Bahasa

Halaman

Hukum

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

Result U

pdate

January 23, 2022

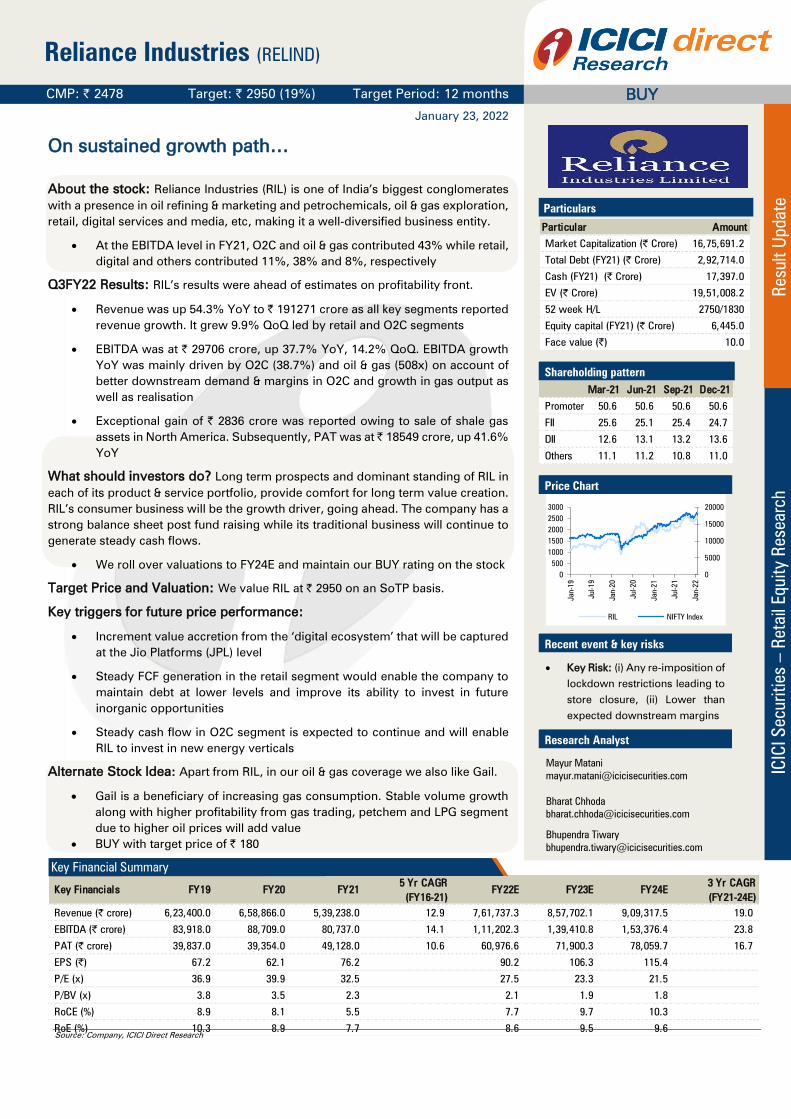

CMP: | 2478 Target: | 2950 (19%) Target Period: 12 months

Reliance Industries (RELIND)

BUY

On sustained growth path…

About the stock: Reliance Industries (RIL) is one of India’s biggest conglomerates

with a presence in oil refining & marketing and petrochemicals, oil & gas exploration,

retail, digital services and media, etc, making it a well-diversified business entity.

At the EBITDA level in FY21, O2C and oil & gas contributed 43% while retail,

digital and others contributed 11%, 38% and 8%, respectively

Q3FY22 Results: RIL’s results were ahead of estimates on profitability front.

Revenue was up 54.3% YoY to | 191271 crore as all key segments reported

revenue growth. It grew 9.9% QoQ led by retail and O2C segments

EBITDA was at | 29706 crore, up 37.7% YoY, 14.2% QoQ. EBITDA growth

YoY was mainly driven by O2C (38.7%) and oil & gas (508x) on account of

better downstream demand & margins in O2C and growth in gas output as

well as realisation

Exceptional gain of | 2836 crore was reported owing to sale of shale gas

assets in North America. Subsequently, PAT was at | 18549 crore, up 41.6%

YoY

What should investors do? Long term prospects and dominant standing of RIL in

each of its product & service portfolio, provide comfort for long term value creation.

RIL’s consumer business will be the growth driver, going ahead. The company has a

strong balance sheet post fund raising while its traditional business will continue to

generate steady cash flows.

We roll over valuations to FY24E and maintain our BUY rating on the stock

Target Price and Valuation: We value RIL at | 2950 on an SoTP basis.

Key triggers for future price performance:

Increment value accretion from the ‘digital ecosystem’ that will be captured

at the Jio Platforms (JPL) level

Steady FCF generation in the retail segment would enable the company to

maintain debt at lower levels and improve its ability to invest in future

inorganic opportunities

Steady cash flow in O2C segment is expected to continue and will enable

RIL to invest in new energy verticals

Alternate Stock Idea: Apart from RIL, in our oil & gas coverage we also like Gail.

