ABC TRANSPORT PLC - Trombino

77

ABC TRANSPORT PLC ANNUAL REPORT AND ACCOUNTS 31 DECEMBER 2014

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of ABC TRANSPORT PLC - Trombino

ABC TRANSPORT PLC

ANNUAL REPORT AND ACCOUNTS31 DECEMBER 2014

ANNUAL REPORT AND ACCOUNTSFOR THE YEAR ENDED 31 DECEMBER 2014

INDEX Page

Corporate information i

Report of the Directors ii - v

Independent Auditors' Report 1

Consolidated and separate statements of profit or loss 2

Consolidated and separate statements of other comprehensive 3

Consolidated and separate statements of financial position 4

Consolidated and separate statements of changes in equity 5

Consolidated and separate statements of cash flows 6

Notes to the Financial Statements 7 - 64

Statement of value added – Group 65

Statement of value added – Company 66

Five year financial summary – Group 67

Five year financial summary – Company 68

ABC TRANSPORT PLC

ABC TRANSPORT PLC

COMPANY REGISTRATION NUMBER 219970

DIRECTORS, OFFICERS AND PROFESSIONAL ADVISERS

DIRECTORS: Mr. Olumide Obayomi - ChairmanMr. Frank Nneji - Managing DirectorMr. Jude Nneji - Deputy Managing DirectorMrs. Uche Ohimai-Ehimiahe - Non-Executive DirectorAlh. Kabiru Yusuf - Non-Executive DirectorMr. John Okoro - Non-Executive Director

SECRETARY/LEGAL:ADVISER Vivian C. Okpe

REGISTERED KM 5, MCC/Uratta Road, Umuoba UrattaOFFICE: P.O. BOX 2575, Owerri Imo State

Tel: 080396600958, 08053002000,Fax: 083-231275E-mail: [email protected]

AUDITORS: PKF Professional ServicesPKF House, 205A ObanikoroIkorodu Road, Lagos. Nigeria

PRINCIPAL Fidelity Bank PlcBANKERS: Zenith Bank Plc

Diamond Bank PlcGuaranty Trust Bank Plc

REGISTRAR First Registrars Nigeria LimitedPlot 2, Abebe Village RoadIganmu, Lagos

i

ABC TRANSPORT PLC

REPORT OF THE DIRECTORSFOR THE YEAR ENDED 31 DECEMBER 2014

1 RESULT Group Company N’000 N’000

(Loss)/profit for the year after taxation #REF! #REF!

2 LEGAL FORM

3 PRINCIPAL ACTIVITIES

4 DIRECTORS AND DIRECTORS’ INTERESTS

5 DIRECTORS’ RESPONSIBILITIES

- proper accounting records are maintained;

- applicable accounting standards are followed;- suitable accounting policies are adopted and consistently applied;- judgments and estimates made are reasonable and prudent; and

The Directors submit their report together with the audited financial statements forthe year ended 31 December 2014.

- Internal control procedures are instituted which, as far as is reasonablypossible, safeguard the assets and prevent and detect fraud and other irregularities.

ABC Transport Plc was incorporated as a Private Limited Company on April 5, 1993and was converted to a Public Limited Liability Company on November 21, 2005. Theshares were quoted on the Nigerian Stock Exchange on December 20, 2006. Asapproved by the Shareholders at the Annual General Meeting of August 12th 2011,the Company’s name was changed from Associated Bus Company Plc to ABCTransport Plc in 2011.

No Director has any disclose-able interest in contracts in which the company wasinvolved during the year under review.

The Directors are responsible for the preparation of the financial statements whichgive a true and fair view of the state of affairs of the Company at the end of eachfinancial year and of the profit or loss for that period and which comply with theCompanies and Allied Matters Act CAP C20 LFN 2004. In doing so they ensure that:

- internal control procedures are instituted which as far as is reasonablypossible, safeguard the assets and prevent and detect fraud and other irregularities;

- the going concern basis is used, unless it is inappropriate to presume thatthe Company will continue in business.

Principal activity of the company is road transportation. It provides both long and short haulbus services; consolidated cargo and haulage services within Nigeria and West African sub-region

ii

ABC TRANSPORT PLC

REPORT OF THE DIRECTORS (continued)

6 DIRECTORS’ SHAREHOLDING AS AT 31 DECEMBER 2014:

Name Direct IndirectMr. Olumide Obayomi - 100,000 - 5,200,000Mr. Frank Nneji - 560,000,000 - -Mr. Jude Nneji - 12,000,000 - -Alhaji Kabiru Yusuf - 1,000,000 - -(Rep: Mrs. Uche Ohimai-Ehimiahe) 15,401,203 - 258,661,359Mr. John Okoro - 765,386 - -

7 PROPERTY, PLANT & EQUIPMENT

8 POST BALANCE SHEET EVENTS

9 MAJOR SUPPLIERS:The Company’s significant local suppliers are:

Conoil Company LimitedEterna Oil Nig. PlcCummins West Africa LtdMcquintus LtsMichelin Tyre Co. LtdPalm Petroleum LtdLeventis Nig. Ltd

10 DONATIONS

NUNAA Owerri Branch Outstanding Donation - 1,000,000Ascend Foundation book Launch - 20,000Corporate Gifts - 961,000Donation to Fadeyi Youths - 284,000Ogunsakin Ben Tosin book Launch - 10,000

2,275,000

Staff Wedding, Gifts & Condolence/Burial Assistance 3,456,274

There are no significant post balance sheet events which have not been provided for in theseaccounts.

The following amounts have been given by way of donations and gifts during the year underreview.

There was no donation or gift made to any political party, political association or for any politicalpurpose in the course of the year under review.

Holdings

Movements in property,plant and equipment during the year are shown in Note 15 to thefinancial statements.

iii

ABC TRANSPORT PLC

REPORT OF THE DIRECTORS (continued)

11 EMPLOYMENT AND EMPLOYEES

1. Employment and Employees

2. Employment of Disabled Persons

3. Work Environment

4. Employee Involvement, Development and Training

Employees are adequately rewarded and motivated to achieve results.

5. Health, safety at work and welfare of employees

Career development of each employee and succession planning are major priorities ofthe company. The employees of the company attend short and long term trainingprogrammes which are tailored to meet the needs of both the employee and company.

The company considers the health, safety and welfare of its employees of paramountimportance. In demonstration of this, the company has a group life insurance policy,pension scheme and has retained the services of healthcare providers across variouslocations. Safety standards are adhered to in the workplace. The employees of thecompany are currently enrolled by the company to the National Health InsuranceScheme.

ABC Transport Plc is an equal opportunity employer concerned with the retention of staffand strives to remain the employer of choice within the road transport sector. Thecompany provides a total compensation package that enables it to attract and retainhighly skilled and qualified employees while recognizing the need to mange payrollcosts.

The Company has reviewed its employment policy in line with the needs of the business.A policy of the Company stipulates that there should be no discrimination in consideringapplications for employment including those from disabled persons. All employeeswhether or not disabled are given equal opportunities to develop. As at 31 December2014, ABC Transport Plc had a total of three (3) persons in its employment.

The Company endeavours to ensure a safe working environment for its employees.Health and safety regulations are in force within the Company’s premises andemployees are aware of existing regulations. Subsidies are provided to all levels ofemployees for medical, transportation, housing etc

Training workshops and seminars are organized regularly for employees at all levels.The Company is committed to keeping employees informed regarding its progress andperformance and the views of the employees are sought particularly with respect tomatters which directly affect them.

The company places considerable value in the involvement of its employees in theattainment of its goals and has continued to keep them as fully informed as possibleregarding the company’s performance and progress. Formal meetings are held amongststaff within the operational zones and suggestions and opinions of employees aresought and considered on the general operations of the company as well as mattersaffecting them employees.

iv

ABC TRANSPORT PLC

REPORT OF THE DIRECTORS (continued)

6. Safety Policy

11 AUDITORS

BY ORDER OF THE BOARD

Vivian C. OkpeCompany Secretary/Legal Adviser

Imo State, Nigeria.18th March 2015

ABC Transport Plc places a premium on the safety of its passengers and crew whilein transit. To this end, the company organizes quarterly safety re-orientation andtraining programmes for its crew. All the vehicles in our fleet are fitted with trackingdevices which monitor speed as the movement of the vehicles. For the period underreview, the accident rate of the company’s fleet was well within acceptable limits,with a large number of the recorded accidents attributable to the errors andmiscalculations of other road users.

At the Annual General Meeting of 2014, upon the retirement of the then externalauditors (Messer Akintola Williams Deloitte). A resolution to appoint PKFProfessional Services as the company's Auditors was propopsed and duly passed. Aresolution will be proposed authorising the Directors to determine their remuneration.

v

INDEPENDENT AUDITORS' REPORTTO THE MEMBERS OF ABC TRANSPORT PLC

Report on the Consolidated Financial Statements

Directors’ Responsibility for the Financial Statements

Auditors’ Responsibility

Opinion

Olatunji O. Ogundeyin, FRC/2013/ICAN/02224For: PKF Professional ServicesChartered AccountantsLagos, NigeriaDate: 25 March 2015

The company and its subsidiaries have kept proper books of account which are in agreement with theconsolidated financial position and statements of comprehensive income as it appears from ourexamination of their records.

