Bahasa

Halaman

Hukum

1

Attila Marján – Lorina Buda: V4, A Modern Mitteleuropa

The paper highlights the similarities and differences in the development paths of the four so

called Visegrad countries (Poland, Hungary, Czech Republic, Slovakia, leaving countries like

Slovenis, Croatia out) focussing on the economic policies of the period of 2004-2014,

representing the first decade of their EU-membership, providing insight in their economic

policy decisions.

Introduction

There are diverse and contrasting interpretations and connotations of the concept of

Mitteleuropa. It served as an idealistic model for a multicultural, multinational region with

common features and geopolitical realities that is situated between the German and Russian

power bloc. The Central-European Federation was the ultimate political vision of this line of

thought. This somewhat nostalgic interpretation was invented and maintained by mainly the

liberal intelligentsia of the late Habsburg era. There is although another Mitteleuropa vision of

Prussian origin - that found its way to mainstream German geopolitical strategy during World

War I. - as a pan-Germanist imperium spreading way into East-Europe. This paper has no

intention to engage in the academic debate on this subject. It chooses the Visegrad 4 countries

as key nation states of this region of Mitteleuropa in its narrow geographical sense because of

geopolitical realities.

In 1335 when the first summit in Visegrad took place, Casimir III of Poland, Charles I of

Hungary, and John I of Bohemia had two objectives: to strengthen their economic and

political cooperation and to form a regional alliance to counter the power of the duke of

Austria and of the Holy Roman Emperor. Some seven hundred years later in a completely

different Europe regional cooperation still has a lot to offer but it has had several impediments

to flourish in central Europe.

The modern times cooperation in the V4 group since its formation in 1991 in a Hungarian

town called Visegrad has had its ups and downs: it almost fell apart in December 2003 in

2

Copenhagen when EU accession terms were to be finalized: a killing competition took place

among the four on who gets the most of the cohesion and agricultural funds.

The group of four central European EU member states, if counted as a single nation state, V4

(64,3 million inhabitants) would rank 22nd in the world and second in Europe, moreover it is

the seventh largest economy in Europe and the 15th globally. Before the introduction of the

double majority voting system they together have had equal number of weighted votes with

Germany and France put together. From November 2014, the double majority has been

replaced the old weighted voting system. According to the new rule the support of 55% of the

Member States representing 65 % of the overall population of the European Union will be

required. The new system significantly modifies the power distribution by strengthening the

influence of big Member States – with a population of 60 million; Spain and Poland will lose

their big Member State status and medium-sized countries’ - between 2 and 11 million

inhabitants - voting power will be reduced dramatically. In the new double majority system

the ability of countries with large population to block decisions will be significantly

reinforced, while small countries’ ability to prevent negative decisions will come to an end.

Germany and France will gain increased blocking capacities but V4 countries will not be able

to form any blocking coalition any longer. Even the new Member States joined in 2004 and

2007 will not be able to block decisions under the new system1. Nevertheless one has to bear

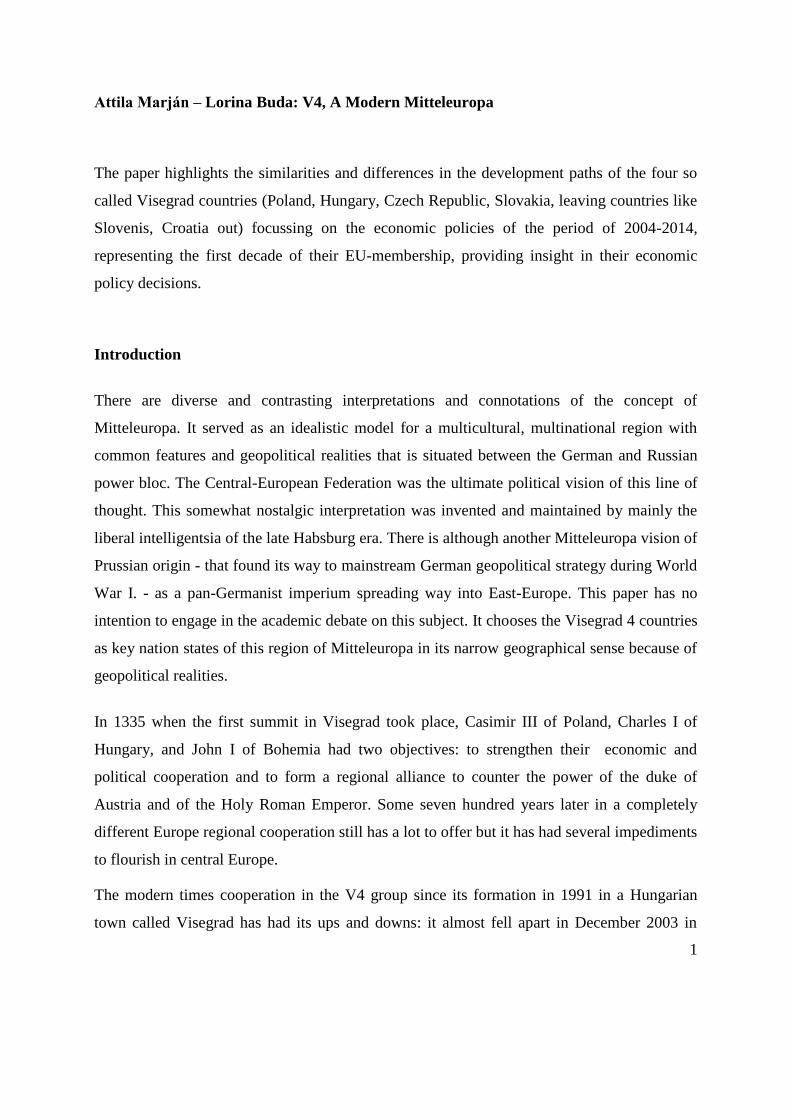

in mind that these countries stand for not more than 5 percent of the EU’s GDP (see graph

below)

Graph 1. Size of the V4 countries as per total EU GDP

1 Attila Marján: EU-rule changes force a Visegad re-think. Europe’s World. 2014. Spring

3

Before a county-by-country analysis the most important features of the V4 group that

demonstrate the similarities and differences are worth quoting for a deeper understanding of

this region:

1. 20th

century history and the mostly unsuccessful settling of its consequences is still a

decisive feature of the present of these countries;

2. There is no genuine socio-economic, cultural and political cohesion among these

countries. The V4 co-operation is more of an empty shell. This is partly a consequence

of the troubled past of these region;

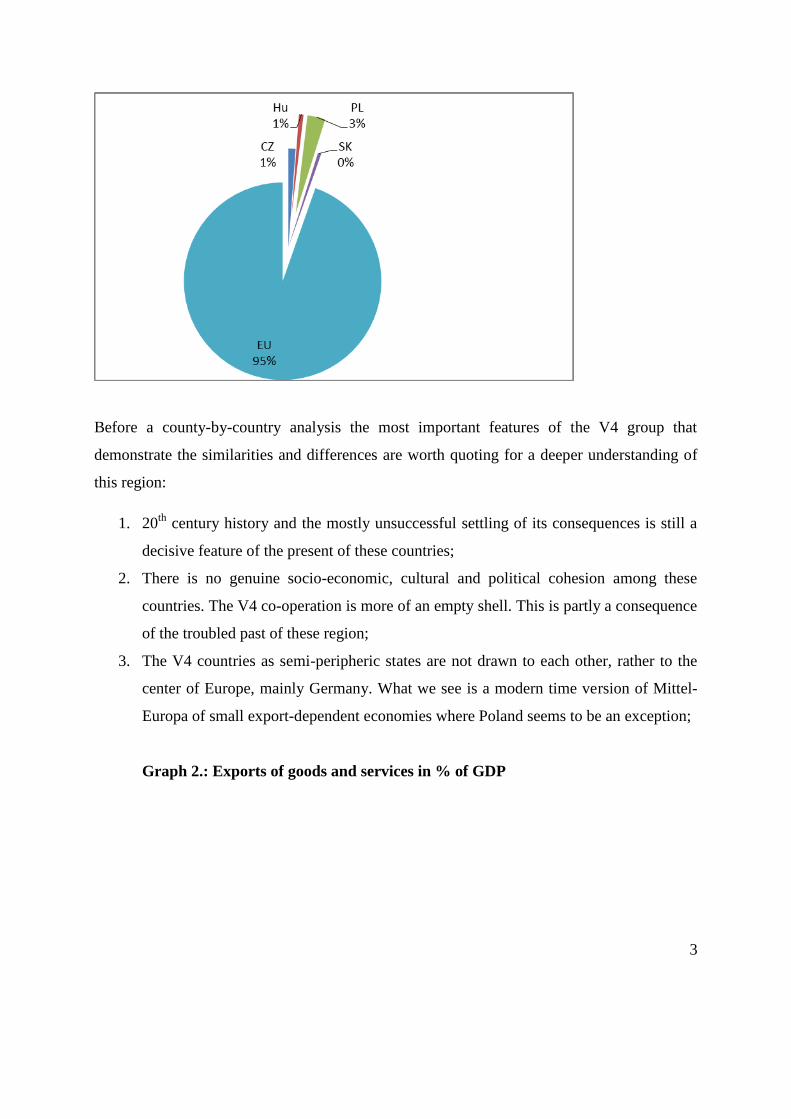

3. The V4 countries as semi-peripheric states are not drawn to each other, rather to the

center of Europe, mainly Germany. What we see is a modern time version of Mittel-

Europa of small export-dependent economies where Poland seems to be an exception;

Graph 2.: Exports of goods and services in % of GDP

4

Source:

http://ec.europa.eu/eurostat/eurostat/tgm/table.do?tab=table&init=1&plugin=1&langu

age=en&pcode=tet00003

4. The above nevertheless means that these countries are practically the economic supply

backwaters of the German economic sphere;

5. Still EU membership represents a historic chance of geopolitical stability and

economic and societal modernisation for these countries;

6. This region needs (would have needed) a special political approach from the EU since

its genuine integration is hindered by factors that cannot normally detected and

handled (lack of strong civic net and traditions, no self-organising and self-protecing

power of the society, weakness of civil society, inherited regional geopolitical tensions

etc.) through the normal EU accession toolbox.

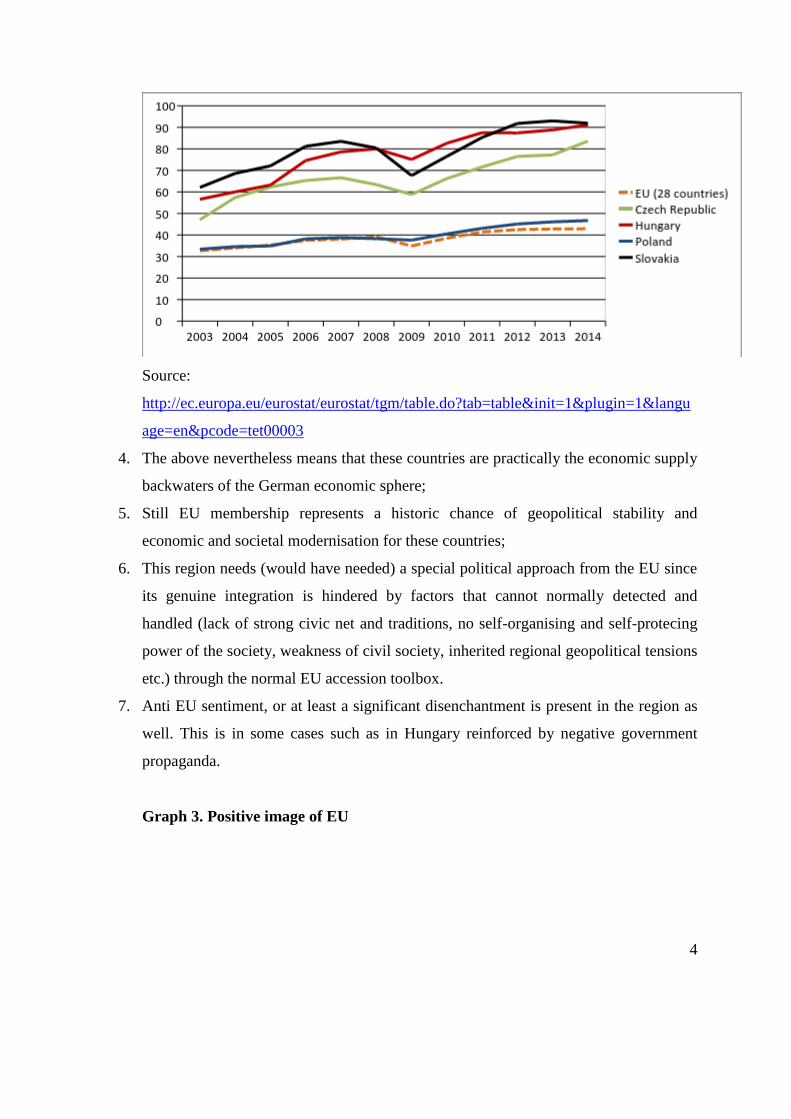

7. Anti EU sentiment, or at least a significant disenchantment is present in the region as

well. This is in some cases such as in Hungary reinforced by negative government

propaganda.

