02 03 What Is An Audit PM 00

24

A U D I T What is an Audit? What is an Audit?

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of 02 03 What Is An Audit PM 00

A U D I T

What is an Audit? What is an Audit?

WHAT IS THE FIRST THING YOU THINK OF WHEN YOU HEAR THE WORD…

AIRPORT

AGENDA What is an Audit? The concept of Materiality and What it Means on the Audit

Why Do We Perform an Audit? Format of the Financial Statements Users of Financial Statements Learning points

AGENDA What is an Audit? The concept of Materiality and What it Means on the Audit

Why Do We Perform an Audit? Format of the Financial Statements Users of Financial Statements Learning points

THE PURPOSE OF AN AUDITThe purpose of an audit is to enhance the degree of confidence of intended users in the financial statements. This is achieved by the expression of an opinion by the auditor on whether the financial statements are prepared, in all material respects, in accordance with the applicable financial reporting framework.

[clarified ISA 200.3]

EXERCISE – 3 MINUTES What does this term mean on an audit?

“Reasonable assurance”

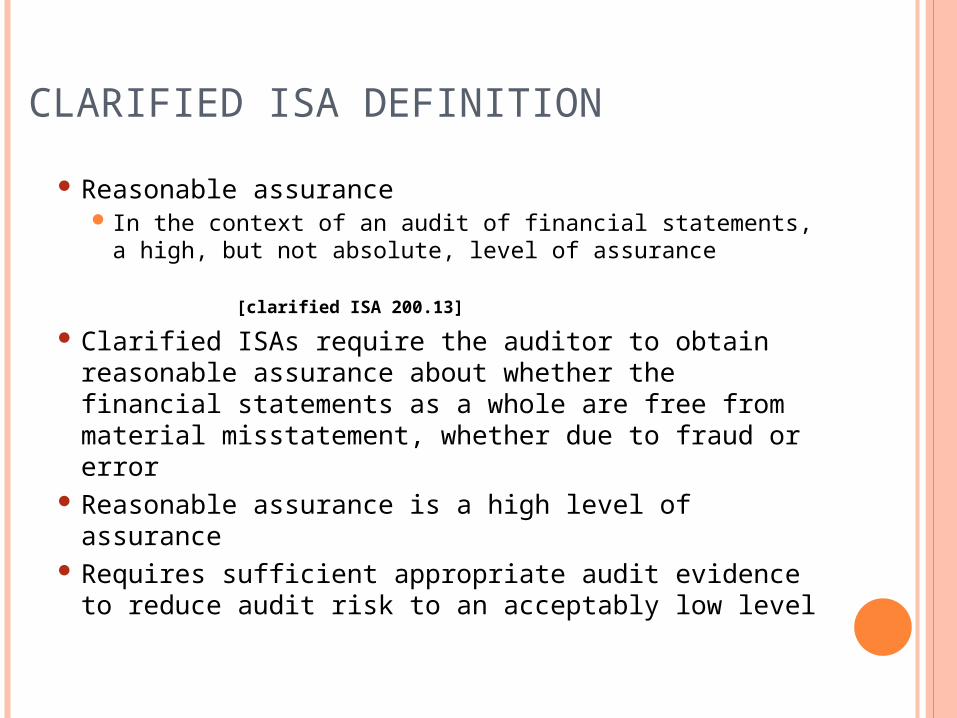

CLARIFIED ISA DEFINITION Reasonable assurance

In the context of an audit of financial statements, a high, but not absolute, level of assurance [clarified ISA 200.13]

Clarified ISAs require the auditor to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error

Reasonable assurance is a high level of assurance

Requires sufficient appropriate audit evidence to reduce audit risk to an acceptably low level

INDEPENDENCE

In mind In appearance

and…

WHICH COLUMN BEST DESCRIBES THE RESPONSIBILITIES OF AN AUDITOR?

