Bahasa

Halaman

Hukum

1

“PERFORMANCE EVALUATION OF URBAN CO-

OPERATIVE BANK - A CASE STUDY OF DEVGIRI URBAN

CO-OPERATIVE BANKS LTD. AURANGABAD”

DISSERTATION SUBMITTED

TO

DR.BABASAHEB AMBEDKAR MARATHWADA UNIVERSITY,

AURANGABAD.

FOR THE DEGREE OF

MASTER OF PHILOSOPHY

IN

DEPARTMENT OF COMMERCE

BY

MR. KALE BILAS SAKHARAM

UNDER THE GUIDANCE OF

PROF. M. A. LOKHANDE

PROFESSOR AND HEAD, DEPARTMENT OF COMMERCE,

DR.BABASAHEB AMBEDKAR MARATHWADA UNIVERSITY,

AURANGABAD.

2

2013-2014

DECLARATION

I hereby declare that this research entitled “Performance Evaluation of

Urban Co-operative Banks – A case Study of Devgiri Urban Co-

operative Banks Ltd. Aurangabad” Submitted for the award of the

Master Of Philosophy degree in the faculty of commerce, to the Dr.

Babasaheb Ambedkar Marathwada University, Aurangabad is of

original nature. I further declare that best of my knowledge and belief

this research work has not been submitted earlier for the award of any

degree of this or any other university.

Date: - / / 2014 (Kale Bilas Sakharam).

Place: - Aurangabad (Research Student)

3

CERTIFICATE

This is to certify that the dissertation entitled “Performance Evaluation

of Urban Co-operative Banks - A case Study of Devgiri Urban Co-

operative Banks Ltd. Aurangabad” is the bonafide research work was

carried out by Kale Bilas Sakharam student of M.Phil department of

commerce under the my supervision Dr.Babasaheb Ambedkar

Marathwada University, Aurangabad, during the year 2013-14 in partial

fulfillment of the requirements for the award of the degree of Master of

Philosophy and that the dissertation has not found any other similar title.

Date: - / /2014. Guide

Place: - Aurangabad. Prof. M.A. Lokhande.

4

ACKNOWLEDGEMENT

First of all I am thankful to my research guide Prof. M. A. Lokhande under whose

guidance this study was conducted. It was on account of his encouragement and

suggestions that this work has come up in the present from.

I am also thankful to Dr. Sayyed Azharuddin, Dr. Veena R. Humbe, Dr. Vilas

Epper, Dr. N.S.Rathi, Dr. J.R.Suryawanshi of Department of Commerce,

Dr.Babasaheb Ambedkar Marathwada University, Aurangabad for their guidance

as and when needed for the completion of this study.

I am deeply indebted to my father Sakharam Kale and Mother Smt. Sukhashalabai

Kale, Limbaji, Vilas, Kailas (Brother) for their good blessing and continue

encouragement to my education and without whose blessing I could never have

stood in my life.

I am very thankful to my friends Kaldate Krishna, Ughade Ashok, Jagdale

Rameshwar, Chate Hanumant, Dabhade Vishawanath, Kaldate Madhukar,

Dombale Sunil, Tonde Adinath, Hake Deepak and Dhawle Nitin who help me in

completing the present study and to those friends whose good wishes were with

me.

I am thankful to Akade Abhishek, Pawar Mama, Raju Lokhande and Gaikawad

Mama non teaching staff members of Dept of commerce, Dr. B. A. M. U, A ‘Bad.

Lastly, I am thankful to all of them who have directly and indirectly helped me in

completing the present study.

Date: - / / 2014. Kale Bilas Sakharam

Place: - Aurangabad. (Research Student)

5

Table of Contents

Chapter No. Particular Page No.

Declaration II

Certificate III

Acknowledgements IV

List of Tables V

List of Charts & Diagrams VI

I Introduction 01-24

II Research Methodology & Literature Review 25-68

III Analysis and Interpretation of Data 69-102

IV Observations and Suggestions 103-110

Bibliography 111-115

Abbreviations 116-117

6

LIST OF TABLES

Table No Name of Tables Page No.

1.1 Urban Co-operative Bank in Maharashtra 20

1.2 Grade wise Distribution of UCBs in Maharashtra 21

1.3 Comparative Statistics of Cooperative Societies In Maharashtra 23-24

3.1 Growth Trend of capital/Liability position of DUCB 71-72

3.2 Growth Trend of Asset/Property position of DUCB 72-73

3.3 Per year Share of the Total Fund of Liability 74-75

3.4 Per year Share of the Total Fund of Asset 75-76

3.5 Capital Adequacy 76-77

3.6 Mixer of Bank Deposits on 2008-2013 (Share of Total fund Deposits) 77-78

3.7 Net Growth and Mixer of Bank Deposits on 2008-2013. 79-80

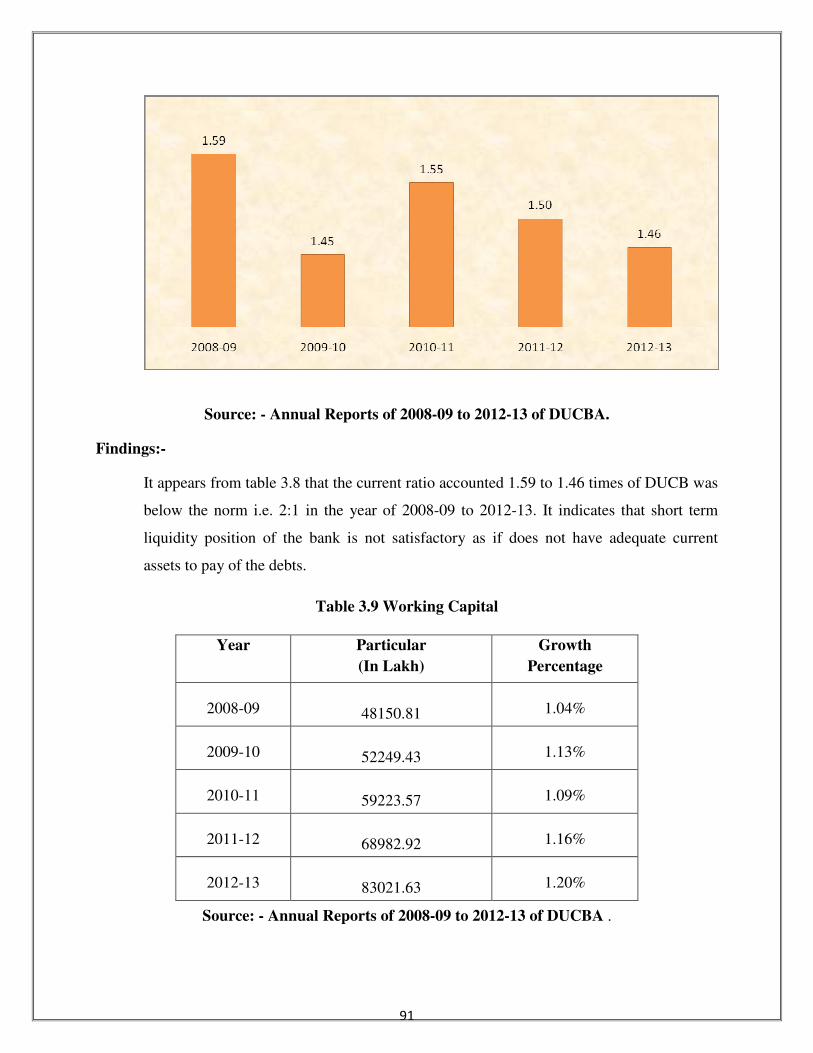

3.8 Short term liquidity position of DUCB 81

3.9 Working Capital 82

3.10 Fixed Assets to Proprietary Fund Ratio 83

3.11 Debt Equity Ratio 84

3.12 Fixed Asset to Current Asset 85

3.13 Working Capital to Net Worth 86

3.14 Solvency Ratio 87

3.15 Fixed Asset to Net worth Ratio 88

3.16 Earning Per Shares (EPS). 89

3.17 Proprietary Ratio. 90

3.18 Profitability Ratio 91

3.19 Non Performing Assets Ratio 92

3.20 Price Earnings Ratio 93

3.21 Dividend Yield Ratio 94

3.22 Dividend Payout Ratio 95

3.23 Interests on Deposits 96

3.24 Interests on Loan 97

3.25 Interests on Investment 98

3.26 Growth trend of Net Profit 99

3.27 Comparative 5 year growth of DUCBA 100-102

7

LIST OF DIGRAMS AND CHARTS

Chart No Name of Diagrams and Charts Page No.

