Alternative Banking and Recovery from Crisis

56

Alternat Ku Paper to be p tive Banking and Recovery from Crisis urt Mettenheim & Olivier Butzbach presented to the Progressive Economy Foru 5-7 March 2014, Brussels um

Transcript of Alternative Banking and Recovery from Crisis

Alternative Banking and Recovery from Crisis

Kurt Mettenheim

Paper to be presented to the Progressive Economy Forum

Alternative Banking and Recovery from Crisis

Kurt Mettenheim & Olivier Butzbach

Paper to be presented to the Progressive Economy Forum

5-7 March 2014, Brussels

Paper to be presented to the Progressive Economy Forum

Alternative Banking and Recovery

Abstract This paper examines the unexpected back to the future modernization of social and public banking across Europe since 2000 provide policy options to recover from crises, sustain ssustainable development. Recent research and international and domestic policy making debates have begun to recognizebanks, cooperative banks and special purpose baignored by a policy consensus on the virtues of privatization and liberalization and scorned by most economists as inefficient banksinvestment banks acting as directliberalization of banking and monetary union in Europe,privatized or demutualized, have realized competitive advantages to sustain market share and modernize while seeking to recast their social missions and policy mandates for the 21century. The paper will report statistical evidence from BANKSCOPEbank change, and comparative case studies to clarify competitive advantage and of alternative banks since 2000of this back to the future modernization of social and public banking for policy debates and strategies for recovery from crisis in Europe and abroad. Kurt Mettenheim Social and Legal Sciences DepartmentSão Paulo Business School Escola de Administração de Empresas de São Paulo, Fundação Getulio Vargas (FGV-EAESP)Av 9 de Julho 2029 01313-902 São Paulo, SP, Brazil +55 11 3799 7858 / 7805 with [email protected] www.fgv.academia.edu/kurtvonmettenheimwww.pickeringchatto.com/brazil

Acknowledgments Support for research came fromresearch fund of the Fundação GetulioFoundation, for a conference on alternative banking and social inclusion at the Bellagio Center in July 2011 and research residencies for the meetings of the Society for the A(2012) and Milan (2013).

Alternative Banking and Recovery from Crisis

2

Alternative Banking and Recovery from Crisis

the unexpected back to the future modernization of social and public since 2000 and explores how alternative banking institutions may

provide policy options to recover from crises, sustain social inclusion and accelerate sustainable development. Recent research and international and domestic policy making

tes have begun to recognize the important role of non-joint stock banks such as savings banks, cooperative banks and special purpose banks. For decades, these institutions

onsensus on the virtues of privatization and liberalization and scorned by fficient banks doomed to be replaced by private commercial and

investment banks acting as direct intermediaries in capital markets. To the contrary, since liberalization of banking and monetary union in Europe, alternative banks, where not privatized or demutualized, have realized competitive advantages to sustain market share and

king to recast their social missions and policy mandates for the 21report statistical evidence from BANKSCOPE, other data sources

bank change, and comparative case studies to clarify the institutional foundations of alternative banks since 2000. We also explore the implications

back to the future modernization of social and public banking for banking theory, policy debates and strategies for recovery from crisis in Europe and abroad.

Olivier Butzbach Social and Legal Sciences Department King's College London

Department of Management de Administração de Empresas de São Paulo, Franklin-Wilkins Building

EAESP) 150 Stamford Street SE1 9NH London United Kingdom

+55 11 3799 7858 / 7805 with Sandra [email protected]

www.fgv.academia.edu/kurtvonmettenheim www.pickeringchatto.com/alternat

m: The Second University of Naples, Italy; GGetulio Vargas Sao Paulo Business School;

on alternative banking and social inclusion at the Bellagio Center research residencies for the authors. We also thank fellowociety for the Advancement of Socio-Economics, in Paris

Alternative Banking and Recovery from Crisis

the unexpected back to the future modernization of social and public and explores how alternative banking institutions may

ocial inclusion and accelerate sustainable development. Recent research and international and domestic policy making

joint stock banks such as savings nks. For decades, these institutions were

onsensus on the virtues of privatization and liberalization and scorned by doomed to be replaced by private commercial and

intermediaries in capital markets. To the contrary, since alternative banks, where not

privatized or demutualized, have realized competitive advantages to sustain market share and king to recast their social missions and policy mandates for the 21st

other data sources on the institutional foundations of

explore the implications banking theory,

policy debates and strategies for recovery from crisis in Europe and abroad.

www.pickeringchatto.com/alternative

GVpesquisa, the and the Rockefeller

on alternative banking and social inclusion at the Bellagio Center We also thank fellow participants at

in Paris (2009), Boston

Executive Summary Introduction 1 Defining and differentiating alternative banks 2 Alternative bank histories

2.1. Italy 2.2. Germany 2.3 Postal Savings Banks

3 Alternative banks after liberalization, deregulation, privatizations and IT revolution

3.1 Back to the future of alternative banking 4 Why alternative banks matter

4.1 Institutions for social and economic development4.2 Alternative banks buffer systemic stability

5 Explaining competitive advantages of alternative banks with banking theory

5.1 Alternative banking and agency theory5.2 Managers-shareholders agency conflicts5.3 Other agency conflicts

6 Alternative banks mitigate information asymmetries through relationship banking 7 Alternative bank funding, equity, reserves and patrimony 8 The sustainable business models of alternative banks 9 Alternative banks smooth inter 10 Conclusion References Appendices

Alternative Banking and Recovery from Crisis

3

Table of Contents

1 Defining and differentiating alternative banks

ostal Savings Banks

Alternative banks after liberalization, deregulation, privatizations and IT revolutione future of alternative banking

Why alternative banks matter .1 Institutions for social and economic development .2 Alternative banks buffer systemic stability

5 Explaining competitive advantages of alternative banks with banking theory5.1 Alternative banking and agency theory

shareholders agency conflicts 5.3 Other agency conflicts

information asymmetries through relationship banking

7 Alternative bank funding, equity, reserves and patrimony

8 The sustainable business models of alternative banks

9 Alternative banks smooth inter-temporal risk

Alternative Banking and Recovery from Crisis

page 4

5

7

8 9 10 14

Alternative banks after liberalization, deregulation, privatizations and IT revolution 15 16

18 19 19

5 Explaining competitive advantages of alternative banks with banking theory 20 22 23 27

information asymmetries through relationship banking 30

32

33

34

35

37

49

Executive Summary Unlike business models of private banks based on profit maximization, shareholder governance and executive-centered management, alternative banks (such as cooperative banks, government savings banks and special purpose banks), share busion sustained returns for long-term horizons; corporate missions that include social and public policy goals; and stakeholder-oriented, boardrecent research suggests that alternative banks have ebanks in terms of efficiency, profitability and risk management. This counters core ideas in contemporary banking theory and bank regulation about the superiority of private, marketbased banking. Concepts and theories frbanks outperform private banks in terms of deposits, reducing information asymmetries, and ameliorating agency conflicts. However, heterodox theories of the firm and institutional foundations of competitive advantage further clarify the historical, social, and organizational advantages (and risks) of alternative banks. Recent research on alternative banksEurope and beyond. First, on a systemic level, alternative banks matter. Compared to banking systems that rely almost exclusively on private commercial and investment banking, the more traditional and socially oriented business models of alternative banks help aand crises caused by the excesses of profit maximizing private banks. Second, alternative banks increase diversity in banking systems. Recent debates among policy-makers and academics emphasize the This warrants a whole chapter in work by academics long interested in nonin policy debates, Andrew Haldane. While agreement has emerand the need to encourage it in banking systems, few ideas have emerged about how toabout this, mostly because of the pgovernment persists in believing they can cThis paper explores how diversehistory and persisted through the most variedcompetitors. This suggests that more than liberalization is needed. banks and "biodiversity" in banking banks through specific regulation

On the level of policy opportunities, tof alternative banks in the 21st century social forces. Local and regional savings banks (and their shared wholesale groups) help citizens and small and medium enterprises secure access to banking and credit that otherwise would suffer financial exclusion and credit rationing. Cooperative banks embedded in local and regional socisocial, regional and cultural missions at the heart of corporate identities and governance.

Special purpose banks provide powerful comparative advantagebecause, as banks, these institutions multiply official deposits by tw(rounding Basel capital reserve requirements)many European governments amidst crisis. Special purpose banks also increase public control over policy implementation through contrtransparent overview from regulatory authorities, the media and press and public.

