A Report On National Life Insurance Company Submitted To: Fatema-Tuz-Zohora

60

A Report On National Life Insurance Company

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of A Report On National Life Insurance Company Submitted To: Fatema-Tuz-Zohora

A Report

On

National Life InsuranceCompany

Submitted To:Fatema-Tuz-Zohora

Department of Marketing

University of Barisal

Submitted

By:

Group: “Flora “

4th Semester

Department of Marketing

University of Barisal

Date of Submission: September 19,2013.

UNIVERSITY OF BARISAL

Department of MarketingGroup Name: Flora

4th SemesterSession: 2011-2012

Group Members

SL Name Id No.

.01 Amina (c) 392

02 Afroza Khanam 386

03 Nishat Zahan Nowshin 384

04 Nishat Binta Kader 383

05 Md.Al-Mamun 361

06 Rubayat Hossain Sujon 339

Letter of transmittal19th September, 2013

Fatema-Tuz-Zohora

Lecturer,

Department of Marketing,

University of Barisal

Subject: Submission of report on “National Life InsuranceCompany”.

Dear Madam,

With great pleasure, we, the members of Flora Group would like tosubmit our project report on “National Life Insurance Companyltd”. We are grateful to you for giving us the opportunity to

work on an Insurance company. We gave our level best to make thereport with information and facts. Despite of some setbacks, withour dedication, we were able to finish the report on time withquality.

We tried our best to make the report possible, and we sincerelyhope that, our report and presentation on “National LifeInsurance Company ltd” will be satisfactory to you.

Sincerely Yours,

On behalf of the group members of

Flora Group

AcknowledgementAt first, we are thankful to “Almighty Allah” for His endlessblessing, without it we won’t be able to deliver the report.

We tried our best to make the report. All the group members haveworked heart and soul in making of the report. We are grateful tothe Almighty that we were able to finish the report on time. We

like to acknowledge the people who gave us all the help that weneed to do this report. Our utmost thanks to the courseinstructor Fatema-Tuz-Zohora for her support and motivation, weare able to finish the report. She helped us to understand thetopic and she helped us to overcome all the obstacles forfinishing the report. Our also want to thank the honorableteachers of the Department of Marketing for their continuoussupport and for giving us the opportunity to learn about the lifeinsurance and the companies procedure. With due respect, we liketo thank the Vice Chancellor. We used many facilities to completethe report and we want give our regards to the whole Universityof Barisal. We tried our level best. But there could be somemistake and we are apologized for any unwanted mistake.

Our efforts were great and we follow the instructions to finishthe report. We appreciate all the help that we get, without themthis report will not be possible.

Executive Summery

National Life Insurance Limited, a general insurance company started

its operation in 12th February, 1985. From the establishment the

company is being operated successfully. This report consists an

elaborated discussion about the insurance industry background of

Bangladesh, present situation of the insurance industry, the analysis

of premium of ‘United Insurance Limited’, risk determining factors and

also the customer analysis about the policies and financial

performance analysis. After preparing this report we have suggested

the company where they can make good and what they can do. The

financial performance analysis shows the companies efficiency year to

year.

Table of contentsChapter Particulars

Title flyTitle Page Letter of TransmittalAcknowledgementExecutive Summary

Chapter-1 Introduction1.1 Introduction1.2 Objectives of the study1.3 Methodology of the study1.4 Limitations of the studyChapter-2 Company overview2.1 Company introduction2.2 Historical Background (In regard of

Bangladesh)2.3 Company’s Vision, mission, goal &

objectives

2.4 Management team2.5 Organization Structure2.6 Branches & offices2.7 Company’s performance & growth2.8 Capital & expenditure2.9 Challenges 2.10 Future plansChapter-3 Insurance policies & conditions3.1 Insurance policies3.2 Policy conditions3.3 Contents of agreement3.4 Elements of insurance contract Chapter-4 Risk issues of NLI company4.1 Definition of risk4.2 Types of risk4.3 Risk measurement tools4.4 Risk management processChapter-5 Insurance pricing, claim settlement,

Insurance marketing & reinsurance5.1 Pricing tools5.2 Pricing process 5.3 Pricing elements5.4 Claim settlement procedure5.5 Insurance marketing techniques 5.6 Reinsurance management Chapter-6 Company Analysis 6.1 SWOT Analysis

Strength

Weakness Opportunities Threats of the company Situational analysis

Chapter -7 Finding , Recommendation & Conclusion 7.1 Findings from Performance Analysis7.2 Concluding Remarks

BibliographyReferences

Introduction Insurance is essentially a collective endeavor under which alarge number of individuals agree to share the loss which a fewof them would incur in future. This means insurance protectsthose unfortunates who suffer heavy financial impact ofanticipated misfortunes by distributing the loss among many whoare exposed to the risk of similar misfortunes.

This report has been prepared as requirement of the insurance andrisk management course.We tried our level best to undertake thefield study very consciously and definitely enjoyed our work. Ithas helped us to understand the theoretical part more easily andin our future career. We believe, this field study willcontribute a lot.

Objectives of the study The objectives can be described in two ways:

Broad objectives:

In this study our fundamental motive is to find out how thelife insurance helps to protect losses though life insuranceis not contract of indemnity. We can also know howthe elementsof life insurance policies vary from each other.

Specific objectives:

The main objective is to know the overall process of aninsurance Company.

To fulfill academic requirement & apply theoreticalknowledge in practical field.

To add value to life.

To gather the practical experience about the activities ofan insurance Company.

To find out the life insurance risk factors & premiums.

To find the policies those are used by the National LifeInsurance Company.

To know the revenue growth, earnings &cash generation of theinsurance Company.

To find out available services of the company.

Scope of the study: This study is based on previous five years performance of thecompany & scenario of Bangladesh from 2007 to 2011. It covers-

The overall company profiles.

Life insurance policy in Bangladesh

Risk factors & premiums.

Merits & problems in insurance policy.

Most of the part of the report is prepared based on thequalitative data & the performance analysis is based onquantitative data.

Methodology of the study

This report has been prepared on the basis of experiencegathered during the period of semester. For preparing thisreport, we have also got information from annual report andwebsite of the National Life Insurance Company. We havepresented my experience and findings by using different chartand tables, which are presented in the analysis part.

Relevant data for this report has been collected primarily bydirect investigation of different records, papers, documents,and operational process and different. The interviews wereadministered by formal and informal discussion. No structuredquestionnaire has been used. Information regarding officeactivities of the insurance has been collected throughconsulting records and discussion.

Data Sources:

The information and data for this report have been collectedfrom both the primary and secondary sources.

The primary sources are as follows:

Face-to-face conversation with the respective officerand stuffs of the branch and head office.

Face-to-face conversation with clients who visited thebranch.

Practical work experience in the different desk of thedepartment of the branch covered.

Relevant field study as provided by the officer concern.

The secondary sources are as follows: Annual Report of National Life Insurance Company. Website of the NLIC. Different manual published by NLIC. Different circular sent by head office.

Limitations of the study

In case of collecting the data, we faced a lot of problems.The limitations of the study that we faced in case ofpreparing the report are as follows.

Difficult to collect the information Shortage of time-collected information was complex and

unsorted. Up to date information were not available. Every organization has their own secrecy that is not

rivaled to others.

Finally first experience may also act constants in theway of meticulous exploration on the report.

Despite these limitations, we have tried our best toprepare the report. If you find any mistakes please consider itcordially.

