Bahasa

Halaman

Hukum

VENTURA COUNTY EMPLOYEES’ RETIREMENT ASSOCIATION

BOARD OF RETIREMENT

BUSINESS MEETING

JUNE 19, 2017

AGENDA PLACE: Ventura County Employees' Retirement Association

Second Floor Boardroom 1190 South Victoria Avenue Ventura, CA 93003

TIME: 9:00 a.m. Members of the public may comment on any item under the Board’s jurisdiction by filling out a speaker form and presenting it to the Clerk. Unless otherwise directed by the Chair, comments related to items on the agenda will be heard when the Board considers that item. Comments related to items not on the agenda will generally be heard at the time designated for Public Comment.

ITEM:

I. CALL TO ORDER

Master Page No.

II. APPROVAL OF AGENDA

1 – 3

Welcome of Newly Elected General Member, Maeve Fox.

III. APPROVAL OF MINUTES

A. Disability Minutes of June 5, 2017 4 – 11

IV. CONSENT AGENDA

A. Approve Regular and Deferred Retirements and Survivors Continuances for the Month of May 2017.

12

B. Receive and File Report of Checks Disbursed in May 2017.

13 – 17

C. Receive and File Budget Summary for FY 2016-17 Month Ending May 31, 2017.

18

Business Meeting Agenda - II. APPROVAL OF AGENDA & WELCOME OF NEWLY ELECTED GENERAL MEMBER

MASTER PAGE NO. 1 of 202

BOARD OF RETIREMENT JUNE 19, 2017 AGENDA BUSINESS MEETING PAGE 2

IV. CONSENT AGENDA (continued)

D. Receive and File Statement of Fiduciary Net Position, Statement of Changes in Fiduciary Net Position, Schedule of Investments and Cash Equivalents, and Schedule of Investment Management Fees for the Period Ending April 30, 2017.

19 – 24

V. INVESTMENT MANAGER PRESENTATIONS

A. Receive Annual Investment Presentation, Parametric, Justin Henne and Ben Lazarus.

25 – 53

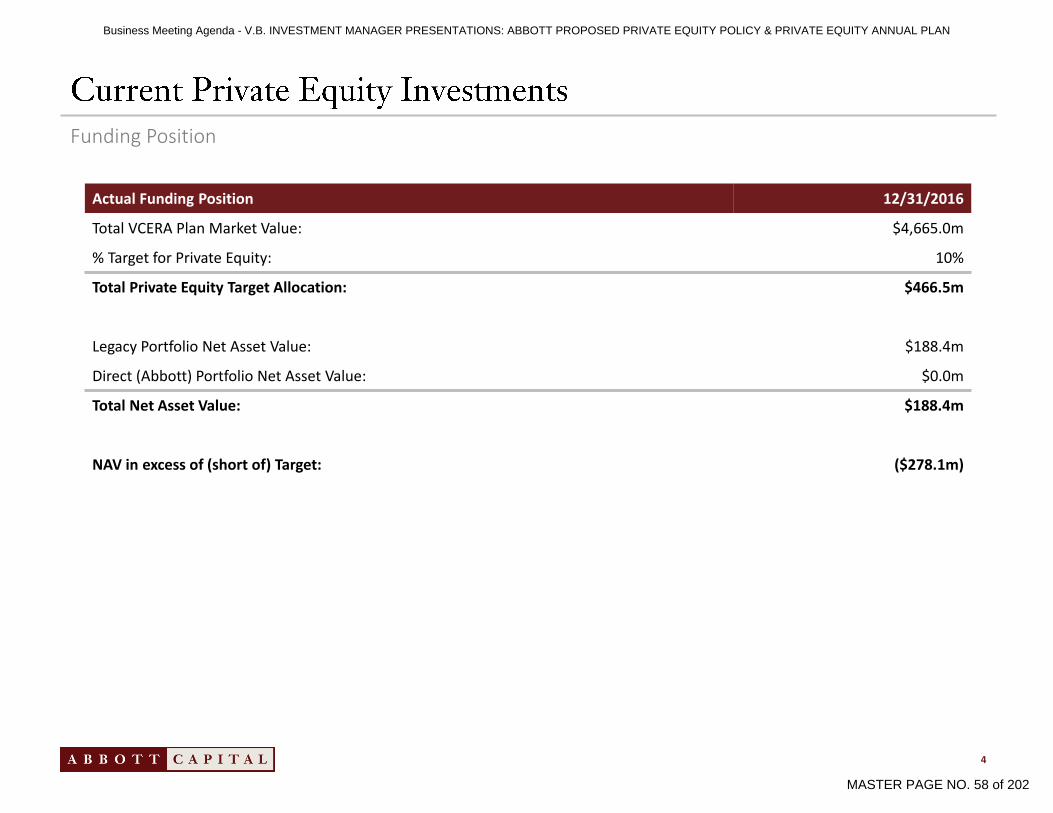

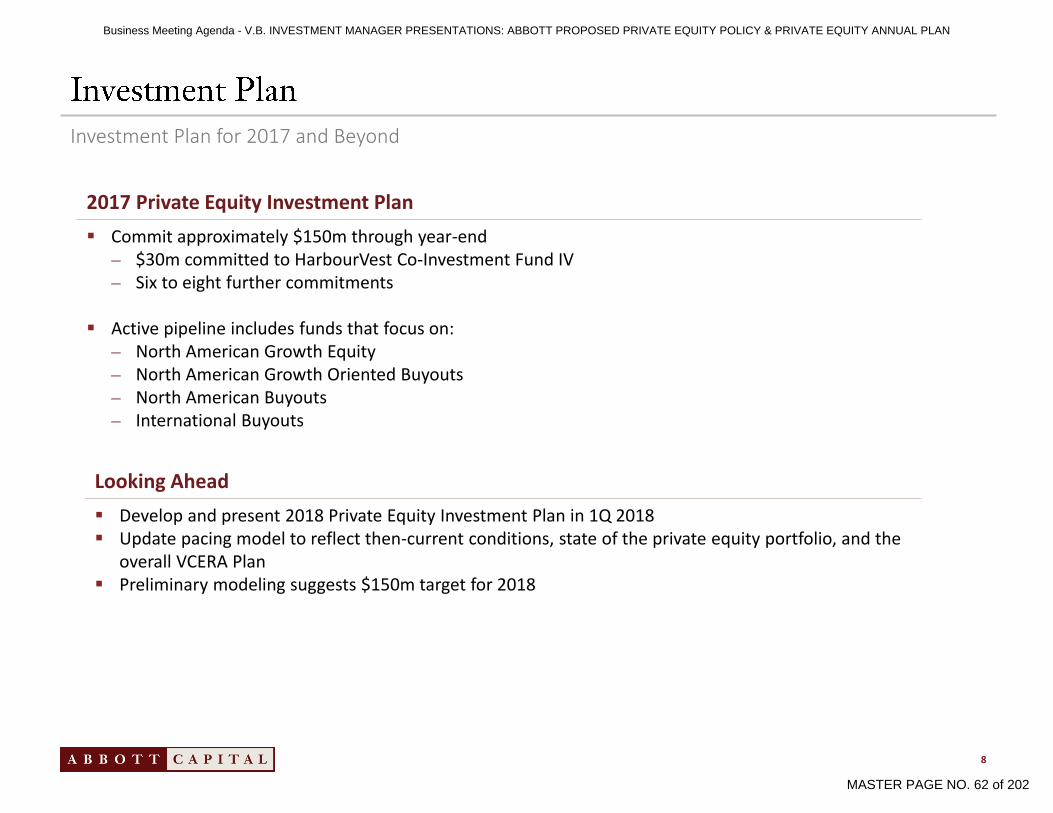

B. Proposed Private Equity Investment Policy and Proposed Private Equity Investment Annual Plan – Abbott Capital Management: Charles Van Horne and Matthew Smith; VCERA – Dan Gallagher

