Bahasa

Halaman

Hukum

Definition - What are Financial Statements?Financial Statements represent a formal record of the financial activities of an entity. These are written reports that quantify the financial strength, performance and liquidity of a company. Financial Statements reflect the financial effects of business transactions and events on the entity.

Four Types of Financial StatementsThe four main types of financial statements are:

1. Statement of Financial Position

Statement of Financial Position, also known as the Balance Sheet, presents the financial position of an entity at a given date. It is comprised of the following three elements:

Assets: Something a business owns or controls (e.g. cash, inventory, plant and machinery, etc)

Liabilities: Something a business owes to someone (e.g. creditors, bank loans, etc)

Equity: What the business owes to its owners. This represents the amount of capital that remains in the business after its assets are used to pay off its outstanding liabilities. Equity therefore represents the difference between the assets and liabilities.View detailed explanation and Example of Statement of Financial Position

2. Income Statement

Income Statement, also known as the Profit and Loss Statement, reports the company's financial performance in terms of net profit or loss over a specified period. Income Statement is composed of the following two elements:

Income: What the business has earned over a period (e.g. sales revenue, dividendincome, etc)

Expense: The cost incurred by the business over a period (e.g. salaries and wages, depreciation, rental charges, etc)Net profit or loss is arrived by deducting expenses from income.

View detailed explanation and Example of Income Statement3. Cash Flow Statement

Cash Flow Statement, presents the movement in cash and bank balances over a period. The movement in cash flows is classified into the following segments:

Operating Activities: Represents the cash flow from primary activities of a business.

Investing Activities: Represents cash flow from the purchase and sale of assets other than inventories (e.g. purchase of a factory plant)

Financing Activities: Represents cash flow generated or spent on raising and repaying share capital and debt together with the payments of interest and dividends.View detailed explanation and Example of Cash Flow Statement

4. Statement of Changes in Equity

Statement of Changes in Equity, also known as the Statement of Retained Earnings, details the movement in owners' equity over a period. The movement in owners' equity is derived from the following components:

Net Profit or loss during the period as reported in the income statement Share capital issued or repaid during the period Dividend payments Gains or losses recognized directly in equity (e.g. revaluation surpluses) Effects of a change in accounting policy or correction of accounting error

- See more at: http://accounting-simplified.com/financial/statements/types.html#sthash.faJZ2bPE.dpuf

Cash payment transactions

1. Purchase of assets in cash

1a. Purchased merchandise and paid $2,000 in cash

debit credit

merchandise 2,000 cash 2,000

debit: increase in assets (merchandise)credit: decrease in assets (cash)

1b. Purchased an equipment and paid $15,000 in cash

debit credit

equipment 15,000 cash 15,000

debit: increase in assets (equipment)credit: decrease in assets (cash)

2. Repayment of liabilities in cash

2a. Repaid $7,000 of bank loans

debit credit

borrowings 7,000 cash 7,000

debit: decrease in liabilities (borrowings)

credit: decrease in assets (cash)

2b. Paid $3,000 accounts payable

debit credit

accounts payable 3,000 cash 3,000

debit: decrease in liabilities (accounts payable)credit: decrease in assets (cash)

3. Payment of expenses in cash

3a. Paid $3,500 rent expense

debit credit

rent expense 3,500 cash 3,500

debit: increase in expenses (rent expense)credit: decrease in assets (cash)

3b. Paid $6,000 salaries expense

debit credit

salaries expense 6,000 cash 6,000

debit: increase in expenses (salaries expense)credit: decrease in assets (cash)

Cash receipt transactions

4. Sale of assets in cash

4a. Sold merchandise and received $6,500 in cash

debit credit

cash 6,500 sales 6,500

debit: increase in assets (cash)

credit: increase in revenue (sales)

The cost of merchandise sold was 5,100

debit credit

cost of goods sold

5,100

merchandise 5,100debit: increase in assets (cash)credit: increase in revenue (sales)

4b. Sold an equipment and received $8,600 in cash

The book value of the equipment was $8,000

debit credit

cash 8,600 equipment 8,000 gain on sale of equipment

600

debit: increase in assets (cash)credit: increase in revenue (sales)

5. Borrowing money

5a. Borrowed $9,000 in cash

debit credit

cash 9,000 borrowings 9,000

debit: increase in assets (cash)credit: increase in liabilities (borrowings)

