Africa Dialogues- NAIROBI - Global Sustainable Electricity ...

409

e8-GEF-UNDESA Financing Sustainable Electrification Dialogues HCB Initiative 1 Financing Sustainable Electrification Workshop -Africa Dialogues- NAIROBI A few lessons learned from an innovative concept for rural electrification : EDF’ s experience on RESCOS Christine HEURAUX EDF Head of Energy Access Programme April 13, 2010

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Africa Dialogues- NAIROBI - Global Sustainable Electricity ...

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n D

ialo

gues

HC

B In

itiat

ive

1

Financing Sustainable Electrification Workshop

-Africa Dialogues-NAIROBI

A few lessons learned from an innovative concept for rural electrification : EDF’ s experience on RESCOS

Christine HEURAUXEDF

Head of Energy Access Programme

April 13, 2010

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n D

ialo

gues

HC

B In

itiat

ive

2

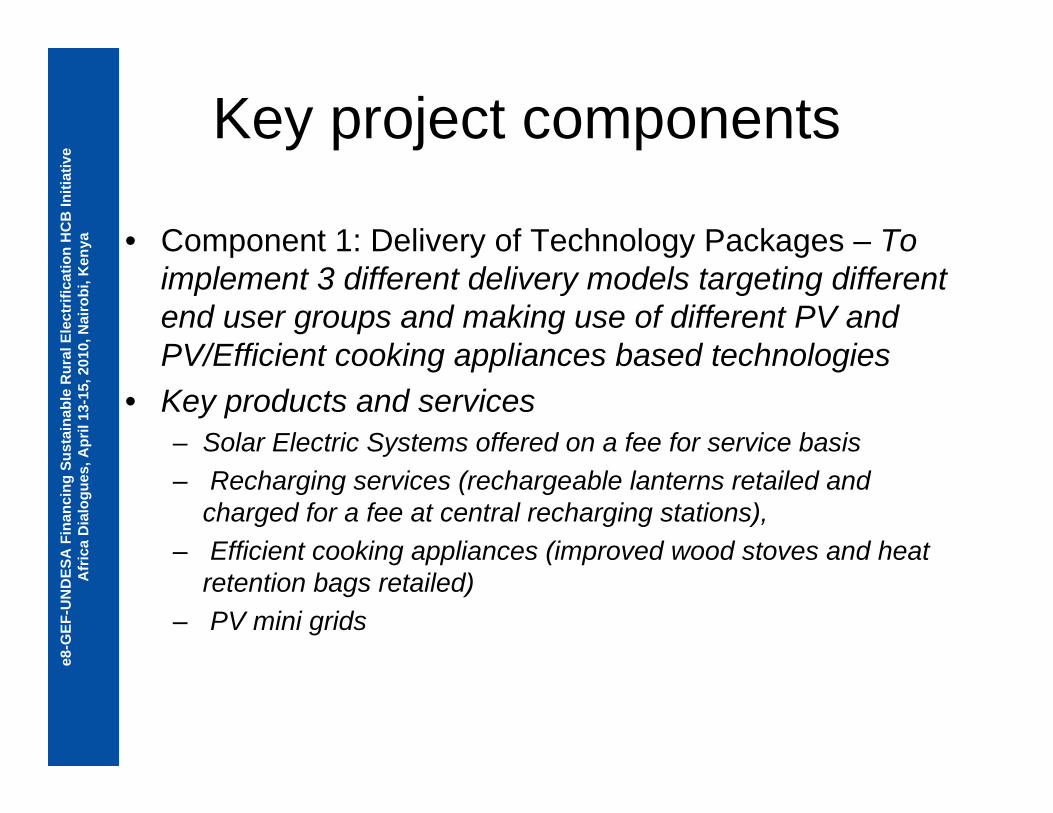

Summary

• Background ………………………………..……………………………………………………………...2-3

• RESCO concept… a model among others ……………………………....……..…..4-5

• What did we learn? First lessons learnt ……… ……………………….……...…….6

• Governments have a key role to play, but all players must committhemselves on a long-term basis ………………………….…………………………..…..7

• Financing must be reliable and flexible …………………………….…………………..8

• The objectives of Access to Energy should be precisely defined….9

• To sum up: a few questions to launch the discussion on the financing of sustainable electrification…………………………………………………10

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n D

ialo

gues

HC

B In

itiat

ive

3

Background 1/2Facts

• Electricity sector: capital intensive + long-term industry (both for big projects and RE)

Everybody now agrees: electrification can’t be for free

• Electricity is both: a growth driver + a market commodity

It requires both government subsidies + obeys to laws of supply and demand which determine the price

• Rural electrification in developing countries - and specifically in Africa - targets low income populations (<1-2 US$/day); low consumption consumers (60-120kWh/year); sparse low density housing

Consequences• Need to create an economical model which should be

profitable > sustainable > replicable

= on the scale of needs

• Need to associate skills of several families of actors:

- local governments

- financial institutions and investors

- private operators from the energy sector

- NGOs and institutions

= for a better allocation of risks and experience-sharing

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n D

ialo

gues

HC

B In

itiat

ive

4

Background 2/2

4 key fundamentals for starting a sustainable electrification programme, on which everybody now agrees:

• An appropriate institutional and legal framework and agreements with national and local authorities on a long term basis

• A local anchorage through local partners and locally trained capacities

• A viable financial model mixing investment, subsidies and adapted tariffs (tailor-made)

• A bottom-up approach to choose the right equipments and technologies at the right place and at the right time

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n D

ialo

gues

HC

B In

itiat

ive

5

RESCO concept… A model among others 1/2

On the basis of the fundamentals described and experimented in the mid'90s, EDF and several partners decided to build a new economical concept called RESCO - Rural Electrification Services Company.

• Local company – under local law – managed by local people

• Agreements with national and local authorities with a long term commitment (15 to 20 years)

• To (generate and) supply energy on a defined area ( concessional approach)

• To sell a range of "decentralised" energy-based services – not just kWh –Electricity, lighting, water pumps, gas, refrigeration, telephone, etc…

• … to at least 10 to 15 000 customers (around 100 000 people) …

• … in a professional manner …

• … while remaining financially viable.

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n D

ialo

gues

HC

B In

itiat

ive

6

* FRES (NUON Foundation) owns 100% of Yéelen Kura since end of 2008 (20% of the capital should be transferred to the salaries).** Korayé Kurumba was transferred in mid 2009 to the EIG GoléKanu owned to 100% by the salaries.

Mali

South Africa

Morocco

Yéelen Kura : EDF, NUON*2 450 clients44 100 people

KES : EDF, TOTAL, CALULO9 800 clients58 800 people

Temasol : EDF, TOTAL, TENESOL26 600 clients186 200 people

KorayéKurumba** : EDF, TOTAL2 000 clients36 000 people

As of February 2010: 325 000 people gotaccess to electricity in 3 countries through 4 RESCOs

RESCO concept… A model among others 2/2

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n D

ialo

gues

HC

B In

itiat

ive

7

What did we learn?First lessons learned

RESCO is an operational model which convinced different governments and is now adopted by them.

What are the challenges to be tackled?

The first assessment of the model is positive but further enhancement is needed

• Although the figures are encouraging, they remain modest

(325 000 people versus 500 million/1,6 billion without access to electricity in Africa and worldwide)

• Still in a learning process

• Very fragile structures

The discussions that follow should address 3 main points: • Commitment of the actors

• How to secure sustainable financing

• The goal of access to energy programme

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n D

ialo

gues

HC

B In

itiat

ive

8

Governments have a key role to play, but all players must commit themselves on a long-term basis

The challenges of rural electrification requires the commitment of several kinds ofplayers

• Local governments and authorities, who draft and implement the regulatory and institutional frameworks that govern economic developments, the creation of infrastructures, secure investments, organize training of human resources and foster the emergence of local entrepreneurs and investors

• Major financial institutions and investors who provide funding and canalise international funding.

• Energy players who contribute their expertise in training, choice of technologies etc.

• NGOs, individual and local communities that participate in rural electrification operations. Key role of the government to achieve a balanced PPP

This commitment must be held over the long term (min. 10 years)

• Long-lasting processes: it takes time to elaborate, implement the legal framework, create the relevant institutions

Business plans have to face variability of economy worldwide

• Small structures can’t afford irregularity and uncertainty of subsidies and tariffs.

Flexibility and long term commitment are needed and may involve all players

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n D

ialo

gues

HC

B In

itiat

ive

9

Financing must be reliable and flexible

Rural electrification financing combines:• subsidies: must be predictable, reliable, regularly paid

• investments: must be secured

• tariffs: must - be adapted to the capacity of the clients to pay

- ensure the operation of the RESCO over the long term

Requires: a continuous discussion and a balanced agreement between public authority

(application of regulatory framework; definition of tariffs; payment of subsidies) and private sector (to find the right equilibrium between services and development/profit)

the business plan should be updated according to the constraints, knowing that the implementation of the RE programmes may take several years.

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n D

ialo

gues

HC

B In

itiat

ive

10

The objectives of Access to Energy should be precisely defined

Improve comfort and quality of life (lighting, health, education)

and/or

Create activities to generate economical revenues

This will determine 3 main choices :• Technological

• Institutional and regulatory

• Economical

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n D

ialo

gues

HC

B In

itiat

ive

11

To sum up: a few questions to launch the discussion on the conditions for a sustainable

access to energy

• Which kind of commitments for which kind of players?

• Which technologies are more suitable for sustainable programmes?

• Which kind of financial models are the most adapted to launch a local

development ?

• Which kind of models are replicable independently from local specificities ?

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n D

ialo

gues

HC

B In

itiat

ive

12

THANK YOU FOR YOUR ATTENTION

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

e8-GEF-UNDESA Financing Sustainable Electrification

Africa DialoguesNairobi, Kenya, April 13-15, 2010

RWE's perspectives&

CDM Fuel Switch and Energy Efficiency Lusaka, Zambia

Antonio Aguilera LagosHead of Carbon Credit Purchase &

Portfolio ManagementRWE Power AG, Germany

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

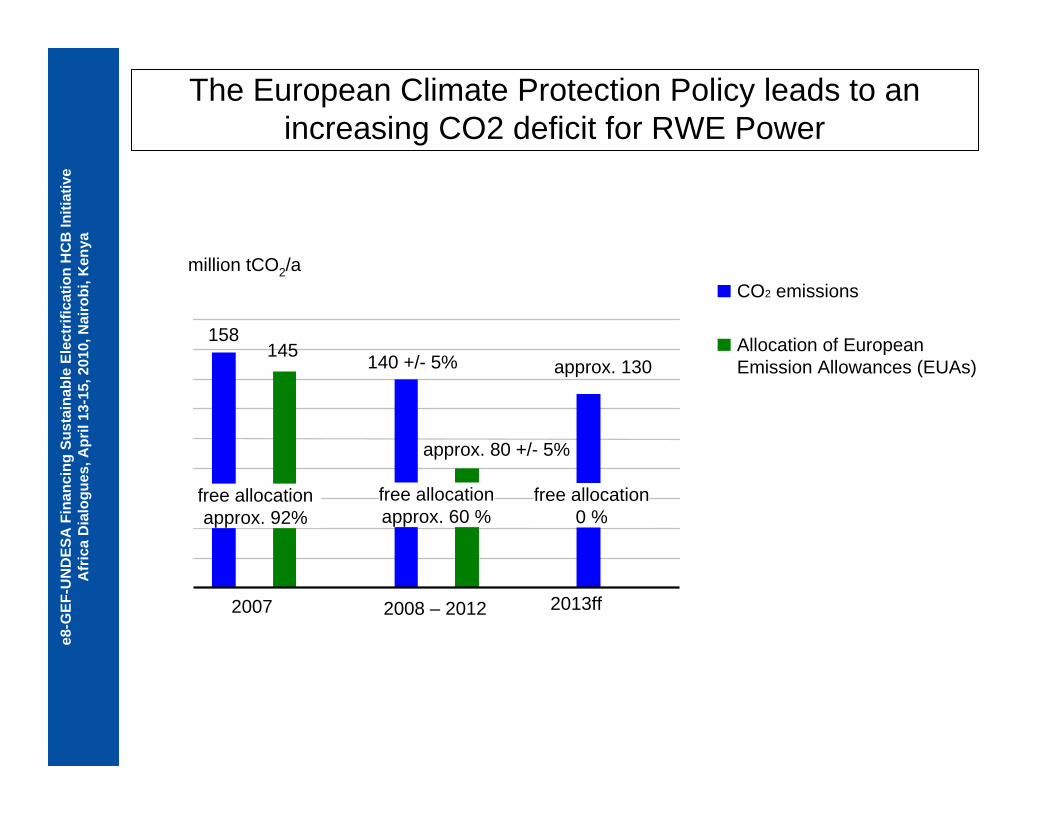

The European Climate Protection Policy leads to an increasing CO2 deficit for RWE Power

