4965 FIM-Session 2

47

Financial Institutions and Markets Session 2

-

Upload

nist-odisha -

Category

Documents

-

view

2 -

download

0

Transcript of 4965 FIM-Session 2

Financial Institutions and Markets

Session 2

• Financial Markets – overview

2

3

Financial Markets• What is a financial market?

– A financial market is a market where financial assets are traded.

• Although the existence of financial market is not a necessary condition for the creation and exchange of a financial asset, in most economies financial assets are created and subsequently traded within some kind of organized financial market structure.

4

Principal Function of financial markets

• The main function ( similar to that we pointed out for a financial asset, but on an aggregate scale)– To transfer surplus funds from the ‘savers’( or deficit spending units in the economy) to the ‘borrowers’ (or surplus spending units in the economy) through the direct finance route.

– Objective : to make necessary funds available for investment in productive assets in the economy

5

Financial markets : Other functions

• The interactions of buyers and sellers in a financial market determine the price of the traded asset. This is called the price discovery-process.

• Secondly, financial markets provide a mechanism for an investor to sell a financial asset. Because of this feature, it is said that a financial market offers liquidity.– In the absence of liquidity, the owner will be forced to hold a debt instrument until it matures and an equity instrument until the company is either voluntarily or involuntarily liquidated.

6

Financial markets : Other functions .. Contd..

• Thirdly, a financial market reduces the search and Information costs of transacting. – Search costs represent explicit costs, such as the money spent to advertise the desire to sell or purchase a financial asset, and implicit costs, such as the value of time spent in locating a counterparty. The presence of some form of organized financial market reduces search costs.

– Information costs are those entailed with assessing the Investment merits of a financial asset; that is, the amount and the likelihood of the cash flow expected- to be generated.

7

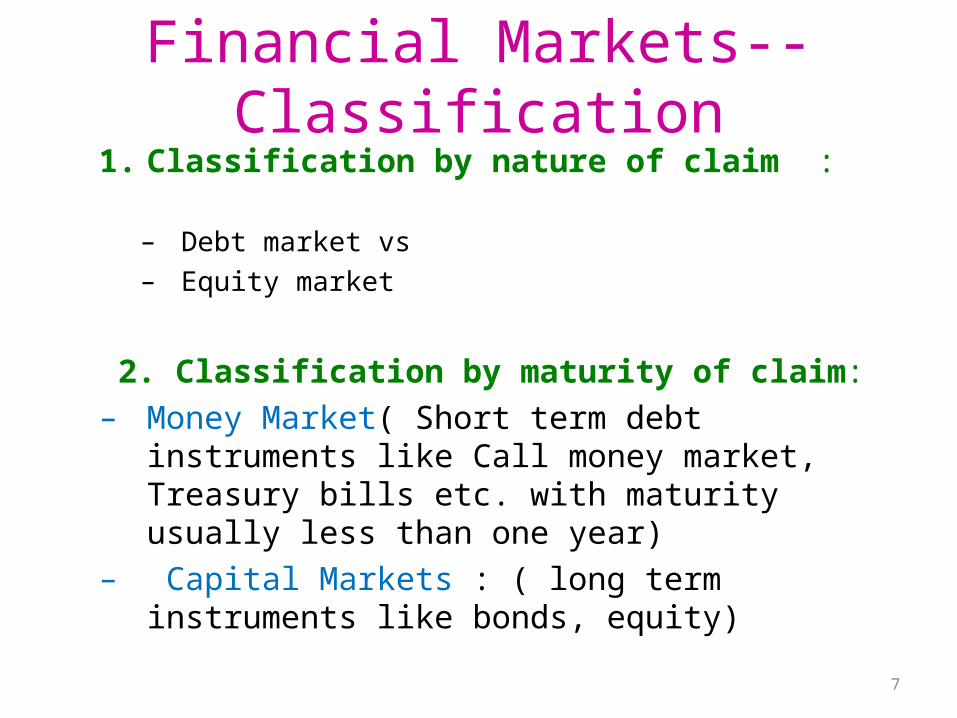

Financial Markets--Classification

1. Classification by nature of claim : – Debt market vs – Equity market

2. Classification by maturity of claim: – Money Market( Short term debt

instruments like Call money market, Treasury bills etc. with maturity usually less than one year)

– Capital Markets : ( long term instruments like bonds, equity)

8

Financial Markets—Classification contd..

