An Online Publication of the ABA Tax Section CONTENTS

64

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868. An Online Publication of the ABA Tax Section Winter • March 2021 • Vol. 40 No. 2 CONTENTS FROM THE CHAIR Moving Forward in 2021 ......................................... 1 PRACTICE POINTS Avoiding an Adverse Tax Impact on Death of an S Corporation Shareholder .......................................... 3 State Taxation of Employees Working Remotely from Another State ......................................................... 8 POLICY POINT The TCJA’s International Tax Schemes ..................... 10 AT COURT NY Uber Driver a Covered “Employee” for Unemployment Insurance Purposes; CA Prop. 22 Provides Limited Employment Benefits to Gig Workers; U.S. Labor Dept. Defines “Independent Contractor” .......................................................... 19 PRO BONO MATTERS Marketing Conundrums for Virtual IRS Events........... 25 Military State Tax Guide Now Available .................... 29 YOUNG LAWYERS CORNER Encouraging Work and Eliminating Poverty: Comparing American and Canadian Family Tax Benefits ............. 30 Winners of the 20th Annual Law Student Tax Challenge ............................................................. 38 THE INCOMPETENT AUTHORITY: QUESTIONS AND ANSWERS ................................................... 40 PEOPLE IN TAX PODCAST Juan Vasquez, Heather Fincher, and Sharon Heck ..... 44 TAX BITS Tax Laws.............................................................. 45 IN THE STACKS Tax Section to Publish 8th Edition of Effectively Representing Your Client Before the IRS ................. 46 SECTION NEWS & ANNOUNCEMENTS ................. 48 • Tax Section Offers Expanded Virtual 2021 May Tax Meeting • Report of the Nominating Committee: 2020-2021 Nominees • Seeking Nominations for Vice Chair of Membership, Diversity, and Inclusion: A Message from the Chair of the Nominating Committee • 2020 Distinguished Service Award Recipient: L. Paige Marvel • Government Submissions Boxscore • Call for Applications: Diversity and Inclusion Scholarships to Virtual 2021 May Tax Meeting • The Tax Lawyer—Winter 2021 Issue Now Available • The Practical Tax Lawyer—March 2021 Issue Now Available • Support the Section’s Public Service Efforts with a Contribution to the TAPS Endowment • Get Involved in ATT SECTION EVENTS & PROMOTIONS Section Meeting & CLE Calendar ............................. 59 Section CLE Products ............................................ 59 Sponsorship Opportunities ..................................... 60 SPONSORSHIP ACKNOWLEDGEMENTS Virtual 2021 Midyear Tax Meeting .......................... 61 Thomson Reuters | Publishing Sponsor ................... 62

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of An Online Publication of the ABA Tax Section CONTENTS

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

An Online Publication of the ABA Tax Section Winter • March 2021 • Vol. 40 No. 2

CONTENTS

FROM THE CHAIRMoving Forward in 2021 ......................................... 1

PRACTICE POINTSAvoiding an Adverse Tax Impact on Death of an S Corporation Shareholder .......................................... 3

State Taxation of Employees Working Remotely from Another State ......................................................... 8

POLICY POINTThe TCJA’s International Tax Schemes ..................... 10

AT COURTNY Uber Driver a Covered “Employee” for Unemployment Insurance Purposes; CA Prop. 22 Provides Limited Employment Benefits to Gig Workers; U.S. Labor Dept. Defines “Independent Contractor” .......................................................... 19

PRO BONO MATTERSMarketing Conundrums for Virtual IRS Events ........... 25

Military State Tax Guide Now Available .................... 29

YOUNG LAWYERS CORNEREncouraging Work and Eliminating Poverty: Comparing American and Canadian Family Tax Benefits ............. 30

Winners of the 20th Annual Law Student Tax Challenge ............................................................. 38

THE INCOMPETENT AUTHORITY: QUESTIONS AND ANSWERS ................................................... 40

PEOPLE IN TAX PODCASTJuan Vasquez, Heather Fincher, and Sharon Heck ..... 44

TAX BITSTax Laws .............................................................. 45

IN THE STACKSTax Section to Publish 8th Edition of Effectively Representing Your Client Before the IRS ................. 46

SECTION NEWS & ANNOUNCEMENTS ................. 48

• Tax Section Offers Expanded Virtual 2021 May TaxMeeting

• Report of the Nominating Committee: 2020-2021Nominees

• Seeking Nominations for Vice Chair of Membership,Diversity, and Inclusion: A Message from the Chair ofthe Nominating Committee

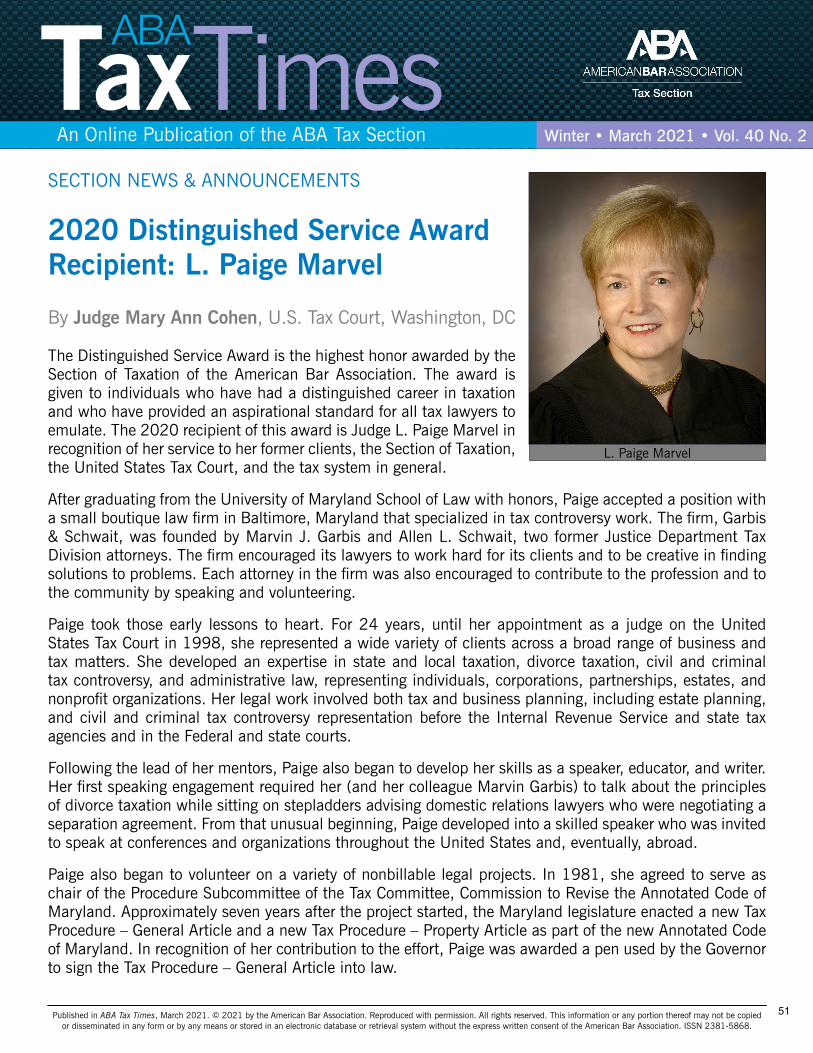

• 2020 Distinguished Service Award Recipient:L. Paige Marvel

• Government Submissions Boxscore

• Call for Applications: Diversity and InclusionScholarships to Virtual 2021 May Tax Meeting

• The Tax Lawyer—Winter 2021 Issue Now Available

• The Practical Tax Lawyer—March 2021 Issue NowAvailable

• Support the Section’s Public Service Efforts with aContribution to the TAPS Endowment

