1. Editorial - Zawar Associates

16

Visit us on www.zawarassociates.c com For free Subscription write to rgzawar@gmai il.com Page 1

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of 1. Editorial - Zawar Associates

Visit us on www.zawarassociates.com For free Subscription write to [email protected]

Visit us on www.zawarassociates.com For free Subscription write to [email protected] Visit us on www.zawarassociates.com For free Subscription write to [email protected] Page 1

Visit us on www.zawarassociates.com For free Subscription write to [email protected] Page 2

1. Editorial

2. Law Update

3. Notifications/Circular

4. What knowledge should house maker

have?

5. Hindu Undivided Family and Its

Constitution

6. Health Tips

7. Social Work

8. Ram Krishna Hari

9. You Wrote it

Visit us on www.zawarassociates.com For free Subscription write to [email protected] Page 3

Degrowth: A Theory of Social Rationality —

1. Editorial

The period after WWII saw an unprecedented

upsurge in economic expansion. Its cascading effect

was almost shaping into a sort of the model for a

strong and balanced growth, conducive to social

progress all across with its accumulative process of

capital and wealth. Capital and Wealth were seen as

the guarantors of full employment, and hence highly

celebrated.GDP was invented as the quantitative

measure of wealth output during this period. Quaintly

enough, the romance with such growth and

development aspirations, did not last longer. The

‘Thirty Glorious Years’ period came to an end by mid-

1960s. There was a realization that what had

happened, had happened because of the easy access

to cheap natural resources of the Southern

hemisphere and such growth was exerting severe

pressure on the environment. There was also an

observation that this process accentuates a massive

deskilling and rationalization of labour, which presaged

dehumanization of production activity. That realization

gave rise to the human centric focus of production,

under a strong social protest from social and economic

rightists. It was beginning of the discourse on post-

capitalism.

The classical style of factorization of production,

focuses more on the capital and labour, downplaying

the importance of the resources drawn from the

Nature, especially the Matter and Energy. The over-

use of resources was accelerating ecological

deterioration, leading to cumulated crises. This gave

rise to the public outcry and debate on the very

purpose and character of growth. Thinkers started

insisting on the minimalistic approach toward life-

style. The focus of the debate got sharper after the

claimed outcomes of globalization and promises of

abundance, prosperity and peace, started falling

through; and leaving a pronounced sequence of a

nightmarish poverty and inequality.

The East-West divide, already existed, now the

North-South divide became shriller. The impact

of resource depletion could be seen in climate

change, biodiversity loss, reduced sense of well-

being and a spurred succession of environmental

disasters and industrial accidents. That caused

the cracks in the ideological foundation of

growth. It became evident that promises are

remote and the threats are real. Global

warming, triggered by increasing emissions of

greenhouse gases due to increased use of fossil

fuels for increased production, were seen as the

causal agent for such degeneration.

Thinkers and activists opened a discourse

against the growth and development and gave it

the name of degrowth. Some thinkers construed

it to be negative in its approach smacking of a

‘negative growth’; so they prefer calling it ‘post-

growth’, ‘a-growth’, ‘anti-growth’, or ‘breaking

the addiction to growth’. Whatever the

onomastics, the idea of degrowth cannot be

constricted to the boundaries of an economic

concept, but to be seen as an aspect of socio-

economic studies in a new political and social

imagination. It has raised a fundamental

question as to whether life and nature can

coexist together, and if yes; how inclusively they

can? It is not about finding an alternative, but

constructing a matrix for alternatives; seeking to

promote reduction of consumption of natural

resources and energy to restrike an equilibrium

in the cycle of the biosphere ecosystems.

Visit us on www.zawarassociates.com For free Subscription write to [email protected] Page 4

The ideology of degrowth basically challenges human conscience against a rising cult of consumerism. It

conveys the idea of minimalism as a core value to save the planet earth and human interest, together; but it

is neither closer to the concept of 3BLnor the green growth. These two are alternative ideas of economic

growth that are blended with environmental sustainability. Degrowth crusaders believe that as long as

fixation with economic growth remains a predominant goal, it can’t be decoupled from resource use; at the

most it would attempt some replenishment. That’s how the green economists present it for low-carbon and

sustainable development. A main driver for green growth is the transition towards sustainable energy

systems. It rolls out a plan that envisages creating opportunities for employment in sectors such as

renewable energy, green agriculture, or sustainable forestry. This is why green growth is not considered a

solution to cope with the limits of natural resources. In ultimate analysis, it remains a means of perpetuating

growth and capital accumulation! There is another alternative of circular economy which looks, to some

extent, proximate to degrowth. It postulates recycling and reuse of material and attempts to better account

for planetary boundaries. It sregenerative approach contrasts the traditional linear approach of "take, make,

dispose" model of production. Circular systems employ reuse, sharing, repairing, refurbishing,

remanufacturing and recycling to create a closed-loop system to minimize the use of resource inputs. It

insists on minimizing the creation of waste, pollution and carbon emissions. The circular economy aims at

keeping products, equipment and infrastructure in use for longer, thus improving the productivity of these

resources. Waste materials and energy become the input for other processes: either as components or as

recovered resources for another industrial process or as regenerative resources for nature.

There is a competition for the unsustainable

patterns of consumption in these two groups, resulting

into an incompatibility. It is essentially a conflict

between the capitalism of the former group and the

developmental aspirations of the emerging economic

group which is generally composed of the ‘emerging

middle and lower classes’. Curiously enough, the

‘consuming tastes’ are common all across the sectoral

chain of north-south and developed-developing. The

complexity of consumption is leveling out the classes.

There is a single ‘global class of consumers’. It is a real

time social emotional learning for developmental

economists and degrowth discourse assumes the

dimension of a new field of study, which is

interdisciplinary and addresses to analyze everyday

human life and the essential character and nature of

all systems of development. It is the starting point for

an endpoint management of human ecology. It’s not

about inventing a new political and social imagination;

Gandhi’s entire philosophy is based on the practice of

such frugal existence; opposite the ideology of post-

modern growth and development. Growth, after all, is

not just a matter of economy; it is a vision of societal

rationality.

