Ashley's.pdf - Bindura University of Science Education

68

BINDURA UNIVERSITY OF SCIENCE EDUCATION FACULTY OF COMMERCE DEPARTMENT OF ACCOUNTANCY THE LEVEL OF EXPOSURE TO VAT BY SMES IN MARONDERA TOWN PRESENTED BY: ASHLEY S. CHEKERA B1542724 A DISSERTATION SUBMITTED IN PARTIAL FULFILMENT OF THE REQUIREMENTS OF THE BACHELOR OF ACCOUNTANCY HONORS DEGREE OF BINDURA UNIVERSITY OF SCIENCE EDUCATION. FACULTY OF COMMERCE APRIL 2019

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Ashley's.pdf - Bindura University of Science Education

BINDURA UNIVERSITY OF SCIENCE EDUCATION

FACULTY OF COMMERCE

DEPARTMENT OF ACCOUNTANCY

THE LEVEL OF EXPOSURE TO VAT BY SMES IN MARONDERA TOWN

PRESENTED BY:

ASHLEY S. CHEKERA

B1542724

A DISSERTATION SUBMITTED IN PARTIAL FULFILMENT OF THE

REQUIREMENTS OF THE BACHELOR OF ACCOUNTANCY HONORS

DEGREE OF BINDURA UNIVERSITY OF SCIENCE EDUCATION.

FACULTY OF COMMERCE

APRIL 2019

i

RELEASE FORM

Name of Student : Ashley S. Chekera

Dissertation Title : The Level of exposure to VAT

by SMEs in

Marondera Town.

Degree Title : Bachelor of Accountancy

(Honours)

Degree

Year This Degree Granted : 2019

Permission is hereby granted to Bindura University of Science Education Library to

produce single copies of this dissertation and to lend or sell such copies for scholarly

or scientific research purpose only. The author reserves other publication rights and

neither non-extensive extracts from it may be printed or reproduced without the

author’s written permission.

SIGNED:

..............................................................

PERMANENT ADDRESS: 2520 Glen Norah A,

Glen Norah, Harare

ii

APPROVAL FORM

Title of Dissertation

The level exposure to VAT by SMEs in Marondera town.

To be completed by student.

I certify that this dissertation meets the preparation guidelines as presented in the

faculty guide and instructions for typing dissertations.

Signature of student.............................................. Date......................................

To be completed by the supervisor.

This dissertation is suitable for submission to the faculty. This dissertation should be

checked for conformity with the faculty guidelines.

Signature of Supervisor...................................................

Date................................

To be completed by chairperson of the department.

I certify to the best of my knowledge, that the required procedures have been followed

and the preparation criteria has been met for this dissertation.

Signature of chairperson....................................................

Date.....................................

iii

DEDICATION

I dedicate this research project to my family and friends. Thank you for your

unwavering support. To you the reader, this work is also dedicated.

iv

ABSTRACT

This study was carried out to determine the level of exposure to value added tax by

small-to-medium enterprises (SMEs) in Marondera town. The research objectives of

this research were to assess the level of awareness to VAT by SMEs, to assess the level

of VAT compliance by SMEs, to identify possible causes of VAT non-compliance

among SMEs and to determine the effect of VAT registration on the profitability of

SMEs. The descriptive research design was used with a sample size of 50 out of a target

population of 127 SMEs. Stratified random sampling was used to group the sample into

4 strata namely; hotel and catering, clothing, retail and furniture making industry. The

questionnaire with a seven-point Likert scale was used to gather data. SPSS version 25

and descriptive statistics were used to analyse data collected and it was presented with

the help of graphs, pie charts and tables. The research findings showed that there is a

significant negative (r=-0.036) correlation between the compliance level and level of

awareness to VAT. Liquidity problems and too much paper work associated with VAT

compliance were found to be major reasons for VAT non-compliance. It was also

revealed that SMEs lack knowledge and understanding on VAT issues. The findings

showed that VAT registration has an influence on the profitability of a firm. The

research therefore recommended that ZIMRA has to make awareness campaigns and

training schemes to impart knowledge among SMEs. The government has to also find

ways to reduce compliance costs on VAT compliance so as to improve the level of

compliance among SMEs.

v

ACKNOWLEDGEMENTS

I feel much honoured to have completed successfully this research project in partial

fulfilment of the requirements of my study in Bachelor of Accountancy Honours

degree.

First and foremost I would like to thank Almighty God for the spiritual guidance,

support and protection throughout my years of study, “For we are nothing but a speck

of dust in his hands.”

My heartfelt gratitude goes to my family especially my mom and younger brother for

their unwavering moral and financial support during my academic endeavours. I

would like to extend my utmost gratitude and appreciation to my beloved friends to

mention in particular, Clementine, Rumbidzai, Ruwarashe and Dolly for their

assistance throughout my years of study.

I am extremely indebted to my supervisor, who patiently guided me throughout this

project and for his factual review of the project. His comments, suggestions and useful

guidance have been invaluable inputs that improved the quality of my research; I

remain ever grateful and thankful to him.

MAY GOD BLESS YOU ALL!!!!

vi

Table of Contents

RELEASE FORM ........................................................................................................... i

APPROVAL FORM ...................................................................................................... ii

DEDICATION .............................................................................................................. iii

ABSTRACT .................................................................................................................. iv

ACKNOWLEDGEMENTS ........................................................................................... v

LIST OF ABBREVIATIONS ...................................................................................... xii

CHAPTER 1 .................................................................................................................. 1

INTRODUCTION ...................................................................................................... 1

1.0 Introduction .......................................................................................................... 1

1.1 Background of the study ................................................................................... 1

1.2 Statement of problem ........................................................................................... 2

1.3 Research objectives .............................................................................................. 2

1.4 Research Questions .............................................................................................. 3

1.5 Hypothesis ................................................................................................................ 3

1.6 Significance of the Study ..................................................................................... 3

1.7 Assumptions ......................................................................................................... 4

1.8 Delimitations of the study .................................................................................... 4

1.9 Limitations of the study ........................................................................................ 4

CHAPTER II .................................................................................................................. 5

LITERATURE REVIEW ........................................................................................... 5

2.0 Introduction .......................................................................................................... 6

2.1 Theoretical Literature ........................................................................................... 6

2.1.0 Definition of SMEs ........................................................................................ 6

2.1.1 Characteristics of SMEs. ............................................................................... 7

2.2 Taxation for SMEs ............................................................................................... 8

2.2.1 History of VAT .............................................................................................. 9

2.2.2 Advantages of VAT ....................................................................................... 9

2.2.3 Drawbacks of VAT ...................................................................................... 10

2.3 VAT registration in Zimbabwe. ......................................................................... 10

2.4 Zimbabwe’s VAT design ................................................................................... 11

2.4.1 Zimbabwe’s VAT system ................................................................................ 12

2.4.2 VAT calculation........................................................................................... 13

2.5 Level of VAT Compliance among SMEs .......................................................... 13

vii

2.5.1 Factors affecting VAT compliance in SMEs ............................................... 14

2.7 Theories of Tax Compliance .............................................................................. 18

2.7.1 Economic based theories ............................................................................. 18

2.7 Empirical Evidence ............................................................................................ 19

2.8 Gap Analysis ...................................................................................................... 22

CHAPTER III .............................................................................................................. 23

3.0 Introduction ........................................................................................................ 24

3.1 Research Design ................................................................................................. 24

3.1.1 Descriptive Research ................................................................................... 24

3.2 Population ........................................................................................................... 25

3.3 Sample and Sample size ..................................................................................... 25

3.4 Sampling Techniques ......................................................................................... 26

3.4.1 Justification of Stratified Sampling ............................................................. 27

3.5 Data Sources ....................................................................................................... 27

3.5.1Primary Source ............................................................................................. 27

3.6 Research Instruments ......................................................................................... 28

3.6.1 Questionnaires ............................................................................................. 28

3.7 Data Validity ................................................................................................... 29

3.8 Data Reliability ............................................................................................... 29

3.9 Data collection procedure ................................................................................... 30

3.10 Data presentation and analysis ......................................................................... 30

3.11 Summary .......................................................................................................... 30

CHAPTER IV .............................................................................................................. 30

DATA PRESENTATION AND ANALYSIS ............................................................. 30

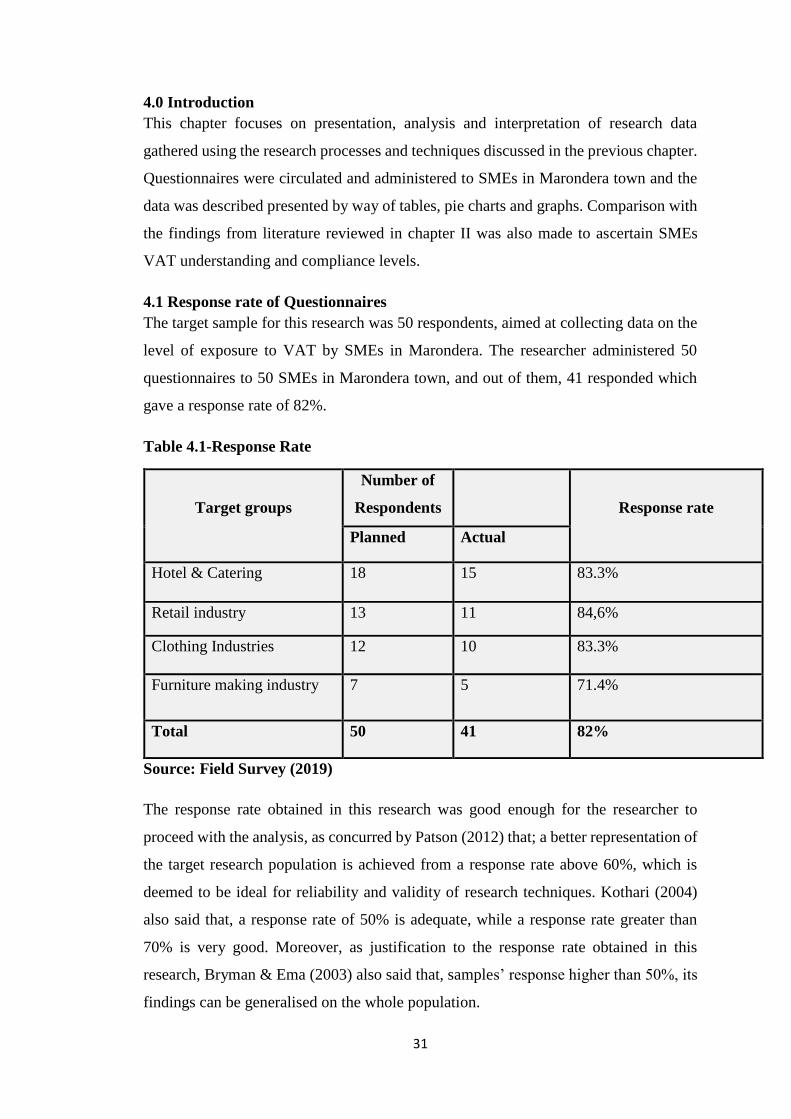

4.0 Introduction ........................................................................................................ 31

