2019-05-15 FPRS Board Agenda and Packet - City of Pasadena

463

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of 2019-05-15 FPRS Board Agenda and Packet - City of Pasadena

bjazmines

Typewritten Text

mprice

Typewritten Text

DATE: 5/15/19 ITEM #: 3

PASADENA FIRE AND POLICE RETIREMENT SYSTEM

MONTHLY ALLOWANCE ROLL - TOTALS

MONTH 2017-2018 2018-2019 Notes

JULY 1,080,895.48 1,087,861.08 a., b.

AUGUST 1,072,450.04 1,087,861.08

SEPTEMBER 1,073,179.24 1,087,861.08

OCTOBER 1,067,418.15 1,082,715.19 c.

NOVEMBER 1,073,865.44 1,086,317.32 d. e.

DECEMBER 1,071,271.25 1,068,434.20 f. g. h.

JANUARY 1,069,560.74 1,069,961.18 g.

FEBRUARY 1,069,560.74 1,060,113.61 i. j. k.

MARCH 1,066,101.66 1,048,594.93 l. m. n. o.

APRIL 1,062,125.72 1,047,879.22 p.

MAY 1,058,324.10 0.00

JUNE 1,057,281.28 0.00

Refund Checks -4,015.13 0.00

Prior Year Accruals Paid -2,859.76 0.00

FY TOTALS 12,815,158.95 10,727,598.89

COL BENEFITS

INCLUDED ABOVE 6,772,116.67 5,777,150.79

COL - % Of Total 53% 54%

a. 2% COLA applied to all members and beneficiaries.

b. C. Freeman has an accrual (from FY 2017) of $2,654.95

d. H. Heidner, surviving spouse of J. Heidner, passed 10/19/2018. She was not a payee.

f. C. Long passed 12/2/2018. Final payment to estate on 12/31/18. Surviving spouse, Nancy Long.

g. R. Stone passed 12/3/2018. Final payment to estate on 1/31/19. No survivor.

h. R. Patterson passed 12/14/2018. Final payment will be paid to estate. Surviving spouse, Carol Patterson.

i. M. Parillo passed 2/14/2019. Final payment will be paid to estate. No survivor.

j. R. Vis passed 2/14/2019. Final payment will be paid to estate. Surviving spouse, Sharon Vis.

k. R. Shultz passed 2/18/2019. Final payment will be paid to estate. No survivor.

l. M. Nelson passed 2/17/2019. Final payment on 2/28/19. No survivor.

m. D. Smith passed 3/1/2019. Final payment will be paid to estate. No survivor.

n. C. Smith, QDRO of D. Smith, passed 3/1/2019. Final payment will be paid.

o. S. Tellez replacement check for un-deposited check, passed 1/4/2015. Payment made to estate.

p. D. McClanahan passed 3/16/2019. Final payment on 3/31/19. Surviving spouse, Evelyn McClanahan.

Y:\Office Docs\Budget\FY 2019 Budget\[FY19 GL Detail FYTD 2019-5-8.xlsx]Journal Detail Export (2)

c. A. Cauchon passed 9/21/2018, ACH reversal processed in Oct. 2018. Final payment to estate on

11/30/18. No survivor.

e. F. Galligan, surviving spouse of James Galligan, passed 9/21/2018. She was a payee and the System

was informed by U.S. Bank's monthly death audit on 11/26/18. The estate has a debt to the System.

mprice

Typewritten Text

DATE: 5/15/19 ITEM #: 4

1OPINION AND ANALYSIS OF KEY ECONOMIC AND INVESTMENT ISSUES

Bill Hackney, CFA

April 10, 2019

How is your mood lately? Despite rising incomes, low

unemployment, falling poverty rates, and one of the

greatest bull markets in history, there is increasing evidence

that many of us are . . . well, going bonkers.

Last summer, Barnes and Noble reported a 25% surge in

sales of books about anxiety. Nothing more relaxing than

reading a book about anxiety at the beach, I suppose.

According to the World Health Organization, about 300

million people worldwide suffer from anxiety disorder. Here

in the US, 40 million adults, about one in five of us, suffer

from this malady.

Despite being one of the wealthiest and safest countries on

earth, the US, with 4% of the world’s population, accounts

for 13% of global anxiety disorders. And the diagnosis

of and prescriptions for anxiety disorders are on a steep

rise. The American Psychiatric Association reports 39% of

Americans said they were more anxious last year than the

year before.

The WHO study found there wasn’t much difference

between rich and poor nations when it came to the

prevalence of depression, but there was a difference when

it came to anxiety. Rich nations tended to be more anxious

than poor ones, with the US leading the way. Researchers

have linked increased anxiety to the pursuit of money, looks

and social status (stereotypically American pursuits) as well

as to increased loneliness and use of social media.

Fortunately, there is a wide variety of prescription drugs to

treat anxiety. It is estimated that one in six Americans takes

some kind of psychiatric drug—mostly antidepressants. But

America’s psychological problems are more serious than

just anxiety. Deaths of despair—suicide, drug overdoses and

liver cirrhosis—are tragically on the increase in the US.

Nobel Prize winning Economist Angus Deaton and his wife

Princeton professor Anne Case made news a few years

ago when they reported mortality rates among white,

working-class Americans are going up in contrast to other

demographic groups. Said Deaton, “You can find episodes

like the flu epidemic or wartimes when mortality rates

go up, but sustained increases in mortality for any major

group in society are really quite rare. It’s an indication that

something is very wrong.”

High

Anxiety

bjazmines

Typewritten Text

Date: 5/15/19 Item#: 6a

bjazmines

Typewritten Text

2OPINION AND ANALYSIS OF KEY ECONOMIC AND INVESTMENT ISSUES

Building on the work of Case and Deaton, the University of

Chicago published last month, “Men without Work: Why are

They So Unhappy in the US Compared to Other Places?” The

key finding: “Prime-aged males out of the labor force in

the US are the least hopeful and most stressed and angry

compared to the same group in other regions, including the

Middle East.”

What’s driving all this anxiety, deaths of despair and

disaffected workforce dropouts? Probably the usual

suspects. Dislocations caused by globalization—pressure

on wages, jobs lost due to plant relocations. Concerns

about immigration. Declining trust in bedrock American

institutions—education, media, religion, government and

capitalism. Cultural factors like loneliness and addiction to

social media.

I am not a psychologist, but I do know that psychology

can have a major impact on the capital markets, causing

them to “overshoot” both on the upside and the

downside. What’s more, the fragile psyche of the American

electorate—and the electorates of many countries—does

impact politics and government policy. In the near-term,

our nation’s declining psychological health is unlikely to

have much effect on the markets: Our economy is strong,

monetary policy is accommodative and our collective

mental condition is a somewhat nebulous force that is slow

moving and difficult to measure. Longer term, say 2020 and

beyond, I believe America’s mental state could threaten the

markets and the economy.

First, let’s look at near-term economic and stock market

conditions. Here the news is decidedly more upbeat. In

March the bull market in stocks turned ten years old and

it is not yet showing many of the late-cycle behaviors

(troublesome inflation and weakening labor markets) which

typically signal the end is nigh.

Exhibit 1 shows my five stock market indicators at the end

of the first quarter of 2019 (S&P 500, 2834) compared with

the end of the third quarter of 2018 (S&P 500, 2914). Of

course, between these two periods, there was a massive

stock market correction followed by an impressive rebound.

Closing prices for the respective quarters, however, were

within 3% of each other.

Note what has changed over the past six months.

Valuations have improved. The market’s price/earnings ratio

dropped by about 3X, thanks to robust earnings growth

due in part to the 2017 tax act (put into effect in 2018). The

economy has gotten a little weaker. The trend in the US

leading economic index flatlined over the last five months

Exhibit 1: Our indicators suggest the US stock market still has modest upside potential.

Indicator Rationale September 30, 2018 March 31, 2019

Short- vs. long-term interest rates

When short-term interest rates rise to meet or exceed long-term rates, monetary policy is usually tight enough to eventually cause a recession.

Fed funds rate is below 10-year T- note, but gap is narrowing

Fed funds rate is below 10-year T-note, but gap is narrowing

Widening spread between high- and low-qualitybond yields

A widening spread between junk bond yields and Treasuries indicates deteriorating credit market conditions.

Credit Spreads are still narrow

Credit Spreads are still narrow

Rising wage inflationWhen wages rise at a 4% annual rate, it is difficult for the Fed to keep core inflation near its 2% goal. So the Fed usually tightens policy aggressively.

Wage growth is 2.9% and beginning to accelerate

Wage growth is 3.2%

S&P 500 P/E ratioover 20 times

Price/earnings ratios over 20 times trailing four quarter earnings makes stocks vulnerable to rising interest rates and inflation.

P/E is 20.7 times P/E is 17.5 times

Downturn in Leading Economic Index®

The Conference Board’s LEI has peaked and turned down in advance of each recession since 1960. Average lead time is 13 months.

Strong uptrend Flat trend last five months

Sources: Bureau of Labor Statistics, Bloomberg, The Conference Board, Atlanta Capital

3OPINION AND ANALYSIS OF KEY ECONOMIC AND INVESTMENT ISSUES

following a protracted period of strength. Not surprising

given the sharp slowdown in the global economy in recent

months.

None of my indicators are negative, but three are flashing

a cautious yellow. The yield curve is very flat and has

remained so for several months. See Exhibit 2. A brief

inversion occurred in March but did not persist. I would be

more concerned about this indicator if it were confirmed

by a sustained rise in credit spreads, which, so far, has not

occurred.

Wage inflation continues to creep higher but is below the

4.0% threshold which would set off a bigger inflation alarm.

Given the recent favorable economic news from the US and

China, the Leading Economic Index seems unlikely to turn

sharply lower anytime soon. If it did, a recession could be

eight to 21 months away based on the history of this index.

The remaining months of 2019 are likely to be a benign,

but unexciting environment for equity investors and a

tricky one for bond investors. Inflation pressures from

rising energy prices and tight labor markets should push

longer-dated fixed income yields higher and keep the yield

curve from inverting. Higher inflation will also keep price/

earnings ratios from expanding. Global economic growth

will remain sluggish as will corporate earnings. In an

environment of no P/E expansion and maybe 5% earnings

growth, I can see the potential for the S&P 500® to hit 2975

this year (17.5 times $170 in earnings).

While the Trump Administration may pull the proverbial

“rabbit out of the hat” with a China trade deal later this

year, American business could face new uncertainties of

higher taxes and tighter regulations if there is a significant

change of leadership in Washington following the 2020

elections.

Here are three key issues that give me high anxiety as we

approach 2020.

A major change in tax policy with unintended

consequences. Anti-capitalist sentiment in the US is high.

In an effort to “punish the rich,” the US could implement

tax policies that could wreck the stock market. Can the rich

afford to pay more in taxes? Of course, they can. It’s clear

to virtually everyone that a return of the Democrats to the

White House will result in higher taxes of some sort. But it

is important to consider what types of income or property

should be taxed. Higher taxes on dividends and capital

gains are often discussed because stocks are perceived to

be owned primarily by the rich. Tax stocks and you avoid

hitting the little guy, so the reasoning goes. However,

taxable individuals and corporations make up a massive

Exhibit 2: Mind the Gaps! The gaps between short and long-term interest rates and low and high quality bonds provide

Sources: Bloomberg, ICE® BofA ML® US High Yield Index, Atlanta Capital as of 3/31/19.

0%

5%

10%

15%

20%

25%

0%

5%

10%

15%

20%

25%

1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

90-Day Treasury Bill Yield 10-Yr Treasury Note Yield High Yield (Junk) Bond Yield Recessions

Today, credit spreads are narrow and the yield curve is flat, but not inverted

Junk bond yields rise relative to Treasury yields

Short-term interest rates rise above long-term rates.

important signals for equity investors.

