A Collaborative Effort AGuideTo BIOTECHNOLOGY FINANCE FirstEdition

247

A Collaborative Effort MINNESOTA DEPARTMENT OF EMPLOYMENT AND ECONOMIC DEVELOPMENT A Guide To BIOTECHNOLOGY FINANCE First Edition

Transcript of A Collaborative Effort AGuideTo BIOTECHNOLOGY FINANCE FirstEdition

A Collaborative Effort

MINNESOTA DEPARTMENT OF EMPLOYMENT AND ECONOMIC DEVELOPMENT

A Guide To

BIOTECHNOLOGYFINANCE First Edition

Aɯ&ÜÐËÌɯ3Öɯ!(.3$"'-.+.&8ɯ%(- -"$is available without charge from the Minnesota Department of Employment and Economic Development, ɯ2ÔÈÓÓɯ!ÜÚÐÕÌÚÚɯ ÚÚÐÚÛÈÕÊÌɯ.ÍÍÐÊÌȮɯƕÚÛɯ-ÈÛÐÖÕÈÓɯ!ÈÕÒɯ!ÜÐÓËÐÕÎȮ 332 Minnesota Street, 2ÜÐÛÌɯ$ɪƖƔƔȮɯSt. Paul, MN 55101ɪƕƗƙƕȭ3ÌÓÌ×ÏÖÕÌȯɯȹƚƙƕȺɯƖƙƝɪƛƘƛƚɯÖÙɯȹƜƔƔȺɯƗƕƔɪƜƗƖƗɯɧɯ%ÈßɯȹƚƙƕȺɯƖƝƚɪƙƖƜƛɯ$ÔÈÐÓȯɯËÌÌËȭÔÕÚÉÈÖɑÚÛÈÛÌȭÔÕȭÜÚɯɧɯ6ÌÉÚÐÛÌȯɯÞÞÞȭ×ÖÚÐÛÐÝÌÓàÔÐÕÕÌÚÖÛÈȭÊÖÔɤÔÕÚÉÈÖ ɯ4×ÖÕɯÙÌØÜÌÚÛȮɯÛÏÐÚɯ×ÜÉÓÐÊÈÛÐÖÕɯÊÈÕɯÉÌɯÔÈËÌɯÈÝÈÐÓÈÉÓÌɯÐÕɯÈÓÛÌÙÕÈÛÐÝÌɯÍÖÙÔÈÛÚɯÉàɯÊÖÕÛÈÊÛÐÕÎɯȹƚƙƕȺɯƖƙƝɪƛƘƛƚȭɯ3ÏÌɯ,ÐÕÕÌÚÖÛÈɯ#Ì×ÈÙÛÔÌÕÛɯÖÍɯ$Ô×ÓÖàÔÌÕÛɯÈÕËɯ$ÊÖÕÖÔÐÊɯ#ÌÝÌÓÖ×ÔÌÕÛɯÐÚɯÈÕɯÌØÜÈÓɯÖ××ÖÙÛÜÕÐÛàɯÌÔ×ÓÖàÌÙɯÈÕËɯÚÌÙÝÐÊÌɯ×ÙÖÝÐËÌÙȭɯ

Printed on Recycled PaperWith a Minimum of 10% Postconsumer Waste

A Guide ToBIOTECHNOLOGYFINANCE

First Edition

August 2005

A Collaborative EffortMinnesota Department of Employment and Economic DevelopmentLindquist & Vennum P.L.L.P.

© Copyright 2005, Minnesota Department of Employment and Economic Development andLindquist & Vennum P.L.L.P.ISBN 1-888404-40-X

FOREWORD

Biotechnology is on the forefront of a technological explosion. Indeed, this has already beendubbed the “Century of Biology.” In little more than a dozen years, the biotechnologyindustry has grown from a handful of companies to a $40 billion worldwide industry thatincreasingly has an impact on a broad spectrum of fields including, health care, agricultureand energy production. Waves of new products, including those that help save lives, growdisease resistant foods and produce environmentally friendly fuels, are coming to market.

The expansion of the industry is being driven by three global demographic trends: a growingpopulation, longer life expectancies and an increasing percentage of elderly people in thetotal population. Developing and manufacturing biotechnology medicines and products,however, is a complex and costly process. Research and development, for example, now costbiotech companies up to $100,000 per employee annually.

To capitalize on the extraordinary opportunities presented by the industry, biotechnologycompanies must be on the cutting edge of modern financing. Success increasingly dependson knowledge of the specific issues that affect the industry and creative strategies thatdevelop from that understanding. Whether in early stages of growth or more mature phasesof development, companies are eager to attract grants, investment and corporate partners.

This Guide is a most welcome addition to the biotechnology entrepreneur ’s toolkit. Itprovides the fundamentals of financing for this evolving field in a concise manner withoutglossing over the details that provide the reader with a greater understanding of thecomplexity of the issues. In that sense, it is truly a guide, and not merely an introduction, tothis exciting new field.

Don Gerhardt, CEO, Medical Alley / MNBIO

i

ACKNOWLEDGEMENTS

The Minnesota Department of Employment and Economic Development and Lindquist &Vennum PLLP are pleased to make available this collaborative publication on biotechnologyfinance.

The following attorneys from Lindquist & Vennum’s Life Sciences Group contributed theirexpertise as authors of the specific sections listed below and, where noted, as editor of theGuide:

Stanley J. Duran, editor . . . . . . . . . . . . . . . . . . . . . . .Business Structures, Debt, Strategic AlliancesTerrance A. Costello . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Tax and Tax CreditsJonathan R. Flora . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Tax and Tax CreditsJoel H. Green . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .FDA Considerations, Strategic AlliancesRyan M. Hoch . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Business StructuresJoseph J. Humke . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Strategic AlliancesEldri L. Johnson . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Stem CellsMark D. Larsen . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Regulatory and Legal OversightJonathan B. Levy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Public Capital FormationBruce H. Little . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Intellectual PropertyJames A. Lodoen . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Distress StageMark S. McNeil . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .International, Import/ExportMarian J. Rainville . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Genetic EngineeringGretchen M. Randall . . . . . . . . . . . . . . . . . . . . .International, Import/Export, Genetic EngineeringBarbara Lano Rummel . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Strategic AlliancesRebecca B. Sandberg . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Private Capital FormationSheva J. Sanders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .ReimbursementJeffrey N. Saunders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Private Capital FormationGeorge H. Singer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Distress StageRobert E. Tunheim . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .SBIR/STTR ProgramsEdward J. Wegerson . . . . . . . . . . . . . . . . . . . . . . . . . .Management Equity Incentive CompensationBarbara J. Wood . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .FDA ConsiderationsJennifer L. Wuollet . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Cloning

Contributing editors at Lindquist & Vennum include Meghan M. Elliott, Thomas G. Lovett, IV,Barbara Lano Rummel, Christopher R. Sullivan, Wallace G. Hilke, Dennis M. O’Malley andGregory L. Wolsky. Other contributing staff at Lindquist & Vennum include Jill M. LaMere,Donna-lee Borovansky, Leslie A. Loar, and Kathleen M. Nydegger.

ii

Special thanks go to the following individuals who assisted in the writing or reviewing ofsections of this Guide or who provided important input on content and subject mattertreatment.

Dr. Lise W. DuranVice President and General Manager,Regenerative TechnologiesSurmodics, Inc.

