1 77 X - World Bank Documents & Reports

228

177 X World Baik Discussion Papers The Regulatory Impediments to the Private Industrial Sector Development in Asla A Comparative Study Deena R. Khatkhate Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of 1 77 X - World Bank Documents & Reports

1 77 X World Baik Discussion Papers

The RegulatoryImpediments to thePrivate IndustrialSector Developmentin AslaA Comparative Study

Deena R. Khatkhate

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Recent World Bank Discussion Papers

No. 118 Improving the Performance of Soviet Enterprises. John Nellis

No. 119 Public Enterprise Reform: Lessonsfrom the Past and Issuesfor the Future. Ahmed Galal

No. 120 The Information Technology Revolution and Economic Development. Nagy K. Hanna

No. 121 Promotitng Rural Cooperatives in Developing Countries: The Case of Sub-Saharan Africa. Avishay Braverman,J. LuisGuasch, Monika Huppi, and Lorenz Pohlmeier

No. 122 Performance Evaluationfor Public Enterprises. Leroy P. Jones

No. 123 Urban Housing Reform in China: An Economic Analysis. George S. Tolley

No. 124 The New Fiscal Federalism in Brazil. Anwar Shah

No. 125 Housing Reform in Socialist Economies. Bertrand Renaud

No. 126 Agricultural Technology in Sub-Saharan Africa: A Workshop on Research Issues. Suzanne Gnaegy andJock R.Anderson, editors

No. 127 Using Indigenous Knowledge in Agricultural Development. D. Michael Warren

No. 128 Research on Irrigation and Drainage Technologies: Fifteen Years of World Bank Experience. Raed Safadi andHerve Plusquellec

No. 129 Rent Control in Developing Countries. Stephen Malpezzi and Gwendolyn Ball

No. 130 Patterns of Direct Foreign Investment in China. Zafar Shah Khan

No. 131 A New View of Economic Growth: Four Lectures. Maurice FG. Scott

No. 132 Adjusting Educational Policies: Conserving Resources While Raising School Quality. Bruce Fuller and Aklilu Habte,editors

No. 133 Letting Girls Learn: Promising Approaches in Primary and Secondary Education. Barbara Herz, K. Subbarao,Masooma Habib, and Laura Raney

No. 134 Forest Economics and Policy Analysis: An Overview. William F. Hyde and David H. Newman, with a contributionby Roger A. Sedjo

No. 135 A Strategyfor Fisheries Development. Eduardo Loayza, in collaboration with Lucian M. Sprague

No. 136 Strengthening Public Service Accountability: A Conceptual Framework. Samuel Paul

No. 137 Deferred Cost Recoveryfor Higher Education: Student Loan Programs in Developing Countries. Douglas Albrechtand Adrian Ziderman

No. 138 Coal Pricing in China: Issues and Reform Strategy. Yves Albouy

No. 139 Portfolio Performance of Selected Social Security Institutes in Latin America. Carmelo Mesa-Lago

No. 140 Social Security and Prospectsfor Equity in Latin America. Carmelo Mesa-Lago

No. 141 China's Foreign Trade and Comparative Advantage: Prospects, Problems, and Policy Implications. Alexander J. Yeats

No. 142 Restructuring Socialist Industry: Poland's Experience in 1990. Homi J. Kharas

No. 143 China: Industrial Policiesfor an Economy in Transition. Inderjit Singh

No. 144 Reforming Prices: The Experience of China, Hungary, and Poland. Anand Rajaram

No. 145 Developing Mongolia. Shahid Yusuf and Shahidjaved Burki

No. 146 Sino-Japanese Economic Relationships: Trade, Direct Investment, and Future Strategy. Shuichi Ono

(Continued on the inside back cover.)

1 77 IESI World Bank Discussion Papers

The RegulatoryImpediments to thePrivate IndustrialSector Developmentin AsiaA Comparative Study

Deena R. Khatkhate

The World BankWashington, D.C.

Copyright c 1992The International Bank for Reconstructionand Development/THE WORLD BANK1818 H Street, N.W.Washington, D.C. 20433, U.SA.

All rights reservedMamifactured in the United States of AmericaFirst printing September 1992

Discsion Papers present results of country analysis or research that is circulated to encourage discussionand comment vwthin the development community. To present these results with the least possible delay, thetypescript of this paper has not been prepared in accordance with the procedures appropriate to formalpdnted texts, and the World Bank accepts no responsibility for errors.

The findis, interpretations, and conclusions expressed in this paper are entirely those of the author(s) andshould not be attributed in any manner to the Wodd Bank, to its affiliated organizations, or to members ofits Board of Executive Directors or the countries they represent. The World Bank does not guarantee theaccuracy of the data included in this publication and accepts no responsibility whatsoever for anyconsequence of their use. Any maps that accompany the text have been prepared solely for the convenienceof readers; the designations and presentation of material in them do not imply the expression of any opinionwhatsoever on the part of the World Bank, its affiliates, or its Board or member countries concening thelepl stau of any country, territory, city, or area or of the authorities thereof or concerning the delimitationof its boundades or its national affiliation.

The material in this publication is copyrighted. Requests for permission to reproduce portions of it shouldbe sent to the Office of the Publisher at the address shown in the copyright notice above. The World Bankencourages dissemination of its work and will normally give permission prompdy and, when thereproduction is for noncommercial purposes, without asking a fee. Permission to copy portions for classroomuse is ganted through the Copyright Clearance Center, 27 Congress Street, Salem, Massachusetts 01970, U.SA.

The complete backlist of publcations from the World Bank is shown in the annual Index of Publications,which contins an alphabetical tide lst (with full orderng information) and indexes of subjects, authors, andcountries and regions. The latest edition is available free of charge from the Distribution Unit, Office of thePublisher, Department F, The World Bank, 1818 H Street, N.W., Washington, D.C. 20433, U.S.A., orfrom Publications, The World Bank, 66, avenue d'I6na, 75116 Paris, France.

ISSN: 0259-210X

Deena R. Khatchate is a consultant in the Industry, Trade and Finance Division of the World Bank's AsiaTechnical Department.

lbnry of Congru Cataloging-in-Publication Data

Khatkhate, Deena R.The regulatory impediments to the private industrial sector

development in Asia: a comparative study / Deena Khatchate.p. cn. - (World Bank discussion papers; 177)

ISBN 0-8213-2221-41. Industry and state-Asia, Southeastern. 2. Industry and state-South Asia. I. Tide. II. Series.HD3616.A773K48 1992338.954-dc2O 92-23555

CIP

- iii -

FOREWORD

The World Bank has come to focus more sharply than in the past onrole of the private sector in member countries. There has been a great deal ofdiscussion on this issue within the Bank with a view to understanding the natureof impediments to the private industrial sector development and to explore afresh approach to promoting that vital sector as an engine of growth. One of theways to clearly perceive the issues is to develop a regional overview of theprivate sector role in some of the countries, where its progress is held back bya variety of regulatory policies. The underlying idea of this study is not somuch to deal with all the relevant policies, such as financial and trade regimesaffecting the private sector or the privatization of public sector as to bringin sharp relief the impediments placed in its development by industrial licensingpolicies, direct foreign investment policies, labor market constraints, pricecontrols and distorted promotional policies. While doing so, it would be helpfulfor the Bank, to know what changes in these policies have occurred, how they haveimpacted on the private sector and what needs to be done in future. However,since the regulatory policies may have different implications in differentcountries, it is rewarding to present a comparative picture in regard to thecountries covered as done in this study. The countries - Bangladesh, India,Indonesia, the Philippines and Sri Lanka are chosen because they provide a mixof countries which need more vigorous and well defined policies to promote theprivate sector.

