Appendix L: Urban Decay Analysis - City of Atascadero

75

City of Atascadero - Del Rio Road Commercial Area Specific Plan Draft EIR Michael Brandman Associates F:\Brandman\Projects\36220001\3 - Draft EIR\released\36220001 Sec99-00 Appendix Dividers.doc Appendix L: Urban Decay Analysis

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Appendix L: Urban Decay Analysis - City of Atascadero

City of Atascadero - Del Rio Road Commercial Area Specific Plan Draft EIR

Michael Brandman Associates F:\Brandman\Projects\36220001\3 - Draft EIR\released\36220001 Sec99-00 Appendix Dividers.doc

Appendix L: Urban Decay Analysis

URBAN DECAY ANALYSIS FOR

DEL RIO SPECIFIC PLAN AREA IN CITY OF ATASCADERO, CA

Prepared for: Michael Brandman Associates

Prepared by: Bay Area Economics

December 2010

Table of Contents Introduction and Summary of Findings......................................................................1

Background and Study Purpose ................................................................................................ 1 Project Description .................................................................................................................... 1 Study Methodology ................................................................................................................... 2 Findings Regarding Urban Decay ............................................................................................. 3 Report Organization .................................................................................................................. 6

Demographic Overview................................................................................................7 Definition of Market Area ......................................................................................................... 7 Population Trends.................................................................................................................... 10 Household Trends.................................................................................................................... 12 Resident Income ...................................................................................................................... 13

Inventory of Existing Competitive Retail ..................................................................14 Overview of Existing Retail Real Estate Market..................................................................... 14 Overview of Primary Market Area Retail Nodes .................................................................... 15 Inventory by Type of Store ..................................................................................................... 19

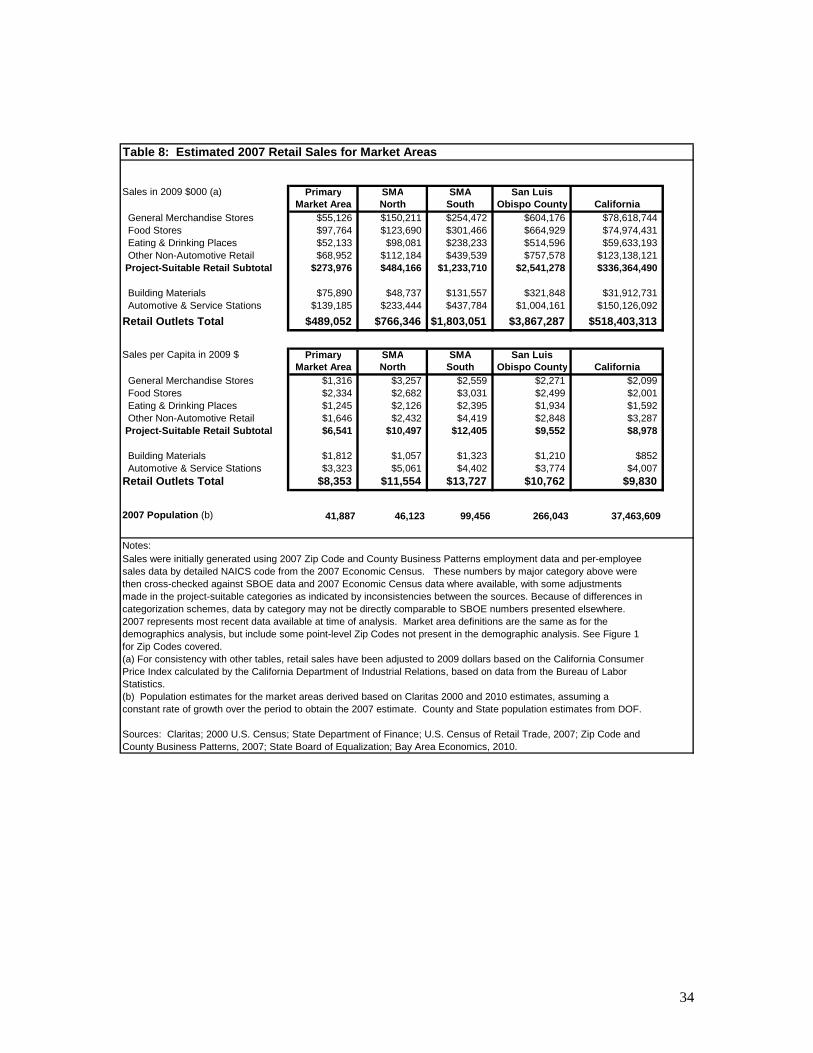

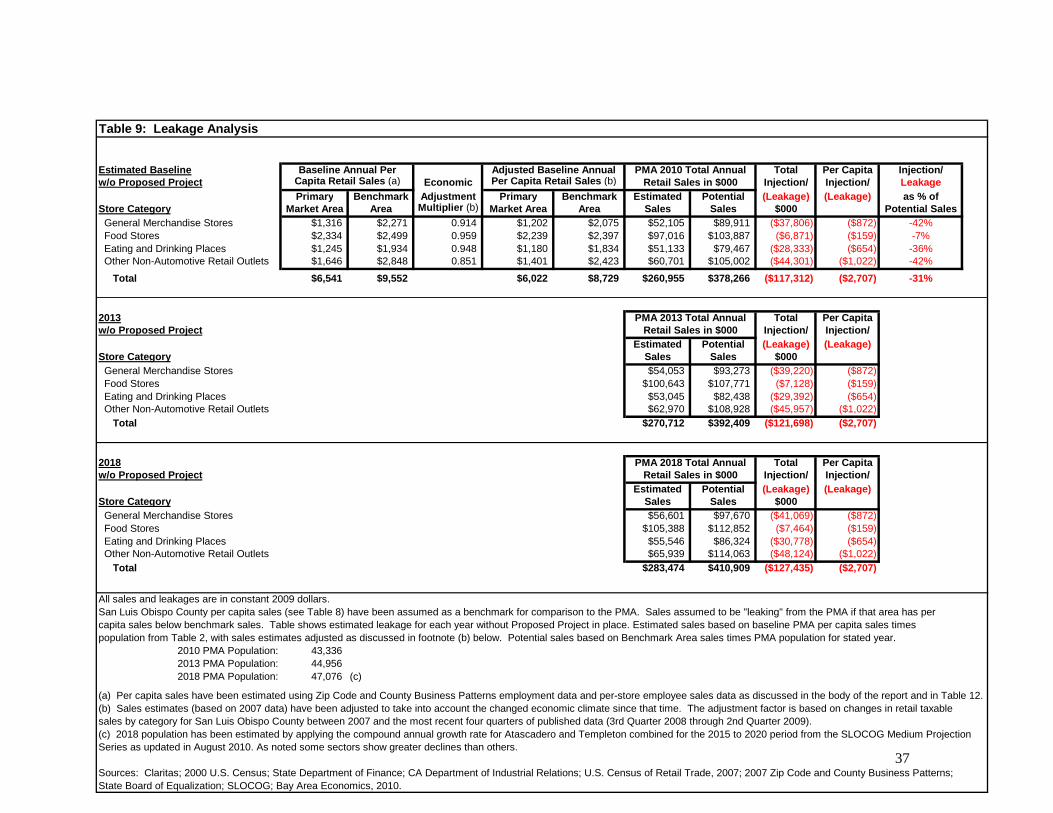

Retail Sales Analysis ..................................................................................................23 Retail Sales Trends in San Luis Obispo County and Cities in the Market Areas.................... 23 Per Capita Taxable Retail Sales .............................................................................................. 28 Estimated Retail Sales in the Market Areas ............................................................................ 31 Leakage Analysis for the Primary Market Area...................................................................... 35

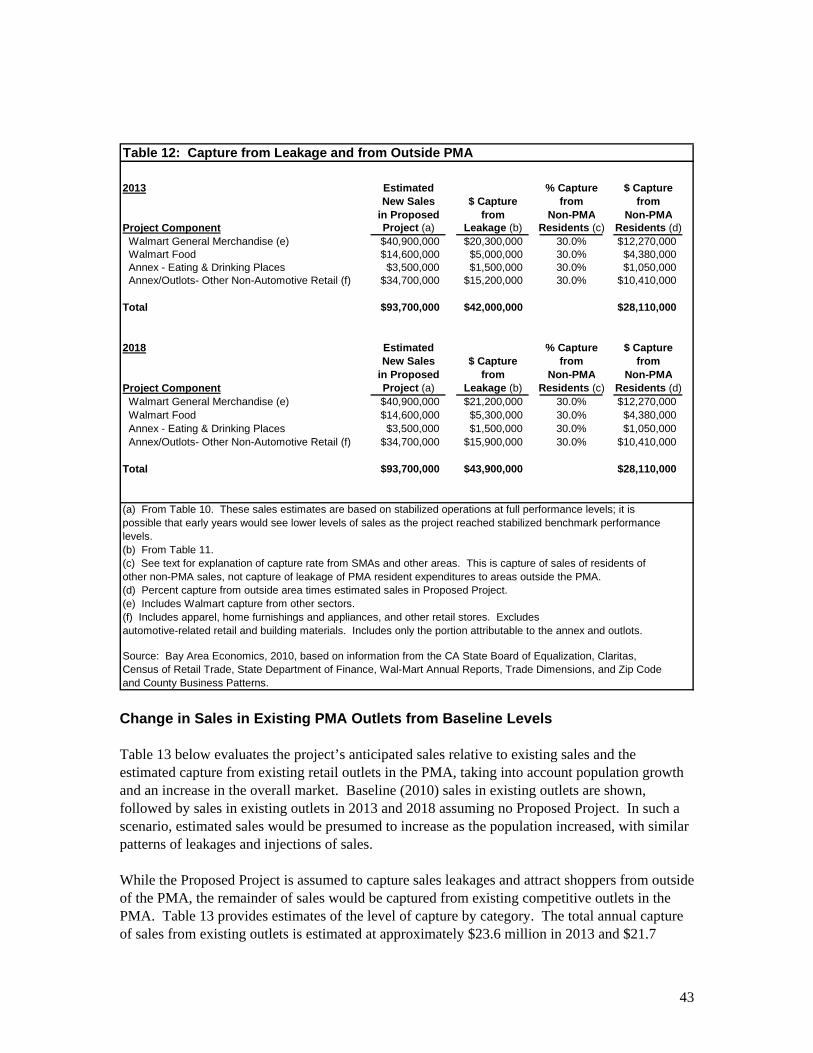

Impacts of Proposed Project on Existing Retail Outlets.........................................38 Overview ................................................................................................................................. 38 Estimated Sales at Project Opening......................................................................................... 39 Potential Capture of Leakage by Proposed Project ................................................................. 40

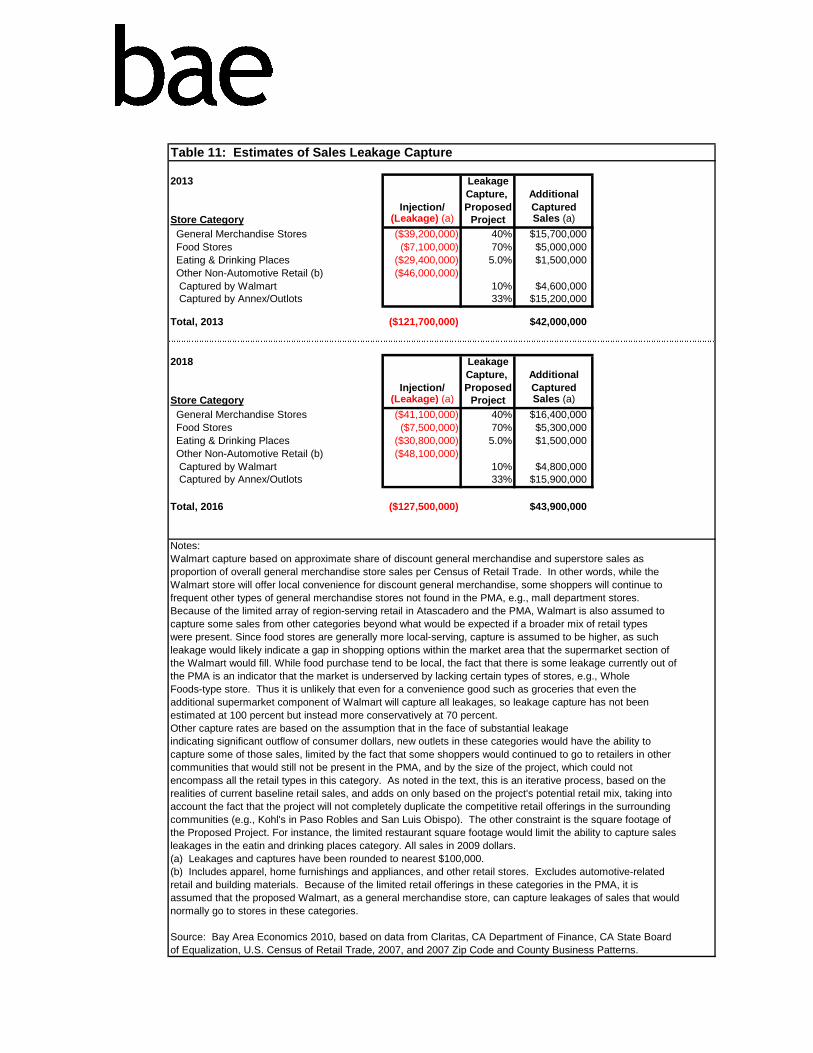

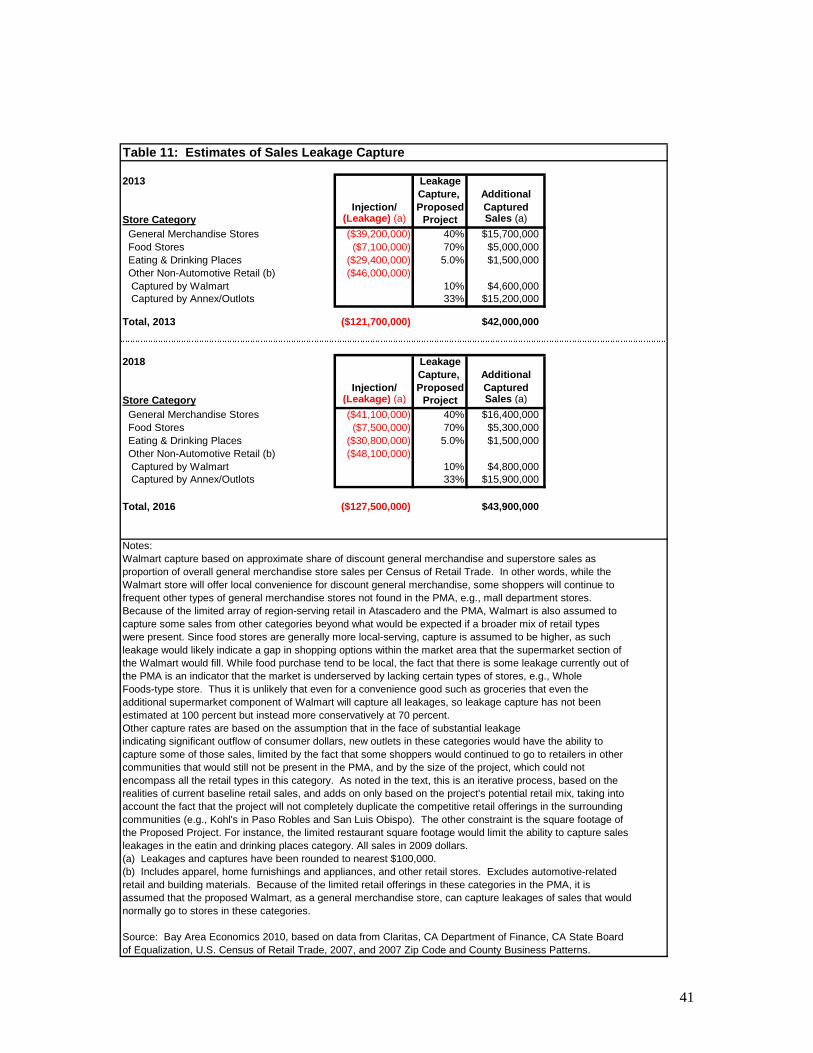

Table 11: Estimates of Sales Leakage Capture

2013 LeakageCapture, Additional

Injection/ Proposed CapturedStore Category (Leakage) (a) Project Sales (a) General Merchandise Stores ($39,200,000) 40% $15,700,000 Food Stores ($7,100,000) 70% $5,000,000 Eating & Drinking Places ($29,400,000) 5.0% $1,500,000 Other Non-Automotive Retail (b) ($46,000,000) Captured by Walmart 10% $4,600,000 Captured by Annex/Outlots 33% $15,200,000

Total, 2013 ($121,700,000) $42,000,000

2018 LeakageCapture, Additional

Injection/ Proposed CapturedStore Category (Leakage) (a) Project Sales (a) General Merchandise Stores ($41,100,000) 40% $16,400,000 Food Stores ($7,500,000) 70% $5,300,000 Eating & Drinking Places ($30,800,000) 5.0% $1,500,000 Other Non-Automotive Retail (b) ($48,100,000) Captured by Walmart 10% $4,800,000 Captured by Annex/Outlots 33% $15,900,000

Total, 2016 ($127,500,000) $43,900,000

Notes:Walmart capture based on approximate share of discount general merchandise and superstore sales asproportion of overall general merchandise store sales per Census of Retail Trade. In other words, while theWalmart store will offer local convenience for discount general merchandise, some shoppers will continue tofrequent other types of general merchandise stores not found in the PMA, e.g., mall department stores. Because of the limited array of region-serving retail in Atascadero and the PMA, Walmart is also assumed tocapture some sales from other categories beyond what would be expected if a broader mix of retail typeswere present. Since food stores are generally more local-serving, capture is assumed to be higher, as suchleakage would likely indicate a gap in shopping options within the market area that the supermarket section ofthe Walmart would fill. While food purchase tend to be local, the fact that there is some leakage currently out ofthe PMA is an indicator that the market is underserved by lacking certain types of stores, e.g., WholeFoods-type store. Thus it is unlikely that even for a convenience good such as groceries that even theadditional supermarket component of Walmart will capture all leakages, so leakage capture has not beenestimated at 100 percent but instead more conservatively at 70 percent.Other capture rates are based on the assumption that in the face of substantial leakageindicating significant outflow of consumer dollars, new outlets in these categories would have the ability tocapture some of those sales, limited by the fact that some shoppers would continued to go to retailers in othercommunities that would still not be present in the PMA, and by the size of the project, which could notencompass all the retail types in this category. As noted in the text, this is an iterative process, based on therealities of current baseline retail sales, and adds on only based on the project's potential retail mix, taking intoaccount the fact that the project will not completely duplicate the competitive retail offerings in the surroundingcommunities (e.g., Kohl's in Paso Robles and San Luis Obispo). The other constraint is the square footage ofthe Proposed Project. For instance, the limited restaurant square footage would limit the ability to capture salesleakages in the eatin and drinking places category. All sales in 2009 dollars.(a) Leakages and captures have been rounded to nearest $100,000.(b) Includes apparel, home furnishings and appliances, and other retail stores. Excludes automotive-relatedretail and building materials. Because of the limited retail offerings in these categories in the PMA, it isassumed that the proposed Walmart, as a general merchandise store, can capture leakages of sales that wouldnormally go to stores in these categories.

