Annual Report for the Year Ended 31 December 2018

519

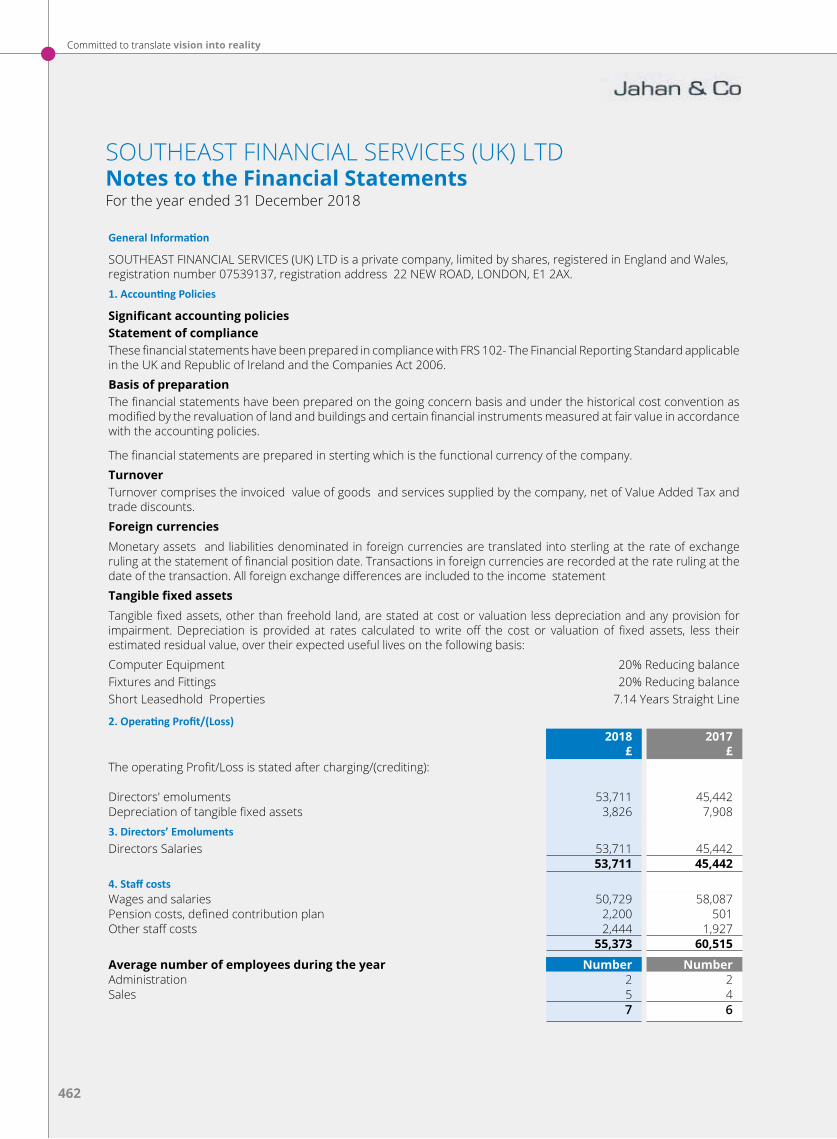

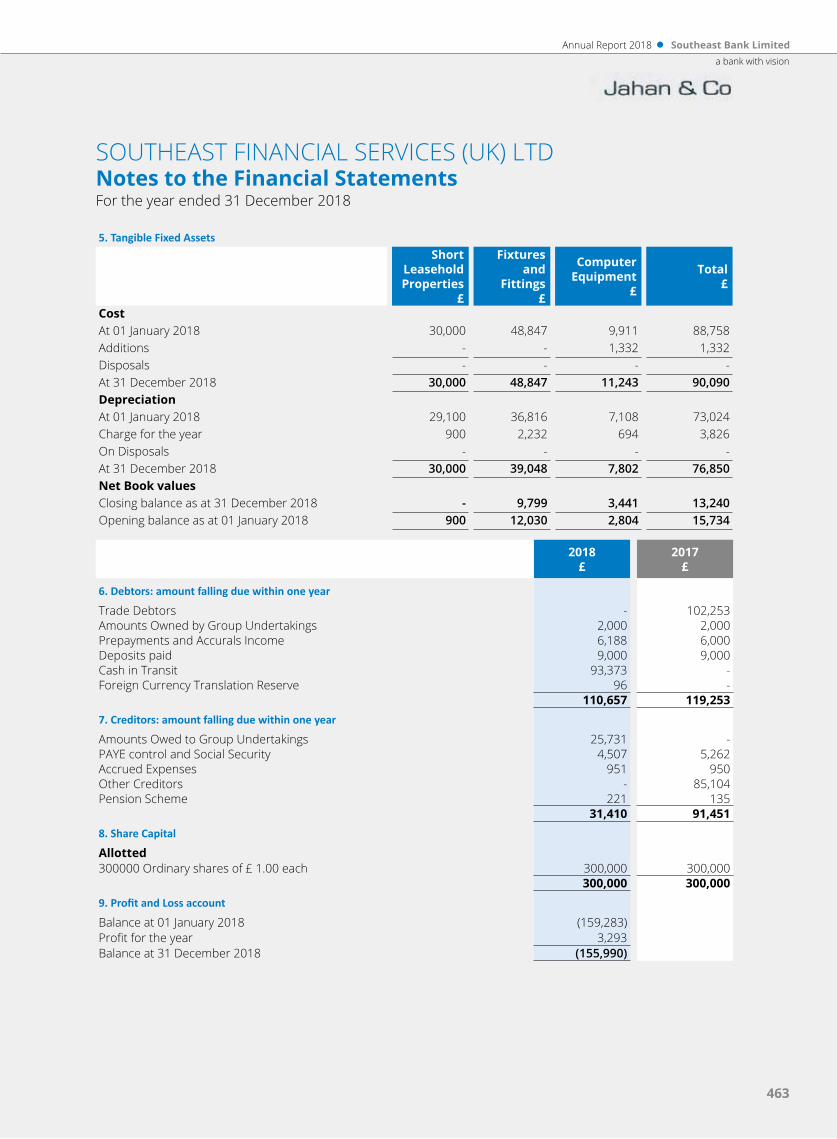

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Annual Report for the Year Ended 31 December 2018

Committed to

TranslateVision Into

Reality

“A bank with vision” is our brand slogan. Our vision to be a premier banking institution of the country and contribute significantly to the national economy was adopted with remarkable foresight in 1995 at the time of inception of the bank. It clearly demonstrates who we are, what we want to become and what we are expected to do. It serves as a beacon to determine our mission and strategies to reach our goals and achieve our vision. It pulls in ideas within the organizations as well as from all stakeholders, generates innovations, provides incentives for excellence in service and above all reiterates the tremendous role of a banking institution for the growth of our national economy through promotion of productive investment. Our vision also reminds us to pursue proactive thinking and adaptability to change in response to emerging opportunities and challenging socioeconomic environment at home and abroad.

At Southeast Bank Limited we continuously design and align our business models keeping in mind our vision, strategies, the aspirations of our stakeholders and above all the need for sustainable development of the economy for greater benefit of the people at large. We relentlessly strive to achieve further excellence in our corporate governance culture and regulatory compliance as well as promote professionalism in our workforce because we believe these are the foundations of sustainable development of our institution. We always keep in mind the dynamic nature of business environment and redesign our lending and deposit mobilization strategies so that they meet the needs of our customers and national development goals not only for the present generation but also for the generations to come.

With clear vision in view, the bank is becoming more and more profitable, flexible, innovative and better structured with attractive products and services for customers at large and skilled, dynamic and dedicated workforce always ready to extend those exceptional services. We are committed to put together all our actions in a dynamic way to transform our vision into reality.

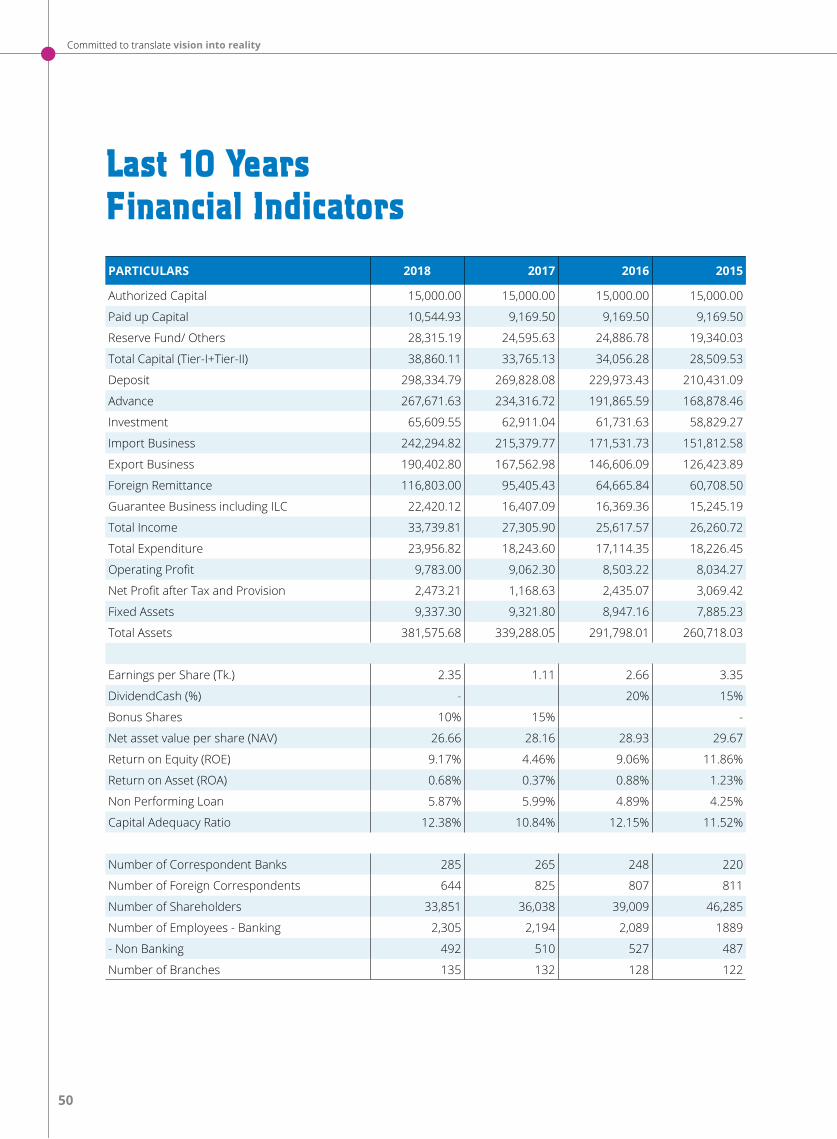

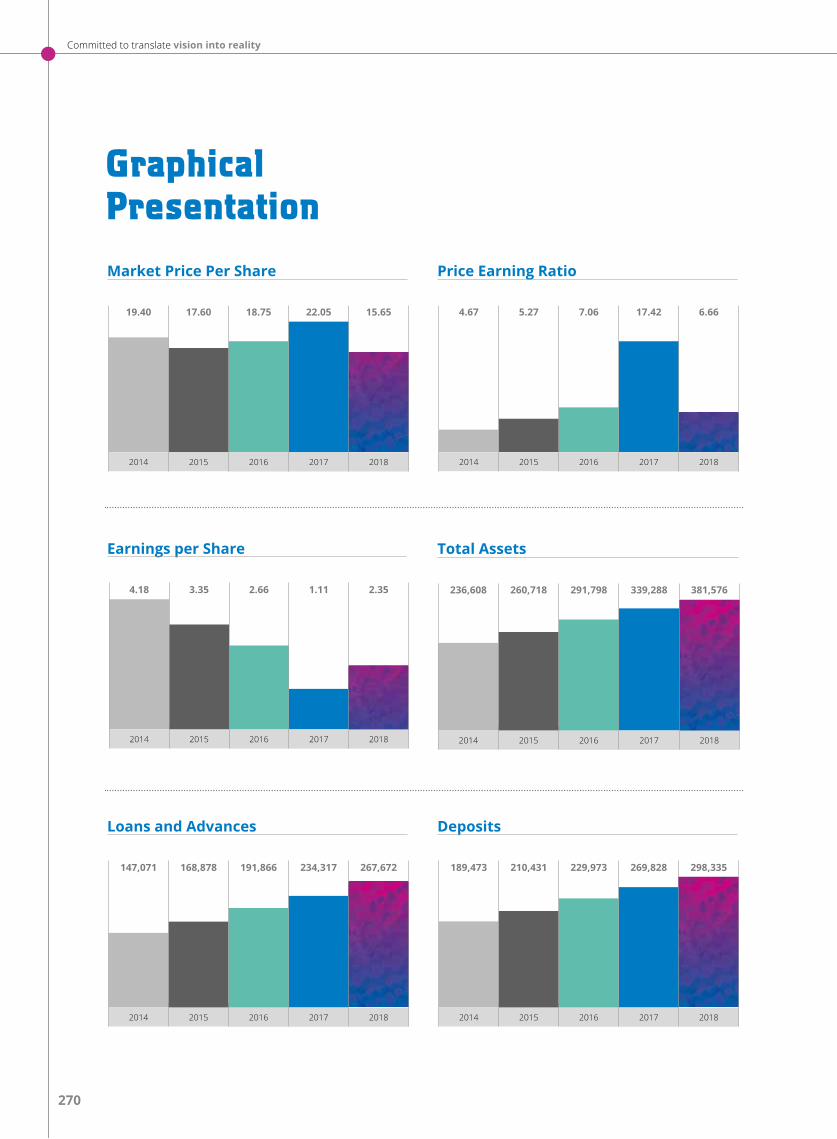

Financial IndicatorsFinancial Overviews - Last 5 Years

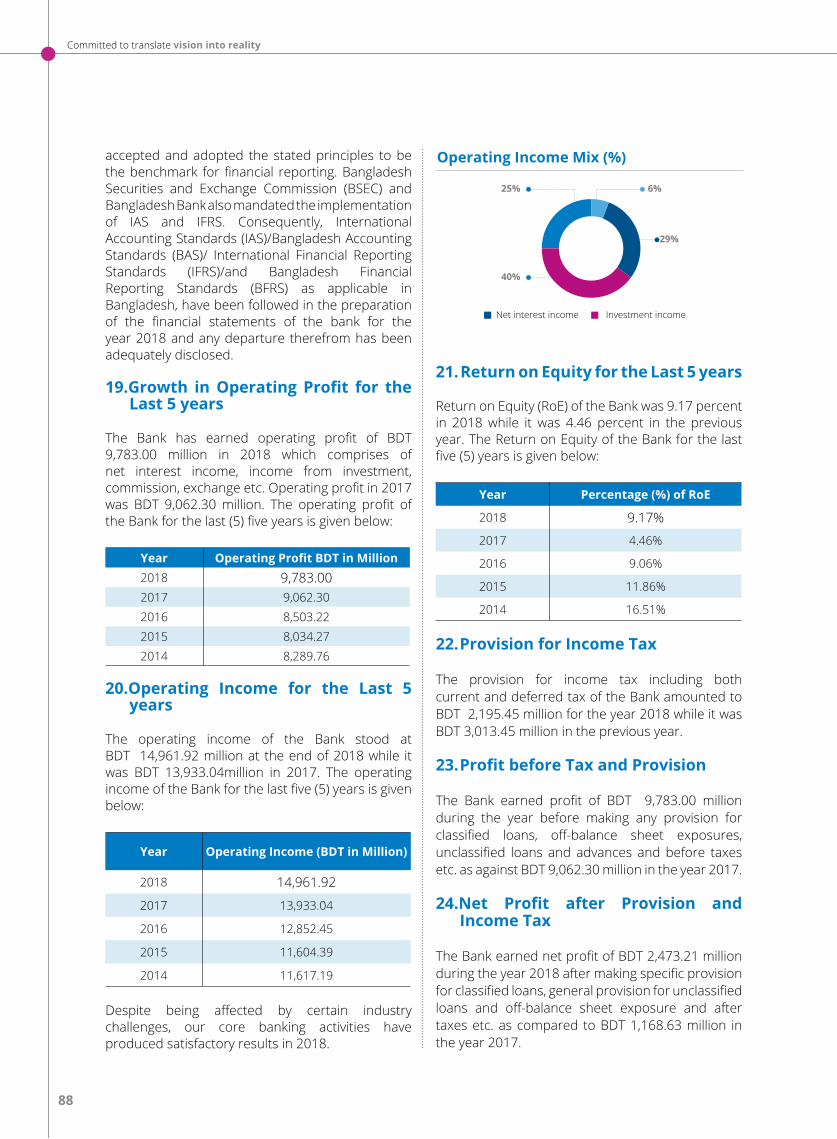

236,608 260,718 291,798 339,288 381,576

Total Assets(BDT in million)

2014 2015 2016 20182017

8,290 8,034 8,503 9,062 9,783

Profit before Provision (BDT in million)

2014 2015 2016 20182017

4.18 3.35 2.66 1.11 2.35

Earnings per Share (EPS)

2014 2015 2016 20182017

12.41% 11.52% 12.15% 10.84% 12.38%

Total Capital to Risk WeightedAssets Ratio

2014 2015 2016 20182017

147,071 168,878 191,866 234,317 267,672

Total Loans and Advances(BDT in million)

2014 2015 2016 20182017

3,837 3,069 2,435 1,169 2,473

Profit after Tax(BDT in million)

2014 2015 2016 20182017

1.67% 1.23% 0.88% 0.37% 0.69%

Return on Assets (RoA)

2014 2015 2016 20182017

1.82% 1.31% 0.92% 0.39% 0.79%

Return on Average Risk WeightedAssets (RRWA)

2014 2015 2016 20182017

Committed to translate vision into reality

Non-Financial IndicatorsNon-Financial Overviews - Last 5 Years

A) IN TERMS OF COMPETITIVENESS

416,823 468,154 570,196 638,139 702,019

Number of Deposit Customers

2014 2015 2016 20182017

74,8

43

98,8

18

50,4

38

134,

255

61,3

27

174,

271

201,

310

102,

000

76,7

83

43,5

13

Number of Cardholders

2014 2015 2016 20182017

Debit Cardholders Credit Cardholders

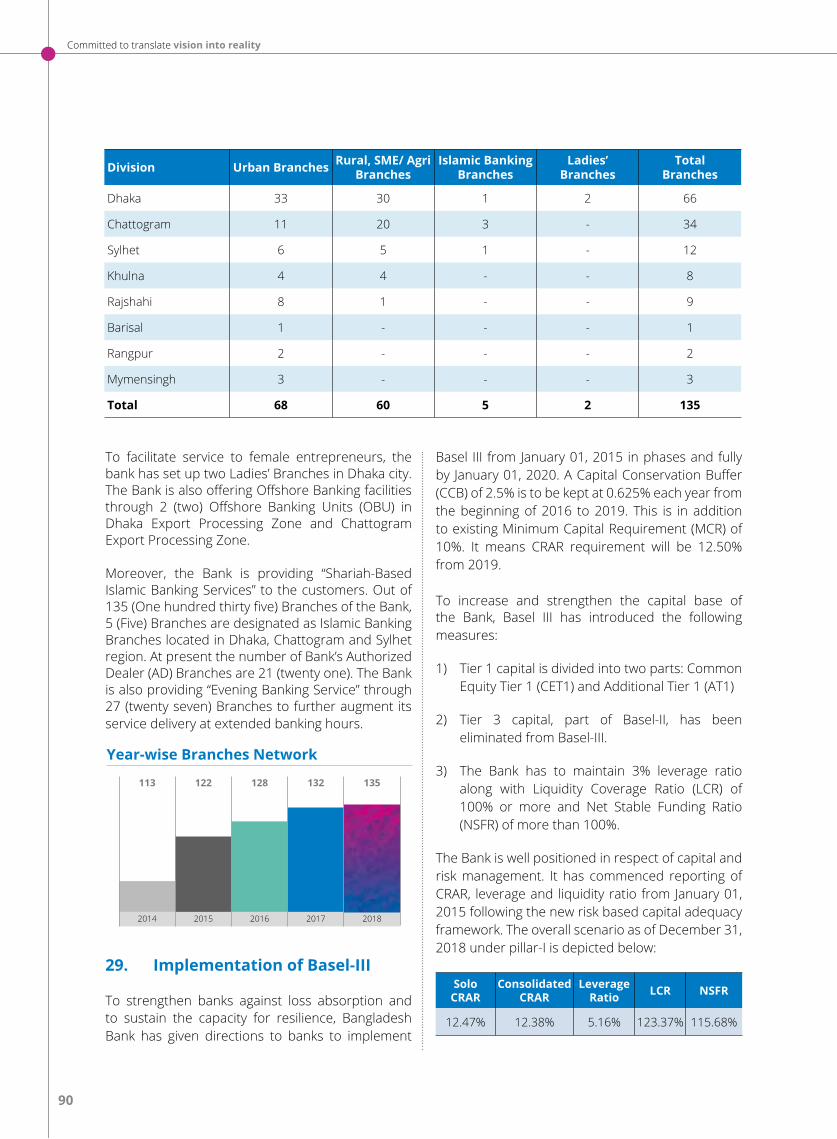

113 122 128 132 135

Number of Branches

2014 2015 2016 20182017

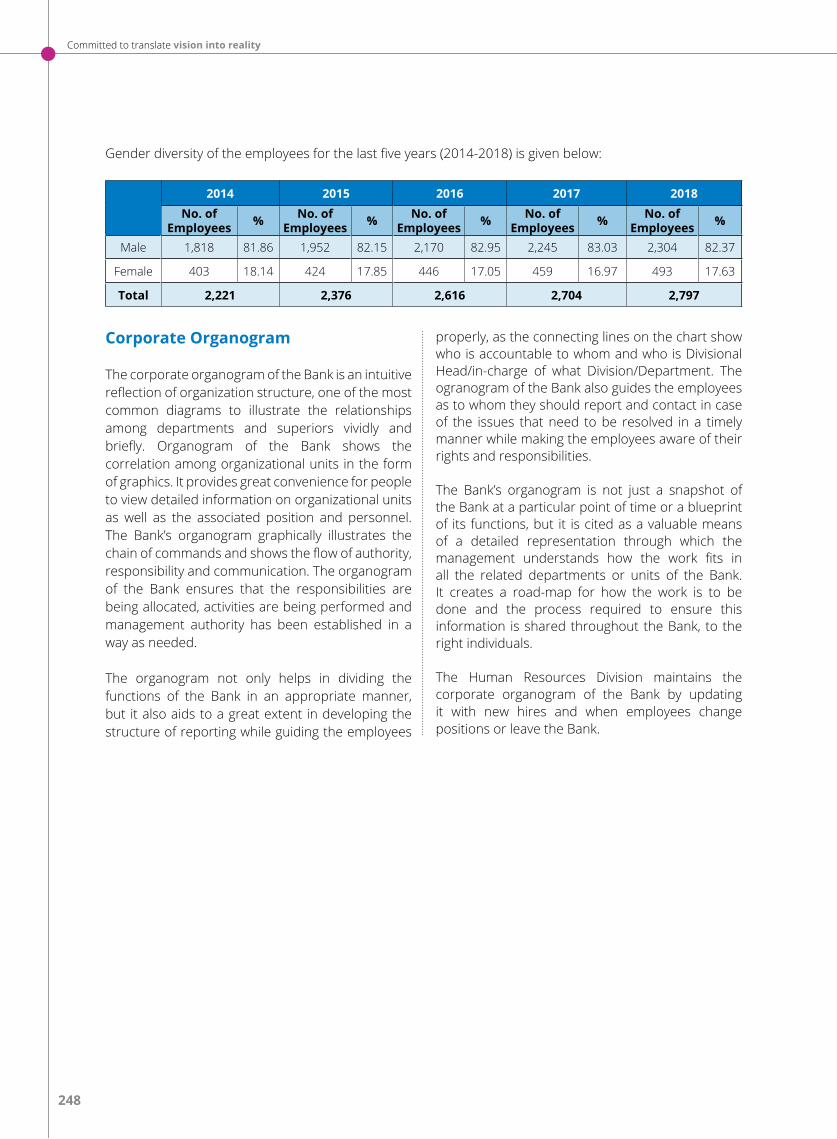

2,221 2,376 2,616 2,704 2,797

Number of Employees

2014 2015 2016 20182017

11,789 13,025 14,155 15,563 16,739

Size of Loan Customers

2014 2015 2016 20182017

114 128 174 189 152

Number of Women Entrepreneurs

2014 2015 2016 20182017

790 811 807 825 644

Number of Foreign Correspondents

2014 2015 2016 20182017

58,169 46,285 39,009 36,038 33,851

Number of Shareholders

2014 2015 2016 20182017

Annual Report 2018 Southeast Bank Limiteda bank with vision

Non-Financial IndicatorsNon-Financial Overviews - Last 5 Years

B) IN TERMS OF ACTIVITY LEVEL

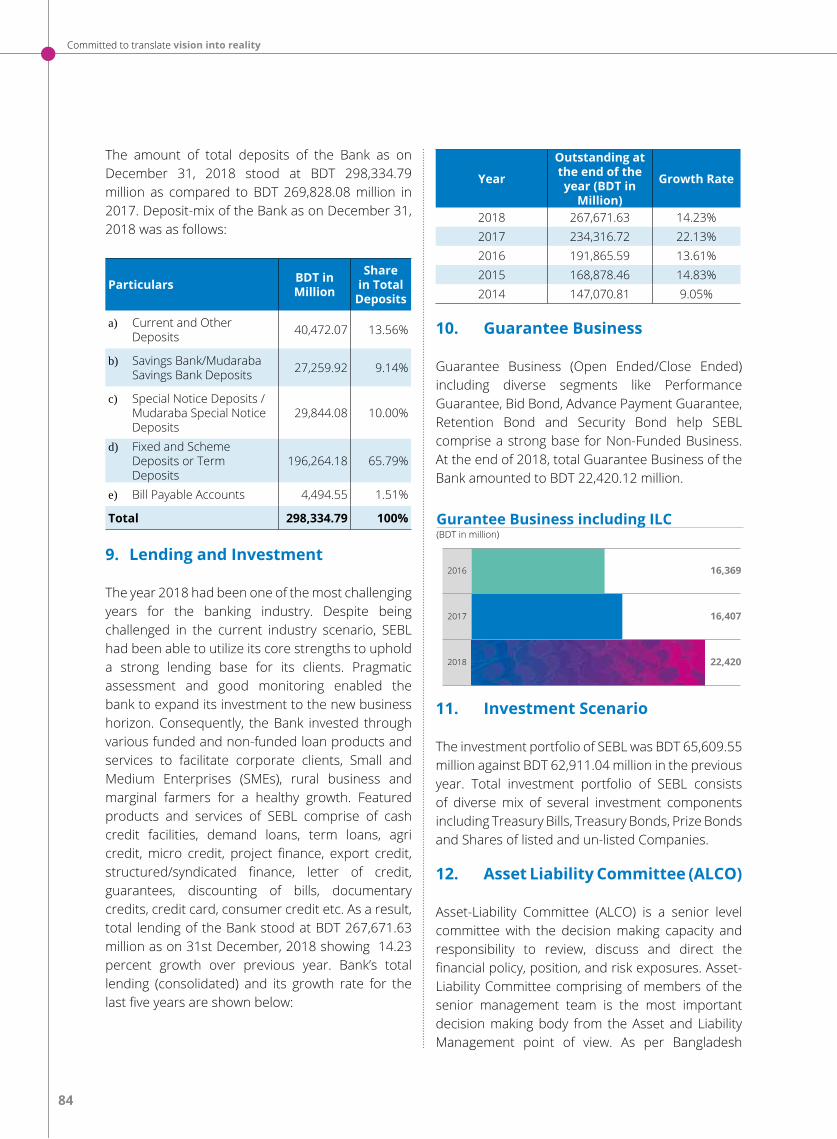

63,421 66,239 73,037 85,353 91,041

Number of Loans Disbursed

2014 2015 2016 20182017

Number of Bad Debt Collected

64

129

4

153

7

147

94

13

52

2014 2015 2016 20182017

Classified Loans Written Off Loans

2.73 2.65 2.56 2.87 2.95

97.27 97.35 97.4497.13 97.05

Market Share of SEBL Deposit (in percent)

