Session 2 ..Fire Insurance ..2012

16

1 Session 2

Transcript of Session 2 ..Fire Insurance ..2012

1

Session 2

Specified perils & all risk concept

2

Property insurance can be given, in the international market on the following

basis : Specific perils policy & All risk Policy Specific perils policy : The perils are

listed out and the exclusions are also mentioned .

All risk policy : Named exclusions …anything not mentioned under

exclusions are deemed to be covered Specific perils

policy is known as “Standard fire and special perils

policy”

The all risk policy is known as

“industrial all risk policy”

In Indian market :

Standard fire and special perils policy…basket of 12 perils

3

FLEXA group

Nat Cat group

Other perils

•Fire •Lightning •Explosion excluding that of boilers and steam generating vessels•Aircraft damage

•Flood , inundation, storm , cyclone , hurricane, typhoon tempest, tornado, hailstorm•Subsidence ,landslide &Rockslide

•Impact damage by Rail/ Road animal or vehicle.•Riot , strike , Malicious damage.•Leakage from Sprinkler Installation• Bush fire •Missile testing operations•Bursting / overflowing of pipes , tanks & apparatus

4

Fire in insurance parlance needs compliance of 3 requirements : 1.There must be actual ignition2.Fire should be accidental 3.There must be something which ought not to be on fire

Presence of

flames is

essentialFire lit for a

specific purpose is NOT a fire

1. Own fermentation, natural heating or spontaneous combustion

2. Undergoing any heating or drying process3. Insured property being burnt by order of

Public authority

Are damages caused by soot/ smoke/ heat or by fire brigade while fighting fire , covered under the policy ??

What is not covered under the peril “fire “?

5

Lightning : Only direct damages caused due to

theimpact of lightning are

covered ..irrespective of whether there is a fire or not

Damages caused by high voltage which passes and causes induced

damages ( in electronic/ electrical equipments

IS NOT COVEREDExplosion/ Implosion :

Explosion is a covered peril other than explosion of boilers or apparatus

generating steam..i.e. only chemical explosion is covered

and not physical explosion( other than domestic boiler )

•Boiler explodes and damages other machineryDamage to boiler not covered ..others covered •Other vessel explodes, damages boiler and other machineryDamage to all assets are covered

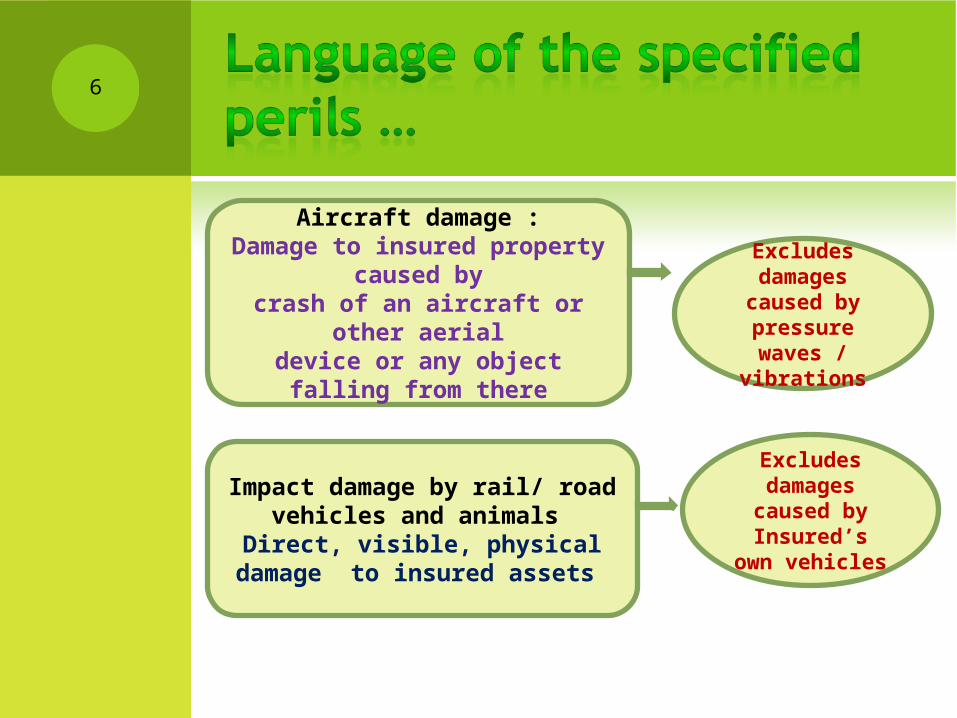

6

Aircraft damage :Damage to insured property

caused bycrash of an aircraft or

other aerialdevice or any object falling from there

Excludes damages caused by pressure waves /

vibrations

Impact damage by rail/ road vehicles and animals

Direct, visible, physical damage to insured assets

Excludes damages caused by Insured’s

own vehicles

7

Riot , strike and Malicious damage

Direct, visible, physical damage causedby external violent means

Any loss due to peaceful

protests or denial of access is NOT covered

A riot is a form of civil disorder characterized often by what is thought of as disorganized groups lashing out in a sudden and intense rash of violence against authority, property or people

In England and Wales , 12 or more persons who are present together use or threaten unlawful violence for a common purpose Under US federal Law , assembling of 3 or more persons indulging inviolence/ threats