4OPINION AND ANALYSIS OF KEY ECONOMIC AND INVESTMENT ISSUES

amount of ownership of US equities. A tax scheme aimed at

the equity market will depress stock prices and hurt non-tax

paying equity owners as well. What about underfunded

state and local pension funds? These funds and most other

pension funds have 60% to 70% of their assets in stocks

and equity-like investments (private equity, hedge funds,

etc.) A major tax increase targeting stocks could precipitate

a municipal financial crisis in my view.

Liquidity in the capital markets dries up. Liquidity

measures how quickly a security can be bought or sold,

at a price close to the last transaction. Since the Great

Recession, liquidity in the stock and bond markets

has been reduced as the Dodd-Frank Act raised capital

requirements for banks and broker/dealers, thus reducing

their incentive to hold securities on their balance sheets

and “make markets.” Liquidity is influenced by investor

psychology and market structure. Add an anxious investor

class to a broker/dealer network not willing to assume

much risk and you get a market panic like the fourth

quarter of 2018. Stock prices dropped 20%, the market for

junk bonds and initial public offerings virtually shut down

and credit spreads on investment grade debt widened

significantly. Anxious investors can spark increased price

volatility which can cause more panic and more volatility.

The fourth quarter market debacle was not an isolated

event. It was a warning shot!

Inflation creeps up, surprising everyone including the

Fed. One key reason for the remarkable longevity of the

current economic and market cycle is that the US economy

never got overheated, forcing the Fed to tighten monetary

policy aggressively. Whenever our economy got up a full

head of steam, something came along to slow it down

and tame inflationary pressures. Most recently it was the

weakness in the Chinese and European economies, with

a little help from the Fed. Still, through it all, the labor

market remained strong and wage inflation continued to

trend higher. Now, it’s practically conventional wisdom that

inflation is dead and the Fed is finished with its tightening

cycle. What a surprise to the markets if this wasn’t true.

With the last year of his first term fast approaching,

President Trump has every incentive to stimulate the

economy. Is a surprising burst of inflation around the

corner? I am anxious to find out. Any unexpected uptick in

inflation could lead to a liquidity driven panic in the bond

market . . . which would eventually impact the stock market

. . . and then the economy.

Good grief! Where’s my Xanax?

This material is presented for informational and illustrative purposes only and should not be construed as investment advice, a recommendation to purchase or sell specific securities, or to adopt any particular investment strategy. The opinions expressed herein are those of the author and do not necessarily reflect the views of other employees at Atlanta Capital Management. Any current investment views and opinions/analyses expressed constitute judgments as of the date of this material and are subject to change at any time without notice. Index and commodity changes are based on price-only percentage change. This material has been prepared on the basis of publicly available information, internally developed data, and other third party sources believed to be reliable. However, no assurances are provided regarding the reliability of such information and Atlanta Capital has not sought to independently verify information taken from public and third party sources. This material may contain statements that are not historical facts, referred to as forward-looking statements. Future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions. Investing entails risks and there can be no assurance that any forecasts or opinions expressed in this material will be realized. ICE® BofA ML® US High Yield Index is an unmanaged index of below investment grade U.S. corporate bonds. ICE® BofA ML® indexes not for redistribution or other uses; provided “as is,” without warranties and with no liability. BofAML® is a licensed registered trademark of Bank of America Corporation in the United States and other countries. It is not possible to directly invest in an index. Past performance does not predict future results.

Atlanta Capital Management Co., LLC | 1075 Peachtree Street NE, Suite 2100, Atlanta, Georgia 30309 | Tel: 404.876.9411 | atlcap.com

│ │ │ │

bjazmines

Typewritten Text

bjazmines

Typewritten Text

Date: 5/15/19 Item#: 6a

•

•

•

•

Assets under management

1

•

•

•

│

│

│

│ │

│

2

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

(3%)

0%

3%

6%

9%

12%

15%

Russell 2000® Index by Earnings Stability

Five-Year Rolling CAGR of As Reported Earnings

3

4

•

•

•

•

•

•

•

•

•

•

•

•

•

•

5

•

•

•

•

•

•

•

•

•

•

•

6

7

+

+

+

+

+

+

–

–

–

–

–

8

9

10

11

12

•

•

•

•

•

•

•

13

14

15

Appendix

Portfolio Administration ReviewInvestment Summary,

Holdings and Transactions

16

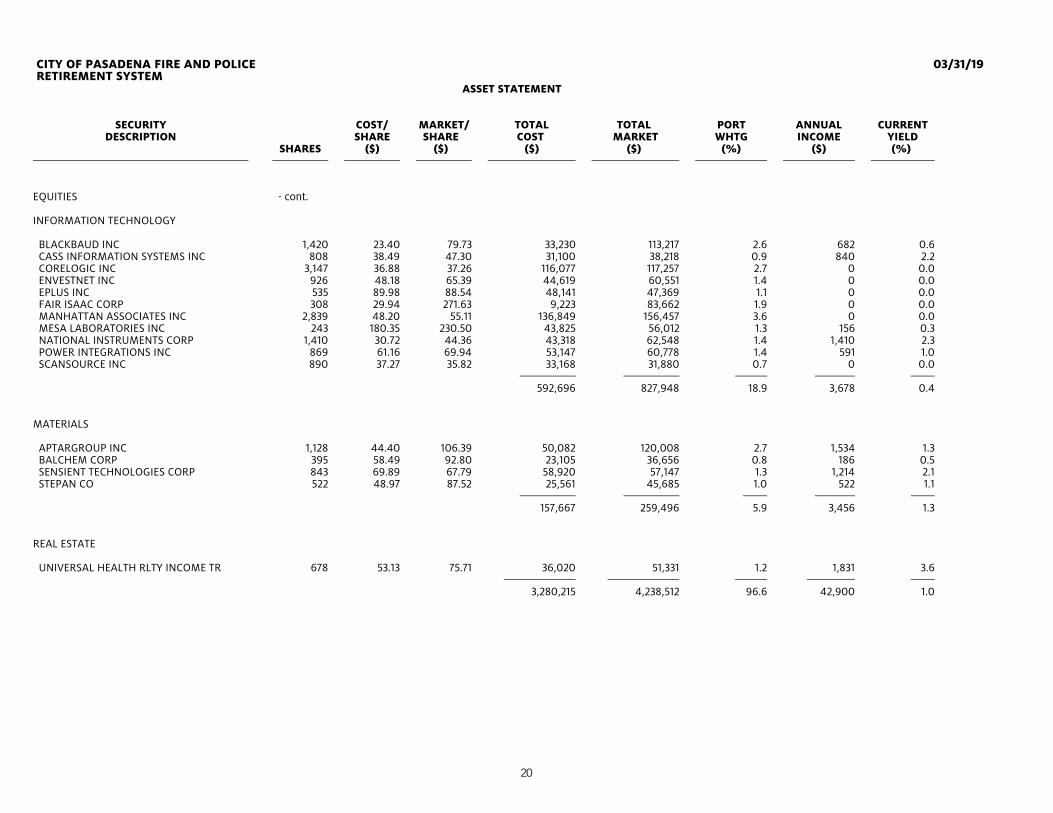

CITY OF PASADENA FIRE AND POLICE 03/31/19 RETIREMENT SYSTEM

INVESTMENT SUMMARY

TOTAL TOTAL PORT ANNUAL CURRENTCOST MARKET WGHT INCOME YIELD ($) ($) (%) ($) (%)

EQUITIES

CONSUMER DISCRETIONARY 459,315 636,313 14.5 4,405 0.7CONSUMER STAPLES 303,830 435,964 9.9 4,923 1.1ENERGY 59,791 39,431 0.9 0 0.0FINANCIALS 619,544 759,126 17.3 16,820 2.2HEALTH CARE 249,972 260,402 5.9 1,490 0.6INDUSTRIALS 801,381 968,499 22.1 6,297 0.7INFORMATION TECHNOLOGY 592,696 827,948 18.9 3,678 0.4MATERIALS 157,667 259,496 5.9 3,456 1.3REAL ESTATE 36,020 51,331 1.2 1,831 3.6 EQUITIES 3,280,215 4,238,512 96.6 42,900 1.0

INVESTABLE CASH

EQUITY CASH 147,982 147,982 3.4 3,478 2.4 TOTAL INVESTMENTS 3,428,197 4,386,493 100.0 46,378 1.1

ACCRUED DIVIDENDS 2,318

______________

TOTAL PORTFOLIO 4,388,811

______________

17

CITY OF PASADENA FIRE AND POLICE 03/31/19 RETIREMENT SYSTEM

ASSET STATEMENT

SECURITY COST/ MARKET/ TOTAL TOTAL PORT ANNUAL CURRENTDESCRIPTION SHARE SHARE COST MARKET WHTG INCOME YIELD

SHARES ($) ($) ($) ($) (%) ($) (%)

EQUITIES

CONSUMER DISCRETIONARY

CHOICE HOTELS INT'L INC 1,656 61.26 77.74 101,441 128,737 2.9 1,424 1.1 COLUMBIA SPORTSWEAR CO 735 38.87 104.18 28,566 76,572 1.7 706 0.9 DORMAN PRODUCTS INC 1,171 50.14 88.09 58,715 103,153 2.4 0 0.0 FRONTDOOR INC 1,870 30.36 34.42 56,765 64,365 1.5 0 0.0 MONRO INC 840 63.19 86.52 53,082 72,677 1.7 672 0.9 POOL CORP 337 78.24 164.97 26,367 55,595 1.3 607 1.1 SALLY BEAUTY HOLDINGS INC 2,510 19.92 18.41 49,991 46,209 1.1 0 0.0 WOLVERINE WORLD WIDE INC 2,491 33.88 35.73 84,387 89,003 2.0 996 1.1

459,315 636,313 14.5 4,405 0.7

CONSUMER STAPLES

CASEY'S GEN'L STORES INC 1,022 95.39 128.77 97,488 131,603 3.0 1,186 0.9 CENTRAL GARDEN & PET CO 1,439 33.68 25.56 48,461 36,781 0.8 0 0.0 INTER PARFUMS INC 1,324 28.87 75.87 38,221 100,452 2.3 1,456 1.4 J&J SNACK FOODS CORP 774 118.09 158.84 91,398 122,942 2.8 1,548 1.3 LANCASTER COLONY CORP 282 100.22 156.69 28,262 44,187 1.0 733 1.7

303,830 435,964 9.9 4,923 1.1

ENERGY

DRIL-QUIP INC 860 69.52 45.85 59,791 39,431 0.9 0 0.0

FINANCIALS

ARTISAN PARTNERS ASSET MGMT INC 1,386 45.38 25.17 62,896 34,886 0.8 3,105 8.9 CADENCE BANCORPORATION 3,103 15.85 18.55 49,169 57,561 1.3 2,172 3.8 IBERIABANK CORP 843 63.28 71.71 53,347 60,452 1.4 1,450 2.4 KINSALE CAPITAL GROUP INC 728 47.41 68.57 34,512 49,919 1.1 233 0.5 MORNINGSTAR INC 800 50.67 125.99 40,535 100,792 2.3 896 0.9 NAVIGATORS GROUP INC 1,160 46.53 69.87 53,979 81,049 1.8 325 0.4 PINNACLE FINANCIAL PARTNERS 1,110 43.56 54.70 48,355 60,717 1.4 710 1.2 PROSPERITY BANCSHARES INC 1,074 54.57 69.06 58,607 74,170 1.7 1,761 2.4 RLI CORP 765 49.72 71.75 38,034 54,889 1.3 673 1.2 SOUTH STATE CORP 1,199 86.97 68.34 104,277 81,940 1.9 1,822 2.2

18

CITY OF PASADENA FIRE AND POLICE 03/31/19 RETIREMENT SYSTEM

ASSET STATEMENT

SECURITY COST/ MARKET/ TOTAL TOTAL PORT ANNUAL CURRENTDESCRIPTION SHARE SHARE COST MARKET WHTG INCOME YIELD

SHARES ($) ($) ($) ($) (%) ($) (%)

EQUITIES - cont.

FINANCIALS - cont.