Source: Bay Area Economics 2010, based on data from Claritas, CA Department of Finance, CA State Boardof Equalization, U.S. Census of Retail Trade, 2007, and 2007 Zip Code and County Business Patterns.

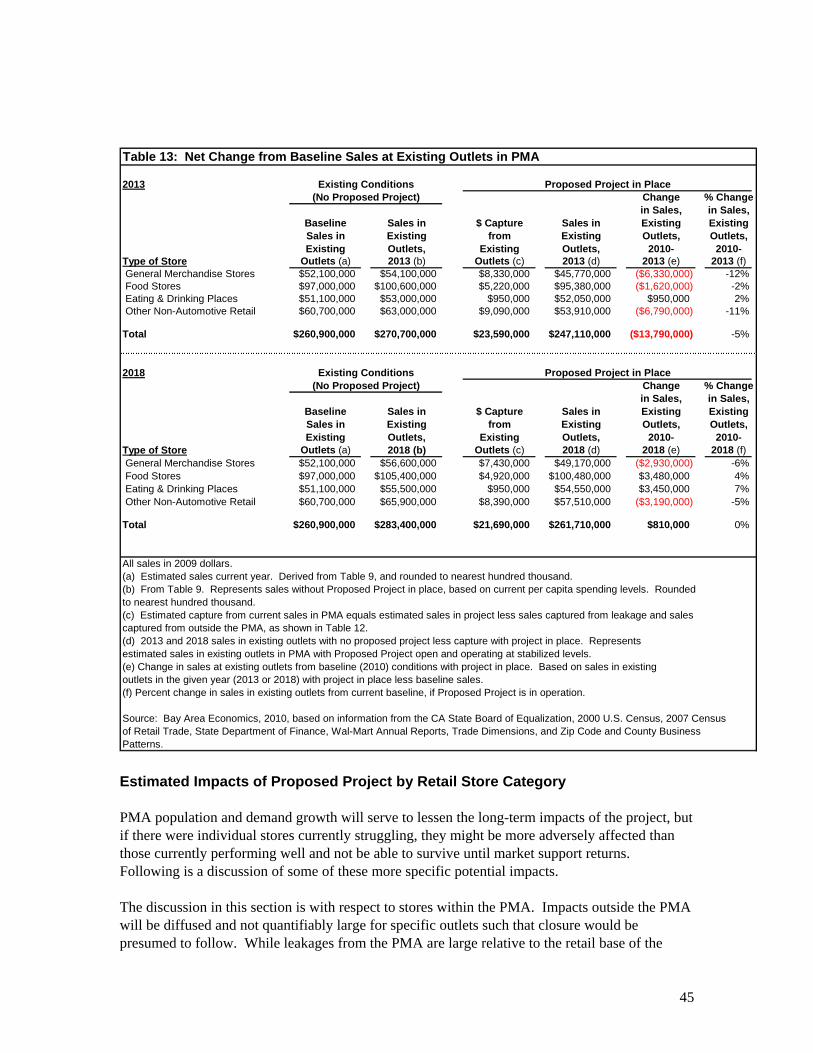

Capture of Sales from Outside the Primary Market Area ....................................................... 41 Capture of Sales from Outside the Primary Market Area ....................................................... 42 Change in Sales in Existing PMA Outlets from Baseline Levels............................................ 43 Estimated Impacts of Proposed Project by Retail Store Category .......................................... 45 Impacts outside the Primary Market Area............................................................................... 49 Cumulative Impacts................................................................................................................. 49 Findings Regarding Urban Decay ........................................................................................... 53

Appendices .................................................................................................................56

1

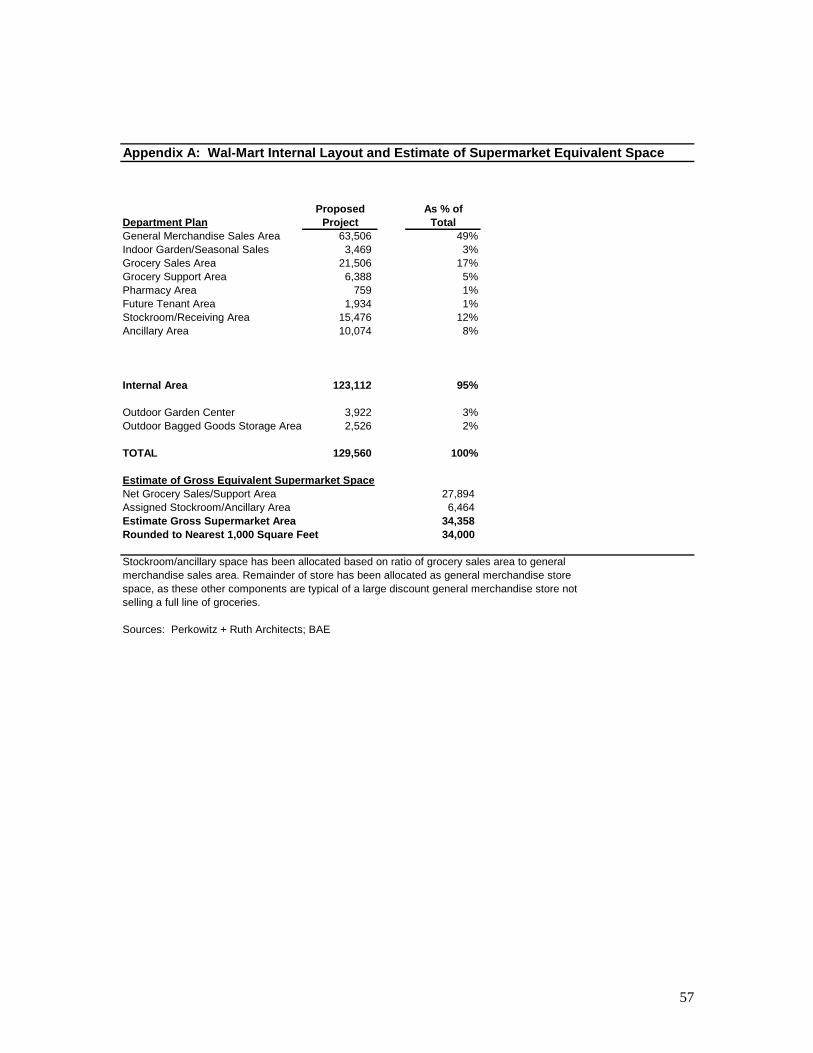

INTRODUCTION AND SUMMARY OF FINDINGS Background and Study Purpose The City of Atascadero (the “City”) is current completing an EIR for the Del Rio Specific Plan Area (the “Proposed Project”), which includes 260,460 square feet of new retail development on various parcels at or near the intersection of El Camino Real and Del Rio Road. The Proposed Project includes commercial as well as residential uses. The City has retained Michael Brandman Associates to complete an Environmental Impact Report (“EIR”). Michael Brandman Associates has retained Bay Area Economics (“BAE”) to undertake a market impact analysis for the retail portion of this project as part of the EIR process, since economic impacts could conceivably lead to urban decay, a potentially significant environmental impact. In this context, urban decay would result only if all of the following occurred: (1) the project results in an economic impact so severe that stores might close as a result; (2) buildings and/or properties, rather than being reused within a reasonable time, would remain vacant; and (3) such vacancies would cause the buildings and/or properties to deteriorate, and lead to the physical decline of the buildings and/or nearby real estate. The business closures and vacancies would have to be significant enough in scale (i.e., in terms of the total square footage affected and/or the loss of key “anchor” tenants) that they would be presumed to lead to significant physical deterioration. Physical deterioration includes, but is not limited to, abandoned buildings and commercial sites, boarded doors and windows, long-term unauthorized use of properties and parking lots, extensive gang or offensive graffiti painted on buildings, dumping of refuse or overturned dumpsters on properties, dead trees or shrubbery, extensive litter, uncontrolled weed growth, and homeless encampments. It should be noted that BAE’s analysis uses the most recently available information at the time of analysis (July/August 2010). This represents a reasonable effort to establish baseline conditions per CEQA. BAE recognizes that over the course of the EIR process, conditions may change rapidly, especially in the current economic environment; BAE attempts to take that into consideration, but future economic conditions may vary from those assumed here. Project Description The Proposed Project as specified for this analysis covers only the retail/commercial component of the project. The largest single component is a Walmart store assumed at 129,560 square feet inclusive of its outdoor garden center. The Walmart site includes two outlots with the potential for an additional 5,000 square feet of building space of unspecified commercial usage. The remainder of the commercial development is the “Annex,” which includes an additional 120,900 square feet of retail/commercial space which is largely unspecified as to tenant mix. The development plan is outlined in Table 1, with detail provided for the internal layout of the Walmart in Appendix A. The supermarket-equivalent space inside the Walmart is estimated at a gross area of 34,000 square feet, including grocery sales, support, and an allocation of stockroom

2

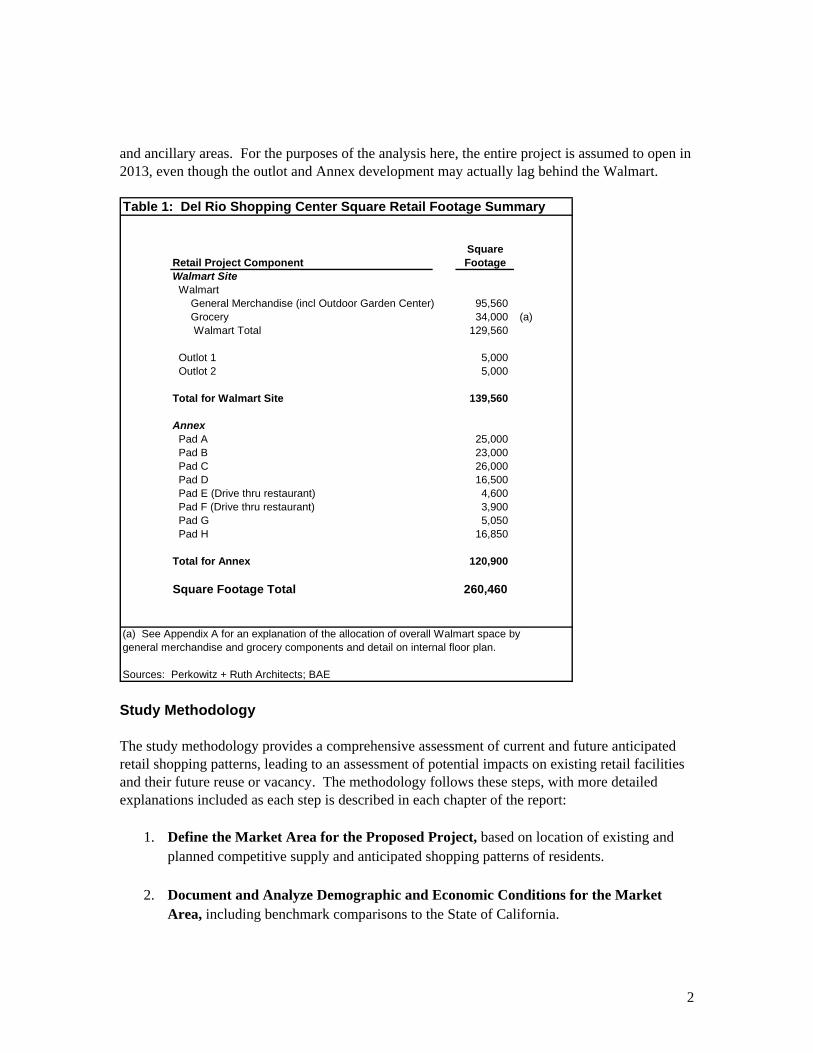

and ancillary areas. For the purposes of the analysis here, the entire project is assumed to open in 2013, even though the outlot and Annex development may actually lag behind the Walmart. Table 1: Del Rio Shopping Center Square Retail Footage Summary

SquareRetail Project Component FootageWalmart Site Walmart General Merchandise (incl Outdoor Garden Center) 95,560 Grocery 34,000 (a) Walmart Total 129,560

Outlot 1 5,000 Outlot 2 5,000

Total for Walmart Site 139,560

Annex Pad A 25,000 Pad B 23,000 Pad C 26,000 Pad D 16,500 Pad E (Drive thru restaurant) 4,600 Pad F (Drive thru restaurant) 3,900 Pad G 5,050 Pad H 16,850

Total for Annex 120,900

Square Footage Total 260,460

(a) See Appendix A for an explanation of the allocation of overall Walmart space bygeneral merchandise and grocery components and detail on internal floor plan.

Sources: Perkowitz + Ruth Architects; BAE Study Methodology The study methodology provides a comprehensive assessment of current and future anticipated retail shopping patterns, leading to an assessment of potential impacts on existing retail facilities and their future reuse or vacancy. The methodology follows these steps, with more detailed explanations included as each step is described in each chapter of the report:

1. Define the Market Area for the Proposed Project, based on location of existing and planned competitive supply and anticipated shopping patterns of residents.

2. Document and Analyze Demographic and Economic Conditions for the Market Area, including benchmark comparisons to the State of California.

3

3. Document and Analyze Existing Retail Space, including key competitive supply and existing vacancies.

4. Document and Evaluate Existing Retail Sales Trends, in order to understand local market area characteristics and variations within the market area or by store category.

5. Estimate Existing Sales Trends and Leakage Out of the Market Area, specifically for the retail categories potentially impacted by the Proposed Project.

6. Estimate Impact of Proposed Project on Market Area Sales, including when the project opens in 2013, and again in 2018 as population in the market area grows.

7. Estimate the Impacts of the Proposed Project on Existing Stores, based on any potential decline in sales for existing stores, as well as the effects of future growth and increased demand in the market area.

8. Assess the Potential for Urban Decay It should be noted that the methodology is based on an actual total sales approach, using estimated actual retail sales as the most reliable indicator of potential sales and resulting potential impacts on existing stores, in turn leading to possible urban decay. BAE relies on estimates of actual sales rather than inventories of existing store space (i.e., supply), due to the variability of existing supply information, the variability of individual store owners choosing to operate oversized or undersized stores relative to their profit margins, and other factors affecting supply of space such as sudden vacancies unrelated to dwindling demand for merchandise (e.g., lost their lease, death in the family, over-leveraged other assets resulting in store closure, etc.). Findings Regarding Urban Decay Urban decay depends on a causal chain as follows:

• The project results in an economic impact so severe that stores might close as a result; • Buildings and/or properties, rather than being reused within a reasonable time, would

remain vacant; and • Such vacancies would be significant enough in scale (in terms of total square footage

affected and/or the loss of key “anchor” tenants”) and duration to cause the buildings and/or properties to deteriorate, and lead to the physical decline of the buildings and/or nearby real estate. The business closures and vacancies would have to be significant enough in scale (i.e., in terms of the total square footage affected and/or the loss of key “anchor” tenants) that they would be presumed to lead to significant physical deterioration. Physical deterioration includes, but is not limited to, abandoned buildings and commercial sites, boarded doors and windows, long-term unauthorized use of properties and parking lots, extensive gang or offensive graffiti painted on buildings, dumping of refuse or overturned dumpsters on properties, dead trees or shrubbery, extensive litter, uncontrolled weed growth, and homeless encampments.

4

Project Alone The analysis here finds that that the first link in this chain, store closure, is not a likely result from the Proposed Project alone, so the causal chain to urban decay does not exist. Outside the PMA, any impacts from additional sales capture would be spread among many outlets spread across the large retail bases in Paso Robles, San Luis Obispo city, and elsewhere, with no potential for closure indicated for any particular retail outlet. Furthermore, existing vacant retail spaces in Atascadero appear to be well-maintained, even for spaces vacant for extended periods. Thus, while the market will be see some short-term readjustments in response to the Proposed Project, long-term vacancy and urban decay are not seen as a likely outcome. It is important to note that City of Atascadero enforces various ordinances related to property maintenance which would further reduce the potential for urban decay. The City actively prohibits conditions which would result in urban decay through its Municipal Code, including but not limited to Section 5-14, which deals with graffiti, Section 6-7, which prohibits the storage of abandoned or dismantled vehicles, Section 6-13, which prohibits vegetative growth or refuse accumulations which become public safety hazards, and Section 8-7, which covers building code violations. The Code provides for the declaration of deteriorating conditions as a public nuisance, and provides enforcement and abatement as generally described in Title 12, which provides for hearings and fines for noncompliance. The City’s Community Development Director has confirmed with BAE that the City actively enforces its ordinances with respect to properties with the kinds of physical conditions linked to urban decay.