- Dr.Shivshankar Mishra, Professor Emeritus

Amid this cacophony, the neo-capitalist theory

came up with the argument that there exists a

similar propensity to reduce the pressure on

resources at the micro-economic and micro-

sectorial level through the use of new, green

technologies that improve technical and economic

efficiency, though the macro context of the globe

may appear different. Efficiency to perform better

in a given sector per unit produced and consumed is

offset by an increase in the scale. This argument is

dismissed on grounds that it is a surreptitious way

of perpetuating growth and capital accumulation

model in the name of the green growth theory and

hence not a solution to cope up with the limits of

natural resources.

The truth is that the external limits of all economic

models of production and consumption are

bounded by the limits of the biosphere, which is the

purveyor of matter and energytoall the subsystems.

The limits of the biosphere are again constricted by

the limits of the stratosphere, which itself is

shrinking in its size and width, and that increases

the woes for life on the planet.

These scientific facts apart, the quest among

developing economies to catch up with the

developed economies in terms of consumption is

intensifying.

Visit us on www.zawarassociates.com For free Subscription write to [email protected] Page 5

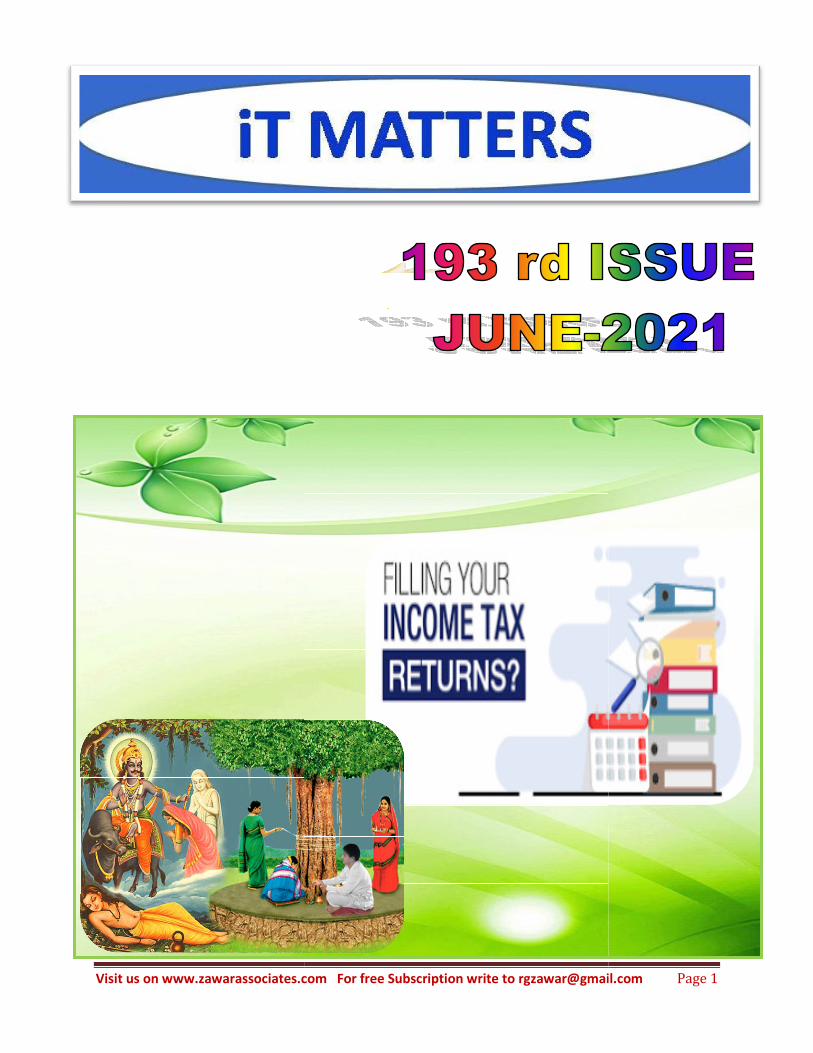

CONCEPT OF LOSSES UNDER THE INCOME-TAX ACT, 1961

2. Law Update

G. Loss in case of convertion of proprietary concern/firm

into a company (section 72A (4))

Sub-section (4) has been inserted with effect from the

A.Y. 1999-2000 which states that in case of succession of a

business where a firm is succeeded by a company fulfilling the

condition u/s. 47 (xiii) or a proprietary concern is succeeded by

a company fulfilling the condition u/s. 47(xiv), the accumulated

loss and the unabsorbed depreciation of the predecessor firm

or proprietary concern as the case may be, shall be deemed to

be the loss and unabsorbed depreciation for the successor

company for the previous year in which the business

reorganization took place.

If the specified condition u/s. 47 (xiii) and 47 (xiv) are not

complied with, then brought forward loss and unabsorbed

depreciation which has been set-off shall be treated as the

income of the successor company chargeable to tax in the

year in which such condition are not complied with.

One of the conditions for carry forward of the loss the firm is that the aggregate of the

shareholding in the company of the partners of the firm is not less than 50 per cent of

the total voting power In the company and their shareholdings continue to be such for a

period of 5 years from the date of the succession.

H. Section 78: carry forward and set off of losses in case of change in the constitution

of firm or on succession:-

Section 78(1):- Change in the constitution

when a change has occurred in the constitution of a firm, then nothing shall entitle

the firm to have carry forward and set-off so much of the loss proportionate to the

share of the retired or deceased partner as exceeds his share of profits, if any, of the

previous year in the firm. No partner can also avail the benefit of the said loss.

