Emotion-based learning: insights from the Iowa Gambling Task

1

This is a pre-print version of an article published in

Computers in Human Behavior

DOI: 10.1016/j.chb.2012.02.024

Available at: http://dx.doi.org/10.1016/j.chb.2012.02.024

A digital revolution: Comparison of demographic profiles, attitudes

and gambling behavior of Internet and non-Internet gamblers

Sally Gainsbury¹, Robert Wood², Alex Russell³, Nerilee Hing¹, &

Alex Blaszczynski³ ¹ Centre for Gambling Education & Research, Southern Cross University

P.O. Box 157, Lismore NSW 2480, Australia

Email: [email protected]

Email: [email protected]

² University of Lethbridge

4401 University Drive, Lethbridge, AB, Canada, T1K 3M4

Email: [email protected]

³ School of Psychology, University of Sydney

Brennan MacCallum Building (A18), University of Sydney NSW 2006, Australia

Email: [email protected]

Email: [email protected]

Please address all correspondence to:

Dr. Sally Gainsbury

Centre for Gambling Education & Research, Southern Cross University

P.O. Box 157, Lismore NSW 2480, Australia

Email: [email protected]

Abstract Internet gambling is one of the fastest growing sectors of ecommerce and rapidly growing as a

mode of gambling. Although Internet gambling is characterized by high levels of customer

choice, little is known about Internet gamblers or their engagement with Internet and non-

Internet forms of gambling. Regulators are struggling to respond to Internet gambling given that

little is known about the impact of this mode of gambling on the existing gambling market, who

is gambling online and how. This paper presents one of the largest studies of Internet gambling;

an online survey completed by 6,682 Australian gamblers. Results show that Internet gamblers

are a heterogeneous group, although there is a tendency for Internet gamblers to be male, have

high incomes and be well educated. Internet gamblers have more positive attitudes towards

gambling and are more highly involved gamblers, engaging in many different gambling activities

in both online and offline forms. However, a proportion of Internet gamblers prefer the privacy

and anonymity of Internet gambling and do not like land-based venues, suggesting that Internet

gambling is creating a new market of gambling customers. Understanding the impact of this new

mode of gamblers on existing gamblers and new players is important to contribute to the

appropriate regulation of this activity.

2

Keywords: online gambling, Internet, wagering, characteristics, survey, motivations

Highlights

We surveyed 6,682 Australian gamblers to compare Internet and non-Internet gamblers

We examined total gambling behaviour and impact of Internet gambling

Internet gamblers play multiple forms and have more positive attitudes towards gambling

Internet gamblers are motivated by the convenience of online sites and greater privacy

Internet gamblers may represent a new customer base that may shift from land-based play

1. Introduction

Substantial consumer research has been conducted on Internet-based purchases and behaviors.

However, a significantly neglected area relates to the use of Internet gambling, and little is

known about how consumers transition to, and engage in, Internet gambling. Thus, the purpose

of this paper is to explore the characteristics of Internet gamblers compared to non-Internet

gamblers, as well as to examine the wider context of Internet gambling and the attitudes and

motivations for this activity.

1.1 Internet gambling industry

Internet gambling is a rapidly growing and evolving phenomenon that has a substantial impact

on gambling and related entertainment, tourism and hospitality industries. The term Internet

gambling is often used interchangeably with online gambling and refers to all forms of gambling

(including wagering) via the Internet through varied media including computers, mobile phones

and wireless devices. In December 2011, there were approximately 2,680 Internet gambling

sites, the majority being privately owned and regulated by offshore locations to provide services

to customers located in wide-ranging geographical regions [1]. Global Internet gambling gross

market win (i.e., stakes wagered less prizes) is expected to reach US$33 billion in 2011 and

exceed US$43 billion by 2015 [2,3]. The global Internet gambling market appears to be

3

outpacing casino gambling, growing at a rate of approximately 12% per annum, and represents

an increasingly important segment (around 9%) of the gambling market [4-6].

Although the land-based gambling industry has experienced a decline, expenditure on Internet

gambling appears to be increasing. For example, Britain‟s biggest bookmaker, William Hill,

reported a 28% rise in Internet gambling revenue in the third quarter of 2011, in contrast to a 3%

decline at its retail business [7]. Similarly, Canadian operator Loto-Quebec reported a marginal

decline in revenue for the six months to September 2011, although its recently launched Internet

gambling site appears to be popular and profitable [8]. North Americans were estimated to spend

over US$5 billion on Internet gambling in 2011 despite regulations prohibiting this mode of

gambling and efforts to enforce these [9].

1.2 Growth factors for Internet gambling

The growth of Internet gambling is driven by several factors. Firstly, the majority of the

population now enjoys Internet access through cheap, fast broadband connections at home, in the

workplace, in libraries, at educational institutions, and in Internet cafes. This is demonstrated by

Internet penetration rates in North America, Europe and Oceania, which range from 58% to 78%

[10]. Additionally, the reduced costs of mobile technology, including smart phones, wireless

devices, and mobile applications (apps) provide Internet access in essentially any location using

3G/4G networks and available Wi-Fi services. Consequently, consumers are becoming more

Internet and technology savvy and trustful of Internet sites, products and services. Recent polls

indicate that 71% of American adults use the Internet to purchase products and 61% use Internet

banking [11]. Use and trust in Internet payment systems are additional key factors supporting

4

growth of Internet gambling. According to Online Casino City [1], there are 217 different

payment methods offered by Internet betting sites, with credit and debit card payments being the

most popular, followed by bank and money transfers and use of third-party payment processers

(such as PayPal and NetTeller, which provide additional levels of security and identity

protection).

The volume of information available on the Internet, availability of tutorials, instructions and

practice or „free play‟ sites, and the ability for peers to share content, allows novice bettors to

feel highly informed and to gather tips and statistics to guide their betting. Very small bets can

also be placed, and many sites offer practice games to enable beginners to gain confidence before

depositing funds. Moreover, initial deposits are typically matched by operators and credits and

bonuses usually have to be played through several times before they can be withdrawn, which

may increase participation and expenditure. The use of „skins‟ allows the presentation and theme

of a site to be modified, while the underlying games and systems remain the same. This enables

an operator to tailor sites for targeted customer groups, for example by modifying the color of a

site‟s background and including a variety of motifs (e.g., shopping, cars, royal, roman) designed

to appeal to different age, gender, and cultural groups.

1.3 Internet gambling regulation and participation

One substantial barrier that continues to limit the growth and uptake of Internet gambling is the

various jurisdictional policies that exist worldwide. The rapid growth of Internet gambling has

outpaced many laws created to regulate gambling activities [12] . Currently, international

jurisdictions have a range of policies that vary from prohibition (which can target operators,

5

players or both), restricted regulation (closed systems or government ownership), or open

regulation. Given the difficulties in enforcing prohibition, the growing awareness of revenue lost

to offshore operators, the recognition of consumer demand, and the importance of ensuring

responsible gambling and player protection, it is likely that the regulation of Internet gambling

will become increasingly liberalized in the years ahead

Liberalization of Internet gambling is likely to increase participation and subsequent revenues for

operators and governments through direct ownership or taxation [12]. The reported increases in

participation and expenditure on Internet gambling sites suggest clear consumer demand for

these products. Internet gamblers appear to gamble on the Internet in addition to other forms of

gambling, including terrestrial play [13]. However, if customers gamble from home they may be

less likely to visit terrestrial gambling venues, thereby impacting associated retail, hospitality,

entertainment, and tourism industries. There are few detailed, comprehensive, robust studies of

Internet gamblers that consider their wider gambling behavior and the impact of this medium.

Few national prevalence studies have been conducted, but international estimates indicate that

between 1-13% of adults gamble online [14-18]. Nonetheless, the growth and availability of

Internet gambling is predicted to continue to increase. Given the potential psychological impact

that may be caused by this mode of gambling [19], further attention is warranted.

Australia appears to be a particularly strong market for Internet wagering, with a solid cultural

acceptance of betting, high level of Internet penetration (over 85%) and increasing uptake of

smart phone technology [20,21]. Internet gambling has been available to Australians since the

1990s, although the Interactive Gambling Act of 2001 prohibited all forms of interactive

6

gambling with the exception of wagering and lottery through licensed providers. The inadequacy

of regulatory restrictions and compliance is evident in the apparent absence of prosecutions for

breaches of the Act [20]. Licensed operators have taken advantage of the lack of marketing

restrictions of Internet gambling products, resulting in a massive increase in the prominence of

advertising for Internet gambling, particularly noticeable through association with sporting

events and codes. These allow targeting of the potential market of sports fans by betting

operators [22] and appear to be having some success; for example, major Internet bookmaker,

Centrebet, reported an increase in new Australian depositing clients by 92%, and an increase in

active clients by 46%, in the first half of the 2011, compared to 2010 financial year [23]. Despite

declines in betting from European markets, Australian clients increased Internet betting by 62%

between 2010 and 2011 [23]. Australians were estimated to spend over AUD$968 million in

2010 on illegal Internet casino, poker and bingo sites and over AUD$600 million on Internet

sports betting [16], although these figures likely underestimate the size of Internet gambling

market.

