101) financial Management (101) Financial Management

15

(101) financial Management 1 (101) Financial Management (Wesfarmer’s Analysis Ratios for the annual report of 2010/2011) Lecturer name: Dr. Azra Fatima Submission Date: Sep, 18, 2014 Student Name: Nagwa Alagami Student Id: 874507

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of 101) financial Management (101) Financial Management

(101) financial Management

1

(101) Financial Management

(Wesfarmer’s Analysis Ratios for the annual report of 2010/2011)

Lecturer name: Dr. Azra Fatima

Submission Date: Sep, 18, 2014

Student Name: Nagwa Alagami

Student Id: 874507

(101) financial Management

2

Table of Contents:

Executive Summary………………………………………………………………………………….…...Page 3

Introduction……………………………………-………………………………………………………...Page4

1) Short-term Solvency or Liquidity Ratios…..........................................................................................Page 5

A) Current Ratio……………………………………………………………....…………………………Page 5

B) Quick Ratio……………………………………………….………….………………………………Page 5

C) Cash Flow from Operations to Current Liabilities………………………………..…………………Page 5

2) Efficiency Ratios……………………..………………………………………………………………Page 6

A) Debtors’ Turnover……………………………………………………………...……………………Page 6

B) Average Days Sales Uncollected…………………………………………………..………………..Page 6

C) Inventory Turnover………………………………………………………………….………………Page 7

D) Inventory Turnover in Days…………………………………………………………………………Page 7

3) Profitability Ratios……………………………………………………….…………….……………Page 8

A) Net Profit Margin………………………………………………………………………..…………Page 8

B) Interest Cost as a percentage of Sales………………………………………………………………Page 8

C) Asset Turnover…………………………………………………………………………...…………Page 8

D) Return in Assets………………………………………………..………………………..…………Page 9

E) Return on Ordinary Shareholders’ Equity……………..………….……………………….………Page 9

4) Long-Term Solvency or Financing Ratios……………………………………….……………….Page 10

A) Debt to Equity………………………………………………………………………..……………Page 10

B) Debt to Total Assets……………………………………….……………….………………………Page 10

C) Interest Coverage……………………………………….…………………..………………………Page 10

D) Cash Flow from Operations to Total Liabilities……………………….…………………...………Page 11

5) Market-Based Investment and Other Ratios……………………………………………….………Page 11

A) Price/Earnings (P/E)………………………………… …………………….…………………..…Page 11

B) Dividend Yield…………………………………………………………….………………………Page 12

C) Dividend Cover……………………………………………………………………………………Page 12

D) Net Tangible Asset Backing…………………………………………….…………………………Page 12

Conclusion……………………………………………………………………………………….……Page 14

References……………………………………………………………………………………….. Page 15

(101) financial Management

3

Executive Summary

Wesfarmer is one of the most stable Australian cooperation companies, which is able to build

strong business with efficient performance, it has a significant assets portfolio, from the value end of

retail to direct and indirect exposure to the resource sector, they can afford establishing new

businesses and work efficiently with the most sensitive changes around them.

the last two year performance analysis showed that Wesfarmer able to create a long term investment

business strategy, they reduced the cost by managing time, and controlling inventory turnover and

products storage to make sure that all liabilities are covered, the equity managed to reflect as

improvement between 2010 to 2011, that reflect to good profit for ordinary shared Given a preference

by many shareholders to receive dividends in the form of shares.

Wesfarmers Operating lease incentives are recognized as a liability when received and released to

earnings on a straight line basis over the lease term. Fixed rate increases to lease payments,

excluding contingent or index based rental increases, such as turnover rental and other similar

increases, are recognized on a straight line basis over the lease term.

In general the financial analysis for the last two years shows that Wesfarmer is a company that has a

strong financial system, is able to come over the different circumstances, and has a goodwill that

help the company to gain trust of shareholders and the market.

(101) financial Management

4

Introduction:

Wesfarmer started originally as farmer company in western area of Australia, then expanded the

business including supermarket and department stores offices supplier, chemical supply, energy

,insurance and fertilizers , then they build large profit from investing on industrial products, the

company build trust with their own shareholders(Webpage 2011b).

As a limited share company have invest with heavy weight in Australia as per the country law

and the result also demonstrates how we truly reflect a cross-section of the Australian economy,

Wesfarmer resource oriented businesses performed very well, despite adverse weather events,

while retailers at the staples and value end of the market performed better than those relying on

need more discretionary spending(Webpage 2011a).

