ FY 2005

KPL Share PriceHang Seng IndexHang Seng Properties Sub-index

FY 2004

KPL Share PriceHang Seng IndexHang Seng Properties Sub-index

KPL Share Price

High: HK$21.95

Low: HK$15.30

Average: HK$18.73

Year’s High PE: 13.5x

Year’s Low PE: 9.4x

Average PE: 11.5x

Hang Seng Index Average PE: 14.5x

Hang Seng Properties Sub-indexAverage PE: 12.4x

KPL Share Price

High: HK$16.90

Low: HK$9.60

Average: HK$13.50

Year’s High PE: 50.6x

Year’s Low PE: 28.7x

Average PE: 40.3x

Hang Seng Index Average PE: 17.7x

Hang Seng Properties Sub-indexAverage PE: 20.5x

SHARE PRICES PERFORMANCES

HK$

8

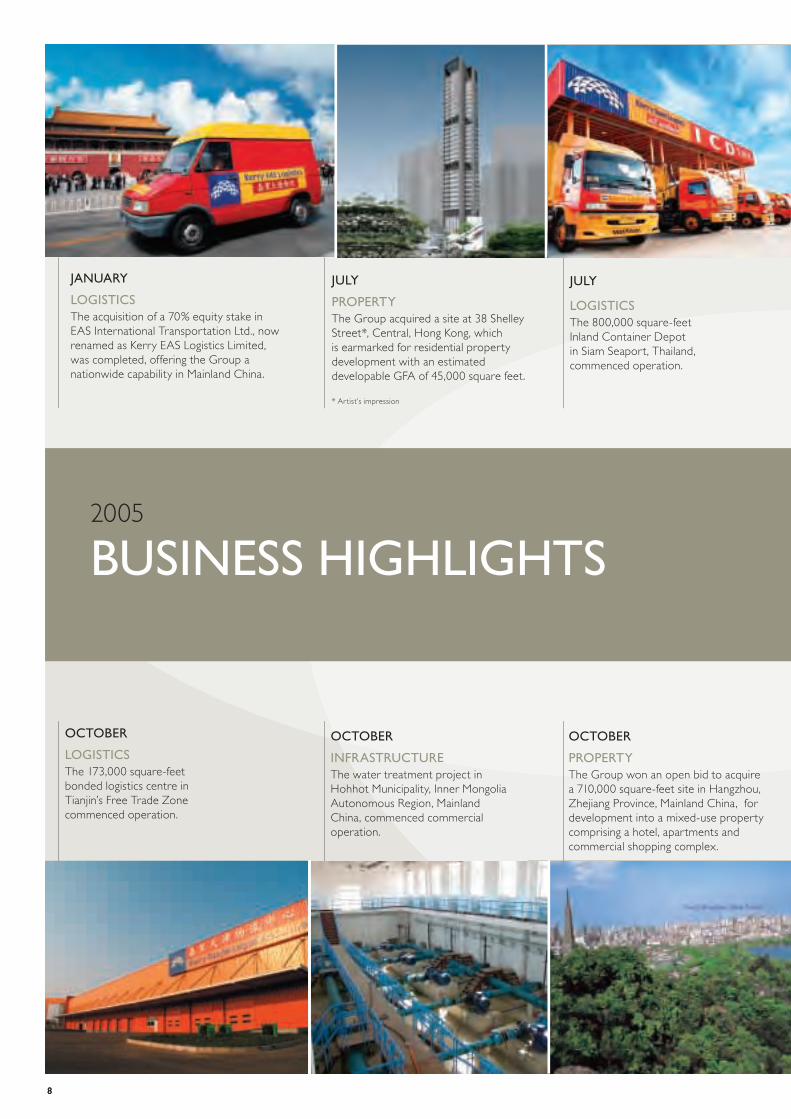

2005

BUSINESS HIGHLIGHTS

JANUARY

LOGISTICSThe acquisition of a 70% equity stake in EAS International Transportation Ltd., now renamed as Kerry EAS Logistics Limited, was completed, offering the Group a nationwide capability in Mainland China.

JULY

PROPERTYThe Group acquired a site at 38 Shelley Street*, Central, Hong Kong, which is earmarked for residential property development with an estimated developable GFA of 45,000 square feet.

* Artist’s impression

OCTOBER

LOGISTICSThe 173,000 square-feet bonded logistics centre in Tianjin’s Free Trade Zone commenced operation.

OCTOBER

INFRASTRUCTUREThe water treatment project in Hohhot Municipality, Inner Mongolia Autonomous Region, Mainland China, commenced commercial operation.

OCTOBER

PROPERTYThe Group won an open bid to acquire a 710,000 square-feet site in Hangzhou, Zhejiang Province, Mainland China, for development into a mixed-use property comprising a hotel, apartments and commercial shopping complex.

JULY

LOGISTICSThe 800,000 square-feet Inland Container Depot in Siam Seaport, Thailand, commenced operation.

8

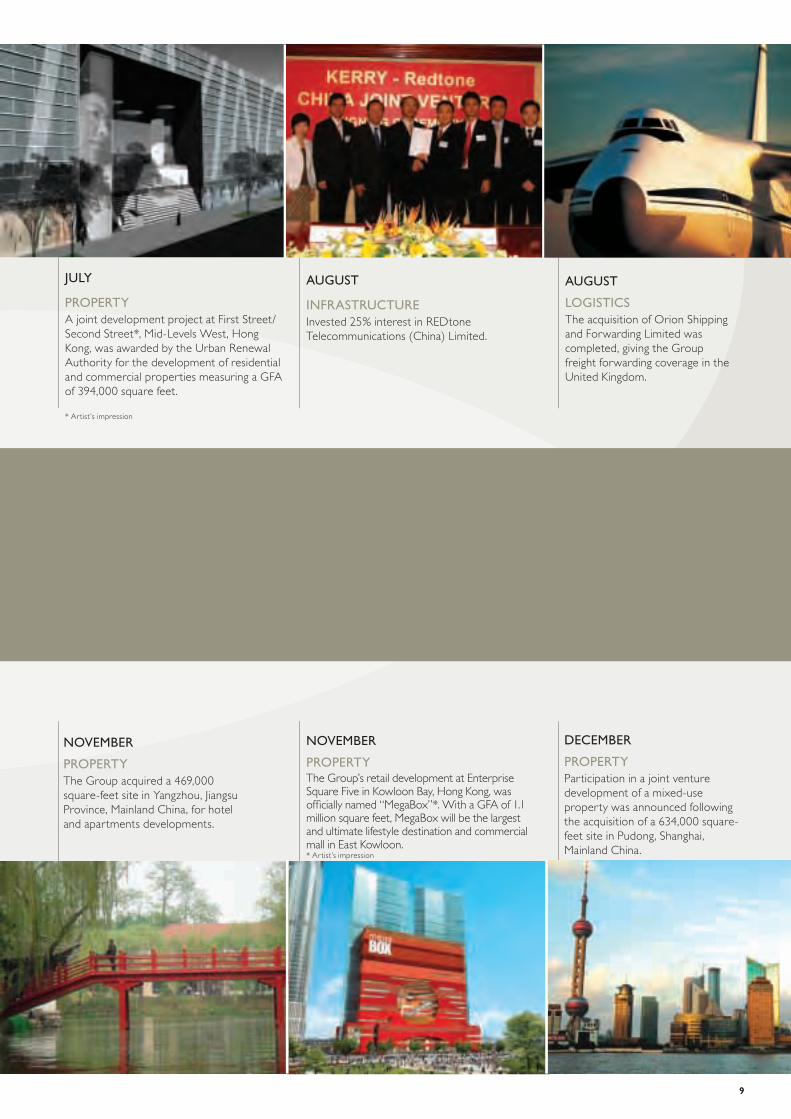

9

JULY

PROPERTYA joint development project at First Street/Second Street*, Mid-Levels West, Hong Kong, was awarded by the Urban Renewal Authority for the development of residential and commercial properties measuring a GFA of 394,000 square feet.

* Artist’s impression

AUGUST

INFRASTRUCTUREInvested 25% interest in REDtone Telecommunications (China) Limited.

AUGUST

LOGISTICSThe acquisition of Orion Shipping and Forwarding Limited was completed, giving the Group freight forwarding coverage in the United Kingdom.

NOVEMBER

PROPERTYThe Group’s retail development at Enterprise Square Five in Kowloon Bay, Hong Kong, was offi cially named “MegaBox”*. With a GFA of 1.1 million square feet, MegaBox will be the largest and ultimate lifestyle destination and commercial mall in East Kowloon.* Artist’s impression

DECEMBER

PROPERTYParticipation in a joint venture development of a mixed-use property was announced following the acquisition of a 634,000 square-feet site in Pudong, Shanghai, Mainland China.

NOVEMBER

PROPERTYThe Group acquired a 469,000 square-feet site in Yangzhou, Jiangsu Province, Mainland China, for hotel and apartments developments.

9

10

It gives me great pleasure to report to shareholders the annual results of Kerry Properties Limited (the “Company”), its subsidiaries and associated companies (collectively, the “Group”) for the year ended 31 December 2005.

RESULTSThe Group’s profi t attributable to shareholders for the year ended 31 December 2005 was HK$3,067 million, representing an increase of 35% compared with HK$2,271 million reported for 2004. The increase in the Group’s earnings is attributable to the 29% increase in earnings contribution from the Hong Kong property business, the 16% increase from the logistics business and the increase in fair values of investment properties which were recognized in the Group’s income statement during the year.