In our opinion, the consolidated financial statements present fairly, in all material respects the consolidatedfinancial position of ABC Transport Plc (“the Company”) and its subsidiaries (together “the Group”)at 31 December 2014, and of their financial performance and cash flows for the year then ended, inaccordance with the Companies and Allied Matters Act, Cap C20, LFN 2004 and in the manner required bythe International Financial Reporting Standards in compliance with the Financial Reporting Council ofNigeria Act, No 6, 2011.

We have audited the accompanying consolidated financial statements of ABC Transport Plc, (theCompany”) and its subsidiaries (together “the Group”) which comprise the consolidated statements offinancial position at 31 December 2014, the consolidated income statements, consolidated statements ofchanges in equity, consolidated statements of cash flows for the year ended, a summary of significantaccounting policies, and other explanatory information.

The Directors are responsible for the preparation and fair presentation of these consolidated financialstatements in accordance with the Companies and Allied Matters Act, Cap C20, LFN 2004 and in themanner required by the International Financial Reporting Standards in compliance with the FinancialReporting Council of Nigeria Act, No 6, 2011, and for such internal control as the Directors determine arenecessary to enable the preparation of consolidated financial statements that are free from materialmisstatement whether due to fraud or error

Our responsibility is to express an opinion on these consolidated financial statements based on our audit.We conducted our audit in accordance with International Standards on Auditing. Those standards requirethat we comply with ethical requirements and plan and perform the audit to obtain reasonable assuranceabout whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in theconsolidated financial statements. The procedures selected depend on the auditors’ judgment, includingthe assessment of the risks of material misstatement of the consolidated financial statements, whether dueto fraud or error. In making those risk assessments, the auditors consider internal control relevant to theentity’s preparation and fair presentation of the consolidated financial statements in order to design auditprocedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion onthe effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness ofaccounting policies used and the reasonableness of accounting estimates made by the Directors, as wellas evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for ouraudit opinion.

1

1

ABC TRANSPORT PLC

CONSOLIDATED STATEMENTS OF PROFIT OR LOSSFOR THE YEAR ENDED 31 DECEMBER 2014

2014 2013 2014 2013Continuing operations Notes N'000 N'000 N'000 N'000

Revenue 6.1 7,347,873 6,656,947 6,846,024 6,636,859Cost of sales #REF! #REF! #REF! #REF!

Gross profit #REF! #REF! #REF! #REF!

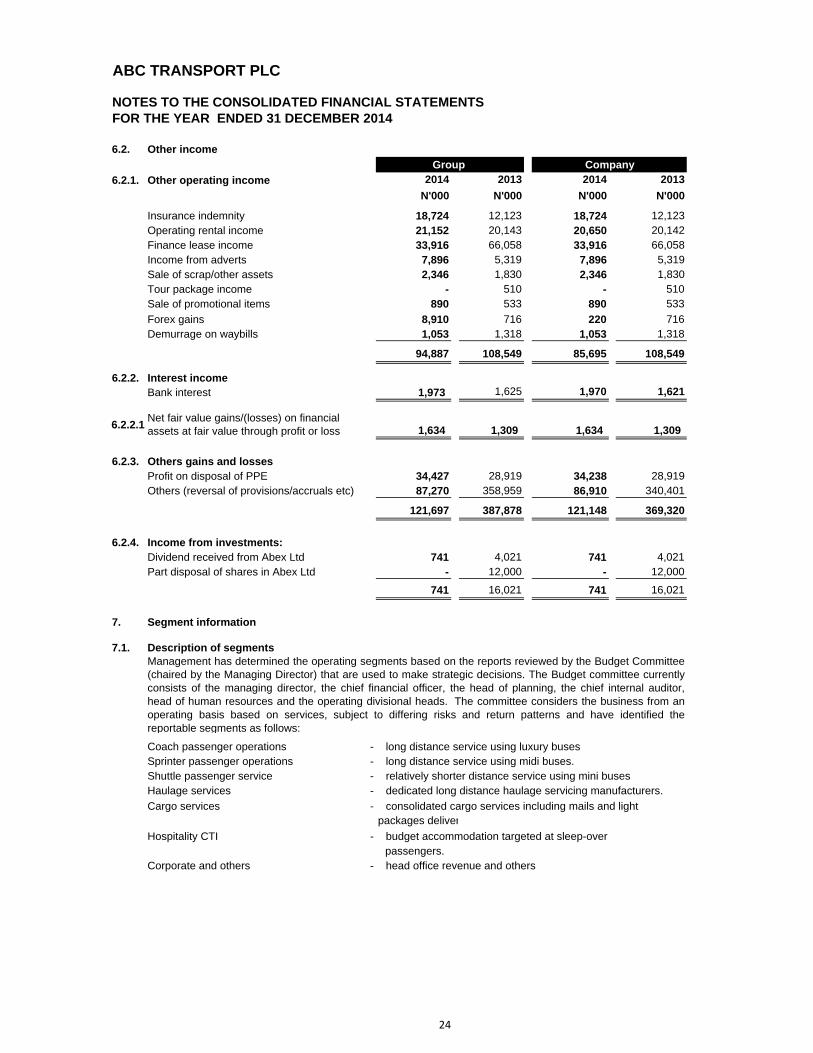

Administrative expenses #REF! #REF! #REF! #REF!Other operating income 6.2.1. 94,887 108,549 85,699 108,549Interest income 6.2.2. 1,973 1,625 1,970 1,621Net fair value gains/(losses) on financial assets atfair value through profit or loss 6.2.2.1 1,634 1,309 1,634 1,309

Income from investments 6.2.4. 741 16,021 741 16,021Impairment losses 9. (9,883) (14,479) (9,883) (14,479)Other gains and losses 6.2.3. 121,697 387,878 121,148 369,320Finance costs 10. (444,442) (243,158) (414,011) (243,158)

(Loss)/profit before tax #REF! #REF! #REF! #REF!

Income tax expenses 11. (113,253) (216,258) (113,264) (213,725)

(Loss)/profit from continuing operations #REF! #REF! #REF! #REF!

Attributable to:Equity shareholders #REF! #REF! #REF! #REF!Non-controlling interests (51,029) (10,977) - -

#REF! #REF! #REF! #REF!

Basic and diluted (loss)/earnings per share(Kobo) 12.1. #REF! #REF! #REF! #REF!

Group Company

2

ABC TRANSPORT PLC

CONSOLIDATED AND SEPARATE STATEMENTS OF OTHER COMPREHENSIVE INCOMEFOR THE YEAR ENDED 31 DECEMBER 2014

2014 2013 2014 2013Notes N'000 N'000 N'000 N'000

(Loss)/profit for the year #REF! #REF! #REF! #REF!

Items that may be reclassified subsequentlyto profit or loss

Foreign exchange translation gains/losses, net of tax 25. 2,055 (2,580) - -

Net actuarial losses on defined benefit plans, net of tax 30. (14,734) (33,920) (14,154) (33,806)

Other comprehensive loss (12,679) (36,500) (14,154) (33,806)

Total comprehensive (loss)/ income for the year #REF! #REF! #REF! #REF!

Attributable to:

Equity shareholders #REF! #REF! #REF! #REF!Non-controlling interests 27. (51,150) (11,016) - -

#REF! #REF! #REF! #REF!

Group Company

3

ABC TRANSPORT PLCCONSOLIDATED STATEMENTS OF FINANCIAL POSITIONFOR THE YEAR ENDED 31 DECEMBER 2014

2014 2013 2014 2013Non-current assets Note N'000 N'000 N'000 N'000Deferred tax asset 11.3 60,543 59,864 59,864 59,864Intangible assets 14. 21,046 17,308 21,046 17,308Property, plant and equipment 15. 4,403,699 3,733,804 4,407,840 3,737,954Investment in subsidiaries 16. - - 11,520 6,520Other investments 17. 1,845 1,845 1,845 1,845Financial assets - FVTPL 17.2. 18,093 16,459 18,093 16,459Finance lease receivables 18. 16,987 62,263 16,987 62,263

4,522,213 3,891,543 4,537,195 3,902,213Current assetsInventories 19. 995,647 291,693 185,976 208,526Finance lease receivables 18. 13,096 36,415 13,096 36,415Trade and other receivables 20. 491,778 526,944 594,941 438,605Other assets 21 329,051 733,439 300,992 1,021,291Cash and bank balances 23. 84,074 152,234 47,278 107,570

1,913,646 1,740,725 1,142,283 1,812,407

Non- current assets held for sale 22. - - - -

Total assets 6,435,859 5,632,268 5,679,478 5,714,620

Equity and reservesIssued share capital 24.1 753,500 753,500 753,500 753,500Share premium 24.2 582,068 582,068 582,068 582,068Retained earnings 26.1 #REF! #REF! #REF! #REF!Other comprehensive income reserve 25. (67,884) (55,467) (58,284) (44,130)

Shareholder's fund #REF! #REF! #REF! #REF!Non-controlling interests 27. (58,544) (7,394) - -

Total equity and reserves #REF! #REF! #REF! #REF!

Non-current liabilitiesLong-term borrowings 28. 875,754 876,043 875,754 876,043Finance lease obligations 29. 62,075 118,374 62,075 118,374Post employment benefits - defined benefits 30.1. 238,873 211,393 236,876 210,455Provisions 31. 38,035 36,204 38,035 36,204Deferred tax 11.3 - - - -

1,214,737 1,242,014 1,212,740 1,241,076Current liabilitiesShort term borrowings 28. 1,467,903 857,652 804,882 857,652Finance lease obligations 29. 128,520 156,018 128,520 156,018Post employment benefits - defined contribution 30.1. 127,821 63,367 127,821 63,367Current taxation liabilities 11.2 231,947 231,297 231,279 229,861Trade and other payables 32. 1,106,447 664,642 992,076 663,999Deferred income 33. 15,529 29,052 15,529 29,052Bank overdrafts 23.1 339,823 108,912 159,874 108,912

3,417,990 2,110,940 2,459,981 2,108,861

Total liabilities 4,632,727 3,352,954 3,672,721 3,349,937Total equity and liabilities #REF! #REF! #REF! #REF!