As per the annual report of 2010 / 2011 we did Ratio Analysis and compared with the last years

report to check:

Short term Solvency and Liquidity Ratios

Efficiency Ratios.

Profitability Ratios.

Long term Solvency or Financing Ratios.

Market based investment and other Ratios.

(101) financial Management

5

1) Liquidity Ratios:

A) Current Ration:

Current Ratio = Current Assets / Current Liabilities

Year Current

Assets

Current Liabilities Calculation Current Ratio

2010 $m 9,674 7,852 9,674/7,852 1.23

2011 $m 10,218 8,722 10,218/8,722 1.17

It’s clear that the liquids able to satisfy contingencies and uncertainties. The ratio shows that the

short-term solvency of business if a firm can pay the current liabilities when due, also noticed an

increase on the current liabilities and decrease in the last year Ratio so, Wesfarmer able to cover

their liabilities.

B) Quick Ratio:

Quick Ratio = (Current assets - Inventory) / Current Liabilities

Year Current

Assets

Inventory Current

Liabilities

Calculation Quick Ratio

2010

$m

9,674 4,658 7,852 (9,674-4,658) /7,852 0.64

2011

$m

10,218 4,987 8,722 (10,218-4,987)/8,722 0.60

The quick ratio is decreasing from 0.64 down to 0.6. The quick ratio does not include inventory

and prepaid expenses in the calculation. So, a business's quick ratio will be lower than its current

ratio. Wesfarmer needs to sell more to pay in short term liabilities quickly.

C) Cash Flow Ratio: (Cash Flow from Operations to Current Liabilities)

*Operating Cash Flow Ratio = Cash Flow / Current Liabilities

Year Cash Flow Current Liabilities Calculation *Ratio

2010 $m 3,327 7,852 3,327/7,852 0.42 or 42%

2011 $m 2,917 8,722 2,917/8,722 0.33 or 33%

(101) financial Management

6

The cash flow ratio is decreasing from 2010 to 2011and that decrease in cash from operating activities

of current liabilities in short period mentioned percentage. The working capital is increasing in the asset

amount, Wesfarmer could be affected, so new solutions should be found.

2)Efficiency Ratios:

A) Debtors’ Turnover:

Debtors’ Turnover = Net Sales / Average Debtors

Net Sales = Revenue – Interest

o 2010: 51,827 – 149 = 51,678

o 2011: 54,875 – 145 = 54,730

Average Debtor:

o 2010: (2009 + 2010/2 = (1893 + 1767)/2 = 1830

o 2011: (2010 + 2011)/2 = (1767 + 2149)/2 = 1958

Year Net Sales Average Debtors Calculation Debtors’ Turnover

2010 $m 51,678 1830 51,678/1830 28.2 times

2011 $m 54,730 1958 54,730/1958 28 times

Wesfarmer have maintained the ratio related to time, a clear drop from 28.2 time down to 28 which

indicates the debtor turnover either remain same or there is no progress.

B) Average Days Sales Uncollected:

Average Days Sales Uncollected = Days in Year / Debtors’ Turnover

Year Days in Year Debtors’ Turnover Calculation Av Days Sales

Uncollected

2010 $m 365 28.2 365/28.2 12.9 days

2011 $m 365 28 365/28 13 days

(101) financial Management

7

Wesfarmer did maintain the company credit of collection day’s average for their receivable and

that will be reflected on their inventories. So Wesfarmer could have the same inventories of the last

year period.

C) Inventory Turnover:

Inventory Turnover = Cost of Sales / Average Inventory

Inventory Turnover is the number of times inventory is turned over into sales during the year or

the number of days it takes to sell the inventory. (Demonstrating Value)

Average Inventory:

o 2010: (2009 + 2010/2 = (4,665 + 4,658)/2 = 4,661

o 2011: (2010 + 2011)/2 = (4,658 + 4,987)/2 = 4,82

Year

Cost of Sales Average Inventory Calculation Inventory Turnover

2010 $m 49,865 4,661 49,865/4,661 10.698

2011 $m 52,891 4,822 52,891/4,822 10.968

The inventory turnover grows up from 10.698 up to 10.968 which show increasing demand on

the company from last operation period, but increasing the cost of sale indicates lack of

inventory and losing sales because of inadequate stock on hand.

