ABJ ISS-92(PG1-47).indd - The Asian Banker

96

1 ISSUE 92 The Asian Banker Sustainability strained The annual definitive ranking and survey of Asia Pacific’s largest and strongest banks The Asian Banker 300 2009-2010 Edition www.theasianbanker.com SPECIAL EDITION ISSUE 92 SEPTEMBER 2009

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of ABJ ISS-92(PG1-47).indd - The Asian Banker

1 ISSUE 92 The Asian Banker

Sustainability strainedThe annual defi nitive ranking and survey of Asia Pacifi c’s largest and strongest banks

The Asian Banker 3002009-2010 Edition

w w w . t h e a s i a n b a n k e r . c o m

S P E C I A L E D I T I O N I S S U E 9 2 S E P T E M B E R 2 0 0 9

ABJ ISS-92(PG1-47).indd 1ABJ ISS-92(PG1-47).indd 1 8/28/09 1:02:49 AM8/28/09 1:02:49 AM

2 ISSUE 92The Asian Banker

THE ASIAN BANKERStreamlined Corporate Actions Processingdelivered by best of breed components forthe complete event management lifecycle,from golden record creation to entitlements.

Isn’t it time to drive down the cost of your operations?

TLM® Corporate Actions is the award-winning solution used by the world’s mostdemanding financial institutions to deliver complete, timely and accurate eventprocessing. It reduces the need for manual intervention, to greatly reduce theoperational risk inherent in processing corporate actions and create more efficient and proactive operations through:

• The rapid capture, cleansing and distribution of data, regardless of source or format, to create a normalised and reliable golden record

• Workflow-based validation and processing of mandatory events and fullyintegrated Diary to efficiently manage voluntary events

• Unique, thin client, Election Management capability enabling fund managers to determine their action in real time

Contact us today to discover how to deliver clarity and predictability across theentire event management process.

+1 (866) 603-1893 (Americas)+44 (0)800 279 5465 (UK)+65 6 224 76 89 (Asia Pacific)

smartstream-stp.com

Account Reconciliations

Cash & Liquidity Management

Compliance Management

Corporate Actions Processing

Hosted Reconciliations (SaaS)

OTC Derivatives Processing

Reconciliations

Trade Finance

Trade Process Management

Treasury Confirmations

Utilities Data Management

ABJ ISS-92(PG1-47).indd 2ABJ ISS-92(PG1-47).indd 2 8/28/09 1:03:03 AM8/28/09 1:03:03 AM

3 ISSUE 92 The Asian Banker

CONTENTSThe Asian Banker Journal is published ten times a year by

Incorporated in Singapore as T.A.B. International Pte Ltd

12

The Asian Banker 300Chinese banks have surged while Japanese banks are in decline

57

Asia Pacifi c’s Strongest BanksBanks in emerging markets are in a better positionto pull in deposits and push out loans

72

Country CapsulesWe assess the performance of the banking markets in14 countries in the Asia Pacifi c region

Founder and PresidentEmmanuel Daniel [email protected]

DirectorCharmaine [email protected]

Director and PublisherCaroline Grimont [email protected]

Managing EditorPeter Hofl ich phofl [email protected]

Writer David Hendrickson [email protected]

Research ManagersChristian Kapfer [email protected] Liu [email protected]

ResearchersNancy Duan [email protected] Yuandong [email protected] Zink [email protected]

Research AnalystAldo Joson [email protected]

Graphics & LayoutValen Siew Tel: (65) 6236 [email protected]

Sales & AdvertisingEunice Foong Tel: (65) 6236 [email protected]

Marie Aquino Tel: (65) 6236 [email protected]

Circulation & Subscription SalesJerome Ong Tel: (65) 6236 [email protected]

Production CoordinatorJanet Chan Tel: (65) 6236 [email protected]

Printed in Singapore byPrint & Print Pte Ltd

MICA (P) 071/07/2009 (Singapore)KDN PPS 1301/09/2009 (028064) (Malaysia)ISSN 02189615

Copyright and ReprintsCopyright Protected. Reproduction of any material in The Asian Banker Journal in any form is prohibited except with written permission from the publisher.

For reprints, please e-mail: [email protected]

Head Offi ce:10 Hoe Chiang Road, #14-06 Keppel Towers Singapore 089315Tel: (65) 6236 6522 (Editorial); (65) 6236 6509/12 (Sales/Marketing); (65) 6236 6175 (Subscriptions); Fax: (65) 6236 6530

Sales Offi ces and Representatives:

ChinaJoanna Woo Tel: (86) 10 5869 [email protected]

#2805 Tower 12, Jianwai SOHO, 39 Dong San Huan Zhong Road, Chaoyang District, Beijing 100022Tel: (86) 10 5869 3492 Fax: (86) 10 5869 3491

Europe & North AmericaJenny A. Swift [email protected]

10 The Beanlands, Wanborough,Wiltshire, SN4 OEJ, United KingdomTel: (44) 179 379 0926 (London) Tel: (1) 917 210 8064 (New York)Mobile: (44) 7788 416 938

MalaysiaNo. 55-6, The Boulevard, Mid Valley City,Lingkaran Syed Putra, 59200 Kuala Lumpur, MalaysiaTel: (6) 03 2284 7110 Fax: (6) 03 2284 5300

Middle EastNicholas [email protected]

PO BOX 124628 DubaiUnited Arab EmiratesTel: (971) 50 452 1800Fax: (971) 4 361 7930

The Asian Banker 3002009-2010 EditionSustainability strainedThe annual defi nitive ranking and survey of Asia Pacifi c’s largest and strongest banks

ABJ ISS-92(PG1-47).indd 3ABJ ISS-92(PG1-47).indd 3 8/28/09 5:05:59 PM8/28/09 5:05:59 PM

4 ISSUE 92The Asian Banker

THE ASIAN BANKER

❏ Subscribe to THE ASIAN BANKER JOURNAL I will get:

I WOULD LIKE TO

To receive our e-newsletters, sign up at www.theasianbanker.com

Please fax your subscription to +65 6236 6530

For enquiries, please contact:Tel: +65 6236 6175, E-mail: [email protected] to: T.A.B. International Pte Ltd 10 Hoe Chiang Road, #14-06 Keppel Towers, Singapore 089315

Cancellation Policy: No refunds for cancellation of The Asian Banker subscriptions, although

credit for other products can be arranged.

Ten issues of THE ASIAN BANKER JOURNAL Online access to web edition for up to fi ve executives

(subscribed issues)

Name:

Job Title:

Organisation:

Address:

Postal Code: Country:

Direct Tel: Fax:

E-mail:

❏ Amex ❏ Diners Club ❏ MasterCard ❏ Visa ❏ JCB

Card No: Expiry Date:

Cardholder’s Name:

(if different from the above)

❏ Non-negotiable cheque made payable to: “TAB International Pte Ltd”

❏ Bank transfer to: Development Bank of Singapore Suntec City Branch, 3 Temasek Boulevard,

Singapore 038983 Account No: 074-001420-8 Account Name: T.A.B. International Pte Ltd

❏ Invoice me (only for corporate account). Payment must be made within 5 working days upon receipt of invoice.

Signature: Date:(as in credit card, if applicable.)

I WISH TO PAY BY (PLEASE COMPLETE THIS SECTION)

❏ US$360 per year

❏ US$330 per year on auto-renewal. Save US$30!

❏ US$520 for 2 years on auto-renewal at US$260 per year. Save US$200!

The Asian Banker (incorporated as TAB Inter-national Pte Ltd in Singapore) is a research and intelligence company dedicated to providing com-plete and up-to-date information on strategic de-velopments in the fi nancial services industry in the Asia Pacifi c region. The company offers a unique combination of the skills of researchers and writers to develop a keen perspective on strategic issues and drivers in the industry through three key divi-sion entities:

The Asian Banker Journal is the fl agship regional pub-lication covering industry best practices. The publication has become the defi nitive commentator on develop-ments in Asia Pacifi c’s fi nancial services industry.

Asian Banker Research offers a wide range of in-telligence-based reports and research products for the banking and fi nancial services community. It is designed to provide senior management with critical business intelligence to secure a market leader posi-tion in the industry.

Asian Banker Forums organises conferences and roundtables for senior executives on key areas of development in the industry. Many of these events are conducted by invitation only. The company’s fl agship event is The Asian Banker Summit, inau-gurated in 2000 and attended by delegates from around the region.

WHO WE ARE

SUBSCRIPTION FORM6 An important note Metamorphosis now

8 Trendwatch Honing the edge

17 List of Asia Pacifi c’s largest banks

22 Ranking of Asia Pacifi c’s largest banks

48 The largest banks in Greater China

50 The largest banks in South and Southeast Asia

51 Performance rankings

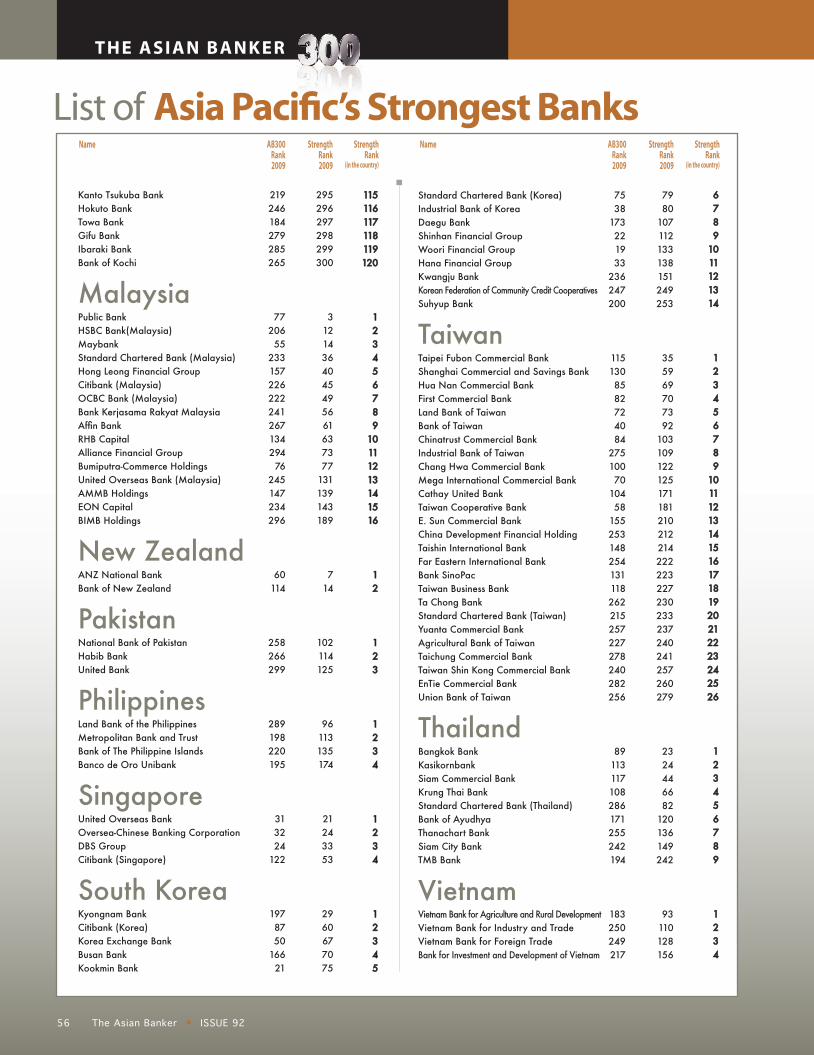

54 List of Asia Pacifi c’s strongest banks

60 Ranking of Asia Pacifi c’s strongest banks

94 The Final Word

ABJ ISS-92(PG1-47).indd 4ABJ ISS-92(PG1-47).indd 4 8/28/09 5:12:07 PM8/28/09 5:12:07 PM

5 ISSUE 92 The Asian Banker

It all adds up to better value!With our tailored solutions, we can help you optimize yourbranch processes and substantially reduce branch costs. Our flexible tools make it easyfor you to create and manage a customer-oriented portfolio with attractive value-addedservices. And our comprehensive consulting, innovative IT solutions and first-class out-sourcing services offer you results for better customer care and maximum efficiency inyour branches. As one of the world’s leading providers of multichannel solutions, we canhelp you move beyond the boundaries of your branch network. Call us at +65 6740 2610or visit our website at www.wincor-nixdorf.com

EXPERIENCE MEETS VISION.

BANK ON SUCCESS.BANK ON OPTIMIZED BRANCHES.

