06-Depresiasi keekonomian migas

66

Depresiasi syamsul irham DEPRESIASI 1. Depresiasi dalam Laporan Keuangan 2. Depresiasi dalam Cash Flow 3. Depresiasi dalam Cost Recovery (PSC term’s) 4. Pengertian Depresiasi 5. Metode Depresiasi

-

Upload

firstyan-dhika-aldani -

Category

Documents

-

view

134 -

download

11

description

petroleum economic

Transcript of 06-Depresiasi keekonomian migas

Depresiasi

syamsul irham

DEPRESIASI

1. Depresiasi dalam Laporan Keuangan

2. Depresiasi dalam Cash Flow

3. Depresiasi dalam Cost Recovery (PSC term’s)

4. Pengertian Depresiasi

5. Metode Depresiasi

Depresiasi

syamsul irham

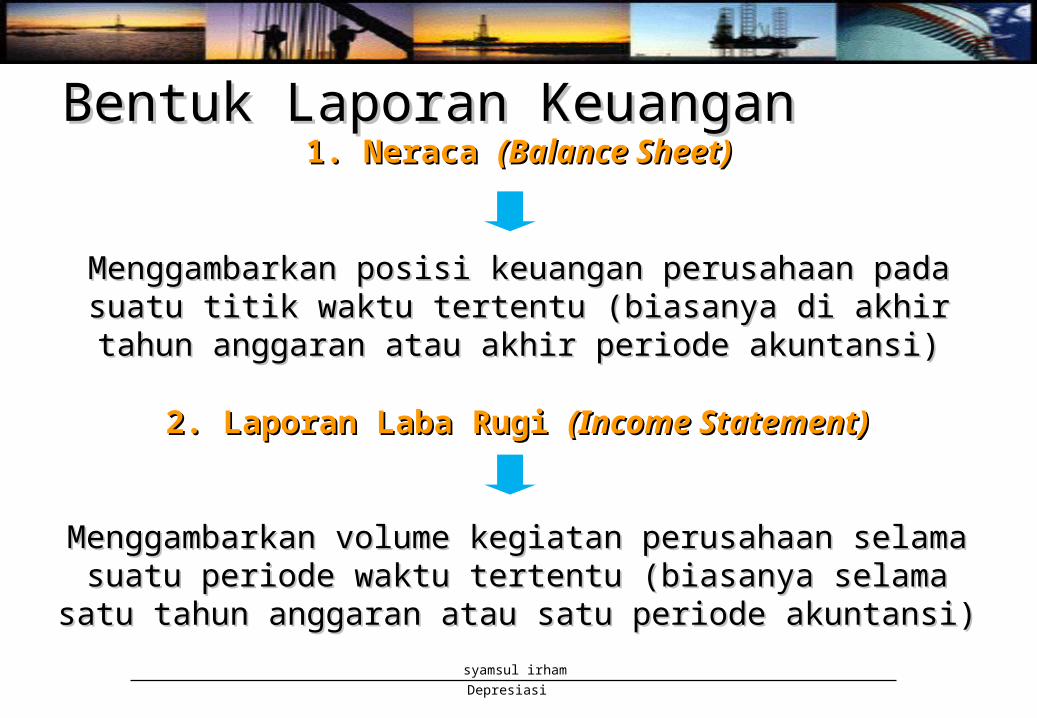

2. Laporan Laba Rugi 2. Laporan Laba Rugi (Income Statement)(Income Statement)

Menggambarkan volume kegiatan perusahaan selama suatu periode Menggambarkan volume kegiatan perusahaan selama suatu periode waktu tertentu (biasanya selama satu tahun anggaran atau satu periode waktu tertentu (biasanya selama satu tahun anggaran atau satu periode

akuntansi)akuntansi)

Bentuk Laporan KeuanganBentuk Laporan Keuangan1. Neraca 1. Neraca (Balance Sheet)(Balance Sheet)

Menggambarkan posisi keuangan perusahaan pada suatu titik waktu Menggambarkan posisi keuangan perusahaan pada suatu titik waktu tertentu (biasanya di akhir tahun anggaran atau akhir periode akuntansi)tertentu (biasanya di akhir tahun anggaran atau akhir periode akuntansi)

Depresiasi

syamsul irham

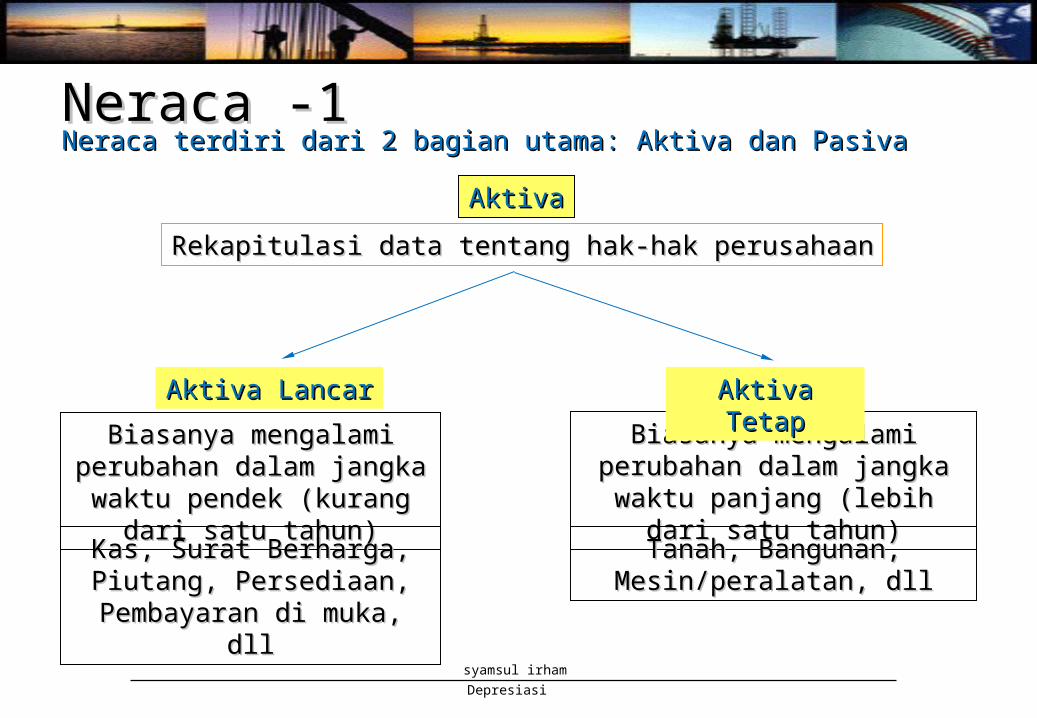

Neraca -1Neraca -1Neraca terdiri dari 2 bagian utama: Aktiva dan PasivaNeraca terdiri dari 2 bagian utama: Aktiva dan Pasiva

Rekapitulasi data tentang hak-hak perusahaanRekapitulasi data tentang hak-hak perusahaan

AktivaAktiva

Biasanya mengalami perubahan Biasanya mengalami perubahan dalam jangka waktu panjang (lebih dalam jangka waktu panjang (lebih

dari satu tahun)dari satu tahun)

Aktiva TetapAktiva Tetap

Biasanya mengalami perubahan Biasanya mengalami perubahan dalam jangka waktu pendek dalam jangka waktu pendek

(kurang dari satu tahun)(kurang dari satu tahun)

Aktiva LancarAktiva Lancar

Kas, Surat Berharga, Piutang, Kas, Surat Berharga, Piutang, Persediaan, Pembayaran di muka, Persediaan, Pembayaran di muka,

dlldll

Tanah, Bangunan, Mesin/peralatan, Tanah, Bangunan, Mesin/peralatan, dlldll

Depresiasi

syamsul irham

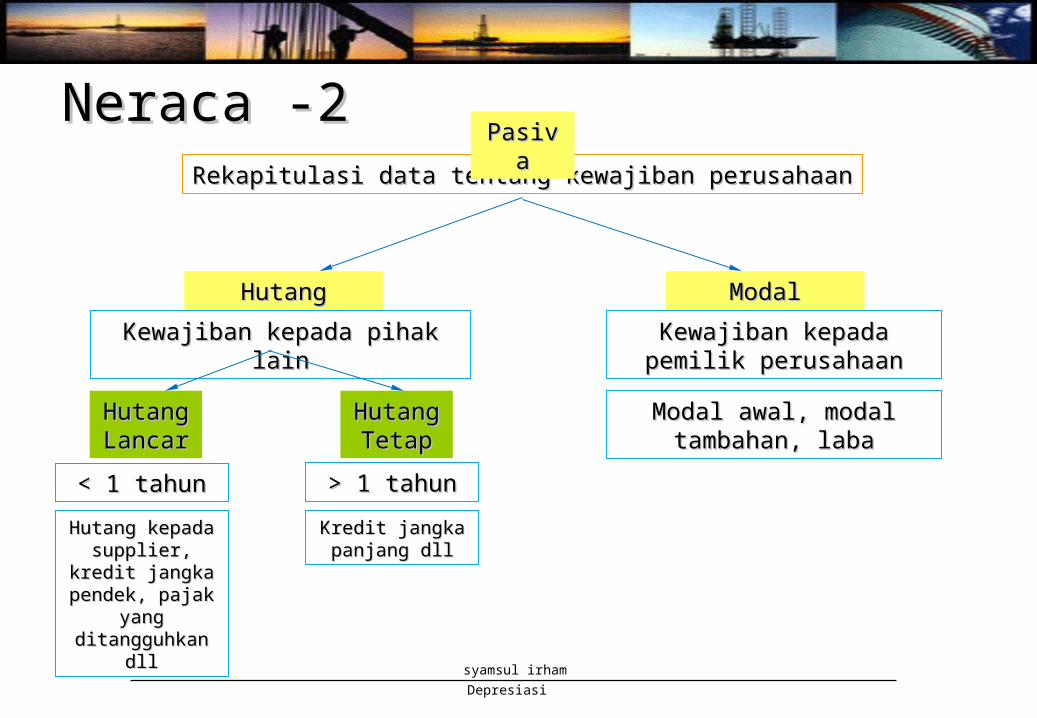

Neraca -2Neraca -2Rekapitulasi data tentang kewajiban perusahaanRekapitulasi data tentang kewajiban perusahaan

PasivaPasiva

Kewajiban kepada pemilik Kewajiban kepada pemilik perusahaanperusahaan

ModalModal

Kewajiban kepada pihak lainKewajiban kepada pihak lain

HutangHutang

Modal awal, modal tambahan, Modal awal, modal tambahan, labalaba

< 1 tahun< 1 tahun

Hutang Hutang LancarLancar

> 1 tahun> 1 tahun

Hutang Hutang TetapTetap

Hutang kepada Hutang kepada supplier, kredit supplier, kredit jangka pendek, jangka pendek,

pajak yang pajak yang ditangguhkan dllditangguhkan dll

Kredit jangka Kredit jangka panjang dllpanjang dll

Depresiasi

syamsul irham

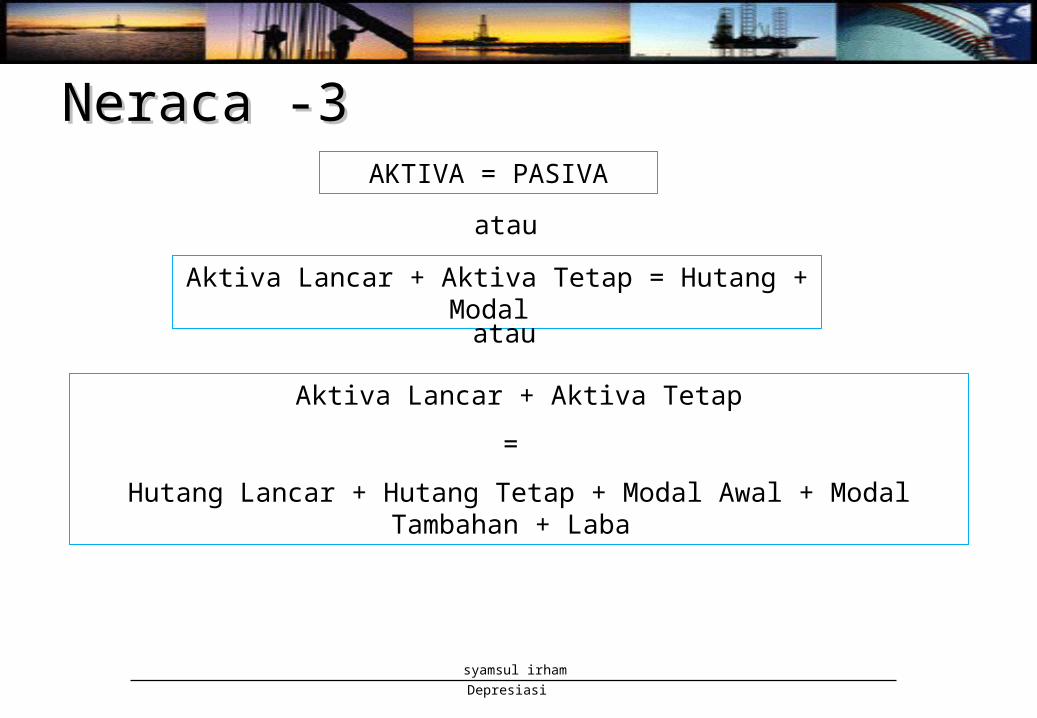

Neraca -3Neraca -3AKTIVA = PASIVA

Aktiva Lancar + Aktiva Tetap = Hutang + Modal

Aktiva Lancar + Aktiva Tetap

=

Hutang Lancar + Hutang Tetap + Modal Awal + Modal Tambahan + Laba

atau

atau

Depresiasi

syamsul irham

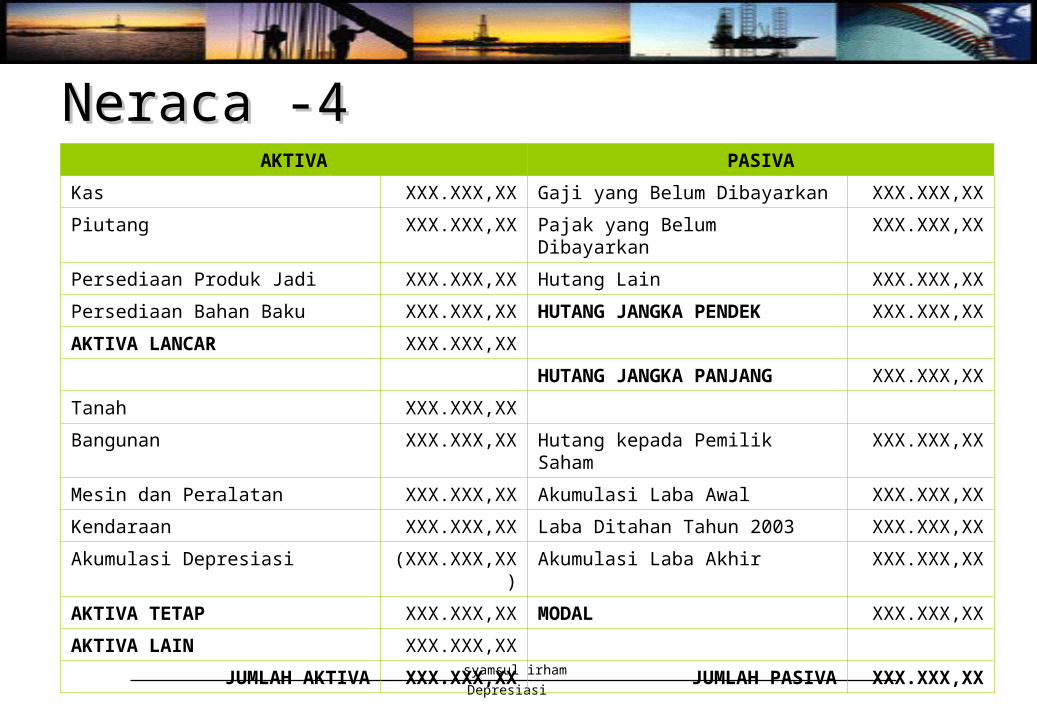

AKTIVA PASIVA

Kas XXX.XXX,XX Gaji yang Belum Dibayarkan XXX.XXX,XX

Piutang XXX.XXX,XX Pajak yang Belum Dibayarkan XXX.XXX,XX

Persediaan Produk Jadi XXX.XXX,XX Hutang Lain XXX.XXX,XX

Persediaan Bahan Baku XXX.XXX,XX HUTANG JANGKA PENDEK XXX.XXX,XX

AKTIVA LANCAR XXX.XXX,XX

HUTANG JANGKA PANJANG XXX.XXX,XX

Tanah XXX.XXX,XX

Bangunan XXX.XXX,XX Hutang kepada Pemilik Saham XXX.XXX,XX

Mesin dan Peralatan XXX.XXX,XX Akumulasi Laba Awal XXX.XXX,XX

Kendaraan XXX.XXX,XX Laba Ditahan Tahun 2003 XXX.XXX,XX

Akumulasi Depresiasi (XXX.XXX,XX)

Akumulasi Laba Akhir XXX.XXX,XX

AKTIVA TETAP XXX.XXX,XX MODAL XXX.XXX,XX

AKTIVA LAIN XXX.XXX,XX

JUMLAH AKTIVA XXX.XXX,XX

JUMLAH PASIVA XXX.XXX,XX

Neraca -4Neraca -4

Depresiasi

syamsul irham

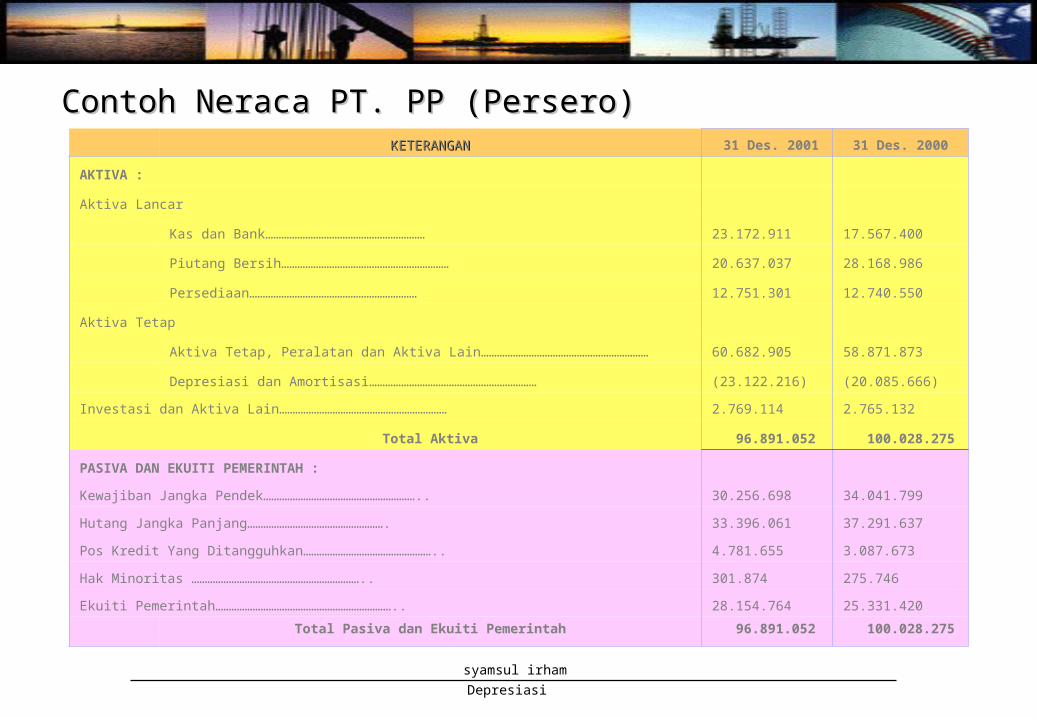

Contoh Neraca PT. PP (Persero)Contoh Neraca PT. PP (Persero)KETERANGANKETERANGAN 31 Des. 2001 31 Des. 2000