1. Staff Letter.

54

2. Abbott Capital Management Presentation.

55 – 64

3. Proposed Private Equity Investment Policy. RECOMMENDED ACTION: Approve and Adopt.

65 – 72

4. Proposed Private Equity Investment Annual Plan. RECOMMENDED ACTION: Approve and Adopt.

73 – 81

VI. INVESTMENT INFORMATION

A. NEPC – Allan Martin and Tony Ferrera. VCERA – Dan Gallagher, Chief Investment Officer.

1. Preliminary Performance Report Month Ending May 31, 2017. RECOMMENDED ACTION: Receive and file.

82 – 89

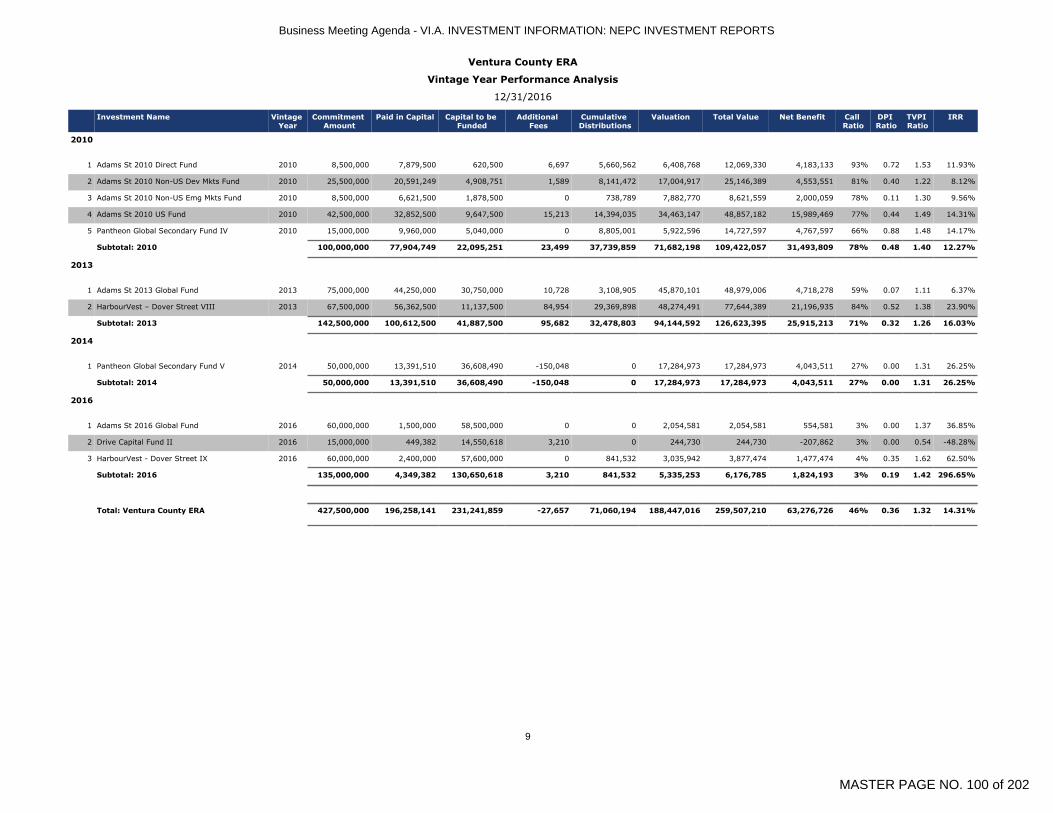

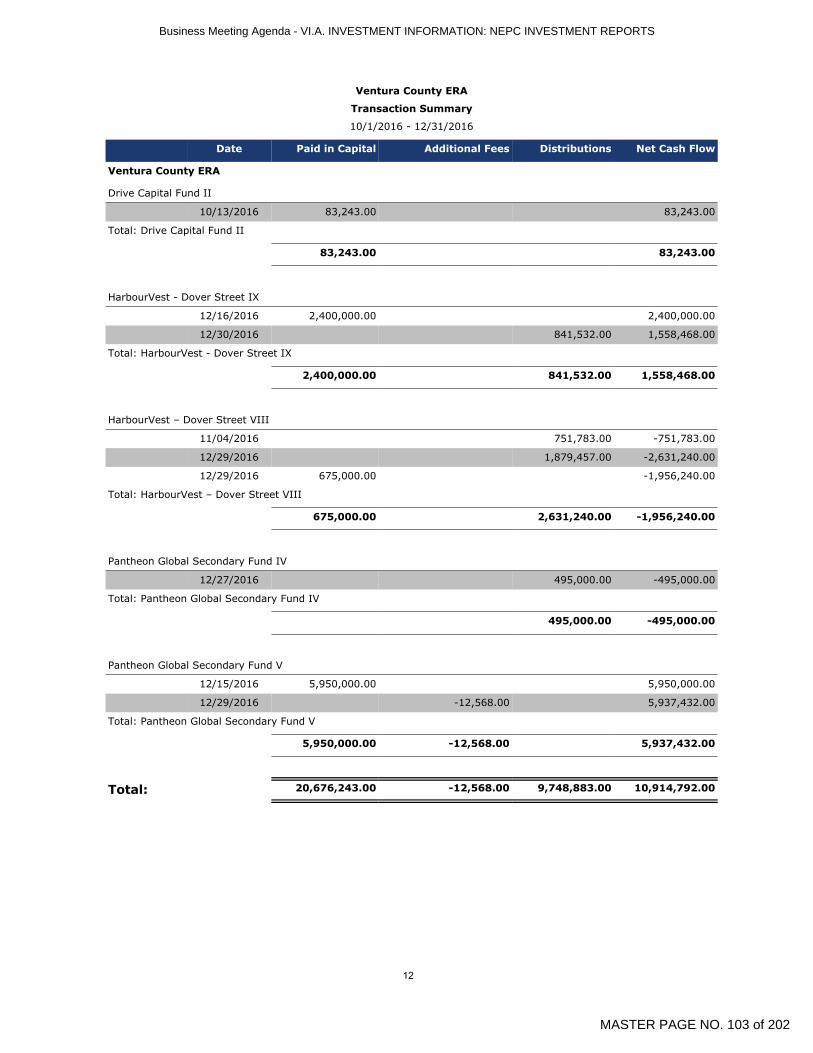

2. Fourth Quarter 2016 Private Markets Review – Private Equity. RECOMMENDED ACTION: Receive and file.

90 – 104

VII. OLD BUSINESS

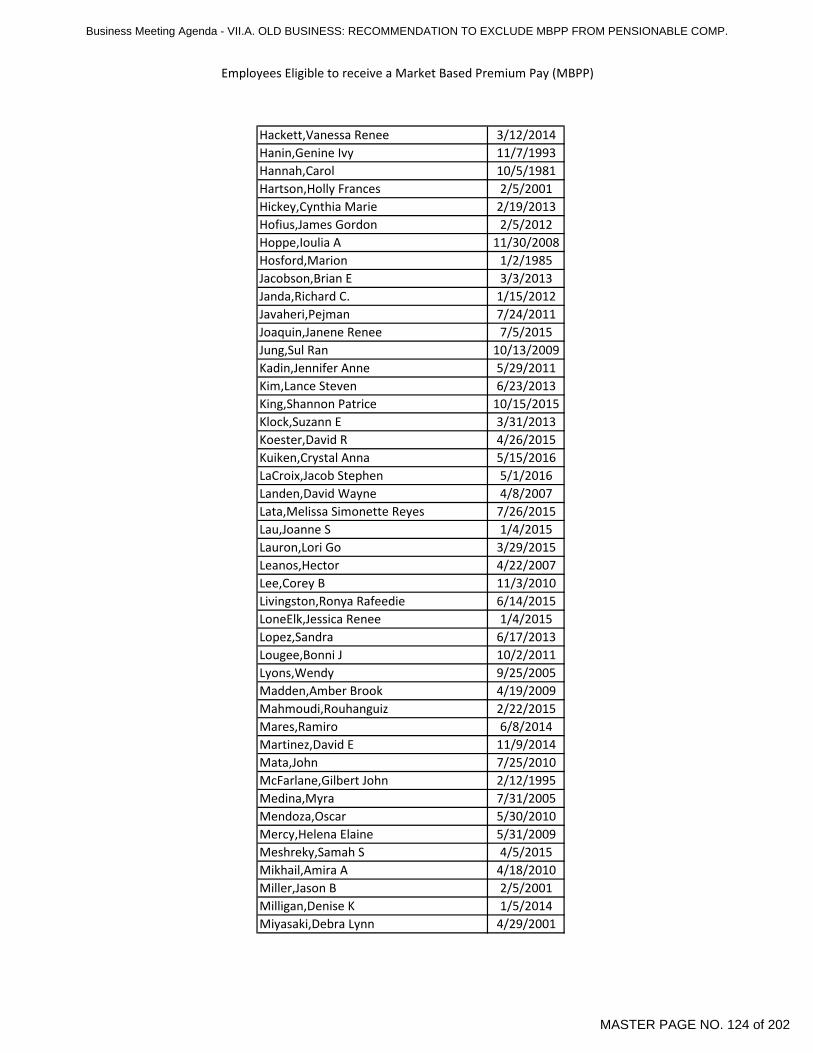

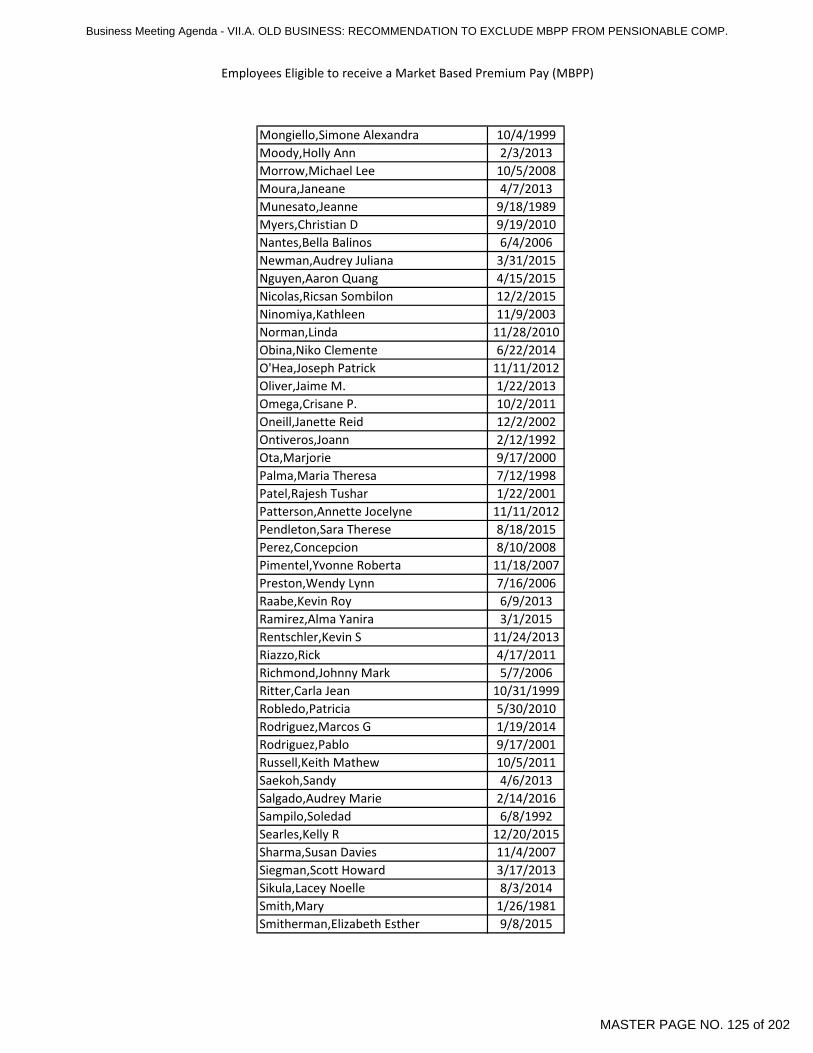

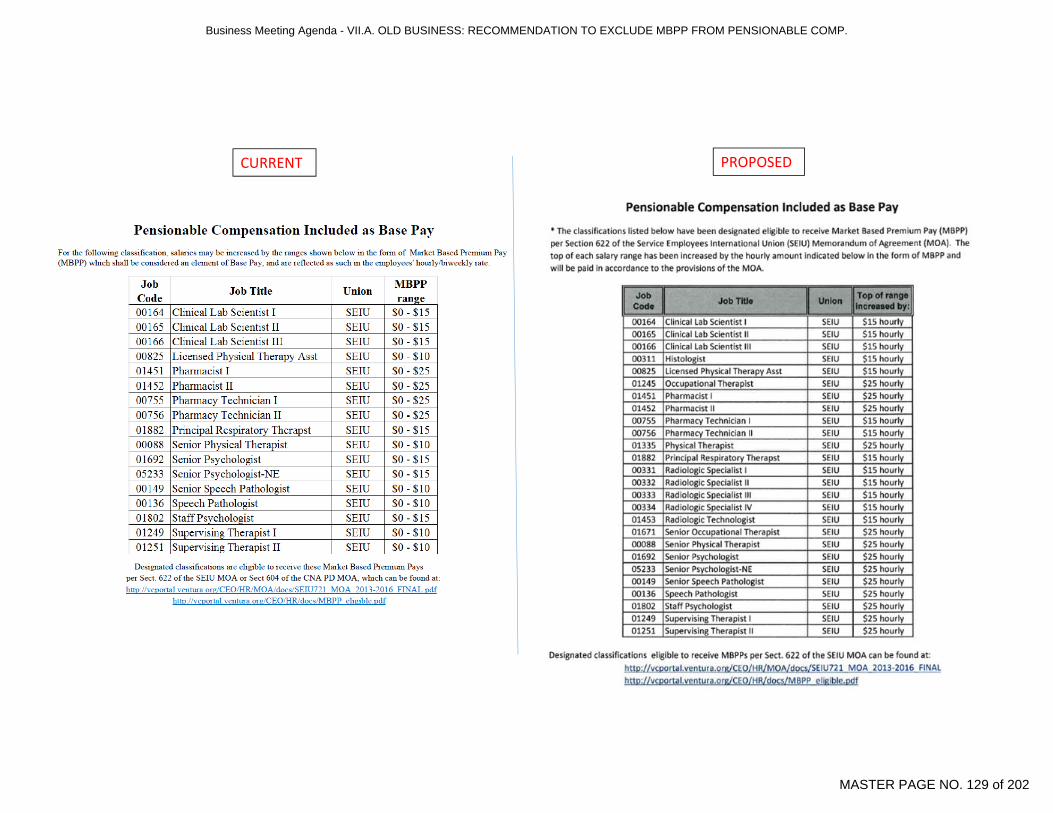

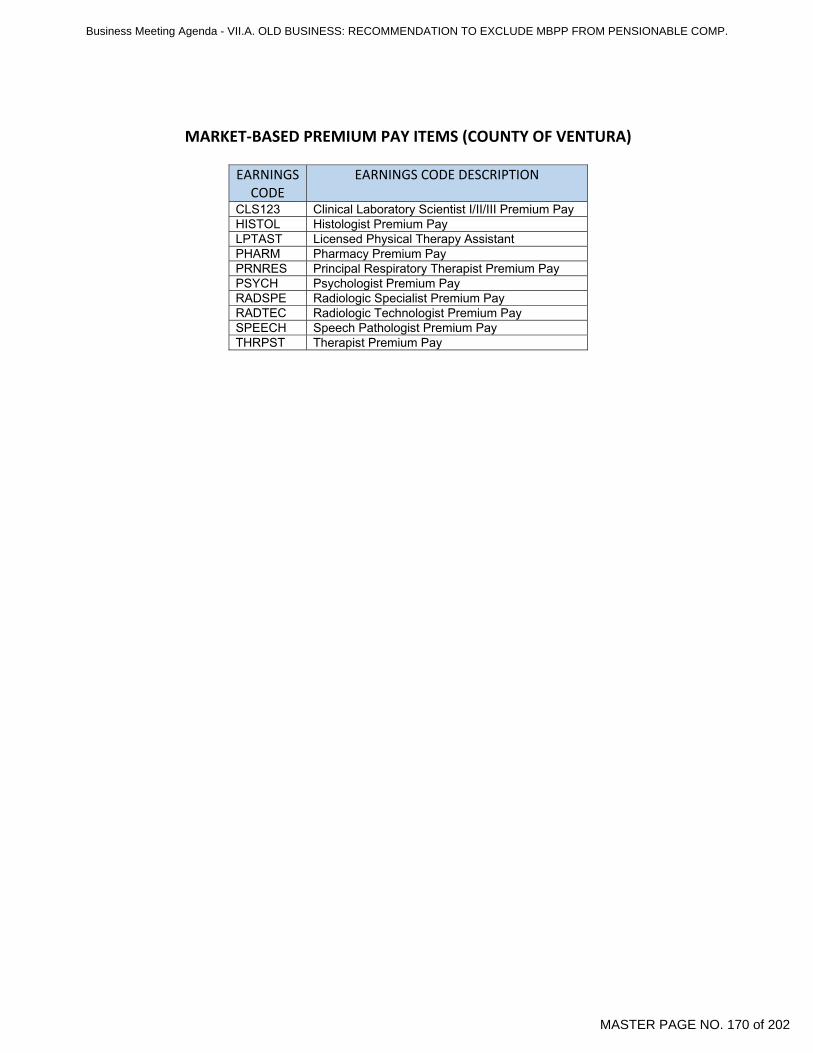

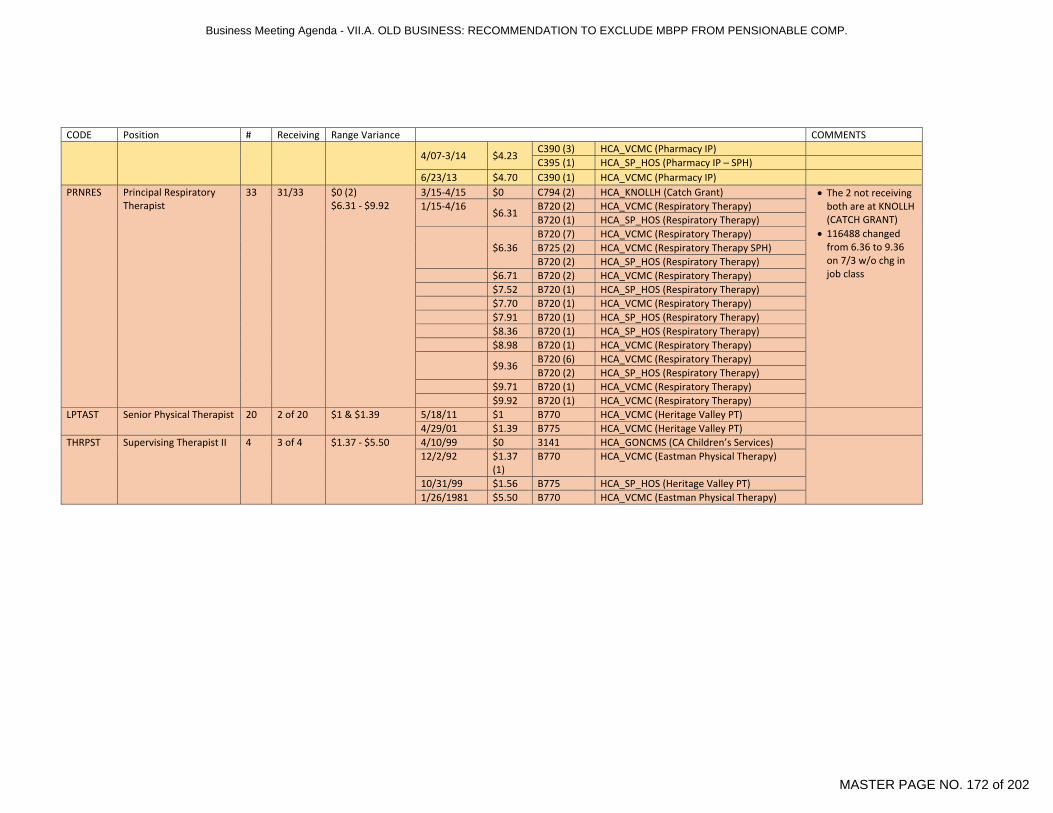

A. Determine Compliance of County’s Proposed Publicly-Available Pay Schedule for Market-Based Premium Pay (MBPP) and Determine Pensionability of MBPP under PEPRA. RECOMMENDED ACTION: EXCLUDE MBPP FROM PENSIONABLE COMPENSATION DUE TO DEFICIENCY IN MEETING PEPRA CRITERIA. Time: 10:30 a.m.