ABJ ISS-92(PG1-47).indd 5ABJ ISS-92(PG1-47).indd 5 8/28/09 1:03:07 AM8/28/09 1:03:07 AM

THE ASIAN BANKER

6 ISSUE 92The Asian Banker

AN IMPORTANT NOTE

Metamorphosis now

It gives me great pleasure to announce that Peter Hoflich has been appointed the managing editor

for all of The Asian Banker publications businesses. He also carries the prestigious title of editor

of The Asian Banker Journal. Peter takes over from Elena Torrijos, who saw the print publication

through the most recent phase of its development as the leading banking publication representing

the Asia Pacific region, and definitely one of the leading publications of its kind—this is not what

we say about ourselves, this is what our readers and the industry at large say about us.

Peter takes over the publication business at a momentous time in the revolution taking place in

the publication industry as a whole. When we say “all of The Asian Banker’s publications,” we refer

not just to The Asian Banker Journal, but to The Asian Banker Interactive, The Banking Conversation

and a host of data-driven publications we are driving online. The format of The Asian Banker Journal

is already being changed to accommodate this transformation that is taking place in the way readers

procure and access intelligence in the industry.

We have also become great users of Twitter, LinkedIn and even Facebook to keep our community

highly personal, informing readers of upcoming interviews with leading personalities around the

world. Visitors to our main website www.theasianbanker.com would immediately recognise how The

Asian Banker brand name has grown, and the fact that we have unparalleled access to leaders from

around the world.

Peter is, of course, no stranger to the industry. He has been with The Asian Banker since 2003 and

I am the first to recognise that he has become the most connected person in the industry, surpass-

ing the goodwill that even I had in the early years. I depend on him for insights on the background

of personalities he knows personally, as well as on trends in the industry.

His incredible sense of organisation (derived from his German heritage) and his affability (being

Canadian, of course) makes him a great journalist. It prepares him uniquely for this new phase in

the publication industry, where foundation work is more crucial than ever before when the publica-

tion industry was just print. I enjoy working with him and have a tremendous regard for his sense

of ownership over the information that he provides his readers.

In the meantime, my own role in the publication business is limited to being the anchor of the world-

wide interviews we do on a new initiative you can visit on www.thebankingconversation.com. Even here,

Peter plays a crucial role in selecting the people we choose to interview. I would encourage readers to

visit our related sites to see how we have transformed and how the new media is confirming something

that we suspected all along—that The Asian Banker is a world class publication, and now with a world

class editor. Please join me in congratulating Peter in this new phase in his professional life!

6 ISSUE 92The Asian Banker

ABJ ISS-92(PG1-47).indd 6ABJ ISS-92(PG1-47).indd 6 8/28/09 6:12:07 PM8/28/09 6:12:07 PM

7 ISSUE 92 The Asian Banker

As leading technology providers of financial services solutions, IBM and

ACI Worldwide have helped financial institutions worldwide build some of

the most sophisticated and flexible payment systems in use today.

Drawing on decades of experience

in application software and

infrastructure optimisation, IBM

and ACI have formed a strategic

relationship to ensure customers

can adapt to changing payment

requirements.

To learn more, visit www.ibm.com or www.aciworldwide.com.

Agile payment solutions from IBM and ACI

Agile Payment Solutions: Wholesale Payments . Financial Crime Management . Retail Payments . Merchant Retail

A unified solution that initiates, manages, secures and operates payments.

Visit us at stand 1E12 inExhibit Hall 1.

www.ibm.com www.aciworldwide.com

ABJ ISS-92(PG1-47).indd 7ABJ ISS-92(PG1-47).indd 7 8/28/09 1:03:14 AM8/28/09 1:03:14 AM

THE ASIAN BANKER

8 ISSUE 92The Asian Banker

The Asian Banker 300 (AB300) has been a product for The Asian Banker for eight years, and this

is the fifth that I’ve seen it assembled. Every year the process is an amazing thing to behold,

as the research team brings the numbers together, gives them a life of their own—and then forces

them to tell their stories.

But this year the experience has been different in many ways. Externally, we are seeing the first

set of mid-crisis performance numbers for Asian banks that can help us assess the state of Asia’s

banks relative to that of their suffering peers in the US and Europe, and gauge their strengths and

weaknesses. Internally, we are also seeing a new AB300 team forming around senior research analyst

Yi Yuandong, who has not only designed powerful analytical tools to

crunch the numbers with, but is gearing up to expand the list to 500

banks for a new online edition that will for the first time compare

the banks of Australia, East Asia, South Asia and Southeast Asia

with the banks of the Middle East and Central Asia. The expanded

ranking will also include countries like Bangladesh, Cambodia

and Sri Lanka, whose largest banks have always been too small to

make it onto our traditional list of 300 banks, but whose inclusion

allows us to apply them to our strength formula and evaluate them

alongside the other banks.

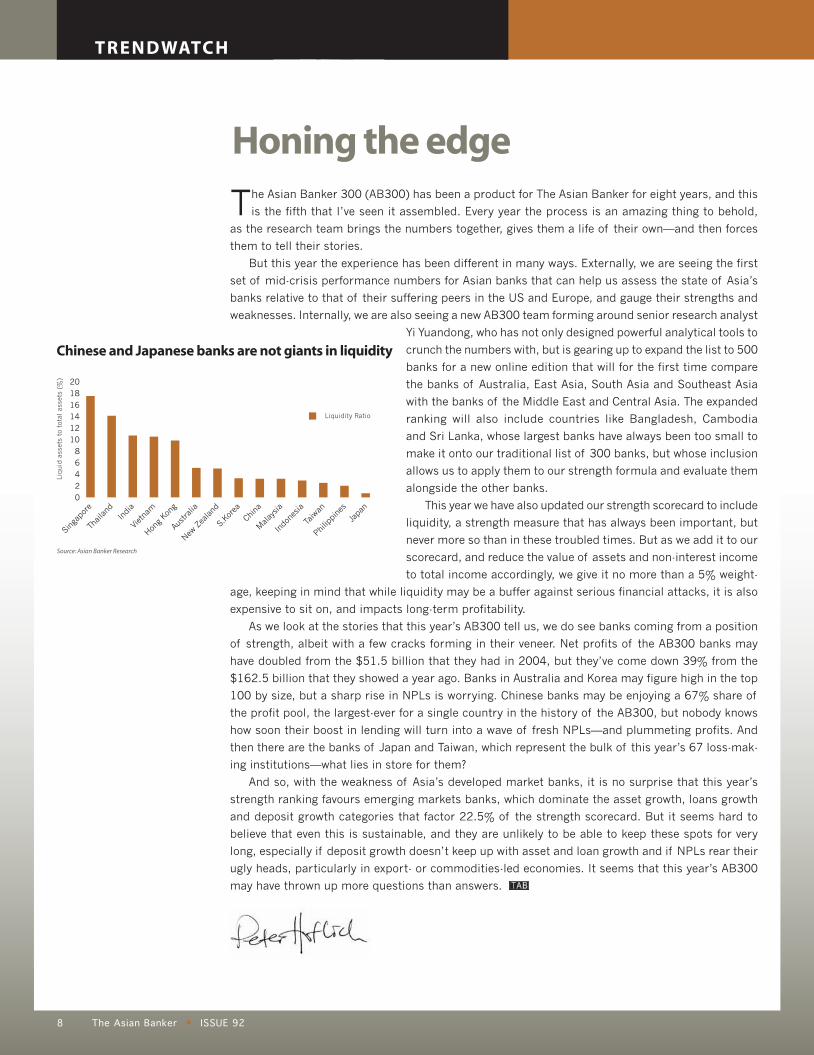

This year we have also updated our strength scorecard to include

liquidity, a strength measure that has always been important, but

never more so than in these troubled times. But as we add it to our

scorecard, and reduce the value of assets and non-interest income

to total income accordingly, we give it no more than a 5% weight-

age, keeping in mind that while liquidity may be a buffer against serious financial attacks, it is also

expensive to sit on, and impacts long-term profitability.

As we look at the stories that this year’s AB300 tell us, we do see banks coming from a position

of strength, albeit with a few cracks forming in their veneer. Net profits of the AB300 banks may

have doubled from the $51.5 billion that they had in 2004, but they’ve come down 39% from the

$162.5 billion that they showed a year ago. Banks in Australia and Korea may figure high in the top

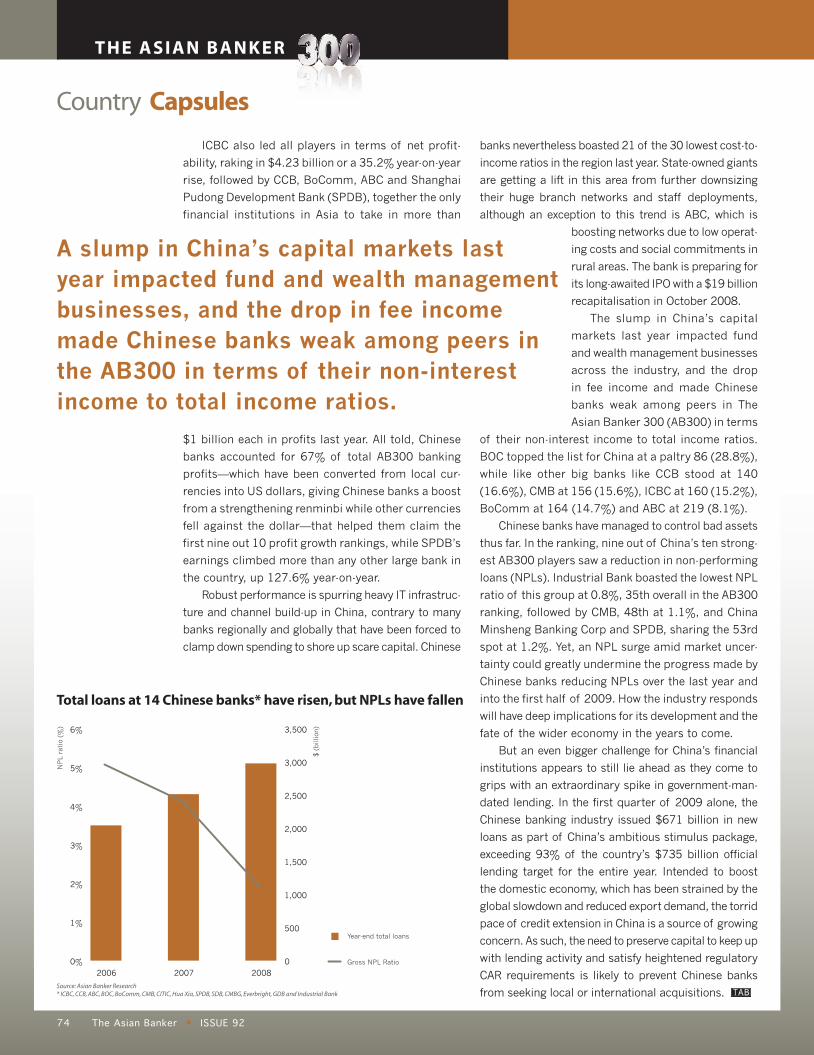

100 by size, but a sharp rise in NPLs is worrying. Chinese banks may be enjoying a 67% share of

the profit pool, the largest-ever for a single country in the history of the AB300, but nobody knows

how soon their boost in lending will turn into a wave of fresh NPLs—and plummeting profits. And

then there are the banks of Japan and Taiwan, which represent the bulk of this year’s 67 loss-mak-

ing institutions—what lies in store for them?

And so, with the weakness of Asia’s developed market banks, it is no surprise that this year’s

strength ranking favours emerging markets banks, which dominate the asset growth, loans growth

and deposit growth categories that factor 22.5% of the strength scorecard. But it seems hard to

believe that even this is sustainable, and they are unlikely to be able to keep these spots for very

long, especially if deposit growth doesn’t keep up with asset and loan growth and if NPLs rear their

ugly heads, particularly in export- or commodities-led economies. It seems that this year’s AB300

may have thrown up more questions than answers.

TRENDWATCH

Honing the edge

Chinese and Japanese banks are not giants in liquidity

Source: Asian Banker Research

02

468

10121416

1820

Sing

apor

e

Thailand

Indi

a

Viet

nam

Hong

Kong

Austra

lia

New Z

ealand

S.Ko

rea

China

Malay

sia

Indo

nesia

Taiw

an

Philip

pine

s

Japa

n

Liquid

ass

ets

to t

otal

ass

ets

(%)

Liquidity Ratio

ABJ ISS-92(PG1-47).indd 8ABJ ISS-92(PG1-47).indd 8 8/28/09 1:03:15 AM8/28/09 1:03:15 AM

9 ISSUE 92 The Asian Banker

Software inf rastructure for rapid change. customers ears of e perience asda

Learn more at www.tibco.com

Software nc. rights reser ed.

