Makalah Aktiva Tetap

31

PT. KAMAN SEJAHTERA Jalan Serang Raya No. 01, Banten Jawa Barat Disusun Oleh : KARTIKA XI AKUNTANSI 1

-

Upload

kartikarodhatul -

Category

Documents

-

view

99 -

download

2

description

kartika

Transcript of Makalah Aktiva Tetap

PT. KAMAN SEJAHTERAJalan Serang Raya No. 01, Banten Jawa Barat

Disusun Oleh :KARTIKA

XI AKUNTANSI 1

Puji syukur saya panjatkan kepada Tuhan Yang MahaKuasa, atas limpahan karunia, rahmat, taufik dan hidayah-Nya dalam mengabdi dan menyumbangkan pikiran untuk nusa, bangsa, dan negara, khususnya melalui bidang pendidikan.

Sesuai dengan judulnya fixed assets (Aktiva Tetap), maka makalah ini sangat sesuai untuk dipakai selain siswa SMK Kelompok Bisnis dan Manajemen ( semester l dan ll ), juga oleh orang yang ingin memahami penyusutan aktiva tetap atau siapa saja yang dalam pekerjaannya dan jabatannya secara langsung maupun tidak langsung berhubungan dengan proses/hasil pekerjaan akuntansi.

Dalam kesempatan ini saya mengucapkan terima kasih kepada semua pihak yanglangsung maupun tidak langsung memungkinkan terbuatnya makalah ini.

Seperti kata pepatah “ Tidak Ada Gading Yang Tidak Retak”, maka buku inipun saya yakini masih banyak kekurangan meskipun saya telah berusaha menyusunnya sebaik mungkin, untuk itu saya mohon maaf dan saran serta kritik untuk perbaikan makalah ini dalam penerbitan berikutnya sangat saya harapkan, untuk itu sebelum dan sesudahnya disampaikan terima kasih.

Akhirnya semoga makalah ini bermanfaat bagi siapa saja yang membacanya, khusus bagi yang ingin memahami AKTIVA TETAP untuk Perusahan Dagang.

Jakarta, Oktober 2013Penulis

Kartika

KATA PENGANTAR 1

AKTIVA TETAP :a) PENGERTIAN 4b) CIRI-CIRI 4

PENYUSUTAN :a) PENGERTIAN 4b) MACAM-MACAM 4c) FAKTOR PENYUSUTAN 4

METODE GARIS LURUS :a) PENGERTIAN 5b) RUMUS 5c) CONTOH SOAL 5

METODE JUMLAH ANGKA TAHUN :a) PENGERTIAN 7b) RUMUS 7c) CONTOH SOAL 7

METODE SALDO MENURUN GANDA :a) PENGERTIAN 9b) RUMUS 9c) CONTOH SOAL 9

METODE UNIT PRODUKSI :a) PENGERTIAN 11b) RUMUS 11c) CONTOH SOAL 11

METODE JAM KERJA :a) PENGERTIAN 13b) RUMUS 13

c) CONTOH SOAL 13

PENGHENTIAN AKTIVA TETAP :a) PENGERTIAN 15b) MACAM- MACAM 15

PENGHENTIAN DIBUANG :a) PENGERTIAN 16b) CONTOH SOAL 16

PENGHENTIAN DIJUAL :a) PENGERTIAN 17b) CONTOH SOAL 17

PENGHENTIAN TUKAR TAMBAH SEJENIS :a) PENGERTIAN 18b) CONTOH SOAL 18

PENGHENTIAN TUKAR TAMBAH TIDAK SEJENIS :a) PENGERTIAN 20b) CONTOH SOAL 20

DAFTAR PUSTAKA 22

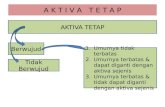

Aktiva tetap adalah aktiva berujud yang digunakan dlaam operasi perusahaan dan tidak dimaksudkan untuk dijual dalam rangka kegiatan normal perusahaan. Aktiva semacam ini biasanya diharapkan dapat memberi manfaat pada perusahaan selama bertahun-tahun. Manfaat yang diberikan aktiva tetap umumnya semakin lama semakim menurun, kecuali manfaat yang diberikan oleh tanah.Aktiva tetap memiliki ciri-ciri sebagai berikut :

a) dibeli atau dimiliki oleh perusahaan dengan tujuan untuk membantu operasional perusahaan dan bukan untuk tujuan dijualkembali.

b) harta tetap ini dapt dipakai atau dimanfaatkan secara berulang-ulang.

c) umur manfaat dari harta ini lebih dari satu tahun.

