Bahasa

Halaman

Hukum

Data mining for decision support on customer insolvencyin telecommunications business

S. Daskalaki a, I. Kopanas b, M. Goudara a, N. Avouris b,*

a Department of Engineering Sciences, University of Patras, Rio Patras GR-26500, Greeceb Department of Electrical and Computer Engineering, University of Patras, Rio Patras GR-26500, Greece

Abstract

This paper reports on the findings of a research project that had the objective to build a decision support system to

handle customer insolvency for a large telecommunication company. Prediction of customer insolvency, well in ad-

vance, and with an accuracy that could make this prediction useful in business terms, was one of the core objectives of

the study. In the paper the process of building such a predictive model through knowledge discovery and data mining

techniques in vast amounts of heterogeneous as well as noisy data is described. The reported findings are very

promising, making the proposed model a useful tool in the decision making process, while some of the discussed

problems and limitations are of interest to researchers who intend to use data mining approaches in other similar real-

life problems.

� 2002 Elsevier Science B.V. All rights reserved.

Keywords: Decision support systems; Predictive data mining; Classification; Customer insolvency

1. Introduction

Telecommunication companies, as well as other

service-providing companies, often suffer from in-

solvent customers who use the provided serviceswithout paying their dues. Companies in tele-

communications business take precautions against

these customers; however, in most cases this refers

to measures applied quite late, often with no sig-

nificant effect. As a result many unpaid bills end up

in the account of uncollectible debts. Thus, failure

of some customers to pay their dues results in con-

siderable loss of revenue for the company. Detec-

tion and prevention of this behavior is an objective

of prime importance for the industry. This is es-

pecially important today that strong competitionis building in many sectors of the telecommuni-

cations industry as monopolies cease to exist.

A model, capable of predicting insolvent be-

havior of customers well in advance, being avail-

able, can be a useful decision support tool for a

service-providing company. However building

such a model is not a trivial process. The research

reported here sets as its prime objective to studythe feasibility of building such a tool for a major

telecommunications operator using data mining

techniques.

European Journal of Operational Research 145 (2003) 239–255

www.elsevier.com/locate/dsw

*Corresponding author.

E-mail addresses: [email protected] (S. Daskalaki), ikop-

[email protected] (I. Kopanas), [email protected]

tras.gr (M. Goudara), [email protected] (N. Avouris).

0377-2217/03/$ - see front matter � 2002 Elsevier Science B.V. All rights reserved.

PII: S0377-2217 (02 )00532-5

The decision to use data mining techniques in

this study is based on the observation that tele-

communication companies collect high volumes of

data relating to different aspects of the interaction

that takes place between the company and its

customers. While in most cases dispersed, thesedata when inter-related may contain valuable in-

formation relating to the insolvency-prediction

problem. Examples of such data are: (a) customer

profiles, (b) usage of the offered service, and (c)

financial transactions of the customers with the

company.

Like fraudsters in other fraud detection prob-

lems, it is assumed that insolvent customers on theaverage behave differently from the rest of the

customers, especially during a critical period pre-

ceding the due-date for payment. The goal is

therefore to reveal those behavioral patterns, which

may distinguish these customers from the rest.

When this information is combined with other

features the whole process may result to rules that

lead to predictions for possible insolvencies. Forthe purposes of this research an experiment was

performed, to prove the hypothesis that in some

cases customer insolvency could be detected much

earlier than it is done today and this in fact may

save the company a considerable amount of lost

revenue.

Some of the inherent limitations that make this

a particularly difficult problem, as identified earlyin the study, were the following:

(a) Insolvent customer�s behavior can be eitherthe result of fraudulence or due to factors beyond

the customer�s will (force majeure, social factorsetc.). The premise of the changing customer be-

havior is obviously related to the former case and

not the latter. Prediction of the second case is

particularly hard, while its existence makes iden-tification of the former cases more difficult.

(b) The available data sets, as often is the case

with real life problems, represent the individual

customer in a limited and distorted way. This is

because the source of our information is exclu-

sively the telecommunication company and the

information that this company can maintain on its

customers. For various ethical and legal reasons,this information cannot be inter-related to other

sources of information; so the customer is repre-

sented as user of the particular service, with no

means of revealing other social or financial aspects

that might had influenced the individual�s behaviorpatterns and might had strong impact towards an

insolvent behavior.(c) In the available large data set, many pa-

rameters can be defined, often deduced from pri-

mary transactional data, which can describe the

behavior of a customer of a modern telecommu-

nications company. Selection of the most relevant

ones for our problem is a tedious process that can

be partly based on statistical analysis tools and

techniques and partly on understanding the sig-nificance of the parameters in the given problem by

the researchers involved. So the process of identi-

fying a subset of these parameters, and subse-

quently using adequate tools for selecting the most

relevant ones is a crucial and important phase,

often directly related to the particular problem and

not easily reproducible.

The outlined difficulties of the problem arecompensated by the fact that there is already a rich

literature on studies with some similarities with

our problem as discussed in Section 2 of the paper.

Also, data mining techniques have matured during

the last years and examples of successful applica-

tion in various areas have been reported. Fur-

thermore, this particular study has been based on a

meticulous and long process of knowledge dis-covery in data found in a multitude of information

systems of the telecommunications operator, as

described in Section 3 of the paper. As discussed in

this paper, statistical analysis and data mining

techniques were used as part of this knowledge

discovery process.

The findings of the study, outlined in the paper,

are significant, since it has been shown that theassumption of differentiation in customer behavior

between insolvent and solvent customers is true. In

particular it has been shown that by using various

data mining techniques, like discriminant analysis,

decision trees and neural networks, it is possible to

predict insolvencies in such a way that this pre-

diction can be operationally useful for the decision

support process of the telecommunications busi-ness relating to this problem.

240 S. Daskalaki et al. / European Journal of Operational Research 145 (2003) 239–255

2. Review of similar problems

Business literature quite often refers to cus-

tomer insolvencies (e.g. Brockett et al., 1997;

Canalli, 2001), however in their terms the cus-tomer almost always refers to corporations, which

become financially delinquent to its creditors and

eventually declare bankruptcy. For our problem,

the telephone company has very limited informa-

tion regarding the financial situation of its cus-

tomers. On the contrary, there are records on

customer transactions either through the billing

department or through the switching centers. Inthat sense, the prediction of customer insolvency

for a telecommunication company as a problem is

closer to the fraud detection problems appearing

in mobile and conventional communications as well

as in credit or calling card operations. The fraud

problems reviewed here carry several common

characteristics, which are summarized below.

• Significant loss of revenue for the company that

provides the service, sometimes exceeding the al-

lowable percentage of the gross margin set as

upper limit for companies in their corresponding

sectors.

• Unpredictability of human behavior, which

makes the problem of fraud detection quite dif-

ficult in general. Fraud detection procedures re-quire study of data that express human behavior

and it is the task of the fraud detector to distin-

guish legitimate from fraudulent behavior.

• Information can be retrieved only after processing

huge amounts of data, which may in fact origi-

nate from several different sources of the com-

pany involved. From previous studies in the

area of fraud detection it is obvious that thedata required are the everyday customer trans-

actions, like the call detail records (CDRs) and

customer purchases. Information regarding

these transactions are routinely collected from

information systems for different purposes, like

billing, customer servicing, etc., however, they

are very important for studying the behavioral

differences between fraudsters and normal cus-tomers. In many cases these data by themselves

are not enough for extracting useful information

and data from other sources in the company is

additionally needed.

• Fraudulent cases are rare compared to the legit-

imate ones. This fact creates an additional diffi-

culty in training algorithms for fraud detection.

In the following, we briefly review studies on

similar problems appearing in the mobile com-

munications, conventional communications and

credit card sectors.

2.1. Fraud in mobile communications

Fraud in telecommunications in general is quite

a common phenomenon, because there is a low

detection risk and in most cases no special equip-

ment is needed; most importantly, however, be-

cause selling the access to the network may create

revenue for the fraudsters (Hoath, 1998).

In mobile telecommunications networks fraudappears with several forms. Some of them may

disappear with the help of technological advances

in the mobile phone and network technology,

however several new others will appear. Service

providers loose a considerable amount of money

and detection of fraud attempts becomes of prime

priority for them. Knowledge discovery along

with data mining techniques promise to provideeffective tools for addressing some of these prob-

lems.