• Get Involved in ATT

SECTION EVENTS & PROMOTIONSSection Meeting & CLE Calendar ............................. 59

Section CLE Products ............................................ 59

Sponsorship Opportunities ..................................... 60

SPONSORSHIP ACKNOWLEDGEMENTSVirtual 2021 Midyear Tax Meeting .......................... 61

Thomson Reuters | Publishing Sponsor ................... 62

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESWinter • March 2021 • Vol. 40 No. 2

EDITORIAL BOARD

COUNCIL DIRECTORT. Keith Fogg

SUPERVISING EDITORLinda M. Beale

INTERVIEW EDITORSTameka E. LesterJeremiah Coder

PODCAST EDITORJames Creech

PRO BONO MATTERS EDITORSAndrew RobersonGina Ahn

AT COURT EDITORT. Keith Fogg

PRODUCTION EDITORSGregory Peacock Todd Reitzel

ASSOCIATE EDITORSJaye CalhounAndy HowlettGuinevere MooreDavid PrattDaniel M. ReachRobert S. SteinbergRobert W. Wood

HYPERTEXT CITATIONS & LINKS

As a service to our readers, ATT authors are encouraged to include hyperlinks to publicly available content within their articles. In addition, certain articles may also contain hypertext citation linking to Westlaw created with Drafting Assistant from Thomson Reuters. Thomson Reuters Legal is the Publishing Sponsor of the ABA Tax Section, and this software usage is implemented in connection with the Section’s sponsorship and marketing agreements with Thomson Reuters. Neither the ABA nor ABA Sections endorse non-ABA products or services. Check if you have access to Drafting Assistant by contacting your Thomson Reuters representative.

EDITORIAL POLICY

ABA Tax Times (ATT) is published at least four times a year featuring articles covering a wide range of tax topics and areas of tax practice, interviews with diverse tax practitioners, Committee reports, Tax Section comment submissions to the government, and other news and information of professional interest to Tax Section members and other readers.

ATT is presented in digital-only format and is distributed by e-mail to Tax Section members as a benefit of membership. To learn more about joining the ABA and the Tax Section, visit http://www.americanbar.org/groups/taxation/membership.html.

ABA Tax Times welcomes the submission of manuscripts from Tax Section members. ATT does not accept articles that have been published previously or are scheduled for publication elsewhere. Publication decisions will be based on editorial consideration of topical timeliness, legal accuracy, quality of writing, tone, and consistency with ATT’s editorial policy. ATT reserves the right to accept or reject any manuscript and to condition acceptance upon revision to conform to its criteria. Members interested in authoring an article are encouraged to contact Professor Linda M. Beale, ATT Supervising Editor, at [email protected].

ATT articles and reports reflect the views of the individuals or committees that prepare them and do not necessarily represent the position of the Tax Section, the American Bar Association, or the editors of ATT. The articles and other content published in ATT are intended for educational and informational purposes only and are not to be considered legal advice. Readers are responsible for seeking professional advice from their own legal counsel.

Authors of accepted articles must sign a standard ABA copyright release form, which gives the ABA exclusive rights to first publication. Authors retain the rights to republish their articles elsewhere (including on the SSRN network) after their articles appear in ATT, with appropriate citation to ATT.

Further information regarding the submission guidelines, including organization, hyperlinks, and article length, is available here: http://www.americanbar.org/groups/taxation/publications/abataxtimes_home/att_editorial.html.

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

An Online Publication of the ABA Tax Section Winter • March 2021 • Vol. 40 No. 2

FROM THE CHAIR

Moving Forward in 2021

By Joan C. Arnold, Troutman Pepper, Philadelphia, PA

Happy 2021! I was more than happy to see 2020 in the rearview window, but I’m still waiting for the electric switch to be thrown to put 2021 in a new light. Somehow the ball dropping on New Year’s Eve just didn’t make it happen. I’m still working from home, still doing more Zoom calls than I care to, and still trying to chart our path as an organization without the ability to have in-person meetings.

But 2020 wasn’t all bad. On a personal level, we welcomed our first grandchild, which makes me remember what joy is all about. She is now almost one, and through the use of facetime, pictures and videos, it’s almost like we have been there to see her grow. Almost.

On a professional level, I realized how fortunate I am to have built up decades of relationships with clients and colleagues in the tax field. It sustains me through the trying times. I wonder, though, how those are faring who have many fewer years of experience and fewer colleagues to lean on. How can we make the Tax Section relevant to them, not just for substantive offerings but for the nurturing of a career and the person carrying out the career? How can we reach out to a broader, more diverse community to better advance and support the role of tax lawyers in the profession and break down implicit bias?

Improving Virtual Meetings

As the Tax Section, we are doing more than just wondering. At our all-virtual Midyear Tax Meeting, we included an increased number of networking events with the goal of inviting more people into the mix. I know that in one event that I attended there were more than a few lawyers new to the field who were there to make contacts and develop their career paths. The Women in Tax Forum held a session on developing executive presence, and it had more than 300 attendees registered.

Our attendance this year was 1,578, exceeding last year’s Midyear Tax Meeting by 400. This year’s attendance included 126 students, up from 29 students the previous year. We would not have achieved those numbers had we not been virtual. Just as at the fall meeting, we had very robust participation from the government, with 532 registered attendees.

Addressing Diversity and Inclusion

We have also been paying close attention to our efforts in advancing diversity. The Tax Section has a Diversity in the Profession Committee (DIPC) that was formed in 2018. The DIPC has taken the lead in developing programs with the goal of addressing both the need for and the means of achieving diversity.

1

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESWinter • March 2021 • Vol. 40 No. 2

For example, the DIPC created the Ginsburg tribute program for the plenary session at the Fall Tax Meeting about the use of a tax case to advance equality. The DIPC has initiated and continues to run the Diversity and Inclusion Scholarship program to support diverse people or people interested in advancing diversity in attending Tax Section meetings.

As a corollary to forming the DIPC, Council in 2018 adopted a revised Diversity and Inclusion Plan. It sets forth our goals and action items for achieving more diversity in our Section. The plan is also summarized here as is relevant to the committees of the Tax Section. I hope you will take some time to read it and act on it.

For me, personally, the focus on diversity has caused me to rethink my vocabulary and how I present issues. For example, when I am making a presentation or teaching, can I get away from examples and terminology that continue to support implicit bias? Do I always need to talk about husband and wife when I want to talk about attribution between spouses? What about using husband and husband? Wife and wife? Would the change of terminology make more people feel welcome in our Section? I am of the view that making a conscious choice to use different examples makes me more aware of my implicit bias and helps to break it down. When the committees are writing those ever-important comments for submission to the government, how can they be more inclusive in their language?

On a Section level, the Council is acting to support our Diversity and Inclusion Plan. Recently, the Council approved creation of a Vice Chair, Membership, Diversity, and Inclusion (VCMDI). This position will work with staff and Section leadership to ensure we meet member needs and continually broaden our diversity and include people of diverse backgrounds in all Section activities. The Nominating Committee seeks nominations for this new Council position; see the announcement in this issue. You will see a greater emphasis on diversity and inclusion as we move forward.

Planning Future Meetings

Speaking of moving forward, our May Tax Meeting will be May 10–14. It will be all virtual. I hope you attended the Midyear Tax Meeting and saw its much-improved virtual meeting technology, which we will also use for the May Tax Meeting. We are planning additional networking events and expanded CLE opportunities. Information can be found here, and I hope to see you there.

As of now, we are looking at the possibility of a blended meeting for the Fall Tax Meeting—some in person and some virtual. The final decision will likely not be made for some time, but we’ll keep you informed.

