An examination of the relationship between service quality perception and customer satisfaction : A...

25

See discussions, stats, and author profiles for this publication at: https://www.researchgate.net/publication/242020859 An examination of the relationship between service quality dimensions, overall internet banking service quality and... Article in Marketing Intelligence & Planning · February 2009 DOI: 10.1108/02634500910928344 CITATIONS 68 READS 1,439 4 authors, including: Michel Roger Mark Rod Carleton University 73 PUBLICATIONS 577 CITATIONS SEE PROFILE Nicholas J. Ashill American University of Sharjah 82 PUBLICATIONS 1,024 CITATIONS SEE PROFILE All content following this page was uploaded by Michel Roger Mark Rod on 26 January 2015. The user has requested enhancement of the downloaded file. All in-text references underlined in blue are linked to publications on ResearchGate, letting you access and read them immediately.

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of An examination of the relationship between service quality perception and customer satisfaction : A...

Seediscussions,stats,andauthorprofilesforthispublicationat:https://www.researchgate.net/publication/242020859

Anexaminationoftherelationshipbetweenservicequalitydimensions,overallinternetbankingservicequalityand...

ArticleinMarketingIntelligence&Planning·February2009

DOI:10.1108/02634500910928344

CITATIONS

68

READS

1,439

4authors,including:

MichelRogerMarkRod

CarletonUniversity

73PUBLICATIONS577CITATIONS

SEEPROFILE

NicholasJ.Ashill

AmericanUniversityofSharjah

82PUBLICATIONS1,024CITATIONS

SEEPROFILE

AllcontentfollowingthispagewasuploadedbyMichelRogerMarkRodon26January2015.

Theuserhasrequestedenhancementofthedownloadedfile.Allin-textreferencesunderlinedinblue

arelinkedtopublicationsonResearchGate,lettingyouaccessandreadthemimmediately.

An examination of the relationshipbetween service quality

dimensions, overall internetbanking service quality and

customer satisfactionA New Zealand study

Michel RodSchool of Marketing & International Business,

Victoria University of Wellington, Wellington, New Zealand

Nicholas J. AshillSchool of Business and Management, American University of Sharjah,

Sharjah, United Arab Emirates, and

Jinyi Shao and Janet CarruthersSchool of Marketing & International Business,

Victoria University of Wellington, Wellington, New Zealand

Abstract

Purpose – The purpose of this paper is to examine the relationships among three dimensions ofservice quality that influence overall internet banking service quality and its subsequent effect oncustomer satisfaction in a New Zealand banking context.

Design/methodology/approach – Internet banking service customers of a national bank inNew Zealand completed a self-administered questionnaire. Data obtained from the customers wereanalysed using the SEM-based partial least squares (PLS) methodology.

Findings – The results show significant relationships among online customer service quality, onlineinformation system quality, banking service product quality, overall internet banking service qualityand customer satisfaction.

Originality/value – Little attention has been given in the literature to understanding the servicequality dimensions that influence overall internet banking service quality and the specific outcome ofcustomer satisfaction. By expanding previous research in internet banking service quality, this paperempirically examines the relationships between three service quality dimensions, overall internetbanking service quality and customer satisfaction.

Keywords Internet, Banking, Customer services quality, Customer satisfaction, Online operations,New Zealand

Paper type Research paper

IntroductionIn service industries in general and in the banking industry, in particular, the internet hasbeen explored and exploited as a means of improving service provision (Jun et al., 2004).

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/0263-4503.htm

Internet bankingservice quality

103

Received May 2008Revised August 2008

Accepted September 2008

Marketing Intelligence & PlanningVol. 27 No. 1, 2009

pp. 103-126q Emerald Group Publishing Limited

0263-4503DOI 10.1108/02634500910928344

Banks are not only competing in traditional banking services, but have also expanded thescope of competition to an e-environment with internet banking services (Gonzalez et al.,2004). These banks are introducing internet banking as an assurance to their customersthat they will be able to maintain a competitive quality of service in the future, in efforts toavoid losing their customers to the branches of foreign banks (Jenkins, 2007). NewZealanders have been avid adopters of internet banking (Fisher, 2001) and offeringinternet banking is no longer regarded as a competitive advantage but a competitivenecessity (Gan et al., 2006). internet banking helps banks to build and maintain closerelationships with their customers, reduces operating and fixed costs (Mols, 2000), andachieves more efficient and enhanced financial performance (DeYoung et al., 2007). Fromthe customer perspective, research has shown that consumers benefit from internetbanking in respect to enhanced control, ease of use, and reduced transaction charges(Unsal and Movassaghi, 2001).

The current research seeks to examine the dimensions and one particularoutcome[1] of internet banking service quality in New Zealand. Specifically, our studyhas two objectives. First, we build on the exploratory work of Jun and Cai (2001) whoidentified three broad conceptual categories related to internet banking service quality,and empirically test the relationships between:

. online customer service quality;

. online information system quality; and

. banking service product quality and overall internet banking service quality.

Second, we examine the relationship between overall internet banking service qualityand customer satisfaction.

In the next section, we present the relevant literature leading to our specific researchhypotheses. This is followed by discussions of the research method and results of theempirical study we conducted in a National Bank in New Zealand. We conclude thepaper with the implications of the results and avenues for future research.

Review of the relevant literatureService quality has been identified as a critical success factor for organisations to buildtheir competitive advantage and increase their competitiveness. Pioneering work byParasuraman et al. (1985) led to a list of ten determinants (reliability; responsiveness;competence; access; courtesy; communication; credibility; security; understanding thecustomer; and tangibles) of service quality as a result of their focus group studies withservice providers and customers which subsequently resulted in the development ofthe SERVQUAL instrument with these ten attributes distilled into five overalldimensions of service quality. The five dimensions of SERVQUAL are (Parasuramanet al., 1988, 1991):

(1) tangibles, which pertain to the physical facilities, equipment, personnel andcommunication materials;

(2) reliability, which refers to the ability to perform the promised servicesdependably and accurately;

(3) responsiveness, which refers to the willingness of service providers to helpcustomers and provide prompt service;

MIP27,1

104

(4) assurance, which relates to the knowledge and courtesy of employees and theirability to convey trust and confidence; and

(5) empathy, which refers to the provision of caring and individualised attention tocustomers.

If one looks to the literature on traditional banking and service quality, work byJohnston (1995) revealed that there are some service quality determinants that arepredominantly satisfiers and others that are predominantly dissatisfiers with the mainsources of satisfaction being attentiveness, responsiveness, care and friendliness. Themain sources of dissatisfaction are integrity, reliability, responsiveness, availabilityand functionality. Subsequent work by Johnston (1997) illustrates that certain actions,such as increasing the speed of processing information and customers, are likely tohave an important effect in terms of pleasing customers; however other activities, suchas improving the reliability of equipment, will lessen dissatisfaction rather than delightcustomers and suggests that it is more important to ensure that the dissatisfiers aredealt with before the satisfiers. Johnson et al. (2008) also illustrate that the influence ofvarious dissatisfies such as inefficiency, chaos, incompetence and isolation on onlinebanking customer satisfaction is mediated by consumer performance ambiguity andconsumer trust in the technology. Thus, in order to maintain and expand theircustomer base, it is critical for banks to understand the criteria consumers use toevaluate internet banking services and how these impact on their perceptions of overallinternet banking service quality, and satisfaction with e-service and banking overall.

This leads to the relationship between service quality and satisfaction. In consumersatisfaction/dissatisfaction literature, expectation – disconfirmation has been givenattention where disconfirmation refers to the difference between prepurchaseexpectations and perceptions of postpurchase (Peter and Olson, 1990). There are twotypes of disconfirmation: negative disconfirmation and positive disconfirmation.Negative disconfirmation occurs when product performance is less than expected,hence consumers are more likely to be dissatisfied, and positive disconfirmation occurswhen product performance is better than expected, which is more likely to result insatisfaction. Specifically, consumer satisfaction is the result of an evaluative processthat compares prepurchase expectations with perceptions of performance during andafter the consumption experience (McQuitty et al., 2000). Despite the cognitiveprocesses, some researchers suggest that affections (Homburg and Giering, 2001) andcumulative experience (Anderson et al., 1994) could contribute to consumer satisfaction.

