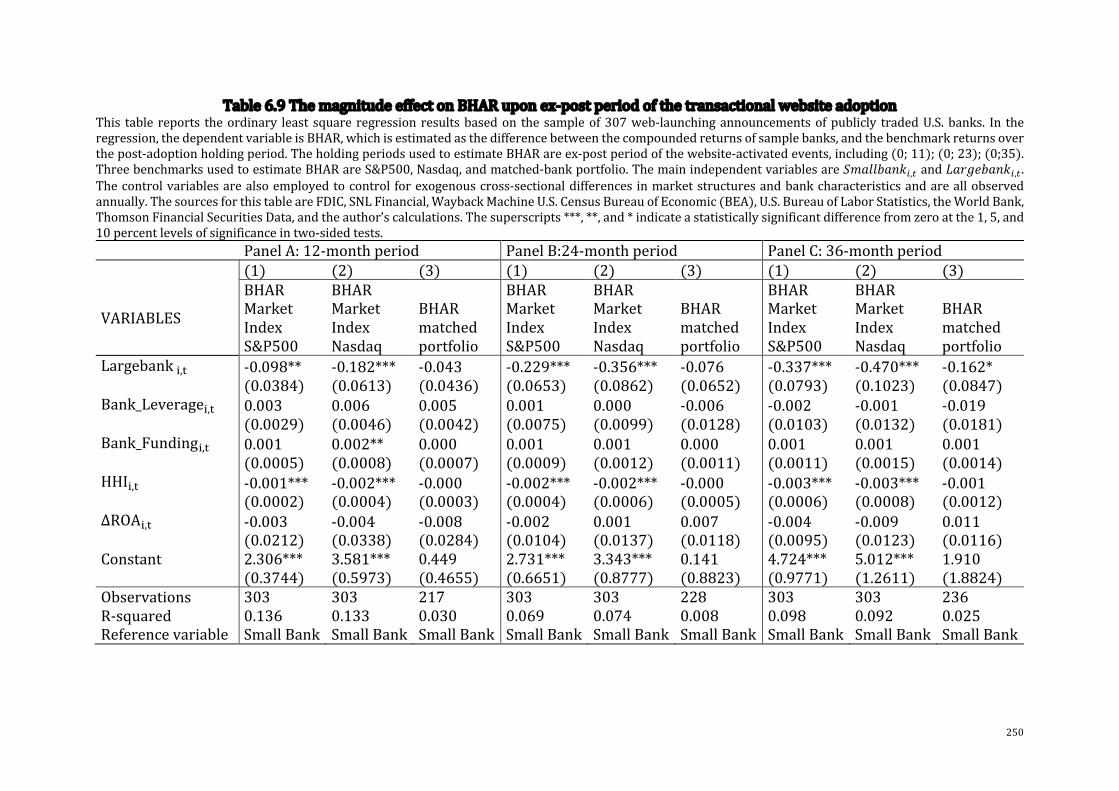

2022 Awarding institution - Research Portal

394

Bangor University DOCTOR OF PHILOSOPHY The Impact of Transactional Website Adoption on Banks’ Performance Dang, Ho Phuong Lan Award date: 2022 Awarding institution: Bangor University Link to publication General rights Copyright and moral rights for the publications made accessible in the public portal are retained by the authors and/or other copyright owners and it is a condition of accessing publications that users recognise and abide by the legal requirements associated with these rights. • Users may download and print one copy of any publication from the public portal for the purpose of private study or research. • You may not further distribute the material or use it for any profit-making activity or commercial gain • You may freely distribute the URL identifying the publication in the public portal ? Take down policy If you believe that this document breaches copyright please contact us providing details, and we will remove access to the work immediately and investigate your claim. Download date: 01. Apr. 2022

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of 2022 Awarding institution - Research Portal

Bangor University

DOCTOR OF PHILOSOPHY

The Impact of Transactional Website Adoption on Banks’ Performance

Dang, Ho Phuong Lan

Award date:2022

Awarding institution:Bangor University

Link to publication

General rightsCopyright and moral rights for the publications made accessible in the public portal are retained by the authors and/or other copyright ownersand it is a condition of accessing publications that users recognise and abide by the legal requirements associated with these rights.

• Users may download and print one copy of any publication from the public portal for the purpose of private study or research. • You may not further distribute the material or use it for any profit-making activity or commercial gain • You may freely distribute the URL identifying the publication in the public portal ?

Take down policyIf you believe that this document breaches copyright please contact us providing details, and we will remove access to the work immediatelyand investigate your claim.

Download date: 01. Apr. 2022

1

TheImpactofTransactionalWebsiteAdoptiononBanks’Performance

ByHoPhuongLanDANG

Ph.D.Thesis

BangorBusinessSchool

BangorUniversity

26thJanuary2022

2

DECLARATION

Iherebydeclare that this thesis is theresultsofmyown investigations,exceptwhere

otherwisestated.Allothersourcesareacknowledgedbybibliographicreferences.This

work has not previously been accepted in substance for any degree and is not being

concurrentlysubmittedincandidatureforanydegreeunless,asagreedbytheUniversity,

forapproveddualawards.

Yrwyfdrwyhynyndatganmaicanlyniadfyymchwilfyhunyw’rthesishwn,aceithrio

lle nodir ynwahanol. Caiff ffynonellau eraill eu cydnabodgandroednodiadauyn rhoi

cyfeiriadaueglur.Nidywsylweddygwaithhwnwedicaeleidderbyno’rblaenargyfer

unrhywradd,acnidyw’ncaeleigyflwynoaryrunprydmewnymgeisiaethamunrhyw

raddonibaieifod,felycytunwydganyBrifysgol,amgymwysteraudeuolcymeradwy.

3

ABSTRACT

The aim of this thesis is to examine the value that the adoption of the transactional

websitehasaddedtobanks’financialperformanceandmarketvalue,overboththeshort

runandlongrun.Followingtheliterature,thisthesisdefinesthetransactionalwebsiteas

abankingwebsitethatallowscustomersto(i)accessinformationand(ii)conductthe

mostbasictransactionsviathesite,atleastbillpaymentsandfundstransfer.

Thisthesisbeginswithanoveldataincluding307fullylistedcommercialbanksintheUS

that launched their transactional website between 1996 and 2010. Following this,

conceptualmodelsareproposedbasedon the resource-basedview.This combination

allows the considerationof the impactof transactionalwebsite adoptionbasedon its

internalstrengthsandthereactionofthemarketandinvestors.

Subsequently, event study and financial measures are the principal methodologies

applied.ItisthefirsttimethatthetwometricsofCumulativeAbnormalReturnandBuy-

and-HoldAbnormalReturnareincorporatedintodigitalbankingliterature,allowingthe

exploitation of market responses and investor behaviour. Furthermore, this thesis

employsfinancialmeasures,alongwithaseriesofregressions,toexaminethestrategic

roleof transactionalwebsite adoption, via its strategic attributes. Strategic attributes,

underthegroundofresource-basedview,willbetherootofthesustainabilityoffirms’

strategy.Itisbecausetheycan(i)deliversuperiorperformanceandcompetitiveedge,

and (ii) preserve value and limit competition. In the banking literature so far, the

adoption of the transactional website is only verified to be profitable, efficient, and

innovativebutnotstrategicandsustainable.

Theresultsbringnewstoriesabouttransactionalwebsiteadoption.Most importantly,

the activation of transactional websites delivers value to both banks’ financial

performance and their market value in both the short- and long-term intervals,

complyingwiththevaluemindsetandsustainabilitymindset.Furthermore, itsatisfies

the conditions of the resource-based view by virtue of its six features, namely value,

appropriability,durability,inimitability,embeddedness,andinterconnectedness.These

features are proved via the way transactional website adoption strengthens the

profitabilityandefficiencyaswellasgeneratesisolatedmechanismstolimitcompetition

(e.g., cumulative experiences, the interconnectedness between transactional website

adoptionandmobilewebsiteadoption).Additionally,thisthesisprovidesnewfindings

oftheimpactofthesizefactor,timingfactorandvicariouslearningbehaviour.Ofwhich,

4

small banks and latecomers tends to achieve more superior performance from their

activation of transactionalwebsites. Furthermore, public information on theprevious

transactional website adoptions becomes an important mechanism for investors’

enhancementinevaluatingofotherwebsiteeventsafterward.

Such evidence suggests that it is time for banks to pay more attention to the value

delivered by their transactional website enablement. At the same time, investor

behaviour,marketresponse,andmulti-channelcombinationarealsowhatbanksshould

focusontodrivetheirsuccessinimplementingtransactionalwebsiteinitiatives.

5

ACKNOWLEDGEMENT

Inthissection,Iwouldliketoexpressmysincerethankstothosewhohaveaccompanied

andhelpedmeduringmydoctoralprogram.

Firstofall,IwouldliketothankBangorUniversityandthecollectiveacademicstaffin

generalfortheirsupport.ThankstoafullscholarshipfromBangorUniversityforhelping

mefulfilmydreamofresearchingadoctorate.

Following this, I would like to extend my sincere and special thanks to my three

supervisors.

Iwould like to expressmydeepest thanks toProf SantiagoCarbo-Valverde.He is the

personwhomostdeeplyinspiredmetoresearchinthebankingandfinancediscipline.

Heisalsoapersonwhohassupportedmealotsincemymaster'sdegree.Santiagohas

accompanied me through many difficulties during my PhD program. He is also my

teachingadvisor,helpingmetoachievemyFHEAdegreeintheprocessofimplementing

my PhD program. With all my gratitude, I want to thank Santiago for his wisdom,

understanding,andsupportthroughouttheyears.

IwouldliketoexpressmydeepgratitudetoDrSaverioStentellaLopeswhohasbeenof

great help inmy PhD thesis. The ideas of the URL data, the long-term buy-and-hold

abnormalreturnsaswellasthestatisticpartsweregreatlysupportedbySaverio.Healso

gaveme great creative inspiration and encouragedme a lot during difficult times of

mine.It canbesaid thatSaverio's ideasare the inspiration for thedevelopmentofmy

knowledge base later. Even when Saverio left Bangor University, he never stopped

helpingandcaringaboutmyPhD.AllIcansayisI'mreallygratefulforthis!

OneofthepeoplewhohadthebiggestinfluenceonmeduringthelastyearsofmyPhD

wasGwion. Iwould liketoextendmygratitudetoGwionforhishelp,whichhaseven

exceededmyexpectations.Hishelpisnotonlyprofessionalbutalsospiritual,whichhelps

mealottoovercomedifficulties.Hehasaccompaniedmethroughmanyupsanddowns

andisapersonwhocalmlysolvesproblemsthatarise.IcanonlysaythatGwion'ssupport

6

has greatly influenced the success of this PhD thesis. I hope he understands I cannot

expressmygratitudeforhishelpbywords.

I know that the abovewords formy supervisors are not never enough.With all my

respect, I thank and admire Santiago, Saverio, and Gwion for their great expertise,

understanding,sincerity,andsupportovertheyears.Iamforevergratefulforthat.You

guysarethebestteachersofmylife.

Iwouldalso like to thankProf.RashaAlsakka forherconcern forPhDstudents'well-

being. Additionally, I would like to thank Prof. Owain, Prof Owain ap Gwilym, Prof

Jonathan Williams, Prof Aziz Jaafar, Prof Edward Shiu, Prof Lynn Hodgkinson, Prof

AndrewHiscock,DrDanialHemmings,DrAlanThomas,DrNoemiMantovan,NiaWyn

Weatherleyfortheirprofessionalassistance.IwouldliketothankBangorUniversity's

academicstaffandotherstafffortheirdedicationtostudents(especiallyJulieBolton).I

wouldliketothanktheInternationalStudentTeam,Visa&Immigrationteam(especially

AlanEdwards),andthecounsellingserviceteamofBangorUniversity.ThankyoutoDr

RosannaRobisonandPGCertteamfororganizingusefulprogramsforus.

Thankyoutomyfamilywhohasbeenwithmethroughmanyupsanddowns.Thankyou

forplacingyourtrustinme.Throughmanyupsanddowns,Irealizethatfamilyisthebest

thingandIwouldliketothankmyparents(VanNghiepandMinhSuong)andmylittle

sister(AnhDang).Pleaseforgivethetimesthatupsetthefamily.Butthewayfromnow

onwillbebrightforme.Thankyoutomygrandmother,aunts(DiBa,DiBon,coHoa),

uncles(cauHai,cauBay),cousins(anhTin,anhSon,chiDiem,Chieu,Be),nephews(Ti,

Chuot),niecesforcaringandlovingme.ThePhDperiodwassobusythat Ididn'tpay

muchattentiontoyouguys.Butsurelymyloveforfamilyandrelativesneverchanges.

Love you forever,mom, dad, little sister, grandma, aunties, uncles, cousins, nephews,

nieces.

Iwouldliketothankmybestfriends.ThankyouPhuDat,VanDai,NgocThuy,TanLoc,

HanaNhi,ThaiNgoc(andhisfamilyandfriends),ThuSang,NgocDiep(andherfriends),

Rachel,Wang,Dong,TienLee(andhis familyandfriends)whohavebeenbymyside.

ThankstoVictoria,mybestfriend,aDr.inLaw,foraccompanyingandhelpingmeover

7

the years. Thanks to Josef for his great help in PhD proofreading. Thanks tomy PhD

colleagues (Summer,Alessio,Tolope,Weifei, Taniyang,Reida, Susan) for theirhelpful

suggestionsandsupport.ThankyoutoalltheotherfriendsinVietnam(especiallyThich

Le,TuanAnh,BaoAnh,MinhKhue,DieuMinh,DaiDuyenandThienPhuc,Lana,Tra,Minh

Quan),intheUK(especiallyJoeandJessica,Stephan,Cecil,Waleed,IoIo,Zelda,Baboo,

Azhar,)andothercountriesfortheirunderstandingandsharing.

Last but not least, I extendmy gratitude to the exminers of this thesis- Dr TimKing

(externalexaminer)andProfessorRashaAlsakka(internalexaminer).Their feedback

didhelptoimprovethisPhDthesispositivelyanditwasabsolutelyvaluablefeedbackfor

me. I firmlybelieve thatmyacademic expertise in the futurewill bepartly improved

thanks to the feedback from the examiners. Please allowme to be grateful for their

attentionandsupport.SpecialthanksalsogotoDrDanialHemming(chair),DrNoemi

Mantovan (as PGR Lead), Professor Andrew Hiscock (Dear of PGR), Prof Owain ap

Gwilym,andJulieBoltonforallthesupportthroughout.

Withallmygratitude,Iwouldliketothankandrememberthehelpinthisheartforever

after.

8

TABLEOFCONTENTS

DECLARATION...................................................................................................................................................2

ABSTRACT............................................................................................................................................................3

ACKNOWLEDGEMENT...................................................................................................................................5

TABLEOFCONTENTS.....................................................................................................................................8

LISTOFTABLES..............................................................................................................................................16

LISTOFFIGURES.............................................................................................................................................18

1 Chapter1:Introduction......................................................................................................................19

1.1 Background....................................................................................................................................19

1.2 MotivationsandAims................................................................................................................23

1.3 Methodology..................................................................................................................................26

1.4 Contribution..................................................................................................................................27

1.5 Structure.........................................................................................................................................28

2 Chapter2:LiteratureReviewandTheoreticalFramework...............................................30

2.1 TheoreticalFramework-Resource-basedView...........................................................30

2.1.1 TheGeneralConceptoftheResource-BasedView.............................................30

2.1.2 ResourcesandCapabilities............................................................................................30

2.1.3 AttributesofStrategicResources...............................................................................32

2.1.4 ImplicationsoftheResource-BasedViewforDigitalBankingAdoption..39

2.2 TheGeneralContextofDigitalization.................................................................................41

2.2.1 DigitalizationintheBankingIndustry.....................................................................41

2.2.2 OpportunitiesandChallengesinBankingDigitalization.................................42

2.3 ValueofDigitalization...............................................................................................................44

2.3.1 ValueofDigitalizationDeliveredtoCustomers...................................................44

2.3.2 ValueofDigitalizationAddedtoBanks’Performance.......................................53

2.4 TheUSbankingevolutionanddigitalizationintheUSbankingindustry..........65

2.4.1 Thederegulationsincethe1990s..............................................................................65

2.4.2 Financialcrisis(2007-2009)........................................................................................69

2.4.3 Post-crisisreforms(2010-2016)...............................................................................69

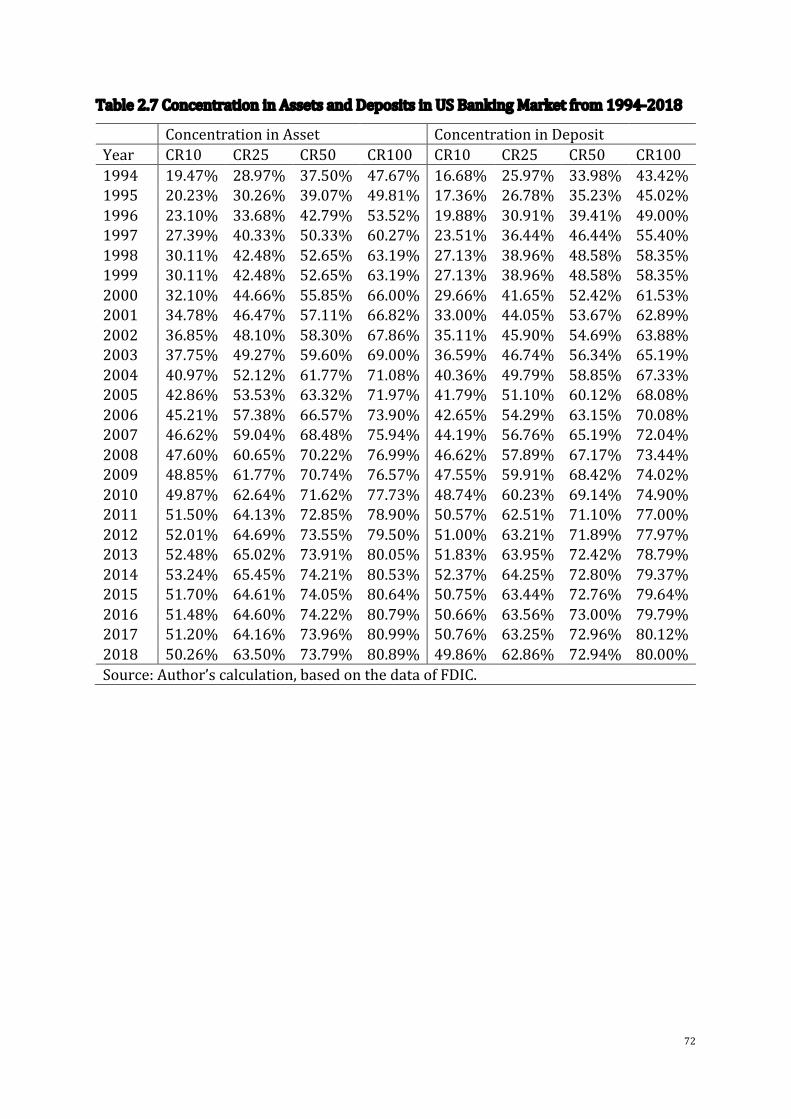

2.4.4 ThecompetitivelandscapeinUSbankingindustry...........................................70

9

2.4.5 TheimportanceofdigitalizationintheUSbankingindustry........................75

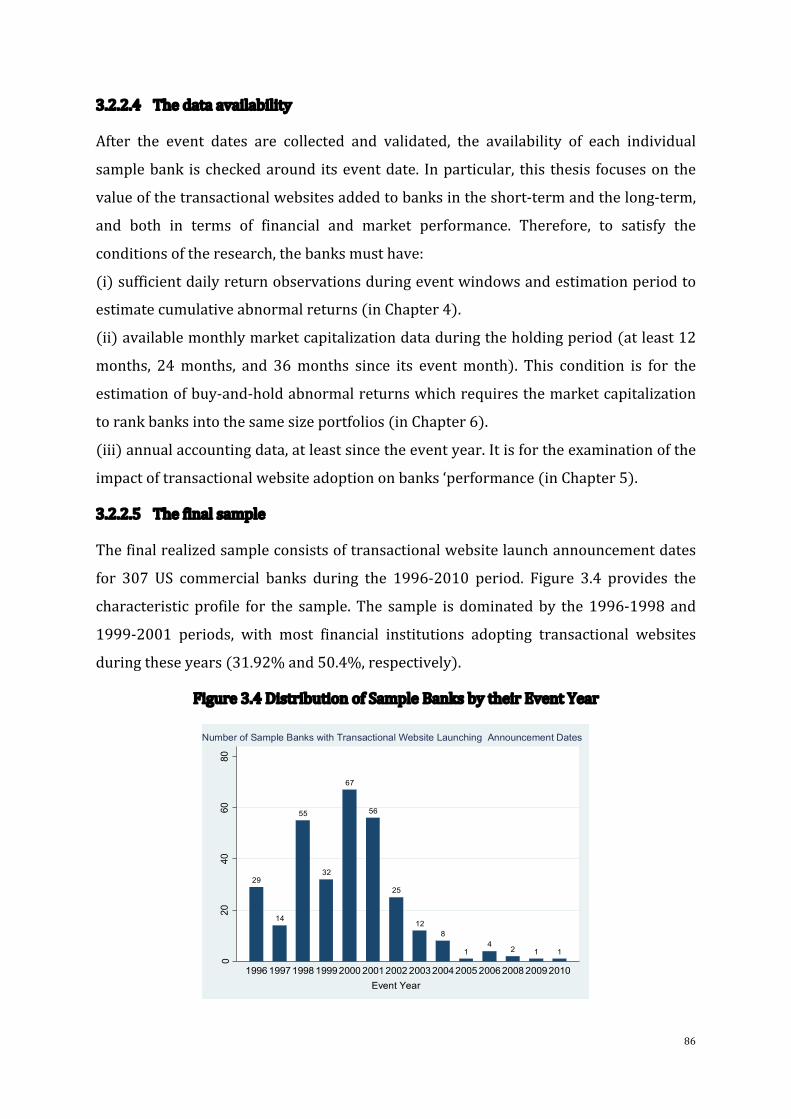

3 Chapter3:DataCollectionandDescription...............................................................................77

3.1 Sampling..........................................................................................................................................77

3.1.1 Thedefinitionoftransactionalwebsiteadoption...............................................77

3.1.2 Themotivationofchoosingthetransactionalwebsite.....................................78

3.2 DataCollection..............................................................................................................................80

3.2.1 Constructingthesampleofbanks..............................................................................80

3.2.2 TheTransactionalWebsiteAdoptionDate............................................................80

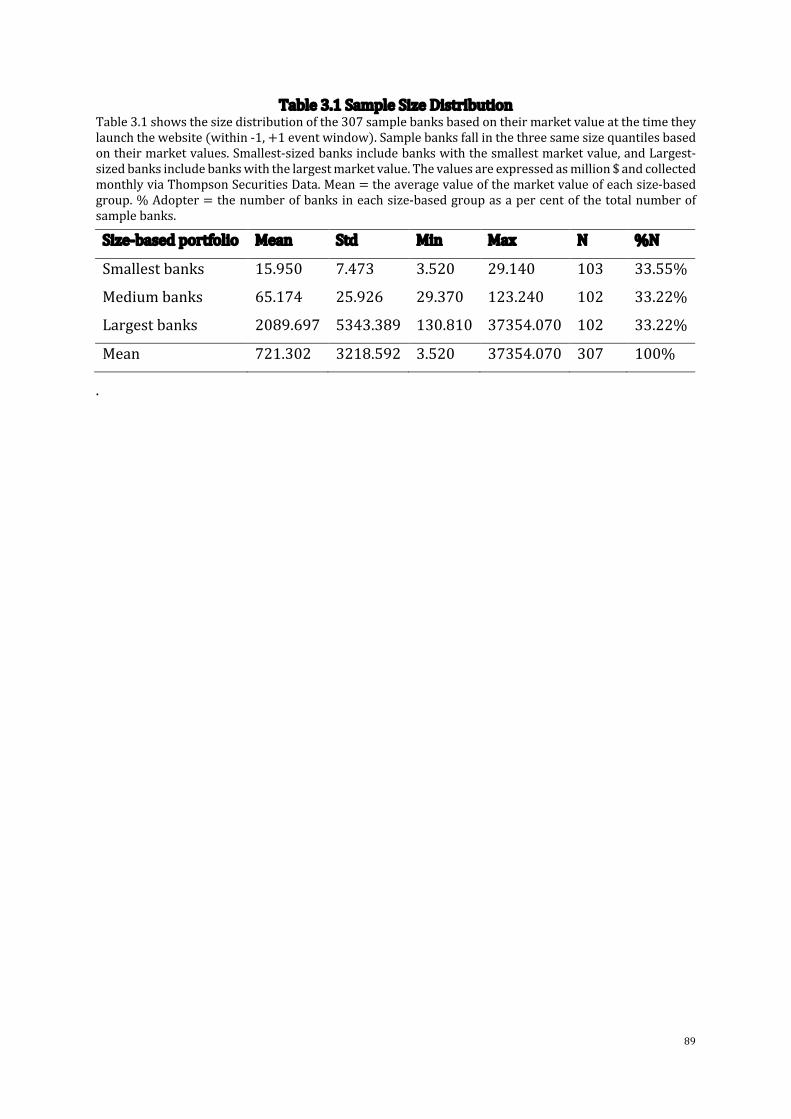

3.3 DataDescription..........................................................................................................................87