1.4 Internet gambling as compared to terrestrial gambling

Despite the many similarities between Internet and terrestrial gambling, Internet gambling does

possess unique features. Internet gambling is highly accessible and convenient; sites operate 24

hours a day, seven days a week and can be accessed through a variety of devices wherever

Internet connections, including 3G networks, are available. Although customers are required to

identify themselves to operators and provide payment details, usernames enable play to be

relatively anonymous and players can create any type of persona they wish. Internet gambling

can be either solitary, with no interaction with other players or staff, or relatively social by

7

utilizing chat functions and message boards. Gambling sites typically offer a vast selection of

games and products, often including a mix of gambling genres; for example, a sports wagering

site enables bets to be placed on numerous international events and also offers casino and poker

as side products for customers. Odds and player returns are typically very competitive and more

rewarding than those offered by terrestrial operators, due to the lower overheads and costs of

running an Internet site. Similarly, players can place very small bets, and play against a much

larger pool of customers, than would be ever available at any single terrestrial venue. As

customers use an account for all betting, details of play history, bets, losses, withdrawals and

deposits are readily available to assist customers to track their gambling. Customers can also

have multiple accounts with different operators. Moreover, in comparison to the relative

geographical restrictions that are endemic to terrestrial gambling, Internet gamblers enjoy the

ease of rapid movement from one Internet venue to another.

An important consideration is whether Internet gamblers, compared to non-Internet gamblers,

represent a unique consumer base. In a study comparing Internet and casino gamblers, Cotte and

Latour [24] found that Internet gamblers engaged in this mode of gambling in a distinctly

different manner than terrestrial casino players. Internet gambling appears to be integrated into

everyday living activities, involve the whole family, but also be used systematically in a more

competitive and less social manner. Monaghan and Derevensky [25] argue that the constant

availability of Internet gambling may lead to excessive time being spent gambling, and also

expose children to this activity, which may normalize gambling and increase the likelihood of

gambling amongst youth. The clear contextual differences reported by players suggested that,

although some gamble online in addition to venue-based play, those with an aversion to

8

terrestrial gambling venues may solely gamble through interactive mediums. Similar motivations

for Internet gambling have been found in other samples of Internet gamblers [26]. However,

Cotte and Latour‟s [24] findings are based on interviews with only 30 gamblers recruited from

Las Vegas, who are likely to be familiar with gambling, and so these results may not be

representative of wider Internet gambling consumption.

Comparison of a large international sample of Internet and non-Internet gamblers supports the

presence of differences between Internet and non-Internet gamblers based on their preferred

medium and engagement with gambling [27]. Gamblers from 105 countries (n=7921, 25%

Internet gamblers) were recruited from Internet gambling portals to complete an online survey A

logistic regression analysis found that characteristics significantly predicting someone being an

Internet gambler were: male gender; being employed; higher household income; younger age;

being single; fewer gambling fallacies (e.g., superstitions, misunderstanding the nature of

randomly determined outcomes); having more positive attitudes toward gambling; higher

gambling expenditure; gambling on a greater number of gambling formats (e.g., casino games,

sports betting, lottery, poker); greater severity of gambling problems; tobacco use; alcohol use;

and illicit drug use. Although these predictors were statistically significant, the use of Internet

gambling was not consistent and demographic characteristics were relatively diverse. The

majority of Internet gamblers also used terrestrial gambling and appeared to be highly involved,

engaging in frequently greater number of gambling formats than terrestrial gamblers (4.1 vs. 2.6)

and reporting higher median monthly gambling expenditures (US$80.00 vs. US$19.26). This

study has made a notable contribution to the understanding of Internet gambling; however, only

25% of participants had ever gambled online and over three-quarters were from the US, where

9

Internet gambling is prohibited so individuals have to be more interested in Internet gambling

and take certain steps to access gambling sites. Therefore, replication of these results in other

jurisdictions and with larger numbers of Internet gamblers is important.

There is a growing body of research examining Internet gamblers and behavioral patterns (e.g.,

28,29). However, these typically do not account for individual‟s wider gambling behavior, which

is a highly important variable in understanding the impact of this new mode of play. The bulk of

research to date on Internet gambling has given little consideration to how Internet gambling is

integrated within a broader spectrum of gambling behavior, creating significant limitations to the

understanding of the impact of this mode of gambling. Analysis of the results of the 2010 British

Gambling Prevalence Survey reveals that Internet gamblers are not a homogenous group of

consumers [17]. These results confirm that Internet gamblers generally also engage in terrestrial

gambling with Internet gambling largely a choice of convenience. This research was based on

national prevalence data, although the original survey only had a 47% response rate providing a

potential bias to results. The final sample was weighted and compared with national population

profiles in an attempt to increase the accuracy of the representation. These results highlight the

importance of examining Internet gambling in the context of all gambling involvement to

examine how this mode of access is integrated with overall patterns of gambling consumption.

This wider consideration will provide a more nuanced understanding of the likely or actual

impact of Internet gambling.

Internet gambling remains a reality that must be addressed by governments and operators in a

socially responsible manner to help protect and reduce the potential harms associated with

10

excessive use [12,20]. The Internet gambling field is characterized by small-scale studies that

often have methodological issues such as the use of non-representative samples limiting the

validity of results and understanding the subsequent nature of, and participation in, Internet

gambling. It is likely that the impact of Internet gambling will vary between jurisdictions based

on regulation, permitted advertising, technology adoption and cultural attitudes. Jurisdictions in

which Internet gambling is prohibited or restricted may benefit from examining the impacts of

Internet gambling in more open regulatory regimes [12]. Greater understanding of the use of

Internet gambling is also highly relevant to various industries and can be used to guide marketing

strategies and interactions with consumers as well as responses to changed consumer behavioral

patterns.

1.5 The current study

This study explores the characteristics of Internet gamblers, in order to determine the extent to

which they represent a distinct sub-group of gambling consumers and the impact of this mode of

play. More specifically, the study provides a comparative examination of gambling participation

levels, frequency and duration of play, gambling expenditure, use of Internet gambling sites, and

patterns of engagement with all forms of gambling. The study also examines gambling attitudes,

beliefs, perceived advantages of Internet gambling, and consequences of Internet gambling.

2. Methods

2.1 Participants

The online survey received responses from 6,682 respondents, with 4,724 completing the entire

survey giving a completion rate of 64.4%. Based on the 5,051 respondents providing full

11

demographic data, respondents were mostly male (86.3%), married (46.0%) and employed full-

time (59.1%). More than a third of respondents reported less than $1,000 household debt, while

household income was fairly evenly spread across all income brackets. Age ranged from 16 to

100 years, with an average of 45.0 years (SD=15.1). More than half reported that they were

from either New South Wales or Queensland. Of the 6,682 respondents, 4,680 (70.0%) reported

that they had gambled at least once on the Internet during the last 12 months. These participants

were classified as Internet gamblers, the remaining participants that had not gambled online on

any form were classified as non-Internet gamblers.

2.2 Procedure

The primary rationale for using an online survey was to generate a large sample of Internet

gamblers, so that their characteristics might be seen and explored in greater detail. Given the

relatively low prevalence of Internet gambling in the general population, other methods of

recruitment, such as telephone surveys, were less likely to generate as large of a sample. For

example, to achieve a sample size of only 179 Internet gamblers in Canada, 8,498 adults were

surveyed over the telephone [27]. By definition, Internet gamblers are active online,

subsequently this was regarded an appropriate recruitment method. A secondary objective of

recruiting participants online was to investigate how Internet gamblers compared to gamblers

that were active online, but did not engage in Internet gambling. The use of a self-selected

sample generated from online advertisements is noted as a limitation to the research. However,

telephone surveys are extremely costly and often exclude mobile phone users that do not have

landlines. Furthermore, evidence suggests that when properly conducted, online surveys generate

data that are as valid, if not more so, than data collected using traditional forms [30,31].

12

For the period between December 2010 and June 2011, banner advertisements containing links

to the survey were placed on a range of Australian websites, including Internet and terrestrial

gambling operators, gambling help and treatment sites, and sites of sporting organizations.

Advertisements were also run on Australian Facebook and Google sites to increase exposure

amongst the general population. The majority of respondents heard about the survey via Internet

gambling websites (58.9%).

