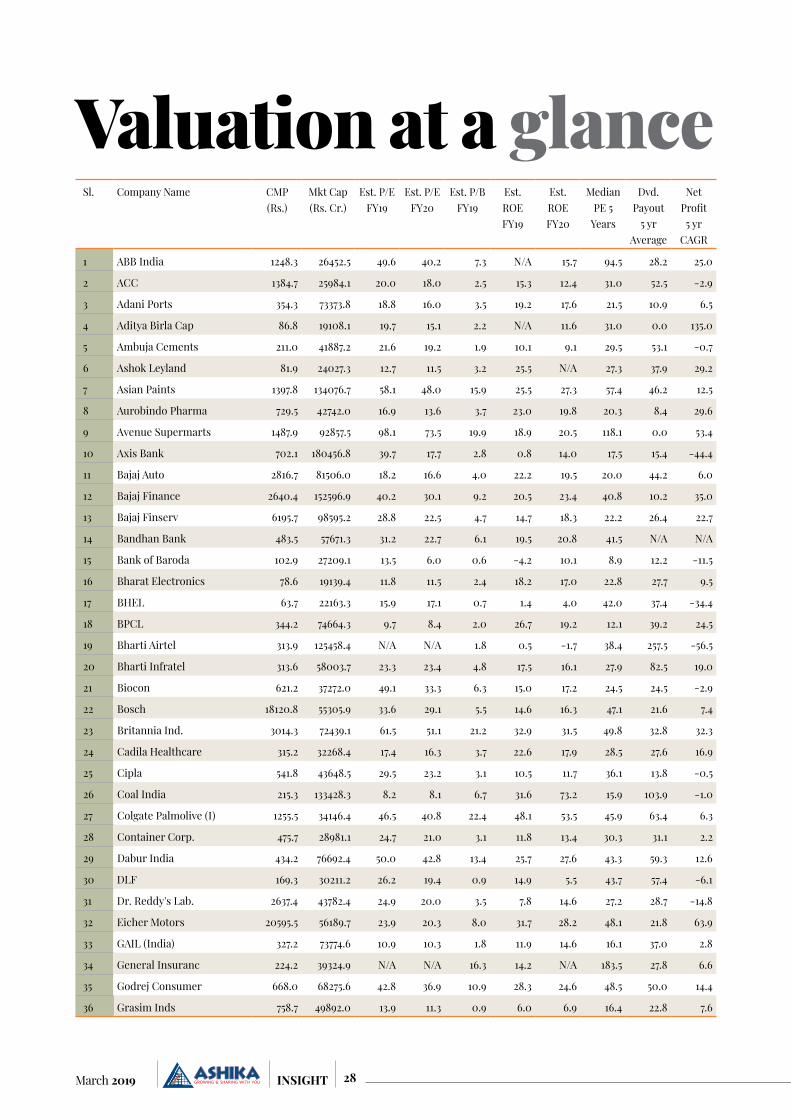

INDIA'S Q3FY19 REPORT CARD - Ashika Group

88

Market Overview Prominent Headlines February 2019 Q&A with CIO Mutual Fund Overview Stock Picks Monthly Insight Performance Valuation at a Glance Q3FY19 Result Analysis Sector Outlook - IT Economy Review Economy Chart Book Management Meet Note Technical View Market Diary Commodity Monthly Round Up World Economic Calendar IN SIGHT March 2019 INDIA’S Q3FY19 REPORT CARD Ashika Group received “BTVI Emerging Company of the Year” Award Mr. Chirag Jain received “BTVI Young Business Leader of the Year” Award Q&A with CIO Mr. Neelesh Surana - Chief Investment Officer - Mirae Asset Global Investments (India) Pvt. Ltd. ITC Ltd. | Tech Mahindra Ltd.

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of INDIA'S Q3FY19 REPORT CARD - Ashika Group

Market OverviewProminent Headlines February 2019Q&A with CIOMutual Fund Overview

Stock PicksMonthly Insight PerformanceValuation at a GlanceQ3FY19 Result Analysis

Sector Outlook - ITEconomy ReviewEconomy Chart BookManagement Meet Note

Technical ViewMarket DiaryCommodity Monthly Round UpWorld Economic Calendar

INSIGHTMarch 2019

INDIA’S Q3FY19 REPORT CARD

Ashika Group received “BTVI Emerging Company of the Year” Award

Mr. Chirag Jain

received “BTVI

Young Business

Leader of the Year”

Award Q&A with CIO

Mr. Neelesh Surana - Chief Investment Officer - Mirae Asset

Global Investments (India) Pvt. Ltd.

ITC Ltd. | Tech Mahindra Ltd.