1. Staff Letter with Attachments. 105 – 181

Business Meeting Agenda - II. APPROVAL OF AGENDA & WELCOME OF NEWLY ELECTED GENERAL MEMBER

MASTER PAGE NO. 2 of 202

BOARD OF RETIREMENT JUNE 19, 2017 AGENDA BUSINESS MEETING PAGE 3

VII. OLD BUSINESS (continued)

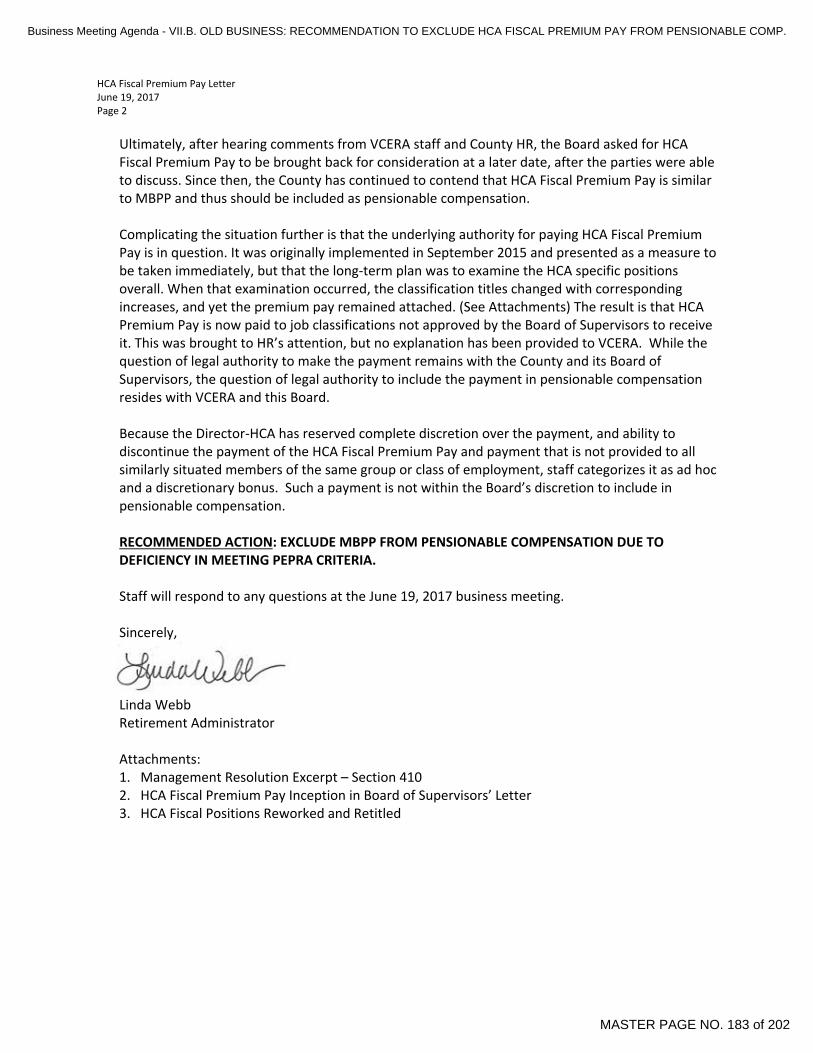

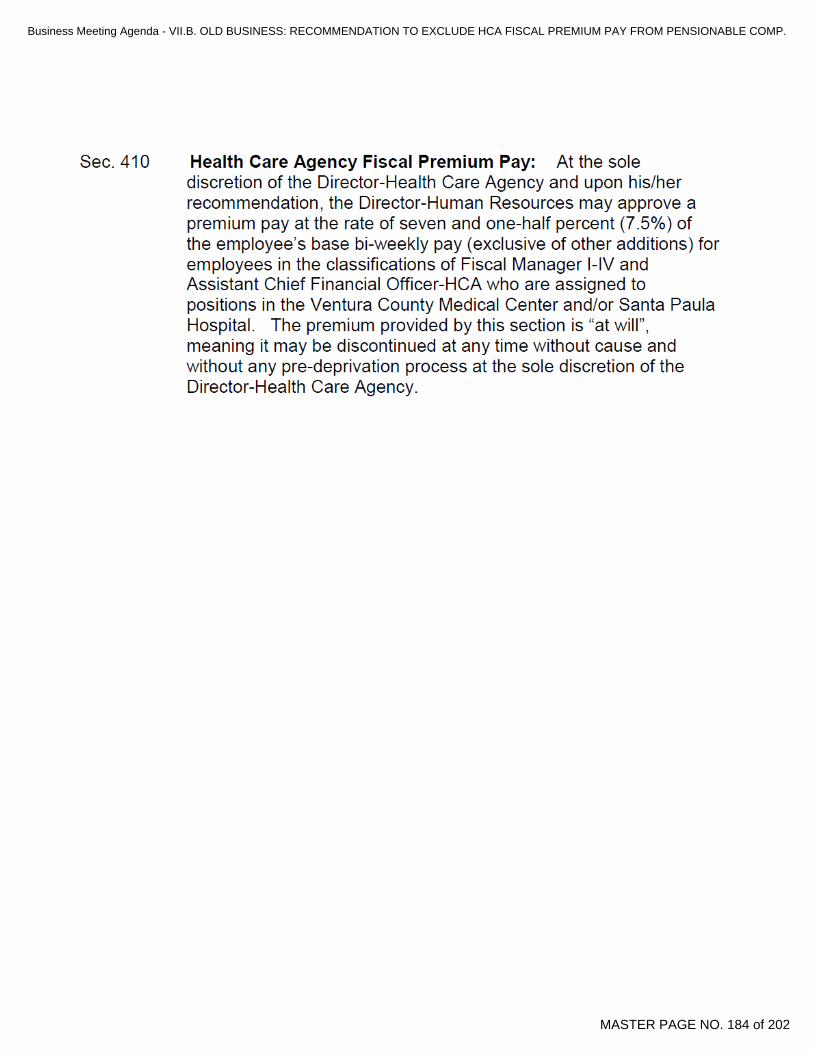

B. Determine Pensionability of HCA Fiscal Premium Pay. RECOMMENDED ACTION: EXCLUDE HCA FISCAL PREMIUM PAY FROM PENSIONABLE COMPENSATION DUE TO DEFICIENCY IN MEETING PEPRA CRITERIA.

1. Staff Letter with Attachments. 182 – 189

VIII. NEW BUSINESS

A. Renewal of Hearing Officer Contracts. RECOMMENDED ACTION: Approve.

1. Staff Letter.

190

2. Proposed Contract. 191 – 192

B. Annual Review of Education and Travel Policy.

1. Staff Letter. 193 – 194

2. Education and Travel Policy Proposed (Redline).

195 – 201

IX. INFORMATIONAL

A. Tortoise Exploring Alternatives with Mariner. 202

X. PUBLIC COMMENT

XI. STAFF COMMENT

XII. BOARD MEMBER COMMENT

XIII. ADJOURNMENT

Business Meeting Agenda - II. APPROVAL OF AGENDA & WELCOME OF NEWLY ELECTED GENERAL MEMBER

MASTER PAGE NO. 3 of 202

VENTURA COUNTY EMPLOYEES’ RETIREMENT ASSOCIATION

BOARD OF RETIREMENT

DISABILITY MEETING

JUNE 5, 2017

MINUTES

DIRECTORS PRESENT:

Tracy Towner, Chair, Alternate Safety Employee Member William W. Wilson, Vice Chair, Public Member Steven Hintz, Treasurer-Tax Collector1 Robert Bianchi, Public Member Craig Winter, General Employee Member Arthur E. Goulet, Retiree Member Will Hoag, Alternate Retiree Member Chris Johnston, Safety Employee Member Ed McCombs, Alternate Public Member

DIRECTORS ABSENT:

Peter C. Foy, Public Member Mike Sedell, Public Member

STAFF PRESENT:

Linda Webb, Retirement Administrator Lori Nemiroff, General Counsel Henry Solis, Chief Financial Officer Dan Gallagher, Chief Investment Officer Karen Scanlan, Accounting Manager I Shalini Nunna, Retirement Benefits Manager Donna Edwards, Retirement Benefits Specialist Stephanie Berkley, Retirement Benefits Specialist Chris Ayala, Program Assistant

PLACE: TIME:

Ventura County Employees' Retirement Association Second Floor Boardroom 1190 South Victoria Avenue Ventura, CA 93003 9:00 a.m.

ITEM:

1 Arrived at 9:04 a.m.

Business Meeting Agenda - III. APPROVAL OF MINUTES

MASTER PAGE NO. 4 of 202

BOARD OF RETIREMENT JUNE 5, 2017 MINUTES DISABILITY MEETING PAGE 2

I. CALL TO ORDER Chair Towner called the Disability Meeting of June 5, 2017, to order at 9:00 a.m.

II. APPROVAL OF AGENDA MOTION: Approve the agenda. Moved by Goulet, seconded by Bianchi. Vote: Motion carried Yes: Bianchi, Goulet, McCombs, Johnston, Wilson, Winter No: - Absent: Foy, Hintz, Sedell

III. APPROVAL OF MINUTES A. Disability & Business Meeting of April 17, 2017. Trustee Bianchi provided a correction to master page 4, where he was listed incorrectly as the Alternate Public Member. Trustee Goulet provided a correction to master page 9, noting that the Board returned to open session following the closed session item. After discussion by the Board, the following motion was made: MOTION: Approve with corrections. Moved by Bianchi, seconded by Goulet. Vote: Motion carried Yes: Bianchi, Goulet, McCombs, Johnston, Wilson, Winter No: - Absent: Foy, Hintz, Sedell

IV. RECEIVE AND FILE PENDING DISABILITY APPLICATION STATUS REPORT MOTION: Receive and File. Moved by Winter, seconded by McCombs. Vote: Motion carried Yes: Bianchi, Goulet, McCombs, Johnston, Wilson, Winter No: - Absent: Foy, Hintz, Sedell

Business Meeting Agenda - III. APPROVAL OF MINUTES

MASTER PAGE NO. 5 of 202

BOARD OF RETIREMENT JUNE 5, 2017 MINUTES DISABILITY MEETING PAGE 3

V. APPLICATIONS FOR DISABILITY RETIREMENT

A. Application Service-Connected Disability Retirement - Jerardo Gomez;

Case No. 16-035.

1. Chief Investment Officer Letter.

2. Application for Service-Connected Disability Retirement, dated

October 27, 2016.

3. Medical Analysis and Recommendation, including Supporting Medical

Documentation, submitted by County of Ventura, Risk Management, in

support of the Application for Service-Connected Disability Retirement,

dated May 22, 2017.

Trustee Hintz arrived at 9:04 a.m.

Paul Hilbun, was present on behalf of County of Ventura Risk Management. The applicant, Jerardo Gomez was not present. After discussion by the Board, the following motion was made: MOTION: Approve Application for Service-Connected Disability Retirement. Moved by Bianchi, seconded by Goulet. Vote: Motion carried Yes: Bianchi, Goulet, Hintz, McCombs, Johnston, Wilson, Winter No: - Absent: Foy, Sedell Both parties agreed to waive preparation of findings of fact and conclusions of law.

B. Application for Non-Service Connected Disability Retirement - Edward Z.

Hosseinipour; Case No. 16-023.

1. Application for Non-Service Connected Disability Retirement, dated

July 22, 2016.

2. Medical Analysis and Recommendation, including Supporting Medical

Documentation, submitted by County of Ventura, Risk Management, in

support of the Application for Non-Service Connected Disability Retirement,

April 3, 2017.

3. Hearing Notice, dated April 10, 2017.

Business Meeting Agenda - III. APPROVAL OF MINUTES

MASTER PAGE NO. 6 of 202

BOARD OF RETIREMENT JUNE 5, 2017 MINUTES DISABILITY MEETING PAGE 4

Paul Hilbun, was present on behalf of County of Ventura Risk Management. The applicant, Edward Z. Hosseinipour was also present. After discussion by the Board, the following motion was made: MOTION: Approve Application for Non-Service Connected Disability Retirement. Moved by Bianchi, seconded by Goulet. Vote: Motion carried Yes: Bianchi, Goulet, Hintz, McCombs, Johnston, Wilson, Winter No: - Absent: Foy, Sedell Both parties agreed to waive preparation of findings of fact and conclusions of law.

VI. OLD BUSINESS

A. Reaffirm Board Action for Merit Increases for General Counsel and Chief Investment Officer.

1. Staff Letter

a. Consideration and Possible Approval of Merit Increase for General Counsel.

Ms. Webb said that at the last meeting the Board authorized merit increases for the General Counsel and Chief Investment Officer, but the agenda had not specifically listed potential increases, which must be done in open session. Therefore, the item was on the agenda so the increases could be formalized and subsequently processed. After discussion by the Board, the following motion was made: MOTION: Approve a 4.76% Merit Increase for the General Counsel. Moved by Goulet, seconded by McCombs. Vote: Motion carried Yes: Bianchi, Goulet, Hintz, McCombs, Johnston, Wilson, Winter No: - Absent: Foy, Sedell

b. Consideration and Possible Approval of Merit Increase for Chief Investment Officer.

After discussion by the Board, the following motion was made:

Business Meeting Agenda - III. APPROVAL OF MINUTES

MASTER PAGE NO. 7 of 202

BOARD OF RETIREMENT JUNE 5, 2017 MINUTES DISABILITY MEETING PAGE 5

MOTION: Approve a 5% Merit Increase for the Chief Investment Officer. Moved by Hintz, seconded by Winter. Vote: Motion carried Yes: Bianchi, Goulet, Hintz, McCombs, Johnston, Wilson, Winter No: - Absent: Foy, Sedell Chair Towner requested a break at 10:00 a.m. Chair Towner left at 10:00 a.m. Vice Chair Wilson acted as Chair in his absence. The Board returned from break at 10:10 a.m.