Barbara CatherallSenior ManagerTauber & Balser

Madeline HarrisBusiness CounselorMinnesota Department ofEmployment and Economic Development

Thomas PareigatVice President,Compliance and Corporate CounselMarshall BankFirst Corporation

We appreciate everyone’s contributions and hard work.

Charles A. Schaffer, Ph.D.Minnesota Department of Employment and Economic Development

Publisher

Stanley J. DuranLindquist & Vennum

Editor

iii

Dr. Mark RobbinsVice President,Legal and Regulatory AffairsUpsher-Smith Laboratories, Inc.

Mitchell SugarmanDirector of Global ReimbursementMedtronic Vascular

Gene GoddardBioscience Industry SpecialistMinnesota Department of Employment and Economic Development

TABLE OF CONTENTS

FOREWORD ................................................................................................................................................i

ACKNOWLEDGMENTS..........................................................................................................................ii

I. INTRODUCTION................................................................................................................................1

A. The Purpose of This Guide ..........................................................................................................1

B. What is “Biotechnology?”............................................................................................................1

C. Legal Advice ..................................................................................................................................2

II. OVERVIEW OF BIOTECHNOLOGY FINANCE............................................................................3

A. The Nature of Finance ..................................................................................................................3

B. Industry Variables That Affect Biotechnology Finance ...........................................................4Lengthy Development Periods.............................................................................................4Reimbursement.......................................................................................................................5Ethical Consideratons ............................................................................................................5International Law and Import/Export Issues ....................................................................6Intellectual Property...............................................................................................................6Tax and Tax Credits ................................................................................................................7

III. CHOICE OF ENTITY AND CORPORATE LIFE CYCLES ............................................................8

A. Choice of Entity: Determining the Appropriate Business Structure .....................................8Types of Ownership – Overview..........................................................................................8Effect on Financing...............................................................................................................20

B. Corporate Life Cycles .................................................................................................................20Start Up Stage........................................................................................................................20Development Stage ..............................................................................................................20Early Commercialization Stage ..........................................................................................21Growth Stage.........................................................................................................................21Mature Stage .........................................................................................................................21Comment ...............................................................................................................................21

IV. BIOTECHNOLOGY FINANCE OPTIONS....................................................................................22

A. Introduction .................................................................................................................................22

B. Private Capital Formation..........................................................................................................22Introduction...........................................................................................................................22Securities and Registration Concerns ................................................................................22

Exemptions from Registration .....................................................................................23Integration.......................................................................................................................27Anti-fraud Considerations............................................................................................27

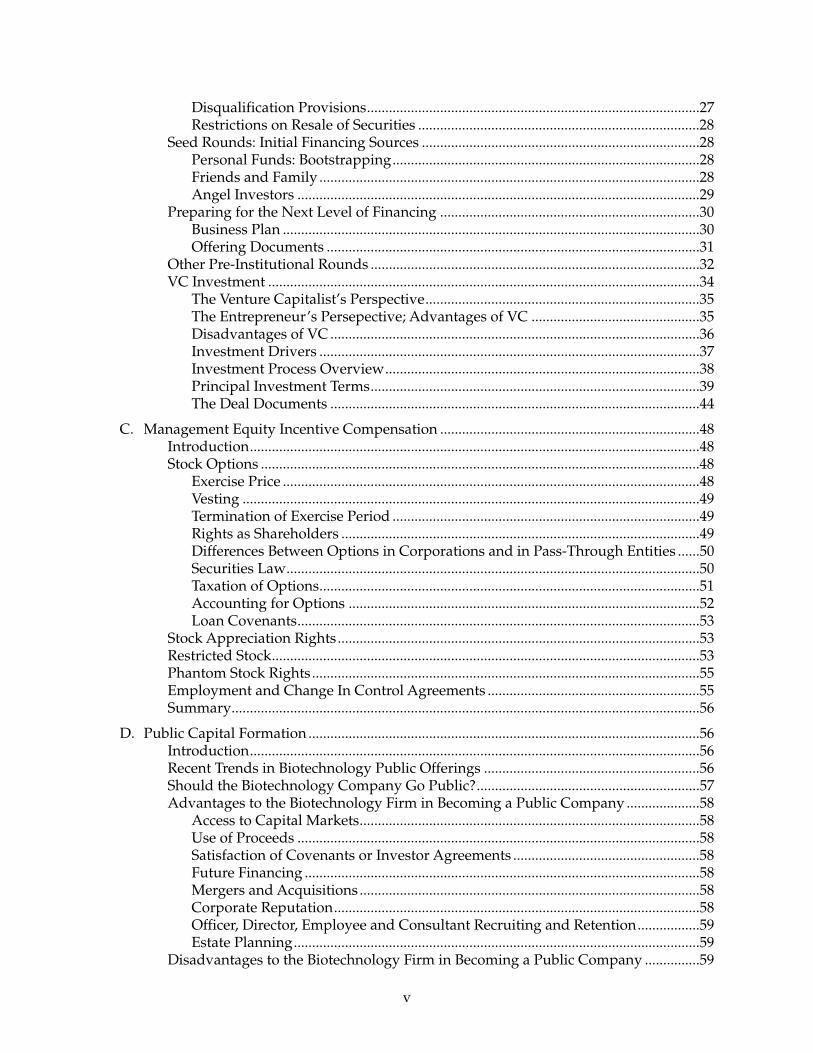

iv

Disqualification Provisions...........................................................................................27Restrictions on Resale of Securities .............................................................................28

Seed Rounds: Initial Financing Sources ............................................................................28Personal Funds: Bootstrapping....................................................................................28Friends and Family ........................................................................................................28Angel Investors ..............................................................................................................29

Preparing for the Next Level of Financing .......................................................................30Business Plan ..................................................................................................................30Offering Documents ......................................................................................................31

Other Pre-Institutional Rounds ..........................................................................................32VC Investment ......................................................................................................................34

The Venture Capitalist’s Perspective...........................................................................35The Entrepreneur’s Persepective; Advantages of VC ..............................................35Disadvantages of VC .....................................................................................................36Investment Drivers ........................................................................................................37Investment Process Overview......................................................................................38Principal Investment Terms..........................................................................................39The Deal Documents .....................................................................................................44

C. Management Equity Incentive Compensation .......................................................................48Introduction...........................................................................................................................48Stock Options ........................................................................................................................48

Exercise Price ..................................................................................................................48Vesting .............................................................................................................................49Termination of Exercise Period ....................................................................................49Rights as Shareholders ..................................................................................................49Differences Between Options in Corporations and in Pass-Through Entities ......50Securities Law.................................................................................................................50Taxation of Options........................................................................................................51Accounting for Options ................................................................................................52Loan Covenants..............................................................................................................53

Stock Appreciation Rights...................................................................................................53Restricted Stock.....................................................................................................................53Phantom Stock Rights..........................................................................................................55Employment and Change In Control Agreements ..........................................................55Summary................................................................................................................................56

D. Public Capital Formation ...........................................................................................................56Introduction...........................................................................................................................56Recent Trends in Biotechnology Public Offerings ...........................................................56Should the Biotechnology Company Go Public?.............................................................57Advantages to the Biotechnology Firm in Becoming a Public Company ....................58

Access to Capital Markets.............................................................................................58Use of Proceeds ..............................................................................................................58Satisfaction of Covenants or Investor Agreements ...................................................58Future Financing ............................................................................................................58Mergers and Acquisitions .............................................................................................58Corporate Reputation....................................................................................................58Officer, Director, Employee and Consultant Recruiting and Retention.................59Estate Planning...............................................................................................................59