2007

158145

free allocationapprox. 92%

140 +/- 5%

2008 – 2012

free allocationapprox. 60 %

CO2 emissions

Allocation of EuropeanEmission Allowances (EUAs)

million tCO2/a

free allocation0 %

2013ff

approx. 130

approx. 80 +/- 5%

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

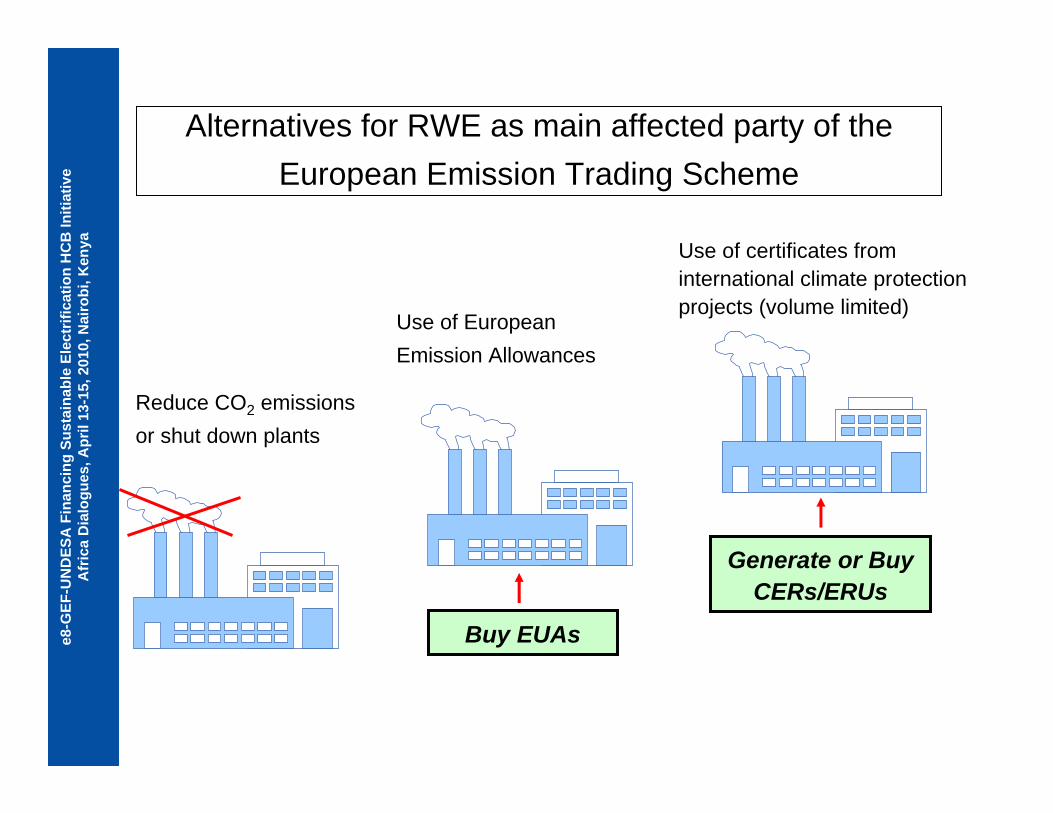

Alternatives for RWE as main affected party of the European Emission Trading Scheme

Reduce CO2 emissionsor shut down plants

Buy EUAs

Generate or Buy CERs/ERUs

Use of European Emission Allowances

Use of certificates from international climate protection projects (volume limited)

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

RWE's climate protection strategy

JI/CDM:Realization of climate protection projects in developing and emerging countries

Renewables:Significant increase of the proportion of renewable energies within the energy generation mix.Investment: 1 bnl. €/a

Energy efficiency:Construction of power plants with higher efficiencies / R&D

Climate friendly power plants:Construction of climate friendlycoal-fired power plants at industrial scale

RWE's components for climate protection

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

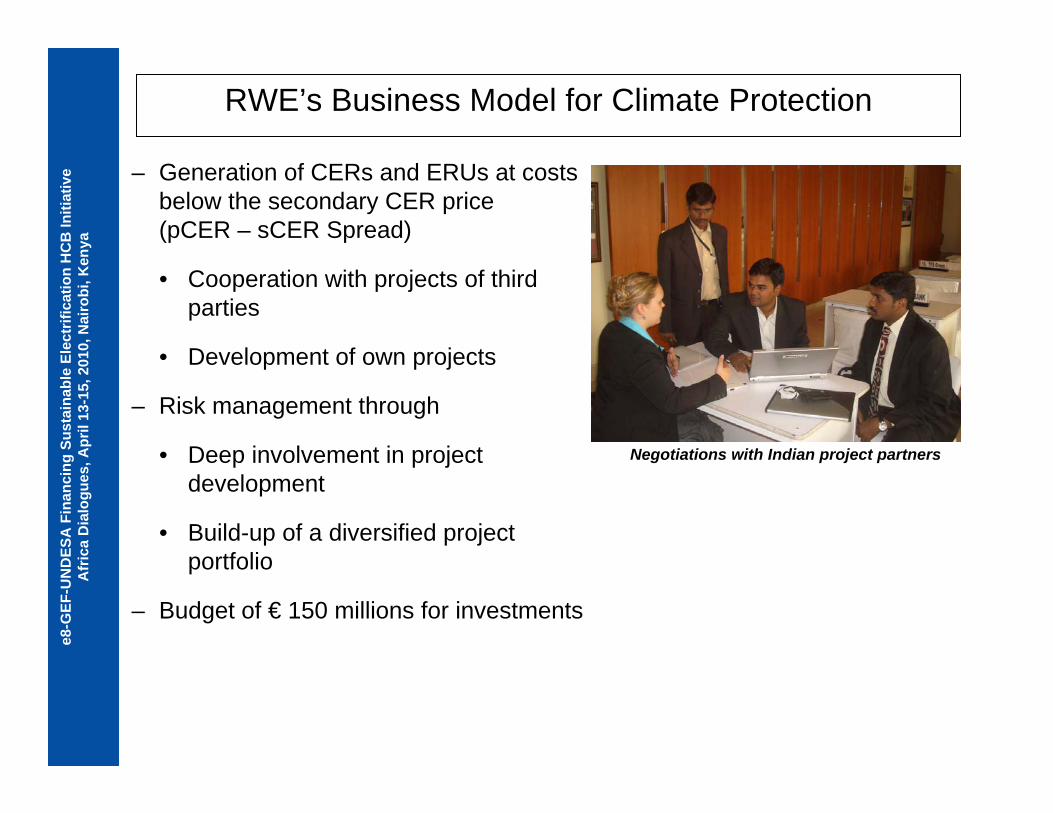

RWE’s Business Model for Climate Protection

Negotiations with Indian project partners

– Generation of CERs and ERUs at costs below the secondary CER price (pCER – sCER Spread)

• Cooperation with projects of third parties

• Development of own projects

– Risk management through

• Deep involvement in project development

• Build-up of a diversified project portfolio

– Budget of € 150 millions for investments

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

RWE's current portfolio of certificates for the CP 1 (2008-12)

* In Operation: All projects which have already issued certificates

** Latest EU-directive for certificates implies no additional Redemption Capacity for RWE Power concerning the years 2013 till 2020, but usage of certificates is still enabled post 2012

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

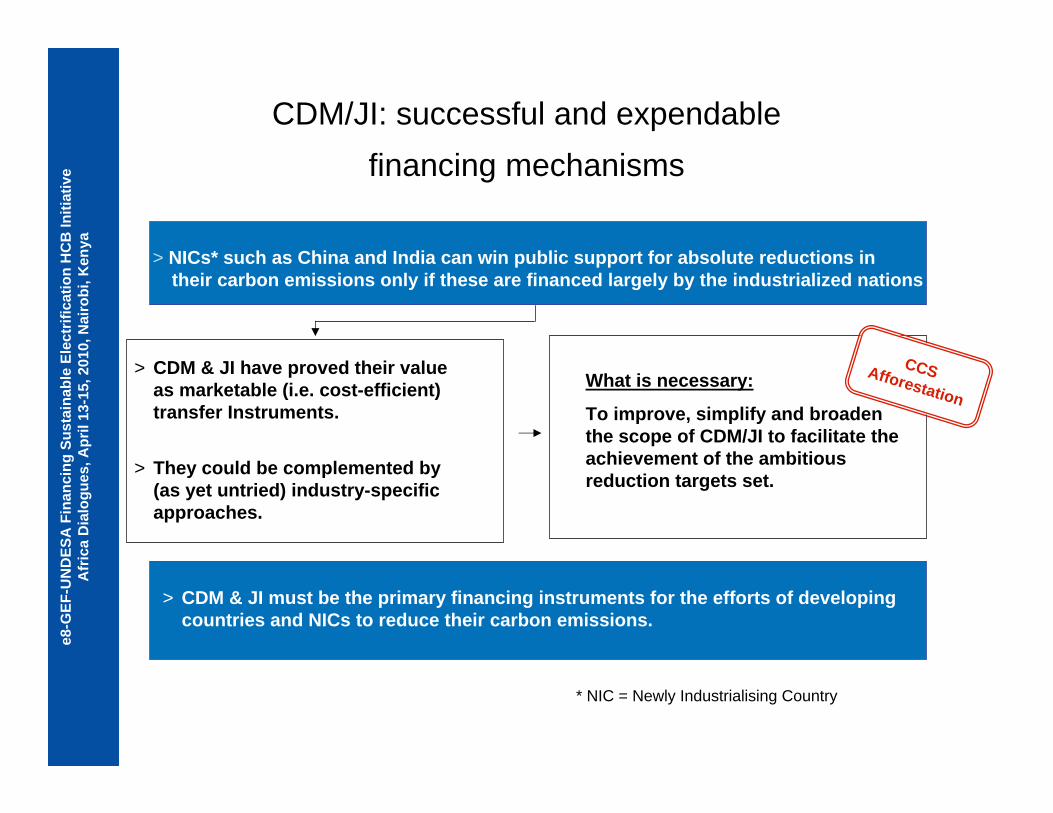

CDM/JI: successful and expendable financing mechanisms

> NICs* such as China and India can win public support for absolute reductions in their carbon emissions only if these are financed largely by the industrialized nations

> CDM & JI have proved their value as marketable (i.e. cost-efficient) transfer Instruments.

> They could be complemented by (as yet untried) industry-specific approaches.

What is necessary:

To improve, simplify and broaden the scope of CDM/JI to facilitate the achievement of the ambitious reduction targets set.

CCSAfforestation

> CDM & JI must be the primary financing instruments for the efforts of developing countries and NICs to reduce their carbon emissions.

