Bahasa

Halaman

Hukum

1

Option Listing, Returns and Volatility: Evidence from Greece

George Filisa,*

, Christos Floros b

and Bruno Eeckels c

a Portsmouth Business School, University of Portsmouth, Portland Street,

Portsmouth, PO1 3DE, UK

b Portsmouth Business School, University of Portsmouth, Portland Street,

Portsmouth, PO1 3DE, UK

c Bournemouth University, Institute of Business and Law, Fern Barrow, Talbot

Campus, Poole, Dorset, BH12 5BB, Bournemouth, UK

Abstract This paper examines the effect of the first introduction of Greek stock options (Greek

Telecommunication Organisation, Intracom, National Bank of Greece and Alpha

Bank) on stock prices and volatility for the period 1999-2002. We examine the

asymmetric information hypothesis using a standard event study methodology and

asymmetric GARCH-type models. Event study results indicate that abnormal returns

existed in the pre-listing period, but tend to disappear in the post-listing period.

Asymmetric Component TGARCH models with GED show that the introduction of

stock options has led to increased volatility (positive effect) for Greek

Telecommunication Organisation, Intracom and National Bank of Greece only (Alpha

Bank shows a positive but insignificant effect). We argue that our results provide

support to the asymmetric information hypothesis, suggesting that the Greek market

has become more efficient after the introduction of stock options.

Keywords: Stock options, returns, volatility, asymmetric component GARCH,

Greece

JEL codes: G15; C32.

* Corresponding author. Email: [email protected]

2

I. Introduction

Derivative markets stabilise spot markets as well as benefit market welfare, by

facilitating risk management, asset allocation and price discovery (Dawson and

Staikouras, 2009). The effects of option listings on return and volatility characteristics

of underlying stocks have been extensively examined but the results of the studies are

conflicting. Different factors, such as the maturity of a stock exchange or the trading

rules and regulations seem to play an important role in the nature of the listing effects.

According to the asymmetric information hypothesis, options may generate a certain

level of impact of the underlying asset prices when the market is incomplete or

exhibits information asymmetry (see Ross, 1976; Stein, 1987; Antoniou and Holmes,

1995). The impact of stock option introduction is expected to be greater to the more

incomplete markets and to those markets that exhibit higher information asymmetry

(Ross, 1976; Stein, 1987). Thus, one would expect the introduction of stock options to

have no effect on the underlying assets if financial markets are complete and

frictionless (Chen and Chang, 2008; Detemple and Jorion, 1990; Grossman, 1988).

Grossman (1988) also explains that listing an option contract increases the underlying

stock’s liquidity, and that the new information arriving from the option market may

serve to stabilise stock market prices. In addition, several authors show that stock

options provide information to the underlying market which makes the prices in the

spot market react more sensitively according to new information due to lower

transaction costs (see Bae et al, 2004; Ross, 1976), thus turning stock markets in

being more efficient. Calado et al. (2005) argue that the introduction of the options

may improve the welfare of previously restricted traders and be associated with a

price effect (see Figlewski and Webb, 1993; Detemple and Selden, 1991;

Bessembinder and Seguin, 1992). Furthermore, Ross (1976) shows that options

3

trading can provide another conduit, where the information is disseminated through

the financial market and affects the set of opportunities faced by investors (see also

Chen and Chang, 2008). According to Harris (1989), an increase in well-informed

speculative trade (i) decreases volatility due to order flow imbalances, and (ii)

increases volatility due to new fundamental information (see also Calado et al., 2005).

In addition, Kumar et al. (1998) report that the introduction of stock options improves

the market quality of the underlying securities by decreasing volatility and the bid-ask

spread, increasing the quoted depth and the trading volume.

In short, due to the asymmetric information hypothesis, when options are introduced

in the market, informed traders will be willing to transfer their funds to the option

market from the spot market. Thus, the option listing is expected to have an effect in

the spot prices (Detemple and Jorion, 1990).

The scope of this study is to examine the effects of stock option1 listing using data

from Greece, an important European emerging market. Although a number of studies

have concentrated on mature markets (U.S, Europe, Japan), this is the first empirical

investigation on the effect of stock options trading on the Greek spot market. Hence, it

is important to study stock option listing effects in emerging spot markets as the

conclusions can be compared with those related to other emerging/mature spot

markets. Further, Greece is the only country in the region of South-East Europe that

has a standardised derivative market, and therefore, this study creates the necessary

background for future research in other similar emerging spot markets from the same

region and elsewhere. In this paper we are solely interested in the first stock option

introduction, the reason being that the uncertainty of such event in a market with no

prior experience of stock option introduction could create significant pricing and

1 Stock options are contracts that grant the holder the right to buy or sell a specific stock at a specific price before the contract expires. Holders of individual stocks can hedge their risk by trading stock options (for more details see Chen and Chang, 2008).

4

volatility effects to the underlying stocks. In addition, it is important for small markets

to be studied as they are usually relatively inefficient. Finally, according to Sahlstrom

(2001, p.21) “evidence from small markets is important, because the benefit of

derivative markets may be greater in relatively inefficient markets”. Such evidence

allows the researchers to evaluate the benefits or drawbacks of derivatives

introduction in various market environments (Sahlstrom, 2001).

This paper examines the behaviour of four stocks, namely National Bank of Greece,

Intracom, Alpha Bank and Greek Telecommunication Organisation, in terms of price

changes and volatility. We employ two different methods, namely an event study

methodology used by Kabir (2000), and an AGARCH methodology which looks at

the market’s reaction to the arrival of different news. The research is primarily

motivated by the lack of similar studies (and the use of the above two methodologies)

to empirically explain the behaviour of European emerging markets.

The paper is organized as follows. In Section 2, the review of literature is presented,

while Section 3 presents the data used. In Section 4, methodology is described and the

findings are interpreted, while conclusions are given in Section 5.

II. Literature Review

There is a broad literature on the impacts of option introduction on the behaviour of

the underlying stocks. Detemple and Jorion (1990) examine the effects of the

introduction of 300 stock options for the period 1973-1986 in the American market.

They find significant stock price increases following option listings for the period

between 1973 and 1982, but no significant effect for the period 1982 to 1986. They

argue that the introduction of stock index options in 1982 may have completed the

market. Conrad (1989) examines the American market for the period 1974 to 1980,

5

and observes that option introductions cause an increase in underlying prices and that

the price increases are positively related to the options market activity.

Sorescu (2000) studies the effects of option introductions for the American market

using a larger sample of 2051 listing events for the period from 1973 to 1995. He

finds positive abnormal return for options listed during 1973 to 1980, and negative

abnormal return for options listed in 1981 and later. Sorescu (2000) argues that the

option effect for the period 1973 to 1995 can be described by a two-regime switching

means with optimal switch date occurring in 1981. To explain this finding, he uses the

argument developed by Detemple and Jorion (1990) on market completion due to the

introduction of index options, and he also stresses the importance of the

implementation of regulatory changes in 1981. Furthermore, Danielsen and Sorescu

(2001) reach to a very interesting conclusion. They argue that non-optioned stocks

tend to be overvalued on average, while option listing lowers the costs of shorting,

and thus causes prices to decline.

Ho and Liu (1997) examine the American option market for the period 1983 to 1990

and observe significant stock prices reversal surrounding option introductions.