Researchers as in Fawcett and Provost (1997)

have studied data from cellular communication

providers. In this work, it is shown that with the

help of knowledge discovery and data mining

techniques it is possible to detect attempts of

cloning fraud with a high degree of accuracy.Other types of fraud have been studied in Burge

et al. (1997) and Shawe-Taylor et al. (1999) and

neural networks have been applied for detecting

attempts for fraud in systems currently used in

Europe. Accessing real data and testing predictive

algorithms often is a problem. Simulation may

then substitute real situation (Barson et al., 1996),

however the effectiveness of the algorithms may bedoubtful.

S. Daskalaki et al. / European Journal of Operational Research 145 (2003) 239–255 241

2.2. Fraud in conventional communications

Several types of fraud have also been identi-

fied in conventional telecommunications services.

Examples of fraud instances include subscriptionfraud, unauthorised calling card usage, fraud

through PBXs, etc. Global losses due to telephone

fraud are estimated to be as high as billions of

dollars a year (Hoath, 1998). Like with mobile

communications, fraudsters take advantage of

technological loopholes in systems; at the same

time they exploit procedures traditionally applied

by telecommunication companies for buildingtrusting relationship with their customers. The

problem of uncollectible debts resulting from un-

reliable/insolvent customers initially has been ad-

dressed in Ezawa and Norton (1995, 1996). In

these article it is reported that detecting unreliable

customers is possible when treated as a classifica-

tion problem, and the proposed classifier is based

on Bayesian networks.Unauthorised calling card usage has been

studied by Yuhas and initial results are reported in

Yuhas (1993). Due to the lack of clearly identified

fraud cases unsupervised learning models have

been adopted for that study. By means of clus-

tering algorithms users of calling cards are

grouped in clusters based on the values of nine

variables, suitably selected to summarize userprofiles.

2.3. Fraud in credit card usage

Studies with data from credit card usage suggest

that fraud in this area may be detected with a

reasonable level of certainty if treated as classifi-

cation problem, where individual transactions areclassified either as potentially fraud or non-fraud

related. Moreover, with the rapid expansion of

e-commerce worldwide scalable techniques sug-

gested by data mining become indispensable in

order to analyse massive amounts of data in a

timely manner (Chan et al., 1999). Fraud cases in

the credit card domain exist due to lost, stolen,

counterfeit or non-received cards, fraudulent ap-plications and exploitation of the mail-order sys-

tem. For all the aforementioned cases classifiers

based on discriminant analysis (Richardson, 1997),

multi-layer perceptron neural networks (Aleskerov

et al., 1997; Dorronsoro et al., 1997; Ghosh and

Reilly, 1994) have been proposed.

Also, in the credit card domain a few billions of

dollars are lost per year for the service providers to

what is referred as charge-off losses, mainly due topersonal bankruptcy. Application of data mining

techniques for knowledge discovery may result to

the construction of a decision tree to be used as

classifier for the accounts reviewed. As reported in

Donato et al. (1999) combining the decision tree

classifier with neural networks, it is possible to

construct a decision support system for on-line

operation with temporal data like customertransactions.

3. Insolvency prediction as the result of a ‘‘knowl-

edge discovery in data’’ process

The bottom line for all studies that have been

reported so far in the area of fraud detection isthat an experiment has to be set to test whether

detection of fraudulent actions is possible and to

decide about the level of accuracy that is possible

to be achieved. In the case of customer insolvency

with conventional communications one may find

certain characteristics that distinguish this prob-

lem from other fraud cases. Specifically, the cus-

tomers are not mobile, so the characteristic ‘‘originof the call’’ is not a useful classifier. On the other

hand, it is often the case that a telephone con-

nection might correspond to multiple users, while

unauthorised use can be a more frequent reason

for a high bill that can lead to insolvency.

A term often used to describe the process of

building a decision support system based in great

extend on large amounts of available data is thatof knowledge discovery from data (KDD). KDD

is defined as the ‘‘nontrivial process of identifying

valid, novel, potentially useful, and ultimately

understandable patterns in data’’ (Frawley et al.,

1991). The study reported in this paper can

be described as a KDD experiment. Following a

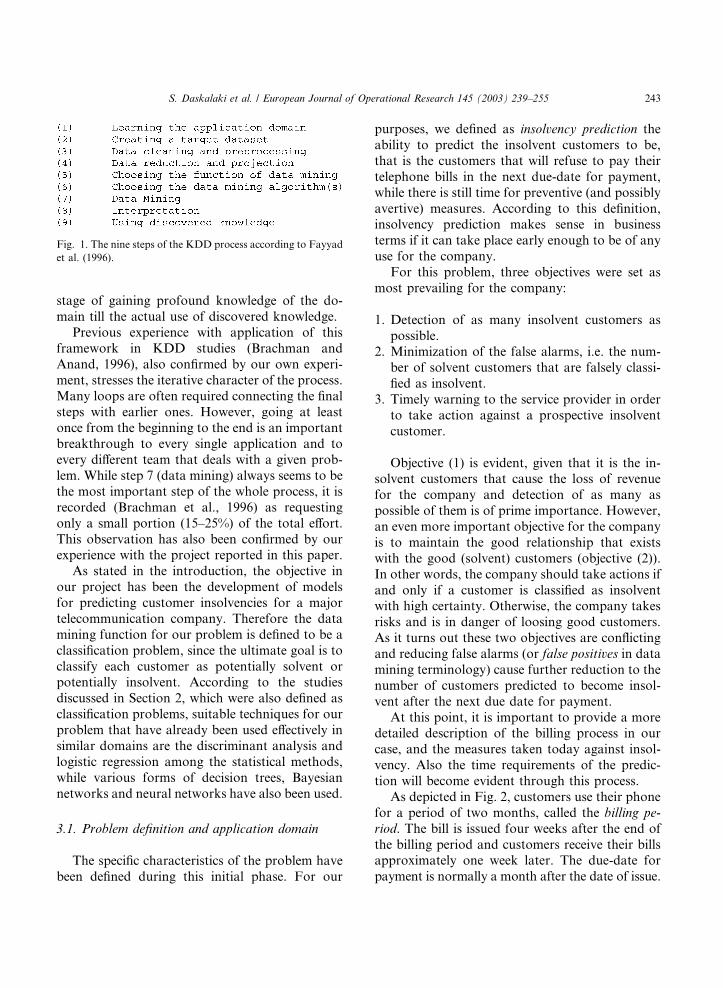

typical KDD framework (Fayyad et al., 1996; Han

and Kamber, 2001), where data mining is the corein the overall process, the experiment went

through all nine steps of Fig. 1, starting from the

242 S. Daskalaki et al. / European Journal of Operational Research 145 (2003) 239–255

stage of gaining profound knowledge of the do-

main till the actual use of discovered knowledge.

Previous experience with application of this

framework in KDD studies (Brachman and

Anand, 1996), also confirmed by our own experi-

ment, stresses the iterative character of the process.

Many loops are often required connecting the final

steps with earlier ones. However, going at leastonce from the beginning to the end is an important

breakthrough to every single application and to

every different team that deals with a given prob-

lem. While step 7 (data mining) always seems to be

the most important step of the whole process, it is

recorded (Brachman et al., 1996) as requesting

only a small portion (15–25%) of the total effort.

This observation has also been confirmed by ourexperience with the project reported in this paper.

As stated in the introduction, the objective in

our project has been the development of models

for predicting customer insolvencies for a major

telecommunication company. Therefore the data

mining function for our problem is defined to be a

classification problem, since the ultimate goal is to

classify each customer as potentially solvent orpotentially insolvent. According to the studies

discussed in Section 2, which were also defined as

classification problems, suitable techniques for our

problem that have already been used effectively in

similar domains are the discriminant analysis and

logistic regression among the statistical methods,

while various forms of decision trees, Bayesian

networks and neural networks have also been used.

3.1. Problem definition and application domain

The specific characteristics of the problem have

been defined during this initial phase. For our

purposes, we defined as insolvency prediction the

ability to predict the insolvent customers to be,

that is the customers that will refuse to pay their

telephone bills in the next due-date for payment,

while there is still time for preventive (and possibly

avertive) measures. According to this definition,insolvency prediction makes sense in business

terms if it can take place early enough to be of any

use for the company.

For this problem, three objectives were set as

most prevailing for the company:

1. Detection of as many insolvent customers as

possible.2. Minimization of the false alarms, i.e. the num-

ber of solvent customers that are falsely classi-

fied as insolvent.

3. Timely warning to the service provider in order

to take action against a prospective insolvent

customer.

Objective (1) is evident, given that it is the in-solvent customers that cause the loss of revenue

for the company and detection of as many as

possible of them is of prime importance. However,

an even more important objective for the company

is to maintain the good relationship that exists

with the good (solvent) customers (objective (2)).