2014 2015 2016 20182017

SEBL Industry other then SEBL

9,656 10,121 10,795 9,382 8,534

Number of New RemittanceCustomers Engaged

2014 2015 2016 20182017

2.79 3.25 2.87 2.91 2.90

97.21 96.75 97.13 97.09 97.10

Market Share of SEBL Advance (in percent)

2014 2015 2016 20182017

SEBL Industry other then SEBL

Committed to translate vision into reality

Non-Financial IndicatorsNon-Financial Overviews - Last 5 Years

C) IN TERMS OF PRODUCTIVITY LEVEL

D) IN TERMS OF QUALITY SERVICE

1.49 1.51 1.60 1.76 1.78

Per Employee Cost (BDT in million)

2014 2015 2016 20182017

2.00% 4.00% 3.00% 2.37%

Average Number of CustomerComplaints Received

2015 2016 20182017

15,942 95,276 159,662 202,809 17,363

Number of Accounts Closed orBecame Dormant

2014 2015 2016 20182017

4,183 4,068 3,690 1,830 1,222

Number of Internet BankingCustomers Engaged

2014 2015 2016 20182017

151,142 138,416 177,260 131,706 149,565

Accounts Opened Trend

2014 2015 2016 20182017

11.00% 3.00% 1.00% 4.44%

Average Number of Service Dropof Call Centre

2015 2016 20182017

a bank with vision

Annual Report 2018 Southeast Bank Limited

Non-Financial IndicatorsNon-Financial Overviews - Last 5 Years

91.87% 92.14% 94.76% 96.31% 96.42%

Customer Satisfaction Level withTechnological Facilities

2014 2015 2016 20182017

82.5% 86% 90.7% 94% 94.8%

Customer Satisfaction Levelwith Bank Staff

2014 2015 2016 20182017

4.98% 4.61% 4.15% 6.02% 7.07%

Employee Turnover Rate

2014 2015 2016 20182017

190 184 136 75 94

Number of Employees Received NewQualifications or Completed Courses

2014 2015 2016 20182017

5.39 2.37 3.26 4.40 4.22

Average Time Taken to Respond toCustomer Inquiry (in minutes)

2014 2015 2016 20182017

Committed to translate vision into reality

Annual Report 2018 Southeast Bank Limiteda bank with vision

BalanceScore Card

BDT in million

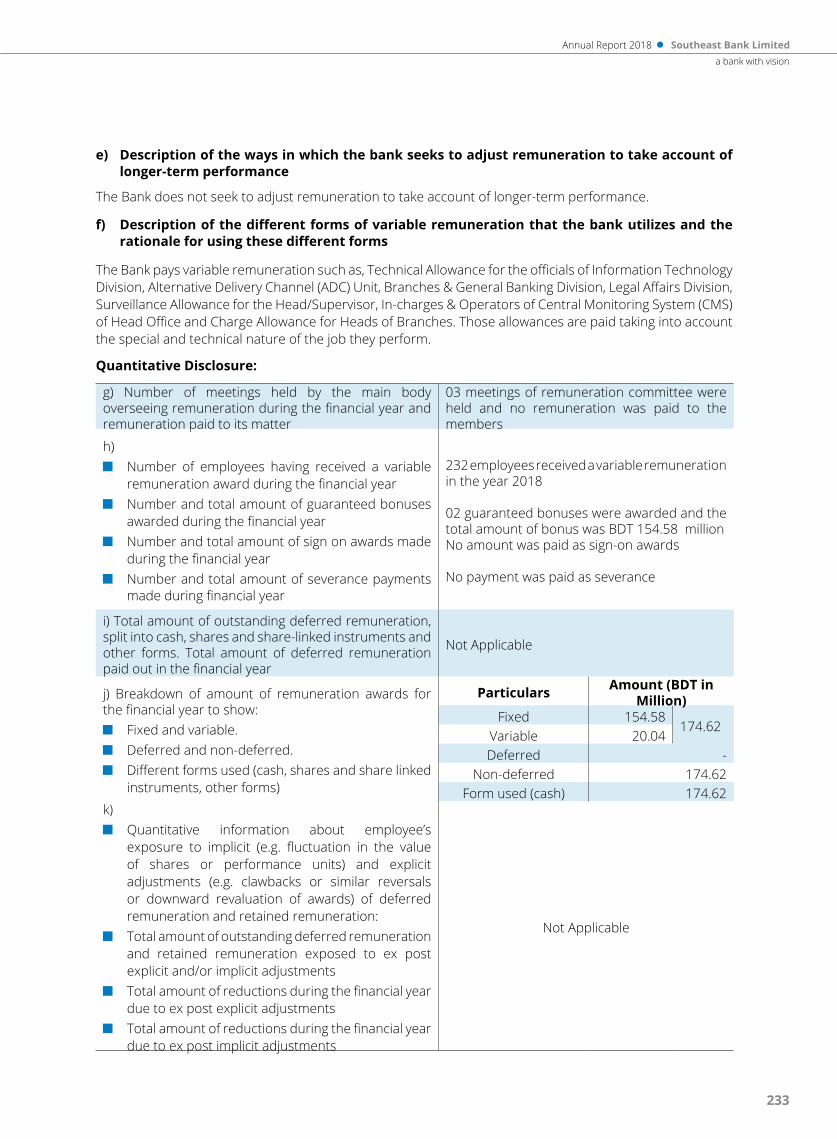

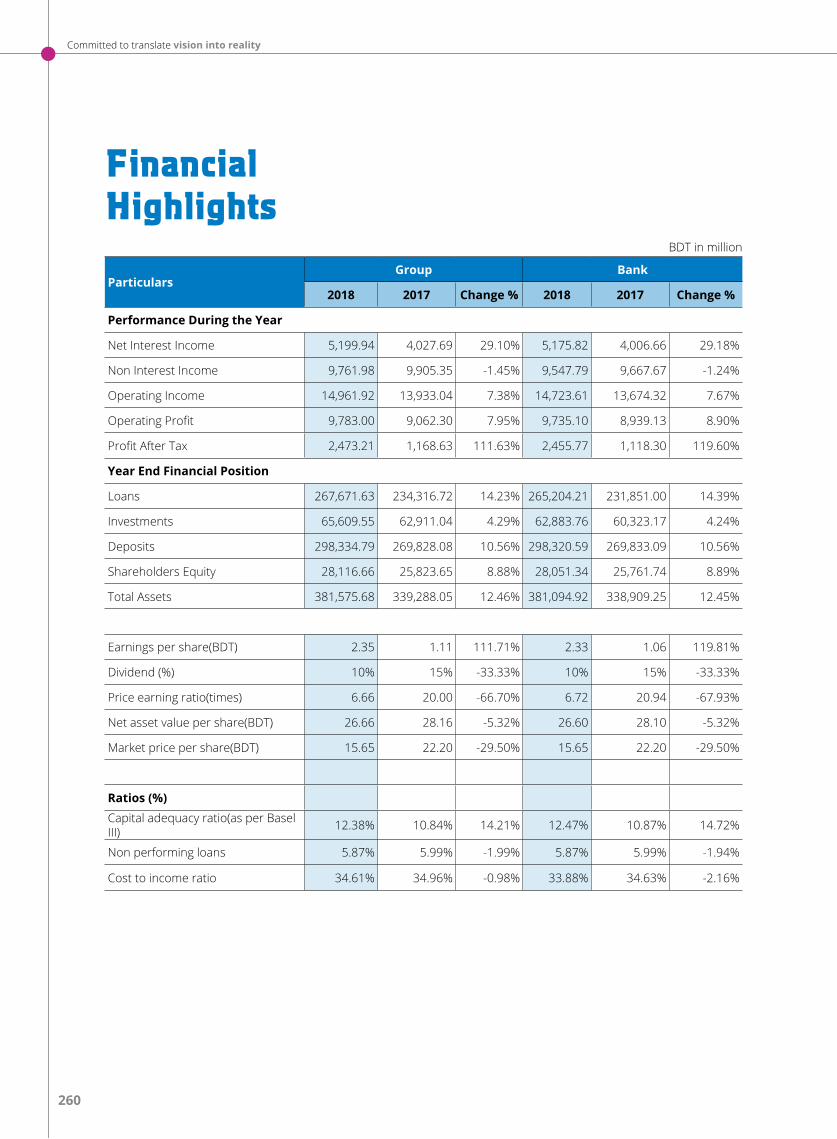

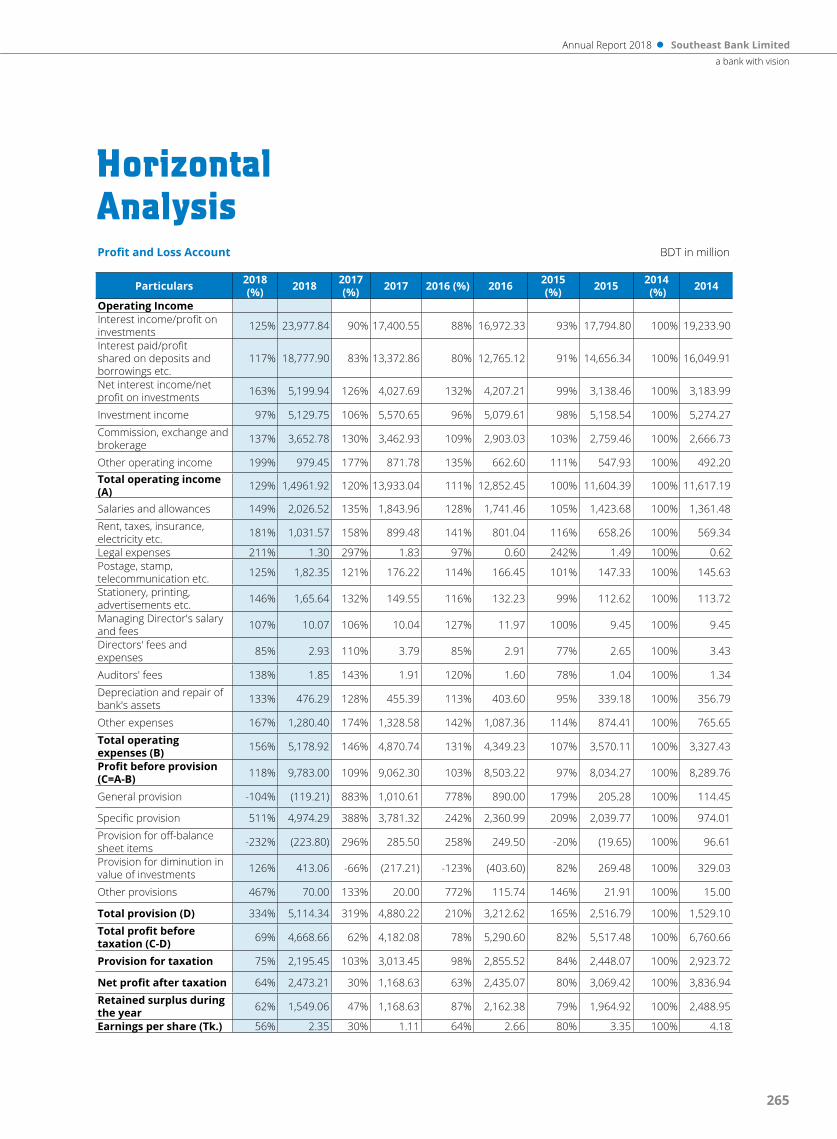

Financial Highlights 2018 2017 2016Financial ResultsRevenue 33,739.81 27,305.90 25,617.57Provision for Credit Losses 9,961.90 6,628.68 3,728.28Operating Expenses 5,178.92 4,870.74 4,349.23Net Revenue 2,473.21 1,168.63 2,435.07Financial Results(%)Reported/Adjusted Efficiency Ratio 34.61% 34.96% 33.84%Return on Common Shareholder's Equity (ROE) 9.17% 4.46% 9.06%Net Interest Margin (NIM) 3.18% 3.42% 3.77%EPS 2.35 1.11 2.66Common Share PerformanceMarket Capitalization 16,450.10 20,356.29 17,146.97Dividends(%)Dividend Yield 0.06 0.07 0.11Reported/Adjusted Dividend Payout Ratio 0.43 1.18 0.75

Revenue

2016 20182017

25,618 27,306 33,740

Net Revenue

2016 20182017

2,435 1,169 2,473

Dividend Yield

2016 20182017

0.11 0.07 0.06

Provision for Credit Losses

2016 20182017

3,728 6,629 9,962

Earnings per Share

2016 20182017

2.66 1.11 2.35

Operating Expenses

2016 20182017

4,349 4,871 5,179

Dividend per Share

2016 20182017

2.00 1.50 1.00

Committed to translate vision into reality

Awards andRecognition

Southeast Bank won “Silver Award” for Corporate Governance Excellence

Southeast Bank Limited has been awarded Silver Award in the “5th ICSB National Award for Corporate Governance Excellence, 2017” in Banking Companies Category by The Institute of Chartered Secretaries of Bangladesh (ICSB). ICSB bestowed the prestigious Award on the Bank for its Corporate Governance practices that came out in the disclosures in the Bank’s Annual Report-2017.

The Institute of Chartered Secretaries of Bangladesh exhaustively analyzed the Bank’s Annual Report-2017 and sieved out the Bank from many aspirants for its outstanding performance, sufficient disclosures for all stakeholders and its commitment to achieving further excellence in corporate governance, and compliance with legal and regulatory requirements.

M. Kamal Hossain, Managing Director of Southeast Bank Limited received the award from Abul Maal Abdul Muhith, MP, Hon’ble Minister, Ministry of Finance, Government of the People’s Republic of Bangladesh in a ceremony held on 10th November 2018 at a local hotel in Dhaka.

The operations of Southeast Bank are built upon unequivocal emphasis on effective Corporate Governance. Its objective is to create, promote and build long-term company value. It is now one of the most disciplined, compliant and admired Bank in the industry. This award will encourage the Bank enormously and put a responsibility upon the Bank Management to keep up the momentum of its performance and to improve governance practices further in the coming years.

Annual Report 2018 Southeast Bank Limiteda bank with vision

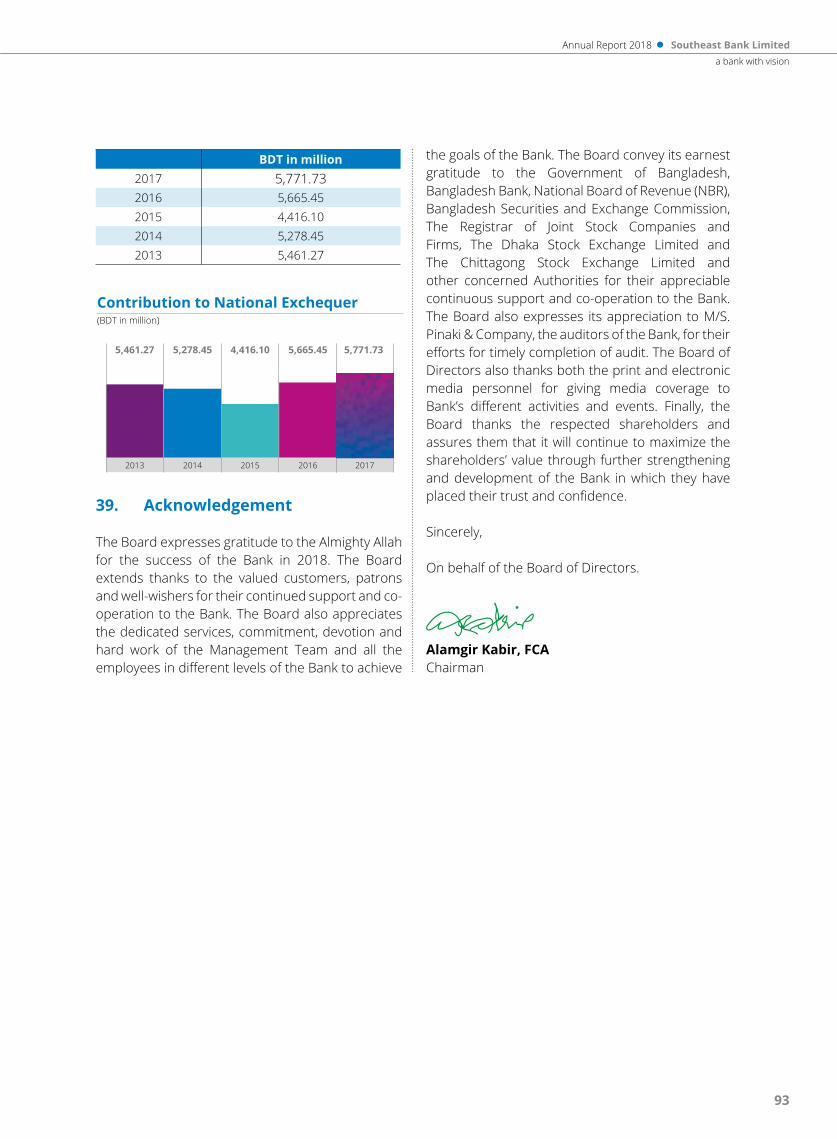

Southeast Bank has been awarded as the country's 4th highest Tax payer in the Banking category.

Southeast Bank Limited has been awarded as the country’s 4th highest Income Tax Payer in the Banking Category for the assessment year 2017-2018. M. A. Mannan, MP, State Minister, Ministry of Finance and Planning handed over the Crest and Tax Card to M. Kamal Hossain, Managing Director, Southeast Bank Limited at the best taxpayer reception ceremony on November 12, 2018. Abul Maal Abdul Muhith, MP, Finance Minister and Md. Mosharraf Hossain Bhuiyan, Chairman, National Board of Revenue were also present at the ceremony.

10

Committed to translate vision into reality

10

Committed to translate vision into reality

Awards andRecognition

11

Annual Report 2018 Southeast Bank Limiteda bank with vision

Awards andRecognition

Annual Report 2018 Southeast Bank Limited

11

a bank with vision

Awards andAwards andRecognitionRecognition

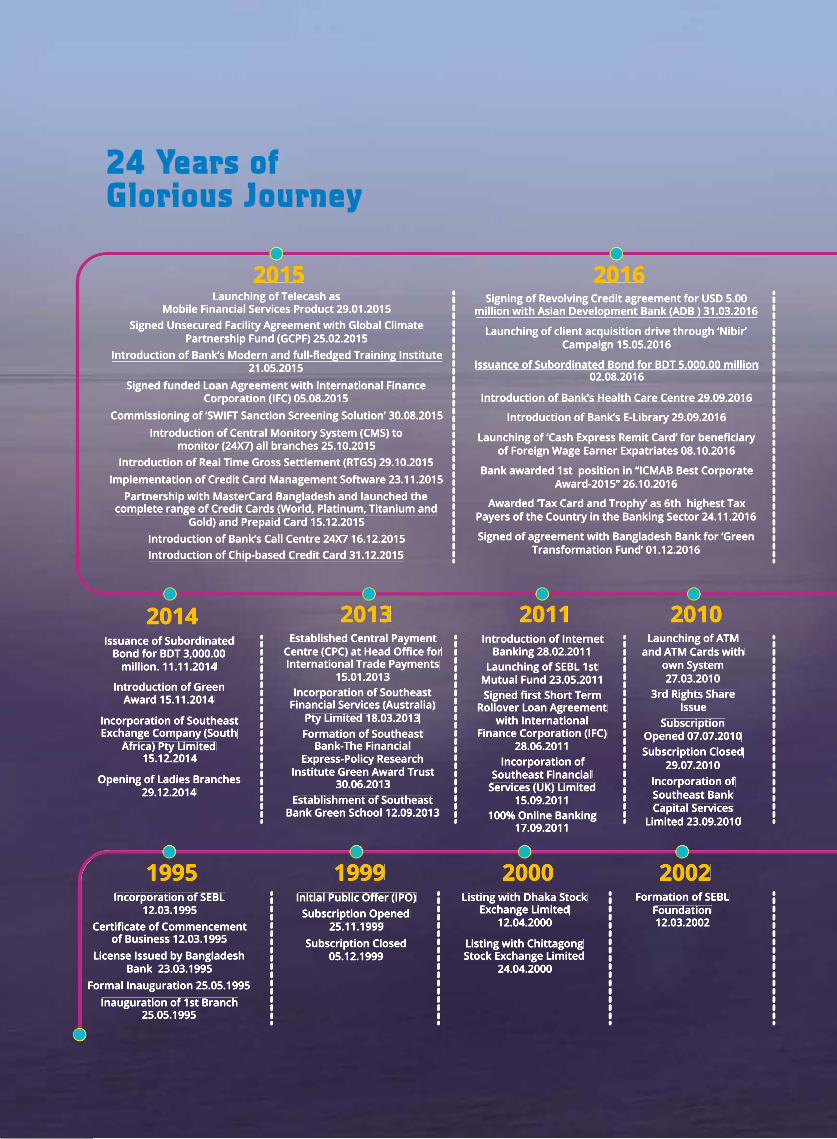

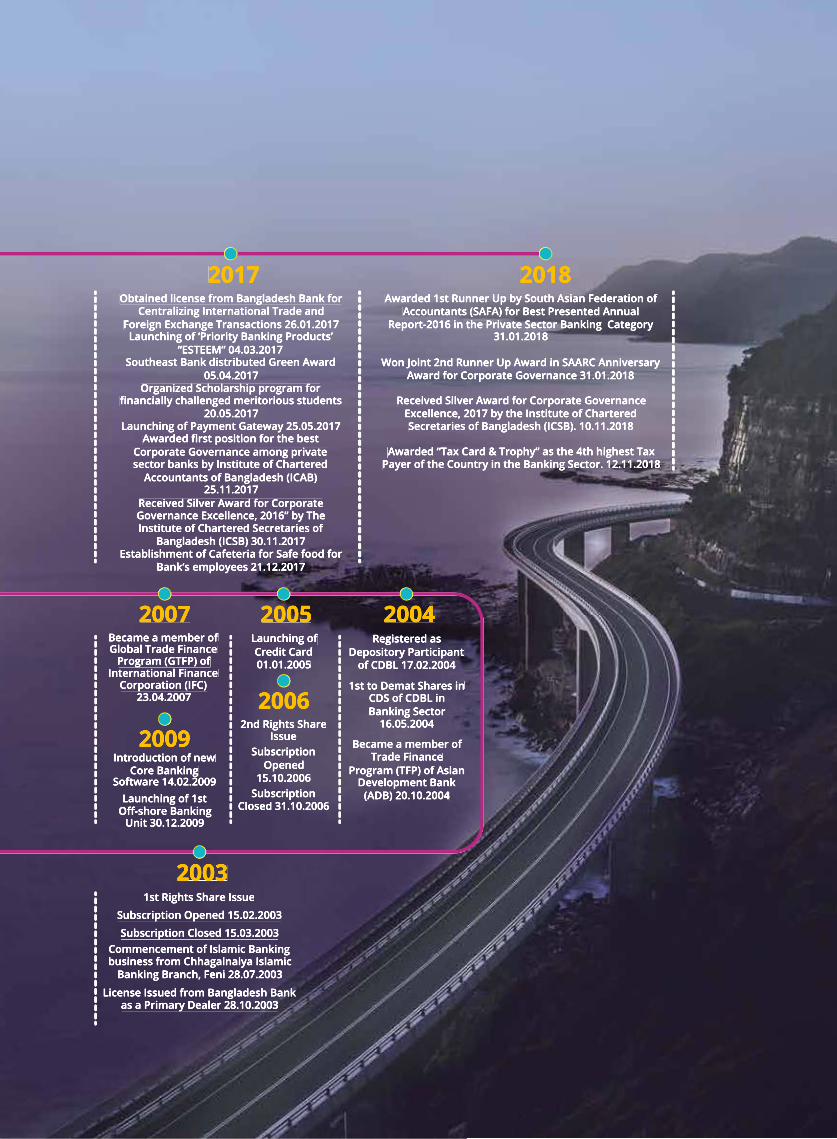

Incorporation of SEBL 12.03.1995

Certificate of Commencement of Business 12.03.1995

License Issued by Bangladesh Bank 23.03.1995

Formal Inauguration 25.05.1995Inauguration of 1st Branch

25.05.1995

1995Initial Public Offer (IPO)

Subscription Opened 25.11.1999

Subscription Closed 05.12.1999

1999Listing with Dhaka Stock

Exchange Limited 12.04.2000

Listing with Chittagong Stock Exchange Limited

24.04.2000

2000Formation of SEBL

Foundation 12.03.2002

2002

Launching of ATM and ATM Cards with

own System 27.03.2010

3rd Rights Share Issue

Subscription Opened 07.07.2010Subscription Closed

29.07.2010Incorporation of Southeast Bank Capital Services

Limited 23.09.2010

2010Introduction of Internet

Banking 28.02.2011Launching of SEBL 1st

Mutual Fund 23.05.2011Signed first Short Term

Rollover Loan Agreement with International

Finance Corporation (IFC) 28.06.2011

Incorporation of Southeast Financial

Services (UK) Limited 15.09.2011

100% Online Banking 17.09.2011

2011Established Central Payment

Centre (CPC) at Head Office for International Trade Payments

15.01.2013Incorporation of Southeast

Financial Services (Australia) Pty Limited 18.03.2013

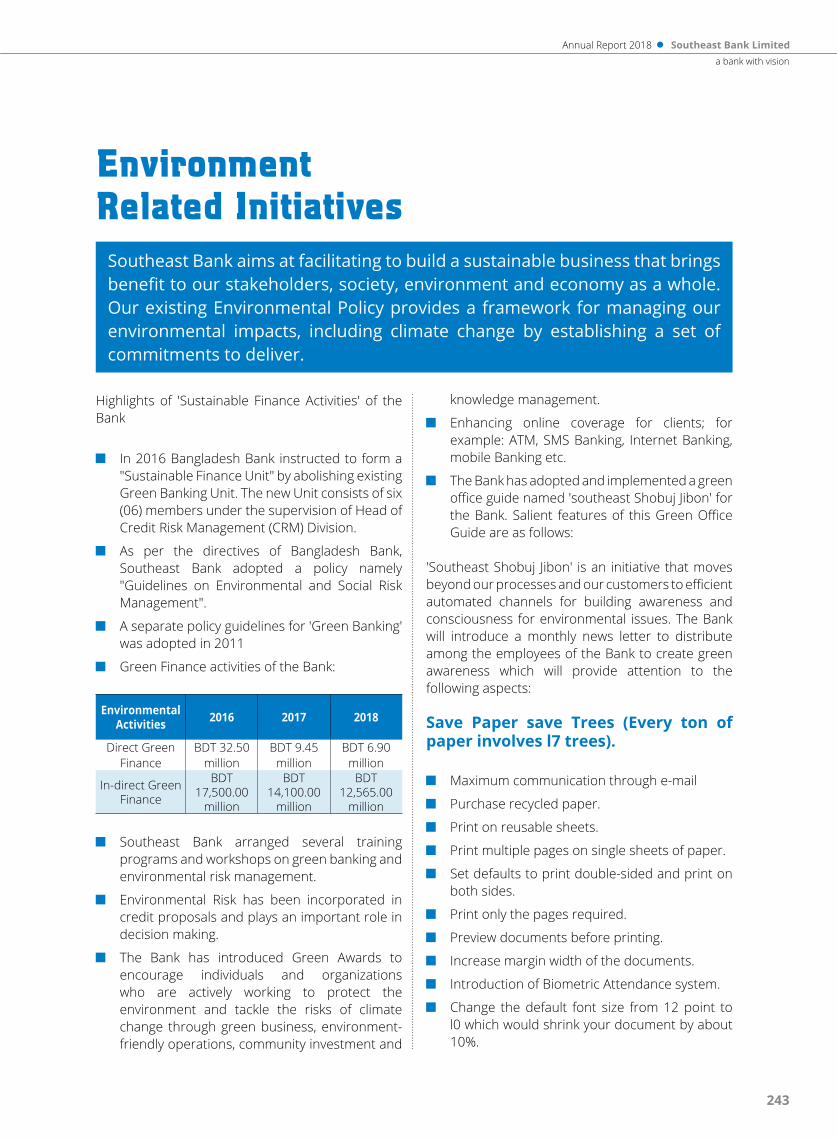

Formation of Southeast Bank-The Financial

Express-Policy Research Institute Green Award Trust

30.06.2013Establishment of Southeast

Bank Green School 12.09.2013

2013Issuance of Subordinated

Bond for BDT 3,000.00 million. 11.11.2014

Introduction of Green Award 15.11.2014

Incorporation of Southeast Exchange Company (South

Africa) Pty Limited 15.12.2014

Opening of Ladies Branches 29.12.2014

2014

Signing of Revolving Credit agreement for USD 5.00 million with Asian Development Bank (ADB ) 31.03.2016

