Bahasa

Halaman

Hukum

ed: CK / sa:JC, PY

Rolling rig-sale bandwagon

Rising rig transactions indicate growing optimism

Industry consolidation has kicked off; positive for

recovery

Improving prospect could catalyse rig delivery

Reiterate BUY on Singapore rigbuilders

Positive indicators of rig market recovery – rising rig sales

volume and mergers. We have observed a strong uptick in

rig transactions over the past 6 months (refer to chart at the

bottom right), which is typically a positive indicator of stronger

demand prospects. The recent establishment of new entrants

(North Drilling, Borr Drilling) as well as rumours of a potential

comeback of Aker Group to the rig-owning space and China

Merchant Group’s hunt for distressed operators, underscore

the growing optimism. The industry has also kick-started the

consolidation wave – Ensco acquiring Atwood; Transocean to

buy Songa – which would accelerate the recovery pace.

More perks to justify relook at Singapore rigbuilders. The

improving rig market could “motivate” rig owners to take

delivery of existing orders and facilitate the disposal of

cancelled units in the second hand market, removing a key

overhang on Singapore rigbuilders. This could free up Keppel

and SMM’s working capital by S$1.5-2.5bn each, lowering

net gearing to 0.3-0.5x, from 0.5-1.0x currently. Both yards’

breakthrough into high-value non-crude solutions (>US$200m

each) – Keppel secured two contracts for LNG-fuelled

containership for US Jones Act market while SMM signed LOI

for at least two large Compressed Gas Liquid carriers –

brightens up the order outlook. Sete Brasil’s rig orders at

Singapore yards could be reactivated in the near future if the

recent submission of a new restructuring plan in end-Aug is

approved.

Reiterate BUYs on Keppel (TP S$7.60) and SMM (S$2.30).

We continue to like Keppel as a proxy to ride on a property

and offshore & marine recovery, while SMM is a pure play to

tap into an O&G recovery. Order wins, which have been

lacking YTD, remain the key re-rating catalysts for both. Our

thesis of yard merger, if it materialises, would be bonus.

(Refer to report “Shipyards: Creating Global Champion”

dated 20 Jul 2017).

STI : 3,225.95

Analyst Pei Hwa HO +65 6682 3714 Glenn Ng +65 6682 2657 [email protected] [email protected]

Keppel Corporation : Diversified conglomerate with core businesses in offshore marine, property investments and development and infrastructure-based activities.

Sembcorp Marine : Principal activities are ship repair, shipbuilding, ship conversion rig building and offshore engineering.

Sembcorp Industries : Focus on Integrated Utilities and Energy, Marine Engineering, Environmental Engineering, Logistics & Engineering & Construction Services.

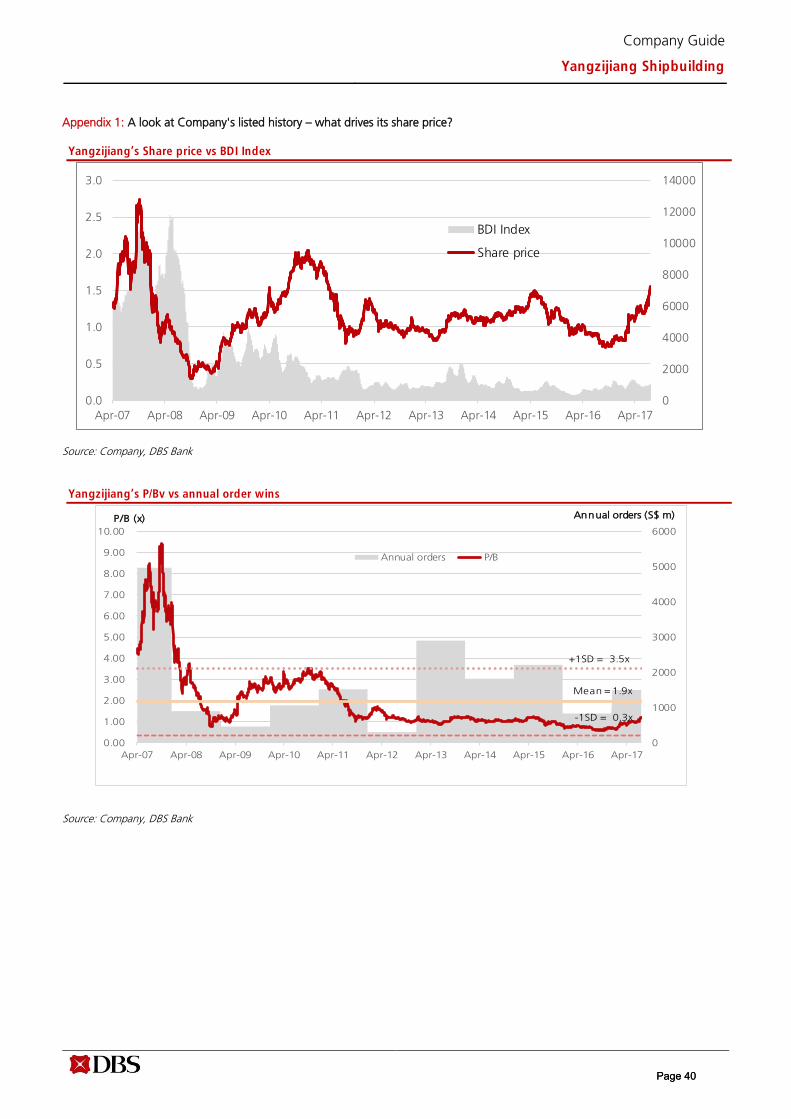

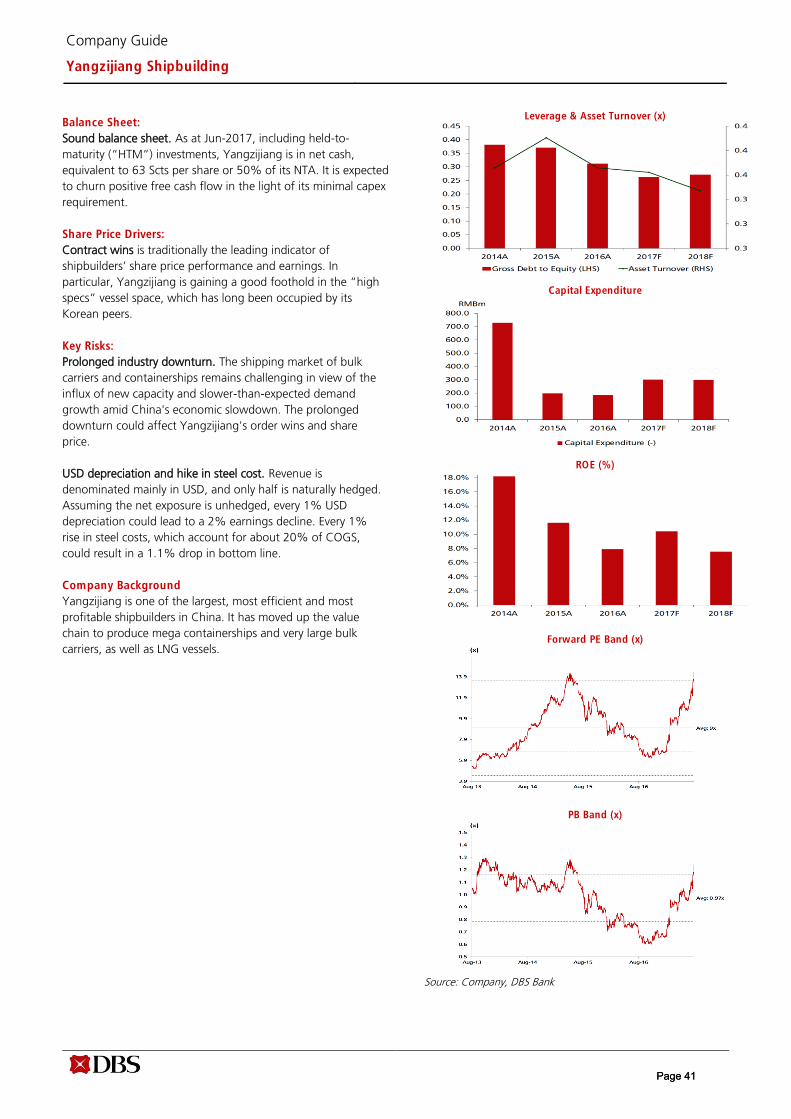

Yangzijiang Shipbuilding (Holdings) Ltd : The largest private containership builder in China who specialises in medium-sized containerships and bulk carriers.

Rig sale volume picking up

Source: Clarksons

1014 14

4 37

1 0 1 2 20

711

15

4

2

13

1

0

5

10

15

20

25

30

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17

Offshore drilling rig unit sales Transocean rig sale to Borr Drilling

Hercules Rig sales

DBS Group Research . Equity 20 Sep 2017

Singapore Industry Focus

Singapore Rigbuilders

Refer to important disclosures at the end of this report

STOCKS

12-mth

Price Mkt Cap Target Price Performance (%)

S$ US$m S$ 3 mth 12 mth Rating

Keppel Corporation

6.38 8,585 7.60 1.4 22.2 BUY

Sembcorp Marine 1.67 2,590 2.30 3.1 33.6 BUY

Sembcorp Industries

2.96 3,920 4.00 (4.2) 14.3 BUY

Yangzijiang Shipbuilding (Holdings) Ltd

1.43 4,050 1.70 16.8 95.2 BUY

Source: DBS Bank, Bloomberg Finance L.P.

Closing price as of 19 Sep 2017

Page 1

Industry Focus

Singapore Rigbuilders

RIG SALE & CONSOLIDATION PICKING UP

RISING SECONDHAND VOLUME

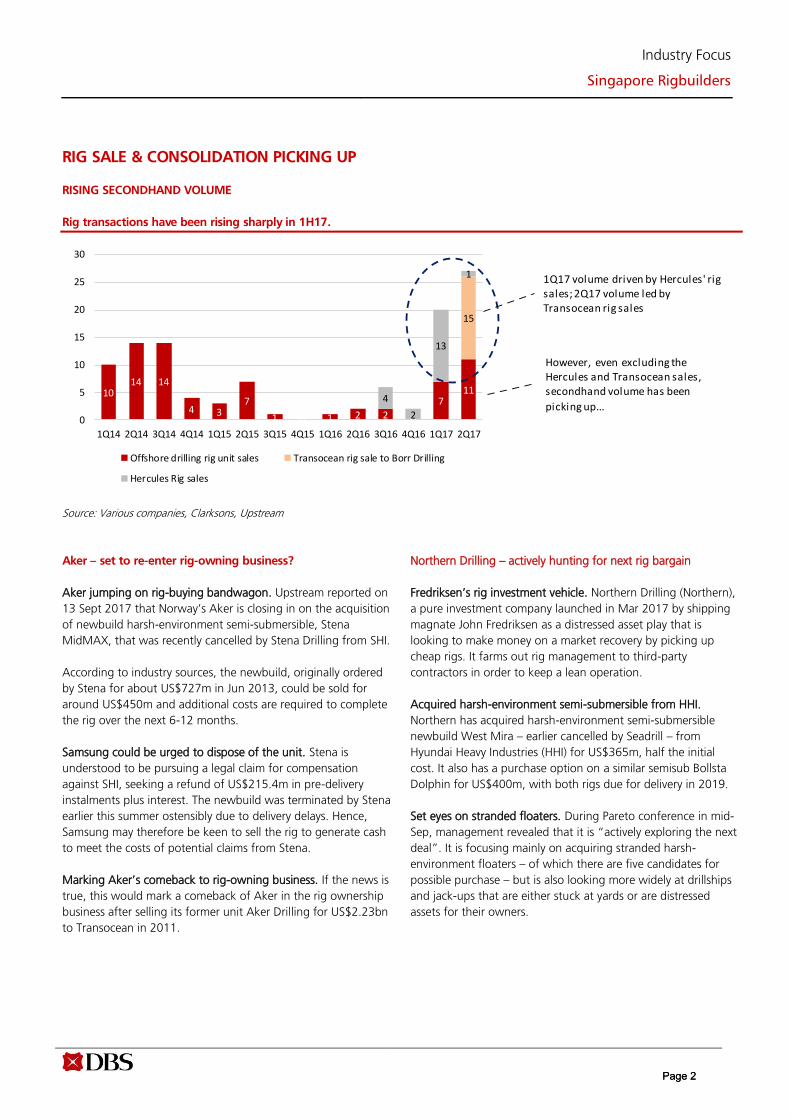

Rig transactions have been rising sharply in 1H17.

Source: Various companies, Clarksons, Upstream

Aker – set to re-enter rig-owning business?

Aker jumping on rig-buying bandwagon. Upstream reported on

13 Sept 2017 that Norway’s Aker is closing in on the acquisition

of newbuild harsh-environment semi-submersible, Stena

MidMAX, that was recently cancelled by Stena Drilling from SHI.

According to industry sources, the newbuild, originally ordered

by Stena for about US$727m in Jun 2013, could be sold for

around US$450m and additional costs are required to complete

the rig over the next 6-12 months.

Samsung could be urged to dispose of the unit. Stena is

understood to be pursuing a legal claim for compensation

against SHI, seeking a refund of US$215.4m in pre-delivery

instalments plus interest. The newbuild was terminated by Stena

earlier this summer ostensibly due to delivery delays. Hence,

Samsung may therefore be keen to sell the rig to generate cash

to meet the costs of potential claims from Stena.

Marking Aker’s comeback to rig-owning business. If the news is

true, this would mark a comeback of Aker in the rig ownership

business after selling its former unit Aker Drilling for US$2.23bn

to Transocean in 2011.

Northern Drilling – actively hunting for next rig bargain

Fredriksen’s rig investment vehicle. Northern Drilling (Northern),

a pure investment company launched in Mar 2017 by shipping

magnate John Fredriksen as a distressed asset play that is

looking to make money on a market recovery by picking up

cheap rigs. It farms out rig management to third-party

contractors in order to keep a lean operation.

Acquired harsh-environment semi-submersible from HHI.

Northern has acquired harsh-environment semi-submersible

newbuild West Mira – earlier cancelled by Seadrill – from

Hyundai Heavy Industries (HHI) for US$365m, half the initial

cost. It also has a purchase option on a similar semisub Bollsta

Dolphin for US$400m, with both rigs due for delivery in 2019.

Set eyes on stranded floaters. During Pareto conference in mid-

Sep, management revealed that it is “actively exploring the next

deal”. It is focusing mainly on acquiring stranded harsh-

environment floaters – of which there are five candidates for

possible purchase – but is also looking more widely at drillships

and jack-ups that are either stuck at yards or are distressed

assets for their owners.

1014 14

4 37

1 0 1 2 20

711

15

4

2

13

1

0

5

10

15

20

25

30

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17

Offshore drilling rig unit sales Transocean rig sale to Borr Drilling

Hercules Rig sales

1Q17 volume driven by Hercules' rig sales; 2Q17 volume led by Transocean rig sales

However, even excluding the Hercules and Transocean sales, secondhand volume has been

picking up...

Page 2Page 2

Industry Focus

Singapore Rigbuilders

Borr Drilling – sees a “window of opportunity” for rig deals

Building high specification jackup empire. Borr Drilling Limited

(Borr), founded in Aug 2016 by John Fredriksen’s ex-associate

Tor Olav Troim and listed on Oslo at end-Aug 2017, has built up

a fleet of 17 premium jack-ups at an average acquisition price of

US$107m/rig, in two rig deals involving Transocean and

bankrupt Hercules Offshore.

Landmark Transocean deal consists of 15 jackups. In Mar 2017,

Borr signed a letter of intent with Transocean for the acquisition

of its entire 15 high-specification jackup rigs for US$1.35bn,

including five newbuilds under construction at Keppel FELS

Limited.

In negotiation for further advantageous jackup deals. Borr is

well-positioned in a price competition for contracts with a

break-even cost per rig that is around 50% lower than its peers.

The new CEO Simon Johnson, who comes on board 1 Aug,

shared at Pareto Securities’ Oil & Offshore conference in Oslo

that Borr will continue to grow their fleet as it sees a “window

of opportunity” for further advantageous rig deals. He further

elaborated that the company is in talks with different players

and “anticipate these discussions to bear fruit”.

Introducing new operator contracting model. Besides the cost

advantage, Borr also aims to differentiate itself from rivals by

offering a new contracting model for operators with features

such as performance incentives based on drilling efficiency, in

collaboration with partner Schlumberger that holds a 20% stake

in Borr.

