2020/21 KSP Policy Consultation Report

358

Presented by the MOEF, Republic of Korea 2020/21 KSP Policy Consultation Report Albania Gas Sector Expansion Strategy for Energy Diversification in Albania

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of 2020/21 KSP Policy Consultation Report

Presented by the MOEF, Republic of Korea

2020/21 KSP Policy Consultation ReportAlbania Gas Sector Expansion Strategy for Energy

Diversification in Albania

Government Publications Registration Number

11-1051000-001116-01

2020/21 KSP Policy Consultation ReportAlbania Gas Sector Expansion Strategy for Energy

Diversification in Albania

Project Title GasSectorExpansionStrategyforEnergyDiversificationinAlbania

Prepared for TheGovernmentofAlbania

In cooperation with Ministry of Infrastructure and Energy (MIE)

Supportedby MinistryofEconomyandFinance(MOEF),RepublicofKorea

KoreaDevelopmentInstitute(KDI)

Preparedby Hanyang University Industry-University Cooperation Foundation (HYU-IUCF)

Project Directors JungwookKim,ExecutiveDirector,CenterforInternationalDevelopment(CID),KDI

SanghoonAhn,FormerExecutiveDirector,CID,KDI

Project Manager KyoungDougKwon,Specialist,CID,KDI

ProjectOfficers HeaweonChoi,SeniorResearchAssociate,DivisionofPolicyConsultation,CID,KDI

Hyeseung Choi, Senior Researcher, Center for Energy Governance & Security, Hanyang University

SeniorAdvisor Joong-KyumKim,FormerCEOofKoreaElectricPowerCorporation

Principal Investigator YounkyooKim,Professor,HanyangUniversity

Authors Chapter1.YounkyooKim,Professor,HanyangUniversity

Chapter2.JinsooKim,AssociateProfessor,HanyangUniversity

NamjinRoh,ResearchFellow,KoreaEnergyEconomicsInstitute

Dritan Spahiu, Local Gas Expert

Chapter3.SungkyuLee,SeniorResearchFellow,KoreaEnergyEconomicsInstitute

Eunmyung Lee, Senior Research Fellow, Hanyang University

Stavri Dhima, Former Head of the Gas Sector, Ministry of Infrastructure and Energy

Chapter4.YounkyooKim,Professor,HanyangUniversity

YoungDooKim,Professor,JeonbukUniversity

WonbaeKim,SeniorResearcher,HanyangUniversity

ArtanLeskoviku,HeadofEnergy,NationalAgencyofNaturalResources

English Editor Editage

2020/21 KSP Policy Consultation Report

GovernmentPublicationsRegistrationNumber11-1051000-001116-01ISBN979-11-5932-658-5 979-11-5932-641-7(set)Copyright ⓒ2021byMinistryofEconomyandFinance,RepublicofKorea

2020/21 KSP Policy Consultation ReportGas Sector Expansion Strategy for Energy

Diversification in Albania

PrefaceTheKnowledgeSharingProgram(KSP) isaknowledge-intensivedevelopmentandeconomic

cooperationprogramdesignedtoshareKorea’sdevelopmentexperienceswithpartnercountries.

Since2004,theMinistryofEconomyandFinanceoftheRepublicofKorea(MOEF)hasbeen

managingKSPforpartnercountriesregardingtheircapacityofpolicybuildingandsustainable

development.Tomeet theneedsofpartnercountries,KSPoffers comprehensivepolicy

consultations through in-depth analysis and training opportunities.

OnbehalfofHanyangUniversity,IwouldliketoexpressourdeepestappreciationtotheMinistry

ofInfrastructureandEnergy(MIE), theGovernmentofAlbaniaandtheKoreaDevelopment

Institute(KDI),andtheMinistryofEconomy&Finance(MOEF)fortheircollaboration inthe

project. In particular, I would like to extend my profound gratitude to H.E. Ilir Bejtja, Vice Minister

of MIE and Illia Gjermani, Director General of Oil and Gas Development of MIE, the Government

ofAlbania.IwouldalsoliketothankMr.EralTrasja,Mr.DritanSpahiu,Dr.StavriDhima,Mr.

ArtanLeskoviku,Dr.MaksimShuli,Mr.AgimNashi,Mrs.EvisÇano,Mrs.RenataAliko,Mr.Arqile

Piperi,Mr.SidritTako,Mr.AlbanIbrahimifortheirunwaveringsupport.Thecompletionofthe

project“GasSectorExpansionStrategyforEnergyDiversificationinAlbania”wouldnothavebeen

possiblewithouttheirdevotion.

IalsowishtothanktheKSPconsultationteam:Dr.Joong-KyumKim(SeniorAdvisorandHead),

ProfessorYounkyooKim(PrincipalInvestigator),andDr.JinsooKim,Dr.NamjinRoh,Dr.Sungkyu

Lee,Mr.EunmyungLee,Dr.YoungDooKim,andMr.WonbaeKim(FellowResearchers) for

producing this report.

Thisprojectbenefitedgreatly fromthecontributionofseveralothersfromboth insideand

outsidetheAlbaniangovernment,suchasDr.FrankUmbach,HeadofResearch,EUCERS/CASSIS,

University of Bonn and Dr. Stephen Blank, Senior Fellow, Foreign Policy Research Institute (FPRI). I

wouldliketoextendmysincereappreciationforallthosewhohavemadevaluablecontributions

to the successful completion of this project. I am also grateful to the Center for International

Development (CID)ofKDI, inparticularDr. JungwookKimandDr.SanghoonAhn (Project

Directors),Dr.KyoungDougKwon(ProjectManager),andMs.HeaweonChoi(ProjectOfficer),for

their hard work and dedication toward the project.

IfirmlybelievethatKSPwillserveasasteppingstonetofurtherelevatemutual learningand

economiccooperationbetweenAlbaniaandKorea,andhopethat itwillcontributetotheir

sustainabledevelopment.

Sung Kyu Ha

Dean

Industry-University Cooperation Foundation

Hanyang University

Contents2020/21KSPwithAlbania ················································································································ 023Executive Summary ·························································································································· 029

Chapter 1 Introduction

Summary ·········································································································································· 0331.ObjectivesandScope ··················································································································· 0342. Methodology ································································································································ 0373.GasSupply,Demand,andMarketinAlbania ············································································· 040 3.1. Energy Supply and Demand ································································································· 040 3.2. Natural Gas Demand Structure ···························································································· 047 3.3. Gas Supply Structure ············································································································· 053 3.4. Gas Market Development ····································································································· 0614. South-East Europe (SEE) Gas Supply and Demand ····································································· 062References ········································································································································ 078

Chapter 2 Long-Term Outlook for Natural Gas Demand/Supply in Albania and the Strategy for Demand Drive of Natural Gas

Summary ·········································································································································· 0851. Introduction ·································································································································· 0862.KoreanExperiencesofNaturalGasDemandModeling····························································· 087 2.1.NaturalGasDemandinKorea ······························································································ 087 2.2.WorldPanelModelofKorea ································································································· 0913.EnergyDemandForecastingModels:Bottom-upvs.Top-down ··············································· 092 3.1.EnergyDemandModelingApproaches ··············································································· 092 3.2.Bottom-upModelandtheGasMasterPlanforAlbania ····················································· 0944. Strategies for Updating Demand Forecasts in the Gas Master Plan ········································· 096 4.1.CurrentStatusofGasDemandinAlbania ··········································································· 096 4.2.OurApproachtoGMPinAlbania ························································································· 1015.ResultsandProposalsforNaturalGasDemandPromotioninAlbania ···································· 104 5.1.Household&ServiceSector ·································································································· 104 5.2.IndustrySector ······················································································································ 106

5.3.TransportSector ···················································································································· 114 5.4.SurveyResults ························································································································ 119 5.5.ConclusionandSuggestions ································································································ 121References ········································································································································ 125

Chapter 3 National Policy Establishment for Natural Gas Industrial Structure and Market Design in Albania