Graph 3. Positive image of EU

5

Source: Eurobarometer (2014): Public opinion in the European Union 82.

http://ec.europa.eu/public_opinion/archives/eb/eb82/eb82_first_en.pdf

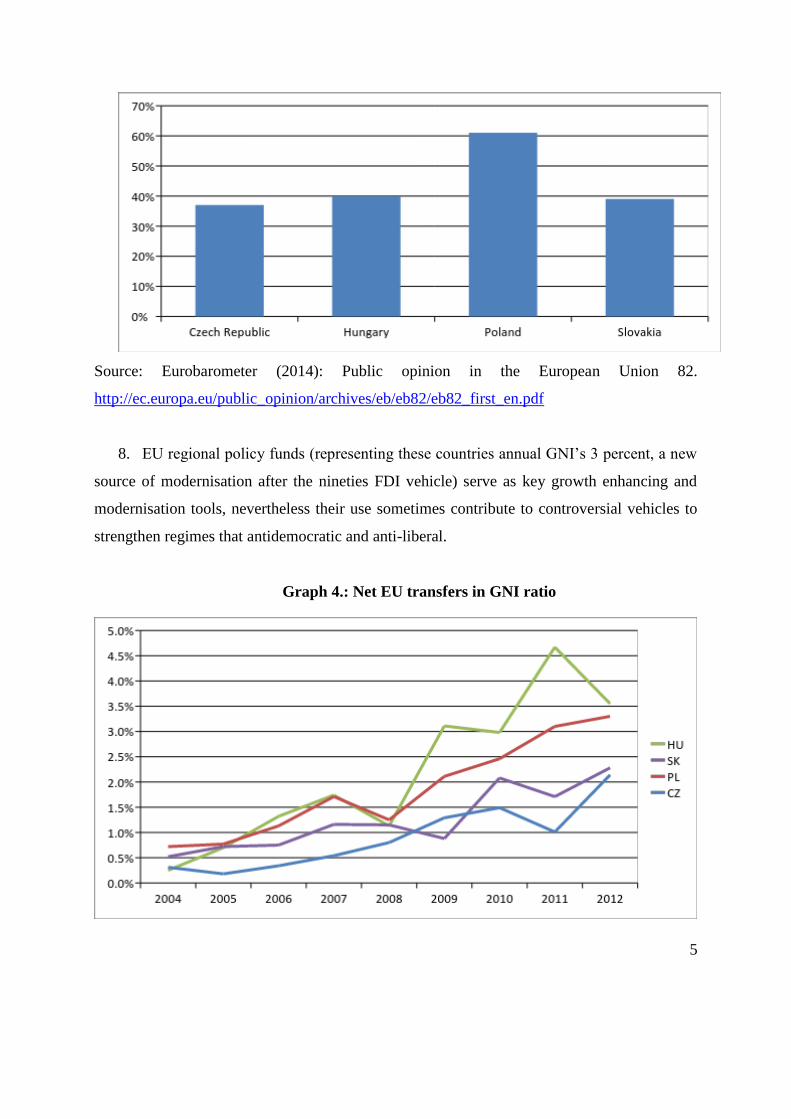

8. EU regional policy funds (representing these countries annual GNI’s 3 percent, a new

source of modernisation after the nineties FDI vehicle) serve as key growth enhancing and

modernisation tools, nevertheless their use sometimes contribute to controversial vehicles to

strengthen regimes that antidemocratic and anti-liberal.

Graph 4.: Net EU transfers in GNI ratio

6

Source: European Commission

9. Although there are very important features that are similar in these countries’

economies and societal webs, different political drives in the different V4 countries

result in rather diverging realities. The most pertinent example is pro-European Poland

and pro-East Hungary: the former is about to achieve its best geopolitical standing

since centuries, while the latter has slipped into a pariah status from its number one

place in the nineties. Moreover Poland started to aim at higher geopolitical objectives

such as creating a new Weimar arrangement in Europe. 2The historically amicable

Polish Hungarian relations froze in February 2015 when the Hungarian prime minister

went to Warsaw to give an explanation why he had received Putin – in the middle of

invading a European country - a few days before. The head of the Polish opposition,

the former ideological ally of the Hungarian pime minister refused to receive the

Hungarian premier which was unthinkable before.

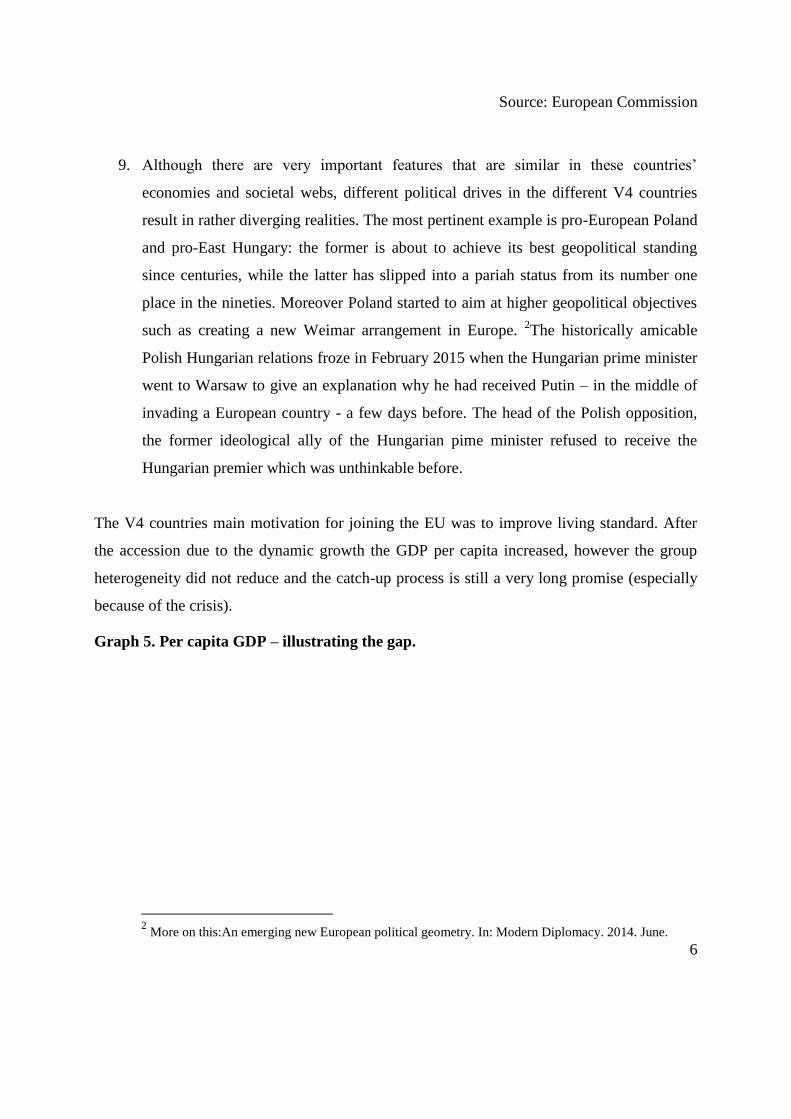

The V4 countries main motivation for joining the EU was to improve living standard. After

the accession due to the dynamic growth the GDP per capita increased, however the group

heterogeneity did not reduce and the catch-up process is still a very long promise (especially

because of the crisis).

Graph 5. Per capita GDP – illustrating the gap.

2 More on this:An emerging new European political geometry. In: Modern Diplomacy. 2014. June.

7

Source: European Commission

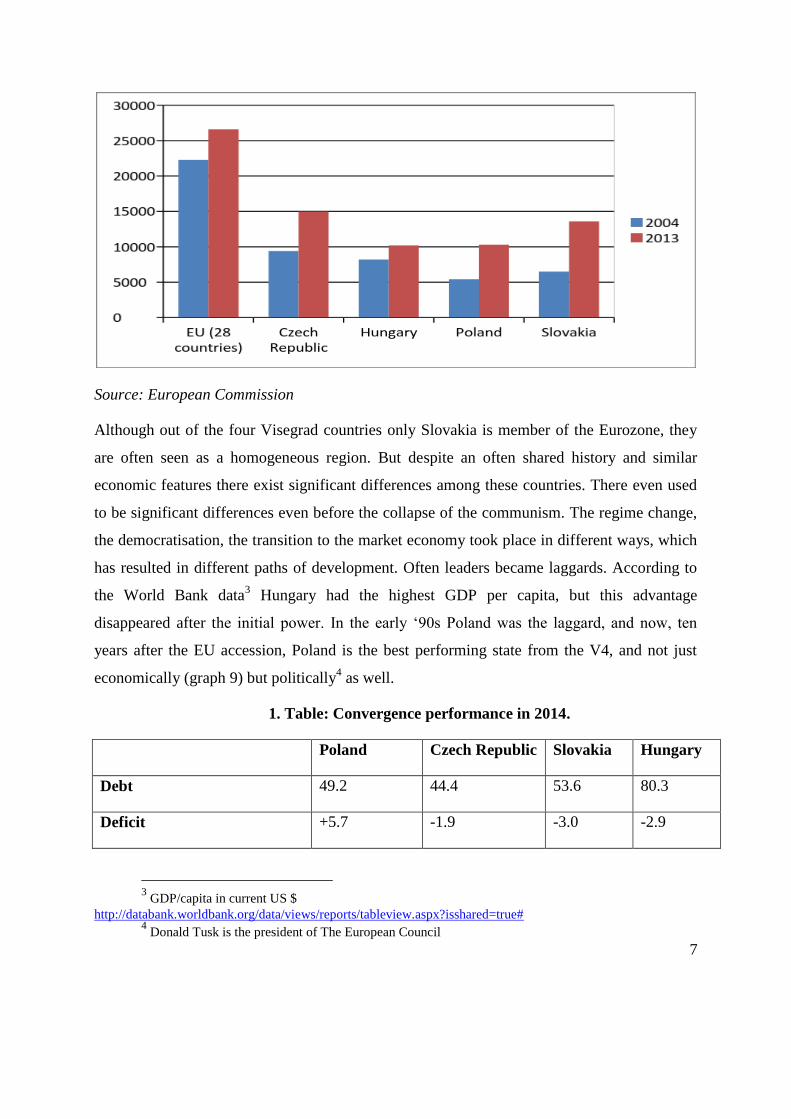

Although out of the four Visegrad countries only Slovakia is member of the Eurozone, they

are often seen as a homogeneous region. But despite an often shared history and similar

economic features there exist significant differences among these countries. There even used

to be significant differences even before the collapse of the communism. The regime change,

the democratisation, the transition to the market economy took place in different ways, which

has resulted in different paths of development. Often leaders became laggards. According to

the World Bank data3 Hungary had the highest GDP per capita, but this advantage

disappeared after the initial power. In the early ‘90s Poland was the laggard, and now, ten

years after the EU accession, Poland is the best performing state from the V4, and not just

economically (graph 9) but politically4 as well.

1. Table: Convergence performance in 2014.

Hungary Slovakia Czech Republic Poland

80.3 53.6 44.4 49.2 Debt

-2.9 -3.0 -1.9 +5.7 Deficit

3 GDP/capita in current US $

http://databank.worldbank.org/data/views/reports/tableview.aspx?isshared=true# 4 Donald Tusk is the president of The European Council

8

1 -0.1 0.9 0.6 Inflation

5.8 2.7 2.2 4.2 Long-term interest rate

No No No Yes Country in excessive deficit

Source: ECB

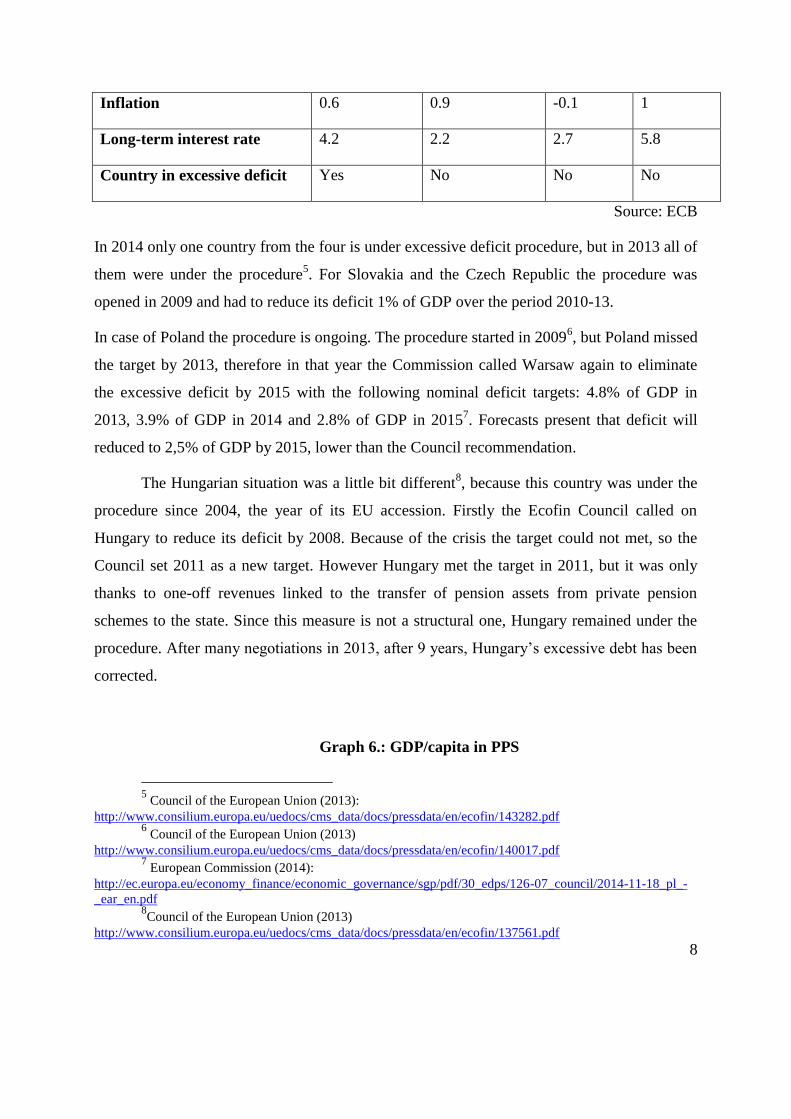

In 2014 only one country from the four is under excessive deficit procedure, but in 2013 all of

them were under the procedure5. For Slovakia and the Czech Republic the procedure was

opened in 2009 and had to reduce its deficit 1% of GDP over the period 2010-13.

In case of Poland the procedure is ongoing. The procedure started in 20096, but Poland missed

the target by 2013, therefore in that year the Commission called Warsaw again to eliminate

the excessive deficit by 2015 with the following nominal deficit targets: 4.8% of GDP in

2013, 3.9% of GDP in 2014 and 2.8% of GDP in 20157. Forecasts present that deficit will

reduced to 2,5% of GDP by 2015, lower than the Council recommendation.