The Moment of Truth

ver customer interaction – hether it s through the call center branch o ce email or eb – is a moment o opportunit . chance to buil or ero e the compan s relationship ith that customer.

s Predictive Customer Interaction Management solution – evelope in collaboration ith Fortune 100 customers in the retail banking sector – uses real-time events to anticipate customer nee s. his improves the e ectiveness o outboun marketing inboun marketing customer service an other relationship management activities. earn more at .tibco.com solutionsin ustr nance

ABJ ISS-92(PG1-47).indd 9ABJ ISS-92(PG1-47).indd 9 8/28/09 1:03:17 AM8/28/09 1:03:17 AM

CO - PUBL I SHED ART ICLE

ISSUE 92The Asian Banker10

Enabling client success with value-added services in a challenging environmentBy leveraging Deutsche Bank’s FX4Cash, fi nancial institutions are able to benefi t from increased business and revenue opportunities by offering value-added services to their corporate clients.

With weak market fundamentals and profi tability, many banks have been scaling back on investments in new product innovation and technology. FI clients are also

reassessing their strategic investments in technology and infrastructure to determine whether they can sustain ongoing investments or consider the option of outsourcing to a strong global provider. However, Deutsche Bank is bucking the trend and continues to invest in the latest technology to expand its suite of innovative cash management prod-ucts globally while ensuring that onshore clients across 17 markets in Asia have access to bespoke services and solutions. “We need to stay on top of clients’ requirements and Deutsche Bank has been proactive in addressing recent challenges with increased focus on technological advancements,” says John Ball, Head of Cash Management Financial Institutions, Asia-Pacifi c.

One product which has been gaining popularity among FI clients is the bank’s cross- currency payment platform, FX4Cash. Launched in the second half of 2008, the solution was designed to enable FI clients to transact large numbers of cross-currency transactions with ease. The FX4Cash platform has recently been enhanced to include 50 additional currencies. “This allows our clients to effect payments in more than 125 currencies via one base account,” says Ball.

Leveraging on its Global Markets’ foreign exchange and Global Transaction Bank-ing’s payments processing expertise, the FX4Cash platform - which is integrated with autobahnFX, the bank’s proprietary foreign exchange trading platform, and the bank’s award-winning Money Transfer New Architecture (MTNA) - was designed to offer cost and effi ciency benefi ts to corporate and FI clients. “FX4Cash is a marriage of Deutsche Bank’s leadership in foreign exchange and its leading cash management capabilities,” said Kefei Chang, Head of FX4Cash, Asia-Pacifi c.

Deutsche Bank’s leadership in foreign exchange further enhances this value proposi-tion. The bank was recently named leading FX bank globally by Euromoney for the fi fth consecutive year, accounting for 20.96% of all market turnover.

In the cash management space where competition is intense, Deutsche Bank is quick to access the potential growth in Asia’s payment space - where local currencies are increas-ingly gaining importance in transaction settlement. The bank is also acutely aware of the multiple regulatory jurisdictions governing FI client requirements across Asia. “FX4Cash is positioned to help our clients increase effi ciencies and minimise costs in cross-currency

John BallHead of Cash Management

- Financial Institutions,

Asia Pacifi c

ABJ ISS-92(PG1-47).indd 10ABJ ISS-92(PG1-47).indd 10 8/28/09 1:03:17 AM8/28/09 1:03:17 AM

ISSUE 92 The Asian Banker 11

settlements across geographies. As a one-stop solution for cross-border currency pay-ments worldwide, clients are drawn to the solution’s benefi ts as it streamlines, automates and controls payables, simplifi es the number of accounts maintained, and minimises as-sociated costs and reconciliation efforts. Clearly, this solution offers clients access to FX price transparency and reduces manual intervention,” added Chang.

Since the launch of FX4Cash in the third quarter of 2008, more than 100 clients have gone live on the platform and have used the solution. One of the early adopters of the FX4Cash platform is Bank CIMB Niaga (CIMB Niaga). With over 655 branches across Indonesia, CIMB Niaga is one of the country’s largest banks and serves a wide range of corporate and retail clients. “FX4Cash has enabled CIMB Niaga to generate additional business and revenue opportunities, reduce costs, create new effi ciencies and gain access to greater choices in managing their cross-currency payments. The benefi ts of FX4Cash will now be available to more corporates through CIMB Niaga’s broad network across Indonesia,” says Chang.

To this end, technological capabilities, scale and network reach remain key success factors for cash management banks. Deutsche Bank’s market leadership has also been confi rmed by recent award wins: Asian Banker Achievement Award for Cash Management and Treasury Services for

Banks and Corporates in The Asian Banker Leadership Awards 2009 Best Overall Cash Management Bank in Asia (2003-2008) as voted by fi nancial institu-

tions in the 2009 Asiamoney Cash Management Poll of Polls.Beyond meeting clients’ requirements, Ball believes in exercising due diligence to iden-

tify opportunities for them in this challenging environment. “FX4Cash will help our clients optimise the effi ciencies in their value chain. Starting last year, clients have been seeking alternative revenue sources with shrinking retail and trading activities. One of their primary concerns is managing thinner margins in the current market environment. By leveraging FX4Cash, our clients stand to benefi t from increased business and revenue opportunities by offering value-added services to their corporate clients,” says Ball.

Kefei ChangHead of FX4Cash Asia Pacifi c

FX4Cash improves effi ciency, saves cost and mitigates risk.

ABJ ISS-92(PG1-47).indd 11ABJ ISS-92(PG1-47).indd 11 8/28/09 1:03:21 AM8/28/09 1:03:21 AM

THE ASIAN BANKER

12 ISSUE 92The Asian Banker

Although The Asian Banker 300 (AB300) has

a somewhat different story to tell every year,

the story invariably will involve China, Asia’s most

dynamic economy. With the region beginning to

suffer economic jitters, China’s banks have clearly

demonstrated the benefit of operating in a large and

protected market: while the Chinese banks only had

37 banks in the AB300 this time—a distant second in

the ranking after Japan, which has 120 entrants—they

stood out in the AB300 for profitability, taking 67%

of the 300 banks’ profits. This was on the back of

having only a 26.8% share of the 300 banks’ assets,

30.7% of the deposits and 24% of the loans.

This growth is relative: the AB300 figures reflect a

currency conversion to US dollars in order to ground

the results in a single currency, and the various in-

terest rate fluctuations render it impossible to make

true apples to apples comparisons. But across the

countries in the Asian Banker 300, the currency trend

was that the Chinese renminbi and the Japanese yen

appreciated against the dollar over their respective

reporting periods, while the Hong Kong dollar and

New Taiwan dollar were flat-ish; the rest of Asia’s cur-

rencies weakened. In keeping with this trend, a very

good year for Chinese banks was amplified not only

by the renminbi strengthening relative to the dollar,

but other countries’ softness to it.

In parallel with the boosting of Chinese banks’

standing in the survey, the help that a strengthening

yen gave Japan’s banks only made their atrocious

results less dismal, as a weakening economy and over-

exposure to stock markets led them to a cumulative

annual loss that represented 25% of the profit pool

of the 300 banks.

Making moneyAs western banks stumble and declare losses, profit-

ability has become a key indicator of business model

sustainability, as well as a litmus test of the secu-

rity of size. This year, 233 of Asia’s banks declared

profit, while 67 showed losses. Among these banks,

56 were Japanese, nine Taiwanese, and one each

from Australia and Hong Kong. Loss-making seemed

chronic at the Taiwanese lenders, seven of which had

also lost money the previous year (likewise, seven

Japanese banks went from a loss to a loss, but they

Justifying sizeChina is the only country that can still demonstrate that size matters—but for how long?

By Peter Hofl ich

ABJ ISS-92(PG1-47).indd 12ABJ ISS-92(PG1-47).indd 12 8/28/09 1:03:23 AM8/28/09 1:03:23 AM

13 ISSUE 92 The Asian Banker

are anomalies as the 49 other loss-making banks had

at least been profitable in 2007). Nevertheless, for

banks that declared losses in 2007 at the height of

the economic cycle, continuing losses in 2008 may

indicate the start of a death spiral. This is particularly

worrisome for Taiwan, which has already seen a round

of failing lenders sold to foreign banks.

Keeping it all relativeThe long-term trends in the AB300 show what a roller

coaster Asia’s banks have been on. In 2007, Japan

and Australia were close in their profitability, exceeded

somewhat by China, while in 2006 and 2005, Japa-

nese banks had been the most profitable by a clear

margin (Australia, China, Hong Kong and Japan are

the only countries that have ever seen their share of

profits in the double digits).

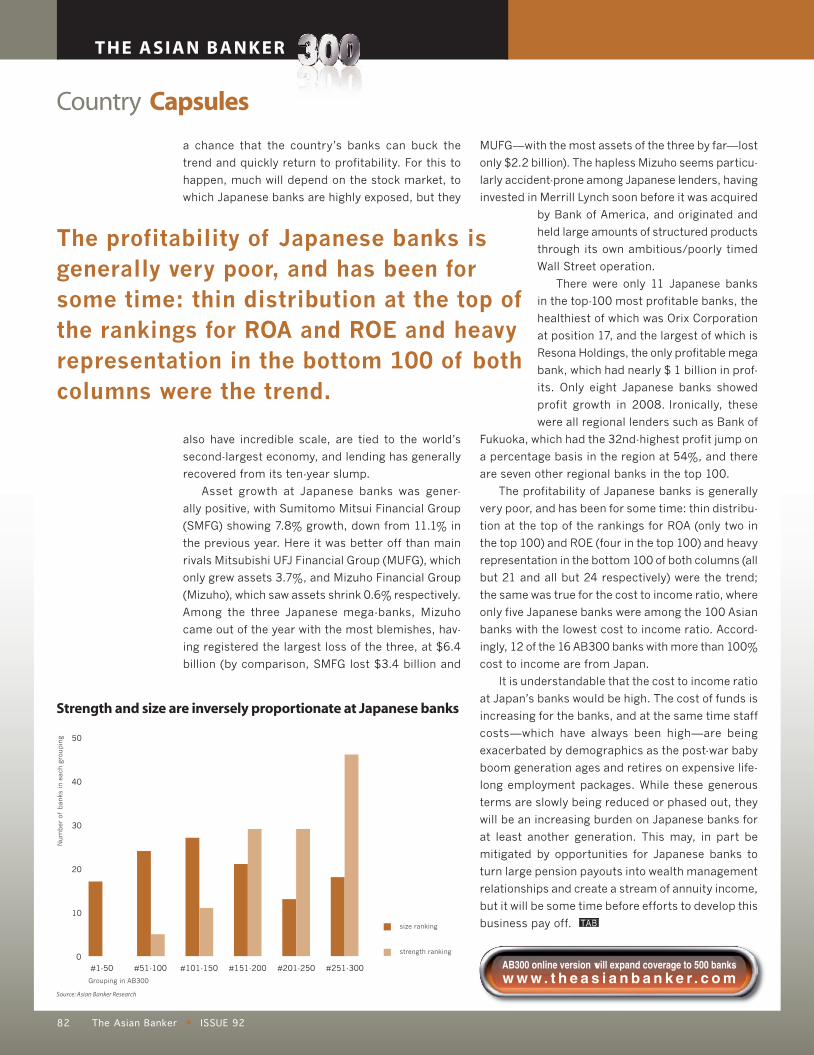

Although Japanese financial institutions will be

the largest for some time to come—the 120 Japanese

banks in the listing hold 43% of the region’s assets, the

only country in the listing besides China to have ever

held a double-digit percentile—they may never again

have the percentage of profitability that they once

had. Even with their disadvantaged currencies, and the

heavy profitability of the Chinese banks, most of the

other countries in Asia gained ground in profitability in

this year’s ranking. Exceptions were South Korea, which

suffered a mini funding and currency crisis, Pakistan,

which suffered severe political problems in a year rife

with political assassination and unrest, and New Zea-

land, which went into recession earlier than any other

country in the Asia Pacific region. Japanese banks also

trail all of the countries in terms of its liquidity as well

as percentage of non-interest income.