Visit us on www.zawarassociates.com For free Subscription write to [email protected] Page 6

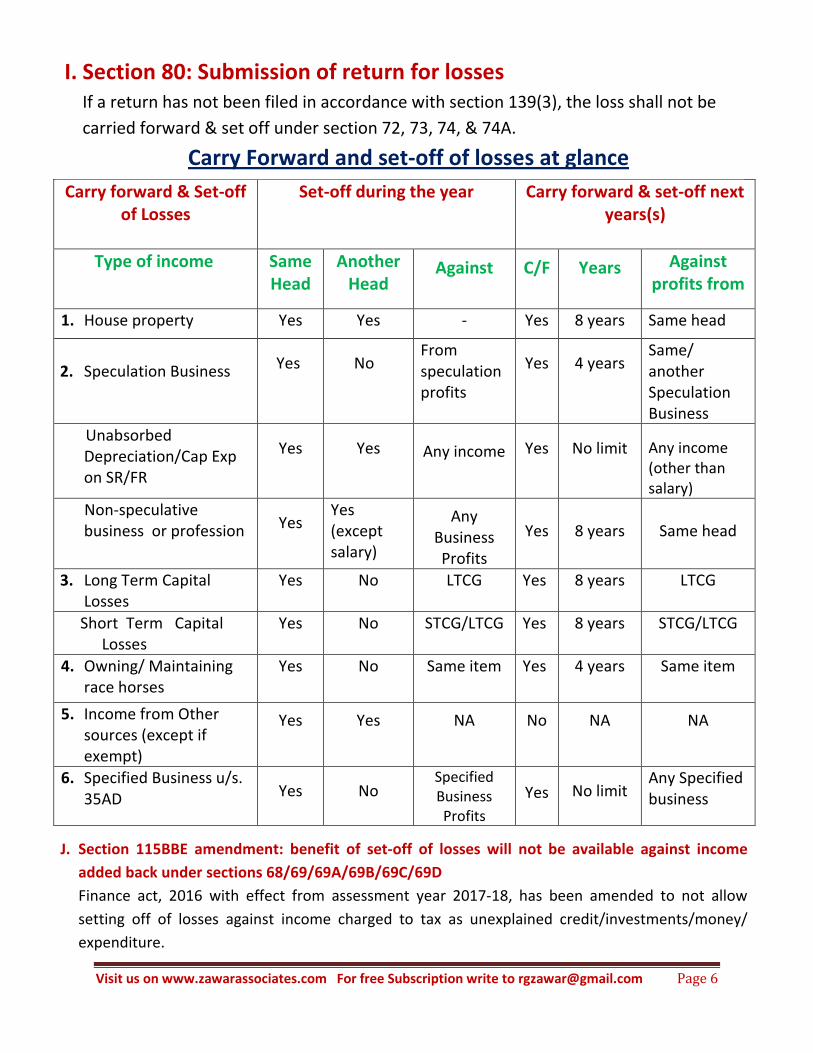

Carry forward & Set-off

of Losses

Set-off during the year Carry forward & set-off next

years(s)

Type of income Same

Head

Another

Head

Against

C/F

Years Against

profits from

1. House property Yes Yes - Yes 8 years Same head

2. Speculation Business

Yes

No From

speculation

profits

Yes

4 years Same/

another

Speculation

Business

Unabsorbed

Depreciation/Cap Exp

on SR/FR

Yes

Yes

Any income

Yes

No limit

Any income

(other than

salary)

Non-speculative

business or profession

Yes Yes

(except

salary)

Any

Business

Profits

Yes

8 years

Same head

3. Long Term Capital

Losses

Yes No LTCG Yes 8 years LTCG

Short Term Capital

Losses

Yes No STCG/LTCG Yes 8 years STCG/LTCG

4. Owning/ Maintaining

race horses

Yes No Same item Yes 4 years Same item

5. Income from Other

sources (except if

exempt)

Yes

Yes

NA

No

NA

NA

6. Specified Business u/s.

35AD

Yes

No Specified

Business

Profits

Yes

No limit Any Specified

business

I. Section 80: Submission of return for losses

If a return has not been filed in accordance with section 139(3), the loss shall not be

carried forward & set off under section 72, 73, 74, & 74A.

Carry Forward and set-off of losses at glance

J. Section 115BBE amendment: benefit of set-off of losses will not be available against income

added back under sections 68/69/69A/69B/69C/69D

Finance act, 2016 with effect from assessment year 2017-18, has been amended to not allow

setting off of losses against income charged to tax as unexplained credit/investments/money/

expenditure.

Visit us on www.zawarassociates.com For free Subscription write to [email protected] Page 7

3. Notifications/Circular

DIRECTORATE OF INCOME TAX (SYSTEMS) ARA Center, Ground Floor, E-2, Jhandewalan Extension,

New Delhi— 110055.

D.O. F. No. Pr. DGIT(S)/486-2020-21 New Delhi, 19th May 2021

Dear

Subject: Launch of new E-filing Portal of the Income Tax Department – Non-availability of e-Filing services from 01.06.2021 to 06.06.2021 Reg.

The Income Tax Department is going to launch its new E-filing portal www.incometax.gov.in on June 7th,

2021. In preparation for this launch and for migration activities, the existing portal of the Department at

www.incometaxindiaefiling.gov.in would not be available for a brief period of 6 days from 1st June to 6th June

2021.

Officers in field including AOs, CIT (A), PCIT interact with taxpayers through E-proceedings over the E-filing

portal directly or through the NeAC/NFAC for:

i. Issue of Notices, SCNs and getting response to various E-Proceedings

ii. Conducting of Video conference or adjournments

iii. Issuing Questionnaires, summons, letters etc

iv. Responding to E-Nivaran or Outstanding Tax demand etc

v. Communicating final orders in Assessment, Appeals, Exemption, Penalties etc

Apart from this Officers access the E-filing portal to view ITRs, Statutory forms, MIS etc.

In preparation for the transition to the new system, the existing E-filing portal will NOT be available to both

taxpayers as well as Departmental Officers for a period of 6 days from 1st June to 6th June 2021. Hence, it is

requested that all officers may be immediately informed about this so that they may not fix any compliance dates

during this period. All Officers may be directed to fix any hearing or compliances only from June 10th

onwards to give

taxpayers time to respond on the new system. If they have already scheduled any hearing or compliance which

requires submissions online during this period, they may prepone or adjourn the hearing and reschedule the work

items after this period, etc.

They may also view/ download any submissions in E-proceedings prior to June 1st and the PDF of any ITRs and

non-ITR forms that may be needed by them in advance so that they can continue to work in ITBA system including

completion of assessment proceedings where no further interaction with taxpayer is necessary. It is clarified that the

ITBA system and the CPC systems will continue to function for assessment related functions. All Orders, notices

issued during this period, however, will be made visible to the taxpayer only after the new portal goes live on June

7th, 2021.

I would also encourage all Officers to complete all their urgent tasks involving interactions with taxpayers prior

to June 1st to avoid the blackout period or typical initial teething issues in the transition. I would like to thank all

officers for their patience during the switch over to the new E-filing portal of the Department and seek your good

wishes.

