Bahasa

Halaman

Hukum

Template Cap Table and Returns Analysis Guide

by Alexander Jarvis

Follow and connect with me

• @ADJBlog

• https://angel.co/alexander-jarvis

• sg.linkedin.com/in/alexanderdjarvis/

• This is a guide to using a template cap table (with returns analysis) that I created

• The cap table enables founders to track ownership from founding up to Series-C

• In addition there is a nifty ‘Returns Waterfall’ tab that enables you to calculate returns to all the shareholders at an exit

• This presentation is going to explain at a high level how to use it • This stuff is complicated so you are going to have to

do reading to really get your head around it

Introduction

• You can download the spreadsheet from my blog here:

http://wp.me/p41jkx-3d

Download

• It is an excel spreadsheet that sets out in a ledger who owns the startup at different periods of time

• It is a list of the shareholders and how much each person owns

• It tells you how much money you will make if you exit, which is what I am sure you want to know!

What is a cap table?

• Think of it this way, when you start out as a founder you own 100% of the company, right? Well you raise a Seed round and now investors have a chunk. How do you know who owns what? The cap table tells you

• Furthermore, by having one properly set out you can truly understand what you own in different scenarios and after all sorts of complex things happen such as effects of liquidation preferences, discounts on convertible debt, the option pool shuffle and more importantly, not confuse ‘basic’ stuff like your ownership being based on post-money valuations and not pre-money

Why do you need a cap table?

• The cap table enables you to understand the ownership of your company and how it evolves across multiple financing rounds, as well as play with all the assumptions to support how you structure your next financing round

• The template accounts for most for what you will typically see with investors. It covers you for: • Initial founder table • Angel investment (Both as convertible debt which converts at Seed

stage and straight priced round) • Seed investment (Assuming 1x strategy preferred liquidation

preference) • Series A, B and C (Again structured as the Seed investment)

• In addition to the cap table, I have integrated a waterfall returns analysis so you can calculate exactly how much people will earn and at different exit valuation scenarios. I have not seen someone do this before, so I think it is pretty cool

What my template cap table does

• As you are no doubt aware, things can get pretty complicated and therefore my model does not account for every scenario

• Assuming you are dealing with reputable investors, you won’t ever really have to change this (Such as account for multiple liquidation preferences and participating preferred shares)

• I do not assume that you will: • Get funded with warrants • Assume there is a vesting schedule on shares (Though there is a

switch to remove unissued shares from the ESOP pool) • Have debt and interest that converts to shares • Have multiple liquidation preferences • Participating preferred shares • Different terms for investors at each stage of funding

What my template cap table does not do

• Your cap table is important. I did this myself and it has not been audited by anyone

• You ultimately will need a lawyer to ratify it • I do not take any responsibility whatsoever with

what you do with it

Important Disclaimer!

Founder Table

• Founders and staff get both/or: • Common stock • Common options

• Common stock is ‘junior’ to preference shares which is what your investors get (Certainly in series-A and after)

• Preference shares are legally a separate ‘class’ • Often they come with special rights, normally either