4.1 Response rate of Questionnaires ........................................................................ 31

4.2 Business Type .................................................................................................... 32

4.3 Form of ownership ............................................................................................. 32

4.4 Business duration ............................................................................................... 33

4.5 The effectiveness of the VAT system in encouraging VAT compliance ........... 35

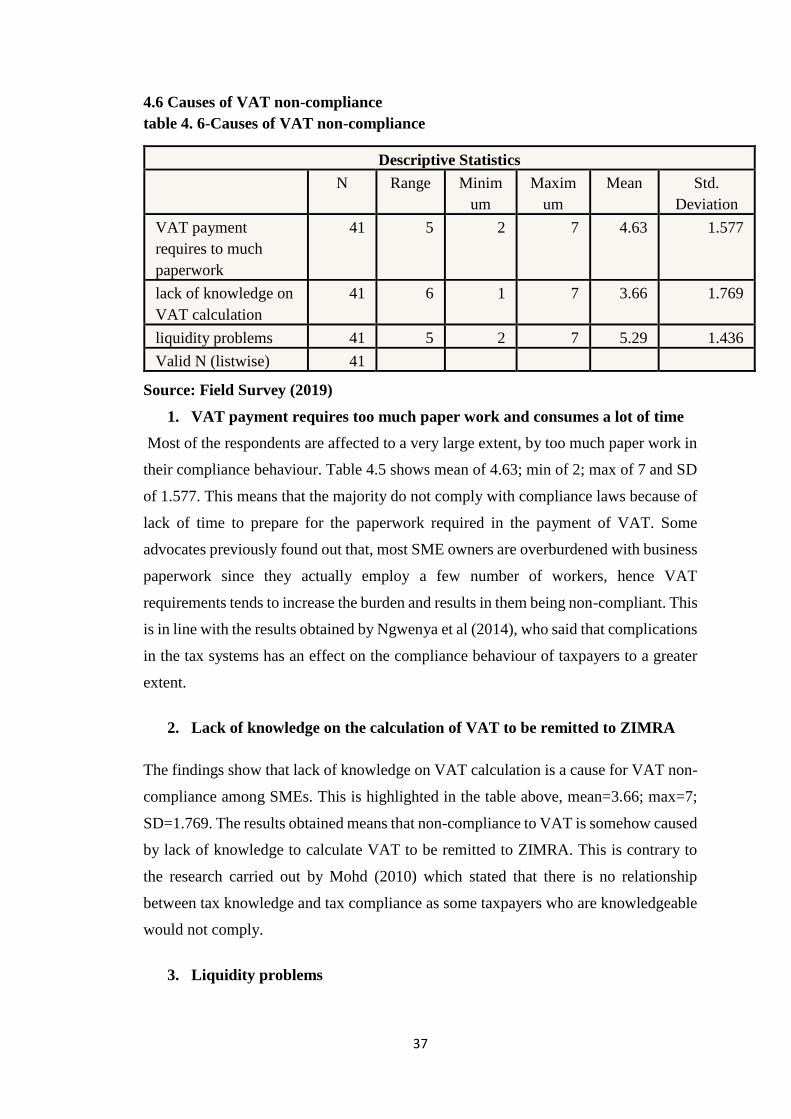

4.6 Causes of VAT non-compliance ........................................................................ 37

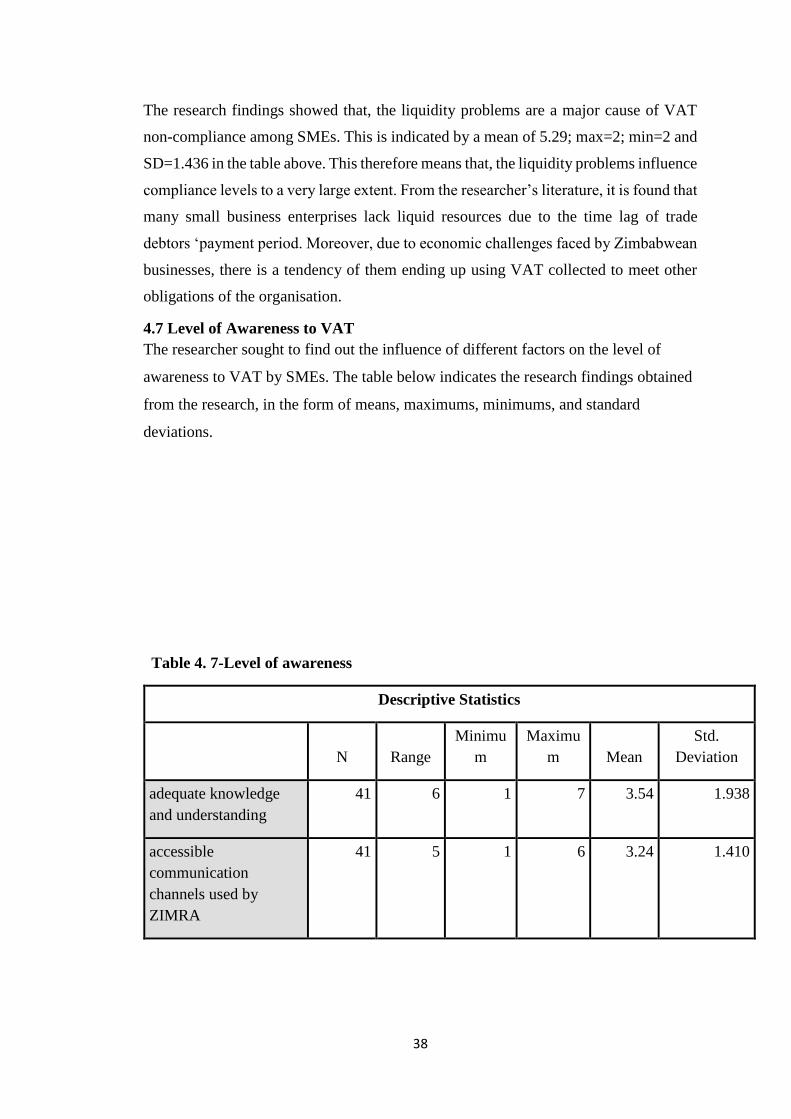

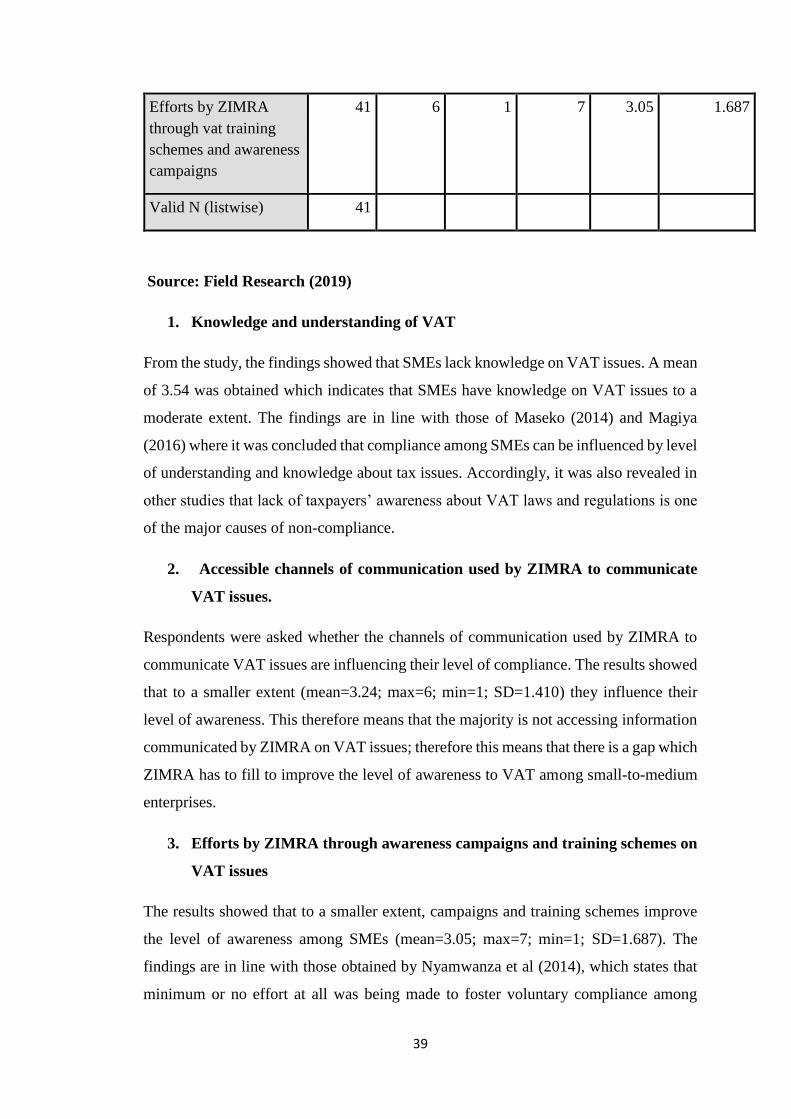

4.7 Level of Awareness to VAT ............................................................................... 38

4.8 The effect of VAT on firm’s profitability .......................................................... 40

viii

4.9 Relationship between VAT compliance and Level of awareness to VAT ......... 41

4.9.1 Hypothesis ................................................................................................... 41

CHAPTER V ............................................................................................................... 43