2.1 COMPANY INRODUCTIONNational Life Insurance Company Limited the first private sectorlife insurance company in Bangladesh. It came into existence asthe first private sector indigenous life insurer after a lengthycomplicated process of preparatory work under the guidance &leadership of Alhaj M. Haider Chowdhury, the founder Chairman ofthe company. He was floated the company with three distinct &definite philosophies. In brief, the first one is to encourage &induce saving of the high/mid income population and especially ofthe low income & marginal group. The low income people usuallyface economic hardship for household food security & healthproblems at certain period of their life. Saving throughinsurance might provide them relief at odds & calamities. Thesecond one is to create & provide employment opportunity for theilliterate/half literate/literate youth of the country. Thethird one is capital formation at national level for investmentto develop dynamism at macro-economy. The members of the Board of Directors imbued with the spirit ofsocial service, which the company stands for, are leaders inother professions & business, such as finance, marketing andprivate enterprise. They are equipped with their specializedknowledge to run the company skillfully & maintain anunparalleled position in the insurance arena.

As a service industry, the company is committed to personalizedservice to its valued customers and will justify their confidenceby prudent and viable economic management and offering absolutesecurity and favorable returns. The company has grown & developed massively & substantially overa period of about 20 years. It has earned name & fame along withpremium for the services it provides to the policy holders. Sinceinception, it has focused on policy holders' satisfaction for thetype, quality & timeliness of the services. The company hasdiversified its products to match customers' needs & preferences.Currently it provides multifarious life assurance products tocater the aspirations & needs as well as religious beliefs of theclients.

2.2 HISTORICAL BACKGROUNDNational Life Insurance Company Limited the first private sectorlife insurance company in Bangladesh, incorporated on 12 February1985 as a public limited company under the Companies Act 1913 toengage in life insurance business according to the provisions ofthe Insurance Act 1938 and Rules 1958 and other applicable lawsand rules. National Life Insurance Co Ltd. formally startedfunctioning on 23 April 1985 following formal approval of theGovt with an authorized capital of Taka 200 million divided into2 million ordinary shares of Taka 100 each. The company is listedwith Dhaka Stock Exchange & Chittagong Stock Exchange Ltd.

This company began operation with 11 staff with a head officecovering few hundred sq. ft. of area at Segunbagicha, Dhaka; buttoday manpower enrollment has reached more than 100,000 staffwith head offices at different locations of Motijheel CommercialArea of Dhaka covering several thousand sq., feet of floor areawith several hundred branch & zonal offices all over the country.In a couple of years, hopefully & definitely, head office of thecompany, will shift to 'NLI Tower' -own high rise building atKawranbazar, at a significant artery point of Dhaka metropolis.

The company has also purchased plots & lands at differentDivisional & District headquarters. In course of time, it willshift to own premises from the rented space gradually & makecommercial utilization of the plots & lands.

2.3 VISION, MISSION, GOAL & OBJECTIVES

VISION & Mission: National Life Insurance Company doesn’t have their mission &vision individually. They set their mission & vision united.These are

In our country the middle class & lower class people can’t enter into saving procedure. So in case of death of earning hand of their family or his inability of income make them helpless & bringto the street. For this reason the life insurance companies come forward for them to increase their saving habit. So this was our main &1st mission to increase the saving.

In our country an uncountable amount of educated, half-educatedyoung generation is unemployed. So our mission is to make them

self-employed by what they want to do willingly. To meet theunemployed people with the employment in cities or villages wasour 2ndmission as well as vision because we hope in near futureit will give us free of unemployment country.

To create the saving & increment of national fund is animportant subject. Saving helps a lot in the canvas of nationaleconomy. So this is our mission to accumulate the fund fornational economy to increase our national income. This was our3rd mission.

To become most caring insurance company with dedication,dynamic, innovation & client’s need based on comprehensiveservice.

The objectives of the National Life Insurance Company Ltd. aregiven below: To render best customer service. To earn premium achieved by making customer satisfaction. To play a major role for the development of insurance

industry. To make the payment of claim quickly. To expand company’s branch. To increase volume & company’s share. Always alive to the needs of the customer & to fulfill their

needs with satisfaction.

2.4 Management team

CHAIRMANMr. Mahmudul Huq Taher

DIRECTORS

Mr. Abdul Monem

Mr. Tofazzal Hossain

Mr. Nader Khan

Mr. Morshed Alam

Mr. Mostafizur RahmanMr. K.M. Habib ZamanMrs. Farzana RahmanMrs. Latifa A. Rana

Mrs. S. F. Rowshan AkhterMr. Mehdadur Rahman Durand

VICE CHAIRMANMr. Md. Imrul Alam

DIRECTORS

Mr. MatiurRahmanMr. Mujibur RahmanMr. K I Hossain

Mr. S. M. Shamsul ArefinMr. Eng. Ali Ahmed

Mr. Mohammad Haroon PatwaryPublic Share Holders Group

INDEPENDENT DIRECTORSMr. M. Haider ChowdhuryMr. Alamgir Kabir, FCA

MANAGING DIRECTOR

Mr. Jamal Mohammed Abu Naser (c.c.)

COMPANY SECRETARY

Mr. Md. Abdul WahabMian

ExecutivesName Designation Division

Jamal Mohammed Abu Naser Managing Director & CEO Managing Director

Dipen Kumar Saha Roy, FCA Deputy Managing Director andCFO

DMD Secretariat

Mr. Sunil Kanti Barua Senior Executive VicePresident

Sales Promotion

Mr. Khasru Chowdhury Senior Executive VicePresident

Sales Promotion

Mr. Kazim Uddin Senior Executive VicePresident

Sales Promotion

Mr. Anwar Hossain SeniorVice President Commission

Md. Nomanul Mehadi Khan SeniorVice President Finace& Accounts

Md. Enamul Haque Senior Vice President Establishment

Engr. Md. AbulKashem Senior Vice President Engineering

Mohammad Abdul WahabMian Company Secretary Board & Share

Mr. Abul Kashem Senior Vice President(Dev.) Sales Promotion

Mr. Khorshed Alam Patwary Senior Vice President(Dev.) NPDI

Mr. Morshedul Alam Chowdhury Senior Vice President(Dev.) Noakhali

Mr. Osman Gani Chowdhury Senior Vice President(Dev.) Patiya

Mr. Sayed Md. Yusuf Senior Vice President(Dev.) Chittagong

Mr. Sadeq Hossain Vice President Sales Promotion

Mr. Fazle Elahy Chowdhury Vice President Audit & Inspection

Mr. Salah Uddin Md. BakiBillah Vice President Policy Service

Mr. Ahmed Hossain Chowdhury Vice President Kandirpar

Mr. Baharuddin Majumder Vice President(Dev.) Newmarket

Mr. Matiar Rahman Vice President(Dev.) Bogra

Mr. Shahabuddin Vice President(Dev.) Kandirpar

Mr. Abul Mansur Ahmed Vice President(Dev.) Dhaka

Mr. Shakhawat Hossain Vice President(Dev.) B-Baria

Kazi Abdul Motin Vice President(Dev.) Area-03

Mr. Borhan Uddin Ahmeed Deputy Vice President Policy Service

Mr. Azizul Hoq Bhuiyan Deputy Vice President Finance & Accounts

Mr. S. l. M. Shahabuddin Deputy Vice President Training

Mr. Kazi Mohammed Mohsin Deputy Vice President Group

Mr. Bani Amin Deputy Vice President Policy Service

Mr. Ashraf Uddin Ahmed Mazumder Deputy Vice President I.T.