* NIC = Newly Industrialising Country

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

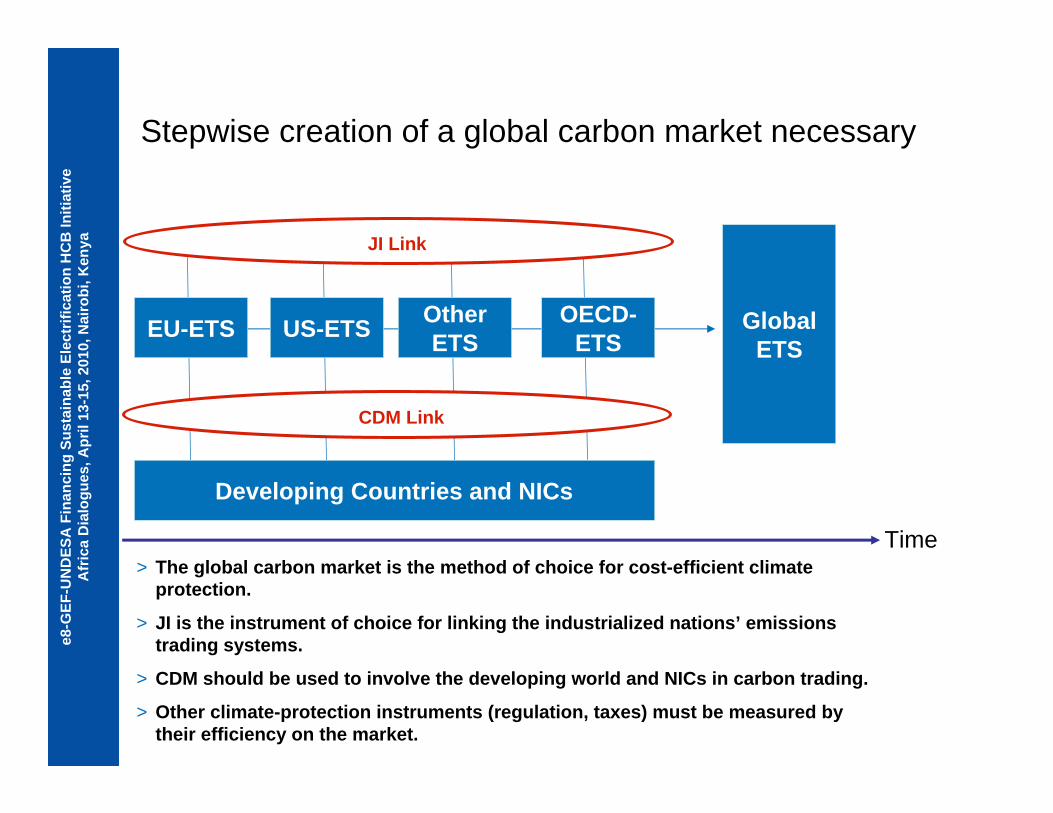

Stepwise creation of a global carbon market necessary

JI Link

Developing Countries and NICs

CDM Link

Global ETS

> The global carbon market is the method of choice for cost-efficient climate protection.

> JI is the instrument of choice for linking the industrialized nations’ emissions trading systems.

> CDM should be used to involve the developing world and NICs in carbon trading.

> Other climate-protection instruments (regulation, taxes) must be measured by their efficiency on the market.

Time

EU-ETS US-ETS OtherETS

OECD-ETS

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

Effective and cost-efficient climate protection is crucial for RWE’s position on the post-Kyoto treaty

> The post-Kyoto treaty must contain binding reduction commitments on a scale large enough to stabilize the global climate.

> The efforts of the global community to reduce carbon emissions must be economically efficient so as not to jeopardize prosperity.

> In the long run, there will have to be a global pricing mechanism for CO2emissions to signal shortages more efficiently and ensure that CO2 avoidance is rewarded.

> The measures adopted must be aimed solely at stabilizing the global climate and not to be burdened with extraneous political objectives.

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

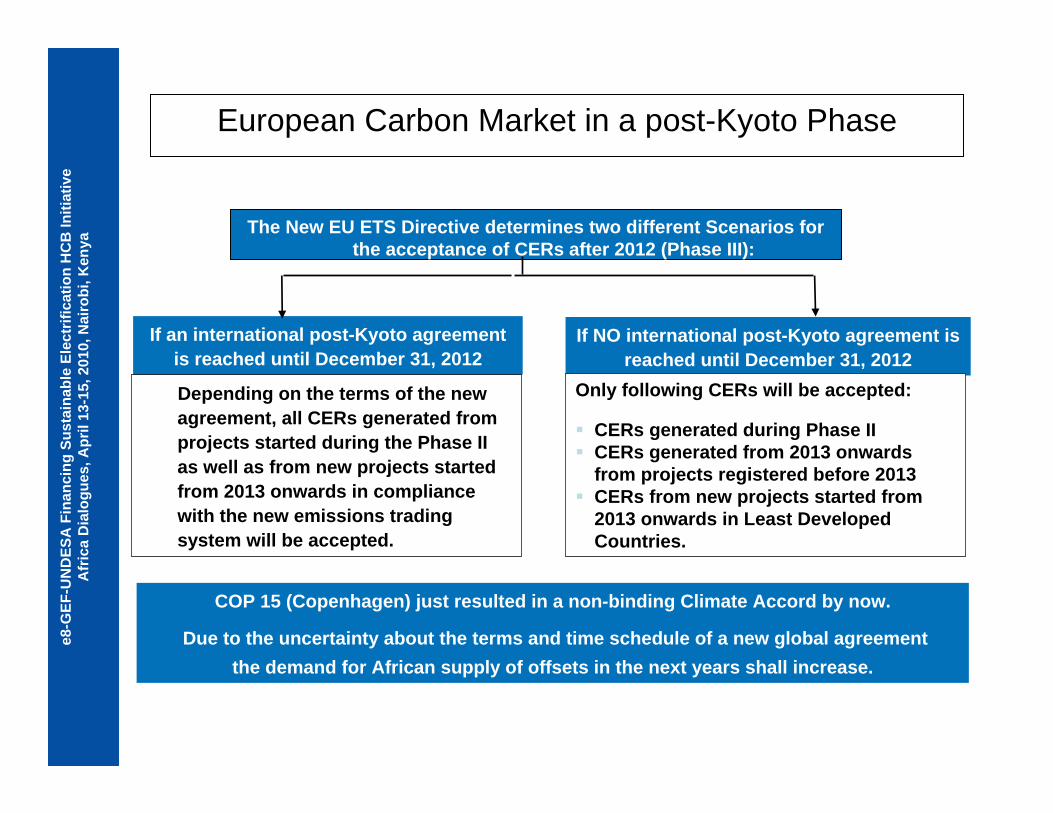

If NO international post-Kyoto agreement is reached until December 31, 2012

European Carbon Market in a post-Kyoto Phase

The New EU ETS Directive determines two different Scenarios for the acceptance of CERs after 2012 (Phase III):

If an international post-Kyoto agreement is reached until December 31, 2012

Only following CERs will be accepted:

CERs generated during Phase II CERs generated from 2013 onwards

from projects registered before 2013 CERs from new projects started from

2013 onwards in Least Developed Countries.

Depending on the terms of the new agreement, all CERs generated from projects started during the Phase II as well as from new projects started from 2013 onwards in compliance with the new emissions trading system will be accepted.

COP 15 (Copenhagen) just resulted in a non-binding Climate Accord by now.

Due to the uncertainty about the terms and time schedule of a new global agreementthe demand for African supply of offsets in the next years shall increase.

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

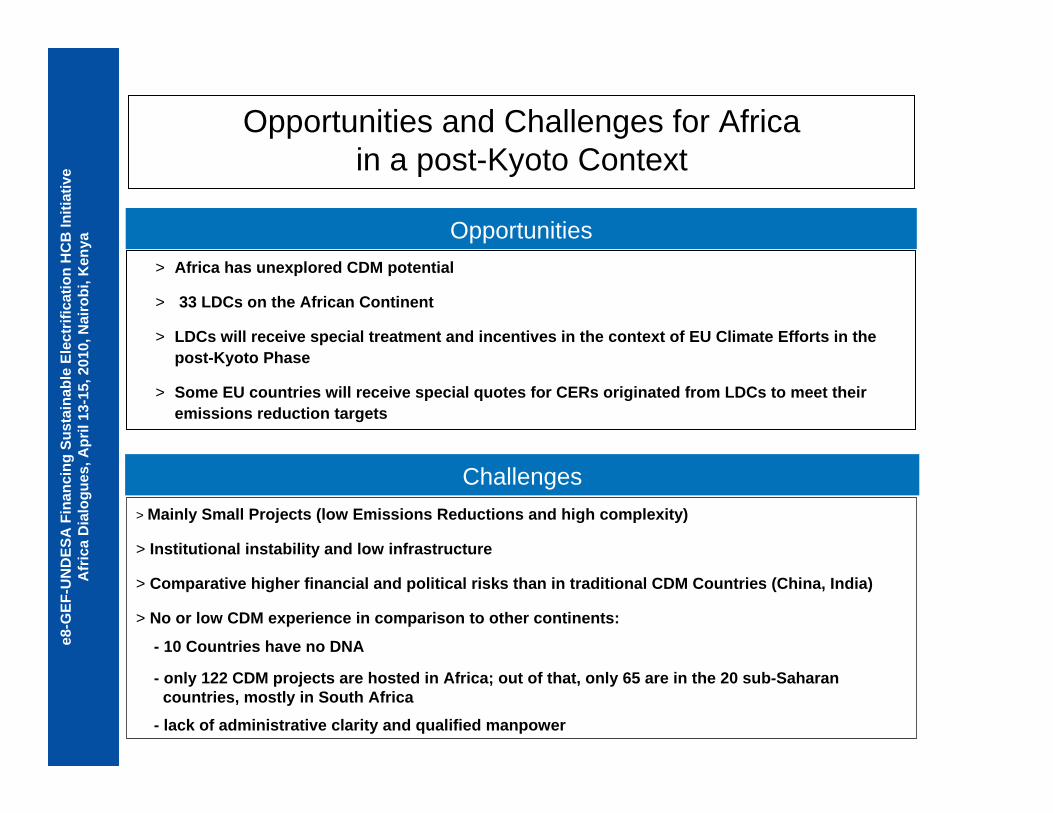

Opportunities and Challenges for Africa in a post-Kyoto Context

> Africa has unexplored CDM potential

> 33 LDCs on the African Continent

> LDCs will receive special treatment and incentives in the context of EU Climate Efforts in the post-Kyoto Phase

> Some EU countries will receive special quotes for CERs originated from LDCs to meet their emissions reduction targets

Opportunities

Challenges> Mainly Small Projects (low Emissions Reductions and high complexity)

> Institutional instability and low infrastructure

> Comparative higher financial and political risks than in traditional CDM Countries (China, India)

> No or low CDM experience in comparison to other continents:

- 10 Countries have no DNA

- only 122 CDM projects are hosted in Africa; out of that, only 65 are in the 20 sub-Saharancountries, mostly in South Africa

- lack of administrative clarity and qualified manpower

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

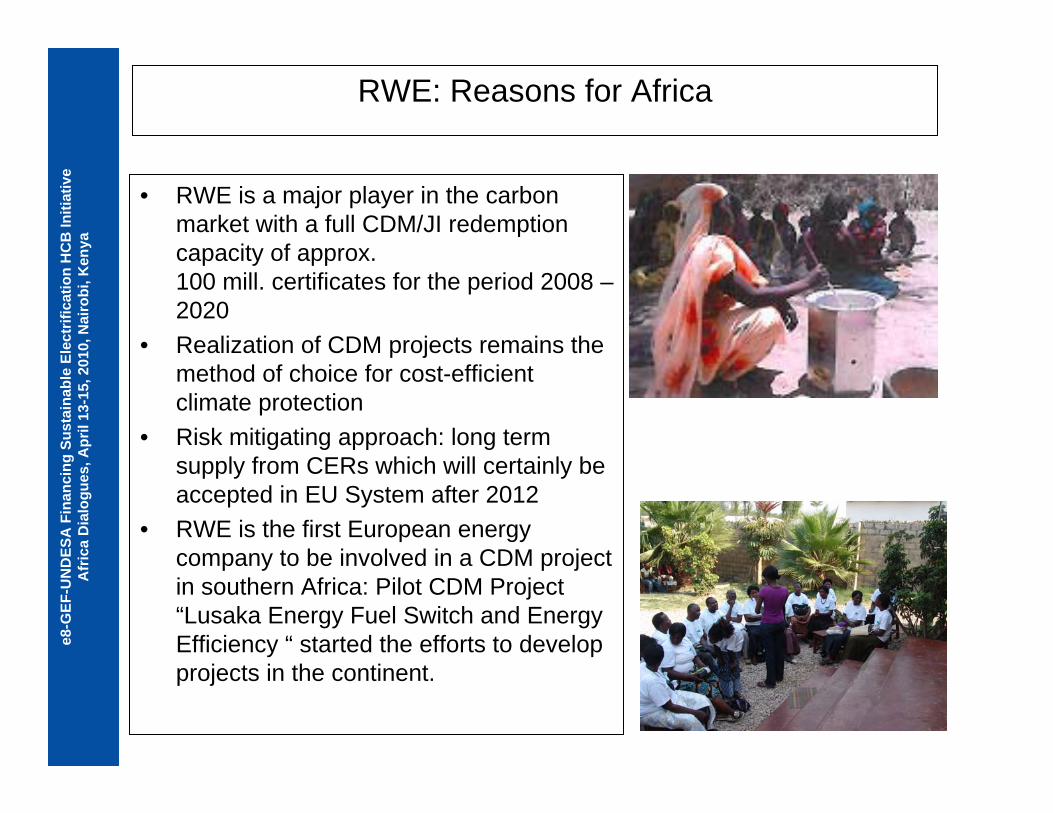

RWE: Reasons for Africa

• RWE is a major player in the carbon market with a full CDM/JI redemption capacity of approx. 100 mill. certificates for the period 2008 –2020

• Realization of CDM projects remains the method of choice for cost-efficient climate protection

• Risk mitigating approach: long term supply from CERs which will certainly be accepted in EU System after 2012

• RWE is the first European energy company to be involved in a CDM project in southern Africa: Pilot CDM Project “Lusaka Energy Fuel Switch and Energy Efficiency “ started the efforts to develop projects in the continent.