5b. Issued a promissory note and received $11,000 in cash

debit credit

cash 11,000 notes payable

11,000

debit: increase in assets (cash)

credit: increase in liabilities (notes payable)

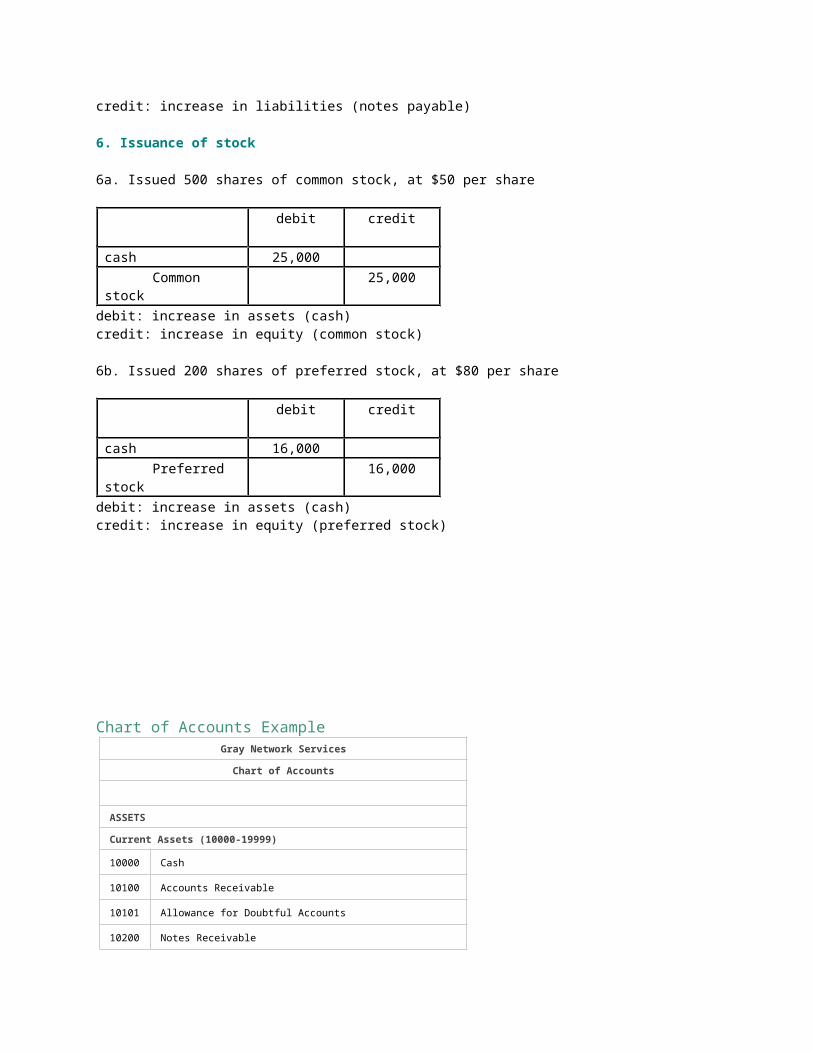

6. Issuance of stock

6a. Issued 500 shares of common stock, at $50 per share

debit credit

cash 25,000 Common stock

25,000

debit: increase in assets (cash)credit: increase in equity (common stock)

6b. Issued 200 shares of preferred stock, at $80 per share

debit credit

cash 16,000 Preferred stock

16,000

debit: increase in assets (cash)credit: increase in equity (preferred stock)

Chart of Accounts ExampleGray Network Services

Chart of Accounts

ASSETS

Current Assets (10000-19999)

10000 Cash

10100 Accounts Receivable

10101 Allowance for Doubtful Accounts

10200 Notes Receivable

10300 Interest Receivable

10400 Service Supplies

Non-Current Assets (20000-29999)

20000 Leasehold Improvements

20100 Furniture and Fixtures

20101 Accumulated Depreciation – Furniture and Fixtures

20200 Service Equipment

20201 Accumulated Depreciation – Service Equipment

LIABILITIES (30000-39999)

30000 Accounts Payable

30100 Notes Payable

30200 Salaries Payable

30300 Rent Payable

30400 Interest Payable

30500 Unearned Revenue

30600 Loans Payable

OWNER'S EQUITY (40000-49999)

40000 Mr. Gray, Capital

40100 Mr. Gray, Drawing

INCOME (50000-59999)

50000 Service Revenue

50100 Interest Income

50200 Gain on Sale of Equipment

EXPENSE (60000-69999)

60000 Rent Expense

60100 Salaries Expense

60200 Supplies Expense

60300 Utilities Expense

60400 Interest Expense

60500 Taxes and Licenses

60600 Depreciation Expense

60700 Doubtful Accounts Expense

70000 Income Summary

Example

Company A was incorporated on January 1, 2010 with an initial capital of 5,000 shares of common stock having $20 par value. During the first month of its operations, the company engaged in following transactions:

Date TransactionJan 2

An amount of $36,000 was paid as advance rent for three months.