Penyusutan adalah proses pengalokasian harga perolehan aktiva tetap menjadi biaya selama masa manfaanya dengan cara yang rasional dan sistematis. Penyusutan dapat dicatat dan dilaporkan dengna menggunakan metode-metode berikut :1. garis lurus2. jumlah angka tahun3. saldo menurun ganda4. unit produksi5. jam kerja

Penyusutan akan mempengaruhi neraca melalui akumulasi penyusutan, dan laporan laba-rugi melalui biaya penyusutan.Penyusutan periodic didasarkan pada tiga factor berikut :1. harga perolehan,2. nilai residu3. umur manfaat

Nilai residu atau biasa disebut dengan nilai sisa adalah taksiran nilai tunai aktiva pada akhir umur manfaat aktiva tersebut. Umur ekonomis atau biasa disebut juga umur manfaat adalah jangka waktu pemakaian aktiva yang diharapkan oleh perusahaan.

Berikut adalaah contoh soal melalui metode-metode penyusutan:

1. Metode Garis Lurus Metode garis lurus adalah metode penyusutan yang menganggap bahwa

harta tetap dimanfaatkan dengan cara yang sama dari tahun ketahun, sehingga besarnya penyusutan harta tetap tiap periode akuntansi adalah sama. Penyusutan dengan cara ini dapat dilakukan dengan memakai rumus sebagai berikut:

KET :P : Penyusutan per periodeHP : Harga Perolehan dari harta tetapNS : Nilai ResiduUE : Umur ekonomis / umur manfaat.

P = HP−NSEU

Example:PT . Kaman is a public transport corporation buses . Vehicle purchases made by the company during the year 2012 are :

On January 1, PT . Kaman Sejahtera purchase price of a vehicle with 2 pieces @ Rp. 45.000.000,-. Dated January 5, 2012 issued under the name of cost with the price of Rp .5.400.000,- and making body of the car with the price of Rp. 6.200.000,-. The purchases made in cash . This vehicle has estimated economic life of 4 years and a residual value of @ Rp. 5.000.000,-.

Then on 6 June 2012, PT . Kaman Sejahtera buy 1 piece of the vehicle at a price of Rp. 50.000.000,-. On 8 June 2012 incurred under the name costs and making body of the car @ Rp .4.600.000,- . This vehicle has a 6 -year economic life the residual value of Rp .10.000.00,-.

Determine depreciation the machine for the first year until the end of the age of the machine ekonomisand depreciation tables using the straight-line method .

Completion : A. ) Depreciation on the machine :

The purchase price ( 2x Rp .45.000.000,- ) = Rp . 90.000.000,-Cost under the name of Rp . 5.400.000,-Karoseri cost Rp . 6.200.000,-

The amount of additional costs = Rp . 11.600.000,- Acquisition price of = Rp. 101 600,000,-

Per - year depreciation = Rp .101 600 000– (2 x Rp .5,000,000 )

4

= Rp .91,600,000

4= Rp. 22,900,000,-

B. ) Table Depreciation :

DATE KETERANGAN DEPRECIATION EXPENSE

ACCUMULATED

DEPRECIATION

BOOK VALUE

31/12/12 Depreciation in 2012

Rp. 22.900.000,-

Rp. 22.900.000,-

Rp. 78,700,000,-

31/12/13 Depreciation in 2013

Rp. 22.900.000,-

Rp. 45,800,000,-

Rp. 55,800,000,-

31/12/14 Depreciation in 2014

Rp. 22.900.000,-

Rp. 68,700,000,-

Rp. 32,900,000,-

31/12/15 Depreciation in 2015

Rp. 22.900.000,-

Rp. 91,600,000,-

Rp. 10,000,000 ,-

SCORE Rp.91.600.000

• A.) Depreciation on purchases in June as follows:Purchase Price = Rp. 50,000,000,-Cost under the name of Rp. 4,600,000Karoseri cost Rp. 4,600,000

Number of Additional Cost = Rp. 9,200,000,-Acquisition price of the machine = Rp 59,200,000,-

Depreciation year 1= 712

x (Rp .59,200,000−Rp .10,000,000)5

= Rp.

5,740,000,

Depreciation of 2 s / d 6 = Rp .59,200,000−Rp .10,000,000

5 = Rp.

9,840,000,-

Depreciation year 7 = 512

x (Rp .59,200,000−Rp .10,000,000)5

= Rp.

4,100,000,- B.) Table Depreciation :

DATE KETERANGAN DEPRECIATION EXPENSE

ACCUMULATED

DEPRECIATION

BOOK VALUE

31/12/2012

Depreciation 1 year

Rp. 5,740,000,-

Rp. 5,740.000,-

Rp.53,460,000,-

31/12/2013

Depreciation 2 year

Rp. 9,840,000,-

Rp. 15,580,000,-

Rp.43,620,000,-

31/12/2014

Depreciation 3 year

Rp. 9,840,000,-

Rp. 25,420,000,-

Rp.33,780,000,-

31/12/2015

Depreciation 4 year

Rp. 9,840,000,-

Rp. 35,260,000,-

Rp.23,940,000,-

31/12/2016

Depreciation 5 year

Rp. 9,840,000,-

Rp. 45,100,000,-

Rp. 14,100,000,-

31/12/2017

Depreciation 6 year

Rp. 4,100,000,-

Rp. 49,200,000,-

Rp.10,000,000,-

SCORE Rp.49,200,000

2. Metode Jumlah Angka Tahun Metode Jumlah Angka Tahun adalah metode yang dapat dicari

dengan cara menjumlahkan semua angka dari umur ekonomis dari harta tetap yang bersangkutan.jumlah angka tahun adalah jumlah dari digit umur ekonomis suatu harta tetap.