The Hungarian situation was a little bit different8, because this country was under the

procedure since 2004, the year of its EU accession. Firstly the Ecofin Council called on

Hungary to reduce its deficit by 2008. Because of the crisis the target could not met, so the

Council set 2011 as a new target. However Hungary met the target in 2011, but it was only

thanks to one-off revenues linked to the transfer of pension assets from private pension

schemes to the state. Since this measure is not a structural one, Hungary remained under the

procedure. After many negotiations in 2013, after 9 years, Hungary’s excessive debt has been

corrected.

Graph 6.: GDP/capita in PPS

5 Council of the European Union (2013):

http://www.consilium.europa.eu/uedocs/cms_data/docs/pressdata/en/ecofin/143282.pdf 6 Council of the European Union (2013)

http://www.consilium.europa.eu/uedocs/cms_data/docs/pressdata/en/ecofin/140017.pdf 7 European Commission (2014):

http://ec.europa.eu/economy_finance/economic_governance/sgp/pdf/30_edps/126-07_council/2014-11-18_pl_-

_ear_en.pdf 8Council of the European Union (2013)

http://www.consilium.europa.eu/uedocs/cms_data/docs/pressdata/en/ecofin/137561.pdf

9

Source: Eurostat

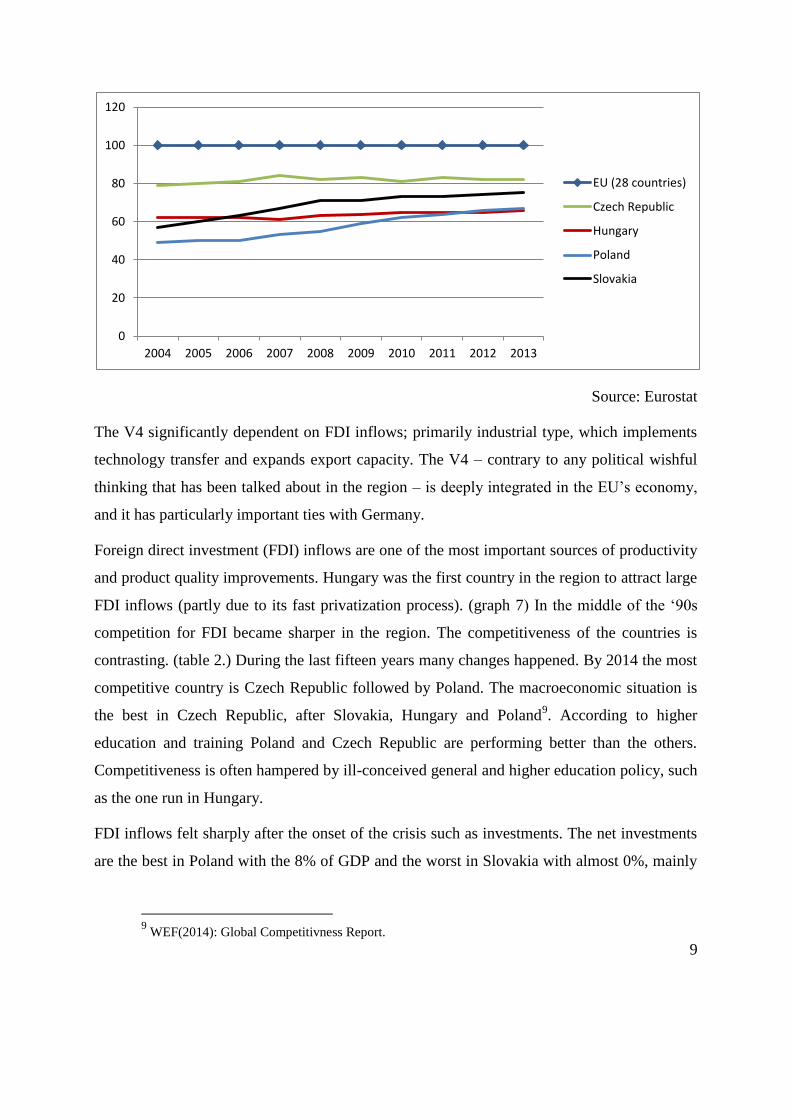

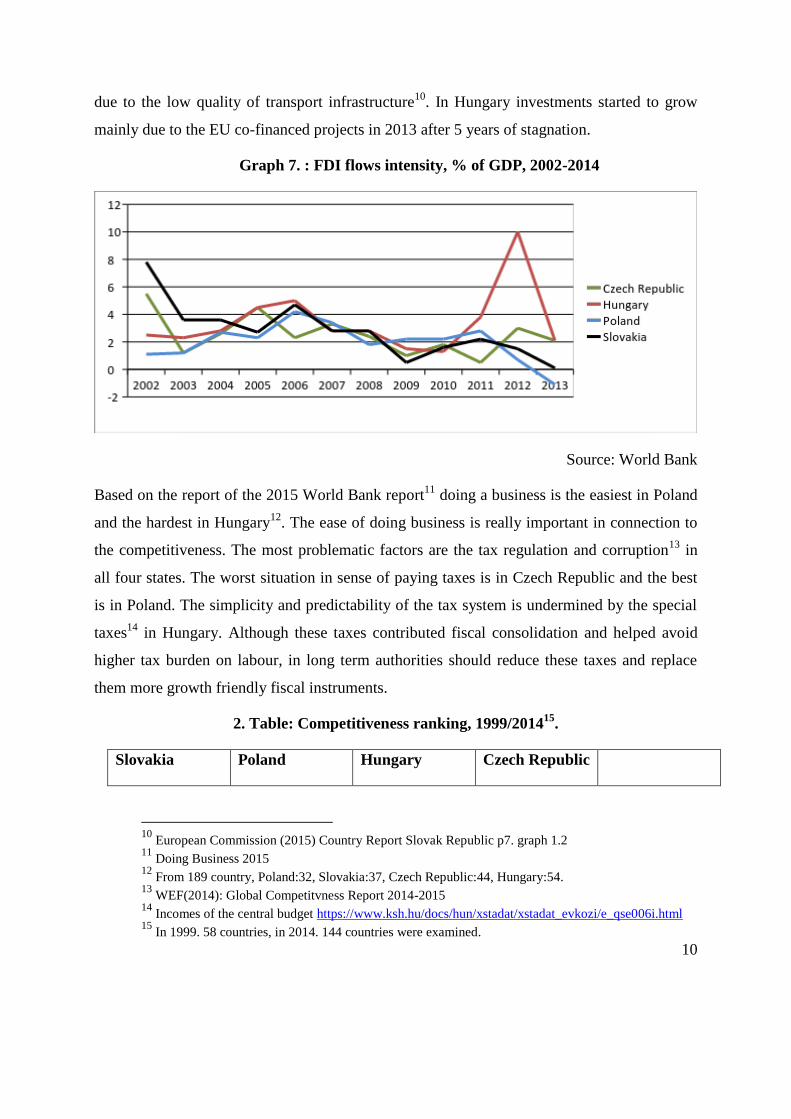

The V4 significantly dependent on FDI inflows; primarily industrial type, which implements

technology transfer and expands export capacity. The V4 – contrary to any political wishful

thinking that has been talked about in the region – is deeply integrated in the EU’s economy,

and it has particularly important ties with Germany.

Foreign direct investment (FDI) inflows are one of the most important sources of productivity

and product quality improvements. Hungary was the first country in the region to attract large

FDI inflows (partly due to its fast privatization process). (graph 7) In the middle of the ‘90s

competition for FDI became sharper in the region. The competitiveness of the countries is

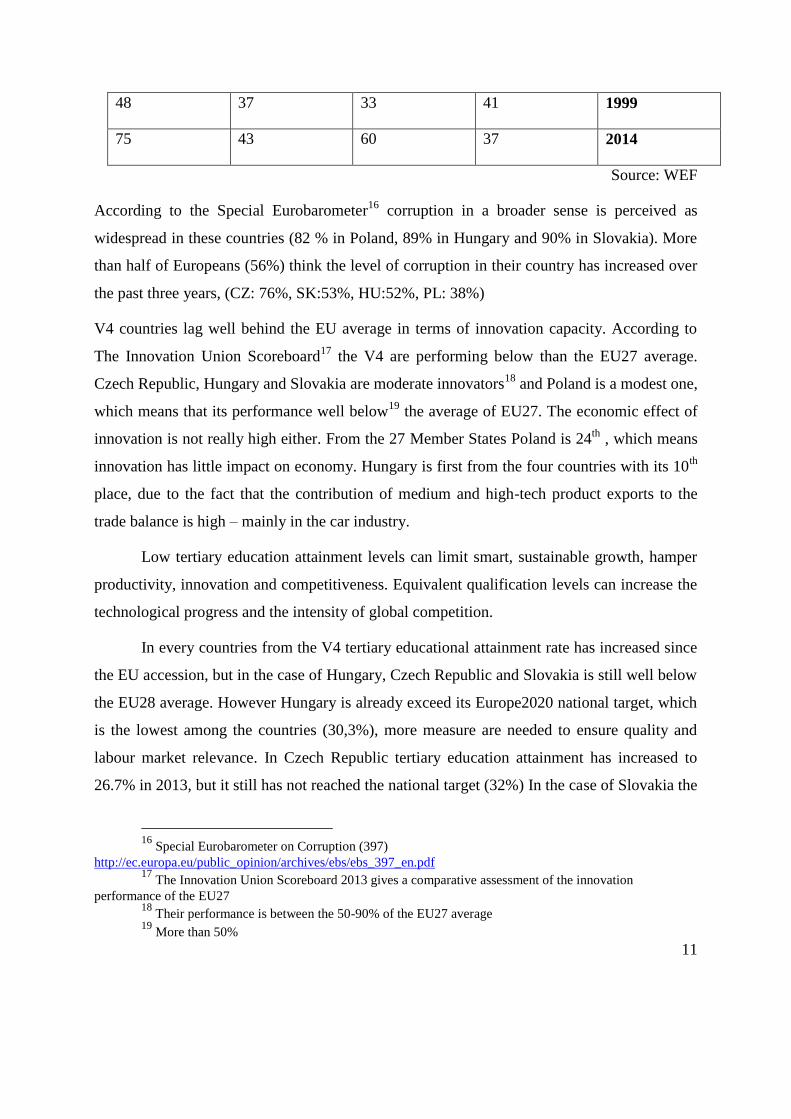

contrasting. (table 2.) During the last fifteen years many changes happened. By 2014 the most

competitive country is Czech Republic followed by Poland. The macroeconomic situation is

the best in Czech Republic, after Slovakia, Hungary and Poland9. According to higher

education and training Poland and Czech Republic are performing better than the others.

Competitiveness is often hampered by ill-conceived general and higher education policy, such

as the one run in Hungary.

FDI inflows felt sharply after the onset of the crisis such as investments. The net investments

are the best in Poland with the 8% of GDP and the worst in Slovakia with almost 0%, mainly

9 WEF(2014): Global Competitivness Report.

0

20

40

60

80

100

120

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

EU (28 countries)

Czech Republic

Hungary

Poland

Slovakia

10

due to the low quality of transport infrastructure10

. In Hungary investments started to grow

mainly due to the EU co-financed projects in 2013 after 5 years of stagnation.

Graph 7. : FDI flows intensity, % of GDP, 2002-2014

Source: World Bank

Based on the report of the 2015 World Bank report11

doing a business is the easiest in Poland

and the hardest in Hungary12

. The ease of doing business is really important in connection to

the competitiveness. The most problematic factors are the tax regulation and corruption13

in

all four states. The worst situation in sense of paying taxes is in Czech Republic and the best

is in Poland. The simplicity and predictability of the tax system is undermined by the special

taxes14

in Hungary. Although these taxes contributed fiscal consolidation and helped avoid

higher tax burden on labour, in long term authorities should reduce these taxes and replace

them more growth friendly fiscal instruments.

2. Table: Competitiveness ranking, 1999/201415

.

Czech Republic Hungary Poland Slovakia

10

European Commission (2015) Country Report Slovak Republic p7. graph 1.2 11

Doing Business 2015 12

From 189 country, Poland:32, Slovakia:37, Czech Republic:44, Hungary:54. 13

WEF(2014): Global Competitvness Report 2014-2015 14

Incomes of the central budget https://www.ksh.hu/docs/hun/xstadat/xstadat_evkozi/e_qse006i.html 15

In 1999. 58 countries, in 2014. 144 countries were examined.

11

1999 41 33 37 48

2014 37 60 43 75

Source: WEF

According to the Special Eurobarometer16

corruption in a broader sense is perceived as

widespread in these countries (82 % in Poland, 89% in Hungary and 90% in Slovakia). More

than half of Europeans (56%) think the level of corruption in their country has increased over

the past three years, (CZ: 76%, SK:53%, HU:52%, PL: 38%)

V4 countries lag well behind the EU average in terms of innovation capacity. According to

The Innovation Union Scoreboard17

the V4 are performing below than the EU27 average.

Czech Republic, Hungary and Slovakia are moderate innovators18

and Poland is a modest one,

which means that its performance well below19

the average of EU27. The economic effect of

innovation is not really high either. From the 27 Member States Poland is 24th

, which means

innovation has little impact on economy. Hungary is first from the four countries with its 10th

place, due to the fact that the contribution of medium and high-tech product exports to the

trade balance is high – mainly in the car industry.