Mr. Md. Belal Hossain Deputy Vice President Underwriting

Md. Harunur Rashid Mozumder Deputy Vice President Policy Service

Mr. Iftekharul Alam Deputy Vice President C D A

Mr. Rohan Ahmed Deputy Vice President Group

Mohammed Ziaur Rahman Actuarial Officer Actuarial

Mr. Monir Ahmed Deputy Vice President(Dev.) Dhaka Zone-01

Md. Dabir Uddin Deputy Vice President(Dev.) Tongi

Mr. Sawrupkumar Shyam Asstt. Vice President Commision

Mr. Mesbah Uddin Asstt. Vice President Commision

Mr. Aminul Islam Asstt. Vice President Law

Mr. Mohd. Mohiuddin Asstt. Vice President Policy Service

Mr. Maksudul Hoque Asstt. Vice President Establishment

Mr. Abdur Rahim Asstt. Vice President Transport

Mr. Md. Nazrul Islam Asstt. Vice President Agency

Mr. A. K. M. Miraj Asstt. Vice President Finance & Accounts

A. M. M. Moiz Uddin Asstt. Vice President I.T.

Mr. Md. Daud Meah Asstt. Vice President Finance & Accounts

Mr. Abul Kalam Bhuiyan Asstt. Vice President Policy Service

Mr. MohdJasim Uddin Asstt. Vice President Islami Takaful

Mr. Mohd Mobinur Rahman Asstt. Vice President Finance & Accounts

Emran Hossain Bhuiyan Asstt. Vice President Finance & Accounts

Md. Abdul Kader Asstt. Vice President Finance & Accounts

Md. Bakhtiar Uddin Asstt. Vice President Engineering

Mr. Morshed Ali Asstt. Vice President(Dev.) CTG.

Md. Seraj-Ud-Daullah Asstt. Vice President(Dev.) Khulna

Mr. Azmal Hoque Asstt. Vice President(Dev.) Hathazari

Aminul Islam Asstt. Vice President(Dev.) Dinajpur

Md. Tazul Islam Asstt. Vice President(Dev.) Barisal

Mizanur Rahman Asstt. Vice President(Dev.) Bogra

Md. Zafar Ahmed Asstt. Vice President(Dev.) Zindabazar

Salim Samjed Ashrafi Asstt. Vice President(Dev) Rauzan M.A

Zinnatun Nahar Asstt. Vice President(Dev.) Jessore.

Md. Khorshed Alam Asstt. Vice President(Dev.) Munshigong

Abdul Mannan Asstt. Vice President(Dev.) Gouripur

Nirmalandu Barai. Asstt. Vice President(Dev.) GoalaBazar

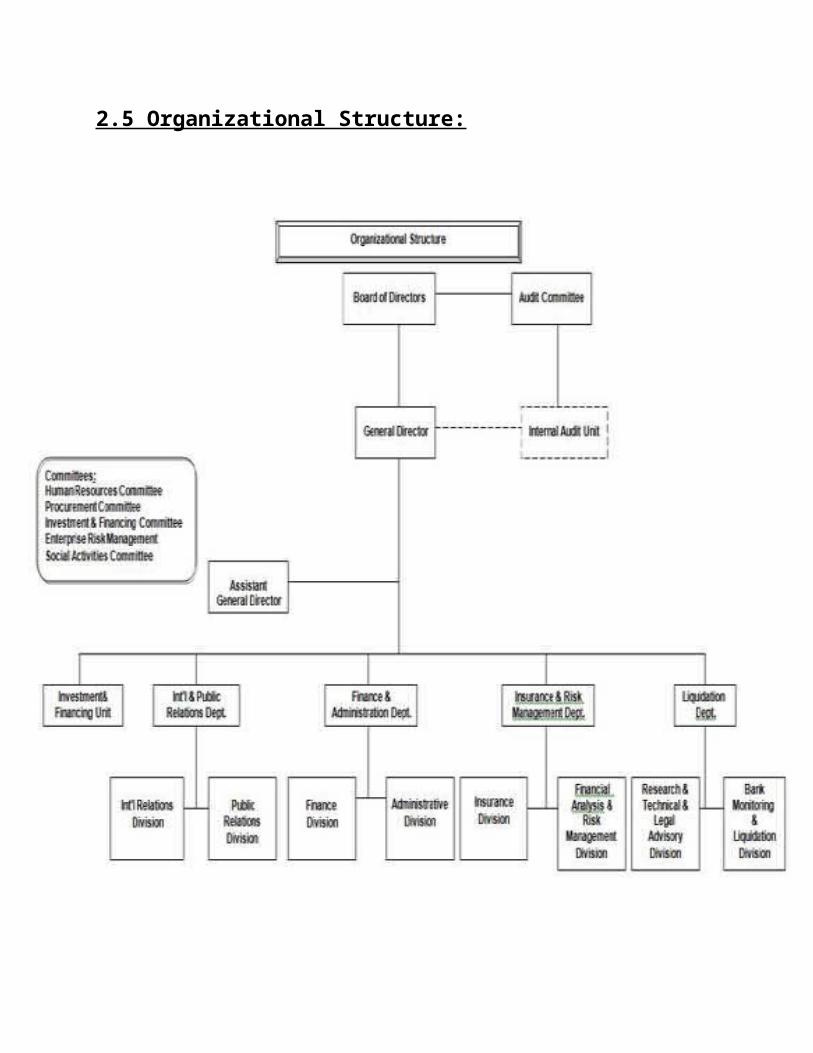

2.5 Organizational Structure:

2.6 Branches & officesBranches Branches

Registered office:NLI Tower,54, KaziNazrul Islam AvenueKarwan Bazar, Dhaka-1215

Rajbari Zone Hazi Super Market (3rd

floor) Thana Road, Pangsha

Motijheel Zone: 79Motijheel C/A, Dhaka-1000 G.P.Kh (1st floor) 49/1.

PragotiSharaniRoad. Shajadpur, Gulshan Dhaka- 1212

Bogra Zone Mastar Para (Thana Bhaban)

Kahalu Upazilla Road, Sonatala

Farmgate Zone: 56 KaziNajrul Islam Avenue

(3rd floor)Karwan bazar, Dhaka-1205

Road No. - 2, Plot No.-1. Mirpur-10, Dhaka-1216

Rajshahi Zone: Molla Plaza (4th floor)

shaheb Bazar GolamMostofaBhaban

Banlamotor Zone: Badsha Plaza,20 Link Road ,

Banglamotor, Dhaka 336 D.I.T Road, Rampura,

Dhaka-1219

Rangpur Zone: Thana Road. Kounia Station Road, Badargonj

Narayangonj Zone: Mid Tower City Complex (3rd

floor) 54 B.B Road, Narayangonj

Chowdhury Bari, Bandar, Narayangonj.

Khulna Zone: Pather Bazar, School Road,

Dighalia Jahid Plaza (1st floor)

Paikgacha

Munshigonj Zone: Sharif Plaza (3rd floor)

MathparaMunshigonj Sreenagar, Munshigonj

Jessore Zone: Bandar Complex (2nd floor)

Benapol Bazar, Sharsha Nowapara, Avoynagar.

Gazipur Zone: Kapasia, Gazipur

Barishal Zone: Akan Vila, Sadar Road,

Banaripara TalukderMahal,

Chargadatali, Gournadi

Manikgonj Zone: Haji Sabed Supper Market

(2nd floor) Jhitka Bazar, Harirampur

Bhola Zone: Zia Super Market (2nd

floor)Sadar Road.

Kishorgonj zone: College Road, Bhairab

Borguna Zone: Patharghata office

2.7 Performance & Growth of the Company:Taka in Million

Particulars 2012 2011 2010 2009 2008Total premium 7028.62 6321.84 6070.3

44718.3

64069.2

0Investment income 2463.09 1712.66 1741.8

81311.1

31060.1

1Claims 3294.39 2558.65 1947.9

71634.2

81385.4

5Management expenses 2100.97 2000.91 1982.6

11534.5

81309.0

3Assets 27919.9

823824.7

520422.49

16285.95

13140.97

Life fund 24186.87

20687.22

17630.52

14039.24

11404.49

Dividend (cash + stock)(%)

30+30 50+10 60 55 50

Premium (%) 11.18 4.14 28.65 15.95 15.02Claims (%) 28.76 31.35 19.19 17.96 2.25Assets (%) 17.19 16.66 25.40 23.93 22.10Life fund (%) 16.92 17.34 25.58 23.10 25.57

Challenges:: Factors in the economy, risk management, keeping costs low

and retaining business in a competitive market are issuesinsurance companies face on a regular basis.