Summary ·········································································································································· 1291. Introduction ·································································································································· 1312.StrategyandTasksforDevelopmentofNaturalGasIndustryofAlbania ································ 132 2.1. Current Situation of Energy Industry and Restructuring Policy of Government ·············· 132 2.2. Energy Pricing System in Electricity and Natural Gas Markets ··········································· 135 2.3.TheEU’sNew“EuropeanGreenDeal”andtheFutureConstraintRoleof NaturalGasforEurope’sEnergySupply ·············································································· 1383.OverviewofKorea'sNaturalGasIndustry ·················································································· 155 3.1. Supply and Demand of Natural Gas ····················································································· 155 3.2. Import of LNG and Supply Infrastructure ············································································ 158 3.3. Hydrogen ······························································································································· 1604.DevelopmentofKorea’sNaturalGasIndustry ··········································································· 160 4.1.EffortstowardsStableEnergySupplyforEconomicDevelopment ···································· 160 4.2. Implementation of the Introduction of LNG and Development of the Gas Market ·········· 163 4.3.SupportviaNaturalGasTariff ······························································································ 169 4.4.FinancialAidstoLNGBusiness ····························································································· 171 4.5.Long-TermEnergySupplyandDemandPlan ······································································ 1725.ComparisonofLawsandRegulationsonNaturalGasinAlbaniaandKorea ··························· 178 5.1.LawsandRegulationsonNaturalGasinAlbania ································································ 178 5.2.LawsandRegulationsonNaturalGasinKorea ·································································· 180 5.3.ComparisonofLawsandRegulationsbetweentheTwoCountries ··································· 1846.Recommendation:TheEstablishmentofaNaturalGas-RelatedAgency ································· 187 6.1.NeedsandStepsRequiredtoEstablishaNaturalGas-RelatedAgency ····························· 187 6.2.EstablishmentofEnergyPolicyandTechnologyThinkTank ·············································· 189 6.3.EstablishmentofOrganizationsRelatedtoGasSafetyandTechnology ··························· 198References ········································································································································ 203

Chapter 4 Albania’s Natural Gas Infrastructure Build-out and Technical Cooperation

Summary ·········································································································································· 2091. Introduction ·································································································································· 2102.Albania’sNationalNaturalGasInfrastructureBuild-out ··························································· 211 2.1. Domestic Resources ·············································································································· 221 2.2. National Infrastructure Build-out ························································································ 2253.Albania’sNaturalGasInfrastructureInterconnectionwithNeighboringCountries ················ 232 3.1.IonianAdriaticPipeline ········································································································· 232 3.2.LNGKrk ·································································································································· 235 3.3. LNG Revithoussa ··················································································································· 236 3.4. Eagle LNG······························································································································· 2374.ComparativeAssessmentofLNGIntroductionMethods ·························································· 239 4.1.FSRUTechnical&EconomicAssessment ············································································· 242 4.2.SSLNGTechnical&EconomicAssessment ··········································································· 278 4.3.SiteAssessment ····················································································································· 3175.RecommendationsforAlbania ···································································································· 331 5.1.StatusofAlbania’sGasSupplySystem ················································································· 331 5.2.HowtoStarttheLNGBusinessinAlbania? ·········································································· 3376.SharingKorea’sKnowledge&ExperienceinNaturalGas&LNGInfrastructure ······················ 343 6.1.Korea’sKnowledge&ExperienceinLNG ············································································· 343 6.2.Korea’sKnowledge&ExperienceinSSLNG ········································································· 3447.TechnicalCooperationbetweenSouthKoreaandAlbania ························································ 349 7.1. Transmission ·························································································································· 349 7.2.Equipment ····························································································································· 350 7.3. LNG Technologies ·················································································································· 3518.RecommendationsfortheDevelopmentofAlbgazSh.a.withBenchmarksonKOGAS ·········· 351References ········································································································································ 354

Contents

Contents l List of Tables

Chapter 1

<Table1-1> ObjectivesoftheProject ························································································· 037<Table1-2> SoutheastEurope–Macroeconomic&EnergySnapshot2016 ··························· 041<Table1-3> AlbaniaTPESperSector,2020-2040 ······································································· 042<Table1-4> AlbaniaTPESperFuel,2020-2040 ·········································································· 042<Table1-5> PotentialNaturalGasConsumptionby2040 ························································ 047<Table1-6> TotalNaturalGasConsumptioninAlbania ···························································· 048<Table1-7> “Non-Binding”PhaseoftheMarketTestof2019 ·················································· 052

Chapter 2

<Table2-1> StructureofPrimaryEnergySupplybySourceinRepublicofKorea ··················· 088<Table2-2> NaturalGasDemandProjectioninKorea ······························································ 090<Table2-3> ComparisonofEnergyDemandModelingApproaches ······································· 093<Table2-4> TotalPrimaryEnergySupplyinAlbania ································································· 097<Table2-5> GDPGrowthinAlbania ··························································································· 097<Table2-6> TotalFinalEnergyConsumptionbySectorinAlbania··········································· 097<Table2-7> TPESbyResourcesinAlbania,NaturalGasScenario ············································ 098<Table2-8> TFECbySectorinAlbania,NaturalGasScenario··················································· 099<Table2-9> PotentialNaturalGasConsumptionin2040(NaturalGasScenario) ··················· 100<Table2-10> PriceLevelofAlternativeFueltoNaturalGas ······················································· 105<Table2-11> PriceLevelofNaturalGasforPriceCompetitiveness ··········································· 105<Table2-12> AssumptionforGDPGrowthandStructure ·························································· 107<Table2-13> TFECbySectorinAlbania,NaturalGasScenario··················································· 110<Table2-14> TFECbyFuelTypeinChemical&PetrochemicalofNon-OECD(2017) ················· 111<Table2-15> TFECbyFuelTypeinSteel&IronIndustryofNon-OECD(2017) ·························· 113<Table2-16> DemandforFertilizerNutrientUseintheWorld ·················································· 114<Table2-17> FertilizersImportsbyNutrientintheAlbania ······················································· 114<Table2-18> TFECinTransportSectorinAlbania(2019) ···························································· 116<Table2-19> WorldLNGBunkeringDemandOutlook ······························································· 118<Table2-20> InlandLNGBunkeringDemandinAlbania ··························································· 119<Table2-21> SurveyPoolfortheNaturalGasDemandAnalysis ··············································· 119<Table2-22> AnticipatedDemandIncreaseby2040 ·································································· 120<Table2-23> RoughEstimationforFutureNaturalGasDemandinAlbanianIndustries········· 121

Contents l List of Tables

<Table2-24> AssumptionsfortheScenariostoUpdatetheGMP ·············································· 122<Table2-25> EstimatedNaturalGasDemandinAlbania ··························································· 123

Chapter 3

<Table3-1> LNGDemandForecastbySectorintheBasicPlan ··············································· 164<Table3-2> MajorDiscussionTopicsbyWorkingGroupDivision ············································ 176

Chapter 4

<Table4-1> DesignGasQuantitiesforSupplyofConsumersonanAnnualBasisin2040 ···· 215<Table4-2> TotalPotentialNaturalGasConsumptioninAlbaniaby2040 ······························ 216<Table4-3> ListofPotentialAnchorLoadswithIndicatedNaturalGasConsumption ··········· 218<Table4-4> ForecastedNaturalGasConsumptioninRefineriesinAlbania ···························· 219<Table4-5> IAPSummary ··········································································································· 234<Table4-6> CapacityTrendofImportTerminalsbyRegion ····················································· 244<Table4-7> FSRUandLandPowerPlants ·················································································· 249<Table4-8> ComparisonofFSUandBMPP ··············································································· 251<Table4-9> FSPPShipStructure ································································································· 253<Table4-10> ClassificationandCharacteristicsofRegasificationFacilities ······························· 254<Table4-11> FSRUProjectStatus(AsoftheEndof2020) ·························································· 262<Table4-12> CapacityComparisonforLandTerminalandFSRU ··············································· 268<Table4-13> ComparisonbetweenOnshoreTerminal,FSRUandCoveredFSRUs ··················· 271<Table4-14> WorldSSLNGMarket,2020–2025 ·········································································· 278<Table4-15> DefiningSSLNGandComparisonswithStandardLNG ········································ 283<Table4-16> LNGImportTerminalsinEurope ············································································ 308<Table4-17> MediterraneanLNGTerminals-SSLNGServices ··················································· 311<Table4-18> CapitalandOperatingCostofSSLNG ···································································· 313<Table4-19> MainAssumptions ··································································································· 315<Table4-20> AssumptionsforDieselReplacementinPowerGenerations ······························· 316<Table4-21> TableofRankings ···································································································· 330<Table4-22> FSRUFleetattheEndof2020 ················································································· 340