In the context of internet banking, there is a growing body of research that haslooked at influences on customer satisfaction. Jayawardhena and Foley (2000b)illustrated that such web site features as speed, web site content and design,navigation, interactivity and security all influence user satisfaction whereas Broderickand Vachirapornpuk (2002) found that the level and nature of customer participationhad the greatest impact on the quality of the service experience and issues such ascustomers’ zone of tolerance, the degree of role understanding by customers andemotional response potentially determined, expected and perceived service quality.Similarly, Lassar et al. (2000) demonstrated that a functional-quality based model did abetter job of predicting customer satisfaction than a SERQUAL instrument for thosecustomers actively involved or highly interested in service delivery. Research thatinvestigates the criteria customers use in evaluating internet banking service quality

Internet bankingservice quality

105

and their satisfaction with the bank overall is still a relatively new area (Jayawardhena,2004; Sohail and Shaikh, 2008). Han and Baek’s (2004) empirical study of onlinebanking in Korea found strong relationships between online banking service, customersatisfaction, and customer retention.

Table I illustrates additional research that has looked at online service quality.Yang and Fang (2004) found that ease of use and usefulness are important factors in

evaluating online service quality. Doll and Torkzadeh (1988) identified five qualitydimensions that have an impact on “end-user” satisfaction in an online environment:content, accuracy, format, ease of use, timeliness. The reliability and validity of thesedimensions were confirmed by Doll et al. (1994) and Hendrickson and Collins (1996).Zeithaml et al. (2001) developed e-SERVQUAL for measuring e-service quality, identifying11 dimensions: access; ease of navigation; efficiency; flexibility; reliability;personalisation; security/privacy; responsiveness; assurance/trust; site aesthetics; andprice knowledge. In terms of a satisfactory online retailing experience, Wolfinbarger andGilly (2002) uncovered four dimensions: web site design, reliability, privacy/security,and customer service. With regard to the success of a web site, Liu and Arnett (2000)suggested four factors. They are: system use, system design quality, information quality,and playfulness. Exploratory research done in the context of online retailing by Jun et al.(2004) revealed reliable/prompt responses, attentiveness, and ease of use had considerableimpacts on both customers perceived overall service quality and satisfaction. It alsoindicated that there is a significant positive relationship between overall service qualityand satisfaction. Thus, from the literature it seems that the key drivers are ease of use andreliability. However, other factors such as accuracy, responsiveness and web site designare also important.

During the past several years, several conceptual and empirical studies have attemptedto address the key attributes of service quality directly or indirectly related to onlineservice and, SERVQUAL has been widely accepted and used in measuring informationsystem service quality (van Dyke et al., 1997). Yang and Jun (2002) redefined the traditionalservice quality dimensions in the context of online services, and suggested an instrumentconsisting of seven online service dimensions (reliability, access, ease of use,personalisation, security, credibility, and responsiveness). Joseph et al. (1999) consideredbanking service quality with respect to technology use, such as ATMs, telephone, and the

Authors Key dimensions discussed

Doll and Torkzadeh (1988) Content, accuracy, format, ease of use, timelinessJun et al. (2004) Reliable/prompt responses, attentiveness, and ease of useLiu and Arnett (2000) System use, system design quality, information quality,

playfulnessParasuraman et al. (2005) Privacy/security; information content and availability; web site

design or graphic style; ease of use; and reliability/fulfillmentPikkarainen et al. (2006) Content, ease of use, accuracyWolfinbarger and Gilly (2002) Web site design, reliability, privacy/security, customer serviceYang and Fang (2004) Ease of use and usefulness are important factors in evaluating

online service qualityZeithaml et al. (2001) Access; ease of navigation; efficiency; flexibility; reliability;

personalisation; security/privacy; responsiveness; assurance/trust;site aesthetics; price knowledge

Table I.Selected online servicequality literature

MIP27,1

106

internet and identified six dimensions. They were convenience/accuracy;feedback/complaint management; efficiency; queue management; accessibility; andcustomisation. A UK study uncovered five key service quality attributes, such as securityrelated issues, convenience, speed and timeliness of the service, and productvariety/diverse features (White and Nteli, 2004). Shamdasani et al. (2008) foundthat perceived control has the strongest influence on service quality evaluations and thatperceived speed of delivery, reliability and enjoyment also have a significant impact onservice quality perceptions.

Although there have been attempts to use the SERVQUAL instrument in traditionalretail banking contexts across different countries (Arasli et al., 2005; Cui et al., 2003;Jabnoun and Al-Tamimi, 2003; Najjar and Bishu, 2006), there has been far lessattention to its utility in assessing service quality and customer satisfaction in aninternet banking context. The research model and hypotheses which guide thisresearch follow. Against this background, we now present our conceptual frameworkand hypotheses drawing upon the extant literature.

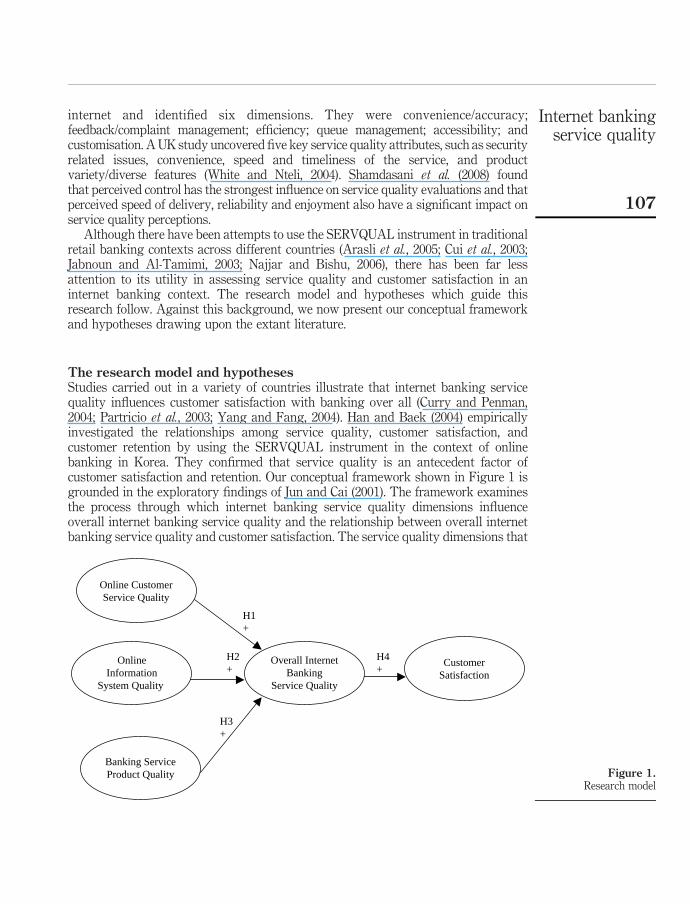

The research model and hypothesesStudies carried out in a variety of countries illustrate that internet banking servicequality influences customer satisfaction with banking over all (Curry and Penman,2004; Partricio et al., 2003; Yang and Fang, 2004). Han and Baek (2004) empiricallyinvestigated the relationships among service quality, customer satisfaction, andcustomer retention by using the SERVQUAL instrument in the context of onlinebanking in Korea. They confirmed that service quality is an antecedent factor ofcustomer satisfaction and retention. Our conceptual framework shown in Figure 1 isgrounded in the exploratory findings of Jun and Cai (2001). The framework examinesthe process through which internet banking service quality dimensions influenceoverall internet banking service quality and the relationship between overall internetbanking service quality and customer satisfaction. The service quality dimensions that

Figure 1.Research model

Online CustomerService Quality

OnlineInformation

System Quality

Banking ServiceProduct Quality

Overall InternetBanking

Service Quality

CustomerSatisfaction

H1+

H2+

H3+

H4+

Internet bankingservice quality

107

influence overall internet banking service quality are: online customer service quality;online system quality; and banking service product quality.

Gap theory suggests that differences between customers’ expectations about theperformance of service providers and their assessments of the actual performance of aspecific firm drive their perception of service quality and these perceptions of servicequality will be influenced by both the interpersonal and non-human interactions withservice providers (Jun and Cai, 2001). The present study subscribes to Jun and Cai(2001, p. 277) in referring to the traditional banking service quality and customerservice literature as “focused on the interpersonal service encounter”, whereas onlineinformation system quality is defined as “concentrated on computer andnetworking-based impersonal interactions, with a particular emphasis on end-usercomputing satisfaction” (Jun and Cai, 2001, p. 277). Similarly, Yang et al. (2004, p. 1153)concluded “the principal goal of information systems service is to enable customers tofunction independently and to conduct numerous transactions on their own. Inaddition, as end-users, consumers often seek desired product and service informationthrough Web sites”. Drawing on the above literature, the current study defines onlineinformation system quality as the extent to which the information system performs itsintended function of enabling customers to carry out transactions and informationsearches online. Following Yang et al. (2004) we define banking service product qualityas the number and relevance to customers of internet banking products and services.Overall, internet banking service quality is conceptualised in the current study as theperceived level of service quality of banking services delivered online (Jun and Cai,2001). Finally, customer satisfaction is defined as customer satisfaction with internetbanking service quality and the bank overall (Jun and Cai, 2001). The hypothesisedrelationships among these variables are discussed below.