Biases in favor of private banking have blinded Europeans from using their longstanding, large alternative banking groups to recover

Alternative Banking and Recovery from Crisis

4

Unlike business models of private banks based on profit maximization, shareholder centered management, alternative banks (such as cooperative

banks, government savings banks and special purpose banks), share business models based term horizons; corporate missions that include social and public oriented, board-centered governance. Strong evidence from

recent research suggests that alternative banks have equaled or outperformed jointbanks in terms of efficiency, profitability and risk management. This counters core ideas in contemporary banking theory and bank regulation about the superiority of private, marketbased banking. Concepts and theories from banking studies help explain how alternative banks outperform private banks in terms of core functions such as creating liquidity, pooling deposits, reducing information asymmetries, and ameliorating agency conflicts. However,

firm and institutional foundations of competitive advantage further clarify the historical, social, and organizational advantages (and risks) of alternative banks.

lternative banks provides new ideas for responses to crisis in First, on a systemic level, alternative banks matter. Compared to banking

systems that rely almost exclusively on private commercial and investment banking, the more traditional and socially oriented business models of alternative banks help aand crises caused by the excesses of profit maximizing private banks.

Second, alternative banks increase diversity in banking systems. Recent debates among makers and academics emphasize the need for diversity or heterogeneity

This warrants a whole chapter in the recent EU ‘Liikanen’ report and is the focus of recent work by academics long interested in non-profit, such as David Lewellyn and a leading figure in policy debates, Andrew Haldane. While agreement has emerged about the value of diversity and the need to encourage it in banking systems, few ideas have emerged about how toabout this, mostly because of the persistence of biases toward market-based

persists in believing they can create diversity by decreasing barriers how diverse types of alternative banks emerged very

through the most varied contexts since, often outperformsts that more than liberalization is needed. The benefits of

in banking require public policies to protect and nurture through specific regulations, tax incentives, and other rules.

icy opportunities, the unexpected back to the future modernization century provides critical policy alternatives for political and

social forces. Local and regional savings banks (and their shared wholesale groups) help izens and small and medium enterprises secure access to banking and credit that otherwise

would suffer financial exclusion and credit rationing. Cooperative banks also remain embedded in local and regional social institutions, specializing in relationship

missions at the heart of corporate identities and governance. Special purpose banks provide powerful comparative advantages for public policy

because, as banks, these institutions multiply official deposits by two and capitalization by ten(rounding Basel capital reserve requirements). This is critical given the fiscal constraints of many European governments amidst crisis. Special purpose banks also increase public control over policy implementation through contractual monitoring and supervision amidst transparent overview from regulatory authorities, the media and press and public.

Biases in favor of private banking have blinded Europeans from using their longstanding, large alternative banking groups to recover from crisis.

Alternative Banking and Recovery from Crisis

Unlike business models of private banks based on profit maximization, shareholder centered management, alternative banks (such as cooperative

ness models based term horizons; corporate missions that include social and public

centered governance. Strong evidence from qualed or outperformed joint-stock

banks in terms of efficiency, profitability and risk management. This counters core ideas in contemporary banking theory and bank regulation about the superiority of private, market-

om banking studies help explain how alternative core functions such as creating liquidity, pooling

deposits, reducing information asymmetries, and ameliorating agency conflicts. However, firm and institutional foundations of competitive advantage further

clarify the historical, social, and organizational advantages (and risks) of alternative banks. responses to crisis in

First, on a systemic level, alternative banks matter. Compared to banking systems that rely almost exclusively on private commercial and investment banking, the more traditional and socially oriented business models of alternative banks help avert asset bubbles

Second, alternative banks increase diversity in banking systems. Recent debates among diversity or heterogeneity in banking.

report and is the focus of recent profit, such as David Lewellyn and a leading figure

ged about the value of diversity and the need to encourage it in banking systems, few ideas have emerged about how to go

based banking (the UK reate diversity by decreasing barriers to entry).

very early in European outperforming for-profit he benefits of alternative

protect and nurture alternative

back to the future modernization policy alternatives for political and

social forces. Local and regional savings banks (and their shared wholesale groups) help izens and small and medium enterprises secure access to banking and credit that otherwise

also remain , specializing in relationship banking with

missions at the heart of corporate identities and governance. for public policy

o and capitalization by ten . This is critical given the fiscal constraints of

many European governments amidst crisis. Special purpose banks also increase public control actual monitoring and supervision amidst

transparent overview from regulatory authorities, the media and press and public. Biases in favor of private banking have blinded Europeans from using their

Introduction

Explanations of the 2007-8 financial crisis (Lo, 2012) and positions in debates about how to regulate banks in its wake rely on implicit or explicit normative assumptions about the business models of banks. Banks used to be seeinstitutions (Allen and Santomero, 2001). However, since contemporary banking theory favours disintermediation in the sense of banks using products and services traded on financial markets credit, and manufacture assets (Berger (2013) review how strategies of marketprolonged recover, while De Jonghe (2010) and Gorton and Metrick (2010) have called for a return to narrow banking (traditional depositregulations to separate investment banking from retail banking such as US, or ring-fencing (UK Independent Commission on Banking, 2011), have, to date, been watered down through compromises with marketappear unable to reverse the trend toward capital market operations in large private banks.Remarkably, both academic research and policy proposals have largely overlooked alternative bank groups, large and small, that avoided the excessive risks and capital marketmaximizing business models blamed for crisis in 2007(Butzbach and Mettenheim, 2014) includes a wide variety of credit institutions such as cooperative banks and credit unions, government savings banks and special purpose (development) banks, building societies, thrifts and mutual savings bconcept of alternative banking is justified because these institutions differ from private banks and share business models based on the following: 1) an absence of profit maximization imperatives and shareholder based governance; returns; 3) business missions that include social and public goods and; 4) stakeholder oriented, board-centered governance.

Several European alternative bank groups strayed from these principles. In Spain, the Cajas (savings banks) helped drive the boom and bust cycle that has devastated the country. In Germany, several Landesbanken global investment banks during the 2000s only to be caught in the 2007Raiffeisen cooperative bank group expanded investment banking and commercial banking operations across Eastern and Central Europe after the collapse of the Soviet Union only to retreat after the recent crisis. In the UK, aggressive growth strategiCoop Bank. Government banks in developing and emerging countries have long drawn criticism for crony credit, poor management and environmental damage. However, many government owned savings banks and development banks in these cofrom capture and mismanagement under military rule and authoritarian regimes to shape growth amidst democratization and reforms, provide counterafter 2008 and, perhaps most importantly, bring vastinto the formal economy while providing new social policies such as basic income (Mettenheim et al, 2013).

The specific experiences of alternative banks vary. However, this article builds on the growing empirical literature that finds alternative banks equal to or superior than jointcompetitors in terms of efficiency, profitability, risk management and other standard criteria used in banking studies. These findings hold in a variety of settings, most ironicallyears after liberalization, deregulation, privatizations and foreign bank entry. Instead of

Alternative Banking and Recovery from Crisis

5

8 financial crisis (Lo, 2012) and positions in debates about how to regulate banks in its wake rely on implicit or explicit normative assumptions about the business models of banks. Banks used to be seen as deposit-taking and loaninstitutions (Allen and Santomero, 2001). However, since Battacharya and Thakor (1993), contemporary banking theory favours disintermediation in the sense of banks using products and services traded on financial markets to manage risk, price assets and liabilities, allocate credit, and manufacture assets (Berger et al, 2010). Contributors to Hardie and Howarth (2013) review how strategies of market-based banking caused financial crisis and have

e Jonghe (2010) and Gorton and Metrick (2010) have called for a return to narrow banking (traditional deposit-taking and loan-making). Proposals for regulations to separate investment banking from retail banking such as the Volcker rule in the

fencing (UK Independent Commission on Banking, 2011), have, to date, been watered down through compromises with market-based views of banking (Lall, 2012) and appear unable to reverse the trend toward capital market operations in large private banks.

rkably, both academic research and policy proposals have largely overlooked alternative bank groups, large and small, that avoided the excessive risks and capital marketmaximizing business models blamed for crisis in 2007-8. The category of (Butzbach and Mettenheim, 2014) includes a wide variety of credit institutions such as cooperative banks and credit unions, government savings banks and special purpose (development) banks, building societies, thrifts and mutual savings banks. However, a broad concept of alternative banking is justified because these institutions differ from private banks and share business models based on the following: 1) an absence of profit maximization

shareholder based governance; 2) long-term business horizons sustained by returns; 3) business missions that include social and public goods and; 4) stakeholder

centered governance. Several European alternative bank groups strayed from these principles. In Spain, the

