A STUDY ON THE DETERMINANT FOR FAMILY TAKAFUL CONSUMPTION

40

A STUDY ON THE DETERMINANT FOR FAMILY TAKAFUL CONSUMPTION NURUL NADIA BINTI HARUN 2009804722 BACHELOR OF BUSINESS ADMINISTRATION (HONS) FINANCE FACULTY OF BUSINESS MANAGEMENT MARA UNIVERSITY OF TECHNOLOGY KELANTAN PROPOSAL

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of A STUDY ON THE DETERMINANT FOR FAMILY TAKAFUL CONSUMPTION

A STUDY ON

THE DETERMINANT FOR FAMILY TAKAFUL CONSUMPTION

NURUL NADIA BINTI HARUN

2009804722

BACHELOR OF BUSINESS ADMINISTRATION (HONS) FINANCE

FACULTY OF BUSINESS MANAGEMENT

MARA UNIVERSITY OF TECHNOLOGY

KELANTAN

PROPOSAL

DECLARATION OF ORIGINAL WORK

BACHELOR OF BUSINESS ADMINISTRATION (HONS) FINANCE

FACULTY OF BUSINESS MANAGEMENT

UNIVERSITI TEKNOLOGI MARA KELANTANG

KAMPUS KOTA BHARU

I, NURUL NADIA BINTI HARUN, (I/C NUMBER: 880920-03-5432)

Hereby declares that:

This work has not previously been accepted insubstance for any degree, locally or overseas, andis not being concurrently submitted for this degreeor any other degrees.

This project paper is the result of my independentwork and investigation except where it is otherwisestated.

2

All verbatim extract have been distinguish byquotation marks and source of my information havebeen specifically acknowledgement.

Signature: ____________________ Date:_________________

LETTER OF TRANSMITTAL

Bachelor in Business Administration (Hons) Finance

Universiti Teknologi Mara (UiTM) Kampus kota bharu,

Kota Bharu,, Kelantan.April 2011

Associate Prof. Safri Bin Ya

The Head of Programme,

Bachelor of Business Administration (Hons) Finance,

Faculty of Business Management

University Teknologi MARA UiTM;

Kota Bharu, Kelantan.

Dear Sir,

3

SUBMISSION OF PROJECT PAPER

Attached is the project paper titled ‘A study on the

determinant for Family Takaful consumption.’ To fulfill

the requirement needed by the Faculty of Business

Management, Universiti Teknologi MARA

Your kindness in accepting the unbounded thesis is very

much appreciated.

Thank you.

Yours sincerely,

…………………………………………….

NURUL NADIA BINTI HARUN

2009804722

Bachelor of Business Administration (Hons) Finance

ABSTRACT

This study attempts to determine the determinants

for Family Takaful consumption, whether population,

interest rate and GDP related to the demand for Family

Takaful. This study uses 10 data that is collected from

annual report of Etiqa Takaful 1997 to 2006. The data

collected was then tested on the multiple regression

4

analysis and then were use to test the hypothesis in this

study.

5

CHAPTER 1:INTRODUCTION

6

1.1 Background of study

The development of Takaful industry

The development of the Takaful industry in Malaysia in

the early 1980s was inspired by the prevailing needs of

the Muslim public for a Shariah-compliant alternative

to conventional insurance, as well as to complement the

operation of the Islamic bank that was established in

1983. It was, to a large extent, triggered by the

decree issued by the Malaysian National Fatwa Committee

which ruled that life insurance in its present form is

a void contract due to the presence of the elements of

Gharar (uncertainty), Riba’ (usury) and Maisir

(gambling). A Special Task Force was established by the

Government in 1982 to study the viability of the

setting up of an Islamic insurance company following

the recommendations of the Task Force, the Takaful Act

was enacted in 1984 and the first Takaful operator was

incorporated in Malaysia in November 1984. The Takaful

industry in Malaysia has consistently registered strong

growth in the last 20 years. It has proven to be

resilient in the face of intense competition from the

7

more advanced insurance industry. The industry has

recorded average annual growth rates of 57.9% and 44%

in assets and net contributions respectively since

1986.