3.1 Growth Trend of capital/Liability position of DUCB 71-72

3.2 Growth Trend of Asset/Property position of DUCB 72-73

3.3 Per year Share of the Total Fund of Liability 74-75

3.4 Per year Share of the Total Fund of Asset 75-76

3.5 Capital Adequacy 76-77

3.6 Mixer of Bank Deposits on 2008-2013 (Share of Total fund Deposits) 77-78

3.7 Net Growth and Mixer of Bank Deposits on 2008-2013. 79-80

3.8 Short term liquidity position of DUCB 81

3.9 Working Capital 82

3.10 Fixed Assets to Proprietary Fund Ratio 83

3.11 Debt Equity Ratio 84

3.12 Fixed Asset to Current Asset 85

3.13 Working Capital to Net Worth 86

3.14 Solvency Ratio 87

3.15 Fixed Asset to Net worth Ratio 88

3.16 Earning Per Shares (EPS). 89

3.17 Proprietary Ratio. 90

3.18 Profitability Ratio 91

3.19 Non Performing Assets Ratio 92

3.20 Price Earnings Ratio 93

3.21 Dividend Yield Ratio 94

3.22 Dividend Payout Ratio 95

3.23 Interests on Deposits 96

3.24 Interests on Loan 97

3.25 Interests on Investment 98

3.26 Growth trend of Net Profit 99

8

Chapter –I

Introduction

Chapter I Introduction Page No

1.1 Co-operative Banks in India 02-03

1.2 History of Co-operative Banks 03-07

1.3 Function of Co-operative Banks:- 08

1.4 Advantages and Role of Co-operative Banking in India 08-09

1.5 Structure of Co-operative Banking in India:- 07

1.6 The 7 Co-operative Principle are;- 10-11

1.7 Urban Co-operative Bank – Concept: 12

1.8 Profile of DUCB 13

1.9 Brief History of Urban Cooperative Banks in India 14-18

1.10 Objectives of the Urban Co-operative Banks:- 18-19

1.11 Role of the UCBs in Indian Banking System: 19-20

1.12 Urban Co-operative Banks in Maharashtra 19-23

Table 1.1 Urban Co-operative Banks in Maharashtra 20

Table 1.2 Grade wise Distribution of UCBs in Maharashtra 21

Table 1.3 Comparative Statistics of co-operative societies in MS 23-24

9

1.1 Co-operative Banks in India:-

The Co-operative Banks are a special type of banking in which people co-operative with

each other with a view to promote their mutual interest. Co-operative means working together. In

this banking organization, people voluntarily co-operative with each other on equal terms to

promote their own economic interest. The year 1904 marked the beginning of the history of

Agricultural Co-operative Banks in India. The Anyonya Co-operative banks in India are

considered as the first Co-operative bank in Asia.

The Co-operative Bank is an important constituent of the Indian Financial System,

judged by the role assigned, the expectations supported to fulfill, their number, and the number

of officers the Co-operative bank operate. Though the Co-operative movement originated in the

west, but the importance of such banks assumed in India is rarely paralleled anywhere else in the

world. The Co-operative banks in India play an important role even today in rural financing. The

business of Co-operative Banks in the urban areas also has increased phenomenally in recent

years due to the sharp increase in the number of primary Co-operative Banks. Co-operative

Banks in India are registered under the Co-operative Societies Act. The Co-operative Banks is

also regulated by the RBI. They are governed by the Banking Regulation Act 1949 and Banking

Laws (co-operative Societies) Act, 1965.

In India the co-operative movement was introduced as a remedy for the proverbial

poverty of the small agriculturalists. It was the government of Madras (Chennai) who grasped

the possibilities of co-operative movement in India. The origin of urban cooperative credit

societies in India can be traced to the close of 19th century. Inspired by the urban co-operative

credit institutions organized in Germany by Mr. Hermann Schulze (1860) and in Italy by Prof.

Luigi Luzzatti (1866), the first urban co-operative credit society named “ANYONYA

SAHAKARI MANDALI” was established in Baroda on 5th

February, 1889, under the guidance

of Shri V.L. Kavthekar. But the co-operative credit societies got legal status only in 1904, when

the govt. of India passed the first “Cooperative credit societies Act, 1904” with a view to

encourage thrift, eradicate rural indebtedness and provide credit to the needy and weaker sections

of the society in rural areas. This act has widened the scope of co-operative enterprises in India.

UCBs oriented and developed as a result of the cooperative movement to provide self

help to needy sections of society. The co-operative movement came into existence in the late

1700s in England where Robert Owen – a great philosopher advocated the establishment of co-

10

operative communities to mitigate the sufferings of the exploited class in the wake of the

industrial revolution. But the modern co-operative movement began in 1844 near Manchester,

England when 28 flannel weavers established “The Rochadale Society of Equitable Pioneers” to

increase their wages.

1.2 History of Co-operative Banks:-

Robert Owen (1771-1858) fathered the co-operation movement. A Welshman who made

his fortune in the cotton trade. Owen believed in putting his workers in a good environment with

access to education for themselves and their children. These ideas were put into effect

successfully in the cotton mills of New Lanark, Scotland. It was here that the first co-operative

store was opened. Spurred on by the success of this, he had the idea of forming “Villages of co-

operation” where workers would drag themselves out of poverty by growing their own food,

making their own clothes and ultimately becoming self – governing. He tried to form such

communities in Orbison in Scotland and in New Harmony, Indiana in the United States of

America, but both communities failed. Although, Owen inspired the co-operative movements,

others such as Dr. William King (1786 – 1865) took his ideas and made them more workable and

practical. King believed in starting small, and realized that the working classes would need to set

up cooperatives for themselves, so he saw his role as one of instruction. He founded a monthly

periodical called The Co-operator, the first edition of which appeared on May 1, 1828. This gave

a mixture of co-operative philosophy and practical advice about running a shop using co-

operative principles. King advised people not to cut themselves off from society, but rather to

form a society within a society and to start with a shop because, “We must go to shop every day

to buy food and necessaries – why then should we not go to our own shop?” He proposed

sensible rules, such as having a weekly account audit, having three trustees and not having

meetings in pubs (to avoid the temptation of drinking profits). A few poor weavers joined

together to form the Rochdale Equitable Pioneers Society at the end of 1843. The Rochdale

Pioneers, as they became know, set out the Rochdale Principles in 1844 which form the basis of

co-operative movement today.

Co-operative communities are now wide spread with one of the largest and most

successful examples being at Mondragon in Basque country of Spain. Co-operatives were also

successful in Yugoslavia under Tito where workers council gained a significant role in

management. In many European countries, co-operative institutions have a predominant market

11

share in the retail banking and insurance businesses. The Indian co-operative movement was

initiated by the government. It spread and diversified with the encouragement and support of the

government. Its present condition on is also to a great extent because of the intrusive

involvement of and interference by the government.

The history of co-operative movement in India is broadly divided into two phases.

That means co-operative movement has passed into two phases. They are-

1) Co –operative movement in pre-independence era.

2) Co-operative movement in post–independence era.

These two phases are briefly discussed below:-

i) Co-operative Movement in pre-independence era:

The pages of Indian history cite many evidences of co-operative activities from earliest

times. However, the first recorded activity began in 1904 when this movement was officially set

up by the British Government. Before that in the year 1892, Derrick Nicholson, tried to find out

ways and means to establish institutions so as to help the agricultural sector. He gave the

suggestions for setting of co-operative societies. Within that decade, India faced a terrible famine

in 1899.

The Government appointed the Second Famine Commission 1901 to suggest measures

for the victims. The commission recommended for a number of development activities and

setting up of new institution. The most important among them was the strong recommendation

for organisation of co-operative societies. The Government had accepted many of the

recommendations and in 1904 “co operative societies Act” were passed. The aim was to help the

rural farmers and artisans by providing short term and long term loans.

These credit societies were organised on the basis of two models, one for rural area and

other for urban area. For the former these were organised on Reinfusion Model while for the

latter it was Schulze Delitzsch Bank Model. Due to this Act a number of Co-operative Societies

grew up in rural area, but they could not function effectively. The major defects were.

i) There was no provision for setting up of Non credit Co-operative Societies in rural area.

12

ii) No special Central agency was created for financing and supervising the activities of

these societies.

iii) The division of the Credit Co-operative Societies into two types rural and urban stood as

a barrier since no specific arrangements could be done for either due to the overlapping

nature of such classification.