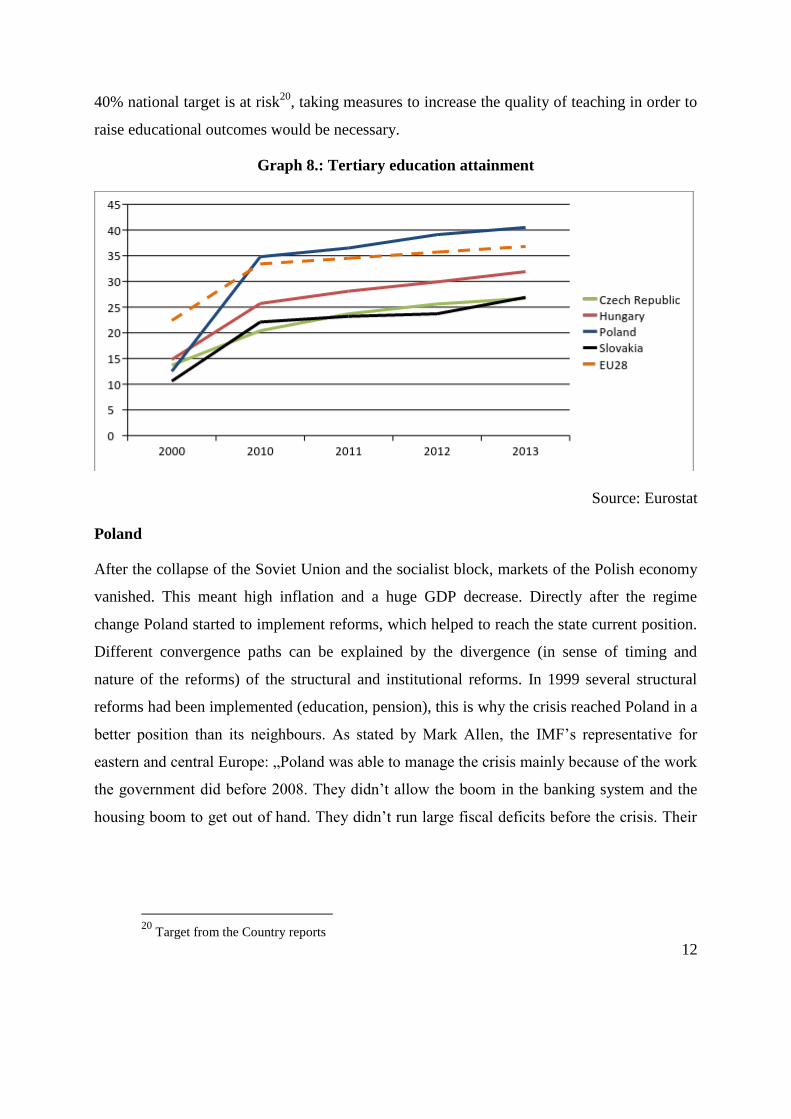

Low tertiary education attainment levels can limit smart, sustainable growth, hamper

productivity, innovation and competitiveness. Equivalent qualification levels can increase the

technological progress and the intensity of global competition.

In every countries from the V4 tertiary educational attainment rate has increased since

the EU accession, but in the case of Hungary, Czech Republic and Slovakia is still well below

the EU28 average. However Hungary is already exceed its Europe2020 national target, which

is the lowest among the countries (30,3%), more measure are needed to ensure quality and

labour market relevance. In Czech Republic tertiary education attainment has increased to

26.7% in 2013, but it still has not reached the national target (32%) In the case of Slovakia the

16

Special Eurobarometer on Corruption (397)

http://ec.europa.eu/public_opinion/archives/ebs/ebs_397_en.pdf 17

The Innovation Union Scoreboard 2013 gives a comparative assessment of the innovation

performance of the EU27 18

Their performance is between the 50-90% of the EU27 average 19

More than 50%

12

40% national target is at risk20

, taking measures to increase the quality of teaching in order to

raise educational outcomes would be necessary.

Graph 8.: Tertiary education attainment

Source: Eurostat

Poland

After the collapse of the Soviet Union and the socialist block, markets of the Polish economy

vanished. This meant high inflation and a huge GDP decrease. Directly after the regime

change Poland started to implement reforms, which helped to reach the state current position.

Different convergence paths can be explained by the divergence (in sense of timing and

nature of the reforms) of the structural and institutional reforms. In 1999 several structural

reforms had been implemented (education, pension), this is why the crisis reached Poland in a

better position than its neighbours. As stated by Mark Allen, the IMF’s representative for

eastern and central Europe: „Poland was able to manage the crisis mainly because of the work

the government did before 2008. They didn’t allow the boom in the banking system and the

housing boom to get out of hand. They didn’t run large fiscal deficits before the crisis. Their

20

Target from the Country reports

13

debt, even though, at close to 55 percent, is a little bit high by emerging market standards, did

not give rise to concern. „21

Following important reforms which have deeply transformed the structure of the economy,

Poland has economically integrated to the eurozone, caught up steadily with the EU15 in

GDP-per-capita terms22

. By 2013, the country had achieved levels of income and quality of

life likely never experienced before. Since the accession GDP increased by 48,6% and 20%

from this growth was reported during the period 2008-201323

. (graph 5.)

Productivity steadily improved24

since the accession, and the labour cost per unit has

decreased25

. Growth is driven by export growth, private consumption, and infrastructure

investments linked to the transfers of EU funds and the 2012 European football

championship. Poland is a fairly big economy with a large domestic market, which makes it

less dependent on exports.

Graph 9.: Real GDP growth rate, 2006-2013

Source: Eurostat

21

IMF(2012): Poland continouses as bright spot in region

http://www.imf.org/external/pubs/ft/survey/so/2012/car020312a.htm 22

GDP per capita http://appsso.eurostat.ec.europa.eu/nui/show.do?dataset=nama_aux_gph&lang=en 23

GDP growth

http://epp.eurostat.ec.europa.eu/tgm/table.do?tab=table&init=1&plugin=1&language=en&pcode=tec00115 24

Productivity

http://epp.eurostat.ec.europa.eu/tgm/refreshTableAction.do;jsessionid=9ea7d07d30e8adf98854aaa14d088119d3

d3b7c2244b.e34OaN8PchaTby0Lc3aNchuMchuNe0?tab=table&plugin=1&pcode=tsdec310&language=en 25

Labour cost

http://epp.eurostat.ec.europa.eu/tgm/table.do?tab=table&init=1&language=en&pcode=tec00130&plugin=1

-8,0

-6,0

-4,0

-2,0

0,0

2,0

4,0

6,0

8,0

10,0

12,0

2006 2007 2008 2009 2010 2011 2012 2013

Czech Republic

Hungary

Poland

Slovakia

14

Overall, the fact that Poland – by far the biggest of the V4 economies - did so well speaks not

only to its strong economic fundamentals, but also to good policy management and sound and

well-chosen economic policies. The results of the economic prosperity of the country were

used by the Polish government to improve the international position of the country, which was

supported by the country image and international political actions (such as the Year of

Chopin, the Polish Presidency of the EU, the Polish-Ukrainian joint organized Football

Championship). Warsaw is trying to obtain the right position, according to its growing

economic weight, both in the international and European arena. Tusk government not only

was able to stabilize the relationship with Berlin, but Poland became one of Germany’s major

allies in the European crisis management.

Warsaw responded to the crisis less sensitively than the international standards. Poland was

the only EU country where negative economic growth26

did not occurred as a result of the

crisis. Poland added significant fiscal stimulus during the crisis. This was one of the major

reasons why Poland did not fall into recession during the crisis. The government enacted a

discretionary fiscal relaxation of 4,5 percent of GDP and allowed the automatic stabilizers to

work27

. As a result, the fiscal deficit rose from less than 2 percent of GDP in 2007 to more

than 7 percent in 2009 (graph 10). Policymakers had considerable room for countercyclical

monetary and fiscal policy, because Poland did not have any severe macroeconomic

imbalances on the eve of the crisis.

Graph 10.: Fiscal deficit, (% of GDP) 2006-2013

26

GDP growth

http://epp.eurostat.ec.europa.eu/tgm/table.do?tab=table&plugin=1&language=en&pcode=tec00115 27

http://ec.europa.eu/economy_finance/eu/forecasts/2014_autumn/pl_en.pdf

15

Source: Eurostat

Although the Polish government debt has increased since the outbreak of the crisis, it is still

under the magic 60% of GDP28

. The general government debt-to-GDP ratio fell from 55.7%

in 2013 to 49.1% in 2014. It is set to amount to 50.1% in 2016. (graph 15)

Poland was granted a precautionary loan under the IMF’ Flexible Credit Line in 2010 but

hasn’t needed to draw on the funds29

, because the government insisted to solve the problems

by structural reforms and cut spending. Significant fiscal consolidation helped to reduce the

deficit and contain government debt. Poland’s fiscal framework contains a public debt rule

which is anchored in the Constitution and limits gross debt to 60% of GDP. Similarly,

monetary policy was accommodative at first, with aggressive cuts in the policy interest rate.

Reflect to the excessive deficit procedure Warsaw has implemented some reforms to

increase state revenues30

:

● increasing VAT rates from 22% to 23% and parallel decreasing the rates for basic food

products from 7% to 5%. Limiting the VAT fraud: reducing the limit authorising tax

payers to the exemption from the obligation to keep cash register, extension of the reverse

charge mechanism and the joint and several liability of the purchaser for tax liabilities of

the supplier of steel products, fuel and non-processed gold

28

Government debt

http://epp.eurostat.ec.europa.eu/tgm/table.do?tab=table&plugin=1&language=en&pcode=tsdde410 29

http://www.imf.org/external/pubs/ft/scr/2012/cr1212.pdf 30

http://ec.europa.eu/economy_finance/economic_governance/sgp/pdf/30_edps/126-07_council/2014-

11-18_pl_-_ear_en.pdf

-10

-8

-6

-4

-2

0

2006 2007 2008 2009 2010 2011 2012 2013

Czech Republic

Hungary

Poland

Slovakia

16

● increasing social security contributions (through limiting the part transfer red to OFE

(Open Pension Funds) in favour of the part transferred to FUS (Social Insurance Fund) –

2011 as well as owing to the increase of the pension insurance contribution in 2012

● introducing a fee for exploiting certain natural deposits of copper and silver

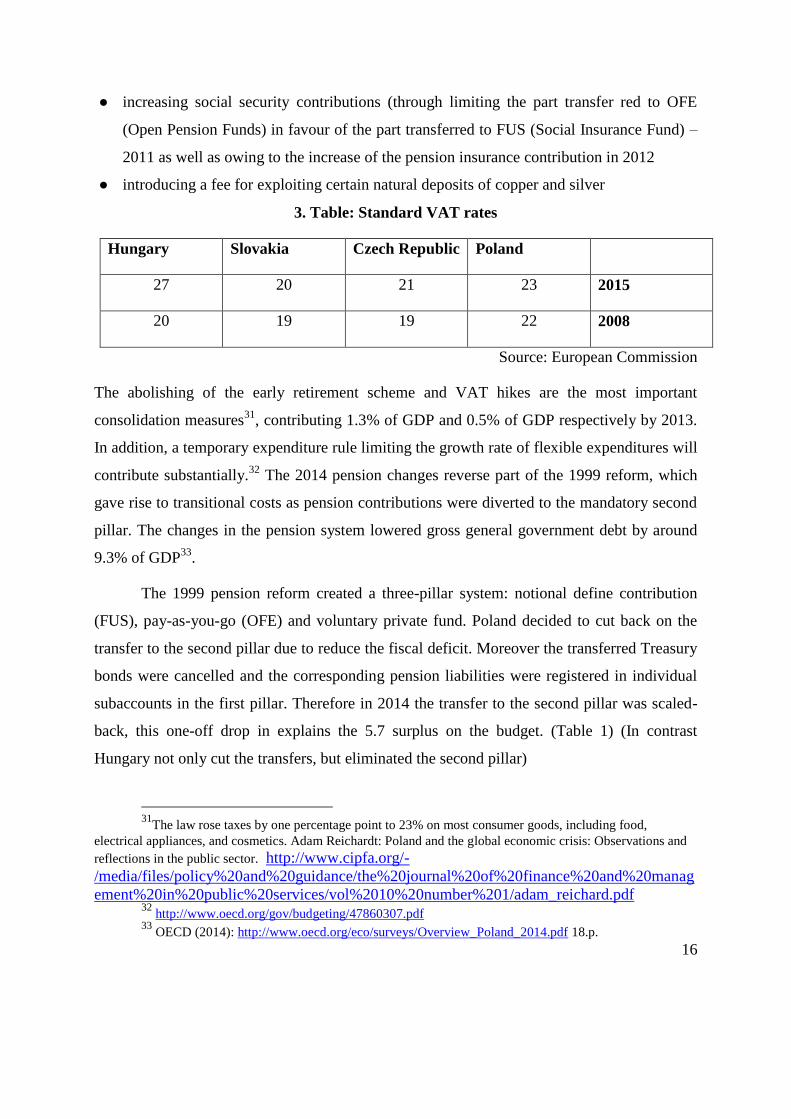

3. Table: Standard VAT rates

Poland Czech Republic Slovakia Hungary

2015 23 21 20 27

2008 22 19 19 20

Source: European Commission

The abolishing of the early retirement scheme and VAT hikes are the most important

consolidation measures31

, contributing 1.3% of GDP and 0.5% of GDP respectively by 2013.

In addition, a temporary expenditure rule limiting the growth rate of flexible expenditures will

contribute substantially.32

The 2014 pension changes reverse part of the 1999 reform, which

gave rise to transitional costs as pension contributions were diverted to the mandatory second

pillar. The changes in the pension system lowered gross general government debt by around

9.3% of GDP33

.

The 1999 pension reform created a three-pillar system: notional define contribution

(FUS), pay-as-you-go (OFE) and voluntary private fund. Poland decided to cut back on the

transfer to the second pillar due to reduce the fiscal deficit. Moreover the transferred Treasury

bonds were cancelled and the corresponding pension liabilities were registered in individual

subaccounts in the first pillar. Therefore in 2014 the transfer to the second pillar was scaled-

back, this one-off drop in explains the 5.7 surplus on the budget. (Table 1) (In contrast

Hungary not only cut the transfers, but eliminated the second pillar)

31

The law rose taxes by one percentage point to 23% on most consumer goods, including food,

electrical appliances, and cosmetics. Adam Reichardt: Poland and the global economic crisis: Observations and

reflections in the public sector. http://www.cipfa.org/-

/media/files/policy%20and%20guidance/the%20journal%20of%20finance%20and%20manag

ement%20in%20public%20services/vol%2010%20number%201/adam_reichard.pdf 32

http://www.oecd.org/gov/budgeting/47860307.pdf 33

OECD (2014): http://www.oecd.org/eco/surveys/Overview_Poland_2014.pdf 18.p.

