Bahasa

Halaman

Hukum

INCOME TAX AND EDUCATIONAL INSTITUTIONS AND UNIVERSITY

S. K. Mishra, Chief Commissioner of Income Tax, Indore

SYNOPSIS1. Introduction – Roll of Income tax Department, + Slide2. Educational activities 10(23C) (iiiab) (iiiad) (vi) 2(15)3. Charitable religious trust/society/InstitutionsSection 11, 12, 12A 12AA 13Section 11(5) 13(2) 13(3)4. Requirement of 10(23C)(vi)5. Case Study6. Comparison of 10(23C)(vi) with 2(15) read with Sec. 11 to 137. Some more case laws to explain - a) Education, b) Solely education purpose and not for profit c) Charitable purpose8. Cases study where 10(23C)(vi) Exemptions denied9. Whether benefit u/s 12A is available even if 10(23C)(vi) rejected 10 Anonymous donations11. TDS provisions.12. Section 80E Deduction for education loan13. Donations for approved research in science, social welfare and statistics.14. Proposed modification in Draft ‘Direct Tax Code’15. Impact on Wealth tax

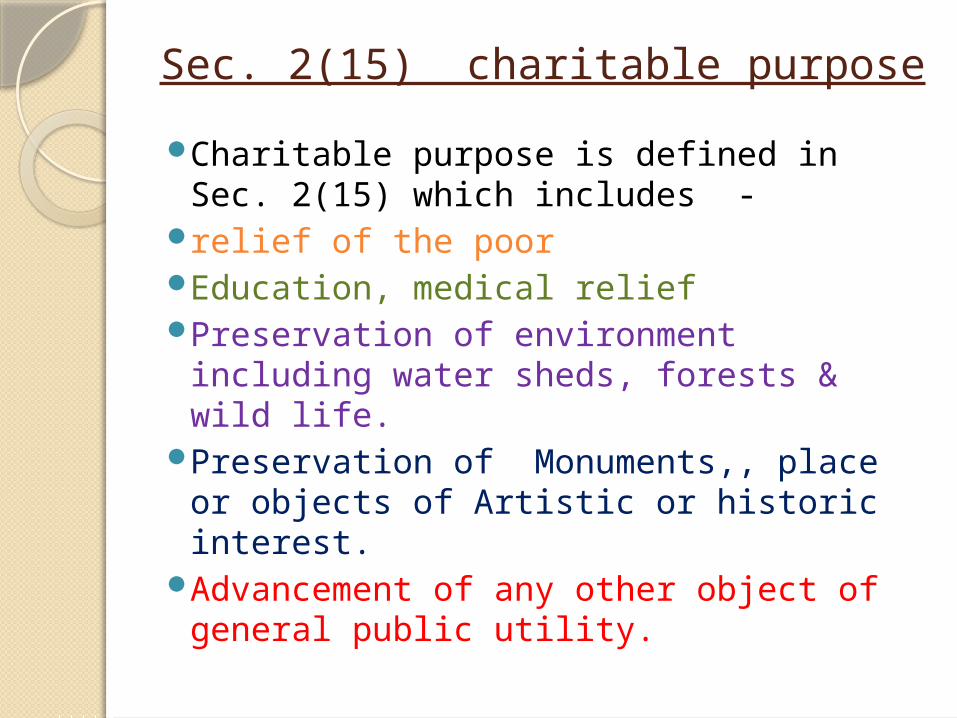

Sec. 2(15) charitable purposeCharitable purpose is defined in Sec. 2(15) which includes -

relief of the poorEducation, medical relief Preservation of environment including water sheds, forests & wild life.

Preservation of Monuments,, place or objects of Artistic or historic interest.

Advancement of any other object of general public utility.

Provided , The advancement of any other object of general public utility

shall not be a charitable purpose, if it involves

the carrying of any activity in the nature of trade, commerce or business or any

activity rendering any service for CESS or Fee or

any other consideration in relation to any trade, commerce or business

provided gross total receipts is Rs. 25 lakhs or less.

Taxation of Charitable Trust/Institution

Section 11 provides the manner in which income is exempt from income-tax.