Gail is a beneficiary of increasing gas consumption. Stable volume growth

along with higher profitability from gas trading, petchem and LPG segment

due to higher oil prices will add value

BUY with target price of | 180

Key Financials FY19 FY20 FY21 5 Yr CAGR

(FY16-21)

FY22E FY23E FY24E 3 Yr CAGR

(FY21-24E)

Revenue (| crore) 6,23,400.0 6,58,866.0 5,39,238.0 12.9 7,61,737.3 8,57,702.1 9,09,317.5 19.0

EBITDA (| crore) 83,918.0 88,709.0 80,737.0 14.1 1,11,202.3 1,39,410.8 1,53,376.4 23.8

PAT (| crore) 39,837.0 39,354.0 49,128.0 10.6 60,976.6 71,900.3 78,059.7 16.7

EPS (|) 67.2 62.1 76.2 90.2 106.3 115.4

P/E (x) 36.9 39.9 32.5 27.5 23.3 21.5

P/BV (x) 3.8 3.5 2.3 2.1 1.9 1.8

RoCE (%) 8.9 8.1 5.5 7.7 9.7 10.3

RoE (%) 10.3 8.9 7.7 8.6 9.5 9.6

Particulars

Particular Amount

Market Capitalization (| Crore) 16,75,691.2

Total Debt (FY21) (| Crore) 2,92,714.0

Cash (FY21) (| Crore) 17,397.0

EV (| Crore) 19,51,008.2

52 week H/L 2750/1830

Equity capital (FY21) (| Crore) 6,445.0

Face value (|) 10.0

Shareholding pattern

Mar-21 Jun-21 Sep-21 Dec-21

Promoter 50.6 50.6 50.6 50.6

FII 25.6 25.1 25.4 24.7

DII 12.6 13.1 13.2 13.6

Others 11.1 11.2 10.8 11.0

Price Chart

Recent event & key risks

Key Risk: (i) Any re-imposition of

lockdown restrictions leading to

store closure, (ii) Lower than

expected downstream margins

Research Analyst

Mayur Matani

Bharat Chhoda

Bhupendra Tiwary

0

5000

10000

15000

20000

0

500

1000

1500

2000

2500

3000

Jan-1

9

Jul-1

9

Jan-2

0

Jul-2

0

Jan-2

1

Jul-21

Jan-2

2

RIL NIFTY Index

Key Financial Summary

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 2

ICICI Direct Research

Result Update | Reliance Industries

Key takeaways of recent quarter & conference call highlights

Segmental details

Reliance Jio

RJio’s Q3 quarterly print was a mixed bag. While SIM consolidation led second

consecutive quarter of net subscriber decline, positive surprise was on tad higher

ARPU growth (also a function of SIM consolidation, where low quality subs churn

might have been seen) and beat at the EBITDA level owing to lower networking

operating costs. Revenues and EBITDA were at | 19347 crore, | 9514 crore, up 3.3%,

5.8% QoQ, respectively. Margins were at 49.2%, up 120 bps QoQ and higher than

our estimates of 48.1%, owing to lower network operating costs, which were down

0.3% QOQ. PAT at | 3615 crore, up 2.5% QoQ, was a tad lower than expected (our

expectations | 3675 crore), owing to higher than anticipated depreciation.

On KPI front, key takeaways were:

o Subscribers: The overall subscriber base (including fibre and

enterprise) was at 421 mn, down 8.5 mn QoQ. While the gross

addition at 34.6 mn was strong, SIM consolidation led to net

customer decline of 8.5 million (churn rate of 3.4%). We also

highlight that Jio’s active sub proportion (VLR) was at ~83.9% in

November vs. peers’ 97.9% and 86.9%, respectively. Thus, some

SIM consolidation impact was imminent. On fibre front, the overall

sub base has crossed 5 million

o ARPU: Given the SIM consolidation (with improved subscriber mix)

and impact of tariff hike undertaken in December (~20-25% hike in

prepaid segment), the ARPU saw a growth of 5.6% QoQ at | 151.6

(our expectations | 149)

o Data/Voice usage: Total minutes grew 4.8% QoQ to 1,149 bn, and

data usage was up 1.9% QoQ to 23,430 bn GB. The company also

attributed the improvement in customer metrics to SIM

consolidation

o Spectrum liabilities repayment: The company has paid | 30,791

crore (~| 10,000 in December, 2021 and remaining in January,

2022), clearing deferred spectrum liabilities acquired in auctions

prior to March 2021 and refinancing of the same at lower interest

rates will result in interest cost saving of | 1,200 crore annually

The company has guided for a transient reduction in SIM base, with Covid

impact on recharge cycle and tariff hikes, owing to consolidation for the low-

usage and inconsistent subscriber base. Furthermore, on expected lines, it

indicated full impact of tariff hike likely to be reflected in ARPU and financials

over next few quarters. We marginally cut our FY23, FY24 topline estimates

by 2.7%, 1.2%, respectively, owing to SIM consolidation impact. However,

bottomline estimates stand upgraded by 1.3%, 4.3% for FY23, FY24,

respectively, given the interest cost savings on account of refinancing of

spectrum liabilities at lower rates. Post any respite on chip shortage, we

expect the subscriber addition traction to recover with JioPhone Next

picking up while ARPU hike benefits will accrue over the next couple of

quarters. We continue to believe Jio’s digital ecosystem lends it a

competitive advantage in the overall communication space, thereby

providing superior legs of growth and valuation pegging

ICICI Securities | Retail Research 3

ICICI Direct Research

Result Update | Reliance Industries

Reliance Retail: Robust store addition trajectory continues

Reliance Retail reported one of its best quarterly performance on account of record

number of store additions (837 added in Q3FY22) and normalisation of footfalls to

pre-Covid levels (95%). Revenues for Q3FY22 crossed the | 50,000 crore mark and

grew 53% YoY (27% QoQ) to | 57714 crore (I-direct estimate: | 52600 crore). Core

retail revenue (excluding connectivity) grew 90% YoY. The management during the

call highlighted that demand was robust across all consumption categories, with

fashion and electronics segment outperforming (2x YoY growth). On the profitability

front, EBITDA margins (excluding other investments) remained constant YoY at

6.1%, with absolute EBITDA increasing 53% YoY to | 3522 crore (I-direct estimate:

| 3576 crore). Other income came in at | 300 crore vs. | 775 crore in Q3FY21. The

company continues to fill white spaces through acquisitions; as it bought 25.8% in

Dunzo for US$200 mn (India’s leading last mile delivery and quick commerce player),

acquired ‘Jaisuryas’ (leading grocery chain in South India), and stakes in ‘Amante’

(premium woman intimate-wear brand), Kalanikethan (leading saree and ethnic wear

retailer). For YTDFY22, it has spent ~| 7600 crore towards acquiring new businesses.

