All India Canara Bank Retirees' Federation(Regd)

108

57 AICBRF - 2 ND Triennial Conference All India Canara Bank Retirees’ Federation (Regd) INFORMATION DOCUMENTS 2 ND TRIENNIAL CONFERENCE FEBRUARY 24-25, 2016 KOCHI (Affiliated to All India Bank Retirees’ Federation)

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of All India Canara Bank Retirees' Federation(Regd)

57AICBRF - 2ND Triennial Conference

All India Canara BankRetirees’ Federation (Regd)

INFORMATION DOCUMENTS2ND TRIENNIAL CONFERENCE

FEBRUARY 24-25, 2016 KOCHI

(Affiliated to All India Bank Retirees’ Federation)

58 AICBRF - 2ND Triennial Conference

LIST OF AIBRF AFFILIATES

PUBLIC SECTOR BANKS (23):

01. ALLAHABAD BANK

02. BANK OF INDIA

03. ANDHRA BANK

04. BANK OF BARODA

05. BANK OF MAHARASHTRA

06. CENTRAL BANK OF INDIA

07. CANARA BANK

08. CORPORATION BANK

09. DENA BANK

10. INDIAN BANK

11. INDIAN OVERSEAS BANK

12. PUNJAB NATIONAL BANK

13. SYNDICATE BANK

14. STATE BANK OF MYSORE

15. STATE BANK OF TRAVANCORE

16. UCO BANK

17. UNITED BANK OF INDIA

18. UNION BANK OF INDIA

19. VIJAYA BANK

20. STATE BANK OF PATIALA RETD OFFICERS’ ASSOCN

21. ALL INDIA STATE BANK OF PATIALA RETD EMPLOYEES’ ASSOCIATION

22. STATE BANK OF INDORE RETD OFFICERS’ ASSOCIATION

23. PUNJAB & SIND BANK

59AICBRF - 2ND Triennial Conference

PRIVATE SECTOR BANKS (14):

01. CATHOLIC SYRIAN BANK

02. ICICI BANK

03. J & K BANK RETD. OFFICERS’ ASSOCN., (PRE-1986)

04. FEDERAL BANK

05. KARUR VYSYA BANK

06. ING VYSYA BANK

07. TAMILNADU MERCANTILE BANK

08. KARNATAKA BANK

09. DHANALAKSHMI BANK

10. HDFC BANK

11. SOUTH INDIAN BANK

12. KERALA GRAMIN BANK

13. J & K BANK PENSIONERS’ WELFARE FEDERATION

14. RATNAKAR BANK

FOREIGN BANKS (2):

01. STANDARD CHARTERED BANK RETIREES’ ASSOCIATION

02. STANCHART BANK RETIREES’ ASSOCIATION

ASSOCIATION/LOCAL BODIES PROVIDING DIRECT MEMBERSHIP (5):

01. M.P. BANK RETIREES’ ASSOCIATION - INDORE

02. BELGAUM BANK RETIREES’ ASSOCIATION

03. ALL KERALA BANK RETIREES’ FEDERATION

04. ANDHRA PRADESH BANK RETIREES’ FEDERATION

05. M.P.BANK RETIREES’ ASSOCIATION - RAIPUR

60 AICBRF - 2ND Triennial Conference

STATE FEDEARTIONS (11):

01. ANDHRA PRADESH

02. GUJARAT

03. KERALA

04. KARNATAKA

05. MAHARSHTRA

06. MADHYA PRADESH AND CHHATISGARH

07. NORTH EASTERN STATES COMPRISING ASSAM, MEGHALAYA, TRIPURA, ARUNACHALPRADESH & NAGALAND

08. ODISHA

09. TAMILNADU

10. UTTAR PRADESH

11. WEST BENGAL

SUMURRY OF AFFILIATES:

PUBLIC SECTOR BANKS 23

01. PRIVATE SECTOR BANKS 14

02. FOREIGN BANKS 02

03. LOCAL ASSOCIATIONS/BODIES 05

TOTAL 44

PRIMARY MEMBERSHIP OF AFFILIATES CROSSED 1,35,000

61AICBRF - 2ND Triennial Conference

IBA CIRCULARS ON PENSION MATTERSSl No.

01

02

03

04

05

06

07

08

09

10

IBA CIR. No.

PD/CIR/76/G(ii)1846

PD/CIR/76/G(ii)/993

PD/CIR/76/6(ii)/1739

PD/CIR/76/G(ii)/1803

PD/CIR/76/G(ii)/1831

PD/CIR/76/G(ii)/2139

PD/CIR/76/G(ii)/285

PD/CIR/76/G(ii)/296

PD/CIR/76/G(ii)/391

PD/CIR/76/G(ii)/392

DATE

18.02.1995

19.09.1995

05.12.1995

13.12.1995

15.12.1995

17.01.1996

30.05.1996

31.05.1996

11.06.1996

12.06.1996

SUBJECT OF THE CIRCULAR

BEPR 1993 NETTING, COMMON DATE FORMAKING COMMUTATION ABSOLUTE, INT.RATE ON CPF ON ACCOUNT OF REFUND

APPROVAL FOR DRAFT PENSION REGULATIONSRECEIVED FROM GOVT. OF INDIA, MoF(BANKING DIVISION)

GUIDELINES FOR SETTLEMENT OF FAMILYPENSION TO FAMILIES OF EMPLOYEESWHOSE WHEREABOUTS ARE NOT KNOWN

MODEL PENSION TRUST DEED & MODELDEED OF VARIATION

NETTING FACILITY TO EMPLOYEES WHORETIRED ON OR AFTER 01.01.1986 BUTBEFORE THE NOTIFIED DATE

CREATION OF PENSION TRUST & AD-HOCPAYMENT OF PENSIONARY BENEFIT, PENDINGIT APPROVAL TO THE TRUST/FUND; “NOOBJECTION” OF CBDT TO TRANSFERACCUMULATED EMPLOYER’S CONTRIBUTIONIN THE PF TO PENSION FUND IN RESPECT OFPENSION OPTEES

RECKONING OF DATE ON WHICH COMMUTATIONBECAME ABSOLUTE IN THE CASE OF THOSEWHO RETIRED BEFORE 01.11.1993.

ENCASHMENT OF LEAVE TO EMPLOYEESWHO SEEK VOLUNTARY RETIREMENT UNDERREGULATION 29 OF BEPR 1995

WAIVER OF INTEREST AFTER 01.04.1995 ONPF AMOUNT TO BE REFUNDED BY RETIREDEMPLOYEES / FAMILY MEMBERS OFDECEASED EMPLOYEES.

SIMILAR GUIDELINES TO PRIVATE SECTORBANKS AS IN SERIAL NUMBER 09

62 AICBRF - 2ND Triennial Conference

11

12

13

14

15

16

17

18

19

20

21

22

23

20.07.1996

05.09.1996

07.09.1996

11.11.1996

19.12.1996

19.06.1997

05.07.1997

12.08.1997

02.01.1998

04.01.1998

19.01.1998

28.07.1998

18.11.1998

DEFINITION OF PAY FOR PENSION -6TH BIPARTITE SETTLEMENT

PROCEDURE FOR PAYMENT OF PENSION TORETIREES SETTLED OUTSIDE INDIA

DELETING STRIKE CLAUSE IN BEPR 1995

PAYMENT OF MINIMUM FP & DR THEREONIN CASES WHERE AGGREGATE OF BASICFAMILY PENSION AND ADDITIONAL FAMILYPENSION FALLS SHORT OF MINIMUMFAMILY PENSION.

NOTIFICATION DATED 06.12.1996

UPDATION OF PENSION IN RESPECT OFTHOSE WHO HAVE DRAWN PARTLY PRE-REVISED AND PARTLY REVISED PAY I.E. AS PERPAY SCALES AS IN V BPS AND VI BPS

CHECK LIST FOR BANK’S MEDICAL OFFICERSWHILE CARRYING OUT MEDICAL EXAMINATIONOF RETIRED EMPLOYEES SEEKING COMMUTATIONOF PENSION.

GOVT’S DECISION ON SETTING UP OF FUND,INVESTMENT OF FUND MONEYS ANDPURCAHSE OF ANNJUITY FROM LIC BY PRIVATESECTOR BANKS

AMENDMENT TO REGULATION 22 (4) (b)BEPR 1995 – DELETION OF CLAUSE RELATINGTO FORFEITURE OF PAST SERVICE FORPARTICIPATION IN STRIKES.

VOLUNTARY RETIREMENT AS PER BEPR1995

PTEs – REFUND OF PF IN RESPECT OF INELIGIBLECASES

REGULN 39 OF BEPR 1995 – COMPUTATIONOF FAMILY PENSION

BEPR 1995 - UPDATION OF PENSION

PD/CIR/76/G(ii)/630

PD/CIR/76/G(ii)/928

PD/CIR/76/G(ii)/943

PD/CIR/76/G(ii)/1381

PD/CIR/76/G(ii)/1696

PD/CIR/76/G(ii)/490

PD/CIR/76/G(ii)/592

PD/CIR/76/G(ii)/821

PD/CIR/76/G(ii)/1545

PD/KVK/85/G(ii)/2037

PD/CIR/76/G(ii)/1638

PD/CIR/76/G(ii)/495

PD/CIR/76/G(ii)/1109

63AICBRF - 2ND Triennial Conference

24

25

26

27

28

29

30

10.12.1998

04.03.1998

02.06.1998

12.06.1998

26.06.1998

28.07.1998

18.11.1998

COUNTING PERIODS OF EXTRAORDINARYLEAVE ON LOP AS QUALIFYING SERVICE FORPENSION – PROSPECTIVE EFFECT OF REGU-LATION 17 PROVIDED THE REQUISITE DIREC-TIVE HAS BEEN GIVEN BY THE SANCTIONINGAUTHORITY

PAYMENT OF PENSION ARREARS FROM01.11.1993 TO ELIGIBLE MEMBERS OF FAM-ILY WHERE THE EMPLOYEE HAD RETIRED BE-FORE 01.11.1993 BUT DIED SUBSEQUENTLYBEFORE NOTIFIED DATE.