Section 12 provides the income of trust or institutions from contributions.

Section 12A provides the conditions as to registration of trusts, etc.

Section 12AA provides the procedure for registration and cancellation.

Section 13 provides that section 11 & 12 not to apply in certain cases i.e. forfeiture of exemption.

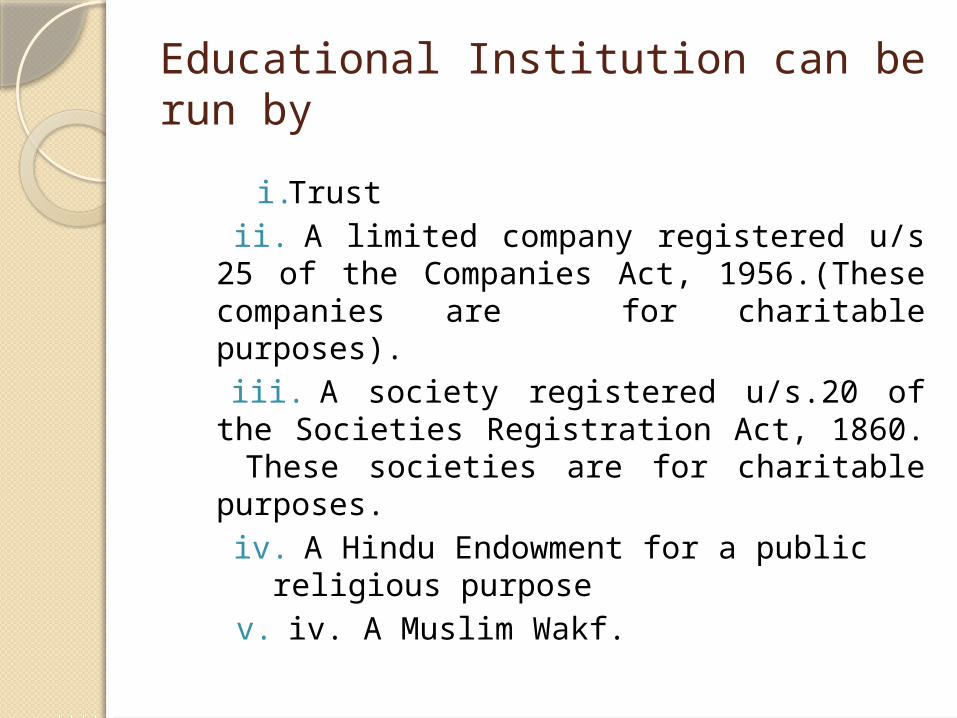

Educational Institution can be run by

i.Trust ii. A limited company registered u/s 25 of the Companies Act, 1956.(These companies are for charitable purposes).iii. A society registered u/s.20 of the Societies Registration Act, 1860. These societies are for charitable purposes.iv. A Hindu Endowment for a public religious purpose v. iv. A Muslim Wakf.

Can the objects of the trust be charitable as well as non

charitableSakthi Charities, 149 ITR 624, and in many other cases, courts opined that for claiming exemption u/s 11 to 13, The trust should exist exclusively for charitable purposes.

Education The Supreme Court in Sole Trustee, Loka Shikshana Trusts v. CIT (1975) 101 ITR 234 held that education’ connotes the process of training and developing the knowledge, skill, mind and character of students by normal schooling. Gujarat High Court held that the element of imparting education to the students or element of normal schooling where there are teachers and taught must be present so as to fall within the meaning of education.

Not educational activityproviding scholarships and financial assistance to students without keeping any control over such students.

coaching classes run on pure commercial principles

Printing Press for Publication Books / News Paper

Providing transport, Canteen or Hostels as Business activity

Provisions Of The Act Relevant For Educational Institution

Sec. 10(23C)

Exemption as an Educational Institution

Sec. 11/12/1

2A

Exemption as a Charitable

Institution

Sec. 35

Expenditure on Scientific Research

Exemption u/s. 10(23C)As per Sec. 10(23C), income of following educational institutions is fully exempt from income tax :

Exemption u/s. 10(23C)

Exemption u/s. 10(23C)

Exemption u/s. 10(23C)