The year 1928 saw a worldwide economic depression. The prices of agricultural

commodities fell down to a great extent and unemployment along with other economic crisis

grew up. The creditors had no way to repay the loan. This brought many co-operative societies in

to a standstill position.

In year 1933, the Reserve Bank of India was set up. The bank took some initiative to

recognise the co-operative movement. It had a separate department for a co-operative credit. It

helped to keep the movement alive which was gradually decaying.

In 1937, the popular Congress Government came to power in several states. The popular

leaders took much more initiative in organising and extending this movement. But much

progress could not do due to outbreak of Second World War. During this time, the ministry

resigned. It was left in the hands of British Government again. But the war itself gave a boost to

co-operative societies. The war brought a sudden increase in the prices of agricultural products

and other food grains.

The rural farmer got extra economic gains. Non credit societies grew up. The working

capital of co-operative societies also increased. The number of different credit and non credit co-

operatives increased rapidly. The co-operative movement gathered momentum. The all India Co-

operative planning Committee in 1945 also worked al lot in this direction.

ii) Co-operative movement in Post independence Era:

After independence for the first 3 years i.e. up to no significant development could be

made. It was mainly due to the problem created by partition and absence of concrete programme

for national re-organisation. However, the leaders of free India could the importance of co-

operative movement for a successful democracy importance was given to strengthen co-

13

operative structure of country and various provisions were made through different Five Year

Plan.

The co-operative movement completed its 50 years dump the first plan. The Golden

Jubilee was celebrated throughout the country with much excitement. This made the people feel

the importance of such a movement. Attention was given to utilise the credit in productive

activities.

The First Plan also recommended for training of personnel's and setting up of Co-

operative Marketing Societies.

The Second Plan laid down proposals for extending co operative activity into various

fields. It gave special emphasis on the warehousing co operatives at the State and Central level.

The Third Plan brought still new areas under Co operative societies. The co operative

society for sugarcane, cotton, spinning, milk supply was proposed. Some concrete steps were

taken to train the personnel's. The co operative training College at Pune and many regional

centres were established to train the workers.

The Fourth Plan emphasised for consolidation of co-operative system. The new

programme for high yielding crops was started. Different credit societies were organised to serve

these programmes.

The Fifth Plan made special provisions for improvement of Central Banks and no viable

primary agricultural societies, re-organising marketing as well as consumer societies. It also

recommended for establishment of Farmer’s Service Societies.

The Sixth Plan laid down a point programme for co-operative societies. It aimed at

transforming the primary village societies to multipurpose societies.

i) To reconstruct the policies and of co-operative so that it can bring about economic

development of people.

ii) To extend co-operative activities to the fields of food processing, poultry farming, dairy

farming, fishery and many other related fields.

14

iii) To give necessary training and guidance for developing skilled the efficient personnel's.

The Seventh Plan has also given more importance on the growth and expansion of co

operative societies to ensure public participation to achieve its main objective i.e. the movement

towards social justice has to be faster and there must be a sharper focus on employment and

poverty alleviation.

1.3 Functions of Co-operative Banks:-

Co-operative Banks basis functions is to provide credit facility to the farmers, artisans,

workers engaged in cottage and small scale industries and other such areas going on in the rural

areas. Cooperative banks also perform the basic function of banking but they differ from

commercial Banks in the following aspects.

1. Commercial Banks are joint stock companies under the company’s act of 1956 or public

sector banks under a separate act of a parliament whenever as co-operative banks were

establishment under the co-operative society’s acts of different states.

2. Commercial Banks structural is branch banking structure whereas co-operative Banks

have a there tier setup, with state co-operative banks at apex level, central District

cooperative banks at district level and primary cooperative Societies at rural level.

3. Only some of the sections of banking regulation act of 1949, are applicable to co-

operative Banks, regulating only in partial control by RBI of Cooperative Banks.

4. Cooperative banks functions on the principle of co-operative and not entirely on

commercial parameters.

5. Cooperative banks in India finance the rural areas under.

- Farming, Cattle, Milk, Hat chery, Personal Finance, Cooperative banks in India finance the

urban areas under, Self employment, Small scale units, and consumer finance.

15

1.4 Advantages or Role of Co-operative Banking in India:-

1. Co-operative Banks give loans to the farmers and artisans at low rate of interest who are

thus saved of the exploitation by the Mahajans. Loans are available only for productive

purposes. Wasteful expenditure is, therefore, avoided.

2. Co-operative Banks give loans to the farmers to buy good seeds, fertilisers and cattle.

These banks also help in the consolidation of land holdings and removal of irrigation and

transport constraints. As a result, agricultural production tends to increase.

3. As a result of co-operative baking income of the farmers has tended to rise, as also their

standards of living in India, co-operative Banks are required to spend 10% of their profit

on rural development. Co-operative Banks thus are an important force behind the rural

up liftmen.

4. Co-operative Banking encourages thrift. Also, small savings of the people are gainfully

used by this.

1.5 Structure of Co-operative Banking in India:-

The Co-operative Banking structure in India is divided into following main 5 Categories.

- Primary Agricultural Credit Societies.

- District Central Co-operative Banks

- State Co-operative Banks or Apex Banks.

- Land Development Banks or State Co-operative Agricultural and Rural.

- Primary Urban Co-operative Banks.

Co-operative banks function on the basis of 'no-profit no-loss'. Co-operative banks, as a

principle, do not pursue the goal of profit maximization. Therefore, these banks do not focus on

16

offering more than the basic banking services. So, co-operative banks finance small borrowers in

industrial and trade sectors, besides professional and salary classes.

• Some cooperative banks in India are more forward than many of the state and private

sector banks.

• According to NAFCUB (National Federation of Urban Co-operative Banks and Credit

Societies Ltd), the total deposits and lending of cooperative banks in India is much more

than old private sector banks and also some new public sector banks.

• This exponential growth of co-operative banks in India is attributed mainly to their much

better local reach, personal interaction with customers, and their ability to catch the

nerve of the local clientele.

Although they are not better than private banks in terms of facilities provided, their interest

rates are definitely competitive. For example, the interest rates on auto loans are anywhere less

than 5%-7% than that offered by private banks.

However, unlike private banks, the documentation process is lengthy if not stringent and

getting a loan approved quickly is rather difficult. The criteria for getting a loan from a UCB are

less stringent than for a loan from a commercial bank. For instance, when taking an education

loan, it does not matter whether the course you are going for is recognized or not.

So, it makes better sense to bank with UCBs today, what with the rates some offer being the

best in the industry. And with the risk of a run minimized, they are almost on an equal footing

with commercial banks when it comes to vying for your attention. However, to get a loan, you

have to be a member of the SCB: own its shares worth at least 2.5 per cent of the loan amount, or

a maximum of Rs. 25,000. This amount earns a return of 12-20 per cent.

According to the International Co-operative Alliance Statement of co-operative identity, a

co-operative is an autonomous association of persons united voluntarily to meet their common

economic, social, and cultural needs and aspirations through a jointly-owned and democratically-

controlled enterprise. Co-operatives are based on the values of self-help, self-responsibility,

democracy, equality, equity and solidarity. In the tradition of their founders, co-operative

17

members believe in the ethical values of honesty, openness, social responsibility and caring for

others.

1.6 The 7 co-operative principles are:

1. Voluntary and open membership

2. Democratic member control

3. Member economic participation

4. Autonomy and independence

5. Education, training and information

6. Co-operation among Co-operatives

7. Concern for Community

A co-operative bank is a financial entity which belongs to its members, who are at the

same time the owners and the customers of their bank. Co-operative banks are often created by

persons belonging to the same local or professional community or sharing a common interest.

Co-operative banks generally provide their members with a wide range of banking and financial

services (loans, deposits, banking accounts...).

Co-operative banks differ from stockholder banks by their organization, their goals, their

values and their governance. In most countries, they are supervised and controlled by banking

authorities and have to respect prudential banking regulations, which put them at a level playing

field with stockholder banks. Depending on countries, this control and supervision can be

implemented directly by state entities or delegated to a co-operative federation or central body.

Even if their organizational rules can vary according to their respective national legislations,

Co-operative banks share common features:

Customer's owned entities: in a co-operative bank, the needs of the customers meet the

needs of the owners, as co-operative bank members are both. As a consequence, the first aim of a

18

Co-operative bank is not to maximize profit but to provide the best possible products and

services to its members. Some co-operative banks only operate with their members but most of

them also admit non-member clients to benefit from their banking and financial services.

