Bahasa

Halaman

Hukum

The Impact of Financial Institutions on Property Rights

– and the Impact of Institutions on Financial Volatility – in Transition Economies

Christopher A. HartwellHead of Global Markets

and Institutional Research25 February, 2014

What are the relationships between financial markets, financial institutions, and other institutions that make up a market economy?

How can we think about institutions quantitatively?

Are there “non-traditional” econometric or quantitative methods that can capture the relationships b/w financial markets and external institutions?

Themes of Today’s Talk

Part I: Financial Institutions and Property Rights

What are institutions? And how do they evolve?The transition contextThe interplay between financial markets and institutionsTesting the relationship and results

Part II: Institutions and Financial Volatility

Going the other way: institutional changes and financial market functioningApplication of volatility models to institutionsThe empirical evidence of institutional volatility

Conclusions

Outline of Presentation

PART I: FINANCIAL INSTITUTIONS AND PROPERTY RIGHTS

Institutions are a set of rules, constraints, and behavioral guidelines, enforced by either formal or informal means external to the individual, which are designed or arise to shape the behavior of individual actors. (Hartwell 2013)

Can be further divided into:– Political: Pertaining to distribution of political power

– Economic: Designed or arising to maximize the utility of principals in the economic sphere, by solely influencing and mediating economic outcomes pertaining to distribution of resources.

– Social: Institutions not explicitly concerned with political power or economic incentives but geared towards behavior and norms outside these spheres

What is an “Institution?”

Under our definition, financial markets are thus also an economic institution

– Like all institutions, they interact with and are influenced by other institutions

– Their emergence is also often conditioned by the presence (or lack) of other institutions

Financial markets are normally an outgrowth of development processes– Stock markets and the like embody the property rights and legal regime of a country up to that point

Financial Markets and Institutions

Historical development of stock markets mirror their times and their societies:

Antwerp Stock Market (1531)Port of Antwerp a center for European commerce

London Stock Exchange (1773)“The City” already a locus of global financial power

New York Stock Exchange (1792)Providing a way for intermediation in the newly independent colonies

In each instance, stock market arose due to needs of other parts of the market

What Begets a Financial Market Most?

Different and clear sequence of institutional creation not present elsewhere:

Many countries in transition started from near-zero formal property rights, but with nascent financial institutions

– Private property outlawed under communism, small-scale and informal property rights could not support a larger market system

Perhaps more accurately, exogenously-given (and not organically-grown) financial markets

– Armenia, Kyrgyzstan, Ukraine, Russia, Romania, Poland, many others all recipients of USAID monies for capital market development

Not necessarily responding to an organic or urgent need as seen throughout history (although this is debatable)

The Transition Context

Given the sequencing and initial conditions in the transition countries of CEE and FSU:

Did the presence and, more crucially, the usage or success of a stock market in transition economies, reinforce the development of supporting institutions - in particular property rights?

Research Question

Long and rich economic, political, anthropological, and sociological history in the creation of property rights

Mijiyawa (2013) distills four schools of thought:

– economic approach: property rights institutions are created when the benefits of their creation exceed their costs (also Demsetz (1967) and North (1971));

– cultural approach: institutional variation reflects the differences in the beliefs of political leaders about what institutions create benefits for society;

– historical approach: cross-country differences in property rights institutions are the by-product of historical accidents; and

– political approach: institutions are chosen by the individuals who control political power to maximize their personal payoffs

This paper focuses on the economic, cultural and political approaches – transition dynamics make historical approaches less relevant

Property Rights and their Determinants

Positively:– Creation of new property rights would be reinforced as

actors see the benefits that come from increased financial intermediation

– Improved financial intermediation helps businesses to form, an entrepreneurial class to emerge that has a vested interest in property rights

– Part of a package of transition (“indivisibility of reforms”) so that countries likely to push through extensive financial reform would also have more comprehensive property rights

Negatively:– Diminishing returns to stock exchange?

Eventually the “outsiders” of the stock exchange become “insiders” to the political process

Support industry- or exchange-specific policies which may advantage the exchange to the exclusion of general property rights

How Might Financial Institutions Influence Property Rights?

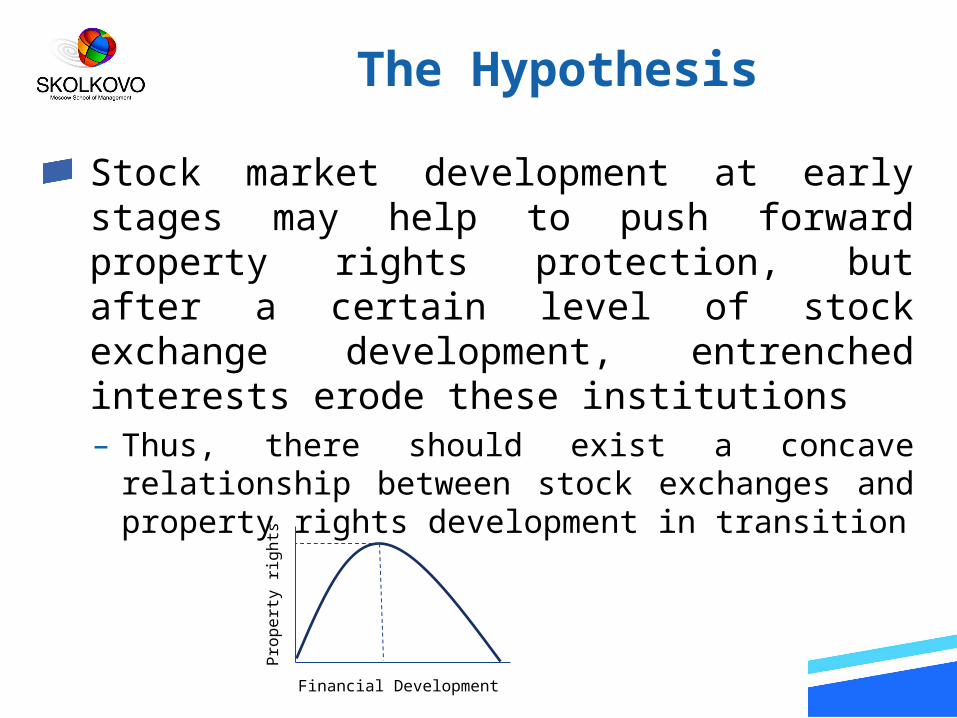

Stock market development at early stages may help to push forward property rights protection, but after a certain level of stock exchange development, entrenched interests erode these institutions– Thus, there should exist a concave relationship between stock exchanges and property rights development in transition