Earnings per share for the year were HK$2.53, representing an increase of 33% compared with HK$1.90 per sharein 2004.

Shareholders should note that these are the fi rst annual results published by the Company following the adoption of a number of new or revised Hong Kong accounting standards which took effect from 1 January 2005. The most signifi cant of these is the adoption of the fair value model in the accounting treatment of investment properties. Set out below are the effects of adopting this accounting policy on the Group’s profi t attributable to shareholders.

The Board has recommended the payment of a fi nal dividend of HK$0.50 per share for the year, with a scrip dividend alternative. Together with the interim dividend of HK$0.20 per share, the total dividend for the year ended 31 December 2005 will be HK$0.70 per share, representing an increase of 17% compared with HK$0.60 per sharein 2004.

HIGHLIGHTS OF THE GROUP’S OPERATIONS IN 2005

I. Property investment and developmentMainland China

Our Mainland China Property Division recorded a net profi t attributable to shareholders of HK$372 million during the year, representing a decrease from HK$548 millionin 2004.

As a result of the Central Government’s policy to relieve pricing pressures, the past year was characterized by a slowdown in residential property sales in Mainland China. However, our investment property portfolio, including Beijing Kerry Centre, Shanghai Kerry Centre and Shenzhen Kerry Centre, continued to enjoy high occupancy rates and generated strong recurrent earnings for the Group. During the year, we also took the opportunity to add quality sites measuring a total developable GFA of 4.6 million square feet to our development land bank.

In October 2005, we entered a joint venture agreement with Shangri-La Asia Limited, Allgreen Properties Limited and Shanghai Lujiazui Finance & Trade Zone Development Co. Ltd. to develop a mixed-use project in Shanghai’s prestigious Pudong District, located near the Shanghai New International Expo Centre. We have a 40.8% interest in this prime development which measures a total of 2.48 million square feet in GFA. This project will complement the

Chairman’s

STATEMENT

Year ended 31 December

2005HK$ million

2004HK$ million Increase

Profi t attributable to shareholders before taking into account the net change in fair values/revaluation surplus of investment properties and related tax effects 1,759 1,580 11%

Add:Net change in fair values/

revaluation surplus of investment properties and related tax effects 1,308 691

Profi t attributable to shareholders 3,067 2,271 35%

Mr Ang Keng LamChairman of the Board of Directors

11

development of Shanghai’s Pudong District in the lead-up to the 2010 Shanghai Expo event.

The Group is also investing in and capitalizing on the growth of major secondary cities which are undergoing economic expansion. We have acquired prime sites in Hangzhou with a buildable GFA of 1.8 million square feet, and in Yangzhou with a buildable GFA of 1 million square feet.

These investments are in line with the Group’s core business strategy of developing large scale mixed-use properties, catering to the needs of the increasingly affl uent consumers in Mainland China.

Hong Kong

Our Hong Kong Property Division recorded a net profi t attributable to shareholders of HK$1,429 million during the year, representing an increase from HK$1,187 millionin 2004.

In 2005, Hong Kong’s strong economy led to a signifi cant upward movement in both residential and offi ce rental rates. The Group capitalized on the high demand for quality offi ce space and luxury residential properties, by selling certain properties at attractive profi t margins during the year.

Before the year end, we have settled the land premiums for the property developments in Ap Lei Chau and Tsuen Wan. Furthermore, the Group acquired a number of prime sites on Hong Kong Island this year; these include one located at Shelley Street in the popular “SOHO” District, and another located at First Street/Second Street in Mid-Levels West. These sites offer excellent development potential for the Group.

During the year, the Group made strong progress with the Enterprise Square Five development in Kowloon Bay. It is a large retail entertainment complex (known as “MegaBox”) with twin tower grade-A offi ces, and is a major component of our property portfolio in Hong Kong. Upon its completion in mid-2007, Enterprise Square Five will become a leading landmark within the district, and will further enhancethe value of the Group’s adjacent existing offi ce and commercial properties.

As at 31 December 2005, properties under development in Hong Kong measured an aggregate GFA of 3.1 million square feet, which provides a strong land bank for our development programme in Hong Kong up to 2009.

Macau

Macau witnessed a thriving economy in 2005. We remain optimistic on the future of Macau and its potential economic growth, and the Group is committed to developing a luxury residential project in the city.

II. Logistics NetworkKerry Logistics Network Limited, the Group’s Logistics Division, recorded net profi t attributable to shareholders of HK$1,085 million during the year, representing an increase from HK$438 million in 2004.

The Logistics Division carried out extensive expansion plans in 2005. In Thailand, we completed the construction of an 800,000 square-feet Inland Container Depot in Siam Seaport, located near Laem Chabang, South of Bangkok. In Europe, we expanded our operations to Spain and also acquired two local companies in the United Kingdom engaged in various logistics services. We entered an agency agreement with Lynden International, a US-based company with offi ces in the United States, Canada, Mexico and Puerto Rico, to develop trans-Pacifi c freight forwarding businesses.

In Mainland China, a major milestone was marked for the division after our acquisition of a 70% equity interest in EAS International Transportation Ltd., now renamed Kerry EAS Logistics Limited (“KEAS”). Established for over 20 years with over 120 offi ces serving over 1,100 cities throughout Mainland China, KEAS is now one of the leading logistics operators in Mainland China. Furthermore, with the completion of a 173,000 square-feet bonded logistics centre in Tianjin’s Free Trade Zone in 2005 along with others strategically located in the Free Trade Zones of Yantian, Beijing and Shanghai’s Waigaoqiao, we now have a bonded logistics centre portfolio of over 1 million square feet in total.

12

Through strategic alliances and acquisitions, our network now covers Mainland China, various parts of Asia, Europe, Australia and North America. We have business operations in 13 countries, and have grown to become a major Asian-based international logistics operator.

In recognition of our outstanding achievements, Kerry Logistics was the winner of the Local (Hong Kong) Logistics Award and the Mainland Logistics (non-SME) Award at the Logistics Awards Hong Kong 2005, organized by the Hong Kong Trade Development Council and four other renowned local trade associations.

III. InfrastructureThe Division recorded net profi t attributable to shareholders of HK$38 million in 2005 (2004: HK$31 million), which is mainly attributable to its investment in the Western Harbour Crossing in Hong Kong. We will continue to focus on investment opportunities in the utilities, energy recycling and environmental protection-related sectors in Mainland China to generate recurrent income for the Group.

PROSPECTS

Mainland China’s economy demonstrated a robust performance in 2005, with GDP growth of 9.9%, a strong export sector and low domestic infl ation. We believe this strong performance will continue in 2006. The introduction of the State Council’s land tender policies has meant increased transparency and better accessibility for foreign investors to acquire land in Mainland China. We believe that the Central and Provincial Governments will continue to invest in more quality infrastructure and allocate more resources to the rural areas, as 2006 marks the fi rst year of the Central Government’s eleventh Five-Year Plan. Under such an economic environment, we expect strong liquidity and increased affordability, fuelling the local demand for quality properties.

Similarly, Hong Kong experienced a year of strong growth. With GDP growth of 7.6%, infl ation maintained at 1% and an overall increase in wage levels, Hong Kong’s property market experienced a rise in demand. Our outlook for 2006 remains positive; this is primarily due to the aforementioned

sustainable economic growth of Mainland China, Hong Kong’s niche in the trade and fi nancial services sectors and its booming tourism industry. The market’s expectation of an end to the interest rate hikes will also have a positive effect on the property sector.

On the logistics front, we aim to widen our global client base and to enhance our international profi le. We will continue to venture into new markets such as India, the Middle East and other parts of Europe, in search of strategic alliances and investments to expand our business network. We will continue to invest in advanced technology for our logistics operations as we believe that technological innovation is paramount in maintaining our competitive advantage inthe industry.

In line with our mission statement of “Aspiring to Excellence”, we will continue to develop a portfolio of premium assets in the property, logistics and infrastructure sectors. With a positive economic outlook for 2006, the Group will participate in development opportunities which we believe not only benefi t the communities we invest in, but also offer optimal fi nancial returns to the Group and to our shareholders.

APPRECIATION

On behalf of the Board, I would like to express my sincere appreciation to the Group’s management and staff for their diligence, loyalty and dedication. I am grateful to the members of the Board for their valuable counsel and guidance, as well as to our investors and strategic partners for their unfailing support and confi dence which has ultimately contributed towards the Group’s success.

Ang Keng Lam

Chairman

Hong Kong, 24 March 2006

CHAIRMAN’S STATEMENT (Continued)

Management Discussion & Analysis

OVERALL RESULTSThe Group continued to demonstrate a strong fi nancial performance during the year ended 31 December 2005. Turnover of the Group for the year was HK$8,009 million, which registered an increase of 57% when compared with the turnover of HK$5,102 million for 2004. The Group’s turnover mainly comprises proceeds from the continuing sales of properties, rental income as well as revenue from hotel operations, warehouse operations and logistics services. The increase in turnover during the year was attributable to the growth in rental income, the improved performance of Beijing Kerry Centre Hotel and the revenue contribution from logistics services.

In accordance with the new Hong Kong accounting standard on accounting for investment properties, the change in fair values of investment properties is recorded in the income statement. During the year ended 31 December 2005, the net change in fair values of the Group’s investment properties and related tax effects in the aggregate amount of HK$1,308 million was recognized in the Group’s consolidated income statement.