Specifically, they find positive cumulative excess returns beginning 100 days prior to

the option introduction and, starting three days before option introduction, negative

excess returns which continue at least 100 days after the introduction day. On the

other hand, Kabir (2000), examining the Dutch market for the period 1978-1993,

finds significant decline in stock prices following the introduction of stock options. St.

Pierre (1998), on the other hand, uses a EGARCH model to characterize the return

generating process of the underlying securities, and shows that the stock conditional

returns distribution is unaffected by option introduction for the period 1973 to 1990.

Further, Mayhew and Mihov (2000) report evidence of negative price effect around

6

the listing period, but not significant, and an increase in volatility after the listing

period on some selected stocks. Evidence from other international markets (Stucki

and Wasserfallen, 1994; Faff and Hillier, 2004) concludes that stock prices tend to

increase around option listing period. Recently, Liu (2009) shows that the listing of

the S&P 100 options results in lower volatility but no price change for the underlying

stocks. According to Liu (2009, p.1045), “it is the informed and speculative portfolio

traders that have migrated from the underlying market to the newly created index

options market when it becomes available”.

The findings of the literature regarding the effects on the underlying volatility also

provide mixed evidence. Kabir (2000) reports no significant effect on the volatility on

the underlying stocks. On the other hand, Conrad (1989) and Sahlstrom (2001) find

lower volatility for the underlying after option listing. Sahlstrom (2001) reports a

decrease in the stock bid-ask spreads in the Finnish market.

Using a sign and sized conditional ARCH model (SSC-GARCH), Becchetti and

Caggese (2000) research the effect of index option introduction for six European

stock markets. They find that the introduction of index option significantly reduces

the impact of negative shocks on conditional volatility of optioned index in five out of

six countries but has no significant impact on relative unconditional volatility in four

out of six countries. St. Pierre (1998), using a function-noise model, shows that option

introduction has no effect on the conditional volatility of the underlying. Mazouz

(2004), using a GARCH (1,1) methodology, reaches the same conclusion. Other

studies on option listing effect on volatility include Freund et al (1994), Bollen

(1998), Skinner (1989) and Cao (1999). Calado et al. (2005) analyse the volatility

effect of the initial exchange-listing of options on the Portuguese stock market using

an OLS regression. They report that the hypothesis that the listing of derivatives has

7

no effect on the total risk of the underlying stocks cannot be rejected. Recently, Chen

and Chang (2008) explain the impact of listing options on the abnormal return and

volatility of the underlying securities in Taiwan. The empirical results show that there

is a short-term positive impact on the underlying stock prices around the time when

the stock options are listed. In particular, they find that there is a weak impact

regarding both the AAR and CAR due to that fact that investors in Taiwan are used to

employing warrants to speculate or hedge. Further, they show that the variance of the

underlying securities, estimated by a GARCH(1,1) model, decreases significantly

over the 10 days after the stock options are introduced, which improves the efficiency

of the market (see also Detemple and Jorion, 1990).

Apart from studies related to stock option listing effect, there is an extensive literature

on the futures listing effects on stock price and volatility. These include, among

others, papers by Floros and Vougas (2006), Ryoo and Smith (2004), Bae et al.

(2004), Bologna and Cavallo (2002), Chang et al. (1999), Antoniou and Holmes

(1995), Harris (1989) and Aggarwal (1988). Results from these studies are also

ambiguous in terms of futures listing effects on stock or index prices and volatilities.

Overall, the literature is not providing strong evidence to allow the support of

Detemple and Jorion’s (1990) argument, which suggests that a positive abnormal

return in spot prices should be expected around the option listing period, due to the

efficiency enhancement that the listing offers to the underlying market. According to

the asymmetric information hypothesis, option listing period should be characterised

by higher abnormal returns in the post-listing period, which in the long run fade away

and by lower volatility in the post-listing period. In the next sections, we describe the

data and methodology used to examine whether the first option listing in the Greek

stock market provides support to the asymmetric information hypothesis.

8

III. Data Description

We use daily prices of the Athens General Index and the four optioned stocks: Greek

Telecommunication Organisation (GTO), National Bank of Greece (NBG), Alpha

Bank (AB) and Intracom (INTRA). The sample covers the period December 1999 to

February 2002 and includes 521 trading days. Closing prices were obtained from

Datastream. The option listing took place the same day (January 7, 2001) for the four

listed firms. The Athens Derivatives Exchange (ADEX) began option contract trading

on the high capitalization index (FTSE/ASE 20) of the Athens Stock Exchange

(ASE), in September 2000. In January 2001, it was the first introduction of stock

option in four listed firms from the high capitalization index, namely National Bank

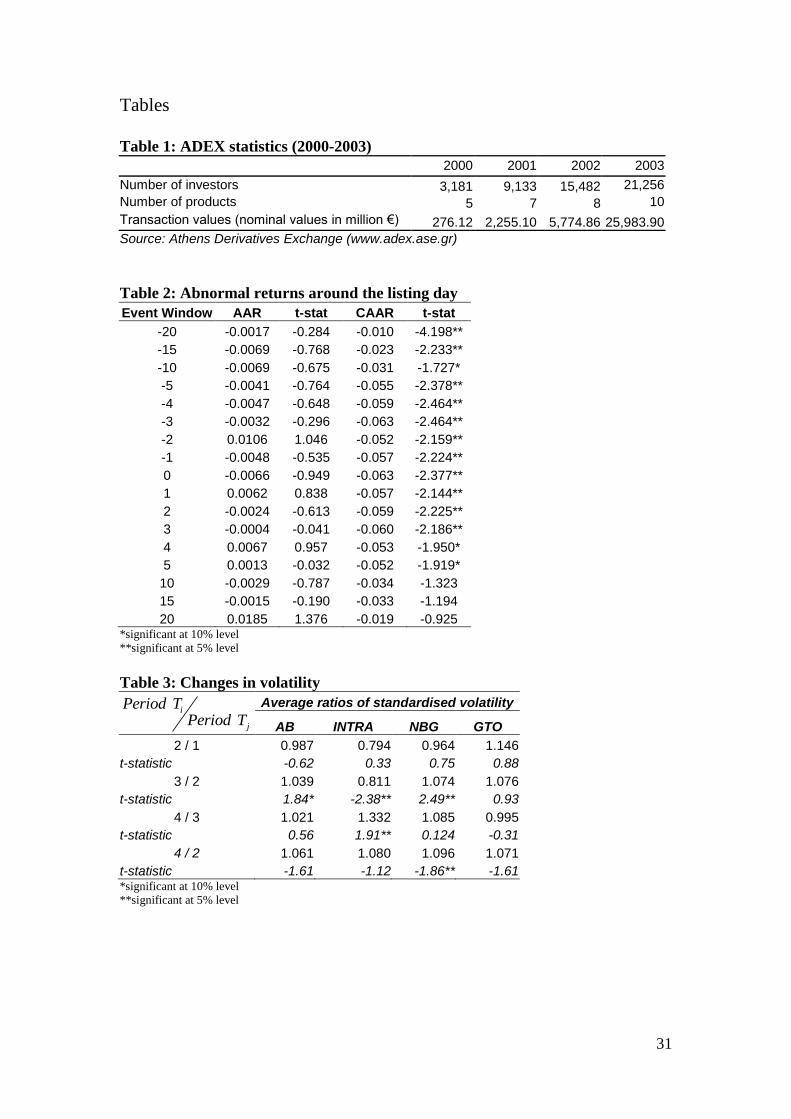

of Greece, Intracom, Alpha Bank and Greek Telecommunication Organisation. Table

1 shows some facts regarding the first four years of ADEX operations. The market

shows a significant increase from one year to the next (2000-2003) and a huge

increase in the transaction values of the market and in the number of investors.