Launching of client acquisition drive through ‘Nibir’ Campaign 15.05.2016

Issuance of Subordinated Bond for BDT 5,000.00 million 02.08.2016

Introduction of Bank’s Health Care Centre 29.09.2016

Introduction of Bank’s E-Library 29.09.2016

Launching of ‘Cash Express Remit Card’ for beneficiary of Foreign Wage Earner Expatriates 08.10.2016

Bank awarded 1st position in “ICMAB Best Corporate Award-2015” 26.10.2016

Awarded ‘Tax Card and Trophy’ as 6th highest Tax Payers of the Country in the Banking Sector 24.11.2016

Signed of agreement with Bangladesh Bank for ‘Green Transformation Fund’ 01.12.2016

20162015Launching of Telecash as

Mobile Financial Services Product 29.01.2015Signed Unsecured Facility Agreement with Global Climate

Partnership Fund (GCPF) 25.02.2015Introduction of Bank’s Modern and full-fledged Training Institute

21.05.2015Signed funded Loan Agreement with International Finance

Corporation (IFC) 05.08.2015Commissioning of ‘SWIFT Sanction Screening Solution’ 30.08.2015

Introduction of Central Monitory System (CMS) tomonitor (24X7) all branches 25.10.2015

Introduction of Real Time Gross Settlement (RTGS) 29.10.2015Implementation of Credit Card Management Software 23.11.2015

Partnership with MasterCard Bangladesh and launched the complete range of Credit Cards (World, Platinum, Titanium and

Gold) and Prepaid Card 15.12.2015Introduction of Bank’s Call Centre 24X7 16.12.2015Introduction of Chip-based Credit Card 31.12.2015

24 Years ofGlorious Journey

1st Rights Share Issue

Subscription Opened 15.02.2003

Subscription Closed 15.03.2003Commencement of Islamic Banking business from Chhagalnaiya Islamic

Banking Branch, Feni 28.07.2003

License Issued from Bangladesh Bankas a Primary Dealer 28.10.2003

2003

Registered as Depository Participant

of CDBL 17.02.2004

1st to Demat Shares in CDS of CDBL in Banking Sector

16.05.2004

Became a member of Trade Finance

Program (TFP) of Asian Development Bank

(ADB) 20.10.2004

2004

2nd Rights Share Issue

Subscription Opened

15.10.2006Subscription

Closed 31.10.2006

2006

Launching of Credit Card 01.01.2005

2005

Introduction of new Core Banking

Software 14.02.2009Launching of 1st

Off-shore Banking Unit 30.12.2009

Became a member of Global Trade Finance

Program (GTFP) of International Finance

Corporation (IFC) 23.04.2007

2009

2007

Obtained license from Bangladesh Bank for Centralizing International Trade and

Foreign Exchange Transactions 26.01.2017Launching of ‘Priority Banking Products’

“ESTEEM” 04.03.2017Southeast Bank distributed Green Award

05.04.2017Organized Scholarship program for

financially challenged meritorious students 20.05.2017

Launching of Payment Gateway 25.05.2017Awarded first position for the best

Corporate Governance among private sector banks by Institute of Chartered

Accountants of Bangladesh (ICAB) 25.11.2017

Received Silver Award for Corporate Governance Excellence, 2016” by The Institute of Chartered Secretaries of

Bangladesh (ICSB) 30.11.2017Establishment of Cafeteria for Safe food for

Bank’s employees 21.12.2017

2017Awarded 1st Runner Up by South Asian Federation of

Accountants (SAFA) for Best Presented Annual Report-2016 in the Private Sector Banking Category

31.01.2018

Won Joint 2nd Runner Up Award in SAARC Anniversary Award for Corporate Governance 31.01.2018

Received Silver Award for Corporate Governance Excellence, 2017 by the Institute of Chartered Secretaries of Bangladesh (ICSB). 10.11.2018

Awarded “Tax Card & Trophy” as the 4th highest Tax Payer of the Country in the Banking Sector. 12.11.2018

2018

14

Letter of Transmittal 16Forward Looking Methodology 17Notice of the 24th Annual General Meeting 19Message from the Chairman 20-25Review from the office of the Managing Director 26-30Integrated Reporting 31-33Corporate Philosophy and Business Model 34-35

VISION AND MISSION Strategic Objectives, Planning and Priorities 37-40Core Values, Code of Conduct and Ethics 41-43Corporate Profile 44-45Group Corporate Structure 46-47Organogram of the Bank 48-49Last 10 Years Financial Indicators 50-51Composition of Board of Directors and its Committees 52-58Brief Profile of Board of Directors 60-71Code of Conduct for Directors 72Policy on reviewing effectiveness of the Board of Directors 73Directors’ Responsibility Statements 74-75

DIRECTORS’ REPORT 77-93

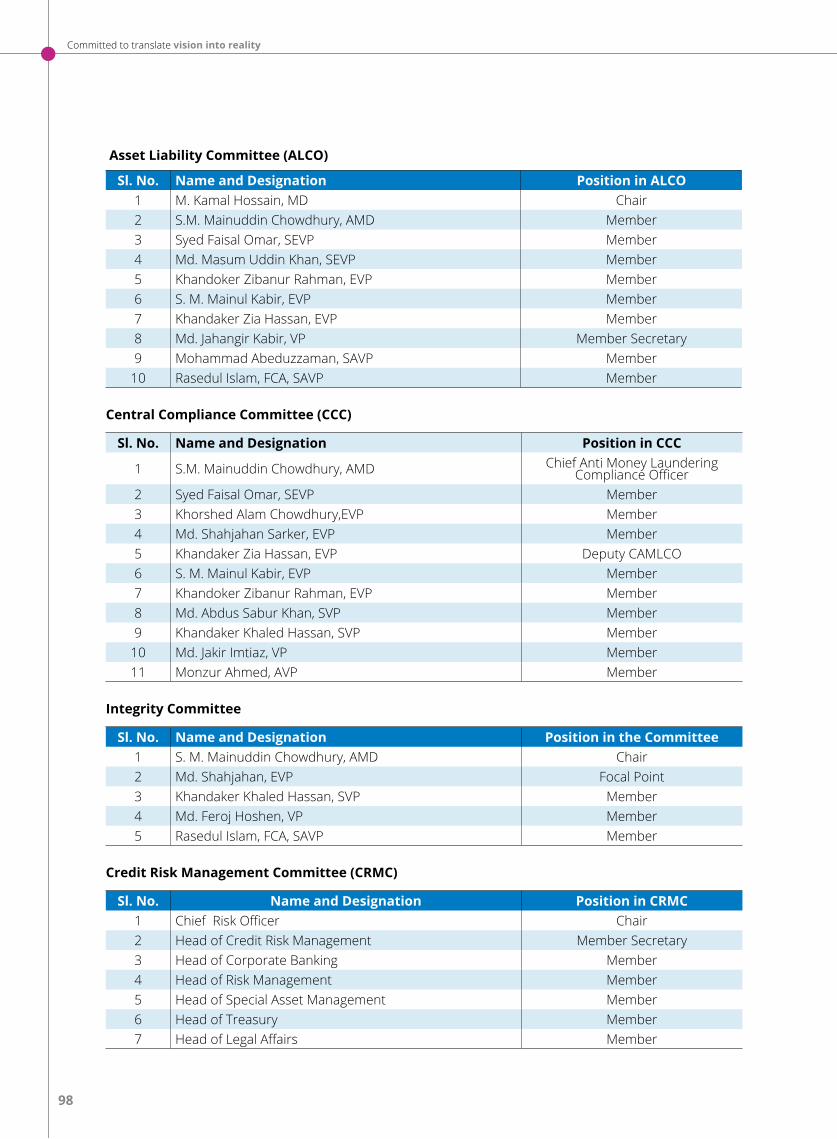

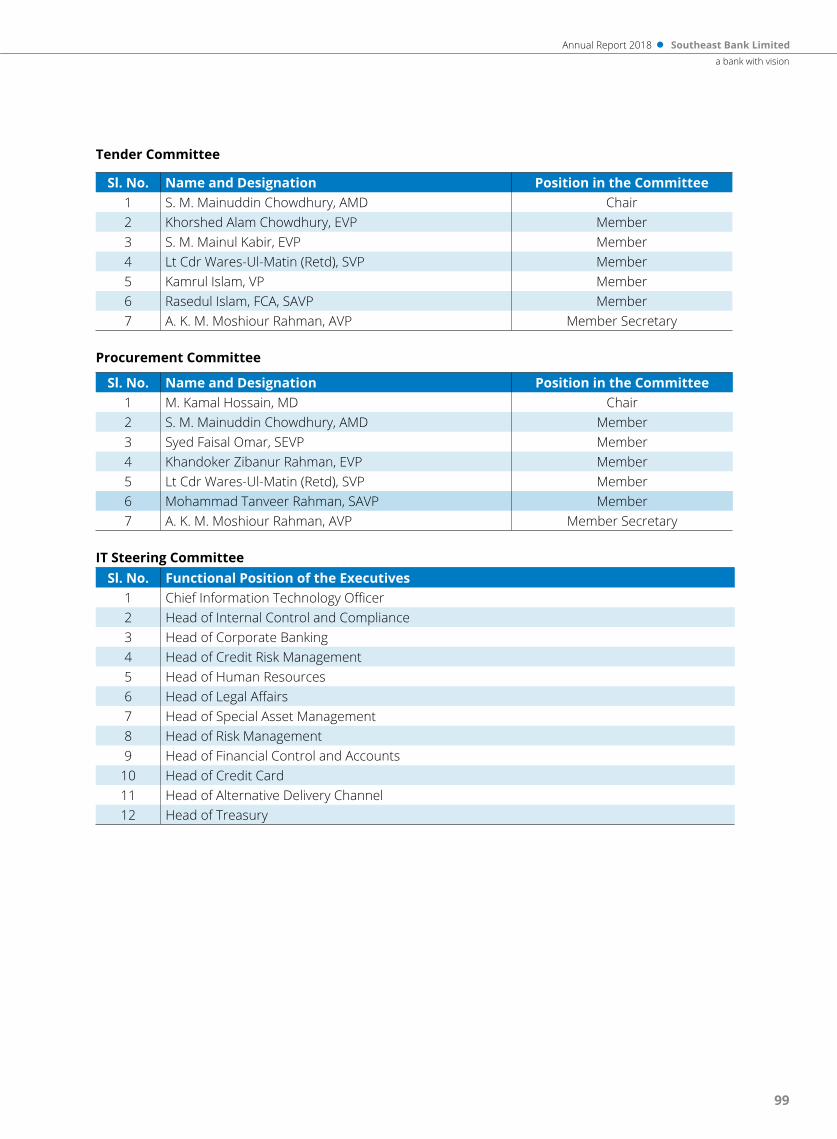

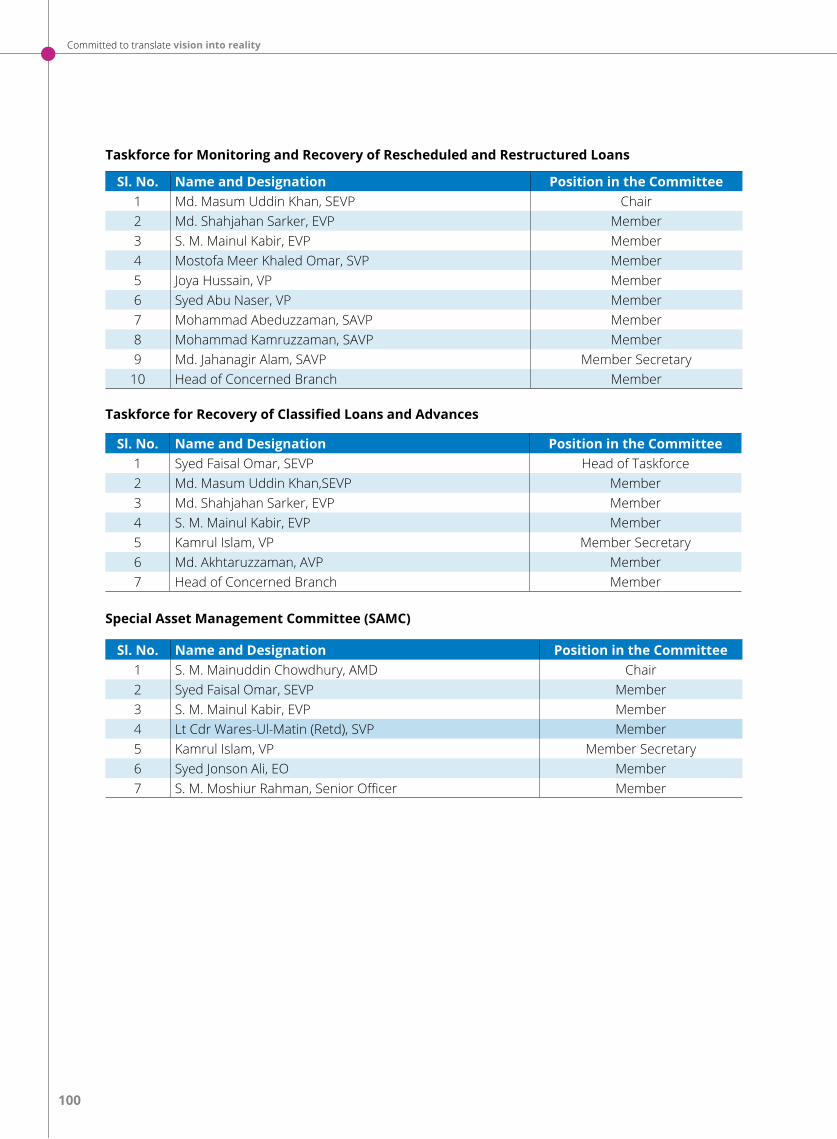

Senior Management Team 94-95Code of Conduct for Senior Management Team 96Committees of the Management 97-100

CORPORATE GOVERNANCE 103-154

Report of the Bank’s Shariah Supervisory Committee 155-156

MANAGEMENT REVIEW, RESPONSIBILITY AND EVALUATION 159-204

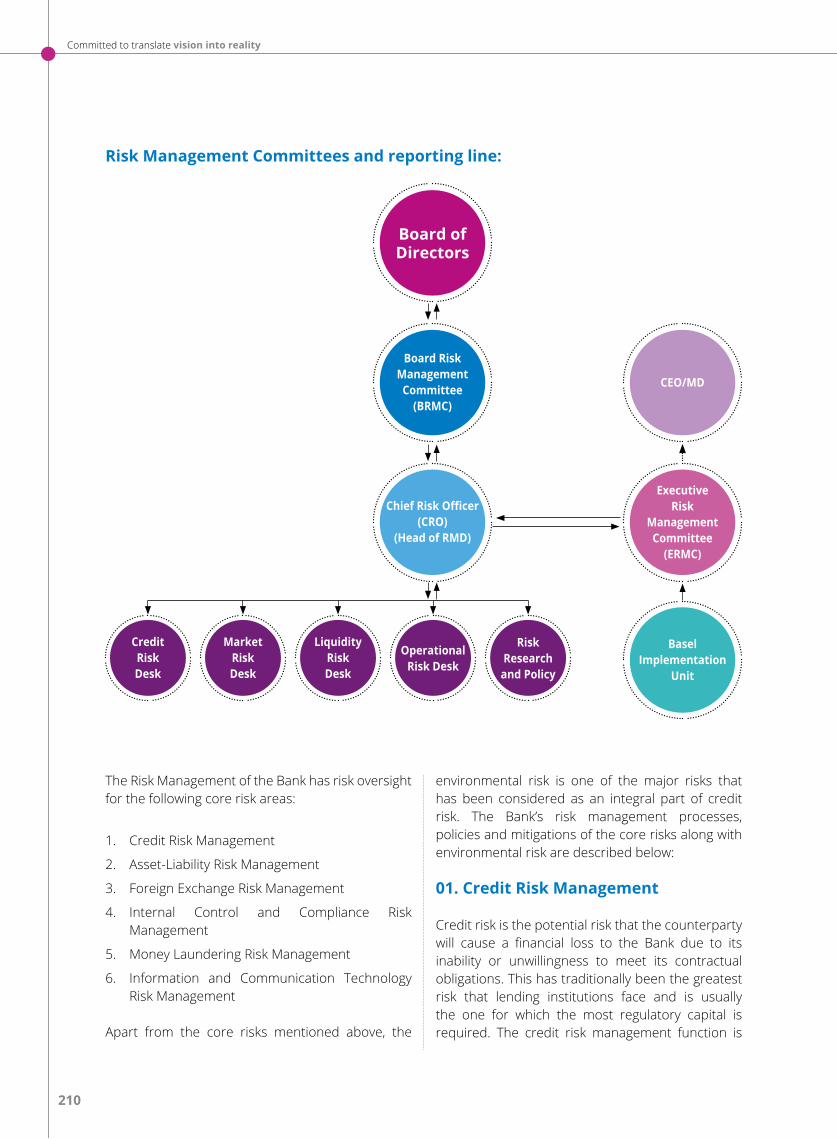

RISK MANAGEMENT AND CONTROL FRAMEWORK Report on Risk Management Framework, Mitigation Methodology and Risk Reporting by Chief Risk Officer

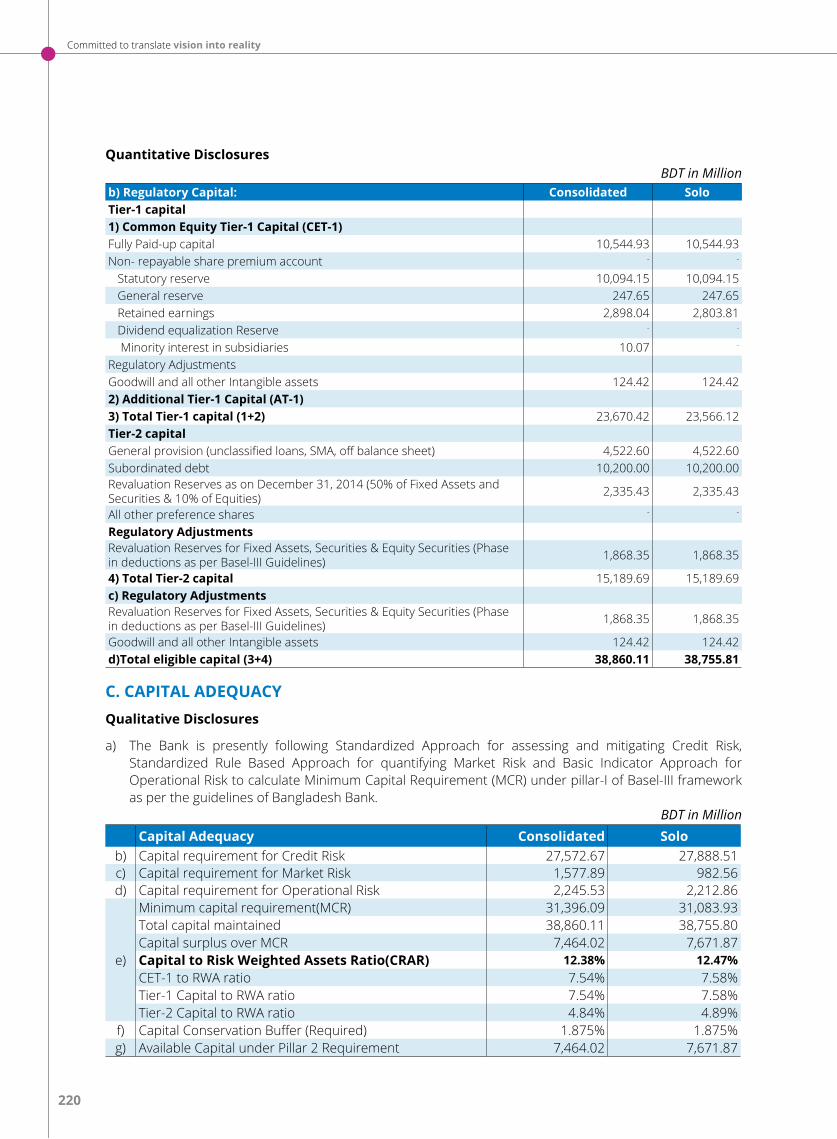

206-217Risk Management in Southeast Bank LimitedDisclosure on Risk Based Capital Adequacy (Basel III) 218-233

