Bahasa

Halaman

Hukum

TRANSI TI ON FIN ANC E, BANK ING AND CURRENCY RESEARCH

The Chinese Banking System: Economic Performanceand Prospects for Future Development

Enrico Geretto Æ Rubens Pauluzzo

Received: 22 July 2008 / Accepted: 4 September 2008 / Published online: 25 February 2009

� Springer-Verlag 2009

Abstract This paper examines the main characteristics of the Chinese banking

industry. In particular, it analyses the main performance indicators of the system

together with some prospects of future development. The paper also considers the

problems related to high levels of non-performing loans and the internationalization

paths of the Chinese banking market. In spite of some recent reforms, further

legislative improvements are required to develop the system and to allow a gradual

opening to foreign competition.

Keywords China � Banking system � Economic performance

JEL Classification F37 � G21

Introduction

The gradual opening of the People’s Republic of China to international markets

raises the problem of how the financial system, and in particular the banking market,

will be able to support this phenomenon (Fishman 2004; Lemoine 2005; Dobson

and Kashyap 2006; Rampini 2006; Chiarlone and Amighini 2007). This paper aims

at deepening the economic performances of the major banks of the People’s

Republic of China and the main problems related to the entire Chinese banking

system.

In particular, after a short examination of the main balance sheet items of the

major Chinese banks, we propose an analytical scheme of the results achieved, in

E. Geretto (&) � R. Pauluzzo

Faculty of Economics, University of Udine, Udine, Italy

e-mail: [email protected]

R. Pauluzzo

e-mail: [email protected]

123

Transit Stud Rev (2009) 16:92–113

DOI 10.1007/s11300-009-0055-4

order to provide a structured evaluation of them. The final section of the paper

analyses the possible future scenarios and specific problems of the banking system.

Structure of the Chinese Banking System

The Chinese banking system is characterized by a pyramid structure. Its top is

represented by the People’s Bank of China (PBOC), established in 1948, with

central bank functions. Since April 2003, the PBOC has been supported by the

China Banking Regulatory Commission (CBRC), established to deal with the

regulatory and supervisory activities, allowing the PBOC to focus exclusively on

monetary policy issues. The core of the Chinese banking system is represented by

the State-Owned Banks, divided into Commercial Banks and State Policy Banks.

Commercial Banks are the four major banks of the country1 (Big four), established

in 1980 by the modernization of PBOC. They include:

• Industrial & Commercial Bank of China;

• Bank of China;

• China Construction Bank;

• Agricultural Bank of China.

The market share of these institutions (52%) is mainly due to their role in

implementing the economic and social policies of the government, as a result of the

firm relationship with State-Owned Enterprises (SOEs). The Big four have several

branches and offices throughout the country, allowing them to maintain large and

stable relations with the market. The government involvement in their management

activities has generated an inefficient costs structure, a weak corporate governance

and high levels of non-performing loans (NPLs).

In order to avoid the risk that the Big four could be used as mere instruments for

financial support to public projects and to focus their activities on better commercial

criteria, three State Policy Banks were established in 1994:

• Agricultural Development Bank of China;

• China Development Bank;

• Export-Import Bank of China.

These banks represent a crucial lever for the Chinese economic development.

They have inherited the typical activities of state banks, but they have not taken

charge of their outstanding debts; their main source of funding is represented by

bonds, placed both on the domestic (National Inter-Bank Bond Market); (CBRC

2005, 2006d, 2007a, b, c), and on the international markets.

Other important bank categories of the Chinese system are represented by Joint

Stock Commercial Banks and City Commercial Banks. Joint Stock Commercial

Banks are owned by the state, local authorities and other investors: some of them

1 Official statistics have been considering a fifth bank, Bank of Communication (BOCOM), in State-owned banks since March 2007. In this study, however, that bank is not considered because its data at the

end of 2006 were not self-important.

The Chinese Banking System 93

123

have placed their shares on stock markets. These commercial banks are authorized

to carry out any banking activities, including currency transactions (Fioroni and

Cianci 2004). In spite of their relatively small size, they are growing at a quick pace,

attracting the interest of foreign banks. Half of the 13 Joint Stock Commercial

Banks in China have a partnership with a foreign investor. City Commercial Banks,

on the other hand, operate exclusively within the main urban centers. Owned by

local governments and local companies, they provide their services to SMEs in

Beijing, Shanghai, Tianjin, Guangzhou and Dalian, which are the most developed

areas of the country.

The Chinese banking system is completed by Rural Credit Cooperatives. There

are almost 40,000 cooperative banks, supporting the activities of outlying SMEs.

Until a few years ago, they were controlled by the Agricultural Bank of China but,

nowadays, they are supervised by the PBOC. The firm connection of such banks to

the local authorities, or to highly politicized public bodies, means that their

management criteria are largely influenced by state mechanisms.

Performance of the Main Credit Institutions

The paper analyses nine Chinese credit institutions: Agricultural Bank of China

(ABC), Bank of China (BOC), Construction Bank of China (CBC), Industrial and

Commercial Bank of China (ICBC), China Development Bank (CDB), Bank of

Communications (BOCOM), China Merchants Bank (CMC), China Minsheng

Banking Corporation (CMBC) and Shenzhen Development Bank (SDB). Their bank

counters are 75,686, more than 90% of total Chinese bank counters. Their

employees are 1,535,579 (83.3% of total bank employees). The funds they manage

represent 84% of the total funds managed by the entire Chinese banking system2

(CBRC 2006a, b, c, d, 2007a, b, c).

In order to better analyze the economic performance of the panel, we consider

the following reclassification of financial statements. Assets are divided into

interest bearing assets (loans) and non-interest bearing assets (cash, fixed assets,

etc.). Liabilities are also divided into interest bearing liabilities (deposits) and

non-interest bearing liabilities (provisions for risks and other charges). As for

income statements, we consider interest net income (the difference between interest

income and interest expenses), intermediation margin (calculated by adding the

commissions and other incomes to the interest net income), profit before tax

(intermediation margin minus commissions and other expenses) and net profit after

tax (profit before tax minus tax income) (Tables 1, 2).

LSþ OA ¼DSþ OLþ EQ

II� IE ¼NIþ CI ¼ IM� CE ¼ PBT� IT ¼ NPAT

2 All data refer to 2005.

94 E. Geretto, R. Pauluzzo

123

Tab

le1

Bal

ance

shee

t2

00

5—

(mil

lio

ns

of€)

Bal

ance

shee

t2

00

5A

BC

BO

CC

BC

ICB

CC

DB

BO

CO

MC

MB

CM

BC

SD

BT

ota

l

Lo

ans

(LS

)2

93

,39

92

26

,03

02

51

,37

93

36

,73

71

79

,82

47

9,7

00

48

,17

83

2,3

98

15

,71

51

,463

,360

Oth

eras

sets

(OA

)2

07

,73

92

72

,14

42

30

,13

03

41

,40

11

9,6

10

69

,64

82

8,9

83

26

,12

17

,63

71

,203

,413

To

tal

asse

ts(T

A)

50

1,1

38

49

8,1

74

48

1,5

10

67

8,1

39

19

9,4

35

14

9,3

48

77

,16

25

8,5

20

23

,35

22

,666

,773

Dep

osi

ts(D

S)

42

4,0

23

38

9,0

37

42

0,5

96

60

2,5

88

14

,37

41

28

,23

46

6,6

36

50

,16

52

1,1

98

2,1

16

,852

Oth

erli

abil

itie

s(O

L)

68,7

53

81,5

52

30,7

28

48,2

53

171,3

52

12,3

40

7,7

94

6,7

31

1,6

23

429,1

28

Tota

lli

abil

itie

s492,7

76

470,5

89

451,3

24

650,8

42

185,7

27

140,5

75

74,4

31

56,8

96

22,8

21

2,5

45,9

80

Ow

ner

’s/S

har

e-hold

ers’

equit

y(E

Q)