Page 3Page 3

Industry Focus

Singapore Rigbuilders

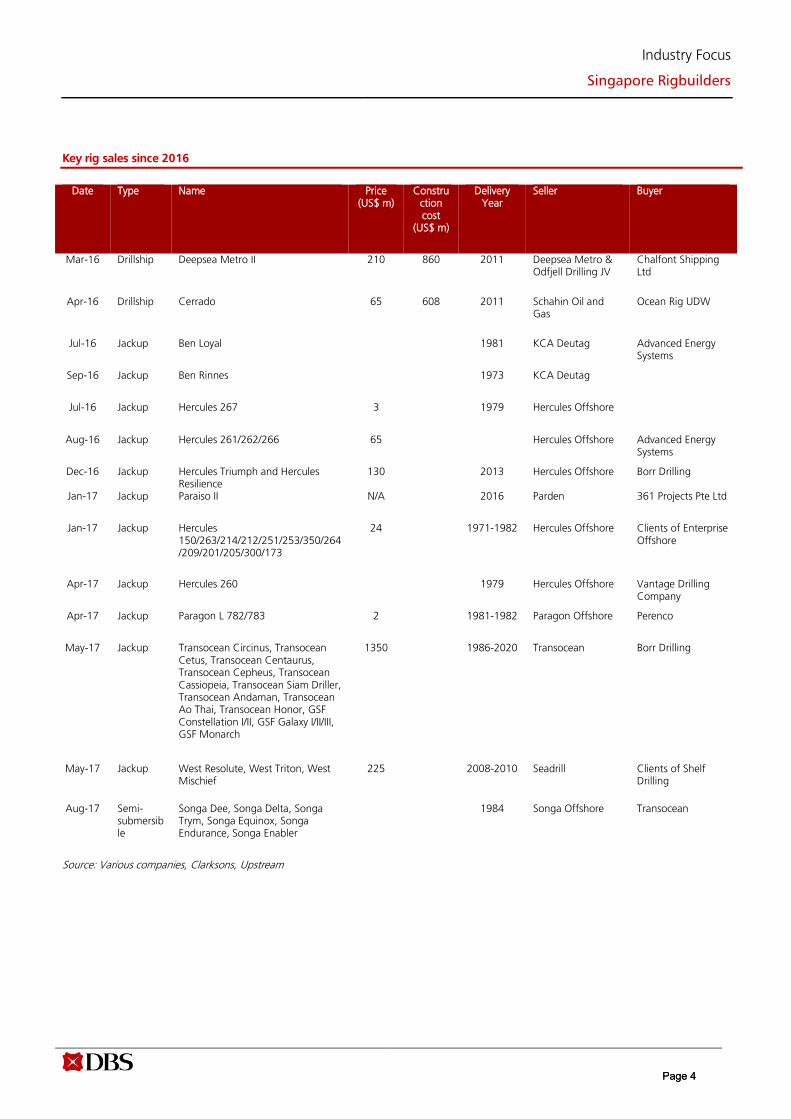

Key rig sales since 2016

Date Type Name Price (US$ m)

Construction cost

(US$ m)

Delivery Year

Seller Buyer

Mar-16 Drillship Deepsea Metro II 210 860 2011 Deepsea Metro & Odfjell Drilling JV

Chalfont Shipping Ltd

Apr-16 Drillship Cerrado 65 608 2011 Schahin Oil and Gas

Ocean Rig UDW

Jul-16 Jackup Ben Loyal 1981 KCA Deutag Advanced Energy Systems

Sep-16 Jackup Ben Rinnes 1973 KCA Deutag

Jul-16 Jackup Hercules 267 3 1979 Hercules Offshore

Aug-16 Jackup Hercules 261/262/266 65 Hercules Offshore Advanced Energy Systems

Dec-16 Jackup Hercules Triumph and Hercules Resilience

130 2013 Hercules Offshore Borr Drilling

Jan-17 Jackup Paraiso II N/A 2016 Parden 361 Projects Pte Ltd

Jan-17 Jackup Hercules 150/263/214/212/251/253/350/264/209/201/205/300/173

24 1971-1982 Hercules Offshore Clients of Enterprise Offshore

Apr-17 Jackup Hercules 260 1979 Hercules Offshore Vantage Drilling Company

Apr-17 Jackup Paragon L 782/783 2 1981-1982 Paragon Offshore Perenco

May-17 Jackup Transocean Circinus, Transocean Cetus, Transocean Centaurus, Transocean Cepheus, Transocean Cassiopeia, Transocean Siam Driller, Transocean Andaman, Transocean Ao Thai, Transocean Honor, GSF Constellation I/II, GSF Galaxy I/II/III, GSF Monarch

1350 1986-2020 Transocean Borr Drilling

May-17 Jackup West Resolute, West Triton, West Mischief

225 2008-2010 Seadrill Clients of Shelf Drilling

Aug-17 Semi-submersible

Songa Dee, Songa Delta, Songa Trym, Songa Equinox, Songa Endurance, Songa Enabler

1984 Songa Offshore Transocean

Source: Various companies, Clarksons, Upstream

Page 4Page 4

Industry Focus

Singapore Rigbuilders

RIG CONSOLIDATION WAVE

Transocean to buy Songa

Transocean pays US$3.4bn for Songa. In mid-Aug 2017,

Transocean Ltd (Transocean) announced that it is acquiring

Songa Offshore (Songa) for US$3.4bn. The offer price of

NOK47.50 per Songa share represents a 37% premium to the

five-day average closing price.

Strengthen positioning in harsh-environment, deepwater rigs.

The transaction strengthens Transocean’s industry-leading

position with the addition of Songa’s four “Cat-D” harsh-

environment, semisubmersible drilling rigs on long-term

contracts with Statoil in Norway. Besides, Songa’s fleet also

includes three additional semisubmersible drilling rigs.

The combined company will operate a fleet of 51 mobile

offshore drilling units, consisting of 30 ultra-deepwater floaters,

11 harsh environment floaters, three deepwater floaters and

seven midwater floaters. Additionally, Transocean has four ultra-

deepwater drillships under construction, including two

contracted with Shell for ten years each.

Cost synergies. The transaction is expected to be earnings

accretive and yields annual expense synergies of approximately

US$40m.

Ensco acquires Atwood

Ensco to acquire Atwood Oceanics in an all-stock deal valued at

about US$863m. Ensco plc (Ensco) and Atwood Oceanics, Inc.

(Atwood) jointly announced in end-May 2017 that they have

entered into a definitive merger agreement under which Ensco

will acquire Atwood in an all-stock transaction.

Offer price premium of 33%. The offer price of US$10.72 per

Atwood share (at a swap ratio of 1.6x Ensco share for every

Atwood share) represents a premium of approximately 33% to

Atwood’s closing price on 26 May.

Potential cost synergies. Post-merger, Ensco and Atwood

shareholders will own approximately 69% and 31%,

respectively, of Ensco. The merged entity is expected to realise

annual pre-tax expense synergies of approximately U$65m for

full-year 2019 and beyond.

Widened product offerings. The deal will provide Ensco with six

ultradeepwater floaters, including four drillships, and five high-

specification jackups. Post-transaction, the combined company

will have a fleet of 63 rigs, including ultradeepwater drillships,

deep and midwater semisubmersibles, and shallow-water

jackups, with a customer base of 27 national oil companies,

supermajors, and independents.

China Merchants Group – from rig-builder to rig-owner?

Looking to acquire distressed offshore rig operators or assets? In

early-Sep 2017, state-owned conglomerate China Merchants

Group is reportedly exploring acquisitions of distressed offshore

rig operators. It is said to have looked at various assets and

companies including Seadrill Ltd (Seadrill) and Shelf Drilling Ltd

(Shelf). These efforts are at an early stage, and China Merchants

may also opt to pick off assets as opposed to full takeovers.

Moving up value chain. The group’s China Merchants Industry

Holdings Co. unit builds semi-submersible rigs and other

offshore equipment. It is also a minority shareholder in the

parent company of CIMC Raffles, which builds drilling platforms

used by oil producers, including China National Petroleum Corp.

RIG MARKET ON RECOVERY TRACK

Brent crude oil prices holding up at the US$55/bbl level; gradual

recovery expected going into 2018. Our forecast of US$50-

55/bbl average Brent price in 2017 looks broadly on track to be

met, with YTD Brent price averaging US$52.2/bbl currently. We

believe the global crude oil rebalancing should accelerate into

2018, driven by demand outstripping supply and thus inventory

drawdowns. Additionally, we think worries over US shale oil

production could be overblown as we see evidence of US shale

productivity gains plateauing, and cash operating costs look to

have bottomed. Thus, we are forecasting an average price of

US$55-60/bbl for Brent in 2018, followed by US$60-65/bbl in

the long term (based on a marginal cost curve analysis).

Industry capital expenditure looks to have bottomed; 2018

could see an upswing. If we look at the capital expenditure

(capex) budgets for 2017 of the eight largest international oil

companies (IOCs), the trend is essentially flattish compared to

2016 (up 1% y-o-y). However, as the oil market rebalances, and

prices stabilise in the US$50-$60/bbl range, we believe oil

majors may consider revising up future capex estimates in 2018,

which could support higher spending in 2H18 and 2019.

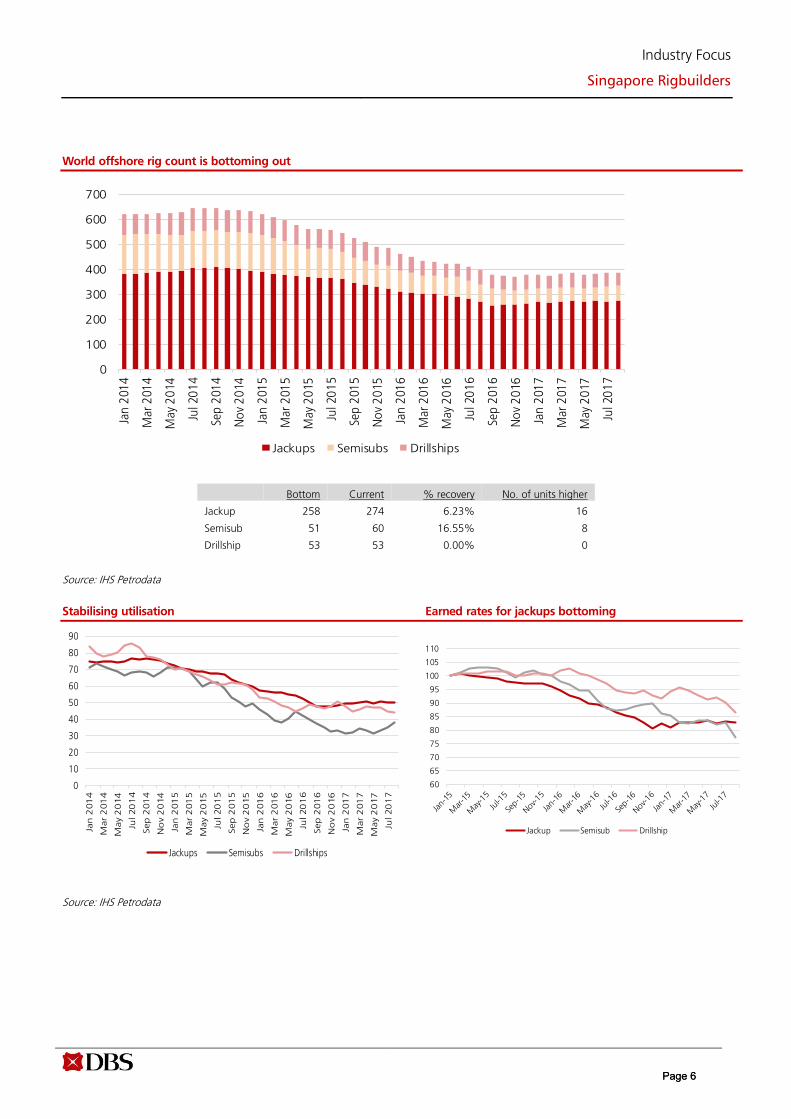

Green shoots of a recovery: offshore working rig count has

bottomed in 1Q17. After falling from a peak of 736 contracted

offshore rigs in April 2014 to 457 rigs in January 2017, the

working rig count has taken a U-shaped upward trajectory since

February 2017, with the rig count as of August 2017 rising

c.6.5% from January’s trough levels. A meaningful rebound in

the working rig count would of course be predicated on oil

majors increasing their capex budgets.

Page 5Page 5

Industry Focus

Singapore Rigbuilders

World offshore rig count is bottoming out

Source: IHS Petrodata

Stabilising utilisation Earned rates for jackups bottoming

Source: IHS Petrodata

Bottom Current % recovery No. of units higher

Jackup 258 274 6.23% 16

Semisub 51 60 16.55% 8

Drillship 53 53 0.00% 0

0

100

200

300

400

500

600

700

Jan

201

4

Mar

201

4

May

20

14

Jul 2

01

4

Sep

201

4

No

v 2

014

Jan

201

5

Mar

201

5

May

20

15

Jul 2

01

5

Sep

201

5

No

v 2

015

Jan

201

6

Mar

201

6

May

20

16

Jul 2

01

6

Sep

201

6

No

v 2

016

Jan

201

7

Mar

201

7

May

20

17

Jul 2

01

7

Jackups Semisubs Drillships

0

10

20

30

40

50

60

70

80

90

Jan

201

4

Mar

201

4

May 2

014

Jul 20

14

Sep

201

4

No

v 2

014

Jan

201

5

Mar

201

5

May 2

015

Jul 20

15

Sep

201

5

No

v 2

015

Jan

201

6

Mar

201

6

May 2

016

Jul 20

16

Sep

201

6

No

v 2

016

Jan

201

7

Mar

201

7

May 2

017

Jul 20

17

Jackups Semisubs Drillships

60

65

70

75

80

85

90

95

100

105

110

Jackup Semisub Drillship

Page 6Page 6

Industry Focus

Singapore Rigbuilders

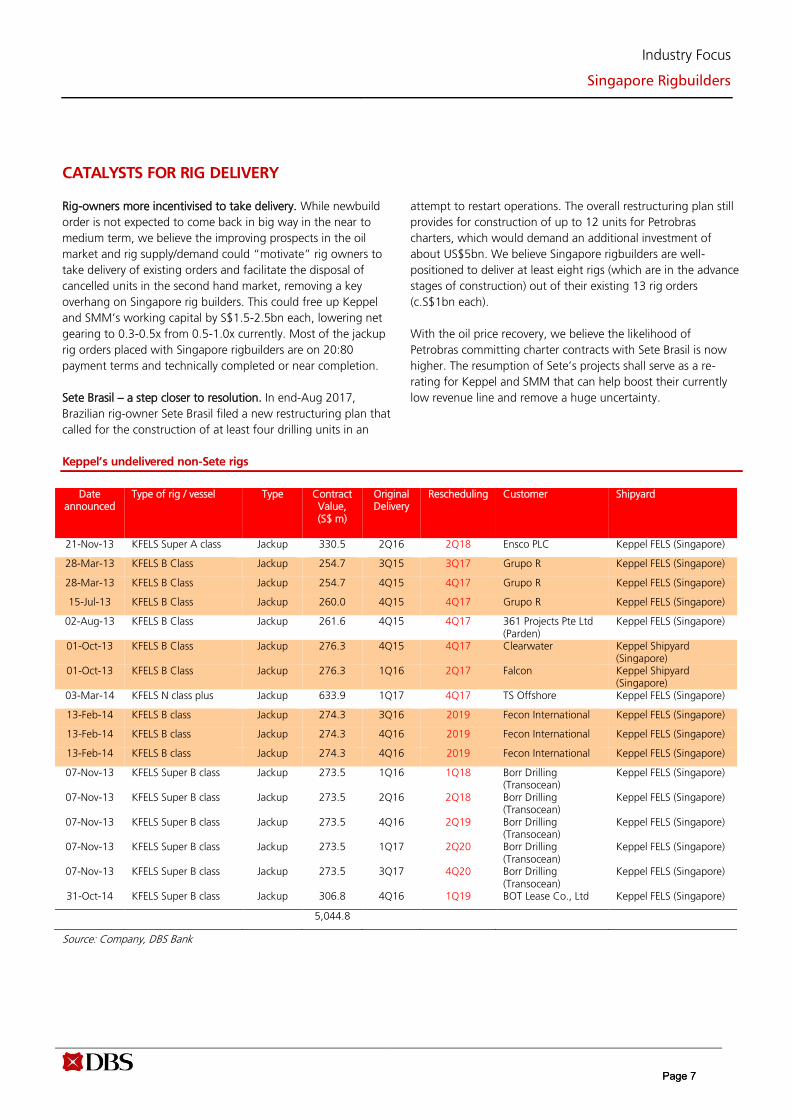

CATALYSTS FOR RIG DELIVERY

Rig-owners more incentivised to take delivery. While newbuild

order is not expected to come back in big way in the near to

medium term, we believe the improving prospects in the oil

market and rig supply/demand could “motivate” rig owners to

take delivery of existing orders and facilitate the disposal of

cancelled units in the second hand market, removing a key

overhang on Singapore rig builders. This could free up Keppel

and SMM’s working capital by S$1.5-2.5bn each, lowering net

gearing to 0.3-0.5x from 0.5-1.0x currently. Most of the jackup

rig orders placed with Singapore rigbuilders are on 20:80

payment terms and technically completed or near completion.

Sete Brasil – a step closer to resolution. In end-Aug 2017,

Brazilian rig-owner Sete Brasil filed a new restructuring plan that

called for the construction of at least four drilling units in an

attempt to restart operations. The overall restructuring plan still

provides for construction of up to 12 units for Petrobras

charters, which would demand an additional investment of

about US$5bn. We believe Singapore rigbuilders are well-

positioned to deliver at least eight rigs (which are in the advance

stages of construction) out of their existing 13 rig orders

(c.S$1bn each).

With the oil price recovery, we believe the likelihood of

Petrobras committing charter contracts with Sete Brasil is now

higher. The resumption of Sete’s projects shall serve as a re-

rating for Keppel and SMM that can help boost their currently

low revenue line and remove a huge uncertainty.