Example :

a) On January 1, 1997 , PD. Kaman buy a car with Rp. 365 000 000,- in cash. Dated January 3, 1997 issued by the costs of purchasing the car is

Rp .30.000.000,-. In the appraisal has economic life age of the car is 6 years with a residual value of Rp .17.000.000,-.

b) On October 28, 1997, PD. Kaman buy a car with a price of Rp . 298 000 000,- in cash. Dated October 29, 1997 issued under the name of cost of Rp .9,000,000 , and transportation - purchase of Rp . 3.000.000,-. On this car has estimated economic life of 7 years with a residual value of Rp .22,000,000,-.

Make the car depreciation method along with the total number of years of depreciation table .

Completion :a) * Depreciation of the car is :

The purchase price of Rp . 365 000 000 , -Costs incurred Rp . 30 ..000.000 , -

The amount of additional costs Rp . 30.000.000 , -Acquisition price of Rp . 395 000

000 , -

Digit year number is : 6 +5 +4 +3 +2 +1 = 21Amount to be depreciated historical cost = Acquisition price of - residual value

= Rp. 395 000 000 - Rp. 17.000.000 = Rp. 378,000,000,-

Depreciation in 1997 = 6

21 x Rp. 378.000.000 = Rp.

108,000,000,-

Depreciation in 1998 = 5

21 x Rp. 378.000.000 = Rp.

90.000.000,-

Depreciation in 1999 = 4

21 x Rp. 378.000.000 = Rp.

72.000.000,-

Depreciation in 2000 = 3

21 x Rp. 378.000.000 = Rp.

54.000.000,-

Depreciation in 2001 = 3

21 x Rp. 378.000.000 = Rp.

54.000.000,-

Depreciation in 2002 = 1

21 x Rp. 378.000.000 = Rp.

18.000.000,-

Table depreciation of the car is :

DATE ACQUISITION PRICE

DEPRECIATION EXPENSE

ACCUMULATED

DEPRECIATION

BOOK VALUE

31/12/97

Rp.395.000.000,-

Rp. 108.000.000,-

Rp. 108.000.000,-

Rp.287.000.000,

31/12/98

Rp.395.000.000,-

Rp. 90.000.000,-

Rp. 198.000.000,-

Rp.197.000.000,-

31/12/99

Rp.395.000.000,-

Rp. 72.000.000,-

Rp. 270.000.000,-

Rp.125.000.000,-

31/12/00

Rp.395.000.000,-

Rp. 54.000.000,-

Rp. 324.000.000,-

Rp.71.000.000,-

31/12/01

Rp.395.000.000,-

Rp. 36.000.000,-

Rp. 360.000.000,-

Rp.35.000.000,-

31/12/02

Rp.395.000.000,-

Rp. 18.000.000,-

Rp. 378.000.000,-

Rp.17.000.000,-

SCORE Rp.378.000.000,

b ) * contraction in October are as follows :purchase price of Rp . 310,000,000,-cost under the name of Rp . 9,750,000,-purchase freight costs Rp . 8,250,000,-

additional amount of Rp . 18,000,000,-acquisition price of Rp . 328,000,000,-

*digit year number is 7 +6 +5 +4 +3 +2 +1 = 28 *amount to be depreciated historical cost = acquisition price of - residual value

= Rp. 328.000.000 – Rp. 20.000.000 = Rp. 308.000.000,-

Depreciation in 1997 = 2

12 x

728

x Rp. 308.000.000 = Rp.

12.833..333,-

Depreciation in 1998 = 6

28 x Rp. 308.000.000 = Rp. 66.000.000,-

Depreciation in 1999 = 5

28 x Rp. 308.000.000 = Rp. 55.000.000,-

Depreciation in 2000 = 4

28 x Rp. 308.000.000 = Rp. 44.000.000,-

Depreciation in 2001 = 3

28 x Rp. 308.000.000 = Rp. 33.000.000,-

Depreciation in 2002 = 2

28 x Rp. 308.000.000 = Rp. 22.000.000,-

Depreciation in 2003 = 1

28 x Rp. 308.000.000 = Rp. 11.000.000,-

Depreciation in 2004 = 1012

x 7

28 x Rp. 308.000.000 = Rp.