5.0Introduction ......................................................................................................... 43

5.2 Conclusions ............................................................................................................ 44

5.3Recommendations ............................................................................................... 45

5.4 Suggestions for further study ............................................................................ 46

REFERENCES ............................................................................................................ 46

ix

LIST OF FIGURES

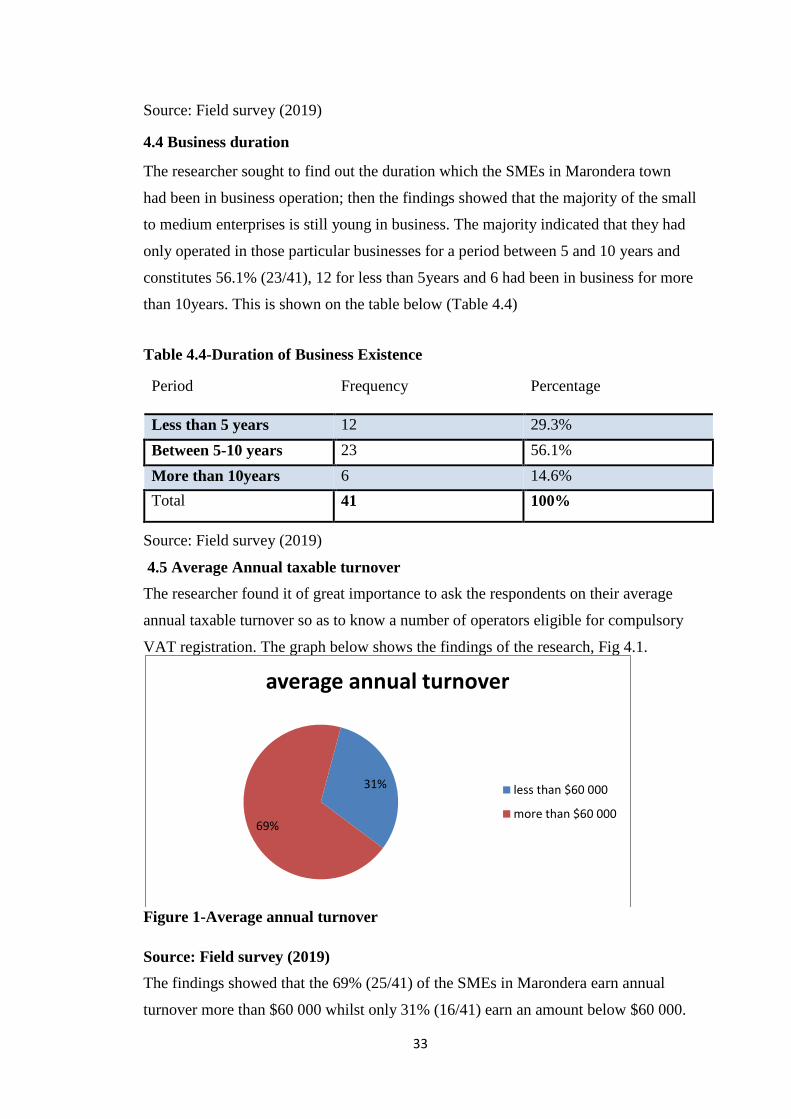

Figure 1-Average annual turnover ............................................................................... 33

Figure 2-VAT registered firms .................................................................................... 34

x

LIST OF TABLES

Table 4. 1-Response Rate............................................................................................. 31

Table 4. 2-Type of Business ........................................................................................ 32

Table 4. 3-Business ownership .................................................................................... 32

Table 4. 4-Duration of Business Existence .................................................................. 33

Table 4. 5-Causes of VAT non-compliance................................................................. 37

Table 4. 6-Level of awareness ..................................................................................... 38

Table 4. 7-VAT registered firms and profitability ....................................................... 40

Table 4. 8-staff training costs on VAT calculation ...... Error! Bookmark not defined.

Table 4. 9-Correlation between VAT awareness and VAT compliance..................... 42

xi

LIST OF APPENDICES

APPENDIX 1-QUESTIONNAIRE ............................................................................. 51

xii

LIST OF ABBREVIATIONS

OECD The Organisation for Economic Co-operation and Development

SMEs Small and Medium Enterprises

ZIMRA Zimbabwe Revenue Authority

AFRODAD African Forum and Network on Debt and Development

VAT Value Added Tax

1

1

CHAPTER 1

INTRODUCTION

1.0 Introduction

This research gives an outline on the level of exposure to VAT by SMEs in Marondera

town. This chapter will provide an outline of the background of study, the statement of

the problem, the objectives of the study, research questions, significance of study,

assumptions, limitations of the study as well as delimitations

1.1 Background of the study

The Government of Zimbabwe largely relies on the funds collected by the Revenue

authority, through tax, that is from, import duties, corporate tax, income tax and value

added tax. It has become a major challenge to the Government, on the sources of funds,

since the greater part of the economy is dominated by informal businesses which

employ few employees. This therefore made VAT newsworthy in today’s economy,

since corporate and income tax are expected to produce less revenue than consumption-

based taxation. Value Added Tax refers to an indirect tax which is levied by government

on local and imported supplies of goods and, or services made by a registered operator,

collected at each stage of production, distribution and importation, (ZIMRA VAT Guide

(2007)2nd Edition).

In 2017 reports showed that, Zimbabwe had $5.7 billion circulating in the informal

sector following a Finscope Micro, SMEs survey, 2012, where there were 2.8million

SME owners employing 2.9 million people and contributing over 60% to the Gross

domestic Product. VAT compliance by SMEs therefore is the newsworthy issue as

Government is in quest of ways to improve efficiency in tax revenue collection. The

speedy expansion of informal sector businesses in Zimbabwe made ZIMRA, to consider

the SMEs crucial in achieving economic growth. According to Treasury, the thrust to

register SMEs for VAT is to enable the established companies to claim for input tax on

goods and services supplied by the SMEs.

2

Since Small and Medium Enterprises are the majority business tax payers in most

developing countries, their level of exposure to VAT directly impact on government tax

revenue collections since they are largely involved in trading of taxable goods and

services. In Zimbabwe, VAT was introduced in January 2004 replacing taxes such as

sales tax, betting tax, gaining tax and import tax (AFRODAD, 2011).The fact that most

SMEs are finding it difficult to get registered by ZIMRA, is somehow an indication lack

of knowledge of VAT, by tax payers.

ZIMRA could earn more tax from the SMEs through Value-added Tax (VAT), since

these businesses solely do not normally employ a large number of people. Therefore the

level of exposure to VAT by SMEs could result in their level of tax compliance.

1.2 Statement of problem

Zimbabwe Revenue Authority is failing to collect a sufficient amount of revenue to

support government’s activities despite the expectations that the VAT system will

counteract underperformance of sales tax and boost the revenue base for the

government. SME owners seem to have little or no knowledge on VAT because there

is minimum co-operation. Adesola(2012) and Glenday (2013) concurred that small

enterprises are allowed to register voluntarily by VAT systems but they are not willing

to register for VAT, hence affects revenue collection negatively. In 2017, government

of Zimbabwe issued a Value Added tax amnesty to allow SMEs to register with ZIMRA

but only 70% complied with a contribution to tax revenue of about 20%

(www.openparly.co.zw). The Government of Zimbabwe still lacks income for the

development of the country and stabilise the economy due to failure by SMEs to remit

VAT to ZIMRA. This in fact presents the need to determine the possible causes of non-

compliance of VAT by the SMEs. An understanding of whether the SME owners have

knowledge and exposure to VAT has not been determined and the gap needs to be filled.

1.3 Research objectives

This study is aimed to achieve the following objectives:

i. To assess the level of awareness to VAT by SMEs.

ii. To assess the level of VAT compliance by SMEs.

iii. To identify possible causes of VAT non-compliance among SMEs

iv. To determine the effect of VAT registration on the profitability of SMEs

3

1.4 Research Questions

i. How does level of awareness to VAT by SMEs affect their level of

compliance?

ii. How effective is the VAT system in encouraging VAT compliance

among SMEs?

iii. What are the possible causes of non-VAT compliance among SMEs?

iv. What are the implications of VAT registration on profitability of SMEs?

1.5 Hypothesis

Ho: there is no relationship between VAT compliance and level of awareness to VAT

H1: there is a relationship between VAT compliance and level of awareness to VAT

1.6 Significance of the Study

To Researcher

This study enabled the researcher to gain much relevant knowledge, invaluable

experience on VAT and greater understanding on SME operations. The research also

provides a future platform for further researches to improve Value Added Tax operation

systems among the SMEs.