INSIDE THIS ISSUE

Marketoverview1 45 Sector -

Information

Technology

6 Q&A with CIO- Neelesh Surana, Mirae Asset Global Investments (India) Private Limited

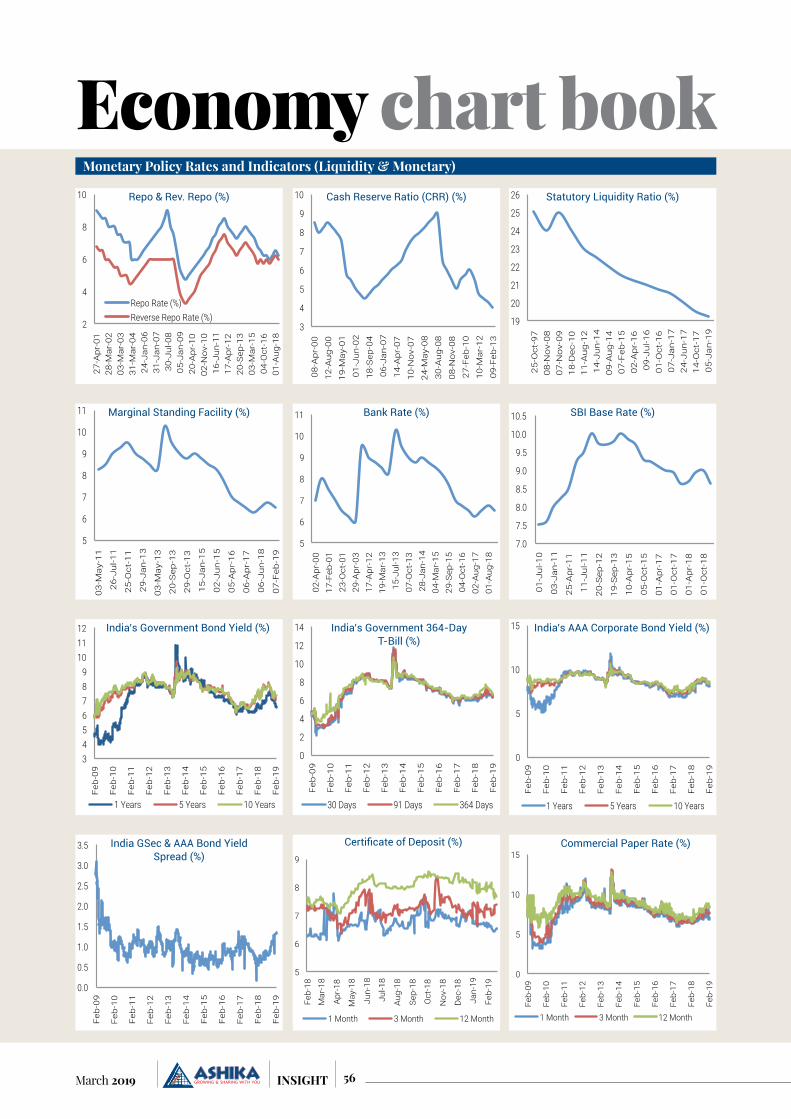

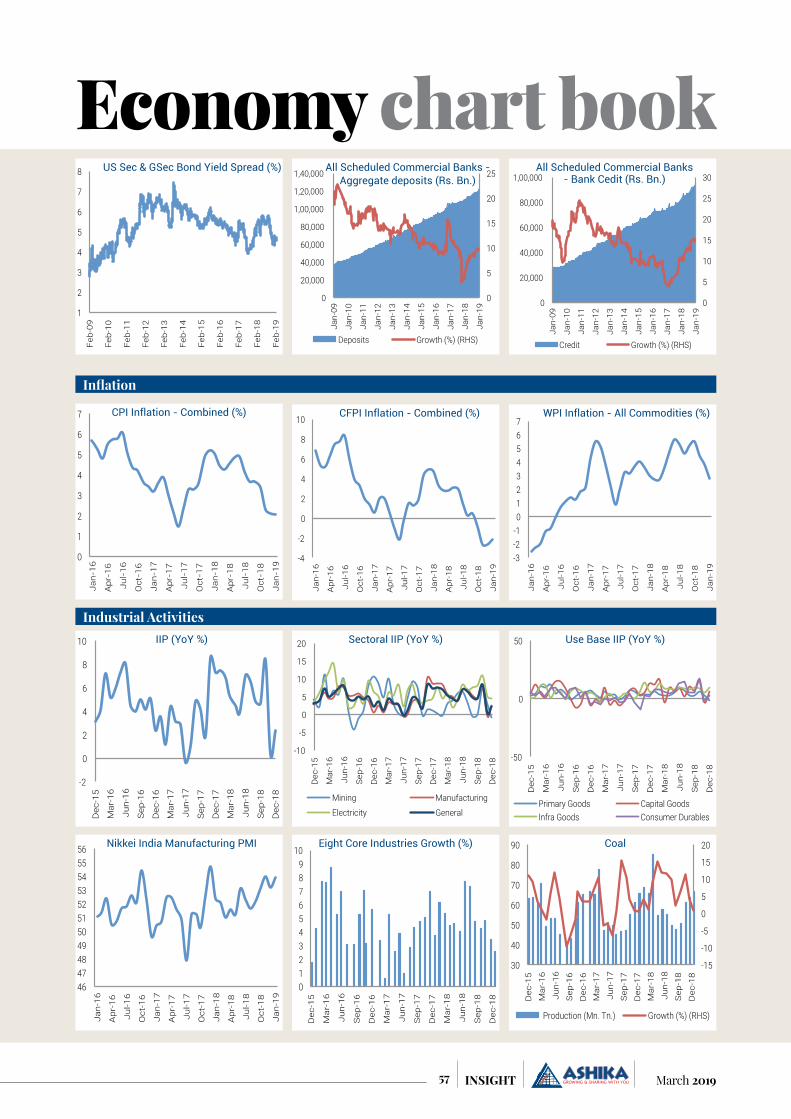

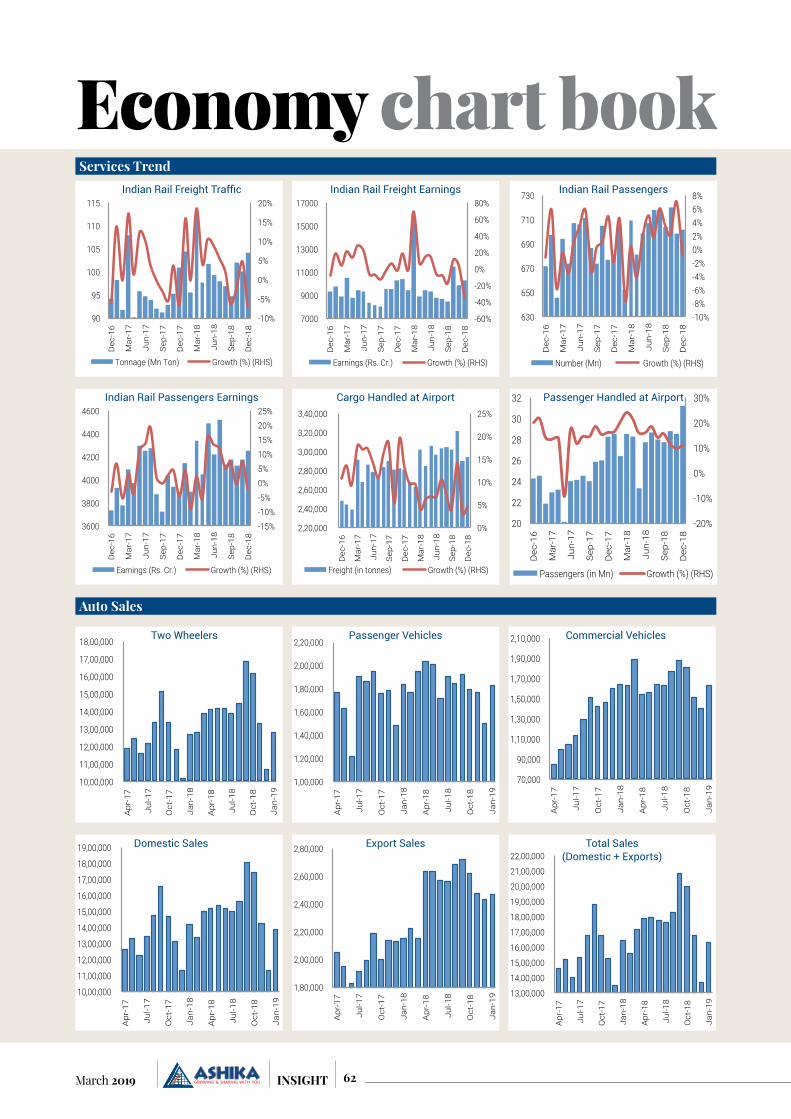

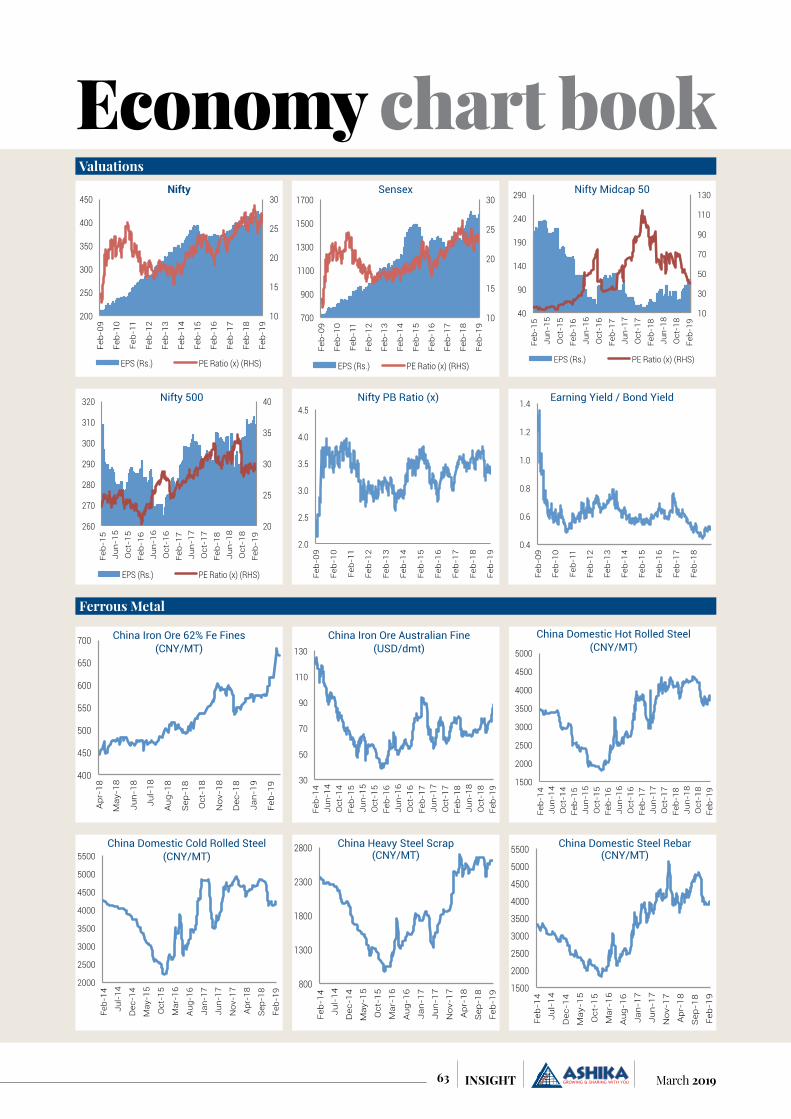

56 Economychart book

14 Stockpicks• ITC Ltd.• Tech Mahindra Ltd.

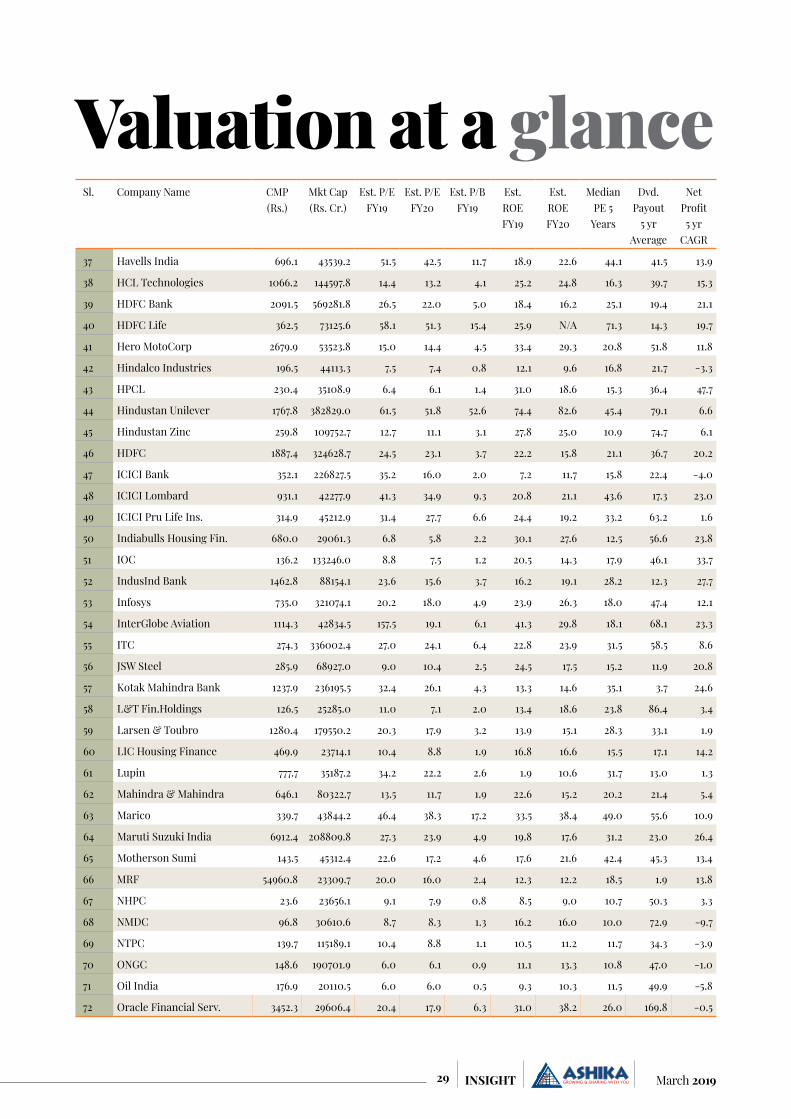

28 Valuationat a glance

76 Technicalview

80 Commoditymonthly round up

Economyreview 52

Mutualfund overview 8 Manage-

mentmeet note• Ajanta Pharma Ltd. 70

Monthlyinsight performance 20

Q3FY19Result Analysis 31

Marketdiary 79

Worldeconomic calendar 82

Prominent headlines February 2019 4PROMINENT

HEADLINES

1 March 2019INSIGHT

MarketOVERVIEW

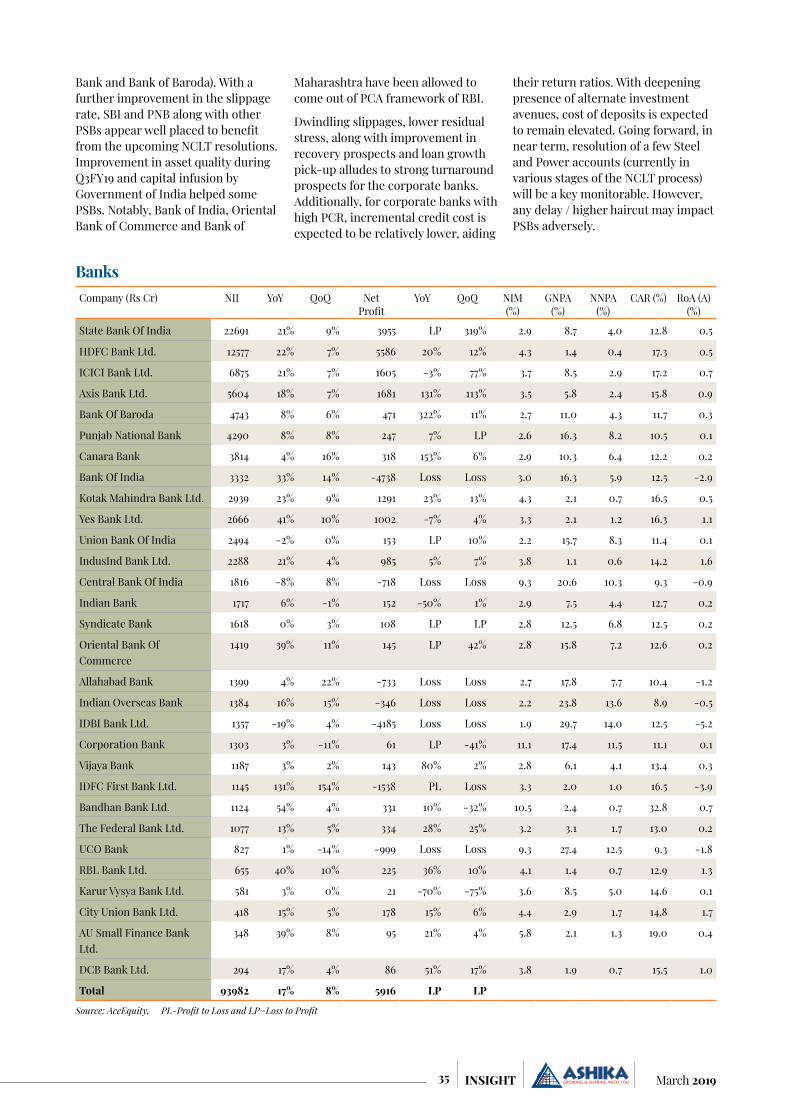

Indian market has to deal with volatility in times ahead as uncertainty prevails with respect to geo political tensions and elections due in April to May. Geopolitical tensions could escalate as India carried out pre-dawn air strikes on terror camps across the Line of Control on 26th February.

2March 2019 INSIGHT

Foreign Secretary, Vijay Gokhale stated that India is firmly and resolutely committed to taking all

measures to fight the menace of terrorism. This excercise was non-military, pre-emptive action was targeted specifically to eliminate terror training camp. The move by India was widely expected given the ghastly attack on Indian soldiers in Jammu and Kashmir’s Pulwama and chances of follow on attacks. The strong statements by Prime Minister, Modi was essentially to send a stern message which promised for strong steps to counter terrorism. Even US President stated that the relation between Indian and Pakistan has stooped to new lows and that a strong answer by India was understandable. Nevertheless, the attacks were not orchestrated to hurt Pakistan but to counter terrorism. India has received support from international partners who have condemned the grievous attacks. Pakistan has rejected India’s claims but promised of a befitting reply for crossing the Line of Control and retaliated by entering Indian airspace on 27th February 2019. Thus, things could remain tense but not expected to turn into war as Pakistan PM signal to resolve issue through talks while India also wants to avoid further escalation of situation. Experts feel the impact of the geopolitical tensions to be modest unless things take an ugly turn. Geopolitical tensions across the border although affects investor sentiments but in reality, have a neutral impact on the earnings and thus could throw out immense opportunities to invest in good businesses in case pessimism hits the roof.

Going by the way markets have behaved, there is still confidence that Narendra Modi will get a second term as Prime Minister of India. The consensus view being that the NDA government will be able to form government with the help of regional parties, however, will not be able to gain majority on its own like that of 2014. Experts believe that the cash transfer move for farmers is a little late and the farmer dissent for the last two to three years will result in

loss of seats in Hindi heartland. The inherent strength of the market could also be on account of an anticipation of a stable government. A stable government is indeed desirable from investor point of view since it provides with the opportunity to carry on with the reforms which drives growth. However, what market is not pricing in at this point of time is a third front kind of government. In India’s history, a third front government has only resulted in re-election in short span of time as different regional parties fail to reach a consensus on account of divergent ideologies and agenda. Thus, clearly markets would be spooked once that is a reality. However, this is too early to predict anything on elections as the early poll results are also about to change as are the sentiments. Besides, a number of regional parties together contributing 100-150 seats have still kept their options opened and could be the swing factor joining the coalition which is in a better position to form government. Going by the past, NDA has the skills to allure coalitions to stick and that process has already started and expected to pick up. However, the final swing could be noticed post announcement of results. In case

two coalitions, UPA and NDA runs neck to neck, this clutch of regional parties will eventually decide the fate. Needless to mention, Uttar Pradesh will be the deciding factor, however the equation remains complex and challenges daunting for BJP to succeed since this time SP and BSP have formed a pre-poll alliance. There are caste divides between SP & BSP party cadres, and this could either work for or against, but nevertheless this could have a diminishing effect on BJP’s vote share in the state. Last time, BJP bagged 73 of 80 seats which is not expected to be repeated. A glimpse of arch rivals forming alliance and succeeding is an example of alliance between RJD and Janata Dal (United) in 2015 Bihar assembly elections which was a success. However, barring the uncertainties, what investors anticipate is a stable government and market has been discounting the same but uncertainties over the outcome have limited upside. Thus, post elections markets will probably find ground and stocks would play on their own based on individual fundamentals.

Good quality stocks with strong fundamentals are often bought when market corrects however not due to earnings concern. The present geopolitical crisis even though heightens will only cast its shadow for medium term and will pass on and thus it makes sense to look at the earnings perspective because that will drive the share prices. For the recently concluded earning season for quarter ended December, there were challenges presented in terms of tight liquidity, high raw material prices, currency volatility and slowdown in government spending (as election draws near) apart from global trade issues. However, weak INR provided support to export oriented sectors as well as Pharm and IT in particular while volumes in consumption space remained strong. Q3FY19 provided with a contrasting picture as the growth was driven by the Banking, financial services and insurance (BFSI) sector as against non-BFSI sector in earlier quarters. Earnings revival in the banking space led by corporate

Good quality stocks with strong fundamentals are often bought when market corrects however not due to earnings concern. The present geopolitical crisis even though heightens will only cast its shadow for medium term and will pass on and thus it makes sense to look at the earnings perspective because that will drive the share prices.

3 March 2019INSIGHT

banks drove BFSI performance and the trend is expected to continue. This is fourth consecutive quarter where Sensex companies (ex-banking) have recorded double digit bottomline growth, amid robust consumer sentiment and peaking commodity prices. Sensex companies (ex-banking) reported a stellar operational performance in Q3FY19 primarily driven by robust consumer demand domestically and uptick in commodity prices thereby benefitting the oil & gas as well as metals space. Net sales in Q3FY19 were up 22% YoY. This coupled with 165 bps improvement in EBITDA margin to 20.1% led to 13% growth in operating profit. Gross margins declined 270 bps YoY. partly compensated by operating leverage benefits like lower employee as well as other expenses. Subsequently Net Profit in Q3FY19 (Ex Tata Motors) was up 17.8% YoY. Going ahead, impact of low commodity prices including crude oil along with stabilisation of rupee may support growth. However, there are significant headwinds as well apart from the geo political and political tensions in the likes of global growth slowdown, domestic liquidity, shift in government spending from capex to rural. Global slowdown will impact companies in the IT and metal space as well as auto exports while

tight domestic liquidity condition will continue to impact NBFCs and shift in government spending will be boon for consumption companies but will slowdown industrials and cement companies in the short term. However, clarity will emerge only after general elections.

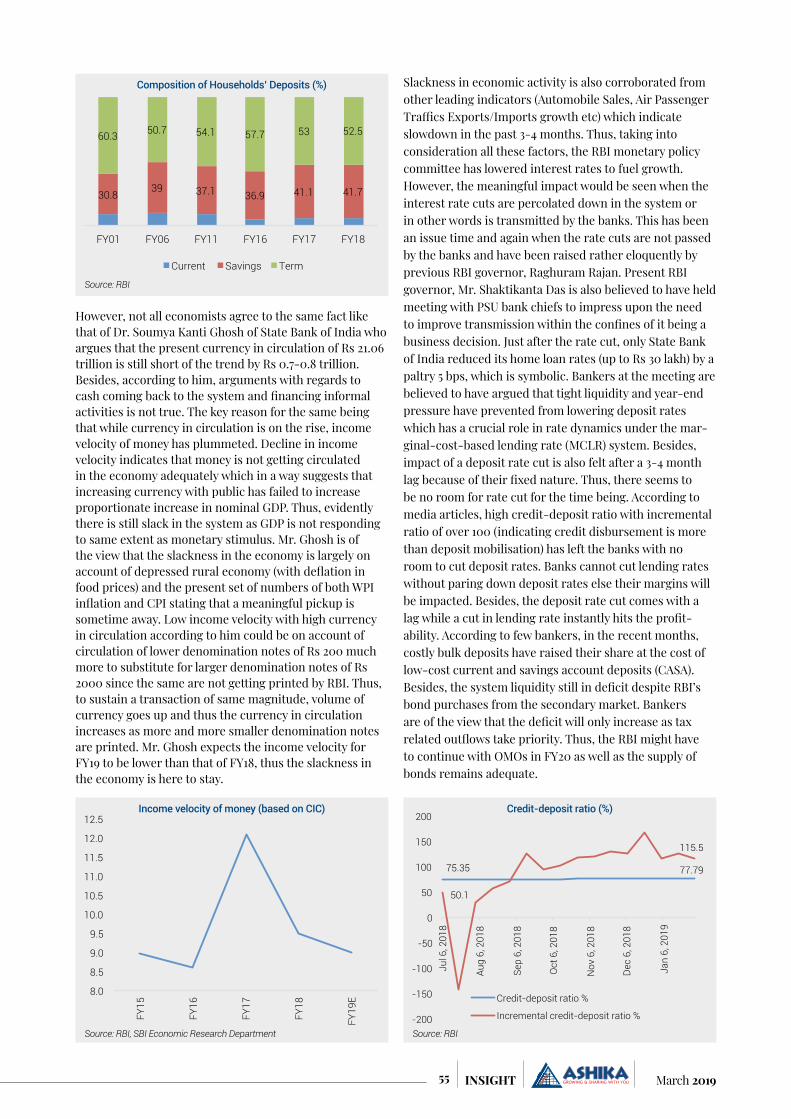

Recent economic indicators for Indian economy however suggest slackness in the economy which has also been highlighted by the RBI in its policy statement. Thus, the RBI in its latest policy lowered repo rates by 25 bps to give growth a chance. However, the key issue with the transmission of interest rates by banks still persists as incremental credit to deposit ratio of the banks is above 100% which suggests that unless deposit rates are lowered, the banks are unable to lower lending rates. Even if the deposit rates are lowered, it takes effect with a lag while the same on the lending rates is immediate which takes a toll on the margins, thus the banks and the RBI are not on the same page of passing on the rate cuts. Besides, the liquidity situation in India remains tight as currency in circulation is on a high. This has prompted RBI to conduct periodic open market operations (OMOs) however the systemic liquidity situation hasn’t improved

materially. Despite higher currency in circulation, the income velocity of money has lowered and is expected to stay low which again suggests slackness in economy. The recent set of data from automobile sales, business activity, online passenger traffic as well as exports suggest weakness. Consumption has been hurt as suggested in Q2FY19 GDP data as well and is not expected to have recovered. However, the inflationary pressures have remained subdued with the decline in food prices while the core inflation has been stubborn. The inflation estimates have actually been lower than RBI’s estimates as well and thus justifies the rate cut. However, going ahead, food prices would recover from low base besides the core inflation is expected to ease. Inflationary pressures could also be witnessed from higher fiscal deficit numbers which stands at 121.5% of the budgeted target for the period April to January. However, in an election year, this is understandable. Stability of Indian rupee is crucial and with the crude oil prices hovering ~USD65/barrel, current account deficit is not expected to breach dangerous levels. However, sustenance of foreign inflows is crucial which again depends on the global economic scenario and the view on global trade.

