AGENDA WASHOE COUNTY, NEVADA OPEB TRUST FUND ...

38

John Sherman, Chairman Darrell Craig, Trustee Paul McArthur, Comptroller/Trustee Terrance Shea, Legal Counsel AGENDA WASHOE COUNTY, NEVADA OPEB TRUST FUND BOARD OF TRUSTEES August 5, 2014 at 9:00 a.m. Room C-110 (Central Conference Room) Washoe County Administrative Complex, Building C 1001 E. 9th Street - Reno, Nevada 89512 NOTE: Items on the agenda may be taken out of order; combined with other items; removed from the agenda; moved to the agenda of another later meeting; moved to or from the Consent section; or may be voted on in a block. Items with a specific time designation will not be heard prior to the stated time, but may be heard later. Items listed in the Consent section of the agenda are voted on as a block and will not be read or considered separately unless removed from the Consent section. Facilities in which this meeting is being held are accessible to the disabled. Persons with disabilities who require special accommodation or assistance (e.g. sign language, interpreters or assisted listening devices) at the meeting should notify the Washoe County Comptroller’s Office at 328-2552, 24 hours prior to the meeting. . Time Limits. Public comments are welcomed during the Public Comment periods for all matters, whether listed on the agenda or not, and are limited to two minutes per person. Additionally, public comment of two minutes per person will be heard during individual action items on the agenda. Persons are invited to submit comments in writing on the agenda items and/or attend and make comment on that item at the Trustee’s meeting. Persons may not allocate unused time to other speakers. Forum Restrictions and Orderly Conduct of Business. The Washoe County OPEB Trust Board of Trustees conducts the business of the OPEB Trust Fund during its meetings. The presiding officer may order the removal of any person whose statement or other conduct disrupts the orderly, efficient or safe conduct of the meeting. Warnings against disruptive comments or behavior may or may not be given prior to removal. The viewpoint of a speaker will not be restricted, but reasonable restrictions may be imposed upon the time, place and manner of speech. Irrelevant and unduly repetitious statements and personal attacks which antagonize or incite others are examples of speech that may be reasonably limited. Responses to Public Comments. The Board of Trustees can deliberate or take action only if a matter has been listed on an agenda properly posted prior to the meeting. During the public comment period, speakers may address matters listed or not listed on the published agenda. The Open Meeting Law does not expressly prohibit responses to public comments by the Board. However, responses from Trustees to unlisted public comment topics could become deliberation on a matter without notice to the public. On the advice of legal counsel and to ensure the public has notice of all matters the Board of Trustees will consider, Trustees may choose not to respond to public comments, except to correct factual inaccuracies, ask for staff action or to ask that a matter be listed on a future agenda. The Board may do this either during the public comment item or during the following item: “*Trustee’s/Staff announcements, requests for information, topics for future agendas and statements relating to items not on the agenda”. This Agenda for the meeting has been posted at the following locations: Washoe County Administration Building (1001 E. 9th Street, Bldg. A), Washoe County Courthouse-Second Judicial District Court (75 Court Street), Washoe County Downtown Reno Library (301 S. Center Street), Sparks Justice Court (1675 Prater Way #107) the Washoe County Website at www.washoecounty.us/finance/OPEB.htm, and the Nevada Public Notice Website (https://notice.nv.gov).

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of AGENDA WASHOE COUNTY, NEVADA OPEB TRUST FUND ...

John Sherman, Chairman Darrell Craig, Trustee Paul McArthur, Comptroller/Trustee

Terrance Shea, Legal Counsel

AGENDA

WASHOE COUNTY, NEVADA OPEB TRUST FUND

BOARD OF TRUSTEES

August 5, 2014 at 9:00 a.m.

Room C-110 (Central Conference Room) Washoe County Administrative Complex, Building C

1001 E. 9th Street - Reno, Nevada 89512

NOTE: Items on the agenda may be taken out of order; combined with other items; removed from the agenda; moved to the agenda of another later meeting; moved to or from the Consent section; or may be voted on in a block. Items with a specific time designation will not be heard prior to the stated time, but may be heard later. Items listed in the Consent section of the agenda are voted on as a block and will not be read or considered separately unless removed from the Consent section. Facilities in which this meeting is being held are accessible to the disabled. Persons with disabilities who require special accommodation or assistance (e.g. sign language, interpreters or assisted listening devices) at the meeting should notify the Washoe County Comptroller’s Office at 328-2552, 24 hours prior to the meeting. . Time Limits. Public comments are welcomed during the Public Comment periods for all matters, whether listed on the agenda or not, and are limited to two minutes per person. Additionally, public comment of two minutes per person will be heard during individual action items on the agenda. Persons are invited to submit comments in writing on the agenda items and/or attend and make comment on that item at the Trustee’s meeting. Persons may not allocate unused time to other speakers. Forum Restrictions and Orderly Conduct of Business. The Washoe County OPEB Trust Board of Trustees conducts the business of the OPEB Trust Fund during its meetings. The presiding officer may order the removal of any person whose statement or other conduct disrupts the orderly, efficient or safe conduct of the meeting. Warnings against disruptive comments or behavior may or may not be given prior to removal. The viewpoint of a speaker will not be restricted, but reasonable restrictions may be imposed upon the time, place and manner of speech. Irrelevant and unduly repetitious statements and personal attacks which antagonize or incite others are examples of speech that may be reasonably limited. Responses to Public Comments. The Board of Trustees can deliberate or take action only if a matter has been listed on an agenda properly posted prior to the meeting. During the public comment period, speakers may address matters listed or not listed on the published agenda. The Open Meeting Law does not expressly prohibit responses to public comments by the Board. However, responses from Trustees to unlisted public comment topics could become deliberation on a matter without notice to the public. On the advice of legal counsel and to ensure the public has notice of all matters the Board of Trustees will consider, Trustees may choose not to respond to public comments, except to correct factual inaccuracies, ask for staff action or to ask that a matter be listed on a future agenda. The Board may do this either during the public comment item or during the following item: “*Trustee’s/Staff announcements, requests for information, topics for future agendas and statements relating to items not on the agenda”. This Agenda for the meeting has been posted at the following locations: Washoe County Administration Building (1001 E. 9th Street, Bldg. A), Washoe County Courthouse-Second Judicial District Court (75 Court Street), Washoe County Downtown Reno Library (301 S. Center Street), Sparks Justice Court (1675 Prater Way #107) the Washoe County Website at www.washoecounty.us/finance/OPEB.htm, and the Nevada Public Notice Website (https://notice.nv.gov).

Washoe County, Nevada OPEB Trust Board of Trustees Meeting Agenda for August 8, 2014 Page 2 of 2

Support documentation for items on the agenda that is provided to the Washoe County, Nevada OPEB Trust Board of Trustees is available to members of the public at the Washoe County Comptroller’s Office (1001 E. 9th Street, Room D-200 Reno, Nevada), Sandra McGarva, Administrative Secretary Supervisor (775) 328-2553; and on the County’s website at http://www.washoecounty.us/finance/OPEB.htm

All items numbered or lettered below are hereby designated for possible action as if the words “for possible action” were written next to each item (NRS 241.020). An item listed with asterisk (*) is an item for which no action will be taken.

* 1. Roll call.

* 2. Public Comments. Comments heard under this item will be limited to two minutes per person and may pertain to matters both on and off the Board of Trustee’s agenda. The Board will also hear public comment during individual action items, with comment limited to two minutes per person. Comments are to be made to the Board as a whole.

3. Introduce and welcome Paul McArthur, CPA MBA Comptroller, to the Board of Trustees, who steps into the position vacated by Cynthia Washburn, effective July 18.

4. Approval of minutes from the April 23, 2014, meeting.

5. Nominate and vote to appoint new Vice Chairman.

6. Review and approve claims processed, administrative expenditures and reimbursements to employersthrough June 30, 2014.

7. Acknowledge receipt of interim financial statements for the period ending June 30, 2014.

8. Review and possible approval of the Budget and the Cash Transfer Plan to the State Retiree BenefitsInvestment Fund for fiscal year 2014/2015.

* 9. Discussion: Audit Services by Kafoury Armstrong & Company for FYE 2014; Chairman and Comptroller to sign their acknowledgement (not usually copied and presented as part of packet, but in anticipation of questions, this item is included for the benefit of Trustees who may wish to discuss).

* 10. Discussion: TMWA merger with Washoe County Water/Utility function.

11. Discuss and determine FY15 OPEB Board of Trustees’ meeting dates and times.

* 12. Trustees’/Staff announcements, requests for information, and topics for future agendas, statements relating to items not on the agenda and any ideas and suggestions for greater efficiency, cost effectiveness and innovation in providing for the benefits of Washoe County, Nevada OPEB Trust participants in accordance with the benefit plans. (No discussion on this item will take place among Trustees.)

* 13. Public Comments. Comments heard under this item will be limited to two minutes per person and may pertain to matters both on and off the Board of Trustee’s agenda. The Board will also hear public comment during individual action items, with comment limited to two minutes per person. Comments are to be made to the Board as a whole.

14. Adjourn.

BOARD OF TRUSTEES, WASHOE COUNTY, NEVADA OPEB TRUST FUND

WEDNESDAY, APRIL 23, 2014, 9:00 A.M.