Democratic member control: co-operative banks are owned and controlled by their

members, who democratically elect the board of directors. Members usually have equal voting

rights, according to the co-operative principle of "one person, one vote".

Profile allocation: in a co-operative bank, a significant part of the yearly profit, benefits

or surplus is usually allocated to constitute reserves. A part of this profit can also be distributed

to the co-operative members, with legal or statutory limitations in most cases. Profit is usually

allocated to members either through a patronage dividend, which is related to the use of the co-

operatives products and services by each member, or through an interest or a dividend, which is

related to the number of shares subscribed by each member.

Co-operative banks are deeply rooted inside local areas and communities. They are

involved in local development and contribute to the sustainable development of their

communities, as their members and management board usually belong to the communities in

which they exercise their activities. By increasing banking access in areas or markets where

other banks are less present - SMEs, farmers in rural areas, middle or low income households in

urban areas - co-operative banks reduce banking exclusion and foster the economic ability of

millions of people. They play an influential role on the economic growth in the countries in

which they work in and increase the efficiency of the international financial system. Their

specific form of enterprise, relying on the above-mentioned principles of organization, has

proven successful both in developed and developing countries.

A word of caution: Only approach those co-operative banks which have a good history.

Since, a lot of co-operative banks have political interests, providing social help is not one of their

priorities sometime.

19

1.7 Urban Co-operative Bank – CONCEPT:

As the name suggests, a bank operating in urban areas on the basis of co-operative

principles is known as Urban Co-operative Bank. There was no well defined concept of an Urban

Co-operative Bank before 1939. Initially UCBs were organized as credit societies in India and

later converted into Urban Banks. It was the Mehta Bhansali Committee (1939) which made the

first attempt to define an Urban Co-operative Bank. Subsequently in 1966, when banking laws

were made applicable to co-operative banks, provision of section 5 [CCV] of Banking

Regulation Act 1949 [As applicable to cooperative societies (AACS)] defined an Urban Co-

operative Bank as a Primary Cooperative

Bank other than a Primary Agricultural Credit Society –

1. The primary objective or principal business of which is the transaction of banking

business,

2. The paid up share capital and reserves of which are not less than one lakh rupees,

3. The by – laws of which do not permit admission of any other co-operative society as a

member.

Provided that this sub – clause shall not apply to the admission of a co-operative

bank as a member by reason of such a Co-operative Bank subscribing to the share capital of such

Co-operative society out of fund provided by the State Government for the purpose.

In short, UCBs are Primary Co-operative Banks organized on Co-operative basis,

operating in metropolitan, urban and semi – urban areas to cater the needs of specific types or

groups of members pertaining to certain class of community, small scale industrial units, trade,

professions, etc. They are of two types: a unit banking type and branch banking type.

Besides providing main banking service to their customers, they also provide various

other banking and subsidiary services to their customers and have developed a nice market for

them to survive.

20

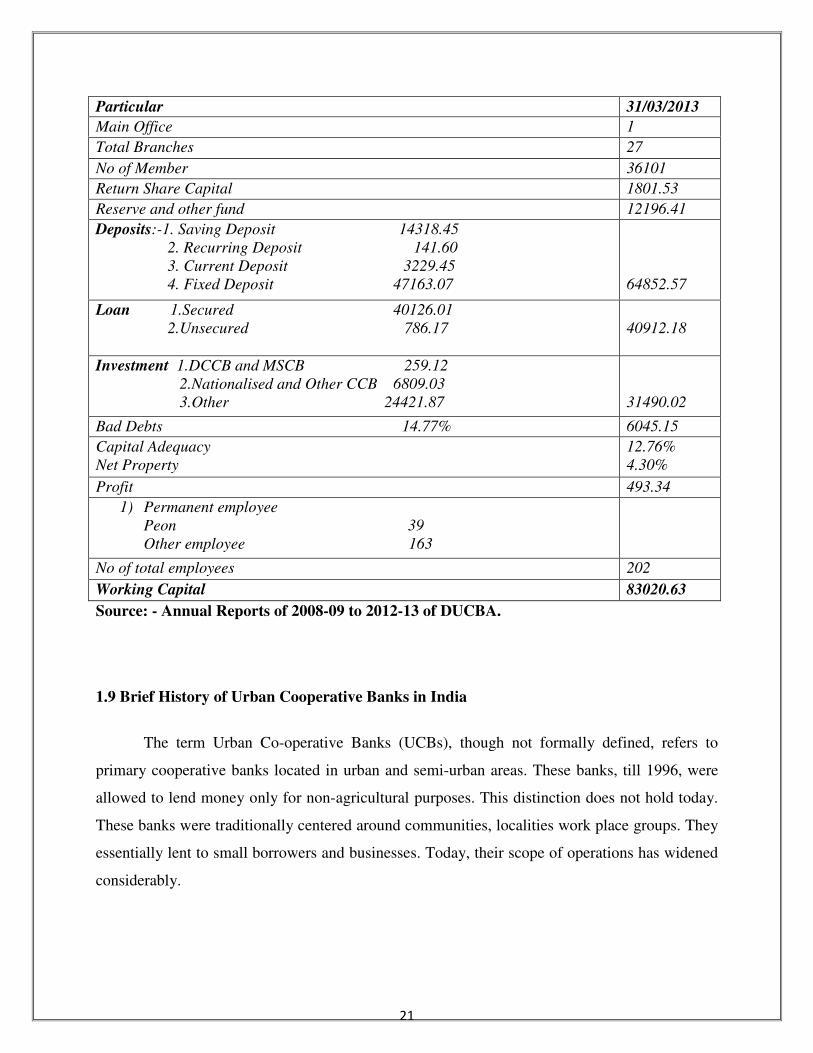

1.8 Profile of Devgiri Urban Co-operative Bank Ltd. Aurangabad

Name of Bank :- Devgiri Urban Cooperative Bank Ltd. Aurangabad

Address :- Earth Complex, Kesarsinghpura, Adalat

Road, Aurangabad-431 001.

Registration No :- AGD/BNK/215/84,

And Date 24/01/1984.

Permission of RBI :- UBD/BNK/312/p,

No and Date 18/05/1984.

Area :- Whole Maharashtra state (In Lakh)

21

Source: - Annual Reports of 2008-09 to 2012-13 of DUCBA.

1.9 Brief History of Urban Cooperative Banks in India

The term Urban Co-operative Banks (UCBs), though not formally defined, refers to

primary cooperative banks located in urban and semi-urban areas. These banks, till 1996, were

allowed to lend money only for non-agricultural purposes. This distinction does not hold today.

These banks were traditionally centered around communities, localities work place groups. They

essentially lent to small borrowers and businesses. Today, their scope of operations has widened

considerably.

Particular 31/03/2013

Main Office 1

Total Branches 27

No of Member 36101

Return Share Capital 1801.53

Reserve and other fund 12196.41

Deposits:-1. Saving Deposit 14318.45

2. Recurring Deposit 141.60

3. Current Deposit 3229.45

4. Fixed Deposit 47163.07

64852.57

Loan 1.Secured 40126.01

2.Unsecured 786.17

40912.18

Investment 1.DCCB and MSCB 259.12

2.Nationalised and Other CCB 6809.03

3.Other 24421.87

31490.02

Bad Debts 14.77% 6045.15

Capital Adequacy

Net Property

12.76%

4.30%

Profit 493.34

1) Permanent employee

Peon 39

Other employee 163

No of total employees 202

Working Capital 83020.63

22

The origins of the urban cooperative banking movement in India can be traced to the

close of nineteenth century when, inspired by the success of the experiments related to the

cooperative movement in Britain and the cooperative credit movement in Germany such

societies were set up in India. Cooperative societies are based on the principles of cooperation, -

mutual help, democratic decision making and open membership. Cooperatives represented a new

and alternative approach to organization as against proprietary firms, partnership firms and joint

stock companies which represent the dominant form of commercial organization.

The Beginnings

The first known mutual aid society in India was probably the ‘Anyonya Sahakari

Mandali’ organized in the erstwhile princely State of Baroda in 1889 under the guidance of

Vithal Laxman also known as Bhausaheb Kavthekar. Urban co-operative credit societies, in their

formative phase came to be organized on a community basis to meet the consumption oriented

credit needs of their members. Salary earners’ societies inculcating habits of thrift and self help

played a significant role in popularizing the movement, especially amongst the middle class as

well as organized labour. From its origins then to today, the thrust of UCBs, historically, has

been to mobilize savings from the middle and low income urban groups and purvey credit to

their members - many of which belonged to weaker sections.

