Bahasa

Halaman

Hukum

India’s uncertainties at presentand its optimism for the future

Luxury markets in Chindia India: Beyond anti-corruption

ISSN : 2233-5609

The views expressed here are those of the authors and do not necessarilyrepresent the official views of POSCO Research Institute.Not for sale.

Copyright © 2011POSCO Research Institute All rights reserved.Production in whole or in part without written permission is strictly prohibited.

Registration number: 강남바 00092Registration date: December 16, 2010

How to contact the Quarterly: [email protected]

Publisher: Kim Joon-Han Published by POSCO Research Institute

Editing Director: Kim Chang-Do Editor-in-Chief: Yoon So-Jin

Printed by Jeong-Moon Printing Co., Ltd.Date of lssue: January 25, 2012

Contents Winter l 2012 l Vol. 05

ColumnIndia’s uncertainties at present and its optimism for the future

Kim Kwang-Ro

Luxury markets in ChindiaChina, a strong hand in the premium market 009

Cho Jun-Hyeon

China’s craze for luxury goods 015

Hong Sun-Young

China’s great cause: “Create Chinese brands” 023

Shim Sang-Hyung

India, no longer a low-end market 029

Cho Choong-Jae

Korean companies in India, bolstering premium strategies 035

Imm Jeong-Seong

India: Beyond anti-corruptionIndian corruption: characteristics and responses 043

Santosh Kumar

Eradicating corruption, a new mission for economic growth 051

Kim Mi-Su

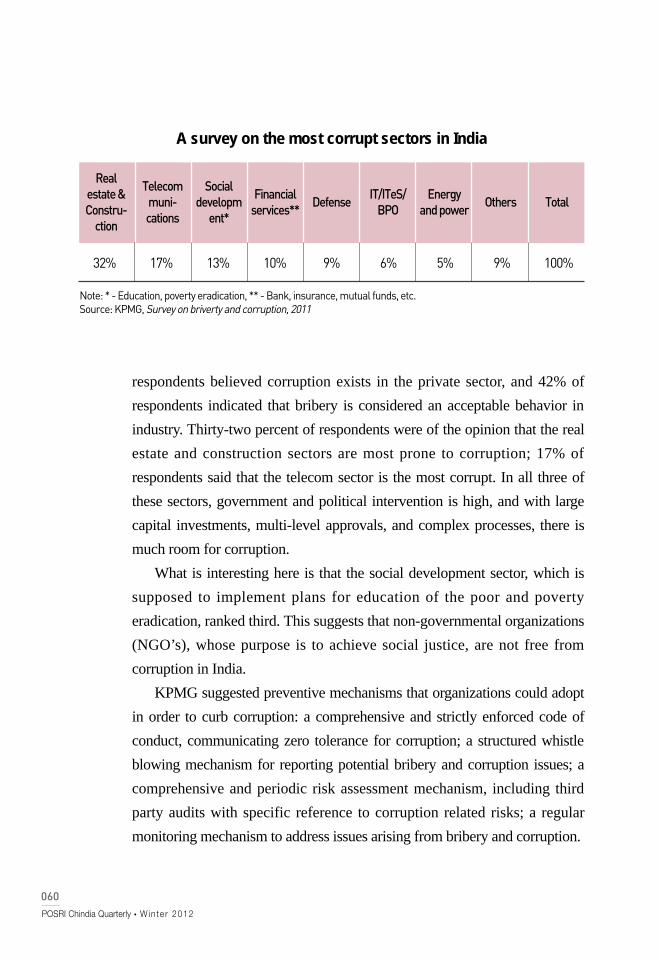

Mounting demand for ethical corporate management 057

Imm Jeong-Seong

04

07

41

Issue analysesWill China be a lifesaver in the eurozone crisis? 067Pyo Han-Hyung

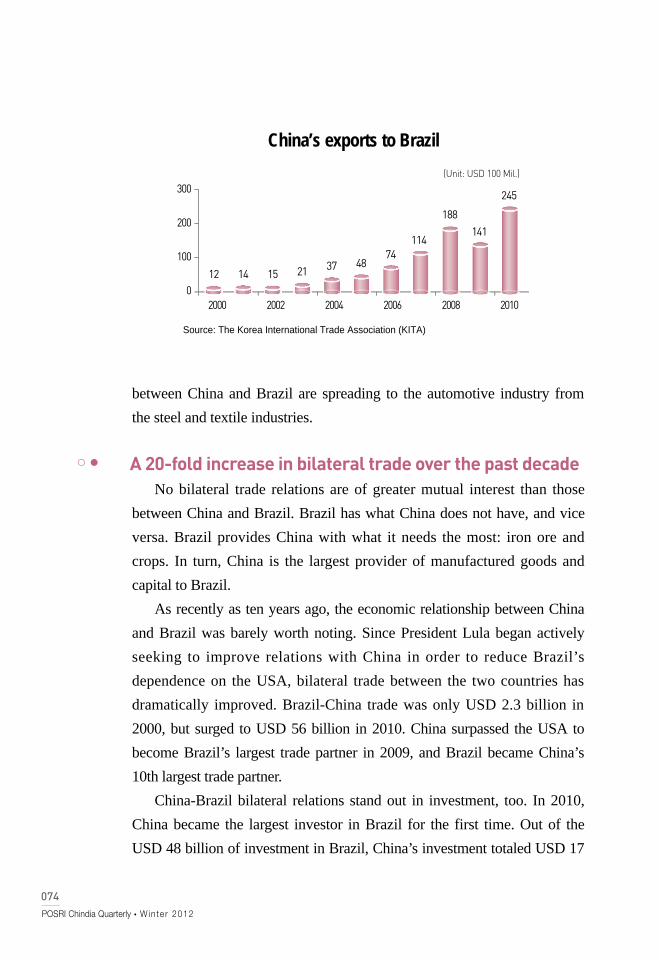

Resurfacing China-Brazil conflicts 073Oh Jung-Hoon

India’s quiet diplomacy seeking a permanent UN Security Council seat 081Kim Chan-Wahn

Chinese private enterprises: advances and drawbacks 087Shim Sang-Hyung

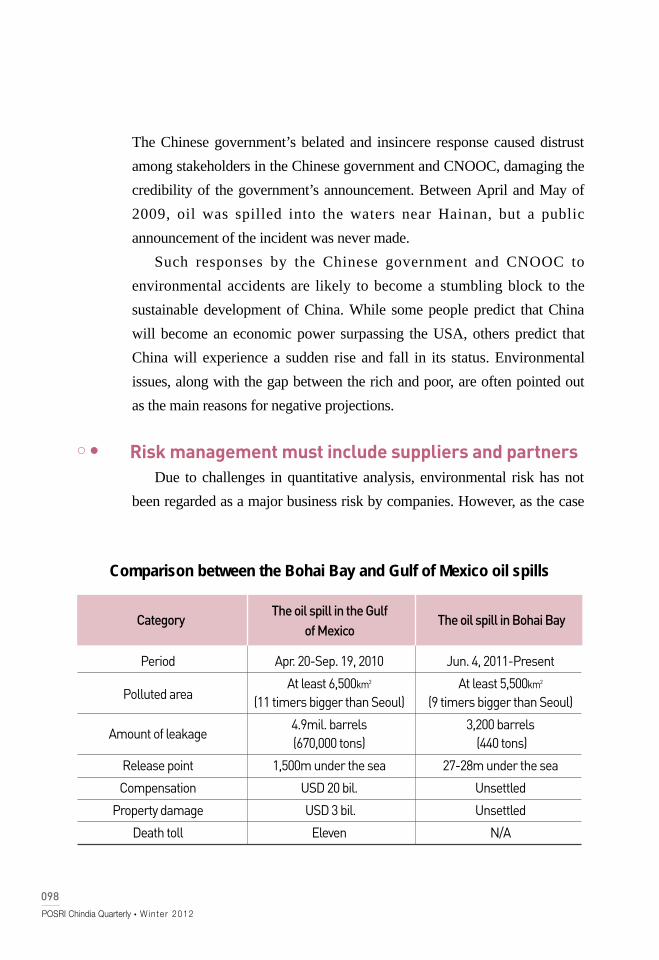

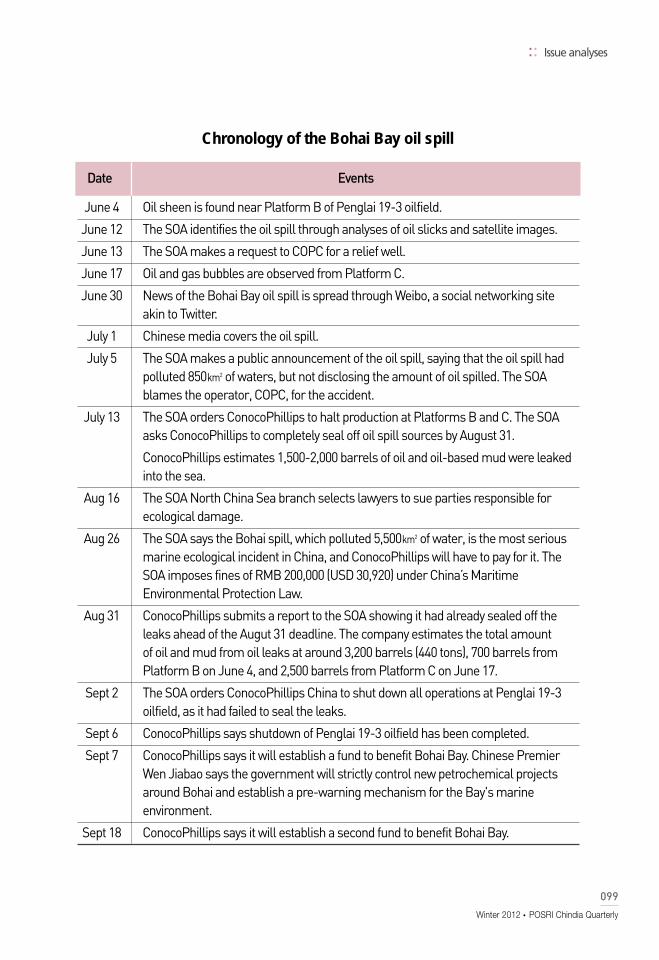

The Bohai Bay oil spill and China’s environmental risks 095Heo Jae-Yong

The heated Indian nuclear energy market 103Ji Yeon-Jung

CorporationsAfter a series of successes, BYD faces risks 113Li Wan-Yong

Interviews: India’s STAR CJ Network and Lock & Lock 119Shin Woo-Kyun, Ham Tae-Wook, Yoo Sung-Won

CultureCultural aspects of parks 126Jang Soo-Hyun

Indians’ synthesizing mindset 130Lee Yong-Hwa

65

111

124

POSRI Chindia Quarterly�Win te r 2012

004

India’s uncertainties at presentand its optimism for the future

Kim Kwang-RoVice Chairman of ONICRA

Recently, the hottest political issues in India include the

amendments to the Indian Expropriation Act and the

eradication of corruption. Land expropriation has always been

a stumbling block for industrial projects in India, and clashes

between residents and public power occur often. However, the Indian

government does not see land expropriation as a security issue, but

basically an issue of changing the minds of local residents. The Indian

Parliament deems that the absolute majority of people protesting land

expropriation are residents whose livelihoods are being threatened.