Relationship between online customer service quality and overall internet banking servicequalityAlthough they do not experience face-to-face interaction with bank staff, onlinecustomers expect to be treated with respect, provided with valuable information bythe web site, and receive prompt and reliable service (Jun and Cai, 2001). Intuitively, weexpect that the quality of interaction between customers and service providers(i.e. banks) will be associated with overall service quality. Previous research hasidentified the relative importance of key dimensions of customer service quality tooverall service quality (Rosen and Karwan, 1994) and in the context of internet banking,Jayawardhena (2004) has developed a number of measures that can be used to measurecustomer service quality in e-banking services across five dimensions, namely, access,web site interface, trust, attention and credibility. The more positive customers’perceptions of online customer service quality in an internet banking environment, thegreater the likelihood that overall online service quality will be perceived to be high.Using the SERVQUAL instrument, Han and Baek (2004) for example, found that therewas a positive relationship between online customer service quality and overall internetbanking service quality. In light of the above we suggest our first hypothesis:

H1. Online customer service quality is positively related to overall internetbanking service quality.

MIP27,1

108

Relationship between online information system quality and overall internet bankingservice qualityOnline information system quality is vital to internet banking users’ perceptions ofoverall internet banking service quality because it is a key enabler of the services theywish to use (Jun and Cai, 2001). If the information system does not perform well,customers are not able to reliably make transactions or access information,compromising their perceptions of service quality (Yang et al., 2004). If the web site isnot informative, or the design of the web site is not user friendly, this will have a negativeimpact on customers’ perceptions of overall internet banking service quality. The moreconveniently customers can interact with the bank through the web site, the safer theironline transactions, and the more error-free the transactions, the better customers’perceptions with the service quality provided online by the bank. Thus, our secondhypothesis is:

H2. Online system quality is positively related to overall internet banking servicequality.

Relationship between banking service product quality and overall internet bankingservice qualityStudies have shown that banking service product quality is an important factor thatinfluences customers’ perceptions of overall banking service quality (Jayawardhenaand Foley, 2000a). Strieter et al. (1999) note that one of the most important developmentsin banking is the increased emphasis on marketing a wide array of financial services.Mols (2000) argues that the characteristics and features of the products offered to thecustomers can attract more new customers. Cho and Park (2001) argue that variety ofproducts influences internet shopper satisfaction. Thus, a wide product range anddiverse features are important in influencing customers’ perceptions of internetbanking service quality (Jun and Cai, 2001; Yang et al., 2004), online customers preferfirms that offer a variety of services and diverse features. Hence, our third hypothesis is:

H3. Banking service product quality is positively related to overall internetbanking service quality.

Relationship between overall internet banking service quality and customer satisfactionThere appears to be a consensus emerging that satisfaction refers to the outcome ofindividual service transactions and the overall service encounter, whereas servicequality is the customer’s overall impression of the relative inferiority/superiority of theorganisation and its services (Johnston, 1995). Numerous studies have shown thatservice quality is positively related to customers’ satisfaction in an online environment(Han and Baek, 2004; Yang and Fang, 2004). Intuitively, the more positive customers’perception of online service quality, the better their overall satisfaction with the bank islikely to be. The strength of this relationship depends on the weight given bycustomers to overall internet banking service quality relative to other attributes of thebank. Thus, our fourth hypothesis is:

H4. Overall internet banking service quality is positively related to customersatisfaction.

Internet bankingservice quality

109

Research methodSampleTo collect the data for the study, a total of 300 individualised questionnaires weredistributed by mail to a systematic random sample of customers of a major NewZealand retail bank with internet banking services as well as branches. This researchemployed a systematic sampling technique. The sample was chosen by selecting arandom starting point and then picking every 100th individual customer in successionfrom the bank’s derived database. Applying this technique, 300 individuals wereselected. These customers were identified as internet banking users at the time of thesurvey and were made aware that the questionnaire related to their online bankingexperiences. By the cut-off date for data collection, 72 usable questionnaires werereturned for a response rate of 24.0 per cent. Just under 55 per cent of the respondentswere female. Just over one-third (33.8 per cent) had secondary education and 54.9 percent had college/university education. Respondents were spread across all age groupswith 15.3 per cent of customers between the ages of 18 and 24, 20.8 per cent betweenthe ages of 25 and 34, 26.4 per cent between the ages of 35 and 44, 25 per cent betweenthe ages of 45 and 54 and 12.5 per cent 55 years and older. These profiles werecomparable to the total population of the bank’s internet customer base.

To ensure that sample bias and nonresponse bias were not present, appropriatecomparisons were made between early and late respondents, and between respondentsand nonrespondents (Armstrong and Overton, 1977). Early and late respondents werecompared on all variables of interest, using traditional t-tests following Armstrong andOverton’s (1977) recommendations. Unpaired t-tests were used to compare the groupmeans to each other. Differences between the means were not statistically significant atthe 0.05 level, indicating that there were no differences between the group means of earlyand late respondents. Hence, it was assumed that non-response bias was not a problem.At the same time, early and late respondents were compared and following therecommendation of Mentzer and Flint (1997), 30 nonrespondents were contacted andasked five questions (survey items) relating to the hypotheses. There was no statisticallysignificant difference between the answers of respondents and nonrespondents to thesequestions.

MeasurementIn designing the survey instrument the relevant writings in the online service qualityliterature were canvassed (Han and Baek, 2004; Yang et al., 2004). The Appendix detailsthe items used to measure each construct. Following Han and Baek (2004), and Jun andCai (2001) we defined and measured online customer service quality and onlineinformation system quality as multidimensional constructs. Specifically, online customerservice quality was operationalised using Han and Baek’s (2004) four dimensions ofonline customer service quality (tangibles, reliability, responsiveness and empathy).Tangibles and reliability were measured with three items each, while responsivenesswas measured with two items and empathy was measured with four items.Online information system quality was operationalised with six dimensions (ease ofuse, accuracy, security/privacy, contents, timeliness, and aesthetics) from the work of Junand Cai (2001). In total, 15 items were used to measure these six dimensions. Bankingproduct service quality was operationalised using five items adapted from the work ofJun and Cai (2001). Overall, internet banking service quality consisted of two items from

MIP27,1

110

the work of Yang et al. (2004): overall online service quality of the bank; and overallperception of the bank as a good supplier of banking services. Finally, customersatisfaction was measured with four items (Yang et al., 2004). Responses to thequestionnaire items were elicited on five-point scales ranging from “5 ¼ strongly agree”to “1 ¼ strongly disagree” (Appendix).

All constructs were deemed reflective constructs since the items reflect the meaningof the construct. Reflective indicators are created under the perspective that they allmeasure the same underlying phenomenon (Chin, 1998). We defined and measuredonline customer service quality as a multidimensional construct and formed compositemeasures for each dimension by averaging scores across items representing thatdimension. Specifically, we used the composite scores of each set of items comprisingtangibles, reliability, responsiveness and empathy to measure online customer servicequality since the use of composite scores to represent the construct as a partialaggregation model acknowledges its multidimensional nature (Bagozzi and Heatherton,1994). Strong correlations among tangibles, reliability, responsiveness, and empathyprovided empirical justification for treating the four as indicators of online customerservice quality. We followed the same procedure for the measurement of onlineinformation system quality. Similarly, strong correlations among ease of use, accuracy,security/privacy, content, timeliness and aesthetics provided empirical justification fortreating the six as indicators of online information system quality.

Owing to the self-report nature of the survey, method variance is identified as apotential issue. Spector (1987) reported that the most frequently found sources of methodvariance in self reports are acquiescence and social desirability bias. The surveyinstrument was also organised into various sections by separating the independent anddependent variables in an effort to reduce single-source method bias (Podsakoff et al.,2003). Reynolds’ (1982) short form of the Marlowe-Crowne Social Desirability Scale(Crowne and Marlowe, 1960) was also included in the survey. Examining thecorrelations of the social desirability measure with all of the items used in the studyrevealed that social desirability bias was not an issue in these data. A further post hoctest for common method bias, a Harman’s (1967) one-factor test was also performed.According to this test, if a single factor emerges or one factor accounts for more than50 per cent of the variance in the variables, common method variance is present(Podsakoff et al., 2003). Our analysis showed that no general factor was present.