UMPQUA HOLDINGS CORP 2,452 13.00 16.50 31,879 40,458 0.9 2,060 5.1 WESTAMERICA BANCORPORATION 1,008 43.60 61.80 43,953 62,294 1.4 1,613 2.6

619,544 759,126 17.3 16,820 2.2

HEALTH CARE

COVETRUS INC 610 33.73 31.85 20,574 19,429 0.4 0 0.0 EMERGENT BIOSOLUTIONS INC 938 60.11 50.52 56,386 47,388 1.1 0 0.0 ICU MEDICAL INC 350 161.34 239.33 56,468 83,766 1.9 0 0.0 INTEGRA LIFESCIENCES HOLDINGS 1,409 43.58 55.72 61,408 78,509 1.8 0 0.0 PATTERSON COMPANIES INC 1,433 38.48 21.85 55,137 31,311 0.7 1,490 4.8

249,972 260,402 5.9 1,490 0.6

INDUSTRIALS

AAON INC 1,182 25.92 46.18 30,641 54,585 1.2 378 0.7 ALAMO GROUP INC 235 96.69 99.94 22,721 23,486 0.5 113 0.5 BEACON ROOFING SUPPLY INC 2,810 38.33 32.16 107,709 90,370 2.1 0 0.0 EXPONENT INC 1,868 22.50 57.72 42,030 107,821 2.5 1,196 1.1 FORWARD AIR CORP 1,167 52.98 64.73 61,833 75,540 1.7 840 1.1 GENERAC HOLDINGS INC 870 55.68 51.23 48,445 44,570 1.0 0 0.0 HURON CONSULTING GROUP INC 1,251 56.50 47.22 70,680 59,072 1.3 0 0.0 KIRBY CORP 1,260 57.19 75.11 72,054 94,639 2.2 0 0.0 LANDSTAR SYSTEM INC 707 62.66 109.39 44,299 77,339 1.8 467 0.6 MOOG INC CL A 1,293 76.66 86.95 99,121 112,426 2.6 1,293 1.2 RAVEN INDUSTRIES INC 1,015 20.35 38.37 20,652 38,946 0.9 528 1.4 SIMPSON MANUFACTURING CO INC 933 70.82 59.27 66,078 55,299 1.3 821 1.5 UNIFIRST CORP 507 126.66 153.50 64,215 77,825 1.8 228 0.3 US ECOLOGY INC 602 47.38 55.98 28,520 33,700 0.8 433 1.3 WELBILT INC 1,397 16.02 16.38 22,382 22,883 0.5 0 0.0

801,381 968,499 22.1 6,297 0.7

19

CITY OF PASADENA FIRE AND POLICE 03/31/19 RETIREMENT SYSTEM

ASSET STATEMENT

SECURITY COST/ MARKET/ TOTAL TOTAL PORT ANNUAL CURRENTDESCRIPTION SHARE SHARE COST MARKET WHTG INCOME YIELD

SHARES ($) ($) ($) ($) (%) ($) (%)

EQUITIES - cont.

INFORMATION TECHNOLOGY

BLACKBAUD INC 1,420 23.40 79.73 33,230 113,217 2.6 682 0.6 CASS INFORMATION SYSTEMS INC 808 38.49 47.30 31,100 38,218 0.9 840 2.2 CORELOGIC INC 3,147 36.88 37.26 116,077 117,257 2.7 0 0.0 ENVESTNET INC 926 48.18 65.39 44,619 60,551 1.4 0 0.0 EPLUS INC 535 89.98 88.54 48,141 47,369 1.1 0 0.0 FAIR ISAAC CORP 308 29.94 271.63 9,223 83,662 1.9 0 0.0 MANHATTAN ASSOCIATES INC 2,839 48.20 55.11 136,849 156,457 3.6 0 0.0 MESA LABORATORIES INC 243 180.35 230.50 43,825 56,012 1.3 156 0.3 NATIONAL INSTRUMENTS CORP 1,410 30.72 44.36 43,318 62,548 1.4 1,410 2.3 POWER INTEGRATIONS INC 869 61.16 69.94 53,147 60,778 1.4 591 1.0 SCANSOURCE INC 890 37.27 35.82 33,168 31,880 0.7 0 0.0

592,696 827,948 18.9 3,678 0.4

MATERIALS

APTARGROUP INC 1,128 44.40 106.39 50,082 120,008 2.7 1,534 1.3 BALCHEM CORP 395 58.49 92.80 23,105 36,656 0.8 186 0.5 SENSIENT TECHNOLOGIES CORP 843 69.89 67.79 58,920 57,147 1.3 1,214 2.1 STEPAN CO 522 48.97 87.52 25,561 45,685 1.0 522 1.1

157,667 259,496 5.9 3,456 1.3

REAL ESTATE

UNIVERSAL HEALTH RLTY INCOME TR 678 53.13 75.71 36,020 51,331 1.2 1,831 3.6 3,280,215 4,238,512 96.6 42,900 1.0

20

CITY OF PASADENA FIRE AND POLICE 03/31/19 RETIREMENT SYSTEM

ASSET STATEMENT

SECURITY COST/ MARKET/ TOTAL TOTAL PORT ANNUAL CURRENTDESCRIPTION SHARE SHARE COST MARKET WHTG INCOME YIELD

SHARES ($) ($) ($) ($) (%) ($) (%)

INVESTABLE CASH

EQUITY CASH 148 0.00 1000.00 147,982 147,982 3.4 3,478 2.4 TOTAL INVESTMENTS 3,428,197 4,386,493 100.0 46,378 1.1

ACCRUED DIVIDENDS 2,318

____________________________

TOTAL PORTFOLIO 4,388,811

____________________________

21

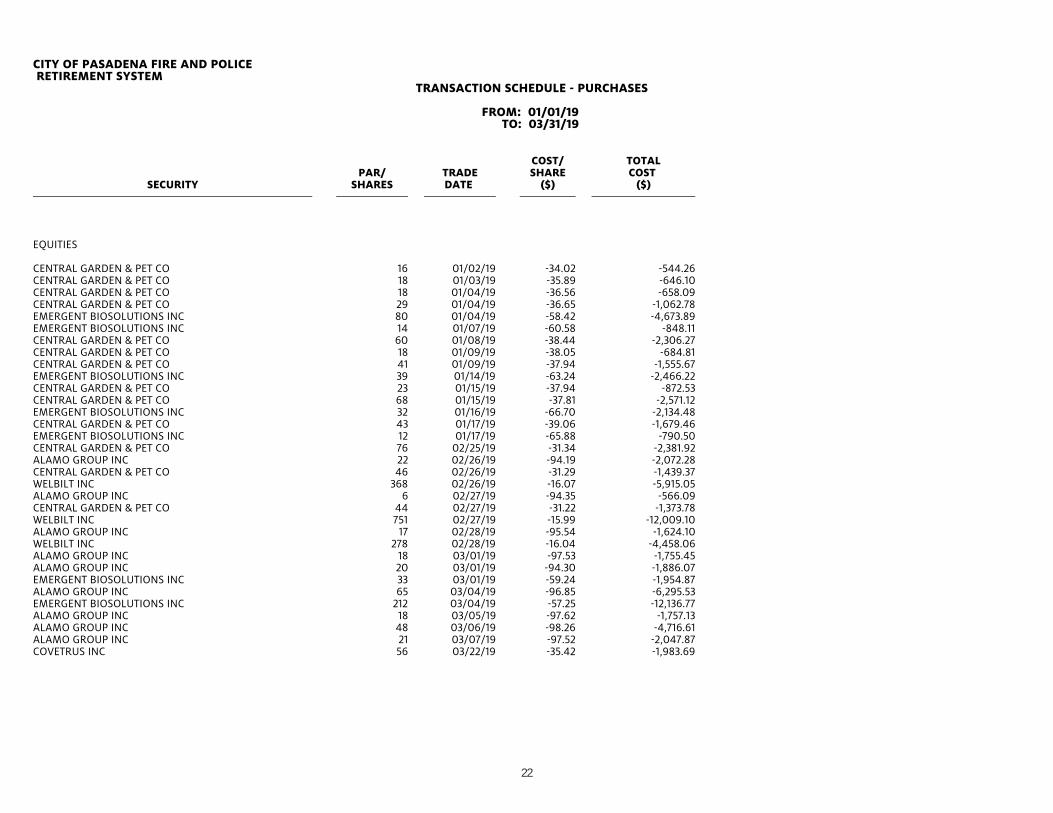

CITY OF PASADENA FIRE AND POLICE RETIREMENT SYSTEM

TRANSACTION SCHEDULE - PURCHASES

FROM: 01/01/19 TO: 03/31/19

COST/ TOTAL PAR/ TRADE SHARE COST

SECURITY SHARES DATE ($) ($)

EQUITIES

CENTRAL GARDEN & PET CO 16 01/02/19 -34.02 -544.26CENTRAL GARDEN & PET CO 18 01/03/19 -35.89 -646.10CENTRAL GARDEN & PET CO 18 01/04/19 -36.56 -658.09CENTRAL GARDEN & PET CO 29 01/04/19 -36.65 -1,062.78EMERGENT BIOSOLUTIONS INC 80 01/04/19 -58.42 -4,673.89EMERGENT BIOSOLUTIONS INC 14 01/07/19 -60.58 -848.11CENTRAL GARDEN & PET CO 60 01/08/19 -38.44 -2,306.27CENTRAL GARDEN & PET CO 18 01/09/19 -38.05 -684.81CENTRAL GARDEN & PET CO 41 01/09/19 -37.94 -1,555.67EMERGENT BIOSOLUTIONS INC 39 01/14/19 -63.24 -2,466.22CENTRAL GARDEN & PET CO 23 01/15/19 -37.94 -872.53CENTRAL GARDEN & PET CO 68 01/15/19 -37.81 -2,571.12EMERGENT BIOSOLUTIONS INC 32 01/16/19 -66.70 -2,134.48CENTRAL GARDEN & PET CO 43 01/17/19 -39.06 -1,679.46EMERGENT BIOSOLUTIONS INC 12 01/17/19 -65.88 -790.50CENTRAL GARDEN & PET CO 76 02/25/19 -31.34 -2,381.92ALAMO GROUP INC 22 02/26/19 -94.19 -2,072.28CENTRAL GARDEN & PET CO 46 02/26/19 -31.29 -1,439.37WELBILT INC 368 02/26/19 -16.07 -5,915.05ALAMO GROUP INC 6 02/27/19 -94.35 -566.09CENTRAL GARDEN & PET CO 44 02/27/19 -31.22 -1,373.78WELBILT INC 751 02/27/19 -15.99 -12,009.10ALAMO GROUP INC 17 02/28/19 -95.54 -1,624.10WELBILT INC 278 02/28/19 -16.04 -4,458.06ALAMO GROUP INC 18 03/01/19 -97.53 -1,755.45ALAMO GROUP INC 20 03/01/19 -94.30 -1,886.07EMERGENT BIOSOLUTIONS INC 33 03/01/19 -59.24 -1,954.87ALAMO GROUP INC 65 03/04/19 -96.85 -6,295.53EMERGENT BIOSOLUTIONS INC 212 03/04/19 -57.25 -12,136.77ALAMO GROUP INC 18 03/05/19 -97.62 -1,757.13ALAMO GROUP INC 48 03/06/19 -98.26 -4,716.61ALAMO GROUP INC 21 03/07/19 -97.52 -2,047.87COVETRUS INC 56 03/22/19 -35.42 -1,983.69

22

CITY OF PASADENA FIRE AND POLICE RETIREMENT SYSTEM

TRANSACTION SCHEDULE - PURCHASES

FROM: 01/01/19 TO: 03/31/19

COST/ TOTAL PAR/ TRADE SHARE COST

SECURITY SHARES DATE ($) ($)

EQUITIES - cont.