To Bindura University of Science Education

This study will help Bindura University students to have a deeper and professional

understanding in VAT. It will also be used by other scholars as literature review and as

a path for further study.

To the Tax Administrators

This research will equip tax administrators on how best they can impart knowledge

about VAT to SME owners, so that there is an improvement in VAT compliance by

those business owners, as well as surpassing their targets. This study therefore will help

in developing and redesigning suitable VAT system and compliance challenges in the

economy.

To the Government

4

The findings of this research will give government a path to initiate and modify the

Revenue Acts to ensure their effectiveness in developing compliance among SMEs.

1.7 Assumptions

This study based on the following assumptions:

Sample selected is a representative of the perception of taxpayers and

their level of exposure.

Responses given by the respondents will be genuine and give all relevant

information.

Information to be provided by respondents is confidential.

1.8 Delimitations of the study

This research was limited on the views and opinions of SMEs in Marondera town; it did

not consider those of big, well established companies. This division is largely

dominated by SME operators than big companies. It focused mainly on the level of

knowledge of VAT by SMEs and their level of compliance as required by the VAT Act.

1.9 Limitations of the study

The subject under study was a bit sensitive; therefore the respondents could not honestly

express their opinions. In addition, because of fear by SME operators that they might

be exposed off for VAT non-compliance, there was no assurance that the respondents

will return all the questionnaires. The research was also limited to public available

information since some information relating to VAT issues cannot be readily available

from ZIMRA offices for confidentiality purposes.

However, to alleviate those limitations, the researcher guaranteed the respondents that

the data collected for this research will be kept with strictest confidentiality. The

researcher had a thorough explanation about the significance of this study to the

respondents and that it is solely for academic purposes and that the researcher was not

a representative of the tax officials.

Definition of terms

SMEs- these are informal business operators that employ a minimum number of five

employees and have an annual turnover less than $1 million (SMEAZ, 2012)

5

VAT- is a type of consumption tax that is placed on a product whenever value is added

at a stage of production and final sale. It is levied on transactions rather than person

(Investopedia, 2013).

Value added tax compliance: refers to the degree to which a tax payer complies or

fails to comply with the tax rules of his or her country (Stiglitz, 1985)

Tax compliance- this refers to the most neutral term to describe the taxpayer’s

willingness to pay their taxes (Kirchler, 2007).

Tax non-compliance - is the failure of the taxpayer to meet tax obligations, irrespective

of whether this is committed intentionally or not (James and Alley, 2002)

CHAPTER II

LITERATURE REVIEW

6

2.0 Introduction

This chapter reviews, explores and cites what other relevant studies of the same subject

matter have found as the researcher tried to find explanations to her findings. Literature

review enables the researcher to detect research gaps in the study at hand and compare

her findings with those of other researchers. Shuttleworth (2009), propounded that,

literature review is a summary and synopsis of a particular area of research, allowing

anybody reading the paper to establish why you are pursuing this particular research

program. To convey the research problem into centre of attention, the study is of two

folds, that is, the theoretical fold which deals with the conceptual elements leading to

the appropriate evaluation criterion and the empirical fold which deals with assessing

previous studies.

2.1 Theoretical Literature

2.1.0 Definition of SMEs

Definition of SMEs differs from one country to another. Advocates found that,

definitions of SMEs differ quite widely from nation to nation, depending on who is

providing the definition. Kim and Gallent, 2002 & Tevera 1998 also suggested that,

there is no commonly accepted definition of SMEs. Different variables are considered

in determining whether an entity is an SME or not, basing on factors such as, number

of employees, turnover levels, capital net assets and capital base, (Hisrich et al, 2004).

Description of SMEs and features were once based on non-current assets mainly but

this was not giving a clear definition, some other items were later on used such as

employment levels, annual turnover, annual balance sheet total and some jurisdictions

still use total assets in addition (Nkwe, 2013). SMEs are categorised into three, which

are, the Small, Micro and medium enterprises.

In Botswana, Small enterprises are defined as those that employ less than 25 workers

and earning an annual sales turnover between P60 000 and P1 500 000, medium

enterprises employ not more than 100 workers and their annual turnover is between P

1 500 000 and P5 000 000 (Nkwe, 2013). An SME in South Africa is defined as any

business with less than two hundred employees, annual turnover of less than ZAR5

million, capital assets of less than ZAR2 million, and with owners who are directly

involved in the management of the business.

7

According to the Small and medium Enterprise Act in Zimbabwe, the Ministry defined

small enterprise as a registered organisation employing 30 to 100 employees. In

addition, the Small Enterprises Development Corporation (SEDCO, 2010) went on to

define small and medium entity as that enterprise employing not more than 100 workers

and earning a maximum turnover of up to $800 000 per annum. Small-medium

enterprises are defined in terms of turnover and value of assets by Small-Medium

Enterprise Association of Zimbabwe (SMEAZ, 2012). The small enterprises are

categorized in a class of those with turnover of less than US$240 000 or assets less than

US$100 000 annually, medium enterprises are those with an annual turnover and assets

above those of small enterprises but less than US$1 million. However, definitions of an

SME vary from one nation to another, there is no collectively approved definition of an

SME therefore, for the purpose of this study, an SME is regarded as an entity that

employs less than 100 people, generating less than US$1 million in annual turnover,

registered or non-registered.

2.1.1 Characteristics of SMEs.

Masarirambi (2013), characterised SMEs in Zimbabwe as diverse collection from small

workshops making furniture, metal parts to medium-sized producers of machinery as

well as service providers such as restaurants, consulting hairdressing and computer

software firms. SME operators have different perspectives in the case of business

structure; some wants to remain small, while others are focused on expansion and

inventive. A number of SME characteristics are discussed below, according to

Matsebula (1996).

i. Ease of entrance

Small enterprises require a low start up capital as compared to bigger ones; therefore

this makes it easier for them to enter into the market. There are fewer barriers to entry

into the informal sector such that at any given time an individual can start venture and

compete in informal sector. (Ojeka, 2012)

ii. Sole or few individual ownership

Small business enterprises are usually run by a sole proprietor and due to lack of funds

to employ more individuals; they employ an average of four depending on the type of

the business, Yanksan (1989). Family labour tends to be the cheapest source of labour

8

to the business. Farell and Fleming, (2000) added that, the majority of the businesses in

the informal sector are dominated by family ownership.

iii. Highly dependent on indigenous resources

SMEs heavily depend or rely on locally sourced resources and usually serve as suppliers

of the local manufacturing companies and also they are usually labour intensive,

Hanefah, Ariff & Kasipillai (2002). Most SME operators lack knowledge of the

international market and exposure, some have a negative perception towards

international markets and has low risk appetite, and this limits them from growing and

earning more foreign currency (ZIMRA, 2015).

iv. Unregulated and competitive markets.

The economy of today is largely dominated with SMEs but they are omnipresent and

flexible hence it is difficult for local authorities and government to regulate the sector.

This therefore results in stiff completion and it is the survival of the fittest from both

the formal and informal competitors. A practical example can be observed at Glenview

area 8 wood complex for furniture manufacturing.

v. Narrow range of source of income

Most SME operators lack collateral security, hence they have a reduced income base

since financial institutions lack trust on them. They cannot borrow large sums of money

from some of the financial institutions hence reduced chances of growth and increased

financial problems.

2.2 Taxation for SMEs

Zimbabwean tax system comprises of different tax heads which are regulated by the

government through a revenue collection board called ZIMRA. Tax collected is

grouped into two categories or types, which are, indirect and direct taxes. Direct taxes

include the corporate tax, Pay As You Earn (PAYE), Investment income tax, capital

gains tax, Estate duty tax and Presumptive tax. On the other hand, indirect tax includes,

Value Added Tax (VAT), Sales tax, Customs and exercise duty. SMEs are therefore

subject to any or all of the mentioned tax obligations. However, this research dwelled

much on VAT in SMEs as they are dominating the Zimbabwean economy through

buying and selling goods.

9

2.2.1 History of VAT

Value Added Tax was first introduced by a German economist during the 18th century.

He devised a sales tax on goods that did not affect the cost of producing or distribution

but rather, it was collected on the absolute price charged to the end user (consumer).

This therefore means that, the tax was always fixed on the final price as it did not matter

how numerous transactions the goods went through.

In 1954, upon the development of the Common Market in Europe (European Union) it

came to a decision that one condition of joining was the imposition of a form of VAT.

Sales tax was later on replaced with VAT, by UK when it joined the European Union

in 1973. In most of the Western European nations, VAT has now become a major part

of the tax structure. www.encylopedia.com.

According to the research done by an economist at the International Monetary fund,

Jean Francois Ruhashynkiko and Richard Stern, the regional Coordinator for Africa at

the International Finance Corporation, World Bank Group, they referred to the incentive

structure of tax system in Africa. The colonial tax system remained the same until the

fiscal crisis of the 1980s in Africa. The introduction of VAT then lately emanate from

the tax recommendations involving flattening tax rates and broadening tax bases. Small

business taxpayers in Africa often pose extraordinary challenges, and they are referred

to as “hard to tax”.

2.2.2 Advantages of VAT

Easy to administer- VAT is collected in every stage of the production line,

therefore it makes it a practical benefit as compared to sales tax. Furthermore,

VAT allows the fiscal authority to evaluate accounted sales of each

intermediate good with reported purchases; hence gives an advantage of easier

enforcement.(J. Aizenman et al, 2005).

J. Aizenman et al, 2005 added that, increased VAT collection points due to

existence of registered traders at each state of production chain thereby

minimising the risk of substantial losses due to evasion and avoidance by single

trader.

Centralisation of the tax refunds as stated by the Zimbabwe Value Added Tax

Act [Chapter 23:12] section 44, that the approval only rests with the

Commissioner General after the provision of an acceptable proof of a

legitimate refund claim, increases revenue security.