In other words, the company should take actions if

and only if a customer is classified as insolventwith high certainty. Otherwise, the company takes

risks and is in danger of loosing good customers.

As it turns out these two objectives are conflicting

and reducing false alarms (or false positives in data

mining terminology) cause further reduction to the

number of customers predicted to become insol-

vent after the next due date for payment.

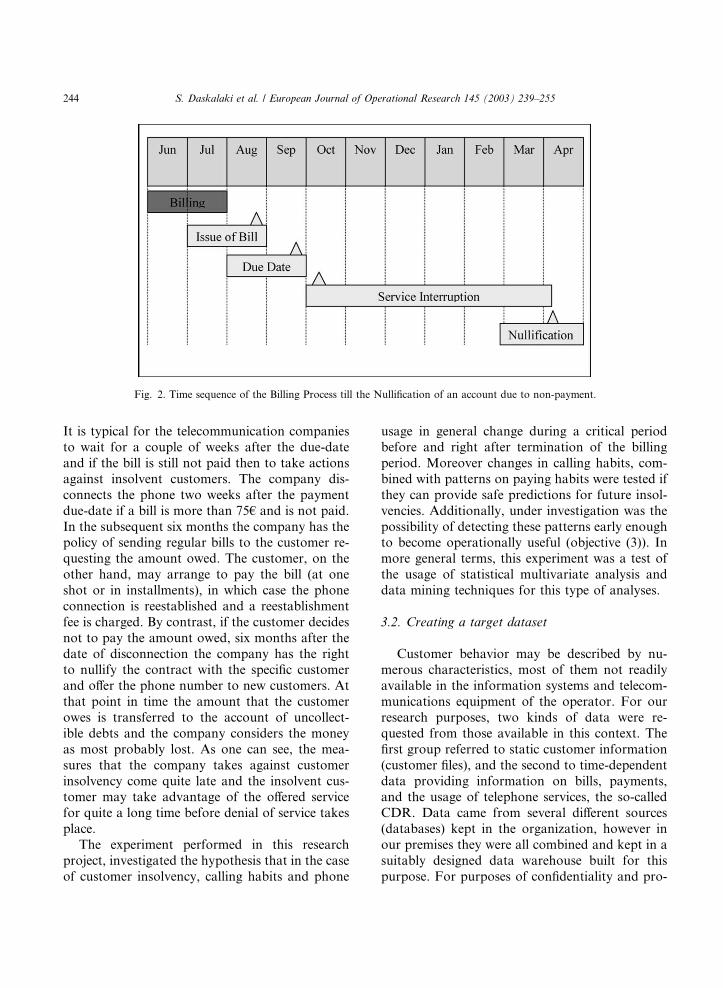

At this point, it is important to provide a moredetailed description of the billing process in our

case, and the measures taken today against insol-

vency. Also the time requirements of the predic-

tion will become evident through this process.

As depicted in Fig. 2, customers use their phone

for a period of two months, called the billing pe-

riod. The bill is issued four weeks after the end of

the billing period and customers receive their billsapproximately one week later. The due-date for

payment is normally a month after the date of issue.

Fig. 1. The nine steps of the KDD process according to Fayyad

et al. (1996).

S. Daskalaki et al. / European Journal of Operational Research 145 (2003) 239–255 243

It is typical for the telecommunication companies

to wait for a couple of weeks after the due-date

and if the bill is still not paid then to take actions

against insolvent customers. The company dis-

connects the phone two weeks after the payment

due-date if a bill is more than 75€ and is not paid.

In the subsequent six months the company has thepolicy of sending regular bills to the customer re-

questing the amount owed. The customer, on the

other hand, may arrange to pay the bill (at one

shot or in installments), in which case the phone

connection is reestablished and a reestablishment

fee is charged. By contrast, if the customer decides

not to pay the amount owed, six months after the

date of disconnection the company has the rightto nullify the contract with the specific customer

and offer the phone number to new customers. At

that point in time the amount that the customer

owes is transferred to the account of uncollect-

ible debts and the company considers the money

as most probably lost. As one can see, the mea-

sures that the company takes against customer

insolvency come quite late and the insolvent cus-tomer may take advantage of the offered service

for quite a long time before denial of service takes

place.

The experiment performed in this research

project, investigated the hypothesis that in the case

of customer insolvency, calling habits and phone

usage in general change during a critical period

before and right after termination of the billing

period. Moreover changes in calling habits, com-

bined with patterns on paying habits were tested if

they can provide safe predictions for future insol-

vencies. Additionally, under investigation was the

possibility of detecting these patterns early enoughto become operationally useful (objective (3)). In

more general terms, this experiment was a test of

the usage of statistical multivariate analysis and

data mining techniques for this type of analyses.

3.2. Creating a target dataset

Customer behavior may be described by nu-merous characteristics, most of them not readily

available in the information systems and telecom-

munications equipment of the operator. For our

research purposes, two kinds of data were re-

quested from those available in this context. The

first group referred to static customer information

(customer files), and the second to time-dependent

data providing information on bills, payments,and the usage of telephone services, the so-called

CDR. Data came from several different sources

(databases) kept in the organization, however in

our premises they were all combined and kept in a

suitably designed data warehouse built for this

purpose. For purposes of confidentiality and pro-

Fig. 2. Time sequence of the Billing Process till the Nullification of an account due to non-payment.

244 S. Daskalaki et al. / European Journal of Operational Research 145 (2003) 239–255

tection of customer privacy, data were codified in a

secure way. To be more specific the raw data used

in this research referred to:

• customer information from customer files,

• usage of phone connection from switching cen-ters,

• billing data from the billing information system,

• reports on payments by customers from the bill-

ing information system,

• reports of phone disconnections due to failure of

payment,

• reports of phone reconnections after payment,

and• reports of permanent nullifications of contracts.

In order to make this study more representative

of a cross-section of customers of the operator,

data were collected from three different geographic

areas, one rural/agricultural, one semi-rural/tou-

ristic and one urban/industrial. Altogether, the

three areas totaled 100,000 customers.In terms of time, the data in the target dataset

covered a span of 17 months. Because of the billing

process described previously, there was a two-

month shift between billing data and telephone

usage records; that is to say billing covered data

from 10/1999 to 2/2001, while the call records re-

spectively spanned from 8/1999 to 12/2000. As an

indication for the size of the data warehouse built,collected data were over 10 GB in raw form.

3.3. Data cleaning and preprocessing

At this stage it was essential to test the quality

of the collected data, to filter out information of

no significance to our study and to inter-relate the

heterogeneous data items in the data warehouse.This has been a tedious process. Examples of the

performed operations during this phase are in-

cluded here.

Very early in our study it was clear that a 50%

decrease of the total volume of the data could be

achieved by eliminating inexpensive calls (charging

less than 0.3€). The elimination of these data did

not affect the result of our research given that thecompany is mostly interested on detecting patterns

of expensive calls placed with the ultimate goal not

to be paid.

However low percentage of corrupted data,

certain error correction procedures were applied

whenever appropriate in order to sanitize the data

from missing or erroneous values. Such problemsarose from lack of integration among information

systems within the organization that provided the

data and the dispersion of data sources. For ex-

ample, the planned dates for service interruption

due to lack of payment not always coincided with

the actual disconnection date but this could be

corrected by checking the CRD records. Also,

some phone accounts did not appear in the recordsof payments, however this information could be

deduced by examining the details in the following

bill.

The synchronization of data was an important

and tedious procedure during this step. The goal

was to study the behavior of all customers during a

period starting several weeks before a billing pe-

riod expires. However, billing periods vary to formdifferent groups of phone accounts. So insolvent

customers appear in different points of time during

the period of our study, so synchronization was

absolutely necessary.

3.4. Data reduction and projection

The data cleaning and pre-processing (e.g. re-cords synchronisation) of the previous phase, re-

vealed a number of cases of insolvent customers

with insufficient information that eventually had

to be eliminated from the data set. The next step

was to group information by phone account, so

manipulation of data became much easier.

The study period for the behavior of insolvent

customers was set to be approximately a periodof seven months before the disconnection of the

phone, which usually occurs six months before

the nullification of the account. The decision for

the length of the study period was based on data

analysis and business requirements. Within the

seven-month study period information regarding

call transactions made by the customer was ag-

gregated by two-week periods.With the help of statistical inference at this

point, a number of features were tested with the

S. Daskalaki et al. / European Journal of Operational Research 145 (2003) 239–255 245

ultimate goal to reveal those characteristics that

were discriminant factors for the two categories of

customers. The ones that did not provide any valid

or useful information in distinguishing solvent

from insolvent customers were eliminated.

