Bahasa

Halaman

Hukum

Important disclosures appear on the last page of this report.

1

Krause Fund Research

Fall 2016

Technology (Beta)

Recommendation: Buy

Analysts

Wenlong Xu

Wenzhu Duan

Company Overview

Cognizant Technology Solutions Co. provide information

technology, consulting and business process services to

businesses. By using its global delivery model, domain

expertise, and portfolio of services, it helps businesses to

combine digital technology in their operation and operate in a

more efficient and innovative manner. In order to keep its

competency, Cognizant adopted business strategies that focus on

reinvestment, unique global delivery model, long-term customer

relationship, and selective strategic acquisitions, joint ventures

and strategic alliances.

Stock Performance Highlights 52-week High $65.91

52-week Low $45.44

Beta Value 1.06

Average Daily Volume 1.143 m

Share Highlights Market Capitalization $32.75 b

Shares Outstanding 606.7 M

Book Value per share $16.97

EPS 2015 $2.67

P/E Ratio 21.09

Dividend Yield N/A

Dividend Payout Ratio N/A

Company Performance Highlights ROA 10.98%

ROE 16.33%

Sales $13.26 b

Financial Ratios Current Ratio 3.56

Debt to Equity 14%

Cognizant Technology

Solutions Corp. (NASDAQ: CTSH)

December 4, 2016 Current Price $54.02

Target Price $75.50

Hard Time for CTSH

As an IT service company, Cognizant is sensitive to the

fluctuation of economic condition. This year is a hard year for

Cognizant. The still-weak global economy slowed the growth of

Cognizant.

Based on the one-year stock performance, Cognizant’s stock

price was mainly influenced by report result and legislation

factors.

Cognizant has outstanding financial conditions. According

to its financial statement, it has a 14% debt to equity ratio, 2.91

current ratio and 0.41 debt to equity ratio. Those financial

indicators show Cognizant has low credit risk.

Worldwide, Cognizant leased 11.7 million square feet and

owned 13.0 million square feet facilities in 24 countries. Those

Facilities guarantees Cognizant’s abilities to attract new

customers and maintain with relationship with old customers.

Although Cognizant did not pay out any dividend and spend

little on stock repurchase, Cognizant keeps obtaining the

comparative advantages through acquisition. According to

Cognizant’s Q3 report, Cognizant has around 4.8 billion cash on

hand. In this year, Cognizant has already acquired six

companies.

Cognizant is able to adjust its focus on time. In 2014,

Cognizant focused on the development of Healthcare segment

and obtained substantially growth in the revenue from healthcare

segment. This year, Cognizant began to focus on its

Manufacturing segment, we believe Cognizant will get succeed

in this industry segment.

The hard time is temporary. We believe as long as the

economic condition upturn, Cognizant’s stock price will also up

rapidly. Therefore, the recommendation we offered is Buy.

One Year Stock Performance

(Soured from: Yahoo Finance Blue: CTSH Red: S&P 500)

Important disclosures appear on the last page of this report.

2

Executive Summary Cognizant has rich distribution channels and many professional

staffs. In addition, Cognizant also provides more than 27

different kinds of personality service for the customers.

Therefore, the demand of IT service plays an important role in

Cognizant’s revenue growth. Although the number of data is

keeping rapid increase, the economic condition slows

Cognizant’s revenue growth down because of the bad

performance of finance industry and healthcare industry.

Furthermore, the majority employees for Cognizant are in India

and 21.4% of the company’s revenue are from foreign country,

the fluctuation of exchange rate would have negative impact on

Cognizant’s salaries expense and revenue stream as the

appreciation of U.S dollar. Therefore, the growth rate for

Cognizant in the following several years would not be kept in a

high level. However, compared with its peer, Cognizant has the

best performance. Although cognizant cannot offer high level

return, the growth rate for this company is stable. If there is a

diversification need or risk-avoiding demand, we recommend a

buy rating for Cognizant Technology Solutions Corp.

Macroeconomic Outlook

Gross Domestic Product

Soured from Factset and World Banki

Gross domestic product is all the finished goods and services

produced within a country’s border in a specific time period,

which is measured by currency. Based on the data in the past 10

years, IT is highly economically sensitive-- it’s more likely to

outperform during periods of economic growth. Historically,

Technology tracks closely with the direction of GDP growth. ii

GDP can be calculated by the function: Y= C+G+I+ (EX-IM).

This function will be used to analyze the GDP growth rate in this

passage. Based on this function, consumer spending(C),

government spending(G), investment(I) and national total net

exports(EX-IM) would be analyzed individually.

Sourced from Worldbankiii

Overview: Based on the World Bank database, from 1961 to

2015, the GDP growth rate in U.S ranges from -2.78% to 7.26%

and the median is 3.3%, which has a downward trend. In short

term, from 2010 to 2015, the GDP growth rate in U.S ranges

from 1.49 to 2.53 and the median is 2.33, which looks relative

flat.

Consumer spending: According to the previous data of consumer

spending, if there is no big problem with the economy, the

consumer spending will increase steady. In the next two years,

the projected consumer spending growth rate will range from

0.8% to 0.4%. The growth rate will decrease gradually. Because

high-tech sector is highly correlated with consumer spending. It

will be discussed more detailed in the following part.

Source from UsFederalBudgetsiv

Government spending: According to data from United States

Censes, the government spending will increase by 6.41% in FY

2016 and 5.46% in FY 2017.v The estimate growth rate looks

steady in the following five years from the chart offered below.

The forecasting is based on the historical tables in the current

presidential budget. We can see that the government has no plan

to implement restrictive fiscal policy.

Important disclosures appear on the last page of this report.

3

Source: Federal Reserve Bank of St. Louisvi

Investment: Investment activity is highly correlated with interest

rate. Based on the statistics offered by FRED, the interest rate is

close to historic low in recent years. From 2010 to now, the

effective federal fund rate ranges from 0.07% to 0.4%.

Generally, low federal rate will incentive investment activity,

but the non-farm employment rate is less than anticipated.

Softening foreign economy and domestic investment makes

Federal Reserve hold the federal fund rate in a low level. In this

condition, the federal fund rate can only increase. This may lead

investment activity weaker. On the other sides, the strengthening

dollar will also decrease the oversea investment on U.S.

NX: NX is the difference between export and import. NX is

highly correlated with exchange rate. Owing to the British

withdrawing from the EU and the emerging market transition,

such as China, U.S dollar become safety currency. However,

although this is a good news for oversea investment, it is a bad

news for net export. High tech industries are a strong industry

for U.S. Last year, U.S high-technology exports was 154.354

Billion, which account for 7% of U.S total export. Therefore, the

perspective for NX would be negative.

Overall, based on the flat growing consumer spending and

government spending, worse investment environment and

negative NX perspective, in short term, the GDP growth rate

will not have drastic change. Additionally, with the moderate

loose monetary policy and moderate fiscal policy. The GDP

growth rate will not decrease too much. Moreover, as the new

present coming into power, there will be more policies to

incentive the economy growth. Projected GDP growth rate

could be 2.8% to 3.5%. For the next 6 months, the GDP growth

rate should be around 3.0%. For the next two years, considering

bolster expectations for Fed rate, the GDP growth rate would

stay at 2.8%.

Consumer Spending

Consumer spending variable measures consumers’ total

consumption of goods and services using their disposable

personal income. In the information technology sector,

consumers are the main end-users of the technology hardware

and equipment. Besides, most semiconductors production is put

into the production of technology hardware and equipment. That

means, almost two third of technology products rely on the

consumption of consumers. A decrease in consumer spending

will tend to influence technology products purchasing more

because they are daily necessities. An increase in consumer

spending will benefit technology sector because it signals excess

money to spend on recreation supplies. Thus, it is important to

follow how much they spend on goods and services and how

much money available for them to spend as a whole.

Source: U.S. Bureau of Economic Analysisvii

As shown in the tables above, In the first quarter of 2016, the

consumer spending has grown 0.41% compare to the last quarter

of 2015. The second quarter of 2016 has seen 1.1% of growth in

consumer spending which is nearly twice than last quarter. The

consumer spending has seen a steady continuing growth in

recent ten years except for a sharp drop during the financial

crisis in 2008. Then, with the recovering and the growth of the

economy, consumer spending is continuing growing. The

quarterly growth rate in 2015 fell from 0.71% to 0.41%, which

shows a slowing growth in 2015. However, the doubled growth

rate in the second quarter of 2016 could be considered as a

signal of a continuing growth of consumer spending shortly. We

don’t think the next quarter of consumer spending growth would

be doubled again. We see the change as a one-time change. In

our opinion, we project the third quarter’s consumer spending

growth will decrease 0.10% which follows the decreasing trend

of 2015. As for the growth for the next two years, we assume the

quarterly growth rate would decrease at a speed of 0.1%

quarterly but never below 0.04% until there is another sharp

increase again in the economy. The reason is that we consider a

one-time sharp increase in consumer spending is reasonable after

a short period. For example, accumulated wealth allows

consumers to buy more during a specific of time. As shown in

figure 2.0, the disposable personal income sees a sharp increase

in the second quarter of 2016 which significantly support the

increase in consumer spending. However, the disposable

personal income is very unlikely to have a sharp increase again

within the two years.

Unemployment Rate

The rate of unemployment is the number of unemployed workers

divided by the total labor force. A low unemployment rate

indicates a strong economic growth. As discussed above,

technology sector usually outperforms market during an

economic growth period. As the chart indicated below, since

average unemployment rate reached its high point of 9.6% in

2010, it has been steadily decreased to 5.3% in 2015.viii From

Important disclosures appear on the last page of this report.

4

January to August 2016, unemployment rate fluctuates in the

range of 4.7% to 5%, reflecting a positive economic growth

from 2015 to 2016.

Decreasing unemployment rate implies an increasing demand of

labor, which lead to rising average income in the U.S. According

to the Bureau of Labor Statistics, the average hourly wage for

private companies increases from $25.12/hour (Aug. 2015) to

$25.73/hour (Aug. 2016). ix As mentioned in the consumer

spending section, increasing household income shows the

growth opportunity for the technology sector.