Present:

John Sherman, Chairman Cynthia Washburn, Trustee

Darrell Craig, Trustee

Staff:

Mary Solorzano, Accounting Manager Sandra McGarva, Secretary

Terrance Shea, Legal Counsel

The Board convenes in regular session at approximately 9:02 a.m. at the Central Conference Room, Building C, of the Washoe County Administrative Complex, 1001 East Ninth Street, Reno, Nevada. Roll is called, there is a quorum. (For the record, Mary Walker, fiscal agent of the Fire entities in OPEB, is also present.) There is no Public Comment. Approve minutes from January 30, 2014 meeting. Trustee Craig moves to approve the minutes of January 30, 2014 as written. There is no public comment. Chairman Sherman seconds the motion. All are in favor, the motion carries. Review and approve claims processed, administrative expenditures and reimbursements to employers through March 31, 2014. Ms. Solorzano directs the Trustees to page 13 of their packet, and indicates there are no surprises in the administrative expenses, largely consisting of payments to Trustees and our quarterly payment to the County for Administrative and Accounting services. It is anticipated that we will come in on budget in Accounting and Administrative services at the end of the year, but she explains the likelihood that we will hit our full budget on the actuarial expenditures is very slim because Milliman typically bills us following provision of the services, which occurs at close to the end of the year. Ms. Solorzano recaps the Washoe County Request for Reimbursement, and notes this is the item being presented for approval. She notes at the bottom of Page 14, where it includes the standard detail of the report, and states the chart displays the full expense of the benefits, how much the retirees are paying, and how much we are reimbursing in the premium. She notes the difference is the net amount that the employer has either contributed or pre-paid, and at this point in time it is still a contribution. There are no questions. Trustee Washburn moves to approve the reimbursement request in the amount of $2,035,997, as well as the Administrative Expenses for the third quarter. Trustee Craig seconds the motion. There is no public comment and no more discussion. All are in favor. The motion carries.

1

Washoe County, Nevada OPEB Trust Fund April 23, 2014 Page 2 of 4 Acknowledge receipt of interim financial statements for the period ending March 31, 2014. Ms. Solorzano begins summarizing the Interim Financial Highlights for the Quarter Ended March 31, 2014, stating the big story for the year is how well the unrealized gains and losses seem to be performing in the RBIF. She states we are currently averaging over 22% if we include those unrealized gains and losses, and 4.17% without. She adds that we have a little bit of interest receivable and the reimbursement payable to Washoe County, which is our other net asset activity. No other significant changes are noted. Chairman Sherman asks Ms. Solorzano to bring the Trustees up to speed on the GASB Rule No. 45 where it says if you don’t contribute your ARC on an annual basis, that anything less than that turns into a liability, and that must be accrued from year to year. He states further that when we first started the Trust, based on the dynamics of the County holding a Special Revenue Fund, we put a lot of money into the Trust. Do we now post a liability or an asset based on that accounting? Ms. Solorzano responds, saying it is not done annually. Trustee Washburn explains that in the Government-wide, because we were given that starting point, we had that money, and we’re probably just within one year of exhausting that asset. Chairman Sherman clarifies that it is still a net asset recorded on the combining statements. He states further that if the County does not budget for, and actually transfer the full ARC into the Trust, eventually that net asset will turn into a liability. That is confirmed. Chairman Sherman states it is interesting to note that Trust Net Assets are in excess of $145 million. Brief discussion. It is noted this amount is double what the Trust started out with a few years ago, and still the largest Trust in the RBIF. Trustee Washburn moves to acknowledge receipt of the interim financial statements for the period ending March 31, 2014. There is no Public Comment. Trustee Craig seconds the motion. All are in favor, the motion carries. Discussion and possible action: revisit proposed cash transfer timing to the Nevada Retiree Benefits Investment Fund for the remainder of the fiscal year. Trustee Washburn asks to note for the record that in March we missed our transfer to the RBIF. She states we had a backup plan and we had two people out, and we missed sending the wire. Additionally, it is noted the County reduced their contribution to the Trust by $2.6 million in order to cover their Association agreements. Chairman Sherman states he wants to discuss Item 7 of the agenda with this item, as he believes it is relative to Item 6, as to the transfer and the tentative budget for FY14/15; Trustee Washburn asks to explain the reduction of the transfer, and states there is actually an off-setting. The County needed to fund the General Fund for Association agreements. They first looked to possible salary sweep activity, but were short to fund the Agreements. So the OPEB took the hit as one of the few big dials they have. However, there also is an acknowledgement that because of the way we were doing the accounting when the Trust was first created, we weren’t reimbursing on a premium basis, we were reimbursing on a total cost basis. Our best estimate of those two years is $2.6 million. The County’s intent is to pay back that $2.6 million that was over reimbursed so that we’re whole.

2

Washoe County, Nevada OPEB Trust Fund April 23, 2014 Page 3 of 4 Chairman Sherman asks how the County will pay the over reimbursement to the Health Fund. Ms. Solorzano states through reduction of requests for reimbursements from the Trust for the fourth quarter and possibly into the first quarter of next year. Chairman Sherman states, as it relates to that, any current estimate on the Health Benefit Fund requirements for FY14/15? Ms. Solorzano states they did not push that through as they are just finalizing their budget yesterday and today. It is noted the costs will go up – the Self-Funded went up almost 11%. There is discussion. It is noted that for the past two years the rates did not change but the cost did go up. Trustee Washburn explains that we did have some favorable claims experience so we are going to use some of the Health Benefits Fund to level out the rate of increase, so it averages out to approximately 4-5% increase on the Self-Funded – less on the HMO because their costs go up at a slower trend, and we are also doing a bigger promotion for the High Deductible Health Plan as a test to see if more people would go for it, as we are seeing the beginnings of lower expense. We did go out with a proposal for increased rates, but those are still in negotiations. Trustee Washburn adds that the ACA tax on the HMO alone is 2.3%. There is also a per-person tax on the Self-Funded. It is noted that this coming year will be the first year for that. Trustee Craig asks how much it is, and Mr. Morgan responds, stating there are two pieces: one is $2 and one is $63, so it is $65 per head per year. Trustee Craig asks if that will be passed on down to the retirees. It is explained that it is all factored into the rate. More discussion. It is noted that the Health Benefits Fund still has a very robust fund balance. Trustee Craig asks how many retirees sit on that negotiating committee. It is noted there is one retiree out of approximately 14 people, but that the Committee’s actual role is in Plan design and not in rate setting. There is discussion. It is noted there are approximately 1,600 retirees, and 2,700 current employees. Trustee Craig thought representation would be a little more balanced. More discussion. It is noted that if we approached the Insurance Negotiating Committee to evaluate for representation on a pro-rata basis – the deputies would likely dominate. Trustee Washburn states the tentative budget is the same as last year’s - $18.7 million. There is discussion with respect to the ARC being funded for FY14/15, and it is anticipated it will. Ms. Solorzano explains that because they missed March and did not have any activity going into the RBIF in May, we added what would have happened in March to May. It is noted that adjustment is indicated on page 24. There is discussion as to if the Trustees want to take action now on the larger than typical sum of Trust funds parked in the County pool. Chairman Sherman moves to change the cash transfer schedule to reflect the addition of $1.5 million for July’s transfer to RBIF. There is no public comment. Trustee Washburn seconds the motion. All are in favor. The motion carries. Trustee Washburn explains, for Discussion: status of employers’ budgets for the upcoming fiscal year and potential impact (Item 7, opened for discussion with Item 6), the budget on the TMFPD/SFD side is

3

Washoe County, Nevada OPEB Trust Fund April 23, 2014 Page 4 of 4 still not determined because they’re still into all of their negotiations. Bids for their Health Benefits Fund came in fairly flat. It is expected their costs will run about the same next year. She states that Human Resources received approval for consulting and professional services efforts to reach out to retirees for educating them about the various options under Medicare, hopefully to encourage retirees to get over onto Medicare. There is more discussion. The objective is to increase and support our Board’s direction to retirees to go onto Medicare when they turn 65. They’ll be enforcing that more as we go forward and helping those people to find the right program. It is noted the policy expecting retirees to go onto Medicare was established in 2010. Ms. Solorzano advises that there is very serious talk about moving to a calendar year for Plan years for retiree and all health benefits for the County. There is discussion on the process of moving to calendar year, but it is noted the employees will like it much better if they don’t have to get hit with their deductible for a half-year period. There is more discussion with respect to how expensive Medicare is, and the collective bargaining agreements include only active employees because once you leave you’re no longer part of the Association. It is noted that this Trust and the Trustees have no voice or authority over the structure of the Health Benefit Plan over retirees specifically. Trustee’s/Staff Announcements, Requests for Information, Topics for Future Agendas, Statements relating to Items not on the Agenda and any ideas and suggestions for greater efficiency, cost effectiveness and innovation in providing for the benefits of Washoe County, Nevada OPEB Trust Participants in accordance with the Benefit Plans. (No discussion on this item will take place among Trustees.) Chairman Sherman states the pending merger of Washoe County’s Water/Utility with Truckee Meadows Water Authority (TMWA) has a retiree health benefits component in it that currently is undergoing analysis. There is going to be some determination and, to some extent, required negotiation as to how retiree health benefits will be treated for those employees who will leave Washoe County and go to TMWA. We’re in the midst of determining the best way to structure that to ensure that nobody is worse off, and whether those employees will go under TMWA’s health retirement benefit or stay with the County’s. He notes it will be perhaps 30 people, which won’t be material to the Trust. He feels, however, that we should give a heads-up to the Trust attorney advising of these negotiations with TMWA, noting that TMWA is structurally different, and it might be both financially and legally prudent as neither of us want to potentially threaten the tax-exempt status of our Trusts, so we need to make sure those things are covered in a thoughtful, due diligence process. There is no Public Comment. As there is no further business, the meeting is adjourned at 9:40 a.m.