Keppel’s undelivered non-Sete rigs

Date announced

Type of rig / vessel Type Contract Value, (S$ m)

Original Delivery

Rescheduling Customer Shipyard

21-Nov-13 KFELS Super A class Jackup 330.5 2Q16 2Q18 Ensco PLC Keppel FELS (Singapore)

28-Mar-13 KFELS B Class Jackup 254.7 3Q15 3Q17 Grupo R Keppel FELS (Singapore)

28-Mar-13 KFELS B Class Jackup 254.7 4Q15 4Q17 Grupo R Keppel FELS (Singapore)

15-Jul-13 KFELS B Class Jackup 260.0 4Q15 4Q17 Grupo R Keppel FELS (Singapore)

02-Aug-13 KFELS B Class Jackup 261.6 4Q15 4Q17 361 Projects Pte Ltd (Parden)

Keppel FELS (Singapore)

01-Oct-13 KFELS B Class Jackup 276.3 4Q15 4Q17 Clearwater Keppel Shipyard (Singapore)

01-Oct-13 KFELS B Class Jackup 276.3 1Q16 2Q17 Falcon Keppel Shipyard (Singapore)

03-Mar-14 KFELS N class plus Jackup 633.9 1Q17 4Q17 TS Offshore Keppel FELS (Singapore)

13-Feb-14 KFELS B class Jackup 274.3 3Q16 2019 Fecon International Keppel FELS (Singapore)

13-Feb-14 KFELS B class Jackup 274.3 4Q16 2019 Fecon International Keppel FELS (Singapore)

13-Feb-14 KFELS B class Jackup 274.3 4Q16 2019 Fecon International Keppel FELS (Singapore)

07-Nov-13 KFELS Super B class Jackup 273.5 1Q16 1Q18 Borr Drilling (Transocean)

Keppel FELS (Singapore)

07-Nov-13 KFELS Super B class Jackup 273.5 2Q16 2Q18 Borr Drilling (Transocean)

Keppel FELS (Singapore)

07-Nov-13 KFELS Super B class Jackup 273.5 4Q16 2Q19 Borr Drilling (Transocean)

Keppel FELS (Singapore)

07-Nov-13 KFELS Super B class Jackup 273.5 1Q17 2Q20 Borr Drilling (Transocean)

Keppel FELS (Singapore)

07-Nov-13 KFELS Super B class Jackup 273.5 3Q17 4Q20 Borr Drilling (Transocean)

Keppel FELS (Singapore)

31-Oct-14 KFELS Super B class Jackup 306.8 4Q16 1Q19 BOT Lease Co., Ltd Keppel FELS (Singapore)

5,044.8

Source: Company, DBS Bank

Page 7Page 7

Industry Focus

Singapore Rigbuilders

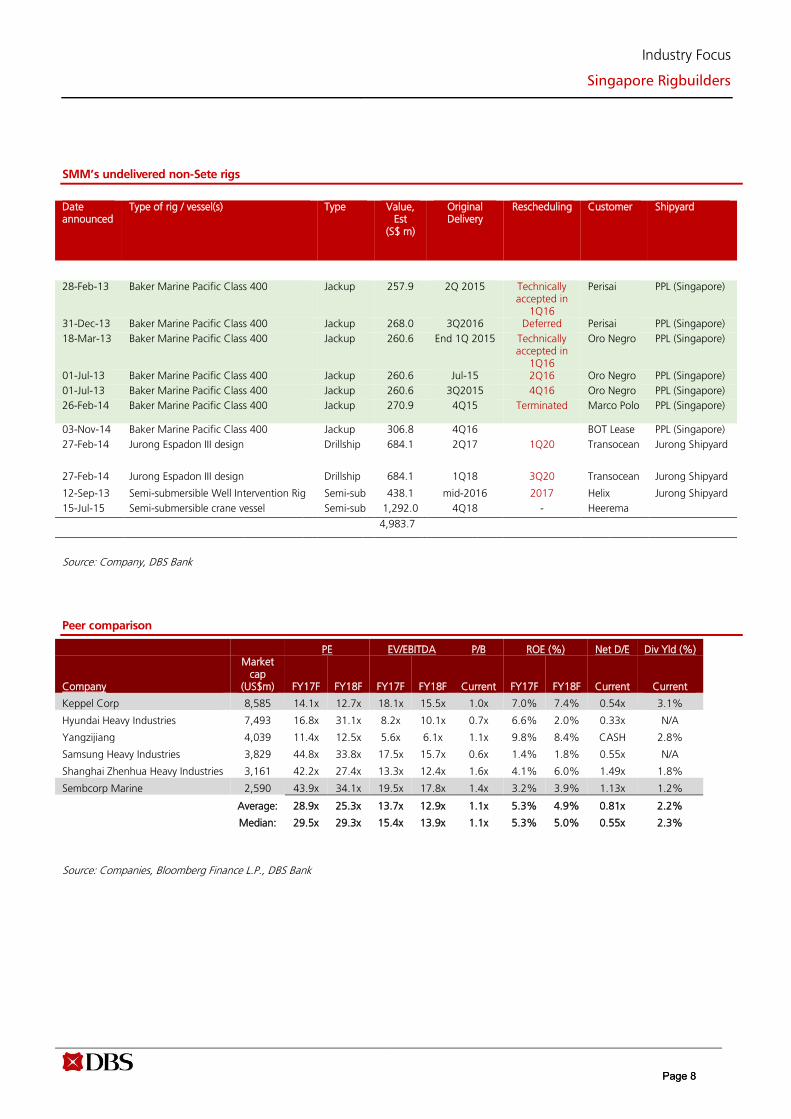

SMM’s undelivered non-Sete rigs

Date announced

Type of rig / vessel(s) Type Value, Est

(S$ m)

Original Delivery

Rescheduling Customer Shipyard

28-Feb-13 Baker Marine Pacific Class 400 Jackup 257.9 2Q 2015 Technically accepted in

1Q16

Perisai PPL (Singapore)

31-Dec-13 Baker Marine Pacific Class 400 Jackup 268.0 3Q2016 Deferred Perisai PPL (Singapore)

18-Mar-13 Baker Marine Pacific Class 400 Jackup 260.6 End 1Q 2015 Technically accepted in

1Q16

Oro Negro PPL (Singapore)

01-Jul-13 Baker Marine Pacific Class 400 Jackup 260.6 Jul-15 2Q16 Oro Negro PPL (Singapore)

01-Jul-13 Baker Marine Pacific Class 400 Jackup 260.6 3Q2015 4Q16 Oro Negro PPL (Singapore)

26-Feb-14 Baker Marine Pacific Class 400 Jackup 270.9 4Q15 Terminated Marco Polo PPL (Singapore)

03-Nov-14 Baker Marine Pacific Class 400 Jackup 306.8 4Q16 BOT Lease PPL (Singapore)

27-Feb-14 Jurong Espadon III design Drillship 684.1 2Q17 1Q20 Transocean Jurong Shipyard

27-Feb-14 Jurong Espadon III design Drillship 684.1 1Q18 3Q20 Transocean Jurong Shipyard

12-Sep-13 Semi-submersible Well Intervention Rig Semi-sub 438.1 mid-2016 2017 Helix Jurong Shipyard

15-Jul-15 Semi-submersible crane vessel Semi-sub 1,292.0 4Q18 - Heerema

4,983.7

Source: Company, DBS Bank

Peer comparison

Source: Companies, Bloomberg Finance L.P., DBS Bank

PE EV/EBITDA P/B ROE (%) Net D/E Div Yld (%)

Company

Market cap

(US$m) FY17F FY18F FY17F FY18F Current FY17F FY18F Current Current

Keppel Corp 8,585 14.1x 12.7x 18.1x 15.5x 1.0x 7.0% 7.4% 0.54x 3.1%

Hyundai Heavy Industries 7,493 16.8x 31.1x 8.2x 10.1x 0.7x 6.6% 2.0% 0.33x N/A

Yangzijiang 4,039 11.4x 12.5x 5.6x 6.1x 1.1x 9.8% 8.4% CASH 2.8%

Samsung Heavy Industries 3,829 44.8x 33.8x 17.5x 15.7x 0.6x 1.4% 1.8% 0.55x N/A

Shanghai Zhenhua Heavy Industries 3,161 42.2x 27.4x 13.3x 12.4x 1.6x 4.1% 6.0% 1.49x 1.8%

Sembcorp Marine 2,590 43.9x 34.1x 19.5x 17.8x 1.4x 3.2% 3.9% 1.13x 1.2%

Average: 28.9x 25.3x 13.7x 12.9x 1.1x 5.3% 4.9% 0.81x 2.2%

Median: 29.5x 29.3x 15.4x 13.9x 1.1x 5.3% 5.0% 0.55x 2.3%

Page 8Page 8

Industry Focus

Singapore Rigbuilders

COMPANY GUIDES

COMPANY GUIDES

Page 9Page 9

ed: JLC / sa:JC, PY

BUY (Upgrade from HOLD)

Last Traded Price ( 20 Jul 2017): S$6.53 (STI : 3,293.13)

Price Target 12-mth: S$7.60 (16% upside) (Prev S$6.00)

Analyst Pei Hwa HO +65 6682 3714 [email protected]

What’s New Keppel closes in on delivery of world’s first FLNG vessel

conversion

A testament to Keppel; smooth operation of this unit

will boost confidence of potential customers

Benefits from improving sentiment on property

Upgrade to BUY; TP lifted to S$7.60

Price Relative

Forecasts and Valuation FY Dec (S$ m) 2015A 2016A 2017F 2018F

Revenue 10,296 6,767 6,568 6,666 EBITDA 2,280 1,392 1,568 1,669 Pre-tax Profit 1,997 1,055 1,202 1,271 Net Profit 1,525 784 907 959 Net Pft (Pre Ex.) 1,476 784 907 959 Net Pft Gth (Pre-ex) (%) 2.2 (46.9) 15.7 5.7 EPS (S cts) 83.9 43.1 49.9 52.7 EPS Pre Ex. (S cts) 81.2 43.1 49.9 52.7 EPS Gth Pre Ex (%) 2 (47) 16 6 Diluted EPS (S cts) 83.6 43.0 49.7 52.5 Net DPS (S cts) 33.9 20.0 20.0 21.1 BV Per Share (S cts) 610 641 671 704 PE (X) 7.8 15.1 13.1 12.4 PE Pre Ex. (X) 8.0 15.1 13.1 12.4 P/Cash Flow (X) nm 36.0 12.0 14.3 EV/EBITDA (X) 8.3 13.8 12.1 11.3 Net Div Yield (%) 5.2 3.1 3.1 3.2 P/Book Value (X) 1.1 1.0 1.0 0.9 Net Debt/Equity (X) 0.5 0.5 0.5 0.5 ROAE (%) 14.2 6.9 7.6 7.7

Earnings Rev (%): - - 4 Consensus EPS (S cts): 47.6 52.0 Other Broker Recs: B: 6 S: 0 H: 12

Source of all data on this page: Company, DBS Bank, Bloomberg Finance L.P

Riding on improving sentiment on property

Upgrade to BUY with higher TP of S$7.60, after raising valuation peg for property segment from 0.85x to 1.0x P/B, in line with larger-cap Singapore developer peers. We have also omitted the 10% conglomerate discount. Property now contributes nearly two-thirds of earnings and valuation. The segment should continue to see promising sales in China, Vietnam and Singapore. Keppel’s decent dividend yield of 3-4% (based on 40% payout ratio) would also lend some support to its share price.

O&M barely breaking even; looking beyond results. O&M’s recurring net earnings plunged from the peak of c.S$260m a quarter in 2014 to barely break even in 1H17 due to lower volume; EBIT margins fell from 14% to 2% during the same period. We opine that investors should look beyond the upcoming quarterly results, which tend to be lumpy and likely to remain weak, given the low order wins over the past 2 years.

Catalysts – Order wins; property re-rating. We expect Keppel to secure S$1.5bn worth of new orders this year, up from S$500m last year. The group is diversifying into non drilling and LNG segments. This is much needed to replenish its orderbook, which has dwindled to S$3.4bn, excluding Sete’s S$4bn orders. Positive sentiment on the property sector could narrow the valuation discount (currently at 15% to book in our SOTP valuation). Management remains optimistic of stronger home sales in China and Vietnam, with 17k ready-to-launch homes in its pipeline through 2019, representing c.3x of its home sales in 2016.

Valuation: Our TP of S$7.60 is based on sum-of-parts valuation: (1) the O&M segment is valued at 1.8x P/BV, (2) infrastructure at 15x PE on FY16F earnings, (3) the property segment at 1.0x P/BV, (4) investment (Keppel Capital) at 15x PATMI, and (5) market values/estimated fair values are used for listed subsidiaries. Our TP translates to 1.1x FY17 P/BV.

Key Risks to Our View: The O&M segment could fare worse than expected. We forecast annual revenues from Keppel O&M to fall to the ~S$2.6bn level in FY17 and FY18, from S$7-8bn during FY12-14. The continued depletion of its orderbook and deferments/cancellations could pose downside risks to our forecast.

At A Glance Issued Capital (m shrs) 1,813

Mkt. Cap (S$m/US$m) 11,838 / 8,651

Major Shareholders (%)

Temasek Holdings Private Ltd 20.5

Aberdeen Asset Management 5.0

Blackrock 4.7

Free Float (%) 69.8

3m Avg. Daily Val (US$m) 13.9

ICB Industry : Oil & Gas / Oil Equipment; Services & Dist

DBS Group Research . Equity 20 Jul 2017

Singapore Company Guide

Keppel CorporationVersion 9 | Bloomberg: KEP SP | Reuters: KPLM.SI Refer to important disclosures at the end of this report

49

69

89

109

129

149

169

189

209

4.2

5.2

6.2

7.2

8.2

9.2

10.2

11.2

Jul-13 Jul-14 Jul-15 Jul-16 Jul-17

Relative IndexS$

Keppel Corporation (LHS) Relative STI (RHS)

Page 10Page 10

Company Guide

Keppel Corporation

WHAT’S NEW

Delivering world’s first FLNG vessel conversion

Keppel hosted a vessel tour and analyst briefing in early July

following the naming ceremony of the world’s first Floating

Liquefied Natural Gas FLNG vessel conversion – Hilli Episeyo

(picture attached). The vessel is expected to be delivered over

the next 2-3 months upon completion of vessel

commissioning.

This is a significant milestone for Keppel:

1) Hilli Episeyo is the world’s first FLNG vessel conversion

project. Keppel’s Korean peers are only constructing newbuild

FLNG vessels.

2) It is a testament to Keppel’s engineering capability,

given the complexity of the project and space constraint, as

the vessel was converted from a 1975-built LNG carrier

3) It showcases Keppel’s industry connection and ability

to stitch up the value chain with key partners, including

customers and end users.

4) With the experience gained from this first FLNGV

conversion project, Keppel is now in a unique position to

provide customers with reliable end-to-end solutions for the

EPC and commissioning of liquefaction unit - FLNG vessel as

well as regasification unit - FSRU (Floating Storage and

Regasification Unit) conversions.

5) Keppel’s converted FLNG vessel is a faster-to-market

and cost-effective solution compared to newbuilds. The

successful delivery and smooth operation of the unit will

boost the confidence of potential customers and attract new

orders for this solution. In the longer term, Keppel’s LNG

solutions are poised to become mainstream products, riding

on the global push towards cleaner energy.

Order wins driven by non-drilling solutions, diversifying into

LNG. Keppel’s FLNG vessel orders from Golar were priced at

over S$900m each. FLNG orders currently account for over

50% of Keppel’s orderbook (S$3.5bn as of end-March 2017).

This is a strategic move to reduce reliance on drilling solutions

and tap on the robust demand growth for natural gas as

cleaner energy. We believe LNG solutions will be a major

order driver for Singapore rigbuilders moving into 2018.

Keppel to ride on sentiment turnaround in the property

sector; raising valuation peg to 1.0x P/BV. Our property

analysts believe that we are at the start of a multi-year

government relaxation cycle in Singapore, which presents a

multi-year re-rating potential for developers. We are raising

our valuation peg for Keppel’s property segment from 0.85x

to 1.0x P/BV, in line with the other large-cap Singapore

developer peers.

Page 11Page 11

Company Guide

Keppel Corporation

CRITICAL DATA POINTS TO WATCH

Critical Factors

Orderbook the key driver of Keppel O&M’s earnings; FLNG and

production facilities to fill the gap. Keppel O&M secured

S$1.8bn in order wins in FY15 and S$500m in FY16, dismal

compared to its 2010 and 2011 peak of S$10bn p.a. Its

orderbook has dwindled to S$3.4bn, from S$5.1bn at end-2015

and S$3.5bn a quarter ago. A declining net orderbook points to

declining earnings ahead. Scrapping of old rigs (>30 years old),

estimated to constitute ~15% of the current fleet globally,

could help push the market back into balance. An oil price

rebound would also improve rig utilisation, spurring capex

spend and order wins. In terms of growth potential, Keppel’s

first-mover advantage in the FLNG conversion market could

provide earnings upside; customer Golar has already awarded

Keppel a third FLNG project.

Residential property sales in China and Vietnam are the main

drivers of Keppel Land’s revenue and earnings. In China, further

relaxation of cooling measures, urbanisation and low mortgage

rates resulting from monetary easing, seem to be encouraging

for residential property sales. Vietnam is another emerging

market for Keppel, accounting for 27% of its home sales in

FY16. Unit sales in Singapore will likely be dampened by weak

buyer sentiment due to the continuing effects of the

government’s tightening measures, a flood of incoming

completions and slowing government land sales (GLS) – factors

which signal falling average selling prices.

The infrastructure division’s earnings buoyed by handover of

problematic assets. The bad-apple situation with Keppel

Infrastructure’s EPC projects has improved with the handover of

the two Greater Manchester EfW (energy-from-waste) plants

and Doha North in 2015. Thus, lower EPC provisions going

forward should boost earnings in the short term.

Value-unlocking divestments can provide earnings upside.

Divestments can free up cash to be invested in more profitable

areas or to pay down debt. In Keppel’s case, it may also reduce

the conglomerate discount on its stock. M1 is a possible

candidate for sale; its fundamentals are uninspiring and our

telecom analyst has downgraded M1 to FULLY VALUED after

removing the 25% M&A premium from its DCF valuation,

following the announcement that M1’s major shareholders

(with a combined stake of 61%) are not going ahead with a

strategic review to dispose of their stake. We estimate Keppel's

stake in M1 to be worth ~S$320m. Injection of infrastructure

assets such as Woodlands Wafer Fab Park into Keppel

Infrastructure Trust (KIT), to whom Keppel Infrastructure acts as

sponsor, could be another alternative.

Sales Trend

Asset Trend

Profitability Trend

Margin Trends (%)

Source: Company, DBS Bank

-30.0%

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

0

2,000

4,000

6,000

8,000

10,000

12,000

2014A 2015A 2016A 2017F 2018F

S$ m

Total Revenue Revenue Growth (%) (YoY)

5,000

10,000

15,000

20,000

25,000

2014A 2015A 2016A 2017F 2018F

S$ m

Net Fixed Assets (Tangible) Total Current Assets

783

1,283

1,783

2,283

2,783

2014A 2015A 2016A 2017F 2018F

S$ m

Operating EBIT Pre tax Profit Net Profit

10%

15%

20%

25%

30%

2014A 2015A 2016A 2017F 2018F

EBITDA Margin % EBIT Margin % Net Income Margin %

Page 12Page 12

Company Guide

Keppel Corporation

Balance Sheet:

Following the privatisation of Keppel Land in 1Q15, Keppel

Corp’s net gearing rose from 0.11x as of end-2014 to 0.42x as

of end-2Q15 and 0.662x as of end-2Q16. The increase in

gearing stems from a lower shareholders' equity and cash

balance as the privatization was largely funded by cash. The

gearing level had declined to 0.58x as of end-2Q17, aided by

capital recycling.