Contents l List of Figures

Chapter 1

[Figure1-1] KSPProcedure ········································································································· 040[Figure1-2] TPESbyEnergySource,2018 ·················································································· 042[Figure1-3] InstalledPowerCapacity,2018 ·············································································· 043[Figure1-4] DistributionofPrimaryEnergySupplybyDemandSector,2018 ························· 044[Figure1-5] ElectricityProduction,ConsumptionandNetImports,2014-2019 ····················· 044[Figure1-6] NetEnergyImports,2014-2018 ············································································· 045[Figure1-7] Albania’sGDPGrowthin2019ComparedwithCountriesinSouthEastEurope ··· 048[Figure1-8] Albania’sEnergyDemandGrowthin2015-2017 ··················································· 049[Figure1-9] Albania’sIndustrialGasDemandGrowthin2019 ················································· 049[Figure1-10] Albania’sDieselPricesin2019················································································ 050[Figure1-11] IndustrialNaturalGasPricesin2019····································································· 051[Figure1-12] Albania’sLPGPricesin2019 ··················································································· 051[Figure1-13] NaturalGasConsumption,2020-2040 ··································································· 052[Figure1-14] GasSupplyGrowthin2015-2017 ··········································································· 053[Figure1-15] NaturalGasUseGrowthinPowerGeneration,2015-2017 ·································· 054[Figure1-16] DryNaturalGasProductionofAlbania ·································································· 054[Figure1-17] GasProductioninAlbania,2009-2018 ··································································· 055[Figure1-18] South-EastEuropeGeography ··············································································· 062[Figure1-19] Russia’sNewGasPipelinesinSouthEasternEurope ············································ 063[Figure1-20] TANAP-TAP-SCPPipeline-Network ·········································································· 065[Figure1-21] EuropeanLNGImportsin2018-2020 ···································································· 071[Figure1-22] PNGvs.LNGImportsinEuropein2019 ································································ 072[Figure 1-23] Potential Export Routes of Gas from the Eastern Mediterranean Export Countries (Israel, Cyprus, and Egypt) ························································· 075[Figure 1-24] Eastern Mediterranean Gas Fields, Gas Pipelines and Egypt’sLNGExportTerminal ·················································································· 076

Chapter 2

[Figure2-1] CityGasDemandbyUsein2019 ············································································ 089[Figure2-2] HistoricalNaturalGasDemandinKorea(1992-2020) ·········································· 089[Figure2-3] MonthlyGasDemandinKorea(2014-2020)·························································· 091[Figure2-4] KoreanOutlookofGenerationOutputShare(TargetScenario)··························· 091

[Figure2-5] AnalysisFrameworkofMAED ················································································· 095[Figure2-6] TotalPrimaryEnergySupplyinAlbania,NaturalGasScenario,2040 ·················· 098[Figure2-7] TotalFinalEnergyConsumptioninAlbania,NaturalGasScenario,2040 ············ 099[Figure2-8] NaturalGasDemandProjectionintheGMPofAlbania ······································· 100[Figure2-9] ASurveyfortheNaturalGasDemandofAlbanianIndustrialSectors ················· 101[Figure2-10] Oil&NaturalGasPriceOutlookinEurope ···························································· 106[Figure2-11] ProjectedGDPGrowthRateofAlbania ·································································· 106[Figure2-12] FinalEnergyConsumptioninAlbaniabyIndustrialSector(2019) ······················· 107[Figure 2-13] Fractional Distillation Unit of Crude Oil ································································· 109[Figure 2-14] Manufacturing Process of Hot Rolled Steel Sheet and Coil ·································· 112[Figure2-15] Harber-BoschProcessFlow ···················································································· 113[Figure2-16] Heavy-dutyVehiclesGHGIntensity ········································································ 115[Figure 2-17] LNG Refueling Sites and LNG HDT Sales in China ················································· 115[Figure2-18] NaturalGasMarketShareinHeavyDutyTrucks ··················································· 116[Figure 2-19] Yearly Development of LNG Fueled Fleet ······························································· 117[Figure2-20] NumberofPortforLNGBunkeringbyStageandRegion ···································· 118

Chapter 3

[Figure3-1] ElectricityPricesforHouseholdCustomersintheRegionalCountries(2019) ···· 137[Figure 3-2] Electricity Prices for Non-Household Customers in the RegionalCountries(2019) ······················································································ 137[Figure 3-3] Previous EU Energy and Climate Policy Goals prior to the EGD ··························· 139[Figure3-4] TheEuropeanGreenDeal(Dec.2019) ··································································· 140[Figure3-5] NextGenerationFundoftheEU ············································································ 141[Figure3-6] GlobalEnergyTransitionInvestments(2004-2020) ·············································· 142[Figure3-7] Renewables-DecliningLevelisedCostofElectricity(2010-2019) ························ 143[Figure3-8] DecliningBatteryCosts ··························································································· 145[Figure3-9] DevelopmentofGreenversusBlueandGreyHydrogenCosts(2020-2030) ······· 152[Figure3-10] TheEU’sHydrogenStrategyinThreeSteps(July2020) ········································ 153[Figure 3-11] Hydrogen Options Based on Energy Resources ···················································· 154[Figure3-12] GrowthRateofTPESandContributionsofNaturalGasinKorea ························ 156[Figure3-13] Korea’sNaturalGasConsumption,2008-2018 ······················································ 157[Figure3-14] Korea’sLNGImportsbySource,2008-2018 ·························································· 158

Contents l List of Figures

[Figure3-15] OverviewofChangesintheKoreanEconomyandEnergySector ······················· 161[Figure3-16] EnergyIndustryStructureofKorea ······································································· 162[Figure3-17] ChangesinTotalPrimaryEnergySupplyofKorea ················································ 162[Figure3-18] NaturalGasBusinessFlowChart ··········································································· 165[Figure3-19] StructureofEnergySpecificFundsinKorea ·························································· 172[Figure3-20] StructureofNationalEnergyPlanbySector ························································· 173[Figure 3-21] Promotion Results of the 3rd Energy Master Plan ················································ 175[Figure 3-22] Promotion of the Basic Plan for Electricity Supply and Demand ·························· 177[Figure3-23] StructureofNationalEnergyPlanbySector ························································· 188[Figure3-24] FamilyTreeofEnergyInstitutesinKorea ······························································ 189[Figure3-25] KEEI’sManagementVisionandStrategies ···························································· 190[Figure3-26] OrganizationofKEEI ······························································································· 191[Figure3-27] OrganizationofKIER ······························································································· 193[Figure3-28] OrganizationofKIGAM ··························································································· 195[Figure3-29] OrganizationofKETEP ···························································································· 197[Figure3-30] OrganizationofKGS ································································································ 199[Figure3-31] OrganizationofKOGAS-Tech ·················································································· 201

Chapter 4

[Figure4-1] TAPRouteandStrategicPartnershipProjects ······················································· 212[Figure4-2] MunicipalitiesandLGUsViableforFurtherScreeningforGasification ··············· 213[Figure4-3] TotalPotentialNaturalGasConsumptioninAlbaniabyConsumptionSector ···· 217[Figure4-4] LocationsofAnchorConsumers ············································································ 218[Figure4-5] ProductionbyOilField ···························································································· 223[Figure4-6] AlbanianExplorationBlocks ··················································································· 225[Figure4-7] AlbanianSectionofIAPRoute ················································································ 233[Figure4-8] LocationofLNGKrk ································································································ 235[Figure 4-9] Revithoussa LNG Terminal ······················································································ 236[Figure4-10] LocationofEagleLNGTerminal ············································································· 238[Figure4-11] ComparisonbetweenFSRUandFSU ····································································· 243[Figure 4-12] Import Terminal Construction and Capacity Change ············································ 244[Figure4-13] ItalyAdriaticLNGTerminal ····················································································· 247[Figure 4-14] Malaysia Sungai Udang Terminal ··········································································· 247