Disadvantages to the Biotechnology Firm in Becoming a Public Company ...............59

v

Liability Risks and Regulatory Scrutiny.....................................................................59Potential for Loss of Control.........................................................................................59Loss of Confidentiality ..................................................................................................60Reporting and Ongoing Compliance ..........................................................................60Initial and Ongoing Expenses ......................................................................................60Pressure to Satisfy Shareholder Expectations ............................................................60Restrictions on Selling Existing Shareholders’ Shares..............................................60

Preparing the Biotechnology Firm for an Initial Public Offering ..................................61Company Readiness ......................................................................................................61Board of Directors ..........................................................................................................61Board Committees .........................................................................................................61State of Incorporation, Minnesota vs. Delaware .......................................................61Control Share Acquisition Act......................................................................................62Business Combination Act............................................................................................62Other Anti-takeover Measures.....................................................................................62

Underwriters .........................................................................................................................63Letter of Intent ................................................................................................................63Offering Size and Price..................................................................................................63Underwriting Commissions.........................................................................................63Underwriter Warrants ...................................................................................................63Reimbursement of Underwriters’ Expenses ..............................................................63Rights of Refusal ............................................................................................................64Lock-Up Agreements.....................................................................................................64Over-allotment Option..................................................................................................64

Offering Publicity .................................................................................................................64Preparing the Registration Statement................................................................................65

Due Diligence Investigation .........................................................................................65SEC Review.....................................................................................................................66Underwriters’ Syndication ...........................................................................................67

Listing Requirements ...........................................................................................................67Closing the Offering.............................................................................................................67Periodic Reporting Requirements ......................................................................................68

Form 10-K........................................................................................................................68Form 10-Q .......................................................................................................................68Form 8-K..........................................................................................................................68Management Discussion and Analysis.......................................................................69Exhibits ............................................................................................................................69Proxy Regulation............................................................................................................69Accurate Books and Records........................................................................................70

Sarbanes-Oxley .....................................................................................................................71Overview.........................................................................................................................71Section 302 Certifications..............................................................................................71Section 906 Criminal Certifications .............................................................................72Management’s Report on Internal Controls and Attestation by

Indepent Auditor .......................................................................................................72Increased Liability Risk and Forfeiture of Bonuses for Certain Restatements......73Audit Committees..........................................................................................................73Financial Experts............................................................................................................73Controls to Ensure Material Transactions are Disclosed..........................................73Off Balance Sheet Transactions ....................................................................................74

vi

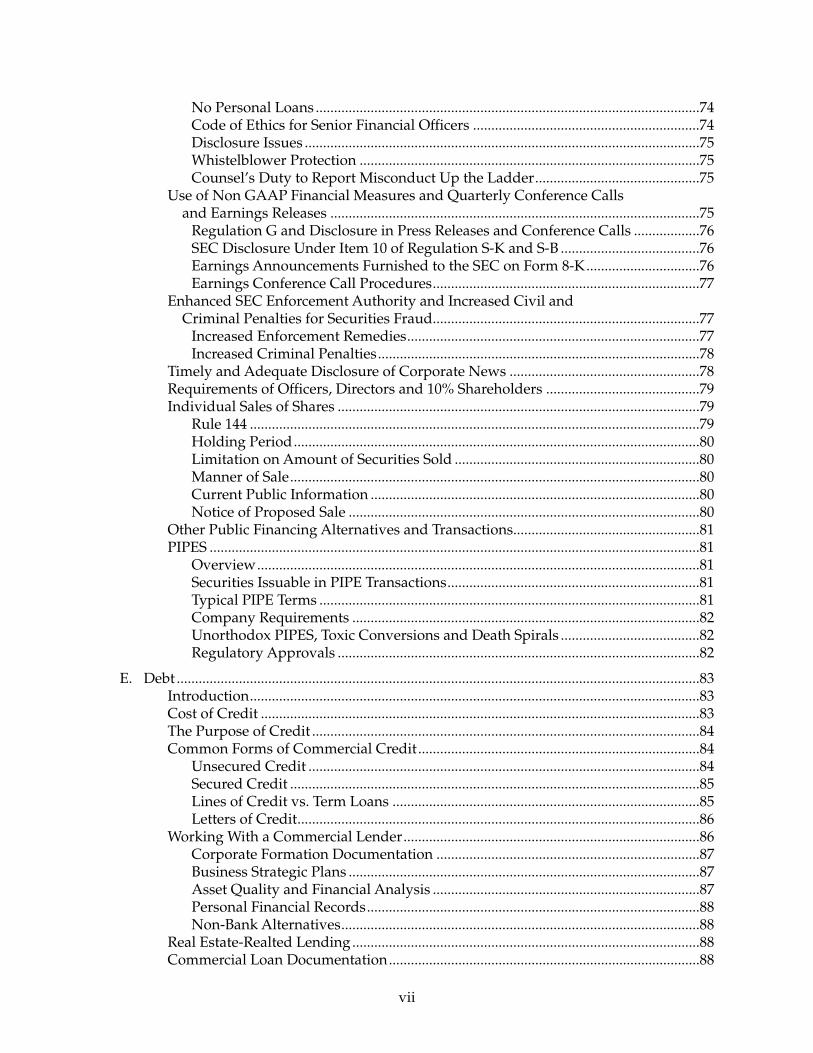

No Personal Loans .........................................................................................................74Code of Ethics for Senior Financial Officers ..............................................................74Disclosure Issues ............................................................................................................75Whistelblower Protection .............................................................................................75Counsel’s Duty to Report Misconduct Up the Ladder.............................................75

Use of Non GAAP Financial Measures and Quarterly Conference Callsand Earnings Releases .....................................................................................................75

Regulation G and Disclosure in Press Releases and Conference Calls ..................76SEC Disclosure Under Item 10 of Regulation S-K and S-B ......................................76Earnings Announcements Furnished to the SEC on Form 8-K...............................76Earnings Conference Call Procedures.........................................................................77

Enhanced SEC Enforcement Authority and Increased Civil andCriminal Penalties for Securities Fraud.........................................................................77

Increased Enforcement Remedies................................................................................77Increased Criminal Penalties........................................................................................78

Timely and Adequate Disclosure of Corporate News ....................................................78Requirements of Officers, Directors and 10% Shareholders ..........................................79Individual Sales of Shares ...................................................................................................79

Rule 144 ...........................................................................................................................79Holding Period...............................................................................................................80Limitation on Amount of Securities Sold ...................................................................80Manner of Sale................................................................................................................80Current Public Information ..........................................................................................80Notice of Proposed Sale ................................................................................................80

Other Public Financing Alternatives and Transactions...................................................81PIPES ......................................................................................................................................81

Overview.........................................................................................................................81Securities Issuable in PIPE Transactions.....................................................................81Typical PIPE Terms ........................................................................................................81Company Requirements ...............................................................................................82Unorthodox PIPES, Toxic Conversions and Death Spirals ......................................82Regulatory Approvals ...................................................................................................82

E. Debt ...............................................................................................................................................83Introduction...........................................................................................................................83Cost of Credit ........................................................................................................................83The Purpose of Credit ..........................................................................................................84Common Forms of Commercial Credit.............................................................................84

Unsecured Credit ...........................................................................................................84Secured Credit ................................................................................................................85Lines of Credit vs. Term Loans ....................................................................................85Letters of Credit..............................................................................................................86