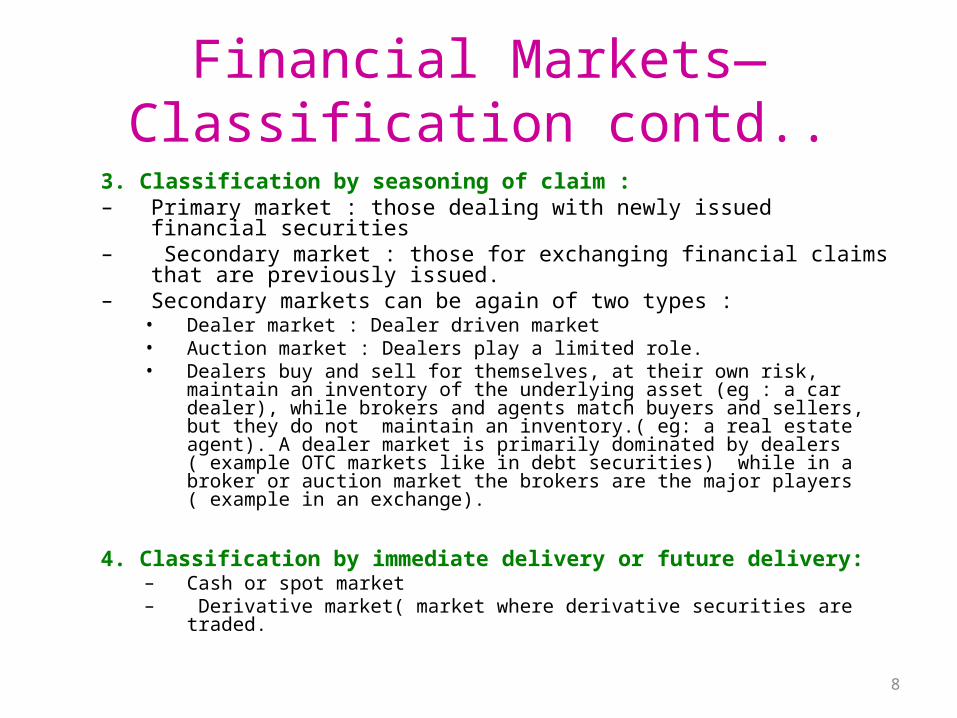

3. Classification by seasoning of claim : – Primary market : those dealing with newly issued

financial securities– Secondary market : those for exchanging financial claims

that are previously issued.– Secondary markets can be again of two types :

• Dealer market : Dealer driven market• Auction market : Dealers play a limited role.• Dealers buy and sell for themselves, at their own risk,

maintain an inventory of the underlying asset (eg : a car dealer), while brokers and agents match buyers and sellers, but they do not maintain an inventory.( eg: a real estate agent). A dealer market is primarily dominated by dealers ( example OTC markets like in debt securities) while in a broker or auction market the brokers are the major players ( example in an exchange).

4. Classification by immediate delivery or future delivery:– Cash or spot market – Derivative market( market where derivative securities are

traded.

• Intermediaries

9

10

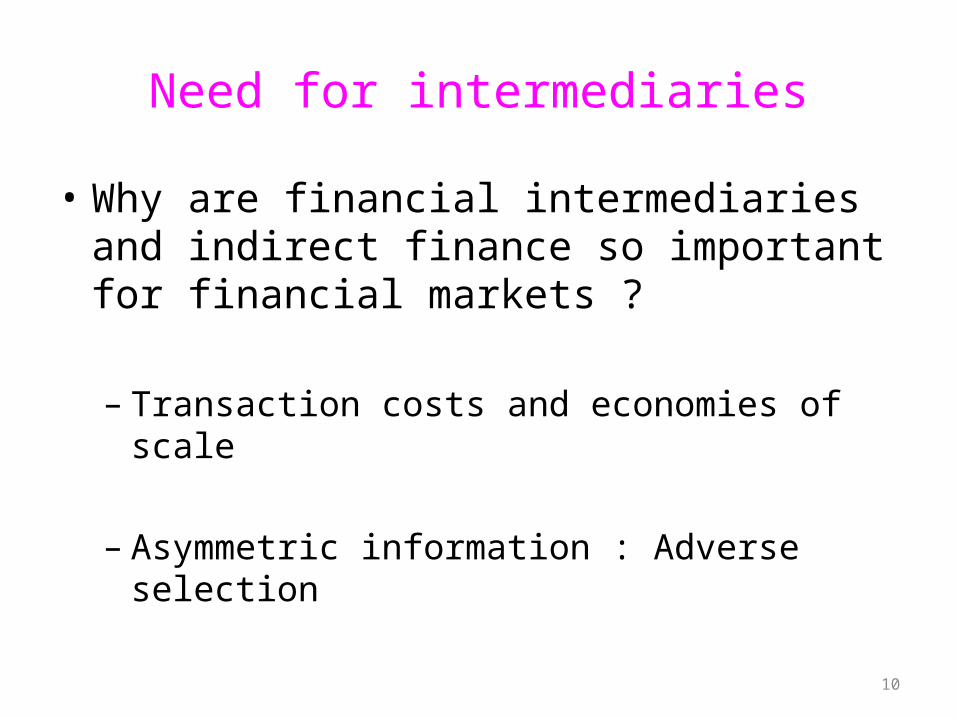

Need for intermediaries

• Why are financial intermediaries and indirect finance so important for financial markets ?