[TABLE 1 HERE]

However, it is clear that the market is very new as it only trades 10 derivative

products and the number of investors and the transaction values are very small

compared to the traditional derivative exchanges such as the CBOE and LIFFE

(statistics for CBOE and LIFFE are not reported here, but are available upon request).

Furthermore, by the time ADEX started to trade options in 2000, the ASE was an

emerging market. As it became a mature market in 2001, it is clear that there could be

some important implications in the underlying and the derivative market. Hence, a

study in the stock option listing effects on price and volatility for Greece is of a

significant importance.

9

IV. Methodology and Results

Effect on Stock Returns

We test the option listing effect on stock returns using a standard event, which can be

found in Kabir (2000). The event window will consist of a period of 20 trading days

around the listing period (-20…0…+20). We argue that 20 trading days are able to

capture the option listing effect around the listing period as it covers a period of

around one calendar month (assuming 20 trading days per month). We use the Market

Model, based on the Capital Asset Pricing Model, in order to estimate the excess daily

returns of the stock, as follows:

it i i mt itR a b R e (1)

We estimate the parameters of the regression equation (1), using 120 trading days

prior the event window (-140, -21). Based on equation 1, the expected stock return

should be as follows:

( ) ( )it i i mtE R a b E R (2)

So, any excess or abnormal return should be calculated by the difference of the actual

return minus the expected return.

ˆˆit it i i mtAR R a b R (3)

Then, we estimate the average abnormal returns (AARt) and the cumulative average

abnormal returns (CAARt) using the following equations:

1

1 N

t it

i

AAR ARN

(4)

where, 1,2,...,i N and 20, 19,...,0,..., 19, 20t

10

1s k

k t

t s

CAAR AAR

(5)

where, 2 41k and , 20, 19,...,0,..., 19, 20t s

We calculate the AARt and CAARt over the event window period (-20, +20). In order

to perform a significance test on the abnormal returns, we standardise first the

abnormal returns, using:

( )

itit

i

ARSAR

s AR (6)

where ( )is AR is the standard deviation of the abnormal returns of stock i in the

estimation period.

We also standardize the CAARt using the following formula:

1 1s k

ik it

t s

SCAR SARk

(7)

The final step is to calculate the t-statistics for the sample. The t-statistics for

standardise abnormal returns and standardised cumulative abnormal returns are

calculated as follows:

1

1N

it

t

t SAR SARN

(8)

1

1N

ik

i

t SCAR SCARN

(9)

Table 2 reports the results of the average abnormal returns and the cumulative average

abnormal returns along with their t-statistics, for the even window period. We can

observe that the cumulative average abnormal returns are negative and they are

significant throughout the pre-listing period.

[TABLE 2 HERE]

11

The overall cumulative abnormal negative returns are 0.57% until the day of the

announcement. The significance of the CAAR could be due to the effect of the

announcement (the announcement of the listing took place on the 7th

of January

2001). So, it could be argued that investors took a sell position regarding the four

stocks in order to assess the effect of the option listing. This can also be supported by

the findings during the post-listing period. After the first 5 days of the post-listing

period we can observe insignificant cumulative abnormal returns (either positive or

negative).

Furthermore, the day of the listing did not produce any significant results, as the

abnormal return on that day was -0.66% percent, yet it was not significant.

Overall, we observe that the option listing in the emerging market of Greece caused

significant negative cumulative abnormal returns in the pre-listing period (-20 days to

-1 day), which continued until 5 days after the introduction of the options. Our

research does not support the evidence of post-listing abnormal returns (positive or

negative), as none of the abnormal returns were significant. However, this is in line

with Liu (2009) and Danielsen and Sorescu (2001) for mature markets; although, due

to the special characteristics of emerging markets (incomplete markets), we would

expect the Greek stocks to exhibit a post-listing significant price change (Ross, 1976;

Stein, 1987; Antoniou and Holmes, 1995; Chen and Chang, 2008). Note that, the

majority of the studies in mature markets exhibit a significant post-listing increase or

decrease in the share prices (see Faff and Hillier, 2004; Detemple and Jorion, 1990).

Our findings support the asymmetric information hypothesis, as the pre-listing

cumulative negative abnormal returns were eliminated in the post listing period. The

elimination of these negative returns can be attributed to the new information that was

transmitted from the option market to the stock market.

12

Effect on Stock Volatility

Using the same data, we use a different methodology to examine any effects of option

listing on volatility. We divide our observations into four periods, as follows:

Period T1: from -260 to -141

Period T2: from -140 to -21

Period T3: from 21 to 140

Period T4: from 141 to 260

The reason for having four periods to examine the stock price volatility is merely

because we want to examine the option listing effect to both long- and short-run (i.e.

using the period T3 we can examine the short run effects in volatility, while using the

period T4 we examine the long-run effects).

We measure volatility for each period independently and for each stock, using the

following formula:

1202

1( ) 252120 1

it i

ti T

R R

R

(10)

where 1,2,...,i N , 1,2,...,125t and 1,2,3 and 4T period . We multiply by 252

(average trading days per year) in order to annualize volatility. We follow the same

method to calculate volatility for the General Index. Then, we standardize the

volatility calculation for each stock by:

,

i Ti T

m T

RSTR

R

(11)

In order to assess the significant difference between volatilities over the four periods,

a standard paired sample t-test is used.

13

Having concluded on the effect of option listing on stock returns, we should assess the

effect on stock volatility. Table 3 reports the results for the four firms individually.

[TABLE 3 HERE]

From the above table, we can observe that in the three out of the four cases (AB,

INTRA and NBG) there was a drop in volatility in period 2 compared to period 1.

Furthermore, we can observe that three firms (AB, NBG and GTO) exhibited higher

volatility in the post-listing period compared to the pre-listing period. The most

important finding is that, for the majority of the firms, the difference in volatility

between period 3 and 2 was significant. This indicates that stock showed a significant

higher volatility in the third period (post-listing period, day 21 to day 140). However,

in the volatility comparison between period 3 and 4 we can notice that for the

majority of the firms there is an insignificant change, showing the increase that was

observed from period 2 to period 3 did not persist in period 4.

The final comparison will be between the periods 2 and 4. In order to assess whether

the change that was observed from period 2 to period 3 still remains, we need to

examine whether the change between period 4 and 2 is significant. From the empirical

results, we notice that the change in volatility is not significant for all firms.

So, overall we conclude that there is an effect from the option listing on stock

volatility (increase in volatility) in the early post-listing period (period 3). This could

be due to the lack of confidence of the Greek investors to the new product as there

was no previous trading experience from the Greek investors. However, higher

volatility in the early post-listing period should not necessarily be interpreted as a

negative effect. Such volatility behaviour could also be justified by the amount of new

information that arrives to the spot market from the newly introduced option market,

14

thus not necessarily due to destabilisation effects (Edwards, 1988). Past research in

mature markets finds evidence of volatility decrease in the post-listing period

(Becchetti and Caggese, 2000; Sahlstrom, 2001; Conrad, 1989). Research in emerging

markets mainly exhibits that stock option listing results to either a reduction in

volatility (Calado et al., 2005) or no effect (Chen and Chang, 2008). Overall, we

argue that our results provide support to the asymmetric information hypothesis, as

we observe a reduction in the stock return volatility during the long run post-listing

period (an exception is the early post-listing period, which shows higher volatility).