Working With a Commercial Lender.................................................................................86Corporate Formation Documentation ........................................................................87Business Strategic Plans ................................................................................................87Asset Quality and Financial Analysis .........................................................................87Personal Financial Records...........................................................................................88Non-Bank Alternatives..................................................................................................88

Real Estate-Realted Lending...............................................................................................88Commercial Loan Documentation.....................................................................................88

vii

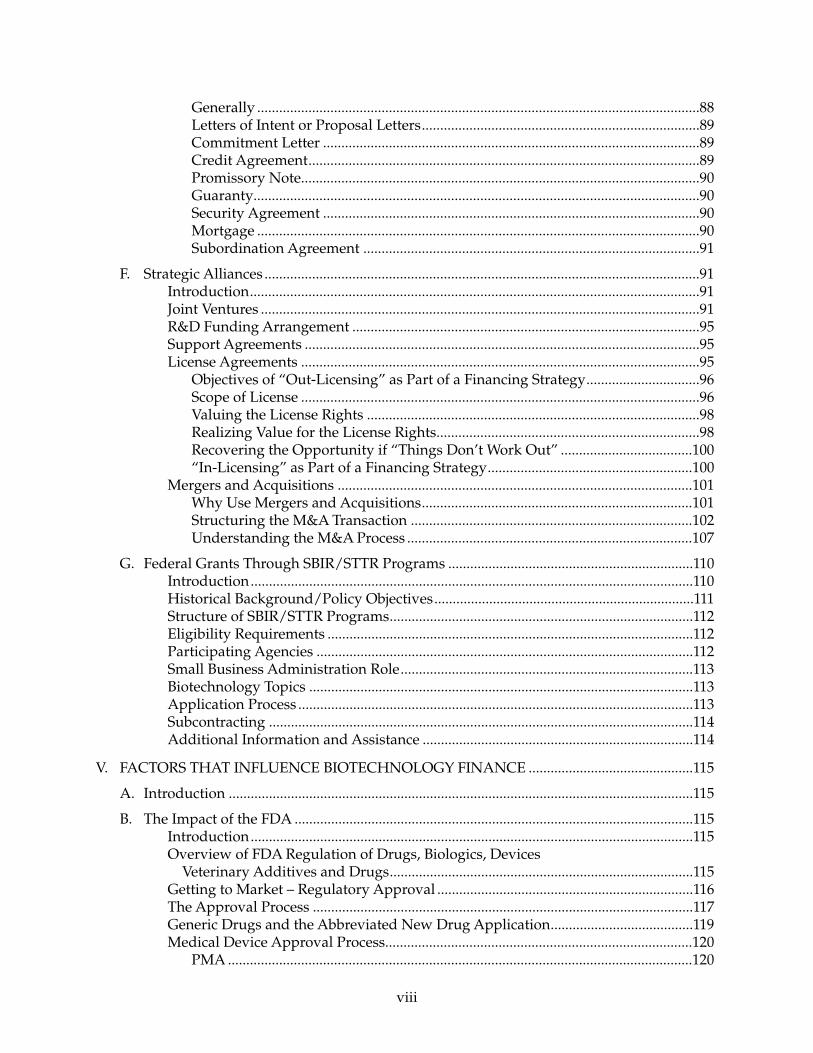

Generally .........................................................................................................................88Letters of Intent or Proposal Letters............................................................................89Commitment Letter .......................................................................................................89Credit Agreement...........................................................................................................89Promissory Note.............................................................................................................90Guaranty..........................................................................................................................90Security Agreement .......................................................................................................90Mortgage .........................................................................................................................90Subordination Agreement ............................................................................................91

F. Strategic Alliances .......................................................................................................................91Introduction...........................................................................................................................91Joint Ventures ........................................................................................................................91R&D Funding Arrangement ...............................................................................................95Support Agreements ............................................................................................................95License Agreements .............................................................................................................95

Objectives of “Out-Licensing” as Part of a Financing Strategy...............................96Scope of License .............................................................................................................96Valuing the License Rights ...........................................................................................98Realizing Value for the License Rights........................................................................98Recovering the Opportunity if “Things Don’t Work Out” ....................................100“In-Licensing” as Part of a Financing Strategy........................................................100

Mergers and Acquisitions .................................................................................................101Why Use Mergers and Acquisitions..........................................................................101Structuring the M&A Transaction .............................................................................102Understanding the M&A Process ..............................................................................107

G. Federal Grants Through SBIR/STTR Programs ...................................................................110Introduction.........................................................................................................................110Historical Background/Policy Objectives.......................................................................111Structure of SBIR/STTR Programs...................................................................................112Eligibility Requirements ....................................................................................................112Participating Agencies .......................................................................................................112Small Business Administration Role................................................................................113Biotechnology Topics .........................................................................................................113Application Process ............................................................................................................113Subcontracting ....................................................................................................................114Additional Information and Assistance ..........................................................................114

V. FACTORS THAT INFLUENCE BIOTECHNOLOGY FINANCE .............................................115

A. Introduction ...............................................................................................................................115

B. The Impact of the FDA .............................................................................................................115Introduction.........................................................................................................................115Overview of FDA Regulation of Drugs, Biologics, Devices

Veterinary Additives and Drugs...................................................................................115Getting to Market – Regulatory Approval ......................................................................116The Approval Process ........................................................................................................117Generic Drugs and the Abbreviated New Drug Application.......................................119Medical Device Approval Process....................................................................................120

PMA ...............................................................................................................................120

viii

510(k)..............................................................................................................................120Investigational Device Exemption.............................................................................120

Adverse Event Reporting to the FDA..............................................................................121Post-Marketing Adverse Drug Experience Reporting............................................121Medical Device Adverse Event Report .....................................................................121

C. Intellectual Property Rights.....................................................................................................121Patents ..................................................................................................................................123

Utility, Novelty and Non-Obviousness ....................................................................123Pharmaceutical Patents ...............................................................................................126Patents In Living Matter .............................................................................................128European Patents .........................................................................................................129Compulsory Licensing of Patents..............................................................................129Governmental Appropriation of Patents..................................................................130Research Exemption ....................................................................................................130Competitor Patents ......................................................................................................130

Copyrights ...........................................................................................................................131International Copyright ..............................................................................................132

Trademarks..........................................................................................................................132Trade Secrets........................................................................................................................133

D. Tax and Tax Credits...................................................................................................................134Introduction.........................................................................................................................134Tax Deductions and Credits..............................................................................................135

Product Development .................................................................................................135Exemptions Applicable to Intellectual Property .....................................................135Section 197 Intangibles ................................................................................................137Credit for Research and Development Expenses ....................................................137Orphan Drug Credit ....................................................................................................139General Business Credit Limitations.........................................................................139Credit for Nonconventional Fuel Production and Biomass ..................................139

Tax Issues Arising from Commercialization...................................................................140Taxable Dispositions....................................................................................................140Tax Free Dispositions...................................................................................................141

Tax Issues Arising from Exit Strategies ...........................................................................142Taxable Sales or Reorganizations of the Company .................................................142Joint Ventures................................................................................................................143Exit Strategies that Avoid Taxable Recognition of Gain or Loss ...........................143

E. U.S. Import/Export Considerations.......................................................................................144Imports into the U.S. ..........................................................................................................144Exports from the U.S. .........................................................................................................146

F. International Regulations and Barriers..................................................................................147Background .........................................................................................................................147International Structures for Legal Control or Standardization....................................149