control or economic in nature • This means you get paid after everyone who has

preference ones

Shares

Founder table

This is the split of the company when you start

Put in name of founders and staff Put in the shares people start out with

New shares get dealt with later

This tells you how much everyone owns…

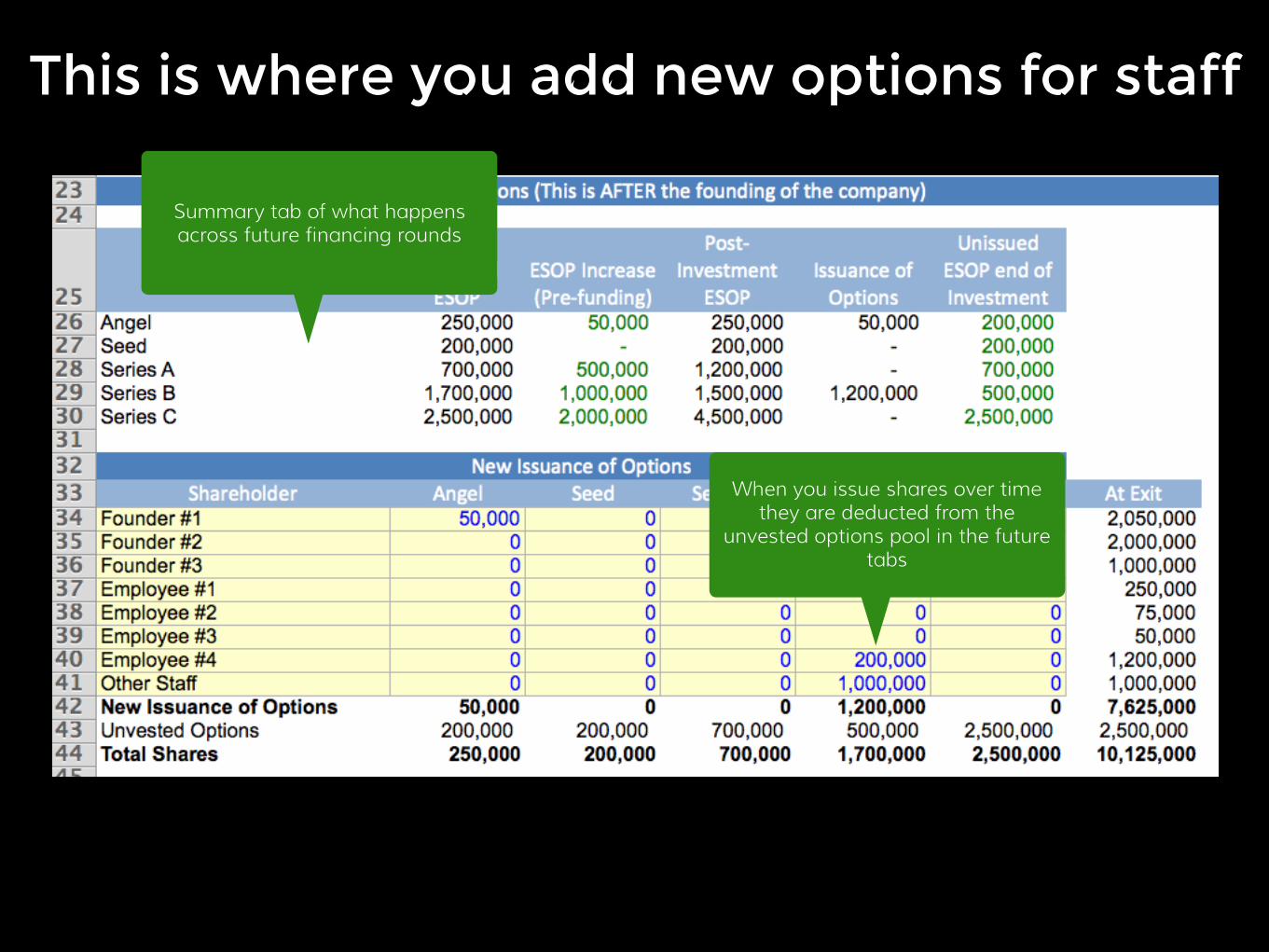

New options

This is where you add new options for staff

When you issue shares over time they are deducted from the

unvested options pool in the future tabs

Summary tab of what happens across future financing rounds

Angel Round

• Your angel round will either be: • Priced round - ‘Angel cap table’ tab • Convertible debt - ‘Angel Convertible’ tab

• I have made two sheets to deal with these • The priced round is the same as all the other

sheets except angels are getting common shares • The convertible debt gets converted to Preference

shares at the discount you negotiate to the Seed Round (Aka the ‘Next qualified financing’) • Why? Well it’s all about negotiation. Assume angels in

a priced round don’t get preference, but in a convertible they want to convert at the same class as the Seed investors