The problem is the stark difference between the amount the government

pays residents for their land and the market price. Some people argue that

farmers should be able to sell their land directly at market prices. Besides the

economic issue, farmers are fundamentally opposed to land expropriation on

the grounds that they would lose their livelihood. It is easy to think the

residents can be persuaded if expropriation is decided lawfully, but one must

CO

LU

MN

Winter 2012�POSRI Chindia Quarterly

005

remember that the residents have been

living on the land since before there

was law. They are fighting against the

laws of the government with the law of

nature. The government cannot turn a

blind eye to their outcries because they

will be judged with votes.

Korean companies should not focus solely on their negotiations with the

Indian government; they must also have a good grasp of the needs of local

residents, the actual land owners. These companies must first try to understand

why local residents might not cooperate despite government agreement. They

should try to win support from local non-governmental organizations, and

create an environment favorable to the coexistence of residents and

companies, offering various programs through the establishment, operation,

and employment of schools or hospitals. Contributing only a building is not

enough; it is important to take charge of the continued operation. The

operating cost for the hospitals one Korean company built when it entered the

Indian market was less than USD 2,000 per month per hospital. In pursuing a

large project, a little sincerity can go a long way.

Corruption in India is not as bad as it looks in general media coverage.

Certain foreign media, including the Wall Street Journal, have deemed that

corruption in India is not too serious, except for mega projects involving the

Indian government. For example, in order to tackle corruption in India, one

high court has recently proposed legalizing fees that would replace bribes.

This was based on the notion that small bribes often help cover expenses

incurred at public offices.

Regardless of the level of corruption in India, corruption is regarded

The current situation in India

may seem chaotic. However,

I believe that India is moving

toward a bright future.

“

“

POSRI Chindia Quarterly�Win te r 2012

006

both in India and overseas as an obstacle to the economic growth of India.

Indian people are showing enthusiastic support for Anna Hazare, who has

gone on hunger strikes for the enactment of the anti-corruption law. Hazare

is revered as the “next Gandhi.”

In order to do good business in India, where bribery is rampant, Korean

companies should handle everything in a lawful and transparent manner.

They should comply with environmental protection regulations as well as

accounting regulations, for instance, and pay taxes responsibly. There

should be no secrets. Korean companies should make no mistakes, as if

there are revenue officers and public officials from the environmental

department among their employees. That way, they will have nothing to

hide from the scrutiny of revenue officers and environmental officers.

The current situation in India may seem chaotic. However, I believe that

India is moving toward a bright future. Paradoxically, Bihar, one of the

poorest states, and Gujarat, whose chief minister has been denied a US visa

due to religious conflicts, stand on the frontline of land expropriation reform

and corruption eradication. The chief ministers of these two Indian states

have been described by Fortune magazine and the Wall Street Journal as

ideal chief ministers for India’s future. More and more politicians will

follow in their footsteps. In addition, bolstered by public opinion against

corruption, Tamil Nadu and West Bengal have elected female chief

ministers. Foreign media are praising India’s democracy wherein the

political powers are judged by public votes.

With only one law enacted, India will not change overnight. Given the

public support for anti-corruption, however, India seems to have a bright future.

I have an optimistic view that India will advance greatly over the next thirty

years, though the pace of advancement may be slower than that of China.

LLuuxxuurryy mmaarrkkeettss

iinn CChhiinnddiiaa

�China, a strong hand in the premiummarket

�China’s craze for luxury goods

�China’s great cause: “Create Chinese brands”

�India, no longer a low-end market

�Korean companies in India, bolstering premium strategies

As liquor reddens a person’s face, gold blackens an official’s

heart. (白酒紅人面 黃金墨吏心) - Chinese Epigrams and

Aphorisms (推句集)

Gold has been a symbol of wealth and treasure throughout the ages all

over the world. Few people would refuse gold. This saying applies not only

to public officials or people with black hearts. The fewer the number of

people privileged to own a treasure, the more precious it becomes. This is

the way of the world.

○● China and India’s premium market growing by 20-30%

“Crouching Tiger”and “Hidden Dragon”loom large in the global

premium and luxury markets. The terms refer not to the movie starring Yun-

Fat Chow (周潤發), but to China and India, which are evolving from the

China, a strong handin the premium market

Winter 2012�POSRI Chindia Quarterly

009

:: Luxury markets in Chindia

Cho Jun-HyeonProfessor of Economics, Pusan National University

POSRI Chindia Quarterly�Win te r 2012

010

“factories of the world”to

the “markets of the world”.

China and India have had a

significant impact on the

world economy for quite

some time. However, their

predominant image has

been one of countries that

manufacture cheap products

at low labor costs.

Things are changing rapidly now. Amidst widespread slowdown in the

global economy, China and India are leading the global consumer market.

This does not mean that their markets are simply big in size. It means that

the two Asian countries are emerging as strong hands not only in the low-

end market, but also in the premium and luxury markets.

In 2010, the global premium market totaled USD 254 billion, showing

an approximately 12% increase year-on-year; however, China’s premium

market is showing an average annual growth rate of 30%, far exceeding the

global average. China is the world’s second largest premium market after

Japan, and it is expected to become the largest in 2014. India’s premium

market has been increasing by 20% annually, and its size is expected to

match that of advanced countries by 2015. Simply put, China and India will

take the lead in the world’s premium and luxury markets in the near future.

○● Low per capita income, high consumption by the rich

Changes happening in China and India are attributed mainly to the rapid

economic growth and rising incomes. However, the more important reason

for the new consumption trend in these countries is changes in income

distribution and demographics.

China and India both have low per capita incomes, but they have large

With more aggressive marketing

strategies and systematic support

from the government and research

institutes, the Korean economy has

much to gain from the premium

markets in China and India.

Winter 2012�POSRI Chindia Quarterly

011

:: Luxury markets in Chindia

populations of luxury consumers. In China, the number of people with more

than RMB 10 million (USD 1.57 million) is around 960,000, and this

number is increasing by 10% each year. The number of people that can

afford premium and luxury goods in China stands at around 160 million, or

12% of the total population. In India, the number of households with an

annual income of over USD 100,000 totals 1.6 million, and their income is

increasing by 14% each year.

The traditional upper-class still constitutes a large proportion of

premium consumers in China and India. This is truer in India, where the

caste system of the past still remains a factor, than it is in China, whose

economy has shifted from the socialist system. However, what is drawing

attention to the new consumption trend in China and India is the nouveau

rich, who have benefited from the economic growth and prefer name brand

and luxury goods to show off their social standing. In the USA and Europe,

luxury goods are consumed mainly by middle-aged and older people, while

in China young adults account for more than 70% of total luxury

consumption. As a result of China’s one child policy, many of the young

generation who were pampered in childhood have higher consumption

tendencies than young people in other countries; they also have a strong

preference for luxury goods. The popular term “moonlight clan”(月光族)

was coined recently to describe people who live from paycheck to paycheck

or spend all of their monthly income. Together with increasing consumption

by young people, women’s rising purchasing power is stimulating luxury

consumption. In about half of Chinese households, income is managed by

the woman of the house.

The emergence of new types of transactions, mainly online, is another

catalyst for the increase in luxury consumption in China and India. In China,

online luxury consumption totaled RMB 3.4 billion in the second quarter of

2011, a 19% increase from the previous quarter. This trend is expected to

continue in the second half of 2011, reaching RMB 16 billion by the end of

POSRI Chindia Quarterly�Win te r 2012

012

2011. A Rapid increase in overseas travel has also bolstered luxury

consumption, as purchasing name brand luxury products overseas can be up

to 30% cheaper than buying them in China.

○● A sharp contrast to contracted luxury markets in the

USA and Europe

The emergence of China and India is changing the landscape of the

global premium market. Japan is still the world’s largest premium market,

with about 40% market share. However, Japan’s luxury market is decreasing

by 5% each year due to economic slowdown. American and European

luxury markets are showing slowing growth trends. The global financial

crisis originated in the USA, and the EU-led sovereign debt crisis is causing

further contraction of the premium market. Under these circumstances, the

growth of the global premium market is being led by emerging economic

powers, including China and India. Although China and India’s premium

markets have shown sharp growth in recent years, they are still quite new

and have remarkable potential to grow further.

Global luxury brands are rushing into China and India. Seven out of the

ten largest shopping centers in the world are located in China. One out of ten

Bentleys, a major luxury car brand, is sold in China. Bentley Motors has

successfully entered the Indian market, and Mercedez-Benz and Rolls-

Royce are following suit. India’s largest luxury brand shop is owned by

Ermenegildo Zegna, a men’s luxury clothing brand. Chanel and Louis

Vuitton, well known luxury brands of high end women’s apparel and

designer products, have large shops in New Delhi, Mumbai, and other big

cities in India.