Paras BothraPresident - Equity ResearchEmail - [email protected]: 022 6611 1704 / 1786Mobile: 98203 97061

India needs fewer and mega banks which are strong because in

every sense, from bor-rowing rates to optimum utilisation, the economies of scale as far as banking sector is concerned are of great help - Arun Jaitley, Finance Minister

Inflation continues to come down on a global basis and provides the

cover for RBI to cut rates. However, in a period of fiscal expansion, cutting rates too aggressively will be adding fuel to the fire. That will lead to a higher price to be paid through inflation down the road. RBI better be very careful on this front - Krishna Memani, chief investment officer at Oppenheimer Funds

The major challenges for the future for the banking sector

remains ensuring inter-mediation by financial institutions is clean be it public sector banks, private sector or NBFC. How do we see that credit rating agencies also become far more accountable because their rating determines the flow of credit. It has impact on yields that’s another area - Rajiv Kumar, Financial Services Secretary

India and Russia are working to address and resolve trade

and investment issues to facilitate and increase private sector coopera-tion between the coun-tries - Suresh Prabhu, Commerce and Industry Minister

Indian equities are the best bet in the emerging market pack

at the moment, despite the nervousness ahead of the general elections and is bullish on technology and consumer-linked stocks in India - Mark Mobius, Founding Partner of Mobius Capital Partners

At the moment, we are not seeing strong inflows

into broad emerging markets although we have addressed the issue of large outflows which was the experience of 2018. I was saying earlier that coming into 2019, the EM positioning was over-weight India and what we are seeing is just a reallocation of the assets away from India towards markets like China, Brazil and Turkey where you are seeing stronger perfor-mance. What we might see is if EM continues to rise, you begin to see some inflows into broader EM funds, perhaps massive allocation by the global investors and then the FII net numbers might start to look a little bit better for India as it gets its share of the flow of capital into emerging markets - Adrian Mowat, EM - Equity Strategist

The risk is that the growing uncer-tainty about the

election outcome in India will lead to a slowdown in the inflows into domestic equity funds, which have been the main driver of the stock market since Modi was elected in May 2014. The latest data shows that such a decline is happening. This is clearly a growing risk in the short term, most particularly as many foreign investors will want to await the outcome of the pending elections - Christopher Wood, managing director and equity strategist at CLSA

Digital opportuni-ties and skills will pave the future of

the IT-BPM industry in India. Digitalisation ini-tiatives are at the core of business transformation and may be less impacted by somewhat lower growth in major econo-mies - Debjani Ghosh, President, Nasscom

Four clouds” or fac-tors undermining economic progress

– namely Brexit uncer-tainty, trade tensions and tariff escalations, global financial tightening and an accelerated slow-down in the Chinese economy. The risks posed by each cloud could create the “perfect economic storm”. We have big risks on the horizon and the clouds that we have signaled about [12 months ago] are getting darker by the day - Christine Lagarde, head of the International Monetary Fund

4March 2019 INSIGHT

PROMINENT HEADLINES FEBRUARY 2019

The country has climbed from seventh slot in

2017 to the third rank in 2018 in the world travel & tourism council’s power and performance index. the tourism sector alone has created nearly 14 million jobs across the country in the last four years alone - KJ Alphons, Union tourism minister

I think the (Indian economic) growth is still going to be higher

than China. We will probably see around 7 per cent, and that itself is a tremendous accomplish-ment. I know unemploy-ment is a real issue, and this is something that whoever comes to power in the next election, is going to have to address very forcefully. They will have to think how to make it work, and that means making it easier for foreign investors to come in - Mark Mobius, Founding Partner of Mobius Capital Partners

Historically, it has been seen that it (election) does

not have a long-standing impact on the markets. Most governments have been progressive and worked for development of the economy and as we go into the event, we think the construct of the Corporate India balance sheet will far outweigh the outcome of the elections - Kenneth Andrade, founder, Old Bridge Capital

The recent macro-economic tailwinds in India have been

especially compelling. Real GDP growth over the last two years has aver-aged 7%, the highest rate among the largest econ-omies in the world. This strong Indian economic performance is buoyed by a well-educated work-force and a pro-growth oriented government. Bold structural reforms, such as the implemen-tation of the GST, and the Insolvency and Bankruptcy Code, have improved governance standards and processes - Jonathan Gray, Presi-dent & COO Blackstone

Corporate debt is currently the leading bogeyman

among the international regulators. It is the thing that looks most likely, like sub-prime. Janet Yellen, the former chair of Fed-eral Reserve, spoke about it recently. The Bank of England released new data showing that it is double what we thought it was — $2.2 trillion, which also happens to be the same as the sub-prime debt - Kenneth Rogoff, professor of Economics at Harvard University

The recent trend of rolling out doles for the farm sector,

including the Union Budget’s basic income scheme, as a “disturbing trend” which will impact fiscal stability, growth and also Centre-state relations - Y V Reddy, former RBI Governor

No other large economy in the world is growing at over 7 per cent year after year, the fundamentals of our economy are sound. We are well set to become a 5 trillion-dollar economy in the near future. We are one of the most open countries for foreign direct investment today. More than 90 per cent of our sectors are now on automatic route for approval. As a result of this and the confidence in India, we have received FDI worth over USD 250 billion over the past four years - Narendra Modi, Prime Minister of India

India is its No.1 priority foreign investment destination and its companies are looking at becoming household names in the country with projects in oil refining, petrochemicals and fertilisers - Khalid Al-Falih, Saudi Oil Minister

5 March 2019INSIGHT

6March 2019 INSIGHT

Q: What is the mood amongst the investors given the geopolitical risks? How do you see the political landscape panning out and how should one position his portfolio considering so much of uncertainty?

A: Typically, investor behaviour swings like a pendulum from greed to fear and the other way. In the times of uncertainty, investors are generally fearful and are greedy during market buoyancy. History has shown us that the periods of uncertainty are generally the best times from investment perspective and building a portfolio. Point to point returns are

highest for the money invested at the peak of uncertainties.

Having said that, the best strategy for a retail investor is to do a periodic investment depending upon his cash flows which will average out / moderate out the impact mood swings of the investor.

So far as the political uncertainty is concerned, as per most experts and media reviews it seems the current NDA regime is expected to come back in power albeit with a lower mandate. Even if the outcome of election is otherwise, larger government policies and long term drivers of Indian

economy will be on a growth path, in our view.

From an Indian investor point of view, all the key risks (a) currency, (b) oil price and (c) interest rates had played out in 2018. 2019 has started on a much better macro backdrop. The Nifty valuations at 16.5x appear reasonable in the backdrop of FY18-20 earnings CAGR of 17%. We continue to stick to our bottom up stock picking strategy and see this as a good opportunity to invest in good quality names available at reasonable valuations.

Q: What’s your outlook on the markets in near-term considering that Budget sops and a rate cut by RBI which failed to lift the sentiments? Do you think there are further rate cuts in the offing?

A: While, the budget seems positive for the consumption sector and rate cuts is positive, normalization of liquidity situation for NBFCs, outcome of US-China trade talks and upcoming general elections, seem to be on top of the investor mind and could influence the markets in near term.

Interest rates are determined by various factors which include (1) inflation and its expectations, (2) fiscal deficit/government borrowings and (3) rate differential versus other economies. While the 2 (inflation and US Fed stance) of these 3 factors are favourable for interest rate cuts, government may struggle to meet its FY20 fiscal deficit which will act as a counter measure to rate cut.

Q: There are increasing chances of a global slowdown unless a truce is arrived at between US & China soon. How much it would impact the Indian markets and sentiments in case of a prolonged delay?

A: The outcome of the truce between US and China is un-determined at this stage. However, based on various news flow it seems the truce may get extended and the imposition of incremental duties may get delayed. Having said that, IMF has projected a slowdown of the global GDP growth rates for the coming year.

Mr. Neelesh Surana - Chief Investment Officer - Mirae Asset Global Investments (India) Private Limited

Q&A WITH CIO

7 March 2019INSIGHT

India’s EXIM trade (exports + imports) is ~30% of its GDP, hence, any meaningful slowdown or prolonged delayed growth will have some impact on the Indian economy. However, India being a largely a domestic oriented economy, any impact would be sector specific and even lesser from the investible universe point of view.

Q: How do see the rupee to play out given the outlook of crude oil prices?

A: The key influencers for rupee movement include crude price (through CAD), external fund flows and relative interest rates.

Given the long-term inflation differential between India and US, rupee is expected to depreciate 3-5% per annum to neutralize the interest rate differential between both the countries.

However, rupee does not depreciate secularly on a yearly basis, but it depreciates sharply by 15%-18% in a block of 4-5 years, as seen in its last 15 years history. Given, ~80% dependence of Indian economy on energy imports and consistent trade deficits, the same patterns should follow in the foreseeable future.

Q: How do you decode the December quarter corporate earnings and your expectations for FY20 & FY21?

A: The aggregate 3QFY19 Revenue/EBITDA/PAT (adjusted for one-off gains/impairments) growth for Nifty is at 23%/5%/10% YoY. At the sector level, Industrials, Healthcare, Financials (private corporate lenders) and Energy delivered earnings beat, while Materials, Utilities, and Autos (ex M&M) disappointed.

Corporate Banks showed a material sequential improvement in the slippage/asset quality trends. This coupled with return of credit growth augurs well for their earnings growth. This provides good visibility on the earnings outlook, as Corporate Banks were one of the key drivers for the earnings miss over the past few years.

As against higher single digit growth in FY19, FY20 consensus Nifty earnings are expected to grow at >25%. The earnings growth for FY20 over FY19 is meaningful and led by financials, Oil & Gas, IT and to some extent auto sector.

Q: Which are the sectors do you think would perform well in upcoming years? Also what is your take on consumer business given such high multiples?

A: The India corporate earnings are on a normalization path post the demonetization and GST disruptions. Over the next 3 years earnings momentum is expected to pick up led by (a) 12-15% nominal GDP growth, (b) NPA provisioning largely done, (c) likely pickup in private capex as industrial utilization nearing 78-80% in 2019/2020 and (d) national elections will be behind us.

We are currently positive on private banks, pharma and consumer sector from the medium-term perspective.

Consumer companies were significantly re-rated post 2008 global financial crisis because of their strong free cash generation capability, higher RoCE and stable growth. While the consumer businesses have rerated in the past, many of the richly valued stocks have corrected in the recent past. We keep evaluating such businesses and make our investment decisions based on appropriate entry points. At Mirae Asset, while building the portfolio, we follow bottom-up approach our stock selection philosophy is guided by growth at reasonable price (GARP).

Q: Do you think the crisis with the NBFCs is over or something bigger is in the offing?

A: The liquidity crisis which started with IL&FS issue while not fully resolved is on a normalization path. With the intervention by RBI and the government, we expect the normalization in the liquidity situation sooner than later.

For NBFC’s, while the funding costs on an average has increased, the NBFCs with strong parentage, good track record and balance sheet are still able to raise funds with relative ease.

Nevertheless, the near-term loan growth could be moderated for some NBFCs. On the margin front, NBFCs operating in niche segments, with ability to pass on the higher interest rates would be able to protect their spreads.

Q: Post correction, is it the right time to get in quality midcaps?

A: The valuation differential between midcaps and large caps have significantly corrected from its peak in December 2017 at a headline level.

The bottom up opportunities are clearly emerging in the midcap segment, however subject to valuation, we continue to be selective and invest in companies where earnings visibility is good and balance sheet/cash flow characteristics are not questionable.

Q: How do investors cope with corporate governance issues even in big names? Any sector specific risk you perceive or any underweight themes you want to highlight in current the market scenario?

A: Corporate governance is a very major issue across all geographies. While there are checks and balances like audit committee, auditors, rating agencies, regulators and whistle blower policies among others put in place in the system to counter the corporate governance issues, but they have not been 100% full proof. While the systematic improvement has taken care of this issue to a large extent over the time period and will only improve from here. In the interim, portfolio diversification is the only way for the investors to counter such issues.

On the sector specific issue, we have been underweight on sectors like public sector banks, infra space and telecom.

* View of Mr. Neelesh Surana (CIO - Mirae AMC) ably assisted by Mr. Harshad Borawake (Head – Research - Mirae Asset & Co-Manager of Mirae Asset India Equity Fund)

8March 2019 INSIGHT

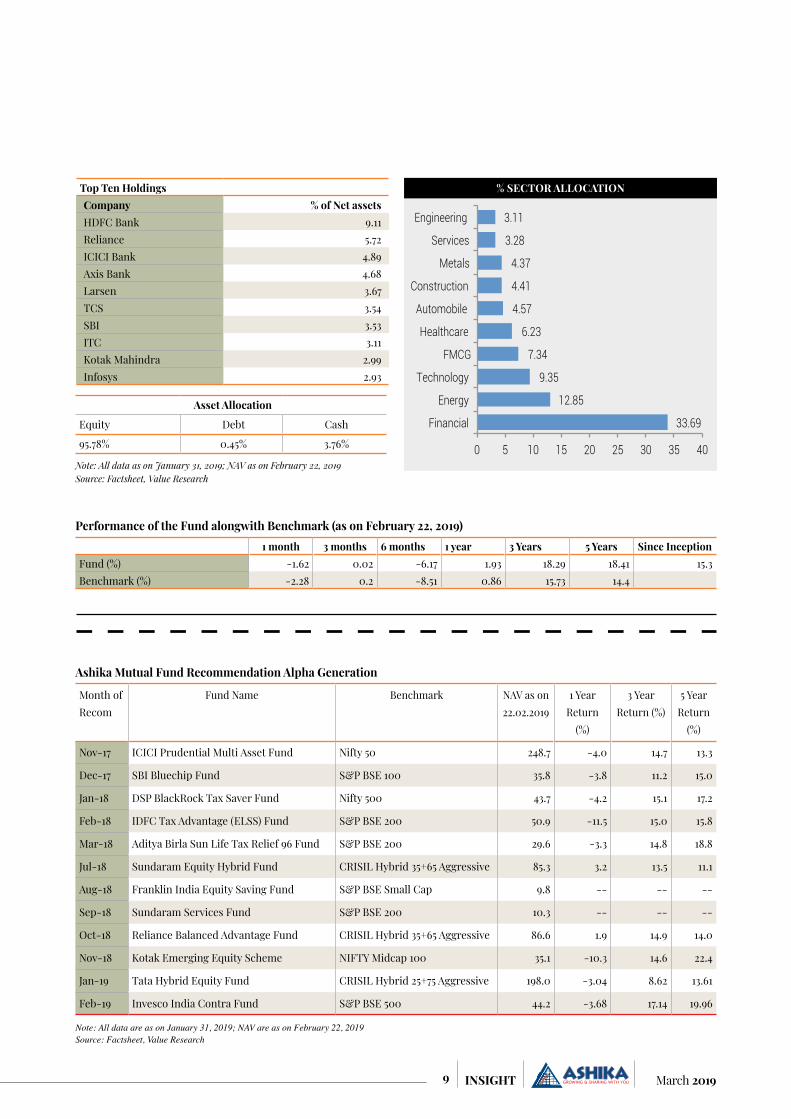

Mutual Fund Overview MIRAE ASSET INDIA EQUITY FUND

Investment ObjectiveThe investment objective of the scheme is to generate long term capital appreciation by capitalizing on potential investment opportunities through predominantly invest-ing in equities, equity related securities. The Scheme does not guarantee or assure any returns. Suitable for investors who are seeking Multicap Investing.

Investment StrategyMirae Asset India Equity Fund is a multicap fund which follows the below strategy:

Investment approach is centered around participating in high quality business upto a reasonable price and holding the same over an extended period of time Has flexibility to invest across sectors, themes & market

caps. Aims to combine consistency of largecaps with

conviction ideas from midcaps. Focuses on companies with sustainable competitive

advantage- Stocks which have strong pricing power and are sector leaders.

Its strategy is based on fundamental bottom-up analysis and results in a well-diversified portfolio, with no sector, stock, theme, or style being disproportionate. Alpha generation is driven mainly by superior stock selection and not sector rotation. The fund’s process combines qualitative parameters and rigourous company analysis with quantitative parameters. The investment philosophy of the fund is built on three core principles: quality businesses with stable earnings, strong management, and attractive valuation.