Angel round tabs

Angel round tabs: Angel Convertible

Angel Convertible tab

Here you issue convertible notes which convert at Seed

Put in the numbers you negotiate, simple

This is something you agree on approximately, and let’s you know

how much is owed till you raise again

This changes automatically when you start putting in numbers into the

Seed round tab It will say “215” if the Seed table is

blank

Where the angel converts in the seed stage

This shows you total amount of cash you actually got

Thats the convertible value it converts into

It’s higher than the $50k investment due to interest and being netted up

from the discount

See the conversion of shares in the Seed tab

And here the angel convertible fits into the summary cap table in the

Seed tab

Angel round tabs: Angel Cap Table

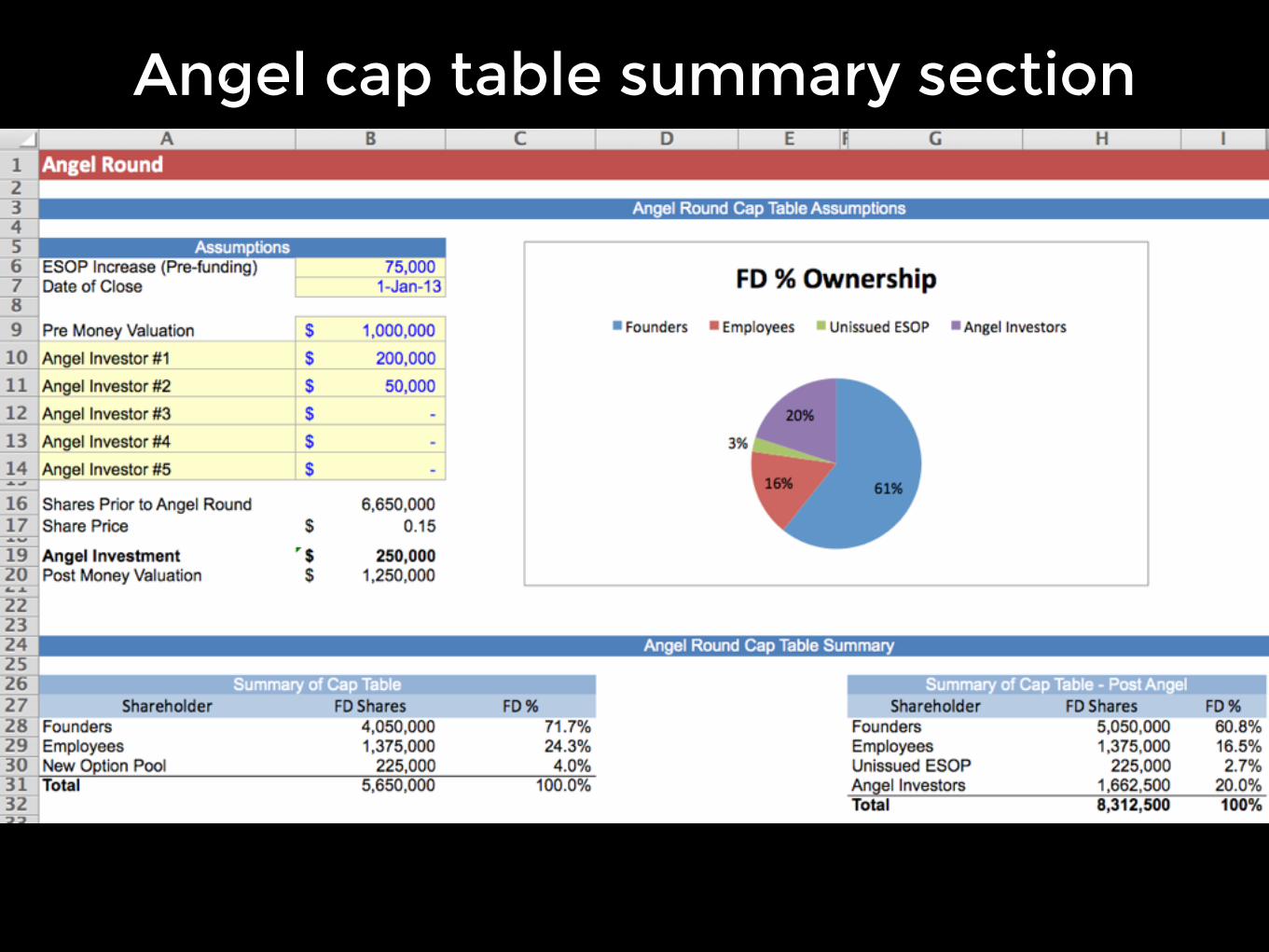

Angel cap table summary section

Put in assumptions and see the resultsHere the investor wants a bigger

ESOP plan This is a option pool for staff

If is also a way to decrease the effective valuation

This is the date you close the round

Premoney + investment = postmoney

Put in how much each investor invests and their name

Summary cap table before investment

Summary cap table AFTER investment

Calculations of Angel round

The right section is what just happened after the angel investment

This shows you the cap table from previous round

note this is 25000 more than before We increased the ESOP in the round

by 75000 but in the founder sheet we issued 50000 shares to Founder

#1. This nets to a 25000 increase

Here is the issuance

Now everyone is getting diluted as we add more shares

There are 2 investors one takes 80% of the shares from

that round

After we issue new shares everyone gets diluted

Seed Round

• Having raised the angel round, the next one is Seed

• The seed round is priced- you agree on a pre-money valuation and investment amount

• The Seed investors get issued a new class of shares call preference shares • Give them ‘economic’ right of a 1x liquidation

preference. Meaning they get their investment back before common shareholders do if they use the right (Optional, they will convert to common if they can make more money)

• This is a straight preferred not participating preferred (Investors don’t ‘double dip’ which is bad for founders)

Seed round

Seed round assumptions

Put in the terms for the new round, note the Convertible note!