VII. NEW BUSINESS

A. Review and Adoption of Proposed Fiscal Year 2017/18 Budget. RECOMMENDED ACTION: Approve. Materials to be provided.

1. Staff Letter.

Ms. Webb and Mr. Solis presented the FY 2017-18 proposed budget. Trustee Goulet expressed concern whether certain proposed expenditures included in the newly created Investment and Other Expenditures budgets were categorized correctly and should be excluded from the administrative spending cap (CAP). More specifically, Trustee Goulet believed that depreciation/amortization should not be excluded from the CAP and requested legal justification. Mr. Solis replied that the budgeted amount for depreciation/amortization represented the allocation of the accumulated costs associated with the recently completed pension administraton system. Mr. Solis further explained that the expenditures in question were excludible from the CAP as they were capitalized during the implementation period and would continue to be excluded from the CAP, as they are amoritized. He also stated that VCERA was following GASB standards specifically related to the treatment of intangible assets and had conferred with counsel regarding the treatment of capital expenditures and whether they should be included or excluded from the CAP. Trustee Goulet stated that VCERA follows the County Employees’ Retirement Law (CERL) and not GASB and did not believe VCERA had to follow GASB. Mr. Solis replied that he would research further and report back. After discussion by the Board, the following motion was made: MOTION: Approve. Moved by Bianchi, seconded by Goulet.

Business Meeting Agenda - III. APPROVAL OF MINUTES

MASTER PAGE NO. 8 of 202

BOARD OF RETIREMENT JUNE 5, 2017 MINUTES DISABILITY MEETING PAGE 6

Vote: Motion carried Yes: Bianchi, Goulet, Hintz, McCombs, Johnston, Wilson, Winter No: - Absent: Foy, Sedell

B. Recommendation to Engage Gabriel, Roeder Smith & Company for Actuarial Audit Services. RECOMMENDED ACTION: Approve.

Ms. Webb reported that the members of the ad hoc committee had reviewed the actuarial audit RFP submissions and recommended engaging Gabriel, Roeder Smith & Company. After discussion by the Board, the following motion was made: MOTION: Approve. Moved by Bianchi, seconded by Goulet. Vote: Motion carried Yes: Bianchi, Goulet, Hintz, McCombs, Johnston, Wilson, Winter No: - Absent: Foy, Sedell

C. Recommendation to Support AB 526 from Trustee Goulet.

1. Letter from Trustee Goulet.

2. Proposed Support Draft.

Chair Towner returned at 10:40 a.m., and acted as Chair for the remainder of the meeting. Trustee Goulet said that the drafted letter indicated that AB 526 is similar to AB 1853 from last session, which would have given CERL systems the ability to establish district status. He said AB 526 would only apply to Sacramento County, but he believed it was important to publicly support the legislation with the proposed draft letter. After discussion by the Board, the following motion was made: MOTION: Approve Support for AB 526. Moved by Goulet, seconded by Johnston. Vote: Motion carried Yes: Bianchi, Goulet, Hintz, McCombs, Johnston, Wilson, Winter No: - Absent: Foy, Sedell

Business Meeting Agenda - III. APPROVAL OF MINUTES

MASTER PAGE NO. 9 of 202

BOARD OF RETIREMENT JUNE 5, 2017 MINUTES DISABILITY MEETING PAGE 7

D. Consideration and Possible Approval of Expedited Process for Retirement Administrator Evaluation.

1. Letter from Will Hoag, Chair, Personnel Review Committee.

Trustee Hoag informed the Board that it was discovered that the Retirement Administrator’s evaluation and possible merit increase had been due in January 2017. Trustee Hoag said that the Board would need to go into a closed session to discuss and then return to an open session to consider a merit increase. General Counsel reminded the Board that they would first need to approve the proposed expedited process approval for the Retirement Administrator and waive the formality of the established evaluation policy before convening into closed session. After discussion by the Board, the following motion was made: MOTION: Approve an Expedited Evaluation Process for the Retirement Administrator and Waive the Formal Evaluation Process. Moved by Hintz, seconded by Bianchi. Vote: Motion carried Yes: Bianchi, Goulet, Hintz, McCombs, Johnston, Wilson, Winter No: - Absent: Foy, Sedell The Board Adjourned to Closed Session at 10:42 a.m.

E. Consideration and Possible Approval of Merit Increase for Linda Webb, Retirement Administrator. This item to be considered following “VIII. Closed Session.”

VIII. CLOSED SESSION

A. PUBLIC EMPLOYEE PERFORMANCE EVALUATION Title: Retirement Administrator (Government Code section 54957(b)(1))

Upon returning to open session at 10:49 a.m., Chair Towner stated that the Board would like to thank Ms. Webb for her outstanding job performance over the past 2 and a half years. After discussion by the Board, the following motion was made: MOTION: Approve a 7.83% Merit Increase for the Retirement Administrator. Moved by Bianchi, seconded by Goulet. Vote: Motion carried

Business Meeting Agenda - III. APPROVAL OF MINUTES

MASTER PAGE NO. 10 of 202

BOARD OF RETIREMENT JUNE 5, 2017 MINUTES DISABILITY MEETING PAGE 8

Yes: Bianchi, Goulet, Hintz, McCombs, Johnston, Wilson, Winter No: - Absent: Foy, Sedell

IX. INFORMATIONAL

A. 2017 Abbott Capital Private Equity Client Conference & Annual Meeting.

B. SACRS UC Berkeley Program.

C. Consent to Assignment of Agreement for REAMS.

D. Nossaman Public Pensions Fiduciaries Forum 2017.

X. PUBLIC COMMENT

None.

XI. STAFF COMMENT

Mr. Gallagher informed the Board that the $30 million allocation to Harbourvest’s Co-Investment Fund IV had been accepted in time for the May 31 fund closing. Mr. Gallagher also said that contract negotiations with Abbott Capital were expected to be completed by the end of the week.

XII. BOARD MEMBER COMMENT

None.

XIII.

ADJOURNMENT The meeting was adjourned at 10:55 a.m.

Respectfully submitted,

___________________________________________ LINDA WEBB, Retirement Administrator

Approved,

__________________________ TRACY TOWNER, Chairman

Business Meeting Agenda - III. APPROVAL OF MINUTES

MASTER PAGE NO. 11 of 202

DATE OF TOTAL OTHER EFFECTIVE

FIRST NAME LAST NAME G/S MEMBERSHIP SERVICE SERVICE DEPARTMENT DATE

Judith E. Allen G 2/11/2007 10.13 Public Works Agency 4/1/2017

Elia Arciniega G 2/4/2002 15.17 Human Services Agency 4/1/2017

Martha Barragan G 1/20/1991 21.90 Human Services Agency 4/9/2017

Valerie Barraza G 12/13/1999 22.38 D=5.0 Auditor-Controller 4/22/2017

Jaime C. Bautista G 3/17/2001 16.08 General Services Agency 4/22/2017

Ross Bonfiglio S 7/25/1982 34.74 Sheriff's Department 3/31/2017

Reem Dajani-Stratton G 9/16/1979 37.13 B=0.1154 Resource Management Agency 4/29/2017

Daniel Farmer S 8/22/2010 5.52 Sheriff's Department 3/17/2017

Gregory Ford G 12/25/1988 28.33 Health Care Agency 4/29/2017

Michael Gram G 6/18/2006 10.07 Health Care Agency 4/29/2017

Olivia Herrera G 2/25/2007 10.15 General Services Agency 4/15/2017

Richard Herrera G 11/16/1992 24.46 * C=5.98 Public Works Agency 4/22/2017

Armand Horgan G 3/11/2007 10.06 Human Services Agency 4/1/2017

Dennis Kanthack G 12/20/1992 23.09 Public Works Agency 3/30/2017

Christina L. Kiefer G 7/30/1995 13.44 * B=0.1151 Fire Protection District 3/31/2017

C=8.33

(deferred)

Carol Kilbey G 10/10/2004 5.87 Health Care Agency 12/10/2012

Robert MacInnes S 8/10/1986 10.22 District Attorney 4/1/2017

Bart Matthews S 3/30/1980 37.01 Fire Protection District 3/26/2017

Linda Mora G 9/21/1986 30.40 A=0.0962 Clerk and Recorder 4/1/2017

Joseph Munoz G 11/5/1995 22.56 B=1.0659 General Services Agency 4/27/2017

Molly M. Pearson G 3/26/1995 6.11 B=0.1123 Air Pollution Control District 4/24/2017

(deferred)

John K. Pena G 7/17/2005 11.56 Public Works Agency 4/10/2017

Scott H. Quady G 8/20/2001 26.30 Regional Sanitation District 4/8/2017

Maria Rangel G 11/2/1986 30.80 B=0.2842 Sheriff's Department 4/28/2017

* C=5.30

Shirley J. Smith G 2/6/2000 13.50 Health Care Agency 5/9/2017

(deferred)

David S. Swenson G 2/25/2007 7.05 A=0.4568 Health Care Agency 4/22/2017

Brian Trushinski G 12/8/2003 13.14 * C=1.6760 Public Works Agency 5/1/2017

(deferred)

Joanne Y. Urasaki G 7/31/2000 16.65 Information Services Department 4/8/2017

Joseph P. Villasana G 8/17/1980 25.73 B=0.2838 Public Defender 4/6/2017

Deborah L. Weigand G 1/8/2006 10.84 Human Services Agency 3/31/2017

Christine Clark G 02/04/2012 5.24 C=10.3075 Health Care Agency 04/27/2017

Amber B. Madden G 10/19/2008 7.38 Health Care Agency 05/20/2017

Joyce L'Heureux G 11/02/2008 8.49 Health Care Agency 05/20/2017

Kimberly D. Prendergast G 06/01/2008 10.14 D=1.8351 Health Care Agency 04/29/2017

Anna Adams

Patsy E. Hulsey

Joanna I. Lange

Joseph F. Marnick

Raul R. Ramirez

Freddie Salinas

* = Member Establishing Reciprocity

A = Previous Membership

B = Other County Service (eg Extra Help)

C = Reciprocal Service

D = Public Service

SURVIVORS' CONTINUANCES:

VENTURA COUNTY EMPLOYEES' RETIREMENT ASSOCIATION

REPORT OF REGULAR AND DEFERRED RETIREMENTS AND SURVIVORS CONTINUANCES

MAY 2017

REGULAR RETIREMENTS:

DEFERRED RETIREMENTS:

Business Meeting Agenda - IV. CONSENT AGENDA

MASTER PAGE NO. 12 of 202

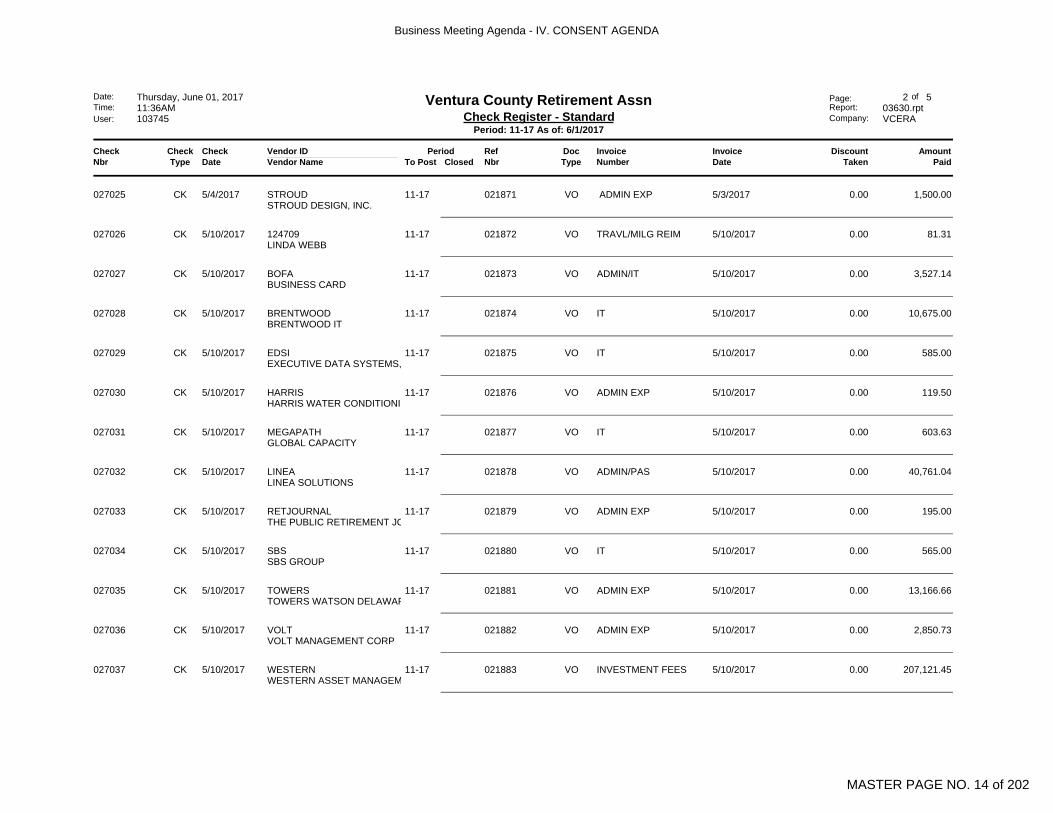

ClosedInvoice Discount AmountDocRefCheck Check InvoiceCheck

Nbr Type DateVendor IDVendor Name Nbr Type Date Taken PaidNumberTo Post

Date:Time:User:

Thursday, June 01, 201711:36AM103745

Page:Report:Company:

1 of 503630.rptVCERA

Ventura County Retirement AssnCheck Register - Standard

Period: 11-17 As of: 6/1/2017

Period

Company: VCERAAcct / Sub: 1002 00

122261VCGINA SIMONELLI

5/3/2017 11-17027012 11-17

108530VCCHRIS WEBB

5/3/2017 11-17027013 11-17

BLACKROCKVCBLACKROCK INSTL TRUST C

5/3/2017 11-17027014 11-17

CUSTOMVCCUSTOM PRINTING

5/3/2017 11-17027015 11-17

SACRSVCSACRS

5/3/2017 11-17027016 11-17

SPRUCEVCSPRUCEGROVE INVESTMEN

5/3/2017 11-17027017 11-17

STROUDVCSTROUD DESIGN, INC.