The study has relied only on the available sources within the Bankand outside and therefore there has remained inevitably several gaps ininformation and data, which seem to have biased some of the analytical points andconclusions. Though the difficulties in developing an analytical framework wererecognized, an attempt was made to discuss the regulatory policies in a mutuallyconsistent and sufficiently representative empirical framework (drawing, ofcourse, on the work done in the academia) germane to developing countries, inwhich interrelations between macroeconomic determinants of private sectordevelopment, the degree of interventionist policies and the relative role ofpublic and private sector are clearly underscored. The approach adopted forpresentation of the material is to discuss the selected regulatory policy aspectswith respect to each of the countries, referring to inter-country variations andto weave the common threads of arguments in the Executive Summary. This approachalso combined the macro-policy discussion with micro analysis of selectedsubsectors, before and after the regulatory reforms affecting them wereiLntroduced. This was done in order to capture the impact of reforms onindustries more concretely and meaningfully, which could not have been possibleif the impact was sought to be assessed only on a macro basis. This study hasyielded some interesting lessons which, I hope, will guide not only the policymakers in these countries but also the Bank staff working in those countries andother countries where the development of private sector is awaiting more focusedattention.

Daniel RitchieDirector

Asia Technical DepartmentAsia Region

- iv -

Acknowldo mant

Th- author would like to acknowledge coments and suggestions on earlierdrafts of this paper by Daniel Ritchie, Ihalid Siraj, Frida Johansen, DipakDasgupata, Nissim Zzekiel, Charleo Draper, Dilip Wagle, N. Hanna and I. Newport.Hemant Saijal provided valuable statistical assistance and prepared the earlydrafts of the country industry studios included in the appendix.

!ables of Onemt5

Exccutivo Summary .............. ..* .......................... . ................... ........ vii

I. Introduction .. .... ............. ................*................. I

II. Private Sector Develoment. its Deterinant and Role ofGovernment Intervention - An Emoirical Fram.work .....0................... . 2

Private Investment and Economic Growth ................................ 3Macroeconomic Determinants of Private Investment in Developing Countries ... 4Limits of Government Intervention ....... ....... . ...... . S

III. Macroeconomic Environment and Trade and Financial c ar Polies .......... .0

Macroeconomic Environment . ...... ... .. * ....................... 10

Trade Policy Reforms ........................................................ 28

Financial Sector Reforms .. ................................................. 32

IV. Domestic Reaulatorv Policy Imoediments to the PrivateIndustrial Development ..................................................... 37

Industrial Policy Framework ... ............... . 37

Consequences of Domestic Regulatory Policy . . 54

V. Industrial PolicX Reform and Its Imoact............................. 66

Industrial Regulatory Policy Reform .............................. ........... 66Impact of Deregulation . ........... .*. ........ s ... .......... . 83

A Micro Approach to Impact of Deregulation on Industry . ............. 102References ................................................................. 104Appendices ...... . .................... 109

vii

EXECUTIVE SUMMARY

Introduction

1. This study, drawing mainly on the existing material within the Bank

group and outside focuses on the domestic regulatory apparatus in five Asiancountries, India, Indonesia, The Philippines, Sri Lanka and Bangladesh inorder to critically examine how it has affected the growth of privateindustrial sector development. The selected countries provide a mix of

countries that are in various stages of modifying and/or dismantling theirdomestic regulatory policies. These are discussed under five topics:(a) industrial licensing; (b) price control policies; (c) labor marketpolicies; (d) policies directed towards direct foreign investments; and(e) the promotional policies in regard to private sector development. To theextent other policies such as trade and financial sector policies are germaneto the private sector development, they have been briefly discussed inappropriate contexts. There are other regulatory obstacles to the privateindustrial development but they could not be discussed for want of relevantinformation. The summary will focus on the salient features of this study,such as its underlying empirical framework, divergence and convergence ofexperiences of the countries covered in the study and some lessons drawn fromtheir experiences.

Determinants of Private Sector Development and Role of GovernmentIntervention - An Empirical Framework

2. Recent empirical research in the field of development economics hasdemonstrated for a sample of 24 developing countries that there is a strongand positive relationship between private sector activity, particularlyprivate sector investment and economic growth. Except when public investmentis in infrastructure, it tends to crowd out private investment. The privatesector, which grows faster through direct and indirect policy measuresdirected at removing constraints and offering incentives of various sortsplays a dominant role in the growth process. In the sample of countrieschosen, which included several Asian countries, it is found that, highestaverage rates of growth were attained with the highest average ratios ofprivate to total investments. More important is the finding that theproductivity growth arising from factors and technical change has been higherLn respect of private investment than in public investment. The capital inprivate investment contributes to productivity, while capital's contributionin public investment has been negative. These experiences generally conformto those of the industrial countries.

:3. On the basis of the experiences of the industrial countries duringthe last four decades, the macroeconomic determinants of private investmentare identified as: (a) macroeconomic stability as represented by lowinflation rate; (b) economic growth and per capita income level; (c) the levelof real interest rates; (d) debt service ratio; and (e) the rate of publicsector investments. The relationship between private sector growth andinflation rate, debt-service ratio and public investment (except when it is ininfrastructure) is negative and the relationship between private investment

viii

and per capita income level and real interest rates is positive. The evidenceon these relationships has been investigated in empirical work on 23 develop-ing countries both by observing the average values during the period of 1975-87 with above and below average private investment rates and by rigorouseconometric tests and it was concluded that the expected relationship betweenprivate investment and the specified determinants is well supported.

4. As regards the limits and nature of government intervention inprivate sector activiLty, the empirical evidence points to the possibility andalso practicability to devise optimal rules for operating regulatory systemwhich while servicing its legitimate purpose will not transcend its limits tothe disadvantage of the private sector development. First, any policyaffecting allocation of resources, and regulation of private sector needs tobe pursued if and only if there is a specified set of procedures or criteriafor deciding what fits within the defined scope of the enunciated economicpolicies. Second, even when there is strong presumption in favor of govern-ment intervention, it is imperative to limit it to minimum necessary scale asefficiency of regulation is scale-determined. Three, from amongst theavailable alternative regulatory sets, it is necessary to go in for one whichwill provide the least scope for rent seeking. This may imply that policiesdirectly controlling private sector are likely to be less efficient thanpolicies that offer incentives for individuals to embark on activities whichare considered desirable. Finally, a regulatory policy involving lowerinformation costs and transparency is a preferred alternative.

Se It is with a general reference to this empirical framework that theregulatory policies as operated in the five Asian countries, and their reformsare discussed below.

Intercountry Experience in Operating Regulatory Policies:Divergence and Converaence

6. The experience in pursuing regulatory policies and their implementa-tion in all these five countries has been unavoidably diverse and yieldedvarying results. The reasons for this difference in performance are many andvaried. The macroeconomic environment is a crucial factor in determining themode of regulatory policies and their outcome. Domestic regulatory reform isa part of an overall reform strategy and its impact therefore is determined byhow well other parts of the reform strategy are dovetailed into the domesticregulatory policy. The success of the policies is also dependent on how theregulatory reforms are designed. At times, in a strict formal sense, reformslook attractive but there are certain features which get built into it,attenuating their efficiency. From this point of view, it is rewarding toreview the experiences of the five countries in a comparative context. Thisapproach may also suggest how certain problems, faced by some of the countriescould be avoided by modification of reform policies in those countries,drawing on the experiences of those where no such problems had arisen; it mayalso enrich the knowledge of those who would be involved in the private sectordevelopment policies at some future date.

7. All the five countries covered in this study--India,Indonesia, ThePhilippines, Sri Lanka and Bangladesh--differfrom each other in almost everyrespect - structure, the stage of development, diversity of output and theexport orientation. India and The Philippines were perhaps much more advanced

ix

in the early 1950s than the other three. But the greatest progress in termsof industrialization and export orientation took place in Indonesia particu-larly since the beginning of 1980e. It also figured most prominently in thefield of economic reform whether it related to financial reform, trade reformor thie industrial regulatory reform. On the other hand, India's reforms werelopsided, confined mainly to the domestic regulatory policies leaving otherareas like the trade and financial sector reform relatively immune from newpolicies until recently. The Philippines, Sri Lanka, and Bangladesh have mademajor dent on their trade and financial sector policies which were, in manyrespects more far-reachingthan in the case of India. In terms of macro-economic situation, Indonesia has been able to maintain a better record since1980, which contributed to the speed of the reform of its trade, financial andindustrial regulatory policies. India, after a long period of stable macro-economic environment ran into serious imbalances in the latter half of 1980s--precisely the period when it embarked on industrial deregulation. ThePhilippines, Sri Lanka, and Bangladesh went through undulating macroeconomicsituation during the 1980s, which, while interfering with their economicreform policies, did not scupper them. In fact, despite the adverse macro-economic situation, these countries persisted with their reforms with varyingdegree of success.