Contents

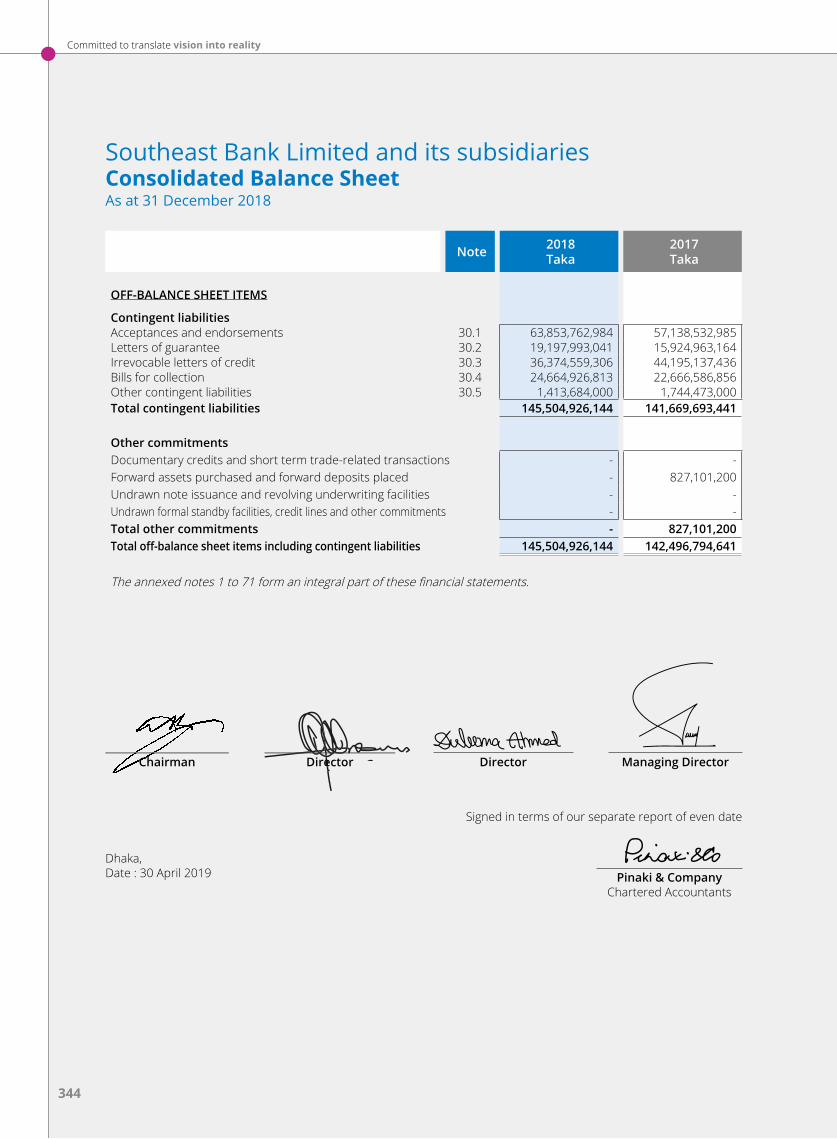

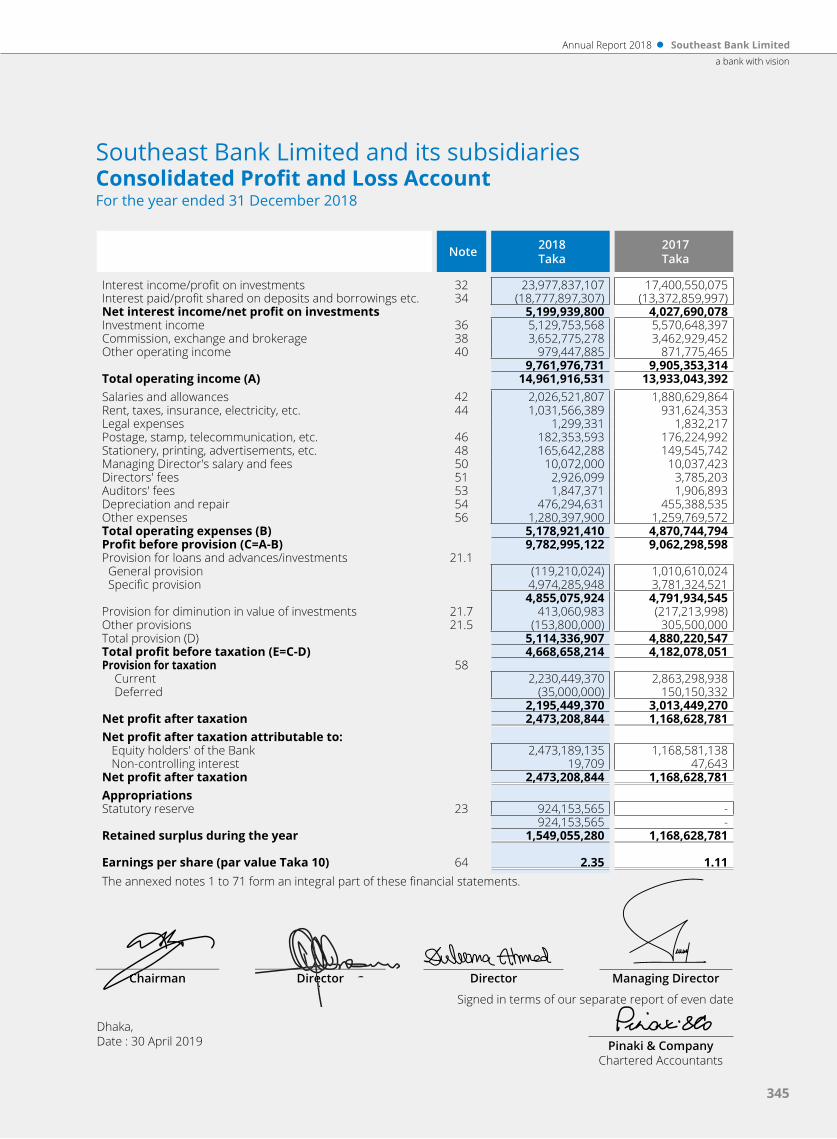

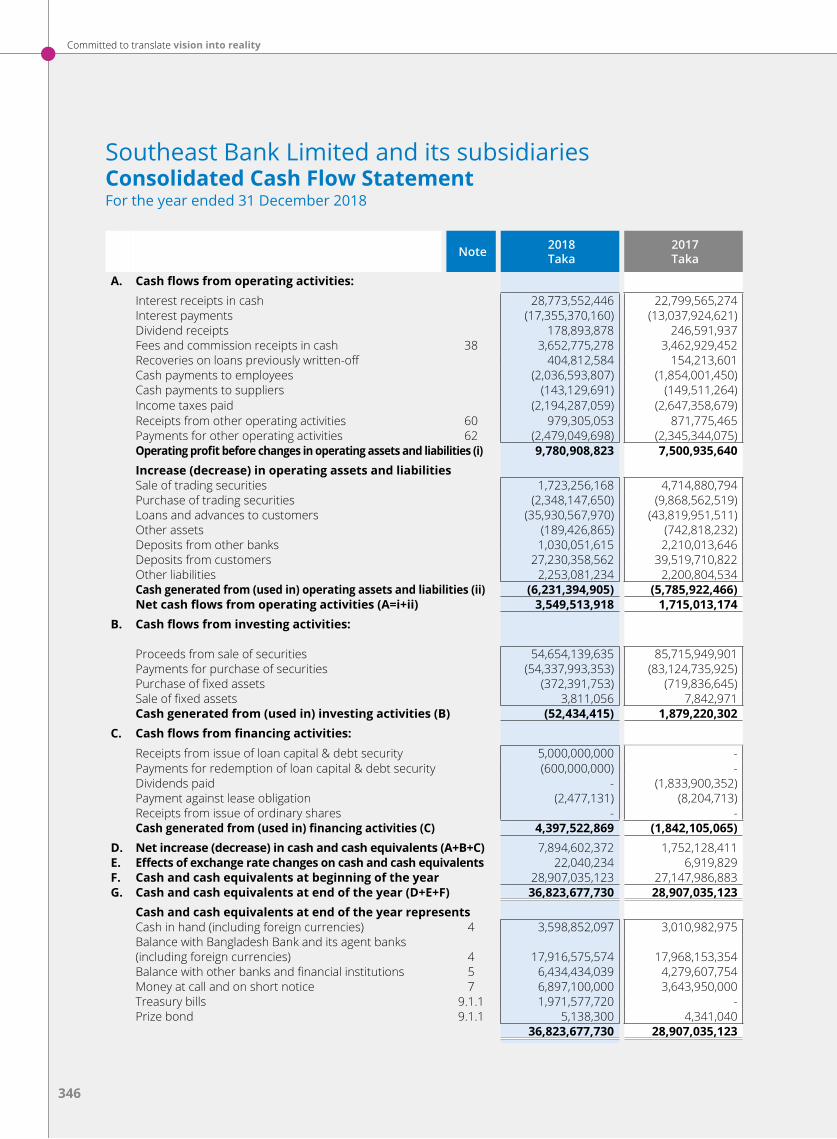

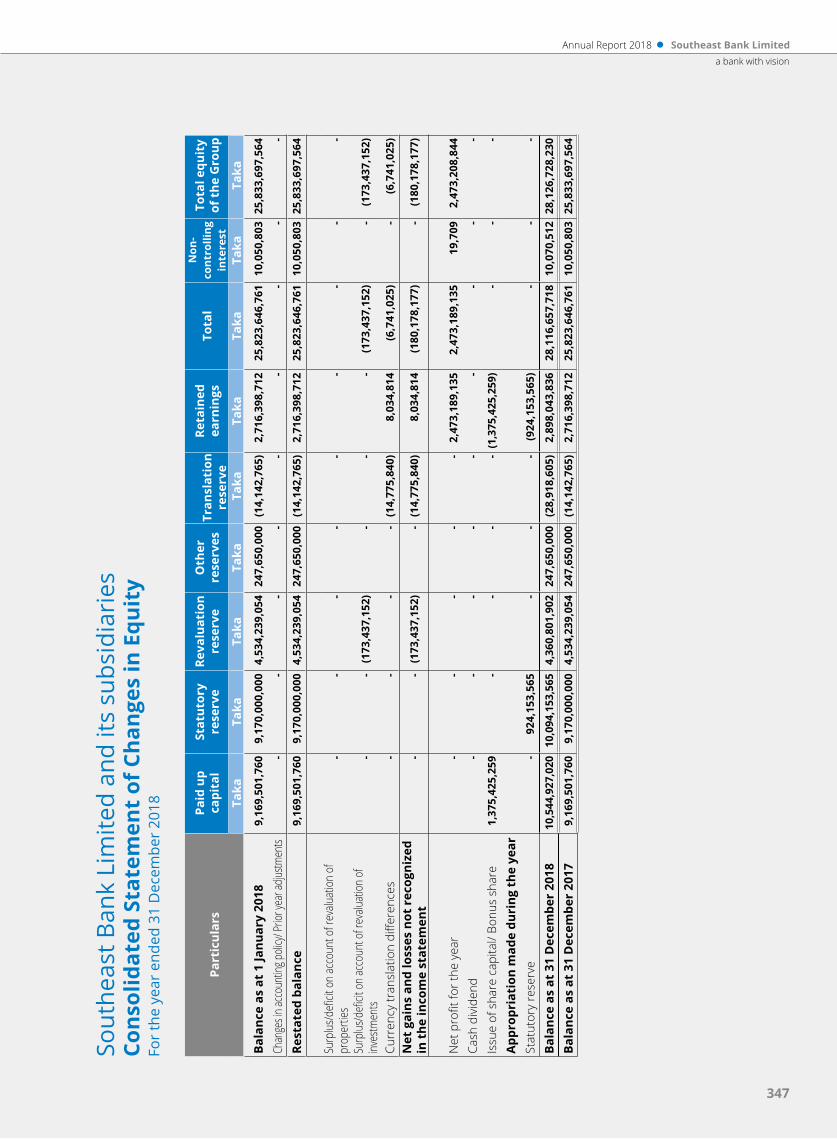

15

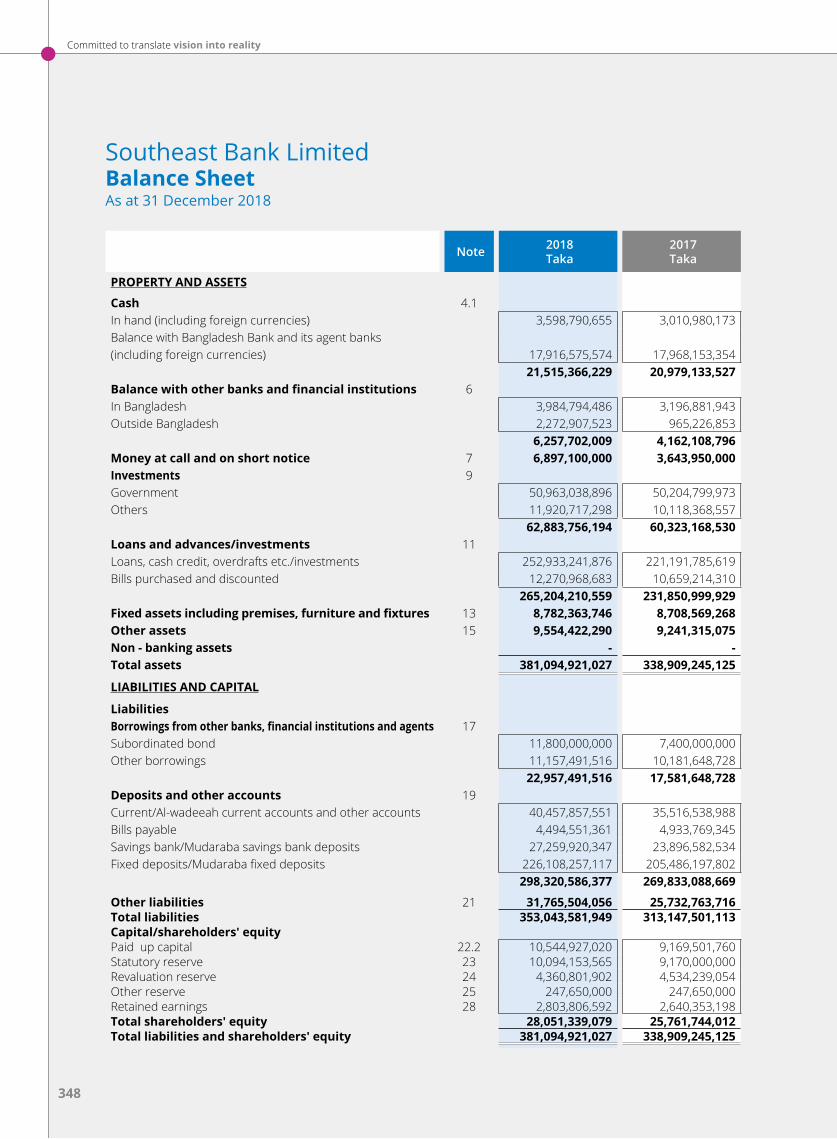

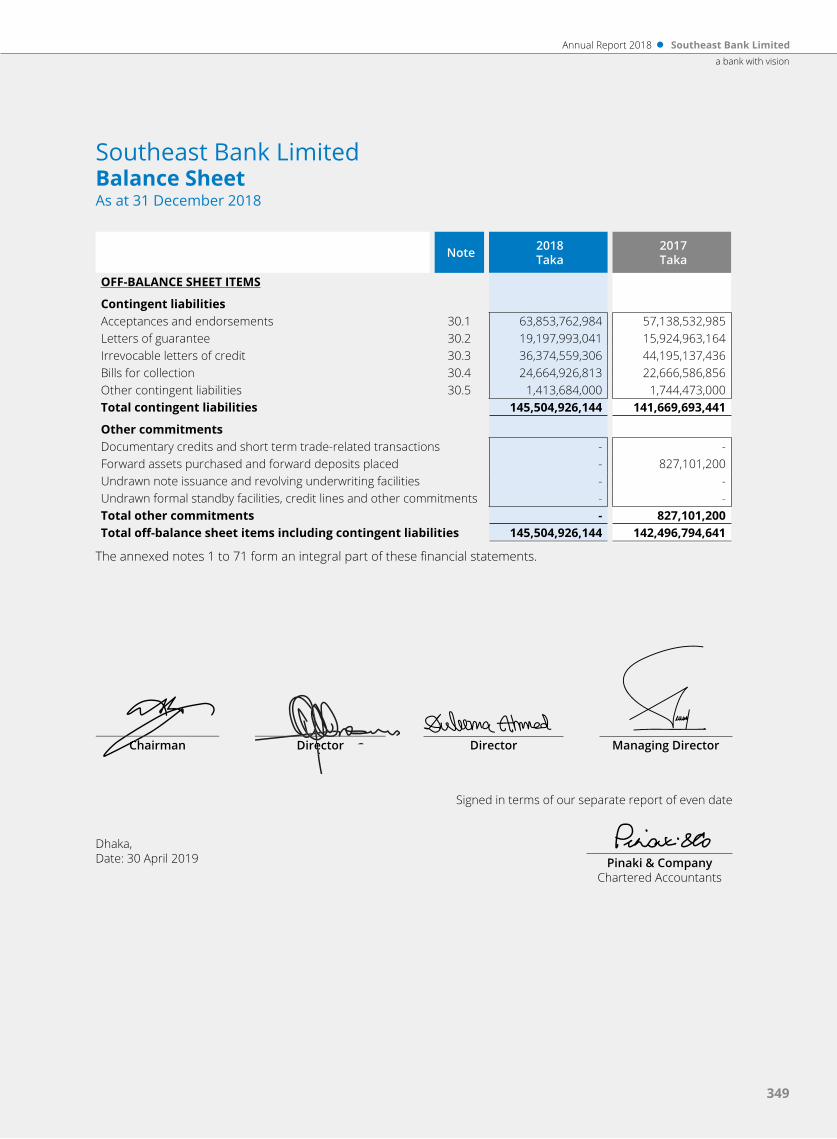

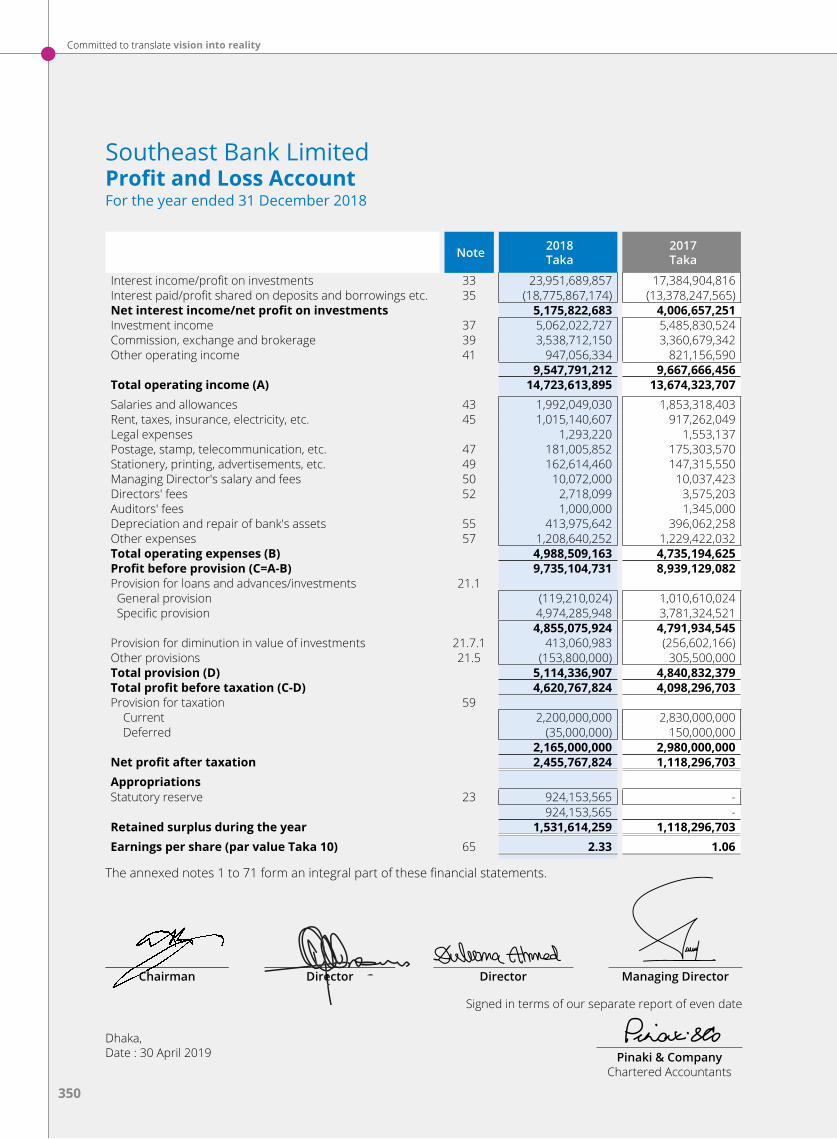

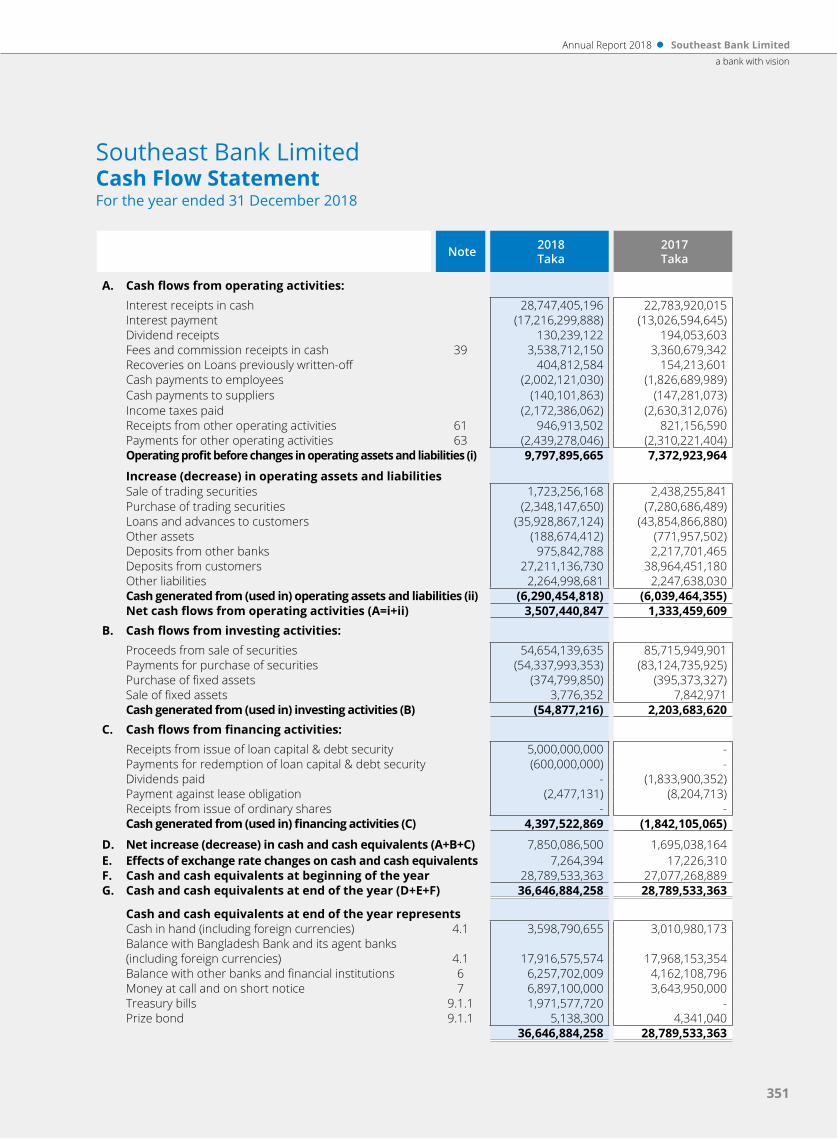

FINANCIAL STATEMENTSIndependent Auditor’s Report to the Shareholders 338Consolidated Balance Sheet 343Consolidated Profit and Loss Account 345Consolidated Cash Flow Statement 346Consolidated Statement of Changes in Equity 347Notes to the Financial Statements 353FINANCIAL STATEMENTS OF ISLAMIC BANKING BRANCHES 424FINANCIAL STATEMENTS OF OFFSHORE BANKING 434FINANCIAL STATEMENTS OF SEBL SUBSIDIARIES 443