No ESOP

This is the value Angel convertible investors get

This is the actual cash that was got

Angel investors now own 15%

Seed investors got 25%

Seed cap table

This is the ownership of your startup post Seed investment now

Seed investors now have a ‘fully diluted’ 24.9%

Preference not common shares have been issues

Fully diluted adds both common and preference

We can see a summary of ownership by category

Series A Cap Table

• Things have gone well and you are now closing your Series-A

• Pre-money has been agreed at $5m, with $1.3m investment

• If you divide the pre-money valuation over the total number of shares post Seed you get the share price that Series A investors are buying at

• The number of shares in total post series-a shares have been issued times by the share price tell you the post money valuation

Series A

Series-A Assumptions

Nothing you havent seen before

Lots new shares in ESOP

Series A investors take 21%

Seed investors diluted to 19%

Here is the share price i mentioned

Series-A cap table

Unissued ESOP is now 725k shares (5%) and we have two Series A investors on the board

Series A investors take 20.6%

Unissued ESOP bigger 5% ESOP

Series B Cap Table

• Its a year later • Pre-money is up to $12m, with $5m investment • The investors want to make the ESOP bigger so

you can issue more shares to staff • The Series-B investors are senior to the Series-A

ones

Series B

Series B assumptions

We issue 1m to the ESOP

Lots new shares in ESOP

Issue new options and expand ESOP

The unissued ESOP nets out

Unissued ESOP now 525k shares

We issued 1.2m options to Employee #4 and the rest of the

staff

Unissued ESOP now 525k shares

Series B cap table

The cap table is getting big now!