8. Despite some differences among countries arising from the differingeconomic structures, stages of devel6pment or the openness of the economies,they are all similar in regard to what they experienced from followingregulatory policies such as industrial licensing, price controls, promotionalpolicies in regard to small scale industries, labor market polices and thepolicies towards FDI. Industrial licensing failed to achieve the objective ofdi,spersal of industry or producing output in cost-effective and profitableways. It did not succeed in preventing products, not intended by the authori-ties nor concentration of industries in, few owners, cities or areas. Pricecontrols proved to be the greatest disincentive for production of thecontrolled commodities in all countries and accounted for latent or openinflationary pressures and widespread rent seeking. Again, these controlswere evaded on a large scale. The import substitution was no doubtaccelerated but it was not only inefficient but also raised the level ofimports in all the five countries, containment of which was the avowedobjective of import substitution strategy. The promotional policies towardssmall scale industries failed to accomplish their goal. The so-called smallscale industries consumed both capital and labor and they came in the way ofhealthy and competitive expansion of the large industry.

9. India's experience in reform policies has been illuminating less forwhat India accomplished in making its economy competitive than for letting innew impulses for efficiency consciousness. A reorientation in governmentpolicies towards industrial development during the 1980s no doubt brought in afresh breeze in otherwise suffocated private enterprise economy and for thefirst time, it was realized by the industrial entrepreneurs that quantitygeneration without quality and competitive pricing would be a futile exercisein the long run when India would have to face outside producers in the worldmarket. And yet it can not be said that the domestic regulatory reform wasfar reaching enough. In point of fact, it was half-hearted, steeped inbureaucratic rigmarole, and essentially opaque. Though the grip of theadministration was somewhat loosened and the implementation of regulatoryregime was made somewhat purposive, "the system remained substantially intact.In some ways, it actually became more complicated, because almost every reform

x

was hedged about with pages of rules to prevent abuse. The folds of India'sregulatory system overlap each other so luxuriously that extreme violence willbe needed to expose even an inch of the economy to daylight".1/

10. One of the major reasons for this rather disappointing outcome wasthe perpetuation of the old trade regime. The high effective rate ofprotection (ERP) in industries benefitting from delicensing, while bearinghigh financial returns ended up in distorting domestic industrial structure,and in insulating it: from foreign competition. One of the glaring exampleswas the implementation of the Phased Manufacturing Program (PMP) which tookaway a great deal of advantages which the industry with or without licensingrequirements could have derived from the relaxed regulatory regime. PMPs hadtwo effects: First, the local content of requirements resulted in uneconomicscales of production and raised the cost of the final production. Second inthose industries where technological innovations could occur rapidly, indigen-ousness of the compcnent industry resulted in a "locked in" effect on thefinal goods. As regards exports, though a variety of incentives wereprovided, they entailed a massive complexity of the schemes, the delays, thetime and money needed to deal with power-conscious bureaucracy. The endresult of all this, was that final impact on private sector industrialdevelopment and the efficiency was much less than it could have been, if tradepolicy regime had undergone reform simultaneously.

il. Equally discouraging and counterproductive was the design of theregulatory reforms. If one step was taken forward towards liberalization, itwas matched by half a step backward to minimize if not completely offset theimpact. This was done by adding a large number of micro conditions to themacro measures, whether the reform related to the large scale organizedindustrial sector or the small. scale industries or their location in backwardregions. This was well illustrated by what was pronounced in the 1990Industrial Policy (though it remained a paper tiger). The effective ceilingon project size for delicensing was raised by 300 percent but at the sametime, a proviso was added that industry-specific delicensing would beeliminated- -i.e. all projects above the size ceiling would be required toobtain license even in Previously delicensed industries. Yet another examplewas that of requirement for Minimum Economic Scale (MES) plants. While theclearance or new investment and most expansion investments conforming to MESstipulation, was automatic, the clearance for projects above MES was not.Similar was the experience in regard to permissible investment in the backwardareas or the small scale industries which were saddled with micro conditionsof one kind or another for availing of every concession offered.

12. The nature of the public sector investment and its uneconomic andinefficient operations detracted considerably from the intended impact of thedomestic deregulation. It was often argued that the private sector industrialperformance was lackluster because of the slowdown in public investment andunless the latter picked up, private sector growth would remain sluggish.However, the public investment that was implicit was in infrastructuralfacilities such as power, communication and transport and not in manufacturingsuch as machinery, steel etc. What actually happened was that the publicsector investment could not increase, where it ought to have, because of the

1/ A Survey of India in the Economist (London), May 4, 1991.

xi

wasteful operation of the public sector manufacturing sector, which failed togenerate internal surpluses. As several studies by Bureau of Industrial Costsand Prices (BICP) have shown, the state owned steel plants, coal mines,

shipyards, machine tool factories and host of similar other enterprises, werebedeviled with egregious overstaffing, obsolete technology, underutilizationof capacity, excessive inventories--allthat would make the enterprise a deadduck. Thus the public investment, even of a desirable kind could notincrease. On the other hand, the high cost of products in vital inputindustries in the public sector was passed on to the captive private sector inthe form of higher prices or higher taxes.

13. Finally, the authorities' piecemeal and firefighting kind ofapproach to domestic deregulation ignored the crucial importance of overdue

labor market reforms. Far from any reform in this sphere, the Governmentsboth central and states were totally apathetic to the problem and took someretrogressive steps such as prohibiting retrenchment in loss-makingindustries. This made not only the exit of loss-making industrial unitsalmost impossible but also prevented other industries which were favorablyimpacted by domestic deregulation from improving their operational efficiencyand to become competitive both in domestic and foreign markets.

14. Nevertheless, the deregulation experiment that India embarked onduring the 1980s, however, faint-hearted was not in vain. It could show in aconvincing fashion what even a small dose of domestic deregulation couldaclhieve in terms of higher industrial performance, economic efficiency,diversity of products and eagerness to compete in international markets. Itopened a window of opportunity to the private sector which exploited theincentives with vigor and when confronted with unresponsive bureaucracies,tried to get round them in legal or illegal ways to demonstrate its intrinsicdynamism. It tested the waters of a less constrictive environment anddeimonstrated to the skeptical government and intelligentsia in general whatcould be accomplished, even with a little chance coming its way. Perhaps themost important benefits that ensued from 1980s deregulation were psychologicaland attitudinal and may help to break the entrenched barriers in the Indianeconomy to rapid growth of the private sector. With new sweeping economicpolicy reforms ushered in by the Government that came to power in June 1991,the Indian private sector may record more efficient growth than in the past.

15. Indonesia, on the other hand, presents a striking contrast to India.The Indonesian experience can be taken as strongly supporting the deregulationpolicies taken in their pristine purity. Its success lay in synchronizing itwith the sound macroeconomic policies, its strong export orientation, theassignment of a central role to the private sector, mutual consistency amongreforms in all areas, trade, financial sector, industrial licensing, land andlabor policy, etc., and deepening the reform process continuously throughextending it to new areas, e.g., maritime deregulation. Appropriate exchangerate adjustment, interest rate deregulation, control of inflation, access toexport credits created the suitable incentive framework, within which theprivate sector could progress rapidly, by exploring new products and newmarkets. Apart from this, the reforms in different areas were not only wellcoordinated but properly sequenced. But for this, the reform process wouldhave stalled either because certain reforms were prematurely set in or certain

others were delayed.

xii

16. With all these reforms, however, Indonesia has not been able toeliminate some other obstacles peculiar to that country, which are even moreformidable than industrial regulatory policies or a trade policy. Unless theyare modified, it cannot be said, in a comparative sense, that Indonesia'sderegulation has progressed faster than in countries like India. First ofthese is the corporate legal framework consisting of antiquated laws unsuitedto modern business practices. The most important weakness of the legalframework has been enforcement of laws which entail several cumbersomeprocedures. So long as these gaps remain, other deregulation measures wouldnot result in achieving what could have been achieved otherwise. Indonesiahas been also amiss in not paying adequate attention to reforms of local levelregulations which have been particularly complex, complicated and incomprehen-sible and have posed more formidable barriers to entry than the investmentlicensing regulations. Since nothing much is done in this area, other majorreforms have been less successful in their intended goals. This throws intobold relief the fact that for any comparative study, the relevance andimplications of restrictive practices, not often captured by commonly adoptedregulatory practices across countries need to be understood in their propercontext. In the absence of information on legal framework and contract lawsin other countries, no meaningful conclusion can be drawn about whether thesecountries performed better or worse than Indonesia.