(savings banks) helped drive the boom and bust cycle that has devastated the country. Landesbanken (provincial government banks) attempted to become

global investment banks during the 2000s only to be caught in the 2007-8 crisis. The Raiffeisen cooperative bank group expanded investment banking and commercial banking operations across Eastern and Central Europe after the collapse of the Soviet Union only to retreat after the recent crisis. In the UK, aggressive growth strategies led to reversals at the

Government banks in developing and emerging countries have long drawn criticism for crony credit, poor management and environmental damage. However, many government owned savings banks and development banks in these countries have recovered from capture and mismanagement under military rule and authoritarian regimes to shape growth amidst democratization and reforms, provide counter-cyclical credit to adjust to crisis after 2008 and, perhaps most importantly, bring vast numbers of previously bankless citizens into the formal economy while providing new social policies such as basic income

The specific experiences of alternative banks vary. However, this article builds on the terature that finds alternative banks equal to or superior than joint

competitors in terms of efficiency, profitability, risk management and other standard criteria used in banking studies. These findings hold in a variety of settings, most ironicall

liberalization, deregulation, privatizations and foreign bank entry. Instead of

Alternative Banking and Recovery from Crisis

8 financial crisis (Lo, 2012) and positions in debates about how to regulate banks in its wake rely on implicit or explicit normative assumptions about the

taking and loan-making Battacharya and Thakor (1993),

contemporary banking theory favours disintermediation in the sense of banks using products to manage risk, price assets and liabilities, allocate

, 2010). Contributors to Hardie and Howarth based banking caused financial crisis and have

e Jonghe (2010) and Gorton and Metrick (2010) have called for a making). Proposals for

the Volcker rule in the fencing (UK Independent Commission on Banking, 2011), have, to date, been

based views of banking (Lall, 2012) and appear unable to reverse the trend toward capital market operations in large private banks.

rkably, both academic research and policy proposals have largely overlooked alternative bank groups, large and small, that avoided the excessive risks and capital market-based, profit

8. The category of alternative banks (Butzbach and Mettenheim, 2014) includes a wide variety of credit institutions such as cooperative banks and credit unions, government savings banks and special purpose

anks. However, a broad concept of alternative banking is justified because these institutions differ from private banks and share business models based on the following: 1) an absence of profit maximization

term business horizons sustained by returns; 3) business missions that include social and public goods and; 4) stakeholder

Several European alternative bank groups strayed from these principles. In Spain, the (savings banks) helped drive the boom and bust cycle that has devastated the country.

(provincial government banks) attempted to become 8 crisis. The Austrian

Raiffeisen cooperative bank group expanded investment banking and commercial banking operations across Eastern and Central Europe after the collapse of the Soviet Union only to

es led to reversals at the Government banks in developing and emerging countries have long drawn

criticism for crony credit, poor management and environmental damage. However, many untries have recovered

from capture and mismanagement under military rule and authoritarian regimes to shape cyclical credit to adjust to crisis

numbers of previously bankless citizens into the formal economy while providing new social policies such as basic income

The specific experiences of alternative banks vary. However, this article builds on the terature that finds alternative banks equal to or superior than joint-stock

competitors in terms of efficiency, profitability, risk management and other standard criteria used in banking studies. These findings hold in a variety of settings, most ironically many

liberalization, deregulation, privatizations and foreign bank entry. Instead of

convergence toward joint-stock private banking, alternative banks have modernized to maintain or expand market shares. We explain this anomaly for neoapproaches and neo-liberal policy designs by focusing on the main features of savings banks, cooperative banks and government special purpose banks. Explanations of alternative bank performance are drawn from banking theory and heterodox reseabanking theory reveal how alternative banks perform the core functions of modern banks such as creating liquidity, pooling deposits, reducing information asymmetries and managing potential agency conflicts. Heterodox theories orevealing further institutional foundations of competitive advantages in alternative banking.Since the 2007-8 financial crisis, a wide variety of scholars and policythe risky business models of private commercial and investment banks (US Government Financial Crisis Inquiry Commission, 2011; Admati and Hellwig, 2013). Although still marginal to policy debates and research in the mainstream disciplines of accounting, political economy, and law, the errors of private banks have nonetheless begun to produce reassessment of alternative banks (Butzbach and Mettenheim, 2014) and raise concern about the lack of organizational diversity in banking Goodhart and Wagner, 2012; Ayadi reassessment pales in comparison to decades of research biased toward private and jointstock banks and policy reforms that sought to reduce or eliminate government and nonbanks and credit institutions through privatizations, demutualization, liberalization, foreign bank entry and deregulation of credit markets.

The bulk of mainstream economists and personnel at international policy making institutions expected alternative banks to disappear, either sooner through privatizations or later as liberalization revealed the greater efficiency of private and foreign banks; or indeed after alternative bank managers would abandon longstanding traditions of social and state banking in favour of profit maximizing, marketcommercial and investment banks. The contrary has ensued. banking groups have, through a variety of strategies, modernized to hold their gmaintaining or gaining market shares in many advanced and developing countries, especially in retail banking (deposits, savings accounts and lending to small and medium enterprises and households). And empirical studies have gone beyond descriptiveshares to show how alternative banks have in many cases equaled or exceeded the performance of private banks in terms of cost, operational efficiency and profitability.

This is a paradox. As Canning et al. put it, “a central issue isarise and survive in a world dominated by investorMost banking studies simply ignore alternative banks. The aim of this paper is, therefore, to propose a consistent framework to explain The paper is organized as follows. Section one defines and differentiates alternative banks from private banks. Section two illustrates histories of alternative banks to introduce their institutional foundations of competitive advantage. Section three explores why alternative banks matter for social and economic development and systemic stability of banking. Section four explores the unexpected realization of competitive advantages by alternative banks afterliberalization, deregulation, privatizations and the revolution in technologies of information and communication that have changed the industry. Section five draws from theories of agency conflicts in banking studies to explain the competitive advantages Section six explores how stakeholder governance embedded in local, regional and national social and political forces mitigate information asymmetries through relationship banking. Section seven briefly explores how alternative banks o

Alternative Banking and Recovery from Crisis

6

stock private banking, alternative banks have modernized to maintain or expand market shares. We explain this anomaly for neo-classi

liberal policy designs by focusing on the main features of savings banks, cooperative banks and government special purpose banks. Explanations of alternative bank performance are drawn from banking theory and heterodox research on firms. Concepts from banking theory reveal how alternative banks perform the core functions of modern banks such as creating liquidity, pooling deposits, reducing information asymmetries and managing

Heterodox theories of the firm expand the scope of analysis by revealing further institutional foundations of competitive advantages in alternative banking.

8 financial crisis, a wide variety of scholars and policy-makers have criticized ls of private commercial and investment banks (US Government

Financial Crisis Inquiry Commission, 2011; Admati and Hellwig, 2013). Although still marginal to policy debates and research in the mainstream disciplines of accounting, political

aw, the errors of private banks have nonetheless begun to produce reassessment of alternative banks (Butzbach and Mettenheim, 2014) and raise concern about the lack of organizational diversity in banking (Michie and Oughton, 2013; Liikanen, 2012;

and Wagner, 2012; Ayadi et al, 2010; Ayadi et al, 2009). However, this belated reassessment pales in comparison to decades of research biased toward private and jointstock banks and policy reforms that sought to reduce or eliminate government and nonbanks and credit institutions through privatizations, demutualization, liberalization, foreign

deregulation of credit markets. The bulk of mainstream economists and personnel at international policy making

ative banks to disappear, either sooner through privatizations or later as liberalization revealed the greater efficiency of private and foreign banks; or indeed after alternative bank managers would abandon longstanding traditions of social and state

ing in favour of profit maximizing, market-based business models taken from private commercial and investment banks. The contrary has ensued. Defying expectations, alternative banking groups have, through a variety of strategies, modernized to hold their gmaintaining or gaining market shares in many advanced and developing countries, especially in retail banking (deposits, savings accounts and lending to small and medium enterprises and households). And empirical studies have gone beyond descriptive evidence from market shares to show how alternative banks have in many cases equaled or exceeded the performance of private banks in terms of cost, operational efficiency and profitability.