3.4 SomeImportantConsiderations...........................................................................................94

3.4.1 Marketreactiontothetransactionalwebsiteadoption...................................94

3.4.2 Banks’spre-announcements........................................................................................95

3.4.3 Survivorshipbias...............................................................................................................96

3.4.4 M&Aactivities.....................................................................................................................97

4 Chapter4:DoTransactionalWebsiteInitiativesAddValuetoBanks?.........................99

4.1 Introduction...................................................................................................................................99

4.2 Literaturereviewandhypothesisdevelopment.........................................................103

4.2.1 Theimpactofdigitalinitiativesonthemarketvalueofbanks....................103

4.2.2 TheMagnitudeEffect.....................................................................................................107

4.2.3 TheInfluenceoftheTimingEffect...........................................................................108

4.3 DataandMethodology............................................................................................................110

4.3.1 Data........................................................................................................................................110

4.3.2 Eventstudymethodology............................................................................................111

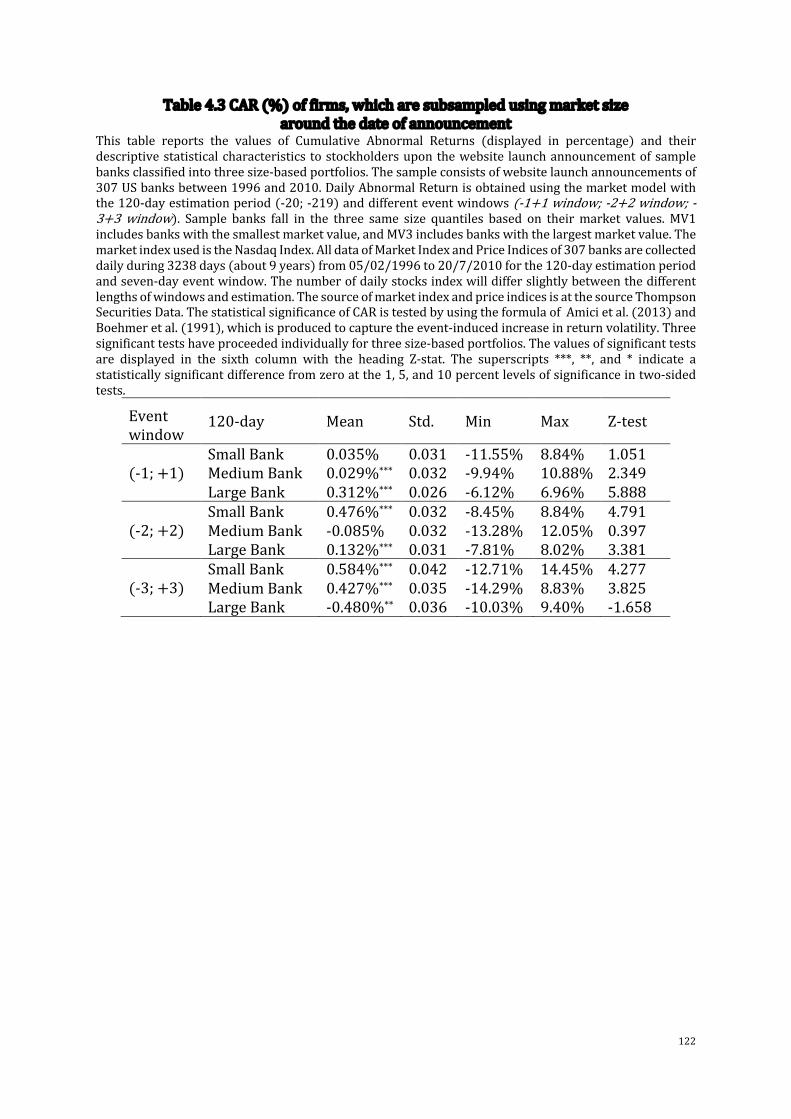

4.4 EmpiricalResultsandDiscussions....................................................................................115

4.4.1 EmpiricalResultsforHypothesis4.1:Wealthcreationoftransactional

websitelauncheventsovertheshortterm.............................................................................115

4.4.2 EmpiricalresultsforHypothesis4.2:Themagnitudeeffectintheshort-

termuponatransactionalwebsitelaunchevent..................................................................116

4.4.3 EmpiricalResultsforHypothesis4.3:Timingeffect........................................118

10

4.5 RobustnessTesting..................................................................................................................124

4.5.1 Alternativeestimationperiods..................................................................................124

4.5.2 Alternativemarketindex.............................................................................................124

4.6 Conclusion....................................................................................................................................125

4.6.1 SummaryofFindings.....................................................................................................125

4.6.2 ManagerialImplications...............................................................................................127

4.6.3 LimitationsandDirectionsforFutureResearch................................................128

5 Chapter5:DoestheAdoptionofTransactionalWebsitesImproveBanks’Financial

Performance?.................................................................................................................................................130

5.1 Introduction.................................................................................................................................130

5.2 LiteratureReview.....................................................................................................................133

5.2.1 Theaccounting-basedapproachanditssuperiority.......................................133

5.2.2 Theaccounting-basedapproachindigitalbankingliterature.....................134

5.2.3 LiteratureGaps.................................................................................................................135

5.3 HypothesesProposal...............................................................................................................139

5.3.1 TheFeaturesofValue,AppropriabilityandDurabilityinTransactional

WebsiteAdoption...............................................................................................................................139

5.3.2 TheFeaturesofEmbeddedness,Interconnectedness,andInimitabilityof

TransactionalWebsiteAdoption..................................................................................................140

5.3.3 Inter-FirmHeterogeneityduetotheSizeEffect................................................144

5.3.4 Inter-FirmHeterogeneityduetotheTimingOrderEffect............................147

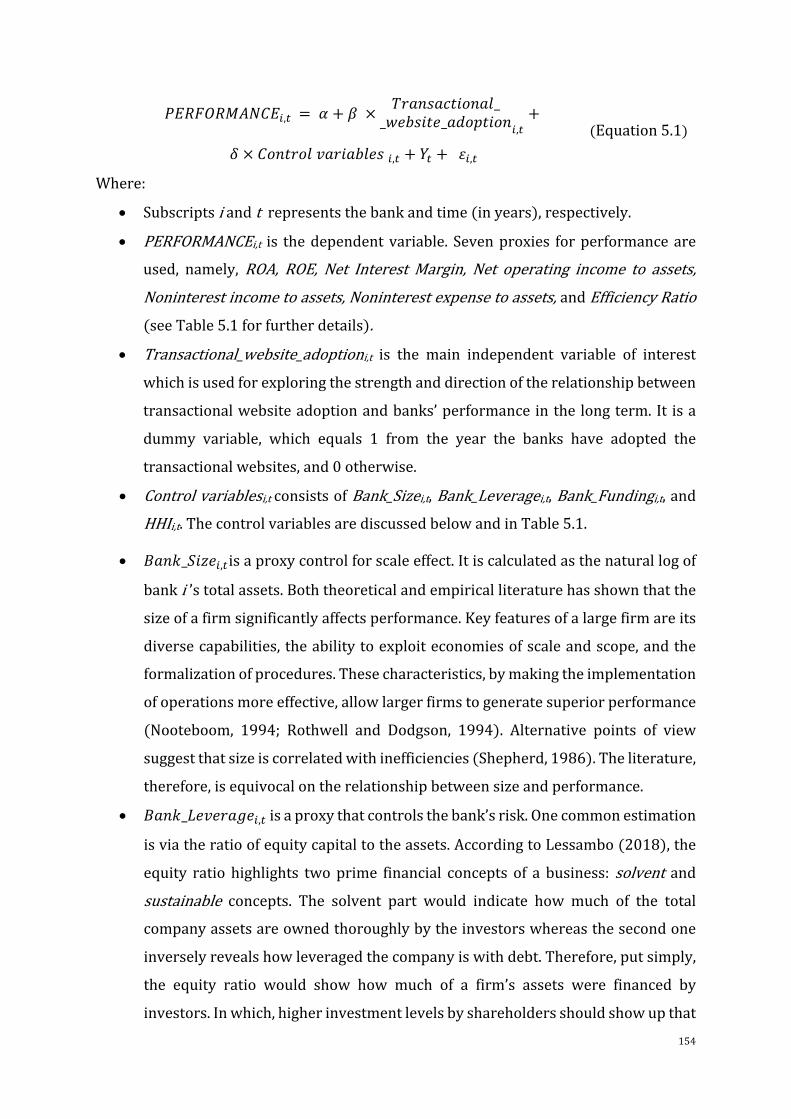

5.4 Data.................................................................................................................................................151

5.4.1 Mobileadoptiondata.....................................................................................................151

5.5 MethodologyandEmpiricalResults.................................................................................153

5.5.1 Hypothesis5.1:Thelong-termimpactoftransactionalwebsiteadoption

onbanks’financialperformance..................................................................................................153

5.5.2 Hypothesis5.2:TheFeaturesofEmbeddedness,Interconnectedness,and

InimitabilityofTransactionalWebsiteAdoption.................................................................164

5.5.3 Hypothesis5.5:TheInter-FirmHeterogeneityAttributedtoSizeEffect178

11

5.5.4 Hypothesis5.4:Inter-firmHeterogeneityAttributedtotheTimingOrder.

186

5.6 Robustnesstest..........................................................................................................................191

5.6.1 Meandifferenceinbanksaccountingperformance.........................................191

5.6.2 Dynamicstesting..............................................................................................................192

5.6.3 Re-categorizationofbanksizeintothreequantiles.........................................193

5.6.4 Re-estimationofallmainequations,usingyear,stateandbank-levelfixed

effect 193

5.7 Conclusion....................................................................................................................................195

5.7.1 SummaryofFindings.....................................................................................................195

5.7.2 MainContributions.........................................................................................................198

5.7.3 ManagerialImplications...............................................................................................200

5.7.4 LimitationsandFutureDiscussion..........................................................................201

6 Chapter6:DoDigitalTransactionalWebsiteInitiativesAddValuetoBanksinLong

Run?...................................................................................................................................................................204

6.1 Introduction.................................................................................................................................204

6.2 LiteratureReview.....................................................................................................................208

6.2.1 Theimpactofdigitaladoptiononbanks’performanceinthelongrun..208

6.2.2 Thegapindigitalbankingliteratureandtheimportanceoflong-term

examination...........................................................................................................................................208

6.2.3 Long-runreturnAnomaliesLiterature..................................................................209

6.2.4 Mainfindingsintheliteratureandthisresearchcontribution...................210

6.3 HypothesisProposal................................................................................................................214

6.3.1 Hypothesis6.1:Wealthcreationoftransactionalwebsiteadoptioninthe

longterm.................................................................................................................................................214

6.3.2 Hypothesis6.2:Theimpactofthe“learningbyobserving”effect.............220

6.3.3 Hypothesis6.3andHypothesis6.4:Theimpactofthemagnitudeeffect

andtimingeffectoverthelongterm..........................................................................................221

6.4 MethodologyandDataDescription...................................................................................222

6.4.1 Estimationoflong-termAbnormalReturns........................................................222

12

6.4.2 MethodologyofHypothesis6.1:TheregressionbetweenBHARand

transactionalwebsiteadoption....................................................................................................230

6.4.3 MethodologyofHypothesis6.2:Theimpactofthe“learningbyobserving”

231

6.4.4 MethodologyofHypothesis6.3:Theimpactofmagnitudeeffectinthe

longrun 232

6.4.5 MethodologyofHypothesis6.4:Theimpactoftimingeffectinthelongrun

233

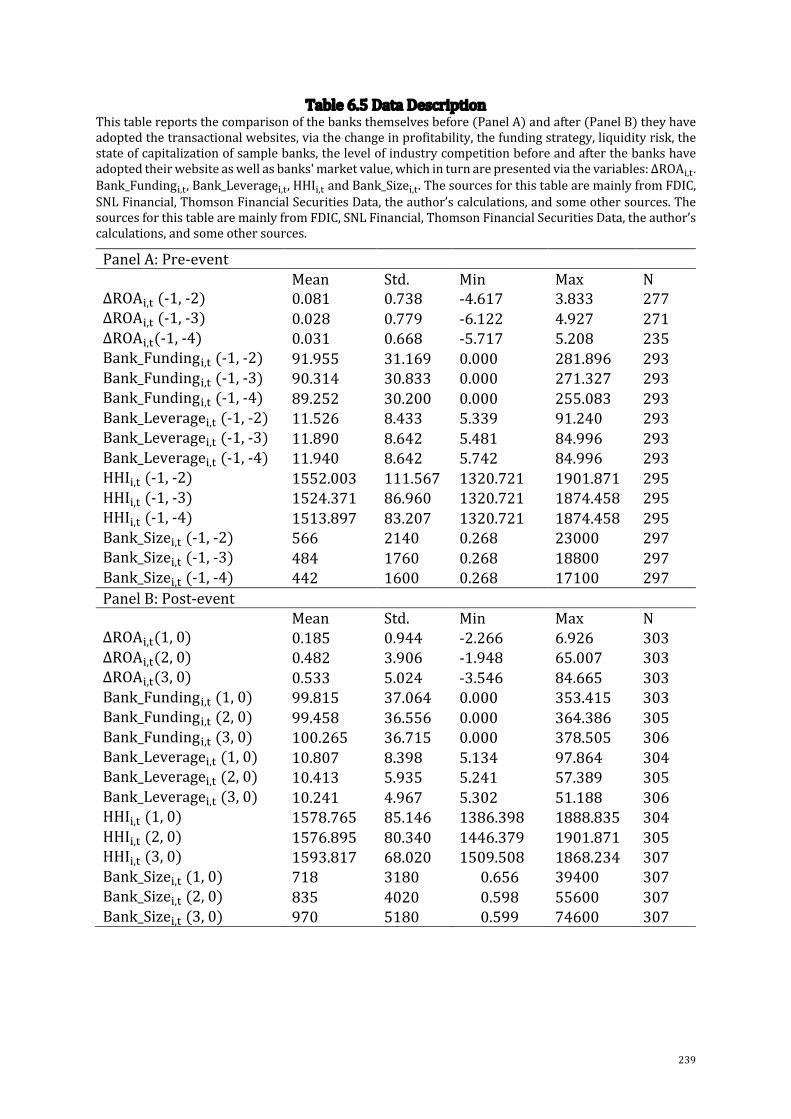

6.4.6 DescriptiveStatistics......................................................................................................237

6.5 EmpiricalResults.......................................................................................................................240

6.5.1 ResultsofHypothesis6.1:Wealthcreationoftransactionalwebsite

adoptioninthelongterm................................................................................................................240

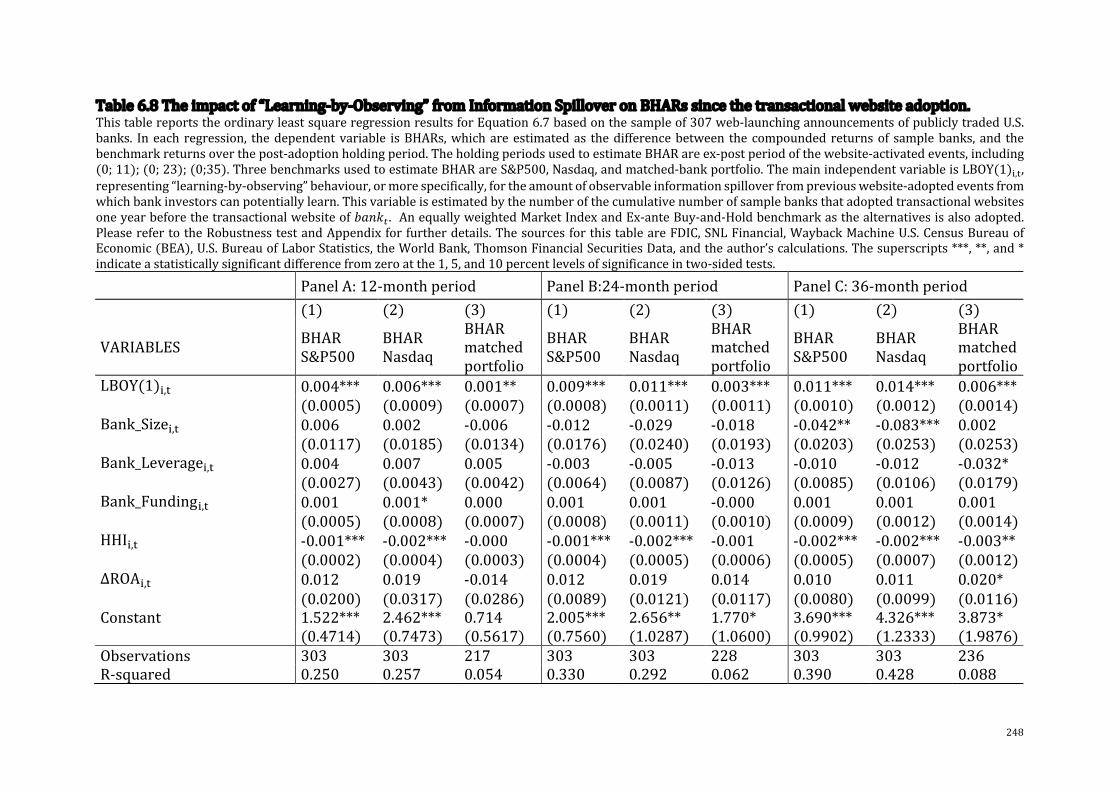

6.5.2 ResultsofHypothesis6.2:Theimpactofthe“learningbyobserving”....245

6.5.3 ResultsofHypothesis6.3:Theimpactofmagnitudeeffectinthelongrun

249

6.5.4 ResultsofHypothesis6.4:Theimpactoftimingeffectinthelongrun...252

6.6 RobustnessTests.......................................................................................................................257

6.6.1 Applicationofalternativebenchmarks..................................................................257

6.6.2 The“Learning-by-observing”effect........................................................................257

6.6.3 Thesizeeffectoverbothex-anteandex-postperiodsoftransactional

websitelaunchingevents................................................................................................................258

6.6.4 Thetimingeffectovertheex-postperiodoftransactionalwebsitelaunch

events. 259

6.6.5 Re-estimationofallmainequations,usingfixedeffects................................260

6.7 Conclusion....................................................................................................................................260

6.7.1 SummaryofFindings.....................................................................................................260

6.7.2 SupportiveLiteratureandFurtherDiscussions.................................................262

6.7.3 ManagerialImplications...............................................................................................264

6.7.4 LimitationsandFutureDiscussions........................................................................266

7 Chapter7:Conclusion......................................................................................................................268

7.1 TheFindingsineachEmpiricalChapter.........................................................................268

13

7.1.1 Chapter4:DoTransactionalWebsiteInitiativesAddValuetoBanks?...268

7.1.2 Chapter5:DoestheAdoptionofTransactionalWebsitesImproveBanks’

FinancialPerformance?....................................................................................................................269

7.1.3 Chapter6:DoDigitalTransactionalWebsiteInitiativesAddValueto

BanksinLongRun?............................................................................................................................270

7.2 ResearchContributions..........................................................................................................272

7.3 ManagerialImplications.........................................................................................................273

7.4 LimitationsandFurtherResearch.....................................................................................275

REFERENCES.................................................................................................................................................277

APPENDIX.......................................................................................................................................................327

AppendixA-AdditionalAnalysesforModelsinChapter4...................................................327

TableA.4.5CumulativeAbnormalReturnuponWebsite-LaunchingAnnouncements,

usingalternativeestimationperiods..............................................................................................328

TableA.4.6CAR(%)offirms,whicharesubsampledusingmarketsizearoundthe

dateofannouncement...........................................................................................................................329

TableA.4.7CumulativeAbnormalReturnuponWebsite-LaunchingAnnouncements,

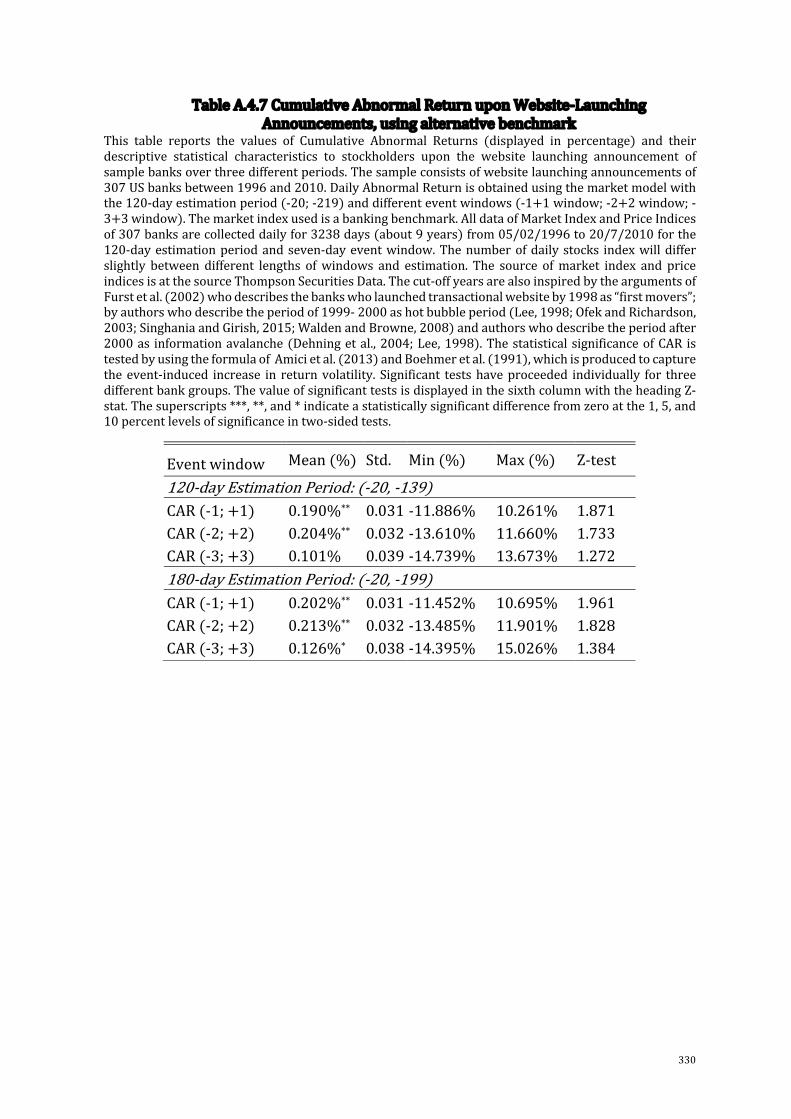

usingalternativebenchmark..............................................................................................................330