Thus, we suggest that there was an improvement of the ASE efficiency, which can be

attributed to the stock option introduction; a finding which is in line with Detemple

and Jorion (1990), who argued that a volatility decrease in the post-listing period

suggests an increase in market efficiency.

Application of GARCH Models

Financial markets appear to be affected by the accumulation of information as

reflected in the prices. Cox (1976) shows that derivative trading has an impact on

price expectations by altering the flow of information into the market2. The present

study offers a new perspective on the issue of the impact of asymmetries on spot

volatility.

Many studies analyse the impact of derivatives trading (e.g. futures effect) using time

series models (the standard GARCH(1,1) model or the GJR model) which test for the

presence of heteroskedasticity and asymmetries (see Floros and Vougas, 2006).

In the literature, a large number of specifications of GARCH models have been

considered to describe the characteristics of financial markets. The simple

2 Cox (1976) defines information content as knowledge regarding random disturbances having an impact on demand in the real economy (see also Dawson and Staikouras, 2009)

15

GARCH(p,q) model, developed by Engle (1982) and extended by Bollerslev (1986)

and Nelson (1991), captures better the tendency of returns to exhibit volatility

clustering, incorporating heteroskedasticity into the estimation procedure (Floros and

Vougas, 2006; Xekalaki and Degiannakis, 2010). However, this specification fails to

measure the impact of negative or positive innovations on conditional volatility.

Furthermore, asymmetric GARCH models introduced to capture asymmetry of data in

where good news and bad news have different predictability for future volatility. In

particular, the Threshold GARCH model (TGARCH) or GJR was introduced by

Zakoian (1994) and Glosten, Jaganathan and Runkle (1993). The specification for the

conditional variance is given by

q

i

p

j

jtjttitit da1 1

2

1

2

1

22 (12)

where 1td if 0t and 0td otherwise.

In GJR, good news ( 0t ) and bad news ( 0t ) have differential effects on the

conditional variance; good news has an impact of a , while bad news has an impact of

a . If 0 then the leverage effect exists and bad news increases volatility, while

if 0 the news impact is asymmetric.

An alternative specification for the conditional volatility process is component

GARCH or CGARCH. Engle and Lee (1993) proposed the CGARCH model in order

to investigate long- and short-run movements of volatility. The conditional variance in

the CGARCH(1,1) model is given by (12.1):

(12.3) )()(

(12.2) )()(

(12.1) )()(

2

1

2

111

1

2

11

2

1

2

2

1

2

1

2

tttt

tttttt

ttt

qqaq

a

16

The component model shows mean reversion to (constant over time), while it

allows mean reversion to a varying level tq , see (12.2) and (12.3). In equations (12.2)

and (12.3), t is volatility and tq is the time varying long run volatility. Equation

(12.2) describes the transitory component, tt q2 , while equation (12.3) describes

the long run component tq , see Floros (2007) and Xekalaki and Degiannakis (2010)

for more details.

Moreover, because of the existence of leverage effect in financial data, Engle and Lee

(1993) considered combining the CGARCH model with TGARCH to allow shocks to

affect the volatility components asymmetrically.

In this study, we analyse the effect of stock options trading on stock price volatility

using a combination of Threshold GARCH and Component GARCH model. In other

words, an extension of CGARCH model, namely the AGARCH or asymmetric

Component GARCH is used. The AGARCH model combines the component model

with the asymmetric TARCH model presented above with asymmetric effects in the

transitory equation. The model is given by:

)()()(

)()(

221

2

1211

2

111

2

1

2

11

2

1

2

11

tttttttttt

ttttt

ttt

zqdqqq

zqq

xR

(13)

where tz1 and tz2 are the exogenous variables and d is the dummy variable indicating

negative shocks. 01 implies transitory leverage effects in the conditional

variance. An additional dummy variable, called Dummy, is added into the conditional

volatility of AGARCH model (as presented in equation 13). The Dummy variable

takes value zero for the pre-options period and one for the post-options period. It

allows us to determine whether stock options prices are related to any change in the

spot volatility. When the coefficient of the Dummy variable is positive (negative) then

17

there is a positive (negative) effect of stock options trading on volatility. According to

Floros and Vougas (2006), assuming that markets are efficient, then the ARCH

parameter can be viewed as ‘news’ coefficient, while the GARCH parameter can be

viewed as ‘old news’ and the persistence coefficient. According to Butterworth

(2000), an increase (decrease) in ARCH suggests that news is reflected in prices more

rapidly (slow), while a reduction in GARCH suggests that old news has a less

persistent effect on prices changes, see Floros and Vougas (2006). An increase in

GARCH suggests greater persistence, while when the sum of ARCH and GARCH

coefficients approaches unity then volatility shocks are persistent.

Other specifications of the GARCH and TGARCH, not reported here, include the

exponential GARCH (EGARCH) and power GARCH (PGARCH). TGARCH,

EGARCH and PGARCH models capture volatility asymmetry, but the Akaike

Information Criterion (AIC) and the Schwarz information criterion in this study select

the simple AGARCH (1,1), which is estimated using the Marquardt algorithm with

the HCC option3.. Due to the fact that the conditional distribution of errors (residuals)

is non-normal, other than normal distributional assumptions should be used to capture

for fat tails in time series (e.g. Student t, GED, GT). In this paper, we consider the

generalised error distribution or GED suggested by Nelson (1991), which allows for

both skewness and leptokurtosis (see Lee and Tse, 1991; Johnson et al., 1995;