64.166.667,-

Depreciation table :

DATE ACQUISITION PRICE

DEPRECIATION EXPENSE

ACCUMULATED

DEPRECIATION

BOOK VALUE

31/12/1997 Rp. 328.000.000,- Rp. 12.833.333,- Rp. 12.833.333,- Rp.315.166.667,-31/12/1998 Rp. 328.000.000,- Rp. 66.000.000,- Rp. 78.833.333,- Rp.249.166.667,-31/12/1999 Rp. 328.000.000,- Rp. 55.000.000,- Rp. 133.833.333,- Rp.194.166.667,-31/12/2000 Rp. 328.000.000,- Rp. 44.000.000,- Rp. 177.833.333,- Rp.150.166.667,-31/12/2001 Rp. 328.000.000,- Rp. 33.000.000,- Rp. 210.833.333,- Rp.117.166.667,-31/12/2002 Rp. 328.000.000,- Rp. 22.000.000,- Rp. 232.833.333,- Rp. 95.166.667,-31/12/2003 Rp. 328.000.000,- Rp. 11.000.000,- Rp. 243.833.333,- Rp. 84.116.667,-28/09/2004 Rp. 328.000.000,- Rp. 64.166.667,- Rp. 308.000.000,- Rp. 20.000.000,-

SCORE Rp.308.000.000,-

3. Metode Saldo Menurun GandaMetode Saldo Menurun Ganda adalah metode yang selalu didasari

pada nilai buku harta tetapyang bersangkutan. Nilai buku dari harta tetap semakin lama akan semakin kecil. Oleh karena itu, biaya penyusutan dengan metode ini makin lama juga akan menjadi semakin kecil. Tarif penyusutan yang sering digunakan adalah tariff metode garis lurus yang dikalikan dua, sehingga metode ini sering disebut metode saldo menurun ganda. Penyusutan dengan metode ini dapat dirumuskan sebagai berikut :

Example :

a) On January 1, 2000, PD. Kaman to buy a machine with a purchase price of Rp. 89,000,000,-. These purchases result in mounting costs of Rp. 6.500.000,- and the trial costs of Rp. 1.500.000,-. In the appraisal has economic life of the machine for 8 years with residual value of Rp. 8.000.000,-.

b) Then, on 2 November 2000, PD. Kaman to buy back a machine with price Rp. 73,000,000,-. The costs to be incurred in the purchase takes for Rp. 8,000,000,-. The machine has an estimated economic life of 5 years with a residual value of Rp. 6,500,000,-.

Make the depreciation of fixed assets and depreciation tables using the double declining balance method.

Completion :

a) * Persentasi straight line = 18

x 100 % = 1,25 %

* Percentase of depreciation = 2 x 1,25 % = 25 %

Penyusutan Pertahun = 2 x Persen Garis Lurus x Nilai Buku

* Depreciation machine are:Purchase price of Rp.

89,000,000,-Installation costs Rp . 6,500,000Trial costs Rp . 1,500,000

Additional amount of Rp . 8,000,000,-

Acquisition price of Rp . 97,000,000,-

Depreciation in l (2000) = 25 % x Rp. 97,000,000 = Rp. 24.250.000,-Depreciation in ll (2001) = 25 % X Rp. 72,750,000 = Rp. 18,187,500,-Depreciation in lll (2002) = 25 % x Rp. 54,562,500 =

Rp .13,640,625,-Depreciation in lV (2003) = 25 % x Rp. 40,921,875 =

Rp .10,230,469,-Depreciation in V (2004) = 25 % x Rp. 30,691,406 = Rp . 7,672,852,-Depreciation in Vl (2005) = 25 % x Rp. 23,018,554 = Rp. 5,754,639,-Depreciation in VII (2006) = 25 % x Rp. 17,263,915 = Rp. 4,315,979,-Depreciation in Vlll (2007) = 25 % x Rp. 12,947,936 = Rp . 3,236,984,

• Table of depreciation :

DATE ACQUISITION PRICE

DEPRECIATION EXPENSE

ACCUMULATED DEPRECIATION

BOOK VALUE

31/12/2000 Rp. 97.000.000 Rp. 24.250.000,- Rp. 24.250.000,- Rp. 72.750.000,- 31/12/2001 Rp. 97.000.000 Rp. 18.187.500,- Rp. 42.437.500,- Rp. 54.562.500,- 31/12/2002 Rp. 97.000.000 Rp. 13.640.625,- Rp. 56.078.125,- Rp. 40.921.875,- 31/12/2003 Rp. 97.000.000 Rp. 10.230.469,- Rp. 66.308.594,- Rp. 30.691.406,- 31/12/2004 Rp. 97.000.000 Rp. 7.672.852,- Rp. 73.981.446,- Rp. 23.018.554,- 31/12/2005 Rp. 97.000.000 Rp. 5.754.639,- Rp. 79.736.085,- Rp. 17.263.915,- 31/12/2006 Rp. 97.000.000 Rp 4.315.979,- Rp. 84.052.064,- Rp. 12.947.936,- 31/12/2007 Rp. 97.000.000 Rp. 3.236.984,- Rp. 87.289.048,- Rp. 9.710.952,-

