Bahasa

Halaman

Hukum

DETERMINANTS OF FORMAL SOURCE OF CREDIT LOAN

REPAYMENT PERFORMANCE OF SMALLHOLDER FARMERS: THE

CASE OF NORTH WESTERN ETHIOPIA, NORTH GONDAR

M. Sc. Thesis

Amare Berhanu

November 2005

Alemaya University

DETERMINANTS OF FORMAL SOURCE OF CREDIT LOAN

REPAYMENT PERFORMANCE OF SMALLHOLDER FARMERS: THE

CASE OF NORTH WESTERN ETHIOPIA, NORTH GONDAR

A Thesis Submitted to the

Department of Agricultural Economics, School of Graduate Studies

ALEMAYA UNIVERSITY

In Partial Fulfillment of the Requirements for the Degree of

MASTER OF SCIENCE IN AGRICULTURE

(AGRICULTURAL ECONOMICS)

By

Amare Berhanu

November 2005

Alemaya University

ii

SCHOOL OF GRADUATE STUDIES

ALEMAYA UNIVERSITY

As members of examining Board of the Final MSc Open Defense, we certify that we have read

and evaluated the thesis prepared by Amare Berhanu entitled DETERMINANTS OF

FORMAL SOURCE OF CREDIT LOAN REPAYMENT PERFORMANCE OF

SMALLHOLDER FARMERS: THE CASE OF NORTH WESTERN

ETHIOPIA, NORTH GONDAR and recommended that it be accepted as fulfilling the

thesis requirement for the degree of Master of Science in Agriculture (Agricultural

Economics).

------------------------------------------- ----------------------- --------------------------

Name of Chairman Signature Date

------------------------------------------- ----------------------- --------------------------

Name of Internal Examiner Signature Date

------------------------------------------- ----------------------- --------------------------

Name of External Examiner Signature Date

Final approval and acceptance of the thesis is contingent upon the submission of the final copy

of the thesis to the Council of Graduate Studies (CGS) through the Department Graduate

Committee (DGC) of the candidate’s major department.

I hereby certify that I have read this thesis prepared under my direction and recommend that it

be accepted as fulfilling the thesis requirement.

------------------------------------------- ----------------------- --------------------------

Name of Major Advisor Signature Date

DEDICATION

To Ethiopian Smallholder Farmers

iv

STATEMENT OF AUTHOR

I hereby declare that this thesis is my bonafide work and that all sources of materials used for

this thesis have been duly acknowledged. This thesis has been submitted in partial fulfillment

of the requirements for an advanced MSc degree at Alemaya University and is deposited at the

University Library to be made available to borrowers under the rules of the library. I solemnly

declare that this thesis is not submitted to any other institution anywhere for the award of any

academic degree, diploma, or certificate.

Brief quotations from this thesis are allowable without special permission provided that

accurate acknowledgement of source is made. Requests for permission for extended quotation

from or reproduction of this manuscript in whole or in part may be granted by the Department

of Agricultural Economics the Dean of the School of Graduate Studies, Alemaya University,

when in his judgment the proposed use of the material is in the interests of scholarship. In all

other instances, however, permission must be obtained from the author.

Name: ---------------------------------- Signature: ----------------

Place: Alemaya University, Alemaya

Date of Submission: ----------------

v

ABBREVIATIONS

A.A. Addis Ababa

ACORD Agency for Co-operation in Research and Development

ACSI Amhara Credit and Saving Institution

AIDB Agricultural and Industrial Development Bank

ANRS Amhara National Regional State

BoFED Bureau of Finance and Economic Development

BoPED Bureau of Planning and Economic Development

CBE Commercial Bank of Ethiopia

CBO Community Based Organizations

CSA Central Statistics Authority

DA Development Agent

DBE Development Bank of Ethiopia

FAO Food and Agriculture Organization

FMSC Farmers Multi Service Cooperative

GDP Dross Domestic Product

Ha Hectare

IFAD International Fund for Agricultural Development

LDCs Less Developed Countries

LPM Linear Probability Model

MASL Meters Above Sea Level

MFI Micro Finance Institution

MLE Maximum Likelihood Estimates

MoFED Ministry of Finance and Economic Development

MTDP Market Town Development Program

NBE National Bank of Ethiopia

NGO Non-Governmental Organization

OLS Ordinary Least Squares

PA Peasants’ Association

vi

POCSSBO Project Office for the Creation of Small Scale Organizations

RoSCA Rotating Saving and Credit Associations

RWSEP Rural Water Supply and Environment Program

SPSS Statistical Package for Social Sciences

SRS Simple Random Sampling

SS Systematic Sampling

TLU Tropical Livestock Unit

TOL Tolerance

UNDP United Nations Development Program

UNECA United Nations Economic Commission for Africa

VIF Variance Inflation Factor

vii

BIOGRAPHY

The author was born in Addis Ababa in 1973. He completed his primary and junior secondary

education at Mekane Heiwot and Miazeya 23 Junior Secondary Schools, respectively and

attended his secondary school education at Yekatit 12 Comprehensive Secondary School

(1987-1991). After passing Ethiopian School Leaving Certificate Examination (ESLCE), he

joined the former Alemaya University of Agriculture in September 1991 and graduated with

B.Sc degree in the field of Agricultural Economics in July 1995.

Starting from September 1995 up to September 2003 he served in different governmental

organizations in Amhara region. Immediately after graduation he was assigned to work in the

then Information for Town Development Project. Then five months later he was employed as

Socio-Economic Expert of Dembia Woreda Council Office. In June 1998 he was transferred to

the Zonal Administrative Office of North Gondar and worked as an Socio-Economic Expert

until July 2002.

Finally, he was transferred to his present Organization, the Rural and Agriculture Office of

Lay Armachiho Woreda, and served as a Head of Credit and Input Desk, from September

2002 until he joined Alemaya University to pursue his postgraduate study in September 2003.

viii

ACKNOWLEDGEMENTS

First and foremost let me praise and honor the almighty God for the opportunity and capacity

given to me to realize my aspiration.

Several individuals and organizations deserve acknowledgement for their contributions to the

study. My foremost appreciation and thanks go to my major advisor, Dr. Bekabil Fuffa for his

close supervision and professional advice and encouragement during the research work. My

heart-felt thanks also go to my co-advisor, Ato Gizachew Ashagrie, for his invaluable

comments and professional advice throughout the course of the research work. He also

deserves especial gratitude for permitting me to use Internet services of Gondar University for

this study.

I would also like to carry my gratitude to Amhara Region Agricultural Research Institute and

Integrated Livestock Development Project for providing me with financial and logistics

support during the process of data collection. In addition, I would like to thank staff members

of Gondar University, ILDP, North Gondar Administrative Zone Office and North Gondar

Rural Development and Agricultural Branch Office for their friendly and dedicated co-

operation. I am indebted to Dr. Belayneh Legesse, Dr. Edelegnaw Walle, Ato Mule Tarekegn,

Ato Megabiaw Tassew, Ato Bekele Hunde, Ato Tesfaye Kebede, Ato Tekeba Yalew for their

invaluable comments, encouragement and advice during the course of my study. My special

thanks are given to my wife, W/ro Asegedech Tezera and our families for their invaluable

encouragement throughout the study period.

My special gratitude goes to the members of the sample farm households, who responded to

numerous questions during the peak time of agricultural activity in the area, some of which

touched on very sensitive issues, such as their possession of assets, access to credit, and level

of debt.

ix

TABLE OF CONTENTS

DEDICATION ......................................................................................................................... iii

STATEMENT OF AUTHOR..................................................................................................iv

ABBREVIATIONS....................................................................................................................v

BIOGRAPHY...........................................................................................................................vii

ACKNOWLEDGEMENTS .................................................................................................. viii

LIST OF TABLES....................................................................................................................xi

LIST OF FIGURES.................................................................................................................xii

LIST OF APPENDICES....................................................................................................... xiii

ABSTRACT..............................................................................................................................xiv

INTRODUCTION .....................................................................................................................1

1.1. Background .....................................................................................................................1

1.2. Statement of the Problem...............................................................................................4

1.3. Objectives of the Study...................................................................................................6

1.4. Significance of the Study................................................................................................7

1.5. Scope and Limitations of the Study ..............................................................................7

1.6. Organization of the Thesis .............................................................................................8

2. LITERATURE REVIEW.....................................................................................................9

2.1. Definition and Theoretical Perspectives of Credit Market.........................................9

2.1.1. Definition and concepts of credit............................................................................9

2.1.2. The Need for Credit...............................................................................................10

2.1.3. Theoretical perspective of credit market.............................................................11

2.1.4. Rural credit, moral hazard and adverse selection..............................................13

2.1.4.1. Adverse selection.............................................................................................15

2.1.4.2. Moral hazard...................................................................................................16

2.2. Situation of Rural Finance in Ethiopia.......................................................................16

2.2.1. The emergence and evolution of formal credit in Ethiopia ...............................17

2.2.1.1. Rural credit before 1975 ................................................................................17

2.2.1.2. Rural credit during the Dergue period.........................................................20

2.2.1.3. Rural credit after the reform period.............................................................21

x

2.2.2. Formal financial institutions in Ethiopia.............................................................23

2.2.2.1. Amhara Credit and Saving Institutions (ACSI) ..........................................24

2.2.2.2.Cooperatives in Ethiopia.................................................................................25

2.2.3. Informal financial sector in Ethiopia...................................................................27

2.3. Empirical studies on loan recovery and defaults......................................................28

3. METHODOLOGY..............................................................................................................33

3.1. Description of the Study Area .....................................................................................33