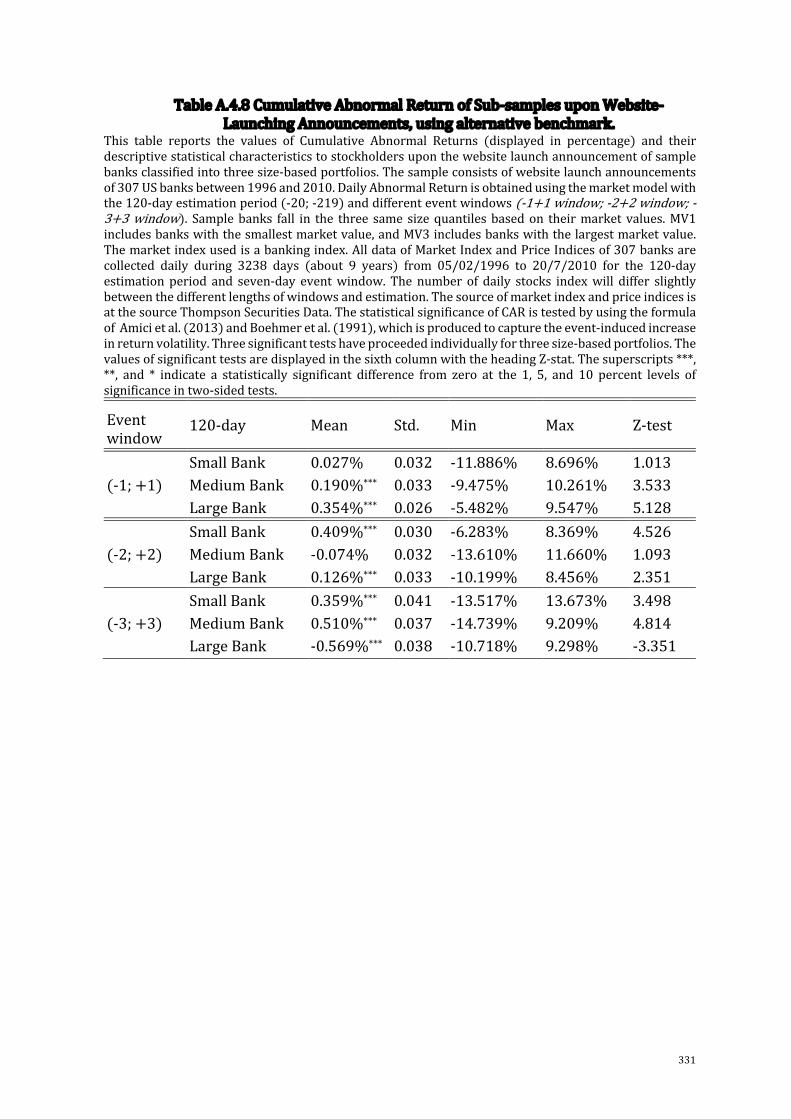

TableA.4.8CumulativeAbnormalReturnofSub-samplesuponWebsite-Launching

Announcements,usingalternativebenchmark..........................................................................331

TableA.4.9CAR(%)ofCumulativeAbnormalReturnofSub-samplesuponWebsite-

LaunchingAnnouncements,usingalternativebenchmark...................................................332

AppendixB-AdditionalAnalysesforModelsinChapter5...................................................333

FigureA.5.4NetInterestMarginforallU.SBanksfrom1986to2020............................334

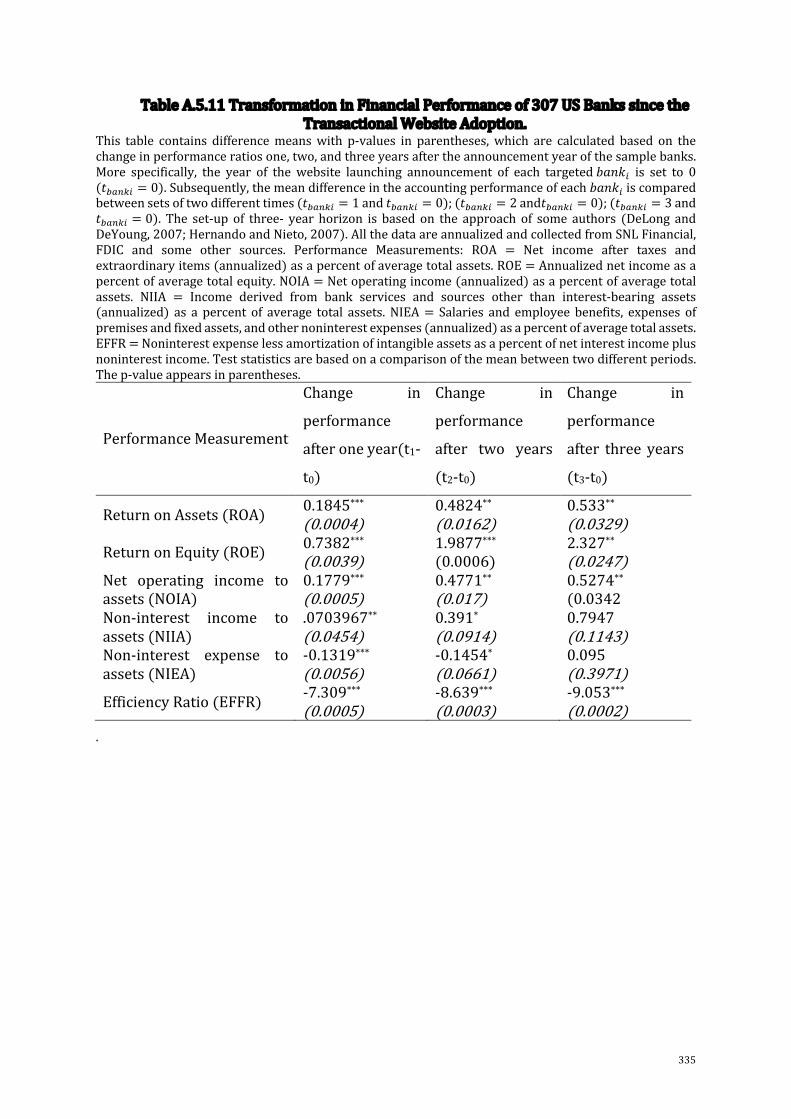

TableA.5.11TransformationinFinancialPerformanceof307USBankssincethe

TransactionalWebsiteAdoption.......................................................................................................335

TableA.5.12DynamicImpactsofTransactionalWebsiteAdoptiononBanks’

Performance...............................................................................................................................................336

TableA.5.13Themagnitudeeffectintransactionalwebsiteadoption,usingthreesize-

basedquantiles.........................................................................................................................................338

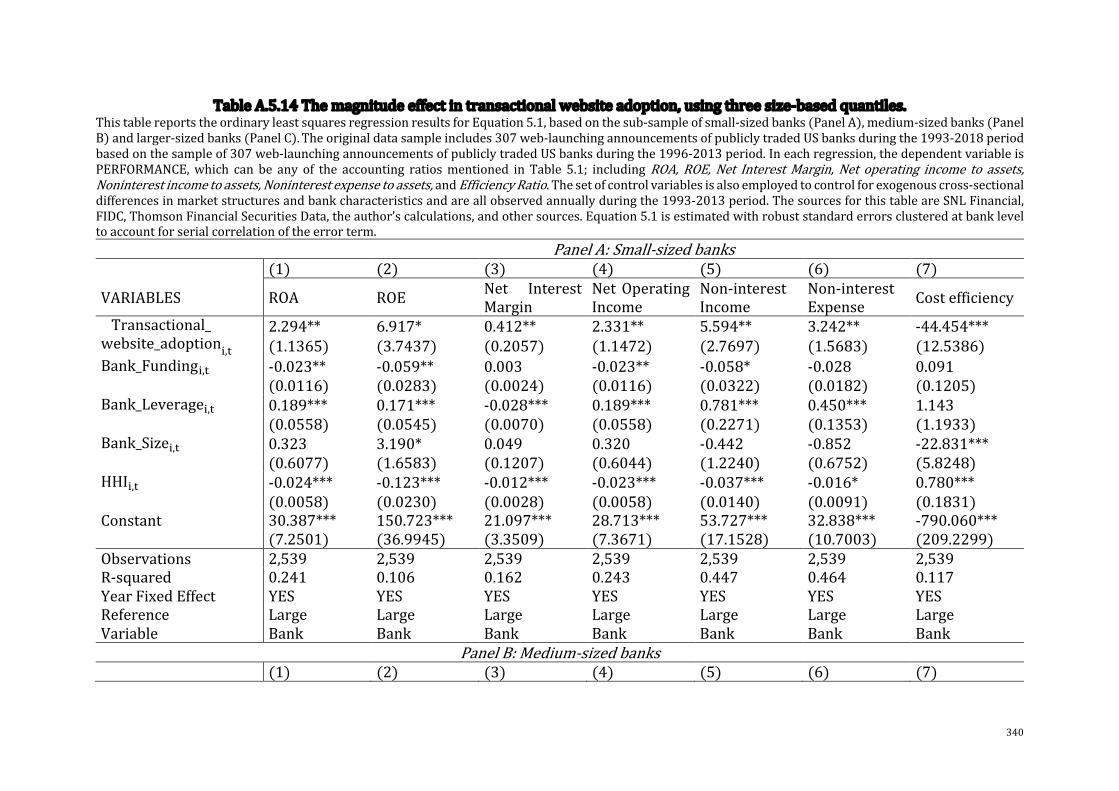

TableA.5.14Themagnitudeeffectintransactionalwebsiteadoption,usingthreesize-

basedquantiles.........................................................................................................................................340

TableA.5.15Variationin“LearningbyBehaviour”Variable................................................343

14

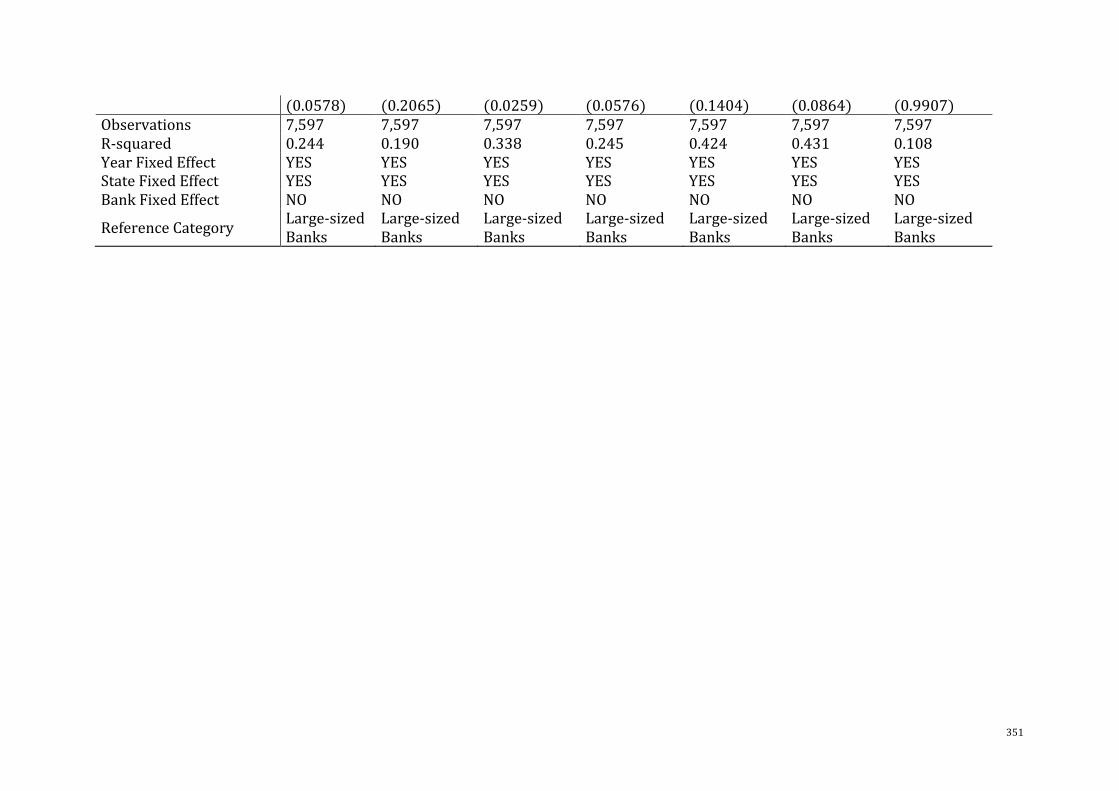

TableA.5.16Re-estimationofEquation5.1,usingYearandStateFixedEffects.........344

TableA.5.17Re-estimationofEquation5.2,usingYearandStateFixedEffect...........345

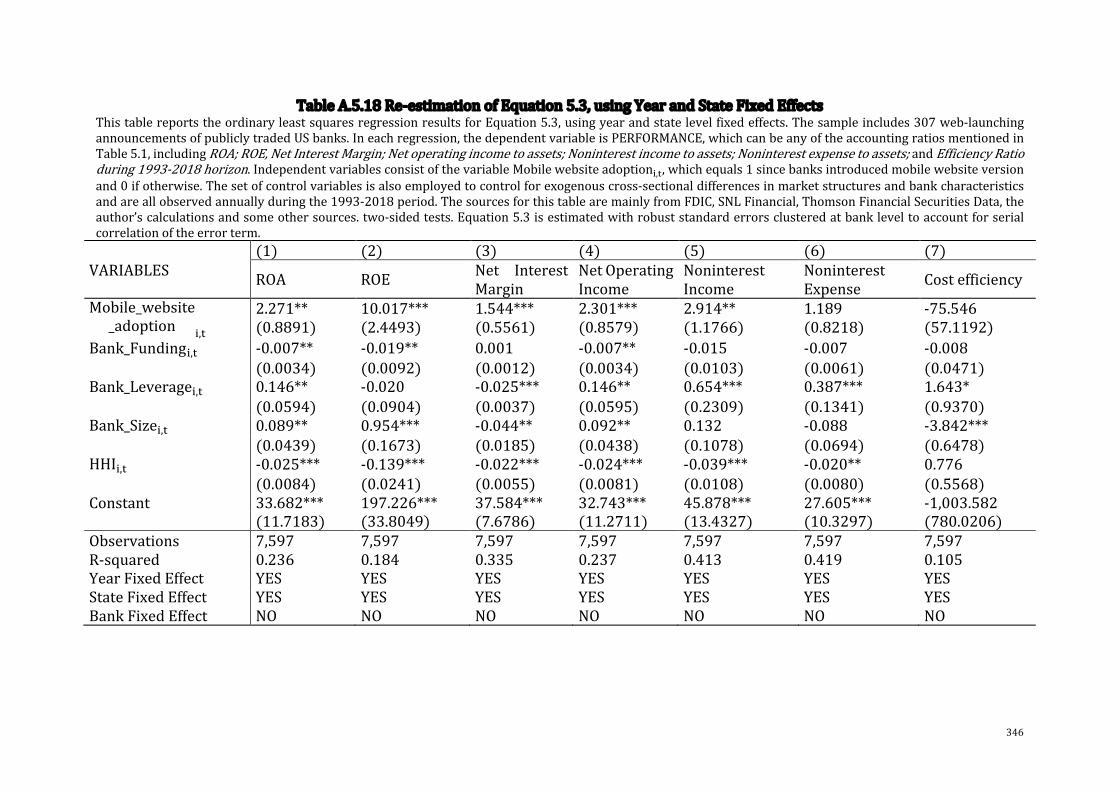

TableA.5.18Re-estimationofEquation5.3,usingYearandStateFixedEffects.........346

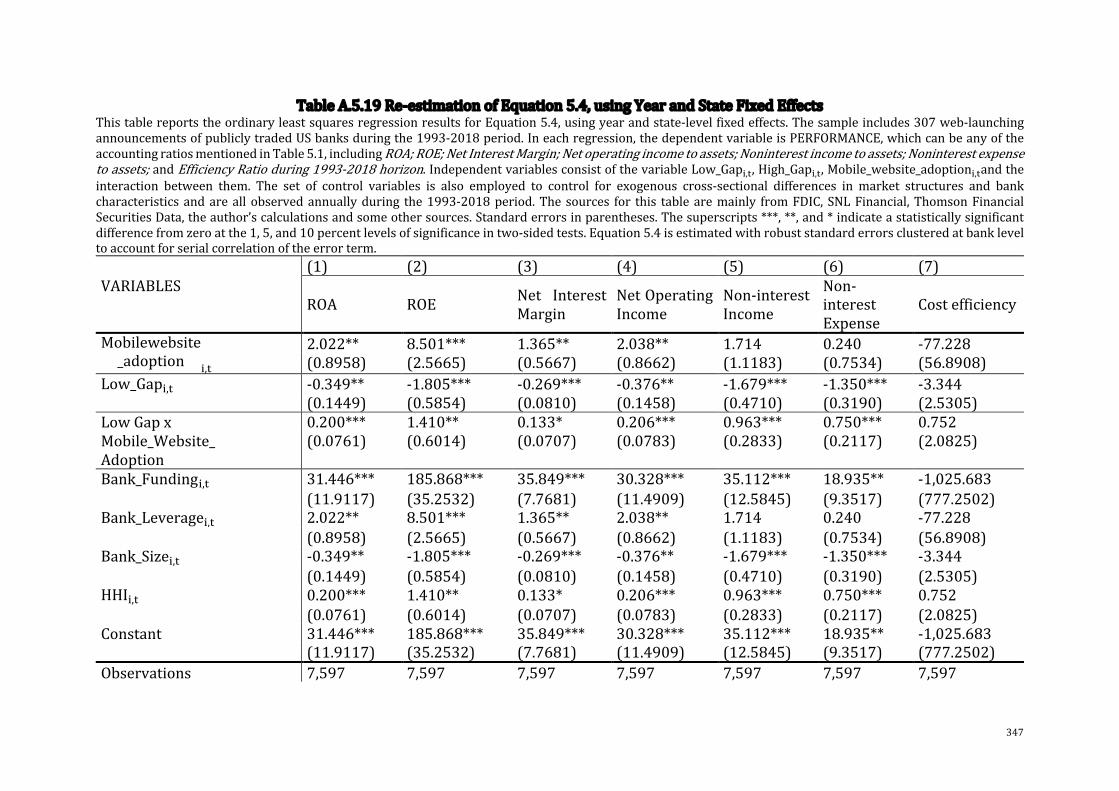

TableA.5.19Re-estimationofEquation5.4,usingYearandStateFixedEffects.........347

TableA.5.20Re-estimationofEquation5.5,usingYearandStateFixedEffects.........349

TableA.5.21Re-estimationofEquation5.6,usingYearandStateFixedEffects.........350

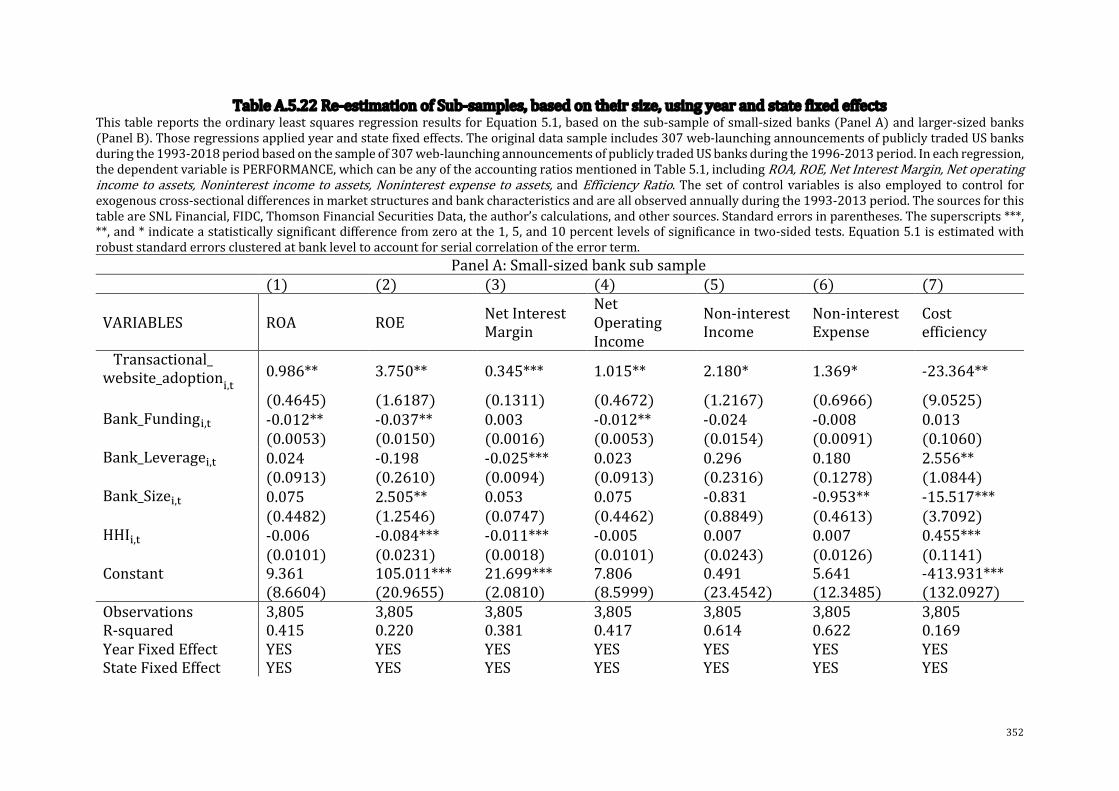

TableA.5.22Re-estimationofSub-samples,basedontheirsize,usingyearandstate

fixedeffects.................................................................................................................................................352