AKTIVA :

Aktiva Lancar

Kas dan Bank…………………………………………………… 23.172.911 17.567.400

Piutang Bersih……………………………………………………… 20.637.037 28.168.986

Persediaan……………………………………………………… 12.751.301 12.740.550

Aktiva Tetap

Aktiva Tetap, Peralatan dan Aktiva Lain……………………………………………………… 60.682.905 58.871.873

Depresiasi dan Amortisasi……………………………………………………… (23.122.216) (20.085.666)Investasi dan Aktiva Lain……………………………………………………… 2.769.114 2.765.132

Total Aktiva 96.891.052 100.028.275

PASIVA DAN EKUITI PEMERINTAH : Kewajiban Jangka Pendek………………………………………………….. 30.256.698 34.041.799 Hutang Jangka Panjang……………………………………………. 33.396.061 37.291.637 Pos Kredit Yang Ditangguhkan………………………………………….. 4.781.655 3.087.673 Hak Minoritas ……………………………………………………….. 301.874 275.746 Ekuiti Pemerintah………………………………………………………….. 28.154.764 25.331.420

Total Pasiva dan Ekuiti Pemerintah 96.891.052 100.028.275

Depresiasi

syamsul irham

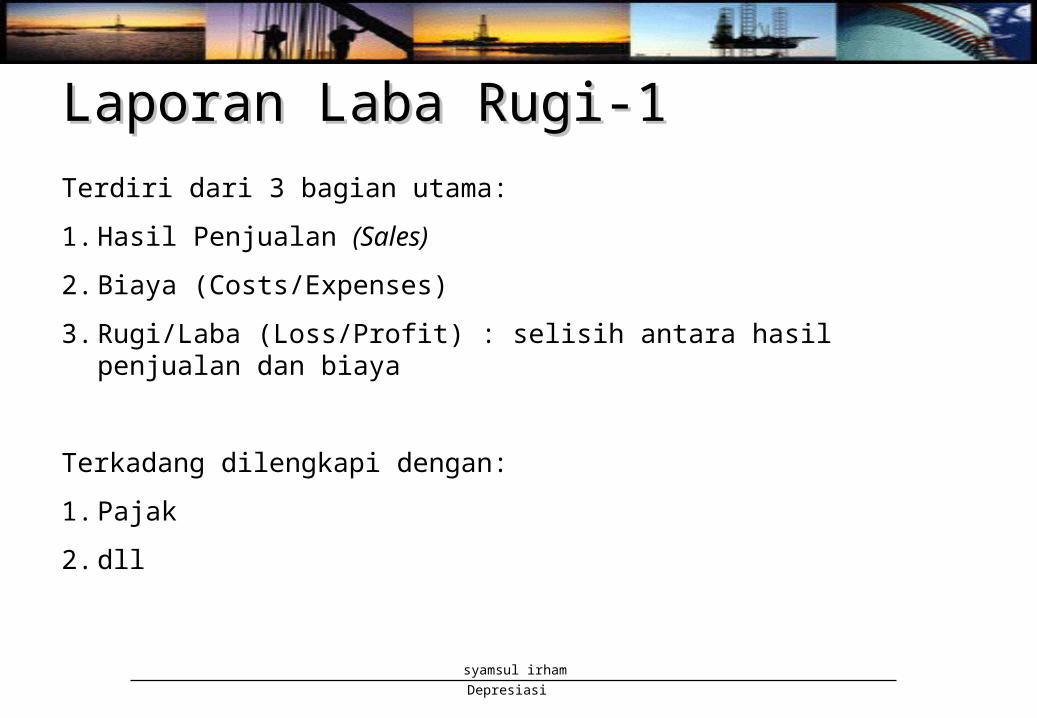

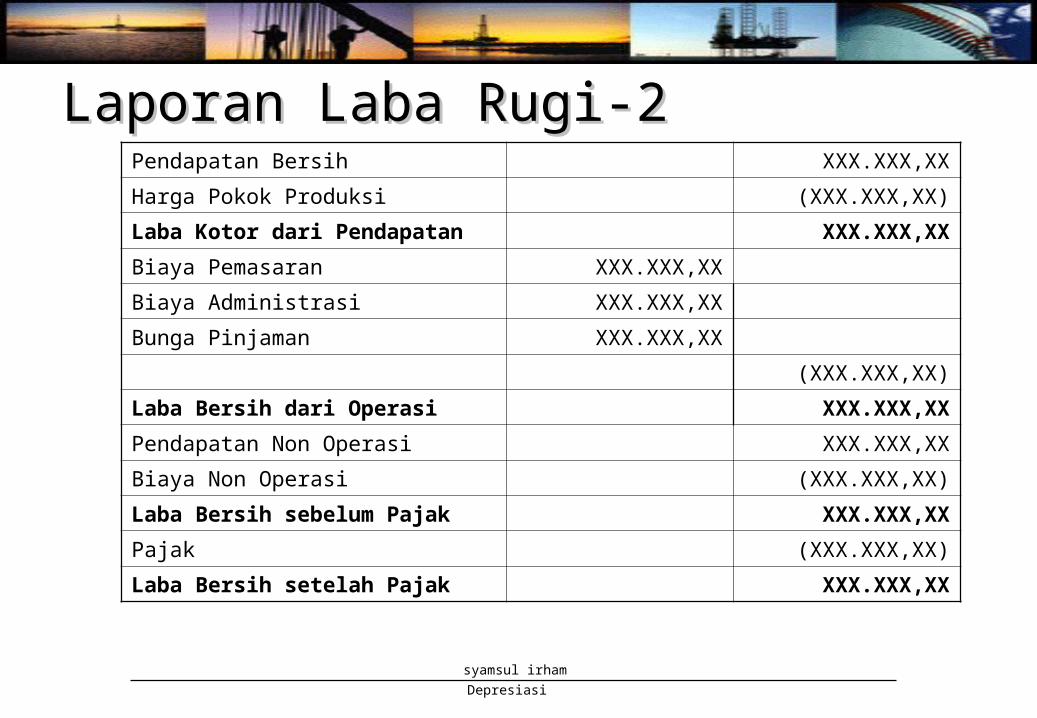

Laporan Laba Rugi-1Laporan Laba Rugi-1Terdiri dari 3 bagian utama:

1. Hasil Penjualan (Sales)

2. Biaya (Costs/Expenses)

3. Rugi/Laba (Loss/Profit) : selisih antara hasil penjualan dan biaya

Terkadang dilengkapi dengan:

1. Pajak

2. dll

Depresiasi

syamsul irham

Laporan Laba Rugi-2Laporan Laba Rugi-2Pendapatan Bersih XXX.XXX,XX

Harga Pokok Produksi (XXX.XXX,XX)

Laba Kotor dari Pendapatan XXX.XXX,XX

Biaya Pemasaran XXX.XXX,XX

Biaya Administrasi XXX.XXX,XX

Bunga Pinjaman XXX.XXX,XX

(XXX.XXX,XX)

Laba Bersih dari Operasi XXX.XXX,XX

Pendapatan Non Operasi XXX.XXX,XX

Biaya Non Operasi (XXX.XXX,XX)

Laba Bersih sebelum Pajak XXX.XXX,XX

Pajak (XXX.XXX,XX)

Laba Bersih setelah Pajak XXX.XXX,XX

Depresiasi

syamsul irham

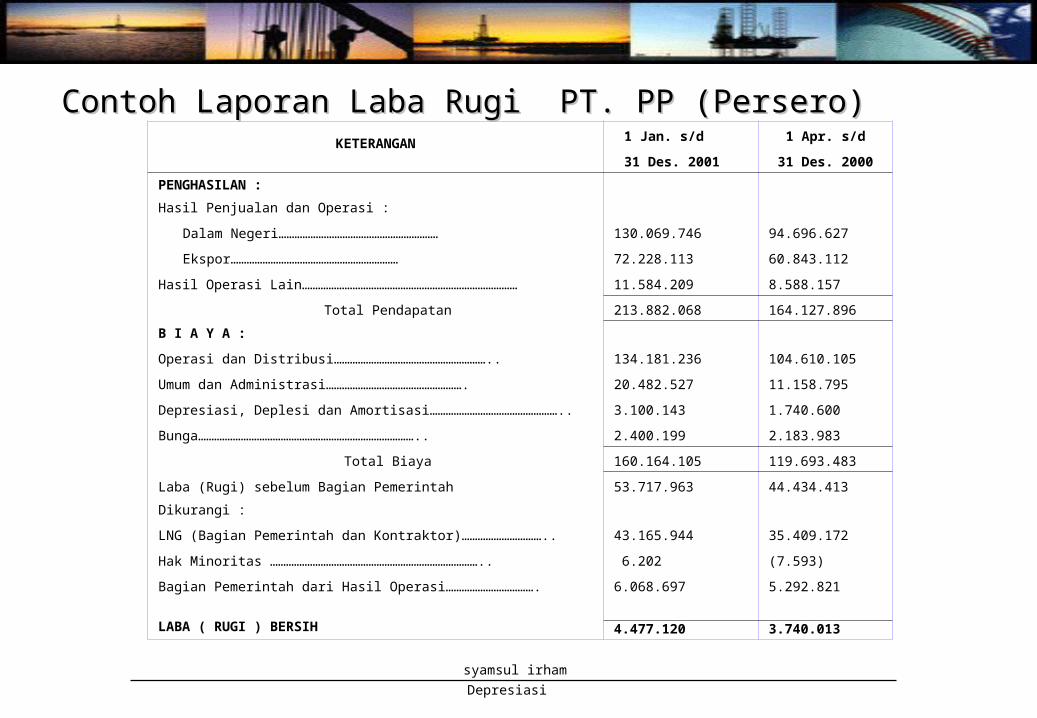

Contoh Laporan Laba Rugi PT. PP (Persero)Contoh Laporan Laba Rugi PT. PP (Persero)

KETERANGAN 1 Jan. s/d 1 Apr. s/d

31 Des. 2001 31 Des. 2000

PENGHASILAN :

Hasil Penjualan dan Operasi :

Dalam Negeri…………………………………………………… 130.069.746 94.696.627

Ekspor……………………………………………………… 72.228.113 60.843.112

Hasil Operasi Lain……………………………………………………………………… 11.584.209 8.588.157

Total Pendapatan 213.882.068 164.127.896

B I A Y A :

Operasi dan Distribusi………………………………………………….. 134.181.236 104.610.105

Umum dan Administrasi……………………………………………. 20.482.527 11.158.795

Depresiasi, Deplesi dan Amortisasi………………………………………….. 3.100.143 1.740.600

Bunga……………………………………………………………………….. 2.400.199 2.183.983

Total Biaya 160.164.105 119.693.483

Laba (Rugi) sebelum Bagian Pemerintah 53.717.963 44.434.413

Dikurangi :

LNG (Bagian Pemerintah dan Kontraktor)………………………….. 43.165.944 35.409.172

Hak Minoritas …………………………………………………………………….. 6.202 (7.593)

Bagian Pemerintah dari Hasil Operasi……………………………. 6.068.697 5.292.821

LABA ( RUGI ) BERSIH 4.477.120 3.740.013

Depresiasi

syamsul irham

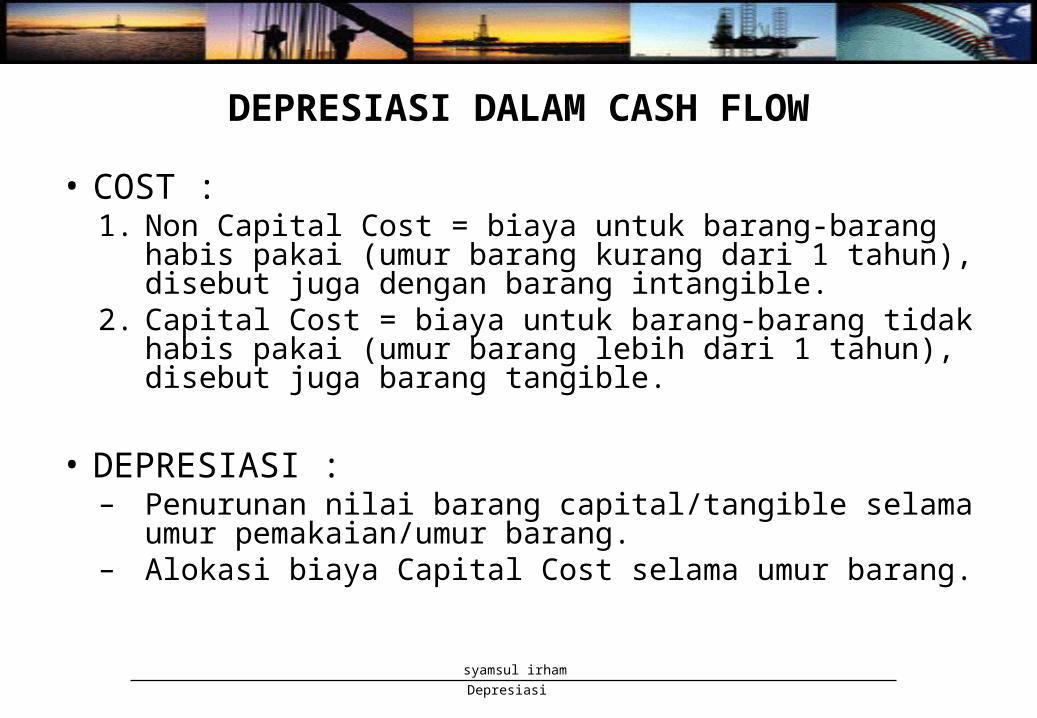

DEPRESIASI DALAM CASH FLOW

• COST :1. Non Capital Cost = biaya untuk barang-barang habis

pakai (umur barang kurang dari 1 tahun), disebut juga dengan barang intangible.

2. Capital Cost = biaya untuk barang-barang tidak habis pakai (umur barang lebih dari 1 tahun), disebut juga barang tangible.

• DEPRESIASI :– Penurunan nilai barang capital/tangible selama umur

pemakaian/umur barang.– Alokasi biaya Capital Cost selama umur barang.

Depresiasi

syamsul irham

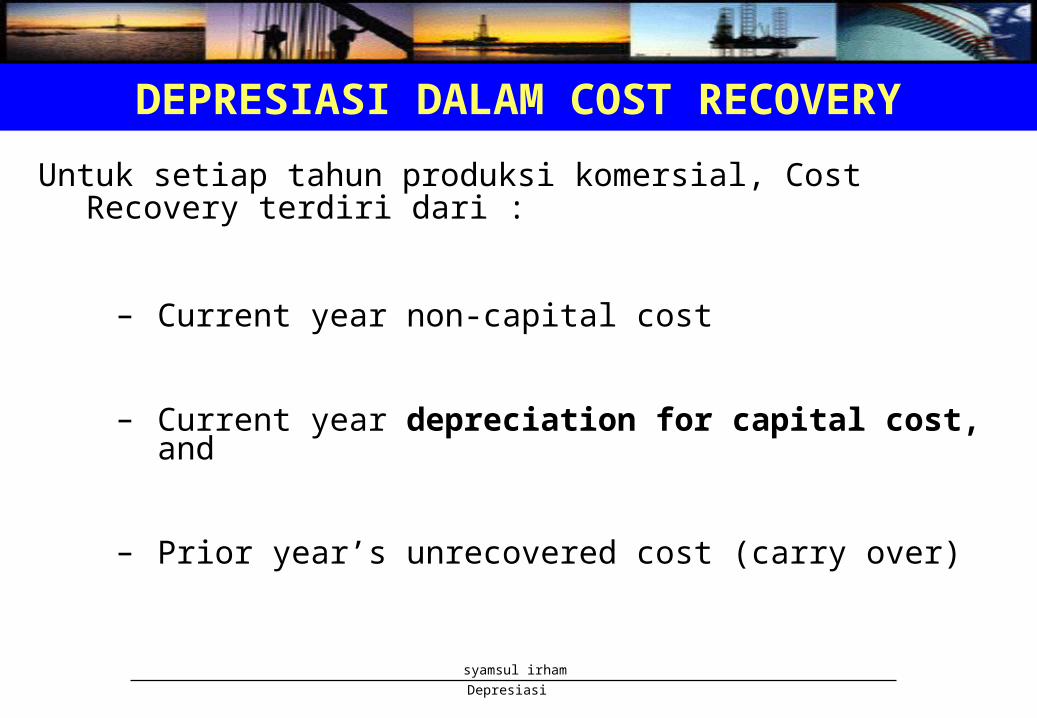

Untuk setiap tahun produksi komersial, Cost Recovery terdiri dari :

– Current year non-capital cost

– Current year depreciation for capital cost, and

– Prior year’s unrecovered cost (carry over)

DEPRESIASI DALAM COST RECOVERY

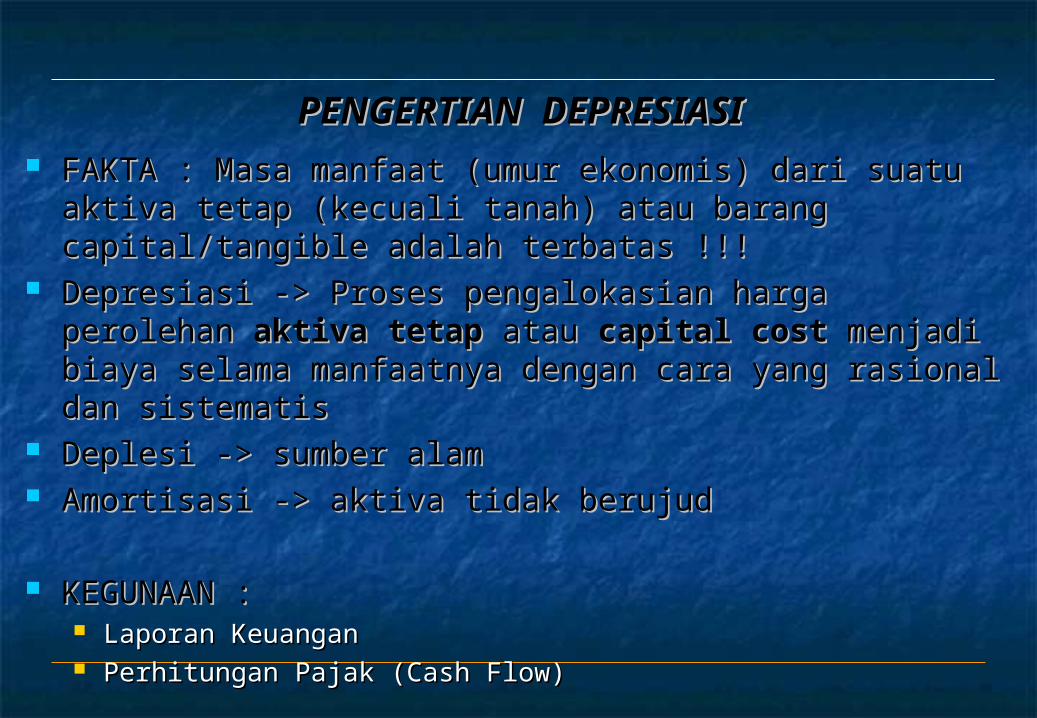

PENGERTIAN DEPRESIASIPENGERTIAN DEPRESIASI FAKTA : Masa manfaat (umur ekonomis) dari suatu aktiva FAKTA : Masa manfaat (umur ekonomis) dari suatu aktiva

tetap (kecuali tanah) atau barang capital/tangible adalah tetap (kecuali tanah) atau barang capital/tangible adalah terbatas !!!terbatas !!!