………………………………………………………………………………………….} Chairman FRC/2013/………………………………………}

………………………………………………………………………………………….} Managing Director/CEO FRC/2013/…………………….}

………………………………………………………………………………………….} Chief Financial Officer FRC/2013/………………………

The accounting policies and explanatory notes on pages 8 to 64 form part of these financial statements

Group Company

The financial statements on pages 2 to 64 were approved by the Board of Directors on 25 March 2015 and signed on itsbehalf by:

4

ABC TRANSPORT PLCCONSOLIDATED STATEMENTS OF CHANGES IN EQUITYFOR THE YEAR ENDED 31 DECEMBER 2014

I. Group Issued Nonshare Share Retained OCI controlling

capital premium earnings reserves interests TotalN'000 N'000 N'000 N'000 N'000 N'000

1 January 2013 753,500 582,068 886,462 (19,006) 3,622 2,206,646

Changes in equity for 2013:(Loss)/loss for the year - - #REF! - (10,977) #REF!Translation loss - - - (2,554) (26) (2,580)Actuarial loss - - - (33,907) (13) (33,920)Dividends relating to 2013 paid during the year - - (195,910) - - (195,910)

31 December 2013 753,500 582,068 #REF! (55,467) (7,394) #REF!

1 January 2014 753,500 582,068 #REF! (55,467) (7,394) #REF!

Changes in equity for 2014:Profit/(loss) for the year - - #REF! - (51,029) #REF!Dividends relating to 2014 paid during the year - - (90,420) - - (90,420)Translation gain/(loss) - - - 2,035 20 2,055Actuarial loss - - - (14,452) (141) (14,593)

31 December 2014 753,500 582,068 #REF! (67,884) (58,544) #REF!

II. Company Issued share Share Retained OCIcapital premium earnings reserves Total

N'000 N'000 N'000 N'000 N'000

1 January 2013 753,500 582,068 914,061 (10,324) 2,239,305

Changes in equity for 2013:Profit/(loss) for the year - - #REF! - #REF!Other comprehensive income - - - (33,806) (33,806)Dividends relating to 2013 paid during the year - - (195,901) (195,901)

31 December 2013 753,500 582,068 #REF! (44,130) #REF!

1 January 2014 753,500 582,068 #REF! (44,130) #REF!

Changes in equity for 2014:(loss)/profit for the year - - #REF! - #REF!Other comprehensive income - - - (14,154) (14,154)Dividends relating to 2014 paid during the year - - (90,420) - (90,420)

31 December 2014 753,500 582,068 #REF! (58,284) #REF!The above consolidated and separate statement of changes in equity should be read in conjunction with the accompanyingnotes.

5

ABC TRANSPORT PLC

CONSOLIDATED STATEMENTS OF CASH FLOWSFOR THE YEAR ENDED 31 DECEMBER 2014

2014 2013 2014 2013Note N'000 N'000 N'000 N'000

Cash flows from operating activitiesCash received from customers, staff andrelated parties 7,383,039 6,128,407 6,689,688 6,259,148Cash paid to suppliers and others (5,830,220) (5,233,108) (4,312,681) (5,377,154)

Cash generated from operations 1,552,819 895,299 2,377,007 881,994Income tax paid (79,750) (101,793) (79,478) (97,909)

Net cash from operating activities 34. 1,473,069 793,506 2,297,529 784,085

Cash flows from investing activities:Investments in financial assets 1,634 1,309 1,634 1,309Purchase of property, plant and equipment 15. (1,941,683) (1,172,114) (1,922,029) (1,171,796)Other movement in PPE 61,130 - 64,778 -Purchase of intangible assets (12,854) (14,237) (12,854) (14,237)Additional investment in subsidiaries - - (5,000) -Proceeds from investments 741 16,021 741 16,021Proceeds on sale of property plant and equipment

73,675 145,366 73,486 145,366

Cash received from investment in finance leases 32,230 84,603 32,230 84,603

Net cash used in investing activities (1,785,127) (939,052) (1,767,014) (938,734)

Cash flows from financing activities:Additional borrowings taken 1,631,035 1,232,880 945,821 1,232,880Repayment of borrowings (999,365) (849,242) (999,362) (849,983)Additional finance leases 124,150 147,185 124,150 147,185Repayment of finance lease obligations (207,947) (138,914) (207,947) (139,048)Interest repaid (444,442) (243,158) (414,011) (243,158)Dividends paid to the company's shareholders (90,420) (195,910) (90,420) (195,910)

Net cash from/ (used in) financing activities 13,011 (47,159) (641,769) (48,035)

Net decrease in cash and cash equivalents (299,047) (192,705) (111,254) (202,684)

Cash and cash equivalents at 1 January 43,298 236,003 (1,342) 201,342

Cash and cash equivalents at 31 December 23. (255,749) 43,298 (112,596) (1,342)

Group Company

6

ABC TRANSPORT PLCNOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2014

1. General information1.1. The Group

1.2. Going concern

2.1 Statement regarding status of compliance with IFRSs

2.2 Basis of preparation

3. Statement of significant accounting policiesThe following are the significant accounting policies adopted by the Group:

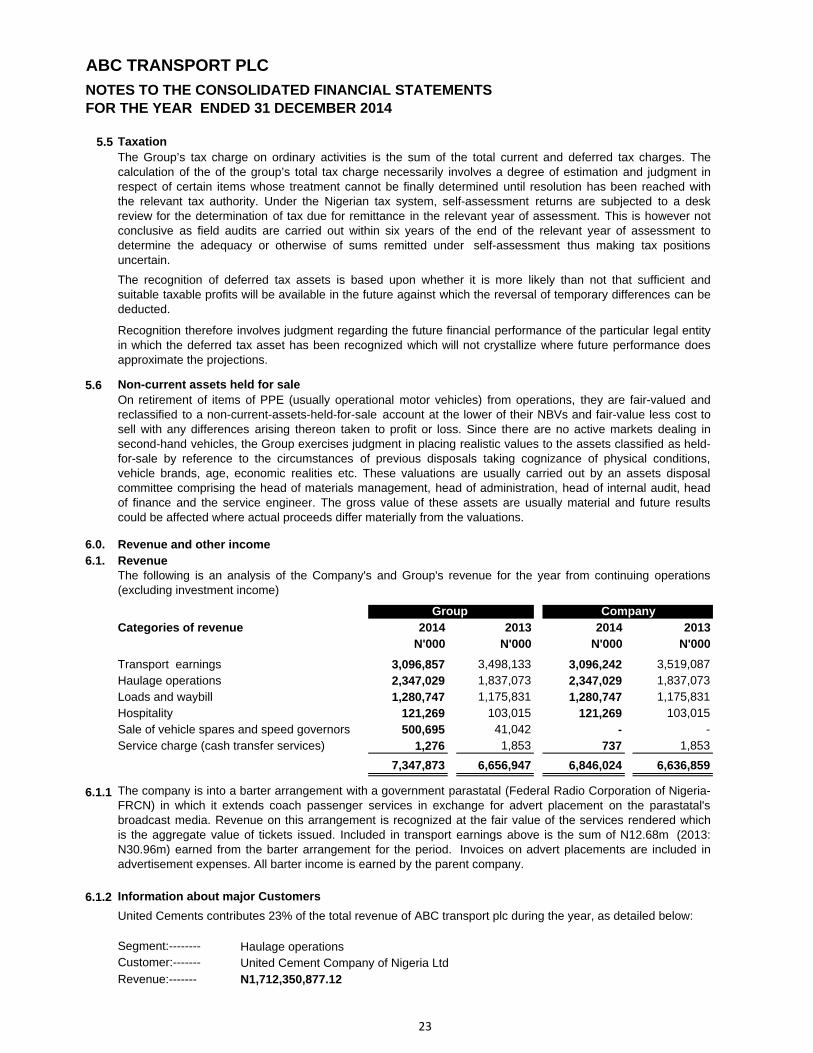

3.1 Revenue

The consolidated financial statements have been prepared in accordance with International Financial ReportingStandards.

Revenue is measured at the fair value of the consideration received or receivable in respect of passengeroperation, cargo services, haulage, hire services and hospitality business.

Revenue received in advance (advance bookings) is treated as a liability, until the service is rendered. Revenuefor cargo items not yet delivered to destination as at the reporting date is equally treated as a liability while allattributable revenue on delivered loads (haulage and cargo) at the end of the reporting period are included inrevenue irrespective of when they are invoiced to the customer.

ABC Transport Plc was incorporated in Nigeria in April 1993 with registered office at Km 5, MCC/Uratta Road,Umuoba Uratta, P.O. Box 2575, Owerri, Imo State. The company’s primary business is road passengertransportation between major cities in the South, North Central and Abuja.In July 2004, the company commenced road passenger transportation on the West Coast between Lagos, Nigeriaand Accra, Ghana. ABC Transport Ghana in which ABC Transport Plc owns a 99% equity stake wasincorporated in 2007 to provide transport services within Ghana and to offer passenger and cargo handlingservices to ABC Transport Plc. ABC Transport Plc is also involved in cargo business across the road passengernetwork and hospitality business at its City Transit Inn (CTI), Abuja. Haulage activities picked up actively for thecompany in the year 2010.