New investors

More dilution

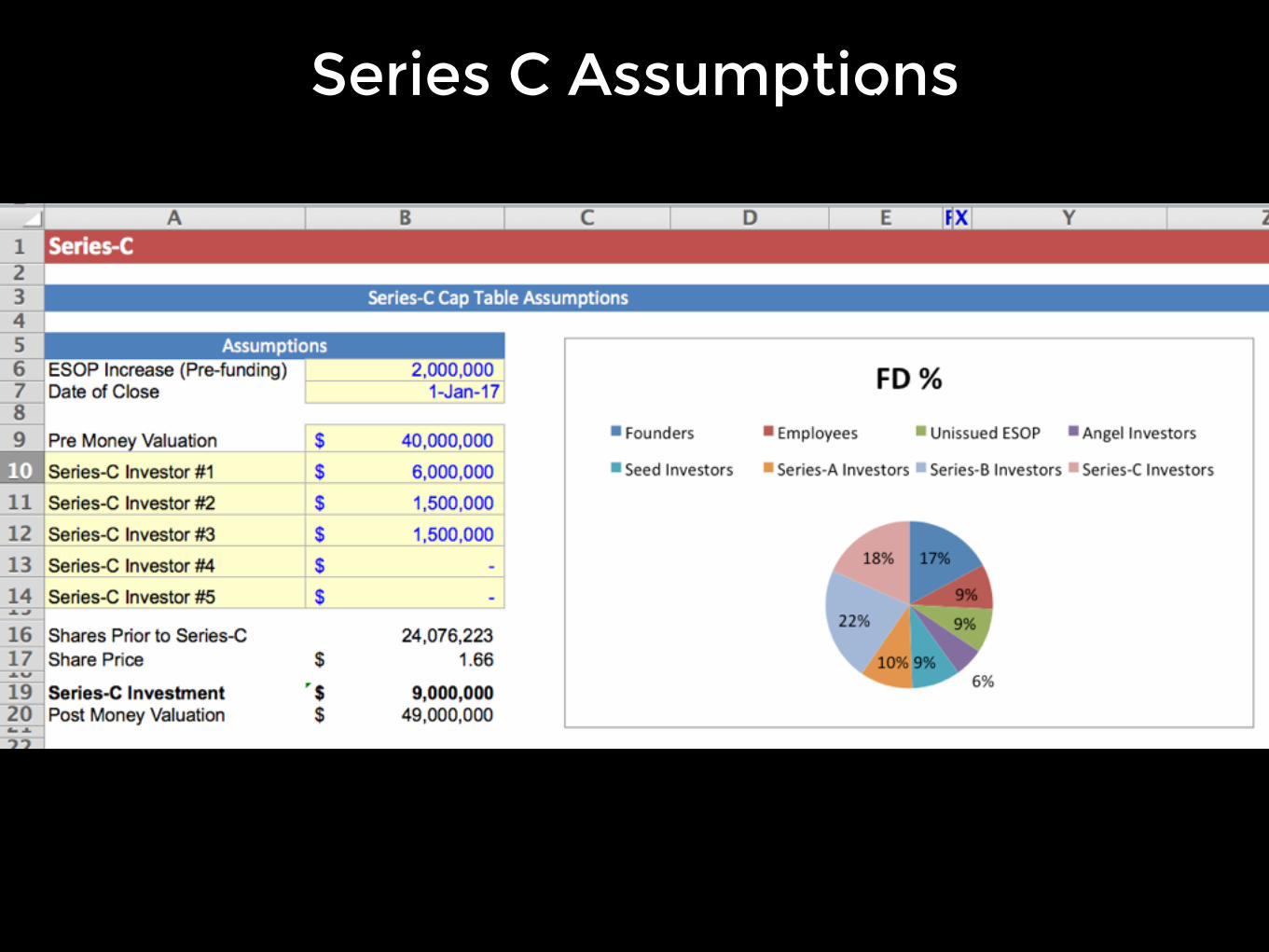

Series C Cap Table

• You raise your Series-C round which is a growth investment to scale your business before your exit

• This is the last round of financing you are going to do (In this model anyway)

• Post this you will be looking at exit opportunities and using the next tab, “Returns Waterfall” to calculate the returns on investment

Series-C

Series C Assumptions

Series C cap table

Returns Waterfall

• After multiple rounds of finance, hard work and some luck, it is time to make money at exit!

• The “Returns Waterfall” will tell you how much money each investor will make for different valuations

• The latest investor typically gets their money back first, so the sheet is a reverse waterfall • You start with the Exit value • Each investor decides if they use their liquidation

preference or not and the money flows down to the common shareholders

Introduction

• Investors asked you to increase the ESOP so you could issue shares to new staff as you need to attract new talent • Investors ask this BEFORE they put in money, so

previous investors are the only ones getting diluted • It also reduced the effective valuation they paid as they

don’t expect all the shares to be issued to new staff • In most cases the entire ESOP will NOT be issued

meaning that the returns are equally divided across all shareholders • Previous investors paid to make the ESOP pool

• The model allows you to remove or leave it in • Expect to remove it

Including the unissued ESOP?

Assumptions

There are only a few variables for you to have to play with

This is summary of your final cap table

This allows you to adjust for unissued options and drives all the

calculations below

This is the ESOP switch FALSE: remove unissued ESOP

TRUE: include whole ESOP

The exit date drives dividend payments (If investors negotiated

them)Dividend % is input here

Series-C get a dividend of 10%

This tells you if the shares are included or not

Summary of investor returns by exit value

The more you sell for the more common get

Common get nothing as liquidation preferences claim all the return

Series-C liquidation preference is taken up to here

The exit value range (Right is more cash!)

% of returns taken by shareholders

Here we can see how much of the money goes to what investor

Series-C get all of it

Common shareholders (Founders and staff) get paid!

Past a certain point, returns are constant to all shareholders in

proportion to ownership

Valuation range

This is the range of exit values

The range

This is your base exit value

This is the increments (+/-) to the central exit value

Series-C preference calculation

This tells you if Series-C take their preference payment or if they convert to common shares and take a %

They aren’t converting to common shares till an exit of $64m so they

take their preference

Convert to common tells you if they convert

Returns for different exit values

Series-C get a dividend payment of 10% so the total preference is more

than $9m

We put the 10% dividend in the assumptions remember?