SCORE Rp. 87.289.048,-

b ) * Depreciation in November are as follows :purchase price of Rp . 73,000,000,-costs incurred Rp . 8,000,000

additional amount of Rp . 8.000.000,-

acquisition price of Rp. 81.000.000,-

Depreciation in l (2000) = 2

12 x 40 % x Rp. 81,000,000 = Rp. 5,400,000,-

Depreciation in ll (2001) = 40 % x Rp. 75,600,000 = Rp. 30,240,000,-Depreciation in lll (2002) = 40 % x Rp. 45,360,000 = Rp .18,114,000,-Depreciation in lV (2003) = 40 % x Rp. 27,216,000 = Rp .10,886,400,-Depreciation in V (2004) = 40 % x Rp . 16,329,600 = Rp. 6,531,840,-

Depreciation in Vl (2005) = 1012

x 40 % x Rp. 81.000.000 = Rp. 3.265.920,-

Depreciation table :

DATE ACQUISITION PRICE

DEPRECIATION EXPENSE

ACCUMULATED DEPRECIATION

BOOK VALUE

31/12/2000 Rp. 81.000.000,- Rp. 5.400.000,- Rp. 5.400.000,- Rp. 75.600.000,-31/12/2001 Rp. 81.000.000,- Rp. 30.240.000,- Rp. 35.640.000,- Rp. 45.360.000,-31/12/2002 Rp. 81.000.000,- Rp. 18.114.000,- Rp. 53.784.000,- Rp. 27.216.000,-31/12/2003 Rp. 81.000.000,- Rp. 10.886.400,- Rp. 64.670.400,- Rp. 16.329.600,-31/12/2004 Rp. 81.000.000,- Rp. 6.531.840,- Rp. 71.202.240,- Rp. 9.797.760,-02/11/2005 Rp. 81.000.000,- Rp. 3.265.920,- Rp. 74.468.160,- Rp. 6.531.840,-

SCORE Rp. 74.468.160,-

4 ) Method Unit ProduksiMetode unit produksi adalah metode perhitungan penyusutan harta tetap

yang didasarkan pada perkiraan kemampuan produksi barang yang akan dihasilkan selama umur manfaat dari harta tetap yang bersangkutan. Metode ini paling banyak diaplikasi pada perhitungan penyusutan harta tetap mesin. Cara perhitungan penyusutan dengan cara ini dapat dirumuskan sebagai berikut :

Example:On January 1 , 1999, PT. Kaman to buy a machine with price Rp.

56,700,000,- and 10% VAT. Incurred in the purchase and installation costs trials Rp.4,000,000, purchase of transport costs Rp. 4,250,000 and insurance fee of Rp. 4.000.000,-. This machine has the estimated economic life of 4 years with a residual value of Rp. 6.750.000,-. During the useful life of this machine will be able to work for 43,200 hours of work and be able to produce 38,000 units of goods , machinery production forecasts for the next 4 years are as follows :

Penyusutan Per-tahun = Unit ProduksiTahunKe−n

Total Produksi x ( Harga Perolehan –

Residu )Penyusutan Per-unit = HargaPerolehan−Residu

Total Produksi x ( Produksi

Tahun Ke-n )

YEARS PRODUCTION UNIT HOURS OF WORK

1999 8.600 3.5002000 7.300 2.3502001 9.200 3.2002002 12.900 3.450

SCORE 38.000 15.000 Hours

Make the depreciation of fixed assets and depreciation tables using the productive output method.

Completion :

a) Depreciation machine are: The purchase price of Rp. 56,700,000,-VAT10% (10% x Rp. 5,.700,000) to Rp. 5,670,000The cost of installing and testing Rp. 4,000,000Purchasefreight costs Rp. 4,250,000Insurance costs Rp . 5,000,000

Total additional cost of Rp . 18,920,000,-Acquisition price of Rp. 75,620,000,-

Penyusutan Per-tahun = Unit ProduksiTahunKe−n

Total Produksi x ( Harga Perolehan –

Residu )

Depreciation in 1999 = 9.500

38.000 x ( Rp. 75,620,000 – Rp. 6,750,000) = Rp.

17,217,500,-

Depreciation in 2000 = 9.200

38.000 x Rp. 68,870,000 = Rp.

16,673,789,-

Depreciation in 2001 = 9.800

38.000 x Rp. 68,870,000 = Rp.

17,761,211,-

Depreciation in 2002 = 9.500

38.000 x Rp. 68,870,000 = Rp.