1

Additionally, the City’s Community Redevelopment Agency provides resources to maintain and improve physical conditions in the City’s commercial areas, particularly the Downtown. The Agency’s Project Area comprises the Downtown and most of the El Camino Real retail corridor through the City, including the site of the Proposed Project development. The Agency has a Downtown Revitalization Plan which includes a Streetscape Project, assistance for the Colony Square project, and funding for graffiti removal. The City also maintains an Office of Economic Development, which assists in the recruitment and expansion of commercial businesses within the City limits. The OED is comprised of key staff members from each of the City's seven departments. The OED has completed the following projects in the past 18 months, indicating a proactive stance toward improving the retail environment and staving off physical decline:

• Downtown commercial building façade improvement grant program. • Building permit fee reduction program for businesses in the Redevelopment Agency area. • Relocation of Cowgirl Café restaurant after they lost their lease, to a vacant restaurant

space at 8300 El Camino Real. • Assistance provided to Auto Zone to find location. Auto Zone is in the process of

moving into 8195 El Camino Real to occupy a building that was vacated when Hollywood Video closed.

1 Personal communication with Warren Frace, Community Development Director for City of Atascadero,

August 26, 2010.

5

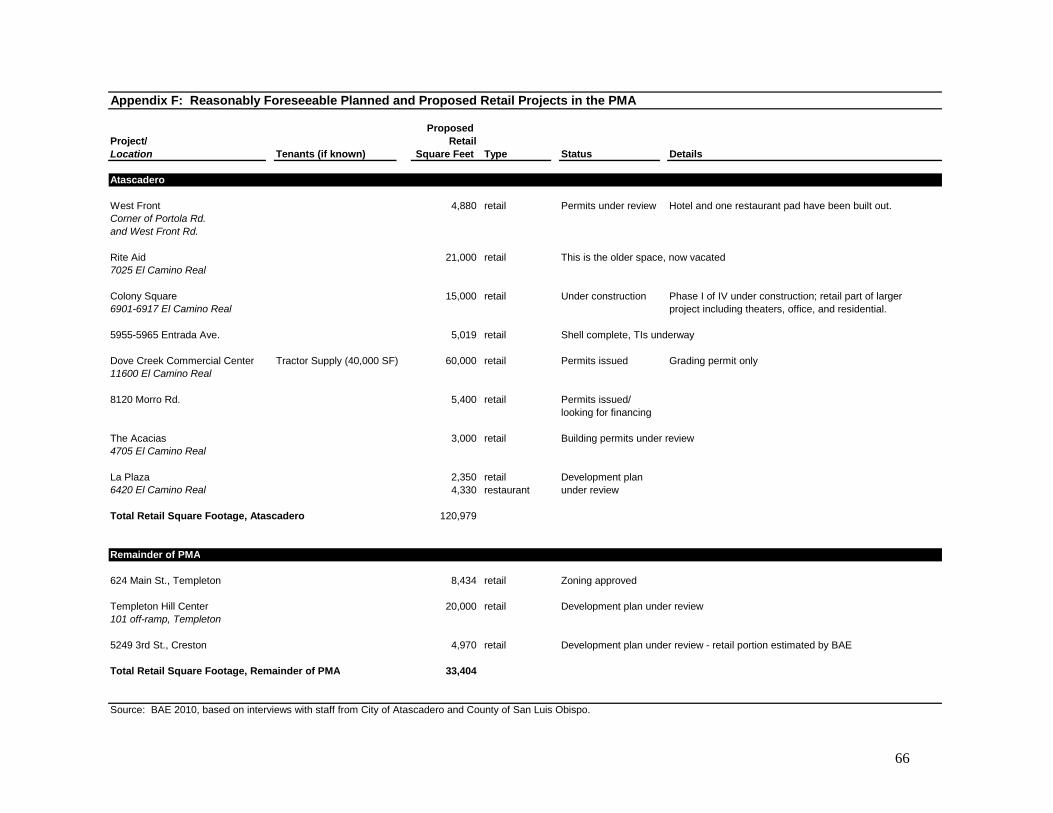

BAE’s own area tour indicates that commercial and retail properties in Atascadero, including vacant properties, are generally well maintained. Site reconnaissance around the area found little evidence of blighted buildings, marred by broken windows, graffiti, rubbish, overgrown vegetation, or other indicators of urban decay. This suggests that both property owners and local government are vigilant about preventing physical deterioration of the community. The notable deteriorated property in Atascadero is the 1.7-acre La Plaza site Downtown as discussed in the Inventory of Existing Competitive Retail above. However, site conditions relate largely to a fire at the property rather than being the result of economic conditions resulting in abandonment. In fact, there is currently a development proposal put forward for this site, the La Plaza project as noted in Appendix F. Another factor that would tend to lessen the potential for urban decay is the likelihood of market corrections as future conditions evolve. Retail spaces such as those in the Proposed Project, are often not developed without commitment from potential tenants. Without those commitments, developers will either cancel or delay projects, often due to the inability to obtain financing. With the exception of Walmart, BAE was not provided with information indicating any tenant commitments for the outlots or the Annex portions of the Proposed Project; in the absence of those commitments the project may not move forward on the schedule assumed here, and the parcels may remain vacant for a longer period of time. In Atascadero, an example of a site that has remained vacant until project commitments are secured can be found in the Home Depot Center, which has had an undeveloped parcel available for several years. However, a vacant parcel such as this does not constitute urban decay. While a tight market might lead to limited re-tenanting in retail uses, in any market there are often retailers trying to enter the market that see vacant spaces in a down market as an opportunity. For example, following the closure of Mervyns’ stores nationally, Kohl’s has chosen to reuse their vacant spaces in many markets, including Lodi, Ukiah, Eureka, and Capitola. Forever 21 re-tenanted a vacant Gottschalks in San Luis Obispo (as well as in other cities). Also in San Luis Obispo, the former Circuit City space in Irish Hills Plaza has provided an opportunity for the New Frontiers Natural Foods to relocate and expand from their current location. As noted previously, in Atascadero itself restaurant and retail users (e.g., Autozone, Cowgirl Café) have shown continued re-tenanting of vacant space even in the short period between BAE’s site tour and this analysis. Thus, even in the current economic climate, there are opportunities for re-tenanting of spaces that continue to be well-maintained and available in the market, reinforcing the likelihood that property owners will not let vacant spaces physically deteriorate. In the event of an owner’s failure to maintain vacated properties in a condition suitable for releasing, past experience indicates that the City of Atascadero will prevent physical deterioration from occurring through active and aggressive enforcement of its Code provisions relating to the abatement of public nuisances due to lack of property maintenance and management. The City of Atascadero has demonstrated its commitment to preventing physical deterioration of commercial properties within the City through its successful enforcement efforts to date, as well as through the actions of its Redevelopment Agency. Based on its past performance and policy commitments, it is reasonable to expect that the City will not allow commercial properties which may become vacant to deteriorate physically.

6

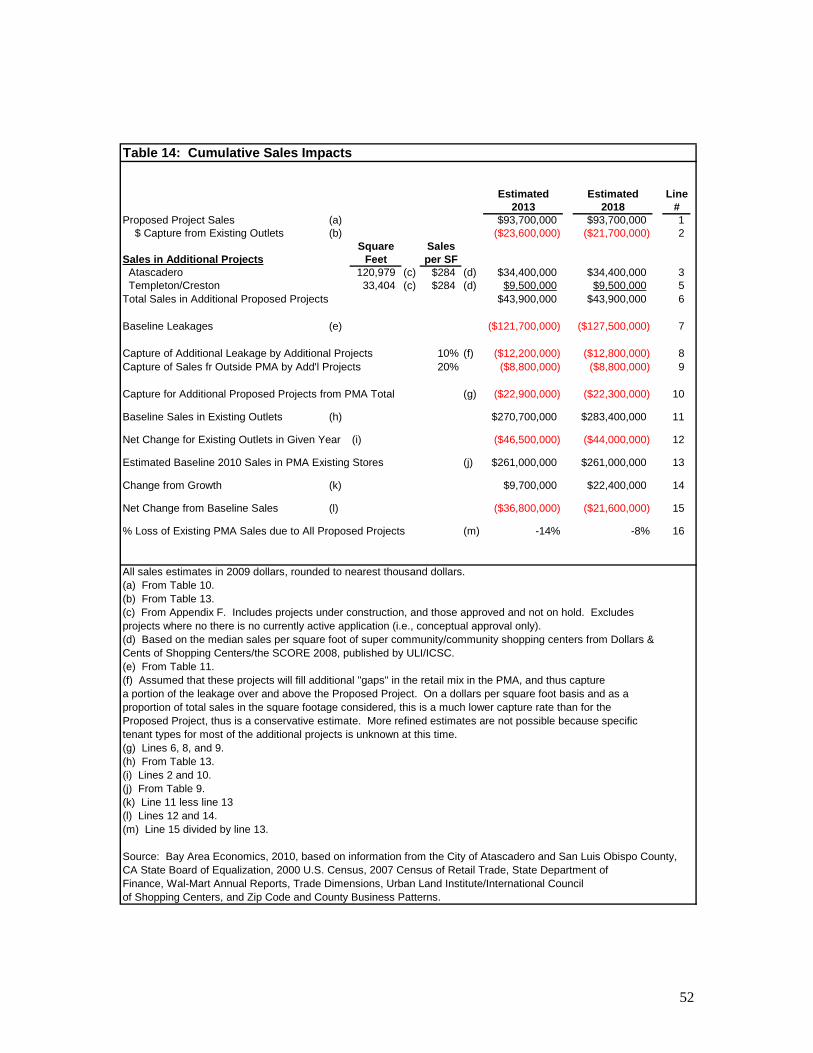

Cumulative Impacts None of the planned and proposed spaces include supermarket or large discount general merchandise store space, so the additional planned and proposed projects do not make it any more likely that a store in these sectors would face closure. Based on the above analysis, there is the potential for overall sales at existing retail outlets in the PMA to decrease in 2013 by 14 percent from baseline levels but improve to an overall estimated decrease of eight percent by 2018 due to a modest increase in the area population. It is not possible, however, to state with certainty that particular outlets or centers are going to be impacted by store closures since much of the tenant mix in the Proposed Project and the other reasonably foreseeable competitive projects is unknown, and in fact, the level of long term loss is such that existing outlets on the whole might survive without closure. The current market shows that there are retailers seeking space for re-tenanting and that even under current conditions, re-tenanting is occurring in the Atascadero area. Additionally, market corrections such as a longer buildout period for the Proposed Project are likely in response to an increase in the available existing inventory. Finally, based on its past performance and policy commitments as discussed above, it is reasonable to expect that the City will not allow commercial properties that may become vacant under cumulative conditions to deteriorate physically such that urban decay would result. Report Organization This report contains the following sections, providing background information and addressing issues of concern: this Introduction and Summary of Findings; Demographic Overview; Inventory of Existing Competitive Retail; Retail Sales Analysis; and Impacts of Proposed Project on Existing Retail Outlets.

7

DEMOGRAPHIC OVERVIEW This section presents background information on current and projected demographic conditions in the City of Atascadero and nearby communities in San Luis Obispo County making up the Proposed Project’s Primary and Secondary Market Areas. Developing a demographic profile of these areas will help in identifying key factors influencing future retail sales in the areas, and to assess the potential impacts of the Proposed Project and any other planned retail projects on existing retail outlets and centers. This discussion will consider the data available in light of current economic context, i.e., the unsettled national and world economies. Data sources considered include the U.S. Census Bureau, the San Luis Obispo Council of Governments, the California State Department of Finance, and Claritas, a private vendor providing estimates of current and future demographic conditions. Definition of Market Area A market area is the geographic region that encompasses most of a retail outlet’s customers. BAE defined the Market Areas for the Proposed Project, based on:

• Physical tour of Atascadero and surrounding areas of San Luis Obispo County • Mapping of existing nearby general merchandise and other competing retail nodes in

nearby locales • Mapping of proposed sites for key planned and proposed competitive retail facilities • An understanding based on experience of retail shopping patterns, particularly for

discount general merchandise and grocery items, as well as the general anticipated shopping patterns of residents

The Proposed Project presents a rather complex situation with respect to defining its market area. The anchor Walmart store will largely determine the customer base for this center. Typically, the market area for a Walmart can be defined based on the location of other nearby Walmarts as well as natural barriers such as gaps between population centers. In the case of this project, the nearest Walmarts are to the north in Paso Robles and to the south in Arroyo Grande. However, neither of these stores is slated to carry a full line of groceries (i.e., a broad array of food items including fresh meats/seafood and produce), so the planned Atascadero store will provide a broader retail mix. As a result, some shoppers will be attracted to this store even though it is not the closest Walmart; in the case of Paso Robles, where the existing Walmart is near the south end of town, and the Atascadero Walmart would only be a few minutes farther away, some shoppers might elect to drive past the Paso Robles store to go to Atascadero. These shoppers would also have to drive by the Target in Paso Robles to reach this proposed store. Thus, while some capture can be assumed, it may be limited due to the existing discount store options in Paso Robles, as well as the broad range of other retail shopping available in that city. As a result, BAE has segmented the secondary market area into northern and southern components, with the northern component consisting of Paso Robles and areas of the County to the north beyond Paso Robles. This area is designated as the Secondary Market Area North (“SMA-N”)

8

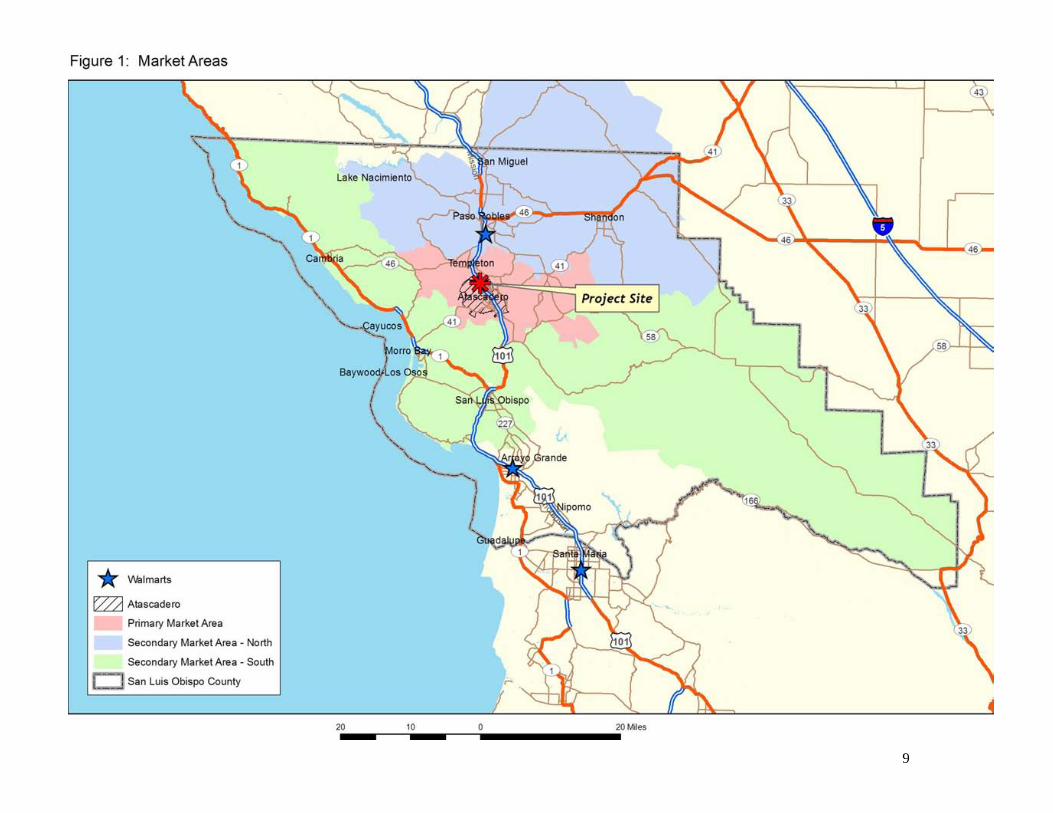

To the south, the Arroyo Grande store is over 30 miles distant, but San Luis Obispo is approximately halfway between the two stores, and while San Luis Obispo currently has no general merchandise discount stores, a Target store is under construction and will be open before the Proposed Project. There is also a Costco, the only warehouse club store in San Luis Obispo County. Additionally to the south and west are the coastal communities including Baywood-Los Osos, Morro Bay, and other communities to the north on State Highway 1. These communities have limited retail, with the mix focused on stores providing everyday items and specialty retail driven by tourism. The proposed store in Atascadero will be the closest Walmart to Morro Bay, and will be a similar distance from the other coastal communities as either the Walmart in Paso Robles or the Walmart in Arroyo Grande (although farther away than the Target in San Luis Obispo city. Further complicating the analysis, San Luis Obispo city, while not offering a Walmart, offers a wide array of other region-serving retail, and is closer to some of these communities than any of the existing or planned Walmarts. Nevertheless, the Atascadero Walmart should attract some shoppers from both San Luis Obispo city and these coastal communities. The combination of San Luis Obispo city and the coastal communities extending from Baywood-Los Osos north to the Monterey County line constitute the southern component of the secondary market area for the Proposed Project, designated as the Secondary Market Area South (“SMA-S”). Beyond these communities to the south, the existing Walmart and other retail in the Arroyo Grande area and beyond in Santa Maria, as well as the greater distances, will effectively limit the attraction of the Proposed Project to potential shoppers. Monterey County directly to the north of the Secondary Market Areas (“SMAs”) is very lightly populated and provides its own retail shopping farther north in Salinas and the Monterey Bay Area, serving the population centers of that County. The Primary Market Area (“PMA”), where the Proposed Project has the potential to attract a higher proportion of shoppers as it is clearly the closest Walmart, is defined as the City of Atascadero and the unincorporated community of Templeton not far to the north of the project site, as well as surrounding rural areas. The market areas have been defined based on Zip Code boundaries, in a split of the market areas as discussed above, and provide a good basis for data analysis due to the availability of data on retail outlets from Zip Code Business Patterns. These areas are shown in Figure 1. As shown, the boundaries of these Zip Codes extend beyond the areas discussed above, but these additional areas are largely unpopulated and have no significant retail concentrations, so their inclusion should not materially affect the analysis.