With global brands rushing in, competition is mounting in China and

India. Complacency, thinking that one pencil for each of the 1.3 billion

people in China equals 1.3 billion pencils sold, is doomed to fail.

Winter 2012�POSRI Chindia Quarterly

013

:: Luxury markets in Chindia

Fortunately for Korea, Chinese and Indian consumers show a strong

preference for Korean products. Korean products are popular and widely

known in China; in India, Korean companies such as Samsung, LG, and

POSCO are perceived as leading premium brands. With more aggressive

marketing strategies and systematic support from the government and

research institutes, the Korean economy has much to gain from the premium

markets in China and India.

Winter 2012�POSRI Chindia Quarterly

015

China’s craze for luxury goods

:: Luxury markets in Chindia

Hong Sun-YoungSenior Researcher of Samsung Economic Research Institute (SERI)

China has undisputedly emerged as one of the world’s largest

consumer markets for luxury goods. China’s luxury market

was merely RMB 5 billion in 1998, but grew almost 11-fold to

RMB 55 billion by 2008. The market has been growing

rapidly, by more than 20% each year since 2008. According to the World

Luxury Association (WLA), China is the second biggest luxury goods

market, with a 27% market share of global luxury goods consumption in

2011, slightly lower than Japan at 29%, and higher than the United States at

14% and Europe at 18%. The WLA also stated that China will overtake

Japan as the world’s top consumer of luxury goods by 2012.

Just as Chinese tourists on shopping sprees have caught everyone’s

attention in Korea, Chinese tourists are now showing off their high

purchasing power in the UK, emerging as major consumers in the UK

luxury market. British media coined the term “the Gucci generation”for

POSRI Chindia Quarterly�Win te r 2012

016

wealthy Chinese tourists who readily buy luxury houses in London,

expensive artwork, and premium wine. Chinese tourists spent roughly GBP

1 billion (USD 1.57 billion) on luxury goods during the 2010 Christmas sale

season in the UK. In the UK, Chinese expenditures accounted for a third of

luxury brand sales, including Louis Vuitton, Gucci, and Burberry. For this

reason, countries such as the USA, the UK, and Japan are doing their best to

attract Chinese travelers through various measures, easing strict visa

restrictions and developing tour programs. The Chinese are now the main

pillar of the global luxury market. The buying power of China’s rich not

only increases profits of luxury brands, but also influences whole economies

and industries.

○● High consumption by women and the younger

generation

The reason the world should pay attention to wealthy Chinese is that the

Chinese premium market is large and growing rapidly. According to World

Bank reports, the top 1% of Chinese households holds 41.4% of national

wealth. Ji Baocheng (紀寶成), President of Renmin University of China,

stated in the National People’s Congress that the richest 10% of Chinese

people own 80% of the country’s collective wealth. In other words, wealth

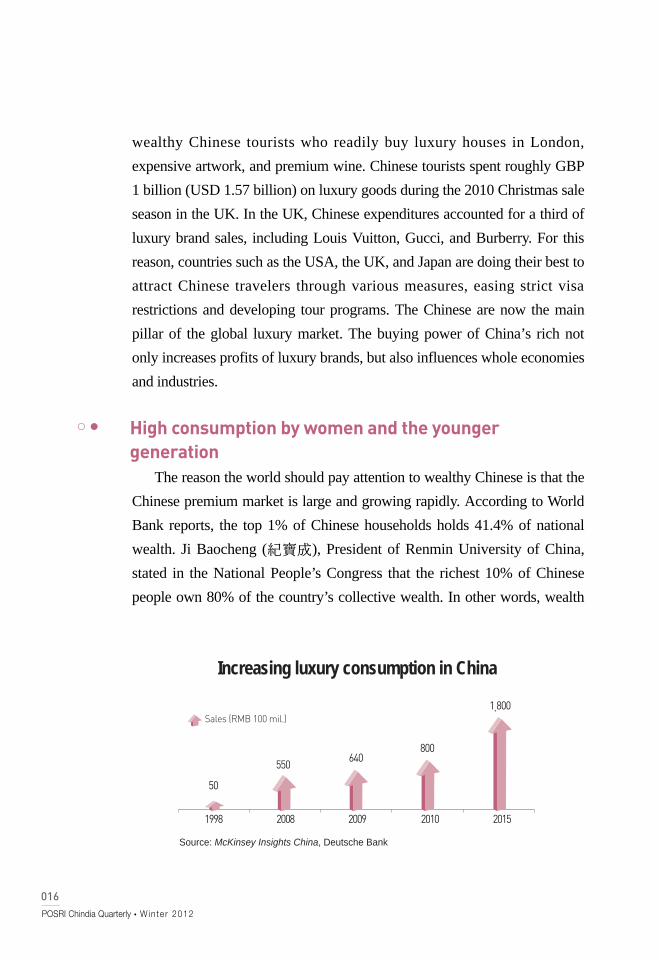

Source: McKinsey Insights China, Deutsche Bank

Increasing luxury consumption in China

Sales (RMB 100 mil.)

1998 2008 2009 2010 2015

50

550640

800

1,800

Winter 2012�POSRI Chindia Quarterly

017

:: Luxury markets in Chindia

in China is more highly concentrated in the high-income bracket than it is in

other countries. Therefore, the rich have high purchasing power out of

proportion to their share of the total population. With China’s economic

growth rate remaining high, the upper class in China is expected to expand

significantly. The number of Chinese people with incomes over USD

10,000 is currently 160 million, 12% of the total population. This is a

threefold increase from 2005. The higher the people’s income, the faster

consumption grows. The average household spending of the wealthiest 10%

increased 4.8-fold from RMB 6,000 in 2005 to RMB 29,000 in 2009 the

highest rate of increase in a four-year time span.

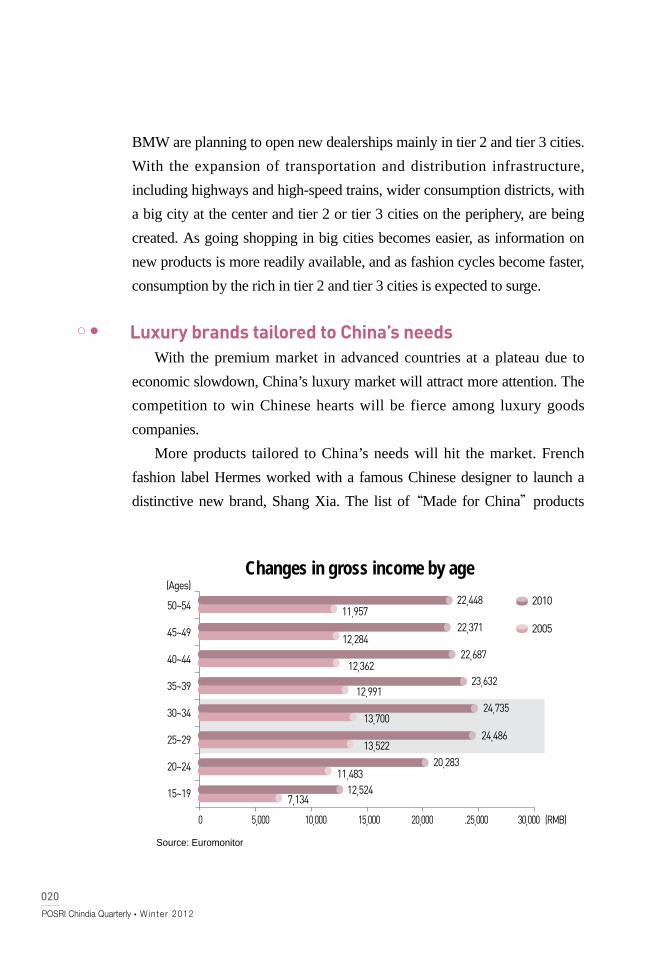

One of the distinctive characteristics of Chinese high income earners is

their young age. Chinese between the ages 25 and 34 have the highest

income, unlike in other countries where the highest income earners are in

their forties. The average age of Chinese billionaires is 39 years old, far

lower than the global average of 54. The reason is presumably that young

Chinese people possess high levels of education and skills. For the same

reason, they are different from other age groups in terms of their preferred

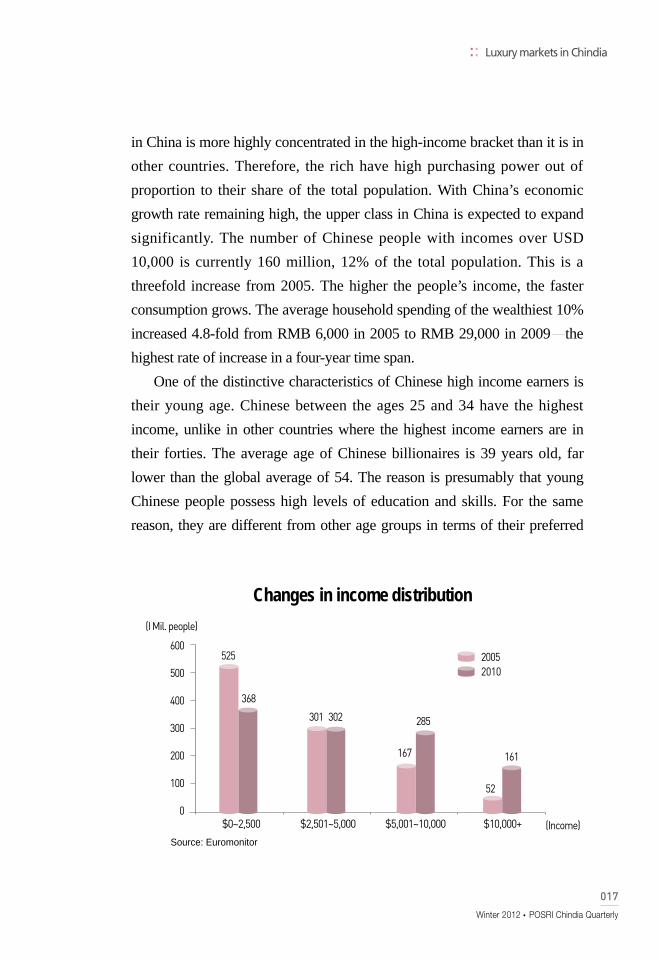

Source: Euromonitor

Changes in income distribution

$0~2,500 $2,501~5,000 $5,001~10,000 $10,000+

600

500

400

300

200

100

0

(I Mil. people)

525

167

285

52

161

368

301 302

20052010

(Income)

POSRI Chindia Quarterly�Win te r 2012

018

brands and brand exposure paths. While middle-aged and older people learn

about luxury goods through acquaintances and conventional media, the

younger generations get information on the Internet and buy luxury goods

through overseas sites or purchasing agency services. The motivation for

buying luxury goods varies from desire to display wealth to the quality and

utility of the product itself to self-satisfaction.

