A GUIDE TO WAVELETS FOR ECONOMISTS

61

A GUIDE TO WAVELETS FOR ECONOMISTS ∗ Patrick M. Crowley Texas A&M University – Corpus Christi Abstract. Wavelet analysis, although used extensively in disciplines such as signal processing, engineering, medical sciences, physics and astronomy, has not fully entered the economics discipline yet. In this survey article, wavelet analysis is introduced in an intuitive manner, and the existing economics and finance literature that utilizes wavelets is surveyed and explored. Extensive examples of exploratory wavelet analysis are given, most using Canadian, US and Finnish industrial production data. Finally, potential and possible future applications for wavelet analysis in economics are discussed. Keywords: Business cycles; Economic growth; Multiresolution analysis; Statisti- cal methodology; Wavelets 1. Introduction The wavelet literature has rapidly expanded over the past 15 years, with over 1600 articles and papers now published using this methodology in a wide variety of disciplines. Applications using wavelets in disciplines other than economics are extensive, with many papers published in areas such as acoustics, astronomy, engineering, forensics, geology, medicine, meteorology, oceanography and physics. Economics (and to a lesser degree, finance) is conspicuous in its absence from this list, largely because for some reason the potential for using wavelets in economic applications has been overlooked. Although some enterprising economists have attempted to use wavelet analysis, given the discipline’s fixation on traditional econometric methods, these papers have not been widely cited and have in fact been largely ignored. The main aim of this survey paper is to shed new light on wavelet analysis by illustrating its usage in applied economic analysis, to highlight the work that has already been done using this methodology, and to suggest future areas where wavelet analysis might be able to make a contribution to our discipline. To maximize accessibility to this material, the discussion paper is pitched at a less technical level than most other introductions to wavelets, although a fairly complete list of references is provided for those who might wish to refer to more technical sources. 1 There are also three other entry points to this literature that are specifically aimed at economists – the excellent book by Gen¸ cay, Sel¸ cuk and Whitcher (2001), an ∗ This article is an extended, corrected and revised version of Bank of Finland Discussion paper 05-01, which possesses the title ‘An Intuitive Guide to Wavelets for Economists’. 0950-0804/07/02 0207–61 JOURNAL OF ECONOMIC SURVEYS Vol. 21, No. 2 C 2007 The Author Journal compilation C 2007 Blackwell Publishing Ltd, 9600 Garsington Road, Oxford OX4 2DQ, UK and 350 Main Street, Malden, MA 02148, USA.

Transcript of A GUIDE TO WAVELETS FOR ECONOMISTS

A GUIDE TO WAVELETS FORECONOMISTS∗

Patrick M. Crowley

Texas A&M University – Corpus Christi

Abstract. Wavelet analysis, although used extensively in disciplines such as signalprocessing, engineering, medical sciences, physics and astronomy, has not fullyentered the economics discipline yet. In this survey article, wavelet analysisis introduced in an intuitive manner, and the existing economics and financeliterature that utilizes wavelets is surveyed and explored. Extensive examples ofexploratory wavelet analysis are given, most using Canadian, US and Finnishindustrial production data. Finally, potential and possible future applications forwavelet analysis in economics are discussed.

Keywords: Business cycles; Economic growth; Multiresolution analysis; Statisti-cal methodology; Wavelets

1. Introduction

The wavelet literature has rapidly expanded over the past 15 years, with over1600 articles and papers now published using this methodology in a wide varietyof disciplines. Applications using wavelets in disciplines other than economicsare extensive, with many papers published in areas such as acoustics, astronomy,engineering, forensics, geology, medicine, meteorology, oceanography and physics.Economics (and to a lesser degree, finance) is conspicuous in its absence from thislist, largely because for some reason the potential for using wavelets in economicapplications has been overlooked. Although some enterprising economists haveattempted to use wavelet analysis, given the discipline’s fixation on traditionaleconometric methods, these papers have not been widely cited and have in factbeen largely ignored. The main aim of this survey paper is to shed new light onwavelet analysis by illustrating its usage in applied economic analysis, to highlightthe work that has already been done using this methodology, and to suggest futureareas where wavelet analysis might be able to make a contribution to our discipline.To maximize accessibility to this material, the discussion paper is pitched at a lesstechnical level than most other introductions to wavelets, although a fairly completelist of references is provided for those who might wish to refer to more technicalsources.1 There are also three other entry points to this literature that are specificallyaimed at economists – the excellent book by Gencay, Selcuk and Whitcher (2001), an

∗This article is an extended, corrected and revised version of Bank of Finland Discussion paper 05-01,

which possesses the title ‘An Intuitive Guide to Wavelets for Economists’.

0950-0804/07/02 0207–61 JOURNAL OF ECONOMIC SURVEYS Vol. 21, No. 2C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd, 9600 Garsington Road, Oxford OX4 2DQ, UKand 350 Main Street, Malden, MA 02148, USA.

208 CROWLEY

article by Ramsey (2002) which provides a nice rationale for wavelets in economics,and a discussion paper by Schleicher (2002).

So, what are wavelets? Wavelets are, by definition, small waves. That is, theybegin at a finite point in time and die out at a later finite point in time. As such theymust, whatever their shape, have a defined number of oscillations and last through acertain period of time or space. Clearly, these small wave-like functions are ideallysuited to locally approximating variables in time or space as they have the ability tobe manipulated by being either ‘stretched’ or ‘squeezed’ so as to mimic the seriesunder investigation.

Wavelets possess many desirable properties, some of which are useful ineconomics and finance, but many of which are not. In this paper the focus is placedon the ability of wavelet analysis to deal with both stationary and nonstationary data,their localization in time and their ability to decompose and analyse fluctuations ina variable.

The survey is organized into seven parts. Part 2 introduces wavelets, part 3describes how wavelet transforms work, and delivers some variations on the basictheme, part 4 describes some applications and extensions that might be of particularinterest to economists, while part 5 looks at wavelets as applied in the frequencydomain. Part 6 then describes the literature in economics and finance to date, andsuggests areas in economics where wavelets might potentially make a contribution,and then part 7 concludes. Economic examples are provided throughout.

2. Wavelets 101

First, we need to dispense with some terminology. A real discrete-time signal isdefined as any real-valued function of the integers. Thus signals differ from variablesin that signals are assumed to be continuous and can be infinite in length, whereasvariables in economics are usually sampled discretely and are assumed to have abeginning point and an end point, and may not be an easily definable function orin fact definable function of the integers. Signals therefore exist as well-definedfunctions, whereas economic and financial variables are usually assumed to haveunknown data-generating processes. Although wavelet analysis has its origins in thesignal processing literature, most of the techniques used in wavelet analysis carryover to the analysis of any variable, whether discretely sampled, or continuous. Inthis survey paper, therefore, we use the terms signal and variable interchangeably.

Most economists are at least vaguely familiar with Fourier analysis, and this is agood starting point as wavelet analysis has various points of similarity and contrastwith Fourier analysis. The Fourier transform is based on the usage of the sum of sineand cosine functions at various wavelengths to represent a given function. One ofthe drawbacks of Fourier transforms though is that it is assumed that the frequencycontent of the function is stationary along the time axis. Imagine a minimalistsymphony (say John Adams or Steve Reich) – the analogue here would be eachinstrument playing a note, with a specific loudness: a0 + a1 cos t + a2 cos 2t+ . . . – to represent this signal one would only need the list of amplitudes (a0,a1, a2, . . .) and the corresponding frequencies (0, 1, 2, . . .). In this sense Fourier

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

GUIDE TO WAVELETS FOR ECONOMISTS 209

analysis involves the projection of a signal onto an orthonormal2 set of trigonometriccomponents. The Fourier transform makes particular sense when projecting over therange (0, 2π ), as Fourier series have infinite energy (they do not die out) and finitepower (they cannot change over time).

Windowed Fourier analysis extends basic Fourier analysis by transforming shortsegments of the signal separately, so that the assumption of no variation over timecan be relaxed. In other words there are breaks where we just repeat the exerciseabove. Once again these are just separate sets of orthonormal components – one setfor each window.

In a sense, wavelets are a further refinement of Fourier analysis, as they arelocalized in both time and their functional components. They thus provide aconvenient and efficient way of representing complex variables or signals, aswavelets can cut data up into different frequency components. They are especiallyuseful where a variable or signal lasts only for a finite time, or shows markedlydifferent behaviour in different time periods. Using the symphonic analogy, waveletscan be thought of representing the symphony by transformations of a basic wavelet,w(t). So at t = 0, if cellos played the same tune twice as fast as the double basses,then the cello would be playing c1w(2t) while the double basses play b1w(t),presumably with b1 ≥ c1. At t = 1, the next bass plays b2 w(t − 1), and thenext cello plays c2 w(2t − 1) starting at t = 0.5. Note that we need twice as manycellos to complete the symphony as double basses, as long as each cello plays thephrase once. If violas played twice as fast as cellos and violins twice as fast asviolas, then obviously this would be eight times as fast as double basses, and ifthere were such an instrument as a hyper-violin, then it would play 16 times fasterthan a double bass. In general the n-violins play ‘scalings’ of w(2nt).

In wavelet analysis, we only need to store the list of amplitudes, as the scalingsautomatically double the frequency. With Fourier analysis a single disturbance affectsall frequencies for the entire length of the series, so that although one can try andmimic a signal (or the symphony) with a complex combination of waves, the signalis still assumed to be ‘homogeneous over time’. In contrast, wavelets have finiteenergy and only last for a short period of time. It is in this sense that wavelets are nothomogenous over time and have ‘compact support’, so that following our analogy,we can analyse changes in the pitch as well as what is played. In wavelet analysis toapproximate series that continue over a long period, functions with compact supportare strung together over the period required, each indexed by location.

2.1 Elementary Wavelets

Wavelets have genders: there are father wavelets φ and mother wavelets ψ . Thefather wavelet integrates to 1 and the mother wavelet integrates to 0∫

φ(t) dt = 1 (1)∫ψ (t) dt = 0 (2)

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

210 CROWLEY

`s8' father, phi(0,0)

0 2 4 6

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

`s8' mother, psi(0,0)

-2 0 2 4

-1.0

-0.5

0.0

0.5

1.0

1.5

Figure 1. Mother and Father Wavelets.

The father wavelet (or scaling function) essentially represents the smooth, trend(low-frequency) part of the signal, whereas the mother wavelets represent the detailed(high-frequency) parts by scale by noting the amount of stretching of the waveletknown as ‘scale’ or ‘dilation’. In diagrammatic terms, father and mother waveletscan be illustrated for the Daubechies wavelet, as shown in Figure 1.

Wavelets also come in various shapes: some are discrete (as in the Haar wavelet –the first wavelet to be proposed many decades ago, which is a square wavelet withcompact support), some are symmetric (such as the Mexican hat wavelet), some arealmost symmetric (such as the symmlet and coiflet), and some are asymmetric (suchas daublets).3 Four are illustrated in Figure 2, where all wavelets are mother wavelets.The upper left-hand wavelet is a Haar wavelet, and this is a discrete symmetricwavelet. The upper right-hand box contains a daublet, which is asymmetric, thelower left-hand box contains a symmlet and the lower right-hand box a coiflet. Thelatter two wavelets are almost symmetric.