17,217,500,-

b) Depreciation Table :

DATE ACQUISITION PRICE

DEPRECIATION EXPENSE

ACCUMULATED

DEPRECIATION

BOOK VALUE

31/12/1999 Rp. 75,620,000,- Rp. 17,217,500,- Rp. 17,217,500,- Rp. 58,402,500,-31/12/2000 Rp. 75,620,000,- Rp. 16,673,789,- Rp. 33,891,289,- Rp. 41,728,711,-31/12/2001 Rp. 75,620,000,- Rp. 17,761,211,- Rp. 51,652,500,- Rp. 23,967,500,-31/12/2002 Rp. 75,620,000,- Rp. 17,217,500,- Rp. 68,870,000 ,- Rp. 6,750,000,-

SCORE Rp. 68,870,000 ,-

5) Metode Jam Kerja

Metode jam kerja adalah metode perhitungan penyusutan harta tetap yang didasari pada perkiraan kemampuan harta tetap yang bersangkutan pekerja selama umur manfaatnya. Metode ini paling banyak diaplikasipada perhitungan penyusutan harta tetap mesin. Cara perhitungan penysuutan dengan cara ini dapat dirumuskan sebagai berikut :

Example:On January 1 , 1999, PT. Kaman to buy a machine with price Rp.

56,700,000,- and 10% VAT. Incurred in the purchase and installation costs trials

Penyusutan Per-tahun = Jam KerjaTahunKe−nTotal Jam Kerja

x ( Harga Perolehan –

Residu )Penyusutan Per-unit =

HargaPerolehan−ResiduTotal JamKerja

x ( Jam Kerja Tahun

Ke-n )

Rp.4,000,000, purchase of transport costs Rp. 4,250,000 and insurance fee of Rp. 4,000,000,-. This machine has the estimated economic life of 4 years with a residual value of Rp. 6,750,000,-. During the useful life of this machine will be able to work for 43,200 hours of work and be able to produce 38,000 units of goods , machinery production forecasts for the next 4 years are as follows :

YEARS PRODUCTION UNIT HOURS OF WORK

1999 8.600 3.5002000 7.300 2.3502001 9.200 3.2002002 12.900 3.450

SCORE 38.000 15.000 Hours

Make the depreciation of fixed assets and depreciation tables using the service hour method.

Completion :

a) Depreciation machine are: The purchase price of Rp. 56,700,000,-VAT10% (10% x Rp. 5,.700,000) to Rp. 5,670,000The cost of installing and testing Rp. 4,000,000Purchasefreight costs Rp. 4,250,000Insurance costs Rp . 5,000,000

Total additional cost of Rp . 18,920,000,-Acquisition price of Rp. 75,620,000,-

Penyusutan Per-unit = HargaPerolehan−Residu

Total JamKerja x ( Jam Kerja Tahun

Ke-n )

Depreciation in 1999 = Rp .68,870,000

15,000 x 3.500 = Rp.

19,283,600,-

Depreciation in 2000 = Rp .68,870,000

15,000 x 2.350 = Rp.

12,947,560,-

Depreciation in 2001 = Rp .68,870,000

15,000 x 3.200 = Rp.

17,630,720,-

Depreciation in 2002 = Rp .68,870,000

15,000 x 3.450 = Rp.

19,008,120,-

b) Depreciation Table :

DATE ACQUISITION PRICE

DEPRECIATION EXPENSE

ACCUMULATED

DEPRECIATION

BOOK VALUE

31/12/1999 Rp. 75,620,000,- Rp. 19,283,600,- Rp. 19,283,600,- Rp.56,336,40031/12/2000 Rp. 75,620,000,- Rp. 12,947,560,- Rp. 32,231,160,- Rp.43,388,84031/12/2001 Rp. 75,620,000,- Rp. 17,630,720,- Rp. 49,861,880,- Rp.25,758,12031/12/2002 Rp. 75,620,000,- Rp. 19,008,120,- Rp. 68,870,000,- Rp. 6,750,000

SCORE Rp. 68,870,000 ,-

Penghentian aktiva tetap adalah jika aktiva tetap yang sudah kurang bermanfaat lagi karena habis umur ekonomisnya atau tidak layak lagi untuk dipakai terus karena sudah

Penghentian Aktiva Tetap

ketinggalan jaman dengan munculnya mesin-mesin baru yang dapat memproduksi barang yang mutunya lebih baik, lebih menghematkan biaya dan kapasitasnya lebih tinggi, maka aktiva lama tersebut harus dihentikan pemakaiannya.

Apabila suatu aktiva tetap akan dihentikan, maka pertama-tama harus ditentukan dahulu nilai buku aktiva tetap tersebut. Nilai buku adalah selisih antara harga perolehan aktiva tetap dengan akumulasi penyusutan pada tanggal yang bersangkutan. Apabila penghentian terjadi pada suatu tanggal tertentu pada suatu tahun, maka penyusutannya harus dihitung sampai dengan saat penghentian terjadi. Selanjutnya nilai buku aktiva tetap harus dihapus dari pembukuan dengan mendebet rekening akumulasi penyusutan dan mengkredit aktiva tetap yang bersangkutan sebesar harga perolehannya.