With regards,

Yours

(Ann.J.Singh)

Principal Director General of Income Tax (Systems)

Central Board of Direct Taxes

To,

All Principal Chief Commissioners of Income Tax,

Chief Commissioners of Income Tax / Directors General of Income Tax

Visit us on www.zawarassociates.com For free Subscription write to [email protected] Page 8

- Arpita Kalani, Solapur

4. What knowledge should house maker have?

heCe efce$eebvees Leebyee, legcner ÛegkeâleeÙe ] heâòeâ IejkeâeceeÛeb %eeve hegjsme veener DeepeÛÙee Homemaker uee DeeefCe

DeepeÛÙee Ùee pandemic situation ceOÙes lej cegUerÛe veener] efleuee SkeâJesU Gòece mJeÙebheekeâ veener Deeuee lejer Ûeeuesue-kegâ"s efyeie[le YouTube Deens vee lÙeeJej heentve keâ® Mekeâles leer heCe yeensjerue peieeÛes knowledge YouTube veener osT Mekeâle] heCe keâe DemeeJeb ns knowledge ? lej Sskeâe, mecepee Ùeoe keâoeefÛele DeepeÛeer heefjefmLeleer heenlee pej Iejeleerue keâlee&/keâceJelÙee heg®<eeuee keâener Peeueb DeeefCe meJe& peyeeyeoejer ¢ee Homemaker Jej ÙesTve he[ueer lej ? DeeefCe leer lej keâener ceeefnleer vemeuÙeeves totally blank Deens] ogmeNÙeeJej DeJeuebyetve Deens] legceÛÙeekeâ[s Yejhegj hewmee / mebheòeer Deens heCe kegâ"s Je keâMeer nsÛe ceeefnleer vemesue lej keâeÙe keâjCeej ? DeeefCe cnCetveÛe leeruee keâener Keeueerue iees°eRÛe knowledge Jej JejÛeb keâe nesF&vee heCe ’’DemeeÙeueeÛe’’ nJeb ]

• ceesyeeF&ue:ceesyeeF&ue:ceesyeeF&ue:ceesyeeF&ue:----

DeepeÛÙee keâeUeleerue meJee&le cenlJeeÛeer iees°] heCe Ùeele heâòeâ keâenermes Application ÛeeueJelee ÙesCes hegjsmeb veener Ùeeletve Homemaker uee searching, online

payment, maps etc. Deeueb heeefnpes Demeb ceuee Jeešleb] cnCepes keâmeb Deeheueb kegâ"s keâenerÛeb De[le veener] DeLee&leÛe ’’ceesyeeF&ue’’ JÙeJeefmLele Ûeeue Jelee Deeuee heeefnpes]

• Bank A/C & banking knowledge:-

GÅee keâener De[ÛeCe DeeuÙeeJej Homemaker uee ns ceenerle heeefnpes keâer DeeheuÙee Iejeleerue meomÙeebÛes keâesCelÙee yeBkesâle Je keâesCeles a/c Deensle Je les keâmes operate keâjeJes] ATM heemeJe[& Ûes ner ceeefnleer leeruee DemeeJeer] ns meJe& nemÙeebmeheo Jeešsue heCe ns iejpesÛe Deens] lÙeeÛeØeceeCes yeBkesâÛes basic JÙeJenej hewmes "sJeCes, keâe"Ces, Ûeskeâ F] Ûeer ner ceeefnleer nJeer] pesCeskeâ®ve leer keâesCeeJejner DeJeuebyetve jenCeej veener]

legcner efJeÛeej keâjle Demeeue keâer, ne keâeÙe ØeMve Peeuee keâe ? keâmeuee ØeMve Deens ne?

meeOeer iees° Deens Homemaker uee lÙee meJe& iees°eRÛe b knowledge Demeues heeefnpes pes Iej meebYeeUCÙeemee"er iejpesÛe Deens] pemes keâer, mJeÙebheekeâ, meeheâmeheâeF&/mJeÛÚlee, IejeÛeer Je IejÛÙeebÛeer keâeUpeer F] F] yejesyej vee? SJnevee legcner Google Jej meÛe& kesâueele vee lejer legcneuee nsÛe Gòej efceUsue] yej ns Peeueb Iej meeYeebUCÙeemee"erÛe Iejeleerue %eeve] heCe efleuee keâener yeensjÛe knowledge vekeâes keâe?

Dejs nes keâer, yeensjÛe heCe %eeve nJesÛe vee efleuee] pemes keâer, Yeepeer ceekexâš kegâ"s Deens-efleLes peeCÙeeÛee jmlee keâesCelee,ogOe [sDejer keâes"s Demeles? efkeâjeCee keâes"gve DeeCeÙeÛee ? Dejs yeme yeme SJe[b knowledge hegjsme Deens keâer Homemaker uee ] DemeÛeb Jeešlebvee DeeheuÙeeuee cnCepesÛe meceepeeuee?

Visit us on www.zawarassociates.com For free Subscription write to [email protected] Page 9

• Insurance :- ne meJee&le cenlJeeÛee Yeeie DeepeÛeer heefjefmLeleer heenlee keâeneRvee lej Deeheuee insurance agent keâesCe Deens ns ner ceeefnleer vemeleb ¢eele lÙee Homemaker Ûeer Ûegkeâ veener ns] Ûegkeâ Deeheueer Deens keâer DeeheCeÛeb leeruee Ùee meJe& iees°eRheemetve otj "sJelees] efleuee insurance egent, insurance premium etc. Ûeer lej ceeefnleer nJeerÛe heCeÛee lÙeeÛeyejesyej keâener DeheIeele PeeuÙeeme efkebâJee ce=lÙet PeeuÙeeme lÙee Insurance Ûee claim keâmee keâjeJee, lÙeemee"er keâesCeeuee YesšeJeb ns osKeerue ceeefnleer Demeueb keâer heg{erue Øeesmesme meesheer nesles Je SveJesUer nesCeejer OeeJeheU šUles]