D) Inventory Turnover in Days:

Inventory Turnover in Days = Days in Year / Inventory Turnover

Year Days in Year Inventory Turnover Calculation Inventory Turnover

2010 $m 365 10.698 365/ 10.698 34.11 days

2011 $m 365 10.968 365/10.968 33.27 days

Wesfarmer is doing the inventory turnover very fast; day’s number increased from the last year

which shows better performance and that is a mark for Wesfarmer that they can manage their

own stock.

.

(101) financial Management

8

3)Profitability ratios:

A) Net Profit Margin:

Net Profit Margin = Net Profit / Sales

Year Net Profit Sales Calculation Net Profit Margin

2010 $m 1565 49,865 1565/ 49,865 0.031

2011 $m 1922 52,861 1922/52,861 0.036

The Net profit has developed from 2010 to 2011, Wesfarmer succeeded to add extra profit, the ratio

measures overall profitability

B) Interest Cost Ratio:

Interest Cost as a percentage of Sales = Interest Expense / Sales

Year Interest

Expense

Sales Calculation Interest Cost as a

Percentage of Sales

2010 $m 654 49,865 654/49,865x100 1.311%

2011 $m 526 52,891 526/52,891 x100 0.994%

It’s clear that, Wesfarmer reduced the cost of interest which means that they could get profit on sales

without need for loans; the interest cost has dropped from 1.3% to 0.994% in 2011 with decrease on

expenses like inventories.

C) Asset Turnover:

Asset Turnover = Sales / Average Total Asset

Average Total Assets

o 2010: (2009 + 2010)/2 = (39,062 + 39236)/2 = 39,149

o 2011: (2010 + 2011)/2 = (39236 + 40814)/2 = 40,025

Year Sales Average Total

Assets

Calculation Asset Turnover

2010 $m 51,485 39,149 51,485/39,149 1.32

2011 $m 54,513 40,025 54,513/40,025 1.36

(101) financial Management

9

Sales in Wesfarmer improved which indicates that they can manage using the available assets

wisely and producing based on its assets. While, increasing from 1.32 to 1.36 reflects the good

sale and success to point high demand products.

D) Return To Asset:

Return in Assets = Net Profit Average / Total Asset

Net Profit Average = Net Profit + Interest + Income Tax

o 2010 = 1,565 + 149 + 2,215 = 3,929

o 2011 = 1,922 + 145 + 2,706 = 4,773

Year Net Profit

Average

Average Total

Assets

Calculation Return on Assets

2010 $m 3,929 39,149 3,929/ 39,149 0.10 or 10%

2011 $m 4,773 40,025 4,773/40,025 0.12 or 12%

Wesfarmer managed to use the asset depending on its demands, Wesfarmer provides a

product that requires minimal additional assets.

E) Return to ordinary Shareholders:

Return on Ordinary Shareholders’ Equity = Net Profit / Average Shareholders’ Equity

Average Shareholders’ Equity

o 2010 = (2009 + 2010)/2 = (24,248 + 24,694)/2 = 24,471

o 2011 = (2010 + 2011)/2 = (24,694 + 25,329)/2 = 25,011

Year Net Profit Shareholders’

Equity

Calculation Return on Ordinary

Shareholders Equity

2010 $m 1,565 24,471 1,565/24,471 0.064 or 6.4%

2011 $m 1,922 25,011 1,922/25,011 0.077 or 7.7%

Wesfarmer managed to generate income for the Shareholders, a clear increasing on 2011 when

comparing with 2010 it sustain on the right direction. Increasing From 2010 of 6.4% up to 7.7%

indicates the right direction of creating profit with minimal base of assets.

(101) financial Management

10

4)Long-Term Solvency or Financing Ratios:

A) Debt to Equity Ratio:

Debt to Equity = Total Liabilities / Total Shareholders’ Equity

Year Total

Liabilities

Total

Shareholders’

Equity

Calculation Debt to Equity

2010 $m 14,542 24,694 14,542/24,694 0.59

2011 $m 15,485 25,329 15,485/25,329 0.61

Wesfarmer increased the liabilities, which keep the company in a high risk if they could not

manage the assets. an increasing trend of debt-to-equity ratio is not safe because it will make the

percentage of assets of a business increasing.