Jan 3

Paid $60,000 cash on the purchase of equipment costing $80,000. The remaining amount was recognized as a one yearnote payable with interest rate of 9%.

Jan 4

Purchased office supplies costing $17,600 on account.

Jan 13

Provided services to its customers and received $28,500 incash.

Jan 13

Paid the accounts payable on the office supplies purchasedon January 4.

Jan 14

Paid wages to its employees for first two weeks of January, aggregating $19,100.

Jan 18

Provided $54,100 worth of services to its customers. They paid $32,900 and promised to pay the remaining amount.

Jan 23

Received $15,300 from customers for the services provided on January 18.

Jan 25

Received $4,000 as an advance payment from customers.

Jan 26

Purchased office supplies costing $5,200 on account.

Jan 28

Paid wages to its employees for the third and fourth week of January: $19,100.

Jan 31

Paid $5,000 as dividends.

Jan 31

Received electricity bill of $2,470.

Jan 31

Received telephone bill of $1,494.

Jan 31

Miscellaneous expenses paid during the month totaled $3,470

The following table shows the journal entries for the above events.

Date Account Debit Credit

Jan 1 Cash 100,0

00

Common Stock 100,0

00Jan 2 Prepaid Rent 36,00

0

Cash 36,000

Jan 3 Equipment 80,00

0

Cash 60,000

Notes Payable 20,000

Jan 4 Office Supplies 17,60

0

Accounts Payable 17,60

0Jan 13 Cash 28,50

0

Service Revenue 28,50

0Jan 13 Accounts Payable 17,60

0

Cash 17,600

Jan 14 Wages Expense 19,10

0

Cash 19,100

Jan 18 Cash 32,90

0

Accounts Receivable

21,200

Service Revenue 54,10

0Jan 23 Cash 15,30

0

Accounts Receivable 15,30

0Jan 25 Cash 4,000

Unearned Revenue 4,000

Jan 26 Office Supplies 5,200

Accounts Payable 5,200

Jan 28 Wages Expense 19,10

0

Cash 19,100

Jan 31 Dividends 5,000

Cash 5,000Jan 31

Electricity Expense 2,470

Utilities Payable 2,470

Jan 31 Telephone Expense 1,494

Utilities Payable 1,494

Jan 31

Miscellaneous Expense 3,470

Cash

Answers to Easy Practice Test

1. A revenue account is credited this period when a. services are provided to a customer this period b. services are provided to the company this period c. services are paid for this period and provided next period d. income is earned last period

A. A revenue account is credited when it is increased. Revenues are recorded with an increase when the revenue is earned this period; a good or service has been provided this period. (b.) is an expense.

2. An expense account is debited this period when a. services are provided to a customer this period b. services are provided to the company this period c. services will be paid for this period and provided next period d. services will be provided to the company next period

B. Expense accounts are debited when they increase. A service provided to the company this period is an increase in to the expense this period.

3. What is recorded when wages are paid to employees who worked this period? a. a debit to an asset and a credit to a liability b. a credit to a revenue and a debit to an asset c. a debit to an expense and a credit to an asset d. a debit to a liability and a credit to a revenue

C. Wages paid to employees who worked this period is an increase to an expense and a decrease to cash. Increasing an expense is a debit and decreasing cash, anasset, is a credit.

4. Dividends earned and not yet received are recorded with a. a debit to an asset and a credit to a liability b. a credit to a revenue and a debit to an asset c. a debit to an expense and a credit to an asset d. a debit to a liability and a credit to cash

B. Earned means it is a revenue. Revenues increase with a credit. Not yet received is a receivable which is an asset. Assets increase with a debit.

5. Using up prepaid rent is recorded with a. a credit to a liability b. a debit to an expense c. a credit to an expense d. a debit to an asset

B. Using up the asset prepaid rent is an expense. An increase to an expense is recorded with a debit. Using an asset is also a decrease to the asset which is recorded with a credit. This is not one of the choices.

