$25,500,000 BANNING UNIF1ED SCHOOL ... - CA.gov

229

NEW ISSUE-FULL BOOK-ENTRY INSURED RATING: S&P: "AA" UNDERLYING RATING: S&P: "A" (See "MISCELLANEOUS - Rating" herein) In the opinion of Bowie, Arneson, Wiles & Giannone, Newport Beach, California ("Bond Counsel"), subject, however, to certain qualifications described herein, and based upon an analysis of existing laws, regulations, rulings and court decisions, and assuming, among other matters, the accuracy of certain representations and compliance with certain covenants, interest on the Bonds is excluded from gross income for federal income tax purposes under Section 103 of the Internal Revenue Code of 1986, as amended. In the farther opinion of Bond Counsel, interest on the Bonds is not an item of tax preference for purposes of the federal alternative minimum taxes imposed on individuals and corporations; however Bond Counsel observes that such interest is included as an aqjustment in the calculation of federal corporate alternative minimum taxable income and may therefore affect a corporation's alternative minimum tax liabilities. In the farther opinion of Bond Counsel, interest on the Bonds is exempt from State of California personal income taxation. Bond Counsel expresses no opinion regarding or concerning any other tax consequences related to the ownership or disposition of the accrual or receipt of interest on the Bonds. See "TAX lvfATTERS - Opinion of Bond Counsel" herein. Dated: Date of Delivery $25,500,000 BANNING UNIF1ED SCHOOL DISTRICT (Riverside County, California) General Obligation Bonds, 2016 Election, Series A Due: August 1, as shown on the inside front cover page This cover page contains certain information for quick reference only. It is not a summary of this issue. Investors must read the entire Official Statement to obtain information essential to the making of an infonned investment decision. Capitalized terms used but not otherwise defined on this cover page shall have the meanings assigned to such terms herein. The Banning Unified School District (Riverside County, California) General Obligation Bonds, 2016 Election, Series A (the "Bonds") were authorized at an election of the registered voters of the Banning Unified School District (the "District'') held on November 8, 2016 (the "2016 Authorization"), at which more than fifty-five percent of the persons voting on the proposition voted to authorize the issuance and sale of not to exceed $25,500,000 principal amount of general obligation bonds of the District. The Bonds are being issued by the County of Riverside on behalf of the District for the purposes of (a) raising money for acquiring and constructing the projects, facilities and equipment set forth in the 2016 Authorization, (b) fi.mding interest on the Bonds, and (c) to pay all necessary legal, financial, printing, insurance and other contingent costs in connection with the issuance, sale and delivery of the Bonds. The Bonds are general obligations of the District payable solely from ad valorem property taxes. The Board of Supervisors of Riverside County is empowered and obligated to annually levy ad valorem taxes, without limitation as to rate or amount, upon all property within the District subject to taxation thereby (except certain personal property which is taxable at limited rates), for the payment of principal of and interest on the Bonds when due. The Bonds will be issued in book-entry form only, and will be initially issued and registered in the name of Cede & Co. as nominee for The Depository Trust Company, New York, New York (collectively referred to herein as "DTC''). Purchasers of the Bonds (the "Beneficial Owners'') will not receive physical certificates representing their interest in the Bonds. The Bonds will be dated as of their date of initial delivery (the "Date of Delivery'') and will be issued as current interest bonds, such that interest thereon will accrue from the Date of Delivery and be payable semiannually on February 1 and August 1 of each year, commencing February 1, 2018. The Bonds are issuable in denominations of $5,000 principal amount or any integral multiple thereof. Payments of principal of and interest on the Bonds will be made by Zions Bank, a division of ZB, National Association as the paying agent, bond registrar and transfer agent for the Bonds (the "Paying Agent''), to DTC for subsequent disbursement to DTC Participants (as defined herein) who will remit such payments to the Beneficial Owners of the Bonds. See "THE BONDS - Book-Entry Only System" herein. The scheduled payment of principal of and interest on the Bonds when due will be guaranteed under an insurance policy to be issued concmrently with the delivery of the Bonds by ASSURED GUARANTY MUNICIPAL CORP. See "THE BONDS - Bond lnsmance" herein and "APPENDIX F - SPECIMEN MUNICIPAL BOND INSURANCE POLICY" attached hereto. The Bonds are subject to optional and mandatory sinking fund redemption as further described herein. Maturity Schedule (see inside front cover page) The Bonds will be offered when, as and if issued and received by the Underwriter, subject to the approval of legality by Bowie, Arneson, Wiles & Giannone, Newport Beach, California, Bond Counsel. Certain legal matters will be passed upon by Stradling Yocca Carlson & Rauth, a Professional Corporation, San Francisco, California, Disclosure Counsel. Certain matters will be passed upon for the Underwriter by Dannis Woliver Kelley, Long Beach, California. The Bonds, in book-entry form, will be available through the facilities of The Depository Trust Company in New York, New York, on or about April 5, 2017. Dated: March 22, 2017.

-

Upload

khangminh22 -

Category

Documents

-

view

7 -

download

0

Transcript of $25,500,000 BANNING UNIF1ED SCHOOL ... - CA.gov

NEW ISSUE-FULL BOOK-ENTRY INSURED RATING: S&P: "AA" UNDERLYING RATING: S&P: "A"

(See "MISCELLANEOUS - Rating" herein)

In the opinion of Bowie, Arneson, Wiles & Giannone, Newport Beach, California ("Bond Counsel"), subject, however, to certain qualifications described herein, and based upon an analysis of existing laws, regulations, rulings and court decisions, and assuming, among other matters, the accuracy of certain representations and compliance with certain covenants, interest on the Bonds is excluded from gross income for federal income tax purposes under Section 103 of the Internal Revenue Code of 1986, as amended. In the farther opinion of Bond Counsel, interest on the Bonds is not an item of tax preference for purposes of the federal alternative minimum taxes imposed on individuals and corporations; however Bond Counsel observes that such interest is included as an aqjustment in the calculation of federal corporate alternative minimum taxable income and may therefore affect a corporation's alternative minimum tax liabilities. In the farther opinion of Bond Counsel, interest on the Bonds is exempt from State of California personal income taxation. Bond Counsel expresses no opinion regarding or concerning any other tax consequences related to the ownership or disposition of the accrual or receipt of interest on the Bonds. See "TAX lvfATTERS - Opinion of Bond Counsel" herein.

Dated: Date of Delivery

$25,500,000 BANNING UNIF1ED SCHOOL DISTRICT

(Riverside County, California) General Obligation Bonds, 2016 Election, Series A

Due: August 1, as shown on the inside front cover page

This cover page contains certain information for quick reference only. It is not a summary of this issue. Investors must read the entire Official Statement to obtain information essential to the making of an infonned investment decision. Capitalized terms used but not otherwise defined on this cover page shall have the meanings assigned to such terms herein.

The Banning Unified School District (Riverside County, California) General Obligation Bonds, 2016 Election, Series A (the "Bonds") were authorized at an election of the registered voters of the Banning Unified School District (the "District'') held on November 8, 2016 (the "2016 Authorization"), at which more than fifty-five percent of the persons voting on the proposition voted to authorize the issuance and sale of not to exceed $25,500,000 principal amount of general obligation bonds of the District. The Bonds are being issued by the County of Riverside on behalf of the District for the purposes of (a) raising money for acquiring and constructing the projects, facilities and equipment set forth in the 2016 Authorization, (b) fi.mding interest on the Bonds, and (c) to pay all necessary legal, financial, printing, insurance and other contingent costs in connection with the issuance, sale and delivery of the Bonds.

The Bonds are general obligations of the District payable solely from ad valorem property taxes. The Board of Supervisors of Riverside County is empowered and obligated to annually levy ad valorem taxes, without limitation as to rate or amount, upon all property within the District subject to taxation thereby (except certain personal property which is taxable at limited rates), for the payment of principal of and interest on the Bonds when due.

The Bonds will be issued in book-entry form only, and will be initially issued and registered in the name of Cede & Co. as nominee for The Depository Trust Company, New York, New York (collectively referred to herein as "DTC''). Purchasers of the Bonds (the "Beneficial Owners'') will not receive physical certificates representing their interest in the Bonds. The Bonds will be dated as of their date of initial delivery (the "Date of Delivery'') and will be issued as current interest bonds, such that interest thereon will accrue from the Date of Delivery and be payable semiannually on February 1 and August 1 of each year, commencing February 1, 2018. The Bonds are issuable in denominations of $5,000 principal amount or any integral multiple thereof.

Payments of principal of and interest on the Bonds will be made by Zions Bank, a division of ZB, National Association as the paying agent, bond registrar and transfer agent for the Bonds (the "Paying Agent''), to DTC for subsequent disbursement to DTC Participants (as defined herein) who will remit such payments to the Beneficial Owners of the Bonds. See "THE BONDS - Book-Entry Only System" herein.

The scheduled payment of principal of and interest on the Bonds when due will be guaranteed under an insurance policy to be issued concmrently with the delivery of the Bonds by ASSURED GUARANTY MUNICIPAL CORP. See "THE BONDS - Bond lnsmance" herein and "APPENDIX F - SPECIMEN MUNICIPAL BOND INSURANCE POLICY" attached hereto.

The Bonds are subject to optional and mandatory sinking fund redemption as further described herein.

Maturity Schedule (see inside front cover page)

The Bonds will be offered when, as and if issued and received by the Underwriter, subject to the approval of legality by Bowie, Arneson, Wiles & Giannone, Newport Beach, California, Bond Counsel. Certain legal matters will be passed upon by Stradling Yocca Carlson & Rauth, a Professional Corporation, San Francisco, California, Disclosure Counsel. Certain matters will be passed upon for the Underwriter by Dannis Woliver Kelley, Long Beach, California. The Bonds, in book-entry form, will be available through the facilities of The Depository Trust Company in New York, New York, on or about April 5, 2017.

Dated: March 22, 2017.