8,3

61

27,5

85

30,1

86

27,2

96

13,7

08

8,7

73

2,7

30

1,6

23

530

120,7

93

Tota

lli

abil

itie

san

deq

uit

y501,1

38

498,1

74

481,5

10

678,1

39

199,4

35

149,3

48

77,1

62

58,5

20

23,3

52

2,6

66,7

73

To

tal

mea

ns

the

tota

lo

fth

esa

mp

le,

no

tth

eto

tal

of

the

enti

resy

stem

The Chinese Banking System 95

123

Tab

le2

Inco

me

stat

emen

t2

00

5—

(mil

lio

ns

of€)

Inco

me

stat

emen

t2005

AB

CB

OC

CB

CIC

BC

CD

BB

OC

OM

CM

BC

MB

CS

DB

Tota

l

Inte

rest

inco

me

(II)

11

,04

21

7,5

77

18

,23

42

5,2

30

9,7

43

5,2

18

2,7

18

1,8

37

91

09

2,5

09

Inte

rest

expen

ses

(I.E

)-

6,4

49

-7

,03

1-

5,9

92

-9

,096

-5

,52

5-

1,9

00

-9

70

-8

21

-3

96

-3

8,1

80

Net

inte

rest

inco

me

(NI)

4,5

93

10

,54

61

2,2

42

16

,13

44

,218

3,3

18

1,7

48

1,0

15

51

45

4,3

29

Com

mis

sions

&oth

erin

com

es(C

I)3,9

92

1,8

12

1,3

62

2,0

85

229

420

300

662

68

10,9

30

Inte

rmed

iati

on

mar

gin

(IM

)8,5

85

12,3

58

13,6

04

18,2

19

4,4

47

3,7

38

2,0

48

1,6

78

582

65,2

59

Com

mis

sions

&oth

erex

pen

ses

(CE

)-

7,7

58

-6

,56

6-

7,7

89

-1

1,5

99

-9

92

-2

,389

-1

,369

-1

,232

-5

20

-4

0,2

14

Pro

fit

bef

ore

tax

(PB

T)

82

75

,79

15

,815

6,6

20

3,4

55

1,3

49

67

84

45

62

25

,04

5

Inco

me

tax

(IT

)-

71

7-

2,3

67

-8

68

-2

,626

-1

,06

2-

37

8-

28

4-

16

1-

30

-8

,493

Net

pro

fit

afte

rta

x(N

PA

T)

10

93

,42

34

,946

3,9

93

2.3

93

97

13

93

28

33

21

6,5

52

AB

CA

gri

cult

ura

lB

ank

of

Chin

a,B

OC

Ban

ko

fC

hin

a,C

BC

Co

nst

ruct

ion

Ban

ko

fC

hin

a,IC

BC

Ind

ust

rial

and

Com

mer

cial

Ban

ko

fC

hin

a,C

DB

Chin

aD

evel

op

men

t

Ban

k,

BO

CO

MB

ank

of

Com

mu

nic

atio

ns,

CM

CC

hin

aM

erch

ants

Ban

k,

CM

BC

Ch

ina

Min

shen

gB

ankin

gC

orp

ora

tio

n,

SD

BS

hen

zhen

Dev

elop

men

tB

ank

So

urc

eC

BR

C,

An

nu

alR

eport

20

06

–2

00

5;

Nat

ion

alB

ure

auo

fS

tati

stic

so

fth

eP

eople

’sR

epub

lic

of

Ch

ina.

Ow

nel

abora

tion

96 E. Geretto, R. Pauluzzo

123

We are therefore able to provide some economic performance indicators:

PBT=EQ ¼ NI=EQð Þ � IM=NIð Þ � PBT=IMð Þ ¼ Gð ÞROE

NPAT=EQ ¼ NI=EQð Þ � IM=NIð Þ � NPAT=IMð Þ ¼ Nð ÞROE

Splitting ROE into three parts makes it easier to understand changes in ROE. In

particular, Gross or Net ROE can be decomposed into interest net income divided

by owner’s/share-holders’ equity (NI/EQ), intermediation margin divided by

interest net income (IM/NI) and profit before tax or net profit after tax divided by

intermediation margin (PBT or NPAT/IM) (Tables 3, 4).

NI/EQ can be analyzed considering its relation with total assets (good proxy for

managed funds):

NI=EQ ¼ NI=TAð Þ � TA=EQð ÞThis allows us to examine, on the one hand, the return on assets (ROA) and, on

the other hand, the leverage of a specific bank.

Because of the central role played by the ratio NI/EQ in the ROE equation, we

would also like to suggest the following decomposition (Table 5):

NI=EQ ¼ II=LSð Þ � LS� DSð Þ=EQ½ �f g þ II=LSð Þ � IE=DSð Þ½ � � DS=EQð Þf gWe consider the determinants of the interest net income, represented by the

spread earned on the share of invested deposits (second addend), and the average

interest rate multiplied by the ratio between net monetary working capital (loans

minus deposits) and owner’s/share-holders’ equity (first addend).

The collected data show a gross return on equity [(G) ROE] of about 21% for the

entire panel in 2005: the burden of taxation is about 7% points [(N)

ROE = 13.70%]. In both cases, this is a significant performance level. The key

factor to the overall profitability is the interest net income: its ratio to the owner’s/

share-holders’ equity is 45%. The influence of commissions and other incomes is

only 20%: this is mainly due to the limited use of banking services by customers

and/or a low supply level by banks (Table 6). Finally, operational costs absorb more

than 60% of the intermediation margin: data show low levels of efficiency

(Tables 7, 8). As stated before, the overall profitability is strongly influenced by the