The company is listed on the Nigerian Stock Exchange (NSE) and is required to prepare its consolidated financialstatements in accordance with the International Financial Reporting standards (IFRS) set by the InternationalAccounting Standards Board (IASB) and adopted by the Federal Republic of Nigeria, under the regulation of theFinancial Reporting Council of Nigeria with effective date of transition to IFRS on 1st January 2011.

The financial statements are prepared on the historical cost basis of accounting other than for certain items ofproperty, plant and equipment that have been stated at deemed cost under the transition rules of IFRS. Certainfinancial instruments are measured at fair value.

The consolidated financial statements are presented in thousands Naira, which is the functional currency of theeconomic environment in which the entity operates.

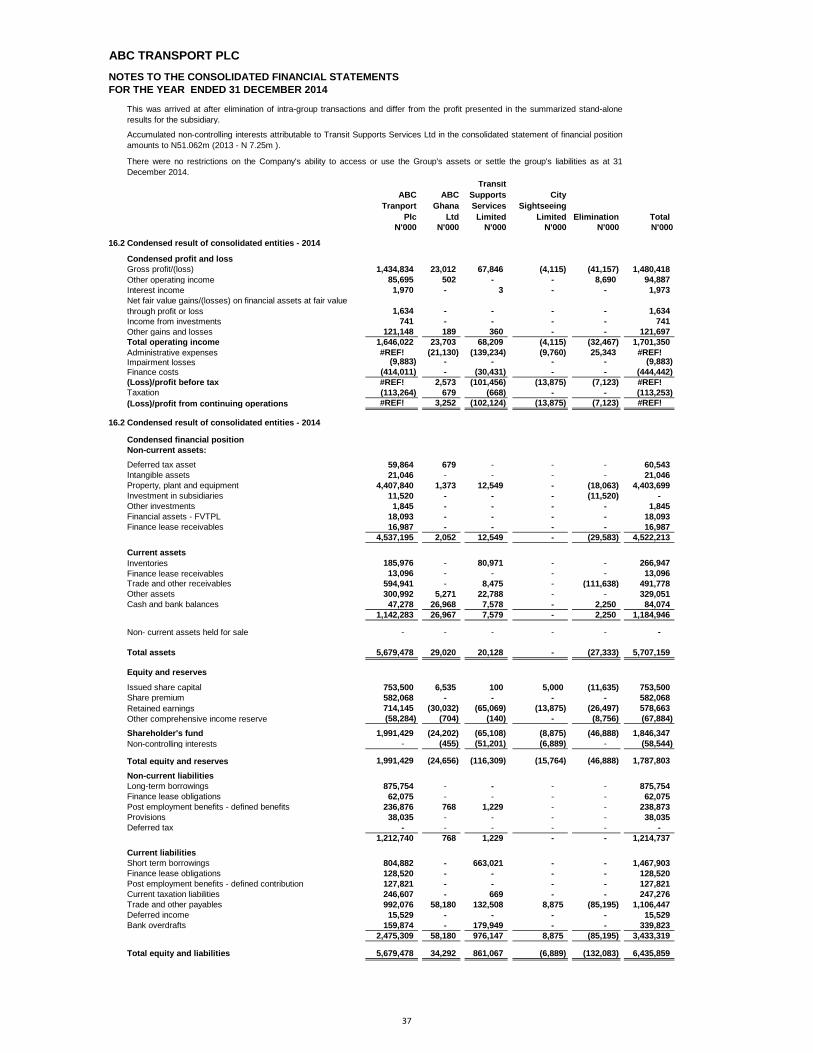

ABC Transport Plc which became a public liability company in 2005 equally owns 50% equity stake in TransitSupports Services Ltd, a trading company engaged in the importation and sales of vehicle spares and installationof motor vehicle speed governing devices, and a 5% stake in ABC Express Courier (ABEX) Ltd. In October2014,Transit Supports Services Ltd commenced the assembly of heavy duty trucks under the automotive policy ofthe Federal Government of Nigeria. The assembly is carried out in partnership with the Shanxi Group ofChina(owners of the SHACMAN franchise) and the Anambra Motor Manufacturing Company of Nigeria.

The Group's management has made an assessment of the Group's ability to continue as a going concern. Whilethe management is satisfied that ABC Transport Plc, ABC Transport Ghana Ltd and Transit Supports Serviceshave the resources and business prospects to continue in business for the forseeable future, however, thebusiness of a new subsidiary, City Sightseeing Ltd floated within the year was suspended because of lowpatronage due to security challenges in the northern part of Nigeria where it was designed to operate. CitySightseeing Ltd ceased operations in December 2014 having operated for only three months. It was resolved thatthe assets and liabilities of City Sightseeing Ltd be acquired by the parent company with effect from December2014 and the financial statements have been prepared on this basis.

The Company floated a new fully owned subsidiary, City SightSeeing Nig. Ltd within the period. City SightSeeingLtd which commenced operations in August 2014 operates a dedicated tour service that takes tourists throughmajor sites attraction in Abuja using specially designed state-of-the-art tour buses

7

ABC TRANSPORT PLCNOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2014

3.2. Customer loyalty programme

3.3. Property, plant and equipment

Useful livesLuxury buses and trucks 5 - 7 yearsTrailer beds 7 - 10 yearsShuttle buses 2 - 5 yearsPool buses 4 - 6 yearsComputers 3 - 5 yearsFurniture and equipment 4 - 5 yearsBuildings 15 - 20 years

Depreciation commences when assets are available for use.

Major refurbishments and renovations are capitalized as part of the item of the property, plant andequipment and are depreciated over the remaining useful lives of the assets. Depreciation is provided onthe cost of assets less any residual value over their estimated useful lives, using the straight-line method, asfollows:

Proceeds from the disposal of property, plant and equipment are excluded from revenue, they form part ofother income as gains or losses from disposal of property, plant and equipment. Gains or losses on theremeasurement of non-current assets classified as held for sale that does not meet the definition ofdiscontinued operations are included in profit or loss from continuing operations.

On presentation of 11 manual tickets or 10 e-tickets, a customer is awarded a free ticket for the next travel,hence revenue from passenger operation (coach) is regarded as a multiple-component sales i.e thecomponents being revenue and award credit.

The Group grants award credits for each sale/travel which is accumulated for each passenger up to thenumber required for redemption of the award. The consideration initially received for each travel is allocatedbetween revenue and the award credit. The consideration allocated to award credits represents the amountthat the entity has received for accepting an obligation to supply awards if customers redeem the credits.This amount reflects both the value of the awards and the Group’s expectations regarding the proportion ofcredits that will be redeemed, i.e. the risk of a claim being made. A customer loyalty award obligation isrecognized as a liability until the Group fulfills its obligations to deliver awards to customers or when the riskof a claim has expired. Claims in respect of a particular year expire at the end of February of the succeedingyear. Hence, revenue relating to award credits is recognized as the risk expires, i.e. based on the number ofaward credits that have been redeemed relative to the total number expected to be redeemed. This is inaccordance with International Financial Reporting Interpretation Committee 13 (IFRIC 13).

Property, plant and equipment are stated at cost less accumulated depreciation and any recognizedimpairment loss. Bus terminals and other buildings are carried at their historical cost less accumulateddepreciation and any impairment loss. Durability of such items is considered before capitalisation. Majorspare parts of motor vehicles which include axle, gear box, engine and body are capitalised when they arereplaced and depreciated over the remaining useful lives of the assets. The values of the replaced parts arederecognised on replacement.

Buildings on leasehold lands are depreciated over their estimated useful lives unless there are indicationsthat the lease will not be renewable at the expiration of the extant lease terms, in which case the buildingsare depreciated over the remaining life of the lease. In such a case a decommissioning cost is capitalisedand discounted over the remaining life of the lease in accordance with IAS 37.

The revalued amounts of land and buildings have been adopted as the deemed cost for these assets. Allother assets have been recognized at their historical costs.

8

ABC TRANSPORT PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2014

3.4. Basis of consolidation

All intra-group transactions, income and expenses are eliminated in full on consolidation.

3.5. InventoriesSpare parts and other stock items are valued at the lower of cost and net realisable value. Cost includespurchase cost and other cost incurred in bringing the stocks to their present location and condition. Theweighted average cost method is used to determine cost.

An executive director in ABC Transport Plc represents the company on the Board of Transit SupportServices Ltd; and ABC Transport Plc is a major customer to Transit Support Services Ltd, which deals onvehicle consumable.

Non-controlling interests represent the portion of profit or loss and net assets of subsidiaries not owned,directly or indirectly by ABC Transport Plc. Non-controlling interests are presented separately in theconsolidated income statement and within equity in the consolidated statement of financial positionseparately from the parent shareholders' equity.

Associates are those entities over which the Group can exercise significant influence, but not control or jointcontrol. Investment in associate is accounted for in the financial statements using the equity method.Investment in the associate is carried in the statement of financial position at cost plus post acquisitionchanges in the Group’s share in the net assets of associate, less any impairment in value. The statement ofprofit or loss reflects the Group’s share of the results of the operations of associate.