Note: All data as on January 31, 2019; NAV as on February 22, 2019Source: Factsheet, Value Research

Important InformationNAV (G) (Rs.) 47.25NAV (D) (Rs.) 16.77Inception Date April 4, 2008Fund size (in Rs cr) 10,343.4Fund Manager Neelesh Surana, Harshad Borawake &

Gaurav MisraEntry load N.AExit Load 1% for redemption within 365 daysBenchmark NIFTY 200 TRIMin Investment Rs.5000Min SIP Investment Rs.1000

Key RatiosBeta 0.96Standard deviation (%) 14.42Sharpe Ratio 0.69Alpha 2.37R Squared 0.97Expense ratio (%) 2.05Portfolio Turnover ratio (%) 53.00Avg Market cap (Rs in cr) 129,741

Fund Features

Consistency of Performance**

Dual Strategy Of Core and Tactical allocation^Capitalize on Long & ShortTerm Opportunities

Risk mitigation to reduce volatility and improve liquidity

RiskMitigation

InvestmentProcess

ActiveManagement

(Core & Tactical)

PortfolioPsychographic

Benchmark

StockSelection

(Bottom-upApproach)

Flexibility to invest across sectors,themes, styles and market caps.

Focused on Good Businesses

9 March 2019INSIGHT

Month of Recom

Fund Name Benchmark NAV as on 22.02.2019

1 Year Return

(%)

3 Year Return (%)

5 Year Return

(%)

Nov-17 ICICI Prudential Multi Asset Fund Nifty 50 248.7 -4.0 14.7 13.3

Dec-17 SBI Bluechip Fund S&P BSE 100 35.8 -3.8 11.2 15.0

Jan-18 DSP BlackRock Tax Saver Fund Nifty 500 43.7 -4.2 15.1 17.2

Feb-18 IDFC Tax Advantage (ELSS) Fund S&P BSE 200 50.9 -11.5 15.0 15.8

Mar-18 Aditya Birla Sun Life Tax Relief 96 Fund S&P BSE 200 29.6 -3.3 14.8 18.8

Jul-18 Sundaram Equity Hybrid Fund CRISIL Hybrid 35+65 Aggressive 85.3 3.2 13.5 11.1

Aug-18 Franklin India Equity Saving Fund S&P BSE Small Cap 9.8 -- -- --

Sep-18 Sundaram Services Fund S&P BSE 200 10.3 -- -- --

Oct-18 Reliance Balanced Advantage Fund CRISIL Hybrid 35+65 Aggressive 86.6 1.9 14.9 14.0

Nov-18 Kotak Emerging Equity Scheme NIFTY Midcap 100 35.1 -10.3 14.6 22.4

Jan-19 Tata Hybrid Equity Fund CRISIL Hybrid 25+75 Aggressive 198.0 -3.04 8.62 13.61

Feb-19 Invesco India Contra Fund S&P BSE 500 44.2 -3.68 17.14 19.96

Ashika Mutual Fund Recommendation Alpha Generation

1 month 3 months 6 months 1 year 3 Years 5 Years Since InceptionFund (%) -1.62 0.02 -6.17 1.93 18.29 18.41 15.3Benchmark (%) -2.28 0.2 -8.51 0.86 15.73 14.4

Performance of the Fund alongwith Benchmark (as on February 22, 2019)

Asset Allocation

Equity Debt Cash

95.78% 0.45% 3.76%

33.69

12.85

9.35

7.34

6.23

4.57

4.41

4.37

3.28

3.11

0 5 10 15 20 25 30 35 40

Financial

Energy

Technology

FMCG

Healthcare

Automobile

Construction

Metals

Services

Engineering

% SECTOR ALLOCATION Top Ten HoldingsCompany % of Net assetsHDFC Bank 9.11Reliance 5.72ICICI Bank 4.89Axis Bank 4.68Larsen 3.67TCS 3.54SBI 3.53ITC 3.11Kotak Mahindra 2.99Infosys 2.93

Note: All data as on January 31, 2019; NAV as on February 22, 2019Source: Factsheet, Value Research

Note: All data are as on January 31, 2019; NAV are as on February 22, 2019Source: Factsheet, Value Research

10March 2019 INSIGHT

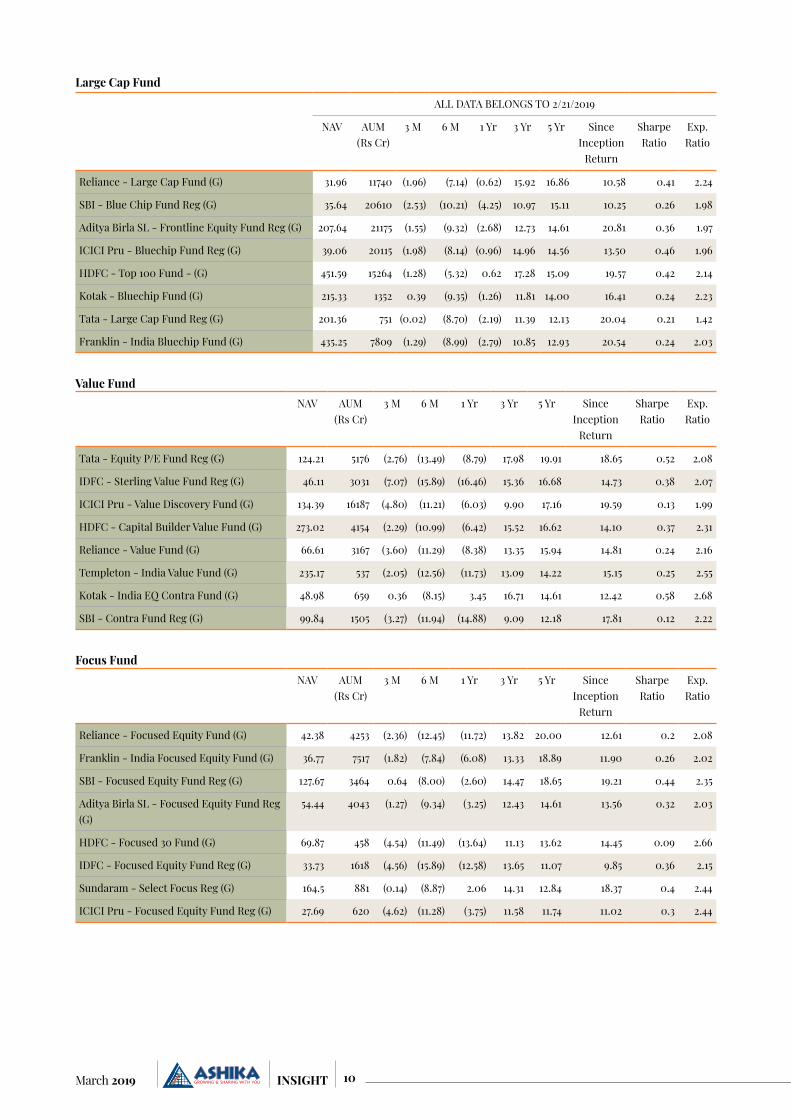

NAV AUM (Rs Cr)

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

Reliance - Focused Equity Fund (G) 42.38 4253 (2.36) (12.45) (11.72) 13.82 20.00 12.61 0.2 2.08

Franklin - India Focused Equity Fund (G) 36.77 7517 (1.82) (7.84) (6.08) 13.33 18.89 11.90 0.26 2.02

SBI - Focused Equity Fund Reg (G) 127.67 3464 0.64 (8.00) (2.60) 14.47 18.65 19.21 0.44 2.35

Aditya Birla SL - Focused Equity Fund Reg (G)

54.44 4043 (1.27) (9.34) (3.25) 12.43 14.61 13.56 0.32 2.03

HDFC - Focused 30 Fund (G) 69.87 458 (4.54) (11.49) (13.64) 11.13 13.62 14.45 0.09 2.66

IDFC - Focused Equity Fund Reg (G) 33.73 1618 (4.56) (15.89) (12.58) 13.65 11.07 9.85 0.36 2.15

Sundaram - Select Focus Reg (G) 164.5 881 (0.14) (8.87) 2.06 14.31 12.84 18.37 0.4 2.44

ICICI Pru - Focused Equity Fund Reg (G) 27.69 620 (4.62) (11.28) (3.75) 11.58 11.74 11.02 0.3 2.44

Focus Fund

NAV AUM (Rs Cr)

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

Tata - Equity P/E Fund Reg (G) 124.21 5176 (2.76) (13.49) (8.79) 17.98 19.91 18.65 0.52 2.08

IDFC - Sterling Value Fund Reg (G) 46.11 3031 (7.07) (15.89) (16.46) 15.36 16.68 14.73 0.38 2.07

ICICI Pru - Value Discovery Fund (G) 134.39 16187 (4.80) (11.21) (6.03) 9.90 17.16 19.59 0.13 1.99

HDFC - Capital Builder Value Fund (G) 273.02 4154 (2.29) (10.99) (6.42) 15.52 16.62 14.10 0.37 2.31

Reliance - Value Fund (G) 66.61 3167 (3.60) (11.29) (8.38) 13.35 15.94 14.81 0.24 2.16

Templeton - India Value Fund (G) 235.17 537 (2.05) (12.56) (11.73) 13.09 14.22 15.15 0.25 2.55

Kotak - India EQ Contra Fund (G) 48.98 659 0.36 (8.15) 3.45 16.71 14.61 12.42 0.58 2.68

SBI - Contra Fund Reg (G) 99.84 1505 (3.27) (11.94) (14.88) 9.09 12.18 17.81 0.12 2.22

Value Fund

ALL DATA BELONGS TO 2/21/2019

NAV AUM (Rs Cr)

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

Reliance - Large Cap Fund (G) 31.96 11740 (1.96) (7.14) (0.62) 15.92 16.86 10.58 0.41 2.24

SBI - Blue Chip Fund Reg (G) 35.64 20610 (2.53) (10.21) (4.25) 10.97 15.11 10.25 0.26 1.98

Aditya Birla SL - Frontline Equity Fund Reg (G) 207.64 21175 (1.55) (9.32) (2.68) 12.73 14.61 20.81 0.36 1.97

ICICI Pru - Bluechip Fund Reg (G) 39.06 20115 (1.98) (8.14) (0.96) 14.96 14.56 13.50 0.46 1.96

HDFC - Top 100 Fund - (G) 451.59 15264 (1.28) (5.32) 0.62 17.28 15.09 19.57 0.42 2.14

Kotak - Bluechip Fund (G) 215.33 1352 0.39 (9.35) (1.26) 11.81 14.00 16.41 0.24 2.23

Tata - Large Cap Fund Reg (G) 201.36 751 (0.02) (8.70) (2.19) 11.39 12.13 20.04 0.21 1.42

Franklin - India Bluechip Fund (G) 435.25 7809 (1.29) (8.99) (2.79) 10.85 12.93 20.54 0.24 2.03

Large Cap Fund

11 March 2019INSIGHT

NAV AUM (Rs Cr)

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

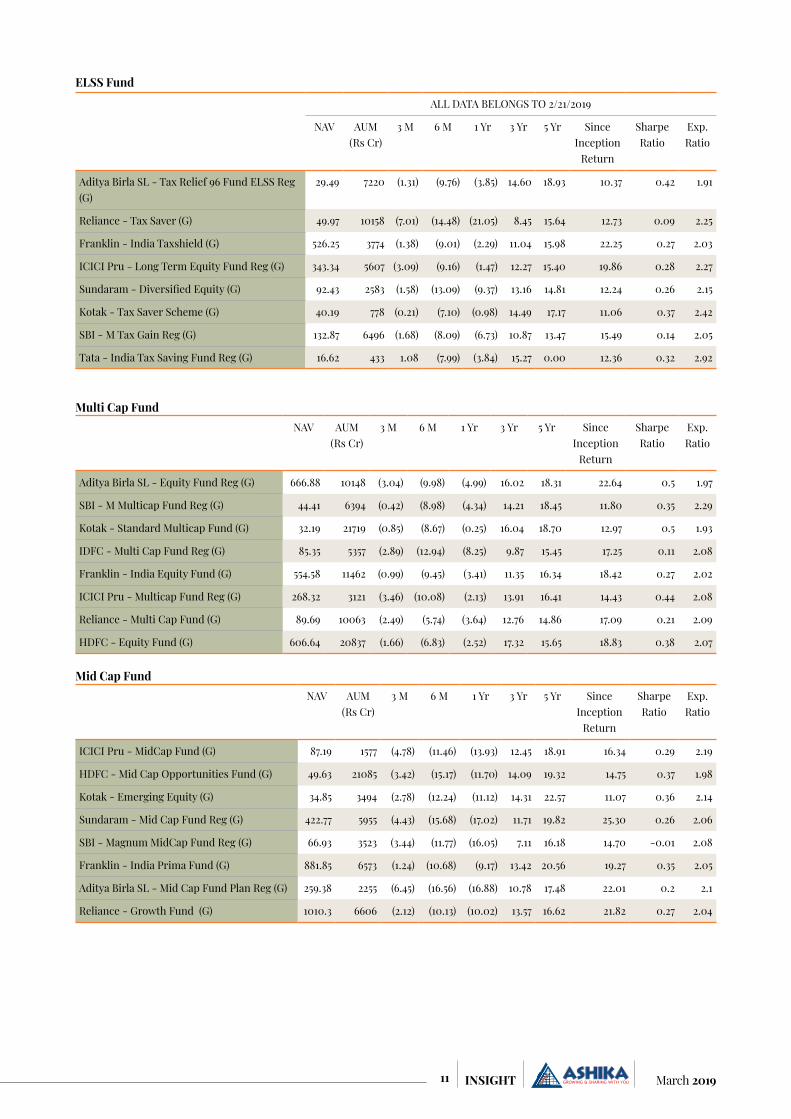

Aditya Birla SL - Equity Fund Reg (G) 666.88 10148 (3.04) (9.98) (4.99) 16.02 18.31 22.64 0.5 1.97

SBI - M Multicap Fund Reg (G) 44.41 6394 (0.42) (8.98) (4.34) 14.21 18.45 11.80 0.35 2.29

Kotak - Standard Multicap Fund (G) 32.19 21719 (0.85) (8.67) (0.25) 16.04 18.70 12.97 0.5 1.93

IDFC - Multi Cap Fund Reg (G) 85.35 5357 (2.89) (12.94) (8.25) 9.87 15.45 17.25 0.11 2.08

Franklin - India Equity Fund (G) 554.58 11462 (0.99) (9.45) (3.41) 11.35 16.34 18.42 0.27 2.02

ICICI Pru - Multicap Fund Reg (G) 268.32 3121 (3.46) (10.08) (2.13) 13.91 16.41 14.43 0.44 2.08

Reliance - Multi Cap Fund (G) 89.69 10063 (2.49) (5.74) (3.64) 12.76 14.86 17.09 0.21 2.09

HDFC - Equity Fund (G) 606.64 20837 (1.66) (6.83) (2.52) 17.32 15.65 18.83 0.38 2.07

Multi Cap Fund

NAV AUM (Rs Cr)

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

ICICI Pru - MidCap Fund (G) 87.19 1577 (4.78) (11.46) (13.93) 12.45 18.91 16.34 0.29 2.19

HDFC - Mid Cap Opportunities Fund (G) 49.63 21085 (3.42) (15.17) (11.70) 14.09 19.32 14.75 0.37 1.98

Kotak - Emerging Equity (G) 34.85 3494 (2.78) (12.24) (11.12) 14.31 22.57 11.07 0.36 2.14

Sundaram - Mid Cap Fund Reg (G) 422.77 5955 (4.43) (15.68) (17.02) 11.71 19.82 25.30 0.26 2.06

SBI - Magnum MidCap Fund Reg (G) 66.93 3523 (3.44) (11.77) (16.05) 7.11 16.18 14.70 -0.01 2.08

Franklin - India Prima Fund (G) 881.85 6573 (1.24) (10.68) (9.17) 13.42 20.56 19.27 0.35 2.05

Aditya Birla SL - Mid Cap Fund Plan Reg (G) 259.38 2255 (6.45) (16.56) (16.88) 10.78 17.48 22.01 0.2 2.1

Reliance - Growth Fund (G) 1010.3 6606 (2.12) (10.13) (10.02) 13.57 16.62 21.82 0.27 2.04

Mid Cap Fund

ALL DATA BELONGS TO 2/21/2019

NAV AUM (Rs Cr)