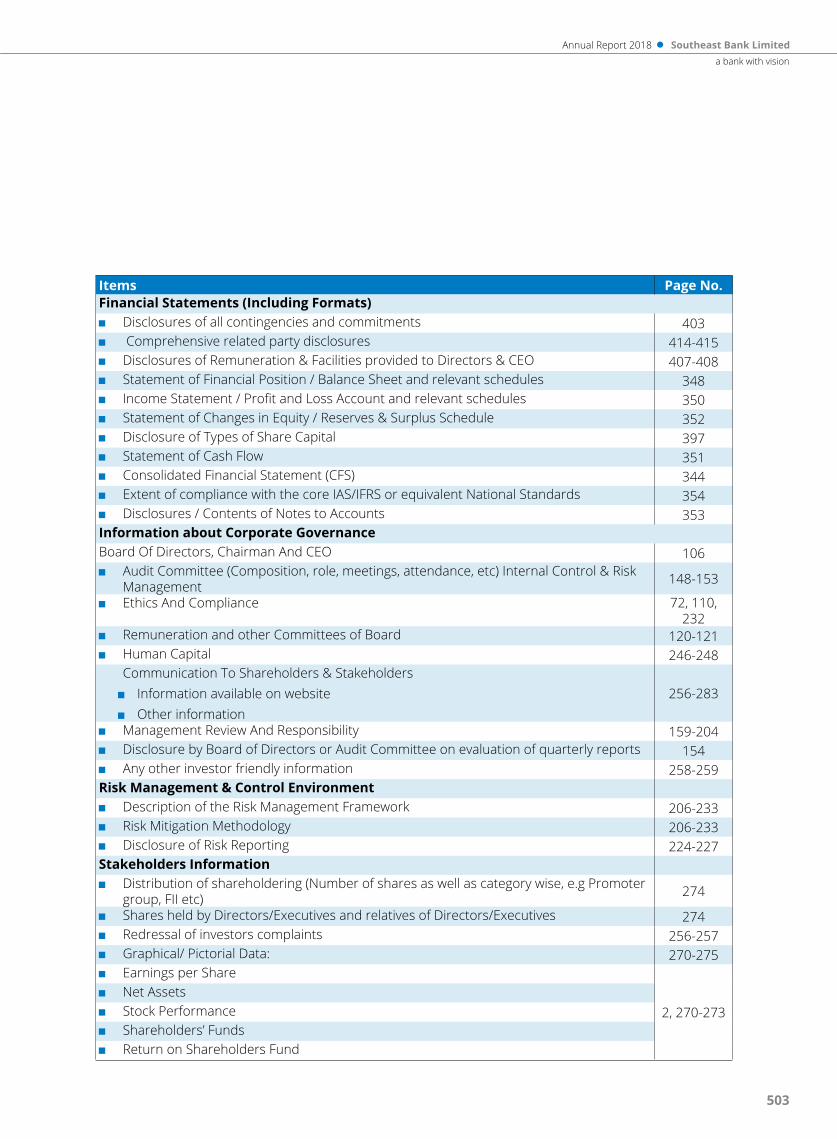

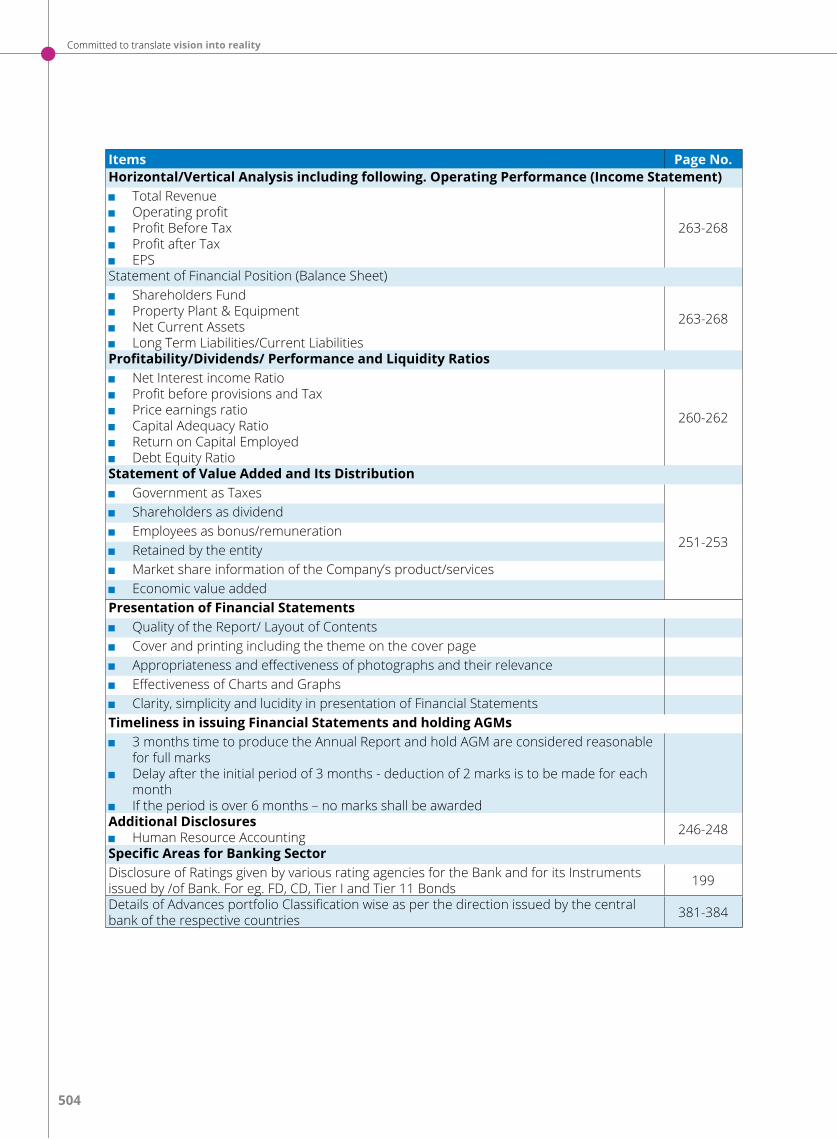

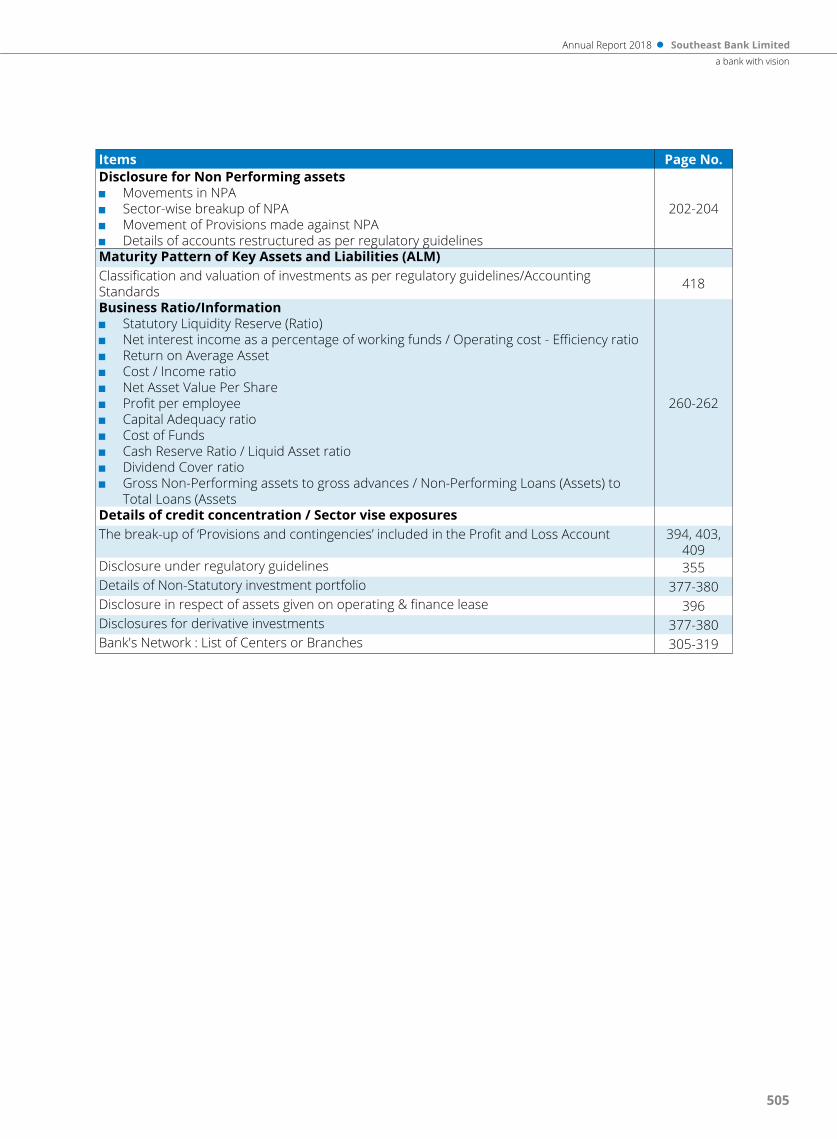

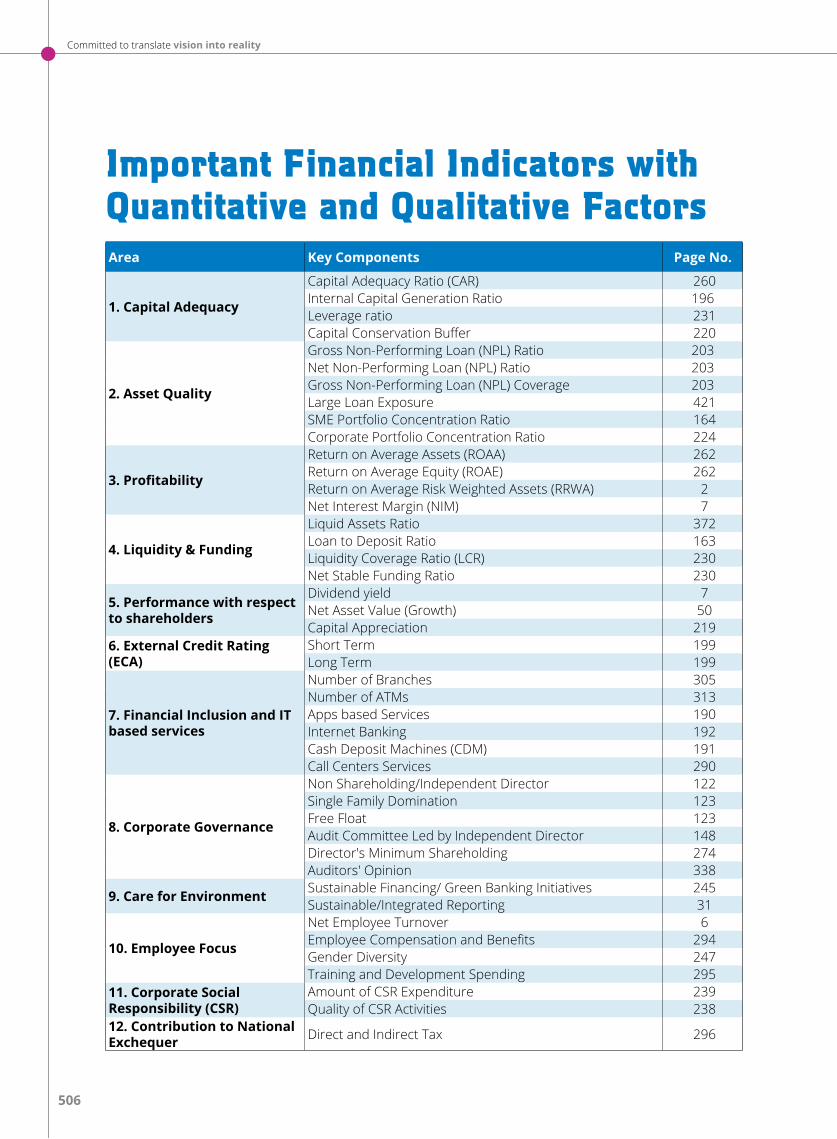

STANDARD DISCLOSURES CHECKLIST 490-506

Events-2018 507-512Proxy Form and Attendance Slip

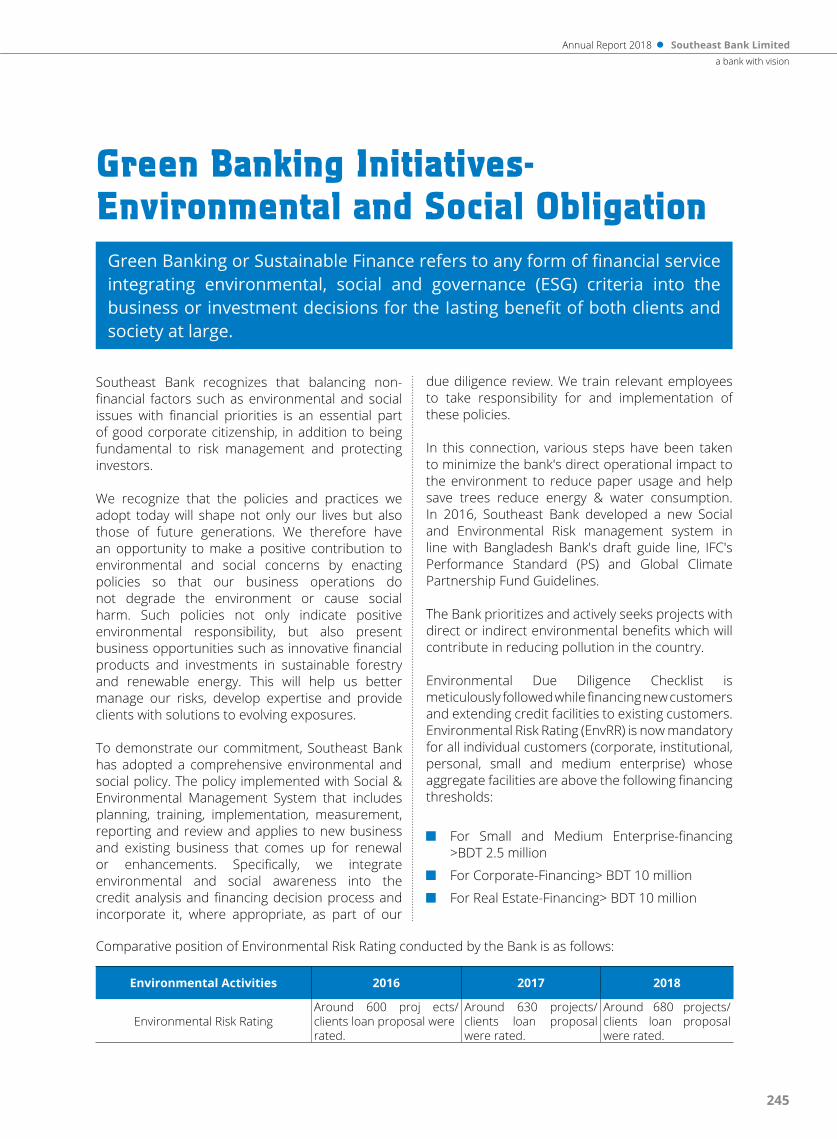

SUSTAINABILITY APPRAISAL AND INTEGRATED REPORTING 236-253

COMMUNICATION TO SHAREHOLDERS & STAKEHOLDERS 256-283

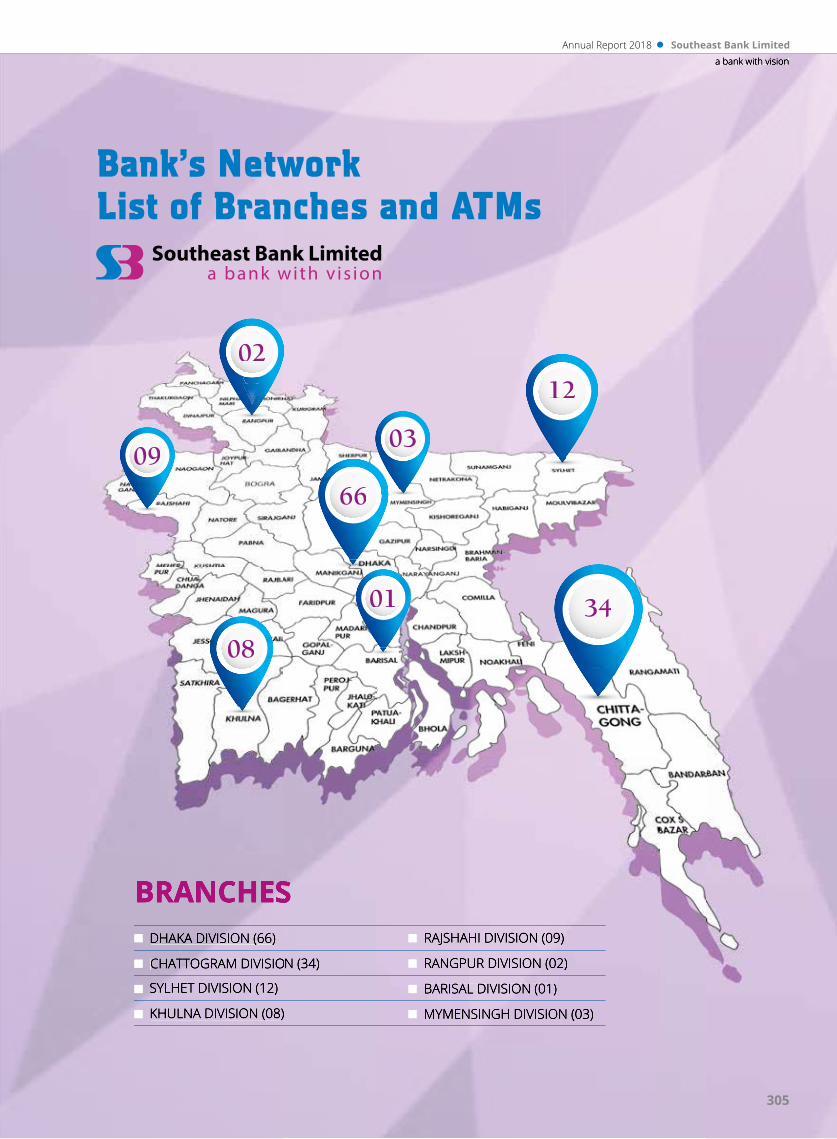

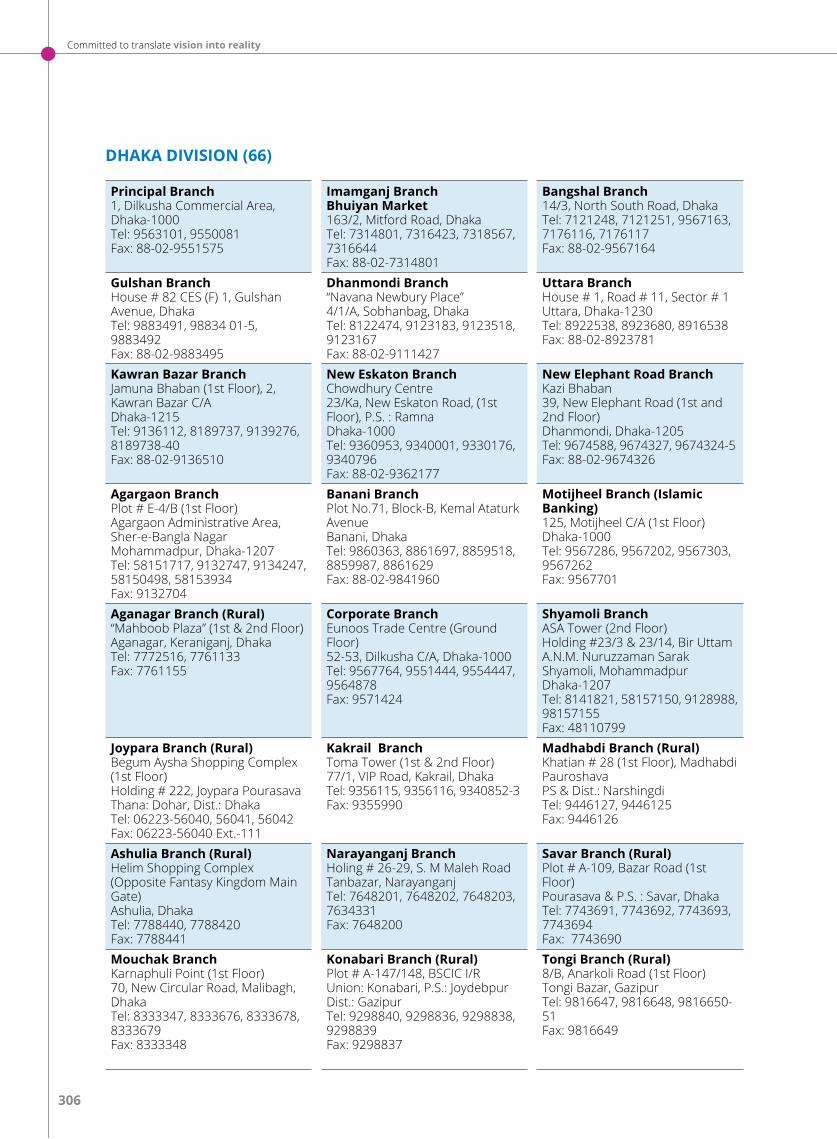

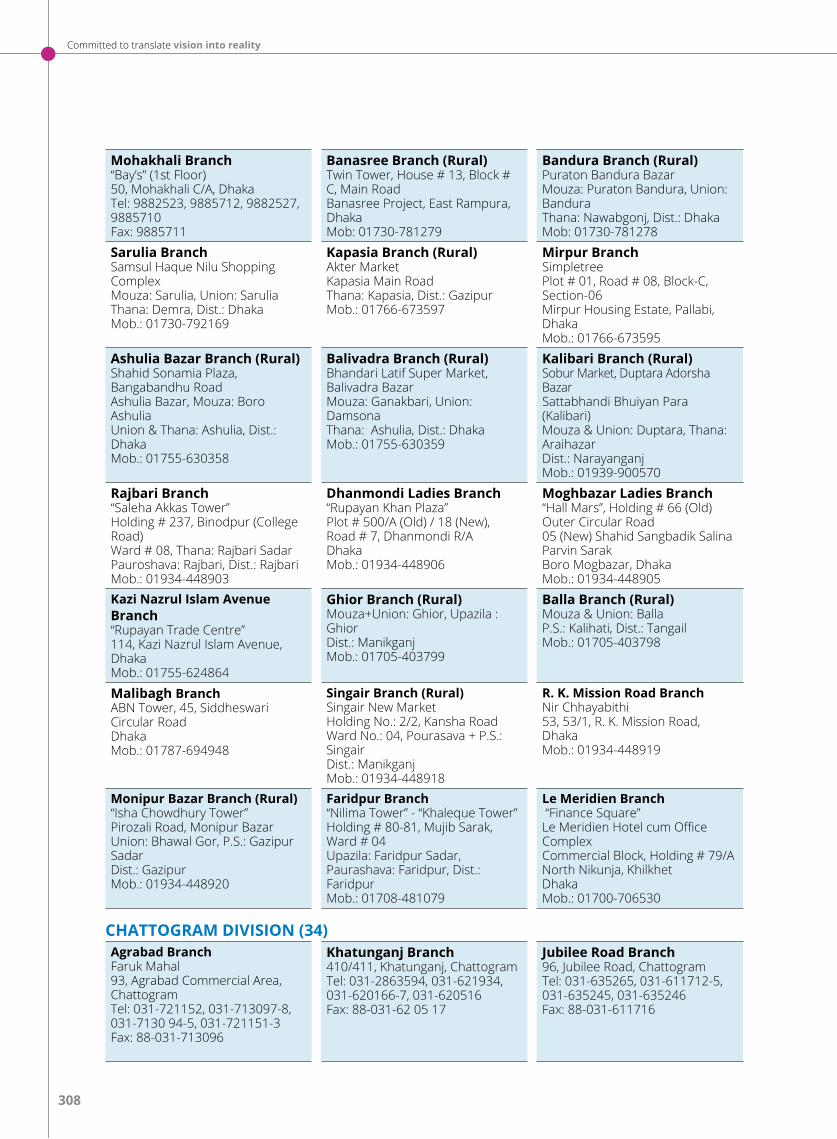

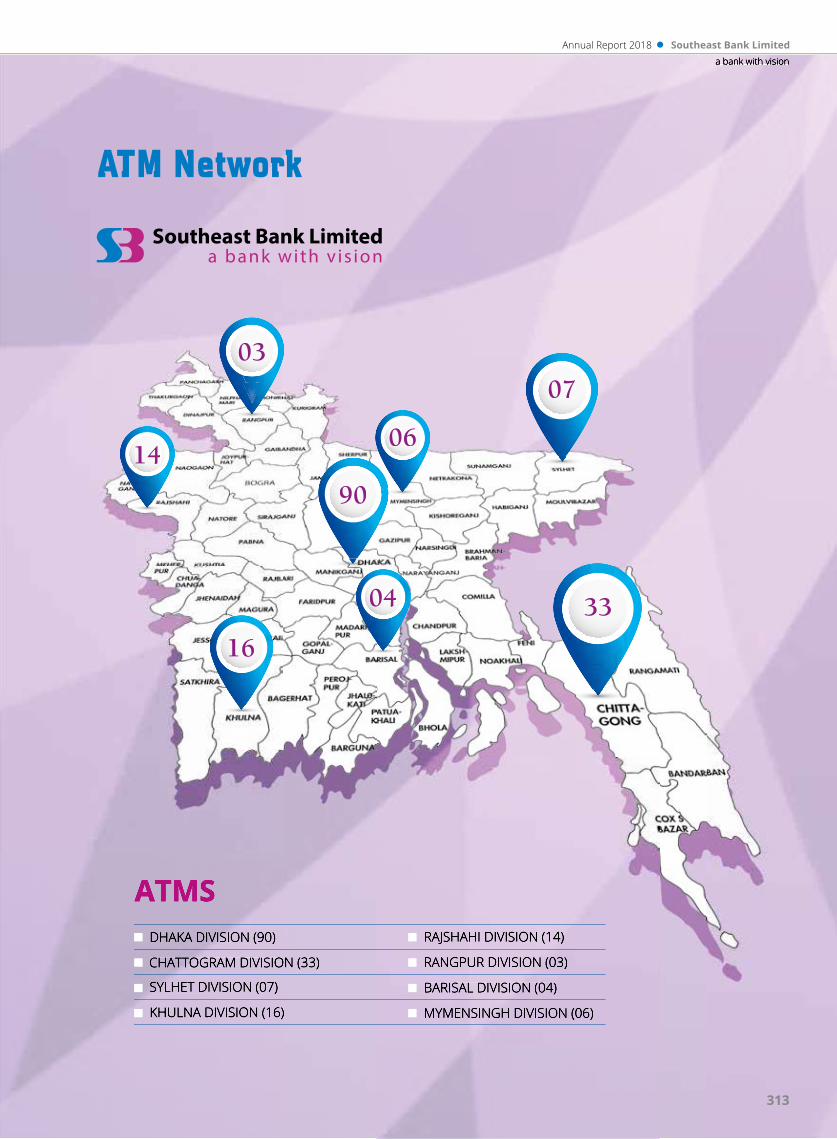

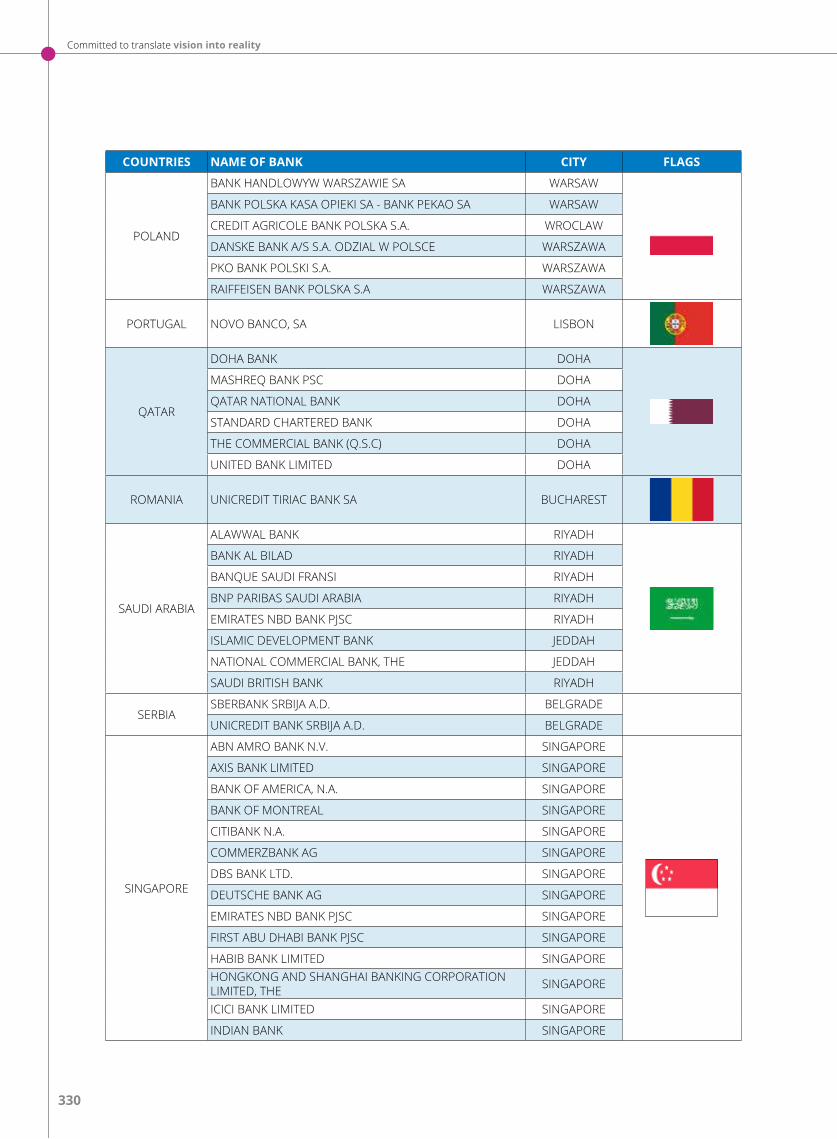

SEBL OUTLOOKProducts and Services 286-288Central Monitoring System - Round the Clock 289Call Center 24 X7X365 290Media Highlights 291-293Caring for the Employees (Health and Safety) 294Career Development Program 295Contribution to National Exchequer 296Empowering Women 297Environment - Responsive Bank 298Southeast Bank Green School 299-301Financial Inclusion: Mobile Banking Services – Telecash 302Connecting Customers 303Service Excellence in Action 304Bank's Network: List of Branches and ATMs 305-319Worldwide Correspondents Network 320-335

16

Committed to translate vision into reality

All Shareholders of Southeast Bank Limited, Bangladesh Bank, Bangladesh Securities and Exchange Commission, The Registrar of Joint Stock Companies and Firms, The Dhaka Stock Exchange Limited and The Chittagong Stock Exchange Limited

Annual Report of Southeast Bank Limited for the Year - 2018

Dear Sirs:

Thank you for supporting us in the preceding years. It is our immense pleasure to lay before you the Bank’s Annual Report-2018 along with the Audited Financial Statements (consolidated and solo) as at and for the year ended on December 31, 2018. The Annual Report-2018 of the Bank comprises Balance Sheet, Profit and Loss Account, Statement of Changes in Equity, Cash Flow Statement along with Notes to the Accounts. We hope that the report will be of use to you today and tomorrow.

Best regards,

Yours sincerely,

A.K.M. Nazmul HaiderCompany Secretary

Letter of Transmittal

17

Annual Report 2018 Southeast Bank Limiteda bank with vision

A forward-looking statement is a statement that contains predictions, projections and possibilities. It relates to future events. It often predicts expected future business and financial performance. It contains words such as ‘expect’, ‘anticipate’, ‘believe’, ‘seek’, ‘will’, ‘may’, ‘would’, ‘presume’, ‘assure’, ‘hope’, so on and so forth. A forward-looking statement naturally addresses matters that are, to certain degrees, uncertain and may not happen. In most cases, a forward-looking statement is made in respect of company’s expected income, earning, business growth, horizontal expansion, cost structure, capital structure, dividends etc. Such a statement is made based on some assumptions about future events which may happen or may not happen.

This Annual Report-2018 of Southeast Bank Limited also contains forward-looking statements. Since there are uncertainties about the occurrence of the future events, those should be treated from that viewpoint in decision-making by the users of the Annual Report.

Forward LookingMethodology

18

Committed to translate vision into reality

20

12

20

13

20

1

4

2 0 1 5

2

01

6

20

17

20

18

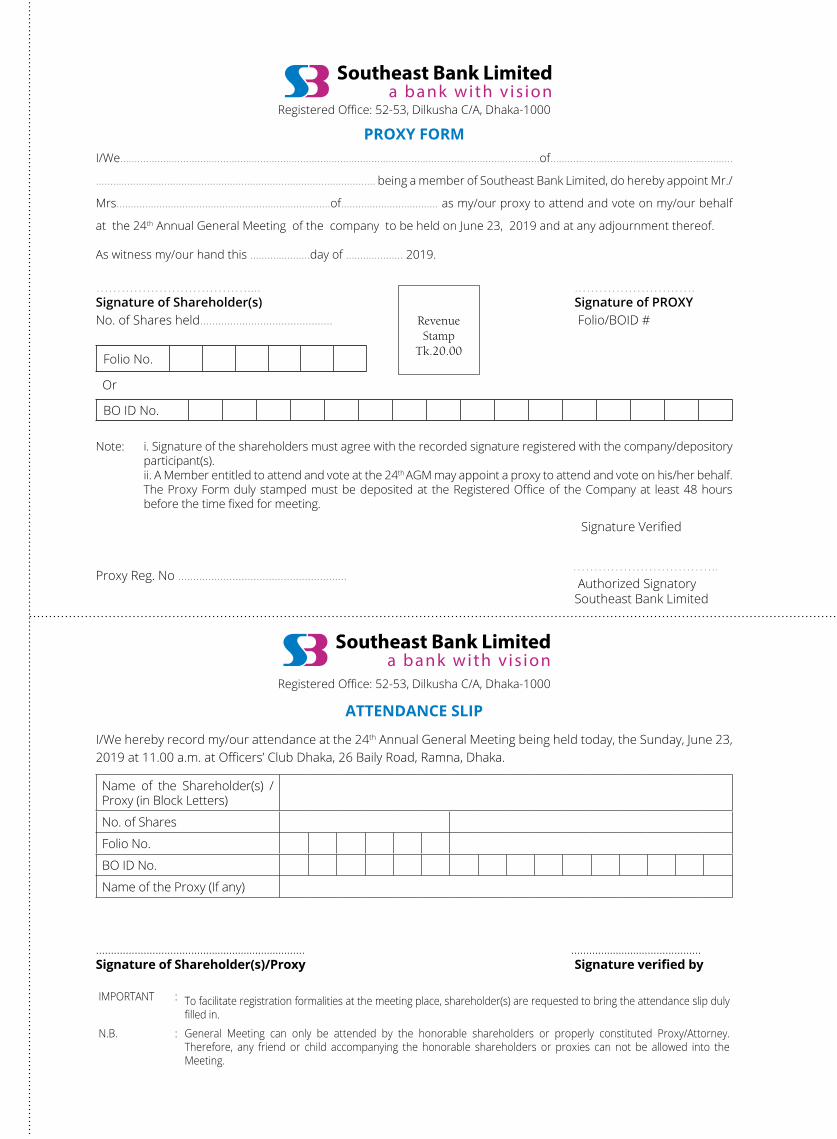

Southeast Bank Lim�ed24th

Annual General Meeting

Venue: Officers’ Club Dhaka26, Baily Road, Ramna,

Dhaka-1000

Date:Sunday, June 23, 2019

at 11.00 a.m.

Notice of the24th Annual General MeetingNotice is hereby given to all members of Southeast Bank Limited that the 24th Annual General Meeting of the Shareholders of the Company will be held on Sunday, June 23, 2019 at 11.00 a.m. at Officers’ Club Dhaka, 26, Baily Road, Ramna, Dhaka-1000 to transact the following business and adopt necessary resolutions:

AGENDA:

1. To receive, consider and adopt the Profit and Loss Accounts of the Company for the year ended on December 31, 2018 and the Balance Sheet as at that date together with the Reports of the Board and the Auditors thereon.

2. To declare dividend for the financial year ended December 31, 2018.

3. To elect / re-elect Directors and to approve the re-appointment of the Independent Director.

4. To appoint Statutory Auditors for the term until the next Annual General Meeting and fix their remuneration.

5. To appoint the Compliance Auditor as per Corporate Governance Code for the year 2019 and fix their remuneration.

6. Miscellaneous, if any, with the permission of the chair.

By order of the Board

Dated: Dhaka A.K.M. Nazmul HaiderMay 30, 2019 Company Secretary

NOTES:

a) The “Record Date” was on Thursday, May 23, 2019.

b) The Shareholders whose name would appear in the CDS/Register of Members of the Company on the Record date shall be entitled to the dividend and attend the AGM.

c) Any member of the Company eligible to attend and vote at the Annual General Meeting may appoint a proxy to attend and vote on his/her behalf. Proxy Form or the Power of Attorney duly signed by the Member and stamped with requisite stamp must be submitted at the Registered Office of the Company at least 48 hours before the meeting.

d) Attendance of the Shareholder/Attorney/Proxy shall be recorded up to 11.00 a.m. at the entrance of the meeting venue. Attendance slip has to be signed and submitted at the Registration Counter. The signature must agree with the recorded signature.

e) Annual Report of the Bank, Attendance Slip, Proxy Form along with the Notice will also be available in the website of the Company at www.southeastbank.com.bd in due course. The Hon’ble Members may also collect the Annual Report, attendance Slip and Proxy Form from the Investors' Relation Department of the Company.

f) All members are requested to update their respective BO Accounts with 12 digits Tax payer’s Identification Number (e-TIN), Bank Account Number, E-mail address, Mailing address and other related information through their respective Depository Participants (DP).

g) As per Bangladesh Securities and Exchange Commission’s Circular No.SEC/CMRRCD/2009-193/154 dated October 24, 2013, and the regulation 24 (2) of the Stock Exchanges (Listing) Regulations-2015 “no benefit in cash or kind, other than in the form of cash dividend or stock dividend, shall be paid to the holders of equity securities” for attending the 24th Annual General Meeting of the Bank.

Annual Report 2018 Southeast Bank Limiteda bank with vision

19

Committed to translate vision into reality

Message from theChairman

20

Annual Report 2018 Southeast Bank Limiteda bank with vision

Bismillahir Rahmanir Rahim

Dear Shareholders,

It is with great pleasure that I heartily welcome you all to the 24th Annual General Meeting of the respected Shareholders of the Bank and sincerely thank you for your continued interest and support for the sustained growth of the Bank over the years. On behalf of the Board of Directors of the Bank, this is my privilege to present before you the Audited Financial Statements for the year ended 31, December, 2018 reflecting the consistent performance of the Bank in respect of operational results and standard of Corporate Governance and regulatory compliance. I would also take this opportunity to highlight our strategies to achieve further operational excellence in our business operations in the future.