[Figure4-15] BrazilPecémFSRUTerminal ··················································································· 248[Figure4-16] ArgentineandLithuanianFSRUTerminals ···························································· 248[Figure 4-17] Toscana FSRU Terminal, Italy ·················································································· 249[Figure4-18] NusantaraandLampungFSRUTerminal,Indonesia ············································ 250[Figure 4-19] FSU and BMPP ········································································································· 251[Figure4-20] LNGCandFSPP ········································································································ 252[Figure 4-21] LNGC, FSU, and BMPP ····························································································· 252[Figure 4-22] Components ············································································································ 253[Figure 4-23] Structure of FSRU Superstructure ·········································································· 255[Figure 4-24] FRSU Income Trend ································································································· 261[Figure4-25] FloatingRegasificationTerminalInstallationTrend ·············································· 261[Figure4-26] FloatingTerminalFacilityCapacityTrend ······························································ 263[Figure 4-27] Trend of FSRU Ships ································································································ 264[Figure4-28] NumberofFSRUShipOwnershipbyOperator ····················································· 267[Figure4-29] NaturalGasLiquefactionProcess ·········································································· 279[Figure4-30] NaturalGasLiquefactionProcessattheReceivingEnd ······································· 280[Figure 4-31] Value Chain of Conventional LNG and SSLNG ······················································· 281[Figure4-32] DefinitionofSSLNG ································································································· 281[Figure 4-33] Standard LNG and SSLNG ······················································································· 282[Figure 4-34] Standard LNG Value Chain······················································································ 283[Figure4-35] LNGValueChain ······································································································ 284[Figure4-36] SSLNGValueChain ·································································································· 285[Figure4-37] SmallScaleLiquefactionPlantinChina ································································· 286[Figure4-38] SmallSatelliteTerminal··························································································· 287[Figure4-39] StorageandRegasificationBarge ·········································································· 288[Figure4-40] MediumScaleTerminal ·························································································· 288[Figure 4-41] Full Containment Tank ···························································································· 290[Figure 4-42] Bullet Tank ··············································································································· 290[Figure4-43] LNGStorageAlternatives ························································································ 291[Figure 4-44] Transporting CNG ···································································································· 292[Figure4-45] LNGvs.CNG ············································································································· 293[Figure4-46] OnshoreReceivingTerminals ················································································· 293[Figure4-47] LocalLiquefactionPlant ·························································································· 294

Contents l List of Figures

[Figure4-48] LNGTrailer49,200Liters,4.8Bar ··········································································· 295[Figure4-49] IntermodalTransportwithISOContainers(20ft) ················································· 295[Figure4-50] IntermodalTransportwithISOContainers ··························································· 295[Figure4-51] 54ISOContainerswithCapacityof43,500Liters ················································· 296[Figure4-52] ORV··························································································································· 297[Figure4-53] SubmergedCombustionVaporizer ········································································ 298[Figure4-54] Shell-and-TubeLNGVaporizer ················································································ 298[Figure4-55] LNGSatelliteStation ······························································································· 299[Figure4-56] LNGMicrobulk ········································································································· 299[Figure4-57] LNG/LCNGVehicleFuelingStation ········································································· 300[Figure4-58] PortsEngagedinLNGBunkeringorStudyingIt ··················································· 301[Figure4-59] LNGColdEnergyUtilization ···················································································· 302[Figure4-60] LNGImportTerminalsOfferingSmallScaleServices ··········································· 310[Figure4-61] CapitalCostsofLNGProjectsandServices ··························································· 313[Figure4-62] SSLNG-BasedGasSupplytoaPowerPlant ··························································· 315[Figure4-63] DieselReplacementinPowerGeneration ····························································· 315[Figure4-64] SSLNG-BasedGasSupplytoIndustries ································································· 316[Figure4-65] MapShowingtheAreaofInvestigation ································································ 319[Figure4-66] IdentifiedLocations ································································································ 321[Figure4-67] SatelliteImageofLocation1 ·················································································· 322[Figure4-68] ArialViewofLocation1 ··························································································· 323[Figure4-69] ViewfromtheNorthtoPortoRomano ·································································· 324[Figure4-70] SatelliteImageofLocation2 ·················································································· 325[Figure4-71] NewlyBuiltTouristHotelsbehindSpilleBeach ····················································· 326[Figure 4-72] Satellite Image of Location 3 ·················································································· 328[Figure4-73] NewlyBuiltHotelneartheVillageofDorezezaeRe ············································· 328[Figure4-74] ViewofSazanIslandLookingWest ········································································ 329[Figure4-75] SatelliteImageofLocation4 ·················································································· 329[Figure4-76] TypicalLNGSupplyChain ······················································································· 334[Figure 4-77] FSRU LNG Unloading Type ······················································································ 335[Figure4-78] SSLNGApplications ································································································· 336[Figure4-79] LNGImportTerminalsSurroundingAlbania ························································· 339

Abbreviation Definition

AAV Ambient Air Vaporizers

AKBN National Agency of Natural Resources (Albanian: Agjencia Kombëtare e Burimeve Natyrore)

ALKOGAP Albania-Kosovo Gas Pipeline

ALL Albanian Lek (Official Currency of Albania)

ALPEX Albanian Power Exchange

API American Petroleum Institute

ARMO Albanian Refining and Marketing of Oil

BCM Billion Cubic Meters

BNEF Bloomberg New Energy Finance

BPLE Basic Plan of The Electricity Supply and Demand

BRUA Bulgaria, Romania, Hungary and Austria (Gas Interconnector)

CAPEX Capital Expenditures

CCGT Combined Cycle Gas Turbine

CCS Carbon Capture and Storage

CEECS Central and Eastern European Countries

CESEC Central and South Eastern Europe Energy Connectivity

CNG Compressed Natural Gas

DCM Decision of The Council of Ministers

DCS Distributed Control System

DME Dimethyl Ether

DSO Distribution System Operator

ECT Energy Community Treaty

EE Energy Efficiency

EEZ Exclusive Economic Zone

EGD European Green Deal

EGMS Energy and Greenhouse Gas Modeling System

List of Abbreviations

Abbreviation Definition

EIB European Investment Bank

EMGP East Mediterranean Gas Pipeline

ENTSOG European Network of Transmission System Operators

EPC Engineering, Procurement and Construction

EPRB Electricity Policy Review Board

ERE Energy Regulatory Authority (Albanian: Enti Rregullator i Energjisë)

ESS Energy Storage System

EU European Union

EUROSTAT Statistical Office of The European Union.

FID Final Investment Decision

FSHU Universal Service Supplier

FSPP Floating Storage Power Plant

FSRU Floating Storage and Regasification Unit

FSU Floating Storage Unit

FTL Free Market Supplier

GDP Gross Domestic Product

GHG Greenhouse Gas

GIS Geopolitical Intelligence Services

GMP(A) Gas Master Plan (of Albania)

GTC Gas Technology Corporation

HDT Heavy Duty Truck

HDV Heavy Duty Vehicles

HIPPS High Integrity Pressure Protection System

HLW High Level Waste

HPP Hydro Power Plant

HVDC High Voltage Direct Current

IAEA International Atomic Energy Agency

List of Abbreviations

Abbreviation Definition

IAP Ionian Adriatic Pipeline

ICED Income Coefficient of Energy Demand

IEA International Energy Agency

IENE Institute of Energy for South East Europe,

IFAAV Intermediate Fluid Ambient Air Vaporizers

IFV Intermediate Fluid Vaporiser

IGB Interconnector Greece-Bulgaria

IGU International Gas Union

IMO International Maritime Organisation

IRENA International Renewable Energy Agency

ISO International Organization for Standardization

JTF Just Transition Fund

KAS Konrad Adenauer Foundation

KDI Korea Development Institute

KEEI Korea Energy Economics Institute

KEPCO Korea Electric Power Corporation

KESH Albanian Power Corporation

KESIS Korea Energy Statistical Information System

KETEP Korea Institute of Energy Technology Evaluation and Planning

KGS Korea Gas Safety Corporation

KGU Korean Gas Union

KIER Korea Institute of Energy Research

KIGAM Korea Institute of Geoscience and Mineral Resources

KIITE Korea Institute of Industrial Technology Evaluation.