Share Price Drivers:

Recovery in oil prices would support the share price. We think

Keppel O&M would benefit if oil prices recover to at least above

the US$55/bbl level, which would trigger more offshore oil &

gas capex spend.

Announcement of new order wins. Strong order win

announcements could push up the share price, as investors

reward greater visibility on revenues and earnings.

Key Risks:

Competition from foreign yards. Keener competition from

Chinese yards – which are usually aggressive in their pricing

and lax with payment terms – as well as Korean peers may

affect order wins and profitability, especially if Keppel starts to

offer concessions to protect market share.

Further deferments possible if oil prices remain subdued. Since

the oil price started declining in mid-2014, we have seen oil

majors and asset owners slash capex spending substantially,

which has hit yards hard. Meanwhile, deliveries of newbuilds

and conversions already under construction are being delayed

– a situation which could worsen if oil prices remain low.

Company Background

Keppel is a diversified conglomerate with its core businesses in

offshore marine (O&M), property investments and

development, and infrastructure-based activities in Singapore

and the region. O&M is the largest segment, typically

contributing about two-thirds of group revenue. It possesses

strong market leadership positions in rigbuilding, particularly

for jackups and semi-submersibles, FPSO conversion, FLNG

conversion, as well as repair and construction of high-end

specialised vessels.

Leverage & Asset Turnover (x)

Capital Expenditure

ROE (%)

Forward PE Band (x)

PB Band (x)

Source: Company, DBS Bank

0.2

0.3

0.3

0.4

0.4

0.5

0.5

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

2014A 2015A 2016A 2017F 2018F

Gross Debt to Equity (LHS) Asset Turnover (RHS)

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

2014A 2015A 2016A 2017F 2018F

Capital Expenditure (-)

S$m

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

2014A 2015A 2016A 2017F 2018F

Avg: 12.7x

+1sd: 13.8x

+2sd: 14.8x

-1sd: 11.6x

-2sd: 10.5x

8.8

9.8

10.8

11.8

12.8

13.8

14.8

15.8

Jul-13 Jul-14 Jul-15 Jul-16 Jul-17

(x)

Avg: 1.39x

+1sd: 1.84x

+2sd: 2.29x

-1sd: 0.93x

-2sd: 0.48x0.4

0.9

1.4

1.9

2.4

Jul-13 Jul-14 Jul-15 Jul-16 Jul-17

(x)

Page 13Page 13

Company Guide

Keppel Corporation

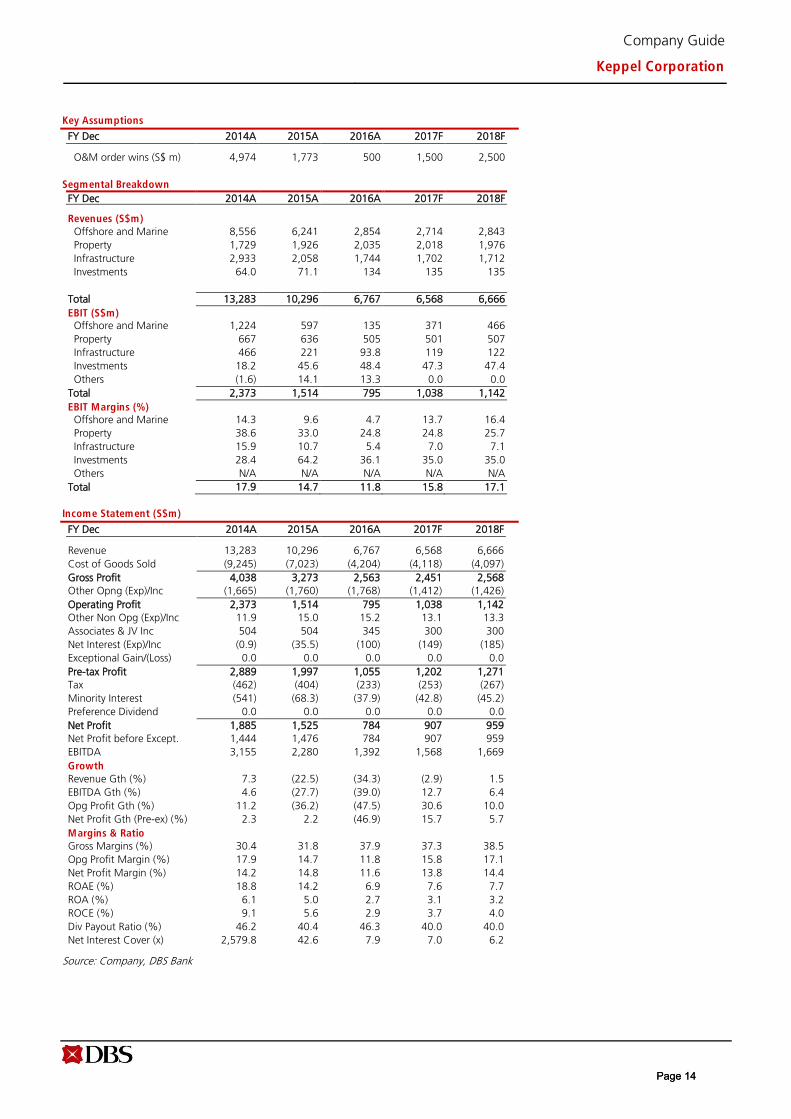

Key Assumptions

FY Dec 2014A 2015A 2016A 2017F 2018F

O&M order wins (S$ m) 4,974 1,773 500 1,500 2,500

Segmental Breakdown

FY Dec 2014A 2015A 2016A 2017F 2018F

Revenues (S$m)

Offshore and Marine 8,556 6,241 2,854 2,714 2,843

Property 1,729 1,926 2,035 2,018 1,976

Infrastructure 2,933 2,058 1,744 1,702 1,712

Investments 64.0 71.1 134 135 135

Total 13,283 10,296 6,767 6,568 6,666

EBIT (S$m) Offshore and Marine 1,224 597 135 371 466

Property 667 636 505 501 507

Infrastructure 466 221 93.8 119 122

Investments 18.2 45.6 48.4 47.3 47.4

Others (1.6) 14.1 13.3 0.0 0.0

Total 2,373 1,514 795 1,038 1,142

EBIT Margins (%) Offshore and Marine 14.3 9.6 4.7 13.7 16.4

Property 38.6 33.0 24.8 24.8 25.7

Infrastructure 15.9 10.7 5.4 7.0 7.1

Investments 28.4 64.2 36.1 35.0 35.0

Others N/A N/A N/A N/A N/A

Total 17.9 14.7 11.8 15.8 17.1

Income Statement (S$m)

FY Dec 2014A 2015A 2016A 2017F 2018F

Revenue 13,283 10,296 6,767 6,568 6,666

Cost of Goods Sold (9,245) (7,023) (4,204) (4,118) (4,097)

Gross Profit 4,038 3,273 2,563 2,451 2,568

Other Opng (Exp)/Inc (1,665) (1,760) (1,768) (1,412) (1,426)

Operating Profit 2,373 1,514 795 1,038 1,142

Other Non Opg (Exp)/Inc 11.9 15.0 15.2 13.1 13.3

Associates & JV Inc 504 504 345 300 300

Net Interest (Exp)/Inc (0.9) (35.5) (100) (149) (185)

Exceptional Gain/(Loss) 0.0 0.0 0.0 0.0 0.0

Pre-tax Profit 2,889 1,997 1,055 1,202 1,271

Tax (462) (404) (233) (253) (267)

Minority Interest (541) (68.3) (37.9) (42.8) (45.2)

Preference Dividend 0.0 0.0 0.0 0.0 0.0

Net Profit 1,885 1,525 784 907 959

Net Profit before Except. 1,444 1,476 784 907 959

EBITDA 3,155 2,280 1,392 1,568 1,669

Growth

Revenue Gth (%) 7.3 (22.5) (34.3) (2.9) 1.5

EBITDA Gth (%) 4.6 (27.7) (39.0) 12.7 6.4

Opg Profit Gth (%) 11.2 (36.2) (47.5) 30.6 10.0

Net Profit Gth (Pre-ex) (%) 2.3 2.2 (46.9) 15.7 5.7

Margins & Ratio

Gross Margins (%) 30.4 31.8 37.9 37.3 38.5

Opg Profit Margin (%) 17.9 14.7 11.8 15.8 17.1

Net Profit Margin (%) 14.2 14.8 11.6 13.8 14.4

ROAE (%) 18.8 14.2 6.9 7.6 7.7

ROA (%) 6.1 5.0 2.7 3.1 3.2

ROCE (%) 9.1 5.6 2.9 3.7 4.0

Div Payout Ratio (%) 46.2 40.4 46.3 40.0 40.0

Net Interest Cover (x) 2,579.8 42.6 7.9 7.0 6.2

Source: Company, DBS Bank

Page 14Page 14

Company Guide

Keppel Corporation

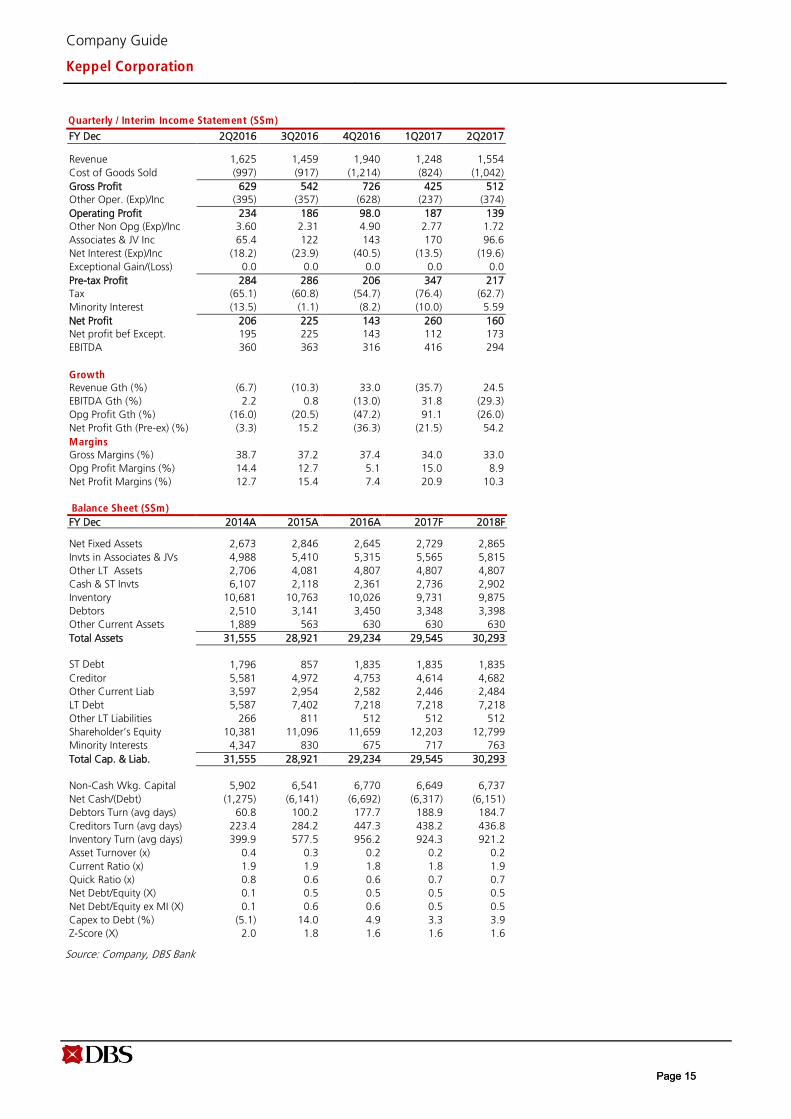

Quarterly / Interim Income Statement (S$m)

FY Dec 2Q2016 3Q2016 4Q2016 1Q2017 2Q2017

Revenue 1,625 1,459 1,940 1,248 1,554

Cost of Goods Sold (997) (917) (1,214) (824) (1,042)

Gross Profit 629 542 726 425 512

Other Oper. (Exp)/Inc (395) (357) (628) (237) (374)

Operating Profit 234 186 98.0 187 139

Other Non Opg (Exp)/Inc 3.60 2.31 4.90 2.77 1.72

Associates & JV Inc 65.4 122 143 170 96.6

Net Interest (Exp)/Inc (18.2) (23.9) (40.5) (13.5) (19.6)

Exceptional Gain/(Loss) 0.0 0.0 0.0 0.0 0.0

Pre-tax Profit 284 286 206 347 217

Tax (65.1) (60.8) (54.7) (76.4) (62.7)

Minority Interest (13.5) (1.1) (8.2) (10.0) 5.59

Net Profit 206 225 143 260 160

Net profit bef Except. 195 225 143 112 173

EBITDA 360 363 316 416 294

Growth

Revenue Gth (%) (6.7) (10.3) 33.0 (35.7) 24.5

EBITDA Gth (%) 2.2 0.8 (13.0) 31.8 (29.3)

Opg Profit Gth (%) (16.0) (20.5) (47.2) 91.1 (26.0)

Net Profit Gth (Pre-ex) (%) (3.3) 15.2 (36.3) (21.5) 54.2

Margins

Gross Margins (%) 38.7 37.2 37.4 34.0 33.0

Opg Profit Margins (%) 14.4 12.7 5.1 15.0 8.9

Net Profit Margins (%) 12.7 15.4 7.4 20.9 10.3

Balance Sheet (S$m)

FY Dec 2014A 2015A 2016A 2017F 2018F

Net Fixed Assets 2,673 2,846 2,645 2,729 2,865

Invts in Associates & JVs 4,988 5,410 5,315 5,565 5,815

Other LT Assets 2,706 4,081 4,807 4,807 4,807

Cash & ST Invts 6,107 2,118 2,361 2,736 2,902

Inventory 10,681 10,763 10,026 9,731 9,875

Debtors 2,510 3,141 3,450 3,348 3,398

Other Current Assets 1,889 563 630 630 630

Total Assets 31,555 28,921 29,234 29,545 30,293

ST Debt 1,796 857 1,835 1,835 1,835

Creditor 5,581 4,972 4,753 4,614 4,682

Other Current Liab 3,597 2,954 2,582 2,446 2,484

LT Debt 5,587 7,402 7,218 7,218 7,218

Other LT Liabilities 266 811 512 512 512

Shareholder’s Equity 10,381 11,096 11,659 12,203 12,799

Minority Interests 4,347 830 675 717 763

Total Cap. & Liab. 31,555 28,921 29,234 29,545 30,293

Non-Cash Wkg. Capital 5,902 6,541 6,770 6,649 6,737

Net Cash/(Debt) (1,275) (6,141) (6,692) (6,317) (6,151)

Debtors Turn (avg days) 60.8 100.2 177.7 188.9 184.7

Creditors Turn (avg days) 223.4 284.2 447.3 438.2 436.8

Inventory Turn (avg days) 399.9 577.5 956.2 924.3 921.2

Asset Turnover (x) 0.4 0.3 0.2 0.2 0.2

Current Ratio (x) 1.9 1.9 1.8 1.8 1.9

Quick Ratio (x) 0.8 0.6 0.6 0.7 0.7

Net Debt/Equity (X) 0.1 0.5 0.5 0.5 0.5

Net Debt/Equity ex MI (X) 0.1 0.6 0.6 0.5 0.5

Capex to Debt (%) (5.1) 14.0 4.9 3.3 3.9

Z-Score (X) 2.0 1.8 1.6 1.6 1.6

Source: Company, DBS Bank

Page 15Page 15

Company Guide

Keppel Corporation

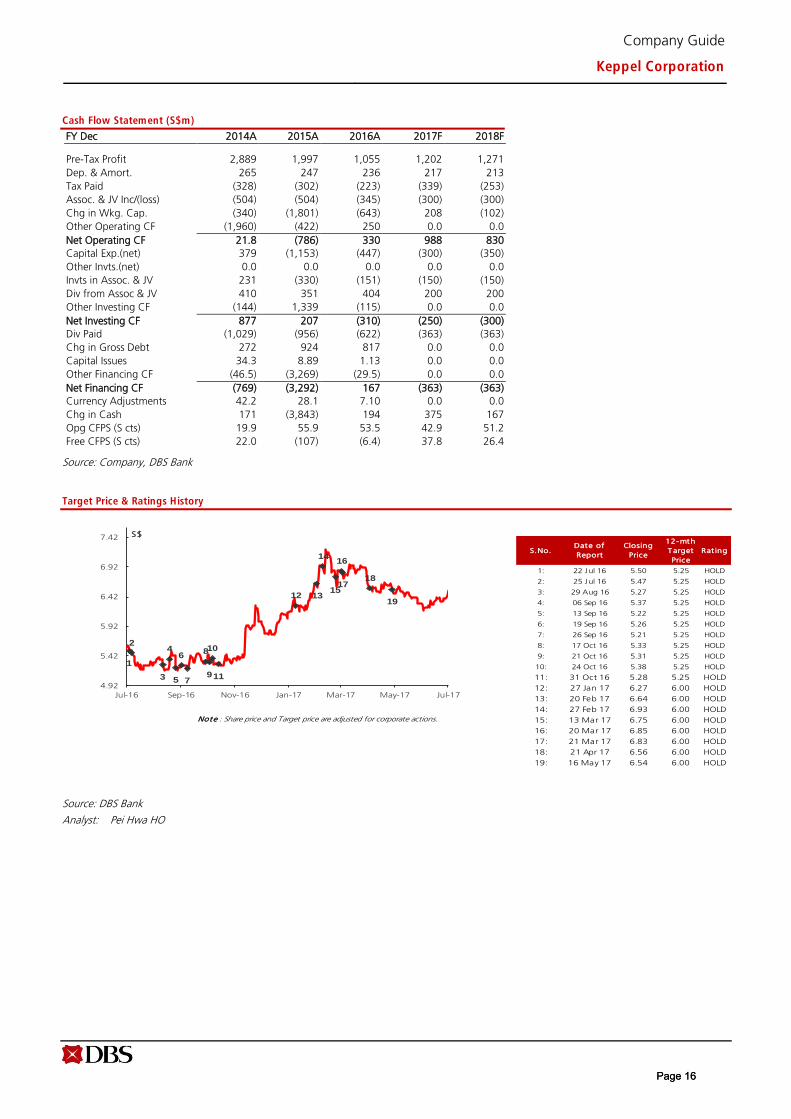

Cash Flow Statement (S$m)