Uncertainty regarding the economy along with changes inhow people do business keep this industry on its toes asit strives to meet the demands of consumers and ensurelong-term success.

Challenging in insurance claim may be necessary to coverdamages to people’s health or property. Insurancecompanies are in business to take in more money inpremiums than they pay out in claims.

In general, a company won't be shy to fight back againstpeoples appeals to get a higher claim settlement. If you'dlike to try to get more money out of your insurancecompany, be prepared for a battle that could take monthsor years to resolve.

Future plans:

In every kind of business or organization or companies have theirown future plan to develop his or her business. The future plansof the National Life Insurance Company Ltd. are given below

To capture the customer united insurance company willadd more policy to give more facilities as well asservice.

To give claim settlement when the claim occurs asquicker than other insurance company.

By opening new policy and branches UICL need manpowerthat mean unemployment problem will reduce.

To provide the policies to the mass people of thecountry.

To exceed present target for better future profit.

To become one of the market leader.

3.1 Insurance policiesThere are different kinds of insurance policies that aremaintained in Federal Insurance Company covering differentperils. They are stated below:Endowment Insurance It’s a safest and surest method of guaranteed cash provisioneither at a specified time or at death (Allah forbid). Underthese policies, the sum insured plus bonuses are payable at theend of the specified number of years or at death of the lifeinsured if earlier. Premiums are payable for the specified numberof years or till death, if earlier. Age of the policy holder onmaturity should not be more than Age 70 years. The benefits underthe plan can be further increased by attaching supplementarycovers. This policy can be taken for 10, 15, 20, 25, 30 0r 35years.Anticipated Endowment Insurance

This is a modified form of endowment assurance and is also called‘Three Payment Plan’. Besides fulfilling the long-term financialneeds, it also helps in meeting the short-term financialexigencies. As the name suggests, the plan offers three paymentsthroughout term of the policy. The plan offers survival benefits equal to 25% of sum insured oncompletion of 1/3rd and 2/3rd term of the policy. If thepolicyholder does not withdraw the survival benefits, a veryattractive special reversionary bonus is available. On completionof term of the policy, the remaining 50% sum insured plus accruedbonuses shall be payable.

Child Protection InsuranceThis is a joint life assurance and covers the lives of child andeither of the parents. If the policyholder and the child bothsurvive full term of the policy, sum insured and accrued bonusesbecome payable. If the policyholder dies (Allah Forbid) beforecompletion of term of the policy the payment of premiums ceasesand the child is paid an income of Taka 100/- per thousand sumsinsured per annum till the completion of the policy term. Oncompletion of policy term, sum insured inclusive of bonusesaccrued till the death of the policyholder is paid to the child. If the child dies (Allah Forbid) before maturity of the policy orduring lifetime of the policyholder, the death claim is payableto the policyholder depends on the age of death of the child. Five Payment Endowment Insurance (With Profits)

is given for 10, 15, 20, 25 & 30 years term (with profit). Thisplan provides 10% sum assured upon expiry of one fifth of theterm, 15% sum assured upon expiry of two fifth of the term, 20%sum assured upon expiry of three fifth of the term, 25% sumassured upon expiry of four fifth of the term, and the remaining30% of the sum assured along with accrued interest is paid atmaturity.

Whole Life Insurance (With Profits)

This plan is mainly devised to create an estate for the heirs of thepolicyholder as the plan basically provides for payment of sum assuredplus bonuses on the death of the policyholder. However, consideringthe increased longevity of the Bangladesh population, the Corporationhas amended the above provision, thereby providing for payment of sumassured plus bonuses in the form of maturity claim on completion ofage 85 years or on expiry of term.

Double Endowment policy

Under this policy, if the life assured dies (Allah Forbid) duringthe endowment period, the basic sum assured is payable and if hesurvives to the end of the term, double of the sum assured ispaid. The premium, are generally quoted according to theendowment period, irrespective of the age at entry subject toprovision that maturity age is not beyond 65 years.

Double Security Insurance (With Profits)

Under this policy premium is payable until policy holder dies(Allah Forbid) or on expiry of the term. On expiry of termprinciple amount with bonus is given. If policy holders dies(Allah Forbid) before the expiry of term then for every tk 1000double will be given. But bonus will be counted on principalamount tk 1000. This policy range is 12, 15, 20 or 25 years.

Children Education Security Plan

This is a joint life assurance and covers the lives of child andeither of the parents. If the policyholder and the child bothsurvive full term of the policy, sum insured and accrued bonusesbecome payable. If the policyholder dies (Allah Forbid) beforecompletion of term of the policy the payment of premiums ceasesand the child is paid an income of Tk 10/- per thousand sumsinsured per annum till the completion of the policy term. Oncompletion of policy term, sum insured inclusive of bonusesaccrued till the death of the policyholder is paid to the child.This policy can be taken for 10, 15 or 20 years.

Pension Plan (Without Profit)Pensions are provided at quarterly intervals from an agedesignated by the policyholder for life, guaranteed for a minimum

period of 10 years i.e. if the pensioner dies (Allah Forbid)anytime within 10 years his designated nominee will get pensionfor remaining term of 10 years. Before pension starts, if thepolicyholder dies (Allah Forbid), 10 times the annual pension ispaid as a lump-sum to his nominee and the policy is terminatedupon such payment. Family Income Rider-FIRThis policy can be taken only under endowment policy. Under thispolicy if policy holder dies (Allah Forbid) then on principleamount 25% bonus, 10% half yearly installment until expiry ofterm and 75% will be given on the expiry of term. This policy isavailable in 10, 15, 20 and 25 years.BAHUMUKHI BIMA (With Profits)Under this policy holder of the policy can get assurance for oldage, his family member, his child’s education and for marriage.If policy holders dies (Allah Forbid) before term then familymember will get monthly income of 1% of sum assured, will begiven 10% of the sum assured once and 90% will be given afterexpiry of term. If policy holder survives till expiry of deaththan he will be given sum assured with bonus.BONDHOKI BIMA (without profits)Mortgage Life Insurance is a form of insurance specificallydesigned to protect a repayment mortgage. If the policyholderwere to die (Allah Forbid) while the mortgage life insurance wasin force, the policy would pay out a capital sum that will bejust sufficient to repay the outstanding mortgage.Mortgage life insurance is supposed to protect the borrower'sability to repay the mortgage for the lifetime of the mortgage.This is in contrast to Private mortgage insurance, which is meantto protect the lender against the risk of default on the part ofthe borrower.Group InsuranceNational Life offers a host of Group-Life Insurance schemes from which an organization/ employer may choose for benefits of its members/employees, as may best serve their interest according to organizational setup.

To be treated as a group, the following criteria need to be fulfilled: i) A “Group” Should comprise of at least 15 members ii) It should be a legitimately organized body iii) Group clientsof National Life Insurance Company Limited include iv) Semi-Government organization, autonomous bodies v) Private, Non-Government Organizations (NGO's) vi) Educational & Financial Institutions vii) Public Limited Companies viii) Associations, Business organizations etc. Monthly Deposit Scheme InsuranceThis policy can be taken by age of 18 to 45 years and policyamount can be of tk 6000 to tk 50000. Term of the policy is 10years and maximum age on maturity should not be more than 70years. Actuary decides the amount of bonus should be given. Iffor any reason premium is not payable before 1 year than policyamount will not be paid.