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

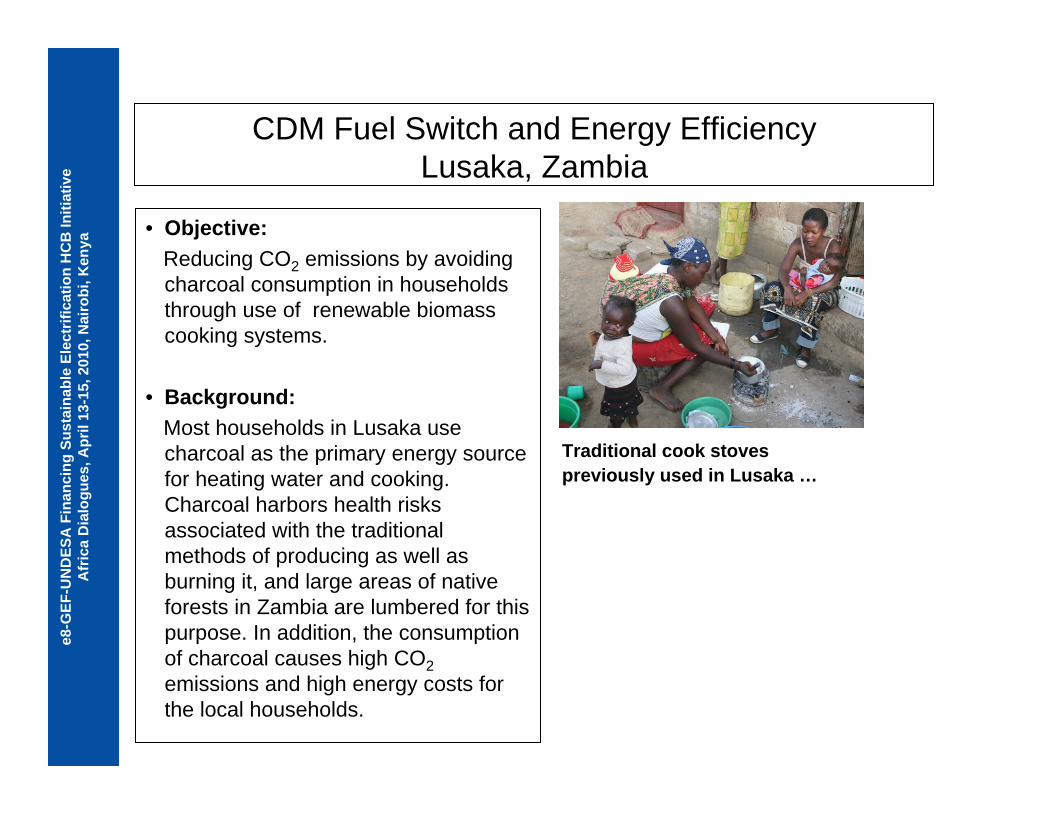

CDM Fuel Switch and Energy EfficiencyLusaka, Zambia

• Objective:Reducing CO2 emissions by avoiding charcoal consumption in households through use of renewable biomass cooking systems.

• Background: Most households in Lusaka use charcoal as the primary energy source for heating water and cooking. Charcoal harbors health risks associated with the traditional methods of producing as well as burning it, and large areas of native forests in Zambia are lumbered for this purpose. In addition, the consumption of charcoal causes high CO2emissions and high energy costs for the local households.

Traditional cook stoves previously used in Lusaka …

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

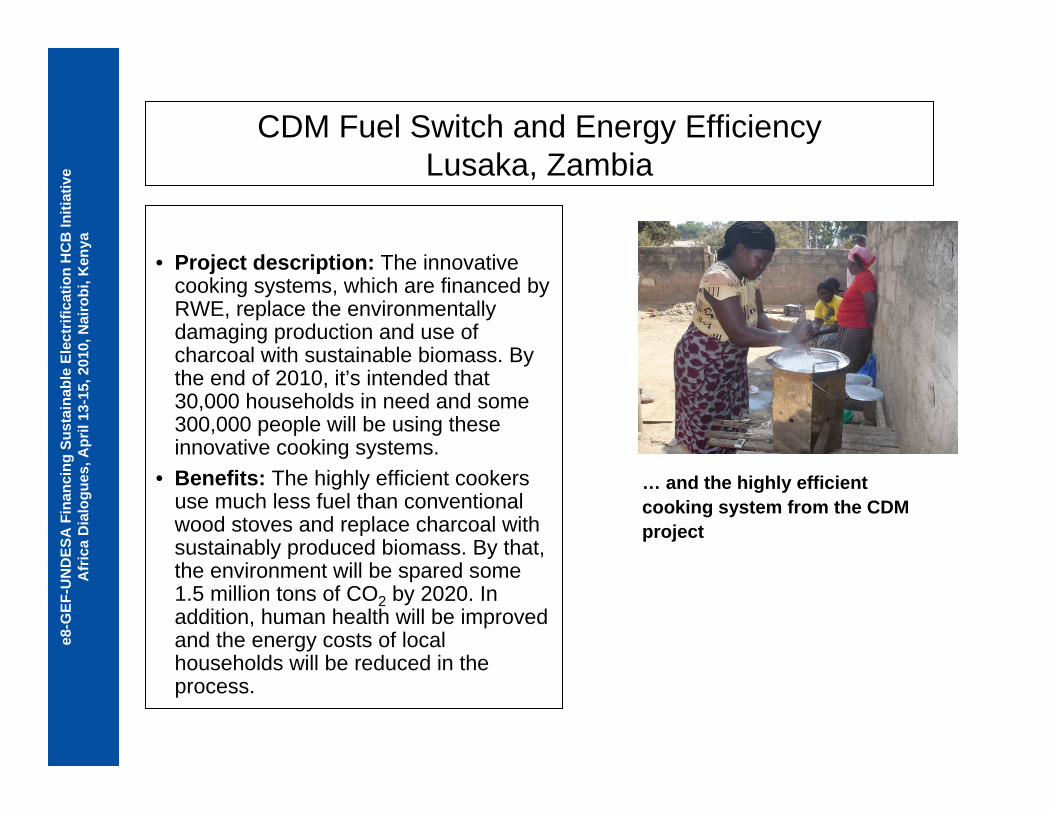

CDM Fuel Switch and Energy Efficiency Lusaka, Zambia

• Project description: The innovative cooking systems, which are financed by RWE, replace the environmentally damaging production and use of charcoal with sustainable biomass. By the end of 2010, it’s intended that 30,000 households in need and some 300,000 people will be using these innovative cooking systems.

• Benefits: The highly efficient cookers use much less fuel than conventional wood stoves and replace charcoal with sustainably produced biomass. By that, the environment will be spared some 1.5 million tons of CO2 by 2020. In addition, human health will be improved and the energy costs of local households will be reduced in the process.

… and the highly efficient cooking system from the CDM project

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

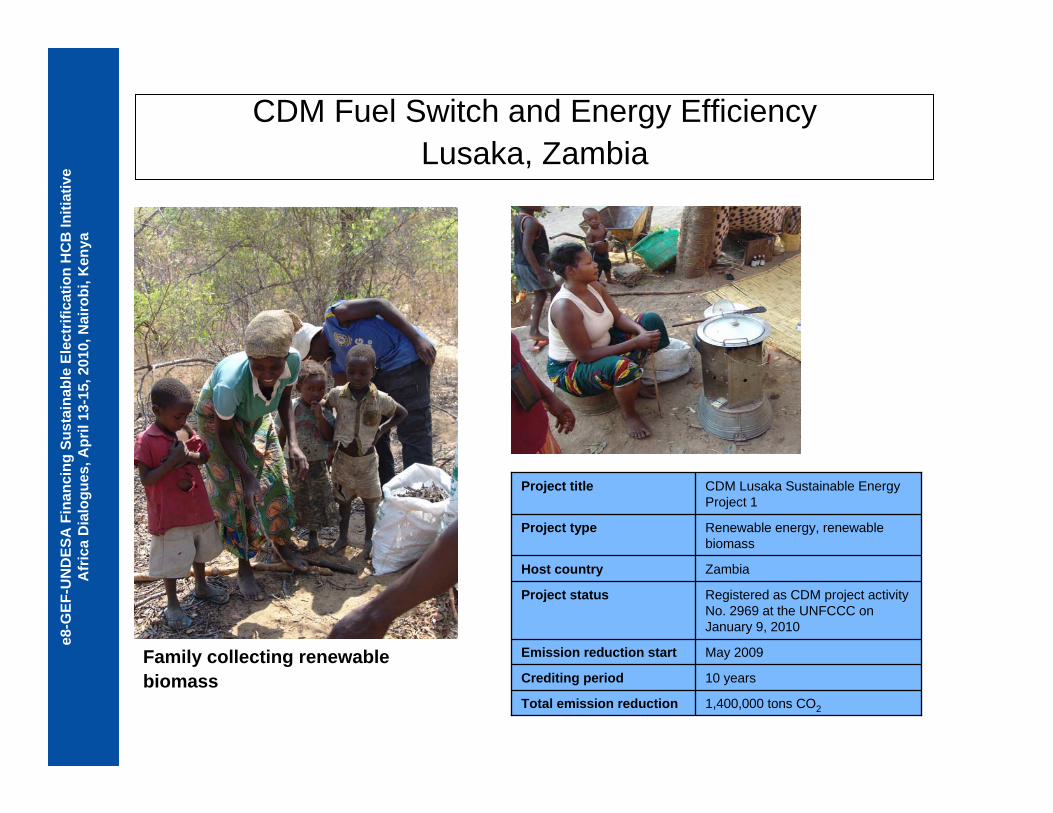

CDM Fuel Switch and Energy EfficiencyLusaka, Zambia

10 yearsCrediting period

1,400,000 tons CO2Total emission reduction

Registered as CDM project activity No. 2969 at the UNFCCC on January 9, 2010

Project status

May 2009Emission reduction start

ZambiaHost country

Renewable energy, renewable biomass

Project type

CDM Lusaka Sustainable Energy Project 1

Project title

Family collecting renewable biomass

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

Benefits of a partnership

A partnership with RWE offers project developers significant benefits: • RWE is a trustworthy and reliable business partner. RWE is financial secure and

buys CERs/ERUs to meet its own long-term reduction obligations in Europe.

• RWE can support you financially.

• RWE is willing, as a project partner, to assume project risks in the implementation of CDM projects.

• RWE has been developing experience in the execution of its own CDM and JI projects since 1999.

• RWE offers you technological expertise in the most important GHG avoidance methods, which are a crucial success factor in the implementation of CDM projects.

• RWE supports you in the entire CDM process: from preparing the PDD all the way to the issue of certificates.

Please discuss your potential CDM projects with us.

Suitable financing schemes and regulations for rural electrification

Financing Sustainable Rural Electrification, Africa Dialogues

Workshop E8, GEF, UNDESANairobi, 13-15 April 2010

Simon RollandPolicy and Development Officer, Alliance for Rural Electrification

2Simon Rolland, Workshop E8, GEF, UNDESA Nairobi, 13-15 April 2010

ARE promotes and provides efficient renewable solutions for rural electrification in developing countries.

• The Alliance attracts and unites all relevant private actors in order to speak with one voice about rural electrification with renewable energies.

• The Alliance generates technical and financial solutions about rural electrification in developing countries.

• ARE communicates and advocates for rural electrification using RET and convinces all relevant stakeholders.