Indicative of the type of work performed at thisstage are the following statistical tests:

1. Each telephone account belongs uniquely to

one out of twenty three categories (examples

of categories are: domestic, business, public

schools, payphone, etc.). A chi-square hypothe-

sis testing was performed for checking indepen-

dence of the distribution of phone accountsamong the different categories for the two

classes of customers. The hypothesis was re-

jected (p-value� 0:001), concluding that cate-gories of the accounts are not independent of

the customer class.

2. The average amount owed on the bi-monthly

bills was calculated for all solvent and insolvent

customers and was significantly higher for theclass of insolvent customers. This finding was

consistent throughout all different categories

of telephone connections. To support this a hy-

pothesis testing for homogeneity of the ‘‘aver-

age amount owed’’ for the two classes of

customers and the different categories was per-

formed. The hypothesis was rejected (p-

value� 0:001) supporting the conjecture statedabove.

3. For each customer the ‘‘extra charges’’ on the

bi-monthly bills were calculated by comparing

the total charges for the phone usage and the

service offered with the actual amount of the bill

to reveal charges resulting from previous bills,

charges from purchases of other products of

the company (like phone handsets, mobilehandsets, entries in yellow pages, etc.). The hy-

pothesis test performed for homogeneity of this

feature across the two classes of customers and

across the different categories of accounts again

rejected the hypothesis (with a p-value� 0:01)concluding significant differences between the

two classes.

4. Finally, the feature ‘‘payment by installments’’was studied by providing the number of times

a customer had requested payment by install-

ments during the study period. The hypothesis

for equal proportions of customers between

the two classes was rejected, indicating signifi-

cant differences between the two classes of cus-

tomers.

All previously mentioned tests were performed

in the original dataset, however in order to create

customer profiles, and even more so in order to

study the usage of the phone for customers of the

two classes it was important to create a smaller

and more manageable dataset projecting all char-

acteristics from the original one.

3.5. Defining the data mining function and feature

selection

As mentioned earlier, the problem of predicting

customer insolvency may be viewed as a classifi-

cation problem, where each customer is classified

in one of two classes: most possibly solvent or most

possibly insolvent with respect to the following due-

date of payment and the attitude towards the

amount owed in the following six months. As a

classification problem, it carried the following

characteristics:

• The distribution of customers between the two

classes was very uneven in the original dataset:approximately 99.3% were solvent customer

and 0.7% insolvent customers per billing period

in a given group of accounts.

• The absolute number of insolvencies in our data

set was very small, because only a few insol-

vency cases arise in every given billing period.

• The misclassifications for the two classes of cus-

tomers carried different costs, following objec-tives (1) and (2) set in the beginning of our

project and discussed in Section 3.1.

As discussed by Weiss and Provost (2001),

classification problems with these characteristics

are particularly difficult to solve. Therefore, a new

dataset had to be created specifically for the data

mining function through a stratified samplingprocedure for the solvent customers. This is a

recommended procedure in similar problems

(Chan and Stolfo, 1998). In this new dataset the

246 S. Daskalaki et al. / European Journal of Operational Research 145 (2003) 239–255

distribution of customers between the two classes

was altered to approximately 90% of solvent cus-

tomer and 10% of insolvent customers. The new

distribution between the classes was achieved by

maintaining all cases of insolvent customers in the

original data set, while for the solvent customers astratified sampling was performed. Our goal was

to create a representative sample of the solvent

customers, so that the algorithms would be trained

sufficiently well. Therefore, the triad of character-

istics geographic area, type of phone connection,

and group of the phone account were used for

sampling strata. These three characteristics had to

be carried in the sample with the same proportionsas in the original dataset in order (a) to maintain

the three distinct geographic areas in the reduced

data set, mentioned in Section 3.2, (b) to represent

the different types of phone connections, see

analysis in Section 3.4 and (c) to eliminate sea-

sonality associated with groups of phone accounts,

discussed in Section 3.3.

The result of this procedure was a dataset con-sisting of 2066 cases in total (solvent and insolvent).

For these cases a number of primary and secondary

features were created. After a data analysis phase,

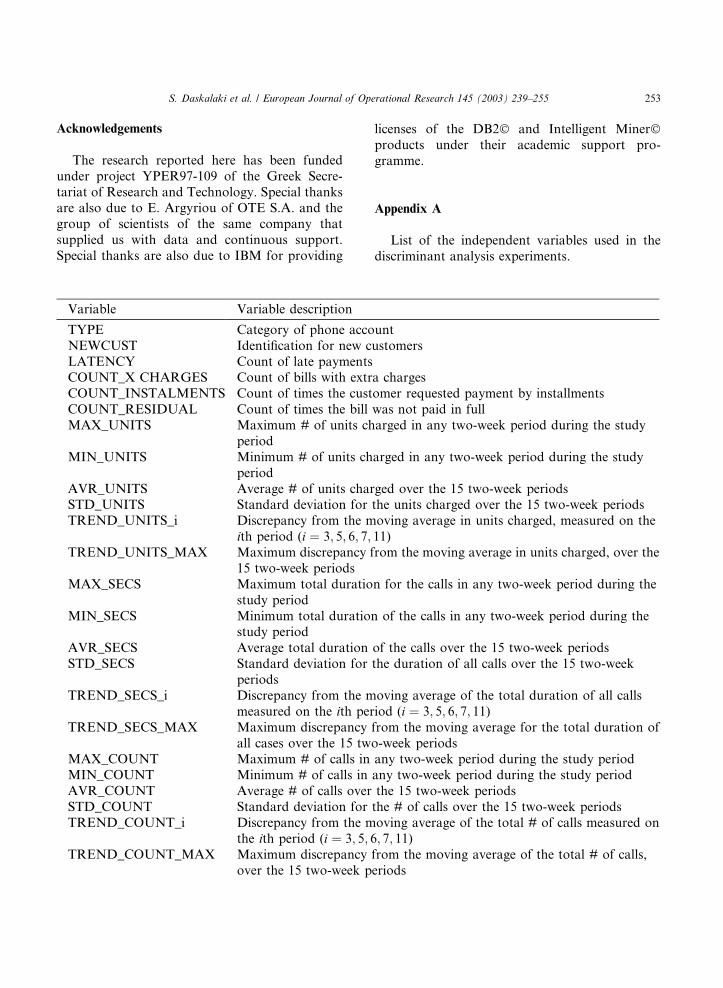

briefly outlined in the following, 46 variables,

shown in the Appendix, were selected as candi-

date discriminating factors. Two of those variables

(TYPE, NEWCUST) describe the account, four

(LATENCY, COUNT_X_CHARGES, COUNT_INSTALMENTS, andCOUNT_RESIDUAL) the

behavior of the customer towards previous phone

bills, and the remaining 40 summarizes the call

habits of the customers over 15 two-week periods.

The selection of the last 40 variables was based on

a data analysis performed on the new reduced

dataset.

An adequate study period was established foreach phone account, called critical period during

which patterns of customer behavior were to be

observed. For the accounts that were nullified due

to non-payment, the critical period was defined to

be the last 15 two-week periods before interruption

of service. For the accounts that were not nullified,

the critical period was defined to be a period of

similar length prior to a possible date of inter-ruption had they not paid a certain bill. For each

account there were six possible dates per year for

service interruption, out of which one was selected

in random.