KOGAS Korea Gas Corporation

KOGAS-TECH Korea Gas Technology Corporation

KOSTT Transmission System Operator of The Republic of Kosovo

List of Abbreviations

Abbreviation Definition

KPE Korea Power Exchange

KSP Knowledge Sharing Program

KTOE Kilotonne of Oil Equivalent

LCNG Liquid to Compressed Natural Gas

LEAP Long-range Energy Alternatives Planning

LGU Local Government Unit

LNG Liquefied Natural Gas

LPG Liquefied Petroleum Gas

MAED Model for Analysis of Energy Demand

MCM Million Cubic Meter

MIE Ministry of Infrastructure and Energy of Albania

MMBTU Metric Million British Thermal Unit

MOEF Ministry of Economy and Finance of the Republic of Korea

MOTIE Ministry of Trade, Industry and Energy

NBC National Business Center

NDC Nationally Determined Contribution

NECPS National Energy and Climate Plans

NGH Natural Gas Hydrate

NGVA European Natural Gas Vehicle Association

NGVS Natural Gas Vehicles

NREAP Albania's National Renewable Energy Action Plans

O&M Operation and Maintenance

OECD Organisation for Economic Co-operation and Development

OPEX Operational Expenditures

ORF Onshore Receiving Facility

ORV Open Rack Vaporiser

OSHEE (or OSSH) Albanian Power Distribution Operator

Abbreviation Definition

OST Transmission System Operator

PCIS Projects of Common Interest

PECI Project of Energy Community Interest

PFD Process Flow Diagram

PID Piping & Instrument Flow Diagram

PIG Pipeline Inspection Gauge

PMI Project of Mutual Interest

PNG Pipeline Natural Gas

PRMS Pressure Reducing and Metering Station

PV Photovoltaic

R&D Research and Development

RCT Reverse Cooling Tower

RECAP Regional Project Energy Security and Climate Change Asia-Pacific

RES Renewable Energy Sources

SCP South Caucasus Pipeline

SCV Submerged Combustion Vaporiser

SEE/CEE Southeast and Central Europe

SGC Southern Gas Corridor

SOCAR State Oil Company of The Azerbaijan

SSLNG Small Scale LNG

STV Shell and Tube Vaporisers

TANAP Trans-Anatolian Pipeline

TAP Trans Adriatic Pipeline

TBP Trans-Balkan Pipeline

TFC Total Final Consumption

TPES Total Primary Energy Supply

TPP Thermo Power Plant

List of Abbreviations

Abbreviation Definition

TSO Transmission System Operator

TYNDP Ten Year Network Development Plan

UAE United Arab Emirates

UNECE United Nations Economic Commission for Europe

UNEP United Nations Environment Programme

UNFCCC United Nations Framework Convention on Climate Change

USA United States of America

USAID United States Agency for International Development

USD United States Dollar

VAT Value-added Tax

WB World Bank

WB6 Western Balkans 6

WBIF Western Balkans Investment Framework

WEO World Energy Outlook

2020/21 KSP with AlbaniaHyeseung Choi (Hanyang University)

023

2020/21 KSP with Albania

Albania is one of the fastest growing economy in the western Balkan region with an economic growth rate of 4% in 2018. One of the biggest impediment of economic growth in Albania is its current energy situation. Albania has been heavily relying on diesel and heavy oil as the primary sources of energy for transportation and industry to satisfy its increasing energy demand. Comparatively, Albania’s gas market size is one of the smallest in the western Balkan region, recording 15 million cubic meters in production and consumption in 2015. As a Contracting Party of the Energy Community and a signatory to the Energy Charter, Albania faces the need to diversify its energy sources, such as using natural gas, to maintain the supply and demand of LNG.

Accordingly, upon the Ministry of Infrastructure and Energy (MIE) of Albania’s submission of the KSP demand survey, the Ministry of Economy and Finance (MOEF) of the Republic of Korea conducted a review session of the proposal for diversifying the energy sector of Albania. The “Policy to facilitate the role of natural gas in the energy sector in Albania” was thus confirmed.

The main objectives of the 2020/21 KSP with Albania is to support its government in diversifying energy sources apart from imported petroleum and achieving energy independence. Furthermore, it aims to support Albania to efficiently manage the existing and new gas fields, and increase the institutional and technical expertise of its energy institutions. Based on the Republic of Korea’s past experience in the field of natural gas development, the Korean Research Team has provided policy directions and recommendations on three sub-topics. The details of the project, including the sub-topics and main project participants are listed below.

2020/21 KSP with AlbaniaHyeseung Choi (Hanyang University)

Gas Sector Expansion Strategy for Energy Diversification in Albania

024

Sub-Topics Researchers Local Consultants

Long-Term Outlook for Natural Gas Demand/Supply in Albania and

the Strategy for Demand-Drive of Natural Gas

Jinsoo Kim(Associate Professor, Hanyang University)

Namjin Roh(Research Fellow,

Korea Energy Economics Institute)

Dritan Spahiu(Local Gas Expert)

National Policy Establishment for Natural Gas Industrial Structure

and Market Design in Albania

Sungkyu Lee(Senior Research Fellow,

Korea Energy Economics Institute)Eunmyung Lee

(Senior Research Fellow, Hanyang University)

Stavri Dhima(Former Head of Gas Sector,

Ministry of Infrastructure and Energy)

Albania’s Natural Gas Infrastructure Build-out and Technical Cooperation

Younkyoo Kim(Professor, Hanyang University)

Young Doo Kim(Professor, Jeonbuk University)

Wonbae Kim(Senior Researcher,

Hanyang University)

Artan Leskoviku(Head of Energy,

National Agency of Natural Resources)

• Senior Advisor: Joong-Kyum Kim, Former CEO of Korea Electric Power Corporation• Project Manager: Kyoung Doug Kwon, Specialist, CID, KDI• Principal Investigator: Younkyoo Kim, Professor, Hanyang University

Due to the COVID-19 pandemic, activities of the 2020/21 KSP with Albania were conducted online. Aside from official activities, both the Korean and Albanian delegations ensured effective communication, through email exchanges and organizing online meetings if required.

The 2020/21 KSP with Albania was officially launched online on December 10, 2020 via ‛Launching Seminar and High-level Meeting’ in the presence of Dr. Joong-Kyum Kim, Senior Advisor and Head of 2020/21 KSP with Albania from the Korean side, and H.E. Ilir Bejtja, Deputy Minister of MIE. High-level Officials from both sides discussed policy priorities of Albania. The main goal of the Launching Seminar was to exchange ideas and set the goals of the KSP with the Albanian government and KSP Research Team. Mr. Illia Gjermani, the Petroleum Director of MIE gave a thorough presentation on the overview of the Energy Sector and Demand from the Albanian Government. This Seminar facilitated the Korean Research Team to understand the scope of this research, which is in line with policy priorities of Albania.

After three months of preliminary research by the Korean Research Team, the participants of the 2020/21 KSP with Albania gathered online to conduct ‛KSP Policy Seminar and In-depth Study’ on March 11th. High-level Officials from both sides also joined the Policy Seminar, where Dr. Joong-Kyum Kim, Senior Advisor and Head of 2020/21 KSP with Albania

025

delivered opening remarks, followed by welcoming remarks by H.E. Ilir Bejtja of MIE and congratulatory remarks by Ambassador Soosuk Lim of the Embassy of Republic of Korea to Greece. Experts from various Albanian affiliated institutions such as Energy Regulatory Authority (ERE), National Agency of Natural Resources (AKBN), Albpetrol, and Albgaz joined the Policy Seminar to provide the Korean Research Team with necessary information and materials. For each of the three sub-topics, the Korean researchers presented their preliminary findings to the Albanian delegation. Then, three local experts delivered presentations on 1) Status of supply and demand of natural gas and other energy sources in Albania, 2) development of the gas sector and real targets of national policy for energy diversification in Albania, and 3) Albania’s natural gas infrastructure. The discussion and Q&A sessions were held with experts from affiliated institutions.