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

Aditya Birla SL - Tax Relief 96 Fund ELSS Reg (G)

29.49 7220 (1.31) (9.76) (3.85) 14.60 18.93 10.37 0.42 1.91

Reliance - Tax Saver (G) 49.97 10158 (7.01) (14.48) (21.05) 8.45 15.64 12.73 0.09 2.25

Franklin - India Taxshield (G) 526.25 3774 (1.38) (9.01) (2.29) 11.04 15.98 22.25 0.27 2.03

ICICI Pru - Long Term Equity Fund Reg (G) 343.34 5607 (3.09) (9.16) (1.47) 12.27 15.40 19.86 0.28 2.27

Sundaram - Diversified Equity (G) 92.43 2583 (1.58) (13.09) (9.37) 13.16 14.81 12.24 0.26 2.15

Kotak - Tax Saver Scheme (G) 40.19 778 (0.21) (7.10) (0.98) 14.49 17.17 11.06 0.37 2.42

SBI - M Tax Gain Reg (G) 132.87 6496 (1.68) (8.09) (6.73) 10.87 13.47 15.49 0.14 2.05

Tata - India Tax Saving Fund Reg (G) 16.62 433 1.08 (7.99) (3.84) 15.27 0.00 12.36 0.32 2.92

ELSS Fund

12March 2019 INSIGHT

ALL DATA BELONGS TO 2/21/2019

NAV AUM (Rs Cr)

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

Reliance - Small Cap Fund (G) 35.99 7461 (8.71) (17.63) (20.46) 16.17 24.99 16.27 0.38 2.3

SBI - Small Cap Fund Reg (G) 47.22 1438 (4.45) (14.54) (19.35) 16.16 27.90 17.84 0.41 2.49

Franklin - India Smaller Companies Fund (G)

49 6983 (5.25) (15.42) (18.19) 11.34 20.75 12.88 0.24 2.02

Sundaram - Small Cap Fund Reg (G) 72.55 1088 (6.39) (18.29) (29.95) 7.05 19.50 15.18 -0.02 2.33

Aditya Birla SL - Small Cap Fund Reg (G) 30.55 2232 (8.83) (20.88) (26.40) 11.22 17.87 9.98 0.26 2.06

HDFC - Small Cap Fund (G) 39.82 6013 (4.77) (11.35) (12.12) 19.74 19.32 13.55 0.56 2.16

Kotak - Smallcap Fund (G) 64.21 1067 (5.10) (14.54) (17.79) 10.99 18.67 14.21 0.22 2.34

ICICI Pru - Smallcap Fund Reg (G) 21.59 176 (6.42) (17.06) (25.58) 6.71 10.95 7.01 0.04 2.61

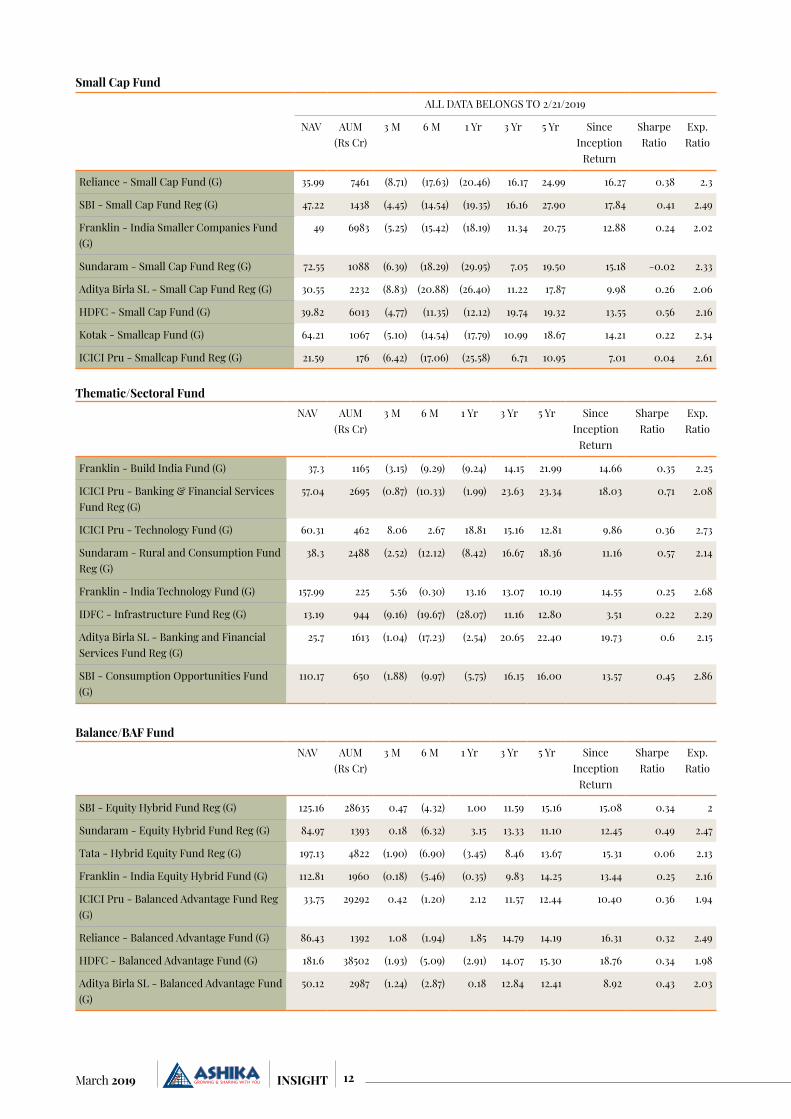

Small Cap Fund

NAV AUM (Rs Cr)

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

Franklin - Build India Fund (G) 37.3 1165 (3.15) (9.29) (9.24) 14.15 21.99 14.66 0.35 2.25

ICICI Pru - Banking & Financial Services Fund Reg (G)

57.04 2695 (0.87) (10.33) (1.99) 23.63 23.34 18.03 0.71 2.08

ICICI Pru - Technology Fund (G) 60.31 462 8.06 2.67 18.81 15.16 12.81 9.86 0.36 2.73

Sundaram - Rural and Consumption Fund Reg (G)

38.3 2488 (2.52) (12.12) (8.42) 16.67 18.36 11.16 0.57 2.14

Franklin - India Technology Fund (G) 157.99 225 5.56 (0.30) 13.16 13.07 10.19 14.55 0.25 2.68

IDFC - Infrastructure Fund Reg (G) 13.19 944 (9.16) (19.67) (28.07) 11.16 12.80 3.51 0.22 2.29

Aditya Birla SL - Banking and Financial Services Fund Reg (G)

25.7 1613 (1.04) (17.23) (2.54) 20.65 22.40 19.73 0.6 2.15

SBI - Consumption Opportunities Fund (G)

110.17 650 (1.88) (9.97) (5.75) 16.15 16.00 13.57 0.45 2.86

Thematic/Sectoral Fund

NAV AUM (Rs Cr)

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

SBI - Equity Hybrid Fund Reg (G) 125.16 28635 0.47 (4.32) 1.00 11.59 15.16 15.08 0.34 2

Sundaram - Equity Hybrid Fund Reg (G) 84.97 1393 0.18 (6.32) 3.15 13.33 11.10 12.45 0.49 2.47

Tata - Hybrid Equity Fund Reg (G) 197.13 4822 (1.90) (6.90) (3.45) 8.46 13.67 15.31 0.06 2.13

Franklin - India Equity Hybrid Fund (G) 112.81 1960 (0.18) (5.46) (0.35) 9.83 14.25 13.44 0.25 2.16

ICICI Pru - Balanced Advantage Fund Reg (G)

33.75 29292 0.42 (1.20) 2.12 11.57 12.44 10.40 0.36 1.94

Reliance - Balanced Advantage Fund (G) 86.43 1392 1.08 (1.94) 1.85 14.79 14.19 16.31 0.32 2.49

HDFC - Balanced Advantage Fund (G) 181.6 38502 (1.93) (5.09) (2.91) 14.07 15.30 18.76 0.34 1.98

Aditya Birla SL - Balanced Advantage Fund (G)

50.12 2987 (1.24) (2.87) 0.18 12.84 12.41 8.92 0.43 2.03

Balance/BAF Fund

13 March 2019INSIGHT

ALL DATA BELONGS TO 2/21/2019

NAV AUM (Rs Cr)

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

Aditya Birla SL - Equity Savings Fund Reg (G)

12.76 1281 (1.39) (0.47) (5.34) 3.12 8.05 5.86 0.16 2.19

HDFC - Equity Savings Fund (G) 35.21 6499 (1.21) (0.21) (1.33) 5.41 11.75 9.13 0.57 1.94

ICICI Pru - Equity Savings Fund (G) 13.26 2044 (0.45) 0.61 1.30 5.29 9.81 6.99 0.39 1.34

Kotak - Equity Savings Fund Reg (G) 13.79 2287 (0.44) 0.94 (0.66) 7.09 8.64 7.52 0.42 2.18

Reliance - Equity Savings Fund Reg (G) 12.28 2265 (1.81) (1.23) (4.64) 4.55 8.00 5.65 0.06 2.03

SBI - Equity Savings Fund Reg (G) 12.46 2336 (0.42) 0.58 (2.76) 4.64 7.41 5.99 0.04 2.02

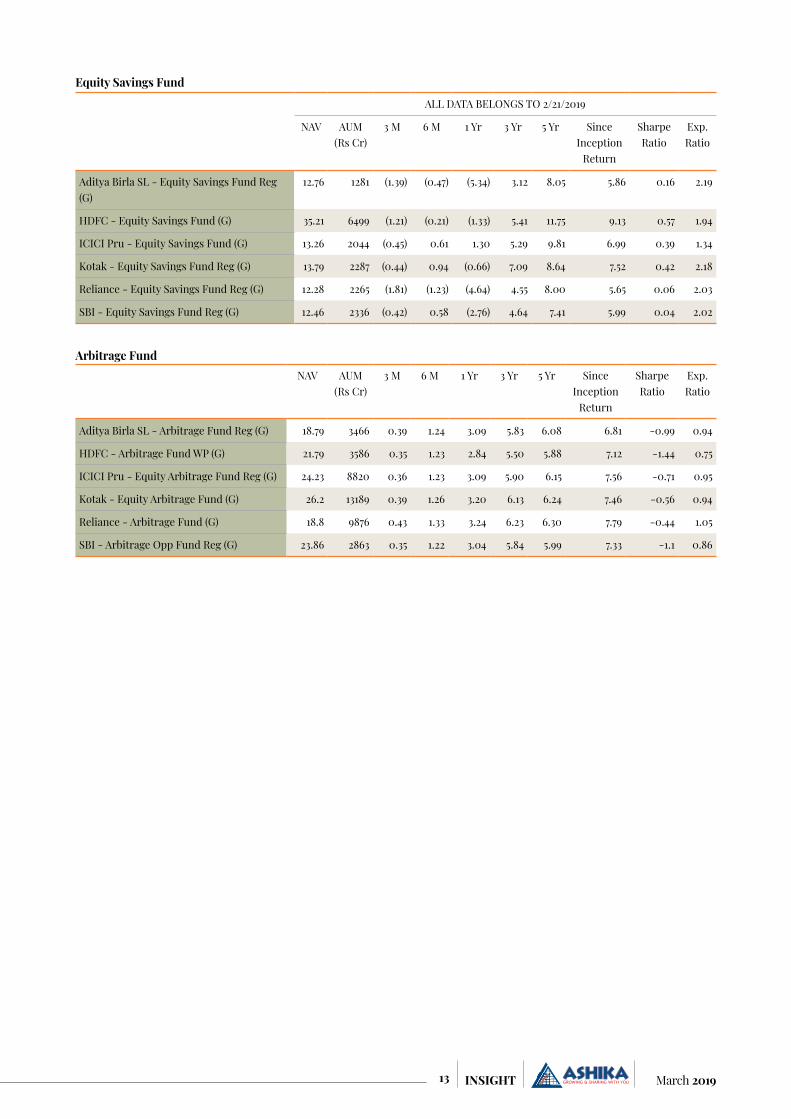

Equity Savings Fund

NAV AUM (Rs Cr)

3 M 6 M 1 Yr 3 Yr 5 Yr Since Inception

Return

Sharpe Ratio

Exp. Ratio

Aditya Birla SL - Arbitrage Fund Reg (G) 18.79 3466 0.39 1.24 3.09 5.83 6.08 6.81 -0.99 0.94

HDFC - Arbitrage Fund WP (G) 21.79 3586 0.35 1.23 2.84 5.50 5.88 7.12 -1.44 0.75

ICICI Pru - Equity Arbitrage Fund Reg (G) 24.23 8820 0.36 1.23 3.09 5.90 6.15 7.56 -0.71 0.95

Kotak - Equity Arbitrage Fund (G) 26.2 13189 0.39 1.26 3.20 6.13 6.24 7.46 -0.56 0.94

Reliance - Arbitrage Fund (G) 18.8 9876 0.43 1.33 3.24 6.23 6.30 7.79 -0.44 1.05

SBI - Arbitrage Opp Fund Reg (G) 23.86 2863 0.35 1.22 3.04 5.84 5.99 7.33 -1.1 0.86

Arbitrage Fund

14March 2019 INSIGHT

CMP: Rs 275 Rating: BUY Target: Rs 319

Investment RationaleCigarette Business, still the key revenue driverThe $11 billion cigarette market in India is dominated by 3 key players with ITC being the market leader and has been put under extremely stringent tobacco control regulations. Despite an extremely challenging

operating environment, the company consolidated its leadership position in the industry through innovative and varied consumer preferences. Some of the key recent initiatives include the launch of innovative variants viz., Classic’ Rich & Smooth (triple segment filter with superior filtration), Classic Verve low smell

(demi slim format), `Hollywood’ (triple segment filter) and `Flake’ Taste Pro (dual segment filter). The company’s cigarette segment witnessed volume growth of around 8% in Q3FY19 led by 64mm while the 69mm segment contributed 38-39% of cigarette sales volume and remaining ~20% was contributed by Long &

Company InformationBSE Code 500875NSE Code ITCBloomberg Code ITC INISIN INE154A01025Market Cap (Rs. Cr) 338,899.40Outstanding shares (Cr) 1,224.7052-wk Hi/Lo (Rs.) 322.7/251.3Avg. daily volume (1yr. on NSE) 11,244,750Face Value (Rs.) 1Book Value (Rs) 43.7

FII 17.1%

Others 44.9%

DII 38.1%

Shareholding pattern as of December 2018

STOCK PICKS

ITC Ltd.

15 March 2019INSIGHT

King size segments. Volume growth is back after stable pricing environment and recovered strongly from negative base (-5% in Q3FY18). Going ahead, stability in GST rates remains the key factor for sustenance of demand in the cigarette business. Cigarette EBIT margin in Q3FY19 was however impacted on account of higher cost of leaf tobacco crop and an increase in capsule cigarettes in the overall mix. Nevertheless, cigarette business remains as the highest contributor to revenues as well as operating profit (EBIT) with contribution of 42% and 84% respectively.

FMCG business-on strong growth trajectoryIn order to reduce its dependence on the highly taxed cigarette business and to diversify, it has steadily built a strong FMCG business franchisee which now contributes ~26% of revenues. The company expects that next leg of growth will come from this segment and has set an ambitious target to achieve Rs 1 lakh crore business in FMCG vertical by 2030. The FMCG business has been growing at a CAGR of 10% for the last five years. In a very short span of time ITC’s products have assumed market leadership – Aashirvaad is No. 1 in Branded Atta, Sunfeast is No. 1 in Premium Cream Biscuits, Bingo is No. 1 in the Bridges segment of Snack Foods. Other ITC brands are

also gaining significant consumer franchise. YiPPee being No. 2 in Noodles, Engage- No. 2 in Deodorants and Mangaldeep is No. 2 in Agarbattis and No. 1 in the Dhoop Segment. From being loss making at EBIT level as of FY13, FMCG business has slowly and gradually gained traction and presently contributes ~1.8% of consolidated EBIT. To make digital presence felt, ITC would start its own e-commerce operation for premium and niche products. The online store will complement its efforts to sell through online channel partners and marketplaces. ITC has also launched an e-store and an app for stationary products. The

company has continuously made investments in the FMCG business leveraging strong cashflows from cigarette business and intends to make fresh investment of Rs 1700 crore in West Bengal which would include a personal care products manufacturing line. The company will also expand its Dhulagarh facility and milk productivity improvement and procurement programme in the state. Hence with stabilizing trade channels and improving rural demand amid government effort to boost farm income, it can be expected that company’s non-cigarette business to deliver strong performance in coming years.