Source: Bureau of Labor Statisticsx

As the unemployment rate fluctuates during the first 8 months of

the year, we think it’s reasonable that it stays at 5% for next two

quarters. According to Goldman Sachs, it’s more than likely that

the Fed will increase interest rate this month.xi In the long run,

with a higher interest rate, the economic growth rate will slow

down. However, we do think that the U.S. economy will

continue to grow, but with a slower and a healthier outlook. As

an indicator of the economy growth rate, unemployment is likely

to follow the trend. We expect the unemployment rate to

decrease 0.2% per year for the upcoming 2-3 years. To sum up,

in short-term, the unemployment rate will keep at 4.9%/. In

long-term, the unemployment rate will keep decrease to 4.2%.

Federal Fund Rate

Source from: Factsetxii

According to the chart above, there is a reverse relationship

between Fed Fund rate and Market return. Because of the

recovery of the economy, the anticipation of the rise of Fed

Fund rate get stronger. The PMI index in Nov 2016 is 54.5,

this is a strong signal of economic recovery.

Source: Federal Reserve Bank of St. Louisxiii

Due to the Fed Fund rate is the historical low, the rate could

only be increase. Therefore, we believe the federal fund rate

will increase to 0.65~0.90 in December 2016. In the next

five years, we think the Federal Fund rate will increase to

3%, which is negative to the IT industry.

Capital Outlook

Source from: Yahoo Finance

xiv

The chart above shows the performances of S&P 500 and S&P

500 IT Sector. Historically, there is a strong positive relationship

between the IT sector and the U.S Equities. Based on top

technology companies’ performance, we regard the industry a

“high beta” play, which was 1.73 relative to S&P 500 index

beta. xv In other words, the IT sector outperforms the board

market during an upward trend and underperforms during a

downward trend. Therefore, in the long run, if we hold an

optimistic opinion on the overall market (S&P 500), then it is a

good choice to invest in the technology sector as its value will

increase better than the overall market. Therefore, we predict

that the IT sector will benefit from the low federal fund rate to

expand business in the short run period. Also, a slight increase in

the federal fund rate will increase some financial institutions’

revenues and profits, which in turn they will increase investment

and purchase on technology products or services. Thus, in the

long term, we think the IT sector will still outperform the stock

market and experience an upward trend. In order to better

analyze the capital market, we decide to choose IT sector (a high

Important disclosures appear on the last page of this report.

5

beat player) and Industries sector (has a similar beta with the

market) to compare the performance of the market. In the

following six months, we think the S$P 500 index will be at the

level of 2250. In long-term, the next five years, the index could

increase to 2300.

Industry Analysis

Overview

Data processing and hosting services is a sub-industry under the

IT services sector. Firms in this industry mainly provide

infrastructures and services to facilitate IT related activities.

They offer business process management, application services,

data storage and management, IT support, website hosting,

automated data entry service, network management, etc. The

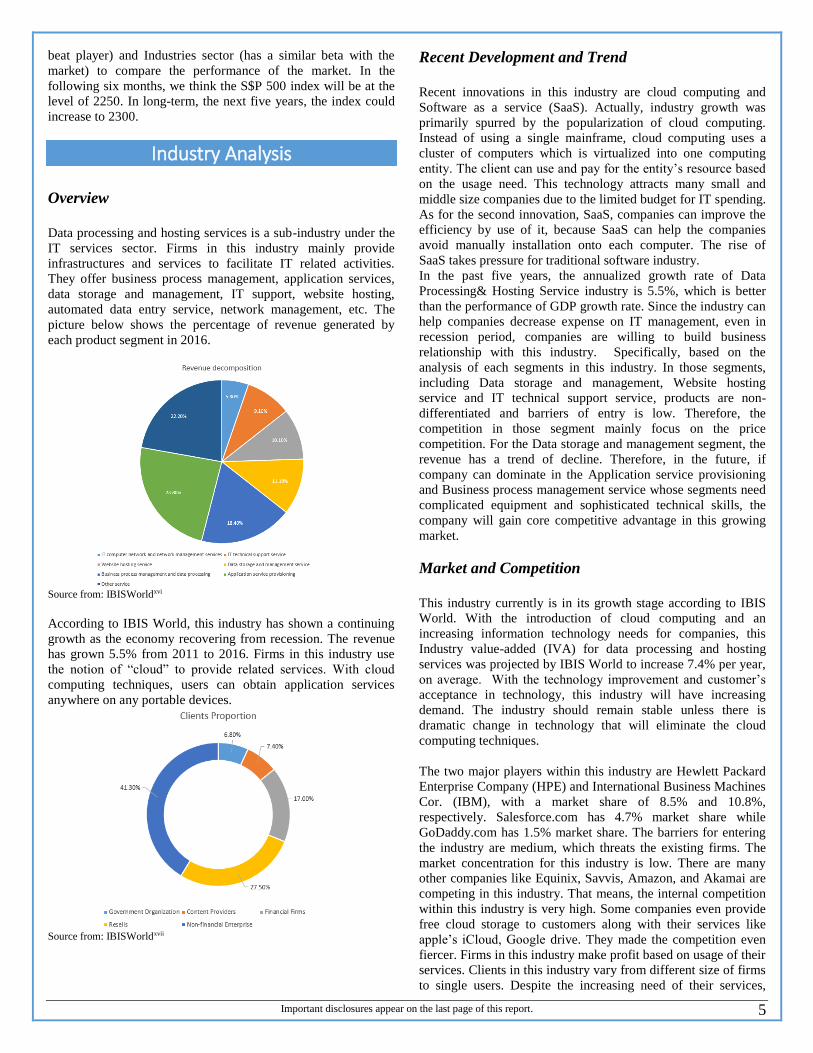

picture below shows the percentage of revenue generated by

each product segment in 2016.

Source from: IBISWorldxvi

According to IBIS World, this industry has shown a continuing

growth as the economy recovering from recession. The revenue

has grown 5.5% from 2011 to 2016. Firms in this industry use

the notion of “cloud” to provide related services. With cloud

computing techniques, users can obtain application services

anywhere on any portable devices.

Source from: IBISWorldxvii

Recent Development and Trend

Recent innovations in this industry are cloud computing and

Software as a service (SaaS). Actually, industry growth was

primarily spurred by the popularization of cloud computing.

Instead of using a single mainframe, cloud computing uses a

cluster of computers which is virtualized into one computing

entity. The client can use and pay for the entity’s resource based

on the usage need. This technology attracts many small and

middle size companies due to the limited budget for IT spending.

As for the second innovation, SaaS, companies can improve the

efficiency by use of it, because SaaS can help the companies

avoid manually installation onto each computer. The rise of

SaaS takes pressure for traditional software industry.

In the past five years, the annualized growth rate of Data

Processing& Hosting Service industry is 5.5%, which is better

than the performance of GDP growth rate. Since the industry can

help companies decrease expense on IT management, even in

recession period, companies are willing to build business

relationship with this industry. Specifically, based on the

analysis of each segments in this industry. In those segments,

including Data storage and management, Website hosting

service and IT technical support service, products are non-

differentiated and barriers of entry is low. Therefore, the

competition in those segment mainly focus on the price

competition. For the Data storage and management segment, the

revenue has a trend of decline. Therefore, in the future, if

company can dominate in the Application service provisioning

and Business process management service whose segments need

complicated equipment and sophisticated technical skills, the

company will gain core competitive advantage in this growing

market.

Market and Competition

This industry currently is in its growth stage according to IBIS

World. With the introduction of cloud computing and an

increasing information technology needs for companies, this

Industry value-added (IVA) for data processing and hosting

services was projected by IBIS World to increase 7.4% per year,

on average. With the technology improvement and customer’s

acceptance in technology, this industry will have increasing

demand. The industry should remain stable unless there is

dramatic change in technology that will eliminate the cloud

computing techniques.

The two major players within this industry are Hewlett Packard

Enterprise Company (HPE) and International Business Machines

Cor. (IBM), with a market share of 8.5% and 10.8%,

respectively. Salesforce.com has 4.7% market share while

GoDaddy.com has 1.5% market share. The barriers for entering

the industry are medium, which threats the existing firms. The

market concentration for this industry is low. There are many

other companies like Equinix, Savvis, Amazon, and Akamai are

competing in this industry. That means, the internal competition

within this industry is very high. Some companies even provide

free cloud storage to customers along with their services like

apple’s iCloud, Google drive. They made the competition even

fiercer. Firms in this industry make profit based on usage of their

services. Clients in this industry vary from different size of firms

to single users. Despite the increasing need of their services,

Important disclosures appear on the last page of this report.

6

clients hold their decision in choosing their services. That

means, the bargaining power is highly controlled in their clients.

With many service providers, firms will have less pricing power,

meaning they have to compete for price in order to attract new

users and maintain old users.

Although there are no substitutes for these services, the external

competition in this industry is high. For instance, medium to

large clients like big firms and organizations may choose to

build their IT infrastructure and IT department depending on

their financial status. This external competition will significantly

influence the market because large users (non-financial

enterprise, financial firms, and government organizations)

accounts for 58.1% of the total market.

There are less supply threats within this industry. Without any

reliance on raw materials, it mainly depends on technology

advance like improvement in computer hardware as well as

technical expertise.

Better-positioned firms

In this industry, firms that mainly focus on application service

provisioning, business process management (BPO), and data

storage and management services are considered as better

positioned. Firstly, as shown in figure 2, 53.3% of revenue

generated in this industry is come from these three service

segments. Secondly, these services require service providers to

have complicated equipment and sophisticated technical skills.

Thus, big service providers are more likely to be selected by

large firms and companies, who are the major market in this

industry, due to their company scale and reputation. Thirdly,

they tend to build long-term relationship and sign long-term

contracts with business, meaning fewer threats in losing

customers. For example, for BPO services, businesses would not

end the relationship easily because one change or delay in

business process will influence the business as a whole. The

direct benefit for these service providers is they have customer

loyalty and pricing power. Also, businesses today want to be

more efficient in their business process and fear of falling behind

competitors. They are seeking these services actively. It also

gives potential development and sustainability to this industry.