4

WASHOE COUNTY, NEVADA OPEB TRUST

Administrative Expense Detail - YTD Actual vs. Annual Budget

For the Year Ended June 30, 2014 - unaudited

Washoe Co State of Nevada Sierra FPD

Retiree Health Public Employee FPD Retiree Retiree

Benefit Benefit Group Medical Group Medical 2014

Program Plan Plan Plan Total

BUDGET

Administrative Expenses

Actuarial valuations $ 15,000 $ 3,000 $ 9,000 $ 9,000 $ 36,000

Accounting and

administrative services 6,770 6,770 6,769 6,769 27,078

Audit fees 1,500 1,500 1,500 1,500 6,000

Trustee fees 100 100 100 100 400

Operating Expenses 200 200 200 200 800

$ 23,570 $ 11,570 $ 17,569 $ 17,569 $ 70,278

ACTUAL

Administrative Expenses

Actuarial valuations $ 2,235 $ 630 $ 16,250 $ 1,250 $ 20,365

Accounting and

administrative services 6,770 6,770 6,769 6,769 27,078

Audit fees 1,500 1,500 1,500 1,500 6,000

Trustee fees 160 160 160 160 640

Legal fees - - - - -

Operating Expenses - - - - -

$ 10,665 $ 9,060 $ 24,679 $ 9,679 $ 54,083

VARIANCE

Administrative Expenses

Actuarial valuations $ 12,765 $ 2,370 $ (7,250) $ 7,750 $ 15,635

Accounting and

administrative services - - - - -

Audit fees - - - - -

Trustee fees (60) (60) (60) (60) (240)

Legal fees - - - - -

Operating Expenses 200 200 200 200 800

$ 12,905 $ 2,510 $ (7,110) $ 7,890 $ 16,195

Truckee Meadows

5

WASHOE COUNTY, NEVADA OPEB TRUST

Washoe Co. State of Nevada

Retiree Health Public Employee

Benefit Plan Benefit Plan Total

Trust portion of retiree premiums $ 1,962,890 $ - $ 1,962,890

Cost for PEBP participants - 72,856 72,856

Requested reimbursement $ 1,962,890 $ 72,856 $ 2,035,746

Review of Average Cost per Participant by Coverage Type

Average

Average # Premium Monthly Cost

Plan Participants Total per Participant

PPO with Medicare 318 388,325 407.05

PPO without Medicare 631 1,034,758 546.62

Subtotal - PPO 949 1,423,083

HMO with Medicare 67 71,845 357.44

HMO without Medicare 288 450,816 521.78

Subtotal - HMO 355 522,661

Senior Care Plus 78 17,146 73.27

State PEBS 280 72,856 86.73

Total - all plans 1,662 2,035,746

Historical Comparison of Benefits Expense vs. Premium Reimbursements - WCRHBP

Benefits Retiree Pmts / Premium Reimb over/

Expense Misc Revenue Reimbursement (under) net exp

Fiscal Year 2013:

Q1 FY13 $ 2,157,310 $ (775,716) $ 1,870,582 $ 488,988

Q2 FY13 3,370,959 (750,107) 1,876,053 (744,799)

Q3 FY13 3,071,262 (1,224,128) 1,888,976 41,842

Q4 FY13 4,302,528 (606,105) 1,895,307 (1,801,116)

Total FY2013 $ 12,902,059 $ (3,356,056) $ 7,530,918 $ (2,015,085)

Fiscal year 2014:

Q1 FY14 $ 2,027,172 $ (832,254) $ 1,931,143 $ 736,225

Q2 FY14 4,566,136 (1,020,094) 1,941,728 (1,604,314)

Q3 FY14 2,187,617 (759,729) 1,958,334 530,446

Q4 FY14 4,673,531 (757,037) 1,962,890 (1,953,604)

Total FY2014 $ 13,454,456 $ (3,369,114) $ 7,794,095 $ (2,291,247)

Review of Washoe County Request for Reimbursement

For the Quarter Ended June 30, 2014

6

Washoe County, Nevada OPEB Trust Fund Financial Highlights for the Quarter Ended June 30, 2014 - Unaudited

All $ in Thousands unless otherwise noted.

Prepared by Washoe County Comptroller’s Office 7/30/14

Net Assets by Plan

• Net assets have increased by $30.7 million year-to-date to $154.3 million, due to investment income and prefunding contributions from employers. The trust holds $150.9 million in the State RBIF pool.

• Other net assets include amounts due from Washoe County for prefunding, less balances payable to employers for retiree coverage.

• Reimbursements to Washoe County for the WCRHBP reflect the employer portion of retiree premiums. The year-to-date difference between premiums and the actual cost paid by the County for retiree health benefits is recorded as contributions for incurred cost.

Change in Plan Net Assets

• Investment income includes $17.76 million from unrealized gains in the State RBIF pool due to fluctuations in the fair value of investments.

Budget Comparison

• Prefunding includes $545,000 from SFPD that was not budgeted. • Investment income in the State RBIF pool is currently averaging 19.82% including unrealized gains, 4.05%

without.

State RBIF WC-Pool Other-Net Net Assets

WC-RHBP 143,375$ 98$ 3,011$ 146,484$ WC-PEBP 2,566 10 31 2,607

TMFPD 4,011 79 (108) 3,982

SFPD 930 304 1 1,235

150,882$ 491$ 2,935$ 154,308$

WC-RHBP WC-PEBP TMFPD SFPD TOTAL

Additions:

Prefunding 15,683$ 417$ -$ 545$ 16,645$

Investment income, net of expense 21,284 381 619 121 22,405

Plan members, other 3,369 - - 8 3,377

Contrib. for incurred cost 2,291 - - - 2,291

42,627 798 619 674 44,718

Deductions:Benefits Paid 13,454 310 186 13 13,963

Administrative 11 9 25 10 55

13,465 319 211 23 14,018

Net change in Plan Net Assets 29,162$ 479$ 408$ 651$ 30,700$

Budget YTD Act % Bud Variance

Additions:

Prefunding 18,700$ 16,645$ 89% (2,055)$

Investment income, net of expense - 22,405 0% 22,405

Plan members, other 3,585 3,377 94% (208)

Contrib. for incurred cost 2,288 2,291 100% 3

24,573 44,718 182% 20,145

Deductions:

Benefits Paid 14,132 13,963 99% 169

Administrative 70 55 79% 15

14,202 14,018 99% 184

Net change in Plan Net Assets 10,371$ 30,700$ 296% 20,329$

7

TMFPD

Retiree Group

Medical Plan

SFPD

Retiree Group

Medical Plan Total

Assets

Cash and investments:

Washoe County Investment Pool $ 98,067 $ 9,995 $ 78,566 $ 304,210 $ 490,838

State of NV RBIF 143,374,562 2,565,611 4,010,573 929,851 150,880,597

Accounts receivable 4,970,660 104,340 - - 5,075,000

Interest receivable 3,268 113 206 837 4,424

Total Assets 148,446,557 2,680,059 4,089,345 1,234,898 156,450,859

Liabilities

Accounts payable 1,963,050 72,856 107,786 - 2,143,692

Net assets held in trust for other

postemployment benefits $ 146,483,507 $ 2,607,203 $ 3,981,559 $ 1,234,898 $ 154,307,167

WASHOE COUNTY, NEVADA OPEB TRUST FUND

AS OF JUNE 30, 2014 - UNAUDITED

State of Nevada

Public Employee

Benefit Plan

Washoe Co.

Retiree Health

Benefit Plan

STATEMENTS OF PLAN NET ASSETS

8

WASHOE COUNTY, NEVADA OPEB TRUST FUND

STATEMENT OF CHANGES IN PLAN NET ASSETS

FOR THE YEAR ENDED JUNE 30, 2014 - UNAUDITED

(WITH COMPARATIVE AMOUNTS FOR THE YEAR ENDED JUNE 30, 2013)

Combined Trust

Budget Actual Act % Variance 6/30/2013

Additions

Contributions

Employer:

Prefunding $ 18,700,000 $ 16,644,869 89.01% $ (2,055,131) $ 17,400,000

Contributions for incurred cost 2,287,500 2,291,247 100.16% 3,747 2,015,085

Plan member 3,015,000 2,923,133 96.95% (91,867) 2,575,989

Other 570,000 454,313 79.70% (115,687) 789,732

Total Contributions 24,572,500 22,313,562 90.81% (2,258,938) 22,780,806

Investment Income

Interest and dividends 49,500 3,835,908 7749.31% 3,786,408 3,189,327

Net increase (decrease) in fair value

of investments - 18,625,689 18,625,689 9,624,225

49,500 22,461,597 45376.96% 22,412,097 12,813,552

Less investment expense 49,500 56,585 114.31% (7,085) 47,917

Net Investment Income - 22,405,012 22,405,012 12,765,635

Total Additions 24,572,500 44,718,574 181.99% 20,146,074 35,546,441

Deductions

Benefits 14,131,500 13,964,082 98.82% 167,418 13,420,831

Administrative expense 70,278 54,083 76.96% 16,195 69,759

Total Deductions 14,201,778 14,018,165 98.71% 183,613 13,490,590

Net Change in Plan Net Assets 10,370,722 30,700,409 296.03% 20,329,687 22,055,851

Net Assets Held in Trust for Other

Postemployment Benefits

Beginning of year 123,606,758 123,606,758 - 101,550,907

End of Period $ 133,977,480 $ 154,307,167 $ 20,329,687 $ 123,606,758

9

WASHOE COUNTY, NEVADA OPEB TRUST FUND

STATEMENT OF CHANGES IN PLAN NET ASSETS

FOR THE YEAR ENDED JUNE 30, 2014 - UNAUDITED

(WITH COMPARATIVE AMOUNTS FOR THE YEAR ENDED JUNE 30, 2013)

Washoe County - Retiree Health Benefit Plan

Budget Actual Act % Variance 6/30/2013

Additions

Contributions

Employer:

Prefunding $ 18,282,610 $ 15,682,610 85.78% $ (2,600,000) $ 17,011,626

Contributions for incurred cost 2,287,500 2,291,247 100.16% 3,747 2,015,085

Plan member 3,015,000 2,914,801 96.68% (100,199) 2,566,324

Other 570,000 454,313 79.70% (115,687) 789,732

Total Contributions 24,155,110 21,342,971 88.36% (2,812,139) 22,382,767

Investment Income

Interest and dividends 46,500 3,641,185 7830.51% 3,594,685 3,016,926

Net increase (decrease) in fair value

of investments - 17,695,720 17,695,720 9,121,339

46,500 21,336,905 45885.82% 21,290,405 12,138,265

Less investment expense 46,500 53,515 115.09% (7,015) 45,156

Net Investment Income - 21,283,390 21,283,390 12,093,109

Total Additions 24,155,110 42,626,361 176.47% 18,471,251 34,475,876

Deductions

Benefits 13,601,500 13,454,456 98.92% 147,044 12,902,059

Administrative expense 23,570 10,665 45.25% 12,905 27,395

Total Deductions 13,625,070 13,465,121 98.83% 159,949 12,929,454

Net Change in Plan Net Assets 10,530,040 29,161,240 276.93% 18,631,200 21,546,422

Net Assets Held in Trust for Other

Postemployment Benefits

Beginning of year 117,322,267 117,322,267 - 95,775,845

End of Period $ 127,852,307 $ 146,483,507 $ 18,631,200 $ 117,322,267

10

WASHOE COUNTY, NEVADA OPEB TRUST FUND

STATEMENT OF CHANGES IN PLAN NET ASSETS

FOR THE YEAR ENDED JUNE 30, 2014 - UNAUDITED

(WITH COMPARATIVE AMOUNTS FOR THE YEAR ENDED JUNE 30, 2013)

Washoe County - NV PEBS Plan

Budget Actual Act % Variance 6/30/2013

Additions

Contributions

Employer:

Prefunding $ 417,390 $ 417,390 100.00% $ - $ 388,374

Total Contributions 417,390 417,390 100.00% - 388,374

Investment Income

Interest and dividends 1,000 65,419 6541.90% 64,419 58,502

Net increase (decrease) in fair value

of investments - 316,933 316,933 172,489

1,000 382,352 38235.20% 381,352 230,991

Less investment expense 1,000 976 97.60% 24 914

Net Investment Income - 381,376 381,376 230,077

Total Additions 417,390 798,766 191.37% 381,376 618,451

Deductions

Benefits 320,000 310,442 97.01% 9,558 315,315

Administrative expense 11,570 9,060 78.31% 2,510 13,480

Total Deductions 331,570 319,502 96.36% 12,068 328,795

Net Change in Plan Net Assets 85,820 479,264 393,444 289,656

Net Assets Held in Trust for Other

Postemployment Benefits

Beginning of year 2,127,939 2,127,939 - 1,838,283

End of Period $ 2,213,759 $ 2,607,203 $ 393,444 $ 2,127,939

11

WASHOE COUNTY, NEVADA OPEB TRUST FUND

STATEMENT OF CHANGES IN PLAN NET ASSETS

FOR THE YEAR ENDED JUNE 30, 2014 - UNAUDITED

(WITH COMPARATIVE AMOUNTS FOR THE YEAR ENDED JUNE 30, 2013)

Truckee Meadows FPD - Retiree Group Med Plan

Budget Actual Act % Variance 6/30/2013

Additions

Contributions

Employer:

Prefunding $ - $ - $ - $ -

Total Contributions - - - -

Investment Income

Interest and dividends 1,500 106,316 7087.73% 104,816 97,899

Net increase (decrease) in fair value

of investments - 514,711 514,711 282,449

1,500 621,027 41401.80% 619,527 380,348

Less investment expense 1,500 1,630 108.67% (130) 1,605

Net Investment Income - 619,397 619,397 378,743

Total Additions - 619,397 619,397 378,743

Deductions

Benefits 200,000 186,242 93.12% 13,758 196,013

Administrative expense 17,569 24,679 140.47% (7,110) 8,979

Total Deductions 217,569 210,921 96.94% 6,648 204,992

Net Change in Plan Net Assets (217,569) 408,476 (187.75%) 626,045 173,751

Net Assets Held in Trust for Other

Postemployment Benefits

Beginning of year 3,573,083 3,573,083 - 3,399,332

End of Period $ 3,355,514 $ 3,981,559 $ 626,045 3,573,083

12

WASHOE COUNTY, NEVADA OPEB TRUST FUND

STATEMENT OF CHANGES IN PLAN NET ASSETS

FOR THE YEAR ENDED JUNE 30, 2014 - UNAUDITED

(WITH COMPARATIVE AMOUNTS FOR THE YEAR ENDED JUNE 30, 2013)

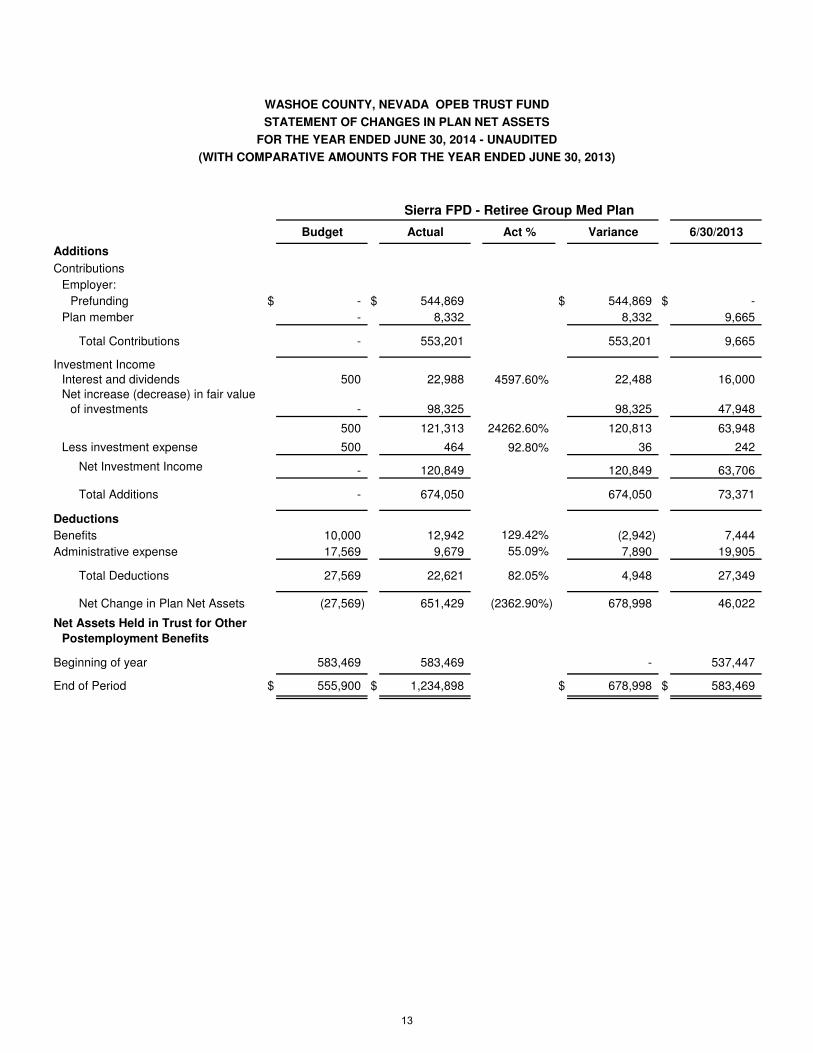

Sierra FPD - Retiree Group Med Plan

Budget Actual Act % Variance 6/30/2013

Additions

Contributions

Employer:

Prefunding $ - $ 544,869 $ 544,869 $ -

Plan member - 8,332 8,332 9,665

Total Contributions - 553,201 553,201 9,665

Investment Income

Interest and dividends 500 22,988 4597.60% 22,488 16,000

Net increase (decrease) in fair value

of investments - 98,325 98,325 47,948

500 121,313 24262.60% 120,813 63,948

Less investment expense 500 464 92.80% 36 242

Net Investment Income - 120,849 120,849 63,706

Total Additions - 674,050 674,050 73,371

Deductions

Benefits 10,000 12,942 129.42% (2,942) 7,444

Administrative expense 17,569 9,679 55.09% 7,890 19,905

Total Deductions 27,569 22,621 82.05% 4,948 27,349

Net Change in Plan Net Assets (27,569) 651,429 (2362.90%) 678,998 46,022

Net Assets Held in Trust for Other

Postemployment Benefits

Beginning of year 583,469 583,469 - 537,447

End of Period $ 555,900 $ 1,234,898 $ 678,998 $ 583,469

13

WA

SH

OE

CO

UN

TY

, N

EV

AD

A

OP

EB

TR

US

T F

UN

D

RE

CO

MM

EN

DE

D B

UD

GE

T

FO

R T

HE

YE

AR

EN

DE

D J

UN

E 3

0,

20

15

Tru

ck

ee

Wa

sh

oe

Co

Sta

te o

f N

eva

da

Me

ad

ow

sS

ierr

a F

ire

Re

tire

e H

ea

lth

Pu

bli

c E

mp

loye

eF

PD

Re

tire

eR

eti

ree

20

13

20

14

20

15

Be

ne

fit

Be

ne

fit

Gro

up

Me

dic

al

Gro

up

Me

dic

al

Ac

tua

lE

TC

To

tal

Pro

gra

mP

lan

Pla

nP

lan

Ad

dit

ion

sC

on

trib

utio

ns

Em

plo

yer:

Pre

fun

din

g$

17

,40

0,0

00

$1

6,6

44

,86

9

$

18

,70

0,0

00

$

18

,30

3,8

72

$

39

6,1

28

$-

$-

Co

ntr

ibu

tio

ns f

or

incu

rre

d c

ost

2,0

15

,08

5

2,2

91

,24

7

2,2

87

,50

0

2

,28

7,5

00

-

-

-

P

lan

me

mb

er

2,5

75

,98

9

2,9

23

,13

3

3,0

24

,00

0

3

,01

5,0

00

-

-

9,0

00

Oth

er

78

9,7

32

4

54

,31

3

57

0,0

00

57

0,0

00

-

-

-

To

tal C

on

trib

utio

ns

22

,78

0,8

06

22

,31

3,5

62

24

,58

1,5

00

2

4,1

76

,37

2

39

6,1

28

-

9

,00

0

Inve

stm

en

t In

co

me

:

Inve

stm

en

t e

arn

ing

s1

2,8

13

,55

2

2

2,4

61

,59

7

5

8,1

50

5

5,0

00

1

,00

0

1

,65

0

5

00

Le

ss in

vestm

en

t e

xp

en

se

(47

,91

7)

(5

6,5

85

)

(58

,15

0)

(55

,00

0)

(1,0

00

)

(1,6

50

)

(50

0)

Ne

t In

vestm

en

t In

co

me

12

,76

5,6

35

22

,40

5,0

12

-

-

-

-

-

To

tal A

dd

itio

ns

35

,54

6,4

41

44

,71

8,5

74

24

,58

1,5

00

2

4,1

76

,37

2

39

6,1

28

-

9

,00

0

De

du

cti

on

sB

en

efits

13

,42

0,8

31

13

,96

4,0

82

14

,13

5,3

50

1

3,6

01

,50

0

32

0,0

00

20

0,0

00

13

,85

0

Ad

min

istr

ative

exp

en

se

69

,75

9

5

4,0

83

60

,72

6

22

,80

7

10

,80

7

9,3

06

17

,80

6

To

tal D

ed

uctio

ns

13

,49

0,5

90

14

,01

8,1

65

14

,19

6,0

76

1

3,6

24

,30

7

33

0,8

07

20

9,3

06

31

,65

6

Ne

t C

ha

ng

e in

Pla

n N

et

Asse

ts2

2,0

55

,85

1

3

0,7

00

,40

9

1

0,3

85

,42

4

10

,55

2,0

65

6

5,3

21

(2

09

,30

6)

(2

2,6

56

)

Ne

t A

ss

ets

He

ld i

n T

rus

tfo

r O

the

r P

oste

mp

loym

en

tB

en

efits

Be

gin

nin

g o

f ye

ar

10

1,5

50

,90

7

12

3,6

06

,75

8

15

4,3

07

,16

7

1

46

,48

3,5

07

2,6

07

,20

3

3

,98

1,5

59

1,2

34

,89

8

En

d o

f ye

ar

$1

23

,60

6,7

58

$

15

4,3

07

,16

7

$1

64

,69

2,5

91

$1

57

,03

5,5

72

$2

,67

2,5

24

$3

,77

2,2

53

$1

,21

2,2

42

20

15

Re

co

mm

en

de

d B

ud

ge

t

14

WA

SH

OE

CO

UN

TY

, N

EV

AD

A O

PE

B T

RU

ST

PR

OP

OS

ED

AD

MIN

IST

RA

TIV

E E

XP

EN

SE

BU

DG

ET

FIS

CA

L Y

EA

R E

ND

ING

JU

NE

30

, 2

01

5

Wa

sh

oe

Co

Sta

te o

f N

eva

da

Sie

rra

FP

D

Re

tire

e H

ea

lth

Pu

bli

c E

mp

loye

eF

PD

Re

tire

eR

eti

ree

Be

ne

fit

Be

ne

fit

Gro

up

Me

dic

al

Gro

up

Me

dic

al

20

15

Pro

gra

mP

lan

Pla

nP

lan

To

tal

Ad

min

istr

ative

Exp

en

se

sA

ctu

ari

al va

lua

tio

ns

$1

5,0

00

$

3,0

00

$1

,50

0

$

10

,00

0

$2

9,5

00

A

cco

un

tin

g a

nd

ad

min

istr

ative

se

rvic

es

6,0

67

6,0

67

6,0

66

6,0

66

24

,26

6

Au

dit f

ee

s1

,66

0

1

,66

0

1

,66

0

1

,66

0

6

,64

0

T

ruste

e f

ee

s8

0

80

8

0

80

3

20

Oth

er

op

era

tin

g e

xpe

nse

s-

-

-

-

-

$2

2,8

07

$

10

,80

7

$9

,30

6

$

17

,80

6

$6

0,7

26

Tru

ck

ee

Me

ad

ow

s

15

Wash

oe C

ou

nty

, N

evad

a O

PE

B T

rust

Fu

nd

Cash

Flo

w P

roje

cti

on

s a

nd

Pla

nn

ed

Tra

nsfe

rs t

o t

he S

tate

In

vestm

en

t F

un

d (

RB

IF)

for

FY

2015

Pro

po

sed

8/5

/14

Pre

fun

din

g

Co

ntr

ibu

tio

ns

Dir

ect

Exp

en

ses

Reim

bu

rse

Em

plo

yers

Cash

Ch

an

ge

Trs

frs t

o

RB

IF

Cash

in

WC

Po

ol

Cash

in

RB

IFT

ota

l C

ash

&

Investm

ts*

Be

gin

nin

g b

ala

nce

490,8

38

$

150,8

80,5

97

$

151,3

71,4

35

$

Jul-

14

Tru

ste

e M

ee

tin

g-

(6,2

16)

-

(6,2

16)

-

484,6

22

150,8

80,5

97

151,3

65,2

19

Aug

5,0

75,0

00

(6

,216)

(2,0

35,9

06)

3,0

32,8

78

-

3,5

17,5

00

150,8

80,5

97

154,3

98,0

97

Sep

-

(5

6,2

16)

-

(5

6,2

16)

2,0

15,0

00

1,4

46,2

84

152,9

95,5

97

154,4

41,8

81

Oct

Tru

ste

e M

ee

tin

g4,6

75,0

00

(6

,216)

(2,0

30,0

00)

2,6

38,7

84

2,0

15,0

00

2,0

70,0

68

155,0

10,5

97

157,0

80,6

65

Nov

-

(6

,216)

-

(6,2

16)

1,5

15,0

00

548,8

52

156,5

25,5

97

157,0

74,4

49

Dec

-

(5

6,2

16)

-

(5

6,2

16)

-

492,6

36

156,5

25,5

97

157,0

18,2

33

Jan

Tru

ste

e M

ee

tin

g4,6

75,0

00

(6

,216)

(2,0

30,0

00)

2,6

38,7

84

907,0

00

2,2

24,4

20

157,4

32,5

97

159,6

57,0

17

Feb

-

(6

,216)

-

(6,2

16)

907,0

00

1,3

11,2

04

158,3

39,5

97

159,6

50,8

01

Mar

-

(5

6,2

16)

-

(5

6,2

16)

907,0

00

347,9

88

159,3

46,5

97

159,6

94,5

85

Apr

Tru

ste

e M

ee

tin

g4,6

75,0

00

(6

,216)

(2,0

30,0

00)

2,6

38,7

84

907,0

00

2,0

79,7

72

160,2

53,5

97

162,3

33,3

69

May

-

(6

,216)

-

(6,2

16)

907,0

00

1,1

66,5

56

161,1

60,5

97

162,3

27,1

53

Jun

-

(5

6,2

00)

-

(5

6,2

00)

907,0

00

203,3

56

162,0

67,5

97

162,2

70,9

53

Jul-

15

Tru

ste

e M

eeting

4,6

75,0

00

-

(2

,030,0

00)

2,6

45,0

00

-

2,8

48,3

56

162,0

67,5

97

164,9

15,9

53

Cash f

low

tota

l23,7

75,0

00

(274,5

76)

(10,1

55,9

06)

13,3

44,5

18

10,9

87,0

00

Less:

Pm

ts r

ela

ted t

o F

Y14

(5,0

75,0

00)

2,0

35,9

06

FY

15 B

udget

18,7

00,0

00

(8,1

20,0

00)

Key

Assum

ptions:

Only

key

changes in c

ash f

low

are

show

n.

TM

FP

D -

Quart

erl

y paym

ents

to C

ity

of

Reno,

based o

n F

Y14 a

ctu

al -

paid

in last

month

of

each q

uart

er.

Tra

nsfe

rs t

o R

BIF

will

be r

evi

ew

ed q

uart

erl

y fo

r possib

le a

dju

stm

ent.

WC

RH

BP

PE

BP

WC

Tota

l

WC

co

ntr

ibu

tio

n18,3

03,8

72

396,1

28

18,7

00,0

00

A

llo

c. b

ase

d o

n U

AA

L /

pa

id i

n q

ua

rte

rly

in

cre

me

nts

P:\

OP

EB

\20

15

\OP

EB

Tra

nsf

ers

FY

15

.xls

m

16

Wash

oe C

ou

nty

, N

evad

a O

PE

B T

rust

Fu

nd

Cash

Flo

w P

roje

cti

on

s a

nd

Pla

nn

ed

Tra

nsfe

rs t

o t

he S

tate

In

vestm

en

t F

un

d (

RB

IF)

for

FY

2015

Pro

po

sed

8/5

/14

WC

RH

BP

Pre

fun

din

g

Co

ntr

ibu

tio

ns

Dir

ect

Exp

en

ses

Reim

bu

rse

Em

plo

yers

Cash

Ch

an

ge

Trs

frs t

o

RB

IF

Cash

in

WC

Po

ol

Cash

in

RB

IFT

ota

l C

ash

&

Invest.