3.1.1 Amhara National Regional State...........................................................................33

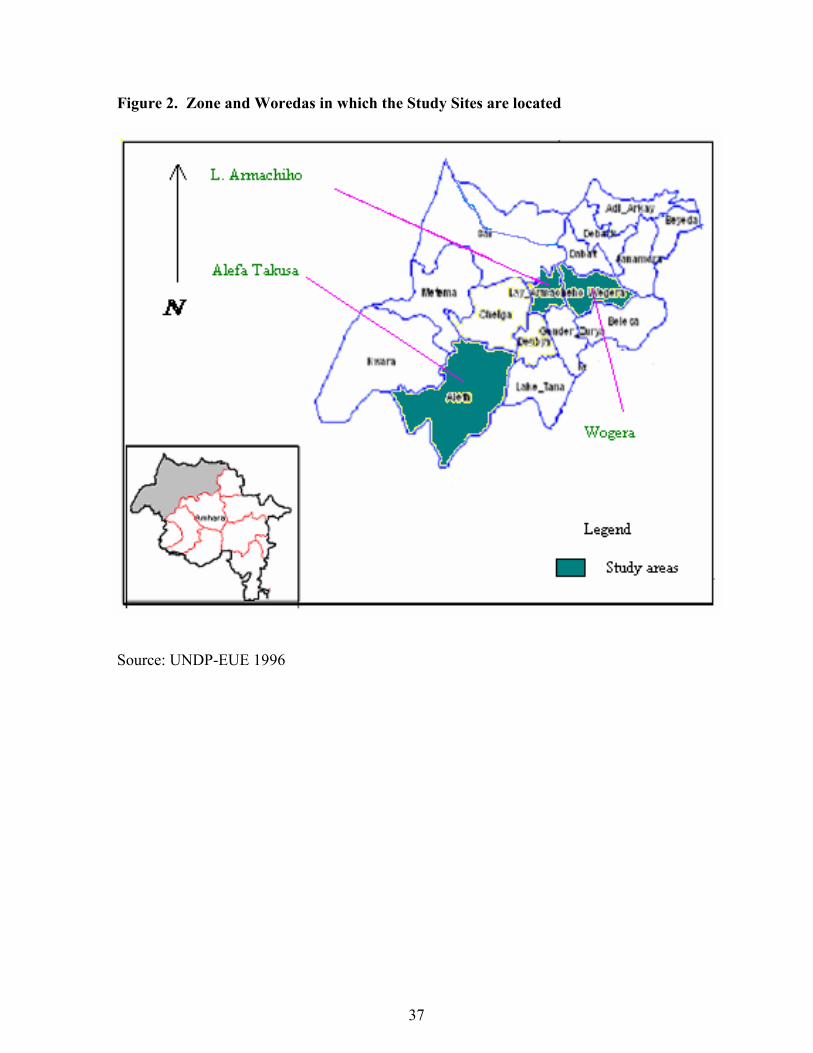

3.1.2. North Gondar Administrative Zone ....................................................................35

3.1.2.1. Population characteristics..............................................................................35

3.1.2.2. Farming system...............................................................................................35

3.1.2.3. Climate and topography ................................................................................36

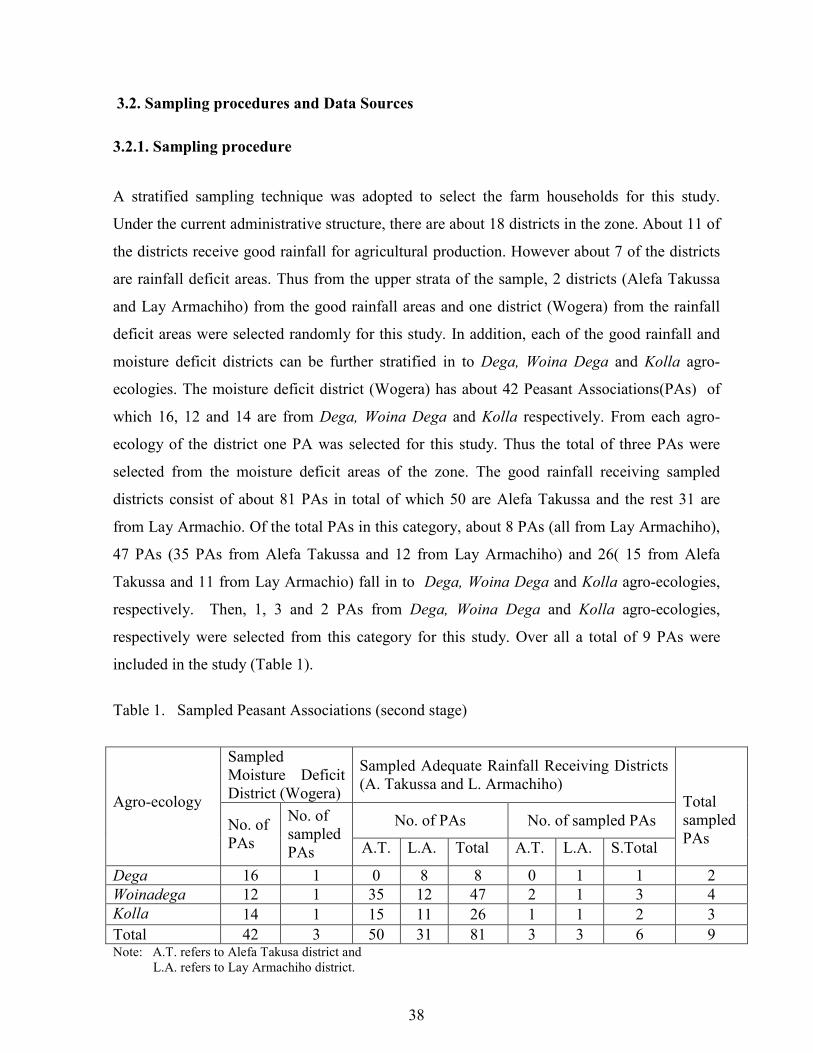

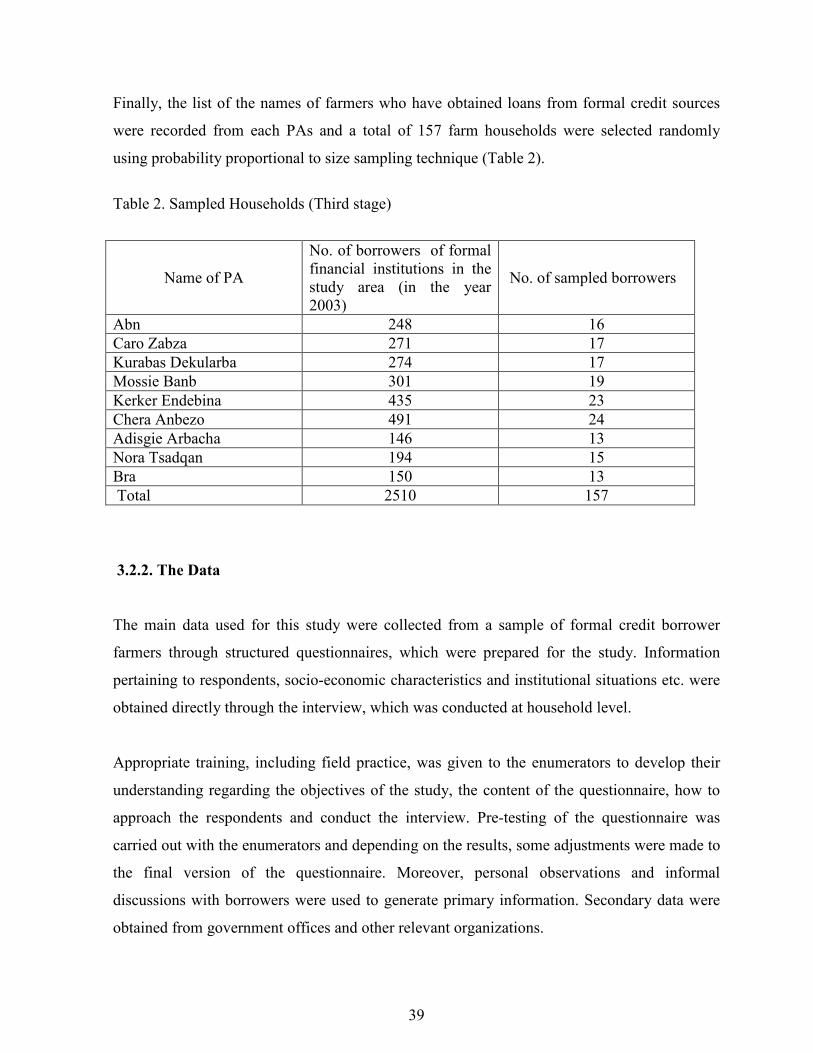

3.2. Sampling procedures and Data Sources.....................................................................38

3.2.1. Sampling procedure ..............................................................................................38

3.3. Variable Specification and Hypotheses ......................................................................40

3.4. Methods of Data Analysis ............................................................................................44

3.4.1. Descriptive statistics ..............................................................................................44

3.4.2. Econometric model ................................................................................................44

4. RESULTS AND DISCUSSION..........................................................................................49

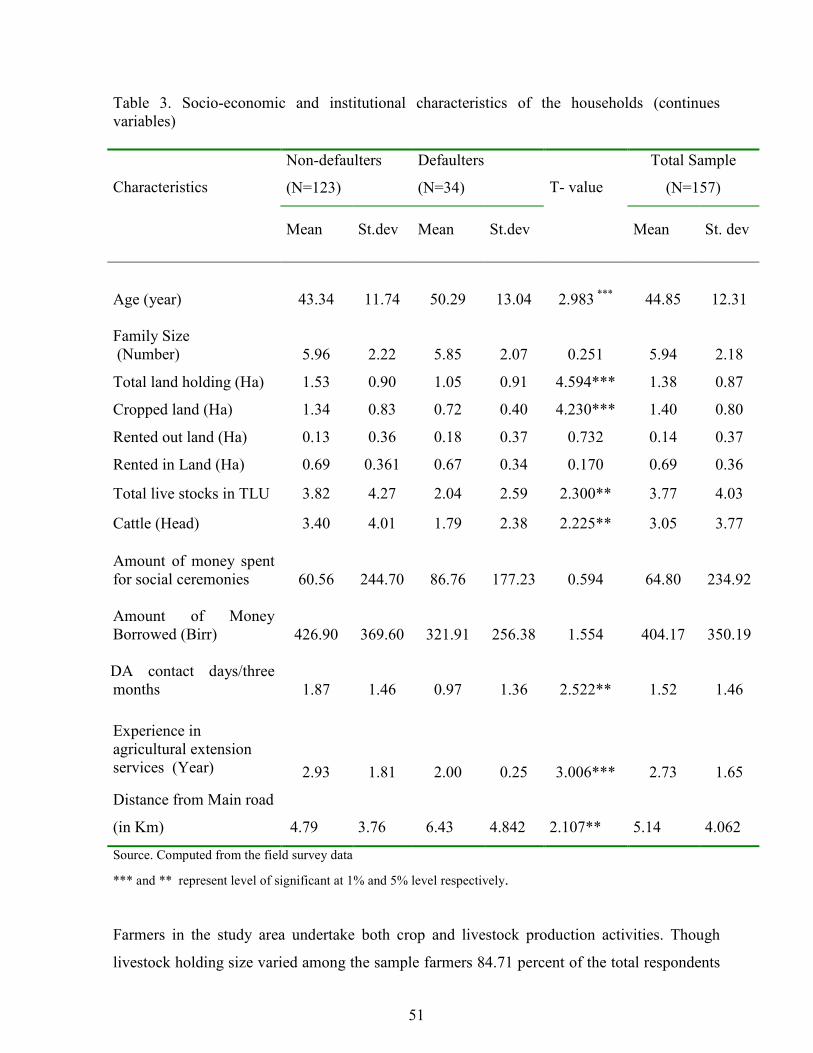

4.1. Results of Descriptive Statistics Analysis ...................................................................49

4.1.1 Source of Credit ......................................................................................................54