The Hypothesis

Prop

erty

rig

hts

Financial Development

Where Y is property rights, STOCK is a measure of stock market development, INST are other institutions that can affect property rights development, and MACRO is a vector of macroeconomic variables (lagged one period)

Time dummies included

Within groups (fixed-effects) specification, due to the “moderate N, large T” nature of the panel

Driscoll and Kraay (1998) standard errors to account for heteroskedasticity and autocorrelation (as the Driscoll and Kraay errors are also designed specifically for “large T” datasets such as this one)

Breusch-Pagan (1980) LM test of independence shows spatial correlation amongst the countries. Luckily, as noted by Hoechle (2007), the non-parametric covariance matrix estimation procedure of Driscoll-Kraay adjusted standard errors is designed precisely to correct for this dependence

The Econometric Examination

Contract-intensive money– Used by inter alia Clague et. al (1996, 1999), Dollar and

Kraay (2003), Knack, Kugler, and Manning (2003), Fortin (2010), Compton and Giedeman (2011), and Hartwell (2013),

– Proportion of money held outside the formal banking sector:

– Higher numbers indicate more money in the formal financial sector, and thus higher property rights

– Clague et. al (1999:200) note, “Where citizens believe that there is sufficient third-party enforcement, they are more likely to allow other parties to hold their money in exchange for some compensation.”

Measuring Property Rights: the Dependent Variable

How would we define the level of “financial development?” Is it:

How big the stock market is? – Maybe bigger is better? Proxied here by growth in stock

market capitalization as a percentage of GDP

How successful the stock market is? – Maybe size doesn’t matter ; a large but failing stock

exchange could also have a drag on property rights. Here I use the change in stock returns over the period.

How volatile the stock market is?– Perhaps the demonstration effect of equity volatility may

negatively impact property rights throughout the real economy. Proxied as the sum of daily squared returns, aggregated monthly

Which Facet of the Stock Market Matters?

A new database of monthly data for transition economies with stock exchange returns and volatility over a shifting window from 1989-2012Stock data from Bloomberg, Datastream, CEICProperty Rights data from IMF IFSInstitutional data from ICRG Political Risk IndicatorsMacroeconomic variables from IMF IFS

The Data

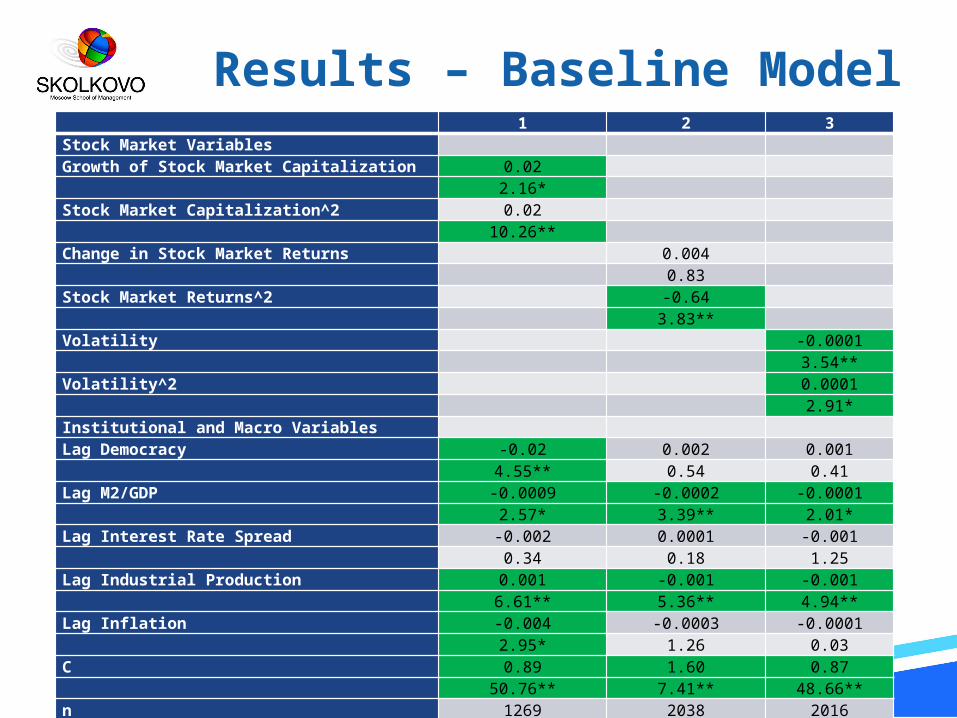

Results – Baseline Model 1 2 3Stock Market Variables Growth of Stock Market Capitalization 0.02 2.16* Stock Market Capitalization^2 0.02 10.26** Change in Stock Market Returns 0.004 0.83 Stock Market Returns^2 -0.64 3.83** Volatility -0.0001 3.54**Volatility^2 0.0001 2.91*Institutional and Macro Variables Lag Democracy -0.02 0.002 0.001

4.55** 0.54 0.41Lag M2/GDP -0.0009 -0.0002 -0.0001 2.57* 3.39** 2.01*Lag Interest Rate Spread -0.002 0.0001 -0.001 0.34 0.18 1.25Lag Industrial Production 0.001 -0.001 -0.001 6.61** 5.36** 4.94**Lag Inflation -0.004 -0.0003 -0.0001 2.95* 1.26 0.03C 0.89 1.60 0.87 50.76** 7.41** 48.66**n 1269 2038 2016R-squared 0.39 0.23 0.20Time Dummies? yes yes yes