• Financial knowledge:-

legcner cnCeeue ÙeeÛeer keâeÙe iejpe ? heCe ns osKeeue eflelekeâÛeb cenlJeeÛe Deens] Homemaker uee efveoeve Deeheueb Iej ÛeeueCÙeemee"er monthly efkeâleer KeÛe& Ùeslees ¢eeÛeer ceeefnleer DemeeÙeueeÛeb nJeer] ¢eele efMe#eCe, Deew<eOes, KeeCes-efheCes ,ceveesjbpeve F] Jej nesCeeNÙee KeÛee&Ûeer Deboepes ceeefnleer DemeeÙeuee nJeer] peCeskeâ®ve GÅee iejpe he[ueerÛe lej ¢eeÛe Homemaker JÙeJeefmLeleheCes financial planning keâ®ve saving ner keâ® Mekeâleerue] DeeefCe Homemaker Ûe Demeles peer JeeÙeheâU KeÛe& šekegâve saving keâ® Mekeâles] Skeâoe efleuee involve keâ®ve lej hene vekeäkeâerÛe legcneuee Úeve result efceUsue] [believe me]

• iegbleJeCegkeâer yeöue:iegbleJeCegkeâer yeöue:iegbleJeCegkeâer yeöue:iegbleJeCegkeâer yeöue:---- DeeheCe hewmes kegâ"s iegbleJeuesues Deens] DeeefCe efkeâleer: cnCepesÛe DeeheCe] hewmes yeBkesâle FD mJe®heele "sJeuesues Deens keâer shares,debt DeMee ceOÙes iegbleJeuesues Deensle ÙeeÛeer osKeerue ceeefnleer leeruee vekeäkeâerÛe Åee DeeefCe legceÛÙee securities Demeleerue lej D-mat A/C, broker etc Ûeer ceeefnleer nJeer] ns ¢ee mee"er keâer De[ÛeCeerÛÙee JesUsme ns encash keâjCÙeemee"er leeruee vekeäkeâerÛe meeshes peeF&ue.

• About loan:- DeeheCe kegâCeeuee hewmes Gmeves efouesues Deensle efkebâJee keâesCeekeâ[tve Iesleuesues Deens ÙeeÛeerner ceeefnleer "sJeeJeer] keâejCe

lÙee mebyebOeerle JÙeJenej keâjleevee keâesCelÙeener Øekeâejs heâmeJesefiejer meceesjerue JÙeòeâer keâ[tve nesT veÙes]

• about vehicle:-

Deepekeâeue peJeUheeme meJeË ie=efnCeeRvee 2wheeler & 4wheeler ÛeeueJelee Ùesles] heCe lÙeeleuÙee 1 % DeMee Deensle keâer pÙeebvee lÙee iee[eryeöue ceeefnleer Demeles] Deelee Ùee iee[er yeöue keâeÙe ceeefnleer DemeeJeer lej ner iee[er keâesCeeÛÙee veeJeeJej Deens] ?lÙeeÛe insurance DeheIeele Peeuee lej les claim keâmeb keâjeJeb?. Renew keâmeb Je keâesCeekeâ[s keâjeJe etc.

Jejerue Ùee meJe& iees°eRÛeer Lees[erheâej ceeefnleer Skeâe ie=efnCeeruee DemeeJeer Demeb Deecnebuee Jeešleb] legcneuee ner DeMee keâener iees°eRÛeer ceeefnleer osKeerue ie=efnCeeruee DemeeJeer] peer Ùeele veceto veener Demes Jeešleb Demesue, DeMee keâener iees°eRÛeer ceeefnleer Demesue lej Deecnebuee vekeäkeâerÛe keâUJee! DeeheCe lÙee meJe& JeeÛekeâebheÙeËle heesnÛeJeCÙeeÛee ØeÙelve keâ®] OevÙeJeeo] OevÙeJeeo] OevÙeJeeo] OevÙeJeeo] !!

Visit us on www.zawarassociates.com For free Subscription write to [email protected] Page 10

5. Hindu Undivided Family and Its Constitution

Q.57 Is it not necessary for the other coparceners to agree in order to entitle a

coparcener to claim for a partition?

Ans.: It is not necessary that other coparceners should agree to the partition sought

by one of the coparceners but merely because one member severs his relations

with others there is no severance between others (CIT vs. Govindlal Mathurbhai

Oza (1982) 13 ITR 711 (Guj.) The other members continue to remain joint

However on account of over-riding provision contained u/s. 171(9) of the I.T.

Act such partial partition shall not be recognized as valid for income-tax

assessment.

Q.58 Does a partition take place at the time of death of a coparcener?

Ans.: A partition is an act effected inter vivos between the parties agreeing to the

partition A death of a coparcener cannot bring about an automatic partition and

on such a death the other surviving members continues to remain joint However

under the provisions of 56 of Hindu succession Act there is a deemed partition for

a limited purpose of determining the share of the deceased coparcener for the

purpose of succession under the Act. The right of a female heir to the interest

inherited by her in the family property gets fixed on the death of a male member

under section 6 of the Act but she cannot be treated as having ceased to be a

member of the family without her volition as otherwise it will lead to strange

results which could not have been in the contemplation of parliament when it

enacted that provision and which might also not be in the interest of such female

heirs. The female heir shall have the option to separate herself or to continue in

the family as long as she wishes as its member though she has acquired an

indefeasible interest in a specific share of the family property which would remain

undiminished whatever may be the subsequent changes in the composition of the

membership of the family (Refer state of Maharashtra vs. Narayan Rao Sham Rao

Deshmukh (1987) 163 ITR 31 (SC) Ahar Devi & Others vs. Parmeshwari Devi &

Others AIR 2006 SC 3332 .

Visit us on www.zawarassociates.com For free Subscription write to [email protected]

Q.59 Can a widow or wife claim partition?

Ans.: A widow steps in the shoes of her husband

Hindu Woman’s Rights to property Act

claim the partition on the death of her husband there can be a valid partition

between a widowed mother and son (Refer Ram Narain paliwar vs. CIT (1986) 162

ITR 539 (P&H); CIT vs. Mulchand Sukmal jain (1993) 200 IT

However a wife during the lifetime of her husband

case there is a partition, she shall get share equal to that of her son and husband

(Refer : Kundanlal vs. CIT (1981) 129ITR 755 (P&H)

दै�नक

सकाळी उठ�यावर �श क�न झा�यावर

�वारे वर ओढाव े

व लगेच जोर जोरान े२-3 वेळा �शकं�न

असे 2-3 वेळा करावे.