FY Dec 2014A 2015A 2016A 2017F 2018F

Pre-Tax Profit 2,889 1,997 1,055 1,202 1,271

Dep. & Amort. 265 247 236 217 213

Tax Paid (328) (302) (223) (339) (253)

Assoc. & JV Inc/(loss) (504) (504) (345) (300) (300)

Chg in Wkg. Cap. (340) (1,801) (643) 208 (102)

Other Operating CF (1,960) (422) 250 0.0 0.0

Net Operating CF 21.8 (786) 330 988 830

Capital Exp.(net) 379 (1,153) (447) (300) (350)

Other Invts.(net) 0.0 0.0 0.0 0.0 0.0

Invts in Assoc. & JV 231 (330) (151) (150) (150)

Div from Assoc & JV 410 351 404 200 200

Other Investing CF (144) 1,339 (115) 0.0 0.0

Net Investing CF 877 207 (310) (250) (300)

Div Paid (1,029) (956) (622) (363) (363)

Chg in Gross Debt 272 924 817 0.0 0.0

Capital Issues 34.3 8.89 1.13 0.0 0.0

Other Financing CF (46.5) (3,269) (29.5) 0.0 0.0

Net Financing CF (769) (3,292) 167 (363) (363)

Currency Adjustments 42.2 28.1 7.10 0.0 0.0

Chg in Cash 171 (3,843) 194 375 167

Opg CFPS (S cts) 19.9 55.9 53.5 42.9 51.2

Free CFPS (S cts) 22.0 (107) (6.4) 37.8 26.4

Source: Company, DBS Bank

Target Price & Ratings History

Source: DBS Bank

Analyst: Pei Hwa HO

S.No.Date of

Report

Closing

Price

12-mth

Target

Price

Rat ing

1: 22 Jul 16 5.50 5.25 HOLD

2: 25 Jul 16 5.47 5.25 HOLD

3: 29 Aug 16 5.27 5.25 HOLD

4: 06 Sep 16 5.37 5.25 HOLD

5: 13 Sep 16 5.22 5.25 HOLD

6: 19 Sep 16 5.26 5.25 HOLD

7: 26 Sep 16 5.21 5.25 HOLD

8: 17 Oct 16 5.33 5.25 HOLD

9: 21 Oct 16 5.31 5.25 HOLD

10: 24 Oct 16 5.38 5.25 HOLD

11: 31 Oct 16 5.28 5.25 HOLD

12: 27 Jan 17 6.27 6.00 HOLD

13: 20 Feb 17 6.64 6.00 HOLD

14: 27 Feb 17 6.93 6.00 HOLD

Note : Share price and Target price are adjusted for corporate actions. 15: 13 Mar 17 6.75 6.00 HOLD

16: 20 Mar 17 6.85 6.00 HOLD

17: 21 Mar 17 6.83 6.00 HOLD

18: 21 Apr 17 6.56 6.00 HOLD

19: 16 May 17 6.54 6.00 HOLD

1

2

3

4

5

6

7

8

9

10

11

12 13

14

15

16

1718

19

4.92

5.42

5.92

6.42

6.92

7.42

Jul-16 Sep-16 Nov-16 Jan-17 Mar-17 May-17 Jul-17

S$

Page 16Page 16

ed: JS / sa:JC, PY

BUYLast Traded Price ( 3 Aug 2017): S$3.22 (STI : 3,342.92) Price Target 12-mth: S$4.00 (24% upside) (Prev S$4.10)

Analyst Pei Hwa HO +65 6682 3714 [email protected]

What’s New • 2Q hit by India’s refinancing cost and Marine’s forex

loss

• Singapore Utilities and Urban Development strongerthan expected

• Declared interim dividend of 3 Scts per share

• Maintain BUY; TP adjusted to S$4.00 followingmarginal earnings revisions

Price Relative

Forecasts and Valuation FY Dec (S$ m) 2015A 2016A 2017F 2018F Revenue 9,545 7,907 7,178 7,899 EBITDA 590 1,305 1,317 1,374 Pre-tax Profit 426 537 518 568 Net Profit 549 395 380 425 Net Pft (Pre Ex.) 123 407 380 425 Net Pft Gth (Pre-ex) (%) (84.6) 230.1 (6.7) 11.9 EPS (S cts) 30.7 22.1 21.2 23.8 EPS Pre Ex. (S cts) 6.91 22.8 21.2 23.8 EPS Gth Pre Ex (%) (85) 230 (7) 12 Diluted EPS (S cts) 30.5 21.9 21.1 23.6 Net DPS (S cts) 11.0 7.99 6.80 7.61 BV Per Share (S cts) 360 375 388 405 PE (X) 10.5 14.6 15.2 13.5 PE Pre Ex. (X) 46.6 14.1 15.2 13.5 P/Cash Flow (X) nm 6.6 11.0 2.6 EV/EBITDA (X) 21.3 11.2 11.5 10.2 Net Div Yield (%) 3.4 2.5 2.1 2.4 P/Book Value (X) 0.9 0.9 0.8 0.8 Net Debt/Equity (X) 0.6 0.9 0.9 0.8 ROAE (%) 9.1 6.0 5.6 6.0 Earnings Rev (%): (4) (1) Consensus EPS (S cts): 22.0 26.3 Other Broker Recs: B: 7 S: 3 H: 5

Source of all data on this page: Company, DBS Bank, Bloomberg Finance L.P

Look forward to review outcome in 4Q Maintain BUY; TP adjusted slightly to S$4.00, after trimming FY17/18F earnings by 4%/1.5% to reflect larger losses at its second power plant in India. While weakness in India may take longer to resolve, we continue to like Sembcorp Industries (SCI) as it offers a unique value proposition as a proxy to ride the cyclical O&M upturn, and is supported by a defensive utilities business. Our S$4.00 TP translates to 1.1x P/BV, which we believe is fair in view of its 6% ROE and 2% dividend yield. The stock offers 24% potential upside.

Strategic review gives rise to speculation. Under the helm of the new CEO, SCI is undertaking a complete review of businesses and strategic direction, focusing on performance, sustainability and value creation. The review is expected to be concluded in 4Q17. While it is premature to shed more light on the future direction of SCI, this may revive market speculation on potential rationalisation of SCI, Sembcorp Marine (SMM) and Keppel Corporation (Keppel).

Where we differ: “Big three rationalisation theory” and long-term growth prospects of utilities. Since Aug-2015, we have flagged the potential merger between Keppel’s O&M arm and SMM during the structural downturn. The potential spin-off of its marine arm could re-rate SCI’s undervalued utilities business that is currently overshadowed by a weak marine outlook. We believe in the long-term growth prospects of SCI’s utilities arm, which has expanded its global footprint and recently made forays into key emerging markets – India, Bangladesh and Myanmar.

Valuation: Given its diverse earnings stream and various listed assets, we derive our fair value for SCI based on the sum of its different parts: market valuations of its stakes in listed companies Sembcorp Marine (SGX-listed, 60.6% stake), Gallant Venture (SGX-listed, 11.96% stake) and Salalah (Muscat stock exchange, 40% stake) as well as earnings from utilities and urban development. For its holding company position, we have applied a 10% conglomerate discount to the reappraised net asset value (RNAV). We derive a TP of S$4.00, translating to 1.1x P/BV.

Key Risks to Our View: Key risks to earnings are further deferments/cancellations of marine projects, deterioration of Singapore's power spark spreads, and execution hiccups at its Indian power plants.

At A Glance Issued Capital (m shrs) 1,784 Mkt. Cap (S$m/US$m) 5,746 / 4,229 Major Shareholders (%) Temasek Holdings Pte Ltd 49.5 Mondrian Investment Partners Ltd 4.9

Free Float (%) 45.6 3m Avg. Daily Val (US$m) 6.7 ICB Industry : Oil & Gas / Oil Equipment; Services & Dist

DBS Group Research . Equity 4 Aug 2017

Singapore Company Guide

Sembcorp Industries Version 14 | Bloomberg: SCI SP | Reuters: SCIL.SI Refer to important disclosures at the end of this report

Page 17Page 17

Company Guide

Sembcorp Industries

WHAT’S NEW

Hit by refinancing cost and forex loss

2Q17 hit by India’s refinancing cost and Marine’s forex loss. Group net profit came in at S$55.3m (-36% y-o-y) in 2Q17, dragged by S$33.9m prepayment penalty for India’s Sembcorp Gayathri Power (SGPL) plant as previously guided and Marine’s S$34.3m forex loss (attributable to SCI: S$20m). This brings 1H17 group earnings to S$174.4m, making up 44% of our full year forecast.

SMM reported 51% y-o-y lower headline net profit of S$5.6m (attributable to SCI: S$3.4m), though the drag was mainly from large FX losses of S$34.3m due to the revaluation of the Brazilian yard’s liabilities denominated in US dollar to Brazilian Real, as well as revaluation of other assets and liabilities from USD to SGD. Without the FX loss, net profit would have come in at c. S$38m – more or less flat q-o-q. On a positive note, EBIT margin rose from 1.8% in 1Q17 to 4.3% this quarter. Stripping out the FX losses, the improvement would have been more pronounced, with adjusted EBIT margin at 9.6% for 2Q17.

India’s power sector could take longer to improve. Losses at the SGPL plant (the first unit commenced operations in Nov-2016 and second unit in Feb-2017) widened by S$3m to S$29m in 2Q17 due to weaker spot tariffs. The plant incurred relatively high startup loss of S$27m in 4Q16 and S$55m in 1H17. Earnings could be volatile in the absence of long-term Power Purchase Agreement (PPAs) and coal cost pass-through mechanism, while short term market is competitive in the near term. Management expects India’s power sector to take another 2-3 years to resolve current power oversupply led by structural issues.

Refinancing India’s loan: short term pain, long term gain. Management has refinanced its Indian loan (Thermal Powertech Corporation India (TPCIL) in 2H16 and SGPL in 1H17) as part of its efforts to lower operational cost. As a result, SGPL incurred one-off prepayment penalty of S$39.1m in 1H17. But, this is expected to lower future interest cost by 300bps to around 10-11%, resulting in interest savings of c.S$40m p.a. for SGPL plant.

Earnings revision. We have lowered our FY17-18 net profit forecasts by 3.8/1.5% largely to reflect the bigger than expected losses at SGPL.

Some bright spots. Utilities business in Singapore was stronger than expected, and net profit rose 45% y-o-y and 22% q-o-q to S$41.7m in 2Q17, thanks to the stronger centralised utilities and gas business. This was partly driven by the resumption of a customer’s (JAC) plant. Urban Development also posted stellar 1H17 earnings with net profit surging 5.2x in 1H17 as land sales picked up.

Declared interim dividend of 3 Scts, down from 4 Scts last year. Management intends to maintain the 30% payout ratio while attempting to conserve cash for investment.

Page 18Page 18

Company Guide

Sembcorp Industries

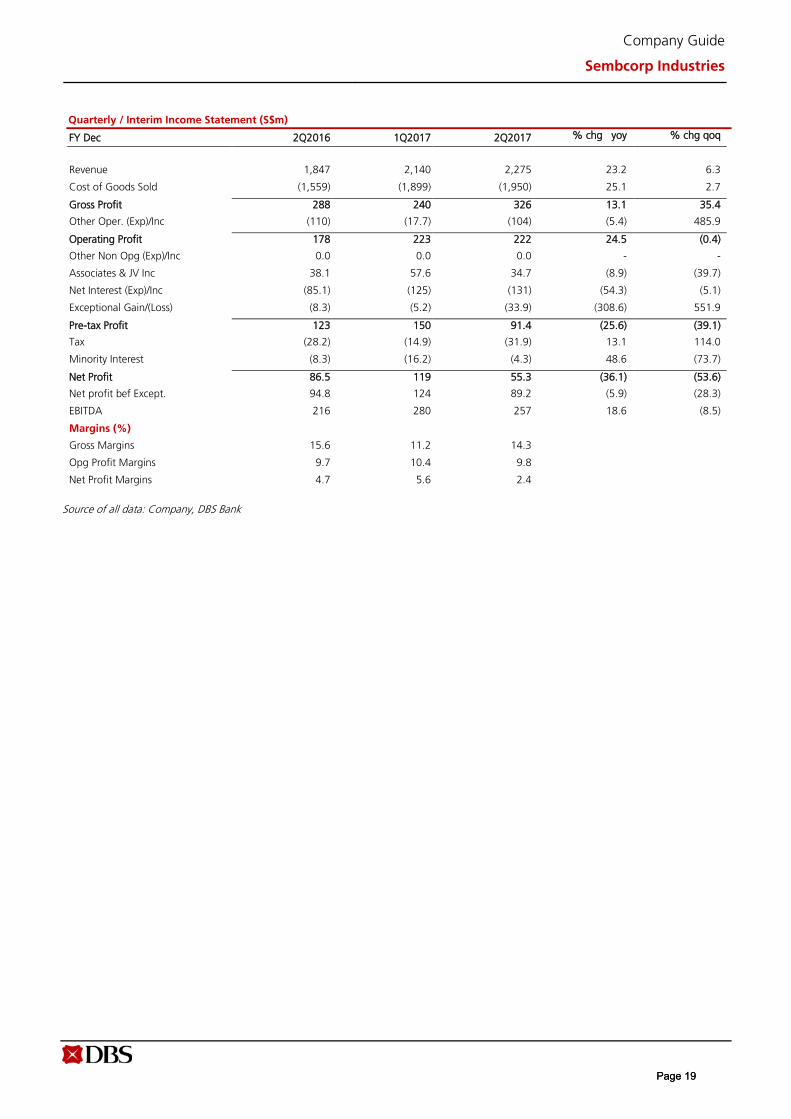

Quarterly / Interim Income Statement (S$m)

FY Dec 2Q2016 1Q2017 2Q2017 % chg yoy % chg qoq

Revenue 1,847 2,140 2,275 23.2 6.3

Cost of Goods Sold (1,559) (1,899) (1,950) 25.1 2.7

Gross Profit 288 240 326 13.1 35.4

Other Oper. (Exp)/Inc (110) (17.7) (104) (5.4) 485.9

Operating Profit 178 223 222 24.5 (0.4)

Other Non Opg (Exp)/Inc 0.0 0.0 0.0 - -

Associates & JV Inc 38.1 57.6 34.7 (8.9) (39.7)

Net Interest (Exp)/Inc (85.1) (125) (131) (54.3) (5.1)

Exceptional Gain/(Loss) (8.3) (5.2) (33.9) (308.6) 551.9

Pre-tax Profit 123 150 91.4 (25.6) (39.1)

Tax (28.2) (14.9) (31.9) 13.1 114.0

Minority Interest (8.3) (16.2) (4.3) 48.6 (73.7)

Net Profit 86.5 119 55.3 (36.1) (53.6)

Net profit bef Except. 94.8 124 89.2 (5.9) (28.3)

EBITDA 216 280 257 18.6 (8.5)

Margins (%)

Gross Margins 15.6 11.2 14.3

Opg Profit Margins 9.7 10.4 9.8

Net Profit Margins 4.7 5.6 2.4

Source of all data: Company, DBS Bank

Page 19Page 19

Company Guide

Sembcorp Industries

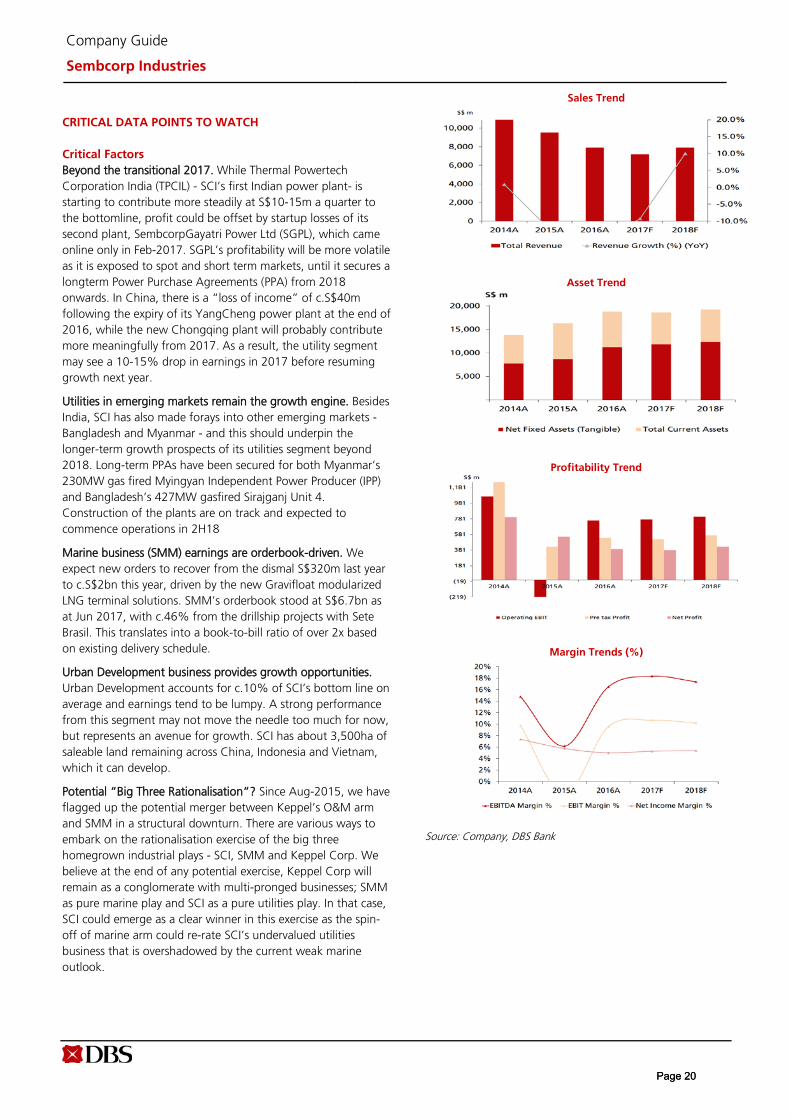

CRITICAL DATA POINTS TO WATCH

Critical Factors Beyond the transitional 2017. While Thermal Powertech Corporation India (TPCIL) - SCI’s first Indian power plant- is starting to contribute more steadily at S$10-15m a quarter to the bottomline, profit could be offset by startup losses of its second plant, SembcorpGayatri Power Ltd (SGPL), which came online only in Feb-2017. SGPL’s profitability will be more volatile as it is exposed to spot and short term markets, until it secures a longterm Power Purchase Agreements (PPA) from 2018 onwards. In China, there is a “loss of income” of c.S$40m following the expiry of its YangCheng power plant at the end of 2016, while the new Chongqing plant will probably contribute more meaningfully from 2017. As a result, the utility segment may see a 10-15% drop in earnings in 2017 before resuming growth next year.