10

Wider tax base- VAT is nonaligned as it does not discriminate between

industries or between capital and revenue expenses of the business. This

therefore increases the tax base to the government as compared to sales tax.

High level of tax compliance is expected from traders as the tax authority has

a higher visibility under the VAT system.

Competitive exports- direct exports are exposed at a special rate of 0%,

therefore the prices of goods exported does not include VAT which make them

more competitive internationally.

2.2.3 Drawbacks of VAT

Increase the aggregate tax burden to taxpayers- it is evidenced that VAT

increases the tax burden by 50% in Europe, M Keen et al (2007. He further

stated that, as firms try to keep their product prices competitive, they tend to cut

other factor costs such labour costs by shifting to capital intensive.

Advocates of VAT suggest that VAT has a number of disadvantages. It is

believed that it is inflationary, regressive, complex, costly to administer, comply

with and in practice discriminatory.

Inflationary- imposition of tax on consumption may raise prices of goods

indefinitely so that the traders maintain their profit margins.

Regressive- VAT lacks fairness, as the tax charged on consumption is the same,

whether on low-income earners and high –income earners. This is regressive in

the sense that the percentage of VAT charged to low-income persons tends to

be higher than that of the high-income earners.

Complexity- different rates and exemptions of VAT has been practically proved

to be complex in many different countries. This also increases the cost of

administering VAT by both the government and the business enterprises.

Accounting cost- the VAT system largely relies on the invoices and this

relatively requires the upkeep of detailed records of all tax invoices by the

registered operators. This increases the work and burden to the registered

operators.

2.3 VAT registration in Zimbabwe.

Value Added Tax (VAT) is an indirect tax on consumption, charged on the supply of

taxable goods and services and its effect is independent of the level of profits. VAT can

11

be charged by any person registered or required to be registered for VAT, carrying on

trade as defined in the legislation (www.zimra.co.zw). Input tax is the VAT paid on

purchases of taxable supplies made by the registered operator. Output tax is charged on

the sales made by the registered operator on taxable supplies. VAT refunded or payable

to ZIMRA is calculated by the registered operator, by deducting output tax from input

tax. VAT refund occurs when the output tax is less than the input tax and VAT payable,

when output tax is more than input tax.

VAT registration is compulsory to traders whose taxable supplies exceed or are likely

to exceed $60, 000.00 in a period of 12months. It is also voluntary to traders whose

taxable supplies do not meet or exceed the $60, 000.00 and have not in past failed to

comply with the legislation (ZIMRA 2004). In the case that the operator meets or

exceeds a turnover threshold level but fails to register, the Commissioner General of

ZIMRA will apply Section 23(4) (b) of VAT Act. The operator will therefore be

registered compulsorily by the Commissioner General and will be entitled to pay the

VAT due, interest and penalties on the computed debt (ZIMRA 2014).

ZIMRA (2014), clearly stated that, traders who will be solely dealing in exempt supplies

specified in terms of Section 11 (a-j) of VAT act, may be excluded from registration of

VAT. In addition, an employee providing service to his/her employer or conducting

private or recreational pursuit or hobby whose taxable turnover does not meet or exceed

$60 000,00 annually are not liable to be registered operators for VAT purposes

(ZIMRA, 2014).

2.4 Zimbabwe’s VAT design

The Zimbabwe’s VAT Act [Chapter 23:12] states that, the administering and

management of VAT rest with ZIMRA which is chiefly headed by the Commissioner

General of Revenues. The Minister of Finance appoints the Commissioner General with

the power vested in him/her by the Government of Zimbabwe. VAT is charged on local

and imported supplies of goods and or, services made by a registered operator. Taxable

supplies are defined in the ZIMRA VAT Guide (2007) as supplies that are chargeable

at a standard rate of 15%. Some goods are zero rated supplies, of which VAT is charged

at 0%. Zero rated supplies include foodstuffs such as; uncooked beef, uncooked fish,

milk and milk products, fresh birds, eggs, plain bread, mealie-meal etc. VAT Act also

states that, supplies of goods and services on which VAT is not chargeable and not form

12

part of the taxable turnover are exempt supplies. Examples of exempt supplies include

financial services, provision of electricity and piped water for domestic use, rates

charged by Local Authorities, educational services, medical services supplied by any

person on institution and fuel.

2.4.1 Zimbabwe’s VAT system

The filing, submission and payment processes of VAT differ from one country to

another. Most countries are said to have a single stated day on which they remit their

taxes as it is believed to be time consuming, Liam et al (2001). They further stated that,

this payment date, which is the due date, is characterised by long queues at banks for

deposits and at the offices where the returns are submitted.

In Zimbabwe, tax payers are arranged into four categories, that is, category A to D as

outlined in the VAT Act Chapter 23:12, Section 27. Submission of returns and payment

for VAT to the Commissioner is required to be done in accordance with the stated tax

periods.

Category A: Two-month period ending on the 1st day of January, March, May,

July, September and November.

Category B: A two-month period ending on the last day of; February, April,

June, August, October and December.

Category C: Monthly basis submission of VAT returns, (One month tax period)

Category D: This category is meant for registered traders in farming, with

turnover not more than or not likely to exceed the prescribed amount per annum.

Also registered tax payers will be allowed upon approval of a written application

to the Commissioner.

However, due to hyperinflation in Zimbabwe to date, all tax payers are to comply with

category C requirements. According to ZIMRA website www.zimra.co.zw, the

registered operator is obliged to calculate and remit VAT due to the Commissioner

General of ZIMRA on or before the 25th of every month.

VAT returns can be physically submitted to the authority offices, through post offices,

or electronically. Zimbabwean VAT system allows tax payers to submit returns online

and payments should be made through the banks, www.zimra.co.zw.

13

2.4.2 VAT calculation

Value added tax is charged on goods rather than persons’ income. There are two

recommended methods of calculating VAT which are: Subtractive procedure and

Addictive procedure.

i. Subtractive Procedure

This method of calculating VAT is the one used in Zimbabwe, where the taxpayer

simply has to subtract the input tax from the output tax and determine VAT payable

or refundable thereof (ZIMRA website, www.zimra.co.zw). VAT collected from

selling the products is the output tax and that incurred in acquiring taxable supplies

is the input tax. Subtractive method can be expressed as follows:

VAT Due/ Refundable = output tax – Input tax

Therefore, VAT liability under this method is the amount payable by a trader for

VAT, determined through subtracting VAT paid on purchases (input tax) from VAT

collected on sales (output tax), I.N Grand et al (2001).

ii. Addictive Procedure

The second method of calculating VAT has been stated by R.W Lindholm (1976) as the

Addictive procedure. This method determines taxable value added by finding the

difference between selling price and the purchase price. The tax base applied to VAT

under this procedure is the total payment of the factors of production, which are income

to the owners of production.

2.5 Level of VAT Compliance among SMEs

Tax compliance can be defined as the most neutral term to describe taxpayers’

willingness to pay their taxes, Kirchler (2007). Singh (2003) also defined tax

compliance as person’s act of filing returns, declaring all taxable income accurately and

disbursing all payable taxes within a stipulated time without waiting for any follow ups

from the authority. VAT compliance therefore simply means that, the firm is registered

as required by the law, file the returns on time, accurately reports complete information

to determine VAT due or refundable, keeps proper books of accounts and remit all

amounts due as and when required by the authority.

14

Most existing large or macro business enterprises were at one point small businesses;

therefore SMEs of today are future large companies. Thus, today’s SMEs have to be

nurtured to ensure highest level of compliance among them for a better tomorrow.

2.5.1 Factors affecting VAT compliance in SMEs

a) Income level

Income levels of taxpayers tend to play an important role in decision making upon

compliance. Income levels differ from one business to another depending on the

business activities involved in that business. Low-income earners tend to be less

compliant than those high-income earners since their income would be sufficient to

meet the organisational commitments (Torgler, 2007). VAT still stands as the most

important sources of revenue on which registered taxpayers invest before remitting to

the tax authorities. Ainsworth & Madhazhovaral, (2010) advocated that, increases in

VAT rates give rise to an advanced spread of fraudulent schemes due to availability of

significant amounts of VAT supposed to be payable to tax authorities. Financially

struggling firms have increased chances of evading from tax as an alternative source of

finance to the business operations and fail to remit VAT withheld from customers

(output tax), International Monetary Fund, 2009)

Furthermore, taxpayers can take advantage of inflation rates and make exaggerated

claims for credit for input tax because an inflated amount increases the net income and

fraudulently reducing the tax liability and minimise tax due to revenue authorities.

Businesses minimize VAT liability may be minimised by overstating purchase costs or

understate sales proceeds, (Slenmrod & Gillitzer, 2013). Keen & Smith (2007)

propounded that some business activities may be omitted from the company’s books

allowing them to understate the sales made and also understate their purchases thereby

reducing their tax liability.

In addition, with the aim to maximise income levels, taxpayers tends to exaggerate the

tax liability through misallocations of taxable supplies to lower-taxed categories, (GTZ,

2010; Keen & Smith 2007). The issue of underreporting is more likely in high-income

earners than low-income taxpayers since they contribute a considerable proportion to

VAT revenue, thereby giving them greater chances to misreport since it is more likely

to deter them from evading due to loss of potential revenue, (Franzoni, 1999).

15

Duverne, (1990) gave a practical example which happened in France whereby from the

audited VAT operators, 66% had understated the value of taxable sales having 25% of

them fraudulently reported and 40% had overstated the value of taxable inputs having

aim of income maximisation thus signifying the impact of income to level of

compliance.