17. The Philippines' case is typical of how proforma reform processesprogress. It has pursued reform on a wide front--notbold but in a rightdirection. As a result the private sector investment increased substantiallyand a considerable impetus was given to the labor-intensive techniques ofproduction. The export-oriented projects however began to decline because themacroeconomic policies, particularly the real exchange rate policy ran counterto the basic thrust of the reform policies--theexperience not too differentfrom that of India, where the industrial deregulation coincided with worseningof the balance of payments and precisely for the same reasons as in thePhilippines, viz., iLnconsistent macroeconomic policies as reflected inwidening fiscal deficit. The Philippine's experience in regard to foreigndirect investment can be contrasted with that of Indonesia. Both liberalizedpolicies toward foreign investment in intent, incentive and direction but withdifferent results. Indonesia emerged as a beneficiary on a larger scale whilethe Philippines was left on the fringe. The reason was, apart from thepolitical instability which was beyond the control of the authorities, thehesitant implementation of the DFI policy. There was a strong perception thatthe policy operated on a case-by-casebasis, providing misleading signalsabout the discretionary authorities. This was also accompanied by theapprehension about "60-40" rule that restricted foreign ownership in projectsto 40 percent- -againan experience analogous to what happened in India.

18. Sri Lanka typified a case where far reaching economic reforms wereintroduced in 1977, but a pay-off in terms of results was small. This wasbecause the authorities lost the momentum of reforms, being preoccupied withthe problem of macro management of the economy, which became serious due torapid expansion of the public sector and consequent widening of fiscaldeficit. In fact Sri Lanka's experience throws in bold relief the criticalimportance of the need to maintain macroeconomic stability as a preconditionfor the progress and success of reform policies. Sri Lanka's reforms were onwide front-financial sector, trade and industrial sector, but they did notsucceed as much as they could have if the authorities were more adept inmaintaining suitable macroeconomic environment.

xiii

19. Bangladesh represents a somewhat different case where despitegenerous and varied incentive system in regard to foreign investment, theimpact on DIP was moderate. Though in the 1980e, several export-orientedindustries were established, the flow of foreign investment was discouraged bylimited resource base, small domestic market, inadequacy of physical andsocial infrastructural facilities, relatively high production costs, poorlabor discipline and above all the unreliable legal system. In fact thenumber of foreign firms in the manufacturing sector declined. Thisdemonstrates that much more than the formal incentive scheme is required forindustrial promotion and a piecemeal approach to deregulation is perhapscounterproductive. Unfortunately, firmer conclusions about the reform impactsin Sri Lanka and Bangladesh could not be drawn in absence of reliable informa-tion and data.

20. What emerges from the reform experiences in the countries is thatthe impediments in private sector development should not be interpreted asarising from any particular set of policies in a particular area; they areimbedded in the economic and industrial environment, institutional andadministrative arrangements and procedures, lack of internal mobility of laborand capital, and cultural and sociological attitudes. Thus the problem ofimpediment should be seen as a whole and the approach to their removal shouldbe multi-dimensional.

What Do We Learn?

21. First of all, the economies which strive to grow rapidly through amedium of private sector have to maintain macroeconomic balances as indicatedby sustainable balance of payments deficit, minimization of external debt-overhang, declining fiscal deficit and reasonably stable inflation rates. Inabsence of this, a stab at regulatory reforms would not only not yield optimalresults but would in fact weaken reforms. After all, deregulation is notwithout costs in the short and medium term. Since the manufacturing sectorunder constricting regulatory regime develops a great deal of featherbedding,the whiff of reform creates initially viability problems for the sector and ata second remove for the financial sector. This is because the financialsystem, comes under heavy strain and stress with collapsing borrowing industryand ends with a large amount of non-performing loans. Thus the financialcrisis with a large amount of bad loans looms large in normal circumstances inregulated economies but it becomes even more unmanageable if the macroeconomicsituation is adverse to begin with. Apart from this, real incentives for theprivate sector emanate from a stable economic situation which assures growingmarkets, scope for enterprise, and innate urge for seeking profit opportuni-tiies and these incentives are stronger than the disincentives stemming fromre,gulatory system per se.

22. The second lesson is that a holistic approach to deregulation ismore productive than a partial deregulation in any one sphere say inindustrial policy which is divorced from any reform in other areas. If forinstance, domestic deregulation frees industry, it does not reap the competi-tive benefits fully unless the domestic industry faces the challenges frominternational markets. This means, domestic deregulation should proceed Diaassu with liberalization of trade and tariffs. If resource allocation

between traded and home goods is to be influenced, it should better be done byusing economy-wide instruments such as appropriate real exchange rate policy,rather than specific quotas and differentiated tariffs and so on. However,

xiv

the governments in the countries studied except Indonesia have been slow ontrade reforms on the ostensible ground that the major sources of revenue wouldbe lost to the governments with the elimination of tariffs. If that is thecase, then a policy of instituting a uniform tariff across all imports wouldbe a better alternative. That would give separate exchange rates for exportsand imports (without resulting in different exchange rates for differentimports). The merit of such a policy of associating trade reform withdomestic deregulation would have a more efficiency-enhancing impact on thedomestic manufacturing sector.

23. Three, the evidence gathered from the countries also indicates thatit is difficult to resort to selective intervention as a general propositionas opposed to the functional intervention. The critical element in allregulatory policies, especially of selective type which involves favoring onetype of activity over the other competing one is the exercise of discretion.Although some principles or rules can be devised to govern the intervention ofselective type, they tend to become non-operational for two reasons. First itis impossible, even in theory to come up with a set of principles or rule forall myriad categories of regulations that are mutually consistent with themultiple goals of the industrial policy framework, which in themselves are notentirely consistent. This means that the first operating rule mentioned inpara. 4 that any policy regulating private economic activity needs to bepursued if and only if there is a specified set of procedures or criterion forwhat should be included or excluded is often violated. This was borne out bywhat happened in India. Most of the state intervention was devised to assisteither small scale industry or a project helping the poor. In practice, thecoverage expanded so much that selectivity was lost in the process ofimplementation. Thie same was the experience in Indonesia, the Philippines andSri Lanka, where the targeted industries far from benefitting from interven-tion in terms of productivity and profitability, remained in crutches almostperennially. For another, the problem of translating whatever rules there areinto operational decisions is "a problem of orwellian dimensions." Theallocative mechanism is largely in the form of quantitative restrictions. Itis true that regulatory policy of selective type achieved impressive resultsin Korea and Japan. However, much of the success that it met with is to beascribed to the institutional, historical, sociological and cultural factorsspecific to these countries and it is unrealistic to generalize its beneficialimpact for other countries. In India for example, the intervention began withselectivity approachi, in early stages of its development but it soon becamemore generic resulti.ng in perverse incentive system. If a selective interven-tion becomes ineluctable at all, it should be done in such a way that theintervened industries are exposed to market discipline as much as the Koreanindustry was.