Before signing off, I need to give a great shout-out of thanks to our staff. They have done an incredible job to pivot from in-person meetings to virtual meetings, and they work tirelessly to make them better each time.

Thanks for reading and, as always, please contact me if you have any comments, suggestions, or questions. ■

2

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

An Online Publication of the ABA Tax Section Winter • March 2021 • Vol. 40 No. 2

PRACTICE POINT

Avoiding an Adverse Tax Impact on Death of an S Corporation Shareholder

By Herbert R. Fineburg and Charles A. McCauley III, Offit Kurman, P.A., Philadelphia, PA

I. Introduction

One of the main reasons to consider a partnership for owning a business rather than an S Corporation is the adverse impact upon death if the business is held by an S Corporation. Now there are solutions to this problem for S Corporation shareholders that tax advisers need to add to their toolbox. These solutions convert the tax status of the business from an S Corporation to a partnership for federal tax purposes, in a federal income tax-neutral manner. This can be accomplished through liquidation in

the case of a deceased shareholder or reorganization prior to death of a shareholder.

A. Upon the Death of an S Corporation Owner

Specifically, upon the death of an S Corporation owner, the heirs are denied the benefits of receiving a step-up in bases in underlying corporate assets to fair market value. In a partnership, the heirs receive a full income tax-free step-up in basis for all of the underling partnership assets and the benefits of obtaining the income tax shelter from new large depreciation deductions. However, in an S Corporation when the owner dies, the shareholder heirs only receive a step-up of basis in the corporate stock equal to the fair market value of the company at the date of death. The underlying S Corporation assets retain the same pre-death tax bases even though the decedent estates in both cases have the same federal estate tax implications and costs. Therefore, the S Corporation heirs should consider promptly liquidating the corporation to also achieve an income-tax neutral stepped-up basis for the company’s assets. This same technique can also be considered if a surviving shareholder buys out the estate of a deceased shareholder.

B. Prior to Death of an S Corporation Owner

Alternatively, with proper tax and estate planning the S Corporation shareholders have reorganization options prior to death of an S Corporation shareholder to avoid heirs being denied the benefits of receiving a step-up in bases in underlying corporate assets to fair market value upon death. The reorganization options include, but are not limited to (i) a contribution by the S Corporation of its assets to a limited partnership or limited liability company in return for issuance of a preferred interest in such entity, or (ii) a sale of the assets of the S Corporation to a limited partnership or limited liability company in consideration of a note payable to the S Corporation. If the shareholder recently purchased the stock of an S Corporation without an IRC Section

3

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESWinter • March 2021 • Vol. 40 No. 2

338 Election, there is a statutory merger of the S Corporation into a limited partnership or limited liability company with such entity surviving the merger. This achieves the same result as the heirs of an estate who have a high stock basis without the underlying S Corporation assets having a stepped-up basis.

II. Achieving Step-up in Basis upon a Shareholder’s Death Through Liquidation

For the estate of an S Corporation shareholder, one of the major problems is the inability of the estate, and thus the heirs as shareholders, to achieve a step-up in basis for the underlying corporate assets. Upon death, the shareholder’s estate receives a stepped-up basis in the shareholder’s stock only equal to the fair market value of the company on the date of death. In contrast, a tax partnership (including a limited liability company (LLC) taxed as a partnership) obtains a stepped-up basis for the decedent’s partnership interest and for the decedent’s proportional interest in the underlying partnership assets through an election under sections 736 and 754.

S corporations can consider the planning option of liquidating the S Corporation or liquidating the S Corporation through a merger. Because partnership status is generally preferable to the S Corporation structure for tax purposes, the estate or heirs can also use this event to convert from an S Corporation to a partnership without the usual tax consequences of such a conversion. Under this planning technique, estates and the heirs holding S corporation stock have a unique opportunity to achieve multiple tax benefits. This article describes how this conversion to partnership status and stepped-up basis in assets can be structured with little, if any, tax cost to the estate and heirs. When an S Corporation liquidates, the corporation is treated as having sold all of its assets for their fair market value, typically resulting in taxable S Corporation gain. Likewise, the estate is treated as having sold its S Corporation stock for an amount equal to the fair market value of the assets it receives in the liquidation distribution from the S Corporation.

Fortunately, when the S Corporation recognizes taxable gain, that gain increases the estate’s basis in the stock in an amount equal to the taxable gain recognized by the S Corporation. This taxable gain is reported to the estate on the corporation’s final Schedule K-1 (Form 1020S). The estate’s tax basis in its S Corporation stock is increased to the fair market value of the S Corporation stock upon the death of the shareholder and further increased as a result of the deemed sale of the S Corporation stock upon the liquidation.

Simultaneous with the increase in basis from the liquidation, the estate recognizes a taxable loss equal to the taxable gain reported to the estate on the corporation’s final Schedule K-1. The loss on the deemed sale of the S Corporation stock in the liquidation is reported on the estate’s or heirs’ Schedule D (Form 1040 or 1041). Typically, the S Corporation gain on the Schedule K-1 (Form 1020S) reported on Schedule E (Form 1040 or 141) and the loss on the Schedule D (Form 1040 or 1041) will net out with no tax due by the estate or its heirs for the S Corporation gain on liquidation. Remarkably, the business will have a new step-up in basis in all of its assets which the heirs can contribute tax-free to a new partnership.

Consider the following hypothetical facts. Sam has two heirs and he owns 100% of Hardware Corporation (taxed as an S Corporation) with a basis in his stock of $5,000. When Sam dies, Hardware Corporation is worth $10 million and has a basis in its assets of $10,000. As a result of Sam’s death, Sam’s estate now has a stepped-up tax basis in the Hardware Corporation stock of $10 million (the fair market value of the stock on Sam’s death).

If Sam’s two heirs liquidate the corporation, Hardware Corporation will recognize gain in the amount of $9,990,000 from the deemed sale of its assets ($10 million value minus $10,000 basis). Hardware Corporation will report a gain of $9,990,000 to Sam’s estate on a Schedule K-1 (Form 1020S). Upon

4

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESWinter • March 2021 • Vol. 40 No. 2

recognition of this gain by Hardware Corporation, Sam’s estate basis in the stock will increase by $9,900,000 because of the deemed sale gain, giving Sam’s estate an aggregate tax basis in the stock of $19,990,000 ($9,990,000 deemed sale gain + $10,000,000 step up to fair market value on death). The liquidation of Hardware Corporation on the Schedule D of Sam’s heirs will be reported as a loss of $9,990,000, calculated as the difference between the fair market value of the Hardware Corporation assets received by Sam’s heirs of $10 million and Sam’s estate’s stock basis of $19,990,000

It is anticipated that the Schedule K-1 gain recognized by Sam’s estate of $9,990,000 on Schedule E of the Form 1041 and the Schedule D loss on the Form 1041 recognized by Sam’s estate of $9,990,000 will mostly off-set each other even though they are reported on different Schedules. Some difference may occur because the Schedule D loss will be a capital loss but some of the gain on the Schedule K-1 may be ordinary income recapture. The benefit of the large depreciation or amortization deductions for the assets with stepped-up basis will far exceed the modest tax cost. To utilize the depreciation, Sam’s heirs can contribute the $10 million in assets tax-free to a new partnership (or LLC taxed as a partnership) under section 721. The benefit to the new partnership is the ability to depreciate $10 million of asset basis in the partnership compared to the $10,000 of asset basis in an unliquidated Hardware Corporation.

III. Reorganization Prior to Death Through Contribution to a Partnership for a Preferred Return

Another tax planning strategy available prior to the death of the S Corporation shareholder is a reorganization involving the contribution by the S Corporation of its assets to an entity electing to be taxed as a partnership in return for issuance of a preferred interest in the newly formed entity.