Advertisements highlighted the interactive nature of the survey and contained phrases such as

„See how your gambling knowledge, attitudes, and behavior compares to other Australians‟

included the logos of the two universities involved in the research. Clicking on the advertisement

directed participants to the online gambling survey home page, which included an informative

consent preamble outlining the purpose of the survey, and reminding potential participants of the

voluntary and anonymous nature of their participation. Respective university human research

ethics committees approved the research.

2.3 Measures

An online survey adapted from the instrument used by Wood & Williams [27] in a large-scale

Internet gambling study that recruited 12,521 adults from 105 countries was used for purposes of

this study. The measures were purposefully created for this study and their psychometric

properties have not been validated, although future research will use the results to improve these

measures. The vast majority of questions were fixed-choice, some allowed multiple options, and

free-response to enable participants to provide feedback. The survey contained several sections:

13

a) Gambling Behavior Scale. Participation in nine different gambling activities/forms was

measured, including: instant win scratch tickets, lottery tickets and keno, betting on

sporting events, betting on dog or horse races, bingo, games of skill, poker (against

individuals), electronic gaming machines, casino table games, Internet casino games.

Participants indicated how often they engaged in each form (seven options ranging from

„4 or more times a week‟ to „not at all in the past 12 months‟). Non-participants were not

shown the remaining questions for that form. Those that had participated at least „less

than once a month‟ indicated their average monthly spend (defined as „how much you are

ahead or behind, or your net win (+) or loss (-) in an average MONTH in the past 12

months‟), and their use of the Internet for that form of gambling, Participants were also

asked how often they drank alcohol or used illegal drugs when gambling with five

response options ranging from „never‟ to „always‟.

b) Internet Gambling Questions. The first question in this section asked participants where

they primarily gamble online and included a response option: “I have never gambled on

the Internet”. Participants that selected this response skipped the remainder of this

question and were classified as non-Internet gamblers. The remaining participants were

classified as Internet gamblers and completed 12 questions including: the year they first

gambled online, time of day typically gamble online, preferred medium for online

gambling, and the association between Internet gambling and negative consequences

(impact of Internet gambling on sleep, eating patterns, gambling expenditure).

Participants were asked to nominate the factors that motivated them to choose an Internet

gambling site and the advantages and disadvantages of Internet gambling compared to

14

land-based play. For these questions a list of factors was generated based on previous

research although participants could provide additional feedback.

c) Gambling Attitudes Scale. Three questions were asked in this section: Beliefs about the

harms versus benefits (5 response options ranging from „The harm far outweighs the

benefits‟ to „The benefits far outweigh the harm‟); morality of gambling („Do you believe

that gambling is morally wrong?‟ response options include „no‟, „yes‟ and „unsure/don‟t

know); and appropriate policy concerning legalization (four response options „All types

of gambling should be legal‟, „All types of gambling should be legal‟, „All types of

gambling should be illegal‟, „Unsure/don't know‟). Responses were coded and summed to

produce a total score range of -3 to +3 with positive scores denoting positive attitudes,

negative scores denoting negative attitudes and neutral scores (0) denoting neutral views

or participants being unsure of their views.

The number of questions answered by each participant varied, as some questions were only

shown to participants based on previous responses. Additional questions were included in the

online survey but are not included in the analyses presented in this paper so are not described

here. The online survey was interactive and provided feedback to participants. The purpose of

this was to ensure that the questionnaire was engaging and interesting to assist with recruitment

and retention of participants. Participants were asked about the perceived usefulness and impact

on the interactive feedback provided in the survey and provided general demographic

information. The mean time to complete the survey was 12 minutes 23 seconds (SD = 9.0

minutes). The vast majority of participants (90%) complete the survey in 20 minutes or less. A

very small proportion (1%) spent over an hour completing the survey, however as participants

15

completed the survey at their leisure the completion times indicate that some started the survey

and came back to it several hours later.

2.4 Analysis

Due to the large sample size, an alpha of 0.001 was used and effect sizes are reported for all t-

tests and chi-squares. For t-tests, Cohen‟s d is reported, where 0.2 indicates a small effect, 0.5 a

medium effect and 0.8 a large effect. For chi-square, the (phi) coefficient was used, where

values between -0.3 and 0.3 may be treated as trivial associations. Analysis was limited to

quantitative results as the free-response options were included to ensure that no major variables

were inadvertently excluded and to guide subsequent research.

3. Results

3.1 Demographics

As shown in table 1, Internet gamblers were not significantly different in age to non-Internet

gamblers. A higher proportion of Internet gamblers were male (92.2%) compared to non-Internet

gamblers (73.0%), 2

(1, N=5,050) = 334.17, p < 0.001, although the effect size is small, = 0.26

with females being underrepresented in the overall sample. The demographics also differ

between Internet and non-Internet gamblers in terms of: marital status, 2

(4, N=5,001) = 47.81, p

< 0.001, = 0.09; current employment status, 2

(6, N=4,909) = 104.23, p < 0.001, = 0.15; and

household income, 2

(11, N=4,913) = 100.19, p < 0.001, = 0.14. As all tests reported here

have more than one degree of freedom, standardized residuals were examined to determine

where the differences lie, using a standardized residual of 2 as an indicator. More Internet

gamblers tend to be married compared to non-Internet gamblers, while more non-Internet

16

gamblers tend to be divorced or separated or never married, compared to Internet gamblers. In

terms of employment status, a higher proportion of Internet gamblers are employed full-time and

a lower proportion of Internet gamblers are employed part-time, unemployed, homemakers and

full-time students. In terms of income, the pattern of results suggests that Internet gamblers have

higher incomes than non-Internet gamblers. Approximately 15% of Internet gamblers reported

household incomes over $150,000, in comparison to a proportion of 10% among non-Internet

gamblers. Additionally, there were a greater proportion of Internet gamblers in each household

income bracket over $50,000.

Insert table 1 about here

3.2 Gambling behavior

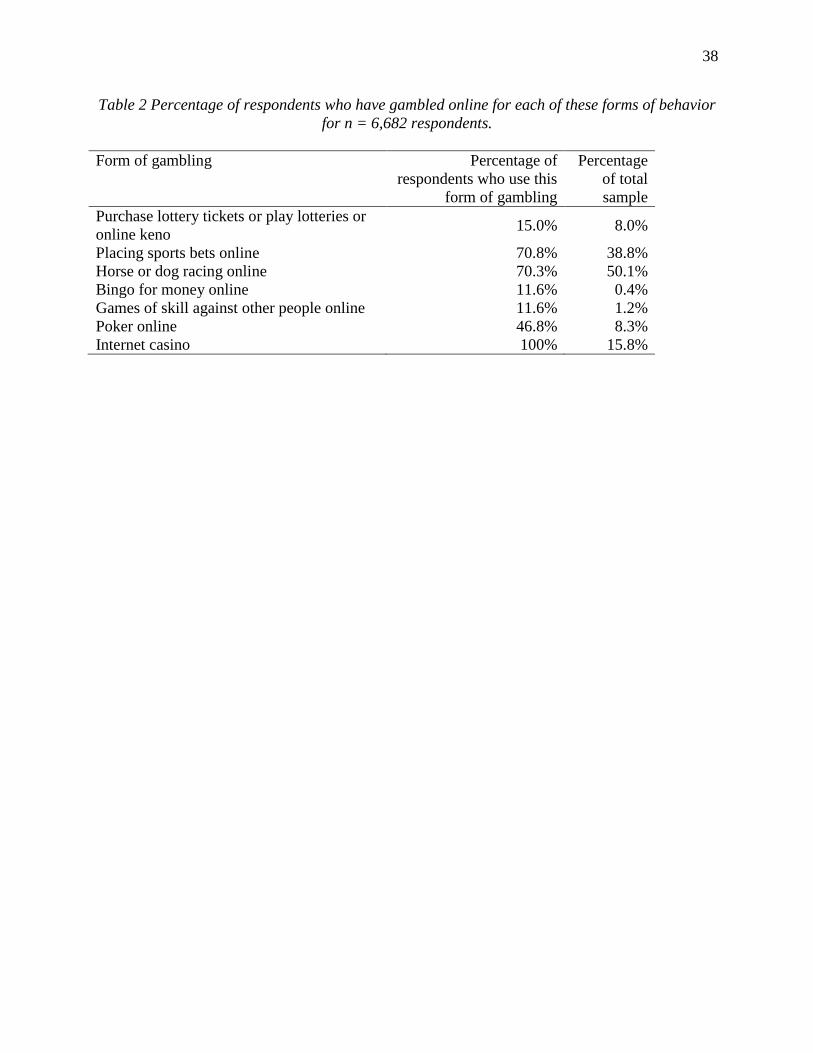

In terms of involvement in Internet gambling, participants were most likely to use Internet race

wagering (50.1%) and sports betting (38.8%) with Internet casino games (15.8%), Internet poker

(8.3%), and Internet lottery (8.0%) used by a smaller proportion of gamblers. Amongst

participants that engaged in each form of gambling, Internet wagering on sports (70.8%) and

races (70.3%) were still the most likely form of Internet gambling, although 46.8% of poker

players used Internet poker sites and 15.0% of those buying lottery tickets or playing keno did so

online (table 2).