Be

gin

nin

g b

ala

nce

98,0

67

$

143,3

74,5

62

$

143,4

72,6

29

$

Jul-

14

Tru

ste

e M

ee

tin

g-

(1,9

01)

-

(1,9

01)

-

96,1

66

143,3

74,5

62

143,4

70,7

28

Aug

4,9

70,6

60

(1

,901)

(1,9

63,0

50)

3,0

05,7

09

-

3,1

01,8

75

143,3

74,5

62

146,4

76,4

37

Sep

-

(1

,901)

-

(1,9

01)

2,0

00,0

00

1,0

99,9

74

145,3

74,5

62

146,4

74,5

36

Oct

Tru

ste

e M

ee

tin

g4,5

75,9

68

(1

,901)

(1,9

50,0

00)

2,6

24,0

67

2,0

00,0

00

1,7

24,0

41

147,3

74,5

62

149,0

98,6

03

Nov

-

(1

,901)

-

(1,9

01)

1,5

00,0

00

222,1

40

148,8

74,5

62

149,0

96,7

02

Dec

-

(1

,901)

-

(1,9

01)

-

220,2

39

148,8

74,5

62

149,0

94,8

01

Jan

Tru

ste

e M

ee

tin

g4,5

75,9

68

(1

,901)

(1,9

50,0

00)

2,6

24,0

67

900,0

00

1,9

44,3

06

149,7

74,5

62

151,7

18,8

68

Feb

-

(1

,901)

-

(1,9

01)

900,0

00

1,0

42,4

05

150,6

74,5

62

151,7

16,9

67

Mar

-

(1

,901)

-

(1,9

01)

900,0

00

140,5

04

151,5

74,5

62

151,7

15,0

66

Apr

Tru

ste

e M

ee

tin

g4,5

75,9

68

(1

,901)

(1,9

50,0

00)

2,6

24,0

67

900,0

00

1,8

64,5

71

152,4

74,5

62

154,3

39,1

33

May

-

(1

,901)

-

(1,9

01)

900,0

00

962,6

70

153,3

74,5

62

154,3

37,2

32

Jun

-

(1

,896)

-

(1,8

96)

900,0

00

60,7

74

154,2

74,5

62

154,3

35,3

36

Jul-

15

Tru

ste

e M

ee

tin

g4,5

75,9

68

-

(1

,950,0

00)

2,6

25,9

68

-

2,6

86,7

42

154,2

74,5

62

156,9

61,3

04

Cash f

low

tota

l23,2

74,5

32

(22,8

07)

(9

,763,0

50)

13,4

88,6

75

10,9

00,0

00

Less:

Pm

ts r

ela

ted t

o F

Y14

(4,9

70,6

60)

1,9

63,0

50

FY

15 B

udget

18,3

03,8

72

(7,8

00,0

00)

PE

BP

Pre

fun

din

g

Co

ntr

ibu

tio

ns

Dir

ect

Exp

en

ses

Reim

bu

rse

Em

plo

yers

Cash

Ch

an

ge

Trs

frs t

o

RB

IF

Cash

in

WC

Po

ol

Cash

in

RB

IFT

ota

l C

ash

&

Invest.

Be

gin

nin

g b

ala

nce

9,9

95

$

2,5

65,6

11

$

2,5

75,6

06

$

Jul-

14

Tru

ste

e M

ee

tin

g-

(901)

-

(901)

-

9,0

94

2,5

65,6

11

2,5

74,7

05

Aug

104,3

40

(901)

(72,8

56)

30,5

83

-

39,6

77

2,5

65,6

11

2,6

05,2

88

Sep

-

(9

01)

-

(901)

15,0

00

23,7

76

2,5

80,6

11

2,6

04,3

87

Oct

Tru

ste

e M

ee

tin

g99,0

32

(9

01)

(80,0

00)

18,1

31

15,0

00

26,9

07

2,5

95,6

11

2,6

22,5

18

Nov

-

(9

01)

-

(901)

15,0

00

11,0

06

2,6

10,6

11

2,6

21,6

17

Dec

-

(9

01)

-

(901)

-

10,1

05

2,6

10,6

11

2,6

20,7

16

Jan

Tru

ste

e M

ee

tin

g99,0

32

(9

01)

(80,0

00)

18,1

31

7,0

00

21,2

36

2,6

17,6

11

2,6

38,8

47

Feb

-

(9

01)

-

(901)

7,0

00

13,3

35

2,6

24,6

11

2,6

37,9

46

Mar

-

(9

01)

-

(901)

7,0

00

5,4

34

2,6

31,6

11

2,6

37,0

45

Apr

Tru

ste

e M

ee

tin

g99,0

32

(9

01)

(80,0

00)

18,1

31

7,0

00

16,5

65

2,6

38,6

11

2,6

55,1

76

May

-

(9

01)

-

(901)

7,0

00

8,6

64

2,6

45,6

11

2,6

54,2

75

Jun

-

(8

96)

-

(896)

7,0

00

768

2,6

52,6

11

2,6

53,3

79

Jul-

15

Tru

ste

e M

ee

tin

g99,0

32

(8

0,0

00)

19,0

32

-

19,8

00

2,6

52,6

11

2,6

72,4

11

Cash f

low

tota

l500,4

68

(10,8

07)

(3

92,8

56)

96,8

05

87,0

00

Less:

Pm

ts r

ela

ted t

o F

Y14

(104,3

40)

72,8

56

FY

15 B

udget

396,1

28

(320,0

00)

P:\

OP

EB

\20

15

\OP

EB

Tra

nsf

ers

FY

15

.xls

m

17

Wash

oe C

ou

nty

, N

evad

a O

PE

B T

rust

Fu

nd

Cash

Flo

w P

roje

cti

on

s a

nd

Pla

nn

ed

Tra

nsfe

rs t

o t

he S

tate

In

vestm

en

t F

un

d (

RB

IF)

for

FY

2015

Pro

po

sed

8/5

/14

TM

FP

D

Pre

fun

din

g

Co

ntr

ibu

tio

ns

Dir

ect

Exp

en

ses

Reim

bu

rse

Em

plo

yers

Cash

Ch

an

ge

Trs

frs t

o

RB

IF

Cash

in

WC

Po

ol*

Cash

in

RB

IF*

To

tal

Cash

&

Invest.

Be

gin

nin

g b

ala

nce

78,5

66

$

4,0

10,5

73

$

4,0

89,1

39

$

Jul-

14

Tru

ste

e M

ee

tin

g-

(776)

-

(776)

-

127,7

90

4,0

60,5

73

4,1

88,3

63

Aug

-

(7

76)

-

(776)

-

127,0

14

4,0

60,5

73

4,1

87,5

87

Sep

-

(5

0,7

76)

-

(5

0,7

76)

-

76,2

38

4,0

60,5

73

4,1

36,8

11

Oct

Tru

ste

e M

ee

tin

g-

(776)

-

(776)

-

75,4

62

4,0

60,5

73

4,1

36,0

35

Nov

-

(7

76)

-

(776)

-

74,6

86

4,0

60,5

73

4,1

35,2

59

Dec

-

(5

0,7

76)

-

(5

0,7

76)

-

23,9

10

4,0

60,5

73

4,0

84,4

83

Jan

Tru

ste

e M

ee

tin

g-

(776)

-

(776)

-

23,1

34

4,0

60,5

73

4,0

83,7

07

Feb

-

(7

76)

-

(776)

-

22,3

58

4,0

60,5

73

4,0

82,9

31

Mar

-

(5

0,7

76)

-

(5

0,7

76)

-

71,5

82

4,0

60,5

73

4,1

32,1

55

Apr

Tru

ste

e M

ee

tin

g-

(776)

-

(776)

-

70,8

06

4,0

60,5

73

4,1

31,3

79

May

-

(7

76)

-

(776)

-

70,0

30

4,0

60,5

73

4,1

30,6

03

Jun

-

(5

0,7

70)

-

(5

0,7

70)

-

19,2

60

4,0

60,5

73

4,0

79,8

33

Jul-

15

Tota

l-

(209,3

06)

-

(209,3

06)

-

SF

PD

Pre

fun

din

g

Co

ntr

ibu

tio

ns

Dir

ect

Exp

en

ses

Reim

bu

rse

Em

plo

yers

Cash

Ch

an

ge

Trs

frs t

o

RB

IF

Cash

in

WC

Po

ol*

Cash

in

RB

IF*

To

tal

Cash

&

Invest.

Be

gin

nin

g b

ala

nce

304,2

10

$

929,8

51

$

1,2

34,0

61

$

Jul-

14

Tru

ste

e M

ee

tin

g-

(2,6

38)

-

(2,6

38)

-

251,5

72

979,8

51

1,2

31,4

23

Aug

-

(2

,638)

-

(2,6

38)

-

248,9

34

979,8

51

1,2

28,7

85

Sep

-

(2

,638)

-

(2,6

38)

-

246,2

96

979,8

51

1,2

26,1

47

Oct

Tru

ste

e M

ee

tin

g-

(2,6

38)

-

(2,6

38)

-

243,6

58

979,8

51

1,2

23,5

09

Nov

-

(2

,638)

-

(2,6

38)

-

241,0

20

979,8

51

1,2

20,8

71

Dec

-

(2

,638)

-

(2,6

38)

-

238,3

82

979,8

51

1,2

18,2

33

Jan

Tru

ste

e M

ee

tin

g-

(2,6

38)

-

(2,6

38)

-

235,7

44

979,8

51

1,2

15,5

95

Feb

-

(2

,638)

-

(2,6

38)

-

233,1

06

979,8

51

1,2

12,9

57

Mar

-

(2

,638)

-

(2,6

38)

-

130,4

68

1,0

79,8

51

1,2

10,3

19

Apr

Tru

ste

e M

ee

tin

g-

(2,6

38)

-

(2,6

38)

-

127,8

30

1,0

79,8

51

1,2

07,6

81

May

-

(2

,638)

-

(2,6

38)

-

125,1

92

1,0

79,8

51

1,2

05,0

43

Jun

-

(2

,638)

-

(2,6

38)

-

122,5

54

1,0

79,8

51

1,2

02,4

05

Jul-

15

Tota

l-

(31,6

56)

-

(3

1,6

56)

-

* C

ash b

ala

nces in T

MF

PD

and S

FP

D r

eflect

reallo

cations o

f P

ool and R

BIF

cash in J

uly

and D

ecem

ber.