Following Podsakoff et al. (2003), we also specified, besides substantive factors, acommon method factor whose indicators include all the principal construct items in theresearch model. The result is the proportion of the variance explained by the commonmethod. Our results showed that the average explained variance of substantiveindicators is 0.77, while the average method-based variance is 0.04. The subsequentratio of substantive variance to method variance is 19.5:1, with no significant methodfactor loadings detected for all but two items at p , 0.05. This analysis also supportsthe conclusion that common method bias did not impact our results. Furthermore, thestructural model results reported later show different levels of significance for pathcoefficients, which prior work suggests provides additional evidence that commonmethod bias did not influence the statistical results (Patnayakuni et al., 2006).

The next step in data analysis involved model estimation using the soft-modellingSEM methodology partial least squares (PLS Graph version 3.00). PLS has a rigorousmathematics base, but the mathematical model is soft in that it makes no

Internet bankingservice quality

111

measurement, distributional or sample size assumptions. Lohmoller (1989) argues thatit is neither the concepts nor the models nor even the estimation techniques that are“soft”, only the distributional assumptions. Results are also restricted to predictiveinferences, i.e. prediction not causality (Wold, 1985) because conditions of a closedsystem are not met. We justify our use of PLS given the small sample size and our useof measures that are not well established but are grounded in exploratory research(Chin and Newstead, 1999).

Means and standard deviations of the model constructs are shown in Table II.Frequency analysis of the 21 measures indicated no problems of floor or ceiling effectsin the measurements. The usable response number (n ¼ 72) is also above therecommended minimum required for model estimation. PLS requires a minimumsample size that equals ten times the greater of the number of items comprising themost complex formative construct or the largest number of predictors leading to anendogenous construct (Barclay et al., 1995). In this study, the most complex regressioninvolved three predictors leading to the endogenous construct, overall internet banking

Variable Factor loading

Overall internet banking service qualityic ¼ 0.93, mean score ¼ 4.27, a ¼ 0.86, SD ¼ 0.76, AVE ¼ 0.870Ovosq 0.9255Ovexp 0.9395Customer satisfactionic ¼ 0.92, mean score ¼ 4.42, a ¼ 0.88, SD ¼ 0.63, AVE ¼ 0.740Ovservic 0.8955Ovsatis 0.8560Ovproduc 0.8821Ovxyz 0.8034Online customer service qualityic ¼ 0.91, mean score ¼ 4.09, a ¼ 0.86, SD ¼ 0.64, AVE ¼ 0.706Reliabit 0.8840Response 0.8278Tangible 0.7587Empathy 0.8844Online information system qualityic ¼ 0.92, mean score ¼ 4.26, a ¼ 0.87, SD ¼ 0.63, AVE ¼ 0.649Aestheti 0.7560Timeline 0.7777Contents 0.7944Easeofus 0.8499Security 0.7601Accuracy 0.8872Banking service product qualityic ¼ 0.90, mean score ¼ 4.08, a ¼ 0.86, SD ¼ 0.74, AVE ¼ 0.644Range 0.7129Features 0.8510Free 0.7604Function 0.8254Menu 0.8538

Notes: “ic” is internal consistency measure; a is Cronbach’s a; AVE is average variance extracted

Table II.Convergent anddiscriminant validity ofthe model constructs

MIP27,1

112

service quality, thus indicating that the minimum sample requirement for statisticalanalysis is 30 usable responses.

The test of the measurement model includes the estimation of convergent anddiscriminant validity of the instrument items. Convergent validity of the measurementmodel was assessed by three measures: item reliability, construct (composite) reliability,and average variance extracted (AVE) (Fornell and Larcker, 1981). Item reliability wasevaluated by the size of the loadings of the measures on their corresponding constructs.The loadings should be at least 0.60 and ideally at 0.7 or above (Chin, 1998) indicatingeach measure is accounting for 50 per cent or more of the variance of the underlyinglatent variable (Fornell and Larcker, 1981). Table II shows that all loadings exceeded0.70, thus indicating adequate convergent validity.

Composite reliability was assessed on the basis of internal consistency. The internalconsistency measure is similar to Cronbach’s a. Cronbach’s a assumes parallelmeasures, and represents a lower bound of composite reliability (Chin, 1998). Fornell andLarcker (1981) suggested that the measure of internal consistency is better thanCronbach’sa since it uses the item loadings obtained within the nomological network orcausal model. Table II illustrates that the composite reliability was satisfactory.

Convergent validity is adequate when constructs have an AVE of at least 0.50(Fornell and Larcker, 1981). When AVE is greater than 0.50, the variance shared with aconstruct and its measures is greater than the error. As shown in Table II all theconstructs have an AVE score above 0.50.

Discriminant validity was assessed using two methods. First, we examined thecross-loadings of the constructs and the measures; second, we compared the squareroot of the AVE for each construct with the correlation between the construct and otherconstructs in the model. Going down the columns in Table III, the correlations of theconstruct with its measures were higher than the correlations with any other measures.Similarly, going across the rows in the table, the correlations of the measures with itsconstruct were higher than the correlations with any other construct.

Chin (1998) states that if the square root of the AVE for each construct is larger thanthe correlation between the construct and any other construct in the model, then themeasures should be considered to have adequate discriminant validity. Table IV showsall constructs in the estimated model satisfied this criterion. Since none of theoff-diagonal elements exceeded the respective diagonal element, the criteria fordiscriminant validity were considered satisfied.

Overall, the measurement model results provided support for convergent anddiscriminant validities of the measures used in this research.

ResultsThe structural model was evaluated using the R 2 for the dependent constructs and thesize, t-statistics and significance level for the structural path coefficients. Thet-statistics were estimated using the bootstrap resampling procedure (100 resamples).The results of the structural model are shown in Table V.

The results demonstrate that the structural model explains 64.3 per cent of thevariance in overall internet banking service quality and 68.4 per cent of the variance incustomer satisfaction. The results show that online customer service quality and onlineinformation system quality are significantly and positively related to overall internetbanking service quality. Thus, H1 and H2 are supported. Although banking service

Internet bankingservice quality

113

product quality does not have a significant relationship with overall internet bankingservice quality ( p , 0.05) the relationship is marginally supported at p , 0.10. Thus,there is marginal support for H3. The structural model results also show a significantand positive relationship between perceptions of overall internet banking servicequality and customer satisfaction. Therefore, H4 is supported.

Overall internetbanking service

qualityCustomer

satisfaction

Onlinecustomerservicequality

Onlineinformation

system quality

Bankingserviceproductquality

Overall internetbanking servicequality 0.933Customersatisfaction 0.827 0.860Online customerservice quality 0.706 0.737 0.840Onlineinformationsystem quality 0.775 0.753 0.776 0.806Banking serviceproduct quality 0.664 0.731 0.675 0.708 0.802

Note: Square root of AVE in the diagonal

Table IV.Correlation amongconstruct scores

Measures

Overall internetbanking service

qualityCustomer

satisfactionOnline customerservice quality

Onlineinformation

system qualityBanking serviceproduct quality

Ovosq 0.9255 20.053 0.009 20.058 20.060Ovexp 0.9395 0.048 20.008 0.052 0.050Ovservic 20.027 0.8955 20.001 20.063 20.097Ovsatis 0.059 0.8560 0.005 0.120 0.059Ovproduc 20.034 0.8821 20.041 0.016 0.063Ovxyz 20.004 0.8034 0.039 20.087 20.030Reliabit 0.008 20.059 0.8840 0.031 20.036Response 20.059 20.062 0.8278 20.071 20.120Tangible 0.085 0.107 0.7587 0.094 0.081Empathy 20.047 0.006 0.8844 20.070 0.062Aestheti 0.026 0.070 0.080 0.7560 0.038Timeline 20.100 20.129 20.011 0.7777 20.028Contents 20.026 0.014 20.047 0.7944 0.011Easeofus 0.018 0.009 20.010 0.8499 20.010Security 0.073 0.048 20.053 0.7601 20.007Accuracy 20.016 20.035 0.039 0.8872 20.005Range 0.040 20.010 0.086 20.015 0.7129Features 20.063 20.046 20.002 20.001 0.8510Free 20.121 20.090 0.016 20.024 0.7604Function 0.089 0.113 20.062 0.067 0.8254Menu 0.003 20.015 20.018 20.043 0.8538

Table III.Correlation betweenmeasures and constructs

MIP27,1

114

Finally, we performed the Stone-Geisser test of predictive relevance to assess model fitin PLS analysis (Geisser, 1975; Stone, 1974). q-Square is a measure of how well theobserved values are reproduced by the model and its parameter estimates. q-Squaregreater than 0 implies that the model has predictive relevance, whereas q-square lessthan 0 suggest that the model lacks predictive relevance. In our main PLS model,q-square is 0.54 for overall internet banking service quality and 0.48 for customersatisfaction.