(l)

(2)

Maturity (August l)

2018 2019 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037

MATURITY SCHEDULE

BasecusIp 111 : 066617

$25,500,CXXJ BANNING UNIFIED SCHOOL DISTRICT

(Riverside County, California) General Obligation Bonds, 2016 Election, Series A

$10,475,000Serial Bonds

Principal Interest Amount Rate Yield

$965,000 2.000% l.040% 460,000 3.000 l.250

80,000 4.000 l.700 120,000 4.000 l.930 165,000 4.000 2.140 205,000 4.000 2.320 255,000 5.000 2.470 305,000 5.000 2.590 365,000 5.000 2.700 425,000 4.000 2.94d2) 485,000 3.000 3.230 545,000 3.125 3.340 610,000 5.000 3.l9d2) 685,000 5.000 3.27d2) 770,000 5.000 3.34d2) 860,000 5.000 3.4002) 955,000 5.000 3.45d2)

1,055,000 5.000 3.49d2) l, 165,000 3.625 3.890

CUSIP"'

JUG JV4 JW2 JX0 JY8 JZS KA8 KB6 KC4 KD2 KEO KF7 KGS KH3 KJ9 KK6 KL4 KM2 KN0

$7,665,000-5.250% Term Bonds due August l, 2042 -Yield 1500% "': CUSI P"': K PS

$7,360,000-4.000% Term Bonds due August l, 2046-Yield 4.030%; CUSI P"': KQ3

CUSI P is a registered traderrarkof the American Bankers Association. CUSIP data herein is provided by CUSIP Global Services ("CGS"), managed by S&P Capital IQ on behalf of The American Bankers Association. This data is not intended to create a database and does not serve in any way as a substitute for the CGS database. CUSIP numbers have been as~gned by an independent company not affiliated with the Distric~ the Financial Advisor or the Underwriter and are included solely for the convenience of the registered o.vners of the applicable Bonds. None of the Distric~ the Financial Advisor or the Underwriter is responsible for the selection or uses of these CUSIP nurrtiers, and no representation is trade as to their correctrless on the applicable Bonds or as included herein. The CUSIP nurrtier for a specific maturity is subject to being changed after the execution and delivery of the Bonds as a result of various subsequent actions including, but not lirrited to, a refunding in whole or in part or as a result of the prcx:urerrent of secondruy rrarket ix>rtfolio insurance or other sirrilar enhancerrent by investors that is applicable to all or a portion of certain rm.turities of the Bonds. Yieldtocall at par on August l, 2027.

This Official Statement does not constitute an offering of any security otherthan the original offering of the Bonds of the District No dealer, broker, salesperson or other person has been authorized by the District to give any information or to make any representations other than as contained in this Official Statement, and if given or made, such other information or representation not so authorized should not be relied upon as having been given or authorized by the District.

The issuance and sale of the Bonds have not been registered under the Securities Act of 1933 or the Securities Exchange Act of 1934, both as amended, in reliance upon exemptions prCNided thereunder by Sections 3(a)2 and 3(a)12, respectively. This Official Statement does not constitute an offer to sell or a solicitation of an offer to buy in any state in which such offer or solicitation is not authorized or in which the person making such offer or solicitation is not qualified to do so or to any person to whom it is unlawful to make such offer or solicitation.

The information set forth herein, other than that prCNided by the District, has been obtained from sources which are believed to be reliable, but is not guaranteed as to accuracy or completeness, and is not to be construed as a representation by the District. The information and expressions of opinions herein are subject to change without notice and neither delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in the affairs of the District since the date hereof. This Official Statement is subrritted in connection with the sale of the Bonds referred to herein and may not be reproduced or used, in whole or in part, for any other purpose.

When used in this Official Statement and in any continuing disclosure by the District in any press release and in any oral statement made with the apprCNal of an authorized officer of the District or any other entity described or referenced in this Official Statement, the words or phrases "will likely result," "are expected to," "will continue," "is anticipated," "estirrate," "project," "forecast," "expect," "intend" and sinilar expressions identify "forward looking statements'' within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements are subject to risks and uncertainties that could cause actual results to differ materially from those contemplated in such forward-looking statements. Any forecast is subject to such uncertainties. Inevitably, some assumptions used to develop the forecasts will not be realized and unanticipated events and circumstances may occur. Therefore, there are Ii kely to be differences between forecasts and actual results, and those differences may be material.

The Underwriter has prCNided the follcwing sentence for inclusion in this Official Statement "The Underwriter has revie.ved the information in this Official Statement in accordance with, and as part of, its responsibilities to investors under the federal securities laws as applied to the facts and circumstances of this transaction, but the Underwriter does not guarantee the accuracy or completeness of such information."

IN CONNECTION WITH THIS OFFERING, THE UNDERWRITER MAY OVER ALLOT OR EFFECT TRANSACTIONS WHICH STABILIZE OR MAINTAIN THE MARKET PRICE OF THE BONDS AT A LEVEL ABOVE THAT WHICH MIGHT OTHERWISE PREVAIL IN THE OPEN MARKET. SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUED AT ANY TIME. THE UNDERWRITER MAY OFFER AND SELL THE BONDS TO CERTAIN DEALERS AND DEALER BANKS AND BANKS ACTING AS AGENT AT PRICES LOWER THAN THE PUBLIC OFFERING PRICES STATED ON THE INSIDE COVER PAGE HEREOF AND SAID PUBLIC OFFERING PRICES MAY BE CHANGED FROM TIME TO TIME BY THE UNDERWRITER.

The District maintains a website. Hcwever, the information presented on the District's website is not incorporated into this Official Statement by any reference, and should not be relied upon in making investment decisions with respect to the Bonds.

Assured Guaranty Municipal Corp. ("AGM") makes no representation regarding the Bonds or the advisability of investing in the Bonds. In addition, AGM has not independently verified, makes no representation regarding, and does not accept any responsibility for the accuracy or completeness of this Official Statement or any information or disclosure contained herein, or orritted herefrom, other than with respect to the accuracy of the information regardingAGM supplied by AGM and presented under the heading "THE BONDS -Bond Insurance'' herein and in "APPENDIX F - SPECIMEN MUNICIPAL BOND INSURANCE POLICY" attached hereto.

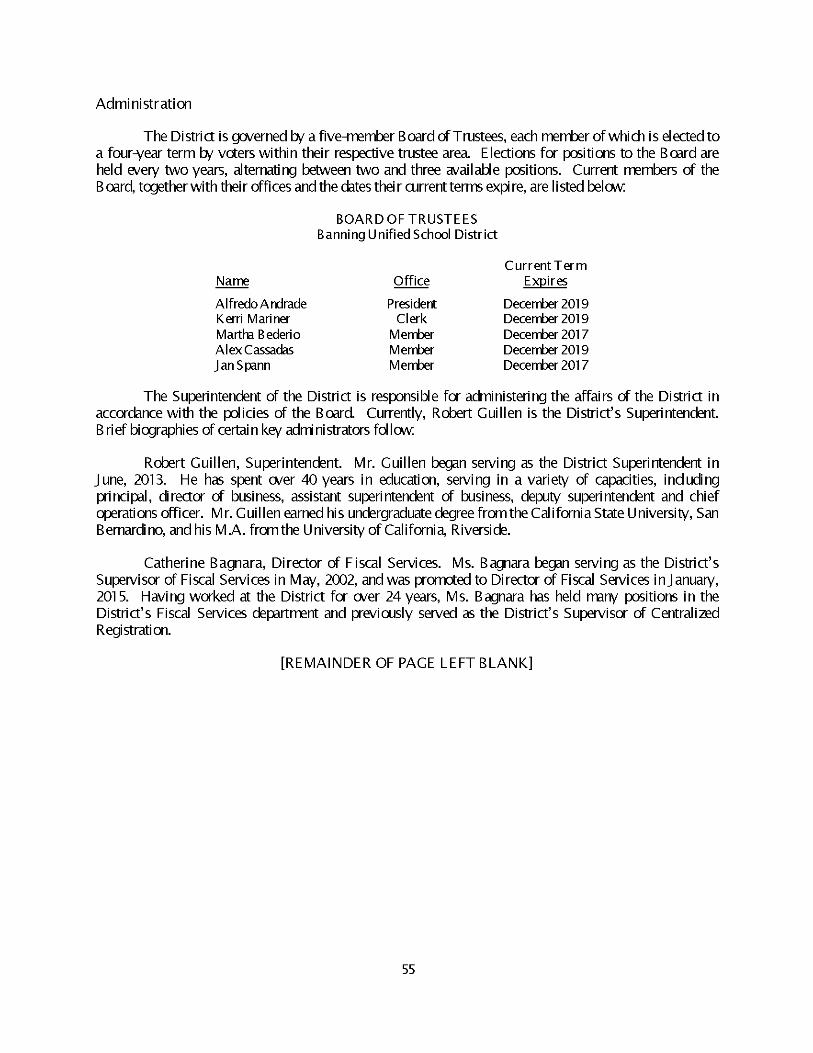

BANNING UNIFIED SCHOOL DISTRICT

Board of Trustees

Alfredo Andrade, President Kerri Mariner, Clerk

Martha B ederi o, M errber Alex Cassadas, Merrber

J an Spann, Merrber

District Administration

RobertT. Guillen, Superintendent Catherine Bagnara, Director of Fiscal Seivices Christina Hoff, Supervisor of Fiscal Seivices

PROFESSIONAL SERVICES

Bond Counsel

BCM/ie, Arneson, Wiles & Giannone Ne\\,1]0rt Beach, California

Disclosure Counsel

Stradling Y occa Carl son & Rauth, a Professional Corporation San Francisco, California

Financial Advisor

Dale Scott & Company Inc. San Francisco, California

PAYING AGENT

Zions Bank, a division of ZB, National Association Los Angeles, California

TABLE OF CONTENTS

INTRODUCTION ....................................................................................................................................................... 1

GENERAL ................................................................................................................................................................... 1 PURPOSES OF THE BONDS ........................................................................................................................................... 1

AUTHORITY FOR ISSUANCE OF THE BONDS ................................................................................................................ 2

SOURCES OF PAYMENT FOR THE BONDS .................................................................................................................... 2

DESCRIPTION OF THE BONDS ...................................................................................................................................... 2

TAX MATTERS ........................................................................................................................................................... 3

OFFERING AND DELIVERY OF THE BONDS .................................................................................................................. 3 BOND OWNER'S RISKS ............................................................................................................................................... 3

CONTINUING DISCLOSURE ......................................................................................................................................... 3

PROFESSIONALS INVOLVED IN THE OFFERING ............................................................................................................ 4

FORWARD LOOKING STATEMENTS ............................................................................................................................. 4

OTHER INFORMATION ................................................................................................................................................ 4

THE BONDS ................................................................................................................................................................ 5

AUTHORITY FOR ISSUANCE ........................................................................................................................................ 5 SECURITY AND SOURCES OF PAYMENT ...................................................................................................................... 5