Table 3 Gross ROE

2005 NI/EQ * IM/NI * PBT/IM (G) ROE %

ABC 0.5493 * 1.8691 * 0.0963 0.0989 9.89

BOC 0.3823 * 1.1718 * 0.4687 0.2100 21.00

CBC 0.4056 * 1.1113 * 0.4274 0.1926 19.26

ICBC 0.5911 * 1.1292 * 0.3634 0.2425 24.25

CDB 0.3077 * 1.0543 * 0.7769 0.2520 25.20

BOCOM 0.3782 * 1.1266 * 0.3609 0.1538 15.38

CMB 0.6403 * 1.1716 * 0.3315 0.2487 24.87

CMBC 0.6260 * 1.6516 * 0.2658 0.2748 27.48

SDB 0.9680 * 1.1323 * 0.1065 0.1168 11.68

Total 0.4498 * 1.2012 * 0.3838 0.2073 20.73

The Chinese Banking System 97

123

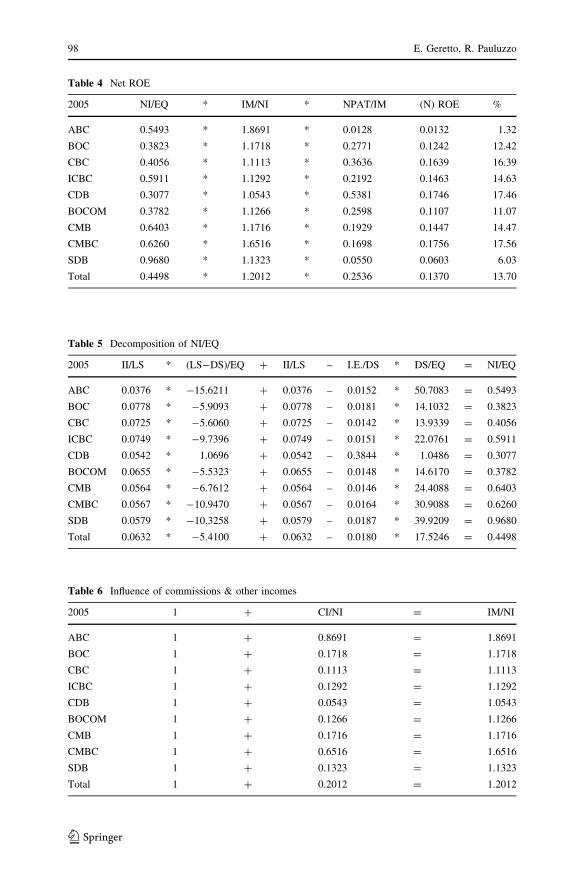

Table 5 Decomposition of NI/EQ

2005 II/LS * (LS-DS)/EQ ? II/LS – I.E./DS * DS/EQ = NI/EQ

ABC 0.0376 * -15.6211 ? 0.0376 – 0.0152 * 50.7083 = 0.5493

BOC 0.0778 * -5.9093 ? 0.0778 – 0.0181 * 14.1032 = 0.3823

CBC 0.0725 * -5.6060 ? 0.0725 – 0.0142 * 13.9339 = 0.4056

ICBC 0.0749 * -9.7396 ? 0.0749 – 0.0151 * 22.0761 = 0.5911

CDB 0.0542 * 1.0696 ? 0.0542 – 0.3844 * 1.0486 = 0.3077

BOCOM 0.0655 * -5.5323 ? 0.0655 – 0.0148 * 14.6170 = 0.3782

CMB 0.0564 * -6.7612 ? 0.0564 – 0.0146 * 24.4088 = 0.6403

CMBC 0.0567 * -10.9470 ? 0.0567 – 0.0164 * 30.9088 = 0.6260

SDB 0.0579 * -10.3258 ? 0.0579 – 0.0187 * 39.9209 = 0.9680

Total 0.0632 * -5.4100 ? 0.0632 – 0.0180 * 17.5246 = 0.4498

Table 6 Influence of commissions & other incomes

2005 1 ? CI/NI = IM/NI

ABC 1 ? 0.8691 = 1.8691

BOC 1 ? 0.1718 = 1.1718

CBC 1 ? 0.1113 = 1.1113

ICBC 1 ? 0.1292 = 1.1292

CDB 1 ? 0.0543 = 1.0543

BOCOM 1 ? 0.1266 = 1.1266

CMB 1 ? 0.1716 = 1.1716

CMBC 1 ? 0.6516 = 1.6516

SDB 1 ? 0.1323 = 1.1323

Total 1 ? 0.2012 = 1.2012

Table 4 Net ROE

2005 NI/EQ * IM/NI * NPAT/IM (N) ROE %

ABC 0.5493 * 1.8691 * 0.0128 0.0132 1.32

BOC 0.3823 * 1.1718 * 0.2771 0.1242 12.42

CBC 0.4056 * 1.1113 * 0.3636 0.1639 16.39

ICBC 0.5911 * 1.1292 * 0.2192 0.1463 14.63

CDB 0.3077 * 1.0543 * 0.5381 0.1746 17.46

BOCOM 0.3782 * 1.1266 * 0.2598 0.1107 11.07

CMB 0.6403 * 1.1716 * 0.1929 0.1447 14.47

CMBC 0.6260 * 1.6516 * 0.1698 0.1756 17.56

SDB 0.9680 * 1.1323 * 0.0550 0.0603 6.03

Total 0.4498 * 1.2012 * 0.2536 0.1370 13.70

98 E. Geretto, R. Pauluzzo

123

Table 7 Influence of commissions & other expenses

2005 1 – CE/IM = PBT/IM

ABC 1 – 0.9037 = 0.0963

BOC 1 – 0.5313 = 0.4687

CBC 1 – 0.5726 = 0.4274

ICBC 1 – 0.6366 = 0.3634

CDB 1 – 0.2231 = 0.7769

BOCOM 1 – 0.6391 = 0.3609

CMB 1 – 0.6685 = 0.3315

CMBC 1 – 0.7342 = 0.2658

SDB 1 – 0.8935 = 0.1065

Total 1 – 0.6162 = 0.3838

Table 8 Influence of commissions & other income and income tax

2005 1 – CE ? IT/IM = NPAT/IM

ABC 1 – 0.9872 = 0.0128

BOC 1 – 0.7229 = 0.2771

CBC 1 – 0.6364 = 0.3636

ICBC 1 – 0.7808 = 0.2192

CDB 1 – 0.4619 = 0.5381

BOCOM 1 – 0.7402 = 0.2598

CMB 1 – 0.8071 = 0.1929

CMBC 1 – 0.8302 = 0.1698

SDB 1 – 0.9450 = 0.0550

Total 1 – 0.7464 = 0.2536

Table 9 ROA and Leverage

2005 NI/TA * TA/EQ = NI/EQ

ABC 0.0092 * 59.9304 = 0.5493

BOC 0.0212 * 18.0596 = 0.3823

CBC 0.0254 * 15.9519 = 0.4056

ICBC 0.0238 * 24.8439 = 0.5911

CDB 0.0211 * 14.5487 = 0.3077

BOCOM 0.0222 * 17.0236 = 0.3782

CMB 0.0227 * 28.2641 = 0.6403

CMBC 0.0174 * 36.0561 = 0.6260

SDB 0.0220 * 43.9774 = 0.9680

Total 0.0204 * 22.0772 = 0.4498

The Chinese Banking System 99

123

Ta

ble

10

Bal

ance

shee

t2

00

6—

(mil

lio

ns

of€)

Bal

ance

shee

t2

00

6A

BC

BO

CC

BC

ICB

CC

DB

BO

CO

MC

MB

CM

BC

SD

BT

OT

AL

Lo

ans

(LS

)3

01

,80

22

27

,40

02

69

,20

53

43

,79

61

94

,09

28

8,5

57

53

,44

94

2,9

05

17

,04

81

,538

,25

4

Oth

eras

sets

21

8,0

73

29

0,6

58

25

7,8

65

38

6,6

78

31

,04

77

8,5

10

37

,41

62

5,2

37

8,3

01

1,3

33

,78

6

To

tal

asse

ts(T

A)

51

9,8

75

51

8,0

59

52

7,0

70

73

0,4

74

22

5,1

39

16

7,0

68

90

,86

56

8,1

42

25

,35

02

,872

,04

0

Dep

osi

ts(D

S)

46

0,1

85

39

8,4

15

45

6,5

34

61

7,8

85

15

,10

91

38

,17

47

5,2

73

56

,74

72

2,5

90

2,2

40

,91

2

Oth

erL

iabil

itie

s5

1,5

18

78

,99

73

8,4

61

66

,76

81

94

,64

22

0,0

63

10

,23

29

,517

2,1

30

47

2,3

28

To

tal

liab

ilit

ies

51

1,7

03

47

7,4

12

49

4,9

95

68

4,6

53

20

9,7

51

15

8,2

37

85

,50

56

6,2

64

24

,72

02

,713

,24

0

Ow

ner

’s/S

har

e-h

old

ers’

equ

ity

(EQ

)8

,172

40

,64

63

2,0

75

45

,82

01

5,3

88

8,8

30

5,3

60

1,8

78

63

01

58

,80

0

To

tal

liab

ilit

ies

and

equ

ity

51

9,8

75

51

8,0

59

52

7,0

70

73

0,4

74

22

5,1

39

16

7,0

68

90

,86

56

8,1

42

25

,35

02

,872

,04

0

100 E. Geretto, R. Pauluzzo

123

Ta

ble

11

Inco

me

stat

emen

t2

00

6—

(mil

lio

ns

of€)

Inco

me

stat

emen

t2

00

6A

BC

BO

CC

BC

ICB

CC

DB

BO

CO

MC

MB

CM

BC

SD

BT

ota

l

Inte

rest

inco

me

(II)

14

,68

12

0,8

84

20

,93

42

6,5

53

11

,29

66

,279

3,3

07

2,6

62

1,1

24

10

7,7

20

Inte

rest

expen

ses

(I.E

)-

7,6

70

-9

,14

1-

7,2

79

-1

0,6

84

-6

,143

-2

,407

-1

,214

-1

,089

-4

93

-4

6,1

20

Net

inte

rest

inco

mb

e(N

I)7

,01

01

1,7

43

13

,65

51

5,8

69

5,1

53

3,8

72

2,0

92

1,5

73

63

16

1,6

00

Co

mm

issi

on

s&

oth

erin

com

es(C

I)4

,49

72

,11

51

,623

2,0

16

48

94

57

37

31

46

87

11

,80

3

Inte

rmed

iati

on

mar

gin

(IM

)1

1,5

08

13

,85

81

5,2

78

17

,88

55

,642

4,3

29

2,4

66

1,7

19

71

87

3,4

03

Com

mis

sions

&oth

erex

pen

ses

(CE

)-

10

,32

1-

7,3

39

-8

,885

-1

0,8

73

-1

,727

-2

,636

-1

,484

-1

,201

-5

24

-4

4,9

90

Pro

fit

bef

ore

tax

(PB

T)