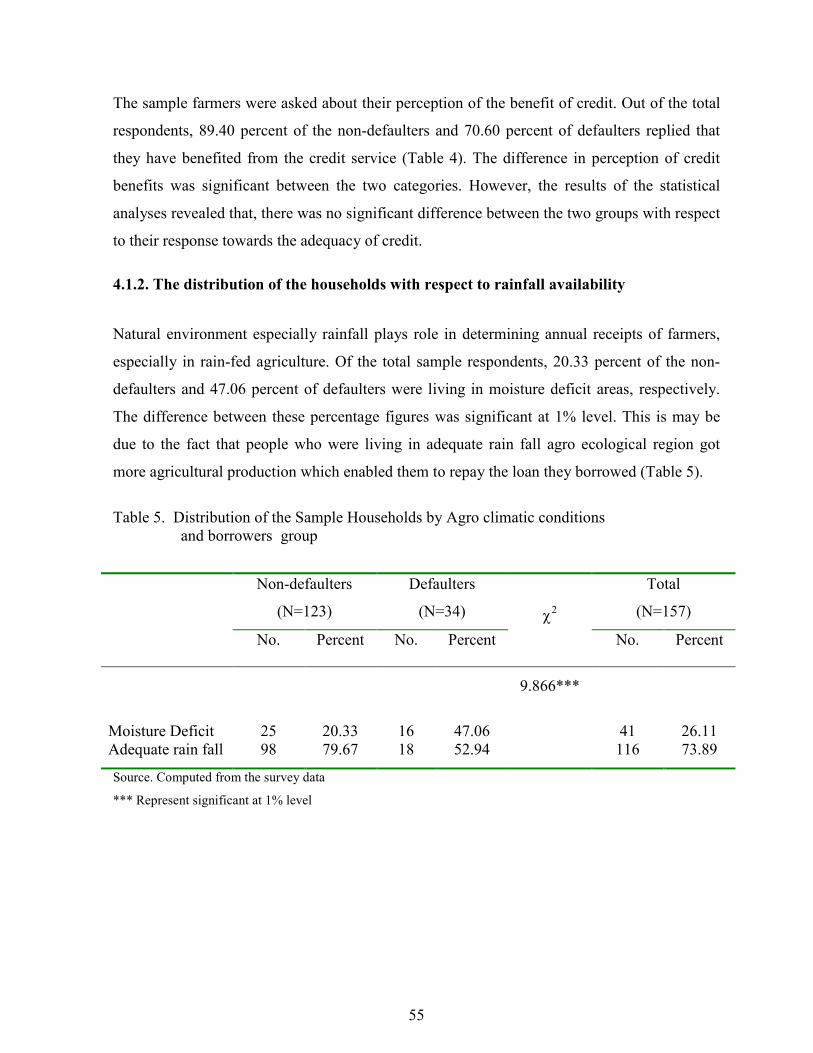

4.1.2. The distribution of the households with respect to rainfall availability...........55

4.1.3. Major agricultural production problems in the area.........................................56

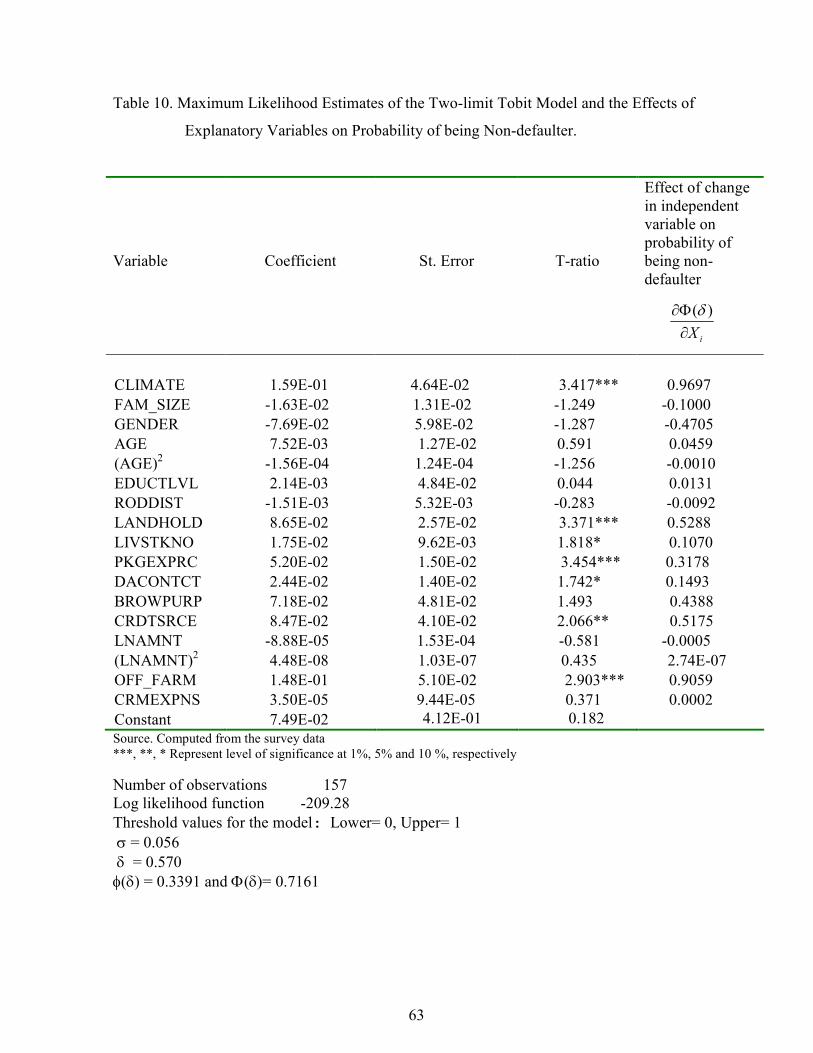

4.2. Results of the Econometric Model ..............................................................................57

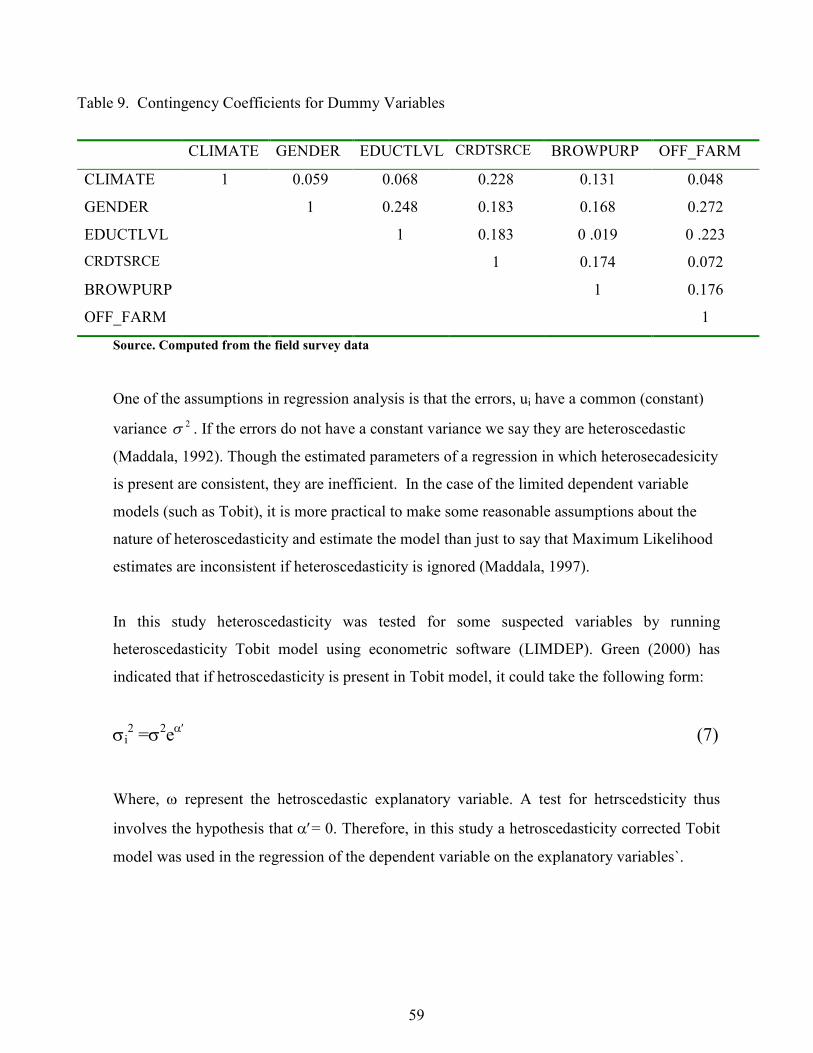

4.2.1. Multicollinearity and Hetroscedasticity Diagnosis.............................................57

4.2.2. Determinants of probability of being non-defaulter and degree of loan

recovery ............................................................................................................................60

5. CONCLUSIONS AND POLICY IMPLICATIONS ........................................................65

6. REFERENCES ....................................................................................................................68

7. APPENDICES......................................................................................................................76

xi

LIST OF TABLES

Table 1. Sampled Peasant Associations (second stage) ...........................................................38

Table 2. Sampled Households (Third stage) ............................................................................39

Table 3. Socio-economic and institutional characteristics of the households (continues

variables) ...........................................................................................................................51

Table 4. Socio-economic and institutional characteristics of the sample households (discrete

variables)…………………………………………………………………………………54

Table 5. Distribution of the Sample Households by Agro climatic conditions........................55