21

Alamgir Kabir, FCAChairman

22

Committed to translate vision into reality

1. Synoptic Review of Financial Performance: 2018

By the grace of Almighty Allah (SWT), Southeast Bank Limited (SEBL) delivered strong operating performance and cost efficiencies as well as significant returns and growth in all key business indicators in 2018. I am pleased to announce another set of record results in 2018. During the year, despite many challenges, the bank made a notable growth through reshaping our business strategies and processes and remodeling our service quality and delivery channel. A glimpse of the performance is shown below:

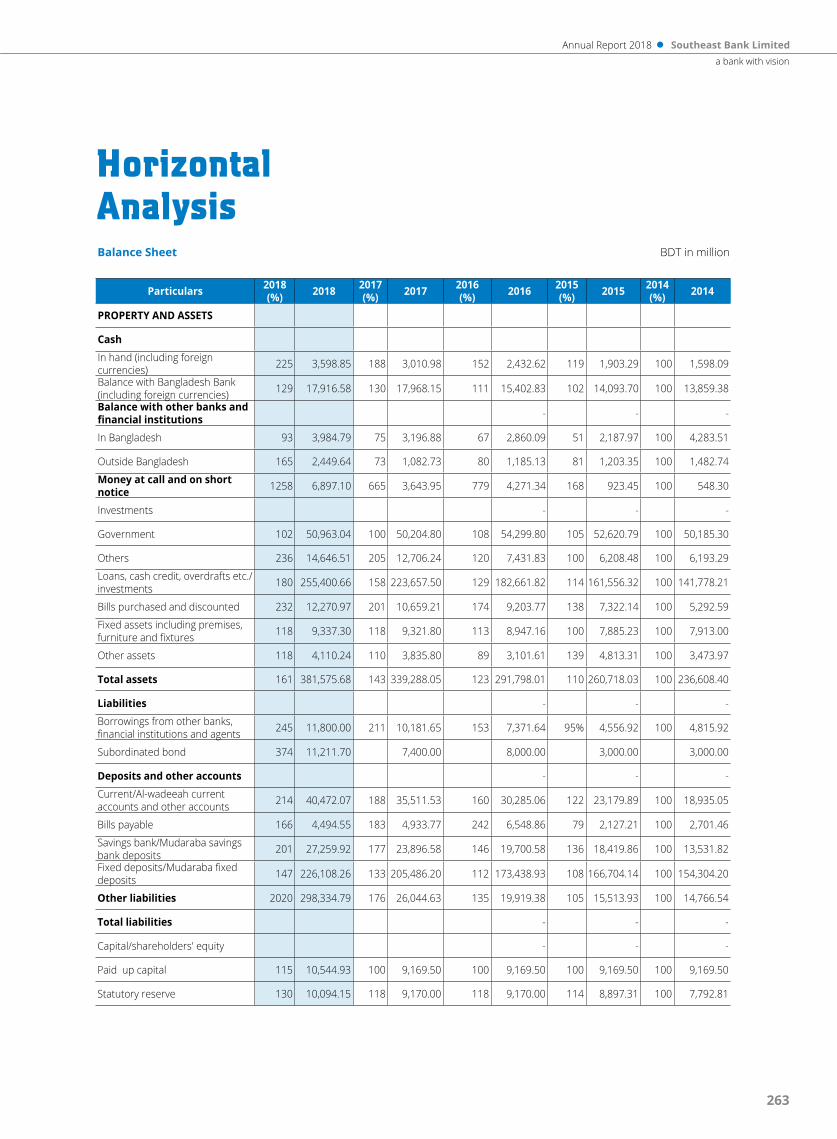

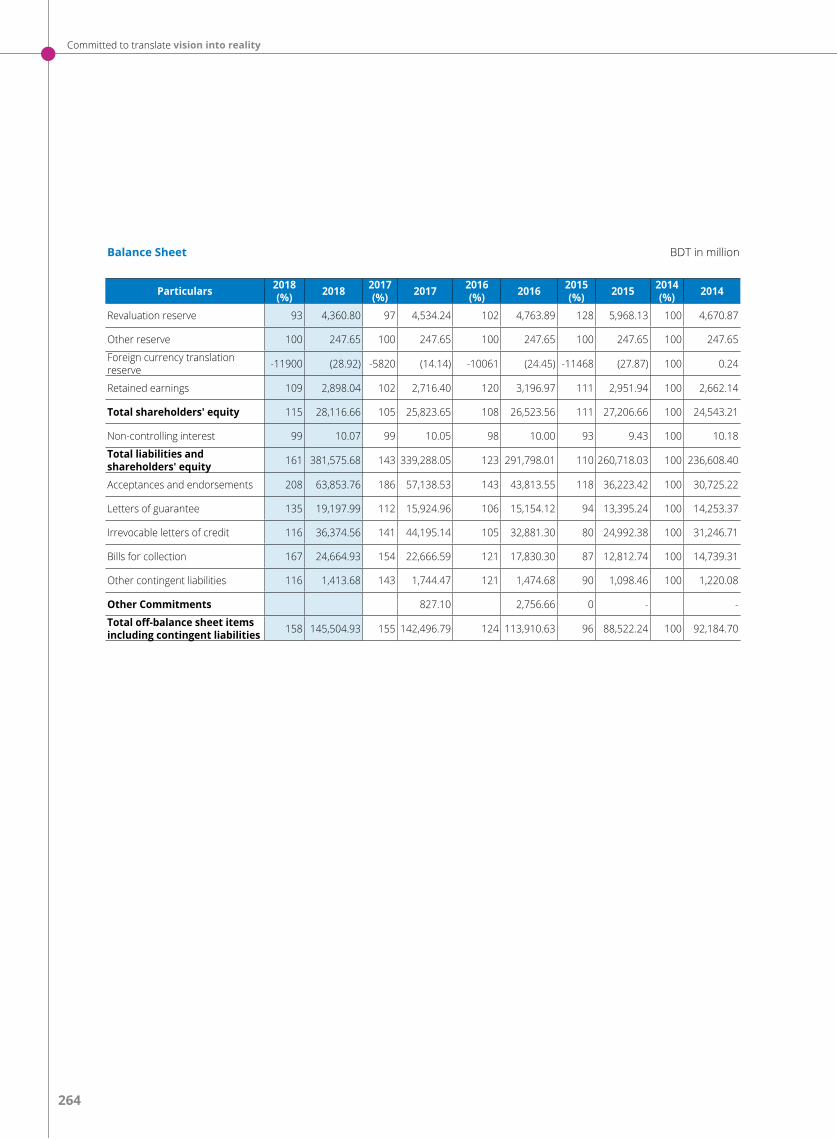

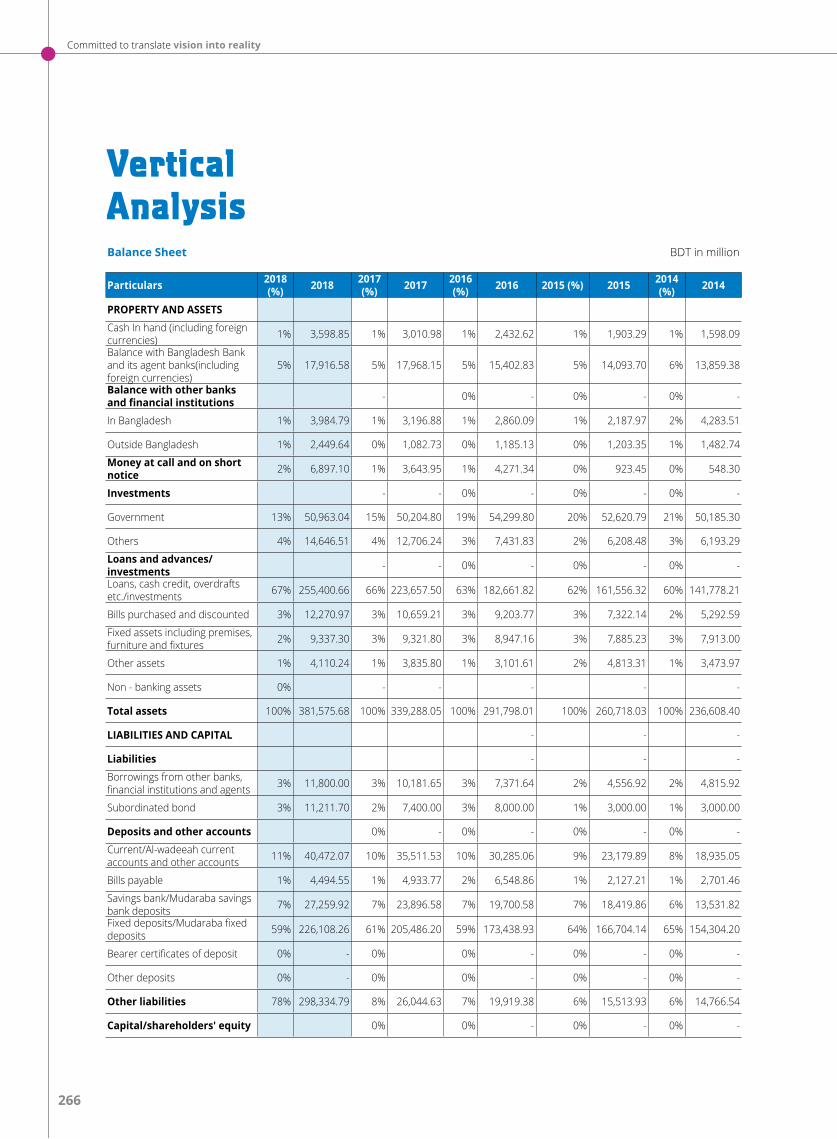

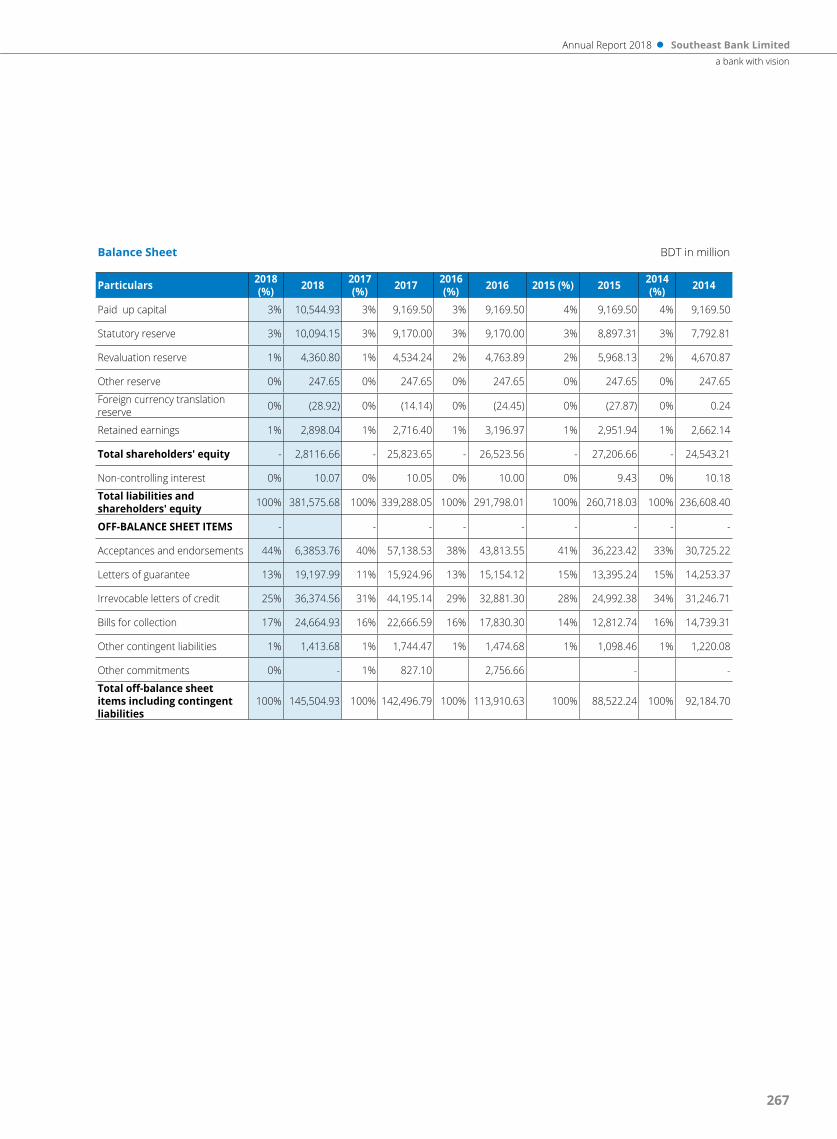

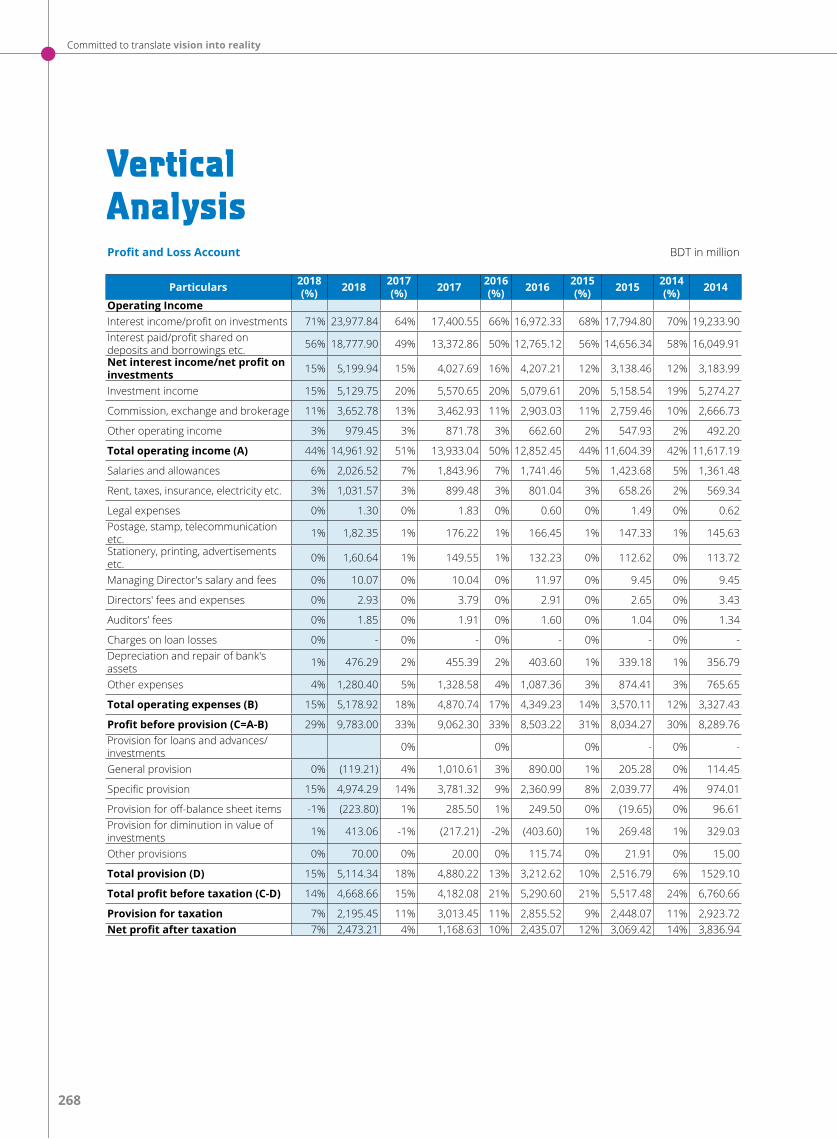

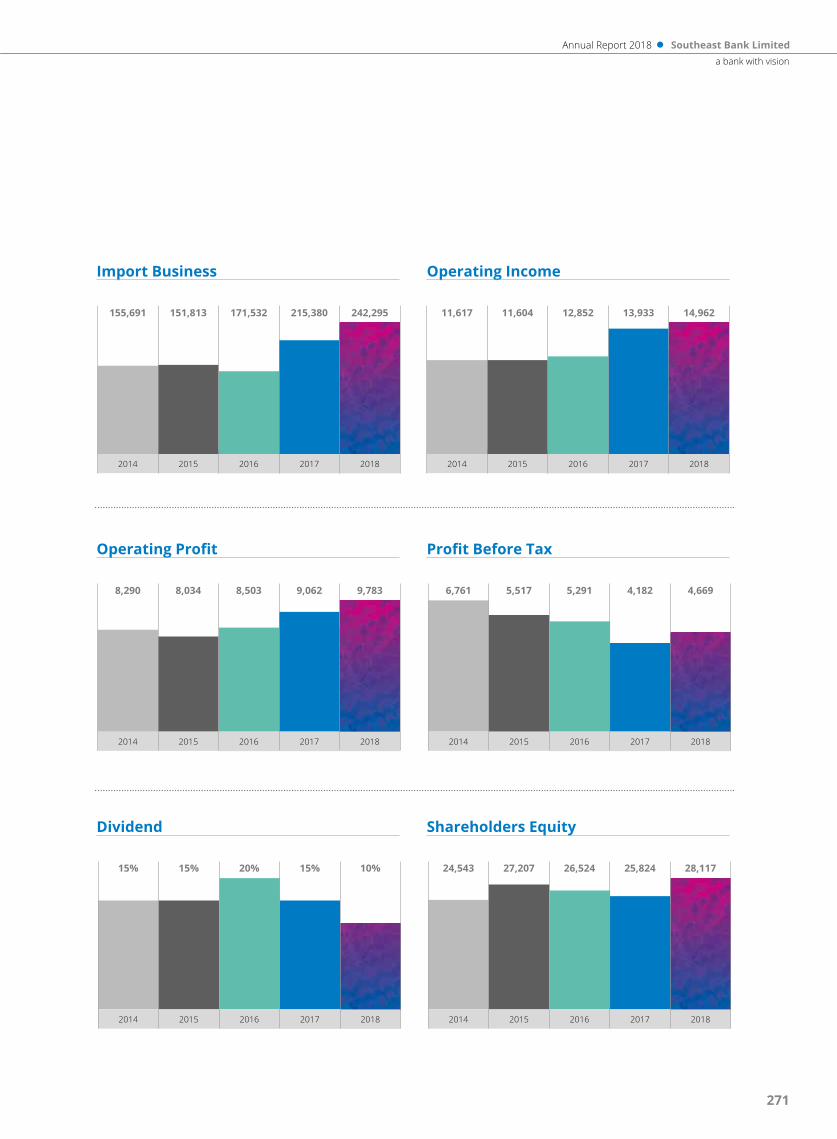

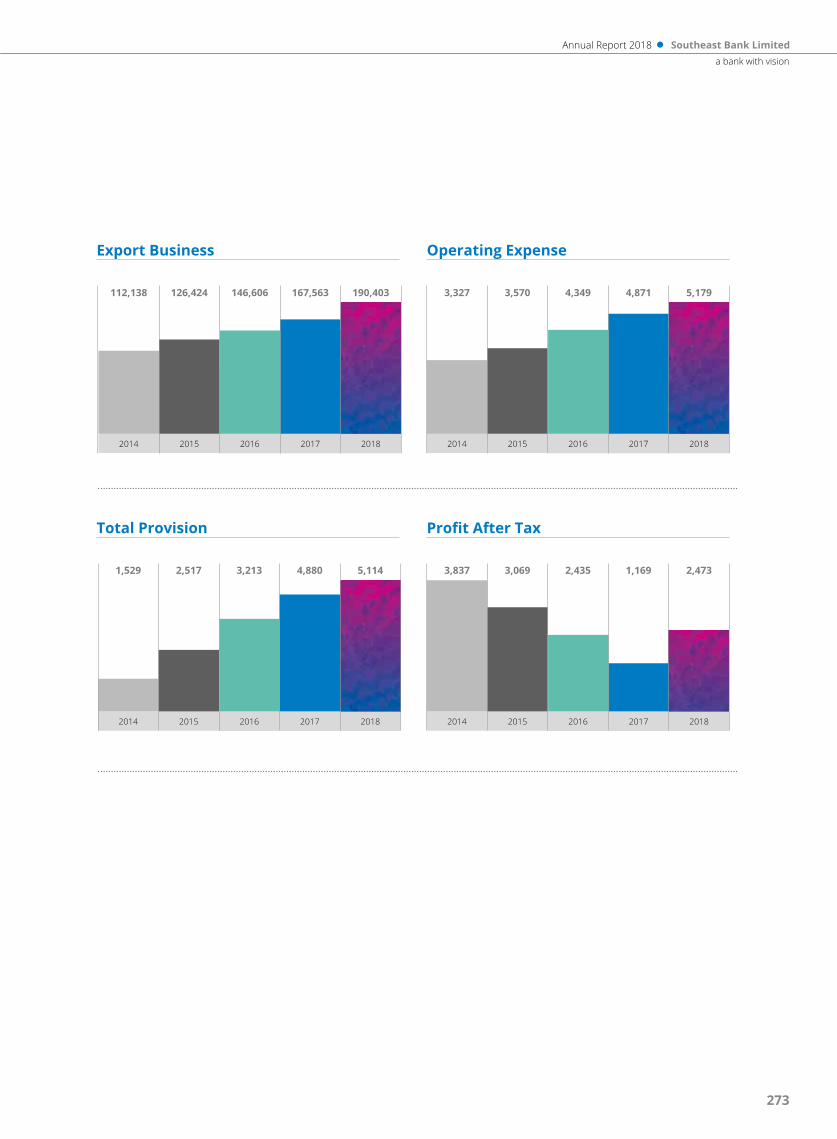

Bank’s total loans and advances portfolio increased by 14.23 percent to BDT 33,354.91 million in 2018, over BDT 234,316.72 million in 2017. Bank’s total asset increased by 12.46 percent to BDT 42,287.62 million in 2018, over BDT 339,288.05 million in 2017. The Bank’s total deposit increased by 10.56 percent to BDT 28,506.72 million in 2018, over BDT 269,828.08 million in 2017. During the year 2018, the Bank made an operating profit of BDT 9,783.00 million as against BDT 9,062.30 million in 2017.

There was increase of cost of fund (COF) and it reached 7.81 percent at year end. The total deposit of the Bank including Islamic Banking Deposits increased by 10.56 percent over that of last year. It led to a healthy Loan to Deposit Ratio of 81.55 percent. The net interest margin of the Bank reached 3.81 percent at the end of 2018. The Bank was able to increase Net Interest Income to BDT 5,199.94 million in 2018 from BDT 4,027.69 million in 2017. Fees and other income during the year 2018 had a good growth of 6.86 percent over that of 2017. The good contribution of Fees and other income to Bank’s total income is a clear testimony of Bank’s strength. We are looking forward to building better and innovative processes and structures to gain a competitive advantage for brighter business result in the coming days.

2. Governance and Transparency

One of the basic policies of Southeast Bank Limited is to strengthen its corporate governance status by practicing efficient corporate governance and compliance processes through meeting all regulatory requirements. We have established ourselves as one of the most compliant banks in the industry by establishing responsible management

system and strengthening supervision. The prime objective of Bank’s Corporate Governance system is to enhance stakeholders’ value by pursuing responsible and ethical practices of business and upholding high standard of disclosure and transparency.

Our Annual Report contains adequate disclosures reflecting compliance of all applicable Accounting Standards. In recognition, over the past few years Southeast Bank received a number of awards from distinguished institutions on corporate governance and quality of disclosure and transparency reflected in the Annual Report. An elaborate report on Corporate Governance of the Bank in 2018 is included in this Annual Report.

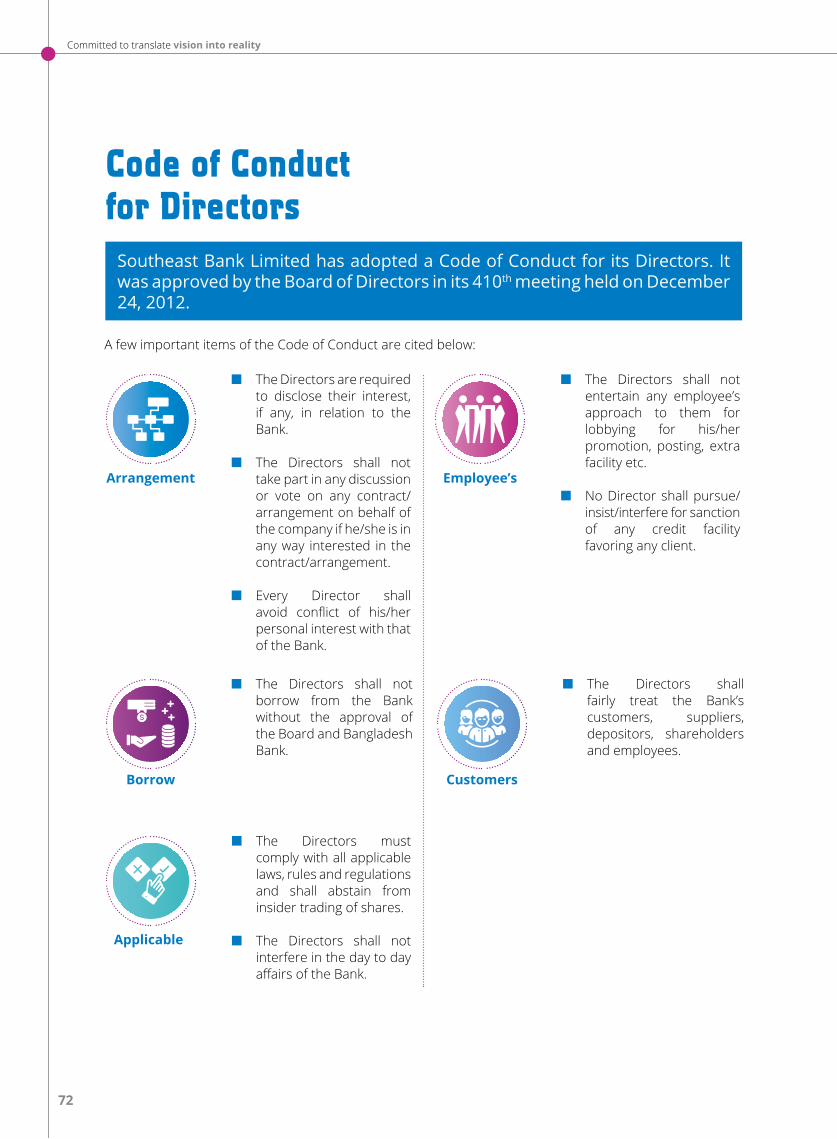

3. Code of Conduct of Directors

The Board of Directors of the Bank in its 410th meeting held on December 24, 2012, inter alia approved, the Code of Conduct for the Directors of the Bank. The Directors are sincere in abiding by the Code of Conduct. There had not been any breach of the Code of Conduct by any Director of the Bank. The Directors are regularly apprised of the relevant guidelines given by the regulatory authorities so that they can discharge their responsibilities effectively and efficiently.

4. Customers - Our Partners of Progress

Our first and the highest priority is to provide quick and effective services and maximum satisfaction to the customers and we always work for new and better ways to serve them. This ideology is widely practiced in the Bank.

Our customers need a trustworthy partner and that we are. As a partner of progress, we provide them financial flexibility and service diversity. With our profound understanding of the business and needs of our customers and the challenges being faced by them, we focus on delivering highly customized products and services. Southeast Bank has become a synonym of quality banking services and products. It has a diverse array of products and services tailored carefully to cater to the needs of all segments of customers in the industry through a fair deal. We always emphasize on long term ethical customer relationship considering high productivity through professional team work, creativity and customer-focused marketing.

Our operational strategies are structured with intelligent planning to address the special and

23

Annual Report 2018 Southeast Bank Limiteda bank with vision

often complex needs of the customers. It is our ongoing endeavor to understand the unique requirements of our customers and to cater to these requirements to the best of our abilities. We regularly carry out required research, analysis and survey to find out what the customers expect. We obtain meaningful and actionable feedback from customers and use it to improve our services and exceed the expectations of our customers by offering new products and technology-based support. Our customers increasingly want solutions rather than products.

The Bank has also developed and implemented AML and CFT compliance policy. Under the policy, customer due diligence is being done, transactions of clients are being monitored, reporting to regulatory authority is being made, sanction lists are being screened while allowing any transaction and utmost care is being exercised in case of handling walk-in and unknown customers. We have also successfully introduced a ‘Customer Charter’ in line with the guidelines of the Bangladesh Bank. We spend money on things that matter to them and add value to the Bank in terms of image and profit.