1,1

86

6,5

19

6,3

93

7,0

11

3,9

15

1,6

93

98

15

18

19

42

8,4

13

Inco

me

tax

(IT

)-

62

1-

1,9

32

-1

,887

-2

,15

8-

1,2

25

-5

00

-3

20

-1

45

-6

7-

8,8

55

Net

pro

fit

afte

rta

x(N

P)

56

54

,58

74

,506

4,8

52

2,6

90

1,1

94

66

13

73

12

71

9,5

58

AB

CA

gri

cult

ura

lB

ank

of

Ch

ina,

BO

CB

ank

of

Ch

ina,

CB

CC

on

stru

ctio

nB

ank

of

Ch

ina,

ICB

CIn

du

stri

alan

dC

om

mer

cial

Ban

ko

fC

hin

a,C

DB

Ch

ina

Dev

elo

pm

ent

Ban

k,

BO

CO

MB

ank

of

Com

munic

atio

ns,

CM

CC

hin

aM

erch

ants

Ban

k,

CM

BC

Ch

ina

Min

shen

gB

ank

ing

Co

rpo

rati

on

,S

DB

Sh

enzh

enD

evel

op

men

tB

ank

So

urc

eC

BR

C,

An

nu

alR

eport

20

06

–2

00

5;

Nat

ion

alB

ure

auo

fS

tati

stic

so

fth

eP

eop

le’s

Rep

ub

lic

of

Ch

ina.

Ow

nel

abora

tio

n

The Chinese Banking System 101

123

Table 13 Net ROE

2006 NI/EQ * IM/NI * NPAT/IM (N) ROE %

ABC 0.8579 * 1.6414 * 0.0492 0.0693 6.93

BOC 0.2889 * 1.1801 * 0.3310 0.1129 11.29

CBC 0.4257 * 1.1189 * 0.2949 0.1405 14.05

ICBC 0.3463 * 1.1270 * 0.2714 0.1059 10.59

CDB 0.3349 * 1.0949 * 0.4768 0.1748 17.48

BOCOM 0.4385 * 1.1180 * 0.2756 0.1351 13.51

CMB 0.3905 * 1.1782 * 0.2685 0.1235 12.35

CMBC 0.8376 * 1.0928 * 0.2170 0.1986 19.86

SDB 1.0016 * 1.1379 * 0.1769 0.2016 20.16

Total 0.3879 * 1.1916 * 0.2664 0.1232 12.32

Table 14 ROA and Leverage

2006 NI/TA * TA/EQ = NI/EQ

ABC 0.0135 * 63.6166 = 0.8579

BOC 0.0227 * 12.7456 = 0.2889

CBC 0.0259 * 16.4324 = 0.4257

ICBC 0.0217 * 15.9419 = 0.3463

CDB 0.0229 * 14.6308 = 0.3349

BOCOM 0.0232 * 18.9204 = 0.4385

CMB 0.0230 * 16.9524 = 0.3905

CMBC 0.0231 * 36.2843 = 0.8376

SDB 0.0249 * 40.2381 = 1.0016

Total 0.0214 * 18.0859 = 0.3879

Table 12 Gross ROE

2006 NI/EQ * IM/NI * PBT/IM (G) ROE %

ABC 0.8579 * 1.6414 * 0.1031 0.1453 14.53

BOC 0.2889 * 1.1801 * 0.4704 0.1604 16.04

CBC 0.4257 * 1.1189 * 0.4184 0.1993 19.93

ICBC 0.3463 * 1.1270 * 0.3921 0.1530 15.30

CDB 0.3349 * 1.0949 * 0.6939 0.2544 25.44

BOCOM 0.4385 * 1.1180 * 0.3911 0.1917 19.17

CMB 0.3905 * 1.1782 * 0.3982 0.1832 18.32

CMBC 0.8376 * 1.0928 * 0.3013 0.2758 27.58

SDB 1.0016 * 1.1379 * 0.2702 0.3079 30.79

Total 0.3879 * 1.1916 * 0.3871 0.1789 17.89

102 E. Geretto, R. Pauluzzo

123

Table 15 Influence of commissions & other income

2006 1 ? CI/NI = IM/NI

ABC 1 ? 0.6414 = 1.6414

BOC 1 ? 0.1801 = 1.1801

CBC 1 ? 0.1189 = 1.1189

ICBC 1 ? 0.1270 = 1.1270

CDB 1 ? 0.0949 = 1.0949

BOCOM 1 ? 0.1180 = 1.1180

CMB 1 ? 0.1782 = 1.1782

CMBC 1 ? 0.0928 = 1.0928

SDB 1 ? 0.1379 = 1.1379

Total 1 ? 0.1916 = 1.1916

Table 16 Influence of commissions & other expenses

2006 1 – CE/IM = PBT/IM

ABC 1 – 0.8969 = 0.1031

BOC 1 – 0.5296 = 0.4704

CBC 1 – 0.5816 = 0.4184

ICBC 1 – 0.6079 = 0.3921

CDB 1 – 0.3061 = 0.6939

BOCOM 1 – 0.6089 = 0.3911

CMB 1 – 0.6018 = 0.3982

CMBC 1 – 0.6987 = 0.3013

SDB 1 – 0.7298 = 0.2702

Total 1 – 0.6129 = 0.3871

Table 17 Influence of commissions & other income and income tax

2006 1 – CE ? IT/IM = NPAT/IM

ABC 1 – 0.9508 = 0.0492

BOC 1 – 0.6690 = 0.3310

CBC 1 – 0.7051 = 0.2949

ICBC 1 – 0.7286 = 0.2714

CDB 1 – 0.5232 = 0.4768

BOCOM 1 – 0.7244 = 0.2756

CMB 1 – 0.7315 = 0.2685

CMBC 1 – 0.7830 = 0.2170

SDB 1 – 0.8231 = 0.1769

Total 1 – 0.7336 = 0.2664

The Chinese Banking System 103

123

Table 18 Decomposition of NI/EQ

2006 II/LS * (LS-DS)/EQ ? II/LS – I.E./DS * DS/EQ = NI/EQ

ABC 0.0486 * -19.3812 ? 0.0486 – 0.0167 * 56.3124 = 0.8579

BOC 0.0918 * -4.2074 ? 0.0918 – 0.0229 * 9.8021 = 0.2889

CBC 0.0778 * -5.8403 ? 0.0778 – 0.0159 * 14.2333 = 0.4257

ICBC 0.0772 * -5.9817 ? 0.0772 – 0.0173 * 13.4848 = 0.3463

CDB 0.0582 * 11.6313 ? 0.0582 – 0.4066 * 0.9819 = 0.3349

BOCOM 0.0709 * -5.6191 ? 0.0709 – 0.0174 * 15.6482 = 0.4385

CMB 0.0619 * -4.0716 ? 0.0619 – 0.0161 * 14.0435 = 0.3905

CMBC 0.0620 * -7.3706 ? 0.0620 – 0.0192 * 30.2167 = 0.8376

SDB 0.0659 * -8.7968 ? 0.0659 – 0.0218 * 35.8571 = 1.0016

Total 0.0700 * -4.4248 ? 0.0700 – 0.0206 * 14.1115 = 0.3879

Table 19 NPLs of commercial banks (millions of €)

Banks I Quarter 2006 II Quarter 2006 III Quarter 2006 IV Quarter 2006

NPLs % NPLs % NPLs % NPLs %

SOCBs 109,113.52 9.78 103,864.61 9.47 105,511.32 9.31 102,486.67 9.22

JSCBs 15,253.76 3.92 12,014.04 3.09 11,677.29 2.91 11,363.63 2.81

Major commercial banks 124,367.28 8.26 115,878.66 7.80 117,188.60 7.64 113,850.29 7.51