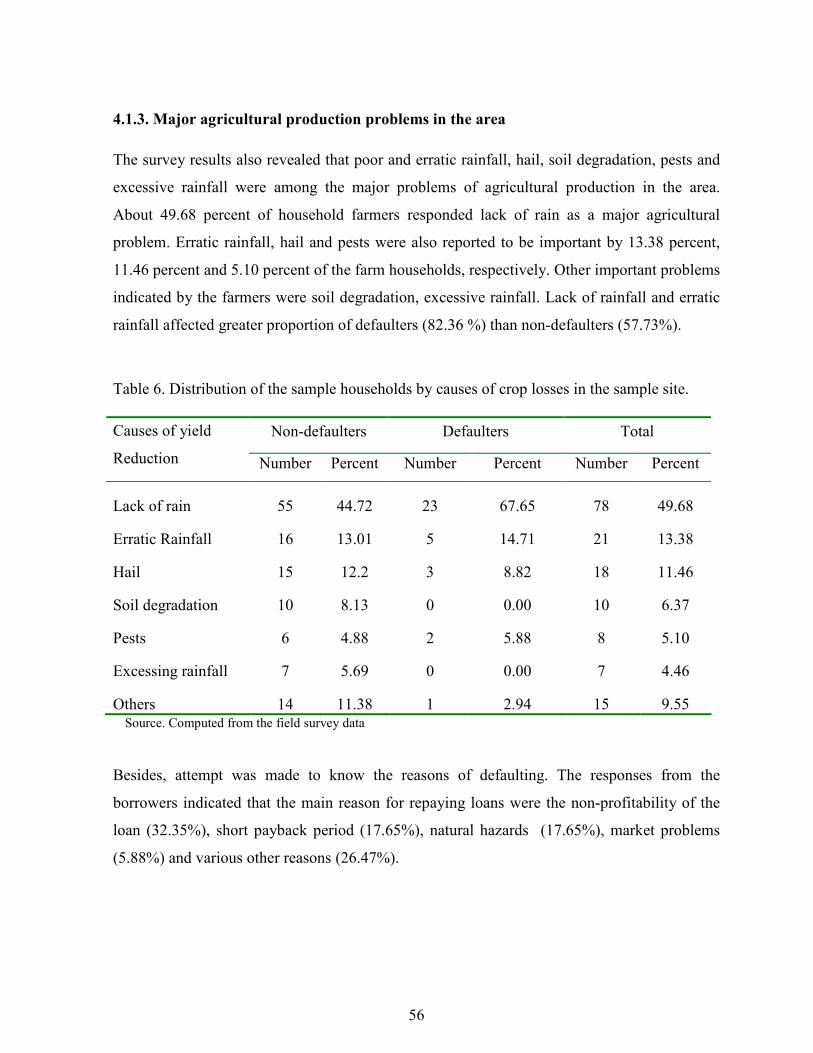

Table 6. Distribution of the sample households by causes of crop losses in the sample site. ..56

Table 7. Borrowers' responses on main reason for not repaying the loan ................................57

Table 8. VIF of the Continuous Explanatory Variables used in the study ...............................58

Table 9. Contingency Coefficients for Dummy Variables .......................................................59

Table 10. Maximum Likelihood Estimates of the Two-limit Tobit Model and the Effects of

Explanatory Variables on Probability of being Non-defaulter…………………………..63

Table 11. Marginal effects of Independent variables on rate of repayment ..............................64

xii

LIST OF FIGURES

Figure 1. Location of ANRS in Ethiopia 34

Figure 2. Zone and Woredas in which the Study Sites are located 37

xiii

LIST OF APPENDICES

Appendix 1. Capital and Branch Network of the Banking System in Ethiopia ........................77

Appendix 2. Branch Network of Insurance Companies ...........................................................77

Appendix 3. Micro Finance Institutions Operating in Ethiopia as of June 2003 (NBE)..........78

Appendix 4. Conversion Factors for Livestock Units ..............................................................79

Appendix 5. Survey Questionnaire............................................................................................80

xiv

DETERMINANTS OF FORMAL SOURCE OF CREDIT LOAN

REPAYMENT PERFORMANCE OF SMALLHOLDER FARMERS: THE

CASE OF NORTH WESTERN ETHIOPIA, NORTH GONDAR

By: Amare Berhanu

ABSTRACT

Delivering productive credit to the rural poor has been a hotly pursued but problem-plagued

undertaking. No other concern than loan default has an acute effect on the success of credit

programs in rural areas. Loan default is a crucial problem of rural financial services.

Therefore, the major concern of this study was to identify the major socio-economic,

institutional and natural factors that affect loan repayment capacity of smallholder farmers in

North Gondar of Amahara regional state. The main data used for this study were collected

from a sample of formal credit borrower farmers in the zone through structured questionnaire.

A total of 157 farm households cases were included in the final analysis. In addition,

secondary data were collected from different organizations and pertinent publication in order

to elaborate the present situation of rural credit in Ethiopia. Two-limit Tobit model was

employed to analyze factors influencing loan repayment and intensity of loan recovery among

smallholder farmers in the zone. A total of seventeen explanatory variables were included in

the model of which seven variables were found to be significant. These were agro ecology of

the study area, size of land holding, total number of livestock, number of years of experience

in agricultural extension services, number of extension contact days, credit source, and

income from off-farm activities. Therefore, consideration of these factors is vital as it provides

information that would enable to undertake effective measures with the aim of improving loan

repayment in the zone. It would also enable lenders and policy makers to have information as

to where and how to channel efforts in order to minimize loan default.

INTRODUCTION

1.1. Background

Ethiopia is a landlocked country in the horn of Africa, bounded by Eritrea in the North, in the

West by Sudan, in the South by Kenya and in the East by Somalia and Djibouti. It lies within

the tropics between 3°24` and 14°53` North; and 32°42` and 48°12` East. The country covers

1,120,000 square kilometers and the population is estimated at about 77 million in 2005,

which makes it the third most populous country in Africa. Ethiopia has reasonably good

resource potential for agricultural development- biodiversity, water resources, minerals, etc.

Yet, it is faced with complex poverty, which is broad, deep, and structural. The proportion of

the population below the poverty line is 44 per cent in 1999/2000 (MoFED, 2002)

In spite of the huge agricultural potential, the growth in agricultural production has not been

able to keep pace with that of the demand. Great proportion of cultivated land is held by

subsistence farmers who produce about 97% of the national agricultural output (Welday,

1999). The small-scale farmers, however, produce a little ‘surplus’ over their requirement and,

hence, could not adequately feed the population out of the agricultural sector. Experiences

over the past four decades had shown that in drought affected years farmers are the ones who

suffer from hunger /famine.

The contributing factors to the low level of productivity are many but poor and backward

technology is the principal one. Production methods have remained unchanged for thousands

of years. Times and methods of sowing crops are the same as those mentioned in the books

explaining the history of Ethiopia; the implements and tools for tilling, harvesting, threshing,

and winnowing are identical with, if improved a little better than, those described in the

ancient books. In brief, Ethiopia’s agriculture is characterized by extremely limited capital

resources, the use of traditional methods of production and, thus, low productivity of resources

2

involved in the production process. These characteristics tend to perpetuate the existing

situation whereby agriculture has not been able to feed the country's fast-growing population

and cannot therefore make a substantial contribution to economic growth.

According to Timmer (1988), the first step for economic development is 'getting agriculture

moving'. Moshar (1966) has classified the facilities and services involved in the modernization

of agriculture into two groups viz. the essentials and the accelerators. The former, as the name

implies, must be present to enable a farmer to adopt an innovation; and the latter are those that

may be important to get an innovation adopted. Credit is one of the five accelerators that

Mosher (1966) listed.

With introduction of new production technologies, the financial needs of farmers have

increased manifold in Ethiopia. Steady agricultural development depends upon the continuous

increase in farm investment. Most of the time, especially during the take-off stage of

agricultural development, heavy investment cannot be made by the farmers out of their own

funds because of their present level of incomes. Moreover, there exists no significant margin

of income that can be channeled into the agricultural sector to undertake development

activities. Thus, here comes the importance and significance of the availability of rural credit

to bridge the gap between owned and required capital (Singh et al., 1985).

It is important, however, that these borrowed funds be invested for productive purposes and

generate additional income to be repaid to the lending institutions to have sustainable and

viable production process. But increase in default rate is one of the major problems of lending

institutions (Singh et al., 1985). According to Bekele (2001), in Ethiopia loan repayment was

not a serious problem prior to 1990 and became a serious issue after 1990. For instance, it has

been reported that loan recovery ratio in Ethiopia declined from 54% in 1990 to 37% in 1991

and further dropped to 15% in 1992.

Delivering productive credit to the rural poor has been a hotly pursued but problem plagued

undertaking. Providing low –cost, efficient credit services and recovering a high percentage of

loans granted are the ideal aims in rural finance (Wenner, 1995). This is because low

repayment performance discourages the lender to promote and extend credit to large and

fragmented farm households. Therefore, a thorough investigation of the various aspects of

3

loan defaults, source of credit and condition of loan provision are of great importance both for

policy makers and lending institutions. Hence, this study was undertaken to analyze the

determinants of loan repayment from formal sources in North Gondar Administrative Zone.

4

1.2. Statement of the Problem

In the subsistence agriculture and low-income countries like Ethiopia, where smallholder

farming dominates the overall national economy, smallholder farmers are facing severe

shortage of financial resources to purchase productive agricultural inputs. The price of inputs

is going up every year. Consequently, the dependence of the subsistence farmers on financial

institutions for credit has become substantially higher nowadays.

Failure by farmers to repay their loans in time or to repay them at all is a serious problem

facing both agricultural credit institutions and smallholder farmers. According to Hunte

(1996), loan default is a tragedy because failing to implement appropriate lending strategies

and credible credit policies often result in demise of credit institutions.

The Amhara National Regional State (ANRS) is amongst the ten autonomous regions of the

Federal Democratic Republic of Ethiopia. It is the second largely populated region of the

country next to Oromia. According to population projection of BoFED for the year 2003, the

total population of the region is estimated to be 17,687,760. The agricultural sector employs

90% of the working force and contributes 65.8% to the regional GDP. Majority of the

community is involved in mixed farming. Cereals are the predominant agriculture produce

accounting for 74% of the total cultivated land and 83% of the grain production (RWSEP,

2001). Widespread poverty and food insecurity are prevalent in many parts of the region. Lack

of well-established and sustainable financial institutions is one of the root causes of acute

poverty in the rural areas of the region. Lack of access to financial services makes the rural

households to be less acceptable of new technologies leading to low agricultural productivity

and food security.

In North Gonder Zone the Regional Government and Non-Governmental organizations extend

credit facilities to farming households to narrow the gap between the required and the owned

capital to use improved agricultural technologies that would increase production and

productivity. However, there is a series loan repayment problem in the area. For instance,

according to North Gondar Rural Development Office second Quarter Report (2003/2004);

about 8.3 million Birr loan, which was given from 1996 to 2002, has not been repaid.

5

Although there are such severe problems, factors that affect loan repayment performance of

small holders from formal sources have not been studied in the area.

Therefore, this study was initiated with the main objective of analyzing the determinants of

formal source of credit loan repayment performance of smallholder farmers in North Gondar

Administrative Zone.

6

1.3. Objectives of the Study

Te general objective of this study is to analyze the extent to which formal source of credit non-

default and default rates are associated with different personal, socio-economic and

institutional characteristic of farm households in Gondar Zone of Amhara Region.

The specific objectives are:

1. To identify the sources of credit and purpose of the loan among smallholder farmers in the

zone.

2. To determine the extent of defaults in the repayment of formal source of credit loans offered

to smallholder farmers in the study area.