GENERAL PROVISIONS ............................................................................................................................................... 6

BOND INSURANCE ...................................................................................................................................................... 7 ANNUAL DEBTSERVICE ........................................................................................................................................... 10

APPLICATION AND INVESTMENT OF BOND PROCEEDS .............................................................................................. 10

REDEMPTION ............................................................................................................................................................ 11

BOOK-ENTRY ONLY SYSTEM ................................................................................................................................... 15 DISCONTINUATION OF BOOK-ENTRY ONLY SYSTEM; REGISTRATION,

PAYMENT AND TRANSFER OF BONDS .................................................................................................................... 17 DEFEASANCE ........................................................................................................................................................... 17

ESTIMATED SOURCES AND USES OF FUNDS ................................................................................................ 18

TAX BASE FOR REPAYMENT OF BONDS ........................................................................................................ 19

ADVALOREM PROPERTY TAXATION ......................................................................................................................... 19

ASSESSED VALUATIONS ........................................................................................................................................... 20 APPEALS AND ADJUSTMENTS OF ASSESSED VALUATIONS ....................................................................................... 21

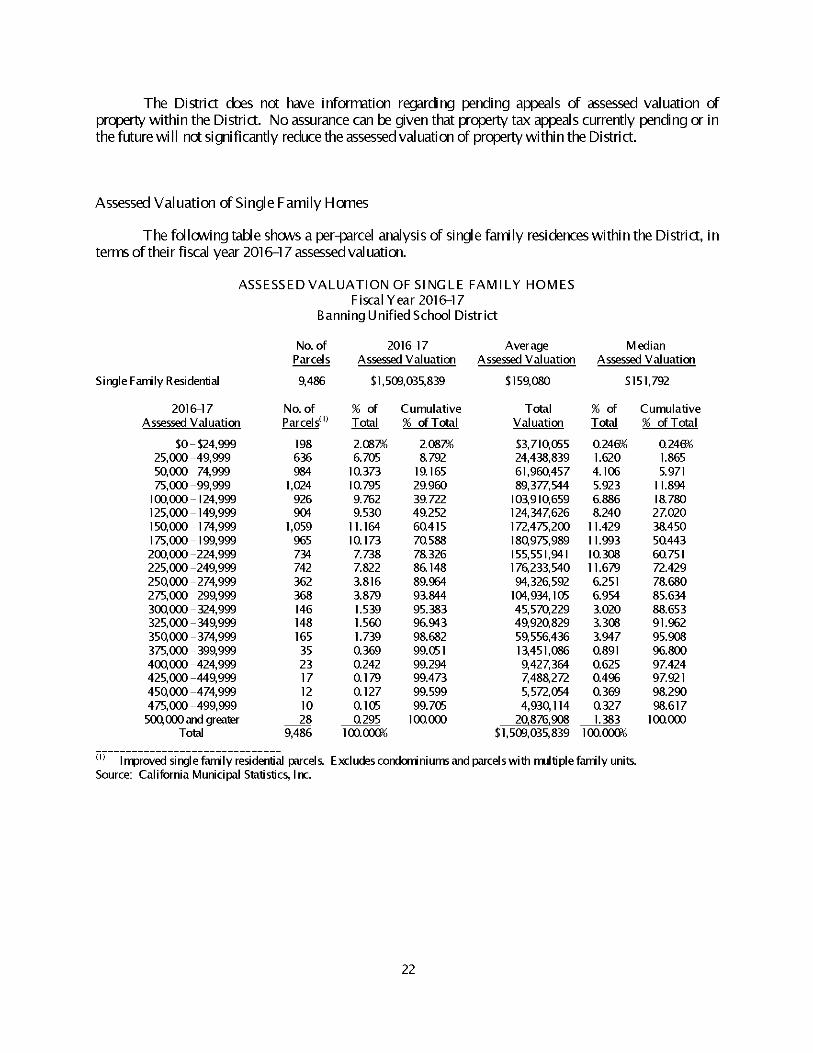

ASSESSED VALUATION OF SINGLE FAMILY HOMES ................................................................................................. 22

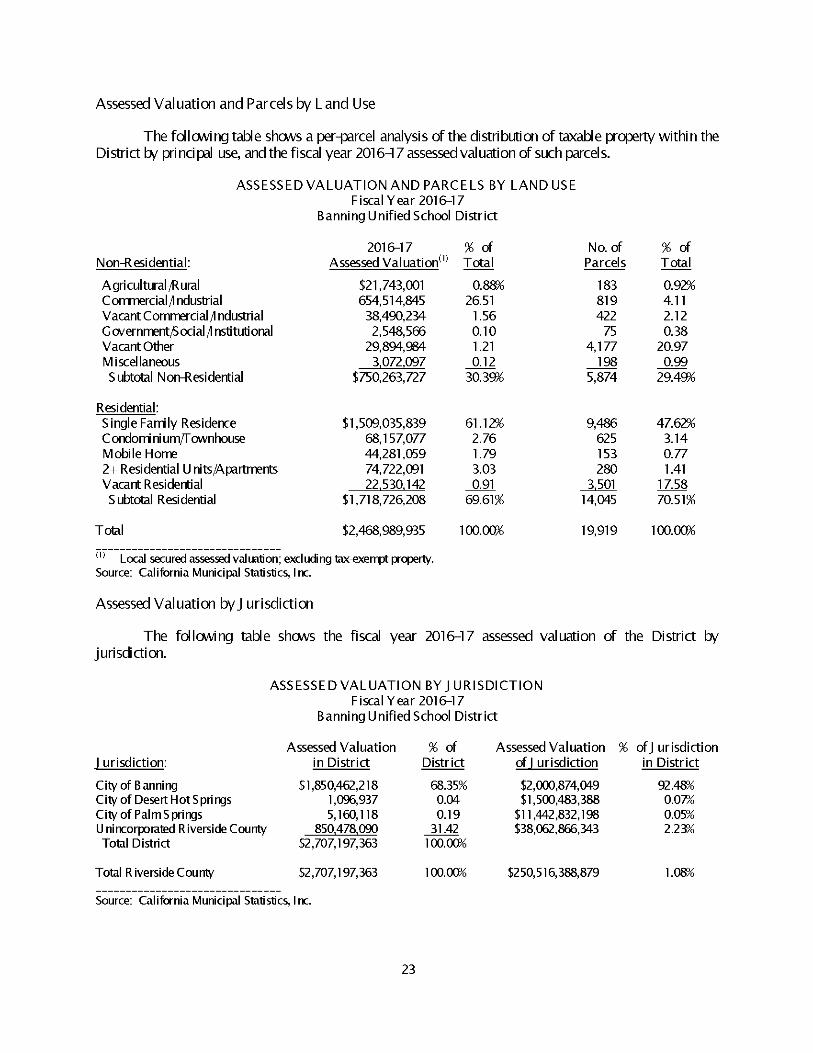

ASSESSED VALUATION AND PARCELS BY LAND USE ............................................................................................... 23 ASSESSED VALUATION BY JURISDICTION ................................................................................................................. 23

TAX LEVIES, COLLECTIONS AND DELINQUENCIES ................................................................................................... 24 ALTERNATIVE METHOD OF TAX APPORTIONMENT-"TEETER PLAN" ...................................................................... 24

TAX RATES .............................................................................................................................................................. 25

PRINCIPAL TAXPAYERS ............................................................................................................................................ 26

STATEMENT OF DIRECT AND OVERLAPPING DEBT ................................................................................................... 26

CONSTITUTIONAL AND STATUTORY PROVISIONS AFFECTING DISTRICT REVENUES AND APPROPRIATIONS ............................................................................................. 28

ARTICLE XII IA OF THE CALIFORNIA CONSTITUTION ............................................................................................... 28

LEGISLATION IMPLEMENTING ARTICLE XII IA ......................................................................................................... 29

UNITARY PROPERTY ................................................................................................................................................ 29

ARTICLE XII IB OF THE CALIFORNIA CONSTITUTION ............................................................................................... 29

ARTICLE XII IC AND ARTICLE X IIID OF THE CALIFORNIA CONSTITUTION .............................................................. 30

PROPOSITION 26 ....................................................................................................................................................... 31

PROPOSITIONS 98AND 111 ....................................................................................................................................... 31

PROPOSITION 39 ....................................................................................................................................................... 33

PROPOSITION lA AND PROPOSITION 22 .................................................................................................................... 34

JARVIS VS. CONNELL .................................................................................................................................................. 34

PROPOSITIONS 30AND 55 ......................................................................................................................................... 35

TABLE OF CONTENTS (cont'd)

PROPOSITION 2 ......................................................................................................................................................... 35

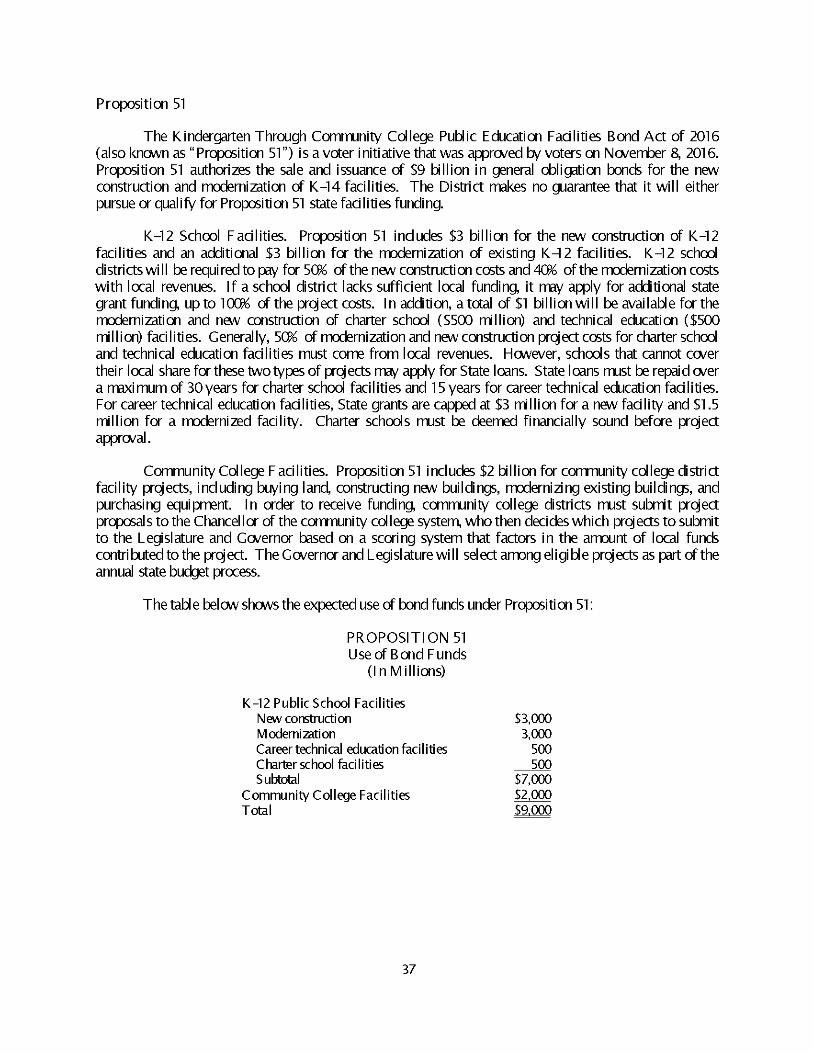

PROPOSITION 51 ....................................................................................................................................................... 37