The useful lives of the assets are reviewed at least at each financial year end and, if expectation differsfrom previous estimates, the change is accounted for as a change in accounting estimate in accordancewith IAS 8. Asset classified as held for sale are carried at the lower of carrying amount and fair value lesscost to sell in accordance with IFRS 5. Items of PPE classified as held for sale are not depreciated inaccordance with IFRS 5 non-current assets held for sale and discontinued operations.

The gain or loss arising on the disposal or retirement of an asset is determined as the difference betweenthe sales proceeds and the carrying amount of the asset and is recognised in other income.

Borrowing costs relating to self constructed items of property, plant and equipment are capitalised in linewith IAS 23 borrowing costs.

The consolidated financial statements incorporate the financial statement of ABC Transport Plc and itssubsidiaries made up to 31 December each year.

Subsidiaries are entities over which the Group has power to govern the financial and operating policies,generally accompanying a shareholding of more than one half of the voting rights.

Although the equity interest of the Group in Transit Support Service Ltd is 50%, control is predicated on thefact that: The managing director of ABC Transport Plc owns the other 50% equity of the equity shares and isequally the managing director of Transit Support Services Ltd:

9

ABC TRANSPORT PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2014

3.6. Impairment

Indicators of impairment

3.7. ProvisionsThe Group recognises a provision if, and only if:

i. A present obligation (legal or constructive) has arisen as a result of past event,ii. Payment is probable (more likely than not), andiii. The amount can be reliably estimated.

3.8. Foreign currencies

Provision for settlement of litigation is measured at the most likely amount payable, as advised by theGroup’s solicitors. Provision for warranties is measured at a probability weighted expected value. Bothmeasurements are at discounted present values using a pre- tax discount rate that reflects the currentmarket assessment of the time value of money specific to the liability.

The functional currency of the Group is Naira. Transactions in currencies other than naira are recorded atthe rates of exchange prevailing on the dates of the transactions. Foreign exchange gain and lossesresulting from the settlement of such transactions and from the translation at year end exchange rates ofmonetary assets and liabilities denominated in foreign currency are recognised in the statement of othercomprehensive income.

A possible obligation i.e. a contingent liability is disclosed but not accrued. However, disclosure is notmade if payment is remote.

At each reporting date, the Group reviews the carrying amounts of its assets to determine whether there isany indication that those assets have suffered an impairment loss. If any such indication exists, therecoverable amount of the asset is estimated in order to determine the extent of the impairment loss (ifany). Recoverable amount is the higher of fair value less costs to sell and value in use. In assessing valuein use, the estimated future cash flows are discounted to their present value using a pre-tax discount ratethat reflects current market assessments of the time value of money.

Where the asset does not generate cash flows that are independent from other assets, the Groupestimates the recoverable amount of the cash-generating unit to which the asset belongs. If the asset doesnot belong to a cash generating unit, its fair value is determined and compared to its carrying amount todetermine its recoverable amount. If the recoverable amount of an asset (or cash-generating unit) isestimated to be less than its carrying amount, the carrying amount of the asset (cash-generating unit) isreduced to its recoverable amount. An impairment loss is recognised as an expense immediately, unlessthe relevant asset is carried at a revalued amount, in which case the impairment loss is treated as arevaluation decrease to the extent of previous revaluation gains, with any residual impairment recognisedas an expense.Where an impairment loss subsequently reverses, the carrying amount of the asset (cash-generating unit)is increased to the revised estimate of its recoverable amount, but so that the increased carrying amountdoes not exceed the carrying amount that would have been determined had no impairment loss beenrecognised for the asset (cash-generating unit) in prior years. A reversal of an impairment loss isrecognised as income immediately, unless the relevant asset is carried at a revalued amount, in whichcase the reversal of the impairment loss is treated as a revaluation increase.

The Group’s motor vehicle performance report provides the primary reference for motor vehiclesimpairment review. The report has such indicators as number of breakdowns per vehicle, sparesconsumption per vehicle, number of operation run per vehicle, accidented vehicles etc. Secondaryindicators include market prices and the general economic situation in the country.

10

ABC TRANSPORT PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2014

3.9. Taxation/deferred tax assets

3.10. Financial instruments

Trade and other receivables

Borrowings

Trade and other payables

Effective interest method

Loans and borrowings are initially measured at fair value, net of direct transaction costs. Subsequently, loansand borrowings are measured at amortised cost, which is calculated by taking into account any discount orpremium on settlement.

Trade and other payables are initially measured at fair value, and are subsequently measured at amortisedcost using the effective interest method.

The effective interest method is a method of calculating the amortised cost of a financial asset or liability and ofallocating interest income or expense over the relevant period. The effective interest rate is the rate that exactlydiscounts estimated future cash receipts or payments over the expected life of the financial asset or liability.

Judgment is required to determine the amount of deferred tax assets that can be recognized, based upon thelikely timing and level of future taxable profits, together with future tax planning strategies.

Assets and liabilities of ABC Ghana limited are translated from its functional currency into naira at theexchange rate prevailing at the reporting date. Trading results are translated at the average rate for theperiod. Exchange differences arising on the consolidation of the net assets of ABC Ghana limited are dealt withthrough the foreign currency translation reserve, while those arising from trading transactions are dealt with inthe statement of profit or loss. On disposal of a business, the cumulative exchange differences previouslyrecognised in the foreign currency translation reserve relating to that business are transferred to the statementof profit or loss as part of gain or loss on disposal.

Current tax assets and liabilities are measured at the amount expected to be recovered from or paid to taxationauthorities.

Deferred tax is determined using the tax rates that have been enacted or substantially enacted by the reportingdate and which are expected to apply when related deferred tax asset is realised or deferred tax liability issettled. Deferred tax assets are recognised to the extent that it is probable that future taxable profits will beavailable against which the temporary differences can be utilised.

Financial assets and financial liabilities in respect of financial instruments are recognised on the Company’sbalance sheet when the Company becomes a party to the contractual provisions of the instrument. Financialliabilities and equity instruments are classified according to the substance of the contractual arrangementsentered into.

Deferred tax is provided in full, using the liability method, on temporary differences arising between the taxbases of assets and liabilities and their carrying amounts in the consolidated financial statements.

Trade receivables do not carry any interest and are stated at their nominal value as reduced by appropriateallowances for estimated irrecoverable amounts. Estimated irrecoverable amounts are based on the ageing ofthe receivable balances and historical experience. Individual trade receivables are written-off whenmanagement deems them not to be collectible.

11

ABC TRANSPORT PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2014

Held to maturity (HTM) investments

Available-for-sale (AFS) financial assets

Held for trading (HFT) financial assets

Financial instruments at fair value through profit or loss

Impairment of financial assets

Assets carried at amortized cost

The Company first assesses whether objective evidence of impairment exists individually for financialassets that are individually significant, and individually or collectively for financial assets that are not anindividually assessed financial asset, whether significant or not, and the asset is included in a group offinancial assets with similar credit risk characteristics and that group of financial assets is collectivelyassessed for impairment. Assets that are individually assessed for impairment and for which animpairment loss is or continues to be recognized are not included in a collective assessment ofimpairment.

If, in a subsequent period, the amount of the impairment loss decreases and the decrease can be relatedobjectively to an event occurring after the impairment was recognized, the previously recognizedimpairment loss is reversed. Any subsequent reversal of an impairment loss is recognized in the incomestatement, to the extent that the carrying value of the asset does not exceed its amortized cost at reversaldate.

Financial instruments are classified in this category if these result from trading activities or derivativestransaction that are not accounted for as accounting hedges, or when the Company elects to designate afinancial instrument under this category.

HTM investments are non-derivative financial assets with fixed or determinable payments and fixedmaturities wherein the Company has the positive intention and ability to hold to maturity. HTM investmentsare carried at cost or amortized cost in the balance sheets. Amortization is determined by using theeffective interest rate method.

AFS financial assets are non-derivatives that are either designated in this category or not classified in anyof the other categories. AFS financial assets are carried at fair value in the balance sheets. Changes inthe fair value of such assets are accounted for in equity only when the investment is derecognized orwhen the investment is determined to be impaired at which time the cumulative gain or loss previouslyreported in equity is included in the statements of income.

The fair value of financial instruments that are actively traded in organized financial market is determinedby reference to quoted market bid prices at the close of business on the balance sheet date. For financialinstruments where there is no active market, except for investment in unquoted equity securities, fair valueis determined using valuation techniques. Such techniques include using recent arm’s-length markettransactions; reference to the current market value of another instrument, which is substantially the same;discounted cash flow analysis; and option pricing models. In the absence of a reliable basis fordetermining fair value, investments in unquoted equity securities are carried at cost, net of impairment.

The Company assesses at each balance sheet date whether a financial asset or group of financial assetsis impaired.

If there is objective evidence that an impairment loss on loans and receivables carried at amortized costhas been incurred, the amount of the loss is measured as the difference between the asset’s carryingamount and the present value of estimated future cash flows (excluding future credit losses that have notbeen incurred) discounted at the financial asset’s original effective interest rate (i.e the effective interestrate computed at initial recognition). The carrying amount of the asset shall be reduced either directly orthrough use of an allowance account. The amount of the loss shall be recognized in profit or loss.