PAYMENT OF MINIMUM PENSION AND DRIN CASES WHERE BASIC PENSION IS LESSTHAN ADMISSIBLE MINIMUM PENSION BUTAGGREGATE OF BASIC PENSION AND ADDI-TIONAL PENSION IS MORE THAN THE MINI-MUM PENSION.

FORMULA/METHOD FOR TRANSFER OF THESECURITIES RELATING TO INVESTMENT OF PFMONEYS TO PENSION FUND BASED ON AV-ERAGE MATURITY AND AVERAGE YIELD

REVISION IN THE UPPER LIMIT ON THEEMPLOYER’S ANNUAL CONTRIBUTION TOPENSION FUND FROM 25% TO 27% OF THEEMPLOYEE’S PAY FOR EACH YEAR.

RATE OF FAMILY PENSION IN CASES WHERETHE PENSION AUTHORISED TO THE EM-PLOYEE ON HIS RETIREMENT IS LESS THANTHE AMOUNT OF FAMILY PENSION AT ORDI-NARY RATES.

OPTN TO DRAW PENSION WITH REFERENCETO PAY AS PER SCALES IN EXISTANCE PRIORTO 01.11.1992/ 01.07.1993 IN CASES WHERECONSEQUENT UPON UPDATION OF PEN-SION, THE AGGREGATE OF BASIC PENSION& D.R. REDUCED.

PD/CIR/76/G(ii)/1778

PD/CIR/76/G(ii)/1939

PD/CIR/76/G(ii)/191

PD/CIR/76/G(ii)/221

PD/CIR/76/G(ii)/289

PD/CIR/76/G(ii)/495

PD/CIR/76/G(ii)/1109

64 AICBRF - 2ND Triennial Conference

31

32

33

34

35

36

37

38

39

40

WHEREVER PENSIONER OPTED TO DRAWPENSION ON PRE-REVISED SCALES OF PAYAND HAS BEEN PAID ACCORDINGLY, FP IN HISCASE WILL ALSO HAVE TO BE ARRIVED AT BYRECKONING THE PAY THAT HAS BEEN RECKONEDFOR ARRIVING AT AVERAGE EMOLUMENTSFOR PENSION.

“PAY” TO BE RECKONED FOR AVERAGEEMOLUMENTS IN THE CASE OF EMPLOYEEWHO RETIRES ON SUPERANNUATIONWHILE ON DEPUTATION TO ANOTHERORGANISATION.

OPTION BETWEEN MILITARY FAMILY PEN-SION AND FAMILY PENSION UNDER BEPR1995 (PL. REF TO SL. Nos. 26 & 28)

DEARNESS RELIEF ON EX-GRATIA

BROKEN PERIOD OF SERVICE OF LESS THANONE YEAR BUT MORE THAN 6 MONTHS , NOTTO BE RECKONED FOR DETERMINING MINIMUMSERICE REQUIRED TO MAKE AN EMPLOYEEELIGIBLE FOR PENSION (PL REFER TOREGULATION 18)

WHAT CONSTITUTES INITIATION OF DEPARTMENTALPROCEEDINGS / INSITUTION OF JUDICIALPROCEEDINGS?

CLARIFICATION ON DRAWAL OF MILITARYFAMILY PENSION BY THOSE WHO DRAWNFAMILY PENSION UNDER BEPR 1995 (PL. SEESL. Nos. 23 & 28)

PAYMENT OF PROVISIONAL PENSION WHERETHERE IS LIKELY DELAY IN PROCESSING OFPENSION PAPERS AND GRANT OF FINALPENSION.

AS IN SL. Nos. 23 & 26

GRANTING EX-GRATIA TO SURVIVING PRE-01.01.1986 RETIREES

PD/CIR/76/G(ii)/1492

PD/CIR/76/G(ii)/1521

PD/CIR/76/G(ii)/212

PD/CIR/76/G(ii)/76

PD/CIR/76/G2/797

PD/CIR/76/G2/1136

PD/CIR/76/G2/1218

PD/CIR/76/G2/1655

PD/CIR/76/G2/1805

PD/CIR/76/G(ii)/67

04.01.1999

11.01.1999

13.05.1999

17.05.1999

14.08.1999

12.10.1999

30.10.1999

15.01.2000

10.02.2000

17.04.2000

65AICBRF - 2ND Triennial Conference

BPS/27.03.2000 – COMPTN OF PENSION

GRANT OF PENSIONARY BENEFITS TO OFFICERSWHO VOLUNTARILY RETIRED FROM SERVICESOF THE BANK DURING THE PERIOD01.01.1986 TO 31.10.1993

COMPUTATION OF PENSION CONSEQUENTTO WAGE REVISION OF WORKMEN – BPSDATED 27.03.2000

COMPUTATION OF AVERAGE EMOLUMENTS– RECKONING OF DA AT 1616 POINTS

METHOD OF COMPUTATION OF PENSIONCONSEQUENT UPON PAY REVISION OFOFFICERS IN TERMS OF JOINT NOTE DATED14.12.1999 AND OF WORKMEN IN TERMS OF7TH BPS DATED 27.03.2000

BENEFITS OF REGLN 29 (5) NOT AVAILABLEFOR VRS OPTEES UNDER VRS 2000

DR-PENSN– RE-EMPLOYED EX-SERVICEMEN

AMENDMENTS TO REGLN 28 OF BEPR 1995PRO-RATA PENSION IN CASE OF RETIREMENTPRIOR TO ATTAINING AGE OF SUPERANNUATIONUNDER A SPECIFIC SCHEME OF THE BANK.

GUIDELINES FOR GRANTING COMPASSIONATEALLOWANCE UNDER REGULATION 31 OFBEPR 1995.

PROPOSED AMENDMENTS TO BEPR 1995 &GAZETTEE NOTIFICATION TO BE ISSUED

AMENDMENTS TO BEPR 1995 – RECTIFICATIONOF DISCREPANCIES

RECTIFICATION OF ERRORS & OMISSIONS INDRAFT NOTIFICATION OF AMENDMENTS

41

42

43

44

45

46

47

48

49

50

51

52

03.05.2000

01.06.2000

04.09.2000

27.09.2000

23.10.2000

25.01.2001

19.03.2001

05.12.2001

08.01.2002

23.01.2002

05.02.2002

02.03.2002

PD/CIR/76/G(2)/163

PD/CIR/76/G2/394

PD/CIR/76/G(ii)/938

PD/CIR/76/G(ii)/1106

PD/CIR/76/G2/1284

PD/CIR/76/G2/1766

PD/CIR/76/G2/589/2045

PD/CIR/76/G2/1128

PD/CIR/76/G2/1242

PD/CIR/76/G(ii)/1317

PD/CIR/76/G(ii)/1387

PD/CIR/76/G(ii)/1524

66 AICBRF - 2ND Triennial Conference

EXAMPLES ON UPDATION OF FP/ADDNL FPIN RESPECT OF EMPLOYEES WHO WERE INTHE SERVICE OF THE BANK ON OR AFTER01.01.1986 AND HAD DIED WHILE IN SERVICEON OR BEFORE 31.10.1987 OR HAD RETIREDON OR BEFORE 31.10.1987, BUT DIED.

PROCEDURE TO ARRIVE AT PENSION PAYABLETO PART-TIME EMPLOYEES ON SCALE WAGES

NO IMPACT ON AVERAGE EMOLUMENTS FORPARTICIPATION IN STRIKE WITH LOP

COMMUTATION OF PENSION AND EFFECTIVEDATE OF COMMENCEMENT OF PAYMENT OFRESIDUAL PENSION

PENSION UNDER 8TH BIPARTITE SETLEMENT

RE-DEFINITION OF PAY AS PER BPS/JN DATED02.06.2005

CONSTITUTION OF GRIEVANCES REDRESSALCELL IN BANKS

PENSION OPTION – SHARING OF COST

ANOTHER PENSION OPTION – IMPLEMENTNOF 9TH BPS & JOINT NOTE DT. 27.04.2010

NEW PENSION SCHEME FOR THOSE JOININGBANKS ON OR AFTER 01.04.2010

PENSION FOR THOSE RETIRED BETWEEN01.11.2007 TO 31.07.2008

ANOTHER PENSION OPTION TO OFFICERSRETIRED UNDER VRS AS PER OSR

CORRIGENDUM TO IBA CIRCULAR ONANOTHER PENSION OPTION TO OFFICERSRETIRED UNDER VRS AS PER OSR

INCREASE IN EX-GRATIA AMOUNT TO PRE 86RETIREES & SURVIVING SPOUSES

53

54

55

56

57

58

59

60

61

62

63

64

65

66

PD/CIR/76/G2/1558

PD/CIR/76/G2/105

PD/GSN/SBT/G2/276

PD/CIR/76/G2/337

RECORD NOTE

PD/76/D/G2/2005-06/557

CIR/HR & IR/G2/2008-09/3059

RECORD NOTE

CIR/HR & IR/G2/665/90/2010-11/999

CIR/HR & IR/G2(DC)/2010-11/1036

CIR/HR & IR/G2/2010-11/1502

CIR/HR & IR/2012-13/G2/6213

CIR/HR & IR/2012-13/ G2/6219

CIR/HR & IR/G3/2013-14/8613

07.03.2002

19.04.2002

22.05.2002

28.06.2003

22.06.2005

28.06.2005

30.03.2009

27.11.2009

10.08.2010

23.09.2010

13.10.2010

09.11.2012

12.11.2012

06.01.2014

67AICBRF - 2ND Triennial Conference

COMPASSIONATE JOBS IN PSBs

ENCASHMENT OF PL ON COMPULSORYRETIREMENT

CALCULATION OF PENSION FOR THOSERETIRED BETWEEN 01.11.2012 AND31.07.2013

SUPERANNUATION BENEFITS TO THOSEIMPOSED WITH PUNISHMENT OF REMOVAL /DISCHARGED FROM BANK SERVICE

FITMENT FORMULA ON PROMOTION OFSUBSTAFF TO CLERICAL CADRE

FITMENT FORMULA ON PROMOTION OFCLERICAL TO OFFICER CADRE

REVISION OF HALTING ALLOWANCE

TA/DA TO SERVING/RETD EMPLOYEES FORATTENDING DISCIPLINARY / CRIMINALPROCEEDINGS AS CHARGED OFFICER,PROSECUTING / DEFENCE WITNESS.