But it is not just Japan that has suffered, the

entire region has seen total profits stagger, dropping

to only $99 billion, a level not seen since 2004. And

while assets and deposits continue to grow, loans

have fallen too. With the drop in lending, and with

margins tightening in aggressive lending markets

such as China, profits in 2009 will probably continue

to weaken.

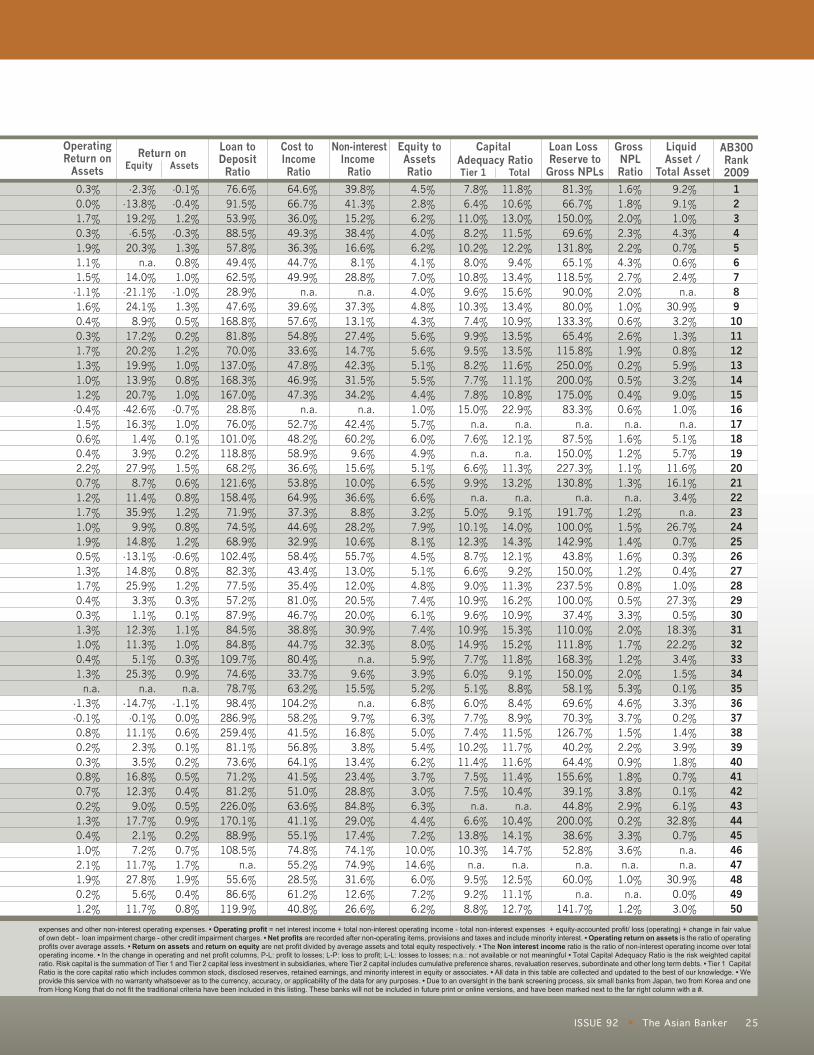

What is The Asian Banker 300?Now in its eighth year, The Asian Banker 300 (AB300) is an annual study of the financial and business per-

formance of the commercial banking industry in the Asia Pacific region. The study comprises two different

lists: the first ranks the top 300 banks in the region by asset size, while the second ranks the same 300 banks

by strength—an evaluation that is based on a belief that a strong bank demonstrates long-term profitability

from its core businesses.

Which banks are included?The Asian Banker ranks financial institutions by asset size and focuses on Asia Pacific banks east of Iran. We

publish online an expanded version of this list, The Asian Banker 500, which includes banks from the Middle

East and Central Asia as well. The focus of the list is on commercial banks and financial holding companies

with a significant proportion of activity in commercial banking; the AB300 does not include central banks,

policy banks or finance companies.

How do we collect and treat the data? Bank annual reports and statistics provided by central banks or industry associations are our main sources

of data. In the absence of up-to-date annual reports, we contact banks directly to source financial results.

Consolidated figures are used for banking groups, except when non-banking activities account for a substantial

portion of the consolidated figures. All figures are converted into US dollars using rates current at the end

of the banks’ respective financial years.

Who puts The AB300 together? The team of researchers who created the AB300 is led by Yi Yuandong. With quantitative

analytical skills honed by a background in consulting, Yuandong has guided the team in

scouring a broad range of data sources for robust figures, while also constructing a powerful

analytical platform that will be expanded to all of the 500 banks in the ranking’s interactive

online version.

(Continued on page 16)

ABJ ISS-92(PG1-47).indd 13ABJ ISS-92(PG1-47).indd 13 8/28/09 1:03:27 AM8/28/09 1:03:27 AM

CO - PUBL I SHED ART ICLE

ISSUE 92The Asian Banker14

Banks that have spent large amounts of money acquiring new customers report that up to 30% of these are lost in the fi rst year. Given that acquiring new customers is a

far more expensive process than keeping existing ones, the key question must be: “Why do people change banks and how can you minimise the chances of them leaving?”

A recent Forrester report highlights the importance of consistent, high quality customer service when it states that “each interaction represents an opportunity to keep or lose your most important customers”.

For a bank, those interactions could be with real people (at the branch or call centre) or with self-service channels (ATMs and online). At the branch, a bad experience could mean a rude member of staff or having to wait in line. At an ATM, it could be the machine being ‘down’ or a particular service not being available.

In all cases, the frustrated customer leaves with a lower opinion of the bank and will be more receptive to a competitor’s timely piece of marketing. With a lost opportunity goes an entire customer relationship with all the cross-selling opportunities involved.

The bottom line is that a large bank could experience a swing in revenue by as much as $242 million, depending on the level of customer experience it provides.

The good news is that the channel through which banks can most easily differentiate themselves is also the most visible and most likely to attract the customers of other fi nancial institutions—the ATM network.

Other banks’ customers may never walk into your branches, visit your website or ring your call centre. But they may use your ATMs once a week or more, making them the public face of your brand.

The average customer uses an ATM fi ve times a month. That’s fi ve opportunities to impress. For banks that have failed to keep pace with the latest technology developments, it could also represent fi ve situations where the customer will leave dissatisfi ed, either with the range of services, the speed of the transaction or with the availability of the ATM to complete the transaction they require.

Today’s ‘iPhone lifestyles’ mean consumers expect quick, slick services to be available wherever and whenever they want them.

For an institution that wishes to differentiate itself from the competition the message is simple: your self-service channel needs to do more, be more attractive, easier to use, faster and more reliable.

A recent Aite study demonstrated that “the age of banks’ ATMs affects ATM channel service performance.” They found 75% of bank executives who managed a network with an average ATM age of less than fi ve years ranked their network in the top quartile, whereas only 55% of bankers with an ATM channel more than six years old did so.

Our own latest generation of ATMs—NCR SelfServ—provides banks with a key com-petitive advantage in delivering the services customers require. Whether it’s in terms of functionality, delivery, ease of use, speed, reliability or enhanced security, the new ATMs have incorporated customer needs into the design.

Retaining customers with modern self-service

The latest generation of ATMs delivers the key services sought by banks’ customers

“Each interaction

represents an

opportunity to keep

or lose your most

important customers”.

Forrester

ABJ ISS-92(PG1-47).indd 14ABJ ISS-92(PG1-47).indd 14 8/28/09 1:03:32 AM8/28/09 1:03:32 AM

ISSUE 92 The Asian Banker 15

Functionality. Adding new features and functionality are of key importance. As well as providing the services customers increasingly require, such as automated deposit and bill payment, another key ele-ment of customer service is personalisation of ATM transactions. Speed to market for new ATMs and new transactions is vital to ensuring best in class service. Looking forward, as new payment mechanisms evolve, it is also important that developments such as contactless cards and mobile payments can be integrated.

Availability. Availability is about delivering transactions that are 100% successful every time and thereby ensuring satisfi ed customers. Equally important is ensuring this is done in a cost-effective manner, using com-prehensive performance information to enable best practice management of the self service network.

In order to ensure maximum ATM availability remote servicing is key, avoiding time consuming call-outs. Firmware updates and ‘soft’ upgrades are downloadable to the ATM without the need for a site visit. And these days that’s not all—NCR SelfServ is the only ATM to offer self-healing capabilities, providing an automatic return to service for ‘soft’ failures, reducing downtime from two to three hours, to 10 to 15 minutes. In busy locations, where every minute counts, this is a massive advance.

An examination of ATM downtime reveals that over half of all downtime is due to low-level maintenance tasks such as clearing card or paper jams. With NCR SelfServ, this has been addressed by the introduction of interactive full motion video allowing on-the-spot training and speeding up the process.

“Our ATM channel plays a key part in how our customers perceive us, and maintaining the highest levels of availability is key to providing exceptional customer service” says Fatih Bektasoglu, business unit manager at Garanti Bank in Turkey. “With unique technologies, NCR has enabled us to provide 24/7 availability and provide superior service to our customers”.

Confi dence. It is essential that customers are confi dent in using the ATMs. The intro-duction of superior security features limits customer exposure to fraud and, for the bank, lessens the possibility of being targeted for attack, with the attendant negative publicity. The latest generation of NCR ATMs has a unique portfolio of security features to protect the ATM at every possible point of compromise.

Convenience and Speed. Though such measures are not always clear to customers, one more obvious benefi t is improvements in the ease of use and speed of transactions. China Bank’s SelfServ ATMs in the Philippines have cut cash withdrawal times by a third, to about 30 seconds, reducing queues and improving the customer experience.

Carol L. Chua, assistant vice president and head of China Bank’s ATM center division, says, “This new technology from NCR is already enhancing our customers’ experience. Almost immediately after we installed our fi rst SelfServ machine, we got customer feedback saying this machine was far, far faster than its predecessor. We’re very pleased.”

Responsibility. One other thing that customers increasingly expect from their banks is a sense of corporate responsibility, adopting policies to reduce environmental impact. SelfServ ATMs deploy dual-roll two-sided thermal printing technology (2ST). This is patented to print on both sides of a thermal paper receipt, reducing paper consumption up to 45%. The dual roll also means no more ‘out of paper’ calls and eliminates up to 20% waste per roll.

In the current environment, customer loyalty is paramount, and at a time when only exceptional service will suffi ce, NCR’s technologically advanced SelfServ ATMs exceed expectations, enabling broad functionality, high levels of availability, fast, secure transac-tions and low operating costs. Smart capital expenditure can generate the exceptional service that will help your customers remain your customers.

Stuart ButtarManaging Director

NCR South-East Asia

Contact details: Stuart ButtarManaging DirectorNCR South East [email protected]

Other banks’ customers

may never walk into

your branches or visit

your website, but they

may use your ATMs once

a week. Your ATM,

are your public face.