12

ABC TRANSPORT PLCNOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2014

Assets carried at cost

Available-for-sale financial assets

Derecognition of financial assets and financial liabilities

- the right to receive cash flows from the assets have been expired; or-

3.11. Segmental reporting

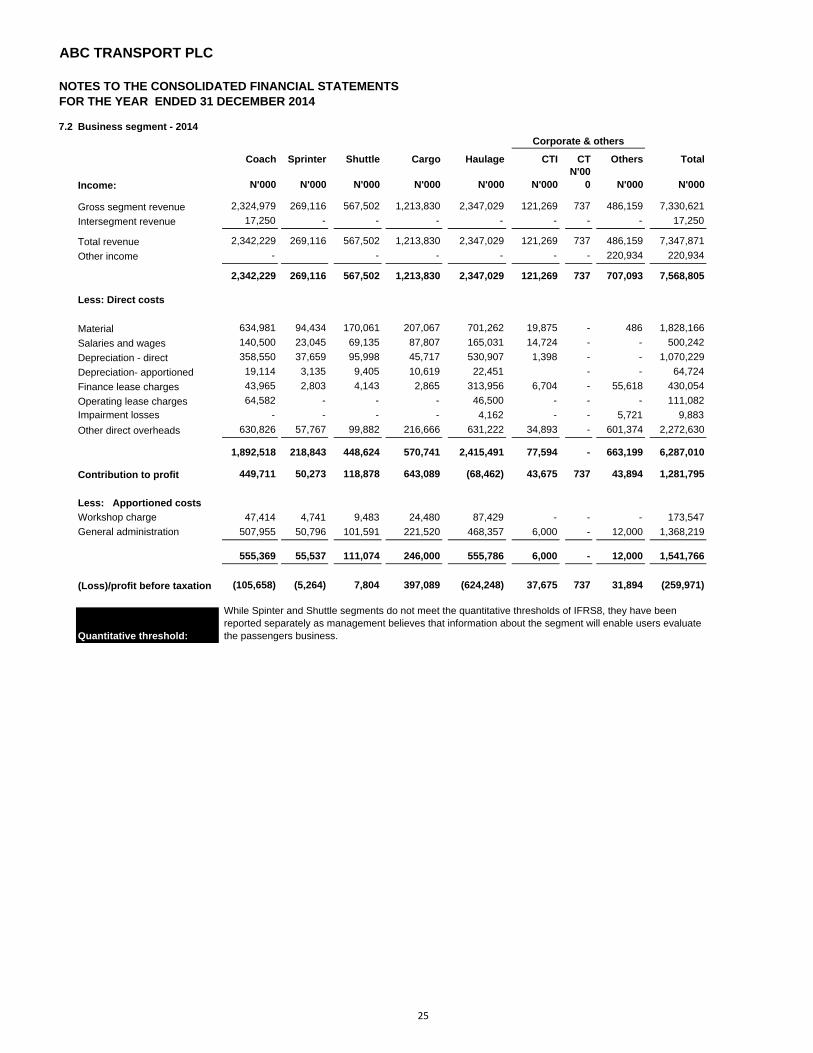

The Group is primarily organized on a business basis and it includes the following:Coach operationShuttle operationSprinter operationHaulage service;Cargo service andHospitality services.

A financial liability is derecognized when the obligation under the liability is discharged or cancelled orexpires. Where an existing financial liability is replaced by another from the same lender or substantiallydifference terms, or terms of an existing liability are substantially modified, such an exchange ormodification is treated as a derecognition of the original liability and the recognition of a new liability, andthe difference in the respective carrying amounts is recognized in the income statement.

The management of ABC Transport Plc has determined the operating segments of the Group basedupon the information provided to the Managing Director who is considered to be the chief operatingdecision maker.

This is consistent with the way the group manages itself and the format of the Group’s internal financialreporting. The second analysis is presented according to the geographic markets comprising Nigeria andGhana. The Group’s geographical segments are determined by the location of the Group’s assets andoperations.

A financial asset (or, where applicable a part of a financial asset or part of a group of similar financialassets) is derecognized where:

the Company retains the rights to receive cash flows from the asset, but has assumed anobligation to pay them in full without material delay to a third party under a “pass-through”arrangement; or the Company has transferred its rights to receive cash flows from the asset andeither (a) transferred substantially the risks and rewards of the asset, or (b) has neithertransferred nor retained substantially all the risks and rewards of the asset, but has transferredcontrol of the asset. Where the Company has transferred its right to received cash flows from anasset and has neither transferred not retained substantially all the risks and rewards of the assetnor transferred control of the asset, the asset is recognized to the extent of the Company’scontinuing involvement in the asset.

If there is objective evidence that an impairment loss on an unquoted equity instrument that is not carriedat fair value because its fair value cannot be reliably measured, or on a derivative asset that is linked toand must be settled by delivery of such an unquoted equity instrument has been incurred, the amount ofthe loss is measured as the difference between the asset’s carrying amount and the present value ofestimated future cash flows discounted at the current market rate of return for similar financial assets.

If an available-for-sale financial asset is impaired, an amount comprising the difference between its cost(net of any principal payment and amortization) and its current fair value, less any impairment losspreviously recognized in profit or loss, is transferred from equity to the statement of income. Reversals inrespect of equity instruments classified as available-for-sale are not recognized in statement of income.Reversals of impairment losses on debt instruments are reversed through profit or loss if the increase infair value of the instrument can be objectively related to an event occurring after the impairment loss wasrecognized in income statement.

13

This is consistent with the way the group manages itself and the format of the Group’s internal financialreporting. The second analysis is presented according to the geographic markets comprising Nigeria andGhana. The Group’s geographical segments are determined by the location of the Group’s assets andoperations.

13

ABC TRANSPORT PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2014

3.12. Trade and other receivables

3.13.

3.14 LeasesLeases are classified as finance leases whenever the terms of the lease transfers substantially all therisks and rewards of ownership to the lessee. All other leases are classified as operating leases. Assetsheld under finance leases are included in the statement of financial position at fair value, or, if lower, atthe present value of the minimum lease payments, each determined at inception of the lease lessdepreciation and impairment losses. These assets are depreciated over the shorter of the asset’s usefullife and the lease term. Where the lease term is shorter than the useful lives of the assets and there is areasonable expectation that ownership will be obtained after the expiration of the lease term, the assetsare depreciated over their useful lives.

The finance charges are allocated over the period of the lease in proportion to the capital amountoutstanding.

Trade and other receivables are recognised and carried at the lower of their original value andrecoverable amount. Allowance is made where there is evidence that the balances will not be recoveredin full.

The Group operates a funded contributory pension scheme in accordance with the Pension Reform Act,2004, where both employer and employee contribute 7.5% each of the sum of the employee’s basicsalary, housing and transport allowances. The Group’s portion is charged to the statement of profit orloss. The Group also operates an unfunded gratuity scheme for the benefit of its employees. Provision forthe scheme is reviewed annually in line with the actuarial gratuity computations at the end of eachfinancial year. IAS 19 paragraph 51 on employee benefits allows the Group to use estimates, averagesand computational short cuts to provide reliable approximations to the liability, in conformity with theprojected unit credit method.

The cost of the defined benefit plan is determined using actuarial valuation method as valued byprofessional actuaries. The actuarial valuation involves making assumptions about discount rates, futuresalary increases, mortality rates and future pension increases. Due to the long term nature of theseplans, such estimates are subject to significant uncertainty.

The undiscounted amount of short-term benefits which include wages and salaries, bonuses and otherallowances attributable to services which have been rendered by employees in the period are recognisedas an expense. Any difference between the amount expensed and cash payments made is treated asliability or prepayment. Provisions are made for un-lapsed compensated leave of absence not yet takenby employees as at the reporting date.

Retirement benefit cost, defined benefit obligation and short term employee benefit

14

ABC TRANSPORT PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 20143.15 Cash and cash equivalents

3.16. Share premiumThis relates to issue of the shares of ABC Transport Plc.

3.17. ReservesThe translation reserve:

3.18. Government grants

3.19 Share Capital

4. New and revised IFRSs in issue but not yet effective

4.1 IFRS 14 Regulatory Defferal Accounts

a.

b.

c.

Rate regulation: A framework for establishing the prices that can be charged to customers for goods andservices and that framework is subject to oversight and / or approval by a rate - regulator.

Rate regulator: An authorised body that is empowered by statute or regulation to establish the rate orrange of rates that bind an entity. The rate regulator may be a third-party body or a related party of theentity, including the entity's own govening board, if that body is required by statute or regulation to setrates both in the interest of customers and to ensure the overall financial viability of the entity.

Regulatory deferral account balance: The balance of any expense (or income) account would not berecognised as an asset or a liability in accordance with other standards, but that qualifies for deferralbecause it is included, or is expected to be included, by the rate regulator in establishing the rate(s) thatcan be charged to adopter of IFRS.This standard will however not affect the Group's financial statementsas the Company is not a first time customers.

Government grants are recognized where there is reasonable assurance that the group will comply withthe conditions attaching to it, and that the grant will be received. Where government grant is by theextension of interest free loans or below-market rate of interest, the benefit of the interest free/belowmarket interest rate is measured as the difference between the initial carrying value of the loandetermined in accordance with IAS 39 and the proceeds received. Government grants are recognized inthe profit or loss on a systematic basis over the periods in which the group recognizes as expenses therelated costs for which the grants are intended to compensate.

Cash comprises cash in hand and demand deposits. Cash equivalents are short-term highly liquidinvestments with a maturity of less than 90 days that are readily convertible to known amounts of cashand subject to insignificant risk of changes in value.

The translation reserve comprises all foreign currency differences arising from the translation of the netassets of overseas operations.