Insert table 2 about here

The Internet gamblers in this study, as a group, were found to be more versatile gamblers than

their terrestrial counterparts. Indeed, reports of past year involvement indicate that Internet

gamblers participated in 4.96 (SD = 2.56) of the 10 different gambling forms surveyed, which

17

was significantly higher than the 3.27 (SD = 1.95) different forms of gambling on average for

non-Internet gamblers, t(4882.59) = 29.33, p < 0.001, d = 0.75. When considering weekly

gambling behavior, more non-Internet gamblers (19.0%) used electronic gaming machines

compared to Internet gamblers (14.0%), although the effect size for this suggests the difference is

small. However, as shown in table 3, on a weekly basis, more Internet gamblers wagered on

sporting events and horse and dog races, played poker and Internet casino games compared to

non-Internet gamblers.

Insert table 3 about here

In terms of monthly win/loss on different types of gambling, there were no significant

differences between Internet and non-Internet gamblers. This may partly be due to the large

variance in the data, but the median wins/losses for each type of gambling appear to be quite

similar. The sum of expenditure stated for each type of gambling was weakly and negatively

correlated with estimations of overall monthly gambling spend (r = -0.161, N = 846, p < 0.001)

for the non-Internet gambling group, whereas for the Internet group, there was no significant

correlation (r = 0.011, N = 1,774, p = 0.64). There was a significant difference between Internet

and non-Internet gamblers in terms of their highest frequency of gambling 2

(6, N=6,682) =

725.89, p < 0.001, = 0.33. Examination of table 4 suggests that Internet gamblers appear to

gamble more frequently than non-Internet gamblers.

Insert table 4 about here

18

3.3 Alcohol and drug use when gambling

Approximately 75.0% of Internet gamblers reported drinking alcohol on some gambling

occasions, compared to 66.3% of non-Internet gamblers, 2

(1, N=5,837) = 49.25, p < 0.001, =

0.09. Internet gamblers were also more likely to report using drugs on at least some occasions

(9.4%) compared to non-Internet gamblers (6.3%), 2

(1, N=5,845) = 16.41, p < 0.001, = 0.05.

3.4 Gambling Attitudes

Internet gamblers (M = 0.74, SD = 1.56) had significantly more positive attitudes to gambling

than non-Internet gamblers (M = -0.06, SD = 1.63), t(4359) = 15.72, p < 0.001, d = 0.50. A

greater proportion of non-Internet gamblers (68.5%) than Internet gamblers (50.2%) believed

that the harms of gambling outweigh the benefits to society, 2

(4, N=4,326) = 184.70, p < 0.001,

= 0.21. Similarly, non-Internet gamblers (11.0%) were more likely to believe that gambling is

morally wrong than Internet gamblers (4.5%), 2

(2, N=4,353) = 139.42, p < 0.001, = 0.18.

Reported opinions about legalized gambling demonstrated high levels of uncertainty amongst

participants with 62.8% of all participants indicating either that some types of gambling should

be legal or that they were unsure or did not know. Internet gamblers (37.5%) were more likely

than non-Internet gamblers (27.0%) to indicate that all types of gambling should be legal, 2

(2,

N=4,355) = 58.09, p < 0.001, = 0.12.

3.5 Internet use

Questions about Internet use were only asked of participants who indicated that they had

gambled online at least once in the past 12 months. Half of the Internet gamblers that responded

to the survey indicated that they first gambled online in or before 2006, with approximately 200

19

participants reporting first gambling online in 1995 (the earliest year cited) and another

substantial uptake in 2000. Responses indicate that the number of gamblers taking up Internet

gambling is increasing progressively each year. The vast majority of Internet gamblers (94.9%)

gambled online from home and only a minority typically gambled from work (3.2%). The

majority (60.2%) reported gambling from midday to 6pm, with a further 28.4% gambling

between 6pm and midnight. The majority of Internet gamblers preferred to use computers for

Internet gambling (84.0%), with only 5.5% of respondents stating that they preferred to gamble

online with their mobile phone.

Measurement of the proportion of gambling conducted online for each type of activity was

somewhat problematic due to methodological limitations, (respondents could give percentage

responses that sum to more than 100%).. Still, those identified as Internet gamblers reported that

they conducted 74.3% of their sports betting online by computer and 72.4% of their horse and

dog racing betting online. Internet gamblers indicated that 21.5% of sports betting and 23.1% of

race wagering was typically conducted online using mobile phones. Betting at terrestrial

agencies accounted for only 29.6% of sports betting and 32.7% of race wagering and the

telephone was used for 11.0% of sports and 12.7% of race wagering. Internet gamblers also

reported that they do the majority of their other forms of gambling online, including buying

lottery tickets (60.0%), playing bingo (60.3%), playing games of skill (65.4%) and playing poker

(70.7%).

In terms of length of gambling sessions, the distributions were skewed, with some players having

very long sessions, for example, up to 12 consecutive hours of Internet poker. The median

20

session of bingo lasted approximately half an hour, while the average Internet casino visit was

approximately an hour. Games of skill against others were played in sessions lasting

approximately one and a half hours, while the median Internet poker session was around two

hours.

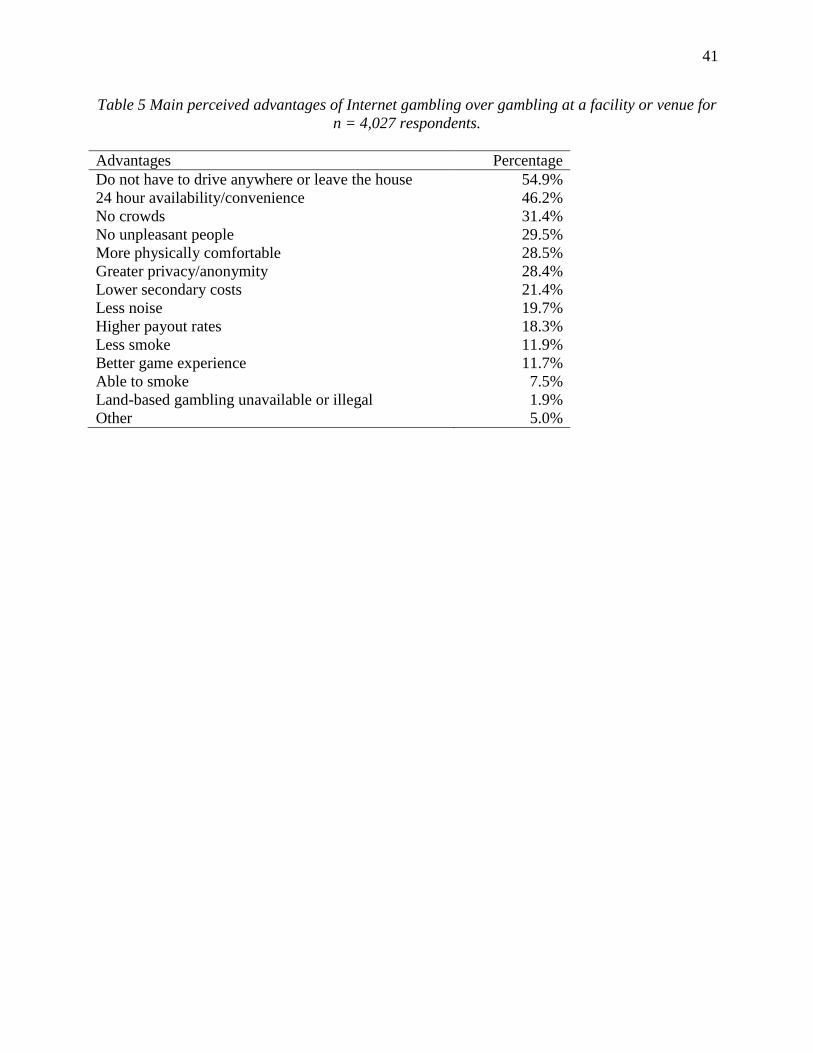

3.6 Motivations for Internet gambling

Most Internet gamblers considered the fact that they do not have to drive anywhere or leave the

house (54.9%) as an advantage over gambling in a facility (table 5), followed by 24 hour

availability and convenience (46.2%) and the lack of crowds (31.4%), unpleasant people (29.5%)

and greater privacy and anonymity (28.4%). Physical comfort was also an important factor

(28.5%). The first two advantages listed were also the most common responses as to why

respondents started gambling on the Internet in the first place. Lower secondary costs, less noise

and higher payout rates were noted by approximately one-fifth of Internet gamblers. Terrestrial

gambling being unavailable or illegal was nominated as an advantage by approximately 2% of

Internet gamblers.