17

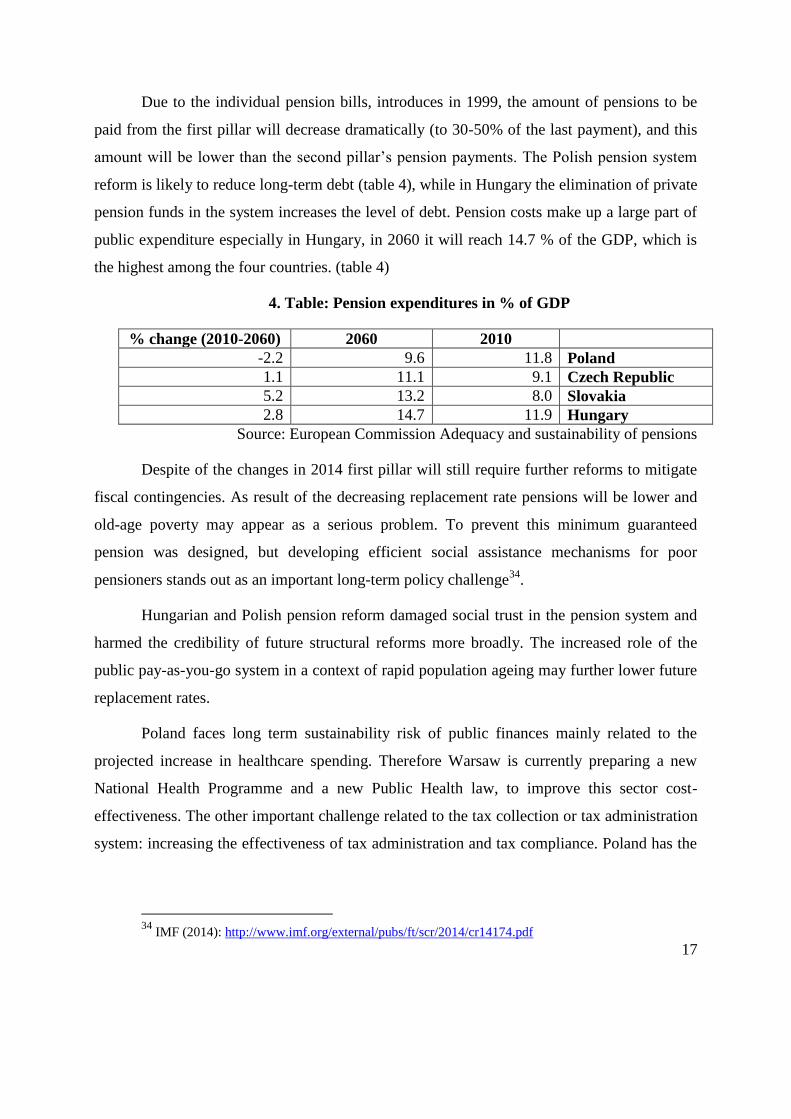

Due to the individual pension bills, introduces in 1999, the amount of pensions to be

paid from the first pillar will decrease dramatically (to 30-50% of the last payment), and this

amount will be lower than the second pillar’s pension payments. The Polish pension system

reform is likely to reduce long-term debt (table 4), while in Hungary the elimination of private

pension funds in the system increases the level of debt. Pension costs make up a large part of

public expenditure especially in Hungary, in 2060 it will reach 14.7 % of the GDP, which is

the highest among the four countries. (table 4)

4. Table: Pension expenditures in % of GDP

2010 2060 % change (2010-2060)

Poland 11.8 9.6 -2.2

Czech Republic 9.1 11.1 1.1

Slovakia 8.0 13.2 5.2

Hungary 11.9 14.7 2.8

Source: European Commission Adequacy and sustainability of pensions

Despite of the changes in 2014 first pillar will still require further reforms to mitigate

fiscal contingencies. As result of the decreasing replacement rate pensions will be lower and

old-age poverty may appear as a serious problem. To prevent this minimum guaranteed

pension was designed, but developing efficient social assistance mechanisms for poor

pensioners stands out as an important long-term policy challenge34

.

Hungarian and Polish pension reform damaged social trust in the pension system and

harmed the credibility of future structural reforms more broadly. The increased role of the

public pay-as-you-go system in a context of rapid population ageing may further lower future

replacement rates.

Poland faces long term sustainability risk of public finances mainly related to the

projected increase in healthcare spending. Therefore Warsaw is currently preparing a new

National Health Programme and a new Public Health law, to improve this sector cost-

effectiveness. The other important challenge related to the tax collection or tax administration

system: increasing the effectiveness of tax administration and tax compliance. Poland has the

34

IMF (2014): http://www.imf.org/external/pubs/ft/scr/2014/cr14174.pdf

18

second highest (after the Slovak Republic) cost for tax administration per net revenue

collection35

.

The country’s growth in the last decade was remarkable. (Graph 9) In order to be able

to continue this tendency further steps will be needed, such as improving the business climate

and innovation capacity of the Polish companies. Medium technology sectors using cheap and

comparatively low-skilled labour, which can undermine the future growth. The ratio of Gross

Value Added is lower than the other V4 countries36

. Firms with a higher technological content

tend to grow faster than low-technology sectors.

Some of the reforms not involve either significant budgetary or distributional costs;

others are more complex and need better preparation. Fortunately necessary reforms have

been implemented always. The challenge is not only identifying the needful measures, but to

find the way of political economy to implement them.

Czech Republic

The Czech economy started to grow in 2010 with 2,7 %, but after the growing tendency the

economy dropped back. (graph 9) Thanks to the decrease of the export and internal

consumption (private and public). Real incomes felt due to government measures, such as

freezing wages and cutting back allowances and benefits. Like all the V4 countries, the Czech

growth is depending on external conditions. The majority of its manufacturing exports are

directed to Germany and Western European countries. The Czech economy exited the

recession and started to recover during the second half of 2013, primarily driven by domestic

demand and growth in export markets. Real GDP growth is expected to be stronger in 2015

and 2016 with the remaining main driver: domestic demand.

35

European Commission (2014) Taxation.

http://ec.europa.eu/europe2020/pdf/themes/02_taxation_02.pdf 36

GVA: Ratio og GVA produced in high- and medium-high-technology industries to medium- and low

technology sectors. ECFIN (2014): Country Focus: Securing Poland’s economic succes: A good time for

reforms. http://ec.europa.eu/economy_finance/publications/country_focus/2014/pdf/cf_vol11_issue9_en.pdf

19

A sharp fiscal adjustment led to an exit from the Excessive Deficit Procedure37

(EDP) and

kept debt levels contained, but exacerbated the recession. The adjustment was driven mainly

by a compression of capital expenditure, partly due to implementation bottlenecks, while an

increase in VAT rates helped boost revenue. As a result of the measures and also to one-off

factors, the overall fiscal deficit narrowed from 4.2 percent of GDP in 2012 to 1.5 percent in

2013. (graph 10)

In 2014 the new Czech government has decided to adopt a fiscal policy that aims at keeping

the public deficit below 3% GDP and a reform agenda focussed on promoting external

competitiveness, investment, exports, infrastructures and quality of public services, which

were recommended by the European Commission also38

.

With respect to pensions, the government aims to propose to withdraw the second

pillar, as well as introducing measures to ensure the long-term stability of the public pension

system and an adequate level of pensions. The pension system is currently relatively

successful in preventing old-age poverty. Contrary to the Polish and Hungarian example,

Prague not dismantled but created a second pillar to its pension system in 2013. Although it is

a pity that due to the low participation and minimalized political support it is going to be

demolished in 2016.

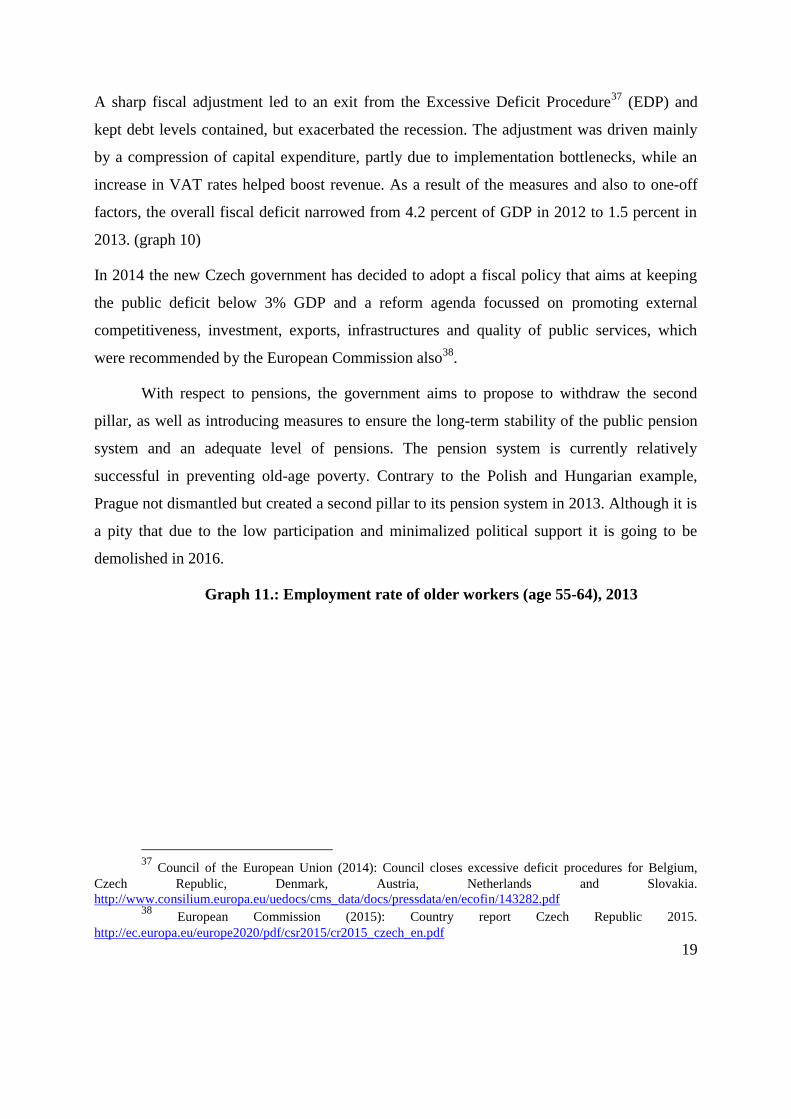

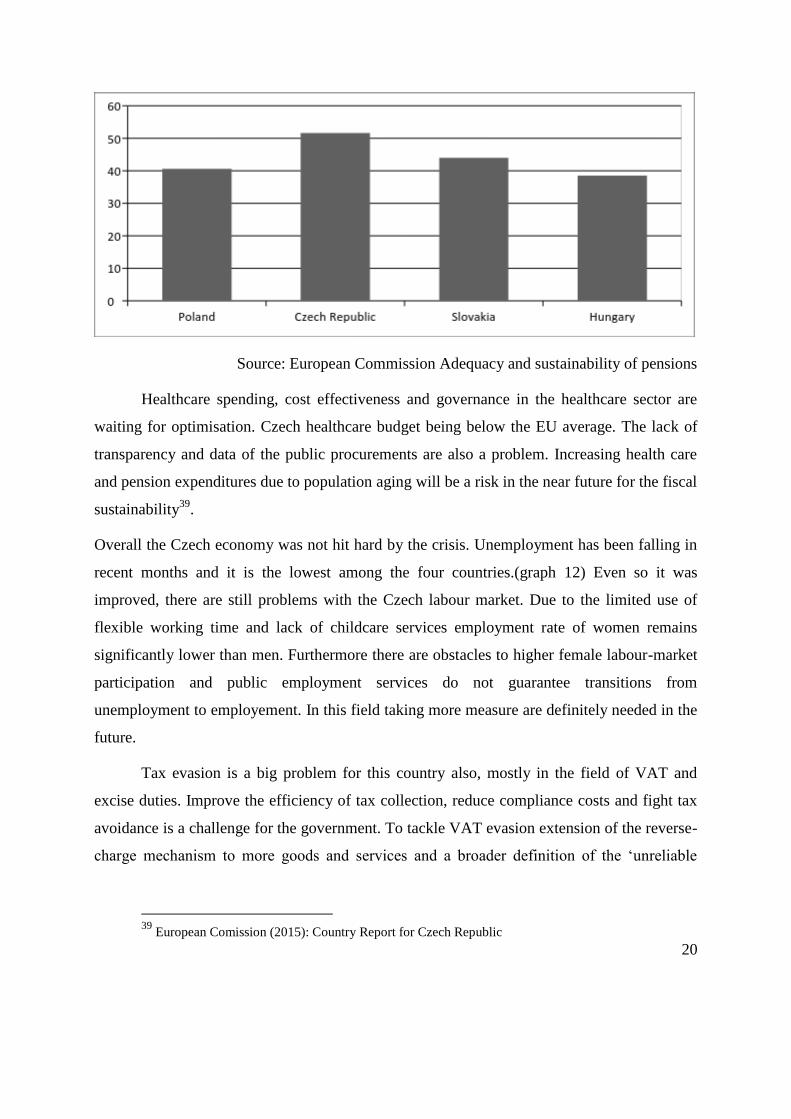

Graph 11.: Employment rate of older workers (age 55-64), 2013

37

Council of the European Union (2014): Council closes excessive deficit procedures for Belgium,

Czech Republic, Denmark, Austria, Netherlands and Slovakia.

http://www.consilium.europa.eu/uedocs/cms_data/docs/pressdata/en/ecofin/143282.pdf 38

European Commission (2015): Country report Czech Republic 2015.

http://ec.europa.eu/europe2020/pdf/csr2015/cr2015_czech_en.pdf

20

Source: European Commission Adequacy and sustainability of pensions

Healthcare spending, cost effectiveness and governance in the healthcare sector are

waiting for optimisation. Czech healthcare budget being below the EU average. The lack of

transparency and data of the public procurements are also a problem. Increasing health care

and pension expenditures due to population aging will be a risk in the near future for the fiscal

sustainability39

.