As Canning et al. put it, “a central issue is why notarise and survive in a world dominated by investor-owned banks, run for profit” (2003: 244). Most banking studies simply ignore alternative banks. The aim of this paper is, therefore, to propose a consistent framework to explain this unexpected persistence of alternative banks.The paper is organized as follows. Section one defines and differentiates alternative banks from private banks. Section two illustrates histories of alternative banks to introduce their

tions of competitive advantage. Section three explores why alternative banks matter for social and economic development and systemic stability of banking. Section four explores the unexpected realization of competitive advantages by alternative banks afterliberalization, deregulation, privatizations and the revolution in technologies of information and communication that have changed the industry. Section five draws from theories of agency conflicts in banking studies to explain the competitive advantages Section six explores how stakeholder governance embedded in local, regional and national social and political forces mitigate information asymmetries through relationship banking. Section seven briefly explores how alternative banks obtain funding and hold equity, reserves

Alternative Banking and Recovery from Crisis

stock private banking, alternative banks have modernized to classical economic

liberal policy designs by focusing on the main features of savings banks, cooperative banks and government special purpose banks. Explanations of alternative bank

rch on firms. Concepts from banking theory reveal how alternative banks perform the core functions of modern banks such as creating liquidity, pooling deposits, reducing information asymmetries and managing

f the firm expand the scope of analysis by revealing further institutional foundations of competitive advantages in alternative banking.

makers have criticized ls of private commercial and investment banks (US Government

Financial Crisis Inquiry Commission, 2011; Admati and Hellwig, 2013). Although still marginal to policy debates and research in the mainstream disciplines of accounting, political

aw, the errors of private banks have nonetheless begun to produce reassessment of alternative banks (Butzbach and Mettenheim, 2014) and raise concern about

(Michie and Oughton, 2013; Liikanen, 2012; However, this belated

reassessment pales in comparison to decades of research biased toward private and joint-stock banks and policy reforms that sought to reduce or eliminate government and non-profit banks and credit institutions through privatizations, demutualization, liberalization, foreign

The bulk of mainstream economists and personnel at international policy making ative banks to disappear, either sooner through privatizations or

later as liberalization revealed the greater efficiency of private and foreign banks; or indeed after alternative bank managers would abandon longstanding traditions of social and state

based business models taken from private Defying expectations, alternative

banking groups have, through a variety of strategies, modernized to hold their ground - maintaining or gaining market shares in many advanced and developing countries, especially in retail banking (deposits, savings accounts and lending to small and medium enterprises

evidence from market shares to show how alternative banks have in many cases equaled or exceeded the performance of private banks in terms of cost, operational efficiency and profitability.

why not-for-profit banks owned banks, run for profit” (2003: 244).

Most banking studies simply ignore alternative banks. The aim of this paper is, therefore, to this unexpected persistence of alternative banks.

The paper is organized as follows. Section one defines and differentiates alternative banks from private banks. Section two illustrates histories of alternative banks to introduce their

tions of competitive advantage. Section three explores why alternative banks matter for social and economic development and systemic stability of banking. Section four explores the unexpected realization of competitive advantages by alternative banks after liberalization, deregulation, privatizations and the revolution in technologies of information and communication that have changed the industry. Section five draws from theories of agency conflicts in banking studies to explain the competitive advantages of alternative banks. Section six explores how stakeholder governance embedded in local, regional and national social and political forces mitigate information asymmetries through relationship banking.

btain funding and hold equity, reserves

and patrimony differently than private banks. Section eight summarizes the sustainable business models of alternative banks, while section nine reviews recent research suggesting that alternative banks may smooth intfindings and argues for extending the scope of banking studies through further analysis of alternative banks and research on the institutional foundations of competitive advantage in banking.

1) Defining and differentiating alternative banks

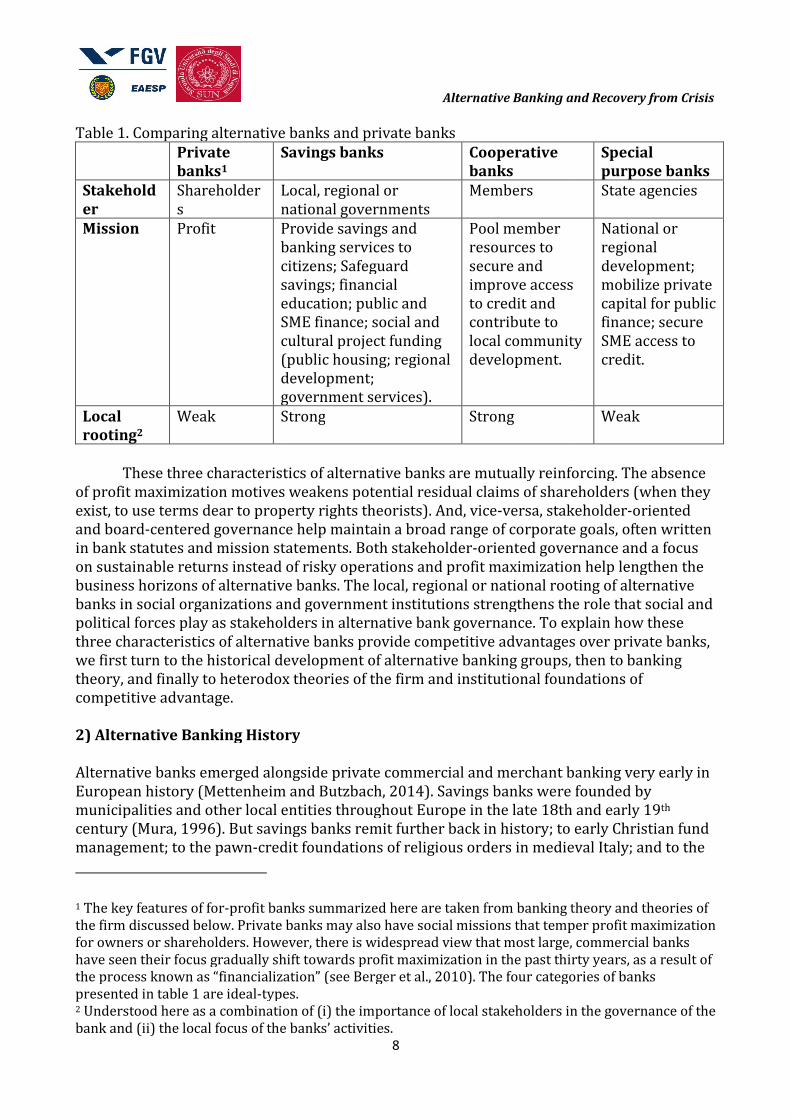

The concept of alternative banks encompasses a broad, heterogeneous set of financial institutions including cooperative banks and savings banks, credit unions, mutual savings associations, government development bankmay appear to have little in common. How can we compare, for instance, small British building societies or local (sometimes “single window”) Italian cooperative banks with a financial Behemoth such as the Netdifferences, alternative banks share three core characteristics that differ from what is often seen as the typical bank in academic research and policy making debates: the jointprofit universal bank. The three core characteristics of alternative banks are:

Corporate Purpose: Alternative banks are notshareholder value or returns for owners. This does not mean that alternative banks do not make profits: they do, and have been found to be However, the corporate missions of alternative banks retain a broad range of explicitly stated objectives, to be sustained by returns, such as favoring economic and sociafinancing local projects, making credit available to poorer households or small businesses, and providing long term investments in social and cultural capital and public policies.

Governance Structure: The governance of alternative banks isboard-centered in the sense that they: (a) are not run for the exclusive benefit of shareholders; (b) are controlled by a broader range of stakeholders than for(members in the case of mutuals, credit unions and cooprepresentatives (and often clients) in the case of savings banks, and regional or national governments in the case of special purpose or development banks, and; (c) are managed by corporate boards that keep executives and staff under joint-stock banks.

Business Models: The business models of alternative banks differ from private bank business models along two crucial dimensions: (a) more cautious, longsustain social and public policy missions through returns, and; (b) corporate cultures and missions that value the social, cultural and developmental needs of their geographic areas or functionally defined members and clients.