This type of reorganization can be illustrated by a case study and diagram in which the S Corporation (Hardware Inc.) forms an LLC taxed as a partnership (Hardware LLC) into which it transfers all of its operating assets. After the reorganization the S Corporation owner Fred Smoot, through his revocable living trust, continues to hold 100% of the outstanding shares of Hardware Inc., and directly and indirectly, owns all of the interests in Hardware LLC.

The steps to complete the reorganization are as follows. First, Hardware LLC issues a preferred membership interest to Hardware Inc. equal to the estimated value of the business ($14.0 million). The preferred interest has a liquidation preference and could also have a cumulative dividend. The preferred interest holder may also have the option to claim all or some of a distribution of profits or permit all or some of a distribution of profits to be allocated to the holders of common interests. Hardware LLC also issues a majority of Hardware LLC common interests to Fred Smoot: those common interests have a value of zero (assuming the preferred interest equals the value of the entire business). As part of Hardware’s reorganization plans, Hardware LLC’s key officers and executives may receive a grant and award of restricted common interests to enable them to share in the value creation going forward while isolating the existing business value with the preferred interest holder.

Other than the company designation as an LLC as opposed to a corporation and a contingent unvested restricted grant and award to key management to enable them to share in value creation going forward, nothing has changed. The staff, location, emails, phone numbers and all other details of Hardware as well as current contracts and other agreements remain unchanged. As a result of the reorganization, Mr. Smoot is able to remain in control of his business, isolate his prior accretion of wealth and provide valuable equity incentive grants to his key employees.

5

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESWinter • March 2021 • Vol. 40 No. 2

Fig. 1: Ownership of Hardware Holdings, Inc., A Delaware Limited Liability Company

IV. Reorganization Prior to Death: A Sale of Assets for a Note

Another tax and estate planning strategy to consider is the sale of the assets of an S Corporation (or C Corporation) to a limited partnership (or LLC taxed as a partnership) for a note payable to the S Corporation. (After the reorganization, the C Corporation can make an S Corporation election).

The following case study and diagram illustrates this tax and estate planning strategy. On December 18, 2019, Hardware Inc. (a C Corporation) changed its name to Hardware Holdings Inc. and formed Hardware Holdings LLC as a subsidiary. On December 31, 2019, Hardware Holdings Inc. sold all of its assets (except cash) to Hardware Holdings LLC, based upon the appraised value of the assets as determined by outside accountants. The sale was represented by a 121-month promissory note for tangible assets and a separate 121-month promissory note for section 197 intangibles. In addition, the LLC executed a line-of-credit note payable to the corporation so that cash would be available to the LLC. The sale of assets also included the corporation’s marketable securities, which the LLC required to secure its loan. Immediately after the sale on December 31, 2019, the LLC membership interests were distributed to all of the shareholders pro-rata. Because the LLC’s assets were encumbered by promissory notes for 100% of their fair market value, the net value of the LLC interests was reported to be zero dollars. Effective January 1, 2020, Hardware Holdings Inc. elected to be taxed as an S corporation. The foregoing transactions were approved by all of the shareholders and directors of Hardware Holdings Inc. at annual and special meetings held on December 11, 2019.

6

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESWinter • March 2021 • Vol. 40 No. 2

Fig. 2: Sale of Assets and Distribution of LLC Membership Interests

■

7

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

An Online Publication of the ABA Tax Section Winter • March 2021 • Vol. 40 No. 2

PRACTICE POINT

State Taxation of Employees Working Remotely from Another State

By Michael McLoughlin, Kean Miller LLP, New Orleans, LA

Even though New York and Massachusetts have restricted out-of-state commuters from coming back to their pre-pandemic offices to work, they still expect them to pay personal income taxes to the state as if they were working in the state. That is, the two states are taxing nonresidents as if they continued to commute to work every day even if they do not set foot in the state and do all of their work remotely from a home office. Not surprisingly, the home states where those commuters live and (now) work are fighting back against what they see as a money grab by states that do not have any right to the tax revenue.

On October 19, 2020, New Hampshire filed a petition with the U.S. Supreme Court to overturn an April 2020 Massachusetts emergency regulation1 that requires nonresidents who were working in Massachusetts when the pandemic started, many of whom live in New Hampshire, to continue to pay Massachusetts’ personal income tax even though they have not been commuting to Massachusetts since early 2020 and will likely continue to work from home for the foreseeable future. On December 22, 2020, New Jersey—joined by Connecticut, Hawaii, and Iowa—filed an amici curiae brief supporting New Hampshire’s petition. In late January, the Supreme Court asked the Acting Solicitor General to weigh in on the debate.2 A date for argument before the Supreme Court has not yet been set.

The New Hampshire petition asserts that the Massachusetts emergency regulation violates the Commerce and Due Process constitutional provisions by imposing income tax on New Hampshire residents despite the fact that the individuals did not enter Massachusetts to work during the period at issue. Specifically, the Massachusetts regulation requires individuals who were employees performing services in Massachusetts immediately prior to the start of the pandemic to continue to pay Massachusetts personal income tax even if they are now working from home in another state due to the effects and restrictions from the pandemic. This rule could potentially result in an individual who does not enter Massachusetts for a single day in 2021 being considered to have nexus there and to be subject to income tax there, simply because that person once actually conducted the work in Massachusetts.

New Hampshire argues that Massachusetts is effectively eliminating what it has called the “New Hampshire Advantage”—i.e., the fact that a resident of New Hampshire who works in New Hampshire does not have to pay a traditional personal income tax. Thus, New Hampshire claims that Massachusetts is impermissibly

1 Massachusetts Source Income of Non-Residents Telecommuting due to the COVID-19 Pandemic, 830 CMR 62.5A.3.2 See, e.g., Mike Shaikh & Michael Tedesco, Scotus Invites Acting Solicitor General to Weigh In on Ongoing Dispute Between Massachusetts and New Hampshire Regarding Controversial COVID-19 Sourcing Rule, SaltSavvy (Jan. 27, 2021).

8

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESWinter • March 2021 • Vol. 40 No. 2

interfering with New Hampshire’s right to provide its residents a planned tax benefit from working inside the state.

New Jersey elected to file an amicus brief supporting New Hampshire because it is fighting a similar battle with New York. New York has long required nonresident individuals who work for New York companies but perform their services outside of the state to pay New York personal income tax unless it was a “necessity” that the employee work outside the state. If the individual worked outside the state purely for the employee’s convenience, then the individual was required to continue to pay New York taxes. The New York Department of Taxation and Finance has recently confirmed that nonresidents who are working from home because they cannot return to their New York offices due to COVID-19 must still pay New York income tax unless a bona fide office has been established from which the employee telecommutes.

The problems that result from this taxation of non-residents for states like New Hampshire, which does not impose a personal income tax, and New Jersey, which provides a credit to residents for taxes paid to other states, are slightly different. As noted, New Hampshire claims that Massachusetts is eliminating the advantage of not having to pay an income tax that the New Hampshire legislature has provided to its residents who work in New Hampshire. New Jersey, on the other hand, asserts that it is losing tax revenue to New York on income earned by its residents who are working full time in New Jersey because New Jersey residents receive a credit against taxes owed to New Jersey for taxes they pay to other states.