P:\

OP

EB

\20

15

\OP

EB

Tra

nsf

ers

FY

15

.xls

m

18

19

20

21

22

23

650 California Street, 17th Floor San Francisco, CA 94108-2702 USA

Tel +1 415 403 1333 Fax +1 415 403 1334

milliman.com

July 23, 2014 Ms. Mary Solorzano Accounting Manager Washoe County Comptroller’s Office 1001 East Ninth Street Reno, Nevada 89512 Estimate of Retiree Health Plan Liability for County Employees Transferring to TMWA Dear Ms. Solorzano: As requested, we have estimated the County’s current retiree health plan liability for 29 County employees who have accepted positions with the Truckee Meadows Water Authority (TMWA). The liabilities shown in the table below are based on the same plan provisions and assumptions (summarized in the attached appendices) to be used for the valuation of retiree health and life benefits for Washoe County as of July 1, 2014. The liabilities shown below represent the County’s liability if the employees were to remain employed by the County. If all employees terminate employment with the County and commence employment with TMWA, the County would no longer have a retiree health and life benefit liability for the 29 employees assuming no employees elect to apply for and receive retiree health benefits from the County upon transferring to TMWA.

July 1, 2014

Number of Employees 29

Present Value of Benefits $ 2,462,000

Actuarial Accrued Liability $ 1,590,000

Normal Cost $ 111,000

The items shown in the table above are defined as follows: The Present Value of Benefits is the present value of projected benefits (projected claims less retiree contributions) discounted at the valuation interest rate (7.0%). The Actuarial Accrued Liability (AAL) is the present value of benefits that are attributed to past service only. The portion attributed to future employee service is excluded. For active employees, this is equal to the present value of benefits prorated by service to the valuation date over projected service at the expected retirement age. The Normal Cost is that portion of the County provided benefit attributable to employee service in the current year. Employees are assumed to have an equal portion of the present value of benefits attributed to each year of service from date of hire to expected retirement age.

24

Mary Solorzano July 23, 2014 Page 2

This work product was prepared solely for the Washoe County for the purposes described herein and may not be appropriate to use for other purposes. Milliman does not intend to benefit and assumes no duty or liability to other parties who receive this work. Milliman recommends that third parties hire their own actuary or other

qualified professional when reviewing Milliman work product.

Milliman

In preparing our report, we relied, without audit, on information (some oral and some in writing) supplied by Washoe County’s staff. This information includes but not limited to employee census data, financial information and plan provisions. While Milliman has not audited the financial and census data, they have been reviewed for reasonableness and are, in our opinion, sufficient and reliable for the purposes of our calculations. If any of this information as summarized in this report is inaccurate or incomplete, the results shown could be materially affected and this report may need to be revised. All costs, liabilities, rates of interest, and other factors for the County have been determined on the basis of actuarial assumptions and methods which are individually reasonable (taking into account the experience of the County and reasonable expectations); and which, in combination, offer our best estimate of anticipated experience affecting the County. Further, in our opinion, each actuarial assumption used is reasonably related to the experience of the Plan and to reasonable expectations which, in combination, represent our best estimate of anticipated experience for the County. This valuation report is only an estimate of liability as of a single date. It can neither predict the Plan’s future condition nor guarantee future financial soundness. Actuarial valuations do not affect the ultimate cost of Plan benefits, only the timing of County contributions. While the valuation is based on an array of individually reasonable assumptions, other assumption sets may also be reasonable and valuation results based on those assumptions would be different. No one set of assumptions is uniquely correct. Determining results using alternative assumptions is outside the scope of our engagement. Future actuarial measurements may differ significantly from the current measurements presented in this report due to such factors as the following: plan experience differing from that anticipated by the economic or demographic assumptions; changes in economic or demographic assumptions; and changes in plan provisions or applicable law. Due to the limited scope of our assignment, we did not perform an analysis of the potential range of future measurements. The County has the final decision regarding the appropriateness of the assumptions and actuarial cost methods. Actuarial computations presented in this report are for purposes described herein. Determinations for other purposes may be significantly different from the results contained in this report. Accordingly, additional determinations may be needed for other purposes. Milliman’s work is prepared solely for the internal business use of the Washoe County. To the extent that Milliman's work is not subject to disclosure under applicable public records laws, Milliman’s work may not be provided to third parties without Milliman's prior written consent. Milliman does not intend to benefit or create a legal duty to any third party recipient of its work product. Milliman’s consent to release its work product to any third party may be conditioned on the third party signing a Release, subject to the following exceptions:

a) The Washoe County may provide a copy of Milliman’s work, in its entirety, to the County's professional service advisors who are subject to a duty of confidentiality and who agree to not use Milliman’s work for any purpose other than to benefit the County.

b) The Washoe County may provide a copy of Milliman’s work, in its entirety, to other

governmental entities, as required by law. No third party recipient of Milliman's work product should rely upon Milliman's work product. Such recipients should engage qualified professionals for advice appropriate to their own specific needs.

25

Mary Solorzano July 23, 2014 Page 3

This work product was prepared solely for the Washoe County for the purposes described herein and may not be appropriate to use for other purposes. Milliman does not intend to benefit and assumes no duty or liability to other parties who receive this work. Milliman recommends that third parties hire their own actuary or other

qualified professional when reviewing Milliman work product.

Milliman

The consultants who worked on this assignment are actuaries. Milliman’s advice is not intended to be a substitute for qualified legal or accounting counsel. The signing actuary is independent of the plan sponsor. We are not aware of any relationship that would impair the objectivity of our work. On the basis of the foregoing, we hereby certify that, to the best of our knowledge and belief, the report is complete and accurate and has been prepared in accordance with generally recognized and accepted actuarial principles and practices which are consistent with the applicable Actuarial Standards of Practice of the American Academy of Actuaries. The undersigned is a member of the American Academy of Actuaries and meets the Qualification Standards of the American Academy of Actuaries to render the actuarial opinion contained herein. If you have any questions, please give me a call at (415) 394-3740. Sincerely, John R. Botsford, FSA, MAAA Consulting Actuary JRB/dyu n:\was\corr\2014\was0714-tmwa.doc

26

This work product was prepared solely for the Washoe County for the purposes described herein and may not be appropriate to use for other purposes. Milliman does not intend to benefit and assumes no duty or liability to other parties who receive this work. Milliman recommends that third parties hire their own actuary or other

qualified professional when reviewing Milliman work product.

Milliman

Milliman Client Report APPENDICES

Appendix A. Summary of Benefits Below is a summary of our understanding of the County's retiree benefit program.

Eligibility All employees who retire from County employment and receive monthly payments under the Public Employees Retirement System (PERS) of Nevada are eligible to participate in the plan. In addition, employees who have terminated employment prior to retirement may enroll in the County's health coverage upon commencing retirement if the County is that individual's last public employer. These persons must show evidence of good health and are subject to a 12 month pre-existing condition limitation. Retiree health and welfare benefits are provided under three contribution “tiers”. Tier 1 includes all employees employed on July 1, 1996 and hired prior to the dates shown in the table. Tier 2 includes all employees hired after the Tier 1 “exclusion” dates in the table below and before July 1, 2010. Tier 3 includes all employees hired on or after July 1, 2010.

Employee Association

Tier 1 Exclusion Date for Employees Hired After

Confidential (non-represented) September 17, 1997

WCEA (non-supervisory) September 17, 1997

WCEA (supervisory) September 17, 1997

WCSDA (non-supervisory) January 1, 1998

WCSSDA (supervisory) July 1, 1998

WCDA (investigators) February 11, 1998

WCPAA (attorneys) April 29, 1998

Non-represented attorneys in DA/PD April 29, 1998

WCNA (nurses) August 26, 1998

WC Elected Officials September 29, 1999

In order to draw a PERS benefit, an employee must meet certain age and service requirements described below: Regular Members age 65 with 5 years service, or age 60 with 10 years service, or at any

age with 30 years service. Sheriffs age 65 with 5 years service, or age 55 with 10 years service, or age 50

with 20 years service, or at any age with 30 years service. Disabled Members 5 years service and totally unable to perform current job or any

comparable job for which the member is qualified by training and experience, because of injury or illness of a permanent nature.

Benefit Plans

27

This work product was prepared solely for the Washoe County for the purposes described herein and may not be appropriate to use for other purposes. Milliman does not intend to benefit and assumes no duty or liability to other parties who receive this work. Milliman recommends that third parties hire their own actuary or other

qualified professional when reviewing Milliman work product.

Milliman

Milliman Client Report APPENDICES

Medical Identical benefits as provided to active employees. Retirees can elect coverage under either the Self-Funded Group Health Plan or the HMO Health Plan. Medicare eligible retirees may also choose the Senior Coverage Plan. The Group Health Plan has full coordination of benefits integration with Medicare.

Prescription Drug Identical benefits as provided to active employees. Vision Identical benefits as provided to active employees. Dental Retirees after 1/1/96 have the option, upon retirement, to retain dental

benefits with the retiree paying the full premium.