Another characteristic of China’s rich is a high proportion of women.

Women are given the same opportunities in education and society as men,

hence Chinese women’s income level is higher than that of women in other

countries. The Hurun Research Institute (胡潤) released a report showing

that China has over 875,000 multimillionaires, up 6.1% from the previous

year, and one third of them are women. Female consumers show high

purchasing power in the premium market. According to a McKinsey & Co.

survey, women accounted for more than half of the USD 15 billion in

Chinese luxury goods sales in 2010, an increase from 45% in 2008. The

average female luxury consumer in China also spent 22% more in 2010 than

in 2008, while men spent only 10% more.

Source: Euromonitor

Spending increase by income level

Lowest Low Medium-low Medium Medium-high High Highest(0~10%) (10~20%) (20~40%) (40~60%) (60~80%) (80~90%) (90~100%)

30,000

25,000

20,000

15,000

10,000

5,000

0

(RMB)

2,0614,901

2,516

6,743

2,334

8,739

3,446

11,320

4,046

14,964

4,666

19,264

6,033

29,00419952009

(Income)

Winter 2012�POSRI Chindia Quarterly

019

:: Luxury markets in Chindia

Wealthy Chinese women

have an impact on male-

dominated markets, such as

cars and high-end spirits, as

well as cosmetics and

designer clothing. Maserati,

a well-known Italian luxury

sports car manufacturer, sold

400 cars in China last year, 50% more than the previous year. Women

account for 30% of Maserati’s sales in China, compared to less than 10% in

Europe. Ferrari and Lamborghini also reported that the percentage of

women buying their cars in China is more than double the global average.

More women buy whisky in China than in the West. Companies in the

related industries are modifying their marketing strategies, developing

products tailored to women, for example.

○● The preference for luxury brands spreading to small

and medium-sized cities

The number of rich people has been growing in tier 2 and tier 3 cities. In

the decade starting in 2000, the urbanization rate in China surged from

34.8% to 46.6%. In tier 2 and tier 3 cities, opportunities for economic

growth and employment have expanded due to government investment in

infrastructure, such as the Rise of Central China Plan and China Western

Development, combined with the relocation of plants looking for cheap

labor costs. Approximately 30% of the well-to-do in China currently live in

big cities, including Beijing, Shanghai, Guangzhou, and Shenzhen, but by

2015, about 75% are expected to live in tier 2 or tier 3 cities.

Luxury brands are actively entering tier 2 and tier 3 cities in response to

changing consumer demographics. Louis Vuitton and Gucci are expanding

into cities like Chengdu, Chongqing, and Changsha, while Volkswagen and

With the premium market in

advanced countries at a plateau due

to economic slowdown, China’s

luxury market will attract more

attention.

POSRI Chindia Quarterly�Win te r 2012

020

BMW are planning to open new dealerships mainly in tier 2 and tier 3 cities.

With the expansion of transportation and distribution infrastructure,

including highways and high-speed trains, wider consumption districts, with

a big city at the center and tier 2 or tier 3 cities on the periphery, are being

created. As going shopping in big cities becomes easier, as information on

new products is more readily available, and as fashion cycles become faster,

consumption by the rich in tier 2 and tier 3 cities is expected to surge.

○● Luxury brands tailored to China’s needs

With the premium market in advanced countries at a plateau due to

economic slowdown, China’s luxury market will attract more attention. The

competition to win Chinese hearts will be fierce among luxury goods

companies.

More products tailored to China’s needs will hit the market. French

fashion label Hermes worked with a famous Chinese designer to launch a

distinctive new brand, Shang Xia. The list of “Made for China”products

Source: Euromonitor

Changes in gross income by age

0 5,000 10,000 15,000 20,000 .25,000 30,000

(Ages)

50~54

45~49

40~44

35~39

30~34

25~29

20~24

15~19

(RMB)

22,44811,957

12,28422,687

12,362

12,99123,632

24,735

24,486

20,283

12,524

13,700

13,522

11,483

7,134

22,371

2010

2005

Winter 2012�POSRI Chindia Quarterly

021

:: Luxury markets in Chindia

goes on: dENiZEN by Levi’s was designed to fit the slim Chinese body

type, and the new long-wheelbase BMW 5 Series Sedan was designed to

cater to the Chinese preference for big sedans.

These products will play a major role in the companies’ entry into

regions outside of China as well. A US-based manufacturer of sanitary ware

released Numi, a smart toilet, targeting Chinese consumers. Because

bathrooms in China are typically cold, Numi issues warm air from a floor-

level vent to heat the floor and warm the user’s feet. It is also equipped with

a touch screen to control various functions, including music, video games,

and e-books, in order to satisfy the Chinese taste for entertainment. Milan-

based Yoox.com, which sells discount designer fashion online, has selected

China as a test market for its standby service, a system Yoox has arranged

with FedEx where the deliverer waits at the door in case the customer is

dissatisfied with the delivered product and decides to return the item to

Yoox. If this service is successful in China, Yoox’s largest market, the

company will expand the service to other countries.

Currently, there are many companies differentiating themselves with

products tailored to the Chinese. However, after some time, the products

themselves become insufficient to make a company stand out. At that point,

the most important asset might be the differentiated brand image the

company has come to own. Recently, South Korean fashion retailer E-Land

Group, which has been growing by approximately 50% each year, recorded

KRW 1.2 trillion in sales in China alone. In order to boost its brand image in

the Chinese market, E-Land acquired Mandarina Duck, an Italian-based

brand that offers luxury luggage and travel accessories, and established a

joint venture partnership with Kate Spade, an American fashion label. The

Chinese consumer market has great potential, and, therefore, companies

should focus on brand management centered on the Chinese premium

market, in addition to developing products tailored for the Chinese

market.

Winter 2012�POSRI Chindia Quarterly

023

China’s great cause:“Create Chinese brands”

:: Luxury markets in Chindia

Shim Sang-HyungSenior Business Analyst of POSCO Research Institute

Transformers is an American film franchise that depicts the

showdown between the Autobots, who try to save the Earth

and Humanity, and the Decepticons, who try to control

Humanity. The third film in the series, with sports cars

transforming into sleek robots and other eye-catching visual effects, hit the

box office last summer and drew 7.4 million viewers in Korea alone.

Something caught my attention in the scenes that take place at the

company where Sam, the main protagonist, is employed. Various notebook

computer models bearing the Lenovo logo appear throughout the scenes.

Lenovo pursued an indirect advertising strategy for maximum publicity

effect by becoming one of the official sponsors of the movie. As former

installments of the series have become mega hits, the competition for and

costs of being a sponsor must have been enormous. At the entrances of

theaters in Korea, images of Lenovo products were displayed with the line

POSRI Chindia Quarterly�Win te r 2012

024

“transformable and innovative like Transformers”. Demand for Lenovo

products among Korean consumers has reportedly increased since the

movie’s release. Lenovo has been extremely successful in exposing

consumers to the company and creating a brand image.

○● Desire to become a multinational brand

Chinese PC manufacturer Lianxiang (�想) acquired IBM’s Personal

Computing Division in 2004 and changed its name to “Lenovo”, a name

derived from the “Le-”from “legend”and “novo”, the pseudo-Latin for

“new”. For a while, Lenovo had a difficult time with post-merger

integration and saw its margins declining. However, with its sales for the

second quarter of 2011 up 23.1% year-on-year, Lenovo became the world’s

third largest PC vendor, boasting the highest growth rate in the global PC

industry in the last seven years.

Lenovo has something to worry about, though. While 80% of sales in its

PC operation, which accounts for 60% of the company’s business, comes

from China, only about 6% comes from the USA. This means that the

dramatic development over the last two years is only attributed to the robust

Chinese domestic market; this blurs the iconic “China Power”image of

Lenovo, which leapfrogged into a global technology brand with the

acquisition of IBM, the leader of the PC industry. In May of 2011, Lenovo

decided to build a new plant through a joint venture with Japanese

electronics company NEC. In addition, by acquiring German computer and

consumer electronics maker Medion, Lenovo strengthened production and

distribution bases in advanced countries and set out to promote the company

and its brand. These efforts have a single reason. Lenovo is driven by a

strong desire to become a multinational company with a world-class brand.

The Chinese government is offering active policy support to aid brand

strategies of Chinese companies. This support came from the idea that it is

imperative to build independent, innovative capabilities and to create world-

Winter 2012�POSRI Chindia Quarterly

025

:: Luxury markets in Chindia

class brands in order to elevate China’s position from the low-to-middle

levels of the global manufacturing value chain, boosting its international

competitiveness. It is very common for global brands to produce parts and

materials in China and finish processing and assembling there, but China

possesses few products with their own brand power.

The Chinese government added to its 12th Five-Year Plan the goals of

establishing a global sales network and nurturing Chinese brands to a global

level, showing its commitment to becoming a “brand power nation”. Earlier

this year, China’s Ministry of Industry and Information Technology

announced policies to support overseas trademark registration and patent

applications for Chinese brands in order to solidify the footing of Chinese

electronics brands, and to encourage Chinese electronics companies to

Ranking Brand IndustryBrand value

(RMB 100 Mil.)