Table 1 on the following pagethree core features for three types of alternative banks, in addition to for

Alternative Banking and Recovery from Crisis

7

and patrimony differently than private banks. Section eight summarizes the sustainable business models of alternative banks, while section nine reviews recent research suggesting that alternative banks may smooth inter-temporal risk. The conclusion synthesizes recent findings and argues for extending the scope of banking studies through further analysis of alternative banks and research on the institutional foundations of competitive advantage in

and differentiating alternative banks

The concept of alternative banks encompasses a broad, heterogeneous set of financial institutions including cooperative banks and savings banks, credit unions, mutual savings associations, government development banks and special purpose banks. These institutions may appear to have little in common. How can we compare, for instance, small British building societies or local (sometimes “single window”) Italian cooperative banks with a financial Behemoth such as the Netherland Rabobank, or French Crédit Agricole? Despite their differences, alternative banks share three core characteristics that differ from what is often seen as the typical bank in academic research and policy making debates: the joint

niversal bank. The three core characteristics of alternative banks are:

: Alternative banks are not-for-profit, i.e. they do not aim to maximize shareholder value or returns for owners. This does not mean that alternative banks do not

they do, and have been found to be more profitable than for-However, the corporate missions of alternative banks retain a broad range of explicitly stated objectives, to be sustained by returns, such as favoring economic and sociafinancing local projects, making credit available to poorer households or small businesses, and providing long term investments in social and cultural capital and public policies.

: The governance of alternative banks is stakeholdercentered in the sense that they: (a) are not run for the exclusive benefit of

(b) are controlled by a broader range of stakeholders than for(members in the case of mutuals, credit unions and cooperatives), government representatives (and often clients) in the case of savings banks, and regional or national governments in the case of special purpose or development banks, and; (c) are managed by corporate boards that keep executives and staff under closer supervision and control than

: The business models of alternative banks differ from private bank business models along two crucial dimensions: (a) more cautious, long-term oriented strategies to

public policy missions through returns, and; (b) corporate cultures and missions that value the social, cultural and developmental needs of their geographic areas or functionally defined members and clients.

on the following page summarizes the specificities presented by each of these three core features for three types of alternative banks, in addition to for-

Alternative Banking and Recovery from Crisis

and patrimony differently than private banks. Section eight summarizes the sustainable business models of alternative banks, while section nine reviews recent research suggesting

temporal risk. The conclusion synthesizes recent findings and argues for extending the scope of banking studies through further analysis of alternative banks and research on the institutional foundations of competitive advantage in

The concept of alternative banks encompasses a broad, heterogeneous set of financial institutions including cooperative banks and savings banks, credit unions, mutual savings

s and special purpose banks. These institutions may appear to have little in common. How can we compare, for instance, small British building societies or local (sometimes “single window”) Italian cooperative banks with a

herland Rabobank, or French Crédit Agricole? Despite their differences, alternative banks share three core characteristics that differ from what is often seen as the typical bank in academic research and policy making debates: the joint-stock, for-

niversal bank. The three core characteristics of alternative banks are:

profit, i.e. they do not aim to maximize shareholder value or returns for owners. This does not mean that alternative banks do not

-profit banks. However, the corporate missions of alternative banks retain a broad range of explicitly stated objectives, to be sustained by returns, such as favoring economic and social development, financing local projects, making credit available to poorer households or small businesses, and providing long term investments in social and cultural capital and public policies.

stakeholder-oriented and centered in the sense that they: (a) are not run for the exclusive benefit of

(b) are controlled by a broader range of stakeholders than for-profit banks eratives), government

representatives (and often clients) in the case of savings banks, and regional or national governments in the case of special purpose or development banks, and; (c) are managed by

closer supervision and control than

: The business models of alternative banks differ from private bank business term oriented strategies to

public policy missions through returns, and; (b) corporate cultures and missions that value the social, cultural and developmental needs of their geographic areas or

pecificities presented by each of these -profit banks.

Table 1. Comparing alternative banks and private banks Private

banks1

Savings banks

Stakehold

er

Shareholders

Local, regional or national governments

Mission Profit Provide savings and banking services to citizens; Safeguard savings; financial education; public and SME finance; social and cultural projec(public housing; regional development; government services).

Local

rooting2

Weak Strong

These three characteristics of alternative banks are mutually reinforcing. The absence

of profit maximization motives weakens potential residual claims of shareholders (when they exist, to use terms dear to property rights theorists). And, viceand board-centered governance help maintain a broad range of corporate goals, often written in bank statutes and mission statements. Both stakeholderon sustainable returns instead of risky operations and profit maximization help lengthen the business horizons of alternative banks. The local, regional or national rooting of alternative banks in social organizations and government instpolitical forces play as stakeholders in alternative bank governance. To explain how these three characteristics of alternative banks provide competitive advantages over private banks, we first turn to the historical development of alternative banking groups, then to banking theory, and finally to heterodox theories of the firm and institutional foundations of competitive advantage.

2) Alternative Banking History

Alternative banks emerged alongside private coEuropean history (Mettenheim and Butzbach, 2014). Savings banks were founded by municipalities and other local entities throughout Europe in the late 18th and early 19century (Mura, 1996). But savings banks remanagement; to the pawn-credit foundations of religious orders in medieval Italy; and to the

1 The key features of for-profit bankthe firm discussed below. Private banks may also have social missions that temper profit maximization for owners or shareholders. However, there is widespread view that most large, commercial have seen their focus gradually shift towards profit maximization in the past thirty years, as a result of the process known as “financialization” (see Berger et al., 2010). The four categories of banks presented in table 1 are ideal-types.2 Understood here as a combination of (i) the importance of local stakeholders in the governance of the bank and (ii) the local focus of the banks’ activities.

Alternative Banking and Recovery from Crisis

8

Table 1. Comparing alternative banks and private banks Savings banks Cooperative

banks

Local, regional or national governments

Members

Provide savings and banking services to citizens; Safeguard savings; financial education; public and SME finance; social and cultural project funding (public housing; regional development; government services).

Pool member resources to secure and improve access to credit and contribute to local community development.

Strong Strong

These three characteristics of alternative banks are mutually reinforcing. The absence of profit maximization motives weakens potential residual claims of shareholders (when they

xist, to use terms dear to property rights theorists). And, vice-versa, stakeholdercentered governance help maintain a broad range of corporate goals, often written

in bank statutes and mission statements. Both stakeholder-oriented governance and a focus on sustainable returns instead of risky operations and profit maximization help lengthen the business horizons of alternative banks. The local, regional or national rooting of alternative banks in social organizations and government institutions strengthens the role that social and political forces play as stakeholders in alternative bank governance. To explain how these three characteristics of alternative banks provide competitive advantages over private banks,

orical development of alternative banking groups, then to banking theory, and finally to heterodox theories of the firm and institutional foundations of

2) Alternative Banking History

Alternative banks emerged alongside private commercial and merchant banking very early in European history (Mettenheim and Butzbach, 2014). Savings banks were founded by municipalities and other local entities throughout Europe in the late 18th and early 19century (Mura, 1996). But savings banks remit further back in history; to early Christian fund

credit foundations of religious orders in medieval Italy; and to the

profit banks summarized here are taken from banking theory and theories of the firm discussed below. Private banks may also have social missions that temper profit maximization for owners or shareholders. However, there is widespread view that most large, commercial have seen their focus gradually shift towards profit maximization in the past thirty years, as a result of the process known as “financialization” (see Berger et al., 2010). The four categories of banks

types. ood here as a combination of (i) the importance of local stakeholders in the governance of the

bank and (ii) the local focus of the banks’ activities.

Alternative Banking and Recovery from Crisis

Special

purpose banks

State agencies

improve access

local community

National or regional development; mobilize private capital for public finance; secure SME access to credit.