SUPERANNUATION BENEFITS TO EMPLOYEESREMOVED / COMPULSORILY RETD /DISCHARGED FROM SERVICE

31.12.2014

11.05.2015

08.06.2015

30.06.2015

07.08.2015

07.08.2015

15.09.2015

19.11.2015

23.12.2015

CIR/HR&IR/2014-25/532/1108HR&IR/76/H7/E9/755

CIR/HR&IR/G2/2015/S-2016/874

CIR/HR&IR/KU/M1/1004

CIR/HR&IR/515/2015-2016/1194

CIR/HR&IR/582/2015-16/1195

HR&IR/CIR/2015-2016/E/(ix)/1348HR&IR/CIR/2015-2016/E9/M1/1641

HR&IR/CIR/2015-16/M1/1852

67

68

69

70

71

72

73

74

75

68 AICBRF - 2ND Triennial Conference

GOVERNMENT OF INDIA INSTRUCTIONS TOPSBs ON PENSION MATTERS

SL. No. LETTER NUMBER DATE PARTICULARS

F.No.4/8/14/96-IRF.4/8/16/96-IR

F.4/8/16/98-IRF.No.11/3/92-IRF.4/4/6/99-IR

F.4/8/4/22/98-IR

F.4/8/22/2001-IR

F.No.5/7/2003-ECB& PRG.I., M.F.F.No.1(7)(2)/ 2003/ TA/11O.M.No.1(7)(2)/2003/TA/ 67-74F.No.9/11/2005-IR

F.No.4/9/1-2014-IR(Pt)

F.No.4/1/1/2015-IRDFSF.No.6

F.No.4/2/2/2015-IRDFS

29.06.199606.08.1996

14.10.199826.11.199828.07.2000

05.02.2002

19.02.2002

22.12.2003

07.01.2004

04.02.2004

12.01.2014

05.01.2015

20.08.2015

01.01.2016

02.01.2016

PENSION AS PER 6TH BPSREGULATION 26 OF BEPR 1995 - ADDITION TOQUALIFYNG SERVICE IN SPECIAL CIRCUMSTANCES.—DO—AMOUNT OF EX-GRATIAADMISSIBILITY OF TA UNDER VRS IN TERMSOF REGLN 29 OF BEPR 1995. (PVT SECTORBANKS ADVISED VIDE CIRCULAR No: PD/CIR/76/E9/831 DATED 10.08.2000SERVICE RENDERED IN BANKS/ FINANCIALINSTITUTIONS CANNOT BE COUNTED ASQUALIFYING SERVICE UNDER GOVERNMENTFOR PENSION AND VICE-VERSA.ADMISSION TO THE PENSION FUND OF AN OFFICEROR A WORKMEN EMPLOYEE WHO COULDNOT EXERCISE OPTION FOR PENSION BECAUSEHE/SHE STOOD EITHER DISMISSED ORCOMPULSORILY RETIRED ON 29.09.1995, BUTLATER GOT REINSTATED EITHER DUE TO DECISIONOF THE COURT OR APPELLATE AUTHORITY.DEFINED CONTRIBUTION PENSION – NEWPENSION SCHEMEOPERATIONALISATION OF NEW PENSIONSYSTEM FROM 01.01.2004—DO—

ENGAGEMENT OF RETD OFFICERS ASADVISORS/CONSULTANTSFREEDOM OF NON-INTERFERENCE OF PSBsON COMMERCIAL DECISIONS/TRANSFERS/POSTINGSNOTIFICATION OF 2nd & 4th SATURDAY AS HOLI-DAYS.GAZETTE NOTIFICATIN ON PAYMENT OFBONUS AMENDMENT ACT 2015INITIATING PROCESS FOR 11th BIPARTITEWAGE NEGOTATIONS

1

345

6

7

8

9

10

2

11

12

13

14

15

69AICBRF - 2ND Triennial Conference

70 AICBRF - 2ND Triennial Conference

71AICBRF - 2ND Triennial Conference

72 AICBRF - 2ND Triennial Conference

73AICBRF - 2ND Triennial Conference

74 AICBRF - 2ND Triennial Conference

75AICBRF - 2ND Triennial Conference

76 AICBRF - 2ND Triennial Conference

77AICBRF - 2ND Triennial Conference

78 AICBRF - 2ND Triennial Conference

79AICBRF - 2ND Triennial Conference

CANARA BANK EMPLOYEES’ PENSION FUND

GROWTH OF PENSION FUND CORPUS

FINANCIAL YEAR PENSION FUND CORPUS IN CRORES

1995 - 1996

1996 - 1997

1997 - 1998

1998 - 1999

1999 - 2000

2000 - 2001

2001 - 2002

2002 - 2003

2003 - 2004

2004 - 2005

2005 - 2006

2006 - 2007

2007 - 2008

2008 - 2009

2009 - 2010

2010 - 2011

2011 - 2012

2012 - 2013

2013 - 2014

2014 - 2015

0000.00

0174.36

0213.71

0250.72

0301.62

0370.75

0526.19

0638.51

0748.34

0905.92

1136.81

1380.50

2661.24

3019.32

3384.34

7189.14

7781.25

8345.31

8767.00

9644.00

80 AICBRF - 2ND Triennial Conference

81AICBRF - 2ND Triennial Conference

82 AICBRF - 2ND Triennial Conference

83AICBRF - 2ND Triennial Conference

84 AICBRF - 2ND Triennial Conference

85AICBRF - 2ND Triennial Conference

Claim Applicationto be submitted

Claim Applicationto be submitted

Claim Applicationto be submitted

Claim Applicationto be submitted

Claim Applicationto be submitted

DischargeReceipt to besubmited.

86 AICBRF - 2ND Triennial Conference

87AICBRF - 2ND Triennial Conference

RATE

OF

FAM

ILY P

ENSI

ON

- TA

BLE

AS P

ER 5

TH B

PSAS

PER

6TH

BPS

AS P

ER 7

TH B

PS

Cess

atio

n 01

-01-

86 to

31-

10-9

2 (W

)Ce

ssat

ion

01-0

1-86

to 3

0-06

-93

(O)

Cess

atio

n 01

-11-

92 to

31-

03-9

8 (W

)Ce

ssat

ion

01-0

7-93

to 3

1-03

-98

(O)

Cess

atio

n 01

-04-

98 to

31-

10-0

2(B

oth

W &

O)

Scal

e of

pay

last

dra

wn

1. U

pto

Rs.1

500/

-

(Min

. 375

)

2. R

s.15

01/-

to R

s.30

00/-

(Min

. 450

)

3. A

bove

Rs.

3000

/-

(Min

. 600

)

Rate

of F

P

30%

(Max

. 450

)

20%

(Max

. 600

)

15%

(Max

. 125

0)

Scal

e of

pay

last

dra

wn

1. U

pto

Rs.2

870/

-

(Min

. 720

)

2. R

s.28

71/-

to R

s.57

40/-

(Min

. 860

)

3. A

bove

Rs.

5740

/-

(Min

. 115

0)

Rate

of F

P

30%

(Max

. 860

)

20%

(Max

. 115

0)

15%

(Max

. 240

0)

Scal

e of

pay

last

dra

wn

1. U

pto

Rs.4

040/

-

(Min

. 101

5)

2. R

s.40

40/-

to R

s.80

80/-

(Min

. 121

2)

3. A

bove

Rs.