Size of the stock market (capitalization), appears to reinforce property rights, albeit slowly

– increasing stock market size results in an unmitigated positive effect, with a net accelerating effect greater than a linear increase alone

Stock market performance, has a positive but insignificant relationship with property rights

– Quadratic term for stock market performance (returns) shows a powerful concave relationship

Financial market turmoil has an unequivocal negative effect on property rights in transition

– Surprising result: volatility has a strong negative effect at first, turning into a positive effect on property rights at higher levels of volatility

Summary of Results

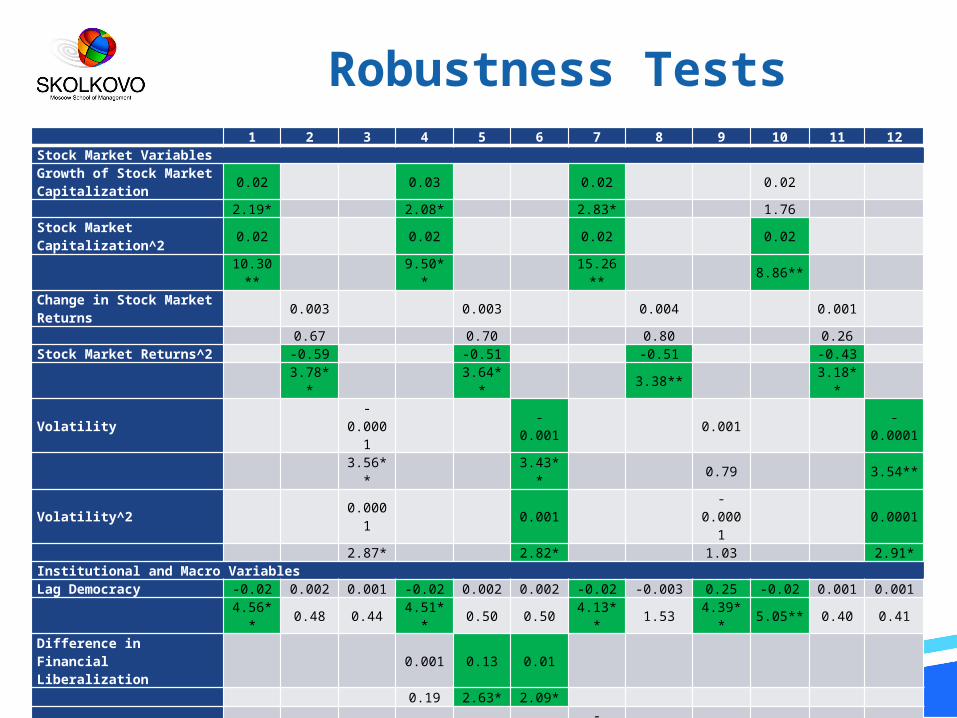

Robustness Tests 1 2 3 4 5 6 7 8 9 10 11 12Stock Market VariablesGrowth of Stock Market Capitalization 0.02 0.03 0.02 0.02

2.19* 2.08* 2.83* 1.76 Stock Market Capitalization^2 0.02 0.02 0.02 0.02

10.30** 9.50*

* 15.26** 8.86**

Change in Stock Market Returns 0.003 0.003 0.004 0.001

0.67 0.70 0.80 0.26 Stock Market Returns^2 -0.59 -0.51 -0.51 -0.43

3.78** 3.64*

* 3.38** 3.18**

Volatility -

0.0001

-0.001 0.001 -

0.0001

3.56** 3.43*

* 0.79 3.54**

Volatility^2 0.0001 0.001

-0.0001

0.0001

2.87* 2.82* 1.03 2.91*Institutional and Macro VariablesLag Democracy -0.02 0.002 0.001 -0.02 0.002 0.002 -0.02 -0.003 0.25 -0.02 0.001 0.001

4.56** 0.48 0.44 4.51*

* 0.50 0.50 4.13** 1.53 4.39*

* 5.05** 0.40 0.41

Difference in Financial Liberalization

0.001 0.13 0.01

0.19 2.63* 2.09*

Change in Private Credit to GDP

-0.0001

-0.0001 0.002

0.58 0.32 0.08 Initial Level of Executive Constraints 0.15 0.15 0.14

57.04**

52.47**

48.66**

C 0.89 0.89 0.88 0.89 1.42 0.87 0.92 0.83 4.80

51.21**

48.54**

49.29**

44.98**

7.97**

56.22**

46.17** 40.88** 10.89

**

n 1266 2010 2013 1259 1939 1934 1031 1558 1579 1236 1963 2016R-squared 0.39 0.22 0.20 0.39 0.26 0.20 0.65 0.32 0.81 0.37 0.25 0.20Time Dummies? yes yes yes yes yes yes yes yes yes yes yes yes

In transition economies, yes, bigger stock markets do correlate with property rights, but the scale of the effect is smallStock market performance generally doesn’t matter for the development of property rights, as larger gains in the stock market may be viewed as outliers– On the other hand, incremental gains could reinforce

incremental institutional changes via a feedback effect Volatility seems to be harmful in building support for property rights at the outset, but healthy at higher levels of rights

Tentative Conclusions

Accounting for endogeneity?– Success of financial markets themselves determined by other

factors, perhaps the same that determined the path of property rights in transition

– An IV-GMM approach might be interesting here, if good instruments can be identified (one of the reasons I haven’t done it as of yet)

Is there a way to measure participation in the stock market?

– Perhaps a democratized stock market is the key for the link between financial markets and property rights

Do these results hold for other emerging markets (not just transition economies)?Can we econometrically and theoretically model the continuing interactions between financial and other institutions?

For the Future (Still a Work in Progress!)

PART II: INSTITUTIONS AND FINANCIAL VOLATILITY

Institutional development is influenced by financial markets… but how do the changes in external institutions affect financial market performance?– Financial markets may have been

established via exogenous support, but their operation would be affected by changes in external policies and institutions exogenous to the influence of stock markets

– The reality of an economy and polity in flux may provide feedback effects to the financial markets

Institutions and Financial Markets: Going

the Other Way

Did economic and political institutions have a discernible effect on financial sector volatility during the transition period?