9

10

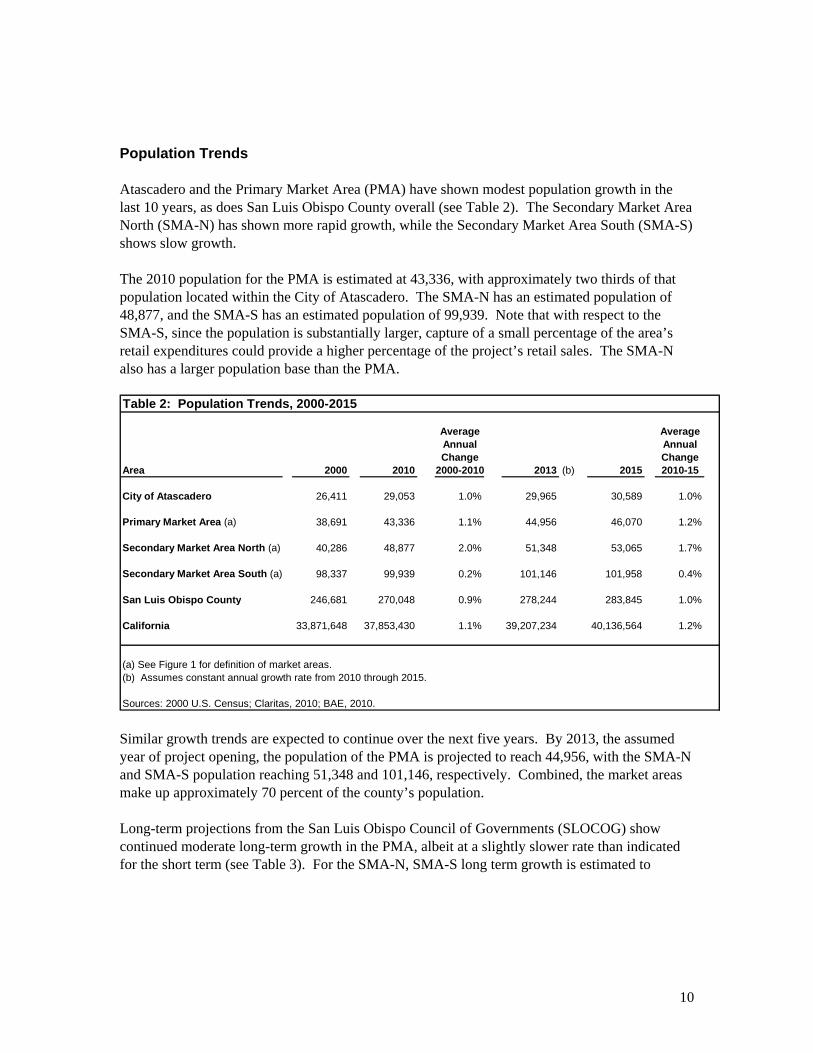

Population Trends Atascadero and the Primary Market Area (PMA) have shown modest population growth in the last 10 years, as does San Luis Obispo County overall (see Table 2). The Secondary Market Area North (SMA-N) has shown more rapid growth, while the Secondary Market Area South (SMA-S) shows slow growth. The 2010 population for the PMA is estimated at 43,336, with approximately two thirds of that population located within the City of Atascadero. The SMA-N has an estimated population of 48,877, and the SMA-S has an estimated population of 99,939. Note that with respect to the SMA-S, since the population is substantially larger, capture of a small percentage of the area’s retail expenditures could provide a higher percentage of the project’s retail sales. The SMA-N also has a larger population base than the PMA. Table 2: Population Trends, 2000-2015

Average AverageAnnual AnnualChange Change

Area 2000 2010 2000-2010 2013 (b) 2015 2010-15

City of Atascadero 26,411 29,053 1.0% 29,965 30,589 1.0%

Primary Market Area (a) 38,691 43,336 1.1% 44,956 46,070 1.2%

Secondary Market Area North (a) 40,286 48,877 2.0% 51,348 53,065 1.7%

Secondary Market Area South (a) 98,337 99,939 0.2% 101,146 101,958 0.4%

San Luis Obispo County 246,681 270,048 0.9% 278,244 283,845 1.0%

California 33,871,648 37,853,430 1.1% 39,207,234 40,136,564 1.2%

(a) See Figure 1 for definition of market areas.(b) Assumes constant annual growth rate from 2010 through 2015.

Sources: 2000 U.S. Census; Claritas, 2010; BAE, 2010. Similar growth trends are expected to continue over the next five years. By 2013, the assumed year of project opening, the population of the PMA is projected to reach 44,956, with the SMA-N and SMA-S population reaching 51,348 and 101,146, respectively. Combined, the market areas make up approximately 70 percent of the county’s population. Long-term projections from the San Luis Obispo Council of Governments (SLOCOG) show continued moderate long-term growth in the PMA, albeit at a slightly slower rate than indicated for the short term (see Table 3). For the SMA-N, SMA-S long term growth is estimated to

11

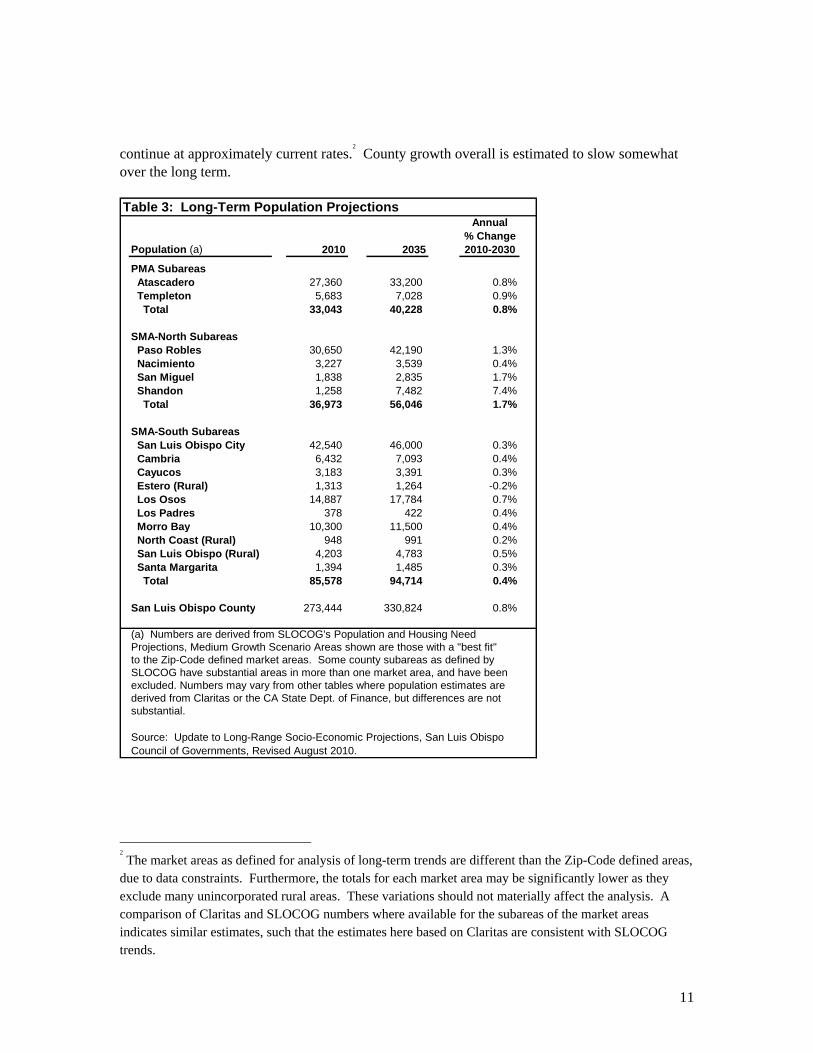

continue at approximately current rates.2 County growth overall is estimated to slow somewhat

over the long term. Table 3: Long-Term Population Projections

Annual% Change

Population (a) 2010 2035 2010-2030

PMA Subareas Atascadero 27,360 33,200 0.8% Templeton 5,683 7,028 0.9% Total 33,043 40,228 0.8%

SMA-North Subareas Paso Robles 30,650 42,190 1.3% Nacimiento 3,227 3,539 0.4% San Miguel 1,838 2,835 1.7% Shandon 1,258 7,482 7.4% Total 36,973 56,046 1.7%

SMA-South Subareas San Luis Obispo City 42,540 46,000 0.3% Cambria 6,432 7,093 0.4% Cayucos 3,183 3,391 0.3% Estero (Rural) 1,313 1,264 -0.2% Los Osos 14,887 17,784 0.7% Los Padres 378 422 0.4% Morro Bay 10,300 11,500 0.4% North Coast (Rural) 948 991 0.2% San Luis Obispo (Rural) 4,203 4,783 0.5% Santa Margarita 1,394 1,485 0.3% Total 85,578 94,714 0.4%

San Luis Obispo County 273,444 330,824 0.8%

(a) Numbers are derived from SLOCOG's Population and Housing NeedProjections, Medium Growth Scenario Areas shown are those with a "best fit"to the Zip-Code defined market areas. Some county subareas as defined bySLOCOG have substantial areas in more than one market area, and have beenexcluded. Numbers may vary from other tables where population estimates arederived from Claritas or the CA State Dept. of Finance, but differences are notsubstantial.

Source: Update to Long-Range Socio-Economic Projections, San Luis ObispoCouncil of Governments, Revised August 2010.

2 The market areas as defined for analysis of long-term trends are different than the Zip-Code defined areas,

due to data constraints. Furthermore, the totals for each market area may be significantly lower as they exclude many unincorporated rural areas. These variations should not materially affect the analysis. A comparison of Claritas and SLOCOG numbers where available for the subareas of the market areas indicates similar estimates, such that the estimates here based on Claritas are consistent with SLOCOG trends.

12

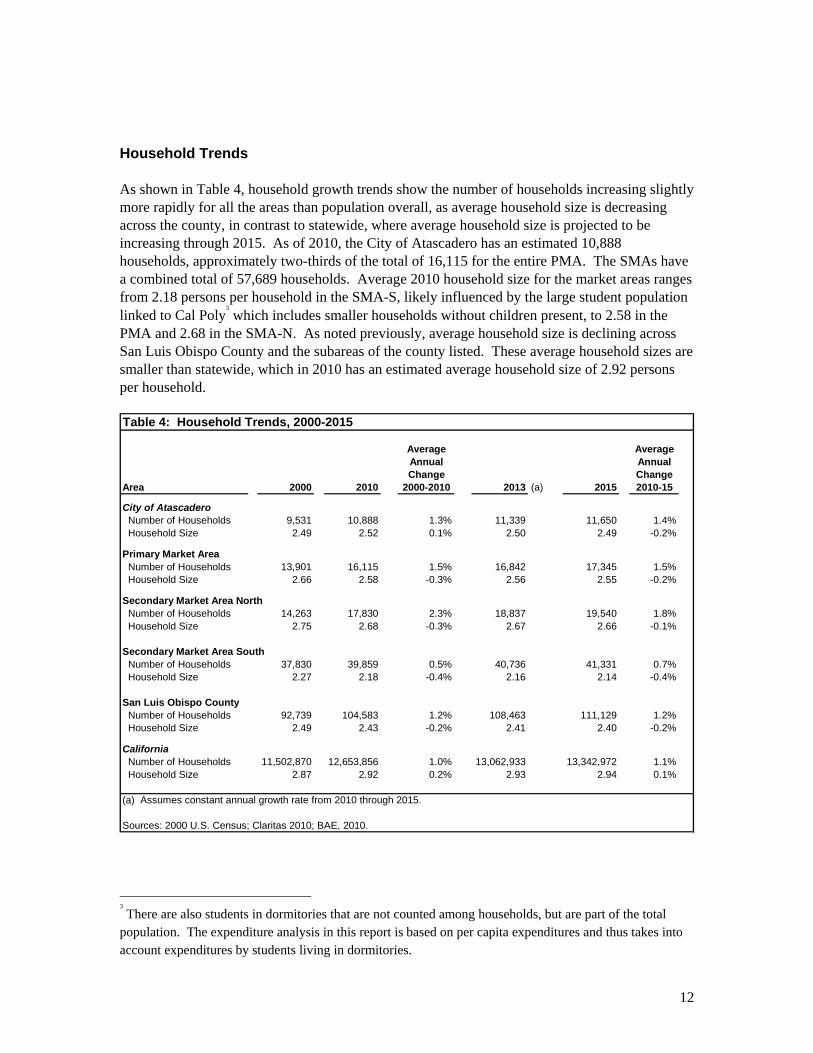

Household Trends As shown in Table 4, household growth trends show the number of households increasing slightly more rapidly for all the areas than population overall, as average household size is decreasing across the county, in contrast to statewide, where average household size is projected to be increasing through 2015. As of 2010, the City of Atascadero has an estimated 10,888 households, approximately two-thirds of the total of 16,115 for the entire PMA. The SMAs have a combined total of 57,689 households. Average 2010 household size for the market areas ranges from 2.18 persons per household in the SMA-S, likely influenced by the large student population linked to Cal Poly

3 which includes smaller households without children present, to 2.58 in the

PMA and 2.68 in the SMA-N. As noted previously, average household size is declining across San Luis Obispo County and the subareas of the county listed. These average household sizes are smaller than statewide, which in 2010 has an estimated average household size of 2.92 persons per household. Table 4: Household Trends, 2000-2015

Average AverageAnnual AnnualChange Change

Area 2000 2010 2000-2010 2013 (a) 2015 2010-15

City of Atascadero Number of Households 9,531 10,888 1.3% 11,339 11,650 1.4% Household Size 2.49 2.52 0.1% 2.50 2.49 -0.2%

Primary Market Area Number of Households 13,901 16,115 1.5% 16,842 17,345 1.5% Household Size 2.66 2.58 -0.3% 2.56 2.55 -0.2%

Secondary Market Area North Number of Households 14,263 17,830 2.3% 18,837 19,540 1.8% Household Size 2.75 2.68 -0.3% 2.67 2.66 -0.1%

Secondary Market Area South Number of Households 37,830 39,859 0.5% 40,736 41,331 0.7% Household Size 2.27 2.18 -0.4% 2.16 2.14 -0.4%

San Luis Obispo County Number of Households 92,739 104,583 1.2% 108,463 111,129 1.2% Household Size 2.49 2.43 -0.2% 2.41 2.40 -0.2%

California Number of Households 11,502,870 12,653,856 1.0% 13,062,933 13,342,972 1.1% Household Size 2.87 2.92 0.2% 2.93 2.94 0.1%

(a) Assumes constant annual growth rate from 2010 through 2015.

Sources: 2000 U.S. Census; Claritas 2010; BAE, 2010.

3 There are also students in dormitories that are not counted among households, but are part of the total

population. The expenditure analysis in this report is based on per capita expenditures and thus takes into account expenditures by students living in dormitories.

13

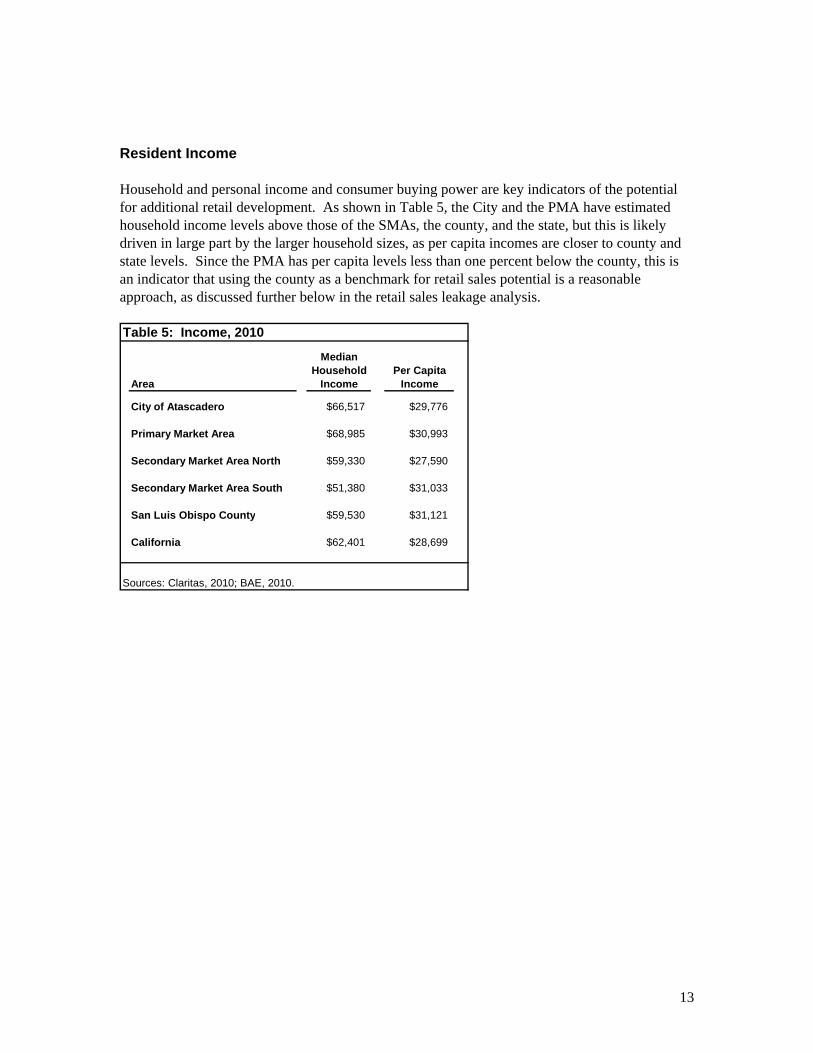

Resident Income Household and personal income and consumer buying power are key indicators of the potential for additional retail development. As shown in Table 5, the City and the PMA have estimated household income levels above those of the SMAs, the county, and the state, but this is likely driven in large part by the larger household sizes, as per capita incomes are closer to county and state levels. Since the PMA has per capita levels less than one percent below the county, this is an indicator that using the county as a benchmark for retail sales potential is a reasonable approach, as discussed further below in the retail sales leakage analysis. Table 5: Income, 2010

MedianHousehold Per Capita

Area Income Income

City of Atascadero $66,517 $29,776

Primary Market Area $68,985 $30,993

Secondary Market Area North $59,330 $27,590

Secondary Market Area South $51,380 $31,033

San Luis Obispo County $59,530 $31,121

California $62,401 $28,699

Sources: Claritas, 2010; BAE, 2010.