Section 146 of Indian Penal code defines “rioting”…. Unlawful assembly ( Five or more persons having common illegal purpose ) using force or violence Malicious act : the deliberate and intentional harming of property; damaged caused due to personal grouse or ill will….not defined in IPC

8

STFI: Storm , typhoon, tempest, tornado, cyclone , hurricane , flood, inundation, hailstorm

Storm----violent disturbance of the atmosphere with

thunder or strong wind or heavy rainfall----Tempest, typhoon, hurricane, cyclone all

are “violent storms”Flood---- temporary covering of land areas by water due to

overflow of surface bodies of water or as a result of

local torrential rain. It is a condition of water course in

which the water level or the discharge exceeds a

certain average or normal value

9

•Mere cracking or settlement of the building unless entire building collapses•Damages during alterations, demolitions, repair •Defective design/defective construction•Settlement or movement of made up ground•Coastal/ river erosion

EXCLUDES :

The perils include rockslide also along with Landslide and subsidence but excludes the following:

10

Leakage from sprinkler installations …… covers Damage by water as a result of accidental discharge or leak from an automatic sprinkler installationExclude damages in respect of buildings which are empty or not in use or are under repair or when the sprinkler is being repaired or being removed for repairBush fire : Would mean any fire originating from small dry bushes or unwanted growth of vegetation in and around factories, offices, residence etc …excluding loss or damage caused by forest fires

11

• War( also warlike situations ) group of perils including civil commotion • Damages caused by radioactive contamination , leakage from nuclear reactors , caused by nuclear wastes , ionising radiations•Goods held in trust , money, securities , stamps , documents , computer records, plans, designs, patterns , moulds, explosives ….unless specifically mentioned on the policy.• Damage to any property which have been insured under a separate marine policy .• Pollution and contamination..excluding pollution or contamination arising out of perils insured under the policy OR perils which itself results form pollution and contamination

12

•Loss or damage caused by change of temperature to stocks in cold storage •Electrical exclusion •Loss of earnings, loss by delay, loss of market share , consequential loss •Spoilage damage as a result of cessation/ retardation/ interruption of process or operation caused by an insured peril .•Theft during or after the operation of an insured peril•Volcanic eruptions/ other convulsions of nature , earthquake.•Loss or damage to property, if they are removed to any other building , other than the one which is covered ---- only exception ---machinery / equipment sent for repairs / cleaning/ renovation for a max period of 60 days •Terrorism•Architects/ surveyor’s / consulting engineer’s fees AND removal of debris expenses , following operation of insured perils ABOVE …3% and 1% of claim amount respectively

Is there an excess under the fire policy ?

Deductibles under a fire policy

13

The deductibles vary based on the sum insured ..increase with the increase in the

exposure SUM INSURED SLAB..applicable per location

DEDUCTIBLE ( EXCESS )

Up to 10 crores 5% of claim amount minimum of Rs 10,000

Above 10 crores and up to 100 crores

5% of claim amount minimum of Rs 25,000

Above 100 crores and up to 1500 crores

5% of claim amount minimum of Rs 500,000

Above 1500 crores and up to 2500 crores

5% of claim amount minimum of Rs 2,500,000

Above 2500 crores 5% of claim amount minimum of Rs 5,000,000

General conditions under a fire policy

141. Mis -representation, mis - description

or non disclosure of material facts would result in the policy being voidable

2. Policy shall cease after 7 days , if a building or part of the building

collapses / falls or is displaced , without any of the insured perils having operated …however on specific written

request ( within the 7 days period) the insurer might consider continuing with

the cover ….but maybe on revised terms .3. Policy ceases to attach under any of the

following situations ( unless insured has sought an approval from insurer )

a. Alteration of the trade / manufacturing process , change in occupancy, or other circumstances which has increased the

nature of risk b. Building unoccupied for more than 30 days

( not applicable for residential dwelling )

c. If interest passes to somebody else from the insured ( other than by will or

through law )

General conditions under a fire policy

154. Marine clause :..Policy does not cover any

loss or damage to property which is covered under a MARINE POLICY , other than any balance amount

left after settlement of the marine claim.5. Cancellation of Policy : Policy can be

cancelled on request of INSURED … refund on SHORT PERIOD BASIS . Policy can also be cancelled by INSURER after giving 15 days notice …refund on

PRO RATA BASIS .6. Claims related conditions :

a.Written notice of claim with full details within 15 days

b.Cooperation with and full access to premises and documents/ records to o insurer’s

representatives at the time of survey , after a claim has been intimated .

c.No liability after 12 months 7. Rights of Insurers after claim…

8. Fraud….policy void 9. Condition of Reinstatement … option lies with

insurer that in case they want , instead of paying the monetary claim , they can decide to

reinstate the property to the condition prior to loss, at their expense

General conditions under a fire policy

1610. Condition of Average : Applicability of Under-insurance .. Every item, if more than

one, of the policy shall be separately subject to this condition.

11. Principle of contribution in fire insurance …. More than one insurance policy covering same property …each policy pays a proportionate share of the loss ( in the

ratio of the respective sum insured and total sum insured )

12. Subrogation of rights of insured for recovery from any third party , in favour of Insurer , subsequent to settlement of the

claim by the Insurer .13. Condition of Arbitration …as per

Provisions and Conciliation act of 1996.14. All communications between insurer and

insured would be in writing .15. Automatic reinstatement of sum insured : Irrespective of the number of claims under

the policy , the sum insured should be maintained during the currency of the policy