The enactment of Cooperative Credit Societies Act, 1904, however, gave the real impetus

to the movement. The first urban cooperative credit society was registered in Canjeevaram

(Kanjivaram) in the erstwhile Madras province in October, 1904. Amongst the prominent credit

societies were the Pioneer Urban in Bombay (November 11, 1905), the No.1 Military Accounts

Mutual Help Co-operative

Credit Society in Poona (January 9, 1906). Cosmos in Poona (January 18, 1906), Gokak

Urban (February 15, 1906) and Belgaum Pioneer (February 23, 1906) in the Belgaum district,

the Kanakavli-Math Co-operative Credit Society and the Varavade Weavers’ Urban Credit

Society (March 13, 1906) in the South Ratnagiri (now Sindhudurg) district. The most prominent

amongst the early credit societies was the Bombay Urban Co-operative Credit Society,

sponsored by Vithaldas Thackersey and Lallubhai Samaldas established on January 23, 1906.

23

The Cooperative Credit Societies Act, 1904 was amended in 1912, with a view to broad

basing it to enable organization of non-credit societies. The Maclagan Committee of 1915 was

appointed to review their performance and suggest measures for strengthening them. The

committee observed that such institutions were eminently suited to cater to the needs of the

lower and middle income strata of society and would inculcate the principles of banking amongst

the middle classes. The committee also felt that the urban cooperative credit movement was

more viable than agricultural credit societies. The recommendations of the Committee went a

long way in establishing the urban cooperative credit movement in its own right.

In the present day context, it is of interest to recall that during the banking crisis of 1913-

14, when no fewer than 57 joint stock banks collapsed, there was a there was a flight of deposits

from joint stock banks to cooperative urban banks. Maclagan Committee chronicled this event

thus:

“As a matter of fact, the crisis had a contrary effect, and in most provinces, there was a

movement to withdraw deposits from non-cooperatives and place them in cooperative

institutions, the distinction between two classes of security being well appreciated and a

preference being given to the latter owing partly to the local character and publicity of

cooperative institutions but mainly, we think, to the connection of Government with Cooperative

movement”.

Under State Purview

The constitutional reforms which led to the passing of the Government of India Act in

1919 transferred the subject of “Cooperation” from Government of India to the Provincial

Governments. The Government of Bombay passed the first State Cooperative Societies Act in

1925 “which not only gave the movement its size and shape but was a pace setter of cooperative

activities and stressed the basic concept of thrift, self help and mutual aid.” Other States

followed. This marked the beginning of the second phase in the history of Cooperative Credit

Institutions.

24

There was the general realization that urban banks have an important role to play in

economic construction. This was asserted by a host of committees. The Indian Central Banking

Enquiry Committee (1931) felt that urban banks have a duty to help the small business and

middle class people. The Mehta-Bhansali Committee (1939), recommended that those societies

which had fulfilled the criteria of banking should be allowed to work as banks and recommended

an Association for these banks. The Co-operative Planning Committee (1946) went on record to

say that urban banks have been the best agencies for small people in whom Joint stock banks are

not generally interested. The Rural Banking Enquiry Committee (1950), impressed by the low

cost of establishment and operations recommended the establishment of such banks even in

places smaller than taluka towns.

The first study of Urban Co-operative Banks was taken up by RBI in the year 1958-59.

The Report published in 1961 acknowledged the widespread and financially sound framework of

urban co-operative banks; emphasized the need to establish primary urban cooperative banks in

new centers and suggested that State Governments lend active support to their development. In

1963, Varde Committee recommended that such banks should be organized at all Urban Centers

with a population of 1 lakh or more and not by any single community or caste. The committee

introduced the concept of minimum capital requirement and the criteria of population for

defining the urban centre where UCBs were incorporated.

Duality of Control

However, concerns regarding the professionalism of urban cooperative banks gave rise to

the view that they should be better regulated. Large cooperative banks with paid-up share capital

and reserves of Rs.1 lakh were brought under the perview of the Banking Regulation Act 1949

with effect from 1st March, 1966 and within the ambit of the Reserve Bank’s supervision. This

marked the beginning of an era of duality of control over these banks. Banking related functions

(viz. licensing, area of operations, interest rates etc.) were to be governed by RBI and

registration, management, audit and liquidation, etc. governed by State Governments as per the

25

provisions of respective State Acts. In 1968, UCBS were extended the benefits of Deposit

Insurance.

Towards the late 1960s there was much debate regarding the promotion of the small scale

industries. UCBs came to be seen as important players in this context. The Working Group on

Industrial Financing through Co-operative Banks, (1968 known as Damry Group) attempted to

broaden the scope of activities of urban co-operative banks by recommending that these banks

should finance the small and cottage industries. This was reiterated by the Banking Commissions

(1969).

The Madhavdas Committee (1979) evaluated the role played by urban co-operative banks

in greater details and drew a roadmap for their future role recommending support from RBI and

Government in the establishment of such banks in backward areas and prescribing viability

standards.

The Hate Working Group (1981) desired better utilization of banks' surplus funds and

that the percentage of the Cash Reserve Ratio (CRR) & the Statutory Liquidity Ratio (SLR) of

these banks should be brought at par with commercial banks, in a phased manner. While the

Marathe Committee (1992) redefined the viability norms and ushered in the era of liberalization,

the Madhava Rao Committee (1999) focused on consolidation, control of sickness, better

professional standards in urban co-operative banks and sought to align the urban banking

movement with commercial banks.

A feature of the urban banking movement has been its heterogeneous character and its

uneven geographical spread with most banks concentrated in the states of Gujarat, Karnataka,

Maharashtra, and Tamil Nadu. While most banks are unit banks without any branch network,

some of the large banks have established their presence in many states when at their behest

multi-state banking was allowed in 1985. Some of these banks are also Authorized Dealers in

Foreign Exchange

Recent Developments

26

Over the years, primary (urban) cooperative banks have registered a significant growth in

number, size and volume of business handled. As on 31st March, 2003 there were 2,104 UCBs

of which 56 were scheduled banks. About 79 percent of these are located in five states, - Andhra

Pradesh, Gujarat, Karnataka, Maharashtra and Tamil Nadu. Recently the problems faced by a

few large UCBs have highlighted some of the difficulties these banks face and policy endeavors’

are geared to consolidating and strengthening this sector and improving governance.

1645 Urban Cooperative Bank with more than 8150 branches across India. The aggregate

deposit exceeded Rs. 2.00 lakh crores.

Source: Adapted from a paper by O.P. Sharma, formerly of the History Cell.

1.10 Objectives of the Urban Co-operative Banks:-

The UCBs are generally considered as “Small People’s Bank” and they are organized for

promoting thrift and co-operation among the lower and middle strata of the society. The

objectives of the UCBs are summarized in two categories, which are as follow:

[A] Principal objectives:

(i) To promote thrift, self help and mutual co-operation among the members,

(ii) To mobilize resources i.e. to borrow funds form members and non members to utilize for

giving loans to their members,

(iii) To provide credit to the members at reasonable rates for productive purposes,

(iv) To undertake collection of bills drawn, cheques, drafts, etc. accepted or endorsed by

members and approved constituents, to remit funds and to discount cheques and bills of

approved members subject to rules and by laws on their behalf,

(v) To arrange for safe custody of valuables and documents of members and constituents,

and

(vi) To provide all other banking and subsidiary services.

[B] Subsidiary Objectives:

(i) To give possible help and necessary guidance to traders, artisans etc. who are members of

the bank,

27

(ii) To do every kind of trust and agency business and particularly do the work of investment

of funds, sale of properties and of recovery and acceptance of money,

(iii) To undertake every kind of banking and sharaffi business and also give bank guarantee

and letters of credit on behalf of members.

1.11 Role of the UCBs in Indian Banking System:

The performance of the co-operative banking sector as a whole has attracted considerable

attention in recent years. Today they have become an important constituent of the Indian

financial system and cover a large segment of society because of their “PROMPT,

PERSONALIZED AND COURTEOUS SERVICE”. They take the responsibility of covering the

unmonitored sector neglected by commercial banks and are called “purveyors of credit to small

and medium enterprises”. They provide service with no bars of castes, creed, religion, language,

etc. and thus spread the feeling of “Unity in Diversity”. Some UCBs operate beyond their state of

registration and are governed by the Multi State Co-operative Societies Act, 1984. In addition to

their traditional retail banking business, some have also taken up diversified activities like stock

investment scheme, opening and maintenance of nonresident and ordinary rupee accounts,

merchant banking etc. They owe responsibility not only towards customers but also towards

employees and society.