Weak

These three characteristics of alternative banks are mutually reinforcing. The absence of profit maximization motives weakens potential residual claims of shareholders (when they

versa, stakeholder-oriented centered governance help maintain a broad range of corporate goals, often written

rnance and a focus on sustainable returns instead of risky operations and profit maximization help lengthen the business horizons of alternative banks. The local, regional or national rooting of alternative

itutions strengthens the role that social and political forces play as stakeholders in alternative bank governance. To explain how these three characteristics of alternative banks provide competitive advantages over private banks,

orical development of alternative banking groups, then to banking theory, and finally to heterodox theories of the firm and institutional foundations of

mmercial and merchant banking very early in European history (Mettenheim and Butzbach, 2014). Savings banks were founded by municipalities and other local entities throughout Europe in the late 18th and early 19th

mit further back in history; to early Christian fund credit foundations of religious orders in medieval Italy; and to the

s summarized here are taken from banking theory and theories of the firm discussed below. Private banks may also have social missions that temper profit maximization for owners or shareholders. However, there is widespread view that most large, commercial banks have seen their focus gradually shift towards profit maximization in the past thirty years, as a result of the process known as “financialization” (see Berger et al., 2010). The four categories of banks

ood here as a combination of (i) the importance of local stakeholders in the governance of the

Monti di pieta savings and pawn banks founded throughout Italy in the 15(Menhegin, 1986). Raiffeisen and SchultzGerman speaking areas after hunger and economic crisis ravaged small farmers and communities in the late 1840s. Development banks were created throughout Europe during the 19th century and developing countries in the 20accelerate industrialization (Aghion, 1999; Zysman, 1983; Diamond, 1957). In Europe, (and European colonies), government postal banks rapidly improved access to payment services and savings accounts after the 1860s. Alternative banks were captured in the 20Prime ministers eager to bypass parliaments tapped postal savings deposits for public finance and war. Fascist and Stalinist governments took over, often by force, cooperative basavings banks. From 1945-80, alternative banks were instrumental for recovery from war and sustaining growth across Europe (Shonfield, 1965); remaining critical institutions for complementary relations (Schmidt and Tyrell, 2001) with public savingsand other core features of Welfare States. The following sections indicate the importance of alternative banking histories and the need for further research.

2.1. Italy

Alternative banks retained substantial market shares during the lareforms in the 1990s transformed most banks into jointTable 2 reports the credit provided by different types of banks in Italy from 1861During this period, private banks decline from just oshare of credit in Italy. While savings banks and Monti di pieta, popular banks and credit cooperatives maintained substantial shares of lending during this period of development and credit market deepening, newlymarket share to over 13 percent by 1910. Table 2) Italian Credit Institution Loans, 1861

Savings Banks &Year Private Monti di pietà1861 38.7 38.71870 47.1 137.41880 213.0 234.01890 362.3 391.91900 331.9 367.41910 1.029.7 857.7

Source: De Bonis et al (2012) “New Time Series on the Activity of Banks and Other Financial Institutions from 1861 to 2011.” The importance of branch office networks for relational banking and other institutional foundations of competitive advantage are discussed below. Tbranch offices held by different types of banks in Italy from 1936bank share of branch office networks declines to below half of the total number. Instead, credit institutes, national-interest banks, pbanks expand their shares of branch offices in the posteconomy.

Alternative Banking and Recovery from Crisis

9

Monti di pieta savings and pawn banks founded throughout Italy in the 15n and Schultz-Delitz credit cooperatives were founded across

German speaking areas after hunger and economic crisis ravaged small farmers and communities in the late 1840s. Development banks were created throughout Europe during

ping countries in the 20th century to finance infrastructure and accelerate industrialization (Aghion, 1999; Zysman, 1983; Diamond, 1957). In Europe, (and European colonies), government postal banks rapidly improved access to payment services

ccounts after the 1860s. Alternative banks were captured in the 20Prime ministers eager to bypass parliaments tapped postal savings deposits for public finance and war. Fascist and Stalinist governments took over, often by force, cooperative ba

80, alternative banks were instrumental for recovery from war and sustaining growth across Europe (Shonfield, 1965); remaining critical institutions for complementary relations (Schmidt and Tyrell, 2001) with public savings, pension programs and other core features of Welfare States. The following sections indicate the importance of alternative banking histories and the need for further research.

Alternative banks retained substantial market shares during the late 19th reforms in the 1990s transformed most banks into joint-stock firms through privatizations. Table 2 reports the credit provided by different types of banks in Italy from 1861During this period, private banks decline from just over half market share to a third of market share of credit in Italy. While savings banks and Monti di pieta, popular banks and credit cooperatives maintained substantial shares of lending during this period of development and credit market deepening, newly founded government special credit institutes increased market share to over 13 percent by 1910.

Table 2) Italian Credit Institution Loans, 1861-1910 (billion euros)

Savings Banks & Popular Banks & Gov. SpecialMonti di pietà Credit Coops Cred. Institutes

38.7 1.5137.4 20.4 23.3234.0 92.7 144.6391.9 209.1 427.0367.4 234.4 349.1857.7 652.1 379.2

al (2012) “New Time Series on the Activity of Banks and Other Financial Institutions from 1861 to 2011.”

The importance of branch office networks for relational banking and other institutional foundations of competitive advantage are discussed below. Table 3 reports the number of branch offices held by different types of banks in Italy from 1936-1966. Again, the private bank share of branch office networks declines to below half of the total number. Instead,

interest banks, popular coops, savings and Monti, and rural savings banks expand their shares of branch offices in the post-war period of growth and social

Alternative Banking and Recovery from Crisis

Monti di pieta savings and pawn banks founded throughout Italy in the 15th century Delitz credit cooperatives were founded across

German speaking areas after hunger and economic crisis ravaged small farmers and communities in the late 1840s. Development banks were created throughout Europe during

century to finance infrastructure and accelerate industrialization (Aghion, 1999; Zysman, 1983; Diamond, 1957). In Europe, (and European colonies), government postal banks rapidly improved access to payment services

ccounts after the 1860s. Alternative banks were captured in the 20th century. Prime ministers eager to bypass parliaments tapped postal savings deposits for public finance and war. Fascist and Stalinist governments took over, often by force, cooperative banks and

80, alternative banks were instrumental for recovery from war and sustaining growth across Europe (Shonfield, 1965); remaining critical institutions for

, pension programs and other core features of Welfare States. The following sections indicate the importance of

century until stock firms through privatizations.

Table 2 reports the credit provided by different types of banks in Italy from 1861-1910. ver half market share to a third of market

share of credit in Italy. While savings banks and Monti di pieta, popular banks and credit cooperatives maintained substantial shares of lending during this period of development and

founded government special credit institutes increased

Total 79.0

228.3 684.2

1.390.3 1.282.8 2.918.7

al (2012) “New Time Series on the Activity of Banks and Other Financial

The importance of branch office networks for relational banking and other institutional able 3 reports the number of

1966. Again, the private bank share of branch office networks declines to below half of the total number. Instead,

opular coops, savings and Monti, and rural savings war period of growth and social

Table 3) Branch Offices of Types of Banks, Italy 1936

Year J-Stock* Credit Co´s* Other*1936 1929 22151940 1502 16961950 1778 19431960 2087 22291966 2334 2459

*=private banks Fonte: Banca d'Italia, (1977). Struttura funzionale e territoriale del sistema bancario italiano 1936-1974, Rome 1977.

In Italy, reforms during the 1990s and 2000s privdirected government credit channels in favour of private banking. However, instead of wholesale privatization, shares were allocated to savings banks foundations designed to continue the social and cultural missions of savibank change across Europe. 2.2. Germany Alternative banking in Germany emerged during the 19shares since. Indeed, studies of banking in Germany use the concept of three pillars describe the largely equal market shares, since the 19(pillar one), cooperative banks (pillar two) and local and regional government savings banks (pillar three) (Schmidt et al, 2014). Table 4) German Sparkasse Sav

Year Banks Offices Accounts1839 85 1845 157 1850 234 2781471855 323 4235421865 517 9195131875 1005 22091011885 1318 1485 42094531895 1493 2448 68766641900 1490 2828 86707091910 1711 4619 129003041913 1765 5268 14417642

Balance = Millon marks, Avg and per cap Balance = marksSource: Büschegen, H. E. (1983: 399).

Sparkasse savings banks, the third pillar, grew from 85 institutions in 1839 to 1765 mostly municipal government banks by 1920savings accounts, number of accounts per 100 residents and balance per capita population suggest that past debates about public savings banks in Germany remain relevant for

Alternative Banking and Recovery from Crisis

10

Table 3) Branch Offices of Types of Banks, Italy 1936-1966

Credit National Popular Savings &

Other* Institutes Banks Coops Monti192 935 607 1161 1536136 996 577 946 1664109 1183 661 1142 2131114 1371 737 1476 2632

96 1501 791 1695 2940

Struttura funzionale e territoriale del sistema , Rome 1977.