The Alliance for Rural ElectrificationMission and Objectives

3Simon Rolland, Workshop E8, GEF, UNDESA Nairobi, 13-15 April 2010

ARE: Our Members

Acciona Solar IsofotonASIF IT Power

BP Solar KXNConergy Outback PowerEcotècnia PhaesunEnersys Q cells

European Photovoltiac Industry Association (EPIA)

Scatec Solar

European Renewable Energy Council (EREC) SharpEuropean Small‐Hydro Assocation (ESHA) SMAEuropean Wind Energy Association (EWEA) Solar Pack

Fondazione Madre Agnese Solaria Energia y Medio AmbienteFortis Wind Solarworld

Global Wind Energy Council (GWEC) StecaGuascor Solar Studer Innotec

IDAE SunlabobInnovation Energie Développement (IED) Trama TecnoambientalInstitute for Solar Energy Systems (ISE) University of SouthamptonInstitute for Sustainable Power, Inc. University of Twente

4Simon Rolland, Workshop E8, GEF, UNDESA Nairobi, 13-15 April 2010

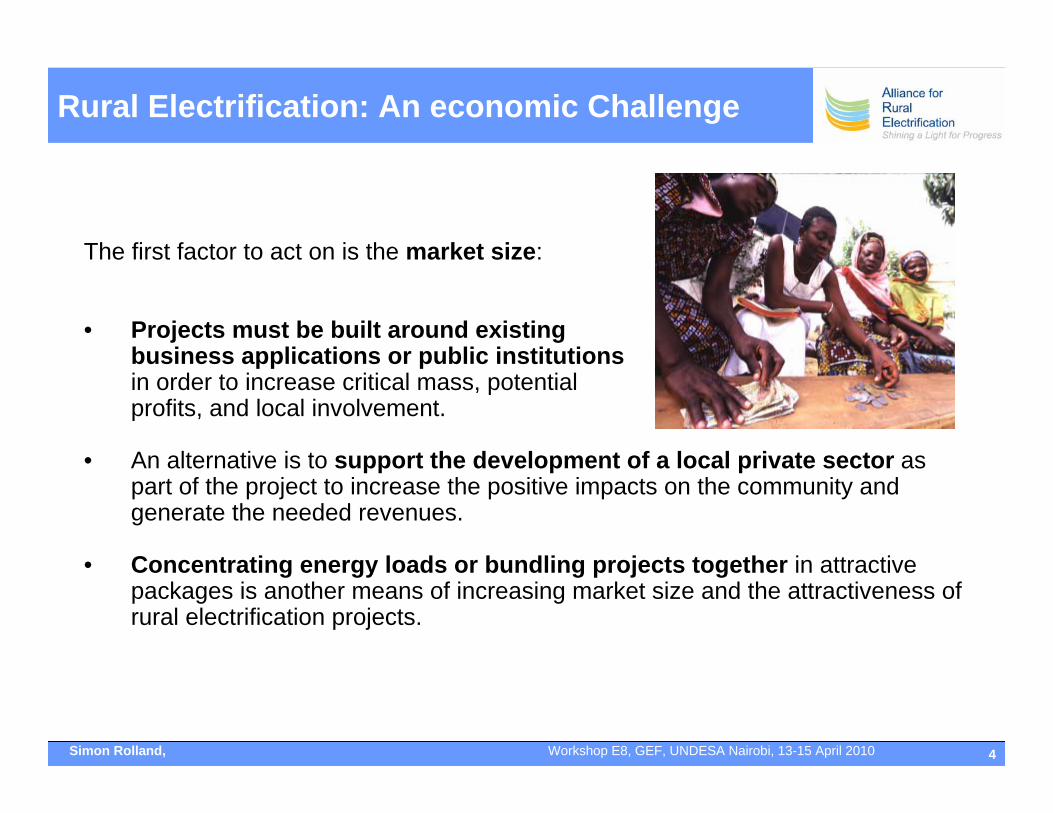

The first factor to act on is the market size:

• Projects must be built around existing business applications or public institutionsin order to increase critical mass, potential profits, and local involvement.

• An alternative is to support the development of a local private sector as part of the project to increase the positive impacts on the community and generate the needed revenues.

• Concentrating energy loads or bundling projects together in attractive packages is another means of increasing market size and the attractiveness of rural electrification projects.

Rural Electrification: An economic Challenge

5Simon Rolland, Workshop E8, GEF, UNDESA Nairobi, 13-15 April 2010

Rural Electrification: An economic Challenge

The second and main factor are tariffs and subsidies:

• Sustainable rural electrification tariff must at least cover the running and replacement costs (break-even tariff), even though the opportunity for profit is key to attract private operators (financially viable tariffs).

• Tariffs must maintain the balance between commercial viability and consumers’ ability and willingness to pay.

• Smart combinations of subsidies are key to attract operators and ensure project sustainability.

• Subsidies can support the investment, the connection, the operation costs and the output: Investment subsidies are a good solution if they go along with a good tariff structure; whereas OBA schemes if adequately planned are powerful instruments to leverage private investments and ensure O&M.

• Other forms of support can also be offered to project developers: tax credits; low import duties; site surveys; market studies; and capacity-building.

6Simon Rolland, Workshop E8, GEF, UNDESA Nairobi, 13-15 April 2010

Rural Electrification: A regulation Challenge

Regulation has to be an instrument favoring new projects. It needs to be light and flexible for small power producer in terms of standards and tariffs. It also has to protect rural consumers.

PPA regulation is especially important:

- PPAs must be fair and binding to protect every actor equally.

- PPAs should be as standardized as possible.

- PPAs should be signed over longer period of time and should be flexible and revisable when it comes to tariff.

7Simon Rolland, Workshop E8, GEF, UNDESA Nairobi, 13-15 April 2010

Rural Electrification: A political Challenge

• Access to electricity must rank high on the development agenda

• Access to electricity should follow a reliable long term strategy and the legal framework must allow for private and local initiatives

• Subsidies for fossil fuels should be phased out or transferred to the RETs. Trade barriers should be removed, as a pre-condition of the involvement of the funding of the project.

• A close dialogue between policymakers, the private sector and representatives of rural communities is indispensable for sustainable policies (Better education/communication on RETs).

8Simon Rolland, Workshop E8, GEF, UNDESA Nairobi, 13-15 April 2010

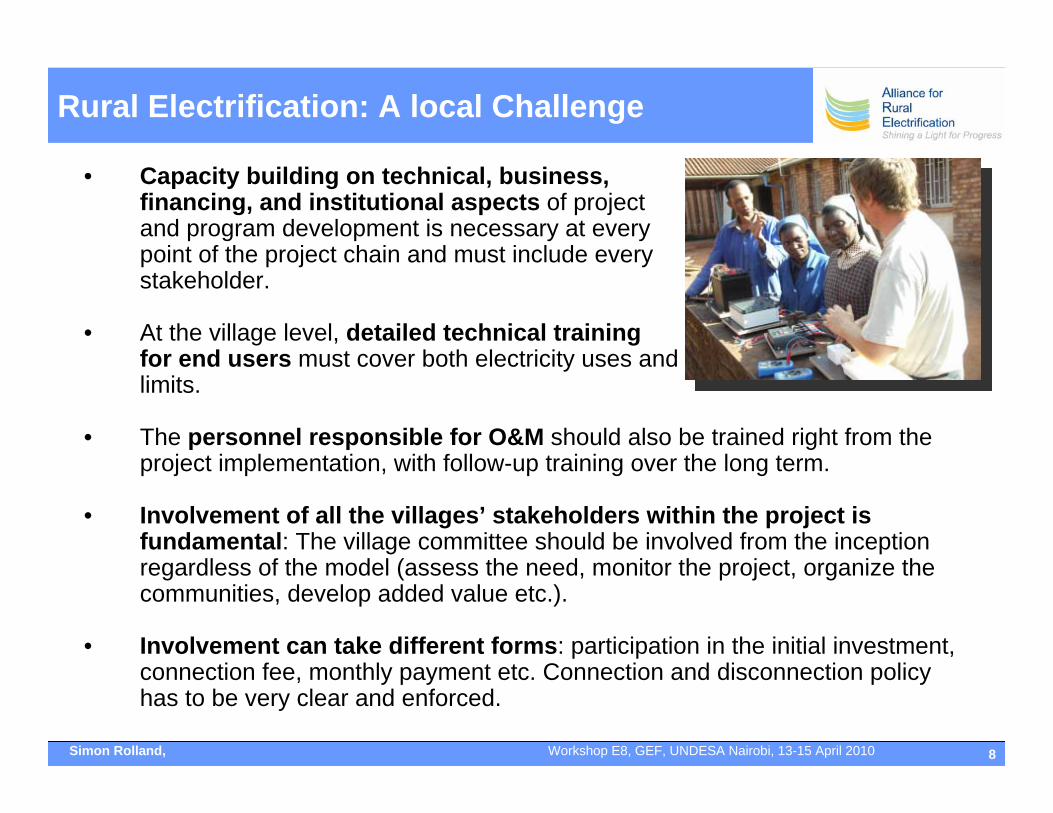

Rural Electrification: A local Challenge

• Capacity building on technical, business, financing, and institutional aspects of project and program development is necessary at every point of the project chain and must include every stakeholder.

• At the village level, detailed technical training for end users must cover both electricity uses and limits.

• The personnel responsible for O&M should also be trained right from the project implementation, with follow-up training over the long term.

• Involvement of all the villages’ stakeholders within the project is fundamental: The village committee should be involved from the inception regardless of the model (assess the need, monitor the project, organize the communities, develop added value etc.).

• Involvement can take different forms: participation in the initial investment, connection fee, monthly payment etc. Connection and disconnection policy has to be very clear and enforced.

9Simon Rolland, Workshop E8, GEF, UNDESA Nairobi, 13-15 April 2010

Alliance for Rural Electrification

Rue d’Arlon 63‐65,

1040 Brussels, Belgium

T +32 2 400 10 52

www.ruralelec.org Pho

to c

redi

t: A

RE

mem

bers

THANK YOU!

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le R

ural

Ele

ctrif

icat

ion

HC

B In

itiat

ive

Afr

ica

Dia

logu

es, A

pril

13-1

5, 2

010,

Nai

robi

, Ken

ya Peri-urban Electrification

By Connie SmyserSmyser Associates

e8-GEF-UNDESA Financing Rural Sustainable Electrification

Africa Dialogues Nairobi, Kenya, April 13-15, 2010

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le R

ural

Ele

ctrif

icat

ion

HC

B In

itiat

ive

Afr

ica

Dia

logu

es, A

pril

13-1

5, 2

010,

Nai

robi

, Ken

ya

Outline

• What is peri-urban electrification and where does it fit?

• What is the success rate and is it sustainable?

• What factors influence success?• Business opportunities and barriers to

investment• Finance options

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le R

ural

Ele

ctrif

icat

ion

HC

B In

itiat

ive

Afr

ica

Dia

logu

es, A

pril

13-1

5, 2

010,

Nai

robi

, Ken

ya

Where Does Peri-urban Electrification Fit?

•• DefinitionDefinition– NOT suburban– Poor, informal, contiguous to urban area, few or no

services, tenancy issues, may or may not be temporary

•• What is the key difference from a slum?What is the key difference from a slum?– Distinction is blurry. Little difference except for

location and possibly characteristics of inhabitants. Ex. Townships in S. Africa are government sanctioned but conditions are slumlike and most often on the far edges of cities.

– For this talk, examples from slums and peri-urban situations will be used, referring to urban electrification

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le R

ural

Ele

ctrif

icat

ion

HC

B In

itiat

ive

Afr

ica

Dia

logu

es, A

pril

13-1

5, 2

010,

Nai

robi

, Ken

ya

How does this affect electrification needs and supply?

•• Potential customer perspectivePotential customer perspective, great willingness to connect legally but many barriers.

•• GovernmentsGovernments may “lump” urban areas in with either rural or urban slum electrification. BUT: Policies may be radically different.– Ex. Brazil Luz para Todos is rural while a separate program and policies

exist for urban “favelas” (slums).– But, in P-U areas alternatives to electricity are more like slums than

rural areas, e.g., little access to fuel wood, likely to have LPG etc. – P-U/slum solutions range from programs such as Morocco’s (Villes sans

Bidonvilles, i.e., eradication) to those in Latin America that favor acceptance, upgrading in situ, and granting tenancy and other rights.

•• Degree of FormalityDegree of Formality of the area may matter. – Ex: settlements on rights of way would be considered temporary and

therefore ineligible while those informal areas that could be legally developed may become eligible, creating inequalities among areas.

•• Municipalities become key partnersMunicipalities become key partners.