The scaling or dilation property of wavelets is particularly important in exploratoryanalysis of time series. Consider a double sequence of functions

ψ (t) = 1√sψ

(t − u

s

)(3)

where s is a sequence of scales. The term 1√s

ensures that the norm of ψ (·) is equal

to one. The function ψ (·) is then centred at u with scale s. In wavelet language,we would say that the energy of ψ (·) is concentrated in a neighbourhood of u with

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

GUIDE TO WAVELETS FOR ECONOMISTS 211

`haar' mother, psi(0,0)

0.0 0.2 0.4 0.6 0.8 1.0

-1.0

-0.5

0.0

0.5

1.0

`d12' mother, psi(0,0)

-4 -2 0 2 4

-1.0

-0.5

0.0

0.5

1.0

`s12' mother, psi(0,0)

-4 -2 0 2 4 6

-1.0

-0.5

0.0

0.5

1.0

1.5

`c12' mother, psi(0,0)

-4 -2 0 2 4

6

6

-0.5

0.0

0.5

1.0

1.5

Figure 2. Families of Wavelets.

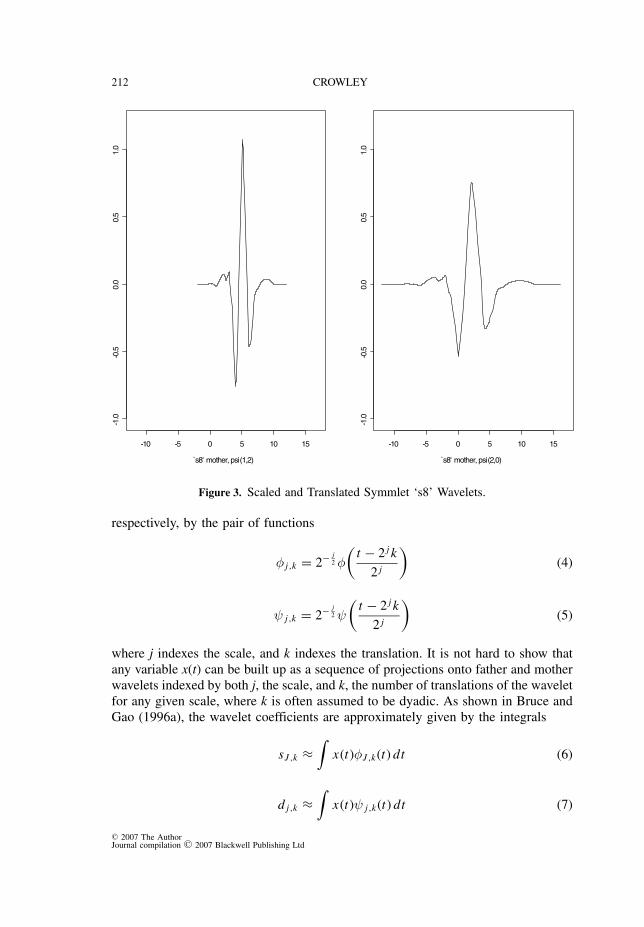

size proportional to s. As s increases the length of support in terms of t increases.So, for example, when u = 0, the support of ψ (·) for s = 1 is [d, − d]. As s isincreased, the support widens to [sd, −sd].4 Scaling is particularly useful in the timedomain, as the choice of scale indicates the ‘packets’ used to represent any givenvariable or signal. A broad support wavelet yields information on variable or signalvariations on a large scale, whereas a small support wavelet yields information onsignal variations on a small scale. The important point here is that as projectionsare orthogonal, wavelets at a given scale are not affected by features of a signal atscales that require narrower support. Lastly, using the language introduced above, ifa wavelet is shifted on the time line, this is referred to as translation or shift of u.An example of the dilation and translation property of wavelets is shown in Figure3. The left-hand box contains a symmlet of dilation 8, scale 1, shifted 2 to the right,while the right-hand box contains the same symmlet with scale 2 and no translation.

2.2 Multiresolution Decomposition

The main feature of wavelet analysis is that it enables the researcher to separateout a variable or signal into its constituent multiresolution components. In order toretain tractability (many wavelets have an extremely complicated functional form),assume we are dealing with symmlets; then the father and mother pair can be given,

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

212 CROWLEY

`s8' mother, psi(1,2)

-10 -5 0 5 10 15

-1.0

-0.5

0.0

0.5

1.0

`s8' mother, psi(2,0)

-10 -5 0 5 10 15

-1.0

-0.5

0.0

0.5

1.0

Figure 3. Scaled and Translated Symmlet ‘s8’ Wavelets.

respectively, by the pair of functions

φ j,k = 2− j2 φ

(t − 2 j k

2 j

)(4)

ψ j,k = 2− j2 ψ

(t − 2 j k

2 j

)(5)

where j indexes the scale, and k indexes the translation. It is not hard to show thatany variable x(t) can be built up as a sequence of projections onto father and motherwavelets indexed by both j, the scale, and k, the number of translations of the waveletfor any given scale, where k is often assumed to be dyadic. As shown in Bruce andGao (1996a), the wavelet coefficients are approximately given by the integrals

sJ ,k ≈∫

x(t)φJ ,k(t) dt (6)

d j,k ≈∫

x(t)ψ j,k(t) dt (7)

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

GUIDE TO WAVELETS FOR ECONOMISTS 213

j = 1, 2, . . . J such that J is the maximum scale sustainable with the data to hand.A multiresolution representation of x(t) is now given by

x(t) =∑

k

sJ ,kφJ ,k(t) +∑

k

dJ ,kψ J ,k(t)

+∑

k

dJ−1,kψ J−1,k(t) + · · · +∑

k

d1,kψ1,k(t) (8)

where the basis functions φ J,k(t) and ψ J,k(t) are assumed to be orthogonal, that is∫φJ ,k(t)φJ ,k ′ (t) = δk,k ′∫ψ J ,k(t)φJ ,k ′ (t) = 0∫ψ J ,k(t)ψ J ′

,k ′ (t) = δk,k ′ δ j, j ′ (9)

where δ i, j = 1 if i = j and δ i, j = 0 if i �= j . Note that when the number ofobservations is dyadic, the number of coefficients of each type is given by

• at the finest scale 21: there are n2coefficients labeled d 1,k .• at the next scale 22: there are n

22 coefficients labeled d 2,k .• at the coarsest scale 2J : there are n2J coefficients d J,k and s J,k .

In wavelet language, each of these coefficients is called an ‘atom’ and thecoefficients for each scale are termed a ‘crystal’.5 The multiresolution decomposition(MRD) of the variable or signal x(t) is then given by

{SJ , DJ , DJ−1, . . . D1} (10)

where SJ is the first term on the right hand side of equation 8, DJ is the secondterm etc.

For ease of exposition, the informal description above assumes a continuous signal,which in signal processing is usually the case, but in economics although variableswe use for analysis represent continuous ‘real-time signals’, they are invariablysampled at pre-ordained points in time. The continuous version of the wavelettransform (known as the CWT) assumes an underlying continuous signal, whereasa discrete wavelet transform (DWT) assumes a variable or signal consisting ofobservations sampled at evenly spaced points in time. Apart from a later sectionin the paper, only the DWT (or variations on the DWT) will be used from this pointonwards.

The interpretation of the MRD using the DWT is of interest in terms ofunderstanding the frequency at which activity in the time series occurs. For example,with a monthly or daily time series, Table 1 shows the interpretation of the differentscale crystals.

Note five things from Table 1:

(1) The number of observations dictates the number of scale crystals that can beproduced – only j scales can be used given that the number of observations, N ≥

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

214 CROWLEY

Table 1. Frequency interpretation of MRD scale levels.

Annual Monthly DailyScale frequency frequency frequencycrystals resolution resolution resolution

d1 2–4 2–4 2–4d2 4–8 4–8 4–8d3 8–16 8–16=8m–1yr4m 8–16d4 16–32 16–32=1yr4m–2yr8m 16–32=3wds1d–6wks2dd5 32–64 32–64=2yr8m–5yr4m 32–64=6wks 2d–12wks 4dd6 64–128 64–128=5yr4m–10yr8m 64–128=12wks 4d–25wks 3dd7 128–256 128–256=10yr8m–21yr4m 128–256=25wks 3d–51wks 1dd8 256–512 etc etc

2 j . Using the example given in this paper of industrial production, we have1024 monthly observations, so the maximum number of scales is in theoryj = 9. If there are only 256 observations, then no more then seven crystalscan be produced, but as the highest scale (lowest frequency crystal) can onlyjust be resolved, it is usually recommended that only six crystals be produced.With 512 monthly observations, the d7 crystal can be produced, and the trendcrystal (or ‘wavelet smooth’), denoted s7 will yield further fluctuations fromtrend for all periodicities above a 256-month period.

(2) The choice of wavelet used in the analysis also figures into the number ofscale crystals that can be produced. Say you have a choice between an ‘s4’and an ‘s8’ wavelet for the MRD analysis. An ‘s4’ wavelet means that thesymmetric wavelet starts with a width of four observations for its support –this corresponds to the wavelet used to obtain the d1 crystals.6 Using an s4wavelet with annual or quarterly data will still capture the correct periodicities,but will enable the researcher to decompose to higher-order scales. Clearly thehigher the frequency of data, the more likely the researcher is to use a longersupported wavelet though, as very short wavelets are unlikely to yield anyadditional information.

(3) Wavelet MRD analysis assumes that data are sampled at equally spacedintervals. The frequency resolution interpretation is more difficult with dailydata, as daily (or hourly or even more frequently sampled) data are not evenlysampled. Note that with yearly data the resolution limit on a d3 crystal is halfthe time period on the minimum frequency picked up by a d5 crystal. Clearlythis would not be the case when using daily data though assuming 5 days tothe week.

(4) Existing stylized facts need to be taken into account when applying an MRDto economic data. For example, as economists know that business cycles lastfor a decade at the most, it does not make sense to decompose a series beyondthis level if conventional business cycles are the main concern – so with annualdata it would not make sense to use anything more than the d3 scale crystals

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

GUIDE TO WAVELETS FOR ECONOMISTS 215

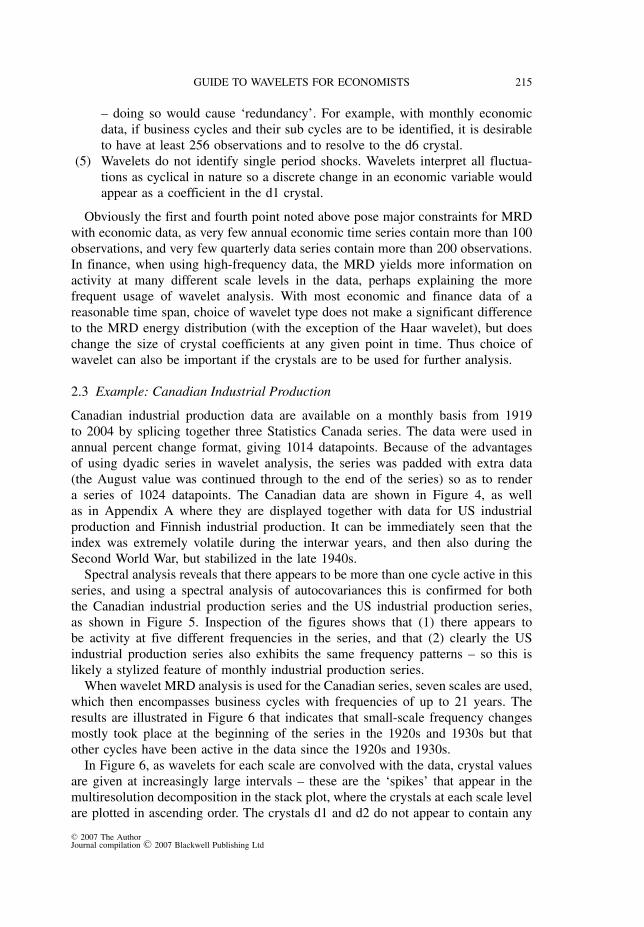

– doing so would cause ‘redundancy’. For example, with monthly economicdata, if business cycles and their sub cycles are to be identified, it is desirableto have at least 256 observations and to resolve to the d6 crystal.