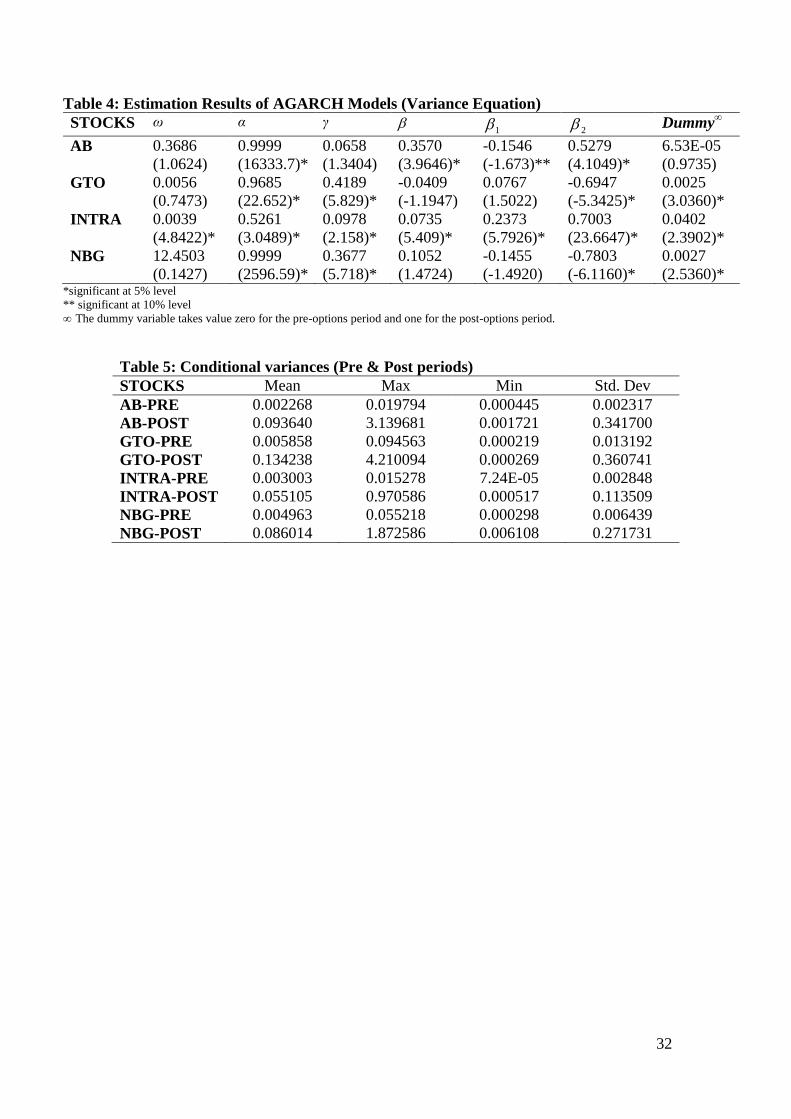

Xekalaki and Degiannakis, 2010). In Table 4, selected AGARCH models with a

Dummy variable in the conditional variance equation are reported4. There is a positive

effect of stock options trading on stock market volatility. The effect is statistically

significant (Dummy variable is positive), and therefore, there is an increase in

3 To estimate AGARCH models, an iterative procedure is used upon the method of Marquardt algorithm, and Heteroskedasticity Consistent Covariance (HCC) option is used to compute quasi maximum likelyhood (QML) covariances and standard errors

using the methods described by Bollerslev and Wolldridge (1992). 4 Results from TGARCH, EGARCH and PGARCH are qualitatively similar to ACARCH results and they are available upon request.

18

volatility associated with the stock options introduction. This is not true for Alpha

Bank, where the Dummy variable is positive but not significant. Further, for all cases,

the sum of ARCH and GARCH coefficients is very close to one (in absolute terms),

indicating that volatility shocks are quite persistent. A large sum of the coefficients in

the conditional variance equations implies that a large positive or a large negative

return will lead future forecasts of the variance to be high. The coefficient of the

lagged squared returns is always positive and statistically significant for AB and

INTRA, while it is insignificant for NBG and GTO. Therefore, strong ARCH effects

are apparent for AB and INTRA stocks. Also, the coefficient of lagged conditional

variance is significantly positive and less than one for AB and INTRA, indicating that

the positive impact of ‘old’ news on volatility is significant. The magnitude of the

coefficient 2 is especially high for INTRA, indicating a long memory in the

variance. . Note that the coefficient 2 is negatively significant for GTO and NBG,

which implies a negative impact of news on volatility. Furthermore, the coefficient 1

implies significant transitory leverage effects in the conditional variance for INTRA

only.

[TABLE 4 HERE]

The next step is to examine and compare the values of ARCH and GARCH terms as

well as the volatility (conditional variances) parameters for the pre-stock options and

the post-stock options periods. The estimation results of GARCH models (pre- and

post-periods)5 suggest an increase in GARCH indicating a greater persistence effect

of old news on prices changes of GTO, AB and NBG (this is not applied to INTRA).

5 The results from the GARCH models using pre- and post samples are available upon request.

19

Furthermore, the results show a decrease in ARCH for all stocks suggesting that news

is reflected in prices more slowly.

Descriptive statistics of conditional variances from the AGARCH(1,1) models, are

presented in Table 5. It is clear that the variances are much higher in the post-stock

options periods than in the pre-stock options periods (for all cases). In other words,

we find higher market volatility after stock options introduction in the Greek stock

market. This is in line with our previous findings.

[TABLE 5 HERE]