The company in YTDFY22 added ~1778 stores (850, 1369 added in FY21, FY20,

respectively) taking total store count to 14412 (40.0 million sq ft). The company also

added 73 new supply chain locations to strengthen its omni-channel play. Digital

commerce orders (up 2x YoY) and merchant partnerships (up 4x YoY) continue to

scale new highs. While the new strain has resulted in sporadic disruptions, the

company expects to accelerate the growth momentum with normalisation of the

operating environment. Reliance Retail’s widespread physical store network would

further enhance its omni channel capabilities and position it as a frontrunner to

garner consistent business growth by capturing a larger pie of the Indian retail sector

opportunity. We roll our estimates to FY24E and model in revenue, EBITDA CAGR of

25% and 36% in FY21-24E.

Fashion & lifestyle:

Apparel and footwear registered highest quarterly sales with sales up 2x

YoY driven by festive and winter-wear. Footfalls back to pre-Covid levels

with conversion ratio and average transaction higher than pre-Covid levels

Trends “Small Town” (tier III/!V cities) launched its 500th

store with highest

ever monthly sales.

AJIO sustained its strong track record (3x YoY), with monthly active users

up 2x YoY. The business grew its catalogue 2x YoY by adding national and

regional brands to its offerings

In the luxury/premium brands business, revenue grew 2x YoY with

resumption of mall stores and pick up in footfalls

Grocery:

Grocery continued its growth trajectory and registered all-time high revenue

and record store sales driven by higher bill values and footfall recovery

JioMart created new high with 10x growth in merchant base

Launched experiential premium gourmet superstore. ‘Freshpik’, in JioWorld

drive in Mumbai. Expansion planned in this format

Consumer electronics:

Consumer electronics registered its best ever Diwali sales with conversion

and average basket value at record high. Revenues doubled YoY, boosted

from sale of devices

Broad based double double-digit growth across all key categories like

phones, TVs and home appliances

ICICI Securities | Retail Research 4

ICICI Direct Research

Result Update | Reliance Industries

Energy segments

O2C profitability marginally below estimates; E&P growth continues

O2C revenue was at | 131427 crore, up 56.8% YoY, 9.1% QoQ, ahead of

our estimate of | 124448 crore. Higher demand across key segments led to

revenue growth

EBITDA grew 38.7% YoY (6.4% QoQ) to | 13530 crore, marginally below

our estimate of | 14570 crore, mainly due to increase in feedstock prices.

On a QoQ basis, higher feedstock and product prices limited growth in

EBITDA

O2C EBITDA is expected at | 52748.1 crore in FY22E. Going ahead, we

estimate O2C EBITDA at | 60296.6 crore and | 61565 crore in FY23E and

FY24E, respectively, as we estimate stability in GRMs with economic

recovery over medium term

E&P segment revenue was driven by increase in realisation for gas output

from KG basin. Revenue at | 2599 crore was up 493.7% YoY (and 55.7%

QoQ). Domestic production was 42.2 BCFe, up 1% QoQ

Both KG-D6 and CBM realisation improved QoQ. KG-D6 realisation

increased 69% post revision in gas prices in October that led to EBITDA

growth. EBITDA was at | 2033 crore vs. EBITDA of | 1071 crore in Q2FY22

and EBITDA of | 4 crore in Q3FY21

We revise estimates taking into account current oil & gas prices trend. Gas

realisation is expected to remain healthy in the near term, which augurs well

for the segment. E&P EBITDA is expected at | 5371.2 crore. Going ahead,

we estimate E&P EBITDA at | 10129.8 crore and | 12204.9 crore in FY23E

and FY24E, respectively.

ICICI Securities | Retail Research 5

ICICI Direct Research

Result Update | Reliance Industries

Exhibit 1: Variance Analysis

Q3FY22 Q3FY22E Q3FY21 YoY (% ) Q2FY22 QoQ (% ) Comments

Total Revenues 1,91,271.0 1,79,317.6 1,23,997.0 54.3 1,74,104.0 9.9Above estimates mainly on account of higher than

expected O2C and retail revenue

Raw materials costs 1,26,169.0 1,14,092.2 72,249.0 74.6 1,13,429.0 11.2

Employees Cost 4,660.0 4,583.5 4,244.0 9.8 4,580.0 1.7

Other Expenses 30,736.0 30,331.4 25,938.0 18.5 -15,578.0 -297.3

Total Expenditure 1,61,565.0 1,49,007.1 1,02,431.0 57.7 1,02,431.0 57.7

EBITDA 29,706.0 30,310.5 21,566.0 37.7 26,020.0 14.2 Broadly in line with expectations

EBITDA margins (%) 15.5 16.9 17.4 -186 bps 14.9 59 bps

Depreciation 7,683.0 7,378.0 6,665.0 15.3 7,230.0 6.3

EBIT 22,023.0 22,932.5 14,901.0 47.8 18,790.0 17.2

Interest 3,812.0 3,250.0 4,326.0 -11.9 3,819.0 -0.2

Other Income 4,180.0 4,000.0 4,528.0 -7.7 4,263.0 -1.9

Extra Ordinary Item 2,836.0 0.0 -121.0 NA 0.0 NAExceptional gain on account of sale of shale gas assets

in North America

PBT 25,227.0 23,682.5 14,982.0 68.4 19,234.0 31.2

Total Tax 4,688.0 5,968.0 88.0 5,227.3 3,755.0 24.8

PAT 18,549.0 15,615.0 13,101.0 41.6 13,680.0 35.6

Key Metrics

Exchange rate (|/$) 75.0 75.0 73.8 1.6 74.1 1.2

ARPU (|) 151.6 149.3 151.0 0.4 143.6 5.6

Subscribers (mn) 421.0 437.5 410.8 2.5 429.5 -2.0

Retail revenue (| crore) 57717.0 52599.0 36887.0 56.5 45450.0 27.0 Store addition: 837, footfalls: 95%

Retail EBITDA (| crore) 3835.0 3963.0 3102.0 23.6 2923.0 31.2EBITDA margins (excluding other investments) remained

constant YoY at 6.1%.