14

INVENTORY OF EXISTING COMPETITIVE RETAIL This chapter profiles existing retail space in the Primary Market Area, including retail centers, Downtown Atascadero, and other supply potentially competitive with the Proposed Project. The profile is based on an area tour, interviews with brokers handling retail properties, and additional research including online searches and contacts with store operators and city staff. Overview of Existing Retail Real Estate Market In any retail market, existing retail space is vacated on a regular basis due to functional obsolescence or the general cycle of retail closures and openings over time. For instance, until recently there has been a long-term trend in the supermarket industry toward larger stores and consolidation, with older stores reused by “second generation” tenants such as dollar stores, furniture outlets, and even non-retail uses such as fitness centers.

4 Thus any retail market is likely

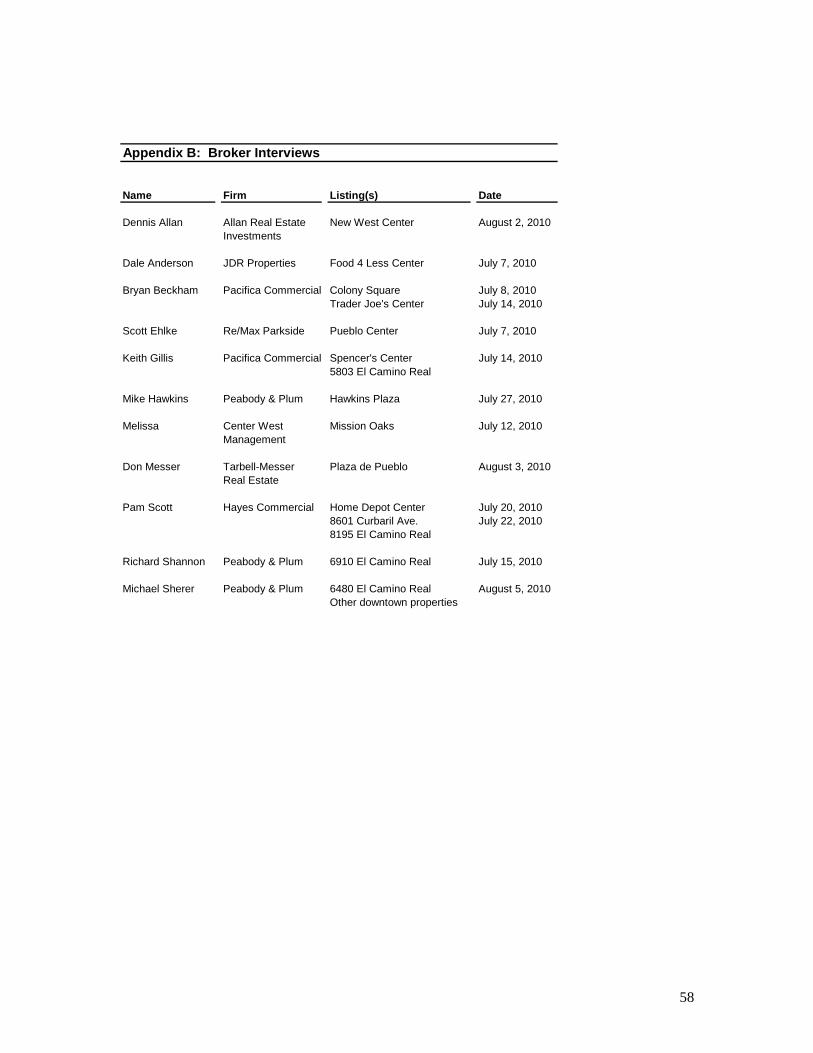

to have a certain amount of vacant space due to normal turnover and changes in retailing, and vacancies alone do not necessarily indicate urban decay or physical deterioration. Following is an analysis of overall retail estate conditions in the region, based in part on interviews with brokers handling retail properties and on an area tour. The retail areas of the PMA are almost entirely situated along old Highway 101, El Camino Real in Atascadero and, to a very limited degree, Main Street in Templeton. In Atascadero, El Camino Real from Santa Rosa Avenue through the Downtown is a long strip largely composed of retail and commercial centers as well as stand-alone retail and commercial uses. The larger centers are anchored by supermarkets; all of the City’s existing supermarkets are on El Camino Real south of Downtown. North of Downtown, the retail is more scattered, with various free-standing uses and centers between Downtown and the northern boundary of the City. In Templeton, there is a limited amount of retail along Main Street, as well as the only substantial retail center in the PMA not in the El Camino Real/Main Street corridor, the Vineyard Center anchored by Trader Joe’s on Rossi Road near the Vineyard Drive exit from Highway 101. For a listing of major retail centers in Atascadero and Templeton, see Appendix H. As part of its analysis, BAE contacted real estate brokers active in the local retail market.

5

According to these brokers, retail leasing activity in Atascadero has been slow, as might be expected under current conditions. Many vacancies have attracted little or no interest. Atascadero has limited space of a size large enough to be attractive to large national tenants, and in fact the most sought-after spaces currently are smaller spaces ranging from less than 1,000 square feet up to 3,000 square feet, with local “mom & pop” businesses, especially restaurants, being the most likely tenants. One broker stated that the city lacked spaces in the 10,000 square-foot range, and the brokers noted that much of the retail is in aging smaller strip centers. Stand- 4 More recently, niche grocery stores such as Trader Joe’s, Fresh & Easy, Grocery Outlet, and ethnic

supermarkets have started to occupy smaller spaces that are either new or that have been vacated by supermarket chain stores, in some cases subdividing the supermarket space and only using a portion of it. 5 See Appendix B for a list of brokers interviewed.

15

alone properties with good parking and high visibility on El Camino Real are also seen as more attractive. While none of the brokers tracked all properties in the PMA, vacancy estimates ranged from 10 percent up to 40 percent, with most estimates in the 10 to 20 percent range; the high end estimates were from a broker focused on Downtown. While some brokers indicated that vacancies were higher than usual currently, others noted that the limited number of additions to the overall retail inventory over the last few years even as the area has experienced modest growth in demand has kept vacancies down. Some also stated that Atascadero has tended to have chronically higher vacancies than surrounding cities, and many of the vacancies noted by these brokers were in fact vacancies of well over one year. Overall, the retail in Atascadero is seen as largely being local-serving, with shoppers venturing to nearby Paso Robles and elsewhere for major shopping trips. While some indicated that individual businesses could be impacted by the presence of Walmart, most brokers stated that overall it would improve the retail climate in the City and help in attracting larger national-tenants, especially to the north end of town, as more shoppers stay in town, and the City develops more of an ability to attract shoppers from outlying communities such as Morro Bay. Overview of Primary Market Area Retail Nodes The discussion that follows puts PMA retail centers in three major geographic categories: El Camino Real south of Downtown; Downtown Atascadero; and Other Key Retail Centers. El Camino Real South of Downtown This area contains the bulk of Atascadero’s existing retail development, including over a dozen shopping centers of various sizes as well as many free-standing businesses. The larger centers are anchored by the City’s four existing supermarkets, and the City’s three consumer-oriented drug stores are all located in this area.

6 Also along this strip are two major hardware/home

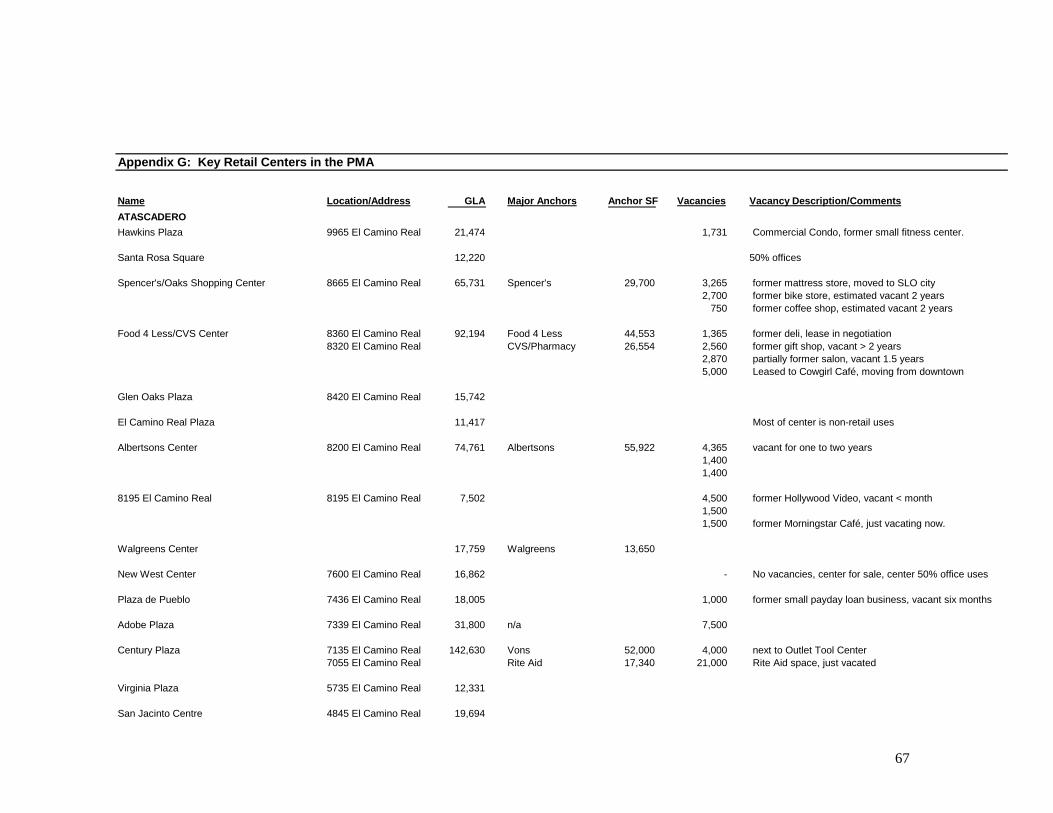

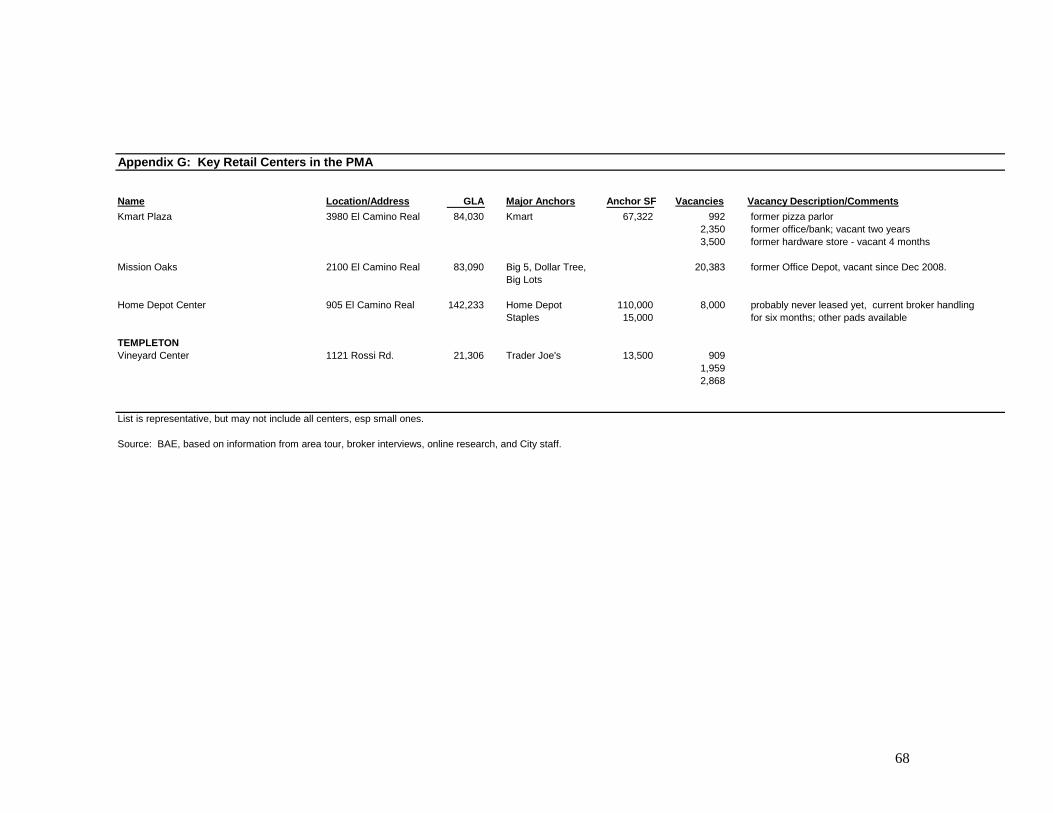

improvement businesses, and numerous other retail outlets, restaurants, and service businesses. Based on estimates from various sources, at the time of BAE’s area tour there were approximately 525,000 square feet in the inventoried centers, with approximately 75,000 square feet of vacant space (see Appendix G for details), for a vacancy rate of approximately 14 percent.

7

These vacancies range in size from less than 1,000 square feet to the recently vacated Rite Aid space of 21,000 square feet. Vacancies are scattered along the corridor. Vacancies in this area appear to be well-maintained in tenant-ready condition, and the market is still active, as several spaces that were vacant at the time of BAE’s area tour have since been re-tenanted. For instance, 6 Further discussion of supermarkets and general merchandise stores, including these drug stores, is found

later in this chapter. 7 Note that this vacancy rate is based on an inventory that is not all-inclusive, since the source data is not

all-inclusive with respect to square footages for free-standing retail properties. For instance it excludes the two hardware stores, and other freestanding businesses. While most of these other properties appear occupied, at the time of BAE’s area tour there were also some free-standing vacancies, including the former Wendy’s and Carl’s Jr. restaurant pads. Overall, while a precise rate is not known for these free-standing spaces, on the ground observation indicates that the vacancy is not substantially different than for the space in centers.

16

the small 8195 El Camino Real center had several vacancies, including a former Hollywood Video and restaurant, but this center is again fully leased, with an Autozone store coming in, according to City staff.

8 Additionally, the Cowgirl Café, which lost the lease at its downtown

location to another restaurant, has relocated to a vacant restaurant space at 8300 El Camino Real. Downtown Atascadero Downtown Atascadero has a number and variety of retail offerings. As in many older downtown districts, the mix of establishments has evolved toward small specialty retail, restaurants, entertainment, and business and personal services. This has been in response to regional competition dating back to the development of strip centers and the earliest malls, as major shopping trips for both convenience and comparison goods has shifted away from downtown areas throughout the U.S. For the purposes of the analysis here, this area is roughly bordered by Mercedes Avenue/Highway 41, Highway 101, extending to the northwest on El Camino Real to Rosario Avenue to include Virginia Plaza, and by Lewis Avenue/South Mall/Capistrano Avenue. The core area of the Downtown is on El Camino Real, Traffic Way, and Entrada Avenue. The uses consist largely of small independent retailers, restaurants, and service-oriented businesses. The Carlton Hotel is the “landmark” commercial building of the area. The area also includes the currently vacant historic City Hall as well the building currently housing city offices. The Carlton is a key anchor structure; at the time of BAE’s area tour in the summer of 2010, the first-floor restaurant and lounge had recently closed because of financial difficulties, but the restaurant re-opened in October 2010. Key businesses include Mobley’s Moto X and Boardshop, a sporting goods shop specializing in motocross and surfing equipment, and Grisanti Hardware. Other businesses include a mix of service businesses, specialty shops, and galleries. The Downtown area currently has a large number of vacancies, especially on the southwest side of El Camino Real, where the width of El Camino Real and traffic serve to isolate the area from the remainder of Downtown, and businesses are stretched along El Camino Real sandwiched between the street and Highway 101 rather than being in a more pedestrian-friendly configuration on city blocks.

9 These include two former restaurants

10 and the property southeast of the former

Jack-in-the-Box that is in disrepair and fenced off following a structure fire a few years ago that destroyed the largest building on site. While this property could properly be described as being in urban decay if it were abandoned with no prospects for future development, it is currently for sale or lease. In fact, a development proposal for the 1.7-acre site, which consists of multiple parcels, 8 Based on personal communication with Jim Lewis, Assistant City Manager, and Warren Frace,

Community Development Director. 9 BAE did not attempt to estimate total square footages for the scattered properties Downtown, but

vacancies here appear higher than the 14 percent estimated for the centers on El Camino Real south of Downtown. 10

One of these restaurant spaces, a former Denny’s, will be re-tenanted by a Bob’s Big Boy, according to local news reports from November 2010. (“Lon Allan: Bob's Big Boy to open in Atascadero,” SanLuisObispo.com/The Tribune, November 22, 2010, http://www.sanluisobispo.com/2010/11/22/1380132/more-tasty-news-for-atascadero.html.) This location, across the street from the Colony Square Development, is well situated to capture business from patrons of the theater complex.

17

is currently under review by the City. The broker representing the property stated that the remaining buildings are in some cases heavily damaged, and would have to be removed for any re-use of the property. There are other vacancies scattered throughout the Downtown area. Most of these properties appear to be well-maintained. One property (the former Hardwoods Showroom) had a boarded-up window at the time of BAE’s area tour, and one property on the strip near Mobley’s appears to have substantial water damage in the interior, but the exterior front façade is still in good condition. There is also a major development project underway, the Colony Square development at the corner of Mercedes Avenue and El Camino Real. This project upon completion is slated to include a ten-screen state-of-the art movie complex, 75,000 square feet of retail/restaurant space, office space, housing, and a parking structure, in an effort to create a strong destination attraction in Downtown Atascadero. The project has a compact “New Urbanist” design, rather than being a sprawling suburban shopping center with a large open parking lot. Currently, the movie complex and a first phase of retail are under construction. As noted above, the broker handling the retail leasing reports strong interest from several restaurant chains. This project is likely to create a dynamic for the Downtown very different from current conditions, if it is successful in attracting patrons and shoppers. The additional foot traffic in the area would prove beneficial for all of the Downtown area, and the development of this project confirms the shift of Downtown Atascadero to a business niche not directly competitive with the offerings proposed for the Del Rio Specific Plan Area. Other Key Retail Centers There are several other major retail nodes worth noting in Atascadero and Templeton. These include the Kmart Center, Mission Oaks, the Home Depot Center, the Vineyard Center, and downtown Templeton. While there are other nodes, they tend to be either scattered outlets of smaller stand-alone retailers or restaurants, or centers focused more on service businesses than retail. The Kmart Center totals slightly less than 85,000 square feet, including the 67,322 square-foot Kmart. Vacancies are currently estimated at 6,842 square feet, or eight percent of the center total (albeit a substantial portion of the non-anchor space). While some of this space has been vacant for an extended period, it is well-maintained. The Kmart store is the PMA’s only large discount general merchandise store, and would be a direct competitor to the proposed Walmart.