तसेच दसु!या नाकपुडीन ेह% कराव.े

नाकाम'ये रा(भर *चटकून बसलेल% संपूण/

तसेच करोणा 0कंवा त1सम इतर 3वषाणू

5दवसभर नाकाकडे हाथ जाणार नाह%. Raja G Life Guide

Visit us on www.zawarassociates.com For free Subscription write to [email protected]

Q.59 Can a widow or wife claim partition?

A widow steps in the shoes of her husband. Earlier on account of the

Hindu Woman’s Rights to property Act, 1937 and now being a heir in class I can

claim the partition on the death of her husband there can be a valid partition

between a widowed mother and son (Refer Ram Narain paliwar vs. CIT (1986) 162

ITR 539 (P&H); CIT vs. Mulchand Sukmal jain (1993) 200 ITR 528 (Gauhati);

However a wife during the lifetime of her husband, cannot claim a partition but in

she shall get share equal to that of her son and husband

(Refer : Kundanlal vs. CIT (1981) 129ITR 755 (P&H)

- To be continue next month

दै�नक कर�या यो�य शु�द���या - २

स�ूम नेती/न�य

झा�यावर, एका हाता8या ओंजुळम'ये पाणी घेऊन ते पाणी

�शकं�न थ;ब ना थ;ब पाणी काढून टाकावे.

संपूण/ घाण बाहेर पडत.े

3वषाणू नाकापुडी8या जवळपास अस�यास तेह% बाहेर फेकले

.

Visit us on www.zawarassociates.com For free Subscription write to [email protected] Page 11

Earlier on account of the

1937 and now being a heir in class I can

claim the partition on the death of her husband there can be a valid partition

between a widowed mother and son (Refer Ram Narain paliwar vs. CIT (1986) 162

R 528 (Gauhati);

cannot claim a partition but in

she shall get share equal to that of her son and husband

inue next month

पाणी एका नाकपुडी

फेकले जातील.

Visit us on www.zawarassociates.com For free Subscription write to [email protected] Page 12

FOOD AND NUTRITION Choosing disease-fighting Foods

6. Health Tips

Research indicates that eating certain foods can help

lower your risk of several diseases.

• Eat at least four servings of vegetables a day Vegetables are loaded with vitamins and minerals, contain fiber,

have no cholesterol, and are low in fat and calories. They’re a great

source of phytochemicals, substances that appear to help reduce

the risk of chronic diseases such as heart disease, cancer and

diabetes. Eat a variety to get all the health benefits.

• Eat at least three servings of fruits a day

Fruits are filled with vitamins, minerals, antioxidants and fiber. Except for a few, such as avocado and coconut, they’re virtually free of fat. Fruits are a major source of flavonoids, substances that may help lower the risk of cardiovascular disease and cancer. Choose a variety of fruits to get the most health benefits.

• Eat foods high in omega-3s

Eating at least two servings (about 3 ounces each) a week of fish that are rich in omega-3 fatty acids — such as salmon, trout, tuna, herring and sardines — can help reduce your risk of heart disease. Instead of frying, bake or grill the fish. Note: The Food and Drug Administration (FDA) advises pregnant women, nursing mothers and children to avoid king mackerel, shark, swordfish and tilefish (golden bass or golden snapper), which are higher in mercury. Tuna steak and albacore tuna generally have more mercury than canned light tuna. Plant sources of omega-3s include canola oil, flaxseed (ground and oil), soybeans and walnuts (whole and oil).

• Choose whole-grain foods Eating whole grains may lower your risk of cardiovascular disease, type 2 diabetes and cancer. In addition to the more familiar whole-grain breads and cereals, add variety to your diet with hulled barley, brown rice, buckwheat, bulgur, millet, quinoa, whole-wheat pasta and wild rice.

Visit us on www.zawarassociates.com For free Subscription write to [email protected] Page 13

7. SOCIAL Work

meceepekeâejCemeceepekeâejCemeceepekeâejCemeceepekeâejCe

Deepe nce Úesšs-Úesšs ØeceeCe ces Deveskeâ «eghe yeves ngÙes osKeles nw~

Tvekeâer yeveeJeš keâYeer peeleerhej DeeOeeefjle nw, keâYeer JÙeJemeeÙehej, keâYeer ieeBJehej, keâYeer SjerÙee F. hej DeeOeeefjle nesleer nw~ meYeer «eghe ces meYeemeoes keâer FÛÚe meceepe kesâ ef}Ùes kegâÚ keâeÙe& keâjves keâer nesleer nw~ “keâewvemee keâeÙe& neLe ces }s?” Fme efJe<eÙe hej peye ÛeÛee& nesleer nw; lees meeceevÙele;

’’ceveesjbpeve’’ ’’Ûeej efoJeejer kesâ Deboj kesâ Kes}/iesce’’ ’’[e@keäšjer me}en leLee F}epe’’ ’’Deejece keâer meheâj’’ FlÙeeoer, FlÙeeoer

Øekeâej kesâ keâeÙeex keâes yengcele efce}lee nw~.Swmes ner keâeÙeexkeâes yengcele efce}ves keâe keâejCe, Fme Øekeâej kesâ Projects ces Dehes#eerle peeoe mes peeoe }esiees keâe menYeeie~ Deewj keâeÙe&keâlee& keâer Ùen FÛÚe nesleer nw keâer, cew peye Flevee meceÙe os jne ngb lees peeoelej }esie Fmeces çeeceer} nes~

efheâj Fve keâeÙeex keâe yepesš yeveeÙee peelee nw~ yepesš ces meYeer keâe Deveg«en Quality leLee Quantity hej neslee nw~ Deleb ces yepesš kesâ Collection keâer yeele Deeleer nw~ hewmes ceebieves keâer yeele nesleer nw ~ hewmees kesâ ef}Ùes meceepe ces Iegceves keâer yeele Deeleer nw, leye pÙeeoelej meYeemeo Fmeces mes Dehevee Deieb efvekeâe}ves keâer, Ùee efheâj Deheves ner pesye mes jkeäkeâce osves keâer keâesçeerçe keâjles nw~