1 Industrial and Commercial Bank of China Bank 2162.85

2 State Grid ( ) Power 1876.96

3 China Mobile ( ) Telecommunications 1829.67

4 CCTV Broadcasting 1261.29

5 China Life ( ) Insurance 1035.51

6 China National Petroleum Petroleum 1006.23

7 Sinochem Petroleum 958.57

8 Huawei Telecommunications 867.46

9 First Automobile Works (FAW) Automotive 842.66

10 Lenovo Electronics 825.91

Source: china.org.cn (June 30, 2011)

Top 10 of China’s 500 most valuable brands in 2011

POSRI Chindia Quarterly�Win te r 2012

026

participate in overseas exhibitions and take part in M&A’s and joint ventures

with foreign companies.

○● Global brands dominating China’s premium market

The 2011 list of China’s 500 most valuable brands, released in June of

2011, shows that most of the highest ranked companies are large, state-

owned infrastructure enterprises (banks, power, petroleum, etc.), including

the Industrial Commercial Bank of China, which ranked first. The only

consumer goods companies on

the list are First Automobile

Works (FAW) (中 一汽) at 9th

and Lenovo, which ranked 10th.

On the other hand, the average

market share of the top ten

brands in the Chinese consumer

goods market was 69.9%,

according to the 2010 statistics

of the National Bureau of

Statistics of China. This figure shows that brand consumption has taken root

with Chinese consumers. In terms of home appliances, the market share of

the top 10 brands was 81.3%, showing the strong influence of brands on

consumption. The market share of food brands was approximately 70%,

while that of cultural and office product brands was about 80%.

With few high-end Chinese brands, global luxury brands, such as

Burberry, Hugo Boss, and Armani, had the highest growth in sales in the

women’s apparel market, which grew by almost 30% last year. As wealthy

Chinese come to prefer high-end goods in line with their increasing incomes

and standard of living, their consumption of luxury goods also increases─

a big windfall for foreign companies.

The changing consumption pattern of the Chinese is also well reflected

It is imperative to create world-

class brands in order to elevate

China’s position from the low-to-

middle levels of the global

manufacturing value chain.

Winter 2012�POSRI Chindia Quarterly

027

:: Luxury markets in Chindia

in their consumption of automobiles, a good example of durable goods with

rising sales. Thanks to Chinese government policies that nurture local

automakers, Chinese automakers, including Chery Motors and Geely

Motors, seemed to make modest progress in the mid-2000s. Later, Chinese

consumers with growing buying power chose cars manufactured by foreign-

invested joint ventures, such as Volkswagen, GM, and Hyundai Motors.

Having been nudged aside in the areas of quality, design, and brand power,

Chinese carmakers have been pursuing strategies to acquire technologies

and brands quickly through M&A’s with companies from advanced

countries. Following Geely’s acquisition of Volvo in 2010, Zhejiang

Youngman Lotus Automobile (浙江靑年) bought shares of SAAB in June

of 2011. Chinese firms’ M&A’s of advanced companies in the consumer

goods sector will increase in the future. In particular, companies in Europe

are expected to be potential target companies, rather than those in the USA,

which has strict M&A regulations for companies having strategic products

or advanced technologies.

○● A brand power nation─a long and treacherous way to go

In the early stage of a brand lifecycle, the brand becomes a guarantee of

quality. In the next stage, the individuality and preferences of the consumer

are well reflected in the brand. Going one stage further, the brand ownership

creates personal identities, and brands create social values and hierarchy. In

the final stage, the values of the brand are extended beyond the product and

become the encompassing image of the company (Tan & Ming, 2003). Only

when companies pursue a range of carefully planned brand strategies over a

long time will they be able to reach a level of brand power as high as that of

Apple. This is why expectations come hand in hand with worries about the

haste of Chinese companies and of the government to satisfy their craving

for brand power.

Winter 2012�POSRI Chindia Quarterly

029

India, no longer a low-end market

Cho Choong-JaeTeam Leader of South Asia TeamKorea Institute for International Economic Policy (KIEP)

Whenever I go to India for business, I make some time to

drop by the shopping malls, where I can feel the

changes happening in India, directly or indirectly,

especially changes in consumption trends and

corporate response strategies.

Some time ago, the look of appliance stores changed completely. First of

all, the television sets on display have changed. CRT TV’s with their

bulging backs are hard to find; instead, an array of flat panel TV’s is on

display. Screen sizes have become much larger, and home theater systems

are shown. In terms of televisions, stores in India look not that different

from those in Korea.

What about food and beverage stores? Coffee products are now on sale

in India, a country of tea; coffee mixes with creamer and sugar have hit the

market. Various types of coffee are displayed according to flavor and area of

origin, including Brazil, Columbia, and Kilimanjaro. Teas with special

:: Luxury markets in Chindia

POSRI Chindia Quarterly�Win te r 2012

030

functions are found on tea selves: tea that is good for health, tea that is good

for the brain and weight-loss, and tea that can be steeped in cold water. In

the dried noodle section, many types of cup noodles are displayed along

with other types of instant noodles.

Liquor stores were once barely noticeable in India, a sober country.

Things have changed now. Many different types of beer can be found in

various containers and volumes. At some stores, wine accounts for more

than half the products on display. There seem to be six to eight types of wine

which are all made in India. Almost all shopping centers have multiplex

cinemas with elegant cafes and cozy rest areas.

Scenery has changed on the road, too. In the past, taxis in Delhi were

mostly Ambassadors made by Hindustan Motors. Now the street is a much

more diversified and upscale scene with various types of taxis, such as Tata

Indica and Indigo, and Hyundai Santro. For passenger cars, Suzuki Maruti

800 was ubiquitous on Indian streets in the past; now there are other types of

vehicles, with a rising number of luxury cars.

○● Craze for luxury goods

In a nutshell, India’s consumption market trend that is identifiable at

shopping malls and on the street is high quality, high-functionality, and high

price. This trend is called “premiumization”. The increasing market demand

for premium brands is called “premiumization of the market”or “trading-up”;

these kinds of products are called “premium products”or “trade-up products”.

By taking the sales of premium products into consideration, it is easy to

recognize how high and strong India’s passion for premium products is. In

the Indian automotive market, passenger vehicles are classified into four to

six types according to engine displacement: mini, compact, mid-size,

executive, luxury, etc. Among them, compact cars have the largest market

share, followed by mid-size cars. Mid-size cars are much higher-end and

more expensive than compact cars. However, the share of compact cars has

Winter 2012�POSRI Chindia Quarterly

031

:: Luxury markets in Chindia

recently decreased, while that of mid-size cars has noticeably increased. The

market share of compact cars was 75% for January to August of 2009, and

74.1% for the entire year of 2009, but this figure dropped to 72.9% for

January to July of 2010, and to 70.9% year-on-year. It dropped by four

percentage points over the past two years. For the same period, the share of

mid-size cars rose by 1.9 percentage points, from 18.1% to 20.0%.

The same is true for two-wheeled vehicles. Up until 2001, motorcycles

made up 68.7% of the two-wheeled vehicle market, but in 2010, this figure

increased to 76.5%. By contrast, the share of scooters and mopeds (a

combination of motorcycle and bicycle) has dropped from 31.3% to 23.5%

in the same period. Motorcycles are more luxurious than scooters or mopeds

in terms of price, performance, and engine size.

○● A 30% increase in sales of flat panel TV’s and double-

door refrigerators

“Premiumization”in sales trends is well reflected in Diwali, India’s

biggest festival and shopping occasion. According to the Retailers

Source: CEIC

Changing shares of two-wheeled vehicles in India

9080706050403020100

68.7

31.324.2 22.3 20.0 17.6 16.8 20.4 21.6 21.7 23.5

75.8 77.7 80.0 82.4 83.2 79.6 78.4 78.3 76.5

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Motorcycles Scooters and mopeds

(Unit: %)

POSRI Chindia Quarterly�Win te r 2012

032

Association of India (RAI), the 2010 Diwali season resulted in big gains for

retailers, with sales rising by 50-80% compared to 2010. The rise was

attributed to surges in the price of gold and premium product sales. Also, the

Diwali season saw an increase of 25-30% in sales per retailer for premium

consumer products like flat panel TV’s and double-door refrigerators.

DisplaySearch, a global leader in display market research, predicts that

between 2012 and 2013, the sales of flat panel plasma displays will surpass

that of bulky CRT’s, whose current market share is 75%.

In biscuits and cooking oil, premium products that emphasize health and

convenience are gaining ground. Parle Products, India’s leading

manufacturer of biscuits and confections, had only 15% of the market share

of premium products four years ago, but this figure currently stands at

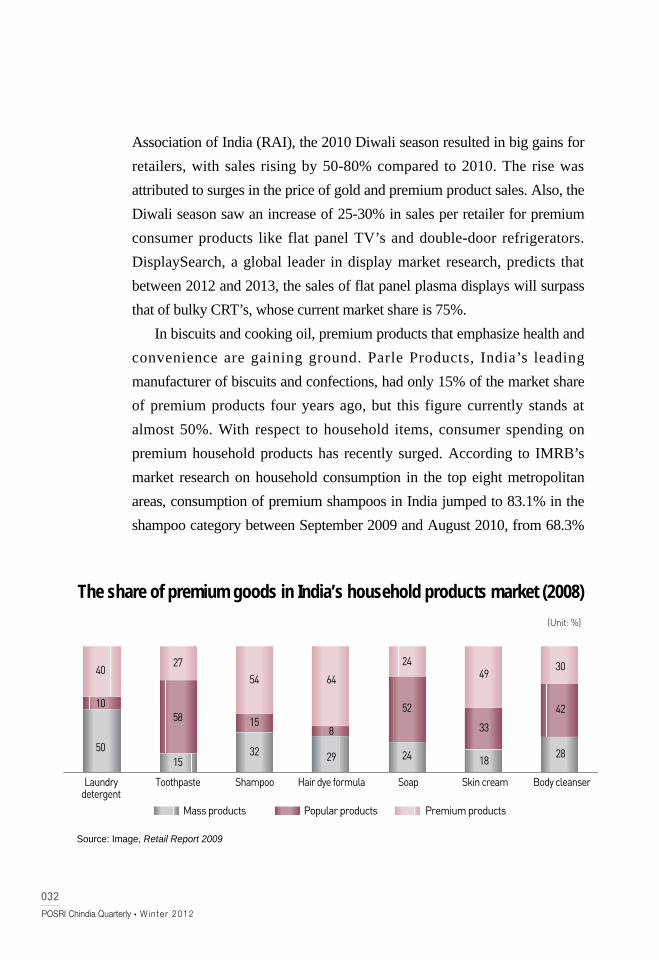

almost 50%. With respect to household items, consumer spending on

premium household products has recently surged. According to IMRB’s

market research on household consumption in the top eight metropolitan

areas, consumption of premium shampoos in India jumped to 83.1% in the

shampoo category between September 2009 and August 2010, from 68.3%

Source: Image, Retail Report 2009

The share of premium goods in India’s household products market (2008)

(Unit: %)

Laundrydetergent

Toothpaste Shampoo Hair dye formula Soap Skin cream Body cleanser

5015

58

2754

15

32 29

8

64

24

24

52

49

33

18

30

42

28

10

40

Mass products Popular products Premium products

Winter 2012�POSRI Chindia Quarterly

033

:: Luxury markets in Chindia

between September

2008 and August 2009.