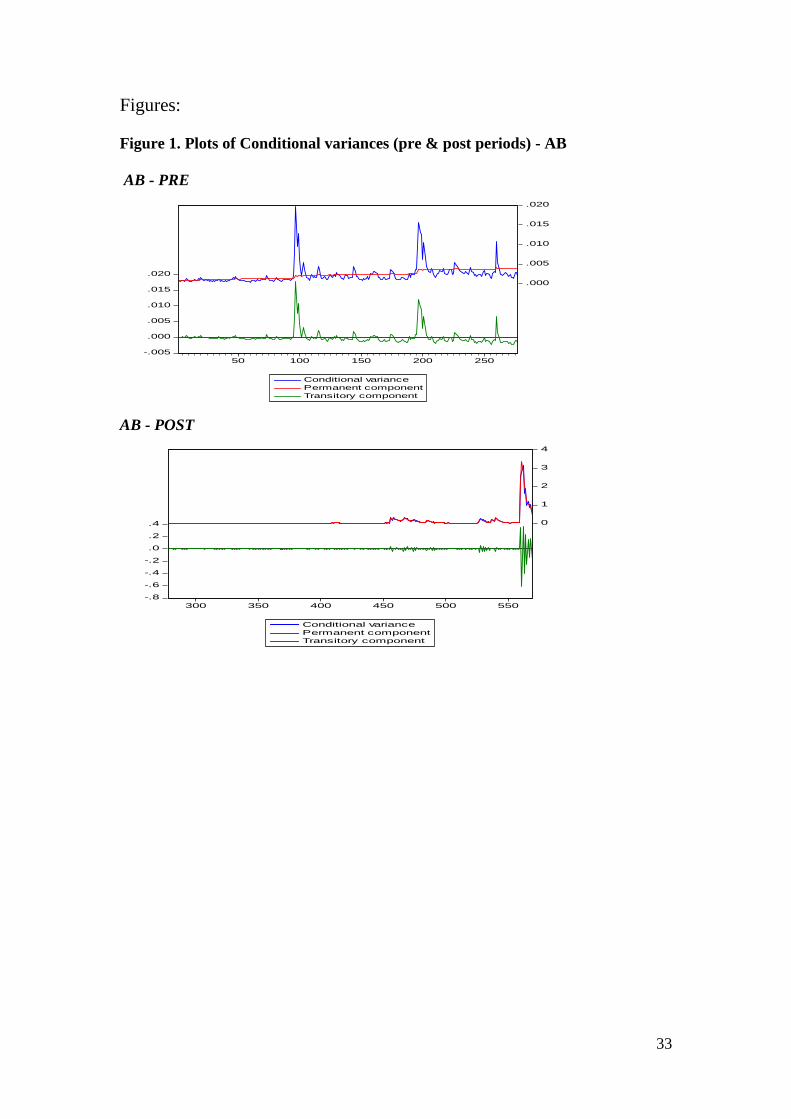

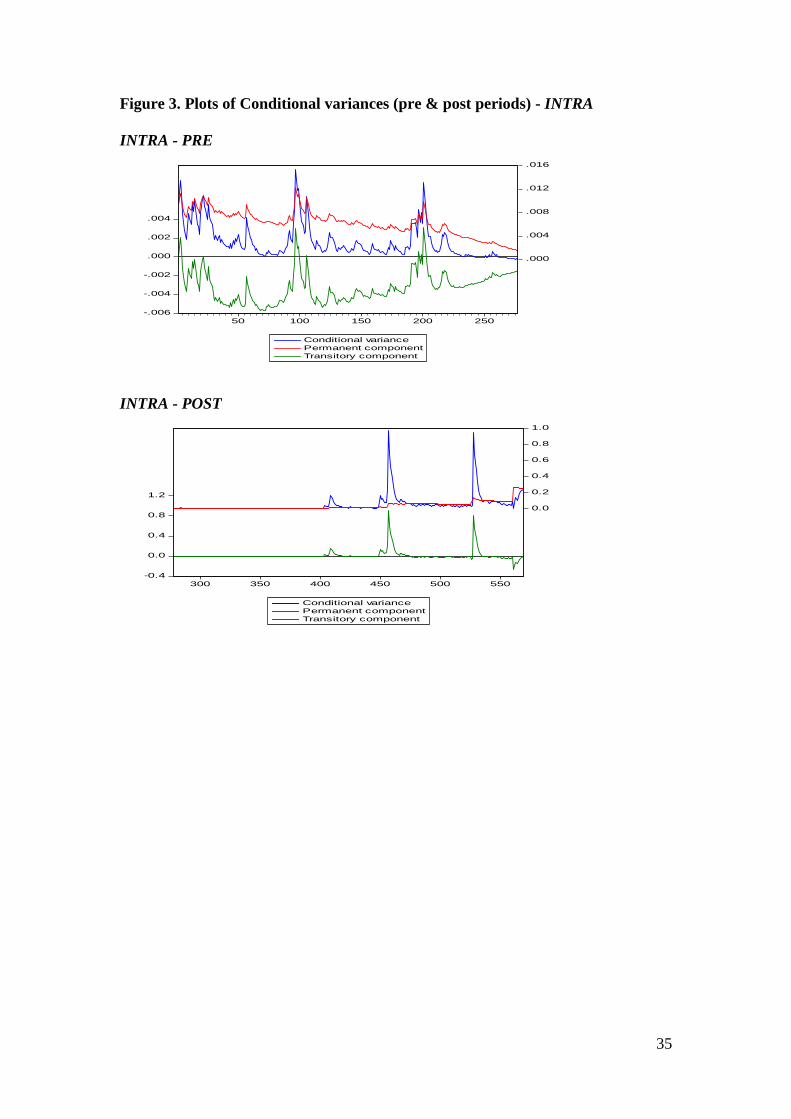

Finally, Figures 1-4 present the conditional variances for all cases before and after the

introduction of stock options trading in Greece. The results confirm that the

introduction of stock options has led to increased volatility (hence, positive effect) for

all four stocks (we again find that there is not a significant increase for AB).

[FIGURE 1 HERE]

[FIGURE 2 HERE]

[FIGURE 3 HERE]

[FIGURE 4 HERE]

AGARCH modelling reaches the same conclusion with the event study methodology,

which strengthens the robustness of our results.

V. Conclusion

Given that spot and derivatives markets are linked by arbitrage operations, then

derivatives markets would convey information to the cash market (Dawson and

Staikouras, 2009). Researchers show that the price of an underlying asset may become

more volatile after derivative introduction because increased speculators and

20

uninformed traders bring imperfect information into the derivative market (Chang and

Liao, 2010). Further, Ma and Rao (1988) argue that the volatility of underlying assets

declines if the derivative market generates a migration of noisy traders from the

underlying asset market (or enhances the information efficiency by hedging), see also

Chao and Liao (2010, p. 1388).

The listing of stock options can provide additional information to the underlying

market. Hence, the prices in the spot market may react more sensitively due to new

information, lower transaction costs, highly-leveraged properties and an absence of

short selling constraints in relation to the options (Chen and Chang, 2008). According

to Ho et al. (1995), after stock options are listed, investors absorb the new

information, while Kumar et al. (1998) report that the introduction of stock options

improves the market quality of the underlying securities by decreasing volatility and

the bid-ask spread, increasing the quoted depth and the trading volume. Furthermore,

Bansal et al. (1989) show that the introduction of stock options does not change the

systematic risk of the underlying securities.

Past empirical studies provide mixed results when they test the option listing effect on

price returns and volatility (Liu, 2009; Chen and Chang, 2008; Calado et al., 2005). In

this paper, we examine the effects of option listing on stock returns and volatility for

the Greek market. Our study further contributes to the research as it uses data from an

emerging market and is also the first to focus on the Greek option market, ADEX. We

investigate this issue using two empirical methods: an event study methodology and

AGARCH models. The research is primarily motivated by the lack of similar studies

(and the use of two different methodologies) on European emerging markets.

Our results indicate strong evidence that option listings exercise influence on stock

returns and volatility. In particular, our findings support the asymmetric information

21

hypothesis, as the pre-listing cumulative negative abnormal returns were eliminated in

the post-listing period. The elimination of these negative returns can be attributed to

the new information that was transmitted from the option market to the stock market.

In addition, there is some effect on volatility in the post-listing period, where stock

volatility increased in the short-term. A possible explanation of this increase in

volatility may be the uncertainty of the investors facing for the first time Greek stock

options. According to Calado et al. (2005. p. 913), “an increase in volatility would

constitute a good reason to pressure to further regulate derivatives trading in

general”. On the other hand, such volatility behaviour could also be justified by the

amount of new information that arrives to the Greek spot market from the newly

introduced option market, thus not necessarily due to destabilisation effects (Edwards,

1988); an explanation which is consistent with the asymmetric information

hypothesis. Under AGARCH methodology, we confirm the findings of the event

study methodology. In particular, we find that three firms (GTO, NBG and INTRA)

exhibited significant higher volatility in the post-listing period compared to the pre-

listing period (AB also exhibited a higher volatility in the post-listing period but it

was not significant). The estimation results of AGARCH models (pre- and post-

periods) indicate a greater persistence effect of old news on prices changes of GTO,

AB and NBG. Further, we find that news is reflected in prices more slowly for all

stocks.

These results do not support the majority of previous findings in terms of option

listing effects on stock prices in emerging and mature stock markets, as most studies

have identified increased post-listing stock returns (see, inter alia, Conrad, 1989 –

US: CBOE and AOE; Detemple and Jorion, 1990 – US: S&P500; Sorescu, 2000 –

22

US: CBOE, AMEX, NYSE; Chen and Chang, 2008 – Taiwan: TAIFEX). However,

our results are in line with Liu (2009 – US: S&P100).

In terms of option listing effects on stock return volatility our study provides support

to the majority of the previous studies in both mature and emerging stock markets; i.e.

a decrease in stock return volatility in the post-listing period (see, inter alia, Conrad,

1989– US: CBOE and AOE; Detemple and Jorion, 1990– US: S&P500; Becchetti and

Caggese, 2000 – UK, The Netherlands, Switzerland, Austria, Germany and France:

Euronext, Eurex and ATX; Sahlstrom, 2001 – Finland: HEX; Calado et al., 2005 –

Portugal: Euronext).

Overall, we argue that our results provide support to the asymmetric information

hypothesis, suggesting that the Greek stock market has become more efficient in the

post-listing period and that information from ADEX to ASE can be disseminated due

to investors’ behaviour after the introduction of stock options. Hence, the Greek stock

market reacts more sensitively according to the new information due to lower

transaction costs (see, Bae et al., 2004). This should be helpful to accurately value

options and other derivatives products. Moreover, our findings help investors,

financial managers and modelers dealing with options markets understand the changes

in the Greek capital market. Future research needs to investigate the persistence of

options effect in the longer run as well as explore the relationships among price,

volatility, market depth and trading volume using modern quantitative methods.