(5) Wavelets do not identify single period shocks. Wavelets interpret all fluctua-tions as cyclical in nature so a discrete change in an economic variable wouldappear as a coefficient in the d1 crystal.

Obviously the first and fourth point noted above pose major constraints for MRDwith economic data, as very few annual economic time series contain more than 100observations, and very few quarterly data series contain more than 200 observations.In finance, when using high-frequency data, the MRD yields more information onactivity at many different scale levels in the data, perhaps explaining the morefrequent usage of wavelet analysis. With most economic and finance data of areasonable time span, choice of wavelet type does not make a significant differenceto the MRD energy distribution (with the exception of the Haar wavelet), but doeschange the size of crystal coefficients at any given point in time. Thus choice ofwavelet can also be important if the crystals are to be used for further analysis.

2.3 Example: Canadian Industrial Production

Canadian industrial production data are available on a monthly basis from 1919to 2004 by splicing together three Statistics Canada series. The data were used inannual percent change format, giving 1014 datapoints. Because of the advantagesof using dyadic series in wavelet analysis, the series was padded with extra data(the August value was continued through to the end of the series) so as to rendera series of 1024 datapoints. The Canadian data are shown in Figure 4, as wellas in Appendix A where they are displayed together with data for US industrialproduction and Finnish industrial production. It can be immediately seen that theindex was extremely volatile during the interwar years, and then also during theSecond World War, but stabilized in the late 1940s.

Spectral analysis reveals that there appears to be more than one cycle active in thisseries, and using a spectral analysis of autocovariances this is confirmed for boththe Canadian industrial production series and the US industrial production series,as shown in Figure 5. Inspection of the figures shows that (1) there appears tobe activity at five different frequencies in the series, and that (2) clearly the USindustrial production series also exhibits the same frequency patterns – so this islikely a stylized feature of monthly industrial production series.

When wavelet MRD analysis is used for the Canadian series, seven scales are used,which then encompasses business cycles with frequencies of up to 21 years. Theresults are illustrated in Figure 6 that indicates that small-scale frequency changesmostly took place at the beginning of the series in the 1920s and 1930s but thatother cycles have been active in the data since the 1920s and 1930s.

In Figure 6, as wavelets for each scale are convolved with the data, crystal valuesare given at increasingly large intervals – these are the ‘spikes’ that appear in themultiresolution decomposition in the stack plot, where the crystals at each scale levelare plotted in ascending order. The crystals d1 and d2 do not appear to contain any

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

216 CROWLEY

1920 1929 1938 1947 1956 1965 1974 1983 1992 2001

0100

200

300

400

SA

IPIn

d$C

AN

IPIS

A

1920 1929 1938 1947 1956 1965 1974 1983 1992 2001

-20

-10

010

20

30

40

IPS

A$C

AN

IPS

A

Figure 4. Canadian Industrial Production (sa): 1919–2004.

discernable cycles, d3 appears to have contained some explanatory power duringthe 1920s and 1930s, but now most variability is to be found in crystals d4 to d7and s7 (due to the size of the crystal coefficients). The cyclical interpretation ofthese crystals corroborates the spectra obtained in Figure 5 as four separate cyclesare identified (crystals d4, d5, d6 and d7), with crystals d1 to d3 containing mostlynoise. Crystal s7 is interpreted as a trend or drift variable, and does not capture anydistinct cycles in the data.

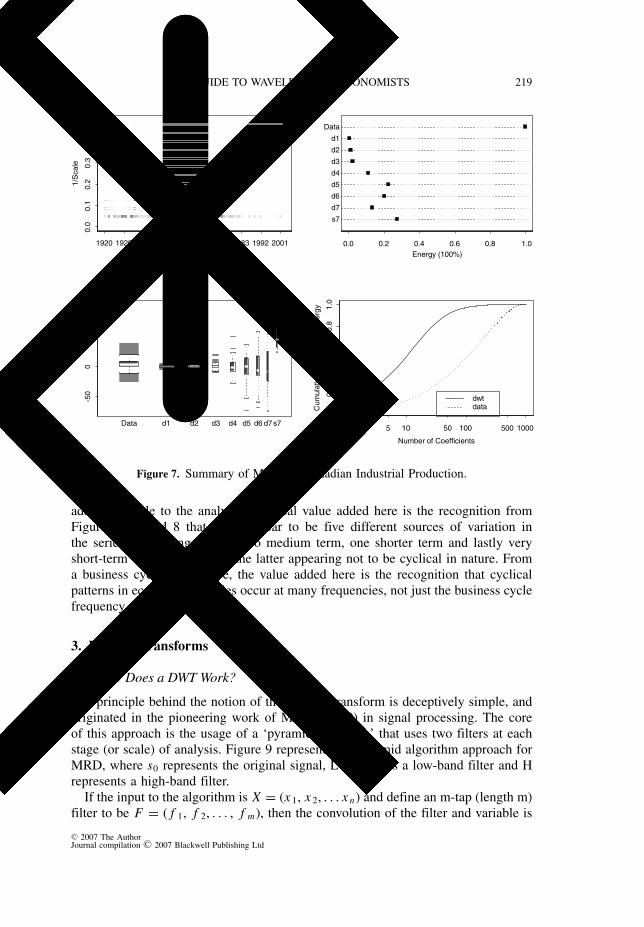

There are various ways of looking at the resulting DWT in graphical terms asshown in Figure 7. First, in the upper left plot a time-frequency graph shows activityin each scale through time. The y-axis is the inverse of scale – so large-scale (dilated)wavelets are given by flat wide boxes, and small-scale (very compact) wavelets aregiven by tall thin boxes. Each box should have the same area. This illustrates thelocalization in time of both large-scale and small-scale wavelets. The colour of theboxes reflects the size of the crystal coefficients – in this schema green, black andbrown represent increasingly large coefficient sizes. Second, in the upper right-handpanel, a dot chart shows the percentage of energy by crystal for scale j , E j , whichis given by

Edj = 1

E

n2 j∑

k=1

d2j,k (11)

where d refers to the detail crystals and E is the total energy of the series. Orthogonalwavelets are energy (variance) preserving, so that

E = Esj +

j∑i=1

Edi (12)

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

GUIDE TO WAVELETS FOR ECONOMISTS 217

0.0 0.1 0.2 0.3 0.4 0.5

frequency

-40

-20

020

spectr

um

bandwidth= 0.000281909 , 95% C.I. is ( -5.87588 , 17.5667 )dB

0.0 0.1 0.2 0.3 0.4 0.5

frequency

-40

-20

020

spectr

um

bandwidth= 0.000281909 , 95% C.I. is ( -5.87588 , 17.5667 )dB

0.0 0.1 0.2 0.3 0.4 0.5

frequency

-10

010

20

30

spectr

um

0.0 0.1 0.2 0.3 0.4 0.5

frequency

-10

010

20

30

spectr

um

Figure 5. Spectra for Canadian and US Industrial Production.

where Esj is the energy of the smooth. As already noted, crystals d4, d5, d6, d7

and s7 contain most of the series energy. For the bottom left-hand panel, a box plotshould be self explanatory, and here the width of the boxes represents the number ofdata points or coefficients. Lastly the bottom right-hand figure shows an energy plotthat provides the cumulative energy function for the data and the DWT. Clearly theDWT contains the salient information about the series much better than the originaluntransformed data, which helps to explain why wavelets are so popular as a meansof data compression. Note also from Figure 6 that the individual detail crystals havemean of zero, so that the energy of each crystal is nothing more than the varianceof the crystal coefficients. Hence the energy distribution in Figure 7 (top left-handbox) represents a variance decomposition by frequency for the series under analysis.Another measure often referred to in the signal processing literature is power, whichhere would be defined as just the average squared value of the crystal coefficients,or Ed

j /n2 j from equation (11).

2.4 Multiresolution Analysis (MRA)

The sequence of partial sums of crystals

Sj−1(t) = SJ (t) + DJ (t) + DJ−1(t) + · · · + D j (t) (13)

provides a multiresolution approximation (MRA) to the variable. This works bybuilding up the series from the highest numbered (coarsest) scale downwards. An

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

218 CROWLEY

1920 1931 1942 1953 1964 1975 1986 1997 2008

s7

d7

d6

d5

d4

d3

d2

d1

Position

Figure 6. DWT for Canadian Industrial Production.

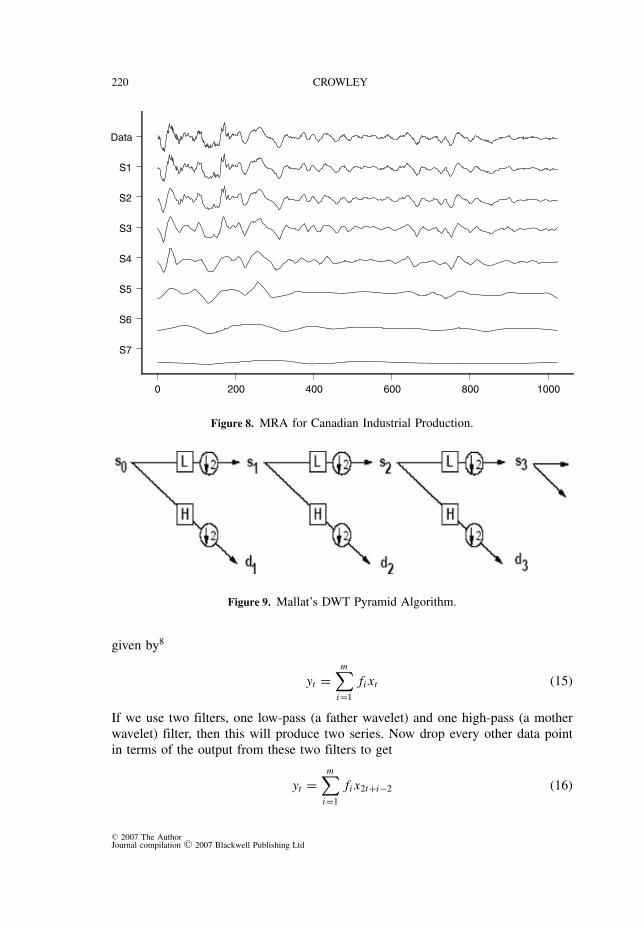

MRA therefore could be viewed as a filtered version of the series that retains themost important parts of the series, but de-noises the series to a greater or lesserdegree. Indeed, because wavelet analysis essentially filters certain information atdifferent scales, many of those involved in the development of wavelets label themfilters (of limited bandwidth).7 To show how the inverse discrete wavelet transform(IDWT) can approximate the series by acting as a band-pass filter, a smooth MRArepresentation of the data using the 4–6 scale crystals is calculated as follows

S4 = S6 + D6 + D5 (14)

Clearly one could also reconstruct the signal again by adding lower scale crystalsto equation (14). One interesting application in wavelet analysis, given that wehave determined which crystals are most relevant for describing Canadian industrialproduction, is to invert the wavelet transform so as to reconstruct the series usingan MRA. If this is done, Figure 8 shows what is obtained. S7 represents s7 crystal,but then when d7 is superimposed, S6 is obtained, etc.