Catalyst for Growth/Change

Number of mobile internet connections: Owing to the

popularization of smartphone since 2007, mobile broadband

connection has skyrocketed. In the past five years, from 2011 to

2015, the compound growth rate of mobile internet connections

is 13.1%. The number of mobile internet connections increase

from 130.72 million to 242.00 million. The increase of mobile

internet connections created a great many of data. Facing the

countless data, many companies seek help from third-party

provider. In the next five years, although the smartphone market

is about saturation, the estimated compound growth rate is

5.1%,xviii which offers a chance for Data Processing& Hosting

Service industry.

Percentage of services conduced online: This driver is the most

direct driver for this industry. This driver reflects “the increasing

use by consumers and businesses of the internet for services they

used pay for in a physical form”.xix This number increased from

7.05% to 12.68% from 2011 to 2015. Based on the perspective

of IBISWorld, this number will increase constantly from 12.68%

to 19.47% in 2020.

Key Investment Positive or Negatives

Investment Positive:

As the amount of data increasing, the requirement of IT

infrastructure becomes more complex, and professional.

Outsourcing the IT need is the best choice for many

new or large companies.

From 2008 to now, the growth rate for this industry is

positive, which has an annualized growth rate of 6.7%.

Even though in the 2008 financial crisis, this industry

has a growth rate of 9.3%.

Business processing outsourcing is cost saving for firms

and a new trend for today’s businesses, and many firms

will outsource their un-core business process to save

time and money.

Investment Negative:

In the past five years, the compound annualized growth

rate for this industry is 6.48%, which is under-

performance compared with S&P 500 Index.

The data safety is an unavoidable issue for this industry.

How the companies in this industry will protect the

client’s data from losing and stealing is an issue.

Technology changes fast and unpredictable. Adoption

of new computing technology may change the whole

industry.

Company Analysis

Overview and Business Description

Cognizant Technology Solutions Co. provide information

technology, consulting and business process services to

businesses. By using its global delivery model, domain

expertise, and portfolio of services, it helps businesses to

combine digital technology in their operation and operate in a

more efficient and innovative manner. In order to keep its

competency, Cognizant adopted business strategies that focus on

reinvestment, unique global delivery model, long-term customer

relationship, and selective strategic acquisitions, joint ventures

and strategic alliances.

The company reported a net income of $1623.6 million during

the fiscal year ended Dec. 2015. An increase of 12.8% over

2015. Cognizant recently releases its third-quarter net income of

444.4 million as of Sept.30, 2015. An increase of 11.9% over the

third quarter in 2015. Management projected its fiscal 2016

revenue to be in the range of $13.47 billion to $13.53 billion.

Important disclosures appear on the last page of this report.

7

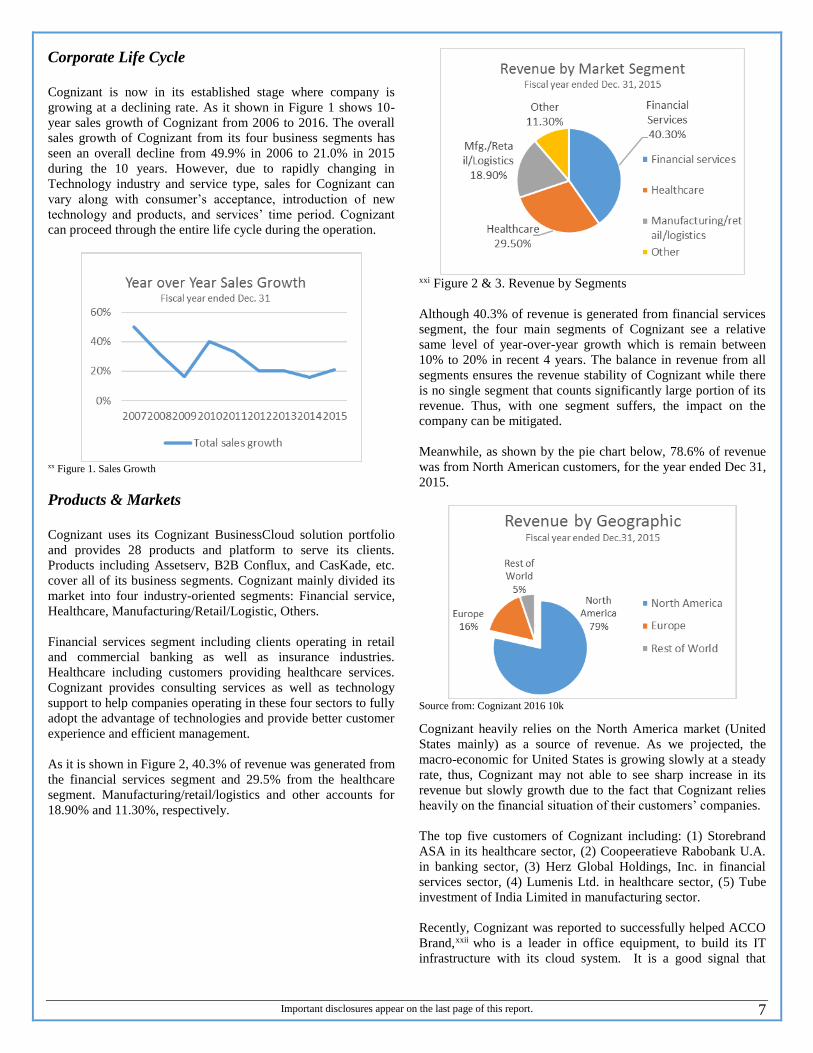

Corporate Life Cycle

Cognizant is now in its established stage where company is

growing at a declining rate. As it shown in Figure 1 shows 10-

year sales growth of Cognizant from 2006 to 2016. The overall

sales growth of Cognizant from its four business segments has

seen an overall decline from 49.9% in 2006 to 21.0% in 2015

during the 10 years. However, due to rapidly changing in

Technology industry and service type, sales for Cognizant can

vary along with consumer’s acceptance, introduction of new

technology and products, and services’ time period. Cognizant

can proceed through the entire life cycle during the operation.

xx Figure 1. Sales Growth

Products & Markets

Cognizant uses its Cognizant BusinessCloud solution portfolio

and provides 28 products and platform to serve its clients.

Products including Assetserv, B2B Conflux, and CasKade, etc.

cover all of its business segments. Cognizant mainly divided its

market into four industry-oriented segments: Financial service,

Healthcare, Manufacturing/Retail/Logistic, Others.

Financial services segment including clients operating in retail

and commercial banking as well as insurance industries.

Healthcare including customers providing healthcare services.

Cognizant provides consulting services as well as technology

support to help companies operating in these four sectors to fully

adopt the advantage of technologies and provide better customer

experience and efficient management.

As it is shown in Figure 2, 40.3% of revenue was generated from

the financial services segment and 29.5% from the healthcare

segment. Manufacturing/retail/logistics and other accounts for

18.90% and 11.30%, respectively.

xxi Figure 2 & 3. Revenue by Segments

Although 40.3% of revenue is generated from financial services

segment, the four main segments of Cognizant see a relative

same level of year-over-year growth which is remain between

10% to 20% in recent 4 years. The balance in revenue from all

segments ensures the revenue stability of Cognizant while there

is no single segment that counts significantly large portion of its

revenue. Thus, with one segment suffers, the impact on the

company can be mitigated.

Meanwhile, as shown by the pie chart below, 78.6% of revenue

was from North American customers, for the year ended Dec 31,

2015.

Source from: Cognizant 2016 10k

Cognizant heavily relies on the North America market (United

States mainly) as a source of revenue. As we projected, the

macro-economic for United States is growing slowly at a steady

rate, thus, Cognizant may not able to see sharp increase in its

revenue but slowly growth due to the fact that Cognizant relies

heavily on the financial situation of their customers’ companies.

The top five customers of Cognizant including: (1) Storebrand

ASA in its healthcare sector, (2) Coopeeratieve Rabobank U.A.

in banking sector, (3) Herz Global Holdings, Inc. in financial

services sector, (4) Lumenis Ltd. in healthcare sector, (5) Tube

investment of India Limited in manufacturing sector.

Recently, Cognizant was reported to successfully helped ACCO

Brand,xxii who is a leader in office equipment, to build its IT

infrastructure with its cloud system. It is a good signal that

Important disclosures appear on the last page of this report.

8

Cognizant pays effort in developing relationship with other big

supplier in its business segments.

Marketing Strategy

Cognizant generates sales from direct selling using sales

representatives, referrals, and returning customers. Cognizant is

a B2B type operation. That means Cognizant heavily relies on its

sales representative to introduce their services and products in

order to build relationships. It highly relies on the capability of

their sales force in order to compete for new and returning

customers. The high dependence on sales force would increase

the risk of generating fewer sales with poor performance of sales

representative. The SG&A expense of Cognizant remains at a

constant level of around 20% of sales during 2011 to 2015. We

think the constant level of SG&A spending should be able for

Cognizant to sustain its current growth.

Revenue stream & cost structure

As a global leader in business and technology services,

Cognizant primary offers personalized service to the customers.

Price structures for Cognizant are based on expectations and

assumptions regarding the cost and complexity of work

performing. Cognizant predominantly contract to customers on a

time-and-materials basis or on a fixed-price basis. Fixed-price

contract accounts for around 36.5% revenue of Cognizant in

2015.

The cost of Cognizant mainly focuses on cost of revenue and

SG&A expense. Cost of revenue accounts for 72.4% of

operating expense and 59.9% of total revenue while SG&A

expense accounts for 24.4% of operating expense and 20.2% of

total revenue. The primarily cost for Cognizant is cost of

revenue.

Cognizant’s cost of revenue primarily consists of salaries,

incentive-based compensation, payroll taxes, employee benefits,

immigration and project-related travel for technology personnel,

subcontracting and sales commissions related to revenues. The

cost of revenue increased by 21.2% during 2015 as compared to

an increase of 16.6% during 2014. The increase mainly leaded

by the increase in compensation and benefits cost. Similarly, the

SG&A expenses includes salaries, incentive-based

compensation, stock-based compensation expense, payroll taxes,

employee benefits, immigration, travel, marketing,

communications, management, finance, administrative and

occupancy cost. Compensation and benefit cost also accounts for

the primarily increase in SG&A expense. Overall, human

resource accounts for huge expenditure of Cognizant. The

compensation and benefit, which includes incentive-based

compensation cost, increased rapidly.