Swmee keâjves kesâ efheÚs Tvekesâ Deheves-Deheves hegJe& DevegYeJe nesles nw~ Jewmes lees ceeveJe meceepe efØeÙe nw, Fmeef}Ùes Fme lejn kesâ keâeÙe& efmehe&â Fmeer oçekeâ ces Ûe} jns nw Ssmeer yeele vener~ Fefleneme ces keâF& çeleeyoerÙees mes Fme lejn kesâ meceepe keâeÙe& nesles DeeÙes nw~ Fefleneme ves cee$e efmehe&â Gvner keâeÙeeX keâes njmeceÙe Carry forword leLee Brought forward keâerÙee nw pees keâeÙe& meceepe ces }byeer meceÙe lekeâ TheÙeesieer jns nw~ efpemekeâe Deemej, Ùee efpemekesâ heâ} }byes meceÙelekeâ efce}les jns nes~

Visit us on www.zawarassociates.com For free Subscription write to [email protected] Page 14

efvemeie& keâe efveÙece Yeer Ùener nw~ Deehe Deheves Iej kesâ DeeBieve ces cesLeer, keâeWLeeryeerj, hee}keâ Swmes hes[ }ieebDees lees, hes[ npeejes DeeÙeWies ~ Skeâ mes ome yeej meyedpeer ces ye[e DeeveboYeer oskeâjpeeÙeWies~ hejbleg Deehe Skeâ ner Deece keâe hes[ }ieeDees lees Deehekeâe heesleeYeer Deehekeâe veece }sles ngÙes Deece KeeÙesiee~ Fmeer lejn meceepe keâeÙe&ces Yeer keâce meceÙe Deevebo osvesJee}s Project ces menYeeie ye[e efce}lee nw~ Deewj }byes meceÙelekeâ ØeYeeJe keâjvesJee}s Projects ces menYeeie keâce efce}lee nw~ hen}s Jeie& ces DeevesJee}s Projects keâer veeWo kegâÚ SMS, email leLee Phone Call lekeâ efmeceerle nesleer nw~

ogmejs ogmejs ogmejs ogmejs Jeie& kesâ Jeie& kesâ Jeie& kesâ Jeie& kesâ Projects efkeâ veeWo Fefleneme ces çeskeâ[es Je<e& lekeâ jnleer nw~efkeâ veeWo Fefleneme ces çeskeâ[es Je<e& lekeâ jnleer nw~efkeâ veeWo Fefleneme ces çeskeâ[es Je<e& lekeâ jnleer nw~efkeâ veeWo Fefleneme ces çeskeâ[es Je<e& lekeâ jnleer nw~

1.1.1.1. yee} ieieebOej efle}keâ ves çeg® efkeâÙee ieCeheleer cenesmleJe nes, 2.2.2.2. meeefJeef$eyeeF& hegâ}s ves çeg® keâer }[efkeâÙees keâer mkegâ} nes, 3.3.3.3. [eB.nsie[sJeej leLee [eB. ieesefJe}keâjb ieg®peer ves çeg® efkeâÙee RSS keâeÙe& nes, 4.4.4.4. [eB. Deebyes[keâj ves çe®g efkeâÙee oef}le keâeÙe& nes, 5.5.5.5. ceoj lesjsmee keâe keâeÙe& nes, Ùee 6.6.6.6. [eB. jece ceveesnj }esefnÙeekeâe keâeÙe& nes, Fve meYeer keâeÙeex keâer Fefleneme ves veeWo }er nw~ Deewj

meceepe ces ye[s yeo}eJe Fve keâeÙeex kesâ keâejCe DeeÙes nw~ Deleb: cesjer Deehe meYeer mes Ùener efJevebleer nw, keâer Deehe meYeer }esie Deehekesâ efpeJeCe keâe Flevee yengceguÙe meceÙe oskeâj meceepe keâeÙe& keâjves nslet, De}ie De}ie iegÇhe ces çeeceer} ngÙes nes~ lees keäÙees ve nce Tleves ner meceÙe ces Swmes keâeÙeex keâes neLees ces }s efpememes nceejs keâeÙeex keâer veeWo }svee Fefleneme keâes DeefveJeeÙe& nesiee~

Ùen yeele pe®j nw, Swmes keâeÙeex ces Deehekeâes Public

Response keâce jnsiee, efheâj Yeer cegPes efJeßJeeme nw , keâer Deehekeâes Delebjerkeâ meceeOeeve efce}siee ~ çeebleer efce}sieer~

~nefj DeeWce~~nefj DeeWce~~nefj DeeWce~~nefj DeeWce~

CA. Rajendra G. Zawar.

AURANGABAD

Visit us on www.zawarassociates.com For free Subscription write to [email protected] Page 15