Discussion and managerial implicationsBased on the work of Jun and Cai (2001), Han and Baek (2004) and Yang et al. (2004),this research presented a model to explain how three dimensions of internet bankingservice quality influence perceptions of overall internet banking service quality, andhow these overall perceptions of internet service quality influence customers’satisfaction. All hypotheses were confirmed albeit with H3 marginally. Our resultssuggest that online information system quality is a significantly stronger predictor ofoverall internet banking service quality than both online customer service quality andbanking service product quality individually and when combined.

The significant relationship between online customer service quality and overallinternet banking service quality indicates that the quality of customer service isimportant for banks in the context of internet banking. Even in the absence offace-to-face interactions, reliability, responsiveness, tangibles and empathy are stillimportant to customers. These dimensions directly affect customer perceptions ofoverall internet banking service quality which influences overall customer satisfactionwith the bank.

Online information system quality is also significantly related to overall internetbanking service quality perceptions. A high-performance information system enablescustomers to conduct banking transactions on their own through the computer system.Without direct interaction with bank staff, ease of use, accuracy, security, timeliness,contents and aesthetics are critical to enhancing customer perception of overall internetbanking service quality. The strong positive association between overall internetbanking service quality and customer satisfaction suggests that when overall internetbanking service quality is perceived to be high, customers are more likely to besatisfied with their online service and consequently will be more satisfied with theirbank. Overall, the contribution that this research makes is in examining five relevantand important constructs in one model. Specifically, we empirically examine the

Proposedeffect

Pathcoefficient

Observedt-value

Sig.level

Overall internet banking service quality ( R 2 ¼ 0.643)H1. Online customer service quality þ 0.208 1.9562 * *

H2. Online information system quality þ 0.485 3.6163 * * *

H3. Banking service product quality þ 0.180 1.4533 *

Customer satisfaction ( R 2 ¼ 0.684)H4. Overall internet banking service quality þ 0.827 24.5843 * * *

Notes: p-values: *, 2 , 0.10; * *, 2 , 0.050; * * *, 2 , 0.001

Table V.Structural (inner) model

results

Internet bankingservice quality

115

relationship between three service quality dimensions, overall internet banking servicequality and customer satisfaction in a New Zealand context. This exploration ofthose service quality dimensions that lead to overall internet banking service qualityand its effect on overall satisfaction is a novel contribution to the literature.

The research findings suggest a number of implications for online banking servicesmanagement. This includes the need for managers to acknowledge that the provisionof online service quality is an expectation of bank customers. It is possible thatcustomers see online service as separate to their relationship with other bankingactivities (and the bank as a whole) and merely perceive it as an expected service. Thefindings suggest the following specific directions for managers regarding onlinebanking service provision:

. When assessing online service quality, managers should not employ generalmeasures of online service quality, but should ensure that they are evaluating allaspects of their specific online service where there may be a need to useindustry-specific measures.

. Online banking service providers should continually monitor the level offulfilment of personal needs and satisfaction with the organisation of the site ifthey wish customers to remain loyal to the online service.

. Finally, there is a need to look beyond simply providing good online service sitesto build strong, enduring relationships with customers.

Conclusions and future researchIt has been argued that internet banking helps banks to build and maintain closerelationships with their customers and reduces operating and fixed costs (Mols, 2000),with daily and frequent internet banking users emphasising “ease of use” and“aesthetics” for electronic fund transfer and foreign exchange transactions (Kam andRiquelme, 2007). Recent research demonstrates that as customers become moreacclimatised to internet banking; they use these services more often and we arebeginning to see attempts to investigate internet banking service quality and customersatisfaction in a global context. In a Malaysian internet banking context, Poon (2008)found that convenience of usage, accessibility, features availability, bank managementand image, security, privacy, design, content, speed, and fees and were significant withrespect to the users’ adoption of e-banking services; with privacy and security being themajor sources of dissatisfaction and accessibility, convenience, design and content beingsources of satisfaction. In Estonia, continued usage of internet banking services isdependent upon perceived usefulness (Eriksson and Nilsson, 2007). Shi and Fang (2006)showed that attributes including information quality, transaction speed, and securityplay significant roles in influencing attitude towards the adoption of internet banking inTaiwan. In Qatar, although recent research demonstrates that in order to attract moreusers to internet banking, in addition to ease of use, it is critical to develop secure andprivate internet banking systems that are trustworthy (Kassim and Abdullah, 2006).In Saudi Arabia, efficiency and security, fulfillment and responsiveness were found toinfluence customers’ perceptions of service quality (Sohail and Shaikh, 2008). In a UKcontext, Jayawardhena and Foley (2000b) illustrated that such web site features asspeed, web site content and design, navigation, interactivity and security all influenceuser satisfaction. More recent work in the area corroborates such factors as usefulness,

MIP27,1

116

ease of use, reliability, security, responsiveness, and continuous improvement in (Liaoand Cheung, 2008) and credibility, efficiency, problem handling and security (Siu andMou, 2005) in a Hong Kong internet banking context but to date, relatively little researchhas investigated the criteria customers use in evaluating overall internet bankingservice quality as a precursor to their overall satisfaction with the bank. This studyaddresses this paucity and examines the service quality dimensions that lead to overallinternet banking service quality and its resulting impact on overall customersatisfaction in a national bank in New Zealand.

In this study, the assurance dimension of SERVQUAL was dropped in the contextof online banking due to the unique features of online services. Online bankingcustomers heavily rely on the non-human interface of banking services. Thus, theirevaluations of service quality are mainly influenced by the features and the security ofonline bank web sites and they cannot accurately assess the assurance dimension ofSERVQUAL which is defined by the knowledge and courtesy of administrators (Hanand Baek, 2004). The study builds on previous research (Jun and Cai, 2001; Han andBaek, 2004; Yang et al., 2004) and extends this work by examining the relationshipsamong three quality constructs (online customer service quality, online informationsystem quality, and banking service product quality), overall internet banking servicequality, and customer satisfaction. In doing so, the study makes a contribution tounderstanding the key determinants of overall internet banking service quality.

The findings of this study have a number of implications for managers. Onlinecustomer service quality positively influences customers’ perceptions of overall internetbanking service quality offered by the bank. Consequently, bank management shouldplace emphasis on offering reliable, responsible, tangible and empathic customerservice. Moreover, the study reveals that online information system quality is the mostsignificant predictor of overall internet banking service quality. This suggests thatmanagement should ensure that the internet banking environment; especially the website as interface between the bank and its customers, has the navigational and visualcharacteristics, as well as practical considerations necessary for security and ease of use.Furthermore, overall internet banking service quality is strongly related to overallcustomer satisfaction with the bank. This suggests the relevance of delivering highquality service online to maintain and/or increase customers’ satisfaction with the bank.

With respect to study limitations, although the sample has the strength of being arandom sample of real world banking customers, the sample size may be consideredsmall. The data collection was part of the third author’s honours dissertation researchand as such, there were certain time and resource constraints. For this reason, a largersample size is desirable in future research. The sample is skewed to a particular ethnicgroup with 83.1 per cent of the respondents being European New Zealanders. Althoughthis is likely to be representative of the bank’s customer base, future research couldfocus on diversifying the samples across different ethic groups, gender, income, andeducation. Business-to-business internet banking service quality could also beinvestigated.