ABJ ISS-92(PG1-47).indd 15ABJ ISS-92(PG1-47).indd 15 8/28/09 1:03:33 AM8/28/09 1:03:33 AM

THE ASIAN BANKER

16 ISSUE 92The Asian Banker

THE ASIAN BANKER

16 ISSUE 92The Asian Banker

Chinese banks were the most profi table by far

1,858.4

6,697.2

1,074.3

956.9

115.3

10,951.8

391.4

108.3

27.8

55.1

465.3

1,187.7

851.3

228.9

56.2

25,026

12.6%

67.5%

11.1%

9.5%

1.9%

-25.3%

4.7%

1.1%

0.5%

0.4%

4.6%

6.3%

2.0%

2.4%

0.6%

100%

12.5

66.9

11.0

9.4

1.9

-25.1

4.7

1.1

0.5

0.4

4.5

6.2

2.0

2.4

0.6

99

4.3%

30.7%

4.3%

4.0%

0.5%

44.0%

1.6%

0.3%

0.1%

0.2%

1.6%

3.4%

3.6%

1.0%

0.2%

100%

748.50

5,313.71

749.05

696.55

93.28

7,619.51

285.64

59.62

20.22

43.01

282.01

593.97

619.51

171.81

39.25

17,336

9.1%

24.0%

3.0%

4.0%

0.5%

44.0%

1.7%

0.6%

0.1%

0.2%

1.6%

5.8%

3.9%

1.2%

0.3%

100%

1,214.3

3,194.3

403.5

538.1

61.3

5,871.9

226.7

86.6

15.8

24.5

219.8

772.5

514.2

155.2

36.2

13,335

7.4%

26.8%

4.3%

3.8%

0.5%

43.8%

1.6%

0.4%

0.1%

0.2%

1.9%

4.7%

3.4%

0.9%

0.2%

100%

Australia

China

Hong Kong

India

Indonesia

Japan

Malaysia

New Zealand

Pakistan

Philippines

Singapore

S.Korea

Taiwan

Thailand

Vietnam

TOTAL

13

37

15

27

6

120

16

2

3

4

4

14

26

9

4

300

CountryNumber of banks in AB300

Total Assets ($bn)

Share of Total Assets

Total Loans ($bn)

Share of Total Loans

Share of Total Deposits

Total Net Profit ($bn)

Share of TotalNet Profit

Total Deposits ($bn)

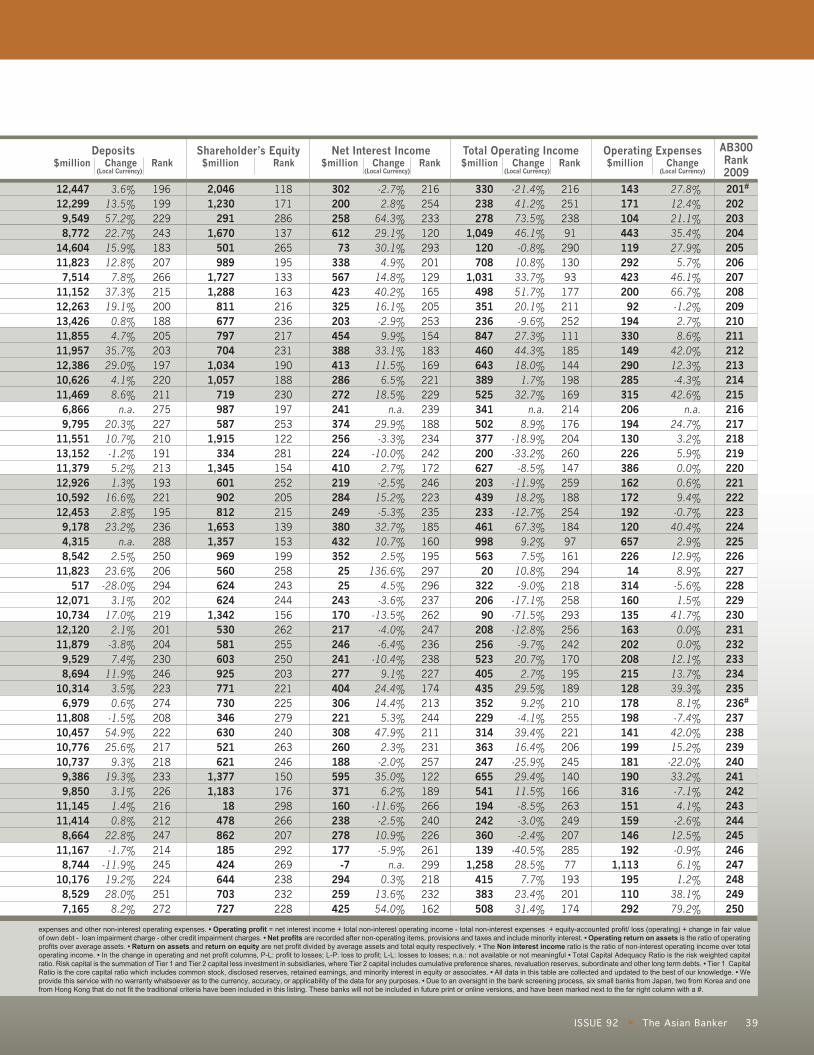

Source: Asian Banker Research

Getting realIn 2008, it was typically banks in emerging markets

that focussed on the fundamentals of banking: taking

deposits and dispersing loans. This makes greater

sense these days anyway, now that the call for “back-

to-basics, boring” banking has become deafening.

The highest-growing banks in deposits were typi-

cally the Chinese banks, and 39 of the fifty fastest-

growing banks are from emerging markets. Among the

developed market banks, Korean institutions were the

most aggressive in gathering deposits, with several

large Korean banks such as Standard Chartered Korea

and Woori Financial Group engaged in significant de-

posit-gathering exercises. Standard Chartered Bank

also aggressively sought deposits in Hong Kong, its

second-largest market after South Korea.

(Continued from page 13)

AB300 online version will expand coverage to 500 banksw w w . t h e a s i a n b a n k e r . c o m

The story is even more polarised in the case of

loans, where developed market banks hold only six

of the top fifty positions, and where Indian banks like

HDFC Bank—which took over Centurion Bank of Pun-

jab—and Central Bank of India, Indian Bank, Axis Bank

and Bank of Baroda pushed out loans at percentages

from 34% to 56% greater than the previous year.

With banks in developed markets laying low in

lending, it remains to be seen where aggressive lend-

ing will lead Asia’s emerging market banks in this era

of economic uncertainty. But this will surely start to

become apparent by next year’s AB300.

ABJ ISS-92(PG1-47).indd 16ABJ ISS-92(PG1-47).indd 16 8/28/09 1:03:35 AM8/28/09 1:03:35 AM

17 ISSUE 92 The Asian Banker

A Affi n Bank Malaysia 267Agricultural Bank of Taiwan Taiwan 227Agricultural Bank of China China 6Aichi Bank Japan 139Akita Bank Japan 154Allahabad Bank India 177Alliance Financial Group Malaysia 294AMMB Holdings Malaysia 147Andhra Bank India 248ANZ National Bank New Zealand 60Aomori Bank Japan 159Aozora Bank4 Japan 65Ashikaga Bank Japan 92Australia and New Zealand Banking Group Australia 14Awa Bank Japan 138AXIS Bank India 133

B Banco de Oro Unibank Philippines 195Bangkok Bank Thailand 89Bank Central Asia Indonesia 168Bank CIMB Niaga5 Indonesia 268Bank Danamon Indonesia 263Bank for Investment and Development of Vietnam Vietnam 217Bank Kerjasama Rakyat Malaysia Malaysia 241Bank Mandiri Indonesia 129Bank Negara Indonesia Indonesia 185Bank of Ayudhya Thailand 171Bank of Beijing China 74Bank of Baroda India 90Bank of Communications China 12Bank of China China 7Bank of Dalian China 235Bank of East Asia Hong Kong 80Bank of East Asia (China) China 191Bank of Fukuoka Japan 49Bank of Hangzhou China 212Bank of Ikeda Japan 140Bank of India India 93Bank of Iwate Japan 144Bank of Jiangsu China 123Bank of Kochi Japan 265Bank of Kyoto Japan 59Bank of Maharashtra India 239Bank of Nagoya Japan 124Bank of Nanjing China 224Bank of New Zealand New Zealand 114Bank of Ningbo China 208Bank of Okinawa Japan 199Bank of Queensland Australia 174Bank of Saga Japan 170Bank of Shanghai China 78Bank of Taiwan Taiwan 40Bank of the Philippine Islands Philippines 220Bank of the Ryukyus Japan 196Bank of Tianjin China 209Bank of Western Australia2 Australia 94Bank of Yokohama Japan 30Bank Rakyat Indonesia Indonesia 167Beijing Rural Commercial Bank China 142Bank SinoPac Taiwan 131Bendigo and Adelaide Bank1 Australia 125BIMB Holdings Malaysia 296

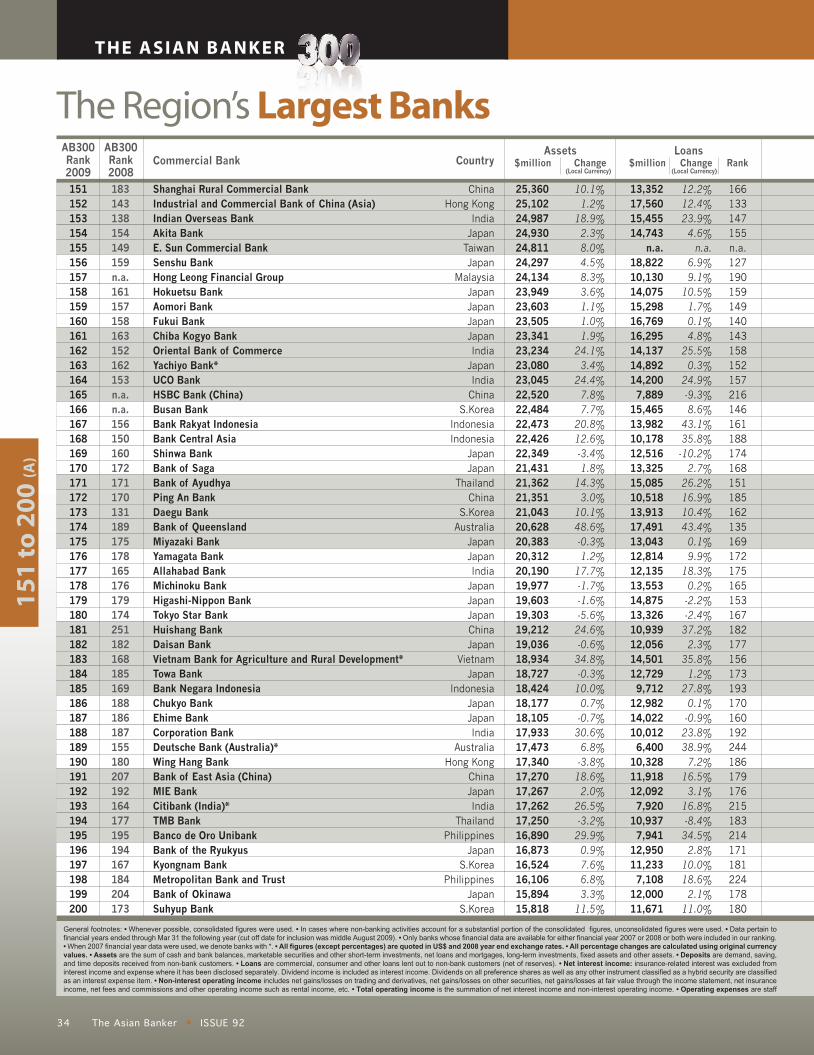

List of Asia Pacifi c’s Largest Banks

Biwako Bank Japan 243BOC Hong Kong Holdings Hong Kong 29Bumiputra-Commerce Holdings Malaysia 76Busan Bank S.Korea 166

C Canara Bank India 96Cathay United Bank Taiwan 104Central Bank of India India 150Chang Hwa Commercial Bank Taiwan 100Changsha City Commercial Bank China 292Chiba Kogyo Bank Japan 161Chiba Bank Japan 39China Bohai Bank China 272China CITIC Bank China 25China Construction Bank China 5China Development Financial Holding Taiwan 253China Everbright Bank China 34China Merchants Bank China 20China Minsheng Banking Corporation China 27China Zheshang Bank China 238Chinatrust Commercial Bank Taiwan 84Chinese Mercantile Bank China 270Chong Hing Bank Hong Kong 277Chugoku Bank Japan 69Chukyo Bank Japan 186Chuo Mitsui Trust Holdings Japan 26Citibank (Australia) Australia 225Citibank (Hong Kong) Hong Kong 211Citibank (India) India 193Citibank (Japan) Japan 62Citibank (Korea) S.Korea 87Citibank (Malaysia) Malaysia 226Citibank (Singapore) Singapore 122CITIC Ka Wah Bank Hong Kong 202Commonwealth Bank of Australia2 Australia 13Corporation Bank India 188

D Daegu Bank S.Korea 173Dah Sing Banking Group Hong Kong 214Daisan Bank Japan 182Daishi Bank Japan 91DBS Group Singapore 24Dena Bank India 261Deutsche Bank (Australia) Australia 189Dongguan City Commercial Bank China 271

E eBANK Japan 276Ehime Bank Japan 187Eighteenth Bank Japan 149EnTie Commercial Bank Taiwan 282EON Capital Malaysia 234Evergrowing Bank China 203E. Sun Commercial Bank Taiwan 155

F Far Eastern International Bank Taiwan 254First Bank of Toyama Japan 251First Commercial Bank Taiwan 82Fubon Bank (Hong Kong) Hong Kong 281

Name Country Rank Name Country Rank

ABJ ISS-92(PG1-47).indd 17ABJ ISS-92(PG1-47).indd 17 8/28/09 1:03:36 AM8/28/09 1:03:36 AM