Other businesses to support margin expansionApart from cigarette and FMCG, the other significant mark for the company is in the Paperboards, Paper and Packaging and hotel businesses. In the paper business, ITC has emerged as a strong household name with ‘classmate’ brand (No. 1 in Notebooks) and packaging business is driven by FMCG, liquor and legal cigarette industry. In FY18, the business was hit due to GST implementation thus resulting in 2% decline in revenues, however it has turned around and posted growth of 9% in FY19 so far. It has a steady state contribution of ~6% to the consolidated EBIT and has continued this trend for last few years. Steady prices and benign input costs is expected to support margin expansion in paper & packaging business. Hotel business for ITC is a profitable one with revenue growth in the range of 5-6% annually for the last five years. Although, small, accounting for ~2-3% of consolidated revenue and EBIT contribution of ~1%, the hotel business is profitable with EBIT margins ~10% and has scope of expansion driven by improvement of around 4-5% in average room rate (ARR). Besides, higher occupancy levels (greater than 60%) will ensure steady run rate of revenues going ahead.

In order to reduce its dependence on the highly taxed cigarette business and to diversify, it has steadily built a strong FMCG business franchisee which now contributes ~26% of revenues.

ITC Ltd 3 yr Price Chart

150

200

250

300

350

400

Feb-

16

Apr-

16

Jun-

16

Aug-

16

Oct

-16

Dec

-16

Feb-

17

Apr-

17

Jun-

17

Aug-

17

Oct

-17

Dec

-17

Feb-

18

Apr-

18

Jun-

18

Aug-

18

Oct

-18

Dec

-18

Feb-

19

16March 2019 INSIGHT

Strong financials & healthy balance sheetOver the years, ITC reported strong financial growth with revenue growing at 8.6% CAGR between FY13-FY18. EBITDA and PAT grew by 8% CAGR during the same period. ITC is a virtually debt free company with stable growth in operating cash flows. Steady net profitability margins aided the company to sustain an average RoE of 28% in past 5 years. Company even registered consistent growth in FCF in last five years, thus can fund any capex without leveraging its balance sheet. Further, company has good track record of paying dividend to its shareholders and thus maintained an average dividend yield of 1.98% in past 5 years. Financially, ITC is well placed to capitalize any growth opportunities emerge in its business verticals.

Q3FY19 result HighlightsGross Revenue for the quarter stood at Rs. 11340.15 crores, representing a growth of 15.1% driven mainly by FMCG-Others, Agri Business and Paperboards, Paper & Packaging. Cigarette revenues grew 9.6% yoy (driven by volume growth of 7.5%), while FMCG, Hotels, Agri, and paperboard businesses reported revenue growth of 11.5%, 11.7%, 25.7% and 20.5% yoy, respectively. EBITDA grew by 11.2% yoy to Rs 4,325.8 crores while EBITDA margin, contracted by 127bps yoy to 38.5%. cigarette EBIT grew 8.8% yoy, while FMCG (others) reported a strong EBIT growth of 63.1% yoy followed by paperboard and hotels at 23.8% and 10.1%, respectively. However, agri segment’s EBIT declined by 14.8% yoy on shortage of Leaf Tobacco in AP (Andhra Pradesh) and adverse

crop quality. Profit after Tax before considering exceptional items, grew by 13.8%, which was 17-quarter high.

Key Risks Operating in highly regulated

cigarette business, thus any strict regulation or increase in tax rate could adversely impact its cigarette business, which is currently the main profit contributor of the company.

Company’s other business verticals are directly linked with consumption growth, thus any slowdown in domestic economy could hurt its business growth.

ValuationITC’s latest set of results instills confidence with broad-based growth across all business segments. Cigarette volumes sustained as stable prices induced demand and non-cigarette business also performed well driven by FMCG and paper businesses. Stability in GST rates remains the key factor for sustenance of demand in the cigarette business while margin expansion is expected to be driven by FMCG, paper and Hotels business. With strong operating cash flows driving capacity expansions across business segments, we have a positive view on the company and thus we recommend our investors to BUY the scrip with target of Rs 319 from 12 months investment perspective. At the CMP, the scrip is valued at P/E multiple of 24.3x on Bloomberg consensus EPS of Rs 11.4.

Particulars (in Rs Cr) FY17 FY18 FY19E FY20E

Revenue 42,360 43,123 47,474 52,495

Growth (%) 9.2% 1.8% 10.1% 10.6%

EBITDA 15,449 16,496 18,252 20,588

EBITDA Margin (%) 36.5% 38.3% 38.4% 39.2%

Net profit 10,299 11,280 12,426 13,992

Net Profit Margin (%) 24.3% 26.2% 26.2% 26.7%

EPS (Rs) 8.5 9.2 10.2 11.4

Source: Bloomberg consensus

17 March 2019INSIGHT

STOCK PICKS

Tech Mahindra Ltd.CMP: Rs 825 Rating: BUY Target: Rs 960

Company InformationBSE Code 532755NSE Code TECHMBloomberg Code TECHM INISIN INE669C01036Market Cap (Rs. Cr) 81683Outstanding shares(Cr) 98.152-wk Hi/Lo (Rs.) 840.0 / 602.4Avg. daily volume (1yr. on NSE) 3,287,472Face Value(Rs.) 5.0Book Value 209.1

Investment RationaleTurnaround in Telecom verticalTelecom vertical which has been declining/flat for several quarters came back strong in last two quarters. Telecom which contributes 41% of revenue, grew 2.5% QoQ in USD in Q3FY19. Tech M’s Telecom vertical

has shown three consecutive years of tepid performance over FY15-FY18 led by ramp down in LCC (Acquired entity), Pricing pressure in Top client (AT&T), softness in Comviva and client specific weakness (KPN deal ramp down). Communication vertical organic USD revenues (ex-LCC) remained tepid for three consecutive

years (up 0.5% CAGR over FY15-FY18). It is expected that worst is behind for Communication vertical and recent large deal wins in 1HFY19 should render stability for this vertical performance. While Telecom pickup has already been visible in Q2FY19, it is expected that communication vertical will have a turnaround

Promoters 35.9%

DII 13.0%

FII 38.5%Others 12.6%

Share holding pattern as on December 2018

18March 2019 INSIGHT

performance going forward on the back of strong deal momentum, absence of revenue pruning at LCC and huge spends related to 5G roll out. The management highlighted that the telecom vertical would continue to grow in Q4FY19E, led by recent deal wins.

Better placed to capitalize on 5G opportunity5G is a large opportunity for which the company is well-positioned due to investments in network capability through LCC, investments in platforms and IP and investments in partnerships to develop an eco-system play, viz. Intel, Rakuten, stake in Altio Star, among others. This positions it well to capitalise on the 5G opportunity across networks and IT services. Deal wins were healthy with total consideration value (TCV) of $440 million includes US$240mn in the communications vertical and rest in the Enterprise segment. Taking into consideration strong deal wins in 9MFY19 (~US$1.2bn) accompanied by continued momentum in communication. Given its early investments, the communication deals have been spread across digital, network, software transformation and spending relating to the preparation for upcoming 5G transformation. Further, investment relating to 5G is expected to pick-up pace during H2FY20E on account of new capex

for strengthening of infrastructure and network, laying out of digital platform for customer management/ devices and automation to control the operating expenses. Going ahead, it is expected that 5G investments and modernization of existing systems by telecom operators, including pre-5G network transformation initiatives will be the key growth drivers in the Telecom Vertical.

Operating performance on an uptick TechM continues to deliver better operating margin performance for the last seven consecutive quarters, with an improvement of 650 bps in EBIT margins as compared to Q1FY18. Operating margins came in at a multi-quarter high at 19.3% (post 20.2% in Q3FY15) on the back of opti-misation of SG&A expenses (13.8% as % of revenue in Q3FY19) and benefit of increase in utilisation (rose 100 bps to 82%). The management said it would be comfortable in keeping SG&A as proportion of revenues in range of 14-14.5% though it may see quarterly volatility. The management also believes that there is scope for further improvement in margins, led by improvement business mix, increase in offshore revenue mix and improvement in profitability of portfolio companies to nearly dou-ble-digit levels. Further, incremental contribution from high margin digital segment (now 33% of revenues) and

healthy growth in the same (10% QoQ) along with healthy profitability in business process services would bode well for margins going ahead. Cost rationalisation in acquired companies could also give further boost to mar-gins. The management is confident of the improvement in EBIT margin to sustain, driven by operational efficiencies and improvement in profitability of acquired companies.

Strong client addition to sustain growthTech Mahindra’s strong clients addition across segments reduces dependency over particular clients and makes business structure more robust. This also helps maintain steady operating margins over longer period of time. Client addition during the recent quarters remained high which denotes rising demand for automation among different verticals. During Q3FY19 Tech Mahindra added 5 new clients taking total active clients counts to 935. During Q3FY19, Tech Mahindra have 416 clients in $1mn+bucket, 157 clients in $5mn+, 88 clients in $10mn+ and 20 clients in $20mn+ bucket. Total clients in the $50 mn+ clients bracket is 18.

First-ever share buybackTech Mahindra has approved its first-ever buy-back proposal worth Rs. 19.56 bn at a price of Rs. 950/share which is 9.2% of TechM’s net worth and ~29% of cash and investments as of Q3FY19-end. This makes TechM the last of the Top-5 IT majors to announce a buy-back and all having done so on more than one occasion. Importantly, this signals a shift in capital allocation policy, and such buy-backs could become a more regular feature for the company, going forward, as has been the case with each of the other four top-tier IT firms. At Rs. 950, TechM will buy back 20.585mn equity shares, which implies 2.1% of total shares outstand-ing. The company has fixed March 6, 2019 as the record date for the purpose of ascertaining shareholder eligibility to participate in the buy-back. Assuming buyback is successful and the entire Rs. 19.56 bn is utilised for the buy-back, after adjusting for lower other income, there will be a ~0.5% improvement in EPS. On the

Tech Mahindra Ltd. Price Chart

0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000 18,000

350 400 450 500 550 600 650 700 750 800 850

Feb-

16

May

-16

Aug-

16

Nov

-16

Feb-

17

May

-17

Aug-

17

Nov

-17

Feb-

18

May

-18

Aug-

18

Nov

-18

Feb-

19

Volume (000's) (RHS) TechM

19 March 2019INSIGHT

other hand, RoE should see improve-ment of >50 bps. It is believed that the buy-back will provides confidence on management’s view of underlying business strength, and will boost sentiment.

Steady quarterly performanceTech Mahindra reported Q3FY19 numbers above consensus estimates on all fronts. Rupee revenue came at Rs 8,944 crore, up by 3.6% QoQ. Dollar revenue came at USD 1,261 million, up by 3.5% QoQ while in Constant Currency terms revenue growth was up 4.3% QoQ. Revenue growth was led by BPO services with revenue growth of 13% QoQ at Rs 754.2 crore, while IT segment growth during the quarter was 3% QoQ at Rs 8,189.5 crore. Dig-ital revenues were up 10% QoQ and accounted to 33% of total revenues and remains the key growth driver. EBIT came at Rs 1,439 crore, up by 8.7% QoQ with EBIT margin at 16.10%, marginally improved by 76 bps QoQ. On EBIT front, IT services recorded a growth of 7% QoQ at Rs 1580 core, while BPO segment witnessed a de-growth of 2% QoQ at Rs 142.6 crore. Management cited that there was tax reversal benefit of 7.5% during the quarter. Net profitability came at Rs 1,203 crore, up by 13.0% QoQ led by better performance at operating level and lower tax rate. Total headcount at 121,842; up 3,451 QoQ. The Active Client count stood at 935 in Q3, up by 5 QoQ. Free cash flow of USD 160.3 million; cash conversion to PAT at 94%. Cash and Cash equivalent of USD 1,251.8 million as of Dec 31,2018.

Key Risk Delay in telecom spend can impact

company’s performance High exposure to Europe may

impact growth Adverse cross-currency

movements.

ValuationTech Mahindra has posted strong numbers in last few quarters with both revenue growth and margin expansion led by healthy deal wins. Going ahead it is expected that the company will post better perfor-mance in FY20 led by strong revival in

communication, continued deal wins and improvement in enterprise seg-ment. The communication segment (~41% of revenue) which was facing challenges for the past two years due to slow growth in LCC acquisition, tepid performance of Comviva and price cuts in its large account (AT&T), however with deal wins in last 2 quarters especially in area like Telco, OTT and media players will result in strong growth ahead. Further, given its diversified offerings in the telecom space, it is expected that TechM is well placed to capitalise the 5G opportunity across networks and IT services. Company has guided for healthy growth in telecom going ahead, aided by strong deal wins, healthy deal pipeline and 5G related opportunity. Moreover, the Company has consistently improved its margins since the last seven quarters led by multiple levers and aims for further margin expansion going forward led by changing business mix, increas-ing adoption of automation and improvement in portfolio companies’ margins. Going ahead, rising demand across geographies and across dif-ferent verticals helps Tech Mahindra to attain higher growth momentum. Along with robust business structure, healthy deal pipeline and revitaliza-tion of key business segment make Tech Mahindra a safer bet to invest in. Also, recent buyback announce-ments augur well for return ratios of the company. Thus, we recommend our investors to BUY the scrip with target of Rs. 960 from 12-18 months investment perspective. At the CMP, the scrip is valued at P/E multiple of 15.1x on Bloomberg consensus EPS of Rs. 55.

Particulars (in Rs Cr) FY18 FY19E FY20E FY21E

Net Sales 30772.9 34988.8 38627.6 42181.4

Growth (%) 5.6 13.7 10.4 9.2

EBITDA 4682.5 6437.9 7146.1 7803.6

EBITDA Margin (%) 15.2 18.4 18.5 18.5

Net profit 3786.1 4338.6 4867.1 5399.2

Net Profit Margin (%) 12.3 12.4 12.6 12.8

EPS (Rs) 43.0 44.2 49.6 55.0

Consensus Estimate: Bloomberg, Ashika Research

Tech Mahindra has posted strong numbers in last few quarters with both revenue growth and margin expansion led by healthy deal wins. Going ahead it is expected that the company will post better performance in FY20 led by strong revival in communication, continued deal wins and improvement in enterprise segment.

20March 2019 INSIGHT

Monthly Insight Recommendation Performance Sheet

21 March 2019INSIGHT

Our recommendation includes stocks across the sectors that are generating alpha return for our investors. For the last 10 years we have been consistent in generating superior return for our clients through our prestigious monthly insight recommendations. Since January 2012 we have recom-mended 271 stocks out of which 226 has achieved target. Success ratio stands at 84%. Out of these 135 stocks have given a return of more than 100%. During this period the Nifty has given a return of 127% from current

price and a return of 147% from its all time high.