European Directive 2001/18.......................................................................................149The Cartagena Protocol and Codex Guidelines ......................................................150

Country-Specific Implementations of the Cartagena Protocol ....................................151Japan ..............................................................................................................................152Mexico............................................................................................................................152Canada...........................................................................................................................152

ix

China..............................................................................................................................153Conclusion...........................................................................................................................154

G. Genetic Engineering .................................................................................................................155Introduction.........................................................................................................................155Laws, Regulations and Government Initiatives Affecting Finance.............................155

Federal Laws, Rules and Regulations .......................................................................156Federal Government Initiatives .................................................................................160State Laws, Rules and Regulations and Initiatives .................................................161Intellectual Property Laws and Issues ......................................................................163Legal Arrangements ....................................................................................................165

International Issues; Trade Barriers Affecting Finance .................................................165Overview.......................................................................................................................165Human Applications ...................................................................................................165Agricultural Applications ...........................................................................................166Conclusion ....................................................................................................................167

Ethical and Social Issues Affecting Finance....................................................................168Conclusion...........................................................................................................................170

H. Stem Cells...................................................................................................................................171Introduction.........................................................................................................................171Legal Restrictions on Stem Cell Research .......................................................................171

Restrictions in Minnesota ...........................................................................................171Federal Restrictions .....................................................................................................172Other States...................................................................................................................172

Public Funding of Stem Cell Research ............................................................................173Funding in Minnesota .................................................................................................173Federal Funding ...........................................................................................................174Other State Funding ....................................................................................................174

Private Funding ..................................................................................................................175Current Trends ....................................................................................................................175

I. Cloning .......................................................................................................................................176Introduction.........................................................................................................................176Primary Types of Cloning .................................................................................................176Cloning of Humans............................................................................................................176

Federal Regulation.......................................................................................................177Regulation by States ....................................................................................................177International Regulation .............................................................................................178Effect on Corporate Finance .......................................................................................178Agricultural...................................................................................................................178Plant Cloning ................................................................................................................178Non-Human Animal Cloning ....................................................................................179Use of Cloned Plant and Non-Human Animals......................................................179Effects on Corporate Finance .....................................................................................179

J. Reimbursement .........................................................................................................................179Introduction.........................................................................................................................179Overriding Considerations ...............................................................................................181Reimbursement Systems ...................................................................................................182Coding, Coverage & Payment ..........................................................................................183

Coding ...........................................................................................................................184

x

Coverage .......................................................................................................................184Payment.........................................................................................................................186

Communicating About Reimbursement .........................................................................186Conclusion...........................................................................................................................187

K. Regulatory and Law Enforcement Oversight of Biotechnology Firms .............................187Fraud and Abuse in the HHS Context.............................................................................187Health and Human Services Office of Inspector General.............................................188Statutory Bases for Liability and Exposure for FDA Fraud and Abuse......................189

False Statements and Fraudulent Claims .................................................................189Title 42 Crimes..............................................................................................................190Anti-Kickback Act........................................................................................................190Conspiracies and Schemes to Defraud .....................................................................191False Claims Act, Qui Tam Cases and Whistleblowers ...........................................191

Recent Developments Regarding Securities and Investor Fraud................................192Conclusion...........................................................................................................................193

L. Distress Stage.............................................................................................................................193Introduction.........................................................................................................................193Potential Liability for the Board of Directors .................................................................193

General ..........................................................................................................................193Zone of Insolvency.......................................................................................................194

Alternative Responses to Distress....................................................................................197Out-of-Court Restructuring........................................................................................197Receivership..................................................................................................................198Chapter 7 Bankruptcy .................................................................................................198Chapter 11 Bankruptcy................................................................................................199

Selected Bankruptcy Topics ..............................................................................................199Involuntary Bankruptcy Proceeding.........................................................................199Debtor-in-Possession ...................................................................................................200Automatic Stay .............................................................................................................200Proceeds from Inventory or Collateral Cannot be Used Without

Court Approval ........................................................................................................200Transactions Must Generally be in the Ordinary Course of Business..................201Preferential Transfers...................................................................................................201Fraudulent Transfers ...................................................................................................201Contract or Lease Terminations .................................................................................202Intellectual Property Licenses in Bankruptcy ..........................................................202

NOTES .....................................................................................................................................................205

GLOSSARY OF DEFINED TERMS......................................................................................................229

xi

I. INTRODUCTION

A. The Purpose of This Guide

This Guide provides a practical business and legal roadmap for understanding the financingoptions available to biotechnology companies and the circumstances in which these optionsare available. Biotechnology finance options are shaped not only by factors that affect allbusinesses, but also by a set of variables that apply specifically to this industry. In theoverview that follows, we discuss these variables and the manner in which they may affectthe financing decisions of the biotechnology company. Later in the Guide, we provide a moredetailed discussion of each of these specific factors. Depending on the circumstances acompany faces, some of these factors may be more important than others in charting asuccessful financing strategy.

The heart of the book, of course, is the section on the financing options available tobiotechnology companies and the related discussion of the requirements or restrictions thatapply to the use of each of those alternatives. Because many options are based on thestructure of the company and the company’s stage of development, we provide a detailedexplanation of the choice of business entities available to biotechnology companies in thechapter immediately preceding the finance section. We also provide a discussion of thevarious stages of the company’s life cycle. An understanding of a company’s stage ofdevelopment is critical to determining the most appropriate sources and methods offinancing.

B. What is “Biotechnology?”

Throughout this Guide, “biotechnology” is used to describe the science of developing andmanufacturing new products derived from living organisms or parts of living organisms(e.g., cells, genes or proteins). Evolving technologies in healthcare, however, are causing aconvergence of the pharmaceutical, medical device and biotechnology fields. The resultingnew product platforms (i.e., products resulting from combining cellular byproducts withdevices) are contemplated here as a segment within biotechnology.

In the glossary at the end of the Guide, we have labored to provide very specific definitionsfor the various scientific, industrial, governmental, financial, legal and other terms used inthe field.

1

C. Legal Advice

Although we have worked hard to summarize the most important issues affectingbiotechnology finance today, this Guide is only intended to be a general summary and doesnot constitute legal advice. Appropriate legal advice can only be rendered upon a specific setof facts. Lindquist & Vennum PLLP and the Minnesota Small Business Assistance Officecannot and do not assume responsibility for decisions based upon the information providedin this Guide. You should consult with legal counsel for specific advice regarding your situationbefore acting on any matter. As this Guide suggests, there are many issues to consider inbiotechnology finance.

To ensure compliance with requirements imposed by the U.S. Treasury, we inform you thatany U.S. federal tax advice contained in this Guide is not intended or written to be used, andcannot be used, for the purpose of avoiding penalties under the Internal Revenue Code of1986, as amended (“Code”), or promoting, marketing or recommending to another party anytransaction or matter that is contained in this Guide.

2

II. OVERVIEW OF BIOTECHNOLOGY FINANCE

A. The Nature of FinanceFinance is the science of money management.1 As a practical matter, biotechnologycompanies are primarily concerned with that aspect of financing that involves the allocationof resources. Financing is required to fund operations, develop products and successfullyenter the market.

Like corporate finance in general, biotechnology finance is fundamentally driven by therelationship between risk and return. Risk is defined as the degree of uncertainty of return onan asset while return is defined as the change in the value of a portfolio of assets over anevaluation period, including any distributions made from the portfolio during that period.2

The basic rule of finance is that the greater the business entity’s risk, the greater the returnrequired by investors.