Double Installment Jono Insurance (with profit)In this policy after a fixed period of time in two installmentsum assured with interest is given which helps economically smallincome people. To enter into this contract age of the policyholder should be 20 to 45 years. Maximum age of the policy holderon expiry should not be more than 57 years. Minimum premiumshould be tk 104.40 to maximum tk 2610. Minimum policy amountshould be 12000 to maximum tk 300,000. Term of the policy is 12years.Denmohor InsurancePremiums deposited will be refunded with profits if any pluspremiums payable up to maturity date from the date of death willalso be refunded. On maturity if the policyholder survives fullsum assured with accrued bonuses with be paid. For 10, 15 0r 20years this policy can be taken. This sum assured will be given towife of policy holder. Age of the policy holder on maturityshould not be more than Age 70 years.Hajj Insurance

On maturity if the policyholder survives full sum assured withaccrued bonuses with be paid. Premiums deposited will be refundedwith profits if any plus premiums payable up to maturity datefrom the date of death will also be refunded. This policy termcan be 10, 15 or 20 years. Age of the policy holder on maturityshould not be more than Age 70 years. In case of half annuallypremium then 2% more premium will be taken and it will be taxfree. Takaful contract amount will not be less than tk 100,000.Three Payment Insurance (Takaful)Under these policies, the sum insured plus profit are payable atthe end of the specified number of years or at death of the lifeinsured if earlier. Premiums are payable for the specified numberof years or till death, if earlier. This plan provides 25% sumassured upon expiry of one fourth of the term, 25% sum assuredupon expiry of two fourth of the term, and the remaining 50% ofthe sum assured along with accrued profits is paid at maturity.This policy term can be for 12, 15, 18, 21 or 24 years. In thispolicy annual premium is at least tk 2000.

Four Payment Insurance (Takaful)Under these policies, the sum insured plus profit are payable atthe end of the specified number of years or at death of the lifeinsured if earlier. Premiums are payable for the specified numberof years or till death, if earlier. This plan provides 15% of sumassured upon expiry of one fourth of the term, 20% of sumassured upon expiry of two fourth of the term, 25% of sum assuredupon expiry of third fourth of the term and the remaining 40% ofthe sum assured along with accrued profits is paid at maturity.Available term for this policy is 12, 16, 20, 24 and 28 years. Inthis policy annual premium is at least tk 2000.

3.2 POLICY CONDITION

Incontestability: The policy will become incontestable afterexpiry of two years from the date of commencement of risk orfrom the date of revival of the lapsed policy unless for

nondisclosure of material facts or fraud committed by the Proposer/insured.

Travel, Residence and Occupation: The Policy is free from all restrictions as to travel, residence and occupation.

Commencement of Policy: The Policy shall not be enforcing until the company has received the first Premium. This payment is due and payable as on the date of commencement ofrisk whether it is a single premium or the first of a seriesof periodical premiums.

Days of Grace: For payment of renewal premium thirty days ofgrace are allowed if death occurs within the days of grace and before payment of premium the policy will be treated as valid and effectual subject to deduction of the unpaid premiums.

Payment of Premiums: All premiums are payable in advance to the Company in full the insured bearing remittance charges, if any The actual date of receipt of the premium by the Company will be treated as the date of payment.

Revival of Lapsed Policies: When a policy which has not acquired a surrender value lapses through nonpayment of premium within the days of grace the same can be revived within five years on payment of all arrears of premium together with interest at a rate not exceeding the prevailing Bank Rate on proof being given at the cost of theinsured to the satisfaction of the Company of the good health and continued eligibility of the life for insurance.

Special Revival Scheme: If a policy is discontinued before acquiring the Surrender Value and the Policyholder is unableto Pay the arrear of premiums together with interest subjectto satisfactory evidence of insurability being furnished to the Company at the Policyholder’s cost the Policy may be revived by advancing the Commencement/Maturity date of the policy and by charging the required special revival fee and premiums for enhanced age of the insured. This benefit is available only once during the whole policy term.

Receipts for Premiums: No receipt shall be valid unless it is on an official printed form bearing the signature of an Authorized Officer of the Company.

Non-forfeiture of Policies: After the payment of two consecutive years full premium the Policy shall not lapse orbecome void for omission to pay any premium and the Company offers anyone of the following Options as has been indicatedby the Policyholder in writing before the cessation of premium if no Option is exercised by the Policyholder, then Option A stated below will operate. Option A: Make the Policy Paid-up for a reduced Sum Insured after advancing one year’s premium, subject to the availability of the Surrender Value without the obligation to pay future premiums and if the policy is and-profit one without the right to participate in future Bonus. Option B: keep the Policy in full force by advancing thepremium at such rate of interest as the Company from time totime determine until the Surrender Value is exhausted.

Proof of Age: Must be the proved to the satisfactory of theCompany before any benefit is paid under the within mentioned policy. In the event of discrepancy or inaccuracy in age, adjustment will be made in premium provided the age is within the insurable age limit of the Company and provided the statement thereof was not fraudulent made and provide the proposer/life insured did not suppress facts which it was material to disclose, otherwise the policy willbe null and void and the premiums paid will stand fortified.

Surrender Value and Loan: A policy of life insurance, if enforce, shall acquire after all premiums have been paid forat least two consecutive years a Cash surrender Value which will be quoted on application, and this Value may be taken by Policyholder at such rate of interest as the Company may from time to time determine.

Payment of Claims: Claims are paid at the Principal Places of Business or the Head Office of the Company promptly on proof of age, death and title.

Suicide: Death by suicide does not vitiate the policies of the Company unless such death occurs within one year from the date of issue of the policy or Revival and even in such event the bonafide interests acquired by assignment shall

not be effected provided notice in writing of the assignmentor change shall have been received by the Company at least three calendar months prior to the death.

Notice of Assignment and Nomination: All notices of Assignment or Nomination or Cancellation or Changes of Nomination must state the date and purport thereof be sent to the Head Office of the Company at Dhaka. The Company on receipt of the usual fee will acknowledge such Notices whichshould be lodged in duplicate. Every Nomination shall be deemed to have been made pursuant to Section 39 of the Insurance Act 1938. In recording an Assignment the Company does not accept any responsibly or express any opinion as tothe validity or legal effect of the Assignment.

Policyholder’s Directors: Subject to the Insurance Act, 1938 and the Rules made there under a policyholder may seek election as a Policyholder’s Director.

Lien Clause: Notwithstanding anything herein contained to the country, it is hereby agreed & declared that in the event of the life insured happening during currency of the policy at any time within the first years, the amount payable will be less by of the sum insured & bonuses

Pregnancy Clause: In the event of death of the insured ladytaking place within the policy term from the date of commencement of risk due to any cause directly or indirectlyattributed to the first pregnancy, the company’s liability shall be limited only to refund of the premiums received without interest exclusive of first year premium or extra

3.3 Contents of agreement

In National Life Insurance Company there are a lot of things thatare included in an agreement of insurer & insured which are knownas contents of agreement. It includes detail information of theinsurance contract. They are described below:

I) Name of the proposer in Bengali and English (In blockletters)

II) Father’s / Husband’s Name

III) Mother’s Name

IV) Occupation

V) If service holder name of the post or employer

I) Residential Address (Also in English block letters)

II) Permanent Address

Age nearest Birthday……….years………………..birthplace………….nationality………………

Along with any certificate that helps to prove age.

I) Sum to be Assured Tk.

II) Table No. & Term

III) Installment System: Annually…..Half Annually……

IV) Detail of Deposition of Money

For Extra benefit mark right

Accidental Death Insurance

Accidental Death and Disability insurance

Family Security Insurance

Name of the Person giving Premium (other than holder thaninsurable interest description must be given)

Educational Level

Surrender Value

Description of other life insurance of proposer if any

I) Nominee’s Name and Signature

II) Guardians’ Name and Signature if minor

I) Description of any other pending proposal in this orother insurance company

II) Description of denial or stopped or extra condition orextra premium of other insurance

I) Description of any dangerous occupation o any possibilityof joining

II) Description of any threat on life

Some question be to answered before medical report is given

At last a declaration is given that the proposer isgiving all the information truthfully and he understands all

the condition and he is agreed to it. Signature of theproposer is given below.