The issue is an important one for the Supreme Court to resolve. The problem is not likely to go away soon, and residents of New Hampshire and New Jersey who are affected by the Massachusetts and New York provisions, respectively, do not have an adequate state forum in which to protest the imposition of the taxes at issue. Moreover, even if pandemic restrictions end within the next six to twelve months, many people will likely choose to continue to work remotely from their homes in these and other states, and employers will likely support that decision, as they realize that they save money by doing so. If states continue to struggle with declining tax revenues in 2021 and 2022, there will likely be even fiercer competition for those tax revenues between states where the employer and its primary offices are located and those whose residents, prior to the pandemic, regularly commuted to those states for work. ■

9

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

An Online Publication of the ABA Tax Section Winter • March 2021 • Vol. 40 No. 2

POLICY POINT

The TCJA’s International Tax Schemes

By Benjamin M. Willis, Tax Analysts Contributing Editor to TaxNoTes

The tax bill signed into law by then-President Trump on December 22, 2017 (TCJA, an acronym for the “Tax Cuts and Jobs Act” unofficial title) is the most expansive and complex international tax reform made in a single piece of congressional legislation. The TCJA is plagued with ambiguities, gaps, uncertainties, and errors. The current economic crisis stemming from the COVID-19 pandemic makes one thing clearer than ever about the TCJA’s provisions: the need to fix them.

Taxpayers have begun to bring forward cases attacking the validity of the new international tax rules. These cases expose the inept lack of coordination among the various relevant statutory rules. Treasury simply will not be able to provide taxpayer certainty through regulations integrating scattered, incoherent, and nonexistent policies to argue that the clearly disjointed provisions sufficiently resemble an organized scheme. Congress placed an unfair burden on Treasury to expect it to justify these partisan piecemeal provisions cobbled together at lightning speed. Ultimately, this lack of coherence will result in taxpayer wins, which was perhaps the underlying unifying goal of the TCJA, which used explicit and implicit tax cuts (available through planning) to find more favorable revenue estimates but should not be allowed to survive a more thoughtful Congress.

This article makes the case that the claim that the TCJA’s international tax provisions represent a coherent statutory scheme is patently false: it is essentially one of those “alternative facts” concocted by the prior administration to conceal the true winners and losers of its single significant legislative achievement. The provisions fluctuate in their application to controlled foreign corporations (CFCs) and specified foreign corporations (SFCs) and their owners, which sometimes must only be corporations and sometimes include individuals and passthrough entities.1 The effective dates, like the provisions’ scope, do not align. Contrary to Treasury’s amusing concoction, the TCJA in no way created an “interlocking statutory scheme” through sections 245, 965, 951A, and subpart F.2 This is becoming ever clearer as the lawsuits begin to surface.

I. The Cases Against the TCJA Rules

On November 11, 2020 in Moore v. U.S., the U.S. District Court for the Western District of Washington incorrectly determined that the TCJA’s change to “a territorial tax model” is “a change in subpart F to

1 A specified foreign corporation is CFC or any foreign corporation with a corporate U.S. shareholder. Section 965(e)(1). A CFC is foreign corporation more than 50 percent owned, by vote or value, by U.S. shareholders. Section 957(a). A U.S. shareholder is a U.S. person that owns 10 percent, by vote or value, of a foreign corporation. Section 951(b). 2 See T.D. 9865, explaining why section 245A should be narrowed.

10

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESWinter • March 2021 • Vol. 40 No. 2

incentivize U.S. taxpayers to repatriate foreign earnings.” The Moore court went on to explain that section 965’s mandatory repatriation tax (MRT) is not a wholly new tax but merely resolves an uncertainty because “it was unclear when and if a CFC’s earnings attributable to U.S. shareholders would be subject to U.S. tax. The TCJA and MRT remove that uncertainty.” This is the essence of the notion—that the TCJA’s international tax provisions flow from a seamless integrated statutory scheme—promulgated by the Trump Treasury in order to market the legislation as well as conceal its winners and losers.

A week after the court’s decision in Moore, Liberty Global, Inc. (a U.S. subsidiary of U.K. telecommunications giant Liberty Global PLC) sued after the government denied its section 245A deduction for the 2018 tax year.3 Liberty Global argues that “the section 245A Temporary Regulations are substantively and procedurally invalid” and that they are “contrary to the controlling statutes.” It asserts that the regulations improperly disallow the section 245A territorial dividends-received deduction (DRD) because such disallowance rules are “not found in or supported by the statute.”

These two cases have more in common than one would think at first blush. While Moore is focused on the unconstitutionality of section 965’s repatriation tax and Liberty Global on the invalidity of the section 245A regulations, the best argument supporting the taxpayers is that the TCJA’s plain language (muddled as it is) simply does not support the government’s positions.

Section 965 was not intended to remove the uncertainty of timing of taxation of a CFC’s earnings and profits: the section does not even apply to CFCs. Subpart F, of course, is the part of the Code that deals with CFCs and something of which the government could argue realistically that taxpayers had notice. To qualify as a CFC, a foreign corporation must be more than 50 percent owned by U.S. shareholders. Section 965’s new jurisdictional link, in contrast, is merely predicated on a single corporate U.S. shareholder owning 10 percent of a foreign corporation, an unusually limited jurisdictional link for international taxation. How could a foreign corporation or its owners anticipate that subpart F would (i) be expanded to govern corporations for which a de minimis portion of stock is owned by U.S. shareholders and (ii) result in retroactive taxation of 30 years of earnings and profits (E&P) that in no way reflect earnings accrued to the current 10-percent shareholder. That shareholder could well hold loss shares rather than shares with any built-in gain or other accession to wealth.4

This situation is worsened since E&P are not the same as taxable income, and the distortion is increased when decades of E&P become subject to a transition tax, raising the question whether the TCJA reflects an appropriate understanding of income. E&P is a poor barometer of income for shareholders that do not receive dividends. For example, E&P doesn’t take into account unrecognized losses.5 On an annual basis, subpart F generally withstood scrutiny as a way to flow income through to a block of majority U.S. shareholders. In contrast, forcing a minority individual shareholder to take into account decades of E&P of a majority foreign-owned corporation with neither prior notice nor any of the benefits from the new statutory scheme raises serious concerns. Given the 30 years at issue in the Liberty Global case, it is certainly possible that individuals were required to pick up income on loss shares for which there was no accession to wealth. If the E&P had been required to be adjusted, as is done under section 877A by taking into account

3 Liberty Global Inc. v. United States, No. 1:20-cv-03501 (D. CO, Nov. 27, 2020).4 Tony Nitti, “Glenshaw Glass and Defining Income,” 170 Tax Notes Federal 1257 (Feb. 22, 2021) (“Glenshaw Glass [348 U.S. 426 (1955)], however, established a general principle and corresponding three-part test that are critical to applying the tax law: The 16th Amendment grants Congress the power to tax all realized gains, and thus any item that (1) increases the wealth of a taxpayer, (2) is realized, and (3) the taxpayer has control over is income unless specifically exempted by statute.”)5 § 312(f) (indicating that only recognized losses are taken into account to determine current earnings and profits).

11

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESWinter • March 2021 • Vol. 40 No. 2

unrecognized losses upon a jurisdictional shift, a stronger argument could be made that the tax was in fact reaching actual income.

This brings us back to Liberty Global and whether the so-called gap period created by different effective dates for section 245A and the new subpart F rules can be altered by Treasury’s complex regulations that disallow a section 245A DRD. Ultimately, the justification for a regulatory fix, after a proper technical correction failed, illustrates clearly that the TCJA’s international provisions are no part of an integrated statutory scheme.