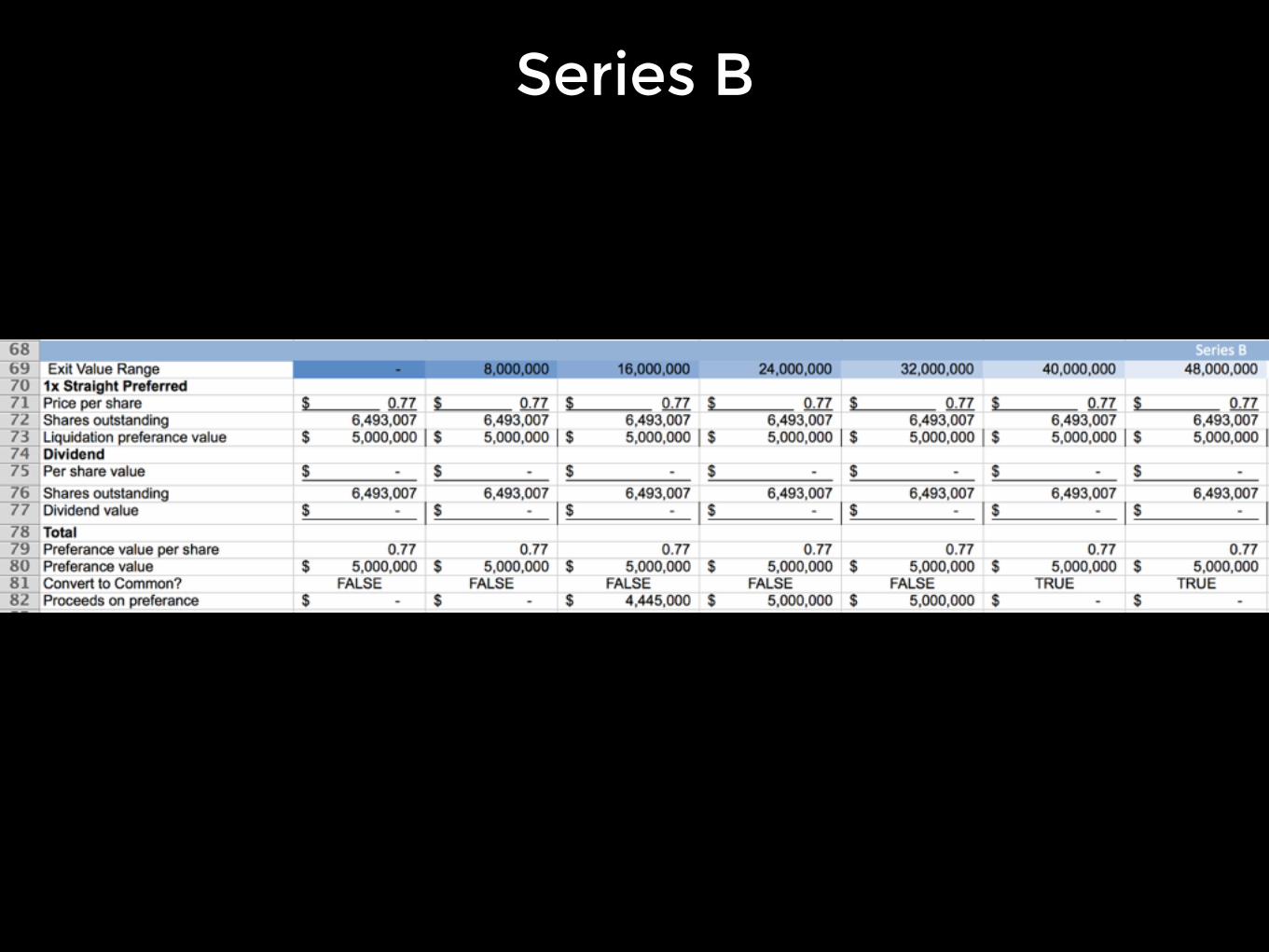

Series B

Series B are next in the waterfall

Preference payment Here they convert to common

No dividend being paid

B, A and Seed get calculated in the same manner

Preference payment summary

At the end of the waterfall you see preference paid and remaining proceeds for common shareholders

Preferences paid

Amount for common shares to get return

Common share returns summary

After adjusting for preference share payments you can see how much common shareholders get paid

Common get nothing

% of what is left getting paid to the shareholders

The number of shares ‘what is left’ is divided to common shares

Preferences are not taken, investors convert to common

$ payment to common shareholders

Total proceeds to all investors

We see here the actual amount each shareholder gets

This shows common plus preference payments as a % of total proceeds

This is the dollar value payment to investors

Ths is the per share return to investors

This shows the multiple of their investment they make

Seed investors get a 5.6x return on investment

1x return is the liquidation preference at work

Print sheets

• These sheets are simply a summary you can print out of the cap tables

Summary

Series-A

Series-B

Series-C

Enjoy!

Copyright © 2022 FDOKUMEN