Few of the stocks recommended by us have given stellar returns which are TCS Ltd, Maruti Suzuki, Kotak Mahindra Bank, L&T, Axis Bank, Indusind Bank, M & M, Ultratech Cement, Bajaj Finserv, Godrej Con-sumer, Godrej Consumer Prod, BPCL, Britannia, Britannia Industries, Tata Motors, Adani Ports, Hero MotoCorp, Dabur India, Tech M, Motherson Sumi, Shree Cement, Bharti InfraTel, Pidilite Ind., Zee Entertainment,

Lupin, Cadila Helthcare, HPCL, Dr. Reddy Lab, Ashok Leyland, Aurobindo Pharma, Havels India, Petronet LNG, MRF, UPL, Sun TV, L&T Finance, Divis Lab, Berger Paints, Berger India, Gruh Finance, Torrent Pharma, LIC Housing Fin, Emami, Exide Inds, Dewan Housing, Whirlpool India, Graphite India, Cummins India, Indraprastha Gas, Tata Global, SKS Microfinance, Glenmark Pharma, Indian Bank, Godrej Properties, Castrol India, Abbott India, Info Edge (India), AIA Engineering, MRPL,

Target Achieved 84%

Calls Open 6%

Exit / Booked 10%

Total Call: 271

Success Rate

Return Classification

More than 100% Return 50% - 135 stocks

50-25% Return 13% - 34 stocks

Less than 25% Return 20% - 55 stocks

100-50% Return 17% - 47 stocks

22March 2019 INSIGHT

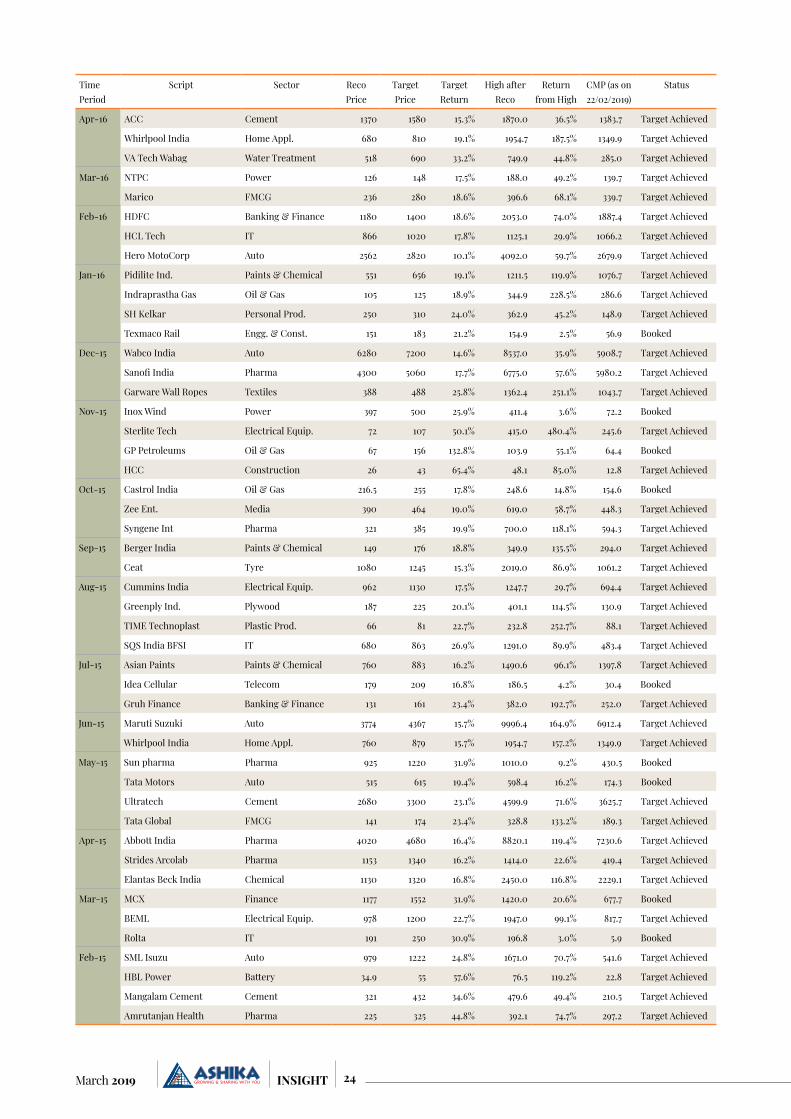

TimePeriod

Script Sector RecoPrice

TargetPrice

TargetReturn

High afterReco

Returnfrom High

CMP (as on 22/02/2019)

Status

Mar-19 ITC Ltd. FMCG 275 319 16.0%

Tech Mahindra IT 825 907 16.4%

Feb-19 HDFC Bank Banking 2090 2407 15.2% 2155.0 3.1% 2091.5

Pfizer Pharma 3039 3490 14.8% 3153.0 3.8% 3005.7

Jan-19 United Spirits FMCG 640 735 14.8% 644.9 0.8% 533.3

Abbott India Pharma 7480 8580 14.7% 8325.0 11.3% 7230.6

Indraprastha Gas Oil & Gas 262 315 20.2% 311.4 18.9% 286.6

Dec-18 Berger Paints Paints 319 369 15.7% 344.9 8.1% 294.0

Cummins India Capital Goods 776 889 14.6% 884.2 13.9% 694.4 Target Achieved

Nov-18 Nestlé India FMCG 9680 11370 17.5% 11751.0 21.4% 10685.5 Target Achieved

Dabur India FMCG 385 470 22.1% 464.2 20.6% 435.4 Target Achieved

Oct-18 Godrej Consumer FMCG 768 910 18.5% 849.9 10.7% 668.0

Dr. Lal PathLabs Pharma 954 1125 17.9% 1125.0 17.9% 1032.7 Target Achieved

Sep-18 Bharat Forge Auto 665 752 13.1% 693.9 4.3% 489.2 Booked

ABB India Electrical Equip. 1322 1510 14.2% 1517.0 14.8% 1248.3 Target Achieved

Whirlpool of India Consumar Durables 1795 2033 13.3% 1954.7 8.9% 1349.9

Aug-18 Cipla Pharma 625 715 14.4% 678.5 8.6% 541.3

Marico FMCG 351 408 16.2% 396.6 13.0% 339.7

Jul-18 Procter & Gamble Hygiene FMCG 9900 11100 12.1% 11337.0 14.5% 10174.9 Target Achieved

Dishman Carbogen Pharma 261 307 17.6% 314.8 20.6% 188.5 Target Achieved

Jun-18 Nestle India FMCG 9519 10900 14.5% 11751.0 23.4% 10685.5 Target Achieved

CESC Power 802 1020 27.2% 732.8 -8.6% 673.6

Bata India Footware 764 890 16.5% 1320.0 72.8% 1313.0 Target Achieved

May-18 ITC FMCG 280 324 15.7% 323.0 15.3% 274.3 Target Achieved

Tata Chemical Chemicals 762 890 16.8% 787.5 3.3% 564.8

Apr-18 Voltas Consumar Durables 620 720 16.1% 664.7 7.2% 531.3

Mar-18 Infosys IT 571 667 16.8% 772.3 35.2% 735.0 Target Achieved

Britannia Industries FMCG 4960 5690 14.7% 6934.4 39.8% 3012.8 Target Achieved

Feb-18 Power Grid Power 192 223 16.1% 216.0 12.5% 181.9

Godrej Consumer FMCG 701 804 14.7% 1017.7 45.2% 668.0 Target Achieved

Jan-18 Solar Industries Chemicals 1182 1480 25.2% 1300.0 10.0% 937.8

Maharshtra Seamless Engg. & Const. 505 585 15.8% 552.0 9.3% 465.5 Booked

Dec-17 Petronet LNG Oil & Gas 251 297 18.3% 275.1 9.6% 215.4

Hindustan Copper Metals & Mining 95 116 22.1% 110.5 16.3% 45.1 Booked

Nov-17 KNR Constructions Engg. & Const. 249 297 19.3% 349.0 40.2% 195.6 Target Achieved

Indian Hotels Co. Hotels 107 127 18.7% 161.0 50.4% 142.9 Target Achieved

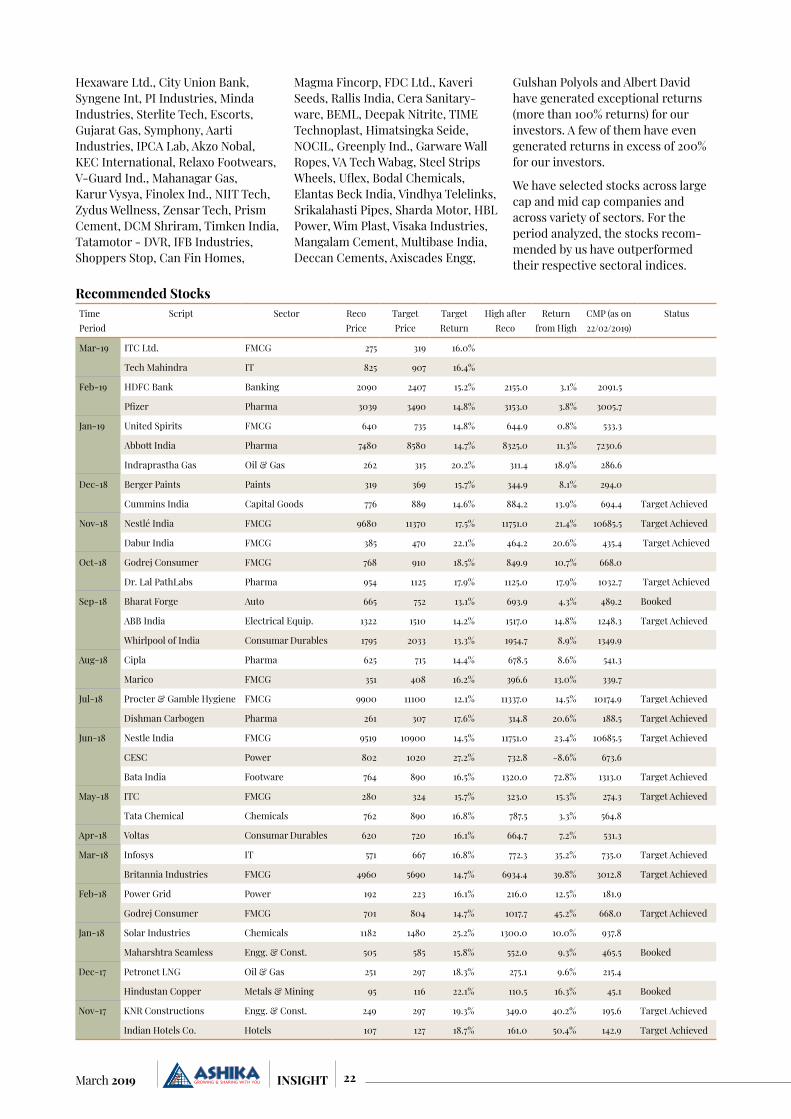

Recommended Stocks

Hexaware Ltd., City Union Bank, Syngene Int, PI Industries, Minda Industries, Sterlite Tech, Escorts, Gujarat Gas, Symphony, Aarti Industries, IPCA Lab, Akzo Nobal, KEC International, Relaxo Footwears, V-Guard Ind., Mahanagar Gas, Karur Vysya, Finolex Ind., NIIT Tech, Zydus Wellness, Zensar Tech, Prism Cement, DCM Shriram, Timken India, Tatamotor - DVR, IFB Industries, Shoppers Stop, Can Fin Homes,

Magma Fincorp, FDC Ltd., Kaveri Seeds, Rallis India, Cera Sanitary-ware, BEML, Deepak Nitrite, TIME Technoplast, Himatsingka Seide, NOCIL, Greenply Ind., Garware Wall Ropes, VA Tech Wabag, Steel Strips Wheels, Uflex, Bodal Chemicals, Elantas Beck India, Vindhya Telelinks, Srikalahasti Pipes, Sharda Motor, HBL Power, Wim Plast, Visaka Industries, Mangalam Cement, Multibase India, Deccan Cements, Axiscades Engg,

Gulshan Polyols and Albert David have generated exceptional returns (more than 100% returns) for our investors. A few of them have even generated returns in excess of 200% for our investors.

We have selected stocks across large cap and mid cap companies and across variety of sectors. For the period analyzed, the stocks recom-mended by us have outperformed their respective sectoral indices.

23 March 2019INSIGHT

TimePeriod

Script Sector RecoPrice

TargetPrice

TargetReturn

High afterReco

Returnfrom High

CMP (as on 22/02/2019)

Status

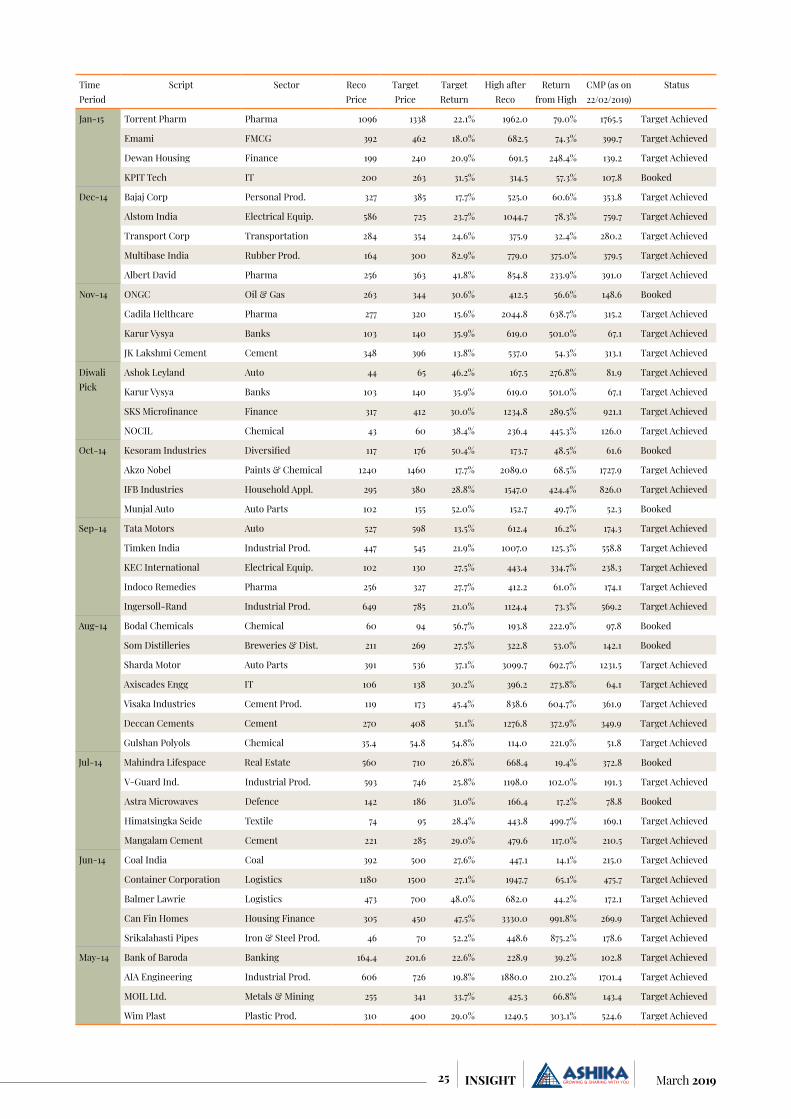

Oct-17 CDSL Banking & Finance 340 424 24.7% 396.9 16.7% 210.1 Booked

Karur Vysya Banking & Finance 125 145 15.8% 150.4 20.5% 67.1 Booked

Sep-17 Hindustan Unilever FMCG 1217 1379 13.3% 1869.5 53.6% 1768.6 Target Achieved

NMDC Metals & Mining 126 142 12.7% 162.7 29.1% 96.8 Target Achieved

Aug-17 Kaveri Seed Agricultural Prod. 683 790 15.7% 708.0 3.7% 402.9 Booked

Indraprastha Gas Oil & Gas 234 280 19.7% 344.9 47.4% 286.6 Target Achieved

Jul-17 Greaves Cotton Auto 159 193 21.4% 170.8 7.4% 119.0 Booked

Apollo Tyres Tyre 240 278 15.8% 307.3 28.0% 210.2 Target Achieved

Jun-17 Bosch Auto 23325 27442 17.7% 25240.0 8.2% 18120.8 Booked

Relaxo Footwears Footwear 458 571 24.7% 873.6 90.7% 731.3 Target Achieved

May-17 PNC Infratech Engg. & Const. 155 200 29.0% 228.3 47.3% 131.0 Target Achieved

PI Industries Chemical 866 1028 18.7% 1034.0 19.4% 905.2 Target Achieved

Apr-17 Akzo Nobel Paints & Chemical 1862 2135 14.7% 2089.0 12.2% 1727.9 Booked

Crompton Greaves Household Appl. 211 244 15.6% 295.0 39.8% 209.5 Target Achieved

Mar-17 Manappuram Finance Banking & Finance 95 120 26.3% 130.5 37.3% 112.9 Target Achieved

Deepak Nitrite Chemical 107 124 15.9% 305.0 185.0% 216.9 Target Achieved

Feb-17 Dewan Housing Banking & Finance 290 341 17.6% 691.5 138.4% 139.2 Target Achieved