COVETRUS INC 74 03/22/19 -35.02 -2,591.12COVETRUS INC 480 03/25/19 -33.33 -15,999.07

-108,458.22

23

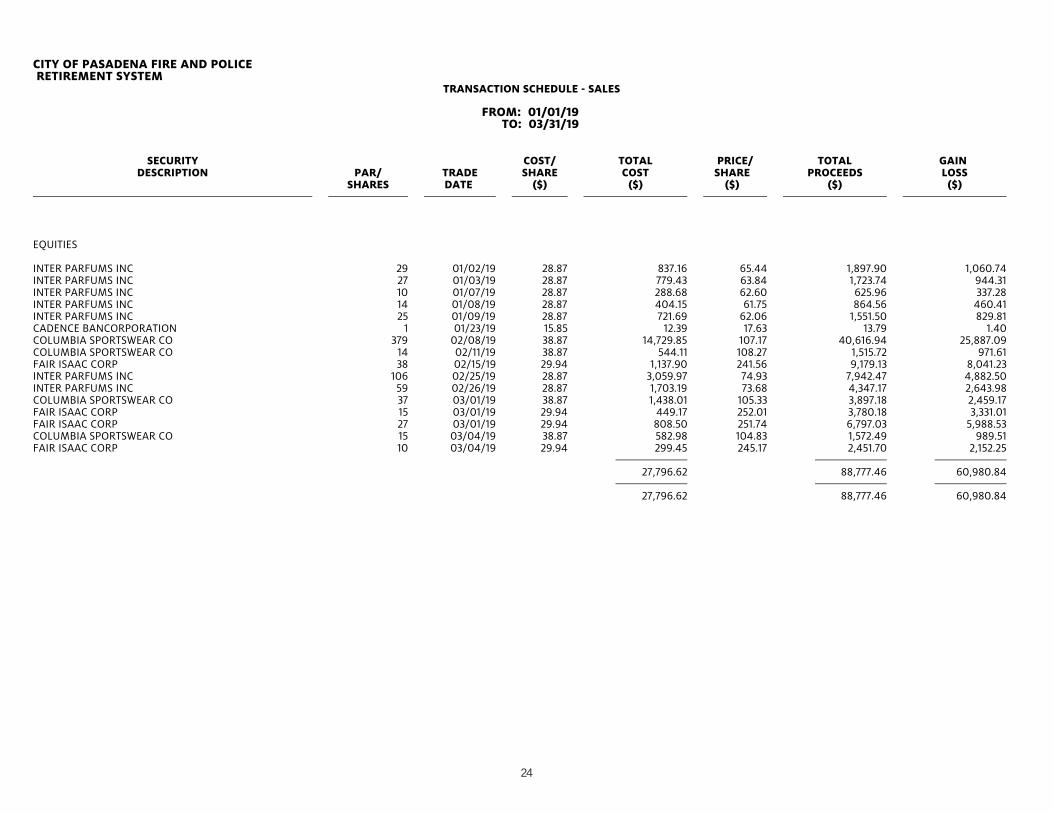

CITY OF PASADENA FIRE AND POLICE RETIREMENT SYSTEM

TRANSACTION SCHEDULE - SALES

FROM: 01/01/19 TO: 03/31/19

SECURITY COST/ TOTAL PRICE/ TOTAL GAIN DESCRIPTION PAR/ TRADE SHARE COST SHARE PROCEEDS LOSS

SHARES DATE ($) ($) ($) ($) ($)

EQUITIES

INTER PARFUMS INC 29 01/02/19 28.87 837.16 65.44 1,897.90 1,060.74INTER PARFUMS INC 27 01/03/19 28.87 779.43 63.84 1,723.74 944.31INTER PARFUMS INC 10 01/07/19 28.87 288.68 62.60 625.96 337.28INTER PARFUMS INC 14 01/08/19 28.87 404.15 61.75 864.56 460.41INTER PARFUMS INC 25 01/09/19 28.87 721.69 62.06 1,551.50 829.81CADENCE BANCORPORATION 1 01/23/19 15.85 12.39 17.63 13.79 1.40COLUMBIA SPORTSWEAR CO 379 02/08/19 38.87 14,729.85 107.17 40,616.94 25,887.09COLUMBIA SPORTSWEAR CO 14 02/11/19 38.87 544.11 108.27 1,515.72 971.61FAIR ISAAC CORP 38 02/15/19 29.94 1,137.90 241.56 9,179.13 8,041.23INTER PARFUMS INC 106 02/25/19 28.87 3,059.97 74.93 7,942.47 4,882.50INTER PARFUMS INC 59 02/26/19 28.87 1,703.19 73.68 4,347.17 2,643.98COLUMBIA SPORTSWEAR CO 37 03/01/19 38.87 1,438.01 105.33 3,897.18 2,459.17FAIR ISAAC CORP 15 03/01/19 29.94 449.17 252.01 3,780.18 3,331.01FAIR ISAAC CORP 27 03/01/19 29.94 808.50 251.74 6,797.03 5,988.53COLUMBIA SPORTSWEAR CO 15 03/04/19 38.87 582.98 104.83 1,572.49 989.51FAIR ISAAC CORP 10 03/04/19 29.94 299.45 245.17 2,451.70 2,152.25

27,796.62 88,777.46 60,980.84 27,796.62 88,777.46 60,980.84

24

Appendix

Proxy Report

25

City of Pasadena Fire and Police Retirement SystemReporting Period: 01/01/2019 to 03/31/2019

UniFirst Corp.Meeting Date: 01/08/2019 Record Date: 11/16/2018 Shares Voted: 456

Issue VoteProposal Number

Elect Director Phillip L. Cohen1.1 For

Elect Director Cynthia Croatti1.2 For

2 Ratify Ernst & Young LLP as Auditors For

Sally Beauty Holdings, Inc.Meeting Date: 01/31/2019 Record Date: 12/06/2018 Shares Voted: 2,510

Issue VoteProposal Number

1.1 Elect Director Christian A. Brickman For

Elect Director Marshall E. Eisenberg1.2 For

Elect Director Diana S. Ferguson1.3 For

Elect Director David W. Gibbs1.4 For

Elect Director Linda Heasley1.5 For

Elect Director Joseph C. Magnacca1.6 For

Elect Director Robert R. McMaster1.7 For

Elect Director John A. Miller1.8 For

Elect Director P. Kelly Mooney1.9 For

Elect Director Susan R. Mulder1.10 For

Elect Director Denise Paulonis1.11 For

Elect Director Edward W. Rabin1.12 For

Advisory Vote to Ratify Named Executive Officers' Compensation

2 For

Approve Omnibus Stock Plan3 For

4 Ratify KPMG LLP as Auditors For

J&J Snack Foods Corp.Meeting Date: 02/05/2019 Record Date: 12/11/2018 Shares Voted: 774

Issue VoteProposal Number

1 Elect Director Vincent Melchiorre For

2 Advisory Vote to Ratify Named Executive Officers' Compensation

For

Beacon Roofing Supply, Inc.Meeting Date: 02/12/2019 Record Date: 12/18/2018 Shares Voted: 2,810

Issue VoteProposal Number

1.1 Elect Director Robert R. Buck For

Elect Director Paul M. Isabella1.2 For

Elect Director Carl T. Berquist1.3 For

Elect Director Barbara G. Fast1.4 For

Elect Director Richard W. Frost1.5 For

Elect Director Alan Gershenhorn1.6 For

Elect Director Philip W. Knisely1.7 For

Elect Director Robert M. McLaughlin1.8 For

Elect Director Neil S. Novich1.9 For

Elect Director Stuart A. Randle1.10 For

Elect Director Nathan K. Sleeper1.11 For

Elect Director Douglas L. Young1.12 For

Ratify Ernst & Young LLP as Auditors2 For

3 Advisory Vote to Ratify Named Executive Officers' Compensation

For

Central Garden & Pet Co.Meeting Date: 02/12/2019 Record Date: 12/14/2018 Shares Voted: 465

Issue VoteProposal Number

1.1 Elect Director John B. Balousek For

Elect Director William E. Brown1.2 Withhold

Elect Director Thomas J. Colligan1.3 For

Elect Director Michael J. Edwards1.4 For

Elect Director John E. Hanson1.5 For

Elect Director Brooks M. Pennington, III1.6 Withhold

Elect Director John R. Ranelli1.7 Withhold

Elect Director George C. Roeth1.8 Withhold

Elect Director Mary Beth Springer1.9 For

2 Ratify Deloitte & Touche LLP as Auditors For

26

Moog, Inc.Meeting Date: 02/12/2019 Record Date: 12/18/2018 Shares Voted: 1,293

Issue VoteProposal Number

1 Elect Director Bradley R. Lawrence For

2 Ratify Ernst & Young LLP as Auditors For

Fair Isaac Corp.Meeting Date: 02/28/2019 Record Date: 01/02/2019 Shares Voted: 398

Issue VoteProposal Number

1a Elect Director A. George Battle For

Elect Director Braden R. Kelly1b For

Elect Director James D. Kirsner1c For

Elect Director William J. Lansing1d For

Elect Director Eva Manolis1e For

Elect Director Marc F. McMorris1f For

Elect Director Joanna Rees1g For

Elect Director David A. Rey1h For

Approve Qualified Employee Stock Purchase Plan2 For

Amend Omnibus Stock Plan3 For

Advisory Vote to Ratify Named Executive Officers' Compensation

4 For

Ratify Deloitte & Touche LLP as Auditors5 For

Other Business6 For

27

EuroPacific Growth Fund®As of March 31, 2019

Consider for a core international allocation.

Executive Summary

Implementation guidance:

The fund's investment objective is to provide long-term growth of capital.Fund Objective:

• EuroPacific Growth advanced in the first quarter, outpacing its primary benchmark, MSCI ACWI ex USA, which finished up 10.31%.

• Stock selection drove nearly all of the excess return for EuroPacific Growth relative to the benchmark, as both sector and regional selection detracted fromresults. That was primarily due to the fund's average cash weighting of about 7% amid a strong market rally.

• Japanese companies in the portfolio were the leading contributors overall, by country, with strength from both Softbank on news of a stock buyback andDaiichi Sankyo on an announced agreement with AstraZeneca to develop and sell one of their cancer drugs.

• Not all companies in Japan contributed as the biggest company detractor was Sony, which reported weak numbers due to declining sales of its PS4 gamingconsole. International Airlines Group, or IAG, which is the parent of British Airways as well as a number of other European airlines, also detracted from resultsas Brexit concerns weighed on investor sentiment.

• Emerging markets collectively helped the fund with strength from a number of technology and consumer-related companies. In particular, those from SouthKorea and India led the way.

• While the fund's technology holdings push its orientation toward the growth style, broad positioning in many other sectors exhibits a less growth-orientedfootprint than many peers -- having less exposure in industrials, consumer staples and health care as examples. The market has generally continued to favorgrowth stocks, and this orientation, while helpful to results relative to the index is unhelpful to peer group rankings in the short run.

Invests in attractively valued companies in developed and emerging markets that are positioned to benefit frominnovation, global economic growth, increasing consumer demand or a turnaround in business conditions.Distinguishing characteristics:

1

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.© 2019 Capital Group. All rights reserved

mprice

Typewritten Text

DATE: 5/15/19 ITEM #: 6b

EuroPacific Growth Fund®As of March 31, 2019

Figures shown are past results for Class F-1, F-2, F-3 and R-6 shares and are not predictive of results in future periods. Current and future results may be lower or higher than those shown. Share prices and returns will vary, so investors may lose money. Investing for short periods makes losses more likely. For current information and month-end results, visit americanfunds.com or americanfundsretirement.com.

Returns Total returns Average annual total returns Expense Ratio

For periods ended March 31, 2019 (%) 3 mo YTD 1 year 3 years 5 years 10 years Lifetime

EuroPacific Growth Fund F-1 13.11 13.11 -5.01 8.91 3.88 9.55 10.42 0.85

EuroPacific Growth Fund F-2 13.18 13.18 -4.75 9.22 4.16 9.84 10.70 0.58

EuroPacific Growth Fund F-3 13.21 13.21 -4.65 9.32 4.27 9.95 10.86 0.49

EuroPacific Growth Fund R-6 13.20 13.20 -4.66 9.33 4.27 9.95 10.81 0.49

Historical Benchmarks Index* 10.31 10.31 -4.22 8.09 2.57 8.85 8.18 ---MSCI All Country World ex USA Index** 10.31 10.31 -4.22 8.09 2.57 8.85 --- ---Lipper International Funds Average 10.84 10.84 -5.77 6.65 2.14 8.80 8.51 ---

Fund inception: April 16, 1984

Market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index. Lipper averages reflect the current composition of all eligible mutualfunds (all share classes) within a given category. There have been periods when the fund has lagged the indexes.