24. Four, the regulatory system worked best when it was confined to asmall part of the functioning of industry as the efficiency of regulations isscale-determined. In all the countries covered in the study but more particu-larly in India and Indonesia, the intervention was not only in almost allsegments of industry but also all aspects of their organization. The creditwas regulated, output size was controlled, management was directed, locationwas determined, the marketing of products was planned and all that is done bythe bureaucracy of the Government whose motivations and attitudes weregoverned by law and order ethos of the governance than by commercial andtechnological considerations. Here again, second optimal rule of interventionmentioned earlier was not observed.

xv

25. Five, the promotional policy particularly in regard to small scaleindustry through reservation of products and so on, while being promotionaltowards inefficient industry tends to discourage capacity creation in andcompetition from large scale industry whether or not the product of the smallscale sector is competitive in terms of cost and quality. The mill sector ofIndia's textile industry and its exports were destroyed in part by suchpolicy, while the small scale industry could not stand on its feet. India'sexperience in this arealhas been one of unending woes for the small scalesector. Even after prolonged period of subsidization of all sorts, the numberof small scale units turning sick mounted over the years. If the assuredcredit access to imports and other needed inputs for getting enterpriserunning and going, are maintained as easy and equitable, there is no furtherincentive needed to be provided through reservation of products and throughtaxing of large-scale sector products. The focus should be on access issueand not on subsidies, taxes or reservation.

26. Six, the domestic regulating policy, while being a major impedimentto the private industrial development is one among many. Even more importantmeasures are needed to be directed towards creating a legal and institutionalinfrastructure for the smooth functioning of the private sector. This hasbeen well illustrated by the Indonesian experience. Though Indonesia'sindustrial policy, trade and financial sector reforms were deep and sweeping,they failed to get a full pay-off as Indonesia lagged in changing itscorporate law and other laws vital to trade and industry. Similar was thecase with issues of land and property rights. In some ways, the reform ofthese laws became more imperative than industrial deregulation. Othercountries like the Philippines, Bangladesh may have had these problems but theinformation on their legal framework and property rights could not beobtained. If allowance is made for it, perhaps, their situation may be foundto be even worse than that of Indonesia.

27,, Seven, the policy towards foreign investment has been liberalized inAsian countries but it succeeded most in some like Indonesia in inducinginflow of foreign investment. This means that the intent of the FDI policyand other factors related to it are more important than mere formal liberal-ization of ownership in foreign investment. Oftentimes, the foreigninvestment policy liberalization is accompanied by stipulation of conditionsrequiring foreign firms to export a certain part of their output. While thisis understandable in view of the foreign exchange constraints in thesecountries, it is interpreted by foreign investors as unduly binding on theiroperations. If a free and competitive markets are maintained within thecountries, the foreign firms would naturally remain cost effective, in whichcase their products will automatically compete with similar productsmanufactured internationally and the conditions for compulsory exports willbecome redundant. If the foreign firms are not competitive, then there issomething wrong with a whole set of domestic policies which still stall theemiergence of competitive markets.

28, Eight, reform of regulatory policies is of course an imperative butcredibility of these policies is even more important. It has been a commonexperience in deregulating countries that the policies are often changedbackward and forward, which create a great deal of uncertainty in theinvestor's mind as to whether the new reformed policies would stay the courseor would be reversed. It is therefore necessary that the governments refrainfrom changing the direction of their reform policies once they are set in

xvi

motion. If the authorities consider that economic fundamentals are such thatthey make reversal unavoidable, they should, from the start, introduce reformsin discrete steps so that they would stay put even if economic situationchanges for worse.

29. Ten, the labor market policy changes cannot be shirked if thederegulation is to take hold . Facilitation of exit is as much crucial asentry which is addressed by deregulation. However, the experience shows thatin most countries, there is a certain lethargy in dealing up-front with laborretrenchment which inevitably follows deregulation. Much can be learnt inthis regard from thie Swedish labor market policies. Anticipating laborretrenchment, the government can organize retraining programs for retrenchedlabor to prepare them for new kinds of jobs, through paying them remunerationless than the wages in the previous employment. In addition to this, employ-ment schemes paid for with wage goods, tried in countries like India can beimplemented. In short, labor market reforms should be considered as a sinaqua non of the industrial policy reform.

30. Eleven, though all the countries under examination had introduced avariety of incentive schemes - fiscal, credit, marketing and technical, theywere either inadequate or overborne by a set of direct regulations . If theemphasis were mainly on the former, the rent seeking could have been much lessand industrial growth would have been higher. As observed the countries usedindustrial licensing and price and foreign controls as the main instrumentsfor directing investment; allowing the manufactures to indulge more incircumventing these controls rather than in producing what was targeted by thestate.

31. Twelve, most of the regulations used and implemented underlinedbroad goals about industries to be promoted and the assistance provided tothem, while details of these policies were enshrined in rules and regulationsknown only to those who administered those policies. This was particularly soin regard to industrial licensing and foreign exchange allocations and thepolicies to ward foreign direct investment. This lack of transparency inregulatory mechanisms, gave undue powers to the administration and encouragedthe special interests group in the private sector to appropriate licenses orforeign exchange allocations through personal contacts with the concernedauthorities. The most glaring example of this was that of India. There wasbroad eligibility criteria for issue of industrial licensing, which emphasizedwide dispersal of owinership of industry. However, as it turned out, thelicenses issued got concentrated in only a few big industrialists, therebydefeating the very criterion used to prevent it.

32. Finally, this paper recognizes but could not discuss for want ofinformation how much importance should be attached to the transaction costsarising from interactions between the private sector and the Government on theone hand and those between different firms within the private sector. It iswidely believed that transaction costs, described also as "cost of doingbusiness" may be even a more deterring factor for industrial growth than theregulatory policies. With the reduction of these transaction costs, therigour of regulations may not be felt to the same extent as is generallybelieved. One study, though preliminary, found that there is a regularcorrelation between the cost of communications - a particular subject of

xvii

transaction cost and export growth.2/ For lack of required data for the

countries, these hypotheses could not be tested, though there is a strong casefor in in-depth study of this aspect in any liberalization policies that areto be formulated for the developing countries or countries in transitions from

a socialist to market oriented system.

2/ D. Laland U. Patel, "Transaction Costs or the Cost of Doing Business.Empirical Estimates for Some Developing Countries" (Unpublished) 1992.

I. INTRODUCTION

1.1 In the early thinking on the economic problems of developingcountries and development policy, there was a pronounced bias in favor of thepublic sector as an instrument of development and income distribution andgovernmental intervention to regulate the incipient private sector so as makeit conform to the certain predetermined investment priorities. A strong faithin the Government's power was reinforced by the inchoate stage of privateenterprise and initiative in the early phases of development, uncongenialeconomic environment, inadequacy and rigidities of the money and capitalmarkets to finance new enterprises and the lumpiness of new investments.

1.2 There has been recently a marked turnaround in the approach todevelopment policy. The realization that policies, with a subordinate roleassigned to the private sector introduced many unintended distortions in mostof the developing countries, which culminated ineluctably in an all round risein economic and social costs of development, thereby drying up the mainspringsof productivity growth. The accumulated experiences of a relative failure ofthe public sector including its regulatory policies acquired sharpness ofrelevance when the centrally planned economies with comprehensiveinterventionist regimes, collapsed in quick succession. The unresponsivebureaucracy, a maze of controls and regulations, unaccountability inmanagement and the inability to react to changing opportunities and pricesignals, both internal and external tended to sap the vitality of theeconomies and as a result these countries reached a point of no return. By arule of elimination, therefore, a sustained and dynamic development of theprivate sector became an only viable option for the progress of theseeconomies.

1.3 There were also positive factors which imparted urgency to relianceon the private sector as the main engine of growth. The rapid development ofthe newly industrialized countries in Asia (NICs) demonstrated the vigorousnature of the private sector-led growth and the legitimate role of thegovernment in clearly defining rules to intervene in cases of market failureand in provision of public goods, including legal and institutionalfoundations, education and certain infrastructural investment. The otherdevelopment was that international markets became more integrated with greatermobility of factors of goods, more efficient flow of information and rapidtechnological change so that any country desiring to progress had to develop acapacity to respond, in a rational way, to international prices, costs andtechnical changes.

1.4 Recognizing this new configuration of economic and institutionalforces, developing countries, came to focus on the importance of stablemacroeconomic environment free from constricting trade, financial andindustrial regimes in order to facilitate growth of the private enterprise.