Insert table 5 about here

The main perceived disadvantages of Internet gambling (table 6) were that it is too convenient

(29.9%) and that it is easier to spend more money (27.8%). Approximately 15% of Internet

gamblers indicated that Internet gambling had a poorer social atmosphere and was more

addictive than terrestrial gambling.

21

Insert table 6 about here

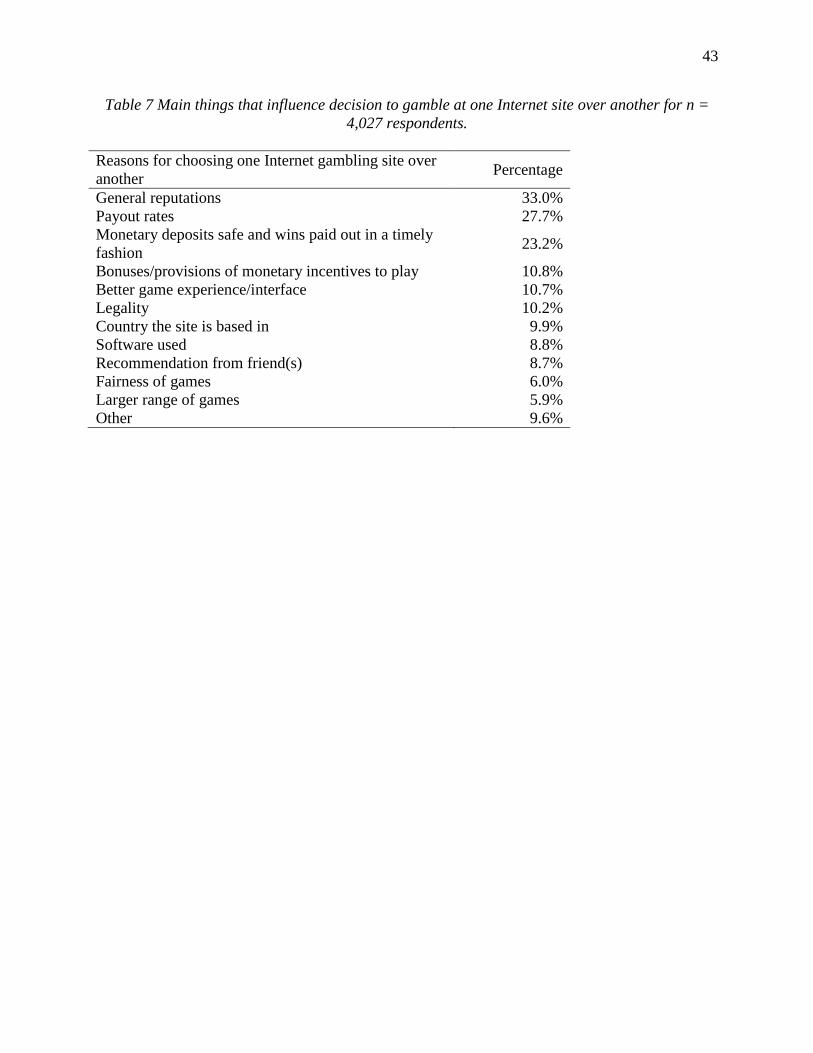

The most popular reasons for choosing one Internet gaming site over another (table 7) were:

general reputations (33.0%), payout rates (27.7%), and monetary deposits being safe with wins

paid out in a timely fashion (23.2%). Bonuses and incentives and superior game interfaces were

nominated by approximately 11% of Internet gamblers as a motivator for choosing a particular

site with legality, the country a site is based in, software used and personal recommendations

indicated by 10% or fewer of Internet gamblers.

Insert table 7 about here

The most popular sites to buy Lottery tickets or to play Internet Keno were Australian-based

sites, indicated as preferred sites by 92.5% of respondents that engaged in these forms of Internet

gambling. Similarly, for those using Internet sports betting and race wagering, a preference was

shown for Australian sites. However, this may also reflect the recruitment directly from several

Australian wagering sites. For all other forms of Internet gambling, as there are no legal

Australian sites that are available, participants used offshore sites.

3.7 Characteristics Statistically Differentiating Internet Gamblers from Non-Internet

Gamblers

A logistic regression was conducted investigating characteristics differentiating Internet

gamblers from non-Internet gamblers. A total of 13 predictor variables were used: gender, state

22

of residence, employment status, marital status, household income, alcohol use, illicit drug use,

level of education, household debt, age, gambling expenditure, number of different gambling

behaviors and gambling attitudes.

As only fifty-seven respondents indicated that they had not entered high school, they

were collapsed into a group with those who had not completed high school as a “less than high

school” group. All categorical variables were dummy coded using the following reference

groups: gender (female), state (ACT), employment status (on leave or other), marital status

(married) and education level (less than high school).

All continuous variables were checked for skewness and corrected with the following

transformations: debt (square root transformation) and number of gambling behaviors (square

root transformation). The skewness of gambling expenditure and gambling attitude could not be

corrected. Gambling expenditure was particularly leptokurtic, which was reduced by winsoring

the extreme 1% of values (114 values in total). There were no issues with the age or household

income variables. Of the 6,682 respondents considered for the analysis, there were missing data

for 2,851 cases (42.7%), so mean or mode replacement of missing values was not used. Instead,

missing values were excluded on a listwise basis, leaving 3,831 respondents in the analysis. Of

these, 2,602 were Internet gamblers and 1, 229 were non-Internet gamblers.

The test of the overall model with 13 predictors was statistically significant, 2

(31, N=3,831) =

633.80, p < 0.001 indicating that, altogether, these predictors reliably distinguish between

Internet gamblers and non-Internet gamblers. Overall prediction success is 73.6% and is

particularly good for Internet gamblers (92.2%), but less so for non-Internet gamblers (34.1%).

23

Table 8 outlines the predictor variables, including regression coefficients, Wald statistics,

significance and odds ratio for each of the predictors, including dummy variables. Controlling

for all other variables in the model, the significant predictors that differentiate Internet gamblers

from non-Internet gamblers (using alpha = 0.01) were: female gender, state, employment status

(particularly the unemployed and full-time students compared to those on leave/other), higher

household income, higher number of gambling behaviors and a more positive attitude to

gambling. The gender finding is surprising and may have been due to the relatively small number

of female gamblers in general, particularly female Internet gamblers, so the analysis was re-run

without gender. The pattern of significant predictors did not change.

Insert table 8 about here

3.8 Survey feedback

Most respondents who provided feedback found the survey at least somewhat useful (72.2%),

and 16.5% reported that they expected their gambling to decrease in next couple of months as a

result of the normative feedback provided comparing their responses to those of others taking the

survey matched by age and gender. There were no significant differences in survey feedback

between Internet and non-Internet gamblers.

4. Discussion

4.1 Demographics

The results are consistent with previous studies suggesting that Internet gamblers are more likely

to be male, have higher incomes, work full-time and are married or co-habitating [26,27,32-40].

24

Internet gamblers, compared to non-Internet gamblers, appear to be more likely to be situated in

the higher socio-economic strata and may subsequently have greater disposable income.

However, it should be stated that Internet gamblers nonetheless comprise a heterogeneous group,

who embody a range of demographic characteristics. This is reflected in the contrasting findings,

from the logistic regression, that being unemployed or a student predicted Internet gambling as

well as higher household income. The predominance of males in the Internet gambling group

may also be reflective of the unequal gender ratio of the survey and placement of links

predominately on betting sites, which are typically used by males.

4.2 Gambling involvement

The majority of Internet gambling by those surveyed appears to be conducted at sports and race

wagering sites. This is not surprising, given that these sites are legal, regulated and heavily

advertised and were involved in the recruitment of participants. However, a substantial

proportion of the surveyed gamblers are also using offshore casino games and poker sites,

indicating the ineffectiveness of existing regulation prohibiting operators from providing Internet

gambling to Australians. Among poker players almost half report gambling online, suggesting

that there is a reasonable degree of customer demand for these services. Participation in other

forms of Internet gambling is relatively low at this time however, legalization and advertising of

these would likely increase participation rates.