B) Debt to Total Asset Ratio:

Debt to Total Assets = Total Liabilities / Total Assets

Year Total Liabilities Total Assets Calculation Debt to Equity

2010 $m 14,542 39,236 14,542/39,236 0.37

2011 $m 15,485 40,814 15,485/40,814 0.38

the debt to equity is increasing , it provides Wesfarmer more values of asset and keep low risk with

loans to maintain their liabilities ,the total liabilities increased and shares also up and that reflecting on

more liabilities on to cover all debts.(“Financial Ratio Analysis Articles” 2014).

C) Interest Cover Ratio:

Interest Coverage = Net Profit + Income Tax + Interest (EBIT)/Interest Expense

Year Net Profit + Income Tax

+ Interest

Interest

Expense

Calculation Debt to Equity

2010 $m 1,565 + 2,215 + 149 654 3,929/654 6.007

2011 $m 1,922 + 2,706 + 145 526 4773/526 9.074

(101) financial Management

11

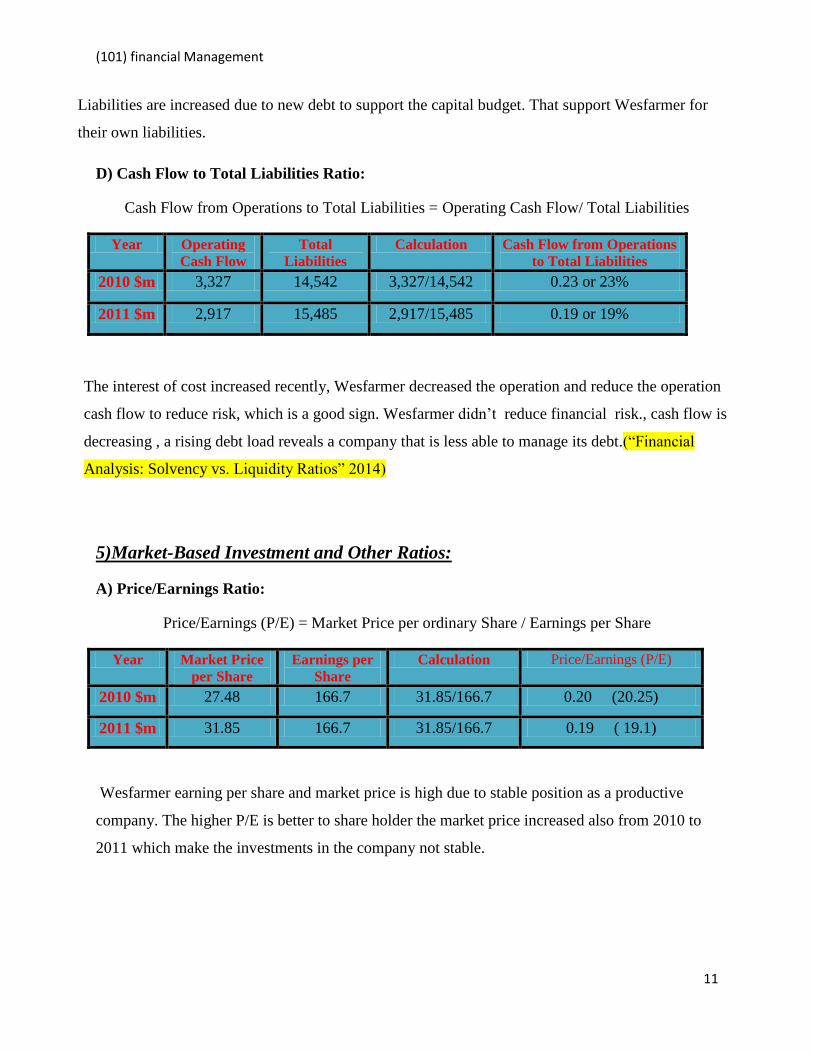

Liabilities are increased due to new debt to support the capital budget. That support Wesfarmer for

their own liabilities.