5. Risk Management

Recognizing the crucial role of risk management for sustainable growth, the Bank has developed necessary systems and processes for assessment and management of all potential strategic and operational risks in the light of Bangladesh Bank’s Risk Management Guidelines.

Southeast Bank builds its approach to risk management on the concept of three lines of defence, signifying a clear division of responsibilities between the risk owners and control functions. Strategically, Board of Directors, through the Board Risk Management Committee and the senior management team, sets up risk governance structure and risk philosophy, endorses risk strategies and reviews and approves risk policies as well as the risk threshold in line with the bank’s risk appetite. These limits are continuously monitored by an experienced risk management team and overseen by Board Risk Management Committee. The Risk Management Committee of the Board reviews and monitors the overall risk management system of the Bank and reports to the Board from time to time. The risk management system of SEBL has been described in “Risk Management Report” section of this annual report.

6. Internal Control System

The Bank management is held responsible for putting in place a sound system of internal controls to safeguard stakeholders’ interest. Board of Directors of Southeast Bank Limited has the ultimate responsibility to make significant policies to ensure compliance at all levels in the bank’s day-to-day activities. The Audit Committee of the Bank reviews on regular basis adequacy and effectiveness of the system of internal controls in compliance with the guidelines of Regulatory Authorities. The Internal Control & Compliance Division (ICCD) has been organized in line with the guidelines of the regulatory Authority. It reports directly to the Audit Committee and ensures compliance of all internal control systems and procedures and directives given by the Audit Committee and the Board of Directors.

There is maker and checker concept with due areas of accountability for each and every transaction and segment of work in the Bank. The internal control system is designed to meet the purposes of completeness, accuracy, reliability of financial transactions, justification and reasonableness of Bank’s operational aspects.

7. Credit Policy of SEBL

Southeast Bank has a comprehensive credit policy encompassing both Conventional and Islamic banking modes of lending. It comprises clearly stated universal and basic operating concepts, policies and standards for credit operations in accordance with bank’s business objectives and rules of conduct of credit in line with the guidelines of Bangladesh Bank. We promote understanding of and strict adherence to our credit policy among all our concerned employees. Our assessment for corporate loan or investment involves varieties of financial analyses including cash flow to predict an enterprise’s capability of loan or investment repayment and its prospect. While assessing credit worthiness, we focus on a number of principles considering qualitative and quantitative judgment including, but not limited to, borrowers’ background and character, risk factors, purpose of the credit or investment facility, tenor of the Bank’s exposure, security offered, business segment scenario, pricing, national policy etc. While approving a loan or investment, we try to ensure that our power of sanctioning a loan or investment does never over-power our fair judgment. The credit policy

24

Committed to translate vision into reality

focuses on inclusive and productive use of credit with distinct attention to adequacy of credit flows to agriculture, SMEs, Women entrepreneurship and we are also keen to move fast for green banking to protect environment. The total volume credit grew by 14.23% at the end of the year 2018.

8. Our Unique Advantage: Our Human Capital

Southeast Bank Limited has always pursued a balanced Human Resource policy. We facilitate greater engagement and reap all the competitive advantage that a productive and skillful manpower provides. We continue to strengthen our workforce management practices. Our people are undoubtedly the core asset of our bank and we acknowledge their hard work and dedication in elevating our bank to where it is today. We are always conscious of the importance of retaining and attracting the best talents. Our human resource management policies are designed on the principles of care, capacity building, knowledge sharing and fairness. Besides hiring best resource on purely merit basis, performance of every staff member is evaluated on a uniform benchmark to help promote a culture of merit and fairplay in the organization.

We provide useful behavioral framework for resolution of dilemma that our employees individually encounter while doing their everyday activities. We help them make responsible and consistent professional decisions selflessly. We provide a competitive compensation and incentive package to motivate our employees. The employees are provided with adequate opportunities for their professional development at home and abroad.

9. Calibrating our Strategic Path for the years to come

We have navigated in the banking sector of Bangladesh for the last 24 years. As we step into the realms of 2019, we are shaping our strategies to better suit the changing economic and financial market scenario and taking pragmatic steps to accelerate growth. We are well-positioned on a firm platform to progress further in our chosen areas of operations. Over the years, we have built up a strong foundation for the future to deliver a leading performance and competitive returns that our shareholders want to see. Our success truly portrays that we keep a watchful eye and analyze our strengths and weaknesses to meet the emerging

challenges to our business operations and also grab the opportunities as and when they arise. We are committed to embrace technological change and innovations to further develop attractive value propositions to our clients. We will continue to strive to improve further our operational efficiency with the main focus on creating wealth for shareholders.

10. Adding to our list of Accolades and Achievements: Symbol of Inspiration

Southeast Bank greatly weighs good corporate governance and operational excellence. These are our fundamental requirements in our aspiration to remain a leading banking institution in our country. We do have strategy, intent and ability to take the Bank forward further. In recognition, The Institute of Chartered Secretaries of Bangladesh (ICSB) awarded our Bank Second Position (Silver Award) for continuous commitment to Corporate Governance Excellence for the year 2017.

Southeast Bank Limited received Tax Card and Crest from National Board of Revenue (NBR), Ministry of Finance, Government of the People’s Republic of Bangladesh. Southeast Bank was given the country’s 4th highest Tax Payers Award in the Banking Institutions Category for the assessment year 2017-2018.

11. Caring about Our Communities for Societal Upliftment

We believe that a stable environment and a strong economy are correlated and preconditions for progress of the country. The Bank is closely related with the communities where it runs its business. We always extend our hands towards underprivileged groups of the society and consistently promote social and economic upliftment of the people at the hour of need. Our focus is on sports, arts & culture, education, and entrepreneurship and on identifying the links between them. We launched and contributed in different programs with the desire to generate more social impact through our activities. Our CSR goes far beyond charity and the engagements of our CSR are steadily increasing in depth and diversity both in expenditures, financial inclusion drives, greening the internal practices and processes, and in lending to environment friendly projects.

We acknowledge our social responsibility well and align our business strategies with our culture. SEBL

25

Annual Report 2018 Southeast Bank Limiteda bank with vision

is working towards improving the energy efficiency of its operations and optimizing the use of natural resources. Moreover, the Bank has created a Trust in association with The Financial Express and Policy Research Institute as part of its Corporate Social Responsibility (CSR) to create awareness in green retention and green business.

We created Southeast Bank Foundation to carry out CSR related activities in a most organized way. We are serving the society as part of our Corporate Social Responsibility (CSR) by giving stipends to poor and meritorious students, distributing warm clothes to winter-hit people and contributing to the different relief funds. In the year 2018, we spent BDT 208.53 million for activities related to CSR which is inclusive of the CSR expenditures incurred by Southeast Bank Foundation. During the year the Bank made significant donations to the Prime Minister’s Relief Fund for helping cold and flood hit people across the country including displaced Rohingyas, development of cultural activities, sponsoring Jubo games and so on.

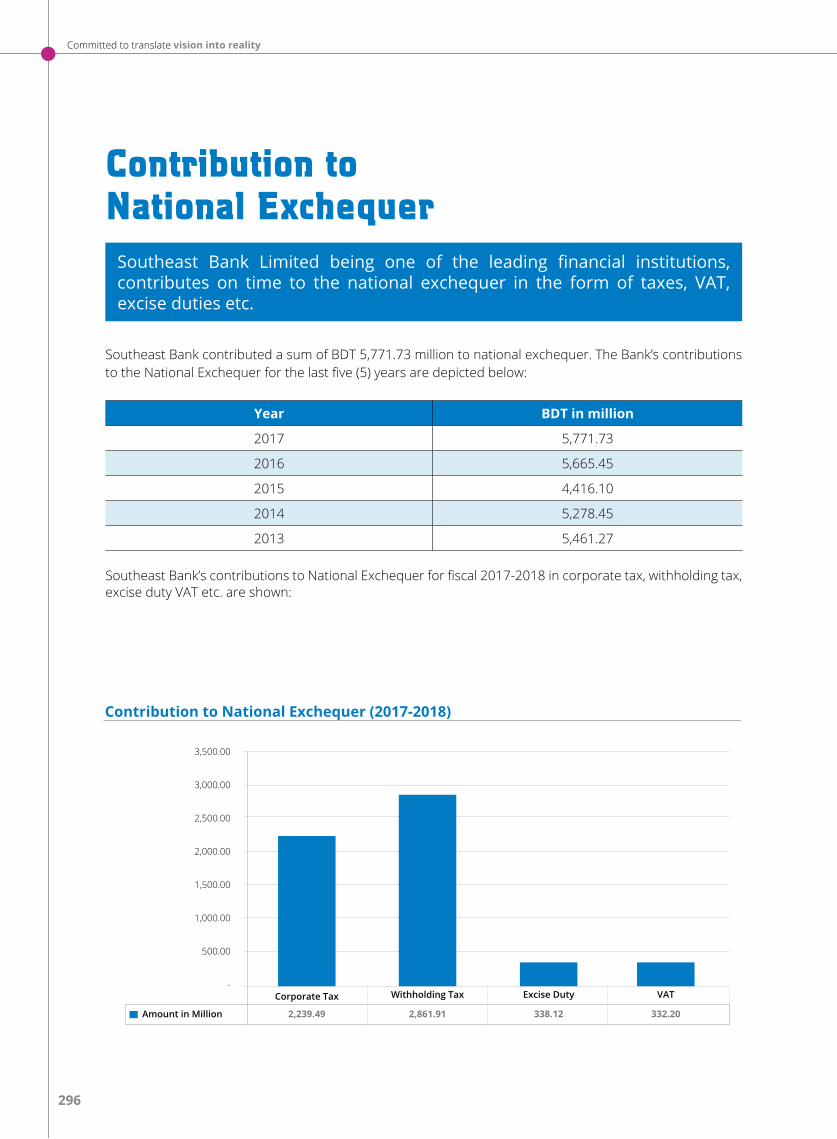

As a Bank born and bred in Bangladesh, we have also a deep commitment to the Country’s economic development and preservation of the environment. We believe our conscious choice of protecting the environment today will lead to a better and sustainable tomorrow. We are also one of the leading tax payers of the country. We contribute to the society by paying taxes to the national exchequer timely. During the year 2017-2018 we contributed an amount of BDT 5,771.73 million to the National Exchequer.

12. Acknowledge Our Stakeholders

I am thankful to the Almighty Allah for the business success of the Bank in 2018 amid competitive and challenging business environment. I also take the opportunity to thank the Directors of the Bank for their support and guidance during the year under review. Their collective wisdom substantially contributed to our success. I also thank our Management and the members of the staff under the leadership of the Managing Director for their loyalty, support and relentless efforts for Bank’s qualitative and quantitative improvements. I respect their zeal to work hard to reach newer heights of success. Our shareholders’ unflinching support and confidence are vital to the Bank’s continued growth and development. We thank them and pledge to maintain the Bank’s legacy.

I conclude by conveying my very sincere and special thanks to our valued customers, patrons, well wishers, the Government of the People’s Republic of Bangladesh, Bangladesh Bank, Registrar of Joint Stock Companies and Firms, the Bangladesh Securities and Exchange Commission, the Dhaka Stock Exchange Limited, the Chittagong Stock Exchange Limited and all others concerned for their unwavering support and co-operation.

I also look forward to their continued support, co-operation and guidance in the days ahead. I reiterate with firm commitment that we will remain disciplined, compliant and result-oriented in all our endeavors and in return seek their continued cooperation.

Finally, I thank the respected shareholders for attending the 24th Annual General Meeting and contributing significantly to the deliberations and adoption of resolutions against the agenda.

May the Almighty Allah bestow on us His infinite blessings.

Allah Hafiz.

Thank you once again for being with us.

With warm regards,

Alamgir Kabir, FCA Chairman

Committed to translate vision into reality

We are delighted to present the Bank’s operating results for 2018 which is the evidence of sustainable business growth of the bank. 2018 was a very challenging year for banks. By the grace of almighty Allah, Southeast Bank’s performance for the year remained stable with good momentum for growth. We have consolidated our position over the years through emphasis on effective execution of our strategies, sensible decision making, robust risk management framework and good governance practices. Our operating results are impressive and we expect the same momentum to continue in the days to come. Prudent direction and guidance of the Board of Directors and acumen and dedication of our experienced management team played a key role in our business performance.

Review from the office of the Managing Director

26

Annual Report 2018 Southeast Bank Limiteda bank with vision

M. Kamal HossainManaging Director

27

28

Committed to translate vision into reality

Economic Reflection

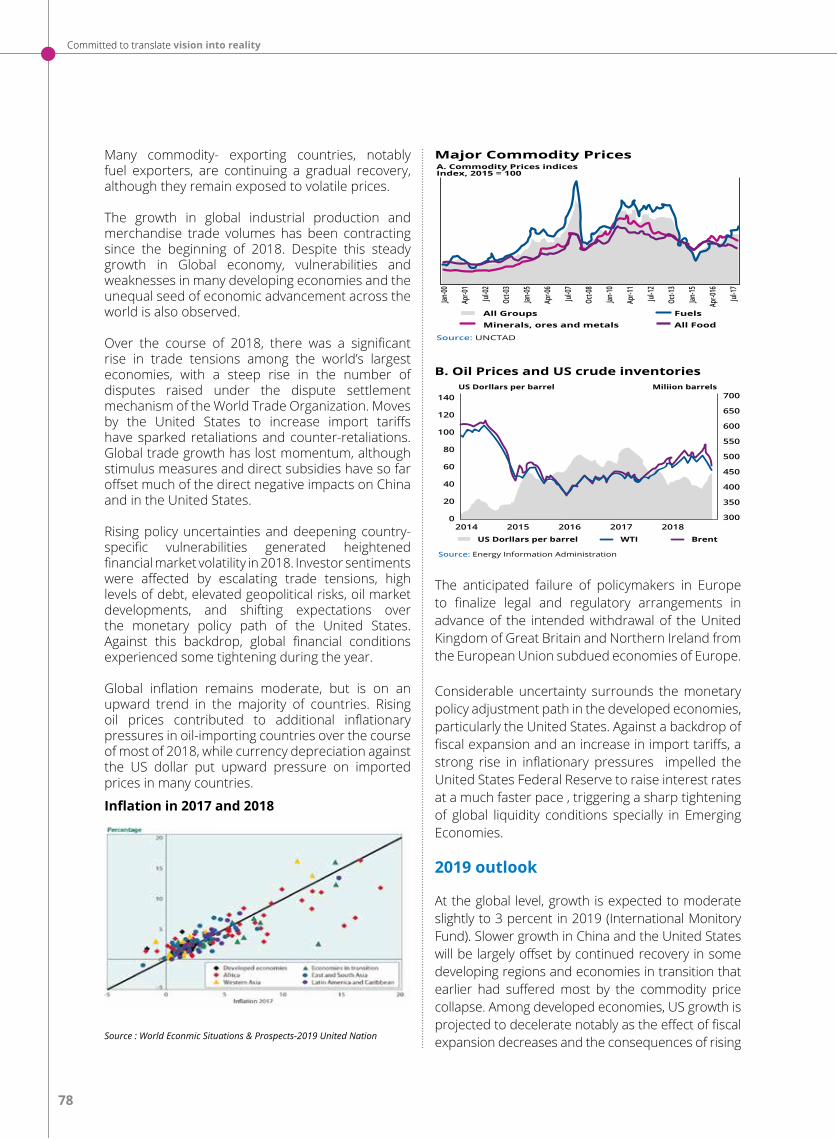

In 2018, the global economy recovered at a faster speed than expected, with the developed economies like USA, Europe and Japan growing well. China and India grew faster than the other emerging economies. Brazil, Russia and other emerging markets also remained on a faster growth track. The developed economies, typically the USA, tightened their monetary policies and a majority of the emerging markets remained stable despite somewhat loose monetary policies. Global economic growth improved during 2018 with expansion in both advanced and developing economies. Geopolitical developments in various regions might also affect the economy and financial markets through their impact on commodity prices, risk appetite and capital flows.

2018 was election year but Bangladesh’s economy continued to gain momentum, aided by decisive policy decisions taken by the Government of Bangladesh in the last few years. The accommodative monetary policy stance, increase in development spending, growth in private sector credit, easing energy supply, continuing work on infrastructure and energy projects and growth oriented policies were primarily instrumental in achieving the recent performance of the economy. The large-scale manufacturing growth picked up momentum and agriculture sector achieved its growth target mainly due to supportive policies and increased agriculture credit disbursements. Stable exchange rate and oil prices in local market during 2018 helped contain inflation at an expected level.

Bangladesh’s economic prospects for 2019 seem promising. Therefore, the GDP growth target of 7.80% for fiscal 2018-2019 appears attainable. Manufacturing sector is expected to benefit from higher development spending, improvement in political and security conditions and the trend of low cost of borrowings. To support the acceleration in the economy, banking sector of Bangladesh will need to keep pace with it.

Business and Achievements

Under the low interest rate regime, significant emphasis has been given on productivity improvements to improve overall efficiency. These actions, along with an overall control on costs, allowed the Bank to meet its business objectives.

Despite the challenging landscape, low interest rate and intense market competition, Southeast Bank managed to deliver on various key performance indicators. Some of those achievements are depicted below:

Southeast Bank achieved operating profit (before provisions and tax) of BDT 9,783.00 million for the year 2018 compared to last year’s BDT 9,062.30 million which is 7.95 percent higher than last year. Net profit after taxation reached BDT 2,473.21 million for 2018, a 116.63 percent rise over 1,168.63 million from last year. Earnings per share for 2018 is BDT 2.35 compared to BDT 1.11 of 2017.

Bank’s balance sheet increased by 12.46 percent over December 2017. The Bank added BDT 28,506.72 million to its deposits base in 2018. As such, total deposit base of the Bank reached BDT 298,334.79 million with 34.22 percent low cost deposit at the end of 2018.

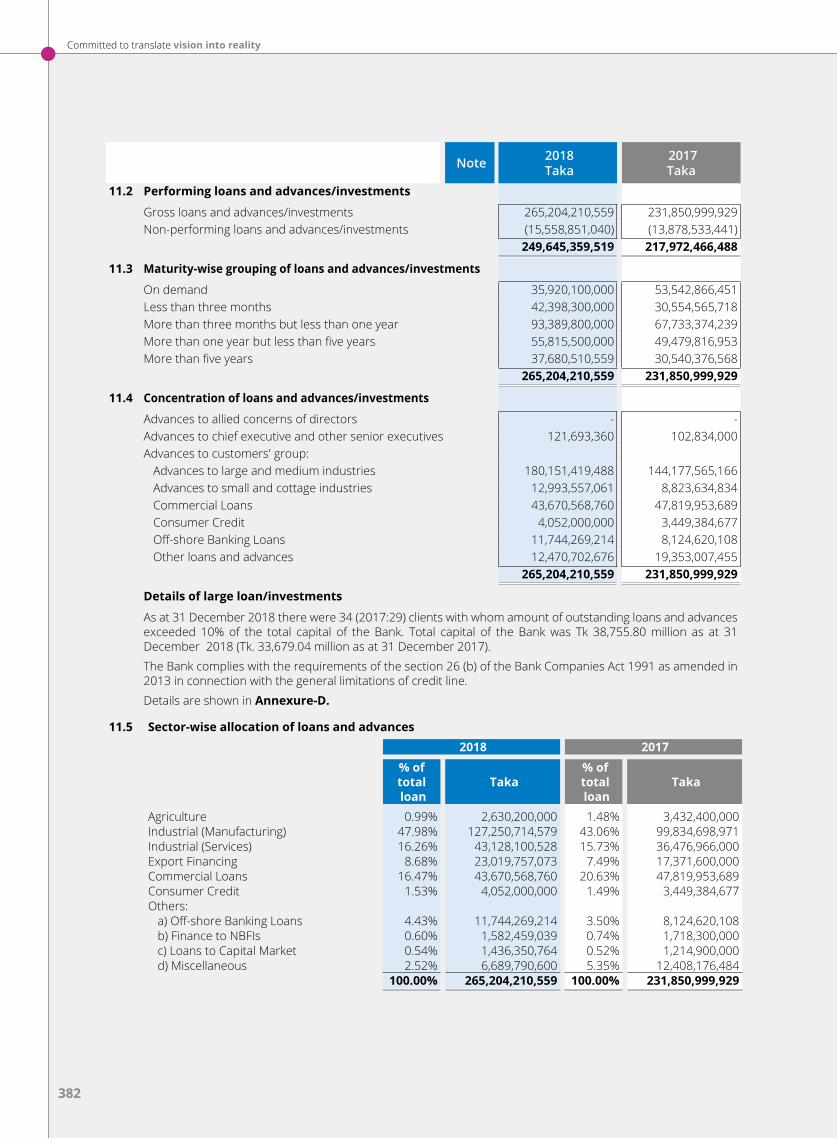

Bank’s aggregate loan portfolio grew by 14.23 percent during the year in an environment of low interest rates. As such total loan portfolio reached BDT 267,671.63 million at the end of the year. The Bank has continued to improve the credit portfolio mix towards retail, SME and higher rated corporate loans. The proportion of SME loans in the portfolio increased to 86.49 percent as on December 31, 2018.

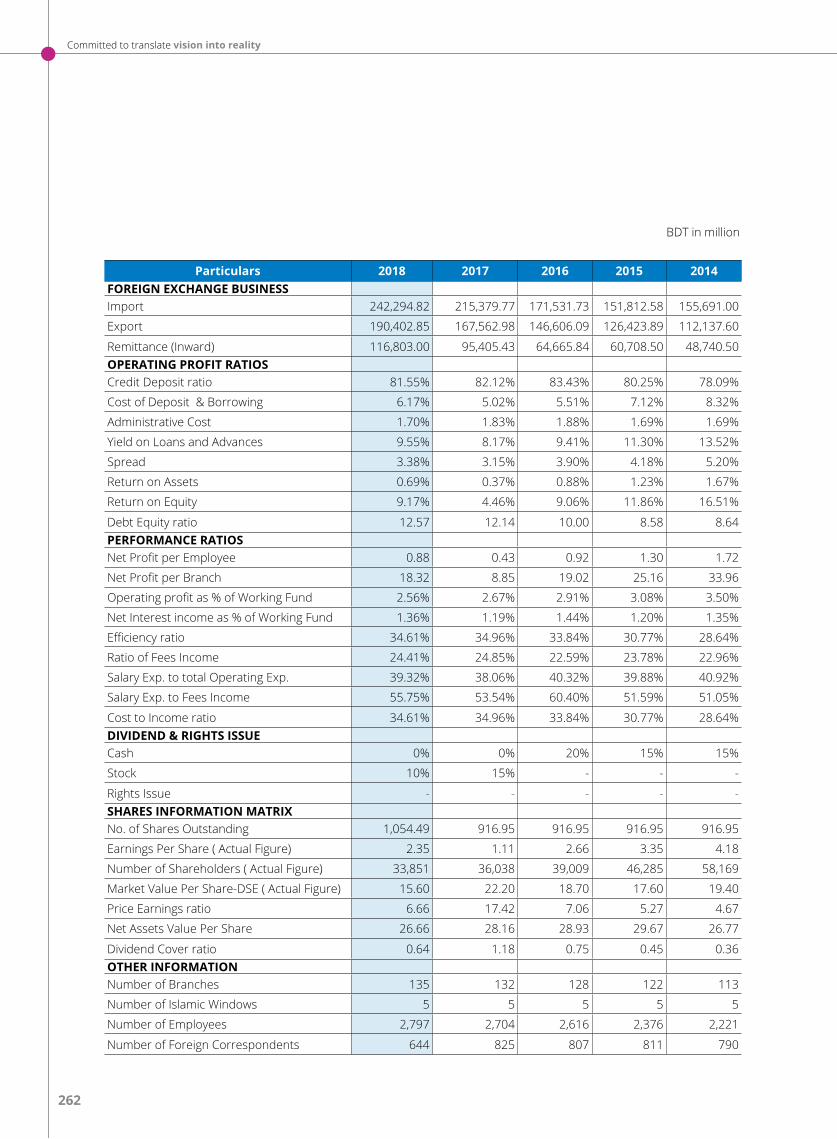

In 2018, total Import business grew by 12.50 percent to BDT 242,294.82 million and export business by 13.63 percent to BDT 190,402.80 million.

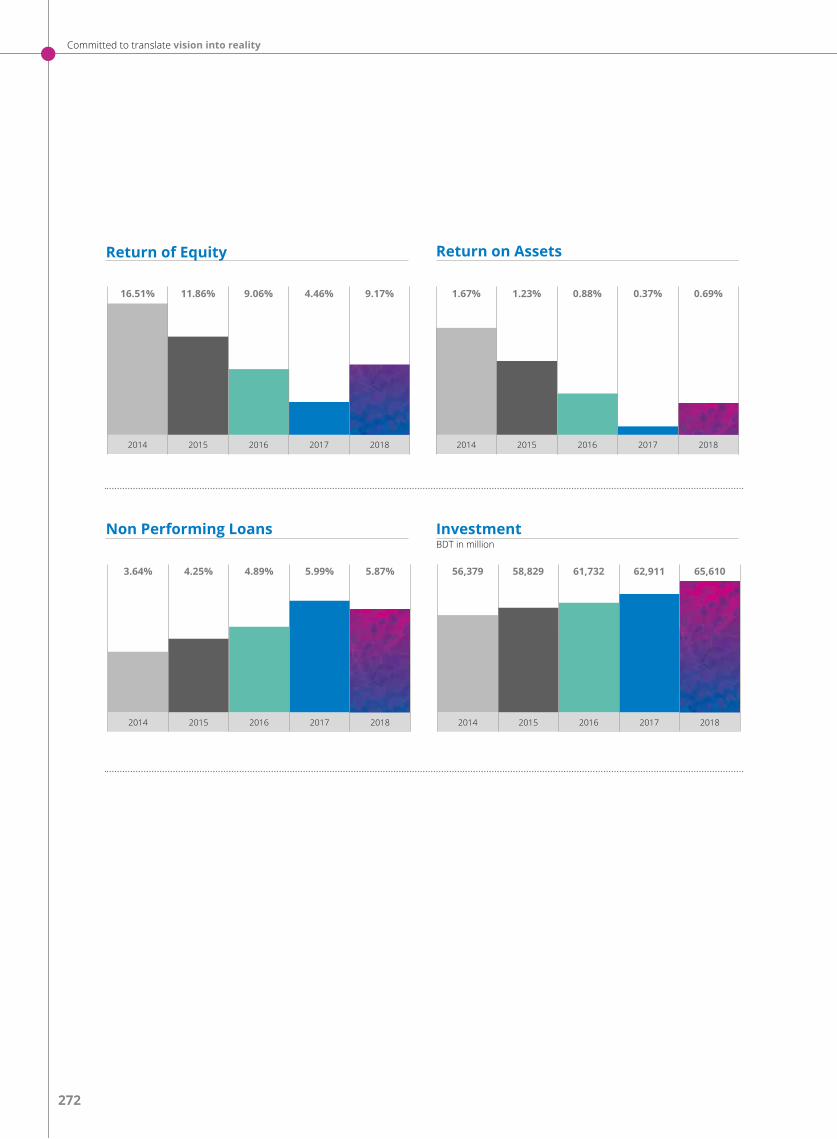

While loan growth was accelerated, we kept a sharp eye on portfolio quality. As a result, the Non-performing loan’s ratio reduced to 5.87 percent.

The Bank has added over almost 64,000 deposit customers to its base. Total deposit customer of our bank stood around at 700,000 at the end of the year.

The Bank has been able to increase its market share in the remittance business which grew from BDT 95,405.43 million as on December 31, 2017 to BDT116,803.00 million as on December 31, 2018.

29

Annual Report 2018 Southeast Bank Limiteda bank with vision

Asset Quality

Banking sector is reeling under bad loans and heavy provision burden. To a certain extent, we are also exposed to this problem. As on December 31, 2018 Southeast Bank reported Gross Non-Performing Loans (GNPLs) of BDT 15,558.85 million as against BDT 13,878.53 million as on December 31, 2017. Southeast Bank has taken multidimensional initiatives for reducing non-performing loans. We hope the process of resolution of the asset quality pressures and NPL issues is likely to witness substantial progress in the days ahead.