The research did not examine the relationship between customer satisfaction andcustomer retention. Future research could look at the relationships among overallinternet banking service quality, customer satisfaction and customer retention. Theseresearch findings would provide insights for banking service providers to keep theirexisting customer base and increase their profitability. Another avenue for future

Internet bankingservice quality

117

research is to examine the dimensions and outcome of internet banking service quality ina wider sample of banks, perhaps in different countries or even to try test the hypothesesin multiple service contexts, i.e. services delivered through internet channels (e.g. traveland insurance agents) in order to extend the model’s generalisability. The study did notcompare customer perceptions of internet banking service quality between internet-only banks versus bricks-and-mortar banks. Customers may have differentexpectations and perceptions of internet banking service quality from internet -onlybanks versus bricks-and mortar banks. The work of Lassar et al. (2000) suggests thatcustomers who use internet-only banking may be more “highly involved” than othersand without knowing whether our sample of customers use other banking channels,they may place more emphasis on some dimensions rather than others (e.g. the speed ofthe service delivery). Similarly, Eriksson and Nilsson (2007) found that ongoing use ofonline banking is negatively affected by multichannel satisfaction and customers do notseparate the service offerings of online channels from other channels.

An additional acknowledgement is that there has been academic debate over thestructure and conceptualisation of the SERVQUAL measurement tool, despite its useby practitioners in services. While service quality evaluations involve both processquality and outcome quality dimensions, SERVQUAL measures only the processquality dimensions, i.e. that it does not address the service encounter outcomes (Buttle,1996; Mangold and Babakus, 1991; Richard and Allaway, 1993) and it does not providegood measures of the importance of service attributes and dimensions. Thus, there isno academic consensus as to the nature or content of the service quality dimensions(Brady and Cronin, 2001; Cronin and Taylor, 1992) except that service quality is amultidimensional construct (Gronroos, 2001; Zineldin, 2002).

Finally, methodological limitation should be noted in that while many of the expectedrelationships have been observed here and are consistent with a theory of causality;these relationships do not demonstrate causality, since alternative explanations cannotbe ruled out. Thus, some might argue that the assumed relationship between servicequality leading to overall satisfaction might in fact, be in the opposite direction.

Note

1. Other possible outcomes that have been investigated in the literature include trust, loyalty,commitment or dissatisfaction/switching, bank preference (Floh and Treiblmaier, 2006).

References

Anderson, E.W., Fornell, C. and Lehmann, D.R. (1994), “Customer satisfaction, market share andprofitability”, Journal of Marketing, Vol. 58 No. 3, pp. 53-66.

Arasli, H., Katircioglu, S.T. and Mehtap-Smadi, S. (2005), “A comparison of service quality in thebanking industry: some evidence from Turkish- and Greek-speaking areas in Cyprus”,The International Journal of Bank Marketing, Vol. 23 Nos 6/7, pp. 508-26.

Armstrong, S.J. and Overton, T.S. (1977), “Estimating nonresponse bias in mail surveys”,Journal of Marketing Research, Vol. 14 No. 3, pp. 396-402.

Bagozzi, R.P. and Heatherton, T.F. (1994), “A general approach to representing multifacetedpersonality constructs: application to state self-esteem”, Structural Equation Modelling,Vol. 1 No. 1, pp. 35-67.

MIP27,1

118

Barclay, D., Higgins, C. and Thompson, R. (1995), “The partial least squares (PLS), approach tocausal modeling: personal computer adoption and use as an illustration (withcommentaries)”, Technology Studies, Vol. 2 No. 2, pp. 285-324.

Brady, M.K. and Cronin, J.J. Jr (2001), “Some new thoughts on conceptualizing perceived servicequality: a hierarchical approach”, Journal of Marketing, Vol. 65 No. 3, pp. 34-49.

Broderick, A.J. and Vachirapornpuk, S. (2002), “Service quality in internet banking: theimportance of customer role”, Marketing Intelligence & Planning, Vol. 20 No. 6, pp. 327-35.

Buttle, F. (1996), “SERVQUAL: review, critique, research agenda”, European Journal ofMarketing, Vol. 30 No. 1, pp. 8-34.

Chin, W.W. (1998), “Issues and opinion on structural equation modelling”, MIS Quarterly, Vol. 22No. 1, pp. 7-16.

Chin, W.W. and Newstead, P. (1999), “Structural equation modeling analysis with small samplesusing partial least squares”, in Hoyle, R. (Ed.), Statistical Strategies for Small SampleResearch, Sage, Thousand Oaks, CA, pp. 307-41.

Cho, N. and Park, S. (2001), “Development of electronic commerce user-consumer satisfactionindex (ecusi) for internet shopping”, Industrial Management & Data Systems, Vol. 101No. 8, pp. 400-5.

Cronin, J. and Taylor, S. (1992), “Measuring service quality: a reexamination and extension”,Journal of Marketing, Vol. 56 No. 3, pp. 55-68.

Crowne, D. and Marlowe, D. (1960), The Approved Motive, Wiley, New York, NY.

Cui, C.C., Lewis, B.R. and Park, W. (2003), “Service quality measurement in the banking sector inSouth Korea”, The International Journal of Bank Marketing, Vol. 21 Nos 4/5, pp. 191-201.

Curry, A. and Penman, S. (2004), “The relative importance of technology in enhancing customerrelationships in banking – a Scottish perspective”, Managing Service Quality, Vol. 14 No. 4,pp. 331-41.

DeYoung, R., Lang, W. and Nolle, D. (2007), “How the internet affects output and performance atcommunity banks”, Journal of Banking & Finance, Vol. 31 No. 4, pp. 1033-60.

Doll, W.J. and Torkzadeh, G. (1988), “The measurement of end-user computing satisfaction”, MISQuarterly, Vol. 12 No. 2, pp. 259-74.

Doll, W.J., Xia, W. and Torkzadeh, G. (1994), “A confirmatory factor analysis of the end-usercomputing satisfaction instrument”, MIS Quarterly, Vol. 18 No. 4, pp. 43-461.

Eriksson, K. and Nilsson, D. (2007), “Determinants of the continued use of self-servicetechnology: the case of internet banking”, Technovation, Vol. 27 No. 4, pp. 159-67.

Fisher, C. (2001), “Electronic banking: are you exposed?”, Chartered Accountants Journal ofNew Zealand, Vol. 80 No. 11, p. 15.

Floh, A. and Treiblmaier, H. (2006), “What keeps the e-banking customer loyal? A multigroupanalysis of the moderating role of consumer characteristics on e-loyalty in the financialservice industry”, Journal of Electronic Commerce Research, Vol. 7 No. 2, pp. 97-110.

Fornell, C. and Larcker, D.F. (1981), “Structural equation models with unobservable variablesand measurement error”, Journal of Marketing Research, Vol. 18 No. 3, pp. 39-50.

Gan, C., Clemes, M., Limsombunchai, V. and Weng, A. (2006), “A logit analysis of electronicbanking in New Zealand”, International Journal of Bank Marketing, Vol. 24 No. 6,pp. 360-83.

Geisser, S. (1975), “The predictive sample reuse method with applications”, Journal of theAmerican Statistical Association, Vol. 70, pp. 320-8.

Internet bankingservice quality

119

Gonzalez, M.E., Quesada, G., Picado, F. and Eckelman, C.A. (2004), “Customer satisfaction usingqfd: an e-banking case”, Managing Service Quality, Vol. 14 No. 4, pp. 317-30.

Gronroos, C. (2001), “The perceived service quality concept a mistake?”, Managing ServiceQuality, Vol. 11 No. 3, pp. 150-2.

Han, S. and Baek, S. (2004), “Antecedents and consequences of service quality in online banking:an application of the SERVQUAL instrument”, Advances in Consumer Research, Vol. 31,pp. 208-14.

Harman, H. (1967), Modern Factor Analysis, University of Chicago Press, Chicago, IL.

Hendrickson, A.R. and Collins, M.R. (1996), “An assessment of structure and causation of ISusage”, The Database for Advances in Information Systems, Vol. 27 No. 2, pp. 61-7.

Homburg, C. and Giering, A. (2001), “Personal characteristics as moderators of the relationshipbetween customer satisfaction and loyalty – an empirical analysis”, Psychology &Marketing, Vol. 18 No. 1, pp. 43-66.

Jabnoun, N. and Al-Tamimi, H. (2003), “Measuring perceived service quality at UAE commercialbanks”, The International Journal of Quality & Reliability Management, Vol. 20 Nos 4/5,pp. 458-72.

Jayawardhena, C. (2004), “Measurement of service quality in internet delivered services: thedevelopment and validation of an instrument”, Journal of Marketing Management, Vol. 20Nos 1/2, pp. 185-209.

Jayawardhena, C. and Foley, P. (2000a), “Overcoming constraints on electronic commerce:internet payment systems”, Journal of General Management, Vol. 24 No. 2, pp. 19-35.