The effect on the Group’s profi t attributable to shareholders due to the net change in fair values/revaluation surplus of the Group’s investment properties and related tax effects is as follows:

Excluding the effect of the net change in fair values/revaluation surplus of the Group’s investment properties and related tax effects, the 11% year-on-year increase in the profi t attributable to shareholders is mainly attributable to the Hong Kong Property Division and the Logistics Network Division, which demonstrated a year-on-year increase of 29% and 16%, respectively.

13

Year ended 31 December

2005HK$ million

2004HK$ million Increase

Profi t attributable to shareholders before taking into account the net change in fair values/revaluation surplus of investment properties and related tax effects 1,759 1,580 11%

Add:Net change in fair values/

revaluation surplus of investment properties and related tax effects 1,308 691

Profi t attributable to shareholders 3,067 2,271 35%

14

OVERVIEW

During the year ended 31 December 2005, the Group acquired a number of new property sites in Hong Kong and Mainland China. These acquisitions effectively increased the Group’s land bank, and enabled the Group to reap the benefi ts of the positive outlook of the property sectors in these territories.

As at 31 December 2005, the Group maintained a portfolio (measured in gross fl oor area (“GFA”)) comprising 16.17 million square feet (2004: 11.03 million square feet) of properties under development, 7.47 million square feet (2004: 7.48 million square feet) of completed investment properties and 0.22 million square feet (2004: 0.56 million square feet) of properties held for sale. Such a portfolio provides the Group with an opportunity to enjoy the attractive fi nancial returns arising from the sales of properties, as well as from leased properties. This portfolio will generate a strong sales and recurrent income maintaining the Group’s positive growth momentum going forward.

PROPERTY PORTFOLIO COMPOSITION24.37 million square feet of GFA

Investment Properties/Hotel Property

7.98 million square feet

33%

67%

29%

23%

48%

11%20%

17%

52%Hong Kong

OverseasMainland ChinaMacau

By Location

Review of

PROPERTY BUSINESSBalanced Portfolio, Premium Brand, Delivering Quality,Regional Focus.

Management Discussion & Analysis

Properties Under Development/Held for Sale

16.39 million square feet

15

MAINLAND CHINA PROPERTY DIVISION

During the year ended 31 December 2005, the Mainland China Property Division reported turnover of HK$1,012 million (2004: HK$1,351 million) and a net profi t attributable to the Group of HK$372 million (2004: HK$548 million), after taking into account the increase in fair values of investment properties (after deferred taxation) of HK$77 million (2004: HK$107 million). Excluding the effect of the increase in fair value of investment properties (after deferred taxation), net profi t attributable to the Group amounted to HK$295 million (2004: HK$441 million). The decrease in turnover and net profi t in 2005 is mainly due to the decrease in the sales of properties in Mainland China compared with 2004.

The Division remains extremely selective in its choice of new investments. In terms of new property developments, prime locations are preferred where land supply is relatively restricted, in order to ensure sustainable asset value and strong resilience during periods of market uncertainties. Behind this strategy also lies a long-standing mission for the Group to build on its expertise and reputation in Mainland China’s property market in creating a profi le of strategically-located, high-end properties in élite neighbourhoods.

The Group continues to focus on the development of large-scale, mixed-use property projects in key locations. The cross-marketing effect between the various categories of a mixed-use property development project will inevitably enhance property values and rental rates.

Investment PropertiesDuring the year ended 31 December 2005, the Group’s portfolio of investment properties in Mainland China generated rental turnover and operating profi t from rental activities of HK$542 million and HK$428 million, respectively (2004: HK$493 million and HK$363 million, respectively).

The Group’s investment property portfolio in Mainland China as at 31 December 2005 comprised an aggregate GFA of 3.33 million square feet (2004: 3.37 million square feet). The geographical distribution of the Group’s investment properties in Mainland China is set out in the table below.

PROPERTY PORTFOLIO COMPOSITION

Mainland China (sq.ft.) Hong Kong (sq.ft.) Macau (sq.ft.) Overseas (sq.ft.) Total GFA (sq.ft.)

Investment Properties 3,334,070 1,803,751 - 2,336,897 7,474,718

Properties Under Development 8,446,719 3,146,151 2,800,000 1,780,695 16,173,565

Properties Held for Sale 27,714 179,068 - 13,304 220,086

Hotel Property 499,642 - - - 499,642

Total GFA 12,308,145 5,128,970 2,800,000 4,130,896 24,368,011

INVESTMENT PROPERTIES IN MAINLAND CHINA

Beijing (sq.ft.) Shanghai (sq.ft.) Shenzhen (sq.ft.) Fuzhou (sq.ft.) Total GFA (sq.ft.)

Offi ce 814,665 632,259 132,204 - 1,579,128

Commercial 184,998 400,707 107,256 63,986 756,947

Residential 277,330 148,688 - - 426,018

Carparks & Others 194,698 235,075 142,204 - 571,977

Total GFA 1,471,691 1,416,729 381,664 63,986 3,334,070

16

As at 31 December 2005, the Group’s investment property portfolio of offi ce, commercial and residential properties achieved occupancy rates of 95%, 92% and 72%, respectively (2004: 97%, 97% and 72%, respectively). Highlights of the occupancy rates of the Group’s major investment properties in Mainland China as at 31 December 2005 were as follows:

OCCUPANCY RATES OF MAJOR INVESTMENT PROPERTIES IN MAINLAND CHINA

Property

Occupancy rateas at

31 December 2005

Occupancy rateas at

31 December 2004

Beijing Kerry Centre 89% 89%

Shanghai Kerry Centre 91% 89%

Shenzhen Kerry Centre 96% 96%

Kerry Everbright City Phase I 95% 98%

Sales of Completed PropertiesSales of completed properties during the year ended 31 December 2005 contributed turnover and operating profi t of HK$149 million and HK$37 million, respectively (2004: HK$595 million and HK$196 million, respectively).

Turnover and profi t contributions from property sales in Mainland China recorded during 2005 were generated mainly from the sales of units of Arcadia Court and Regency Park Phase IIIB in Shenzhen and Central Residences in Fuzhou.

Properties under DevelopmentThe Group made key investments in Mainland China during the year ended 31 December 2005, with a view to develop a balanced portfolio of properties for sale, development and investment. The Group continues to build on its strong presence in Shanghai, Beijing and Shenzhen, and has begun to explore property development opportunities in major secondary cities which are experiencing economic growth in order to tap into their market potential and increasingly affl uent consumer sectors.

In relation to the mixed-use property development project in Jingan District, Shanghai, the Company and Shangri-La Asia Limited (“SA”) jointly announced in December 2005 that all the underlying contract approvals had been obtained

REVIEW OF PROPERTY BUSINESS (Continued)

Futian Offi ce,*Shenzhen, Mainland China (right)

Kerry Everbright City Phase II,* Shanghai, Mainland China (far right)

* Artist’s impression

PROPERTIES UNDER DEVELOPMENT IN MAINLAND CHINA

Shanghai (sq.ft.)

Shenzhen (sq.ft.)

Beihai (sq.ft.)

Hangzhou (sq.ft.)

Yangzhou (sq.ft.)

Manzhouli (sq.ft.)

Total GFA upon completion

(sq.ft.)

Residential 1,367,638 - - - - - 1,367,638

Apartments 328,747 - - 376,740 494,283 627,444 1,827,214

Offi ce 1,076,372 807,300 - - - - 1,883,672

Commercial 384,737 - 77,350 861,120 - 88,868 1,412,075

Hotel 825,900 - - 592,020 538,200 - 1,956,120

Total GFA upon completion 3,983,394 807,300 77,350 1,829,880 1,032,483 716,312 8,446,719

Management Discussion & Analysis

17

from the PRC Government, apart from one supplemental contract relating to one of the sites within the project. Accordingly, the deadline for the execution of all the underlying contracts for the project was extended to 30 June 2006 (or such other date as the Company and SA may agree). Development and construction works of the project are expected to commence in the fourth quarter of 2006.

Completion of Central Residences Phase II, a luxury residential development in Changning District, Shanghai, is scheduled for the second quarter of 2006. Structural, mechanical and electrical works have been completed and interior fi nishes are in progress. The project will have a total developable GFA of 641,000 square feet.

Upon completion, the mixed-use Kerry Everbright City Phase II development in Shanghai will deliver a total GFA of 1,576,000 square feet, and is designated for offi ce, residential and retail purposes. With the Phase IIa foundation works completed and basement works in progress, the residential towers are expected to be completed in the second quarter of 2007. Phase IIb foundation works are currently in progress.

In Shenzhen, development of the 807,000 square-feet grade-A offi ce complex in Futian Central District is scheduled for completion in the third quarter of 2007. Meanwhile, development of a 323,000 square-feet site in Manzhouli, Inner Mongolia, is expected to be completed by 2009.

MAINLAND CHINA

PROPERTY PORTFOLIO12.31 million square feet of GFA

Investment Properties/Hotel Property

3.84 million square feet

Properties under Development/Held for Sale

8.47 million square feet

1%

47%

10%

22%

12%8%

Shenzhen

ShanghaiBeijingHangzhou

Fuzhou/Beihai

YangzhouManzhouli

By location

Hotel

CommercialOffi ceResidential

ApartmentsCarparks & others

By type

13%20%

41%

11%

15%

37%

51%

10%

2%

17%

23%

22%

22%

16%

31%

69%

18

In November 2005, the Group announced its successful acquisition from the Hangzhou Bureau of Land Resources of a site in Xia Cheng District, Hangzhou, Zhejiang Province. The total developable site area is 710,000 square feet, offering a total buildable GFA of 1,830,000 square feet and will be earmarked for a mixed-use development comprising a hotel, apartments and a commercial shopping complex. It is scheduled for completion in 2009. The site is strategically located close to the famous Xihu (West Lake) tourist attraction and the major commercial district along Yan An Road. The rapid economic growth of the Yangtze River Delta Region is expected to generate a strong demand for high-end residential and commercial properties in the area including Hangzhou, giving the Group a competitive advantage with long-term growth prospects.