Elements of insurance contract

The elements of insurance contract include both the elements ofgeneral & special contract. They are described below:Offer and Acceptance

There must be a lawful offer by one party and a lawful acceptanceof the offer by the other party or parties. The adjective“lawful” implies that the offer and acceptance must conform tothe rules laid down in the Bangladesh Contract Act regardingoffer and acceptance.

Intention to create Legal Relationship

There must be an intention (among the parties) that the agreementshall result in or create legal relations. An agreement to dineat a friend’s house is not an agreement intended to create legalrelations and is not a contract.

Lawful Consideration

Subject to certain exceptions, an agreement is legallyenforceable only when each of the parties to it gives somethingand gets something. An agreement to do something for nothing isusually not enforceable by law. The something given or obtainedis called consideration.

Capacity of parties

The parties to an agreement must be legally capable of enteringinto an agreement; otherwise it cannot be enforced by a court oflaw. If any of the parties to the agreement suffers from any suchdisability, the agreement is not enforceable by law.

Free Consent

In order to be enforceable, an agreement must be based on thefree consent of all the parties. A person guilty of coercion,undue influence etc. cannot enforce the agreement. The otherparty (aggrieved party) can enforce it.

Legality of the Object

The object for which the agreement has been entered into must notbe illegal, or immoral or opposed to public policy.

Certainty

The agreement must not be vague. It must be possible to ascertainthe meaning of the agreement, for otherwise it cannot beenforced.

Void Agreements

An agreement so made must not have been expressly declared to bevoid. Under Bangladesh Contract Act there are five categories ofagreement which are expressly declared to be void.

Writing, Registration and Legal Formalities

The contract need to be in written, registered and maintain legalformalities to be enforceable by law.

4.1 Definition of Risk:Risk is a concept which relate to human expectation. It denotesto a potential negative impact to an asset or somecharacteristics of value that may arise from some present processor from future event.People express risk in different ways. To some, it is chance orprobability of loss, to others; it may be uncertain situation or

deviations or what statisticians call dispersions from theexpectation. In most of the terminology the term risk includeexposure to adverse situation.Risk is therefore incidental to life. Some people livedangerously. While others exercise is extreme caution.Nevertheless, the happing of fortuitous events or element cannotbe avoided, although its effect may be either good or bad.

Types of risk:

There are mainly two types of risks-

Uninsurable risk :If the insurance can be purchased at higher premium, thereshould not be any uninsurable risk. After investing all thefactors affecting the risk, the life insurance companyshould be able to give each due consideration and determinethe premium charge for the insurance.

Insurable risk: The insurable risk are those which after the selectionprocess can be carried out but any insurer although therecan be different terms and conditions for different policyholders.There are further three types of insurable risk. They are-

Standard risk: The standard risk related to the normal life where there is no much or no less risk.

Sub-standard risk: Sub-standard risk is that risk whichis higher though insurable than the standard risk.

Super-standard risk: The super-standard risk is presentwhere there is lower risk than the standard risk.

Risk management tools:

The following tools are used in National Life insurance Companyto manage risks-

Age: the age of the life to be assured is the mostimportant factor to affect mortality. The premium isdetermined at every year of the completion of age.

Build: build refers to physique of the proposed life &includes height, weight & the distribution of weight &chest expansion.

Physical condition: the physical condition of the age lifeproposed has a direct bearing on the mortality of the life.The conditions are sight, hearing, heart, lungs, tonsils,teeth, kidneys etc.

Personal history: the personal history of the life proposedwould reveal the possibility of death to him. The historymust be connected with the health record, past habit,insurance history etc.

Family history: family history also requires information ofhabit, health, occupation & insurance of other familymembers. It may be good or poor.

Occupation: if the occupation is hazardous because he maysuffer at any time while at work.

Residence: the residence also affects the risk. The riskwill be lesser in a good climate area & more in a badclimate although the difference is narrowed down.

Present habits: the present habits of the prosper affectsthe risk. Drunkards & non-temperate persons cause increasein mortality.

Morals: it has been observed that the departure from thecommonly accepted standards of ethical & moral conductinvolve extra mortality.

Economic status: it is essential to examine that the family& business circumstances of the proponents are such as tojustify the amount of insurance applied for.

Risk Management Process

1. Establish the context:Establish the context include planning and remainder of theprocess and mapping out the scope of exercise the identity andobjectives of stakeholders, the basis upon which risk will beevaluated and defining a framework for the process, and agendafor identification and analysis.2. Identification:After establishing the context, the next step in the process ofmapping risk is to identify potential risks. Risks are aboutevents that, when triggered, will cause problems. Hence, riskidentification can start with source of problems or with theproblems itself.

Source analysis Problem analysis Event

The several of risk identification are: Checklist method Financial method Flowchart method On-site inspections Interaction with others Contract analysis Statistical record of losses

3. Assessment:Once risk has been identified they must then be assessed as totheir potential severity of loss and to the probability ofoccurrence. These quantities can be either simple to measure, incase of the value of a lost building, or impossible to know forsure in the case of the probability of an unlikely event

occurring. The fundamental difficulty in risk assessment isdetermining the rate of occurrence since statistical informationis not available on all kinds of past incidents. Numerousdifferent formulas exist, but perhaps the most widely acceptedformula for risk qualification is Rate of occurrence.4. Potential risk treatment:Once the risk have been identified and assessed, all techniquesto manage the risk fall into one or more of these four majorcategories:

Risk transfer Risk avoidance Risk retention Risk control

A. Risk transfer:Risk transfer means that the expected party transfers whole orpart of losses consequential risk exposure to another party for acost. Apart from insurance device there are some other techniquesby which the risk may be transferred.B. Risk avoidance:Avoid the risk or circumstances which may lead to losses inanother way, includes not performing an activity that could carryrisk.C. Risk retention:Risk retention implies that the losses arising due to a riskexposure shall be retained or assumed by the party or theorganization. There may have two types of risk retention

Self-insurance Captive insurance

D. Risk control: Risk can be control either by avoidance or by controlling.However as a concept these can be segregated into two

Before occurrence of losses After occurrence of losses

5. Create the plan:Decide the combination and method to be used for each risk. Eachrisk management decision should be recorded and approved by theappropriate level of management. A good management plan shouldcontain a schedule for control and implementation and responsiblepersons for those actions.6. Implementation:Follow all the planned method for mitigating the effect of therisk. Purchase insurance policy for the risk that have beendecided to transfer to an insurer, avoid all the risk that can beavoided without sacrificing the entity’s goal, reduce others andretain the rest.7. Review and evaluation of the plan:Initial risk management will never be perfect. Practiceexperience and actual loss result, will necessitate changes inthe plan and contribute information to allow possible differentdecision to be made in dealing with the risk being faced.

5.1: Pricing Tools:Pricing tools mean techniques or methods of calculating price or premium. There are mainly two types of pricing tools to calculatepremium. These two techniques are Net Single Premium and Gross Premium. National Life Insurance Company uses both of the tools to calculate their price or premium.

For Net Single Premium National Life Insurance Company uses Mortality Table of Different age, amount of claim per death. Thenthey use to convert it into present value using present value factor. They calculate both Net Single Premium for Term Policy and different Endowment Policies as well as Deferred Annuities.

Gross Premium is that premium which is charged by the insured to meet the amount of claims and expenses. The Gross Premium

includes the Net Premium and loading expenses. Loading is the process of adding the Net expense with Net Premium.

5.2: Pricing Process: Process means the method of calculating premium. In case of calculating premium different insurance companies follow different methods. National Life Insurance Company also use a procedure to calculate their premium. They follow some specific chart which are structured for one thousand taka insurance policyin case of different insurance policies. And all the charts differ from one policy to another policy. In the chart the premium rate depends on the age of the insurer and on the maturity period. National Life Insurance Company takes a rate from their chart depending on the age and the maturity period, then they multiply it with the policy value and divided by one thousand.