23

References

Aggarwal, R. (1988) Stock Index Futures and Cash Market Volatility, Review of

Futures Markets, 7, 290–299.

Antoniou, A. and Holmes, P. (1995) Futures Trading, Information and Spot Price

Volatility: Evidence for the FTSE 100 Stock Index Futures Contract using GARCH,

Journal of Banking & Finance, 19, 117–129.

Bae, S. C., Kwon, T. H. and Park, J. W. (2004) Futures Trading, Spot Market

Volatility, and Market Efficiency: the Case of the Korean Index Futures Markets,

Journal of Futures Markets, 24, 1195–1228.

Bansal, V. K., Pruitt, S. and Wei, K. C. J. (1989) An empirical reexamination of the

impact of CBOE option initiation on the volatility and trading volume of the

underlying equities: 1973-1986, Finance Review, 24, 19-29.

Bechetti, L. and Caggese, A. (2000) Effects of index option introduction on stock

index volatility: a procedure for empirical testing based on SSC-GARCH models,

Applied Financial Economics, 10, 323-341.

Bessembinder, H. and Seguin, P. J. (1992) Futures-trading activity and stock price

volatility, Journal of Finance, XLVII, 2015-34.

Bollen, N. P. B. (1998) A Note on the Impact of Options on Stock Return Volatility,

Journal of Banking and Finance, 22, 1181-1191.

24

Bollerslev, T. (1986) Generalised autoregressive conditional heteroscedasticity,

Journal of Econometrics, 31, 307-27.

Bollerslev, T. and Wooldridge, J. (1992) Quasi-maximum likelihood estimation and

inference in dynamic models with time-varying covariances, Econometric Reviews,

11, 143-172.

Bologna, P. and Cavallo, L. (2002) Does the Introduction of Stock Index Futures

Effectively Reduce Stock Market Volatility? Is the ‘Futures Effect’ Immediate?

Evidence from the Italian Stock Exchange using GARCH, Applied Financial

Economics, 12, 183–192.

Butterworth, D. (2000) The impact of futures trading on underlying stock index

volatility: the case of the FTSE Mid 250 contract, Applied Economics Letters, 7, 439-

444.

Calado, J. P. T., Garcia, M. T. M. and Pereira, S. E. T. M. (2005) An empirical

analysis of the effects of options and futures listing on the underlying stocks’ return

volatility: the Portuguese case, Applied Financial Economics, 15, 907-13.

Cao, H. H. (1999) The Effect of Derivative Assets on Information on Information

Acquisition and Price Behavior in a Rational Expectations Equilibrium, Review of

Financial Studies, 12, 131-163.

25

Chang, E. C., Cheng, J. and Pinegar, J. M. (1999) Does Futures Trading Increase

Stock Market Volatility? The Case of the Nikkei Stock Index Futures Markets,

Journal of Banking and Finance, 23, 727–753.

Chang, J. J. and Liao, S. L. (2010) Warrant introduction effects on stock return

processes, Applied Financial Economics, 20, 1377-1395.

Chen, D. H. and Chang, P. H. (2008) The impact of listing stock options on the

underlying securities: the case of Taiwan, Applied Financial Economics, 18, 1161-

1172.

Conrad, J. (1989) The price effect of option introduction, The Journal of Finance, 44,

487-498.

Danielsen, B. R. and Sorescu, M. S. (2001) Why Do Option Introductions Depress

Stock Prices? A Study of Diminishing Short Sale Constraints, Journal of Financial

and Quantitative Analysis, 36, 451-484.

Dawson, P. and Staikouras, S. K. (2009) The impact of volatility derivatives on

S&P500 volatility, The Journal of Futures Markets, 29(12), 1190-1213.

Detemple, J. and Jorion, P. (1990) Option listing and stock returns: An empirical

analysis, Journal of Banking and Finance, 14, 781-801.

26

Detemple, J. and Selden, L. (1991) A general equilibrium analysis of option and stock

market interactions, International Economic Review, 32, 279-303.

Edwards, E. R. (1988) Does futures trading increase stock market volatility?,

Financial Analysts Journal, 44, 63-69.

Engle, R. F. (1982) Autoregressive conditional heteroscedasticity with estimates of

the variance of UK inflation, Econometrica, 50, 987-1008.

Engle, R. F. and Lee, G. G. J. (1993) A permanent and transitory component model of

stock return volatility. Discussion paper 9244, Department of Economics, University

of California, San Diego.

Faff, R. and Hillier, D. (2004) Complete markets, Informed trading and Equity option

introductions, Journal of Banking and Finance, 29, 1359-1384.

Figlewski, S. and Webb, G. P. (1993) Options, short sales, and market completeness,

Journal of Finance, XLVII, 761-77.

Floros, C. (2007) The use of GARCH models for the calculation of minimum capital

risk requirements: International evidence, International Journal of Managerial

Finance, 3(4), 360-371.

27

Floros, C. and Vougas, V. D. (2006) Index futures trading, information and stock

market volatility: The case of Greece, Derivatives Use, Trading & Regulation, 12,

146-166.

Freund, S., McCann, P. D. and Webb, P. G. (1994) A Regression Analysis of the

Effects of Option Introduction on Stock Variances, Journal of Derivatives, 1, 25-38.

Glosten, L. R., Jaganathan, R., and Runkle, D. (1993) On the relation between the

expected value and the volatility of the normal excess return on stocks, Journal of

Finance, 48, 1779-1801.

Grossman, D. J. (1988) An analysis of the implications for stock and futures price

volatility of program trading and dynamic hedging strategies, Journal of Business, 61,

275-98.

Harris, L. (1989) S&P500 Cash Stock Price Volatilities, Journal of Finance, 44,

1155–1175.

Ho, L. C., Hassell, J. M. and Swidler, S. (1995) An empirical examination of the

dispersion and accuracy of analyst forecasts surrounding option listing, Review of

Financial Economics, 4, 171-85.

Ho, L. C. J. and Liu, C. S. (1997) A reexamination of price behavior surrounding

option introduction, Quarterly Journal of Business and Economics, 36, 39-50.

28

Johnson, N.L., Kotz, S. and Balakrishnan, N. (1995) Continuous univariate

distributions, Vol. 2, 2nd

edition, New York: John Wiley & Sons Inc.

Kabir, R. (2000) The price and volatility effects of stock option introduction: a

reexamination, Research in Banking and Finance, 1, 261-279.

Kumar, R., Sarin, A. and Shastri, K. (1998) The impact of options trading on the

market quality of the underlying security: an empirical analysis, Journal of Finance,

53, 717-32.

Lee, T. K. Y. and Tse, Y. K. (1991) Term structure of interest rates in the Singapore

Asian dollar market, Journal of Applied Econometrics, 6, 143-152.

Liu, S. (2009) The impacts of index options on the underlying stocks: the case of the

S&P 100, The Quarterly Review of Economics and Finance, 49, 1034-1046.

Ma, C. K. and Rao, R. P. (1988) Information asymmetry and options trading, The

Financial Review, 23, 39-51.

Mayhew, S. and Mihov, V. (2000) Another Look at Option Listing Effects,

EconWPA, Finance Series 0004002, Available from:

http://129.3.20.41/eps/fin/papers/0004/0004002.pdf [accessed by 12 July 2009]

29

Mazouz, K. (2004) The effect of CBOE option listing on the volatility of NYSE

traded stocks: a time-varying variance approach, Journal of Empirical Finance, 11,

695–708.