The Moore decision was incorrect because a CFC isn’t relevant for section 965’s tax, and this tax is certainly far more than a clarification of how a CFC’s earnings should be taxed. A CFC also isn’t relevant for section 245A’s territorial DRD, which is even further removed from subpart F: instead of using the CFC definition of U.S. shareholder that includes individual and passthrough owners, the section 245A territorial tax system only applies to a domestic corporation that owns 10 percent of the foreign corporation. These differences that expand the application of the repatriation tax and minimize the territorial DRD concurrently expand and narrow pre-existing subpart F principles, providing clear evidence of a failure to coordinate the provisions in TCJA’s so-called statutory scheme.

The other international TJCA provisions not at issue in these two cases further illustrate the lack of a coherent statutory scheme. The new subpart F provisions—including section 951A’s global intangible low-taxed income (GILTI) as well as section 965’s repatriation tax—care not who the U.S. shareholder is, while the new deductions—the 50 percent GILTI deduction and 37.5 percent foreign-derived intangible income (FDII) deduction—are only available for domestic corporations. Together, these completely different provisions maximize income for individuals and provide deductions only to corporations so it is unsurprising that neither the provisions’ terms nor their effective dates align.

II. The Disjointed International Provisions of the TCJA.

A. Transition Tax under Section 965

Section 965 imposes a one-time transition tax on post-1986 untaxed foreign E&P of foreign corporations (called “deferred foreign income corporations” or DFICs) owned by U.S. shareholders (including individuals and passthrough entities). Those individuals and pass-through U.S. shareholders of corporations that are not CFCs are likely to have little ability to extract distributions from the DFICs because of the 10-percent ownership threshold. Nonetheless, the transition tax applies to prior foreign earnings without regard to whether any of those profits are actually repatriated. (As already noted, the taxable amount does not accurately reflect income since it fails to take into account up to 30 years of unrecognized losses.)

The applicable tax rate is 15.5 percent for cash and certain cash equivalents and 8 percent for illiquid assets. The reduced tax rate for illiquid assets acknowledges the difficulty the foreign corporation would have securing cash to pay dividends to be used to pay the mandatory repatriation tax. Similarly recognizing the hardship that lumpsum payments of the repatriation tax would cause, the provision allows the repatriation tax to be paid over an eight-year period, with back-loaded payments ensuring that the bulk of payment occurs in the last three years.

While section 965 was enacted in the subpart F section of the Code to give the appearance of taxpayer notice and thus address constitutionality concerns, section 965’s tax on the E&P of DFICs represents a stark contrast to the CFC regime in which U.S. shareholders were required to own more than 50 percent of the corporation and thus could generally compel a distribution and were only taxed currently on “bad”

12

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESWinter • March 2021 • Vol. 40 No. 2

(e.g., passive) earnings. This inability to compel a distribution had also been addressed in the 1986 passive foreign investment corporation (PFIC) reforms to the Code in another situation resulting in pass-through treatment to shareholders of passive earnings, because Congress recognized that “the U.S. investors may not have sufficient ownership in the PFIC to compel distributions.”6 For PFICs, both the qualified electing fund (QEF) and mark-to-market (MTM) rules provide PFIC owners with considerable flexibility compared to the default regime.

In sum, the section 965 tax applies to an inaccurate measure of a corporation’s untaxed foreign earnings at an incredibly low rate that benefits large taxpayers but hurts many less liquid taxpayers.

Constitutionality Concerns

The title of section 965 is “Treatment of deferred foreign income upon transition to participation exemption system of taxation”. Yet section 965 taxes those individuals and passthrough entities who do not participate in the exemption system. Section 245A, which is described in the legislative history as the “provision [that] generally establishes a participation exemption system for foreign income,” applies only to domestic corporations.7 This is where constitutional concerns arise.

A new tax regime for expatriating individuals was adopted in 2008, as part of the HEART Act.8 Section 877A provides for a mark-to-market tax on the net gain in property of expatriating U.S. citizens, generally applied as though the person’s property were sold at its fair market value on the day before expatriation.9 The underlying legislative history explored the constitutionality of the tax and explained that a change in a taxpayer’s jurisdictional rights under section 877A is a realization event that permits immediate taxation of built-in gains, even without a transfer to another owner.

[W]hen property effectively is transferred to a new legal situs that alters the taxpayer’s, and the Government’s, legal relationship to the property ... it is possible to characterize expatriation as being accompanied by a ‘realization’ with respect to certain assets in view of the change of the legal attributes of such assets, so that Government’s inchoate interest in its receiving its share of any increase in value need not be extinguished.10

This realization argument was drafted in response to “opposing views on the validity” of the tax based on the Sixteenth Amendment, principles of international law, and whether economic gains have nexus to the

6 H.R. Conf. Rep. No. 99-841, 1986-3 C.B. (PART 4) 1.7 H.R. Rep. No. 115-446 (2017) (“The provision generally establishes a participation exemption system for foreign income. This exemption is provided for by means of a 100-percent deduction for the foreign-source portion of dividends received from specified 10-percent owned foreign corporations by domestic corporations that are United States shareholders of those foreign corporations within the meaning of section 951(b) (referred to here as ‘participation DRD’). A specified 10-percent owned foreign corporation is any foreign corporation with respect to which any domestic corporation is a United States shareholder.”).8 Heroes Earnings Assistance and Relief Tax Act Of 2008, P.L. 110-245 (June 17, 2008).9 Joint Committee on Taxation Report, JCX-44-08 (“Such individuals are subject to income tax on the net unrealized gain in their property as if the property had been sold for its fair market value on the day before the expatriation or residency termination (‘mark-to-market tax’)”).10 Joint Committee on Taxation, Issues Presented By Proposals To Modify The Tax Treatment Of Expatriation, JCS-17-95 (June 1, 1995) (providing a comprehensive discussion of the realization requirement with a focus on retroactivity, notice, and change in jurisdictional taxing rights as a realization).

13

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESWinter • March 2021 • Vol. 40 No. 2

United States.11 The TCJA’s new international tax provisions seem designed to fall within this description of a realization event due to the change in jurisdictional taxing rights arising from the new quasi-territorial regime. This justification does not appear to apply, however, for taxpayers who do not fall within the scope of section 245A’s participation exemption. Thus, it is not surprising that noncorporate taxpayers are arguing against the constitutionality of application to them of section 965.12

B. Territorial DRD under Section 245A’s Participation Exemption

Although individuals pay the repatriation tax designed for a transition to section 245A’s territorial deduction, they do not benefit from dividend deductions. Nor is the section 245A deduction limited to CFC distributions to shareholders that are taxed under subpart F. Section 245A provides a 100-percent dividends-received deduction to transition to the TCJA’s hybrid territorial regime equal to the foreign-source portion of any dividend received from a specified 10-percent-owned foreign corporation by its U.S. corporate shareholder.

The regulations impose taxes on some offshore earnings in apparent inconsistency with the statutory language, on the grounds that the statutory language as written inadvertently confers a benefit unintended by Congress. The unintended taxpayer benefit arises because section 245A applies to distributions after December 31, 2017, whereas the GILTI provision (discussed further below) is effective for the first tax year beginning after December 31, 2017. Treasury essentially argues that its regulatory grant requires it to read the provisions as intending to leave no gap. Strict textualists will counter, nonetheless, that the regulatory grant should not be able to disregard the difference in wording even if its impact is to provide an unreasonable benefit not intended by Congress. Further, even though Congress acted with undue haste, including without the benefit of any hearings or the ability for congressional representatives, their staffs, and the tax committees adequately to scrutinize the legislative language, it can be argued that the drafters should have been aware of the different wording of the effective dates, the common use of fiscal years rather than calendar years as the taxable year for C corporations, and the gap in time creating the benefit because of the difference in wording.