There are many different types of business risk to consider and hundreds of variables thatmay affect these risks. The combination of these risks and variables define the overallrisk/return relationship for a given firm as determined by an investor. The various types ofrisk include, but are not limited to:

• Market Entry: How does the biotechnology firm overcome barriers to entry in theindustry, especially the competitive advantages already in place for existing firms?

• Technology: Will the new product or technology work? Can it be copied or reverseengineered? What factors will cause the technology to become obsolete? How does thebiotechnology company protect its intellectual property and not infringe on theintellectual property of others?

• Regulatory: What kind of government approvals will be required? How long willthese approvals take to obtain and at what cost?

• Market Acceptance: Can the new product be quickly commercialized in sufficientnumbers to penetrate the market? How long will it take?

• Competitive: What effect will competition have on profitability? What will it take interms of sales and revenue to secure and sustain market share?

• Interest Rate: Will interest rates remain stable or will there be wide fluctuations ininterest rates over time? What impact will rates and fluctuations have on operationsand on financing alternatives?

• Currency: Will fluctuations in foreign currency exchange rates affect the product inforeign markets? Will they have an impact on the cost of materials from foreign sources?

3

• Economic Structure: What choices need to be made regarding the organizational, legaland capital structure of the firm?

• Financing: Where will the next round of financing come from and in what form? Whatis the appropriate mix of debt and equity?

Each investor will analyze and consider each of the risk categories and the underlyingvariables to determine a required return. By understanding its investors’ risk/returnanalyses, a biotechnology firm can more successfully determine the most logical path tosecuring effective financing for its development and take appropriate steps to reduce real andperceived risks.

B. Industry Variables That Affect Biotechnology Finance

Several factors have a substantial effect on biotechnology finance. Many of these factorsconspire to drag out the timeline for the development of the company’s product and,consequently, have a negative impact on the ability to successfully obtain necessaryfinancing. Other factors have an impact on risk, early stage development and long-termgoals.

Lengthy Development Periods

Developing any new drug, biologic, or medical device for use in humans can be a long,arduous process. Some studies indicate that the creation of a single new drug may involvethe research and review of thousands of substances, a ten to fifteen year development andtesting process, and a total investment of several hundred million dollars.3,4 The timeline isdictated by the nature of developing complex technologies and the extensive regulatoryand research requirements that apply to these technologies.

The discovery of deoxyribonucleic acid (“DNA”), the molecule carrying the genetic codefor all forms of life, laid the foundation for revolutionary biotechnology advancements.Nevertheless, it took fifty years to develop the computing tools and techniques required tocomplete the mapping of the human genome in 2003. The complicated manufacture ofnew biotechnology products often requires the development of new technologiesinvolving ultra-clean production facilities, component assembly techniques and otherprocesses critical to the success of the product. The technology is often complicated and,by virtue of its originality, creativity and inventiveness, can take years to develop.

The regulatory process to bring new technologies to market also presents a dauntingchallenge to the biotechnology company. According to Standard & Poor’s, of the 10,000substances reviewed and considered for drug development, approximately 250 make it topreclinical laboratory and animal testing.5 Within five or more years, approximately five ofthose substances enter clinical testing on humans, a testing process involving threedistinct phases and several more years of study. A Phase I study to determine a drug’ssafety and level of dosage takes approximately one to two years and involves onehundred to two hundred human volunteers. Phase II involves several hundred human

4

volunteers and a two to three year process designed to identify potential side affects andthe drug’s efficacy. Phase III involves testing the drug on several hundred to severalthousand volunteers in the hopes of identifying potential adverse reactions and long termaffects of the drug. At the end of ten to fifteen years, the Food and Drug Administration(“FDA”) will finally approve one drug for the marketplace.

Having the most thorough biotechnology product approval and regulatory process in theworld adds significant time and expense to the commercial development of the product.Investors, of course, want to see returns as soon as possible. Typically, there is anexpectation of returns or the ability to employ a desirable exit strategy somewhere withinthree to seven years of investment. As a result, certain products with long developmentperiods may only be undertaken by large, well-established biotechnology andpharmaceutical companies or by partnering with these companies.

The promise and potential of these new products, however, appears to be overcominginvestment timidity. Research and development (“R&D”) spending in the biotechnologyindustry segment is among the highest of any U.S. industry group, and it is rising.According to an industry study by Standard & Poor ’s, R&D spending in thebiotechnology industry was $11.0 billion in 2001, $12.5 billion in 2002, $14.5 billion in 2003,and $10.2 billion through the first half of 2004.6 The extreme amount of money required toproduce one new product, coupled with a long development period, means investors willhave to tie up a substantial amount of capital for a longer period of time. The bottom lineis that returns on investment generated by biotechnology companies will need to behigher than those generated from other investments or investors will opt for the otherinvestments.

Reimbursement

The success of many biotechnology products will depend on the ability of the company tosecure payment for the product from the insurance companies, health plans andgovernmental health care programs that provide coverage to the consumer. The ability tosell some products is dependent on an assurance that adequate reimbursement will beavailable. Obtaining reimbursement can be a time-consuming process. A plan to obtainreimbursement should be established as early as possible for any product that will bedependent on revenue from reimbursement.

Ethical Considerations

In the last 50 years, massive strides in technology have caused an explosion in thedevelopment of biotechnology products. The phenomenal advancement in knowledge hasalso led to deep fears about that knowledge, its potential misuse and ethicalconsiderations scarcely imaginable in the middle of the twentieth century.

One of several examples involves a new form of genetically modified corn, or Bt corn.7

This new grain was engineered with a bacterial code that enhanced its ability to repel cornborers and other pests. Sowing Bt corn has the added benefit of reducing the use and

5

amounts of harmful pesticides required to protect other corn hybrids. But Bt corn hasraised genuine practical and philosophical questions such as what are the effects onhumans and the environment of products made with Bt corn? These and similar concernshave led many countries to ban the use and production of genetically modified (“GM”)agricultural products.

Stem cell research, cloning and similar cutting edge technologies raise promise, hope andmany questions. Some of these questions have led to the development of new laws andregulations governing the use of these technologies, and altering the kinds ofbiotechnology products that can be produced using these technologies. Fears over theoutcome of legislative or regulatory restrictions can have a negative impact on securingfinancing.

International Law and Import/Export Issues

It may be necessary for a company to introduce a biotechnology product to the globalmarket because of the nature of the product or to generate a sufficient base of revenue tosupport the costs of development. If so, the company will find itself dealing with a wholenew set of challenges. Going into foreign jurisdictions increases the complexity of productdevelopment and distribution, particularly in the area of GM foods. International treatiesbetween countries, European Union (“EU”) directives, standards set by the UnitedNations, country-specific regulations, trade policy, and protectionism all converge tocreate a complex web of rules for the biotechnology exporter. The governing principle, ifthere is one, is that biotechnology products will be examined on a case-by-case basis byeach country to determine if there is a foreseeable threat to human health, the food supply,or the environment. If a company must be in these markets, financing will be required toendure product testing, multi-agency regulation, and cultural biases againstbiotechnology, particularly GM foods. Similar concerns arise over importingbiotechnology products into the U.S.