18 ISSUE 92The Asian Banker

THE ASIAN BANKER

List of Asia Pacifi c’s Largest BanksName Country Rank Name Country Rank

Fukui Bank Japan 160Fukuoka Financial Group Japan 35

G Gifu Bank Japan 279Guangdong Development Bank China 53Gunma Bank Japan 68

H Habib Bank Pakistan 266Hachijuni Bank Japan 66Hana Financial Group S.Korea 33Hang Seng Bank Hong Kong 48HDFC Bank6 India 109Higashi-Nippon Bank Japan 179Higo Bank Japan 106Hiroshima Bank Japan 64Hokkaido Bank Japan 101Hokkoku Bank Japan 121Hokuetsu Bank Japan 158Hokuhoku Financial Group Japan 42Hokuriku Bank Japan 73Hokuto Bank Japan 246Hokuyo Bank Japan 61Hong Leong Financial Group Malaysia 157Hongkong and Shanghai Banking Corporation Hong Kong 9HSBC Bank (China) China 165HSBC Bank (India) India 204HSBC Bank (Malaysia) Malaysia 206Hua Nan Commercial Bank Taiwan 85Hua Xia Bank China 41Huishang Bank China 181Hyakugo Bank Japan 98Hyakujushi Bank Japan 105

I Ibaraki Bank Japan 285Ibarakiken Credit Cooperative Japan 244ICICI Bank India 46Indian Bank India 213Indian Overseas Bank India 153Industrial and Commercial Bank of China China 3Industrial and Commercial Bank of China (Asia) Hong Kong 152Industrial Bank China 28Industrial Bank of Korea S.Korea 38Industrial Bank of Taiwan Taiwan 275ING Bank (Australia) Australia 126Iyo Bank Japan 79

J Japan Trustee Services Bank Japan 228Jammu and Kashmir Bank India 300Jiangnan Rural Credit Cooperatives of Wuhan China 284Joyo Bank Japan 52Juroku Bank Japan 95

K Kagawa Bank Japan 223Kagoshima Bank Japan 119

Kansai Urban Banking Corporation Japan 110Kanto Tsukuba Bank Japan 219Kasikornbank Thailand 113Keiyo Bank Japan 116Kirayaka Bank Japan 237Kita-Nippon Bank Japan 231Kiyo Holdings Japan 107Kookmin Bank S.Korea 21Korea Exchange Bank S.Korea 50Korean Federation of Community Credit Cooperatives S.Korea 247Kotak Mahindra Bank India 287Krung Thai Bank Thailand 108Kumamoto Family Bank Japan 232Kwangju Bank S.Korea 236Kyongnam Bank S.Korea 197

L Land Bank of the Philippines Philippines 289Land Bank of Taiwan Taiwan 72

M Macquarie Group Australia 43Maybank Malaysia 55Mega International Commercial Bank Taiwan 70Metropolitan Bank and Trust Philippines 198Michinoku Bank Japan 178MIE Bank Japan 192Minato Bank Japan 132Mitsubishi UFJ Financial Group Japan 1Miura Fujisawa Shinkin Bank Japan 295Miyazaki Bank Japan 175Mizuho Financial Group Japan 2Momiji Bank Japan 135Musashino Bank Japan 111

N Nagano Bank Japan 264Nagano Shinkin Bank Japan 293Naganoken Credit Cooperative Japan 288Nanto Bank Japan 86Nanyang Commercial Bank Hong Kong 201National Bank of Pakistan Pakistan 258National Australia Bank Australia 10Nishi-Nippon City Bank Japan 57Norinchukin Bank Japan 8

O OCBC Bank (Malaysia) Malaysia 222Ogaki Kyoritsu Bank Japan 102Oita Bank Japan 136Oriental Bank of Commerce India 162Orix Corporation Japan 47Oversea-Chinese Banking Corporation Singapore 32

P Ping An Bank China 172Public Bank Malaysia 77Punjab and Sind Bank India 280Punjab National Bank India 83

ABJ ISS-92(PG1-47).indd 18ABJ ISS-92(PG1-47).indd 18 8/28/09 1:03:37 AM8/28/09 1:03:37 AM

19 ISSUE 92 The Asian Banker

The branch as the key delivery channel for retail banks

Integrating the branch into Wincor Nixdorf’s ProClassic/Enterprise Retail Banking Solution Suite creates a versatile service platform for innovative retail banks

CO - PUBL I SHED ART ICLE

ISSUE 92 The Asian Banker 19

Contact details: Kasten KemnaRegional Marketing DirectorBanking Division Asia Pacifi cWincor Nixdorf2 Kallang SectorSingapore 349277Phone (65) [email protected]

Innovative Wincor Nixdorf branch design

Case Study: In May 2009, Baden-Württembergische Bank (BW-Bank), deployed ProClassic/Enter-prise Retail Banking Solution Suite (PC/E) in its 200 branches. The bank also rolled out new software to tailor offers to customers’ individual needs via its self-service, online banking and telephone banking channels.

BW-Bank has been operating 330 self-service terminals with PC/E since 2003. In 2006, the bank asked Wincor Nixdorf to extend its use of PC/E to include management of its ATS that will emulate front-offi ce processes . The bank plans to use the Teller Operations solution to handle processes such as teller account management and account transactions.

The use of standard software means that the bank will be able to implement fur-ther developments and changes resulting from legal stipulations or process changes at greater speed than before. In late 2009, BW-Bank will pilot one-to-one marketing software, PC/E Direct Marketing, to establish and personalise contact with customers across all its delivery channels.

Source: Wincor Nixdorf, press release, “BW-Bank adds direct marketing and front-offi ce processes to ProClassic Enterprise”

ProClassic/Enterprise (PC/E) Retail Banking Solution Suite is a modular software suite that focuses on sales and service processes in retail banks. It combines channel delivery,

security, management and optimization, and banking business capabilities, and allows banks to render themselves future-proof and expandable by transforming their IT architectures.

The suite’s net-centric concept ensures that new services and functions are quickly implemented and centrally managed. The packages are based on a service-oriented multi-channel concept that allows individual functions and services to be reused across all delivery channels. Focussing on branches, the following innovative modules are available to optimize processes and maximize return on investment: Teller Operations: Caters to transactions around cash-handling and account-related

services at the counter. This solution makes customer transactions leaner and more effi cient, and eases processes in the branch, such as end-of-day teller closing.

ATS Manager: Smoothly connects the automated teller safe (ATS, also known as TAU or TCR) device with the teller application to ensure secure cash-in and -out transactions at the teller to streamline cash processes in the branch. The software consolidates all cash transactions, linking them to individual customers and teller operators.

Peripheral Management: Optimizes the connection and management of the multiple peripherals that typically exist in a branch, such as card readers, document printers or signature pads. From a central management console, the software can react fl exibly when devices are out of order and provides alternative access.These three software products help banks streamline teller operations and maximize

customer service levels, providing bank staff a seamless and modern user interface to allow time for sales and consulting services.

ABJ ISS-92(PG1-47).indd 19ABJ ISS-92(PG1-47).indd 19 8/28/09 1:03:39 AM8/28/09 1:03:39 AM

20 ISSUE 92The Asian Banker

THE ASIAN BANKER

List of Asia Pacifi c’s Largest BanksName Country Rank Name Country Rank

R Resona Holdings Japan 11RHB Capital Malaysia 134Rokinren Bank Japan 88Rural Credit Cooperatives Union of Shunde China 259

S Saikyo Bank Japan 291San-In Godo Bank Japan 103Sapporo Hokuyo Holdings Japan 54Sendai Bank Japan 283Senshu Bank Japan 156Shanghai Commercial and Savings Bank Taiwan 130Shanghai Commercial Bank Hong Kong 218Shanghai Rural Commercial Bank China 151Shanghai Pudong Development Bank China 23Shenzhen Development Bank China 63Shiga Bank Japan 97Shikoku Bank Japan 143Shimizu Bank Japan 210Shinhan Financial Group S.Korea 22Shinkin Central Bank Japan 16Shinkumi Federation Bank Japan 99Shinsei Bank4 Japan 36Shinwa Bank Japan 169Shizuoka Bank Japan 45Shoko Chukin Bank Japan 37Shonai Bank Japan 260Siam City Bank Thailand 242Siam Commercial Bank Thailand 117Sony Bank Japan 205St George Bank3 Australia 44Standard Chartered Bank (China) China 216Standard Chartered Bank (India) India 207Standard Chartered Bank (Korea) S.Korea 75Standard Chartered Bank (Malaysia) Malaysia 233Standard Chartered Bank (Taiwan) Taiwan 215Standard Chartered Bank (Thailand) Thailand 286Standard Chartered Bank (Hong Kong) Hong Kong 56State Bank of India India 17Suhyup Bank S.Korea 200Sumitomo Mitsui Financial Group Japan 4Sumitomo Trust and Banking Japan 18Suncorp-Metway Australia 67Suruga Bank Japan 120Syndicate Bank India 141

T Ta Chong Bank Taiwan 262Taichung Commercial Bank Taiwan 278

Taiko Bank Japan 221Taipei Fubon Commercial Bank Taiwan 115Taishin International Bank Taiwan 148Taiwan Business Bank Taiwan 118Taiwan Cooperative Bank Taiwan 58Taiwan Shin Kong Commercial Bank Taiwan 240Tajima Bank Japan 273Takinogawa Shinkin Bank Japan 297Thanachart Bank Thailand 255TMB Bank Thailand 194Tochigi Bank Japan 146Toho Bank Japan 128Tokushima Bank Japan 229Tokyo Shinkin Bank Japan 298Tokyo Star Bank Japan 180Tokyo Tomin Bank Japan 145Tomato Bank Japan 269Tottori Bank Japan 274Towa Bank Japan 184Trust and Custody Services Bank Japan 290

U UCO Bank India 164Union Bank of India India 127Union Bank of Taiwan Taiwan 256United Bank Pakistan 299United Bank of India India 252United Overseas Bank (Malaysia) Malaysia 245United Overseas Bank Singapore 31

V Vietnam Bank for Agriculture and Rural Development Vietnam 183Vietnam Bank for Foreign Trade Vietnam 249Vietnam Bank for Industry and Trade Vietnam 250

W Westpac Banking Corporation3 Australia 15Wing Hang Bank Hong Kong 190Wing Lung Bank Hong Kong 230Woori Financial Group S.Korea 19

Y Yachiyo Bank Japan 163Yamagata Bank Japan 176Yamaguchi Financial Group Japan 51Yamanashi Chuo Bank Japan 137Yuanta Commercial Bank Taiwan 257

77 Bank Japan 71

Bank-specifi c footnotes: • 1. Adelaide Bank and Bendigo Bank merged in November, 2008. • 2. Bank of Western Australia was acquired by Commonwealth Bank of Australia in December, 2008. • 3. Westpac Banking Corporation and St George Bank will complete their merger in late 2009. • 4. Aozora Bank and Shinsei Bank will merge in early 2010. • 5. Lippo Bank and Bank Niaga have been merged into Bank CIMB Niaga. • 6. HDFC Bank acquired Centurion Bank of Punjab.