8080

/-

(Min

. 161

6)

Rate

of F

P

30%

(Max

. 121

2)

20%

(Max

. 161

6)

15%

(Max

. 337

8)

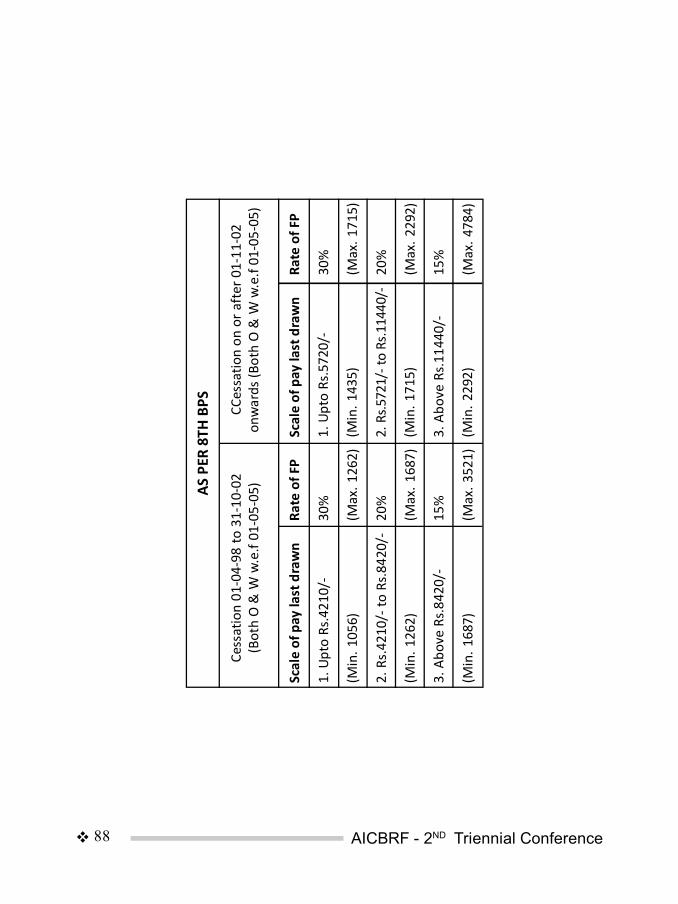

88 AICBRF - 2ND Triennial Conference

AS P

ER 8

TH B

PS CCes

satio

n on

or a

fter

01-

11-0

2on

war

ds (B

oth

O &

W w

.e.f

01-0

5-05

)Ce

ssat

ion

01-0

4-98

to 3

1-10

-02

(Bot

h O

& W

w.e

.f 01

-05-

05)

Scal

e of

pay

last

dra

wn

1. U

pto

Rs.4

210/

-

(Min

. 105

6)

2. R

s.42

10/-

to R

s.84

20/-

(Min

. 126

2)

3. A

bove

Rs.

8420

/-

(Min

. 168

7)

Rate

of F

P

30%

(Max

. 126

2)

20%

(Max

. 168

7)

15%

(Max

. 352

1)

Scal

e of

pay

last

dra

wn

1. U

pto

Rs.5

720/

-

(Min

. 143

5)

2. R

s.572

1/- t

o Rs

.114

40/-

(Min

. 171

5)

3. A

bove

Rs.

1144

0/-

(Min

. 229

2)

Rate

of F

P

30%

(Max

. 171

5)

20%

(Max

. 229

2)

15%

(Max

. 478

4)

89AICBRF - 2ND Triennial Conference

Not

e: In

the

case

of P

art-t

ime

empl

oyee

s, th

e m

inim

um a

mou

nt o

f Fam

ily P

ensio

n an

d th

e m

axim

um a

mou

nt o

f Fam

ilyPe

nsio

n sh

all b

e in

pro

port

ion

to th

e ra

te o

f sca

le w

ages

dra

wn

by th

e em

ploy

ee.

Min

imum

Pen

sion

:

In r

espe

ct o

f em

ploy

ees

othe

r th

an P

art-t

ime

empl

oyee

s w

ho r

etire

d on

or

afte

r 01

-11-

2007

, the

am

ount

of M

inim

umPe

nsio

n sh

all b

e Rs

.1,7

79/-

p.m

. In

resp

ect o

f Par

t-tim

e em

ploy

ees w

ho re

tired

on

or a

fter 0

1-11

-200

7, m

inim

um p

ensio

npa

yabl

e sh

all b

e as

follo

ws:

AS P

ER 9

TH B

PS (B

oth

O &

W)

Cess

atio

n on

or a

fter 0

1-11

-200

7 on

war

ds

Scal

e of

pay

last

dra

wn

1. U

pto

Rs.7

090/

-

(Min

. 177

9)

2. R

s.70

91/-

to R

s.14

180/

-

(Min

. 218

6)

3. A

bove

Rs.

1418

1/-

(Min

. 284

1)

Rate

of F

P

30%

(Max

. 218

6)

20%

(Max

. 284

1)

15%

(Max

. 593

0)

Scal

e of

PTE

Min

imum

Pen

sion

1/3

Scal

e W

ages

Rs.5

95/-

p.

m.

½ S

cale

Wag

esRs

.892

/-

p.m

.

¾ S

cale

Wag

esRs

.133

9/- p

.m.

90 AICBRF - 2ND Triennial Conference

In re

spec

t of e

mpl

oyee

s (ot

her t

han

part

-tim

e em

ploy

ees)

who

retir

e/re

tired

from

serv

ice

on o

r aft

er 0

1.11

.201

2 th

e or

dina

ryra

te o

f pen

sion

shal

l be

as u

nder

:

Not

e:- I

n th

e ca

se o

f par

t-tim

e em

ploy

ees,

the

min

imum

am

ount

of f

amily

pen

sion

and

the

max

imum

am

ount

of f

amily

pens

ion

shal

l be

in p

ropo

rtio

n to

the

rate

of s

cale

wag

es d

raw

n by

the

empl

oyee

.

(IV) M

INIM

UM

PEN

SIO

N: I

n re

spec

t of e

mpl

oyee

s oth

er th

an p

art-t

ime

empl

oyee

s, w

ho re

tired

on

or a

fter

01/

11/2

012,

the

amou

nt o

f min

imum

pen

sion

shal

l be

Rs.2

,785

p.m

. In

resp

ect o

f par

t-tim

e em

ploy

ees w

ho re

tired

on

or a

fter 0

1/11

/201

2,th

e m

inim

um p

ensio

n pa

yabl

e sh

all b

e Rs

.932

p.m

. in

resp

ect o

f par

t-tim

e em

ploy

ees

draw

ing

1/3

scal

e w

ages

, Rs.

1,39

7p.

m. i

n re

spec

t of p

art-t

ime

empl

oyee

s dra

win

g ½

scal

e w

ages

and

Rs.

2,0

96 p

.m. i

n re

spec

t of p

art-t

ime

empl

oyee

s dra

win

g¾

scal

e w

ages

.

AS P

ER 1

0th B

PS B

OTH

FO

R 0

& W

CESS

ATIO

N O

N O

R AF

TER

01.1

1.20

12 O

NW

ARD

S

Scal

e of

Pay

per

mon

th

Upto

Rs.

11,1

00/-

From

Rs.

11,1

01/-

to R

s. 2

2,20

0/-

Abov

e Rs

.22,

200/

-

Amou

nt o

f Mon

thly

Fam

ily P

ensio

n

30 p

er c

ent o

f the

‘pay

’ sub

ject

to a

Min

imum

of R

s. 2

,785

/- p

er m

onth

.

20 p

er c

ent o

f the

‘pay

’ sub

ject

to a

Min

imum

of R

s.3,

422/

- per

mon

th.

15 p

er c

ent o

f the

‘pay

’ sub

ject

to a

Min

imum

of R

s.4,

448/

- per

mon

th a

ndM

axim

um o

f Rs.

9,28

4/- p

er m

onth

.

91AICBRF - 2ND Triennial Conference

CON

SUM

ER P

RICE

IND

EX F

IGU

RES

BASE

198

2 =

100

YEAR

JAN

FEB

MAR

APR

MAY

JUN

JUL

AUG

SEPT

OCT

NO

VD

ECAV

G19

8816

616

816

619

8916

516

516

616

716

917

017

217

417

617

617

617

517

119

9017

417

517

718

018

218

518

919

019

119

519

819

918

619

9120

220

220

120

220

420

921

421

722

122

322

522

521

219

9222

822

922

923

123

423

624

224

224

324

424

424

323

719

9324

124

124

324

524

625

025

325

625

926

226

526

425

219

9426

326

526

726

927

227

728

128

428

828

929

128

927

819

9528

929

129

329

530

030

631

331

531

731

932

131

730

619

9631

531

631

932

432

833

333

934

334

434

634

935

033

419

9735

035

035

135

435

235

535

835

936

136

536

637

235

819

9838

438

238

038

338

939

941

141

342

043

343

842

940

519

9942

041

541

441

541

942

042

442

642

943

743

843

142

420

0043

143

043

443

844

044

244

544

344

444

945

044

644

120

0144

544

344

544

845

145

746

346

646

546

847

246

945

820

0246

746

646

846

947

247

648

148

448

548

748

948

447

720

0348

348

448

749

349

449

750

149

949

950

350

450

249

620

0450

450

450

450

450

851

251

752

252

352

652

552

151

420

0552

652

652

552

952

752

953

854

054

254

855

355

053

6

92 AICBRF - 2ND Triennial Conference

BASE

200

1 =

100

NEW

YEAR

JAN

FEB

MAR

APR

MAY

JUN

JUL

AUG

SEP

OCT

NO

VD

ECAV

G20

0611

911

911

912

012

112

312

412

412

512

712

712

712

320

0712

712

812

712

812

913

013

213

313

313

413

413

413

120

0813

413

513

713

813

914

014

314

514

614

814

814

714

220

0914

814

814

815

015

115

316

016

216

316

516

816

915

720

1017

217

017

017

017

217

417

817

817

918

118

218

517

820

1118

818

518

518

618

718

919

319

419

719

819

919

719

120

1219

819

920

120

520

620

821

221

421

521

721

821

920

920

1322

122

322

422

622

823

123

523

723

824

124

323

923

220

1423

723

823

924

224

424

625

225

225

325

325

325

325

320

1525

425

325

425

625

826

126

326

426

626

927

026

926

1.4

93AICBRF - 2ND Triennial Conference

Taxability of Medical Reimbursement Received andMedical Expenses Paid from Income Tax Perspective

All of us in our day to day life are incurring medical expenses either for ourself or for thedependent family members like spouse, children, parents, brothers and sisters.

In this article we are going to talk about the funding of these medical expenses andincome tax treatment of these expenses and reimbursements thereof (if any).