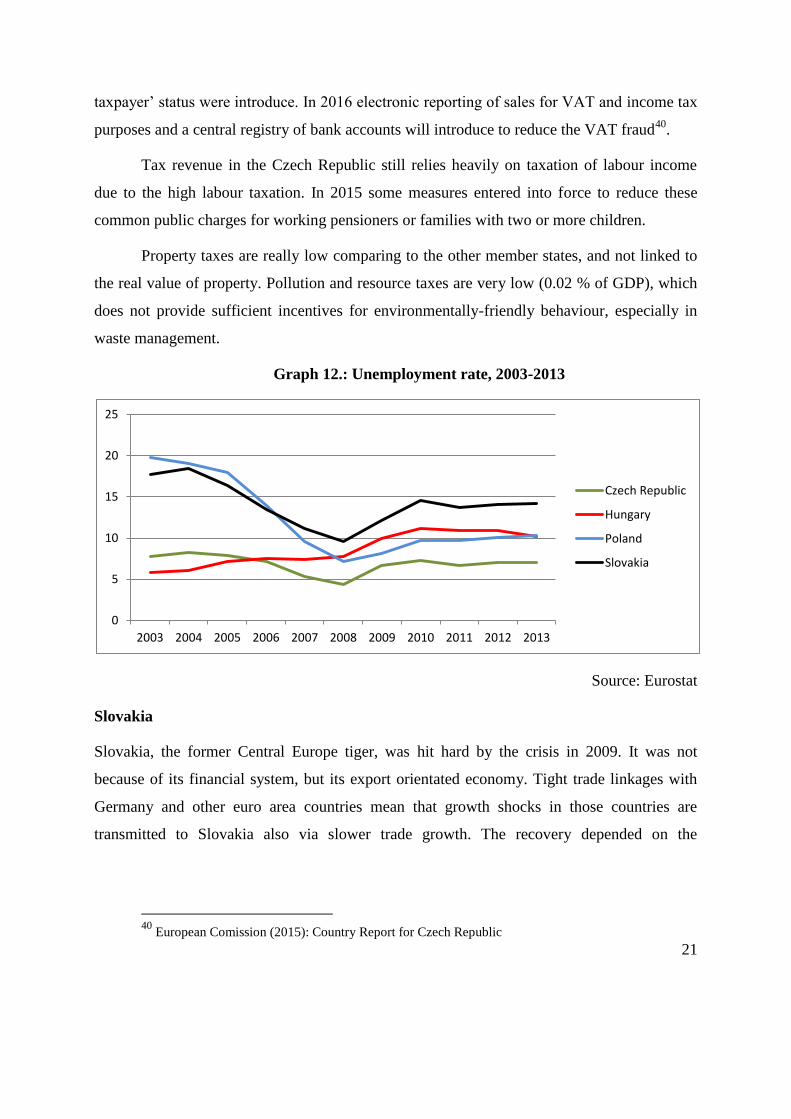

Overall the Czech economy was not hit hard by the crisis. Unemployment has been falling in

recent months and it is the lowest among the four countries.(graph 12) Even so it was

improved, there are still problems with the Czech labour market. Due to the limited use of

flexible working time and lack of childcare services employment rate of women remains

significantly lower than men. Furthermore there are obstacles to higher female labour-market

participation and public employment services do not guarantee transitions from

unemployment to employement. In this field taking more measure are definitely needed in the

future.

Tax evasion is a big problem for this country also, mostly in the field of VAT and

excise duties. Improve the efficiency of tax collection, reduce compliance costs and fight tax

avoidance is a challenge for the government. To tackle VAT evasion extension of the reverse-

charge mechanism to more goods and services and a broader definition of the ʻunreliable

39

European Comission (2015): Country Report for Czech Republic

21

taxpayerʼ status were introduce. In 2016 electronic reporting of sales for VAT and income tax

purposes and a central registry of bank accounts will introduce to reduce the VAT fraud40

.

Tax revenue in the Czech Republic still relies heavily on taxation of labour income

due to the high labour taxation. In 2015 some measures entered into force to reduce these

common public charges for working pensioners or families with two or more children.

Property taxes are really low comparing to the other member states, and not linked to

the real value of property. Pollution and resource taxes are very low (0.02 % of GDP), which

does not provide sufficient incentives for environmentally-friendly behaviour, especially in

waste management.

Graph 12.: Unemployment rate, 2003-2013

Source: Eurostat

Slovakia

Slovakia, the former Central Europe tiger, was hit hard by the crisis in 2009. It was not

because of its financial system, but its export orientated economy. Tight trade linkages with

Germany and other euro area countries mean that growth shocks in those countries are

transmitted to Slovakia also via slower trade growth. The recovery depended on the

40

European Comission (2015): Country Report for Czech Republic

0

5

10

15

20

25

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Czech Republic

Hungary

Poland

Slovakia

22

improvement of euro area confidence, and it was driven by the export41

and domestic

demand42

.

Slovakia is the only eurozone member from the V4. The Slovak koruna joined the Exchange

Rate Mechanism (ERM II) on 28 November 2005. On 1 January 2009 Slovakia joined

eurozone with hope it will provide some protection against negative impact of global

downturn.43

. Slovakia faced the financial crisis with lower vulnerabilities than other countries.

Euro membership also meant early participation in all collective crisis-related measures and

hence much more financial and capital market stability.

General government deficit increased after the outbreak of the crisis and reached 8% of GDP

in 2009, which has resulted an excessive debt procedure in the country. Due to this procedure

many macroeconomic developments happened.

Strong fiscal consolidation contributed to confidence financial markets in Slovakia. However,

it has also undercut domestic drivers of growth, in particular as public investment spending

has fallen and tax rates have risen. As a consequence of budget consolidation, low income

growth, stagnating employment, deteriorating terms-of-trade and the increase in servicing

costs of loans as a percentage of income, domestic demand felt back.

Responding to the crisis many changes happened. Slovakia also reformed its pension

system, but not the way as Hungary and Poland. The general pension fund reform improved

the long term sustainability of the pension finance. The reform included automatic increase in

the statutory retirement age depending on life expectancy, change in the indexation of pension

benefits, strengthening solidarity in awarding new pensions and changes to the maximum

assessment base for the payment of social insurance contributions. Moreover the reform

introduced the fourth type of pension fund, so-called index -linked, whose performance will

replicate developments in one or more stock market indices. The proposed change enables

41

Export growth is still very dependent on the situation in automotive and consumer electronics

sectors, and competition from neighbouring countries has become fiercer 42

Domestic demand depends on income growth generated by the foreign-owned export sector, but it is

not well developed. 43

EC (2014a) Slovakia and the euro:

http://ec.europa.eu/economy_finance/euro/countries/slovakia_en.htm

23

savers to divide their savings into two pension funds, one of which must be a bond pension

fund44

.

Slovakia implemented tax reforms in 2013 that replaced the flat income tax with a

progressive one45

, which should promote greater equity; and phasing out lower taxation of the

self-employed should reduce tax avoidance. Furthermore the corporate income tax rate has

been raised from 19% to 23%.

Due to the fight against tax fraud VAT effective rate increased with 2%. VAT control

statement, compulsory down-payment on VAT were introduces, and inspection on VAT

audit46

were emphasized. According to the national target of VAT collection effectiveness has

to reach 72% by 2020, this was 53% in 201247

. The implicit tax rate on labour is the lowest

among the four countries, and lower than the EU28 average; but real estate and environment

taxes are a problem is Slovakia as well as the other countries48

.

Unemployment has remained high, and still the highest among the four countries. (graph 12.)

High unemployment rate can undermine the growth. A significant part of unemployment is

located in more remote rural regions with a low population density. Despite of this fact

mobility of unemployed people are low due to the high living and housing cost and weak

travelling infrastructure. Unemployment had reached 20 per cent of labour force in the early

2000s. However, strong growth and convergence brought a reduction in the unemployment

rate to a low of 10 % in 2008. Following this, the fall in exports in 2008/9 was associated with

a new increase in unemployment to nearly 15 per cent. Nowadays it reached 12,4%, but it still

above the EU average (9,9%). The jobless recovery and the high unemployment rate illustrate

imbalances in the economy. The most problematic groups are women, Roma and young

people. 60% of the unemployements are low skilled and long-term unemployed. Due to its

structural nature unemployment rate will remain around 12%49

.

44

Stability Programme for the Slovak Republic 2014-2017.

http://ec.europa.eu/europe2020/pdf/csr2014/sp2014_slovakia_en.pdf 45

new tax rates: 19% and 25% 46

80% of all tax audit were VAT audit 47

http://ec.europa.eu/europe2020/pdf/csr2014/nrp2014_slovakia_en.pdf 48

European Cimmission (2015) Country Report Slovakia 49

European Commission (2015): Country Report Slovakia

24

In order to increase employment rate Slovakia should increase the quality and

attainment of education, because low skilled workers and women have particularly low

employment rates. The high ratio (6,4%) of early school leavers, especially for Roma people,

calling for targeted measures also.

Prior to the financial crisis, Slovakia succeeded in reducing public debt levels. Government

debt has risen sharply since the 2009 global crisis and is now running into constitutional debt

ceilings. (graph 15) Slovakia adopted a complex fiscal legislative reform in December 201150

.

Fiscal Responsibility Constitutional Act introduces debt brakes, new institutional framework

(Council for Budget Responsibility and two committees – for macroeconomic forecasts and

for tax forecasts), and transparency rules. The purpose of the Act is to, first, entrench certain

fundamental fiscal rules in the legal system, and second to create competences and obligations

for public authorities that would otherwise being prevented by other constitutional provisions

or constitutionally problematic or insufficient.

To help plunging car industry government also introduced car-scrapping bonus to boost car

sales, mirroring similar subsidies in France and Germany. The first wave was launched in

early March and the second in April. Government allocated 55 million euro to subsidy

purchase of 44,200 new cars51

.

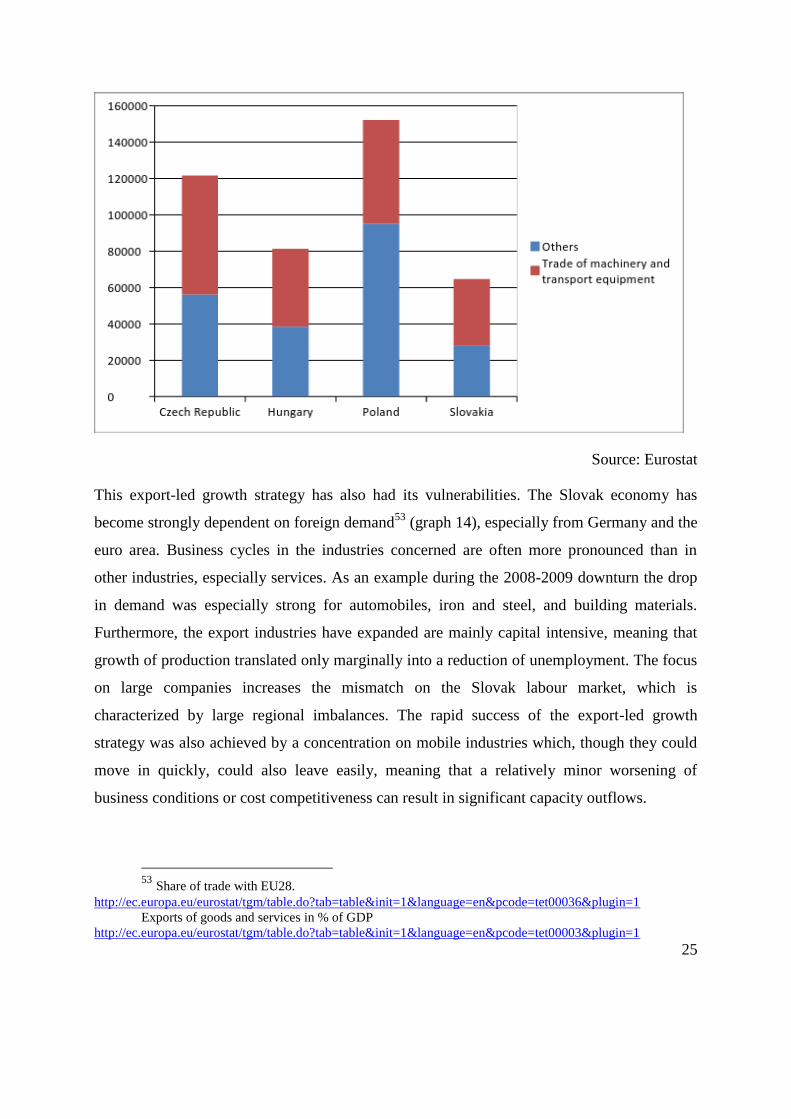

Export (mainly manufacturing) industries have received special attention in Slovakia too.

Various measures were used to attract foreign direct investors. Automobile industry has

grown almost from nothing in Slovakia during the past eleven years, which has become the

most important exporting industry. It gives the GDP’s ¼, and the export’s 1/3. Unit labour

costs declined52

in all major export industries between 1998 and 2007. This is in line with the

dominating importance of price competiveness for Slovak exports.