Overview of Takaful

Takaful is a system of Islamic insurance based on the

principle of mutual cooperation (ta’awun) and donation

(tabarru’), where the risk is shared collectively and

voluntarily by the group of participants. It is derived

from an Arabic word meaning ‘joint guarantee’ or

‘guaranteeing each other’ (Mahmood, 2008). It is an

arrangement by a group of people with common interests

to guarantee or protect each other from certain defined

misfortunes such as premature death, disability and

8

property damages (Obaidulllah, 2005). Under Takaful

schemes, participants mutually agree to guarantee and

to protect each other against a defined loss or damage,

by jointly providing financial assistance to any

members suffering from a loss.

As a concept, insurance does not contradict the Islamic

principles since it is essentially a system of mutual

help. However, the operation of conventional insurance

involves the elements of uncertainty (gharar) and

gambling (maysir) in the contract of insurance, and

usury (riba) in its investment activities, which do not

conform to the requirements of Shariah. Gharar, may

exist with regard to the scope of coverage, terms of

the contract and source of the claim payments. Maysir,

may arise from any speculative element present in a

contract, such as an unequal exchange of the amount of

money. Riba, or excessive profit, may arise from

financial interest received from the investment of

funds collected from the participants. Avoidance of

these elements is essential in an insurance system

acceptable by the Syariah, and this is where Takaful

9

differs with the conventional insurance. Takaful

arrangement embraces the elements of mutual

cooperation, shared responsibility, mutual protection,

and joint indemnity (Central Bank of Malaysia, Takaful

Industry Review, 2005).

Takaful is a system of Islamic insurance based on the

principle of mutual cooperation (ta’awun) and donation

(tabarru’), where the risk is shared collectively and

voluntarily by the group of participants. In a Takaful

transaction, the party called the participant (insured),

who pays a particular amount of money known as

contribution (premium) to another, who is known as

Takaful operator (insurer) with a mutual agreement that,

the operator is under a legal responsibility to provide

the participant with a financial security against

unexpected loss or damage caused to the subject matter

of the policy should one occurs within the agreed

period of the policy. Takaful is designed to provide

protection against individual and businesses.

10

According to The Banker (2001), the Islamic insurance

sector or Takaful has expanded in many major markets and

in Muslim dominated countries around the world. Among

the Top 25 companies in the world, ranked by The

Banker, Brunei’s Takaful IBB Bd is first followed by

SCA’s of Iran Insurance Company and Malaysia’s Syarikat

Takaful Malaysia Berhad with Shariah compliant assets

worth US31.5 billion, US1.5 billion and US824.8 million

respectively, while the GCC companies, is led by Saudi

Arabia’s Company for Cooperative Insurance. The impact

of Islamization has not only been felt where Islam is

practiced, but also in countries where the Muslim

population has increased tremendously and this is

particularly true in the Western world, Europe and

North America.

This study is to investigate on what could be the main

determinant for the demand of Family Takaful products.

Nowadays, people are very concern about choosing the

products that we have in the market.

11

What is Family Takaful?

Family Takaful provides people with both a protection

policy and long-term savings for peace of mind. The

people or the beneficiary will be provided with

financial benefits if they suffer a tragedy. At the

same time, they will enjoy an investment return because

part of their contribution will be deposited in an

account for the purpose of savings. They have a choice

of maturity periods and there is no forfeiture in the

event of cancellation. They are also entitled to

personal tax relief when participate in family Takaful.