In November 2005, the Group also acquired a land site in Yangzhou, Jiangsu Province. The site has an area of 469,000 square feet and offers a total buildable GFA of 1,032,000square feet for hotel and apartment developments, which are scheduled for completion in 2009.

In December 2005, the Group jointly announced with SA the acquisition of a 634,000 square-feet site in Pudong, Shanghai, to be developed into a mixed-use property comprising hotel, offi ces, serviced suites/serviced apartments, commercial properties and related ancillary facilities. The site is located adjacent to the Shanghai New International Expo Centre. The site is expected to offer an above-ground buildable GFA of 2,476,000 square feet, and is scheduled for completion in 2009. The Group has a 40.8% interest in this joint venture project, for which the Group’s maximum commitment is US$240,720,000 (approximately HK$1,877,616,000).

Based on the new projects mentioned above, the Group acquired four land sites with a total buildable GFA measuring 4.6 million square feet during the year which comprisethe following:

REVIEW OF PROPERTY BUSINESS (Continued)

TOTAL BUILDABLE GFA OF LAND SITES ACQUIRED DURING THE YEAR

Project Location Usage Group’s Interest

Group’s attributable buildable GFAas at 31 December 2005

(sq.ft.)

Manzhouli Apartments/ Commercial

Manzhouli, Inner Mongolia Apartments/Commercial 100% 716,312

Hangzhou Complex Development Hangzhou Apartments/Commercial/ Hotel

100% 1,829,880

Yangzhou Complex Development Yangzhou Apartments/Hotel 100% 1,032,483

Shanghai New International Expo Complex Development

Pudong, Shanghai Offi ce/Apartments/ Commercial/Hotel

40.8% 1,010,094

Total buildable GFA 4,588,769

Management Discussion & Analysis

19

Beijing Kerry Centre,Beijing, Mainland China (far left)

Mid-Levels residential properties, Hong Kong (left)

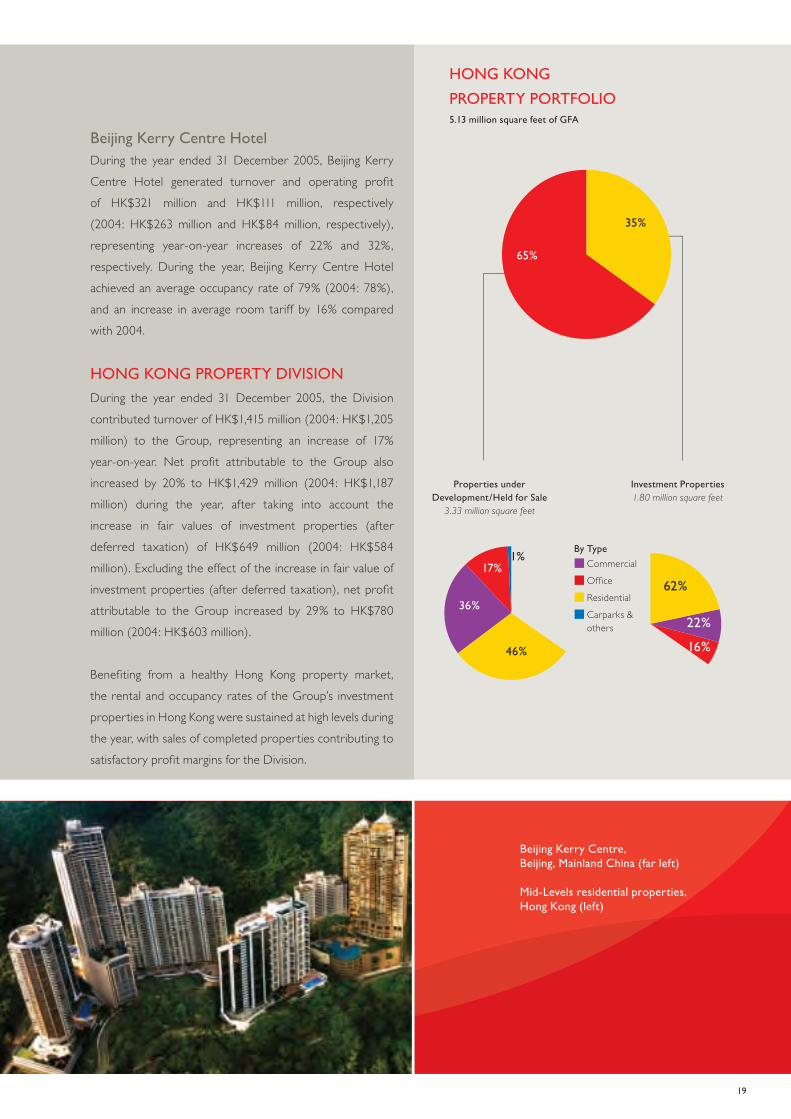

Beijing Kerry Centre HotelDuring the year ended 31 December 2005, Beijing Kerry Centre Hotel generated turnover and operating profi t of HK$321 million and HK$111 million, respectively (2004: HK$263 million and HK$84 million, respectively), representing year-on-year increases of 22% and 32%, respectively. During the year, Beijing Kerry Centre Hotel achieved an average occupancy rate of 79% (2004: 78%), and an increase in average room tariff by 16% compared with 2004.

HONG KONG PROPERTY DIVISION

During the year ended 31 December 2005, the Division contributed turnover of HK$1,415 million (2004: HK$1,205 million) to the Group, representing an increase of 17% year-on-year. Net profi t attributable to the Group alsoincreased by 20% to HK$1,429 million (2004: HK$1,187 million) during the year, after taking into account the increase in fair values of investment properties (after deferred taxation) of HK$649 million (2004: HK$584 million). Excluding the effect of the increase in fair value of investment properties (after deferred taxation), net profi t attributable to the Group increased by 29% to HK$780 million (2004: HK$603 million).

Benefi ting from a healthy Hong Kong property market, the rental and occupancy rates of the Group’s investment properties in Hong Kong were sustained at high levels during the year, with sales of completed properties contributing to satisfactory profi t margins for the Division.

HONG KONG

PROPERTY PORTFOLIO5.13 million square feet of GFA

Investment Properties1.80 million square feet

Properties under Development/Held for Sale

3.33 million square feet

1%

36%

46%

17%

Carparks & others

CommercialOffi ceResidential

By Type

22%

16%

62%

35%

65%

20

Investment PropertiesThe Group’s premium portfolio of investment properties continue to provide steady income and earnings contributions to the Group. During the year ended 31 December 2005, the Group’s portfolio of investment properties in Hong Kong generated rental turnover of HK$352 million (2004: HK$303 million) and operating profi t of HK$135 million (2004 : HK$111 million).

As at 31 December 2005, the Group held an investment property portfolio in Hong Kong measuring an aggregate GFA of 1.8 million square feet which comprisesthe following:

INVESTMENT PROPERTIES IN HONG KONG

Total GFA (sq.ft.)

Residential 1,117,697

Commercial 391,594

Offi ce 294,460

Total GFA 1,803,751

As at 31 December 2005, the Group’s investment property portfolio of offi ce, commercial and residential properties achieved occupancy rates of 96%, 94% and 93%, respectively (2004 : 93%, 89% and 97%, respectively).

The brand was created to address the Group’s value-added services for tenants of its prestigious residential investment properties. This initiative is currently being replicated throughout the Group’s fast-growing networks in Hong Kong and Mainland China.To extend its service pledge, the Group has introducednew cross-boundary tenant benefi ts and other exclusive lifestyle services.

Sales of Completed PropertiesSales of completed properties during the year ended 31 December 2005 were HK$1,063 million (2004: HK$902 million), representing an increase of 18% year-on-year. The turnover in 2005 was mainly generated from the sales of (i) the remaining residential units at Constellation Cove; (ii) certain units at Tregunter Towers on a strata-title basis; (iii) one luxury residential unit at Branksome Crest, Mid-Levels; (iv) offi ce units at Enterprise Square Three, Kowloon Bay; and (v) the Group’s entire property interests in AXA Centre, an offi ce property in Wanchai. The Division generated operating profi t of HK$516 million from property sales during the year (2004: HK$312 million), which represents an increase of 65% year-on-year.

REVIEW OF PROPERTY BUSINESS (Continued)

15 Homantin Hill Road,Ho Man Tin, Kowloon, Hong Kong (right)

The Ball Atrium of MegaBox*,Kowloon Bay, Hong Kong (far right)

* Artist’s impression

Management Discussion & Analysis

21

Properties under ConstructionEnterprise Square Five is another major grade-A retail, entertainment and offi ce project in the Group’s development blueprint. The development has a planned GFA of 1.6 million square feet, of which 1.1 million square feet have been assigned to accommodate MegaBox, a proprietary family destination and the largest commercial mall in East Kowloon. Pre-leasing activities of MegaBox

commenced in the fourth quarter of 2005, whilst the pre-leasing activities of the offi ce properties of Enterprise Square Five is expected to commence in the third quarter of 2006. With a scheduled completion date of mid-2007, Enterprise Square Five is expected to add further value to the Group’s existing portfolio of quality properties in Kowloon Bay, and will certainly enhance the Group’s presence and profi le in the Kowloon Bay area.