O2C EBITDA (| crore) 13530.0 14569.7 9756.0 38.7 12720.0 6.4 Lower than estimates

E&P EBITDA (| crore) 2033.0 1564.8 4.0 50,725.0 1071.0 89.8

Source: Company, ICICI Direct Research

Exhibit 2: Change in estimates

(| Crore) Old New % Change Old New % Change

Revenue 752856.0 761737.3 1.2 855223.1 857702.1 0.3

EBITDA 1,11,763.0 1,11,202.3 -0.5 142895.1 1,39,410.8 -2.4Marginal revision in estimates across key segments led

to change in estimates

EBITDA Margin (%) 14.8 14.6 -25 bps 16.7 16.3 -45 bps

PAT 57,867.7 60,976.6 5.4 74189.3 71,900.3 -3.1

EPS (|) 85.6 90.2 5.4 109.7 106.3 -3.1

FY22E FY23E

Source: Company, ICICI Direct Research

Exhibit 3: Assumptions

FY20 FY21 FY22E FY23E FY22E FY23E

Exchange rate (|/$) 70.8 74.0 74.3 74.5 74.2 74.0

ARPU (|) 130.4 143.1 146.3 163.2 146.3 163.2

Subscribers 387.5 426.2 434.4 463.4 458.4 476.9 Realigned estimates post Q3FY22 results

Retail revenue (| crore) 163029.0 153818.0 197167.0 255661.0 193571.0 246317.0

Retail EBITDA (| crore) 9695.0 9842.0 12780.0 17774.4 13271.0 18596.1

O2C EBITDA (| crore) 53803.0 38170.0 52748.1 60296.6 52608.5 61396.6

E&P EBITDA (| crore) 353.0 258.0 5371.2 10129.8 5208.5 10998.4

Gas output (mmscmd) 9.8 8.3 15.1 16.4 16.1 20.1Revised gas output estimates post sale of shale gas

assets

Current Earl ier

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 6

ICICI Direct Research

Result Update | Reliance Industries

Exhibit 4: Jio Variance Analysis

Q3FY22 Q3FY22E Q3FY21 Q2FY22 YoY (% ) QoQ (% ) Comments

Revenue 19,347 19,387 18,492 18,735 4.6 3.3Topline in line as lower sub was offset by superior

ARPU

Other Income 155 17 52 14 198.1 1,007.1

Network operating expenses 6,243 6,476 5,653 6,264 10.4 -0.3

Access charges 229 220 1,549 217 -85.2 5.5

Employee cost 361 360 343 355 5.2 1.7

Selling & Distribution expenses 269 267 298 264 -9.7 1.9

Other expenses 479 461 496 452

EBITDA 9,514 9,333 8,114 8,989 17.3 5.8EBITDA beat owing to lower networking operating

costs

EBITDA Margin (%) 49.2 48.1 43.9 48.0 530 bps 120 bps

Depreciation 3,568 3,208 2,910 3,188 22.6 11.9

Interest 1,254 1,213 850 1,084 47.5 11.9

Exceptional Items 0 0 0 0 NA NA

Total Tax 1,232 1,253 1,115 1,203 10.5 2.4

PAT 3,615 3,675 3,291 3,528 9.8 2.5

Subs (mn) 421 438 411 430 2.5 -2.0

While tha gross addition at 34.6 mn was robust, SIM

consolidation led to net customer decline of 8.5

million

ARPU (|) 152 149 151 144 0.4 5.6ARPU growth was driven by partial pass through of