Final regulations state that the international “framework confirms that the section 245A deduction is intended to apply to residual E&P that is not subject to section 965 and properly determined to be exempt from current taxation under the GILTI and subpart F regimes.”13 This counters the statutory interpretation

11 The Joint Committee includes a clear statement of the issues raised:How one views the concept of ‘realization” is the key factor underlying the above two opposing views on the validity, under both the Sixteenth Amendment and human rights principles of international law, of the expatriation tax proposals. A secondary conceptual issue underlying the opposing views is when is it appropriate to view the income tax system and the estate and gift tax systems as separate from each other (such that determining the proper treatment of gain under one system is independent of the tax consequences that flow under the other systems) or as part of a comprehensive, inter-connected regime designed to ensure taxation, at least in the long-run, of economic gains that have a nexus to the United States, even if current income taxation of some gains is deferred for administrative or policy reasons.

Id. See also Reuven S. Avi-Yonah, Is GILTI Constitutional? 170 Tax NoTes Federal 283 (Jan. 11, 2021)(noting that arguments for unconstitutionality “rest on the assertion that deemed dividends are economically equivalent to taxing a CFC on foreign-source income, which is unconstitutional under the jurisdictional limits of Cook and is also a violation of international law”).12 See, e.g., Andrew Velarde, Silver’s Transition Tax Summary Judgment Briefing Draws to a Close, 99 Tax NoTes INT’l 1100 (Aug. 24, 2020)(noting that the reasons the taxpayers sue felt unduly harmed cannot be ignored).13 T.D. 9909 (Aug. 21, 2020).

14

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESWinter • March 2021 • Vol. 40 No. 2

principles espoused in Gitlitz,14 the Constitution’s separation of powers, and which branch of government legislates.15

C. Global Intangible Low-Taxed Income under Section 951A

Section 951A requires U.S. shareholders (those who own 10-percent or more by vote or value, taking into account direct, indirect and constructive ownership) of any CFC to include their GILTI in respect of their direct or indirect ownership in gross income. The provision is designed to tax earnings that exceed a deemed return on qualified business asset investment (QBAI) and thus operates effectively as a minimum average foreign tax.16 The tax base comprises the aggregate net income (with adjustments) of the CFC less a deemed 10-percent rate of return on QBAI. Section 951A applies to the tax years of foreign corporations beginning after December 31, 2017. As previously discussed, the different effective date for section 951A compared to section 965, without the regulatory guidance discussed here, creates a gap period for fiscal-year corporations.

GILTI is treated as Subpart F income. Consequently, unless individual U.S. shareholders make a section 962 election,17 the GILTI amount will be subject to tax at their individual rates without the benefit of indirect foreign tax credits or the GILTI deduction (described in the next section). In some cases they would be eligible for lower rates on qualified dividends.

D. FDII and GILTI Deductions under Section 250

Section 250 creates a 37.5 percent deduction for FDII, which reduces the effective tax rate for qualifying income from the (new) standard 21 percent corporate rate to 13.125 percent. The section also allows an initial 50 percent deduction for GILTI income as determined under section 951A, resulting in a GILTI tax rate for corporations generally at 10.5 percent (half of the 21% current corporate tax rate). Both deductions are available only for domestic corporations.

The separate and distinct FDII deduction subsidizes foreign purchases from U.S. corporations, while the GILTI deduction merely reduces this includable type of subpart F income for certain domestic corporate shareholders. Any U.S. corporation can take advantage of the FDII export subsidy regardless of whether it has controlled foreign corporations or GILTI income. They are each stand-alone deductions that can each benefit taxpayers.

14 Gitlitz v. Commissioner, 531 U.S. 206 (2001) (deciding to follow the plain language of the law notwithstanding it provided a “double windfall” and disagreeing with the logic of the lone dissenting judge, Justice Stephen Breyer, who argued we “should read ambiguous statutes as closing, not maintaining, tax loopholes. Such is an appropriate understanding of Congress’ likely intent.”). 15 Willis, “Congress Expands Gitlitz to Triple Tax Benefits for PPP,” 170 Tax Notes Federal 293 (Jan. 11, 2021) (“Congress just spent months debating the proper tax benefits that should stem from PPP loans, and their conclusion was that the Gitlitz benefits were appropriate and aren’t a loophole that Breyer thought would likely be unintended by Congress. The point is that courts (and others) should be wary before making assumptions about Congress’s likely intent on tax and economic policy. The approach the Court almost unanimously rejected in Gitlitz is simply not administrable and defies the allocation of power between the courts and Congress. The potential loss of revenue Breyer was concerned with should be addressed by a concerted effort to close the tax gap. Legislative efforts along these lines now look quite likely, given Democrats will effectively control both chambers of Congress and an economic recovery later this year is probable.”).16 See, e.g., Jasper L. Cummings, Jr., GILTI Puts Territoriality in Doubt, 159 Tax Notes 161 (Apr. 9, 2018) (“As for GILTI, Republicans used a version of ‘race to the bottom’ that intricately combined drastically cutting the U.S. corporate tax rate and currently taxing foreign active income earned in countries with relatively low tax rates. Evidently, they hope U.S. corporations will locate operations in countries with rates just high enough to mostly avoid GILTI and maybe encourage foreign tax cuts — which would generate calls for more U.S. rate reductions, known in Republican circles as a ‘virtuous cycle.’”).17 The section 962 election results in a section 78 gross-up that increases the GILTI amount by the creditable foreign tax. There is also a U.S. dividend tax on any actual distribution of earnings that were subject to the U.S. tax on the GILTI amount.

15

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESWinter • March 2021 • Vol. 40 No. 2

III. The Regulations Are Even More Disjointed

In Liberty Global Inc. v. United States, No. 1:20-cv-03501, Liberty Global argues that the section 245A regulations are invalid and are contrary to the controlling statutes. It asserts that the regulations improperly disallow the section 245A territorial DRD because that disallowance is not found in or supported by the statute. The fact that the effective date of the provision encouraging movement of property into the U.S. applies before the GILTI regime’s taxing provision kicks in is not unreasonable: the provisions were not coordinated and do not even apply to the same types of taxpayers. Both the foreign corporations (specified foreign corporations for the DRD and CFCs for subpart F and GILTI) as well as their owners (corporations for the DRD and any U.S. shareholder for subpart F and GILTI) are different.

The executive branch was unable to obtain congressional passage of a technical correction to resolve the conflicting effective dates for the DRD under section 245A and the GILTI regime under section 951A. In lieu of those technical corrections, Treasury has tried to achieve the same result through interpretation intended to coordinate the two regimes. The problem Treasury has is that section 245A explicitly allows a domestic corporation the benefit of a 100-percent DRD for the foreign-source portion of a dividend received from a CFC after December 31, 2017, even if that dividend had not also borne the burden of taxation under the GILTI rules. The taxpayer benefit Treasury claims was unintended stems from the fact that section 245A applies to distributions after December 31, 2017, whereas GILTI is effective for the first tax year beginning after December 31, 2017.

The differing effective date language, likely an implicit tax cut, results in a benefit for corporations with taxable years that are not calendar years. The gap period favors large non-calendar fiscal-year multinational corporations by allowing taxpayers to step up basis in qualified business asset investment and intangibles and generate earnings and profits for tax-free dividends relying on the 100-percent section 245A DRD before GILTI is effective. That also allows increased future depreciation and amortization deductions from the stepped-up basis to offset tested income under GILTI.