– Transaction costs and economies of scale

– Asymmetric information : Adverse selection

11

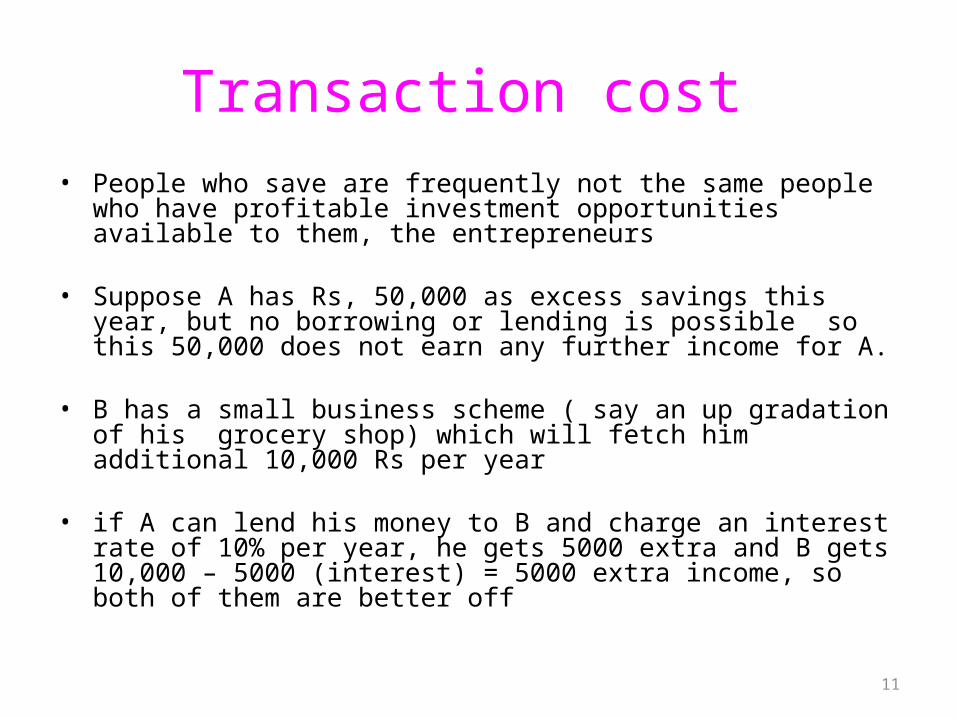

Transaction cost • People who save are frequently not the same people

who have profitable investment opportunities available to them, the entrepreneurs

• Suppose A has Rs, 50,000 as excess savings this year, but no borrowing or lending is possible so this 50,000 does not earn any further income for A.

• B has a small business scheme ( say an up gradation of his grocery shop) which will fetch him additional 10,000 Rs per year

• if A can lend his money to B and charge an interest rate of 10% per year, he gets 5000 extra and B gets 10,000 – 5000 (interest) = 5000 extra income, so both of them are better off

12

Transaction costs… contd…

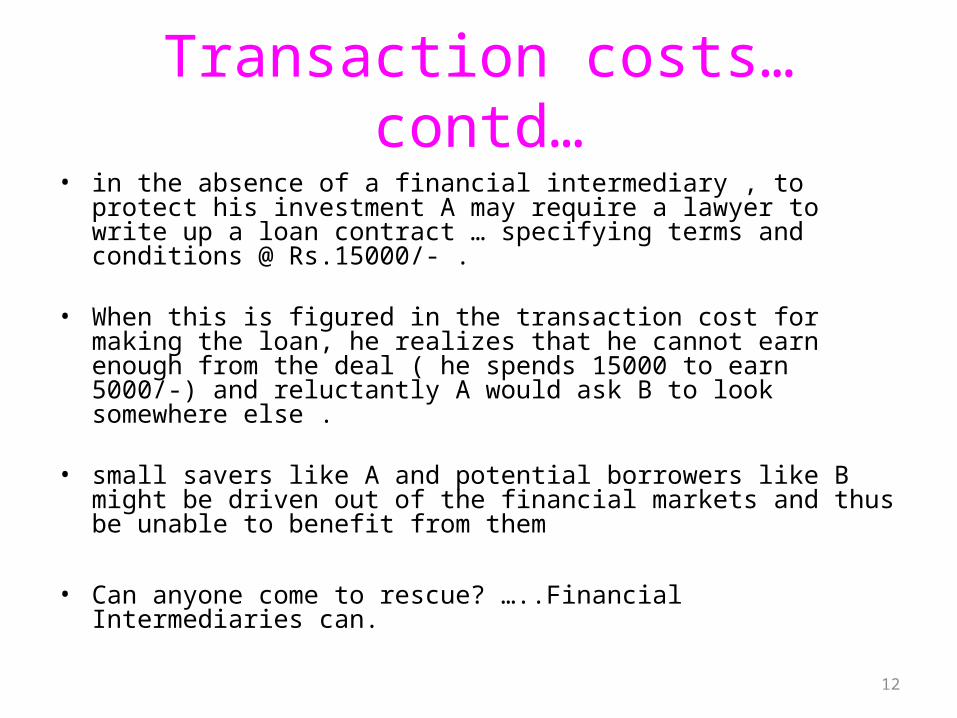

• in the absence of a financial intermediary , to protect his investment A may require a lawyer to write up a loan contract … specifying terms and conditions @ Rs.15000/- .

• When this is figured in the transaction cost for

making the loan, he realizes that he cannot earn enough from the deal ( he spends 15000 to earn 5000/-) and reluctantly A would ask B to look somewhere else .

• small savers like A and potential borrowers like B might be driven out of the financial markets and thus be unable to benefit from them

• Can anyone come to rescue? …..Financial Intermediaries can.

13

Transaction costs.. Contd..