The company has not applied the following new and revised IFRSs that have been issued but are not yeteffective at the reporting period (Earlier application is permitted in some cases)

IFRS 14 was originally issued in January 2014 and applies to an entity's first annual IFRS financialstatements for a period beginning on or after 1 January 2016.The objective of IFRS 14 is to specify thefinancial reporting requirements for 'regulatory deferral account balances' that arise when an entityprovides goods or services to customers at a price or rate that is subject to rate regulation. IFRS 14 isdesigned as a limited scope Standard to provide an interim short-term solution for rate-regulated entitiesthat have not yet adopted IFRS. Its purpose is to allow rate-regulated entities adopting IFRS for the firsttime to avoid changes in accounting policies in respect of regulatory deferral accounts until such time asthe International Accounting Standards Board (IASB) can complete its comprehensive project on rateregulated activities.

The company has one class of shares, ordinary shares and are classified as equity. Incremental costdirectly attributable to issue of ordinary shares are recognized as a deduction from equity, net of taxeffects.

15

ABC TRANSPORT PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2014

4.2 IFRS 15 Revenue from contracts with customers

4.3 IFRS 9 Financial Instrument (final version)

The package of improvements introduce by the final version includes:1. A logical model for classification and measurement.2. A single, forward looking ' expected loss' impairment model.

3. A substantially- reformed approach to hedge accountingThis final version supersedes all previous versions ( IFRS 9 (2009) or (2010) or (2013) or IFRS 9 (2014),subject to specific time frame.

It was originally issued in May 2014 and its effective date is reporting period beginning on or after January 1,2017. The objective of IFRS 15 is to establish the principles that an entity shall apply to report usefulinformation to users of financial statement about the nature,amount,timing and uncertainty of revenue andcash flows arising from a contract with a customer. It is a converged standard on the recognition of revenuefrom contracts with customers issued by IASB and FASB. The standard will improve the financial reporting ofrevenue and improve comparability of the top line in financial statements globally. The areas that could havesignificant inpacts / challenges for entities are highlighted below.

Variable consideration: Entities might agree to provide goods or services for consideration that variescertain future events occurring or not occurring.Those amounts are often not recognised as revenue until thecontigency is resolved. Now an estimate of variable consideration is included in the transaction price if it ishighly probable that the amount will not result in a significant revenue reversal if estimates changes. Thisamount is recognised as revenue when goods or services are transferred to the customer.

Allocation of transaction price based on relative stand-alone selling price: Entities that sell multiplegoods or services in a single arrangement must allocate the consideration to each of those goods orservices.This allocation is based on the price an entity would charge a customer on a stand-alone basis foreach good or service.

Time value of money: Some contracts provide the customer or the entity with a significant financing benefit(explicitly or implicitly). This occur when performance and payment occur at significantly different times. Thetransaction price should be adjusted for time value of money , if the contracts includes a significant financingcomponent. Adoption of this standard is not expected to have a material effect on the way the Grouppresently accounts for its contracts with customers.

(Effective for annual periods beginning on or after January 1,2018, with early adoption permitted.)

Transfer of control: Obtaining control of goods and services by cutomer entails recognition of revenue theseller / provider.This control means ability to direct the use of and obtain the benefits from the good orservice. The standard gives guidance and clarification on whether revenue should be recognised over time orat a point in time.

IFRS 9 is a new standard for financial instruments that is ultimately intended to replace IAS 39 in its entirety.

16

ABC TRANSPORT PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2014

4 Classification and measurement of financial assets and financial liabilities

5

6

7 Expected loss impairment model

8 Hedge Accounting

Although, IFRS 9 treatment of financial assets are still similar to that of IAS 39 Financial Instruments:recognition and measurement, thus: amortized cost, fair value through other comprehensive income(FVTOCI) and fair value through profit or loss (FVTPL). Now, criteria for classification into the appropriatemeasurement category are significantly different. Embedded derivatives are no longer seperated fromfinancial assets hosts. The final version of IFRS 9 introduces a new classification and measurementcategory of FVTOCI for debt instruments that meet the following two conditions:

The financial asset is held within a business model whose objective is achieved by both collectingcontractual cash flows and selling financial assets

The impairment model in IFRS 9 is based on the concept of providing for expected losses at inception of acontract, except in the case of purchased or originaed credit-impaired financial assets, where expectedcredit losses are incorporated into the effective interest rate. Financial assets measured at amortised cost;Financial assets mandatorily measured at FVTOCI; Loan commitments when there is a present obligationto extend credit (except where these are measured at FVTPL); Financial guarantee contracts to which IFRS9 is applied (except those measured at FVTPL); Lease receivables within the scope of IAS 17 Leases; andContract assets within the scope of IFRS 15 Revenue from Contracts with Customers (i.e. rights toconsideration following transfer of goods or services). Expected credit losses are required to be measuredthrough a loss allowance at an amount equal to: The 12-month expected credit losses (expected creditlosses that result from those default events on the financial instrument that are possible within 12 monthsafter the reporting date); or Full lifetime expected credit losses (expected credit losses that result from allpossible default events over the life of the financial instrument).

The significant improvement is majorly to align accounting more closely with risk management.Theobjective is to represent in the financial statements the effect of an entity's risk management activities whenthey use financial instrument to manage exposures arising from particular risks and those risks could affectprofit or loss, or other comprehensive income. The fundamental improvements on IAS 39 were in the areasof: objective, hedge items, hedging instruments, effectiveness assessment,discontinuation andrebalancing,groups and net positions and presentation and disclosure. The group is not commited atadopting the standard earlier and in its eventual adoption will not hesitate to make adequate disclosures.

Business model test

Cash flow characteristics testThe contractual terms of the financial asset give rise on specified dates to cash flows that are solelypayments of principal and interest on the principal amount outstanding. Unless, on initial recognition, it isdesignated at fair value through profit or loss to address an accounting The final Standard also addsguidance on how to determine whether financial assets are held under a business model that is 'hold tocollect' or 'hold to collect and sell', also under contractual cash flow characteristics test it clarify that inbasic lending arrangements the most significant elements of interest are consideration for the time value ofmoney and credit risk.

18

ABC TRANSPORT PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2014

4.4 Accounting for Acquisitions of Interests in Joint Operations (Amendments to IFRS 11)(Effective for annual periods beginning on or after January 1,2016.)

4.5(Effective for annual periods beginning on or after January 1,2016.)

4.6(Effective for annual periods beginning on or after January 1,2016.)Amends IFRS 10 Consolidated Financial Statements and IAS 28 Investments in Associates and JointVentures (2011) to clarify the treatment of the sale or contribution of assets from an investor to itsassociate or joint venture, as follows: Require full recognition in the investor's financial statements ofgains and losses arising on the sale or contribution of assets that constitute a business (as defined inIFRS 3 Business combinations) Require the partial recognition of gains and losses where the assets donot constitute a business, i.e. a gain or loss is recognised only to the extent of the unrelated investors'interests in that associate or joint venture. The amendment will not have impact on the financial staementas there were no transaction of this nature during 2014 financial year.

Amends IFRS 11 Joint Arrangements to require an acquirer of an interest in a joint operation in which theactivity constitutes a business (as defined in IFRS 3 Business combinations) to: Apply all of the businesscombinations accounting principles in IFRS 3 and other IFRSs, except for those principles that conflictwith the guidance in IFRS 11. Disclose the information required by IFRS 3 and other IFRSs for businesscombinations. The amendments apply both to the initial acquisition of an interest in joint operation, andthe acquisition of an additional interest in a joint operation (in the latter case, previously held interests arenot remeasured). The application of the standard will not have effect on the financial statement as thegroup is not involve in any joint operation arrangement presently.

Amends IAS 16 Property, Plant and Equipment and IAS 38 Intangible Assets to: Clarify that a depreciationmethod that is based on revenue that is generated by an activity that includes the use of an asset is notappropriate for property, plant and equipment. Introduce a rebuttable presumption that an amortisationmethod that is based on the revenue generated by an activity that includes the use of an intangible assetis in appropriate, which can only be overcome in limited circumstances where the intangible asset isexpressed as a measure of revenue, or when it can be, demonstrated that revenue and the consumptionof the economic benefits of the intangible asset are highly correlated. The company systematicallyallocate depreciable amount of an asset over its useful lives, so the amendement will not have any impacton her financial statement.

Clarification of Acceptable Methods of Depreciation and Amortisation (Amendments to IAS 16 andIAS 38)

Sale or Contribution of Assets between an Investor and its Associate or Joint Venture (Amendmentsto to IFRS 10 and IAS 28)

18

ABC TRANSPORT PLCNOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2014

4.7 Amendments in issue applicable for financial year beginning on or after july 1, 2014.i Defined Benefit plans: Employee Contributions (Amendments to IAS 19)

ii Annual improvements to IFRSs 2010-2012 Cycle-various standardsiii Annual improvements to IFRSs 2011-2013 Cycle-various standards

It involves the following standards and the specifics:IFRS 1;IFRS version that a first-time adopter can applyIFRS 2;The meaning of 'Vesting condition'IFRS 3;The classification and measurement of contingent consiseration.IFRS 8; Disclosure on the aggregation of operating segments.IFRS 13;Measurement of short term receivables and payables.IAS 16 & 38; Reinstatement accumulated depreciation (amortization) on revaluation.IAS 24;definition of 'related party'IAS 40; Interrelationship of IFRS 3 and IAS 40

4.7.2 IFRS 10 consolidation financial statements

4.7.3 IFRS 11 joint arrangements

The amendments are relevant only to defined benefit plans that involves contributions from employeesor third parties meeting certain criteria. It further clarify how service linked contributions fromemployees or third parties should be included in determining net current service cost and the definedbenefit obligation. The group defined benefit scheme is funded by the employer only therby making theamendment irrelevant to the group.