Depresiasi -> Proses pengalokasian harga perolehan Depresiasi -> Proses pengalokasian harga perolehan aktiva tetap aktiva tetap atau atau capital cost capital cost menjadi biaya selama menjadi biaya selama manfaatnya dengan cara yang rasional dan sistematismanfaatnya dengan cara yang rasional dan sistematis

Deplesi -> sumber alamDeplesi -> sumber alam Amortisasi -> aktiva tidak berujudAmortisasi -> aktiva tidak berujud

KEGUNAAN :KEGUNAAN : Laporan KeuanganLaporan Keuangan Perhitungan Pajak (Cash Flow)Perhitungan Pajak (Cash Flow)

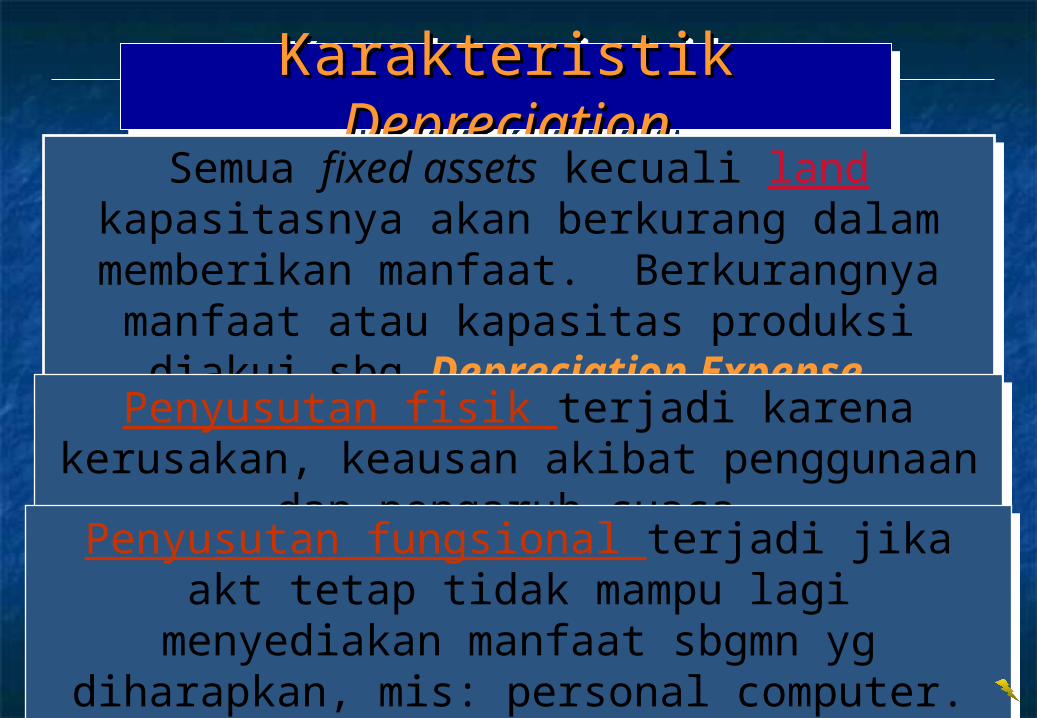

Karakteristik Karakteristik DepreciationDepreciationKarakteristik Karakteristik DepreciationDepreciationSemua fixed assets kecuali land kapasitasnya akan

berkurang dalam memberikan manfaat. Berkurangnya manfaat atau kapasitas produksi diakui

sbg Depreciation Expense.

Semua fixed assets kecuali land kapasitasnya akan berkurang dalam memberikan manfaat.

Berkurangnya manfaat atau kapasitas produksi diakui sbg Depreciation Expense.

Penyusutan fisik terjadi karena kerusakan, keausan akibat penggunaan dan pengaruh cuaca.

Penyusutan fisik terjadi karena kerusakan, keausan akibat penggunaan dan pengaruh cuaca.

Penyusutan fungsional terjadi jika akt tetap tidak mampu lagi menyediakan manfaat sbgmn yg

diharapkan, mis: personal computer.

Penyusutan fungsional terjadi jika akt tetap tidak mampu lagi menyediakan manfaat sbgmn yg

diharapkan, mis: personal computer.

TanahTanahTanahTanah

Tanah mempunyai umur ekonomis yang tidak terbatas, oleh karenanya

tidak dilakukan depresiasi.

Gedung/BangunanGedung/BangunanGedung/BangunanGedung/Bangunan

Gedung mempunyai umur yang terbatas, sehingga harus Gedung mempunyai umur yang terbatas, sehingga harus dilakukan depresiasi. dilakukan depresiasi.

PeralatanPeralatanPeralatanPeralatan

Sama seperti gedung,

peralatan juga mempunyai

umur ekonomis yang terbatas

sehingga harus dilakukan

depresiasi pula.

Depresiasi

syamsul irham

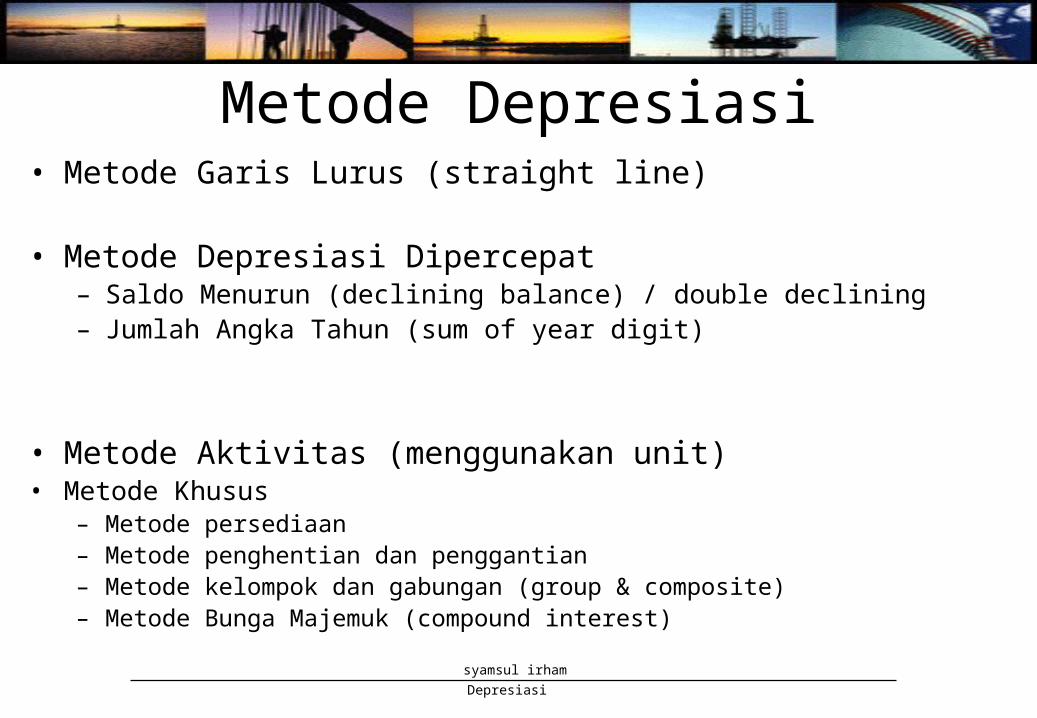

Metode Depresiasi• Metode Garis Lurus (straight line)

• Metode Depresiasi Dipercepat– Saldo Menurun (declining balance) / double declining – Jumlah Angka Tahun (sum of year digit)

• Metode Aktivitas (menggunakan unit)• Metode Khusus

– Metode persediaan – Metode penghentian dan penggantian– Metode kelompok dan gabungan (group & composite)– Metode Bunga Majemuk (compound interest)

Depresiasi

syamsul irham

• Hal penting yang harus diperhatikan:– harga perolehan– nilai residu / nilai sisa– masa manfaat / umur aktiva– Metode Depresiasi

• Dasar Depresiasi = Harga perolehan - Nilai sisa

Depresiasi

syamsul irham

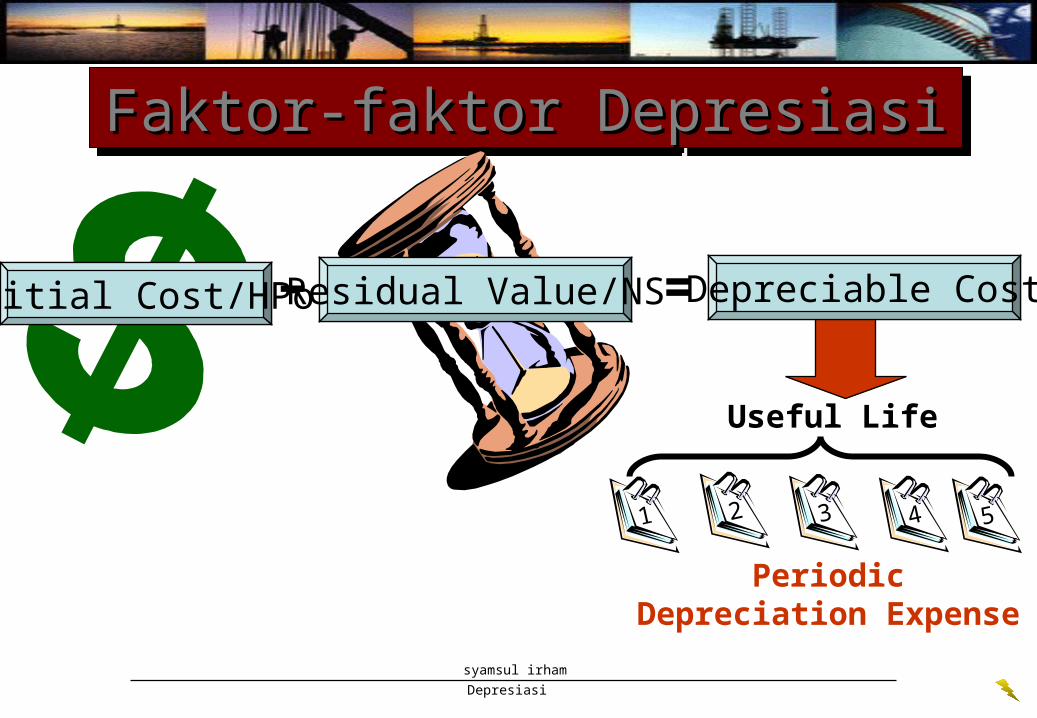

Faktor-faktor DepresiasiFaktor-faktor DepresiasiFaktor-faktor DepresiasiFaktor-faktor Depresiasi

Initial Cost/HPo Residual Value/NS- = Depreciable Cost

Useful Life

1

Periodic Depreciation Expense

2 3 4 5

Depresiasi

syamsul irham

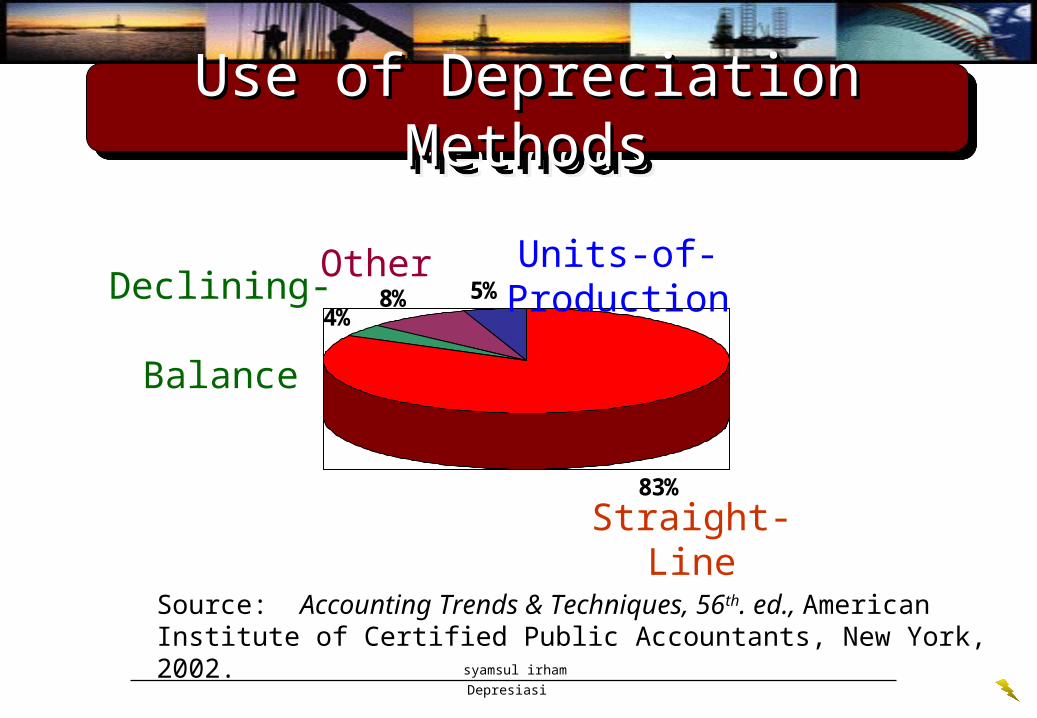

83%

4%8% 5%

Straight-Line

Declining- Balance

Other Units-of-Production

Source: Accounting Trends & Techniques, 56th. ed., American Institute of Certified Public Accountants, New York, 2002.

Use of Depreciation MethodsUse of Depreciation MethodsUse of Depreciation MethodsUse of Depreciation Methods