For each account and for every two-week pe-

riod in the critical period several variables were

defined by counting the total number of units

charged to the account, the total amount of timethat the phone was utilized, the number of phone

calls made, and the total count of different num-

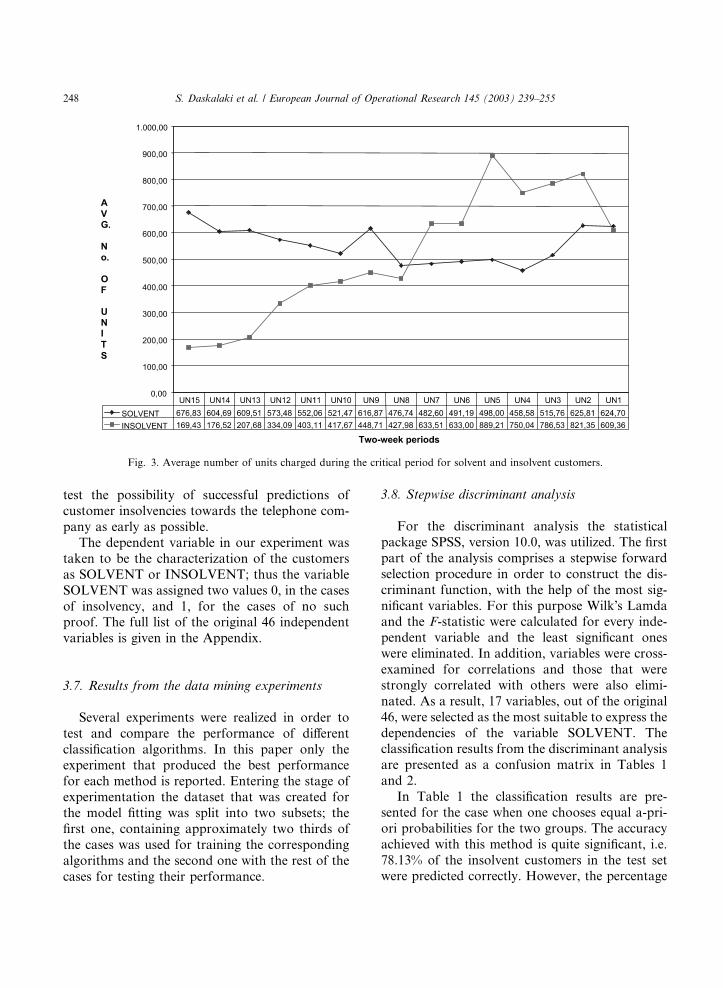

bers that were called during that period. Fig. 3

shows one of these variables, the average number

of units charged during their corresponding critical

periods, for the solvent and the insolvent custom-

ers, respectively. A clearly different average be-

havioral pattern in the two populations emergesfrom this figure. On the average the solvent cus-

tomers were charged approximately the same

amount of units during all periods, ranging from

460 units to 680 units. On the contrary, the in-

solvent customers on the average were charged

significantly less units than the solvent during the

first eight two-week periods and afterwards their

behavior changed resulting to significantly moreunits than the solvent customers.

The conclusion of this phase of the study was to

create several new variables describing the usage of

each phone account, compared to a moving aver-

age of four previous two-week periods. Therefore,

as mentioned earlier, many new variables were

created, out of which the 46 variables in the Ap-

pendix were chosen as most prominent. As will beexplained in Section 3.6, the set of the variables

was further reduced with the help of the stepwise

discriminant analysis.

3.6. Selection of classification algorithms

At this stage of our research we tried a number

of alternative classification algorithms for testingour hypothesis, using the reduced dataset and the

selected variables as candidate discriminating

features. The algorithms used in the study were

discriminant analysis, decision trees and neu-

ral networks. Each one of them gives a different

classifier, a linear one produced by the discrimi-

nant analysis, a non-linear by the neural network,

and a rule-based classifier by the decision tree.These algorithms were applied to the dataset cre-

ated for the model fitting with the ultimate goal to

S. Daskalaki et al. / European Journal of Operational Research 145 (2003) 239–255 247

test the possibility of successful predictions of

customer insolvencies towards the telephone com-

pany as early as possible.

The dependent variable in our experiment was

taken to be the characterization of the customers

as SOLVENT or INSOLVENT; thus the variable

SOLVENT was assigned two values 0, in the cases

of insolvency, and 1, for the cases of no suchproof. The full list of the original 46 independent

variables is given in the Appendix.

3.7. Results from the data mining experiments

Several experiments were realized in order to

test and compare the performance of different

classification algorithms. In this paper only theexperiment that produced the best performance

for each method is reported. Entering the stage of

experimentation the dataset that was created for

the model fitting was split into two subsets; the

first one, containing approximately two thirds of

the cases was used for training the corresponding

algorithms and the second one with the rest of the

cases for testing their performance.

3.8. Stepwise discriminant analysis

For the discriminant analysis the statistical

package SPSS, version 10.0, was utilized. The first

part of the analysis comprises a stepwise forward

selection procedure in order to construct the dis-

criminant function, with the help of the most sig-

nificant variables. For this purpose Wilk�s Lamdaand the F-statistic were calculated for every inde-

pendent variable and the least significant ones

were eliminated. In addition, variables were cross-

examined for correlations and those that were

strongly correlated with others were also elimi-

nated. As a result, 17 variables, out of the original

46, were selected as the most suitable to express the

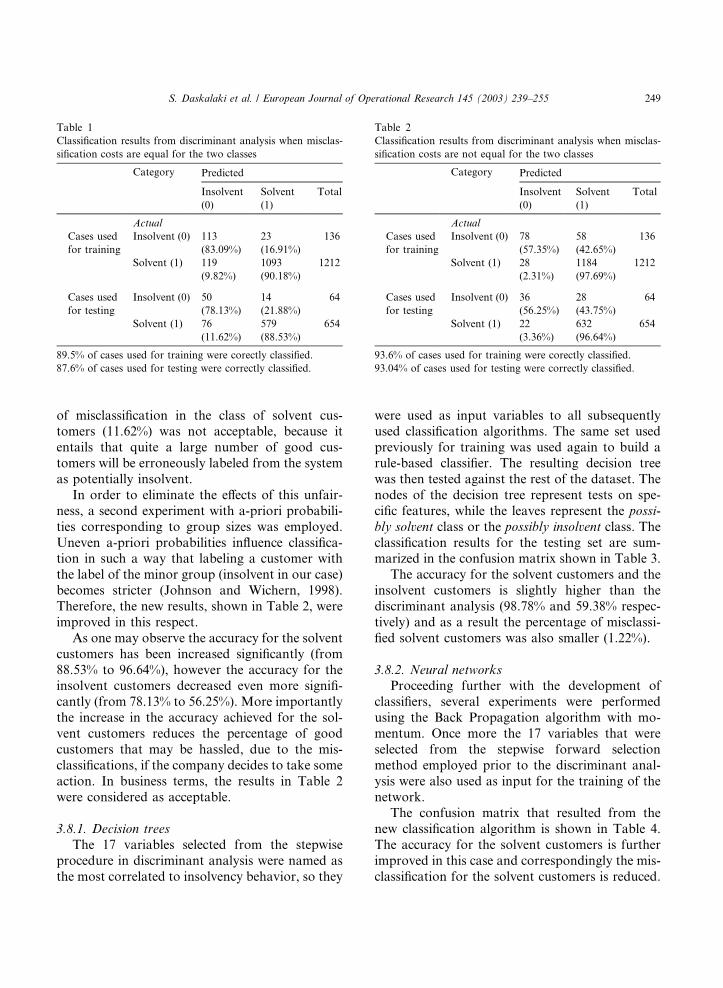

dependencies of the variable SOLVENT. Theclassification results from the discriminant analysis

are presented as a confusion matrix in Tables 1

and 2.

In Table 1 the classification results are pre-

sented for the case when one chooses equal a-pri-

ori probabilities for the two groups. The accuracy

achieved with this method is quite significant, i.e.

78.13% of the insolvent customers in the test setwere predicted correctly. However, the percentage

Fig. 3. Average number of units charged during the critical period for solvent and insolvent customers.

248 S. Daskalaki et al. / European Journal of Operational Research 145 (2003) 239–255

of misclassification in the class of solvent cus-tomers (11.62%) was not acceptable, because it

entails that quite a large number of good cus-

tomers will be erroneously labeled from the system

as potentially insolvent.

In order to eliminate the effects of this unfair-

ness, a second experiment with a-priori probabili-

ties corresponding to group sizes was employed.

Uneven a-priori probabilities influence classifica-tion in such a way that labeling a customer with

the label of the minor group (insolvent in our case)

becomes stricter (Johnson and Wichern, 1998).

Therefore, the new results, shown in Table 2, were

improved in this respect.

As one may observe the accuracy for the solvent

customers has been increased significantly (from

88.53% to 96.64%), however the accuracy for theinsolvent customers decreased even more signifi-

cantly (from 78.13% to 56.25%). More importantly

the increase in the accuracy achieved for the sol-

vent customers reduces the percentage of good

customers that may be hassled, due to the mis-

classifications, if the company decides to take some

action. In business terms, the results in Table 2

were considered as acceptable.