3. To identify factors which affect formal source of credit loan repayment performance of

smallholders in the zone and determine their relative importance.

7

1.4. Significance of the Study

Funds extended for the purpose of augmenting capital of small farmers should be used for the

intended goal and finally be repaid to the lending institution in order to have viable, strong and

sustainable agricultural credit schemes and efficient operation mechanisms year after year.

Contrary to this fact, it has been reported in various literatures that loan default is a critical

problem of formal financial institutions in Ethiopia. Nonetheless, little has been attempted in

identifying specific important factors that should be treated to reduce this national problem.

Therefore, studies on the factors which affect loan repayment performance are vital to enable

governmental and non governmental financial institutions, policy makers, policy

implementers, as well as borrowers to have knowledge as to where and how to channel efforts

in order to minimize loan defaults and help to design successful credit programs in the study

area and outside of it. Moreover, the study would provide micro level information for those

who would like to conduct detailed and comprehensive studies on rural credit.

1.5. Scope and Limitations of the Study

This study was conducted in Gondar Zone of Amhara Regional State in Ethiopia. As stated in

the objectives, the main aim of this study is to identify important demographic, scio-economic

and institutional factors that affect loan repayment performance of smallholder farmers that

borrowed from formal credit sources. Accordingly, the study was conducted in three districts

of the zone and 157 randomly selected households that were users of credit from formal

sources during the 2003 agricultural production year were included in the study. Primary data

on the above main categories of variables were collected using structured questionnaire.

Descriptive statistics and two-limit Tobit econometric model were used to analyze the

primary data collected. Sixteen independent and one dependent, variables were selected for

analytical purpose.

This study is concerned with the analysis of the main determinants of formal credit source loan

repayment performance of North Gondar Administrative Zone small-scale farmers and did not

consider the loan repayment performance of the farmers in the area from informal credit

8

sources. However, the analysis of the loan repayment performance of the farmers from

informal credit sources could generate useful information that might help in channeling

financial resources to the farmers of the zone. Future research topics focusing on this could

thus generate useful information for policy makers, lending institutions and other stakeholders

working in rural development areas.

1.6. Organization of the Thesis

The remaining parts of the thesis are organized as follows. Chapter two presents review of

literature that includes definitions of concepts, the need for credit, overview of the financial

system in Ethiopia and empirical studies on loan repayment performance. Chapter three

presents the research methodologies employed in the study. Results obtained are presented and

discussed in detail in chapter four. Finally, chapter five presents summary and policy

implications of the research.

9

2. LITERATURE REVIEW

Conceptual and Analytical Models of Credit repayment as well as knowledge of past research

endeavors are essential for detailed analysis of determinants of loan repayment. In this chapter,

definitions of important terms of credit and finance, emergence and evolution of credit market

in Ethiopia, empirical studies on determinants of loan repayment at the global as well as at

country level are presented.

2.1. Definition and Theoretical Perspectives of Credit Market

2.1.1. Definition and concepts of credit

The Concise Mc Graw-Hill Dictionary of Modern Economics defines credit as an exchange of

goods and services for a promise of the future payment. It also indicates that credit is

necessary in a dynamic economy because of the time that elapses between the production of a

good and its ultimate sale and consumption and credit bridges this gap. The risk in extending

credit is the probability that future payment by the borrower will not be made (Greenwal &

Associates, 1983).

Financial institutions are private or governmental organizations, which serve the purpose of

accumulating funds from savers and channeling them to individual households, and business

looking for credit. Financial institutions are composed of deposit-type institutions (bank and

non-bank contractual saving institutions), personal and business financial companies,

government and quasi-government agencies, and miscellaneous lenders. Financial institutions

that receive funds from savers and lend them to borrowers are called financial intermediaries.

In broad sense, the term financial intermediary is applicable to all financial institutions

including commercial banks. These intermediaries pool money from savers and channel them

to individuals, mutual saving banks, saving and loan associations, insurance companies, and

pension trusts. In narrow sense, however, it excludes commercial banks (Greenwald &

Assocates, 1983). Formal financial institutions can be defined as institutions that are regulated

10

by central bank supervisory authorities for licensing and credit policy implementations. They

usually use legal documentation or the legal system to enforce their regulations.

2.1.2. The Need for Credit

Credit is the key means to have access to inputs in many development programs. This is

particularly true for rural development because so long as sufficient credit is not provided to

the development programs of weaker sections of the society, the goal of development may not

be achieved.

As a result of high population pressure in rural areas of developing countries, like Ethiopia,

increasing of additional productive land is difficult implying the need of improving farm level

productivity through intensification. This involves as pointed out by Jama and Kulundu

(1992), use of improved farm inputs such as fertilizers and improved seeds besides improved

tillage and husbandry practices. These inputs are not available on the farm and some farmers

are not able to purchase them due to lack of finance. Moreover, most of the commercial inputs

are expensive and hence smallholder farmers cannot afford to buy them from their own cash

earnings. It is, therefore, generally acknowledged that agricultural credit to smallholder

farmers can help to improve their farm productivity through use of improved farm inputs.

A number of researchers (Adams &Graham, 1981; Gongalez-Vega, 1977; FAO, 1996)

reported the requirement of credit facilities to small holders of less developed countries

(LDCs) for production and consumption smoothing. Governments of LDCs and aid agencies

have spent a large amount of money to this sector. The motivation has been the belief that

loans are an essential part of various input packages that were prescribed as part of agricultural

investment projects designed to introduce modern technologies and thus stimulate change and

growth in agriculture.

Kumer et al. (1978) from India also indicated that the needs for credit in the case of majority

of cultivators arises from inadequate savings to finance various activities on their farm.

Moreover, while their income accrues during limited period of the year, their expenses are

11

spread throughout the year. This implies that expenditure on inputs have to be incurred much

in advance of the income from resulting outputs. Producers meet these expenditures out of

their past savings and when these savings fall short of the requirement, they borrow if they

could manage getting. Some studies in Ethiopia showed that credit increased productivity in

agriculture by enabling farmers to adopt improved technologies. For instance, the study by

Wolday (1999) showed that farmers who had access to credit were more likely to use

improved seeds than those who had no access to credit.

According to Kebede (1995), credit makes traditional agriculture more productive through the

purchase of farm equipment and other agricultural inputs, the introduction of modern irrigation

system and other technological developments. Credit can also be used as an instrument for

market stability. Rural farmers can build their bargaining power by establishing storage

facilities and providing transport system acquired through credit. Credit plays a key role in

covering consumption deficits of farm households. This would, in turn, enable the farm family

to work efficiently in agricultural activities. Credit can farther be used as an income transfer

mechanism to remove the inequalities in income distribution among the small, middle, and big

farmers. Moreover, credit encourages savings and savings held with rural financial institutions

that could be channeled to farmers for use in agricultural production. Credit also creates

employment opportunities for rural farmers.

Rural households in Ethiopia need credit for investment in a range of on-farm, off-farm and

off_farm activities. There is potentially a huge demand for credit from 10-12 million rural

families, which is hardly met at present (IFAD, 2001). Most productive activities are seasonal

and there is equally strong credit demand for consumption smoothing.

2.1.3. Theoretical perspective of credit market

A major economic problem in developing countries is financial intermediation, the

mobilization of capital from one group (savers/lenders) and its simultaneous allocation to meet

the needs of another group (borrowers/entrepreneurs) (Christensen, 1993). Critical for efficient

capital mobilization and allocation, financial intermediation can be performed through various

forms of instrument. The three most important ones are equities (stocks), long-term (bonds),

and short-term loans (credit) (Stiglitz, 1989). In most developing countries, because of the

12

relative under-development of first two forms of instruments, credit markets for short term

loans become the major means of financial intermediation. The capital mobilization function

of credit markets is, however, constrained by several factors. First when there is a lack of

macroeconomic stability, as experienced by many Latin American countries during the 1970s

and 1980s, people prefer to invest in fixed assets- real estate, jewelry, etc… or to save in

foreign currencies overseas, instead of depositing local currencies in domestic institutions.

Second, savers are willing to deposit money in saving institutions only if they believe that they

will be able to withdraw the money according to pre specified terms. The risk of bank closure

and the availability of deposit insurance become important considerations for potential

depositors. In many countries, governments establish banking regulations such as capital and

reserve requirement to ensure the ability of banks to meet withdrawal demand.

Third, government regulations create opportunities for political abuses. In some developing

countries, for example: banking system is tightly controlled by government officials who see it

as a convenient source of cheap credit for their own expenditure projects and their favored

political clients ( Hanke and Walters, 1991). Offering mostly negative real interest rates to

depositors, the banking system is not an attractive saving avenue for most people (McKinnon,

1973). The limitation of the formal banking system may be compensated by informal credit

arrangements that offer higher returns for depositors, but these informal arrangements are

usually limited in scale and lack legal protection for depositors.

In addition to overcoming obstacles for capital mobilization, credit markets need to overcome

information problems associated with credit allocation (Stiglitz, 1989). First, because of the

potential for default, lenders need to solve the selection problem-screening loan applications

based not just on how much interest the borrowers are willing to pay, but another probability

of default. Second, enforcement problems related to the ability of lenders to ensure that

borrowers will actually repay principals and interests at specific times. Third, loan counteracts

need to include a variety of provisions other than interest rates. Non-price terms such as

collateral and other kinds of restrictive covenants, like market interlinkage, are often needed to

create appropriate incentives for loan repayment.

13

2.1.4. Rural credit, moral hazard and adverse selection

According to Conning and Udry (2005), contracting under asymmetric information lead to

several obvious questions such as, as to why the financial markets and risk sharing

arrangements often fail to achieve efficient exchange even in small village communities, as to

what explains the structure and organization of actual financial markets and why are

diversified outside financial intermediaries such as banks and insurance companies often

reluctant or slow to enter rural financial markets.

Accordingly, the defining characteristic of all financial contracts is that they involve the

exchange of state-contingent promises. But the fear that promises may be broken can limit the

set of credible promises that a would-be issuer can commit to keeping. In a world of complete

markets this problem was abstracted away by simply assuming that all potential contract

breaches could be immediately detected and causelessly deterred, but most of the modern

literature on financial contracting focuses on how asymmetric information and limited

enforcement problems may together limit the set of feasible commitments. This theory has

proven powerful and rich at providing insights with which to interpret the shape of real world

financial contracts and institutional arrangements Conning and Udry (2005).

While the theoretical literature on asymmetric information and imperfect enforcement is rich,

there has been comparatively little empirical work that attempts to characterize the exact

nature and extent of imperfect information in rural financial markets (ibid, PP.32). Chiappori

(forthcoming) is a useful review of relevant literature in the developed country context. Aleem

(1990) provides dramatic direct evidence of the 33 importance of screening costs for lenders.