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le R

ural

Ele

ctrif

icat

ion

HC

B In

itiat

ive

Afr

ica

Dia

logu

es, A

pril

13-1

5, 2

010,

Nai

robi

, Ken

ya

The Distribution Company Perspective

•• Proximity, access to supply and safetyProximity, access to supply and safety are main distinctions. Mounting a program can be quite different in terms of costs, type of actions taken and likely effectiveness.

•• Proximity:Proximity:– Close to existing distribution grid means likely rampant theft and

excessive usage. Company will need to implement a set of actions that “take back” the concession area along with making necessary distribution system upgrades

– Far from the grid (or war torn) means dramatically higher costs of grid installation and expanding O&M activities and personnel AND planning for inevitable attempts to steal electricity.

•• Are structures electrifiable?Are structures electrifiable? Where there is a will, there is a way, but adds costs.

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le R

ural

Ele

ctrif

icat

ion

HC

B In

itiat

ive

Afr

ica

Dia

logu

es, A

pril

13-1

5, 2

010,

Nai

robi

, Ken

ya

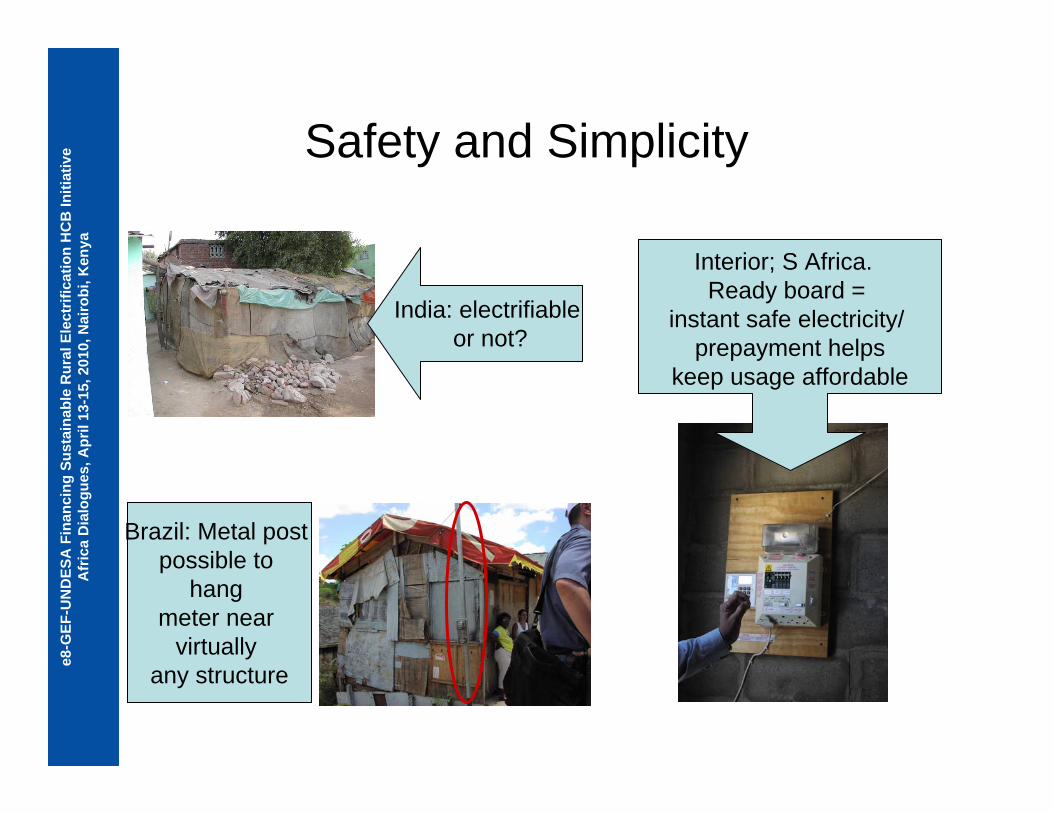

Safety and Simplicity

India: electrifiableor not?

Interior; S Africa. Ready board =

instant safe electricity/ prepayment helps

keep usage affordable

Brazil: Metal post possible to

hang meter near

virtually any structure

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le R

ural

Ele

ctrif

icat

ion

HC

B In

itiat

ive

Afr

ica

Dia

logu

es, A

pril

13-1

5, 2

010,

Nai

robi

, Ken

ya

What is the success rate and is it sustainable?

•• Some notable failures but others unqualified successesSome notable failures but others unqualified successes•• Morocco: Morocco: ““temporarytemporary”” electrificationelectrification

– 93% of the communities electrified with payment performance 96% of billing. ROI less than one year.

•• AmplaAmpla/Brazil High tech solutions/Brazil High tech solutions– Investment actually reduced tariffs by 1.23% in the 2009. – Theft reduced to <5% and non-payment virtually eliminated where technology

applied– 40% decrease in kWh used – 3.4 percentage point drop in losses– Chile, Peru, Argentina, Colombia and many companies in Brazil have similar

successes.

•• Mozambique:Mozambique: Prepayment systemPrepayment system plus commercial management improvements

– Number of customers more than doubled in 4 years; – Collection rate improved from 75% in 1995 to 94% in 2005;– Average consumption per customer dropped from 148 kWh to 124 kWh– Total distribution losses decreased from 43% to 18% between 1995 and 2005.

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le R

ural

Ele

ctrif

icat

ion

HC

B In

itiat

ive

Afr

ica

Dia

logu

es, A

pril

13-1

5, 2

010,

Nai

robi

, Ken

ya

Components of Success

•• Effective antiEffective anti--theft technologytheft technology tailored to the socio-economic character of the area targeted. Can range from simply making meter bypass harder to total reconfiguration of the grid and replacing conventional meters with electronic meters with remote reading and disconnection.

•• SocioSocio--economic Solutionseconomic Solutions– Social Partnership (“We deliverYou pay”)– Know your community– Community based service “agents” (intermediaries)– Making it easier to pay connection fees/bills, e.g. payments over time for

connection to helping customer to become eligible for low income tariff.– Energy efficiency assistance; internal improvements, e.g., rewiring for safety,

efficiency– Economic development assistance– Community and individual legal assistance (e.g., for land title or equivalent)

•• Appropriate support and realistic policies applied by governmentAppropriate support and realistic policies applied by governmentss•• Business plans that management and financiers can trustBusiness plans that management and financiers can trust

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le R

ural

Ele

ctrif

icat

ion

HC

B In

itiat

ive

Afr

ica

Dia

logu

es, A

pril

13-1

5, 2

010,

Nai

robi

, Ken

ya

Government Policies & MarketConditions Affect ROI

NET REVENUE & PAYBACK FOR PILOT CASES AND SENSITIVITIES

0200,000400,000600,000800,000

1,000,0001,200,0001,400,0001,600,000

BASE CASE

BASE with

O&M

12%

debt

50%

debt

No S

ubsid

iesNo re

sale

No Avo

ided C

osts, N

o res

ale

No S

ubs,

No AC, N

o Res

ale

Base, Optimistic and Pessimistic Cases and Sensitivities

Net R

even

ue U

S$

0.00

5.00

10.00

15.00

20.00

25.00

30.00

Payb

ack

(yea

rs)

RevenuesPayback

Based on data from USAID SELR Brazil Project 2007

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le R

ural

Ele

ctrif

icat

ion

HC

B In

itiat

ive

Afr

ica

Dia

logu

es, A

pril

13-1

5, 2

010,

Nai

robi

, Ken

ya

Effect of EE Measures on Usage and Bill

0

10

20

30

40

50

60

70

80

90

0-100 101-150 151-200 201-300 >300Consumption Blocks (kWh)

Avg

Billin

g wi

th T

axes

0%

5%

10%

15%

20%

25%

Perc

ent o

f Sala

ry

Total monthly billBill after EE Savings% of Salary% of salary after EE

Less than 5% of salary is considered affordable and likely to Less than 5% of salary is considered affordable and likely to reduce temptation to stealreduce temptation to steal

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le R

ural

Ele

ctrif

icat

ion

HC

B In

itiat

ive

Afr

ica

Dia

logu

es, A

pril

13-1

5, 2

010,

Nai

robi

, Ken

ya

Results Achieved

•• Legal & Safe Access Legal & Safe Access to electricity for millions achieved

•• Technical and nonTechnical and non--technical lossestechnical losses dramatically reduced

•• RevenuesRevenues increased through improved payment performance and sales to non-subsidized customers

•• Energy efficiencyEnergy efficiency: typical reductions in usage for those formerly stealing are from 20 to 50%; EE assistance can dramatically increase savings. Saved power can be sold to full tariff customers.

•• Bottom lineBottom line: long term effort to meet a permanent challenge can make significant improvements in company viability dependingon the scale of the interventions -- but investments will be necessary.

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le R

ural

Ele

ctrif

icat

ion

HC

B In

itiat

ive

Afr

ica

Dia

logu

es, A

pril

13-1

5, 2

010,

Nai

robi

, Ken

ya

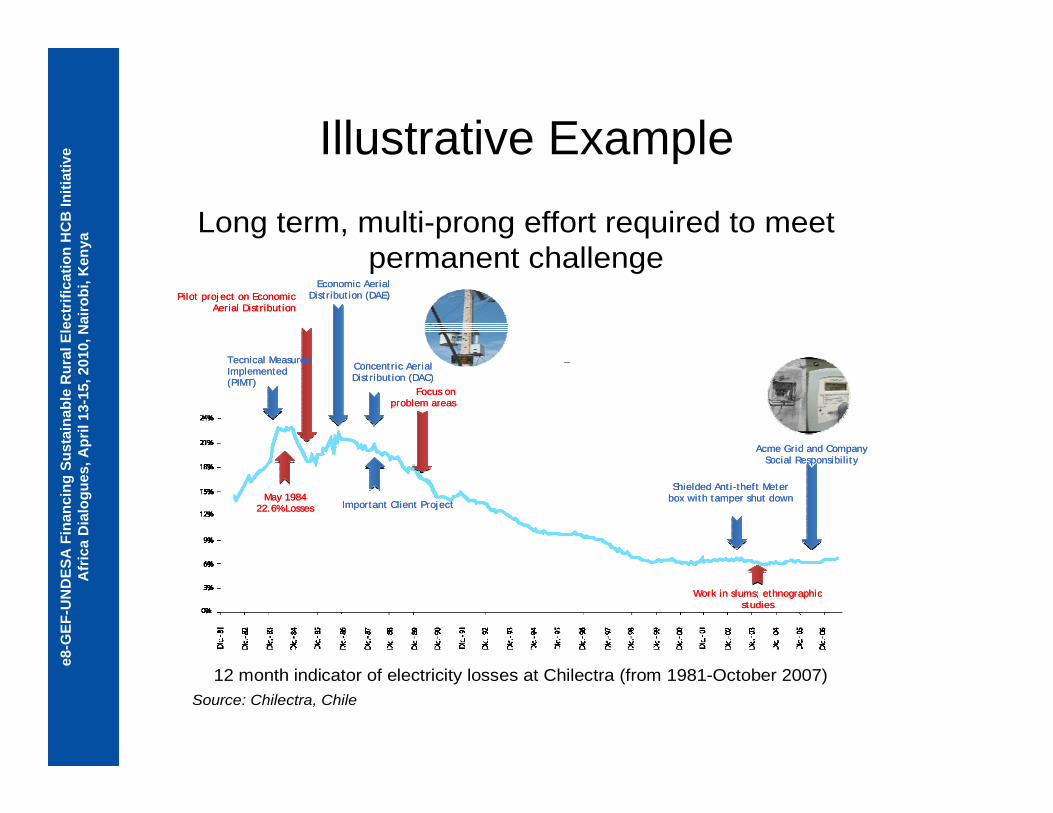

Illustrative ExampleLong term, multi-prong effort required to meet

permanent challenge

May 198422.6% Losses

May 198422.6% Losses

Pilot project on EconomicAerial Distribution

Pilot project on EconomicAerial Distribution

Economic AerialDistribution (DAE)

Economic AerialDistribution (DAE)

Important Client ProjectImportant Client Project

Concentric AerialDistribution (DAC)Concentric AerialDistribution (DAC)

Focus onproblem areas

Focus onproblem areas

Shielded Anti-theft Meter box with tamper shut downShielded Anti-theft Meter

box with tamper shut down

Work in slums; ethnographicstudies

Work in slums; ethnographicstudies

Acme Grid and CompanySocial Responsibility

Acme Grid and CompanySocial Responsibility

12 month indicator of electricity losses at Chilectra (from 1981-October 2007)

Tecnical MeasuresImplemented(PIMT)

Tecnical MeasuresImplemented(PIMT)

Source: Chilectra, Chile

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le R

ural

Ele

ctrif

icat

ion

HC

B In

itiat

ive

Afr

ica

Dia

logu

es, A

pril

13-1

5, 2

010,

Nai

robi

, Ken

ya

Barriers and Problems

•• Low electrification ratesLow electrification rates make it hard to justify serving low income when higher income/consuming households and businesses cannot gain access

•• Poor cost recovery and/or no source of funds for Poor cost recovery and/or no source of funds for infrastructureinfrastructure

•• Poor commercial systems Poor commercial systems undermine effectiveness•• GraftGraft undermines value of intervention •• Incentives lackingIncentives lacking for distribution companies to begin

tackling the problem or continue vigilance and community engagement.