IFRS 10 replaces the parts of IAS 27 Consolidated and Separate Financial Statements that deal withconsolidated financial statements. SIC-12 Consolidation – Special Purpose Entities will be withdrawnupon the effective date of IFRS 10. Under IFRS 10, there is only one basis for consolidation, that is,control. In addition, IFRS 10 includes a new definition of control that contains three elements: (a)power over an investee, (b) exposure, or rights, to variable returns from its involvement with theinvestee, and (c) the ability to use its power over the investee to affect the amount of the investor'sreturns. Extensive guidance has been added in IFRS 10 to deal with complex scenarios.

The directors of the Company made an assessment as at the date of initial application of IFRS 10 (i.e.1 January 2013) as to whether or not the Group has control over the subsidiaries in accordance withthe new definition of control and the related guidance set out in IFRS 10. The directors concluded thatit has had control over the subsidiaries since the acquisition on the basis that the Company has themajority share holding in the subsidiaries and there are no hindrances or arrangements that wouldgive control to the non-controlling interest holders. Therefore, in accordance with the requirements ofIFRS 10, the subsidiaries have been subsidiaries of the Company since 2011.

IFRS 11 replaces IAS 31 Interests in Joint Ventures. IFRS 11 deals with how a joint arrangement ofwhich two or more parties have joint control should be classified. SIC-13 Jointly Controlled Entities –Non-monetary Contributions by Ventures will be withdrawn upon the effective date of IFRS 11. IFRS11 is concerned principally with addressing two aspects of IAS 31: first, that the structure of thearrangement was the only determinant of the accounting, and second, that an entity had a choice ofaccounting treatment for interests in jointly controlled entities.The application of this standard had no material impact on the disclosures or on the amountsrecognised in the consolidated financial statements as the Group does not currently hold any JointArrangement contract

The group have not adopted the amendments early but the eventual adoption will not have significantinfluence on the annual report.

19

ABC TRANSPORT PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2014

4.7.4 IFRS 12 Disclosure of interests in other entities

4.8. New IFRS pronouncements adopted.4.8.1 Amendments to IFRS 10,IFRS 12 and IAS 27

(Effective for annual periods beginning on or after 1 January 2014)

4.8.2 Amendments to IAS 32 Offsetting Financial Assets and Financial Liabilities.(Effective for annual periods beginning on or after 1 January 2014)

4.8.3(Effective for annual periods beginning on or after 1 January 2014)

4.8.4 IFRIC 12 Levies(Effective for annual periods beginning on or after 1 January 2014)This provide guidance on when to recognise a liability for a levy imposed by government, both for levies thatare accounted for in accordance with IAS 37 Provisions, Contigent Liabilities, and Contigent Assets and thosewhere the timing and amount of the levy is certain. The application of these standards does not have anysignificant or material effect on the amounts and disclosures in the financial statement.

Amendments to IAS 36 Recoverable Amount Disclosures for Non-Financial Assets.

IFRS 12 is a disclosure standard and is applicable to entities that have interests in subsidiaries, jointarrangements, associates and/or unconsolidated structured entities. In general, the disclosure requirements inIFRS 12 are more extensive than those in the current standards. IFRS 12 replaces the disclosurerequirements in IAS 27, IAS 28 and IAS 31 except for the disclosure requirements that apply only whenpreparing Separate financial statements, which are included in IAS 27 Separate financial statements.

IFRS 12 is a disclosure standard and is applicable to entities that have interests in subsidiaries, jointarrangements, associates and/or unconsolidated structured entities. In general, the application of IFRS 12 hasresulted in more extensive disclosures in the consolidated financial statements

The amendments to IFRS 10 introduce an exception from the requirement to consolidate subidiaries for aninvestment entity.In terms of exception, an entity is required to measure its interests in subsidiaries at fairvalue through profit or loss. The exception does not apply to subsidiaries of investment entities that provideservices that relate to the investment entity's investment activities. None of the subsidiaries in the groupqualifies as 'investment entity'.

The amendments to IAS 32 clarify existing application issues relating to the offseting requirements.Specifically,the amendments clarify the meaning of 'currently has a legally enforceable right of set-off,'simultaneous realisation and settlement', 'offsetting of collateral amounts' and 'the unit of account for applyingthe offsetting requirements'. The company is aware of retrospective application of the amendments.There isno offsetting arrangement in the group.

The amendment reduces the circumstances in which the recoverable amount of assets or cash generatingunits is required to be disclosed, clarify the disclosure required and to introduce an explicit requirement todisclose the discount rate used in determining impair ment (or reversals) where recoverable amount (based onfair value less cost of disposal) is determined using a present value technique. Disclosure requirementfollowed in the presentation of the financial statement

20

ABC TRANSPORT PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2014

5.0 Critical accounting estimates

5.1 Property, plant and equipment

Estimation of useful life

YearsFreehold buildings 20Motor vehicles 5 - 7Furniture and equipment 5Flat beds 7Furniture, fixtures and equipment 5

PPE is stated at fair value less accumulated depreciation and any impairment losses. Depreciation iscalculated to write off the fair value of PPE other than land and work-in-progress on a straight-line basisover the estimated useful life of the respective classes of assets at the following annual rates:

The preparation of financial statements in conformity with IFRS requires management to makejudgments, estimates and assumptions that affect the reported amounts of assets, liabilities, disclosure ofcontingent assets and liabilities at the date of the financial statements and the reported amounts ofrevenues and expenses during the reporting period. Actual results could differ from those estimates. Keyestimates were made in the area of impairment of assets held for sale, contingent liability, provision fordefined benefit plan and general allowance on trade receivables.

The charge in respect of periodic depreciation is derived after determining an estimate of an asset’sexpected useful life and the expected residual value at the end of its life. Increasing an asset’s expectedlife or it’s residual value would result in the reduced depreciation charge in the consolidated incomestatement.

Property, plant and equipment represent the most significant proportion of the asset base of the group,accounting for about 80% of the Group’s total assets. Therefore the estimates and assumptions made todetermine their carrying value and related depreciation are critical to the Group’s financial position andperformance.

The Group prepares its consolidated financial statements in accordance with IFRS, the application whichoften requires judgments to be made by management when formulating the Group’s financial positionand results. Under IFRS, the directors are required to adopt those accounting policies most appropriateto the Group’s circumstances for the purpose of presenting fairly the Group’s financial position, financialperformance and cash flows.

In determining and applying accounting policies, judgment is often required in respect of items where thechoice of specific policy, accounting estimate or assumption to be followed could materially affect thereported results or net assets position of the Group should it later be determined that a different choicewould be more appropriate.

Management considers the accounting estimates and assumptions discussed below to be its criticalaccounting estimates and accordingly provides an explanation of each below.

The discussions below should also be read in conjunction with the Group’s disclosure of significantaccounting policies.

21

ABC TRANSPORT PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2014

5.2 Provisions and contingent liabilities

5.3 Allowances for trade receivables

5.4 Defined benefit obligation

The useful lives and residual values of motor vehicles are determined by management based onhistorical experience as well as anticipation of future events and circumstances which may impact theiruseful lives such as utility, nature of the road infrastructure, and changes in automobile technology.

Buildings on owned land are depreciated over the period management expects to derive benefit from theiruse and this period is reviewed annually for appropriateness. Judgment is however applied on the usefullives of buildings constructed on lands held on short-term leases which are only depreciated over a periodextending beyond the expiry of the lease if there is reasonable expectation that the lease will be renewed.Depreciation charged in the income statement together with the carrying amounts will differ significantlyshould an expected renewal of short-term fail to materialize. This is in view of the under-provisionresulting from the shorter useful lives and the possible impacts of un-capitalized decommissioning costs.

The group exercises judgment in measuring and recognizing allowance for trade receivables

Impairment allowance is made when there is objective evidence that the company/group will not be ableto collect the debts. The allowance raised is the amount needed to reduce the carrying value to thepresent value of expected future cash receipts.

Receivables resulting from barter arrangements are not subject to the aged-analysis above as judgmentis exercised by management in determining the position of such receivables.

The Group operates an unfunded defined benefit scheme which entitles staff who put in a minimumqualifying working period of five years to gratuity upon leaving the employment of the company. IAS 19requires the application of the Projected Unit Credit Method for actuarial valuations. Actuarialmeasurements involve the use of several demographic projections regarding mortality, rates of employeeturnover etc and financial projections in the area of future salaries and benefit levels, discount rate,inflation etc.

Withholding tax credit notes receivable aged 18 months and above are considered doubtful for collectionand are subjected to a 100% provision. No provisioning is made for credit notes aged below 18 months asthey are considered collectible going by the present timeframe between the remittance of deductions andproduction of the credit notes by the Federal Inland Revenue Service.

The uncertainty underlying these assumptions about the future is likely to make actual payments differfrom liabilities carried in the statement of financial position.

Provisions are recognised when the Group has a present obligation (legal or constructive) as a result of apast event, it is probable that the Group will be required to settle the obligation, and a reliable estimate canbe made of the amount of the obligation.

The amount recognised as a provision is the best estimate of the consideration required to settle thepresent obligation at the end of the reporting period, taking into account the risks and uncertaintiessurrounding the obligation. When a provision is measured using the cash flows estimated to settle thepresent obligation, its carrying amount is the present value of those cash flows (when the effect of thetime value of money is material).