FUTURE INITIATIVES ................................................................................................................................................ 38

DISTRICT FINANCIAL INFORMATION ............................................................................................................ 38

STATE FUNDING OF EDUCATION .............................................................................................................................. 38

OTHER REVENUE SOURCES ...................................................................................................................................... 43

STATE DISSOLUTION OF REDEVELOPMENT AGENCIES ............................................................................................. 43

BUDGET PROCESS .................................................................................................................................................... 45

ACCOUNTING PRACTICES ......................................................................................................................................... 48

COMPARATIVE FINANCIAL STATEMENTS ................................................................................................................. 48

STATE BUDGET MEASURES ...................................................................................................................................... 50

BANNING UNIFIEDSCHOOL DISTRICT .......................................................................................................... 54

INTRODUCTION ........................................................................................................................................................ 54

ADMINISTRATION ..................................................................................................................................................... 55

ENROLLMENT AND ADA .......................................................................................................................................... 56 LABOR RELATIONS .................................................................................................................................................. 56

DISTRICT RETIREMENT SYSTEMS ............................................................................................................................. 57

OTHER POST-EMPLOYMENT BENEFITS ..................................................................................................................... 63

PARTICIPATION INJOINT POWERS AUTHORITIES ...................................................................................................... 64 DISTRICT DEBT STRUCTURE .................................................................................................................................... 65

TAX MATTERS ........................................................................................................................................................ 67

OPINION OF BOND COUNSEL .................................................................................................................................... 67

ORIGINAL ISSUE DISCOUNT; PREMIUM BONDS ........................................................................................................ 68

IMPACT OF LEGISLATIVE PROPOSALS, CLARIFICATIONS OF THE CODE AND COURT DECISIONS ON TAX EXEMPTION ................................................................................................................ 68

INTERNAL REVENUE SERVICE AUDIT OF TAX -EXEMPT BOND ISSUES ...................................................................... 69

INFORMATION REPORTING AND BACKUPWITHHOLDING ......................................................................................... 69

LEGAL MATTERS .................................................................................................................................................. 69

LEGALITY FOR INVESTMENT IN CALIFORNIA ........................................................................................................... 69

EXPANDED REPORTING REQUIREMENTS .................................................................................................................. 70 CONTINUING DISCLOSURE ....................................................................................................................................... 70

No LITIGATION ........................................................................................................................................................ 71

FINANCIAL STATEMENTS ......................................................................................................................................... 72

LEGAL OPINION ....................................................................................................................................................... 72

MISCELLANEOUS .................................................................................................................................................. 72

RATING .................................................................................................................................................................... 72

UNDERWRITING ....................................................................................................................................................... 73 ADDITIONAL INFORMATION ..................................................................................................................................... 74

APPENDIX A: FORM OF OPINION OF BOND COUNSEL ........................................................................................... A-1

APPENDIX B: 2015-16AUDITED FINANCIAL STATEMENTS OF THE DISTRICT ...................................................... B-1

APPENDIX C: FORM OF CONTINUING DISCLOSURE CERTIFICATE ........................................................................ C-1

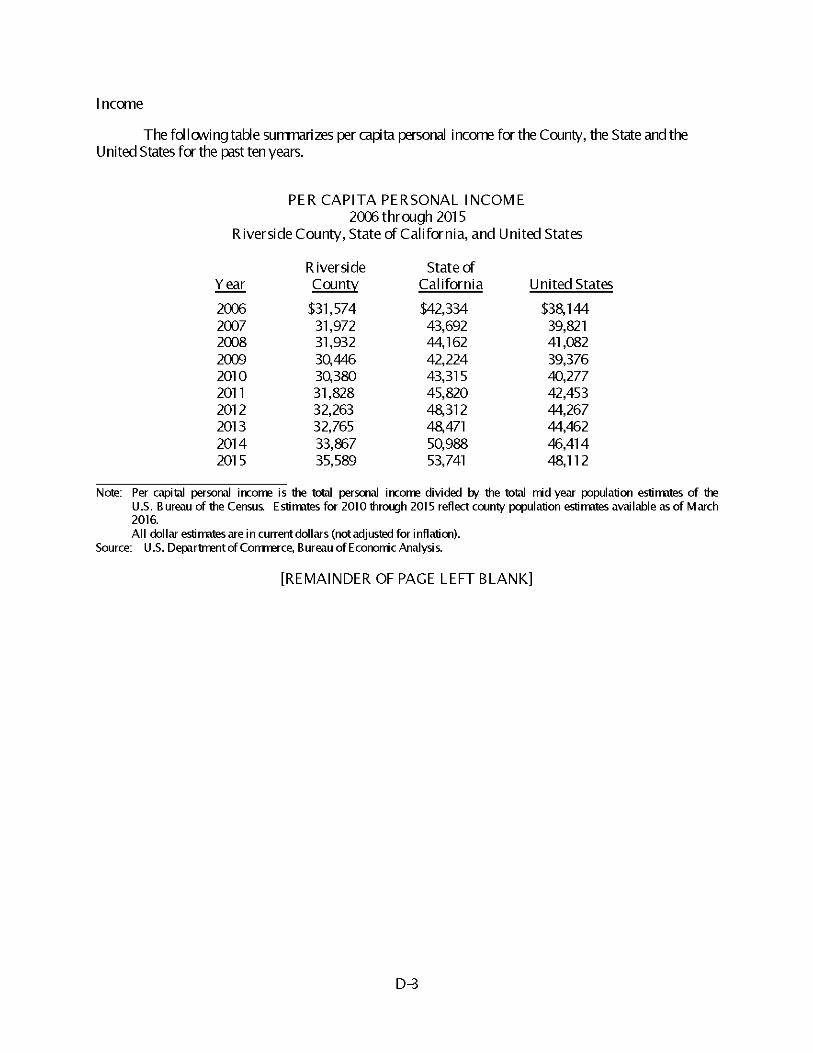

APPENDIX D: ECONOMIC AND DEMOGRAPHIC INFORMATION FOR THE CITY OF BANNING AND RIVERSIDE COUNTY ....................................................................................... D-1

APPENDIX E: RIVERSIDE COUNTY INVESTMENT POOL ....................................................................................... E-1

APPENDIX F: SPECIMEN MUNICIPAL BOND INSURANCE POLICY ......................................................................... F-1

ii

$2S,SOO,OOO BANNING UNIFIED SCHOOL DISTRICT

(Riverside County, California) General Obligation Bonds, 2016 Election, Series A

INTRODUCTION

This Official Statement, which includes the cover i:age, inside front cover page and appendices hereto, provides inforrration in connection with the sale of the Banning Unified School District (Riverside County, California) General Obligation Bonds, 2016Election, Series A (the"Bonds'').

This Introduction is not a surnrrary of this Official Statement. It is only a brief description of and guide to, and is qualified Or, more corrplete and detailed inforrration contained in the entire Official Statement, including the ewer i:age, inside front cover i:age and appendices hereto, and the documents surnrrari:zed or described herein. A full review should be rrade of the entire Official Statement. The offering of the Bonds to potential investors is rrade only 0y means of the entire Official Statement.

General

The Banning Unified School District (the "District'') was established in 1877, and ewers approxirrately 303 square miles in the communities of Cabazon, Whitewater, Poppet Flats and the Morongo Indian Reservation as well as the City of Banning. The District is located in the western portion of Riverside County (the "County"), approxirrately 80 nil es east of Los Angeles and 34 nil es east of the City of Riverside. The District currently operates five elementary schools (transitional kindergarten through grade 5), one middle school (grades 6--S), one comprehensive high school (grades 9-12), one continuation high school, a K-12 Independent Study School, and one adult education program For fiscal year 2016-17, the District's average daily attendance ("ADA") is 4,2S2 students, and taxable property within the District has a fiscal year 2016-17 assessed valuation of $2,707,197,363.

The District is gwerned 0y a five--rrember Board of Trustees (the "Board'), each member of which is elected to a four-year term 0y voters within their respective trustee area. Elections for positions to the Board are held every two years, alternating between two and three available positions. The management and policies of the District are adninistered 0y a Superintendent appointed 0y the Board who is responsible for day-to-day District operations as well as the supervision of the District's other personnel. Robert Gui 11 en is currently the District Superintendent.

For more inforrration regarding the District generally, see "DISTRICT FINANCIAL INFORMATION" and "BANNING UNIFIED SCHOOL DISTRICT" herein, and for more inforrration regarding the District's assessed valuation, see "TAX BASE FOR REPAYMENT OF BONDS" herein.

Purposes of the Bonds

The Bonds are being issued 0y the District forthe purposes of (a) raising money for acquiring and constructing the prqjects, faci Ii ties and equi prnent set forth in the 2016 Authorization (defined herein), (b) funding interest on the Bonds and (c) to l'.0-Y all necessary legal, financial, printing, insurance and other contingent costs in connection with the issuance, sale and delivery of the Bonds. See "THE BONDS -Application and Investment of Bond Proceeds" and "ESTIMATED SOURCES AND USES OF FUNDS" herein.

Authority for Issuance of the Bonds

The Bonds are issued b,t the County in the narre of the District pursuant to certain prwisions of the Gwemrrent Code of the State of California (the "Govemrrent Code'') and applicable provisions of the Education Code of the State of California (the" Education Code") and pursuant to resolutions adopted b,t the County Board of Supervisors of Riverside County (the "County Board') and the Board. See ''THE BONDS -Authority for Issuance" herein.