There are primarily three ways of funding your medical expenses:

1) To pay medical expenses out of your own source (It happens in case of non-in-sured self employed persons or for non-insured salaried people where employerdoes not provide any medical benefit)

2) Medical reimbursement provided by employer (in case of salaried people only)

3) Medical reimbursement provided by medical insurance company against themediclaim policies taken (applicable for both salaried as well as non-salariedpeople).

1) Income Tax treatment in case of self financed medical expenses:

In case of self financed medical expenses (i.e from own source) there is no income tothe person who has incurred expenses. Hence the question of chargeability of tax does notarise.

Now the question arises, “Whether such expenses can be treated as allowable expendi-ture under Income Tax”?

In case of salaried person who is not provided with any medical benefit by his employerand who does not have any medical insurance policy, no income tax benefit of medicalexpenses will be available to them.

In case of self employed persons, medical expenses incurred on him or his dependentfamily members would be treated as personal expenses and would not be allowed as busi-ness expenditure (as held by Delhi High Court in the case of Shanti Bhushan vs Commis-sioner Of Income Tax ).

So in case of sole proprietorship and partnership business the medical expenses in-curred by the proprietor or partner would be a disallowable expenses. However if theyprovide medical facilities to their employees then such medical expenses for employeesonly will be allowable expenditure for Income Tax calculation.

However in the case of a company even the directors are treated as employees of thecompany since the company has a separate legal entity, so medical expenses incurred by

94 AICBRF - 2ND Triennial Conference

directors and reimbursed by the company would be an allowable expenditure for the com-pany.

2) Income Tax treatment in case of salaried person who are provided with medical benefit:

This is dealt in section 17(2) of the Income Tax Act as perquisite.

The whole amount of expenses incurred by the employer will be allowable expenditureto such employer under Income Tax Act.

In case of salaried person who is provided with medical allowance the whole amountwill be taxable.

The medical facility in India provided to the employee or his dependent relative (i,echildren, spouse, brothers, sister and parents) by his employer will not be chargeable totax to the extent of the following:

a) Medical facility provided in a Hospital owned/maintained by the employer.

b) Medical facility provided in a Hospital of Central Government/ State Government/local authority.

c) Medical facility provided in a Private hospital if it is also recommended by theGovernment for the treatment of Government employees,

d) Medical facility provided for Specified medical facility (given in rule 3A) in a hospi-tal approved by the Chief Commissioner of Income Tax.

e) Health insurance premium – Medical insurance premium paid on behalf of theemployee or reimbursed to the employee by the employer is not chargeable totax in the hands of the employee.

f) Any other facility in India – Any other expenditure incurred or reimbursed by theemployer for providing medical facility in India is not chargeable to tax up to Rs.15,000 in aggregate per assessment year (fixed medical allowance is fully charge-able to tax).

For medical facility provided outside India the following perquisite will not be charge-able to tax subject to the condition mentioned therein:

95AICBRF - 2ND Triennial Conference

Perquisite not chargeable to tax

Medical treatment of employee or anymember of family of such employeeoutside India

Cost of stay abroad of employee or anymember of the fami ly for medicaltreatment & cost of stay of oneattendant who accompanies the patientin connection with such treatment

Cost on travel of the employee/anymember of his fami ly and oneattendant who accompanies the patientin connection with treatment outsideIndia

Conditions to be satisfied

Expenditure shall be excluded fromthe perquisite only to the extentpermitted by the Reserve Bank of India

Expenditure shall be excluded from theperquisite only to the extent permittedby the Reserve Bank of India.

Expenditure shall be excluded fromperquisite only in the case of anemployee whose gross total income, ascomputed before including therein theexpenditure on travelling, does notexceed Rs. 2,00,000/-

3) Income Tax treatment in case of medical insurance reimbursement under mediclaimpolicy (for both salaried as well as non-salaried people):

Money received through a claim under a medical policy is only a reimbursement ofexpenditure already incurred by the policyholder. As this does not amount to profit orincome for the insured person, this money is not taxable.

Apart from that any amount paid as medical insurance premium will be allowed asdeduction u/s 80D to the maximum of Rs 60,000 (detail below) provided payment is madeby cheque;

Type of Deduction

Basic Deduction

Additional Deduction

For

Self, Spouse ordependant children

Parents

Senior Citizen

Rs.30,000/-

Rs.30,000/-

Others

Rs.20,000/-

Rs.20,000/-

Hence we can summarise the above provisions as below:

1) In case of self employed person he cannot claim any tax benefit of medical ex-penses incurred on him or his family as it would be treated as his personal expen-diture.

2) Any amount received from the Insurance company under a medical policy will notbe treated as income of the insured person as it is not a profit or income to theinsured person but only a reimbursement.

96 AICBRF - 2ND Triennial Conference

3) For salaried employees any amount received as medical allowance will be fullytaxable but medical reimbursement to the extent of Rs 15,000 per assessmentyear will not be taxable.

4) For salaried employees if the employer pays medical insurance premium on be-half of the employee or give reimbursement of medical insurance premium toemployee then this amount will not be chargeable to tax in the hands of em-ployee.

5) Medical facility provided in Govt hospital / hospital maintained by employer / Govtrecommended hospital will not be taxable in hands of employee.

6) Medical facility provided for specified diseases in a Hospital approved by the ChiefCommissioner of Income Tax will not be taxable in hands of employee.

7) For medical insurance premium paid the maximum deduction of Rs 60,000 can beavailed u/s 80D.

Source: http://taxguru.in

97AICBRF - 2ND Triennial Conference

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY,PART–II, SECTION 3, SUB-SECTION (ii)]

Government of IndiaMinistry of Finance

Department of Revenue(Central Board of Direct Taxes)

(Income-tax)

NOTIFICATION

New Delhi, the 12th October, 2015

S.O.2791(E). – In exercise of the powers conferred by section 295, read with section80DDB of the Income-tax Act, 1961 (43 of 1961), the Central Board of Direct Taxes herebymakes the following rules further to amend the Income-tax Rules, 1962, namely:-

1. (1) These rules may be called the Income-tax (15th Amendment) Rules, 2015.

(2) They shall come into force on the date of publication in the Official Gazette.

2. In the Income-tax Rules, 1962 (hereinafter referred to as the said rules), in rule11DD, for sub-rules (2) and (3), the following sub-rules shall be substituted, namely:-

“(2) The prescription in respect of the diseases or ailments specified in sub-rule (1) shallbe issued by the following specialists:-

(a) for diseases or ailments mentioned in clause (i) of sub-rule (1) - a Neurologisthaving a Doctorate of Medicine (D.M.) degree in Neurology or any equivalent de-gree, which is recognised by the Medical Council of India;

(b) for diseases or ailments mentioned in clause (ii) of sub-rule (1) - an Oncologisthaving a Doctorate of Medicine (D.M.) degree in Oncology or any equivalent de-gree which is recognised by the Medical Council of India;

(c) for diseases or ailments mentioned in clause (iii) of sub-rule (1) - any specialisthaving a post-graduate degree in General or Internal Medicine, or any equivalentdegree which is recognised by the Medical Council of India;

(d) for diseases or ailments mentioned in clause (iv) of sub-rule (1) - a Nephrologisthaving a Doctorate of Medicine(D.M.) degree in Nephrology or a Urologist havinga Master of Chirurgiae(M.Ch.) degree in Urology or any equivalent degree, whichis recognised by the Medical Council of India;

98 AICBRF - 2ND Triennial Conference

(e) for diseases or ailments mentioned in clause (v) of sub-rule (1) – a specialist hav-ing a Doctorate of Medicine (D.M.) degree in Hematology or any equivalent de-gree, which is recognised by the Medical Council of India:

Provided that where in respect of any diseases or ailments specified in sub - rule (1),the patient is receiving the treatment in a Government hospital, the prescription may beissued by any specialist working full-time in that hospital and having a post - graduatedegree in General or Internal Medicine or any equivalent degree, which is recognised bythe Medical Council of India.

(3) The prescription referred to in sub-rule(2) shall contain the name and age of thepatient, name of the disease or ailment along with the name, address, registration numberand the qualification of the specialist issuing the prescription:

Provided that where the patient is receiving the treatment in a Government hospital,such prescription shall also contain the name and address of the Government hospital.”

3. In the said rules, in Appendix-II, Form No. 10-I shall be omitted.

[Notification No.78 /2015/F. No.142/20/2015-TPL]

(ArjuGarodia)

Under Secretary (TPL)

Note .—The principal rules were published in the Gazette of India vide notification num-ber S.O. 969(E), dated the 26th March, 1962, and was last amended by vide notificationnumber. S.O. 2663(E), dated the 29th October, 2015.

99AICBRF - 2ND Triennial Conference

100 AICBRF - 2ND Triennial Conference

101AICBRF - 2ND Triennial Conference

OUR JOURNEY SO FAR & THRISSUR BECKONS

Can we escape history?

History is the record of human endeavours, achievements and defaults. History is madenot by individuals, but by the masses. It is their score card. That being the case, We, as anOrganisation, impacted history in our own humble, yet unique style.

The history of Retirees’ Associations is the sum total of the experience of the retiredbank employees for improving their post-retiral life. Its pages are filled with agonisingstruggles, sacrifices, successes and set-backs. With this understanding, we present brieflythe saga of struggle for pension and Bank Retirees’ Movement.

Pension for bank employees was demanded in 1950s & 1960s before Sastry/DesaiTribunals and has been a pending issue since V Bipartite Settlement (1989) in the bankingindustry. Pension issue was one of the principal demands of nationwide bankmen’s strikeaction on 11.08.1989. Since it was felt that achieving pension as a third retirement benefitseemed to be beyond the realm of realities, it was decided that pension with insulationagainst inflation in lieu of bank’s contribution to Provident Fund was to be pursued.