5/3/2017 11-17027018 11-17

122261 57.800.00TRAVL/MILG REIM 5/3/2017CKGINA SIMONELLI

5/4/2017 VO027019 02186511-17

108530 76.990.00TRAVL/MIL REIMB 5/3/2017CKCHRIS WEBB

5/4/2017 VO027020 02186611-17

BLACKROCK 245,805.210.00INVESTMENT FEES 5/3/2017CKBLACKROCK INSTL TRUST C

5/4/2017 VO027021 02186711-17

CUSTOM 1,179.310.00ADMIN EXP 5/3/2017CKCUSTOM PRINTING

5/4/2017 VO027022 02186811-17

SACRS 1,080.000.00ADMIN EXP 5/3/2017CKSACRS

5/4/2017 VO027023 02186911-17

SPRUCE 61,253.870.00INVESTMENT FEES 5/3/2017CKSPRUCEGROVE INVESTMEN

5/4/2017 VO027024 02187011-17

VOIDED CHECKS

Business Meeting Agenda - IV. CONSENT AGENDA

MASTER PAGE NO. 13 of 202

ClosedInvoice Discount AmountDocRefCheck Check InvoiceCheck

Nbr Type DateVendor IDVendor Name Nbr Type Date Taken PaidNumberTo Post

Date:Time:User:

Thursday, June 01, 201711:36AM103745

Page:Report:Company:

2 of 503630.rptVCERA

Ventura County Retirement AssnCheck Register - Standard

Period: 11-17 As of: 6/1/2017

Period

STROUD 1,500.000.00 ADMIN EXP 5/3/2017CKSTROUD DESIGN, INC.

5/4/2017 VO027025 02187111-17

124709 81.310.00TRAVL/MILG REIM 5/10/2017CKLINDA WEBB

5/10/2017 VO027026 02187211-17

BOFA 3,527.140.00ADMIN/IT 5/10/2017CKBUSINESS CARD

5/10/2017 VO027027 02187311-17

BRENTWOOD 10,675.000.00IT 5/10/2017CKBRENTWOOD IT

5/10/2017 VO027028 02187411-17

EDSI 585.000.00IT 5/10/2017CKEXECUTIVE DATA SYSTEMS,

5/10/2017 VO027029 02187511-17

HARRIS 119.500.00ADMIN EXP 5/10/2017CKHARRIS WATER CONDITIONIN

5/10/2017 VO027030 02187611-17

MEGAPATH 603.630.00IT 5/10/2017CKGLOBAL CAPACITY

5/10/2017 VO027031 02187711-17

LINEA 40,761.040.00ADMIN/PAS 5/10/2017CKLINEA SOLUTIONS

5/10/2017 VO027032 02187811-17

RETJOURNAL 195.000.00ADMIN EXP 5/10/2017CKTHE PUBLIC RETIREMENT JO

5/10/2017 VO027033 02187911-17

SBS 565.000.00IT 5/10/2017CKSBS GROUP

5/10/2017 VO027034 02188011-17

TOWERS 13,166.660.00ADMIN EXP 5/10/2017CKTOWERS WATSON DELAWAR

5/10/2017 VO027035 02188111-17

VOLT 2,850.730.00ADMIN EXP 5/10/2017CKVOLT MANAGEMENT CORP

5/10/2017 VO027036 02188211-17

WESTERN 207,121.450.00INVESTMENT FEES 5/10/2017CKWESTERN ASSET MANAGEM

5/10/2017 VO027037 02188311-17

Business Meeting Agenda - IV. CONSENT AGENDA

MASTER PAGE NO. 14 of 202

ClosedInvoice Discount AmountDocRefCheck Check InvoiceCheck

Nbr Type DateVendor IDVendor Name Nbr Type Date Taken PaidNumberTo Post

Date:Time:User:

Thursday, June 01, 201711:36AM103745

Page:Report:Company:

3 of 503630.rptVCERA

Ventura County Retirement AssnCheck Register - Standard

Period: 11-17 As of: 6/1/2017

Period

CLIFTON 40,067.000.00INVESTMENT FEES 5/10/2017CKPARAMETRIC PORTFOLIO AS

5/10/2017 VO027038 02188411-17

ADP 2,876.280.00ADMIN EXP 5/18/2017CKADP, LLC

5/18/2017 VO027039 02188511-17

ACCESS 334.280.00ADMIN EXP 5/18/2017CKACCESS INFORMATION MANA

5/18/2017 VO027040 02188611-17

BARNEY 315.000.00ADMIN EXP 5/18/2017CKA.B.U. COURT REPORTING, IN

5/18/2017 VO027041 02188711-17

AT&T 346.180.00IT 5/18/2017CKAT&T MOBILITY

5/18/2017 VO027042 02188811-17

REUTERS 357.000.00IT 5/18/2017CKTHOMSON REUTERS- WEST

5/18/2017 VO027043 02188911-17

SBS 3,125.050.00IT 5/18/2017CKSBS GROUP

5/18/2017 VO027044 02189011-17

SHRED-IT 145.860.00ADMIN EXP 5/18/2017CKSHRED-IT USA

5/18/2017 VO027045 02189111-17

TWC 294.990.00IT 5/18/2017CKTIME WARNER CABLE

5/18/2017 VO027046 02189211-17

102661 1,123.360.00TRAVEL REIMB 5/24/2017CKLORI NEMIROFF

5/24/2017 VO027047 02189411-17

104238 1,058.560.00TRAVEL REIMB 5/24/2017CKTRACY TOWNER

5/24/2017 VO027048 02189511-17

124709 1,541.990.00TRAVEL REIMB 5/24/2017CKLINDA WEBB

5/24/2017 VO027049 02189611-17

124968 1,487.060.00TRAVEL REIMB 5/24/2017CKDAN GALLAGHER

5/24/2017 VO027050 02189711-17

990002 1,328.120.00TRAVEL REIMB 5/24/2017CKARTHUR E. GOULET

5/24/2017 VO027051 02189811-17

Business Meeting Agenda - IV. CONSENT AGENDA

MASTER PAGE NO. 15 of 202

ClosedInvoice Discount AmountDocRefCheck Check InvoiceCheck

Nbr Type DateVendor IDVendor Name Nbr Type Date Taken PaidNumberTo Post

Date:Time:User:

Thursday, June 01, 201711:36AM103745

Page:Report:Company:

4 of 503630.rptVCERA

Ventura County Retirement AssnCheck Register - Standard

Period: 11-17 As of: 6/1/2017

Period

ADP 2,892.110.00ADMIN EXP 5/24/2017CKADP, LLC

5/24/2017 VO027052 02189911-17

MF 16,989.750.00ADMIN EXP 5/24/2017CKM.F. DAILY CORPORATION

5/24/2017 VO027053 02190011-17

PRUDENTIAL 136,763.210.00INVESTMENT FEES 5/24/2017CKPRUDENTIAL INSURANCE

5/24/2017 VO027054 02190111-17

SBS 3,587.500.00IT 5/24/2017CKSBS GROUP

5/24/2017 VO027055 02190211-17

SEGAL 3,554.000.00ACTUARY FEES 5/24/2017CKSEGAL CONSULTING

5/24/2017 VO027056 02190311-17

VITECH 88,990.000.00PAS 5/24/2017CKVITECH SYSTEMS GROUP, IN

5/24/2017 VO027057 02190411-17

VOLT 2,150.130.00ADMIN EXP 5/24/2017CKVOLT MANAGEMENT CORP

5/24/2017 VO027058 02190511-17

107666 12.250.00ADMIN EXP 5/31/2017CKSHALINI NUNNA

5/31/2017 VO027059 02190611-17

990004 640.860.00TRAVEL REIMB 5/31/2017CKWILL HOAG

5/31/2017 VO027060 02190711-17

AYALA 875.000.00ADMIN EXP 5/31/2017CKIRENE P. AYALA

5/31/2017 VO027061 02190811-17

FEDEX 38.280.00ADMIN EXP 5/31/2017CKFEDEX

5/31/2017 VO027062 02191011-17

NOSSAMAN 414.400.00LEGAL FEES 5/31/2017CKNOSSAMAN LLP

5/31/2017 VO027063 02191111-17

CDW GOVERN 215.500.00IT 5/31/2017CKCDW GOVERNMENT

5/31/2017 VO027064 02191211-17

Business Meeting Agenda - IV. CONSENT AGENDA

MASTER PAGE NO. 16 of 202

ClosedInvoice Discount AmountDocRefCheck Check InvoiceCheck

Nbr Type DateVendor IDVendor Name Nbr Type Date Taken PaidNumberTo Post

Date:Time:User:

Thursday, June 01, 201711:36AM103745

Page:Report:Company:

5 of 503630.rptVCERA

Ventura County Retirement AssnCheck Register - Standard

Period: 11-17 As of: 6/1/2017

Period

NOVANIS 16,730.000.00PAS 5/31/2017CKNOVANIS

5/31/2017 VO027065 02191311-17

CORPORATE 1,714.890.00ADMIN EXP 5/31/2017CKSTAPLES ADVANTAGE

5/31/2017 VO027066 02191411-17

VITECH 93,896.740.00PAS 5/31/2017CKVITECH SYSTEMS GROUP, IN

5/31/2017 VO027067 02191511-17

Check Count: 56 Acct Sub Total: 1,015,069.99

Amount PaidCountCheck Type1,015,069.9949Regular

0.000Hand

0.007Void

0.000Stub

Zero 0.000Mask 0 0.00Total: 56 1,015,069.99

Electronic Payment 0 0.00

Company Total 1,015,069.99Company Disc Total 0.00

Business Meeting Agenda - IV. CONSENT AGENDA

MASTER PAGE NO. 17 of 202

VENTURA COUNTY EMPLOYEES' RETIREMENT ASSOCIATION BUDGET SUMMARY FISCAL YEAR 2016-2017

May 2017- 91.67% of Fiscal Year Expended

Adopted AdjustedEXPENDITURE DESCRIPTIONS 2016/2017 2016/2017 Year to Date Available Percent

Budget Budget May-17 Expended Balance ExpendedSalaries & Benefits: Salaries 2,370,800.00$ 2,512,612.00$ 201,978.07$ 2,150,264.13$ 362,347.87$ 85.58% Extra-Help 192,400.00 192,400.00 17,200.86 140,132.60 52,267.40 72.83% Overtime 3,000.00 3,000.00 0.00 31.47 2,968.53 1.05% Supplemental Payments 74,400.00 75,322.00 3,341.50 44,024.52 31,297.48 58.45% Vacation Redemption 131,300.00 191,300.00 7,578.04 168,246.99 23,053.01 87.95% Retirement Contributions 432,100.00 437,235.00 37,988.38 380,744.78 56,490.22 87.08% OASDI Contributions 141,800.00 143,515.00 13,025.53 121,970.73 21,544.27 84.99% FICA-Medicare 37,800.00 38,202.00 3,046.35 33,767.67 4,434.33 88.39% Retiree Health Benefit 4,000.00 4,000.00 0.00 3,970.75 29.25 99.27% Group Health Insurance 194,300.00 197,212.00 17,350.00 180,495.47 16,716.53 91.52% Life Insurance/Mgmt 1,100.00 1,125.00 86.50 971.34 153.66 86.34% Unemployment Insurance 2,400.00 2,427.00 201.95 2,140.81 286.19 88.21% Management Disability Insurance 18,400.00 18,609.00 1,326.12 14,539.80 4,069.20 78.13% Worker' Compensation Insurance 19,900.00 20,138.00 1,619.30 17,783.43 2,354.57 88.31% 401K Plan Contribution 48,600.00 49,403.00 4,685.90 49,737.13 (334.13) 100.68% Transfers In 135,500.00 135,500.00 0.00 23,668.92 111,831.08 17.47% Transfers Out (135,500.00) (135,500.00) 0.00 (23,668.92) (111,831.08) 17.47%

Total Salaries & Benefits 3,672,300.00$ 3,886,500.00$ 309,428.50$ 3,308,821.62$ 577,678.38$ 85.14%

Services & Supplies: Telecommunication Services - ISF 35,400.00$ 35,400.00$ 3,144.75$ 32,840.90$ 2,559.10$ 92.77% General Insurance - ISF 13,100.00 13,100.00 0.00 13,079.00 21.00 99.84% Office Equipment Maintenance 2,000.00 2,000.00 0.00 672.00 1,328.00 33.60% Membership and Dues 14,700.00 14,700.00 0.00 13,437.00 1,263.00 91.41% Education Allowance 8,000.00 8,000.00 0.00 2,000.00 6,000.00 25.00% Cost Allocation Charges 89,500.00 89,500.00 0.00 89,508.00 (8.00) 100.01% Printing Services - Not ISF 12,000.00 12,000.00 1,179.31 3,515.84 8,484.16 29.30% Books & Publications 3,000.00 3,000.00 195.00 1,302.52 1,697.48 43.42% Office Supplies 20,000.00 20,000.00 1,757.74 14,531.67 5,468.33 72.66% Postage & Express 60,000.00 60,000.00 50.53 51,078.16 8,921.84 85.13% Printing Charges - ISF 18,000.00 18,000.00 0.00 4,157.60 13,842.40 23.10% Copy Machine Services - ISF 4,500.00 4,500.00 684.24 1,831.44 2,668.56 40.70% Board Member Fees 13,300.00 13,300.00 1,200.00 10,200.00 3,100.00 76.69% Professional Services 1,292,100.00 938,200.00 44,622.49 657,182.67 281,017.33 70.05% Storage Charges 4,200.00 4,200.00 334.28 3,882.19 317.81 92.43% Equipment 6,000.00 6,000.00 0.00 15,331.78 (9,331.78) 255.53% Office Lease Payments 205,000.00 205,000.00 16,989.75 186,827.06 18,172.94 91.14% Private Vehicle Mileage 12,500.00 12,500.00 1,768.47 11,659.10 840.90 93.27% Conference, Seminar and Travel 138,400.00 138,400.00 10,982.96 88,482.89 49,917.11 63.93% Furniture 15,000.00 15,000.00 0.00 1,658.76 13,341.24 11.06% Facilities Charges 13,300.00 13,300.00 220.00 3,100.00 10,200.00 23.31% Judgement & Damages 0.00 0.00 0.00 0.00 0.00 #DIV/0! Transfers In 20,000.00 20,000.00 0.00 2,501.18 17,498.82 12.51% Transfers Out (20,000.00) (20,000.00) 0.00 (2,501.18) (17,498.82) 12.51%