Core Assets

I would like to acknowledge the hard work and dedication of all members of Southeast Bank, who are undoubtedly the core asset of our bank. It is my utmost belief that committed and professional team is the main strategic advantage of Southeast Bank over its peers. The talents, passion and commitment of our people, The Southeast Family, has been the cornerstone of our sustained success over the years. We are fortunate to have a diverse group of qualified, trained and dedicated employees across Bangladesh.

Customer Centricity

Customer satisfaction is at the heart of our operations. With a thrust to achieve operational excellence, we continue to invest in our people so that we can collectively provide quality and reliable customer service efficiently with meticulous attention towards regulatory compliance.

Technological Progress

Technological leadership is an absolute must for the delivery of value to all our stakeholders amidst rapidly changing life styles and paradigms. Southeast Bank is committed to place cutting edge technology at the forefront of our delivery channels and operations. While driving technology to new heights, we must remain ever vigilant about information and cyber security. Southeast Bank makes continuous efforts to strengthen its ability to prevent, detect and respond to cyber-attacks by improving governance and leveraging technology advancements. In the process, recently, southeast Bank has further strengthened its security

system especially for online transaction through introduction of Two Factor Authentication (2FA), One Time Password (OTP) etc.

Network Building

Our branch footprint comprises of 135 branches with the addition of 03 new branches opened during 2018. Through our network of 113 conventional branches, 05 Islamic banking branches, 15 SME and Agri Branches, 02 Ladies Branches and 02 Off-shore Banking units, we reach our customers spread across the country. We also have a fast growing Alternative Delivery Channel (ADC) which extends the Bank’s reach beyond its branch network.

Capital Management

The Bank is taking all necessary steps to remain fully compliant with the Basel III transition plan, which includes raising the Capital to Risk-weighted Asset Ratio (CRAR) threshold by the end of 2018. Tier 1 common equity capital ratio exceeds the minimum requirement of Basel-III standards. As such the CRAR of the Bank stood at 12.38 percent as on December 31, 2018 which is well above the regulatory requirement of 11.875%.

Financial Attributes

The Bank always prepares consolidated financial statements of the Bank and its subsidiaries. Side by side, separate financial statements of the Bank is prepared in accordance with Bangladesh Financial Reporting Standards (BFRSs), the requirements of the Bank Companies Act, 1991, the rules and regulations issued by Bangladesh Bank (BB), the Companies Act, 1994, the Securities and Exchange Rules, 1987 and other applicable laws and regulations. Significant accounting policies and estimations detailing nature of the components of financial statements are adequately disclosed. Any significant changes, if made, are aptly addressed along with its impact in the financial statement in Section 3 of Notes to the Financial Statements.

Important financial indicators of current year are presented in comparison with performance of the bank in preceding five years. A thorough presentation comparing with prior years’ business performance has been shown in this report under segment ‘Stakeholders’ Information.

30

Committed to translate vision into reality

Looking Ahead

We remain hopeful that stable political environment and the Government multidimensional approach to accelerate economic growth will help create congenial environment for business growth in years ahead.

The environment in which we operate is evolving rapidly and we remain prepared to navigate the challenges and capitalize on the opportunities. The environment of low interest rates and resulting compression on banking spread is likely to continue in the foreseeable future, however industry driven loan growth, along with an off-take in export led manufacturing and private sector credit will present opportunities for which Southeast Bank is well positioned.

In the light of the outlook for the Banking Sector in general, our Bank will be focusing on NPL reduction and to improve efficiency and productivity. Bank is poised to improve the fundamentals and post strong results in 2019.

Strategies

In 2018, the Bank continued to focus on its strategic priorities of improving the portfolio quality and taming down non-performing loans. Within portfolio quality, the emphasis was on improving the portfolio mix with a focus on retail and SME lending, lending to higher rated corporate, resolution of stressed borrowers and proactive monitoring of loan portfolios across businesses. In 2019, the Bank would aim at risk calibrated profitable growth through focusing on the following areas:

The Bank would focus on sustaining its robust deposit base and increasing the proportion of low cost deposits.

The priority would be on growing the retail, SME and higher rated corporate portfolio with a focus on enhancing the customer franchise.

The bank would maintain strong Credit Monitoring with a view to arresting fresh slippage of any loan.

Recovery against Non-performing loans especially rescheduled, classified and written-off loans would be strengthened to further consolidate the credit portfolio.

The Bank would continue to invest in technology and preserve its digital leadership by offering best in class digital products to customers and automating internal processes to increase efficiency.

The Bank would maintain a strong capital position with a view to maintaining strong Capital to Risk-weighted Asset Ratio.

The Bank would leverage all capabilities to be the trusted partner in serving the customers and become the banker of choice.

Note of Thanks

I take this opportunity to thank the members of the Board and Bangladesh Bank for their valuable support and guidance as the Bank continues to face challenging times. I am thankful to our investors for the trust that they have placed in the Bank. The excellent results for 2018 would not have been possible without the loyalty of our customers who have continued to build stronger relationships and patronize our products and service offerings. On behalf of the Bank, I express my appreciation to all our customers and most importantly I would like to acknowledge our employees whose painstaking commitment, hard work and dedication has enabled successful delivery of our promise to all our stakeholders. It is the support and encouragement of all our stakeholders that enhances our strength and helps us stay focused on our goal.

M. Kamal HossainManaging Director

31

Annual Report 2018 Southeast Bank Limiteda bank with vision

IntegratedReporting

The Bank through its pragmatic operation and ethical banking has embedded the idea of integrated thinking in its overall strategic attributes. The very aspect of sustainable growth has evolved in the entity’s outlook. Therefore, the bank takes pride in integrating social and environmental growth in the overall business operation to achieve both social and corporate goals.

Scope and Boundary of the Report

The Integrated Report covers the period from January 01, 2018 to December 31, 2018. This report aims to provide a transparent and balanced appraisal of the material issues that faced our business during the year under review and that impacted our ongoing ability to create value. The Financial information regarding sustainable value addition has been presented in respective segments along with independent audit reports and evaluation. Non-financial issues and information regarding the bank had been demonstrated throughout the report in different segments narrated as Non-financial indicators, Sustainability Report, Director’s Report, etc. During preparation of the report there had been no material change in the reporting of financial and non-financial issues regarding the bank.

We have prepared and presented financial statements and other reports in compliance with the requirements of

Bank Company Act, 1991 (Amended upto 2018)

Bangladesh Bank Regulations

The Companies Act 1994

Bangladesh Accounting Standards

Bangladesh Financial Reporting Standards (BFRS)

Financial Institutions Act 1993

Securities and Exchange Rules 1987

The Income Tax Ordinance, 1984

And other applicable laws and regulations of the bank

Materiality

Southeast Bank Limited has always been vigilant in addressing the material issues which have substantial impact on the strategic direction and operation of our business. Several non-financial parameters and our performance in the relevant parameters were disclosed considering their materiality in decision making and formulation of strategic directions. Environmental obligation and financial inclusion having substantial material impacts were prioritized through disclosure of explicit steps taken by the bank.

An integrated report is a concise communication about how an organization’s strategy, governance, performance and prospects, in the context of its external environment, lead to the creation of value in the short, medium and long term. Modern business world has embraced this form of reporting as a part of its responsible and proactive sense of communicating with its stakeholders. Southeast Bank Limited has already transformed its integrated thinking into a set of disclosures termed as Integrated Report. The Bank has always been proactive in its strategies in the form of taking into account the integrated thinking in business ideology and value creation. The Bank does believe in dealing with our clientele with the best practice of responsible banking along with the idea of creating sustainable value for all the stakeholders.

32

Committed to translate vision into reality

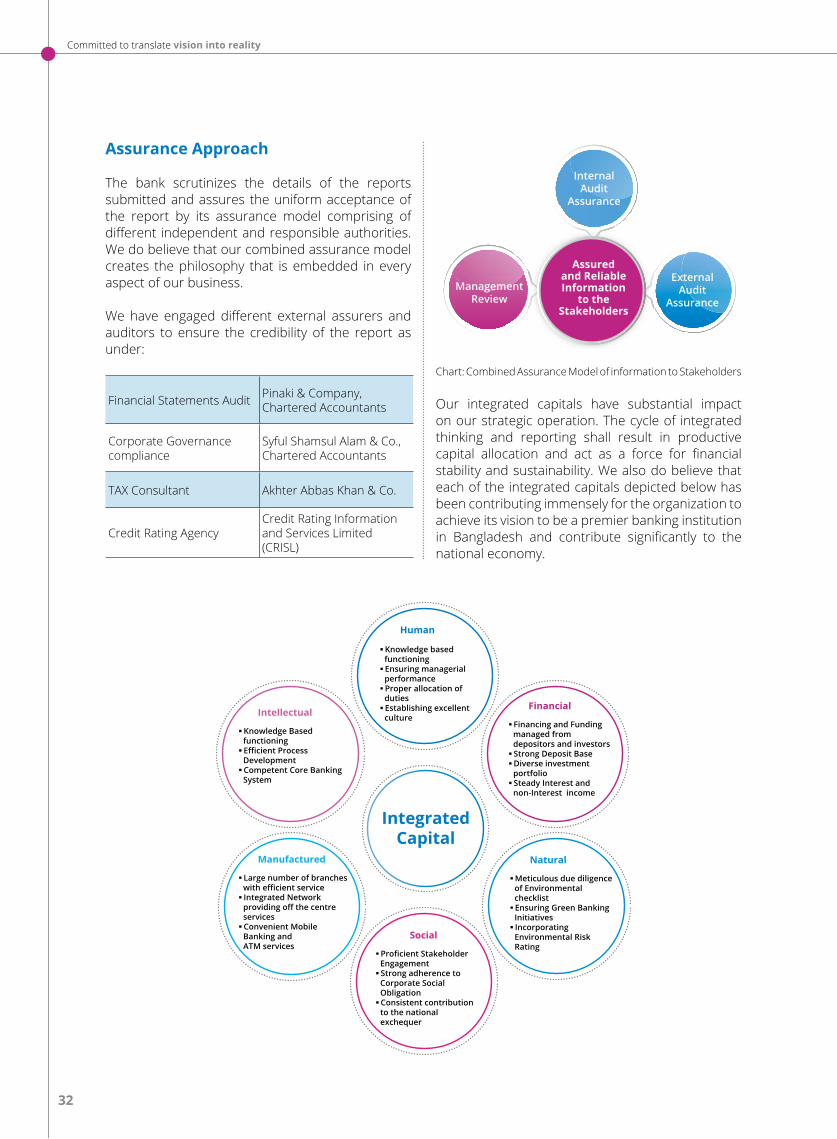

Assurance Approach

The bank scrutinizes the details of the reports submitted and assures the uniform acceptance of the report by its assurance model comprising of different independent and responsible authorities. We do believe that our combined assurance model creates the philosophy that is embedded in every aspect of our business.

We have engaged different external assurers and auditors to ensure the credibility of the report as under:

Financial Statements Audit Pinaki & Company, Chartered Accountants

Corporate Governance compliance

Syful Shamsul Alam & Co., Chartered Accountants

TAX Consultant Akhter Abbas Khan & Co.

Credit Rating AgencyCredit Rating Information and Services Limited (CRISL)

Management Review

External Audit

Assurance

InternalAudit

Assurance

Assuredand Reliable Information

to the Stakeholders

Chart: Combined Assurance Model of information to Stakeholders

Our integrated capitals have substantial impact on our strategic operation. The cycle of integrated thinking and reporting shall result in productive capital allocation and act as a force for financial stability and sustainability. We also do believe that each of the integrated capitals depicted below has been contributing immensely for the organization to achieve its vision to be a premier banking institution in Bangladesh and contribute significantly to the national economy.

Knowledge based functioning Ensuring managerial

performance Proper allocation of

duties Establishing excellent

culture Financing and Funding

managed from depositors and investors Strong Deposit Base Diverse investment

portfolio Steady Interest and

non-Interest income

Financial

Meticulous due diligence of Environmental checklist Ensuring Green Banking

Initiatives Incorporating

Environmental Risk Rating

Natural

Proficient Stakeholder Engagement Strong adherence to

Corporate Social Obligation Consistent contribution

to the national exchequer

Social

Large number of branches with efficient service Integrated Network

providing off the centre services Convenient Mobile

Banking and ATM services

Manufactured

Knowledge Based functioning Efficient Process

Development Competent Core Banking

System

Intellectual

IntegratedCapital

Human

33

Annual Report 2018 Southeast Bank Limiteda bank with vision

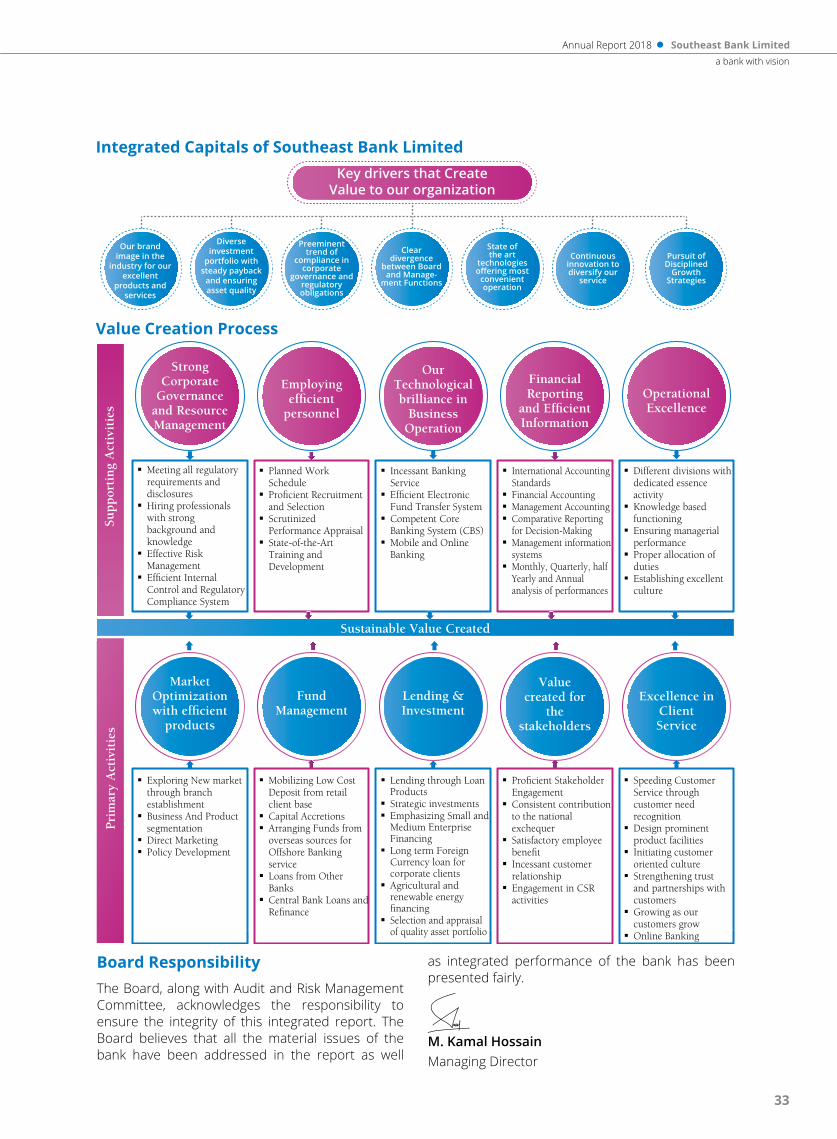

Integrated Capitals of Southeast Bank Limited

Value Creation Process

Our brand image in the

industry for our excellent

products and services

Diverse investment

portfolio with steady payback

and ensuring asset quality

Preeminent trend of

compliance in corporate

governance and regulatory obligations

Clear divergence

between Board and Manage-

ment Functions

State ofthe art

technologies offering most

convenient operation

Continuous innovation to diversify our

service

Pursuit of Disciplined

Growth Strategies

Key drivers that CreateValue to our organization

Pri

mar

y A

ctiv

itie

s

Sustainable Value Created

Sup

por

tin

g A

ctiv

itie

s

Our Technological brilliance in

Business Operation

Financial Reporting

and Efficient Information

Operational Excellence

Employing efficient

personnel

Market Optimization with efficient

products

Lending & Investment

Value created for

the stakeholders

Excellence in Client Service

Fund Management

� Meeting all regulatory requirements and disclosures

� Hiring professionals with strong background and knowledge

� Effective Risk Management

� Efficient Internal Control and Regulatory Compliance System

� Planned Work Schedule

� Proficient Recruitment and Selection

� Scrutinized Performance Appraisal

� State-of-the-Art Training and Development

� Incessant Banking Service

� Efficient Electronic Fund Transfer System

� Competent Core Banking System (CBS)

� Mobile and Online Banking

� International Accounting Standards

� Financial Accounting� Management Accounting� Comparative Reporting

for Decision-Making� Management information

systems� Monthly, Quarterly, half

Yearly and Annual analysis of performances

� Different divisions with dedicated essence activity

� Knowledge based functioning

� Ensuring managerial performance

� Proper allocation of duties

� Establishing excellent culture

� Exploring New market through branch establishment

� Business And Product segmentation

� Direct Marketing� Policy Development

� Mobilizing Low Cost Deposit from retail client base

� Capital Accretions� Arranging Funds from

overseas sources for Offshore Banking service

� Loans from Other Banks

� Central Bank Loans and Refinance

� Lending through Loan Products

� Strategic investments� Emphasizing Small and

Medium Enterprise Financing

� Long term Foreign Currency loan for corporate clients

� Agricultural and renewable energy financing

� Selection and appraisal of quality asset portfolio

� Proficient Stakeholder Engagement

� Consistent contribution to the national exchequer

� Satisfactory employee benefit

� Incessant customer relationship

� Engagement in CSR activities

� Speeding Customer Service through customer need recognition

� Design prominent product facilities

� Initiating customer oriented culture

� Strengthening trust and partnerships with

customers� Growing as our

customers grow� Online Banking

StrongCorporate

Governanceand Resource Management

Board ResponsibilityThe Board, along with Audit and Risk Management Committee, acknowledges the responsibility to ensure the integrity of this integrated report. The Board believes that all the material issues of the bank have been addressed in the report as well

as integrated performance of the bank has been presented fairly.

M. Kamal HossainManaging Director

34

Committed to translate vision into reality

Corporate Philosophyand Business Model

CUSTOMERS

Our company philosophy is simple. It is customer-friendly and fully responsive to customer needs and expectations. We carry out required research, analysis and survey to find out what the customers expect. We leverage technology and expertise to provide the best services and convenience to the customers. We spend money on things that matter to them and add value to the Bank in terms of image and profit. That is why our customer-base has been steadily expanding over the years.

HUMAN RESOURCE

Our people are smart, professional, well-qualified, energetic and sincere. They are passionate about what they do. Since they enjoy their work, it becomes easy for them to work hard. They do not follow any set model, rather they create models. They completely own what they plan and do. They have a longing to be significant. So, they are a part of something noble and purposeful.

COMMUNICATION

Our philosophy is to reduce lines and layers of communication. We believe in free flow of ideas within the Management Team. The Senior Management Team is also open to ideas suggested by the lower level executives and officers. At the same time, our decision making process is short but quick.

CONTROL MECHANISM

Our control mechanism is practiced at all levels. We strive to control the behavior of the employees. Our control mechanism is closely linked to efficiency, quality, innovation and responsiveness to customers.

QUALITY AND PRODUCTIVITY

Our philosophy is geared towards boosting productivity and maintaining a reliable high quality service standard. In the process of delivery of service, co-ordination is the essence of our business. Our philosophy is to achieve our goals through a combination of budgetary control, pay for performance, incentive system, unique corporate culture etc. It continuously stresses key values.

SUCCESS

Our people work hard to succeed. Success is a good fortune. It comes from their aspiration, desperation, perspiration and inspiration. As our people do more, they earn more and get more.

BUILDING FUTURE

Our philosophy is to make decisions today to improve performance tomorrow. We know a company which is successful has to continue to be successful. We do not fear our future, we shape it by our corporate conduct. Our hope is far greater than our fear.

Our corporate philosophy centers around our corporate missions, business domain and management goals. We devote our talent and technology to the creation of value for our stakeholders. Everyday our people bring this philosophy to life and to their work. Our philosophy cannot be bound by a few words or issues. Yet we narrate the followings:

35

Annual Report 2018 Southeast Bank Limiteda bank with vision

Business Model Canvas of Southeast Bank Limited

Key Partners

Customers Shareholders Employees Regulators Strategic Partners

Key Activities

Deposit Services Lending International Trade Services Remittance Service Treasury Solutions Islamic Banking Service Off-shore Banking

Key Resources

Highly Professional & Experienced Board Nationwide Network Worldwide Correspondent Network Highly Skilled Staff Dedicated Service Attitude Wide Range of Products Strong IT architecture Strong Capital Base

Cost Structure

Interest Expense Operating Expense Capital Expenditure

Revenue Streams

Interest Income Investment Income Fees, Commission etc. Other Operating Income

Customer Segments

KYC – Know Your Customer Personal Visit Phone Call/ Email/ SMS Automated Services Special Campaign In-depth Analysis Individual Solution Continual Review Research & Development Receiving Feedback

Delivery Channels

Branches ATMs Internet Banking Mobile Banking Call Center Subsidiary Companies

Customer Segments

Corporate Clients Small & Medium Enterprises Non-Banking Financial Institutions Banks Individuals/ Retail Clients Institutional Clients Govt. & Non-Govt. Organizations

Value Proposition

Complete Solution of Business Needs One Stop Service for Personal Banking Innovative Tailor-made Products Timely, Cost-effective & Superior Services Geographically Well-spread Availability

36

Committed to translate vision into reality

37

Annual Report 2018 Southeast Bank Limiteda bank with vision

Vision

To be a premier banking institution in Bangladesh and contribute significantly to the national economy.

Mission Statements

High quality financial services with state of the art technology.

Customer Service Excellence / Prompt Customer Service.

Sustainable growth strategy.

High ethical standards in business.

Steady return on shareholders’ equity.

Innovative banking at a competitive price.

Attraction and retention of quality human resource.

Commitment to Corporate Social Responsibility

38

Committed to translate vision into reality

StrategicObjectives

Priorities followedin 2018

a) Maintaining a high quality assets portfolio to achieve strong and sustainable returns and to continuously build shareholders’ value.

b) Maintaining adequate capital in line with risk appetite of the Bank.

c) Strengthening trust and partnerships with customers by focusing on the Bank’s core values of quality customer service, professionalism, teamwork and integrity.

d) Hiring professionals with strong background and knowledge.

e) Strengthening technologies that reduce operational risks and promote the implementation of best practices in the industry.

f) Developing innovative products and services that attract our targeted customers and market segments.

g) Exploring new avenues for growth and profitability.

h) Practicing efficient risk management principles in line with all six core risks in banking

operation, green banking and environmental risk management.

i) Practicing efficient corporate governance and compliance processes through meeting all regulatory requirements and disclosures in line with national and international best practices by ensuring best internal control monitoring practices.

j) Upholding Bank’s brand image as a customer friendly bank through efficient and prompt customer service, product diversification with a view to establishing a long term profitable relationship with our customers.

k) Serving the society as part of our Corporate Social Responsibility (CSR) by giving stipends to poor students, distributing warm clothes to winter-hit people, providing financial assistance to disadvantaged people and contributing to different relief funds. We also contribute to the society by paying taxes to the national exchequer timely.

l) Extending banking services to the un-banked people for financial inclusion for meeting socio-economic requirements.

The Bank had the following plans and road-map for business success in 2018.

i) Excellence in banking operations through maintaining strong fundamentals of Capital Adequacy, Business Diversification and Exploring Non-Funded Business

ii) Prudent Asset Management

iii) Prudent Liability Management

iv) Excellence in Delivering Customer Service

v) Effective Risk Management

vi) Effective IT Framework and System

vii) Efficient Internal Control and Regulatory Compliance System

viii) Strong Human Resource Base

ix) Going green in the future of banking

39

Annual Report 2018 Southeast Bank Limiteda bank with vision

Strategic priorities- Growth in areas of strength

Sustainable revenue growth comes from our ability to build relationships with our customers, and creating niche markets. We do this by providing our customers with exceptional service.

Diversification and increasing loan clients and maintaining quality assets

Export expansion and diversification Promoting Islamic banking through conventional

branches Emphasizing Small and Medium Enterprises

financing. Agricultural & Rural Credit through Micro

Financial Institutions Sustainable financing for Energy efficiency and

renewable energy projects Arranging funds from overseas sources for Off-

shore banking service and long term foreign currency loans for corporate clients.

Integrated marketing development initiative by creation of customer oriented culture

Remittance as a source of foreign currency

Strategic priorities - Resilience and flexibility

SEBL is committed to consolidate its solid capital base to support the risks associated with our diversified businesses, while still providing investors with superior returns. We actively manage our capital to support the execution of our business strategies. Our goal is to achieve the lowest cost of capital by managing its mix and by building our base through earnings and selective capital issues.

expediting borrowers’ rating,

concentrating on lending portfolio having lower capital charge,

strengthening internal Capital adequacy assessment process (ICAP)

Preemptive preparation for Basel –III compliance

StrategicPriorities

SEBL will keep on growing as a leading Bank of Bangladesh, in spite of existence of external challenges: first because we have a farsighted Board, vibrant management and an enthusiastic & skilled group of employee base that is committed to working together to provide our customers with excellent service; second, because we are building on a solid foundation of key strengths, including a strong capital base, and excellent risk and cost management skills; third, because we are strategically diversifying our business lines, products and locations; and finally, because we have a clear focus on our strategy and where we need to direct our efforts. Our strategic focus– is built around a few key priorities that will guide our actions as we move forward over the next several years. They will serve as a roadmap to help us navigate through the new landscape in which we are now operating. Sustainable revenue growth, capital management, leadership, prudent risk & appetite management, efficiency & expense management – will be the pillars of our strategy in upcoming years. They will play a critical role in our success and, given the ongoing market uncertainty, they deserve a prominent place in our strategic framework.

40

Committed to translate vision into reality

Revising the capital allocation to business in line with revised capital adequacy target ratios

At SEBL, we are known for our risk management culture, characterized by a pragmatic approach and rigorous processes. We make a point of knowing our customers. But at the heart of our strength is experience and good judgment.

For Credit Risk-our focus is to develop a strategic business plan for appetite management and structured policy guideline and framework in order to manage default loans.

Ensuring effective risk management system specially prudent management of Asset Liability risk, Foreign Exchange risk and Operational risk

Ensuring meticulous compliance of disbursement procedures and monitoring and follow-up of each loan by the Branch managers to ensure in timely recovery of the same

Strengthening recovery drive to bring down the NPL at a minimum level

Ensuring efficient internal control and regulatory compliance in all levels of banking operations.

Strategic priorities for Leading Customer Experiences

Ensuring quality customer service at primary distribution channel such as Branch and development of alternative delivery channels to improve customer experiences.

Developing and upgrading customized asset, liability and transaction products for Retail, SME and Corporate clients.

Mobilizing low cost sustainable deposits from retail and institutional client base

Increasing client base for financial inclusion and wider market penetration.

Strategic priorities for Leadership/HR capacity development

SEBL’s success depends on having the right leaders to execute our strategy. For this reason, leadership

remains one of our strategic priorities. Our leadership strategy continues to build competitive advantage through comprehensive development programs and tools.

Hiring the best talents in different arenas of Banking

Fostering a culture of creativity, innovation and diversity with a view to sustainable business growth.

Developing Human resource by rendering training and motivation. so that they remain capable to lead new initiatives

Creating Alignment between the leadership development strategy and the business strategy

Key Performance indicator (KPI) based evaluation system

Developing Human resource management system to transform the organization

Efficiency and expense management-

Expense management is a traditional strength at SEBL – and today, it’s more important than ever. While revenue growth is ultimately decided by our customers & external factors, expenses are something we can control. Across SEBL, we are carefully monitoring our spending and looking for ways to improve productivity by being innovative and doing more with less :

Clear Cost saving strategies

Business process reengineering (BPR) in different Business and operational areas to improve efficiency.

Optimizing efficiency by Budgetary control

Paperless banking

Implementing Green office Guide

41

Annual Report 2018 Southeast Bank Limiteda bank with vision

Our Values, Core Values, Core Strengths & Core Competencies

Our ValuesOur Values Serve as a compass for our action and describe our direction.

Core Strengths Professionally Strong Board of Directors

Strong Capital Base