Do other macroeconomic variables found to already have an impact in the literature on volatility have more or less of an effect in the presence of market-supporting institutions?

Did the volatility of these institutions and their changes during the transition period affect financial markets? Put simply, did institutional volatility feed through to financial volatility?

Three Research Questions for Part II

Literature has focused on answering the question if institutions influence financial sector development and activity

– The overwhelming consensus is “of course,” see Demirgüç-Kunt and Levine (1996), Claessens and Laeven (2003), Beck and Levine (2008), Andrianaivo and Yartey (2009)

Another stream focuses on institutional changes and effect on growth

– Brunetti and Weder (1998) find that constitutional changes (i.e. political volatility) are negatively correlated with growth

– Svensson (1998) finds political institutional volatility have negative effect on investment

– Berggren, Bergh, and Bjornskov (2011) find institutional instability in legal and policy institutions in rich countries actually contributes significantly to higher growth rates, while instability of social institutions is a drag on growth across all countries.

Challenge is bringing the two together – this paper!

Previous Literature: Institutions and Financial

Performance

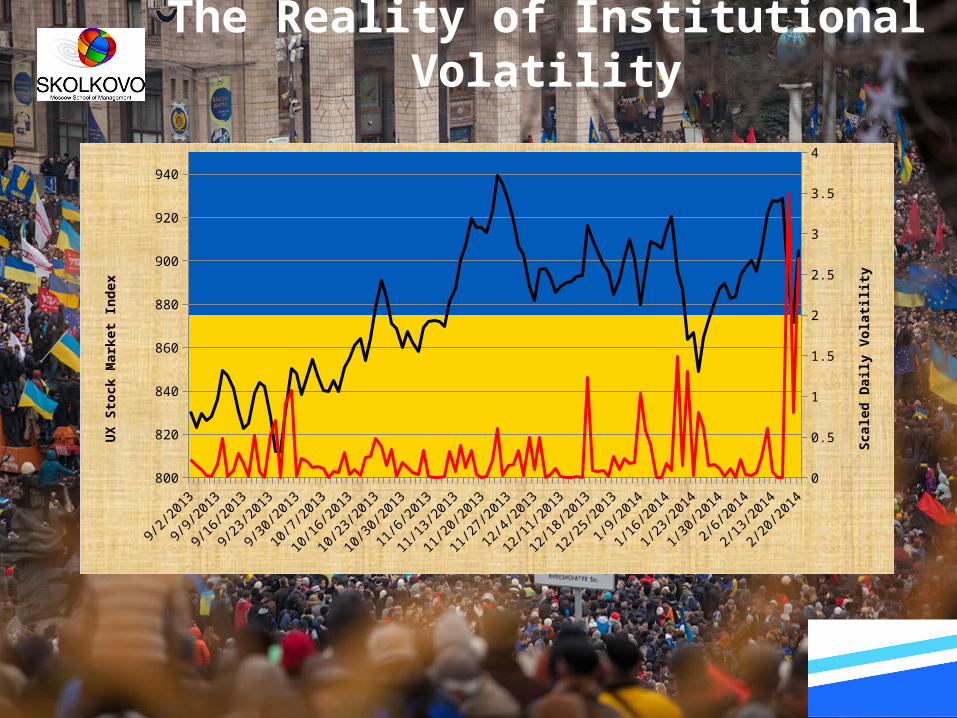

The Reality of Institutional Volatility

9/2/2013

9/9/2013

9/16/2013

9/23/2013

9/30/2013

10/7/2013

10/16/2013

10/23/2013

10/30/2013

11/6/2013

11/13/2013

11/20/2013

11/27/2013

12/4/2013

12/11/2013

12/18/2013

12/25/2013

1/9/2014

1/16/2014

1/23/2014

1/30/2014

2/6/2014

2/13/2014

2/20/2014

800

820

840

860

880

900

920

940

0

0.5

1

1.5

2

2.5

3

3.5

4

UX S

tock

Marke

t In

dex

Scal

ed D

aily

Vol

atil

ity

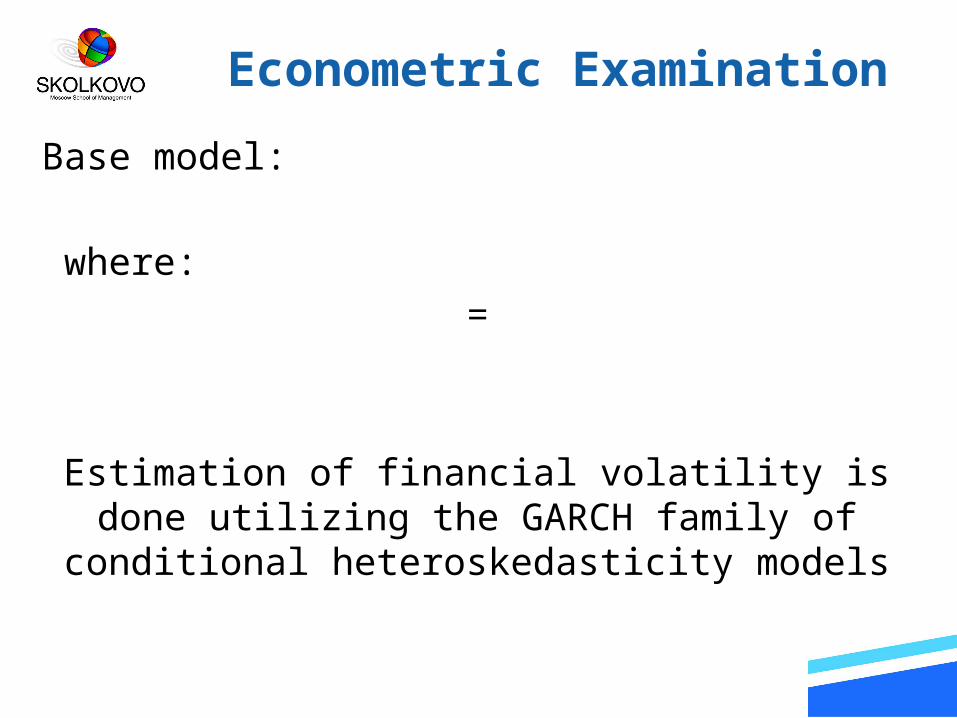

Base model:

where: =

Estimation of financial volatility is done utilizing the GARCH family of

conditional heteroskedasticity models

Econometric Examination

Yes, but…

Wait, (G)ARCH Models and Institutions?