11

The approximately 20,000 square-foot San Jacinto Centre contains a specialty pharmacy and other non-retail businesses and is thus not seen as competitive in the mainstream retail market. There were no vacancies noted in the center at the time of BAE’s area tour. Mission Oaks is directly across El Camino Real from the proposed Walmart site and totals approximately 83,000 square feet. This center was originally built as an outlet center, but currently suffers from high vacancy, including a space of over 20,000 square feet formerly occupied by Office Depot for little more than a year. Tenants in this center include Big Lots, 11

See further discussion below focused on general merchandise stores.

18

Game Stop, Big 5, Famous Footwear, Dollar Tree, as well as some smaller tenants such as Subway. The center contains one other vacant space in addition to the former Office Depot. The vacant spaces appear to be well-maintained; the broker contacted regarding this center indicated that prospects for leasing would improve upon approvals and completion of the Walmart. At the very north end of Atascadero is the 142,000 square-foot Home Depot center. The anchor store makes up over two-thirds of the building area, with Staples occupying a separate building of approximately 15,000 square feet. There are two other outbuildings, one with 8,000 square feet of available space. There is one unbuilt pad space, as well as another vacant lot available for an additional phase of development. In Templeton, there is the recently opened Vineyard Center with Trader Joe’s and several other small tenants. This 21,306 square-foot center has two vacant spaces totaling 2,868 square feet. Downtown Templeton has a hardware store and limited other retail and restaurants in smaller historic structures along Main Street. Many of the outlets appear to be visitor-oriented.

19

Inventory by Type of Store The Proposed Project has the potential to capture some of the substantial retail leakages as discussed below, but it will also capture sales from its most direct competitors in the PMA, especially the established supermarkets and general merchandise outlets. Following is a discussion of key competitors in the categories of food stores and general merchandise stores in the PMA, with a brief discussion of retail in other sectors. The analysis with respect to Walmart impacts focuses on larger competitors, stores that are functionally similar to that proposed store. For example, any smaller food stores such as convenience stores and specialty food stores are assumed to have a level of sales that already accounts for supermarket-type competition; an additional large supermarket-equivalent space is unlikely to draw a substantial number of shoppers away from these smaller food stores, which survive by focusing on a different market niche than major supermarkets, such as convenience or specialty goods. Furthermore, vacancies in small non-anchor spaces are unlikely to lead to closure of adjacent businesses and result in urban decay, since these vacancies in scattered smaller stores alone are less likely to result in a “downward spiral” to urban decay than the loss of the major anchor of a shopping center or district that serves to attract customers to the smaller ancillary businesses. The retail market responds regularly to scattered small vacancies as part of the normal business cycle, so vacancy of any smaller retail space is far less likely to lead to urban decay. Food Stores The Proposed Project would include space equivalent in function and layout to a supermarket, so the existing supermarkets in the PMA would be directly competitive with the Walmart, and would be most likely to be impacted by the Proposed Project as a result. At the time of analysis in July/August 2010, there were five supermarkets operating within the PMA, four in Atascadero and one in Templeton, as shown in Table 6. These include Albertsons, Vons, Spencer’s Fresh Market, and Food 4 Less in Atascadero, and Trader Joe’s in Templeton. The Albertsons and Vons are conventional national chain supermarkets, of approximately 56,000 and 52,000 square feet, respectively. The Food 4 Less is a 44,553 square-foot warehouse-style store that is part of a national brand, but with regional ownership.

12 Spencer’s is a small regional chain with five

stores, four in San Luis Obispo County and one in Santa Maria; the Atascadero store is approximately 30,000 square feet. Trader Joe’s is an expanding California-based chain with three stores in San Luis Obispo County, and numerous stores throughout the state and elsewhere. Trader Joe’s stores tend to be smaller than conventional supermarkets at less than 15,000 square feet, and offers unique brands and items often not found in other supermarkets at relatively low cost. Trader Joe’s stores typically have much higher sales per square foot than conventional supermarkets. The Templeton store is no exception, with extremely strong sales in a space estimated at 13,500 square feet. Overall, these stores total slightly less than 200,000 square feet of gross retail space. All of these stores appear to be well-maintained and clean. These stores dominate the food store category in the area; there are few other food stores of any size in the PMA. 12

The Food 4 Less in Atascadero is owned by PAQ, Inc, of Stockton, which owns 12 Food 4 Less stores in the Central Valley and San Luis Obispo County. Nationally, Kroger, a major national chain, owns many Food 4 Less-branded stores.

20

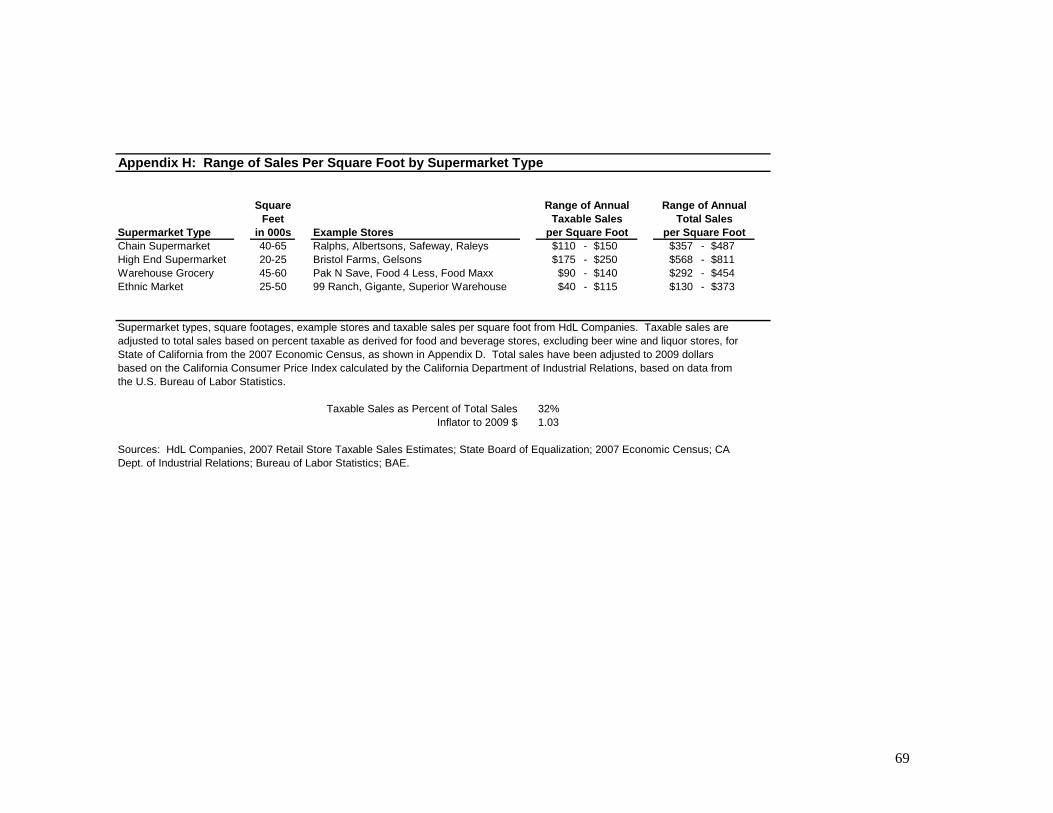

To determine sales for these stores in order to assess current performance, BAE contacted store representatives. None of the stores contacted was willing to share sales figures, which are usually considered proprietary, although some respondents shared impressions of their general sales strength and overall market conditions. Alternatively, BAE relied on the following: site visits to get a sense of overall traffic; data from Trade Dimensions, a vendor of store-by-store retail sales data acquired through various means including industry insiders; and published retail sales data for the food store category. Published taxable sales data and Zip Code Business patterns as well as the 2007 Census of Retail Trade provided a sense of the overall sales levels. BAE estimates the overall sales at these existing directly competitive supermarkets at approximately $90 million to $100 million annually, or approximately $460 to $510 per square foot.

13 This is in the range of

the median annual sales per square foot of $486 for supermarkets in super community/community shopping centers from Dollars & Cents of Shopping Centers/The SCORE 2008.

14 Trader Joe’s is

skewing this average upward, with annual sales likely greater than $1,000 per square foot. For the remaining markets, the Albertsons, Vons, and Food 4 Less are estimated to have sales in a range around the Dollars & Cents median, with Spencer’s sales at a somewhat lower level. However, as a smaller regional store, Spencer’s may have a lower hurdle rate for profitability, and as noted, the median is not a measure of profitability nor should it ever be applied as a “break-even” benchmark. Profitability information can vary considerably by individual store as well as company based on a broad range of factors including rent, financing, and labor costs. This is indicated by the broad range in sales per square foot for supermarkets. For instance, based on data derived from a survey by the HdL Companies on taxable retail sales by store type, total annual sales per square foot for various types of supermarkets in California are estimated to range from $130 to $811 (see Appendix H).

13

It should be noted that due to nondisclosure agreements, BAE cannot publish the individual store sales estimates from Trade Dimensions, which are estimates in any case rather than precise statements of sales levels. The overall estimate here should be taken as having some level of imprecision rather than as exact estimates of sales, and are not based on disclosure of individual store sales by store management in any case. 14

Published by Urban Land Institute/International Council of Shopping Centers, 2008. Note that there appears to be some variability in this estimate over time; only two years earlier, the preceding version of this publication listed the same data point as $392. The substantial change between the 2006 and 2008 publications may relate in part to sampling and data collection issues (total sample size of stores was in the 125 to 150 stores range) rather than such a large increase in sales.

21

Table 6: Competitive Supermarkets in the Primary Market Area

GrossSquare

FeetAlbertsons 8200 El Camino Real Atascadero 55,922

Vons 7135 El Camino Real Atascadero 52,000

Spencer's Fresh Market 8665 El Camino Real Atascadero 29,700

Food 4 Less 8360 El Camino Real Atascadero 44,553

Trader Joe's 1111 Rossi Rd Templeton 13,500

Total Estimated Supermarket Space in PMA 195,675

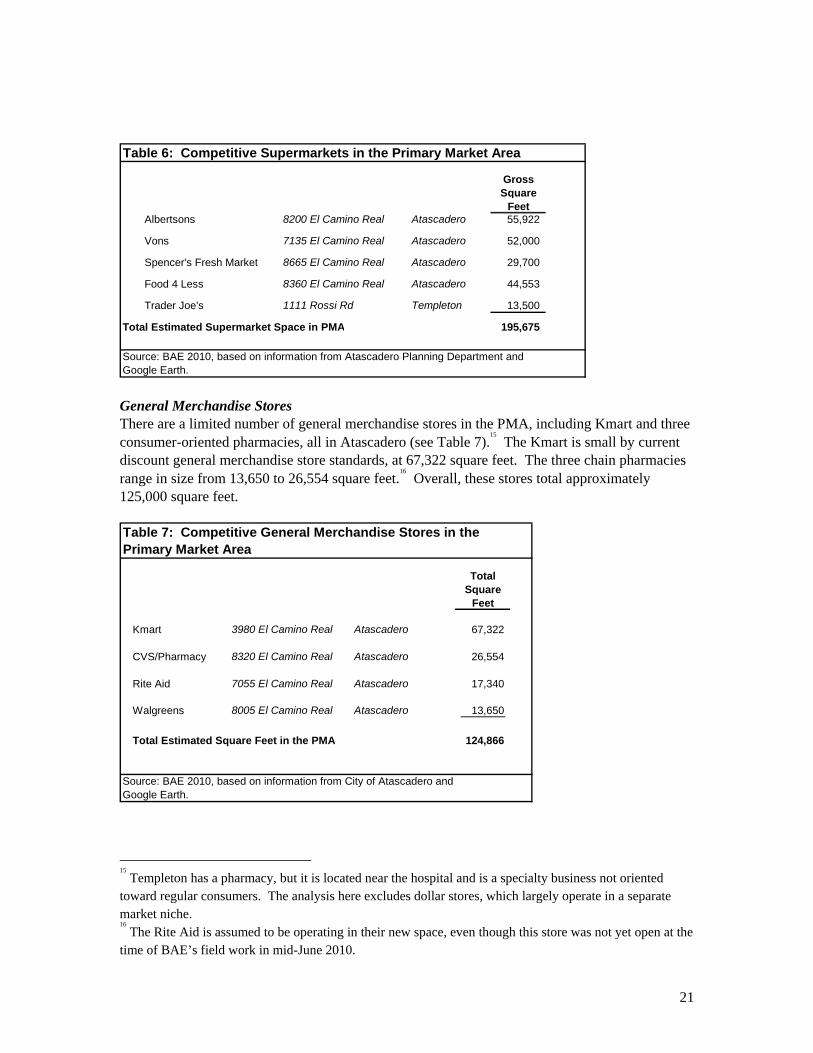

Source: BAE 2010, based on information from Atascadero Planning Department andGoogle Earth. General Merchandise Stores There are a limited number of general merchandise stores in the PMA, including Kmart and three consumer-oriented pharmacies, all in Atascadero (see Table 7).

15 The Kmart is small by current

discount general merchandise store standards, at 67,322 square feet. The three chain pharmacies range in size from 13,650 to 26,554 square feet.

16 Overall, these stores total approximately

125,000 square feet.

TotalSquare

Feet

Kmart 3980 El Camino Real Atascadero 67,322

CVS/Pharmacy 8320 El Camino Real Atascadero 26,554

Rite Aid 7055 El Camino Real Atascadero 17,340

Walgreens 8005 El Camino Real Atascadero 13,650

Total Estimated Square Feet in the PMA 124,866

Source: BAE 2010, based on information from City of Atascadero andGoogle Earth.

Table 7: Competitive General Merchandise Stores in the Primary Market Area

15

Templeton has a pharmacy, but it is located near the hospital and is a specialty business not oriented toward regular consumers. The analysis here excludes dollar stores, which largely operate in a separate market niche. 16

The Rite Aid is assumed to be operating in their new space, even though this store was not yet open at the time of BAE’s field work in mid-June 2010.

22

Using sources similar to those for the food stores, BAE estimates that these four stores have total annual sales of between $37.5 and $42.5 million, or approximately $300 to $340 per square foot. The sales performance average is pulled down by Kmart, but this store appears to be performing well above Kmart norms, most likely due to the lack of a direct competitor in the PMA.

17

Beyond the PMA, large general merchandise discount stores such as Walmart and Target can be found along the Highway 101 corridor in Paso Robles and Arroyo Grande. There are no large discount general merchandise stores in San Luis Obispo city or the coastal communities in the SMA-S. San Luis Obispo city, however, has more conventional department-type stores as well as the County’s only Costco. Given this lack of larger general merchandise competitors and their presence in nearby cities, for other than everyday shopping, PMA residents have a strong incentive to shop outside the area when seeking items found at general merchandise stores. This indicates a strong likelihood of significant sales leakages from the PMA. Other Retail In the eating and drinking places category, there are many smaller outlets scattered throughout the PMA, in a mix including fast food franchises and locally owned businesses. However, as noted in the leakage analysis below, even for this category the PMA appears under-retailed, particularly for national chain sit-down restaurants. Among other retail sectors of interest, the City’s retail consists largely of smaller outlets, with the exception of a few mid-size national chain stores in Mission Oaks and the Home Depot Center. Based on the Zip Code Business Patterns data from 2007, in the relevant non-automotive retail categories there are only four stores in the PMA with 20 or more employees, including one appliance store, one sporting goods store, one office supply store, and one beer, wine, and liquor store.

17

Based on Sears Holding Company’s most recent 10-K Annual Report (for 2009), Kmart sales nationally average only $125 per square foot annually.

23

RETAIL SALES ANALYSIS This section examines retail trends in Atascadero and the market areas. Data from the incorporated cities within the market areas are presented, along with comparative data from San Luis Obispo County and California. The analysis presents an overview of retail sales, and then focuses on the key categories of food stores and general merchandise stores that represent the primary competition with the Proposed Project’s major component, the Walmart store. A discussion of sales in other key retail store categories is also presented. A leakage analysis for the Primary Market Area is undertaken to identify the relative strength of major retail sectors, in comparison to each other and to the county overall. The primary source of information on general retail expenditures in California is the taxable retail sales data published by the State Board of Equalization (SBOE). SBOE publishes Taxable Sales in California, a quarterly and annual publication that reports taxable sales by major store categories by city and county. With adjustments made to take into account nontaxable sales such as food and prescriptions, this source usually offers the best baseline data for jurisdictions for which it is available. The most recent published annual data available at the time of this analysis were from 2008; additionally data from the first two quarters of 2009 are available, but SBOE has undertaken a major reclassification of businesses that makes comparisons with earlier data and a continued time series difficult if not impossible. The lag in data reporting must be taken into consideration, especially in light of the currently unsettled economic climate. Because of the limitations with SBOE data with respect to availability for unincorporated areas which make up a large portion of all the Market Areas, the leakage analysis itself utilizes estimates based on Zip Code and County Business Patterns employment data benchmarked to adjusted data on sales per employee from the 2007 Census of Retail Trade, with adjustments by category made based on crosschecks with the Census of Retail Trade and SBOE data. Retail Sales Trends in San Luis Obispo County and Cities in the Market Areas The following section presents SBOE-derived retail sales data from Atascadero, San Luis Obispo city, and Paso Robles, which are the incorporated places within the market areas for which the state publishes retail sales data by major store category,

18 and which, based on the location of

residents as well as most retail outlets, account for a large proportion of the retail sales in the PMA and the SMAs. For comparative purposes sales data from San Luis Obispo County and the State of California are also presented. All data are presented in constant 2009 dollars, based on the California Consumer Price Index. Taxable sales have been adjusted for the general merchandise and food store categories based on a factor derived from a comparison of taxable sales as reported by SBOE and total retail sales as reported by the Census of Retail Trade. Finally, the static estimate based on Zip Code Business Patterns is presented and discussed; this estimate relies on the most recent data available from that source, from 2007. 18

Data for Morro Bay are not published by retail store category.