Utilities in emerging markets remain the growth engine. Besides India, SCI has also made forays into other emerging markets - Bangladesh and Myanmar - and this should underpin the longer-term growth prospects of its utilities segment beyond 2018. Long-term PPAs have been secured for both Myanmar’s 230MW gas fired Myingyan Independent Power Producer (IPP) and Bangladesh’s 427MW gasfired Sirajganj Unit 4. Construction of the plants are on track and expected to commence operations in 2H18

Marine business (SMM) earnings are orderbook-driven. We expect new orders to recover from the dismal S$320m last year to c.S$2bn this year, driven by the new Gravifloat modularized LNG terminal solutions. SMM’s orderbook stood at S$6.7bn as at Jun 2017, with c.46% from the drillship projects with Sete Brasil. This translates into a book-to-bill ratio of over 2x based on existing delivery schedule.

Urban Development business provides growth opportunities. Urban Development accounts for c.10% of SCI’s bottom line on average and earnings tend to be lumpy. A strong performance from this segment may not move the needle too much for now, but represents an avenue for growth. SCI has about 3,500ha of saleable land remaining across China, Indonesia and Vietnam, which it can develop.

Potential “Big Three Rationalisation”? Since Aug-2015, we have flagged up the potential merger between Keppel’s O&M arm and SMM in a structural downturn. There are various ways to embark on the rationalisation exercise of the big three homegrown industrial plays - SCI, SMM and Keppel Corp. We believe at the end of any potential exercise, Keppel Corp will remain as a conglomerate with multi-pronged businesses; SMM as pure marine play and SCI as a pure utilities play. In that case, SCI could emerge as a clear winner in this exercise as the spin-off of marine arm could re-rate SCI’s undervalued utilities business that is overshadowed by the current weak marine outlook.

Sales Trend

Asset Trend

Profitability Trend

Margin Trends (%)

Source: Company, DBS Bank

Page 20Page 20

Company Guide

Sembcorp Industries

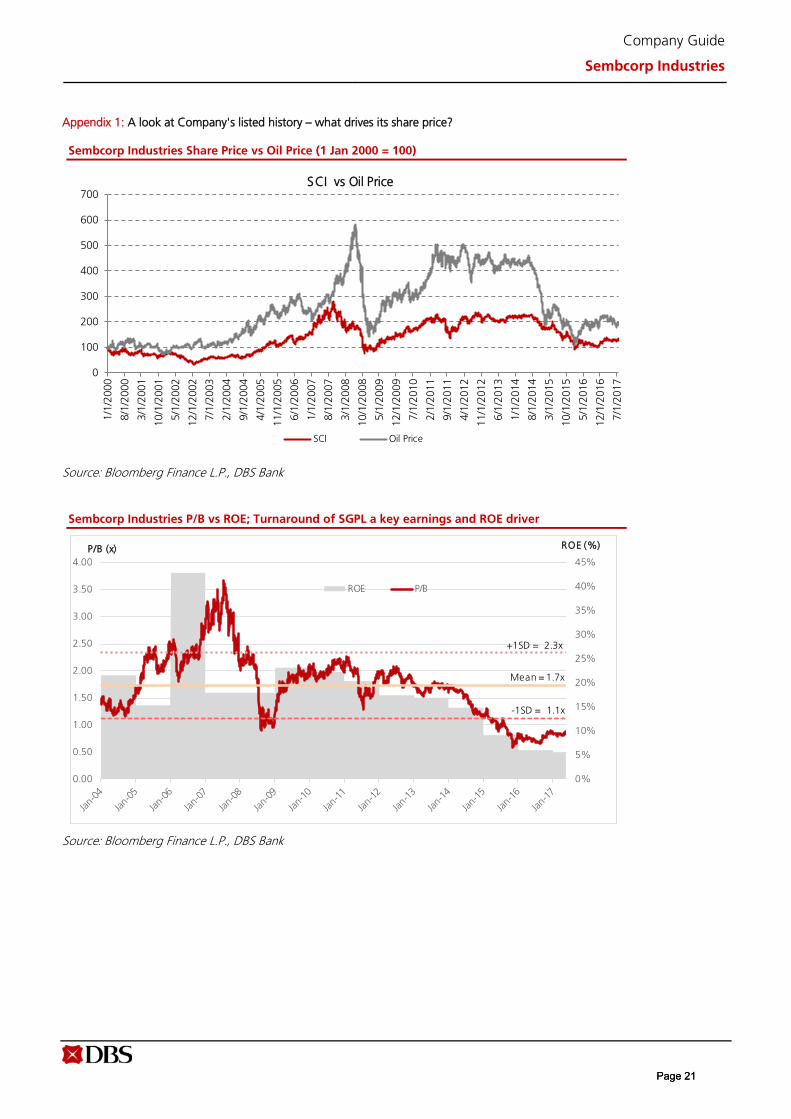

Appendix 1: A look at Company's listed history – what drives its share price?

Sembcorp Industries Share Price vs Oil Price (1 Jan 2000 = 100)

Source: Bloomberg Finance L.P., DBS Bank

Sembcorp Industries P/B vs ROE; Turnaround of SGPL a key earnings and ROE driver

Source: Bloomberg Finance L.P., DBS Bank

0

100

200

300

400

500

600

700

1/1/

2000

8/1/

2000

3/1/

2001

10/1

/200

1

5/1/

2002

12/1

/200

2

7/1/

2003

2/1/

2004

9/1/

2004

4/1/

2005

11/1

/200

5

6/1/

2006

1/1/

2007

8/1/

2007

3/1/

2008

10/1

/200

8

5/1/

2009

12/1

/200

9

7/1/

2010

2/1/

2011

9/1/

2011

4/1/

2012

11/1

/201

2

6/1/

2013

1/1/

2014

8/1/

2014

3/1/

2015

10/1

/201

5

5/1/

2016

12/1

/201

6

7/1/

2017

SCI vs Oil Price

SCI Oil Price

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

ROE P/B

Mean = 1.7x

-1SD = 1.1x

ROE (%)P/B (x)

+1SD = 2.3x

Page 21Page 21

Company Guide

Sembcorp Industries

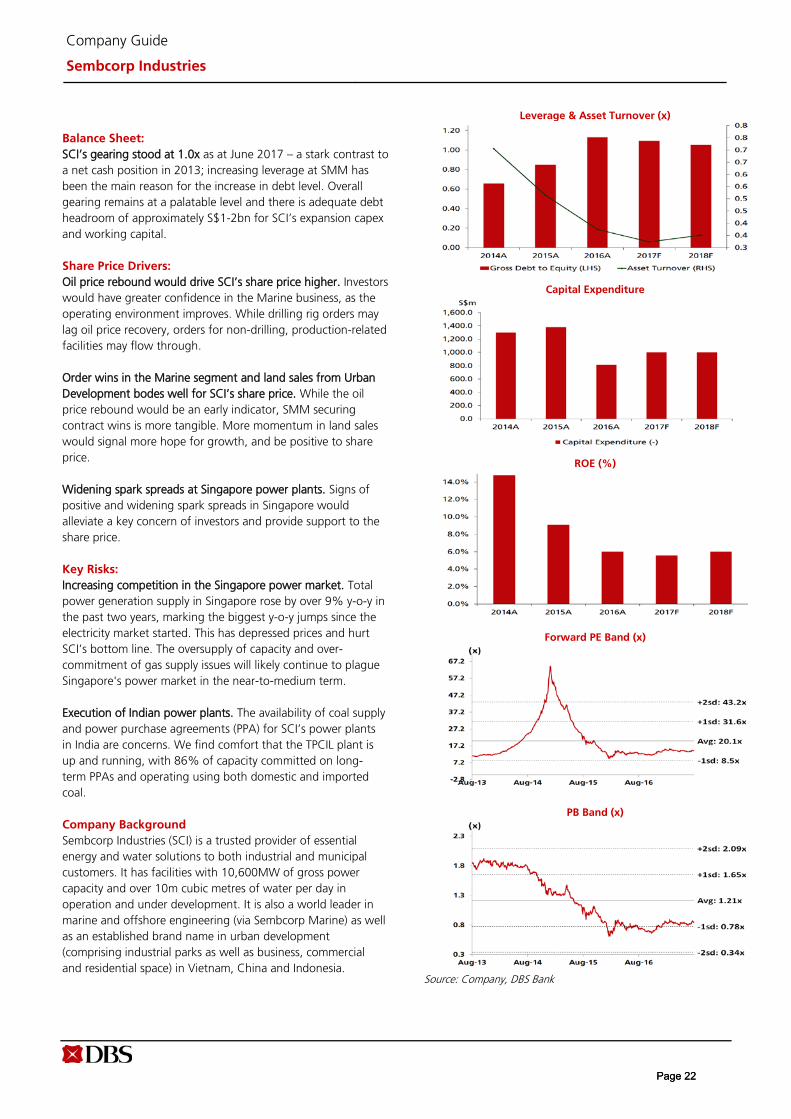

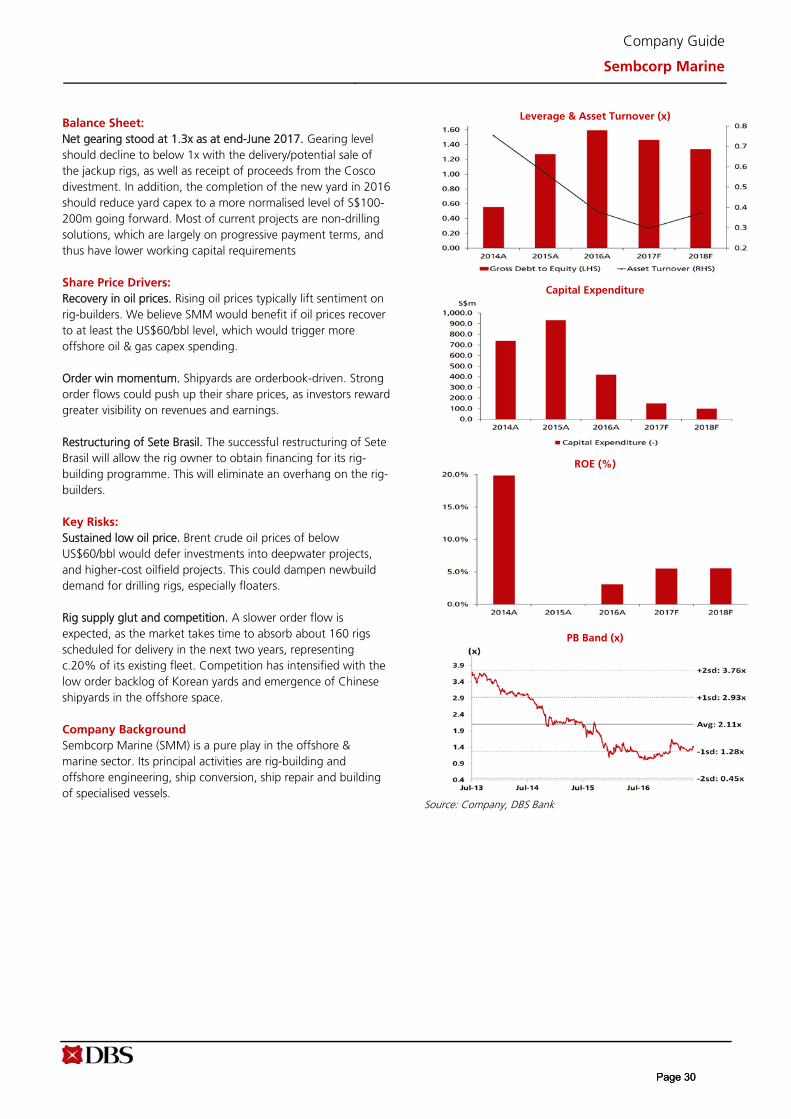

Balance Sheet: SCI’s gearing stood at 1.0x as at June 2017 – a stark contrast to a net cash position in 2013; increasing leverage at SMM has been the main reason for the increase in debt level. Overall gearing remains at a palatable level and there is adequate debt headroom of approximately S$1-2bn for SCI’s expansion capex and working capital.

Share Price Drivers: Oil price rebound would drive SCI’s share price higher. Investors would have greater confidence in the Marine business, as the operating environment improves. While drilling rig orders may lag oil price recovery, orders for non-drilling, production-related facilities may flow through.

Order wins in the Marine segment and land sales from Urban Development bodes well for SCI’s share price. While the oil price rebound would be an early indicator, SMM securing contract wins is more tangible. More momentum in land sales would signal more hope for growth, and be positive to share price.

Widening spark spreads at Singapore power plants. Signs of positive and widening spark spreads in Singapore would alleviate a key concern of investors and provide support to the share price.

Key Risks: Increasing competition in the Singapore power market. Total power generation supply in Singapore rose by over 9% y-o-y in the past two years, marking the biggest y-o-y jumps since the electricity market started. This has depressed prices and hurt SCI’s bottom line. The oversupply of capacity and over-commitment of gas supply issues will likely continue to plague Singapore's power market in the near-to-medium term.

Execution of Indian power plants. The availability of coal supply and power purchase agreements (PPA) for SCI’s power plants in India are concerns. We find comfort that the TPCIL plant is up and running, with 86% of capacity committed on long-term PPAs and operating using both domestic and imported coal.

Company Background Sembcorp Industries (SCI) is a trusted provider of essential energy and water solutions to both industrial and municipal customers. It has facilities with 10,600MW of gross power capacity and over 10m cubic metres of water per day in operation and under development. It is also a world leader in marine and offshore engineering (via Sembcorp Marine) as well as an established brand name in urban development (comprising industrial parks as well as business, commercial and residential space) in Vietnam, China and Indonesia.

Leverage & Asset Turnover (x)

Capital Expenditure

ROE (%)

Forward PE Band (x)

PB Band (x)

Source: Company, DBS Bank

Page 22Page 22

Company Guide

Sembcorp Industries

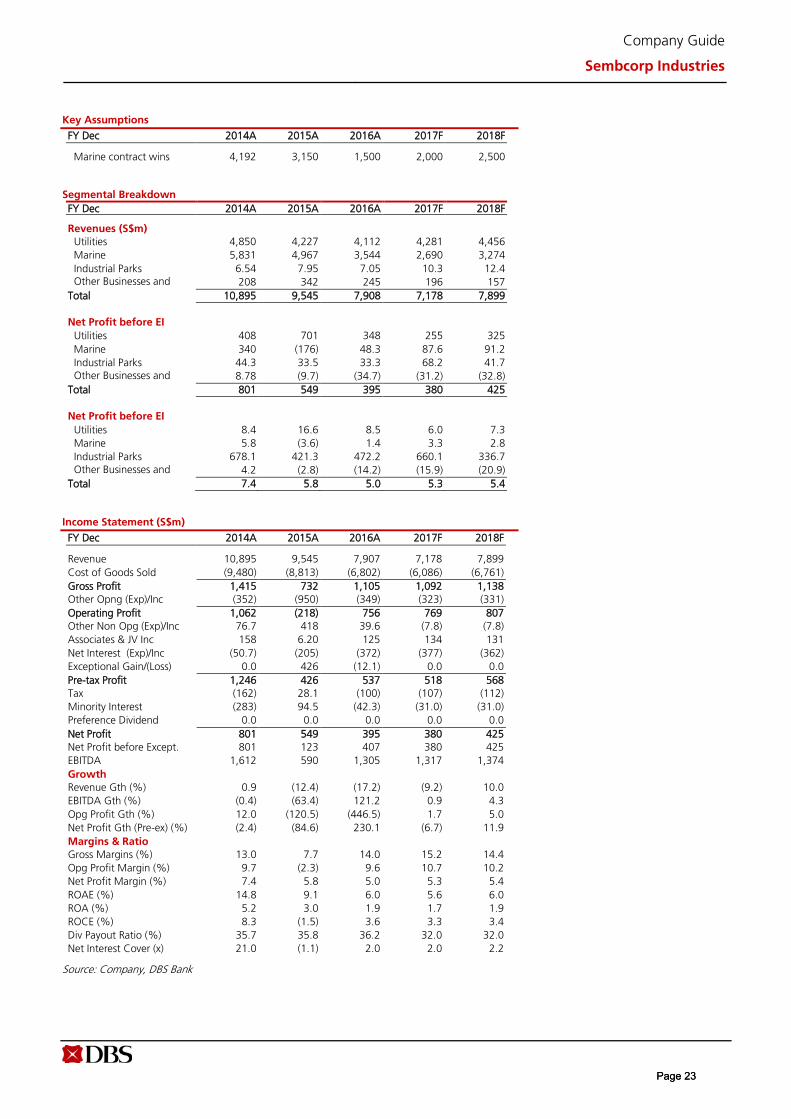

Key Assumptions

FY Dec 2014A 2015A 2016A 2017F 2018F

Marine contract wins 4,192 3,150 1,500 2,000 2,500

Segmental Breakdown FY Dec 2014A 2015A 2016A 2017F 2018F

Revenues (S$m) Utilities 4,850 4,227 4,112 4,281 4,456 Marine 5,831 4,967 3,544 2,690 3,274 Industrial Parks 6.54 7.95 7.05 10.3 12.4 Other Businesses and 208 342 245 196 157 Total 10,895 9,545 7,908 7,178 7,899

Net Profit before EI Utilities 408 701 348 255 325

Marine 340 (176) 48.3 87.6 91.2 Industrial Parks 44.3 33.5 33.3 68.2 41.7 Other Businesses and

8.78 (9.7) (34.7) (31.2) (32.8)