Klonner (2004) shows that asymmetric information has dramatic consequences for bidding

patterns in (high-value) ROSCA auctions in a village in Southern India. Gine and Klonner

(2003) examine the role of imperfect information regarding borrower type for the structure of

financial markets in a coastal village in Tamil Nadu. They show that uncertainty about

(fishing) entrepreneurs’ ability slows the pace of costly technological innovation for relatively

poor entrepreneurs.

14

Karlan and Zinman (2004) use a randomized intervention to identify the extent of adverse

selection and moral hazard in a South African credit market. They find that about 40% of defaults

in this market can be attributed to one of these types of asymmetric information.

Asymmetric information makes it difficult for a would-be creditor or insurer to be sure

whether the expected probability distribution over state-contingent payoffs associated with a

contract promise is the one being represented by the seller or not, as in the case of adverse

selection (private information about the agent or the project’s characteristics) or moral hazard

(private information about whether a specified action or contingency has occurred or not). In

practice variants of each of these problems may be the concern.

A farmer may promise to work diligently to repay a loan but when that farmer’s harvest fails

and he declares a default a lender may not be able to tell whether this was due to just bad luck

or to the farmer’s mishandling of the loan. Lenders and insurers may also not be able to very

easily verify whether the farmer’s reported harvest failure is genuine or misrepresented.

In each of these cases the problem turns around to bite the borrower or the insuree who will

have a hard time obtaining credit or insurance from any source in the first place unless they

find a way of credibly signaling their commitment.

Problems of commitment can also arise however even when information is perfect and

symmetric because even though actions and outcomes are observed, agents may still be able to

simply renege or walk away from their commitments unless they face credible and effective

sanctions to dissuade such opportunistic default. Some literature refers to this last problem of

opportunistic default as the problem of ‘limited commitment’ (e.g. Ligon et al 1999; Paulson

et al 2003) yet many contracting problems involve an agent’s limited ability to commit to

fulfilling elements of a contract, whether it be to truthfully reveal their type (adverse

selection), to take a specified action (ex-ante moral hazard), to truthfully report an outcome

(ex-post moral hazard), or to deliver on a promise (opportunistic default). Each of these

problems is related and are all believed to play important roles in shaping the pattern of

financial contracting everywhere (Conning and Udry, 2005).

15

According to Ghosh and Mookherjee (1999), in adverse selection concept, defaults arise

involuntarily, owing to adverse income or wealth shocks that make borrowers unable to repay

their loans. The moral hazard in contrast stresses problems with contract enforcement:

borrowers may not repay their loans even if they have the means to do so. Both explain how

borrowing constraints endogenously arise in order to mitigate these incentive problems, even

in the absence of exogenous restrictions on interest rate flexibility.

In line with the above descriptions, the two important problems associated with financial

markets, i.e. adverse selection and moral hazard are discussed.

2.1.4.1. Adverse selection

According to Akerlof (1970), in the usual case, a key condition for the existence of adverse

selection is an asymmetry of information. In Economics, information asymmetry occurs when

one party to a transaction has more or better information than the other party.

The adverse selection theory of credit markets originated with the paper by Stiglitz and Weiss

(1981) (as sighted by Ghosh and Mookherjee 1999). The theory rests on two main

assumptions: that lenders cannot distinguish between borrowers of different degrees of risk,

and that loan contracts are subject to limited liability (i.e., if project returns are less than debt

obligations, the borrower bears no responsibility to pay out of pocket).

Adverse selection arises when borrowers have characteristics that are unobservable to the

lender but affect the probability of being able to repay the loan (Karlan and Zinman, 2004). A

lender can try to deal with this information problem directly, by trying to assess these

characteristics, or indirectly by offering loan terms that only good risks will accept. The

typical method for separating good risks from bad risks is to ask the borrower to pledge

collateral. Risky borrowers are likely to fail more often and lose their collateral. If the bank

offers two different contracts, one with high interest rates and low collateral and the other with

the opposite, risky borrowers will select the former and safe borrowers the latter. But poor

people by definition do not have assets that make useful collateral, meaning that lenders have

no effective way to separate good risks from bad. Group lending deals with adverse selection

by drawing on local information networks to achieve the equivalent of gathering direct

16

information on borrowers and using differences in loan terms to separate good from bad

borrowers (Eston and Gersovitz, 1981).

2.1.4.2. Moral hazard

The problem of moral hazard is immense for formal sector lending but even moneylenders

have not fully overcome it although they can distinguish between bad luck and poor

performance, especially when their clients reside in the same villages Mohiuddin (1993).

According to Gould and Lazear (2002), moral hazard is a problem and it results when one

party insures another against some event over which the insured party has some control.

Once a borrower has taken a loan, the project’s payoff depends in part on the borrower’s

actions, including levels of labor and other inputs. Ordinarily, we would expect the borrower

to choose these actions such that the marginal benefit of each action equals its marginal cost.

That is not necessarily the case with asymmetric information. In the absence of collateral, the

lender and borrower do not have the same objectives because the borrower does not fully

internalize the cost of project failure. Moreover, the lender cannot stipulate perfectly how the

borrower should run the project, in part, because some of the borrower’s actions are not

costlessly observable.

According to Mohiuddin (1993), problem of moral hazard is solved in formal sector poverty

lending by tying credit and savings together, by having a built-in mechanism for emergency

fund to handle unforeseen shocks (due to weather or price changes), and by its emphasis on

borrower-initiated lending to avoid loan use in risky unknown ventures where markets or input

supplies are uncertain.

2.2. Situation of Rural Finance in Ethiopia

Rural finance in Ethiopia, as in other developing countries, has dualistic features. Both formal

and informal saving and credit arrangements exist in the country. The second and the most

important in the rural areas is the informal sources which are categorized as commercial (those

who lend money on short term basis to obtain profit) and non-commercial (lenders that

generally include friends, relatives and neighbors).

17

2.2.1. The emergence and evolution of formal credit in Ethiopia

The formal sources are financial institutions that are set up legally and engaged in the

provision of credit and mobilization of savings. These institutions are regulated and controlled

by the National Bank of Ethiopia (NBE).

Here we can categorize evolution of formal rural credit services in Ethiopia by three period of

times; i.e. rural credit in Ethiopia before 1975, during the Derge period and after Derge

regime.

2.2.1.1. Rural credit before 1975

The present banking systems and formal credits structure can be traced back to 1905 when the

National Bank of Egypt established the Bank of Abyssinia, the first bank in Ethiopia. The

Bank of Abyssinia was liquidated by the imperial decree of August 29, 1931 and was replaced

by the Bank of Ethiopia with 60% of the capital owned by the government and 40% by the

general public. The Bank of Ethiopia was also closed in 1935 following the Italian invasion,

and Ethiopia had no banking system of its own until 1942 when the State Bank of Ethiopia,

authorized by the imperial charter, was established with a capital of 1 million Maria Theresa,

fully subscribed by the Ministry of Finance.

Following the creation of the Ministry of Agriculture in 1943, the Agricultural Bank of

Ethiopia was established to accelerate agricultural development by assisting small landholders

whose farms had been devastated during the Italian occupation through loans for purchase of

seeds, livestock and implements and to repair or reconstruct their homes and farm buildings

(Tesfaye, 1993). Public banks were supposed to mobilize resources and channel them in

accordance with the Second Five years Development Plan. The Plan identified, which

identified (i) agriculture as the leading economic activity, (ii) Mining, manufacturing and

power as “the most propulsive sectors. The Plan made a distinction between credit for

investment and current transactions and gave priority in investment credits to “directly

productive” economic activities. The Plan also allowed for interest rate discrimination

between borrowers favoring businesses that are in conformity with the Plan. Credit access was

not to be discriminated by ownership. Instead, the Plan explicitly recognized the private and

18

public sectors as equally important. Regarding rural finance, the share of agriculture reflected

the importance attached to it in the Plan. Subsistence and large-scale and mechanized

agriculture together were to receive about half of the bank credit. Subsistence agriculture was

transformed through (a) the introduction of improved tools and implements, modern

techniques, and better seeds; (b) credit, price and tax policies; and (c) land reform and

agricultural services (Assefa, 2004).

Accordingly, farmers were to be assisted to produce more marketable surpluses, and thereby

develop the subsistence agricultural sector into a monetized one. Credit for farm tools and

implements were to be extended by the Development Bank of Ethiopia not directly but

through the then Grain Corporation or Farmers’ Cooperatives. These institutions were to

receive credit funds and then buy the implements and supply them to farmers on credit (to be

repaid in kind) or lease or sell them on credit if they are expensive - such as selectors,

threshing machines, winnowers, etc… (to be repaid in cash). It was explicitly stated that credit

was to be provided only in goods and services, the reason being to ensure that it is used only

for productive purposes. These practices were expected to raise production as a result of rapid

application of efficient implements and lead to commercialization of peasant agriculture due to

increased marketable agricultural output. Priority for credit among farmers was to be

determined by the co-operatives with advice from extension agents.

Banks were also to extend credit to commercial farms for modern tools, fattening, etc... and

fishing co-operatives at favorable terms. High collateral as high as 200% of the loan, mainly in

the form of real property and machinery, and guarantor requirements, in the face of

widespread tenancy, land title problems e.g. communal land, rist system, etc..., proved to be

the major hindrances. Of the total DBE loans disbursed during 1951-69, only 42 per cent went

to agriculture, of which small farmers received only 7.5 per cent. The successor of DBE, the

AIDB whose objective, among others, was to mobilize funds and extend medium- and long-

term agricultural credit, did not do a better job in terms of reaching farmers with credit either.

19

In fact, its credit policy disqualified peasant farmers in areas away from the main road, without

many borrowers, required property collateral (which should be insured at the borrowers

expense) ranging 100 to 200% of the amount borrowed, and/or personal guarantor; and

required borrower farmers to sell their output to its subsidiary at fixed prices as a means of

enforcing repayment (Tesfaye, 1993). The implication of these on peasant farmers’ credit

access is clear. While the share of agriculture in AIDB total credit during 1970/71-74/75 was

high, averaging about 65 per cent, peasant farmers did not benefit much. It mainly went to

dairy development projects, large farmers, co-operatives of commercial farmers, etc….

The comprehensive and minimum Agricultural Extension package programs, which were

intended to support small farmers by, among other things, organizing them in a way that

makes it easier and less costly for the AIDB to provide credit, did not achieve much in terms

of reaching small farmers partly due to the stringent requirements involved such as high down

payment (25 to 75%), two reputable guarantors (one of them the landlord in case of tenant

borrowers), and signed lease agreement and partly due to incentive problems associated with

the share cropping arrangement that prevailed and marketing problems. Just like what

happened in most credit programs of other countries, benefits mainly accrued to the non-target

groups (landlords, large landowners/big cultivators, merchants, etc.). Overall, the extent of

exclusion was well recognized by the AIDB board so much so that in 1974 it decided to

introduce a small farmers credit program on pilot basis but was not implemented as it was

overtaken by events of the revolution (Tesfaye, 1993).