To add on, Zimbabwean VAT system is based on the invoices, both the purchases and

sales. However, in the case that there are delays in the payment of goods by the credit

customer, VAT bill will burden the registered operator, which might result in VAT non-

compliance, (Ainsworth & Madzharova, 2012:12).

b) Administrative procedures

Administrative procedures are measures or aims designed by a tax authority to

effectively and efficiently manage the tax system at the same time discharging its

responsibilities. These actions influence the level of compliance of business operators.

i. Mode or method of remitting VAT

Complex and time consuming modes of payment reduce the level of compliance to VAT

by business enterprises. Countries with online payment for VAT tends to have less

compliance challenges as it takes less time on average to comply as compared to those

ones who do not, (PricewaterhouseCoopers, 2010). Manual and traditional ways of

remitting tax to tax authorities is prone to errors, therefore countries with electronic tax

systems reduces errors, improves efficiency, takes less processing time and reduces

administration costs, (Araki & Claus, 2014:42, Ernst & Young, 2014 &

PricewaterhouseCoopers, 2013).

ii. Frequency of VAT returns requirement.

The rate of recurrence and number of returns at which VAT returns are required affects

the length of time period taken by the taxpayer to comply. Depending on the category

taxpayer is in, the VAT returns in Zimbabwe are required on monthly basis or after two

months. As evidenced that time taken to comply is more than that of where returns are

required, either semi-annually or quarterly. PricewaterhouseCoopers confirmed this

through an analysis which proved that in economies where returns are filed in a monthly

basis compliance took more time than those filed quarterly or semi-annually,

16

(PricewaterhouseCoopers, 2010). The fact that the Zimbabwean taxpayers are required

to remit on or before 25th of the following month, implicates the compliance time.

iii. Details of Transactions

Contents required by the Tax Administrators on the VAT returns affect the rate of

compliance by SMEs. The more and complex the transactions required, the lesser the

rate of compliance because more time will be needed to compile the information. Ernst

& Young, (2014) propounded that, economies that requires taxpayers to submit any

additional information makes compliance obligations extremely onerous. Zimbabwean

VAT Act requires the taxpayers to submit the purchases made with the corresponding

list of supplies, their invoice numbers and VAT registration numbers which were made,

also the original invoices will be required when there is need for inspection at the

operator’s office, (ZIMRA, 2014). Evans et al as cited by Maseko (2014) agreed to the

fact that poor record keeping results in higher costs of compliance for SMEs in terms

of time that is considered to be scarce thereby encouraging SMEs to remain informal

and thereby not comply with tax legislature

iv. Number of tax Administrators

The number of tax administrators in an economy greatly affects the time taken to

comply by taxpayers, (PricewaterhouseCoopers, 2013). Specialisation in tax

administrators in different types of tax increases VAT compliance time, it is evidenced

that, for nations or economies where value added tax is administered by the same tax

authority as the one that deals with corporate income tax, compliance is easier,

(PricewaterhouseCoopers, 2010 & 2013).

c) VAT understanding by taxpayers

Value Added Tax compliance behaviour is greatly influenced by tax understanding in

taxpayers. VAT understanding is determined by the level of taxpayer to interpret

taxation laws and Acts, their willingness and ability to comply. Kasipillai (2003)

elaborated that, the tax understanding that relay to compliance is the general

understanding about taxation regulations and information pertaining to the opportunity

to evade tax. Informing taxpayers on how and where the money collected is spent by

the government, its role in national development and how VAT Act is applied is helpful

in public awareness to VAT, (Mohd, 2010). Hite and Hasseldine (2001) emphasised

17

that, it is the duty of the tax Authorities to have teachings on tax courses because it has

an impact of understanding on compliance.

d) Taxpayer’s Attitude

According to Ajzen’s (1991) Theory of Planned Behaviour, attitude is defined as an

individual’s own personal views about behaviour. To relate with VAT, taxpayers’

attitudes can be explained as either positive or negative views of tax compliance

behaviour. VAT compliance would mean positive views and non-compliance represents

negative views. Taxpayers’ attitude differs significantly, some comply, but some do not

even keep proper documentation required for VAT purposes. Bradley (1994) also

proposed that attitude on a person’s own tax avoidance, and attitude concerning other

persons’ elusive behaviours are considerable. For instance, utilizing state income to, for

example, primary amenities like health, electricity and public transport will increase the

propensity to comply on a voluntary basis.

2.6 Causes of VAT non-compliance

a) VAT compliance costs

Sandford, Godwin and Hardwick defined tax compliance costs as, “the costs incurred

by taxpayers and third parties in meeting the requirements laid upon them in complying

with a given structure and level of tax”. Research carried out by Eichfelder and

Vaillancourt, reviewed that tax compliance costs tend to be high internationally and it

is a problem not limited to a specific nation or specific country. These costs are also

believed to be much regressive and have a great impact on smaller enterprises relative

to their size.

Schmidt et al, (2007) propounded that, it is an overburden to the SME owners on top

of the existing workloads to go through all their paperwork and keep them updated on

legislation he went on to add that, unlike larger enterprises, SMEs has to go over manual

checks and filing which often is associated with higher variable costs.

b) Lack of knowledge of VAT by SMES

From the view of Schmidt et al (2007), stated that most SME owners lacks knowledge

and awareness of what needs to be done and also distorted individual perceptions of

potential costs and benefits of complying with VAT. They further suggested that

18

information from the authority on VAT issues usually is disseminated via the Internet,

which normally SMEs does not make use of, therefore increases the rate of unawareness

of tax regulations.

c) Complex VAT systems

In a research carried out by S. Smulders & C. Evans (2016), they stated that many

advocates found VAT system designs to be a contributing factor to VAT non-

compliance. The use of single against multiple rates, registration thresholds, numerous

exemptions and zero-rated items, invoicing, bookkeeping requirements and special

rules for small businesses; can all influence VAT compliance. In addition, Eichfelder

and Vaillancourt also concurred that, other factors that influence VAT compliance

includes frequency of reporting, documentation requirements and cost of audits, appeals

and litigation levels.

2.7 Theories of Tax Compliance

Tax compliance among tax payers can be classified in different tax theories depending

on the nature and basis of compliance behaviour of tax payers. One of these theories is

the economic based theory which emphasises on incentives (Trivedi and Shehata,

2005). This research is based on the economic based theories.

2.7.1 Economic based theories

This theory has a basic assumption that people are free-riders and voluntary contribution

to the government is quite a problem unless the threat of punishment makes it sensible.

According to Trivedi and Shehata (2005) as quoted by Omweri et al (2010), concurred

that taxpayers maximises moral utility by weighing economic consequences of various

compliant alternatives such as whether or not to evade tax, the chances of being detected

and the consequences thereof, then make a choice on the alternatives that gives the

highest after-tax profit. Economic based theory is therefore based on the idea that

taxpayers’ behaviour towards compliance is influenced by economic aims and

objectives such as profit maximization and the likelihood of detection. Therefore to

increase value added tax compliance level, audits and penalties for non compliance

should be increased as it increases the likelihood of detection.

19

2.7 Empirical Evidence

2.7.1 O. Zivanai, F. Chari & C. Nyakurimwa: Tax compliance challenges in

fulfilling tax obligations among SMEs in Zimbabwe: A survey of SMEs in Bindura

(2015)

The research was carried out to assess tax compliance issues in SMEs in fulfilling their

tax obligations. A survey of SMEs in Bindura town was used as a sample for the

investigation. The foremost objectives of the study were to verify on the causes of tax

compliance or non-compliance among SMEs and to assess the effectiveness of the

presumptive tax system in formalisation of informal sector. A sample size of 30 SMEs

was used with 5 strata. The findings of the study concluded that, the majority of informal

traders are not tax compliant due to apparent high tax rates, low chance of detection,

lack of confidence in revenue authority and the fact that most informal traders are

evading taxes. Recommendations made were; to give tax benefits to large companies

for trading with compliant SMEs, use tax agents, have tax audits, enforce tax laws and

launch awareness campaigns on presumptive tax, as this would help SMEs to be

compliant.

2.7.2 M. N. Thiga & W. Muturi (2015): Factors that influence compliance with tax

laws among Small and Medium Sized Enterprises in Kenya

The study aimed at analysing the factors influencing tax compliance among SMEs in

Kenya. A sample size of 400 SMEs, in Kiambu County, was drawn from a target

population of 2541 in Kenya. Results extracted from that research showed that tax rates

and tax compliance costs are the major contributing factors in tax compliance. It further

revealed that, low tax rates and low tax compliance are associated with high levels of

tax compliance. Furthermore, the study concluded that tax compliance cost have the

most momentous effect on tax compliance. The study recommended that the revenue

authority should, implement more tax incentives, improve tax awareness, set out

favourable tax rates, increase tax penalties and reduce tax compliance costs.

2.7.3 Akinboade O. A. (2015): Correlates of tax compliance of Small and Medium

Size Businesses in Cameroon.

The objective of the study was to assess tax compliance by small and medium size

businesses in Cameroon. A sample size of 575 SME operators was investigated, from

20

two different regions, Central and Littoral. The results of the study showed that, high

registration cost and time-consuming processes promote non-compliance of SME

operators. The perception that the taxpayer has to go through many departments in the

process reduces the probability of compliance. This study recommended that,

perceiving the tax system as easy to understand and consistent promotes tax compliance.

In addition, good response to enquiries by tax authorities during registration process is

believed to improve tax compliance.

2.7.4Amayi G C and Machogu B J (2013): The effects of taxpayer education on

voluntary tax compliance among SMEs in Mwanza City- Tanzania.