6. Cash paid for salaries owed to employees for working last month isrecorded with a. a debit to a liability

b. a credit to an expense c. a credit to a revenue d. a debit to an expense

A. Paying for an amount owed is a decrease to cash and a decrease to the liability.Assets are decreased with a credit and liabilities are decreased with a debit. The expense was recorded last period with a debit when the service was provided.

7. Depreciation expense is recorded in the same transaction as a. a credit to equipment b. a credit to accumulated depreciation c. a credit to accrued expenses d. a credit to prepaid expenses

B. Accumulated depreciation is the account that is always credited when recordingdepreciation expense. This account is the total of all prior years’ depreciation expense. Accumulated depreciation is a contra asset account which means it is opposite of an asset. Assets increase with a debit, so accumulated depreciation is increased with a credit (opposite).

8. An increase to an expense will be recorded in the same transaction with a. a credit to a liability b. a debit to a liability c. a credit to a revenue d. a credit to owner’s equity A. The expense must be paid for now or paid for later. The expense is a debit, so the other account must be a credit. Payment now decreases the asset cash. Decreasing an asset is done with a credit which is not one of the choices. Payinglater increases a liability which is done with a credit (b). A revenue and expense is not recorded together in the same journal entry.

9. The company issued stock to investors. Which of the following is done to record this transaction? a. credit owner’s equity and debit retained earnings b. debit an asset and credit an asset c. credit an assets and debit a liability d. debit an asset and credit owner’s equity

D. Issuing stock to investors increases cash, recorded with a debit, and increases common stock, recorded with a credit.

10. The company purchases a truck and pays cash. Which of the following is doneto record this transaction? a. debit cash and credit truck b. debit truck and credit accounts payable c. debit truck and credit cash d. debit truck expense and credit cash

C. Truck increases and cash decreases. Both are assets. The truck increases with a debit and the cash decreases with a credit.

11. Journal entries are used for the purpose of a. recording transactions only b. recording and summarizing transactions c. determining if the accounting equation balances d. listing all the account names used

A. Journal entries are made to record transactions. T accounts summarize transactions to get account balances that are reported on the financial statements. Recording debits and credits properly will balance the accounting equation (c.) A trial balance lists all account names used.

12. Which of the following transactions requires a credit to a liability account? a. purchase an asset and pay cash b. purchase an asset and agree to pay later c. issue common stock d. repay a liability

B. A credit to a liability account is an increase. An increase to a liability occurs when the company borrows to purchase an asset and pays later. Repaying a liability is a debit to the liability (d.) (a. & c.) do not impact a liability.

13. The account name debited when the company pays a supplier is a. accounts receivable b. accounts payable c. supplies d. cash

B. Owing a supplier is called accounts payable. Cash is credited when payment ismade. Accounts payable is debited.

14. The account name debited when the company collects from a customer is a. cash b. accounts payable c. accounts receivable d. none of the above

A. Amounts owed from the customer is accounts receivable. The customer pays cashto the company. Cash is increased (debit) and accounts receivable is decreased (credit); both are assets.

15. Account names that will not be used to record the same transaction are a. cash and accounts receivable b. cash and inventory c. accounts receivable and accounts payable d. accounts payable and cash

C. The company can not owe someone and be owed as a result of the same transaction. The other choices are cash being paid or collected, which are commontransactions.

16. Record journal entries for following transactions. After recording the transactions, prepare a “T account” and balance the cash account.