Jayawardhena, C. and Foley, P. (2000b), “Change in banking sector – the case of internet bankingin the UK”, Internet Research Electronic Networking Application and Policy, Vol. 10 No. 1,pp. 19-30.

Jenkins, H. (2007), “Adopting internet banking services in a small island state: assurance of bankservice quality”, Managing Service Quality, Vol. 17 No. 5, pp. 523-37.

Johnson, D., Bardhi, F. and Dunn, D. (2008), “Understanding how technology paradoxes affectcustomer satisfaction with self-service technology: the role of performance ambiguity andtrust in technology”, Psychology & Marketing, Vol. 25 No. 5, pp. 416-43.

Johnston, R. (1995), “The determinants of service quality: satisfiers and dissatisfiers”,International Journal of Service Industry Management, Vol. 6 No. 5, pp. 53-71.

Johnston, R. (1997), “Identifying the critical determinants of service quality in retail banking:importance and effect”, The International Journal of Bank Marketing, Vol. 15 No. 4,pp. 111-6.

Joseph, M., McClure, C. and Joseph, B. (1999), “Service quality in the banking sector: the impact oftechnology on service delivery”, The International Journal of Bank Marketing, Vol. 17No. 4, pp. 182-93.

Jun, M. and Cai, S. (2001), “The key determinants of internet banking service quality: a contentanalysis”, The International Journal of Banking Marketing, Vol. 19 No. 7, pp. 276-91.

Jun, M., Yang, Z. and Kim, D. (2004), “Customers’ perceptions of online retailing service qualityand their satisfaction”, International Journal of Quality & Reliability Management, Vol. 21No. 8, pp. 817-40.

Kam, B. and Riquelme, H. (2007), “An exploratory study of length and frequency of internetbanking usage”, Journal of Theoretical and Applied Electronic Commerce Research, Vol. 2No. 1, pp. 76-85.

MIP27,1

120

Kassim, N. and Abdullah, A. (2006), “The influence of attraction on internet banking:an extension to the trust-relationship commitment model”, International Journal of BankMarketing, Vol. 24 No. 6, pp. 424-42.

Lassar, W.M., Manolis, C. and Winsor, R.D. (2000), “Service quality perspectives and satisfactionin private banking”, International Journal of Bank Marketing, Vol. 18 No. 4, pp. 244-71.

Liao, Z. and Cheung, M.T. (2008), “Measuring consumer satisfaction in internet banking: a coreframework”, Association for Computing Machinery. Communications of the ACM, Vol. 51No. 4, pp. 47-51.

Liu, C. and Arnett, K.P. (2000), “Exploring the factors associated with web site success in thecontext of electronic commerce’”, Information & Management, Vol. 38 No. 1, pp. 23-33.

Lohmoller, J.B. (1989), Latent Variable Path Modelling with Partial Least Squares,Physica-Verlag, Heidelberg.

McQuitty, S., Finn, A. and Wiley, J.B. (2000), “Systematically varying consumer satisfaction andits implications for product choice”, Academy of Marketing Science Review, Vol. 2000No. 10, pp. 1-16.

Mangold, W.G. and Babakus, E. (1991), “Service quality: the front-stage vs. the back-stageperspective”, Journal of Services Marketing, Vol. 5 No. 4, pp. 59-70.

Mentzer, J.T. and Flint, D.J. (1997), “Validity in logistics research”, Journal of Business Logisitics,Vol. 18 No. 1, pp. 199-216.

Mols, N.P. (2000), “The internet and banks’ strategic distribution channel decisions”,International Journal of Bank Marketing, Vol. 17 No. 6, pp. 295-300.

Najjar, L. and Bishu, R.R. (2006), “Service quality: a case study of a bank”, The QualityManagement Journal, Vol. 13 No. 3, pp. 35-44.

Parasuraman, A., Zeithaml, V.A. and Berry, L.L. (1985), “A conceptual model of service qualityand its implications for future research”, Journal of Marking, Vol. 49 No. 4, pp. 41-50.

Parasuraman, A., Zeithaml, V.A. and Berry, L.L. (1988), “SERVQUAL: a multi item scale formeasuring consumer perception of service quality”, Journal of Retailing, Vol. 64 No. 1,pp. 12-40.

Parasuraman, A., Zeithaml, V.A. and Berry, L.L. (1991), “Refinement and reassessment of theSERVQUAL scale”, Journal of Retailing, Vol. 67 No. 4, pp. 420-50.

Parasuraman, A., Zeithaml, V.A. and Malhotra, A. (2005), “E-S-QUAL: a multiple-item scale forassessing electronic service quality”, Journal of Service Research, Vol. 7 No. 3, pp. 213-33.

Partricio, L., Fisk, R.P. and e Cunha, J.F. (2003), “Improving satisfaction with bank serviceofferings: measuring the contribution of each delivery channel”, Managing Service Quality,Vol. 13 No. 6, pp. 471-82.

Patnayakuni, R., Rai, A. and Seth, N. (2006), “Relational antecedents of information flowintegration for supply chain coordination”, Journal of Management Information Systems,Vol. 23 No. 1, pp. 13-49.

Peter, J.P. and Olson, J.C. (1990), Consumer Behavior and Marketing Strategy, Irwin, Homewood, IL.

Pikkarainen, K., Pikkarainen, T., Karjaluoto, H. and Pahnila, S. (2006), “The measurement ofend-user computing satisfaction of online banking services: empirical evidence fromFinland”, The International Journal of Bank Marketing, Vol. 24 Nos 2/3, pp. 158-72.

Podsakoff, P.M., Mackenzie, S.B., Lee, J. and Podsakoff, N.P. (2003), “Common method biases inbehavioral research: a critical review of the literature and recommended remedies”, Journalof Applied Psychology, Vol. 88 No. 5, pp. 879-903.

Internet bankingservice quality

121

Poon, W-C. (2008), “Users’ adoption of e-banking services: the Malaysian perspective”, Journal ofBusiness & Industrial Marketing, Vol. 23 No. 1, pp. 59-69.

Reynolds, W.M. (1982), “Development of reliable and valid short forms of the marlowe-crownesocial desirability scale”, Journal of Clinical Psychology, Vol. 38 No. 1, pp. 119-25.

Richard, M.D. and Allaway, A.W. (1993), “Service quality attributes and choice behavior”,Journal of Services Marketing, Vol. 7 No. 1, pp. 59-68.

Rosen, L.D. and Karwan, K.R. (1994), “Prioritizing the dimensions of service quality”,International Journal of Service Industry Management, Vol. 5 No. 4, pp. 39-52.

Shamdasani, P., Mukherjee, A. and Malhotra, N. (2008), “Antecedents and consequences ofservice quality in consumer evaluation of self-service internet technologies”, The ServiceIndustries Journal, Vol. 28 No. 1, pp. 117-38.

Shi, Y. and Fang, K. (2006), “Effects of network quality attributes on customer adoptionintentions of internet banking”, Total Quality Management, Vol. 17 No. 1, pp. 61-77.

Siu, N. and Mou, J. (2005), “Measuring service quality in internet banking: the case ofHong Kong”, Journal of International Consumer Marketing, Vol. 17 No. 4, pp. 99-116.

Sohail, M. and Shaikh, N. (2008), “Internet banking and quality of service”, Online InformationReview, Vol. 32 No. 1, pp. 58-72.

Spector, P.E. (1987), “Method variance as an artifact in self-reported affect and perceptions atwork: myth or significant problem?”, Journal of Applied Psychology, Vol. 72 No. 3,pp. 438-43.

Stone, M. (1974), “Cross-validatory choice and assessment of statistical predictions”, Journal ofthe Royal Statistical Society, Vol. 36 No. 2, pp. 111-33.

Strieter, J., Gupta, A.K., Raj, S.P. and Wilemon, D. (1999), “Product management and themarketing of financial services”, International Journal of Bank Marketing, Vol. 17 No. 7,pp. 342-55.

Unsal, F. and Movassaghi, H. (2001), “Impact of internet on financial services industry: a casestudy of on-line investing”, Internet Research: Electronic Networking Applications andPolicy, Vol. 12 No. 3, pp. 221-34.

van Dyke, T.P., Kappelman, L.A. and Prybutok, V.R. (1997), “Measuring information systemsservice quality: concerns on the use of the SERVQUAL questionnaire”, MIS Quarterly,Vol. 21 No. 2, pp. 195-208.

White, H. and Nteli, F. (2004), “Internet banking in the UK: why are there not more customers?”,Journal of Financial Services Marketing, Vol. 9 No. 1, pp. 49-56.