The researchers aimed at establishing the level of tax education, tax compliance level

and how tax education affects voluntary compliance among SMEs in Mwanza city-

Tanzania. Twenty-five questionnaires were used to collect data using descriptive survey

method. The research findings showed that the majority have basic tax education which

helped them to gain knowledge and awareness of their rights and obligations on taxation

issues and procedures for remitting taxes. The findings also showed that the level of

taxpayer education affect compliance and it was concluded that the two are positively

related. The researchers recommended that government should make efforts to impart

tax knowledge to individuals and to the business environment. They also suggested that

taxation should be educated at all levels of education, that is, from primary school

upwards with an aim to promote voluntary compliance.

2.7.5 Maseko N. (2014): the impact of personal tax knowledge and compliance costs

on tax compliance behaviour of SMEs in Zimbabwe, Harare, Bindura and

Chitungwiza.

The study was designed to investigate on how SMEs’ unique business conditions,

perceptions towards tax, levels of personal tax knowledge and compliance costs affect

their tax compliance behaviour. A sample size of 13 taxpayers was used, and a

qualitative research design was adopted. Primary research was used to collect data

through face-to-face interviews. Results from the study indicated that business

conditions encompassed by SMEs are different from those of bigger companies, and

this therefore makes them bear high tax compliance decisions. The study then concluded

that, to improve voluntary tax compliance by SMEs, ZIMRA is recommended to update

21

taxpayers with information on tax rates, tax credits and tax allowances through the print

media and press in order to improve the levels of personal tax knowledge.

2.7.6 Faridy, N, et al (2014): Complexity, Compliance costs and Non-Compliance

with VAT by Small and Medium Enterprises in Bangladesh: Is there a

Relationship?

The study aimed at investigating the nature and extent of the relationships between the

complexity of VAT legislation, the costs of compliance with VAT and non-compliance

with VAT legislation by SMEs in Bangladesh. It was gathered by way of focus groups

through interviews and survey through a purposive sample of SME taxpayers in

Bangladesh. The results of this research revealed that, the complexity in VAT law and

compliance costs are the most significant factors influencing VAT non-compliance in

SMEs. In addition, audits and penalties have been found to have less effect on VAT

non-compliance for non-compliant taxpayers. This therefore revealed that, to get rid of

VAT non-compliance through audits and penalties appeared to be complicated. The

study also revealed that, reduction in compliance cost would not essentially improve

compliance by non-compliant VAT payers, but it might for compliant VAT payers.

2.7.7 Nyamwanza T, et al (2014): An analysis of SME’s Attitudes and Practices

Towards Tax Compliance in Zimbabwe.

The study was carried out to assess the level of tax compliance among SMEs and impact

on business operations, to assess the communication methods used in informing SMEs

about regulatory developments and to assess the importance of regulatory compliance

for SMEs and its costs. A sample of fifty businesses in the retail sector in Gweru was

used to gather data about this research. The findings from this research revealed that,

least efforts are being put in place to impose compliance and also the tax collection

officials are corrupted, their level of corruption is high. Contrary to a research made by

Faridy et al (2014), penalties have been found to be the most effective in enforcing

compliance. The research also recommended that, publicity through radios, televisions

and pamphlets should be increased by authorities. Furthermore, ZIMRA is

recommended to give business people more formal tax education to enhance

understanding of tax obligations and compliance.

22

2.7.8Nungi Nkwe (2013): Tax Payers’ Attitude and Compliance Behaviour among

SMEs in Botswana.

The research sought to identify, the level of tax compliance of the taxpayers in relation

to their attitude and behaviour; to identify the factors that influence their attitudes; to

determine link between attitudes and tax compliance behaviour and then recommend

ways to improve compliance of tax through development of improved taxpayers’

attitudes among SMEs in Botswana. 200 taxpayers were randomly selected and sampled

with a total of 180 responses to questionnaires, that is, 90%. There was a moderate

gender distribution from the taxpayers who responded, with 99 being male counterparts

and 81 female. Descriptive statistics were used to analyze data collected and statistical

tools were used to present data. It was concluded that, the taxpayers’ attitude towards

tax affect their tax compliance behaviour.

2.7.9 Deshmukh’ M. S. (2012): The effect of value added tax (VAT) on the

profitability of manufacturing firms: a study of United Cement Company of

Nigeria Ltd (UNICEM).

The study aimed at obtaining information about the significance and implementation of

the value added tax on the profitability of manufacturing firms. A sample of 222 persons

was used to collect data through a descriptive research design. Questionnaires were used

to gather data and the results indicated that there is a significant relationship or effect

of VAT on the profitability and cost of production in firms. VAT is believed to cause a

reduction in the profitability of manufacturing firms and increases the cost of

production. Based on the research findings, it is suggested that value added tax should

be easy to comply with.

2.8 Gap Analysis

It has been noted that there is a gap in what literature says about VAT knowledge and

compliance in SMES. Although many authors have carried out similar researches

worldwide, the researcher considers the study of significance due to a number of

reasons. Through research, the author found that the economy of Zimbabwe is ever

changing and is facing a lot of challenges which are resulting in activities from small

scale operators. Secondly, several researchers focused more on income tax compliance

in SMES and less on VAT compliance, therefore the researcher dedicated her time to

study this so as to identity the level of VAT knowledge and compliance levels in SMES.

23

In addition, previous researches on VAT knowledge were carried out in developed

countries; however, this research was carried out in a developing nation, Zimbabwe so

as to surpass its revenue base through VAT compliance by SMES.

2.8 Summary

This chapter robustly discussed and re-examined on associated literature in relation to

the research study.

CHAPTER III

RESEARCH METHODOLOGY

24

3.0 Introduction

The credibility, reliability and appropriateness of research findings depend mainly on

the research methods used in collecting and analysing data. Research methodology

refers to a plan of action, strategies, processes or design behind the use of desired

outcomes. This chapter presents and gives justification on the research design, target

population, the sample and sampling designs, the designing and administration of data

collection instruments employed in the study. The research methodology focused on

Marondera small-medium business enterprises.

3.1 Research Design

A research design can be defined as a plan on how one goes about answering the

objectives of the research study (Bryman and Bell, 2007). Cooper and Schindler (2003;

146) viewed it as a plan and structure of investigation so conceived as to obtain answers

to research questions. In simpler terms research design gives a framework for plan of

action to the research plan. A research design can be categorised into various ways, for

instance, explanatory, descriptive or causal. The researcher used descriptive research

technique, which was found to be the most suitable in answering the research questions

on compliance of VAT. As elaborated by another scholar, research design has to provide

answers for questions like: what techniques were used to gather data? How were

constraints dealt with?

3.1.1 Descriptive Research

This type of research design is used when a researcher desire to know the characteristics

of a certain phenomena on a particular problem. Hashemi and Babaii (2013) pointed

out that descriptive research design describes the attitudes, feelings, views and

behaviours of a certain group of persons at a give place and time. Macdonald &

Headlam (2012) concurred that descriptive survey is one of the best method researchers

can use to collect data from the primary source for purpose of describing a population.

Descriptive research enabled the researcher to gather first hand data or original data as

she used questionnaires to collect information for the study. It seems to be the most

appropriate research design because Stangor (2014) highlighted that descriptive

research design allows the researcher to define and examine behaviour accurately and

also Macdonald & Headlam (2012) added that it enables the researcher to assess

attitudes and orientations in an outsized population.

25

This type is formally designed to gather simple data to investigate possible relationships

between two or more variables and in making predictions about future events. The

researcher opted for descriptive research because it is economic in terms of cost and

time and also, more data could be gathered through questionnaires increasing its

reliability. Moreover, the researcher could efficiently devote much of her time on a

selected regional area, or target group, that is, Marondera town.

However, descriptive research design has been argued by Creswell (2014) saying that,

there are high risks of asking unnecessary questions. Questions to be asked the public

has to be general questions, which accommodate the general public, hence this increases

the risk of asking unfitting questions. This research therefore tried to minimize that risk

through asking simple standard questions.

3.2 Population

There are two categories of population in research that exists, that is, the target

population and the study population, Rajasekat and Philominthan (2003). Flowler

(2013) alluded that, a study population is a group of individuals with one or more similar

physiognomies from which the researcher gather data about the problem. A target

population is described as a well-defined collection of individuals or objects known to

have the same features, Treece (2004). The target population in this study constituted

of SMEs in Marondera. The population in this study constitutes all SMEs in Zimbabwe

which recently were found to be 2.8million registered operators by a survey done by

FinScope in 2012 ( FinScope Zimbabwe, 2012). The target population in this study

constitutes of 127 SMEs.

3.3 Sample and Sample size

A sample refers to a subset of the population which represents typical features and main

characteristics of a population. The smaller the sample size, the more risky it is for

sampling error. For the purpose of this study, the researcher used a sample of 50 SMEs.

According to Jalil (2013), a reliable sample must be thirty percent and above of the

targeted population and in this research the sample size was 39%.