Intellectual Property

Intellectual property is fundamental to the financing strategy of a biotechnology company.Among a company’s most valuable assets are the right and ability to develop and exploitexisting or new inventions, trade secrets, proprietary information and know-how. Todevelop an effective financing strategy, a biotechnology entrepreneur must consider theintellectual property it might develop, acquire, or license. It is equally important for thecompany to develop a thorough knowledge of the competing intellectual property that isor may be owned or under development by other companies or entrepreneurs in the samefield. Additionally, before venturing into a discrete area of biotechnology, a company mustdevelop a thorough understanding of government regulations, scholastic research, andinformation in the worldwide public domain that may have an effect on contemplateddevelopments. The value of existing or proposed intellectual property is contingent bothupon the availability of legal protection and upon the immediate and long-term demandfor new developments in that area of biotechnology.

6

Tax and Tax Credits

The tax issues that are relevant to a biotechnology company will typically depend on thestage at which the company is positioned in its life cycle. For example, during its earlyyears, a biotechnology company is likely to make substantial R&D expenditures before itgenerates significant revenue. The primary tax issues it faces during this period involveidentifying and exploiting available tax deductions and tax credits. The Code provides avariety of incentives that may apply to R&D expenditures in the form of both taxdeductions and tax credits.

As a biotechnology company progresses in its life cycle, significant tax issues may arise asit commercializes and exploits the patents and technology it develops and owns. Theserevenue-generating operations will produce another set of tax issues. For example, thedecision whether to license or sell a patent may produce fundamentally different taxconsequences.

The exit strategy to be used by the company’s investors will raise yet another set of taxissues and potential tax liabilities. For example, there are a variety of exit strategiesavailable to investors, ranging from an outright sale of technology to a tax-freereorganization. Each alternative generates different tax consequences, which in turn willhave a significant economic impact on the investors.

7

III. CHOICE OF ENTITY AND CORPORATE LIFE CYCLES

A. Choice of Entity: Determining the Appropriate Business Structure

One of the first strategic financial decisions of a biotechnology business is selecting the mostappropriate form of business structure. This choice of entity will affect: how the organizationand its owners are taxed; how the organization and the owners may be exposed to or maylimit their liability to others; and the ability for the organization to raise capital. Complicatingthe choice of entity decision is the fact that the optimal form for a start-up stage companymay not be the optimal form of entity when the business becomes a mature stage company.Therefore, business owners must consider both the current and the long-term needs of theorganization. Altering the form of entity under which a business operates is sometimesdifficult from a governance and tax perspective, and sometimes may be accomplished understate law only through a merger or conversion. Consequently, the decision regarding theform of entity must be reviewed carefully and undertaken only after a thorough examinationof the short and long term plans of the business.

Types of Ownership – Overview

The primary types of ownership structure include sole proprietorship, generalpartnership, limited partnership, limited liability partnership, limited liability company,and corporation (both C corporation and S corporation). Each type varies in terms of theformalities required to form the organization, the extent of liability of the owners toothers, management and governance requirements, taxation of the organization and itsowners and available exit strategies.

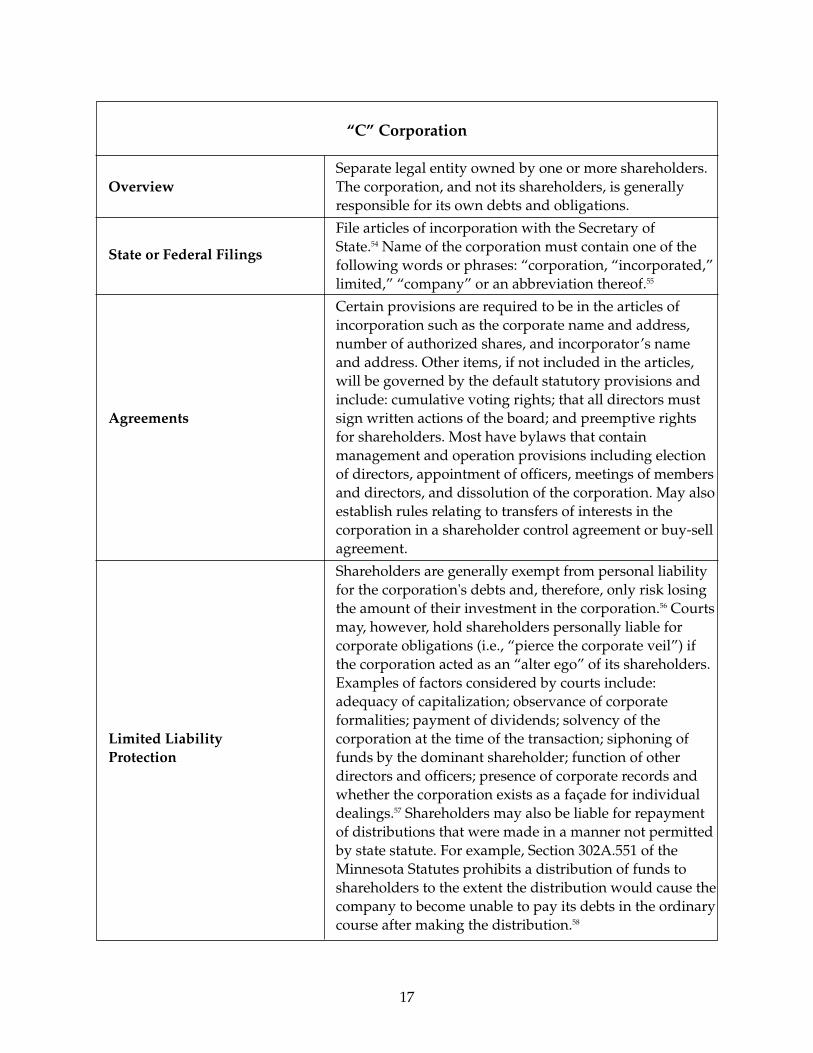

The most basic form of business ownership available is the sole proprietorship, which is abusiness operation owned and managed by a single individual. Very few formalities arerequired, but the owner is personally responsible for the liabilities of the organization.Similarly, a general partnership can be formed relatively informally between two or morepersons intending to carry on a business for a profit. The owners of a general partnershipare each personally liable for all obligations of the partnership. In order to limit potentialliability of the owners, business owners would need to consider forming a limitedpartnership (which imposes liability obligations on the general partners but limits theliability of the limited partners), a limited liability partnership (which extends the liabilityprotection to each member of the partnership), a corporation or a limited liabilitycompany. A corporation is a separate entity from its owners. Consequently, the owners aregenerally insulated from liability beyond the capital contributions made to purchaseshares of stock of the corporation. The corporation as a separate entity faces additional