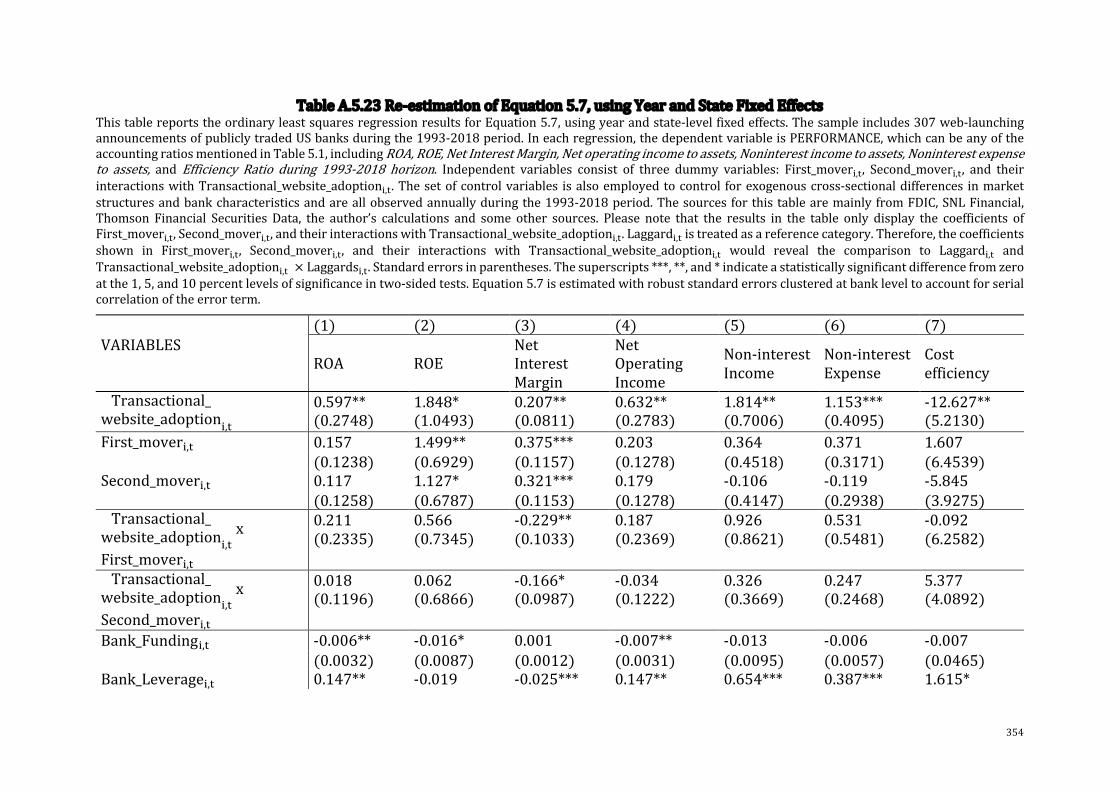

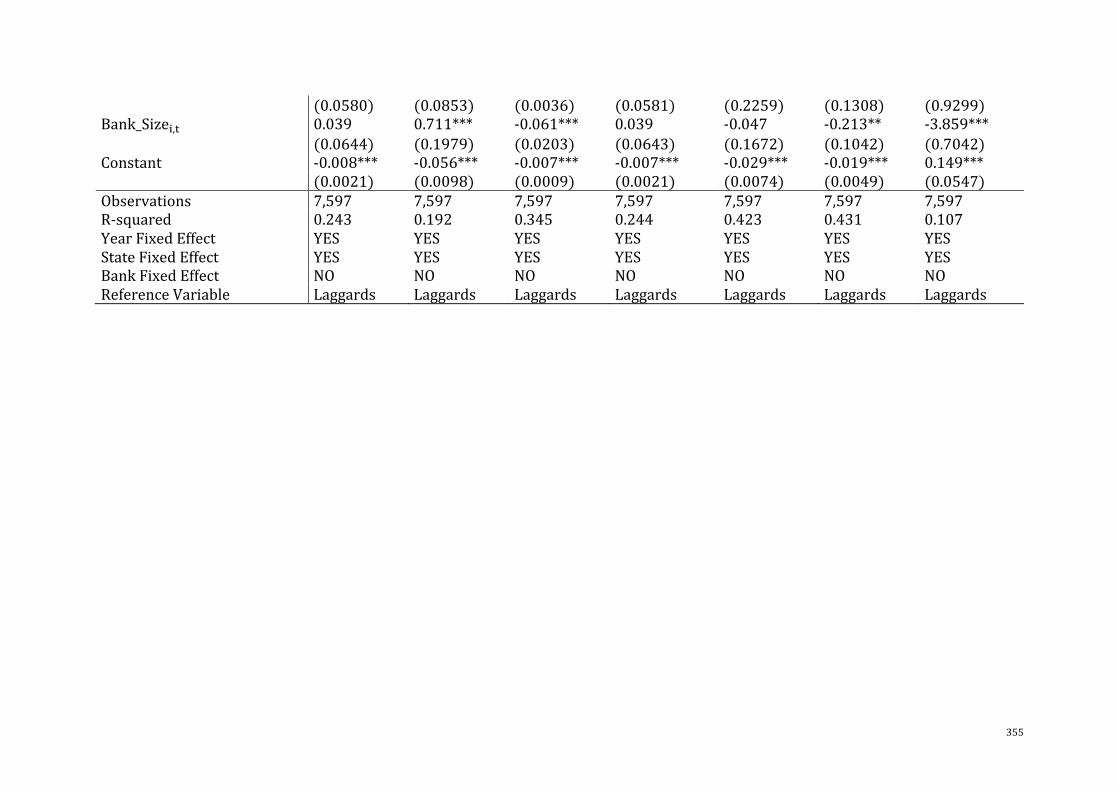

TableA.5.23Re-estimationofEquation5.7,usingYearandStateFixedEffects.........354

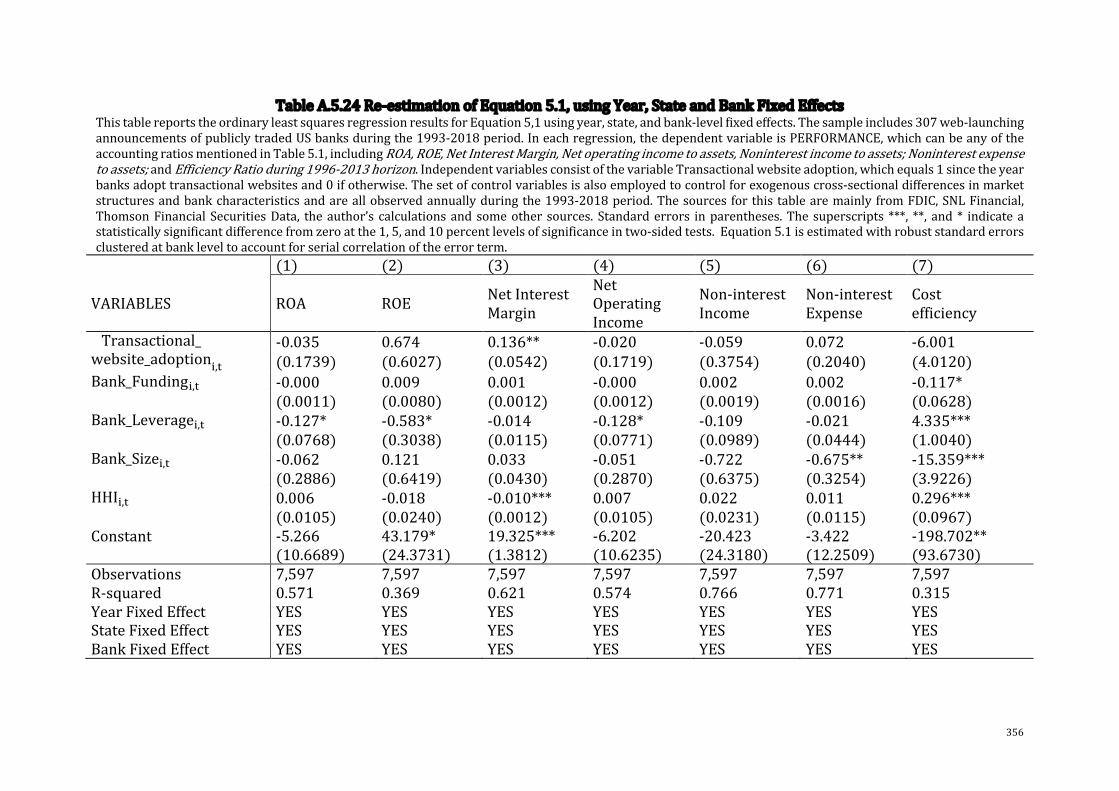

TableA.5.24Re-estimationofEquation5.1,usingYear,StateandBankFixedEffects

..........................................................................................................................................................................356

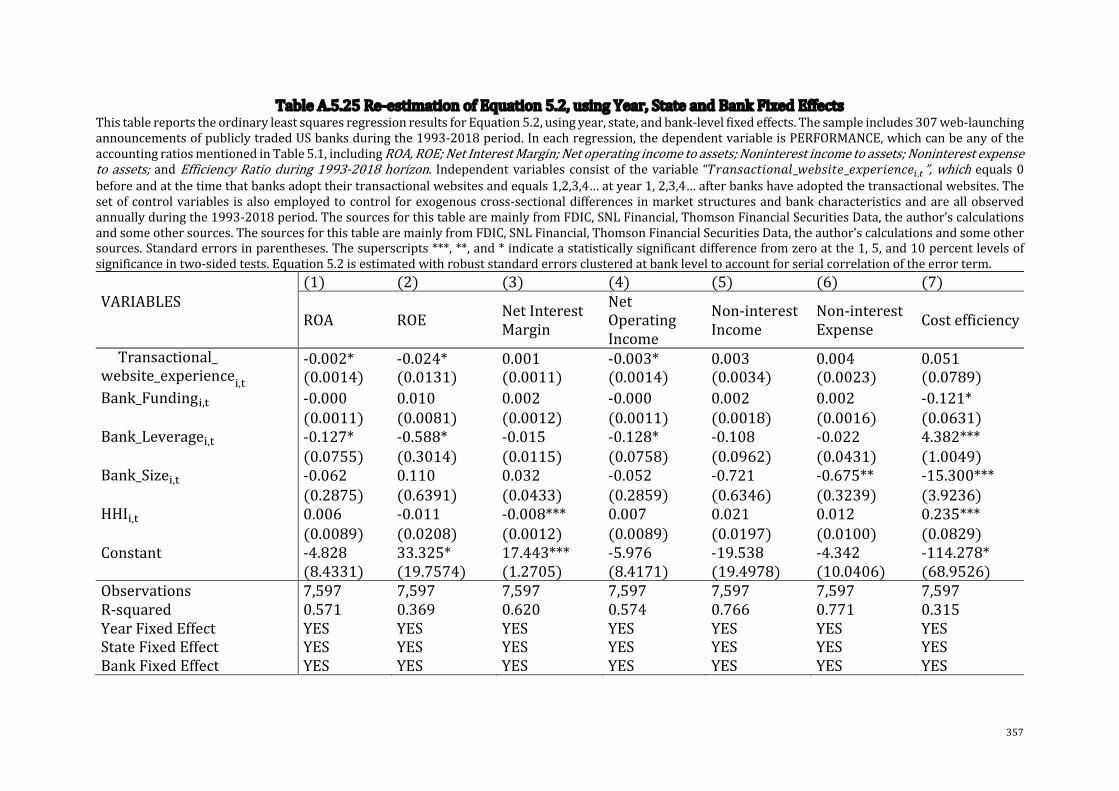

TableA.5.25Re-estimationofEquation5.2,usingYear,StateandBankFixedEffects

..........................................................................................................................................................................357

TableA.5.26Re-estimationofEquation5.3,usingYear,StateandBankFixedEffects

..........................................................................................................................................................................358

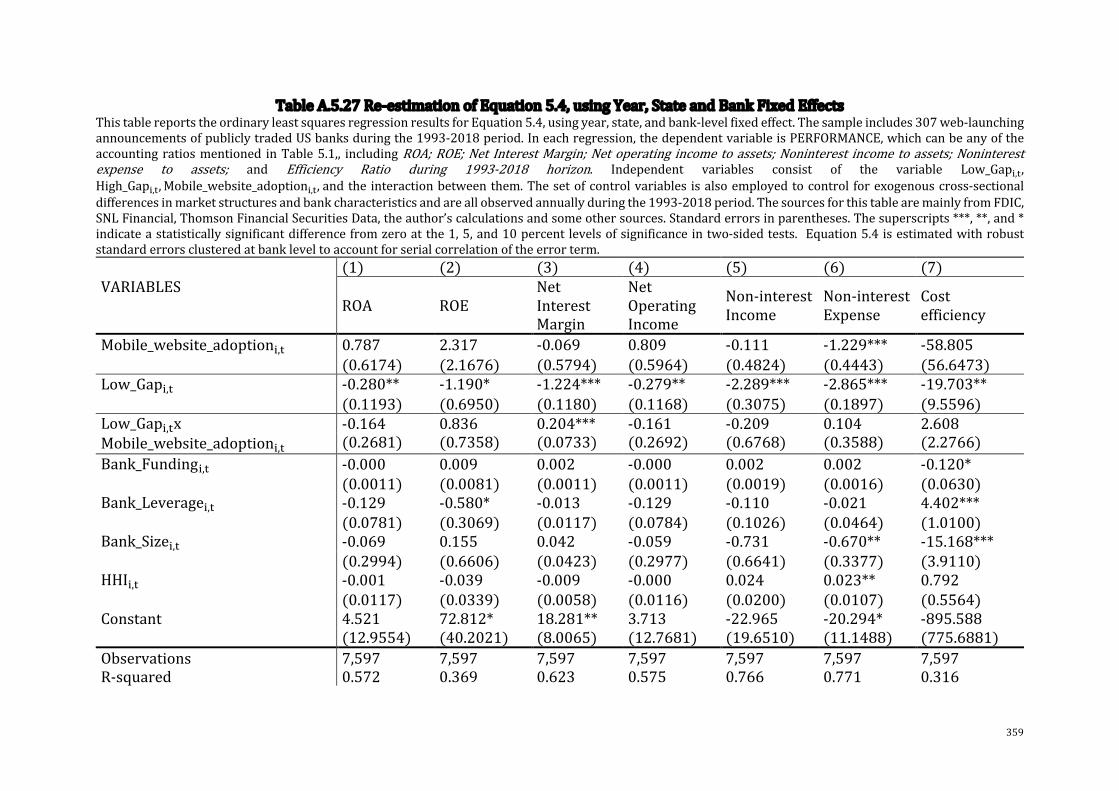

TableA.5.27Re-estimationofEquation5.4,usingYear,StateandBankFixedEffects

..........................................................................................................................................................................359

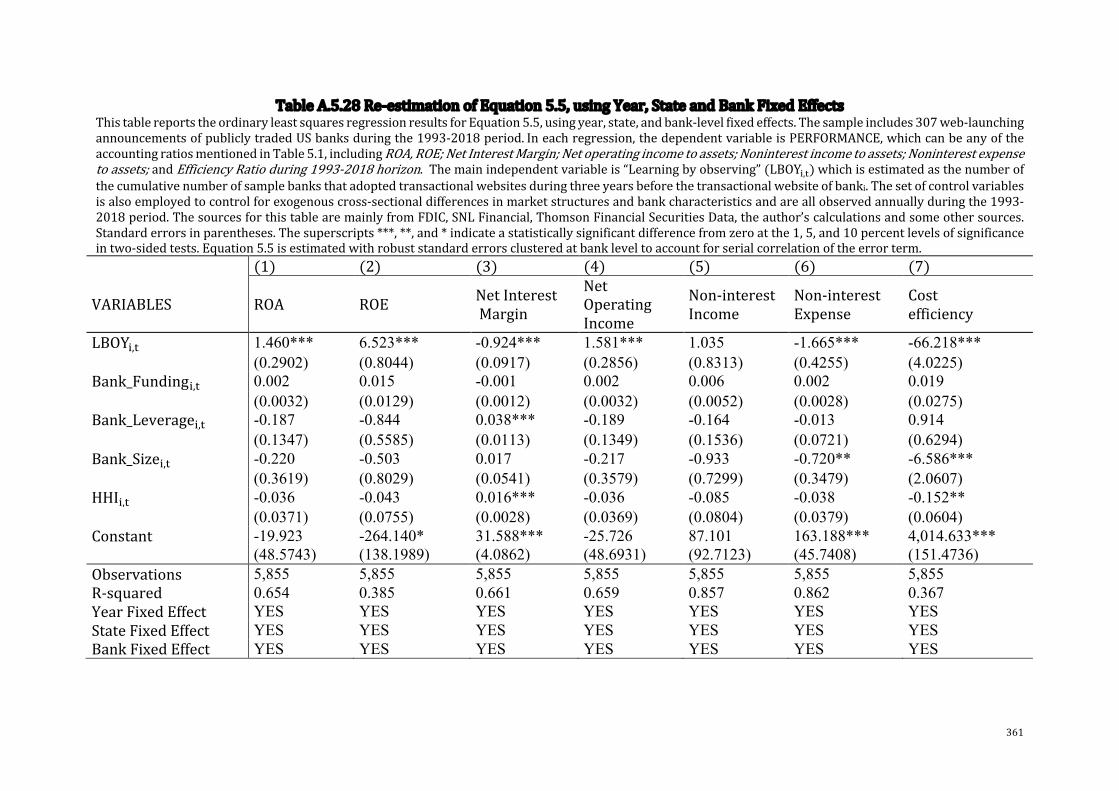

TableA.5.28Re-estimationofEquation5.5,usingYear,StateandBankFixedEffects

..........................................................................................................................................................................361

TableA.5.29Re-estimationofEquation5.6,usingYear,StateandBankFixedEffects

..........................................................................................................................................................................362

TableA.5.30Re-estimationofSub-samples,basedontheirsize,usingyear,stateand

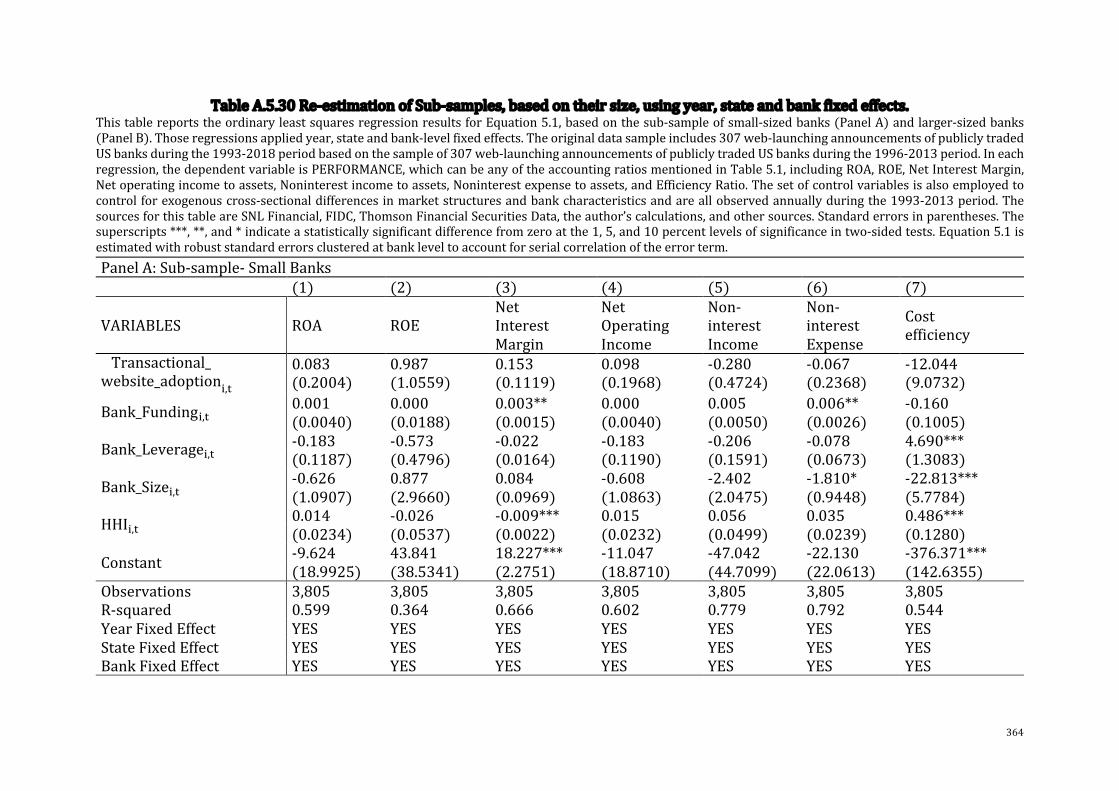

bankfixedeffects.....................................................................................................................................364

TableA.5.31Re-estimationofEquation5.7,usingYear,StateandBankFixedEffects

..........................................................................................................................................................................366

AppendixC-AdditionalAnalysesforModelsinChapter6...................................................368

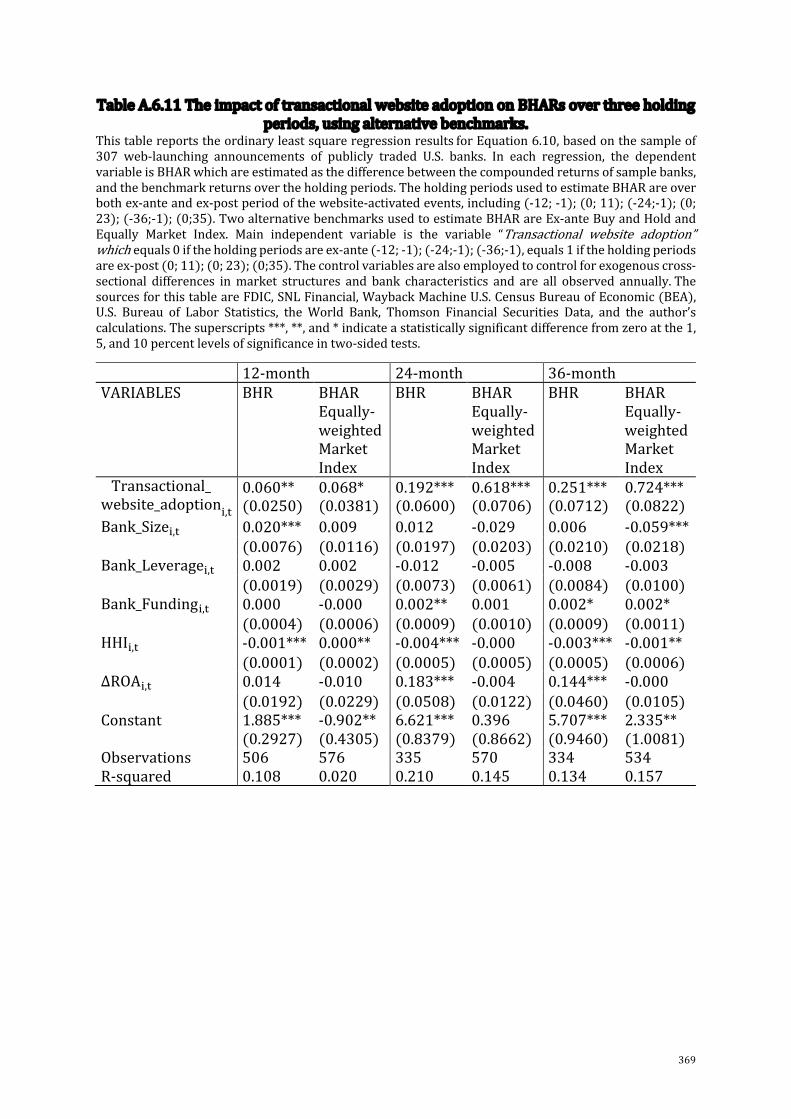

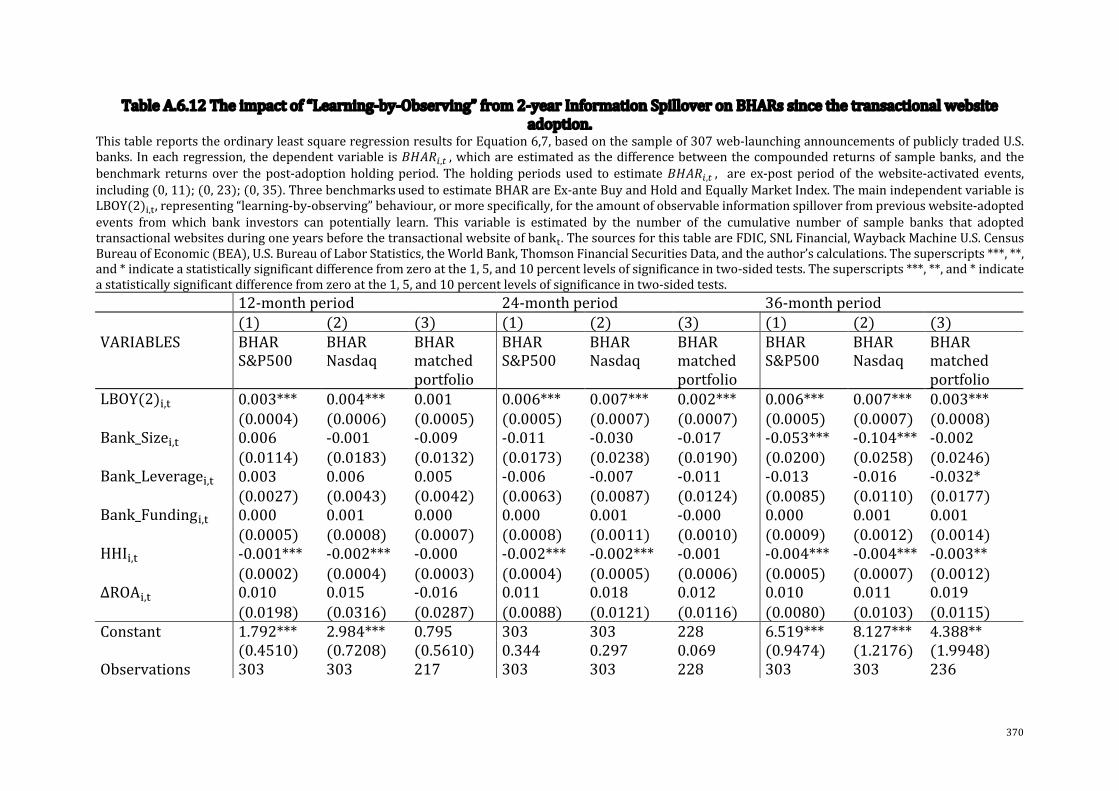

TableA.6.11TheimpactoftransactionalwebsiteadoptiononBHARsoverthree

holdingperiods,usingalternativebenchmarks.........................................................................369

TableA.6.12Theimpactof“Learning-by-Observing”from2-yearInformation

SpilloveronBHARssincethetransactionalwebsiteadoption............................................370

TableA.6.13Theimpactof“Learning-by-Observing”from3-yearInformation

SpilloveronBHARs.................................................................................................................................372

sincethetransactionalwebsiteadoption......................................................................................372

15

TableA.6.14ThemagnitudeeffectonBHARuponex-anteandex-postperiodofthe

transactionalwebsiteadoption.........................................................................................................373