Technical corrections were not an option to salvage the partisan overhaul of the U.S. international tax system squeezed through the Senate with 51 votes through the budget reconciliation process. Accordingly, Treasury opted to resolve the issue through an interpretation of the statutory provisions necessary to carry out the congressional purpose. It was a tall tale to say the least. But what better way to help conceal hidden tax cuts used to meet budget reconciliation restrictions than spending government resources to write rules to disavow them. The fact that the rules were certain to fail doesn’t change the narrative – it only changed the financial statements of the well-informed. Perhaps the gap period satiated large constituents who were promised a 20 percent corporate tax rate.18 Conjecture aside, it can’t be denied that the TCJA is filled with massive congressionally intended benefits for large corporations that took many months to decipher. And back to the point, why would anyone think that immediate DRD benefits provided to corporate 10 percent owners of specified foreign corporations were meant to align with the GILTI regime’s delayed detriments to CFCs and their corporate, passthrough, and individual U.S. shareholders.

The June 2019 temporary19 and proposed20 regulations describe the provisions to address the gap period succinctly:

18 Scott A. Hodge, “Replacing the 20 Percent Corporate Rate with Rates of 21 or 22 Percent Has Real Economic Consequences,” Tax Foundation (Dec. 8, 2017).19 Treasury Decision 9865, 84 FR 28398, as corrected at 84 FR 38866 (June 18, 2019).20 Proposed Regulations, REG-106282-18 (June 18, 2019).

16

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESWinter • March 2021 • Vol. 40 No. 2

Section 245A is designed to operate residually, such that the section 245A deduction generally applies to any earnings of a CFC to the extent that they are not first subject to the subpart F regime, the GILTI regime, or the exclusions provided in section 245A(c)(3) (and were not subject to section 965). That is, the text of the subpart F and GILTI rules explicitly defines the types of income to which they apply, and section 245A applies to any remaining untaxed foreign earnings. Under ordinary circumstances, this formulation works appropriately, as earnings are first subject to the subpart F or GILTI regimes before the determination of dividends to which section 245A could potentially apply. However, in certain atypical circumstances, a literal application of section 245A (read in isolation) could result in the section 245A deduction applying to earnings and profits of a CFC attributable to the types of income addressed by the subpart F or GILTI regimes — the specific types of earnings that Congress described as presenting base erosion concerns. These circumstances arise when a CFC’s fiscal year results in a mismatch between the effective date for GILTI and the final measurement date under section 965 or involve unanticipated interactions between section 245A and the rules for allocating subpart F income and GILTI when there is a change in ownership of a CFC.

Why does Treasury think section 245A should not be applied based on its literal meaning? Because of “atypical” circumstances. What circumstances are so “atypical” they could render the words of Congress meaningless? A C corporation with a non-calendar fiscal year. It is as quixotic as Don Quixote charging at a windmill thinking it was a giant.

Treasury said in its 2019 temporary regulations that “where the literal effect of section 245A would reverse the intended effect of the subpart F and GILTI regimes, this conflict is best resolved, and the structure of the statutory scheme is best preserved, by limiting section 245A’s effect.”

Section 245A(g), which the final regulations rely on, provides that the “Secretary shall prescribe such regulations or other guidance as may be necessary or appropriate to carry out the provisions of this section.” The final regulations describe the need to coordinate section 245A and section 965 as limiting the availability of the section 245A deduction “in certain limited circumstances where the effect would be contrary to the appropriate application of those provisions in the context of the Act’s integrated approach to the taxation of income, or E&P generated by income, of a CFC.”21

The term “appropriate” in section 245A(g) is broader than the “necessary” rules permitted by section 7805(a).22 Nevertheless, in my view the section 245A regulations at issue are in no way “appropriate to carry out” the section’s provisions. As shown in this analysis, Subpart F, GILTI, and section 965 do not apply to the same taxpayers as section 245A nor does section 245A require the foreign corporation to be a CFC. The transaction tax in section 965 applies to individual and passthrough owners. These provisions are sufficiently different that the Treasury’s efforts to reconcile them seem both overbroad and unauthorized.

It thus seems likely that courts will find Treasury Regulation section 1.245A-5 invalid.23 It is my view that Treasury cannot exercise its discretionary authority to draft regulations to cover up mistakes that should

21 Treasury Decision 9909, at 10 (Aug. 21, 2019).22 Section 7805(a) states: “Except where such authority is expressly given by this title to any person other than an officer or employee of the Treasury Department, the Secretary shall prescribe all needful rules and regulations for the enforcement of this title, including all rules and regulations as may be necessary by reason of any alteration of law in relation to internal revenue.”23 For a fuller discussion on the regulatory provisions, see Willis The Territorial DRD Regs Are Invalid, 164 Tax NoTes Federal 2265 (Sept. 30, 2019).

17

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

ABA TAX TIMESWinter • March 2021 • Vol. 40 No. 2

have been addressed through legislative technical corrections, even if the only way the TCJA could be salvaged as a reasonable international corporate scheme was for Treasury and the IRS to draft rules to complete the law. While it was once thought that these Herculean regulatory efforts could work, most now recognize that the task was impossible. Ultimately, it is taxpayers who will bear the burden of the TCJA’s taxing provisions—not solely by interpreting the burdensome regulations propping up the new laws but also by predicting which regulations the courts are most likely to invalidate as overreaching. This is why within days of the release of the temporary DRD regulations, practitioners warned that the participation exemption anti-abuse rule would spur litigation. Practitioners explored the uphill battle Treasury will have in defending these regulations even with its arguments about aggressive tax planning, when taxpayers should be able to rely on the effective dates provided in the statute for any change in law.24

IV. Conclusion

Treasury’s efforts represent the interests of the Treasury secretary as a member of the president’s cabinet to vigorously defend the administration’s trade policies. Treasury is clearly striving to protect executive branch goals and statements and ensure that a hastily drafted statute makes sense. Treasury took on the impossible task of making appropriate connections between the allowed deductions under sections 245A and 250 and the GILTI inclusions that Congress left undone in its haste, yet Treasury cannot ignore the law. As these broad reaches of regulatory discretion accumulate, TCJA interpretation loses any semblance of credibility.

This article argues therefore that the temporary and proposed section 245A regulations should be found invalid. Treasury should not be able to use its interpretative authority to expand the GILTI penalty tax in regulations promulgated under a Code provision intended to provide a 100-percent deduction to create a territorial tax system. These new retroactive burdens go beyond the language of the statute and, although uncertain, may well surpass congressional intent. Taxpayers will inevitably challenge the regulations in the courts, and it is almost certain that taxpayers will prevail. Congress should act now to remedy the statutory TCJA mess. ■

24 See Willis, GILTI as Charged: FDII Regulations Prove Harmful Tax Export Subsidy, 162 Tax NoTes 1481 (Mar. 25, 2019).

18

Published in ABA Tax Times, March 2021. © 2021 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. ISSN 2381-5868.

An Online Publication of the ABA Tax Section Winter • March 2021 • Vol. 40 No. 2

AT COURT

NY Uber Driver a Covered “Employee” for Unemployment Insurance Purposes; CA Prop. 22 Provides Limited Employment Benefits to Gig Workers; U.S. Labor Dept. Defines “Independent Contractor”

By Edward Leyden, Leyden Law LLC, Bowie, MD

The last third of 2020 saw several important developments in the arena of worker classification. For a general review of the classification issue, see the article published in the summer edition of ABA Tax Times.1

I. New York Decision on Uber Drivers

In the last weeks of the year, an intermediate appellate court for New York held, in the Matter of the Claim of Colin Lowry (Uber Tech., Inc. – Commissioner of Labor),2 that Uber Technologies, Inc. (Uber) exercises sufficient control over the drivers who utilize the company’s smart phone application (app) as to establish an employment relationship. This ruling comes in the wake of a decision in June 2020 by the New York Court of Appeals (New York’s highest court) in Matter of Vega (Postmates, Inc. – Commissioner of Labor)3 that a courier for an app-based delivery service was an employee for purposes of New York State Unemployment Insurance.