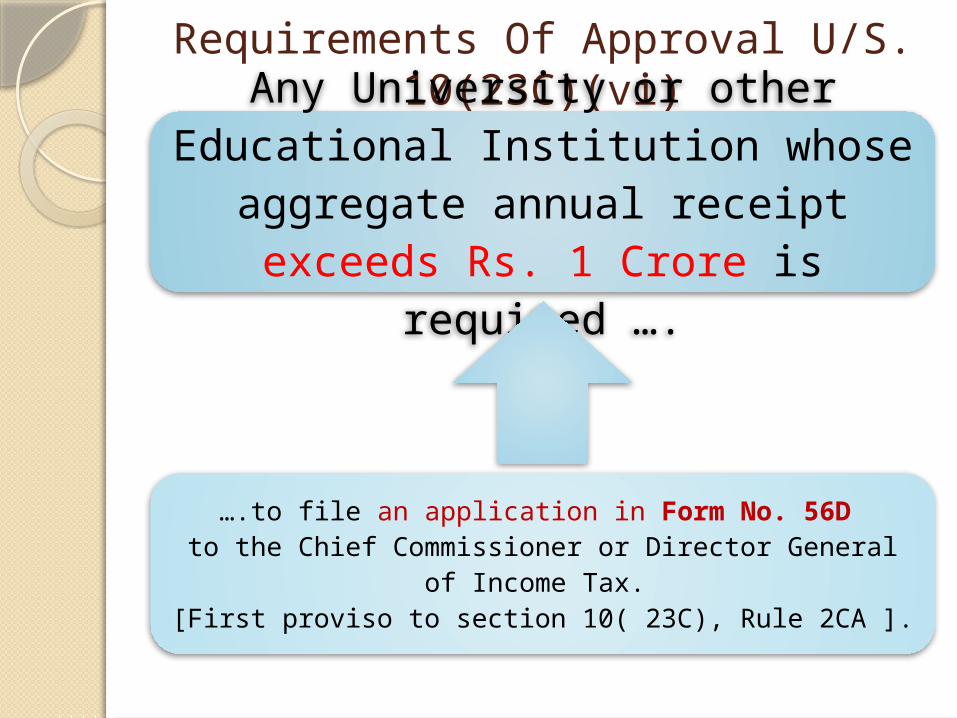

Requirements Of Approval U/S. 10(23C)(vi)Any University or other

Educational Institution whose aggregate annual receipt exceeds Rs. 1 Crore is

required ….

….to file an application in Form No. 56D to the Chief Commissioner or Director General

of Income Tax. [First proviso to section 10( 23C), Rule 2CA ].

Approval u/s. 10(23)(c )(vi)

Chief Commissioner or Director General of Income Tax ..may call for

such documents (including audited annual accounts) or information, to satisfy itself about the

genuineness of the activities

and may also make such enquires as it deems necessary [Second proviso to section 10( 23C)].

Approval u/s. 10(23)(c )(vi)Any university or other educational institution

under section 10(23C)(vi), shall….

apply its income or accumulate wholly and exclusively for the objects for which it is

established

and in case more than 15% of income is accumulated, the period of accumulation of the amount exceeding 15% of its Income, in no case shall exceed 5 years. [Third Proviso to section

10(23C)]

Investment of fundsThe university or other

educational institution under section 10(23C)(vi)

can not invest or deposit its funds otherwise than in any one or more of the forms or modes specified in sub-section

(5) of section 11.

Business Income If the Educational Institution as

specified u/s 10(23C)(vi) carries on any business then…

……exemption shall be available in respect of business income only if the business is incidental to the attainment of its objectives and

…separate books of accounts are maintained by it in respect of such

business . [Seventh Proviso to section 10(23C)].

Other requirements in form 56DThe form is to be submitted in 4 copies alongwith a enclosure and be sent to the authorized CCIT/DGIT

Copies of the following documents should be annexed:- Deed of Trust/ Memorandum and Articles of Association or other documents showing legal status of the Enterprises.

List of the major office bearers including settler and members of the Governing Body.

Photocopies of the registration u/s 12A if any. Photocopy of the latest certificate u/s 80G. True copies of the Assessment Orders passed in last 3 years.