The share of premium

skin creams rose to

13.9% from 6.5% in

the same period, and

that of premium talcum

powders rose to 7.9%

from 6.2%.

According to India’s retail and distribution institution, in 2008 premium

shampoos and hair dye formulas accounted for more than half of total sales

in their categories, and premium laundry detergents and skin creams

accounted for more than 40% of total sales. Premiumization in men’s shoes,

which seemed slow to react to latest trends and premium products, is

happening rapidly. India’s footwear market grows by about 9% annually, but

the growth rate of premium brands such as Bata and Reebok reaches 20%.

Premium footwear accounts for half of total footwear sales in India.

○● Premiumization, faster than expected

Indian consumers prefer premium products for the same reasons as

consumers in other countries and regions. What is distinctive here is that the

rate of premiumization in India is faster and more widespread than

expected. As the middle class has broadened and their consumption pattern

has changed from “saving”to “satisfaction”or “value”, premiumization is

increasing. When consumers are willing to pay extra money for superior

products, the phenomenon of premiumization, or trading-up, begins.

Premiumization accelerates further when people earn more and their desire

for a better life and more convenience becomes stronger, and when

corporate competition becomes fiercer and product lifecycles become

shorter.

A company’s share in the Indian

premium market has become a

determinant for not only short-term

results but also for its long-term

growth.

POSRI Chindia Quarterly�Win te r 2012

034

Due to India’s high growth rates since 2003, household income has

increased astronomically. Statistics of Global Insight, a leading provider of

global economic outlook, show that India’s per capita income surpassed

USD 400 in 1996, and took seven years to reach USD 500 in 2003.

However, per capita income has grown by more than USD 100 every year

since 2003, to a record of about USD 1,350 in 2010. With household

income rising, the middle class and their purchasing power are also

expanding. A McKinsey report predicted that the number of Indian middle

class with an annual household income of USD 4,500-11,300 will reach 250

million in 2015, a 450% increase from 45 million in 2005. Indian

consumption patterns are bound to change.

When income increases, consumption naturally increases, resulting in

conspicuous consumption. Consumers are willing to pay a much higher

price for essentially the same product; this is called the Veblen effect. In

addition, the bandwagon effect arises when consumer demand concentrates

on commodities that reflect higher preference. This is a snapshot of the

Indian market. Companies never miss such an opportunity. They rush to

release products with new functions, high quality, and convenience,

accelerating the premiumization even further. A company’s share in the

Indian premium market has become a determinant for not only short-term

results but also for its long-term growth.

Winter 2012�POSRI Chindia Quarterly

035

Korean companies in India,bolstering premium strategies

:: Luxury markets in Chindia

Imm Jeong-SeongSenior Business Analyst of POSCO Research Institute

○● Home appliance makers─early entry, belated returns

In July 2010, LG Electronics announced that it would shift its business

strategy in India to premium marketing─trimming the number of models in

its CRT range of color TV’s from 54 to 32, and focusing more on LCD and

PDP flat screen TV’s. It also plans to increase production of premium home

appliances, including double-door refrigerators, drum laundry machines,

and stand-alone air-conditioners. LG Electronics noted the reason for the

change to its business strategy: “Our market share is going to fall in the

short term, but in the long term, the Indian consumer market is going

premium.”In India, LG Electronics currently has the largest market share in

refrigerators, laundry machines, air-conditioners, and microwaves, but with

its profits deteriorating, it was forced to make this decision in order to

survive in the fast-paced, ever-changing Indian market.

POSRI Chindia Quarterly�Win te r 2012

036

Meanwhile, after some ups and downs since entering the Indian

premium market in 2005, Samsung Electronics is finally smiling. In 2006,

Samsung stopped manufacturing CRT TV’s and shifted its focus to

premium models such as flat screen TV’s─a move criticized in and out of

the company for many years. However, its bold move, removing or reducing

low-technology and low value-added product lines, and changing its product

portfolio to include premium and high value-added products, is now bearing

positive results in its sales, profits, and brand image. In the mobile phone

market in particular, where expansion was twofold that of the general home

electronics market, Samsung was able to surpass LG in sales of 2010 as a

result of its premium strategy.

However, the situation does not allow Samsung to remain complacent.

Japanese companies, such as Sony, Panasonic, and Daikin, which have been

waiting for the Indian premium market to open, are stepping up the

offensive by building large plants in India, localizing products, expanding

distribution channels, and bolstering their brand images. Retreating is not an

option, since India’s low-end market is already dominated by domestic

companies, including Videocon and Onida, and Chinese makers such as

Haier.

○● Auto makers with expanded portfolios

The pattern of changes in India’s automotive market is more

complicated. Just when the market dominated by compact cars was replaced

by one dominated by mid-size cars, India’s Tata Motors rolled out the Tata

Nano, the world’s cheapest car at INR 100,000. Global car makers followed

suit, starting to sell compact cars or mini cars: Toyota (Etios, 1,200cc, INR

400,000), Nissan (mini cars priced at INR 130,000), GM, Ford and others.

Under the circumstances, Hyundai Motors, the second largest car maker in

India, was forced to strengthen its ultra low-cost product line. Hyundai

Motors plans to complete the development of a new 800cc car model priced

Winter 2012�POSRI Chindia Quarterly

037

:: Luxury markets in Chindia

at INR 200,000. “Hyundai produces high-quality cars. Hyundai has strong

dealer networks and more than 80% brand awareness, so it will continue to

grow in India based on its strong compact car business,”said Park Han-

Woo, the head of Hyundai Motors India (HMI). Meanwhile, in response to

the premiumization of the Indian market, Hyundai plans to manufacture

Santa Fe, Avante, and Sonata in India, becoming the first automaker to offer

a complete lineup in India.

The recent situation, wherein the Indian government’s consistent

increase of interest rates has led to falling demand for vehicles, will be a

good opportunity for Hyundai to strengthen its internal system. Hyundai

plans to unveil new types of cars and focus on promoting its brand

awareness, instead of building new plants. Therefore, Hyundai has a

competitive edge on its competitors, which have to build new plants or

expand existing facilities amidst an economic downturn.

○● High-end and low-end markets─catching two birds at

once

Not all companies should focus on India’s increasing demand for

premium products as the three large Korean companies have done. The

market share of some low-end products accounts for 70-90% of the total

market. Companies should decide their target markets after analyzing

market size, competition structure, and their own competitive edge.

Bain & Co., a consulting firm, advises companies doing business in

India to target both high-end and mass markets. Companies need to pursue

economies of scale in production, distribution, and brand-building. To this

end, it is advantageous for companies to focus not only on the luxury market

but also on the mass market, dealing with a multitude of consumers.

This advice may seem unrealistic for many Korean companies.

However, interpreting the premium strategy might change their minds about

the advice. One Samsung employee in India said that Samsung’s premium

POSRI Chindia Quarterly�Win te r 2012

038

strategy is to set the price of its

products at least one dollar

higher than that of its

competitors’. For example,

Samsung sells cheap twin tub

washing machines, but with its

silver nanotechnology, the

product sells for five to six dollars more than its competing products. This is

a strategy of adopting distinct functions (or localization of products), or

employing new technologies, and making use of superior design and good

brand image, thus leading consumers to open their purses.

Identifying Indian consumers’ distinctive characteristics is a good way

to survive in an Indian market with more premium products and stronger

emphasis on brand power. When Indians buy products, they put more

weight on value than price. This is true for all Indians, from the lower class

to the upper class. Indians buy products only when they feel the value of

the product they are paying for. Good function and quality is a must, and

price should be low or reasonable. Due to this attitude of Indians, big

Korean companies, such as LG Electronics, Samsung Electronics, and

Hyundai Motors, which sell almost the same products in India as they sell

in Korea, have been hailed in India for the past decade. Therefore, Korean

small-sized enterprises with inferior brand power to Japanese or Western

companies should roll out products of good quality that enable Indian

consumers to feel the value beyond price, at a cheaper price than their

competitors. Also, they should provide quality customer service. By doing

so, small-sized enterprises will be able to win consumer trust and promote

their brand image.

Indians are talkative and like to collect information. Because India is a

community-based society, recommendations by family and friends are the

largest factor in making purchasing decisions. In other words, word of

After some ups and downs since

entering the Indian premium market

in 2005, Samsung Electronics is

finally smiling.

Winter 2012�POSRI Chindia Quarterly

039

:: Luxury markets in Chindia

mouth works better than expensive product campaigns, advertisements, or

promotions. To this end, media such as the Internet or social network

services (SNS) are useful. Korean SME’s must seek a strategy of first

targeting consumer groups with great influence, including opinion leaders or

industry leaders, whose words will spread far and wide.