Primary (Urban) co-operative banks play an important role in meeting the growing credit

needs of urban and semi – urban areas. UCBs mobilize savings from the middle and lower

income groups and purvey credit to small borrowers, including weaker sections of the society.

The number of UCBs stood at 1872 at the end of March 2005, including 79 salary earners banks

and 119 Mahila banks. Total no. of scheduled UCBs was 55 at the end of March 2005.

Scheduled UCBs are under closer regulatory and supervisory framework of the Reserve Bank.

Various entities in the urban co-operative banking sector display a high degree of

heterogeneity in terms of deposits / assets base, areas of operation and nature of business. In

view of its importance, it is imperative that the sector emerges as a sound and healthy network of

jointly owned, democratically controlled and professionally managed institutions. In order to

achieve these objectives, the Reserve Bank took a series of policy initiatives in 2004-05. The

most significant initiative in this regard the vision Document and Medium Term Frame work

(MTF) for UCBs. With a view to protecting depositors interest and avoid contagion on the one

hand, and enabling UCBs to provide useful service to local communities and public at large on

28

the other, a draft vision document was prepared and placed in public domain for eliciting

comments. Based on the feedback received from different quarters, the necessary modifications

were carried out in the vision documents to involve as the medium – term frame work for the

sector.

1.12 Urban Co-Operative Banks in Maharashtra:-

Urban Co-Operative banks are an important part of the financial system in Maharashtra.

Despite of being a Bank registered under the Banking Regulation Act 1949, these institutions are

necessarily " the Co-Operative societies and are registered under the Maharashtra Co-Operative

Societies Act 1960." The Co-Operative Banks were established over 100 years ago and were

brought under the purview of Reserve Bank of India, by amending the Banking Regulation Act

1949 vide the amendment in the year 1966. Role of Maharashtra in Urban Co-Operative

Banking sector.

Table 1.1 Urban Co-operative Banks in Maharashtra as on (Rs in Crores)

Source: - maharashtra.gov.in

Note: - Figure in brackets indicates percentage to all India total.

Reserve Bank of India conducts regular inspection of UCBs. They have developed

gradation system for UCBs whereby banks are classified into 4 grades on the basis of CRAR,

Profit/Loss & N.P.A.s. Gradation of UCBs in Maharashtra is as follows :-

Table 1.2 Grade wise Distribution of UCBs in Maharashtra

Grade 31/3/200 8 31/3/20 09 31/3/2010 31/3/2011

Grade I 200 255 274 301

Grade II 190 139 128 105

31/3/2011 India Maharashtra Percentage

Urban Co-Operative Banks (Nos) 1645 539 32.77%

Scheduled banks (Nos) 53 38 71.70%

Non scheduled banks (Nos) 1592 501 31.47%

Multistate banks (Nos) 42 23 54.76%

Share Capital (Rs) 6267 2700 43.08%

Own funds (Rs) 26260 12200 46.46%

Deposits (Rs) 212031 138124 64.14%

Advances (Rs) 136341 90260 66.20%

29

Grade III 99 101 87 78

Grade IV 114 82 64 55

Total

603

577

553

539

Source: - maharashtra.gov.in

Reserve Bank of India impose directions like restriction on declaration of dividend,

reduction of exposure limit etc. for the grade III & grade IV banks.

It needs to strengthen these banks. In March 2005, the Reserve Bank prepared a draft

Vision document for UCBs which, inter alia, discussed the problems of the sector and

highlighted the issue of dual regulatory mechanism which restricted the ability of the

Reserve Bank in handling the weaknesses of entities in the sector. In order to address the

problem of dual control, Vision document proposed the adoption of a consultative

approach for deciding the future set up of weak and sick banks in State.

Objectives:-

1. To rationalize the existing regulatory and supervisory approach keeping in view the

heterogeneous character of entities in the sector.

2. To facilitate focused and continuous system of supervision through enhanced use of

technology.

3. To enhance professionalism and improve the quality of governance in UCBs by

providing training for skill up-gradation as also by including large depositors in the

decision making process / management of banks.

4. To put in place a mechanism that addresses the problems of dual control, given the

present legal framework, and the time consuming process in bringing requisite legislative

changes.

5. To put in place a consultative arrangement for identifying weak but potentially viable

entities in the sector and provide a framework for their being nurtured back to health

including, if necessary, through a process of consolidation.

6. To identify the unviable entities in the sector and provide an exit path for such entities.

30

In terms of the Vision document, the Reserve Bank and the State Government have signed MOU

on 13/12/2006 to ensure greater convergence of approach of the two agencies entrusted with the

regulation and supervision of UCBs. As part of the MOU, it was decided to set up State level

Task Force for Co-operative Urban Banks (TAFCUB) comprising representatives of the Reserve

Bank, State Government and federation/association of UCBs.

The TAFCUB was entrusted.

1) To identify and draw a time bound action plan for the revival of potentially viable Urban

Co-Operative banks and non disruptive exit for non viable UCBs.

2) To facilitate human resource development and IT initiatives in UCBs.

Since 4th January 2007, aprox. 10 to 12 banks were discussed in each meeting. In these

TAFCUB meetings approximately 400 Urban coop. Banks were discussed. After taking detailed

review of these banks, necessary suggestions / directions were issued such as Liquidation,

Appointment of Administrator & exploration for Merger etc.

41 weak Co-Operative banks were merged into financially sound Co-Operative banks thereby

deposits of Approx.3100 crores were secured.

96 banks are taken into liquidation of which depositors of 84 banks are given their deposits back

through insurance claims. In case of remaining banks the preparation of claims are in progress.

Co-Operative banking in India has made substantial progress in dissemination of banking

services based on Co-Operative principles. In view of the special thrust on financial inclusion,

Co-Operative banking has acquired renewed significance in the Indian financial system. The

focus of the recent policy measures, therefore, has once again shifted to the strengthening of Co-

operative banking in India.

Table 1.3 Comparative Statistics of Co-operative Societies in Maharashtra (Rs in Crores)

Particular 2006-07 2007-08 2008-09 2009-10 2010-11

No. Of Societies 200740

-

205553

(02.39%)

212344

(03.30%)

218320

(02.81%)

244306

(11.90%)

No. of Members(Lakh) 476 505 517 542 539

31

- (06.09%) (02.37%) (04.83%) (-0.56%)

Share Capital 12565

-

12809

(01.94%)

14969

(16.86%)

15015

(00.30%)

20543

(36.82%)

Deposits 99792

-

104162

(04.37%)

118024

(13.31%)

128579

(08.94%)

132490

(03.04%)

Working Capital 202207

-

205110

(01.44%)

236401

(15.26%)

246162

(04.13%)

244834

(-0.56%)

Loan & Advances(Net) 82450

-

88166

(06.93%)

82556

(-6.37%)

78190

(-5.29%)

100681

(28.76%)

Sty’s In Profit

i. Number

ii. Profit (Amt)

62880

-

2067

-

63147

(00.42%)

2135

(03.29%)

67950

(07.61%)

2787

(30.54%)

68021

(00.10%)

7212

(158.77%)

70363

(03.44%)

3661

(-49.24%)

Sty In Loss

i. Number

ii. Loss(Amt)

51575

-

3361

-

55257

(07.14%)

4051

(20.53%)

58387

(05.67%)

3558

(-12.17%)

60215

(03.13%)

3569

(00.30%)

59636

(-0.97%)

4526

(26.81%)

Source: - co-operative movement at a Glance in Maharashtra, various issues.

Note: - 1. Figure in the brackets shows the percentage growth over the previous year.

2. The year 2006-07 is an assumed as base year.

The above table 1 shows the comparative statistics of the co-operatives in the state of

Maharashtra during last five years have growth remarkable. The number of societies stood at

2,05,553 in 2007-08, and increased position 2,44,306 in 2010-11, the growth in number of co-

operative was 02.39% to 11.90 % respectively during the over the previous year. Working

capital shown progress in amount as it was Rs. 2,05,110 crores in 2007-08, increased put Rs.

2,44,834 crores in 2010-11, but growth percentage showed decreased 1.44% to -0.56%

respectively during over the previous year. Net advanced by co-operatives showed little progress

Rs. 88,166 crores 2007-08 increased Rs. 1,00,681 crores in 2010-11, there was positive growth

6.93% in 2007-08, increased 28.76% in 2010-11. Number of cooperatives in profit increased

from 62,147 in 2007-08 to increase Rs. 70,363 in 2010-11, amount of profit was Rs. 2,135 crores

32

in 2007-08 increased put Rs. 3,661 crores in 2010-11, shows positive progress 0.42% to 3.44%.