The graph below shows the cash and cash equivalent balances

relative to cash used in share repurchases and debt.

Source from: Factsetxxiii

Cognizant holds 4949.5 millions of cash which consists 37.88%

of its total assets. Besides spending the cash on cost of services

(salaries, R&D), SG&A, Cognizant mainly uses its cash to do

merger & acquisitions and share repurchases to sustain the

growth of the company.

From Cognizant’s cost structure, we see a risk associate with

Cognizant’s acquisition. Although acquisitions might be able to

give Cognizant a short-term growth in its financial performance,

the ongoing performance of acquisition is subject to the risk of

the economy and management.

Distribution and Customer Support

The development and delivery centers and technical

professionals are positioned globally, primarily in India.

Cognizant holds global delivery centers that using the global

network to serve its clients. This strategy helps Cognizant avoid

various risks, including regulatory, economic and political

instability, potentially unfavorable tax etc. Additionally,

according to the corporation strategy, Cognizant plans to open

additional sales and marketing offices globally to support the

demand of their clients and markets.

Cognizant provide on-site, at local or in country, at regional, and

at global services delivery centers to ensure every touch with

customers. Currently, cognizant have 300 strategic clients been

served through its global delivery system.

Suppliers and raw materials

Cognizant has a total of 11 suppliers, including 4 technology

service companies, which are BlackLine, Inc., Information

Corporation, Interxion Holding N.V., and Jacada Ltd.; 3 finance

companies including Custodian REIT PLC, Ascendas India

Trust, and IRSA Inversiones. one producer manufacturing

company named Blue Star limited; one electronic technology

company named Top Image Systems Ltd.; one commercial

service company which is Medidate Solutions, Inc.; and the last

one is Tata Communications limited in communication. In the

sector of Technology Service, there are 4 suppliers, which means

Cognizant has plenty of suppliers in the Technology Service.

However, in other area, Cognizant has limited choice of their

suppliers.

There are no raw materials due to Cognizant is a service

company, what Cognizant offers to the clients are intellectual

property. Therefore, the ability to continually hire, assimilate,

motivate and retain the best talent possible in the industry is

Important disclosures appear on the last page of this report.

9

critical important for Cognizant. Based on CTSH 2015 annually

report, Cognizant has developed strong relationships with key

university around world. Moreover, Cognizant established an

active lateral recruiting program in North America, Europe and

India and an on-campus recruiting program in North America.

Additionally, Cognizant also plans to hire experienced

professionals from competing IT service firms and already

invests heavily in training programs for improving personal

professional growth for their employees. As a result, we see a

good health development in its human resources.

Competition Environment

Cognizant faces intense competitions in the IT services and

outsourcing market. Not only the market segments is broad and

with many local firms specializing in system integration,

traditional consulting, application software design, facilities

management, but also Cognizant faces a lot of direct

competitors, including Infosys, Capgemini, Tata consultancy,

Wipro, and Computer Sciences. While small companies have its

advantage in lower price due to the scale of work, large

competitors may have similar or even greater technical resource

and reputation that attracts customers. Cognizant is competing

for both customers and human resources within the industry. In

order to remain competitive, Cognizant must show a competitive

advantage in its products, service delivery, research and

development, and technical expertise.

The global delivery system put Cognizant in the foreign labor

cost risk. If the labor cost in India rises, it will significantly

increase its labor costs. However, we do not see trend in

increasing labor cost in India. Cognizant still expose to the

associate foreign risk related to the changes in India government

policies.

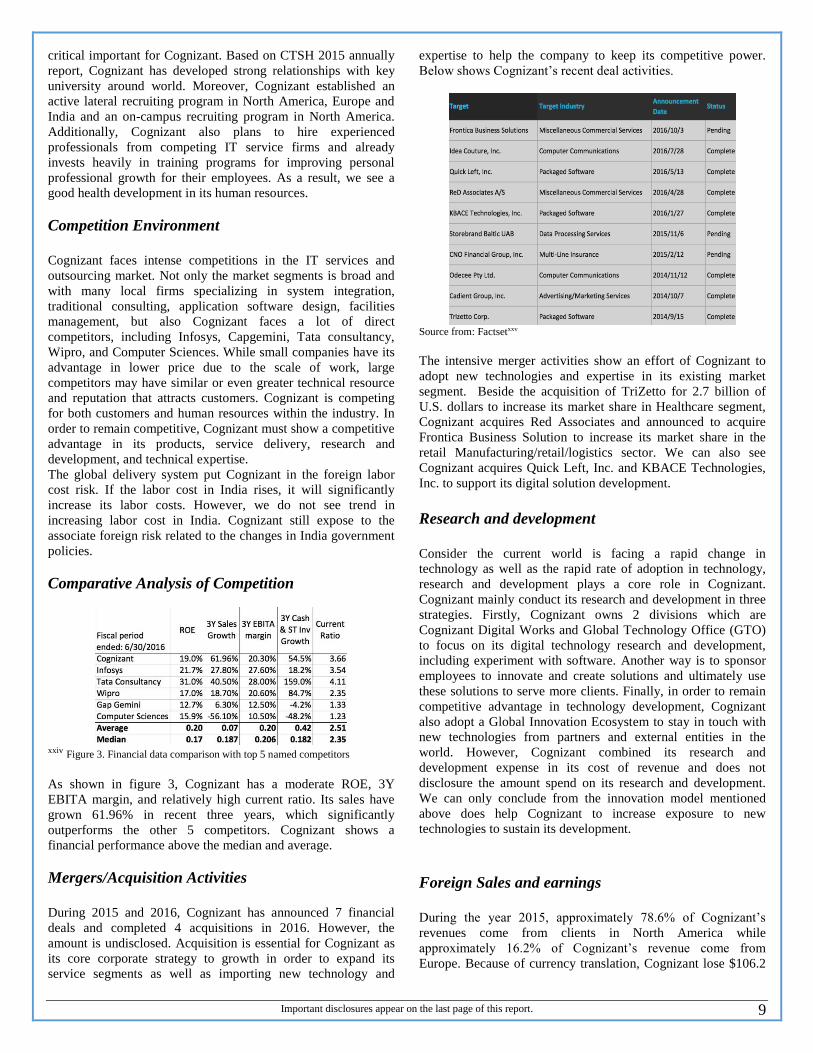

Comparative Analysis of Competition

xxiv Figure 3. Financial data comparison with top 5 named competitors

As shown in figure 3, Cognizant has a moderate ROE, 3Y

EBITA margin, and relatively high current ratio. Its sales have

grown 61.96% in recent three years, which significantly

outperforms the other 5 competitors. Cognizant shows a

financial performance above the median and average.

Mergers/Acquisition Activities

During 2015 and 2016, Cognizant has announced 7 financial

deals and completed 4 acquisitions in 2016. However, the

amount is undisclosed. Acquisition is essential for Cognizant as

its core corporate strategy to growth in order to expand its

service segments as well as importing new technology and

expertise to help the company to keep its competitive power.

Below shows Cognizant’s recent deal activities.

Source from: Factsetxxv

The intensive merger activities show an effort of Cognizant to

adopt new technologies and expertise in its existing market

segment. Beside the acquisition of TriZetto for 2.7 billion of

U.S. dollars to increase its market share in Healthcare segment,

Cognizant acquires Red Associates and announced to acquire

Frontica Business Solution to increase its market share in the

retail Manufacturing/retail/logistics sector. We can also see

Cognizant acquires Quick Left, Inc. and KBACE Technologies,

Inc. to support its digital solution development.

Research and development

Consider the current world is facing a rapid change in

technology as well as the rapid rate of adoption in technology,

research and development plays a core role in Cognizant.

Cognizant mainly conduct its research and development in three

strategies. Firstly, Cognizant owns 2 divisions which are

Cognizant Digital Works and Global Technology Office (GTO)

to focus on its digital technology research and development,

including experiment with software. Another way is to sponsor

employees to innovate and create solutions and ultimately use

these solutions to serve more clients. Finally, in order to remain

competitive advantage in technology development, Cognizant

also adopt a Global Innovation Ecosystem to stay in touch with

new technologies from partners and external entities in the

world. However, Cognizant combined its research and

development expense in its cost of revenue and does not

disclosure the amount spend on its research and development.

We can only conclude from the innovation model mentioned

above does help Cognizant to increase exposure to new

technologies to sustain its development.

Foreign Sales and earnings

During the year 2015, approximately 78.6% of Cognizant’s

revenues come from clients in North America while

approximately 16.2% of Cognizant’s revenue come from

Europe. Because of currency translation, Cognizant lose $106.2

Important disclosures appear on the last page of this report.

10

million net of tax. The fluctuations of exchange rate may cause a

number of adverse effects on the company.

Government regulation:

Government regulation can influence Cognizant’s business from

three aspects: off-shore outsourcing, immigration and

regulations of their client’s industry, such as financial service

industry and healthcare industry.

Considering offshore outsourcing may lead the loss of job

domestically, this issue is a topic of political discussion in the

U.S. If the economy gets worse, Cognizant would suffer from

the prohibition or limitation of offshore outsourcing. Many

professional employees are from developing country. If U.S has

restricted immigration policy, it will be harder for Cognizant

hiring their desire people. Financial service and healthcare

industry accounts for almost 60% of Cognizant’s revenue. The

profit decreases in those industry would negatively influence

Cognizant’s revenue.

Personnel

There are approximate 221700 employees in Cognizant at the

end of 2015, with 40800 persons in North America, 8600

persons in European region and 162500 persons in India. Based

on those number, the majority of employees are in India, which

saves a great many of salaries expense for Cognizant.

Additionally, the depreciation of Indian rupee in 2015 also bring

many benefits to Cognizant.

The average age of Cognizant’s Executive officers are 51.15

years old. Their rich management experience will help the

company development better. However, considering their age, it

may be hard for them to follow the rapid changes of current

technology.