It was reported that what puzzled the employees of Samsung the most

when they launched a premium strategy in India was that they could not

distinguish consumers who would shop premium goods. If Korean

companies want to advance in the Indian market, which still seems to be in

fog, they must study the Indian market thoroughly, including Indian

consumers, competing companies, and distribution structure, as well as

monitor changes in the Indian market meticulously.

IInnddiiaa:: BBeeyyoonndd

aannttii--ccoorrrruuppttiioonn

�Indian corruption: characteristics and responses

�Eradicating corruption, a new missionfor economic growth

�Mounting demand for ethical corporatemanagement

Winter 2012�POSRI Chindia Quarterly

043

Indian corruption: characteristics and responses

:: India: Beyond anti-corruption

Santosh KumarBusiness Analyst of POSCO Research Institute, Delhi Office

Transparency International ranked India 87th out of 178

countries, along with countries like Albania, Jamaica, and

Liberia, in the Corruption Perception Index 2010. Corruption is

ubiquitous in India. Corruption, which largely means bribery, is

intertwined with inefficiency, unaccountability, and the feudal mindset of

public administrators. Bribery makes the decision-making process very slow

and sluggish, and the whole system very insensitive. Corruption in the public

sector─bureaucracy, judiciary, and legislature─is so rampant that an aam

admi (common man) believes that corruption is a normal part of governance.

Once, bribes were paid only to do wrong things, but now bribes are paid not

only to do wrong things but also to do right things on time. Corruption exists

at every level of public administration. Private sector corruption is equally

high in India. The Satyam case was a massive private sector fraud.

○● Corruption from lower to higher bureaucracy

Corruption is extremely high in the lower bureaucracy. No application

POSRI Chindia Quarterly�Win te r 2012

044

moves without high denomination currency notes attached to it. If an aam

admi has to get a driver’s license, passport, birth certificate, death certificate,

ration card, gas connection, electricity connection, water connection, PAN

card, etc., he normally has to bribe the officials who are in charge of issuing

these documents. For these documents, the bribe amount ranges from INR

100 to 10,000 under normal circumstances. If one pays four to five times

more, he can get a driver’s license on the same day and a passport in 10 days.

There are a number of touts working for the government officials. The

corruption in the lower bureaucracy may sound petty but the instances are

numerous. This is the corruption that hits the aam aadmi directly.

Corruption has become so ingrained and institutionalized in the Indian

system that it looks very normal. Corruption is accepted and tolerated by

saying ‘chalta hai’ (it is OK). If government officers demand bribes, people

think ‘chalta hai’ so long as they do the work. When government officers

demand bribes, it is rare that an aam admi protests. Corruption is not just one

way, but two ways. People are also eager to give bribes to get things done.

In the higher bureaucracy, corruption is camouflaged but much larger in

scale than in the lower bureaucracy. Most of the bigger scams are committed

in the higher bureaucracy. Though the higher bureaucracy corruption does

not directly hit the aam aadmi, it causes loss to the government’s exchequer.

The 2G spectrum scam is the latest example of higher bureaucracy scams.

Unlike corruption in the lower bureaucracy, corruption is not so open and

direct here. The ministers and senior bureaucrats use lobbyists and brokers

to crack deals with interested parties. Companies in the private sector are

often confronted with this kind of corruption when they are looking for

government tenders, approvals, and clearances.

○● Public sector corruption

The popular presumption is that everyone ‘from peons to the PM’ is

corrupt in India. Congress Prime Minister Narsimha Rao was found guilty

Winter 2012�POSRI Chindia Quarterly

045

:: India: Beyond anti-corruption

of scams in the 1990s. Some ministers and bureaucrats of the current UPA

government are in jail for being involved in scams. Certain public

institutions are extremely corrupt.

Civic bodies like panchayats and municipalities are the centers of

corruption at the grassroot level. Ironically, these institutions were built and

strengthened to reduce local corruption and red-tapism. Today, panchayats

get lots of funds from the government for development works in rural areas,

but most of the funds are siphoned off by panchayat officials and

middlemen. City municipalities have the power to grant a number of petty

approvals and clearances, such as approving the design of a house, water

connections, and ration cards. This gives enough scope to the municipal

officials to demand bribes. The Municipal Corporation of Delhi is one of the

most corrupt civic institutions in India.

The police department, which is responsible for protecting people and

enforcing the law, is one of the most corrupt institutions in India. It is very

common that when an aggrieved person goes to the police station to file a

criminal complaint, the police officer refuses to file the complaint unless a

bribe is paid to him. The transport department is another very corrupt

institution. The officials of the transport department make a lot of extra

money from vehicle registrations and from issuing driver’s licenses. Traffic

police in India are equally corrupt. It is very common on Indian roads for a

traffic policeman to stop a vehicle and demand unreasonable documents to

elicit a bribe.

Corruption is very high in the lower judiciary compared to the higher

ones. It is very easy to influence the judges in the lower judiciary, especially

in the countryside. Court clerks are very corrupt. There is a very strong

nexus between the criminals, lawyers and court officers. While I was

working in the Delhi courts, I met a person whose wife, while having an

illicit relationship with a policeman, got her living husband declared dead by

the court.

POSRI Chindia Quarterly�Win te r 2012

046

Rural financial institutions, which disburse loans to farmers, are very

corrupt. For example, if the government has sanctioned a INR 50,000 loan

to a farmer, the financial institution will grant him only INR 40,000 and

keep the remaining INR 10,000. The farmers are not less clever. They

happily take INR 40,000 and do not mind giving INR 10,000 to the officer

of the financial institution because they never take a loan with the intention

of repaying it. They will wait for the next election, before which the

government usually waives off farmers’ loans to attract the farmers’ votes. It

is a vicious cycle.

India, rich with mineral resources, has a very lucrative mining business.

There is a very strong mining lobby in Indian politics. The mining

department has the power to grant and renew mining leases to the

companies that dig out the minerals. Usually, there is large-scale corruption

in granting and renewing mining leases. After paying bribes, mining is

allowed by the mining department even after mining leases expire. The

Madhu Koda Case in Jharkhand and the Reddy Brothers’ Case in Karnataka

are burning examples of massive corruption in the mining department.

India’s real estate sector is another corrupt area. There is an extremely

strong nexus between the housing department and private builders. The

private builders bribe the housing department to get approvals and

clearances to develop housing complexes. Sometimes, the builders start

booking flats for a location which actually does not exist. Recently, leading

private builders booked flats and collected millions of rupees from desperate

middle class buyers by selling flats in the NOIDA (New Okhla Industrial

Development Authority) extension. Later it was revealed that there was no

such place as the NOIDA extension. Whenever the housing department

allocates flats to middle class buyers, there are large scale unfair practices of

distributing the flats to influential people or to those who pay bribes. The

Delhi Development Authority (DDA), Delhi’s housing department, is often

blamed for malpractice in allotment.

Winter 2012�POSRI Chindia Quarterly

047

:: India: Beyond anti-corruption

○● Private sector corruption

When public sector institutions are corrupt, it is not possible for private

sector organizations to remain immune to corruption. The Indian private

sector also has massive corruption. There are two aspects of private sector

corruption. Firstly, the private sector pays bribes to government ministers

and bureaucrats to get approvals and licences. The 2G spectrum scam,

wherein the private sector

bribed telecom minister A.

Raja and senior telecom

bureaucrats of the central

government, is the most

perfect recent example of this.

There is a collusive nexus

among politicians, lobbyists,

and businesses. The infamous Radia Tape has exposed how businessmen

like Ratan Tata influenced the appointment of A. Raja as telecom minister

for a second time in the UPA government. Political ties of big business

houses to politicians such as Ambani and Jindal are well known. Secondly,

there is another aspect that shows that there is corruption within private

companies. There are a number of instances like the Satyam Fraud Case and

the Citibank Fraud Case. There are a number of benami (fake) companies

doing business in India. Tax evasion and CEOs inflating the costs of

purchase orders are very common. However, internal corruption within

private companies usually gets suppressed so long as it does not involve the

interests of aam admi.

○● Regional Variation

Corruption is more or less everywhere in India but it is usually higher in

less developed regions like East India and North India than in West India

and South India. Poorer states, such as Jharkhand, Bihar, Orissa, West

The issue of corruption is very

complex and deep-rooted in the

Indian system. It is not easy to

reduce or eliminate corruption all

of a sudden. It will take time, as

reform is needed in many areas.

POSRI Chindia Quarterly�Win te r 2012

048

Bengal, and Uttar Pradesh, are comparatively more affected by corruption

than prosperous states, such as Gujarat, Tamil Nadu, and Kerala. High

poverty and high illiteracy may be responsible for higher corruption in the

eastern and northern states. However, there are also exceptions. Prosperous

states like Punjab, Haryana, Delhi, Maharashtra, and Karnataka are also

corrupt.

○● Reasons for corruption

Firstly, one of the main reasons for corruption in India is the supply-

demand mismatch. Supply is lower than demand. This supply-demand

mismatch is mostly artificial. For example, nowadays more and more

Indians are travelling abroad. So, there is more and more demand for

passports. However, the passport counters in the passport office are not

proportionate to the demand. There is a very long queue in the passport

office. In order to avoid the long queue, people pay bribes. Secondly,

political leaders are elected, but elections themselves are full of corruption.

Almost all political parties issue tickets to candidates after taking huge

money. How can these candidates be expected not to be corrupt once they

become ministers? And where the ministers are corrupt, the bureaucrats will

follow suit. Thirdly, Indian people not only tolerate but also promote

corruption. It is rare that people protest against corruption. They accept it as

a normal part of affairs. People also willingly offer bribes to government

officials as a sign of gratitude. Fourthly, in the rush for development, the

Indian education system has become technical and job-oriented. Moral

education has significantly declined in schools and colleges. Family does

not play an important role in urban areas. Values and ethics are not so

emphasized by family or schools anymore. Money-making has become the

goal of life. Fifthly, laws and procedures are very complex in India. It is not

easy for an aam admi to understand laws and procedures. This necessitates

middlemen. Sixthly, the salary of government officials is comparatively low

Winter 2012�POSRI Chindia Quarterly

049

:: India: Beyond anti-corruption

in India. They do not feel satisfied with their incomes and are tempted to

resort to corruption. Finally, illiteracy is also one of the main reasons for

corruption. It is easy to cajole illiterate people into paying bribes by scaring

them with the law.