Number of societies in loss increased from 55,257 in 2007-08 to increase 59,636 in 2010-11,

percentage of societies in loss decreased by 7.14% in 2006-07 to -0.97 % in 2010-11. However

the amount of loss increased from Rs. 4,051 crores in 2007-08 to Rs. 4,526 crores in 2010-11,

but the percentage increased from 20.53% in 2007-08 to 26.81 % in 2010-11, shows a good sign.

References:-

1. Upendra Rai (2011):-“Banking Awareness”, Arihant publications (India)

Limited, ISBN-978-81-8348-908-9.

2. Dr.K.V.S.N, Jawahar Babu, B.Muniraja Selkhar,(2012):-“ The Emerging Urban Co-

Operative Banks (Ucbs) In India”, IOSR Journal of Business and Management

(IOSRJBM)ISSN: 2278-487X Volume 2, Issue 5 (July-Aug. 2012), PP 01-05.

3. www.rbi.org.in

4. B. D. Patil (2013): “Growth and Progress of Co-Operative Movement In

Maharashtra”, Online International Interdisciplinary Research Journal, ISSN2249-9598,

Volume-III, Issue-VI, Nov-Dec2013

Chapter -II

33

Research Methodology and Literature Review

(A) Research Methodology:-

Chapter II Research Methodology and Literature Review

Page No

A 2.1 Meaning of Research 26

2.2 Objective Of Study 27

2.3 Period of the Study 27

2.4 Data Collection 27-28

2.5 Scope of the Study 28

2.6 Concept of Performance Evaluation 28-29

2.7 Concept of Financial Statement 29-30

2.58 Balance Sheet 30-31

2.9 Income Statement 31-32

2.10 Statement of Retaining Earning 32

2.11 Statement of Sources and Uses of Funds 32

2.12 The Concept of Financial Analysis 32-33

2.13 Significance of Financial Analysis 33

2.14 Comparative Financial Statement Analysis 33

2.15 Trend Analysis 34

2.16 Ratio Analysis 34-41

2.17 Fund Flow Analysis 41-42

B Literature Review 43-68

34

2.1 MEANING OF RESEARCH

Research in common parlance refers to a search for knowledge. Once can also define research as

a scientific and systematic search for pertinent information on a specific topic. In fact, research is

an art of scientific investigation. The Advanced Learner’s Dictionary of Current English lays

down the meaning of research as “a careful investigation or inquiry specially through search for

new facts in any branch of knowledge.”1 Redman and Mory define research as a “systematized

effort to gain new knowledge.”2 Some people consider research as a movement, a movement

from the known to the unknown. It is actually a voyage of discovery. We all possess the vital

instinct of inquisitiveness for, when the unknown confronts us, we wonder and our

inquisitiveness makes us probe and attain full and fuller understanding of the unknown. This

inquisitiveness is the mother of all knowledge and the method, which man employs for obtaining

the knowledge of whatever the unknown, can be termed as research.

Research is an academic activity and as such the term should be used in a technical sense.

According to Clifford Woody research comprises defining and redefining problems, formulating

hypothesis or suggested solutions; collecting, organizing and evaluating data; making deductions

and reaching conclusions; and at last carefully testing the conclusions to determine whether they

fit the formulating hypothesis. D. Slazenger and M. Stephenson in the Encyclopedia of Social

Sciences define research as “the manipulation of things, concepts or symbols for the purpose of

generalizing to extend, correct or verify knowledge, whether that knowledge aids in construction

of theory or in the practice of an art.”3 Research is, thus, an original contribution to the existing

stock of knowledge making for its advancement. It is the pursuits of truth with the help of study,

observation, comparison and experiment. In short, the search for knowledge through objective

and systematic method of finding solution to a problem is research. The systematic approach

concerning generalization and the formulation of a theory is also research. As such the term

‘research’ refers to the systematic method.

2.2 Objectives of the Study

35

To examine the profitability and operating efficiency regarding saving and advances of the

Urban Co-operative Banks.

1. To review the progress of UCBs in Maharashtra.

2. To study the financial position of DUCBA.

3. To study the growth trend of DUCBA.

4. To study the advancing patterns in the DUCBA.

5. To make suggestions for improving profitability.

2.3 Period of Study: -

The present study covers the span of five year i.e. from 2009- 2013 this period of selected

for study because the complete data for the entire period is available. This period is considered

adequate to study trends and conclusions.

2.4 DATA COLLECTION:-

In order to complete the research study data has been collected through the annual report of the

Devgiri Urban Cooperative Bank Ltd Aurangabad.

I) Primary Data:-

Primary Data collected by the Annual Reports of Devgiri Urban Cooperative

Bank Ltd in Aurangabad.

II) Secondary Data:-

For the purpose of the secondary data were collection by the sources such as Books,

journals, Reports, Magazines, News paper, Thesis, Dissertation and government and Non

government publication related to the topic of the study. In relation to secondary data

collection the e-media also helped, like internet, web sites, email etc, these are facilitate to

finding the secondary data.

36

(III) Data Analysis:-

For the purpose of analyzing the data it has been complied and tabulated in a systematic

manner. As per the need of the study i.e. graphs, charts, and statistical and mathematical tools

has been used.

2.5 Scope of the Study:-

1. Operational Scope:-

The focus of the study is on evaluating the financial performance of DUCB.

2. Geographical Scope:-

The study is considered to the Aurangabad where in DUCB is operating.

3. Temporary Scope: - The study covers five years period i.e. 2008-09 to 2012-13.

2.6 Concept of Performance Evaluation -

Business enterprise are created for achieving one or more objectives profit motive being

the most dominant among all objectives for accomplishing its objectives efficiently and

effectively, the firm needs resources which must be optimally utilized. The firm faces the

question of the use and allocation of resources at two levels first at the macro level, the firm has

to compete for purposes with other firms in the capital market. The Criterion used by the capital

market to allocate resources is efficiency, which is conventionally measured in terms of profit. A

firm would thus succeed to obtain funds from the capital market if it has been profitable in the

past or has a profit making potential in the future. The capital market consists of investors

individuals and institutional who decided about the allocation of funds to the firm on the basis of

information regarding the financial performance of the firm. Accounting through its financial

reports furnishes this information to investor's financial reports or statement in the form of

balance sheet and profit and loss account inform investors how the firm has performed.

37

The firm has been able to gather resources from the capital market at the Micro level if its

internal operations, it has to decide allocation of resources to its various projects; activities and

assets. The firm needs relevant information for making decisions of internal use of resources.

Financial information is needed by investor's creditors, management, Govt., and society.

Financial information is required to predict, compare, and evaluate the firm earnings obviate.

The financial information includes the financial statement, Balance sheet, profit and loss

account income statement etc. From the financial information which have been received from

the financial statement and tested the profitability and efficiently of firm or enterprises which is

called performance appraisal. The accounting system identities and gathers relevant data from

the financial statement. The process of data accumulation involves recording and analysis of

economic events financial statement also performance the measurement function. The firm

performs apprised from the financial statement financial statement is a basic of the enterprise

which is used for investors and outsiders to take decision and valued it. Thus performance

appraisal of the firm can be done by the financial statement.

2.7 Concept of Financial Statements: -

The term financial statements have a very ancient historical background. It is as old as the

term Accountancy. But it did not enjoy any significance during the last few decades because the

scope of business was limited as ownership and management consisted of the self same group of

business who was responsible for the fruits of their business. With liberalization and

globalization in the world today, financial statements are increasingly studied and used by

various classes of people who are directly or indirectly related and interested primarily in the

short term liquidity of the firms and its ability to need the debts as and when they full due, long

term lenders are concerned about the ability of the firm to service its debts over the next three to

ten years; while shareholders and potentials investors are interested in the yield and safety of

their funds. Importance of financial statement has also increased due to government regulations,

awareness about. The American Institutes of Certified Public Chartered Accountant states that

''Financial statement reflect a combination of recorded facts, accounting conventions and

personal judgments and the judgments and conventions applied affect them materially the social

rights among consumers and labor union, increasing insecurity of investors funds etc.'' However

38

now it is obligatory for every organization to prepare financial statements as per the annual

report.