As the third official stage, ‘Interim Reporting and Policy Practitioners’ Workshop’ was held online on May 31, 2021. Again, Interim Reporting of 2020/21 KSP with Albania began with opening remarks by Dr. Joong-Kyum Kim, Senior Advisor and Head of 2020/21 KSP with Albania, followed by welcoming remarks by H.E. Ilir Bejtja of MIE. The aim of the interim reporting was to receive feedbacks on the tentative final policy recommendations from the Korean Research Team.

Following the interim reporting, the Korean Research Team hosted a two-day online Workshop arranged for Albanian policy practitioners on June 1–2, 2021. The Korean Research Team considered the topics that were of interest to the Albanian policy practitioners. A total of four lectures were delivered. First, Dr. Ho-Mu Lee, the Director of Research Planning & Coordination of KEEI delivered his presentation on ‘Introduction to Korea Energy Economics Institute (KEEI): History, role and organization.’ Second, Mr. Wonbae Kim, Former Director of Pyeongtaek LNG Terminal, KOGAS presented on ‘Safety Measures for Natural Gas Pipeline Infrastructure System.’ Third, Dr. Euyseok Yang, Senior Research Fellow of KEEI made a presentation on ‘Direction of Energy Transition Policy and Development of Hydrogen Economy: Korea.’ Lastly, Dr. Stephen Blank, Senior Fellow of Foreign Policy Research Institute presented on ‘Southeast Europe Energy Security and Implications for Albania.’

As the last stage of 2020/21 KSP with Albania, ‘Final Reporting Workshop and Senior Policy Dialogue’ was launched on July 27, 2021. As the Head of the Korean side, Dr. Joong-Kyum Kim, Senior Advisor and Head of 2020/21 KSP with Albania delivered welcoming remarks, appreciating the active participation of all the participants to make 2020/21 KSP with Albania a success. As the Head of the Albanian side, H.E. Ilir Bejtja of MIE hoped that 2020/21 KSP with Albania will prove to be the first milestone in energy diversification

2020/21 KSP with Albania

Gas Sector Expansion Strategy for Energy Diversification in Albania

026

of Albania. Ambassador Jung Il Lee of the Republic of Korea to Greece delivered a congratulatory speech, emphasizing on continued economic cooperation between Albania and Korea. Following the remarks by high-level officials from both countries, the Korean researchers presented the result of policy consultation to top policy makers and relevant officials of Albania.

Executive Summary YounkyooKim(HanyangUniversity)

029

Based on the Korean experience, this report introduces the natural gas demand models and structure of gas consumption in energy-intensive industries in the context of Long-Term Energy Demand Outlook for 2040. Estimation for natural gas demand in different sectors can be more convincing and reliable by understanding the energy demand structure in each industry. The following three possible scenarios have been proposed to update the natural gas demand of the GMP of Albania: Low Economic Feasibility, Base, and Active Market Development.

The report proposes the following policy suggestions for the Albanian government to promote the natural gas demand and realize the “Active market development” scenario in Albania:

- Securing the price competitiveness of natural gas is of utmost importance to ensure the successful promotion of natural gas. As evident from survey responses and theories on energy demand modeling, there is an evident willingness to change energy sources and fuels if the price and infrastructure costs remain reasonable.

- Climate crisis and GHG emission reduction is a global megatrend, and the Albanian government and industries need to consider the climate issues. Therefore, survey responses suggest that electrification and power generation by natural gas and fuel substitution is not a choice; it is the only option we have. Renewables could be the future of power generation, but it is difficult to supply all electricity demand from renewables only.

- Natural gas supply infrastructure is essential for price competitiveness as well accessibility. We propose promising options in Chapter 4. but giving a clear policy signal to the possible consumers, including industries, is also important.

- The estimated demand in our study has some limitations: the number of respondents of the survey is limited, the data is not sufficient to analyze the demand with

Executive SummaryYounkyooKim(HanyangUniversity)

Executive Summ

ary

Gas Sector Expansion Strategy for Energy Diversification in Albania

030

econometric or bottom-up models (e.g., the price level of each energy sources), and we do not have enough resources to develop a national energy demand model, especially for electricity. We believe that the Albanian government can handle all these limitations in the future with our suggestions in the other sections.

The report compares laws and regulations on natural gas of Korea and Albania to establish national policies related to the natural gas industrial structure and market design. Energy-related laws and regulations of Albania, including natural gas, have been well enacted and revised in line with the EU's legal framework, backed by EU’s policy consulting support. Restructuring of the energy industry is also being implemented within the guidelines of the EU. Korea has more than 40 years of experiences in the field of gas industry development and safety management. As the natural gas industry develops and market expands in Albania, the need for establishing related laws, regulations, and organization in business activities and safety management sectors will increase substantially.

The report identifies the necessity to establish energy policy and technology think tank as government-affiliated research institutes for their active and effective role in ensuring energy security improvement and energy industry development. It proposes establishing organizations related to gas safety and technology such as the Korea Gas Safety Corporation (KGS) and the Korea Gas Technology Corporation (KOGAS-Tech). Government-funded research institutes such as Korea Energy Economics Institute (KEEI), Korea Institute of Energy Research (KIER), Korea Institute of Geoscience and Mineral Resources (KIGAM), and Korea Institute of Energy Technology Evaluation and Planning (KETEP), are conducting research activities to propose various policy and investment alternatives to the government and energy businesses for quickly responding to changing international energy landscape and developing new technologies. In Korea, certain public enterprises are in charge of the safety of natural gas supply and technology development. KGS is a governmental testing, inspection, and education organization. KOGAS-Tech was established to install reliable and safe natural gas supply facility and reduce the industry’s reliance on foreign technology through technical development in the engineering sector as a subsidiary of Korea Gas Corporation (KOGAS). Korea’s institutions and organization that support the government and energy business could be useful for the stable development of the Albanian natural gas industry.

To expedite and facilitate the gasification of Albania, the Government of Albania is recommended to consider LNG import options along with ensuring pipeline infrastructure development. There are three LNG import methods.

031

1. On shore LNG Import (Regasification) Terminal2. Floating Storage Regasification Unit (FSRU), Floating Storage Unit (FSU), etc.3. On Shore Small Scale LNG (SSLNG)

In Albania, the uses of SSLNG emerges as a solution to feed isolated areas that are not connected to the gas grid, where residential, industrial, and commercial sectors are present. The development of the pipeline transmission and distribution systems alone does not ensure a supply of gas to the two major natural gas consumption centers: the triangle of Fier-Vlora-Ballsh and the region of Durres and Tirana.

LNG technologies are readily possible for “fast-track” implementation of mini LNG facilities, with relatively low investments compared to pipelines or large- scale onshore LNG facilities. Areas limited by a lack of pipeline infrastructure in Albania can be enabled by SSLNG, which can facilitate the rapid establishment of power plants, oil and gas exploration and refining, fertilizers, the food industry, ceramics, etc.

ALBGAZ's development plan, which benchmarked Korea's Gas Corporation, is also presented. Safe and efficient construction by presenting examples of improvements that Korea Gas Corporation has experienced and improved while constructing and operating facilities for about 40 years.

It is also important to select key employees of ALBGAZ and receive training in Korea as part of the capacity-building program. Currently, KOGAS is an important benchmarking target because construction and operation are being pursued at the same time. By proposing to the Albanian government to train LNG procurement experts and to operate a separate LNG procurement department within ALBGAZ, it will be recommended to strengthen the capacity of policy and technical personnel and technical skills for stable and economical natural gas procurement.