12

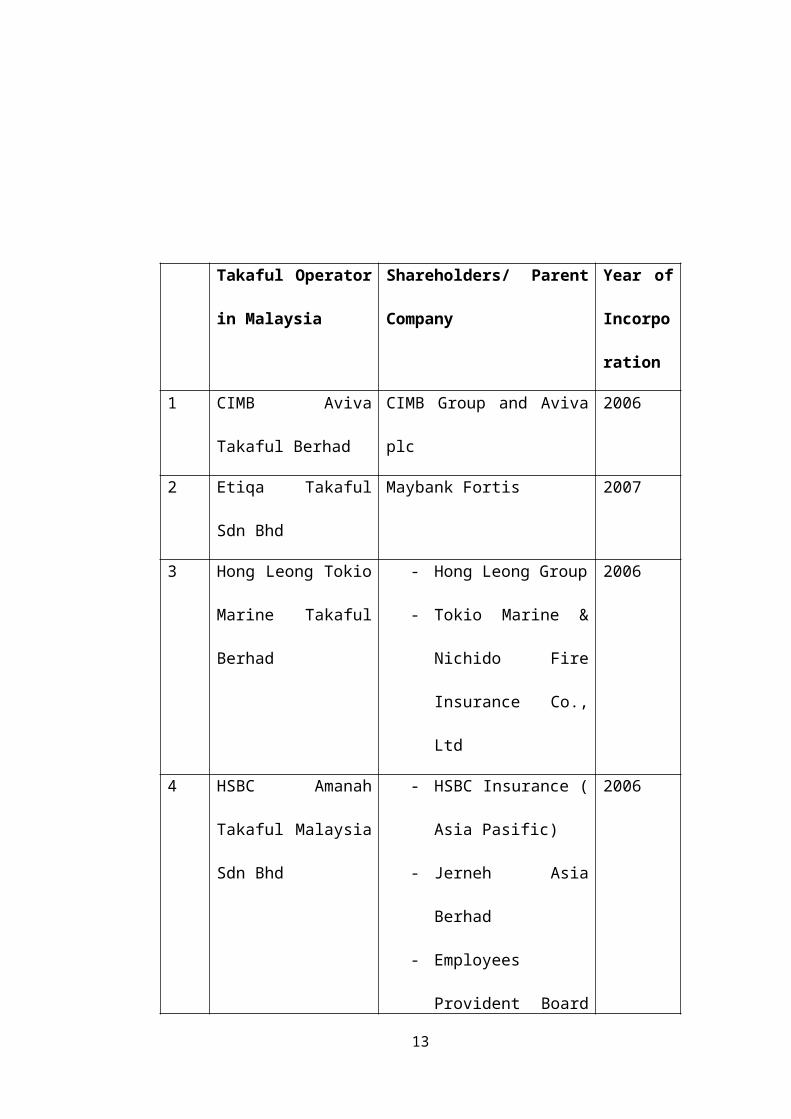

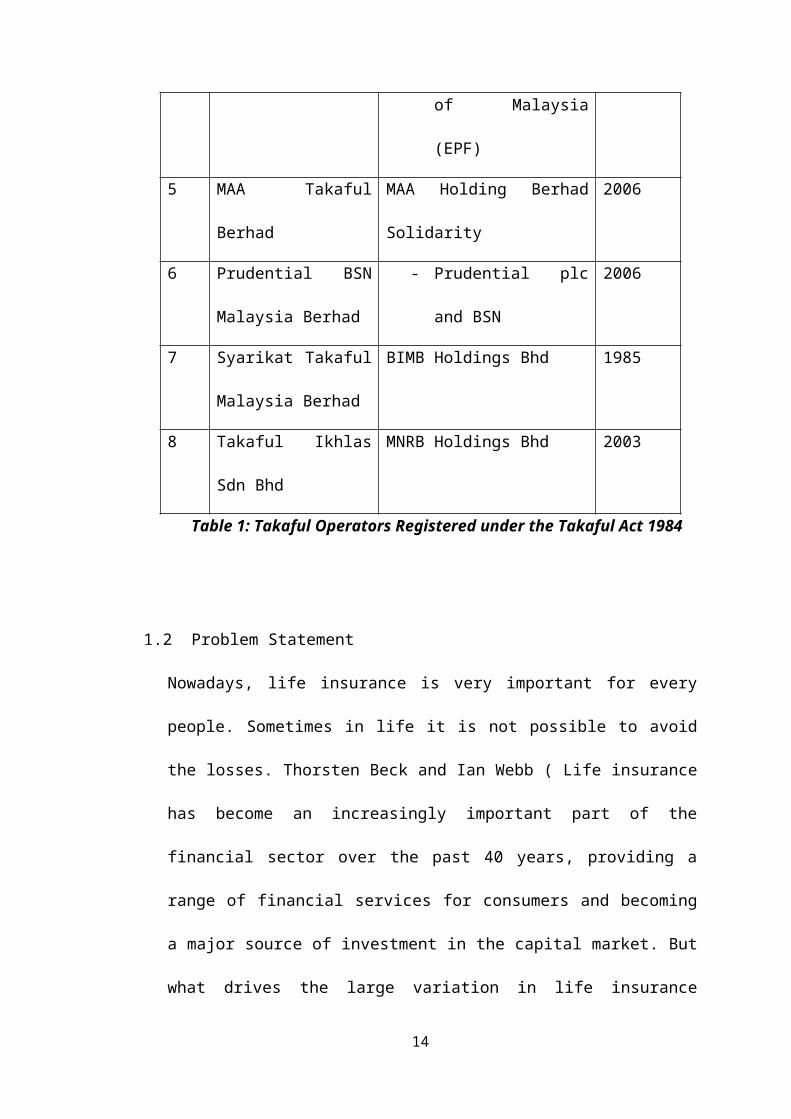

Takaful Operator

in Malaysia

Shareholders/ Parent

Company

Year of

Incorpo

ration

1 CIMB Aviva

Takaful Berhad

CIMB Group and Aviva

plc

2006

2 Etiqa Takaful

Sdn Bhd

Maybank Fortis 2007

3 Hong Leong Tokio

Marine Takaful

Berhad

- Hong Leong Group

- Tokio Marine &

Nichido Fire

Insurance Co.,

Ltd

2006

4 HSBC Amanah

Takaful Malaysia

Sdn Bhd

- HSBC Insurance (

Asia Pasific)

- Jerneh Asia

Berhad

- Employees

Provident Board

2006

13

of Malaysia

(EPF)

5 MAA Takaful

Berhad

MAA Holding Berhad

Solidarity

2006

6 Prudential BSN

Malaysia Berhad

- Prudential plc

and BSN

2006

7 Syarikat Takaful

Malaysia Berhad

BIMB Holdings Bhd 1985

8 Takaful Ikhlas

Sdn Bhd

MNRB Holdings Bhd 2003

Table 1: Takaful Operators Registered under the Takaful Act 1984

1.2 Problem Statement

Nowadays, life insurance is very important for every

people. Sometimes in life it is not possible to avoid

the losses. Thorsten Beck and Ian Webb ( Life insurance

has become an increasingly important part of the

financial sector over the past 40 years, providing a

range of financial services for consumers and becoming

a major source of investment in the capital market. But

what drives the large variation in life insurance

14

consumption across countries remains unclear. For

example people may become ill. They may die of illness

or accidents or their homes or other property may

undergo damage or theft. So in all these cases and they

have to face the loss of income or savings. So

insurance is a manner of financially insuring that if

such an incident comes about then the loss does not

affect the present well being of the person. Insurance

plays an important role in sharing the risks of people

in an affordable form. It helps the people to quickly

recover from damages and losses.

Recognizes the importance of insurance to the user,

Islamic Insurance was introduced to satisfy Muslim