Total 801 549 395 380 425

Net Profit before EI Utilities 8.4 16.6 8.5 6.0 7.3

Marine 5.8 (3.6) 1.4 3.3 2.8 Industrial Parks 678.1 421.3 472.2 660.1 336.7 Other Businesses and

4.2 (2.8) (14.2) (15.9) (20.9)

Total 7.4 5.8 5.0 5.3 5.4

Income Statement (S$m)

FY Dec 2014A 2015A 2016A 2017F 2018F

Revenue 10,895 9,545 7,907 7,178 7,899 Cost of Goods Sold (9,480) (8,813) (6,802) (6,086) (6,761) Gross Profit 1,415 732 1,105 1,092 1,138 Other Opng (Exp)/Inc (352) (950) (349) (323) (331) Operating Profit 1,062 (218) 756 769 807 Other Non Opg (Exp)/Inc 76.7 418 39.6 (7.8) (7.8) Associates & JV Inc 158 6.20 125 134 131 Net Interest (Exp)/Inc (50.7) (205) (372) (377) (362) Exceptional Gain/(Loss) 0.0 426 (12.1) 0.0 0.0 Pre-tax Profit 1,246 426 537 518 568 Tax (162) 28.1 (100) (107) (112) Minority Interest (283) 94.5 (42.3) (31.0) (31.0) Preference Dividend 0.0 0.0 0.0 0.0 0.0 Net Profit 801 549 395 380 425 Net Profit before Except. 801 123 407 380 425 EBITDA 1,612 590 1,305 1,317 1,374 Growth Revenue Gth (%) 0.9 (12.4) (17.2) (9.2) 10.0 EBITDA Gth (%) (0.4) (63.4) 121.2 0.9 4.3 Opg Profit Gth (%) 12.0 (120.5) (446.5) 1.7 5.0 Net Profit Gth (Pre-ex) (%) (2.4) (84.6) 230.1 (6.7) 11.9 Margins & Ratio Gross Margins (%) 13.0 7.7 14.0 15.2 14.4 Opg Profit Margin (%) 9.7 (2.3) 9.6 10.7 10.2 Net Profit Margin (%) 7.4 5.8 5.0 5.3 5.4 ROAE (%) 14.8 9.1 6.0 5.6 6.0 ROA (%) 5.2 3.0 1.9 1.7 1.9 ROCE (%) 8.3 (1.5) 3.6 3.3 3.4 Div Payout Ratio (%) 35.7 35.8 36.2 32.0 32.0 Net Interest Cover (x) 21.0 (1.1) 2.0 2.0 2.2

Source: Company, DBS Bank

Page 23Page 23

Company Guide

Sembcorp Industries

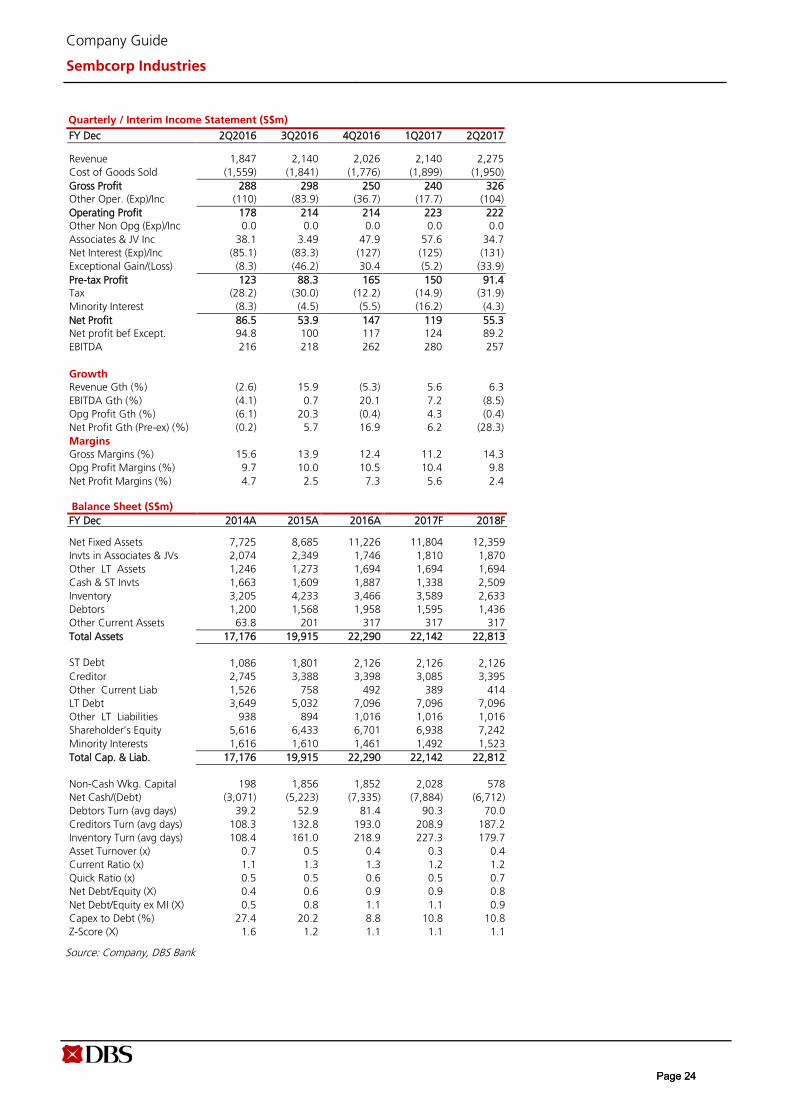

Quarterly / Interim Income Statement (S$m)

FY Dec 2Q2016 3Q2016 4Q2016 1Q2017 2Q2017

Revenue 1,847 2,140 2,026 2,140 2,275 Cost of Goods Sold (1,559) (1,841) (1,776) (1,899) (1,950) Gross Profit 288 298 250 240 326 Other Oper. (Exp)/Inc (110) (83.9) (36.7) (17.7) (104) Operating Profit 178 214 214 223 222 Other Non Opg (Exp)/Inc 0.0 0.0 0.0 0.0 0.0 Associates & JV Inc 38.1 3.49 47.9 57.6 34.7 Net Interest (Exp)/Inc (85.1) (83.3) (127) (125) (131) Exceptional Gain/(Loss) (8.3) (46.2) 30.4 (5.2) (33.9) Pre-tax Profit 123 88.3 165 150 91.4 Tax (28.2) (30.0) (12.2) (14.9) (31.9) Minority Interest (8.3) (4.5) (5.5) (16.2) (4.3) Net Profit 86.5 53.9 147 119 55.3 Net profit bef Except. 94.8 100 117 124 89.2 EBITDA 216 218 262 280 257

Growth Revenue Gth (%) (2.6) 15.9 (5.3) 5.6 6.3 EBITDA Gth (%) (4.1) 0.7 20.1 7.2 (8.5) Opg Profit Gth (%) (6.1) 20.3 (0.4) 4.3 (0.4) Net Profit Gth (Pre-ex) (%) (0.2) 5.7 16.9 6.2 (28.3) Margins Gross Margins (%) 15.6 13.9 12.4 11.2 14.3 Opg Profit Margins (%) 9.7 10.0 10.5 10.4 9.8 Net Profit Margins (%) 4.7 2.5 7.3 5.6 2.4

Balance Sheet (S$m) FY Dec 2014A 2015A 2016A 2017F 2018F

Net Fixed Assets 7,725 8,685 11,226 11,804 12,359 Invts in Associates & JVs 2,074 2,349 1,746 1,810 1,870 Other LT Assets 1,246 1,273 1,694 1,694 1,694 Cash & ST Invts 1,663 1,609 1,887 1,338 2,509 Inventory 3,205 4,233 3,466 3,589 2,633 Debtors 1,200 1,568 1,958 1,595 1,436 Other Current Assets 63.8 201 317 317 317 Total Assets 17,176 19,915 22,290 22,142 22,813

ST Debt 1,086 1,801 2,126 2,126 2,126 Creditor 2,745 3,388 3,398 3,085 3,395 Other Current Liab 1,526 758 492 389 414 LT Debt 3,649 5,032 7,096 7,096 7,096 Other LT Liabilities 938 894 1,016 1,016 1,016 Shareholder’s Equity 5,616 6,433 6,701 6,938 7,242 Minority Interests 1,616 1,610 1,461 1,492 1,523 Total Cap. & Liab. 17,176 19,915 22,290 22,142 22,812

Non-Cash Wkg. Capital 198 1,856 1,852 2,028 578 Net Cash/(Debt) (3,071) (5,223) (7,335) (7,884) (6,712) Debtors Turn (avg days) 39.2 52.9 81.4 90.3 70.0 Creditors Turn (avg days) 108.3 132.8 193.0 208.9 187.2 Inventory Turn (avg days) 108.4 161.0 218.9 227.3 179.7 Asset Turnover (x) 0.7 0.5 0.4 0.3 0.4 Current Ratio (x) 1.1 1.3 1.3 1.2 1.2 Quick Ratio (x) 0.5 0.5 0.6 0.5 0.7 Net Debt/Equity (X) 0.4 0.6 0.9 0.9 0.8 Net Debt/Equity ex MI (X) 0.5 0.8 1.1 1.1 0.9 Capex to Debt (%) 27.4 20.2 8.8 10.8 10.8 Z-Score (X) 1.6 1.2 1.1 1.1 1.1

Source: Company, DBS Bank

Page 24Page 24

Company Guide

Sembcorp Industries

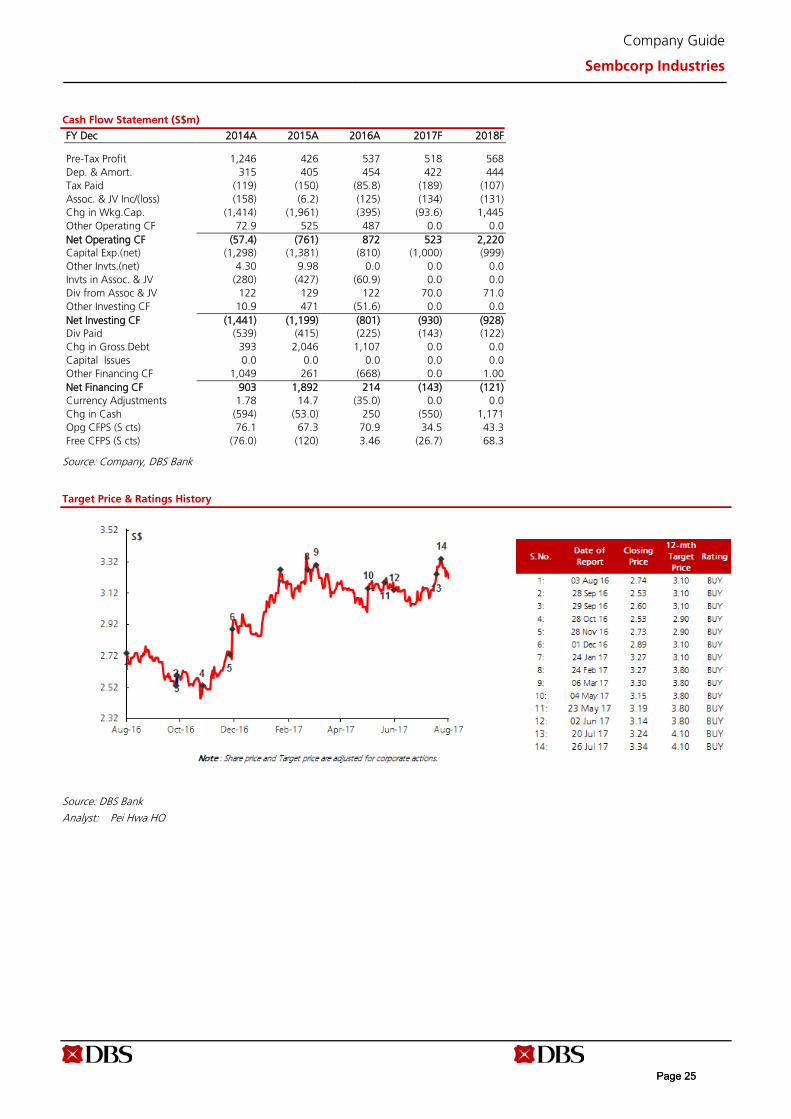

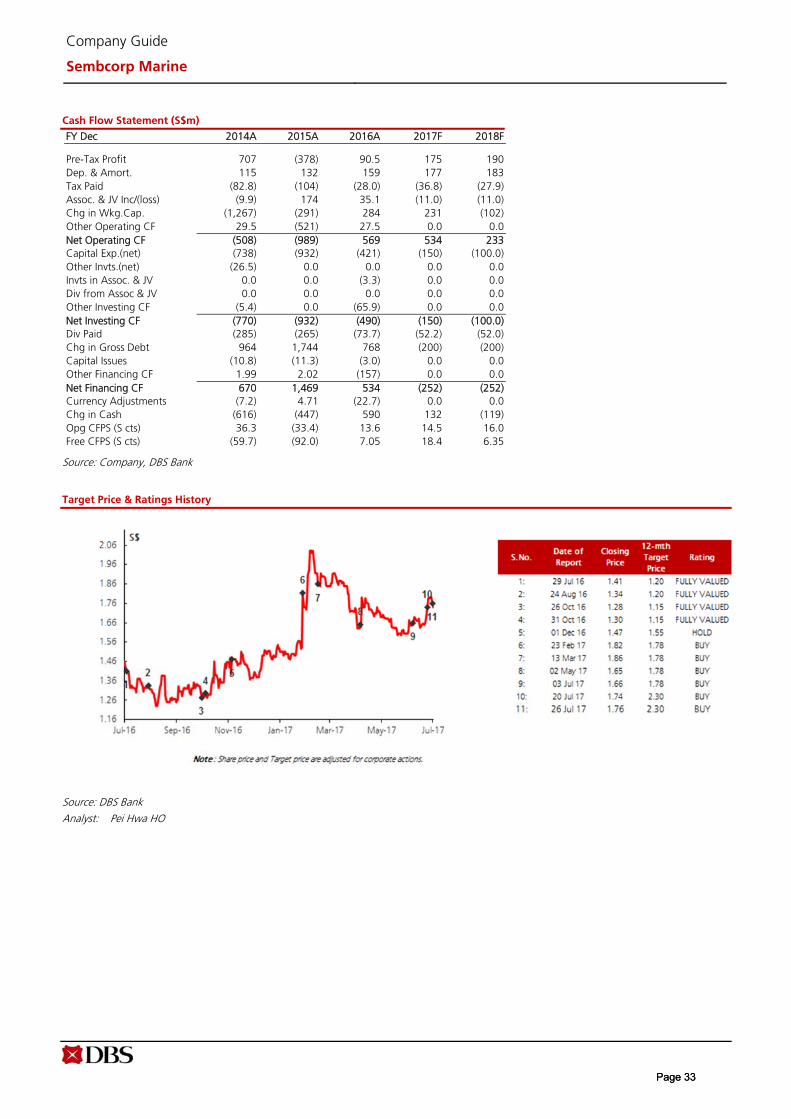

Cash Flow Statement (S$m)

FY Dec 2014A 2015A 2016A 2017F 2018F

Pre-Tax Profit 1,246 426 537 518 568 Dep. & Amort. 315 405 454 422 444 Tax Paid (119) (150) (85.8) (189) (107) Assoc. & JV Inc/(loss) (158) (6.2) (125) (134) (131) Chg in Wkg.Cap. (1,414) (1,961) (395) (93.6) 1,445 Other Operating CF 72.9 525 487 0.0 0.0 Net Operating CF (57.4) (761) 872 523 2,220 Capital Exp.(net) (1,298) (1,381) (810) (1,000) (999) Other Invts.(net) 4.30 9.98 0.0 0.0 0.0 Invts in Assoc. & JV (280) (427) (60.9) 0.0 0.0 Div from Assoc & JV 122 129 122 70.0 71.0 Other Investing CF 10.9 471 (51.6) 0.0 0.0 Net Investing CF (1,441) (1,199) (801) (930) (928) Div Paid (539) (415) (225) (143) (122) Chg in Gross Debt 393 2,046 1,107 0.0 0.0 Capital Issues 0.0 0.0 0.0 0.0 0.0 Other Financing CF 1,049 261 (668) 0.0 1.00 Net Financing CF 903 1,892 214 (143) (121) Currency Adjustments 1.78 14.7 (35.0) 0.0 0.0 Chg in Cash (594) (53.0) 250 (550) 1,171 Opg CFPS (S cts) 76.1 67.3 70.9 34.5 43.3 Free CFPS (S cts) (76.0) (120) 3.46 (26.7) 68.3

Source: Company, DBS Bank

Target Price & Ratings History

Source: DBS Bank

Analyst: Pei Hwa HO

Page 25Page 25

ed: JLC / sa:JC, PY

BUYLast Traded Price ( 27 Jul 2017): S$1.74 (STI : 3,354.71) Price Target 12-mth: S$2.30 (32% upside)

Analyst Pei Hwa HO +65 6682 3714 [email protected]

What’s New Stripping out forex losses, core profit would have been

S$38m and EBIT margin would have climbed to 9.6%

Management remains positive on order wins; FPSOenquiries picked up

An interim dividend of 1Sct was declared

Reiterate BUY; TP S$2.30

Price Relative

Forecasts and Valuation FY Dec (S$ m) 2015A 2016A 2017F 2018F Revenue 4,968 3,545 2,690 3,274 EBITDA (216) 312 393 471 Pre-tax Profit (378) 90.5 175 190 Net Profit (290) 78.8 145 150 Net Pft (Pre Ex.) (290) 78.8 105 150 Net Pft Gth (Pre-ex) (%) nm nm 32.7 43.5 EPS (S cts) (13.9) 3.77 6.91 7.18 EPS Pre Ex. (S cts) (13.9) 3.77 5.00 7.18 EPS Gth Pre Ex (%) (152) (127) 33 43 Diluted EPS (S cts) (13.9) 3.77 6.92 7.18 Net DPS (S cts) 6.00 2.50 2.49 2.51 BV Per Share (S cts) 120 123 127 132 PE (X) nm 46.2 25.2 24.2 PE Pre Ex. (X) nm 46.2 34.8 24.2 P/Cash Flow (X) nm 6.4 6.8 15.6 EV/EBITDA (X) nm 21.1 15.9 13.1 Net Div Yield (%) 3.4 1.4 1.4 1.4 P/Book Value (X) 1.4 1.4 1.4 1.3 Net Debt/Equity (X) 1.0 1.1 0.9 0.9 ROAE (%) (10.6) 3.1 5.5 5.5

Earnings Rev (%): - - Consensus EPS (S cts): 4.5 6.2 Other Broker Recs: B: 6 S: 6 H: 7

Source of all data on this page: Company, DBS Bank, Bloomberg Finance L.P

Stay tuned for order recovery

Maintain BUY; TP S$2.30, based on 1.8x FY17 P/BV (1SD below mean). Stripping out forex losses in 2Q17, SMM saw EBIT margin rebound to 9.6% and PATMI inch up to S$38m,. We continue to see rerating catalysts stemming from: 1) SMM as a pure play to ride the oil-price recovery towards 2H; 2) sizeable new orders for non-drilling solutions, in particular FPSOs and Gravifloat’s modularised LNG terminals; 3) the conclusion of jackup sales; 4) the reactivation of Sete’s projects; and 5) SMM being a potential M&A play arising from a consolidation of Singapore yards.