Sources of Payment for the Bonds

The Bonds are general obligations of the District payable solely from ad valorem property taxes. The Board of Supervisors of the County is errpcwered and obligated to levy such ad valorem taxes, without limitation as to rate or arnount, upon all property within the District sul::iject to taxation thereb,t (except certain personal property which is taxable at linited rates), for the payrrent of principal of and interest on the Bonds when due. See ''THE BONDS -Security and Sources of Payrrent" and "TAX BASE FOR REPAYMENT OF BONDS" herein.

Description of the Bonds

Farm and Registration. The Bonds will be issued in fully registered form only, without coupons. The Bonds will be initially registered in the narre of Cede & Co., as noninee of The Depository Trust Corrpany, NewY ork, New Yark (the" DTC"), who will act as securities depository for the Bonds. See "THE BONDS -General Prwisions" and "THE BONDS -Book-Entry Only System' herein. Purchasers of the Bonds (the "Beneficial owners") will not receive physical certificates representing their interests in the Bands purchased, but wi 11 instead receive credit balances on the books of their respective nominees. In the event that the book-entry only system described belo.v is no longer used with respect to the Bonds, the Bonds will be registered in accordance with the Resolution (as defined herein). See ''THE BONDS -Discontinuation of Book-Entry Only System; Registration, Payrrent and Transfer of Bonds" herein.

So long as Cede & Co. is the registered o.vner of the Bonds, as nominee of DTC, references herein to the" Owners," "Bondo.vners" or "Holders" of the Bonds (other than under the caption "TAX MATTERS" and in APPENDIX A) will mean Cede& Co. and will not mean the Beneficial Owners of the Bands.

Denominations. Individual purchases of interests in the Bonds will be available to purchasers of the Bonds in the denominations of $5,000 principal arnount, or any integral multiple thereof.

Redemption. The Bonds are sul::iject to optional redemption and mandatory sinking fund redemption prior to their stated maturity dates as further described herein. See ''THE BONDS -Redemption" herein.

Payrrents. The Bonds will be dated as of the date of their initial delivery (the "Date of Delivery"). Interest on the Bonds accrues from the Date of Delivery, and is payable semiannually on each February 1 and August 1, comrrencing February 1, 2018 (each, a "Bond Payrrent Date''). Principal of the B ands is payable on August 1, in the amounts and years as sho.vn on the i nsi de front ewer page hereof. Payrrents of the principal of and interest on the Bonds will be rnade b,t Zions Bank, a division of ZB, National Association, as the paying agent, registrar and transfer agent for the Bonds (the "Paying Agent"), to DTC for subsequent disburserrent through DTC Participants (as defined herein) to the B enefi ci al owners of the Bands.

2

Insurance. Concurrently with the delivery of the Bonds, Assured Guaranty Municipc1.I Corp. ("ACM") will issue a rnunicipc1.I bond insurance policy for the Bonds (the "Policy"), which Policy guarantees the scheduled pc1.yment of pri nci pc1.I of and interest on the Bands when due. See ''THE BONDS -Bond Insurance" herein and "APPENDIX F -SPECIMEN MUNICIPAL BOND INSURANCE POL I CY " attached hereto.

Tax Matters

In the opinion of Bo.vie, Arneson, Wiles & Giannone, Newport Beach, California, Bond Counsel, sul::iject, ho.vever, to certain qualifications described herein, and based upon an analysis of existing laws, regulations, rulings and court decisions, and assuming, arnong other rratters, the accuracy of certain representations and cornpl iance with certain cwenants, interest on the Bands is excluded frorn gross income for federal income tax purposes under Section 103 of the Internal Revenue Code of 1986, as amended (the "Code"). In the further opinion of Bond Counsel interest on the Bonds is not an itern of tax preference for purposes of the federal alternative rninirnurn taxes imposed on individuals and corporations; ho.vever Bond Counsel observes that such interest is included as an aqjustment in the calculation of federal corporate alternative ninirnurn taxable income and rray therefore affect a corporation's alternative ninirnurntax liabilities. In the further opinion of Bond Counsel, interest on the Bonds is exerrpt frorn State of California personal income taxation. Bond Counsel expresses no opinion regarding or concerni ng any other tax consequences related to the o.vnershi p or di sposi ti on of the accrual or receipt of interest on the Bonds. See "TAX MATTERS -Opinion of Bond Counsel" herein.

Offering and Delivery of the Bands

The Bonds are offered when, as and if issued, sul::iject to apprwal as to their legality b,t Bond Counsel. It is anticipated that the Bonds in book-entry forrn will be available for delivery through the facilities of DTC in NewY ork, NewY ork, on or about April 5, 2017.

Bond Owner's Risks

The Bonds are general obligations of the District payable solely frorn ad valorern property taxes which rray be levied on all taxable property in the District, without linitation as to rate or arnount (except with respect to certai n personal property which is taxable at Ii ni ted rates). For rnore cornpl ete inforrration regarding the District's financial condition and taxation of property within the District, see "TAX BASE FOR REPAYMENT OF BONDS," "DISTRICT FINANCIAL INFORMATION" and "BANNING UNIFIED SCHOOL DISTRICT" herein.

Continuing Disclosure

The District has covenanted that it will comply with and carry out the prwisions of that certain Continuing Disclosure Certificate relating to the Bonds. Pursuant thereto, the District will cwenant for the benefit of the OWners and Beneficial owners of the Bonds to rrake available certain financial inforrration and operating data relating to the District and to prwide notices of the occurrence of certain listed events, in compliance with Securities and Exchange Cornnission Rule 15c2-12(b)(5) (the" Rule''). The specific nature of the inforrration to be rrade available and of the notices of listed events is summarized belo.v under "LEGAL MATTERS -Continuing Disclosure" herein and "APPENDIX C -FORM OF CONTINUING DISCLOSURE CERTIFICATE" attached hereto.

3

Professionals Involved in the Offering

Bo.vie, Arneson, W i I es & Ci annone, Newport Beach, California, is acting as Bond Counsel to the District with respect to the Bonds. Certain legal matters will be passed upon 0y Stradling Y occa Carlson & Rauth, a Professional Corporation, San Francisco, California, as Disclosure Counsel. Dale Scott & Corrpany Inc., San Francisco, California is acting as Financial Acwisor to the District with respect to the Bonds. Bo.vie, Arneson, Wiles & Giannone, Stradling Y occa Carlson & Rauth, a Professional Corporation and Dale Scott & Corrp3.ny Inc. will receive compensation from the District contingent upon the sale and delivery of the Bonds.

Forward Looking Statements

Certain statements included or incorporated 0y reference in this Official Statement constitute "forward-looking statements" within the meaning of the United States Private Securities Litigation Reform Act of 1995, Section 21 E of the United States Securities Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended. Such statements are generally identifiable 0y the terninology used such as" plan," "intend," "expect," "estimate," "prqject," "budget" or other sinilar words. Such forward-looking statements include, but are not linited to, certain statements contained in the information regarding the District herein.

THE ACHIEVEMENTS OF CERTAIN RESULTS OR OTHER EXPECTATIONS CONTAINED IN SUCH FORWARD-LOOKING STATEMENTS INVOLVE KNOWN AND UNKNOWN RISKS, UNCERTAINTIES AND OTHER FACTORS WHICH MAY CAUSE ACTUAL RESULTS, PERFORMANCE OR ACHIEVEMENTS DESCRIBED TO BE MATERIALLY DIFFERENT FROM ANY FUTURE RESULTS, PERFORMANCE OR ACHIEVEMENTS EXPRESSED OR IMPLIED BY SUCH FORWARD-LOOKING STATEMENTS. THE DISTRICT DOES NOT PLAN TO ISSUE ANY UPDATES OR REVISIONS TO THE FORWARD-LOOKING STATEMENTS SET FORTH IN THIS OFFICIAL STATEMENT.

Other Information

This Official Statement speaks only as of its date, and the information contained herein is sul::iject to change. Copies of documents referred to herein and information concerning the Bonds are available from the Banning Unified School District, 161 West Williams Street, Banning, California 92220, telephone: (951) 922-2706. The District may irrpose a charge for copying, mailing and handling.

No dealer, broker, salesperson or other person has been authorized 0y the District to give any information or to make any representations other than as contained herein and, if given or made, such other information or representations must not be relied upon as having been authorized 0y the District. This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the Bonds 0y a person in any jurisdiction in which it is unlawful for such person to make such an offer, solicitation or sale.

This Official Statement is not to be construed as a contract with the purchasers of the Bonds. Statements contained in this Official Statement which involve estimates, forecasts or matters of opinion, whether or not expressly so described herein, are intended solely as such and are not to be construed as representations of fact. The summaries and references to documents, statutes and constitutional prwisions referred to herein do not purport to be comprehensive or definitive, and are qualified in their entireties 0y reference to each such documents, statutes and constitutional prwisions.

4

The inforrration set forth herein, other than that prwided 0y the District, has been obtained from official sources which are believed to be reliable but it is not guaranteed as to accuracy or completeness, and is not to be construed as a representation 0y the District. The inforrration and expressions of opinions herein are sul::iject to change without notice and neither delivery of this Official Statement nor any sale rrade hereunder shall, under any circumstances, create any implication that there has been no change in the affairs of the District since the date hereof. This Official Statement is subnined in connection with the sale of the Bands referred to herei n and rray not be reproduced or used, in whole or i n part, for any other purpose.

Capitalized terms used but not otherwise defined herein shall have the meanings assigned to such terms i n the R esol uti on (defined bel cw) .

THE BONDS

Authority for Issuance

The Bonds are being issued pursuant to the prwisions of Article 4.5 of Chapter 3 of Part 1 of Division 2 of Title 5 of the Government Code, certain prwisions of the Education Code, Article XI I IA of the State Constitution and pursuant to resolutions adopted 0y the County Board on March 7, 2017 (the "Resolution") and the Board on February 16, 2017.

The District received authorization at an election held on Nwember 8, 2016, 0y the requisite 55% or more of the votes cast 0y eligible voters of the District to issue not to exceed $25,500,000 aggregate principal amount of general obligation bonds (the" 2016 Authorization"). The Bonds are the first series of bonds issued under the 2016 Authorization, and, follo.ving the issuance thereof, none of the 2016 A uthori zati on wi 11 rerrai n uni ssued.