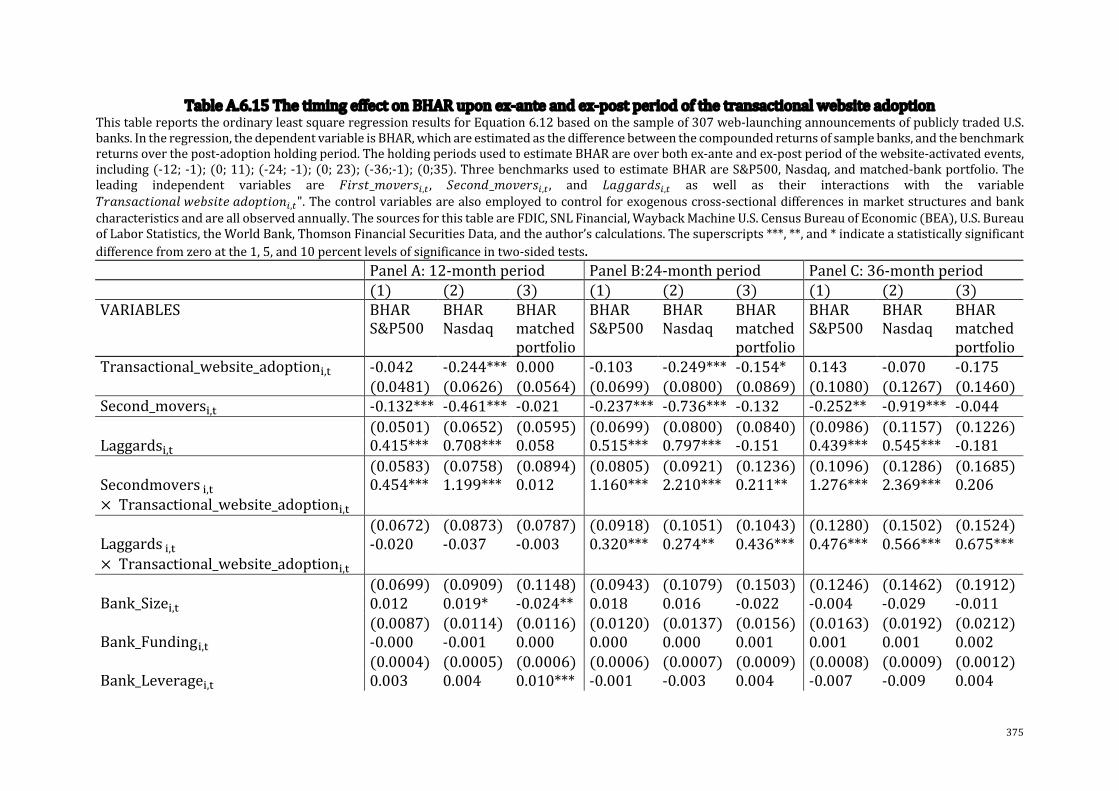

TableA.6.15ThetimingeffectonBHARuponex-anteandex-postperiodofthe

transactionalwebsiteadoption.........................................................................................................375

TableA.6.16Re-estimationofEquation6.6,usingfixedeffects..........................................377

TableA.6.17Re-estimationofEquation6.7,usingfixedeffects..........................................381

TableA.6.18Re-estimationofEquation6.8,usingfixedeffects..........................................385

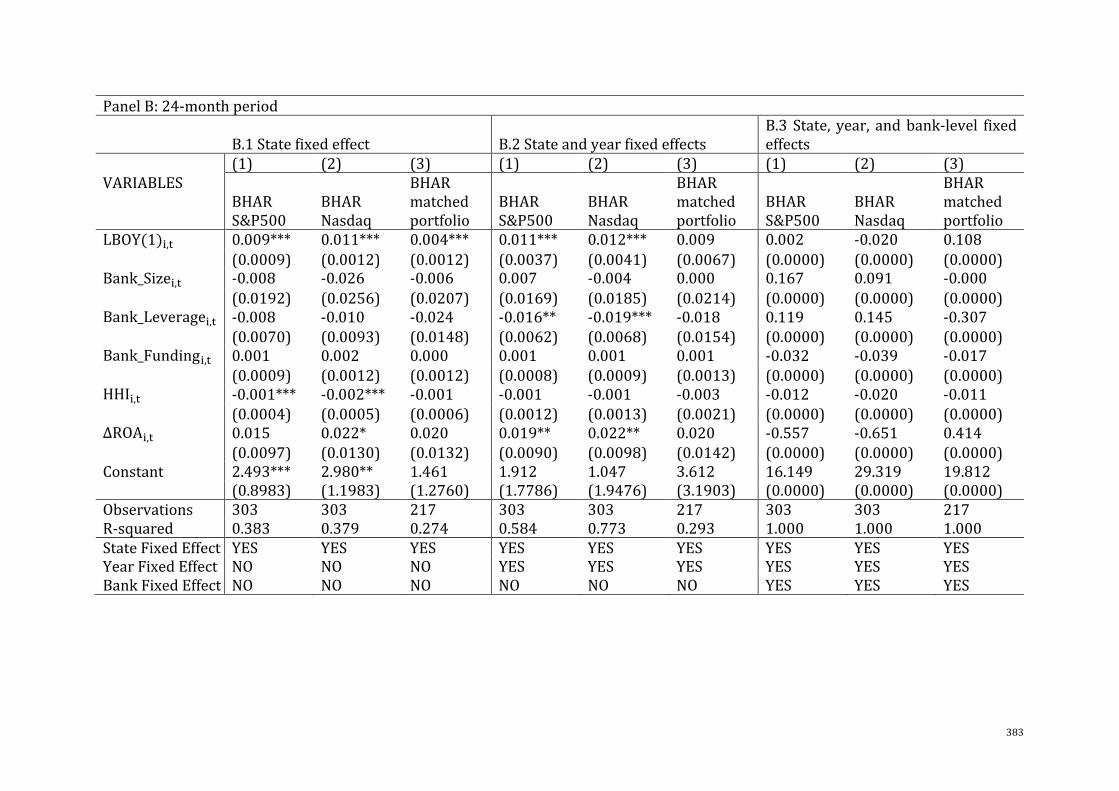

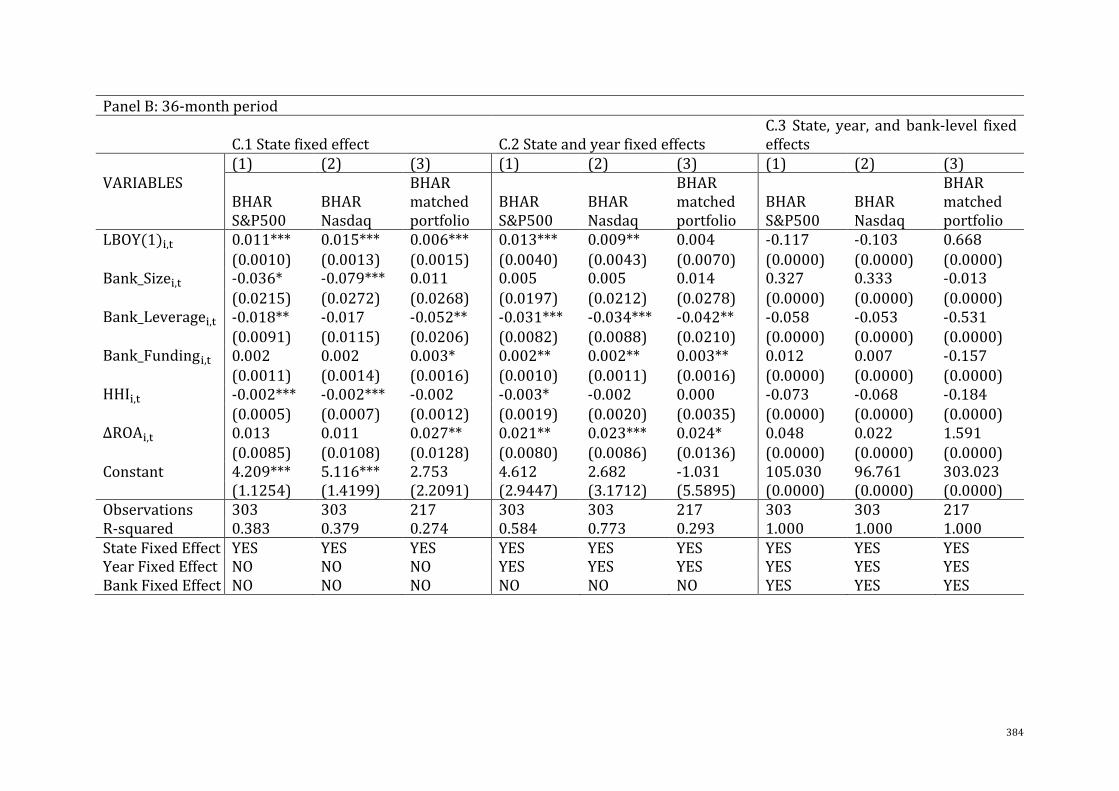

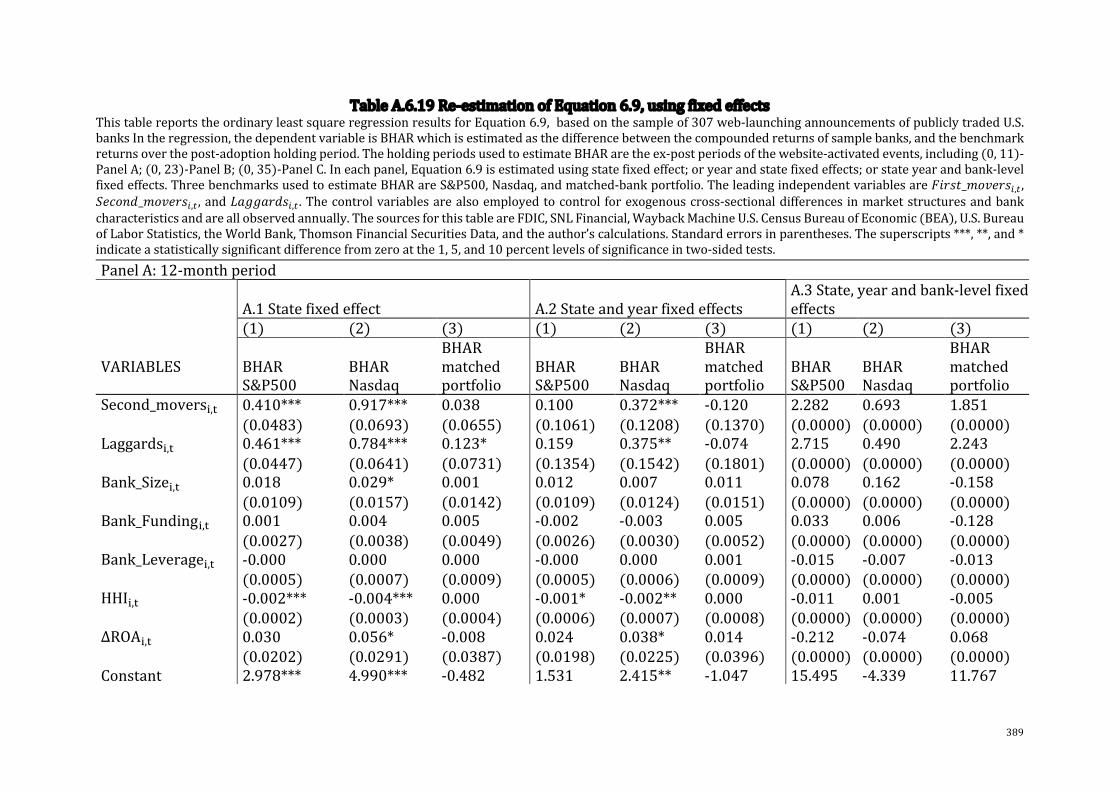

TableA.6.19Re-estimationofEquation6.9,usingfixedeffects..........................................389

16

LISTOFTABLES

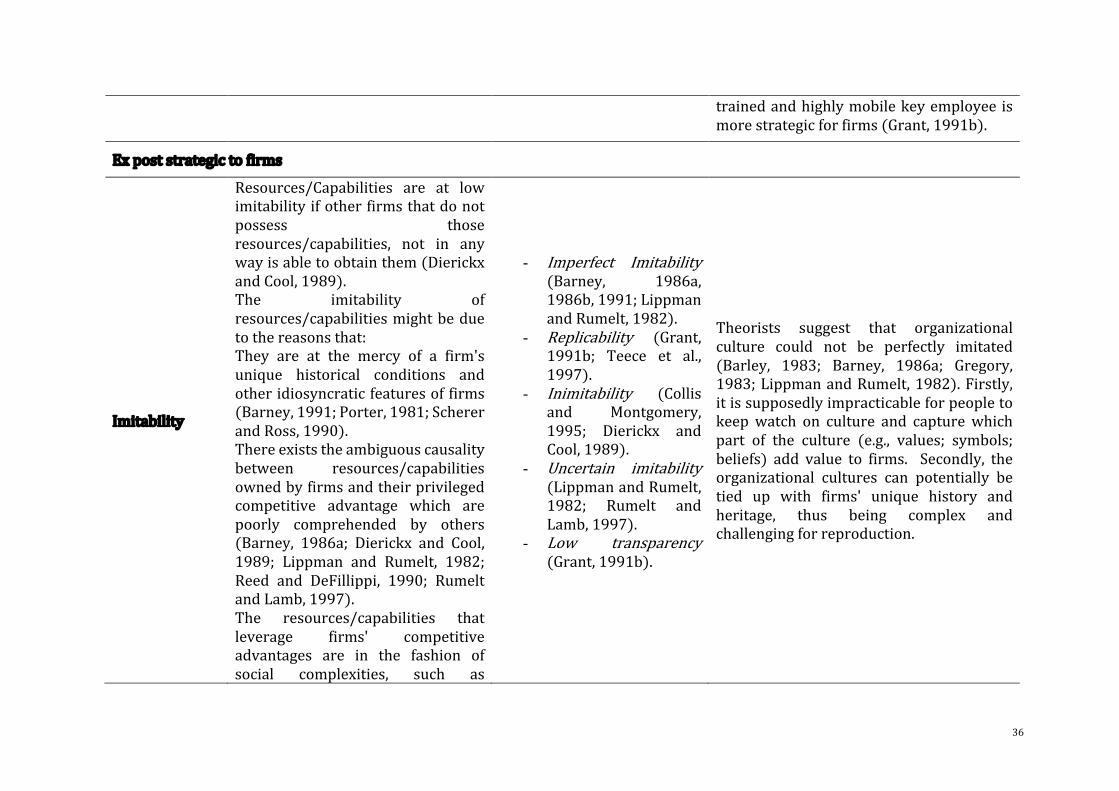

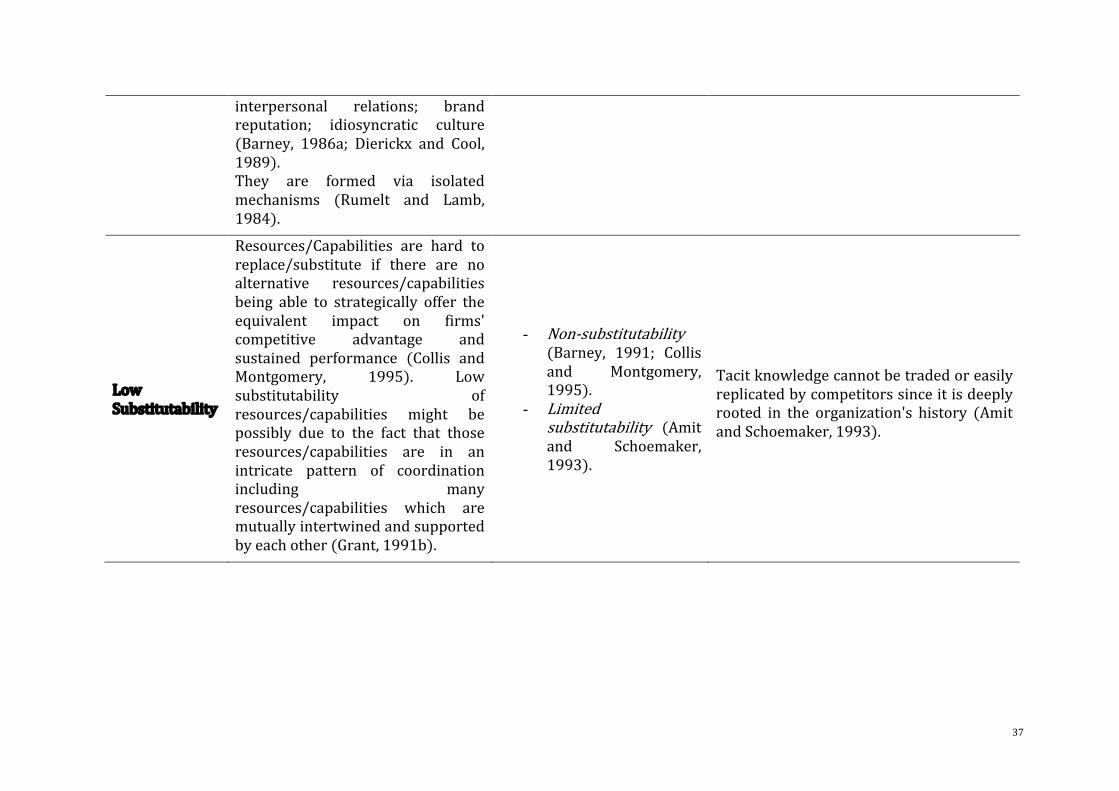

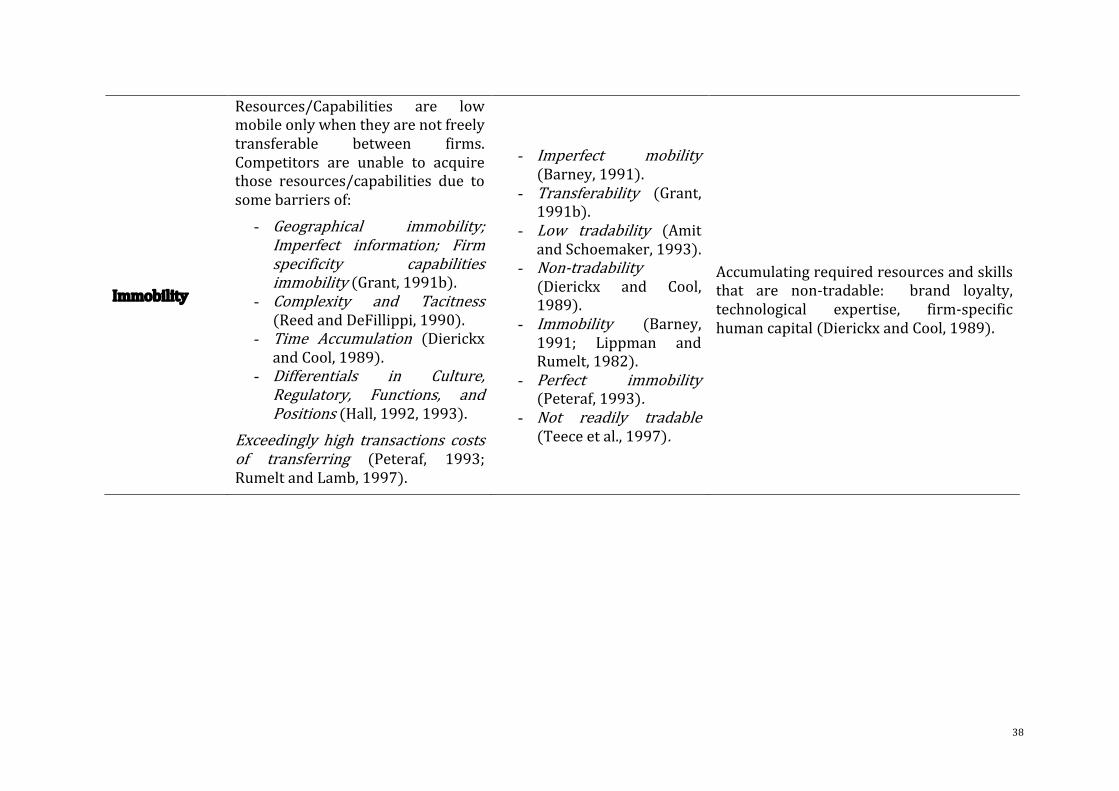

Table2.1StrategicAttributesofResourcesandCapabilities......................................................35

Table2.2StrategicAttributesofDigitalAdoptionandInfluenceonCustomerBehaviour

inUse....................................................................................................................................................................49

Table2.3DigitalBankingAdoptionandtheImpactonCustomerOutcomes......................55

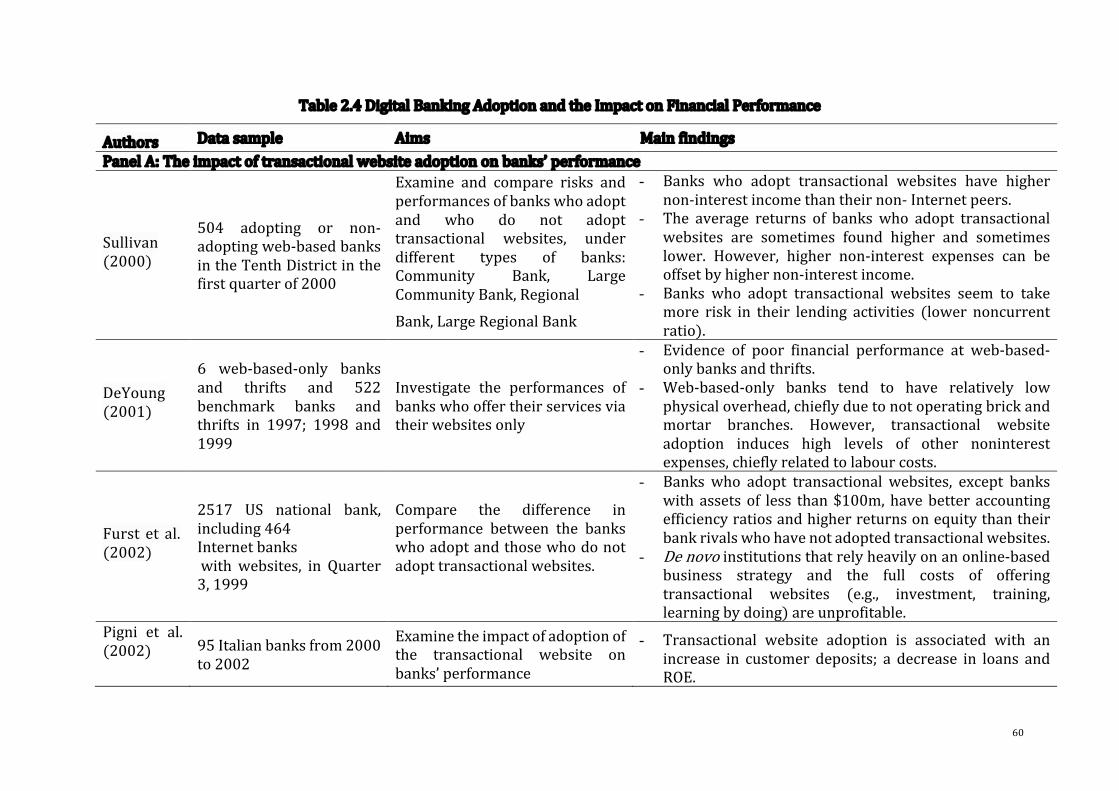

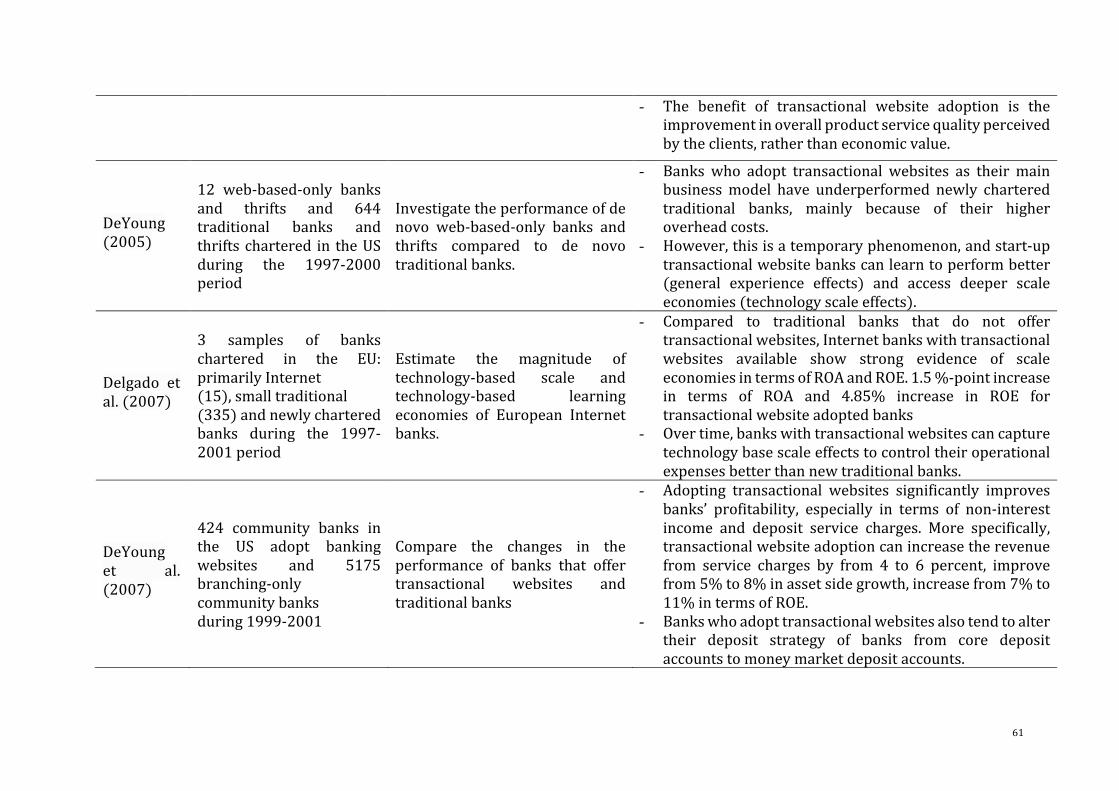

Table2.4DigitalBankingAdoptionandtheImpactonFinancialPerformance.................60