Copies of Audited Accounts and Balance Sheets for the last 3 years alongwith note on examination of accounts.

Note on the activities as reflected in the accounts and annual reports with special reference to the appropriation income towards the object clause:

Any donation from the foreign country under foreign contribution regulation act, 1976.

The other information required in form no. 56D include

information about total income, voluntary contribution received, amount of income utilized wholly and exclusively for education, amount accumulated for the objects for future,

details of modes in which funds are invested/deposited showing nature, value and income from the investments:

details of funds not invested in prescribed mode u/s 11(5)

whether any business is being carried out- give details

other details include any shares/securities, other properties purchase by the institute from any interested persons as specified in sec. 13(2)

whether any part of the income or property of the institute used or applied, directly or indirectly to confer any benefit, amenity, perquisite to any interested person as specified in sec.13(3)

The taxable income if benefit denied u/s 10(23C)(vi).

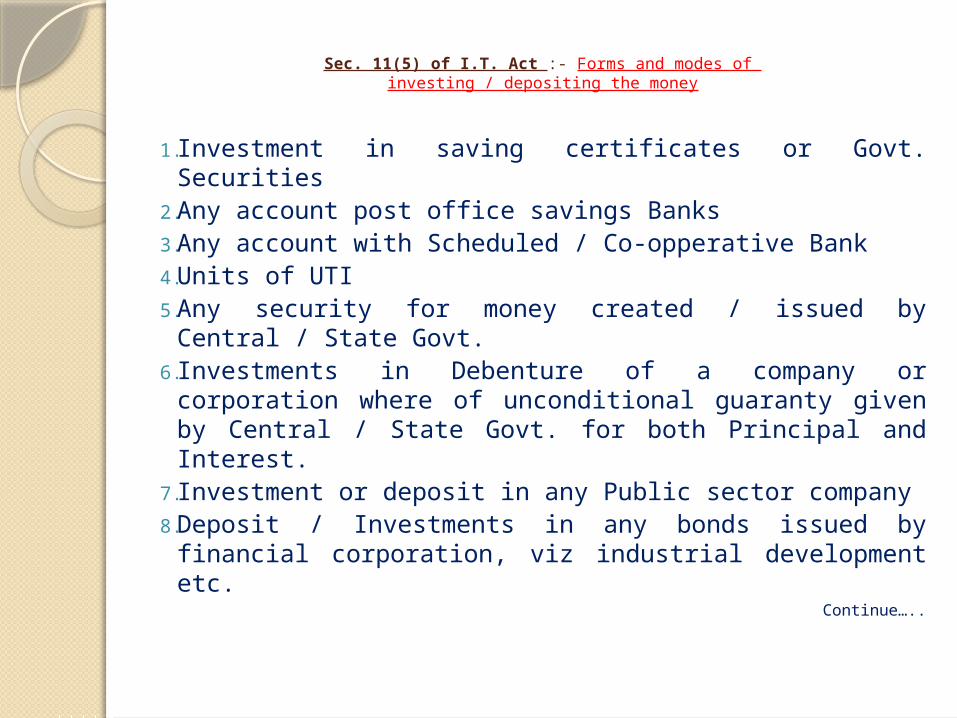

Sec. 11(5) of I.T. Act :- Forms and modes of investing / depositing the money

1.Investment in saving certificates or Govt. Securities

2.Any account post office savings Banks 3.Any account with Scheduled / Co-opperative Bank 4.Units of UTI5.Any security for money created / issued by Central / State Govt.

6.Investments in Debenture of a company or corporation where of unconditional guaranty given by Central / State Govt. for both Principal and Interest.

7.Investment or deposit in any Public sector company8.Deposit / Investments in any bonds issued by financial corporation, viz industrial development etc.

Continue…..

9.Deposit / Investment in bonds issued by Indian Public Company with the main object of providing Long Term finance for construction or purchase of houses.