*Returns reflect results of the fund's current and former benchmark indexes: MSCI All Country World ex USA Index, April 2007-present; MSCI EAFE Index, fund inception-March 2007.Results reflect net dividends.**Results reflect gross dividends through December 31, 2000 and net dividends thereafter.We offer a range of share classes designed to meet the needs of retirement plan sponsors and participants. The different share classes incorporate varying levels of advisorcompensation and service provider payments. Because Class R-6 shares do not include any recordkeeping payments, expenses are lower and results are higher. Other share classesthat include recordkeeping costs have higher expenses and lower results than Class R-6.

Investment results assume all distributions are reinvested and reflect applicable fees and expenses. When applicable, investment results reflect fee waivers and/or expensereimbursements, without which results would have been lower. Please see americanfunds.com for more information. Certain share classes were offered after the inception dates ofsome funds. Results for these share classes prior to the dates of first sale are hypothetical based on Class A share results without a sales charge, adjusted for estimated annualexpenses. (Inception date: Class F-1, March 15, 2001; Class F-2, August 1, 2008; Class F-3, January 27, 2017; Class R-6, May 1, 2009.) Results for certain funds with an inception dateafter the share class inception also include hypothetical returns because those funds' shares sold after the date of first offering. Please see americanfunds.com for more information onspecific expense adjustments and the actual dates of first sale. Expense ratios are as of the fund's prospectus available at the time of publication.

2

EuroPacific Growth Fund®As of March 31, 2019

Quarterly Market review

• Non-U.S. stocks surged over the quarter, rebounding from the steep selloff at the end of 2018. Investor sentiment was boosted by optimism surrounding the tradeconflict between the U.S. and China, as well as an increasingly dovish tone from central banks. Currency movements had a mixed impact on returns: the euro andJapanese yen declined against the U.S. dollar while the British pound rallied amid rising speculation that the U.K. would not leave the European Union without adeal.

• European companies advanced strongly. Rising risk appetite helped stocks overcome signs of slowing economic growth in the eurozone and the uncertaintycaused by the U.K.'s imminent scheduled departure from the EU. The German economy recorded no growth in the final quarter of 2018, while Italy fell into arecession, having delivered two consecutive quarters of negative growth. After ending its bond-buying program in December, the European Central Bank decidedto reinstate its long-term loans to eurozone banks and pledged to hold interest rates until the end of 2020. In general, U.K. companies overcame Brexit-relateduncertainty and joined the global stock market rally.

• Japanese companies delivered solid gains but lagged the broader advance in global stocks amid weak economic data and concerns over trade uncertainty.February's flash estimate of the Nikkei-Markit manufacturing purchasing managers' index slid below the 50 level, indicating that manufacturing activity wascontracting for the first time since August 2016, owing in part to reduced demand from China. Other developed Asia-Pacific markets also rallied, led by double-digit gains in Hong Kong and Australia.

• Companies domiciled in developing economies delivered sizable gains over the quarter, lifted by hopes that the U.S. and China could resolve their tradedifferences. Chinese stocks rebounded after a sharp selloff in 2018, boosted by further stimulus measures from the Chinese authorities as well as a major indexprovider's decision to increase the weighting to Chinese companies in its benchmark index. Brazilian stocks also surged, buoyed by incoming President JairBolsonaro's pledge to liberalize trade and reduce taxes for business. In contrast, Indian stocks advanced but lagged other emerging markets due to rising politicaluncertainty ahead of elections.

3

EuroPacific Growth Fund®

As of March 31, 2019

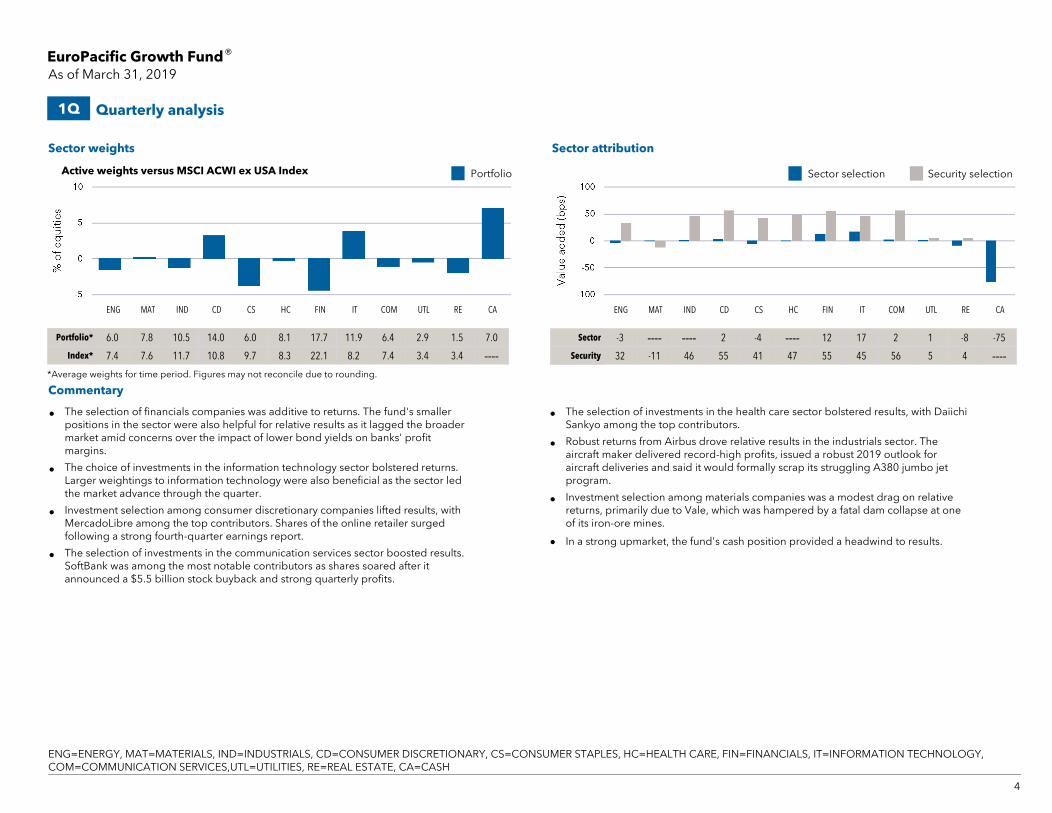

1Q Quarterly analysis

Portfolio* 6.0 7.8 10.5 14.0 6.0 8.1 17.7 11.9 6.4 2.9 1.5 7.0

Index* 7.4 7.6 11.7 10.8 9.7 8.3 22.1 8.2 7.4 3.4 3.4 ----*Average weights for time period. Figures may not reconcile due to rounding.

Sector weights Sector attribution

Commentary

Sector -3 ---- ---- 2 -4 ---- 12 17 2 1 -8 -75

Security 32 -11 46 55 41 47 55 45 56 5 4 ----

Active weights versus MSCI ACWI ex USA Index Portfolio

ENG MAT IND CD CS HC FIN IT COM UTL RE CA

• The selection of financials companies was additive to returns. The fund's smallerpositions in the sector were also helpful for relative results as it lagged the broadermarket amid concerns over the impact of lower bond yields on banks' profitmargins.

• The choice of investments in the information technology sector bolstered returns.Larger weightings to information technology were also beneficial as the sector ledthe market advance through the quarter.

• Investment selection among consumer discretionary companies lifted results, withMercadoLibre among the top contributors. Shares of the online retailer surgedfollowing a strong fourth-quarter earnings report.

• The selection of investments in the communication services sector boosted results.SoftBank was among the most notable contributors as shares soared after itannounced a $5.5 billion stock buyback and strong quarterly profits.

• The selection of investments in the health care sector bolstered results, with DaiichiSankyo among the top contributors.

• Robust returns from Airbus drove relative results in the industrials sector. Theaircraft maker delivered record-high profits, issued a robust 2019 outlook foraircraft deliveries and said it would formally scrap its struggling A380 jumbo jetprogram.

• Investment selection among materials companies was a modest drag on relativereturns, primarily due to Vale, which was hampered by a fatal dam collapse at oneof its iron-ore mines.

• In a strong upmarket, the fund's cash position provided a headwind to results.

Sector selection Security selection

ENG MAT IND CD CS HC FIN IT COM UTL RE CA

4

SM

ENG=ENERGY, MAT=MATERIALS, IND=INDUSTRIALS, CD=CONSUMER DISCRETIONARY, CS=CONSUMER STAPLES, HC=HEALTH CARE, FIN=FINANCIALS, IT=INFORMATION TECHNOLOGY,COM=COMMUNICATION SERVICES,UTL=UTILITIES, RE=REAL ESTATE, CA=CASH

EuroPacific Growth Fund®

As of March 31, 2019

1Q Quarterly analysis

*Average weights for time period. Figures may not reconcile due to rounding.

Regional weights Regional attribution

Commentary

Active weights versus MSCI ACWI ex USA Index

Canada Eurozone Japan EmergingMarkets

OtherEurope

Pacificex Japan

UK USA

Portfolio* 4.0 20.6 12.7 31.1 6.2 7.0 9.2 2.1

Index* 6.8 21.3 16.4 26.0 9.7 8.4 11.4 ----

Canada Eurozone Japan EmergingMarkets

OtherEurope

Pacificex Japan

UK USA

Region -14 4 12 -5 -2 -6 -4 1

Security -3 93 82 108 15 26 25 62

• Positive investment selection in South Korea and India buoyed returns amongcompanies domiciled in developing economies. India's Reliance Industries was anotable contributor.

• The selection of eurozone companies boosted results. France-based Airbus wasamong the top contributors as the aircraft maker delivered record-high profits,issued a robust 2019 outlook for aircraft deliveries and said it would formally scrapits struggling A380 jumbo jet program.

• SoftBank helped lift results among Japanese companies when it announced a $5.5billion stock buyback and strong quarterly profits. Holding Daiichi Sankyo was alsobeneficial as U.K.-listed AstraZeneca has struck a deal worth up to $6.9 billion todevelop and sell one of the Japanese pharmaceutical company's new cancer drugs.

• MercadoLibre was a notable contributor. Shares in the U.S.-listed company, whichoperates an online trading site for Latin American markets, surged following better-than-expected fourth-quarter results.

• Smaller investments in Canadian companies weighed on relative returns, withinvestment selection further hindering relative results.

• In a strong upmarket, the fund's cash position provided a headwind to results.

Portfolio Region selection Security selection

5

SM

EuroPacific Growth Fund®

As of March 31, 2019

Company Portfolio* % Index* % Relative Contribution

Airbus SE 2.42 0.35 0.50

MercadoLibre, Inc. 0.90 0.00 0.46

Reliance Industries Limited 2.31 0.25 0.25

Daiichi Sankyo Company, Limited 0.82 0.10 0.24

SoftBank Group Corp. 0.98 0.35 0.21

Company Portfolio* % Index* % Relative Contribution

Sony Corporation 1.09 0.30 -0.22

ISR: International Consolidated Airlines Group SA 0.68 0.02 -0.19

ISR: Vale S.A. 1.63 0.21 -0.16

EssilorLuxottica SA 0.55 0.18 -0.10

Yamato Holdings Co., Ltd. 0.46 0.04 -0.07

1Q Quarterly analysis

* Average position for quarter; portfolio holdings change. * Average position for quarter; portfolio holdings change.

Commentary Commentary

Airbus

Airbus manufactures aircrafts, helicopters and military equipment. Shares rallied afterthe company beat fourth-quarter earnings forecasts and raised its guidance for planedeliveries and operating profit for 2019. There was also a positive reaction to itsdecision to discontinue production of its loss-making A380 passenger plane.