Executive Summ

ary

Introduction

YounkyooKim(HanyangUniversity)

1.ObjectivesandScope2. Methodology3.GasSupply,Demand,andMarketinAlbania4. South-East Europe (SEE) Gas Supply and Demand

C H A P T E R

01

KeywordsEnergySecurity,EnergyDiversification,NaturalGasDemand,SupplyProjection, Natural Gas Market, Demand-Drive of Natural Gas

033

CHAPTER

01Introduction

Summary

The most urgent question for Albania is how to satisfy its rising energy demand. If Albania is to support its growth, it needs to find additional domestic energy sources. Albania has relatively abundant oil reserves but natural gas reserves have almost been exploited and recoverable reserves seem very limited. Albania has an isolated gas distribution system, which is not connected to international gas transmission systems. Therefore, integration with regional and EU energy markets will be an important step for Albania to meet its growing energy demand.

Albania is among the most vulnerable countries to climate change in the Southeast European region. The government of Albania aims to overcome the imbalance of energy supply and demand by following key strategies and policy measures. For example, diversification of energy sources, precisely through non-hydro renewable energy expansion and gasification.

The Trans Adriatic Pipeline (TAP)—a gas pipeline—is already in operation. Albania has a specific strategic plan for the development of the hydrocarbon sector, especially the natural gas sector. These plans and programs are embodied in the National Energy Strategy for 2018-2030 approved by the Ministerial Committee Decision on July 31, 2018 and the Albanian Gas Master Plan approved by the Ministerial Council on April 2, 2018.

This study aims to illuminate several headwinds and challenges that the future development of Albania's natural gas sector will face along the three respective sub-topics agreed upon by the governments of the Republic of Albania and the Republic of Korea.

The main objectives of the research team are to provide policy directions and recommendations for the policy challenges based on the Republic of Korea’s experience to facilitate the government of Albania’s implementation of the Gas Master Plan. The research

IntroductionYounkyooKim(HanyangUniversity)

Gas Sector Expansion Strategy for Energy Diversification in Albania

034

team has identified the following central questions and objectives corresponding with the three respective sub-topics:

- Long-term Energy Demand Outlook for 2040 and Strategy to Enhance the Role of Natural Gas in Albania.

- Establishment of national policy related to the natural gas industrial structure and market design.

- Feasibility Study on the Introduction of the Liquefied Natural Gas (LNG and SLNG) into Energy Mix in Albania and Technology for the Construction /Operation of Gas Infrastructure.

1. Objectives and Scope

As of 2016, Albania had virtually no gas sector. Its infrastructure was dilapidated to the extent where repair did not make economic sense, and the pattern of settlement of Albania’s citizens with large numbers of sparsely populated settlement worked against an integrated gas network. Therefore, a completely new network was required.1 The TAP pipeline as part of the larger TANAP-TAP project will not only have a significantly positive impact on Albania’s overall economy, but also effectively galvanize the creation of a plan for a new network and relevant projects. Indeed, the gasification plan is clearly inspired by the reports of USAID and a 2016 European funded research on Albania’s gas economy which provided a master plan for Albania’s gasification (henceforth, the Gas Master Plan (GMP)). The GMP identified the energy sector as a strategic growth sector and enabler for the growth of Albania’s economy. It also observed that regardless of its formal status in the overall EU integration project, Albania was bound to accept the corresponding EU Acquis Communautaire in line with the implementation dynamics determined by the (EU’s) Energy Community institutions according to the EnC Treaty’s provisions.

Energy consumption is expected to increase as annual GDP growth is projected at 4% over the next decade. The most urgent question for Albania is how to meet this rising demand. If Albania is to support its growth, it first need to find additional domestic energy sources. Albania has relatively abundant oil reserves; however, its natural gas reserves have almost been exploited and recoverable reserves seem very limited. Albania has an isolated gas distribution system, which is not connected to the international gas transmission systems. Therefore, the integration of regional Albanian and EU energy markets will

1 European Western Balkans Joint Fund, Western Balkans Investment Framework Infrastructure Project Facility Technical Assistance 4 (IPF 4), WB11-ALB-ENE-01 (Gas Master Plan for Albania & Project Identification Plan, 2016), p. 15 (Henceforth Gas Master Plan).

035

CHAPTER

01Introduction

be imperative for Albania to satisfy its growing energy demand for energy. Recently, the Albanian government launched a major investment in the field of energy delivery infrastructure at both national and regional levels.

Albania has also accomplished several feats in terms of energy sector reforms. Its energy sector, especially the electricity sector, is introducing European regulations and institutions. The Trans Adriatic Pipeline (TAP) is already in operation. Albania has a specific strategic plan for the development of the hydrocarbon sector, especially the natural gas sector. These plans and programs are embodied in the National Energy Strategy for 2018-2030 approved by Ministerial Committee Decision on July 31, 2018 and the Albanian Gas Master Plan approved by the Ministerial Council on April 2, 2018.

However, the government will face many challenges in implementing the GMP. One of the most important latest changes is the European Green Deal was introduced by the EU in December 2019. A new ambitious emissions reduction target was established: minus 55% for 2030 (instead of the previous -40%). The EGD has huge implications for the EU’s future energy mix and energy security, including the financing of new energy sources and infrastructures. Even by phasing-out coal in Europe completely, the EU will not be able to achieve its long-term emission reduction goal of minus 95% by 2050. In fact, it needs to reduce its overall gas consumption by 2030.2

Conventionally, it has been believed that for natural gas to play a significant role for gas as a transition fuel, let alone a destination fuel, national governments would have to develop gas-related strategies that encourage its use in the near- and medium-term while facilitating a subsequent orderly transition from gas toward a vast use of renewables.3 In other words, until recently, switching from coal to gas was considered as the most cost-efficient way of securing a major reduction of carbon emissions.

The conventional wisdom may no longer be wise because increasing evidence suggests that it is already cheaper to produce power from renewables than coal or other fuels. For Northern, Western, and even Southern Europe, it almost certainly means that any incremental requirement for power generation will come from renewables.4

Where will the EGD leave natural gas for Albania in the context of the climate

2 Frank Umbach, “Gas Supply Perspectives for Albania under new Conditions of EU Energy and Climate Policies as well as Market Competitiveness Factors,” Manuscript submitted to the Albania KSP research team, April, 2021, p. 2.

3 United Nations Economic Commission for Europe (UNECE), How Natural Gas Can Displace Competing Fuels (Geneva, Switzerland, 2019), p. 5 of Executive Summary.

4 Ibid., p. 7.

Gas Sector Expansion Strategy for Energy Diversification in Albania

036

emergency? Gas does possess distinct advantages that should manifest for at least two decades. The principal concern for Albania is whether the climate emergency will disrupt the supply of water for the production of hydropower, which is the mainstay of energy production. Subsequently, Poland’s desire to secure a “just transition” is instructive for the Government of Albania. A new gas import infrastructure, notably the LNG terminal at Świnoujście and the Baltic line will enable Poland to import Norwegian gas via Denmark, thereby retaining gas’ high share in the energy mix for some years.5