♦Confirms that the financial statements present a true and fair view

♦Corrects all errors in a set of financial statements

♦Involves checking all the controls in an organization to ensure they are working effectively

♦Is responsible for identifying instances of fraud

♦Gives an opinion on whether a set of financial statements give a true and fair view

♦Gives an opinion as to whether the financial statements are prepared in all material respects in accordance with an applicable financial reporting framework

♦Is not responsible for identifying all instances of fraud, but material misstatements, whether due to fraud or error

OVERALL OBJECTIVES OF THE AUDITOR Objectives

Obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error

Express an opinion on whether the financial statements are prepared, in all material respects, in accordance with an applicable financial reporting framework

To report on the financial statements, and communicate as require by the ISAs, in accordance with the auditor’s findings

[clarified ISA 200.11]

♦Responsibilities −Remain independent

−Maintain an attitude of professional skepticism

−Apply professional judgment

−Conduct audits in accordance with the clarified ISAs

AGENDA What is an Audit? The concept of Materiality and What it Means on the Audit

Why Do We Perform an Audit? Format of the Financial Statements Users of Financial Statements Learning points

MATERIALITY Materiality is an amount that represents the size of an omission of misstatement in the financial statements that, in light of the surrounding circumstances, could reasonably be expected to influence the economic decisions of users of financial statements

In general, misstatements, including omissions, are considered to be material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of the financial statements. [clarified ISA 200.6]

MATERIALITY

Materiality $100,000Influences economic decisions of users

Performance Materiality (PM) $70,000

Use to plan and perform our audit .

Audit misstatement

posting threshold (AMPT)

$4,000Summarize audit misstatements over this amount

Figures used for example purposes only

AGENDA What is an Audit? The concept of Materiality and What it Means on the Audit

Why Do We Perform an Audit? Format of the Financial Statements Users of Financial Statements Learning points

WHY DO WE PERFORM AN AUDIT? Users of financial statements Legal and regulatory requirements Financial reporting framework Internal and external reviews Independent audit report

KEY COMPONENTS OF AUDIT REPORTS Title and addressee Introductory paragraph Management’s responsibility for the financial statements

Auditor’s responsibility Auditor’s opinion Other reporting responsibilities Signature of the auditor Date of the auditor’s report and auditor’s address [clarified ISA 700.21-42]

TYPES OF AUDIT REPORTS Unmodified opinion Modified opinion

Qualified Adverse Disclaimer

Modified report Emphasis of matter

AGENDA What is an Audit? The concept of Materiality and What it Means on the Audit

Why Do We Perform an Audit? Format of the Financial Statements Users of Financial Statements Learning points

COMPARATIVE INFORMATION - CLARIFIED ISA 710 The auditor should obtain sufficient appropriate audit evidence about whether the comparative information included in the financial statements has been presented, in all material respects, in accordance with the requirements for comparative information in the applicable financial reporting frameworkDoes comparative information agree with the amounts and disclosures presented in the prior period (provided no restatements)?

Have consistent accounting policies been applied in the current and comparative period (provided no policy changes)?

OTHER INFORMATION – CLARIFIED ISA 720 The financial statements and auditor’s report may be presented together with other unaudited information

The auditor shall read the other information to identify material inconsistencies, if any, with the audited financial statements

Determine whether the audited financial statements or the other information needs to be revised

AGENDA What is an Audit? The concept of Materiality and What it Means on the Audit

Why Do We Perform an Audit? Format of the Financial Statements Users of Financial Statements Learning points

AGENDA What is an Audit? The concept of Materiality and What it Means on the Audit

Why Do We Perform an Audit? Format of the Financial Statements Users of Financial Statements Learning points

WHAT HAVE YOU LEARNED? The objective of an audit is to enhance the confidence of users of the financial statements

An expectation gap exists between the purpose of an audit under clarified ISAs and what the public understands as the auditor’s role

The responsibilities of an auditor, including giving an opinion on whether

a set of financial statements give a true and fair view

WHAT HAVE YOU LEARNED? (CONTINUED) The auditor obtains reasonable assurance, not absolute assurance

Materiality helps us to determine our audit procedures, assess misstatements, assess results of procedures and determine appropriate audit opinion

The auditor may issue an unmodified or modified audit report depending on the circumstances of the audit

Our audit includes consideration of comparative information and other information included with the financial statements

There are various users of the financial statements