tariff hike undertaken in December, 2021

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 7

ICICI Direct Research

Result Update | Reliance Industries

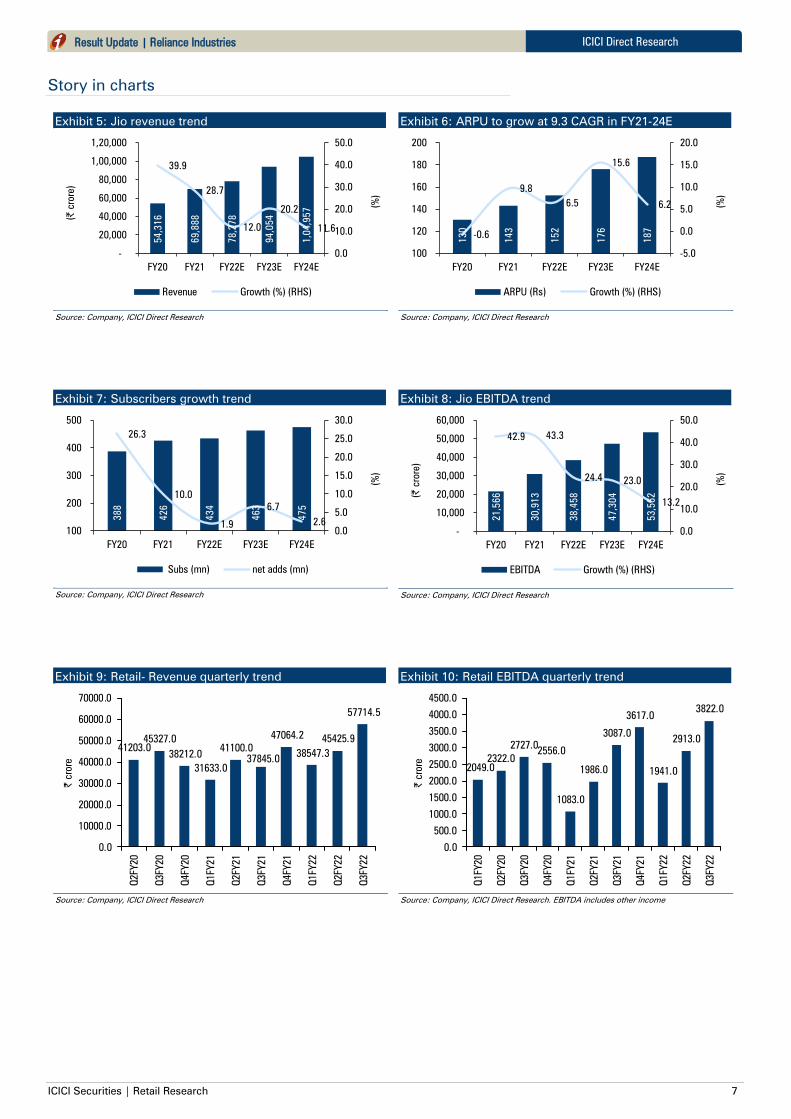

Story in charts

Exhibit 5: Jio revenue trend

Source: Company, ICICI Direct Research

Exhibit 6: ARPU to grow at 9.3 CAGR in FY21-24E

Source: Company, ICICI Direct Research

Exhibit 7: Subscribers growth trend

Source: Company, ICICI Direct Research

Exhibit 8: Jio EBITDA trend

Source: Company, ICICI Direct Research

Exhibit 9: Retail- Revenue quarterly trend

Source: Company, ICICI Direct Research

Exhibit 10: Retail EBITDA quarterly trend

Source: Company, ICICI Direct Research. EBITDA includes other income

54,3

16

69,8

88

78,2

78

94,0

54

1,0

4,9

57

39.9

28.7

12.0

20.2

11.6

0.0

10.0

20.0

30.0

40.0

50.0

-

20,000

40,000

60,000

80,000

1,00,000

1,20,000

FY20 FY21 FY22E FY23E FY24E

(%

)

(|

crore)

Revenue Growth (%) (RHS)

130

143

152

176

187

-0.6

9.8

6.5

15.6

6.2

-5.0

0.0

5.0

10.0

15.0

20.0

100

120

140

160

180

200

FY20 FY21 FY22E FY23E FY24E

(%

)

ARPU (Rs) Growth (%) (RHS)

388

426

434

463

475

26.3

10.0

1.9

6.7

2.6

0.0

5.0

10.0

15.0

20.0

25.0

30.0

100

200

300

400

500

FY20 FY21 FY22E FY23E FY24E

(%

)

Subs (mn) net adds (mn)

21,5

66

30,9

13

38,4

58

47,3

04

53,5

62

42.9 43.3

24.423.0

13.2

0.0

10.0

20.0

30.0

40.0

50.0

-

10,000

20,000

30,000

40,000

50,000

60,000

FY20 FY21 FY22E FY23E FY24E

(%

)

(|

crore)

EBITDA Growth (%) (RHS)

41203.0

45327.0

38212.0

31633.0

41100.0

37845.0

47064.2

38547.3

45425.9

57714.5

0.0

10000.0

20000.0

30000.0

40000.0

50000.0

60000.0

70000.0

Q2FY20

Q3FY20

Q4FY20

Q1FY21

Q2FY21

Q3FY21

Q4FY21

Q1FY22

Q2FY22

Q3FY22

| crore

2049.0

2322.0

2727.02556.0

1083.0

1986.0

3087.0

3617.0

1941.0

2913.0

3822.0

0.0

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

3500.0

4000.0

4500.0

Q1FY20

Q2FY20

Q3FY20

Q4FY20

Q1FY21

Q2FY21

Q3FY21

Q4FY21

Q1FY22

Q2FY22

Q3FY22

| crore

ICICI Securities | Retail Research 8

ICICI Direct Research Result Update | Reliance Industries

Exhibit 11: Consolidated retail revenues CAGR of 25% in FY21-24E

Source: Company, ICICI Direct Research

Exhibit 12: EBITDA expected to grow at 36% CAGR in FY21-24E

Source: Company, ICICI Direct Research. EBITDA excludes other income

Exhibit 13: Robust store addition trajectory in YTDFY22

Source: Company, ICICI Direct Research

21075.033765.0

69198.0

130566.0

162938.0 157642.2

197768.0

255471.5

305852.7

0

30000

60000

90000

120000

150000

180000

210000

240000

270000

300000

330000

FY16 FY17 FY18 FY19 FY20 FY21 FY22E FY23E FY24E

| crore

Consolidated Revenues

857.0 1179.0

2529.0

6201.0

9653.08463.8

11225.3

16795.5

21453.9

4.1

3.5 3.7

4.7

5.9

5.4

5.7

6.6

7.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

0

5000

10000

15000

20000

25000

FY16 FY17 FY18 FY19 FY20 FY21 FY22E FY23E FY24E%

| crore

EBITDA (| crore) EBITDA Margins (%)