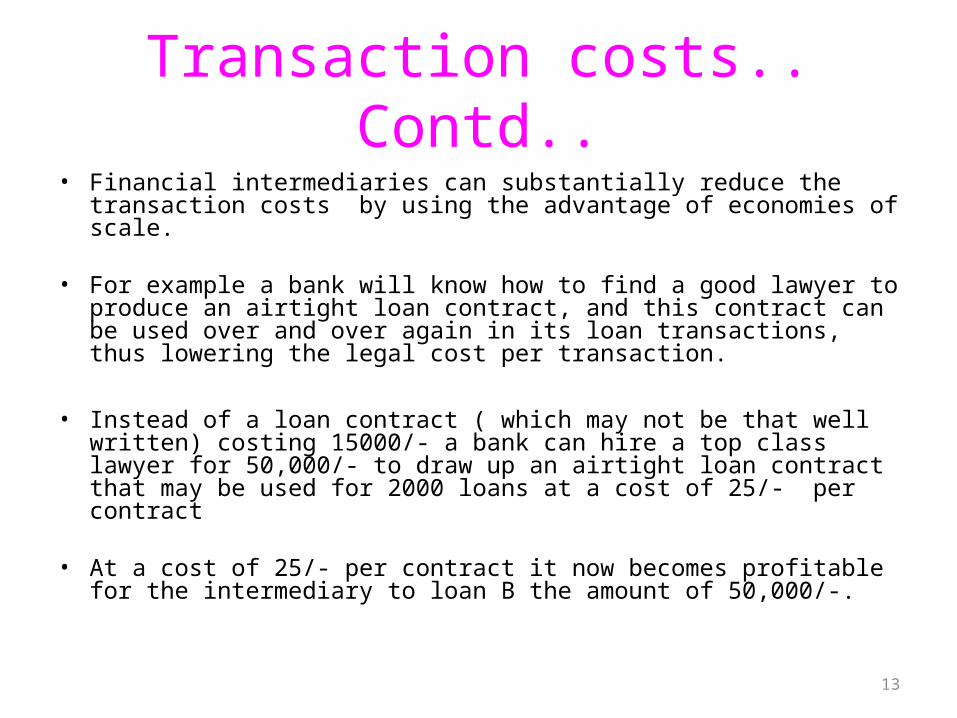

• Financial intermediaries can substantially reduce the transaction costs by using the advantage of economies of scale.

• For example a bank will know how to find a good lawyer to produce an airtight loan contract, and this contract can be used over and over again in its loan transactions, thus lowering the legal cost per transaction.

• Instead of a loan contract ( which may not be that well written) costing 15000/- a bank can hire a top class lawyer for 50,000/- to draw up an airtight loan contract that may be used for 2000 loans at a cost of 25/- per contract

• At a cost of 25/- per contract it now becomes profitable for the intermediary to loan B the amount of 50,000/-.

14

Asymmetric information : adverse selection

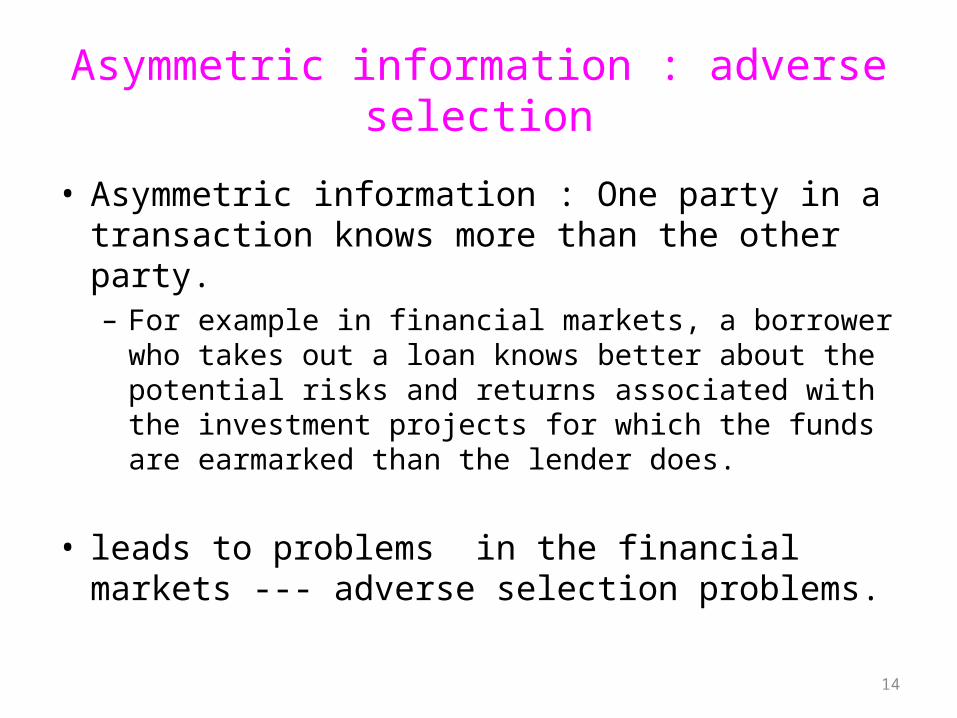

• Asymmetric information : One party in a transaction knows more than the other party. – For example in financial markets, a borrower who takes out a loan knows better about the potential risks and returns associated with the investment projects for which the funds are earmarked than the lender does.

• leads to problems in the financial markets --- adverse selection problems.

15

Adverse selection.. Problem of lemons

• ‘Problem of lemons’– first noted by George Akerlof(1970)— “The market for ‘lemons’: quality, uncertainty and the market mechanism,”– Quarterly Journal of Economics, Vol. 84.

• Lemon’s problem is a market problem caused by information asymmetry leading to failure of the market.

• Popular example can be found with the used car market, insurance companies issuing new policies etc.

16

Problem of lemons—contd..

• Example 1) Used car market : • Suppose you want to purchase an old car --there

are 10 cars on display-5-bad and 5 good. You are not an expert and cannot distinguish between good and bad cars (the only information you are provided is say year of manufacture).

• Suppose the good cars can sell at a min. price of 100k and the bad cars at a min price of 40 k.

• But you will have to quote-How do you quote?

• Now if you want to be overcautious what is your most natural quote?

• quote an average price of say 70 k---• what will happen?

17

Problem of lemons—contd..

• All the good cars will go away and you will be left with only the bad cars in the market----these are the "Lemons "----

• now if you buy one with 70k you will lose out-you do that - get cheated and want to take your hands off the market in future.

• may eventually lead to a complete breakdown of the market.

18

Problem of lemons—contd..

Example 2) Life Insurance :• Suppose that there are two groups among the population, smokers

and non-smokers. • An insurer selling life policies can't tell which is which, so

they set premium at the average level and each pay the same premiums, while people buying insurance know whether they are smokers or not,

• Non-smokers, on the average, are more likely to live longer, while smokers, on the average, are more likely to die younger. So the life policy is a better buy for the smokers' beneficiaries.