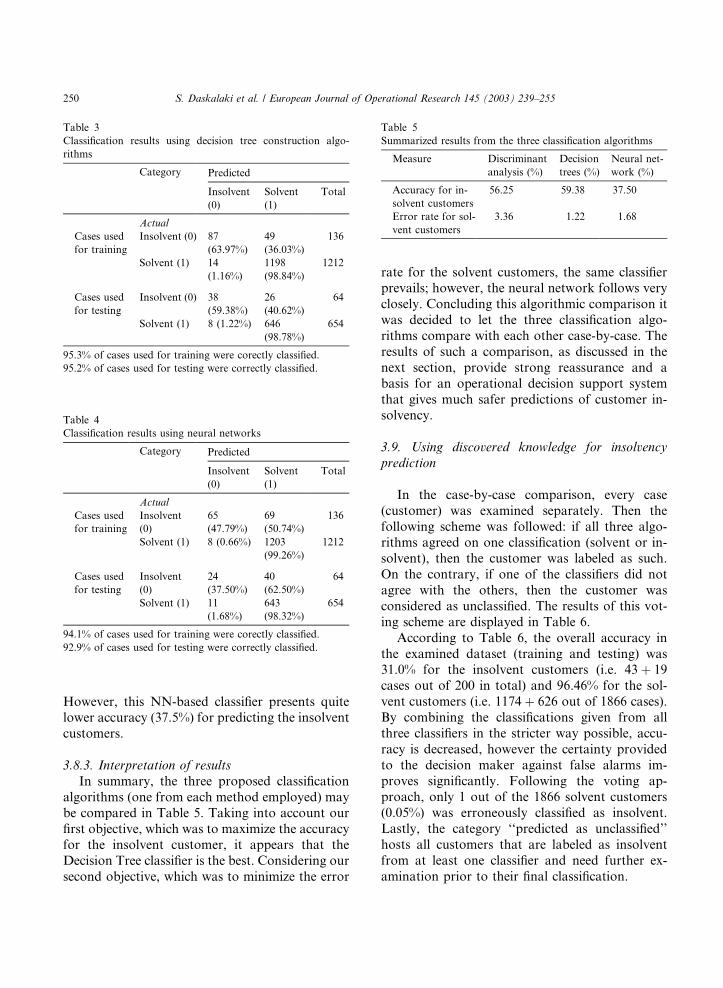

3.8.1. Decision trees

The 17 variables selected from the stepwise

procedure in discriminant analysis were named as

the most correlated to insolvency behavior, so they

were used as input variables to all subsequentlyused classification algorithms. The same set used

previously for training was used again to build a

rule-based classifier. The resulting decision tree

was then tested against the rest of the dataset. The

nodes of the decision tree represent tests on spe-

cific features, while the leaves represent the possi-

bly solvent class or the possibly insolvent class. The

classification results for the testing set are sum-marized in the confusion matrix shown in Table 3.

The accuracy for the solvent customers and the

insolvent customers is slightly higher than the

discriminant analysis (98.78% and 59.38% respec-

tively) and as a result the percentage of misclassi-

fied solvent customers was also smaller (1.22%).

3.8.2. Neural networks

Proceeding further with the development of

classifiers, several experiments were performed

using the Back Propagation algorithm with mo-

mentum. Once more the 17 variables that were

selected from the stepwise forward selection

method employed prior to the discriminant anal-

ysis were also used as input for the training of the

network.The confusion matrix that resulted from the

new classification algorithm is shown in Table 4.

The accuracy for the solvent customers is further

improved in this case and correspondingly the mis-

classification for the solvent customers is reduced.

Table 2

Classification results from discriminant analysis when misclas-

sification costs are not equal for the two classes

Category Predicted

Insolvent

(0)

Solvent

(1)

Total

Actual

Cases used

for training

Insolvent (0) 78

(57.35%)

58

(42.65%)

136

Solvent (1) 28

(2.31%)

1184

(97.69%)

1212

Cases used

for testing

Insolvent (0) 36

(56.25%)

28

(43.75%)

64

Solvent (1) 22

(3.36%)

632

(96.64%)

654

93.6% of cases used for training were corectly classified.

93.04% of cases used for testing were correctly classified.

Table 1

Classification results from discriminant analysis when misclas-

sification costs are equal for the two classes

Category Predicted

Insolvent

(0)

Solvent

(1)

Total

Actual

Cases used

for training

Insolvent (0) 113

(83.09%)

23

(16.91%)

136

Solvent (1) 119

(9.82%)

1093

(90.18%)

1212

Cases used

for testing

Insolvent (0) 50

(78.13%)

14

(21.88%)

64

Solvent (1) 76

(11.62%)

579

(88.53%)

654

89.5% of cases used for training were corectly classified.

87.6% of cases used for testing were correctly classified.

S. Daskalaki et al. / European Journal of Operational Research 145 (2003) 239–255 249

However, this NN-based classifier presents quitelower accuracy (37.5%) for predicting the insolvent

customers.

3.8.3. Interpretation of results

In summary, the three proposed classification

algorithms (one from each method employed) may

be compared in Table 5. Taking into account our

first objective, which was to maximize the accuracyfor the insolvent customer, it appears that the

Decision Tree classifier is the best. Considering our

second objective, which was to minimize the error

rate for the solvent customers, the same classifierprevails; however, the neural network follows very

closely. Concluding this algorithmic comparison it

was decided to let the three classification algo-

rithms compare with each other case-by-case. The

results of such a comparison, as discussed in the

next section, provide strong reassurance and a

basis for an operational decision support system

that gives much safer predictions of customer in-solvency.

3.9. Using discovered knowledge for insolvency

prediction

In the case-by-case comparison, every case

(customer) was examined separately. Then the

following scheme was followed: if all three algo-rithms agreed on one classification (solvent or in-

solvent), then the customer was labeled as such.

On the contrary, if one of the classifiers did not

agree with the others, then the customer was

considered as unclassified. The results of this vot-

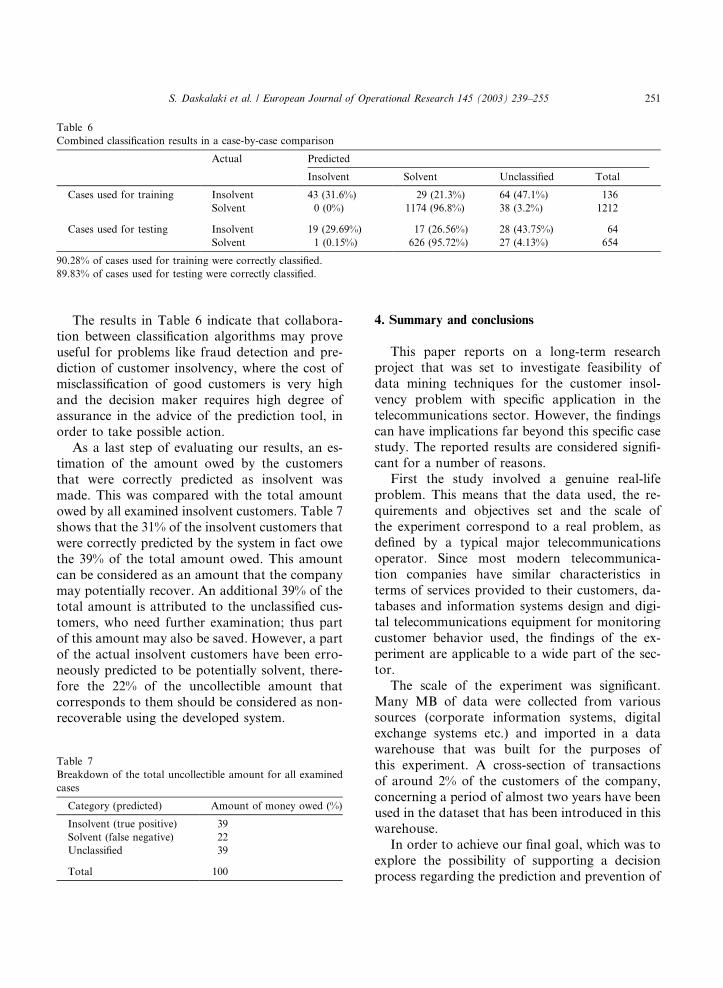

ing scheme are displayed in Table 6.

According to Table 6, the overall accuracy in

the examined dataset (training and testing) was31.0% for the insolvent customers (i.e. 43þ 19

cases out of 200 in total) and 96.46% for the sol-

vent customers (i.e. 1174þ 626 out of 1866 cases).

By combining the classifications given from all

three classifiers in the stricter way possible, accu-

racy is decreased, however the certainty provided

to the decision maker against false alarms im-

proves significantly. Following the voting ap-proach, only 1 out of the 1866 solvent customers

(0.05%) was erroneously classified as insolvent.

Lastly, the category ‘‘predicted as unclassified’’

hosts all customers that are labeled as insolvent

from at least one classifier and need further ex-

amination prior to their final classification.