32453616

7573

10415

11784

12634

14412

0

2000

4000

6000

8000

10000

12000

14000

16000

FY16 FY17 FY18 FY19 FY20 FY21 9MFY22

No. of Stores

ICICI Securities | Retail Research 9

ICICI Direct Research

Result Update | Reliance Industries

Exhibit 14: O2C EBITDA quarterly trend

Source: Company, ICICI Direct Research

Exhibit 15: O2C EBITDA trend

Source: Company, ICICI Direct Research

Exhibit 16: E&P EBITDA quarterly trend

Source: Company, ICICI Direct Research

Exhibit 17: E&P EBITDA trend

Source: Company, ICICI Direct Research

Exhibit 18: Gas production trend

Source: Company, ICICI Direct Research

13568

11961

81668841

9756

1140712231

1272013530

0

2000

4000

6000

8000

10000

12000

14000

16000

Q3FY

20

Q4FY

20

Q1FY

21

Q2FY

21

Q3FY

21

Q4FY

21

Q1FY

22

Q2FY

22

Q3FY

22

| cro

re

53803

38170

52748

6029761565

0

10000

20000

30000

40000

50000

60000

70000

FY20 FY21 FY22E FY23E FY24E

| cro

re

64

-46 -32

-194

4

480

797

1071

2033

-500

0

500

1000

1500

2000

2500

Q3FY

20

Q4FY

20

Q1FY

21

Q2FY

21

Q3FY

21

Q4FY

21

Q1FY

22

Q2FY

22

Q3FY

22

| cro

re

353 258

5371

10130

12205

0

2000

4000

6000

8000

10000

12000

14000

FY20 FY21 FY22E FY23E FY24E

| cro

re

3.02.2

12.9

16.4

20.8

6.8

6.1

2.2

0.0

0.0

0.0

5.0

10.0

15.0

20.0

25.0

FY20 FY21 FY22E FY23E FY24E

mm

scm

d

Domestic Production Shale Gas

ICICI Securities | Retail Research 10

ICICI Direct Research

Result Update | Reliance Industries

Exhibit 19: RIL consolidated revenue

Source: Company, ICICI Direct Research

Exhibit 20: RIL consolidated EBIT

FY20 FY21 FY22E FY23E FY24E

O2C 45191.0 29773.0 44875.1 51296.6 52565.0

Oil & gas -1407.0 -1477.0 2803.2 7229.8 9004.9

Retail 8292.0 7991.0 10575.4 15124.3 18887.2

Digital Services 14634.0 21181.0 26148.0 32451.0 35910.0

Financial Services 811.0 1357.0 933.0 1600.0 1600.0

Others 2671.0 3635.0 4148.0 3800.0 3800.0

Total 70192.0 62460.0 89482.7 111501.8 121767.1

Source: Company, ICICI Direct Research

Exhibit 21: Percentage share of business segments in RIL’s EBIT mix

FY20 FY21 FY22E FY23E FY24E

O2C 64.4% 47.7% 50.1% 46.0% 43.2%

Oil & gas -2.0% -2.4% 3.1% 6.5% 7.4%

Retail 11.8% 12.8% 11.8% 13.6% 15.5%

Digital Services 20.8% 33.9% 29.2% 29.1% 29.5%

Financial Services 1.2% 2.2% 1.0% 1.4% 1.3%

Others 3.8% 5.8% 4.6% 3.4% 3.1%

Total 100% 100% 100% 100% 100%

Source: Company, ICICI Direct Research

Exhibit 22: Valuation

Busienss segments Valuation Methodology Value (| crore) |/share

Energy

Oil to Chemicals 8x FY24E EBITDA 492520 728

Oil & Gas 8x FY24E EBITDA 97639 144

Value of Energy business 590159 873

Consumer Business

Retail (RIL share) 40x FY24E EBITDA 730291 1080

Digital services (RIL share) DCF 530598 785

Value of Consumer business 1260888 1865

Others 154200 228

Net debt 10494 16

Equity value 1994754 2950

Source: Company, ICICI Direct Research

658866

539238

761737

857702

909317

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

1000000

FY20 FY21 FY22E FY23E FY24E

| cro

re

ICICI Securities | Retail Research 11

ICICI Direct Research

Result Update | Reliance Industries

Consolidated Financial Summary

Exhibit 23: Profit and loss statement | crore

(Year-end March) FY21 FY22E FY23E FY24E

Revenue 539238.0 761737.3 857702.1 909317.5

Growth (%) -18.2 41.3 12.6 6.0

(Inc.)/Dec. in stock trade 199915.0 322742.0 312691.4 326865.0

Raw material Costs 92786.0 121972.3 170088.4 180421.8

Employee Costs 14817.0 17791.1 19214.4 20751.5

Excise Duty 72314.0 95712.3 119364.0 126123.0

Other Expenditure 78669.0 92317.3 96933.2 101779.8

Op. Expenditure 4,58,501.0 6,50,535.0 7,18,291.3 7,55,941.1

EBITDA 80737.0 111202.3 139410.8 153376.4

Growth (%) -9.0 37.7 25.4 10.0

Depreciation 26572.0 29667.6 34309.1 38009.3

EBIT 54165.0 81534.7 105101.8 115367.1