MercadoLibre, Inc.

MercadoLibre operates online e-commerce and online auctions, includingmercadolibre.com, the leading e-commerce site for Latin America. Shares surged afterthe company reported strong fourth-quarter results, with both earnings and revenuessurpassing forecasts. MercadoLibre s total number of registered users jumped morethan 25% year-over-year, while new confirmed registered users increased more than75% on a year-over-year basis. Total payments transactions jumped by 72%.

Top five security contributors versus MSCI ACWI ex USA Index Bottom five security contributors versus MSCI ACWI ex USA Index

Sony Corporation

Sony is engaged in the development, design, manufacture and sale of various kinds ofelectronic equipment, instruments and devices for consumer, professional andindustrial markets, as well as game consoles and software. Shares slid after financialresults for the third-quarter fiscal disappointed forecasts as earnings from its gamingbusiness declined, with falling sales of PS4 consoles. Although Sony maintained itsoverall profit forecast for the fiscal year, it lowered guidance for the imaging sensorssegment owing to weakness in the smartphone market.

Vale

Vale engages in the exploration, production and sale of iron ore and nickel in Braziland other countries around the world. Shares slid after hundreds of people were killeddue to the collapse of its Brumadinho dam in Southeast Brazil. Vale subsequentlyannounced various writedowns in relation to the disaster, including $124 millionrelated to the Corrego de Feijao mine, which lies in the vicinity of the dam collapse.Emergency compensation agreements with local authorities were projected to reachup to $520 million. As an interim measure, Vale chief executive Fabio Schvartsman wassucceeded by Eduardo Bartolomeu, who was previously director of base metals.

The mnemonic 'ISR:' indicates that two or more issues of the same issuer have been rolled up and thus what is presented in the report is the Issuer Level data.

6

SM

EuroPacific Growth Fund®

As of December 31, 2018

YTD Year-to-date analysis

Portfolio* 5.5 8.8 9.6 12.5 7.2 7.2 17.2 17.6 3.7 2.6 0.9 7.3

Index* 7.2 8.0 11.8 11.0 9.5 8.1 22.6 10.9 4.7 3.0 3.2 ----*Average weights for time period. Figures may not reconcile due to rounding.

Sector weights Sector attribution

Commentary

Sector -13 ---- 2 -13 -14 -9 14 -14 1 -5 -7 107

Security 13 -42 27 -10 -75 -11 78 -24 -48 30 1 ----

Active weights versus MSCI ACWI ex USA Index Portfolio

• The selection of consumer staples companies dragged on returns, with BritishAmerican Tobacco among the largest detractors. Smaller investments in the sectorfurther hindered results: While consumer staples companies declined over the year,they held up better than the broader market.

• AAC Technologies weighed on results among information technology companies:The company was affected by concerns of slowing demand for smartphones,particularly Apple's iPhone. Nintendo, which moved into the new communicationservices sector in September, was another notable detractor. Larger holdings ininformation technology further hampered results as the sector was among those withthe weakest returns over the year.

• Investment selection among materials companies dampened returns.

• Indian banks HDFC Bank and Kotak Mahindra Bank boosted relative results amongfinancials companies, as did Hong Kong-listed insurer AIA Group. Smaller holdingsin the sector were also helpful for relative results as financials companies lagged thebroader market.

• Investment selection among industrials companies was additive to relative returns.

• The selection of utilities companies bolstered returns. Orsted was among the mostnotable contributors.

Sector selection Security selection

ENG MAT IND CD CS HC FIN IT COM UTL RE CA ENG MAT IND CD CS HC FIN IT COM UTL RE CA

7

SM

ENG=ENERGY, MAT=MATERIALS, IND=INDUSTRIALS, CD=CONSUMER DISCRETIONARY, CS=CONSUMER STAPLES, HC=HEALTH CARE, FIN=FINANCIALS, IT=INFORMATION TECHNOLOGY,COM=COMMUNICATION SERVICES, UTL=UTILITIES, RE=REAL ESTATE, CA=CASH

EuroPacific Growth Fund®

As of December 31, 2018

YTD Year-to-date analysis

*Average weights for time period. Figures may not reconcile due to rounding.

Regional weights Regional attribution

Commentary

Active weights versus MSCI ACWI ex USA Index

Canada Eurozone Japan EmergingMarkets

OtherEurope

Pacificex Japan

UK USA

Portfolio* 3.7 20.7 13.5 30.2 6.1 6.4 10.6 1.4

Index* 6.5 22.4 16.6 25.1 9.3 8.2 12.0 ----

Canada Eurozone Japan EmergingMarkets

OtherEurope

Pacificex Japan

UK USA

Region 12 8 ---- 19 -9 19 ---- 3

Security -33 42 -35 7 15 -22 -138 -3

• The selection of U.K.-listed companies hindered returns. British American Tobaccoand ASOS were among the largest detractors.

• Nintendo weighed on results among Japanese companies.

• Investment selection in Canada dragged on returns, due to select holdings inmaterials and energy companies.

• The selection of eurozone companies boosted relative returns. Investment selectionamong France-based companies lifted relative results, as did having smallerpositions in Germany.

• Holdings of Indian companies were additive to returns among companies domiciledin developing economies. HDFC Bank, Reliance Industries and Kotak Mahindra Bankwere among the top contributors.

Region selection Security selectionPortfolio

8

SM

EuroPacific Growth Fund®

As of December 31, 2018

Company Portfolio* % Index* % Relative Contribution

ISR: HDFC Bank Limited 2.41 0.00 0.45

Reliance Industries Limited 2.08 0.20 0.45

Orsted 0.93 0.06 0.29

Kotak Mahindra Bank Limited 1.08 0.00 0.27

AIA Group Limited 2.56 0.49 0.27

Company Portfolio* % Index* % Relative Contribution

British American Tobacco p.l.c. 1.69 0.56 -0.52

AAC Technologies Holdings Inc. 0.44 0.05 -0.31

Nintendo Co., Ltd. 2.05 0.20 -0.29

ISR: Ryanair Holdings Plc 1.15 0.01 -0.22

ASOS plc 0.36 0.00 -0.21

YTD Year-to-date analysis

* Average position for time period; portfolio holdings change. * Average position for time period; portfolio holdings change.

Commentary Commentary

Kotak Mahindra Bank

Kotak Mahindra Bank is a bank headquartered in Mumbai, India. Shares were driven bystrong growth in customer deposits and loans, as the bank continued to gain marketshare. The bank reported solid profit growth throughout the year. Kotak said it had metits target to double the number of customers to 16 million over the 18-month periodending September 30, 2018. It also reported a decline in its nonperforming loan ratio.

Reliance Industries

Reliance Industries is an India-based conglomerate, with businesses across the energy,petrochemicals and telecommunications sectors. Shares rallied on positive financialresults as earnings from its petrochemical business nearly doubled year-over-year inthe first quarter of its 2019 fiscal year, with the unit experiencing record operatingearnings and substantial improvement in polyester-chain margins. The stock wasadditionally boosted by positive sentiment surrounding its Jio telecom venture, whichcontinued to gain market share and supplanted Vodafone to stand as the secondlargest telecom company by revenue in the Indian market.

Top five security contributors versus MSCI ACWI ex USA Index Bottom five security contributors versus MSCI ACWI ex USA Index

AAC Technologies

AAC Technologies is a vertically integrated manufacturer of miniature technologycomponents and a key supplier to Apple. Shares slid after the company reporteddisappointing results on falling shipments of smartphones, which saw AAC's earningsdecline 21% year-over-year for the nine months ended September 2018. Along with aslowdown in overall demand, AAC was also impacted by higher interest rates and abroader selloff of Hong Kong stocks as the trade dispute between the U.S. and Chinaweighed on sentiment.

British American Tobacco

British American Tobacco (BAT) is one of the world's largest producers of cigarettesand other tobacco products. Shares weakened amid ongoing worries over fallingglobal cigarette demand given the impact of anti-smoking legislation and reports thatthe U.S. Food and Drug Administration (FDA) was moving to ban sales of mentholcigarettes, which account for just over half of BAT's U.S. sales volumes. The FDAbelieves menthol cigarettes are more difficult to quit than regular cigarettes and holdtoo much appeal for younger smokers as they come in various flavors. There were alsocontinuing doubts over the potential of alternative, next-generation products.

The mnemonic 'ISR:' indicates that two or more issues of the same issuer have been rolled up and thus what is presented in the report is the Issuer Level data.

9

SM

EuroPacific Growth Fund®

As of March 31, 2019

Portfolio Positioning Portfolio manager years of experience

Portfolio managers Years with Capital Group Years in profession

Mark E. Denning 36 36

Nicholas J. Grace 25 28

Carl M. Kawaja 27 31

Jonathan Knowles 26 26

Lawrence Kymisis 15 23

Sung Lee 24 24

Jesper Lyckeus 22 23

Andrew B. Suzman 25 25

Christopher Thomsen 21 21

The industrials sector, nearing a 15-year high, has a heavy emphasis in aerospace anddefense, as well as airlines. The fund holds fewer companies here than the index dueprimarily to a lack of exposure in trading, railroad and construction companies. Inaddition, the consumer staples sector is now at a more than a 10-year low on the heelsof weakness in tobacco and resulting trims as conviction waned.

The information technology and consumer discretionary sectors stand out among thefund's largest exposures relative to the index. Semiconductors and electronicequipment & components are a focus in technology, while internet & direct marketingretail and luxury goods are prominent in the consumer discretionary sector. The healthcare sector, recently coming off a multi-year low, continues to garner attention frominvestors for its promising drug pipelines and M&A activity, as well as appealingdefensive characteristics.

The communication services sector, recently changed from telecommunicationservices, now includes additional companies such as Tencent, Naspers, Baidu andNintendo. This shift brings the fund's weight in technology materially lower comparedto previous quarters with minimal impact to the consumer discretionary classification.

The fund's investments in European companies are now at a 15-year low due to weakshare prices and the decision to trim airline holdings as concerns regarding Brexitlingered.

Exposure to emerging markets companies increased to an all-time high of 32.4%, upfrom 31.3%, higher than the index weighting of 26.1%. Our emerging marketsinvestments are concentrated in just a handful of countries with the top 5 capturingnearly all of the fund's exposure: China, India, South Korea, Brazil and Taiwan. Thecompanies have shown strength with broad industry participation. Solid stock selectionresulted in the emerging markets being the fund's top regional contributor during thequarter. Over the longer term, security selection in emerging markets has been aleading regional contributor for the 1-, 3- and 5-year periods, due mostly toinvestments in Indian banks and Chinese internet companies.

10

Although the American Funds are compared to their benchmarks, portfolio managers manage the funds consistent with each fund’s investment objectives.

EuroPacific Growth Fund®

As of March 31, 2019

Attribution methodology disclosure

Equity attribution data was produced using FactSet, a third-party software system,based on daily portfolios. Securities in their initial period of acquisition may not beincluded in this analysis. The analysis includes equity investments only and excludesforward contracts and fixed-income investments, if applicable. It does not account forbuy and sell transactions that might have occurred intraday. As a result, averageportfolio weight percentages are approximate and the actual average portfolio weightpercentages might be higher or lower. Data elements such as pricing, income, marketcap, etc., were provided by FactSet. The index provided for attribution is based onFactSet’s methodology. The index is a broad-based market benchmark and may not beused by Capital Group as the sole comparative index for this fund. Capital believes thesoftware and information from FactSet to be reliable. However, Capital cannot beresponsible for inaccuracies, incomplete information or updating of information byFactSet. Past results are not predictive of results in future periods.

Index definitions

EuroPacific Growth Fund Historical Benchmarks Index returns reflect the results of theMSCI EAFE® Index through 3/31/2007 and the MSCI All Country World ex USA Index,the fund’s current primary benchmark, thereafter. MSCI EAFE® (Europe, Australasia, FarEast) Index is a free float-adjusted market capitalization weighted index that isdesigned to measure developed equity market results, excluding the United States andCanada. MSCI All Country World ex USA Index is a free float-adjusted marketcapitalization weighted index that is designed to measure equity market results in theglobal developed and emerging markets, excluding the United States. The indexconsists of more than 40 developed and emerging market country indexes. Resultsreflect dividends net of withholding taxes. These indexes are unmanaged and,therefore, have no expenses, and their results include reinvested dividends and/ordistributions.