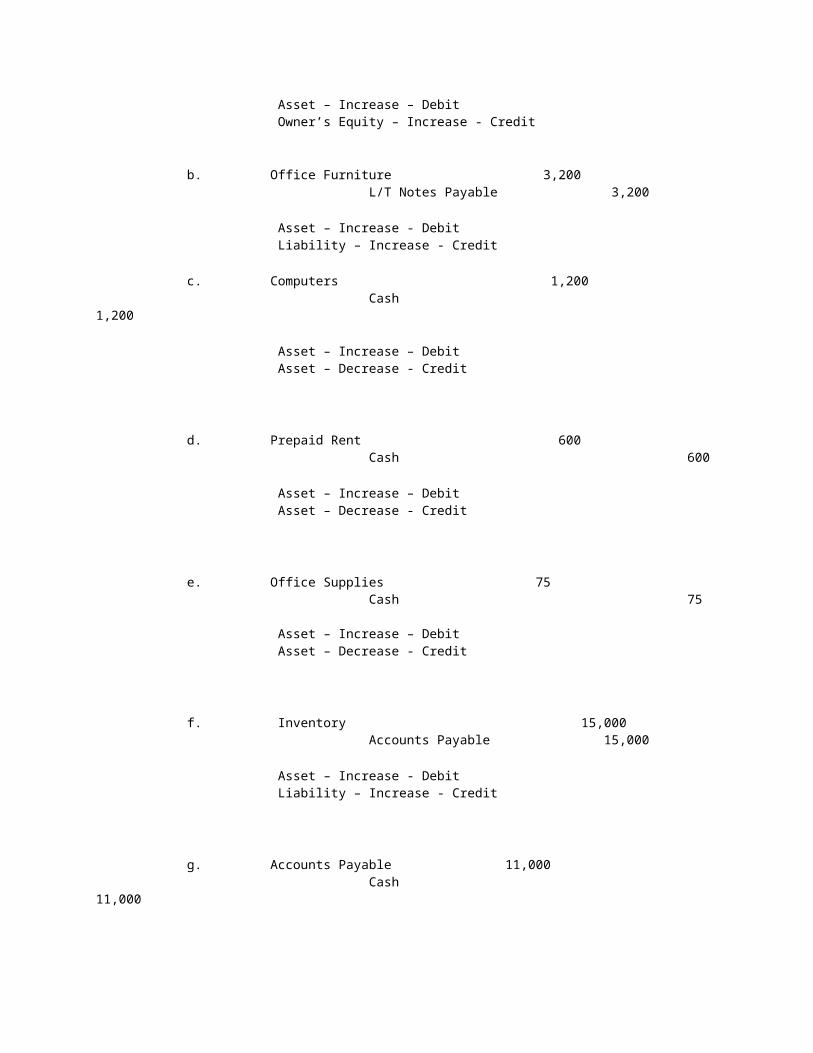

a. Issued stock to investors for $125,000 cash b. Purchased office furniture for $3,200, agree to pay the entire amount in 2 years. c. Purchased computers for the office for $1,200 cash d. Paid for rent for the next 3 months, $600 e. Purchased office supplies for $75 cash f. Purchased inventory on account for $15,000 g. Paid $11,000 to the supplier for the inventory purchased in f. h. Hired employees who will begin work in 2 weeks i. Borrowed $10,000 from the bank to be repaid in 6 months j. Loaned $2,500 to a company who agrees to repay it in 2 years

Answer:

a. Cash 125,000 Common Stock 125,000

Asset – Increase – Debit Owner’s Equity – Increase - Credit

b. Office Furniture 3,200 L/T Notes Payable 3,200

Asset – Increase - Debit Liability – Increase - Credit

c. Computers 1,200 Cash 1,200

Asset – Increase – Debit Asset – Decrease - Credit

d. Prepaid Rent 600 Cash 600

Asset – Increase – Debit Asset – Decrease - Credit

e. Office Supplies 75 Cash 75 Asset – Increase – Debit Asset – Decrease - Credit

f. Inventory 15,000 Accounts Payable 15,000

Asset – Increase - Debit Liability – Increase - Credit

g. Accounts Payable 11,000 Cash 11,000

Liability – Decrease – Debit Asset – Decrease - Credit

h. No entry recorded, no exchange has taken place

i. Cash 10,000 S/T Notes Payable 10,000 Asset – Increase - Debit Liability – Increase - Credit

j. L/T Notes Receivable 2,500 Cash 2,500

Asset – Increase – Debit Asset – Decrease - Credit

Cash ______________________ 125,000 / 1,200 10,000 / 600 / 75 / 11,000 / 2,500 __________ /__________ 135,000 / 15,375 119,625 /

17. Record journal entries for the following transactions. After recording the transactions, prepare a “T account” and balance the accounts payable account.

a. Borrowed $50,000 from the bank, agreed to repay it in 3 years b. Purchased manufacturing equipment for $20,000 cash c. Purchased office furniture on account, $2,700 d. Paid for insurance for the next 6 months, $2,200 e. Repaid $10,000 of the amount borrowed from the bank f. Purchased inventory on account, $15,000 g. Purchased supplies for cash, $100 h. Paid the supplier $14,000 for inventory purchased on account i. Invested $3,000 in a short term investment j. Sold part of the company to investors for $50,000 cash