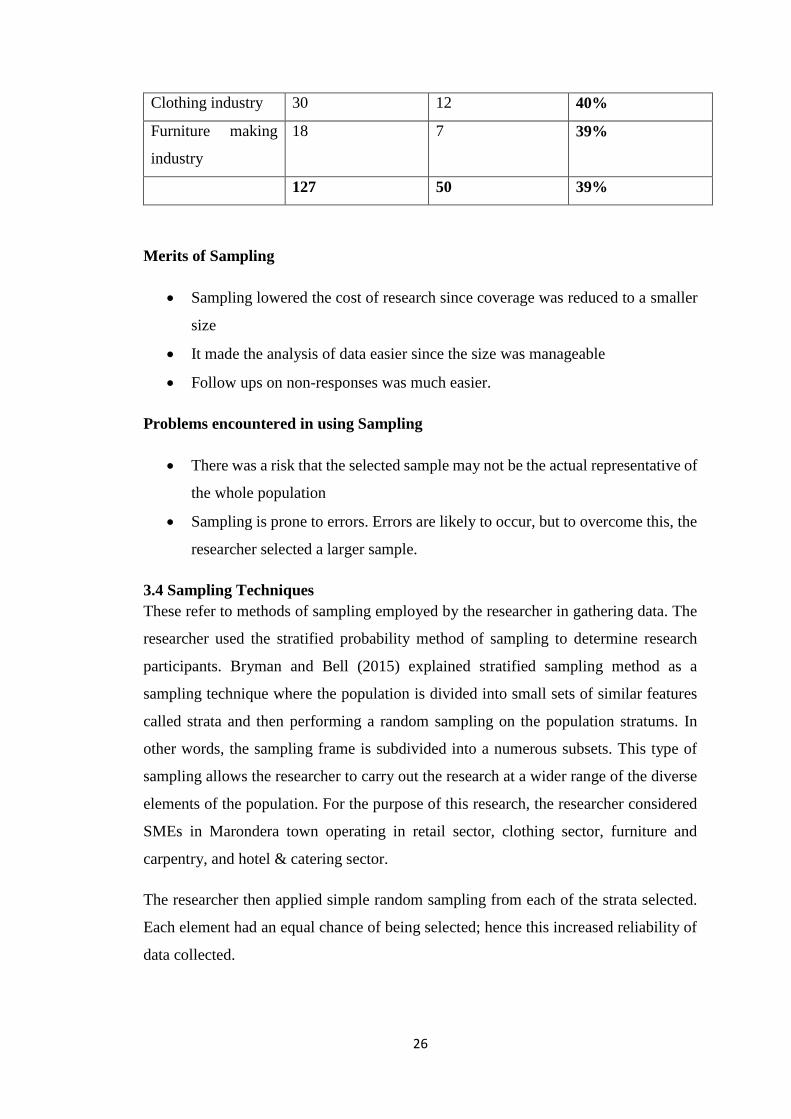

Table 3. 1 - Sample size

Stratum Total population Sample size Sample percentage

Retail 32 13 41%

Hotel & Catering 47 18 38%

26

Clothing industry 30 12 40%

Furniture making

industry

18 7 39%

127 50 39%

Merits of Sampling

Sampling lowered the cost of research since coverage was reduced to a smaller

size

It made the analysis of data easier since the size was manageable

Follow ups on non-responses was much easier.

Problems encountered in using Sampling

There was a risk that the selected sample may not be the actual representative of

the whole population

Sampling is prone to errors. Errors are likely to occur, but to overcome this, the

researcher selected a larger sample.

3.4 Sampling Techniques

These refer to methods of sampling employed by the researcher in gathering data. The

researcher used the stratified probability method of sampling to determine research

participants. Bryman and Bell (2015) explained stratified sampling method as a

sampling technique where the population is divided into small sets of similar features

called strata and then performing a random sampling on the population stratums. In

other words, the sampling frame is subdivided into a numerous subsets. This type of

sampling allows the researcher to carry out the research at a wider range of the diverse

elements of the population. For the purpose of this research, the researcher considered

SMEs in Marondera town operating in retail sector, clothing sector, furniture and

carpentry, and hotel & catering sector.

The researcher then applied simple random sampling from each of the strata selected.

Each element had an equal chance of being selected; hence this increased reliability of

data collected.

27

3.4.1 Justification of Stratified Sampling

Stratified sampling enables robust analysis of each stratum and reduces errors in the

overall sample. It also presents ample data for diverse sub-populations as well as giving

generally more dependable data that gives assurance of representative of the entire

population. Stratified sampling can guarantee that adequate sample points are obtained

to support separate analysis of any subgroup. In argument, Bryman and Bella (2015)

states that, stratified random sampling is difficult in situations where the study

population characteristics are not closely linked.

3.5 Data Sources

Data is useful in a research as it is used to draw up conclusions of the study. It can

however be obtained from two sources namely; primary and secondary data sources.

This research used the primary source only.

3.5.1Primary Source

Zohrabi (2013) defined primary data as data gathered for the first time about the

problem under study. According to Van Nederpelt (2009), primary source of data

consists of new sources of data that is extracted directly from the field work. Primary

data can be obtained through different ways or methods which include issuing out

questionnaires, carrying out interviews and direct observations in the physical ground.

The researcher accomplished primary data source from SMEs through questionnaires,

because this was the most convenient method.

Advantages of Primary data:

Data collected through primary source gave the researcher control over

selection of relevant aspects of the research.

Extraction of new data improved reliability and relevance of research data since

the information gathered was first hand information which is up to date and

collected for the problem at hand, that is VAT non-compliance in SMEs.

It also reduced the level of biased data since it was collected directly from the

SME owners who are currently in the business; they aired out their views as

they are.

Disadvantages of Primary data

28

Analysing primary data was time consuming. The researcher therefore had to

efficiently schedule her time to manage the time required.

Large volumes of data is collected through questionnaires which therefore

increased the burden for data analysis to the researcher, therefore the researcher

had to dedicate more time to analysis of data.

3.6 Research Instruments

Research instruments are referred to as dimensional tools used for collecting data, for

example questionnaires, intended to attain data on a topic of interest from a research

subject, Daas and Arends-Toth (2012). The research under study adopted questionnaires

as the research instrument.

3.6.1 Questionnaires

According to Saunders, Lewis & Thornhill (2012), a questionnaire is a research

instrument that consists of many various questions intended to collect data from the

respondent. Creswell (2014) viewed a questionnaire as a written series of questions the

respondent read, interpret and answer as provided. The researcher distributed the

questionnaires solely to SME operators, using the stratified random sampling. Every

small-medium business enterprise in Marondera had an equal chance of being selected

since they were picked randomly. The questionnaires distributed were self-structured

by the researcher with the help of the knowledge from literature on VAT compliance.

Questions set on questionnaires were closed ended type of questions as the researcher

aimed at quantitative data analysis.

Closed questions enabled the researcher to obtain quantitative type of data, which could

be statistically presented. These types of questions do not allow the respondent to

express his/her views since they only allow them to respond using the given rating scale.

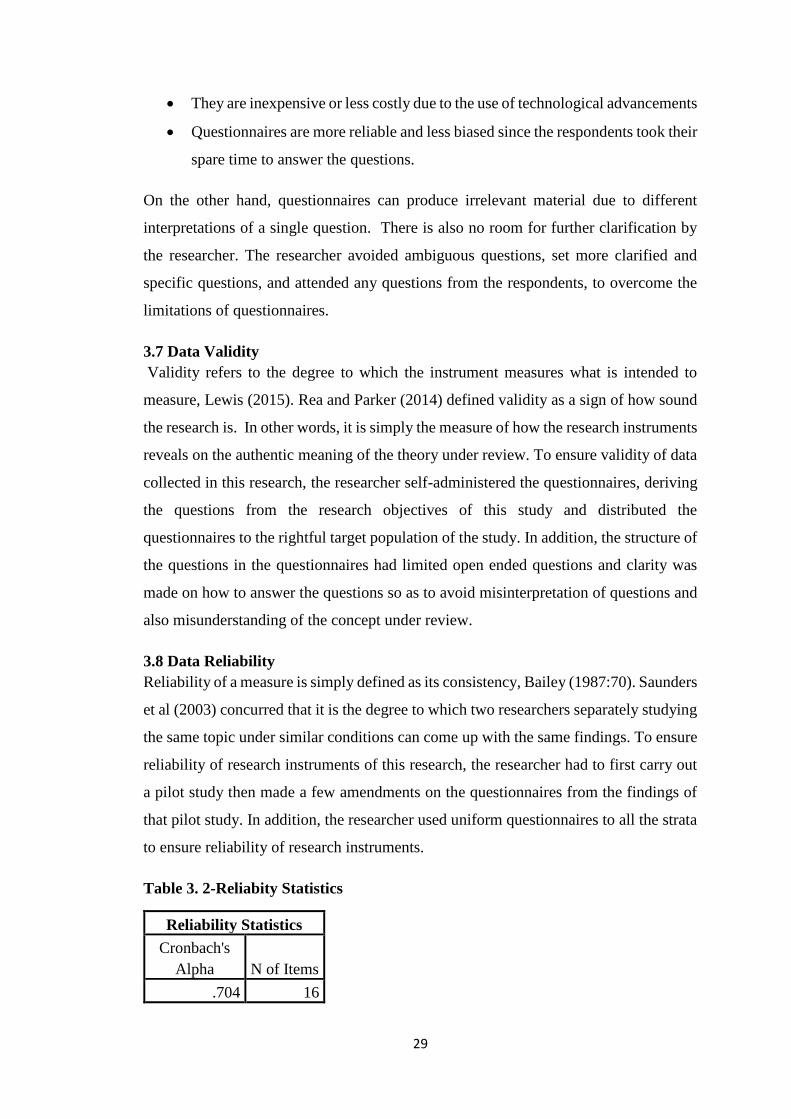

Likert scale was adopted by the researcher in structuring the questionnaires, where the

respondents were required to indicate their degree of agreement through selection of

one of the given responses.

Advantages of Questionnaires

They met the research objectives of the study in question since the questionnaire

allowed the researcher to set a greater number of questions.

They are time saving, considering the time lag the researcher had in carrying out

the study, they were the most suitable research instrument for the research.

29

They are inexpensive or less costly due to the use of technological advancements

Questionnaires are more reliable and less biased since the respondents took their

spare time to answer the questions.

On the other hand, questionnaires can produce irrelevant material due to different

interpretations of a single question. There is also no room for further clarification by

the researcher. The researcher avoided ambiguous questions, set more clarified and

specific questions, and attended any questions from the respondents, to overcome the

limitations of questionnaires.

3.7 Data Validity