City comm. Banks 8,877.93 7.59 8,316.96 6.72 8,067.67 6.07 6,369.12 4.78

Rural commercial banks 1,629.25 6.96 1,637.03 6.64 1,667.90 6.58 1,494.27 5.90

Foreign banks 378.20 0.95 360.07 0.87 354.77 0.81 368.70 0.78

Total 135,252.66 8.03 126,192.71 7.53 127,278.94 7.33 122,082.38 7.09

Next to the values there is the percentage proportion of NPLs of the total loans

Source China Banking Regulatory Commission. Own elaboration

Table 20 Type of NPLs (millions of €)

NPLs classification I Quarter 2006 II Quarter 2006 III Quarter 2006 IV Quarter 2006

NPLs % NPLs % NPLs % NPLs %

Substandard 33,815.48 2.01 30,169.89 1.80 29,213.71 1.68 26,019.31 1.51

Doubtful 51,887.71 3.08 49,572.19 2.96 50,954.35 2.93 50,483.07 2.93

Loss 49,549.46 2.94 46,450.63 2.77 47,110.89 2.71 45,580.00 2.65

Total 135,252.66 8.03 126,192.71 7.53 127,278.94 7.33 122,082.38 7.09

Next to the values there is the percentage proportion of NPLs of the total loans. The loans classification

has five levels: Pass, Special Mention, Substandard, Doubtful, and Loss. The last three categories are

considered NPLs. Cf. C.R.B�C., Statistics, 2007

Source China Banking Regulatory Commission. Own elaboration

104 E. Geretto, R. Pauluzzo

123

interest net income: its decomposition (Table 9) shows the ROA (about 2%)

multiplied by a leverage effect (TA/EQ) equal to 22%. The NI/EQ ratio is positively

influenced by a spread between positive and negative average rates (4.5%), but is

negatively affected by the net monetary working capital.

Net profit after tax in 2006 is lower than the previous year (gross ROE decreases

from 21% to about 17.9%), mainly because of the fall of net interest income, as the

influence of commissions and other incomes and the influence of commissions and

other expenses still remains almost unchanged. As for the NI/EQ ratio, with ROA

remaining equal there is a reduction of the leverage effect; the spread increases (5%

points) and the DS/EQ ratio drops to 14% (Tables 10, 11, 12, 13, 14, 15, 16, 17, 18).

Non-Performing Loans Management

The practice widely followed by several Chinese banks to provide credit on the

basis of patronage favours, rather than actual risk–performance principles, has led to

a high level of outstanding credits (Mallory, 1931; Tam On-Kit, 1992; Tsai, 2000).

The stock of bad loans registered by the Chinese banking system reached RMB

2,400 billion3 at the end of 2003, more than 25% of fund uses. Although this data

reached 7.09% at the end of 2006, it is estimated that more than 60% of this

reduction is due to write-offs related to the transfer of bad loans to asset-

management companies (Gotti Tedeschi 2007) (Tables 19, 20).

Four management companies (AMCs—Asset Management Companies) were

established in 19994 (Chiarlone and Amighini 2007; Malle 2007) to support the

Table 21 NPLs recovered by AMCs (31.12.2005, millions of €)

Data Huarong Great China Orient Cinda Total

Accumulated disposal 25,564.15 27,665.96 13,839.81 21,134.70 88,204.61

Cash recovered 5,713.02 2,872.79 3,362.27 6,600.59 18,548.66

Disposal ratio (%) 69.17 77.88 52.08 63.82 66.74

Asset recovery ratio (%) 26.92 12.90 28.73 34.30 24.58

Cash recovery ratio (%) 22.35 10.39 24.30 31.23 21.03

Accumulated disposal = accumulated amount of cash and non-cash assets recovered as well as loss

incurred by the end of the reporting period, Cash recovered = amount of cash assets recovered, Disposal

ratio = Accumulated disposal/Total NPLs purchased, Asset recovery ration = total assets recovered/

accumulated disposal, Cash recovery ratio = cash recovered/accumulated disposal

Source China Banking Regulatory Commission. Own elaboration

3 Equivalent to about € 229,6 billion (exchange rate: 31.12.2003).4 Cinda for China Construction Bank; Huarong for Industrial and Commercial Bank of China; Orient for

Bank of China and Great Wall and for the Agricultural Bank of China. The AMCs have been subject to a

considerable reform process. In February 2004, the State Council approved a proposal by the Minister of

Finance, according to which the AMCs should be transformed into genuine commercial companies after

2006, the deadline to complete the transfer of debts from the big four. This should ensure that

management companies will be able to use the equity capital in order to purchase non-performing assets

on the basis of commercial criteria: it is widely believed that the reform will lead to the restructuring of

debtor companies in order to attract strategic investors, both domestic and foreign.

The Chinese Banking System 105

123

activity of the Big four. One-hundred and thirty-five billion euros of bad loans (14% of

the GDP of the country) were transferred: however, more than half of NPLs remained

in banks’ portfolios, since only those originated before 1996 were transferred. At the

end of 2005, the AMCs found that 88 billion euros could be recovered,*65% of total

NPLs acquired; nevertheless the cash recovery ratio is still low (21.03%), that is about

18 billion euros. AMCs have different performance levels (Table 21) due to the

different type of their loans. If Great Wall, on the one hand, has acquired low quality

loans from the Agricultural Bank of China, a traditional source of funding for many

rural enterprises, Cinda, on the other hand, has acquired its portfolio from China

Construction Bank, involved in supporting construction projects and urban housing

development (Xu 2005). After a difficult start-up phase, Chinese banks are beginning

to obtain interesting results in doubtful loans management (Xu 2005). In particular,

significant results were achieved by market auctions of bad loans in 2004. The main

buyers of these auctions were the AMCs, often in joint-venture with some of the most

important international financial institutions, such as Morgan Stanley, Goldman

Sachs and Deutsche Bank. Direct sales of NPLs to investors, generally have the form

of individual assets sales, or bulk sales, including negotiated sales and auctions. The

main advantage of these transactions is the immediate liquidity available, often at the

expense of lower recovery values (Table 22).

In order to improve the quality of loan portfolios, China started the first

securitization transactions in 2005. In particular, the Chinese government developed

a regulatory framework, allowing a quick development of the internal market for

asset-backed securities. In order to enter the market, the Big four have received

several aids, mainly in the form of recapitalization, while other banks have been

subject to particular capital-asset constraints (Gyntelberg and Remolona 2006).

These differences explain the interest of the Chinese government in supporting the

main banks of the system, preserving their management and solvency levels, even at

the expense of a fair competition.

Further legislative improvements would be desirable to increase the number of

investors interested in the securitization market. Until a few years ago, Chinese

insurance companies and mutual funds were not allowed to access the asset-backed

securities market, dominated by commercial banks and non-financial private

operators (Gyntelberg and Remolona 2006).

Internationalization of the Banking System

In spite of the negative aspects considered, there are still positive circumstances

that make the Chinese banking market particularly attractive to foreign operators.

The fast growing economy, that should lead to a gradual reduction of bad loans,

government support to a coherent development of the system, as well as high

savings rates5 (IMF 2005), high levels of foreign exchange reserves and a strong

5 Chinese population savings rate, equal to about 25% of disposable income, remains high, despite a low

real interest rate on bank deposits. The high level of savings reflects the demographic development of the

country, with the gradual ageing of the population, the uncertainty regarding the pension benefits, health

care and education, and limited access to credit by individuals for purchasing durable goods and housing.

106 E. Geretto, R. Pauluzzo

123

Tab

le2

2D

irec

tN

PL

ssa

les

tofo

reig

nin

ves

tors

AM

C/B

ank

Yea

rB

oo

kv

alu

eS

ale

val

ue

Sal

ety

pe

Inv

esto

rs

Cin

da

2001

145

mm

.$–1.2

bn.

RM

BN

egoti

ated

Chen

ery

asso

ciat

es

Ori

ent

2001

217

mm

.$–1.8

bn.

RM

B2

1m

m.

$N

egoti

ated

Chen

ery

Ass

oci

ates

Ori

ent

2002

210

mm

.$–1.7

bn.