Interest 21189.0 14278.0 13000.0 13000.0

Other Income 16843.0 16875.0 17400.0 17400.0

PBT 55461.0 86967.7 109501.8 119767.1

Growth (%) 3.5 56.8 25.9 9.4

Tax 1722.0 18266.6 27594.4 30181.3

Minority Interest 4611.0 7724.4 10007.0 11526.1

Reported PAT 49128.0 60976.6 71900.3 78059.7

Growth (%) 24.8 24.1 17.9 8.6

EPS 76.2 90.2 106.3 115.4

Source: Company, ICICI Direct Research

Exhibit 24: Cash flow statement | crore

(Year-end March) FY21 FY22E FY23E FY24E

Profit after Tax 53,739.0 68,701.0 81,907.3 89,585.8

Add: Depreciation 26,572.0 29,667.6 34,309.1 38,009.3

Add: Others -17,122.0 5,275.0 5,275.0 5,275.0

Cash Profit 63,189.0 1,03,643.6 1,21,491.4 1,32,870.1

Increase/(Decrease) in CL -83,978.0 75,805.4 35,967.3 18,452.5

(Increase)/Decrease in CA -55,312.0 -10,357.2 -7,749.2 1,298.1

CF from Operating Activities -76,101.0 1,69,091.8 1,49,709.5 1,52,620.7

Purchase of Fixed Assets 52,019.0 89,882.0 40,240.0 60,000.0

(Inc)/Dec in Investments -88,061.0 -16,854.0 -8,500.0 -8,500.0

Others 87079 8000 8000 8000

CF from Investing Activities -53,001.0 -98,736.0 -40,740.0 -60,500.0

Inc/(Dec) in Loan Funds -81,689.0 -35,000.0 -35,000.0 -35,000.0

Inc/(Dec) in Sh. Cap. & Res. 2,01,189.0 32,153.6 -10,007.0 -11,526.1

Dividend Paid 3921 5071.5 6085.8 6085.8

CF from financing activities 1,15,579.0 -7,917.9 -51,092.8 -52,611.9

Change in cash Eq. -13,523.0 62,437.9 57,876.7 39,508.8

Op. Cash and cash Eq. 30,920.0 17,397.0 79,834.9 1,37,711.6

Cl. Cash and cash Eq. 17,397.0 79,834.9 1,37,711.6 1,77,220.4

Source: Company, ICICI Direct Research

Exhibit 25: Balance Sheet | crore

(Year-end March) FY21 FY22E FY23E FY24E

Source of Funds

Equity Capital 6,445.0 6,762.0 6,762.0 6,762.0

Preference Capital 0.0 0.0 0.0 0.0

Reserves & Surplus 6,93,727.0 7,89,193.1 8,55,007.6 9,26,981.5

Shareholder's Fund 7,00,172.0 7,95,955.1 8,61,769.6 9,33,743.5

Loan Funds 2,92,714.0 2,57,714.0 2,22,714.0 1,87,714.0

Deferred Tax Liability 37,001.0 42,276.0 47,551.0 52,826.0

Minority Interest and others 99,260.0 1,07,260.0 1,15,260.0 1,23,260.0

Source of Funds 11,29,147.0 12,03,205.1 12,47,294.6 12,97,543.5

Application of Funds

Gross Block 7,75,812.0 8,79,812.0 9,34,052.0 9,97,052.0

Less: Acc. Depreciation 2,34,554.0 2,64,221.6 2,98,530.7 3,36,540.0

Net Block 5,41,258.0 6,15,590.4 6,35,521.3 6,60,512.0

Capital WIP 1,25,953.0 1,11,835.0 97,835.0 94,835.0

Total Fixed Assets 6,67,211.0 7,27,425.4 7,33,356.3 7,55,347.0

Investments 3,64,828.0 3,81,682.0 3,90,182.0 3,98,682.0

Inventories 81,672.0 93,912.8 1,05,744.1 1,12,107.6

Debtor 19,014.0 27,130.4 30,548.3 32,386.6

Cash 17,397.0 79,834.9 1,37,711.6 1,77,220.4

Loan & Advance, Other CA 1,71,090.0 1,61,090.0 1,53,590.0 1,44,090.0

Total Current assets 2,89,173.0 3,61,968.1 4,27,594.0 4,65,804.7

Current Liabilities 1,86,936.0 2,60,868.9 2,93,733.6 3,11,410.1

Provisions 5,129.0 7,001.4 10,104.1 10,880.1

Total CL and Provisions 1,92,065.0 2,67,870.4 3,03,837.7 3,22,290.2

Net Working Capital 97,108.0 94,097.7 1,23,756.3 1,43,514.5

Miscellaneous expense 0.0 0.0 0.0 0.0

Application of Funds 11,29,147.0 12,03,205.1 12,47,294.6 12,97,543.5

Source: Company, ICICI Direct Research

Exhibit 26: Key ratios

(Year-end March) FY21 FY22E FY23E FY24E

Per share data (|)

Book Value 1,086.4 1,177.1 1,274.4 1,380.9

Cash per share 27.0 118.1 203.7 262.1

EPS 76.2 90.2 106.3 115.4

Cash EPS 117.5 134.0 157.1 171.6

DPS 7.0 7.5 9.0 9.0

Profitabil ity & Operating Ratios

EBITDA Margin (%) 15.0 14.6 16.3 16.9

PAT Margin (%) 10.0 9.0 9.5 9.9

Fixed Asset Turnover (x) 0.8 1.0 1.2 1.2

Inventory Turnover (Days) 55.3 45.0 45.0 45.0

Debtor (Days) 12.9 13.0 13.0 13.0

Current Liabilities (Days) 126.5 125.0 125.0 125.0

Return Ratios (% )

RoE 7.7 8.6 9.5 9.6

RoCE 5.5 7.7 9.7 10.3

RoIC 5.6 8.4 11.1 12.2

Valuation Ratios (x)