Properties

Intellectual property is crucial for Cognizant. As of December

31, 2015, Cognizant have applied for a total of 596 trademark

registrations in 63 countries. In addition, they have also applied

for 115 U.S. and international patents.

The intangible assets of Cognizant at the end of 2015 is $864.3

million (excluding $2404.7 million goodwill), and deceased

9.37% in 2015. Compared with PPE, the PPE is $1271.4 million

at the end of 2015. The protection of intangible asset is very

important. Cognizant did a good work on it.

SWOT analysis

We summarized the strengths, weakness, opportunities and

threats base on our company analysis.

Strengths:

1. The global delivery system enables Cognizant to reduce the

cost of providing services as well as meet the needs of

customers globally.

2. Cognizant offers 18 services categories like cloud e

services, application services, and consulting in the four

business segment along with 28 existing products and

platforms to meet the demand of customers.

3. Cognizant has a strong financial performance with an

increasing in revenue and relatively steady growth in

revenue growth. With little debt generate, it gives investor a

signal that the financial condition is able to sustain the

growth of Cognizant in the foreseeable future.

Weaknesses:

1. Cognizant heavily relied on its U.S. market as mentioned

before. It makes Cognizant’s performance highly subject to

the change of economic condition of U.S.

2. The intense labor concentration in India makes Cognizant

expose to the risk associate in the foreign policy and foreign

management. The risk can relate to both labor cost and

litigation cost.

3. The intense competition in IT services decreases

Cognizant’s pricing power.

Opportunities:

1. The development of technology of cloud computing, IoS

(Internet of Things), and big data gives Cognizant potential

opportunities to utilize these technologies in developing its

digital solution to customers. Including their data platforms

and applications.

2. The trend of companies adopting new technologies to meet

the competitive environment has also give Cognizant an

opportunity to generate sales.

Threats:

1. High competition in IT services industry give Cognizant a

big pressure to increase its market share. Cognizant have

competitors like Accenture who also has a good financial

performance with effort in increasing their market share.

2. Cognizant is also subject to anti-outsourcing legislation due

to its labor and services centers all located in India. Based

on the new president Trump’s historical statement regards to

outsourcing,xxvi he strongly against outsourcing jobs which

cause American losing job opportunities. We foresee a

potential negative impact would be associated to Cognizant

with Trump in the House. However, it is hard to say

whether his political view can be implemented or not.

Important disclosures appear on the last page of this report.

11

Valuation Analysis

Valuation summary

We utilized four different models to project the future stock

price for Cognizant: (1) Discounted Cash Flow, (2) Economic

Profit, (3) Dividend Discount Model (DDM) and (4) Relative PS

valuation.

According to the Discounted Cash Flow and Economic Profit

model, the estimated stock price is $75.50. According to the

Dividend Discount Model, the projected stock price is $52.45.

According to the Relative PS valuation, the stock price that we

got is $55.81.

Although the stock price projected by the last two methods is

very close to the current stock price $53.95. We choose to use

the result projected by the DCF and EP model. There are several

reasons.

Firstly, according to the 10-K, we can know that Cognizant does

not plan to pay out dividend in the foreseeable future. Besides,

Cognizant also pays little on stock repurchase. Therefore,

Dividend Discount Model cannot totally represent the value

increased to shareholders. It will decrease the estimated stock

price.

Secondly, for the Relative PS valuation, we believe we cannot

get accurate answer from this method. We used Bloomberg to

search the peer companies. Revenue of the peer companies

obtained from North America accounts for at least 70% of their

total revenues. The revenue of peer companies obtained from IT

service industries accounts for at least 80% of their total

revenues. Besides, all of the peer companies are traded in

America exchange. However, although we have a set of pretty

good peer companies. It cannot reflect the actually condition.

Cognizant is a multination enterprise. 20% of its revenue is from

oversea. This makes its background complex. Moreover,

although most of peer companies’ revenue is from IT service,

they weighted not much. In short, because the diversity in this

industry, we cannot get accurate projection by use of PS

valuation model.

Generally, under this condition, DCF and EP methods can best

present the value added by the operation for shareholders.

Income Statement Assumptions

Revenue Decomposition

We identified Cognizant’s revenue by industries. Based on

Cognizant’s 10-K, the revenue was broken into four categories:

(1) financial service, (2) healthcare, (3)

manufacturing/retail/logistics, and (4) others. As Cognizant is a

service industry, the revenue growth is highly correlated to the

IT service demand of those categorized industries. The IT

service demand depends on the growth rate of data and the

specific segment industries. Additionally, although Cognizant is

a multinational enterprise, almost 80% of its revenue comes

from North America (substantially all relates to operations in the

United States). What follows is a forecast on the segments

revenue growth primarily based on the specific industries’ future

perspective in the U.S.

Financial service: Cognizant’s client in this segment includes

banking, investment firms and insurance companies. For the

year 2015, 40.3% of Cognizant’s revenue is from the financial

service segment. However, according to the data form Factset, in

the past five years, the annual growth rate for financial industry

is around 0.05%. Therefore, we believe it is unsustainable for

Cognizant to keep a growth rate like 20% or 30% in the past

several years. Based on the third quarterly report of Cognizant in

2016, revenue from financial service only grew 7.1% compared

with last Q3, due to the fact that banking customers were

negatively affected by the worse economic condition. We

estimate the continuous growth rate for Cognizant in the

financial service industries is 8%.

Healthcare: Healthcare is second biggest revenue source for

Cognizant. It accounts for 29.5% of Cognizant’s revenue in

2015. Cognizant mainly serves healthcare and life science

companies in the healthcare industries. Owing to the Affordable

Care Act, healthcare industries had a strong growth at the year of

2010. However, with the new President Trump coming into

power, the Act will be changed substantially (ABELSON, 2016). xxvii This change will lead healthcare industry into downturn.

Additionally, although in 2015 the revenue from healthcare

sector of Cognizant increased 36.4% compared with 2014, the

amount growth was contributed by the acquisition of TriZetto.

We don’t think the growth rate could last in the following six

years. Based on the Segment revenue statement, the acquisition

does not improve the marginal profits of healthcare segment. To

sum up, we expected the continuous growth rate for healthcare

segment will be around 10%.

Manufacturing/Retail/Logistics: This segments accounts for

18.9% revenue of Cognizant in 2015. The clients in this segment

includes industrial, automotive, process logistics, energy and

utilities, and retail. Considering the two acquisitions Cognizant

made during 2016 as mentioned before are belong to this

business sector, and also the advertisement of emphasis on

Logistics digital solutions on its website during the analysis

period. We foresee the intention of Cognizant to expand the

manufacturing/retail/logistic sector. The effect of acquisition,

without other influences, should be positively reflected in

revenue related to this sector. Thus we projected revenue growth

rate for this sector to increase to 15% in 2017 and then

increasing in slightly decreasing trend.

Other: This sector includes such disparate elements as

communications, information, media and entertainment, and

high technology. This segment accounts for less than 10% of

revenues. Therefore, for this part, we forecasted the revenue

stream based on the other three segments and the economic

condition. We think the continuous growth rate for this segment

is 10%.

Overall, the growth rate of total revenue will be 8.4% at the year

of 2021, with a trend of decline.

Important disclosures appear on the last page of this report.

12

Operating Expenses

Operating expenses includes (1) cost of revenues, (2) SG&A

expense, (3) Depreciation and amortization expense. Different

from the cost structure in other industries, Cognizant’s operating

cost accounts for almost its 80% revenues.

Cost of revenues: cost of revenues consists of salaries, incentive-

based compensation, stock-based compensation expense, payroll

taxes, employee benefits, immigration and project-related travel

for technical personnel subcontracting and sales commissions

related to revenues. Based on the historical data in the past 10

years, we can know that, the cost of revenue is stable at the level

of 56% as the percentage of revenues. Therefore, we projected

the cost of revenues by use of the average of past five years’ cost

of revenue as percentage of revenues, which is 59.07%.

SG&A expense: similar to cost of revenue, SG&A cost consists

of salaries, incentive-based compensation, stock-based

compensation expense, payroll taxes, employee benefits,

immigration, travel, marketing, communications, management,

finance, administrative and occupancy. Based on the historical

data in the past 10 years, we found SG&A expense keeps in a

stable level of 20% as the percentage of revenues. Therefore, we

projected the SG&A by use of the average of past five years’

SG&A expense as percentage of revenues, which is 21.61%.

Depreciation and Amortization: We projected depreciation as

percentage of the gross PPE the previous year. Based on the

historical data, the percentage is 14%.

Due to the acquisition, the intangible assets in 2014 increased

significantly compared with 2013. Therefore, in 2014 the

amortization also increased largely. In Cognizant 10-k, there is

the projected amortization in the following five years. The

amortization was projected by the data from 10-k.

In general, we estimated the operating cost for Cognizant will be

stable around 80 percentage of total revenues in the following

years.

Non-operating gain (expense)

Interest income: Interest income is driven by investment. We

multiplied the total investment by the 10-year T-bond rate to

forecast interest income.

Interest expense: Interest expense is driven by the debt. We

projected interest expense through multiplying the debt by the

cost of debt.

Foreign currency exchange gains(losses): this is a non-operating

account and full of uncertainty. In addition, this only accounts

for a little portion of revenues (losses). We did not forecast this

account.

Provision for income tax

Marginal tax rate: marginal tax rate is used to calculate the

provision for income tax. We forecasted marginal tax rate based

on the average of past five years’ data, which is 26.1%.

Balance Statement Assumption

Cash and cash equivalents: Cash and cash equivalents are

treated as plug account to forecast the cash flow.

Short-term investments: the growth rate for this account is 10-

year T-bond yield.

PPE: the projection of PPE is based on historical capital

expenditure and depreciation. According to the historical data,

the capital expenditure for the recent years has a slight decline

trend. Therefore, we estimated the capital in the following six

years will decrease by 2% per year. Additionally, PPE only

accounts a small portion of total asset, around 13% in the recent

five years.