Emphasizing on three chart procedures are mentioned below under three different policies with examples-

Chart: Endowment Insurance (with Profits)

Yearly Premium Rate for Every Thousand Taka

Age at the nearby birthday

Maturity Period of Insurance10 years

15 years 20 years

25 years 30 years

35 years

25. 107.11 69.70 51.13 39.42 31.91 26.9026. 107.12 69.72 51.16 39.48 32.02 27.06

27. 107.13 69.74 51.21 39.56 32.14 27.2328. 107.14 69.77 51.26 39.65 32.28 27.4329. 107.16 69.81 51.33 39.76 32.44 27.6630. 107.18 69.85 51.42 39.89 32.63 27.9231. 107.21 69.91 51.52 40.04 32.84 28.2032. 107.25 69.98 51.64 40.22 33.08 28.5333. 107.30 70.07 51.78 40.42 33.35 28.8934. 107.37 70.18 51.94 40.65 33.66 29.2935. 107.44 70.30 52.14 40.91 34.00 29.7436. 107.54 70.46 52.36 41.21 34.3937. 107.66 70.63 52.62 41.52 34.8338. 107.80 70.84 52.91 41.54 35.3239. 107.97 71.09 53.24 42.35 35.8640. 108.16 71.76 53.62 42.83 36.4641. 108.39 71.68 54.04 43.3642. 108.65 72.04 53.52 43.9543. 108.96 72.44 55.04 44.6144. 109.29 72.89 55.63 45.3345. 109.67 73.39 56.28 46.1446. 110.09 73.94 57.0047. 110.56 74.55 57.7948. 111.08 75.23 58.6649. 111.65 75.97 59.6350. 112.28 76.78 60.6951. 112.96 77.6852. 113.72 78.6753. 114.55 79.7654. 115.46 80.9555. 116.46 82.28

Let’s assume Mr. X wants to have an endowment policy for 35 years. In the near birthday he will be 25 years old. He wants to take the policy for 30000 taka. So his premium per year will be-

As his age is 25 years old and maturity period of policy is 35 years. Then we get a rate for one thousand taka which is worth 26.90 taka per year.

So for 1000 taka policy holder will have to pay 26.90 taka per year.

For 30000 taka policy holder will have to pay {30000*(26.90/1000)}= 807 taka per year.

Chart: Double security Insurance:

Yearly Premium Rate for Every Thousand Taka

Age at the nearby birthday

Maturity Period of Insurance12 years 15 years 20 years 25 years

20. 110.54 73.18 54.73 43.2821. 110.54 73.20 54.78 43.3822. 110.55 73.23 54.84 43.5223. 110.56 73.26 54.92 43.6724. 110.58 73.30 55.02 43.8525. 110.60 73.36 55.14 44.0726. 110.65 73.45 55.33 44.3727. 110.69 73.57 55.55 44.7328. 110.75 73.71 55.81 45.1529. 110.84 73.90 56.13 46.6430. 110.94 74.10 56.50 46.7931. 111.08 74.37 56.95 46.8232. 111.26 74.69 57.45 47.5333. 111.36 75.08 58.03 48.3334. 111.77 75.54 58.69 49.2435. 112.09 76.08 59.47 50.2436. 112.50 76.70 60.32 51.3937. 112.99 77.40 61.31 52.6338. 113.55 78.22 62.40 54.0339. 114.22 79.15 63.62 55.5840. 114.97 80.19 64.98 57.31

41. 115.84 81.37 66.49 59.1842. 116.82 82.67 68.17 61.2543. 117.94 84.12 70.00 63.5244. 119.17 85.72 72.04 65.9945. 120.52 87.47 74.27 68.7046. 122.02 89.42 76.7047. 123.70 91.54 79.3748. 125.53 93.88 82.2749. 127.52 96.42 85.4650. 129.70 99.20 88.9351. 132.09 102.2552. 134.72 105.5953. 137.70 109.2454. 140.71 113.2155. 144.14 117.57

Let’s assume Mr. X wants to have a Double security Insurance policy for 20 years. In the near birthday he will be 25 years old. He wants to take the policy for 30000 taka. So his premium per year will be-

As his age is 20 years old and maturity period of policy is 25 years. Then we get a rate for one thousand taka which is worth 54.73 taka per year.

So for 1000 taka policy holder will have to pay 54.73 taka per year.

For 30000 taka policy holder will have to pay {30000*(54.73/1000)}= 1641.90 taka per year.

Note: If any policy holder wants to take any extra clause with the principal policy then they will have to give extra amount of money with the principal premium.

5.3: Pricing Elements:

Pricing elements includes all those ingredients or components which are used to calculate premium. National Life Insurance usesmainly three things as their pricing elements. They are mortalitytable, outcome and all expenses. Premium is influenced by this major three things. While calculating premium these are the vitalthings to review or consider.

Mortality table is the table where the survey report of death is available. In this table there are also age, survival rate, and total insured person. Age includes in which age how many people died. Survival rate means the rate of living people among all insured.

Outcome means profit of the organization. National Life InsuranceCompany use to maximize their profit by calculating price more than the claims and all charges. That’s why the exceeding part ofthe price becomes profit of National Life Insurance.

Expenses mean all the cost which will have to bear by the insurance company until the maturity of the policy. There may have different types of expenses- initial expenses, recurring expenses, final expenses, general expenses etc. these types of costs are also included while calculating price.

5.4: Claim settlement procedure: In case of life insurance claim is ask for money which was insured by the insurer after the death or the maturity of the policy. National Life Insurance Company uses some specific procedure to make payment of the claims raised by the policy holder or nominee. To make sure that they are not facing cheat they justify the whole events using the procedure. Their procedures are described below using their given information and their official forms.

Claim settlement if policy holder dies: If the policy holder diesbefore maturity then selected nominees will claim for the insuredamount. It’s a complex process. The process is described below-

Collection and Submission of Claim Form: First of the all nomineeselected by the policy holder need to collect the claim settlement form from the National Life Insurance Company. Then company fills a form with policy holder’s information and policy number. This form contains date of applying for claim, policy no., and some required documents which are needed to submit to the company. And the nominee has to collect all the required documents from different person.In case of National Life Insurance there have six forms to fill up by different person.

Form Filled up by Nominee: A form is to be filled up bynominee where nominee has to input policy no., claim no., the easiest way to go to the policy holders house ex; location, how to go, contact no etc. and also required the claim holders mobile phone no. Filling up the form claim holder has to sign the form at the rightend.

Form filled up by the zonal office/ branch of national life: The form will be filled up by the zonal/ branch manager of the National Life Insurance Company. This form contains claim no, policy no, and all the information of policy holder including his name, father/ husband’s name, nominee’s name, relation with nominee, age at the time of death, occupation, place ofdeath, reason of the death, and comment around death. The manager also has to attest the form including his name, post, and contact no, and signs.

Form filled up by the Doctor: A form is also filled up by the doctor under whose consultation the policy holder took treatment. If the doctor is enlisted with the national life insurance then the doctor has only tomention his code no. If not then he has to fill the form and also has to take witness by the sign of any elite person of society. This form includes a lot of information about his physical condition before and after death, disease of the policy holder, reason of death etc. and at last he has to give some required information about himself and his signature.

Claim form filled up by nominee: This form will be filled up by nominee in front of any identifier and must be signed by the identifier. The identifier will be accepted by the National Life Insurance Company. If the identifier is an senior officer of National Life Insurance, zonal in charge, any teacher of University, Headmaster of high school, lawyer, chairman of municipality or any gadget officer. The most important thing is that the form must be filled up in written form. No symbol will be accepted in this form. Here theamount of claim is mentioned by the nominee and he has to give all the information regarding the policy holder’s death and relationship with the policy holder.Announcement: At the last of the form the nominee will make an announcement that all the filled information are fully true and he did not hide any information and gave those with his full consent and sense. If there are more than one claim holder then they will sign there. Justification: Identifier will check all the information and will mention that all the things are filled up in front of him. Then he will sign with his seal.