24

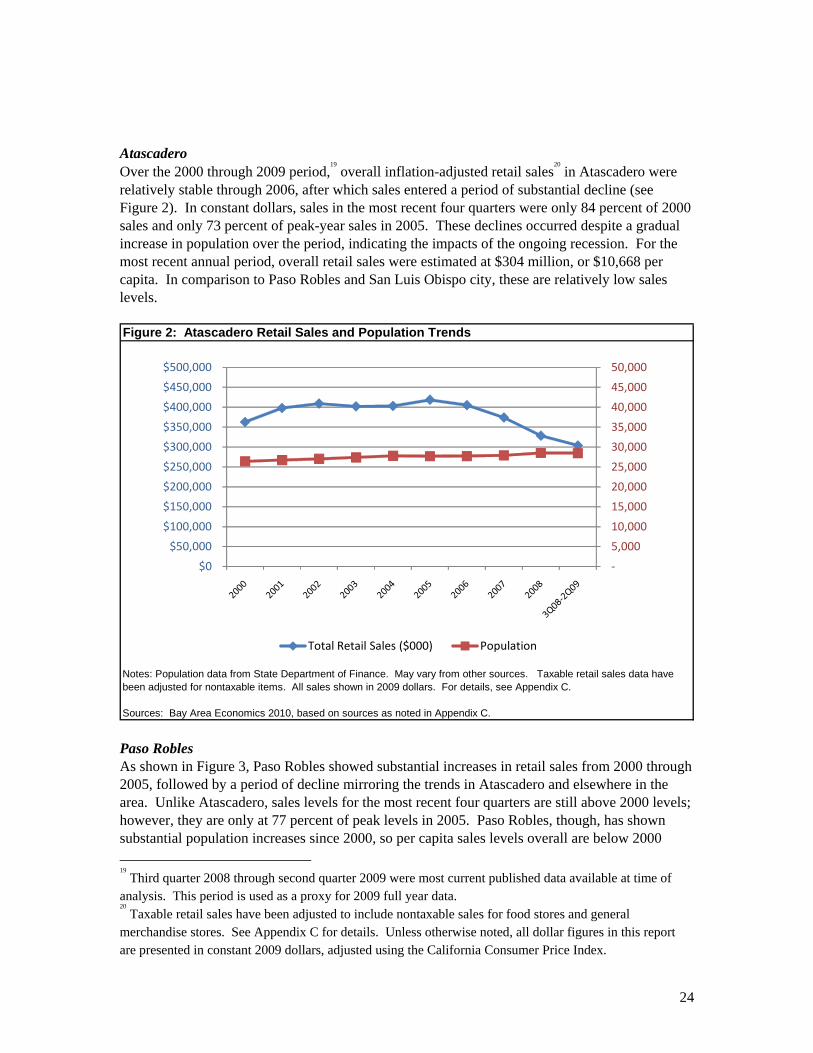

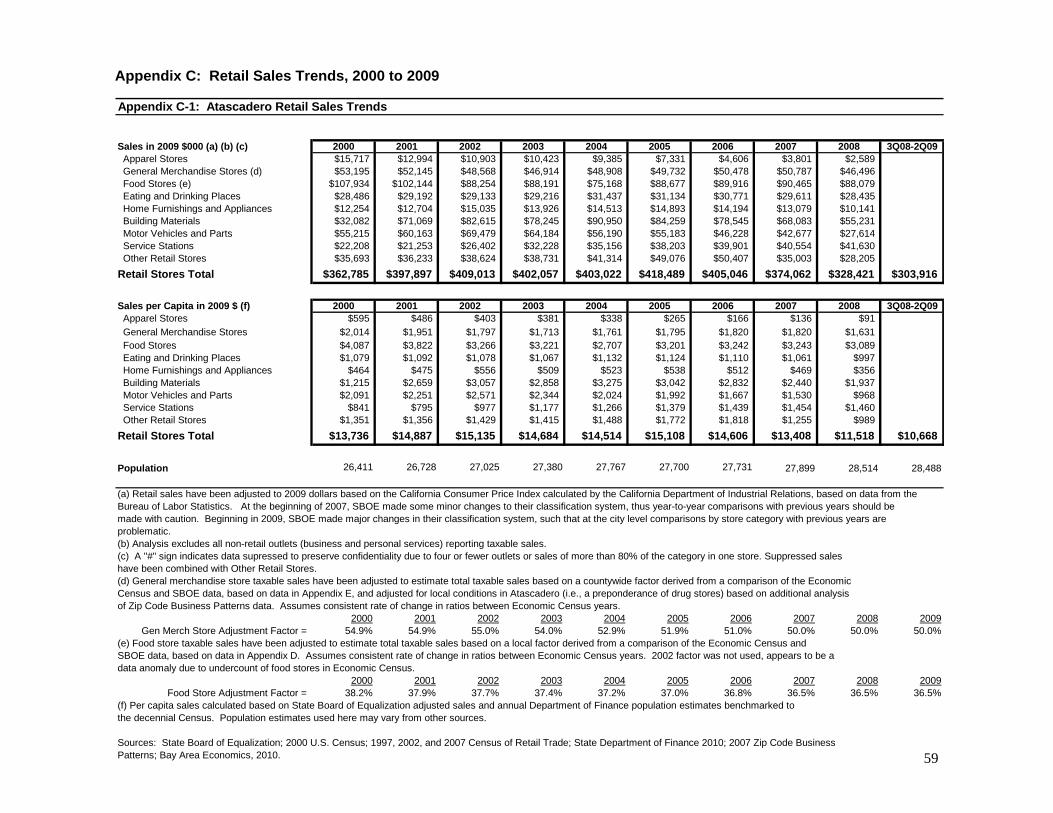

Atascadero Over the 2000 through 2009 period,

19 overall inflation-adjusted retail sales

20 in Atascadero were

relatively stable through 2006, after which sales entered a period of substantial decline (see Figure 2). In constant dollars, sales in the most recent four quarters were only 84 percent of 2000 sales and only 73 percent of peak-year sales in 2005. These declines occurred despite a gradual increase in population over the period, indicating the impacts of the ongoing recession. For the most recent annual period, overall retail sales were estimated at $304 million, or $10,668 per capita. In comparison to Paso Robles and San Luis Obispo city, these are relatively low sales levels. Figure 2: Atascadero Retail Sales and Population Trends

Notes: Population data from State Department of Finance. May vary from other sources. Taxable retail sales data havebeen adjusted for nontaxable items. All sales shown in 2009 dollars. For details, see Appendix C.

Sources: Bay Area Economics 2010, based on sources as noted in Appendix C.

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

Total Retail Sales ($000) Population

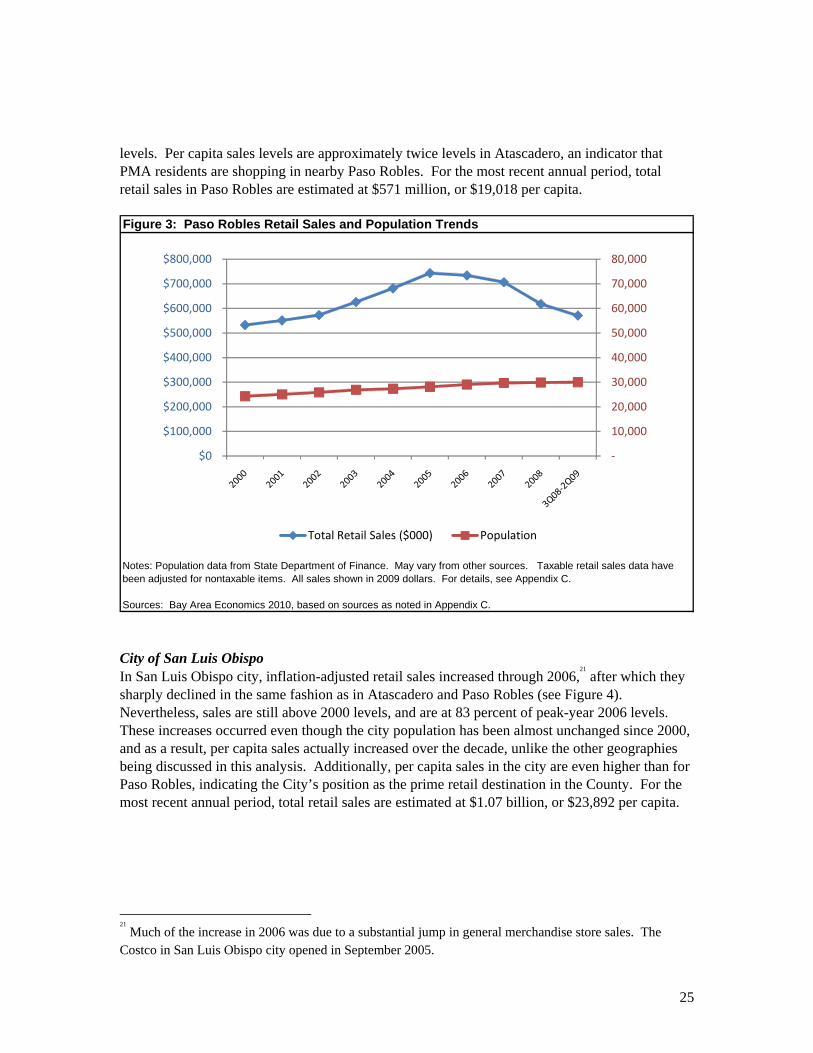

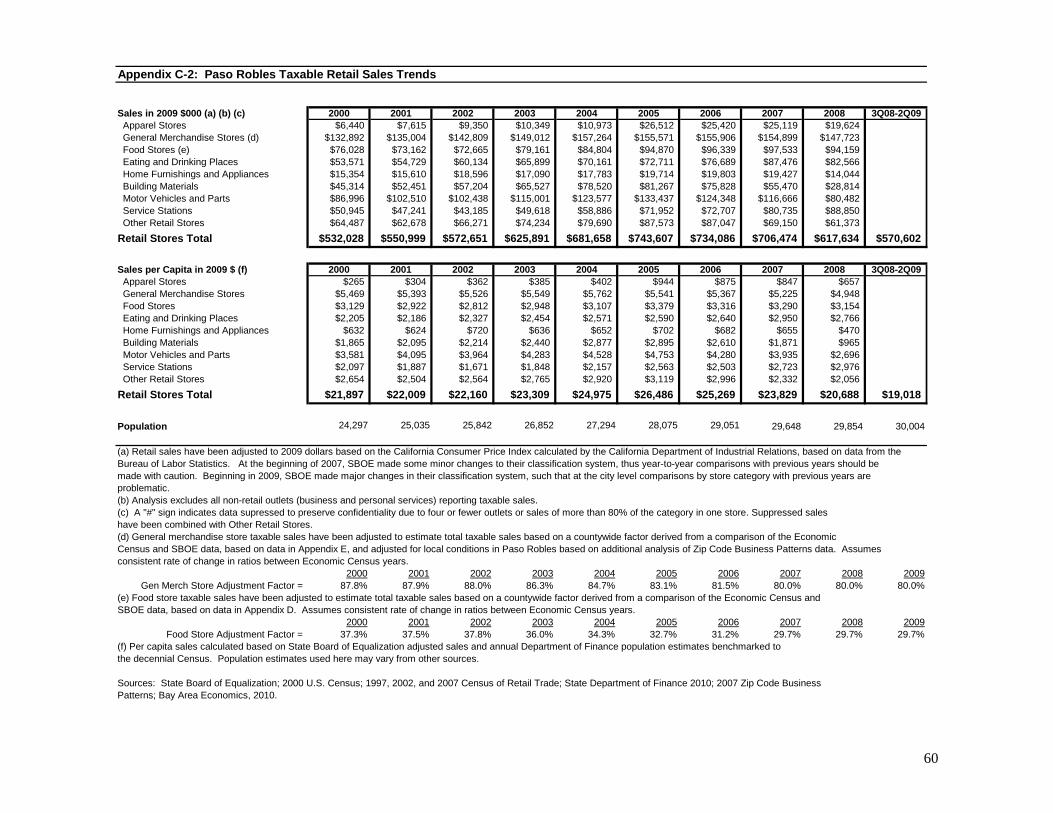

Paso Robles As shown in Figure 3, Paso Robles showed substantial increases in retail sales from 2000 through 2005, followed by a period of decline mirroring the trends in Atascadero and elsewhere in the area. Unlike Atascadero, sales levels for the most recent four quarters are still above 2000 levels; however, they are only at 77 percent of peak levels in 2005. Paso Robles, though, has shown substantial population increases since 2000, so per capita sales levels overall are below 2000 19

Third quarter 2008 through second quarter 2009 were most current published data available at time of analysis. This period is used as a proxy for 2009 full year data. 20

Taxable retail sales have been adjusted to include nontaxable sales for food stores and general merchandise stores. See Appendix C for details. Unless otherwise noted, all dollar figures in this report are presented in constant 2009 dollars, adjusted using the California Consumer Price Index.

25

levels. Per capita sales levels are approximately twice levels in Atascadero, an indicator that PMA residents are shopping in nearby Paso Robles. For the most recent annual period, total retail sales in Paso Robles are estimated at $571 million, or $19,018 per capita. Figure 3: Paso Robles Retail Sales and Population Trends

Notes: Population data from State Department of Finance. May vary from other sources. Taxable retail sales data havebeen adjusted for nontaxable items. All sales shown in 2009 dollars. For details, see Appendix C.

Sources: Bay Area Economics 2010, based on sources as noted in Appendix C.

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

Total Retail Sales ($000) Population

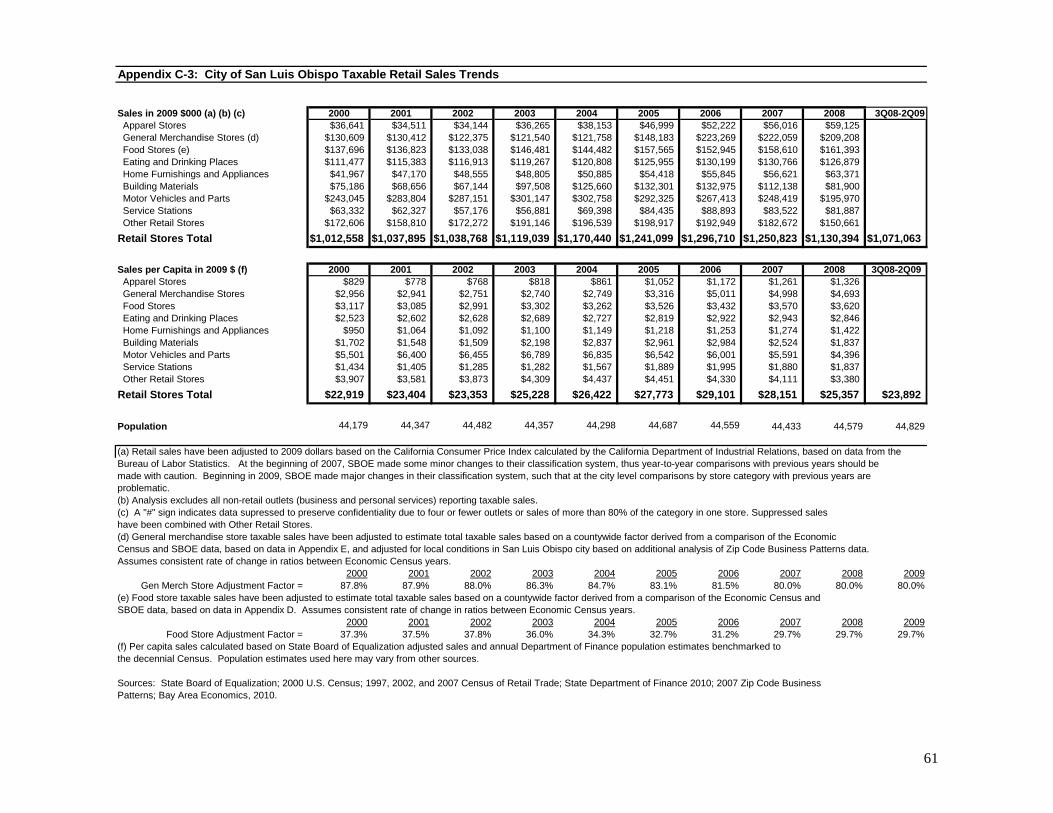

City of San Luis Obispo In San Luis Obispo city, inflation-adjusted retail sales increased through 2006,

21 after which they

sharply declined in the same fashion as in Atascadero and Paso Robles (see Figure 4). Nevertheless, sales are still above 2000 levels, and are at 83 percent of peak-year 2006 levels. These increases occurred even though the city population has been almost unchanged since 2000, and as a result, per capita sales actually increased over the decade, unlike the other geographies being discussed in this analysis. Additionally, per capita sales in the city are even higher than for Paso Robles, indicating the City’s position as the prime retail destination in the County. For the most recent annual period, total retail sales are estimated at $1.07 billion, or $23,892 per capita.

21

Much of the increase in 2006 was due to a substantial jump in general merchandise store sales. The Costco in San Luis Obispo city opened in September 2005.

26

Figure 4: City of San Luis Obispo Retail Sales and Population Trends

Notes: Population data from State Department of Finance. May vary from other sources. Taxable retail sales data havebeen adjusted for nontaxable items. All sales shown in 2009 dollars. For details, see Appendix C.

Sources: Bay Area Economics 2010, based on sources as noted in Appendix C.

