Bahasa

Halaman

Hukum

30QUARTERLY ANALYTICAL REVIEW 3(48)/2012

E C O N O M I C S

w K’ fifteen yearsweremainly backed by

w v. O w 300%

20.5 1995 80 2011. A w w (F 1) w 600% 1995 2012 ( $17.5 $125). T w — w — v K’ x 28 .

Exhausting Opportunities of Extensive Growth as a Factor of Potential Macroeconomic DestabilizationVYACHESLAV DODONOV

T

Fg 1. W B USD [1]

K’ GDP ( USD) v $16.6 $178. T 10%

K v x 3% ’ GDP. T

31QUARTERLY ANALYTICAL REVIEW 3(48)/2012

E C O N O M I C S

Fg 2. C x K’ GDP 19952011 [2]

GDP, USD million

Oil

pric

e, U

SD

Brent oil price, year-end Export, USD million

w GDP x v. F 2 w betweenexports,GDPandworldoilprices,confirmingthatoilpriceshavesignificantlyinfluencedthew .

In themid-2000s another significant growth — w v w v v . Hwv 2008 w K . A v q . Y w w . I tiveexportrevenuesandtaxesdirectlyinfluence

importantindicatorsofpublicfinanceincludingthe v N B N F (F 3).

T v v w w v w . T K’ — v v w (T 1).

T K’ v xv w w w v v x v w v v . Hwv x w w — v w .

1. C w w K’ 19952011

GDP Exports International reserves of the National Bank

Assets of the National Fund

Brent oil price 0.90 0.87 0.92 0.88

180, 000

160, 000

140, 000

120, 000

100, 000

80, 000

60, 000

40, 000

20, 000

0

32QUARTERLY ANALYTICAL REVIEW 3(48)/2012

E C O N O M I C S

Fg 3. C N B’ v N F’ [3]

M v x w v . I S P B I Iv Dv R K 20102014 v “ 2014 w 85 [4]”. T M O G w 130 2020. Hwv v v — 2009 v insignificantincreasesinoilproduction(Figure4).

I 2009 76.5 2010 79.7 2011 80

2012 M O G 81 . T 5% v . Ev w 85 2014 x S P B I Iv Dv w w 1990 2000 w 6.5% ( 2009) 200% 19982009. T q w— — K .

Fg 4. Oilproduction,‘000metrictons[5]

Oil

pric

e, U

SD

Assets of the National Fund, USD millionBrent oil spot price, USD

Gross international reserves, USD million

2012

(Min

istr

y of

Oil

and

Gas

’ for

ecas

t)

60, 000

50, 000

40, 000

30, 000

20, 000

10, 000

0

90, 000

80, 000

70, 000

60, 000

50, 000

40, 000

30, 000

20, 000

10, 000

0

33QUARTERLY ANALYTICAL REVIEW 3(48)/2012

E C O N O M I C S

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Iron ores, sintered and non-sintered, ‘000 metric tons

15,886 17,675 19,281 20,303 19,471 22,263 23,834 21,486 22,281 24,016 24,736

Iron ore pellets, ‘000 metric tons

6,107 7,308 8,849 9,447 7,494 8,473 8,572 6,952 6,182 8,150 7,803

Copper ores, ‘000 metric tons

34,872 36,703 34,887 30,383 34,067 34,082 31,266 32,566 30,594 32,039 34,396

Chrome ores, ‘000 metric tons

2,046 2,370 2,928 3,287 516 4,264 4,590 4,207 4,678 5,092 5,059

Ferroalloys, ‘000 metric tons

1,130 1,235 1,401 1,447 1,530 1,614 1,703 1,590 1,469 1,702 1668

Flat rolled products, ‘000 metric tons

3,888 4,018 3,838 4,040 3,105 3,000 3,441 2,826 2,990 2,900 3108

Unpro-cessed aluminum; aluminum oxide, ‘000 metric tons

1,231 1,387 1,420 1,468 1,505 1,515 1,556 1,714 1,735 1,867 1919

Unpro-cessed lead, metric tons

158,722 162,175 133,178 157,016 135,446 115,974 117,641 105,766 80,994 103,400 111518

Unpro-cessed zinc, metric tons

277,073 286,454 294,566 316,731 357,090 364,821 358,226 365,572 327,873 318,858 319847

Unpro-cessed alloy-free refined copper, met-ric tons

425,670 452,989 432,511 445,268 418,356 427,723 406,091 398,411 312,767 323,368 338524

2. P 20012011 [7]

A K’ — (w 41% 12.1%

K’ x)— w w [6] (T 2).