Jika suatu aktiva tetap sudah tidak dipakai lagi, untuk menghentikan pemakaian aktiva tersebut dapat dilakukan dengan cara :

a) Dibuang atau disingkirkan,b) Dijual,c) Ditukar dengan aktiva yang baru yang sejenis dand) Ditukar dengan aktiva yang baru yang tidak sejenis.

1.Penghentian Dibuang atau Disingkirkan

Dengan dibuangnya aktiva tetap berarti aktiva tersebut harus dikeluarkan dari pembukuan, dengan jurnal :

a. jika sudah habis umur ekonomisnya :

Akumulasi Penyusutan X Rp. XXX

Mesin X Rp. XXX

b. jika belum habis umur ekonomisnya :

Example :In January 2012 an accident which caused the carinto the abyss,

so PT. Kaman Sejahtera had removal of fixed assets. The carwas purchased on January 1, 2010 with acostof Rp. 101,600,000 and accumulated depreciation using the straight-line method of Rp. 45, 800,000with a4-year economic life and residual value of Rp. 10,000,000.asked : termination of fixed assets journals make the car.

Completion :

i) Acquisition price of Rp. 101,600,000Accumulated depreciation Rp. 45,800,000Lossdue todisposal Rp. 55,800,000

ii) Thejournal:Accumulated depreciation Rp. 45,800,000Lossdue todisposal Rp. 55,800,000

Car Rp. 101,600,000

2.Penghentian Dijual

Apabila suatu aktiva tetap dijual, maka nilai buku aktiva tersebut harus dibandingkan dengan hasil penjualannya. Perusahaan mendapat laba, jika hasil penjualan lebih besar dari nilai buku aktiva yang dijual. Sebaliknya, perusahaan menderita rugi, apabila hasil penjualannya lebih kecil daripada nilaibukunya.

Timbulnya laba atau rugi dalam penjualan suatu aktiva tetap sangat umum terjadi. Apabila hasil penjualan sama dengan nilai buku, yang berarti perusahaan tidak mendapat laba atau rugi, maka hal itu hanya terjadi secara kebetulan.Berikut adalah jurnalnya :

a) apabila timbul labaKas Rp. XXXAkumulasi Penyusutan Rp. XXX

Laba Penjualan Rp. XXXMesin Rp. XXX

b) apabila timbul rugiKas Rp. XXXAkumulasi Penyusutan Rp. XXXRugi Penjualan Rp. XXX

Mesin Rp. XXXExample :

Akumulasi Penyusutan X Rp. XXX

Rugi Karena PembuanganRp. XXX

Mesin X Rp. XXX

On January 1,2008 PT. Kaman Sejahtera sell one of the engines of Rp. 25,000,000. The machine was bought on 6th June 2006 with an acquisition cost of Rp. 59,200,00 and accumulated depreciation using the straight-line method of Rp. 21,320,000.make journal termination of fixed assets such machines.

Completion :

i) The sale price Rp. 25,000,000Acquisition price Rp. 59,200,000Accumulated depreciation Rp. 21,320,000

Book value of the machine Rp. 37,880,000Loss due to the removal Rp. 12,880,000

ii) Termination of fixed assets journal are :Cash Rp. 25,000,000Accumulated depreciation Rp. 21,320,000Loss due to the removal Rp. 12,880,000

Machine Rp. 59,200,000

3.Penghentian Tukar Tambah Sejenis

Apabila aktiva tetap ditukar dengan aktiva tetap yang sejenis, maka laba atas pertukaran tidak diakui, sedangkan jika rugi atas pertukaran tersebut harus diakui( perinsip konservatisme ).Berikut adalah jurnalnya :a) Apabila timbul rugi

Mesin (baru) Rp. XXXAkumulasi Penyusutan Rp. XXXRugi pertukaran mesin Rp. XXX

Mesin (lama) Rp. XXXKas Rp. XXX

b) Apabila timbul labaMesin (baru) Rp. XXXAkumulasi Penyusutan Rp. XXX

Mesin (lama) Rp. XXXKas Rp. XXX

Catatan :Laba tidak diakui, maka nilai aktiva baru dicatat sebesar nilai

pengorbanannya ( harga beli – laba yang tidak diakui ).

Example :A machine purchased in January 1987 for Rp. 42,000,000 as at 31

December 1994 have been depreciated Rp. 32,000,000. on the 8th of January 1995 exchanged with similar new machine with the price of Rp.

60,000,000.

Asked:Make the journal termination of fixed assets, if:a) increase the cash of Rp. 55,000,000b) increase the cash of Rp. 47,000,000

Completion :i) The price of a new machine Rp. 60,000,000

price of the old machine Rp. 42,000,000accumulated depreciation Rp. 32,000,000

book value of the old machine Rp. 10,000,000

difference between the book value Rp. 50,000,000

ii) a. add cash of Rp. 55,000,000difference between the book value Rp. 50,000,000add cash Rp. 55,000,000exchange loss ( 5,000,000)

b. add cash of Rp. 47,000,000difference between the book value Rp. 50,000,000add cash Rp. 47,000,000exchange earnings Rp.