Justification: This justification will be made by that person who has no relationship with the policy holder or the claim holder or with the claim amount. And more two people with the same qualification will be the witness. In this form the person will tell everything clearly and honestly what he knows about the policy holder in the first portion. In the second portion he will tell some required information about the claim holders. Justification Announcement: Here the person will tell that he has filled up the form in front of two witnesses and all the information given by him is true and right. He will also announce that the person did not perform suicide. Below of this two witnesses will sign there with their required information.

Description by Recruitment agency: The Company where the policy holder made service, head of the company or

organization will fill up the form with required questions regarding his characteristics in office.At the end he will make an announcement that all the things he described before and information given are true and right in according to their staff record book.Then he will give some of his personal information and sign there with a seal of the office.

Claim settlement after the maturity (if policy holder does not die): If policy holder does not die in the maturity period then it’s not so complex to claim the money of sum insured by the policy holder.

Here policy holder has to make a application from provided by theinsurance company after the maturity of the insurance policy. Then the policy holder has to fill the form with his policy no., and other required information. After that the policy holder willsubmit the form attaching the slips of first and last premium paid by him.

The insurance company will justify all the documents and it will pay all the sum insured to the policy holder.

5.5: Insurance Marketing policy: Marketing is the heart of selling any product or service. It recognizes the product and service to its customers or probable customers. Insurance companies also need to take steps for marketing to introduce their services to the public. Marketing mainly emphasize on advertisement. Generally medium of marketing can be classified into two categories. They are printed medium and electronic medium.

National Life Insurance use both electronic and printed medium. In case of electronic medium they use bill board, and internet. Their services are updated time to time. In case of printed medium they use newspaper only.

The most common and important marketing technique they use is their field worker. Their field workers go door to door and make

their probable customers understand about their policies. It’s the most common and the important medium of marketing technique.

The field workers try to convince their customer to take a policywith providing facilities given by the company.

5.6: Reinsurance management: Reinsurance is the procedure of making insurance of insurance. Incase of reinsurance the ceding company takes all the liability from the primary insurer. Then he distributes risk among other companies who are interested to take the liability to reduce his own risk.

National Life Company has a policy condition of taking insurance worth 5lacs. If any some insured is more than the ceding company can make reinsurance for the exceeding amount of the sum insured.

National Life Insurance use both facultative and treaty contract.In case of facultative contract there have no limitation or reinsurance has no obligation that they might have ta accept the reinsurance contract offered by the ceding company. Here have no obligation that a company must have to take the reinsurance contract. Companies have full right to justify that they should accept the contract or not.

In case of treaty contract treaty has obligation to take responsibility if the value of insurance is more than 5lacs. The National Life Insurance has made treaty contract with only MunichInsurance Company, Germany. When National Life Insurance Companytakes any contract more than 5lacs and if they want to make it reinsurance the Munich Insurance Company is obliged to take the reinsurance contract for the exceeding amount. For 5lacs ceding company or primary insurer, National Life Insurance Company is liable and for the exceeding amount reinsurance Munich Insurance Company is liable.

For both facultative and treaty contract both National Life Company and Munich Insurance Company calculate the actual loss and divide the loss among them in the ratio of liability for claim settlement.

In reinsurance management there is no obligation for ceding company, National Life Insurance to make the insurer known about the treaty company.

6.1SWOT Analysis: National Life Insurance Company has comparatively more external and internal strength than its weakness. Among the existing insurance company in the market it has more opportunities. It also faces some threats from its competitor’s insurance company.

Strength: It has numerous clients.

It is financially established company.

It has a good reputation in the market.

It has skilled manpower for performing itsactivity.

It has long and efficient management cycle.

This company has skilled & long term experiencedmanagement system.

Shareholder’s equity enhancing year by year.

This company maintains well organized data basedsystem for future.

Its reserve increasing year by year.

Now its investment is high volume.

Weakness:At this stage this company has no major weakness.Sometimes it face temporary problem.

During new investment of the company sometimesoccur conflict among the shareholders and companyauthority.

Sometimes it fails to select right clients.

Opportunity As it has huge capital it can easily invest for

new sector.

It can take the advantage of competitor’sweakness.

Now a day peoples are interested about lifeinsurance Company.

It can expand its operation from home to foreigncountry.

It can influence people to take its insurancepolicy.

Threats: There is a huge prospect of the life insurance

business in Bangladesh.

Day by day various insurance companies areestablished so competition is tough.

The rules and regulation of insurance is complex inBangladesh.

The strike of political parties in Bangladesh is abig threat.

Destroy of our national economy.

6.2 SITUATIONAL ANALYSIS:

Situational Analysis provides useful information about a company’s stand-alone risk. In Scenario Analysis we consider

three alternative situations to evaluate the effects on the profit of the organization-

Base Case: This is the normal situation of the economy under

which company usually operates. Premium income and expenses are

set at there most likely values. In our analysis we have

considered year 2005 as the base year.

Best Case: This is the situation of the economy where all of the

variables especially, premium income and expenses are set at

there best reasonably forecasted value, We have considered 25%

probability that the company will operate in best economic

condition.

Worst Case: This is the situation of the economy where all of the

variables especially, premium income and expenses are set at

there worst reasonably forecasted value. We have considered 25%

probability that the company will operate in worst economic

condition.

Table for Scenario Analysis:

Best Case Base Case Worst Case

Particulars (20%increase in

premiumincome &

20%decrease inexpenses)

(actualpremiumincome)

(20%decrease inpremiumincome &

20%increase inexpenses)

Different Insurance Revenue Accounts

21,938,988 18,282,490 14,625,992

Add: Interest Income Other Income

11,112,212 12,74,711

11,112,212 12,74,711

11,112,212 12,74,711

Less: Expenses of Management

(9,854,884) (12,318,605)

(14,782,326)

Profit / Loss for the Year

24,471,027 18,350,808 12,230,589

Interpretation:

From the comparison of above mentioned cases, we have found thecompany is successful to maintain its profitability at differenteconomic conditions.

7.1Finding from performance analysis

1. National Life Insurance Company Ltd Net premium income of2012 is higher than the previous years.

2. The turn over to working capital is lower than theprevious year.

3. The workforce is relatively lower than other insurancecompanies

Recommendation:Studying about this company, we have come to know about somestrength, weakness, opportunities, threats to of this company.So there are some recommendations for the company. Those aregiven below:

They should reach to the remote corner of the country.

They need to take more active stuffs or train their stuffs muchcarefully.

They should try to make their strategy easier, so that thepeople could understand it.

They should not make their policy lengthy.

The computer system they use is needed to improve.

7.2 Concluding Remarks In our effort to prepare this report has not only been anamazing guideline for our future, but also, it has taught us todeal with real life issues like never before. In this little butsignificant journey of ours through this path, we have comeacross people who have immense contribution in the reaching ofour destination.

Finally our special indebtedness is to honorable course teacherFatema-Tuz-Zohora for giving us the opportunity to prepare areport. By doing such report we have gathered a lot of valuable

experiences that will help us in near future. Her advices,guidance, and support helped us enormously to do this researchproperly.

Our last thanks goes to the employees of National Life InsuranceLimited for endless help in providing the information and sharingtheir thoughts.

References and Bibliography 1. Assistant General Manger of National Life Insurance

Company LTD2. Mishra, M N, Insurance principles and practices. Chand &

company ltd, New Delhi, 13th Edition,

3. Annual reports of National life Insurance Company Ltd(2007-2012).

4. Websites WWW.Nationallifeinsurace.com.BD WWW.wikipedia.com WWW.DSE.org WWW.google.com