needs for insurance products. Conventional Insurance

Company nowadays also offers Islamic Insurance

products. This shows that, the demand for Islamic

Insurance (Takaful) is high.

15

In 2007, monthly per capita income in Malaysia is about

RM1900. Approximately 60 percent of the Malaysian

Muslims earn income above RM2000 a month (Department of

Statistics Malaysia, 2007). With the income level

higher than the country’s per capita level, majority of

the Malaysian Muslims may have the financial capacity

to purchase Takaful. Therefore, more aggressive

marketing techniques should be employed by the Takaful

operators to increase penetration rate of Takaful among

the Malaysian Muslim.

Thus, this research is conducted to know the

determinant of Takaful consumption in Malaysia based on

five factors, population, interest rate and Gross

Domestic Product (GDP)

16

1.3 Research Objective

The objective of conducting this research is wanted to

know about the determinant of Takaful products

consumption. Nowadays, we can see that many company

trying to enter the market by introducing different

product and have their own advantage. There are several

objective of doing this research

1.3.1 To determine whether population, interest rate

and Gross Domestic Product (GDP) have significant

relationship with the Takaful consumption.

1.3.2 To identify the most important variable

towards the Family Takaful consumption.

1.4 Scope of study

Focus of this study is on the determinant for the

Takaful consumption. The determinant for Family Takaful

consumption that researcher wants to study is

population, interest rate and GDP. This study will used

data on DataStream at Uitm’s library and from17

Department of Statistic Malaysia. The data for the

demand for Family Takaful was taken from the annual

report of Etiqa Takaful net contribution and then it

would be analyse by using SPSS program as statistical

software. This study will use the data from the year

1997 to 2006.