10. Deposit / Investment in Indian Public Company meant for finance of Urban Infrastructure in India.

11. Investment in immovable Property 12. Deposit with Industrial Development Bank Of

India. 13. Any other from or mode of Investment or Deposit

as may be prescribed. [Rule 17C provides following modes- Mutual fund scheme u/s 10(23D) : Town planning Authority / Bodies of Central / State Govt. : Acquiring equity shares of depository : in shares of National Silk Development Corporation etc. ]

Sec. 13(1) of I.T. Act :- Exemption u/s 11 not available if

Property is held for Pvt. religious purpose & not for general Public

Income for benefit of any particular religious community or caste.

Any part of Income used for giving direct / indirect benefit to a person referred in sec. 13(3)

Any funds are invested/deposited in a manner not specified 11(5)

Any share other than share in a Public sector company/shares prescribed in sec. 11(5)

Exceptions :- Any assets forming part of corpus as on 01.01.1973Any accretion to the shares forming part of corpus,(i) above. Any bonus shares Any debentures of a company or corporation required before 01.01.1983

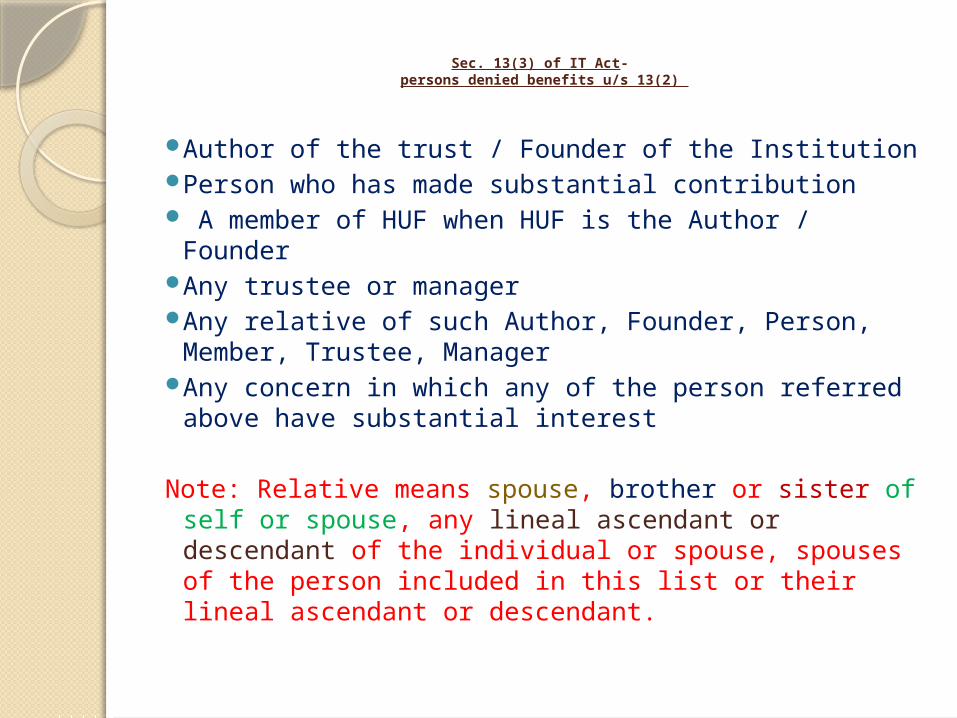

Sec. 13(3) of IT Act- persons denied benefits u/s 13(2)

Author of the trust / Founder of the Institution Person who has made substantial contribution A member of HUF when HUF is the Author / Founder

Any trustee or manager Any relative of such Author, Founder, Person, Member, Trustee, Manager

Any concern in which any of the person referred above have substantial interest

Note: Relative means spouse, brother or sister of self or spouse, any lineal ascendant or descendant of the individual or spouse, spouses of the person included in this list or their lineal ascendant or descendant.

Audit & ReturnIf the income of Educational Institution

exceeds maximum amount which is not chargeable to tax in any previous year

then

it shall get its accounts audited in respect of that year and furnish the audit report in form 10BB along with the return of income.

[Tenth Proviso to section 10(23C)].

Power of WithdrawalIf the activities of such Educational Institution are not found genuine or are not being carried out

in accordance with all or any of the conditions subject to which it was approved….