Again, consistent with previous research [13,27,41], Internet gamblers in this study appear to

participate in a greater variety of gambling formats and be more frequently involved in

gambling. This may indicate that consumers are adding Internet gambling to an existing

25

repertoire of gambling, or conversely, that Internet gambling is facilitating a higher frequency of

gambling given the high accessibility and convenience of this medium. It is likely that both

causal pathways exist. These results highlight the importance of considering the wider context of

gambling behavior when understanding consumer behavior. Despite the lack of homogeneity

among Internet gamblers in terms of patterns of gambling involvement, Internet gamblers are

likely to hold more liberal views of gambling as compared to non-Internet gamblers, which is

consistent with their greater overall gambling involvement.

4.3 Use of Internet gambling

Although interest in Internet gambling has recently increased in Australia, half of the Internet

gamblers surveyed reported first gambling online in the past five years although responses

indicated that Internet gambling has been used for over fifteen years. However, trends indicated

that there is an increasing take-up of Internet gamblers in recent years, which is likely to

continue due to growth factors outlined above. The vast majority of Internet gambling appears to

be occurring from home, using computers, during the afternoon or evening. This is consistent

with interviews with Internet gamblers [24] and suggests that Internet gambling is bringing this

activity into the home, potentially competing with or supplementing existing entertainment

options such as television. The timing of Internet gambling coincides with the broadcast of

sporting and racing events on which the majority of bets are placed. The international nature of

betting means that bets can be placed at any time on sports and races, but it is likely that the

majority of betting is on domestic events and sporting teams. Poker, bingo, and casino games are

also available 24 hours a day, although the majority of play appears to be during typical

recreational hours.

26

Mobile gambling is preferred by a minority of Internet gamblers surveyed, although participants

indicated that mobile phones were used as a secondary medium for Internet gambling. Given the

increased marketing efforts of gambling operators and availability of apps and smart phone use

in Australia, the popularity and use of mobile betting apps is predicted to increase. The global

mobile gambling market was valued at US$2.8 billion in 2010, representing approximately 10%

of the global Internet gambling market and the market is expected to reach US$5.3 billion by

2015 [42]. Mobile apps have been introduced to the Australian market relatively recently due to

rules prohibiting gambling apps from the Apple App Store until the end of 2010 and continued

prohibition in Android app stores. Several Australian gambling operators have now launched

mobile apps, and thus the use of mobile devices for Internet gambling is expected to increase.

Terrestrial venues still account for around a third of betting, and a small proportion of bettors

still use telephone betting. It is likely that a proportion of gamblers will resist Internet gambling

and continue to bet via retail venues, although this may change over time given the importance

and high use of the Internet for everyday activities.

The length of typical Internet gambling sessions indicates why the majority of players surveyed

engage in these activities from the comfort of their own home and through computers. Some

participants reported very long sessions and median sessions of play indicated this was a

continuous activity rather than being used for very short sessions. The length of Internet sports

and race betting sessions were not measured, as it was thought that the time taken to place a bet

online was relatively short and errors may be introduced if time taken to research bets and odds

and watch a sporting event were included. The average length of non-Internet gambling play was

27

also not measured so it is not possible to make comparisons with non-Internet gamblers or

terrestrial sessions of play.

4.4 Motivations for Internet gambling

Respondents‟ perceived advantages of Internet gambling, as opposed to terrestrial gambling, are

consistent with those reported in previous research [18,34,36]. The main advantages cited relate

to convenience and accessibility, which are clear benefits, particularly in Australia where

Internet access is fast, cheap and widely accessible. Indicating that these perceived advantages

are key drivers in the ongoing expansion of the Internet gambling phenomenon, these were also

the primary reasons that respondents provided for their initial decision to begin gambling on the

Internet. Moreover, very few Internet gamblers cited that they could not access terrestrial

gambling, which further highlights the importance of convenience behind the use and uptake of

Internet gambling. A greater proportion of Internet gamblers recruited from an international

sample (14%) indicated that they preferred Internet gambling as terrestrial gambling was not

easily accessible [18], indicating that this is a greater advantage for Internet gambling in some

jurisdictions.

Of interest, slightly less than one-third of Internet gamblers cite a preference of Internet

gambling due to greater physical comfort and not having to be around other patrons, which is

similar to results from an international study indicating that a proportion of Internet gamblers

actually have an aversion to terrestrial venues [26]. These responses may be linked with a desire

for greater privacy and anonymity, but also indicate that Internet gambling sites are attracting

individuals that may not frequent terrestrial facilities and represent a new market of potential

28

consumers. Advantages offered by Internet gambling sites, such as better game interface, greater

variety of betting options, and higher payout rates appeared less important to players overall,

although it is likely that there is a proportion of Internet gamblers, many of whom may be

professional bettors, that perceive these factors as very important.

In terms of disadvantages, it appears that a substantial minority of Internet gamblers believe that

the constant availability and ease of access of Internet gambling sites poses potential risks. This

is consistent with public debate over the potential dangers and risks associated with Internet

gambling, and the responses are congruent with general attitudes that the harms of gambling

somewhat outweigh the benefits. In contrast to Internet gamblers that prefer the setting of

Internet play, a substantial minority of Internet gamblers claim that these sites have a poorer

social atmosphere. This latter result again highlights the tendency for some Internet gamblers to

use this medium mainly for its convenience, rather than because of any perceived superiority in

the social or ambient qualities of Internet play.

Reflecting high levels of trust and comfort, only a minority of Internet gamblers were concerned

with the security of deposits, the certainty of payouts, the legality of Internet gambling, or the

country in which a site is based. This low level of customer concern is somewhat troubling. In

the past, a number of large and well-regarded sites have jeopardized player accounts, as result of

hacking, cheating, customer identity theft, and accounts being frozen with no subsequent refund

to players [43]. Indeed, many offshore sites potentially pose significant risks to Australian-based

gamblers, since very little can be done to resolve disputes, deception, or fraud [12]. Therefore,

public education may be very useful in increasing public understanding of the legality of Internet

29

gambling and the risks of playing on unregulated and offshore sites. Regulated sites should also

ensure that consumers understand the benefits associated with play with licensed operators.

Although legality and jurisdictional context were not cited as reasons for choosing an Internet

gambling site, general reputation, payout rates and the safety of deposits do appear to be of

importance to Internet gamblers. This indicates that, although better rates of return are not seen

as the most important advantage of Internet gambling over terrestrial play, these features are

important in selecting sites. Interestingly, bonuses and incentives motivated only a minority of

players suggesting that trust, safety and consumer protection are important to Internet gamblers.

This is reflected in the choice of Australian-based sites by the majority of participants for their

Internet betting and lottery play. For those playing poker, casino games and bingo on offshore

sites, it indicates a preference for the larger, more reputable operators, which often have self or

regulator-imposed codes of conduct and player protection standards. This was clear from the

responses from Internet poker players that almost exclusively played on two of the largest

international sites. Similarly, those using Internet casinos tended to use relatively well-known

sites.

4.5 Limitations

Due to the self-selected nature of the online survey, the results are not intended to be

representative of the entire population of Australian Internet gamblers. Despite efforts to ensure

that advertisements and links to the surveys were placed on a wide range of sites, this was largely

dependent on cooperation and support from various organizations and individuals. As a

substantial proportion of participants were recruited from Australian wagering sites the responses

30

may not be representative of the wider population of Australian gamblers, thus limiting the

genralizability of the results. In efforts to keep the survey from being too lengthy there were

questions that were not asked. One major subsequent limitation is the lack of detail on frequency

of Internet gambling resulting in all participants who had gambled online at least once in the past

12 months being defined as an Internet gambler. Although this classification has been used in

previous research, it is still a relatively weak variable and does not differentiate between

infrequent and frequent Internet gamblers. Although the instrument used in the present study had

been pilot tested and used in previous research, it has not been validated and so the reliability of

the instrument cannot be demonstrated. Some aspects of Internet gambling were difficult to

measure; in particular, results for questions on expenditure had great variability in responses

making accurate interpretation of results problematic. Research indicates that individuals

perceive and report gambling expenditure in different ways and that, in general, retrospective

estimates of gambling expenditures appear unreliable [44]. The wording used for questions on

expenditure were based on evidence suggesting optimal results, however, the sum on spend for

each form of gambling was only weakly correlated with overall reported spend, indicating that

participants are not very consistent at reporting their net wins and losses. Future research is

already underway to overcome some of these limitations. Specifically, the online survey has

been revised so that participants will be recruited from a wider range of sites and the frequency

of Internet gambling can be determined.

5. Conclusions

Internet gambling represents a highly important development to the gambling industry and is

consistent with the movement to Internet provision of a range of products and services.