Graph 13: The ratio of trade of machinery and transport equipment to total

export in million EUR

50

L’udovít Ódor: Fiscal framework in Slovakia. http://www.oecd.org/gov/budgeting/49778688.pdf 51

http://www.visegrad.info/economic-crisis-in-ceecs/factsheet/economic-crisis.html 52

Nominal unit labour cost

http://ec.europa.eu/eurostat/tgm/table.do?tab=table&init=1&language=en&pcode=tipslm20&plugin=1

25

Source: Eurostat

This export-led growth strategy has also had its vulnerabilities. The Slovak economy has

become strongly dependent on foreign demand53

(graph 14), especially from Germany and the

euro area. Business cycles in the industries concerned are often more pronounced than in

other industries, especially services. As an example during the 2008-2009 downturn the drop

in demand was especially strong for automobiles, iron and steel, and building materials.

Furthermore, the export industries have expanded are mainly capital intensive, meaning that

growth of production translated only marginally into a reduction of unemployment. The focus

on large companies increases the mismatch on the Slovak labour market, which is

characterized by large regional imbalances. The rapid success of the export-led growth

strategy was also achieved by a concentration on mobile industries which, though they could

move in quickly, could also leave easily, meaning that a relatively minor worsening of

business conditions or cost competitiveness can result in significant capacity outflows.

53

Share of trade with EU28.

http://ec.europa.eu/eurostat/tgm/table.do?tab=table&init=1&language=en&pcode=tet00036&plugin=1 Exports of goods and services in % of GDP

http://ec.europa.eu/eurostat/tgm/table.do?tab=table&init=1&language=en&pcode=tet00003&plugin=1

26

However reforms in taxation, pension and healthcare systems can ensure sound public

finances, low investments can undermine Slovakia competitiveness and growth prospect, like

the high unemployment rate. In these two fields significant changes are needed.

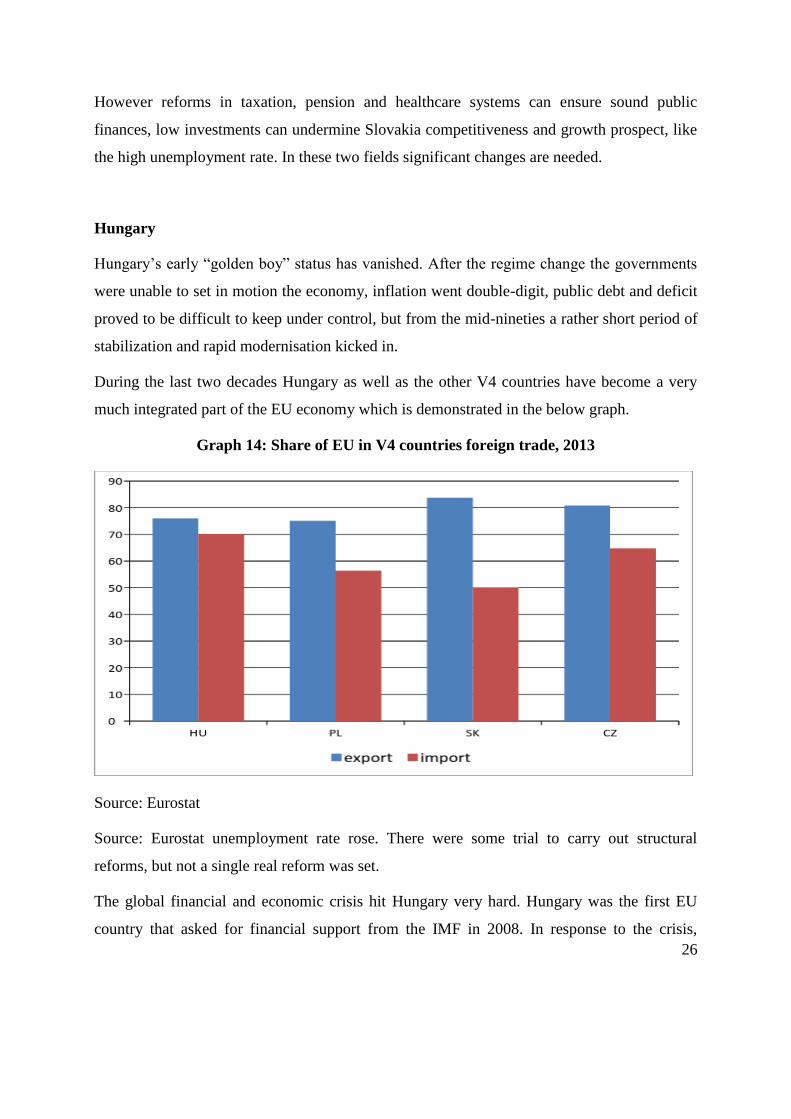

Hungary

Hungary’s early “golden boy” status has vanished. After the regime change the governments

were unable to set in motion the economy, inflation went double-digit, public debt and deficit

proved to be difficult to keep under control, but from the mid-nineties a rather short period of

stabilization and rapid modernisation kicked in.

During the last two decades Hungary as well as the other V4 countries have become a very

much integrated part of the EU economy which is demonstrated in the below graph.

Graph 14: Share of EU in V4 countries foreign trade, 2013

Source: Eurostat

Source: Eurostat unemployment rate rose. There were some trial to carry out structural

reforms, but not a single real reform was set.

The global financial and economic crisis hit Hungary very hard. Hungary was the first EU

country that asked for financial support from the IMF in 2008. In response to the crisis,

27

Hungary took steps at two key areas: fiscal stability and financial stability. The government

took radical steps to diminish costs, and bring the spending to a sustainable rate. All together

spending has to be cut by approximately 5 billion Euros in 2009-2010. The package contained

the elevation of general VAT-rates from 20 to 25 percent (currently it is at 27 percent), with

some exceptions: dairy products, wheat, flour, or starch-made products and district-heating

costs pertain under a preferential, 18 percent tax rate. Excise duty for cigarettes, fuel and

alcohol has grown. The income-tax classes have been changed, so the net income of the most

employees rose. But after the election the government set up a new economic model which is

called unorthodox economic policy.

Hungary’s economy emerged from the 2012 recession and entered to a weak growth path in

2013. This growth is mainly driven by government investment and consumption, and also

exports. Private demand remained weak, and credit to the retail and corporate sectors

continued to contract. Hungary’s medium-term growth prospects remain modest, as private

consumption is still hampered by the ongoing repair of households’ balance sheets; low

employment among low skilled workers and shortcoming in labour and product market; while

the weak business environment continues to weigh on private investment.

Monetary easing has helped to return to growth. The Hungarian National Bank has cuts its

policy rate since 2012 to support demand and credit growth54

. The central bank also

introduced the Funding for Growth Scheme in 2013 with the aim of easing access to finance

for SMEs and improving their credit conditions through the provision of subsidized lending

interest rate. Despite strong take up it is still not clear whether it produce more growth in the

economy or not.

External vulnerabilities have been the key risk of the Hungarian economy. External

debt remains high and large open net position can create more volatility in the future. Growth

potential is held back by low employment among low-skilled and weak investment, making

further structural reforms essential.

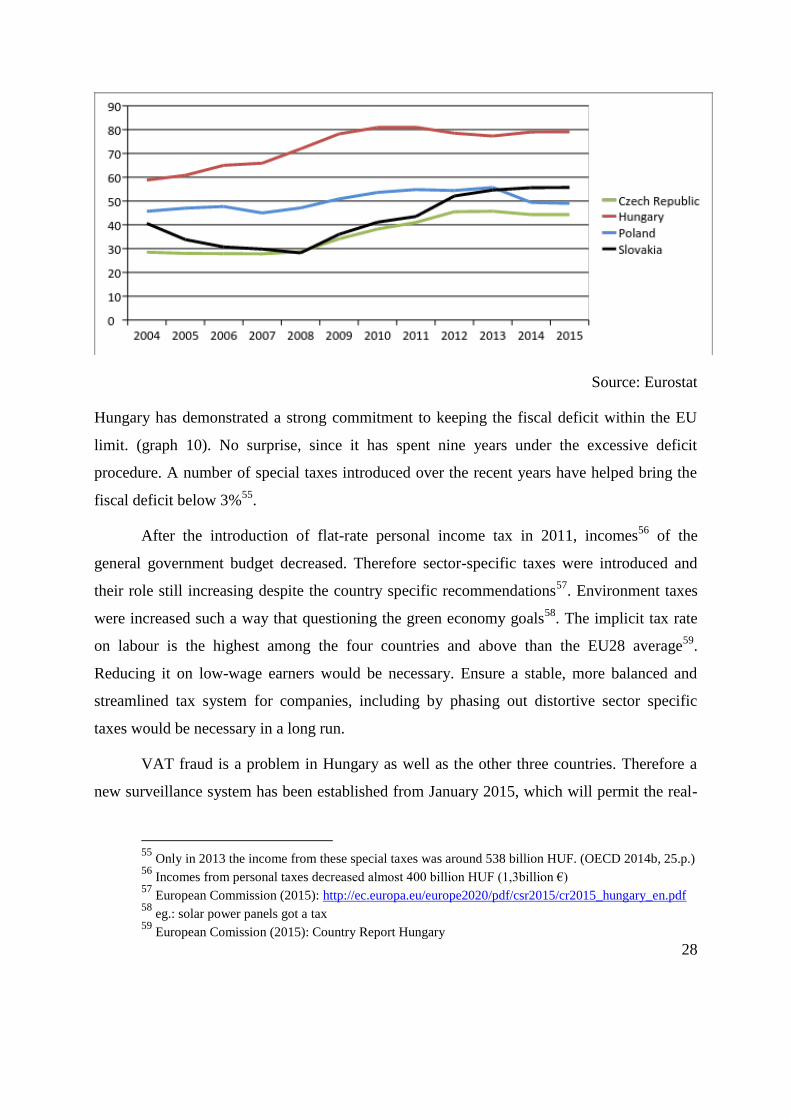

Graph 15.: General government gross debt, %of GDP, 2004-2014

54

Base rate history http://www.mnb.hu/Jegybanki_alapkamat_alakulasa

28

Source: Eurostat

Hungary has demonstrated a strong commitment to keeping the fiscal deficit within the EU

limit. (graph 10). No surprise, since it has spent nine years under the excessive deficit

procedure. A number of special taxes introduced over the recent years have helped bring the

fiscal deficit below 3%55

.

After the introduction of flat-rate personal income tax in 2011, incomes56

of the

general government budget decreased. Therefore sector-specific taxes were introduced and

their role still increasing despite the country specific recommendations57

. Environment taxes

were increased such a way that questioning the green economy goals58

. The implicit tax rate

on labour is the highest among the four countries and above than the EU28 average59

.

Reducing it on low-wage earners would be necessary. Ensure a stable, more balanced and

streamlined tax system for companies, including by phasing out distortive sector specific

taxes would be necessary in a long run.

VAT fraud is a problem in Hungary as well as the other three countries. Therefore a

new surveillance system has been established from January 2015, which will permit the real-

55

Only in 2013 the income from these special taxes was around 538 billion HUF. (OECD 2014b, 25.p.) 56

Incomes from personal taxes decreased almost 400 billion HUF (1,3billion €) 57

European Commission (2015): http://ec.europa.eu/europe2020/pdf/csr2015/cr2015_hungary_en.pdf 58

eg.: solar power panels got a tax 59

European Comission (2015): Country Report Hungary

29

time monitoring of the transport of VAT-liable goods and establishment of on-line links to

cash registers in the retail sector has been completed by the end of 2014.

Regulating the fiscal framework after 2010 has lead to mixed results. Long-term sustainability

is questionable due to incomes after the phasing out of special taxes. Legal actions have to be

taken to improve the transparency of public finances.

The basic feature Hungarian economic policy since 2010 (sometimes misleadingly labelled by

the government as „unorthodox”) is keeping the VAT rate at a very high level (27%) and

more importantly applying one-off sectoral „crisis” taxes imposed on whatever sector that can

be taxed. The application of these taxes (accounting for 2200 billion Hungarian forints (EUR

7,4 billion) together with the nationalisation (i.e.: confiscation) of the second pillar pension

fund assets made it possible to curb the government deficit. These taxes constitute a major

burden on some sectors and seemingly spare the population at least it is more difficult to track

their imposition on the society later by the companies affected through higher fees and other

charges. Here is a list of the nine special tax introduced since 2010:

- special tax on financial institutions;

- special sectoral tax (phased out in 2013);

- utility services tax;

- telecom tax;

- financial transaction tax;

- insurance tax;

- health tax;

- accident tax;

- publicity tax.

Government debt has remained steadily at a high level, which is forecast to be

corrected only at a very slow pace. Despite one-off capital transfers60

that decreased public

debt by around 7% of GDP, and a substantial improvement in the structural balance,

government debt has been broadly stable around 80% of GDP since 2009. This reflects the

effect of a weakened exchange rate, a low growth performance and high financing costs.

(graph 11.) The Hungarian Constitution contains that the gross government debt should not

60

Gathering the private pension fund.

30

exceed 50% of GDP. Until it comes down that level the debt GDP ratio has to decline every

year, after 2016 nominal public debt can increase only by half of expected real GDP growth,

which supposes a counter-cyclical fiscal policy.61

Budgetary risks and the small reduction

path can undermine long-term debt reduction which highlights the importance of fiscal

sustainability and growth friendly economic policy.

The Hungarian export deflators have broadly stagnated since 2000, so far the other V3

countries were able to increase their deflators by around 30% to 70%. All V4 countries are

primarily involved in producing machinery and transport equipment products for exports,

with Poland having a somewhat less concentrated structure compared to the other V3

countries. The Hungarian export performance suggests that the deterioration is primarily

related to tightening supply constraints. This is partly linked to the inability to attract new FDI

inflows but also to the weak spill over linkages between multinationals and domestic

companies. Although recently there have been some large investment projects in the

automobile industry, a marked improvement in the export sector is not expected.

The relapse of Hungary's competitiveness in the export sector is primarily related to the

machinery and transport equipment subsector. (graph 13) Nevertheless, the country continues

to have the highest level of export unit values, thanks to the still competitive product quality

in regional comparison62

.

Although unemployment rate is around 10% (graph 11), increasing employment rate

to reach its Europe2020 national target labour market policy measures are inevitable. Labour

force participation also remains low for women and for old cohort. Maternal employments

rate is the lowest within the OECD63

. The poor overall health status of the Hungarian

population implies that many workers are affected by debilitating health conditions, in

particular at advancing age, this one reason why older workers market participation is low.