…. then the CCIT may at any time after giving reasonable opportunity of being heard withdraw the approval. [Thirteenth

Proviso to section 10(23C)].

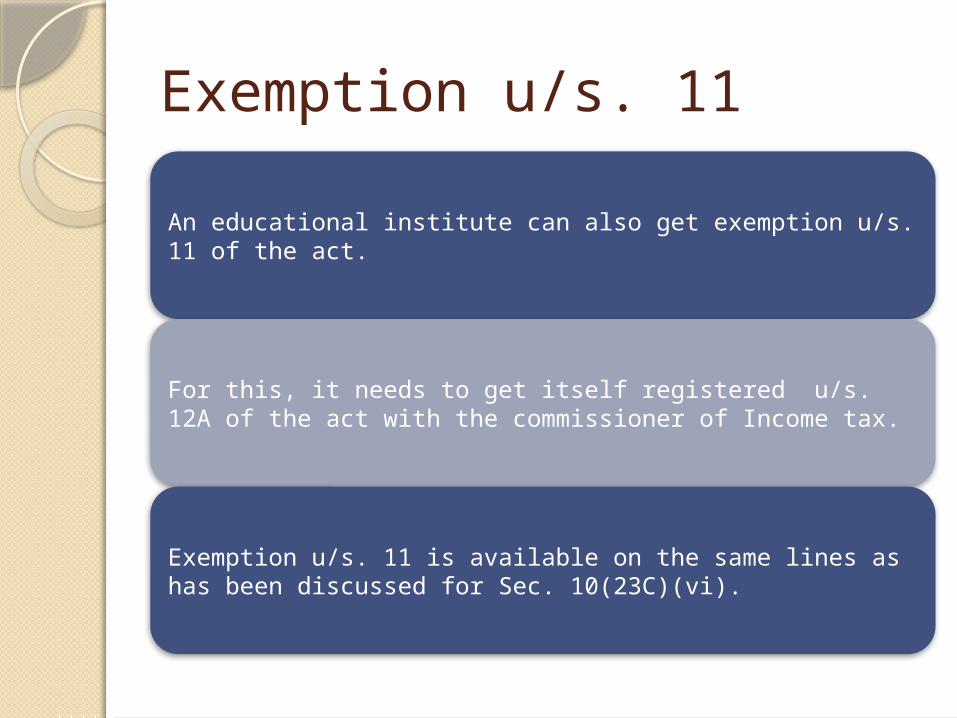

Exemption u/s. 11

An educational institute can also get exemption u/s. 11 of the act.

For this, it needs to get itself registered u/s. 12A of the act with the commissioner of Income tax.

Exemption u/s. 11 is available on the same lines as has been discussed for Sec. 10(23C)(vi).

Anonymous DonationAny anonymous donation received by any university or other educational institution referred to in section 10(23C) (iiiad) and (vi) is not eligible for any exemption.

These donations are taxable @ 30%. Anonymous donation means any voluntary contribution

where the person receiving such contribution does not maintain a record consisting of the identity of the person making such contribution indicating the name and address of the person and other prescribed particulars.

Education Loan

Interest on education loan is deductible u/s 80E, if –

◦ Loan taken by individual, spouse or children

◦ Loan taken from Bank, Financial or charitable institution

◦ No tax benefit on Principal re-payment

◦ Regular full time course or vocational / professional course after Higher Secondary

◦ Deduction allowed upto 08 years

OTHER IMPORTANT ISSUES

CCIT/DGIT have no power to condone delay Order refusing u/s 10(23C)(vi) is non- appealable

If exemption is denied to a institution / trust / fund etc. , then in W.T. , their status is individual for W.T. Computation.

While approving u/s 10(23C)(vi), only essential & reasonable conditions can be imposed, and un- warranted conditions viz not to charge any fee to beneficiary or not to collect exam fee to conduct talent exam etc.

The case laws u/s 10(22) may not be binding u/s 10(23C)(vi) on account of change in legal provisions

If exemption denied u/s 2(15) read with 11-13 for education activity, then no exemption is possible u/s 10(23C).