Answer: a. Cash 50,000 L/T Notes Payable 50,000

Asset – Increase - Debit Liability – Increase - Credit

b. Manufacturing Equipment 20,000 Cash 20,000

Asset – Increase – Debit Asset – Decrease - Credit

c. Office Furniture 2,700 Accounts Payable 2,700

Asset – Increase - Debit Liability – Increase - Credit

d. Prepaid Insurance 2,200 Cash 2,200

Asset – Increase – Debit Asset – Decrease - Credit

e. L/T Notes Payable 10,000 Cash 10,000

Liability – Decrease – Debit Asset – Decrease - Credit

f. Inventory 15,000 Accounts Payable 15,000

Asset – Increase - Debit Liability – Increase - Credit

g. Supplies 100 Cash 100 Asset – Increase – Debit Asset – Decrease - Credit

h. Accounts Payable 14,000 Cash 14,000 Liability – Decrease – Debit Asset – Decrease - Credit

i. S/T Investment 3,000 Cash 3,000 Asset – Increase – Debit Asset – Decrease - Credit

j. Cash 50,000 Common Stock 50,000

Asset – Increase – Debit Owner’s Equity – Increase - Credit

Accounts Payable ______________________ / 2,700 / 15,000 14,000 /

/ / __________ /__________ 14,000 / 17,700_ / 3,700

18. A company had the following transactions during the first month of operations. Record journal entries for these transactions. Determine the balancein the cash account at the end of the first month.

a.) Received $150,000 cash from investors for ownership in the company. b.) Purchased inventory to be sold to customers, $45,000 on account. c.) Rented warehouse space, $6,000 was paid for this month. d.) Sold $5,000 of inventory on account (you have not been paid yet), sales price of $7,500. e.) Acquired office furniture for $3,000 cash f.) Paid $12,000 to employees who worked this month. g.) Acquired manufacturing equipment costing $39,000, paid cash. h.) Paid $700 for janitorial service. i.) Received a $100 utility bill for this month. j.) Collected $7,500 owed from customers.

Answer:

a. Cash 150,000 Common Stock 150,000

Asset – Increase – Debit Owner’s Equity – Increase - Credit

b. Inventory 45,000 Accounts Payable 45,000

Asset – Increase - Debit Liability – Increase - Credit

c. Rent Expense 6,000 Cash 6,000

Expense – Increase – Debit Asset – Decrease - Credit

d. Accounts Receivable 7,500 Sales 7,500

Cost of Goods Sold 5,000 Inventory 5,000

Asset – Increase – Debit Revenue – Increase – Credit Expense – Increase – Debit Asset – Decrease - Credit

e. Office Furniture 3,000 Cash 3,000

Asset – Increase – Debit Asset – Decrease - Credit

f. Salary Expense 12,000 Cash 12,000

Expense – Increase – Debit Asset – Decrease - Credit

g. Manufacturing Equipment 39,000 Cash 39,000

Asset – Increase – Debit Asset – Decrease - Credit

h. Cleaning Expense 700 Cash 700

Expense – Increase – Debit Asset – Decrease - Credit

i. Utility Expense 100 Accounts Payable 100

Expense – Increase - Debit Liability – Increase - Credit

j. Cash 7,500 Accounts Receivable 7,500

Asset – Increase – Debit Asset – Decrease - Credit

Cash ______________________ 150,000 / 6,000 7,500 / 3,000 / 12,000 / 39,000 / 700 __________ /__________ 157,500 / 60,700 96,800 /

For account titles, we will be using the chart of accounts presented in an earlier lesson.All transactions are assumed and simplified for illustration purposes.Note: We will also be using this set of transactions and journal entries in later lessons when we discuss the other steps of the accounting process.Let's start.Transaction #1: On December 1, 2013, Mr. Donald Gray started Gray Network Services by investing $10,000. The journal entry should increase the company's Cash, and establish/increase the capital account of Mr. Gray; hence:

Date2013

Particulars Debit Credit

Dec 1 Cash 10,000

.00

Mr. Gray, Capital 10,000

.00Transaction #2: On December 5, Gray Network Services paid registration and licensing fees for the business, $370.First, we will debit the expense (to increase an expense, you debit it); and then, credit Cash to record the decrease in cash as a result of the payment.