The public works programme has increased employment, but has a poor record in

reintegrating the non-employed to regular work. Like in Slovakia unemployment rate has a

61

http://net.jogtar.hu/jr/gen/hjegy_doc.cgi?docid=A1100425.ATV Article 36. Constitution of Hungary 62

graph 3.12, p23. EC 2014c 63

IMF (2014): http://www.imf.org/external/pubs/ft/scr/2014/cr14156.pdf

31

strong regional profile, which calls for measures to mobilize the workers and create more jobs

in the peripheral regions.

Therefore revision of the public works scheme, creation of a Roma labour market

integration policy scheme and reduction poverty, support the transition between different

stages of education and towards the labour market are should be done in the near future.

Long-term improvements in labour market outcomes will also depend on complimentary

structural reforms, improvements in health care and public education.

Conclusion

The EU as a whole and even more so, the Eurozone was heavily hit by the sovereign debt

crisis, which resulted in way above the mark national debt to GDP ratios. In the light of this

V4 countries’ performance in controlling the national debt was a relative success, although in

absolute terms all of them experienced a rising debt. The analysis of growth trends clearly

show that the dramatic decline in 2009 was followed by consolidation in 2010.

Economic success and political decisions are interlinked to a great extent in the region. This

stems from the fact that politics in general and the direction in which the political class wants

to direct the country is more important in this region in terms of end results both in political

and economic terms. A new government in the V4 countries can have dramatic impact on the

geopolitical, EU-political and economic policy path the country takes. Long-term political

stability is still in nascent form, or in a more pessimistic tone: is a rarity in the region.

V4 countries harnessing the benefits of EU membership differs a lot. Some of the new

members were more successful than others in using EU-accession as an economic and

modernisation leverage by halving the number of people living in poverty and raising the per

capita GDP by almost fifty percent. There is obviously a clear difference in the group when

euro-status is considered. When it comes to EMU issues, the four countries are in different

position and have differing views. The way V4 countries approach the Euro accession and

crisis management is also a mix of economic and political features. These states differ a lot:

Slovakia, a relative latecomer in economic reforms is part of the currency union. Poland,

Hungary and the Czech Republic are not Euro-members. But even this sub-group is divided:

32

Poland intends to join whenever requirements are fulfilled while the Hungarian and the Czech

governments are cool on accession.

The future of the V4 co-operation is dim: clearly the divisive forces are way stronger than the

rather opportunistic cohesive ones (such as the drive to gain as much EU funds as possible).

The case of Hungary is particular, it has maneouvered itself onto a path that leads the country

away not only from the mainstream European political consensus but also from the other

Visegrad countries.

As far as desirable policy actions from the EU’s side vis-à-vis the V4 countries are concerned,

a mix of pragmatist and positivistic engagement is recommended. This would entail taking a

strong stance in relation to the respect of the basic values of Europeaness but also an open and

understanding attitude. Besides the European institutions, Germany will also have to play a

decisive role, not for its own good this time but for the good of this region this time -

hopefully.

References

Constitution of Hungary: Article 36.

http://net.jogtar.hu/jr/gen/hjegy_doc.cgi?docid=A1100425.ATV Last accessed: 20-02-2015

Council of the European Union (2014): Council closes excessive deficit procedures for

Belgium, Czech Republic, Denmark, Austria, Netherlands and Slovakia.

http://www.consilium.europa.eu/uedocs/cms_data/docs/pressdata/en/ecofin/143282.pdf Last

accessed: 20-02-2015

Council of the European Union (2013): Council closes excessive deficit procedures for

Italy, Latvia, Lithuania, Hungary and Romania.

http://www.consilium.europa.eu/uedocs/cms_data/docs/pressdata/en/ecofin/137561.pdf

Council of the European Union (2014): Council closes excessive deficit procedures for

Belgium, Czech Republic, Denmark, Netherlands, Austria and Slovakia

http://www.consilium.europa.eu/uedocs/cms_data/docs/pressdata/en/ecofin/143282.pdf

Council of the European Union (2013) Excessive deficit procedure for Poland:

Insufficient action taken, Council issues new recommendation

http://www.consilium.europa.eu/uedocs/cms_data/docs/pressdata/en/ecofin/140017.pdf

ECB (2014): Convergence Report.

http://www.ecb.europa.eu/pub/pdf/conrep/cr201406en.pdf

33

ECFIN (2014): Country Focus: Securing Poland’s economic success: A good time for

reforms.

http://ec.europa.eu/economy_finance/publications/country_focus/2014/pdf/cf_vol11_issue9_e

n.pdf

Eurobarometer(2014): Public opinion in the European Union 82.

http://ec.europa.eu/public_opinion/archives/eb/eb82/eb82_first_en.pdf

European Commission (2013): Special Eurobarometer on Corruption (397)

http://ec.europa.eu/public_opinion/archives/ebs/ebs_397_en.pdf Last accessed: 20-02-2015

European Commission (2013): The Innovation Union Scoreboard 2013.

http://ec.europa.eu/enterprise/policies/innovation/files/ius-2013_en.pdf Last accessed: 20-02-

2015

European Commission (2014a): Slovakia and the euro:

http://ec.europa.eu/economy_finance/euro/countries/slovakia_en.htm Last accessed: 20-02-

2015

European Commission( 2014b): Economic forecast for Poland

http://ec.europa.eu/economy_finance/eu/forecasts/2014_autumn/pl_en.pdf Last accessed: 20-

02-2015

European Commission (2014c) Macroeconomic imbalances in Hungary 2014.

http://ec.europa.eu/economy_finance/publications/occasional_paper/2014/pdf/ocp180_en.pdf

Last accessed: 20-02-2015

European Commission (2014): Europe 2020 target: Tertiary education attainment.

http://ec.europa.eu/europe2020/pdf/themes/28_tertiary_education_02.pdf

European Commission (2014): Report on action taken by Poland in response to the

Council recommendation of 10 December 2013 in order to bring an end to the situation of

excessive deficit.

http://ec.europa.eu/economy_finance/economic_governance/sgp/pdf/30_edps/126-

07_council/2014-11-18_pl_-_ear_en.pdf

European Commission (2014) Taxation.

http://ec.europa.eu/europe2020/pdf/themes/02_taxation_02.pdf

European Commission (2014): Adequacy and sustainability of pensions

http://ec.europa.eu/europe2020/pdf/themes/04_pensions_02.pdf

European Commission (2014): National Reform Programme of the Slovak Republic

2014 http://ec.europa.eu/europe2020/pdf/csr2014/nrp2014_slovakia_en.pdf

European Commission (2014): Stability Programme for the Slovak Republic 2014-

2017. http://ec.europa.eu/europe2020/pdf/csr2014/sp2014_slovakia_en.pdf

European Commission (2015): VAT Rates applied in the Member States of the

European Union.

34

http://ec.europa.eu/taxation_customs/resources/documents/taxation/vat/how_vat_works/rates/

vat_rates_en.pdf

European Commission (2015): Country report Czech Republic 2015.

http://ec.europa.eu/europe2020/pdf/csr2015/cr2015_czech_en.pdf

European Commission (2015): Country report Hungary 2015.

http://ec.europa.eu/europe2020/pdf/csr2015/cr2015_hungary_en.pdf

European Commission (2015): Country report for Poland 2015.

http://ec.europa.eu/europe2020/pdf/csr2015/cr2015_poland_en.pdf

European Commission (2015): Country report Slovak Republic 2015

http://ec.europa.eu/europe2020/pdf/csr2015/cr2015_slovakia_en.pdf

Eurostat: Nominal unit labour cost

http://ec.europa.eu/eurostat/tgm/table.do?tab=table&init=1&language=en&pcode=tipslm20&

plugin=1 Last accessed: 20-02-2015

Eurostat: Share of trade with EU28.

http://ec.europa.eu/eurostat/tgm/table.do?tab=table&init=1&language=en&pcode=tet00036&

plugin=1 Last accessed: 20-02-2015

Eurostat: Government debt

http://epp.eurostat.ec.europa.eu/tgm/table.do?tab=table&plugin=1&language=en&pcode=tsdd

e410 Last accessed: 20-02-2015

Eurostat: Exports of goods and services in % of GDP

http://ec.europa.eu/eurostat/tgm/table.do?tab=table&init=1&language=en&pcode=tet00003&

plugin=1 Last accessed: 20-02-2015

Eurostat: GDP per capita

http://appsso.eurostat.ec.europa.eu/nui/show.do?dataset=nama_aux_gph&lang=en Last

accessed: 20-02-2015

Eurostat: GDP growth

http://epp.eurostat.ec.europa.eu/tgm/table.do?tab=table&init=1&plugin=1&language=en&pco

de=tec00115 Last accessed: 20-02-2015

Eurostat: Productivity

http://epp.eurostat.ec.europa.eu/tgm/refreshTableAction.do;jsessionid=9ea7d07d30e8adf9885

4aaa14d088119d3d3b7c2244b.e34OaN8PchaTby0Lc3aNchuMchuNe0?tab=table&plugin=1

&pcode=tsdec310&language=en Last accessed: 20-02-2015

Eurostat: Labour cost

http://epp.eurostat.ec.europa.eu/tgm/table.do?tab=table&init=1&language=en&pcode=tec001

30&plugin=1 Last accessed: 20-02-2015

Eurostat: GDP growth

http://epp.eurostat.ec.europa.eu/tgm/table.do?tab=table&plugin=1&language=en&pcode=tec0

0115 Last accessed: 20-02-2015

35

Eurostat: Share of trade with the EU 28

http://ec.europa.eu/eurostat/tgm/table.do?tab=table&init=1&language=en&pcode=tet00036&

plugin=1 Last accessed: 20-02-2015

Eurostat: Long term interest rate:

http://ec.europa.eu/eurostat/tgm/table.do?tab=table&init=1&language=en&pcode=tec00097&

plugin=1

Eurostat: International trade of machinery and transport equipment

http://ec.europa.eu/eurostat/eurostat/tgm/table.do?tab=table&init=1&plugin=1&language=en

&pcode=tet00009

Eurostat: Tertiary education attainment

http://ec.europa.eu/eurostat/tgm/table.do?tab=table&init=1&language=en&pcode=tsdsc480&

plugin=1

Hungarian Central Statistical Office: Incomes of the central budget

https://www.ksh.hu/docs/hun/xstadat/xstadat_evkozi/e_qse006i.html Last accessed: 20-02-

2015

Hungarian National Bank: Base rate history

http://www.mnb.hu/Jegybanki_alapkamat_alakulasa Last accessed: 20-02-2015

IMF (2012): Poland continues as bright spot in region

http://www.imf.org/external/pubs/ft/survey/so/2012/car020312a.htm Last accessed: 20-02-

2015

IMF (2012): Republic of Poland—Review Under the Flexible Credit Line

Arrangement http://www.imf.org/external/pubs/ft/scr/2012/cr1212.pdf Last accessed: 20-02-

2015

IMF (2014):IMF Country Report: Poland.

http://www.imf.org/external/pubs/ft/scr/2014/cr14174.pdf

IMF (2014): Database

http://www.imf.org/external/pubs/ft/weo/2014/02/weodata/weorept.aspx?pr.x=45&pr.

y=13&sy=2001&ey=2015&scsm=1&ssd=1&sort=country&ds=.&br=1&c=964%2C935%2C

936%2C944&s=PPPSH%2CGGXWDG_NGDP&grp=0&a= Last accessed: 20-02-2015

Marján, Attila (2014): The new EU voting system ―The old west-east north south

division. Modern Diplomacy.

http://www.moderndiplomacy.eu/index.php?option=com_k2&view=item&id=454:the-new-

eu-voting-system-the-old-west-east-north-south-division&Itemid=569 Last accessed: 20-02-

2015

Marján, Attila: EU-rule changes force a Visegad re-think. Europe’s World. 2014.

Spring

OECD (2011): Restoring public

financeshttp://www.oecd.org/gov/budgeting/47860307.pdf Last accessed: 20-02-2015

OECD (2014a): Economic Surveys, Poland

http://www.oecd.org/eco/surveys/Overview_Poland_2014.pdf Last accessed: 20-02-2015

36

OECD (2014b): Economic Survey of Hungary.

http://www.oecd.org/eco/surveys/economic-survey-hungary.htm Last accessed: 20-02-2015

Ódor ,L’udovít: Fiscal framework in Slovakia.

http://www.oecd.org/gov/budgeting/49778688.pdf Last accessed: 20-02-2015

Reichardt ,Adam: Poland and the global economic crisis: Observations and reflections

in the public sector. http://www.cipfa.org/-

/media/files/policy%20and%20guidance/the%20journal%20of%20finance%20and%20manag

ement%20in%20public%20services/vol%2010%20number%201/adam_reichard.pdf Last

accessed: 20-02-2015

Visegrad.info (2009): Economic crisis. http://www.visegrad.info/economic-crisis-in-

ceecs/factsheet/economic-crisis.html Last accessed: 20-02-2015

WEF (2014): Global Competitiveness Report 2014-2015

http://www3.weforum.org/docs/WEF_GlobalCompetitivenessReport_2014-15.pdf Last

accessed: 20-02-2015

WEF (1999): Global Competitiveness Report

http://www.cid.harvard.edu/archive/res/gcr_2000_overview.pdf Last accessed: 20-02-2015

World Bank: GDP/capita in current US $

http://databank.worldbank.org/data/views/reports/tableview.aspx?isshared=true# Last

accessed: 20-02-2015

World Bank (2014): Doing Business 2015

http://www.doingbusiness.org/reports/global-reports/doing-business-2015 Last accessed: 20-

02-2015

World Bank (2015): Exports of goods and services % of GDP.

http://databank.worldbank.org/data/views/reports/tableview.aspx?isshared=true# Last

accessed: 20-02-2015

Top Related

Copyright © 2022 FDOKUMEN