In Italy, reforms during the 1990s and 2000s privatized savings banks and reduced directed government credit channels in favour of private banking. However, instead of wholesale privatization, shares were allocated to savings banks foundations designed to continue the social and cultural missions of savings banks. This is just one permutation of

Alternative banking in Germany emerged during the 19th century to retain large market shares since. Indeed, studies of banking in Germany use the concept of three pillars describe the largely equal market shares, since the 19th century, retained by private banks (pillar one), cooperative banks (pillar two) and local and regional government savings banks (pillar three) (Schmidt et al, 2014).

Table 4) German Sparkasse Savings Banks, 1839-1913

AccountsAccts per 100 pop. Balance

Avg. Balance

1838

278147 54 195.4 423542 97 228.7 919513 268 291.3

2209101 8.6 1112 503.4 4209453 14.8 2261 537.1 6876664 21.5 4345 631.9 8670709 25.1 5746 662.6

12900304 32.1 11107 860.1 17642 34.2 13111 909.4

Balance = Millon marks, Avg and per cap Balance = marks Büschegen, H. E. (1983: 399).

Sparkasse savings banks, the third pillar, grew from 85 institutions in 1839 to 1765 mostly municipal government banks by 1920. Historical data on the average balance of savings accounts, number of accounts per 100 residents and balance per capita population suggest that past debates about public savings banks in Germany remain relevant for

Alternative Banking and Recovery from Crisis

Savings & RuralMonti Savings Total1536 1202 76561664 987 68662131 691 77512632 758 92032940 813 10199

Struttura funzionale e territoriale del sistema

atized savings banks and reduced directed government credit channels in favour of private banking. However, instead of wholesale privatization, shares were allocated to savings banks foundations designed to

ngs banks. This is just one permutation of

century to retain large market shares since. Indeed, studies of banking in Germany use the concept of three pillars to

century, retained by private banks (pillar one), cooperative banks (pillar two) and local and regional government savings banks

Balance per-cap. pop.

1.242.373.29

5.613.843.279.5

136.3166.4276.2311.4

Sparkasse savings banks, the third pillar, grew from 85 institutions in 1839 to 1765 . Historical data on the average balance of

savings accounts, number of accounts per 100 residents and balance per capita population suggest that past debates about public savings banks in Germany remain relevant for

discussions of financial inclusion and of the 20th century, the “Sparkasse question” turned on whether increasing values of savings deposits at savings banks indicated drift from social missions that increased risk (because of more volatile middle class and business depositors), or whether traditional clients had instead simply accumulated savings over time. The latter position prevailed, while further debates ensued about the role of small savings of the poor in savings banks helped amelor exacerbate, the business cycle (Seidel, 1909).

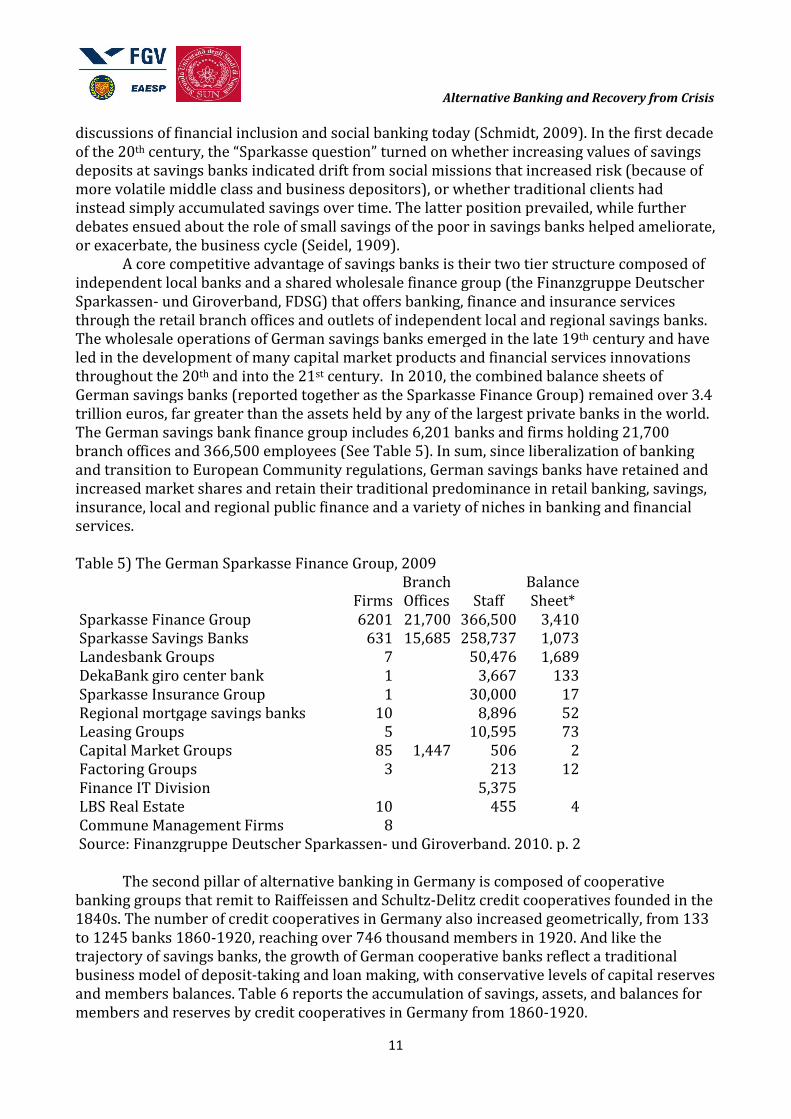

A core competitive advantageindependent local banks and a shared wholesale finance group (the Finanzgruppe Deutscher Sparkassen- und Giroverband, FDSG) that offers banking, finance and insurance services through the retail branch offices and outlets of independent local and regional savings banks. The wholesale operations of German savings banks emerged in the late 19led in the development of many capital market products and financial services innovations throughout the 20th and into the 21German savings banks (reported together as the Sparkasse Finance Group) remained ovtrillion euros, far greater than the assets held by any of the largest private banks in the world. The German savings bank finance group includes 6,201 banks and firms holding 21,700 branch offices and 366,500 employees (See Table 5). In sum, since and transition to European Community regulations, German savings banks have retained and increased market shares and retain their traditional predominance in retail banking, savings, insurance, local and regional public finance anservices. Table 5) The German Sparkasse Finance Group, 2009

Sparkasse Finance Group Sparkasse Savings Banks Landesbank Groups DekaBank giro center bank Sparkasse Insurance Group Regional mortgage savings banksLeasing Groups Capital Market Groups Factoring Groups Finance IT Division LBS Real Estate Commune Management Firms

Source: Finanzgruppe Deutscher Sparkassen

The second pillar of alternative banking in Germany is composed of cooperative banking groups that remit to Raiffeissen and Schultz1840s. The number of credit cooperatives in Germany also increased geometrically, from 133 to 1245 banks 1860-1920, reaching over 746 thousand members in 1920. And like the trajectory of savings banks, the growth of German cooperative banks reflect a traditional business model of deposit-taking and loan making, with conservative levels of capital reserves and members balances. Table 6 reports the accumulation of savings, assemembers and reserves by credit cooperatives in Germany from 1860

Alternative Banking and Recovery from Crisis

11

discussions of financial inclusion and social banking today (Schmidt, 2009). In the first decade century, the “Sparkasse question” turned on whether increasing values of savings

deposits at savings banks indicated drift from social missions that increased risk (because of ile middle class and business depositors), or whether traditional clients had

instead simply accumulated savings over time. The latter position prevailed, while further debates ensued about the role of small savings of the poor in savings banks helped amelor exacerbate, the business cycle (Seidel, 1909).

A core competitive advantage of savings banks is their two tier structure composed of independent local banks and a shared wholesale finance group (the Finanzgruppe Deutscher

rband, FDSG) that offers banking, finance and insurance services through the retail branch offices and outlets of independent local and regional savings banks. The wholesale operations of German savings banks emerged in the late 19

n the development of many capital market products and financial services innovations and into the 21st century. In 2010, the combined balance sheets of

German savings banks (reported together as the Sparkasse Finance Group) remained ovtrillion euros, far greater than the assets held by any of the largest private banks in the world. The German savings bank finance group includes 6,201 banks and firms holding 21,700 branch offices and 366,500 employees (See Table 5). In sum, since liberalization of banking and transition to European Community regulations, German savings banks have retained and increased market shares and retain their traditional predominance in retail banking, savings, insurance, local and regional public finance and a variety of niches in banking and financial

Table 5) The German Sparkasse Finance Group, 2009 Branch Balance

Firms Offices Staff Sheet*6201 21,700 366,500 3,410

631 15,685 258,737 1,0737 50,476 1,6891 3,667 1331 30,000 17

Regional mortgage savings banks 10 8,896 525 10,595 73

85 1,447 506 23 213 12

5,375 10 455 4

8 Source: Finanzgruppe Deutscher Sparkassen- und Giroverband. 2010. p. 2

The second pillar of alternative banking in Germany is composed of cooperative ps that remit to Raiffeissen and Schultz-Delitz credit cooperatives founded in the

1840s. The number of credit cooperatives in Germany also increased geometrically, from 133 1920, reaching over 746 thousand members in 1920. And like the

trajectory of savings banks, the growth of German cooperative banks reflect a traditional taking and loan making, with conservative levels of capital reserves

and members balances. Table 6 reports the accumulation of savings, assets, and balances for members and reserves by credit cooperatives in Germany from 1860-1920.