1.5 Significance

1.5.1 To the researcher.

This research earns the researcher a lot of valuable

knowledge while on others to do your work. After

doing this research, the researcher can compare

those products that Takaful based company offered so

that they do not make mistake in their future time.

1.5.2 To the future researcher

Hopefully this research will be an example or

guidance or reference for them to do better study in

the future. Meaning that, they will have more input

for their research. Find a lot of information and

input from books, journal, article or internet

18

because when we have many input our research will be

more valuable.

1.5.3 To Takaful industry

Takaful company will definitely use this research as

their guidance to find customer. They can use this

research to make further research about the most

important reason to the demand for Family Takaful.

1.6 Limitation

1.6.1 Time constraint

Do not have enough time to do this research because

of doing practical training and need to concentrate

on two things in one time. The researcher needs to

focus on completing this research because it will be

valuable for others. The studies conducted are

accomplished within a short period. In the short

time period it will not be able to obtain more

information for completing the research. Time period

also become a constraint for the researcher to get

more accurate and reliable data.

1.6.2 Lack of information

19

The information for this study is taken from all

sources including via internet but there are small

number of researcher who do related research. There

are small numbers of literature to be reviewed

because most of the journal not specifically related

to this study.

1.6.3 Lack of expertise

Need to learn to use the statistical software

because of lack of expertise to use DataStream and

SPSS program.

1.7 Definition of term

GDP: Gross Domestic Product

INT: Interest rate

POP: Population

20

Chapter 2:LITERATURE

REVIEw

2.0 Literature Review

2.1 Independent Variable21

2.1.1 Population

(Zuriah Abd Rahman), another indicator for Takaful

vibrant growth in the future is the size of the Muslim

market. Experts’ estimate on the number of Muslims in

1999 was 1.2 billion representing between 19.2 to 22

percent of the world’s population and growing at 2.9

percent per year, (2.3 percent growth rate for total

world population), provided by the Council on American-

Islamic Relations in 1999. According to another

estimate, Muslims have grown by more than 235 percent

the last 50 years and now stands at 1.6 billion.

Population size and demographic consideration is

certainly of vital concern for an enterprise before

embarking on a new venture, because the larger the

population, the larger is the potential market size and

the social structure also plays an important role in

dictating demand.

Again research in the area of changes in social

structure also points to a positive relationship, which

shows that the older the population and the lower the

inflation rate, the more people will choose life

22

insurance over other forms of savings (Beenstock et.

al, 1986; Brown and Kim,1993)

Contribution per worker reflects Takaful density within

the labor force. These people are the segment of

population with higher ability to purchase insurance,

and who normally have better education and higher

degree of insurance awareness. They are also more

likely to have greater demand to protect their

dependents through life insurance against financial

difficulties arising from their premature death (Hwang

and Gao, 2003).

In Malaysia, about 53 percent of the population

comprise of Muslims, to whom Takaful plans are mainly

targeted for. In 2007, monthly per capita income in

Malaysia is about RM1900. Approximately 60 percent of

the Malaysian Muslims earn income above RM2000 a month

(Department of Statistics Malaysia, 2007). With the

income level higher than the country’s per capita

level, majority of the Malaysian Muslims may have the

financial capacity to purchase Takaful. Therefore, more

aggressive marketing techniques should be employed by

23

the Takaful operators to increase penetration rate of

Takaful among the Malaysian Muslim.

2.1.2 Interest Rate

Interest rate is expected to have a positive

relationship with Takaful consumption. Higher real

interest rate increases investment returns of the

insurer, thus the insured may enjoy higher benefit from

the policies through higher cash values or dividends.

Similar to the study by Beck and Webb (2003) and

Outreville (1996), this study uses the lending rate to

proxy the long-term interest rate of the country.

(Black and Skipper, 2000)Theories suggest that the

higher the interest rate, the more return can be earned

by the insurers which in turn can increase the value of

a life policy. But some consumers may prefer to invest

in short-term financial instruments during high

interest rate period, which provide higher returns than

the long-term investment in insurance policies.

24

On the other hand, while the real interest rate does

not support the expected negative relationship, the

positive coefficient exhibited by the variable is

consistent with the findings of Beck and Webb (2003).