31

Increasing participation rates and revenue indicate that Internet gambling in all its forms is

meeting consumer demand. Currently, Internet gambling does not appear to be cannibalizing

terrestrial gambling largely because wagering operators can provide Internet services to existing

customers and Internet gamblers actively engage in many types of gambling and also represent a

slightly different customer base to non-Internet gamblers. Some Internet gamblers have an

aversion to terrestrial venues suggesting that this mode is recruiting a new market of consumers,

as well as shifting existing customers away from terrestrial gambling. Subsequently, increased

preference for this mode of access may yield increased participation at the expense of terrestrial

gambling and associated industries. It is highly important for policy makers, operators and all

interested stakeholders to increase their understanding of Internet gamblers and the impact of this

mode of play.

This paper clarifies the use of and engagement with Internet gambling in the wider context of

gambling behavior. The transition to Internet gambling appears to be driven primarily by

convenience and accessibility, which is similar to the use of other products and services online. It

is likely that Internet gamblers also engage with and use other Internet-based products and

activities and this customer base may be relevant to other industries. This research furthers our

understanding of both micro-level processes, such as how consumers choose between Internet

gambling sites, and macro-level processes, such as the global attitudes towards gambling in

general that differ between Internet and non-Internet gamblers.

Acknowledgments

Grateful acknowledgments and thanks are due to the Menzies Foundation for providing Dr.

Gainsbury with an Allied Health Sciences Grant to fund this research. Additional thanks are

made to the individuals and organizations that supported this research through placing

advertisements and links to the online survey on their websites and all participants of the

research.

32

References

[1] Online Casino City. Onlinecasinocity.com. Retrieved, December 23, 2011 from

http://online.casinocity.com/

[2] Global Betting and Gaming Consultants. Global Gaming Report (6th ed.). Castletown, Isle of

Man, British Isles: Author. 2011

[3] S. Holliday. The balance of power in global eGaming. EGR Live, Business Design Centre,

London (2011, May). Retrieved June 10, 2011from

http://www.h2gc.com/news.php?article=H2+Gambling+Capital+Presentations+-

+EGR+Live+May+2011

[4] G. Kelleher. The interactive gambling industry: Key trends 2010. Presentation given at the

iGaming Supershow, Prague, May 25-28, 2010.

[5] Global Betting and Gaming Consultants. Global Gaming Report (5th ed.). Castletown, Isle of

Man, British Isles: Author. 2010

[6] PricewaterhouseCoopers. Global gaming outlook. Retrieved December 5, 2011from

http://www.pwc.com/en_GX/gx/entertainment-media/publications/global-gaming-outlook.jhtml

[7] Stay-at-home Britons turn to TV, gambling. Arab Times. Retrieved November 1, 2011from

http://www.arabtimesonline.com/NewsDetails/tabid/96/smid/414/ArticleID/175625/reftab/73/t/S

tay-at-home-Britons-turn-to-TV-gambling/Default.aspx

[8] Online gaming only bright spot for Loto-Quebec in H1. Gaming Intelligence. Retrieved

November 1, 2011from http://www.gamingintelligence.com/finance/13776-online-gaming-only-

bright-spot-for-loto-quebec-in-h1

[9] H2 Gambling Capital.Gambling goes mobile. London: H2 Gambling Capital. 2011

33

[10] Miniwatts Marketing Group.World Internet users and population stats. Internet World Stats.

March 31, 2011. Retrieved December 21, 2011, from

http://www.internetworldstats.com/stats.htm

[11] Pew Internet & American Life Project.Trend data. Retrieved May 13, 2011from

http://www.pewinternet.org/Trend-Data/Online-Activites-Total.aspx

[12] S. Gainsbury, R. Wood, Internet gambling policy in critical comparative perspective: The

effectiveness of existing regulatory frameworks. International Gambling Studies, 11(2011), 309-

323.

[13] H. Wardle, A. Moody, M. Griffiths, J. Orford, R. Volberg, Defining the online gambler and

patterns of behaviour integration: Evidence from the British Gambling Prevalence Survey 2010.

International Gambling Studies, 11(2011), 339–356.

[14] D.T. Olason, E. Kristjansdottir, H. Einarsdottir, H., Haraldsson, G. Bjarnason, J.

Derevensky, Internet gambling and problem gambling among 13 to 18 year old adolescents in

Iceland. International Journal of Mental Health and Addiction, 9(2011), 257-263.

[15] N. Petry, Internet gambling: An emerging concern in family practice medicine? Fam. Pract.,

23(2006), 421-426.

[16] Productivity Commission (2010). Gambling (Report No. 50). Canberra: Author.

[17] H. Wardle, H.,A. Moody, S. Spence, J. Orford, R. Volberg, D. Jotangia, M. Griffiths, D.

Hussey, F. Dobbie, British gambling prevalence survey 2010. London: National Centre for

Social Research. 2011

[18] R. Wood, R. Williams, Internet gambling: Prevalence, patterns, problems and policy

options. Report prepared for the Ontario Problem Gambling Research Centre: Guelph, ON. 2010

34

[19] S. Monaghan, S. Responsible gambling strategies for Internet gambling: The theoretical and

empirical base of using pop-up messages to encourage self-awareness. Comput. Hum. Behav.

25(2009), 202-207.

[20] S. Gainsbury, Response to the Productivity Commission inquiry report into gambling:

Online gambling and the Interactive Gambling Act. Gambling Research, 22(2010), 3–12.

[21] Nielsen Online. The Australian Internet and Technology Report 2008–2009.Edition 12.

2010

[22] M. Lamont, N. Hing, S. Gainsbury,. Gambling on sport sponsorship: A conceptual

framework for research and regulatory review. Sport Management Review, 14(2011), 246-257.

[23] Centrebet (2011). First-half FY11 results. Sydney: Centrebet.

[24] J. Cotte, K. Latour, Blackjack in the kitchen: Understanding online versus casino gambling.

J. Consum. Res. 35(2009). 742-758.

[25] S. Monaghan, J. Derevensky,. An appraisal of the impact of the depiction of gambling in

society on youth. International Journal of Mental Health and Addiction, 6(2008), 537-550.

[26] R. Wood, R. Williams, Problem Gambling on the Internet: Implications for Internet

Gambling Policy in North America. New Media & Society, 9(2007), 520-542.

[27] R. Wood, R. Williams, A comparative profile of the Internet gambler: Demographic

characteristics, game play patterns, and problem gambling status. New Media & Society,

13(2011), 1123-1141.

[28] D. A. LaPlante, J.H. Kleschinsky, R.A. LaBrie, S.E. Nelson, H.J. Shaffer, Sitting at the

virtual poker table: A prospective epidemiological study of actual Internet poker gambling

behaviour. Comput. Hum. Behav. 25(2009), 711-717.

35

[29] D. LaPlante, A. Schumann, R. LaBrie, H. Shaffer, Population trends in Internet sports

gambling. Comput. Hum. Behav. 24(2008), 2399-2414.

[30] E.T. Miller, D.J. Neal, L.J. Roberts, J.S. Baer, S.O. Cressler, J. Metrik G.A. Marlatt,

Test–retest reliability of alcohol measures: Is there a difference between

Internet-based assessment and traditional methods?, Psychol. Addict. Behav.

16(2002), 56–63.

[31] P.G.M. Van Der Heijden,.G. Van Gils, J. Bouts, J.J. Hox, A comparison of randomized

response, computer-assisted interview and face-to-face direct questioning: Eliciting sensitive

information in the context of welfare and unemployment benefit, sociological methods and

research, 28(2000), 505–537.

[32] American Gaming Association (2006). State of the States 2006: The American Gaming

Association survey of casino entertainment. Retrieved January 4, 2011from

http://www.americangaming.org./survey2006/reference/ref.html

[33] B.J., Bernhard, A.F. Lucas, E. Shampaner, Internet gambling in Nevada. Las Vegas:

International Gaming Institute, University of Nevada, Las Vegas, 2007.

[34] M.D. Griffiths, H. Wardle, J. Orford, K. Sproston, B. Erens, Socio-demographic correlates

of internet gambling: Findings from the 2007 British Gambling Prevalence Survey.

CyberPsychology and Behavior, 12(2009), 199–202.

[35] S. Jime´nez-Murcia, R. Stinchfield, F. Ferna´ndez-Aranda, J. Santamarı´a, R. Granero, E.

Penelo, R. Granero, M. Gómez-Peñaa, N. Aymamí, L. Moragas , A. Soto, J. Menchon, Are

online pathological gamblers different from non-online pathological gamblers on demographics,

gambling problem severity, psychopathology, and personality characteristics? International

Gambling Studies, 11(2011), 325–337.

36

[36] J. McBride, J. Derevensky, Internet gambling behaviour in a sample of online gamblers.

International Journal of Mental Health and Addiction, 7(2009), 149–167.

[37] J. Svensson, R. Romild, Incident Internet gambling in Sweden: Results from the Swedish

longitudinal gambling study. International Gambling Studies, 11(2011), 257–375.