Depresiasi

syamsul irham

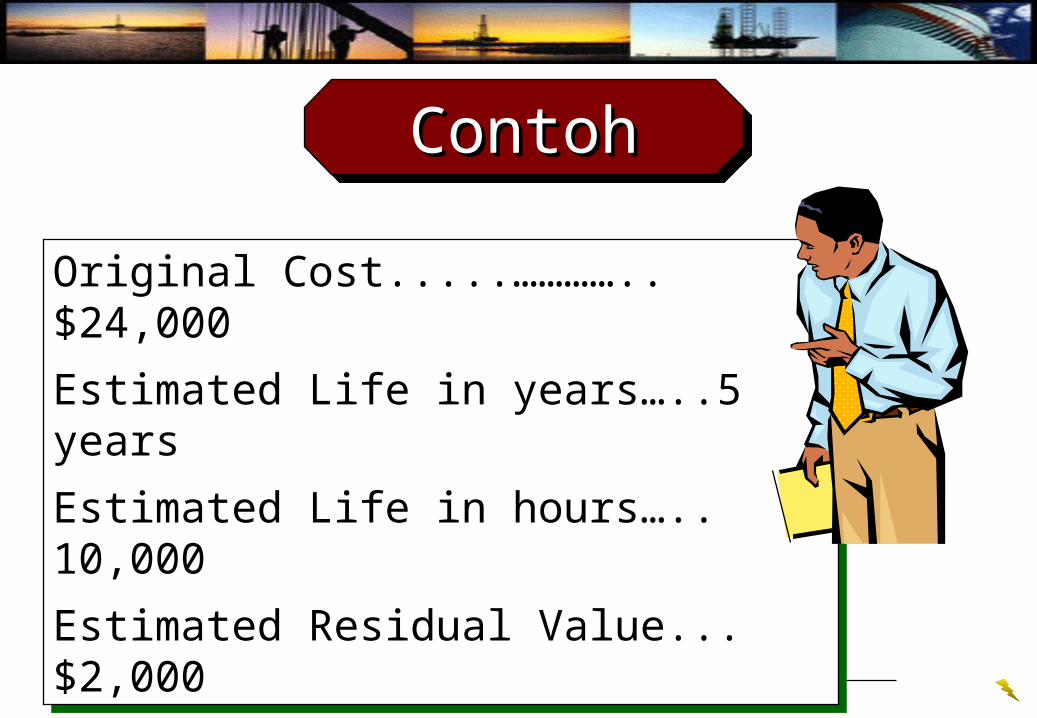

ContohContohContohContoh

Original Cost.....………….. $24,000

Estimated Life in years….. 5 years

Estimated Life in hours….. 10,000

Estimated Residual Value... $2,000

Original Cost.....………….. $24,000

Estimated Life in years….. 5 years

Estimated Life in hours….. 10,000

Estimated Residual Value... $2,000

Depresiasi

syamsul irham

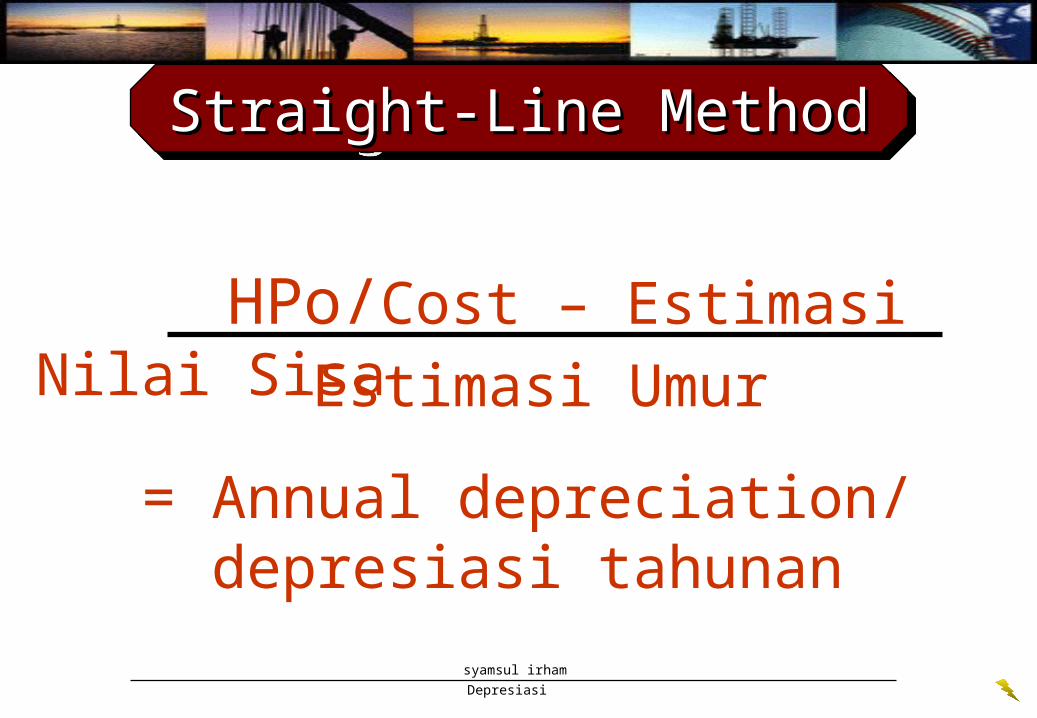

Straight-Line MethodStraight-Line MethodStraight-Line MethodStraight-Line Method

HPo/Cost – Estimasi Nilai Sisa

Estimasi Umur

= Annual depreciation/ depresiasi tahunan

Depresiasi

syamsul irham

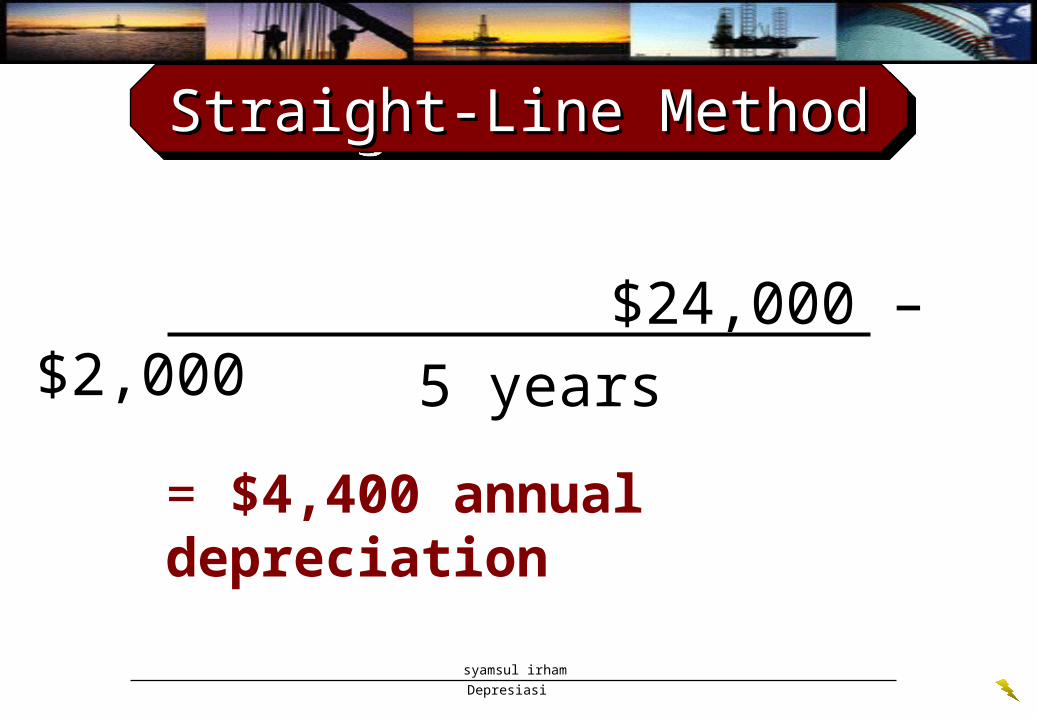

Straight-Line MethodStraight-Line MethodStraight-Line MethodStraight-Line Method

$24,000 – $2,000

5 years

= $4,400 annual depreciation

Depresiasi

syamsul irham

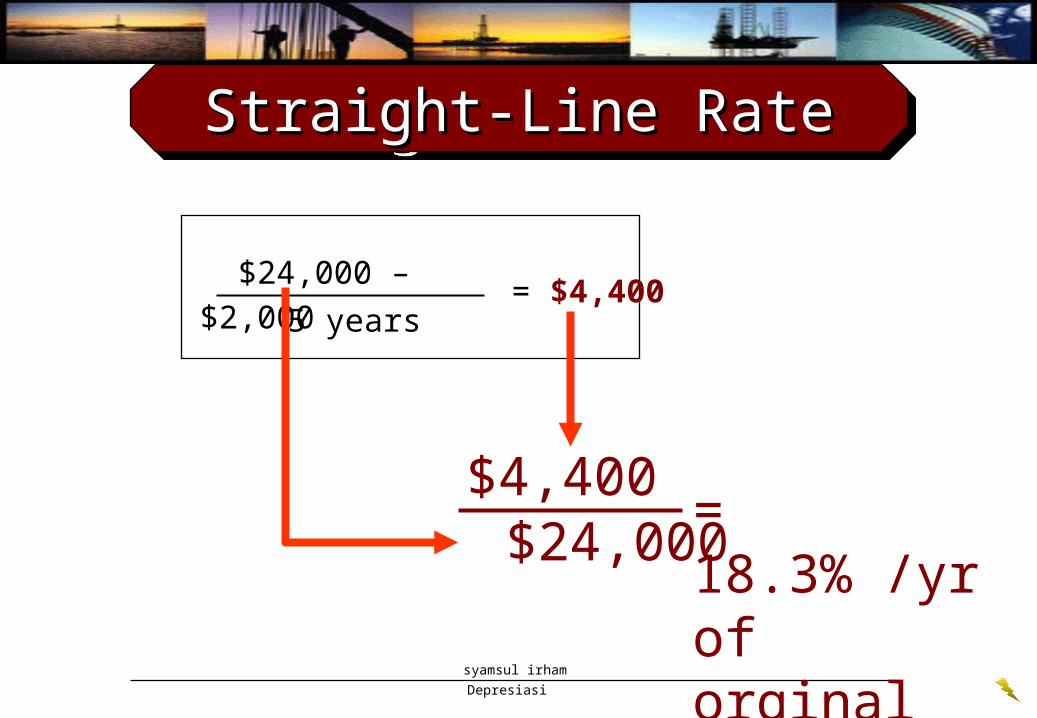

Straight-Line RateStraight-Line RateStraight-Line RateStraight-Line Rate

$24,000 – $2,000

5 years = $4,400

$4,400 $24,000

= 18.3% /yr of orginal cost

Depresiasi

syamsul irham

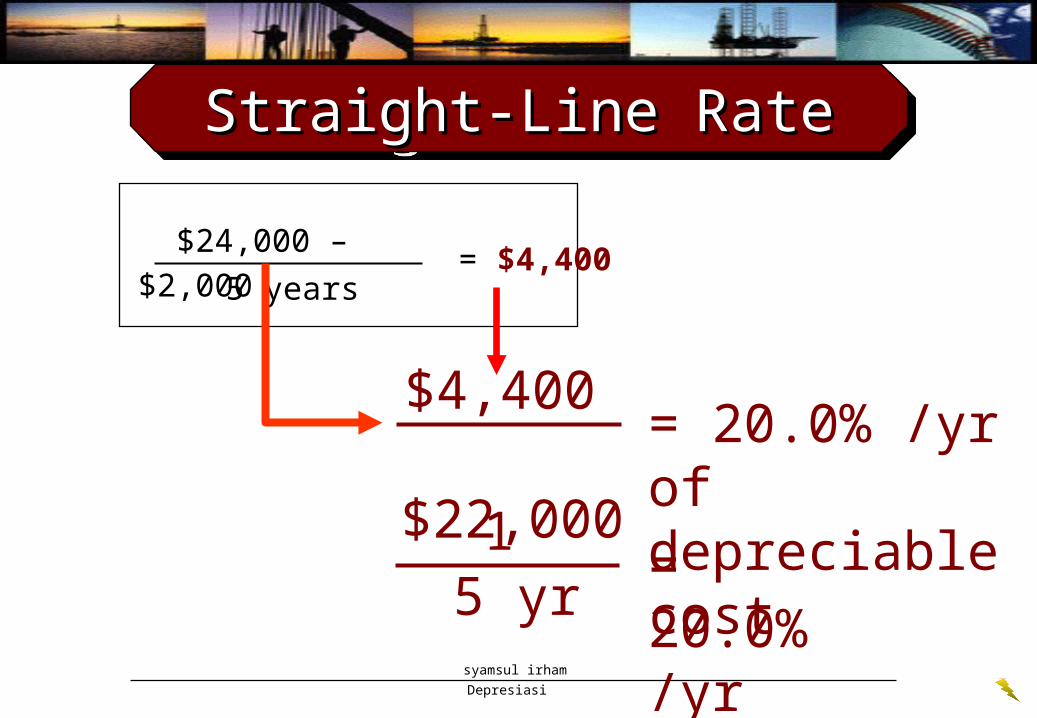

Straight-Line RateStraight-Line RateStraight-Line RateStraight-Line Rate

$24,000 – $2,000

5 years = $4,400

$4,400 $22,000

= 20.0% /yr of depreciable cost

1 5 yr

= 20.0% /yr

Depresiasi

syamsul irham

Straight-Line MethodStraight-Line MethodStraight-Line MethodStraight-Line Method

The straight-line method banyak digunakan perusahaan karena sederhana dan

memberikan alasan yang rasional dalam mentransfer cost ke beban periodik jika

asset yg digunakan memberikan manfaat yg sama

The straight-line method banyak digunakan perusahaan karena sederhana dan

memberikan alasan yang rasional dalam mentransfer cost ke beban periodik jika

asset yg digunakan memberikan manfaat yg sama

Depresiasi

syamsul irham

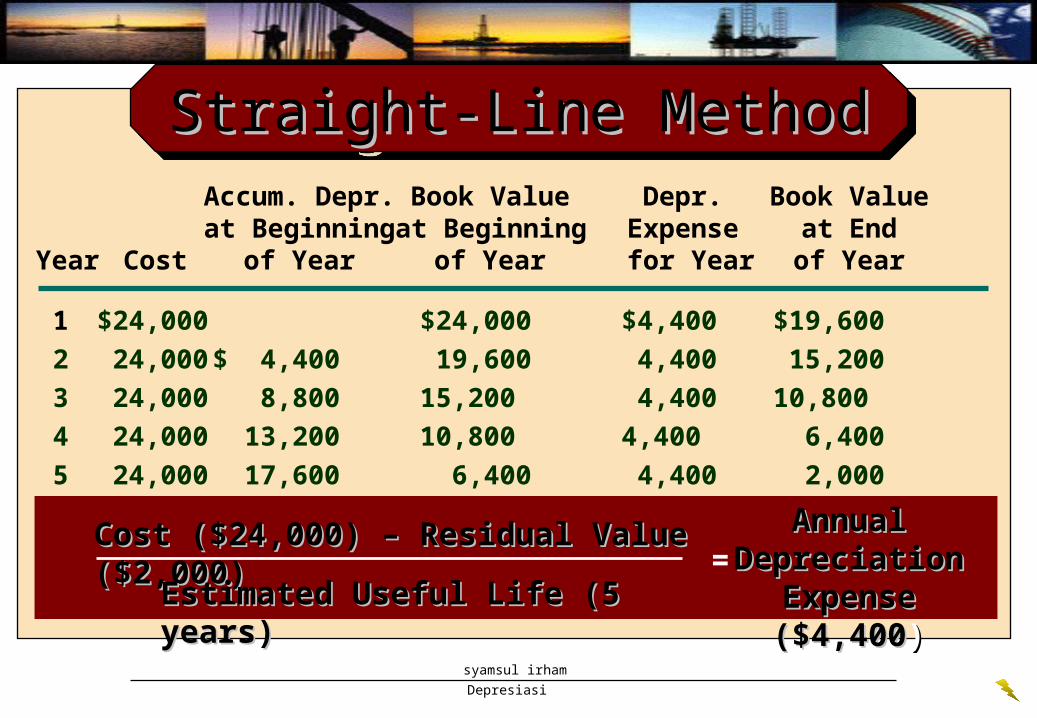

Accum. Depr. Book Value Depr. Book Valueat Beginning at Beginning Expense at End

Year Cost of Year of Year for Year of Year

1 $24,000 $24,000 $4,400 $19,600

2 24,000 $ 4,400 19,600 4,400 15,200

3 24,000 8,800 15,200 4,400 10,800

4 24,000 13,200 10,800 4,400 6,400

5 24,000 17,600 6,400 4,400 2,000

Cost ($24,000) Cost ($24,000) –– Residual Value ($2,000) Residual Value ($2,000)

Estimated Useful Life (5 years)Estimated Useful Life (5 years)=Annual DepreciationAnnual Depreciation

Expense ($4,400Expense ($4,400))

Straight-Line MethodStraight-Line MethodStraight-Line MethodStraight-Line Method

Depresiasi

syamsul irham

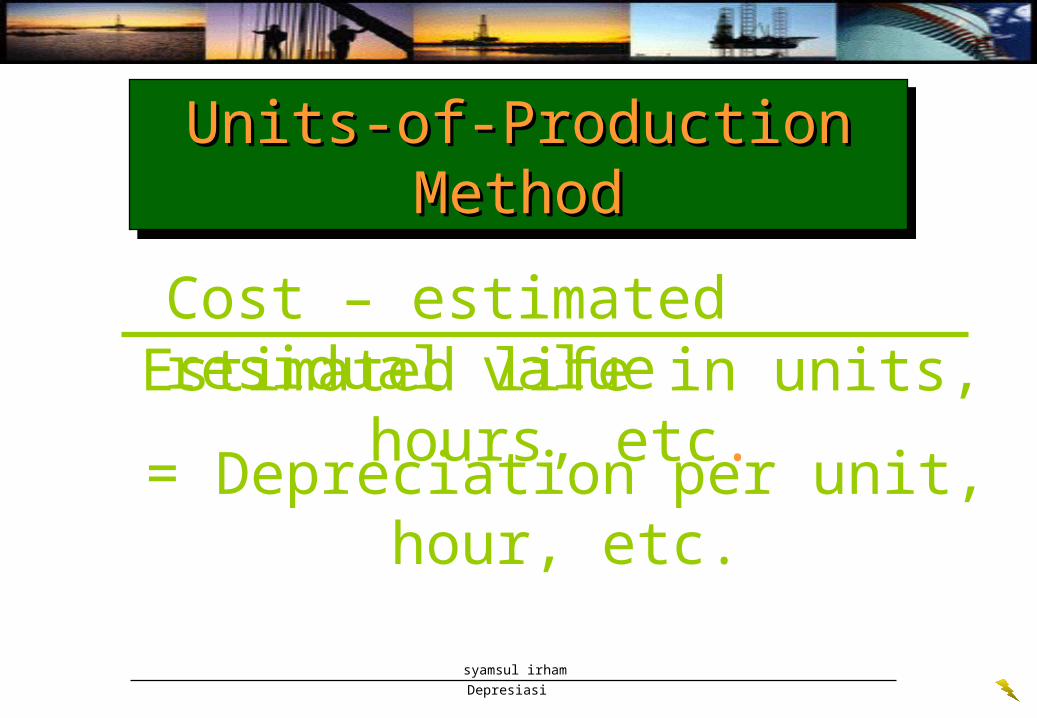

Units-of-Production MethodUnits-of-Production MethodUnits-of-Production MethodUnits-of-Production Method

Cost – estimated residual valueEstimated life in units, hours, etc.

= Depreciation per unit, hour, etc.

Depresiasi

syamsul irham

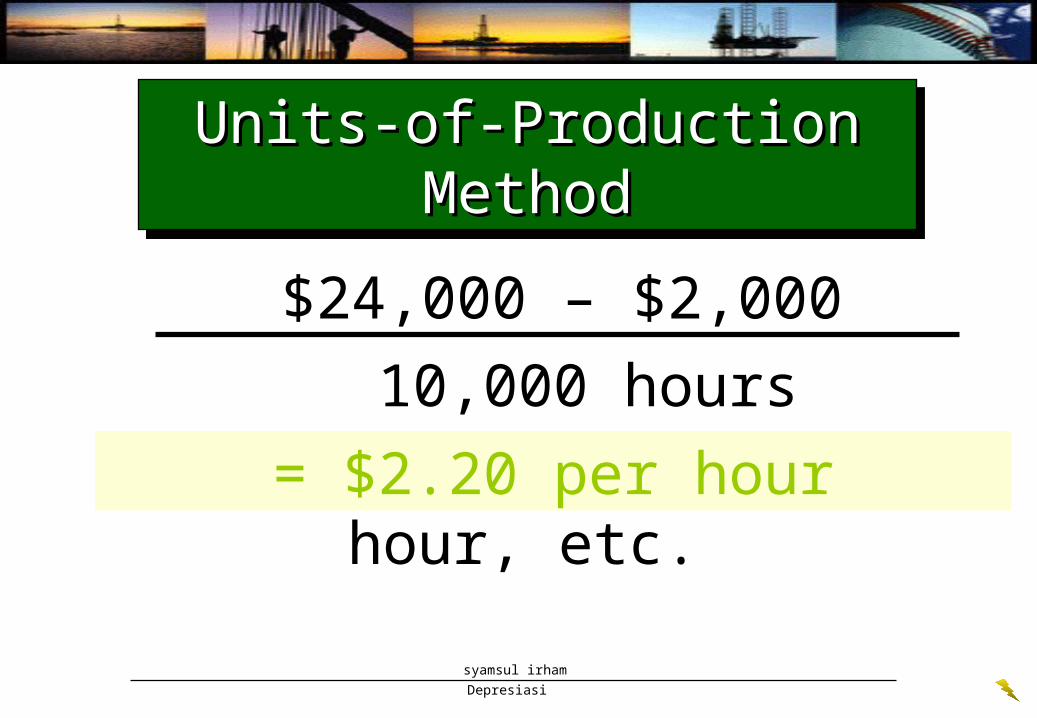

$24,000 – $2,000

10,000 hours

= Depreciation per unit, hour, etc.= $2.20 per hour

Units-of-Production MethodUnits-of-Production MethodUnits-of-Production MethodUnits-of-Production Method

Depresiasi

syamsul irham

The units-of-production method lebih tepat digunakan untuk aktiva tetap yang memberikan manfaat

tidak sama setiap periode.

The units-of-production method lebih tepat digunakan untuk aktiva tetap yang memberikan manfaat

tidak sama setiap periode.