20

2.2.1.2. Rural credit during the Dergue period

After the fall of Emperor Haile Silassie government, the financial system in Ethiopia was

nationalized and restructured based on the 1976 Banking Law. The credit policy was geared

towards the overall policy of the country’s centralized economic management. All elements of

financial repression existed during this period in their severe form: controls on financial prices

(i.e. interest rates and exchange rates) and restrictions/control on new entry into the sector as

well as on the activities and portfolios existing financial institutions. Interest rates on loans to

different economic and social sectors were administratively fixed. The rate structure bears

little relationship with the opportunity cost of capital or the rate of inflation. All financial

institutions were publicly owned and entry was banned, thereby establishing a public

monopoly of the financial sector. Credit policy gave absolute priority to the socialized sector

public enterprises, state farms and cooperatives. Loans and advances by borrowing institutions

over the ten year period between 1981 and 1990 show that on average the government sector

took 36.4% of the total, while 50.3% went to public enterprises and the private sector’s share

was only 8.3% of the total loans and advances made by the banking system during the period.

More than 89 percent of AIDB agricultural loans went to state farms while the rest went to

agricultural co-operatives, with the private peasant sector receiving negligible share.

Discrimination against the private sector was not limited to credit access. The interest rate

schedule explicitly discriminated against the private sector. The NBE set lending rates ranging

between 4.5 – 9.5 percent, depending on the type of ownership and sector.

In many instances, banks have been directed by the NBE to lend for nonviable investments in

the public sector. As a result, most of the funds disbursed to the public enterprises, particularly

state farms, have remained uncollected, leaving the banks with low rate of growth of capital

and reserves. Among the financial institutions, the AIDB suffered serious capital depletion,

with its net capital becoming negative by the end of the 1990 fiscal year. Repayment problem

of the AIDB was so severe (highest 68% in 1988 and lowest of 11% in 1993) that it had to

terminate its agricultural inputs loans to rural households (Wolday, 2003) just as its

predecessor, the DBE, did in 1961. Therefore, the outcome with regard to reaching small rural

borrowers with financial services was disappointing both during the Imperial and Derge

regimes. Within the agricultural sector, registered FMSCs and producers’ cooperatives were

eligible for bank credit except for agricultural input loans. Lack of registration of these

21

cooperatives was the main impediment to the expansion of credit. For instance, as of May

1990, the percentage of registered Service Cooperatives was only 48, while that of the

producers’ cooperatives was only 14. So, the chance of getting credit by small producers was

very low. This is evident from the amount of rural credit that went to the peasant sector, out of

the overall supply of rural credit through both AIDB and CBE during the period 1982 – 1992

only Birr 792 million (9%) went to the peasant sector. Considering the large number of rural

population, the size of land under cultivation and the demand for credit, the volume of loan

extended to this sector was insignificant. Credit delivery systems have been insufficient to

serve the rural people.

2.2.1.3. Rural credit after the reform period

Following the fall of Derge regime, Ethiopia has followed free market economy, which

advocates financial liberalization. Financial liberalization is important component of a

successful development strategy. Both economic theory and practical experience suggest that

financial liberalization can stimulate economic development.

Financial liberalization in Ethiopia began at the end of 1992. The financial reforms undertaken

in Ethiopia include elimination of priority access to credit, interest rate liberalization,

restructuring and introduction of profitability criteria, reduced direct government control on

financial intermediaries and limits bank loans to the government, enhancement of the

supervisory, regulatory and legal infrastructure of the NBE, allowing private financial

intermediaries through new entry of domestic private intermediaries (rather than privatization

of the existing ones) and introduction of treasury bills through auction markets. Prior to 1992,

the interest rate charged to farmers’ cooperatives was 5%, which is below the rate of savings

deposit (6%). Financial institutions were obliged to pay interest margin on deposits from their

own sources. Lending rates that were between 4.5 and 9.5% were raised to 11-15% depending

on the sector until September 1994.

22

Discrimination of credit access and interest rates by type of ownership (i.e. between state

owned enterprises, cooperatives and private firms) was eliminated. Sectoral interest rates

discrimination was reduced, and domestic establishment of private financial institutions was

allowed and encouraged through proclamation number 29/1992. Since January 1995, the NBE

switched to a policy of floors on deposits and ceilings on lending rates, allowing banks to set

interest rates. The NBE revised the floor for saving deposits downwards to 3% from 6% in

2001/02 with an intention of encouraging investment and boost economic activity. Lending

rates quickly followed suit as the minimum-lending rate changed by commercial banks went

down from 10.5% to 7.5% in the same period.

Also, banks have been decentralizing loan decision making in order to reduce transaction costs

of borrowing and reducing screening hence transaction costs of lending. Entry restrictions into

banking were lifted for domestic banks. Entry rules and guidelines have been drawn. The

lending approaches of banks to target beneficiaries could be both a direct type and a two-tier

system. The direct type is in which the Bank extends credit directly to the end user. This could

be an individual person or organization such as cooperatives, government or private

enterprises, which have legal entity. In the two-tier approach, the Bank transfers its financial

resources to end users through other bodies such as cooperatives and peasant associations. In

the case of the first type, the credit beneficiaries enter loan agreements with the bank and are

responsible for repayment of the borrowed loan, whereas in the case of the latter other

intermediaries such as cooperatives or associations sign a loan contract with the bank and

channel the borrowed fund to their members or end users.

In the case of rural Ethiopia, regional governments act as intermediaries between banks and

farmers. These governments use their federally allocated budget as collateral to borrow from

banks and lend these funds to farmers for the purchase of agricultural inputs. This procedure

has enabled banks to lend a great deal of money to farmers. Nevertheless, there have been

cases of default, which have necessitated repayment out of the budget allocations of the

regional administrations. However, the inability of the formal financial sector to provide

adequate financial services to small farmers and the poor in general continued even after the

reform.

23

As compared to other economic sectors the share of agricultural sector in the total credit

disbursed by the banks has continued to be marginal. For instance, the share of agriculture in

the total credit disbursed between 1991/92 and 1997/98 has only been 14.7%, while domestic

trade had 32.2% and industry 13.2%. Recently, the share of agricultural credit stagnated at

around 16% and never exceeded 19% of the total credit disbursed. In addition, it is believed

that almost all of the agricultural credit is of short-term nature, which will have little impact on

long-term investment and transformation of agriculture. The financial resource that flows to

the sector is in general low when compared to the sector’s actual and expected contribution to

the economy growth in agricultural versus non-agricultural (Assefa, 2004).

The absence of an effective peasant institution for credit delivery is the other major problem

associated with the existing credit system in Ethiopia. A typical service cooperative has over 5

to 6 member peasant association or over 1000 member households. It is simply too large to

provide effective screening of borrowers, identify genuine defaulters, generate reliable demand

information, and/or exert any form of peer pressure on members to make timely repayment of

debts. At present, local community participation in screening borrowers and filtering genuine

defaulter is minimal. The authorities and the leaders of FMSCs have no objective means of

assessing the extent of crop loss. Weak cooperatives are also the main reason for the

government intervention in the credit market and diversion of valuable extension time to

administrative affairs. Hence, the effort to restructure FMSCs into smaller groups needs to be

stepped up (Mulat et al., 1998).

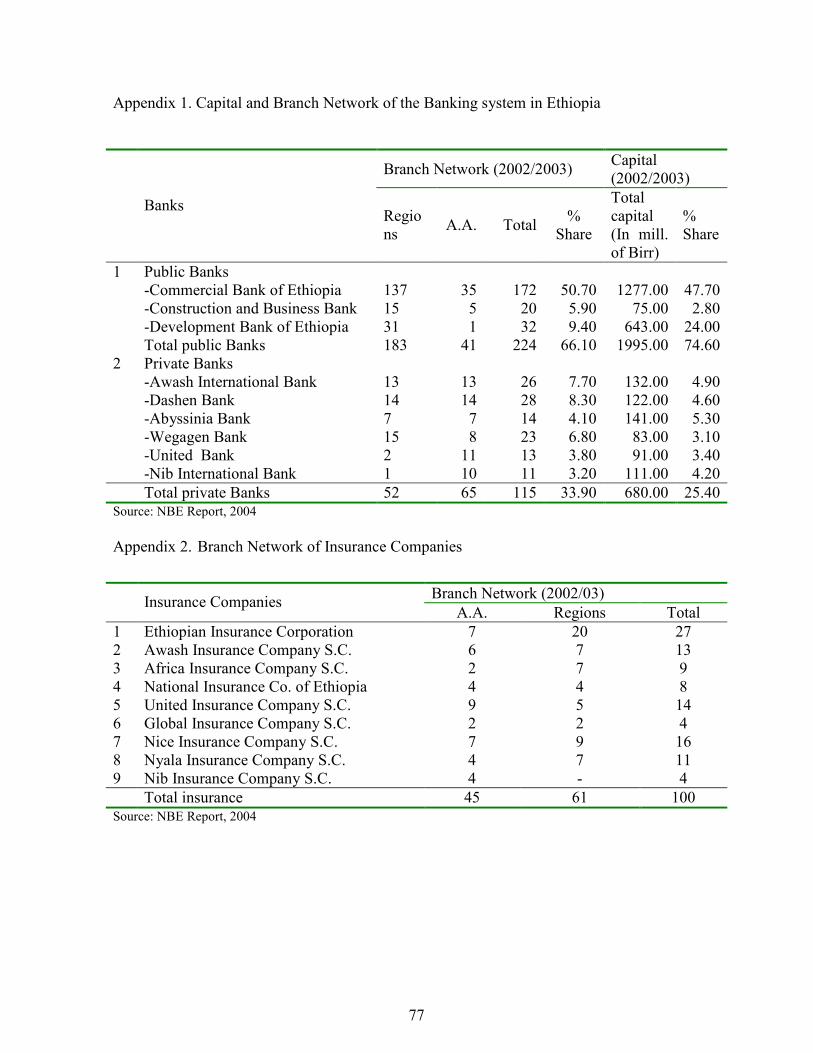

2.2.2. Formal financial institutions in Ethiopia

During fiscal year 2002/03, the numbers of banks where remained nine, of which three were

government owned. The number of insurance companies also stayed at nine, of which one was

state owned (annual report of NBE, 2004). According to the report, foreign entry in to the

financial sector is not allowed until domestic banks attain a certain degree of desired

competitiveness and the National Bank’s supervisory and regulatory capacity is adequately

strengthened.