Wold, H. (1985), “Systems analysis by partial least squares”, in Nijkamp, P., Leitner, L. andWrigley, N. (Eds), Measuring the Unmeasurable, Marinus Nijhoff, Dordrecht, pp. 221-52.

Wolfinbarger, M.F. and Gilly, M.C. (2002), “comQ: dimensionalizing, measuring and predictingquality of the e-tailing experience”, working paper, Marketing Science Institute,Cambridge, MA, pp. 1-51.

Yang, Z. and Fang, X. (2004), “Online service quality dimensions and their relationships withsatisfaction: a content analysis of customer reviews of securities brokerage services”,International Journal of Service Industry Management, Vol. 15 No. 3, pp. 302-26.

Yang, Z. and Jun, M. (2002), “Consumer perception of e-service quality: from internet purchaserand non-purchaser perspectives”, Journal of Business Strategies, Vol. 19 No. 1, pp. 19-41.

Yang, Z., Jun, M. and Peterson, R.T. (2004), “Measuring customer perceived online servicequality: scale development and managerial implications”, International Journal ofOperations & Production Management, Vol. 24 No. 11, pp. 1149-74.

MIP27,1

122

Zeithaml, V.A., Parasuraman, A. and Malhotra, A. (2001), “A conceptual framework forunderstanding e-service quality: implications for future research and managerial practice”,MSI Working Paper Series, No. 00-115, Cambridge, MA, pp. 1-49.

Zineldin, M. (2002), “Managing the age: banking service quality and strategic positioning”,Measuring Business Excellence, Vol. 6 No. 4, pp. 38-43.

Further reading

Devaraj, S., Fan, M. and Kohli, R. (2002), “Antecedents of B2C channel satisfaction andpreference: validation e-commerce metrics”, Information Systems Research, Vol. 13 No. 3,pp. 316-34.

Dixon, M. (1999), “.Com madness: 9 must-know tips for putting your bank online”, America’sCommunity Banker, Vol. 8 No. 6, pp. 12-15.

Jayasuriya, R. (1998), “Measuring service quality in it services: using service encounters to elicitquality dimensions”, Journal of Professional Services Marketing, Vol. 18 No. 1, pp. 11-23.

McKinney, V., Yoon, K. and Zahedi, F. (2002), “The measurement of web-customer satisfaction:an expectation and disconfirmation approach”, Information Systems Research, Vol. 13No. 3, pp. 296-316.

Malhotra, P. and Singh, B. (2006), “The impact of internet banking on bank’s performance: theIndian experience”, South Asian Journal of Management, Vol. 13 No. 4, pp. 25-54.

Sathye, M. (2005), “The impact of internet banking on performance and risk profile: evidencefrom Australian credit unions”, Journal of Banking Regulation, Vol. 6 No. 2, pp. 163-74.

Scullion, M. and Nicholas, D. (2001), “The impact of the web on the stockbroking industry:big bang 2”, Aslib Proceedings, Vol. 53 No. 1, pp. 3-22.

Zeithaml, V.A., Berry, L.L. and Parasuraman, A. (1996), “The behavioural consequences ofservice quality”, Journal of Marketing, Vol. 60 No. 2, pp. 31-46.

(The Appendix Table follows overleaf.)

Internet bankingservice quality

123

Appendix

Construct Sources Dimensions Items

Online customerservice quality

Han and Baek(2004)

Tangibles(tangible)

XYZBANK’s internet banking website provides me with valuableinformationXYZBANK’s internet banking website allows me to find informationeasilyXYZBANK’s internet banking website is visually appealing

Reliability(reliabit)

With my online banking, whenXYZBANK promises to do somethingby a certain time, it does soXYZBANK gets its online serviceright first timeWhen there is a problem with myonline banking, XYZBANK shows asincere interest in solving it

Responsiveness(response)

With my online banking, XYZBANK’sstaff tell me exactly when the service Irequire will be performedFor my online banking, XYZBANK’sstaff give me prompt service

Empathy(empathy)

For my online banking, XYZBANK’sstaff have my best interests at heartFor my online banking, XYZBANK’sstaff understand my specific needsFor my online banking, XYZBANK’sstaff give me personal attentionFor my online banking, the help line ofXYZBANK has operating hoursconvenient to meet my needs

Online informationsystem quality

Jun and Cai(2001) andYang et al. (2004)

Ease of use(easeofus)

The layout of the information inXYZBANK’s internet banking website is easy to followI can easily log on to my accountUsing XYZBANK’s internet bankingweb site requires a lot of effortIt is easy for me to complete atransaction through XYZBANK’sinternet banking web siteI do not encounter long delays whensearching for information onXYZBANK’s internet bankingweb site

Accuracy(accuracy)

My online transactions are alwaysaccurateThe information on XYZBANK’sinternet banking web site is accurate

(continued)Table AI.

MIP27,1

124

Construct Sources Dimensions Items

The online transactions are accuratelydealt with

Security/privacy(security)

I believe that XYZBANK will notmisuse my personal informationI feel safe in my online transactionsthrough XYZBANK’s internetbanking web siteI feel secure in providing sensitiveinformation for online transactionsthrough XYZBANK’s internetbanking web siteI feel the risk associated with onlinetransactions is low throughXYZBANK’s internet banking website

Contents(contents)

My account information onXYZBANK’s internet banking website is well documented and clear

Timeliness(timeline)

The information on XYZBANK’sinternet banking web site is up-to-date

Aesthetics(aestheti)

XYZBANK’s internet banking website is attractive

Banking serviceproduct quality

Jun and Cai (2001) andYang et al. (2004)

XYZBANK provides online serviceswith the features I want (features)XYZBANK provides most of theonline service functions that I need(function)All my online service needs areincluded in the menu options (menu)XYZBANK provides a wide range ofonline service packages (range)XYZBANK provides me many usefulfree online services (free)

Overall internetbanking servicequality

Yang et al. (2004) Overall, the online service quality ofXYZBANK is excellent (ovosq)

Overall, XYZBANK comes up to myexpectations of what makes a goodonline banking supplier (ovexp)

Customer satisfaction Yang et al. (2004) Overall, I am satisfied with myexperience of XYZBANK’s service(ovservic)Overall, I am satisfied withXYZBANK internet-basedtransactions (ovsatis)Overall, I am satisfied with theproducts/services offered byXYZBANK (ovproduc)Overall, I am satisfied withXYZBANK (ovxyz) Table AI.

Internet bankingservice quality

125

About the authorsMichel Rod is a Senior Lecturer in Marketing at University of Victoria of Wellington,New Zealand. His research interests include service recovery performance, burnout, thedevelopment and management of collaborative relationships amongst university, industry, andgovernment organizations within the health sciences sector as well as the commercialisation ofuniversity-developed intellectual property. Rod has published articles in Journal of Retailing andConsumer Services, Journal of Pharmaceutical and Healthcare Marketing, Qualitative MarketResearch: An International Journal, Journal of Information and Knowledge Management, Journalof Entrepreneurship and Innovation, Management Research News, Journal of TransnationalManagement Development, and Science and Public Policy. Michel Rod is the correspondingauthor and can be contacted at: [email protected]

Nicholas J. Ashill is an Associate Professor in Marketing at the American University ofSharjah, United Arab Emirates. Ashill has contributed to such journals as the European Journalof Marketing, Decision Sciences, Journal of Services Marketing, Journal of Strategic Marketing,Journal of Marketing Management, Qualitative Market Research: An International Journal,Journal of Asia-Pacific Business, Journal of Business and Management, International Journal ofBank Marketing and the International Review of Public and Non Profit Marketing.

Jinyi Shao is a former Masters student in Marketing at Victoria University of Wellington,New Zealand.

Janet Carruthers is a Senior Lecturer in Social Marketing and Marketing InformationManagement at Victoria University of Wellington, New Zealand. Her research interests includethe marketing of social change and healthcare marketing. Carruthers has contributed to suchjournals as the Journal of Services Marketing, Journal of Retail and Consumer Services and theInternational Review of Public and Non-Profit Marketing.

MIP27,1

126

To purchase reprints of this article please e-mail: [email protected] visit our web site for further details: www.emeraldinsight.com/reprints

![[D] Diagnóstico e Tratamento das Psicoses (Sem Título e Sem Autor)](https://static.fdokumen.com/doc/165x107/6314fe73511772fe45102b3d/d-diagnostico-e-tratamento-das-psicoses-sem-titulo-e-sem-autor.jpg)