Units-of-Production MethodUnits-of-Production MethodUnits-of-Production MethodUnits-of-Production Method

Depresiasi

syamsul irham

Declining-Balance MethodDeclining-Balance MethodDeclining-Balance MethodDeclining-Balance Method

• Memiliki tingkat depresiasi yang lebih tinggi pada tahun pertama, dan secara bertahap berkurang di tahun berikutnya.

)(

11 ii depresiasikapitalinvestasi

TDepresiasi

Depresiasi

syamsul irham

There’s a shortcut. Simply divide one by the number of

years (1 ÷ 5 = .20).

There’s a shortcut. Simply divide one by the number of

years (1 ÷ 5 = .20).

Declining-Balance MethodDeclining-Balance MethodDeclining-Balance MethodDeclining-Balance Method

determine the straight-line rate

Step 1Step 1

Depresiasi

syamsul irham

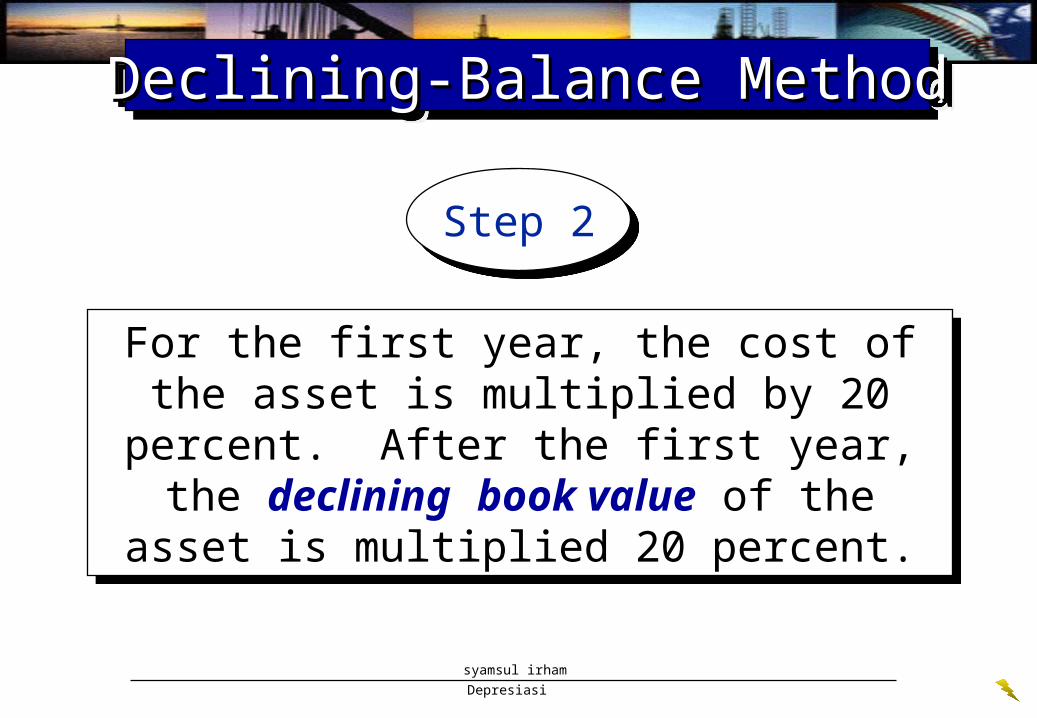

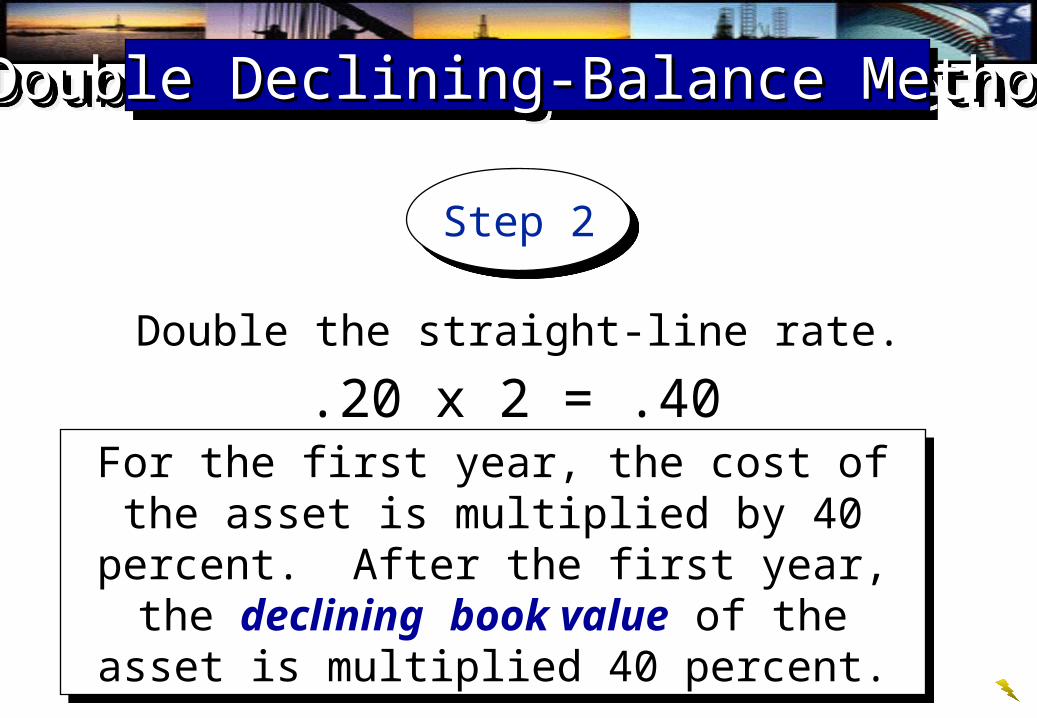

Step 2Step 2

For the first year, the cost of the asset is multiplied by 20 percent. After the first year, the

declining book value of the asset is multiplied 20 percent.

For the first year, the cost of the asset is multiplied by 20 percent. After the first year, the

declining book value of the asset is multiplied 20 percent.

Declining-Balance MethodDeclining-Balance MethodDeclining-Balance MethodDeclining-Balance Method

Depresiasi

syamsul irham

Build a table.

Step 3Step 3

Declining-Balance MethodDeclining-Balance MethodDeclining-Balance MethodDeclining-Balance Method

Depresiasi

syamsul irham

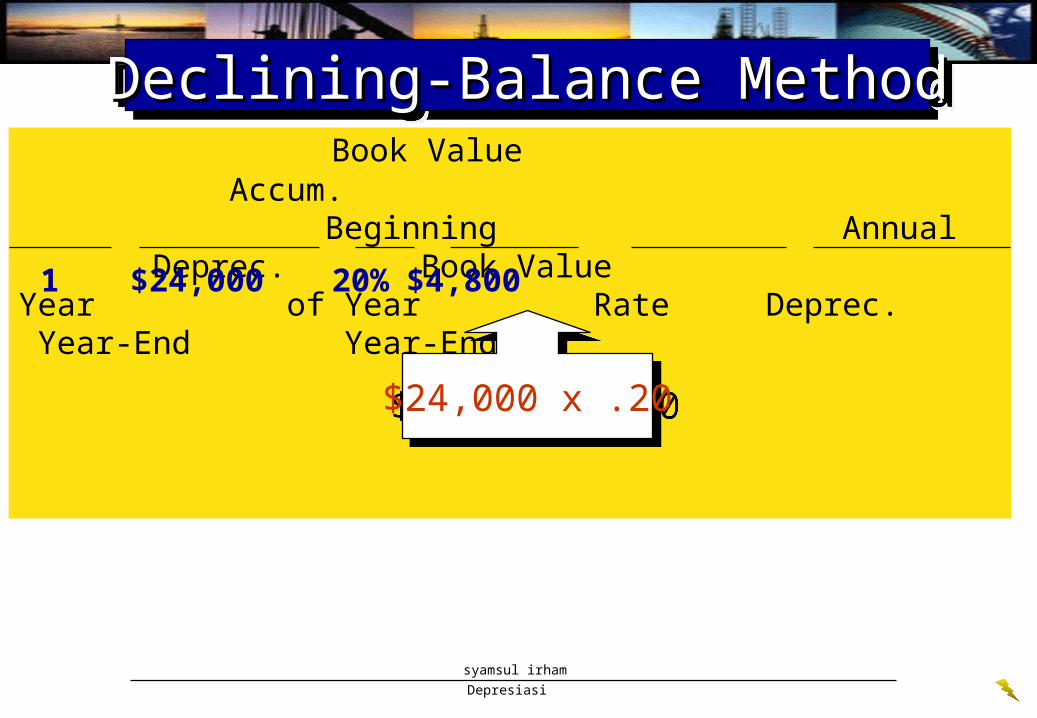

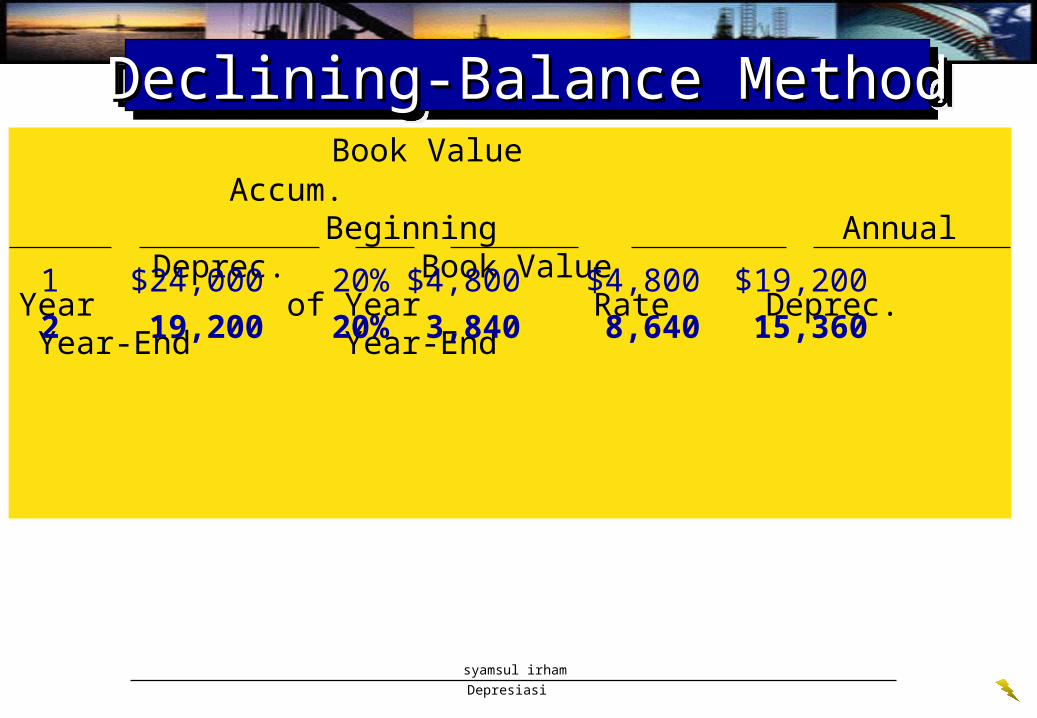

Book Value Accum. Beginning Annual Deprec. Book ValueYear of Year Rate Deprec. Year-End Year-End

1 $24,000 20% $4,800

Declining-Balance MethodDeclining-Balance MethodDeclining-Balance MethodDeclining-Balance Method

$24,000 x .20$24,000 x .20

Depresiasi

syamsul irham

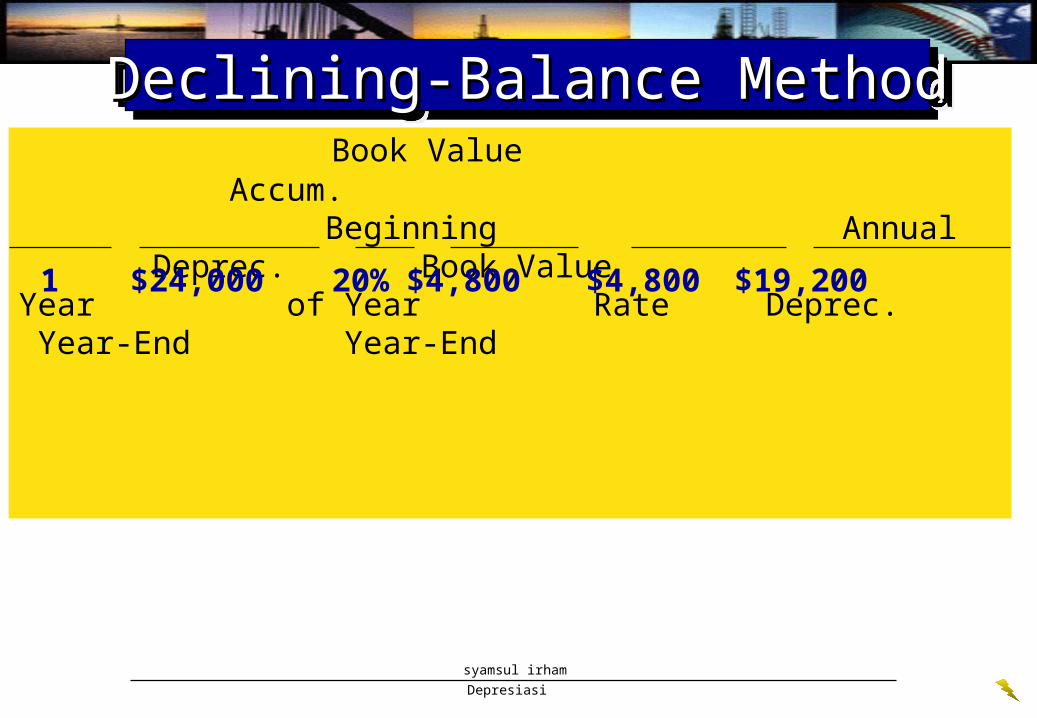

Book Value Accum. Beginning Annual Deprec. Book ValueYear of Year Rate Deprec. Year-End Year-End

1 $24,000 20% $4,800 $4,800 $19,200

Declining-Balance MethodDeclining-Balance MethodDeclining-Balance MethodDeclining-Balance Method

Depresiasi

syamsul irham

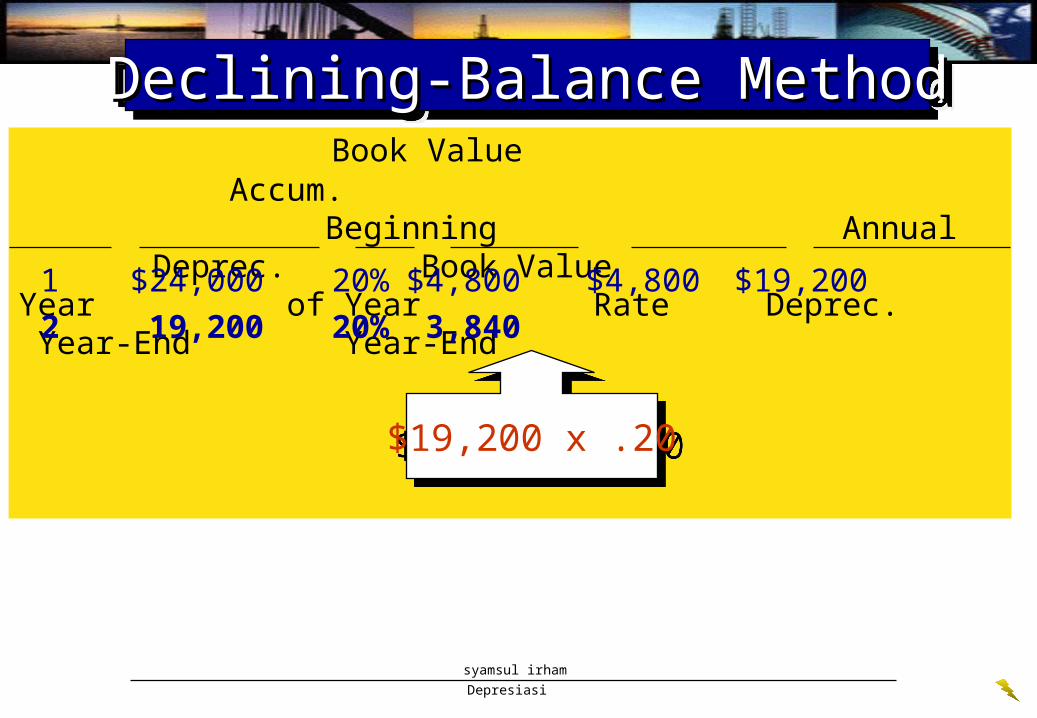

Book Value Accum. Beginning Annual Deprec. Book ValueYear of Year Rate Deprec. Year-End Year-End

1 $24,000 20% $4,800 $4,800 $19,200

2 19,200 20% 3,840

Declining-Balance MethodDeclining-Balance MethodDeclining-Balance MethodDeclining-Balance Method

$19,200 x .20$19,200 x .20

Depresiasi

syamsul irham

Book Value Accum. Beginning Annual Deprec. Book ValueYear of Year Rate Deprec. Year-End Year-End

1 $24,000 20% $4,800 $4,800 $19,200

2 19,200 20% 3,840 8,640 15,360

Declining-Balance MethodDeclining-Balance MethodDeclining-Balance MethodDeclining-Balance Method

Depresiasi

syamsul irham

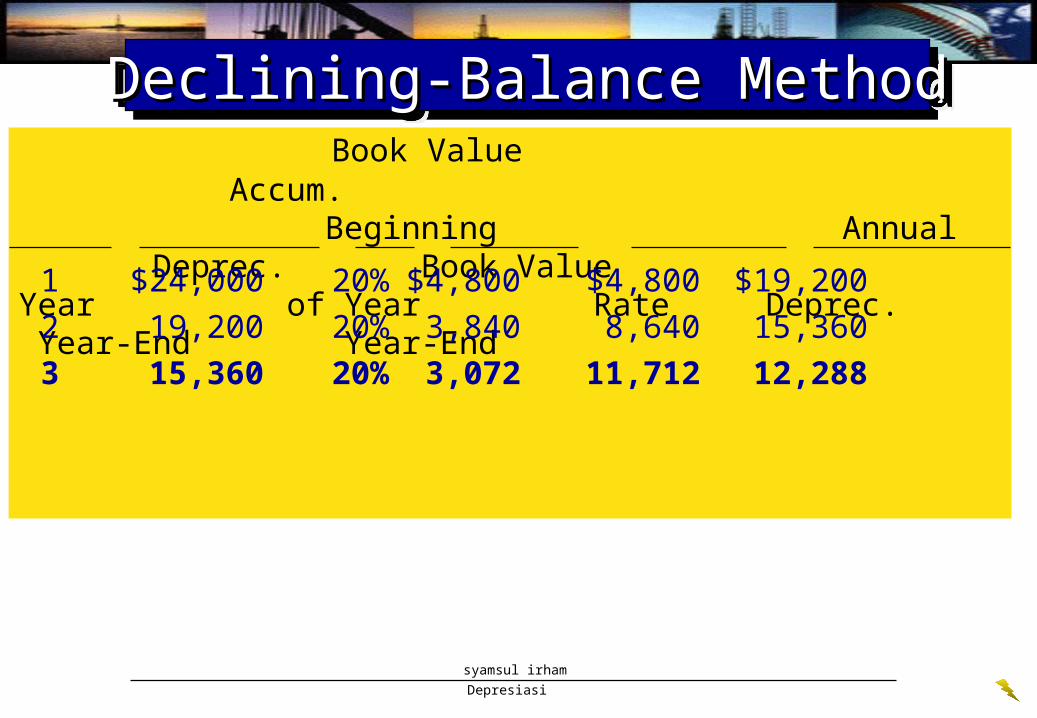

Book Value Accum. Beginning Annual Deprec. Book ValueYear of Year Rate Deprec. Year-End Year-End