Aren’t ARCH models for high-frequency data? And aren’t institutions the definition of

non-high-frequency?

vs.

(G)ARCH models can deal with the specific attributes of financial and institutional volatility that may skew normal econometric

estimation

Institutional shocks can display a high degree of persistence due to their slow-moving and slow-changing nature

The volatility of institutional change is not constant over time

Transition economies are different, as the transition from communism to capitalism is precisely about the replacement of one set of institutions with another.

Difference from Part I – here modeling the processes of financial volatility (the left hand, rather than right hand, side of the equation), including institutional volatility in the conditional variance equation

(G)ARCH Models and Institutions

Asteriou and Price (2001) on political uncertainty and growth in the UK– Use both a GARCH and GARCH in means (GARCH-M) model and find political instability has a highly negative, significant, and persistent effect on GDP growth.

“Spiritual father” of this paper: Campos and Karanasos EL Paper (2008) and JBF Paper (2012)– Examination of political instability on growth in Argentina using PARCH/APARCH methods, finding impact of both formal and informal instability

Previous Uses of GARCH in Institutional Volatility

Modeling

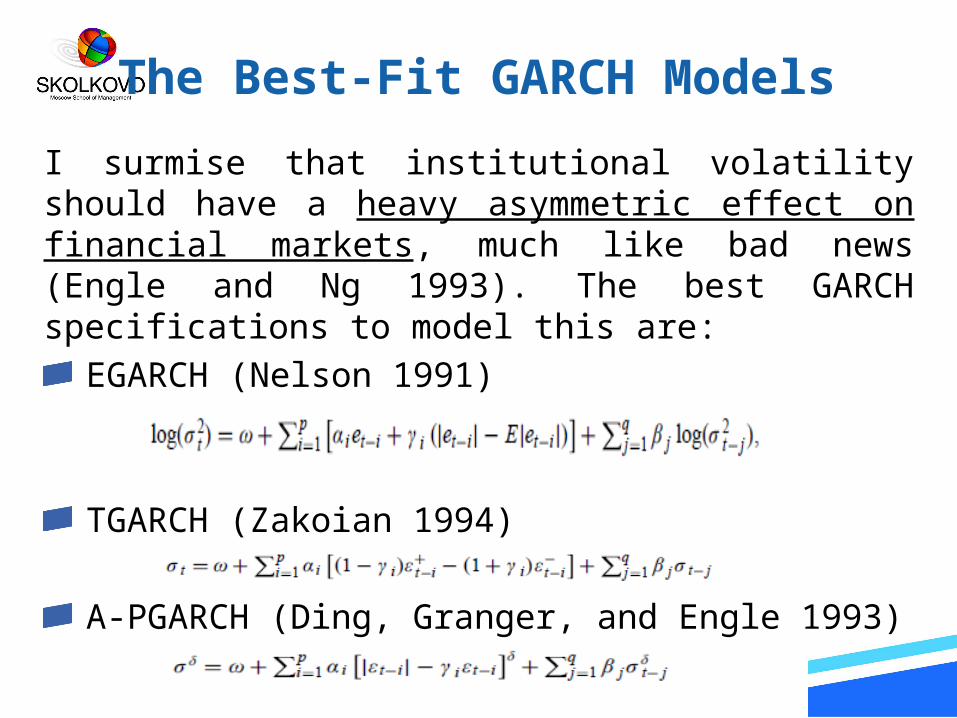

I surmise that institutional volatility should have a heavy asymmetric effect on financial markets, much like bad news (Engle and Ng 1993). The best GARCH specifications to model this are:

EGARCH (Nelson 1991)

TGARCH (Zakoian 1994)

A-PGARCH (Ding, Granger, and Engle 1993)

The Best-Fit GARCH Models

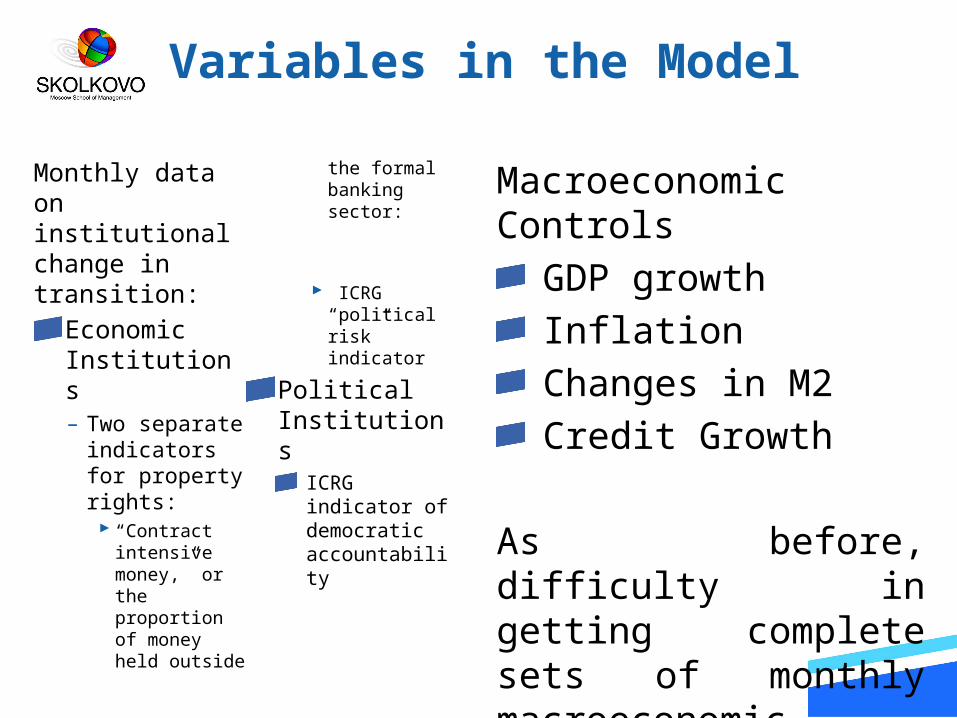

Monthly data on institutional change in transition:

Economic Institutions– Two separate indicators for property rights: “Contract intensive money,” or the proportion of money held outside

the formal banking sector:

ICRG “political risk” indicator

Political Institutions

ICRG indicator of democratic accountability

Macroeconomic Controls

GDP growthInflationChanges in M2Credit Growth

As before, difficulty in getting complete sets of monthly macroeconomic indicators

Variables in the Model

Levels of institutions are included in the conditional mean equation– Lagged property rights and democratic accountability

– “Institutions matter” in the normal econometric sense

Volatility included in the conditional variance, measured in three separate ways– Six-month rolling standard deviation– Three-month rolling standard deviation– Coefficient of variation for both time periods

Institutional Volatility

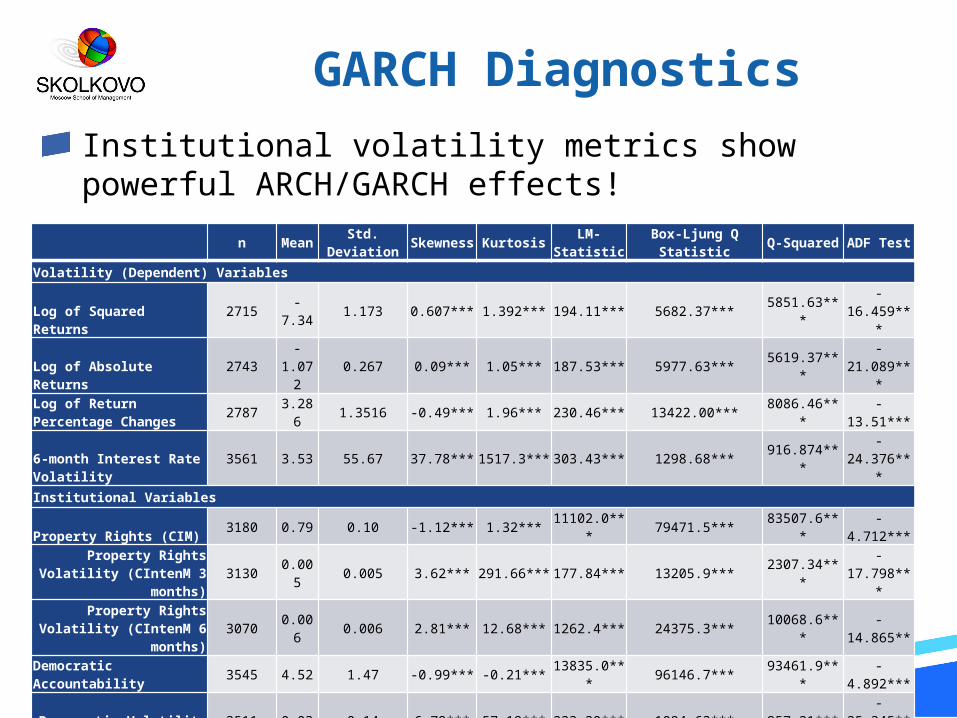

Institutional volatility metrics show powerful ARCH/GARCH effects!

GARCH Diagnostics

n Mean Std. Deviation Skewness Kurtosis LM-

StatisticBox-Ljung Q Statistic Q-Squared ADF Test

Volatility (Dependent) Variables

Log of Squared Returns

2715 -7.34 1.173 0.607*** 1.392*** 194.11*** 5682.37*** 5851.63**

*

-16.459**

*

Log of Absolute Returns

2743-

1.072

0.267 0.09*** 1.05*** 187.53*** 5977.63*** 5619.37***

-21.089**

*Log of Return Percentage Changes 2787 3.28

6 1.3516 -0.49*** 1.96*** 230.46*** 13422.00*** 8086.46***

-13.51***

6-month Interest Rate Volatility

3561 3.53 55.67 37.78*** 1517.3*** 303.43*** 1298.68*** 916.874***

-24.376**

*Institutional Variables

Property Rights (CIM) 3180 0.79 0.10 -1.12*** 1.32*** 11102.0*** 79471.5*** 83507.6**

*-

4.712***Property Rights

Volatility (CIntenM 3 months)

3130 0.005 0.005 3.62*** 291.66*** 177.84*** 13205.9*** 2307.34**

*

-17.798**

*Property Rights

Volatility (CIntenM 6 months)

3070 0.006 0.006 2.81*** 12.68*** 1262.4*** 24375.3*** 10068.6**

*-

14.865**

Democratic Accountability 3545 4.52 1.47 -0.99*** -0.21*** 13835.0**

* 96146.7*** 93461.9***

-4.892***

Democratic Volatility (3 months)

3511 0.03 0.14 6.79*** 57.19*** 223.20*** 1094.63*** 957.21***-

25.345***

Democratic Volatility (6 months)