RM

BN

egoti

ated

Chen

ery

Ass

oci

ates

Hu

aro

ng

20

02

1.3

bn

.$

–1

0.8

bn

.R

MB

87

7.5

mm

.R

MB

Op

enau

ctio

nC

on

sort

ium

led

by

Mo

rgan

Sta

nle

y

Hu

aro

ng

20

02

24

0m

m.

£–

1.9

7b

n.

RM

B1

97

mm

.R

MB

Op

enau

ctio

nG

old

man

Sac

hs

BoC

(Cay

man

)2

00

31

.8b

n.

$–

14.9

bn

.R

MB

Op

enau

ctio

nC

itig

roup

Hu

aro

ng

20

04

2.2

bn

.$

–1

8.4

bn

.R

MB

Op

enau

ctio

nM

org

anS

tan

ley,

Cit

igro

up

,U

BS

,

Go

ldm

anS

ach

s,JP

Mo

rgan

,

Leh

man

,A

oY

iE

r(d

om

esti

c)

CC

B2

00

45

13

mm

.$

–4

.2b

n.

RM

B1

78

mm

.$

–1

.5b

n.

RM

BO

pen

auct

ion

Mo

rgan

Sta

nle

y,

Deu

tsch

eB

ank

To

tal

clo

sed

6.6

bn

.$

CC

B2

00

35

24

mm

.$

–4

.3b

n.

RM

BC

lose

dau

ctio

nM

org

anS

tan

ley

Hu

aro

ng

20

04

21

5m

m.

$–

1.8

bn

.R

MB

Clo

sed

auct

ion

Mo

rgan

Sta

nle

y,

GE

Gre

atW

all

20

04

28

1m

m.

$–

2.3

bn

.R

MB

Neg

oti

ated

Cit

igro

up

Gre

atW

all

20

04

1b

n.

$–

8.3

bn

.R

MB

Go

ldm

anS

ach

s

Gre

atW

all

20

04

Ab

ou

t1

40

mm

.$

Ab

ou

t1

4–

15

mm

.$

Au

ctio

n1

do

mes

tic

and

1in

tern

atio

nal

bu

yer

Ori

ent

20

04

29

0m

m.

$–

2.4

bn

.R

MB

Op

enau

ctio

nC

SF

SB

Cin

da

20

04

29

.7m

m.

$–

24

6m

m.

RM

B1

0.2

mm

.$

–8

5.1

bn

.R

MB

Op

enau

ctio

n1

do

mes

tic

and

1in

tern

atio

nal

bu

yer

To

tal

clo

sed/s

ign

ed2

.5b

n.

$

So

urc

eM

inX

u,

Res

olu

tio

no

fN

on

-Per

form

ing

Lo

ans

inC

hin

a,o

p.

cit.

,p

.4

0

The Chinese Banking System 107

123

net credit position, represent fundamental internal shock absorbers and attract the

investments of large international groups (Meng 1943; D’Agnolo 2001; Aiqun

et al. 2005). In 2003, in the Chinese banking system there were 191 branches of

foreign banks, 2 mixed capital companies, 11 mixed capital fund management

companies and 67 branches of foreign insurance companies. Since then, the

government has aimed at improving the openness of the financial sector to

international operators.6 In order to honour the WTO commitments, the State

Council, the highest administrative authority of the People’s Republic of China,

promulgated the Regulations of the People’s Republic of China on Administration

of Foreign-funded Banks at the end of 2006. These Regulations are formulated for

the purpose of meeting the needs of internationalization and economic develop-

ment of the Chinese system, strengthening and improving supervision and

regulation over foreign-funded banks,7 and promoting safe and sound operations of

the banking industry. In order to establish a wholly foreign-funded bank or a

Chinese-foreign joint venture bank, the minimum registered capital shall be RMB

1 billion8 or an equivalent amount in convertible currencies. When a wholly

foreign-funded bank or a Chinese-foreign joint venture bank establishes a branch

within the territory of the People’s Republic of China, the branch shall receive

from its parent bank a non-callable allocation of not less than RMB 100 million9 or

an equivalent amount in convertible currencies of operating capital. Conversely, a

branch of a foreign bank shall receive from its parent bank a non-callable

allocation of not less than RMB 200 million10 or an equivalent amount in

convertible currencies of operating capital.

When the regulations became effective, foreign banks that met specific prudential

requirements were able to operate in Chinese currency, both in the retail and in the

wholesale market, without any territorial or customer restriction, whereas such

institutions were previously able to operate only in the main cities. However, some

restrictions still persist for the branches of foreign banks: a branch of a foreign bank

6 The pilot project to transform the Bank of China and China Construction Bank into joint-stock

companies is being carried out with the aim of creating modern commercial banks, with share capital, and

internationally competitive. The recapitalization of the three major Chinese banks began in 2003, with a

capital contribution by the People’s Bank of China, amounting to 22.5 billion dollars in the Bank of China

and in the China Construction Bank. The same recapitalization continued in April 2005, with the

contribution of 15 billion dollars to the Industrial and Commercial Bank of China.7 The term foreign-funded banks in these regulations means:

• Wholly foreign-funded bank, funded solely by a foreign bank or jointly with any other foreign

financial institution;

• Chinese-foreign joint venture bank, jointly funded by a foreign financial institution with a Chinese

company or enterprise;

• Branch of a foreign bank;

• Representative office of a foreign bank.

In these Regulations, Wholly foreign-owned banks, Chinese-foreign joint venture banks and the

Branches of a foreign bank are collectively referred to Operational foreign banking entities.8 Equivalent to about € 96.7 million (exchange rate: 01.08.2007).9 Equivalent to about € 9.7 million (exchange rate: 01.08.2007).10 Equivalent to about € 19.3 million (exchange rate: 01.08.2007). The State Council, for prudential

purposes, can raise the above minimum capital requirements.

108 E. Geretto, R. Pauluzzo

123

Ta

ble

23

Op

enin

g-u

pst

ages

of

the

Chin

ese

ban

kin

gsy

stem

toin

tern

atio

nal

com

pet

itio

n:

19

80–

20

06

Sta

ges

Yea

rE

ven

ts

Fir

stst

age

19

80

Jap

anIm

port

and

Ex

port

Ban

kse

tu

pth

efi

rst

fore

ign

ban

kre

pre

sen

tati

ve

offi

cein

Bei

jin

g.

1981

Nan

yan

gC

om

mer

cial

Ban

kse

tup

abra

nch

inS

hen

zhen

asth

efi

rst

oper

atio

nal

fore

ign-

fun

ded

ban

ksi

nce

the

ado

pti

on

of

op

enin

gu

pan

dre

form

po

lice

.

1983

The

Reg

ula

tions

for

the

Est

abli

shm

ent

of

Rep

rese

nta

tive

Offi

ces

inC

hin

aby

Over

seas

Chin

ese

and

Fore

ign

Fin

anci

alIn

stit

uti

ons

wer

epro

mulg

ated

.

19

85

Th

eR

egula

tio

ns

on

the

Ad

min

istr

atio

no

fF

ore

ign

Ban

ks

and

Chin

ese-

fore

ign

Join

t-ven

ture

Ban

ks

inS

pec

ial

Eco

nom

icZ

on

eso

fth

eP

eople

’sR

epub

lic

of

Chin

aw

ere

pro

mu

lgat

ed,

allo

win

gfo

reig

nb

ank

sto

set

up

op

erat

ion

alb

ran

ches

inS

hen

zhen

,Z

hu

hai

,X

iam

en,

Sh

anto

uan

dH

ain

an.

1990

The

Reg

ula

tions

on

the

Adm

inis

trat

ion

of

Fore

ign

Fin

anci

alIn

stit

uti

ons

and

Chin

ese-

fore

ign

Join

t-v

entu

reF

inan

cial

Inst

itu

tio

ns

inS

han

gh

aiw

ere

pro

mu

lgat

ed.