○● Responses of people

In India, the response of the people towards corruption has been largely

one of tolerance and acceptance. Whenever corruption has been exposed in

the government, the people have voted out that government. Otherwise, the

people have accepted corruption as part of their lives. Though there are laws

such as the Prevention of Corruption Act, 1988, they have been largely

ineffective in tackling corruption due to the number of loopholes. Petty

government officials are punished under the law, but not all of the big fishes

are targeted. However, recent exposure of a number of big scams in the

central government, such as the 2G spectrum scam, Commonwealth Games

scam, and cash-for-vote scam, has awakened the public and raised the issue

of corruption within society.

An NGO called India Against Corruption (IAC), led by Anna Hazare,

Arvind Kejriwal, Kiran Bedi, and others, has sparked a people’s movement

against corruption. The IAC is demanding the central government and

Parliament to pass the Jan Lokpal Bill, 2011 (People’s Ombudsman Bill,

2011) to tackle corruption from peons to the PM level. Anna Hazare

conducted hunger strikes twice (in April and August) to force the central

government to adopt the Bill. The hunger strikes of Anna Hazare got

massive support across India, from people of all walks of life. The Anna

Hazare movement has awakened people to the truth that enough is enough

and now is the time to fight corruption. Parliament is now considering

making a strong anti-corruption law. This time, the people’s response to the

anti-corruption movement has been enormous. However, corruption

continues, especially at the lower levels.

POSRI Chindia Quarterly�Win te r 2012

050

○● Implications

The issue of corruption is very complex and deep-rooted in the Indian

system. It is not easy to reduce or eliminate corruption all of a sudden. It will

take time, as reform is needed in many areas. The first good thing that has

happened against corruption is that the people, who used to consider it normal,

have become aware that corruption is problematic. They now understand that

not paying bribes to get things done on time is their basic right.

Corruption is a major political issue, and it impacts voting patterns. It

impacted the voting pattern of people in the elections in Bihar (2010) where

people voted back the corruption-free government of Nitish Kumar. As a

result, Nitish Kumar has gifted Bihar India’s first law that provides time-

bound services to the people, the Right to Services Act, 2011. It also

impacted the assembly elections in Tamil Nadu and West Bengal (2011).

Corruption is going to be a major political issue in the forthcoming

assembly elections in Uttar Pradesh and Gujarat in 2012. Corruption will

dominate the Lok Sabha elections, though they are far off in 2014. Recent

media surveys show that due to corruption the popularity of the congress-led

UPA government has gone down significantly, whereas that of the BJP has

increased significantly.

Winter 2012�POSRI Chindia Quarterly

051

Eradicating corruption, a newmission for economic growth

:: India: Beyond anti-corruption

Kim Mi-SuBusiness Analyst of POSCO Research Institute

Before I went to India to study, people who had lived in India

recommended that I bring small presents like chocolates or

candies. They said that if I gave them to the school

administrative staff, everything would go smoothly. After

living in India for four years, I understand the necessity of such presents. It

is an Indian custom to give a token of appreciation, even for public affairs.

Each year, the World Economic Forum (WEF) publishes the Global

Competitiveness Index (GCI). India ranked 42th in 2006 according to the

GCI, but slid to the 56th position in 2011. Competitiveness is determined by

various pillars, including infrastructure, institutions, macroeconomic

environment, higher education, and training. The institutions pillar measures

the extent of bribery and corruption, and corporate ethics among other

elements. India ranked 83rd on the irregular payments and bribes indicator

in 2010, the first year that category was included, but plunged far below

POSRI Chindia Quarterly�Win te r 2012

052

average to 95th place in 2011. India’s corporate ethics ranking dropped from

61st place in 2008 to 86th in 2011. India’s fall in these rankings is largely

attributed to a series of big scandals in the government and major companies

that became apparent at the end of the last decade.

○● A further drop in the corruption rankings

In a country like India, with rampant bureaucracy, large-scale projects

involve lengthy and complex procedures for acquiring approvals and

licenses. Therefore, many companies pay bribes, under the name of

“express fees,”to public officials in order to run business smoothly and

effectively. In the short term, this kind of bribe might work as lubricant and

have a positive impact on business activities and the economy. In the long

term, however, it harms India’s business environment.

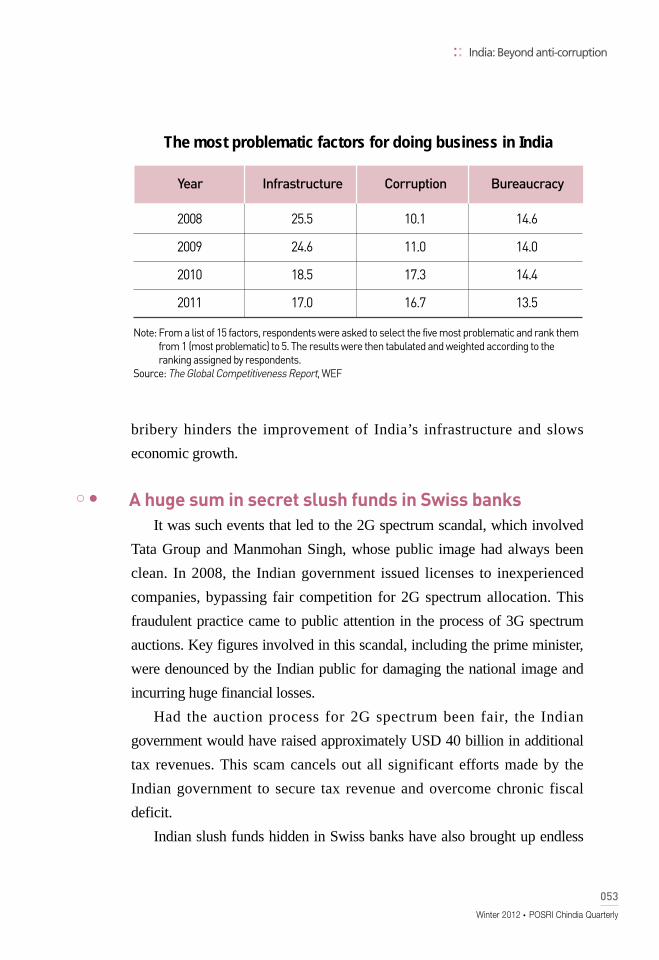

In a survey of Indian businessmen conducted by KPMG Consulting in

2011, nearly 99% of respondents said corruption impedes India’s economic

growth. Comparing the 2011 survey results from China and India, China’s

corruption and bureaucracy scored 8.5 and 10.9 points, respectively, while

those of India scored 16.7 and 13.5 points, respectively.

In India, where bribery has already become a regular practice in doing

business, selecting players through fair competition involves much hassle.

This has been especially true in tenders for massive real estate projects,

including infrastructure construction, and the controversial 2G spectrum

allocation. According to the KPMG report mentioned above, many Indian

businessmen believe that the real estate and construction sectors are most

prone to corruption. This implies that bribery is rampant in massive

construction projects.

The winner of a bid, after bribing public officials, is apt to do

substandard work in order to make up for the unexpected increase in costs,

using inferior construction materials, for instance. Also, businesses that fear

cost increases are often reluctant to invest in infrastructure. In this way,

Winter 2012�POSRI Chindia Quarterly

053

:: India: Beyond anti-corruption

bribery hinders the improvement of India’s infrastructure and slows

economic growth.

○● A huge sum in secret slush funds in Swiss banks

It was such events that led to the 2G spectrum scandal, which involved

Tata Group and Manmohan Singh, whose public image had always been

clean. In 2008, the Indian government issued licenses to inexperienced

companies, bypassing fair competition for 2G spectrum allocation. This

fraudulent practice came to public attention in the process of 3G spectrum

auctions. Key figures involved in this scandal, including the prime minister,

were denounced by the Indian public for damaging the national image and

incurring huge financial losses.

Had the auction process for 2G spectrum been fair, the Indian

government would have raised approximately USD 40 billion in additional

tax revenues. This scam cancels out all significant efforts made by the

Indian government to secure tax revenue and overcome chronic fiscal

deficit.

Indian slush funds hidden in Swiss banks have also brought up endless

Year Infrastructure Corruption Bureaucracy

2008 25.5 10.1 14.6

2009 24.6 11.0 14.0

2010 18.5 17.3 14.4

2011 17.0 16.7 13.5

Note: From a list of 15 factors, respondents were asked to select the five most problematic and rank themfrom 1 (most problematic) to 5. The results were then tabulated and weighted according to theranking assigned by respondents.

Source: The Global Competitiveness Report, WEF

The most problematic factors for doing business in India

POSRI Chindia Quarterly�Win te r 2012

054

debates. The exact amount of

money held in Swiss banks and

the identities of accountholders

have been strictly unknown until

recently. However, while

discussions were taking place on

revision of the Double Taxation

Avoidance Agreement (DTAA)

between India and Switzerland,

it was disclosed that Indians owned the largest number of foreigner-owned

secret accounts in Switzerland. Suspicion is building that the leaders of

society, including high ranking public officials and business leaders, have

sent money overseas to evade taxes and form slush funds.

Reportedly, USD 1.45 trillion of Indian money is deposited in Swiss

banks, which is six times the external debt of India, or 90% of Indian GDP.

This huge sum of money, if it were to return and circulate within the Indian

economy, could help external debt redemption and increase investment,

giving positive impetus to economic growth.

○● Triggering macroeconomic instability

Corruption, which is closely related to increased investment costs and

uncertainty in decision-making, eventually results in a decrease in

investment. Bribes that investors pay to get approvals and licenses for