• Premiums set according to average risk will not be sufficient to cover claims because buyers will be selected for higher risk (buyers carrying less risk are less likely to purchase insurance.)

• So the insurer end up selecting only the ‘lemons’ as its clients. May lead to failure of the business and drive the insurers out of the market completely.

• If the insurance company knew who smokes and who doesn't, it could set rates differently for each group and there would be no adverse selection

19

Problem of lemons—contd..

• Lemons Problem is also important for corporate finance.

• If investors cannot observe the value of the firms before they buy them then they would be willing to pay only an average price for the equity of the firms.

• Given the price is average, selling equity on the market will be

much more attractive to owners of bad firms than to owners of good firms.

• So the true value of the firms that are actually offered on the market will be below the average price commanded.

• This implies that the investors will be generally cheated and should be suspicious that if they are offered equity then it must mean that the firm’s value is more likely to be below the average.

• Hence the investors will no longer be there in the market.

20

Problem of lemons—contd..

• What is the solution ?• Going back to the old car example—

• Get an expert who somehow knows which old car is good and which one is bad.

• He gives his opinion using his expertise ,which one to buy may be against some fee.

• Then you can confidently buy the cars. Both the buyers and the sellers in the market are benefited.

• In case of financial markets ..this expert is the intermediary.

• Example: banks with their credit departments, Credit rating agencies( good at distinguishing between good and bad investment opportunities), investment banks etc.

21

Other roles played by the intermediary

1. Production of information : • Example: • good bank has given money to a

company implies company must be in good position ,o/w they would not have touched it.

22

Other Roles played by the intermediary- contd..

2. Size Intermediation : • Example : I have 100,00 Rs and I want to invest

in Reliance industries But Reliance won’t take it from me due to the reason that they are dealing in crores of Rs. and they don't want to deal with such small bits and pieces. Intermediaries pool many such bits and pieces and may invest the entire sum ( indirect finance route) which could be acceptable to RIL.

3. Temporal Intermediation : • Matching of time • perhaps when I want the money the company may not

be in a position to pay but if I channelise through an intermediary and thousands of others do likewise they may be able to match ( assuming incremental deposit > incremental withdrawal )

23

Role played by the intermediary- contd..

4.Monitoring Difficulty : • Say even if a company like Reliance is ready to take my

small amount of money it is not possible for me to monitor their activities which can be easily done by an intermediary ( say the credit department of a bank)

• A large intermediary is also likely to have much more bargaining power than a small investor in enforcing certain covenants for the company.

5. Risk Intermediation: • With my small money I will not be able to enjoy the

benefits of diversification and reduce the risk of my portfolio. But with an intermediary in place (mutual fund for example ) I can probably buy the units of the fund which with its huge pool of money from many investors like me can ensure considerable diversification----thus I enjoy the benefits of diversification without having to invest a lot of money.

24

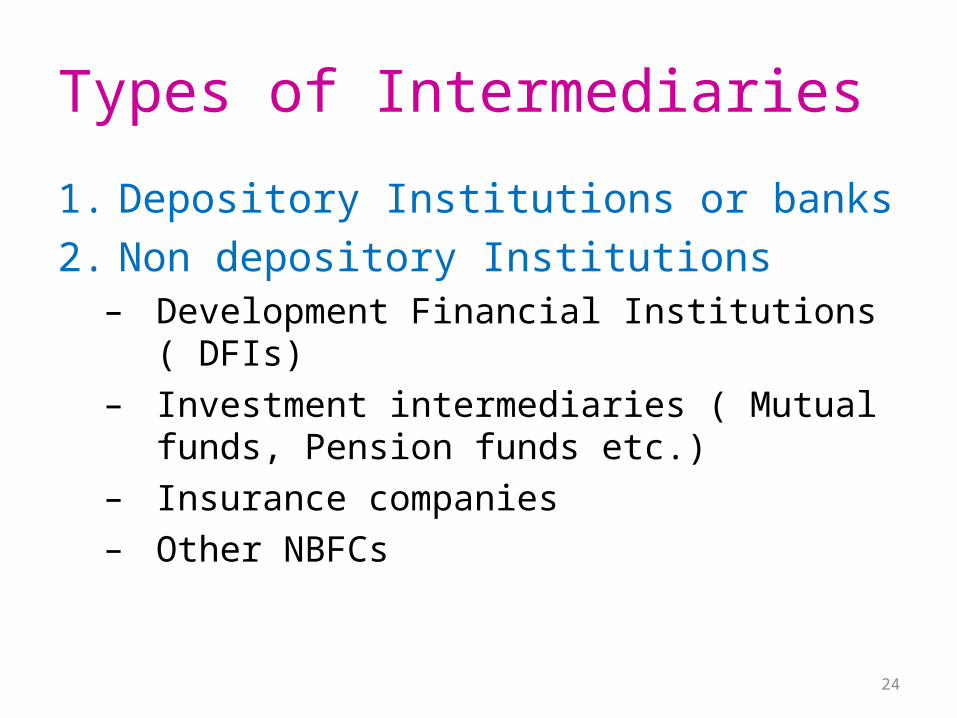

Types of Intermediaries 1. Depository Institutions or banks 2. Non depository Institutions

– Development Financial Institutions ( DFIs)

– Investment intermediaries ( Mutual funds, Pension funds etc.)