PE 32.5 27.5 23.3 21.5

Price to Book Value 2.3 2.1 1.9 1.8

EV/EBITDA 23.2 16.7 12.6 11.0

EV/Sales 3.5 2.4 2.1 1.9

Leverage & Solvency Ratios

Debt to equity (x) 0.4 0.3 0.3 0.2

Interest Coverage (x) 2.6 5.7 8.1 8.9

Debt to EBITDA (x) 3.6 2.3 1.6 1.2

Current Ratio 1.5 1.4 1.4 1.4

Quick ratio 1.1 1.0 1.1 1.1

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 12

ICICI Direct Research

Result Update | Reliance Industries

Exhibit 27: ICICI Direct coverage universe

CMP TP M Cap

(|) (|) (| Cr) FY21 FY22E FY23E FY21 FY22E FY23E FY21 FY22E FY23E FY21 FY22E FY23E FY21 FY22E FY23E

BPCL (BHAPET) 381 520 Buy 79,740 91.0 42.8 40.6 4.2 8.9 9.4 6.2 6.6 6.4 14.8 14.5 13.5 34.9 18.8 16.4

GAIL (India) (GAIL) 144 180 Buy 63,942 11.0 20.8 18.2 13.1 6.9 7.9 10.6 5.2 6.1 8.7 17.9 13.5 10.5 17.4 13.9

Gujarat Gas (GUJGA) 701 645 Hold 48,257 18.5 18.5 23.0 37.8 37.9 30.4 23.5 23.4 19.0 31.7 28.1 30.7 28.5 23.4 24.3

HPCL (HINPET) 310 325 Hold 43,986 70.6 52.6 40.0 4.4 5.9 7.8 5.5 6.3 6.7 15.6 11.3 8.5 29.5 18.6 13.2

Indian Oil Corp (INDOIL) 122 155 Buy 1,12,009 23.8 24.1 18.0 5.1 5.1 6.8 2.9 2.7 3.2 13.3 13.7 10.0 19.8 17.6 12.3

Indraprastha Gas (INDGAS) 425 560 Hold 29,750 14.4 18.1 21.4 29.6 23.4 19.9 19.4 15.9 12.9 20.0 22.0 22.8 17.1 18.7 18.9

Mahanagar Gas (MAHGAS) 853 1120 Hold 8,426 62.7 78.6 101.8 13.6 10.9 8.4 8.5 6.9 4.9 23.1 25.6 28.3 19.2 20.9 22.8

ONGC (ONGC) 164 180 Hold 2,10,467 8.9 30.0 26.6 18.3 5.5 6.2 6.9 4.0 3.2 4.5 12.8 14.4 5.5 16.1 12.8

Petronet LNG (PETLNG) 213 245 Hold 31,950 19.7 19.3 21.2 10.8 11.1 10.0 6.6 6.4 5.7 26.0 24.3 24.7 25.3 23.2 23.5

Reliance Industries (RELIND) 2,478 2,950 Buy 16,75,691 76.2 90.2 106.3 32.5 27.5 23.3 23.2 16.7 12.6 5.5 7.7 9.7 7.7 8.6 9.5

RoCE (% ) RoE (% )

Sector / Company

EPS (|) P/E (x) EV/EBITDA (x)

Rating

Source: Bloomberg, ICICI Direct Research

ICICI Securities | Retail Research 13

ICICI Direct Research

Result Update | Reliance Industries

RATING RATIONALE

ICICI Direct endeavours to provide objective opinions and recommendations. ICICI Direct assigns ratings to its

stocks according -to their notional target price vs. current market price and then categorizes them as Buy, Hold,

Reduce and Sell. The performance horizon is two years unless specified and the notional target price is defined

as the analysts' valuation for a stock

Buy: >15%

Hold: -5% to 15%;

Reduce: -15% to -5%;

Sell: <-15%

Pankaj Pandey Head – Research [email protected]

ICICI Direct Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

ICICI Securities | Retail Research 14

ICICI Direct Research

Result Update | Reliance Industries

ANALYST CERTIFICATION

I/We, Mayur Matani, MBA, Bharat Chhoda, MBA, Bhupendra Tiwary, MBA, Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect

our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. It is also confirmed that

above mentioned Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months and do not serve as an officer, director or employee of the companies

mentioned in the report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products.

ICICI Securities is Sebi registered stock broker, merchant banker, investment adviser, portfolio manager and Research Analyst. ICICI Securities is registered with Insurance Regulatory Development Authority of India Limited (IRDAI)

as a composite corporate agent and with PFRDA as a Point of Presence. ICICI Securities Limited Research Analyst SEBI Registration Number – INH000000990. ICICI Securities Limited SEBI Registration is INZ000183631 for stock

broker. ICICI Securities is a subsidiary of ICICI Bank which is India’s largest private sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture

capital fund management, etc. (“associates”), the details in respect of which are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking and other business relationship

with a significant percentage of companies covered by our Investment Research Department. ICICI Securities and its analysts, persons reporting to analysts and their relatives are generally prohibited from maintaining a financial

interest in the securities or derivatives of any companies that the analysts cover.

Recommendation in reports based on technical and derivative analysis centre on studying charts of a stock's price movement, outstanding positions, trading volume etc. as opposed to focusing on a company's fundamentals and, as

such, may not match with the recommendation in fundamental reports. Investors may visit icicidirect.com to view the Fundamental and Technical Research Reports.

Our proprietary trading and investment businesses may make investment decisions that are inconsistent with the recommendations expressed herein.

ICICI Securities Limited has two independent equity research groups: Institutional Research and Retail Research. This report has been prepared by the Retail Research. The views and opinions expressed in this document may or may

not match or may be contrary with the views, estimates, rating, and target price of the Institutional Research.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected

recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would

endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI

Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in

circumstances where ICICI Securities might be acting in an advisory capacity to this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein

is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers

simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting

and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who

must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient.

The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities

whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks

associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-

managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any compensation or other

benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts and their relatives have any material conflict of

interest at the time of publication of this report.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the publication of

the research report.

Since associates of ICICI Securities and ICICI Securities as a entity are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or

use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in

all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.

Top Related

Copyright © 2022 FDOKUMEN