8

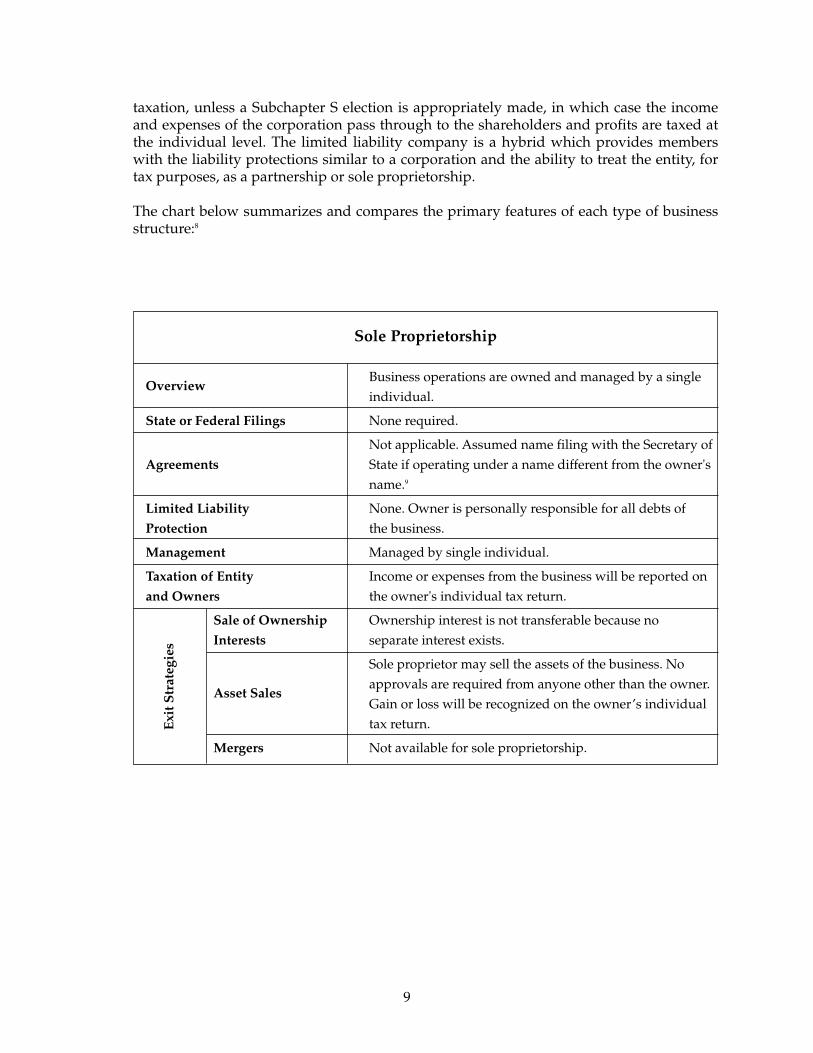

Sole Proprietorship

Business operations are owned and managed by a singleOverview

individual.

State or Federal Filings None required.

Not applicable. Assumed name filing with the Secretary of Agreements State if operating under a name different from the owner's

name.9

Limited Liability None. Owner is personally responsible for all debts of Protection the business.

Management Managed by single individual.

Taxation of Entity Income or expenses from the business will be reported onand Owners the owner's individual tax return.

Sale of Ownership Ownership interest is not transferable because noInterests separate interest exists.

Sole proprietor may sell the assets of the business. No approvals are required from anyone other than the owner.

Asset SalesGain or loss will be recognized on the owner’s individual tax return.

Mergers Not available for sole proprietorship.

taxation, unless a Subchapter S election is appropriately made, in which case the incomeand expenses of the corporation pass through to the shareholders and profits are taxed atthe individual level. The limited liability company is a hybrid which provides memberswith the liability protections similar to a corporation and the ability to treat the entity, fortax purposes, as a partnership or sole proprietorship.

The chart below summarizes and compares the primary features of each type of businessstructure:8

9

Exi

t Str

ateg

ies

10

General Partnership

Formed upon an “association of two or more persons to carry on as co-owners a business for profit.”10 Because no Overviewwritten agreement is required, a general partnership could be formed unintentionally.

None required. Assumed name filing must be made with State or Federal Filings Secretary of State if partnership operates under any name

other than names of individual partners.11

Many partnerships enter into a written partnership agreement that addresses issues such as: the allocation anddistribution of profits and losses; the duties,

Agreements responsibilities and activities of the managing partner and the other partners; the capital contributions of each partner; the methods for resolving management disputes; and the basis for removing a partner.

None. Owners are each personally liable for all obligationsof the partnership.12 The potential liability of each partner Limited Liabilityis unlimited, regardless of the partner's investment in the Protectionpartnership or whether the partner was involved in, or consented to, the events giving rise to the liability.

Decentralized management. The partners are entitled to make decisions on matters affecting partnership business (generally by majority vote, but sometimes, unanimous approval is required).13 The right to share in

Management decision-making process can make the management of the partnership cumbersome. As a result, the partnership agreement may centralize some management decisions in a management committee or other smaller group of partners.

Partnership pays no federal income tax. The income or lossof the partnership is included on each partner's tax return and each partner is required to pay the associated taxes Taxation of Entityregardless of whether distributions have been made to the and Ownerspartner. Partners are entitled to an equal profit distributionunless the written partnership agreement revises the distribution amounts.

11

A partner is entitled to transfer his or her share of the partnership’s profits and losses and his or her right to receive distributions.14 The right to participate in the governance of the partnership and certain other rights are not transferable.15 The exchange or termination of interests in a partnership may cause the partnership to dissolve. The transfer of a partner’s financial rights will not Sale of Ownershipgenerally trigger dissolution of the partnership under stateInterestslaw.16 Partnership agreements generally contain provisions relating to the transfer of interests that may supersede these statutory provisions, including votes required for transfer and providing other partners a right to purchase the interests prior to transfer. When a partner sells his or her ownership interest, he or she will often be required to recognize gain or loss on the sale.

Subject to contrary provisions in a partnership agreement,property held may be transferred to a third party bymeans of an instrument of transfer executed by any partner.17 If the property is partnership property held in the

Asset Sales name of an individual partner, that person generally must assign the property.18 Gains and losses on sales of assets at the partnership level will generally not be subject to tax at the entity level, but will be passed through to the partners or members for recognition.

A general partnership may engage in a merger with another general partnership, a limited liability partnership or a limited partnership.19 In order to effect the merger, the parties must enter into a plan of merger that, among other things, sets forth the terms of the merger. The merger plan

Mergers must be approved by all parties to the agreement, and requires unanimous agreement of the partners or other vote as required under the partnership agreement.20

Following the merger, the surviving partnership must file a statement of merger with the Secretary of State setting forth certain terms of the merger.21

Exi

t Str

ateg

ies

12

Limited Partnership

Consists of two type of partners: general partners and Overviewlimited partners.

File a certificate of limited partnership with the Secretary of State.22 Name must contain the phrase “limited

State or Federal Filings partnership” or the abbreviations “LP” or “L.P.”23

Required to make an annual filing with the Secretary of State.24

Agreements Same as General Partnership.

Partial. General partners are personally responsible for all debts and obligations of the partnership,25 unless they limit their exposure through a “limited liability limited partnership.” Limited partners do not have the right or Limited Liabilitypower to act for or bind the limited partnership26 and Protectionlimited partners are not personally responsible for the obligations of the partnership even if the limited partner participates in management and control of the partnership.27

General partners are vested with the management responsibility and control and if there is more than one general partner, the decisions are made by a majority vote of the general partners. A unanimous vote of all partners

Management is required to amend the partnership agreement, amend the certificate of limited partnership and to sell or dispose of substantially all of the partnership assets unless the limited partnership agreement revises these requirements.28

Limited partnership pays no federal income tax. The income or loss of the partnership is included on each partner's tax return and each partner is required to pay the Taxation of Entityassociated taxes, regardless of whether distributions have and Ownersbeen made to the partner. Partners are entitled to receive distributions based upon the value of their respective contributions to the entity.29

Partners in a limited partnership may only transfer their rights to receive distributions.30 This transfer will not constitute an event that would disassociate the partner or cause dissolution of the partnership under state law.31

However, a transferee’s rights need not be recognized by the limited partnership until the limited partnership receives notice of the transfer. A person receiving an interest in the limited partnership may obtain full rights of

Sale of Ownership a limited partner only after receiving consent of all Interests partners.32 Persons acquiring partnership interests may