Short-term and long-term debt: Throughout ten years, Cognizant

had short-term debt and long-term debt only in the years of 2014

and 2015. From the 10-k of FY15, we can know that the short-

term debt is from revolving facility and the long-term debt is for

the acquisition of TriZetto. Those activities do not occur too

often, so we project Cognizant will pay off the short-term debt in

the next year and long-term debt in 2019, based on the

summarizes of the long-term debt balances in 2016 10-k.

Common equity: the account common equity consists of

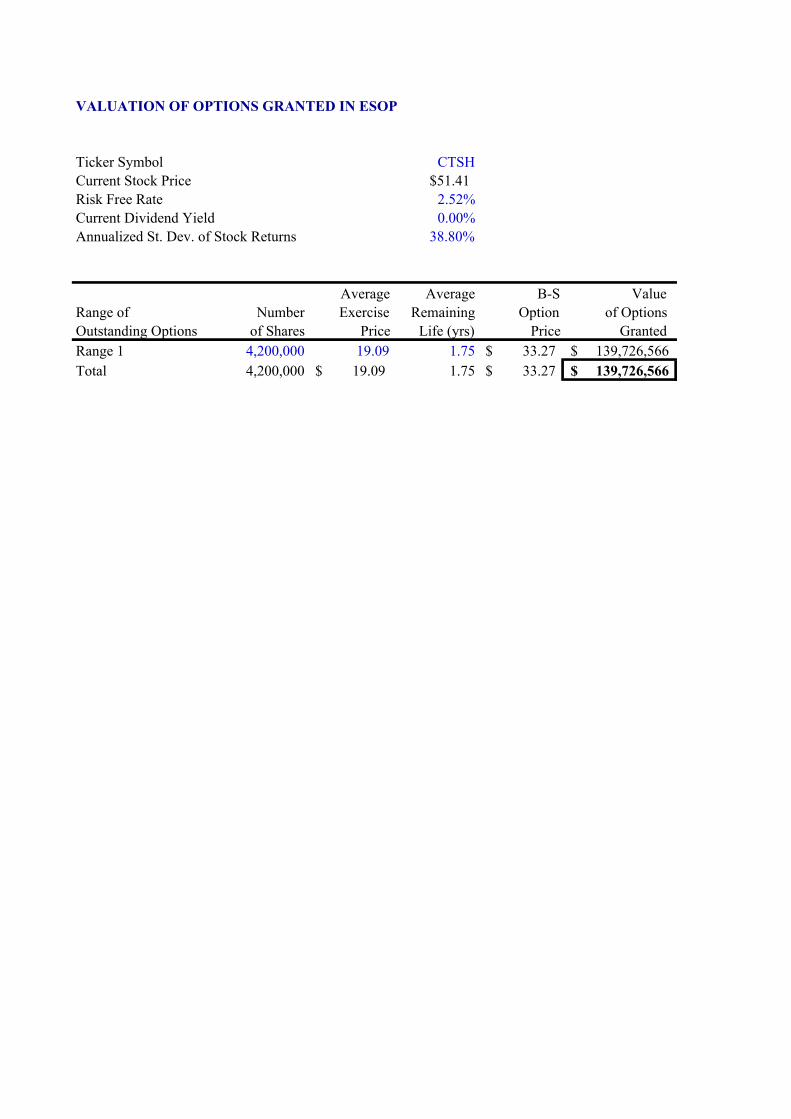

Additional paid-in capital and common stock. Common stock

was projected by the increase effect on ESOP and decrease

effect on share repurchase. The calculation process is provided

in the attached sheet labeled “share changes.”

Dividend: Cognizant has never declared or paid any cash

dividends on the class A common stock. For retaining any future

earnings to finance the growth of its business, Cognizant will not

pay any dividends in the foreseeable future.

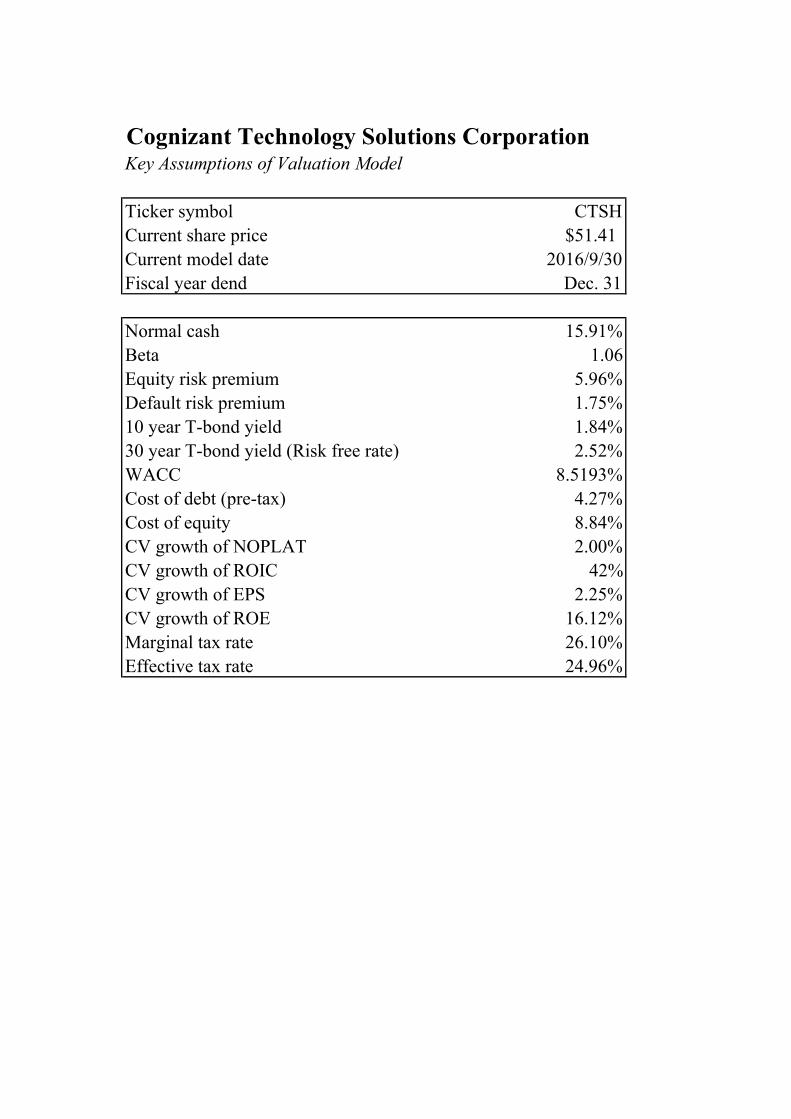

Weighted Average Cost of Capital (WACC)

Cognizant’s weighted average cost of capital (WACC) was

calculated at 8.52% (see the attached document labeled “WACC

calculation” for calculation). The weight of Equity is 94.4% and

the weight of debt is 5.6%. The marginal tax rate is 26.1%,

which has been projected by calculating the tax provision.

Cost of Equity

Beta: from the Bloomberg system, we found the beta for

Cognizant is 1.06.

Risk free rate: we used 30-year T-bond yield as our risk free

rate, which is 2.52%.

Equity risk premium: we chose S&P 500 as our benchmark. By

use of the past 50 years’ monthly return, we got the historical

market return is 8.48%. Then, we subtracted the market return to

risk free rate and got the risk premium which is 5.96%.

Important disclosures appear on the last page of this report.

13

By use of the function: , we can

get the cost of equity is 8.84%

Cost of debt

The debt of Cognizant consists of three parts: (1) short-term

debt, (2) long-term debt and (3) PV of operating lease.

Cognizant does not issue any publically traded debt. Besides,

Cognizant’s competitors also do not have publically traded debt.

Because Cognizant’s debt is not publically available, in order to

find Cognizant’s debt, we need use the default risk premium.

According to Bloomberg, we know that the rating level for

Cognizant is A-. From the default premium table, we can know

that the default risk premium for Cognizant is 1.75%. Adding to

the risk free rate, we can get the cost of debt for Cognizant is

4.27%.

Sensitive Analysis We did six sensitive analyses which is shown in attached

document. Below we explained four sensitivity table: (1) CV

growth rate of ROIC vs. CV growth of NOPLAT, (2) SG&A

expense as % of sales vs. Cost of revenue as % of sales, (3)

Default risk premium vs. Equity risk premium, (4) Equity risk

premium to Risk free rate.

CV growth rate of ROIC to CV growth of NOPLAT

75.50$ 1.50% 1.75% 2.00% 2.25% 2.50%

38.0% 71.69 73.37 75.18 77.14 79.26

40.0% 71.80 73.51 75.35 77.33 79.48

42.0% 71.91 73.64 75.50 77.51 79.69

44.0% 72.00 73.75 75.63 77.67 79.87

46.0% 72.09 73.86 75.76 77.81 80.04

CV growth of ROIC

CV growth of NOPLAT

When the CV growth of NOPLAT keeps constant, the stock

price increases as the CV growth of ROIC increase. The range of

the stock price is from 75.18 to 75.76 while the range of CV

growth of ROIC is from 38% to 46%. When the CV growth of

ROIC keeps constant, the stock price increases as the CV growth

of NOPLAT increase. The range of the stock price is 71.91 to

79.69 while the range of CV growth of NOPLAT is from 1.5%

to 2.5%. It is obviously that compared with CV growth of ROIC,

the stock price is more sensitive to CV growth of NOPLAT.

SG&A expense as % of sales to Cost of revenue as % of sales

75.50$ 57.07% 58.07% 59.07% 60.07% 61.07%

19.61% 91.40 87.43 83.45 79.47 75.50

20.61% 87.43 83.45 79.47 75.50 71.52

21.61% 83.45 79.47 75.50 71.52 67.55

22.61% 79.47 75.50 71.52 67.55 63.57

23.61% 75.50 71.52 67.55 63.57 59.59

S&G expense as % of sales

Cost of revenue as % of sales

When cost of revenue as % sales keeps constant, the stock price

decrease rapidly as the SG&A expense as % of sales increase.

The stock price range is from 91.4 to 75.5 while the range of

SG&A is from 19.61% to 23.61%. On the other hand, when

SG&A expense as % of sales keeps constant, the stick price also

decreases rapidly as the cost of revenue as % of sales increase.