Nelson, D. (1991) Conditional heteroskedasticity in asset returns: A new approach,

Econometrica, 59, 347-370.

Ross, S. (1976) Options and efficiency, Quarterly Journal of Economics, 90, 75-89.

Ryoo, H. J. and Smith, G. (2004) The Impact of Stock Index Futures on the Korean

Stock Market, Applied Financial Economics, 14, 243–251.

Sahlstrom, P. (2001) Impact of stock option listings on return and risk characteristics

in Finland, International Review of Financial Analysis, 10, 19-36.

Skinner, D. J. (1989) Options Markets and Stock Return Volatility, Journal of

Financial Economics, 23, 61-78.

Sorescu, S. (2000) The effect of options on stock prices: 1973 to 1995, The Journal of

Finance, 55,487-514.

St. Pierre, E. (1998) The impact of option introduction on the conditional return of

underlying securities, The Financial Review, 33, 105-118.

Stein, J. C. (1987) Informational externalities and welfare-reducing speculation,

Journal of Political Economy, 95, 1123-45.

30

Stucki, T. and Wasserfallen, W. (1994) Stock and Option Markets, The Swiss

Evidence, Journal of Banking and Finance, 18, 881-893.

Xekalaki, E. and Degiannakis, S. (2010) ARCH Models for Financial Applications.

John Wiley & Sons, New York.

Zakoian, J. M. (1994) Threshold heteroscedastic models, Journal of Economic

Dynamics and Control, 18, 931-955.

31

Tables

Table 1: ADEX statistics (2000-2003)

2000 2001 2002 2003

Number of investors 3,181 9,133 15,482 21,256

Number of products 5 7 8 10

Transaction values (nominal values in million €) 276.12 2,255.10 5,774.86 25,983.90

Source: Athens Derivatives Exchange (www.adex.ase.gr)

Table 2: Abnormal returns around the listing day

Event Window AAR t-stat CAAR t-stat

-20 -0.0017 -0.284 -0.010 -4.198**

-15 -0.0069 -0.768 -0.023 -2.233**

-10 -0.0069 -0.675 -0.031 -1.727*

-5 -0.0041 -0.764 -0.055 -2.378**

-4 -0.0047 -0.648 -0.059 -2.464**

-3 -0.0032 -0.296 -0.063 -2.464**

-2 0.0106 1.046 -0.052 -2.159**

-1 -0.0048 -0.535 -0.057 -2.224**

0 -0.0066 -0.949 -0.063 -2.377**

1 0.0062 0.838 -0.057 -2.144**

2 -0.0024 -0.613 -0.059 -2.225**

3 -0.0004 -0.041 -0.060 -2.186**

4 0.0067 0.957 -0.053 -1.950*

5 0.0013 -0.032 -0.052 -1.919*

10 -0.0029 -0.787 -0.034 -1.323

15 -0.0015 -0.190 -0.033 -1.194

20 0.0185 1.376 -0.019 -0.925 *significant at 10% level

**significant at 5% level

Table 3: Changes in volatility

i

j

Period TPeriod T

Average ratios of standardised volatility

AB INTRA NBG GTO

2 / 1 0.987 0.794 0.964 1.146

t-statistic -0.62 0.33 0.75 0.88

3 / 2 1.039 0.811 1.074 1.076

t-statistic 1.84* -2.38** 2.49** 0.93

4 / 3 1.021 1.332 1.085 0.995

t-statistic 0.56 1.91** 0.124 -0.31

4 / 2 1.061 1.080 1.096 1.071

t-statistic -1.61 -1.12 -1.86** -1.61 *significant at 10% level

**significant at 5% level

32

Table 4: Estimation Results of AGARCH Models (Variance Equation)

STOCKS ω α γ 1 2 Dummy

∞

AB 0.3686

(1.0624)

0.9999

(16333.7)*

0.0658

(1.3404)

0.3570

(3.9646)*

-0.1546

(-1.673)**

0.5279

(4.1049)*

6.53E-05

(0.9735)

GTO 0.0056

(0.7473)

0.9685

(22.652)*

0.4189

(5.829)*

-0.0409

(-1.1947)

0.0767

(1.5022)

-0.6947

(-5.3425)*

0.0025

(3.0360)*

INTRA 0.0039

(4.8422)*

0.5261

(3.0489)*

0.0978

(2.158)*

0.0735

(5.409)*

0.2373

(5.7926)*

0.7003

(23.6647)*

0.0402

(2.3902)*

NBG 12.4503

(0.1427)

0.9999

(2596.59)*

0.3677

(5.718)*

0.1052

(1.4724)

-0.1455

(-1.4920)

-0.7803

(-6.1160)*

0.0027

(2.5360)* *significant at 5% level

** significant at 10% level

∞ The dummy variable takes value zero for the pre-options period and one for the post-options period.

Table 5: Conditional variances (Pre & Post periods)

STOCKS Mean Max Min Std. Dev

AB-PRE 0.002268 0.019794 0.000445 0.002317

AB-POST 0.093640 3.139681 0.001721 0.341700

GTO-PRE 0.005858 0.094563 0.000219 0.013192

GTO-POST 0.134238 4.210094 0.000269 0.360741

INTRA-PRE 0.003003 0.015278 7.24E-05 0.002848

INTRA-POST 0.055105 0.970586 0.000517 0.113509

NBG-PRE 0.004963 0.055218 0.000298 0.006439

NBG-POST 0.086014 1.872586 0.006108 0.271731

33

Figures:

Figure 1. Plots of Conditional variances (pre & post periods) - AB

AB - PRE

-.005

.000

.005

.010

.015

.020

.000

.005

.010

.015

.020

50 100 150 200 250

Conditional variance

Permanent component

Transitory component

AB - POST

-.8

-.6

-.4

-.2

.0

.2

.4 0

1

2

3

4

300 350 400 450 500 550

Conditional variance

Permanent component

Transitory component

34

Figure 2. Plots of Conditional variances (pre & post periods) - GTO

GTO - PRE

-.02

.00

.02

.04

.06

.00

.02

.04

.06

.08

.10

50 100 150 200 250

Conditional variance

Permanent component

Transitory component

GTO - POST

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

0

1

2

3

4

5

300 350 400 450 500 550

Conditional variance

Permanent component

Transitory component

35

Figure 3. Plots of Conditional variances (pre & post periods) - INTRA

INTRA - PRE

-.006

-.004

-.002

.000

.002

.004

.000

.004

.008

.012

.016

50 100 150 200 250

Conditional variance

Permanent component

Transitory component

INTRA - POST

-0.4

0.0

0.4

0.8

1.2

0.0

0.2

0.4

0.6

0.8

1.0

300 350 400 450 500 550

Conditional variance

Permanent component

Transitory component

36

Figure 4. Plots of Conditional variances (pre & post periods) - NBG

NBG - PRE

-.02

.00

.02

.04

.06

-.02

.00

.02

.04

.06

50 100 150 200 250

Conditional variance

Permanent component

Transitory component

NBG - POST

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

-1

0

1

2

3

4

300 350 400 450 500 550

Conditional variance

Permanent component

Transitory component

Top Related

Copyright © 2022 FDOKUMEN