Table2.5USBankingStructurefrom1990-2018............................................................................67

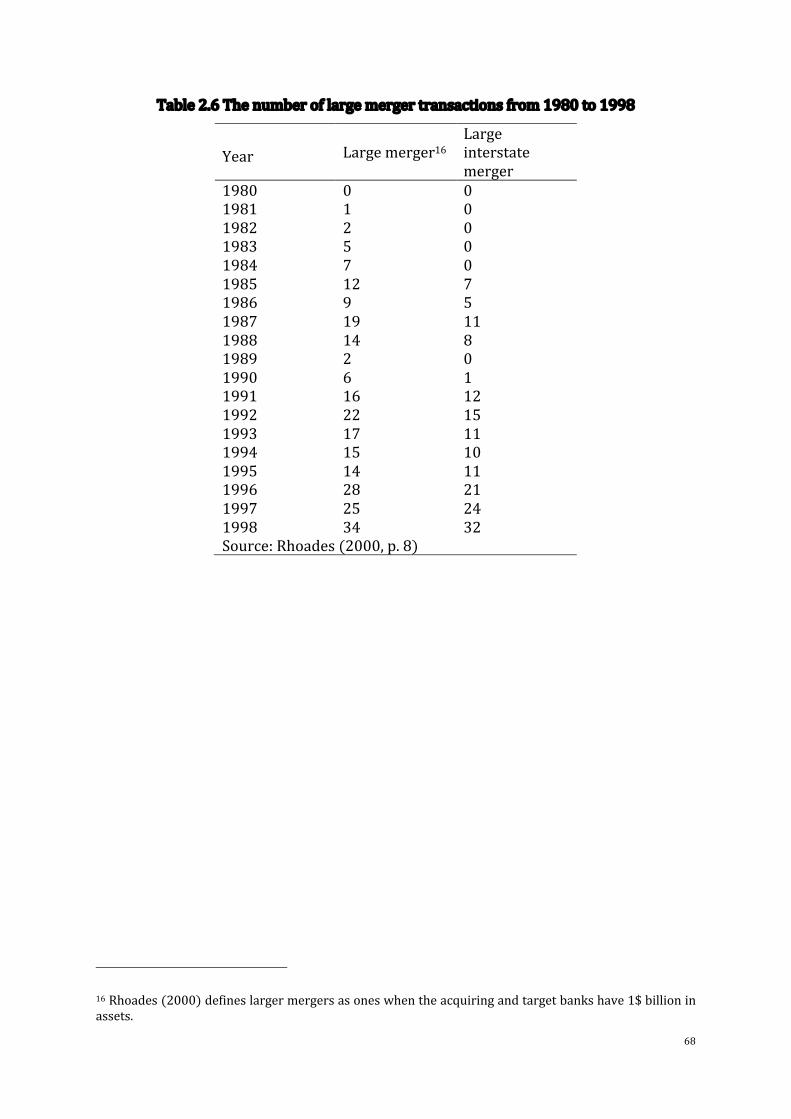

Table2.6Thenumberoflargemergertransactionsfrom1980to1998...............................68

Table2.7ConcentrationinAssetsandDepositsinUSBankingMarketfrom1994-2018

.................................................................................................................................................................................72

Table3.1SampleSizeDistribution.........................................................................................................89

Table3.2BankCharterandSizeDistribution....................................................................................90

Table3.3EventdateandBanksizeDistribution..............................................................................91

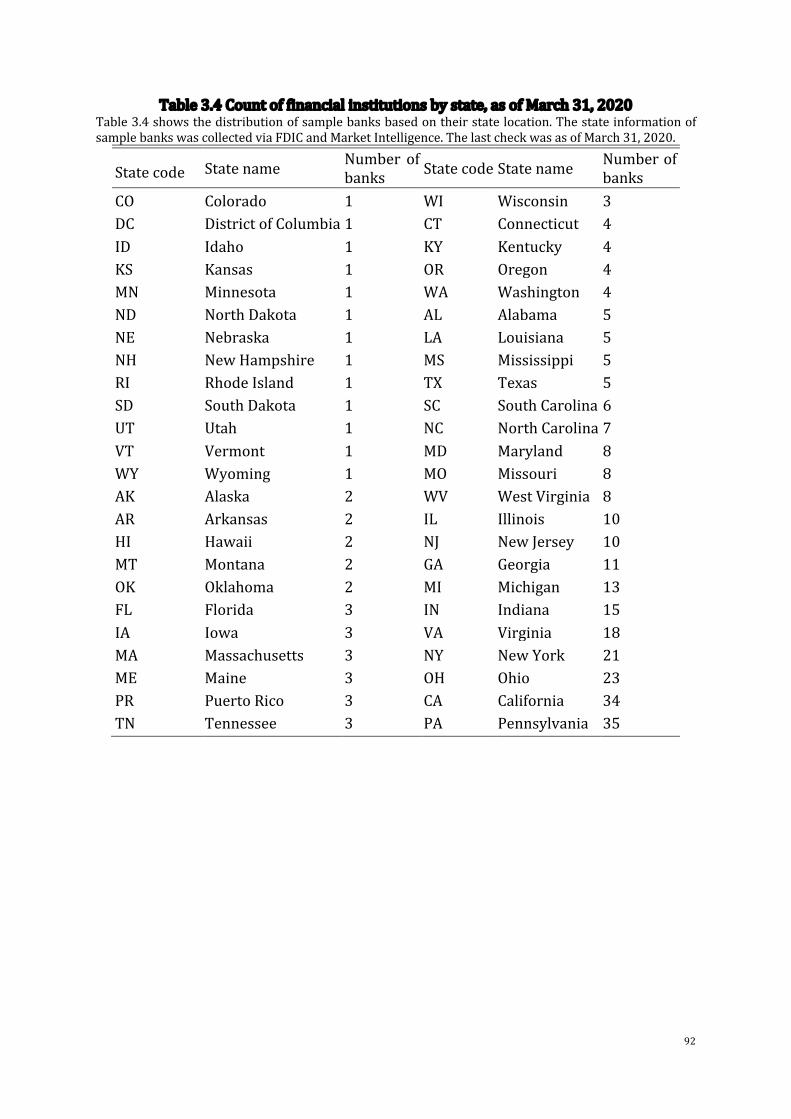

Table3.4Countoffinancialinstitutionsbystate,asofMarch31,2020................................92

Table4.1SummaryofEventDatesandTestPeriodsforAbnormalReturns.....................114

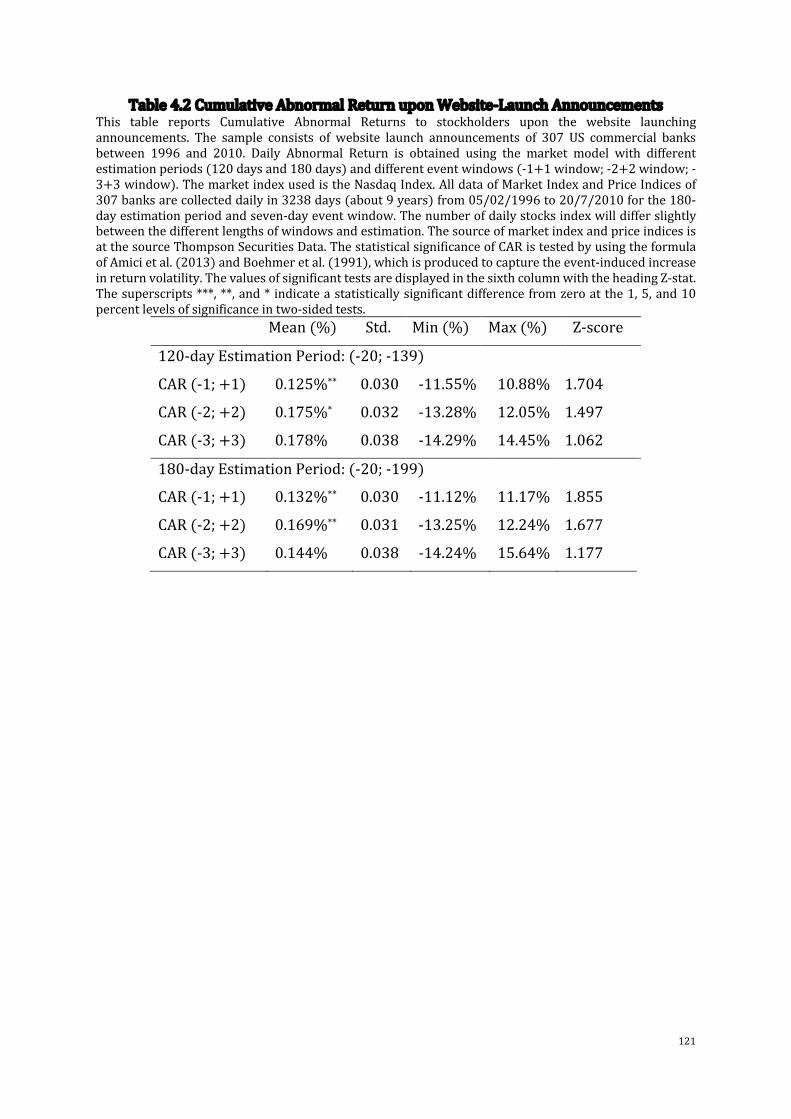

Table4.2CumulativeAbnormalReturnuponWebsite-LaunchAnnouncements...........121

Table4.3CAR(%)offirms,whicharesubsampledusingmarketsize.................................122

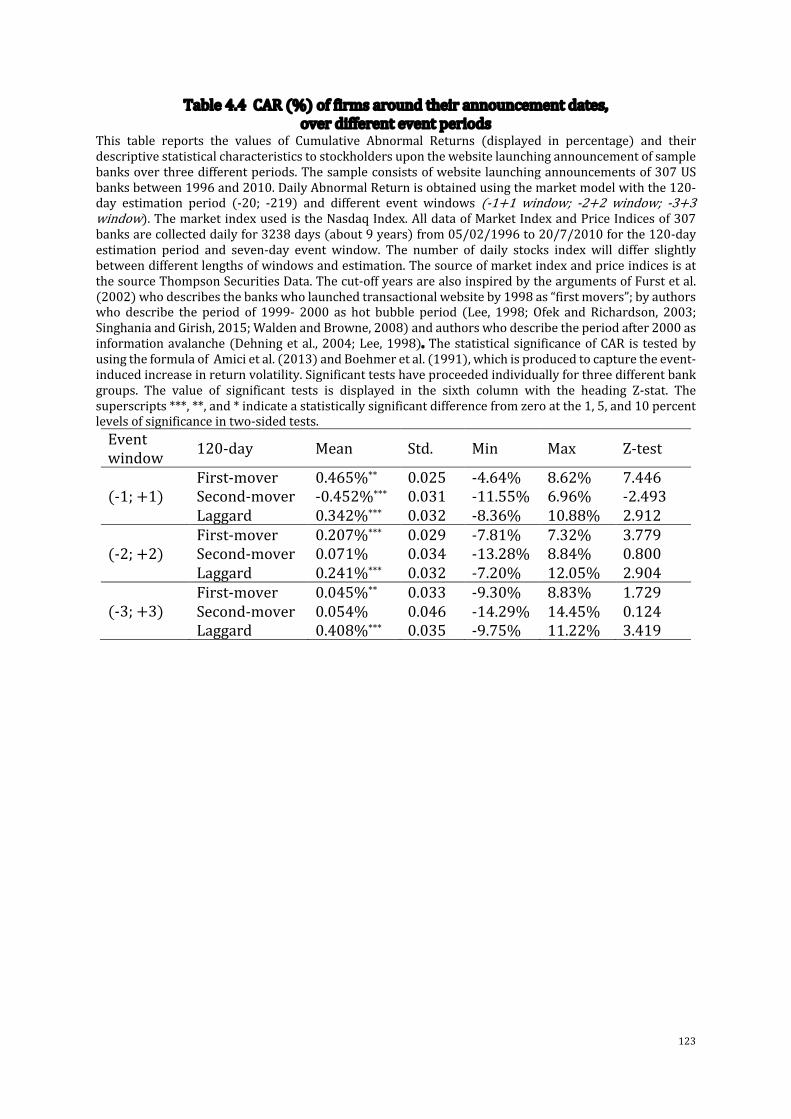

Table4.4CAR(%)offirmsaroundtheirannouncementdates,.............................................123

Table5.1SummaryofVariables.............................................................................................................156

Table5.2Pre-adoptionandPost-adoptionPerformanceofSampleBanks........................160

Table5.3Theimpactoftransactionalwebsiteadoptiononthefinancialperformanceof

banks..................................................................................................................................................................163

Table5.4Theoverall impactof transactionalwebsiteadoptions’experienceonbanks’

performance....................................................................................................................................................166

Table5.5Theimpactofmobilewebsiteadoptiononbanks’performance........................171

Table5.6Theimpactofinterconnectednessbetweentransactionalwebsiteadoptionand

mobilewebsiteadoptiononbanks’performance..........................................................................172

Table5.7Theimpactof“learningby-observing”onbanks’performance..........................177

Table5.8Theimpactofsizeeffectonbanks’performance.......................................................182

Table5.9Themagnitudeimpactinadoptingtransactionalwebsite-Sub-samples........184

Table5.10Theimpactoftimingeffectinadoptingthetransactionalwebsite..................189

Table6.1Literatureontheimpactsofdigitaladoptiononbanks’performanceinthelong

run.......................................................................................................................................................................212

17

Table 6.2 Proposed Strategic Resources and Capabilities of Transactional Website

Adoption...........................................................................................................................................................217

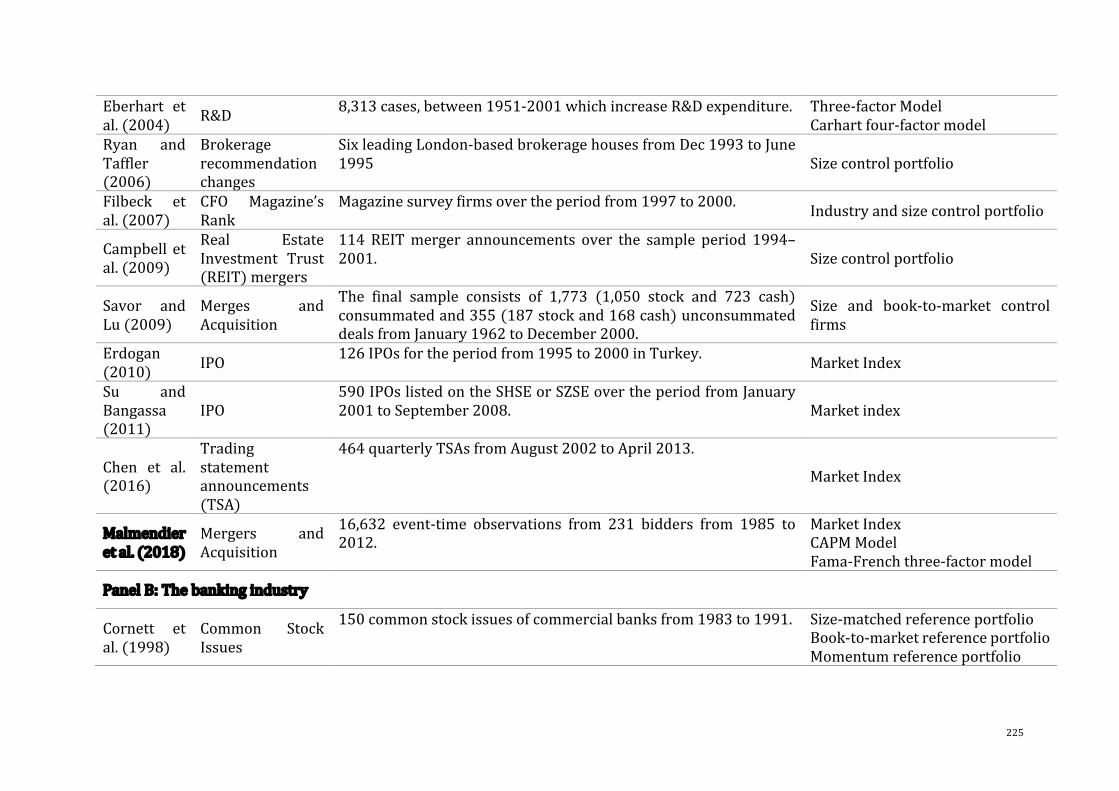

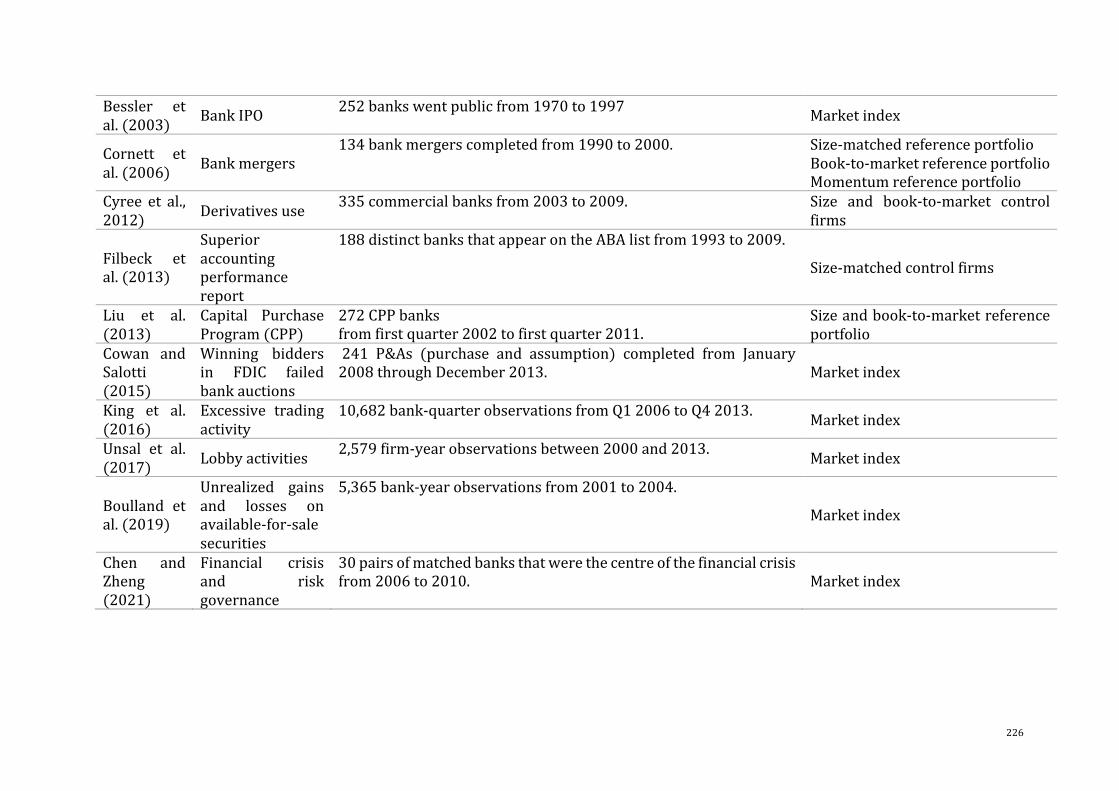

Table6.3Summaryofstudiesanalysinglong-runabnormalstockreturns.......................224

Table6.4SummaryofVariables.............................................................................................................234

Table6.5DataDescription.......................................................................................................................239

Table6.6Buy-and-HoldAbnormalReturns(BHARs)upon......................................................243

Table6.7The impact of transactionalwebsite adoptiononBHARsover threeholding

periods...............................................................................................................................................................244

Table6.8Theimpactof“Learning-by-Observing”fromInformationSpilloveronBHARs

sincethetransactionalwebsiteadoption..........................................................................................248

Table6.9ThemagnitudeeffectonBHARuponex-postperiodofthetransactionalwebsite

adoption............................................................................................................................................................250

Table6.10ThetimingeffectonBHARuponex-postperiodofthetransactionalwebsite

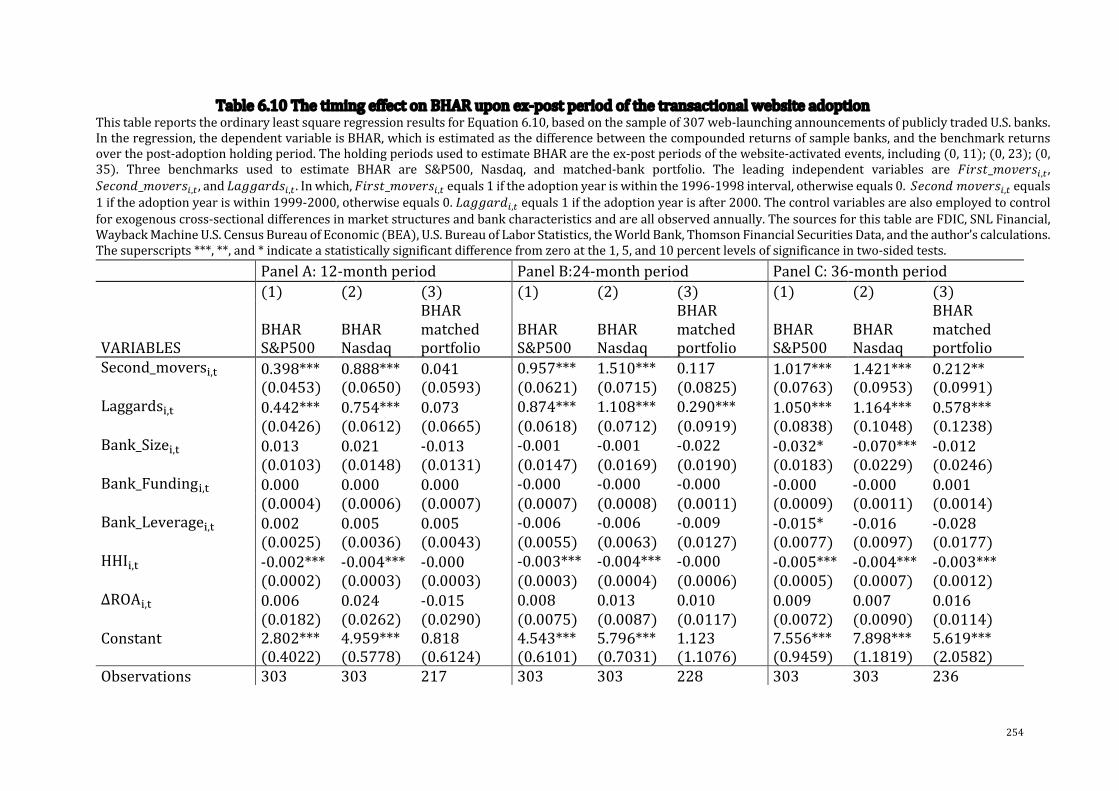

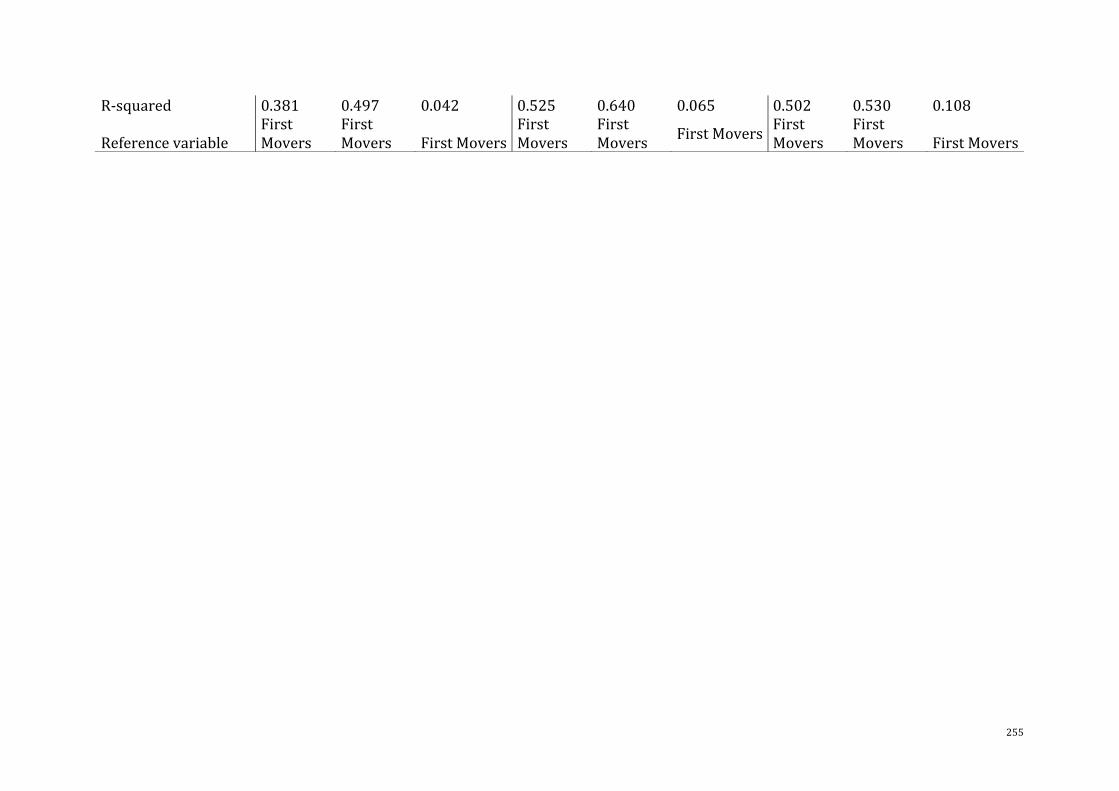

adoption............................................................................................................................................................254