When pension was introduced in November 1990 in RBI in lieu of bank’s contributionto PF with option to the existing employees, AIBEA and AIBOA started pursuing the issuefor introduction of similar pension linked to consumer price index. IBA agreed in principlefor introduction of pension as a second retirement benefit. But nothing happened tillFebruary 1992. AIBEA observed “Pension Day” on 05.02.1993. Counter programmes wereorganised by the Co-ordination Committee. These two programmes divided the employeesinto two almost equal camps much to the joy of the Government and bankers. Well meaningefforts to coordinate with other organisations failed, followed by high voltage campaign ofcalumnies and slanders against mainstream bank employees’ movement.

Despite tall claims of adversaries, the movement did not lose sight of the objective andcontinued its course for achieving pension as a social security measure. On 20.05.1993,IBA offered Pension as a second benefit which was accepted by AIBEA & AIBOA. TheMinutes were signed with an understanding to sign the Settlement/Joint Note within twomonths. Those who opposed Pension in lieu of PF approached Hyderabad High Court andobtained stay order against signing the Settlement on Pension. When the stay got vacated,the Co-ordinating Committee which was christened earlier as Joint Action Council (JAC)gave a call for an indefinite strike. This made IBA to drag its feet in finalising the Settlement.AIBEA and AIBOA reacted with a call for strike action on 28.10.1993. Events took place ata faster pace and with the intervention of Dr. Abrar Ahmed, the then Minister of Statefor Finance, the strike call was deferred. On 29.10.1993, a Settlement and Joint Note forintroduction of index linked pension scheme were signed. The 3rd benefit camp gave uptheir demand and signed the same settlement subsequently.

102 AICBRF - 2ND Triennial Conference

Finalisation of Pension Settlement & Joint Note constitutes a saga of prolonged strugglefor the mainstream bank employees’ movement. Never before, an issue has been so muchemotive and subject matter of intense debate across the country. The Government unilaterallyand in consultation with IBA, formulated a Pension Scheme. On 29.09.1995, Governmentasked the Nationalised Banks to adopt Pension Regulations as prepared by them in therespective Bank Boards. The Government Scheme contained a retrograde provision of notcounting the past services of an employee for pension, in the event of participation instrike. This was thwarted and the dream of Pension came true.

Has this saga of struggle narrated in brief, any message to convey to us? Yes, it has. BankRetirees initially were under the impression that they could convince the IBA/Govt. throughpersonal prayers and petitions appealing to their good senses. Seldom did they realisethen that neither their emotional outbursts nor their individual pleadings will evokesatisfactory response from the powers that be. That is the lesson they learnt.

It was only through their own experience, bank retirees realised the need for unity. Itnot only gave them the numerical strength but also infused them with more confidenceand courage. With this new awareness, the retirees forged ahead towards unity. The movementof bank retirees does not conform to any form or norm. It has been an evolution by itself.The growth of the organisations is both horizontal and vertical; unitary and federal;State-wise and all-India Bank-wise etc; the formation of organisations was essentiallyinfluenced by compulsion of circumstances.

FORMATION OF A.I.B.R.F.

When Pension became part of service condition in the banking industry, the number ofpensioners started growing. To take care of these pensioners and their problems,Bank-wise Unions initiated steps to form Bank-wise All India Retirees’ Association/Organisation covering all categories of retired employees without any differentiation andit was thought fit that such organisation of retirees would be independent without affiliationto serving Unions, which would extend support and assistance in proper implementationof Pension and Welfare Schemes for the benefit of retired bank employees. Thus AIBRFwas founded on 01.05.1994 at Ahmedabad with Sri Romesh Chander Chakraborty asFounder General Secretary. Since then, AIBRF has been organising the retirees in variousbanks with a view to promoting the interest and welfare of retired bank employees acrossthe country. In the evolutionary process, AIBRF took the initiative and formed industrylevel Forum known as United Forum of Bank Retirees’ Organisations to represent theentire bank retirees’ community at industry level before IBA and the Government.

Thus, Retirees’ movement evolved over a period of time in banking industry. Time hascome for us to uphold and carry forward this legacy with maturity. The period, which wehad passed through since we met last in our 3rd Triennial Conference at Kolkata in 2012 hasto be properly analysed and understood for carrying out more effectively our OrganisationalTasks in the days to come.

103AICBRF - 2ND Triennial Conference

Securing another Pension option for Retirees by joining UFBU’s struggle, ParliamentaryCommittee’s recommendations and the IBA subsequently directing to constitute Griev-ances Redressal Cell in Banks, extending notional weightage of upto 5 years to SVRS retir-ees in other PSBs on grounds of interpretation of provisions of Pension Regulations, En-hancing amount of Ex-gratia to Pre-1986 Retirees and their Spouses are major achieve-ments of AIBRF. However, persisting discriminations, denial of Pension option in 2010 tothose who were Compulsorily Retired and Resigned still continue, resulting in gross injus-tice in their post-retiral life.

Taking note of the persisting wrongs heaped on past retirees and also the need to im-prove pensionary benefits in line with RBI Pension Scheme and Central Govt. PensionScheme, Retirees Charter of Demands was formulated long before UFBU constituentsfinalised their Charter of Demands for 10th Bipartite/7th Joint Note Wage Revision. In theabsence of any structured forum, AIBRF submitted its Charter of Demands to IBA, besideseach constituent of UFBU explaining the logic behind our demands. This organizationaleffort was rewarded by all bank unions by way of including retirees’ core issues in theircommon Charter of Demands. In fact, for the first time, UFBU invited AIBRF General Secre-tary for attending its meeting held at Chennai on 04-07-2013. When talks of wage revisionwere in progress between IBA & UFBU, AIBRF was in live contacts with UFBU leaders throughpersonal telephonic contacts, visits and/or written communications.

Another important demand of AIBRF was that AIBRF be given hearing by IBA on issueshaving a bearing on the interests of retirees. For this purpose, AIBRF met the Chief Officialsof the Department of Financial Services twice. Govt. too forwarded AIBRF’s representationto IBA with the direction of taking necessary action. Finding no response, AIBRF organizedbank retirees across the country and held “Maha Dharna” at Jantar Mantar, New Delhi on07.03.2014 to press our demands. Massive Dharna was scintillating success.

Bank retirees were happy when issues of Pension Updation, 100% Neutralisation of DAto Pre-01.11.2002 pensioners, improvement in Family Pension, Uniform HospitalisationScheme for bank retirees were formally discussed on 14th March and 13th June 2014. Circu-lar No.24/14.06.2014 issued by the Convener, UFBU, categorically mentioned that the is-sue of uniform rate of DA has been sent to Government of India for its approval. IBA waspositive on improvement in family pension upon determination of financial impact andapproval from Govt. So long so good was the scenario picturised before bank retirees.

Just a week before signing the 10th BPS, AIBRF was informed that in the 10th Bipartitewage negotiations, retired employees would get uniform hospitalization scheme on cer-tain conditions and no monetary benefit would flow to past retirees. AIBRF immediatelyswung into action, met the Hon’ble Finance Minister and other officials of DFS with therequest to issue direction to IBA to give an opportunity for hearing long pending issues/grievances of retirees, besides seeking to expedite approval sought by IBA on 100%Neutralisation of DA to Pre-Nov. 2002 pensioners.

104 AICBRF - 2ND Triennial Conference

Apprehension of AIBRF proved right when 10th BPS signed on 25.05.2015 showed thedoor to retirees. News that Record Note dated 25.05.2015 was mutually signed, virtuallynegating all retirees’ issues was a bolt from the blue to the retirees. Record Note furtherdeclared that Pension was only a welfare measure, some sort of bounty/charity and cannotbe negotiated upon. This is contrary to plethora of Supreme Court judgements that Pensionwas not a charity, but an obligation on the part of employer as deferred wages.

Justifiably, both the rank and file across the country and the leadership of AIBRF feltdeeply disappointed over this totally unexpected turn of event, disheartened but notdemoralised. On 25.05.2015, AIBRF in a deputation before Chairman of IBA submittedmemorandum demanding that our view points be heard by IBA. IBA also expressed thatthey would talk with AIBRF after some time. We hope that with the election of IBA Chairman,AIBRF shall get opportunity to pursue retirees’ demands.

Side by side, AIBRF decided to give memorandum to Chief of all Public Sector Banks,most of whom received the same from our affiliates. Large number of bank retirees areagitating in front of Headquarters of various banks in support of our demands, besideswriting to DFS that their voice be heard.

With regard to Pensioners retired during 7th BPS period, IBA modified definition of “Pay”and their basic pension was determined less than 50% of last 10 months average. In the 8th

BPS, IBA introduced differential treatment of DA neutralization to Pre-Nov. 2002 pensioners.In the 9th BPS, IBA denied pension option to certain category of retirees. There was noloud voice of protest or large-scale resentment then. But, this time in the post - 10th BPSperiod, anger and anguish of bank retirees are echoed in every nook and corner of thecountry. AIBRF as a growing organization with accountability to its retiree members hasbrought this difference in perspective and approach of the retired employees, from beingsubmissive to vociferous against IBA on ignoring retirees’ issues.

Thus bank retirees under the banner of AIBRF are pushed to war path across the countryreacting strongly against the IBA’s delaying tactics in dealing with retirees’ issues. But it isimperative that we need to maintain cordial relation with the UFBU and its retirees-friendlyconstituents for carrying forward our pending demands. Alongside, effective implementationof our agitational programmes will also bring desired results in the near future.