1 $24,000 20% $4,800 $4,800 $19,200

2 19,200 20% 3,840 8,640 15,360

3 15,360 20% 3,072 11,712 12,288

Declining-Balance MethodDeclining-Balance MethodDeclining-Balance MethodDeclining-Balance Method

Depresiasi

syamsul irham

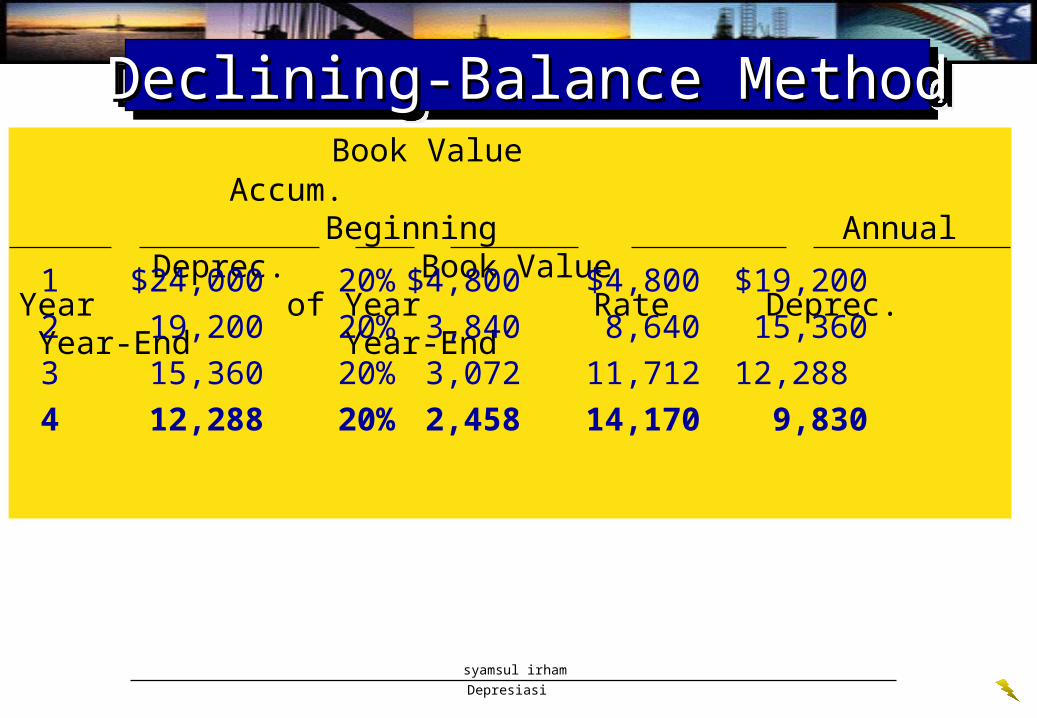

Book Value Accum. Beginning Annual Deprec. Book ValueYear of Year Rate Deprec. Year-End Year-End

1 $24,000 20% $4,800 $4,800 $19,200

2 19,200 20% 3,840 8,640 15,360

3 15,360 20% 3,072 11,712 12,288

4 12,288 20% 2,458 14,170 9,830

Declining-Balance MethodDeclining-Balance MethodDeclining-Balance MethodDeclining-Balance Method

Depresiasi

syamsul irham

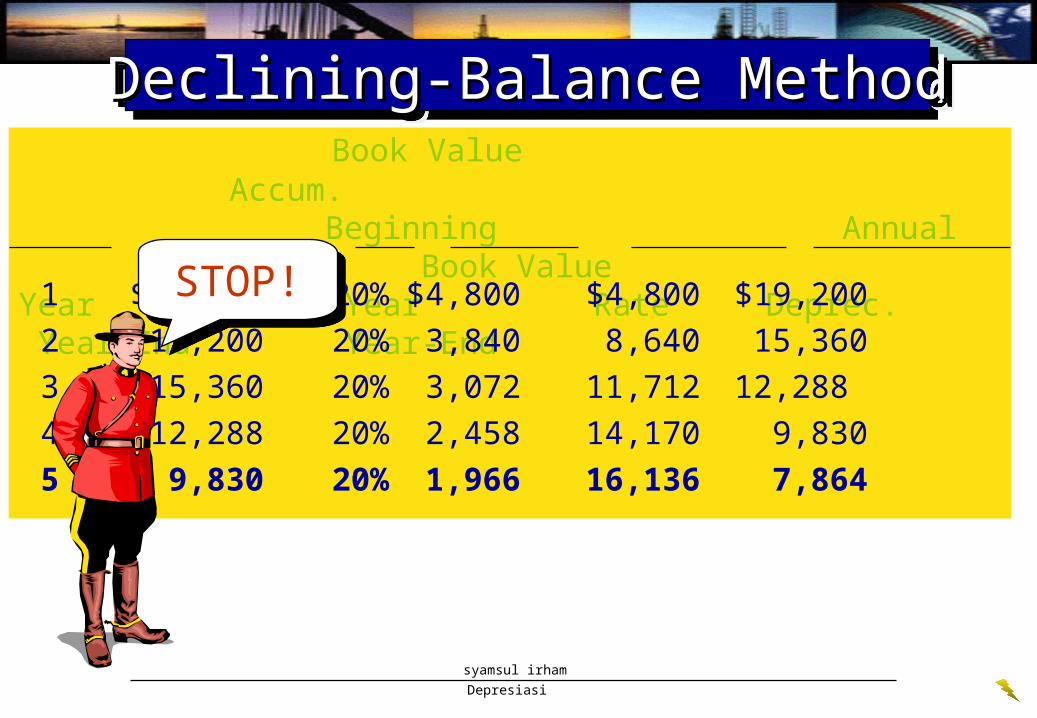

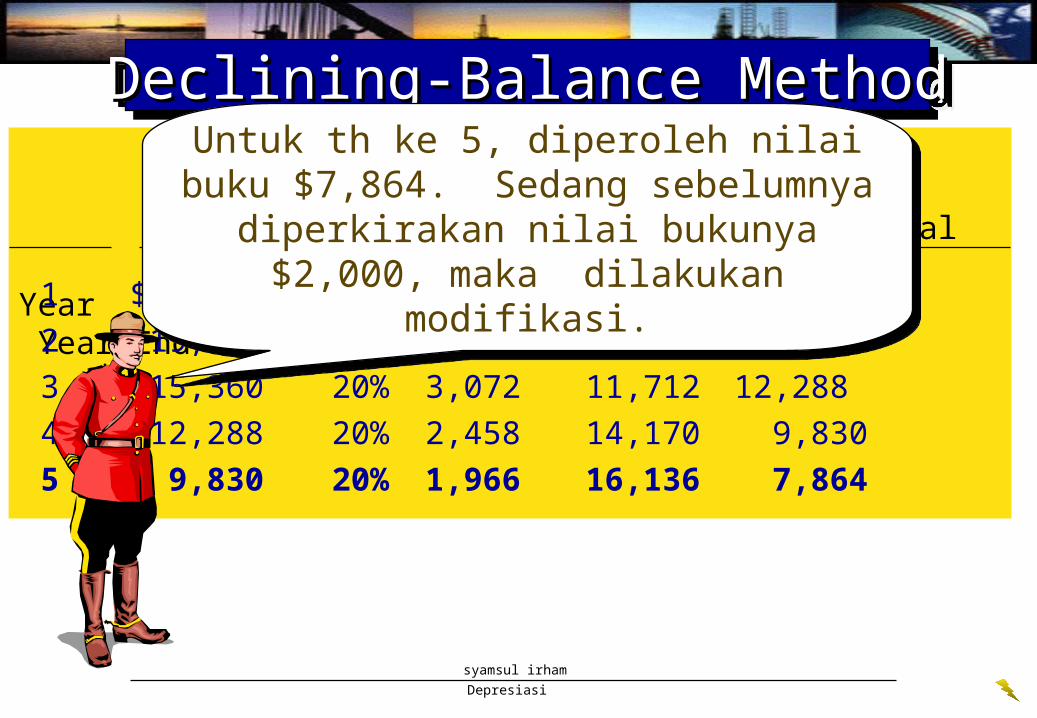

Book Value Accum. Beginning Annual Deprec. Book ValueYear of Year Rate Deprec. Year-End Year-End

1 $24,000 20% $4,800 $4,800 $19,200

2 19,200 20% 3,840 8,640 15,360

3 15,360 20% 3,072 11,712 12,288

4 12,288 20% 2,458 14,170 9,830

5 9,830 20% 1,966 16,136 7,864

STOP!STOP!

Declining-Balance MethodDeclining-Balance MethodDeclining-Balance MethodDeclining-Balance Method

Depresiasi

syamsul irham

Book Value Accum. Beginning Annual Deprec. Book ValueYear of Year Rate Deprec. Year-End Year-End

1 $24,000 20% $4,800 $4,800 $19,200

2 19,200 20% 3,840 8,640 15,360

3 15,360 20% 3,072 11,712 12,288

4 12,288 20% 2,458 14,170 9,830

5 9,830 20% 1,966 16,136 7,864

Declining-Balance MethodDeclining-Balance MethodDeclining-Balance MethodDeclining-Balance Method

Untuk th ke 5, diperoleh nilai buku $7,864. Sedang sebelumnya diperkirakan nilai

bukunya $2,000, maka dilakukan modifikasi.

Untuk th ke 5, diperoleh nilai buku $7,864. Sedang sebelumnya diperkirakan nilai

bukunya $2,000, maka dilakukan modifikasi.

Depresiasi

syamsul irham

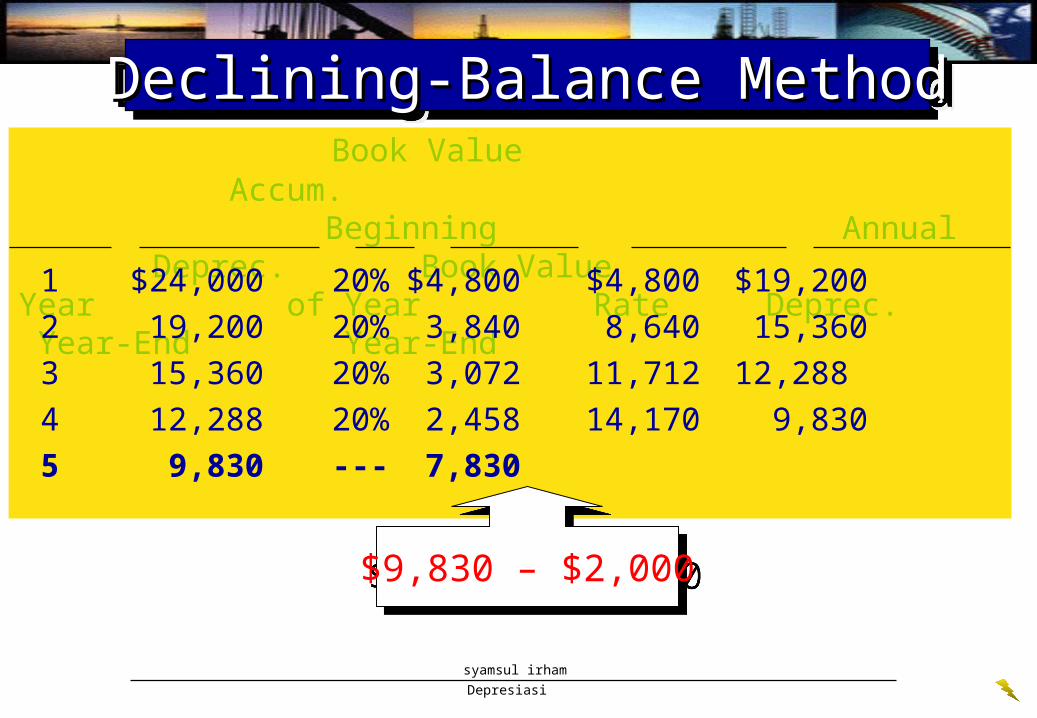

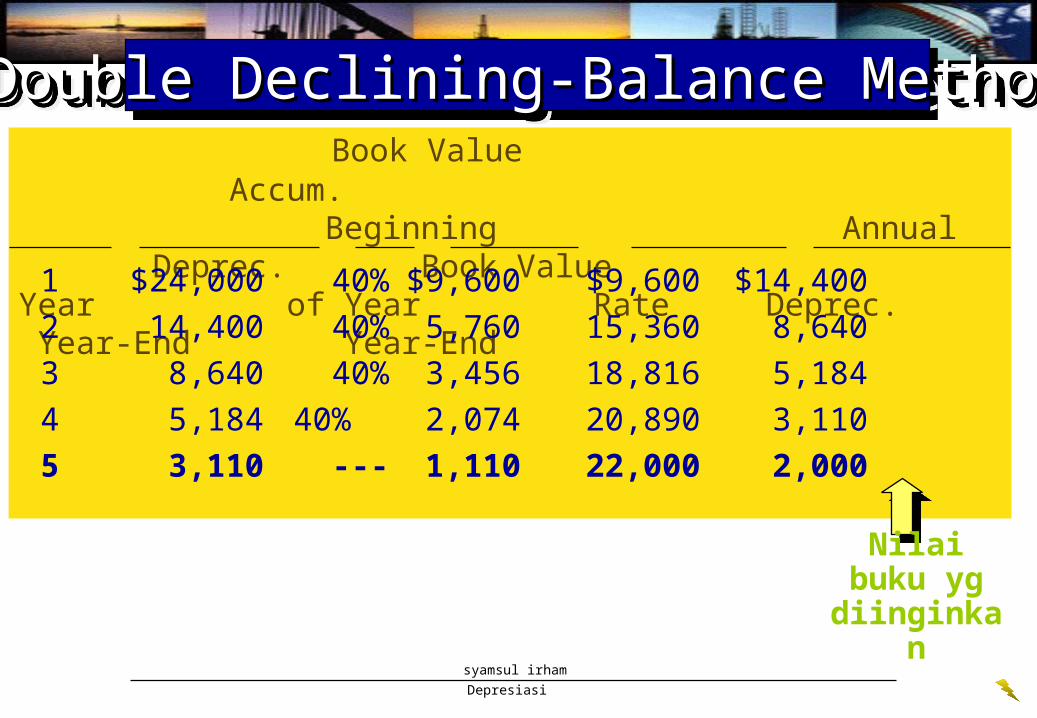

Book Value Accum. Beginning Annual Deprec. Book ValueYear of Year Rate Deprec. Year-End Year-End

1 $24,000 20% $4,800 $4,800 $19,200

2 19,200 20% 3,840 8,640 15,360

3 15,360 20% 3,072 11,712 12,288

4 12,288 20% 2,458 14,170 9,830

5 9,830 --- 7,830

Declining-Balance MethodDeclining-Balance MethodDeclining-Balance MethodDeclining-Balance Method

$9,830 – $2,000$9,830 – $2,000

Depresiasi

syamsul irham

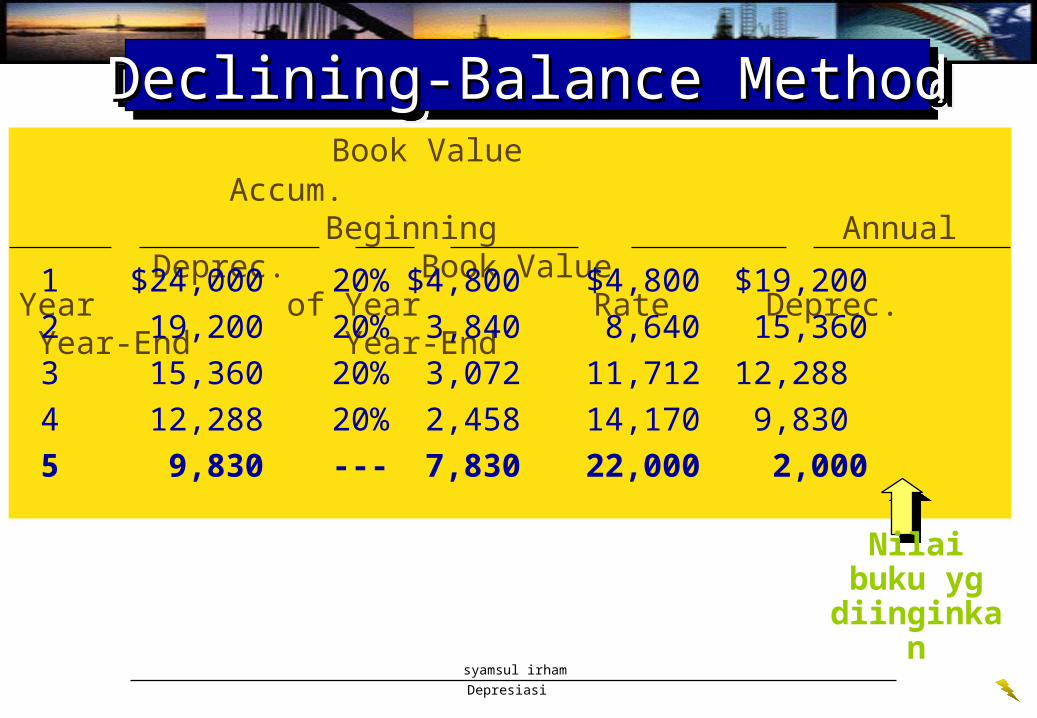

Book Value Accum. Beginning Annual Deprec. Book ValueYear of Year Rate Deprec. Year-End Year-End

1 $24,000 20% $4,800 $4,800 $19,200

2 19,200 20% 3,840 8,640 15,360

3 15,360 20% 3,072 11,712 12,288

4 12,288 20% 2,458 14,170 9,830

5 9,830 --- 7,830 22,000 2,000

Nilai buku yg diinginkan

Declining-Balance MethodDeclining-Balance MethodDeclining-Balance MethodDeclining-Balance Method

Depresiasi

syamsul irham

Double Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance Method

• hampir sama dengan Declining Balance Method, perbedaannya hanya terletak pada laju depresiasi metode ini dua kali lebih besar dari metode declining balance..