Table 3

Classification results using decision tree construction algo-

rithms

Category Predicted

Insolvent

(0)

Solvent

(1)

Total

Actual

Cases used

for training

Insolvent (0) 87

(63.97%)

49

(36.03%)

136

Solvent (1) 14

(1.16%)

1198

(98.84%)

1212

Cases used

for testing

Insolvent (0) 38

(59.38%)

26

(40.62%)

64

Solvent (1) 8 (1.22%) 646

(98.78%)

654

95.3% of cases used for training were corectly classified.

95.2% of cases used for testing were correctly classified.

Table 4

Classification results using neural networks

Category Predicted

Insolvent

(0)

Solvent

(1)

Total

Actual

Cases used

for training

Insolvent

(0)

65

(47.79%)

69

(50.74%)

136

Solvent (1) 8 (0.66%) 1203

(99.26%)

1212

Cases used

for testing

Insolvent

(0)

24

(37.50%)

40

(62.50%)

64

Solvent (1) 11

(1.68%)

643

(98.32%)

654

94.1% of cases used for training were corectly classified.

92.9% of cases used for testing were correctly classified.

Table 5

Summarized results from the three classification algorithms

Measure Discriminant

analysis (%)

Decision

trees (%)

Neural net-

work (%)

Accuracy for in-

solvent customers

56.25 59.38 37.50

Error rate for sol-

vent customers

3.36 1.22 1.68

250 S. Daskalaki et al. / European Journal of Operational Research 145 (2003) 239–255

The results in Table 6 indicate that collabora-tion between classification algorithms may prove

useful for problems like fraud detection and pre-

diction of customer insolvency, where the cost of

misclassification of good customers is very high

and the decision maker requires high degree of

assurance in the advice of the prediction tool, in

order to take possible action.

As a last step of evaluating our results, an es-timation of the amount owed by the customers

that were correctly predicted as insolvent was

made. This was compared with the total amount

owed by all examined insolvent customers. Table 7

shows that the 31% of the insolvent customers that

were correctly predicted by the system in fact owe

the 39% of the total amount owed. This amount

can be considered as an amount that the companymay potentially recover. An additional 39% of the

total amount is attributed to the unclassified cus-

tomers, who need further examination; thus part

of this amount may also be saved. However, a part

of the actual insolvent customers have been erro-

neously predicted to be potentially solvent, there-

fore the 22% of the uncollectible amount that

corresponds to them should be considered as non-recoverable using the developed system.

4. Summary and conclusions

This paper reports on a long-term research

project that was set to investigate feasibility of

data mining techniques for the customer insol-

vency problem with specific application in the

telecommunications sector. However, the findings

can have implications far beyond this specific casestudy. The reported results are considered signifi-

cant for a number of reasons.

First the study involved a genuine real-life

problem. This means that the data used, the re-

quirements and objectives set and the scale of

the experiment correspond to a real problem, as

defined by a typical major telecommunications

operator. Since most modern telecommunica-tion companies have similar characteristics in

terms of services provided to their customers, da-

tabases and information systems design and digi-

tal telecommunications equipment for monitoring

customer behavior used, the findings of the ex-

periment are applicable to a wide part of the sec-

tor.

The scale of the experiment was significant.Many MB of data were collected from various

sources (corporate information systems, digital

exchange systems etc.) and imported in a data

warehouse that was built for the purposes of

this experiment. A cross-section of transactions

of around 2% of the customers of the company,

concerning a period of almost two years have been

used in the dataset that has been introduced in thiswarehouse.

In order to achieve our final goal, which was to

explore the possibility of supporting a decision

process regarding the prediction and prevention of

Table 7

Breakdown of the total uncollectible amount for all examined

cases

Category (predicted) Amount of money owed (%)

Insolvent (true positive) 39

Solvent (false negative) 22

Unclassified 39

Total 100

Table 6

Combined classification results in a case-by-case comparison

Actual Predicted

Insolvent Solvent Unclassified Total

Cases used for training Insolvent 43 (31.6%) 29 (21.3%) 64 (47.1%) 136

Solvent 0 (0%) 1174 (96.8%) 38 (3.2%) 1212

Cases used for testing Insolvent 19 (29.69%) 17 (26.56%) 28 (43.75%) 64

Solvent 1 (0.15%) 626 (95.72%) 27 (4.13%) 654

90.28% of cases used for training were correctly classified.

89.83% of cases used for testing were correctly classified.

S. Daskalaki et al. / European Journal of Operational Research 145 (2003) 239–255 251

future insolvencies from customers a Knowledge

Discovery Data Project was set up and was exe-

cuted from the beginning to the end. The phases

of the knowledge discovery process, relating to

data collection, data quality control, data reduc-

tion and projection and adequate feature selection,i.e. the preparation of the main data mining phase

were confirmed to be the most time consuming and

tedious ones. It is estimated that around 10% of

human and time resources were dedicated to the

initial problem definition phase, 75% to data col-

lection and preparation phase, while only 15% was

devoted to the creation of the prediction model

and evaluation of its performance as a decisionsupport tool. Moreover, throughout this project, it

was recognized that domain experts were contin-

uously providing expertise and intuition by di-

recting and pointing to the matters that were

important for the company and its customers. In

that sense domain knowledge played a significant

role that is not easy to evaluate in exact terms

(Kopanas et al., 2002).It was also shown that the original steps of the

process required a mixture of tools and experts

intuition, relating to the problem of defining the

data set characteristics and selecting adequate

variables describing the required modeling fea-

tures. In the discussion included in Section 3 of the

paper, some of the techniques used in our case for

determining the dataset used and the variablesshown in the Appendix, have been described.

However a more detailed description of the pro-

cess, which in some extend is specific to the char-

acteristics of this particular problem, is beyond the

scope of this overview paper.

The data mining experiment was a multi-stage

process. Various algorithms were tested in order to

establish which one is most suitable for ourproblem and this particular dataset. First a feature

selection was performed using the stepwise for-

ward selection procedure in discriminant analysis.

Through this phase the original 46 variables were

reduced to 17. The selected features were subse-

quently used for the construction of classifiers,

based on a decision tree and a back propagation

neural network algorithm. This way the con-struction of these classifiers was more focused. In

general the three algorithms used had a compar-

ative performance, a conclusion often reached in

similar experiments (Kalapanidas and Avouris,

2001). However, the strict requirements of the

operator in terms of accepted misclassification rate

of positive examples, made the selection of the

adequate algorithm more difficult. Imposing thisrestriction, none of the algorithms used was con-

sidered satisfactory for business use. However

application of a combined algorithm increased the

confidence of the classification prediction, by re-

ducing significantly the false positive rate. The

telephone company considered this performance

satisfactory and the proposed architecture could

become the core component of a decision sup-port system that can provide advices on future

customer insolvencies. By translating the perfor-

mance of the latter system in terms of possible

recollected revenues for the company, it was

shown that the predicted insolvent cases corre-

sponded to a higher percentage of revenue than

percentage of insolvent customer cases. Overall the

performance of the proposed system should beconsidered very good, since the accuracy of the

predictions compare very well with other reported

experiments in similar problems (Ezawa and

Norton, 1995), or in credit card fraud detection

problems (Richardson, 1997) but at a much higher

level of assurance.

Finally an interesting discussion concerns the

degree to which the reported study can be gener-alized and reused in other problems. Some of the

findings and specific techniques used are of general

value, like the two-phase data mining approach

used, the discussion on the knowledge discov-

ery method etc. More specifically, a large class

of problems relating to fraud detection in the ser-

vice industry, which bear many similar character-

istics to the one described here, can be based on avery similar process, where apart from the initial

stages of problem definition and original variables

selection, the rest of the process can be repeated.

Finally, for the specific problem of customer in-

solvency in telecommunication companies, the re-

ported experiment is highly reusable, except of

deviations in the syntactic and semantic definition

of the operator�s data. A parametric tool to handlesuch deviations is one of the objectives of further

research.

252 S. Daskalaki et al. / European Journal of Operational Research 145 (2003) 239–255

Acknowledgements

The research reported here has been funded

under project YPER97-109 of the Greek Secre-

tariat of Research and Technology. Special thanksare also due to E. Argyriou of OTE S.A. and the

group of scientists of the same company that

supplied us with data and continuous support.

Special thanks are also due to IBM for providing

licenses of the DB2� and Intelligent Miner�products under their academic support pro-

gramme.

Appendix A

List of the independent variables used in the

discriminant analysis experiments.