Friends! Set-backs we have suffered should enable us to review our past for rectifyingour shortcomings. It cannot dampen our spirit and determination. On the contrary theyshould steel us further and make us realise as to how arduously we should move forwardas a responsible Organisation. Bank Retirees are more than ever willing to rise to the occasionand march to fight against injustice. When we recapitulate history, we are aware thathistory is not a mere narration of events. It reminds us of the past, spurs us into purposefulactivity for the present and gives us hope for a promising future.

You, I and all of us will be happy to note that our National Organisation AIBRF hasdistinction of 44 Bank wise Retirees’ Federations/Associations as Affiliates with total

105AICBRF - 2ND Triennial Conference

membership crossing 1,25,000. This growth indicates that AIBRF has become an householdname in the family of bank retirees. Thousands of Delegates and Observers are to participatein the Mass Rally on 26.11.2015 and thereafter assemble in the Delegates’ Sessionrepresenting various Banks/States across the country on November 27, 2015 at Thrissur.

In this congregation, we fervently hope:

1. Our 4th Triennial Conference would provide right and clear perspective for projectingbefore bank retirees, infuse further vigour to the movement of retired bankemployees, impart more clarity on prioritising long pending issues of bank retireesand show the way forward;

2. General Council would rise to the occasion in generating requisite enthusiasm andmore confidence in us for carrying forward bank retirees’ movement in the daysto come;

3. Our Delegates’ Session at Thrissur would seriously address vexatious issues of 100%Neutralisation of DA, Family Pension, Pension Updation etc., which are dear tovery old bank retirees and show the path we have to traverse in our enlightenedself interest, so as to culminate in resolving the long pending issues as expeditiouslyas possible;

4. Quality and content of deliberations in the Conference would take us nearer tofinding solution to the issues more particularly of the old retirees in the nearfuture, so that they could enjoy the benefits, which they rightly deserve in theirlife time;

5. The Conference would unfailingly do something tangible to improve the pitiablecondition of spouses of our compatriots, whose rate of Family Pension remainwithout any increase for about 20 years and

6. General Council would formulate its strategy for securing another pension optionfor all Retirees who were denied pension option earlier.

In this historic task of shaping the destiny of bank retirees, let each and every one of usmove forward to contribute our best in further strengthening the mainstream of the BankRetirees Movement Viz: All India Bank Retirees’ Federation and foster the spirit of “allcadre unity” amidst retired bank employees for espousing their cause more effectively, sothat future retirees will always remember the present bank retirees as those who havegiven their best for the welfare of future retirees.

And so the Caravan Marches on …………………….

With Conference Greetings,

(S.V.Srinivasan) DGS, AIBRF

106 AICBRF - 2ND Triennial Conference

107AICBRF - 2ND Triennial Conference

108 AICBRF - 2ND Triennial Conference

109AICBRF - 2ND Triennial Conference

Retirement Benefits - Legal perspective

As the present case is concerned with superannuation pension, a brief history of itsinitial introduction in early stages and continued existence till today may be illuminating.Superannuation is the most descriptive word of all but has become obsolescent because itseems ponderous. Its genesis can be traced to the first Act of Parliament (in U.K.) to beconcerned with the provision of pensions generally in public offices. It was passed in 1810.The Act which substantively devoted itself exclusively to the problem of superannuationpension was superannuation Act of 1834. These are landmarks in pension history becausethey attempted for the first time to establish a comprehensive and uniform scheme for all,whom we may now call civil servants. Even before the 19th century, the problem ofproviding for public servants who are unable, through old age or incapacity, to continueworking, has been recognised, but methods of dealing with the problem varied fromsociety to society and even occasionally from department to department.

A political society which has a goal of setting up of a welfare State, would introduce andhas in fact introduced as a welfare measure, wherein the retiral benefit is grounded on‘considerations of State obligation to its citizens who having rendered service during theuseful span of life must not be left to penury in their old age, but the evolving concept ofsocial security is a later day development’.

Let us therefore examine what are the goals that pension scheme seeks to subserve? Apension scheme consistent with available resources must provide that the pensioner wouldbe able to live: (i) free from want, with decency, independence and self-respect, and (ii) ata standard equivalent at the pre-retirement level. This approach may merit the criticismthat if a developing country like India cannot provide an employee while rendering servicea living wage, how can one be assured of it in retirement ? This can be aptly illustrated bya small illustration. A man with a broken arm asked his doctor whether he will be able toplay the piano after the cast is removed. When assured that he will, the patient replied,‘that is funny, I could not before’. It appears that determining the minimum amountrequired for living decently is difficult, selecting the percentage representing the properratio between earnings and the retirement income is harder. But it is imperative to notethat as self sufficiency declines the need for his attendance or institutional care grows.Many are literally surviving now than in the past. We owe it to them and ourselves thatthey live, not merely exist. The philosophy prevailing in a given society at various stages ofits development profoundly influences its social objectives. These objectives are in turn adeterminant of a social policy. The law is one of the chief instruments whereby the socialpolicies are implemented and pension is paid according to rules which can be said toprovide social security law by which it is meant those legal mechanisms primarilyconcerned to ensure the provision for the individual of a cash income adequate, whentaken along with the benefits in kind provided by other social services (such as free medicalaid) to ensure for him a culturally acceptable minimum standard of living when the normalmeans of doing so failed’. (See Social Security law by Prof. Harry Calvert, p. 1).

110 AICBRF - 2ND Triennial Conference

The concept, history and evolution of pension are extracted from the Judgment ofConstitution Bench (of Hon’ble Supreme Court) in D S Nakara & others Vs Government ofIndia on the 17th December, 1982. This Judgment was a path breaking decision, whichbrought miles of smiles on the faces of crores of Senior Citizens of this country. Thousandsof cases in this country with regard to Pension are decided on the basis of this Judgment.Efforts of Shri D S Nakara and others who have secured this Judgment on the 17th December,1982, which is now being celebrated as ‘PENSIONERS’ DAY’, deserves to be commended.

Now, on account of this decision, Central, State and Defence Pensions are gettingrevised along with revision of salary and allowances of employees.

The same decision in D S Nakara also brought out another principle decided in DeokiNandan Prasad v.State of Bihar & Ors Ors.,[1971] Supp. S.C.R. 634

The antiquated notion of pension being a bounty a gratuitous payment depending uponthe sweet will or grace of the employer not claimable as a right and, therefore, no right topension can be enforced through Court has been swept under the carpet by the decisionof the Constitution Bench in Deoki Nandan Prasad v. State of Bihar & Ors. (1) wherein thisCourt authoritatively ruled that pension is a right and the payment of it does not dependupon the discretion of the Government but is governed by the rules and a Governmentservant coming within those rules is entitled to claim pension. It was further held that thegrant of pension does not depend upon any one’s discretion. It is only for the purpose ofquantifying the amount having regard to service and other allied matters that it may benecessary for the authority to pass an order to that effect but the right to receive pensionflows to the officer not because of any such order but by virtue of the rules. This view wasreaffirmed in State of Punjab & Anr. v. Iqbal Singh (1).

The applicability of Judgment in D S Nakara and if applicable, to what extent and inwhat areas of Bank Employees’ Pension Scheme is highly debatable.

Deoki Nandan Prasad v.State of Bihar & Ors Ors. also connected Pension to Property. Itis observed by the Hon’ble Court as :

Having due regard to the above decisions, we are of the opinion that the right of thepetitioner to receive pension is property under Art. 31(1) and by a mere executive orderthe State had no power to withhold the same. Similarly, the said claim is also propertyunder Art. 19(1)(f) and it is not saved by sub-article (5) of Art. 19.

Right to property was Fundamental Right, it was also a part of Article 19 & 31. It wasmoved to Article 300A by 44th Constitutional amendment during 1979. Now, right toproperty is only a Constitutional Right.

Hon’ble Supreme Court, in State of Jharkhand Vs Jitendra Kumar Srivastava, consideringthis aspect of Pension, being a property which is a Constitutional Right, decided as under :

111AICBRF - 2ND Triennial Conference

14. Article 300 A of the Constitution of India reads as under:

“300A Persons not to be deprived of property save by authority of law. - Noperson shall be deprived of his property save by authority of law.”

Once we proceed on that premise, the answer to the question posed by us in thebeginning of this judgment becomes too obvious. A person cannot be deprived ofthis pension without the authority of law, which is the Constitutional mandateenshrined in Article 300A of the Constitution. It follows that attempt of the appellantto take away a part of pension or gratuity or even leave encashment without anystatutory provision and under the umbrage of administrative instruction cannotbe countenanced.

15. It hardly needs to be emphasized that the executive instructions are not havingstatutory character and, therefore, cannot be termed as “law” within the meaningof aforesaid Article 300A. On the basis of such a circular, which is not having forceof law, the appellant cannot withhold - even a part of pension or gratuity. As wenoticed above, so far as statutory rules are concerned, there is no provision forwithholding pension or gratuity in the given situation. Had there been any suchprovision in these rules, the position would have been different.

Pension in Banks is conceptually different from Pension of Government employees.Before, introduction of pension in Banks in 1995, consequent to Settlement signedon the 29th October, 1993, very few Banks had pension scheme. Since, the presentscheme is far superior to the schemes existed then, with exception of State Bankof India, every other Bank is now covered by this Pension Scheme, which replacedcontributory Provident Fund Scheme. But, payment of Pension to Governmentemployees is a legacy of British rule. Over a period of time Central Governmentpension has undergone changes from 1/80th of emoluments with maximum pensionof Rs.8,100/- per annum plus Dearness Relief thereon to present formula. Aliberalised pension formula for Central Government pensioners was notified onthe 25th May, 1979. Pension calculation formula was revised with effect from1.4.1979. This one decision changed everything with regard to Pension. Landmarkdecision by Constitution Bench in D S Nakara Vs Union of India was decided, whichchanged the treatment of Government Pension. But, this decision questions thevalidity of discrimination while passing this order dated 25th May, 1979.