5 Taxes and Licenses 370.00

Cash 370.00

Transaction #3: On December 6, the company acquired tables, chairs, shelves, and otherfixtures for a total of $3,000. The entire amount was paid in cash.There is an increase in an asset account (Furniture and Fixtures) in exchange for a decrease in another asset (Cash).

6 Furniture and Fixtures

3,000.00

Cash 3,000.00

Transaction #4: On December 7, the company acquired service equipment at $16,000. The company paid a 50% down payment and the balance will be paid after 60 days.This will result in a compound journal entry. There is an increase in an asset account (debit Service Equipment, $16,000), a decrease in another asset (credit Cash, $8,000 – the

amount paid), and an increase in a liability account (credit Accounts Payable, $8,000 – the balance to be paid after 60 days).

7 Service Equipment 16,000.00

Cash 8,000.00

Accounts Payable 8,000.00

Transaction #5: Also on December 7, Gray Network Services purchased service supplieson account amounting to $1,500.The company received supplies thus we will record a debit to increase supplies. By theterms "on account", it means that the amount has not yet been paid; and so, it is recorded as a liability of the company.

7 Service Supplies 1,500.00

Accounts Payable 1,500.00

Transaction #6: On December 9, the company received $1,900 for services rendered. We will then record an increase in cash (debit the cash account) and increase in income (credit the income account).

9 Cash 1,900.00

Service Revenue 1,900.00

Transaction #7: On December 12, the company rendered services on account, $4,250.00. As per agreement with the customer, the amount is to be collected after 5 days. Under the accrual basis of accounting, income is recorded when earned.In this transaction, the services have been fully rendered (meaning, we made an income; we just haven't collected it yet.) Hence, we record an increase in income and an increase in a receivable account.

12

Accounts Receivable

4,250.00

Service Revenue 4,250.00

Transaction #8: On December 14, Mr. Gray invested an additional $3,200.00 into the business. The entry would be similar to what we did in transaction #1, i.e. increase cash and increase the capital account of the owner.

14 Cash 3,200

.00

Mr. Gray, Capital 3,200

.00Transaction #9: Rendered services to a big corporation on December 15. As per agreement, the $3,400 amount due will be collected after 30 days.

15

Accounts Receivable

3,400.00

Service Revenue 3,400.00

Transaction #10: On December 17, the company collected from the customer in transaction #7. We will record an increase in cash by debiting it. Then, we will credit accounts receivable to decrease it. We are actually reducing the receivable since it has already been collected.

17 Cash 4,250

.00

Accounts Receivable 4,250

.00Transaction #11: On December 20, the company paid some of its liability in transaction#5 by issuing a check. The company paid $500 of the $1,500 payable.To record this transaction, we will debit Accounts Payable for $500 to decrease it by that amount. Then, we will credit cash to decrease it as a result of the payment. The entry would be:

20 Accounts Payable 500.0

0

Cash 500.00

The balance of the accounts payable in transaction number #6 would now be $1,000 credit ($1,500initial credit and now a $500 debit).Transaction #12: On December 25, the owner withdrew cash due to an emergency need. Mr.Gray withdrew $7,000 from the company.Naturally, there is a decrease in Cash since the company paid Mr. Gray $7,000. And, wewill increase/record withdrawals (Mr. Gray, Drawing) for the said amount.

25 Mr. Gray, Drawings 7,000

.00

Cash 7,000.00

Transaction # 13: On December 29, the company paid rent for December, $ 1,500. Again, we will record the expense by debiting it and decrease cash by crediting it.

29 Rent Expense 1,500

.00

Cash 1,500.00

Transaction #14: On December 30, the company acquired a $12,000 short-term bank loan; the entire amount plus a 10% interest is payable after 1 year.Again, the company received cash so we increase it by debiting Cash. The company now has a liability (Loans Payable). We increase it by crediting the liability account.

30 Cash 12,000

.00

Loans Payable 12,000.00

Transaction #15: On December 31, the company paid salaries to its employees, $3,500.For this transaction, we will record/increase the expense account by debiting it and decrease cash by crediting it. (Note: This is a simplified entry to present the payment of salaries. In actual practice, different payroll accounting methods are applied.)

31 Salaries Expense 3,500

.00

Cash 3,500.00

There you have it. You should be getting the hang of it by now. If not, then you can always go back to the examples above. Remember that accounting skills require practiceand exposure.

Top Related

Copyright © 2022 FDOKUMEN