If exemption under 1st proviso to sec. 2(15) is denied then income become would taxable even when approval u/s 10(23C)(vi) not withdrawn

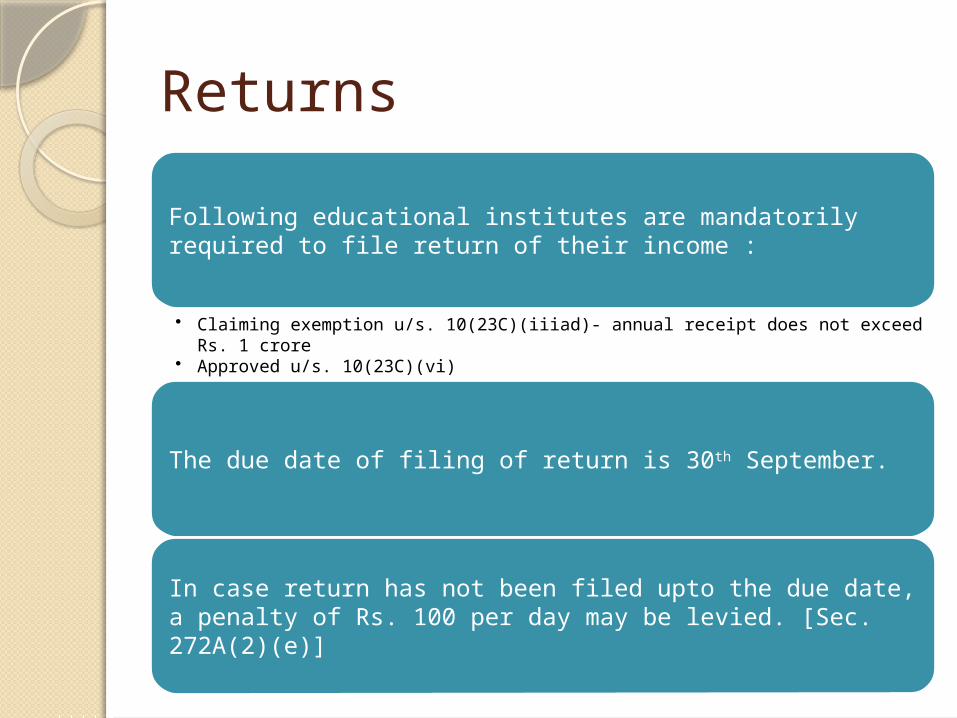

ReturnsFollowing educational institutes are mandatorily required to file return of their income :

• Claiming exemption u/s. 10(23C)(iiiad)- annual receipt does not exceed Rs. 1 crore

• Approved u/s. 10(23C)(vi)

The due date of filing of return is 30th September.

In case return has not been filed upto the due date, a penalty of Rs. 100 per day may be levied. [Sec. 272A(2)(e)]

T.D.S provisions

Even if income of an educational institute is exempt from tax, they are not automatically exempt from TD.S..

As such any person paying any money to them , which is covered by the T.D.S. provisions, shall make TDS from such payment.

E.g., Bank paying interest on FD to these institutes shall deduct tax from such interest.

To gain exemption from T.D.S., educational institutes need to apply to Assessing Officer u/s. 197.

T.D.S. from Payments made

If educational institutes make such payments, which are liable for TDS, they need to deduct tax from such at the appropriate rate.

• Salary• Contract- Construction, Security, Catering etc.• Rent• Consultancy and other professional services fees

Following are some of the payments, typically made by the educational institutes which require TDS to be made :

Direct Tax Code Bill 2010Non Profit Organization defined as

i)Established for the benefit of general public. ii)Actually carries on charitable activity during the F.Y.

iii)Actual beneficiary are general Public.