ABJ ISS-92(PG1-47).indd 20ABJ ISS-92(PG1-47).indd 20 8/28/09 1:03:45 AM8/28/09 1:03:45 AM

21 ISSUE 92 The Asian Banker

ABJ ISS-92(PG1-47).indd 21ABJ ISS-92(PG1-47).indd 21 8/28/09 1:03:46 AM8/28/09 1:03:46 AM

22 ISSUE 92The Asian Banker

THE ASIAN BANKER

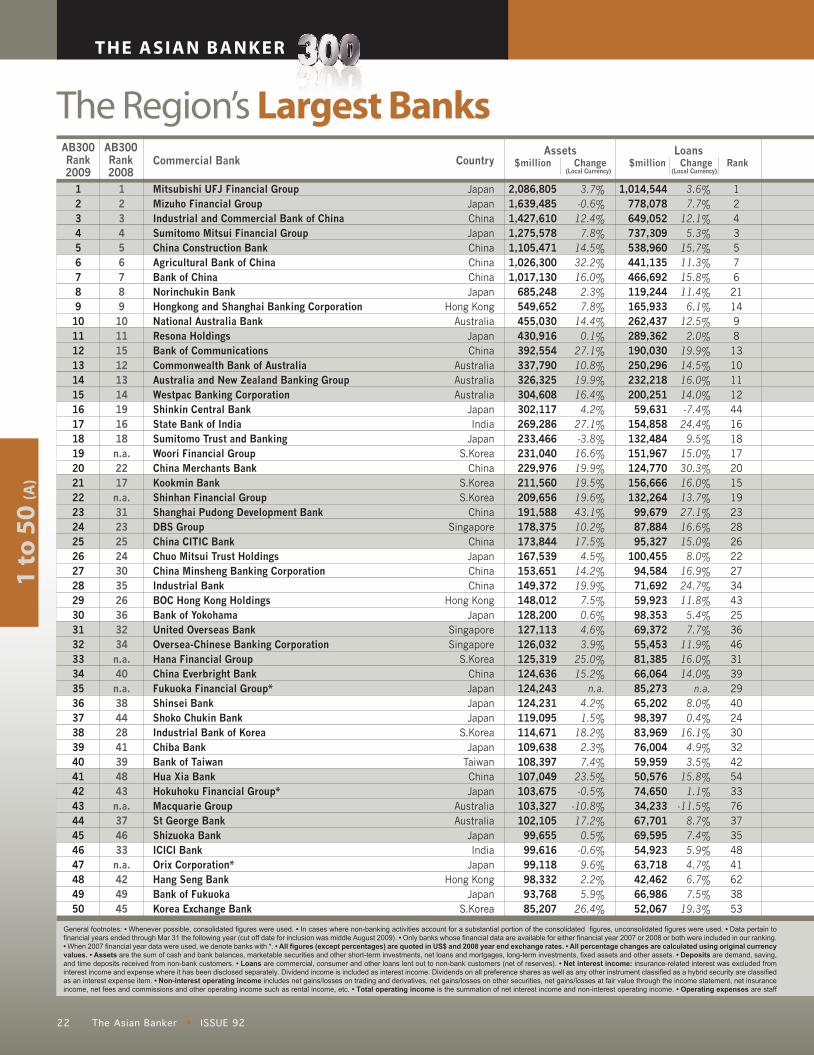

The Region’s Largest Banks

1 t

o 5

0 (A

)

2,086,8051,639,4851,427,6101,275,5781,105,4711,026,3001,017,130

685,248549,652455,030430,916392,554337,790326,325304,608302,117269,286233,466231,040229,976211,560209,656191,588178,375173,844167,539153,651149,372148,012128,200127,113126,032125,319124,636124,243124,231119,095114,671109,638108,397107,049103,675103,327102,105

99,65599,61699,11898,33293,76885,207

1,014,544778,078649,052737,309538,960441,135466,692119,244165,933262,437289,362190,030250,296232,218200,251

59,631154,858132,484151,967124,770156,666132,264

99,67987,88495,327

100,45594,58471,69259,92398,35369,37255,45381,38566,06485,27365,20298,39783,96976,00459,95950,57674,65034,23367,70169,59554,92363,71842,46266,98652,067

3.7%-0.6%12.4%7.8%14.5%32.2%16.0%2.3%7.8%14.4%0.1%27.1%10.8%19.9%16.4%4.2%27.1%-3.8%16.6%19.9%19.5%19.6%43.1%10.2%17.5%4.5%14.2%19.9%7.5%0.6%4.6%3.9%25.0%15.2%n.a.

4.2%1.5%18.2%2.3%7.4%23.5%-0.5%-10.8%17.2%0.5%-0.6%9.6%2.2%5.9%26.4%

3.6%7.7%12.1%5.3%15.7%11.3%15.8%11.4%6.1%12.5%2.0%19.9%14.5%16.0%14.0%-7.4%24.4%9.5%15.0%30.3%16.0%13.7%27.1%16.6%15.0%8.0%16.9%24.7%11.8%5.4%7.7%11.9%16.0%14.0%n.a.

8.0%0.4%16.1%4.9%3.5%15.8%1.1%

-11.5%8.7%7.4%5.9%4.7%6.7%7.5%19.3%

1243576

211498

131011124416181720151923282622273443253646313929402430324254337637354841623853

JapanJapanChinaJapanChinaChinaChinaJapan

Hong KongAustralia

JapanChina

AustraliaAustraliaAustralia

JapanIndia

JapanS.Korea

ChinaS.KoreaS.Korea

ChinaSingapore

ChinaJapanChinaChina

Hong KongJapan

SingaporeSingapore

S.KoreaChinaJapanJapanJapan

S.KoreaJapan

TaiwanChinaJapan

AustraliaAustralia

JapanIndia

JapanHong Kong

JapanS.Korea

General footnotes: • Whenever possible, consolidated figures were used. • In cases where non-banking activities account for a substantial portion of the consolidated figures, unconsolidated figures were used. • Data pertain to financial years ended through Mar 31 the following year (cut off date for inclusion was middle August 2009). • Only banks whose financial data are available for either financial year 2007 or 2008 or both were included in our ranking.• When 2007 financial year data were used, we denote banks with *. • All figures (except percentages) are quoted in US$ and 2008 year end exchange rates. • All percentage changes are calculated using original currency values. • Assets are the sum of cash and bank balances, marketable securities and other short-term investments, net loans and mortgages, long-term investments, fixed assets and other assets. • Deposits are demand, saving, and time deposits received from non-bank customers. • Loans are commercial, consumer and other loans lent out to non-bank customers (net of reserves). • Net interest income: insurance-related interest was excluded from interest income and expense where it has been disclosed separately. Dividend income is included as interest income. Dividends on all preference shares as well as any other instrument classified as a hybrid security are classified as an interest expense item. • Non-interest operating income includes net gains/losses on trading and derivatives, net gains/losses on other securities, net gains/losses at fair value through the income statement, net insurance income, net fees and commissions and other operating income such as rental income, etc. • Total operating income is the summation of net interest income and non-interest operating income. • Operating expenses are staff

Mitsubishi UFJ Financial GroupMizuho Financial GroupIndustrial and Commercial Bank of ChinaSumitomo Mitsui Financial GroupChina Construction BankAgricultural Bank of ChinaBank of ChinaNorinchukin BankHongkong and Shanghai Banking CorporationNational Australia BankResona HoldingsBank of CommunicationsCommonwealth Bank of AustraliaAustralia and New Zealand Banking GroupWestpac Banking CorporationShinkin Central BankState Bank of IndiaSumitomo Trust and BankingWoori Financial GroupChina Merchants BankKookmin BankShinhan Financial GroupShanghai Pudong Development BankDBS GroupChina CITIC BankChuo Mitsui Trust HoldingsChina Minsheng Banking CorporationIndustrial BankBOC Hong Kong HoldingsBank of YokohamaUnited Overseas BankOversea-Chinese Banking CorporationHana Financial GroupChina Everbright BankFukuoka Financial Group*Shinsei BankShoko Chukin BankIndustrial Bank of KoreaChiba BankBank of TaiwanHua Xia BankHokuhoku Financial Group*Macquarie GroupSt George BankShizuoka BankICICI BankOrix Corporation*Hang Seng BankBank of FukuokaKorea Exchange Bank

123456789

1011121314151617181920212223242526272829303132333435363738394041424344454647484950

123456789

101115121314191618n.a.2217n.a.31232524303526363234n.a.40n.a.38442841394843n.a.374633n.a.424945

AB300Rank2009

AB300Rank2008

Commercial Bank CountryAssets

$million ChangeLoans

$million Change Rank(Local Currency)(Local Currency)

ABJ ISS-92(PG1-47).indd 22ABJ ISS-92(PG1-47).indd 22 8/28/09 1:03:47 AM8/28/09 1:03:47 AM

23 ISSUE 92 The Asian Banker

123456789

1011121314151617181920212223242526272829303132333435363738394041424344454647484950

35,92019,69845,38623,74939,46830,87433,491-5,40316,032

8,5967,728

11,3079,5377,8947,543-467

10,4164,8225,4448,1266,5339,2125,0574,1735,9072,8085,0854,3533,2932,6283,6202,8682,2953,6141,9632,1101,4523,3331,688

8242,5772,0894,1442,3891,7317,7735,3093,0781,4582,724

23,19113,14316,31711,71814,33613,81516,721

1,2746,7434,9524,2373,7964,5593,8213,565

4945,4842,3263,2062,9763,5125,9761,8871,8861,9451,6402,2051,5402,6681,2271,4321,2831,8451,2181,2402,199

8451,383

959541

1,0681,0662,669

982953

5,8172,930

877892

1,113

-7.0%8.9%21.2%2.4%22.2%17.7%17.4%

-316.1%1.6%

-20.1%-4.7%23.1%8.3%5.8%7.7%

-144.3%19.4%7.6%-7.2%35.3%-9.3%-1.5%33.6%-2.2%44.4%-12.1%37.9%35.2%-6.3%1.5%7.9%0.5%

-20.3%23.2%n.a.

-22.3%-6.6%2.1%

-13.2%-80.5%23.5%1.1%

-14.7%7.3%9.0%10.1%-1.4%-6.3%-2.1%11.2%

3716254

3008

13179

111518

2981025211419122427203723263240293544305448733162

11342492843601622337139

-2.5%6.1%19.8%8.5%12.0%57.2%29.0%1.6%10.8%-0.6%-0.4%19.9%14.7%11.9%13.7%-5.3%11.0%4.0%9.0%41.7%5.1%89.8%32.4%-5.8%36.2%6.9%28.8%30.1%108.8%8.7%1.5%9.4%18.8%29.8%n.a.

16.5%4.1%5.4%0.9%

-85.8%26.6%3.4%

-27.9%4.3%4.3%4.2%7.0%2.2%6.1%5.6%

1,323,963850,463

1,203,208832,722932,888892,141746,702413,144348,630155,454353,805271,526182,696137,983119,944207,215203,653131,229127,924182,988128,820

83,496138,603118,023138,389

98,118114,976

92,530104,698111,936

82,11065,36974,21388,545

108,40766,25234,29932,36793,67881,41871,01491,91015,15039,79678,24650,626

n.a.76,37377,33343,425

-1.0%1.3%19.0%4.0%19.4%15.3%16.0%-3.4%4.5%10.2%1.5%20.4%20.4%13.9%13.6%1.0%30.7%0.3%38.2%32.5%14.2%20.1%23.4%11.1%20.2%9.0%17.1%25.3%1.5%1.9%10.5%6.0%16.9%11.9%n.a.

15.0%17.2%8.2%1.5%21.1%10.6%-0.4%38.6%18.9%1.3%-7.0%n.a.

8.3%3.2%36.4%

15263478

10169

1115192312132022142134172418292531282635474033274699

10330364432

174833762n.a.393872

21,62611,56638,48614,63132,90928,36223,840

-81110,047

7,4685,6079,6495,5055,4074,963

8355,9961,9184,9196,8605,8785,8434,6142,9955,2811,2434,4253,8322,6172,1022,5011,9432,4073,2681,6582,2371,3112,7731,624

7141,9741,488

6301,6961,4292,0151,3322,1051,2742,001

7.0%0.6%17.2%10.9%16.7%23.1%6.7%

-135.4%16.9%13.8%-2.6%22.1%12.9%7.4%14.4%17.2%23.3%7.6%19.2%38.3%4.8%11.7%30.4%4.6%37.9%8.8%33.9%25.6%4.5%3.4%20.4%23.7%11.6%25.7%n.a.

48.1%-8.3%13.6%4.4%38.3%20.0%-0.7%10.3%12.6%8.3%17.2%0.2%10.4%5.3%17.7%

5716234

3008

10159

161719891238201113142125186422232733283729244331582644

1043648

11442513455326135

expenses and other non-interest operating expenses. • Operating profit = net interest income + total non-interest operating income - total non-interest expenses + equity-accounted profit/ loss (operating) + change in fair value of own debt - loan impairment charge - other credit impairment charges. • Net profits are recorded after non-operating items, provisions and taxes and include minority interest. • Operating return on assets is the ratio of operating profits over average assets. • Return on assets and return on equity are net profit divided by average assets and total equity respectively. • Τhe Non interest income ratio is the ratio of non-interest operating income over total operating income. • In the change in operating and net profit columns, P-L: profit to losses; L-P: loss to profit; L-L: losses to losses; n.a.: not available or not meaningful • Total Capital Adequacy Ratio is the risk weighted capital ratio. Risk capital is the summation of Tier 1 and Tier 2 capital less investment in subsidiaries, where Tier 2 capital includes cumulative preference shares, revaluation reserves, subordinate and other long term debts. • Tier 1 Capital Ratio is the core capital ratio which includes common stock, disclosed reserves, retained earnings, and minority interest in equity or associates. • All data in this table are collected and updated to the best of our knowledge. • Weprovide this service with no warranty whatsoever as to the currency, accuracy, or applicability of the data for any purposes. • Due to an oversight in the bank screening process, six small banks from Japan, two from Korea and one from Hong Kong that do not fit the traditional criteria have been included in this listing. These banks will not be included in future print or online versions, and have been marked next to the far right column with a #.