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

Total Retail Sales ($000) Population

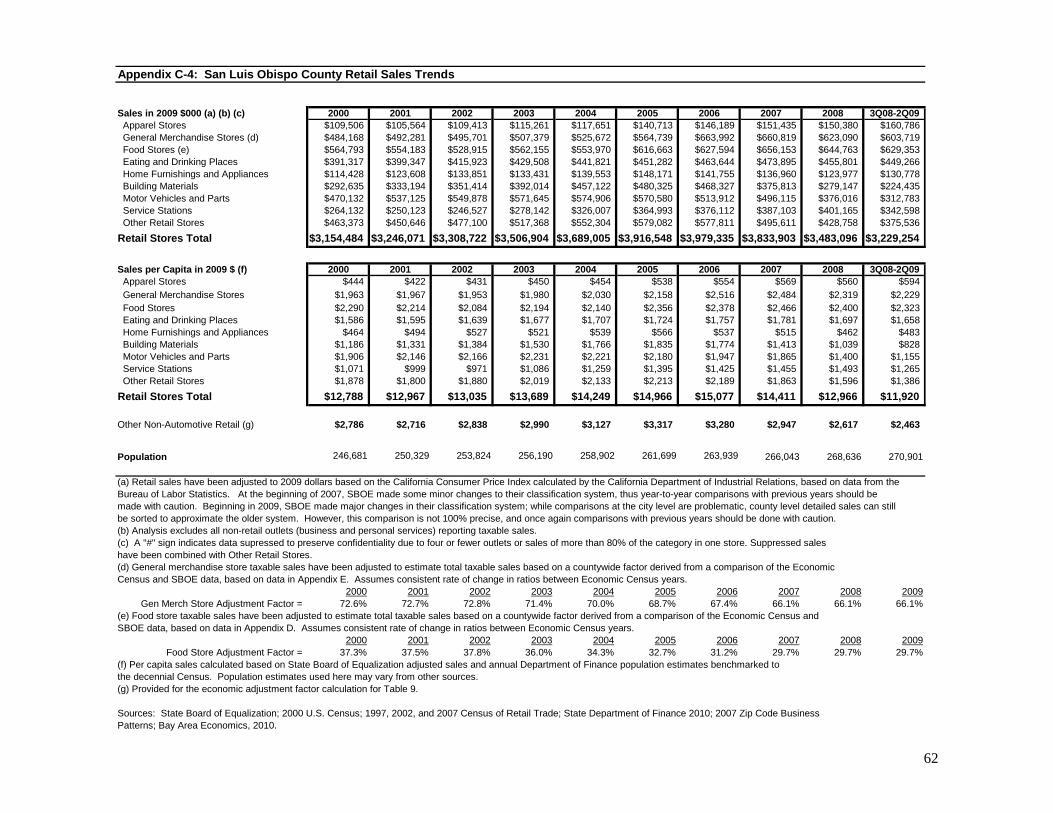

San Luis Obispo County Trends in San Luis Obispo County are similar to those for the City of San Luis Obispo, as shown in Figure 5. Retail sales increased annually from 2000 through 2006, after which a decline ensued. Total sales in the most recent reported annual period were $3.22 billion, down from $3.98 billion in 2006, but slightly higher than in 2000. Annual per capita sales also peaked in 2006, and have since declined to $11,920, 93 percent of the level in 2000. As context, Atascadero’s share of countywide total retail sales in 2009 is estimated at nine percent, with the City having 11 percent of the County’s population. Per capita sales in Atascadero are 88 percent of Countywide levels.

27

Figure 5: San Luis Obispo County Retail Sales and Population Trends

Notes: Population data from State Department of Finance. May vary from other sources. Taxable retail sales data havebeen adjusted for nontaxable items. All sales shown in 2009 dollars. For details, see Appendix C.

Sources: Bay Area Economics 2010, based on sources as noted in Appendix C.

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

$4,500,000

Total Retail Sales ($000) Population

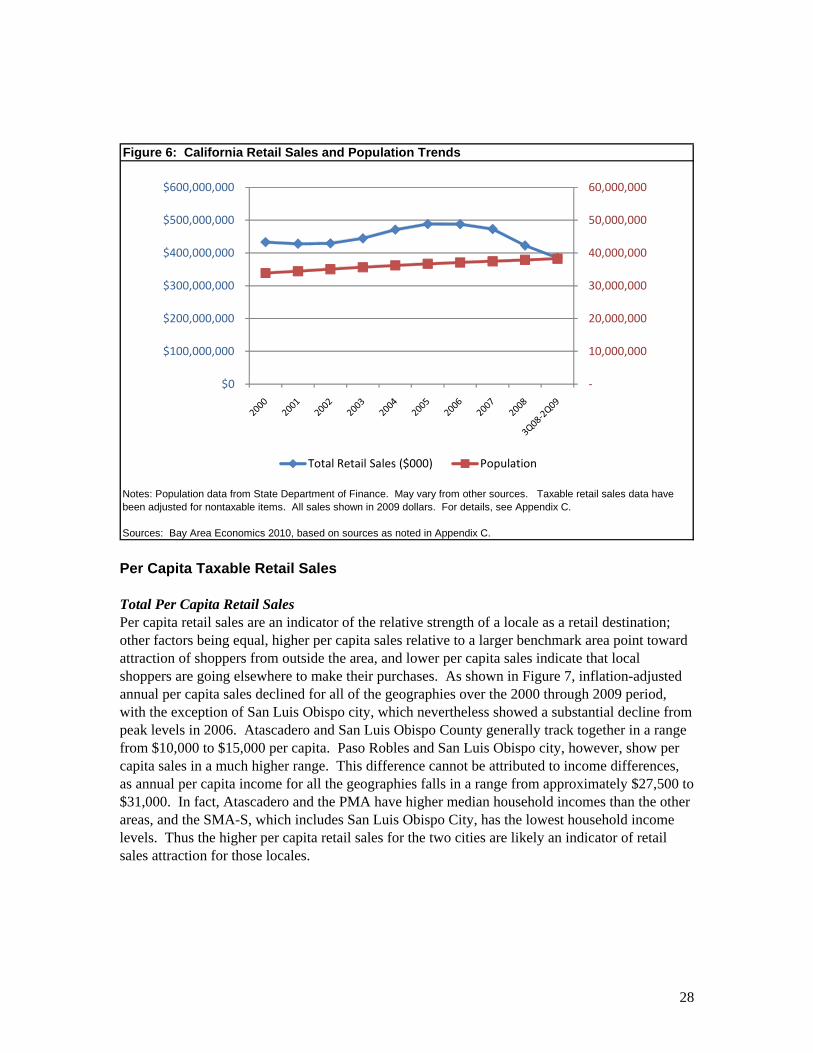

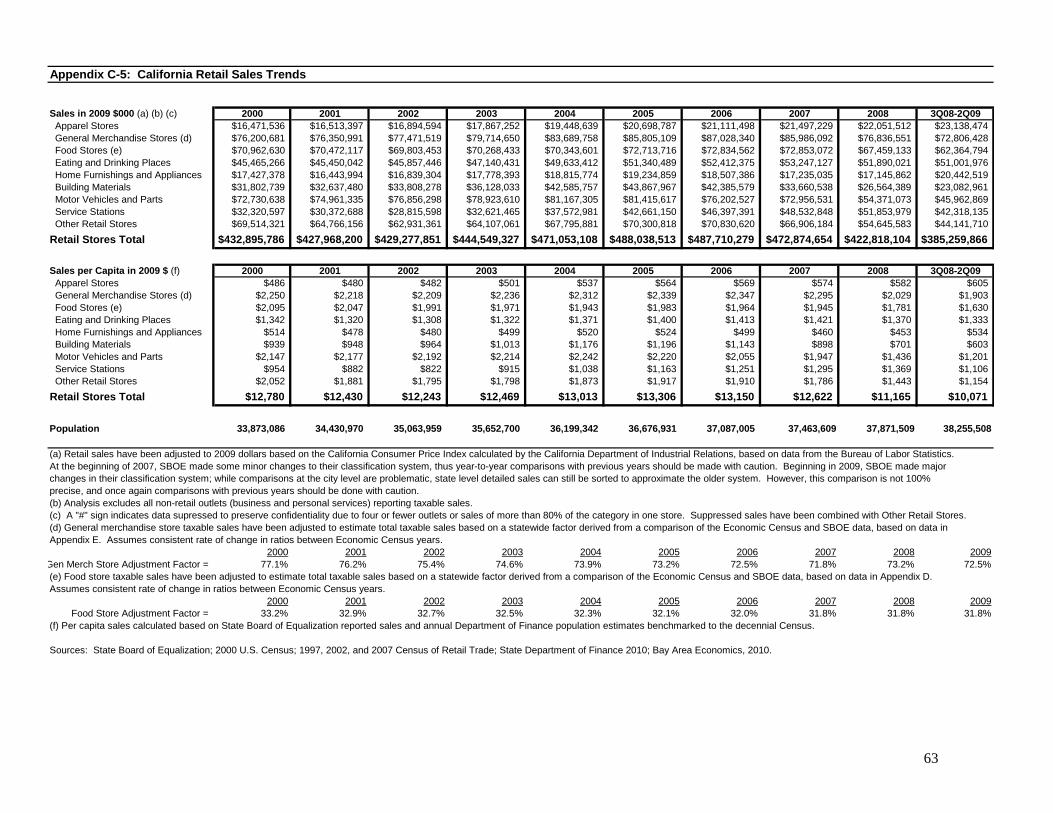

California As shown in Figure 6, retail sales levels for California were relatively flat from 2000 through 2002, reflecting the dot-com bust and post 9/11 decline, effects of which were apparently not as greatly felt in San Luis Obispo County, which continued to show increase during that period. Statewide sales then increased through 2005, with declines since that year. Annual estimated sales of $385 million for the most recent four quarters reported are only slightly above inflation-adjusted 2000 levels, even though the population of the state increased by 13 percent in the same period. As a result, annual per capita sales are only 79 percent of 2000 levels, at $10,071.

28

Figure 6: California Retail Sales and Population Trends

Notes: Population data from State Department of Finance. May vary from other sources. Taxable retail sales data havebeen adjusted for nontaxable items. All sales shown in 2009 dollars. For details, see Appendix C.

Sources: Bay Area Economics 2010, based on sources as noted in Appendix C.

-

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

$0

$100,000,000

$200,000,000

$300,000,000

$400,000,000

$500,000,000

$600,000,000

Total Retail Sales ($000) Population

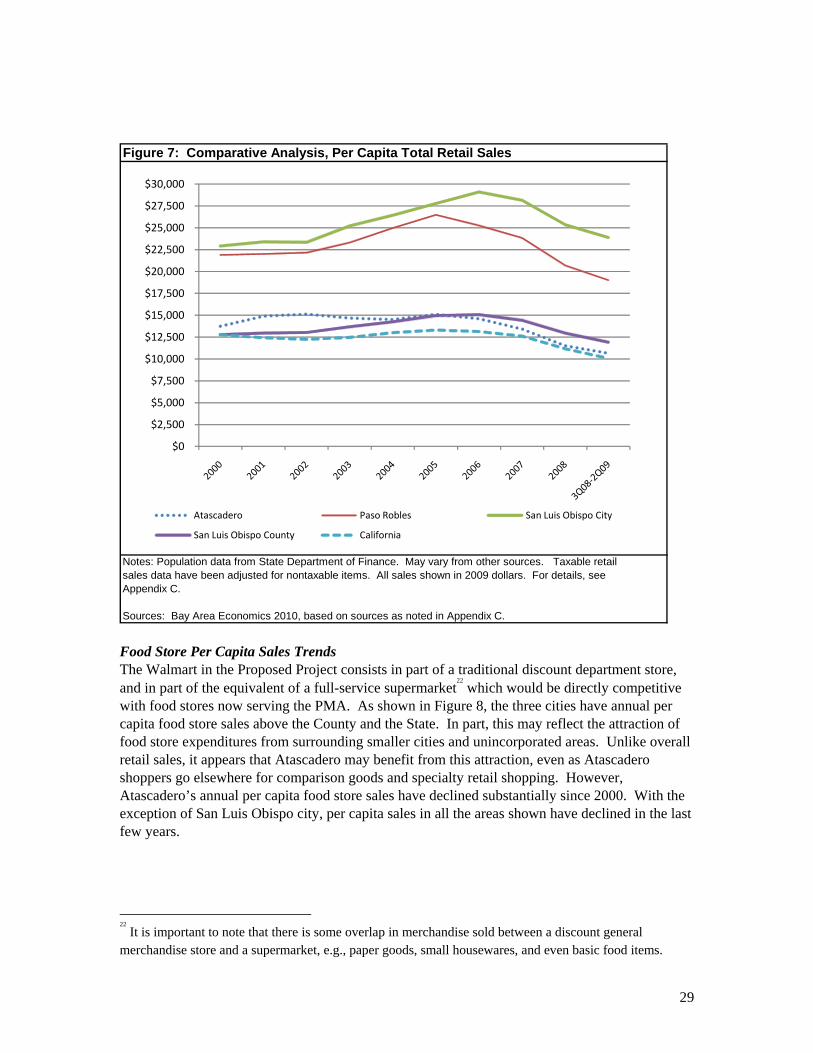

Per Capita Taxable Retail Sales Total Per Capita Retail Sales Per capita retail sales are an indicator of the relative strength of a locale as a retail destination; other factors being equal, higher per capita sales relative to a larger benchmark area point toward attraction of shoppers from outside the area, and lower per capita sales indicate that local shoppers are going elsewhere to make their purchases. As shown in Figure 7, inflation-adjusted annual per capita sales declined for all of the geographies over the 2000 through 2009 period, with the exception of San Luis Obispo city, which nevertheless showed a substantial decline from peak levels in 2006. Atascadero and San Luis Obispo County generally track together in a range from $10,000 to $15,000 per capita. Paso Robles and San Luis Obispo city, however, show per capita sales in a much higher range. This difference cannot be attributed to income differences, as annual per capita income for all the geographies falls in a range from approximately $27,500 to $31,000. In fact, Atascadero and the PMA have higher median household incomes than the other areas, and the SMA-S, which includes San Luis Obispo City, has the lowest household income levels. Thus the higher per capita retail sales for the two cities are likely an indicator of retail sales attraction for those locales.

29

Figure 7: Comparative Analysis, Per Capita Total Retail Sales

Notes: Population data from State Department of Finance. May vary from other sources. Taxable retailsales data have been adjusted for nontaxable items. All sales shown in 2009 dollars. For details, seeAppendix C.

Sources: Bay Area Economics 2010, based on sources as noted in Appendix C.

$0

$2,500

$5,000

$7,500

$10,000

$12,500

$15,000

$17,500

$20,000

$22,500

$25,000

$27,500

$30,000

Atascadero Paso Robles San Luis Obispo City

San Luis Obispo County California

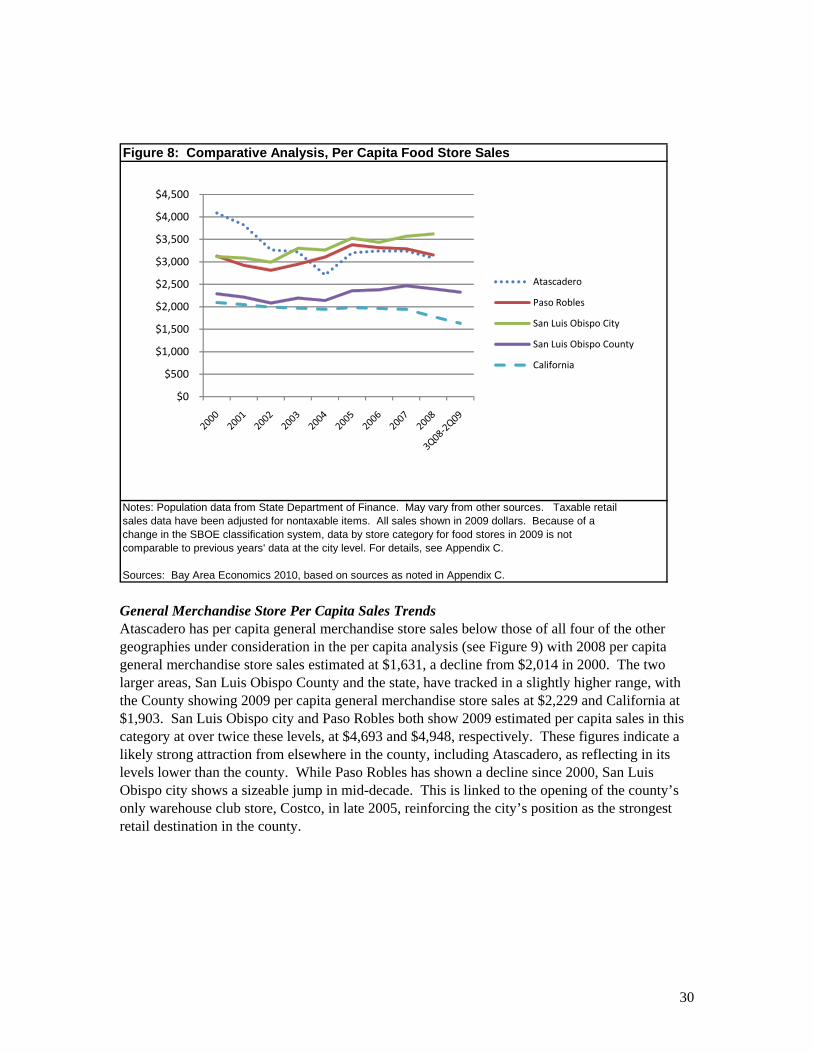

Food Store Per Capita Sales Trends The Walmart in the Proposed Project consists in part of a traditional discount department store, and in part of the equivalent of a full-service supermarket

22 which would be directly competitive

with food stores now serving the PMA. As shown in Figure 8, the three cities have annual per capita food store sales above the County and the State. In part, this may reflect the attraction of food store expenditures from surrounding smaller cities and unincorporated areas. Unlike overall retail sales, it appears that Atascadero may benefit from this attraction, even as Atascadero shoppers go elsewhere for comparison goods and specialty retail shopping. However, Atascadero’s annual per capita food store sales have declined substantially since 2000. With the exception of San Luis Obispo city, per capita sales in all the areas shown have declined in the last few years.

22

It is important to note that there is some overlap in merchandise sold between a discount general merchandise store and a supermarket, e.g., paper goods, small housewares, and even basic food items.

30

Figure 8: Comparative Analysis, Per Capita Food Store Sales