18

LISTOFFIGURES

Figure2.1Trend inConcentration inAssets andDeposits inUSBankingSystem from

1994-2018.........................................................................................................................................................73

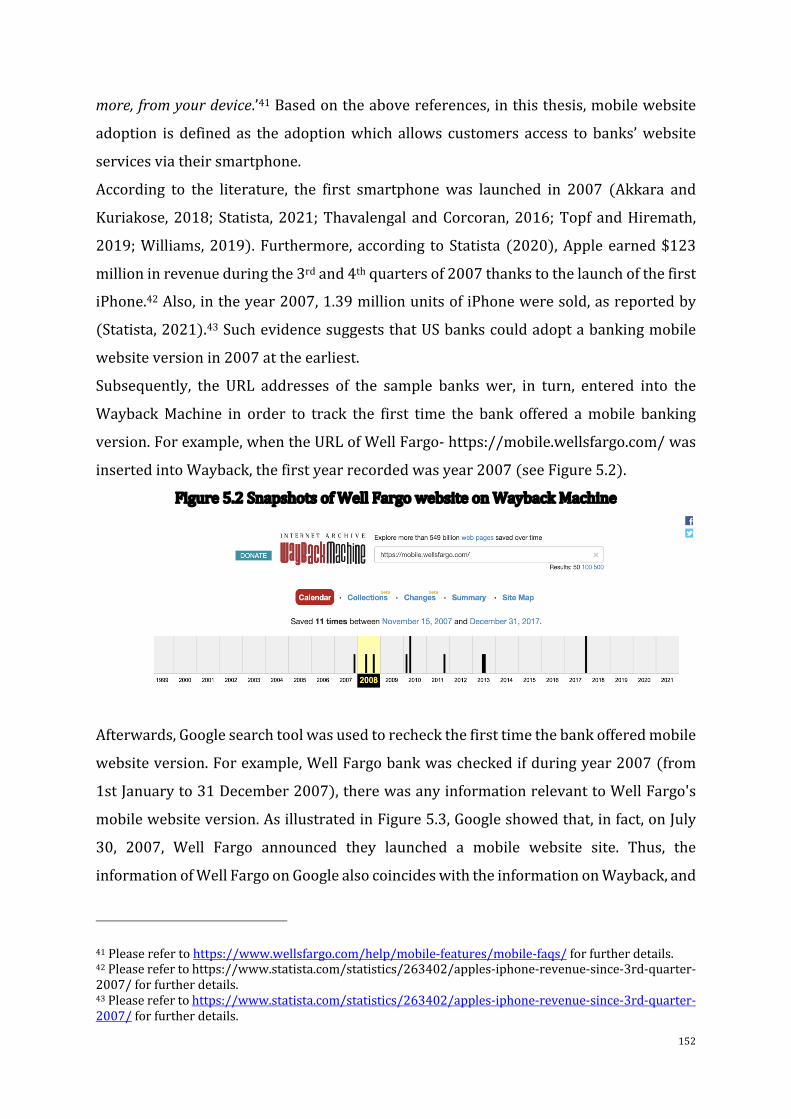

Figure3.1SnapshotsofWellFargowebsiteonWaybackMachine..........................................84

Figure3.2HistoricalWellFargowebsitepageviaitsfirstsnapshot.......................................84

Figure3.3HistoricalWellFargowebsitepageviaitsfirstsnapshot.......................................85

Figure3.4DistributionofSampleBanksbytheirEventYear.....................................................86

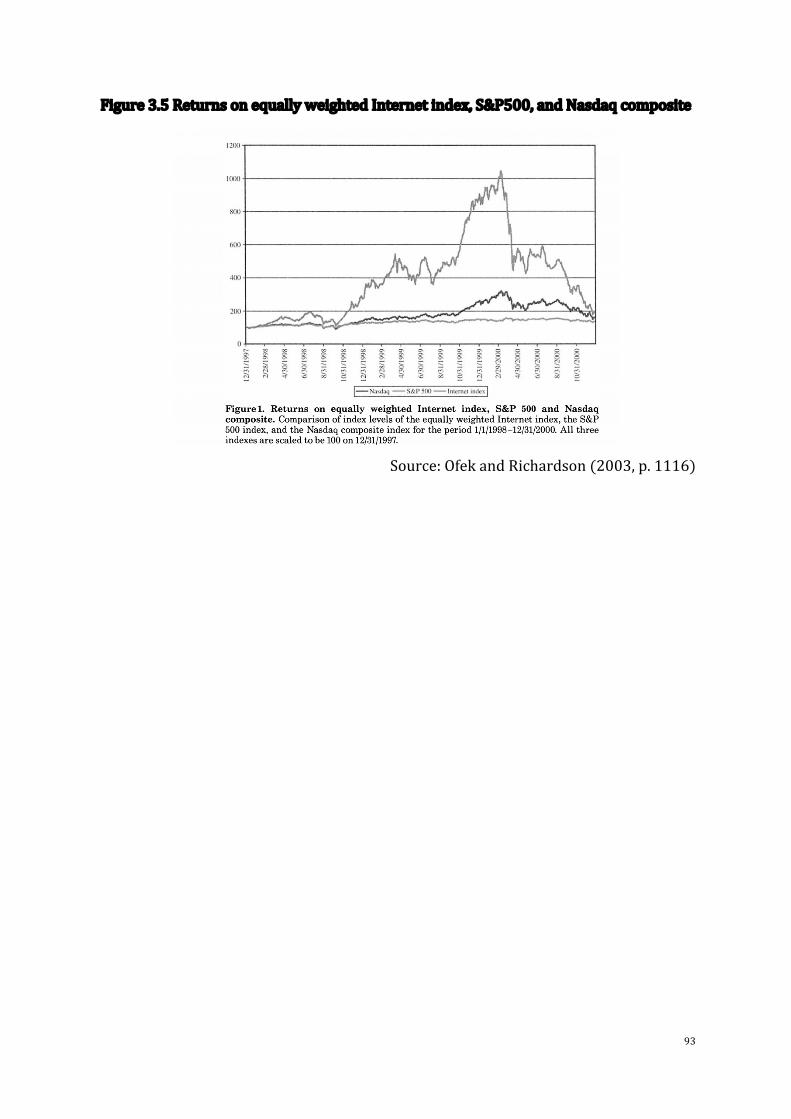

Figure3.5ReturnsonequallyweightedInternetindex,S&P500,andNasdaqcomposite

.................................................................................................................................................................................93

Figure4.1Theinvolvementofinternalfactors(resourcesandcapabilities)andexternal

factors(marketandinvestors)ininfluencingbankperformance..........................................106

Figure5.1FrameworkofResearchHypotheses.............................................................................150

Figure5.2SnapshotsofWellFargowebsiteonWaybackMachine........................................152

Figure5.3ScreenshotofWellsFargo'sMobileWebsiteInformation....................................153

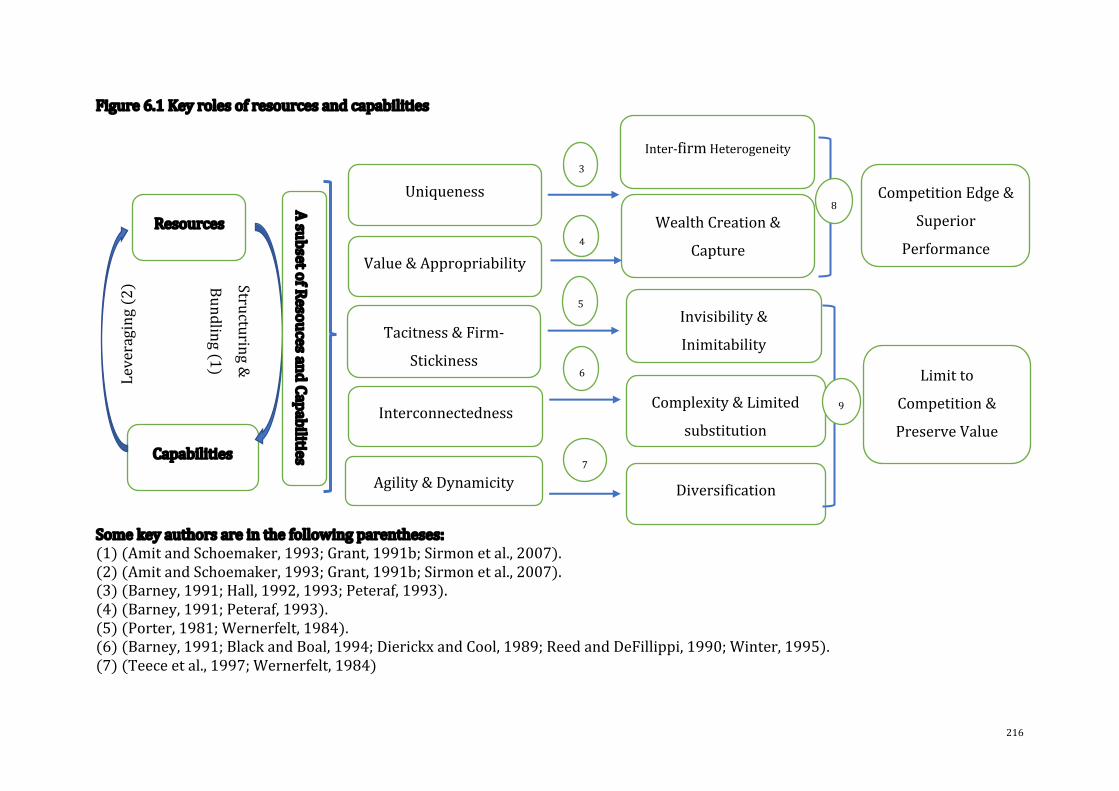

Figure6.1Keyrolesofresourcesandcapabilities.........................................................................216

Figure6.2TheenlargementofthesizeeffectonBHARsofsmallandlargebanks.........251

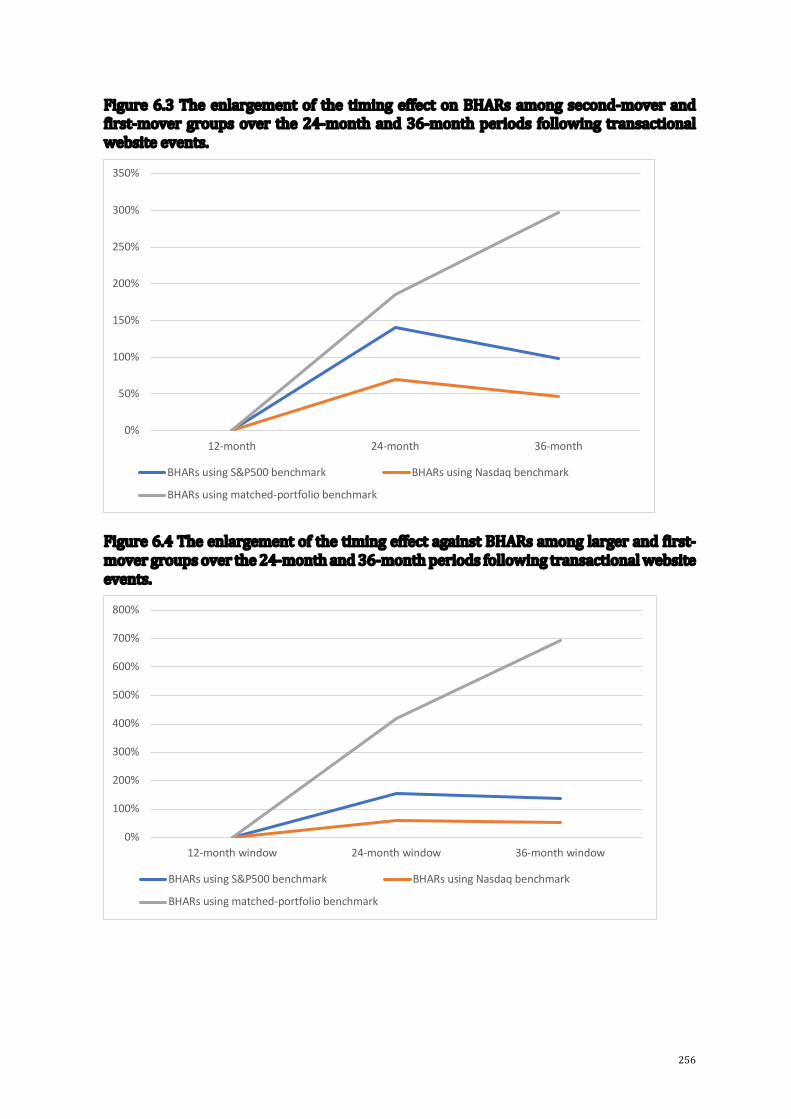

Figure6.3TheenlargementofthetimingeffectonBHARsamongsecond-moverandfirst-

movergroupsoverthe24-monthand36-monthperiodsfollowingtransactionalwebsite

events.................................................................................................................................................................256

Figure6.4TheenlargementofthetimingeffectagainstBHARsamonglargerandfirst-

movergroupsoverthe24-monthand36-monthperiodsfollowingtransactionalwebsite

events.................................................................................................................................................................256

19

1 Chapter1:Introduction

1.1 Background

Globalspendingondigitaltransformationisestimatedtoamountto$2.3trillionby2023,

asreportedbyIDC(2019).95%ofcustomerinteractionswillbecontrolledbyArtificial

Intelligence systems by 2025, as reported by Servion (2018). 59%of enterprises are

afraidthattheyarelateintheirdigitaltransformationefforts,andonly7%ofbusinesses

believetheyhavefullysettheirdigitaltransformationsinmotion,asreportedbyForbes

(2019).These areonly a fewoutof themany statisticsdepicting the current stateof

digitalizationandtheenormousandevolvingexpansionofdigitalactivities intoevery

cornerofsocietyandindustry.Indeed,nowadays,digitalizationintegratesintoalmostall

corporate strategies as well as alters the scale and scope of various aspects of

organizations(Bharadwajetal.,2013;BirgitandElsa,2019;GroverandKohli,2012;Hess

etal.,2016;Ngaietal.,2011;Pagani,2013).

The banking industry is certainly not on the sidelines of this digital transformation.

Indeed,thefinancialsectorisamongthetopthreeindustriesfordigitaltransformation,

with93%ofbusinessesalreadyimplementingadigital-firstbusinessstrategyaccording

toIDG(2018).By2024,mobileandonlinebankingareanticipatedtohavegrownby54%

comparedto2020,withmorethan3.6billioncustomersusingtheseservices(Juniper

Research, 2020). Academic studies also provide evidence that the re-configuration of

financial institutions take intoaccount thesemassivedigitaldisruptions isproceeding

vigorously and diversely, with omnichannel integration and diversification in digital

products/servicesmorestreamlinedprocesses,andbetterservicedeliverywithfewer

mistakesandmoreagileemployees(Carbó-Valverdeetal.,2020;Kelly,2014;Siaetal.,

2016).

Thedigitaltransformationofthebankingindustry,however,hasprovokedanumberof

concerns.Asoftoday,banksarefacinganumberofpressures,suchas:(i)thethreatfrom

digitaldisruptiongeneratedbytheFinTechandBigTechindustries;(ii)nichenewmarket

entrantswithinnovativebusinessmodels;(iii)furtherlegalregulations;(iv)theperilsof

Blockchain;and(v)therisingdemandofdigitallysavvycustomerswhoareincreasingly

awareofbankingcapabilitiestoofferthemdigitalfinancialservices(Carbó-Valverdeet

al.,2020;NättiandLähteenmäki,2016;Siaetal.,2016;Swacha-Lech,2017).Forexample,

banksaroundtheworldlosemorethan$1trilliontocybercrimeseachyear,asreported

20

byAccenture(2019).Databreaches increasedby480%in2018(compared to2017),

equatingtoalossofabout$3.86billionaccordingtoFinancialTimes(2018).Thethreat

fromthedigitaldisruptionofFinTechsandBigTechsisestimatedtodestroysignificant

valueforbanksatleast30-50%ofthenetprofitofbanks(Siaetal.,2016).Therecent

global survey of Deloitte in 2018 shows that 56% of surveyed customers leave their

primarybankinthenexttwoyearsastheyfindbetterpricing,lowerfees,or/andmore

personalizedservicesaswellasmoreattractive loyaltyandreward/programatother

banks.

Underavarietyofpressuressuchascosts,traditionalandinterdisciplinarycompetitors,

aswell as cybersecurity risks, banks are now having problemswithwhere their key

digitalprioritiesshouldbe.“Banksstruggletodeliverinnovativefunctionalitiesandare

stillhesitatingaboutkeyprioritiestopursue”asdescribedbyDeloitte(2019).Moreover,

thepressureisnowcomingfrominvestors,analysts,andmanagementteamswhomay

raise questions about the lack of progress coming from their investments. “Financial

institutions are struggling to make and deliver on the investments they need to be

successfulin10years’timewhiledeliveringvalueforshareholdersintheshort-term”,

saidWyman(2020,p.4).Consideringthis,forthepresenttime,itisessentialtofindthe

preferreddigitaldirectionforfinancialinstitutions.

Most recently, a numberof researchpapers specifically emphasize the role of aweb-

basedbankingchannel.Thesedocumentsshowthatweb-basedbanking is indeedstill

playinganintegralroleinthebankingdeliverysystem,despitethedominanceofmobile

banking and banking applications. More specifically, the report of Deloitte (2018)

concerningitsglobalsurveytakinginMay2018revealsthat94%ofsurveyedcustomers

using mobile banking services use their PC/laptop to access their online banking

platformsatleastonceamonth.1Amongthem,upto38%prefertousetheirlaptopsto

maketransfers,only10%lowerthanthosewhoprefertouseamobilephoneforthesame

transactions.Morenotably,up to53%ofcustomerswilluse theircomputers tomake

1 Please access to the report via https://www2.deloitte.com/us/en/insights/industry/financial-services/online-banking-usage-in-mobile-centric-world.html.Also,forfurtherinformationconcerningthesurveyofDeloitte(2018),pleaseaccesstohttps://www2.deloitte.com/us/en/insights/industry/financial-services/digital-transformation-in-banking-global-customer-survey.html. In which, 17,100 bankingconsumersacross17countriesinMay2018weresurveyedbytheDeloitteCentreforFinancialServicestoestimatethecurrentstateofbanks’digitalengagement.

21

international transactions, comparedwith 24% of customers whowill do it on their

phones.ThesurveyofDeloittealso figuresoutseveralreasonswhyweb-basedonline

banking still plays a vital role in the mobile-centric era which are security and

convenience.ThesefindingsareinlinewiththerecentacademicstudyofCarbó-Valverde

et al. (2020) which reveals that perceived safety influences consumers’ adoption

decisionswhentheygotodigitalbanking.Moreinterestingly,theresultsrevealthatan

averageof58.97%ofcustomersfeelssafeorverysafewithonlinebankingwhilethat

percentageisonly44.29%formobilebanking.Meanwhile,customersfeelthatitiseasier

touseonlinebankingovermobilebanking(66.86versus63.59).2

Thesementioneddocumentssuggest thatwebsite-basedbankinghasan irreplaceable

roledespitetheadventanddominanceofmobilebankingapps.AsDeloitte(2018)states

“Therearepotentialchallengesifbanksallowmobilebankingtoeclipseonlinebanking

fully”,aquestionwasraisedastowhetherthetransactionalwebsiteinitiativeisexactly

what investorsand theoristsexpected,whichwillpotentiallygeneratebothshortand

long-termreturnsforfinancialinstitutionsontheirpathofdigitalization?Intheacademic

worldsofar,however,therearestillsomegapsasfollow:

Firstly,therearethreemainliteraturelinesinthefieldofdigitalbankingasfollows.The

firststreamfocusesonthefeaturesofdigitaladoptionswhichmaysignificantlyinfluence

customerbehaviour,suchasusefulness,easeofuseandsafety(Aliyuetal.,2014;Gerrard

andBarton,2003;Lee,2009;Liuetal.,2011;MannandSahni,2011;Royetal.,2017).The

secondstreamfocusesontheimpactofadigitaladoptionaddedtocustomeroutcomes,

such as higher customer revenue and lower customer costs (Gensler et al., 2012),

increasedengagementinonlineactivities(HittandFrei,2002;StraderandHendrickson,

2001;Xueetal.,2011),andsuperiorcustomerexperience(MbamaandEzepue,2018).

Thethirdstreamfocusesonthefinancialbenefitsofadigitaladoptionaddedtobanks.

Morespecifically,viaadigitaladoptionbankscanbenefitintermsof:(i)newrevenue

streams;(ii)non-interestactivitiesdiversification;and(iii)effectivenessandefficiency

2Conciselyput,theresearchofCarbó-Valverdeetal.(2020)isalsoinlinewithotherstudiesthatfoundthatonline/Internetbankingbringssomeadvantages(e.g.easeofuse,usefulness,safety),whichsignificantlyincrease customer outcomes (e.g. higher customer revenue and lower customer costs, increasedengagement in online activities, superior customer experience, customer satisfaction and trust andcustomerefficiency).(AhmadandAl-Zu’bi,2011;Buelletal.,2010;Dabholkar,1996;FirdousandFarooqi,2017;HittandFrei,2002;MannandSahni,2011;MbamaandEzepue,2018;Xuetal.,2013;Xueetal.,2011).PleasereferChapter2,Section2.3.1forfurtherdiscussion.

22

(Al-HawariandWard,2006;Cicirettietal.,2009;Delgadoetal.,2007;DeYoung,2005;

DeYoungetal.,2007;Furstetal.,2002;GohandKauffman,2015;HernandoandNieto,

2007;MbamaandEzepue,2018;Momparleretal.,2013;Pignietal.,2002;Scottetal.,

2017;Sullivan,2000;Xueetal.,2007).

Nevertheless,theseaboveliteraturestreamsfacesomechallenges.Firstly,fromtheangle

of some theories that take into account firms' capabilities and competencies (e.g.,

resource-basedtheoryorknowledge-basedtheory),customervalueisnecessarybutnot

sufficient to spell out all the mechanisms determining the performance of firms.3

Secondly, the financial metrics are in low frequency by reason of being reported

periodically. Besides, it has been emphasized that there exists intangible strategic

resourcesandcapabilitieswhichareunderlyingmuchofthesuccessofthefirmbutare

virtually invisible on financial statements and thereby, tortuous to be tracked and

evaluated.4

So far, very little attention paid to the market value of a digital adoption which is

evaluatedbythemarketandinvestors.Accordingtoboththeoreticalandempiricalwork,

investorshavetheroleofdetecting,evaluatingandpredicting(Balasubramanianetal.,

2005;Benbunan-FichandFich,2004;Deaneetal.,2019;SabherwalandSabherwal,2005;

Xiaetal.,2016).Marketreactionsandinvestors’actionsareperceivedassuperiorasthey

canofferevaluationsinthemostcomprehensivemannerandattheearliestopportunity

(Fama,1970,1998,2021;Malkiel,1989).Moreover,thevisionarycapabilityisameritof

market judgment,potentiallybringing to light the intangiblevaluesofevents thatare

latent behind the accounting figures. Market evaluation and investor participation,

however,arestillmostlyinaccessibletodigitalbankingliteratureinboththeshort-run

andlong-run.