Putting the wavelet analysis of the Canadian industrial production series together,it is now quite apparent that crystals d7, d6, d5 and d4 largely show the movementof the series. Adding d3 (to get S3 in Figure 8), adds very little to explainingany movement in the series (except perhaps towards the beginning), and if shorterterm fluctuations are desired, then clearly s2 captures some more of the noise but

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

GUIDE TO WAVELETS FOR ECONOMISTS 219

1920 1929 1938 1947 1956 1965 1974 1983 1992 2001

Time

0.0

0.1

0.2

0.3

0.4

0.5

1/S

cale

0.0 0.2 0.4 0.6 0.8 1.0

Energy (100%)

Data

d1

d2

d3

d4

d5

d6

d7

s7

-50

050

100

Data d1 d2 d3 d4 d5 d6 d7 s71 5 10 50 100 500 1000

Number of Coefficients

0.0

0.2

0.4

0.6

0.8

1.0

Cum

ula

tive P

roport

ional E

nerg

y

dwtdata

Figure 7. Summary of MRD for Canadian Industrial Production.

adds very little to the analysis. The real value added here is the recognition fromFigures 5, 7 and 8 that there appear to be five different sources of variation inthe series – one longer term, two medium term, one shorter term and lastly veryshort-term ‘noise’ variations, the latter appearing not to be cyclical in nature. Froma business cycle perspective, the value added here is the recognition that cyclicalpatterns in economic variables occur at many frequencies, not just the business cyclefrequency.

3. Wavelet Transforms

3.1 How Does a DWT Work?

The principle behind the notion of the wavelet transform is deceptively simple, andoriginated in the pioneering work of Mallat (1989) in signal processing. The coreof this approach is the usage of a ‘pyramid algorithm’ that uses two filters at eachstage (or scale) of analysis. Figure 9 represents the pyramid algorithm approach forMRD, where s0 represents the original signal, L represents a low-band filter and Hrepresents a high-band filter.

If the input to the algorithm is X = (x 1, x 2, . . . x n) and define an m-tap (length m)filter to be F = ( f 1, f 2, . . . , f m), then the convolution of the filter and variable is

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

220 CROWLEY

0 200 400 600 800 1000

S7

S6

S5

S4

S3

S2

S1

Data

Figure 8. MRA for Canadian Industrial Production.

Figure 9. Mallat’s DWT Pyramid Algorithm.

given by8

yt =m∑

i=1

fi xt (15)

If we use two filters, one low-pass (a father wavelet) and one high-pass (a motherwavelet) filter, then this will produce two series. Now drop every other data pointin terms of the output from these two filters to get

yt =m∑

i=1

fi x2t+i−2 (16)

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

GUIDE TO WAVELETS FOR ECONOMISTS 221

Figure 10. The IDWT (MRA) Algorithm.

Figure 11. Wavelet Packet Tree.

The output will be s1 for the low-pass filter and d1 for the high-pass filter. Thesedetails coefficients are kept, and s1 is now put through a further high-pass andlow-pass filter, etc., to finally produce

d j = WH ,↓(s j−1) (17)

a set of j detail coefficients and

s j = WL,↓(s j−1) (18)

a set of level j smooth coefficients. The choice of filter obviously aligns with thechoice of wavelet here. This is the output given by the MRD of a variable. Toconstruct an MRA an inverse DWT needs to be performed. In algorithm terms, thisis shown as Figure 10. Here the crystals are taken and convolved with a synthesisfilter, and at the same time ‘upsampled’ by inserting zeros between every other valueof the filter input. The smoothed coefficients for scale j − 1 are obtained as

s j−1 = WL,↑(s j ) + WH ,↑(d j ) (19)

where W F,↑ is an upsampling convolution operator for filter F.

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

222 CROWLEY

3.2 Wavelet Packet Transforms

One important extension to wavelet analysis was introduced by Ronald Coifman andothers (Coifman et al., 1990). Wavelet packets are a generalization of wavelets, asthey take a wavelet of a specific scale and add oscillations. Following the notationused above, in mathematical terms they can be represented as functions W j,b,k

where j corresponds to the scale/resolution level, k corresponds to the translationand b indicates the oscillation index.9 A discrete wavelet packet table is shownschematically in Figure 11, unfortunately using slightly different notation than usedin previous sections. The first line of the figure gives the original data, variable orsignal. The data are first filtered (convolved) with a high-level filter to get A1 and alow-level filter to get D1. The wavelet packet transform then departs with the DWTby continuing to apply high-level and low-level filters to these crystals, with theresult that wavelets with oscillations are introduced. Mathematically these waveletpacket basis functions can be written as

W j,b,k = 2− j/2Wb(2− j t − k) (20)

and the theoretical wavelet packet coefficients can be given as approximately

w j,b,k ≈∫

W j,b,k(t) f (t) dt (21)

Put another way, a wavelet packet crystal w j,b can be written as a vector

w j,b = (w j,b,1, w j,b,2, . . . , w j,b, n2 j

)′ (22)

where w j,b is the result of selecting n linearly independent rows from a matrix W,such that

w = Wx (23)

where x is the original signal/series.Wavelet packet functions are illustrated in Figure 12. The first step in doing

wavelet packet analysis is to use a wavelet packet table. Suppose the series of interesthas n observations, where n is a multiple of 2 j (i.e. dyadic), then the wavelet packettable will have J + 1 resolution levels where J is the maximum resolution level(– level 0 refers to the original series). If the (J + 1) resolution levels are stackedin order, a table of n (J + 1) coefficients is obtained. At level J the table has ncoefficients divided into 2 j coefficient blocks (crystals). In other words, each rowrepresents a certain scale, and as you read across the wavelet packet table you seewavelet filters with increasing large numbers of oscillations at that scale. Thesedifferent wavelet filters arise because of the different feasible permutations of fatherand mother wavelets which increase in number as scale increases. Using Canadianindustrial production data, a wavelet packet transform tends to suggest that the zerooscillation wavelets characterize the series fairly well, so the improvement over aDWT by using a packet transform might not be worthwhile, as the DWT uses singleoscillation wavelets at all scales.10 One of the more interesting uses of waveletpacket transforms is to characterize a series in terms of a particular set of crystalsof a certain scale. So, for example, using an inverse wavelet packet transform with

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

GUIDE TO WAVELETS FOR ECONOMISTS 223

`s8' father, phi(0,0)

0 2 4 6

-0.2

0.4

0.8

1.2

`s8' mother, psi(0,0)

-2 0 2 4

-1.0

0.0

1.0

`s8' wavelet packet, W(0,2,0)

-4 -2 0 2

-1.0

0.0

1.0

`s8' wavelet packet, W(0,3,0)

-2 0 2 4

-1.5

0.0

1.0

`s8' wavelet packet, W(0,4,0)

-4 -2 0 2

-10

1

`s8' wavelet packet, W(0,5,0)

-4 -2 0 2

-10

12

`s8' wavelet packet, W(0,6,0)

-4 -2 0 2

-10

12

`s8' wavelet packet, W(0,7,0)

-2 0 2 4

-10

1

Figure 12. Daubechies Wavelet Packet Functions.

say level 4 crystals, a reconstruction of a series can be made. This is done in Figure13 for the Canadian industrial production series.

Figure 14 presents the time-frequency plot for the level 4 packet transform forthe Canadian industrial production series, and compares it with the original time-frequency plot for the DWT. First note that in the left-hand plot in the panel, theboxes are exactly of the same size – that is because all the crystals are level 4, butrepresenting different numbers of oscillations. In Figure 13 there are 16 crystals,and these are stacked up in the left-hand panel of Figure 14 – once again, waveletswith large numbers of oscillations tend to have significant coefficients only for thefirst part of the series.

3.3 Optimal Transforms

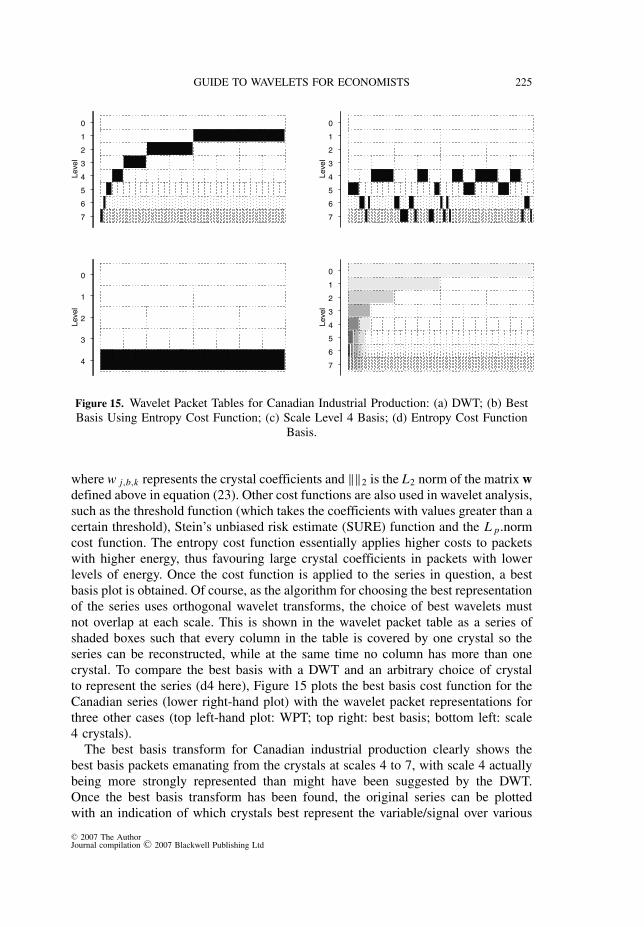

Coifman and Wickerhauser (1992) developed a ‘best basis’ algorithm for selectingthe most suitable bases for signal representation using a wavelet packet table. Thebest basis algorithm finds the wavelet packet transforms W that minimizes a costfunction C

C(W ) =∑j,b∈I

C(w j,b) (24)

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

224 CROWLEY

0 200 400 600 800 1000

w4.15

w4.14

w4.13

w4.12

w4.11

w4.10

w4.9

w4.8

w4.7

w4.6

w4.5

w4.4

w4.3

w4.2

w4.1

w4.0

iwpt

Figure 13. Level 4 Packet Transform for Canadian Industrial Production.

0 200 400 600 800 1000Time

0.0

0.1

0.2

0.3

0.4

0.5

Fre

quency

0 200 400 600 800 1000Time

0.0

0.1

0.2

0.3

0.4

0.5

Fre

quency

Figure 14. Time-frequency Plots for Canadian Industrial Production (a) Level 4 DWPTand (b) DWT.

where I is the set of index pairs (j, b) of the crystals in the transform W. Typically,the entropy cost function is used, in which case the cost function is of the form

Centropyj,b =

∑k

[w j,b,k∥∥w0,0

∥∥2

]2

log

⎧⎨⎩[

w j,b,k∥∥w0,0

∥∥2

]2⎫⎬⎭ (25)

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

GUIDE TO WAVELETS FOR ECONOMISTS 225

7

6

5

4

3

2

1

0

Level

7

6

5

4

3

2

1

0

Level

4

3

2

1

0

Level

7

6

5

4

3

2

1

0

Level

Figure 15. Wavelet Packet Tables for Canadian Industrial Production: (a) DWT; (b) BestBasis Using Entropy Cost Function; (c) Scale Level 4 Basis; (d) Entropy Cost Function

Basis.

where w j,b,k represents the crystal coefficients and ‖‖2 is the L2 norm of the matrix wdefined above in equation (23). Other cost functions are also used in wavelet analysis,such as the threshold function (which takes the coefficients with values greater than acertain threshold), Stein’s unbiased risk estimate (SURE) function and the L p.normcost function. The entropy cost function essentially applies higher costs to packetswith higher energy, thus favouring large crystal coefficients in packets with lowerlevels of energy. Once the cost function is applied to the series in question, a bestbasis plot is obtained. Of course, as the algorithm for choosing the best representationof the series uses orthogonal wavelet transforms, the choice of best wavelets mustnot overlap at each scale. This is shown in the wavelet packet table as a series ofshaded boxes such that every column in the table is covered by one crystal so theseries can be reconstructed, while at the same time no column has more than onecrystal. To compare the best basis with a DWT and an arbitrary choice of crystalto represent the series (d4 here), Figure 15 plots the best basis cost function for theCanadian series (lower right-hand plot) with the wavelet packet representations forthree other cases (top left-hand plot: WPT; top right: best basis; bottom left: scale4 crystals).