– Insurance companies – Other NBFCs

25

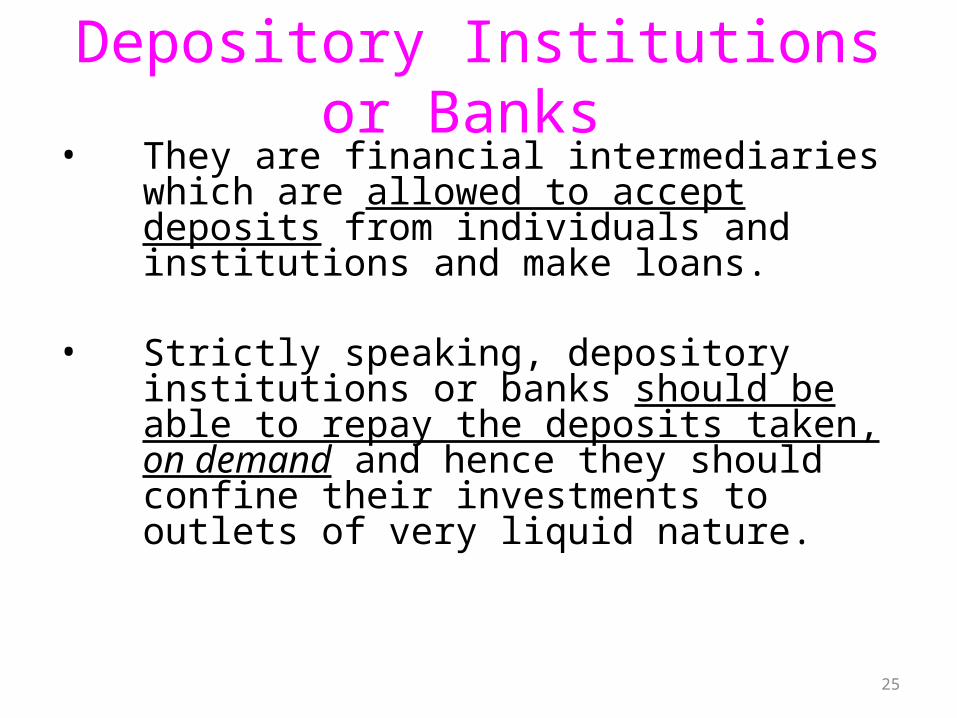

Depository Institutions or Banks

• They are financial intermediaries which are allowed to accept deposits from individuals and institutions and make loans.

• Strictly speaking, depository institutions or banks should be able to repay the deposits taken, on demand and hence they should confine their investments to outlets of very liquid nature.

26

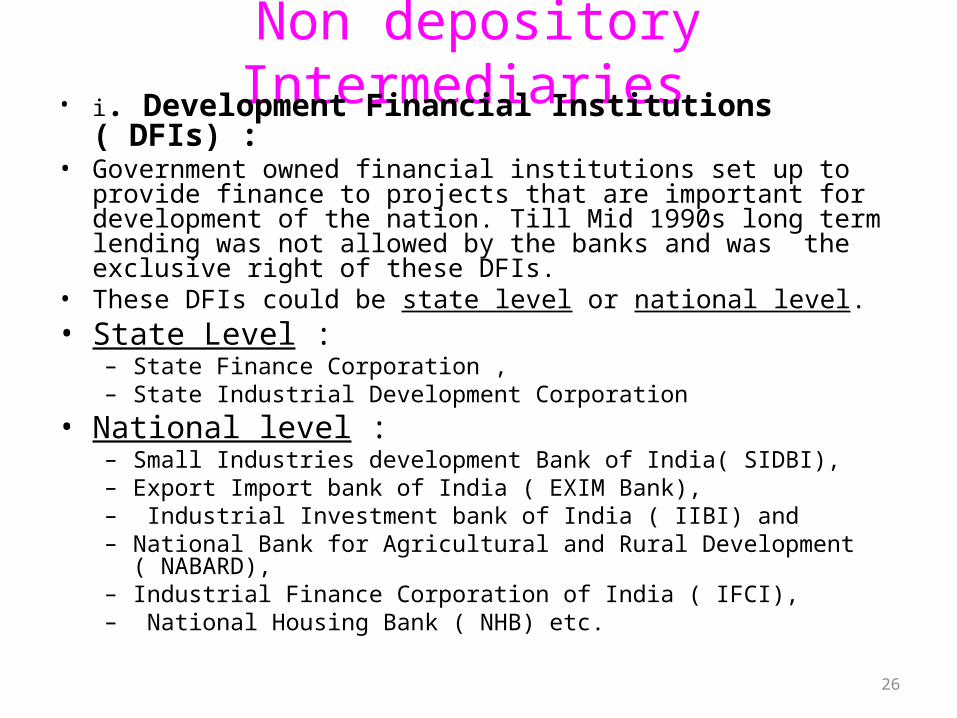

Non depository Intermediaries • i. Development Financial Institutions

( DFIs) : • Government owned financial institutions set up to

provide finance to projects that are important for development of the nation. Till Mid 1990s long term lending was not allowed by the banks and was the exclusive right of these DFIs.

• These DFIs could be state level or national level.• State Level :

– State Finance Corporation , – State Industrial Development Corporation

• National level : – Small Industries development Bank of India( SIDBI), – Export Import bank of India ( EXIM Bank),– Industrial Investment bank of India ( IIBI) and – National Bank for Agricultural and Rural Development

( NABARD), – Industrial Finance Corporation of India ( IFCI),– National Housing Bank ( NHB) etc.

27

Non depository Intermediaries.. Contd..