Intermsoftransactionalwebsiteadoption,inparticular,therehasbeenlittlequantitative

analysis of more extended up-to-date examinations concerning the impact of

transactional website adoption on banks’ performance. The value that transactional

3Coyne(1986)andHall(1993)suggestthatnotonlydotheproductand/ordeliverysystemattributestocustomersneedtobesignificant,buttheyalsoneedtobetheresultofacapabilitydifferentialwhichwillendure.4 ItamiandRoehl(1991)pointout that therearesome intangibleassetsare lessreadilyandhardly tomeasureespeciallysomeincrementalvaluesaddedtoemployee’sskillsandknowledge.Forexample,itishard to reflect in financial statement the enhancing experience of customer service department afterdealingwithabundleofnon-standardizedproblemsofcustomers.

23

websiteshaveaddedtofinancialinstitutionshasbeensofarmostlyscopedwithinthe

earlystageofInternetbankingand/orovertheshortormediumterm(Delgadoetal.,

2007;DeYoungetal.,2007;Furstetal.,2000a;Sullivan,2000).Furthermore,thereisa

lackofemphasisonthestrategicattributesof transactionalwebsiteadoptionthrough

clarification of its sustainable values.More specifically, previous studies consider the

transactionalwebsiteasanadditionalchannelthatcomplementstraditionalbranching

channelsratherthanastrategicbankingdeliverychannel(Cicirettietal.,2009).Several

otherstudiesfocusonsomeparticularfeaturesoftransactionalwebsiteadoption,such

asinnovation(DeYoungetal.,2007;Pignietal.,2002),efficiencyandeffectiveness(Furst

etal.,2002),diversification(DeYoungetal.,2007;Pignietal.,2002).Sofar, littlepaid

attentiontothestrategicattributesoftransactionalwebsiteswhichcouldbetherootof

banks’economicbenefitsovertime,assuggestedbytheperspectiveofresource-based

view.

1.2 MotivationsandAims

Basedonthebackgroundindigitalbankingdisciplineasdiscussedabove,thisthesisaims

atexaminingthevalueoftransactionalwebsiteadoptioninboththemarketperspective

and financial perspective, inboth the short run and long run.This thesis is primarily

motivated by: (i) The important and unreplaceable role of transactionalwebsites, as

suggested by the literature; (ii) Some gaps in digital banking literature; and (iii) The

importanceofexaminationinboththeshortandlongrun.

Firstly, the advent of the transactional website is an important mark in the digital

transformation route of the banking industry. Before the advent of transactional

websites,financialtransactionswereconductedthroughface-to-faceinteractions.Since

theactivationoftransactionalwebsites,bankscanstartofferingtheirservicesatanytime

andanywheregeographicallymoreeffectively(Nathetal.,2001).Therefore,sincethe

activationofbankingwebsites, thebankwouldhavegradually formedthe firstdigital

capabilitiesandresourcesofitsown.5Overtime,digitalcapabilitiesandresourcesfrom

thetransactionalwebsitecanalsobetransferredandinterconnectedwithotherdigital

5SomedigitalcapabilitiesandresourcesofInternetbankingareinformationquality,system'sintegration,assuggestedbyOliveiraetal.(2016).

24

bankingdeliverychannels.6Furthermore,recentdocumentsalsohighlightthatwebsite-

basedbankinghas an irreplaceable role despite the advent anddominance ofmobile

bankingapps(Carbó-Valverdeetal.,2020;Deloitte,2018).

Secondly,thereissomelackindigitalbankingliteratureingeneralandinthescopeof

transactionalwebsiteadoption:(i)Thereislittleattentionpaidtomarketparticipantsin

evaluatingthevalueofdigitalbankingadoptionwhicharesuggestedmoreimmediate,

comprehensive and predictive; (ii) Literature so far only focuses on early stage of

transactional website adoption as well as the short to medium-term impact of this

adoptiononbank’sperformance;and(iii)Relativelylittleisknownaboutthestrategic

attributesofdigitaladoptionandtransactionalwebsiteadoptionwhicharesuggestedby

theresource-basedviewastherootofthesuperiorperformanceoffirms.

Thirdly, the perspective of resource-based view emphasises the importance of both

short-andlong-termexaminationoftheimpactofaninitiative.Alsosuggestedbysome

studies,withoutshort-termwealthdelivered,coupledwithalackofvisionordiscipline,

neither managers nor investors would want to waste their resources on further

strategies.7 In this case, the evaluation of market and investors in the short run is

importantasitsimultaneouslyreflectsamosttimelyintrinsicvalueaswellasindicates

thepredictionsofthefuturebenefitsofthatportfolio(suchassustainability,potential

growth, transformative benefits). By contrast, as the financial ratios are reported

periodically, the short-term intrinsic value of a portfolio is hard to be captured

immediately.Furthermore,by improvingthemarketvalue intheshortrun,bankscan

satisfytheircurrentshareholdersandgaintheirconfidence.8Fromthat,bankscanbetter

plantheircapitalstrategytopursuelonger-termgoals.Butcertainly,allbusinessentities

expectvaluecreationandsustainablegrowthofthebusinessovertime.Therefore,the

proof in short-term value is vital but not adequate to convince managers and

stakeholders to keep focusing on a particular portfolio. It is the case of transactional

6Forexample,Oliveiraetal.(2002)statesthatInternetbankingplaysanimportantroleinformingthecombinativecapabilitiesofservicequality,delivery,theflexibilityofbankinge-services.7Accordingtorecentreports,whatinvestorsexpecttobeforthcomingisawell-fundedorientationintosmallbut sustainabledigital initiativeswhichcancreateeconomic rents in the short runandpreservesustainable earnings and competitive advantages in the long run (Accenture, 2019; Wyman, 2020).Furthermore,asclaimedbyWyman(2020,p.5),"Currentvalueswillbringtransparency,controllability,andcontinuouseliminationoffailinginvestments".8Forexample,empiricalfindingsofSwitzerandCao(2011)showthathighshareholderconfidencevalueisassociatedwithhigherfirms’economicvalueadded.

25

websiteadoptionasaconcernmayberaisedastoifthetransactionalwebsitestilladds

valuetobanksoverthe longrun.Forexample,nowadays, thedigitalbankingdelivery

system tends tobedominatedbydigitalmobile banking andmobile applications, the

managersmaybeconcernedifthevalueoftransactionalwebsitesmaygraduallyerode,

whichmightgiveanindicationofthe impactthatdigitalmobile initiativeshaveinthe

longrun.

Followingpreviousstudies(Dandapanietal.,2018;DeYoungetal.,2007;Eglandetal.,

1998;Furstetal.,2000a;OCC,2000,2019),thisthesisdefinesatransactionalwebsiteas

a site which allows customers to access information and perform the most basic

transactions,includingpayingthebillandtransferringfunds.9,10Thisthesisthenseeks

to address the following researchquestionswhich are in turnpresented in empirical

Chapters4,5and6:

(i)“Whetherornotthetransactionalwebsiteeventsgainedasignificantresponsefrom

themarket in the short term. If applicable,what storyabout the implementationof a

transactionalwebsitewouldberevealed?”

(ii) “Does the transactional website strategically deliver value to a bank’s financial

performanceovertime?Ifthatisthecase,wheredoesthevaluecomefrom?”and

(iii)“Dotransactionalwebsiteinitiativescreatevalueforfinancialinstitutionsinthelong

run? What will be revealed about the transactional website adoption behind the

investor’sbuy-and-holdstrategy?”

Moreconcretely,Chapter4 intends toaddresshowthemarketreacts to transactional

website-enabled events in the short run, reflected through excess returns earned by

banks surrounding their transactionalwebsite-enabled events. In addition, Chapter 4

aimstoexaminesomemoderatingeffectsthatpossiblydifferentiateperformanceamong

banksaswellasalterthewaythemarketreactstotransactionalwebsitelaunchevents,

includingthemagnitudeeffectandtimingeffect.Thereafter,Chapter5isdevotedtothe

impact of transactionalwebsite adoption on the financial performance of banks over

time.Sixattributesoftransactionalwebsiteadoptionbasedontheresource-basedview

9Thisdefinitionisthebasisforthevalidationoftransactionalwebsiteeventdatesofthesamplebanks.MoredetailisdiscussedinChapter3,Section3.2.2.10MorediscussiononthedefinitionoftransactionalwebsiteisprovidedinChapter3,especiallySection3.1.1. Also please refer to Sections 3.1.1 and 3.1.2 for further discussions on the reason of choosingtransactionalwebsiteadoptionastheunitofanalysisaswellasmoreliteraturereviewontransactionalwebsiteadoptioninparticular.

26

are then examined, namely value, appropriability, durability, embeddedness,

inimitability, and interconnectedness. Such attributes clarify the strategic role of the

transactionalwebsite.Theheterogeneityamongbanksisalsotestedwhichispotentially

attributedtothesizeeffectandtimingordereffect.Finally,Chapter6aimstoexamine

howtheinvestorsevaluatetransactionalwebsiteadoptionthroughtheirbuy-and-hold

strategy in relation to the abovebenchmarks.This chapter also strives to answer the

questionoftowhatextentthetransactionalwebsiteadoptionimpactsthebuy-and-hold

abnormal returns (BHAR)which are treated as a proxy for banks’ long-termmarket

performance. Learning-by-observing, size effect and timing order effect are also

objectivesofthatchapter.

1.3 Methodology

Thefollowingmethodologyisappliedbasedonthedataof307fullylistedcommercial

banksintheUSmarket.

Firstly, Chapter 4 applies event studymethodology to estimateCumulativeAbnormal

Returnsearnedbybankssurroundingtheir launchevents.Morecharacteristically, the

marketmodelhasbeenconstructeduponseveralshort-runwindows[including(-1,+1);

(-2,+2);(-3,+3)]anddifferentestimationperiods(including-120days,-180days,-200

days, -300 days). On the foundation of the efficientmarket hypothesis (Fama, 1998),

event study is a great tool to recognize the added value of a specific corporate event

thanks to its ability to react immediately, precisely, and predicatively to themarket.

Today, event study has become one of themostwell-liked approaches, and iswidely

applied inmany disciplines (e.g., IT investments, e-commerce, security breach, M&A,

innovation,R&D,corporateawards).

Secondly, Chapter 5 employs a series of regression analysis to measure the direct

relationshipbetween transactionalwebsiteadoptionand the financialperformanceof

banksoveryears.Regressionanalysisisareliablemethodtoconfidentlydetermineifa

transactionalwebsite is a strategic digital initiative by estimating the effect of its six

attributes: value, appropriation, durability, embeddedness, inimitability, and

interconnectedness.Thesesixfeaturesaretestedtosatisfytheresource-basedview:(i)

competitive advantage and superior performance, and (ii) limit competition and

preservethevalue.

27

Finally, the event-time approach with the Buy-and-Hold Abnormal Return (BHAR)

metric,accompaniedbyregressionanalysisisthefoundationofChapter6.Tomeasure

BHAR,fivedifferentbenchmarksareapplied,includingthreemarketindices,anex-ante

buy-and-holdportfolioandanon-eventsize-matchedcontrolfirmportfolio.BHARisalso

treatedastheproxyofbanks’long-termperformancetofacilitatefurtherexaminationof

thedirecteffectsoftransactionalwebsiteadoption,informationspillovereffect,timing

effect,andsizeeffectonbanks’long-termperformance.

1.4 Contribution

(i) Firstly, in terms of data, this thesis provides exclusive data from 307 fully listed

commercial banks in the US market, concerning their transactional website launch

announcements from 1996-2010. Based on this data, this thesis becomes the first to

enable the participation ofmarkets and investors in evaluating transactionalwebsite

eventsasthefirstdigitalinitiativeoffinancialinstitutions.Also,basedonthisdataset,

themostup-to-dateaccountingdataisprovidedforthesamplebanksfrom1993-2018,

accordinglyauthenticatingtheimpactsoftransactionalwebsitesontheperformanceof

banksinamoresystematicandupdatedmannerinbankingliterature.

(ii)Secondly,intermsofmethodology,thisthesisisthefirstindigitalbankingliterature

puttheevent-timeapproachaccompaniedbytwometricsCumulativeAbnormalReturn

(CAR)(fortheshort-termhorizon)andBuy-and-HoldAnormalReturn(BHAR)(forthe

long-termhorizon)intopractice.CARandBHARarewidelyknownastworobustmetrics

for tracking down market evaluation and investor actions as well as offering an

evaluationofthevalueofeventsinatimely,relevant,accurate,andforward-lookingway.

Unfortunately,bothmetricsarestilluntappedindigitalbankingduetodataconstraints

and the rigour of benchmark selection. Furthermore, this thesis applies some non-

parametricbenchmarkswhicharewell-suited to situationswhere theassumptionsof

parametricstatisticsarenotmet,whichistypicallythecaseforsmallsamplesizes.

(iii)Thirdly,intermsoffindings,thisthesisprovidesempiricalresultswhich:

-Confirmthattransactionalwebsitesimprovemarketperformanceandfinancial

performanceofbanksinboththeshort-termandlong-termperspectives.Therewarding

featuresoftheadoptionofdigitaltransactionalwebsitesareconfirmedbythepositive

market reaction in the short runwith positive cumulative abnormal returns, positive

28

financialperformancethroughouttheyearsandpositiveinvestorevaluationinthelong

runthroughtheirbuy-and-holdstrategy.

- Confirm the impact and strategic role of transactional website adoption via

providing empirical results for six strategic attributes of the transactional websites’

adoption including value, appropriability, durability, embeddedness, inimitability, and

interconnectedness. Through possession of the six above-mentioned attributes, the

transactionalwebsitedeservesappreciationasastrategicdigitalinitiativeofbanksthat

cangenerateandpreservewealthoverthelong-term.Besidesthis,theempiricalfindings

provide a new understanding of the intangible attributes of transactional website

adoption,whicharebeyondthetwostandardattributesdetectedbypreviousstudies-

innovativenessandprofitability.

- Prove the rationality of themarket and investors in evaluating transactional

website portfolio. The verifying evidence includes (i) the existence of learning-by-

observingbehaviourofinvestorsthroughtheinformationspillovermechanism,(ii)the

existence of efficient or semi-efficient markets as the information spillover effect

becomes a learning mechanism of investors (iii) consistency between investors’

predictionsintheshortrunandinvestors’actionsinthelongrunand(iv)consistency

betweentheevaluationofinvestorsandactualfinancialperformanceofbanks.

(iv)Finally, thisthesisbringssomeimplications intermsofconceptualanalysis.More

specifically,thisthesisprovidesconceptualmodelson(i)theroleofinvestorsand(ii)on

howthe internal components (e.g., resourcesandcapabilitiesofdigital initiative)and

externalcomponents(marketandinvestors)interact.Alistofresourcesandcapabilities

of transactionalwebsites (e.g., digital culture, tacitdigitalknowledge,digitalnetwork,

digitalhuman) isalsosuggestedby this thesis tosupport therationalityofmarket. In

short, the conceptual analyses of this thesis have applied the crossover between the

resource-basedview,theefficientmarkethypothesisandmarketsignallinghypothesisto

explainhowtheinternalfactorsandexternalfactorscaninteracttogetherinthecaseof

transactionalwebsiteadoption.Theseconceptshavesofarreceivedlittleattentioninthe

literature.

1.5 Structure

The overall structure of this thesis takes the form of seven chapters, including this

introductorychapter.Chapter2providesthereviewonkeyconceptsandimplicationsof

29

resource-basedviewasthemaintheoreticalframeworkofthisthesis.Afterwards,that

chapterdiscussesonthemostrecentliteraturestreamsrelevanttothevalueofdigital

adoption in general and transactional website adoption in particular as well as the

landscapeofUSbankingindustryduringtheresearchperiod.Subsequently,Chapter3

discussesindetailtheformulationandthedescriptivestatisticsoftheresearchsample

andeventdates.Chapters4,5and6,inturn,provideempiricalresultstoachieveresearch

questions and objectives.More pointedly, Chapter 4 examines the short-termmarket

reactiontowardsthebank’stransactionalwebsiteeventssurroundingthetimetheyare

announced to the market. Subsequently, Chapters 5 and 6 investigate the impact of

transactionalwebsiteadoptiononbanks’performanceinthelongrun,inturnthrough

accountingmeasures(Chapter5)andBHARsmetric(Chapter6).Finally,Chapter7gives

a summaryof themain findingsof eachof theprevious chapters,main contributions,

managerialimplications,researchlimitationsandsomesuggestionsforfurtherresearch

inthefuture.

30

2 Chapter2:LiteratureReviewandTheoreticalFramework

2.1 TheoreticalFramework-Resource-basedView

Theresource-basedviewisthemaintheoreticalframeworkinthisresearch.Thissection

firstly discusses some key concepts of the resource-based view. After that, it will be

followedbythediscussiononwhytheresource-basedviewis important inthedigital

bankingliteratureandhowdotheconceptsrelatetotheaimsandobjectivesofthethesis.

2.1.1 TheGeneralConceptoftheResource-BasedView

At the heart of the resource-based view, the underlying source of firms' competitive

advantages and sustainable success is their idiosyncratic competencies (Amit and

Schoemaker,1993;Barney,1991;Petoeraf,1993).Organizationsarestronglybelievedto

gaineconomicrentsonlyinthecasethattheyareabletoefficientlyleveragetheirown

resources and capabilities which possess strategic features, such as value, firm-

specificity, inimitability, durability, appropriability, limited substitutability (Amit and

Schoemaker,1993;Barney,1991;CollisandMontgomery,1995;DierickxandCool,1989;

Grant,1991b;LippmanandRumelt,1982;Peteraf,1993;RumeltandLamb,1997).

Theresource-basedliteraturealsoconsiderstheimportanceofthemarket,e.g.,Rumelt

andLamb(1997,p.141)saythattheopportunitiesforfirmstoearnsuperiorrentmight

"jumpbehind"iffirmsdonotorareslowtoreacttounexpectedchangesinthemarket,

such as the changes in technology, regulation, consumer behaviour and so forth. In

another study, Amit and Schoemaker (1993) suggest "strategic industry factors"

significantly influence the path of firms' success, including involvement of market

participants(e.g.customers,stakeholders)aswellasthedynamicoftheeconomy.

2.1.2 ResourcesandCapabilities

"Resourcesarecrownjewelsandneedtobeprotectedastheyplayapivotalroleinthe

competitivestrategywhichthefirmpursues"(Grant,1991b,p.129).

Atfirst,resourcesaretheprimemoverofsuperiorperformance.Itiswidelyadmittedby

boththeoristsandempiricaladvocatesoftheresource-basedviewthatresources,dueto

the features specific to firms and their idiosyncrasies, have the ability to create

differentiationamongfirmsandaccordinglyendowfirmswithacompetitiveadvantage

(Barney,1991;Porter,1990)andinter-firmprofitdifferentiations(Grant,1991b;Winter,

1995). Therefore, in the language of the resource-based view, by focusing on the

31

exploitationofsuchundertaking-specificfactorsanddistinctivecompetenciesasinner

strengths,firmsareputtingthemselvesonasuccessfulpathwithsuperiorperformance

(Barney, 1991; Peteraf, 1993; Porter, 1990). For illustration, a substantial amount of

attentionhasbeenpaid to the conceptofknowledgeasoneof themostvaluableand

fundamental resources of the firm. Knowledge is believed to be the basis of a firm’s

superiorperformancenotonlybecausetheyaretheguideforanyactionandanystrategy

of the firm, but also because they are implicit, casually ambiguous, unique to firms,

socially involved and challenging for any external observation. Thereby, the rewards

firms obtain from their knowledge are differential economic rents and competitive

position(Hall,1993;OlavarrietaandFriedmann,1999;SpenderandGrant,1996;Teece,

1988).Conversely,firmsarefoundtoquitepossiblylosetheircompetitiveedgeifthey

emphasize investment without cautiously considering their tacit knowledge

(Johannessenetal.,2001;NonakaandTakeuchi,1995).

Asasecondpoint,resourcesareacompetitivebarriertoprotectthevalueof thefirm

sustained over time. This then suggests there are three features enabling resources

operating through this mechanism. Firstly, it is emphasized by Grant (1991a) that

resources,alongwithcapabilities,givedirectiontothefirmtodefineitself, identifyits

mission, strategy, targeted customers, andmarket.11 Similarly, Grant (1991b, p. 543)

assertsthat"thecompetitiveadvantageisprimarilyconcernedwithexploitingsuperior

resources and capabilities". Itmeans that by understanding and deploying resources

efficiently as inner strength, firms are able to direct themselves to cope with the

uncertaintyofthemarketaswellasthethreatfromtheirrivals.Secondly,resourceshave

thepowertolimitcompetitionthankstothefeaturesofspecificity,tacitness,complexity,

and stickiness to the firmwith time, thereby being a stumbling block to imitation or

substitution(Wernerfelt,1984).

Moreover, some authors call attention to the interconnectedness of resources as an

essential feature in limiting the competition (Barney, 1991; Black and Boal, 1994;

11Grant(1991a)reinforcesthispointbyrecallingTheodoreLevitt'ssuggestionthatenterprisesshouldre-definetheirservedmarketsmorebroadlytomanagetheriskofmarketchange.TheodoreLevitsuggeststhatrailroadsshouldnotbemerelyawareofthemasrailroadbusinessesbuttransportationbusinesseswhichallowthemtodiversifytheirbusinessandregulatethemselvesinthedynamicofexternalmarket.Grant(1991a)hasarguedagainstthisideabyquestioningwhetheritisreasonableforarailroadbusinesstodevelopsuccessfullyinrail,airorcarbusinesses.Hepointsoutthatthelineenterpriseisstillappropriatein the construction andmanagement of oil and gas pipelines as this somehow is compatiblewith theresourcesandcapabilitiesofrailroadsenterprise.

32

DierickxandCool,1989;Winter,1995).ItisclaimedbyWinter(1995,p.14)that"the

valueofidiosyncraticresourcestothefirm--i.e.,thepresentvalueoftheirfuturerent

streamsareaffectedbythefactthattheirpossibleusesincludethedevelopmentofmore

idiosyncraticresources".Theimplicationisthattheinterconnectednessamongspecific

resources within firms offers an additional advantage: an increase in the structural

complexity and ambiguous causalitywith the firm'sperformance. In thismanner, the

interconnectedness of resources would be considered as an isolating mechanism to

protectthefirm'srentsfromunfavourableimitationorreplicationofmovesfromothers

(Barney,1991).

Finally,resourcesarefoundtobeaninstrumentforfacilitatingdiversification.Wernerfelt

(1984)createdtheresource-productmatrix,whichindicatesthedynamicityofresources

inallocatingproducts/servicespreferabletoeachparticularmarket.Ittherebyshowsthe

roleofresourcesinrewardingfirmswithgrowthopportunitiesaswellasthedynamic

capabilitytoadapttodifferentmarkets.

Intermsofcapabilities,theyaregenerallydefinedasfirms'abilitytoemploy,combine,

and deploy their appropriate resources with the pursuit of an efficient and effective

ending.Putdifferently,"thecapabilitiesofafirmarewhatitcandoasaresultofteamsof

resources working together" (Grant, 1991b, p. 120). Amit and Schoemaker (1993)

distinguish capabilities from resources by proposing the role of capabilities towards

organizational systems and the responsiveness to themarket. They put forward that

thesecapabilitiesassisttheorganizationinshorteningthedevelopmentcycle,facilitating

innovation,andactivating flexibilities for repeatedprocesses.Also, capabilitiesenable

firmstoidentify,acknowledge,comprehendandpredictthemarket;accordingly,firms

gainbetterresponsivenesstowardthemarket.Grant(1991a)definescapabilitiesasthe

meansthroughwhichafirm’sresourcesarecoordinated.Resourcesenhancecapabilities

inlong-runadvantage(Winter,1995).Therefore,itisworthhighlightingthatthereisno

separatingoperationbetweenorganizationalresourcesandcapabilities.Instead,theyare

inanintertwinedandmutuallysupportiverelationship.