)(2

1 ii depresiasikapitalinvestasiT

Depresiasi

Depresiasi

syamsul irham

There’s a shortcut. Simply divide one by the number of

years (1 ÷ 5 = .20).

There’s a shortcut. Simply divide one by the number of

years (1 ÷ 5 = .20).

Double Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance Method

determine the straight-line rate

Step 1Step 1

Depresiasi

syamsul irham

Double the straight-line rate.

Step 2Step 2

.20 x 2 = .40

For the first year, the cost of the asset is multiplied by 40 percent. After the first year, the

declining book value of the asset is multiplied 40 percent.

For the first year, the cost of the asset is multiplied by 40 percent. After the first year, the

declining book value of the asset is multiplied 40 percent.

Double Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance Method

Depresiasi

syamsul irham

Build a table.

Step 3Step 3

Double Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance Method

Depresiasi

syamsul irham

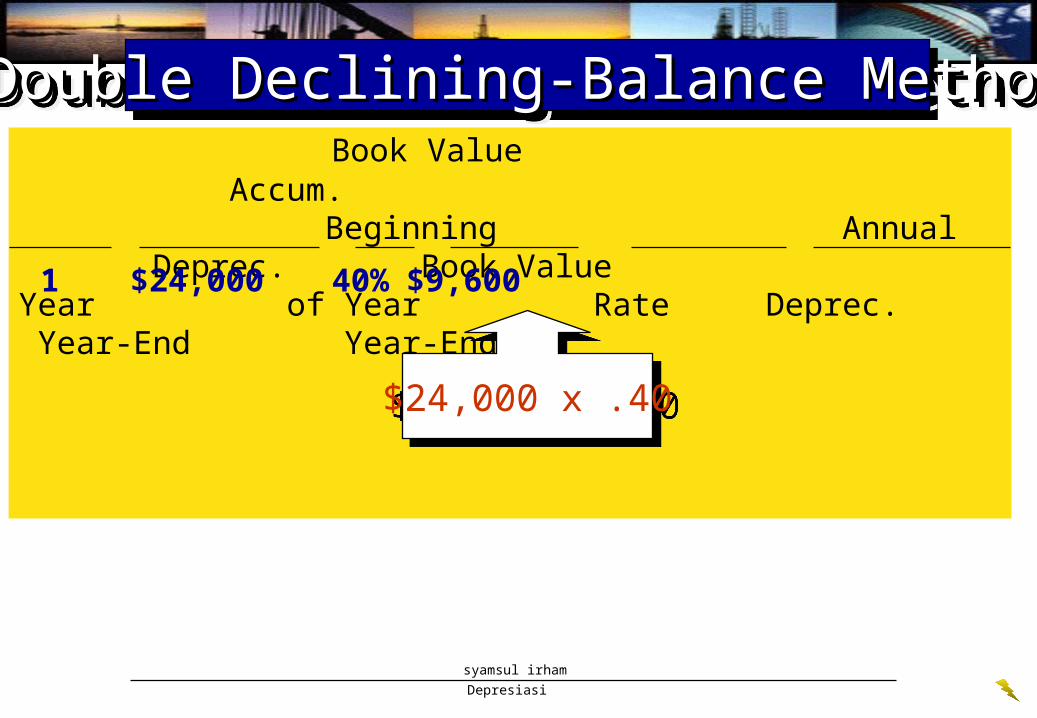

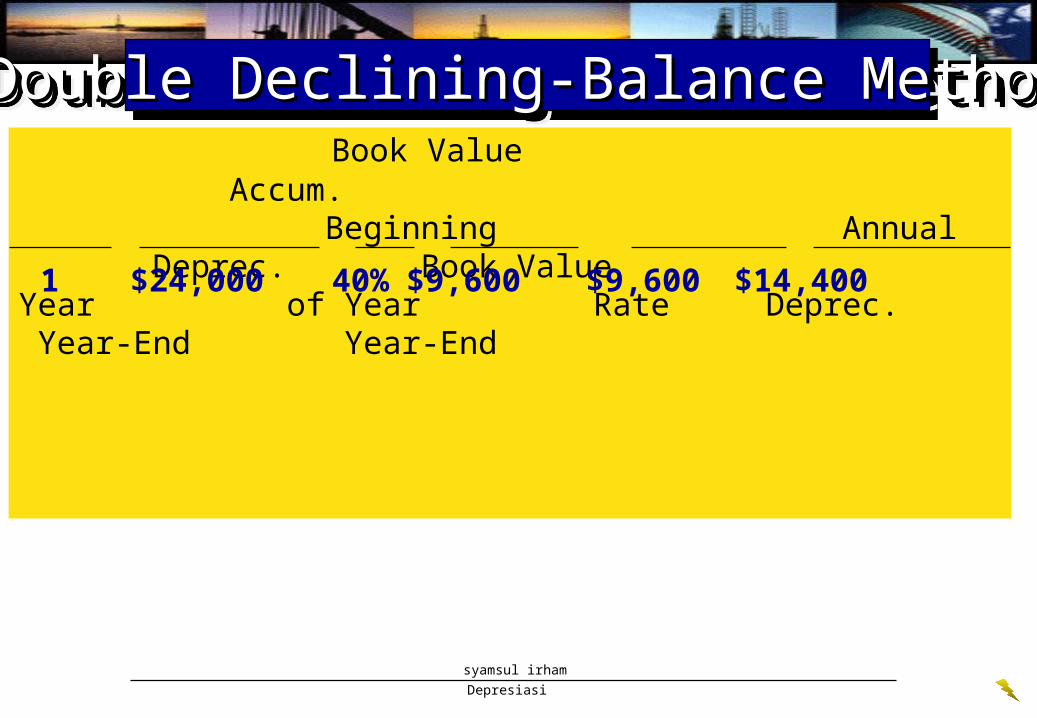

Book Value Accum. Beginning Annual Deprec. Book ValueYear of Year Rate Deprec. Year-End Year-End

1 $24,000 40% $9,600

Double Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance Method

$24,000 x .40$24,000 x .40

Depresiasi

syamsul irham

Book Value Accum. Beginning Annual Deprec. Book ValueYear of Year Rate Deprec. Year-End Year-End

1 $24,000 40% $9,600 $9,600 $14,400

Double Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance Method

Depresiasi

syamsul irham

Book Value Accum. Beginning Annual Deprec. Book ValueYear of Year Rate Deprec. Year-End Year-End

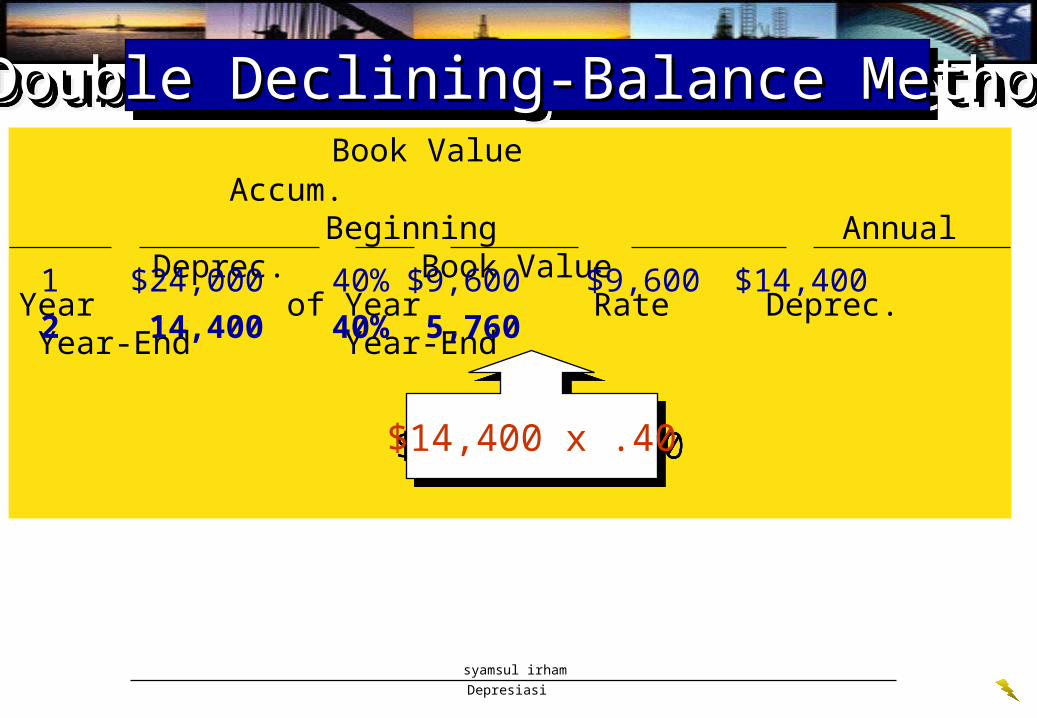

1 $24,000 40% $9,600 $9,600 $14,400

2 14,400 40% 5,760

Double Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance Method

$14,400 x .40$14,400 x .40

Depresiasi

syamsul irham

Book Value Accum. Beginning Annual Deprec. Book ValueYear of Year Rate Deprec. Year-End Year-End

1 $24,000 40% $9,600 $9,600 $14,400

2 14,400 40% 5,760 15,360 8,640

Double Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance Method

Depresiasi

syamsul irham

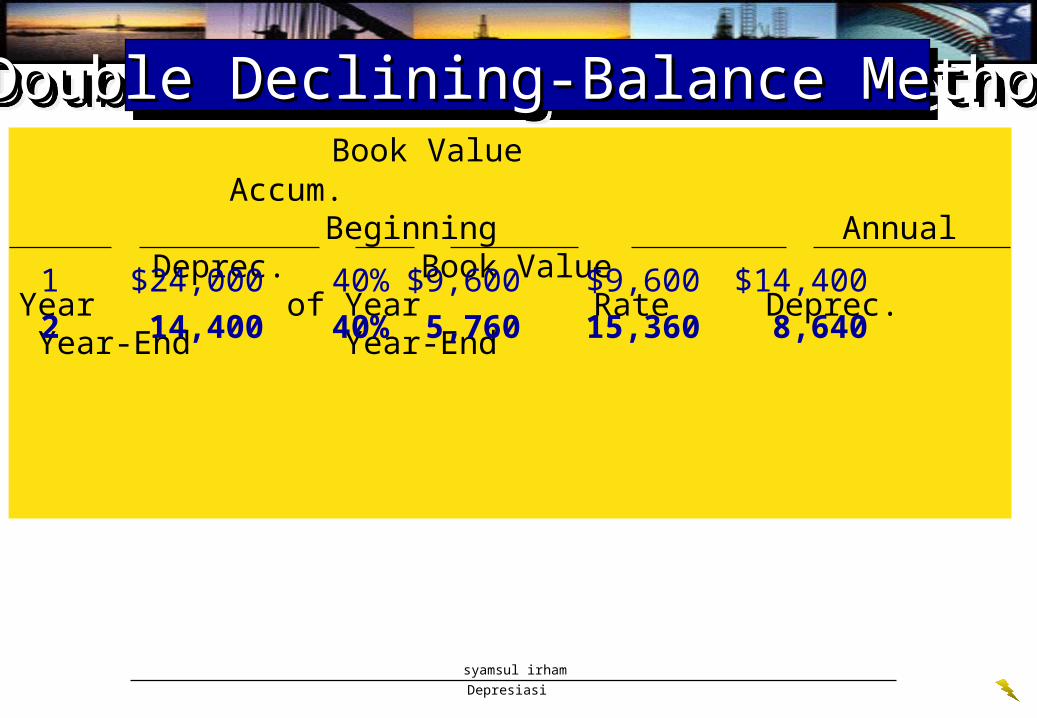

Book Value Accum. Beginning Annual Deprec. Book ValueYear of Year Rate Deprec. Year-End Year-End

1 $24,000 40% $9,600 $9,600 $14,400

2 14,400 40% 5,760 15,360 8,640

3 8,640 40% 3,456 18,816 5,184

Double Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance Method

Depresiasi

syamsul irham

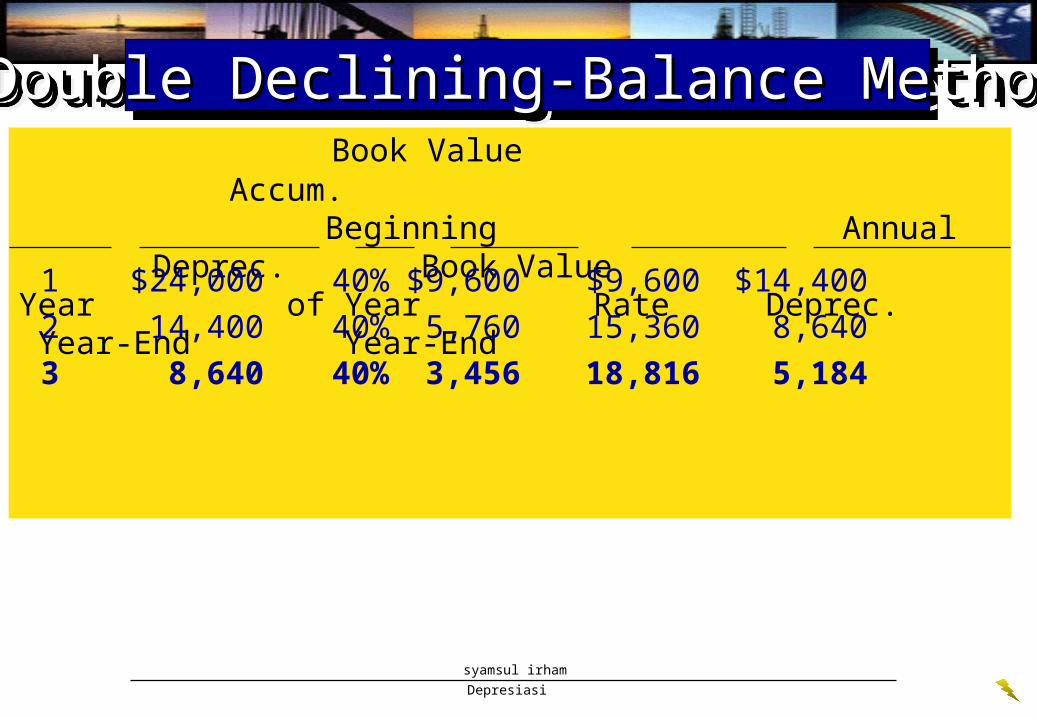

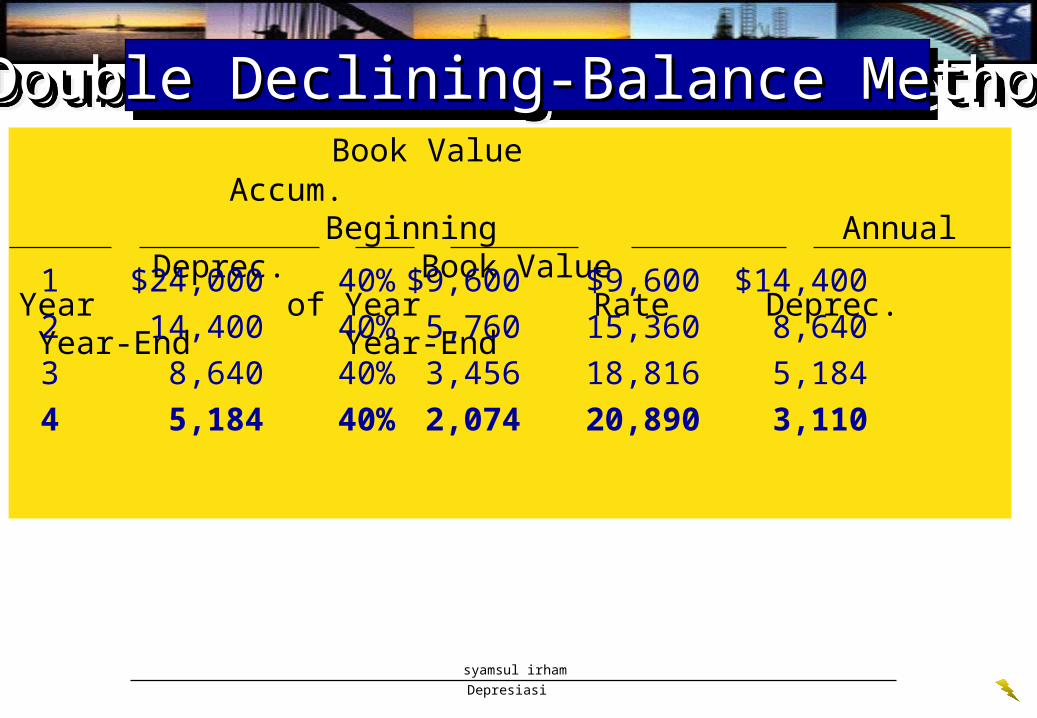

Book Value Accum. Beginning Annual Deprec. Book ValueYear of Year Rate Deprec. Year-End Year-End

1 $24,000 40% $9,600 $9,600 $14,400

2 14,400 40% 5,760 15,360 8,640

3 8,640 40% 3,456 18,816 5,184

4 5,184 40% 2,074 20,890 3,110

Double Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance Method

Depresiasi

syamsul irham

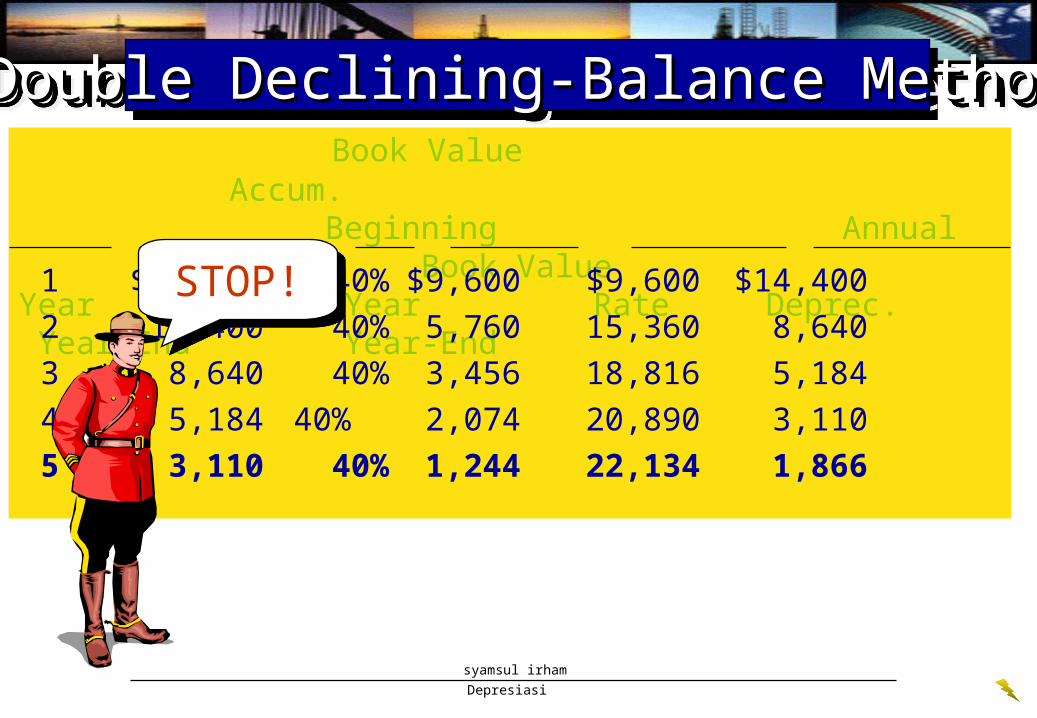

Book Value Accum. Beginning Annual Deprec. Book ValueYear of Year Rate Deprec. Year-End Year-End

1 $24,000 40% $9,600 $9,600 $14,400

2 14,400 40% 5,760 15,360 8,640

3 8,640 40% 3,456 18,816 5,184

4 5,184 40% 2,074 20,890 3,110

5 3,110 40% 1,244 22,134 1,866

STOP!STOP!