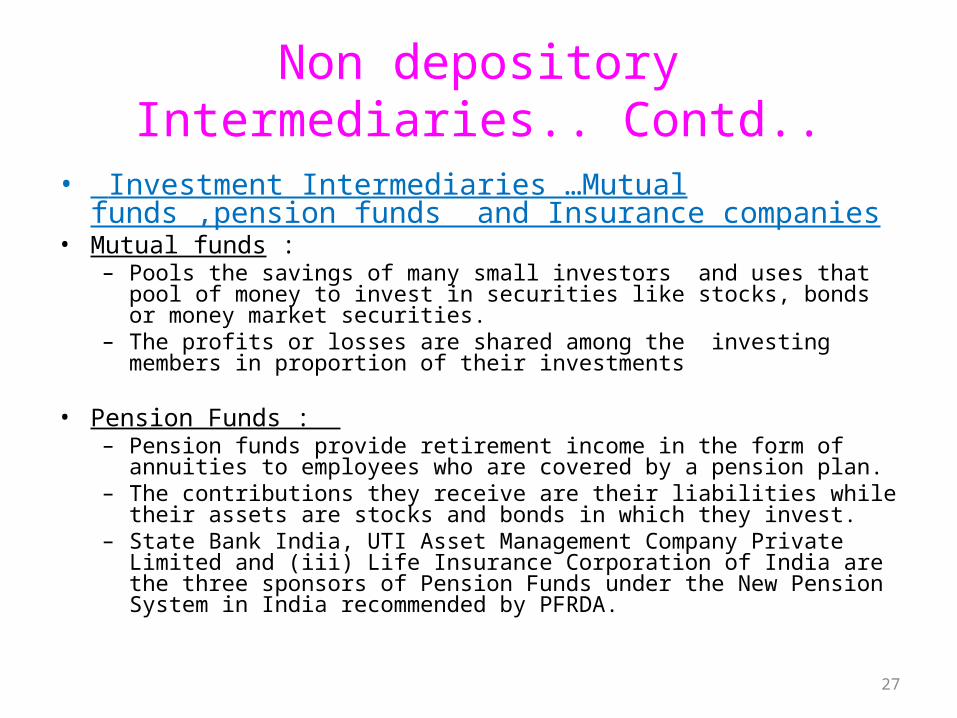

• Investment Intermediaries …Mutual funds ,pension funds and Insurance companies

• Mutual funds : – Pools the savings of many small investors and uses that

pool of money to invest in securities like stocks, bonds or money market securities.

– The profits or losses are shared among the investing members in proportion of their investments

• Pension Funds : – Pension funds provide retirement income in the form of

annuities to employees who are covered by a pension plan. – The contributions they receive are their liabilities while

their assets are stocks and bonds in which they invest. – State Bank India, UTI Asset Management Company Private

Limited and (iii) Life Insurance Corporation of India are the three sponsors of Pension Funds under the New Pension System in India recommended by PFRDA.

28

Non depository Intermediaries.. Contd..

• iii) Insurance Companies : • Essentially invest the savings of the policy holders ( insurance premiums) and in exchange promise them risk protection and /or a specified sum at a later stage. – Life insurance companies : provide this promised sum in the event of maturity or death of the policy holder.

– General insurance : provides this sum upon the happening of a certain event ( eg : a theft or a fire etc. )

• They differ from mutual funds in that, the main business of mutual funds is investment in securities to ensure a return to the unit holders but for insurance companies payments to policy holders may be only incidental to the happening of certain events.

29

Other Non Banking Financial Companies

• They provide a variety of fund -based or non –fund-based(advisory) services.

• Most of the funds raised are in the form of public time deposits .

• Following are some of the principal NBFCs:

– Leasing companies – Hire Purchase and consumer finance companies – Housing finance companies– Venture capital funds– Credit rating agencies – Factoring and forfaiting organizations.– Depositories

30

MARKETS

• Equity and Equity Markets

Types of Equity securities

• Common Equity • Preferred Equity

31

32

Common Equity as security

• Salient properties of common stock –

• that makes them different from the other kinds of securities – – Discretionary Dividend Payments – Residual Claim– Limited Liability– Voting rights

33

Price of Equity… a recap • Price of equity or stock: • The value or price of any financial asset( or any asset) is the PV of the cash flows from the asset.

• Price or value of an equity is also the PV of the cash flows expected from it---– Dividends and – final sale price – which basically boils down to the PV of all future expected dividends(??)

34

Risk of equity.. A recap• Risk from investing in a stock is the uncertainty in the expected cash flows.

• Risk of a stock or equity has two principal components : – Systematic risk and – Unsystematic risk.

• Systematic risk: Risk or uncertainty that is going to affect all the stocks or securities in general. This kind of risk cannot be diversified away. Also called ‘market risk’.– Example : Political/social/economic events affecting the entire economy, change in interest rate, inflation or purchasing power adversely affected etc.

35

Risk of equity a recap …..contd..

• Unsystematic risk component: – risk that is specific to the company– can be diversified away by adding more and more stocks in a portfolio with little correlation with each other.

– an event that might adversely affect one might suitably affect the other thereby canceling out the company specific risk or unsystematic risk.

36

Risk of equity a recap …..contd..

• Unsystematic or firm specific risk can be again :– business risk or – finance risk.

• Business risk of the firm is the total risk or uncertainty inherent in the business of the firm.

• Finance risk is the additional amount of risk placed on the common stockholders as a result of the decision to finance with debt and or preferred stock.( fixed obligation)

• Use of debt and preferred stock ( financial leverage) concentrates the business risk on the common stockholders and makes the common stock riskier.

Preferred Equity • Preferred stock is a ‘hybrid security’ : • It has characteristics of both a bond and a common

stock. • The bond like characteristic is that the income from a

preferred stock is a fixed rate of dividend per year although sometimes a preference shareholder may be guaranteed a minimum fixed dividend on the share with an additional variable component depending on the extent of profit made during the year.