Total Services & Supplies 1,980,000.00$ 1,626,100.00$ 83,129.52$ 1,206,278.58$ 419,821.42$ 74.18%

Total Sal, Ben, Serv & Supp 5,652,300.00$ 5,512,600.00$ 392,558.02$ 4,515,100.20$ 997,499.80$ 81.91%

Technology: Computer Hardware 45,000.00$ 65,000.00$ 514.28$ 5,011.48 59,988.52$ 7.71% Computer Software 216,000.00 216,000.00 4,849.35 76,123.12 139,876.88 35.24% Systems & Application Support 449,000.00 474,000.00 11,810.48 280,874.32 193,125.68 59.26% Pension Administration System 353,000.00 937,100.00 228,177.78 931,115.65 5,984.35 99.36%

Total Technology 1,063,000.00$ 1,692,100.00$ 245,351.89$ 1,293,124.57$ 398,975.43$ 76.42%

Contingency 786,000.00$ 296,600.00$ -$ -$ 296,600.00$ 0.00%

Total Current Year 7,501,300.00$ 7,501,300.00$ 637,909.91$ 5,808,224.77$ 1,693,075.23$ 77.43%

Business Meeting Agenda - IV. CONSENT AGENDA

MASTER PAGE NO. 18 of 202

ACCRUED INTEREST AND DIVIDENDS 4,051,774SECURITY SALES 9,427,719MISCELLANEOUS 28,455

DOMESTIC EQUITY SECURITIES 129,435,938DOMESTIC EQUITY INDEX FUNDS 1,376,862,960INTERNATIONAL EQUITY SECURITIES 399,662,361INTERNATIONAL EQUITY INDEX FUNDS 377,478,397GLOBAL EQUITY 523,340,508PRIVATE EQUITY 185,979,327DOMESTIC FIXED INCOME - CORE PLUS 719,391,179DOMESTIC FIXED INCOME - U.S. INDEX 218,739,475REAL ESTATE 386,654,349ALTERNATIVES 414,844,987CASH OVERLAY - PARAMETRIC (9,963)

SECURITY PURCHASES PAYABLE 19,342,254ACCOUNTS PAYABLE 584,443TAX WITHHOLDING PAYABLE 3,076,580PREPAID CONTRIBUTIONS 10,465,564

Business Meeting Agenda - IV. CONSENT AGENDA

MASTER PAGE NO. 19 of 202

EMPLOYER $153,450,170EMPLOYEE 58,411,036

NET APPRECIATION (DEPRECIATION) IN FAIR VALUE OF INVESTMENTS 471,480,133INTEREST INCOME 11,840,939DIVIDEND INCOME 11,329,004REAL ESTATE OPERATING INCOME, NET 12,494,260SECURITY LENDING INCOME 463,695

MANAGEMENT & CUSTODIAL FEES 11,033,255SECURITIES LENDING BORROWER REBATES 229,778SECURITIES LENDING MANAGEMENT FEES 73,404

BENEFIT PAYMENTS 211,657,027MEMBER REFUNDS 4,262,466ADMINISTRATIVE EXPENSES 5,158,881

Business Meeting Agenda - IV. CONSENT AGENDA

MASTER PAGE NO. 20 of 202

WESTERN ASSET INDEX PLUS $129,435,938 $42,632,159

BLACKROCK - US EQUITY MARKET 1,322,004,711 0BLACKROCK - EXTENDED EQUITY 54,858,249 0

SPRUCEGROVE 205,143,030 0HEXAVEST 86,359,284 0WALTER SCOTT 108,160,047 0

BLACKROCK - ACWIXUS 377,478,397 0

BLACKROCK - GLOBAL INDEX 523,340,508 0

ADAMS STREET 112,481,828 0PANTHEON 22,922,569 0HARBOURVEST 50,077,303 0DRIVE CAPITAL 497,627 0

LOOMIS SAYLES AND COMPANY 76,150,939 2,426,024LOOMIS SAYLES - ALPHA 45,074,515 0REAMS 305,130,070 475WESTERN ASSET MANAGEMENT 293,035,655 5,114,694

BLACKROCK - US DEBT INDEX 218,739,475 0

PRUDENTIAL REAL ESTATE 136,969,399 2,218RREEF 180,164 0UBS REALTY 249,504,786 0

Business Meeting Agenda - IV. CONSENT AGENDA

MASTER PAGE NO. 21 of 202

BRIDGEWATER 289,772,725 0TORTOISE (MLP's) 125,072,262 2,927,109

Business Meeting Agenda - IV. CONSENT AGENDA

MASTER PAGE NO. 22 of 202

BLACKROCK - US EQUITY $194,580BLACKROCK - EXTENDED EQUITY 15,415WESTERN ASSET INDEX PLUS 219,698

BLACKROCK - ACWIXUS 245,258SPRUCEGROVE 461,883HEXAVEST 279,030WALTER SCOTT 648,328

GRANTHAM MAYO VAN OTTERLOO (GMO) 297,518BLACKROCK - GLOBAL INDEX 121,979

ADAMS STREET 1,308,365DRIVE CAPITAL 175,000HARBOURVEST 713,510PANTHEON 450,035

BLACKROCK - US DEBT INDEX 90,630LOOMIS, SAYLES AND COMPANY 227,003LOOMIS ALPHA 132,104REAMS ASSET MANAGEMENT 396,320WESTERN ASSET MANAGEMENT 393,559

PRUDENTIAL REAL ESTATE ADVISORS 865,836RREEF 3,437UBS REALTY 1,784,156

BRIDGEWATER 832,985TORTOISE 578,551

BORROWERS REBATE 229,778MANAGEMENT FEES 73,404

Business Meeting Agenda - IV. CONSENT AGENDA

MASTER PAGE NO. 23 of 202

INVESTMENT CONSULTANT 221,658INVESTMENT CUSTODIAN 246,335

Business Meeting Agenda - IV. CONSENT AGENDA

MASTER PAGE NO. 24 of 202

PERFORMANCE REVIEW

VENTURA COUNTY EMPLOYEES’ RETIREMENT ASSOCCIATION (VCERA)

June 19, 2017

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 25 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

Firm Overview 3

PIOS® (Policy Implementation Overlay Service)*

– Program Review for VCERA 11

Risks 21

Appendices 23

TABLE OF CONTENTS

*PIOS is a trademark registered in the U.S. Patent and Trademark Office.

Portfolio Management

Justin Henne, CFA

Managing Director – Customized

Exposure Management

952.767.7718

Business Development

Ben Lazarus, CFA

Senior Director – Institutional Relationships

952.767.7707

Parametric MN Client Service

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 26 of 202

3This material has been prepared for the exclusive use of VCERA

in a one-on-one presentation only.

FIRM OVERVIEW

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 27 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

WHO WE ARE

Parametric is divided into two segments: Parametric Investment & Overlay Strategies and Parametric Custom Tax-Managed & Centralized

Portfolio Management. For compliance with the Global Investment Performance Standards (GIPS®), the Firm is defined and held out to the

public as Parametric Investment & Overlay Strategies.

*As of 3/31/2017. Includes AUM of Parametric Investment & Overlay Strategies and Parametric Custom Tax-Managed & Centralized Portfolio Management.

Seattle, WA Minneapolis, MN Westport, CT

• Leaders in rules-based, engineered

portfolio solutions

• Strategies ranging from index tracking

portfolios to managed smart beta

• Ability to incorporate responsible investing

themes

• Founded 1987

• A subsidiary of Eaton Vance Corp.

since 2003

• Pioneers in overlay strategies and

custom risk management solutions

(formerly The Clifton Group)

• Innovative product solutions in real asset

and liquid alternatives

• Founded 1972

• Acquired by Parametric in 2012

• Specialists in option portfolio

management

• Provide product-based and custom

option overlay solutions

• Founded 2002

• A part of Parametric since 2007

We provide systematic, disciplined portfolio management solutions

We offer investment solutions through our three investment centers:

> Parametric Portfolio Associates®

LLC (“Parametric”) is a majority-owned subsidiary of Eaton Vance Corp.

> Parametric equity ownership is broadly distributed among senior management and investment professionals.

> Approximately $197.7 Billion in assets under management; 85 investment professionals*.

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 28 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

KEY DIFFERENTIATORS

Aligned investment philosophy across three investment centers, where we:

• Dismiss traditional market forecasts

• Seek to add value through portfolio construction

• Implement a disciplined, transparent investment process, with extensive

risk management

Self-managed, with a culture of innovation and pragmatism

Deep, experienced, and stable team

Client-centered with a focus on service

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 29 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

PARAMETRIC INVESTMENT PLATFORM

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 30 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

ASSETS UNDER MANAGEMENT AS OF MARCH 31, 2017

Institutional Assets by Client Type Institutional Assets by Asset Class

Parametric Volatility Risk Premium Strategies’ assets total $12.4 Billion, and are included in US Equity and Developed Global Equity asset classes, depending on the referenced equity

index.

All numbers are approximate as of 3/31/2017.

Parametric is divided into two segments: Parametric Investment & Overlay Strategies and Parametric Custom Tax-Managed & Centralized Portfolio Management. For compliance with

the Global Investment Performance Standards (GIPS®), the Firm is defined and held out to the public as Parametric Investment & Overlay Strategies. Parametric Investment & Overlay

Strategies provides rules-based investment management services to institutional investors, individual clients and registered investment vehicles. For a complete list and description of

composites, please contact us at 206.694.5575. Total Institutional Assets presented above include assets from the Parametric Investment & Overlay Strategies segment. Please refer to

the GIPS® Presentation and the Disclosures included at the end of this presentation for additional important information.

Total Institutional Assets $116.6 BillionConsists of Funded and Overlay Assets

Corporate & Healthcare

$34.7

Foundation & Endowment

$36.8

Public & Taft-Hartley$29.8

Sub-Advised$15.4

Commodity$3.9

Developed Global Equity

$11.5

Developed International

Equity$9.9

Emerging Markets Equity

$16.4

Fixed Income$40.3

US Equity$34.6

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 31 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

REPRESENTATIVE CLIENT LIST AS OF MARCH 31, 2017

It is not known whether the listed clients approve or disapprove of the adviser. The partial list of clients included herein were selected as being representative of the different types of

institutional clients and businesses serviced by Parametric. Performance-based data was not a determining factor in their selection.

>Public

Alaska Retirement Management Board

Arizona State Retirement System

California State Teachers’ Retirement System

East Bay Municipal Utility District

Fairfax County Retirement Systems

Houston Police Officers’ Pension System

Manhattan & Bronx Surface Transit Operating Authority Pension Plan

Marin County Employees’ Retirement Association

Massachusetts Pension Reserves Investment Management Board

New Mexico Public Employees' Retirement Association

Oakland Police and Fire Retirement System

San Joaquin County Employees’ Retirement Association

San Luis Obispo County

San Mateo County Employees’ Retirement Association

Seattle City Employees’ Retirement System

Wisconsin Investment Board

>Endowments

Indiana University & Foundation

Pepperdine University

Texas Christian University

University of Minnesota Foundation

University of Missouri System

University of Pittsburgh

University of St. Thomas

Regents of the University of Michigan

>Faith Based

Covenant Ministries of Benevolence

Ministers & Missionaries’ Benefit Board of American Baptist Churches

Pension Fund of the Christian Church

>Healthcare

Advocate Health Care Network

Allina Health

North Memorial Health Care

OhioHealth Corporation

Trinity Health

>Taft-Hartley

Board of Trustees ABC-NABET Retirement Trust Fund

Boilermaker-Blacksmith National Pension Trust

Central Laborers’ Pension Fund

Electrical Workers, IBEW, Pacific Coast Fund

Chicago Laborers’ Pension & Welfare Funds

National Retirement Fund

Teamsters, Western Pennsylvania

>Foundations

Auburn University

The Doris Duke Charitable Foundation & Related Entities

The John D. & Catherine T. MacArthur Foundation

The McKnight Foundation

>Corporate

Cargill, Inc.

Macy's, Inc.

3M Company

Nestlé USA, Inc.

Eversource Energy

Target Corporation

United Technologies Corporation

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 32 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

1 Dedicated resources at the Minneapolis Investment Center location with additional compliance resources available in the Seattle Investment Center.2 For overlay services programs, the absolute value of futures and swap based synthetic index exposure is included as assets under management. For Enhancement/Risk Control

programs, the notional hedge target value of the options positions held for clients is included in assets under management.

THE MINNEAPOLIS INVESTMENT CENTER UPDATE (3/31/17)

The Minneapolis Investment Center Highlights: Q117

• As of 3/31/2017, assets under management were approximately $197.75 billion2 for the firm, and $88.48 billion for the

Minneapolis Investment Center.

• During Q117, The Minneapolis Investment Center welcomed 9 new clients in Custom Overlay and 29 to our Volatility Risk

Premium suite.

• Over the last year, the equity market has experienced several instances of sharp pullbacks followed by a quick recovery.

Many clients who utilize Parametric to synthetically rebalance portfolio exposures in a disciplined manner added a

meaningful amount of incremental return with lower risk relative to policy targets.

• In December 2016, Parametric Portfolio Associates LLC and Research Affiliates, LLC announced a partnership to provide a

Systematic Global Macro strategy to institutional separate accounts.