The best basis transform for Canadian industrial production clearly shows thebest basis packets emanating from the crystals at scales 4 to 7, with scale 4 actuallybeing more strongly represented than might have been suggested by the DWT.Once the best basis transform has been found, the original series can be plottedwith an indication of which crystals best represent the variable/signal over various

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

226 CROWLEY

w5

.0

w6

.4

w7

.12

w6

.7

w4

.3

w6

.17

w7

.37

w7

.39

w7

.41

w6

.22

w7

.47

w7

.56

w7

.58

w5

.15

w7

.66

w6

.34

w7

.71

w5

.20

w4

.11

w5

.26

w4

.14

w7

.12

1

w6

.62

w7

.12

7

-50

05

01

00

Figure 16. Time Representation of Canadian Industrial Production Using Best BasisPacket Selection.

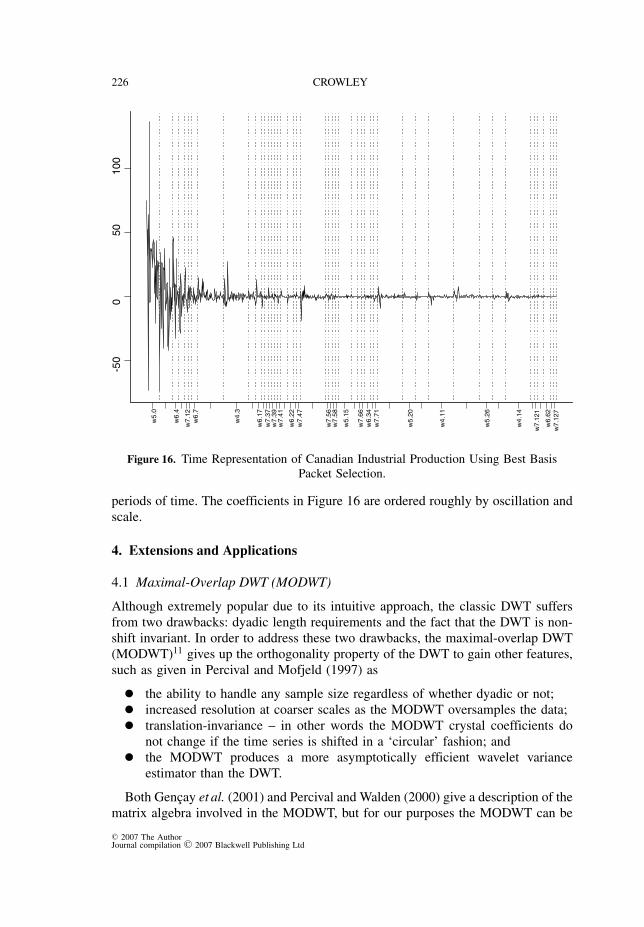

periods of time. The coefficients in Figure 16 are ordered roughly by oscillation andscale.

4. Extensions and Applications

4.1 Maximal-Overlap DWT (MODWT)

Although extremely popular due to its intuitive approach, the classic DWT suffersfrom two drawbacks: dyadic length requirements and the fact that the DWT is non-shift invariant. In order to address these two drawbacks, the maximal-overlap DWT(MODWT)11 gives up the orthogonality property of the DWT to gain other features,such as given in Percival and Mofjeld (1997) as

• the ability to handle any sample size regardless of whether dyadic or not;• increased resolution at coarser scales as the MODWT oversamples the data;• translation-invariance – in other words the MODWT crystal coefficients donot change if the time series is shifted in a ‘circular’ fashion; and• the MODWT produces a more asymptotically efficient wavelet varianceestimator than the DWT.

Both Gencay et al. (2001) and Percival and Walden (2000) give a description of thematrix algebra involved in the MODWT, but for our purposes the MODWT can be

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

GUIDE TO WAVELETS FOR ECONOMISTS 227

1920 1929 1938 1947 1956 1965 1974 1983 1992 2001 2010

s7{-381}

d7{-445}

d6{-221}

d5{-109}

d4{-53}

d3{-25}

d2{-11}

d1{-4}

Position

Figure 17. MODWT for Canadian Industrial Production.

described simply by referring back to Figure 9. In contrast to the DWT, the MODWTsimply skips the downsampling after filtering the data, and everything else describedin the section on MRDs using DWTs above follows through, including the energy(variance) preserving property and the ability to reconstruct the data using MRA withan inverse MODWT. A simple derivation of the MODWT following both Gencayet al. (2001) and Percival and Walden (2000) can be found in Appendix C. Figure17 shows the MODWT for Canadian industrial production. Clearly the resolutiondramatically increases for the coarser scales, and now the intermediate cycles aremore clearly apparent in the data.

One of the problems with the DWT is that the calculations of crystals occur atroughly half the length of the wavelet basis (length) into the series at any givenscale. Thus in Figure 6 crystal coefficients start further and further along the timeaxis as the scale level increases. As the MODWT is shift invariant, the MRD willnot change with a circular shift in the time series, so that each scale crystal can beappropriately shifted so that the coefficients approximately line up with the originaldata (known as ‘zero phase’ in the signalling literature). This is done by shifting thescales to the left by increasingly large amounts as the scale order increases, as they-axis of figure 17 shows.

Although the MODWT has a number of highly desirable properties, the transformleads to a large amount of ‘redundancy’, as even though the transform is energypreserving, the distribution of energy is clearly inferior to the original data. Similaranalysis can be done with MODWTs as with DWTs and Appendix C shows an

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

228 CROWLEY

0 200 400 600 800 1000

Level 7

Level 6

Level 5

Level 4

Level 3

Level 2

Level 1

Level 0

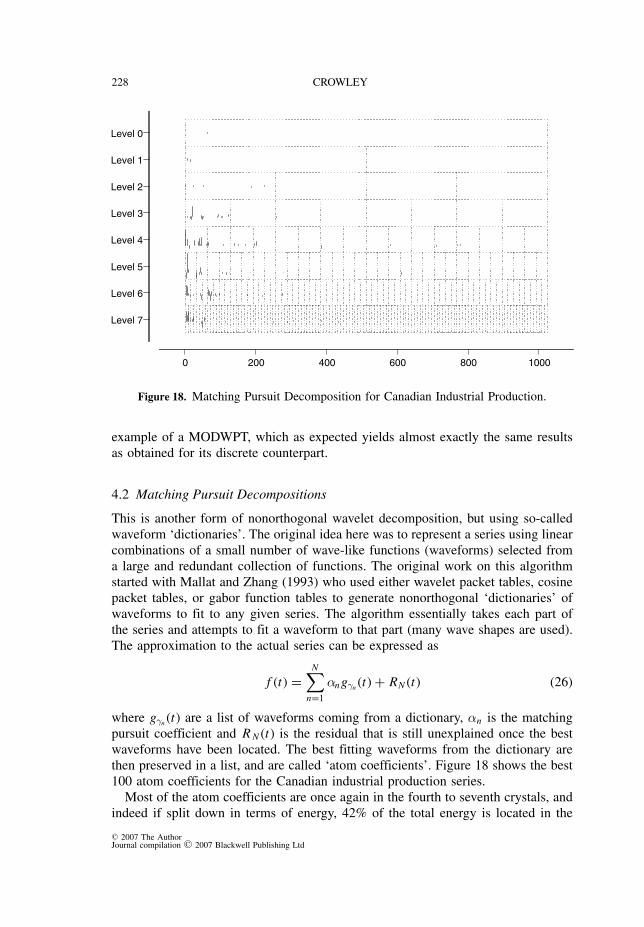

Figure 18. Matching Pursuit Decomposition for Canadian Industrial Production.

example of a MODWPT, which as expected yields almost exactly the same resultsas obtained for its discrete counterpart.

4.2 Matching Pursuit Decompositions

This is another form of nonorthogonal wavelet decomposition, but using so-calledwaveform ‘dictionaries’. The original idea here was to represent a series using linearcombinations of a small number of wave-like functions (waveforms) selected froma large and redundant collection of functions. The original work on this algorithmstarted with Mallat and Zhang (1993) who used either wavelet packet tables, cosinepacket tables, or gabor function tables to generate nonorthogonal ‘dictionaries’ ofwaveforms to fit to any given series. The algorithm essentially takes each part ofthe series and attempts to fit a waveform to that part (many wave shapes are used).The approximation to the actual series can be expressed as

f (t) =N∑

n=1

αngγn (t) + RN (t) (26)

where gγn (t) are a list of waveforms coming from a dictionary, αn is the matchingpursuit coefficient and R N (t) is the residual that is still unexplained once the bestwaveforms have been located. The best fitting waveforms from the dictionary arethen preserved in a list, and are called ‘atom coefficients’. Figure 18 shows the best100 atom coefficients for the Canadian industrial production series.

Most of the atom coefficients are once again in the fourth to seventh crystals, andindeed if split down in terms of energy, 42% of the total energy is located in the

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

GUIDE TO WAVELETS FOR ECONOMISTS 229

0 200 400 600 800 1000

Others

W7.0.7

W6.4.2

W4.0.7

W5.1.1

W5.0.4

W7.6.3

W4.0.40

W4.0.48

W6.0.6

W3.0.21

W7.1.1

W7.0.4

W6.0.3

W4.0.2

W5.0.8

Approx

0 200 400 600 800 1000

Others

S6.10

D5.24

S6.9

D4.11

D6.3

D5.2

S6.8

D6.1

D6.4

S6.6

D6.5

D5.1

S6.1

S6.3

S6.4

Approx

Figure 19. Top 15 Atoms for Canadian Industrial Production: (a) Matching Pursuit and(b) DWT.

scale level 4 atoms. It is noteworthy that the matching pursuit algorithm actuallygives the scale 3 atoms 18% of the energy and scales 5 and 6 around 15% each,which is a somewhat different result than we have obtained when using the DWT,as with the DWT the level 3 crystal had little explanatory power but the level 7had significant explanatory power. Figure 19 compares the top 15 crystals from thematching pursuit algorithm with the top 15 from the DWT.

Clearly the matching pursuit algorithm does a better job of matching waveformsto the series than the DWT. It uses a much richer collection of waveforms than theDWT, which is always limited to one particular wavelet form.

4.3 Wavelet Shrinkage

Donoho and Johnstone (1995) first introduced the idea of wavelet shrinkage in orderto denoise a time series. The basic idea is to shrink wavelet crystal coefficients, eitherproportionately or selectively, so as to remove certain features of the time series. Theinitial version of the waveshrink algorithm was able to denoise signals by shrinkingthe detail coefficients in the lower-order scales, and then applying the inverse DWTto recover a denoised version of the series. The methodology was then extended todifferent types of shrinkage function, notably so-called ‘soft’ and ‘hard’ shrinkage(reviewed in Bruce and Gao (1995)).