Sec

ond

stag

e1

99

4T

he

Reg

ula

tio

ns

of

the

Peo

ple

’sR

epub

lic

of

Ch

ina

on

the

Ad

min

istr

atio

no

fF

ore

ign

Fin

anci

alIn

stit

uti

on

sw

ere

pro

mu

lgat

edas

the

firs

tre

gu

lati

on

sst

andar

diz

ing

fore

ign

ban

ks

beh

avio

rin

Ch

ina,

incl

ud

ing

mar

ket

acce

ssre

qu

irem

ents

and

sup

erv

iso

ryst

andar

ds

for

fore

ign

ban

ks

op

erat

ing

inC

hin

a.

1996

The

Pro

vis

ional

Reg

ula

tions

for

Fore

ign

Fin

anci

alIn

stit

uti

ons

toU

nder

take

RM

BB

usi

nes

s

on

AT

rial

Bas

isin

Sh

ang

hai

Pu

do

ng

Are

aw

ere

pro

mu

lgat

ed,

allo

win

gfo

reig

nb

ank

sto

un

der

tak

eR

MB

bu

sin

ess

tofo

reig

nen

terp

rise

san

dre

sid

ents

on

atr

ial

bas

isin

Sh

ang

hai

Pu

do

ng

area

.

19

98

Th

eC

ircu

lar

of

Issu

esC

on

cern

ing

the

Ap

pro

val

toF

ore

ign

Ban

ks

toE

ng

age

inth

eIn

ter-

ban

k

Borr

ow

ing

inC

hin

aw

asis

sued

,al

low

ing

fore

ign

ban

ks

acce

ssto

dom

esti

cin

ter-

ban

k

off

erin

gm

arket

,an

dto

engag

ein

RM

Bin

ter-

ban

ktr

adin

gan

dca

shtr

ansa

ctio

n.

19

98

Sh

enzh

enw

asap

pro

ved

tob

ea

seco

nd

tria

lci

tyw

her

efo

reig

nb

ank

sco

uld

star

tR

MB

bu

sin

ess.

19

99

Th

eC

ircu

lar

abo

ut

Ex

pan

din

gF

ore

ign

Ban

ks’

RM

BB

usi

nes

sS

cope

inS

han

gh

aian

d

Sh

enzh

enw

asis

sued

,re

lax

ing

the

geo

gra

ph

ical

and

vo

lum

ere

stri

ctio

ns

of

RM

Bb

usi

nes

s

for

fore

ign

ban

ks,

and

allo

win

gth

emto

bo

rro

wR

MB

cap

ital

from

oth

erb

ank

sw

ith

the

mat

uri

tyo

fm

ore

than

1y

ear.

The Chinese Banking System 109

123

Ta

ble

23

con

tin

ued

Sta

ges

Yea

rE

ven

ts

Th

ird

Sta

ge

20

01

Ch

ina

join

edth

eW

TO

.T

he

geo

gra

phic

alan

dcu

sto

mer

rest

rict

ion

so

nfo

reig

ncu

rren

cyfo

r

fore

ign

ban

ks

wer

ere

mo

ved

.F

ore

ign

ban

ks

wer

eal

low

edto

un

der

tak

efo

reig

ncu

rren

cy

busi

nes

sto

Chin

ese

ente

rpri

ses

and

resi

den

ts,

and

tounder

take

RM

Bbusi

nes

sin

Shan

ghai

,

Sh

enzh

en,

Tia

nji

n,

and

Dal

ian

.

20

01

Th

eR

egu

lati

on

so

fth

eP

eop

le’s

Rep

ub

lic

of

Ch

ina

on

the

Ad

min

istr

atio

no

fF

ore

ign

Fin

anci

alIn

stit

uti

ons

(Am

ended

)w

ere

publi

cize

d.

20

02

Th

eR

ule

sfo

rIm

ple

men

tin

gth

eR

egu

lati

on

so

fth

eP

eop

le’s

Rep

ub

lic

of

Ch

ina

on

the

Adm

inis

trat

ion

of

Fore

ign

Fin

anci

alIn

stit

uti

ons

(Am

ended

)w

ere

publi

cize

d.

20

02

RM

Bb

usi

nes

sw

aso

pen

edto

fore

ign

ban

ks

infi

ve

citi

esi.

e.G

uan

gzh

ou

,Q

ing

dao

,Z

hu

hai

,

Nan

jin

gan

dW

uh

an.

20

03

RM

Bb

usi

nes

sw

aso

pen

edto

fore

ign

ban

ks

info

ur

citi

esi.

e.Ji

nan

,F

uzh

ou

,C

hen

gd

uan

d

Cho

ng

qin

g.

Fo

reig

nb

ank

sw

ere

per

mit

ted

tou

nd

erta

ke

corp

ora

teR

MB

bu

sin

ess

inal

lth

e

citi

esw

her

eR

MB

bu

sin

ess

was

op

ened

tofo

reig

nco

mp

etit

ion

.

2003

The

Reg

ula

tions

on

Equit

yIn

ves

tmen

tof

Fore

ign

Fin

anci

alIn

stit

uti

ons

inC

hin

ese

Fin

anci

al

Intu

itio

ns

wer

ep

rom

ulg

ated

,st

ipu

lati

ng

the

qu

alifi

cati

on

so

fth

ein

ves

tors

and

the

pro

port

ion

of

shar

esth

eyco

uld

hold

inth

eC

hin

ese

ban

ks.

20

04

RM

Bb

usi

nes

sw

aso

pen

edto

fore

ign

ban

ks

infi

ve

citi

esi.

e.K

un

min

g,

Bei

jin

g,

Xia

men

,

Sh

eny

ang

and

Xi’

an.

20

05

RM

Bb

usi

nes

sw

aso

pen

edto

fore

ign

ban

ks

inse

ven

citi

esi.

e.S

han

tou

,N

ing

bo

,H

arbin

,

Chan

gch

un

,L

anzh

ou

,Y

inch

uan

,an

dN

ann

ing

.

2006

The

Reg

ula

tions

of

the

Peo

ple

’sR

epubli

cof

Chin

aon

Adm

inis

trat

ion

of

Fore

ign-f

unded

Ban

ks

and

its

imp

lem

enti

ng

rule

sw

ere

mad

ep

ub

lic.

20

06

Th

eg

eog

rap

hic

alan

dcu

stom

erre

stri

ctio

ns

of

RM

Bb

usi

nes

so

nfo

reig

nb

ank

sw

ere

rem

oved

,

thus

allo

win

gfo

reig

nb

ank

sto

off

erR

MB

bu

sin

ess

toal

lk

ind

so

fcu

stom

ers.

Th

en

on

-

pru

den

tial

rest

rict

ion

so

nfo

reig

nb

ank

s’o

per

atio

ns

inC

hin

aw

ere

also

rem

ov

ed.

So

urc

eC

hin

aB

ankin

gR

egula

tory

Co

mm

issi

on

,R

eport

on

the

Op

enin

g-u

po

fth

eC

hin

ese

Ban

kin

gS

ecto

r,h

ttp

://w

ww

.cb

rc.g

ov.c

n,

25

Jan

uar

y2

00

7

110 E. Geretto, R. Pauluzzo

123

may receive a time deposit of not less than RMB 1 million11 from a Chinese citizen

within the territory of China; they are also not allowed to distribute credit cards to

private operators. Foreign financial institutions, interested in operating in local

currency, will be able to have at least three years’ working experience in the

territory of the PBOC and should have achieved positive results for at least two

consecutive years prior to the application. The limit, according to which the total

amount of foreign exchange deposits taken within the Chinese territory by a foreign-

funded financial institution shall not exceed 70% of its total foreign exchange assets

within the Chinese territory, has been abolished. This restriction has been replaced

with the requirement that the total domestic assets of a foreign bank branch shall not

be less than its total domestic liabilities. Several measures were also introduced in

order to increase the supervision and inspection powers of government credit

authorities. In this regard, there are specific provisions regarding internal control

systems, corporate disclosure, corporate governance, and anti-money laundering

rules. Therefore, foreign-funded banks are considered comparable to Chinese

commercial banks (Standing Committee of the Tenth National People’s Congress

2003): the main differences lie in the authorization mechanisms and in their feasible

activities (Table 23).