Alternative Banking and Recovery from Crisis

social banking today (Schmidt, 2009). In the first decade century, the “Sparkasse question” turned on whether increasing values of savings

deposits at savings banks indicated drift from social missions that increased risk (because of ile middle class and business depositors), or whether traditional clients had

instead simply accumulated savings over time. The latter position prevailed, while further debates ensued about the role of small savings of the poor in savings banks helped ameliorate,

of savings banks is their two tier structure composed of independent local banks and a shared wholesale finance group (the Finanzgruppe Deutscher

rband, FDSG) that offers banking, finance and insurance services through the retail branch offices and outlets of independent local and regional savings banks. The wholesale operations of German savings banks emerged in the late 19th century and have

n the development of many capital market products and financial services innovations century. In 2010, the combined balance sheets of

German savings banks (reported together as the Sparkasse Finance Group) remained over 3.4 trillion euros, far greater than the assets held by any of the largest private banks in the world. The German savings bank finance group includes 6,201 banks and firms holding 21,700

liberalization of banking and transition to European Community regulations, German savings banks have retained and increased market shares and retain their traditional predominance in retail banking, savings,

anking and financial

Balance Sheet*

3,410 73

1,689 133

17 52 73

2 12

4

und Giroverband. 2010. p. 2

The second pillar of alternative banking in Germany is composed of cooperative Delitz credit cooperatives founded in the

1840s. The number of credit cooperatives in Germany also increased geometrically, from 133 1920, reaching over 746 thousand members in 1920. And like the

trajectory of savings banks, the growth of German cooperative banks reflect a traditional taking and loan making, with conservative levels of capital reserves

ts, and balances for 1920.

Table 6) German Credit Cooperatives, 1860

Year Coops Members Assets Credit1860 133 316031870 740 314656 1871880 905 460656 4931890 1072 518003 6201900 870 511061 8061910 939 600387 14771920 1245 746058 7158

Source: Deutsche Bundesbank. (Frankfurt: Deutsche Bundesbank, 1976), pp. 344

The “three pillars” expression actually underestimates the importance of alternative banking in Germany because it omits federal and provincial government special purposbanks. German special purpose banks retain an additional 10 percent market share of banking in the country, depending on the sector, product and service (Schmidt et al, 2014; Krahnen and Schmidt, 2005; Deeg, 1999). Table 7 reports the balance sheet, numbownership of the twenty special purpose banks in Germany in 2010. These institutions held 834.4 billion euros on balance sheets with 12,730 employees, serving provincial Lande and federal governments by leading bank consortia and tapping capublic sector and home finance, and construction of public buildings, infrastructure modernization, environmental investments and the greening of industry, and health and other social service provision. Table 7) German Special Purpose Banks, 2010

Federal Government Special Purpose BanksKfW Bank Group Landwirtschaftliche Rentenbank State Government Special Purpose Ban

Investitionsbank Schleswig-Holstein Bremer Aufbau-Bank Hamburgische WohnungsbaukreditanstaltNBank Invest. und Förderbank NiedersachsenNRW Bank (Nordrhein Westfalen Bank)Investitions- und Strukturbank RheinlandLTH, Landestreuhandbank RheinlandSIKB Saarländische InvestitionskreditbankL-Bank, Landeskreditbank Baden-WürttembergLfA Förderbank Bayern Bayerische LandesbodenkreditanstaltLandesförderinstitut Mecklenburg-VorpommernInvestitionsbank Berlin Investitions Bank des Landes BrandenburgInvestionsbank Sachsen-Anhalt Thüringer Aufbaubank Sächsische Aufbaubank Förderbank Wirtschafts- und Infrastrukturbank Total 12,730 834.4Source: Association of German Public * billion euros **100% where % not reported

Alternative Banking and Recovery from Crisis

12

) German Credit Cooperatives, 1860-1920 Savings Member

Credit Deposits Balance Reserves 7 1 0

166 131 40 4438 353 102 16538 438 117 28672 586 133 45

1202 1084 216 944026 6480 391 164

Source: Deutsche Bundesbank. Deutsches Geld- und Bankwesen in Zahlen 1876(Frankfurt: Deutsche Bundesbank, 1976), pp. 344-5

The “three pillars” expression actually underestimates the importance of alternative banking in Germany because it omits federal and provincial government special purposbanks. German special purpose banks retain an additional 10 percent market share of banking in the country, depending on the sector, product and service (Schmidt et al, 2014; Krahnen and Schmidt, 2005; Deeg, 1999). Table 7 reports the balance sheet, number of staff and ownership of the twenty special purpose banks in Germany in 2010. These institutions held 834.4 billion euros on balance sheets with 12,730 employees, serving provincial Lande and federal governments by leading bank consortia and tapping capital markets, especially in public sector and home finance, and construction of public buildings, infrastructure modernization, environmental investments and the greening of industry, and health and other

l Purpose Banks, 2010 Balance

Federal Government Special Purpose Banks Staff Sheet* Majority Ownership**4600 400.1 80% Fed. 20% State Govts.

218 75.8 Fed. Govt.State Government Special Purpose Banks

460 16.7 Schleswig55 1.3 Bremen Holding

Hamburgische Wohnungsbaukreditanstalt 185 5.1 Hamburg NBank Invest. und Förderbank Niedersachsen 426 5.7 Niedersachsen

Nordrhein Westfalen Bank) 1224 161 98.6% Nordrheinund Strukturbank Rheinland-Pfalz 186 8.5 Rhein-Pfalz

LTH, Landestreuhandbank Rheinland-Pfalz 98 1.9 Rhein-PfalzSIKB Saarländische Investitionskreditbank 66 1.2 51% Saar

Württemberg 1230 59.7 Baden-Württemberg344 19.4 Freistaat Bayern

Bayerische Landesbodenkreditanstalt 227 21.2 Bayrischen esbankVorpommern 246 2.5 NORD LB

673 20.4 Berlin Investitions Bank des Landes Brandenburg 505 11.8 50% Brandenburg, 50% NRW Bank

349 1.3 NORD/LB336 2.5 Freistaat Thüringen

905 8.7 Freistaat Sachsen 397 9.6 Landesbank Hessen

Total 12,730 834.4 Source: Association of German Public Sector Banks (Bundesverband Öffentlicher Banken Deutschlands, VÖB)

not reported

Alternative Banking and Recovery from Crisis

und Bankwesen in Zahlen 1876-1975.

The “three pillars” expression actually underestimates the importance of alternative banking in Germany because it omits federal and provincial government special purpose banks. German special purpose banks retain an additional 10 percent market share of banking in the country, depending on the sector, product and service (Schmidt et al, 2014; Krahnen

er of staff and ownership of the twenty special purpose banks in Germany in 2010. These institutions held 834.4 billion euros on balance sheets with 12,730 employees, serving provincial Lande and

pital markets, especially in public sector and home finance, and construction of public buildings, infrastructure modernization, environmental investments and the greening of industry, and health and other

Majority Ownership** 80% Fed. 20% State Govts. Fed. Govt.

Schleswig-Holstein Bremen Holding Hamburg Niedersachsen 98.6% Nordrhein-Westfalen

Pfalz Pfalz

51% Saar Württemberg

Freistaat Bayern Bayrischen esbank NORD LB

50% Brandenburg, 50% NRW Bank NORD/LB Freistaat Thüringen Freistaat Sachsen Landesbank Hessen-Thüringen

Sector Banks (Bundesverband Öffentlicher Banken Deutschlands, VÖB)