After, every Bipartite Settlement, on account of Pay revision, the pension of thosewho have already retired during the settlement period also gets revised. The basisfor revision of pension is implementation or extension of benefit that has alreadybeen sanctioned. But, alteration in Dearness Relief formula for pensioners, postsettlement is without legal basis.

Next controversy, which is still being litigated is with regard to computation ofBasic Pension of Bank employees, who retired during the period from 1.4.1998 to

112 AICBRF - 2ND Triennial Conference

31.10.2002. The Joint Note dated 14th December, 1999 and Bipartite Settlementdate 27th March, 2000 provided for altering the method of calculation of BasicPension. Average of last ten months’ Aggregate of Pre-revised Pay and DearnessAllowance thereon calculated upto 1616 points of AICPI formed basis for calculationof Basic Pension. This is in variation with the formula of calculating Basic Pensionbased on last ten months’ average ‘Pay’. Consequently, the Basic Pension of thosewho retired during this period was reduced from 50% of Basic Pay (Regulation 35)drawn to 41.5% of Basic Pay drawn. The original method of calculation of BasicPension based on last ten months pay was restored, when 8th Bipartite Settlementwas signed on the 2nd June, 2005. Pension was also recalculated with effect from1.5.2005 and arrears was also paid. But, Commutation and arrears were also notpaid.

In the meantime, several retirees approached several High Courts. Appeals againstdecision of three High Courts have reached Supreme Court. Of these three, decisionof Madras High Court in Bank of Baroda & Ors Vs G Palani and the decision ofKarnataka High Court in Vijaya Bank & Ors Vs Suvasini Setty are in favour ofPensioners, whereas, remaining batch decided by Delhi High Court in AIBREA VsUOI went against Pensioners. There are several other petitions are pendingbefore various High Court. The Judgment of Division Bench of Karnataka High Court,headed by present Supreme Court Judge, Justice Vikramjit Sen, considered variousaspects of Law.

We must emphasis forthwith that the so-called Joint Note was at best an inchoateagreement, a mere proposal, which would attain legal sanctity only on the amendmentsto the Officers’ Service Regulations and Bank Employees’ Pension Regulations, 1995being carried out.

13. Constitution Benches of the Supreme Court in Indian Ex - Services League - Vs - Unionof India (1991) 2 Supreme Court Cases 104 and thereafter in Chairman, RailwayBoard - Vs - C.R.Rangadhamaiah, (1997) 6 Supreme Court Cases 623 have enunciatedthat “reckonable emoluments which are the basis for computation of pension areto be taken on the basis of emoluments payable at the time of retirement”.

It seems evident to us that the primary point in the negotiations was the increasewage / salary fixation, and pension was dealt with en passant, as one consequentialor incidental offshoot.’

22. Without reference to P. Sadagopan, a larger Bench came to the same conclusionin K. Kuppusamy - Vs - State of Tamil Nadu, (1998) (8) Supreme Court Cases 469,wherein it spoke thus - “Statutory rules cannot be overridden by executive ordersor executive practice. Merely because the Government had taken a decision toamend the rules does not mean that the rule stood obliterated. Till the rule isamended, the rule applies. Even today the amendment has not been effected. As

113AICBRF - 2ND Triennial Conference

and when it is effected ordinarily it would be prospective in nature unless expresslyor by necessary implication. found to be retrospective” It would be apposite tomention here that the State Bank of Mysore has not amended its Pension Regulationstill date.

The services of the workman are also governed by several standing orders andBipartite Settlements which have the force of law.

It is sought to be argued that the legality of Bipartite Settlement has been affirmedby their Lordships in the above paragraph. We think that this is not the ratio of theJudgement.

Yet another controversy which has affected Ex-employees is pension to those whoresigned from Services of the Banks. Before, Pension Settlement was signed on 29thOctober, 1993, resignation and retirement were two methods of exit. Officers’Service Regulations, 1979 provided for voluntary retirement. There was no suchprovision available for Award Staff. UCO Bank Vs Sanwar Mal ((2004) 4 SCC 412) isthe first case, involving Bank resignees to reach the Apex Court, where Bank wonand resignees lost. Banks continue to quote this Judgment, till Judgment in SheelKumar Jain v. New India Assurance Company Limited and Ors. (2011) 12 SCC 197wherein it is decided that forfeiture clause as per Regulation 22 of Bank Employees’Pension Regulations, cannot be invoked if the employee has resigned after servingfor a period of 20 years or more. This Judgment ensured catena of judgmentsfavouring Bank resignees. One among those is the decision in Vijaya Bank Vs CNarasimhappa. In this case, CMD of Vijaya Bank had to stand as an Accused inContempt Petition filed by the petitioners. 22 petitioners are pensioners now.Thereafter, one adverse Judgment in M R Prabhakar Vs Canara Bank, (2012) 9 SCC671 triggered series of Judgments against resignees. In the meantime, two morefavourable Judgments of Supreme Court, Shahsikala Devi Vs Central Bank of Indiaand Asger Ibrahim Amin Vs LIC of India have brought smiles back on the face ofResignees.

Minutes of meetings held prior to notification of Pension Regulations, reveal thatvoluntary resignations, where resignees are entitled to terminal benefits were notunder the sweep of forfeiture clause under Regulation

22. A little more focus while formulating Pension Regulations, would have broughtmany more benefits.

Another dispute was payment of pension/extension of pension option to thosewho retired under VRS-2001 after serving for a period in excess of 15 years, butless than 20 years, in Associate Banks of State Bank of India. This issue was alsosettled in favour of retirees in State Bank of Patiala Vs Pritham Singh Bedi. Afterthe Judgment, the Bank sought to restrict the benefit to those who had served

114 AICBRF - 2ND Triennial Conference

more than 19 years and 6 months. A clarification petition was also filed. SupremeCourt directed the Bank to file Review Petition. Review Petition, earlier ClarificationPetition sought differentiating retirees who had served more than 19 years and 6months and less than that period, but more than 15 years. The Court rejected thecontention of the Bank and allowed pension to every retiree who had served morethan 15 years. Now, after adverse Judgment in Madras High Court and Kerala HighCourt, State Bank of India has decided to extend the benefit to all similarly placedretirees in Associate Banks.

Incidentally, many banks had not paid pension to those who had served for morethan 19 years and 6 months, despite the Judgment by Apex Court in Indian BankVs N Venkataramani. This Judgment in State Bank of Patiala Vs Pritham Singh Bedinot only settled this controversy, but also that of payment of pension in terms ofRegulation 29, duly adding service, notionally, upto five years in respect of thosewho had served for a period in excess of 19 years and 6 months, but less than 20years.

While Indian Bank Vs N Venkataramani brought efforts of IBA, by insertion of clause

“Provided that provisions of this regulation shall not apply for determining theminimum service required to make an employee eligible for pension.”

to deny broken period benefit as available under Regulation 18 to naught, PrithamSingh Bedi ensured payment of 5 year benefit to those who had served for morethan 19 years & 6 months, but less than 20 years, as the court clearly decided thatthose who had served for more than 19 years & 6 months are eligible for pensionunder Regulations 29.

On the 30th June, 2015, IBA advised member Banks who are parties to BipartiteSettlement dated 10.04.2002/27.5.2002 to implement Judgment of Hon’bleSupreme Court in Bank of Baroda Vs S K Kool (D) through LRs and Bank of BarodaVs Girish Shantilal Shukla. Following sentences extracted from S K Kool’s Judgmentexplains, how provisions have to be harmonized. When harmonised, those whoare inflicted with punishment under clause 6(b) and 6(d) are entitled to everysuperannuation benefit, including pension:

The Regulation does not entitle every employee to pensionary benefits. Its applicationand eligibility is provided under Chapter II of the Regulation whereas Chapter IVdeals with qualifying service. An employee who has rendered a minimum of tenyears of service and fulfils other conditions only can qualify for pension in terms ofArticle 14 of the Regulation. Therefore, the expression “as would be due otherwise”would mean only such employees who are eligible and have put in minimum numberof years of service to qualify for pension. However, such of the employees who arenot eligible and have not put in required number of years of qualifying service

115AICBRF - 2ND Triennial Conference

shall not be entitled to the superannuation benefit though removed from servicein terms of clause 6(b) of the Bipartite Settlement. Clause 6(b) came to be insertedas one of the punishments on account of the Bipartite Settlement. It provides forpayment of superannuation benefits as would be due otherwise. The BipartiteSettlement tends to provide a punishment which gives superannuation benefitsotherwise due. The construction canvassed by the employer shall give nothing tothe employees in any event. Will it not be a fraud Bipartite Settlement? Obviouslyit would be. From the conspectus of what we have observed we have no doubtthat such of the employees who are otherwise eligible for superannuation benefitare removed from service in terms of clause 6(b) of the Bipartite Settlement shallbe entitled to superannuation benefits. This is the only construction which wouldharmonise the two provisions. It is well settled rule of construction that in case ofapparent conflict between the two provisions, they should be so interpreted thatthe effect is given to both. Hence, we are of the opinion that such of the employeeswho are otherwise entitled to superannuation benefits under the Regulation ifvisited with the penalty of removal from service with superannuation benefitsshall be entitled for those benefits and such of the employees though visited withthe same penalty but are not eligible for superannuation benefits under the Regulationshall not be entitled to that.

Accordingly, we hold that the employee’s heirs are entitled to superannuation benefits.

Said IBA letter has advised Banks to amend Regulation 22 (1) to incorporate changes.Still, there is no clarity wordings of the proposed amendment. However, sameregulation cannot assign different meaning to same set of words. Eventually, thisbenefit have to be extended to retired Officers also.