1.5 The principal objective is to study the domestic regulatoryapparatus in five Asian countries, India, Indonesia, Sri Lanka, thePlhilippines and Bangladesh, for a critical examination of how it has affected

- 2 -

the private industrial sector development. The selected countries are invarious stages of modifying their domestic regulatory policies. An attemptwill be made to synthesize their experiences in such a way that more generalpolicy conclusions can be drawn by policymakers as well as Bank staff foraccelerating private sector industrial development. The regulatory policieswill be discussed under five topics: (a) industrial licensing; (b) pricecontrol policies; (c)> labor market policies; (d) policies directed towardsforeign private investment; and (c) the promotional policies in regard toprivate sector development. There are other obstacles to the industrialdevelopment but they could not be discussed for want of relevant information.Left out also will be other major factors such as trade and financial sectorpolicies. These are important, but there are already Bank documents onfinancial restructuring and trade policy loans. Their linkages with domesticregulatory policies will be nevertheless referred to briefly in appropriatecontexts.

1.6 Section II will present a broad empirical framework in which privatesector development, its determinants, its links with economic growth and thelimits of governmental intervention to regulate the private sector, can beviewed in their interconnectedness. This provides a backdrop to thesubsequent country specific and inter-county experience in regard to theimplementation and consequences of domestic regulatory policies. Perspectivesprovided by this discussion on private sector development will hopefullydemonstrate that the need to orient economic policies to facilitate privateinvestment comes from the experiences of the developing countries over asufficiently long period and not from the subjective judgements or ideologicalpreferences. Section III describes the macroeconomic contexts of thecountries' covered to emphasize that in the absence of appropriate economicenvironment, deregulation by itself would not help to promote privateinvestment. Likewise, the key features of trade and financial policies willbe highlighted and the progress made in liberalization of those policies willbe referred to in so far as they have a bearing on domestic deregulation.

1.7 Section IV deals with domestic industrial regulatory policies ineach of the countries allowing a comparative perspective. Discussion willcenter, mainly, on how these regulations are implemented and theirconsequences for private industrial sector investment. Section V will focuson reform episodes and how they have impacted on the private industrialsector. In order to measure the impact, criteria such as concentrationratios, effective protection, domestic resource cost, total factor as well aslabor productivity are used, depending upon data availability. To the extentpossible, individual country studies, in appendices to the main text, will beused in comparing experiences at a micro level.

II. PRIVATE SECTOR DEVELOPMENT. ITS DETERMINANTS AND ROLE OFGOVERNMENTAL INTERVENTION - AN EMPIRICAL FRAMEWORK

2.1 With growth failure in a wide range of developing countries inrecent years and a striking success in only a few, convictions of theeconomists, policy makers and the multilateral lending institutions have grown

in favor of greater reliance on the market in the allocation and use ofresources. This has come to imply that a sustained higher rate of economicgrowth requires stable and traditional macroeconomic policies, liberalizationof goods and factor markets, greater flexibility in the operation of financialsystems and an enhanced role for the private sector in economic management1/In what follows, this empirical evidence on all possible obstacles will beanalyzed drawing on the existing body of research so as to bring in sharprelief of what determines the development of the private sector and thereforegrowth in the developing countries.

Private Investment and Economic Growth

2.2 In a recent study by Khan and Reinhart 2/ a simple growth model isf-ormulated for a cross-section sample of 24 developing countries i./ duringthe 1970s to estimate separately the effects on growth of public sector andprivate sector investment. Until recently, not much was known of theempirical relevance in the developing world of a bias toward the privatesector, except in regard to a positive relationship between trade andfinancial liberalization on the one hand and economic growth on the other.The latter relationships are normally perceived as operating through increasedprivate saving and investment. Now new research in the field of developmenteconomics has brought ample statistical evidence to show a strong and positiverelationship between the private sector activity, particularly private sectorinvestment, and economic growth. It has also by now become clear that public:Lnvestment, except when it is in infrastructure tends to crowd out private:Lnvestment. The sample chosen is so diverse that the conclusions based on itcan be taken as sufficiently valid for many Asian developing countries. Themodel yielded results strongly supporting direct policy measures and indirectones aimed at removing the impediments to private sector development.

2.3 First of all, the private investment plays a dominant role in growthprocess. This means that public investment of omnibus type covering.manufacturing activities has generally no direct effect on growth except inextremely underdeveloped economies and the direct effects of privateinvestment far outweigh those of the public sector investment. In most of the:24 developing countries which include Indonesia, Sri Lanka and NICs, with theIhighest average ratios of private to total investment also recorded the

*lJ Corbo V., Goldstein M and Khan M.S. (eds), Growth Oriented AdiustmentPrograms (Washington, DC. International Monetary Fund and the WorldBank, 1987)

2J Khan M.S. and Reinhart C., "Private Investment and Economic Growth indeveloping countries" World Development volume 18, Number 1.Januaxy. 1990.

3J The countries are Chile, Haiti, Argentina, Bolivia, Sri Lanka, Panama,Honduras, Trinidad and Tobago, Mexico, Venezuela, Barbados, Guatemala,Columbia, Turkey, Costa Rica, Dominican Republic, Indonesia, Ecuador,Thailand, Malaysia, Paraguay, Brazil, Singapore and South Korea.

- 4 -

highest average growth rates. Second result with even wider significance, isthat the productivity growth, arising from factors and technical change ishigher in respect of private investment than in public investment. Thecapital in private investment contributes to productivity, while capital'scontribution in public investment is negative and therefore offsets thecapital productivity in private investment. Judging by several criteria, beit contribution to growth or the increase in factor productivity, or outwardmarket-orientation of the production system or technical change, the privateinvestment has been shown empirically to score over the public investment indeveloping countries. These results generally conform to the experiences inthe industrial countries,/ indicating thereby that the growth process, doesnot vary significantly as between developed and developing countries.

2.4 While private sector investment is shown to be efficiency-superiorto public investment, there are certain exceptions. Public investment ininfrastructure, like roads, communication, etc., far from crowding outprivate investment and offsetting the private sector's contribution to growth,actually complements the private investment and consequently helps to enhancefactor productivity. Only public investment in manufacture competes withprivate investment for resources and markets. Since its contribution isnegative in this type of activity, overall growth is adversely affected.V.

Macroeconomic Determinants of Private Investment in DeveloRing Countries

2.5 The rate of private investment is determined by a host of factors.The regulatory industrial, trade and financial sector policies are only someof them. Unless other factors, in a way more fundamental, work in favor ofprivate sector development, modification of regulatory policies by itself,while helpful, will fail to deliver much. Hence, there may not be one to onerelationship between removal of regulatory impediments and private investmentgrowth. On the basis of the experiences of the industrial countries duringthe last four decades:, the macroeconomic determinants of private investmentare identified as (a) macroeconomic stability as represented by low inflationrate; (b) economic growth and per capita income level; (c) the level of realinterest rates; (d) the debt-service ratio or the magnitude of external debtin relation to GDP; and (e) the rate of public sector investment. For ahealthy private sector promotion, a stable macroeconomic environment is aprecondition; it covers a whole range of variables such as fiscal balance andexternal balance. High inflation rate which can be taken as a proxy formacroeconomic stability or lack of it adversely affects private investment byincreasing the riskinetss of longer-term investment projects, reducing theaverage maturity of commercial lending and distorting the information content

Chenery H., Robinson S., and Syrquin M., Industrialization and Growth. AComparative Studv (Washington, D.C., Oxford University Press for theWorld Bank), 1986.

2/ Blejer M. and Khan M.S. "Government Policy and Private Investment inDeveloping Countries "IMF Staff PaDers, Vol. 31, Number 2, June 1983.