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le R

ural

Ele

ctrif

icat

ion

HC

B In

itiat

ive

Afr

ica

Dia

logu

es, A

pril

13-1

5, 2

010,

Nai

robi

, Ken

ya

Financing Options

•• Cash FlowCash Flow: Many urban electrification projects done out of cash flow because that is the habit of the company; regulators approve return on investment in the tariff structure for necessary infrastructure for electrification and other related hardware.

•• Graduation to commercial loansGraduation to commercial loans: Some companies have graduated from self-financed pilots to commercial loans for such investments

•• Equipment manufacturersEquipment manufacturers: Prepayment meter manufacturers provide finance for prepayment meters and adjunct systems

•• Donors:Donors:– World Bank

• GPOBA provides financial assistance on the customer side to subsidize part of connection costs and internal rewiring for safety purposes.

• The African Electrification Initiative is providing assistance to urban and rural projects. • ESMAP and Cities Alliance are targeting 3 countries in Africa for urban electrification.• Specific urban components in energy sector loans.

– European Union, USAID, other bi-laterals•• Special purpose government fundsSpecial purpose government funds set up for extra costs of serving low

income or remote customers under obligations to serve those customers.

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le R

ural

Ele

ctrif

icat

ion

HC

B In

itiat

ive

Afr

ica

Dia

logu

es, A

pril

13-1

5, 2

010,

Nai

robi

, Ken

ya

Thank You!Thank You!

Connie SmyserSmyser Associates

[email protected] me for bibliography and URLs for

materials relating to peri-urban and slum electrification

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya e8-GEF-UNDESA

Financing Sustainable Electrification

Africa DialoguesNairobi, Kenya, April 13-15, 2010

Africa Energy Access Initiative and the South African Experience

Coretta MagongoaExecutive Manager,

Eskom/ Energy Poverty Action

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

Background• South Africa electricity sector is fully regulated - Eskom – the national power utility

– generates 95% of the electricity. • In 2009, maximum installed capacity reached 43 650 MW which represents close

to 40% of the African continent’s total installed capacity. Electricity is produced mainly from coal (94%).

• National plans are in place to expand the power supply, effectively doubling installed generation to some 80 000 MW by 2025 with associated grid expansion and strengthening.

• In 2009, 75% electrification was achieved –– 88% urban and 55% rural populations. (Electrification is registered as

electrification of households and not as the number of people) • South Africa’s electrification has been achieved mainly through grid extension• In the future, more renewable sources may facilitate further electrification if

barriers to their widespread use are overcome.

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

• 1990-1993 Eskom performed 380 000 connections

• 1994 - Target set by Government for 1,75m by year 2000.

• 2001 to date - over 3,5 million households electrified

– Connection every 30 seconds, pole every 10 seconds, 200m cable every minute.

– 1000 projects - 200 simultaneously each year.

As a result of the optimisation of the technical aspects of the design and construction, the cost per connection reduced in realterms. This resulted in the average cost per connection for grid being below the cost of non grid solar panels.

SA Electrification Programme –Post Apartheid

Due to Apartheid each city, town and village had established areas with good service delivery, and areas with poor or no service delivery. To date, there are still areas without basic services such as water, sanitation and access to electricity and these are not only in rural areas.

In 1994, after the first free election was held, it was estimated that approximately 6 million households were without electricity and the Government embarked on massive electrification drive:

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

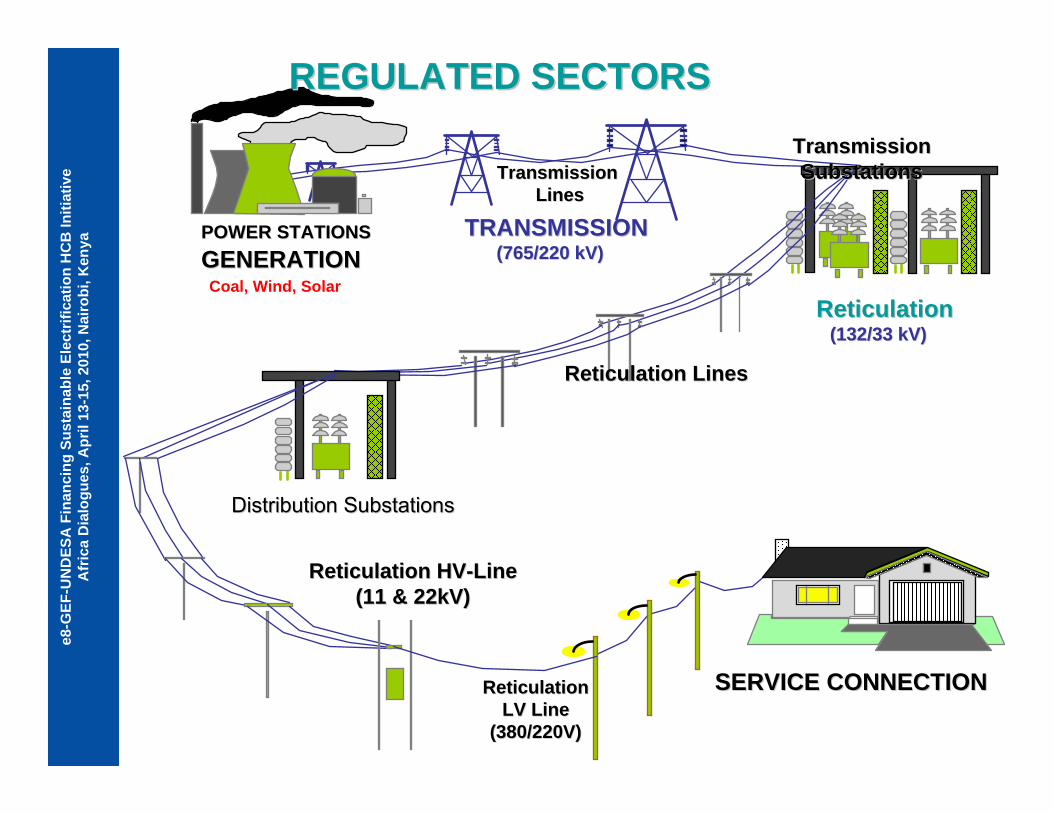

enya POWER STATIONSPOWER STATIONS

GENERATIONGENERATION

Transmission Transmission LinesLines

Transmission Transmission SubstationsSubstations

Reticulation LinesReticulation Lines

SERVICE CONNECTIONSERVICE CONNECTION

Reticulation HVReticulation HV--LineLine(11 & 22kV)(11 & 22kV)

TRANSMISSIONTRANSMISSION(765/220 kV)(765/220 kV)

ReticulationReticulation(132/33 kV)(132/33 kV)

ReticulationReticulationLV LineLV Line

(380/220V)(380/220V)

Distribution SubstationsDistribution Substations

REGULATED SECTORSREGULATED SECTORS

Coal, Wind, Solar

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

• The governance of the electricity sector is the responsibility of the Department of Energy (DoE).

• In 1994, Parliament approved a plan to ensure equal access to basic services for all South Africans.

• The National Energy Regulator, was given the task to develop and oversee the implementation of the Integrated National Electrification Programme (INEP).

• Eskom was tasked by National Energy Regulator of South Africa (NERSA) and later by DoE) to undertake the implementation through the use of contractors as part of any other Eskom business.

• Municipalities are now responsible for reticulation and distribution of electricity to households as well as to small businesses.

• Eskom maintains direct supply of electricity to larger industries• Non-grid electrification is provided by concessionaires. • Only in 2009 has renewable energy officially been accepted as “real” power when

the first national feed-in tariff scheme was established by NERSA.

Legal and regulatory frameworks;

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya • The main funding of the National Electrification Programme is through the

National Budget and not through cross-subsidies.

• Once households are electrified, consumers are billed by the municipalities.

• External donor agencies, in particular the German KfW, support the electrification of schools and clinics.

• Also NORAD, the Norwegian agency for development co-operation, provides support in the form of capacity building, for example to monitor sale and management of electricity, also at the municipal level.

Funding Options

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

• Policies and funds are allocated to ensure that areas or individual houses that cannot be connected to the grid can be serviced through different means of modern energy applications such as solar PV.

• But, Poor policy implementation and lack of clear financial and legal regimes have constrained the development and introduction of new renewable energy sources such as solar, wind, modern bioenergy, etc.

• A key government priority is the issues around the 1.7 million households living in informal settlements be addressed first (by their respective municipal councils):

– either the areas must be formalised, or the inhabitants must be moved to other formalised human settlements before they can be included in the INEP.

• The DoE’s policy guideline addresses this matter, and a plan and its budget are in place to enable connection before 2014 if the Department of Housing or the municipality arrange for people to live in formalised housing.

Financial and energy policy environment

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

Tariffs• South Africa has amongst the lowest electricity tariffs in the world.• As a result, it has not been financially feasible for South Africa − to install new

power generation. • In South Africa alone, the generation margin was only 4% in 2008, leading to

endless power cuts and systematic load shedding. • Tariff increases are now being implemented commencing this month for 2010/11

at 24.8% which translates to ZAR 0.42 (USD 0.067) per kWh• There been considerations on differential tariff increases to protect the poor, a

“home-light” tariff for the low income sector, a similar tariff for small, micro and medium-sized enterprises (SMMEs), and time-of-use tariffs.

• This debate is in line with South Africa’s rural electrification agenda, as new power generation will be necessary to service more households

• NERSA published the REFIT (Renewable Energy Feed In Tariff) in March 2009:• Supports government target of 10 000GWh from renewable energy

sources by 2013 • Four technologies under REFIT Phase I:

0.900.94

2.101.25

R/kWhWind1Concentrated solar power trough with 6 hours storage2

Landfill gas4Small hydro (less than 10 MW)3

Technology

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

• Due to the low cost of grid in South Africa and the excess capacity of generation in the 1990s, Distributed generation option such as diesel or biomass generators, was not economically viable. On average, it proved always more optimum to supply the area with grid.

• Off-grid electrification is carried out by private-sector service providers (concessionaires)

• The non-grid electrification programme which expected to install 300 000 Solar Home System (SHS) (the photovoltaic panel with a battery that could supply lights and radios) in 1998 has not managed to reach its objective. To date, only around 50 000 SHS have been installed

Reason:• Lack of political will• Non-payment of bills• Lack of expected government capital subsidies delayed much of the work. • Decision making, concerning the definition of a non-grid area has also caused delays

and costs to the concessionaires. • Lack of Renewable technology acceptance by Communities• These difficulties have weakened the financial stability of the concessionaires and

delayed the installation process.

Green Technology options, associated costs, risk and opportunities;

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

• In 2008, Eskom launched a programme to subsidise solar water heating (SWH)• The subsidy level was too low and required massive administration and control

systems so that the programme has had little success. • Since 2008 some municipalities have introduced SWH as a way of avoiding load

shedding by Eskom. • Feed-in tariff offers an incentive for grid-connected renewable energy.• Free basic electricity provision for the first 50kWh of consumption per month • Prepaid electricity meters form part of the installation for all new connections, meters

are used to reduce the problem of non-payment.

Subsidies and cost reduction incentives

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

• The DoE monitors the implementation of electrification through field checks and similar direct follow-ups and initiates corrective measures when results are not as planned.

• But there has been an implementation deficit at the DoE because of insufficient capacity and poor co-ordination between the non-grid component of INEP and the Renewable Energy Directorate, which is impeding the efficiency of the Department.

• In the case of non-grid electrification, non-acceptance of renewable energy systems as a solution for the provision of electricity is slowing down the electrification process.

• Experience with non-grid electrification through solar heating systems (SHS) has taught a lesson that solar panels are subject to theft and vandalism.