[38] R.A. Volberg, K.L. Nysse-Carris, D.R. Gerstein, 2006 California problem gambling

prevalence survey: Final report. Submitted to the California Department of Alcohol and Drug

Problems, Office of Problem and Pathological Gambling 2006.

[39] C. Woodruff, S. Gregory, Profile of Internet gamblers: Betting on the future. UNLV

Gaming Research & Review Journal, 9(2005), 1-14.

[40] R. Woolley,Mapping internet gambling: Emerging modes of online participation in

wagering and sports betting. International Gambling Studies, 3(2003), 3-21.

[41] South Australian Centre for Economic Studies, Social and economic impact study into

gambling in Tasmania 2008: Fact sheets. 2008 Retrieved from

dhhs.tas.gov.au/__data/assets/pdf_file/0015/33027/Vol_2_Fact_Sheets.pdf

[42] H2 Gambling Capital , New H2 eGaming dataset now available. Retrieved June 14,

2011from http://www.h2gc.com/news.php?article=New+H2+eGaming+Dataset+Now+Available

[43] J.L. McMullan, A. Rege, Online crime and internet gambling. Journal of Gambling Issues,

24(2010), 54-85.

[44] R. Wood, R. Williams, How much money do you spend on gambling? The comparative

validity of questions wordings used to assess gambling expenditure. International Journal of

Social Research Methodology, 10(2007), 63-77.

37

Table 1. Demographic profile of Non-Internet gamblers and Internet gamblers for n = 5,050

respondents

Non-Internet

gamblers

(N=1,705)

Internet

gamblers

(N=3,345)

Gender

Male 73.7% 92.8%

Female 26.3% 7.2%

p < 0.001 (2

= 334.17, df = 1)

Age bracket

Under 18 0.2% 0.1%

18-19 4.2% 1.0%

20-29 20.9% 16.9%

30-39 14.7% 17.6%

40-49 17.4% 23.0%

50-59 25.3% 22.2%

60-69 13.2% 14.7%

70-79 3.5% 3.8%

80 or older 0.6% 0.7%

p < 0.001 (2

= 94.85, df = 8)

Marital status

Married 41.6% 48.3%

Living with partner 15.1% 17.6%

Widowed 1.6% 1.6%

Divorced or separated 11.5% 9.1%

Never married 30.2% 23.4%

p < 0.001 (2

= 47.81, df = 4)

Current employment status

Employed full-time 54.3% 61.6%

Employed part-time 13.6% 9.0%

Unemployed and seeking work 5.0% 2.4%

Retired 11.0% 14.6%

Homemaker 2.3% 1.1%

Full-time student 7.2% 3.7%

Sick leave, maternity leave, on strike, on

disability OR other 6.7% 7.6%

p < 0.001 (2

= 104.23, df = 6)

38

Table 2 Percentage of respondents who have gambled online for each of these forms of behavior

for n = 6,682 respondents.

Form of gambling Percentage of

respondents who use this

form of gambling

Percentage

of total

sample

Purchase lottery tickets or play lotteries or

online keno 15.0% 8.0%

Placing sports bets online 70.8% 38.8%

Horse or dog racing online 70.3% 50.1%

Bingo for money online 11.6% 0.4%

Games of skill against other people online 11.6% 1.2%

Poker online 46.8% 8.3%

Internet casino 100% 15.8%

39

Table 3 Past year and weekly gambling involvement by Internet and non-Internet gamblers for n

= 6,682 respondents.

Any past year

involvement

Weekly involvement in

past year

Non-Internet

gamblers

Internet

gamblers

Non-Internet

gamblers

Internet

gamblers

Instant win scratch

tickets 45.1% 48.8% 5.9% 5.8%

Lottery tickets 56.5% 66.9% 17.7% 20.9%

Sporting events 42.0% 77.0% 16.9% 42.2%

Horse and dog racing 62.6% 94.1% 35.4% 73.8%

Bingo for money 8.5% 19.5% 1.1% 0.9%

Games of skill (not

including poker) 13.2% 27.2% 2.6% 2.8%

Poker (against

individuals) 15.4% 37.8% 2.6% 10.2%

Slot machines, pokies,

electronic gambling

machines

57.5% 60.2% 19.0% 14.0%

Table games at a

casino 23.6% 43.0% 2.1% 2.1%

Internet casino 0% 21.3% 0% 1.8%

Average number of

games played 3.27 4.96 1.01 1.65

Total valid responses 2,002 4,680 1,999 4,279

40

Table 4 Highest gambling frequency, taken as highest response to any form of gambling for n =

6,682 respondents.

Highest gambling frequency Non-Internet gambler Internet gambler

4 or more times a week 19.3% 43.1%

2-3 times a week 18.4% 21.3%

Once a week 18.7% 15.0%

2-3 times a month 9.7% 5.3%

Once a month 8.4% 2.8%

Less than once a month 18.0% 3.9%

Not at all in the past 12 months 7.5% 8.6%

Total valid responses 2,002 4,680

41

Table 5 Main perceived advantages of Internet gambling over gambling at a facility or venue for

n = 4,027 respondents.

Advantages Percentage

Do not have to drive anywhere or leave the house 54.9%

24 hour availability/convenience 46.2%

No crowds 31.4%

No unpleasant people 29.5%

More physically comfortable 28.5%

Greater privacy/anonymity 28.4%

Lower secondary costs 21.4%

Less noise 19.7%

Higher payout rates 18.3%

Less smoke 11.9%

Better game experience 11.7%

Able to smoke 7.5%

Land-based gambling unavailable or illegal 1.9%

Other 5.0%

42

Table 6 Perceived disadvantages of Internet gambling over gambling at a facility or venue for n

= 4,027 respondents.

Disadvantages Percentage

Too convenient 29.9%

Easier to spend more money 27.8%

Poorer physical atmosphere 10.3%

Poorer social atmosphere 15.1%

More addictive 14.9%

Worry about monetary deposits being safe and/or

having wins paid out in a timely fashion 12.3%

Difficulty verifying fairness of games 10.3%

Poorer game experience (not as fun, etc) 9.8%

Lack of face-to-face contact makes betting more

difficult 6.7%

Difficulty excluding underage gamblers 5.3%

Illegality 2.9%

Other 7.5%

43

Table 7 Main things that influence decision to gamble at one Internet site over another for n =

4,027 respondents.

Reasons for choosing one Internet gambling site over

another Percentage

General reputations 33.0%

Payout rates 27.7%

Monetary deposits safe and wins paid out in a timely

fashion 23.2%

Bonuses/provisions of monetary incentives to play 10.8%

Better game experience/interface 10.7%

Legality 10.2%

Country the site is based in 9.9%

Software used 8.8%

Recommendation from friend(s) 8.7%

Fairness of games 6.0%

Larger range of games 5.9%

Other 9.6%

44

Table 8 Logistic regression of characteristics differentiating Internet gamblers from non-Internet

gamblers for n = 6,682.

Predictor B Wald Significance

Odds

Ratio

Gender -1.301 121.104 <0.001 .272

State 46.13 <0.001

New South Wales .030 .011 .918 1.031

Victoria -.662 4.686 .030 .516

Queensland -.309 1.106 .293 .734

South Australia .060 .040 .842 1.062

Western Australia -.040 .012 .911 .961

Tasmania -.788 3.526 .060 .455

Northern Territory -.773 2.891 .089 .461

Employment Status 31.06 <0.001

Employed full-time .356 5.351 .021 1.428

Employed part-time .393 4.668 .031 1.481

Unemployed/seeking work .781 10.364 .001 2.183

Retired -.261 1.898 .168 .770

Homemaker .066 .038 .846 1.068

Full-time student .668 8.409 .004 1.950

Marital Status 5.98 .200

Living with partner -.241 4.322 .038 .786

Widowed -.336 1.135 .287 .715

Divorced or separated .023 .028 .866 1.023

Never married -.044 .137 .711 .957

Household income .059 17.179 <0.001 1.060

Alcohol Use .189 4.293 .038 1.208

Drug Use -.008 .004 .950 .992

Education level 5.89 .317

Completed high school -.133 1.016 .314 .876

Some technical school,

College or university -.010 .004 .949 .990

Completed technical school,

College or diploma -.084 .403 .526 .920

Completed undergraduate

University degree -.114 .641 .423 .892

Professional degree .173 1.185 .276 1.189

Household debt .027 1.486 .223 1.028

Age .000 .003 .955 1.000

Expenditure .000 3.010 .083 1.000

45

Number of gambling

behaviours .913 78.056 <0.001 2.492

Gambling attitude .223 80.835 <0.001 1.249

Copyright © 2022 FDOKUMEN