In mathematical terms, following the notation of Bruce et al. (1995) these differenttypes of shrinkage can be defined by application of a shrinkage function to the crystal

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

230 CROWLEY

coefficients such that

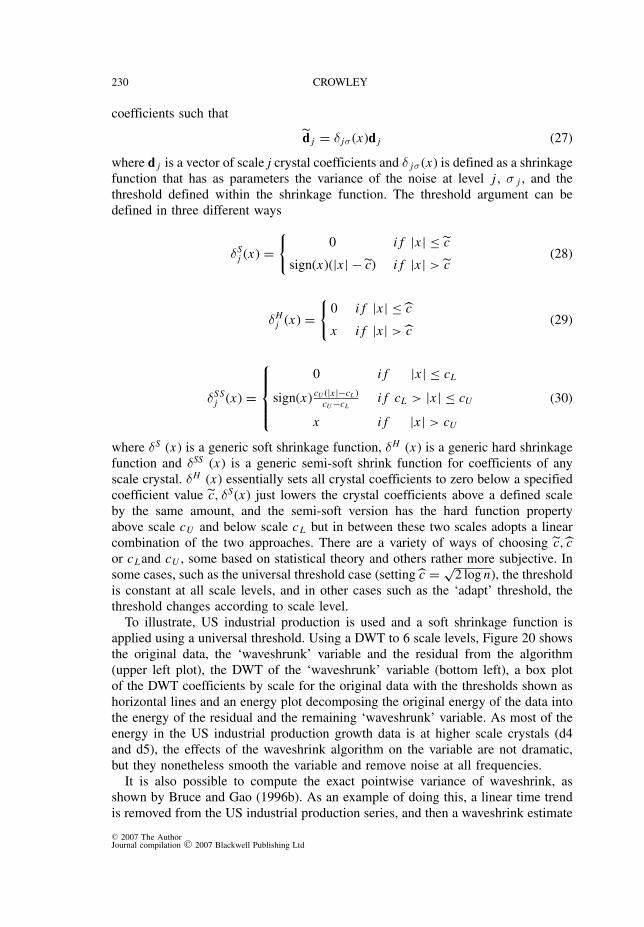

d j = δ jσ (x)d j (27)

where d j is a vector of scale j crystal coefficients and δ jσ (x) is defined as a shrinkagefunction that has as parameters the variance of the noise at level j , σ j , and thethreshold defined within the shrinkage function. The threshold argument can bedefined in three different ways

δSj (x) =

{0 i f |x | ≤ c

sign(x)(|x | − c) i f |x | > c(28)

δHj (x) =

{0 i f |x | ≤ c

x i f |x | > c(29)

δSSj (x) =

⎧⎪⎪⎨⎪⎪⎩0 i f |x | ≤ cL

sign(x) cU (|x |−cL )cU −cL

i f cL > |x | ≤ cU

x i f |x | > cU

(30)

where δS (x) is a generic soft shrinkage function, δH (x) is a generic hard shrinkagefunction and δSS (x) is a generic semi-soft shrink function for coefficients of anyscale crystal. δH (x) essentially sets all crystal coefficients to zero below a specifiedcoefficient value c, δS(x) just lowers the crystal coefficients above a defined scaleby the same amount, and the semi-soft version has the hard function propertyabove scale cU and below scale cL but in between these two scales adopts a linearcombination of the two approaches. There are a variety of ways of choosing c, cor cLand cU , some based on statistical theory and others rather more subjective. Insome cases, such as the universal threshold case (setting c = √

2 log n), the thresholdis constant at all scale levels, and in other cases such as the ‘adapt’ threshold, thethreshold changes according to scale level.

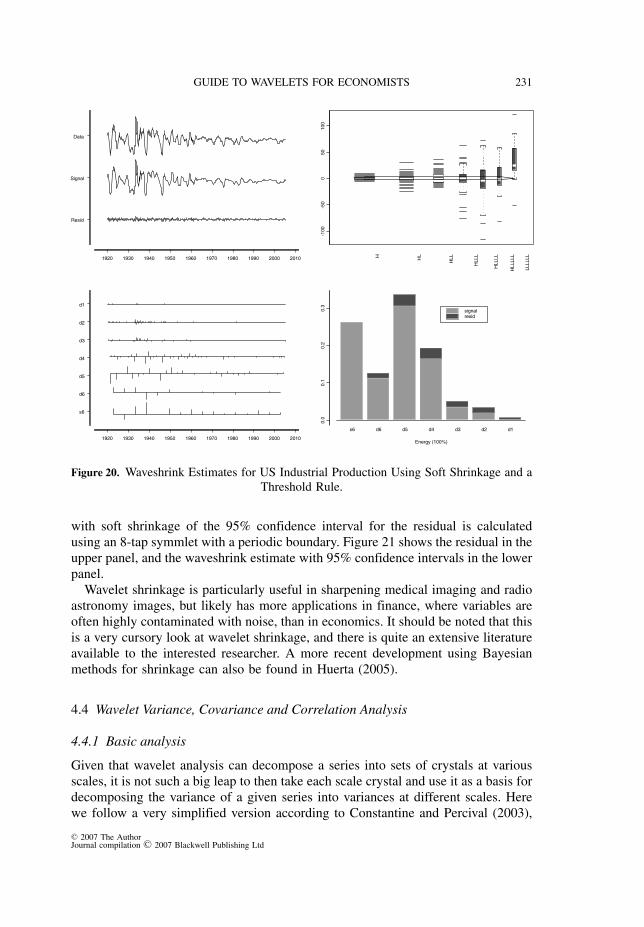

To illustrate, US industrial production is used and a soft shrinkage function isapplied using a universal threshold. Using a DWT to 6 scale levels, Figure 20 showsthe original data, the ‘waveshrunk’ variable and the residual from the algorithm(upper left plot), the DWT of the ‘waveshrunk’ variable (bottom left), a box plotof the DWT coefficients by scale for the original data with the thresholds shown ashorizontal lines and an energy plot decomposing the original energy of the data intothe energy of the residual and the remaining ‘waveshrunk’ variable. As most of theenergy in the US industrial production growth data is at higher scale crystals (d4and d5), the effects of the waveshrink algorithm on the variable are not dramatic,but they nonetheless smooth the variable and remove noise at all frequencies.

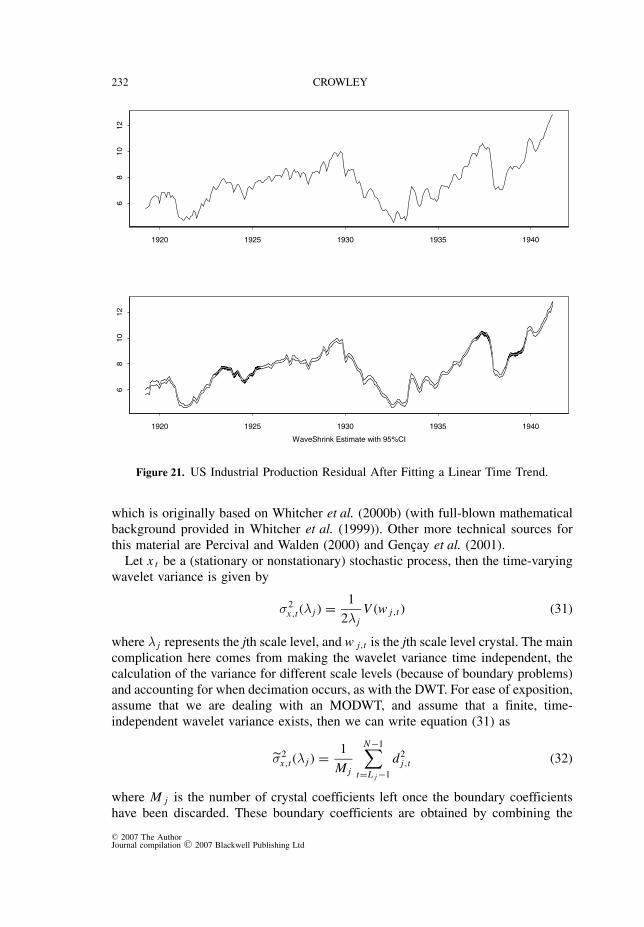

It is also possible to compute the exact pointwise variance of waveshrink, asshown by Bruce and Gao (1996b). As an example of doing this, a linear time trendis removed from the US industrial production series, and then a waveshrink estimate

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

GUIDE TO WAVELETS FOR ECONOMISTS 231

1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

Resid

Signal

Data

-100

-50

050

100

H

HL

HLL

HLLL

HLLLL

HLLLLL

LLLLLL

1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

s6

d6

d5

d4

d3

d2

d1

0.0

0.1

0.2

0.3

s6 d6 d5 d4 d3 d2 d1

Energy (100%)

signalresid

Figure 20. Waveshrink Estimates for US Industrial Production Using Soft Shrinkage and aThreshold Rule.

with soft shrinkage of the 95% confidence interval for the residual is calculatedusing an 8-tap symmlet with a periodic boundary. Figure 21 shows the residual in theupper panel, and the waveshrink estimate with 95% confidence intervals in the lowerpanel.

Wavelet shrinkage is particularly useful in sharpening medical imaging and radioastronomy images, but likely has more applications in finance, where variables areoften highly contaminated with noise, than in economics. It should be noted that thisis a very cursory look at wavelet shrinkage, and there is quite an extensive literatureavailable to the interested researcher. A more recent development using Bayesianmethods for shrinkage can also be found in Huerta (2005).

4.4 Wavelet Variance, Covariance and Correlation Analysis

4.4.1 Basic analysis

Given that wavelet analysis can decompose a series into sets of crystals at variousscales, it is not such a big leap to then take each scale crystal and use it as a basis fordecomposing the variance of a given series into variances at different scales. Herewe follow a very simplified version according to Constantine and Percival (2003),

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

232 CROWLEY

1920 1925 1930 1935 1940

68

10

12

1920 1925 1930 1935 1940

WaveShrink Estimate with 95%CI

68

10

12

Figure 21. US Industrial Production Residual After Fitting a Linear Time Trend.

which is originally based on Whitcher et al. (2000b) (with full-blown mathematicalbackground provided in Whitcher et al. (1999)). Other more technical sources forthis material are Percival and Walden (2000) and Gencay et al. (2001).

Let x t be a (stationary or nonstationary) stochastic process, then the time-varyingwavelet variance is given by

σ2x,t (λ j ) = 1

2λ jV (w j,t ) (31)

where λ j represents the jth scale level, and w j,t is the jth scale level crystal. The maincomplication here comes from making the wavelet variance time independent, thecalculation of the variance for different scale levels (because of boundary problems)and accounting for when decimation occurs, as with the DWT. For ease of exposition,assume that we are dealing with an MODWT, and assume that a finite, time-independent wavelet variance exists, then we can write equation (31) as

σ2x,t (λ j ) = 1

M j

N−1∑t=L j −1

d2j,t (32)

where M j is the number of crystal coefficients left once the boundary coefficientshave been discarded. These boundary coefficients are obtained by combining the

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

GUIDE TO WAVELETS FOR ECONOMISTS 233

beginning and end of the series to obtain the full set of MODWT coefficients, butif these are included in the calculation of the variance this would imply biasedness.If L j is the width of the wavelet (filter) used at scale j, then we can calculate M j

as (N − L j + 1).12

Calculation of confidence intervals is a little more tricky. Here the approach isto first assume that d j ∼ i id(0, σ2

j ) with a Gaussian distribution, so that the sum of

squares of d j is distributed as κχ2η , and then to approximate what the distribution

would look like if the d j are correlated with each other (as they are likely to be).This is done by approximating η so that the random variable (σ2

x,t χ2η)/η has roughly

the same variance as σ2x,t – hence η is not an actual degrees of freedom parameter,

but rather is known as an ‘equivalent degrees of freedom’ or EDOF. There are threeways of estimating the EDOF in the literature, and these can be summarized as(1) based on large sample theory, (2) based on a priori knowledge of the spectraldensity function and (3) based on a band-pass approximation. Gencay et al. (2001)show that if d j is not Gaussian distributed then by maintaining this assumption thiscan lead to narrower confidence intervals than should be the case.