The SG&A expense as % of sales and Cost of revenue as % of

sales have the same impact on stock price. Additionally, the

stock price is highly sensitive to the two variables. 1% change

of either variable will makes around $4 change on stock price.

Therefore, the operating efficiency should be noticed to forecast

the stock price for Cognizant.

Default risk premium to Equity risk premium

75.50$ 5.76% 5.86% 5.96% 6.06% 6.16%

1.35% 78.07 76.83 75.63 74.47 73.34

1.55% 78.00 76.76 75.56 74.40 73.28

1.75% 77.93 76.69 75.50 74.34 73.21

1.95% 77.86 76.62 75.43 74.28 73.15

2.15% 77.78 76.56 75.37 74.21 73.09

Default risk premium

Equity risk premium

When the equity premium is held constant, if the default risk

premium changes from 1.55% to 1.95, the stock price will

decrease from 75.56 to 75.43. On the other hand, when the

default risk premium is held constant, if the equity risk premium

changes from 5.76% to 6.16%, the stock price will decrease

from 77.93 to 73.21. Therefore, compared with default risk

premium, the stock price is more sensitive to equity risk

premium. This is caused by the low leverage ratio for Cognizant.

Equity risk premium to Risk free rate

75.50$ 2.32% 2.42% 2.52% 2.62% 2.72%

5.76% 80.44 79.17 77.93 76.73 75.56

5.86% 79.13 77.89 76.69 75.53 74.40

5.96% 77.86 76.66 75.50 74.37 73.28

6.06% 76.63 75.46 74.34 73.25 72.19

6.16% 75.43 74.31 73.21 72.15 71.13

Equity risk premium

30 year T-bond yield (Risk free rate)

When the equity risk premium is held constant, 0.4% increase of

risk free rate will lead the stock price decrease from 77.86 to

73.28. On the other hand, when the risk free rate is held

constant, 0.4% increase of equity risk premium will lead the

stock price decrease from 77.93 to 73.21. Generally, the two

variables have the same effect on the stock price and the stock

price is sensitive to the two variables. The reason why this

happened is that Cognizant has a low beta, which is 1.06.

Therefore, the percentage change of equity premium and risk

free rate will lead the same change to stock price.

Important disclosures appear on the last page of this report.

14

Important Disclaimer

This report was created by students enrolled in the Security

Analysis (6F:112) class at the University of Iowa. The report

was originally created to offer an internal investment

recommendation for the University of Iowa Krause Fund and its

advisory board. The report also provides potential employers and

other interested parties an example of the students’ skills,

knowledge and abilities. Members of the Krause Fund are not

registered investment advisors, brokers or officially licensed

financial professionals. The investment advice contained in this

report does not represent an offer or solicitation to buy or sell

any of the securities mentioned. Unless otherwise noted, facts

and figures included in this report are from publicly available

sources. This report is not a complete compilation of data, and

its accuracy is not guaranteed. From time to time, the University

of Iowa, its faculty, staff, students, or the Krause Fund may hold

a financial interest in the companies mentioned in this report.

Important disclosures appear on the last page of this report.

15

Reference i Factset ii Erne, B., Teufel, A. (2010). Fisher Investments on

Technology. Hoboken, N.J: John Wiley & Sons. February

1, 2015. iii Worldbank iv http://www.usgovernmentspending.com/ v Usfederalbudget

<http://www.usfederalbudget.us/federal_budget_estimated> vi Federal Reserve Bank of St. Louis

<https://fred.stlouisfed.org/series/FEDFUNDS> vii U.S. Bureau of Economic Analysis

<http://www.tradingeconomics.com/united-states/disposable-

personal-income> viii Bureau of Labor Statistics <

http://data.bls.gov/timeseries/LNS14000000> ix Bureau of Labor Statistics <

http://www.bls.gov/opub/ee/2016/ces/summarytable_201608

.pdf> xhttp://data.bls.gov/timeseries/LNU04000000?years_option=

all_years&periods_option=specific_periods&periods=Annua

l+Data xi Fortune <http://fortune.com/2016/09/06/goldman-sachs-

interest-rates/> xii Factset xiii Federal Reserve Bank of St. Louis

<https://fred.stlouisfed.org/series/FEDFUNDS> xiv Factset xv Erne, B., Teufel, A. (2010). Fisher Investments on

Technology. Hoboken, N.J: John Wiley & Sons. February

1, 2015. xvi IBISWorld xvii IBISWorld xviiiIBISWorld<http://clients1.ibisworld.com.proxy.lib.uiowa.

edu/reports/us/industry/default.aspx?entid=1281> xixIBISWorld<http://clients1.ibisworld.com.proxy.lib.uiowa.e

du/reports/us/industry/default.aspx?entid=1281> xx Figure 1: obtained and generated from Factset xxi Figure 2: Cognizant 2016 proxy statement xxii Bloomberghttp://www.bloomberg.com/press-

releases/2016-11-10/cognizant-cloud-enables-office-product-

leader-acco-brands-it-infrastructure-and-builds-the-

foundation-for-digital-enterprise xxiii factset xxiv Figure 3: Financial data comparison. Data collected from

Factset. xxv Factset xxvi http://www.motherjones.com/politics/2016/03/donald-

trump-outsourcing-flip-flop xxviixxviixxviixxvii

xxvii http://www.motherjones.com/politics/2016/03/donald-

trump-outsourcing-flip-flop

ABELSONREED. The New York Times. nytimes:

http://www.nytimes.com/2016/11/12/business/insurers-

unprepared-for-obamacare-repeal.html?_r=0

Cognizant Technology Solutions CorporationKey Assumptions of Valuation Model

Ticker symbol CTSHCurrent share price $51.41Current model date 2016/9/30Fiscal year dend Dec. 31

Normal cash 15.91%Beta 1.06Equity risk premium 5.96%Default risk premium 1.75%10 year T-bond yield 1.84%30 year T-bond yield (Risk free rate) 2.52%WACC 8.5193%Cost of debt (pre-tax) 4.27%Cost of equity 8.84%CV growth of NOPLAT 2.00%CV growth of ROIC 42%CV growth of EPS 2.25%CV growth of ROE 16.12%Marginal tax rate 26.10%Effective tax rate 24.96%

Cognizant Technology Solutions CorporationRevenue Decomposition(in millions) Fiscal Years Ending Dec. 31 2013 2014 2015 2016E 2017E 2018E 2019E 2020E 2021E

365 Days 365 Days 365 Days 366 Days 365 Days 365 Days 365 Days 366 Days 365 DaysRevenue By Industry

Financial Services 3,717.6 4,285.6 5,002.9 5703.3 6604.4 7555.5 8499.9 9417.9 10171.3YoY Growth 22.5% 15.3% 16.7% 14.0% 15.8% 14.4% 12.5% 10.8% 8.0%Healthcare 2,264.8 2,689.4 3,667.5 4034.3 4514.3 4988.3 5522.1 6101.9 6712.1YoY Growth 17.1% 18.7% 36.4% 10.0% 11.9% 10.5% 10.7% 10.5% 10.0%Manufacturing/Retail/Logistics 1,868.3 2,093.6 2,343.9 2653.3 3051.3 3524.2 4017.6 4560.0 5152.8YoY Growth 24.7% 12.1% 12.0% 13.2% 15.0% 15.5% 14.0% 13.5% 13.0%Other 992.5 1,194.1 1,401.7 1612.0 1839.2 2093.1 2363.1 2672.6 2939.9YoY Growth 13.1% 20.3% 17.4% 15.0% 14.1% 13.8% 12.9% 13.1% 10.0%Total 8843.2 10262.7 12416.0 14002.81 16009.28 18161.09 20402.67 22752.42 24976.11YoY Growth 20.4% 16.1% 21.0% 12.8% 14.3% 13.4% 12.3% 11.5% 9.8%

Segment operating profitFinancial Service 1,212.1 1,320.1 1,641.9Segment Profit Margin 32.6% 30.8% 32.8%Healthcare 829.9 851.0 1,200.0Segment Profit Margin 36.6% 31.6% 32.7%Manufacturing/Retail/Logistics 630.3 685.7 802.7Segment Profit Margin 33.7% 32.8% 34.2%Other 318.3 391.9 453.7Segment Profit Margin 32.1% 32.8% 32.4%

Total segment operating profit 2,990.6 3,248.7 4,098.3Less: unallocated costs 1,312.7 1,363.8 1,956.3Income from operations 1,677.9 1,884.9 2,142.0

Cognizant Technology Solutions CorporationIncome Statement (in millions, except per share data) Fiscal Years Ending Dec. 31 2013 2014 2015 2016E 2017E 2018E 2019E 2020E 2021ERevenues 8,843.19 10,262.70 12,416.00 14,002.81 16,009.28 18,161.09 20,402.67 22,752.42 24,976.11Operating expenses Cost of revenues exclusive of depreciation and amortization expense (5,265.47) (6,141.12) (7,440.20) (8,271.46) (9,456.68) (10,727.76) (12,051.86) (13,439.86) (14,753.39) Selling, general and administrative expenses (1,727.61) (2,037.02) (2,508.60) (3,026.01) (3,459.61) (3,924.61) (4,409.02) (4,916.80) (5,397.34) Depreciation expense (147.57) (165.99) (230.63) (178.00) (192.03) (203.32) (212.27) (219.22) (224.46) Amortization expense (24.64) (33.67) (94.57) (96.10) (93.20) (85.80) (83.50) (76.30) (78.60)Income from operations 1,677.91 1,884.90 2,142.00 2,431.25 2,807.76 3,219.60 3,646.02 4,100.25 4,522.32Other income (expense), net Interest income 48.90 62.44 83.70 91.07 113.90 148.27 177.80 226.85 282.72 Interest expense - (2.47) (17.70) (54.98) (34.16) (29.89) - - - Foreign currency exchange gains (losses), net (41.10) (20.38) (42.60) - - - - - - Other, net 2.20 (0.45) (1.80) - - - - - - Total other income (expense), net 10.00 39.15 21.60 36.09 79.74 118.38 177.80 226.85 282.72 Income before provision for income taxes 1,687.91 1,924.05 2,163.60 2,467.34 2,887.50 3,337.98 3,823.82 4,327.10 4,805.04 Provision for income taxes (459.34) (484.76) (540.00) (643.98) (753.64) (871.21) (998.02) (1,129.37) (1,254.12) Net income 1,228.57 1,439.29 1,623.60 1,823.36 2,133.86 2,466.77 2,825.81 3,197.72 3,550.93