Minneapolis Investment Center:

New Client RelationshipsQ117

Custom Overlay 9

Volatility Risk Premium 29

Total 38

Minneapolis Investment Center:

PersonnelTotal

Investments 38

Marketing / Reporting / Sales 10

Accounting / Operations 23

Information Technology 12

Client Service / Documentation / Management 6

Compliance1 / Risk Management 4

Total 93

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 33 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

THE MINNEAPOLIS AND WESTPORT INVESTMENT CENTERS:

INVESTMENTS

Effective Date: 6/5/2017

INVESTMENT SUPPORT

Ben Adams Ashley Boecker Shane Claugherty Bill Heffernan James Ostrem Tim Post Ryan Spengler Colt Wolfram

Isaac Beckel Max Chisaka Arthur Harris David Mattson Patrick Persons John Schneider Heather Wolf

Jack Hansen, CFA

Chief Investment Officer

Minneapolis and Westport

Investment Centers

Justin Henne, CFA

Managing Director – Customized Exposure Management

Alex Braun, CFA

Portfolio Manager

Macki Anderson

Assoc. Portfolio Manager

Antony Motl, CFA

Portfolio Manager

Dan Wamre, CFA

Sr. Portfolio Manager

Jan Mowbray, CFA

Assoc. Portfolio Manager

Clint Talmo, CFA

Sr. Portfolio Manager

Dane Fickel

Assoc. Portfolio Manager

Jason Nelson, CFA

Portfolio Manager

Ricky Fong, CFA

Portfolio Manager

Drew Carlson, CFA

Assoc. Portfolio Manager

CUSTOMIZED EXPOSURE MANAGEMENT

Larry Berman

Managing Director –

Trading – Westport

Investment Center

Brendan Lanahan

VP – Trader

Mike Kelly

Managing Director

Thomas Lee, CFA

Managing Director – Investment Strategy & Research

Minneapolis and Westport Investment Centers

Alex Zweber, CFA

Portfolio Manager

Jay Strohmaier, CFA

Managing Director

Michael Zaslavsky

Assoc. Portfolio Manager

Chris Haskamp, CFA

Sr. Portfolio Manager

Greg Liebl, CFA

Portfolio Manager

Ken Everding

Managing Director –

Research – Westport

Investment Center

Wei Ge, Ph.D., CFA

Sr. Researcher

ENGINEERED ALPHA STRATEGIES

Yuepeng “Perry” Li,

CFA

Assoc. Portfolio Manager

Joe Zeck, CFA

Assoc. Portfolio Manager

Justin Horner, CFA

Assoc. Portfolio Manager

James Thorson, CFA

Assoc. Portfolio Manager

Tyler Nowicki

Assoc. Portfolio Manager

Allie Neese, CFA

Assoc. Portfolio Manager

Adam SwinneyAssoc. Portfolio Manager

Westport Minneapolis

Zach Olsen, CFA

Assoc. Portfolio Manager

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 34 of 202

11This material has been prepared for the exclusive use of VCERA

in a one-on-one presentation only.

PROGRAM REVIEW FOR VCERA

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 35 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

IMPLEMENTATION CHALLENGES PARAMETRIC OVERLAY COMPONENT 1

• Performance drag due to liquidity needs /

inefficient cash flow process• Fund Cash Securitization

• Residual manager cash balance

performance drag• Manager Cash Securitization

• Exposure management needs related to

manager transitions

• Overlay Transition / Reallocation

Management

• Meaningful deviation from policy targets • Rebalancing

• Unique exposure needs • Outsourced Exposure Management

ADDRESSING IMPLEMENTATION CHALLENGES

Most portfolios have one or more

policy implementation challenges

that may prevent the portfolio from

meeting its objectives

An overlay adds value by alleviating

the inefficiencies created by policy

implementation challenges

An overlay

application for each

implementation

challenge

TARGET ASSET ALLOCATIONOVERLAY

Implementation Challenges Overlay Value Added

TARGET ASSET ALLOCATION

1 Client selects from the Parametric Overlay Component(s) based on unique needs and objectives. Additional Parametric Overlay Components including Currency Exposure

Management and Interest Rate Management are also available.

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 36 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

OVERALL PROGRAM RESULTS

1 Net of management fees and net of transaction costs. April 2017 fees are estimated. Past performance is not indicative of future results.

Note: Fee schedule for overlay assets only is: First $25M @ .15% annually, next $75M @ .10%, above $100M @ .04%, with a minimum annual fee of $50,000.

Please refer to disclosures on the last page.

Program Results

• Market environment through April 30, 2017 produced a synthetic index overlay return1

of $48,823,971 or 0.17% of fund assets since inception.

‒ Benefit-to-cost (net of fees) of 53 to 1.

• Unwanted cash exposure was dramatically reduced.

• Portfolio tracking working well with high level of confidence in portfolio reports.

• Improved tracking error versus benchmark index thus lowering performance risk.

• The overlay program is in compliance with the current investment guidelines.

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 37 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

PROGRAM HIGHLIGHTS

Highlights

• Deployed the $170M contribution via the overlay program on July 1, 2016

• Maintained transition exposure of approximately $200M for the liquidations of PIMCO

Global and Loomis Sayles Global from January 2016 to September 2016 when it was

used to fund three Blackrock allocations

• Bridged a $210M exposure gap related to the full redemption of GMO and

subsequent funding of Blackrock MSCI ACWI Index Fund from 9/28/16 through

10/13/16

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 38 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

FUND CASH SECURITIZATION

Please refer to disclosures in Appendices. The deduction of an advisory fee would reduce an investor’s return. Past performance is not indicative of future results. For illustrative

purposes only. Source: Parametric; Date: 6/6/2017

CHALLENGE

Holding cash to facilitate liquidity needs results in tracking error relative to

the investment policy and creates long-term expected performance drag

EXPECTED BENEFITS

• Increase expected return

• Reduced transaction costs

• Increase day-to-day liquidity

• Simplify the management of inflows and outflows resulting in time

savings for staff

FUND LEVEL CASH RESULTS1

Fund Level Cash Balance

VCERA IMPLEMENTATION

Fund level cash balances are invested with the objective of reducing the

Fund’s deviation from the target asset allocation

Gain/Loss Summary

April ‘17 $1,404,253

YTD $5,087,206

Since 1/1/2014 $219,981

Average:

$92,657,057

1 Returns are through 4/30/2017 and gross of management fees.$0

$50,000,000

$100,000,000

$150,000,000

$200,000,000

$250,000,000

Fund Cash Average

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 39 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

MANAGER CASH SECURITIZATION

CHALLENGE

Residual or transactional manager cash exposure (e.g. 1-3% of portfolio)

creates an expected long-term performance drag

EXPECTED BENEFITS

• Increase expected return

• Ability to customize cash overlay for each manager

• Maintain exposure across multiple asset classes

Gain/Loss Summary

April ‘17 $58,182

YTD $460,161

Since 1/1/2014 ($263,206)

MANAGER CASH RESULTS1

Manager Cash Balance

VCERA IMPLEMENTATION

Manager cash balances are invested with the objective of reducing the

Fund’s deviation from the target asset allocation

Please refer to disclosures in Appendices. The deduction of an advisory fee would reduce an investor’s return. Past performance is not indicative of future results. For illustrative

purposes only. Source: Parametric; Date: 6/6/2017

Average:

$6,552,6641 Returns are through 4/30/2017 and gross of management fees.

$0

$5,000,000

$10,000,000

$15,000,000

$20,000,000

$25,000,000

$30,000,000

$35,000,000

$40,000,000

Manager Cash Average

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 40 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

TRANSITION / REALLOCATION MANAGEMENT

CHALLENGE

Manager changes, manager reallocations, liquidation of illiquid holdings

(e.g. hedge funds), change to target allocations, etc. which cause the fund

to meaningfully deviate from target exposures

EXPECTED BENEFITS

• Mitigation of exposure gaps which reduces performance risk

• The manager termination point can be accelerated or new manager

search period can be extended as long as needed without losing

targeted market exposure

• Note: Parametric works closely with transition service providers but

does not transition physical portfolio holdings

TRANSITION RESULTS1

VCERA IMPLEMENTATION

Reduce or eliminate exposure gaps using index overlays or ETF’s

1 Returns are through 4/30/2017 and gross of management fees.

Please refer to disclosures in Appendices. The deduction of an advisory fee would reduce an investor’s return. Past performance is not indicative of future results. For illustrative

purposes only. Source: Parametric; Date: 6/6/2017

Gain/Loss Summary

April ‘17 $0

YTD $0

Since 1/1/2014 $18,102,644

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 41 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

REBALANCING

CHALLENGE

Asset class exposures which deviate meaningfully from long-term policy

targets or short-term tactical preferences may result in unwanted

exposures and increased tracking error

EXPECTED BENEFITS

• Reduced transaction costs

• Timely and efficient reallocation of portfolio exposures

• Reduction of tracking error versus policy mix

VCERA IMPLEMENTATION

In addition to using cash to move exposures closer to the Fund’s target

asset allocation, short futures positions can be utilized for rebalancing

purposes. Additionally, if the Fund’s exposures deviate from target by a

predetermined threshold, a full rebalance trade is implemented

1 Returns are through 4/30/2017 and gross of management fees.

Please refer to disclosures in Appendices. The deduction of an advisory fee would reduce an investor’s return. Past performance is not indicative of future results. For illustrative

purposes only. Source: Parametric; Date: 6/6/2017

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 42 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

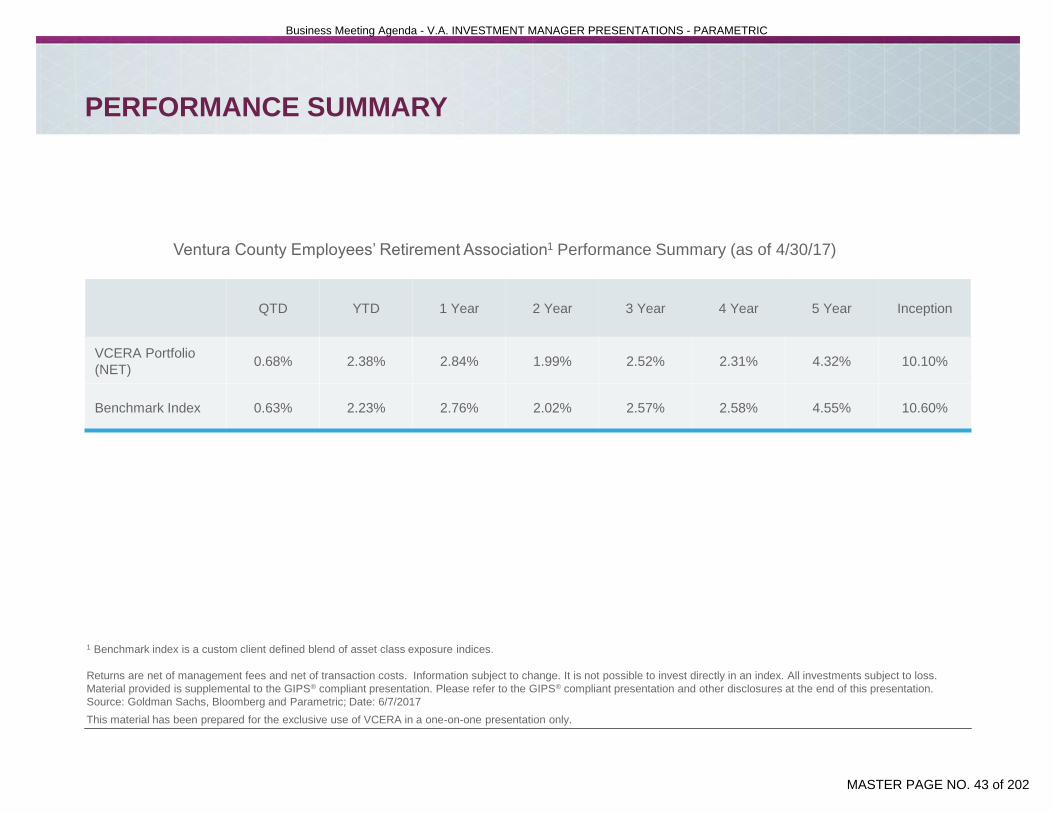

PERFORMANCE SUMMARY

1 Benchmark index is a custom client defined blend of asset class exposure indices.

Returns are net of management fees and net of transaction costs. Information subject to change. It is not possible to invest directly in an index. All investments subject to loss.

Material provided is supplemental to the GIPS® compliant presentation. Please refer to the GIPS® compliant presentation and other disclosures at the end of this presentation.

Source: Goldman Sachs, Bloomberg and Parametric; Date: 6/7/2017

QTD YTD 1 Year 2 Year 3 Year 4 Year 5 Year Inception

VCERA Portfolio

(NET)0.68% 2.38% 2.84% 1.99% 2.52% 2.31% 4.32% 10.10%

Benchmark Index 0.63% 2.23% 2.76% 2.02% 2.57% 2.58% 4.55% 10.60%

Ventura County Employees’ Retirement Association1 Performance Summary (as of 4/30/17)

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 43 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

VCERA GAIN / LOSS SUMMARY (4/30/17)

Returns are gross of management fees. The deduction of an advisory fee would reduce investor’s return. Information subject to change. It is not possible to invest directly in an index.

All investments subject to loss. Material provided is supplemental to the GIPS® compliant presentation. Please refer to the GIPS® compliant presentation and other disclosures at the

end of this presentation. Source: Goldman Sachs, Bloomberg, and Parametric; Date: 5/31/2017.

PIOS Incremental Return (Inception to Date)

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 44 of 202

21This material has been prepared for the exclusive use of VCERA

in a one-on-one presentation only.

RISKS

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 45 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

OVERLAY SERVICES: WHAT ARE THE RISKS?

1 PIOS (Policy Implementation Overlay Service) is a trademark registered in the U.S. Patent and Trademark Office.

Risk Description How Parametric Mitigates

Market Market performs in a way that was not anticipated. For example,

cash outperforms capital markets.