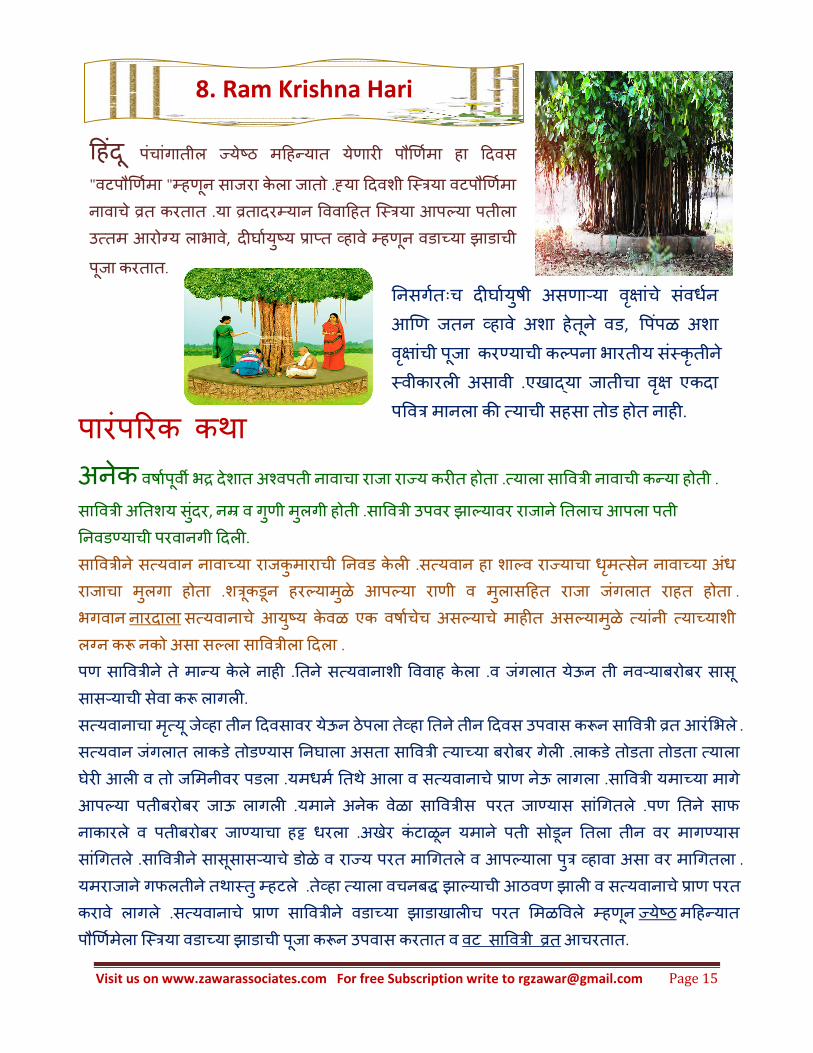

पारंप>रक कथा अनेक वषा/पूव? भ@ देशात अAवपती नावाचा राजा राBय कर%त होता .1याला सा3व(ी नावाची कCया होती .

सा3व(ी अDतशय सुंदर, नE व गुणी मुलगी होती .सा3व(ी उपवर झा�यावर राजान ेDतलाच आपला पती

DनवडGयाची परवानगी 5दल%.

सा3व(ीन ेस1यवान नावा8या राजकुमाराची Dनवड केल% .स1यवान हा शा�व राBयाचा धमृ1सेन नावा8या अधं

राजाचा मुलगा होता .श(कूडून हर�यामुळे आप�या राणी व मुलास5हत राजा जंगलात राहत होता .

भगवान नारदाला स1यवानाच े आयुJय केवळ एक वषा/चचे अस�याच े माह%त अस�यामुळे 1यांनी 1या8याशी

लKन क� नको असा स�ला सा3व(ीला 5दला .

पण सा3व(ीन ेते माCय केले नाह% .Dतन ेस1यवानाशी 3ववाह केला .व जंगलात येऊन ती नव!याबरोबर सासू

सास!याची सेवा क� लागल%.

स1यवानाचा म1ृयू जेLहा तीन 5दवसावर येऊन ठेपला तLेहा Dतन ेतीन 5दवस उपवास क�न सा3व(ी Mत आरं�भले .

स1यवान जंगलात लाकड ेतोडGयास Dनघाला असता सा3व(ी 1या8या बरोबर गेल% .लाकड ेतोडता तोडता 1याला

घेर% आल% व तो ज�मनीवर पडला .यमधम/ Dतथे आला व स1यवानाच ेNाण नेऊ लागला .सा3व(ी यमा8या मागे

आप�या पतीबरोबर जाऊ लागल% .यमान े अनेक वळेा सा3व(ीस परत जाGयास सां*गतले .पण Dतन े साफ

नाकारले व पतीबरोबर जाGयाचा हO धरला .अखेर कंटाळून यमाने पती सोडून Dतला तीन वर मागGयास

सां*गतले .सा3व(ीन ेसासूसास!याच ेडोळे व राBय परत मा*गतले व आप�याला पु( Lहावा असा वर मा*गतला .

यमराजान ेगफलतीने तथाQतु Rहटले . तेLहा 1याला वचनबS झा�याची आठवण झाल% व स1यवानाच ेNाण परत

कराव े लागले .स1यवानाच े Nाण सा3व(ीन े वडा8या झाडाखाल%च परत �मळ3वले Rहणून BयेJठ म5हCयात

पौUण/मेला िQ(या वडा8या झाडाची पूजा क�न उपवास करतात व वट सा3व(ी Mत आचरतात.

8. Ram Krishna Hari

5हदं ू पंचांगातील BयेJठ म5हCयात येणार% पौUण/मा हा 5दवस

"वटपौUण/मा "Rहणून साजरा केला जातो .Wया 5दवशी िQ(या वटपौUण/मा

नावाच ेMत करतात .या MतादरRयान 3ववा5हत िQ(या आप�या पतीला

उ1तम आरोKय लाभाव,े द%घा/युJय NाXत Lहावे Rहणून वडा8या झाडाची

पूजा करतात.

Dनसग/तःच द%घा/युषी असणा!या वZृांचे संवध/न

आUण जतन Lहावे अशा हेतूने वड, 3पपंळ अशा

वZृांची पूजा करGयाची क�पना भारतीय संQकृतीने

Qवीकारल% असावी .एखा�या जातीचा वZृ एकदा

प3व( मानला क[ 1याची सहसा तोड होत नाह%.

Visit us on www.zawarassociates.com For free Subscription write to [email protected] Page 16

CA Zawar,

Thanks for providing useful information regarding IT matter in

FY 2021_2022 ok Adv. Rajendra Sharma

Sir,

It matter issues are worth to go through. Very useful covering

latest professional updates along with obligation to be complied

with and focusing social issues also. It is unique and deserve for

laudable appreciation.

With regards,

CA Bhagwandas V. Kudal, Solapur

DISCLAIMER iT MATTERS is a monthly bulletin for the benefit of associates of ZAWAR ASSOCIATES. It is especially meant for updating the

knowledge of associates and circulates the information among its associates. The bulletin may contain such

research/advice/opinion/information/fact provided by any associate member or moderator. Every content of the bulletin is always

subject to the accuracy and of the description of facts.

ZAWAR ASSOCIATES, its owner do not claim that contains in bulletin obtained after reading as a complete and accurate disclosure of

relevant fact(s).

Considering all above facts any transaction based on above bulletin may not complete without confirming proper

statue/authority/person. Therefore any action/transaction taken on basis of this bulletin does not imply the accuracy or value.

Further the Owners are not liable for any damages or costs suffered due to action/transaction based on information of this bulletin.

For seeking any Clarification you may mail only to [email protected]

ADDRESS: “RAJWADA” 41/42,

GANDHI NAGAR, STATION

ROAD, AURANGABAD.

Email ID

0240-2350301/5

9146060001/2

Contact Us