But in the modern accounting system ''The statement of retained earnings, ''Earning Per

Shares” (EPS) and statement of change in financial position” are also considered as important

financial statements. It is very well known that the financial statements basically refer to balance

sheet and profit and loss account or income statement, of course these two basic statement are

supported by a number of schedule, annexure supplement statements explanatory notes,

footnotes etc. Therefore all these financial statements are having good amount of their

importance in the annual accounts of an organization. These statements are prepared on the basis

of the transactions that have taken place during the accounting period.

As financial statements are the final products of accounting work, done during the

financial period, they can be termed as summarized reports of accounting transactions. They are

prepared for the purpose o presenting a periodic review of the progress made by the enterprise or

management. ''The Financial Statement reflects a combination of recorded facts, accounting

conventions and personal judgments, and the judgments and conventions applied affect them

materially.'' Thus financial statements are the supported statements are a mirror image of the

position of an enterprise regarding earning, profit ability to operate in future, change in it's owns

goals and attain at targeted level. Thus they portray a picture of success or failure of the business

that reflects the effectiveness and efficiency of management. In short financial statements are the

pillars of accounting systems.

2.8 Balance sheet:-

The concept of Balance sheet is an old as the concept of accounting. The first balance

sheet was prepared in 1340 (2). Balance sheet is one of the most significant financial statements

the It indicates the financial condition or the state of affairs of a business at a Particular moment

of time Balance sheet contains information about resources and obligations of a business entity

and about its owners interest in the business at a particular point of time. Assets and Liabilities

are shown in the balance sheet. It also indicates the properties and obligations of a business

entity. It is based on the equation.

Net Assets = Total Assets – Total Liabilities

39

It provides a snapshot of the financial position of the firm at the close of the firm’s

accounting period. In joint stock companies, the balance sheet is prepared as per section 211 of

companies’ act 1956, In banking sector however it is prepared as prescribed in the third schedule

under section 29 of Banking Regulation Act 1949 but in Co-Operative banking sector there is no

any format is prescribed by the Banking Regulations act 1949.

According to I.M. Pandey following are three important functions of Balance sheet

(a) It gives a summary of the firm’s assets and liabilities.

(b) It is a measure of the firm’s liquidity.

(c) It is a measure of the firm’s solvency.

A balance sheet contains information about the assets liabilities and owner’s interest in

the business at a particular point of time. Suppose a balance sheet of a firm prepared as on 31st

March 2003 reveals the financial position on this specific date “The balance sheet is a statement

which reports the values of properties owned by the enterprise and claims of creditors and

owners against these properties.” Thus balance sheet is a statement of assets, liabilities and

owner’s equities at their respective book values of a business firm as on a specific date. In short

it can be said that a balance sheet is a “Status Report” indicating the financial condition of an

enterprise. It can be prepared in horizontal vertical or step format.

2.9 Income Statement: -

Income statement termed as a profit and loss Account is a financial statement. A balance

sheet as discussed above indicates firm’s financial position at a specific date. Hence it is

considered as a very significant statement by bankers and lenders. But it fails to indicate whether

firm is making profit or losing money. Therefore creditors and financial analysts have recently

started paying more attention to earning capacity of the firm which is reflected by profit and loss

account or income statement. It is a scoreboard of the firm’s performance during a period of

time. It is a flow statement.

According to Guthman H.G. “The statement of profit and loss is the condensed and

classified record of the gains and losses causing change in the owner's interest for a period of

time” Income statement indicates the result of business operations during two balance sheet

40

dates. This net result of may be favorable or unfavorable. If favorable the result, is net profit and

if unfavorable the result, is net loss. In other words it is a summary report of income and

expenses incurred in the regular course of business during a particular accounting period. The

income statement shows the incomes and expenses of a business enterprise over a period of time

and then gives final figures representing the amount of profit or loss for the accounting period. It

is the performance report of an enterprise indicating change in income and expenses due to

business operations conducted during a particular accounting period and suggest a long range

view of a business and shows where it is leading to. The income statement can also be presented

in a vertical or horizontal form.

2.10 Statement of Retained Earning: -

Statement of retained earning indicates the cause and magnitude of changes in the

retained earnings of the concur during the year. It begins with the amount of accumulated profits

and concludes with the amount of undistributed earnings. It is prepared to show the amount of

profits transferred to reserves, payment of interim dividend, proposed dividend and

appropriations. It follows the income statement and provides a link between the income

statement and the balance sheet.

2.11 Statement of Sources and Uses of Funds: -

It is a statement summarizing the financing and investing activities of an enterprise

indicating where the financial resources have come from and where they have gone. It measures

the changes that occur in assets, liabilities and other accounting aspects of business operations

and trace the reasons for such changes.

2.12 The Concept of Financial Analysis:-

Financial statements are only the means of providing general information regarding

operational results and financial position of a business. These statements merely contain

financial data about business events which do not reveal any significant conclusions such as

efficiency of the management, strength and weakness of the firm, index of future progress etc.

The analysis is done by properly establishing the relationship between the items of balance sheet

41

and profit and loss account. The first task of financial analysis to determine the information

contained in the financial statement. The second step is to arrange information in a way to

highlights significant relationship. The final step is interpretation and drawing of inferences and

conclusions. Thus financial analysis is the process of selection, reviewing and evaluation of the

accounting information.

2.13 Significance of Financial Analysis: -

The Basic limitations of the traditional financial statements comprising the balance sheet

and the profit and loss account is that they do not give all the information related to the financial

operations of a firm. Nevertheless they provide some extremely useful information to the extent

that the balance sheet is a mirror of the financial position on a particular date in terms of the

structure of assets, liabilities and owner’s equity and so on and the profit and loss account shows

the result of operations during the year. Thus the financial statements provide a summarized

view of the financial position and operations of a firm. Therefore; much can be learnt about a

firm from a careful examination of its financial statements as invaluable documents performance

report. The analysis of financial statement is, thus an important aid to financial analysis. The

focus of financial analysis is on key figures in the financial statements and the significant

relationship that exist between them

2.14 Comparative Financial Statement Analysis: -

Comparative financial statements are statements of financial position of a concern so

designed as to facilitate comparison of different accounting variables and thereby draw useful

conduciveness. According to the M.R. Agrawal “Comparative financial statements are those

statements which summarize and present related accounting data for a number of years

incorporating therein the changes (absolute or relative or both) in individual item.10 In these

statements, the financial data for two or more years are placed and presented in adjacent

columns. So that it may provide a true perspective in order to facilitate period comparison. It is

also comparative financial statements are usually prepared with special columns indicating

absolute data for each of the period and changes in it terms of rupees as well as in terms of

percentages. The comparative financial statements is to ascertain the changes accruing year by

42

year in each item of assets, liabilities and net worth shown in the financial statements of a

business firm and whether such changes are favorable or adverse.

1.15 Trend Analysis: -

A study based on trend percentage is known as trend analysis. Trend analysis indicates

the trend of progress during past several years. Trend percentages are helpful in making a

comparative study of financial statements for several years as it indicates increase or decrease in

an item along with the magnitude of change in percentage. According to R. A. Kennedy and S.

Y. Mc Mullen “For the purpose of financial appraisal, an effective use of financial ratios can be

made by observing the behavior of ratios over period of time”.11 As one of the management

tools, the importance of looking into tendency of events between financial statements prepared at

different period cannot be lost sight of where the business was? Where the business is ? And

where the business will be? All these uses being clearly revealed through trend analysis.

According to M.R. Agrawal “The trend analysis is the method of analyzing financial position of

a business on the basis of changes in the items of financial statement of successive years in

comparison a specific date or period commencement of study.

2.16 Ratio Analysis: -

Analysis of financial statement based on ratios is known as ratio analysis. Ratio analysis

is a technique of presenting internal and external events affecting the business transaction

relating to its operations, operating results and attainment of pre-determined goals and objectives

of a business in brief and summary form.

According to Belverd-E-Needless “Ratio guides or short cuts that are useful in

evaluating the financial position and operations of a company and in comparing them with

previous years or with other companies. The primary purpose of ratio is to point out areas for

further investigations. They should be used in connection with a general understanding of the

company and its environment.

Various Ratios;-

Current Ratio:-

43

The current ratio is balance-sheet financial performance measure of company liquidity. The

current ratio indicates a company's ability to meet short-term debt obligations. The current ratio

measures whether or not a firm has enough resources to pay its debts over the next 12 months.

Potential creditors use this ratio in determining whether or not to make short-term loans. The

current ratio can also give a sense of the efficiency of a company's operating cycle or its ability

to turn its product into cash. The current ratio is also known as the working capital ratio.

Calculation (formula)