MSCI All Country World ex USA Index is a free float-adjusted market capitalizationweighted index that is designed to measure equity market results in the globaldeveloped and emerging markets, excluding the United States. The index consists ofmore than 40 developed and emerging market country indexes. Results reflectdividends gross of withholding taxes through December 31, 2000, and dividends netof withholding taxes thereafter. This index is unmanaged, and its results includereinvested dividends and/or distributions but do not reflect the effect of sales charges,commissions, account fees, expenses or taxes. This index was not in existence as of thedate the fund began investment operations; therefore, lifetime results are not available.

Lipper International Funds Average is composed of funds that invest assets in securitieswith primary trading markets outside the United States. The results of the underlyingfunds in the average include the reinvestment of dividends and capital gaindistributions, as well as brokerage commissions paid by the funds for portfoliotransactions and other fund expenses, but do not reflect the effect of sales charges,account fees or taxes.

Investors should carefully consider investment objectives, risks, charges and expenses. This and other important information is contained in the fund prospectus and summary prospectus, which can be obtained from a financial professional and should be read carefully before investing. Investing outside the United States involves riskssuch as currency fluctuations, periods of illiquidity and price volatility, as more fully described in the prospectus. These risks may be heightened in connection withinvestments in developing countries.

Important Information

MSCI has not approved, reviewed or produced this report, makes no express orimplied warranties or representations and is not liable whatsoever for any data in thereport. You may not redistribute the MSCI data or use it as a basis for other indices orinvestment products.

Source: Thomson Reuters Lipper

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartialinvestment or fiduciary advice.All Capital Group trademarks referenced are registered trademarks owned by The Capital Group Companies, Inc. or an affiliated company. All other company and product namesmentioned are the trademarks or registered trademarks of their respective companies.Cash/cash and equivalents/cash and money market may include short-term securities, accrued income and other assets less liabilities as well as currencies. It may also includeinvestments in money market or similar funds, which may be managed by the investment adviser or its affiliates that are not offered to the public.Securities offered through American Funds Distributors, Inc.

11Lit. No. ITGEQSX-016-0419O CGD/10219-S67023 © 2019 Capital Group. All rights reserved.

Institutional and Intermediary Quarterly Update

Presentation

I. Update on Dodge & CoxII. Stock Fund OverviewIII. International Stock Fund OverviewIV. Global Stock Fund OverviewV. Balanced Fund OverviewVI. Income Fund OverviewVII. Global Bond Fund Overview

This presentation was prepared for a prospective shareholder of the Dodge & Cox Funds and must be accompanied or preceded by a current prospectus and/or summary prospectus for the relevant fund(s). Dodge & Cox does not guarantee the future performance of any account (including Dodge & Cox Funds) or any specific level of performance, the success of any investment decision or strategy that Dodge & Cox may use, or the success of Dodge & Cox's overall management of an account. Investment decisions made for a client's account by Dodge & Cox are subject to various market, currency, economic, political, and business risks (foreign investing, especially in developing countries, has special risks such as currency and market volatility and political and social instability), and those investment decisions will not always be profitable. While every effort is made to ensure accuracy, no representation is made that all information in this presentation is accurate or complete. Neither the information nor any opinion expressed in this presentation constitutes an offer to buy or sell the securities mentioned. This information is the confidential and proprietary product of Dodge & Cox. Any unauthorized use, reproduction, or disclosure is strictly prohibited.

First Quarter 2019

E-1110-070918-100511 | DODGE & COX Investment Managers | San Francisco

mprice

Typewritten Text

DATE: 5/15/19 ITEM #: 6c

Key Characteristics of Our Organization

Over 85 Years of Investment ExperienceDodge & Cox was founded in 1930. We have a stable and well-qualified team of investment professionals, most of whom have spent their entire careers at Dodge & Cox.

Independent OrganizationOwnership of Dodge & Cox is limited to active employees of the firm. Currently there are 76 shareholders and 280(a) total employees.

One BusinessDodge & Cox is solely in the business of investing our clients’ assets. We apply a consistent investment approach to managing equity, debt, and balanced portfolios.

Single Investment Office LocationWe maintain close communication among our investment professionals by managing investments from one office in San Francisco.

Independent Research StaffThorough fundamental analysis of each investment allows us to make independent, long-term decisions for our clients’ portfolios.

(a) Includes employees of wholly owned subsidiary Dodge & Cox Worldwide Investments Ltd. (UK).

E-325-040219-100611 |

March 31, 2019

DODGE & COX Investment Managers | San Francisco 1

Dodge & Cox’s Focused Investment Strategies ($ in Billions)

$307.6 in Total Assets: $174.4 in Equities / $133.2 in Fixed Income

March 31, 2019

Before investing in any Dodge & Cox Fund, you should carefully consider the Fund’s investment objectives, risks, and charges and expenses. To obtain a Fund’s prospectus and summary prospectus, which contain this and other important information, visit dodgeandcox.com or call 800-621-3979. Please read the prospectus and summary prospectus carefully before investing.

Dodge & Cox Funds: $202.5 Billion Separate Accounts: $98.5 Billion

Fixed Income $69.9

Equity$24.3

Balanced$4.3

Core SA $27.8

Liability Hedging$26.8

Other $4.2

Non-U.S. Funds (Irish UCITS): $6.6 Billion

E-353-041219-110718 |

Stock Fund$69.9

Income Fund$56.6

International Stock Fund$51.1

Balanced Fund$15.2

Global Stock Fund$9.5

Global Bond Fund$250 Million

Global Stock$4.2

US Stock$2.1

Global Bond$347 Million

Stable Value $11.1

DODGE & COX Investment Managers | San Francisco 2

Experienced, Integrated, and Stable Investment Team March 31, 2019

Years of experience at Dodge & Cox are updated annually in May

Fixed Income Team / Years at D&C / CoverageDana Emery 35 CEO, President, Co-Director of Fixed IncomeThomas Dugan 24 SVP, Co-Director of Fixed IncomeStephanie Notowich 23 Structured Products Sector CommitteeLarissa Roesch 21 Credit Sector CommitteeJames Dignan 19 MBS/ABS AnalysisE. Saul Peña 18 Portfolio Transitions, Credit TradingLucy Johns 16 Global Bonds, Credit Sector CommitteeJay Stock 16 Treasury/Derivatives Trading, SystemsAdam Rubinson 16 Credit ResearchDamon Blechen 16 Credit Trading/Analysis, Global Bonds Anthony Brekke 15 Credit ResearchNils Reuter 15 MBS/ABS Analysis/Trading Kristina Sormark 14 Credit Trading/AnalysisLinda Chong 13 MBS/ABS Analysis/Trading, Global BondsNicholas Lockwood 11 Munis, Treasury/Derivatives Trading Allen Feldman 11 MBS/ABS Analysis/Trading, SystemsMichael Kiedel 10 Credit ResearchMatthew Schefer 10 Credit Research, Global BondsMasato Nakagawa 6 MBS/ABS Analysis/Trading Mimi Yang 4 Macro, Currency, Global BondsJessica Corr 4 Credit Trading/AnalysisJose Ursua 3 Macro, Currency, Global BondsDavid Strasburg 3 Credit ResearchSamir Amso 3 Credit Trading/Analysis, Global BondsDustin Seely 2 MBS/ABS Analysis/Trading Thomas Powers 2 Macro, Currency, Global BondsShane Cox 2 Treasury/Derivatives Trading, Global Bonds

Global Research Team / Years at D&C / CoverageBryan Cameron 35 SVP, Director of ResearchCharles Pohl 34 Chairman and CIOWendell Birkhofer 31 SVP, TMT Sector CommitteeLynn Poole 31 Healthcare/Consumer Sector CommitteeDiana Strandberg 30 SVP, Director of International EquityKevin Johnson 29 Energy/Industrials Sector CommitteeSteven Cassriel 26 Energy/Industrials Sector CommitteeDavid Hoeft 25 SVP, Associate CIOSteven Voorhis 22 Pharmaceuticals, Assoc. Dir. of ResearchJohn Iannuccillo 21 Aerospace, Elec. Equip., Forest ProductsMario DiPrisco 20 Finance Sector CommitteeRoger Kuo 20 SVP, Internet, MediaKeiko Horkan 18 Banks, Specialty/Consumer FinanceKarol Marcin 18 InsuranceAmanda Nelson 18 Electric Utilities, PipelinesLily Beischer 17 Cosmetics, Apparel, Retail Richard Callister 16 Machinery, Medical DevicesEnglebert Bangayan 16 Commercial Services, Oil/Oil ServicesRaymond Mertens 15 Healthcare Services, Consumer Philippe Barret, Jr. 14 Banks, Asset Managers, BrokersKarim Fakhry 12 Biotech & Pharma, AppliancesKathleen McCarthy 11 Beverages, Building Products, TobaccoParitosh Somani 11 IT Hardware & Services, MiningEmily Han 11 Quantitative AnalysisTae Yamaura 10 Components, Semiconductors, JapanArun Palakurthy 10 Electronics, Semiconductors, Telecom Benjamin Garosi 9 Chemicals, Transportation, AutosSalil Phadnis 7 Energy/Oil, Homebuilders, REITs, HotelsSophie Chen 6 Telecom Equipment, ChinaRobert Turley 5 Asset Allocation, Portfolio StrategyRameez Dossa 5 Banks, IT SoftwareKevin Glowalla 5 TelecomNate Liao New ChinaRaja Patnaik New Portfolio Strategy

U.S. Equity Investment CommitteeBryan Cameron 35 Steven Voorhis 22Charles Pohl 34 Karol Marcin 18Wendell Birkhofer 31 Philippe Barret 14Diana Strandberg 30 Kathleen McCarthy 11

David Hoeft 25 Benjamin Garosi 9

Average Tenure: 23

International Equity Investment CommitteeBryan Cameron 35 Keiko Horkan 18Charles Pohl 34 Richard Callister 16Diana Strandberg 30 Englebert Bangayan 16Mario DiPrisco 20 Raymond Mertens 15Roger Kuo 20 Average Tenure: 23

Global Equity Investment CommitteeCharles Pohl 34 Roger Kuo 20Diana Strandberg 30 Karol Marcin 18David Hoeft 25 Lily Beischer 17Steven Voorhis 22 Average Tenure: 24

U.S. Fixed Income Investment CommitteeDana Emery 35 Adam Rubinson 16Thomas Dugan 24 Anthony Brekke 15Larissa Roesch 21 Nils Reuter 15James Dignan 19 Michael Kiedel 10

Lucy Johns 16 Average Tenure: 19

Global Fixed Income Investment CommitteeDana Emery 35 Lucy Johns 16Thomas Dugan 24 Adam Rubinson 16James Dignan 19 Matthew Schefer 10

Average Tenure: 20

E-1182-040919-112111 | DODGE & COX Investment Managers | San Francisco 3

Dodge & Cox Funds Performance Results March 31, 2019

Average Annual Total Returns for Periods Ended March 31, 2019

E-1775-040319-061814 |

(a) Unannualized rate of total return. (b) Since Global Stock Fund’s inception on May 1, 2008 through March 31, 2019: 5.23% vs. 5.28% MSCI World Index vs. 4.82% MSCI ACWI Index. (c) Since International Stock Fund’s inception on May 1, 2001 through March 31, 2019: 6.86% vs. 4.46% MSCI EAFE Index vs. 5.14% MSCI ACWI free ex USA. (d) A private fund managed by Dodge & Cox with proprietary assets was reorganized into the Dodge & Cox Global Bond Fund on April 30, 2014. Any Fund portfolio characteristics, performance, or attribution information for periods prior to May 1, 2014, are those of the private fund. (e) Since Global Bond Fund’s inception on December 5, 2012 through March 31, 2019: 2.79% compared to 0.66% for the Bloomberg Barclays Global Aggregate Bond Index. The Combined Index reflects an unmanaged portfolio (rebalanced monthly) of 60% of the S&P 500 Index, which is market capitalization-weighted index of 500 large-capitalization stocks commonly used to represent the U.S. equity market, and 40% of the Bloomberg Barclays U.S. Aggregate Bond Index (BBG Barclays U.S. Agg), which is a widely recognized, unmanaged index of U.S. dollar-denominated, investment-grade, taxable fixed income securities. Returns represent past performance and do not guarantee future results. Investment return and share price will fluctuate with market conditions, and investors may have a gain or loss when shares are sold. Fund performance changes over time and currently may be significantly lower than stated above. Performance is updated and published monthly. Before investing in any Dodge & Cox Fund, you should carefully consider the Fund’s investment objectives, risks, and charges and expenses. To obtain a Fund’s prospectus and summary prospectus, which contain this and other important information, or for current month-end performance figures, visit dodgeandcox.com or call 800-621-3979. Please read the prospectus and summary prospectus carefully before investing.