D) Cash Flow to Total Liabilities Ratio:

Cash Flow from Operations to Total Liabilities = Operating Cash Flow/ Total Liabilities

Year Operating

Cash Flow

Total

Liabilities

Calculation Cash Flow from Operations

to Total Liabilities

2010 $m 3,327 14,542 3,327/14,542 0.23 or 23%

2011 $m 2,917 15,485 2,917/15,485 0.19 or 19%

The interest of cost increased recently, Wesfarmer decreased the operation and reduce the operation

cash flow to reduce risk, which is a good sign. Wesfarmer didn’t reduce financial risk., cash flow is

decreasing , a rising debt load reveals a company that is less able to manage its debt.(“Financial

Analysis: Solvency vs. Liquidity Ratios” 2014)

5)Market-Based Investment and Other Ratios:

A) Price/Earnings Ratio:

Price/Earnings (P/E) = Market Price per ordinary Share / Earnings per Share

Year Market Price

per Share

Earnings per

Share

Calculation Price/Earnings (P/E)

2010 $m 27.48 166.7 31.85/166.7 0.20 (20.25)

2011 $m 31.85 166.7 31.85/166.7 0.19 ( 19.1)

Wesfarmer earning per share and market price is high due to stable position as a productive

company. The higher P/E is better to share holder the market price increased also from 2010 to

2011 which make the investments in the company not stable.

(101) financial Management

12

B) Dividend Yield Ratio:

Dividend Yield = Dividend per ordinary Share / Market Price per ordinary Share

Year Dividend per

Share

Market Price

per Share

Calculation Dividend Yield

2010 $m 125 27.48 125/27.48 4.55

2011 $m 150 31.85 150/31.85 4.71

Wesfarmer got good feedback with win/ win idea by getting a profit despite the risk of the

liabilities on the company.

C) Dividend Cover Ratio:

Dividend Cover = Earnings per Share / Dividend per Share

Year Earnings per

Share

Dividend per

Share

Calculation Dividend Cover

2010 $m 135.7 125 135.7/125 1.08

2011 $m 166.7 150 166.7/150 1.11

Dividend cover in Wesfarmer increased for the last year which supports the share dividend trust

to invest more in the company.

D) Net Tangible Asset Ratio:

Net Tangible Asset Backing = Net Tangible Assets / Balance of Number of Ordinary Shares

issued for Accounting purposes

Net Tangible Assets = Total Assets – Intangible Assets – (good will)

o 2010: 24,694 – 4,328 – 16,206 = 41.60

o 2011: 25,329 – 4,353 – 16,227 = 74.49

(101) financial Management

13

Year Net Tangible

Assets

Balance of

Ordinary Shares

Calculation Net Tangible

Asset Backing

2010 $m 41.60 11.52 41.60/11.52 3.609

2011 $m 74.49 11.52 74.49/11.52 4.118

Wesfarmer have a good evidence to move forward starting investments, the net tangible assets

indicates the good investment environment to create good profit.

(101) financial Management

14

Conclusion:

The combinations of stable and successful business Wesfarmer ensure to establish long term

satisfactory equity for the shareholder and added value in practical function on operating new

business.

Wesfarmers maintains a flexible financing structure and able to take advantages by using loans for

new investment opportunities that may arise. Also the risk was shows when the interest of cost

increased significant from 2010 to 2011 and that reflect in short term plan as risk reflect on

decreasing asset of capital and seem and objectives of planning to be maintain on long run.

As risk management Wesfarmer requires hedging and identifying foreign exchange exposures the

firm relating and belong to sales or purchases or when highly probable forecast transactions. Before

hedging the divisions are also taking into account their competitive position and how to protect and

sustain on same principles of earnings and protect from sudden currency movements, Wesfarmer

shows stable to increase in P/E investment Ratio which reflect relatively in the dividend yield and

that indicate high potential of growth with related expanding projects, also is stable financial as

long term despite risk available on short term plans.

(101) financial Management

15

References

AcountingExplained.com, 2013. Financial Acounting. [Online]

Available at: htp:/acountingexplained.com/financial/

[Acesed 26 June 2013].

Investopedia US, A Division of ValueClick, Inc, 2013. Investopedia. [Online]

Available at: htp:/www.investopedia.com/

[Acesed 21 June 2013].

Peavier, R., 2012. Financial Ratio Analysis Tutorial 101. [Online]

Available at: htp:/bizfinance.about.com/od/yourfinancialpositon/s/financial-ratio-analysis-

tutorial- 101.htm

[Acesed 1 July 2013].

Reports

Anderson, R., 2013. Financial Management Study Guide. 5th ed. Melbourne: Chifley Business

School.

Wesfarmer, 2011. Annual Report 2011,Wesfarmer.