5 -

of relative prices. For this reason the relationship between high domesticinflation and private investment is expected to be negative. The per capitaincome, on the other hand, is considered to be a positive function of privateinivestment because at higher level of incomes, more is saved and invested. Asfor the real interest rates, there should be a positive relationship betweenthe real deposit rates and private investment contrary to what was believedearlier on the basis of a neoclassical theory of investment. With high levelofE real interest rates, the private investors are encouraged to accumulatelarger money balances before undertaking investment projects because of thelimited access to credit and equity markets. Finally, the presence of a largeexternal debt burden is considered to adversely affect private investmentbecause large debt-service payments preempt savings required to financeinvestment, a high ratio of external debt to GDP reduces the incentive forinvestment i/ and difficulties in meeting debt-service obligations, tend toreduce the trade financing a country obtains. As regards the publicinvestment, it helps promote private investment, only if it is ininfrastructure as observed earlier. The evidence on these relationships hasbeen addressed both by observing the average values during the period of 1975-87 in twenty-three developing countries 2/ with above and below averageprivate investment rates and by rigorous econometric tests for the samecountries and for the same period.I/ There is support for the expectedrelationship between private investment and the five factors specified above.

Limits of Goverement Interventio

2.6 In addition to the economic determinants of private investment,there are other factors such as Government intervention which helps or hampersprivate sector development. The governments in developing countries haveaLdopted a wide array of instruments of intervention like industrial licensing,trade and price controls, labor market regulation etc., on the ostensibleground of promoting the private sector. Their generalized experiences overalmost four decades was unsavory. On the other hand, in a few countries, morestrikingly the newly industrialized countries in Asia (NICs), the emergingdlevelopment picture was totally different. The activist state, going beyondthe prescribed neutral regulatory regime of neoclassical vintage, has played acatalytic role in strengthening the crucial learning process and offsettingthe externalities, in addition to being a surrogate for missing capitalmnarkets as well documented by Westphal.2/ However, the charisma for

§/ Froot K., and Krugman P., Market Based Debt Reduction For DevelopingCountries: Principles and Prospects (Unpublished) Cambridge, Mass.:National Bureau of Economic Research, 1990.

Z/ The 23 countries are Argentina, Bolivia, Brazil, Chile, Columbia, CostaRica, Ecuador, Guatemala, India, Kenya, the Republic of Korea, Mexico,Pakistan, Peru, the Philippines, Singaporo, Sri Lanka, Thailand, Tunisia,Turkey, Uruguay, Venezuela and Zimbabwe.

l/ Greene J. and Villanueva D., *Private Investment In Developing Countries:An Empirical Analysis' IMF Staff Pagers, Vol. 38, Number 1, March 1991.

i/ Westphal L., "Industrial Policy in an Export-propelled Economy: Lessons

-6-

interventionist policies, overtly similar to those the NICs followed, but withtotally retarding and retrogressive consequences, has worn off. It is nowrealized that the earlier plea of development economists for interventionistregime was not enouglh, as one has to grapple with the issue of micro-management of the invested capital and the organizational and incentiveaspects of facilitating the learning process.

2.7 Focussing on the legitimate role of the instruments of interventionhelps to gain a perspective on why these instruments tend to overreachthemselves, losing sight of their assigned tasks in the process. Theseinstruments have conspicuously succeeded, when they have worked closely andcontinuously with the markets, and when the states remained alert using thesignals emanating from world markets, to maintain dynamic efficiency in firmsand to prevent thereby infant industries from turning into inefficientgeriatric lobbies.1Q/t However convinced one may be of the pervasiveness ofmarket failures in developing countries, one must recognize the vitaldisciplining function of competition in encouraging quick learning and costand quality consciousness.

2.8 Admittedly, the success of intervention schemes, where it occurredhas to be ascribed to certain historical, sociological and societal factors,which are specific to certain countries and cannot be easily replicatedelsewhere. In general, there has been a substantial evidence that failure ofGovernment, when it intervenes is larger in scale than the marketfailures.;lj The reasons for government failure are to be found in theself-centeredness of the agents of governments which administer the policies,the lack of benevolence of government as an institution and the high cost ofgovernment intervention. First, when economic interventions create somethingthat is to be allocated at less than its value by any kind of governmentprocess, resources will be invariably diverted to capture the rights to theitems of value. It generates rent-seeking and what is relevant is that theeconomic cost of many policies--minimum wages, legislation, import licensing,quantitative restrictions, credit rationing, etc.--are far greater when rent-seeking takes place than traditional welfare cost analyses would indicate. Insome instances, policies that might appear desirable to meet noneconomicobjectives, or even to correct "market failures," may result in a situationeven less satisfactory than that prevailing before the policy was put in play.

2.9 Second, whenever a government policy has clearly identifiablebeneficiaries and/or victims, those groups will tend to organize in support or

from South Korea's Experience". The Journal of Economic Perspectives,Vol. 4, Number 3, Summer, 1990.

1Q Bardhan P., "Symposium on the State and Economic Development". TheJournal of Economic PersRectives, Vol. 4, Number 3, Summer, 1990.

1J/ This discussion draws on Anne Krueger's interesting contribution to thesymposium on "The State and Economic Development" that appeared in "TheJournal of EconoMic Literature, Vol. 4, Number 3, Summer, 1990."

opposition to the policies and then lobby for increasing the value of the gainor reducing the value of the losses from those policies. An initial politicalequilibrium may not be a long term equilibrium, as newly formed pressure orinterest groups work increasingly for favorable, or less favorable treatment.For example, once a system of protection against imports is in place,protected producers will generally lobby for higher tariffs and/a lowerquotas, using contrasts with other levels of protection and other arguments.Likewise, initially unprotected groups will begin lobbying for protection, onthe ground, that this case is at least as strong as that of already protectedinterest. More generally, there will be a tendency for increasingproliferation of categories and of policy instruments as various groups assertconflicting and competing claims and this proliferation should be counted as acost of the original policy.

2.10 The group normally administering the policies comes into existence,if no other unit was in existence or if it does, it is expanded with newpowers. Either way, a part of the government usually becomes an advocate formaintaining functions involved and in many cases, extending them. Thoseadministering the policies necessarily believe that they are doing somethingimportant, and also know that discontinuance of the function would result in aloss of jobs for some and of bureaucratic power for others.12/

2.11 Third, it is necessary to differentiate between the interests ofdifferent groups and institutions within the Government. Those organizationsof the Government which are preoccupied with spending will spawn programs andpolicies for access to more funds, while the controlling ministries such asfinance ministries would try to curb them. In this respect ideology becomingan important determinant of what is and what is not generally acceptable.Obviously in democratic societies, policymakers within governments haveautonomy only in so far as the voters acquiesce in their activities, whetherthat permission is of out of ignorance or out of sanction for their activity.InI non democratic regimes, the question of such permission does not arise; thepolicy making bureaucracy is the final arbiter.

2.12 Apart from these inadequacies of Government in managing marketfailure situations, there are certain deficiencies endemic to the regulatorymechanism itself. First there are the sources of misinformation - informationasymmetrics between regulations and those affected by regulations, whetherproducer or consumers; regulatory rigidities that grow out of the tendency forproducers and consumers to develop property rights in particular regulatory

12V Political scientists call it an "iron triangleu of bureaucrats,politicians and voters. The bureaucrats have interest in extending thisscope of their activities, making them visible to the voters; politiciansseek re-election and thus support or at least do not oppose bureaucraticactivities supporting services to the constituents. Voters are madecognizant of the services by bureaucrats and therefore support both thebureaucrats and the politicians (see for application of this concept toIndia. J. Bhagwati, "Poverty and Public Policy", World DeveloDment, May1988).

- 8 -

outcomes; the unintended consequences of what can be called "regulatory firefighting" reacting to unanticipated side effects of previous regulatoryactions and the pursuit of self-interest by those responsible for regulations.The regulatory asymmetry arises because producers have a far greater knowledgeof average and marginal costs, changes in technological conditions and oftheir own degree of managerial inadequacies than do the regulators. Bymanipulating information-access to their advantage, they are able to distortthe regulatory process. The rigidity stems from the fact that the regulatoryapparatus cannot ad'just in response with speed, when economic conditionschange and then involves the economic system in losses. The third type ofregulatory misdirection and regulatory fire-fighting arises because regulatorysystem is often constructed on the premise that regulated entities and theircustomers and competitors will respond passively to regulations, whereasprofit maximizing behavior generally requires that they invest resources tomitigate regulatory impact. This leads to a creeping regulation, a situationin which more and more complex, costly and far-reaching regulations becomeunavoidable to achieve the original regulatory goal.