24

The numbers of bank branches reached 339, of which 172 or about 51 percent belong to the

Commercial Bank of Ethiopia. Despite modest branch expansion, Ethiopia remains as one of

the under-banked countries even at sub-Saharan African countries standard. The bank branch

to population ratio was 1:20,400 during 2002/03. Similarly, total capital of the banking system

reached Birr 2.7 billion, of which about 75 percent was hold by government owned banks.

Commercial Bank of Ethiopia accounted for more than 47 percent of total capital of the

banking system (excluding NBE), NBE (2004) (Annex 1).

At the same time, total branches of insurance companies reached 106 at the end of the fiscal

year (2002/03). Yet geographical distribution of bank and insurance branches was highly

skewed to major towns and cities. Nearly 42 percent of insurance and 31 percent of bank

branches were located in Addis Ababa (Annex 2).

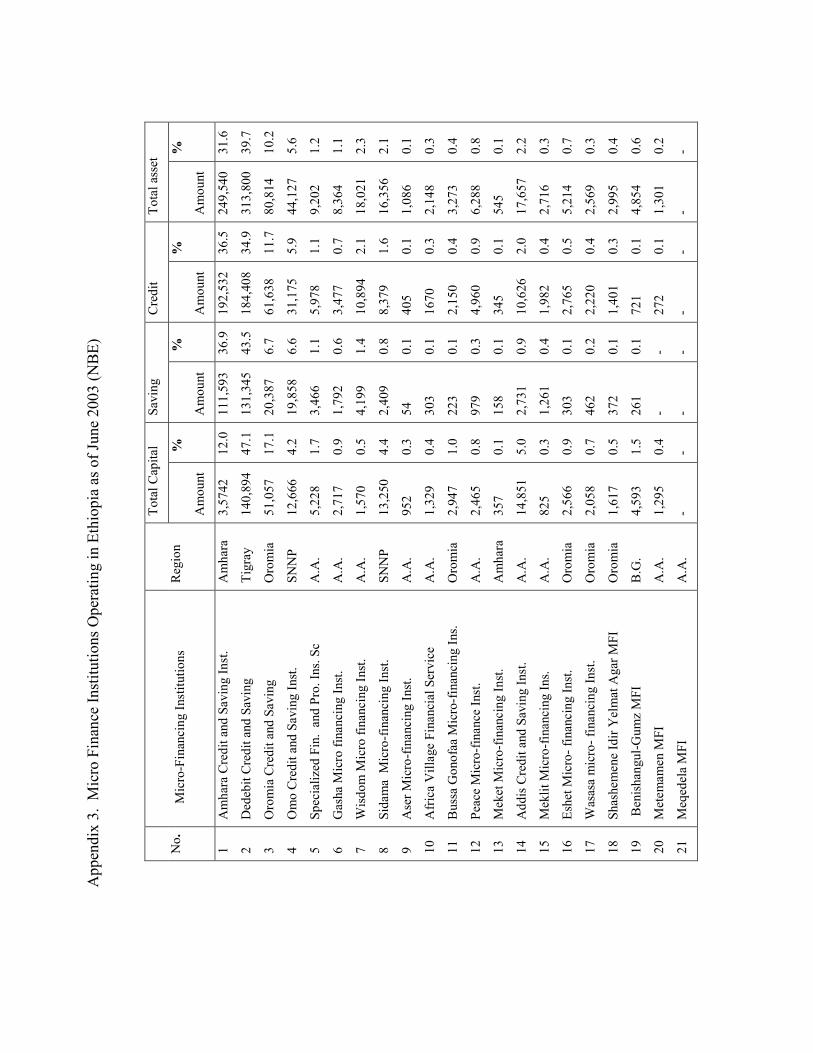

The number of micro-finance Institutions (MFI’s) that operated in the country has reached 22

at the end fiscal year 2002/03, (NBE, 2004). Their total capital stood at Birr 299 million, they

mobilized deposits of Birr 302 million, advanced loans of Birr 528 million and total assets at

Birr 791 million, by the end of the fiscal year. Of the total MFI’s, 10 were operating in Addis

Ababa, 5 in Oromia, 2 in Amhara. The bggest MFI namely , Dedebit Credit and Savings

Institution alone accounted for 47.1 percent of the total capital, 43.5 percent of savings, 34.9

percent of credit and 39.7 percent of the total asset of MFI’s. Amhara Credit and Saving

Institution is the third biggest MFI after Dedabit and Oromia Credit and Saving Institutions

(Annex 3).

2.2.2.1. Amhara Credit and Saving Institutions (ACSI)

Amhara credit and saving institution (ACSI) is a largest micro-finance in the region, which

provides micro credit and saving, and money transfer services. Since its inception in 1995

ACSI has been helped so many poor households live a moderately specified well being. At the

beginning it started its credit services as a local NGO for most vulnerable part of the society.

The institution stretched throughout the region in all woredas and covers about 20 percent of

kebeles as of May 2004. Since its establishment ACSI served more than 482, 083, loan clients

and currently it has about 288, 681 active loan clients and 449, 345 active saving clients BoRD

(2003).

25

It’s extending credit for small-scale enterprises agricultural inputs and housing construction

and maintenance for government employees. The main target groups of the institution are the

productive poor households, which fulfill the eligible criteria of creditworthiness.

According to BoRD (2003), the minimum loan size that provided by the institution is 150 Birr

while a maximum of 15,000 Birr. Most loans are basically have a one year duration. In

addition it changes 18 % interest rate for its loans. It has also model, which is a group pressure

as a loan guarantee methodology to provide credit service to the rural poor. In addition to

group lending ACSI implemented individual lending for government employees for residential

house construction.

2.2.2.2.Cooperatives in Ethiopia

Cooperation is the way of life of Ethiopians and has a long year of experience. This

cooperation may be cultural or religious organizations that make the population a close tie. For

example, iddir /focuses on funeral celebration/, ikuib /which helps for saving money and self

help to the members/, and wenfiel / which is focused on the cooperation on labor peak times

like in the time of harvest, wedding etc./.

However, a modern cooperative in Ethiopia was started at the time of emperor Hileselasie first

in 1961. During this time the first cooperative legal action was made and it is known by

Decree number 44/1961. The second attempt towards legal cooperatives was in 1964, and the

time was the end of first Five Year Development Plan. The first cooperative organization legal

proclamation known as proclamation number 241/1964 was declared. Based on this

proclamation 158 cooperatives were established with 33, 400 members and 9, 970, 600 Birr

total capital.

In 1974 Emperor Haileselasie government fall and was replaced by a socialist type of

government. This government proclaimed cooperative organization proclamation in 1978, and

it is called proclamation number 138/1978. Up to 1990 there were 10,524 different types of

cooperatives with 4,529,259 members and combined capital of Birr 465,467,428 throughout

the country. From these cooperatives 80% were rural cooperatives.

26

During the 1991 change of the government, the negative view towards cooperatives was

manifested in the actions of the farmers of looting and destroying FMSCs property and

records. The FMSCs themselves became notorious for waste and mismanagement. According

to Dessalegn (1994) more than 24 million Birr was misappropriated by those FMSCs, which

the ministry of agriculture had audited. That was almost certainly just the tip of the iceberg,

given that audits were carried out on fewer than 25% of cooperatives.

Wolday (2003) revealed that, the present Government, which was not very sympathetic to

cooperatives initiated by the former government, issued a proclamation in 1995 to reactivate

cooperative movement in the country. Member-led co-operatives are thought to be necessary

to reduce transaction costs and enhance the bargaining position of small farmer. However, in

1994 there was an attempt to strengthen the rural cooperatives. Among the basic action the

government took in this time was the proclamation of agricultural cooperatives, proclamation

no 85/1994.

Cooperative societies now provide a wide range of services, including the supply of inputs,

output marketing and distribute consumer goods. But bad experiences in the past, insufficient

capital, lack of managerial skills and inadequate support from CPB/ offices have not helped

the cooperative movement.

In 2004, the total number of cooperatives reached 7, 640 with 3,762,969 members and total

capital of Birr 316,140,725. The number of agricultural cooperatives was 54% of the total

cooperatives.

In ANRS a total of 1,025 FMSCs with combined capital has reached 45,132,744 Birr on July

2002. In 2004 around 622 (60.68%) FMSCs are actively engaged in agricultural input credit

extension activity. They administered most of the fund borrowed by the regional government

from commercial banks. They administer more than 80% of the input credit in year 2004 in the

region (ARCPB, 2005). The cooperatives have accumulated experiences in credit extension

and repayment collection.

27

2.2.3. Informal financial sector in Ethiopia

According to G/Yohannes (2000), compared with the formal financial institutions, informal

lending is by far the most important source of finance to the rural and urban population. In

recent years, the informal sector has continued to assume increased prominence mainly due to

restrictive rules and regulations of the formal financial sector. The operations of the informal

sector derive their rules and regulations from the country’s culture and customs. Informal

sector transactions are conducted on the basis of trust and intimate knowledge of customers.

The common cultural background and the mutual obligations and fervent bonds of family and

kinship, all operate to promote the trust, accountability and moral responsibility that is lacking

in the official banking system.

Besides, the informal lenders have easy access to information (at reasonable cost) about their

borrowers with whom they have social relations. This permits credit contracts to play a more

direct role in enforcing repayment. Also, the fact that collateral is rarely used in the informal

sector enables it to flexibly satisfy financial needs that cannot be met by the formal financial

institutions (G/Yohannes, 2000).

Nevertheless, the informal sector is not without limitations. Despite its flexibility, rapidity and

transparency of procedures, not only are there scarcities of loanable fund for investment, but

also the interest rates charged on these loans are often exorbitant. The informal financial sector

often embraces a wide group of individuals and institutions whose financial transaction are

generally not subject to direct control by the country’s key monetary and financial policy

instruments. Individual economic entities in the informal sector include moneylenders, money-

keepers, tradesmen, friends and relatives, neighbors, etc….

28

2.3. Empirical studies on loan recovery and defaults

Knowledge of determinants of loan repayment is undoubtedly important for it provides

information to be the lender on the incentives available for the borrower to comply with

repayment schedules. Loan repayment performance is affected by a number of socioeconomic,

institutional and natural factors. Some of which are believed to impact on repayment

negatively while others have positive impact. Various studies have been carried out

concerning loan repayment performance of borrowers in several countries. The following

presents the findings of studies on loan repayment performance.

Major socioeconomic variables that affect credit repayment include education, age of

household head, family size, gender of household head, etc…. Family size is expected to

affect loan repayment performance positively. This is because farmers with more families may

have more labor force for more diversified sources of income. For instance, Schreiner and

Nagarajan (1997), in a case study in Gambia,reported that large households are better in credit