3460 0.05 0.18 4.33*** 23.04*** 2054.6*** 5641.35*** 4824.33***

-23.158**

*

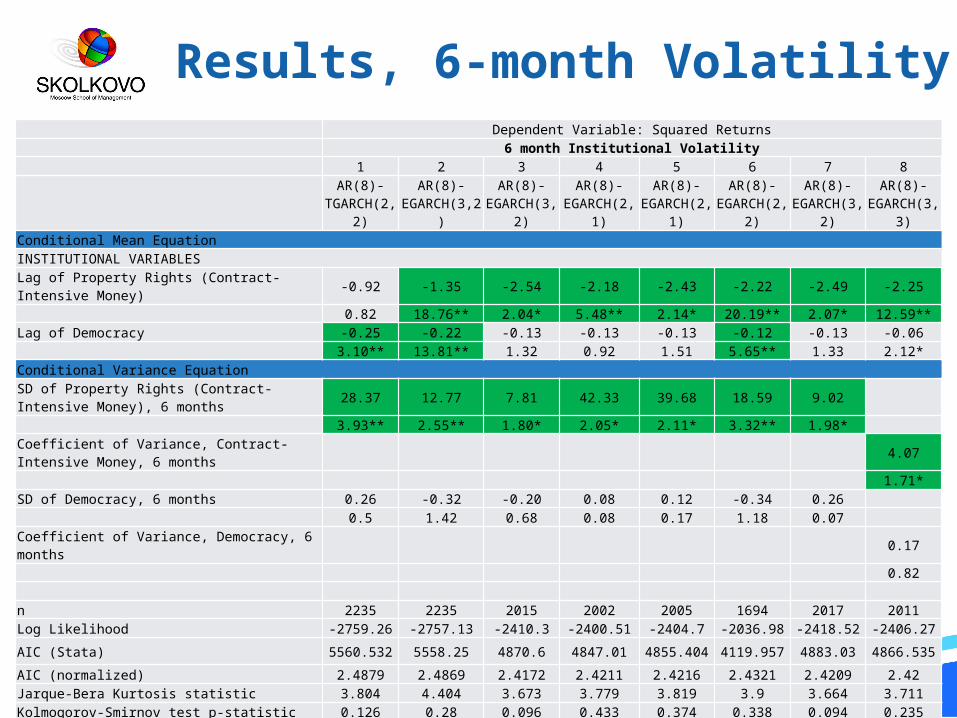

Dependent Variable: Squared Returns6 month Institutional Volatility

1 2 3 4 5 6 7 8

AR(8)-

TGARCH(2,2)

AR(8)-EGARCH(3,2

)

AR(8)-EGARCH(3,

2)

AR(8)-EGARCH(2,

1)

AR(8)-EGARCH(2,

1)

AR(8)-EGARCH(2,

2)

AR(8)-EGARCH(3,

2)

AR(8)-EGARCH(3,

3)Conditional Mean EquationINSTITUTIONAL VARIABLESLag of Property Rights (Contract-Intensive Money) -0.92 -1.35 -2.54 -2.18 -2.43 -2.22 -2.49 -2.25

0.82 18.76** 2.04* 5.48** 2.14* 20.19** 2.07* 12.59**Lag of Democracy -0.25 -0.22 -0.13 -0.13 -0.13 -0.12 -0.13 -0.06 3.10** 13.81** 1.32 0.92 1.51 5.65** 1.33 2.12*Conditional Variance EquationSD of Property Rights (Contract-Intensive Money), 6 months 28.37 12.77 7.81 42.33 39.68 18.59 9.02

3.93** 2.55** 1.80* 2.05* 2.11* 3.32** 1.98* Coefficient of Variance, Contract-Intensive Money, 6 months 4.07

1.71*SD of Democracy, 6 months 0.26 -0.32 -0.20 0.08 0.12 -0.34 0.26

0.5 1.42 0.68 0.08 0.17 1.18 0.07 Coefficient of Variance, Democracy, 6 months 0.17

0.82

n 2235 2235 2015 2002 2005 1694 2017 2011Log Likelihood -2759.26 -2757.13 -2410.3 -2400.51 -2404.7 -2036.98 -2418.52 -2406.27AIC (Stata) 5560.532 5558.25 4870.6 4847.01 4855.404 4119.957 4883.03 4866.535AIC (normalized) 2.4879 2.4869 2.4172 2.4211 2.4216 2.4321 2.4209 2.42Jarque-Bera Kurtosis statistic 3.804 4.404 3.673 3.779 3.819 3.9 3.664 3.711Kolmogorov-Smirnov test p-statistic 0.126 0.28 0.096 0.433 0.374 0.338 0.094 0.235

Results, 6-month Volatility

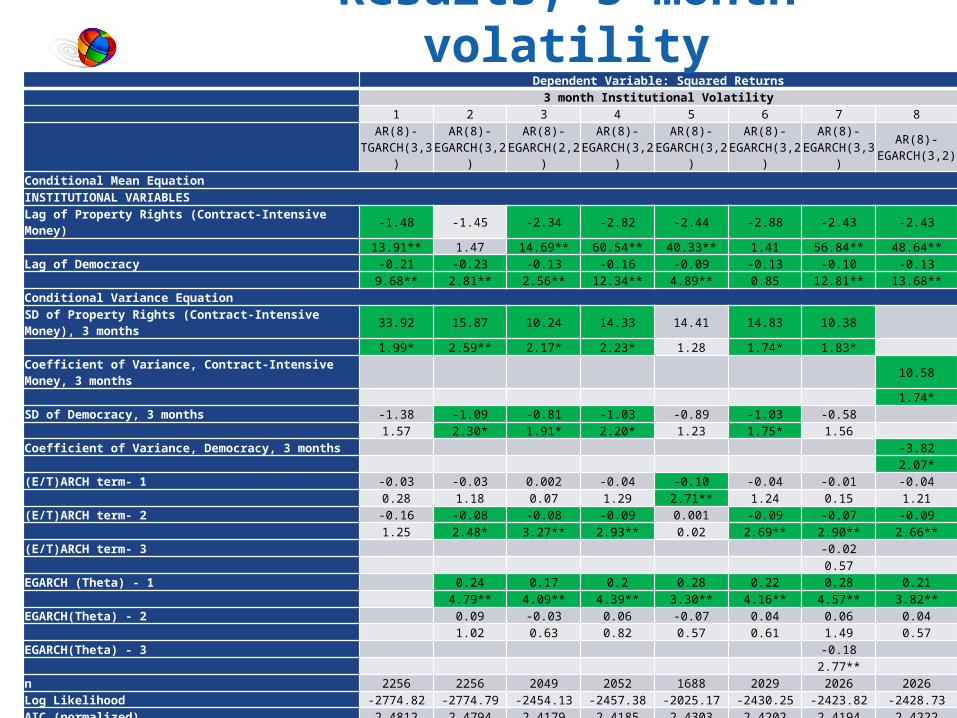

Dependent Variable: Squared Returns3 month Institutional Volatility

1 2 3 4 5 6 7 8

AR(8)-

TGARCH(3,3)