Security and Sources of Payment

The Bonds are general obligations of the District payable solely from ad valorem property taxes. The Board of Supervisors of the County is empo.vered and obligated to annually levy ad valorem property taxes upon all property sul::iject to taxation 0y the District, without linitation as to rate or amount (except certain personal property which is taxable at linited rates), for the payment of principal of and interest on the Bonds when due. The levy rray include allo.vance for an annual reserve, established for the purpose of avoiding fluctuating tax levies. The County, ho.vever, is not obligated to establish such a reserve, and the District can rrake no representation that such reserve will be established 0y the County or that such a reserve, if previously established 0y the County, will be maintained in the future.

Such taxes will be levied annually in addition to all other taxes during the period that the Bonds are outstanding i n an amount sufficient to pay the pri nci pal of and i nterest on the B ands when due. Such taxes, when collected, will be placed 0y the County in the Debt Service Fund (as defined herein), which is required to be segregated and maintained 0y the County and which is designated for the payment of the Bonds, and interest thereon when due, and for no other purpose. Pursuant to the Resolution, the District has pledged funds on deposit in the Debt Service Fund to the payment of the Bonds. Although the County is obligated to levy ad valorem property taxes for the payment of the Bonds as described abOJe, and will rraintain the Debt Service Fund, none of the Bonds are a debt of the County.

Pursuant to Section 53515 of the Gwernment Code, the Bonds will be secured 0y a statutory lien on al I revenues received pursuant to the I evy and col I ecti on of ad val orem property taxes for the payment thereof. The lien automatically attaches, without further action or authorization 0y the Board, and is valid and binding from the ti me the Bands are executed and delivered. The revenues received pursuant to the

5

levy and collection of the ad valorem proi:erty tax will be immediately sul::iject to the lien, and such lien will be enforceable against the District, its successor, transferees and creditors, and all other pm:ies asserting rights therein, irrespective of whether such pm:ies have notice of the lien and without the need for physical delivery, recordation, filing or further act.

The moneys in the Debt Service Fund, to the extent necessary to pay the principal of and interest on the Bonds as the same becorre due and payable, will be transferred to the Paying Agent. The Paying Agent will in turn remit the funds to DTC for remittance of such principc1.I and interest to its Participc1.nts for subsequent di sburserrent to the B enefi ci al ONners of the Bands.

The amount of the annual ad val orem property taxes I evi ed b,t the County to repay the Bands wi 11 be deternined b,t the relationship between the assessed valuation of taxable property in the District and the amount of debt service due on the Bonds in any year. Fluctuations in the annual debt service on the Bonds and the assessed value of taxable property in the District may cause the annual tax rate to fluctuate. E cononi c and other factors beyond the District's control, such as general market decline in I and values, disruption in financial markets that may reduce the availability of financing for purchasers of property, reclassification of property to a class exempt from taxation, whether b,t o.vnership or use (such as exemptions for property o.vned b,t the State and local agencies and property used for qualified education, hospital, charitable or religious purposes), or the complete or pc1.rti al destruction of the taxable proi:erty caused b,t a natural or man made disaster, such as earthquake, flood, fi re, drought or taxi c contani nation, could cause a reduction in the assessed value of taxable property within the District and necessitate a corresponding increase in the annual tax rate. For further information regarding the District's assessed valuation, tax rates, werlapping debt, and other matters concerning taxation, see "CONSTITUTIONAL AND STATUTORY PROVISIONS AFFECTING DISTRICT REVENUES AND APPROPRIATIONS -Article XIIIA of the California Constitution" and "TAX BASE FOR REPAYMENT OF BONDS -AssessedValuations" herein.

General Prwisions

The Bonds will be issued in book-€ntry form only, and will be initially issued and registered in the narre of Cede& Co. as noninee for DTC. See"- Book-Entry Only System' herein. Beneficial ONners will not receive certificates representing their interest in the Bonds. The Bonds will be dated as of the Date of Delivery.

Interest on the Bands accrues from the Date of Delivery and is payable seni annually on each Band Payrrent Date, commencing February 1, 2018. Interest on the Bands wi 11 be computed on the basis of a 36o-clay year of twelve, 3o-clay months. Each Bond will bear interest from the Bond Payrrent Date next preceding the date of authentication thereof uni ess it is authenticated as of a day duri ng the i:eri od from the 16th day of the month next preceding any Band Payrrent Date to that Band Payrrent Date, inclusive, in which event it will bear interest from such Bond Payrrent Date, or unless it is authenticated on or beforeJ anuary 15, 2018, in which event it will bear interest from the Date of Delivery. The Bonds are issuable in denominations of $5,000 principc1.I amount or any integral multiple thereof, and mature on August 1, in the years and amounts set forth ai the inside ewer pc1.ge hereof.

Payrrent. The principc1.I of the Bonds will be pc1.yable in lawful money of the United States of Arrerica to the registered ONner thereof, upon the surrender thereof at the principc1.I office of the Paying Agent. The interest on the Bonds will be pc1.yable in lawful money to the i:erson whose narre api:ears on the bond registration books of the Paying Agent as the registered ONner thereof as of the close of business on the 15th day of the month preceding any Bond Payrrent Date (a "Record Date"), whether or not such day is a business day, such interest to be paid b,t check mailed on such Bond Payrrent Date to such registered ONner at such registered ONner's address as it api:ears on such registration books or at

6

such address as the registered ONner rray have filed with the Paying Agent forthat purpose on or before such Record Date. The interest payrrents on the Bonds will be rrade in imrrediately available funds (e.g., b,t wire transfer) to any registered ONner of at least $1,000,000 of such outstanding Bonds who shall have requested i n wri ti ng such rrethod of payrrent of interest on such Bands prior to the close of business on the Record Date i mrrediately preceding any Band Payrrent Date.

Bond Insurance

Bond Insurance Policy. Concurrently with the issuance of the Bonds, ACM will issue the Policy. The Policy guarantees the scheduled payrrent of principai of and interest on the Bonds when due as set forth in the form of the Policy included as APPENDIX F to this Official Staterrent.

The Policy is not cwered b,t any insurance security or guaranty fund established under New York, California, Connecticut or Florida insurance law.

Considerations Regarding Bond Insurance. In the event of a default in the payrrent of principai of or interest on the i nsured portion of such Bands, when al I or sorre becomes due, any ONner of such insured Bonds may have a claim underthe Policy secured in connection with the Bonds. The Policy rray not insure agai nst rederrpti on preni um, if any, with respect to the B ands.

I n the event that AG M is unable to rrake payrrents of pri nci pai of or interest on the B ands, as such payrrents become due under any applicable Policy, such Bonds will be payable solely as otherwise descri bed herei n. I n the event that AG M becomes obi i gated to malke payrrents with respect to the Bands, no assurance can be given that such event would not acwersely affect the rrarket price of such Bonds or the rrarketabllity or liqJidity of such Bonds.

As a result of obtaining the Policy, the long-term ratings on the Bonds will be dependent in part on the financial strength of ACM and its claim paying ability. Such Bond Insurer's financial strength and claims paying ability are predicated upon a number of factors which could change wer tirre. No assurance is given that the long-term ratings of ACM and of the ratings on the Bonds insured b,t ACM will not be sul::iject to do.vngrade, and such event could acwersely affect the market price of the Bonds, or the rrarketabllity or liquidity for such Bonds.

Neither the District or Underwriter have rrade independent investigations into the claims paying abi Ii ty of AG M and no assurance or representation regardi ng the fi nanci al strength or prqj ected fi nanci al strength of ACM is given. Thus, when making an investrrent decision, potential investors should carefully consider the ability of the District to pay principal and interest on the Bonds, and the claims paying ability of ACM, particularly werthe life of the investrrent.

Assured Guaranty Municipal Corp. ACM is a Ne.v York doniciled financial guaranty insurance company and an indirect subsidiary of Assured Guaranty Ltd. ("AGL"), a Bermuda-based holding company whose shares are publicly traded and are listed on the NewY ark Stock Exchange under the syrrbol "AGO". AGL, through its operating subsidiaries, prwides credit enhancerrent products to the U.S. and global public finance, infrastructure and structured finance rrarkets. Neither AGL nor any of its shareholders or affi I i ates, other than AG M , is obi i gated to pay any debts of AG M or any cl ai ms under any i nsurance policy issued b,t AG M .

AGM's financial strength is rated "AA" (stalble outlook) b,t S&P Glolbal Ratings, a business unit of Standard & Poor's Financial Services LLC ("S&P"), "AA-+'' (stable outlook) b,t Kroll Bond Rating Agency, Inc. ("KBRA") and "A2'' (stable outlook) b,t Moody's Investors Service, Inc. ("Moody's"). Each rating of ACM should be evaluated independently. An explanation of the significance of the above

7

ratings rray be obtained from the applicable rating agency. The above ratings are not recomrrendations to buy, sell or hold any security, and such ratings are sul::iject to revision or withdriM'al at any tirre b,t the rating agencies, including withdrawal initiated at the request of ACM in its sole discretion. In addition, the rati ng agencies rray at any ti rre change AG M 's I ong-term rati ng out I oaks or pl ace such rati ngs on a watch Ii st for possi bl e dcwngrade i n the near term Any do.vnward revision or withdrawal of any of the above ratings, the assignrrent of a negative outlook to such ratings or the placerrent of such ratings on a negative watch list rray have an adJerse effect on the rrarket price of any security guaranteed b,t ACM. ACM only guarantees scheduled principal and scheduled interest payrrents payable b,t the issuer of bonds insured b,t ACM on the date(s) when such amounts were initially scheduled to becorre due and payable (sul::iject to and in accordance with the terms of the relevant insurance policy), and does not guarantee the rrarket price or liquidity of the securities it insures, nor does it guarantee that the ratings on such securities wi 11 not be revised or with drawn.

Current Financial Strength Ratings.

OnJ uly 27, 2016, S&P issued a credit rating report in which it affirmed ACM 's financial strength rating of "AA" (stable outlook). ACM can give no assurance as to any further ratings action that S&P rray take.

On August 8, 2016, Moody's published a credit opinion affirning its existing insurance financial strength rating of "A2'' (stable outlook) on ACM. ACM can give no assurance as to any further ratings action that Moody's rray take.

On December 14, 2016, KBRA issued a financial guaranty surveillance report in which it affirrred AGM's insurance financial strength rating of "AA-+'' (stable outlook). ACM can give no assurance as to any further ratings action that KBRA rray take.