Life Insurance Life insurance coverage is provided to those retirees enrolling in either of the health care benefit plans offered by the County. The amount of coverage provided for the retiree varies according to the retiree’s age as indicated below: Under age 65 $ 20,000 Age 65 to 69 13,000 Age 70 and over 7,000 The amount of coverage provided to covered dependents and surviving spouses of deceased retirees is indicated below: Spouse $ 1,000 Child under 14 days none Child 14 days to 6 months 100 Child 6 months and over 1,000

Dependents’ Benefits Coverage is available for dependents of the retiree including a spouse and any unmarried children who are under age 19, age 19 through 24 if full-time students, or disabled and incapable of self-support.

Survivor Benefits Upon the death of the retiree, benefits may be continued to the surviving spouse for his/her remaining lifetime. Spouses are required to pay 100% of the premium.

28

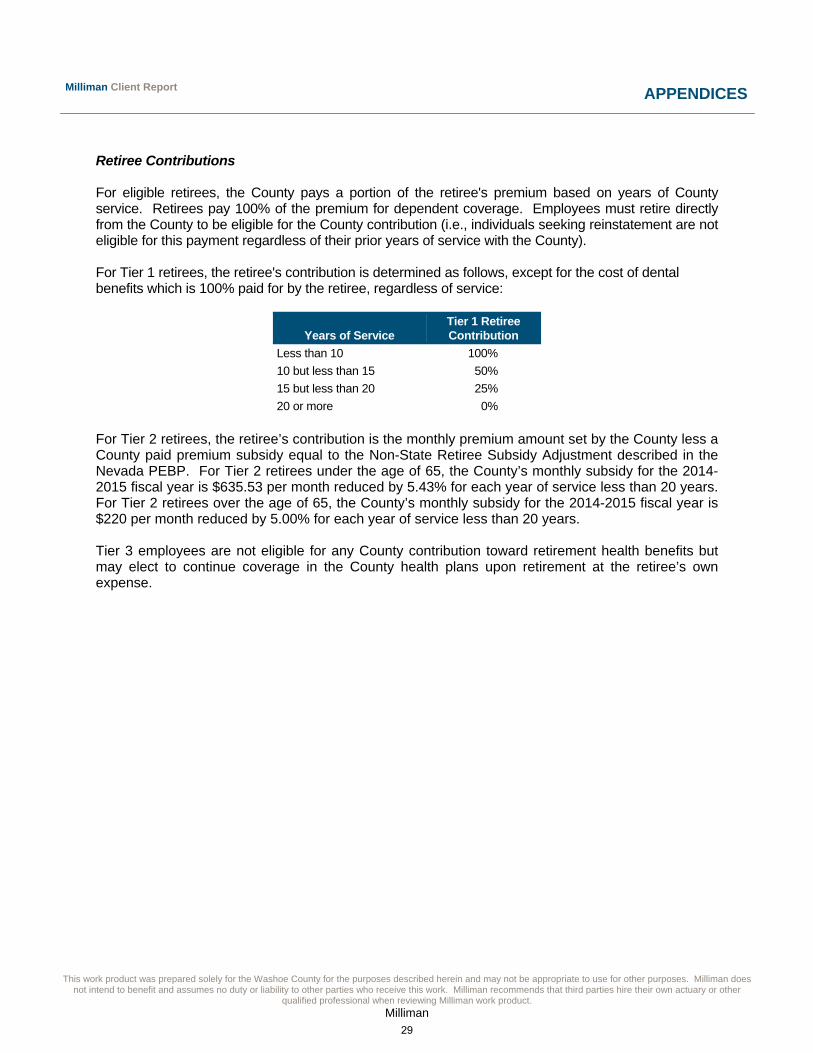

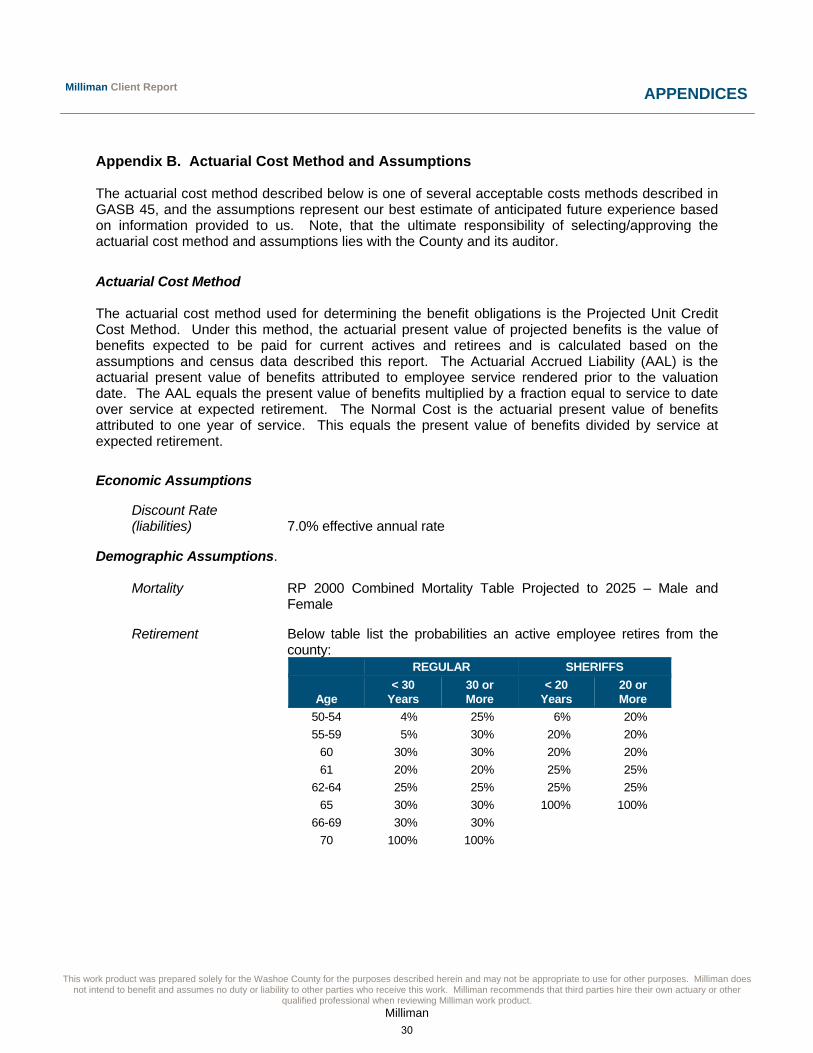

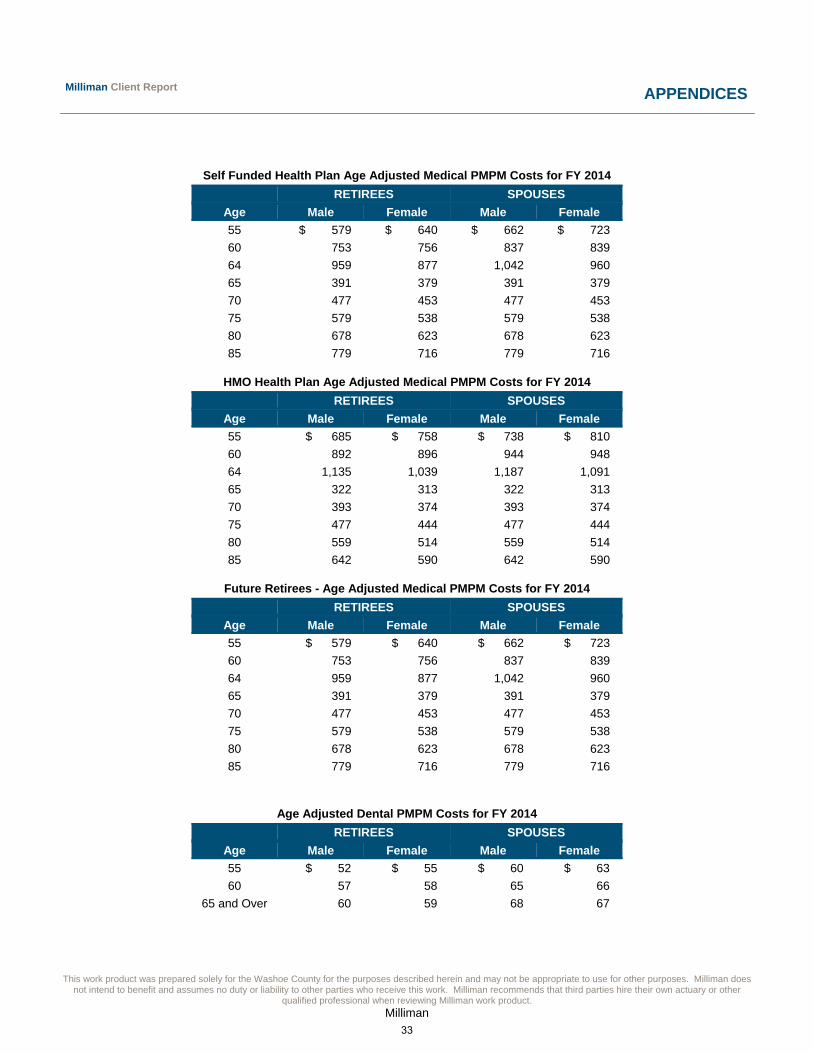

This work product was prepared solely for the Washoe County for the purposes described herein and may not be appropriate to use for other purposes. Milliman does not intend to benefit and assumes no duty or liability to other parties who receive this work. Milliman recommends that third parties hire their own actuary or other

qualified professional when reviewing Milliman work product.

Milliman

Milliman Client Report APPENDICES