The Group’s high-end residential property project at 15 Homantin Hill Road, Kowloon, is scheduled for completion in the second quarter of 2006. This project will add a further 155,000 square feet of GFA to the Group’s prominent residential portfolio in Hong Kong.

In July 2005, the Group acquired a site in Central Mid-Levels at No. 38 Shelley Street. A residential tower with commercial facilities, measuring an estimated developable GFA of 45,000 square feet, is scheduled for completion at the end of 2007.

Properties under PlanningHong Kong

The redevelopment of No. 5 and No. 9 Yuk Yat Street in To Kwa Wan, Kowloon, progressed further. With thedemolition plan approved by Buildings Department, the demolition work has commenced in March 2006. Construction works are expected to commence in the fourth quarter of 2006, with completion scheduled for the fourth quarter of 2009. The site has a developable GFA of 163,000 square feet and has been earmarked for residential and commercial purposes.

22

The Group has completed its site investigation work in respect of a site located at First Street/Second Street Mid-Levels West, Hong Kong. This 394,000 square-feet residential and commercial development, which is a joint development with the Urban Renewal Authority, is scheduled for completion in the fourth quarter of 2008. This development will become a landmark in the Mid-Levels West which has a well-established neighbourhood of commercial activities as well as élite secondary and tertiary education.

Furthermore, in December 2005, the Group acquired a property with GFA measuring 37,000 square feet, located at 26-30 Des Voeux Road West, Hong Kong for redevelopment purposes.

During the year, the Group paid the land premium for the 398,000 square-feet residential property development project in Kwok Shui Road, Tsuen Wan. Project planning has progressed according to schedule and with commencement of construction in the third quarter of 2006, the project is scheduled for completion by the second quarter of 2009. Furthermore, the Group also paid the land premium for the residential property development project in Ap Lei Chau, in which the Group has a 35% interest. The Group has an attributable share of GFA measuring 320,000 square feet in this development project, which is scheduled for completion by the second quarter of 2009.

MacauNegotiations with the Macau SAR Government on the Group’s land acquisition made further progress during the year. The Group commenced discussions with the Macau SAR Government on the conceptual design for the planned residential development for a maximum GFA of 2,800,000 square feet, and approval is expected to be granted in the coming months.

The residential property development project in Macau has been conceived in line with the Macau SAR Government’s objective of providing a low to medium-density, high-quality living environment in Macau. With Macau’s growing economy and its progressive integration with the Pearl River Delta Region driven by infrastructure investments and positive economic performances, the Group remains optimistic about the future prospects of the property market in Macau.

REVIEW OF PROPERTY BUSINESS (Continued)

First Street/Second Street Project*,Mid-Levels West, Hong Kong (left)

Jacksons Landing, Sydney, Australia (right)

* Artist’s impression

Management Discussion & Analysis

23

OVERSEAS PROPERTY DIVISION

During the year ended 31 December 2005, the Overseas Property Division generated a net profi t to the Group of HK$68 million (2004: HK$27 million). The signifi cant increase in the Group’s share of profi t from this Division is mainly attributable to a reduction in the deferred taxation rate in respect of revaluation gain on investment properties, and the change in fair value of investment properties during the year.

As at 31 December 2005, the Group had an investment property portfolio of 2.34 million square feet (2004: 2.23 million square feet) in the Philippines, and a portfolio of

properties held for development and for sale of 1.8 million square feet (2004: 1.8 million square feet) in Australia and the Philippines.

AustraliaAs at 31 December 2005, sales of 868 units (2004: 837 units) of the Group’s 25%-owned Jacksons Landing project were completed, representing 85% of a total of 1,024 units available for sale. This project, located at the Pyrmont Peninsula in Sydney, covers a site of 12 hectares and is designated for residential and commercial property development.

OVERSEAS PROPERTY PORTFOLIO

Australia (sq.ft.) The Philippines (sq.ft.) Total GFA (sq.ft.)

Investment Properties

Hotel lease - 191,832 191,832

Shopping centre lease - 240,697 240,697

Carpark lease - 211,203 211,203

Shopping centre - 1,191,763 1,191,763

Commercial - 11,316 11,316

Offi ce - 174,522 174,522

Carpark and others - 315,564 315,564

Sub-total - 2,336,897 2,336,897

Properties under Development/Held for Sale

Residential 151,851 1,606,288 1,758,139

Offi ce 35,860 - 35,860

Sub-total 187,711 1,606,288 1,793,999

Total GFA 187,711 3,943,185 4,130,896

24

Shangri-La Plaza Mall,Manila, The Philippines (left)

Lobby of Kerry Residence,Beijing, Mainland China (centre)

Swimming Pool of Branksome Crest,Mid-Levels, Hong Kong (far right)

The PhilippinesThe Group’s investments in property interests in the Philippines continue to be held through its 73.88% aggregate direct and indirect interests in EDSA Properties Holdings Inc. (“EPHI”). EPHI is listed on the Philippines Stock Exchange and holds a 78.72% interest in the Shangri-La Plaza Mall, Manila, and indirect interests in The Enterprise Centre, an offi ce and commercial property in Makati, Manila’s fi nancial district.

As at 31 December 2005, the Shangri-La Plaza Mall reported an occupancy rate of 96% (2004: 98%), whilst the occupancy rate at The Enterprise Centre was 96% (2004: 87%).

The Shang Grand Tower in Manila, in which EPHI holds a 67% benefi cial interest, was completed in the fi rst quarter of 2006. As at 31 December 2005, 84% (2004: 53%) of the units of The Shang Grand Tower was sold. Development of The St. Francis Towers project, which is designed to deliver approximately 1,200 residential units from the project’s two 60-storey towers, is scheduled for completion at the end of 2008.

OUTLOOKMainland ChinaThe year 2005 witnessed a continuation of the Group’s expansion policy into Mainland China’s property market. Despite the State Council’s policies to control overheating in property markets in the metropolitan cities, the Group remains optimistic about Mainland China’s property market in the long term. This is primarily due to the continuing economic growth of Mainland China and the constantly improving living standards of the urban community.

Land reform policies launched by the State Council at the end of 2004 and higher resettlement costs have raised public awareness of the increased protection being afforded by civil rights, which make land clearance more diffi cult and hence result in a more restricted land supply. This will, in turn, lead to greater stability in property prices in the future.

Moreover, the property market in Mainland China will continue to be supported by the increasing level of foreign investments, which generate a continuous demand for quality residential, offi ce and commercial properties. To this end, the Group will maintain its strategy in the development of high-end mixed-use properties in the primary and major secondary cities in order to accommodate the demand from both domestic and foreign users.

REVIEW OF PROPERTY BUSINESS (Continued)

Management Discussion & Analysis

25

Looking ahead, the Group will continue to explore development opportunities in the primary and major secondary cities in Mainland China, which are enjoying economic growth and hence an increasingly affl uent consumer sector. The Group plans to apply its successful business model and established track record which have worked in property developments in Beijing, Shanghai and Shenzhen, so as to take advantage of the new opportunities offered by the major secondary cities.

Hong KongThe Group holds a positive future outlook of the Hong Kong property market, which is reinforced by the growing Hong Kong economy, the stabilized unemployment rate, improved household wealth and affordability, and the expectation of an end to the interest rate hikes in 2006. On the other hand, land supply through the application system with the Hong Kong Government, or by way of private tenders or public auctions, have proceeded in an orderly manner creating a favourable demand and supply dynamics for Hong Kong’s property market.

Despite the recent softening in property sales, the long term prospects for luxury and high-end properties are expected to remain positive. The Directors maintain the view that rental rates and property prices for luxury residences and grade-A offi ces will maintain an upward trend.

Capitalizing on the positive outlook for the property market, the Group will continue to explore development opportunities of high-end properties to uphold the Group’s status as a leading developer of premium properties. Furthermore, as part of the Group’s ongoing marketing strategy, the Group will continue to leverage off its

brand to cover both its existing and future luxury property portfolio.

26

Review of

LOGISTICS BUSINESSAsia Based, China Focus, Global Network.

OVERVIEW

During the year ended 31 December 2005, the Division recorded a turnover of HK$5,541 million which represents a strong growth of 121% when compared with HK$2,502 million in 2004. Profi t attributable to shareholders for the year amounted to HK$1,085 million (2004: HK$438 million). Excluding the effects of the increase in fair values of the warehouse properties, logistics centres and buildings (after deferred taxation) of HK$578 million (2004: nil), profi t for the year attributable to operations amounted to HK$507 million which represents a growth of 16% when compared with 2004 and of which (i) HK$163 million (2004: HK$176 million) was contributed by warehousing operations; (ii) HK$129 million (2004: HK$74 million) was contributed by logistics operations; and (iii) HK$215 million (2004: HK$188 million) was contributed by the Division’s investments in associated companies.

Under the name of Kerry Logistics Network Limited (“Kerry Logistics”), the Division operates a portfolio of warehouses, logistics centres and port facilities of over 16 million square feet and a truck fl eet of over 2,000 vehicles, with operations in more than 150 cities in 13 countries worldwide.

LOGISTICS AND DISTRIBUTIONBeing recognized as a key logistics player in the Asia region, Kerry Logistics strives to strengthen and expand its logistics presence across the world. During the year, the volumes of both air and sea cargoes handled by Kerry Logistics have more than doubled in growth when compared with 2004.