Basic EPS 2.03 2.37 2.67 2.98 3.48 4.00 4.57 5.15 5.70 Weighted average number of common shares outstanding—Basic 604.10 608.10 609.10 611.50 613.90 616.30 618.70 621.10 623.50 Dividend per share - - - - - - - -

Cognizant Technology Solutions CorporationCommon Size Income Statement

Fiscal Years Ending Dec. 31 2013 2014 2015 2016E 2017E 2018E 2019E 2020E 2021ERevenues 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%Operating expenses Cost of revenues exclusive of depreciation and amortization expense -59.54% -59.84% -59.92% -59.07% -59.07% -59.07% -59.07% -59.07% -59.07% Selling, general and administrative expenses -19.54% -19.85% -20.20% -21.61% -21.61% -21.61% -21.61% -21.61% -21.61% Depreciation and amortization expense -0.28% -0.33% -0.76% -0.69% -0.58% -0.47% -0.41% -0.34% -0.31%Income from operations 18.97% 18.37% 17.25% 17.36% 17.54% 17.73% 17.87% 18.02% 18.11%Other income (expense), net Interest income 0.55% 0.61% 0.67% 0.65% 0.71% 0.82% 0.87% 1.00% 1.13% Interest expense 0.00% -0.02% -0.14% -0.39% -0.21% -0.16% 0.00% 0.00% 0.00% Foreign currency exchange gains (losses), net -0.46% -0.20% -0.34% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% Other, net 0.02% 0.00% -0.01% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Total other income (expense), net 0.11% 0.38% 0.17% 0.26% 0.50% 0.65% 0.87% 1.00% 1.13%Income before provision for income taxes 19.09% 18.75% 17.43% 17.62% 18.04% 18.38% 18.74% 19.02% 19.24%Provision for income taxes -5.19% -4.72% -4.35% -4.60% -4.71% -4.80% -4.89% -4.96% -5.02%Net income 13.89% 14.02% 13.08% 13.02% 13.33% 13.58% 13.85% 14.05% 14.22%

Cognizant Technology Solutions CorporationBalance Sheet(in millions, except par values) Fiscal Years Ending Dec. 31 2013 2014 2015 2016E 2017E 2018E 2019E 2020E 2021E

AssetsCurrent assets: Cash and cash equivalents 2,213.01 2,010.10 2,125.20 3,313.72 5,129.23 6,679.99 9,290.73 12,271.28 15,384.58 Short-term investments 1,534.47 1,764.60 2,824.30 2,876.27 2,929.19 2,983.09 3,037.98 3,093.88 3,150.80 Trade accounts receivable, net 1,648.79 1,968.68 2,252.60 2,646.07 3,025.23 3,431.85 3,855.44 4,299.47 4,719.67 Unbilled accounts receivable 226.49 324.58 369.00 360.51 412.17 467.57 525.28 585.77 643.02 Deferred income tax assets, net 256.23 - - - - - - - - Other current assets 268.91 352.61 337.50 488.31 558.28 633.32 711.49 793.43 870.98 Total current assets 6,147.89 6,420.57 7,908.60 9,684.88 12,054.10 14,195.81 17,420.91 21,043.82 24,769.05Property and equipment, net 1,081.16 1,247.20 1,271.40 1,371.66 1,452.32 1,516.23 1,565.85 1,603.29 1,854.81Goodwill 444.24 2,413.56 2,404.70 2,404.70 2,404.70 2,404.70 2,404.70 2,404.70 2,404.70Intangible assets, net 131.27 953.75 864.30 871.21 878.18 885.21 892.29 899.43 906.63 Deferred income tax assets, net 147.15 234.20 347.80 392.15 447.92 512.39 586.25 669.82 762.62 Other noncurrent assets 183.01 209.66 268.60 272.63 276.72 280.87 285.08 289.36 293.70 Total assets 8,134.73 11,479.04 13,065.40 14,997.24 17,513.94 19,795.22 23,155.08 26,910.42 30,991.50

Liabilities and Stockholders' EquityCurrent liabilities: Accounts payable 113.39 145.69 165.30 187.43 214.28 243.09 273.09 304.54 334.31 Deferred revenue 182.89 224.11 323.70 418.49 478.46 542.76 609.76 679.98 746.44 Short-term debt - 700.00 406.30 - - - - - - Accrued expenses and other current liabilities 1,478.22 1,522.29 1,818.40 2,192.32 2,506.46 2,843.36 3,194.31 3,562.19 3,910.34 Total current liabilities 1,774.51 2,592.09 2,713.70 2,798.24 3,199.20 3,629.21 4,077.15 4,546.71 4,991.08 Deferred revenue, noncurrent - 81.00 49.30 - - - - - - Deferred income tax liabilities, net 21.17 11.80 3.30 - - - - - - Long-term debt - 937.50 881.20 800.00 700.00 - - - -Other noncurrent liabilities 203.25 116.42 139.80 251.72 287.78 326.47 366.76 409.00 448.97 Total liabilities 1,998.93 3,738.82 3,787.30 3,849.96 4,186.99 3,955.67 4,443.91 4,955.71 5,440.05 Stockholders' equity:

Preferred stock, $0.10 par value, 15.0 shares authorized, none issued - - - - - - - - - Common euqity 549.68 561.70 459.10 504.92 550.73 596.55 642.36 688.18 734.00 Retained earnings 5,862.37 7,301.60 8,925.20 10,748.56 12,882.42 15,349.19 18,175.00 21,372.73 24,923.65 Accumulated other comprehensive income (loss) (276.26) (123.07) (106.20) (106.20) (106.20) (106.20) (106.20) (106.20) (106.20)

Total stockholders' equity 6,135.79 7,740.23 9,278.10 11,147.28 13,326.96 15,839.54 18,711.16 21,954.71 25,551.45 Total liabilities and stockholders' equity 8,134.72 11,479.05 13,065.40 14,997.24 17,513.94 19,795.22 23,155.08 26,910.42 30,991.50

Cognizant Technology Solutions CorporationCommon Size Balance Sheet

Fiscal Years Ending Dec. 31 2013 2014 2015 2016E 2017E 2018E 2019E 2020E 2021E

AssetsCurrent assets: Cash and cash equivalents 25.03% 19.59% 17.12% 23.66% 32.04% 36.78% 45.54% 53.93% 61.60% Short-term investments 17.35% 17.19% 22.75% 20.54% 18.30% 16.43% 14.89% 13.60% 12.62% Trade accounts receivable, net 18.64% 19.18% 18.14% 18.90% 18.90% 18.90% 18.90% 18.90% 18.90% Unbilled accounts receivable 2.56% 3.16% 2.97% 2.57% 2.57% 2.57% 2.57% 2.57% 2.57% Deferred income tax assets, net 2.90% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% Other current assets 3.04% 3.44% 2.72% 3.49% 3.49% 3.49% 3.49% 3.49% 3.49% Total current assets 69.52% 62.56% 63.70% 69.16% 75.29% 78.17% 85.39% 92.49% 99.17%Property and equipment, net 12.23% 12.15% 10.24% 9.80% 9.07% 8.35% 7.67% 7.05% 7.43%Long-term investment 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Goodwill 5.02% 23.52% 19.37% 17.17% 15.02% 13.24% 11.79% 10.57% 9.63%Intangible assets, net 1.48% 9.29% 6.96% 6.22% 5.49% 4.87% 4.37% 3.95% 3.63%Deferred income tax assets, net 1.66% 2.28% 2.80% 2.80% 2.80% 2.82% 2.87% 2.94% 3.05%Other noncurrent assets 2.07% 2.04% 2.16% 1.95% 1.73% 1.55% 1.40% 1.27% 1.18% Total assets 91.99% 111.85% 105.23% 107.10% 109.40% 109.00% 113.49% 118.27% 124.08%

Liabilities and Stockholders' EquityCurrent liabilities: Accounts payable 1.28% 1.42% 1.33% 1.34% 1.34% 1.34% 1.34% 1.34% 1.34% Deferred revenue 2.07% 1.95% 2.48% 2.79% 2.73% 2.74% 2.63% 2.53% 2.41% Short-term debt 0.00% 6.10% 3.11% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% Accrued expenses and other current liabilities 16.72% 13.26% 13.92% 14.62% 14.31% 14.36% 13.80% 13.24% 12.62% Total current liabilities 20.07% 22.58% 20.77% 18.66% 18.27% 18.33% 17.61% 16.90% 16.10%Deferred revenue, noncurrent 0.00% 0.71% 0.38% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Deferred income tax liabilities, net 0.24% 0.10% 0.03% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Long-term debt 0.00% 8.17% 6.74% 5.33% 4.00% 0.00% 0.00% 0.00% 0.00%Other noncurrent liabilities 2.30% 1.01% 1.07% 1.68% 1.64% 1.65% 1.58% 1.52% 1.45% Total liabilities 22.60% 36.43% 30.50% 27.49% 26.15% 21.78% 21.78% 21.78% 21.78%Stockholders' equity:

Preferred stock, $0.10 par value, 15.0 shares authorized, none issued 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Common equity 6.22% 5.47% 3.70% 3.61% 3.44% 3.28% 3.15% 3.02% 2.94%Retained earnings 66.29% 71.15% 71.88% 76.76% 80.47% 84.52% 89.08% 93.94% 99.79%Accumulated other comprehensive income (loss) -3.12% -1.07% -0.81% -0.71% -0.61% -0.54% -0.46% -0.39% -0.34%

Total stockholders' equity 69.38% 75.42% 74.73% 79.61% 83.25% 87.22% 91.71% 96.49% 102.30% Total liabilities and stockholders' equity 91.99% 111.85% 105.23% 107.10% 109.40% 109.00% 113.49% 118.27% 124.08%