Double Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance Method

Depresiasi

syamsul irham

Book Value Accum. Beginning Annual Deprec. Book ValueYear of Year Rate Deprec. Year-End Year-End

1 $24,000 40% $9,600 $9,600 $14,400

2 14,400 40% 5,760 15,360 8,640

3 8,640 40% 3,456 18,816 5,184

4 5,184 40% 2,074 20,890 3,110

5 3,110 40% 1,244 22,134 1,866

Double Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance Method

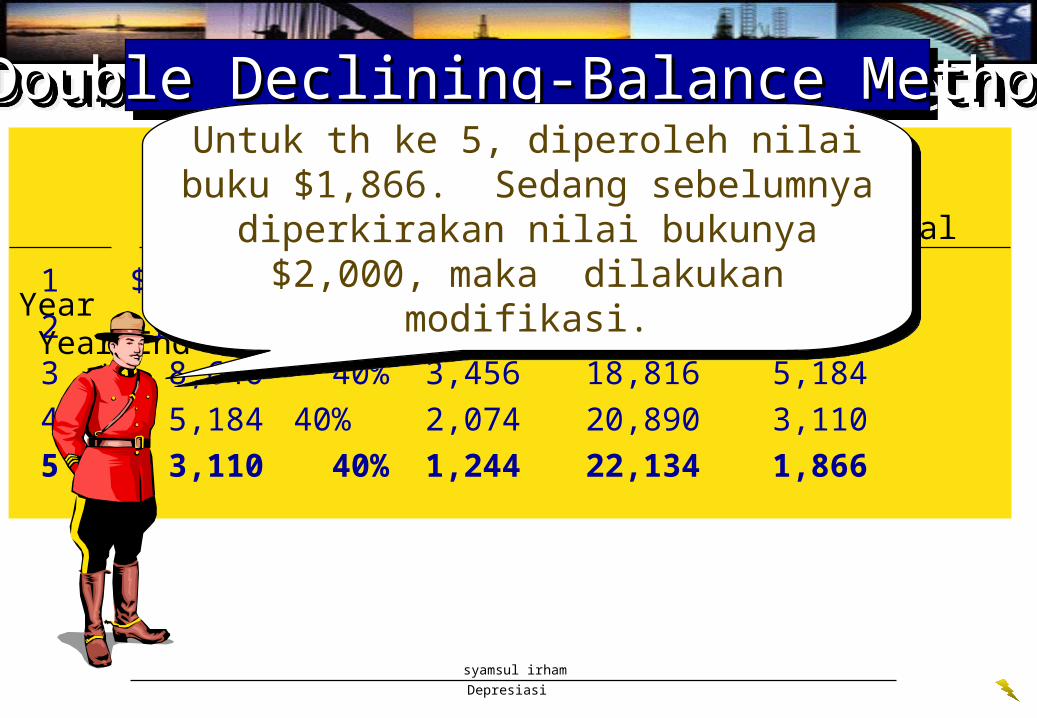

Untuk th ke 5, diperoleh nilai buku $1,866. Sedang sebelumnya diperkirakan nilai

bukunya $2,000, maka dilakukan modifikasi.

Untuk th ke 5, diperoleh nilai buku $1,866. Sedang sebelumnya diperkirakan nilai

bukunya $2,000, maka dilakukan modifikasi.

Depresiasi

syamsul irham

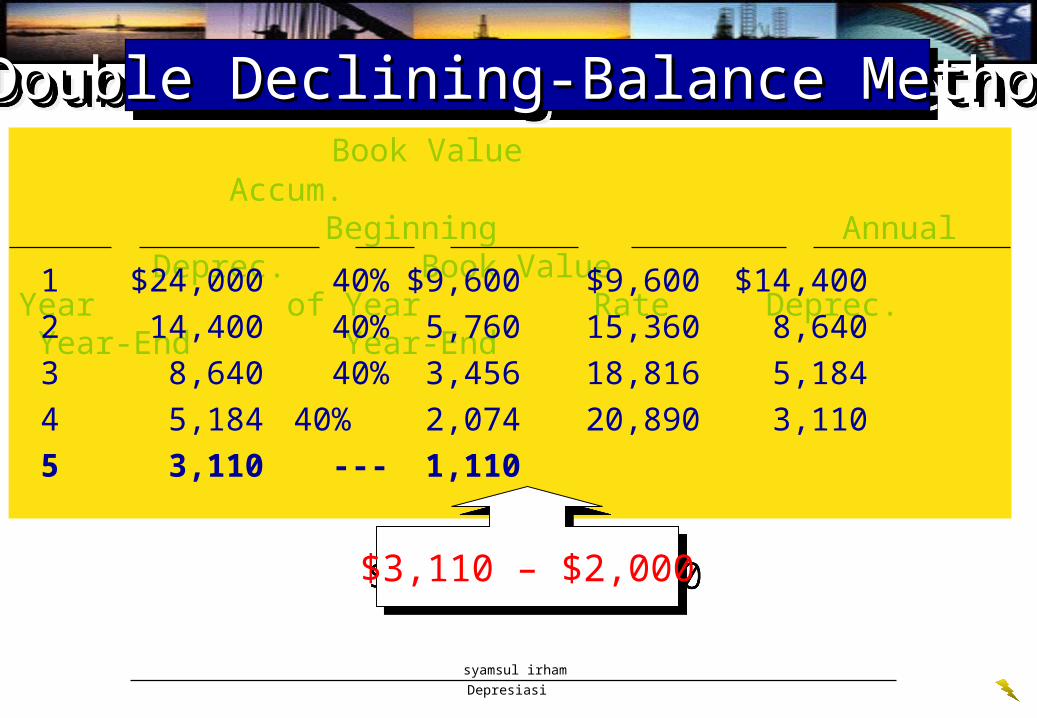

Book Value Accum. Beginning Annual Deprec. Book ValueYear of Year Rate Deprec. Year-End Year-End

1 $24,000 40% $9,600 $9,600 $14,400

2 14,400 40% 5,760 15,360 8,640

3 8,640 40% 3,456 18,816 5,184

4 5,184 40% 2,074 20,890 3,110

5 3,110 --- 1,110

Double Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance Method

$3,110 – $2,000$3,110 – $2,000

Depresiasi

syamsul irham

Book Value Accum. Beginning Annual Deprec. Book ValueYear of Year Rate Deprec. Year-End Year-End

1 $24,000 40% $9,600 $9,600 $14,400

2 14,400 40% 5,760 15,360 8,640

3 8,640 40% 3,456 18,816 5,184

4 5,184 40% 2,074 20,890 3,110

5 3,110 --- 1,110 22,000 2,000

Nilai buku yg diinginkan

Double Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance MethodDouble Declining-Balance Method

Depresiasi

syamsul irham

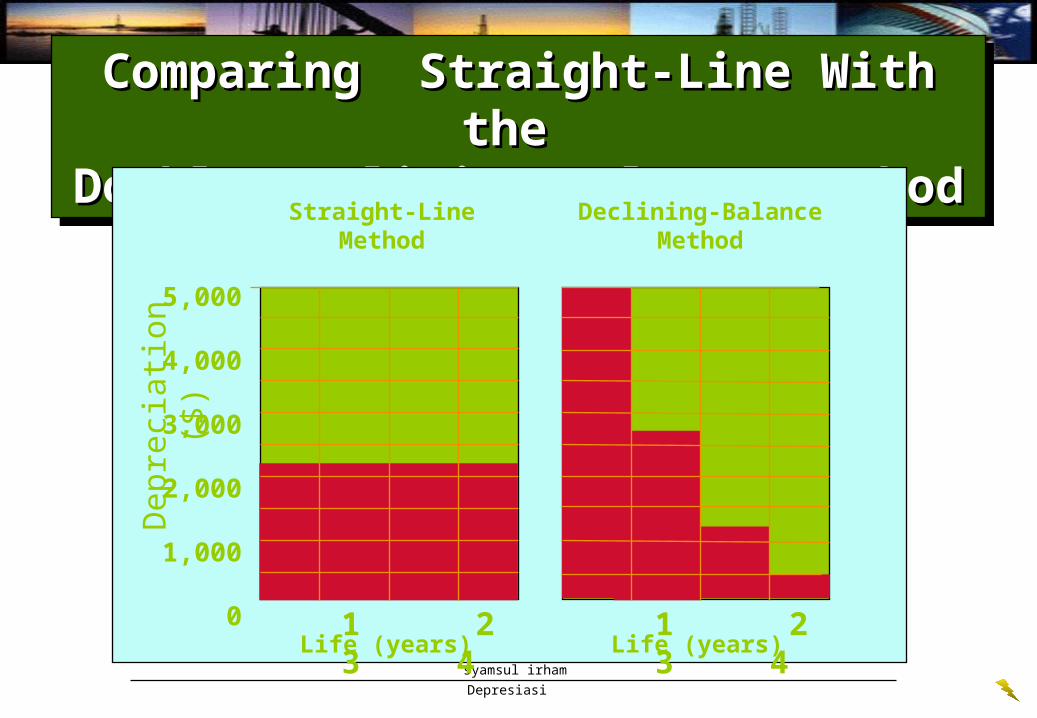

Comparing Straight-Line With the Comparing Straight-Line With the Double Declining-Balance MethodDouble Declining-Balance Method

Comparing Straight-Line With the Comparing Straight-Line With the Double Declining-Balance MethodDouble Declining-Balance Method

Straight-LineMethod

Dep

reci

atio

n ($

) 5,000

4,000

3,000

2,000

1,000

0Life (years)

Declining-BalanceMethod

Life (years) 1 2 3 4 1 2 3 4

Depresiasi

syamsul irham

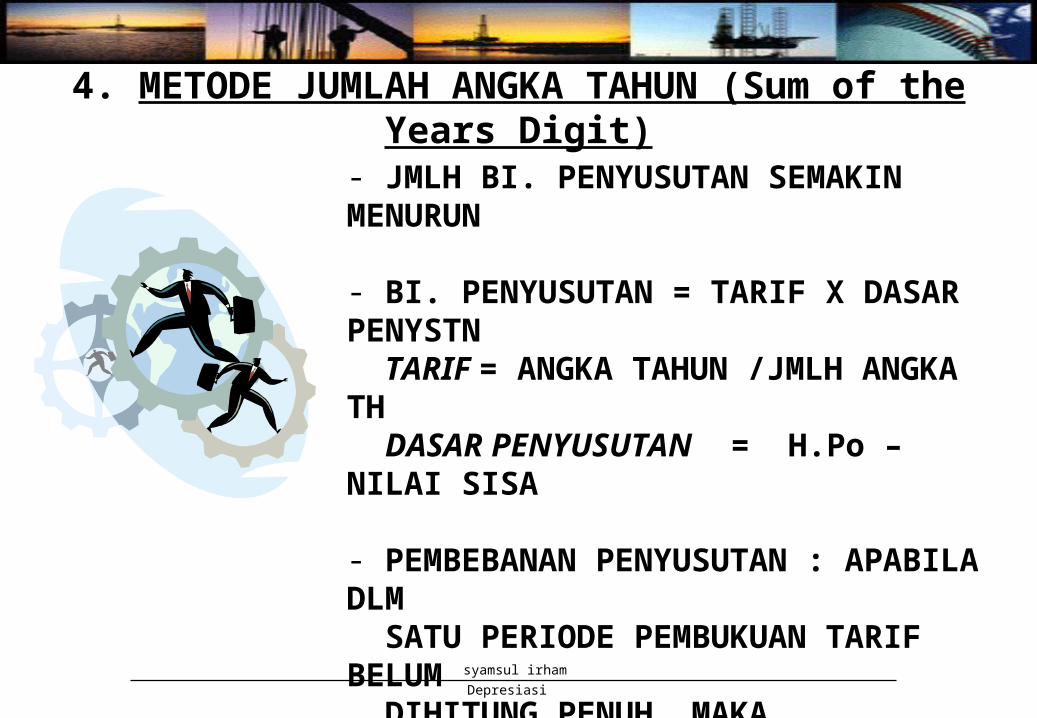

4. METODE JUMLAH ANGKA TAHUN (Sum of the Years Digit)

- JMLH BI. PENYUSUTAN SEMAKIN MENURUN

- BI. PENYUSUTAN = TARIF X DASAR PENYSTN TARIF = ANGKA TAHUN /JMLH ANGKA TH DASAR PENYUSUTAN = H.Po – NILAI SISA

- PEMBEBANAN PENYUSUTAN : APABILA DLM SATU PERIODE PEMBUKUAN TARIF BELUM DIHITUNG PENUH, MAKA KEKURANGANNYA DIBEBANKAN TAHUN BERIKUTNYA.

Depresiasi

syamsul irham

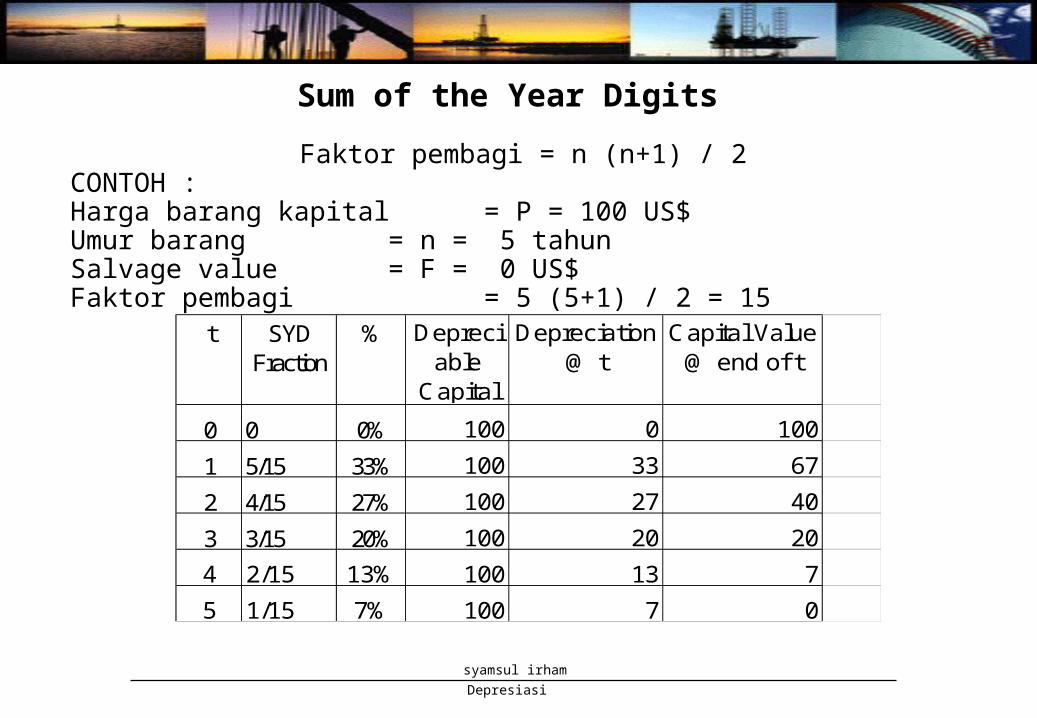

Sum of the Year Digits

Faktor pembagi = n (n+1) / 2CONTOH :Harga barang kapital = P = 100 US$Umur barang = n = 5 tahunSalvage value = F = 0 US$ Faktor pembagi = 5 (5+1) / 2 = 15

t SYD Fraction

% Depreciable

Capital

Depreciation @ t

Capital Value @ end of t

0 0 0% 100 0 100

1 5/15 33% 100 33 67

2 4/15 27% 100 27 40

3 3/15 20% 100 20 20

4 2/15 13% 100 13 7

5 1/15 7% 100 7 0

Depresiasi

syamsul irham

Pemilihan Metode Depresiasi

• Idealnya: pilih metode yang mampu mencocokkan (match) antara pendapatan dan biaya– Jika pendapatan yang dihasilkan dari aktiva

konstan -> garis lurus– Jika pendapatan yang dihasilkan dari aktiva

menurun -> metode dipercepat

Depresiasi

syamsul irham

Pemilihan Metode Depresiasi

• Faktor lain, dalam pemilihan metode:– Praktis– Pengaruh laba dan nilai buku– Pertimbangan pajak

• Dalam Akuntansi : Metode dapat dipilih bebas tetapi harus konsisten

• Dalam KKS Migas : Metode depresiasi yang dipakai ditetapkan dalam kontrak

Depresiasi

syamsul irham

Deplesi

• Sumber Alam (minyak bumi, tambang lainnya, kayu)-> aktiva yang dapat habis, dikonsumsi secara fisik selama periode penggunaan dan tidak menyisakan karakter fisik

• Deplesi -> untuk menghapus aktiva sumber alam ini, akan mengurangi aktiva sumber alam (bukan menjadi Biaya Deplesi)

• Harga perolehan sumber alam:– cost akuisisi -> harga yang dibayarkan untuk memperoleh hak mencari dan

menemukan sumber alam yang belum ditemukan atau membeli lisensi jika sumber alam ini telah ditemukan

Depresiasi

syamsul irham

– Cost Eksplorasi -> biaya untuk menemukan sumber alam• full cost approach -> gagal dan berhasil diakui• successful effort approach -> hanya yang berhasil diakui

– Cost Pengembangan:• peralatan berujud -> peralatan yang diperlukan untuk menambang sumber alam (biasanya

tidak diikutkan dalam penghitungan deplesi)• cost pengembangan tidak berujud -> biaya yang tidak mempunyai karakter fisik tetapi

diperlukan untuk produksi sumber alam, misal: biaya pengeboran, pembuatan lorong, gua, sumur dsb)

– Cost restorasi(perbaikan) ->diikutkan dalam perhitungan deplesi

• Metode yang digunakan adalah Metode Aktivitas (menggunakan unit)

Deplesi