As an example of calculating wavelet variances for the three industrial productionseries, Figure 22 compares the Canadian and Finnish variances and 95% confidenceintervals by scale using a band-pass approximation to EDOF with those of the US(which are shown in the background). The change in wavelet variance by scale isquite similar for Canada and the US, but Finland’s wavelet variance appears not toshow a similar pattern, even when the US series is adjusted so as to coincide withthe Finnish IP period.

Once the wavelet variance has been derived, the covariance between two economicseries follows, as shown by Whitcher et al. (2000b). The covariance of the seriescan be decomposed by scale, and thus different ‘phases’ between the series can bedetected. Figure 23 shows how the covariance between Canadian and US industrialproduction series and Finnish and US industrial production series breaks down byscale and then Figure 24 shows cross covariances between the Canadian and Finnishseries and their US equivalent.

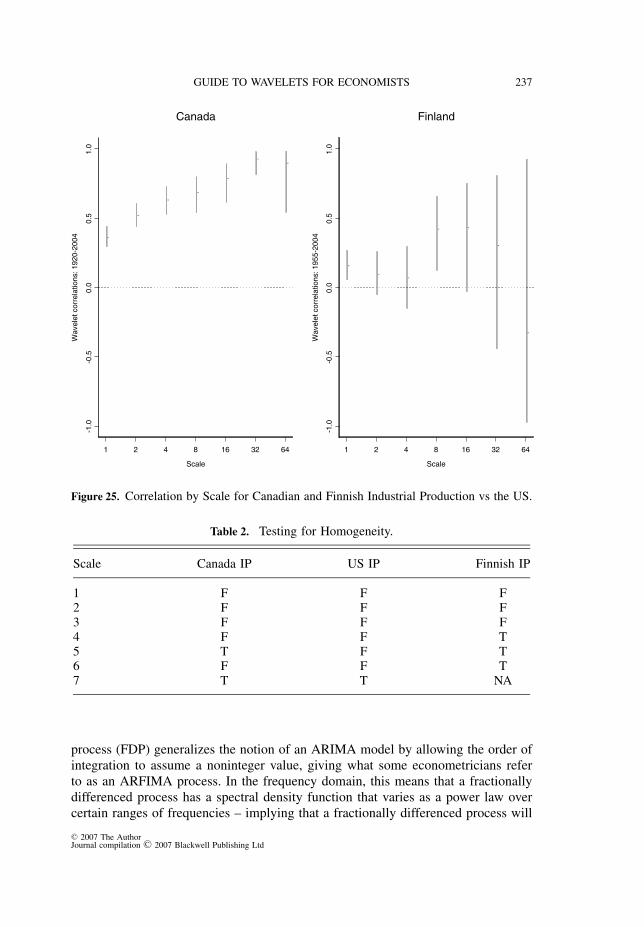

Once covariance by scale has been obtained, the wavelet variances and covariancescan be used together to obtain scale correlations between series. Once again,confidence intervals can be derived for the correlation coefficients by scale (theseare also derived in Whitcher et al. (2000b)). The correlations between the Canadianand Finnish industrial production series and their US counterpart are estimated andplotted in Figure 25 by scale, and then the cross-correlations for up to a 25 monthspan are plotted in Figure 26.

Several interesting points emerge from Figures 25 and 26:

• First, even for time series that are not particularly highly correlated such as thatof Finland and the US, the cyclical nature of the co-correlation at every scaleimplies that there is comovement of business cycles at a variety of differentscales.

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

234 CROWLEY

1 2 4 8 16 32 64

Scale

15

10

50

Wavele

t V

ariance:

1920-2

004

-

-

-

-

--

-

-

-

-

-

-

-

-

Canada

USA

1 2 4 8 16 32 64

Scale

0.5

15

10

Wavele

t V

ariance:

1955-2

004

-

-

-

-

-

-

-

-

-

-

-

-

-

-

Finland

USA

Figure 22. Wavelet Variance by Scale for Canada and Finland IndustrialProduction vs the US.

• Second, for Canada the co-correlation appears to increase as scale increases– this would perhaps be expected for series that are highly correlated (or co-integrated) over time; whereas for Finland, beyond scale 4, the co-correlationdoes not appear to follow any pattern by scale.• Thirdly, as we are comparing crystals for increasingly wide wavelet support,we would expect the positive correlations to persist much longer as lag lengthis increased – this is found to be the case here.• Lastly, at the same lag length the co-correlation can be quite differentaccording to scale (for example for Canada at a lag of 12 months, scales 1–4show negative co-correlation, scale 5 shows zero co-correlation and scales 6and 7 exhibit positive correlation).

4.4.2 Testing for homogeneity

Whitcher et al. (1998) developed a framework for applying a test for homogeneityof variance on a scale-by-scale basis to long-memory processes. A good summaryof the procedure is located in Gencay et al. (2001). The test makes no assumptionabout stationarity of the series and relies on the econometric assumption that thecrystals of coefficients, w j,t for scale j at time t have zero mean and variance σ2

t

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

GUIDE TO WAVELETS FOR ECONOMISTS 235

1 2 4 8 16 32 64

Scale

01

02

03

0

Wa

ve

let

Co

va

ria

nce

: 1

92

0-2

00

4

-

-

-

-

- -

-

Canada

1 2 4 8 16 32 64

Scale

02

46

Wa

ve

let

Co

va

ria

nce

: 1

95

5-2

00

4

- - -

-

-

-

-

Finland

Figure 23. Wavelet Covariance by Scale for Canadian and Finnish IndustrialProduction vs the US.

(λ j ). This allows us to formulate a null hypothesis of

H0 : σ2L j

(λ j ) = σ2L j +1(λ j ) = · · · · = σ2

N−1(λ j ) (33)

against an alternative hypothesis of

HA : σ2L j

(λ j ) = · · · = σ2k (λ j ) �= σ2

k+1(λ j ) = · · · · = σ2N−1(λ j ) (34)

where k is an unknown change point and L j represents the scale once the numberof boundary coefficients have been discarded. The assumption is that the energythroughout the series builds up linearly over time, so that for any crystal, if this isnot the case, then the alternative hypothesis is true.13 The test statistic used to testthis is the D statistic, which has previously been used by Inclan and Tiao (1994) forthe purpose of detecting a change in variance in time series. Define P k as

Pk =∑k

j=1 w2j∑N

j=1 w2j

(35)

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

236 CROWLEY

-20 -10 0 10 20

d7

d6

d5

d4

d3

d2

d1

Canada

Lag-20 -10 0 10 20

d7

d6

d5

d4

d3

d2

d1

Finland

Lag

Figure 24. Cross-covariances for Canadian and Finnish Industrial Production Series vsthe US.

then define the D statistic as D = max (D+, D−) where D+ = (L − Pk) and D− =(Pk − L) where L is the cumulative fraction of a given crystal coefficient to the totalnumber of coefficients in a given crystal. Percentage points for the distribution ofD can be obtained through Monte Carlo simulations, if the number of coefficientsis less than 128 and is obtained through large sample properties. Table 2 showsthe results of applying this test to the industrial production series at a 5% level ofsignificance.

Gencay et al. (2001) provide two examples of tests for homogeneity of variance –one for an IBM stock price and another for multiple changes in variance usingmethodology extending this framework that was developed by Whitcher et al.(2000a).

4.5 Wavelet Analysis of Fractionally Differenced Processes

Granger and Joyeux (1980) first developed the notion of a fractionally differencedtime series and in turn, Jensen (1999, 2000) developed the wavelet approachto estimating the parameters for this type of process. A fractionally differenced

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

GUIDE TO WAVELETS FOR ECONOMISTS 237

1 2 4 8 16 32 64

Scale

-1.0

-0.5

0.0

0.5

1.0

Wavele

t corr

ela

tions: 1920-2

004

Canada

-

-

-

-

-

--

1 2 4 8 16 32 64

Scale

-1.0

-0.5

0.0

0.5

1.0

Wavele

t corr

ela

tions: 1955-2

004

Finland

-

--

- -

-

-

Figure 25. Correlation by Scale for Canadian and Finnish Industrial Production vs the US.

Table 2. Testing for Homogeneity.

Scale Canada IP US IP Finnish IP

1 F F F2 F F F3 F F F4 F F T5 T F T6 F F T7 T T NA

process (FDP) generalizes the notion of an ARIMA model by allowing the order ofintegration to assume a noninteger value, giving what some econometricians referto as an ARFIMA process. In the frequency domain, this means that a fractionallydifferenced process has a spectral density function that varies as a power law overcertain ranges of frequencies – implying that a fractionally differenced process will

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

238 CROWLEY

-20 -10 0 10 20

d7

d6

d5

d4

d3

d2

d1

Canada

Lag-20 -10 0 10 20

d7

d6

d5

d4

d3

d2

d1

Finland

Lag

Figure 26. Cross-correlation for Canadian and Finnish Industrial Production vs the US.

have a linear spectrum when plotted with log scales. A FDP can be defined asdifference stationary if

(1 − B)d xt =d∑

k=0

(d

k

)(−1)k xt−k = εt (36)

where ε t is a white-noise process, d is a real number and(d

k

) = d!k!(d−k)!

=�(d+1)

�(k+1)�(d−k+1), � being Euler’s gamma function. Wavelets can be used to estimate

the fractional difference parameter, d, as the variance of an ARFIMA-type processcan be expressed in the form

σ2x (λ j ) ≈ σ2

ε c(d)[λ j ]2d−1 (37)

where c is a power function of d and d = (d − 0.5). Equation (37) suggests thatto estimate d a least squares regression could be done to the log of an estimate ofthe wavelet variance obtained from an MODWT. This represents the first way ofestimating d, but there is a problem as here the MODWT yields correlated crystals,so the estimate of d would likely be biased upwards.

Another way of estimating the parameters of the FDP is to go back to the DWT,as the scale crystals are uncorrelated, and use the likelihood function for the interior

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

GUIDE TO WAVELETS FOR ECONOMISTS 239

coefficients (in other words after discarding the boundary coefficients). Let d I be avector of length M containing all the DWT wavelet coefficients for all j scales (forwhich there are M j elements for each scale), then the likelihood function for σ2

ε

and d will be (d,σ2

ε | dI) = exp

{( − d′I �

−1dI

dI)/2

}(2π )M/2

∣∣�dI

∣∣1/2(38)

where �dI is the variance–covariance matrix. Using the fact that the waveletcoefficients at different scales are uncorrelated, we can use an approximation tothe variance C j (d,σ2

ε ) so that equation (38) can be rewritten as

(d,σ2

ε | dI) =

J∏j=1

M j −1∏t=0

exp{ − d2

j,t/2C j(d,σ2

ε

)}(2πC j (d,σ2

ε ))1/2(39)

where d j,t is once again a crystal coefficient. Equivalently we can estimate a reducedlog likelihood, such as

�(d | dI ) = M ln(σ2ε (d)) +

J∑j=1

M j ln(C j (d)) (40)

where σ2ε (d) = 1

M

∑Jj=1

1

C j (d)

∑M j −1

t=0 and C j (d) = C j (d,σ2ε )/σ2

ε . Minimizing equa-

tion (40) yields a maximum likelihood estimate for d,d M L E , which can then be

substituted into the definition of σ2ε (d) to obtain an estimate for the variance. Percival

and Walden (2000) devote a whole chapter to the issue of FDPs and provide examplesof MLEs for nonstationary processes, and Constantine and Percival (2003) provideroutines for chopping the series up into blocks to obtain ‘instantaneous’ estimatorsfor the FDP parameters.