Variable Variable description

TYPE Category of phone account

NEWCUST Identification for new customers

LATENCY Count of late paymentsCOUNT_X CHARGES Count of bills with extra charges

COUNT_INSTALMENTS Count of times the customer requested payment by installments

COUNT_RESIDUAL Count of times the bill was not paid in full

MAX_UNITS Maximum # of units charged in any two-week period during the study

period

MIN_UNITS Minimum # of units charged in any two-week period during the study

period

AVR_UNITS Average # of units charged over the 15 two-week periodsSTD_UNITS Standard deviation for the units charged over the 15 two-week periods

TREND_UNITS_i Discrepancy from the moving average in units charged, measured on the

ith period (i ¼ 3; 5; 6; 7; 11)TREND_UNITS_MAX Maximum discrepancy from the moving average in units charged, over the

15 two-week periods

MAX_SECS Maximum total duration for the calls in any two-week period during the

study period

MIN_SECS Minimum total duration of the calls in any two-week period during thestudy period

AVR_SECS Average total duration of the calls over the 15 two-week periods

STD_SECS Standard deviation for the duration of all calls over the 15 two-week

periods

TREND_SECS_i Discrepancy from the moving average of the total duration of all calls

measured on the ith period (i ¼ 3; 5; 6; 7; 11)TREND_SECS_MAX Maximum discrepancy from the moving average for the total duration of

all cases over the 15 two-week periodsMAX_COUNT Maximum # of calls in any two-week period during the study period

MIN_COUNT Minimum # of calls in any two-week period during the study period

AVR_COUNT Average # of calls over the 15 two-week periods

STD_COUNT Standard deviation for the # of calls over the 15 two-week periods

TREND_COUNT_i Discrepancy from the moving average of the total # of calls measured on

the ith period (i ¼ 3; 5; 6; 7; 11)TREND_COUNT_MAX Maximum discrepancy from the moving average of the total # of calls,

over the 15 two-week periods

S. Daskalaki et al. / European Journal of Operational Research 145 (2003) 239–255 253

References

Aleskerov, E., Freisleben, G., Rao, B., 1997. CARDWATCH:

A neural network based database mining system for

credit card fraud detection. In: Proceedings of the 1997

IEEE/IAFE Conference on Computational Intelligence

for Financial Engineering, New York, NY, USA, pp. 89–

95.

Barson, P., Field, S., Davey, N., McAskie, G., Frank, R., 1996.

The detection of fraud in mobile phone networks. Neural

Network World 6 (4), 477–484.

Brachman, R.J., Anand, T., 1996. The process of knowledge

discovery in databases: A human-centered approach. In:

Fayyad, U.M., Piatetsky-Shapiro, G., Smyth, P., Uthurus-

amy, R. (Eds.), Advances in Knowledge Discovery

and Data Mining. AAAI Press/The MIT Press, Menlo Park,

CA.

Brachman, R.J., Khabaza, T., Kloesgen, W., Piatetsky-Shap-

iro, G., Simoudis, E., 1996. Mining business databases.

Communications of the ACM 39 (11), 42–48.

Brockett, P.L., Cooper, W.W., Golden, L.L., Xia, X.,

1997. Case study in applying neural networks to pre-

dicting insolvency for property and casualty insurers.

Journal of the Operational Research Society 48 (12),

1153–1162.

Burge, P., Shawe-Taylor, J., Cooke, C., Moreau, Y., Preneel,

B., Stoermann, C., 1997. Fraud detection and management

in mobile telecommunications networks. In: Proceedings of

the European Conference on Security and Detection, ECOS

�97, London, pp. 91–96.Canalli, E., 2001. Experimenting neural network to forecast

business insolvency. Neural Network World 11 (4), 349–

361.

Chan, P., Stolfo, S., 1998. Toward scalable learning with non-

uniform class and cost distributions: A case study in credit

card fraud detection. In: Proceedings of the 4th Interna-

tional Conference in Knowledge Discovery and Data

Mining, pp. 164–168.

Chan, P., Wei, F., Prodromides, A., Stolfo, S., 1999.

Distributed data mining in credit card fraud detection.

IEEE Intelligent Systems and their Applications 14 (6), 67–

74.

Donato, J., Schryver, J., Hinkel, G., Schmoyer Jr., R., Leuze,

M., Grandy, N., 1999. Mining multi-dimensional data for

decision support. Future Generation Computer Systems 15,

433–441.

Dorronsoro, Z., Ginel, G., Sanchez, C., Santa Cruz, C., 1997.

Neural fraud detection in credit card operations. Transac-

tions on Neural Networks 8 (4), 827–834.

Ezawa, K.J., Norton, S.W., 1995. Knowledge discovery in

telecommunication services data using Bayesian models.

In: Fayyad, U., Uthurusamy, R. (Eds.), Proceedings of First

International Conference onKnowledge Discovery andData

Mining. AAAI Press, Menlo Park, CA, pp. 117–152.

Ezawa, K.J., Norton, S.W., 1996. Constructing Bayesian

networks to predict uncollectible telecommunications ac-

counts. IEEE Expert/Intelligent Systems and their Applica-

tions 11 (5), 45–51.

Fawcett, T., Provost, F., 1997. Adaptive fraud detection. Data

Mining and Knowledge Discovery 1, 291–316.

Fayyad, U.M., Piatetsky-Shapiro, G., Smyth, P., 1996. The

KDD process for extracting useful knowledge from volumes

of data. Communications of the ACM 39 (11).

Frawley, W.J., Piatetsky-Shapiro, G., Matheus, C., 1991.

Knowledge discovery in databases: An overview. In:

Piatetsky-Shapiro, G., Frawley, W.J. (Eds.), Knowledge

Discovery in Databases. AAAI Press/The MIT Press, Menlo

Park, CA.

Ghosh, S., Reilly, D.L., 1994. Credit card fraud detection with

a neural-network. In: Proceedings of the 27th Hawaii

International Conference on Systems Sciences, vol. E. IEEE

Computer Society Press, pp. 621–630.

Han, J., Kamber, M., 2001. Data Mining: Concepts and

Techniques. Academic Press, New York.

Hoath, P., 1998. Telecoms fraud: The gory details. Computer

Fraud & Security (January), 10–14.

Variable Variable description

MAX_DIF Maximum # of different numbers called in any two-week period during the

study period

MIN_DIF Minimum # of different numbers called in any two-week period during the

study periodAVR_DIF Average # of different numbers called over the 15 periods

STD_DIF Standard deviation for the # of different numbers called during the 15 two-

week periods

TREND_DIF_i Discrepancy from the moving average of the # of different numbers called

measured on the ith period (i ¼ 3; 5; 6; 7; 11ÞTREND_DIP_MAX Maximum discrepancy from the moving average of the # of different

numbers called, over the 15 two-week periods

254 S. Daskalaki et al. / European Journal of Operational Research 145 (2003) 239–255

Johnson, R.A., Wichern, D.W., 1998. Applied Multivariate

StatisticalAnalysis. PrenticeHall, Inc., EnglewoodCliffs,NJ.

Kalapanidas, E., Avouris, N., 2001. Short-term air quality

prediction using a case based classifier. Journal of Environ-

mental Modelling and Software 16 (3), 263–272.

Kopanas, I., Avouris, N., Daskalaki, S., 2002. The role

of domain knowledge in a large scale Data Mining Project.

In: Vlahavas, I.P., Spyropoulos, C.D. (Eds.), Methods

and Applications of Artificial Intelligence. Lecture Notes

in AI, LNAI no. 2308. Springer-Verlag, Berlin, pp. 288–

299.

Richardson, R., 1997. Neural networks compared to statistical

techniques. In: Proceedings of the 1997 IEEE/IAFE Con-

ference on Computational Intelligence for Financial Engi-

neering, New York, pp. 89–95.

Shawe-Taylor, J., Howker, K., Burge, P., 1999. Detection of

fraud in mobile telecommunications. Information Security

Technical Report 4 (1), 16–28.

Weiss, G., Provost, F., 2001. The effect of class distribution on

classifier learning, Technical Report ML-TR-43, Depart-

ment of Computer Science, Rutgers University.

Yuhas, B.P., 1993. Toll-fraud detection. In: Aspector, J.,

Goodman, R., Brown, T.X. (Eds.), Proceedings of the

International Workshop on Applications of Neural Net-

works to Telecommunications. Lawrence Erlbaum Associ-

ates, Mahwah, NJ, pp. 239–244.

S. Daskalaki et al. / European Journal of Operational Research 145 (2003) 239–255 255

Top Related

Copyright © 2022 FDOKUMEN