F 2000 of iron and copper ores, ferroalloys, flat rolled w rates.Productionofotheritems,includingrefined . T

. T w . K Iv D C B G P Pj K K A’ C

34QUARTERLY ANALYTICAL REVIEW 3(48)/2012

E C O N O M I C S

C v w v w w 0.5% 1.7% v w 7% 8%. “A ’ v w 25 17 30 w v w q ” [8].

T w K’ 2000— w worldprices—willalsoloseitssignificanceinthex w duringthelastfifteenyears.Withouteventakinginto account the increasingly frequentfinancial x x v w w w $600 2020 x $3000 2030 400% v 20012011.

T w w x $100 (+/$20) ( w ) w. I benotedthatifthereformoftheglobalfinancial v 20082009 w v w . O mainreasonsfortheglobalfinancialturbulenceisv q w v scaleinthelasttenyears,andchangesofitsflowscausefailuresinfinancialmarkets.Ifthereform q ( w v v vv .) w v q . T x K’ x w w w v .

Ex w K’ xv w w v

v v q w:

1. T GDP w 10% 2000. I w w w 34% w w ( v ) wv w x ofthelimitedinflowofexportrevenuesandthis w ;

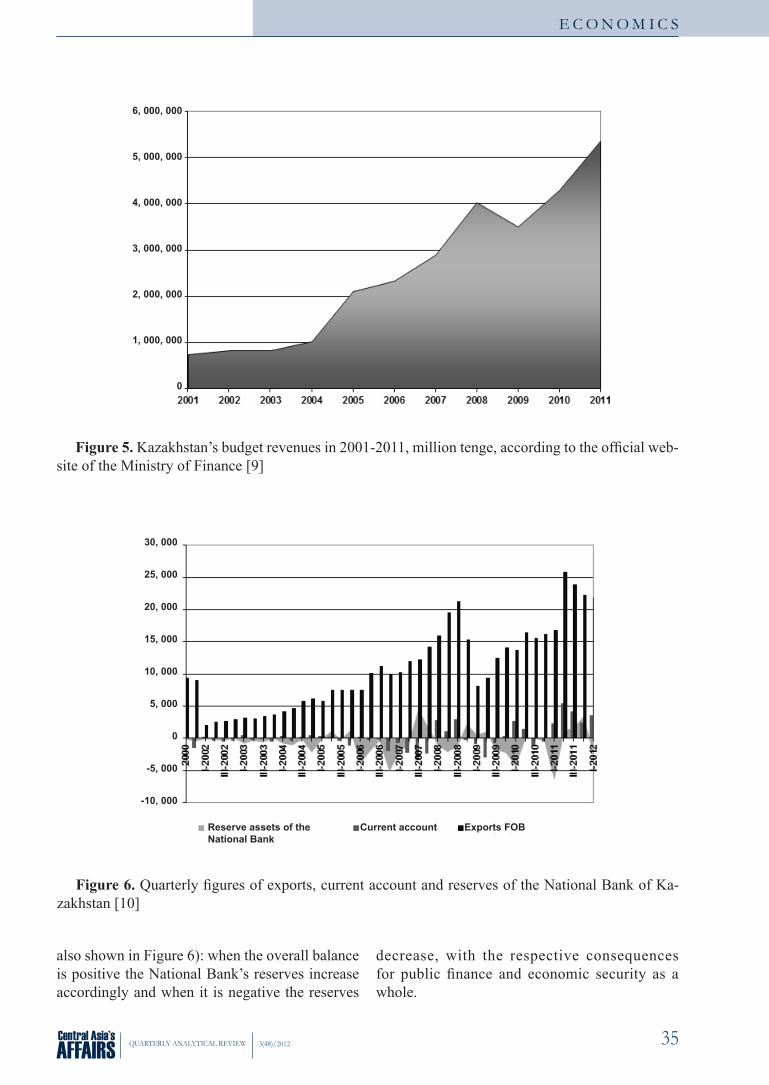

2. S v w w w 2000 w (F 5). A v w x w w w anincreaseinbudgetdeficit.Thecurrentnational 20122014 [9] v w v . Rv x 4346 2011 5311 2014 ( 22.2%) x 5170 5884 (13.8%). Hwv w w q willbedifficulttodealwithbudgetspendingand w q q N F w w ;