Adopting a conservative interpretation, the result for

the log-linear model suggests that a 1% increase in

aggregate per capita income is associated with an

increase of approximately 8:6% in Family Takaful sales.

Cargill and Troxel (1979) examine two kinds of interest

rates in their study: the competing yield on other

savings products and the return earned by life

insurers. The findings on the competing yield are

inconsistent. However, the competing yield tends to be

negatively related to life insurance savings. A higher

interest rate on alternative savings products tends to

cause insurance products to become less attractive as a

savings instrument. The yield on newly issued AAA

utility bonds is used to represent all the competing

rates of return on alternative savings products.

Cargill and Troxel (1979) include the current and

25

twelve-quarter distributed lag variables of competing

yields in their study. The lag variables are included

to reflect the delayed reactions of savers towards new

information regarding interest rates on savings because

changes in interest rates are assumed to produce a

lagged response. Likewise, the findings on the return

earned by life insurers are mixed. However, the return

earned by life insurers is frequently positively

related to life insurance savings. Life insurers

earning a higher rate of return tend to attract

individuals to purchase insurance from them. The yield

on industrial bonds placed privately with a

representative group of life insurance companies is

used as a proxy for the return earned by life insurers.

It is the “new money” rate of return earned by the life

insurers, not the average rate of return on the

invested funds. Similar to the competing yield, the

current and twelve-quarter distributed lags of the

return earned by life insurers are included in the

models to investigate the immediate and lagged

26

responses of changes in interest rates on life

insurance demand.

Outreville (1996) has shown that interest rates such as

the real interest rate and the lending rate are not a

determining factor affecting the demand for life

insurance. The real interest rate is obtained by

subtracting the anticipated inflation from the current

bank discount rate. On the other hand, Rubayah and

Zaidi (2000) investigate three types of interest rates

in their study: the personal savings rate, short-term

interest rate and current interest rate. The personal

savings rate and short-term interest rate are found to

influence significantly and negatively the demand for

life insurance, while the current interest rate is

found to have no significant effect on life insurance

demand. The personal savings rate refers to the

interest rate offered by banks on normal savings, the

short-term interest rate refers to the interest rate on

three-month Treasury Bills, and the current interest

27

rate refers to the base lending rate on bank

borrowings.

Real interest rates have not been systematically

included in all studies. For example, Browne and Kim

(1993) neglect the influence of this variable on life

insurance demand. Outreville (1996) finds the

correlation of real interest rates with life insurance

demand to be almost insignificant. One theoretical

justification for this outcome is that high real

interest rates may decrease the cost of insurance, thus

stimulating its demand. On the other hand, they may

cause consumers to reduce their number of purchases

given the anticipation of higher returns. Beck and Webb

(2003) appear to detect a positive relationship using

average lending rates. However, it can be noted that

lending rates contain a credit risk premium that varies

from one country to another, depending on its credit

default experience. We use the yield on government

bonds (which are virtually free from credit risk) less

the country's rate of inflation to measure real

28

interest rates. In some cases, such as Iceland and

Turkey, where bond markets are nonexistent, bond yields

are replaced by money market rates.

2.1.3 GDP

(Thorsten Beck and Ian Webb), We use real GDP per

capita as well as an indicator of permanent income,

calculated as the predicted value from a regression of

the log of each country’s real GDP per capita on the

time trend. Outreville (1996) finds a significant

positive relationship between financial development and

life insurance penetration. We use the total claims of

deposit money banks on domestic nonfinancial sectors as

a share of GDP as an indicator of banking sector

development.

Outreville (1996) relates the income variable in his

study as the real disposable income per capita. GDP is

used as the basis for the disposable personal income.

29

The income variable is expressed in linear form and in

logarithmic form. (This study use the data on GDP)

Rubayah and Zaidi (2000) examine two types of income

variable in their study, namely GDP and income per

capita. Income per capita is defined as the GDP divided

by the size of the population. In the initial stage,

both the GDP and income per capita are found to have a

positive relationship with the demand for life

insurance but are not significant. It is only when

stepwise regression analysis is applied in the later

stage that GDP appears to have a significant positive

relationship with the demand for life insurance but

income per capita has been aborted. This is because

income per capita contains the element of GDP and

therefore multicollinearity exists because the two

income variables are highly correlated. (This study

also use the data on GDP)

30

31

chapter3:Research

Methodology

3.0 Research methodology

3.1 Research Design

The research design for this study is use secondary

data that taken from DataStream and data from

32

Department of Statistic Malaysia. The data is divided

into two categories namely a) dependent variable: net

contribution of Family Takaful, b) independent

variable: population rate, interest rate and Gross

Domestic Product.