• The stock like characteristic emanates from a bit of residualness in its claim on the assets of the company. In the payment of dividends during the life of the business, as well as during reimbursement during termination of the company, a preference shareholder gets preference over the ordinary shareholder but they are second in line after the debt holders, no payments can be made to the preference shareholders till the debt holder’s payments are cleared.

37

Preference Stock – Types • Participating and non participating : Participating– a

minimum fixed dividend component plus a variable component depending on the profit made. Non Participating – fixed dividend irrespective of the profits made.

• Cumulative vs Non cumulative : In case of the cumulative pref. shares ,if the dividend is not paid in a particular year due to say insufficient profit ,it is cumulatively made good in the following year or years. Thus the preference shareholders are provided additional assurance. For the non cumulative ones there is no such assurance and are thus riskier.

• Redeemable vs irredeemable : The former may be repurchased by the company at a future date while the latter may be permanent like the ordinary shares.

• Convertible preference shares: The preference share may be convertible to ordinary shares in the future on terms and conditions specified in advance.

38

How Stocks are bought and sold.. Stock markets

• Primary market• Secondary market

40

Raising equity money in the primary market

• Why needed ?• Most businesses start as sole proprietorship or small partnership, and initial capital that is required to start a business is usually provided by the entrepreneur himself and his immediate family or friends.

• But one limitation for this set up is that the capital is often small and so when the business needs to grow it is almost always that external equity is needed.

• Advantage of external equity is that the business risk is shared which is not the case with other forms of external financing like debt or preferred equity.

41

Stages/Sources of funding ..initially• When a private company decides to raise equity capital,

it can seek funding from several potential sources : • angel investors :

– First round of private equity for most start ups is often obtained from them . They are rich friends or acquaintances of the entrepreneur. Their capital contribution is often large compared to the capital already employed in the business . As such they obtain substantial equity share of the business .

• Venture capital firms : – Typically institutional investors which specialize in

identifying prospective business ventures and raising money to invest in those ventures.

• Strategic Investors : – Many established corporations purchase equity in younger,

private companies. A corporation that invests in private companies is called many different names like corporate investor/corporate partner/strategic partner/strategic investor etc. Example in 2001 Microsoft invested $51 million in Groove networks as a part of their strategic partnership.

• IPO :– The process of selling stock to the public for the first

time to raise money is called the initial public offering ( IPO).

Why do companies go public?

• Question arises particularly as IPOs are extremely expensive and involve commitment of huge amount of resources ( money and management time and effort) on the part of the company.

• The main reasons could be as follows :• 1)Prestige :

– An IPO is a major accomplishment. The share market , analysts and the press will suddenly begin taking notice.

– Hiring new employees will become easier as publicly traded companies are generally perceived to be more stable than private companies.

– Stock options become much more attractive now and can be offered to cement an employee’s stake in the company.

Why do companies go public?...contd…

• 2) cash Infusion : an IPO typically will raise a lot of money for the company that need not be returned but can be used to build new facilities, invest in new projects, fund research and development and acquisition of new business.

• 3) getting rich : an IPO typically provides the promoters( as well as employees) an opportunity to sell a part of their holdings in the secondary market and reap huge financial benefits. Apple computers went public in 1980. On the first day of trading 40 employees became millionaires.

43

Why do companies go public?...contd…

• 4)Enhanced access to liquidity :An IPO gives the company increased ability to raise even more money. Banks are willing to lend more money and extend credit to publicly traded company.

• 5)Stock as currency : a company can use its stock as a currency to purchase other businesses . Because of the lack of liquidity and because they are hard to value, private companies often have difficulty acquiring new businesses.

44

Some disadvantages of going public

• 1) Expense : – Huge expenses involved in an IPO. Biggest of the expense items is Underwriter’s fees typically ranging between 5-10% of the money raised.

– Plus there are billable hours of attorney’s and accountant’s fees.

– Plus printing costs( mind boggling paperwork is involved) and

– Filing fees with the regulator, listing fees with the exchange etc.

– Time and effort of management of the company in going through the process

45

Some disadvantages of going public… contd…

• 2) Doing business as a public company is more complicated :– Publicly traded companies are required to make certain quarterly and annual filings

– They need a separate department to deal with shareholder’s enquiries

– Need to retain separate attorneys and accountants to handle regulatory compliance.

– Disclosure requirements are much more stringent for a public company

• 3) Dilution of control : – a substantial part of the holding rests with the public after an IPO leading to a dilution in the control on the part of the original owners.

46

47

IPO markets – some figures from 2007 and 2008

• Global IPO activity has more than halved since 2007, according to Ernst & Young’s year-end Global IPO update. During the first 11 months of 2008, a total of 745 IPOs worldwide raised US$95.3 billion in capital. This compares with 1,790 IPOs over the same period in 2007, which raised US$256.9 billion in capital.

• IPO activity has also fallen in emerging markets. BRIC markets recorded 163 deals and US$28.0 billion in capital raised in the first 11 months of 2008. This compares with US$106.8 billion and 365 deals over the same period in 2007.

• Asian IPOs have generated the most capital this year to date (US$29.7 billion) with Greater China accounting for 60% of funds raised in this region.

• India Inc’s capital mobilisation through initial public offerings (IPOs) has hit rock bottom as the total amount raised via this route in 2008 aggregated to only Rs 22,100 crore, the lowest in the last three years.

• In India, capital mobilisation through IPOs witnessed a fall both in terms of volume and value as only 44 transactions worth Rs 22,100 crore were announced compared to a whopping Rs 48,600 crore in 2007.

• Though there was a fall in both value as well as volume, the year 2008 saw several large IPOs across the board including Reliance Power’s Rs 12,590 crore issue - the largest public issue of 2008.