3,000,000

iii) That the journal should be made in the termination of the fixed assets are:a. price of the new machine Rp. 60,000,000

accumulated depreciation Rp. 32,000,000exchange loss Rp. 5,000,000

price of the old machine Rp. 42,000,000

cash Rp. 55,000,000

b. price of the new machine Rp. 57,000,000accumulated depreciation Rp. 32,000,000

price of the old machine Rp. 42,000,000

cash Rp. 47,000,000

4.Penghentian Tukar Tambah Tidak Sejenis

Apabila aktiva tetap ditukar dengan aktiva tetap lain yang tidak sejenis, maka laba atau rugi atas pertukaran diakui. Pertukaran antara aktiva tidak sejenis bisa melibatkan berbgaai macam aktiva. Sebagai contoh, misalnya peralatan angkutan ditukar dengan tanah, atau mobil ditukar dengan mesin pabrik. Dalam hal terjadi pertukaran aktiva tidak sejenis, maka aktiva baru yang diperoleh mempunyai fungsi yang berbeda dengan aktiva yang diserahkan. Oleh karena itu, laba atau rugi harus diakui jika pertukaran terjadi antara aktiva yang tidak sejenis.Berikut adalah jurnalnya :a) Apabila timbul laba :

Mesin (baru) Rp. XXXAkumulasi Penyusutan Rp. XXX

Laba Pertukaran Rp. XXXMesin (lama) Rp. XXXKas Rp. XXX

b) Apabilatimbulrugi :Mesin (baru) Rp. XXXAkumulasi Penyusutan Rp. XXXRugi Pertukaran Rp. XXX

Mesin (lama) Rp. XXXKas Rp. XXX

Example :Atruck with an acquisition cost of Rp. Rp100,000,000 has been

depreciated. 70,000,000 on June 5, 1995 exchange for a bus at a price ofRp. 150,000,000.asked : make the journal termination of fixed assets, if:a) increase the cash of Rp. 130,000,000b) increase the cash of Rp. 115,000,000

Completion:i) The price of bus Rp. 150,000,000

Truck prices Rp. 100,000,000Accumulated depreciation Rp. 70,000,000

Book value oftruck Rp. 30,000,000Difference between the book value Rp. 120,000,000

ii) a. add cash of Rp . 130,000,000 difference between the book value Rp. 120,000,000add cash Rp. 130,000,000exchange loss ( 10,000,000)

b. add cash of Rp . 115,000,000 difference between the book value Rp. 120,000,000add cash Rp. 115,000,000exchange earnings Rp. 5,000,000

iii) that the journal should be madein the termination of the fixed assets are:a. price of bus Rp. 150,000,000

accumulated depreciation Rp. 70,000,000exchange loss Rp. 10,000,000

truck prices Rp. 100,000,000cash Rp. 130,000,000

b. price of bus Rp. 150,000,000accumulated depreciation Rp. 70,000,000

exchange earnings Rp. 5,000,000truck prices Rp. 100,000,000cash Rp. 115,000,000

Jusup, Al. Haryono, M.B.A., Akuntan, Drs. 2005. Dasar-dasar akuntansi jilid 2, edisi 6. Yogyakarta. Bagian Penerbitan Sekolah Tinggi Ilmu Ekonomi YKPN.

Suyoto, Moelyati, Sumardi Drs, Dra. 1999. Akuntansi Keuangan jilid 1, Bandung Titian Ilmu.

www. Google translate.com,

Dari semua hasil makalah saya ini mungkin belum mencapai titik kesempurnaan, mnaka dari itu saya mengucapkan mohonmaaf atas segala kekurangan dari makalah ini.

Dan saya mengucapkan terima kasih atas guru pembimbing saya Ibu Lestari Manurung S,Pd dan teman-teman yang sudah mau membantu sedikit pekerjaan makalah saya ini. Saya berharap agar makalah ini bisa bermanfaat dan dapat dimengerti.

Saya menerima akan kritik dan sarannya terhadap teman-teman atas perhatiannya saya ucapkan terima kasih.

Jakarta, November 2013Penulis

Kartika

Nama : KARTIKATempat, Tanggal Lahir : Jakarta, 05 Juni 1997Alamat Rumah : Jl. Muara Baru Gg. Marlina

Rt. 011/Rw. 017 No. 1 Penjaringan, Jakarta Utara

Anak ke- : 5 (lima) dari 5 BersaudaraLulusan : SDN PENJARINGAN 02

PETANG, SMP NEGERI 21 JAKARTA

Bersekolah : SMK NEGERI 23 JAKARTAKelas : XI AKUNTANSI 1Alamat Sekolah : Jl. Pademangan Timur III Gg. 19

Pademangan, Jakarta UtaraE-mail : [email protected] : @kartika_asmi