3.2 Theoretical Framework

Independent Variable

Dependent Variable

Figure 1: Theoretical framework

33

PopulationInterest RateGDP

3.3 Hypothesis

Ho : There is no significant relationship between

population and demand of Takaful products

H1 : There is a significant relationship between

population and demand of Takaful products

Ho : There is no significant relationship between interest

rate and demand of Takaful products

H1 : There is a significant relationship between interest

rate and demand of Takaful products

Ho : There is no significant relationship between GDP and

demand of Takaful products

H1 : There is a significant relationship between GDP and

demand of Takaful products

34

3.4 Data collection

The data for this research is collect from DataStream,

Department of Statistic and annual report of Etiqa

Takaful (net contribution of Family Takaful). For the

purpose of this research, the researcher used the

secondary data to complete this study. Data for the

demand Family Takaful is collected from Etiqa Takaful

Berhad, researcher only obtained this data because there

is less data from other company. Data for interest rate

is collected from World Bank. Other data is collected

from Datastream at UiTM’s Library

3.4.1 Secondary Data.

Secondary data is defined as the data collected for some

purposes other than the problem in hand (Malhotra, 1999).

In this research, the researcher has used both internal

and external secondary data searching methods in

obtaining the information. 35

3.4.1.1 External sources

The external secondary data are from books, journals,

report and via internet. Many data were taken from

internet because there are limited sources of data from

books, journal and report.

3.4.1.2 Journals/Articles/Report

The researcher has used and referred to journals,

articles and reports to complete the literature review.

The information gathered has helped the researcher to

find out the determinants that might contribute to this

study and help to develop the blueprint of this study as

well as to complete this research.

3.4.1.3 Internet

The researcher has surfed the internet and websites in

order to find more information and to gather the

electronic journals or articles that can help the

researcher to do the research well. The researcher has

surfed yahoo, emerald insight and Google to find the

information required. Through internet also, the36

researcher can find all the information needed. The

researcher also gets data from internet, for example data

of net contribution for family Takaful that get from

Etiqa Takaful Berhad.

3.5 Data Analysis

3.5.1 Multiple Regression Model

Multiple regressions are a statistical technique that

allows us to predict someone’s score on one variable on

the basis of their scores on several other variables. An

example might help. When using multiple regressions in

psychology, many researchers use the term independent

variables to identify those variables that they think

will influence some other dependent variable. The program

that will be used to analyze the data is called SPSS

(Statistical Program for Social Science). SPSS is one of

the most widely available and powerful program to

summarize data and also determine whether there are

significant differences between groups, examine

relationships among variables. For this study, the data

will be analyzed by using the multiple regressions.

37

General form for Multiple Regression Actual (true) Model

Y = B0 + B1x1 + B2x2 + …+ Bnxn + e

Y is the dependent variable

B0 is the actual constant

B1 is the actual coefficient

e is the error term

3.5.2 R, R Square

R is a measure of the correlation between the observed

value and the predicted value of the criterion variable.

R Square (R2), coefficient of determination is the square

of this measure of correlation and indicates the

proportion of the variance in the criterion variable

which is accounted for by our model.

3.5.3 t-statistic

38

The t statistic is a measure of how extreme a statistical

estimate is. You compute this statistic by subtracting

the hypothesized value from the statistical estimate and

then dividing by the estimated standard error. In many,

but not all situation, the hypothesized value would be

zero.

3.5.4 Beta Value

The beta value is a measure of how strongly each

independent variable influences the dependent variable.

The beta is measured in units of standard deviation.

3.5.5 Durbin Watson

Durbin – Watson is the measurement of the correctness of

the model used in the study. Besides that, it also

indicates the strength of the model used. It is measured

through the range from 1.5 and 2.5, which is normally

considered as the best value, as it confirmed that there

is no auto – correlation problem in the model. To

determine the value of d L and d U; it can be refer to the

Durbin Watson correlation table.

39

40