AR(8)-EGARCH(3,2

)

AR(8)-EGARCH(2,2

)

AR(8)-EGARCH(3,2

)

AR(8)-EGARCH(3,2

)

AR(8)-EGARCH(3,2

)

AR(8)-EGARCH(3,3

)

AR(8)-EGARCH(3,2)

Conditional Mean EquationINSTITUTIONAL VARIABLESLag of Property Rights (Contract-Intensive Money) -1.48 -1.45 -2.34 -2.82 -2.44 -2.88 -2.43 -2.43

13.91** 1.47 14.69** 60.54** 40.33** 1.41 56.84** 48.64**Lag of Democracy -0.21 -0.23 -0.13 -0.16 -0.09 -0.13 -0.10 -0.13 9.68** 2.81** 2.56** 12.34** 4.89** 0.85 12.81** 13.68**Conditional Variance EquationSD of Property Rights (Contract-Intensive Money), 3 months 33.92 15.87 10.24 14.33 14.41 14.83 10.38

1.99* 2.59** 2.17* 2.23* 1.28 1.74* 1.83* Coefficient of Variance, Contract-Intensive Money, 3 months 10.58

1.74*SD of Democracy, 3 months -1.38 -1.09 -0.81 -1.03 -0.89 -1.03 -0.58

1.57 2.30* 1.91* 2.20* 1.23 1.75* 1.56 Coefficient of Variance, Democracy, 3 months -3.82

2.07*(E/T)ARCH term- 1 -0.03 -0.03 0.002 -0.04 -0.10 -0.04 -0.01 -0.04 0.28 1.18 0.07 1.29 2.71** 1.24 0.15 1.21(E/T)ARCH term- 2 -0.16 -0.08 -0.08 -0.09 0.001 -0.09 -0.07 -0.09 1.25 2.48* 3.27** 2.93** 0.02 2.69** 2.90** 2.66**(E/T)ARCH term- 3 -0.02 0.57 EGARCH (Theta) - 1 0.24 0.17 0.2 0.28 0.22 0.28 0.21 4.79** 4.09** 4.39** 3.30** 4.16** 4.57** 3.82**EGARCH(Theta) - 2 0.09 -0.03 0.06 -0.07 0.04 0.06 0.04 1.02 0.63 0.82 0.57 0.61 1.49 0.57EGARCH(Theta) - 3 -0.18 2.77** n 2256 2256 2049 2052 1688 2029 2026 2026Log Likelihood -2774.82 -2774.79 -2454.13 -2457.38 -2025.17 -2430.25 -2423.82 -2428.73AIC (normalized) 2.4812 2.4794 2.4179 2.4185 2.4303 2.4202 2.4194 2.4222Jarque-Bera Kurtosis statistic 5.393 5.866 3.708 3.764 3.955 3.798 3.718 3.757Kolmogorov-Smirnov test p-statistic 0.23 0.183 0.429 0.139 0.335 0.286 0.323 0.349Q test p-statistic 0.41 0.4 0.47 0.47 0.63 0.47 0.47 0.47

Distribution Student's T

Student's T GED GED Student's

TStudent's

TStudent's

T Student's T

Results, 3-month volatility

Institutional effects manifest themselves on financial markets both in the conditional mean and the conditional variance– Effect of the levels of property rights and democracy highly significant and with the “correct” sign, i.e more property rights and more democracy lead, on average, to lower volatility

Property rights volatility led to much higher levels of financial volatility, especially when sustained– 6-month variability showed a greater influence than 3-month variability

In 3-month windows, democratic volatility had a dampening effect on financial volatility

– Marginal significance, but perhaps reflecting “wait and see” attitudes

– Also possibly a function of democratic volatility itself v. property rights changes (as we talked about in Part I)

Summary of Results

Utilizing different metrics of financial volatility, results still hold

– Log of absolute returns– Log of return percentage changes– 6-month interest rate volatility

Inclusion of two world volatility metrics also does not change the results

– S&P 500 monthly volatility– Volatility of price of gold

Perhaps not the measurement of financial volatility that is driving the results, but property rights

– Inclusion of ICRG “political risk” indicator as proxy for property rights

– Encompasses investor protection, corruption, conflict (internal and external), the extent of the military in government, law and order, and bureaucratic quality – all central to protecting property

– Results still hold albeit more marginally

Robustness Tests

Better institutions in transition economies lead to lower financial volatility in time-series dataIn EGARCH and TGARCH modeling, institutional effects manifest themselves on financial markets both in the conditional mean and the conditional variance. – In short, better and more stable institutions such

as property rights also made financial stability more likely

Policy ramification! Emphasis should be made (Hartwell (2013)) on “getting the basics right,” protection of private property and a balanced political system quells financial volatility

Conclusions to Part II

CONCLUSIONS

In transition, financial markets influenced the path of property rights, but the changes in property rights also affected financial volatility

– Financial institutions benefit from stable supporting institutions (as the literature has shown), while these supporting institutions themselves can be impacted by financial movements

There must be a way to marry these two strands of research

– If we know that financial markets influence the development of property rights, while changes in property rights influence financial markets, there has to be a unifying theory/model

– How can we think theoretically about institutional influence and interaction? How can we model it?

Quantification of institutions must continue unabated!

Conclusions Overall

DZIĘKUJĘ!

Top Related

Copyright © 2022 FDOKUMEN