2.13 The question therefore is whether the regulatory mechanism can bejettisoned altogether for the many errors of commission or there is somepractical way for sc operating it as to minimize its deleterious featuresaffecting progress of the private sector. Though doing away with regulatorypolicy is the first best policy, it is rarely feasible in the world of realpolitick. Therefore, certain optimal rules of operating regulatory systemwithout its misdirection can be conceived, both on the basis of practicalnecessity and economic efficiency. First of all, any policy affectingallocation of resources, and regulation of private economic activity, needs tobe pursued if and only if there is a specified set of procedures or criteriafor deciding what fits within the defined scope of the enunciated economicpolicies and also an administrative apparatus for implementing that policy.It would help to make a judgement as to the administrative cost andfeasibility of the activity as well as the likelihood that political pressureswill quickly alter the initial chosen process. Second, even when there is astrong presumption in favor of government intervention and conditions favoringits effectiveness, it is imperative to limit it to minimum necessary scalebecause once the intervention enters the scene, it develops a life of its own,diverting some scarce management skills away from where they have greatercomparative advantage. Third, from amongst the available alternativeregulatory sets, it is necessary to go in for one which will provide the leastscope for rent-seeking. This may imply that policies directly controllingprivate economic activity are likely to be less efficacious in terms ofachieving their objectives than policies that offer incentives for individualsto embark on activities which are considered desirable. In other words,intervention policieis aiming at strengthening markets for goods and factors,through incentives are better than control laded intervention policies.Finally, a choice of regulatory policy involving lower information cost andtransparency is a preferred alternative. When the costs of a policy areobscure, special interests in the private sector and government have a greateropportunity to use those policies for their own advantage without incurringthe disapproval of voters and the politicians.

9-

2.14 The broad conclusion that emerges from the foregoing is that whilemarket failure is a pervasive phenomenon in a large number of developingcoamtries, a strong government intervention is not an answer to remove themarket failure. As discussed earlier in this section, economic growth isfaster under conditions of private initiative because productivity growthcomes not only from capital but also technical change and exports. Itsfundamental determinants among others are--low inflation rates, positive realinterest rates, high per capita increase and low foreign debt service ratio.This means that any regulatory policy, if at all deemed essential andunavoidable should be such, in form, substance and direction that thesefundamental determinants of private investment are not stifled. In otherwords, the regulatory policies should be allowed to draw sustenance from theefificiency laden economic determinants, the competitive forces spurring moreinnovations and cost-reducing measures. The question therefore is not whethermarket failure should or should not be met by government intervention; ratherthe issue is how to formulate essential regulatory policies which seek marketguLdance in transmitting their impact on private investment in developingcountries. It is the later which will be discussed in the following sectionsin the light of the empirical and analytical insights presented in thissection.

-10 -

III. MACROECONOMIC ENVIRONMENT AND TRADE AND FINANCIAL REFORM POLICIES

3.1 In this section, a beginning will be made with discussion ofmacroeconomic variables affecting investment and growth to be followed by areference to the trade and financial sector policies in order to spotlighttheir linkages with the domestic regulatory policies - the main focus of thispaper. A comprehension of the interconnectedness of various determinants ofthe private investment and financial sector and trade policies lends aperspective for a realistic assessment of the impact of changes in domesticregulatory policies on the private sector development.

Macroeconomic Environment

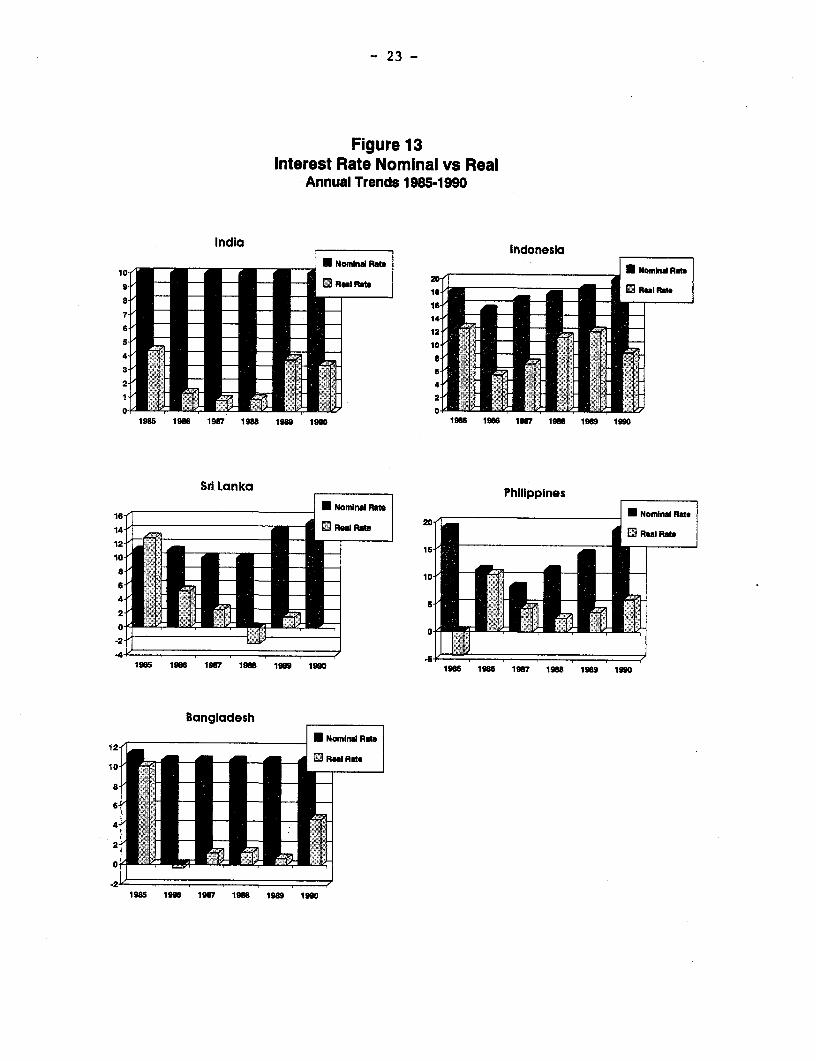

3.2 Macroeconomic picture of the five countries since 1970s is presentedin Figures 1-14a. In terms of macroeconomic situation, Indonesia has beenable to maintain a better record since 1980, which contributed to the speed ofthe reforms of its trade, financial and industrial regulatory policies.India, after a long period of stable macroeconomic environment ran intoserious imbalances in the later half of 1980s - precisely the period when itembarked on industrial deregulation. The Philippines, Sri Lanka, Bangladeshwent through undulating macroeconomic situations during the 1980s, which,while interfering with their economic reform policies, did not scupper them.In fact, despite the adverse macroeconomic situation, these countriescontinued their reforms with varying degree of success.

3.3 India was perhaps the first among developing countries whichembarked on economic development as a deliberate policy in the post-secondWorld War period. 'Yet India's secular growth rate, when seen in relation togrowth rates in some of the developing countries, has been modest at best, anddisappointing at worst. Thus the average real growth rate was only 2.9%during 1961-70, rose to 3.5% during the 1970s: It was only during 1980s whensomewhat liberal trade, financial and regulatory regimes were ushered in thatthe growth rate picked up to the highest decade-wise average of 5.7%, Indiaever experienced. Gross domestic investment as a ratio of GDP reached thehighest level of 23.9% during a decade of 1980s. However, the productivity ofinvestment remained low throughout. The marginal capital/output ratio,inverse measure of investment productivity consistently decreased from 5.40 in1970s to 4.45 in the 1980s. Alongside with rising investment, domestic savingalso rose impressively until mid 1980s, when it reached 23% of GDP and thoughit declined somewhat--mainly due to dissaving by Government sector, remainedhigh by international standards.

3.4 Macroeconomic stability was a characteristic of the Indian economyuntil the early part: of the 1980s, despite large fiscal and external accountdeficits. However, as fiscal deficit began to surge up during the 1980s, the

- 11 -