3 Months Ended(a) YTD(a) 1 Year 3 Years 5 Years 10 Years 20 Years

Stock Fund 10.28% 10.28% 4.30% 14.11% 8.65% 16.14% 9.16%

S&P 500 Index 13.65% 13.65% 9.50% 13.51% 10.91% 15.92% 6.04%

Russell 1000 Value Index 11.93% 11.93% 5.67% 10.45% 7.72% 14.52% 6.68%

Global Stock Fund 9.70% 9.70% -1.55% 11.39% 5.27% 14.33% N.A.(b)

MSCI World Index 12.48% 12.48% 4.01% 10.68% 6.78% 12.38% N.A.(b)

MSCI ACWI Index 12.18% 12.18% 2.60% 10.67% 6.45% 11.98% N.A.(b)

International Stock Fund 9.78% 9.78% -8.00% 7.87% 0.85% 10.25% N.A.(c)

MSCI EAFE Index 9.98% 9.98% -3.71% 7.27% 2.33% 8.96% N.A.(c)

MSCI ACWI ex USA Index 10.31% 10.31% -4.22% 8.09% 2.57% 8.85% N.A.(c)

Balanced Fund 7.80% 7.80% 4.40% 10.38% 6.85% 13.10% 8.11%

Combined Index 9.31% 9.31% 7.78% 8.95% 7.76% 11.15% 5.81%

Income Fund 3.70% 3.70% 4.32% 3.64% 3.15% 5.37% 5.29%

Bloomberg Barclays U.S. Aggregate Bond Index 2.94% 2.94% 4.48% 2.03% 2.74% 3.77% 4.73%

Global Bond Fund(d) 4.69% 4.69% 2.72% 5.49% 2.38% N.A.(e) N.A.

Bloomberg Barclays Global Aggregate Bond Index 2.20% 2.20% -0.38% 1.49% 1.04% N.A.(e) N.A.

DODGE & COX Investment Managers | San Francisco 4

E-10020-041818-031611 |

Dodge & CoxStock Fund Overview

DODGE & COX Investment Managers | San Francisco 5

Dodge & Cox Stock Fund

Fund Overview

Key Characteristics Shared by Dodge & Cox Funds

Low expenses Stable and experienced investment team Consistent investment approach Team decision-making process Historically low turnover resulting from long-term view

March 31, 2019

(a) Excludes negative earners. (b) Excludes Financials and Utilities. (c) Net Cash & Other includes cash, short-term investments, receivables, and payables. Source: Bloomberg LP. Before investing in any Dodge & Cox Fund, you should carefully consider the Fund’s investment objectives, risks, and charges and expenses. To obtain a Fund’s prospectus and summary prospectus, which contain this and other important information, visit www.dodgeandcox.com or call 800-621-3979. Please read the prospectus and summary prospectus carefully before investing. DC

Dodge & Cox Stock Fund (Established January 4, 1965)

Equity Securities96.7%

Net Cash & Other(c)

3.3%

E-833-041319-110211 |

Stock Fund Characteristics

Objective: long-term growth of principal and income Diversified portfolio of 69 securities Long-term investment horizon Well-established companies: Generally with market capitalizations greater than $3 billion Weighted average market capitalization of $148 billion

Below-average valuations Price-to-earnings ratio (forward) of 13.1x(a)

Price-to-sales ratio of 1.5x(b)

Gradual portfolio changes

Total net assets: $69.9 billion Net asset value per share: $183.47 Expense ratio: 0.52%

DODGE & COX Investment Managers | San Francisco 6

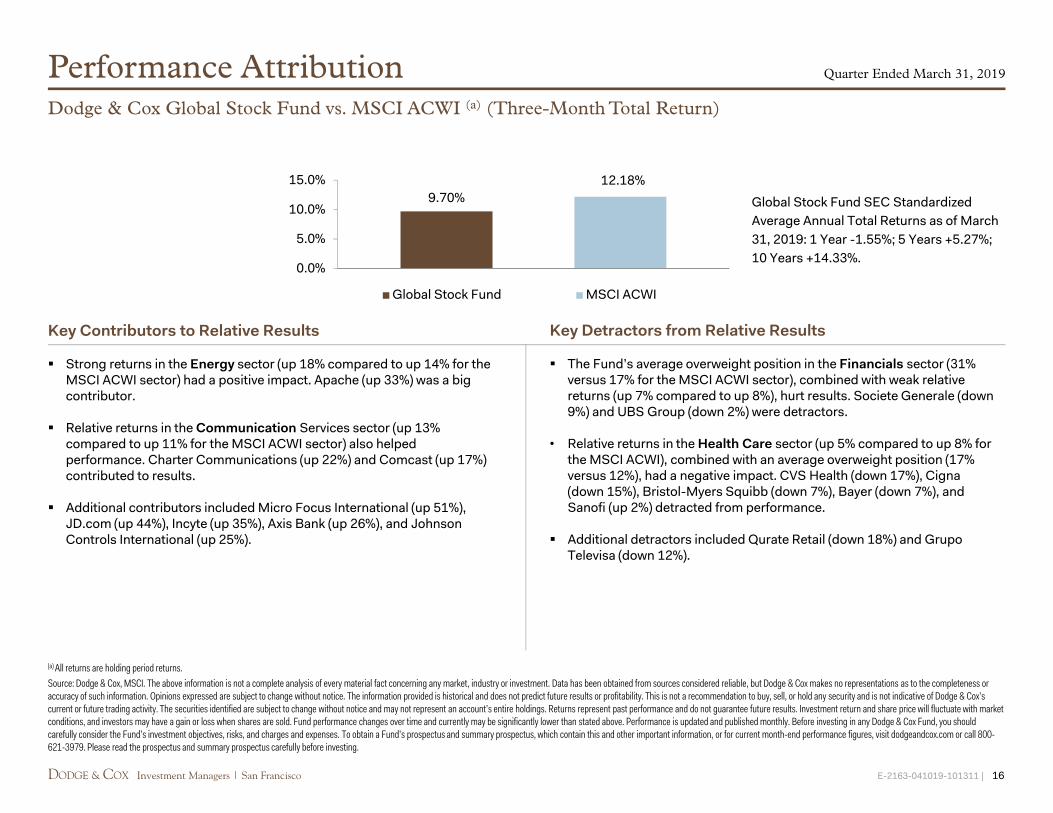

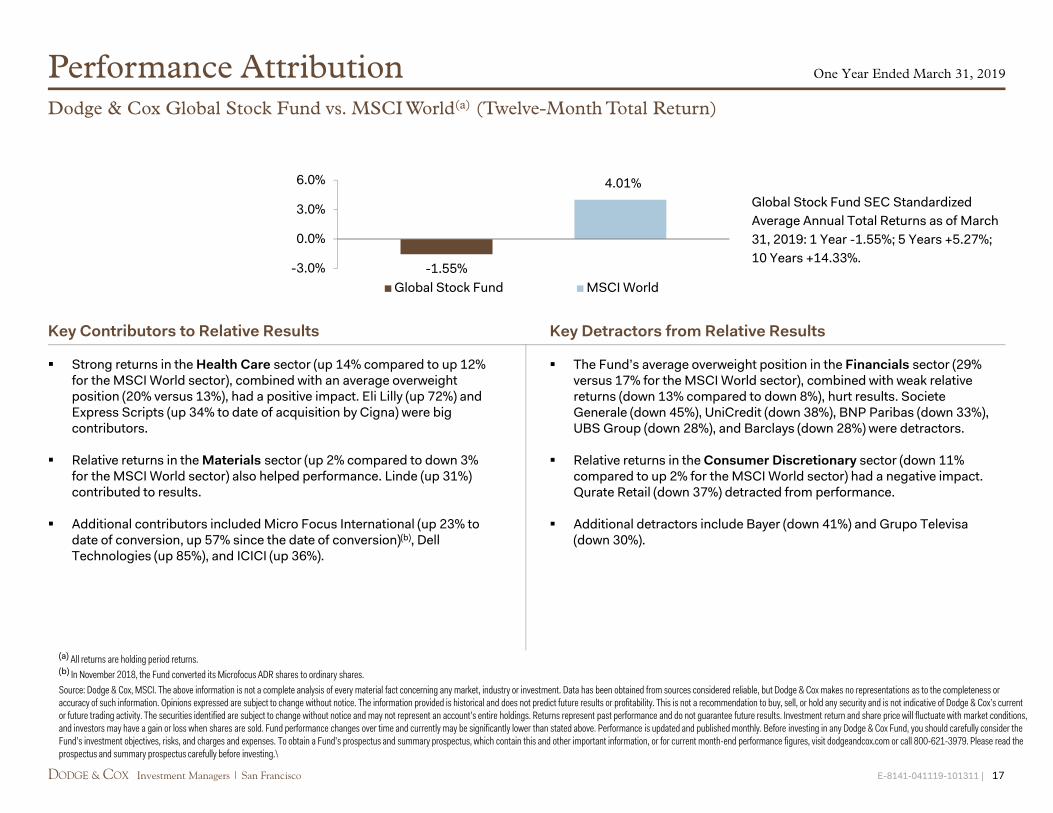

Performance Attribution Quarter Ended March 31, 2019

Source: FactSet. The above information is not a complete analysis of every material fact concerning any market, industry or investment. Data has been obtained from sources considered reliable, but Dodge & Cox makes no representations as to the completeness or accuracy of such information. Opinions expressed are subject to change without notice. The information provided is historical and does not predict future results or profitability. This is not a recommendation to buy, sell, or hold any security and is not indicative of Dodge & Cox’s current or future trading activity. The securities identified are subject to change without notice and may not represent an account’s entire holdings. Returns represent past performance and do not guarantee future results. Investment return and share price will fluctuate with market conditions, and investors may have a gain or loss when shares are sold. Fund performance changes over time and currently may be significantly lower than stated above. Performance is updated and published monthly. Before investing in any Dodge & Cox Fund, you should carefully consider the Fund’s investment objectives, risks, and charges and expenses. To obtain a Fund’s prospectus and summary prospectus, which contain this and other important information, or for current month-end performance figures, visit dodgeandcox.com or call 800-621-3979. Please read the prospectus and summary prospectus carefully before investing.

Dodge & Cox Stock Fund vs. S&P 500 (Three-Month Total Return)

Key Detractors from Relative Results

In the Health Care sector, the Fund’s overweight position (averaging 22% versus 15%) and weaker returns from holdings (up 4% compared to up 7% for the S&P 500 sector) detracted. CVS Health (down 17%), Cigna (down 15%), and Bristol-Myers Squibb (down 7%) performed poorly.

Strong performance from certain large technology and internet related stocks not held by the Fund (e.g., Amazon, Apple) hurt relative results.

Within the Information Technology sector, the Fund’s holdings (up 14%) were not as strong as the S&P 500 sector (up 20%). HP Inc. (down 4%) and Juniper Networks (down 1%) lagged.