The number of products managed by foreign banks were more than 100 at the

beginning of 2007; 115 foreign-funded banks have already gained the permission to

provide RMB services. These banks owned € 78.45 billion in assets, accounting for

1.8% of the total Chinese banking assets. In particular, foreign-funded banks

managed (values expressed in euros):

• € 51.33 billion in foreign currency assets and € 27.12 billion in local currency

assets;

• € 13.51 billion in foreign currency deposits and € 16.6 billion in local currency

deposits;

• € 27.26 billion in foreign currency loans and € 19.48 billion in local currency

loans (CBRC 2007a–d).

Thanks to the new market conditions, several foreign banks have expressed their

interest in acquiring stakes in some Chinese institutions (Tebbutt et al. 2007). The

Hang Seng Bank of Hong Kong has acquired 12% of Industrial Bank of Fujian,

Citigroup has acquired 4.2% of Shanghai Pudong Development Bank and 20% of

Guangdong Development Bank, HSBC has acquired 19.9% of Bank of Commu-

nications and 8% of Bank of Shanghai. Relevant development opportunities have

Newbridge Capital, with 17.9% of Shenzhen Development Bank. Shenzhen

Development Bank has already placed on the market 72.4% of its shares and

Newbridge has become the first foreign investor to control a Chinese bank. Temasek

has also acquired stakes in the Bank of China (4.1%), China Construction Bank

(6%) and China Minsheng Banking Corp. (3.9%): this is a private bank considered a

model for the Chinese banking sector, with low outstanding levels and international

corporate governance standards (Ping 1999; Tomba 2005). Additional holdings are

those acquired by Goldman Sachs, Allianz Capital and American Express in the

11 Equivalent to about € 96,700 (exchange rate: 01.08.2007).

The Chinese Banking System 111

123

Industrial & Commercial Bank of China (7.4%), by Royal Bank of Scotland (8.3%)

and UBS (1.3%) in the Bank of China, by Bank of America (8.5%) in China

Construction Bank, by Deutsche Bank in Hua Xia Bank (7%), by ING in the Bank

of Beijing (19.9%), by Banco Bilbao Vizcaya Argenta in China CITIC Bank (4.8%)

and by the Australia & New Zealand Banking Group, the Commonwealth Bank of

Australia, the Bank of Nova Scotia and BNP in several City Commercial Banks

(Tebbutt et al. 2007). The Chinese government has also encouraged the establish-

ment of foreign-funded banks and joint-ventures, and supported institutional

investors’ operations on stock markets (CSRC 2007). Over the last 3 years, the

number of operators with a QFII license (Qualified Foreign Institutional Investor),

granted by the China Securities Regulatory Commission, has risen from 12 to 52.

This license allows to invest in shares, treasury bonds, convertible bonds, corporate

bonds and closed-end/open-end funds negotiated on the Chinese stock markets.

Conclusion

The analysis of the economic performance of the major banks of the country shows

that the system still lacks of well-developed relationships with the market. This is

mainly due to the brokerage costs for the community (measured by the spread), and

to the low level of commissions and other incomes. At the same time, the

operational management efficiency is not particularly brilliant, because of the high

level of operational costs. The main problem is represented by the volume of NPLs

due to a lending policy based on patronage favours: the solution of this problem lies

in specific regulatory measures and in a different attitude of bank management.

Despite the relevant internationalization and privatization process, there are still

considerable problems, whose solutions will affect the future development and

growth of the Chinese banking and financial system.

On the one hand, the first critical aspect is concerned with the time needed to

implement the required changes. A gradual reform appears the best alternative: the

main risk is to expand the economic gap between developed and inner regions. Too

rapid changes could not ensure the desired results: due to the depth of the issues, too

fast and superficial approaches would leave unanswered questions. On the other

hand, the gradual evolution of the Chinese banking system will probably reduce

government control. Despite the encouraging results in the promotion of access to

small business credit, uncertainties on the final outcome of these measures still

persist: SOEs still have a more favourable treatment, a form of discrimination

against private enterprises, the real growth and development engine for the country.

References

Aiqun P, Pierrepont S, Long A (2005) Export opportunities in the Chinese Banking Industry, CS Market

Research

Chiarlone S, Amighini A (2007) L’economia della Cina. Dalla pianificazione al mercato, Carocci

112 E. Geretto, R. Pauluzzo

123

China Banking Regulatory Commission (2005) Guidelines on bank’s lending to small enterprises.

http://www.cbrc.gov.cn

China Banking Regulatory Commission (2006a) Latest developments in lending to small enterprises.

http://www.cbrc.gov.cn

China Banking Regulatory Commission (2006b) Guidelines on due diligence of commercial banks’

lending to small enterprises (Tentative). http://www.cbrc.gov.cn

China Banking Regulatory Commission (2006c) Regulations of the People’s Republic of China on

administration of foreign-funded banks, Chairman’s Decree of the State Council of the People’s

Republic of China No 478. http://www.cbrc.gov.cn

China Banking Regulatory Commission (2006d) Annual report 2005. http://www.cbrc.gov.cn

China Banking Regulatory Commission (2007a) Rules for implementing the regulations of the People’s

Republic of China on Administration of Foreign-funded Banks, Chairman’s Decree of China

Banking Regulatory Commission No 6, www.cbrc.gov.cn

China Banking Regulatory Commission (2007b) Report on the opening-up of the Chinese Banking

Sector. http://www.cbrc.gov.cn

China Banking Regulatory Commission (2007c) Annual report 2006. http://www.cbrc.gov.cn

China Securities Regulatory Commission (2007) List of QIIFs (as of December 2006), www.csrc.gov.cn

D’Agnolo G (2001) Cina: guida al commercio estero e agli investimenti. Einaudi, Torino

Dobson W, Kashyap AK (2006) The contradiction in China’s gradualist banking reform, Brookings Panel

on Economic Activity, pp 1–39

Fioroni L, Cianci C (2004) Rapporto Rischio paese Cina, Gruppo MPS, Area attivita internazionali—

Servizio rischio paese e controparti estere

Fishman TC (2004) The Chinese century. New York Times Magazine

Gotti Tedeschi C (2007) Il settore bancario in Cina: la crescita del credito e la recente apertura agli

investitori strategici stranieri, Corriere Asia Publishing Ltd

Gyntelberg J, Remolona EM (2006) La cartolarizzazione nella regione Asia-Pacifico: implicazioni per i

rischi di liquidita e di credito, Banca dei Regolamenti Internazionali, Rassegna Trimestrale

International Monetary Fund (2005) World Economic Outlook

Lemoine F (2005) L’economia cinese, Societa editrice il Mulino, Bologna

Malle S (2007) Il profilo economico della Cina oggi, Camera di Commercio di Verona, Convegno

‘‘Verona nel mondo–Report 2007’’

Mallory WH (1931) Rural cooperative credit in China. Quart J Econ 45(3):484–498

Meng CYW (1943) Foreign enterprise in postwar China. Far East Surv 12(22):212–219

On-Kit T (1992) A Private Bank in China: Hui Tong Urban Co-operative Bank, The China Quarterly, No

131, Special Issue: The Chinese Economy in the 1990s, pp 767–777

Ping X (1999) Bank restructuring in China, Bank for International Settlements, pp 124–129

Rampini F (2006) L’impero di Cindia. Strade blu Mondatori, Milano

Standing Committee of the Tenth National People’s Congress (2003) Law of the People’s Republic of

China on Commercial Banks, 27 December 2003

Tebbutt P, Chu C, Lin L (2007) Foreign Banks’ Expansion in China, with a focus on Hong Kong’s Banks,

Fitch Ratings

Tomba L (2005) Una finestra sul Pacifico. Cina. Rischi e opportunita nel settore del credito, Bollettino

della Comunita Scientifica in Australasia, Ambasciata d’Italia, Canberra

Tsai KS (2000) Banquet banking: gender and rotating savings and credit associations in South China. The

China Quarterly, vol 161, pp 142–170

Xu M (2005) Resolution of non-performing loans in China. The Leonard N. Stern School of Business,

Glucksman Institute for Research in Securities Markets

The Chinese Banking System 113

123

Copyright © 2022 FDOKUMEN