In addition to the ISO9001 quality accreditation which the Division has secured since 1998, during the year, Kerry Logistics’ Hong Kong logistics operation was also proud to be awarded the Technology Asset Protection Association Asia Certifi cation in recognition of its high-value electronic and technology products logistics solutions.

Management Discussion & Analysis

27

In Hong Kong, the Division continued to secure large logistics contracts during the year, including an integrated logistics contract with one of the largest wine distributors in Hong Kong. Meanwhile, the Division also assists some high-end fashion brands and chemical clients in establishing their regional logistics hubs in Hong Kong to support their Asian and Mainland China markets.

The trading arm of the Division, KerryFlex Supply Chain Solutions Limited (“KerryFlex”), demonstrated signifi cant growth in its businesses during the year. Supported by the Division’s infrastructure, KerryFlex has a diverse and sizable customer base ranging from healthcare to catering, and lately to fast-moving grocery establishment. In March 2006, KerryFlex completed the acquisition of a 100% interest in a Hong Kong local company which is engaged in the business of import and distribution of non-perishable products for over 50 years. The acquisition enables KerryFlex to establish its foothold in the food service sector, and paves the way for the Division to participate in procurement projects for hotel chains.

China FocusDuring the year, Kerry Logistics further strengthened its logistics foothold in Mainland China by the acquisition of a 70% equity stake in EAS International Transportation Ltd. (now renamed Kerry EAS Logistics Limited (“KEAS”)), which was completed in January 2005. The acquisition marks an important development in the continuing expansion of Kerry Logistics’ network and creates a strong and valuable platform for growth. The acquisition provides Kerry Logistics with a leading nationwide logistics operation network in Mainland China, serving over 1,100 cities in over 32 provinces with over 120 offi ces, 4,000 staff, 1,500 vehicles and over two million square feet of warehouse and logistics facilities.

The fi rst year of operation following the establishment of KEAS has been a success, where the synergies between Kerry Logistics and KEAS begin to materialize. With the integration of KEAS’s business with Kerry Logistics’ existing operations in Mainland China, the KEAS-Kerry Logistics business combination provides the Division with a pan-China coverage of extensive facility infrastructure. With more than 700 operating licenses in Mainland China, the strengthened China network of Kerry Logistics offers a comprehensive range of high-quality logistics solutions to its existing clients. The new KEAS implements a modern management approach to strengthen its existing operational platform, and to support modern logistics demand of its customers. KEAS also intends to expand to overseas markets and reinforce its business growth by tapping into Kerry Logistics’ global network. Other internal re-engineering programme within the combined operations of KEAS and Kerry Logistics, including the restructuring of management systems, agency network and other overseas businesses, are now underway and are scheduled to be completed by the end of 2006.

During the year, construction of the 173,000 square-feet bonded logistics centre in Tianjin’s Free Trade Zone was completed in October 2005. This facility, located near the biggest container hub in Northern China – Tianjin Xingang, incorporates multi-functional warehouses for general cargoes as well as temperature-controlled cargoes and is the Division’s biggest bonded facility in the Northern China region. Commencement of operation is scheduled in the second quarter of 2006.

The construction of the 269,000 square-feet bonded logistics centre in Shenzhen’s Futian Free Trade Zone is also in progress and is scheduled to be completed by the fi rst half of 2006. Meanwhile, the Division is also exploring the possibility to construct its own logistics facilities in other coastal cities in Mainland China, such as Shanghai and Xiamen.

28

Asia BasedDuring the year, Kerry Siam Seaport Limited (“KSSP”) completed the construction of a 800,000 square-feet Inland Container Depot (“ICD”) in Siam Seaport and obtained the offi cial operating license in July 2005. The ICD, together with the container berth expansion which is under construction and is scheduled for completion by late 2006, will spearhead the Division’s efforts in entering the container cargo handling business, and thereby adding value to its existing conventional and bulk cargo services. The extended facility will enable KSSP to handle a maximum of seven ocean vessels at any point in time. Meanwhile, Kerry Logistics is also exploring the possibility of further expanding its warehousing and logistics operations in Thailand through construction of depots and a nationwide distribution network.

2005 also saw a signifi cant growth of Kerry Logistics’ freight forwarding and logistics operations in Singapore, Malaysia and Indonesia in which Kerry Logistics has a 66.67% interest. These business operations commenced in early 2004, and have since developed into sizable operations in their respective regions.

Global NetworkLeveraged off its growing international network, Kerry Logistics is steadily increasing its geographical presence in the European and the United States markets through acquisitions and strategic alliances with key local players.

During the year, Orion Shipping and Forwarding Limited (“Orion”), one of the leading export freight forwarders in the United Kingdom, joined Kerry Logistics’ growing network of freight operation. Founded and based in the United Kingdom with offi ces in Manchester and Birmingham, Orion provides clients with sea, air and long-haul services together with specialist handling of large-scale project cargoes. The acquisition was completed in August 2005 when Kerry Logistics (UK) Limited (“KLUK”), a 91% subsidiary of Kerry Logistics, acquired a 63.5% interest in Orion. Orion and KLUK will be strategically placed to handle the logistics requirements of Kerry Logistics’ clients in the rapidly expanding Asian markets, particularly Mainland China.

In June 2005, Kerry Logistics entered an exclusive contractual agreement with Lynden International (“Lynden”), a leading freight forwarding company in the United States, to combine the sales and operating resources in North America with those in Asia. Such a partnership offers Kerry Logistics’ customers a comprehensive trans-Pacifi c network of services covering Mainland China and various Asian countries.

REVIEW OF LOGISTICS BUSINESS (Continued)

Management Discussion & Analysis

29

Other infrastructure and logistics centres under construction outside Asia includes the construction of a 88,000 square-feet logistics centre in Australia. The facility is scheduled for completion in early 2007.

WAREHOUSING AND DISTRIBUTION CENTRES — HONG KONGThe Division continues to be the single largest warehouse owner and operator in Hong Kong, with a portfolio of13 warehouses occupying an aggregate GFA of 6.74 million square feet. Through continuous service innovation and quality maintenance, the Division’s warehouse portfolio in Hong Kong achieved an occupancy of 97% as at31 December 2005 (2004: 96%).

The increase in market interest rates during 2005 has led to a drop in the overall demand for warehouse space during the year due to the tighter business control of the customers including a reduction in the levels of inventories, particularly with regard to dangerous goods, bonded cargoes and frozen products. Nevertheless, the Division expects a moderate growth in its warehousing operation in Hong Kong, as the continuous re-development of industrial buildings has reduced the supply of general cargo space in the market.

LOGISTICS INFRASTRUCTURE AND ASSOCIATED COMPANIES The Division’s logistics infrastructure investments continue to enjoy satisfactory growth. During the year, Chiwan Container Terminal (“CCT”) and Asia Airfreight Terminal (“AAT”) made very good progress and contributed a steady source of recurrent earnings to the Division.

AAT, being one of the two air cargo terminals located at the Hong Kong International Airport and in which Kerry Logistics has a 15% interest, handled an increased cargo volume throughput of 579,000 tons during the year (2004: 551,000 tons).

2005 was also a record year for CCT, in which Kerry Logistics has a 25% interest. With the construction of new berths and continuous improvement in its operational effi ciency, CCT’s volume throughput reached 3.6 million TEUs (Twenty-Foot Equivalent Units) in 2005. CCT, which is located on the eastern side of the Pearl River Delta in Shekou, Shenzhen, is considered to be one of the most cost-competitive terminals in the Pearl River Delta region.

During the year, the Division’s equity share of profi ts after tax from CCT and AAT and other associated companies amounted to HK$215 million (2004: HK$188 million).

30

INFORMATION TECHNOLOGY

To facilitate the Division’s growth in the higher-end supply chain solutions market, a new initiative “KerrierVISION” was introduced in the second half of 2005 to address the gap between the outsourcing of supply chain management services and the provision of third party logistics services.

“KerrierVISION” is an application platform on top of the existing “Kerrier” family of operational systems. It provides comprehensive visibility throughout the pipeline from both goods and costs perspectives. In addition, the events management engine can orchestrate proactive supply chain management in terms of monitoring control and execution. It enables an accurate and timely decision-makingprocess through the use of business intelligence information facilities. “KerrierVISION” will continue to be the top priority for the Division’s information technology initiatives in the coming year to ensure the Division’s leading position in the logistics market.

In terms of emerging technology, the Division has been working closely with the “Hong Kong R&D Center for Logistics & Supply Chain Management Enabling Technology” on the latest technological developments such as Radio Frequency Identifi cation (RFID), supply chain modelling and industry-specifi c solutions. We are confi dent that Kerry Logistics will continue to maintain its leading position in applying technology in the logistics industry.

In Mainland China, the fi rst phase of the Kerrier Freight Management System (“KerrierFMS”) Enhancement Project was completed during the year. Further enhancement will continue to be made to fi t the business requirements of KEAS. In addition, a reorganization of KEAS’s Beijing Headquarters’ information technology initiatives was also carried out, which will help KEAS’s Beijing Headquarters to demonstrate a more dominant role in the management and development of information technology for application to the logistics industry in Mainland China.

AWARDS AND ACHIEVEMENTS In November 2005, Kerry Logistics was the winner of two major awards in the fi rst Logistics Awards Hong Kong 2005 – namely, the Local (Hong Kong) Logistics Award and the Mainland Logistics (non-SME) Award. Organized by the Hong Kong Trade Development Council and four other renowned local trade associations, the awards recognized and rewarded Kerry Logistics’ outstanding services in the logistics industry in Hong Kong and Mainland China.