Risk and liability mitigation;

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

Challenges•South Africa’s rural electrification challenges are those associated with the transformation of society to erase the inequalities from the past.•Electrification has to address of rural and peri-urban communities and is never profitable as a result private sector participation is minimal•Funding for rural electrification is insufficient and there are limited sources of finance to cater for subsidies.•Not all electricity policies eg. universal access, target poor households (- due to the integration of the poor and the working class).

•There is a challenge with the municipalities’ capacity to deliver and oversee delivery of quality electrification.

•The DoE, is also facing capacity deficits, in monitoring actual performance and to make sure that corrective measures are taken in case of under- or non-performance•Investment is focused on capital infrastructure due to electricity capacity shortages and minimal investment made on development of renewable energy technologies•Structured Planning approach, Housing backlog makes electrification difficult (dplg, housing etc)•Technology Innovations (very high quality standards increase costs & make technologies inaccessible to poor communities, integration of other sources, including grid energy)

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

Regional Cooperation

• Energy Poverty Action (EPA) is an Initiative, which illustrates how international and local cooperation through public-private partnerships (PPPs) and community cooperatives can be successfully deployed to develop market based solutions to rural energy access. • EPA is a Global partnership which has developed a constituency for action: Governments, IFIs (WB, IFC, AfDB) Swedfund, DBSA, private companies, utilities (Eskom, Vattenfal, BC Hydro, Manitoba), global corporations & associations (SANEA).• EPA catalyses market development and facilitates the establishment local capability where utility capacity does not exist.• EPA “not-for-profit” Company provides programme oversight, significant capability building, knowledge and best practice sharing and establishment of institutional capacity. • Rural Electrification Agency is established with central capacity to coordinate and support development of programmes, and to maintain and operate electrification systems. It is linked to policy, regulation, monitoring and enforcement.• The EPA projects are currently being implemented in Lesotho, with South Africa, Namibia and Zambia in the pipeline.

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

Conclusion• Rural economic development needs more than just household electrification. • Constraints on the availability of energy and its affordability affect economic

development, especially in rural areas. • Modern energy services promote economic development by enhancing the

productivity of labour and capital.• In order to achieve rural development objectives, however, there needs to be an

integrated approach to the provision of modern energy services and improved information and telecommunication, education, health and transport services

• In the case of South Africa, the national electrification plan is an integral part of a broader national development plan (also in the Municipal Integrated Development Plans -IDPs).

• Other initiatives are in place to promote growth and job creation, such as through the development of tourism and agriculture.

• Electrifying a new area will open many doors for the rural poor and should take advantage of the parallel government initiatives to stimulate economic growth.

• These initiatives will have more success if they include energy access in their overall objectives.

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

Contact Information:Email: [email protected]

Tel: +27 11 800 2436Fax: +27 860 665 566

Website:www.eskom.co.zaand www.weforum.org/epa

1

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

e8-GEF-UNDESAFinancing Sustainable Electrification

Africa DialoguesNairobi, Kenya, April 13-15, 2010

San Cristobal-Galapagos Wind Project

e8

2

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

The e8 San Cristobal-Galapagos Wind Project

3

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

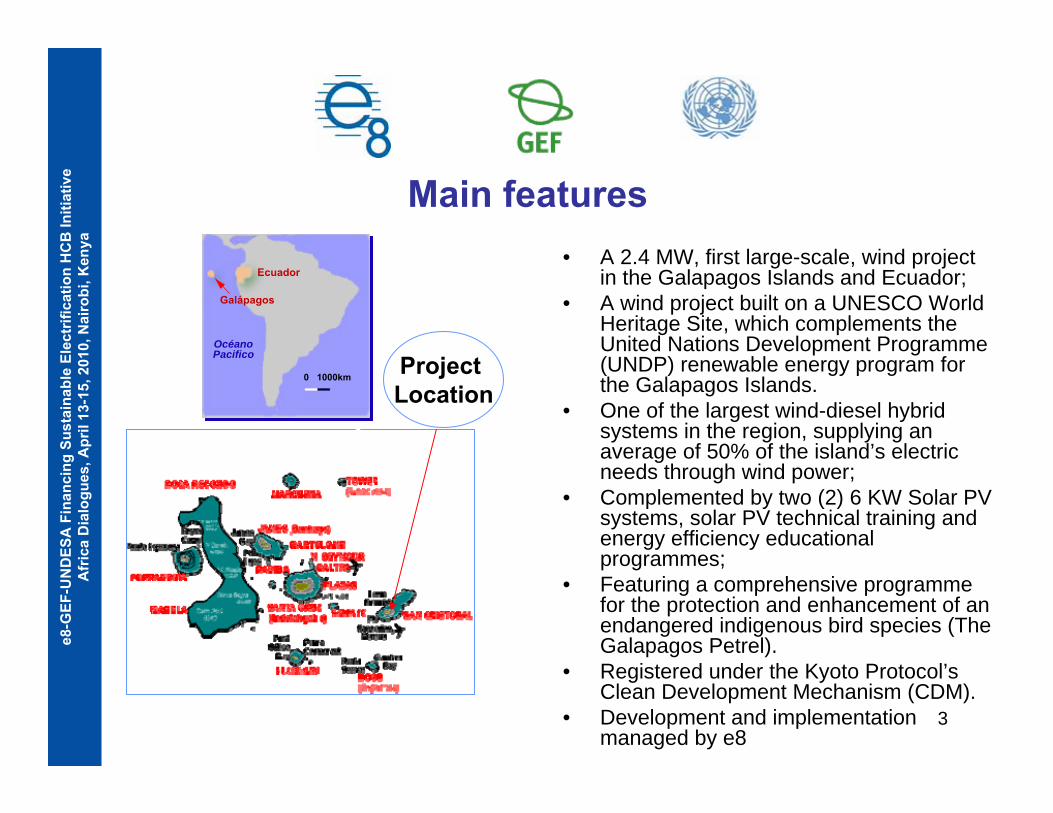

Main features• A 2.4 MW, first large-scale, wind project

in the Galapagos Islands and Ecuador;• A wind project built on a UNESCO World

Heritage Site, which complements the United Nations Development Programme (UNDP) renewable energy program for the Galapagos Islands.

• One of the largest wind-diesel hybrid systems in the region, supplying an average of 50% of the island’s electric needs through wind power;

• Complemented by two (2) 6 KW Solar PV systems, solar PV technical training and energy efficiency educational programmes;

• Featuring a comprehensive programme for the protection and enhancement of an endangered indigenous bird species (The Galapagos Petrel).

• Registered under the Kyoto Protocol’s Clean Development Mechanism (CDM).

• Development and implementation managed by e8

Project Location

0 1000km

Galápagos

Ecuador

OcéanoPacifico

4

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

Project Main Objectives• Reduce the risk of oil spills in a highly vulnerable environment;• Reduce atmospheric fossil-fuel emissions;• Decrease San Cristobal's dependence on diesel fuel;• Transfer technological expertise to local electric utility fro the

operation and maintenance of wind-based power system on a sustained basis;

• Provide a demonstration project model for the promotion and replication of small-scale power systems;

• Contribute to the protection of a unique ecosystem and World Heritage Site

• Increase access of the local population to renewable energy;• Develop public awareness of effective demand-side management

and energy conservation practices.

5

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

Project Timeline

• Concept 1999• Pre- Feasibility Study 2001• Feasibility Study 2005• Limited Notice to Proceed 2005• Full Notice to Proceed 2006• Implementation 2006-2007• Project Closeout 2007• Commissioning Oct. 2007• Inauguration Mar. 2008

6

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

Specific topics•Legal framework•Financial structure•Tariffs•Subsidies•Risk and liability mitigation•Technology issues•Logistical challenges

7

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

Legal and regulatory framework• Energy and rural electrification policies were stable and clear. In spite of

frequent turn over of main Government officers, agreements were fully respected

• Regulatory framework was adequate• Rural Electrification Special Law, established a specific fund for supporting

rural electrification programs• Project developers worked with success together with the National

Electricity Council (CONELEC) in order to allow the use of ruralelectrification funds in renewable energy projects like the Galapagos

• Ecuadorian Electricity Law determines preferred dispatching for electricity from renewable sources. Tariffs regulation establishes a preferred rate for renewable energy in the Galapagos Islands. Both factors were reflected in the PPA signed with Elecgalapagos, the local utility

8

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

Financing the Project (1)• In the 90’s, the Ecuadorian Government declared the need to

promote renewable energy in the Galapagos Islands to replace diesel powered electricity generation

• UNDP committed its support to the Ecuadorian Government to develop a program based on renewable energy for re-electrifying the Galapagos Islands

• A Pre-feasibility report was issued in 2000 by UNDP consultants with identification of renewable resources in the 4 inhabited islands: San Cristobal, Santa Cruz, Isabela and Floreana. Estimated budgets were included.

• Ecuadorian Government and UNDP started to search at international level, potential donors/investors for the development of the Program

9

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

Financing the Project (2)

• Based on previous experiences with UNDP, the e8 companies demonstrated interest in providing financial and technical support to develop the wind project in the San Cristobal island: first site visit was conducted by e8 delegates in November, 2001.

• The e8 companies committed their support, provided that the United Nations Foundation (UNF) also provides a complementary financial support.

• In April, 2003 a Project Document (ProDoc) was signed by the Government of Ecuador, the e8 companies, UNF and UNDP for the development of the Project. Funds from the e8 companies and UNF were provided as grants.

• A Commercial Trust was structured at the same time in order to administrate and manage the project funds. A private Ecuadorian experienced financial agency was designated as the Trustee.

10

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

Financing the Project (3)• The Ecuadorian government contributed with financial resources

from the Rural Electrification Fund (FERUM Fund). FERUM Fund rules were modified to permit financing of renewable energy projects.

• Through a Law in force at the time of Project implementation, itwas possible to receive a percentage of income tax as voluntary donations from Ecuadorian taxpayers.

• Interests earned by funds were also a component of the financialstructure.

• A small financial gap was filled with a short term loan provided with UNF funds through UNDP. Such funds had been provided by UNF for financing other renewable projects in other Galapagos islands.

• Total project cost was USD 10,5 million. • In addition project development and environmental studies were

totally funded and lead by charitable grant and technical expertise from e8 companies.

11

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

Financial structure

Financial structure (millions USD)

e8 ; $5,5 ; 52%

UNF ; $0,3 ; 3%

FERUM ; $3,3 ; 32%

Tax payers ; $0,4 ; 4%

Loan ; $0,6 ; 6%

Interests; $0,3 ; 3%

e8 UNF FERUM Tax payers Loan Interests

12

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

Tariffs (1)

• The Ecuadorian Electricity Council (CONELEC) - the electricity regulator - has established specific tariffs for renewable energies in Ecuador

• For the Galapagos Islands there are special preferential rates, although still not adequate, as explained below.

• The tariff value determined for wind energy is US$ 0,1282 / kWh for the San Cristobal – Galapagos Wind Project

• Above value was fixed by CONELEC after a detailed cost analysis in accordance with the agency criteria based on costs for grid integrated systems. Although the Project developers demonstratedthat such prices are insufficient to cover capital and O&M costs for the San Cristobal project, the regulator did not consider the rationale behind such explanation.

13

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

Tariffs (2)

• Because of such price restriction, the current tariff covers only O&M costs as well as other obligations of the Trust (fund for petrelprotection program, emergency maintenance fund, demobilization fund, seed fund for future re-equipment)

• A PPA has been signed between EOLICSA (the IPP - San Cristobal Wind Project company) and “Elecgalapagos” the local Government Utility, responsible for electricity distribution in the Galapagos

• As mentioned, PPA is based on a rate of US$ 0,1282 / kWh for wind energy delivered to Elecgalapagos, while diesel generated electricity costs approximately US$ 0,17 / kWh to the local utility, based on subsidized fuel delivered at less than 1 USD per gallon(US$ 0.26 / litre).

• Tariffs to final users are regulated by the Ecuadorian Electricity Council (CONELEC)

14

e8-G

EF-U

ND

ESA

Fin

anci

ng S

usta

inab

le E

lect

rific

atio

n H

CB

Initi

ativ

eA

fric

a D

ialo

gues

, Apr

il 13

-15,

201

0, N

airo

bi, K

enya

Subsidies

• Average tariff to final users is US$ 0.09 / kWh, while actual cost to the utility is roughly US$ 0.19 / kWh, including wind component. The difference is being subsided by the Government