CESC Power 750 860 14.7% 825.6 10.1% 673.6 Target Achieved

Jan-17 Persistent Systems IT 616 741 20.3% 915.0 48.5% 601.6 Target Achieved

Dec-16 Britannia Industries FMCG 3010 3522 17.0% 6934.4 130.4% 3012.8 Target Achieved

Berger Paints Paints & Chemical 240 280 16.7% 349.9 45.8% 294.0 Target Achieved

Dishman Pharma Pharma 243 300 23.5% 396.4 63.1% 188.5 Target Achieved

Nov-16 Max Financial Services Banking & Finance 550 650 18.2% 684.0 24.4% 404.5 Target Achieved

Natco Pharma Pharma 575 737 28.2% 1090.0 89.6% 587.2 Target Achieved

Minda Industries Auto 117 151 29.1% 459.0 292.3% 316.0 Target Achieved

Vindhya Telelinks Engg. & Const. 722 900 24.7% 2030.0 181.2% 1396.8 Target Achieved

Oct-16 Credit Analysis Banking & Finance 1314 1543 17.4% 1725.0 31.3% 959.0 Target Achieved

Nilkamal Plastic Prod. 1336 1700 27.2% 2275.0 70.3% 1247.5 Target Achieved

Sep-16 IDFC Bank Banking & Finance 55.4 70 26.4% 83.4 50.5% 45.6 Target Achieved

Mahanagar Gas Oil & Gas 641 748 16.7% 1377.5 114.9% 868.5 Target Achieved

Mercator Diversified 52 71 36.5% 55.3 6.3% 7.0 Booked

Kirloskar Ferrous Iron & Steel Prod. 86 113 31.4% 121.9 41.7% 89.9 Target Achieved

Aug-16 Indian Oil Corp. Oil & Gas 136 155 14.2% 231.5 70.5% 137.2 Target Achieved

LIC Housing Finance Banking & Finance 519 608 17.1% 794.0 53.0% 469.9 Target Achieved

Federal Bank Banking & Finance 65 78 20.0% 127.7 96.4% 79.5 Target Achieved

Unichem Lab Pharma 285 360 26.3% 382.0 34.0% 190.5 Target Achieved

Jul-16 Godrej Properties Construction 365 415 13.7% 920.0 152.1% 724.9 Target Achieved

Capital First Banking & Finance 40 47 16.7% 64.9 62.0% 45.6 Target Achieved

Aarti Industries Chemical 520 620 19.2% 1807.9 247.7% 1409.8 Target Achieved

Steel Strips Wheels Auto 456 578 26.8% 1473.8 223.2% 861.8 Target Achieved

Jun-16 Dabur India FMCG 290 335 15.5% 490.7 69.2% 435.4 Target Achieved

Godrej Consumer Prod FMCG 494 583 18.2% 1017.7 106.1% 668.0 Target Achieved

Glenmark Pharma Pharma 851 985 15.7% 994.0 16.8% 593.0 Target Achieved

Tata Power Co Power 73 85 16.4% 101.8 39.5% 67.1 Target Achieved

May-16 Mahindra & Mahindra Auto 665 775 16.5% 993.0 49.3% 646.6 Target Achieved

PI Industries Paints & Chemical 635 760 19.7% 1034.0 62.8% 905.2 Target Achieved

DCM Shriram Paints & Chemical 157 195 24.2% 628.0 300.0% 365.6 Target Achieved

24March 2019 INSIGHT

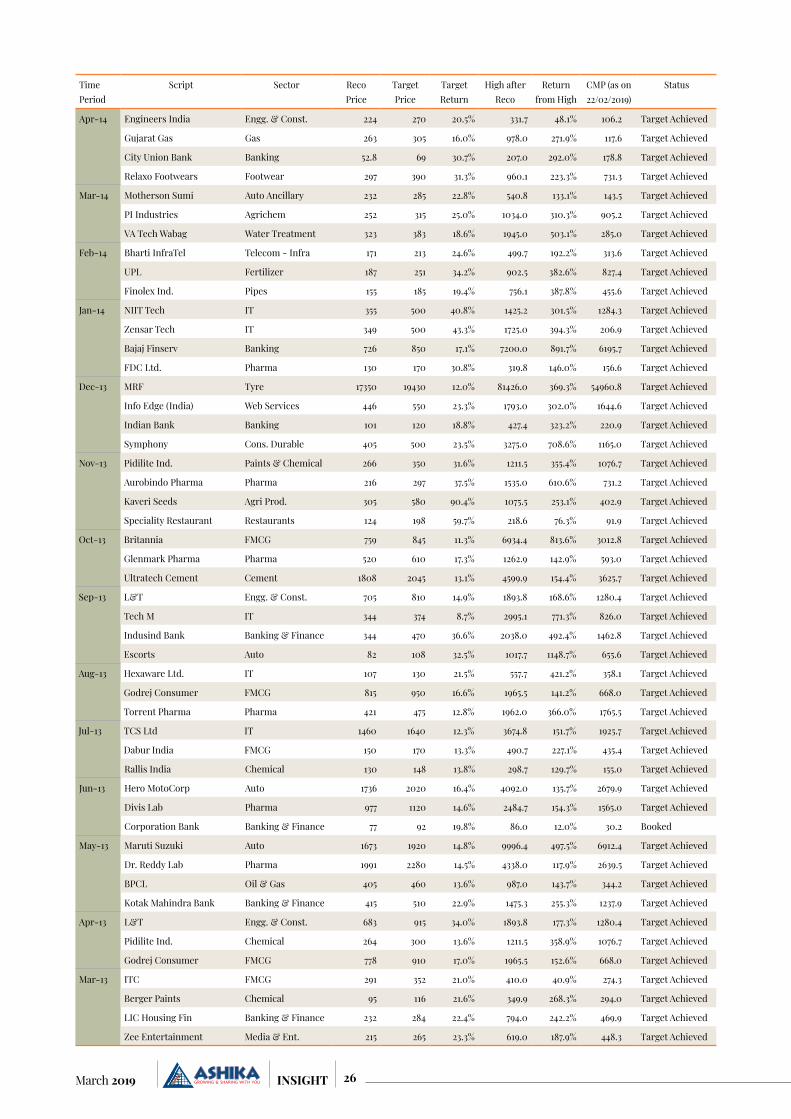

TimePeriod

Script Sector RecoPrice

TargetPrice

TargetReturn

High afterReco

Returnfrom High

CMP (as on 22/02/2019)

Status

Apr-16 ACC Cement 1370 1580 15.3% 1870.0 36.5% 1383.7 Target Achieved

Whirlpool India Home Appl. 680 810 19.1% 1954.7 187.5% 1349.9 Target Achieved

VA Tech Wabag Water Treatment 518 690 33.2% 749.9 44.8% 285.0 Target Achieved

Mar-16 NTPC Power 126 148 17.5% 188.0 49.2% 139.7 Target Achieved

Marico FMCG 236 280 18.6% 396.6 68.1% 339.7 Target Achieved

Feb-16 HDFC Banking & Finance 1180 1400 18.6% 2053.0 74.0% 1887.4 Target Achieved

HCL Tech IT 866 1020 17.8% 1125.1 29.9% 1066.2 Target Achieved

Hero MotoCorp Auto 2562 2820 10.1% 4092.0 59.7% 2679.9 Target Achieved

Jan-16 Pidilite Ind. Paints & Chemical 551 656 19.1% 1211.5 119.9% 1076.7 Target Achieved

Indraprastha Gas Oil & Gas 105 125 18.9% 344.9 228.5% 286.6 Target Achieved

SH Kelkar Personal Prod. 250 310 24.0% 362.9 45.2% 148.9 Target Achieved

Texmaco Rail Engg. & Const. 151 183 21.2% 154.9 2.5% 56.9 Booked

Dec-15 Wabco India Auto 6280 7200 14.6% 8537.0 35.9% 5908.7 Target Achieved

Sanofi India Pharma 4300 5060 17.7% 6775.0 57.6% 5980.2 Target Achieved

Garware Wall Ropes Textiles 388 488 25.8% 1362.4 251.1% 1043.7 Target Achieved

Nov-15 Inox Wind Power 397 500 25.9% 411.4 3.6% 72.2 Booked

Sterlite Tech Electrical Equip. 72 107 50.1% 415.0 480.4% 245.6 Target Achieved

GP Petroleums Oil & Gas 67 156 132.8% 103.9 55.1% 64.4 Booked

HCC Construction 26 43 65.4% 48.1 85.0% 12.8 Target Achieved

Oct-15 Castrol India Oil & Gas 216.5 255 17.8% 248.6 14.8% 154.6 Booked

Zee Ent. Media 390 464 19.0% 619.0 58.7% 448.3 Target Achieved

Syngene Int Pharma 321 385 19.9% 700.0 118.1% 594.3 Target Achieved

Sep-15 Berger India Paints & Chemical 149 176 18.8% 349.9 135.5% 294.0 Target Achieved

Ceat Tyre 1080 1245 15.3% 2019.0 86.9% 1061.2 Target Achieved

Aug-15 Cummins India Electrical Equip. 962 1130 17.5% 1247.7 29.7% 694.4 Target Achieved

Greenply Ind. Plywood 187 225 20.1% 401.1 114.5% 130.9 Target Achieved

TIME Technoplast Plastic Prod. 66 81 22.7% 232.8 252.7% 88.1 Target Achieved

SQS India BFSI IT 680 863 26.9% 1291.0 89.9% 483.4 Target Achieved

Jul-15 Asian Paints Paints & Chemical 760 883 16.2% 1490.6 96.1% 1397.8 Target Achieved

Idea Cellular Telecom 179 209 16.8% 186.5 4.2% 30.4 Booked

Gruh Finance Banking & Finance 131 161 23.4% 382.0 192.7% 252.0 Target Achieved

Jun-15 Maruti Suzuki Auto 3774 4367 15.7% 9996.4 164.9% 6912.4 Target Achieved

Whirlpool India Home Appl. 760 879 15.7% 1954.7 157.2% 1349.9 Target Achieved

May-15 Sun pharma Pharma 925 1220 31.9% 1010.0 9.2% 430.5 Booked

Tata Motors Auto 515 615 19.4% 598.4 16.2% 174.3 Booked

Ultratech Cement 2680 3300 23.1% 4599.9 71.6% 3625.7 Target Achieved

Tata Global FMCG 141 174 23.4% 328.8 133.2% 189.3 Target Achieved

Apr-15 Abbott India Pharma 4020 4680 16.4% 8820.1 119.4% 7230.6 Target Achieved

Strides Arcolab Pharma 1153 1340 16.2% 1414.0 22.6% 419.4 Target Achieved

Elantas Beck India Chemical 1130 1320 16.8% 2450.0 116.8% 2229.1 Target Achieved

Mar-15 MCX Finance 1177 1552 31.9% 1420.0 20.6% 677.7 Booked

BEML Electrical Equip. 978 1200 22.7% 1947.0 99.1% 817.7 Target Achieved

Rolta IT 191 250 30.9% 196.8 3.0% 5.9 Booked

Feb-15 SML Isuzu Auto 979 1222 24.8% 1671.0 70.7% 541.6 Target Achieved

HBL Power Battery 34.9 55 57.6% 76.5 119.2% 22.8 Target Achieved

Mangalam Cement Cement 321 432 34.6% 479.6 49.4% 210.5 Target Achieved

Amrutanjan Health Pharma 225 325 44.8% 392.1 74.7% 297.2 Target Achieved

25 March 2019INSIGHT

TimePeriod

Script Sector RecoPrice

TargetPrice

TargetReturn

High afterReco

Returnfrom High

CMP (as on 22/02/2019)

Status

Jan-15 Torrent Pharm Pharma 1096 1338 22.1% 1962.0 79.0% 1765.5 Target Achieved

Emami FMCG 392 462 18.0% 682.5 74.3% 399.7 Target Achieved

Dewan Housing Finance 199 240 20.9% 691.5 248.4% 139.2 Target Achieved

KPIT Tech IT 200 263 31.5% 314.5 57.3% 107.8 Booked

Dec-14 Bajaj Corp Personal Prod. 327 385 17.7% 525.0 60.6% 353.8 Target Achieved

Alstom India Electrical Equip. 586 725 23.7% 1044.7 78.3% 759.7 Target Achieved

Transport Corp Transportation 284 354 24.6% 375.9 32.4% 280.2 Target Achieved

Multibase India Rubber Prod. 164 300 82.9% 779.0 375.0% 379.5 Target Achieved

Albert David Pharma 256 363 41.8% 854.8 233.9% 391.0 Target Achieved

Nov-14 ONGC Oil & Gas 263 344 30.6% 412.5 56.6% 148.6 Booked

Cadila Helthcare Pharma 277 320 15.6% 2044.8 638.7% 315.2 Target Achieved

Karur Vysya Banks 103 140 35.9% 619.0 501.0% 67.1 Target Achieved

JK Lakshmi Cement Cement 348 396 13.8% 537.0 54.3% 313.1 Target Achieved

Diwali Pick

Ashok Leyland Auto 44 65 46.2% 167.5 276.8% 81.9 Target Achieved

Karur Vysya Banks 103 140 35.9% 619.0 501.0% 67.1 Target Achieved

SKS Microfinance Finance 317 412 30.0% 1234.8 289.5% 921.1 Target Achieved

NOCIL Chemical 43 60 38.4% 236.4 445.3% 126.0 Target Achieved

Oct-14 Kesoram Industries Diversified 117 176 50.4% 173.7 48.5% 61.6 Booked

Akzo Nobel Paints & Chemical 1240 1460 17.7% 2089.0 68.5% 1727.9 Target Achieved

IFB Industries Household Appl. 295 380 28.8% 1547.0 424.4% 826.0 Target Achieved

Munjal Auto Auto Parts 102 155 52.0% 152.7 49.7% 52.3 Booked

Sep-14 Tata Motors Auto 527 598 13.5% 612.4 16.2% 174.3 Target Achieved

Timken India Industrial Prod. 447 545 21.9% 1007.0 125.3% 558.8 Target Achieved

KEC International Electrical Equip. 102 130 27.5% 443.4 334.7% 238.3 Target Achieved

Indoco Remedies Pharma 256 327 27.7% 412.2 61.0% 174.1 Target Achieved

Ingersoll-Rand Industrial Prod. 649 785 21.0% 1124.4 73.3% 569.2 Target Achieved

Aug-14 Bodal Chemicals Chemical 60 94 56.7% 193.8 222.9% 97.8 Booked

Som Distilleries Breweries & Dist. 211 269 27.5% 322.8 53.0% 142.1 Booked

Sharda Motor Auto Parts 391 536 37.1% 3099.7 692.7% 1231.5 Target Achieved

Axiscades Engg IT 106 138 30.2% 396.2 273.8% 64.1 Target Achieved

Visaka Industries Cement Prod. 119 173 45.4% 838.6 604.7% 361.9 Target Achieved

Deccan Cements Cement 270 408 51.1% 1276.8 372.9% 349.9 Target Achieved

Gulshan Polyols Chemical 35.4 54.8 54.8% 114.0 221.9% 51.8 Target Achieved

Jul-14 Mahindra Lifespace Real Estate 560 710 26.8% 668.4 19.4% 372.8 Booked

V-Guard Ind. Industrial Prod. 593 746 25.8% 1198.0 102.0% 191.3 Target Achieved

Astra Microwaves Defence 142 186 31.0% 166.4 17.2% 78.8 Booked

Himatsingka Seide Textile 74 95 28.4% 443.8 499.7% 169.1 Target Achieved

Mangalam Cement Cement 221 285 29.0% 479.6 117.0% 210.5 Target Achieved

Jun-14 Coal India Coal 392 500 27.6% 447.1 14.1% 215.0 Target Achieved

Container Corporation Logistics 1180 1500 27.1% 1947.7 65.1% 475.7 Target Achieved

Balmer Lawrie Logistics 473 700 48.0% 682.0 44.2% 172.1 Target Achieved

Can Fin Homes Housing Finance 305 450 47.5% 3330.0 991.8% 269.9 Target Achieved

Srikalahasti Pipes Iron & Steel Prod. 46 70 52.2% 448.6 875.2% 178.6 Target Achieved

May-14 Bank of Baroda Banking 164.4 201.6 22.6% 228.9 39.2% 102.8 Target Achieved

AIA Engineering Industrial Prod. 606 726 19.8% 1880.0 210.2% 1701.4 Target Achieved