No distinction between any charitable institute or education / Medical

Tax on NPO 15%Tax on NPO refusal 30%

Method of Accountancy Cash System

Accumulation of surplus in excess of 15% (Allowed for 10 years with conditions)

Registration of NPO u/s 93 of Code

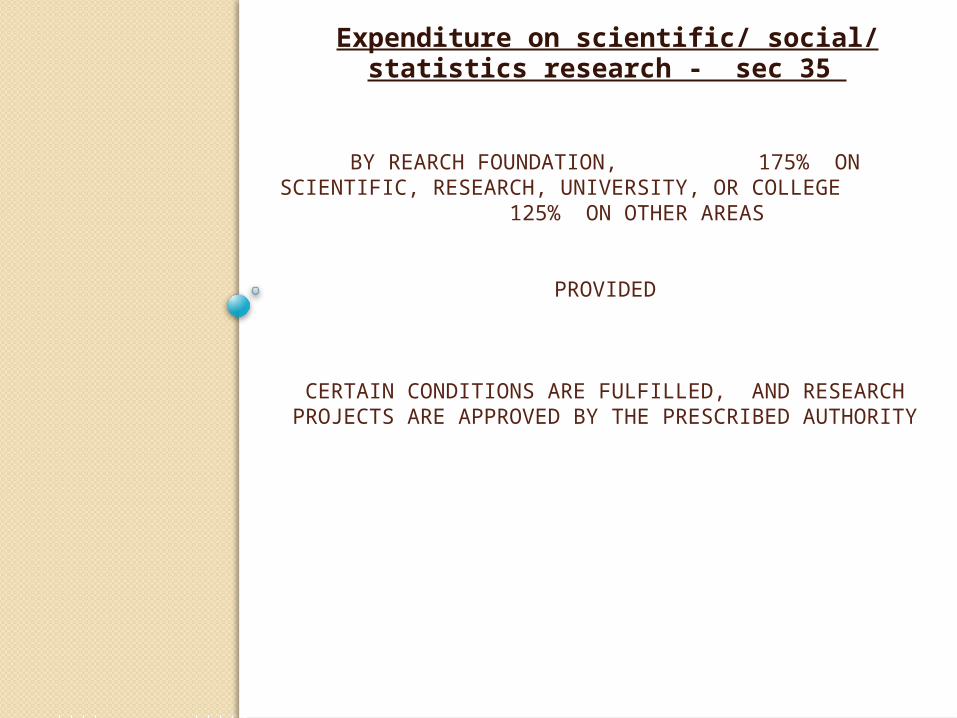

Expenditure On Scientific Research (Sec. 35)

BY REARCH FOUNDATION, 175% ON SCIENTIFIC, RESEARCH, UNIVERSITY, OR COLLEGE

125% ON OTHER AREAS

PROVIDED

CERTAIN CONDITIONS ARE FULFILLED, AND RESEARCH PROJECTS ARE APPROVED BY THE PRESCRIBED AUTHORITY

Expenditure on scientific/ social/ statistics research - sec 35

Deduction to payment for Scientific Research

Approval u/s. 35For the purpose of giving benefit to the donors, the university/ college is required to get itself approved under this section.

Application in form 3CF-II is to be filed for this purpose with commissioner of Income tax.

A copy of application is to be sent to Member (IT), Central Board of Direct Taxes.

Approval u/s. 35

On the application form, CIT may make enquiry

to examinegenuineness of the activity of the association, university, college or other institution.

CIT, within 3 months forward his recommendation to the member (IT), CBDT for approval / rejection

Government – A True Futurist

Government identified

Sectors Finance Act Relevant SectionIndustry & Hotel in Backword areas

1974 80HH

Scientific research & rural development

1980 80GGA

Export Business 1085 80HHC

Infrastructure/tele- communication development

1991 80IA

Software 1991 80HHE

Housing projects 1998 8oHHBA

Health & medical care 1996, 1997 80DD, 80DDA

Government identified Sectors Finance Act Relevant Section

Export of film software 1999 80HHF

BPO & KPO 2000 10A & 10B

Real estate 2004 80IB

Multiplex theater 2002 80IB

Stock market 2004 10(38)

Telecommunication 2001 80IA

Scientific, University college or research foundation

1989 35

Donation for scientific research

1989 80GGA

Research in social& statistics

1912 35, 80GGA

Government knowsWhat needed Infrastructure, Power, hospitals, cold storage, ware houses, packed food, housing, research and development

Where neededBackward areas, developing states, historical places,

When neededTime of investment – decide period of exemptions

Accordingly frame laws & policies

Thanks

Copyright © 2022 FDOKUMEN