Systematic market risk is an inherent part of the PIOS®1 program and can

neither be diversified away nor mitigated. Client specific policy guidelines

are established to clearly define desired market risk based on client asset

allocation targets.

Communication/

Information

Overlay index exposures are maintained based on underlying

investment values provided by one or more third parties. There

are often delays in the receipt of updated information which can

lead to exposure imbalance risks. Inadequate communication

regarding cash flow moves into and out of fund and manager

changes can lead to unwanted asset class exposures and loss.

Parametric establishes communication links with custodial, manager, and

other sources to obtain and verify positions and cash flow data as soon as

it is available. Suspect data may be researched and staff notified.

Margin/Liquidity Potential that the market moves in a manner adverse to the

overlay position causing a mark-to-market loss of capital to the

fund and a resulting need to raise liquidity or to close positions;

this situation could happen at a time when underlying fund or

positions are also declining in value.

Parametric strives to be aware of potential collateral and cash

requirements to reduce the risk of needing to remove positions. Additional

margin requirements are communicated via electronic mail and margin

adequacy is available to the client daily.

Tracking Error Futures (synthetic) index returns do not perfectly track

benchmark index returns. This divergence between the price

behavior of a position or portfolio and the price behavior of a

benchmark is tracking error and impacts performance.

Parametric seeks to minimize tracking error by utilizing liquid futures

contracts with sufficient daily trading volume and open interest. All

derivative contracts will have some tracking error that cannot be mitigated

by an overlay manager.

Leverage Creation of market exposure in excess of underlying collateral

value may lead to significant capital losses and result in position

liquidation.

Parametric obtains daily collateral pool values and adjusts beta overlay

positions to maintain the ratio of total exposure to collateral within a pre-

defined client determined band.

Counterparty Counterparty credit risk on OTC trading. Note: Bilateral centrally

cleared OTC counterparty risk is similar to the clearing risk of

holding futures investments.

Parametric can facilitate the negotiation of ISDA documentation that seeks

to reduce the potential credit risk associated with OTC counterparties.

Parametric monitors credit ratings and credit default swap spreads for all

counterparties used and will inform staff of developments which may

negatively impact credit risk.

Collateral The program may experience losses on the underlying

designated assets in addition to potential losses on the index

market exposure overlaying these assets.

This risk cannot be mitigated by an overlay manager. Parametric

discusses the potential for negative performance in the collateral used for

the overlay prior to alpha transport applications with client.

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 46 of 202

23This material has been prepared for the exclusive use of VCERA

in a one-on-one presentation only.

APPENDICES

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 47 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

EXCHANGE TRADED FUTURES

Characteristics

• Standardized

• Regulated

• Small initial margin

• Marked to market daily (virtually eliminating credit risk)

• Liquid (on average, more notional dollar volume is traded in S&P 500 futures than the average daily volume

of the NYSE each day)

• Efficiently priced with very low transaction costs

• Commonly used by Money Managers, Fund Sponsors, Index Funds, and Hedgers

Counterparty Risk Controls

• All Futures Commission Merchants (“FCM”) (e.g. Goldman Sachs, Citigroup, etc.) post a performance bond,

or deposit, with the clearing house in order to trade

• Performance bonds help to ensure that the FCMs will meet the contractual obligations of the trades they

make

• Brokerage firms require performance bonds, in the form of initial margin, from both the contract buyer and

contract seller

• FCMs must post a security deposit and pledge their assigned shares and memberships to the relevant

exchange thus providing additional incremental credit protection

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 48 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

SYNTHETIC INDICES

1 In the case of style asset exposure needs (i.e. small cap growth), Parametric can manage ETF

exposures to fulfill client needs. Customized nonstandard indexes can be replicated using swaps.

Please note that only broad market (e.g. versus style) futures are available and/or liquid enough for use. Individuals may not invest directly into indexes.

>Domestic Equity1

S&P 500® Index

S&P 400® Mid Cap Index

MSCI USA IMI Index

MSCI Small Cap USA Index

Russell 1000® Index

Russell 2000 ® Index

Russell 3000 ® Index

Wilshire 5000 Index

>Fixed Income

Bloomberg Barclays U.S. Aggregate Bond Index

Bloomberg Barclays U.S. Aggregate Gov/Credit Index

Bloomberg Barclays Intermediate U.S. Gov/Credit Index

Bloomberg Barclays U.S. Long Gov/Credit Index

Bloomberg Barclays U.S. Aggregate Long Treasury Index

Bloomberg Barclays U.S. Long Treasury Index

Bloomberg Barclays U.S. Universal Index

Citi U.S. Broad Investment-Grade (USBIG) Bond Index

BofA Merrill 1-3 Year U.S. Treasury Index

Various Constant Duration Benchmarks

>International Equity

MSCI EAFESM Index

MSCI ACWI ex. U.S.SM

MSCI ACWI ex. U.S. IMI

MSCI Emerging Markets Index

MSCI World ex. U.S.SM

S&P Global Broad Market Index

>Global Equity

MSCI ACWI IMI

MSCI WorldSM

>Commodities

S&P Goldman Sachs Commodity Index

Bloomberg Commodities Index (BCOM)

Custom Commodity Baskets

>International Fixed Income

Citigroup WGBI ex. US

Bloomberg Barclays Global Aggregate Index ex. U.S.

>Currency

Indexes

Individual Currency Exposure

The most often used index benchmarks are as follows:

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 49 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

BIOGRAPHIES: PARAMETRIC

MINNEAPOLIS INVESTMENT CENTER

Orison “Kip” Chaffee, CFA

Managing Principal

Mr. Chaffee is responsible for formulating strategic direction and day-to-day management of the Minneapolis and Westport Investment Centers. Prior to joining Parametric

in 2008*, Kip held a number of executive positions within the financial services industry including VP of Corporate Strategy and Development for Ameriprise Financial

Services and President and COO of Hantz Financial Services. He earned his B.A. in Economics from Harvard University and an MBA with a finance concentration from The

Wharton School of Business. He is a CFA® charterholder and a member of the CFA Society of Minnesota.

Jack Hansen, CFA

Chief Investment Officer

Mr. Hansen leads the investment management department at the Minneapolis Investment Center. Since joining Parametric in 1985*, Jack has managed futures, swaps,

options, and other derivative based programs. He writes and lectures on the use of derivatives in portfolio management. He earned a B.S. degree in Finance and

Economics from Marquette University and a M.S. in Finance from the University of Wisconsin, Madison. He is a CFA® charterholder and member of the CFA Society of

Minnesota.

Justin Henne, CFA

Managing Director – Customized Exposure Management

Mr. Henne leads the investment team responsible for the implementation and enhancement of Parametric’s Customized Exposure Management product. Since joining

Parametric in 2004*, Justin has gained extensive experience trading a wide variety of derivative instruments in order to meet each client’s unique exposure and risk

management objectives. He earned a B.A. in Financial Management from the University of St. Thomas. He is a CFA® charterholder and a member of the CFA Society of

Minnesota.

Thomas Lee, CFA

Managing Director – Investment Strategy and Research

Mr. Lee leads the investment team that oversees investment strategies managed in Parametric’s Minneapolis and Westport Centers. In his current position, Tom directs the

research efforts that support existing strategies and form the foundation for new strategies. He is also chair of the Investment Committee that has oversight of these

strategies. Tom has co-authored articles on topics ranging from liability driven investments to risk parity. Prior to joining Parametric in 1994*, Tom spent two years working

for the Federal Reserve in Washington, D.C. He earned a B.S. in Economics and an MBA in Finance from the University of Minnesota. He is a CFA® charterholder and a

member of the CFA Society of Minnesota.

Jay Strohmaier, CFA

Managing Director

Mr. Strohmaier leads a team of investment professionals responsible for designing, trading and managing institutional portfol ios with an emphasis on Defensive Equity,

hedging, and other asymmetric strategies. He has extensive experience with futures and options-based strategies and has been active in the investment industry since

1984. Prior to rejoining Parametric in 2009*, Jay worked for Cargill, Peregrine Capital Management, and Advantus Capital Management. He earned a B.S. degree in

Agricultural Economics from Washington State University and an M.S. in Applied Economics from the University of Minnesota. He is a CFA® charterholder and a member of

the CFA Society of Minnesota.

*Reflects the year employee was hired by The Clifton Group, which was acquired by Parametric Portfolio Associates® LLC on December 31, 2012.

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 50 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

BIOGRAPHIES: PARAMETRIC

MINNEAPOLIS INVESTMENT CENTER

Christopher Haskamp, CFA

Senior Portfolio Manager

Mr. Haskamp is dedicated to portfolio management and leading research projects in the area of risk management. Chris manages portfolios for the Liability Driven Investing

program as well as for the enhanced index programs. Prior to joining Parametric in 2006*, he spent three years as a scientist at the medical device firm Beckman Coulter

Inc. Chris earned a B.S. in Biochemistry from the University of Minnesota and a M.S. in Chemistry from the University of California, San Diego. Chris earned an MBA in

Finance from the University of Minnesota, Carlson School of Management in May of 2007 and started full time at Parametric in June of 2007. He is a CFA® charterholder

and a member of the CFA Society of Minnesota.

Clint Talmo, CFA

Senior Portfolio Manager

Mr. Talmo is responsible for designing, trading, and managing overlay portfolios with an emphasis on options and OTC swaps. Prior to joining Parametric in 2014, Clint was

a Partner at Aerwulf Asset Management. Previously, he worked for Interlachen Capital Group and EBF & Associates where his responsibilities included research, trading,

and portfolio management. He earned a B.S. in Finance from the University of Colorado. He is a CFA® charterholder and a member of the CFA Society of Minnesota.

Daniel Wamre, CFA

Senior Portfolio Manager

Mr. Wamre leads a team of investment professionals responsible for designing, trading, and managing overlay portfolios. He has extensive experience helping clients and

consultants manage portfolio exposures and risk through futures and options-based strategies. Prior to joining Parametric in 1995* as an intern, and full-time in 1998*, Dan

spent four years as a Platoon Commander/Executive Officer in the United States Marine Corps. Upon completion of graduate school, he spent ten months working as a

commercial banking credit analyst for U.S. Bank in Minneapolis. He earned a B.S. from North Dakota State University and an MBA in Finance from the University of

Minnesota. He is a CFA® charterholder and a member of the CFA Society of Minnesota.

Richard Fong, CFA

Portfolio Manager

Mr. Fong is responsible for designing, trading, and managing overlay portfolios in the Minneapolis Investment Center. Since joining Parametric in 2010*, Ricky has become

a valuable resource supporting management of client LDI and options-based risk management solutions. He earned a B.A. in Financial Economics from Gustavus

Adolphus College. He is a CFA® charterholder and a member of the CFA Society of Minnesota.

Alexander Gomelsky, CFA

Portfolio Manager

Mr. Gomelsky is responsible for designing, trading and managing overlay portfolios as well as serving as an IT leader for the investment area. Prior to joining Parametric in

2009*, Alex worked for Johnson Controls as a Business Analyst within Global Operations and FP&A departments. He earned a B.S. degree in Finance and History from

Boston College. He is a CFA® charterholder and a member of the CFA Society of Minnesota.

*Reflects the year employee was hired by The Clifton Group, which was acquired by Parametric Portfolio Associates® LLC on December 31, 2012.

Business Meeting Agenda - V.A. INVESTMENT MANAGER PRESENTATIONS - PARAMETRIC

MASTER PAGE NO. 51 of 202

This material has been prepared for the exclusive use of VCERA in a one-on-one presentation only.

DISCLOSURE

Parametric Portfolio Associates® LLC (“Parametric”), headquartered in Seattle, Washington, is registered as an investment adviser with the U.S. Securities and Exchange

Commission under the Investment Advisers Act of 1940. Parametric is a leading global asset management firm, providing investment strategies and customized exposure

management directly to institutional investors and indirectly to individual investors through financial intermediaries. Parametric offers a variety of rules-based investment strategies,

including alpha-seeking equity, alternative and options strategies, as well as implementation services, including customized equity, traditional overlay and centralized portfolio

management. Parametric is a majority-owned subsidiary of Eaton Vance Corp. and offers these capabilities through investment centers in Seattle, WA, Minneapolis, MN and

Westport, CT. This material may not be forwarded or reproduced, in whole or in part, without the written consent of Parametric Compliance. Parametric and its affiliates are not

responsible for its use by other parties.

Parametric is divided into two segments: Parametric Investment & Overlay Strategies and Parametric Custom Tax-Managed & Centralized Portfolio Management. For compliance with

the Global Investment Performance Standards (GIPS®), the Firm is defined and held out to the public as Parametric Investment & Overlay Strategies. Parametric Investment &

Overlay Strategies provides rules-based investment management services to institutional investors, individual clients and registered investment vehicles, including Engineered Alpha

Strategies, Specialty Index, and PIOS® (Policy Implementation Overlay Service). The Firm has complied with the GIPS standards retroactive to January 1, 2000.

This information is intended solely to report on investment strategies and opportunities identified by Parametric. Opinions and estimates offered constitute our judgment and are

subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but

do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Past performance does not

indicate future returns. The views and strategies described may not be suitable for all investors. Parametric does not provide legal, tax and/or accounting advice or services. Clients

should consult with their own tax or legal advisor prior to entering into any transaction or strategy described here.

Charts, graphs and other visual presentations and text information were derived from internal, proprietary, and/or service vendor technology sources and/or may have been extracted

from other firm data bases. As a result, the tabulation of certain reports may not precisely match other published data. Data may have originated from various sources including but

not limited to Bloomberg, MSCI/Barra, FactSet, and/or other systems and programs. Please refer to the specific service provider’s web site for complete details on all indices.

Parametric makes no representation or endorsement concerning the accuracy or propriety of information received from any other third party.

Returns presented were generated using Parametric’s proprietary investment methodology as described in Parametric’s Form ADV Part 2A. Returns are unaudited, and may not

correspond to quarterly calculated performance for any other client account in the stated discipline. Returns are calculated in U.S. dollars using the internal rate of return, reflect the

reinvestment of dividends, interest, gains and other income, include transaction costs but exclude account and custodial services fees, and do not take individual investor tax