For more i nforrrati on regardi ng AG M 's financial strength rati ngs and the risks rel ati ng thereto, see AGL'sAnnual Report on Form 10-K for the fiscal year ended December 31, 2016.

Capitalization of ACM.

At December 31, 2016, AGM's policyholders' surplus and contingency reserve were approximately $3,557 nillion and its net unearned prenium reserve was approxirrately $1,328 nil lion. Such amounts represent the corrbi ned surplus, contingency reserve and net unearned preni um reserve of ACM, AGM's wholly o.vned subsidiary Assured Guaranty (Europe) Ltd. and 60.7% of AGM's indirect subsidiary Municipal Assurance Corp.; each amount of surplus, contingency reserve and net unearned preni um reserve for each company was deterni ned in accordance with statutory accounting pri nci pies.

Incorporation of Certain Docurrents W Reference.

Portions of the follo.ving docurrent filed b,t AGL with the Securities and Exchange Commission (the "SEC") that relate to ACM are incorporated b,t reference into this Official Staterrent and shall be deemed to be a part hereof: the Annual Report on Form 10-K forthe fiscal year ended December 31, 2016 (filed b,t AGL with the SEC on February 24, 2017).

A 11 consol i dated fi nanci al staterrents of AG M and al I other i nforrrati on relating to AG M included in, or as exhibits to, docurrents filed b,t AGL with the SEC pursuant to Section 13(a) or 1 S(d) of the Securities Exchange Act of 1934, as arrended, excluding Current Reports or portions thereof "furnished' under Item 2.02 or Item 7.01 of Form 8-K, after the filing of the last docurrent referred to above and before the terni nation of the offeri ng of the B ands shal I be deerred i ncorporated b,t reference

8

into this Official Statement and to be a i:art hereof from the respective dates of filing such documents. Copies of materials incorporated 0y reference are available wer the internet at the SEC's website at http:/MM,w.sec.gcw, at AGL's website at http:/,www.assuredguaranty.corn or will be prwided upon request to Assured Guaranty Municipal Corp.: 1633 B road.vay, New York, New York 10019, Attention: Comrnuni cations Dei:artment (telephone ( 212) 97 4-01 00). Except for the i nformati on referred to abcwe, no information available on or through AGL's website shall be deemed to be i:art of or incorporated in this Official Statement.

Any information regarding ACM included herein under the caption "BOND INSURANCE -Assured Guaranty Muni ci i:al Corp." or included in a document incorporated 0y reference herein (collectively, the "ACM Information") shall be modified or superseded to the extent that any subsequently included ACM Information (either directly or through incorporation 0y reference) modifies or supersedes such previously included ACM Information. Any ACM Information so modified or superseded shall not constitute a i:art of this Official Statement, except as so modified or superseded.

M i scel I aneous Matters.

AG M makes no representation regardi ng the Bands or the ad.ii sabl Ii ty of investing i n the Bands. In addition, ACM has not independently verified, makes no representation regarding, and does not accept any responsibility for the accuracy or corrpleteness of this Official Statement or any information or di sci osure contai ned herei n, or oni tted herefrom, other than with respect to the accuracy of the information regarding ACM supplied 0y ACM and presented under the heading ''THE BONDS -Bond Insurance'' herein.

[REMAINDER OF PAGE LEFT BLANK]

9

Annual Debt Service

The follo.ving table displays the annual debt service requirements of the District for the Bonds ( assumi ng no opti anal redemptions):

Year Ending (August 1)

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040 2041 2042 2043 2044 2045 2046

Annual Principal Payment $965,000 460,000

80,000 120,000 165,000 205,000 255,000 305,000 365,000 425,000 485,000 545,000 610,000 685,000 770,000 860,000 955,000

1,055,000 l, 165,000 1,265,000 1,390,000 1,525,000 1,665,000 1,820,000 1,980,000 2,125,000 2,285,000

970,000 $25,500,000

Annual Interest Payment111

$1,502,738.61 l, 117,225.00 l, 103,425.00 l, 103,425.00 l, 100,225.00 1,095,425.00 1,088,825.00 1,080,625.00 1,067,875.00 1,052,625.00 1,034,375.00 1,017,375.00 1,002,825.00

985,793.76 955,293.76 921,043.76 882,543.76 839,543.76 791,793.76 739,043.76 696,812.50 630,400.00 557,425.00 477,362.50 389,950.00 294,400.00 215,200.00 130,200.00 38,800.00

$23,912,594.93

Total Annual Debt Service Payment

$2,467,738.61 1,577,225.00 l, 103,425.00 l, 183,425.00 1,220,225.00 1,260,425.00 1,293,825.00 1,335,625.00 1,372,875.00 1,417,625.00 1,459,375.00 1,502,375.00 1,547,825.00 l, 595, 793. 76 1,640,293.76 1,691,043.76 1,742,543.76 1,794,543.76 1,846,793.76 1,904,043.76 1,961,812.50 2,020,400.00 2,082,425.00 2,142,362.50 2,209,950.00 2,274,400.00 2,340,200.00 2,415,200.00 1,008,800.00

$49,412,594.93

'" Interest payrrents on the Bonds will be rmde serriannually on February l and August l of each year, comrrencing February l, 201&

See "BANNING UNIFIED SCHOOL DISTRICT -District Debt Structure -General Obligation Bonds" herein for a full table of the annual debt service requirements for the District's outstanding general obi i gati on bonded debt.

Application and Investment of Bond Proceeds

The Bonds are being issued 0y the District forthe purposes of (a) raising money for acquiring and constructing the prqjects, facilities and equipment set forth in the 2016Authorization, (b) funding interest on the Bands and ( c) to pay al I necessary I egal, financial , printing, i nsurance and other conti ngent costs i n connection with the issuance, sale and delivery of the Bonds.

Building Fund. The net proceeds of the sale of the Bonds will be deposited into the fund held b,t the County and designated as the "Banning Unified School District General Obligation Bonds, 2016 Election, Series A Building Fund' (the "Building Fund') and will be applied only for the purposes approved b,t the voters of the District pursuant to the 2016 Authorization. Any interest earnings on

10

rroneys held in the Building Fund will be retained therein. The County will have no responsibility for assuri ng the proper use of the proceeds of the B ands.

Debt Service Fund. Any prenium or accrued interest received b,t the District from the sale of the Bonds will be kept separate and apart in the fund designated as the "Banning Unified School District General Obligation Bonds, 2016 Election, Series A Debt Service Fund' (the "Debt Service Fund'), which fund is held b,t the County for the payment of principal of and interest on the Bands, and for no other purpose. Any interest earnings on rroneys held in the Debt Service Fund will be retained therein. Any excess proceeds of the Bands not needed for authorized purposes for which the Bands are being issued will be transferred to the Debt Service Fund and applied to the payment of the principal of and interest on the Bonds. Pursuant to the Resolution, the District has pledged monies on deposit in the Debt Service Fund to the payment of the Bands. If, after payment in ful I of the Bands, there remain excess proceeds, any such excess amounts will be transferred to the general fund of the District.