REVIEW OF LOGISTICS BUSINESS (Continued)

Management Discussion & Analysis

31

In Mainland China, KEAS was also the winner of several awards in 2005 in recognition of its outstanding performance in air freight, express and logistics services. KEAS was also certifi ed as a “5A” Integrated Logistics Services Company by China Federation of Logistics & Purchasing. KEAS now ranks 7th amongst the top 100 international freight forwarding companies in Mainland China, and ranks 9th amongst the top 50 logistics companies in Mainland China (in terms of turnover in 2004).

OUTLOOK

Leveraging off the strengthened capabilities of the new KEAS, going forward, the Division aims to further reinforce its logistics competitiveness in Mainland China by extending its supply chain management services, further exploring the import and export markets, strengthening its infrastructure, developing its information system and operational expertise, as well as consolidating the Mainland China operations with its overseas agency network. Meanwhile, the Division will also continue to enhance the communication and coordination between its operations in Hong Kong and in Mainland China, in order to provide quality and ‘one-stop-shop’ services to customers on a pan-China scale. On the other hand, the Division will continue to capitalize on the fast-expanding trade between Mainland China and the rest of the world, following the opening up of Mainland China’s logistics market to foreign ownership since late 2005.

Besides the Mainland China market, in view of the continuing consolidation with key players in the global logistics industry, the international logistics and freight forwarding market is expected to undergo rapid changes and increasing competition in the years to come. To cope with these changes, the Division will speed up its globalization process by strengthening its overseas sales network, particularly in the United States, Europe and Australia, in order to maintain Kerry Logistics’ competitiveness with the major global logistics operators worldwide.

32

Review of

INFRASTRUCTUREBUSINESSViable Projects, Environmental Focus,Community Contribution.

OVERVIEW

The Infrastructure Division invests in a range of infrastructure, environmental protection, utilities and energy-related projects in Hong Kong and Mainland China. Through such investments, the Division aims to contribute towards the improvement of the living environment and living standards of the community, as well as the delivery of a steady stream of recurrent income to the Group. During the year ended 31 December 2005, the Division generated net profi t attributable to the Group of HK$38 million(2004: HK$31 million).

HONG KONG

In Hong Kong, the Group has a 15% interest in theWestern Harbour Crossing and a 15% interest in the Cross Harbour Tunnel management contract. The Group’s share of net profi ts from these investments amounted to HK$41 million for the year ended 31 December 2005 (2004: HK$31 million).

MAINLAND CHINADue to the increasing awareness and concerns of the community towards health standards and the quality of life and the increasing demand for energy resources by the community, the Group focuses its investments on environmental protection, utilities and energy-related projects.

Management Discussion & Analysis

33

On 28 February 2005, the Standing Committee of the National People’s Congress endorsed the Renewable Energy Law. The new law, which became effective on 1 January 2006, establishes a platform for the extensive development of renewable energy projects, particularly for commercial uses. Taking into account the market environment and capitalizing on the benefi ts of new policy incentives, the Division continues to focus on projects in three infrastructure areas: water treatment, sewage treatment and municipal solid-waste treatment (including waste-to-energy facilities).

In December 2004, the Group announced its investment in a water treatment project in Hohhot Municipality, Inner Mongolia Autonomous Region. Together with Chemquest (Overseas) Limited (“Chemquest”), a Kuok Group company with a strong and proven background in operating environmental engineering projects across Asia, the Group entered into a 50/50 joint venture known as Kerry CQ JV Environmental Engineering Limited, which has a 26.01% effective interest in a project company engaged in the ownership, operation and maintenance of certain water treatment facilities in Hohhot Municipality. Accordingly, the Group has an effective 13% interest in this project. The maximum total investment amount by Kerry CQ JV Environmental Engineering Limited in this project is RMB143 million (equivalent to approximately HK$138 million), of which the Group’s share is RMB71.5 million (equivalent to approximately HK$69 million). The project commenced commercial operation on 19 October 2005.

In February 2005, the Group tendered for a greenfi eld project to build and operate the fi rst solid waste management facilities in Changzhou, Jiangsu Province. Again, together with Chemquest, the Group entered into a 51/49 joint venture in the establishment of Kerry CQ Waste Incineration Limited which in turn has a 45% interest in a project company, with the remaining 55% interest being held by Golden State Holding Group Corporation and Beijing Golden State Engineering Co., Ltd.. Subsequent to the tender, the project company was chosen by the Changzhou Municipal Government for exclusive negotiation of a concession

agreement. If the terms of the investment are acceptable to the project company as a result of the ongoing negotiations, the project will be undertaken on a build-operate-transfer (BOT) basis, which comprises the building and operation of one of the most advanced incinerator systems in Mainland China.

In August 2005, the Group invested a 25% interest in REDtone Telecommunications (China) Limited (“REDtone China”), which carries out the business operations in Mainland China of REDtone International Bhd., a leading discount telecommunication calls provider in Malaysia. REDtone China plans to invest HK$58.5 million in developing and expanding its operations in the Mainland China market by collaborating with China TieTong Telecommunications Corporation Shanghai Branch Company, in the provision of long-distance, domestic and international discount call packages to mobile phone and fi xed-line subscribers. The Group’s share of investment amount in REDtone China is HK$14.625 million. Capitalizing on the proven success of the business model, experience and expertise of REDtone International Bhd. in Malaysia and the Group’s working knowledge of the Mainland China market, excellent synergies are being offered by the REDtone China joint venture in strengthening the Group’s presence in Mainland China’s telecommunications market.

OUTLOOK

Going forward, the Division will continue to identify and evaluate investment opportunities in commercially viable projects in the utilities, energy recycling and environmental protection-related sectors in Mainland China which will generate strong recurrent income for the Group. In doing so, the Group will leverage off its working knowledge of the Mainland China market and capitalize on the skills and expertise of technical project partners, thereby optimizing fi nancial returns to the Group.

Management Discussion & Analysis

FINANCIAL REVIEW

The Group has centralized funding for all its operationsat the Group level where foreign exchange exposure isalso reviewed and monitored. This policy also achieves better control of treasury operations and lower average cost of funds.

Foreign exchange exposure for the Group is small relative to its total asset base. As at 31 December 2005, total foreign currency borrowings (excluding Renminbi (RMB) borrowings) amounted to the equivalence of HK$652 million and RMB loans amounted to the equivalence of HK$202 million. Therefore, non-RMB total foreign currency borrowings and RMB loans represented approximately 6% and 2%, respectively, of the Group’s total borrowings of HK$11,748 million as at 31 December 2005.

Out of the Group’s total borrowings as at 31 December 2005, HK$1,017 million (representing approximately 9%) was repayable within one year, HK$4,214 million (representing approximately 36%) was repayable within two years, HK$6,514 million (representing approximately 55%) was repayable between three to fi ve years and HK$3 million (representing less than 1%) was repayable over fi ve years. The Group continued to maintain most of its borrowings on an unsecured basis, with unsecured debt accounting for approximately 98% of total borrowings as at 31 December 2005. The Group will continue to obtain fi nancing on an unsecured basis whenever possible, and supplement such borrowings with secured project fi nancing as and when the need arises.

As at 31 December 2005, the gearing ratio for the Group was 36%, based on net debt of HK$9,184 million and shareholder’s equity of HK$25,221 million.

The majority of the Group’s borrowings bear interest costs which are based on fl oating interest rates. As at 31 December 2005, the Group had outstanding interest rate swap contracts which amounted to HK$5.8 billion in total, enabling the Group to hedge its interest rate exposure and to have a more stable interest rate profi le over the next few years.

On 8 April 2005, Wise Insight Finance Limited, a wholly-owned subsidiary of the Company, issued convertible bonds in the aggregate principal amount of HK$2,500,000,000 (the “Convertible Bonds”). The Convertible Bonds are zero coupon-based, have a maturity term of 5 years and are convertible into the Company’s ordinary shares at a conversion price of HK$25.955 per share (subject to adjustments). The issue of the Convertible Bonds provides a fl exible and cost-effi cient funding opportunity which is in the best interest of the Group. Upon conversion of the Convertible Bonds, the capital base of the Company will be enlarged and strengthened which will benefi t the Group’s future growth and developments. On 8 April 2005, Standard & Poor’s awarded the Convertible Bonds with a “BBB-” credit rating.

In terms of the Group’s available fi nancial resources as at 31 December 2005, the Group had total undrawn bank loan and overdraft facilities of HK$3,750 million and net cash on hand of HK$2,564 million. In addition, the generation of strong recurrent cashfl ows from the Group’s investment property portfolio, hotel operation, and logistics, freight forwarding and warehousing businesses provides the Group with a strong fi nancial position, and enables the Group to reap the benefi ts of investment opportunities as and when they arise.

34

The Directors consider that the Group’s property investments in Mainland China benefi t from the upward revaluation of the RMB by 2%, which was announced by the People’s Bank of China in July 2005. Furthermore, the upward revaluation of the RMB has a negligible impact on the Group’s RMB loans, which only represent a very small proportion relative to the Group’s total borrowings.

On 27 June 2005, Standard & Poor’s reaffi rmed a“BBB-” credit rating for Kerry Properties Limited with a stable outlook.