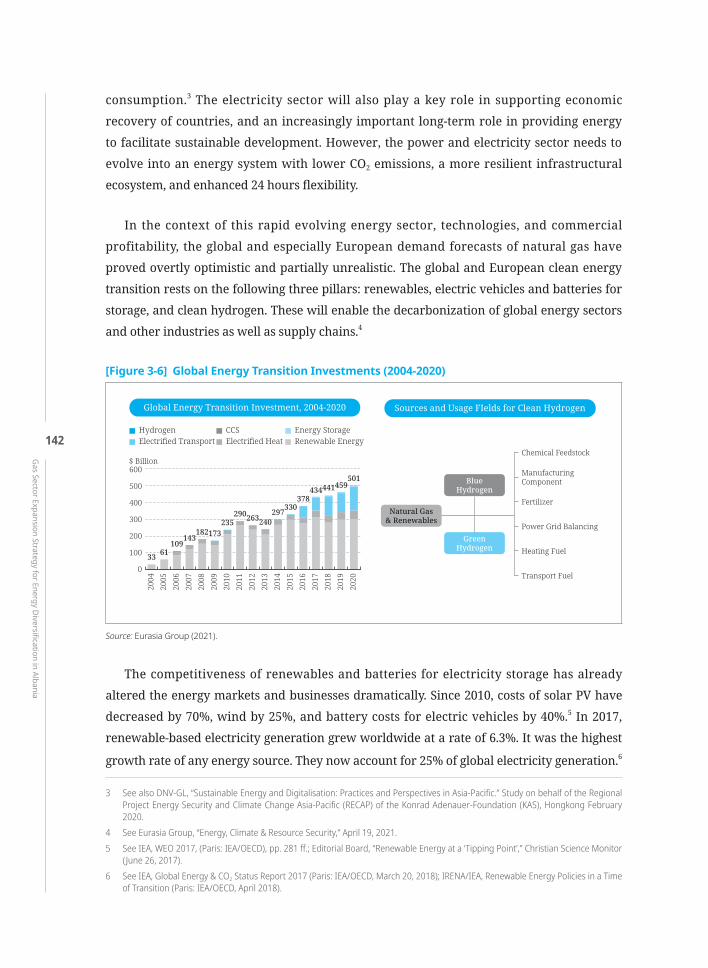

Relatively, Southeast Europe remains Europe’s most polluting and least energy efficient region compared to its GDP. It is energy intensive but also intensive in CO2 per unit of used energy. Southeast Europe will significantly benefit from the introduction and expansion of gas. The countries and districts that will gain most from access to natural gas are Albania, Bosnia-Herzegovina, Kosovo, Montenegro, and North Macedonia, along with southern districts of Croatia and various regions of Serbia.6 LNG will be an important player in the market, due to the plan for new LNG import terminals in the region. The development of small-scale on-shore LNG and floating LNG regasification terminals has the ability to facilitate the emergence of new markets for gas in the western Balkan region. The European Network of Transmission System Operators for Gas (ENTSOG) considers that the potential for LNG supply from all sources will almost double over the next 20 years, from 115 bcm in 2020 to 228 bcm in 2040.7 The maximum capacity for pipeline gas delivery will rise by around 50 bcm.

The development of a functioning and flexible gas market and regional integration of gas market will significantly enable access to natural gas for these countries. However, the implementation of the Southern Gas Corridor project and gas import diversification is not yet complete. Thus, the extent of Russia’s future geo-economic and geopolitical influence through its gas pipeline policy in South Eastern Europe and its opposition to that of EU remains ambiguous. ENTSOG considers that Russia has the potential to expand its pipeline capacity to European customers from the current maximum of 194 bcm/y to 226 bcm/y by 2040.8

The GMP stipulates that natural gas demand in Albania will continue to follow its upward trend supported by its environmental qualities, government investment in the transmission network, and attractiveness for electricity producers. However, the GMP has several caveats. Therefore, building on the major findings from the GMP, this report further investigates the

5 Ibid., p. 7.6 United Nations Economic Commission for Europe (UNECE). The Potential for Natural Gas to Penetrate New Markets (Geneva, Swit-

zerland, 2020), p. 4.7 Ibid., p. 2.8 Ibid.

037

CHAPTER

01Introduction

Albanian energy and gas sector from the perspective of security of gas supply.

This study aims to illuminate several headwinds and challenges that the future development of Albania's natural gas sector will face along the three sub-topics agreed upon by the governments of the Republic of Albania and the Republic of Korea.

The main objectives of the research team are to provide policy directions and recommendations for the policy challenges based on the Republic of Korea’s experience to facilitate the Government of Albania’s implementation of the Gas Master Plan.

The research team has identified central questions and objectives corresponding with the three respective sub-topics.

<Table 1-1> Objectives of the Project

Overarching Topic Policy to Facilitate the Role of Natural Gas in the Energy Sector in Albania

Sub Topic 1

Long-Term Energy Demand Outlook for 2040 and Strategy to Enhance the Role of Natural Gas in Albania- Planning for natural gas supply to the power generation, industry, residential/service

sectors through long-term energy demand forecast by 2040- Establish a plan to construct and establish nationwide natural gas supply networks by

region/time

Sub Topic 2

Establish National Policy Related to the Natural Gas Industrial Structure and Market Design- Institutional framework for the natural gas industry, including the legal system related to

the industrial structure and the corporate form/roles- Policy design for the natural gas market mechanism/rules, such as financing method,

pricing, technology application, supply obligation, etc- (also possibly) Increasing the technical expertise of institutions /entities related to the gas

sector

Sub Topic 3

Feasibility Study on the Introduction of the Liquefied Natural Gas (LNG and SLNG) into Energy Mix in Albania and Technology for the Construction /Operation of Gas Infrastructure- Study on the possibility of the LNG and SLNG project based on the evaluation of the global

LNG market conditions and Albania’s energy supply and demand structure- Sharing Korea’s experience for technical know-how for the construction and operation of

infrastructure facilities such as LNG receiving terminal and nationwide pipeline networks

Source: Author.

2. Methodology

The Knowledge Sharing Program (KSP) is a knowledge-intensive development and economic cooperation program. It is designed to successfully share Korea’s experience in development with partner countries. Since 2004, the Ministry of Economy and Finance of the

Gas Sector Expansion Strategy for Energy Diversification in Albania

038

Republic of Korea (MOEF) has been overseeing KSP for partner countries to facilitate their sustainable development and capacity for policy building. KSP has offered comprehensive policy consultations tailored to the needs of partner countries through in-depth analysis and training opportunities.

In July 2020, upon the submission of the KSP demand survey by the Ministry of Infrastructure and Energy (MIE), the Government of Albania, the MOEF of the Republic of Korea held a review session to propose and confirm the project of increase the abilities of Albanian institutions and entities to enable efficient use of energy sources that are environmentally friendly (with a focus on the natural gas sector). This project aimed to support the Albanian government to diversify energy sources apart from imported petroleum, achieve energy independence, and manage existing or new gas fields. Therefore, the institutional and technical expertise of our energy institutions/entities is extremely important.

The initial project proposal from the Albania government included the following four research sub-topics: 1) to diversify energy sources apart from imported petroleum, 2) to achieve Albania’s energy independence, 3) to better manage existing or new gas fields, and 4) to increase the institutional and technical expertise.

In association with the Korean field experts in the energy sector, we have discussed the current circumstances of Albania’s energy sector and drawn from Korea’s strength. Based on these, the field expert and KDI suggested a revision of the overarching topic and sub-topics, considering that KSP is a policy consultation project that will last for about 10 months. After discussion with the MIE, we agreed to revise the topic as follows:

Based on the revised topics and open bidding process of the Korea Development Institute (KDI) in September 2020, the Center for Energy Governance and Security, Hanyang University, Seoul, Republic of Korea, was designated as the implementing agency in Korea.

The Center for Energy Governance & Security (EGS) was established in 2012 with a major grant from the Korean Ministry of Education. EGS located at Hanyang University’s Seoul Campus, aims to conduct dynamic research on current energy issues while bringing groups of energy experts from major countries in the Asia-Pacific (the United States, China, Japan, Singapore, and Australia) together with an interest and capability to engage in the region. To better understand the notion of ‘global energy governance and energy security’ and the role of Asia, the center disseminates its research by collaborating with leading institutions worldwide through briefings, publications, conferences, and newspaper op-eds.

039

CHAPTER

01Introduction

An international joint team, including researchers from the Korea Energy Economics Institute and other international researchers, was formed according to the Hanyang University’s EGS. The research team comprises Korean experts, policy practitioners, and local consultants. A policy practitioner is a public officer or civil servant who is concerned with related ministerial policies. They are entitled to give (written) comments or opinions on the research proposals, interim reports, and draft of final reports and responsible for organizing networks among the policy institutions or organizations. KSP implementing agency will invite policy practitioner/project manager for the “Interim Reporting & Policy Practitioners’ Workshop,” which will be held in Korea during the program implementation period.

Local consultants in Albania have assisted Korean experts to collect data, review policy documents of the partner country, make preliminary analyses and write a part of the final report with the main author’s (Korean expert) agreement. The scope of work between local consultants and Korean experts is as follows:

- Local consultants are required to provide relevant data and information for effective research, co-author the final report on case-by-case issues, and cooperate with the Korean experts to complete the report.