3. A w . T v v K’ x (F 6) w ( v x F 6 w v w w ). I v w w . T x ( 2008) v v v. T 2005 2006 2006 2007 2010 w x F 6.

T w v ornegative, isfinancedfromthereservesof theN B (

35QUARTERLY ANALYTICAL REVIEW 3(48)/2012

E C O N O M I C S

Fg 5. Kazakhstan’sbudgetrevenuesin2001-2011,milliontenge,accordingtotheofficialweb M F [9]

Reserve assets of the National Bank

Current account Exports FOB

Fg 6. Quarterlyfiguresofexports,currentaccountandreservesoftheNationalBankofKa [10]

w F 6): w v v N B’ v w v v

w v q for public finance and economic security as a w.

6, 000, 000

5, 000, 000

4, 000, 000

3, 000, 000

2, 000, 000

1, 000, 000

0

30, 000

25, 000

20, 000

15, 000

10, 000

5, 000

0

-5, 000

-10, 000

36QUARTERLY ANALYTICAL REVIEW 3(48)/2012

E C O N O M I C S

T v v v w K’ x v v w significantitemsofthebalanceofpayments—thev v — v financialtransactionsaccount,whichreflectsinternationalinvestmentflows,isunstable(Figure7).

T v v v x j ( w ) w repatriate profits abroad (and this is reflected in v ) foreignpartnerstoprovideservices(andthisinflu v ). T x ’ v

x v w w v v . I tionwhenpricesaregrowingthesefiguresremainv w — w v . International investment flows in raw-material K significantextentonexportpricesandwhenthese w v or evenflows outward, resulting in aworsened w v w.

F 7 w v q 2011 ithasremainednegativeeversince.Thisreflects

v x . F q 2011 w v v v v v v $6 N B’ v v q. F A D 2011 N B’ v $7.7 21%. T B $123 $107. A ( q 2012) v w . T w w x—w the2000spricefluctuationswerecompensatedby w x .

Fg 7. QuarterlyfiguresofkeycomponentsofKazakhstan’sbalanceofpayments[11]

Services balance

Balance of trade Balance on investment income

Capital and financial transactions account

15, 000

10, 000

5, 000

0

-5, 000

-10, 000

37QUARTERLY ANALYTICAL REVIEW 3(48)/2012

E C O N O M I C S

A w w x : v w v— v . A thingshappenatthesametimebecauseinthefirst N B w v wv x x . A w v w . T w vmentofnegativetrendssuchasincreasedinflation ’ v debt,theoutflowofcapital,andthedestabilizationofthefinancialsphere.

T x xv w K’ w w w

w ww GDP w ’ . A w x thefirstsignssuchasaslowdowninGDPgrowth w w v . T ww w bedeterminedtoasignificantextentbythespeedofthedevelopmentofnewfields,primarilyKashagan, w w xv w x. Hwv v w v w x intentofifteenyears,therefore,anewstrategyfor w v v j w v .

OURCE:

1. W OPEC C S P FOB W E Ex V (D B). E I A. ://..v

2. K’ S A T..3. N B U.S. E I A.4. S P B I Iv Dv RepublicofKazakhstan for2010-2014.Officialwebsiteof theGovernment R K: ://.v.///12

5. I v R K 19912010. K’ S A: ://.

6. K’ S A A 2012.7. D Q1 2012. JA 2012. I v R

K 19912010. K’ S A: ://.8. T N Dv D H B D K Y

Y. T. 7 J 2012.9. M P N B 20122014. M F oftheRepublicofKazakhstan:http://www.minfin.gov.kz

10. B P K: A. N B R K: ://.

11. B P K: A. N B R K: ://.

Top Related

Copyright © 2022 FDOKUMEN