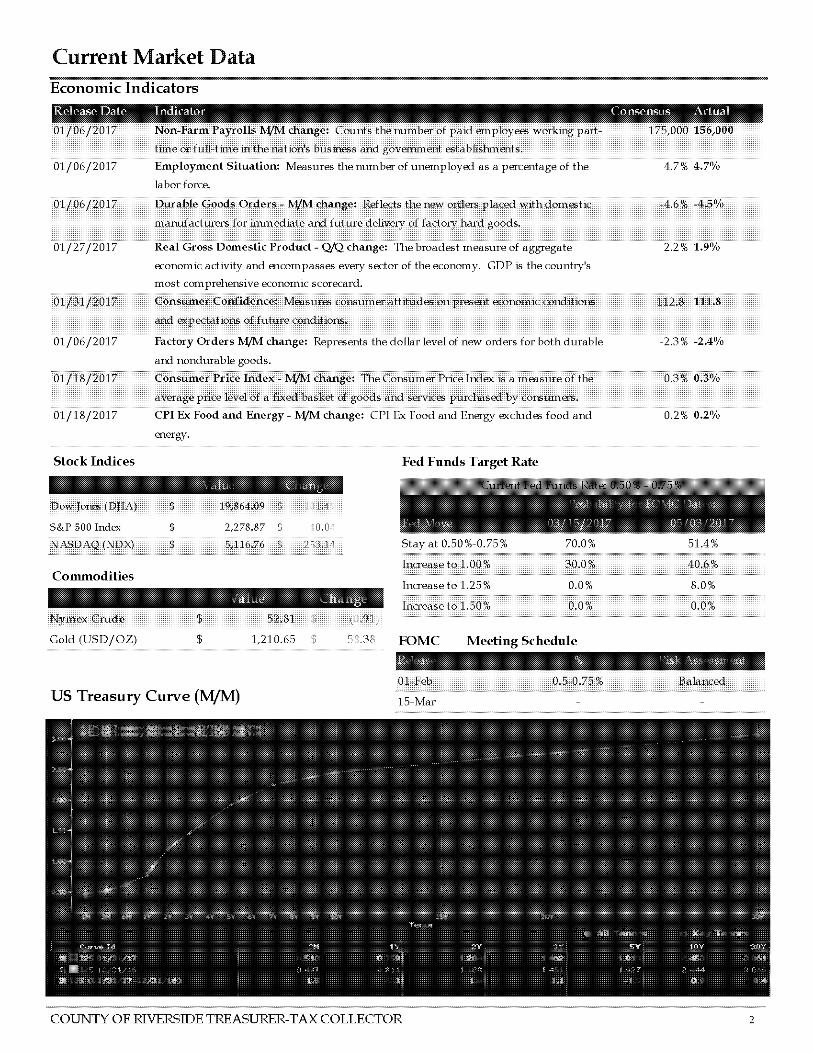

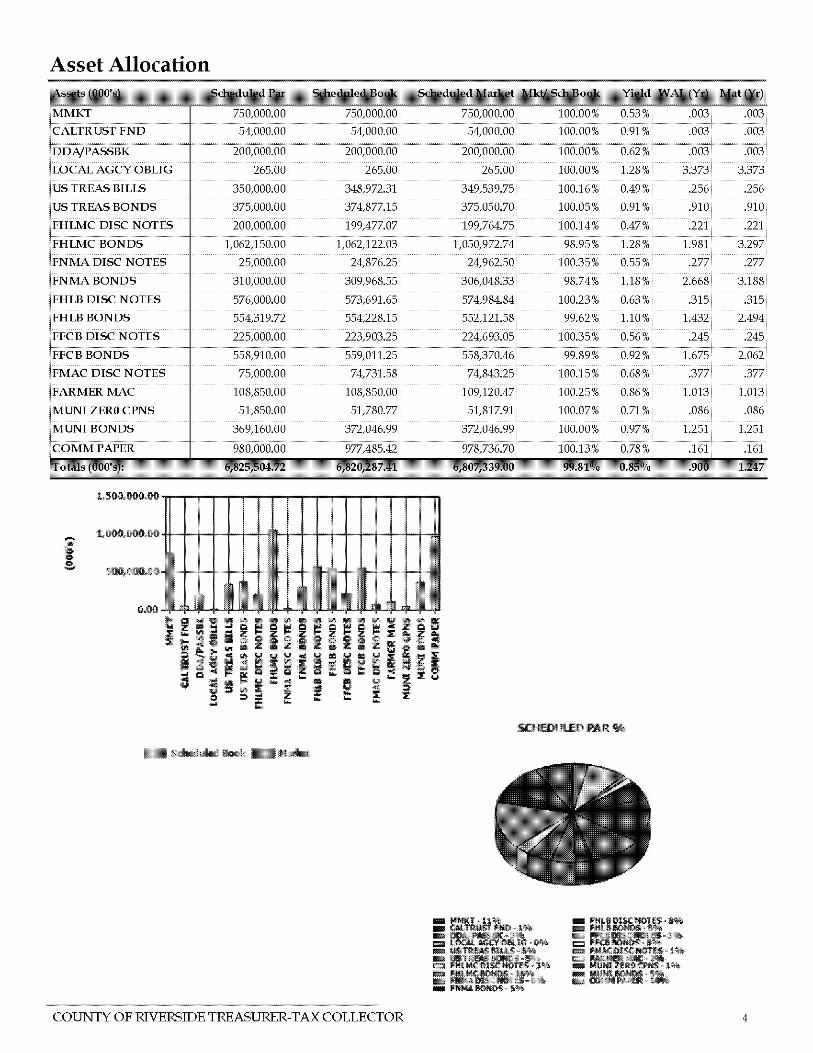

Investment of Proceeds. Moneys in the Building Fund and the Debt Service Fund are expected to be invested through the County's pooled investment fund. See "APPENDIX E - RIVERSIDE COUNTY TREASURY POOL" attached hereto.

Redemption

Optional Redemption. The Bonds maturing on or before August 1, 2027 are not sul::iject to redemption prior to their respective maturity dates. The Bonds maturing on or after August 1, 2028 may be redeemed prior to their respective stated maturity dates at the option of the District, from any source of available funds, as a whole or in part, on any date on or after August 1, 2027, at a redemption price of par, pl us accrued i nterest to the date of redemption.

[REMAINDER OF PAGE LEFT BLANK]

11

Mandatory Sinking Fund Redemption. The term bonds maturing on August 1, 2042 (the" 2042 Term Bonds") and August 1, 2046 (the" 2046Term Bonds," and, together with the 2042 Term Bonds, the "Term Bonds"), are sul::iject to redemption prior to maturity from mandatory sinking fund payments on August 1 of each year, on and after August 1, 2038, at a rederrption price equal to the princi1E amount thereof, together with accrued interest to the date fixed for redemption, without preni um. The pri nci IE amounts represented 0y such Term B ands to be so redeemed, the dates therefor and the fi nal pri nci IE payment date are as indicated in the fol Io.vi ng tables:

(l) Maturity.

-------------------------------(1) Maturity.

2042Term Bonds Redemption Date

(August 1)

2038 2039 2040 2041 204f 11

Principal Amount to be Redeemed

$1,265,000 1,390,000 1,525,000 1,665,000 1,820,000

2046Term Bonds Redemption Date Principal Amount to

(August 1) be Redeemed

2043 2044 2045 2046 11

$1,980,000 2,125,000 2,285,000

970,000

I n the event that a portion of the 2042 Term Bands or 2046 Term Bands is opti anal ly redeemed prior to maturity, the remaining mandatory sinking fund payments sho.vn abcwe shall be reduced proportionately, or as otherwise directed 0y the District, in integral multiples of $5,000 of princi1E amount, in respect of the portion of such Term Bands opti anal ly redeemed.

Selection of Bonds for Redemption. Whenever prwision is made for the optional redemption of Bonds and less than all outstanding Bonds are to be redeemed, the Paying Agent, upon written instruction from the District, will select the Bonds for rederrption as directed 0y the District and if not so directed, in inverse order of maturity. Within a maturity, the Paying Agent will select Bonds for rederrption as directed 0y the District, and if not so directed, 0y lot. Redemption 0y lot will be in such manner as the Paying Agent will deternine; prwided, ho.ve.1er, that the portion of any Bond to be redeemed in part shall be in the princi1E amount of $5,000 or any integral multiple thereof.

Notice of Redemption. When optional redemption is authorized or required pursuant to the Resolution, upon written instruction from the District, the Paying Agent will give notice (a "Redemption Notice") of the redemption of the Bonds. Each Rederrption Notice will specify that the Bonds or a designated portion thereof are to be redeemed; if I ess than al I of the then outstandi ng Bands are to be called for redemption, shall designate the numbers (or state that all Bonds between two stated numbers both inclusive have been called for redemption) and CUSIP numbers, if any, of the Bonds to be redeemed; the date of notice and the date of rederrpti on; the pl ace or pl aces where the redemption wi 11 be made; and descriptive information regarding the Bonds and the specific Bonds to be redeemed, including the dated date, interest rate and stated maturity date of each. Such notice shall further state that on the

12

specified date there shall becorre due and i:ayable upon each Bond to be redeerred, the portion of the Pri nci i:al A nu.mt of such Bond to be redeerred, together with i nterest accrued, to the date of rederrpti on, and rederrpti on preni um( s), if any, and that from and after such date i nterest with respect thereto shal I cease to accrue, as appl i cable.

The Paying Agent will take the follo.ving actions with respect to each such Redemption Notice at least 20 but not more than 45 days prior to the redemption date, such Rederrption Notice will be given to (a) the registered ONners of Bonds, to a Securities Depository, and a national Information Service 0y first class mail; (b) the District, the County, and the respective ONners of any registered Bonds designated for redemption b,t first cl ass mai I, postage prei:ai d, at their addresses appearing on the bond register.

"Informational Services'' rreans the Municii:al Securities Rulemaking Board, through its Electronic Municii:al Market Access (EMMA) system, and, in accordance with then current guidelines of the Securities and Exchange Comnission, such other addresses and;br such other services prwiding information with respect to called bonds as the District may designate in a written request of the District delivered to the Paying Agent.

"Securities Depositories'' rreans the fol lo.vi ng: The Depository Trust Corrpany, with Cede & Co. as its noninee, and in accordance with then current guidelines of the Securities and Exchange Cornnission, such other addresses and;br such other securities depositories as the District may designate in a written request of the District delivered to the Paying Agent.

A certificate of the Paying Agent or the District that a Redemption Notice has been given as provided in the Resolution will be conclusive as against all i:arties. Neither failure to receive or send any Redemption Notice nor any defect in any such Redemption Notice so given will affect the sufficiency of the proceedings for the rederrpti on of the affected Bands. Each check issued or transfer of funds made 0y the Paying Agent for the purpose of redeening Bonds shall bear or include the CUSIP nuniber identifying, b,t issue and maturity, the Bonds being redeemed with the proceeds of such check or other transfer.

Contingent Redemption; Rescission of Redemption. Any Redemption Notice may specify that redemption of the Bands designated for rederrpti on on the specified date wi 11 be sul::ij ect to the receipt b,t the District of monies sufficient to cause such rederrption (and will specify the proposed source of such monies), and the District, the County and the Paying Agent will have no liability to the ONners of any Bonds, or any other i:attv, as a result of the District's failure to redeem the Bonds designated for redemption as a result of insufficient monies therefor.

Additionally, the District may rescind any optional redemption of the Bonds, and notice thereof, for any reason on any date prior to the date fixed for such rederrpti on b,t causi ng written notice of the rescission to be given to the ONners of the Bonds so called for redemption. Notice of rescission of redemption shall be given in the sarre manner in which notice of redemption was originally given. The actual receipt b,t the ONner of any Bond of notice of such rescission shall not be a condition precedent to rescission, and fai I ure to receive such notice or any defect in such notice shal I not affect the validity of the rescission.

Neither the District nor the County will have any liability to the ONners of any Bonds, or any other plrty, as a result of the District's decision to rescind redemption of any Bonds pursuant to the provisions of this subsection.

13

Payment of Redeemed Bonds. When a Rederrption Notice has been given substantially as described above, and, when the amount necessary for the rederrpti on of the Bands cal I ed for rederrpti on ( principal, interest, and premium, if any) is irrevocably set aside for that purpose in the Debt Service Fund, as described in "-Defeasance," the Bonds designated for redemption in such notice will become due and payable on the date fixed for rederrption thereof and upon presentation and surrender of said Bonds at the place specified in the Redemption Notice, said Bonds will be redeemed and paid at the rederrption price out of such fund. All unpaid interest payable at or prior to the redemption date will continue to be payable to the respective ONners, but without interest thereon.

Partial Redemption of Bonds. Upon the surrender of any Bond redeemed in part only, the Paying Agent will execute and delivertothe ONnerthereof a new Bond or Bonds of like series, tenor and maturity and of authorized denoninations equal in principal amount to the unredeemed portion of the Bond surrendered ( the ''Trans fer A mount''). Such partial redemption is val id upon payment of the amount required to be paid to such ONner, and the District will be released and discharged thereupon from all liability to the extent of such payment.

Effect of Notice of Redemption. Notice having been given as described above, and the moneys for the rederrpti on (incl udi ng the interest accrued to the applicable date of rederrpti on) having been set aside as described in "-Defeasance'' herein, the Bonds to be redeemed shall become due and payable on such date of rederrpti on.

If on such redemption date, moneys for the rederrpti on of al I the Bands to be redeemed, together with interest accrued to such rederrption date, shall be held in trust, so as to be available therefor on such rederrption date, and if a Redemption Notice thereof shall have been given as described above, then from and after such rederrpti on date, i nterest on the Bands to be redeemed wi 11 cease to accrue and become payable. All money held forthe redemption of Bonds shall be held in trust for the account of the ONners of the Bands to be so redeemed.