To illustrate wavelets applied to a financial time series, take the British pounddaily series against the US dollar (details given in Appendix D), and after takinglog differences of the series, take the absolute value of the log differences and usean instantaneous parameter estimation of the difference coefficient d. This serieswill likely have long memory as volatility appears in clusters, so that the differencecoefficient is unlikely to be an integer.

Figure 27 plots the instantaneous estimate of the difference coefficient togetherwith a 95% confidence interval band. The mean of the parameter estimates is 0.236,and the mean of the variance estimates for the 10 scale levels estimated is 0.1002.

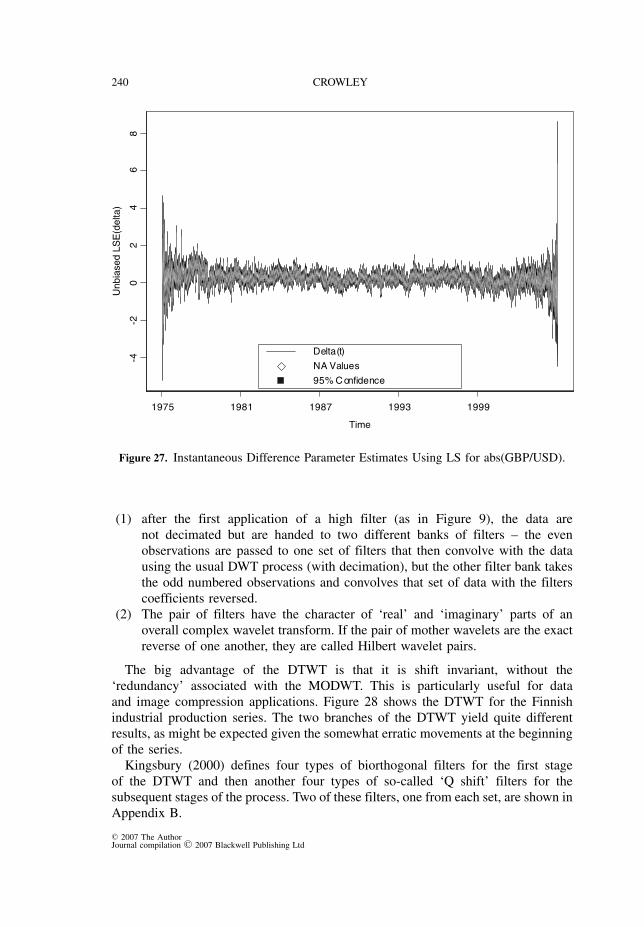

4.6 Dual Tree WTs Using Wavelet Pairs

This is relatively recent research and uses a so-called dual tree wavelet transform(DTWT or complex wavelet transform), developed by Nick Kingsbury (seeKingsbury (1998, 2000)) with particular applications in image compression andreconstruction in mind. The DTWT differs from a traditional DWT in two distinctways:

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

240 CROWLEY

1975 1981 1987 1993 1999

Time

-4-2

02

46

8

Unbia

sed L

SE

(delta)

Delta(t)

NA Values

95% C onfidence

Figure 27. Instantaneous Difference Parameter Estimates Using LS for abs(GBP/USD).

(1) after the first application of a high filter (as in Figure 9), the data arenot decimated but are handed to two different banks of filters – the evenobservations are passed to one set of filters that then convolve with the datausing the usual DWT process (with decimation), but the other filter bank takesthe odd numbered observations and convolves that set of data with the filterscoefficients reversed.

(2) The pair of filters have the character of ‘real’ and ‘imaginary’ parts of anoverall complex wavelet transform. If the pair of mother wavelets are the exactreverse of one another, they are called Hilbert wavelet pairs.

The big advantage of the DTWT is that it is shift invariant, without the‘redundancy’ associated with the MODWT. This is particularly useful for dataand image compression applications. Figure 28 shows the DTWT for the Finnishindustrial production series. The two branches of the DTWT yield quite differentresults, as might be expected given the somewhat erratic movements at the beginningof the series.

Kingsbury (2000) defines four types of biorthogonal filters for the first stageof the DTWT and then another four types of so-called ‘Q shift’ filters for thesubsequent stages of the process. Two of these filters, one from each set, are shown inAppendix B.

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

GUIDE TO WAVELETS FOR ECONOMISTS 241

0 50 100 150 200 250 300

-40-2

00

20

40

60 TreeA

0 50 100 150 200 250 300

-40-2

00

20

40

60 TreeB

0 50 100 150

-40

-20

02

04

06

0

0 50 100 150

-40

-20

02

04

06

0

0 20 40 60

-40

-20

02

04

06

0

0 20 40 60

-40

-20

02

04

06

0

0 10 20 30

-40

-20

02

04

06

0

0 10 20 30

-40

-20

02

04

06

0

5 10 15

-40

-20

02

04

06

0

5 10 15

-40

-20

02

04

06

0

2 4 6 8 10

-40

-20

02

04

06

0

2 4 6 8 10

-40

-20

02

04

06

0

2 4 6 8 10

-40

-20

02

04

06

0

2 4 6 8 10

-40

-20

02

04

06

0

Figure 28. Dual Tree WT for Finnish Industrial Production.

5. Frequency Domain Analysis

5.1 Continuous Wavelet Transforms

Wavelet analysis is neither strictly in the time domain nor in the frequency domain:it straddles both. It is therefore quite natural that wavelets applications have alsobeen developed in the frequency domain using spectral analysis. Perhaps the bestintroduction into the theoretical side of this literature can be found in Lau andWeng (1995) and Chiann and Morettin (1998), while Torrence and Compo (1998)probably provide the most illuminating examples of applications to time series frommeteorology and the atmospheric sciences.

Spectral analysis is perhaps the most commonly known frequency domain toolused by economists (see Collard (1999), Camba and Kapetanios (2001), Valle eAzevedo (2002), Kim and In (2003), Sussmuth (2002) and Hughes and Richter(2004) for some examples), and therefore needs no extended introduction here. Inbrief though, a representation of a covariance stationary process in terms of itsfrequency components can be made using Cramer’s representation, as follows

xt = μ +∫ π

−π

eiωt z(ω) dω (41)

where i = √−1,μ is the mean of the process, ω is measured in radians and z(ω) dωrepresents complex orthogonal increment processes with variance f x (ω), where itcan be shown that

fx (ω) = 1

2π

(γ (0) + 2

∞∑τ=1

γ (τ ) cos(ωτ )

)(42)

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

242 CROWLEY

where γ (τ ) is the autocorrelation function. f x (ω) is also known as the spectrumof a series as it defines a series of orthogonal periodic functions that essentiallyrepresent a decomposition of the variance into an infinite sum of waves of differentfrequencies. Given a large value of f x (ω i ), say at a particular value of ωi , ωi , thisimplies that frequency ωi is a particularly important component of the series.

To intuitively derive the wavelet spectrum, recall using the definition of a motherwavelet convolution from equation (5), that the convolution of the wavelet withthe series renders an expression such as that given in equation (15), and associatedcrystals given by equation (17), then a continuous wavelet transform (CWT) for afrequency index k will analogously yield

Wk(s) =N∑

k=0

xt ψ∗(sωk)eiωk t∂t (43)

where xk is the discrete Fourier transform of x t

xk = 1

(N + 1)

N∑k=0

xt exp

{−2π ikt

N + 1

}(44)

so xk represents the Fourier coefficients, �∗ is the Fourier transform of a normalizedscaling function, �∗, defined as

�∗ ={

t

s

}0.5

�

[t − μ

s

](45)

so that in the frequency domain the CWT W k(s) is essentially the convolution ofthe Fourier coefficients and the Fourier transform of �∗, �∗. The angular frequencyfor ωk in equation (43) is given by

ωk ={ 2πk

(N+1): k ≤ N+1

2

− 2πk(N+1)

: k > N+12

(46)

The CWT, W k(s), can now be split into a real and complex part, � {W k(s)}, and

� {W k(s)}, or amplitude/magnitude, |W k(s)| and phase, tan−1[

�{Wk (s)}�{Wk (s)}

].

To show some examples of wavelet spectra, first Figure 29 shows a three-dimensional plot for the US industrial production series using a log frequency scaleand reversing the time sequencing so as to show the evolution of the spectrum tobest effect.

This CWT spectral plot displays similar characteristics to that of the time-frequency plots of Figure 14, in that the high-frequency content is particularlymarked in the earlier part of the twentieth century, with mostly low-frequency contentevident throughout the entire time period. As might be expected, the ridge lines inthe 3D magnitude plot for the series suggest that there are roughly five distinctfrequencies active in the series, as was already confirmed with the use of a DWT.

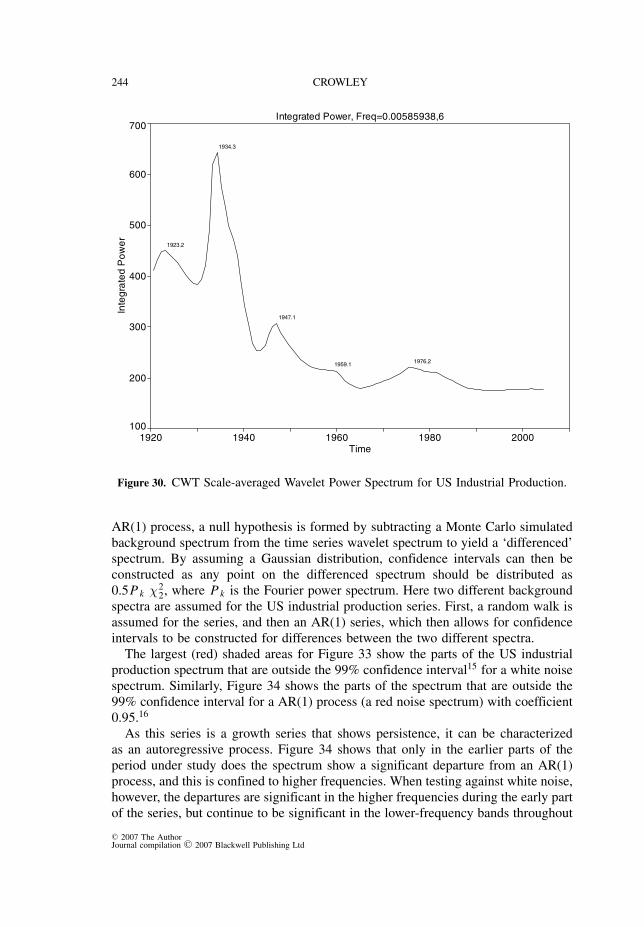

To study phase, it is probably a good strategy to project both 3D plots onto themagnitude or phase axis, respectively, so as to view the plots in terms of theircontours. This is done in Figure 30 first for the scale-averaged (or integrated)

C© 2007 The AuthorJournal compilation C© 2007 Blackwell Publishing Ltd

GUIDE TO WAVELETS FOR ECONOMISTS 243

2010

2000

1990

19801970

19601950

19401930

10

10.1

0.01

Time

Frequency

-50

-500

0

50

50

100

100

150

150

Ma

gnitude

Ma

gnitude

Figure 29. CWT 3D Magnitude Spectrum for US Industrial Production.

power spectrum, |W k(s)|2, which, as expected, shows that the volatile short-termfluctuations in the early part of the series tend to dominate and then in Figure 31 forthe phase contour plot. Figure 32 gives CWT a magnitude contour plot (against logof frequency) using a Paul (complex) wavelet with initial width of 6 months. This isan asymmetric wavelet, and so the frequency is only roughly related to the scale ofthe wavelets, hence the approximation that s−1 is equivalent to the maximum of �

is not analytically correct.14 The contour plots point to several other features fromthe frequency domain, notably