Where we differ: more bullish on SMM’s contract wins. We expect sizeable contracts for LNG solutions to come through in the next 6 months. Order wins, a critical leading indicator for recovery, is set to rise next year with several modularised LNG terminal contracts in the pipeline, each ranging from S$200m-$300m (for importing LNG terminals) to c.S$1bn (for exporting LNG terminals). We expect these to drive SMM’s order wins to the S$2bn mark. SMM has been reportedly in final talks with Chinese conglomerates Poly Group and GCL Group for LNG solutions, as well as Global LNG for a gigantic LNG vessel. This will buck the declining order-book trend, which dipped to S$3.6bn (excluding S$3.12bn Sete orders) in 2Q17.

Disposal of undelivered jackup rigs. SMM has seven outstanding jackup rig orders, which are all at advanced stages of construction. Besides the BOT Lease unit, which will likely be delivered to its customer next year, SMM is in talks with several potential buyers for the five undelivered jackup rigs ordered by financially distressed Perisai and Oro Negro, and one rig terminated by Marco Polo. We believe these rigs have been marked down by c.30% through the provisions made in 4Q15. The successful disposal of these rigs at breakeven price and above will free up capital and eliminate a key overhang on SMM. Valuation: Our target price of S$ 2.30 is based on 1.8x FY17 P/BV, in line with mean of below 1SD since 2004. SMM’s book value was already written down after the massive S$609m provisions in FY15.

Key Risks to Our View: Key downside risks are sustained low oil prices which affect rig count and newbuilding activities, execution risks in new product types, and disposal of jackup rigs at a loss. Upside risk could come from privatisation or M&A activities, as well as the write-back of the provisions from successful deliveries or vessel sales.

At A Glance

Issued Capital (m shrs) 2,090 Mkt. Cap (S$m/US$m) 3,636 / 2,675 Major Shareholders (%) Sembcorp Industries Ltd 61.0 Franklin Resources 5.0

Free Float (%) 34.0 3m Avg. Daily Val (US$m) 5.2 ICB Industry : Oil & Gas / Oil Equipment; Services & Dist

DBS Group Research . Equity 28 Jul 2017

Singapore Company Guide

Sembcorp Marine Version 13 | Bloomberg: SMM SP | Reuters: SCMN.SI Refer to important disclosures at the end of this report

Page 26Page 26

Company Guide

Sembcorp Marine

WHAT’S NEW

2Q showed sequential improvement

SMM reported headline net profits of S$5.6m, though this was mainly due to large FX losses of S$34.3m - on the revaluation of the Brazilian yard’s liabilities denominated in US dollar to Brazilian Real, as well as revaluation of other assets and liabilities from USD to SGD. Without the FX loss, net profit would have come in at c.S$40m – more or less flat q-o-q.

EBIT margin up from 1.8% in 1Q17 to 4.3% this quarter. Stripping out the FX losses, the improvement would have been more pronounced, with adjusted EBIT margin at 9.6% for 2Q17.

YTD order wins at S$75m, but management expects 2017 total wins to surpass 2016’s quantum. While order wins so far this year have been lackluster, management expressed optimism that the full-year orders would come in above 2016’s S$320m secured, although we note that this forecast

may include a variation order on one of the Petrobras FPSOs worth >US$100m. We believe SMM’s Gravifloat LNG terminals provide a unique modular option to customers, and will be the key driver of order wins in the near term. The value of these units can range from S$200-$300m for importing LNG terminals, and up to c.S$1bn for exporting LNG terminals.

Interim dividend of 1.0Scts declared (vs. 1.5Scts interim last year). This translates to a payout ratio of about 46% for 1H16. We believe SMM intends to maintain its dividend payout policy (and assume full-year dividend of 2.5Scts]. Lower gearing upon receipt of the proceeds of the divestment of a 30% in Cosco Shipyard Group should provide some comfort in terms of balance sheet/cashflow management with respect to continued dividend payouts.

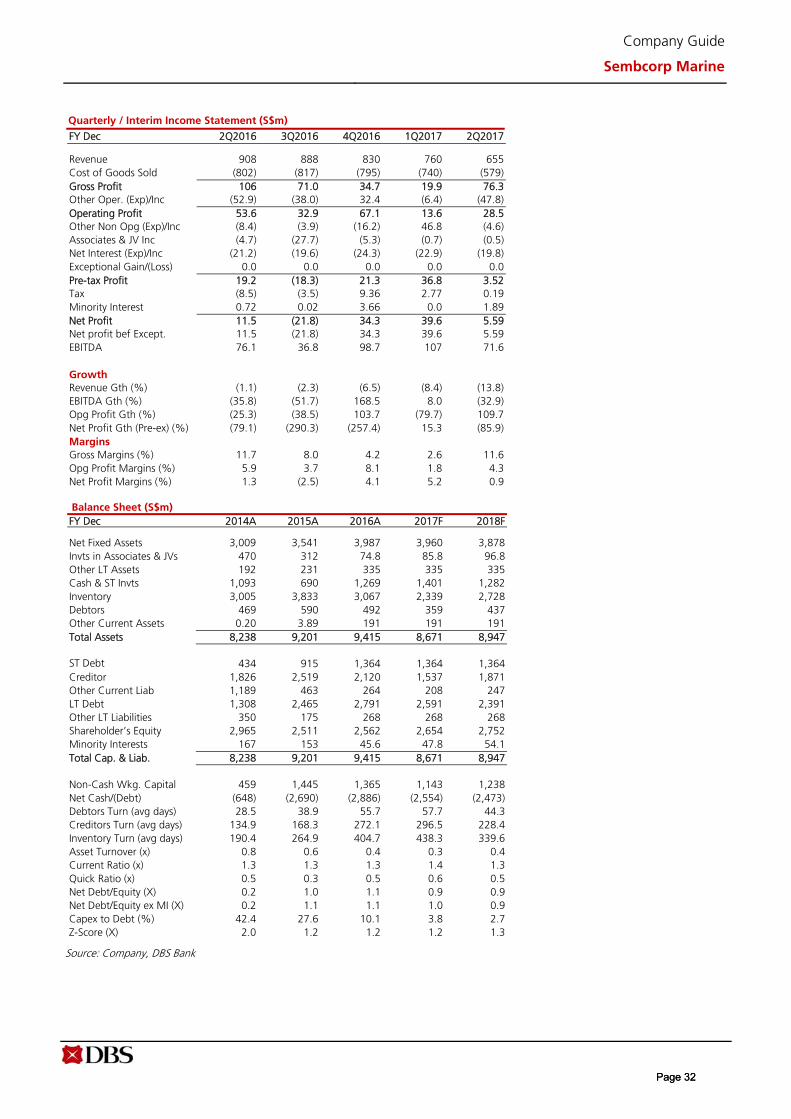

Quarterly / Interim Income Statement (S$m)

FY Dec 2Q2016 1Q2017 2Q2017 % chg yoy % chg qoq

Revenue 908 760 655 (27.8) (13.8)

Cost of Goods Sold (802) (740) (579) (27.8) (21.7)

Gross Profit 106 19.9 76.3 (28.3) 282.6

Other Oper. (Exp)/Inc (52.9) (6.4) (47.8) (9.7) 652.1

Operating Profit 53.6 13.6 28.5 (46.8) 109.7

Other Non Opg (Exp)/Inc (8.4) 46.8 (4.6) 44.5 nm

Associates & JV Inc (4.7) (0.7) (0.5) 89.0 (27.1)

Net Interest (Exp)/Inc (21.2) (22.9) (19.8) 6.7 13.4

Exceptional Gain/(Loss) 0.0 0.0 0.0 - -

Pre-tax Profit 19.2 36.8 3.52 (81.7) (90.4)

Tax (8.5) 2.77 0.19 (102.2) (93.3)

Minority Interest 0.72 0.0 1.89 164.6 nm

Net Profit 11.5 39.6 5.59 (51.2) nm

Net profit bef Except. 11.5 39.6 5.59 (51.2) (85.9)

EBITDA 76.1 107 71.6 (6.0) (32.9)

Margins (%)

Gross Margins 11.7 2.6 11.6

Opg Profit Margins 5.9 1.8 4.3

Net Profit Margins 1.3 5.2 0.9

Source of all data: Company, DBS Bank

Page 27Page 27

Company Guide

Sembcorp Marine

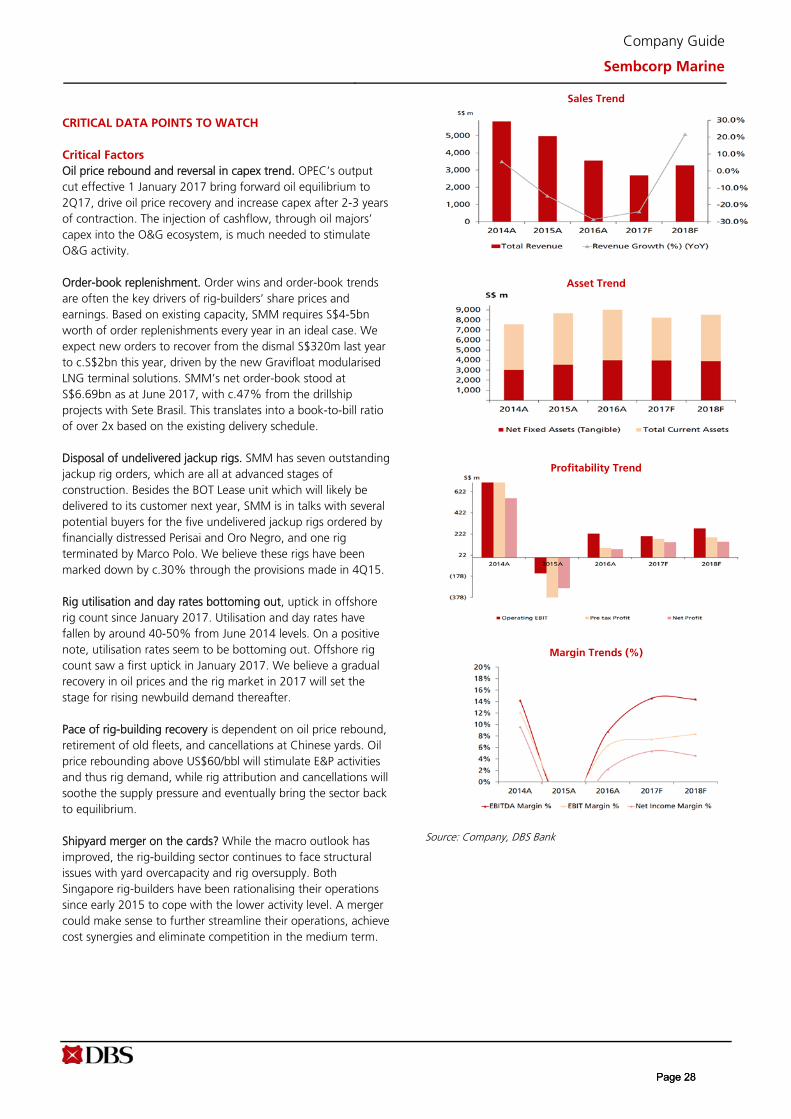

CRITICAL DATA POINTS TO WATCH

Critical Factors

Oil price rebound and reversal in capex trend. OPEC’s output cut effective 1 January 2017 bring forward oil equilibrium to 2Q17, drive oil price recovery and increase capex after 2-3 years of contraction. The injection of cashflow, through oil majors’ capex into the O&G ecosystem, is much needed to stimulate O&G activity.

Order-book replenishment. Order wins and order-book trends are often the key drivers of rig-builders’ share prices and earnings. Based on existing capacity, SMM requires S$4-5bn worth of order replenishments every year in an ideal case. We expect new orders to recover from the dismal S$320m last year to c.S$2bn this year, driven by the new Gravifloat modularised LNG terminal solutions. SMM’s net order-book stood at S$6.69bn as at June 2017, with c.47% from the drillship projects with Sete Brasil. This translates into a book-to-bill ratio of over 2x based on the existing delivery schedule.

Disposal of undelivered jackup rigs. SMM has seven outstanding jackup rig orders, which are all at advanced stages of construction. Besides the BOT Lease unit which will likely be delivered to its customer next year, SMM is in talks with several potential buyers for the five undelivered jackup rigs ordered by financially distressed Perisai and Oro Negro, and one rig terminated by Marco Polo. We believe these rigs have been marked down by c.30% through the provisions made in 4Q15.

Rig utilisation and day rates bottoming out, uptick in offshore rig count since January 2017. Utilisation and day rates have fallen by around 40-50% from June 2014 levels. On a positive note, utilisation rates seem to be bottoming out. Offshore rig count saw a first uptick in January 2017. We believe a gradual recovery in oil prices and the rig market in 2017 will set the stage for rising newbuild demand thereafter.

Pace of rig-building recovery is dependent on oil price rebound, retirement of old fleets, and cancellations at Chinese yards. Oil price rebounding above US$60/bbl will stimulate E&P activities and thus rig demand, while rig attribution and cancellations will soothe the supply pressure and eventually bring the sector back to equilibrium.

Shipyard merger on the cards? While the macro outlook has improved, the rig-building sector continues to face structural issues with yard overcapacity and rig oversupply. Both Singapore rig-builders have been rationalising their operations since early 2015 to cope with the lower activity level. A merger could make sense to further streamline their operations, achieve cost synergies and eliminate competition in the medium term.

Sales Trend

Asset Trend

Profitability Trend

Margin Trends (%)

Source: Company, DBS Bank

Page 28Page 28

Company Guide

Sembcorp Marine

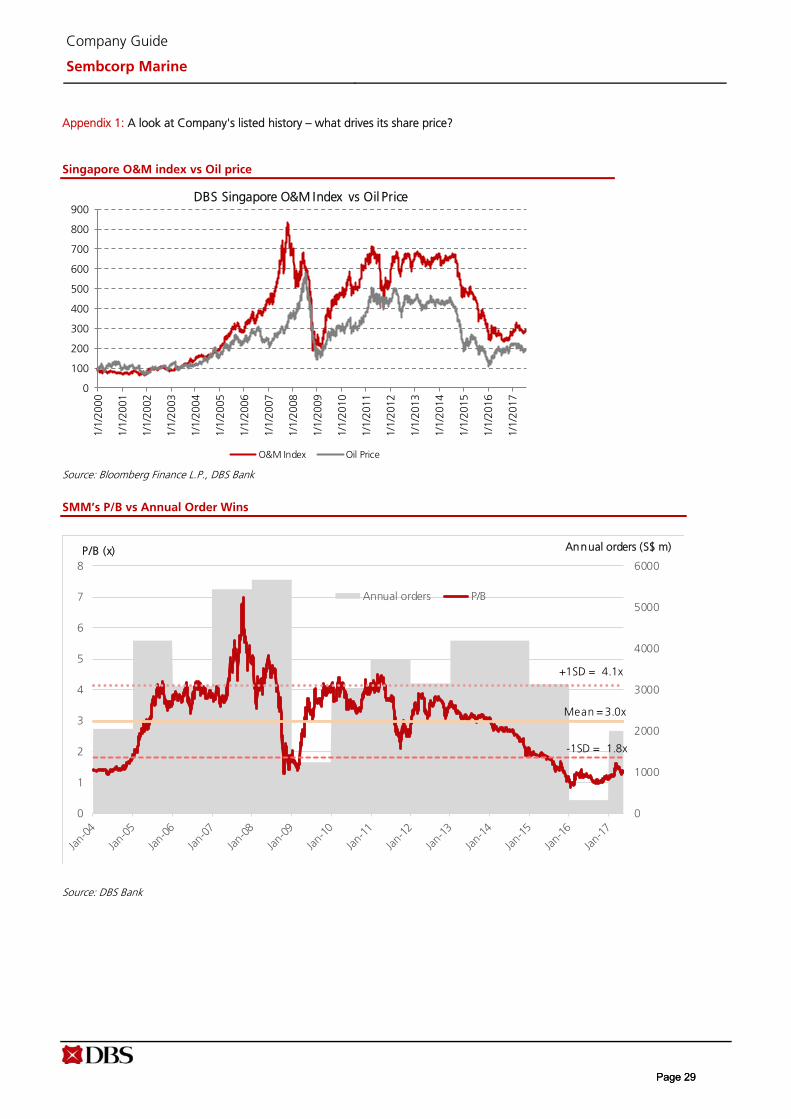

Appendix 1: A look at Company's listed history – what drives its share price?

Singapore O&M index vs Oil price

Source: Bloomberg Finance L.P., DBS Bank

SMM’s P/B vs Annual Order Wins

Source: DBS Bank

0

100

200

300

400

500

600

700

800

900

1/1/

2000

1/1/

2001

1/1/

2002

1/1/

2003

1/1/

2004

1/1/

2005

1/1/

2006

1/1/

2007

1/1/

2008

1/1/

2009

1/1/

2010

1/1/

2011

1/1/

2012

1/1/

2013

1/1/

2014

1/1/

2015

1/1/

2016

1/1/

2017

DBS Singapore O&M Index vs Oil Price

O&M Index Oil Price

0

1000

2000