The Group signed a syndicated loan agreement on 27 February 2006 for an unsecured HK$6 billion revolving loan facility. The interest rate for this facility is HIBOR (Hong Kong Interbank Offered Rate) plus 29 basis points. This facility is for general corporate funding requirements of the Group including refi nancing of a previous HK$4.5 billion syndicated loan facility obtained in January 2002. The facility was launched on 27 February 2006, with participations received from 18 reputable international and local banks and fi nancial institutions.

35

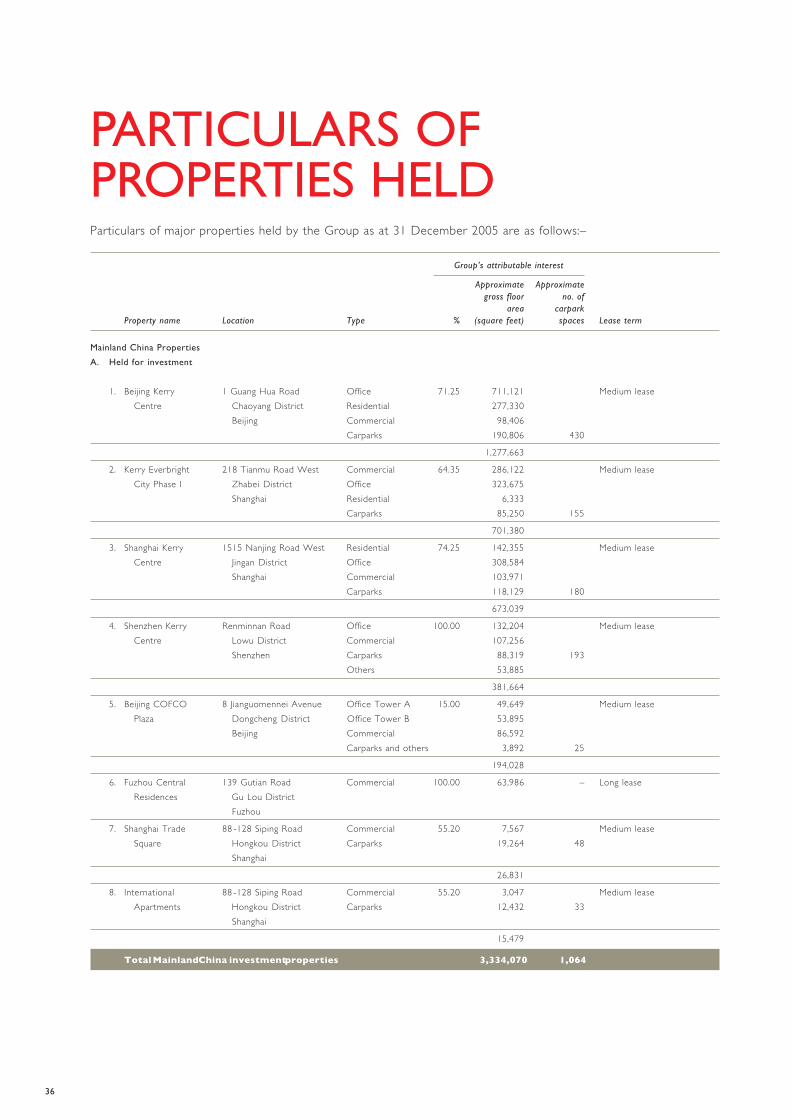

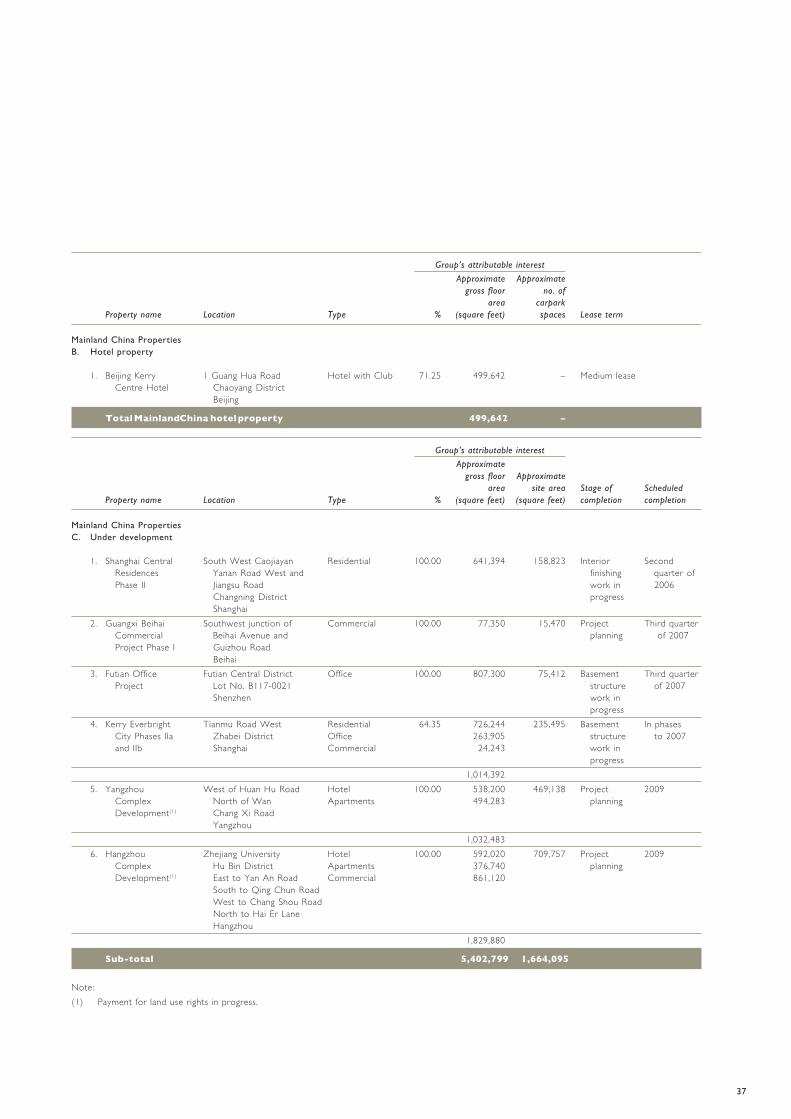

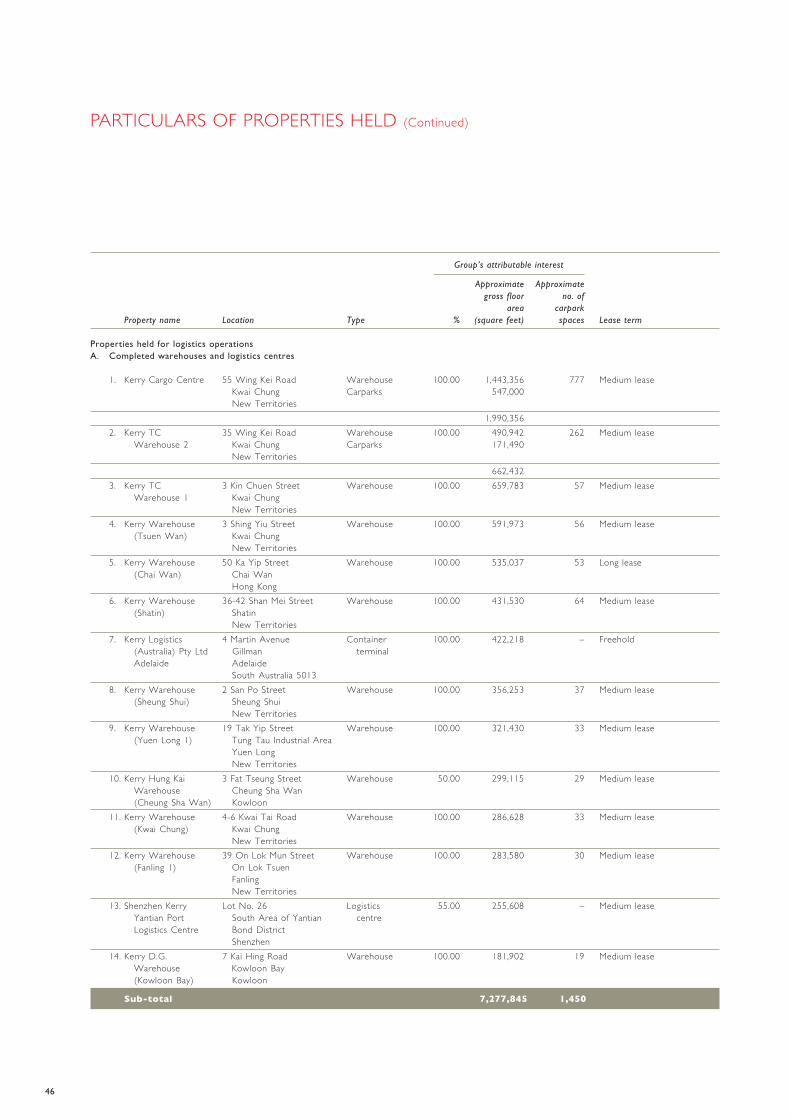

36

PARTICULARS OFPROPERTIES HELDParticulars of major properties held by the Group as at 31 December 2005 are as follows:–

Group’s attributable interest

Approximate Approximategross floor no. of

area carparkProperty name Location Type % (square feet) spaces Lease term

Mainland China Properties

A. Held for investment

1. Beijing Kerry 1 Guang Hua Road Office 71.25 711,121 Medium leaseCentre Chaoyang District Residential 277,330

Beijing Commercial 98,406Carparks 190,806 430

1,277,663