AB300Rank2009

Operating Expenses$million Change

Deposits$million Change Rank

Total Operating Income$million Change Rank

Net Interest Income$million Change Rank

94,44246,13388,75950,81868,41142,51071,67727,46926,48919,49224,00121,96117,25417,79213,490

2,88315,40013,92911,36111,67313,83113,871

6,10214,04713,997

7,5867,8737,173

10,9067,8699,429

10,1437,3844,8626,4268,4577,5075,7295,9256,7444,0123,0936,5434,5107,1909,914

14,4265,9216,7865,307

162547389

1210111413228315192423212042171833313725322826355341303447433963764054362716443849

Shareholder’s Equity$million Rank

(Local Currency) (Local Currency) (Local Currency) (Local Currency)

ABJ ISS-92(PG1-47).indd 23ABJ ISS-92(PG1-47).indd 23 8/28/09 1:03:49 AM8/28/09 1:03:49 AM

24 ISSUE 92The Asian Banker

THE ASIAN BANKER

The Region’s Largest Banks

1 t

o 5

0 (B

)

6,372656

23,7273,556

19,8289,553

14,312-7,3738,7331,7711,4885,9474,3342,9743,332

-1,2403,6941,396

8864,5221,4162,4082,6261,7953,019

8671,9362,339

540368

1,6981,278

4501,476

402-1,611

-119869263256792714288

1,206396

1,0252,0131,807

143948

-46.6%-80.7%24.9%-63.2%19.8%-26.3%-0.3%P-L

-8.6%-66.0%-53.7%16.9%-4.4%-23.1%-5.6%P-L

28.0%-33.8%-63.3%31.3%-57.8%-57.1%42.2%-12.1%35.7%-44.9%17.5%29.8%-76.8%-70.4%-9.7%-23.5%-66.0%1.6%n.a.P-LP-L

-31.9%-70.4%-35.2%9.5%-1.2%-67.9%3.8%

-33.3%19.3%-19.2%-23.2%-72.1%-19.7%

6521

11243

2995

222479

1412

2951027388

261615211341191759812329662573

29627640

1091124548983076321820

15935

JapanJapanChinaJapanChinaChinaChinaJapan

Hong KongAustralia

JapanChina

AustraliaAustraliaAustralia

JapanIndia

JapanS.Korea

ChinaS.KoreaS.Korea

ChinaSingapore

ChinaJapanChinaChina

Hong KongJapan

SingaporeSingapore

S.KoreaChinaJapanJapanJapan

S.KoreaJapan

TaiwanChinaJapan

AustraliaAustralia

JapanIndia

JapanHong Kong

JapanS.Korea

General footnotes: • Whenever possible, consolidated figures were used. • In cases where non-banking activities account for a substantial portion of the consolidated figures, unconsolidated figures were used. • Data pertain to financial years ended through Mar 31 the following year (cut off date for inclusion was middle August 2009). • Only banks whose financial data are available for either financial year 2007 or 2008 or both were included in our ranking.• When 2007 financial year data were used, we denote banks with *. • All figures (except percentages) are quoted in US$ and 2008 year end exchange rates. • All percentage changes are calculated using original currency values. • Assets are the sum of cash and bank balances, marketable securities and other short-term investments, net loans and mortgages, long-term investments, fixed assets and other assets. • Deposits are demand, saving, and time deposits received from non-bank customers. • Loans are commercial, consumer and other loans lent out to non-bank customers (net of reserves). • Net interest income: insurance-related interest was excluded from interest income and expense where it has been disclosed separately. Dividend income is included as interest income. Dividends on all preference shares as well as any other instrument classified as a hybrid security are classified as an interest expense item. • Non-interest operating income includes net gains/losses on trading and derivatives, net gains/losses on other securities, net gains/losses at fair value through the income statement, net insurance income, net fees and commissions and other operating income such as rental income, etc. • Total operating income is the summation of net interest income and non-interest operating income. • Operating expenses are staff

Operating Profit$million Change RankCountry

Mitsubishi UFJ Financial GroupMizuho Financial GroupIndustrial and Commercial Bank of ChinaSumitomo Mitsui Financial GroupChina Construction BankAgricultural Bank of ChinaBank of ChinaNorinchukin BankHongkong and Shanghai Banking CorporationNational Australia BankResona HoldingsBank of CommunicationsCommonwealth Bank of AustraliaAustralia and New Zealand Banking GroupWestpac Banking CorporationShinkin Central BankState Bank of IndiaSumitomo Trust and BankingWoori Financial GroupChina Merchants BankKookmin BankShinhan Financial GroupShanghai Pudong Development BankDBS GroupChina CITIC BankChuo Mitsui Trust HoldingsChina Minsheng Banking CorporationIndustrial BankBOC Hong Kong HoldingsBank of YokohamaUnited Overseas BankOversea-Chinese Banking CorporationHana Financial GroupChina Everbright BankFukuoka Financial Group*Shinsei BankShoko Chukin BankIndustrial Bank of KoreaChiba BankBank of TaiwanHua Xia BankHokuhoku Financial Group*Macquarie GroupSt George BankShizuoka BankICICI BankOrix Corporation*Hang Seng BankBank of FukuokaKorea Exchange Bank

123456789

1011121314151617181920212223242526272829303132333435363738394041424344454647484950

123456789

101115121314191618n.a.2217n.a.31232524303526363234n.a.40n.a.38442841394843n.a.374633n.a.424945

-2,199-6,42016,274-3,48013,555

7,5289,641

-6,3067,0931,928

9804,1683,3412,2732,674

-2,0552,306

201467

3,0651,1581,6081,8311,4721,954-969

1,1461,666

38889

1,3371,251

3841,070

20-1,427

-9607141246449411621814159697

1,6621,819

320621

P-LP-L

35.2%P-L

34.0%17.5%6.2%P-L

-15.8%-47.4%-68.1%39.6%7.2%

-20.9%11.8%

P-L21.3%-79.2%-73.3%37.5%-46.1%-18.2%127.6%-12.9%60.5%

P-L23.6%32.6%-81.0%-88.5%-9.8%-16.0%-63.2%45.2%n.a.P-LP-L

-35.1%-72.6%-33.6%46.1%-4.6%-50.3%0.9%

-60.6%8.5%

-20.6%-24.2%54.9%-18.6%

295300

1298

243

2995

132567

119

2941097478

2218141912

292231657

16520215824

20629323838

1228251543627

1153117156835

Net Profit$million Change Rank

AB300Rank2009

AB300Rank2008

Commercial Bank(Local Currency) (Local Currency)

ABJ ISS-92(PG1-47).indd 24ABJ ISS-92(PG1-47).indd 24 8/28/09 1:03:50 AM8/28/09 1:03:50 AM

25 ISSUE 92 The Asian Banker

123456789

1011121314151617181920212223242526272829303132333435363738394041424344454647484950

-2.3%-13.8%19.2%-6.5%20.3%

n.a.14.0%

-21.1%24.1%

8.9%17.2%20.2%19.9%13.9%20.7%

-42.6%16.3%

1.4%3.9%

27.9%8.7%

11.4%35.9%

9.9%14.8%

-13.1%14.8%25.9%

3.3%1.1%

12.3%11.3%

5.1%25.3%

n.a.-14.7%

-0.1%11.1%

2.3%3.5%

16.8%12.3%

9.0%17.7%

2.1%7.2%

11.7%27.8%

5.6%11.7%

76.6%91.5%53.9%88.5%57.8%49.4%62.5%28.9%47.6%

168.8%81.8%70.0%

137.0%168.3%167.0%

28.8%76.0%

101.0%118.8%

68.2%121.6%158.4%

71.9%74.5%68.9%

102.4%82.3%77.5%57.2%87.9%84.5%84.8%

109.7%74.6%78.7%98.4%

286.9%259.4%

81.1%73.6%71.2%81.2%

226.0%170.1%

88.9%108.5%

n.a.55.6%86.6%

119.9%

4.5%2.8%6.2%4.0%6.2%4.1%7.0%4.0%4.8%4.3%5.6%5.6%5.1%5.5%4.4%1.0%5.7%6.0%4.9%5.1%6.5%6.6%3.2%7.9%8.1%4.5%5.1%4.8%7.4%6.1%7.4%8.0%5.9%3.9%5.2%6.8%6.3%5.0%5.4%6.2%3.7%3.0%6.3%4.4%7.2%

10.0%14.6%

6.0%7.2%6.2%

64.6%66.7%36.0%49.3%36.3%44.7%49.9%

n.a.39.6%57.6%54.8%33.6%47.8%46.9%47.3%

n.a.52.7%48.2%58.9%36.6%53.8%64.9%37.3%44.6%32.9%58.4%43.4%35.4%81.0%46.7%38.8%44.7%80.4%33.7%63.2%

104.2%58.2%41.5%56.8%64.1%41.5%51.0%63.6%41.1%55.1%74.8%55.2%28.5%61.2%40.8%

39.8%41.3%15.2%38.4%16.6%

8.1%28.8%

n.a.37.3%13.1%27.4%14.7%42.3%31.5%34.2%

n.a.42.4%60.2%

9.6%15.6%10.0%36.6%

8.8%28.2%10.6%55.7%13.0%12.0%20.5%20.0%30.9%32.3%

n.a.9.6%

15.5%n.a.

9.7%16.8%

3.8%13.4%23.4%28.8%84.8%29.0%17.4%74.1%74.9%31.6%12.6%26.6%

7.8%6.4%

11.0%8.2%

10.2%8.0%

10.8%9.6%

10.3%7.4%9.9%9.5%8.2%7.7%7.8%

15.0%n.a.

7.6%n.a.

6.6%9.9%

n.a.5.0%

10.1%12.3%

8.7%6.6%9.0%

10.9%9.6%

10.9%14.9%

7.7%6.0%5.1%6.0%7.7%7.4%

10.2%11.4%

7.5%7.5%

n.a.6.6%

13.8%10.3%

n.a. 9.5%9.2%8.8%

11.8%10.6%13.0%11.5%12.2%

9.4%13.4%15.6%13.4%10.9%13.5%13.5%11.6%11.1%10.8%22.9%

n.a.12.1%

n.a.11.3%13.2%

n.a.9.1%

14.0%14.3%12.1%

9.2%11.3%16.2%10.9%15.3%15.2%11.8%

9.1%8.8%8.4%8.9%

11.5%11.7%11.6%11.4%10.4%

n.a.10.4%14.1%14.7%

n.a. 12.5%11.1%12.7%

81.3%66.7%

150.0%69.6%

131.8%65.1%

118.5%90.0%80.0%

133.3%65.4%

115.8%250.0%200.0%175.0%

83.3%n.a.

87.5%150.0%227.3%130.8%

n.a.191.7%100.0%142.9%

43.8%150.0%237.5%100.0%

37.4%110.0%111.8%168.3%150.0%

58.1%69.6%70.3%

126.7%40.2%64.4%

155.6%39.1%44.8%

200.0%38.6%52.8%

n.a.60.0%

n.a.141.7%

1.6%1.8%2.0%2.3%2.2%4.3%2.7%2.0%1.0%0.6%2.6%1.9%0.2%0.5%0.4%0.6%

n.a.1.6%1.2%1.1%1.3%

n.a.1.2%1.5%1.4%1.6%1.2%0.8%0.5%3.3%2.0%1.7%1.2%2.0%5.3%4.6%3.7%1.5%2.2%0.9%1.8%3.8%2.9%0.2%3.3%3.6%n.a.

1.0%n.a.

1.2%

-0.1%-0.4%1.2%

-0.3%1.3%0.8%1.0%

-1.0%1.3%0.5%0.2%1.2%1.0%0.8%1.0%

-0.7%1.0%0.1%0.2%1.5%0.6%0.8%1.2%0.8%1.2%

-0.6%0.8%1.2%0.3%0.1%1.1%1.0%0.3%0.9%

n.a.-1.1%0.0%0.6%0.1%0.2%0.5%0.4%0.5%0.9%0.2%0.7%1.7%1.9%0.4%0.8%

0.3%0.0%1.7%0.3%1.9%1.1%1.5%

-1.1%1.6%0.4%0.3%1.7%1.3%1.0%1.2%

-0.4%1.5%0.6%0.4%2.2%0.7%1.2%1.7%1.0%1.9%0.5%1.3%1.7%0.4%0.3%1.3%1.0%0.4%1.3%

n.a.-1.3%-0.1%0.8%0.2%0.3%0.8%0.7%0.2%1.3%0.4%1.0%2.1%1.9%0.2%1.2%